UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | | | | | | | | | | | | | | | | | | | |

| Investment Company Act file number | 811-08532 |

| |

| AMERICAN CENTURY STRATEGIC ASSET ALLOCATIONS, INC. |

| (Exact name of registrant as specified in charter) |

| |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 |

| (Address of principal executive offices) | (Zip Code) |

| |

JOHN PAK

4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 |

| (Name and address of agent for service) |

| |

| Registrant’s telephone number, including area code: | 816-531-5575 |

| |

| Date of fiscal year end: | 07-31 |

| |

| Date of reporting period: | 07-31-2021 |

ITEM 1. REPORTS TO STOCKHOLDERS.

(a) Provided under separate cover.

| | | | | |

| |

| Annual Report |

| |

| July 31, 2021 |

| |

| Strategic Allocation: Aggressive Fund |

| Investor Class (TWSAX) |

| I Class (AAAIX) |

| A Class (ACVAX) |

| C Class (ASTAX) |

| R Class (AAARX) |

| R5 Class (ASAUX) |

| R6 Class (AAAUX) |

| | | | | |

| President’s Letter | |

| Performance | |

| Portfolio Commentary | |

| Fund Characteristics | |

| Shareholder Fee Example | |

| Schedule of Investments | |

| Statement of Assets and Liabilities | |

| Statement of Operations | |

| Statement of Changes in Net Assets | |

| Notes to Financial Statements | |

| Financial Highlights | |

| Report of Independent Registered Public Accounting Firm | |

| Management | |

| Approval of Management Agreement | |

| Liquidity Risk Management Program | |

| |

| Additional Information | |

| |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Jonathan Thomas

Jonathan Thomas

Dear Investor:

Thank you for reviewing this annual report for the period ended July 31, 2021. Annual reports help convey important information about fund returns, including market factors that affected performance. For additional investment insights, please visit americancentury.com.

Stocks Delivered Strong Gains

Global equities and other risk-on assets rallied for the 12-month period, benefiting from ongoing central bank and federal government support. These programs helped sustain investor confidence and bolster the economic landscape, despite ongoing challenges from COVID-19 and the inconsistent lifting of virus-related restrictions.

In general, data on U.S. manufacturing, employment, housing and corporate earnings remained upbeat during the period. Additionally, expanding COVID-19 vaccine availability and two federal coronavirus aid packages also helped promote investor optimism. Outside the U.S., economies recovered but at a slower pace. Virus outbreaks and slower vaccine rollouts led to lingering lockdowns in some regions.

Against this backdrop, inflation rose, but central banks remained supportive. In the U.S., where annual inflation soared to a 13-year high, the Federal Reserve (Fed) insisted temporary supply chain disruptions and other transient factors were at play. The Fed left interest rates unchanged but hinted it may start hiking rates in 2023, sooner than its previous timetable of 2024.

Despite ongoing pandemic-related challenges, including the emergence of the delta variant of COVID-19, risk assets remained in favor, and global stocks delivered stellar 12-month returns. The U.S. generally outperformed other developed markets, as the S&P 500 Index returned more than 36%. Value stocks generally outperformed growth stocks, while small caps sharply outpaced large caps. The broad U.S. bond market declined modestly, but global bonds delivered a slight gain.

Several Influences Shaping Market Dynamics

The return to pre-pandemic life is progressing, albeit somewhat cautiously due to the spread of the delta variant. As the economy and markets respond to this fluid backdrop, investors will face opportunities and ongoing challenges. Economic growth, inflation, the virus’s trajectory, supply chain normalization and fiscal and monetary policy likely will sway market dynamics.

We appreciate your confidence in us during these extraordinary times. Our firm has a long history of helping clients weather unpredictable markets, and we’re confident we will continue to meet today’s challenges.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

| | | | | | | | | | | | | | | | | | | | | |

| Total Returns as of July 31, 2021 |

| | | | Average Annual Returns | |

| Ticker Symbol | | 1 year | 5 years | 10 years | Since

Inception | Inception Date |

| Investor Class | TWSAX | | 30.04% | 12.76% | 10.18% | — | 2/15/96 |

| S&P 500 Index | — | | 36.45% | 17.34% | 15.33% | — | — |

| Bloomberg Barclays U.S. Aggregate Bond Index | — | | -0.70% | 3.12% | 3.34% | — | — |

| Bloomberg Barclays U.S. 1-3 Month Treasury Bill Index | — | | 0.06% | 1.10% | 0.58% | — | — |

| I Class | AAAIX | | 30.42% | 13.01% | 10.41% | — | 8/1/00 |

| A Class | ACVAX | | | | | | 10/2/96 |

| No sales charge | | | 29.69% | 12.47% | 9.91% | — | |

| With sales charge | | | 22.21% | 11.14% | 9.27% | — | |

| C Class | ASTAX | | 28.76% | 11.63% | 9.09% | — | 11/27/01 |

| R Class | AAARX | | 29.58% | 12.22% | 9.65% | — | 3/31/05 |

| R5 Class | ASAUX | | 30.24% | — | — | 13.47% | 4/10/17 |

| R6 Class | AAAUX | | 30.57% | 13.17% | — | 10.67% | 7/26/13 |

Average annual returns since inception are presented when ten years of performance history is not available.

Fund returns would have been lower if a portion of the fees had not been waived. Extraordinary performance is attributable in part to unusually favorable market conditions and may not be repeated or consistently achieved in the future.

C Class shares will automatically convert to A Class shares after being held for approximately eight years. C Class average annual returns do not reflect this conversion.

Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

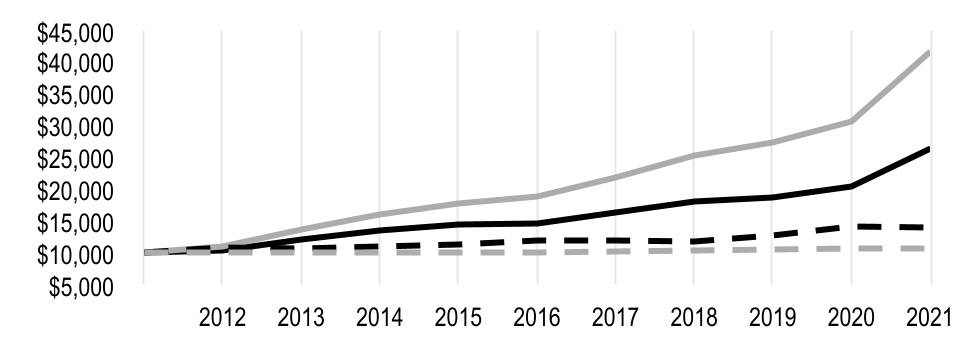

| | |

| Growth of $10,000 Over 10 Years |

| $10,000 investment made July 31, 2011 |

| Performance for other share classes will vary due to differences in fee structure. |

| | | | | |

| Value on July 31, 2021 |

| Investor Class — $26,397 |

|

| S&P 500 Index — $41,689 |

|

| Bloomberg Barclays U.S. Aggregate Bond Index — $13,897 |

|

| Bloomberg Barclays U.S. 1-3 Month Treasury Bill Index — $10,600 |

|

Ending value of Investor Class would have been lower if a portion of the fees had not been waived.

| | | | | | | | | | | | | | | | | | | | |

Total Annual Fund Operating Expenses | | |

| Investor Class | I Class | A Class | C Class | R Class | R5 Class | R6 Class |

| 1.32% | 1.12% | 1.57% | 2.32% | 1.82% | 1.12% | 0.97% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

Portfolio Managers: Rich Weiss, Scott Wilson, Radu Gabudean, Vidya Rajappa and Brian Garbe

Performance Summary

Strategic Allocation: Aggressive returned 30.04%* for the fiscal period ended July 31, 2021. Because of the fund’s strategic exposure to a variety of asset classes, a review of the financial markets helps provide context around performance for the reporting period.

Global financial markets performance was colored by a shift in investor sentiment in late 2020, when investors began to anticipate the rollout of COVID-19 vaccines. Prior to the approval, stock and bond markets had been volatile as the outlook for growth varied with pandemic news. Nevertheless, stimulative fiscal and monetary policies supported the economy and financial markets throughout. The change in sentiment was reflected in equity market performance—gains were initially led by growth-oriented stocks, but then shifted to more economically sensitive value stocks. It was a similar story in fixed-income markets, where risk aversion initially kept yields on government bonds near historic lows. But with the prospect of vaccine distribution and the end of the pandemic, investors generally shifted out of government bonds and into higher-yielding, more procyclical sectors to take advantage of an anticipated economic recovery. Later, however, inflation concerns began to play into investor decisions and contributed to market volatility.

In that environment, broad global equity indices finished the period at or near record highs. In the U.S., stocks generally posted very strong returns. Mid-cap companies led the way, followed by small caps and large caps, while value outperformed growth across all market capitalizations, according to the Russell family of indices. Emerging markets stocks also performed well but lagged the U.S. and developed non-U.S. markets. For the period, the S&P 500 Index gained 36.45%, while the MSCI EAFE Index rose 30.31% and the MSCI Emerging Markets (Net) Index increased 20.64%.

In fixed-income markets, government bonds benefited from concerns about the pandemic early in the period, as investors sought out high-quality, perceived safe-haven investments. In the U.S., unprecedented fiscal and monetary stimulus, and a new tolerance for higher inflation by the Federal Reserve, led to a rise in inflation expectations. As a result, yields on government bonds rose, while inflation-protected and corporate bonds performed well. Later in the period, concerns about a resurgence of COVID-19 and questions about the economic recovery caused government bond yields to decline somewhat. It was a similar story outside the U.S., where yields generally followed the same falling-rising-falling pattern, and ultimately ended the period higher than where they began. Add it all up, and the Bloomberg Barclays Global Aggregate Bond Index ex-USD (Unhedged) returned 1.66% and the Bloomberg Barclays Global Aggregate Bond Index (USD, Hedged) returned 0.23%. By comparison, the Bloomberg Barclays U.S. Aggregate Bond, U.S. High-Yield 2% Issuer Capped Bond and U.S. Treasury Inflation-Protected Securities (TIPS) Indices returned -0.70%, 10.62% and 6.90%, respectively.

Strategic Allocation: Aggressive’s neutral asset mix throughout the period was 79% stocks, 20% bonds and 1% cash-equivalent investments. However, the portfolio’s actual asset weightings varied based on short-term tactical adjustments and fluctuating securities prices.

Tactical Positioning

In an effort to add value and improve the fund’s ability to achieve its objective, we make modest adjustments to the asset allocation. As for regional allocations, because of the speed and success of vaccine rollouts, the U.S. led the economic and earnings recovery. As a result, we maintained our overweight to U.S. stocks relative to non-U.S. markets throughout the period.

*All fund returns referenced in this commentary are for Investor Class shares. Fund returns would have been lower if a portion of the fees had not been waived. Performance for other share classes will vary due to differences in fee structure; when Investor Class performance exceeds that of the fund’s benchmark, other share classes may not. See page 3 for returns for all classes.

Similarly, the continued economic recovery, rising consumer sentiment and indications of higher interest rates all favored value-oriented sectors like financials, materials and industrials over technology and health care. In that environment, we eliminated our long-standing growth overweight and moved to a value overweight during the period. The strong U.S. economic recovery and positive sentiment also pointed us toward a bias in favor of small-cap stocks relative to large.

In fixed income, the rapid economic rebound, higher interest rates and concerns about inflation weighed on government bond markets but favored TIPS and corporate bonds. These conditions benefited our fixed-income allocation, which generally underweighted government bonds in favor of TIPS and higher-yielding sectors such as corporates and select asset-backed securities. Our other tactical allocation decisions also produced positive effects, as U.S. equities outperformed non-U.S. equities, value beat growth and small beat large.

Equity Allocation Performed Well

The equity allocation of Strategic Allocation: Aggressive performed well as all strategies produced positive returns. Key contributions to absolute returns came from U.S. large-cap and value-oriented holdings. While overweight allocations to large-cap value were beneficial, security selection in this category limited gains. Returns were also strongly positive among small-cap value and small-cap growth positions, aided by strong stock selection. Mid-cap equity returns were also positive, though stock selection effects were mixed.

Outside the U.S., large-cap shares and global real estate were significant contributors, while growth-oriented and small-cap holdings made more modest contributions. In global real estate, our decision to overweight this segment during the period added to performance. Security selection was generally positive across the international equity segment and was particularly strong in the international small-cap value allocation.

Fixed-Income Contributed to Performance

In a period when stocks surged to record highs and interest rates rose, the global bond allocation made only a modest, positive contribution to performance. Certain decisions particularly benefited fixed-income returns. For example, worries about resurgent inflation meant that it was beneficial to overweight TIPS. At the same time, expectations of an improving economy also contributed to strong returns in the high-yield market, where we were overweight.

Outlook

The global economic recovery is underway and corporate profits have rebounded sharply, but risks remain. Volatility could spike if investors’ assumptions about inflation, interest rates and corporate earnings disappoint. In addition, the resurgent virus and challenges in terms of vaccine distribution and virus mutation mean we are not out of the woods yet with respect to a sustained global economic recovery. And while the U.S. is leading the recovery in developed markets as easing coronavirus restrictions unleash pent-up consumer demand, emerging markets are improving more gradually as vaccination rates climb. Therefore, we remain neutral in our stock allocations relative to bonds and cash, preferring to stick to our long-term strategic diversification targets.

Within equities, economically sensitive value stocks look appealing relative to growth stocks. We believe the economic recovery that’s driving the rotation from growth to value still has plenty of room to run in the U.S. We also favor small-cap stocks based on several favorable conditions, including stronger U.S. growth relative to non-U.S. economies, low interest rates, tight corporate bond spreads, rising commodity prices and relatively attractive valuations.

In fixed-income markets, our outlook for emerging markets sovereign debt and U.S. securitized bonds is positive. We’re more selective around U.S. credit, U.S. government debt and European debt.

| | | | | |

| JULY 31, 2021 |

Types of Investments in Portfolio | % of net assets |

| Affiliated Funds | 48.8% |

| Common Stocks | 31.8% |

| U.S. Treasury Securities | 5.2% |

| Corporate Bonds | 3.4% |

| Sovereign Governments and Agencies | 2.9% |

| Collateralized Loan Obligations | 0.8% |

| Commercial Paper | 0.5% |

| Municipal Securities | 0.4% |

| Collateralized Mortgage Obligations | 0.4% |

| Asset-Backed Securities | 0.3% |

| Preferred Stocks | 0.3% |

| U.S. Government Agency Mortgage-Backed Securities | 0.1% |

| Exchange-Traded Funds | 0.1% |

| Temporary Cash Investments | 4.3% |

| Temporary Cash Investments - Securities Lending Collateral | 0.1% |

| Other Assets and Liabilities | 0.6% |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from February 1, 2021 to July 31, 2021.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or I Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not through a financial intermediary or employer-sponsored retirement plan account), American Century Investments may charge you a $25.00 annual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $25.00 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments brokerage accounts, you are currently not subject to this fee. If you are subject to the account maintenance fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

| Beginning

Account Value

2/1/21 | Ending

Account Value

7/31/21 | Expenses Paid During Period(1) 2/1/21 - 7/31/21 | Annualized Expense Ratio(1) |

Actual |

| Investor Class | $1,000 | $1,122.20 | $3.53 | 0.67% |

| I Class | $1,000 | $1,123.30 | $2.47 | 0.47% |

| A Class | $1,000 | $1,120.90 | $4.84 | 0.92% |

| C Class | $1,000 | $1,117.30 | $8.77 | 1.67% |

| R Class | $1,000 | $1,121.00 | $6.15 | 1.17% |

| R5 Class | $1,000 | $1,123.30 | $2.47 | 0.47% |

| R6 Class | $1,000 | $1,123.80 | $1.69 | 0.32% |

| Hypothetical |

| Investor Class | $1,000 | $1,021.47 | $3.36 | 0.67% |

| I Class | $1,000 | $1,022.46 | $2.36 | 0.47% |

| A Class | $1,000 | $1,020.23 | $4.61 | 0.92% |

| C Class | $1,000 | $1,016.51 | $8.35 | 1.67% |

| R Class | $1,000 | $1,018.99 | $5.86 | 1.17% |

| R5 Class | $1,000 | $1,022.46 | $2.36 | 0.47% |

| R6 Class | $1,000 | $1,023.21 | $1.61 | 0.32% |

(1)Expenses are equal to the class's annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 181, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. Annualized expense ratio reflects actual expenses, including any applicable fee waivers or expense reimbursements and excluding any acquired fund fees and expenses.

JULY 31, 2021

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

AFFILIATED FUNDS(1) — 48.8% |

|

|

|

| American Century Diversified Corporate Bond ETF | | 288,278 | | $ | 15,244,717 | |

| American Century Focused Dynamic Growth ETF | | 560,733 | | 46,367,012 | |

| American Century Focused Large Cap Value ETF | | 1,010,108 | | 61,895,681 | |

| American Century Quality Diversified International ETF | | 641,891 | | 33,428,207 | |

| American Century STOXX U.S. Quality Growth ETF | | 649,356 | | 47,413,702 | |

| American Century STOXX U.S. Quality Value ETF | | 1,222,230 | | 62,021,083 | |

| Avantis Emerging Markets Equity ETF | | 442,672 | | 29,196,432 | |

| Avantis International Equity ETF | | 499,019 | | 31,772,540 | |

| Avantis International Small Cap Value ETF | | 170,103 | | 11,111,128 | |

| Avantis U.S. Equity ETF | | 814,674 | | 60,978,349 | |

| Avantis U.S. Small Cap Value ETF | | 273,475 | | 20,070,330 | |

TOTAL AFFILIATED FUNDS (Cost $309,495,780) |

| | 419,499,181 | |

| COMMON STOCKS — 31.8% |

|

|

|

| Aerospace and Defense — 0.4% | | | |

Babcock International Group plc(2) | | 65,791 | | 233,830 | |

| BAE Systems plc | | 136,427 | | 1,093,809 | |

CAE, Inc.(2) | | 3,582 | | 109,303 | |

| General Dynamics Corp. | | 4,310 | | 844,889 | |

| Lockheed Martin Corp. | | 1,556 | | 578,319 | |

Mercury Systems, Inc.(2) | | 2,987 | | 197,142 | |

| Safran SA | | 3,561 | | 466,044 | |

| Spirit AeroSystems Holdings, Inc., Class A | | 3,025 | | 130,710 | |

| | | 3,654,046 | |

| Air Freight and Logistics — 0.1% | | | |

| Expeditors International of Washington, Inc. | | 2,182 | | 279,842 | |

| United Parcel Service, Inc., Class B | | 3,140 | | 600,870 | |

| | | 880,712 | |

| Airlines — 0.1% | | | |

Ryanair Holdings plc, ADR(2) | | 2,689 | | 293,208 | |

Southwest Airlines Co.(2) | | 17,871 | | 902,843 | |

| | | 1,196,051 | |

| Auto Components — 0.4% | | | |

Aptiv plc(2) | | 10,664 | | 1,779,288 | |

| BorgWarner, Inc. | | 13,677 | | 669,900 | |

| Bridgestone Corp. | | 6,600 | | 290,762 | |

| Hyundai Mobis Co. Ltd. | | 1,567 | | 364,069 | |

| Linamar Corp. | | 2,335 | | 138,161 | |

| Minth Group Ltd. | | 10,000 | | 42,290 | |

| Sumitomo Rubber Industries Ltd. | | 14,100 | | 189,774 | |

| Valeo SA | | 10,728 | | 310,209 | |

| | | 3,784,453 | |

| Automobiles — 0.3% | | | |

| Bayerische Motoren Werke AG | | 4,404 | | 437,895 | |

| Daimler AG | | 11,496 | | 1,025,897 | |

| Honda Motor Co. Ltd., ADR | | 18,341 | | 588,746 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

Nissan Motor Co. Ltd.(2) | | 84,000 | | $ | 487,522 | |

Tesla, Inc.(2) | | 478 | | 328,482 | |

| | | 2,868,542 | |

| Banks — 1.4% | | | |

AIB Group plc(2) | | 48,655 | | 119,499 | |

Banco Bilbao Vizcaya Argentaria SA(2) | | 64,732 | | 414,380 | |

| Banco Bradesco SA | | 26,763 | | 106,882 | |

| Banco do Brasil SA | | 30,900 | | 187,302 | |

| Bank Central Asia Tbk PT | | 81,400 | | 168,039 | |

| Bank of America Corp. | | 21,972 | | 842,846 | |

| Barclays plc | | 337,468 | | 816,362 | |

| BNP Paribas SA | | 9,602 | | 585,522 | |

| BPER Banca | | 49,178 | | 95,873 | |

| CaixaBank SA | | 143,087 | | 424,955 | |

| Canadian Western Bank | | 4,218 | | 114,984 | |

| Commerce Bancshares, Inc. | | 1,526 | | 107,934 | |

Commerzbank AG(2) | | 21,761 | | 140,140 | |

| Eastern Bankshares, Inc. | | 3,359 | | 61,302 | |

| First Hawaiian, Inc. | | 11,936 | | 328,598 | |

| HDFC Bank Ltd., ADR | | 5,832 | | 411,564 | |

| HSBC Holdings plc | | 84,400 | | 465,853 | |

| JPMorgan Chase & Co. | | 7,056 | | 1,070,960 | |

Jyske Bank A/S(2) | | 1,933 | | 93,796 | |

| M&T Bank Corp. | | 4,312 | | 577,161 | |

| Mitsubishi UFJ Financial Group, Inc. | | 113,800 | | 601,169 | |

| Mizuho Financial Group, Inc. | | 30,650 | | 437,977 | |

| Prosperity Bancshares, Inc. | | 5,446 | | 371,363 | |

| Regions Financial Corp. | | 33,543 | | 645,703 | |

Silvergate Capital Corp., Class A(2) | | 1,306 | | 134,257 | |

| Societe Generale SA | | 9,086 | | 266,090 | |

| Standard Chartered plc (London) | | 21,741 | | 130,333 | |

| Sumitomo Mitsui Financial Group, Inc. | | 11,300 | | 380,912 | |

Triumph Bancorp, Inc.(2) | | 2,508 | | 192,263 | |

| Truist Financial Corp. | | 15,507 | | 844,046 | |

| UniCredit SpA | | 13,585 | | 162,495 | |

Virgin Money UK plc(2) | | 22,970 | | 63,487 | |

| Westamerica Bancorporation | | 5,917 | | 328,689 | |

| | | 11,692,736 | |

| Beverages — 0.2% | | | |

Boston Beer Co., Inc. (The), Class A(2) | | 613 | | 435,230 | |

| MGP Ingredients, Inc. | | 1,553 | | 92,636 | |

| PepsiCo, Inc. | | 5,767 | | 905,131 | |

| Royal Unibrew A/S | | 876 | | 118,710 | |

| | | 1,551,707 | |

| Biotechnology — 0.7% | | | |

| AbbVie, Inc. | | 1,914 | | 222,598 | |

Acceleron Pharma, Inc.(2) | | 945 | | 118,182 | |

ADC Therapeutics SA(2) | | 3,363 | | 70,758 | |

Alnylam Pharmaceuticals, Inc.(2) | | 3,452 | | 617,701 | |

| Amgen, Inc. | | 1,917 | | 463,032 | |

Arcutis Biotherapeutics, Inc.(2) | | 3,325 | | 77,572 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

Arena Pharmaceuticals, Inc.(2) | | 1,112 | | $ | 68,788 | |

Argenx SE, ADR(2) | | 1,358 | | 413,416 | |

Biohaven Pharmaceutical Holding Co. Ltd.(2) | | 1,634 | | 205,900 | |

Blueprint Medicines Corp.(2) | | 1,349 | | 118,537 | |

Bridgebio Pharma, Inc.(2) | | 2,271 | | 121,385 | |

Centessa Pharmaceuticals plc, ADR(2) | | 3,298 | | 68,071 | |

Cytokinetics, Inc.(2) | | 3,030 | | 89,930 | |

Deciphera Pharmaceuticals, Inc.(2) | | 2,590 | | 78,969 | |

Erasca, Inc.(2) | | 2,663 | | 55,923 | |

Fate Therapeutics, Inc.(2) | | 1,138 | | 94,226 | |

FibroGen, Inc.(2) | | 2,455 | | 31,915 | |

Flexion Therapeutics, Inc.(2) | | 6,144 | | 36,434 | |

Global Blood Therapeutics, Inc.(2) | | 2,999 | | 81,963 | |

Halozyme Therapeutics, Inc.(2) | | 3,740 | | 154,574 | |

Heron Therapeutics, Inc.(2) | | 2,868 | | 35,449 | |

Horizon Therapeutics plc(2) | | 7,035 | | 703,641 | |

Immunovant, Inc.(2) | | 2,342 | | 24,497 | |

Insmed, Inc.(2) | | 4,739 | | 116,579 | |

Intellia Therapeutics, Inc.(2) | | 613 | | 86,954 | |

Invitae Corp.(2)(3) | | 2,044 | | 57,212 | |

Iovance Biotherapeutics, Inc.(2) | | 1,105 | | 24,608 | |

KalVista Pharmaceuticals, Inc.(2) | | 2,386 | | 48,054 | |

Karuna Therapeutics, Inc.(2) | | 1,126 | | 128,612 | |

Kinnate Biopharma, Inc.(2)(3) | | 1,504 | | 32,456 | |

Kymera Therapeutics, Inc.(2) | | 1,320 | | 79,438 | |

Natera, Inc.(2) | | 5,847 | | 669,598 | |

Relay Therapeutics, Inc.(2) | | 1,752 | | 56,835 | |

Sigilon Therapeutics, Inc.(2) | | 3,137 | | 15,810 | |

Turning Point Therapeutics, Inc.(2) | | 3,397 | | 216,797 | |

Vertex Pharmaceuticals, Inc.(2) | | 933 | | 188,074 | |

| | | 5,674,488 | |

| Building Products — 0.3% | | | |

| Johnson Controls International plc | | 13,677 | | 976,811 | |

| Masco Corp. | | 6,825 | | 407,521 | |

Masonite International Corp.(2) | | 1,722 | | 194,862 | |

| Sanwa Holdings Corp. | | 5,600 | | 68,148 | |

| Trane Technologies plc | | 5,515 | | 1,122,909 | |

Trex Co., Inc.(2) | | 1,540 | | 149,534 | |

| | | 2,919,785 | |

| Capital Markets — 1.4% | | | |

| Ameriprise Financial, Inc. | | 4,390 | | 1,130,688 | |

| Bank of New York Mellon Corp. (The) | | 28,731 | | 1,474,762 | |

| BlackRock, Inc. | | 661 | | 573,199 | |

| Credit Suisse Group AG | | 50,728 | | 509,274 | |

flatexDEGIRO AG(2) | | 678 | | 81,930 | |

| GCM Grosvenor, Inc., Class A | | 7,764 | | 77,329 | |

| Intercontinental Exchange, Inc. | | 2,576 | | 308,682 | |

| Intermediate Capital Group plc | | 6,499 | | 195,851 | |

| LPL Financial Holdings, Inc. | | 7,647 | | 1,078,533 | |

| MarketAxess Holdings, Inc. | | 1,029 | | 488,950 | |

| Morgan Stanley | | 11,193 | | 1,074,304 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| MSCI, Inc. | | 1,782 | | $ | 1,062,001 | |

| Northern Trust Corp. | | 11,433 | | 1,290,214 | |

Open Lending Corp., Class A(2) | | 6,917 | | 262,846 | |

| Partners Group Holding AG | | 366 | | 625,261 | |

| S&P Global, Inc. | | 1,627 | | 697,528 | |

| State Street Corp. | | 4,154 | | 361,980 | |

| T. Rowe Price Group, Inc. | | 2,945 | | 601,251 | |

| | | 11,894,583 | |

| Chemicals — 0.5% | | | |

| Air Liquide SA | | 2,019 | | 351,121 | |

| Air Products and Chemicals, Inc. | | 1,006 | | 292,776 | |

| Albemarle Corp. | | 1,846 | | 380,350 | |

Axalta Coating Systems Ltd.(2) | | 16,222 | | 488,282 | |

| Corbion NV | | 509 | | 27,865 | |

Diversey Holdings Ltd.(2) | | 9,154 | | 152,689 | |

| Ecolab, Inc. | | 1,333 | | 294,366 | |

| Element Solutions, Inc. | | 28,997 | | 678,240 | |

| Koninklijke DSM NV | | 1,912 | | 385,424 | |

| Linde plc | | 2,495 | | 766,938 | |

OCI NV(2) | | 2,534 | | 61,472 | |

| Sherwin-Williams Co. (The) | | 1,372 | | 399,293 | |

| Zeon Corp. | | 4,600 | | 62,851 | |

| | | 4,341,667 | |

| Commercial Services and Supplies — 0.2% | | | |

| Brink's Co. (The) | | 3,301 | | 254,045 | |

Clean Harbors, Inc.(2) | | 2,534 | | 240,730 | |

Driven Brands Holdings, Inc.(2) | | 8,798 | | 279,952 | |

Elis SA(2) | | 6,484 | | 116,276 | |

| Loomis AB | | 3,849 | | 129,057 | |

| Republic Services, Inc. | | 6,291 | | 744,603 | |

| | | 1,764,663 | |

| Communications Equipment — 0.6% | | | |

Arista Networks, Inc.(2) | | 3,644 | | 1,386,141 | |

| Cisco Systems, Inc. | | 12,769 | | 707,020 | |

F5 Networks, Inc.(2) | | 9,126 | | 1,884,610 | |

| Juniper Networks, Inc. | | 14,237 | | 400,629 | |

| Telefonaktiebolaget LM Ericsson, B Shares | | 33,852 | | 390,455 | |

| | | 4,768,855 | |

Construction and Engineering† | | | |

| Arcadis NV | | 2,651 | | 117,401 | |

| Hazama Ando Corp. | | 10,800 | | 82,162 | |

| | | 199,563 | |

| Construction Materials — 0.1% | | | |

| Buzzi Unicem SpA | | 2,321 | | 61,351 | |

Cemex SAB de CV, ADR(2) | | 74,786 | | 608,010 | |

| Eagle Materials, Inc. | | 1,140 | | 161,105 | |

Summit Materials, Inc., Class A(2) | | 2,631 | | 88,402 | |

| | | 918,868 | |

| Consumer Finance — 0.1% | | | |

| American Express Co. | | 2,922 | | 498,289 | |

goeasy Ltd.(3) | | 971 | | 133,088 | |

| | | 631,377 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Containers and Packaging — 0.5% | | | |

| Amcor plc | | 26,130 | | $ | 302,063 | |

| Avery Dennison Corp. | | 5,198 | | 1,095,115 | |

| Ball Corp. | | 9,994 | | 808,315 | |

| Intertape Polymer Group, Inc. | | 4,918 | | 109,468 | |

| Packaging Corp. of America | | 2,869 | | 405,964 | |

SIG Combibloc Group AG(2) | | 4,408 | | 130,061 | |

| Sonoco Products Co. | | 16,731 | | 1,067,270 | |

| | | 3,918,256 | |

Distributors† | | | |

| D'ieteren Group | | 1,198 | | 192,013 | |

Diversified Consumer Services† | | | |

Chegg, Inc.(2) | | 2,357 | | 208,901 | |

| IDP Education Ltd. | | 4,667 | | 96,706 | |

| | | 305,607 | |

Diversified Financial Services† | | | |

| Zenkoku Hosho Co. Ltd. | | 2,300 | | 104,353 | |

| Diversified Telecommunication Services — 0.1% | | | |

BT Group plc(2) | | 56,365 | | 135,768 | |

| Cellnex Telecom SA | | 11,836 | | 771,904 | |

| Verizon Communications, Inc. | | 4,307 | | 240,245 | |

| | | 1,147,917 | |

| Electric Utilities — 0.5% | | | |

| Edison International | | 17,158 | | 935,111 | |

| Evergy, Inc. | | 5,277 | | 344,166 | |

| Eversource Energy | | 4,255 | | 367,079 | |

| Iberdrola SA | | 30,707 | | 369,561 | |

| NextEra Energy, Inc. | | 13,982 | | 1,089,198 | |

| Pinnacle West Capital Corp. | | 11,301 | | 944,199 | |

| Xcel Energy, Inc. | | 2,281 | | 155,678 | |

| | | 4,204,992 | |

| Electrical Equipment — 0.9% | | | |

| AMETEK, Inc. | | 6,747 | | 938,170 | |

| Eaton Corp. plc | | 2,867 | | 453,129 | |

| Emerson Electric Co. | | 11,762 | | 1,186,668 | |

Generac Holdings, Inc.(2) | | 1,223 | | 512,877 | |

| Hubbell, Inc. | | 3,471 | | 695,797 | |

| Nexans SA | | 1,425 | | 136,392 | |

| nVent Electric plc | | 51,311 | | 1,621,941 | |

Plug Power, Inc.(2) | | 5,358 | | 146,166 | |

| Rockwell Automation, Inc. | | 2,434 | | 748,260 | |

| Schneider Electric SE | | 4,266 | | 714,505 | |

Sensata Technologies Holding plc(2) | | 3,193 | | 187,174 | |

| Ushio, Inc. | | 4,400 | | 78,844 | |

| | | 7,419,923 | |

| Electronic Equipment, Instruments and Components — 0.7% |

| CDW Corp. | | 2,549 | | 467,359 | |

| Cognex Corp. | | 15,422 | | 1,394,303 | |

| Comet Holding AG | | 309 | | 101,180 | |

Fabrinet(2) | | 1,108 | | 104,728 | |

| Hexagon AB, B Shares | | 33,719 | | 558,171 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Jabil, Inc. | | 2,741 | | $ | 163,199 | |

| Keyence Corp. | | 1,000 | | 557,003 | |

Keysight Technologies, Inc.(2) | | 10,408 | | 1,712,636 | |

| National Instruments Corp. | | 2,782 | | 122,714 | |

nLight, Inc.(2) | | 6,145 | | 213,170 | |

Sesa SpA(2) | | 690 | | 122,850 | |

| TE Connectivity Ltd. | | 2,203 | | 324,876 | |

| | | 5,842,189 | |

| Energy Equipment and Services — 0.1% | | | |

| Baker Hughes Co. | | 22,408 | | 475,946 | |

| Schlumberger NV | | 10,963 | | 316,063 | |

| | | 792,009 | |

| Entertainment — 0.4% | | | |

| Activision Blizzard, Inc. | | 2,994 | | 250,358 | |

Live Nation Entertainment, Inc.(2) | | 4,713 | | 371,809 | |

ROBLOX Corp., Class A(2) | | 1,895 | | 145,877 | |

Roku, Inc.(2) | | 2,479 | | 1,061,780 | |

Sea Ltd., ADR(2) | | 1,391 | | 384,138 | |

Walt Disney Co. (The)(2) | | 6,029 | | 1,061,225 | |

Zynga, Inc., Class A(2) | | 58,437 | | 590,214 | |

| | | 3,865,401 | |

| Equity Real Estate Investment Trusts (REITs) — 3.0% | | | |

| American Campus Communities, Inc. | | 5,015 | | 252,305 | |

| Brixmor Property Group, Inc. | | 13,737 | | 316,226 | |

Capital & Counties Properties plc(2) | | 87,955 | | 208,596 | |

| Charter Hall Group | | 28,634 | | 342,172 | |

| Comforia Residential REIT, Inc. | | 58 | | 185,340 | |

| Community Healthcare Trust, Inc. | | 2,326 | | 115,905 | |

| CoreSite Realty Corp. | | 1,680 | | 232,193 | |

| Crown Castle International Corp. | | 924 | | 178,415 | |

| Empire State Realty Trust, Inc., Class A | | 11,433 | | 130,679 | |

| Equinix, Inc. | | 2,013 | | 1,651,485 | |

| Equity Residential | | 8,008 | | 673,713 | |

| Essential Properties Realty Trust, Inc. | | 5,402 | | 160,980 | |

| Essex Property Trust, Inc. | | 3,031 | | 994,471 | |

| Extra Space Storage, Inc. | | 3,791 | | 660,165 | |

| Fibra Uno Administracion SA de CV | | 210,318 | | 228,847 | |

| Global Medical REIT, Inc. | | 7,461 | | 116,093 | |

| Goodman Group | | 45,995 | | 764,996 | |

| Healthcare Trust of America, Inc., Class A | | 21,076 | | 602,563 | |

| Healthpeak Properties, Inc. | | 21,965 | | 812,046 | |

| Ingenia Communities Group | | 46,039 | | 196,511 | |

| Innovative Industrial Properties, Inc. | | 2,857 | | 614,226 | |

| Invincible Investment Corp. | | 437 | | 171,683 | |

| Invitation Homes, Inc. | | 25,511 | | 1,037,788 | |

| Iron Mountain, Inc. | | 7,054 | | 308,683 | |

| Japan Hotel REIT Investment Corp. | | 131 | | 79,885 | |

| Kilroy Realty Corp. | | 4,079 | | 282,552 | |

| Kimco Realty Corp. | | 20,503 | | 437,329 | |

Klepierre SA(2) | | 10,337 | | 250,279 | |

| LaSalle Logiport REIT | | 135 | | 247,266 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Life Storage, Inc. | | 4,783 | | $ | 561,333 | |

| Link REIT | | 37,700 | | 360,274 | |

| Mapletree Commercial Trust | | 133,200 | | 212,063 | |

| Mapletree Logistics Trust | | 111,700 | | 173,913 | |

| MGM Growth Properties LLC, Class A | | 20,107 | | 760,045 | |

| Mitsubishi Estate Logistics REIT Investment Corp. | | 38 | | 175,192 | |

| NETSTREIT Corp. | | 6,500 | | 168,675 | |

| Orix JREIT, Inc. | | 99 | | 188,900 | |

| Prologis, Inc. | | 24,753 | | 3,169,374 | |

| Realty Income Corp. | | 7,632 | | 536,453 | |

| Rexford Industrial Realty, Inc. | | 6,999 | | 430,579 | |

Ryman Hospitality Properties, Inc.(2) | | 2,367 | | 181,549 | |

| SBA Communications Corp. | | 848 | | 289,160 | |

| Segro plc | | 25,305 | | 427,762 | |

Shaftesbury plc(3) | | 25,523 | | 209,215 | |

| Simon Property Group, Inc. | | 5,318 | | 672,833 | |

| SL Green Realty Corp. | | 2,757 | | 205,286 | |

| SOSiLA Logistics REIT, Inc. | | 178 | | 279,341 | |

| Sun Communities, Inc. | | 3,807 | | 746,591 | |

| Tritax Big Box REIT plc | | 45,868 | | 134,190 | |

| UDR, Inc. | | 17,479 | | 961,170 | |

| Urban Edge Properties | | 13,885 | | 263,815 | |

| Ventas, Inc. | | 5,890 | | 352,104 | |

| VICI Properties, Inc. | | 11,122 | | 346,895 | |

| Welltower, Inc. | | 9,347 | | 811,880 | |

| Weyerhaeuser Co. | | 5,108 | | 172,293 | |

| Workspace Group plc | | 21,651 | | 259,333 | |

Xenia Hotels & Resorts, Inc.(2) | | 15,352 | | 271,423 | |

| | | 25,575,033 | |

| Food and Staples Retailing — 0.3% | | | |

| Costco Wholesale Corp. | | 772 | | 331,744 | |

| Koninklijke Ahold Delhaize NV | | 35,076 | | 1,090,332 | |

MARR SpA(2) | | 4,081 | | 94,713 | |

| Matsumotokiyoshi Holdings Co. Ltd. | | 2,600 | | 115,523 | |

| Sysco Corp. | | 11,726 | | 870,069 | |

Zur Rose Group AG(2) | | 1,028 | | 382,249 | |

| | | 2,884,630 | |

| Food Products — 0.4% | | | |

| Bakkafrost P/F | | 1,975 | | 167,840 | |

Beyond Meat, Inc.(2) | | 149 | | 18,282 | |

| Conagra Brands, Inc. | | 31,271 | | 1,047,266 | |

| General Mills, Inc. | | 6,077 | | 357,692 | |

| Glanbia plc | | 7,010 | | 120,342 | |

| J.M. Smucker Co. (The) | | 3,735 | | 489,696 | |

| Kellogg Co. | | 5,982 | | 379,019 | |

| Mondelez International, Inc., Class A | | 7,167 | | 453,384 | |

| Orkla ASA | | 45,122 | | 409,816 | |

Vital Farms, Inc.(2) | | 1,987 | | 34,594 | |

Whole Earth Brands, Inc.(2) | | 9,817 | | 126,247 | |

| | | 3,604,178 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Gas Utilities — 0.1% | | | |

| Atmos Energy Corp. | | 4,770 | | $ | 470,274 | |

| Nippon Gas Co. Ltd. | | 8,800 | | 138,996 | |

| Spire, Inc. | | 6,191 | | 439,252 | |

| | | 1,048,522 | |

| Health Care Equipment and Supplies — 1.2% | | | |

Align Technology, Inc.(2) | | 995 | | 692,321 | |

| Arjo AB, B Shares | | 4,395 | | 55,517 | |

| Baxter International, Inc. | | 4,159 | | 321,699 | |

| Becton Dickinson and Co. | | 2,552 | | 652,674 | |

DexCom, Inc.(2) | | 1,882 | | 970,190 | |

Eargo, Inc.(2)(3) | | 3,304 | | 118,944 | |

Edwards Lifesciences Corp.(2) | | 5,427 | | 609,289 | |

| Elekta AB, B Shares | | 3,911 | | 57,083 | |

Envista Holdings Corp.(2) | | 6,733 | | 290,058 | |

IDEXX Laboratories, Inc.(2) | | 1,879 | | 1,274,958 | |

Inmode Ltd.(2) | | 1,328 | | 150,954 | |

| Koninklijke Philips NV | | 8,711 | | 401,054 | |

| Medtronic plc | | 4,104 | | 538,896 | |

NeuroPace, Inc.(2) | | 4,658 | | 99,215 | |

| Olympus Corp. | | 15,200 | | 312,806 | |

Ortho Clinical Diagnostics Holdings plc(2) | | 9,001 | | 202,252 | |

OrthoPediatrics Corp.(2) | | 1,532 | | 96,271 | |

| ResMed, Inc. | | 485 | | 131,823 | |

Silk Road Medical, Inc.(2) | | 2,974 | | 149,235 | |

Tandem Diabetes Care, Inc.(2) | | 2,525 | | 274,392 | |

| Teleflex, Inc. | | 1,622 | | 644,631 | |

| Zimmer Biomet Holdings, Inc. | | 11,366 | | 1,857,432 | |

| | | 9,901,694 | |

| Health Care Providers and Services — 1.3% | | | |

| Alfresa Holdings Corp. | | 18,000 | | 274,138 | |

Amedisys, Inc.(2) | | 2,417 | | 629,919 | |

| Amvis Holdings, Inc. | | 800 | | 44,151 | |

ATI Physical Therapy, Inc.(2)(3) | | 13,508 | | 46,062 | |

Cano Health, Inc.(2) | | 6,561 | | 70,531 | |

| Cardinal Health, Inc. | | 16,178 | | 960,650 | |

Centene Corp.(2) | | 6,364 | | 436,634 | |

| Chartwell Retirement Residences | | 20,012 | | 210,290 | |

| Cigna Corp. | | 3,123 | | 716,697 | |

Covetrus, Inc.(2) | | 930 | | 23,678 | |

| CVS Health Corp. | | 6,385 | | 525,869 | |

| Encompass Health Corp. | | 11,858 | | 987,178 | |

| Ensign Group, Inc. (The) | | 1,487 | | 126,499 | |

HealthEquity, Inc.(2) | | 3,404 | | 251,828 | |

Henry Schein, Inc.(2) | | 11,680 | | 936,152 | |

| Humana, Inc. | | 626 | | 266,588 | |

| McKesson Corp. | | 3,552 | | 724,004 | |

Option Care Health, Inc.(2) | | 8,066 | | 167,128 | |

| Quest Diagnostics, Inc. | | 8,187 | | 1,160,917 | |

R1 RCM, Inc.(2) | | 22,806 | | 488,276 | |

RadNet, Inc.(2) | | 5,087 | | 186,896 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| UnitedHealth Group, Inc. | | 2,018 | | $ | 831,860 | |

| Universal Health Services, Inc., Class B | | 6,927 | | 1,111,160 | |

| | | 11,177,105 | |

| Health Care Technology — 0.3% | | | |

| Cerner Corp. | | 14,173 | | 1,139,368 | |

Health Catalyst, Inc.(2) | | 4,176 | | 242,459 | |

OptimizeRx Corp.(2) | | 1,868 | | 103,244 | |

Veeva Systems, Inc., Class A(2) | | 3,551 | | 1,181,453 | |

| | | 2,666,524 | |

| Hotels, Restaurants and Leisure — 0.7% | | | |

Autogrill SpA(2)(3) | | 14,626 | | 102,617 | |

Basic-Fit NV(2)(3) | | 2,077 | | 96,002 | |

Booking Holdings, Inc.(2) | | 174 | | 379,017 | |

Brinker International, Inc.(2) | | 2,144 | | 116,505 | |

Chipotle Mexican Grill, Inc.(2) | | 673 | | 1,254,095 | |

| Churchill Downs, Inc. | | 985 | | 183,013 | |

Corporate Travel Management Ltd.(2) | | 4,670 | | 74,552 | |

| Cracker Barrel Old Country Store, Inc. | | 1,335 | | 181,800 | |

Expedia Group, Inc.(2) | | 2,879 | | 463,145 | |

| Food & Life Cos. Ltd. | | 3,600 | | 146,681 | |

Greggs plc(2) | | 3,929 | | 150,551 | |

Hilton Worldwide Holdings, Inc.(2) | | 5,077 | | 667,372 | |

Las Vegas Sands Corp.(2) | | 12,812 | | 542,588 | |

Planet Fitness, Inc., Class A(2) | | 1,930 | | 145,194 | |

SeaWorld Entertainment, Inc.(2) | | 1,683 | | 79,791 | |

Sodexo SA(2) | | 6,576 | | 560,311 | |

| Travel + Leisure Co. | | 604 | | 31,287 | |

Whitbread plc(2) | | 9,629 | | 406,977 | |

| Wingstop, Inc. | | 1,048 | | 179,533 | |

| Wyndham Hotels & Resorts, Inc. | | 2,932 | | 211,280 | |

| | | 5,972,311 | |

| Household Durables — 0.2% | | | |

| Haseko Corp. | | 12,700 | | 171,860 | |

| Man Wah Holdings Ltd. | | 29,200 | | 58,590 | |

| Open House Co. Ltd. | | 11,000 | | 556,157 | |

Sonos, Inc.(2) | | 5,515 | | 184,091 | |

| Taylor Wimpey plc | | 178,294 | | 407,628 | |

| Token Corp. | | 1,000 | | 90,275 | |

| | | 1,468,601 | |

| Household Products — 0.2% | | | |

| Colgate-Palmolive Co. | | 3,468 | | 275,706 | |

| Kimberly-Clark Corp. | | 3,914 | | 531,208 | |

| Procter & Gamble Co. (The) | | 4,698 | | 668,196 | |

| Reynolds Consumer Products, Inc. | | 2,233 | | 63,529 | |

| | | 1,538,639 | |

| Industrial Conglomerates — 0.1% | | | |

| Honeywell International, Inc. | | 3,561 | | 832,526 | |

| Lifco AB, B Shares | | 4,445 | | 130,372 | |

| | | 962,898 | |

| Insurance — 0.8% | | | |

| Aegon NV | | 50,910 | | 216,754 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Aflac, Inc. | | 20,779 | | $ | 1,142,845 | |

| AIA Group Ltd. | | 28,200 | | 337,435 | |

| Allstate Corp. (The) | | 3,948 | | 513,438 | |

| Arthur J. Gallagher & Co. | | 1,651 | | 230,001 | |

| Chubb Ltd. | | 7,487 | | 1,263,356 | |

| Goosehead Insurance, Inc., Class A | | 1,037 | | 124,637 | |

| Hartford Financial Services Group, Inc. (The) | | 4,538 | | 288,708 | |

| Kinsale Capital Group, Inc. | | 1,012 | | 180,789 | |

| Marsh & McLennan Cos., Inc. | | 2,006 | | 295,323 | |

Palomar Holdings, Inc.(2) | | 1,572 | | 128,008 | |

| Prudential Financial, Inc. | | 2,705 | | 271,257 | |

| Reinsurance Group of America, Inc. | | 8,167 | | 899,840 | |

Ryan Specialty Group Holdings, Inc., Class A(2) | | 3,568 | | 105,256 | |

SelectQuote, Inc.(2) | | 19,235 | | 342,383 | |

| Storebrand ASA | | 10,861 | | 93,253 | |

| Travelers Cos., Inc. (The) | | 2,371 | | 353,089 | |

| | | 6,786,372 | |

| Interactive Media and Services — 0.8% | | | |

Alphabet, Inc., Class A(2) | | 1,109 | | 2,988,234 | |

Baidu, Inc., Class A(2) | | 20,600 | | 422,094 | |

| carsales.com Ltd. | | 5,308 | | 85,592 | |

Eventbrite, Inc., Class A(2) | | 6,512 | | 115,718 | |

Facebook, Inc., Class A(2) | | 2,574 | | 917,116 | |

fuboTV, Inc.(2)(3) | | 3,341 | | 87,000 | |

Match Group, Inc.(2) | | 5,968 | | 950,523 | |

Pinterest, Inc., Class A(2) | | 11,262 | | 663,332 | |

QuinStreet, Inc.(2) | | 12,542 | | 230,020 | |

| Tencent Holdings Ltd. | | 8,800 | | 530,712 | |

| | | 6,990,341 | |

| Internet and Direct Marketing Retail — 0.5% | | | |

Alibaba Group Holding Ltd.(2) | | 16,700 | | 407,860 | |

Amazon.com, Inc.(2) | | 716 | | 2,382,554 | |

| ASKUL Corp. | | 3,700 | | 55,852 | |

ASOS plc(2) | | 5,689 | | 300,817 | |

BHG Group AB(2) | | 1,808 | | 27,887 | |

Chewy, Inc., Class A(2)(3) | | 5,913 | | 494,918 | |

Etsy, Inc.(2) | | 3,296 | | 604,849 | |

Revolve Group, Inc.(2) | | 1,807 | | 125,785 | |

| | | 4,400,522 | |

| IT Services — 1.2% | | | |

| Accenture plc, Class A | | 2,264 | | 719,228 | |

Adyen NV(2) | | 250 | | 677,512 | |

| Alten SA | | 815 | | 129,557 | |

| Amdocs Ltd. | | 4,303 | | 331,804 | |

| Atos SE | | 3,526 | | 168,623 | |

| Capgemini SE | | 3,450 | | 745,727 | |

Capita plc(2) | | 138,282 | | 67,745 | |

DigitalOcean Holdings, Inc.(2) | | 2,569 | | 132,304 | |

| Edenred | | 6,614 | | 384,247 | |

Endava plc, ADR(2) | | 1,165 | | 149,842 | |

EPAM Systems, Inc.(2) | | 1,457 | | 815,629 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

Euronet Worldwide, Inc.(2) | | 2,031 | | $ | 290,067 | |

GDS Holdings Ltd., Class A(2) | | 10,900 | | 80,819 | |

I3 Verticals, Inc., Class A(2) | | 6,320 | | 201,734 | |

Indra Sistemas SA(2) | | 17,105 | | 179,063 | |

| Mastercard, Inc., Class A | | 2,252 | | 869,137 | |

| MAXIMUS, Inc. | | 2,932 | | 260,948 | |

Nuvei Corp.(2) | | 1,381 | | 113,242 | |

Okta, Inc.(2) | | 3,608 | | 894,026 | |

PayPal Holdings, Inc.(2) | | 3,531 | | 972,896 | |

Perficient, Inc.(2) | | 1,991 | | 187,731 | |

Repay Holdings Corp.(2) | | 4,118 | | 102,579 | |

Square, Inc., Class A(2) | | 2,527 | | 624,826 | |

Twilio, Inc., Class A(2) | | 1,900 | | 709,821 | |

| Visa, Inc., Class A | | 3,717 | | 915,832 | |

| | | 10,724,939 | |

| Leisure Products — 0.2% | | | |

Accell Group NV(2) | | 1,745 | | 86,417 | |

| BRP, Inc. | | 1,439 | | 120,566 | |

| Brunswick Corp. | | 2,021 | | 210,992 | |

Callaway Golf Co.(2) | | 5,794 | | 183,554 | |

Hayward Holdings, Inc.(2) | | 9,228 | | 222,303 | |

Peloton Interactive, Inc., Class A(2) | | 2,433 | | 287,216 | |

| Polaris, Inc. | | 2,673 | | 350,350 | |

| | | 1,461,398 | |

| Life Sciences Tools and Services — 0.7% | | | |

10X Genomics, Inc., Class A(2) | | 2,678 | | 490,690 | |

| Agilent Technologies, Inc. | | 4,383 | | 671,607 | |

Akoya Biosciences, Inc.(2)(3) | | 2,738 | | 47,477 | |

| Bio-Techne Corp. | | 1,534 | | 739,756 | |

ICON plc(2) | | 1,171 | | 284,869 | |

| Lonza Group AG | | 749 | | 583,190 | |

Mettler-Toledo International, Inc.(2) | | 743 | | 1,094,967 | |

NeoGenomics, Inc.(2) | | 3,895 | | 179,560 | |

Repligen Corp.(2) | | 2,047 | | 502,948 | |

| Thermo Fisher Scientific, Inc. | | 1,137 | | 613,991 | |

Wuxi Biologics Cayman, Inc.(2) | | 30,000 | | 458,227 | |

| | | 5,667,282 | |

| Machinery — 0.8% | | | |

| ANDRITZ AG | | 2,308 | | 127,067 | |

| Astec Industries, Inc. | | 1,873 | | 114,834 | |

| Crane Co. | | 3,923 | | 381,433 | |

| Cummins, Inc. | | 3,356 | | 778,928 | |

Evoqua Water Technologies Corp.(2) | | 5,400 | | 178,254 | |

| FANUC Corp. | | 1,300 | | 291,158 | |

| Graco, Inc. | | 6,496 | | 507,208 | |

IHI Corp.(2) | | 5,700 | | 131,841 | |

| IMI plc | | 8,021 | | 196,233 | |

| Japan Steel Works Ltd. (The) | | 3,000 | | 73,799 | |

Kornit Digital Ltd.(2) | | 1,027 | | 135,728 | |

| Metso Outotec Oyj | | 14,932 | | 169,540 | |

| Oshkosh Corp. | | 4,315 | | 515,858 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| PACCAR, Inc. | | 4,914 | | $ | 407,813 | |

| Parker-Hannifin Corp. | | 5,465 | | 1,705,244 | |

| Rexnord Corp. | | 10,325 | | 581,607 | |

| Techtronic Industries Co. Ltd. | | 31,000 | | 552,801 | |

| Timken Co. (The) | | 2,079 | | 165,280 | |

| Trelleborg AB, B Shares | | 2,718 | | 67,188 | |

| Tsubaki Nakashima Co. Ltd. | | 7,100 | | 107,029 | |

| | | 7,188,843 | |

| Media — 0.3% | | | |

Atresmedia Corp. de Medios de Comunicacion SA(2) | | 16,736 | | 69,190 | |

| Comcast Corp., Class A | | 6,626 | | 389,808 | |

Criteo SA, ADR(2) | | 1,551 | | 60,163 | |

| Fox Corp., Class B | | 23,631 | | 785,494 | |

| Future plc | | 3,638 | | 174,282 | |

Nordic Entertainment Group AB, B Shares(2) | | 1,865 | | 99,593 | |

| ProSiebenSat.1 Media SE | | 2,933 | | 55,724 | |

| Publicis Groupe SA | | 8,165 | | 515,462 | |

Storytel AB(2) | | 1,043 | | 27,007 | |

| WPP plc | | 49,186 | | 636,124 | |

| | | 2,812,847 | |

| Metals and Mining — 0.1% | | | |

| Alamos Gold, Inc. (New York), Class A | | 7,450 | | 60,494 | |

| APERAM SA | | 2,161 | | 135,432 | |

| Mineral Resources Ltd. | | 2,112 | | 97,721 | |

| MMC Norilsk Nickel PJSC | | 1,515 | | 523,638 | |

| Nickel Mines Ltd. | | 31,311 | | 25,264 | |

| OZ Minerals Ltd. | | 4,454 | | 75,512 | |

| Teck Resources Ltd., Class B | | 13,017 | | 297,308 | |

| | | 1,215,369 | |

| Multi-Utilities — 0.1% | | | |

| NorthWestern Corp. | | 13,685 | | 848,333 | |

| Multiline Retail — 0.2% | | | |

Dollar Tree, Inc.(2) | | 7,882 | | 786,545 | |

| Isetan Mitsukoshi Holdings Ltd. | | 16,000 | | 108,344 | |

| Magazine Luiza SA | | 75,876 | | 300,110 | |

Marks & Spencer Group plc(2) | | 38,322 | | 72,142 | |

| Target Corp. | | 1,384 | | 361,293 | |

| | | 1,628,434 | |

| Oil, Gas and Consumable Fuels — 0.6% | | | |

| Cimarex Energy Co. | | 3,749 | | 244,435 | |

| ConocoPhillips | | 27,895 | | 1,563,794 | |

| Devon Energy Corp. | | 17,152 | | 443,208 | |

| Eni SpA | | 17,985 | | 212,684 | |

| Matador Resources Co. | | 4,956 | | 153,140 | |

| Neste Oyj | | 7,363 | | 452,609 | |

| Pioneer Natural Resources Co. | | 2,550 | | 370,693 | |

| Surgutneftegas PJSC, Preference Shares | | 912,892 | | 476,530 | |

| TotalEnergies SE | | 12,519 | | 545,912 | |

Whitecap Resources, Inc.(3) | | 58,475 | | 267,628 | |

| | | 4,730,633 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Paper and Forest Products — 0.1% | | | |

| Mondi plc | | 32,128 | | $ | 890,709 | |

| Personal Products — 0.1% | | | |

| Estee Lauder Cos., Inc. (The), Class A | | 921 | | 307,457 | |

| Shiseido Co. Ltd. | | 7,900 | | 528,002 | |

| | | 835,459 | |

| Pharmaceuticals — 0.8% | | | |

ALK-Abello A/S(2) | | 291 | | 143,465 | |

Arvinas, Inc.(2) | | 1,038 | | 104,942 | |

| AstraZeneca plc | | 2,325 | | 267,165 | |

| AstraZeneca plc, ADR | | 12,963 | | 742,002 | |

Axsome Therapeutics, Inc.(2) | | 1,155 | | 56,121 | |

| Bristol-Myers Squibb Co. | | 9,291 | | 630,580 | |

| Dermapharm Holding SE | | 1,215 | | 97,192 | |

Edgewise Therapeutics, Inc.(2)(3) | | 2,587 | | 45,298 | |

| GlaxoSmithKline plc | | 52,740 | | 1,041,290 | |

Harmony Biosciences Holdings, Inc.(2) | | 1,654 | | 43,269 | |

| Laboratorios Farmaceuticos Rovi SA | | 1,039 | | 73,342 | |

| Merck & Co., Inc. | | 7,172 | | 551,312 | |

| Novartis AG | | 4,083 | | 377,589 | |

| Novo Nordisk A/S, B Shares | | 9,169 | | 848,786 | |

Reata Pharmaceuticals, Inc., Class A(2) | | 583 | | 73,056 | |

| Sanofi | | 2,088 | | 215,217 | |

| Sanofi, ADR | | 12,651 | | 652,286 | |

| Takeda Pharmaceutical Co. Ltd. | | 15,600 | | 519,270 | |

| Zoetis, Inc. | | 2,786 | | 564,722 | |

| | | 7,046,904 | |

| Professional Services — 0.5% | | | |

ASGN, Inc.(2) | | 1,292 | | 130,660 | |

| Bureau Veritas SA | | 11,044 | | 364,714 | |

CoStar Group, Inc.(2) | | 6,000 | | 533,100 | |

| DKSH Holding AG | | 1,277 | | 107,953 | |

| en Japan, Inc. | | 2,500 | | 87,302 | |

First Advantage Corp.(2) | | 8,415 | | 165,018 | |

| IHS Markit Ltd. | | 1,546 | | 180,635 | |

| IR Japan Holdings Ltd. | | 500 | | 61,873 | |

| Jacobs Engineering Group, Inc. | | 5,985 | | 809,471 | |

| Outsourcing, Inc. | | 3,600 | | 68,907 | |

| Recruit Holdings Co. Ltd. | | 12,300 | | 637,517 | |

| Teleperformance | | 1,173 | | 494,767 | |

| TransUnion | | 3,260 | | 391,395 | |

| Verisk Analytics, Inc. | | 2,620 | | 497,643 | |

| | | 4,530,955 | |

| Real Estate Management and Development — 0.3% | | | |

Altus Group Ltd.(3) | | 1,978 | | 93,097 | |

| CapitaLand Ltd. | | 56,200 | | 166,968 | |

| Colliers International Group, Inc. | | 738 | | 94,899 | |

| Colliers International Group, Inc. (Toronto) | | 1,158 | | 148,583 | |

CTP NV(2) | | 9,863 | | 198,812 | |

ESR Cayman Ltd.(2) | | 41,000 | | 144,108 | |

Fastighets AB Balder, B Shares(2) | | 1,400 | | 96,612 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| FirstService Corp. | | 485 | | $ | 90,337 | |

| Newmark Group, Inc., Class A | | 6,083 | | 78,349 | |

| Relo Group, Inc. | | 2,500 | | 55,172 | |

Samhallsbyggnadsbolaget i Norden AB(3) | | 22,962 | | 115,038 | |

| Savills plc | | 5,153 | | 82,300 | |

| Tokyu Fudosan Holdings Corp. | | 43,800 | | 247,266 | |

| Tricon Residential, Inc. | | 38,850 | | 465,540 | |

| VGP NV | | 561 | | 115,495 | |

| | | 2,192,576 | |

| Road and Rail — 0.2% | | | |

| Heartland Express, Inc. | | 22,861 | | 389,323 | |

Nagoya Railroad Co. Ltd.(2) | | 2,600 | | 43,783 | |

| Norfolk Southern Corp. | | 1,663 | | 428,771 | |

| TFI International, Inc. | | 1,191 | | 133,324 | |

| Union Pacific Corp. | | 1,561 | | 341,485 | |

| | | 1,336,686 | |

| Semiconductors and Semiconductor Equipment — 1.1% | | | |

Advanced Micro Devices, Inc.(2) | | 3,312 | | 351,701 | |

Allegro MicroSystems, Inc.(2) | | 2,455 | | 67,292 | |

| Applied Materials, Inc. | | 3,937 | | 550,904 | |

| ASM International NV | | 163 | | 57,850 | |

| ASML Holding NV | | 1,000 | | 764,384 | |

| BE Semiconductor Industries NV | | 1,551 | | 136,114 | |

Enphase Energy, Inc.(2) | | 5,298 | | 1,004,501 | |

Ichor Holdings Ltd.(2) | | 1,967 | | 101,438 | |

| Infineon Technologies AG | | 11,861 | | 453,258 | |

MACOM Technology Solutions Holdings, Inc.(2) | | 3,659 | | 225,833 | |

| Marvell Technology, Inc. | | 14,848 | | 898,453 | |

Nova Ltd.(2) | | 1,589 | | 155,404 | |

| NVIDIA Corp. | | 6,112 | | 1,191,779 | |

Onto Innovation, Inc.(2) | | 2,900 | | 203,232 | |

| Optorun Co. Ltd. | | 800 | | 16,121 | |

| Power Integrations, Inc. | | 910 | | 88,261 | |

Semtech Corp.(2) | | 3,525 | | 218,233 | |

| Skyworks Solutions, Inc. | | 5,591 | | 1,031,595 | |

SOITEC(2) | | 506 | | 121,312 | |

| Taiwan Semiconductor Manufacturing Co. Ltd. | | 38,000 | | 794,181 | |

| Teradyne, Inc. | | 4,261 | | 541,147 | |

| Texas Instruments, Inc. | | 3,406 | | 649,252 | |

| | | 9,622,245 | |

| Software — 2.4% | | | |

Adobe, Inc.(2) | | 1,005 | | 624,738 | |

Atlassian Corp. plc, Class A(2) | | 3,209 | | 1,043,310 | |

Autodesk, Inc.(2) | | 3,157 | | 1,013,808 | |

Cadence Design Systems, Inc.(2) | | 11,475 | | 1,694,284 | |

| CDK Global, Inc. | | 8,061 | | 386,847 | |

Cloudflare, Inc., Class A(2) | | 3,248 | | 385,310 | |

Coupa Software, Inc.(2) | | 1,546 | | 335,482 | |

| Dassault Systemes SE | | 8,440 | | 465,569 | |

Descartes Systems Group, Inc. (The)(2) | | 1,626 | | 117,936 | |

DocuSign, Inc.(2) | | 5,453 | | 1,625,212 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

Everbridge, Inc.(2) | | 691 | | $ | 97,583 | |

Five9, Inc.(2) | | 1,036 | | 208,537 | |

HubSpot, Inc.(2) | | 2,398 | | 1,429,256 | |

Lightspeed POS, Inc.(2) | | 1,106 | | 94,705 | |

| m-up Holdings, Inc. | | 1,800 | | 54,187 | |

Manhattan Associates, Inc.(2) | | 9,956 | | 1,589,276 | |

| Microsoft Corp. | | 17,197 | | 4,899,597 | |

Model N, Inc.(2) | | 4,265 | | 138,058 | |

nCino, Inc.(2) | | 2,346 | | 149,135 | |

| Open Text Corp. | | 9,847 | | 511,158 | |

Palo Alto Networks, Inc.(2) | | 3,808 | | 1,519,582 | |

Paycor HCM, Inc.(2) | | 3,464 | | 95,260 | |

Paylocity Holding Corp.(2) | | 1,039 | | 215,551 | |

RingCentral, Inc., Class A(2) | | 2,240 | | 598,685 | |

SailPoint Technologies Holdings, Inc.(2) | | 4,347 | | 217,307 | |

salesforce.com, Inc.(2) | | 1,629 | | 394,104 | |

Sprinklr, Inc., Class A(2) | | 5,262 | | 101,767 | |

Sprout Social, Inc., Class A(2) | | 3,862 | | 343,100 | |

Workday, Inc., Class A(2) | | 615 | | 144,156 | |

| | | 20,493,500 | |

| Specialty Retail — 0.9% | | | |

| Advance Auto Parts, Inc. | | 5,377 | | 1,140,247 | |

American Eagle Outfitters, Inc.(3) | | 6,747 | | 232,569 | |

Arko Corp.(2) | | 11,987 | | 99,492 | |

Burlington Stores, Inc.(2) | | 3,486 | | 1,167,113 | |

Carvana Co.(2) | | 1,799 | | 607,270 | |

Five Below, Inc.(2) | | 2,536 | | 493,049 | |

Floor & Decor Holdings, Inc., Class A(2) | | 5,633 | | 687,282 | |

| Home Depot, Inc. (The) | | 4,332 | | 1,421,719 | |

Leslie's, Inc.(2) | | 9,637 | | 234,661 | |

| Lithia Motors, Inc. | | 294 | | 110,903 | |

Musti Group Oyj(2) | | 3,117 | | 128,659 | |

National Vision Holdings, Inc.(2) | | 3,511 | | 189,524 | |

| Nextage Co. Ltd. | | 6,400 | | 131,632 | |

| Pets at Home Group plc | | 20,309 | | 131,944 | |

| TJX Cos., Inc. (The) | | 6,250 | | 430,062 | |

| Tractor Supply Co. | | 997 | | 180,387 | |

Watches of Switzerland Group plc(2) | | 10,904 | | 152,505 | |

WH Smith plc(2) | | 2,419 | | 54,558 | |

| | | 7,593,576 | |

| Technology Hardware, Storage and Peripherals — 0.4% | | | |

| Apple, Inc. | | 16,837 | | 2,455,845 | |

| HP, Inc. | | 23,246 | | 671,112 | |

| | | 3,126,957 | |

| Textiles, Apparel and Luxury Goods — 0.5% | | | |

| ANTA Sports Products Ltd. | | 23,000 | | 500,741 | |

| Asics Corp. | | 4,700 | | 103,798 | |

Capri Holdings Ltd.(2) | | 2,633 | | 148,264 | |

Crocs, Inc.(2) | | 2,171 | | 294,844 | |

Dr. Martens plc(2) | | 14,150 | | 85,270 | |

lululemon athletica, Inc.(2) | | 2,606 | | 1,042,843 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| LVMH Moet Hennessy Louis Vuitton SE | | 801 | | $ | 641,334 | |

| NIKE, Inc., Class B | | 5,334 | | 893,498 | |

| Pandora A/S | | 1,302 | | 168,423 | |

| Puma SE | | 4,090 | | 501,718 | |

| VF Corp. | | 3,577 | | 286,875 | |

| | | 4,667,608 | |

Thrifts and Mortgage Finance† | | | |

| Capitol Federal Financial, Inc. | | 15,982 | | 177,240 | |

NMI Holdings, Inc., Class A(2) | | 3,556 | | 78,303 | |

| | | 255,543 | |

| Trading Companies and Distributors — 0.4% | | | |

| AddTech AB, B Shares | | 3,676 | | 76,489 | |

| Ashtead Group plc | | 6,291 | | 470,752 | |

Beacon Roofing Supply, Inc.(2) | | 3,446 | | 184,292 | |

| Diploma plc | | 3,516 | | 144,435 | |

| Electrocomponents plc | | 10,769 | | 152,142 | |

| Finning International, Inc. | | 7,839 | | 202,698 | |

| Grafton Group plc | | 10,988 | | 196,032 | |

| Howden Joinery Group plc | | 13,645 | | 170,038 | |

| MSC Industrial Direct Co., Inc., Class A | | 9,736 | | 868,159 | |

NOW, Inc.(2) | | 5,943 | | 58,657 | |

Seven Group Holdings Ltd.(3) | | 3,801 | | 65,190 | |

| W.W. Grainger, Inc. | | 1,583 | | 703,770 | |

| Yamazen Corp. | | 6,100 | | 57,566 | |

| | | 3,350,220 | |

TOTAL COMMON STOCKS (Cost $182,720,732) |

| | 273,733,142 | |

| U.S. TREASURY SECURITIES — 5.2% |

|

|

|

U.S. Treasury Bills, 0.05%, 9/30/21(4) | | $ | 450,000 | | 449,969 | |

| U.S. Treasury Bonds, 3.00%, 5/15/42 | | 250,000 | | 301,709 | |

| U.S. Treasury Bonds, 3.75%, 11/15/43 | | 40,000 | | 54,102 | |

U.S. Treasury Bonds, 3.125%, 8/15/44(5) | | 1,350,000 | | 1,671,996 | |

| U.S. Treasury Bonds, 3.00%, 5/15/45 | | 100,000 | | 121,840 | |

| U.S. Treasury Bonds, 3.00%, 11/15/45 | | 50,000 | | 61,101 | |

U.S. Treasury Cash Management Bills, 0.04%, 9/16/21(4) | | 440,000 | | 439,979 | |

U.S. Treasury Inflation Indexed Bonds, 2.375%, 1/15/25(5) | | 2,642,799 | | 3,091,572 | |

| U.S. Treasury Inflation Indexed Bonds, 2.00%, 1/15/26 | | 1,560,217 | | 1,859,416 | |

| U.S. Treasury Inflation Indexed Bonds, 2.375%, 1/15/27 | | 267,054 | | 332,990 | |

| U.S. Treasury Inflation Indexed Bonds, 2.50%, 1/15/29 | | 2,696,530 | | 3,558,784 | |

| U.S. Treasury Inflation Indexed Bonds, 2.125%, 2/15/40 | | 448,502 | | 688,420 | |

| U.S. Treasury Inflation Indexed Bonds, 0.75%, 2/15/42 | | 786,515 | | 990,054 | |

| U.S. Treasury Inflation Indexed Bonds, 0.625%, 2/15/43 | | 363,078 | | 448,750 | |

| U.S. Treasury Inflation Indexed Bonds, 1.375%, 2/15/44 | | 1,328,710 | | 1,893,637 | |

| U.S. Treasury Inflation Indexed Bonds, 0.75%, 2/15/45 | | 1,395,082 | | 1,782,968 | |

| U.S. Treasury Inflation Indexed Bonds, 0.875%, 2/15/47 | | 446,204 | | 596,562 | |

| U.S. Treasury Inflation Indexed Bonds, 0.125%, 2/15/51 | | 568,854 | | 654,688 | |

| U.S. Treasury Inflation Indexed Notes, 0.625%, 1/15/24 | | 4,327,688 | | 4,678,185 | |

| U.S. Treasury Inflation Indexed Notes, 0.50%, 4/15/24 | | 3,203,010 | | 3,469,266 | |

| U.S. Treasury Inflation Indexed Notes, 0.125%, 4/15/25 | | 1,928,607 | | 2,103,494 | |

| U.S. Treasury Inflation Indexed Notes, 0.625%, 1/15/26 | | 1,359,912 | | 1,531,839 | |

| U.S. Treasury Inflation Indexed Notes, 0.125%, 4/15/26 | | 3,080,370 | | 3,400,306 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| U.S. Treasury Inflation Indexed Notes, 0.125%, 7/15/26 | | $ | 3,875,661 | | $ | 4,317,915 | |

| U.S. Treasury Inflation Indexed Notes, 0.875%, 1/15/29 | | 373,251 | | 443,739 | |

| U.S. Treasury Inflation Indexed Notes, 0.125%, 1/15/31 | | 3,103,260 | | 3,515,788 | |

U.S. Treasury Notes, 2.00%, 12/31/21(5) | | 200,000 | | 201,598 | |

U.S. Treasury Notes, 2.25%, 8/15/27(5) | | 200,000 | | 216,469 | |

| U.S. Treasury Notes, 0.625%, 5/15/30 | | 1,700,000 | | 1,622,836 | |

TOTAL U.S. TREASURY SECURITIES (Cost $39,660,436) |

| | 44,499,972 | |

| CORPORATE BONDS — 3.4% |

|

|

|

| Aerospace and Defense — 0.1% | | | |

| Boeing Co. (The), 5.81%, 5/1/50 | | 70,000 | | 95,642 | |

Bombardier, Inc., 6.00%, 10/15/22(6) | | 16,000 | | 16,082 | |

| Howmet Aerospace, Inc., 5.125%, 10/1/24 | | 160,000 | | 176,350 | |

| TransDigm, Inc., 6.375%, 6/15/26 | | 50,000 | | 51,750 | |

TransDigm, Inc., 4.625%, 1/15/29(6) | | 290,000 | | 289,649 | |

| | | 629,473 | |

| Airlines — 0.1% | | | |

American Airlines, Inc. / AAdvantage Loyalty IP Ltd., 5.50%, 4/20/26(6) | | 315,000 | | 329,962 | |

| United Airlines Holdings, Inc., 5.00%, 2/1/24 | | 140,000 | | 145,381 | |

| | | 475,343 | |

Auto Components† | | | |

ZF North America Capital, Inc., 4.75%, 4/29/25(6) | | 110,000 | | 119,567 | |

| Automobiles — 0.1% | | | |

| Ford Motor Credit Co. LLC, 3.625%, 6/17/31 | | 370,000 | | 383,918 | |

| General Motors Co., 5.15%, 4/1/38 | | 240,000 | | 295,138 | |

| | | 679,056 | |

| Banks — 0.4% | | | |

| Akbank T.A.S., 5.00%, 10/24/22 | | 70,000 | | 72,012 | |

Avi Funding Co. Ltd., 3.80%, 9/16/25(6) | | 143,000 | | 157,988 | |

| Banco Santander SA, MTN, 2.50%, 3/18/25 | EUR | 100,000 | | 128,829 | |

Banistmo SA, 4.25%, 7/31/27(6) | | $ | 235,000 | | 241,956 | |

| Bank of America Corp., MTN, 2.30%, 7/25/25 | GBP | 100,000 | | 146,874 | |

| Bank of America Corp., MTN, VRN, 2.68%, 6/19/41 | | $ | 370,000 | | 365,821 | |

| Barclays Bank plc, MTN, 6.625%, 3/30/22 | EUR | 50,000 | | 61,912 | |

| CaixaBank SA, MTN, VRN, 2.75%, 7/14/28 | EUR | 100,000 | | 123,959 | |

| CaixaBank SA, MTN, VRN, 2.25%, 4/17/30 | EUR | 100,000 | | 125,002 | |

| Citigroup, Inc., VRN, 3.52%, 10/27/28 | | $ | 220,000 | | 242,622 | |

| Co-Operative Bank plc (The), 4.75%, 11/11/21 (Secured) | GBP | 100,000 | | 140,476 | |

| Commerzbank AG, MTN, 4.00%, 3/23/26 | EUR | 150,000 | | 202,011 | |

| Credit Agricole SA, MTN, 7.375%, 12/18/23 | GBP | 50,000 | | 79,925 | |

| European Financial Stability Facility, MTN, 2.125%, 2/19/24 | EUR | 93,000 | | 117,958 | |

| European Financial Stability Facility, MTN, 0.40%, 5/31/26 | EUR | 200,000 | | 247,498 | |

| ING Groep NV, MTN, 2.125%, 1/10/26 | EUR | 200,000 | | 260,580 | |

Intercorp Financial Services, Inc., 4.125%, 10/19/27(6) | | $ | 170,000 | | 171,800 | |

| Kreditanstalt fuer Wiederaufbau, 4.625%, 1/4/23 | EUR | 75,000 | | 95,685 | |

| Lloyds Bank plc, MTN, 7.625%, 4/22/25 | GBP | 20,000 | | 34,389 | |

| Wells Fargo & Co., VRN, 3.07%, 4/30/41 | | $ | 365,000 | | 383,311 | |

| | | 3,400,608 | |

Beverages† | | | |

| Anheuser-Busch Cos. LLC / Anheuser-Busch InBev Worldwide, Inc., 4.90%, 2/1/46 | | 130,000 | | 166,976 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

| Biotechnology — 0.1% | | | |

| AbbVie, Inc., 4.55%, 3/15/35 | | $ | 40,000 | | $ | 49,158 | |

| AbbVie, Inc., 4.40%, 11/6/42 | | 280,000 | | 345,619 | |

| Gilead Sciences, Inc., 3.65%, 3/1/26 | | 230,000 | | 255,128 | |

| | | 649,905 | |

| Capital Markets — 0.1% | | | |

| Goldman Sachs Group, Inc. (The), 5.50%, 10/12/21 | GBP | 50,000 | | 70,137 | |

| Goldman Sachs Group, Inc. (The), VRN, 1.43%, 3/9/27 | | $ | 125,000 | | 125,674 | |

LPL Holdings, Inc., 4.375%, 5/15/31(6) | | 424,000 | | 435,141 | |

MDGH - GMTN B.V., 3.25%, 4/28/22(6) | | 57,000 | | 58,249 | |

| | | 689,201 | |

Chemicals† | | | |

| Dow Chemical Co. (The), 3.60%, 11/15/50 | | 170,000 | | 189,693 | |

Equate Petrochemical BV, 4.25%, 11/3/26(6) | | 46,000 | | 51,199 | |

| Olin Corp., 5.125%, 9/15/27 | | 70,000 | | 72,977 | |

| | | 313,869 | |

| Commercial Services and Supplies — 0.1% | | | |

Sodexo, Inc., 2.72%, 4/16/31(6) | | 300,000 | | 311,241 | |

| Waste Management, Inc., 2.50%, 11/15/50 | | 120,000 | | 115,888 | |

| | | 427,129 | |

| Consumer Finance — 0.1% | | | |

| Navient Corp., 4.875%, 3/15/28 | | 420,000 | | 424,211 | |

| Containers and Packaging — 0.1% | | | |

Ardagh Metal Packaging Finance USA LLC / Ardagh Metal Packaging Finance plc, 4.00%, 9/1/29(6) | | 145,000 | | 145,544 | |

| Ball Corp., 5.25%, 7/1/25 | | 35,000 | | 39,518 | |

Mauser Packaging Solutions Holding Co., 5.50%, 4/15/24(6) | | 40,000 | | 40,300 | |

Owens-Brockway Glass Container, Inc., 5.875%, 8/15/23(6) | | 40,000 | | 42,982 | |

Sealed Air Corp., 5.125%, 12/1/24(6) | | 105,000 | | 114,251 | |

| | | 382,595 | |

| Diversified Financial Services — 0.1% | | | |

| Allen C Stonecipher Life Insurance Trust, VRDN, 0.12%, 8/6/21 (LOC: Texas Capital Bank and FHLB) | | 155,000 | | 155,000 | |

| Fiore Capital LLC, VRDN, 0.12%, 8/6/21 (LOC: Wells Fargo Bank N.A.) | | 450,000 | | 450,000 | |

| | | 605,000 | |

| Diversified Telecommunication Services — 0.1% | | | |

Altice France SA, 7.375%, 5/1/26(6) | | 140,000 | | 145,775 | |

AT&T, Inc., 3.55%, 9/15/55(6) | | 68,000 | | 70,404 | |

| Hughes Satellite Systems Corp., 5.25%, 8/1/26 | | 100,000 | | 111,950 | |

Level 3 Financing, Inc., 4.625%, 9/15/27(6) | | 185,000 | | 192,426 | |

| Lumen Technologies, Inc., 5.80%, 3/15/22 | | 45,000 | | 46,233 | |

Ooredoo International Finance Ltd., 3.75%, 6/22/26(6) | | 86,000 | | 95,255 | |

Turk Telekomunikasyon AS, 4.875%, 6/19/24(6) | | 115,000 | | 120,565 | |

| Verizon Communications, Inc., 1.75%, 1/20/31 | | 140,000 | | 136,100 | |

| Verizon Communications, Inc., 2.99%, 10/30/56 | | 200,000 | | 194,891 | |

| | | 1,113,599 | |

| Electric Utilities — 0.1% | | | |

| Duke Energy Carolinas LLC, 3.20%, 8/15/49 | | 140,000 | | 152,284 | |

| Duke Energy Florida LLC, 3.85%, 11/15/42 | | 40,000 | | 47,734 | |

| Duke Energy Progress LLC, 4.15%, 12/1/44 | | 40,000 | | 49,453 | |

| Exelon Corp., 4.45%, 4/15/46 | | 20,000 | | 24,931 | |

| | | | | | | | | | | |

| | Shares/Principal Amount | Value |

Greenko Investment Co., 4.875%, 8/16/23(6) | | $ | 57,000 | | $ | 57,674 | |

Israel Electric Corp. Ltd., 6.875%, 6/21/23(6) | | 57,000 | | 63,493 | |

| MidAmerican Energy Co., 4.40%, 10/15/44 | | 60,000 | | 76,055 | |

| NRG Energy, Inc., 7.25%, 5/15/26 | | 75,000 | | 78,111 | |

| PacifiCorp, 2.90%, 6/15/52 | | 60,000 | | 61,352 | |

| Perusahaan Perseroan (Persero) PT Perusahaan Listrik Negara, MTN, 3.00%, 6/30/30 | | 300,000 | | 301,056 | |

| Southern Co. Gas Capital Corp., 3.95%, 10/1/46 | | 20,000 | | 22,967 | |

| Virginia Electric and Power Co., 2.45%, 12/15/50 | | 70,000 | | 66,248 | |

| | | 1,001,358 | |

| Equity Real Estate Investment Trusts (REITs) — 0.1% | | | |

| EPR Properties, 4.95%, 4/15/28 | | 398,000 | | 430,980 | |

IIP Operating Partnership LP, 5.50%, 5/25/26(6) | | 180,000 | | 188,361 | |

Iron Mountain, Inc., 4.875%, 9/15/29(6) | | 355,000 | | 372,384 | |

| MGM Growth Properties Operating Partnership LP / MGP Finance Co-Issuer, Inc., 5.625%, 5/1/24 | | 90,000 | | 97,530 | |

| | | 1,089,255 | |

Food and Staples Retailing† | | | |

| Kroger Co. (The), 3.875%, 10/15/46 | | 80,000 | | 90,198 | |

Food Products† | | | |

Lamb Weston Holdings, Inc., 4.625%, 11/1/24(6) | | 90,000 | | 92,471 | |

MHP SE, 7.75%, 5/10/24(6) | | 71,000 | | 76,819 | |

Post Holdings, Inc., 4.625%, 4/15/30(6) | | 190,000 | | 193,818 | |

| | | 363,108 | |

Gas Utilities† | | | |

| Perusahaan Gas Negara Tbk PT, 5.125%, 5/16/24 | | 114,000 | | 125,987 | |

| Health Care Providers and Services — 0.2% | | | |

CHS / Community Health Systems, Inc., 8.00%, 12/15/27(6) | | 17,000 | | 18,842 | |

CHS / Community Health Systems, Inc., 6.875%, 4/1/28(6) | | 42,000 | | 41,578 | |

| CVS Health Corp., 4.30%, 3/25/28 | | 68,000 | | 78,799 | |

| CVS Health Corp., 4.78%, 3/25/38 | | 40,000 | | 50,291 | |

DaVita, Inc., 4.625%, 6/1/30(6) | | 270,000 | | 279,450 | |

| Kaiser Foundation Hospitals, 3.00%, 6/1/51 | | 70,000 | | 74,310 | |

Team Health Holdings, Inc., 6.375%, 2/1/25(6) | | 45,000 | | 41,794 | |

| Tenet Healthcare Corp., 6.75%, 6/15/23 | | 50,000 | | 54,313 | |

Tenet Healthcare Corp., 6.125%, 10/1/28(6) | | 245,000 | | 261,242 | |

Universal Health Services, Inc., 2.65%, 10/15/30(6) | | 335,000 | | 341,380 | |

| | | 1,241,999 | |

| Hotels, Restaurants and Leisure — 0.1% | | | |

1011778 BC ULC / New Red Finance, Inc., 4.375%, 1/15/28(6) | | 120,000 | | 121,956 | |

Caesars Resort Collection LLC / CRC Finco, Inc., 5.25%, 10/15/25(6) | | 290,000 | | 292,729 | |

Golden Nugget, Inc., 6.75%, 10/15/24(6) | | 140,000 | | 140,525 | |

| MGM Resorts International, 6.00%, 3/15/23 | | 135,000 | | 142,819 | |

| MGM Resorts International, 4.625%, 9/1/26 | | 39,000 | | 40,706 | |

Penn National Gaming, Inc., 5.625%, 1/15/27(6) | | 175,000 | | 181,563 | |

Penn National Gaming, Inc., 4.125%, 7/1/29(6) | | 43,000 | | 42,450 | |