UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8748 |

|

Wanger Advisors Trust |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-617-426-3750 | |

|

Date of fiscal year end: | December 31, 2006 | |

|

Date of reporting period: | June 30, 2006 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders

Wanger U.S. Smaller Companies

2006 Semiannual Report

Wanger U.S. Smaller Companies

2006 Semiannual Report

Table of Contents

| | 1 | | | Understanding Your Expenses | |

|

| | 2 | | | Understanding Our Investment Style | |

|

| | 4 | | | Performance Review | |

|

| | 6 | | | Statement of Investments | |

|

| | 13 | | | Statement of Assets and Liabilities | |

|

| | 13 | | | Statement of Operations | |

|

| | 14 | | | Statements of Changes in Net Assets | |

|

| | 15 | | | Financial Highlights | |

|

| | 16 | | | Notes to Financial Statements | |

|

| | 19 | | | Management Fee Evaluation of the Senior Officer | |

|

| | 24 | | | Board of Trustees and Management of Wanger Advisors Trust | |

|

Columbia Wanger Asset Management, L.P. ("Columbia WAM") is one of the leading global small-cap equity managers in the United States with more than 30 years of small- and mid-cap investment experience. Columbia WAM manages more than $30 billion in equities and is the investment adviser to Wanger U.S. Smaller Companies, Wanger International Small Cap, Wanger Select, Wanger International Select and the Columbia Acorn Family of Funds. Columbia Management Group, LLC ("Columbia Management") is the primary investment management division of Bank of America Corporation. Columbia Management entities furnish investment management services and advises institutional and mutual fund portfolios. Columbia WAM is an SEC-registered investment adviser and indirect, wholly owned subsidiary of Bank of America Corporation.

For more complete information about our funds, including the Columbia Acorn Funds, our fees, risks associated with investing, or expenses, call 1-888-4-WANGER for a prospectus. Read it carefully before you invest or send money. This report is not an offer of the shares of the Columbia Acorn Fund Family.

The discussion in the report of portfolio companies is for illustration only and is not a recommendation of individual stocks. The information is believed to be accurate, but the information and the views of the portfolio managers may change at any time without notice and the portfolio managers may alter a fund's portfolio holdings based on these views and the fund's circumstances at that time.

Wanger U.S. Smaller Companies 2006 Semiannual Report

Understanding Your Expenses

As a Fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory and other Fund expenses. The information on this page is intended to help you understand your ongoing costs of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing the Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the reporting period. The information in the following table is based on an initial investment of $1,000.00, which is invested at the beginning of the reporting period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "actual" column is calculated using actual operating expenses and total return for the Fund. The amount listed in the "hypothetical" column assumes that the return each year is 5% before expenses and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the reporting period. See the "Co mpare with other funds" information for details on using the hypothetical data.

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period.

1. Divide your ending account balance by $1,000.00. For example, if an account balance was $8,600.00 at the end of the period, the result would be 8.6.

2. In the section of the table below titled "Expenses paid during period," you will find a dollar amount in the column labeled "Actual." Multiply this amount by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

January 1, 2006 – June 30, 2006

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid during

period ($) | | Fund's annualized

expense ratio (%)* | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | | |

Wanger U.S. Smaller

Companies | | | 1,000.00 | | | | 1,000.00 | | | | 1,019.98 | | | | 1,020.13 | | | | 4.71 | | | | 4.71 | | | | 0.94 | | |

*For the six months ended June 30, 2006.

Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. As a shareholder of the Fund, you do not incur any transaction costs, such as sales charges, redemption or exchange fees. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund and do not reflect any transactional costs, such as sales charges or redemption or exchange fees, that may be incurred by shareholders of other funds. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate accounts.

1

Wanger U.S. Smaller Companies 2006 Semiannual Report

Understanding Our Investment Style

Why Small and Mid Caps?

Our mission is simple: Invest in good quality, reasonably priced smaller companies that have growth potential and competitive advantages, and hold on to them. We like small companies because they are generally less complicated. Big companies typically have lots of divisions, while most small companies have one division. An added benefit is that sometimes these small companies are undiscovered, which may mean they are undervalued and a potentially good investment. Managers of small companies tend to focus on customers and are acutely aware of competitors. Small-cap stocks are often exciting businesses run by accessible managers, so in addition to the above virtues, they are fun for us to follow.

Though we like small-caps, we don't force sales of successful stocks simply because they appreciated beyond some arbitrary small-cap definition (other small-cap managers may sell at $2 billion capitalizations, for example). The funds we manage could not make strong gains if we simply sold due to size. We let our winners run.

While style classifications can be helpful, we are not style purists. For example, small-cap stocks have outperformed large caps for more than five years, and we think on average they are no longer cheap based on historical valuation. Our analysts have been finding more value among mid-cap names that have the same attributes we like in small caps.

Why Growth-at-a-Reasonable-Price?

At Columbia Wanger Asset Management, we define growth investing styles using the terms Hard Core Value, Growth-at-a-Reasonable-Price (GARP) and Momentum. These terms help define the different ways that an investor can look for returns.

Hard Core Value investors usually buy very cheap stocks, as measured by comparing the stock valuation to the underlying asset values. While this strategy works for a number of competitors who are very good at it, Hard Core Value is not for us. We believe that too often the stocks are very cheap because the underlying businesses are lousy. Successful investing in Hard Core Value largely depends on predicting (or hastening) events such as takeovers, spinouts or turnarounds. Until such an event occurs the stock may be a diminishing asset.

In implementing our Growth-at-a-Reasonable-Price style, our 21 analysts first search for good, growing businesses. We view what we do as investing in companies rather than stocks, and we try to analyze companies as if we were buying the whole business rather than just a fraction of ownership. We define "good, growing businesses" as companies that have sustainable competitive advantages, fine managements, growing markets, and opportunities for market-share gains. Once we've found a good business that has been growing, we follow the company closely and determine if it sells at what we believe is a "reasonable price."

A stock is at a reasonable price if it sells at (or hopefully below) what we believe is its true value. Most growth companies ("growth stock" is a misnomer) are valued by the market based on price-to-earnings (PE) ratios, and comparisons between growth companies are often based on PE-to-growth (PEG) ratios. While that approach makes theoretical sense, reported earnings are often poor measures of underlying economic profits. For example, the costs of employee stock options were not required to be an accounting expense until 2006, so underlying earnings of many companies were overstated. In other cases, companies may have higher free cash flows than suggested by reported earnings. We ask our analysts to look beyond reported earnings and adjust for many factors when using PE ratios or related dividend discount model valuations. Our analysts also use value discipline techniques, calculating potential sell-out or break-up values, whe n it is appropriate to do so.

Often we determine that the stock of a good business that has been growing is not selling at a reasonable price. In those cases we wait—and there have been times that we've waited for years. If valuation is borderline, we can purchase an initial small position and later increase the position or sell the stock depending on fundamentals or valuation. Valuation matters because it enables our shareholders to potentially benefit in two ways: (1) from growth of the underlying business and (2) from growth of a valuation multiplier, such as a PE ratio.

The remaining growth style definition is Momentum. Momentum players (I hesitate to say "investors") look for stocks that have been rising, along with fast earnings growth, and preferably earnings estimate increases. Many Momentum players completely ignore valuation. (Economists label luxury goods as those where demand rises when prices increase, so momentum players are the ultimate luxury goods buyers!) Because Momentum players buy at any price when earnings are good and often sell at any price when earnings are disappointing, we often like to sell our winners to them and sometimes buy their losers—at our dream prices. Momentum can work, especially in bubbles, but it's not for us. It's too far from our mission of investing in good businesses and targeting rational returns.

Just as individual stocks can graduate from small to mid to large caps, they can also move from Hard Core Value to Growth-at-a-Reasonable-Price and then to Momentum. We love to buy stocks in companies not yet recognized as growth businesses. If we can

2

Wanger U.S. Smaller Companies 2006 Semiannual Report

find good companies that we believe are mistakenly priced at Hard Core Value levels, even better. Often our best performing stocks were those that were undiscovered when we bought them, and as they grew, became investor favorites because of their strong business models. We are often challenged (in a good way) when stocks rise to Momentum valuations. The challenge then becomes when to sell. We try to resist significant selling unless we think fundamentals will deteriorate or valuations are entirely inappropriate vs. fundamentals.

Having a sensible investment style is very useful, but it is not enough for long-term success. Other factors, such as our process and the people who make up our investment team, will be discussed in future columns.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, L.P.

The views expressed in "Understanding Our Investment Style" are those of the author. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Wanger Advisors Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Wanger Advisors Fund. References to specific company securities should not be construed as a recommendation or investment advice.

Mid- and small-cap stocks are often more volatile and less liquid than the stocks of larger companies. Small companies may have a shorter history of operations than larger companies and may have a less diversified product line, making them more susceptible to market pressure. Investments in foreign securities have special risks, including political or economic instability, higher costs, different regulations, accounting standards, trading practices and levels of information, and currency exchange rate fluctuations.

3

Wanger U.S. Smaller Companies 2006 Semiannual Report

Performance Review Wanger U.S. Smaller Companies

Robert A. Mohn

Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. For monthly performance updates call 1-888-4-WANGER.

Wanger U.S. Smaller Companies ended the six months up 2.00% (without insurance charges) vs. an 8.21% gain for the Russell 2000 Index. At the end of 2005, Fund returns were well ahead of the index, but market conditions so far in 2006 have provided a headwind to Fund performance. Historically, we have done well in strong markets coming up from the bottom. Alternately, we tend to lag when more speculative stocks spike up in a fully-valued market. That was the market condition the Fund faced going into 2006. The Fund was underrepresented in high-octane names, particularly in the technology and metals sectors and therefore did not get the full benefit of a first quarter surge in small caps. In the final three months of the period, small caps pulled back drastically and the Fund and index were both down over 4.50%.

Eight of the Fund's stocks received takeover offers during the six month period. Two stocks that were impacted, Serologicals and Western Gas Resources, were fairly sizeable positions in the Fund and contributed positively to Fund returns as the stocks bounced on the acquisition news. Serologicals, a producer of biological products and solutions, gained 59% for the six months. Western Gas Resources, a coal seam gas producer and processor, increased 27% year-to-date through June 30.

Other winners for the half year included FMC Technologies, up 57%. FMC makes deep-water oil and gas production systems and has been enjoying robust demand for its products as offshore drilling activity has increased. Genlyte Group, a maker of commercial lighting fixtures, gained 35% for the annual period thanks to improving demand for its product from commercial developers and strong earnings gains. Time Warner Telecom, a provider of fiber-optic data and telephone services, was up 50% for the six months as revenue growth accelerated. Crown Castle International, an owner of cellular communication towers, gained 28% for the half year. Its business has been booming as cellular phone companies grab for more wireless capacity in order to beam internet sites, TV shows and other fun stuff to your cell phone.

Other big percentage winners included Vaalco Energy, an oil and gas producer, up 130% for the half year on higher energy prices. While several Fund retail stocks faltered in the period, Christopher & Banks was the exception. Up 55% for the six months, Christopher & Banks experienced a turnaround as new merchandise was positively received and same-store sales flipped from negative to positive.

On the downside, Neurocrine Biosciences' stock collapsed when the FDA withheld full approval for the high dosage of its sleep medication Indiplon. We sold out of the stock, taking a 65% loss for the six months. Interestingly enough, Neurocrine stock fell an additional 50% after we got out. As mentioned, several retail names were down in the Fund. Chico's FAS, a women's specialty retailer, fell 41% in the half year as new merchandise failed to move and sales came in short. Oxford Industries, a maker of branded and private label apparel, fell 28% for the six months on disappointing sales in its menswear lines.

Two technology names, Avid Technology and CNET Networks also hurt Fund performance. Avid suffered indigestion from an acquisition it made last year and announced delays in new product upgrades. The stock was off 40% for the six months. CNET Networks, a provider of software product reviews and niche technology websites, was off 46% for the half year. CNET's business is driven by new product launches, and two highly anticipated product launches, Microsoft's Vista and Sony's PlayStation 3, were tardy.

The second quarter's pull back in small-cap stocks allowed us to add to positions in fast-growing stocks whose prices fell within our valuation criteria. We continue to take advantage of the many opportunities today's volatile markets offer.

Wanger U.S. Smaller Companies is a diversified fund that invests primarily in the stocks of small- and medium-size U.S. companies. Small-cap stocks are often more volatile and less liquid than the stocks of larger companies. Small companies may have a shorter history of operations than larger companies and may have a less diversified product line, making them more susceptible to market pressure.

As of 6/30/06, the Fund's positions in the stocks mentioned were: Serologicals, 0.9%; Western Gas Resources, 1.1%; FMC Technologies, 2.0%; Genlyte Group, 2.0%; Time Warner Telecom, 1.2%; Crown Castle International, 1.1%; Vaalco Energy, 0.3%; Christopher & Banks, 0.7%; Neurocrine Biosciences, 0.0%; Chico's FAS, 0.7%; Oxford Industries, 1.0%; Avid Technology, 1.8%; CNET Networks, 0.7%.

See next page for index definitions.

4

Wanger U.S. Smaller Companies 2006 Semiannual Report

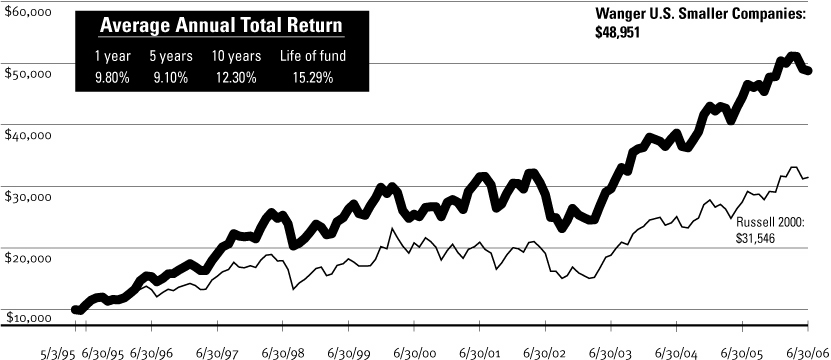

Growth of a $10,000 Investment in

Wanger U.S. Smaller Companies

Total return for each period,

May 3, 1995 (inception date) through June 30, 2006

This graph compares the results of $10,000 invested in Wanger U.S. Smaller Companies on May 3, 1995 (the date the Fund began operations) through June 30, 2006, with the Russell 2000. Dividends and capital gains are reinvested. Performance shown here is past performance, which cannot guarantee future results. Current performance may be higher or lower. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance changes over time. Current returns for the Fund may be different than that shown. For monthly performance updates, please contact us at 1-888-4-WANGER.

Results as of June 30, 2006

| | | 2nd quarter | | Year-to-date | | 1 year | |

Wanger U.S. Smaller

Companies | | | -4.58 | % | | | 2.00 | % | | | 9.80 | % | |

| Russell 2000 | | | -5.02 | | | | 8.21 | | | | 14.58 | | |

| S&P MidCap 400 | | | -3.14 | | | | 4.24 | | | | 12.98 | | |

| S&P 500 | | | -1.44 | | | | 2.71 | | | | 8.63 | | |

NAV as of 6/30/06: $34.38

Performance numbers reflect all Fund expenses but do not include any insurance charge imposed by your insurance company's separate accounts. If performance included the effect of these additional charges, it would be lower.

Due to ongoing market volatility, performance is subject to substantial short-term fluctuations.

The Russell 2000 Index is formed by taking the 3,000 largest U.S. companies and then eliminating the largest 1,000, leaving a mainly small company index. The S&P MidCap 400 is a market value-weighted index of 400 U.S. stocks that are in the next tier down from the S&P 500. The S&P 500 is a broad market-weighted average of blue-chip U.S. companies. All indexes are unmanaged and include reinvested dividends. It is not possible to invest directly in an index.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Top 5 Industries

As a % of net assets, as of 6/30/06

| Information | | | 29.6 | % | |

| Consumer Goods & Services | | | 18.3 | | |

| Industrial Goods | | | 11.9 | | |

| Energy/Minerals | | | 11.6 | | |

| Health Care | | | 10.6 | | |

Top 10 Holdings

As a % of net assets, as of 6/30/06

1. ITT Educational Services

Post-secondary Degree Programs | | 3.9%

| |

2. FMC Technologies

Oil & Gas Well Head Manufacturer | | 2.0

| |

3. Genlyte Group

Commercial Lighting Fixtures | | 2.0

| |

4. Lincare Holdings

Home Health Care Services | | 2.0

| |

5. AmeriCredit

Auto Lending | | 1.9

| |

6. Avid Technology

Digital Nonlinear Editing Software & Systems | | 1.8

| |

7. Alltel

Cellular & Wireline Telephone Services | | 1.7

| |

8. Esco Technologies

Automatic Electric Meter Readers | | 1.6

| |

9. Global Payments

Credit Card Processor | | 1.5

| |

10. Tellabs

Telecommunications Equipment | | 1.5

| |

5

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Common Stocks – 91.2% | | | | | |

| | | Information Group – 29.6% | |

| | | Business Software – 7.8% | |

874,900

| | Avid Technology (b)

Digital Nonlinear Editing Software & Systems | | | $29,160,417

| | |

668,437

| | Kronos (b)

Labor Management Solutions | | | 24,204,104

| | |

535,800

| | Micros Systems (b)

Information Systems for Restaurants & Hotels | | | 23,403,744

| | |

2,280,000

| | Novell (b)

Directory, Operating System & Identity

Management Software | | | 15,116,400

| | |

580,000

| | JDA Software Group (b)

Application/Software & Services for Retailers | | | 8,137,400

| | |

330,800

| | SSA Global Technologies (b)

Enterprise Resource Planning Software | | | 6,410,904

| | |

304,000

| | Concur Technologies (b)

Web Enabled Cost & Expense Management Software | | | 4,702,880

| | |

192,000

| | Progress Software (b)

Application Development Software | | | 4,494,720

| | |

327,200

| | Parametric Technology (b)

Engineering Software & Services | | | 4,158,712

| | |

279,100

| | webMethods (b)

Enterprise Applications Integration Tools | | | 2,754,717

| | |

820,000

| | Indus International (b)

Enterprise Asset Management Software | | | 2,345,200

| | |

51,300

| | MRO Software (b)

Enterprise Maintenance Software | | | 1,029,591

| | |

47,400

| | Witness Systems (b)

Customer Experience Management Software | | | 956,058

| | |

| | | | | | 126,874,847 | | |

| | | Mobile Communications – 5.0% | |

435,192

| | Alltel

Cellular & Wireline Telephone Services | | | 27,778,305

| | |

640,000

| | American Tower (b)

Communications Towers in USA & Mexico | | | 19,916,800

| | |

495,000

| | Crown Castle International (b)

Communications Towers | | | 17,097,300

| | |

2,033,000

| | Dobson Communications (b)

Rural & Small City Cellular Telephone Services | | | 15,715,090

| | |

100,000

| | Openwave Systems (b)

Internet Software for Mobile Devices | | | 1,154,000

| | |

| | | | | | 81,661,495 | | |

Number of

Shares | | | | Value | |

| | | Financial Processors – 2.5% | |

516,880

| | Global Payments (b)

Credit Card Processor | | | $25,094,524

| | |

321,000

| | SEI Investments

Mutual Fund Administration & Investment Management | | | 15,690,480

| | |

| | | | | | 40,785,004 | | |

| | | Computer Hardware and Related

Equipment – 2.4% | |

1,155,000

| | Symbol Technologies

Mobile Computers & Barcode Scanners | | | 12,462,450

| | |

122,800

| | Amphenol

Electronic Connectors | | | 6,871,888

| | |

206,400

| | Nice Systems (Israel) (b)

Audio & Video Recording Solutions | | | 5,808,096

| | |

81,600

| | Rogers (b)

PCB Laminates & High-performance Foams | | | 4,597,344

| | |

415,800

| | Seachange International (b)

Systems for Video On Demand & Ad Insertion | | | 2,893,968

| | |

120,000

| | Intermec (b)

Bar Code & Wireless LAN Systems | | | 2,752,800

| | |

90,000

| | Netgear (b)

Networking Products for Small Business & Home | | | 1,948,500

| | |

50,000

| | Avocent (b)

Computer Control Switches | | | 1,312,500

| | |

301,205

| | SensAble Technologies Series C Pfd. (b) (c)

Sensory Devices for Computer Based Sculpting | | | 3

| | |

1,581,292

| | SensAble Technologies (b) (c)

Sensory Devices for Computer Based Sculpting | | | 16

| | |

| | | | | | 38,647,565 | | |

| | | Business Information and Marketing

Services – 1.7% | |

485,000

| | Ceridian (b)

HR Services & Payment Processing | | | 11,853,400

| | |

443,200

| | Navigant Consulting (b)

Financial Consulting Firm | | | 10,038,480

| | |

65,000

| | Getty Images (b)

Photographs for Publications & Electronic Media | | | 4,128,150

| | |

170,000

| | InfoUSA (b)

Business Data for Sales Leads | | | 1,752,700

| | |

| | | | | | 27,772,730 | | |

See accompanying notes to financial statements.

6

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Telecommunications Equipment – 1.7% | |

1,830,000

| | Tellabs (b)

Telecommunications Equipment | | | $24,357,300

| | |

210,000

| | Andrew (b)

Wireless Infrastructure Equipment | | | 1,860,600

| | |

100,000

| | Symmetricom (b)

Network Timing & Synchronization Devices | | | 707,000

| | |

| | | | | | 26,924,900 | | |

| | | Internet Related – 1.3% | |

1,420,000

| | CNET Networks (b)

Internet Advertising on Niche Websites | | | 11,331,600

| | |

530,000

| | Valueclick (b)

Internet Advertising | | | 8,135,500

| | |

310,000

| | SkillSoft (b)

Web-based Learning Solutions (E-Learning) | | | 1,897,200

| | |

| | | | | | 21,364,300 | | |

| | | Telephone Services – 1.3% | |

1,291,000

| | Time Warner Telecom (b)

Fiber Optic Telephone/Data Service Provider | | | 19,171,350

| | |

65,000

| | Commonwealth Telephone

Rural Phone Franchises & Competing Telco | | | 2,155,400

| | |

| | | | | | 21,326,750 | | |

| | | Semiconductors and Related Equipment – 1.1% | |

615,500

| | Integrated Device Technology (b)

Communications Semiconductors | | | 8,727,790

| | |

670,000

| | Entegris (b)

Semiconductor Wafer Shipping & Handling Products | | | 6,385,100

| | |

70,000

| | Littelfuse (b)

Little Fuses | | | 2,406,600

| | |

125,900

| | IXYS (b)

Power Semiconductors | | | 1,208,640

| | |

| | | | | | 18,728,130 | | |

| | | CATV – 1.0% | |

740,000

| | Discovery Holding (b)

CATV Programming | | | 10,826,200

| | |

1,780,000

| | Gemstar-TV Guide International (b)

TV Program Guides & CATV Programming | | | 6,265,600

| | |

| | | | | | 17,091,800 | | |

Number of

Shares | | | | Value | |

| | | Instrumentation – 0.9% | |

145,000

| | Mettler Toledo International (b)

Laboratory Equipment | | | $8,782,650

| | |

125,000

| | Trimble Navigation (b)

GPS-based Instruments | | | 5,580,000

| | |

| | | | | | 14,362,650 | | |

| | | Radio – 0.8% | |

561,900

| | Salem Communications (b)

Radio Stations for Religious Programming | | | 7,310,319

| | |

260,000

| | Cumulus Media (b)

Radio Stations in Small Cities | | | 2,774,200

| | |

515,000

| | Spanish Broadcasting System (b)

Spanish Language Radio Stations | | | 2,631,650

| | |

| | | | | | 12,716,169 | | |

| | | TV Broadcasting – 0.6% | |

1,030,000

| | Entravision Communications (b)

Spanish Language TV, Radio & Outdoor | | | 8,827,100

| | |

138,500

| | Gray Television

Mid Market Affiliated TV Stations | | | 801,915

| | |

| | | | | | 9,629,015 | | |

| | | Computer Services – 0.5% | |

753,000

| | RCM Technologies (b)(d)

Technology & Engineering Services | | | 3,780,060

| | |

705,500

| | Answerthink (b)

IT Integration & Best Practice Research | | | 2,843,165

| | |

45,000

| | SRA International (b)

Government IT Services | | | 1,198,350

| | |

| | | | | | 7,821,575 | | |

| | | Gaming Equipment – 0.4% | |

205,000

| | Bally Technologies (b)

Slot Machines & Software | | | 3,376,350

| | |

98,500

| | Shuffle Master (b)

Card Shufflers & Casino Games | | | 3,228,830

| | |

| | | | | | 6,605,180 | | |

| | | Contract Manufacturing – 0.4% | |

176,000

| | Plexus (b)

Electronic Manufacturing Services | | | 6,020,960

| | |

See accompanying notes to financial statements.

7

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Television Programming – 0.2% | |

460,000

| | Lions Gate Entertainment (b)

Film & TV Studio | | | $3,933,000

| | |

| | | Publishing – 0.0% | |

13,850

| | Triple Crown Media (b)

Newspapers, Paging & Collegiate Sports Marketing | | | 120,080

| | |

| | | | | Information Group – Total | | | 482,386,150 | | |

| | | Consumer Goods & Services – 18.3% | |

| | | Retail – 6.4% | |

431,000

| | Abercrombie & Fitch

Teen Apparel Retailer | | | 23,890,330 |

| |

635,000

| | Petco Animal Supplies (b)

Pet Supplies & Services | | | 12,973,050 |

| |

450,000

| | Chico's FAS (b)

Women's Specialty Retail | | | 12,141,000 |

| |

409,150

| | Christopher & Banks

Women's Apparel Retailer | | | 11,865,350 |

| |

265,000

| | AnnTaylor Stores (b)

Women's Apparel Retailer | | | 11,495,700 |

| |

190,000

| | Michaels Stores

Craft & Hobby Specialty Retailer | | | 7,835,600 |

| |

390,000

| | Urban Outfitters (b)

Apparel & Home Specialty Retailer | | | 6,821,100 |

| |

163,000

| | Genesco (b)

Multi-concept Branded Footwear Retailer | | | 5,520,810 |

| |

125,000

| | J Crew Group (b)

Multi-channel Branded Retailer | | | 3,431,250 |

| |

445,000

| | Restoration Hardware (b)

Home Furnishing Retailer | | | 3,195,100 |

| |

110,000

| | Aeropostale (b)

Mall-based Teen Retailer | | | 3,177,900 |

| |

150,000

| | Gaiam (b)

Healthy Living Catalogs & E-Commerce | | | 2,103,000 |

| |

| | | | | | | | 104,450,190 | | |

| | | Other Consumer Services – 4.7% | |

972,000

| | ITT Educational Services (b)

Post-secondary Degree Programs | | | 63,967,320 |

| |

426,500

| | Central Parking

Owner, Operator, Manager of Parking Lots & Garages | | | 6,824,000 |

| |

Number of

Shares | | | | Value | |

| | | Other Consumer Services – 4.7% (continued) | |

| | 150,000 | | | Weight Watchers International

Weight Loss Programs | | | $6,133,500

| | |

| | | | | | | | 76,924,820 | | |

| | | Apparel – 2.6% | |

| | 394,200 | | | Oxford Industries

Branded & Private Label Apparel | | | 15,535,422

| | |

| | 459,000

| | | Coach (b)

Designer & Retailer of Branded Leather Accessories | | | 13,724,100

| | |

| | 480,200

| | | Carter's (b)

Children's Branded Apparel | | | 12,691,686

| | |

| | | | | | | | 41,951,208 | | |

| | | Leisure Products – 2.2% | |

| | 366,300 | | | International Speedway

Largest Motorsports Racetrack Owner & Operator | | | 16,985,331

| | |

| | 248,200

| | | Speedway Motorsports

Motorsport Racetrack Owner & Operator | | | 9,367,068

| | |

| | 390,000

| | | Callaway Golf

Premium Golf Clubs & Balls | | | 5,066,100

| | |

| | 106,000

| | | Polaris Industries

Leisure Vehicles & Related Products | | | 4,589,800

| | |

| | | | | | | | 36,008,299 | | |

| | | Nondurables – 0.8% | |

| | 288,000

| | | Scotts Miracle-Gro

Consumer Lawn & Garden Products | | | 12,188,160

| | |

| | 100,000

| | | Prestige Brands Holdings (b)

OTC, Household & Personal Care Products | | | 997,000

| | |

| | | | | | | | 13,185,160 | | |

| | | Furniture and Textiles – 0.8% | |

| | 130,000

| | | HNI

Office Furniture & Fireplaces | | | 5,895,500

| | |

| | 152,000

| | | Herman Miller

Office Furniture | | | 3,917,040

| | |

| | 33,000

| | | Mohawk Industries (b)

Carpet & Flooring | | | 2,321,550

| | |

| | | | | | | | 12,134,090 | | |

| | | Restaurants – 0.4% | |

| | 337,500

| | | Sonic (b)

Quick Service Restaurant | | | 7,016,625

| | |

See accompanying notes to financial statements.

8

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Travel – 0.3% | |

38,200

| | Kerzner International (Bahamas) (b)

Destination Resorts & Casinos | | | $3,028,496

| | |

45,000

| | Vail Resorts (b)

Ski Resort Operator & Developer | | | 1,669,500

| | |

| | | | | | 4,697,996 | | |

| | | Other Durable Goods – 0.1% | |

40,000

| | Cavco Industries (b)

Higher End Manufactured Homes | | | 1,777,600

| | |

| | | Consumer Goods & Services – Total | | | 298,145,988 | | |

| | | Industrial Goods – 11.9% | |

| | | Machinery – 6.1% | |

492,300

| | Esco Technologies (b)

Automatic Electric Meter Readers | | | 26,313,435

| | |

690,600

| | Pentair

Pumps, Water Treatment & Tools | | | 23,611,614

| | |

365,100

| | Nordson

Dispensing Systems for Adhesives & Coatings | | | 17,955,618

| | |

275,000

| | Ametek

Aerospace/Industrial Instruments | | | 13,029,500

| | |

177,300

| | Donaldson

Industrial Air Filtration | | | 6,005,151

| | |

196,000

| | Clarcor

Mobile & Industrial Filters | | | 5,838,840

| | |

189,900

| | K&F Industries Holdings (b)

Aircraft Wheels, Brakes & Fuel Tank Bladders | | | 3,366,927

| | |

132,000

| | Goodman Global (b)

HVAC Equipment Manufacturer | | | 2,003,760

| | |

50,000

| | Kaydon

Specialized Friction & Motion Control Products | | | 1,865,500

| | |

| | | | | | 99,990,345 | | |

| | | Electrical Components – 2.0% | |

453,000

| | Genlyte Group (b)

Commercial Lighting Fixtures | | | 32,810,790

| | |

| | | Construction – 0.8% | |

191,400

| | Florida Rock Industries

Aggregates & Concrete | | | 9,506,838

| | |

35,000

| | Martin Marietta Materials

Aggregates | | | 3,190,250

| | |

| | | | | | 12,697,088 | | |

Number of

Shares | | | | Value | |

| | | Industrial Distribution – 0.6% | |

100,000

| | Aviall (b)

Aircraft Replacement Parts Distributor | | | $4,752,000

| | |

113,000

| | NuCo2 (b)

Bulk Co2 Gas Distribution to Restaurants | | | 2,716,520

| | |

50,000

| | Airgas

Industrial Gas Distributor | | | 1,862,500

| | |

| | | | | | 9,331,020 | | |

| | | Specialty Chemicals – 0.6% | |

407,500

| | Spartech

Plastics Distribution & Compounding | | | 9,209,500

| | |

| | | Outsourcing Services (other than ECM) – 0.5% | |

450,000

| | Quanta Services (b)

Electrical & Telecom Construction Services | | | 7,798,500

| | |

| | | Industrial Materials – 0.5% | |

191,300

| | Mine Safety Appliances

Safety Equipment | | | 7,690,260

| | |

| | | Other Industrial Services – 0.4% | |

130,000

| | Forward Air

Freight Transportation Between Airports | | | 5,294,900

| | |

63,000

| | UTI Worldwide

Global Logistics & Freight Forwarding | | | 1,589,490

| | |

| | | | | | 6,884,390 | | |

| | | Waste Management – 0.3% | |

122,800

| | Waste Connections (b)

Solid Waste Management | | | 4,469,920

| | |

| | | Steel – 0.1% | |

75,000

| | Gibraltar Industries

Steel Processing | | | 2,175,000

| | |

| | | Industrial Goods – Total | | | 193,056,813 | | |

| | | Energy/Minerals – 11.6% | |

| | | Oil Services – 6.5% | |

490,700

| | FMC Technologies (b)

Oil & Gas Well Head Manufacturer | | | 33,102,622

| | |

965,000

| | Chicago Bridge & Iron

Engineering & Construction

for Petrochemicals & LNG | | | 23,304,750

| | |

See accompanying notes to financial statements.

9

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Oil Services – 6.5% (cont) | |

580,000

| | Pride International (b)

Offshore Drilling Contractor | | | $18,113,400

| | |

625,000

| | Hanover Compressor (b)

Natural Gas Compressor Rental & Fabrication | | | 11,737,500

| | |

142,500

| | CARBO Ceramics

Natural Gas Well Stimulants | | | 7,001,025

| | |

112,000

| | Atwood Oceanics (b)

Contract Drilling | | | 5,555,200

| | |

205,000

| | Key Energy Services (b)

Well Worker Services | | | 3,126,250

| | |

457,900

| | Newpark Resources (b)

Drilling Fluid Services | | | 2,816,085

| | |

11,000

| | Helmerich & Payne

Contract Driller | | | 662,860

| | |

| | | | | | 105,419,692 | | |

| | | Oil and Gas Producers – 4.6% | |

400,000

| | Ultra Petroleum (b)

Natural Gas Producer | | | 23,708,000

| | |

296,000

| | Western Gas Resources

Oil & Coal Seam Gas Producer | | | 17,715,600

| | |

416,000

| | Equitable Resources

Natural Gas Producer & Utility | | | 13,936,000

| | |

195,000

| | Quicksilver Resources (b)

Natural Gas & Coal Seam Gas Producer | | | 7,177,950

| | |

193,600

| | Southwestern Energy (b)

Natural Gas Producer | | | 6,032,576

| | |

450,000

| | Vaalco Energy (b)

Oil & Gas Producer | | | 4,392,000

| | |

71,500

| | McMoRan Exploration (b)

Natural Gas Producer & Developer | | | 1,258,400

| | |

| | | | | | 74,220,526 | | |

| | | Oil Refining/Marketing/Distribution – 0.5% | |

185,000

| | Atmos Energy

Dallas Natural Gas Utility | | | 5,163,350

| | |

94,000

| | Oneok

Natural Gas Distribution Pipeline,

Processing & Trading | | | 3,199,760

| | |

| | | | | | 8,363,110 | | |

| | | Energy/Minerals – Total | | | 188,003,328 | | |

Number of

Shares | | | | Value | |

| | | Health Care – 10.6% | |

| | | Health Care Services – 4.4% | |

866,000

| | Lincare Holdings (b)

Home Health Care Services | | | $32,769,440

| | |

258,709

| | Coventry Health Care (b)

HMO | | | 14,213,472

| | |

180,000

| | LCA-Vision

Lasik Surgery Centers | | | 9,523,800

| | |

170,000

| | Charles River Laboratories (b)

Pharmaceutical Research | | | 6,256,000

| | |

205,000

| | United Surgical Partners (b)

Outpatient Surgery Center | | | 6,164,350

| | |

175,000

| | PRA International (b)

Contract Research Organization | | | 3,897,250

| | |

| | | | | | 72,824,312 | | |

| | | Medical Equipment – 2.9% | |

412,000

| | Edwards Lifesciences (b)

Heart Valves | | | 18,717,159

| | |

137,227

| | Advanced Medical Optics (b)

Medical Devices for Eye Care | | | 6,957,409

| | |

190,000

| | Arrow International

Disposable Catheters | | | 6,245,300

| | |

105,000

| | Vital Signs

Anesthesia, Respiratory & Sleep Products | | | 5,200,650

| | |

188,175

| | Intermagnetics General (b)

MRI Equipment Manufacturer | | | 5,076,962

| | |

93,500

| | Orthofix International (b)

Bone Fixation & Stimulation Devices | | | 3,565,155

| | |

75,000

| | PSS World Medical (b)

Medical Supplies Distributor | | | 1,323,750

| | |

| | | | | | 47,086,385 | | |

| | | Hospital/Laboratory Supplies – 2.3% | |

466,000

| | Serologicals (b)

Biomanufacturing & Life Science Research | | | 14,651,040

| | |

235,700

| | ICU Medical (b)

Intravenous Therapy Products | | | 9,955,968

| | |

157,300

| | Diagnostic Products

Immunodiagnostic Kits | | | 9,150,141

| | |

70,700

| | Techne (b)

Cytokines, Antibodies, Other Reagents for Life Sciences | | | 3,600,044

| | |

| | | | | | 37,357,193 | | |

See accompanying notes to financial statements.

10

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of

Shares | | | | Value | |

| | | Biotechnology/Drug Delivery – 1.0% | |

270,000

| | Nektar Therapeutics (b)

Drug Delivery Technologies | | | $4,951,800

| | |

293,000

| | Intermune (b)

Drugs for Hepatitis C, Pulmonary Fibrosis & Cancer | | | 4,819,850

| | |

372,500

| | Ligand Pharmaceuticals (b)

Drugs for Pain, Cancer, Osteoporosis, Diabetes | | | 3,147,625

| | |

315,000

| | Decode genetics (b)

Drugs for Heart Attack, Asthma & Vascular Disease | | | 1,949,850

| | |

50,000

| | Momenta Pharmaceuticals (b)

Sugar Analysis Technology for Drug Design | | | 635,500

| | |

250,000

| | Locus Discovery, Series D Pfd. (c)

High Throughput Rational Drug Design | | | 68,250

| | |

| | | | | | 15,572,875 | | |

| | | Health Care – Total | | | 172,840,765 | | |

| | | Finance – 6.8% | |

| | | Insurance – 3.1% | |

670,500

| | HCC Insurance Holdings

Specialty Insurance | | | 19,739,520

| | |

36,500

| | Markel (b)

Specialty Insurance | | | 12,665,500

| | |

276,000

| | Leucadia National

Insurance Holding Company | | | 8,056,440

| | |

105,000

| | Philadelphia Consolidated Holdings (b)

Specialty Insurance | | | 3,187,800

| | |

87,000

| | Delphi Financial Group

Group Employee Benefit Products & Services | | | 3,163,320

| | |

75,000

| | Endurance Specialty Holdings

Commercial Lines Insurance/Reinsurance | | | 2,400,000

| | |

77,000

| | United America Indemnity (b)

Specialty Insurance | | | 1,604,680

| | |

1,600

| | Eastern Insurance Holdings (b)

Workers Comp & Specialty Insurance | | | 20,480

| | |

| | | | | | 50,837,740 | | |

| | | Finance Companies – 2.5% | |

1,135,400

| | AmeriCredit (b)

Auto Lending | | | 31,700,368

| | |

217,100

| | World Acceptance (b)

Personal Loans | | | 7,711,392

| | |

| | | | | | 39,411,760 | | |

Number of

Shares | | | | Value | |

| | | Banks – 1.0% | |

284,500

| | TCF Financial

Great Lakes Bank | | | $7,525,025

| | |

146,975

| | Chittenden

Vermont & Western Massachusetts Banks | | | 3,799,304

| | |

95,000

| | Greene County Bancshares

Tennessee Bank | | | 2,941,200

| | |

35,000

| | Associated Banc-Corp

Midwest Bank | | | 1,103,550

| | |

20,000

| | First Financial BankShares

West Texas Bank | | | 730,800

| | |

30,000

| | West Bancorporation

Des Moines Commercial Bank | | | 560,100

| | |

| | | | | | 16,659,979 | | |

| | | Savings and Loans – 0.2% | |

110,200

| | Anchor Bancorp Wisconsin

Wisconsin Thrift | | | 3,324,734

| | |

| | | Finance – Total | | | 110,234,213 | | |

| | | Other Industries – 2.4% | |

| | | Real Estate – 1.4% | |

560,000

| | DiamondRock Hospitality

Hotel Owner | | | 8,293,600

| | |

340,000

| | Highland Hospitality

Hotel Owner | | | 4,787,200

| | |

77,500

| | Gaylord Entertainment (b)

Convention Hotels | | | 3,382,100

| | |

150,000

| | Kite Realty Group Trust

Community Shopping Centers | | | 2,338,500

| | |

90,000

| | American Campus Communities

Student Housing | | | 2,236,500

| | |

100,000

| | Crescent Real Estate Equities

Class 'A' Office Buildings | | | 1,856,000

| | |

| | | | | | 22,893,900 | | |

| | | Transportation – 0.5% | |

480,800

| | Heartland Express

Regional Trucker | | | 8,601,512

| | |

See accompanying notes to financial statements.

11

Wanger U.S. Smaller Companies 2006 Semiannual Report

Wanger U.S. Smaller Companies

Statement of Investments (Unaudited) June 30, 2006

Number of Shares

or Principal Amount | | | | Value | |

| | | Regulated Utilities – 0.5% | |

| | 345,000

| | | Northeast Utilities

Utility | | | $7,131,150

| | |

| | | | | Other Industries – Total | | | 38,626,562 | | |

| | | | | Total Common Stock (Cost: $963,921,066) – 91.2% | | | 1,483,293,819 | | |

| Short-Term Obligations – 8.8% | | | |

| $ | 66,000,000 | | | Verizon Global Funding

5.28% – 5.30% Due 7/05/06 – 7/06/06 | | | 65,956,797 | | |

| | 45,000,000 | | | Conocophillips 5.30%

Due 7/03/06 – 7/07/06 | | | 44,974,972 | | |

| | 30,000,000 | | | Countrywide Financial Funding

5.30% Due 7/10/06 | | | 29,960,250 | | |

| | 3,029,000 | | | Repurchase Agreement with State

Street Bank & Trust dated 06/30/06,

due 07/03/06 at 4.93% collateralized by

a Federal Home Loan Bank Note,

maturing 05/22/08, market value

$3,090,000 (repurchase proceeds:

$3,030,244) | | | 3,029,000 | | |

| | | | | (Amortized Cost: $143,921,019) | | | 143,921,019 | | |

| | | | | Total Investments (Cost: $1,107,842,085) – 100.0% (a) | | | 1,627,214,838 | | |

| | | | | Cash and Other Assets Less Liabilities – 0.0% | | | (486,370 | ) | |

| | | | | Total Net Assets – 100.0% | | $ | 1,626,728,468 | | |

Notes to Statements of Investments

(a) At June 30, 2006, for federal income tax purposes cost of investments was $1,107,842,085 and net unrealized appreciation was $519,372,753 consisting of gross unrealized appreciation of $583,357,636 and gross unrealized depreciation of $63,984,883.

(b) Non-income producing security.

(c) Denotes a restricted security, which is subject to restrictions on resale under federal securities laws. These securities are valued in good faith by the Board of Trustees. At June 30, 2006, these securities amounted to $68,269 which represents less than 0.01% of net assets.

Additional information on these securities is as follows:

Security | | Acquisition

Dates | |

Shares | |

Cost | |

Value | |

Locus Discovery,

Series D Pfd. | | 9/5/01 | | | 250,000 | | | $ | 1,000,000 | | | $ | 68,250 | | |

SensAble Technologies

Series C Pfd. | | 4/4/00 | | | 301,205 | | | | 1,000,000 | | | | 3 | | |

SensAble Technologies

Series, common | | 6/28/04 | | | 1,581,292 | | | | 0 | | | | 16 | | |

| | | | | | | | | $ | 2,000,000 | | | $ | 68,269 | | |

(d) An affiliate may include any company in which the Fund owns five percent or more of its outstanding voting shares. On June 30, 2006, the Fund held five percent or more of the outstanding voting securities of the following company:

The aggregate cost and value of this company at June 30, 2006, was $5,474,962 and $3,780,060 respectively. Investments in affiliate companies represent 0.23% of total net assets at June 30, 2006. Investment activity and income amounts related to affiliates during the six months ended June 30, 2006, were as follows:

| Dividend Income | | $ | — | | |

| Net realized gain or loss | | | — | | |

| Change in unrealized gain or loss | | | (60,240 | ) | |

| Purchases | | | — | | |

| Proceeds from sales | | | — | | |

At June 30, 2006, the Fund held investments in the following sectors:

| Sector | | % of

Net Assets | |

| Information Group | | | 29.6 | % | |

| Consumer Goods & Services | | | 18.3 | | |

| Industrial Goods | | | 11.9 | | |

| Energy/Minerals | | | 11.6 | | |

| Health Care | | | 10.6 | | |

| Finance | | | 6.8 | | |

| Other Industries | | | 2.4 | | |

| Short-Term Obligations | | | 8.8 | | |

| Cash and Other Assets Less Liabilities | | | – | | |

| | | | 100.0 | % | |

See accompanying notes to financial statements.

12

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Statement of Assets and Liabilities

June 30, 2006 (Unaudited)

| Assets: | |

| Unaffiliated investments, at cost | | $ | 1,102,367,123 | | |

| Affiliated investments, at cost (See Note 4) | | | 5,474,962 | | |

| Unaffiliated investments, at value | | $ | 1,623,434,778 | | |

| Affiliated investments, at value (See Note 4) | | | 3,780,060 | | |

| Cash | | | 21,812 | | |

| Receivable for: | |

| Investments sold | | | 1,414,341 | | |

| Fund shares sold | | | 2,548,832 | | |

| Interest | | | 415 | | |

| Dividends | | | 464,232 | | |

| Foreign tax reclaims | | | 2,895 | | |

| Total Assets | | | 1,631,667,365 | | |

| Liabilities: | |

| Payable for: | |

| Investments purchased | | | 3,405,530 | | |

| Fund shares repurchased | | | 150,796 | | |

| Investment advisory fee | | | 1,163,706 | | |

| Transfer agent fee | | | 28 | | |

| Trustees' fees | | | 2,135 | | |

| Other liabilities | | | 216,702 | | |

| Total Liabilities | | | 4,938,897 | | |

| Net Assets | | $ | 1,626,728,468 | | |

| Composition of Net Assets: | |

| Paid-in capital | | $ | 1,109,309,181 | | |

| Accumulated net investment loss | | | (445,767 | ) | |

| Accumulated net realized loss | | | (1,575,147 | ) | |

| Net unrealized appreciation on: | |

| Investments | | | 519,372,753 | | |

| Liquidated Security | | | 67,448 | | |

| Net Assets | | $ | 1,626,728,468 | | |

| Fund Shares outstanding | | | 47,317,862 | | |

Net asset value, offering price and redemption

price per share | | $ | 34.38 | | |

Statement of Operations

For the Six Months Ended June 30, 2006 (Unaudited)

| Investment Income: | |

| Dividends (net of foreign taxes withheld of $9,480) | | $ | 3,548,822 | | |

| Interest income | | | 3,581,195 | | |

| Total Investment Income | | | 7,130,017 | | |

| Expenses: | |

| Investment advisory fee | | | 7,223,144 | | |

| Transfer agent fee | | | 249 | | |

| Trustees' fees | | | 69,498 | | |

| Custody fee | | | 26,602 | | |

| Non-recurring costs (See Note 8) | | | 3,624 | | |

| Chief compliance officer expenses (See Note 4) | | | 20,055 | | |

| Other expenses | | | 195,108 | | |

| Total Expenses | | | 7,538,280 | | |

Non-recurring costs assumed by Investment

Adviser (See Note 8) | | | (3,624 | ) | |

| Custody earnings credit | | | (3,977 | ) | |

| Net Expenses | | | 7,530,679 | | |

| Net Investment Loss | | | (400,662 | ) | |

Net Realized and Unrealized Gain (Loss) on

Portfolio Positions: | |

| Net realized loss on investments | | | (1,113,412 | ) | |

Net change in unrealized appreciation

(depreciation) on: | |

| Unaffiliated Investments | | | 28,585,651 | | |

| Affiliated Investments (see note 4) | | | (60,240 | ) | |

| Liquidated Security | | | 7,298 | | |

Net change in unrealized

appreciation (depreciation) | | | 28,532,709 | | |

| Net Gain | | | 27,419,297 | | |

| Net Increase in Net Assets from Operations | | $ | 27,018,635 | | |

See accompanying notes to financial statements.

13

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Statement of Changes in Net Assets

| Increase (Decrease) in Net Assets: | | (Unaudited)

Six months

Ended

June 30,

2006 | | Year Ended

December 31,

2005 | |

| From Operations: | |

| Net investment income (loss) | | $ | (400,662 | ) | | $ | 3,637,119 | | |

| Net realized gain (loss) on investments | | | (1,113,412 | ) | | | 55,808,347 | | |

Net change in unrealized appreciation

on investments | | | 28,532,709 | | | | 84,085,468 | | |

| Net Increase in Net Assets from Operations | | | 27,018,635 | | | | 143,530,934 | | |

| Distributions Declared to Shareholders: | |

| From net investment income: | | | (3,589,922 | ) | | | — | | |

| From net realized gains: | | | (50,639,120 | ) | | | — | | |

| Total Distributions Declared to Shareholders | | | (54,229,042 | ) | | | — | | |

| Share Transactions: | |

| Subscriptions | | | 156,774,798 | | | | 281,666,708 | | |

| Distributions reinvested | | | 54,229,042 | | | | — | | |

| Redemptions | | | (50,760,087 | ) | | | (85,055,673 | ) | |

| Net Increase from Share Transactions | | | 160,243,753 | | | | 196,611,035 | | |

| Total Increase in Net Assets | | | 133,033,346 | | | | 340,141,969 | | |

| Net Assets: | |

| Beginning of period | | | 1,493,695,122 | | | | 1,153,553,153 | | |

| End of period | | $ | 1,626,728,468 | | | $ | 1,493,695,122 | | |

| Undistributed (Accumulated) Net Investment Income (Loss) | | $ | (445,767 | ) | | $ | 3,544,817 | | |

See accompanying notes to financial statements.

14

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Financial Highlights

| | | (Unaudited)

Six Months Ended

June 30, | | Year Ended December 31, | |

| Selected data for a share outstanding throughout each period | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | |

| Net Asset Value, Beginning of Period | | $ | 34.90 | | | $ | 31.37 | | | $ | 26.51 | | | $ | 18.51 | | | $ | 22.25 | | | $ | 19.99 | | |

| Income from Investment Operations: | |

| Net investment income (loss) (a) | | | (0.01 | ) | | | 0.09 | | | | (0.14 | ) | | | (0.11 | ) | | | (0.10 | ) | | | (0.04 | ) | |

| Net realized and unrealized gain (loss) on investments | | | 0.72 | | | | 3.44 | | | | 5.00 | | | | 8.11 | | | | (3.64 | ) | | | 2.31 | | |

| Total from Investment Operations | | | 0.71 | | | | 3.53 | | | | 4.86 | | | | 8.00 | | | | (3.74 | ) | | | 2.27 | | |

| Less Distributions Declared to Shareholders: | |

| From net investment income | | | (0.08 | ) | | | — | | | | — | | | | — | | | | — | | | | (0.01 | ) | |

| From net realized capital gains | | | (1.15 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | |

| Total Distributions Declared to Shareholders | | | (1.23 | ) | | | — | | | | — | | | | — | | | | — | | | | (0.01 | ) | |

| Net Asset Value, End of Period | | $ | 34.38 | | | $ | 34.90 | | | $ | 31.37 | | | $ | 26.51 | | | $ | 18.51 | | | $ | 22.25 | | |

| Total Return (b) | | | 2.00 | %(c) | | | 11.25 | %(d) | | | 18.33 | % | | | 43.22 | % | | | (16.81 | )% | | | 11.39 | % | |

| Ratios to Average Net Assets/Supplemental Data: | |

| Expenses | | | 0.94 | %(e)(f) | | | 0.95 | %(f) | | | 1.00 | %(f) | | | 0.99 | %(f) | | | 1.05 | %(f) | | | 0.99 | % | |

| Net investment income (loss) | | | (0.05 | )%(e)(f) | | | 0.29 | %(f) | | | (0.49 | )%(f) | | | (0.48 | )%(f) | | | (0.47 | )%(f) | | | (0.20 | )% | |

| Waiver | | | — | | | | 0.00 | %(g) | | | — | | | | — | | | | — | | | | — | | |

| Portfolio turnover rate | | | 7 | %(c) | | | 11 | % | | | 15 | % | | | 10 | % | | | 16 | % | | | 18 | % | |

| Net assets, end of period (000's) | | $ | 1,626,728 | | | $ | 1,493,695 | | | $ | 1,153,553 | | | $ | 822,658 | | | $ | 471,726 | | | $ | 498,186 | | |

(a) Net investment income (loss) per share was based upon the average shares outstanding during the period.

(b) Total return at net asset value assuming all distributions are reinvested.

(c) Not annualized.

(d) Had the Investment Adviser not waived a portion of expenses, total return would have been reduced.

(e) Annualized.

(f) The benefits derived from custody fees paid indirectly had no impact.

(g) Rounds to less than 0.01%.

See accompanying notes to financial statements.

15

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Notes to Financial Statements (Unaudited)

1. Nature of Operations

Wanger U.S. Smaller Companies (the "Fund") is a series of Wanger Advisors Trust (the "Trust"), an open-end management investment company organized as a Massachusetts business trust. The investment objective of the Fund is to seek long-term growth of capital. The Fund is available only for allocation to certain life insurance company separate accounts established for the purpose of funding qualified and non-qualified variable annuity contracts, and variable life insurance policies and may also be offered directly to certain types of pension plans and retirement arrangements.

2. Significant Accounting Policies

Security valuation

Securities of the Fund are valued at market value or, if a market quotation for a security is not readily available or is deemed not to be reliable because of events or circumstances that have occurred between the market quotation and the time as of which the security is to be valued, the security is valued at a fair value determined in accordance with procedures established by the Board of Trustees. Securities traded on securities exchanges or in over-the-counter markets in which transaction prices are reported are valued at the last sales price at the time of valuation. If a security is traded principally on the Nasdaq Stock Market Inc., the Nasdaq Official Closing Price will be applied. Securities for which there are no reported sales on the valuation date are valued at the latest bid quotation. Short-term debt obligations having a maturity of 60 days or less from the valuation date are valued on an amortized cost basis, whic h approximates fair value. Securities for which quotations are not readily available and any other assets are valued as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees. The Trust has retained an independent statistical fair value pricing service to assist in the fair valuation process for securities principally traded in a foreign market in order to adjust for possible changes in value that may occur between the close of the foreign exchange and the time at which fund shares are priced. If a security is valued at a "fair value," that value may be different from the last quoted market price for the security.

Repurchase agreements

The Fund may engage in repurchase agreement transactions. The Fund, through its custodians, receives delivery of underlying securities collateralizing each repurchase agreement. The Fund's investment adviser determines that the value of the underlying securities is at all times at least equal to the repurchase price including interest. In the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral may be subject to legal proceedings.

Security transactions and investment income

Security transactions are accounted for on the trade date (date the order to buy or sell is executed) and dividend income is recorded on the ex-dividend date, except that certain dividends from foreign securities are recorded as soon as the information is available to the Fund. Interest income is recorded on an accrual basis and includes amortization of discounts on short-term debt obligations and on long-term debt obligations when required for federal income tax purposes. Realized gains and losses from security transactions are reported on an identified cost basis.

The Fund estimates components of distributions from Real Estate Investment Trusts ("REITS"). Distributions received in excess of income are recorded as a reduction of the cost of the related investments. Results of operations for the year reflect a change in estimate of these components using more current tax reporting received from REIT investments. The change in estimate has no impact on the Fund's net assets.

Restricted Securities

Restricted securities are securities that may only be resold upon registration under federal securities laws or in transactions exempt from registration. In some cases, the issuer of restricted securities has agreed to register such securities for resale at the issuer's expense either upon demand by the Fund or in connection with another registered offering of the securities. Many restricted securities may be resold in the secondary market in transactions exempt from registration. Such restricted securities may be determined to be liquid under criteria established by the Board of Trustees. The Fund will not incur any registration costs upon such resale.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America ("GAAP") requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results may differ from those estimated.

Fund share valuation

Fund shares are sold and redeemed on a continuing basis at net asset value. Net asset value per share is determined daily as of the close of trading on the New York Stock Exchange (the "Exchange") on each day the Exchange is open for trading by dividing the total value of the Fund's investments and other assets, less liabilities, by the number of Fund shares outstanding.

Custody fees/Credits

Custody fees are reduced based on the Fund's cash balances maintained with the custodian. The Fund could have invested a portion of the assets utilized in connection with the expense offset arrangement in an income-producing asset if it had not entered into such an agreement. The amount is disclosed as a reduction of total expenses in the Statement of Operations.

Indemnification

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties which provide general indemnities. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also under the Trust's organizational documents, the Trustees and Officers of the Trust are indemnified against certain liabilities that may arise out of their duties to the Trust. However based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be minimal.

Federal income taxes

The Fund has complied with the provisions of the Internal Revenue Code available to regulated investment companies and, in the manner provided therein, distributes all its taxable income, as well as any net realized gain on sales of investments and foreign currency transactions reportable for federal income tax purposes. Accordingly, the Fund paid no federal income taxes and no federal income tax provision was required.

Distributions to shareholders

Distributions to shareholders are recorded on the ex-date.

3. Federal Tax Information

Capital losses carryforwards of $5,327,851 were utilized during the year ended December 31, 2005.

4. Transactions With Affiliates

Columbia Wanger Asset Management, L.P., ("Columbia WAM") a wholly owned subsidiary of Columbia Management Group, Inc. ("CM"), which in turn is an indirect wholly owned subsidiary of Bank of America Corporation ("BOA"),

16

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Notes to Financial Statements (Unaudited)

furnishes continuing investment supervision to the Fund and is responsible for the overall management of the Fund's business affairs.

Under the Fund's investment management agreement, fees are accrued daily and paid monthly to Columbia WAM at the annual rates shown in the table below:

| Average Daily Net Assets | | Annual Fee Rate | |

| For the first $100 million | | | 0.99 | % | |

| Next $150 million | | | 0.94 | % | |

| In excess of $250 million | | | 0.89 | % | |

For the six months ended June 30, 2006, the Fund's annualized effective investment advisory fee rate was 0.90%.

Certain officers and trustees of the Trust are also officers of Columbia WAM. On June 7, 2006, the board of trustees of Wanger Advisors Trust nominated for election as trustees to the Wanger Advisors Trust board 11 individuals (each a "Nominee" and collectively the "Nominees"). Two of the Nominees are currently trustees of the Trust and the remaining nine Nominees are currently trustees of the Columbia Acorn Trust. A special meeting of the shareholders has been scheduled for September 11, 2006 to vote on the election of the Nominees. Notice of the special meeting, a proxy statement and a proxy card has been mailed to all shareholders of record as of the close of business on July 14, 2006. The Trust makes no direct payments to its officers and trustees who are affiliated with Columbia WAM. For the six months ended June 30, 2006, the Fund paid $69,498 to trustees not affiliated with Columbia WAM.

The Board of Trustees appointed a Chief Compliance Officer to the Fund in accordance with federal securities regulations. The Fund will pay its pro-rata share of the expenses associated with the Office of the Chief Compliance Officer. These expenses are disclosed separately as "Chief compliance officer expenses" in the Statement of Operations.

Columbia Management Distributors, Inc., a wholly owned subsidiary of BOA, serves as the principal underwriter of the Trust and receives no compensation for its services.

Columbia Management Services, Inc. (the "Transfer Agent"), a wholly owned subsidiary of BOA, provides shareholder services to the Fund and has subcontracted with Boston Financial Data Services ("BFDS") to serve as subtransfer agent. For such services, the Transfer Agent receives a fee, paid monthly, at the annual rate of $21.00 per open account. During the period covered by this report, the Transfer Agent has voluntarily waived its right to reimbursement for certain out-of-pocket expenses.

Columbia WAM has delegated to Columbia Management Advisors, LLC, an indirect wholly owned subsidiary of BOA, responsibility to provide certain administrative services to the Fund.

An affiliate may include any company in which a fund owns five percent or more of its outstanding voting shares. On June 30, 2006, the Fund held five percent or more of the outstanding voting securities of one or more companies. Details of investments in those affiliated companies are presented on page 12.

During the six months ended June 30, 2006, the Fund engaged in purchase and sales transactions with funds that have a common investment adviser (or affiliated investment advisers), common Directors/Trustees, and/or common Officers. These purchase and sale transactions complied with provisions of Rule 17a-7 under the Investment Company Act of 1940 and were $5,335 and $0, respectively.

5. Borrowing Arrangements

The Trust participates in a $150,000,000 credit facility, which was entered into to facilitate portfolio liquidity. Interest is charged to each participating fund based on its borrowings at a rate per annum equal to the Federal Funds rate plus 0.50%. In addition, a commitment fee of 0.10% per annum is accrued and apportioned among the participating funds based on their pro-rata portion of the unutilized line of credit. The commitment fee is included in "Other expenses" on the Statement of Operations. No amounts were borrowed under this facility for the six months ended June 30, 2006.

6. Fund Share Transactions

Proceeds and payments on Fund shares as shown in the statement of changes in net assets are in respect of the following numbers of shares:

| | | Six months ended

June 30, 2006 | | Year ended

December 31, 2005 | |

| Shares sold | | | 4,390,839 | | | | 8,661,418 | | |

Shares issued in reinvestment

of dividend distributions | | | 1,565,955 | | | | — | | |

| Less shares redeemed | | | 1,439,076 | | | | 2,637,907 | | |

| Net increase in shares outstanding | | | 4,517,718 | | | | 6,023,511 | | |

7. Investment Transactions

The aggregate cost of purchases and proceeds from sales other than short-term obligations for the six months ended June 30, 2006 were $209,722,034 and $97,255,928.

8. Legal Proceedings

Columbia WAM, Columbia Acorn Trust, another mutual fund family advised by Columbia WAM, and the trustees of Colombia Acorn Trust, are named as defendants in class and derivative complaints which have been consolidated in a Multi-District Action in the federal district court for the District of Maryland (the "MDL Action"). These lawsuits contend that defendants permitted certain investors to market time their trades in certain Columbia Acorn Funds. The MDL Action is ongoing. However, all claims against Columbia Acorn Trust and the independent trustees of Columbia Acorn Trust have been dismissed.

The Columbia Acorn Trust and Columbia WAM are also defendants in a class action lawsuit that alleges, in summary, that the Columbia Acorn Trust and Columbia WAM exposed shareholders of Columbia Acorn International fund to trading by market timers by allegedly (a) failing to properly evaluate daily whether a significant event affecting the value of that fund's securities had occurred after foreign markets had closed but before the calculation of the funds' net asset value ("NAV"); (b) failing to implement the fund's portfolio valuation and share pricing policies and procedures; and (c) failing to know and implement applicable rules and regulations concerning the calculation of NAV (the "Fair Valuation Lawsuit"). The Seventh Circuit ruled that the plaintiffs' state law claims were preempted under federal law resulting in the dismissal of plaintiffs' complaint. Plaintiffs appealed the Seventh Circuit's ruling to the United States S upreme Court.

On March 21, 2005, a class action complaint was filed against the Columbia Acorn Trust and Columbia WAM seeking to rescind the Contingent Deferred Sales Charges assessed upon redemption of Class B shares of Columbia Acorn Funds due to the alleged market timing of the Columbia Acorn Funds. In addition to the rescission of sales charges, plaintiffs seek recovery of actual damages, attorneys' fees and costs. The case has been transferred to the MDL Action in the federal district court of Maryland.

On April 4, 2006, all of the parties to the MDL Action executed a letter settlement agreement intended to fully resolve all of the lawsuits consolidated in the MDL Action as well as the Fair Valuation Lawsuit. The settlement has not yet been finalized or approved by the court.

Columbia WAM, the Columbia Acorn Funds and the trustees of Columbia Acorn Trust are also defendants in a consolidated lawsuit filed in the federal district court of Massachusetts alleging that Columbia WAM used fund assets to make undisclosed payments to brokers as an incentive for the brokers to market the Columbia Acorn Funds over the other mutual funds to investors. The complaint alleges Columbia WAM and the Trustees of the Trust breached certain common laws duties and federal laws.

17

Wanger U.S. Smaller Companies Fund 2006 Semiannual Report

Notes to Financial Statements (Unaudited)

On November 30, 2005, the court dismissed all of the claims alleged against all of the parties in the consolidated complaint. Plaintiffs timely filed a notice of appeal of the district court's dismissal order with the First Circuit Court of Appeals. The parties subsequently executed a settlement term sheet to fully resolve all claims in the litigation. The settlement has not yet been finalized or approved by the court.

The Columbia Acorn Trust and Columbia WAM intend to defend these suits vigorously.

As a result of these matters or any adverse publicity or other developments resulting from them, there may be increased redemptions or reduced sales of Fund shares, which could increase transaction costs or operating expenses, or have other adverse consequences for the Funds.