UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | | | | | |

| Investment Company Act file number | 811-08532 |

| | |

| AMERICAN CENTURY STRATEGIC ASSET ALLOCATIONS, INC. |

| (Exact name of registrant as specified in charter) |

| | |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 |

| (Address of principal executive offices) | (Zip Code) |

| | |

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 |

| (Name and address of agent for service) |

| | |

| Registrant’s telephone number, including area code: | 816-531-5575 |

| | |

| Date of fiscal year end: | 07-31 |

| | |

| Date of reporting period: | 07-31-2019 |

ITEM 1. REPORTS TO STOCKHOLDERS.

|

| |

| | |

| | Annual Report |

| | |

| | July 31, 2019 |

| | |

| | Multi-Asset Income Fund |

| | Investor Class (AMJVX) |

| | I Class (AMJIX) |

| | Y Class (AMJYX) |

| | A Class (AMJAX) |

| | C Class (AMJCX) |

| | R Class (AMJWX) |

| | R5 Class (AMJGX) |

| | R6 Class (AMJRX) |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the fund or your financial intermediary electronically by calling or sending an email request to your appropriate contacts as listed on the back cover of this report.

You may elect to receive all future reports in paper free of charge. You can inform the fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by calling or sending an email request to your appropriate contacts as listed on the back cover of this report. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary.

|

| | |

| President’s Letter | 2 |

|

| Performance | 3 |

|

| Portfolio Commentary | |

|

| Fund Characteristics | |

|

| Shareholder Fee Example | |

|

| Schedule of Investments | |

|

| Statement of Assets and Liabilities | |

|

| Statement of Operations | |

|

| Statement of Changes in Net Assets | |

|

| Notes to Financial Statements | |

|

| Financial Highlights | |

|

| Report of Independent Registered Public Accounting Firm | |

|

| Management | |

|

| Approval of Management Agreement | |

|

| Additional Information | |

|

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Jonathan Thomas

Jonathan Thomas

Dear Investor:

Thank you for reviewing this annual report for the period ended July 31, 2019. Annual reports help convey important details about fund returns, including market factors that affected performance. For additional investment and market insights, please visit our website, americancentury.com.

Stocks Advanced Amid Volatile Climate

Most broad U.S. and global stock indices ended the year with gains. However, these positive results masked wide performance swings. For example, U.S. stocks, as measured by the S&P 500 Index, returned -3.00% in the first half of the period and 11.32% in the second half, leaving the index up 7.99% for the 12 months. Global stocks, as measured by the MSCI All Country World Index, returned -4.71% in the first half, 8.04% in the second half and 2.95% overall. For fixed-income securities, the path to positive performance was smoother, and U.S. and global bonds gained 8.08% and 5.73%, respectively, for the 12 months, according to the Bloomberg Barclays U.S. Aggregate Bond and Global Aggregate Bond indices.

Fed’s Flip Fueled Investor Optimism

Early in the period, mounting concerns about slowing global economic and earnings growth, tariffs and Federal Reserve (Fed) policy soured investor sentiment. After raising rates in September, the Fed hiked again in December and delivered a surprisingly bullish rate-hike outlook that fueled a steep sell-off among riskier assets. Meanwhile, the risk-off climate sparked a flight to quality, and government bond yields plunged.

A key policy pivot from the Fed helped improve investor sentiment beginning in early 2019. The central bank abruptly ended its rate-hike campaign and adopted a dovish tone amid moderating global growth and inflation. Additionally, investors’ worst-case fears about growth, trade and corporate earnings generally eased, which also aided stocks. At the same time, government bond yields continued to fall on moderating global growth data, muted inflation and accommodative central bank policy, including the Fed’s July rate cut. This backdrop supported continued gains for bonds and other interest rate-sensitive assets.

Looking ahead, we expect volatility to remain a formidable factor as investors react to global growth and trade trends, central bank policy and geopolitical developments. We believe this scenario underscores the importance of using professionally managed portfolios in pursuit of investment goals. We appreciate your continued trust and confidence in us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

|

| | | | |

| Total Returns as of July 31, 2019 |

| | | | Average Annual Returns | |

| | Ticker Symbol | 1 year | Since Inception | Inception Date |

| Investor Class | AMJVX | 2.89% | 4.53% | 12/1/14 |

| Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index | — | 6.91% | 5.66% | — |

| Russell 3000 Value Index | — | 4.23% | 7.35% | — |

| Bloomberg Barclays U.S. Aggregate Bond Index | — | 8.08% | 2.83% | — |

| MSCI ACWI ex-U.S. Value Index | — | -5.27% | 1.60% | — |

| Blended Index | — | 5.35% | 5.35% | — |

| I Class | AMJIX | 3.10% | 4.74% | 12/1/14 |

| Y Class | AMJYX | 3.14% | 4.32% | 4/10/17 |

| A Class | AMJAX | | | 12/1/14 |

| No sales charge | | 2.53% | 4.25% | |

| With sales charge | | -3.33% | 2.94% | |

| C Class | AMJCX | 1.77% | 3.49% | 12/1/14 |

| R Class | AMJWX | 2.28% | 4.00% | 12/1/14 |

| R5 Class | AMJGX | 3.10% | 4.21% | 4/10/17 |

| R6 Class | AMJRX | 3.15% | 4.89% | 12/1/14 |

Fund returns would have been lower if a portion of the fees had not been waived. The blended index combines monthly returns of widely known indices. The Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index represents 40%, the Russell 3000 Value Index represents 30%, the Bloomberg Barclays U.S. Aggregate Bond Index represents 20% and the MSCI ACWI ex-U.S. Value Index represents 10% of the blended index.

Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

|

|

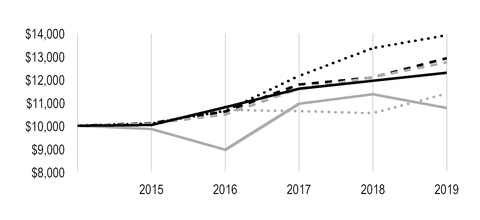

| Growth of $10,000 Over Life of Class |

| $10,000 investment made December 1, 2014 |

| Performance for other share classes will vary due to differences in fee structure. |

|

| |

| Value on July 31, 2019 |

| | Investor Class — $12,297 |

| |

| | Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index — $12,927 |

| |

| | Russel 3000 Value Index — $13,919 |

| |

| | Bloomberg Barclays U.S. Aggregate Bond Index — $11,390 |

| |

| | MSCI ACWI ex-U.S. Value Index — $10,769 |

| |

| | Blended Index — $12,751 |

| |

Ending value of Investor Class would have been lower if a portion of the fees had not been waived.

|

| | | | | | | |

Total Annual Fund Operating Expenses | | |

Investor Class | I Class | Y Class | A Class | C Class | R Class | R5 Class | R6 Class |

| 1.17% | 0.97% | 0.82% | 1.42% | 2.17% | 1.67% | 0.97% | 0.82% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

Portfolio Managers: Rich Weiss, Scott Wilson, Radu Gabudean, Vidya Rajappa and John Donner

Performance Summary

For the fiscal year ended July 31, 2019, Multi-Asset Income returned 2.89%*. The strategy trailed the return of its custom-blended benchmark, which consists of 40% equity and 60% fixed-income investments. Positioning among U.S. fixed-income securities and non-U.S. equities detracted from results relative to the benchmark, while allocations to global real estate investment trusts (REITs) and U.S. equity income were beneficial. As of July 31, 2019, Multi-Asset Income Fund’s 30-day SEC yield was 3.57% after the fee waiver. Without the waiver, the 30-day SEC yield would have been 3.31%. At period-end, the fund’s annual distribution rate was 4.83%.

Fund Strategy and Positioning

The fund’s primary objective is income generation, with long-term capital appreciation as a secondary objective. Our asset allocation strategy diversifies investments directly or indirectly among a range of U.S. and foreign income-oriented equity and fixed-income securities. The fund is not required to allocate its assets in any proportion, but maintains broad allocation ranges of 20% to 80% for equities and 20% to 80% for fixed-income securities to allow the team flexibility in pursuing attractive income-generating opportunities across the globe. To gain exposure to broad investment disciplines and categories, the fund invests in varying combinations of other American Century Investments’ funds (affiliated funds), unaffiliated funds such as exchange-traded funds (ETFs), equity and debt securities and certain derivative instruments. At period-end, the fund’s allocation was 45.5% fixed-income instruments, 41.5% equity (including investments in equity and fixed-income mutual funds and ETFs) and 13% in preferred and convertible securities.

NT High Income Fund was the largest holding in the portfolio throughout the period. We increased the allocation modestly in late 2018, when yield spreads on securities rated below investment grade rose significantly, increasing their appeal in our tactical allocation framework. In 2019, we reduced our exposure to non-U.S. value, as global growth slowed and worries about a potential trade war intensified, contributing to higher volatility in the asset class.

Global Real Estate and U.S. Equity Income Add to Returns

Positioning in the global real estate allocation contributed to performance, aided by positive security selection. Sources of strength were retail REITs and those based in the U.S. Similarly, the U.S. equity income position contributed because of security selection effects, led by consumer staples holdings. The highest income generation came from the NT High Income Fund, global real estate and emerging markets debt allocations.

*All fund returns referenced in this commentary are for Investor Class shares. Fund returns would have been lower if a portion of the fees had not been waived. Performance for other share classes will vary due to differences in fee structure; when Investor Class performance exceeds that of the fund's benchmark, other share classes may not. See page 3 for returns for all share classes.

U.S. Bonds and Non-U.S. Equities Lagged Their Underlying Benchmarks

Notable detraction from performance relative to their underlying benchmarks came from positioning among both investment-grade and high-yield U.S. bonds. Both allocations underperformed their respective benchmarks because of security selection decisions. In the investment-grade slice, it also hurt relative results to have a comparatively short duration at a time when interest rates declined. Duration is a measure of a bond’s price sensitivity to interest rate changes. When interest rates fall, bond prices rise, and the longer the duration, the greater the price increase. A shorter duration provides comparatively less benefit from falling rates.

Non-U.S. equities were another source of weakness, as they generally underperformed U.S. equities and stock choices meant these positions lagged their underlying benchmarks. Security selection in the foreign exchange and equity dividend harvesting sleeves also detracted from relative results.

Outlook

We have a cautious outlook for economic growth, as U.S. industrial production, disposable income and corporate profits have all been declining. In addition, rising tariffs and ongoing trade disputes between the U.S. and many leading economies act as a further drag on growth. Despite this uncertainty, unemployment remains historically low, and sharply lower interest rates should ultimately provide a boost to the economy. What’s more, the U.S. economy remains fairly healthy relative to most other countries, whose economies are expanding more slowly. It should also be noted that we do not feel that a U.S. recession is imminent. Add it all up, and with stock market volatility increasing, trade concerns a wild card and the late stage of the economic cycle, we believe investor expectations should probably be more muted regarding financial market returns going forward.

When considering income, return and risk potential, our outlook at the end of July 2019 had better views on stocks relative to fixed-income alternatives. Within the equity allocation, we had a bias toward emerging markets value equities, global real estate and equity income. Fundamental factors and relative yields support the emerging markets position, while real estate equities are favored relative to bonds because of comparatively attractive yields. Within fixed income, slower growth in the U.S. means it pays to be conscious of credit risk in lower-rated, more economically sensitive issuers. So while the portfolio’s largest absolute allocation was to U.S. high yield, we remain vigilant against volatility in the asset class.

Multi-Asset Income was created to meet the evolving needs of clients who desire a total income solution. We believe that the pursuit of high income today shouldn’t jeopardize the potential for income tomorrow. Our broadly diversified investment approach, combining the best top-down ideas of American Century Investments’ Multi-Asset Strategies team with the bottom-up security selection of our underlying segment management teams, is designed to create an income-generating portfolio optimized for yield, total return and risk.

|

| |

| JULY 31, 2019 |

Types of Investments in Portfolio | % of net assets |

| Affiliated Funds | 50.5% |

| Domestic Common Stocks | 14.2% |

| Foreign Common Stocks* | 8.0% |

| Preferred Stocks | 10.6% |

| Convertible Preferred Stocks | 2.7% |

| Corporate Bonds | 1.6% |

| Exchange-Traded Funds | 1.6% |

| Collateralized Mortgage Obligations | 1.2% |

| Convertible Bonds | 1.1% |

| Commercial Mortgage-Backed Securities | 0.8% |

| Asset-Backed Securities | 0.5% |

| U.S. Treasury Securities | 0.4% |

| Collateralized Loan Obligations | 0.3% |

| Temporary Cash Investments | 6.5% |

| Other Assets and Liabilities | —** |

*Includes depositary shares, dual listed securities and foreign ordinary shares.

**Category is less than 0.05% of total net assets.

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from February 1, 2019 to July 31, 2019.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or I Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

| | | | |

| | Beginning

Account Value

2/1/19 | Ending

Account Value

7/31/19 | Expenses Paid

During Period(1)

2/1/19 - 7/31/19 |

Annualized

Expense Ratio(1) |

Actual | | | | |

| Investor Class | $1,000 | $1,043.70 | $3.40 | 0.67% |

| I Class | $1,000 | $1,044.70 | $2.38 | 0.47% |

| Y Class | $1,000 | $1,045.50 | $1.62 | 0.32% |

| A Class | $1,000 | $1,041.30 | $4.66 | 0.92% |

| C Class | $1,000 | $1,038.50 | $8.44 | 1.67% |

| R Class | $1,000 | $1,040.00 | $5.92 | 1.17% |

| R5 Class | $1,000 | $1,044.70 | $2.38 | 0.47% |

| R6 Class | $1,000 | $1,045.50 | $1.62 | 0.32% |

| Hypothetical | | | | |

| Investor Class | $1,000 | $1,021.47 | $3.36 | 0.67% |

| I Class | $1,000 | $1,022.46 | $2.36 | 0.47% |

| Y Class | $1,000 | $1,023.21 | $1.61 | 0.32% |

| A Class | $1,000 | $1,020.23 | $4.61 | 0.92% |

| C Class | $1,000 | $1,016.51 | $8.35 | 1.67% |

| R Class | $1,000 | $1,018.99 | $5.86 | 1.17% |

| R5 Class | $1,000 | $1,022.46 | $2.36 | 0.47% |

| R6 Class | $1,000 | $1,023.21 | $1.61 | 0.32% |

| |

| (1) | Expenses are equal to the class's annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 181, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. Annualized expense ratio reflects actual expenses, including any applicable fee waivers or expense reimbursements and excluding any acquired fund fees and expenses. |

JULY 31, 2019

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

AFFILIATED FUNDS(1) — 50.5% | | | |

| Emerging Markets Debt Fund R6 Class | | 734,425 |

| $ | 7,652,710 |

|

| Equity Income Fund R6 Class | | 459,302 |

| 4,198,024 |

|

| International Value Fund R6 Class | | 632,015 |

| 4,645,310 |

|

| NT High Income Fund G Class | | 1,311,158 |

| 12,678,901 |

|

| Utilities Fund Investor Class | | 33,004 |

| 588,459 |

|

TOTAL AFFILIATED FUNDS

(Cost $29,467,169) | | | 29,763,404 |

|

| COMMON STOCKS — 22.2% | | | |

| Airlines — 0.1% | | | |

| Eva Airways Corp. | | 64,008 |

| 30,337 |

|

Auto Components† | | | |

| Fuyao Glass Industry Group Co. Ltd., H Shares | | 5,200 |

| 15,818 |

|

| Automobiles — 0.1% | | | |

| Geely Automobile Holdings Ltd. | | 19,000 |

| 28,883 |

|

| Great Wall Motor Co. Ltd., H Shares | | 29,500 |

| 19,907 |

|

| Hyundai Motor Co. Preference Shares | | 105 |

| 6,499 |

|

| Kia Motors Corp. | | 763 |

| 27,965 |

|

| | | | 83,254 |

|

| Banks — 1.7% | | | |

| Absa Group Ltd. | | 900 |

| 9,983 |

|

| Agricultural Bank of China Ltd., H Shares | | 48,000 |

| 19,478 |

|

| AMMB Holdings Bhd | | 36,300 |

| 37,135 |

|

| Banco do Brasil SA | | 2,700 |

| 34,935 |

|

| Banco Santander Mexico SA Institucion de Banca Multiple Grupo Financiero Santand ADR | | 4,800 |

| 34,080 |

|

| Bank Mandiri Persero Tbk PT | | 40,400 |

| 22,873 |

|

| Bank Negara Indonesia Persero Tbk PT | | 18,000 |

| 10,610 |

|

| Bank of China Ltd., H Shares | | 93,000 |

| 37,746 |

|

| Bank of Communications Co. Ltd., H Shares | | 23,000 |

| 16,725 |

|

| China CITIC Bank Corp. Ltd., H Shares | | 26,000 |

| 14,450 |

|

| China Construction Bank Corp., H Shares | | 194,000 |

| 149,356 |

|

| China Merchants Bank Co. Ltd., H Shares | | 3,500 |

| 17,434 |

|

| CIMB Group Holdings Bhd | | 36,100 |

| 44,404 |

|

| Dubai Islamic Bank PJSC | | 6,402 |

| 9,266 |

|

| E.Sun Financial Holding Co. Ltd. | | 11,782 |

| 9,828 |

|

| Grupo Financiero Banorte SAB de CV | | 8,700 |

| 43,523 |

|

| Hana Financial Group, Inc. | | 1,658 |

| 48,633 |

|

| Hong Leong Financial Group Bhd | | 1,900 |

| 8,275 |

|

| Industrial & Commercial Bank of China Ltd., H Shares | | 144,000 |

| 96,928 |

|

| Itau CorpBanca | | 780,417 |

| 6,063 |

|

| Itau Unibanco Holding SA ADR | | 4,500 |

| 41,175 |

|

| Mega Financial Holding Co. Ltd. | | 15,000 |

| 15,462 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| Nedbank Group Ltd. | | 1,859 |

| $ | 31,164 |

|

| Qatar National Bank QPSC | | 6,140 |

| 32,868 |

|

| RHB Bank Bhd | | 20,000 |

| 26,661 |

|

| Shinhan Financial Group Co. Ltd. | | 909 |

| 33,316 |

|

| SinoPac Financial Holdings Co. Ltd. | | 50,000 |

| 19,918 |

|

| Standard Bank Group Ltd. | | 4,283 |

| 53,491 |

|

| Taiwan Business Bank | | 99,000 |

| 42,550 |

|

| Woori Financial Group, Inc. | | 2,871 |

| 31,783 |

|

| | | | 1,000,113 |

|

| Beverages — 0.1% | | | |

| Cia Cervecerias Unidas SA ADR | | 1,000 |

| 27,960 |

|

| Kweichow Moutai Co. Ltd., A Shares | | 100 |

| 14,056 |

|

| Tsingtao Brewery Co. Ltd., H Shares | | 4,000 |

| 23,284 |

|

| | | | 65,300 |

|

| Capital Markets — 0.5% | | | |

| Blackstone Group, Inc. (The), Class A | | 4,722 |

| 226,561 |

|

| Haitong Securities Co. Ltd., A Shares | | 6,200 |

| 12,398 |

|

| Investec Ltd. | | 4,617 |

| 26,318 |

|

| | | | 265,277 |

|

| Chemicals — 0.1% | | | |

| Kumho Petrochemical Co. Ltd. | | 532 |

| 36,619 |

|

| Mexichem SAB de CV | | 4,900 |

| 8,954 |

|

| Petronas Chemicals Group Bhd | | 17,900 |

| 32,430 |

|

| | | | 78,003 |

|

| Construction and Engineering — 0.2% | | | |

| China Communications Services Corp. Ltd., H Shares | | 6,000 |

| 4,196 |

|

| Daelim Industrial Co. Ltd. | | 374 |

| 33,282 |

|

Samsung Engineering Co. Ltd.(2) | | 2,551 |

| 35,338 |

|

| Sinopec Engineering Group Co. Ltd., H Shares | | 23,000 |

| 18,085 |

|

| | | | 90,901 |

|

| Construction Materials — 0.3% | | | |

| Anhui Conch Cement Co. Ltd., H Shares | | 4,000 |

| 23,160 |

|

| Asia Cement Corp. | | 27,000 |

| 36,241 |

|

| China National Building Material Co. Ltd., H Shares | | 24,000 |

| 21,067 |

|

| China Resources Cement Holdings Ltd. | | 28,000 |

| 25,811 |

|

| Taiwan Cement Corp. | | 30,000 |

| 42,961 |

|

| | | | 149,240 |

|

Diversified Financial Services† | | | |

| FirstRand Ltd. | | 3,132 |

| 13,446 |

|

Diversified Telecommunication Services† | | | |

| China Unicom Hong Kong Ltd. | | 10,000 |

| 9,689 |

|

| Telkom SA SOC Ltd. | | 1,748 |

| 10,497 |

|

| | | | 20,186 |

|

| Electric Utilities — 0.6% | | | |

| Centrais Eletricas Brasileiras SA | | 900 |

| 9,244 |

|

| Edison International | | 854 |

| 63,657 |

|

| Enel Americas SA ADR | | 5,000 |

| 41,250 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| Eversource Energy | | 922 |

| $ | 69,943 |

|

| Inter RAO UES PJSC | | 217,000 |

| 15,165 |

|

| Interconexion Electrica SA ESP | | 6,310 |

| 34,464 |

|

| Manila Electric Co. | | 550 |

| 3,943 |

|

| Pinnacle West Capital Corp. | | 766 |

| 69,875 |

|

| Xcel Energy, Inc. | | 1,180 |

| 70,340 |

|

| | | | 377,881 |

|

| Electronic Equipment, Instruments and Components — 0.1% | | |

| Hon Hai Precision Industry Co. Ltd. | | 8,400 |

| 21,123 |

|

Yageo Corp.(2) | | 1,000 |

| 8,440 |

|

| Zhen Ding Technology Holding Ltd. | | 8,000 |

| 29,246 |

|

| | | | 58,809 |

|

| Equity Real Estate Investment Trusts (REITs) — 7.9% | | | |

| Community Healthcare Trust, Inc. | | 6,675 |

| 274,276 |

|

| Essential Properties Realty Trust, Inc. | | 22,001 |

| 464,661 |

|

| Gaming and Leisure Properties, Inc. | | 8,466 |

| 319,253 |

|

| Granite Real Estate Investment Trust | | 8,250 |

| 383,433 |

|

| HCP, Inc. | | 15,534 |

| 496,001 |

|

| Jernigan Capital, Inc. | | 14,254 |

| 282,799 |

|

| Northview Apartment Real Estate Investment Trust | | 16,257 |

| 335,044 |

|

| Spirit Realty Capital, Inc. | | 11,342 |

| 500,409 |

|

| STAG Industrial, Inc. | | 12,959 |

| 385,142 |

|

| STORE Capital Corp. | | 4,810 |

| 164,550 |

|

| VEREIT, Inc. | | 27,462 |

| 250,453 |

|

| VICI Properties, Inc. | | 13,910 |

| 296,839 |

|

| Welltower, Inc. | | 6,176 |

| 513,349 |

|

| | | | 4,666,209 |

|

| Food Products — 0.2% | | | |

| JBS SA | | 6,000 |

| 39,147 |

|

| Standard Foods Corp. | | 9,000 |

| 17,397 |

|

| Uni-President Enterprises Corp. | | 22,000 |

| 57,200 |

|

| | | | 113,744 |

|

| Gas Utilities — 0.3% | | | |

| Atmos Energy Corp. | | 403 |

| 43,943 |

|

| Kunlun Energy Co. Ltd. | | 48,000 |

| 41,868 |

|

| ONE Gas, Inc. | | 427 |

| 38,934 |

|

| Spire, Inc. | | 466 |

| 38,403 |

|

| | | | 163,148 |

|

| Hotels, Restaurants and Leisure — 0.1% | | | |

| Yum China Holdings, Inc. | | 1,030 |

| 46,865 |

|

| Household Products — 0.1% | | | |

Kimberly-Clark de Mexico SAB de CV, A Shares(2) | | 23,200 |

| 48,134 |

|

| Independent Power and Renewable Electricity Producers — 0.1% | |

| Aboitiz Power Corp. | | 59,600 |

| 41,465 |

|

| CGN Power Co. Ltd., H Shares | | 36,000 |

| 10,415 |

|

| Colbun SA | | 73,527 |

| 13,775 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| SDIC Power Holdings Co. Ltd., A Shares | | 8,200 |

| $ | 10,123 |

|

| | | | 75,778 |

|

| Industrial Conglomerates — 0.1% | | | |

| Alfa SAB de CV, Class A | | 30,600 |

| 26,506 |

|

| Shanghai Industrial Holdings Ltd. | | 8,000 |

| 16,439 |

|

| | | | 42,945 |

|

| Insurance — 0.5% | | | |

| China Life Insurance Co. Ltd., A Shares | | 2,400 |

| 10,292 |

|

| China Pacific Insurance Group Co. Ltd., H Shares | | 12,000 |

| 51,442 |

|

| DB Insurance Co. Ltd. | | 558 |

| 26,202 |

|

| Ping An Insurance Group Co. of China Ltd., H Shares | | 11,500 |

| 136,399 |

|

| Powszechny Zaklad Ubezpieczen SA | | 2,969 |

| 31,997 |

|

| Samsung Fire & Marine Insurance Co. Ltd. | | 42 |

| 9,291 |

|

| | | | 265,623 |

|

Interactive Media and Services† | | | |

| Tencent Holdings Ltd. | | 600 |

| 28,062 |

|

Internet and Direct Marketing Retail† | | | |

Alibaba Group Holding Ltd. ADR(2) | | 150 |

| 25,967 |

|

| IT Services — 0.1% | | | |

| Infosys Ltd. ADR | | 2,900 |

| 32,828 |

|

Leisure Products† | | | |

| Giant Manufacturing Co. Ltd. | | 2,000 |

| 15,298 |

|

| Machinery — 0.1% | | | |

| Sany Heavy Industry Co. Ltd., A Shares | | 8,700 |

| 17,749 |

|

| Sinotruk Hong Kong Ltd. | | 11,000 |

| 16,225 |

|

| Weichai Power Co. Ltd., H Shares | | 27,000 |

| 41,804 |

|

| | | | 75,778 |

|

Media† | | | |

| Cheil Worldwide, Inc. | | 700 |

| 15,988 |

|

| Metals and Mining — 0.4% | | | |

| Cia Siderurgica Nacional SA ADR | | 7,500 |

| 32,025 |

|

| Grupo Mexico SAB de CV, Series B | | 2,700 |

| 6,622 |

|

| Korea Zinc Co. Ltd. | | 100 |

| 37,352 |

|

| Kumba Iron Ore Ltd. | | 1,128 |

| 37,371 |

|

| POSCO | | 50 |

| 9,497 |

|

| Vale SA ADR | | 7,500 |

| 97,425 |

|

| | | | 220,292 |

|

| Mortgage Real Estate Investment Trusts (REITs) — 2.4% | | | |

| Blackstone Mortgage Trust, Inc., Class A | | 11,851 |

| 420,947 |

|

| Starwood Property Trust, Inc. | | 21,757 |

| 505,415 |

|

| TPG RE Finance Trust, Inc. | | 25,257 |

| 498,826 |

|

| | | | 1,425,188 |

|

| Multi-Utilities — 0.3% | | | |

| Ameren Corp. | | 883 |

| 66,834 |

|

| NorthWestern Corp. | | 836 |

| 58,453 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| WEC Energy Group, Inc. | | 743 |

| $ | 63,497 |

|

| | | | 188,784 |

|

| Oil, Gas and Consumable Fuels — 4.5% | | | |

| China Petroleum & Chemical Corp., H Shares | | 18,000 |

| 11,595 |

|

| China Shenhua Energy Co. Ltd., H Shares | | 4,000 |

| 7,925 |

|

| CNOOC Ltd. | | 48,000 |

| 78,940 |

|

| Ecopetrol SA ADR | | 1,200 |

| 21,516 |

|

| Energy Transfer LP | | 15,883 |

| 228,398 |

|

| Enterprise Products Partners LP | | 17,174 |

| 517,109 |

|

| EQM Midstream Partners LP | | 4,342 |

| 167,210 |

|

| Gazprom PJSC ADR | | 5,534 |

| 40,568 |

|

| Grupa Lotos SA | | 1,801 |

| 40,596 |

|

| Hess Midstream Partners LP | | 10,215 |

| 205,934 |

|

| LUKOIL PJSC ADR | | 472 |

| 38,807 |

|

| MOL Hungarian Oil & Gas plc | | 4,284 |

| 43,594 |

|

| MPLX LP | | 7,443 |

| 218,452 |

|

| Noble Midstream Partners LP | | 5,632 |

| 174,536 |

|

| Petroleo Brasileiro SA ADR | | 3,690 |

| 50,627 |

|

| Phillips 66 Partners LP | | 4,105 |

| 214,527 |

|

| Plains All American Pipeline LP | | 11,854 |

| 281,888 |

|

| Reliance Industries Ltd. GDR | | 2,544 |

| 85,352 |

|

| Shell Midstream Partners LP | | 10,304 |

| 222,463 |

|

| Yanzhou Coal Mining Co. Ltd., H Shares | | 20,000 |

| 17,677 |

|

| | | | 2,667,714 |

|

Paper and Forest Products† | | | |

| Lee & Man Paper Manufacturing Ltd. | | 27,000 |

| 16,470 |

|

| Personal Products — 0.1% | | | |

| LG Household & Health Care Ltd. Preference Shares | | 51 |

| 34,543 |

|

| Pharmaceuticals — 0.1% | | | |

| Dr Reddy's Laboratories Ltd. ADR | | 500 |

| 18,405 |

|

| Sino Biopharmaceutical Ltd. | | 22,000 |

| 26,748 |

|

| | | | 45,153 |

|

| Real Estate Management and Development — 0.2% | | | |

| Agile Group Holdings Ltd. | | 6,000 |

| 7,759 |

|

| China Vanke Co. Ltd., H Shares | | 4,800 |

| 18,118 |

|

| CIFI Holdings Group Co. Ltd. | | 18,000 |

| 11,422 |

|

| Country Garden Holdings Co. Ltd. | | 20,000 |

| 26,987 |

|

| Longfor Group Holdings Ltd. | | 3,500 |

| 12,869 |

|

| Shui On Land Ltd. | | 126,500 |

| 26,954 |

|

| Sunac China Holdings Ltd. | | 3,000 |

| 13,624 |

|

| | | | 117,733 |

|

| Semiconductors and Semiconductor Equipment — 0.1% | | | |

| Nanya Technology Corp. | | 7,000 |

| 16,580 |

|

| SK Hynix, Inc. | | 353 |

| 22,785 |

|

| Taiwan Semiconductor Manufacturing Co. Ltd. ADR | | 600 |

| 25,578 |

|

| | | | 64,943 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| Technology Hardware, Storage and Peripherals — 0.3% | | | |

| Lenovo Group Ltd. | | 32,000 |

| $ | 25,708 |

|

| Samsung Electronics Co. Ltd. | | 3,482 |

| 132,850 |

|

| Samsung Electronics Co. Ltd. Preference Shares | | 313 |

| 9,751 |

|

| | | | 168,309 |

|

| Transportation Infrastructure — 0.1% | | | |

| International Container Terminal Services, Inc. | | 5,940 |

| 15,784 |

|

| Taiwan High Speed Rail Corp. | | 30,000 |

| 40,060 |

|

| | | | 55,844 |

|

| Water Utilities — 0.1% | | | |

| Cia de Saneamento Basico do Estado de Sao Paulo ADR | | 3,600 |

| 50,076 |

|

| Wireless Telecommunication Services — 0.3% | | | |

| China Mobile Ltd. | | 9,000 |

| 76,609 |

|

| DiGi.Com Bhd | | 40,200 |

| 48,534 |

|

| Globe Telecom, Inc. | | 900 |

| 38,067 |

|

| SK Telecom Co. Ltd. | | 41 |

| 8,575 |

|

| | | | 171,785 |

|

TOTAL COMMON STOCKS

(Cost $12,013,891) | | | 13,091,766 |

|

| PREFERRED STOCKS — 10.6% | | | |

| Banks — 6.0% | | | |

| Bank of America Corp., 5.20% | | 33,000 |

| 33,766 |

|

| Bank of America Corp., 5.875% | | 108,000 |

| 115,058 |

|

| Bank of America Corp., 6.50% | | 418,000 |

| 465,428 |

|

| Citigroup, Inc., 5.95% | | 49,000 |

| 51,537 |

|

| JPMorgan Chase & Co., 5.15% | | 75,000 |

| 76,540 |

|

| JPMorgan Chase & Co., 6.10% | | 186,000 |

| 198,688 |

|

| PNC Capital Trust C, 3.09% | | 679,000 |

| 630,495 |

|

| SunTrust Banks, Inc., 5.125% | | 741,000 |

| 734,257 |

|

| U.S. Bancorp, 5.30% | | 162,000 |

| 170,853 |

|

| U.S. Bancorp, 6.50% | | 15,377 |

| 415,487 |

|

| Wells Fargo & Co., 6.18% | | 633,000 |

| 637,748 |

|

| | | | 3,529,857 |

|

| Capital Markets — 1.6% | | | |

| Bank of New York Mellon Corp. (The), 4.95% | | 260,000 |

| 262,335 |

|

| Charles Schwab Corp. (The), 5.00% | | 675,000 |

| 677,713 |

|

| | | | 940,048 |

|

| Diversified Financial Services — 0.2% | | | |

| JPMorgan Chase & Co., 5.00% | | 76,000 |

| 76,969 |

|

| Voya Financial, Inc., 6.125% | | 60,000 |

| 63,943 |

|

| | | | 140,912 |

|

| Equity Real Estate Investment Trusts (REITs) — 0.9% | | | |

| Kimco Realty Corp., 5.625% | | 530 |

| 13,610 |

|

| Public Storage, 5.40% | | 11,018 |

| 291,316 |

|

| Public Storage, 5.60% | | 7,069 |

| 192,630 |

|

| SITE Centers Corp., 6.25% | | 500 |

| 13,005 |

|

| | | | 510,561 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

Insurance† | | | |

| Progressive Corp. (The), 5.375% | | 17,000 |

| $ | 17,557 |

|

| Mortgage Real Estate Investment Trusts (REITs) — 0.5% | | | |

| Chimera Investment Corp., 8.00% | | 10,474 |

| 278,085 |

|

| Multi-Utilities — 1.3% | | | |

| NextEra Energy Capital Holdings, Inc., 5.25% | | 4,907 |

| 133,520 |

|

| SCE Trust II, 5.10% | | 27,718 |

| 650,264 |

|

| | | | 783,784 |

|

| Oil, Gas and Consumable Fuels — 0.1% | | | |

| Plains All American Pipeline LP, 6.125% | | 68,000 |

| 65,687 |

|

TOTAL PREFERRED STOCKS

(Cost $6,049,160) | | | 6,266,491 |

|

| CONVERTIBLE PREFERRED STOCKS — 2.7% | | | |

| Banks — 0.8% | | | |

| Bank of America Corp., 7.25% | | 143 |

| 202,694 |

|

| Wells Fargo & Co., 7.50% | | 169 |

| 235,005 |

|

| | | | 437,699 |

|

| Chemicals — 0.3% | | | |

| International Flavors & Fragrances, Inc., 6.00%, 9/15/21 | | 3,654 |

| 196,476 |

|

| Equity Real Estate Investment Trusts (REITs) — 0.8% | | | |

| QTS Realty Trust, Inc., 6.50% | | 4,366 |

| 493,838 |

|

| Health Care Equipment and Supplies — 0.6% | | | |

| Becton Dickinson and Co., 6.125%, 5/1/20 | | 4,048 |

| 249,559 |

|

| Danaher Corp., 4.75%, 4/15/22 | | 87 |

| 98,736 |

|

| | | | 348,295 |

|

| Machinery — 0.2% | | | |

| Stanley Black & Decker, Inc., 5.375%, 5/15/20 | | 943 |

| 95,705 |

|

TOTAL CONVERTIBLE PREFERRED STOCKS

(Cost $1,436,564) | | | 1,572,013 |

|

| CORPORATE BONDS — 1.6% | | | |

| Automobiles — 0.1% | | | |

| Ford Motor Co., 4.35%, 12/8/26 | | $ | 45,000 |

| 45,422 |

|

| Banks — 0.1% | | | |

| Wells Fargo & Co., MTN, 4.65%, 11/4/44 | | 50,000 |

| 56,589 |

|

| Biotechnology — 0.1% | | | |

| Amgen, Inc., 4.66%, 6/15/51 | | 40,000 |

| 43,952 |

|

| Consumer Finance — 0.1% | | | |

| Capital One Financial Corp., 3.80%, 1/31/28 | | 40,000 |

| 41,437 |

|

Containers and Packaging† | | | |

| Berry Global, Inc., 5.125%, 7/15/23 | | 20,000 |

| 20,500 |

|

Electronic Equipment, Instruments and Components† | | | |

| Vishay Intertechnology, Inc., 2.25%, 6/15/25 | | 19,000 |

| 17,787 |

|

Energy Equipment and Services† | | | |

| Valaris plc, 8.00%, 1/31/24 | | 11,000 |

| 9,350 |

|

| Entertainment — 0.1% | | | |

Walt Disney Co. (The), 6.90%, 8/15/39(4) | | 25,000 |

| 37,344 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

Equity Real Estate Investment Trusts (REITs)† | | | |

| MGM Growth Properties Operating Partnership LP / MGP Finance Co-Issuer, Inc., 4.50%, 9/1/26 | | $ | 25,000 |

| $ | 25,787 |

|

Food and Staples Retailing† | | | |

| Tesco plc, MTN, 5.50%, 12/13/19 | GBP | 10,000 |

| 12,348 |

|

| Health Care Providers and Services — 0.2% | | | |

| DaVita, Inc., 5.125%, 7/15/24 | | $ | 35,000 |

| 35,219 |

|

| Express Scripts Holding Co., 4.50%, 2/25/26 | | 50,000 |

| 54,132 |

|

| HCA, Inc., 5.00%, 3/15/24 | | 20,000 |

| 21,729 |

|

| | | | 111,080 |

|

| Hotels, Restaurants and Leisure — 0.1% | | | |

International Game Technology plc, 6.25%, 2/15/22(4) | | 35,000 |

| 37,012 |

|

| Household Durables — 0.1% | | | |

| Lennar Corp., 4.75%, 5/30/25 | | 35,000 |

| 36,750 |

|

| Insurance — 0.1% | | | |

| Prudential Financial, Inc., 3.94%, 12/7/49 | | 50,000 |

| 53,078 |

|

| Media — 0.1% | | | |

| Comcast Corp., 4.75%, 3/1/44 | | 25,000 |

| 29,151 |

|

| CSC Holdings LLC, 6.75%, 11/15/21 | | 5,000 |

| 5,362 |

|

| | | | 34,513 |

|

Mortgage Real Estate Investment Trusts (REITs)† | | | |

| Starwood Property Trust, Inc., 5.00%, 12/15/21 | | 20,000 |

| 20,700 |

|

| Multi-Utilities — 0.2% | | | |

| Dominion Energy, Inc., 4.90%, 8/1/41 | | 25,000 |

| 28,893 |

|

| Exelon Generation Co. LLC, 5.60%, 6/15/42 | | 50,000 |

| 57,250 |

|

| Sempra Energy, 3.25%, 6/15/27 | | 50,000 |

| 50,263 |

|

| | | | 136,406 |

|

| Oil, Gas and Consumable Fuels — 0.2% | | | |

| Antero Resources Corp., 5.125%, 12/1/22 | | 20,000 |

| 19,200 |

|

| Kinder Morgan Energy Partners LP, 6.50%, 9/1/39 | | 35,000 |

| 43,394 |

|

| MPLX LP, 4.875%, 12/1/24 | | 47,000 |

| 51,226 |

|

| | | | 113,820 |

|

| Pharmaceuticals — 0.1% | | | |

| Allergan Funding SCS, 4.55%, 3/15/35 | | 40,000 |

| 41,423 |

|

Specialty Retail† | | | |

| Home Depot, Inc. (The), 5.95%, 4/1/41 | | 20,000 |

| 27,372 |

|

Technology Hardware, Storage and Peripherals† | | | |

Dell International LLC / EMC Corp., 5.875%, 6/15/21(4) | | 20,000 |

| 20,353 |

|

Wireless Telecommunication Services† | | | |

| Sprint Communications, Inc., 6.00%, 11/15/22 | | 20,000 |

| 21,300 |

|

TOTAL CORPORATE BONDS

(Cost $908,488) | | | 964,323 |

|

| EXCHANGE-TRADED FUNDS — 1.6% | | | |

| Alerian MLP ETF | | 37,158 |

| 365,263 |

|

| iShares China Large-Cap ETF | | 1,480 |

| 60,828 |

|

| iShares MSCI Emerging Markets ETF | | 2,837 |

| 118,501 |

|

| iShares MSCI India ETF | | 6,090 |

| 200,970 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| iShares MSCI Russia ETF | | 2,250 |

| $ | 87,908 |

|

| iShares MSCI Thailand ETF | | 1,150 |

| 105,800 |

|

TOTAL EXCHANGE-TRADED FUNDS

(Cost $927,205) | | | 939,270 |

|

| COLLATERALIZED MORTGAGE OBLIGATIONS — 1.2% | | | |

| Private Sponsor Collateralized Mortgage Obligations — 0.9% | | |

| Bear Stearns Adjustable Rate Mortgage Trust, Series 2004-12, Class 2A1, VRN, 4.30%, 2/25/35 | | $ | 12,281 |

| 12,524 |

|

| Bear Stearns Adjustable Rate Mortgage Trust, Series 2004-8, Class 2A1, VRN, 4.24%, 11/25/34 | | 3,157 |

| 3,132 |

|

| Chase Mortgage Finance Trust, Series 2007-A2, Class 6A2 SEQ, VRN, 4.52%, 7/25/37 | | 1,209 |

| 1,184 |

|

| Citicorp Mortgage Securities Trust, Series 2007-8, Class 1A3, 6.00%, 9/25/37 | | 3,990 |

| 4,285 |

|

| Citigroup Mortgage Loan Trust, Inc., Series 2004-UST1, Class A5, VRN, 4.40%, 8/25/34 | | 15,044 |

| 15,262 |

|

| Citigroup Mortgage Loan Trust, Inc., Series 2005-4, Class A, VRN, 4.58%, 8/25/35 | | 4,750 |

| 4,903 |

|

| Citigroup Mortgage Loan Trust, Inc., Series 2005-6, Class A2, VRN, 4.55%, (1-year H15T1Y plus 2.15%), 9/25/35 | | 17,553 |

| 18,034 |

|

| Credit Suisse First Boston Mortgage-Backed Pass-Through Certificates, Series 2005-3, Class 1A1, VRN, 5.48%, 7/25/35 | | 6,746 |

| 7,192 |

|

| GSR Mortgage Loan Trust, Series 2005-AR6, Class 2A1, VRN, 4.50%, 9/25/35 | | 15,648 |

| 16,116 |

|

| GSR Mortgage Loan Trust, Series 2005-AR6, Class 4A5, VRN, 4.56%, 9/25/35 | | 10,135 |

| 10,393 |

|

| JPMorgan Mortgage Trust, Series 2005-A4, Class 1A1, VRN, 4.42%, 7/25/35 | | 5,227 |

| 5,302 |

|

| JPMorgan Mortgage Trust, Series 2005-A4, Class 2A1, VRN, 4.38%, 7/25/35 | | 5,016 |

| 5,054 |

|

| JPMorgan Mortgage Trust, Series 2005-A6, Class 7A1, VRN, 4.32%, 8/25/35 | | 3,566 |

| 3,494 |

|

| JPMorgan Mortgage Trust, Series 2005-S2, Class 3A1, VRN, 7.16%, 2/25/32 | | 229 |

| 237 |

|

| MASTR Adjustable Rate Mortgages Trust, Series 2004-13, Class 3A7, VRN, 4.73%, 11/21/34 | | 16,155 |

| 16,865 |

|

Sequoia Mortgage Trust, Series 2017-CH2, Class A10 SEQ, VRN, 4.00%, 12/25/47(4) | | 39,263 |

| 39,697 |

|

| Thornburg Mortgage Securities Trust, Series 2006-4, Class A2B, VRN, 4.49%, 7/25/36 | | 20,385 |

| 19,920 |

|

WaMu Mortgage Pass-Through Certificates, Series 2005-AR3, Class A1, VRN, 4.45%, 3/25/35 | | 7,669 |

| 7,633 |

|

WaMu Mortgage Pass-Through Certificates, Series 2005-AR7, Class A3, VRN, 4.27%, 8/25/35 | | 3,355 |

| 3,428 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2004-A, Class A1, VRN, 5.01%, 2/25/34 | | 7,431 |

| 7,765 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2004-Z, Class 2A2, VRN, 4.97%, 12/25/34 | | 6,759 |

| 6,969 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2005-17, Class 2A1, 5.50%, 1/25/36 | | 61,038 |

| 62,638 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2005-18, Class 1A1, 5.50%, 1/25/36 | | 12,590 |

| 12,652 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2005-AR4, Class 2A1, VRN, 5.10%, 4/25/35 | | 2,231 |

| 2,280 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2005-AR7, Class 1A1, VRN, 5.10%, 5/25/35 | | 3,104 |

| 3,230 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| Wells Fargo Mortgage-Backed Securities Trust, Series 2006-4, Class 2A1, 6.00%, 4/25/36 | | $ | 8,226 |

| $ | 8,257 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2006-6, Class 1A16 SEQ, 5.75%, 5/25/36 | | 14,804 |

| 14,580 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2006-8, Class A10 SEQ, 6.00%, 7/25/36 | | 8,590 |

| 8,707 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2006-8, Class A15, 6.00%, 7/25/36 | | 57,734 |

| 58,522 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR1, Class 2A5 SEQ, VRN, 4.98%, 3/25/36 | | 4,312 |

| 4,296 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR10, Class 1A1, VRN, 5.04%, 7/25/36 | | 2,581 |

| 2,633 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR10, Class 4A1, VRN, 5.18%, 7/25/36 | | 15,485 |

| 15,736 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR10, Class 5A6 SEQ, VRN, 5.02%, 7/25/36 | | 29,902 |

| 30,440 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR12, Class 1A1, VRN, 4.76%, 9/25/36 | | 16,488 |

| 16,833 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR14, Class 2A1, VRN, 4.76%, 10/25/36 | | 8,768 |

| 8,779 |

|

Wells Fargo Mortgage-Backed Securities Trust, Series 2006-AR16, Class A1, VRN, 4.72%, 10/25/36 | | 20,514 |

| 20,548 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2007-11, Class A36, 6.00%, 8/25/37 | | 13,675 |

| 13,879 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2007-15, Class A1, 6.00%, 11/25/37 | | 7,369 |

| 7,505 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2007-4, Class A15, 6.00%, 4/25/37 | | 6,158 |

| 6,248 |

|

| Wells Fargo Mortgage-Backed Securities Trust, Series 2007-7, Class A1, 6.00%, 6/25/37 | | 12,514 |

| 12,823 |

|

| | | | 519,975 |

|

| U.S. Government Agency Collateralized Mortgage Obligations — 0.3% | |

FHLMC, Series 2015-HQ2, Class M3, VRN, 5.52%, (1-month LIBOR plus 3.25%), 5/25/25 | | 50,000 |

| 53,468 |

|

FHLMC, Series 2017-DNA2, Class M1, VRN, 3.47%, (1-month LIBOR plus 1.20%), 10/25/29 | | 35,559 |

| 35,790 |

|

FHLMC, Series 2019-DNA1, Class M1, VRN, 3.30%, (1-month LIBOR plus 0.90%), 1/25/49(4) | | 47,001 |

| 47,155 |

|

FNMA, Series 2014-C02, Class 1M2, VRN, 4.87%, (1-month LIBOR plus 2.60%), 5/25/24 | | 19,742 |

| 20,596 |

|

FNMA, Series 2016-C03, Class 2M2, VRN, 8.17%, (1-month LIBOR plus 5.90%), 10/25/28 | | 4,399 |

| 4,831 |

|

| | | | 161,840 |

|

TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS

(Cost $663,858) | | | 681,815 |

|

| CONVERTIBLE BONDS — 1.1% | | | |

Air Freight and Logistics† | | | |

| Air Transport Services Group, Inc., 1.125%, 10/15/24 | | 19,000 |

| 18,973 |

|

Airlines† | | | |

Citigroup Global Markets Holdings, Inc., (convertible into Southwest Airlines Co.), 6.35%, 9/17/19(3)(4) | | 461 |

| 23,773 |

|

| Biotechnology — 0.1% | | | |

Credit Suisse AG, (convertible into Celgene Corp.), 9.10%, 9/19/19(3)(4) | | 282 |

| 25,224 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| Construction Materials — 0.2% | | | |

Royal Bank of Canada, (convertible into Martin Marietta Materials, Inc.), 6.65%, 8/2/19(3)(4) | | $ | 111 |

| $ | 20,619 |

|

Royal Bank of Canada, (convertible into Martin Marietta Materials, Inc.), 5.60%, 8/12/19(3)(4) | | 21 |

| 3,886 |

|

Wells Fargo Bank N.A., (convertible into Martin Marietta Materials, Inc.), 5.10%, 8/1/19(3)(4) | | 391 |

| 74,099 |

|

| | | | 98,604 |

|

| Diversified Financial Services — 0.1% | | | |

Citigroup Global Markets Holdings, Inc., (convertible into Berkshire Hathaway, Inc., Class B), 1.63%, 8/13/19(3)(4) | | 14 |

| 2,826 |

|

Credit Suisse AG, (convertible into Berkshire Hathaway, Inc., Class B), 1.50%, 12/5/19(3)(4) | | 138 |

| 27,892 |

|

Royal Bank of Canada, (convertible into Berkshire Hathaway, Inc., Class B), 0.90%, 1/23/20(3)(4) | | 72 |

| 15,142 |

|

| | | | 45,860 |

|

| Health Care Technology — 0.1% | | | |

Credit Suisse AG, (convertible into Cerner Corp.), 2.80%, 10/17/19(3)(4) | | 683 |

| 44,879 |

|

Morgan Stanley B.V., (convertible into Cerner Corp.), 1.48%, 10/31/19(3)(4) | | 292 |

| 19,703 |

|

| | | | 64,582 |

|

| Insurance — 0.1% | | | |

AXA SA, 7.25%, 5/15/21(4) | | 54,000 |

| 58,321 |

|

| Semiconductors and Semiconductor Equipment — 0.5% | | | |

| Microchip Technology, Inc., 1.625%, 2/15/27 | | 172,000 |

| 219,610 |

|

| Teradyne, Inc., 1.25%, 12/15/23 | | 43,000 |

| 78,891 |

|

| | | | 298,501 |

|

Software† | | | |

Palo Alto Networks, Inc., 0.75%, 7/1/23(4) | | 14,000 |

| 15,449 |

|

Technology Hardware, Storage and Peripherals† | | | |

Western Digital Corp., 1.50%, 2/1/24(4) | | 9,000 |

| 8,388 |

|

Textiles, Apparel and Luxury Goods† | | | |

UBS AG, (convertible into Ralph Lauren Corp.), 8.65%, 1/23/20(3)(4) | | 116 |

| 12,492 |

|

TOTAL CONVERTIBLE BONDS

(Cost $587,968) | | | 670,167 |

|

| COMMERCIAL MORTGAGE-BACKED SECURITIES — 0.8% | | |

Bank of America Merrill Lynch Commercial Mortgage Securities Trust, Series 2015-200P, Class B, 3.49%, 4/14/33(4) | | 25,000 |

| 26,071 |

|

| Commercial Mortgage Pass-Through Certificates, Series 2014-LC17, Class B, VRN, 4.49%, 10/10/47 | | 10,000 |

| 10,654 |

|

| Commercial Mortgage Pass-Through Certificates, Series 2016-CR28, Class B, VRN, 4.65%, 2/10/49 | | 35,000 |

| 38,436 |

|

| Commercial Mortgage Trust, Series 2015-CR22, Class B, VRN, 3.93%, 3/10/48 | | 25,000 |

| 25,964 |

|

Commercial Mortgage Trust, Series 2017-PANW, Class A SEQ, 3.24%, 10/10/29(4) | | 25,000 |

| 25,813 |

|

Core Industrial Trust, Series 2015-CALW, Class C, 3.56%, 2/10/34(4) | | 25,000 |

| 25,652 |

|

Core Industrial Trust, Series 2015-TEXW, Class B, 3.33%, 2/10/34(4) | | 25,000 |

| 25,614 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

| CSAIL Commercial Mortgage Trust, Series 2017-CX10, Class AS, VRN, 3.67%, 11/15/50 | | $ | 25,000 |

| $ | 26,296 |

|

| GS Mortgage Securities Trust, Series 2015-GC28, Class AS, 3.76%, 2/10/48 | | 15,000 |

| 15,766 |

|

| GS Mortgage Securities Trust, Series 2016-GS2, Class B, VRN, 3.76%, 5/10/49 | | 25,000 |

| 26,121 |

|

Hudson Yards Mortgage Trust, Series 2016-10HY, Class A SEQ, 2.84%, 8/10/38(4) | | 25,000 |

| 25,420 |

|

Hudson Yards Mortgage Trust, Series 2016-10HY, Class B, VRN, 2.98%, 8/10/38(4) | | 10,000 |

| 10,164 |

|

JPMBB Commercial Mortgage Securities Trust, Series 2014-C21, Class B, VRN, 4.34%, 8/15/47 | | 25,000 |

| 26,360 |

|

JPMDB Commercial Mortgage Securities Trust, Series 2017-C5, Class A4 SEQ, 3.41%, 3/15/50 | | 20,000 |

| 21,082 |

|

| JPMorgan Chase Commercial Mortgage Securities Trust, Series 2016-JP2, Class B, 3.46%, 8/15/49 | | 25,000 |

| 25,583 |

|

| JPMorgan Chase Commercial Mortgage Securities Trust, Series 2016-JP3, Class AS, 3.14%, 8/15/49 | | 25,000 |

| 25,454 |

|

| Morgan Stanley Bank of America Merrill Lynch Trust, Series 2017-C34, Class A3 SEQ, 3.28%, 11/15/52 | | 25,000 |

| 26,095 |

|

| UBS Commercial Mortgage Trust, Series 2017-C1, Class A3 SEQ, 3.20%, 6/15/50 | | 50,000 |

| 52,076 |

|

| Wells Fargo Commercial Mortgage Trust, Series 2017-C38, Class A4 SEQ, 3.19%, 7/15/50 | | 25,000 |

| 25,991 |

|

TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES

(Cost $474,955) | | 484,612 |

|

| ASSET-BACKED SECURITIES — 0.5% | | | |

Avis Budget Rental Car Funding AESOP LLC, Series 2015-2A, Class B, 3.42%, 12/20/21(4) | | 25,000 |

| 25,185 |

|

BRE Grand Islander Timeshare Issuer LLC, Series 2017-1A, Class B, 3.24%, 5/25/29(4) | | 13,006 |

| 12,976 |

|

Hilton Grand Vacations Trust, Series 2013-A, Class A SEQ, 2.28%, 1/25/26(4) | | 2,359 |

| 2,358 |

|

Hilton Grand Vacations Trust, Series 2014-AA, Class A SEQ, 1.77%, 11/25/26(4) | | 19,424 |

| 19,320 |

|

Hilton Grand Vacations Trust, Series 2017-AA, Class A SEQ, 2.66%, 12/26/28(4) | | 4,895 |

| 4,910 |

|

Invitation Homes Trust, Series 2017-SFR2, Class A, VRN, 3.16%, (1-month LIBOR plus 0.85%), 12/17/36(4) | | 23,729 |

| 23,715 |

|

Invitation Homes Trust, Series 2017-SFR2, Class B, VRN, 3.46%, (1-month LIBOR plus 1.15%), 12/17/36(4) | | 25,000 |

| 24,998 |

|

Invitation Homes Trust, Series 2018-SFR1, Class C, VRN, 3.56%, (1-month LIBOR plus 1.25%), 3/17/37(4) | | 25,000 |

| 24,948 |

|

Marriott Vacation Club Owner Trust, Series 2012-1A, Class B, VRN, 3.50%, 5/20/30(4) | | 2,582 |

| 2,583 |

|

MVW Owner Trust, Series 2013-1A, Class A SEQ, 2.15%, 4/22/30(4) | | 18,403 |

| 18,346 |

|

MVW Owner Trust, Series 2017-1A, Class B, 2.75%, 12/20/34(4) | | 26,768 |

| 26,617 |

|

Progress Residential Trust, Series 2017-SFR1, Class A SEQ, 2.77%, 8/17/34(4) | | 24,909 |

| 24,927 |

|

Progress Residential Trust, Series 2017-SFR2, Class A SEQ, 2.90%, 12/17/34(4) | | 25,000 |

| 25,024 |

|

Sierra Timeshare Conduit Receivables Funding LLC, Series 2017-1A, Class A SEQ, 2.91%, 3/20/34(4) | | 2,753 |

| 2,776 |

|

Sierra Timeshare Receivables Funding LLC, Series 2015-1A, Class A SEQ, 2.40%, 3/22/32(4) | | 2,797 |

| 2,793 |

|

|

| | | | | | | |

| | | Shares/

Principal Amount | Value |

Sierra Timeshare Receivables Funding LLC, Series 2015-2A, Class A SEQ, 2.43%, 6/20/32(4) | | $ | 6,408 |

| $ | 6,391 |

|

Sierra Timeshare Receivables Funding LLC, Series 2015-3A, Class A SEQ, 2.58%, 9/20/32(4) | | 7,767 |

| 7,754 |

|

Sierra Timeshare Receivables Funding LLC, Series 2016-2A, Class A SEQ, 2.33%, 7/20/33(4) | | 1,966 |

| 1,955 |

|

VSE VOI Mortgage LLC, Series 2016-A, Class A SEQ, 2.54%, 7/20/33(4) | | 18,144 |

| 18,105 |

|

TOTAL ASSET-BACKED SECURITIES

(Cost $275,490) | | | 275,681 |

|

| U.S. TREASURY SECURITIES — 0.4% | | | |

| U.S. Treasury Notes, 2.375%, 2/29/24 (Cost $199,004) | | 200,000 |

| 204,793 |

|

| COLLATERALIZED LOAN OBLIGATIONS — 0.3% | | | |

Carlyle Global Market Strategies CLO Ltd., Series 2014-1A, Class A1R2, VRN, 3.27%, (3-month LIBOR plus 0.97%), 4/17/31(4) | | 50,000 |

| 49,514 |

|

CBAM Ltd., Series 2018-5A, Class B1, VRN, 3.70%, (3-month LIBOR plus 1.40%), 4/17/31(4) | | 25,000 |

| 24,484 |

|

Dryden 41 Senior Loan Fund, Series 2015-41A, Class AR, VRN, 3.27%, (3-month LIBOR plus 0.97%), 4/15/31(4) | | 50,000 |

| 49,487 |

|

Dryden 64 CLO Ltd., Series 2018-64A, Class A, VRN, 3.25%, (3-month LIBOR plus 0.97%), 4/18/31(4) | | 25,000 |

| 24,758 |

|

Sounds Point CLO IV-R Ltd., Series 2013-3RA, Class B, VRN, 4.05%, (3-month LIBOR plus 1.75%), 4/18/31(4) | | 35,000 |

| 34,873 |

|

TOTAL COLLATERALIZED LOAN OBLIGATIONS

(Cost $184,642) | | | 183,116 |

|

| TEMPORARY CASH INVESTMENTS — 6.5% | | | |

| State Street Institutional U.S. Government Money Market Fund, Premier Class | | 3,498,164 |

| 3,498,164 |

|

U.S. Treasury Bills, 2.37%, 11/29/19(5)(6) | | $ | 300,000 |

| 297,972 |

|

TOTAL TEMPORARY CASH INVESTMENTS

(Cost $3,795,856) | | | 3,796,136 |

|

TOTAL INVESTMENT SECURITIES — 100.0%

(Cost $56,984,250) | | | 58,893,587 |

|

OTHER ASSETS AND LIABILITIES† | | | 3,214 |

|

| TOTAL NET ASSETS — 100.0% | | | $ | 58,896,801 |

|

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS

|

| | | | | | | | | | |

| Currency Purchased | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation

(Depreciation) |

| AUD | 665,363 |

| USD | 461,110 |

| Bank of America N.A. | 9/18/19 | $ | (5,360 | ) |

| AUD | 478,475 |

| USD | 335,244 |

| Bank of America N.A. | 9/18/19 | (7,505 | ) |

| AUD | 469,907 |

| USD | 331,129 |

| Bank of America N.A. | 9/18/19 | (9,260 | ) |

| USD | 166,608 |

| AUD | 238,783 |

| Bank of America N.A. | 9/18/19 | 3,050 |

|

| USD | 309,950 |

| AUD | 441,430 |

| Bank of America N.A. | 9/18/19 | 7,586 |

|

| USD | 64,404 |

| AUD | 93,052 |

| Bank of America N.A. | 9/18/19 | 667 |

|

| BRL | 1,856,426 |

| USD | 461,373 |

| Goldman Sachs & Co. | 9/18/19 | 23,361 |

|

| BRL | 71,170 |

| USD | 18,360 |

| Goldman Sachs & Co. | 9/18/19 | 223 |

|

| USD | 24,262 |

| BRL | 94,750 |

| Goldman Sachs & Co. | 9/18/19 | (478 | ) |

| USD | 45,456 |

| BRL | 172,347 |

| Goldman Sachs & Co. | 9/18/19 | 454 |

|

| CAD | 828,285 |

| USD | 615,646 |

| Morgan Stanley | 9/18/19 | 12,510 |

|

|

| | | | | | | | | | |

| Currency Purchased | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation

(Depreciation) |

| USD | 308,715 |

| CAD | 406,575 |

| Morgan Stanley | 9/18/19 | $ | 376 |

|

| USD | 322,697 |

| CAD | 421,710 |

| Morgan Stanley | 9/18/19 | 2,880 |

|

| CHF | 310,080 |

| USD | 310,633 |

| UBS AG | 9/18/19 | 2,421 |

|

| CHF | 475,904 |

| USD | 482,197 |

| UBS AG | 9/18/19 | (1,729 | ) |

| CHF | 324,863 |

| USD | 332,858 |

| UBS AG | 9/18/19 | (4,880 | ) |

| USD | 317,112 |

| CHF | 310,080 |

| UBS AG | 9/18/19 | 4,058 |

|

| USD | 77,518 |

| CHF | 76,659 |

| UBS AG | 9/18/19 | 124 |

|

| CLP | 217,469,749 |

| USD | 317,892 |

| Goldman Sachs & Co. | 9/23/19 | (8,903 | ) |

| USD | 319,879 |

| CLP | 217,469,749 |

| Goldman Sachs & Co. | 9/23/19 | 10,890 |

|

| CNY | 2,242,278 |

| USD | 326,197 |

| Morgan Stanley | 9/18/19 | (1,554 | ) |

| CNY | 2,242,279 |

| USD | 326,197 |

| Morgan Stanley | 9/18/19 | (1,554 | ) |

| CNY | 1,111,546 |

| USD | 161,797 |

| Morgan Stanley | 9/18/19 | (864 | ) |

| USD | 82,321 |

| CNY | 566,669 |

| Morgan Stanley | 9/18/19 | 277 |

|

| USD | 141,419 |

| CNY | 974,097 |

| Morgan Stanley | 9/18/19 | 387 |

|

| COP | 1,034,534,031 |

| USD | 306,467 |

| Goldman Sachs & Co. | 9/18/19 | 7,934 |

|

| USD | 320,337 |

| COP | 1,034,534,031 |

| Goldman Sachs & Co. | 9/18/19 | 5,936 |

|

| USD | 289,615 |

| COP | 939,292,430 |

| Goldman Sachs & Co. | 9/18/19 | 4,158 |

|

| CZK | 7,218,427 |

| USD | 322,309 |

| UBS AG | 9/18/19 | (11,222 | ) |

| CZK | 7,450,078 |

| USD | 329,102 |

| UBS AG | 9/18/19 | (8,031 | ) |

| USD | 320,521 |

| CZK | 7,218,427 |

| UBS AG | 9/18/19 | 9,434 |

|

| USD | 32,540 |

| CZK | 747,380 |

| UBS AG | 9/18/19 | 330 |

|

| USD | 291,194 |

| CZK | 6,702,698 |

| UBS AG | 9/18/19 | 2,333 |

|

| EUR | 138,306 |

| USD | 155,676 |

| JPMorgan Chase Bank N.A. | 9/18/19 | (1,990 | ) |

| EUR | 275,017 |

| USD | 310,544 |

| JPMorgan Chase Bank N.A. | 9/18/19 | (4,945 | ) |

| EUR | 286,054 |

| USD | 322,716 |

| JPMorgan Chase Bank N.A. | 9/18/19 | (4,853 | ) |

| EUR | 290,746 |

| USD | 329,108 |

| JPMorgan Chase Bank N.A. | 9/18/19 | (6,031 | ) |

| USD | 312,732 |

| EUR | 273,249 |

| JPMorgan Chase Bank N.A. | 9/18/19 | 9,098 |

|

| USD | 159,735 |

| EUR | 140,074 |

| JPMorgan Chase Bank N.A. | 9/18/19 | 4,085 |

|

| USD | 322,482 |

| EUR | 286,054 |

| JPMorgan Chase Bank N.A. | 9/18/19 | 4,619 |

|

| USD | 327,502 |

| EUR | 290,746 |

| JPMorgan Chase Bank N.A. | 9/18/19 | 4,425 |

|

| USD | 13,112 |

| GBP | 10,261 |

| Bank of America N.A. | 9/18/19 | 606 |

|

| HUF | 5,042,094 |

| USD | 17,842 |

| UBS AG | 9/18/19 | (679 | ) |

| HUF | 93,481,190 |

| USD | 324,182 |

| UBS AG | 9/18/19 | (5,986 | ) |

| HUF | 13,957,310 |

| USD | 47,666 |

| UBS AG | 9/18/19 | (158 | ) |

| USD | 621,348 |

| HUF | 179,977,291 |

| UBS AG | 9/18/19 | 8,731 |

|

| USD | 10,606 |

| HUF | 3,050,972 |

| UBS AG | 9/18/19 | 221 |

|

| USD | 339,558 |

| HUF | 96,040,336 |

| UBS AG | 9/18/19 | 12,651 |

|

| USD | 15,308 |

| HUF | 4,414,385 |

| UBS AG | 9/18/19 | 282 |

|

| ILS | 1,170,257 |

| USD | 329,427 |

| UBS AG | 9/18/19 | 4,778 |

|

| ILS | 249,115 |

| USD | 70,967 |

| UBS AG | 9/18/19 | 176 |

|

| ILS | 1,025,702 |

| USD | 294,577 |

| UBS AG | 9/18/19 | (1,655 | ) |

| ILS | 1,036,781 |

| USD | 298,114 |

| UBS AG | 9/18/19 | (2,028 | ) |

| USD | 616,637 |

| ILS | 2,220,758 |

| UBS AG | 9/18/19 | (17,572 | ) |

| USD | 25,127 |

| ILS | 90,120 |

| UBS AG | 9/18/19 | (610 | ) |

| USD | 332,173 |

| ILS | 1,170,977 |

| UBS AG | 9/18/19 | (2,237 | ) |

| USD | 293,015 |

| ILS | 1,023,591 |

| UBS AG | 9/18/19 | 696 |

|

|

| | | | | | | | | | |

| Currency Purchased | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation

(Depreciation) |

| JPY | 33,665,311 |

| USD | 312,683 |

| Bank of America N.A. | 9/18/19 | $ | (2,141 | ) |

| JPY | 8,421,350 |

| USD | 77,785 |

| Bank of America N.A. | 9/18/19 | (103 | ) |

| USD | 309,526 |

| JPY | 33,665,311 |

| Bank of America N.A. | 9/18/19 | (1,015 | ) |

| USD | 480,761 |

| JPY | 52,057,272 |

| Bank of America N.A. | 9/18/19 | 565 |

|

| USD | 333,054 |

| JPY | 35,771,956 |

| Bank of America N.A. | 9/18/19 | 3,080 |

|

| KZT | 117,008,666 |

| USD | 301,724 |

| Goldman Sachs & Co. | 9/18/19 | (3 | ) |

| KZT | 64,178,527 |

| USD | 166,524 |

| Goldman Sachs & Co. | 9/18/19 | (1,032 | ) |

| USD | 31,681 |

| KZT | 12,323,835 |

| Goldman Sachs & Co. | 9/18/19 | (98 | ) |

| MXN | 2,947,886 |

| USD | 151,652 |

| Morgan Stanley | 9/18/19 | 984 |

|

| MXN | 6,122,331 |

| USD | 315,389 |

| Morgan Stanley | 9/18/19 | 1,613 |

|

| MXN | 6,079,416 |

| USD | 313,943 |

| Morgan Stanley | 9/18/19 | 837 |

|

| MXN | 5,105,287 |

| USD | 266,602 |

| Morgan Stanley | 9/18/19 | (2,260 | ) |

| USD | 146,774 |

| MXN | 2,947,886 |

| Morgan Stanley | 9/18/19 | (5,861 | ) |

| USD | 316,017 |

| MXN | 6,165,644 |

| Morgan Stanley | 9/18/19 | (3,228 | ) |

| USD | 141,753 |

| MXN | 2,725,904 |

| Morgan Stanley | 9/18/19 | 611 |

|

| MYR | 1,312,321 |

| USD | 318,138 |

| Goldman Sachs & Co. | 9/18/19 | (418 | ) |

| MYR | 991,142 |

| USD | 241,565 |

| Goldman Sachs & Co. | 9/18/19 | (1,604 | ) |

| USD | 47,680 |

| MYR | 196,539 |

| Goldman Sachs & Co. | 9/18/19 | 97 |

|

| NOK | 10,696,793 |

| USD | 1,225,979 |

| Goldman Sachs & Co. | 9/18/19 | (16,633 | ) |

| NOK | 167,933 |

| USD | 19,785 |

| Goldman Sachs & Co. | 9/18/19 | (799 | ) |

| NOK | 2,632,588 |

| USD | 300,882 |

| Goldman Sachs & Co. | 9/18/19 | (3,249 | ) |

| USD | 313,352 |

| NOK | 2,676,280 |

| Goldman Sachs & Co. | 9/18/19 | 10,780 |

|

| USD | 303,505 |

| NOK | 2,591,080 |

| Goldman Sachs & Co. | 9/18/19 | 10,565 |

|

| USD | 60,727 |

| NOK | 528,898 |

| Goldman Sachs & Co. | 9/18/19 | 931 |

|

| NZD | 461,190 |

| USD | 305,843 |

| Bank of America N.A. | 9/18/19 | (2,727 | ) |

| NZD | 242,885 |

| USD | 162,359 |

| Bank of America N.A. | 9/18/19 | (2,724 | ) |

| USD | 459,226 |

| NZD | 704,075 |

| Bank of America N.A. | 9/18/19 | (3,525 | ) |

| PEN | 663,891 |

| USD | 200,753 |

| Goldman Sachs & Co. | 9/18/19 | (216 | ) |

| USD | 457,448 |

| PEN | 1,546,038 |

| Goldman Sachs & Co. | 9/18/19 | (9,553 | ) |

| USD | 481,000 |

| PEN | 1,586,337 |

| Goldman Sachs & Co. | 9/18/19 | 1,825 |

|

| USD | 960,503 |

| PEN | 3,167,451 |

| Goldman Sachs & Co. | 9/18/19 | 3,732 |

|

| USD | 45,147 |

| PEN | 148,675 |

| Goldman Sachs & Co. | 9/18/19 | 238 |

|

| PHP | 1,235,536 |

| USD | 24,164 |

| Goldman Sachs & Co. | 9/18/19 | 48 |

|

| USD | 336,722 |

| PHP | 17,683,318 |

| Goldman Sachs & Co. | 9/18/19 | (9,797 | ) |

| PLN | 146,709 |

| USD | 38,835 |

| Goldman Sachs & Co. | 9/18/19 | (940 | ) |

| PLN | 1,197,896 |

| USD | 321,825 |

| Goldman Sachs & Co. | 9/18/19 | (12,405 | ) |

| PLN | 1,866,575 |

| USD | 493,614 |

| Goldman Sachs & Co. | 9/18/19 | (11,473 | ) |

| PLN | 432,405 |

| USD | 112,711 |

| Goldman Sachs & Co. | 9/18/19 | (1,020 | ) |

| USD | 1,537,978 |

| PLN | 5,909,834 |

| Goldman Sachs & Co. | 9/18/19 | 11,453 |

|

| USD | 25,467 |

| PLN | 96,757 |

| Goldman Sachs & Co. | 9/18/19 | 475 |

|

| USD | 26,036 |

| PLN | 97,500 |

| Goldman Sachs & Co. | 9/18/19 | 852 |

|

| USD | 309,497 |

| PLN | 1,161,759 |

| Goldman Sachs & Co. | 9/18/19 | 9,412 |

|

| USD | 32,927 |

| PLN | 124,573 |

| Goldman Sachs & Co. | 9/18/19 | 750 |

|

| USD | 42,355 |

| PLN | 160,739 |

| Goldman Sachs & Co. | 9/18/19 | 836 |

|

| SEK | 7,356,343 |

| USD | 777,252 |

| Goldman Sachs & Co. | 9/18/19 | (13,156 | ) |

| SEK | 1,441,051 |

| USD | 152,803 |

| Goldman Sachs & Co. | 9/18/19 | (3,122 | ) |

|

| | | | | | | | | | |

| Currency Purchased | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation

(Depreciation) |

| SEK | 259,110 |

| USD | 27,443 |

| Goldman Sachs & Co. | 9/18/19 | $ | (529 | ) |

| USD | 478,747 |

| SEK | 4,474,030 |

| Goldman Sachs & Co. | 9/18/19 | 14,033 |

|

| USD | 46,559 |

| SEK | 440,499 |

| Goldman Sachs & Co. | 9/18/19 | 805 |

|

| USD | 141,911 |

| SEK | 1,351,235 |

| Goldman Sachs & Co. | 9/18/19 | 1,560 |

|

| THB | 3,271,918 |

| USD | 105,973 |

| Goldman Sachs & Co. | 9/18/19 | (82 | ) |

| THB | 9,101,232 |

| USD | 296,699 |

| Goldman Sachs & Co. | 9/18/19 | (2,150 | ) |

| USD | 319,239 |

| THB | 9,832,252 |

| Goldman Sachs & Co. | 9/18/19 | 1,032 |

|

| USD | 236,771 |

| THB | 7,267,698 |

| Goldman Sachs & Co. | 9/18/19 | 1,562 |

|

| USD | 341,428 |

| THB | 10,534,586 |

| Goldman Sachs & Co. | 9/18/19 | 490 |

|

| USD | 163,047 |

| THB | 5,042,072 |

| Goldman Sachs & Co. | 9/18/19 | (133 | ) |

| ZAR | 2,264,974 |

| USD | 152,749 |

| UBS AG | 9/18/19 | 4,264 |

|

| ZAR | 13,434,027 |

| USD | 953,241 |

| UBS AG | 9/18/19 | (21,965 | ) |

| USD | 151,936 |

| ZAR | 2,264,974 |

| UBS AG | 9/18/19 | (5,076 | ) |

| USD | 940,682 |

| ZAR | 13,434,027 |

| UBS AG | 9/18/19 | 9,406 |

|

| | | | | | | $ | (6,528 | ) |

|

| | | | | | | | | | | |

| FUTURES CONTRACTS PURCHASED | | | | |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Underlying

Contract

Value | Unrealized

Appreciation

(Depreciation) |

| U.S. Treasury 10-Year Ultra Notes | 1 | September 2019 | $ | 100,000 |

| $ | 137,844 |

| $ | 2,460 |

|

|

| | | | | | | | | | | |

| FUTURES CONTRACTS SOLD | | | | |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Underlying

Contract

Value | Unrealized

Appreciation

(Depreciation) |

| U.S. Treasury 10-Year Notes | 80 | September 2019 | $ | 8,000,000 |

| $ | 10,193,750 |

| $ | (101,430 | ) |

|

| | | | | | | | | | | | | | | |

| CENTRALLY CLEARED CREDIT DEFAULT SWAP AGREEMENTS |

| Reference Entity | Type‡ | Fixed Rate

Received

(Paid) | Termination

Date | Notional

Amount | Premiums

Paid

(Received) | Unrealized

Appreciation

(Depreciation) | Value^ |

| Markit CDX North America High Yield Index Series 32 | Sell | 5.00% | 6/20/24 | $ | 297,000 |

| $ | 19,942 |

| $ | 4,176 |

| $ | 24,118 |

|

| Markit CDX North America Investment Grade Index Series 32 | Sell | 1.00% | 6/20/24 | $ | 100,000 |

| 2,221 |

| 52 |

| 2,273 |

|

| | | | | | $ | 22,163 |

| $ | 4,228 |

| $ | 26,391 |

|

‡ The maximum potential amount the fund could be required to deliver as a seller of credit protection if a credit event occurs as defined under the terms of the agreement is the notional amount. The maximum potential amount may be partially offset by any recovery values of the reference entities and upfront payments received upon entering into the agreement.