UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08748 | |||||||

| ||||||||

Wanger Advisors Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

227 W. Monroe Street Suite 3000 Chicago, IL |

| 60606 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Mary C. Moynihan Perkins Coie LLP 700 13th Street, NW Suite 600 Washington, DC 20005

Paul B. Goucher, Esq. Columbia Management Investment Advisers, LLC 100 Park Avenue New York, New York 10017

P. Zachary Egan Columbia Acorn Trust 227 West Monroe Street, Suite 3000 Chicago, Illinois 60606 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (312) 634-9200 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2016 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

SEMIANNUAL REPORT

June 30, 2016

COLUMBIA WANGER FUNDS

Managed by Columbia Wanger Asset Management, LLC

WANGER INTERNATIONAL

Wanger International

2016 Semiannual Report

Table of Contents

2 | A View on Brexit | ||||||

| 3 | Understanding Your Expenses | ||||||

4 | Performance Review | ||||||

| 6 | Statement of Investments | ||||||

13 | Statement of Assets and Liabilities | ||||||

13 | Statement of Operations | ||||||

14 | Statement of Changes in Net Assets | ||||||

15 | Financial Highlights | ||||||

16 | Notes to Financial Statements | ||||||

19 | Board Approval of the Advisory Agreement | ||||||

Columbia Wanger Asset Management, LLC (CWAM) is one of the leading global small- and mid-cap equity managers in the United States with over 45 years of small- and mid-cap investment experience. As of June 30, 2016, CWAM managed $17 billion in assets. CWAM is the investment manager to Wanger USA, Wanger International and Wanger Select (together, the Columbia Wanger Funds) and the Columbia Acorn Family of Funds.

An important note: Columbia Wanger Funds are available only through variable annuity contracts and variable life insurance policies issued by participating insurance companies or certain eligible retirement plans. Columbia Wanger Funds are not offered directly to the public and are not available in all contracts, policies or plans. Contact your financial advisor or insurance representative for more information. Columbia Wanger Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA, and are managed by CWAM.

Investors should carefully consider investment objectives, risks and expenses of the Fund before investing. For variable fund and variable contract prospectuses, which contain this and other important information, including the fees and expenses imposed under your contract, investors should contact their financial advisor or insurance representative. Read the prospectus for the Fund and your variable contract carefully before investing.

The views expressed in "A View on Brexit" and in the Performance Review reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Wanger Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Wanger Fund. References to specific company securities should not be construed as a recommendation or investment advice.

1

Wanger International 2016 Semiannual Report

A View on Brexit

Global equity markets were caught on the back foot by the outcome of the UK referendum on continued European Union (EU) membership. The long-term political and economic implications of this decision are potentially vast and impossible to discern at this stage, not least because they will be shaped by how policymakers respond. As investors globally reprice risk and reposition portfolios in light of currency sensitivity and how they expect this outcome to bear differently on sectors, countries and companies, there will be mispricing opportunities. This is good for stock pickers and we expect to be active. We will be looking closely at how strong players in diverse industries might improve their competitive positions, as growth opportunities become more scarce and costs of capital among competitors more differentiated. We expect the relatively high balance sheet and business model quality of the stocks that we hold in the Columbia Wanger Funds to prove helpful in coming quarters because the risk premium has gone up, as evidenced by increased volatility, compressed multiples in some pockets of the market such as European banks, and sharp currency swings.

This political development is nonetheless clearly a negative one. The United Kingdom is the fifth largest economy in the world and the second largest within the EU. It has been a member of the European Economic Community (precursor to the EU) since 1973.i The UK exit raises uncertainties about global growth, heightens risk aversion, and it will preoccupy European policymakers at a time when they are already challenged by anemic growth, high unemployment, refugee immigration flows, and international and domestic security concerns.

While many market observers view the outcome of the referendum as a comment on, and existential threat to, the overall European integration project, it may, rather, reflect a larger process at work, namely increasing middle-class discontent with the perceived consequences of globalization in industrialized democracies. Rising populism and nativist resentments in Europe and the United States could be

harbingers of future policy regimes that place less value on minimizing trade friction, and the mobility of capital and labor, all of which have contributed to global prosperity. The evolving framework for global trade and investment over the last 25 years has been an enormous engine of global growth. During this period, a substantial percentage of the world's population once living within largely economically isolated communist states was integrated into the modern global economy as producers and consumers. This has raised standards of living in emerging markets and reduced the cost of consumer goods in industrialized countries, while creating new and growing markets for the sort of technologically sophisticated exports that support high-paying jobs in industrialized countries.

The Columbia Wanger Funds have benefited meaningfully from these trends. With Brexit, the EU will lose its strongest advocate of economic liberalism, which has served as an important counterpoint to statist perspectives in Germany and France. At a minimum, it appears that domestic policies are poised to pivot toward the populist issue of economic inequality, which in Europe may manifest itself in a slowdown or reversal of structural reforms in EU labor markets, with negative consequences for productivity and, with it, standards of living. Fiscal tightening, where necessary, could be scaled back as a salve to populists, and it seems likely that industrialized countries will see increased constraints on immigration, even where demographically driven labor shortages exist.

While this could well be regarded as overall bad news for asset owners, opportunities will likely present themselves. For many years, the Columbia Wanger Funds have explored how factory automation is deployed to reduce labor costs or to replace labor altogether, trends which could be accelerated by a reduction in immigration. London will fight hard to retain its role as the center of European finance, but bank chiefs are already talking about decamping elsewhere, which could create opportunity in continental European real estate and

construction. As corporate investment decision-making and household spending slow amidst the uncertainty, fiscal stimulus could be sought via public infrastructure projects, which would be good for constructors and suppliers of building materials. Public policy that increases labor's share of income would benefit consumer companies oriented to a lower middle class demographic. Other policy interventions could result in continued ultra-low interest rates, with implications for interest-rate sensitive businesses. In any case, it seems that earnings growth will continue to be a scarce factor in a low-growth world.

P. Zachary Egan

President and Global Chief Investment Officer

Columbia Wanger Asset Management, LLC

i http://ukandeu.ac.uk/fact-figures/when-did-britain-decide-to-join-the-european-union/

2

Wanger International 2016 Semiannual Report

Understanding Your Expenses

As a shareholder, you incur three types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees. There are also ongoing costs, which generally include management fees and other expenses for Wanger International (the Fund). Lastly, there may be additional fees or charges imposed by the insurance company that sponsors your variable annuity and/or variable life insurance product. The following information is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to help you compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in the Fund during the period. The actual and hypothetical information in the table below is based on an initial investment of $1,000 at the beginning of the period indicated and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the Fund's actual operating expenses and total return for the period. You may use the Actual information, together with the amount invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the results by the expenses paid during the period under the Actual column. The amount listed in the "Hypothetical" column assumes a 5% annual rate of return before expenses (which is not the Fund's actual return) and then applies the Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the period. See "Compare with other funds" below for details on how to use the hypothetical data.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Fund with other funds. To do so, compare the hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing cost of investing in a fund only and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical calculations are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. If transaction costs were included in these calculations, your costs would be higher.

January 1, 2016 – June 30, 2016

| Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during period ($) | Fund's annualized expense ratio (%)* | ||||||||||||||||||||||||||||

Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | ||||||||||||||||||||||||||

Wanger International | 1,000.00 | 1,000.00 | 998.40 | 1,019.19 | 5.66 | 5.72 | 1.14 | ||||||||||||||||||||||||

* Expenses paid during the period are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 366.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Fund. Expenses paid during the period do not include any insurance charges imposed by your insurance company's separate account. The hypothetical example provided is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

3

Wanger International 2016 Semiannual Report

Performance Review Wanger International

|

| ||||||

| P. Zachary Egan Co-Portfolio Manager | Louis J. Mendes Co-Portfolio Manager | ||||||

Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. International investing involves certain risks and volatility due to potential political, economic or currency instabilities and different, potentially less stringent, financial and accounting standards than those generally applicable to U.S. issuers. Risks are enhanced for emerging market issuers. Investments in small- and mid-cap companies involve risks and volatility and possible illiquidity greater than investments in larger, more established companies.

Wanger International ended the semiannual period down 0.16%, performing in line with the Fund's primary benchmark, the MSCI ACWI Ex USA Small Cap Index (Net), which was down 0.20%. Major factors impacting markets during the period were the surprise outcome of the Brexit vote in the United Kingdom, continued strong performance from the commodities sector, and signs of strength in a number of developing economies, particularly in Southeast Asia.

As discussed in our letter at the front of this report, the United Kingdom's decision to exit the European Union was somewhat unexpected by global markets and triggered a short-term flight to safety as investors considered the potential consequences of this action. The immediate reaction was a rise in the U.S. dollar and the Japanese yen, while the UK pound fell to its lowest levels in the last 30 years. Renewed discussions of a prolonged low interest rate environment in most developed economies provided a positive jolt to many emerging markets with economies sensitive to global rates. While the Fund declined nearly 9% over the two trading days following the Brexit vote, it regained over half of this drop within a week. As long-term investors, our focus remained on the medium-term impacts this decision could have on Fund holdings, and the adjustments we made to the portfolio were modest. We took advantage of short-term price volatility around Brexit to add to UK self-storage company Big Yellow, where we struggle to see how Brexit will materially change prospects going forward. In continental Europe, the Fund's long-standing strategic underweight in European banks proved positive, as the uncertainty raised by the referendum weighed heavily on these stocks.

One area that performed well throughout the period was commodities. Year to date, the energy and basic materials sectors of the benchmark were up 9% and 13%, respectively, in U.S. dollars (USD). Continued stable economic growth and very low interest rates across developed economies, combined with the positive effects of China's stimulus policies enacted in 2015, have reignited confidence in the underlying price for a number of basic materials. Those emerging markets dependent upon commodity exports outperformed but were modest weights within the Fund and benchmark. Year to date within the Fund's small-cap equity benchmark, Brazil (+48% in USD), Russia (+58% in USD) and South Africa

(+28% in USD) all rallied strongly with strengthening currencies after a mostly dismal 2015 performance. A long-term Fund position in Tahoe Resources, a low-cost silver miner based in Guatemala, was a top contributor in the period, rising 73% on the rebound in silver prices.

Current political uncertainty appears likely to drive a continuation of loose monetary policy in Japan and Europe for the near term. The low interest rate environment is driving a global search for yield, buoying the prices of stable, cash-generative and dividend-paying stocks. Unprecedented intervention to keep interest rates low will eventually reverse, which we believe will make current valuations assigned to these "safe haven" securities hard to justify, particularly where there is little earnings growth. Accordingly, we have worked hard over the period to increase the Fund's exposure to companies with solid earnings growth. We expect these businesses to prove more resilient, should interest rates normalize. If this mean reversion takes longer than expected, this will likely be because of ongoing weak demand globally, in which case companies with growing earnings should command a valuation premium, also not a bad outcome for long-term growth investors. New Fund positions that reflect this focus on growth include DIP, an operator of online websites and mobile applications for temporary job listings in Japan. DIP is capitalizing on an aging Japanese population that is driving a labor shortage; a corporate preference for temporary workers to maintain flexibility and curb costs; and increased user preference for Internet and mobile job listings. Since 2009, full-time workers in Japan have declined by 2.35 million, while part-time jobs have increased by 1.17 million.

Fund holdings are as of the date given, are subject to change at any time, and are not recommendations to buy or sell any security.

4

Wanger International 2016 Semiannual Report

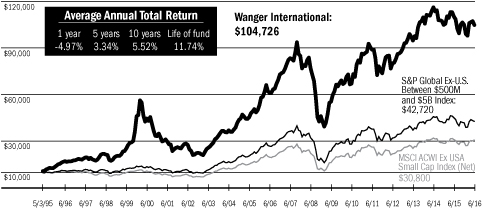

Growth of a $10,000 Investment in Wanger International

May 3, 1995 (inception date) through June 30, 2016

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. For most recent month-end performance updates, please visit investor.columbiathreadneedleus.com.

This graph compares the results of $10,000 invested in Wanger International on May 3, 1995 (the date the Fund began operations) through June 30, 2016, to the MSCI ACWI Ex USA Small Cap Index (Net) and the S&P Global Ex-U.S. Between $500M and $5B Index with dividends and capital gains reinvested. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index.

Top 10 Holdings

As a percentage of net assets, as of 6/30/16

| 1. CCL Industries (Canada) Global Label Converter | 2.0 | % | |||||

| 2. Seria (Japan) 100 Yen Discount Stores | 1.6 | ||||||

| 3. SimCorp (Denmark) Software for Investment Managers | 1.6 | ||||||

| 4. Aurelius (Germany) European Turnaround Investor | 1.5 | ||||||

| 5. Domino's Pizza Enterprises (Australia) Domino's Pizza Operator in Australia & New Zealand | 1.4 | ||||||

| 6. Trelleborg (Sweden) Manufacturer of Sealing, Dampening & Protective Solutions for Industry | 1.4 | ||||||

| 7. Elior Group (France) Contract Caterer & Travel Concessionary | 1.4 | ||||||

| 8. Halma (United Kingdom) Health & Safety Sensor Technology | 1.3 | ||||||

| 9. Ag Growth (Canada) Manufacturer of Augers & Grain Handling Equipment | 1.3 | ||||||

| 10. Distribuidora Internacional de Alimentación (Spain) Discount Retailer in Spain & Latin America | 1.3 | ||||||

Top holdings exclude short-term holdings and cash, if applicable.

Top 5 Countries

As a percentage of net assets, as of 6/30/16

Japan | 22.5 | % | |||||

United Kingdom | 12.2 | ||||||

Germany | 6.9 | ||||||

Canada | 6.4 | ||||||

Sweden | 6.1 | ||||||

Results as of June 30, 2016

2nd quarter* | Year to date* | 1 year | 5 years | 10 years | |||||||||||||||||||

Wanger International | -1.13 | % | -0.16 | % | -4.97 | % | 3.34 | % | 5.52 | % | |||||||||||||

| MSCI ACWI Ex USA Small Cap Index (Net)** | -0.87 | -0.20 | -5.46 | 2.28 | 4.09 | ||||||||||||||||||

| S&P Global Ex-U.S. Between $500M and $5B Index | 0.24 | 1.98 | -5.35 | 2.49 | 4.76 | ||||||||||||||||||

NAV as of 6/30/16: $24.15

* Not annualized.

** The Fund's primary benchmark effective January 1, 2016. Prior to January 1, 2016, the S&P Global Ex-U.S. Between $500M and $5B Index was the Fund's primary benchmark.

Performance numbers reflect all Fund expenses but do not include any fees and expenses imposed under your variable annuity contract or life insurance policy or qualified pension or retirement plan. If performance numbers included the effect of these additional charges, they would be lower.

The Fund's annual operating expense ratio of 1.11% is stated as of the Fund's prospectus dated May 1, 2016, and differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and/or expense reimbursements as well as different time periods used in calculating the ratios.

All results shown assume reinvestment of distributions.

The MSCI ACWI Ex USA Small Cap Index (Net) captures small-cap representation across 22 of 23 developed market countries (excluding the United States) and 23 emerging markets countries. The S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States. Indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

Portfolio characteristics and holdings are subject to change periodically and may not be representative of current characteristics and holdings.

5

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

| Number of Shares | Value | ||||||||||

Equities – 98.0% | |||||||||||

Asia – 41.7% | |||||||||||

Japan – 22.5% | |||||||||||

102,700 | Seria 100 Yen Discount Stores | $ | 8,500,064 | ||||||||

109,600 | FamilyMart Convenience Store Operator | 6,679,165 | |||||||||

477,700 | Aeon Mall Suburban Shopping Mall Developer, Owner & Operator | 6,250,246 | |||||||||

192,900 | Bandai Namco Branded Toys & Related Content | 4,978,077 | |||||||||

84,800 | Yonex (a) Branded Sporting Goods Manufacturer | 4,723,574 | |||||||||

195,771 | Doshisha Consumer Goods Wholesaler | 3,761,055 | |||||||||

319,700 | Ushio Industrial Light Sources | 3,756,022 | |||||||||

44,300 | Hikari Tsushin Office IT/Mobiles/Insurance Distribution | 3,711,163 | |||||||||

133,600 | Glory Currency Handling Systems & Related Equipment | 3,635,199 | |||||||||

228,600 | Santen Pharmaceutical Specialty Pharma (Ophthalmic Medicine) | 3,592,949 | |||||||||

1,074,000 | Seven Bank ATM Processing Services | 3,333,602 | |||||||||

123,400 | DIP Mobile Temporary Job Information Provider | 3,329,291 | |||||||||

379,000 | NOF Specialty Chemicals, Life Science & Rocket Fuels | 3,145,683 | |||||||||

145,200 | Aeon Financial Service Diversified Consumer-related Finance Company in Japan | 3,144,007 | |||||||||

429,300 | iStyle Cosmetics Review Portal & Retailer | 3,089,206 | |||||||||

1,125 | Kenedix Retail REIT Retail REIT in Japan | 3,028,943 | |||||||||

24,450 | Hirose Electric Electrical Connectors | 3,006,518 | |||||||||

82,800 | Japan Airport Terminal (a) Airport Terminal Operator at Haneda | 3,004,089 | |||||||||

2,922 | LaSalle Logiport REIT (b) Logistics REIT in Japan | 2,974,266 | |||||||||

| Number of Shares | Value | ||||||||||

65,020 | Milbon Hair Products for Salons | $ | 2,931,814 | ||||||||

31,900 | Disco Semiconductor Dicing & Grinding Equipment | 2,885,030 | |||||||||

148,000 | Daiseki Waste Disposal & Recycling | 2,862,213 | |||||||||

69,300 | JIN (a) Eyeglasses Retailer | 2,719,748 | |||||||||

162,200 | OSG Consumable Cutting Tools | 2,701,979 | |||||||||

48,500 | OBIC Computer Software | 2,669,747 | |||||||||

90,400 | Nakanishi Dental Tools & Machinery | 2,661,254 | |||||||||

56,000 | Otsuka One-stop IT Services & Office Supplies Provider | 2,618,635 | |||||||||

111,400 | Aica Kogyo Laminated Sheets, Building Materials & Chemical Adhesives | 2,545,861 | |||||||||

77,000 | MonotaRO Online Maintenance, Repair & Operations Goods Distributor in Japan | 2,545,693 | |||||||||

52,000 | Asahi Intecc Medical Guidewires for Surgery | 2,541,054 | |||||||||

126,500 | Icom Two Way Radio Communication Equipment | 2,479,609 | |||||||||

420 | Industrial & Infrastructure Fund Industrial REIT in Japan | 2,341,780 | |||||||||

452,000 | Dowa Holdings Environmental/Recycling, Nonferrous Metals, Electronic Material & Metal Processing | 2,329,759 | |||||||||

244,000 | Yamaguchi Financial Group Regional Bank in Yamaguchi, Fukuoka & Hiroshima | 2,307,336 | |||||||||

180,600 | Kintetsu World Express Airfreight Logistics | 2,187,879 | |||||||||

139,300 | NGK Spark Plug Automobile Parts | 2,102,703 | |||||||||

71,400 | Sega Sammy Holdings Gaming Software/Hardware & Leisure Facilities | 768,985 | |||||||||

121,844,198 | |||||||||||

See accompanying notes to financial statements.

6

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

| Number of Shares | Value | ||||||||||

Korea – 3.9% | |||||||||||

143,008 | Koh Young Technology Inspection Systems for Printed Circuit Boards | $ | 5,108,793 | ||||||||

101,272 | Korea Investment Holdings Brokerage & Asset Management | 3,733,602 | |||||||||

10,330 | KCC Paint & Housing Material Manufacturer | 3,435,921 | |||||||||

114,800 | ModeTour Network Travel Services | 2,770,947 | |||||||||

48,100 | Kepco Plant Service & Engine Power Plant & Grid Maintenance | 2,719,442 | |||||||||

17,922 | Nongshim Holdings Holding Company of Food Conglomerate | 2,291,692 | |||||||||

977 | Orion Corp Confectionery & Snack Manufacturer | 801,946 | |||||||||

20,862,343 | |||||||||||

Taiwan – 3.1% | |||||||||||

386,000 | Silergy Chinese Provider of Analog & Mixed Digital Integrated Circuits | 4,565,830 | |||||||||

140,000 | St. Shine Optical Disposable Contact Lens Original Equipment Manufacturer | 3,163,737 | |||||||||

277,000 | Ginko International Contact Lens Maker in China | 2,893,965 | |||||||||

171,803 | Voltronic Power Uninterruptible Power Supply Products & Solar Inverters | 2,401,628 | |||||||||

302,349 | Advantech Industrial PC & Components | 2,305,491 | |||||||||

104,000 | PChome Online Taiwanese E-commerce Company | 1,152,810 | |||||||||

16,483,461 | |||||||||||

India – 2.8% | |||||||||||

527,518 | Amara Raja Indian Maker of Auto & Industrial Batteries, Mostly for the Replacement Market | 6,804,284 | |||||||||

603,779 | TVS Motor Indian Maker of Scooters, Mopeds, Motorcycles, & Three-wheelers | 2,778,648 | |||||||||

245,385 | United Breweries Indian Brewer | 2,739,092 | |||||||||

| Number of Shares | Value | ||||||||||

399,460 | Zee Entertainment Enterprises Indian Programmer of Pay Television Content | $ | 2,711,451 | ||||||||

15,033,475 | |||||||||||

China – 2.3% | |||||||||||

116,227 | 51job – ADR (a) (b) Integrated Human Resource Services | 3,406,613 | |||||||||

17,300,000 | Jiangnan Group Cable & Wire Manufacturer | 2,778,755 | |||||||||

5,560,000 | AMVIG Holdings Chinese Tobacco Packaging Material Supplier | 2,192,381 | |||||||||

786,000 | TravelSky Technology Chinese Air Travel Transaction Processor | 1,519,512 | |||||||||

4,536,000 | NewOcean Energy Southern China Liquefied Petroleum Gas Distributor | 1,489,648 | |||||||||

6,453,000 | Sihuan Pharmaceutical Holdings Group Chinese Generic Drug Manufacturer | 1,232,614 | |||||||||

12,619,523 | |||||||||||

Singapore – 2.1% | |||||||||||

4,032,673 | Mapletree Commercial Trust Retail & Office Property Landlord | 4,435,851 | |||||||||

8,400,000 | China Everbright Water Waste Water Treatment Operator | 3,978,841 | |||||||||

6,404,900 | SIIC Environment (b) Waste Water Treatment Operator | 2,954,831 | |||||||||

11,369,523 | |||||||||||

Hong Kong – 2.0% | |||||||||||

6,104,000 | Value Partners Mutual Fund Management | 5,652,270 | |||||||||

2,853,000 | Vitasoy International Hong Kong Soy Food Brand | 5,190,089 | |||||||||

10,842,359 | |||||||||||

Philippines – 1.3% | |||||||||||

51,759,301 | Melco Crown (Philippines) Resorts (b) Integrated Resort Operator in Manila | 4,188,930 | |||||||||

3,453,000 | Puregold Price Club Supermarket Operator in the Philippines | 3,093,553 | |||||||||

7,282,483 | |||||||||||

See accompanying notes to financial statements.

7

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

| Number of Shares | Value | ||||||||||

Cambodia – 1.1% | |||||||||||

8,652,000 | Nagacorp Casino & Entertainment Complex in Cambodia | $ | 5,777,223 | ||||||||

Indonesia – 0.6% | |||||||||||

8,839,200 | Link Net Fixed Broadband & CATV Service Provider | 2,724,077 | |||||||||

2,800,000 | Media Nusantara Citra Media Company in Indonesia | 469,749 | |||||||||

3,193,826 | |||||||||||

Total Asia | 225,308,414 | ||||||||||

Europe – 41.5% | |||||||||||

United Kingdom – 12.2% | |||||||||||

535,093 | Halma Health & Safety Sensor Technology | 7,277,806 | |||||||||

460,000 | Shaftesbury London Prime Retail REIT | 5,413,097 | |||||||||

103,000 | Rightmove Internet Real Estate Listings | 5,030,617 | |||||||||

1,292,559 | Regus Rental Office Space in Full Service Business Center | 4,997,867 | |||||||||

1,900,000 | Rentokil Initial Pest Control, Washroom & Workwear Service Provider | 4,906,578 | |||||||||

465,737 | Big Yellow UK Self Storage | 4,849,703 | |||||||||

229,513 | WH Smith Newsprint, Books & General Stationery Retailer | 4,821,725 | |||||||||

1,287,825 | Polypipe Manufacturer of Plastic Piping & Fittings | 4,464,340 | |||||||||

350,902 | Abcam Online Sales of Antibodies | 3,614,986 | |||||||||

776,943 | Domino's Pizza UK & Ireland Pizza Delivery in the UK, Ireland & Switzerland | 3,451,876 | |||||||||

56,865 | Spirax Sarco Steam Systems & Pumps for Manufacturing & Process Industries | 2,847,486 | |||||||||

3,659,853 | Assura UK Primary Health Care Property REIT | 2,679,400 | |||||||||

| Number of Shares | Value | ||||||||||

508,087 | DS Smith Packaging | $ | 2,628,696 | ||||||||

1,210,014 | Connect Group Newspaper & Magazine Distributor | 2,385,405 | |||||||||

609,228 | PureCircle (b) Natural Sweeteners | 2,380,386 | |||||||||

761,673 | Ocado (a) (b) Online Grocery Retailer | 2,350,148 | |||||||||

482,000 | Halfords UK Retailer of Leisure Goods & Auto Parts | 2,072,381 | |||||||||

66,172,497 | |||||||||||

Germany – 6.9% | |||||||||||

136,750 | Aurelius European Turnaround Investor | 8,036,843 | |||||||||

144,425 | Wirecard (a) Online Payment Processing & Risk Management | 6,361,330 | |||||||||

57,781 | MTU Aero Engines Airplane Engine Components & Services | 5,398,358 | |||||||||

59,700 | Fielmann Retail Optician Chain | 4,366,422 | |||||||||

91,367 | NORMA Group Clamps for Automotive & Industrial Applications | 4,329,022 | |||||||||

80,400 | Ströer (a) Out of Home & Online Advertising | 3,698,335 | |||||||||

131,597 | Elringklinger (a) Automobile Components | 2,590,630 | |||||||||

5,316 | Rational Commercial Ovens | 2,460,189 | |||||||||

37,241,129 | |||||||||||

Sweden – 6.1% | |||||||||||

424,154 | Trelleborg Manufacturer of Sealing, Dampening & Protective Solutions for Industry | 7,526,812 | |||||||||

673,803 | Unibet European Online Gaming Operator | 6,190,049 | |||||||||

389,377 | Recipharm (a) Contract Development Manufacturing Organization | 5,442,083 | |||||||||

300,923 | Sweco (a) Engineering Consultants | 5,220,708 | |||||||||

See accompanying notes to financial statements.

8

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

| Number of Shares | Value | ||||||||||

Sweden – 6.1% (cont) | |||||||||||

74,809 | Millicom Telecoms Operator in Latin America & Africa | $ | 4,588,735 | ||||||||

183,503 | Mekonomen (a) Nordic Integrated Wholesaler/Retailer of Automotive Parts & Service | 3,947,374 | |||||||||

22,835 | Byggmax Nordic Discount DIY Retail Chain | 173,407 | |||||||||

33,089,168 | |||||||||||

Spain – 3.3% | |||||||||||

1,220,000 | Distribuidora Internacional de Alimentación Discount Retailer in Spain & Latin America | 7,121,010 | |||||||||

941,860 | Prosegur Security Guards | 5,676,149 | |||||||||

53,000 | Viscofan Sausage Casings Maker | 2,941,536 | |||||||||

83,000 | Bolsas y Mercados Españoles Spanish Stock Markets | 2,332,671 | |||||||||

18,071,366 | |||||||||||

Denmark – 2.6% | |||||||||||

171,577 | SimCorp Software for Investment Managers | 8,420,406 | |||||||||

278,825 | William Demant Holding (b) Manufacture & Distribution of Hearing Aids & Diagnostic Equipment | 5,427,548 | |||||||||

13,847,954 | |||||||||||

Netherlands – 2.4% | |||||||||||

175,987 | Aalberts Industries Flow Control & Heat Treatment | 5,275,785 | |||||||||

66,960 | Gemalto Digital Security Solutions | 4,056,700 | |||||||||

193,387 | Brunel Temporary Specialist & Energy Staffing | 3,530,656 | |||||||||

12,863,141 | |||||||||||

Finland – 2.0% | |||||||||||

332,599 | Tikkurila Decorative & Industrial Paint in Scandinavia, Central & Eastern Europe | 6,022,562 | |||||||||

122,354 | Konecranes Manufacture & Service of Industrial Cranes & Port Handling Equipment | 3,106,085 | |||||||||

| Number of Shares | Value | ||||||||||

405,068 | Sponda Office, Retail & Logistics Properties | $ | 1,763,956 | ||||||||

10,892,603 | |||||||||||

Italy – 1.9% | |||||||||||

96,664 | Brembo High Performance Auto Braking Systems Supplier | 5,324,799 | |||||||||

84,000 | Industria Macchine Automatiche Food & Drugs Packaging & Machinery | 5,056,415 | |||||||||

10,381,214 | |||||||||||

France – 1.9% | |||||||||||

337,514 | Elior Group Contract Caterer & Travel Concessionary | 7,323,766 | |||||||||

7,529 | Eurofins Scientific Food, Pharmaceuticals & Materials Screening & Testing | 2,789,287 | |||||||||

10,113,053 | |||||||||||

Norway – 1.0% | |||||||||||

537,507 | Atea Nordic IT Hardware/Software Reseller & Integrator | 5,122,173 | |||||||||

Belgium – 0.7% | |||||||||||

62,000 | Melexis Analog & Custom IC Designer | 3,895,971 | |||||||||

Switzerland – 0.5% | |||||||||||

7,961 | Inficon Gas Detection Instruments | 2,694,620 | |||||||||

Total Europe | 224,384,889 | ||||||||||

Other Countries – 13.8% | |||||||||||

Canada – 6.4% | |||||||||||

62,716 | CCL Industries Global Label Converter | 10,914,560 | |||||||||

227,742 | Ag Growth Manufacturer of Augers & Grain Handling Equipment | 7,218,573 | |||||||||

132,947 | Vermilion Energy Canadian Exploration & Production Company | 4,233,476 | |||||||||

87,200 | Boardwalk Real Estate Investment Trust Canadian Residential REIT | 3,885,005 | |||||||||

See accompanying notes to financial statements.

9

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

| Number of Shares | Value | ||||||||||

Canada – 6.4% (cont) | |||||||||||

159,000 | Prairie Sky Royalty (a) Canadian Owner of Oil & Gas Mineral Interests | $ | 3,017,671 | ||||||||

111,000 | ShawCor Oil & Gas Pipeline Products | 2,751,910 | |||||||||

215,516 | CAE Flight Simulator Equipment & Training Centers | 2,603,974 | |||||||||

34,625,169 | |||||||||||

Australia – 3.0% | |||||||||||

146,615 | Domino's Pizza Enterprises Domino's Pizza Operator in Australia & New Zealand | 7,544,443 | |||||||||

4,520,881 | TFS Corporation Indian Sandalwood Plantation | 4,775,341 | |||||||||

572,000 | Estia Health Residential Aged Care Facility Operator | 1,983,911 | |||||||||

249,211 | Challenger Financial Annuity Provider in Australia | 1,628,154 | |||||||||

269,796 | Spotless Facility Management & Catering Company | 228,331 | |||||||||

16,160,180 | |||||||||||

United States – 1.3% | |||||||||||

79,814 | LivaNova (b) Neuromodulation & Cardiac Devices | 4,009,057 | |||||||||

93,000 | Cepheid (b) Molecular Diagnostics | 2,859,750 | |||||||||

6,868,807 | |||||||||||

South Africa – 1.2% | |||||||||||

733,480 | Coronation Fund Managers South African Fund Manager | 3,327,214 | |||||||||

356,306 | Famous Brands Quick Service Restaurant & Cafe Franchise System in Africa | 3,072,438 | |||||||||

6,399,652 | |||||||||||

Guatemala – 0.8% | |||||||||||

289,255 | Tahoe Resources Silver & Gold Projects in Guatemala, Canada & Peru | 4,332,276 | |||||||||

| Number of Shares | Value | ||||||||||

Egypt – 0.6% | |||||||||||

658,688 | Commercial International Bank of Egypt Private Universal Bank in Egypt | $ | 2,965,358 | ||||||||

New Zealand – 0.5% | |||||||||||

904,200 | Sky City Entertainment Casino & Entertainment Complex | 2,959,733 | |||||||||

Total Other Countries | 74,311,175 | ||||||||||

Latin America – 1.0% | |||||||||||

Mexico – 1.0% | |||||||||||

34,570 | Grupo Aeroportuario del Sureste – ADR Mexican Airport Operator | 5,515,644 | |||||||||

Total Latin America | 5,515,644 | ||||||||||

| Total Equities (Cost: $450,875,054) – 98.0% | 529,520,122 | (c) | |||||||||

Short-Term Investments – 0.3% | |||||||||||

$ | 1,607,078 | JPMorgan U.S. Government Money Market Fund, IM Shares (7 day yield of 0.29%) | 1,607,078 | ||||||||

| Total Short-Term Investments (Cost: $1,607,078) – 0.3% | 1,607,078 | ||||||||||

Securities Lending Collateral – 3.5% | |||||||||||

19,135,017 | Dreyfus Government Cash Management Fund, Institutional Shares (7 day yield of 0.24%) (d) | 19,135,017 | |||||||||

| Total Securities Lending Collateral (Cost: $19,135,017) – 3.5% | 19,135,017 | ||||||||||

| Total Investments (e) (Cost: $471,617,149) – 101.8% | 550,262,217 | ||||||||||

| Obligation to Return Collateral for Securities Loaned – (3.5)% | (19,135,017 | ) | |||||||||

Cash and Other Assets Less Liabilities – 1.7% | 9,434,651 | ||||||||||

Net Assets – 100.0% | $ | 540,561,851 | |||||||||

ADR = American Depositary Receipts

REIT = Real Estate Investment Trust

See accompanying notes to financial statements.

10

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

> Notes to Statement of Investments

(a) All or a portion of this security was on loan at June 30, 2016. The total market value of securities on loan at June 30, 2016 was $18,401,815.

(b) Non-income producing security.

(c) On June 30, 2016, the Fund's total equity investments were denominated in currencies as follows:

Currency | Value | Percentage of Net Assets | |||||||||

Japanese Yen | $ | 121,844,198 | 22.6 | ||||||||

Euro | 103,458,477 | 19.1 | |||||||||

British Pound | 66,172,497 | 12.3 | |||||||||

Canadian Dollar | 38,957,445 | 7.2 | |||||||||

Swedish Krona | 33,089,168 | 6.1 | |||||||||

| Other currencies less than 5% of total net assets | 165,998,337 | 30.7 | |||||||||

Total Equities | $ | 529,520,122 | 98.0 | ||||||||

(d) Investment made with cash collateral received from securities lending activity.

(e) At June 30, 2016, for federal income tax purposes, the cost of investments was approximately $471,617,149 and net unrealized appreciation was $78,645,068 consisting of gross unrealized appreciation of $106,850,961 and gross unrealized depreciation of $28,205,893.

Fair Value Measurements

Various inputs are used in determining the value of the Fund's investments, following the input prioritization hierarchy established by accounting principles generally accepted in the United States of America (GAAP). These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – prices determined using other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk and others)

• Level 3 – prices determined using significant unobservable inputs where quoted prices or observable inputs are unavailable or less reliable (including management's own assumptions about the factors market participants would use in pricing an investment)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Examples of the types of securities in which the Fund would typically invest and how they are classified within this hierarchy are as follows. Typical Level 1 securities include exchange traded domestic equities, mutual funds whose NAVs are published each day and exchange traded foreign equities that are not statistically fair valued. Typical Level 2 securities include exchange traded foreign equities that are statistically fair valued, forward foreign currency exchange contracts and short-term investments valued at amortized cost. Additionally, securities fair valued by CWAM's Valuation Committee (the Committee) that rely on significant observable inputs are also included in Level 2. Typical Level 3 securities include any security fair valued by the Committee that relies on significant unobservable inputs.

The Committee is responsible for applying the Trust's Portfolio Pricing Policy and the CWAM pricing procedures (the Policies), which are approved by and subject to the oversight of the Board.

The Committee meets as necessary, and no less frequently than quarterly, to determine fair values for securities for which market quotations are not readily available or for which the investment manager believes that available market quotations are unreliable. The Committee also reviews the continuing appropriateness of the Policies. In circumstances where a security has been fair valued, the Committee will also review the continuing appropriateness of the current value of the security. The Policies address, among other things: circumstances under which market quotations will be deemed readily available; selection of third party pricing vendors; appropriate pricing methodologies; events that require fair valuation and fair value techniques; circumstances under which securities will be deemed to pose a potential for stale pricing, including when securities are illiquid, restricted, or in default; and certain delegations of authority to determine fair values to the Fund's investment manager. The Committee may also meet to discuss additional valuation matters, which may include review of back-testing results, review of time-sensitive information or approval of other valuation related actions, and to review the appropriateness of the Policies.

For investments categorized as Level 3, the significant unobservable inputs used in the fair value measurement of the Fund's securities may include: (i) data specific to the issuer or comparable issuers, (ii) general market or specific sector news and (iii) quoted prices and specific or similar security transactions. The Committee considers this data and any changes from prior periods in order to assess the reasonableness of observable and unobservable inputs, any assumptions or internal models used to value those securities and changes in fair value. Significant changes in any of these factors could result in lower or higher fair value measurements. Various factors impact the frequency of monitoring (which may occur as often as daily), however the Committee may determine that changes to inputs, assumptions and models are not required with the same frequency.

The following table summarizes the inputs used, as of June 30, 2016, in valuing the Fund's assets:

Investment Type | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||||||||

Equities | |||||||||||||||||||

Asia | $ | 3,406,613 | $ | 221,901,801 | $ | — | $ | 225,308,414 | |||||||||||

Europe | — | 224,384,889 | — | 224,384,889 | |||||||||||||||

Other Countries | 45,826,252 | 28,484,923 | — | 74,311,175 | |||||||||||||||

Latin America | 5,515,644 | — | — | 5,515,644 | |||||||||||||||

Total Equities | 54,748,509 | 474,771,613 | — | 529,520,122 | |||||||||||||||

| Total Short-Term Investments | 1,607,078 | — | — | 1,607,078 | |||||||||||||||

| Total Securities Lending Collateral | 19,135,017 | — | — | 19,135,017 | |||||||||||||||

Total Investments | $ | 75,490,604 | $ | 474,771,613 | $ | — | $ | 550,262,217 | |||||||||||

The Fund's assets assigned to the Level 2 input category are generally valued using a market approach, in which a security's value is determined through its correlation to prices and information from observable market transactions for similar or identical assets. Foreign equities are generally valued at the last sale price on the foreign exchange or market on which they trade. The Fund may use a statistical fair valuation model, in

See accompanying notes to financial statements.

11

Wanger International 2016 Semiannual Report

Wanger International

Statement of Investments (Unaudited), June 30, 2016

accordance with the policy adopted by the Board, provided by an independent third party to value securities principally traded in foreign markets in order to adjust for possible stale pricing that may occur between the close of the foreign exchanges and the time for valuation. These models take into account available market data including intraday index, ADR, and ETF movements.

There were no transfers of financial assets between Levels 1 and 2 during the period.

Financial assets were transferred from Level 3 to Level 2 as trading resumed during the period.

The following table shows transfers between Level 2 and Level 3 of the fair value hierarchy:

Transfers In | Transfers Out | ||||||||||||||

| Level 2 | Level 3 | Level 2 | Level 3 | ||||||||||||

| $ | 2,776,146 | $ | — | $ | — | $ | 2,776,146 | ||||||||

Transfers into and/or out of Level 3 are determined based on the fair value at the beginning of the period for security positions held throughout the period.

See accompanying notes to financial statements.

12

Wanger International 2016 Semiannual Report

Statement of Assets and Liabilities

June 30, 2016 (Unaudited)

Assets: | |||||||

Investments, at cost | $ | 471,617,149 | |||||

| Investments, at value (including securities on loan of $18,401,815) | $ | 550,262,217 | |||||

Cash | 86,399 | ||||||

Foreign currency (cost of $1,692,854) | 1,693,483 | ||||||

Receivable for: | |||||||

Investments sold | 11,559,568 | ||||||

Fund shares sold | 1,145,615 | ||||||

Securities lending income | 155,948 | ||||||

Dividends | 539,391 | ||||||

Foreign tax reclaims | 459,499 | ||||||

Trustees' deferred compensation plan | 175,875 | ||||||

Prepaid expenses | 35,183 | ||||||

Total Assets | 566,113,178 | ||||||

Liabilities: | |||||||

Collateral on securities loaned | 19,135,017 | ||||||

Payable for: | |||||||

Investments purchased | 4,714,544 | ||||||

Fund shares redeemed | 1,334,738 | ||||||

Investment advisory fee | 13,818 | ||||||

Administration fee | 731 | ||||||

Transfer agent fee | 2 | ||||||

Trustees' fees | 3,572 | ||||||

Custody fee | 72,482 | ||||||

Reports to shareholders | 57,035 | ||||||

Trustees' deferred compensation plan | 175,875 | ||||||

Other liabilities | 43,513 | ||||||

Total Liabilities | 25,551,327 | ||||||

Net Assets | $ | 540,561,851 | |||||

Composition of Net Assets: | |||||||

Paid-in capital | $ | 454,924,677 | |||||

Undistributed net investment income | 1,343,776 | ||||||

Accumulated net realized gain | 5,690,186 | ||||||

Net unrealized appreciation (depreciation) on: | |||||||

Investments | 78,645,068 | ||||||

Foreign currency translations | (41,856 | ) | |||||

Net Assets | $ | 540,561,851 | |||||

Fund Shares Outstanding | 22,380,302 | ||||||

| Net asset value, offering price and redemption price per share | $ | 24.15 | |||||

Statement of Operations

For the Six Months Ended June 30, 2016 (Unaudited)

Investment Income: | |||||||

Dividends (net foreign taxes withheld of $842,339) | $ | 7,366,910 | |||||

Interest | 62 | ||||||

Income from securities lending—net | 463,495 | ||||||

Total Investment Income | 7,830,467 | ||||||

Expenses: | |||||||

Investment advisory fee | 2,584,950 | ||||||

Transfer agent fees | 314 | ||||||

Administration fee | 137,473 | ||||||

Trustees' fees | 27,073 | ||||||

Custody fees | 116,274 | ||||||

Reports to shareholders | 128,007 | ||||||

Audit fees | 34,404 | ||||||

Legal fees | 57,226 | ||||||

Chief compliance officer expenses | 24,832 | ||||||

Commitment fee for line of credit (Note 5) | 10,600 | ||||||

Other expenses | 18,376 | ||||||

Total Expenses | 3,139,529 | ||||||

Net Investment Income | 4,690,938 | ||||||

| Net Realized and Unrealized Gain (Loss) on Investments: | |||||||

Net realized gain (loss) on: | |||||||

Investments | 7,458,765 | ||||||

Foreign currency translations | 50,187 | ||||||

Net realized gain | 7,508,952 | ||||||

Net change in unrealized appreciation (depreciation) on: | |||||||

Investments | (13,794,766 | ) | |||||

Foreign currency translations | (5,186 | ) | |||||

Net change in unrealized depreciation | (13,799,952 | ) | |||||

Net realized and unrealized loss | (6,291,000 | ) | |||||

Net Decrease in Net Assets from Operations | $ | (1,600,062 | ) | ||||

See accompanying notes to financial statements.

13

Wanger International 2016 Semiannual Report

Statements of Changes in Net Assets

Increase (Decrease) in Net Assets | (Unaudited) Six Months Ended June 30, 2016 | Year Ended December 31, 2015 | |||||||||

Operations: | |||||||||||

Net investment income | $ | 4,690,938 | $ | 7,165,545 | |||||||

Net realized gain (loss) on: | |||||||||||

Investments | 7,458,765 | 50,409,289 | |||||||||

Foreign currency translations | 50,187 | (346,363 | ) | ||||||||

Net change in unrealized appreciation (depreciation) on: | |||||||||||

Investments | (13,794,766 | ) | (55,119,081 | ) | |||||||

Foreign currency translations | (5,186 | ) | 29,388 | ||||||||

Net Increase (Decrease) in Net Assets from Operations | (1,600,062 | ) | 2,138,778 | ||||||||

Distributions to Shareholders From: | |||||||||||

Net investment income | (1,831,842 | ) | (9,178,114 | ) | |||||||

Net realized gains | (44,383,757 | ) | (56,072,696 | ) | |||||||

Total Distributions to Shareholders | (46,215,599 | ) | (65,250,810 | ) | |||||||

Share Transactions: | |||||||||||

Subscriptions | 4,322,805 | 12,302,455 | |||||||||

Distributions reinvested | 46,215,599 | 65,250,810 | |||||||||

Redemptions | (48,789,699 | ) | (94,967,225 | ) | |||||||

Net Increase (Decrease) from Share Transactions | 1,748,705 | (17,413,960 | ) | ||||||||

Proceeds from regulatory settlements | — | 131,912 | |||||||||

Total Decrease in Net Assets | (46,066,956 | ) | (80,394,080 | ) | |||||||

Net Assets: | |||||||||||

Beginning of period | 586,628,807 | 667,022,887 | |||||||||

End of period | $ | 540,561,851 | $ | 586,628,807 | |||||||

Undistributed (Overdistributed) net investment income | $ | 1,343,776 | $ | (1,515,320 | ) | ||||||

See accompanying notes to financial statements.

14

Wanger International 2016 Semiannual Report

Financial Highlights

The following table is intended to help you understand the Fund's financial performance. Certain information reflects financial results for a single share held for the periods shown. Per share net investment income (loss) amounts are calculated based on average shares outstanding during the period. Total return assumes reinvestment of all dividends and distributions, if any. Total return does not reflect payment of the expenses that apply to the variable accounts or contract charges, if any. Total return and portfolio turnover are not annualized for periods of less than one year. The portfolio turnover rate is calculated without regard to purchase and sales transactions of short-term instruments and certain derivatives, if any. If such transactions were included, the Fund's portfolio turnover rate may be higher.

| (Unaudited) Six Months Ended June 30, | Year Ended December 31, | ||||||||||||||||||||||||||

Selected data for a share outstanding throughout each period | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||||||||

Net Asset Value, Beginning of Period | $ | 26.32 | $ | 29.07 | $ | 34.55 | $ | 31.19 | $ | 28.79 | $ | 36.16 | |||||||||||||||

Income from Investment Operations: | |||||||||||||||||||||||||||

Net investment income | 0.22 | 0.31 | 0.36 | 0.39 | 0.46 | 0.42 | |||||||||||||||||||||

Net realized and unrealized gain (loss) | (0.16 | ) | (0.09 | ) | (1.56 | ) | 6.18 | 5.27 | (5.31 | ) | |||||||||||||||||

Reimbursement from affiliate | — | — | — | — | — | 0.00 | (a) | ||||||||||||||||||||

Total from Investment Operations | 0.06 | 0.22 | (1.20 | ) | 6.57 | 5.73 | (4.89 | ) | |||||||||||||||||||

Less Distributions to Shareholders: | |||||||||||||||||||||||||||

Net investment income | (0.09 | ) | (0.41 | ) | (0.48 | ) | (0.88 | ) | (0.38 | ) | (1.64 | ) | |||||||||||||||

Net realized gains | (2.14 | ) | (2.57 | ) | (3.80 | ) | (2.33 | ) | (2.95 | ) | (0.84 | ) | |||||||||||||||

Total Distributions to Shareholders | (2.23 | ) | (2.98 | ) | (4.28 | ) | (3.21 | ) | (3.33 | ) | (2.48 | ) | |||||||||||||||

Proceeds from regulatory settlements | — | 0.01 | — | — | — | — | |||||||||||||||||||||

Net Asset Value, End of Period | $ | 24.15 | $ | 26.32 | $ | 29.07 | $ | 34.55 | $ | 31.19 | $ | 28.79 | |||||||||||||||

Total Return | (0.16 | )% | 0.10 | %(b) | (4.40 | )% | 22.37 | % | 21.56 | %(c) | (14.62 | )%(c) | |||||||||||||||

Ratios to Average Net Assets/Supplemental Data: | |||||||||||||||||||||||||||

Total gross expenses (d) | 1.14 | %(e) | 1.12 | % | 1.05 | % | 1.07 | % | 1.08 | % | 1.06 | % | |||||||||||||||

Total net expenses (d) | 1.14 | %(e) | 1.12 | % | 1.05 | % | 1.07 | % | 1.05 | %(f) | 1.00 | %(f) | |||||||||||||||

Net investment income | 1.71 | %(e) | 1.11 | % | 1.10 | % | 1.19 | % | 1.51 | % | 1.25 | % | |||||||||||||||

Portfolio turnover rate | 36 | % | 53 | % | 28 | % | 44 | % | 34 | % | 36 | % | |||||||||||||||

Net assets, end of period (000s) | $ | 540,562 | $ | 586,629 | $ | 667,023 | $ | 784,977 | $ | 702,667 | $ | 682,217 | |||||||||||||||

Notes to Financial Highlights

(a) Rounds to zero.

(b) The Fund received proceeds from regulatory settlements. Had the Fund not received these proceeds, the total return would have been lower by 0.01%.

(c) Had the Investment Manager and/or its affiliates not waived a portion of expenses, total return would have been reduced.

(d) In addition to the fees and expenses that the Fund bears directly, the Fund indirectly bears a pro rata share of the fees and expenses of any other funds in which it invests, if any. Such indirect expenses are not included in the Fund's reported expense ratios.

(e) Annualized.

(f) The benefits derived from custody fees paid indirectly had an impact of less than 0.01%.

See accompanying notes to financial statements.

15

Wanger International 2016 Semiannual Report

Notes to Financial Statements (Unaudited)

1. Nature of Operations

Wanger International (the Fund), a series of Wanger Advisors Trust (the Trust), is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. The investment objective of the Fund is to seek long-term capital appreciation. The Fund is available only for allocation to certain life insurance company separate accounts established for the purpose of funding participating variable annuity contracts and variable life insurance policies and may also be offered directly to certain qualified pension and retirement plans.

2. Summary of Significant Accounting Policies

Basis of preparation

The Fund is an investment company that applies the accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946, Financial Services—Investment Companies (ASC 946). The financial statements are prepared in accordance with U.S. generally accepted accounting principles (GAAP) which requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security valuation

Securities of the Fund are valued at market value or, if a market quotation for a security is not readily available or is deemed not to be reliable because of events or circumstances that have occurred between the market quotation and the time as of which the security is to be valued, the security is valued at its fair value determined in good faith under consistently applied procedures established by the Board of Trustees (the Board). A security traded on a securities exchange or in an over-the-counter market in which transaction prices are reported is valued at the last sales price at the time of valuation. A security traded principally on NASDAQ is valued at the NASDAQ official closing price. Exchange traded funds (ETFs) are valued at their closing net asset value as reported on the applicable exchange. A security for which there is no reported sale on the valuation date is valued at the mean of the latest bid and ask quotations.

Short-term investments maturing in 60 days or less are valued at amortized cost, which approximates market value.

The Trust has retained an independent statistical fair value pricing service that employs a systematic methodology to assist in the fair valuation process for securities principally traded in a foreign market in order to adjust for possible changes in value that may occur between the close of the foreign market and the time as of which the securities are to be valued. If a security is valued at a fair value, that value may be different from the last quoted market price for the security.

Foreign currency translations

Values of investments denominated in foreign currencies are converted into U.S. dollars using the New York spot market rate of exchange at the time of valuation. Purchases and sales of investments and dividend and interest income are translated into U.S. dollars using the spot market rate of exchange prevailing on the respective dates of such transactions. The gain or loss resulting from changes in foreign exchange rates is included with net realized and unrealized gain or loss from investments, as appropriate.

Security transactions and investment income

Security transactions are accounted for on the trade date (date the order to buy or sell is executed) and dividend income is recorded on the ex-dividend date, except

that certain dividends from foreign securities are recorded as soon as the information is available to the Fund. Interest income is recorded on the accrual basis and includes amortization of discounts on debt obligations when required for federal income tax purposes. Realized gains and losses from security transactions are recorded on an identified cost basis.

Awards, if any, from class action litigation related to securities owned may be recorded as a reduction of cost of those securities. If the applicable securities are no longer owned, the proceeds are recorded as realized gains.

The Fund may receive distributions from holdings in equity securities, ETFs, other regulated investment companies (RICs), and real estate investment trusts (REITs), which report information on the tax character of their distributions annually. These distributions are allocated to dividend income, capital gain and return of capital based on actual information reported. Return of capital is recorded as a reduction of the cost basis of securities held. If the Fund no longer owns the applicable securities, return of capital is recorded as a realized gain. With respect to REITs, to the extent actual information has not yet been reported, estimates for return of capital may be made by the Fund's management. Management's estimates are subsequently adjusted when the actual character of the distributions is disclosed by the REITs, which could result in a proportionate change in return of capital to shareholders.

Expenses

General expenses of the Trust are allocated to the Fund and the other series of the Trust based upon relative net assets or other expense allocation methodologies determined by the nature of the expense. Expenses directly attributable to the Fund are charged to the Fund.

Fund share valuation

Fund shares are sold and redeemed on a continuing basis at net asset value. Net asset value per share is determined daily as of the close of trading on the New York Stock Exchange (the Exchange) on each day the Exchange is open for trading by dividing the total value of the Fund's investments and other assets, less liabilities, by the number of Fund shares outstanding.

Securities lending

The Fund may lend securities up to one-third of the value of its total assets to certain approved brokers, dealers and other financial institutions to earn additional income. The Fund retains the benefits of owning the securities, including the economic equivalent of dividends or interest generated by the security. The Fund also receives a fee for the loan. The Fund has the ability to recall the loans at any time and could do so in order to vote proxies or to sell the loaned securities. Each loan is collateralized by cash that exceeded the value of the securities on loan. The market value of the loaned securities is determined daily at the close of business of the Fund and any additional required collateral is delivered to each Fund on the next business day. The Fund has elected to invest the cash collateral in the Dreyfus Government Cash Management Fund. The income earned from the securities lending program is paid to the Fund, net of any fees remitted to Goldman Sachs Agency Lending, the Fund's lending agent, and borrower rebates. The Fund's investment manager, Columbia Wanger Asset Management, LLC (CWAM), does not retain any fees earned by the lending program. Generally, in the event of borrower default, the Fund has the right to use the collateral to offset any losses incurred. In the event the Fund is delayed or prevented from exercising its right to dispose of the collateral, there may be a potential loss to the Fund. Some of these losses may be indemnified by the lending agent. The Fund bears the risk of loss with respect to the investment of collateral. The net lending income earned by the Fund as of June 30, 2016, is included in the Statement of Operations.

16

Wanger International 2016 Semiannual Report

Notes to Financial Statements, continued (Unaudited)

Offsetting of assets and liabilities

The following table presents the Fund's gross and net amount of assets and liabilities available for offset under netting agreements and under a securities lending agreement as well as the related collateral received by the Fund as of June 30, 2016:

| Goldman Sachs ($) | |||||||

Liabilities | |||||||

Collateral on securities loaned | 19,135,017 | ||||||

Total liabilities | 19,135,017 | ||||||

Total financial and derivative net assets | (19,135,017 | ) | |||||

Financial instruments | 18,401,815 | ||||||

Net amount (a) | (733,202 | ) | |||||

(a) Represents the net amount due from/ (to) counterparties in the event of default.

Securities lending transactions

The following table indicates the total amount of securities loaned by type, reconciled to gross liability payable upon return of the securities loaned by the Fund as of June 30, 2016:

| Overnight and Continuous | Up to 30 Days | 30 – 90 Days | Greater than 90 Days ($) | Total ($) | |||||||||||||||||||

| Securities lending transactions | |||||||||||||||||||||||

Equity securities | $ | 18,401,815 | $ | — | $ | — | $ | — | $ | 18,401,815 | |||||||||||||

| Gross amount of recognized liabilities for securities lending (collateral received) | 19,135,017 | ||||||||||||||||||||||

| Amounts due to counterparty | $ | 733,202 | |||||||||||||||||||||

Federal income taxes

The Fund has complied with the provisions of the Internal Revenue Code available to regulated investment companies and, in the manner provided therein, distributes substantially all its taxable income, as well as any net realized gain on sales of investments and foreign currency transactions reportable for federal income tax purposes. Accordingly, the Fund paid no federal income taxes and no federal income tax provision was required.

Foreign capital gains taxes

Gains in certain countries may be subject to foreign taxes at the fund level. The Fund accrues for such foreign taxes on realized and unrealized gains at the appropriate rate for each jurisdiction. The amount, if any, is disclosed as a liability on the Statement of Assets and Liabilities.

Distributions to shareholders

Distributions to shareholders are recorded on the ex-dividend date.

Indemnification

In the normal course of business, the Trust on behalf of the Fund enters into contracts that contain a variety of representations and warranties and that provide general indemnities. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also under the Trust's organizational documents, the trustees and officers of the Trust are indemnified against certain liabilities that may arise out of their duties to the Trust. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be remote.

3. Federal Tax Information

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. Reclassifications are made to the Fund's capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations.

Management is required to determine whether a tax position of the Fund is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any related appeals or litigation processes, based on the technical merits of the position. The tax benefit to be recognized by the Fund is measured as the largest amount of benefit that is greater than fifty percent likely of being realized upon ultimate settlement. Management is not aware of any tax positions in the Fund for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. However, management's conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, new tax laws, regulations, and administrative interpretations (including relevant court decisions). The Fund's federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service.

4. Transactions with Affiliates

CWAM is a wholly owned subsidiary of Columbia Management Investment Advisers, LLC (Columbia Management), which in turn is a wholly owned subsidiary of Ameriprise Financial, Inc. (Ameriprise Financial). CWAM furnishes continuing investment supervision to the Fund and is responsible for the overall management of the Fund's business affairs.

CWAM receives a monthly advisory fee based on the Fund's average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | ||||||

Up to $100 million | 1.10 | % | |||||

$100 million to $250 million | 0.95 | % | |||||

$250 million to $500 million | 0.90 | % | |||||

$500 million to $1 billion | 0.80 | % | |||||

| $1 billion and over | 0.72 | % | |||||

For the six months ended June 30, 2016, the annualized effective investment advisory fee rate, was 0.94% of the Fund's average daily net assets.

CWAM provides administrative services and receives an administration fee from the Fund at the following annual rates:

| Wanger Advisors Trust Aggregate Average Daily Net Assets of the Trust | Annual Fee Rate | ||||||

Up to $4 billion | 0.05 | % | |||||

$4 billion to $6 billion | 0.04 | % | |||||

$6 billion to $8 billion | 0.03 | % | |||||

| $8 billion and over | 0.02 | % | |||||

For the six months ended June 30, 2016, the annualized effective administration fee rate was 0.05% of the Fund's average daily net assets. CWAM has delegated to Columbia Management responsibility to provide certain sub-administrative services to the Fund.

Columbia Management Investment Distributors, Inc. (CMID), a wholly owned subsidiary of Ameriprise Financial, serves as the Fund's distributor and principal underwriter.

Columbia Management Investment Services Corp. (CMIS), a wholly owned subsidiary of Ameriprise Financial, is the transfer agent to the Fund. For its services, the Fund pays CMIS a monthly fee at the annual rate of $21.00 per open account. CMIS also receives reimbursement from the Fund for certain out-of-pocket expenses.

Certain officers and trustees of the Trust are also officers of CWAM. The Trust makes no direct payments to its officers and trustees who are affiliated with CWAM.

17

Wanger International 2016 Semiannual Report

Notes to Financial Statements, continued (Unaudited)

The Board has appointed a Chief Compliance Officer of the Trust in accordance with federal securities regulations. The Fund, along with other affiliated funds, pays its pro-rata share of certain of the expenses associated with the office of the Chief Compliance Officer.

The Trust offers a deferred compensation plan for its independent trustees. Under that plan, a trustee may elect to defer all or a portion of his or her compensation. Amounts deferred are retained by the Trust and may represent an unfunded obligation of the Trust. The value of amounts deferred is determined by reference to the change in value of Class Z shares of one or more series of Columbia Acorn Trust or a money market fund as specified by the trustee. Benefits under the deferred compensation plan are payable in accordance with the plan.

For the six months ended June 30, 2016, the Fund engaged in purchase and sales transactions with funds that have a common investment manager (or affiliated investment managers), common directors/trustees, and/or common officers. Those purchase and sale transactions complied with provisions of Rule 17a-7 under the 1940 Act and were $19,408,444 and $5,462,621, respectively. The sale transactions resulted in a net realized gain of $1,808,732.

5. Borrowing Arrangements

During the period January 1, 2016 through April 28, 2016, the Trust participated in a revolving credit facility in the amount of $400 million with a syndicate of banks led by JPMorgan Chase Bank, N.A., along with Columbia Acorn Trust, another trust managed by CWAM. Effective April 28, 2016, the credit facility was renewed in the amount of $200 million with a syndicate of banks led by JPMorgan Chase Bank, N.A. Under each facility, interest is charged to each participating Fund based on its borrowings at a rate per annum equal to the Federal Funds Rate plus 1.00%. In addition, a commitment fee of 0.08% (before April 28, 2016) and 0.15% (after April 28, 2016) per annum of the unutilized line of credit is accrued and apportioned among the participating Funds based on their relative net assets. The commitment fee is disclosed as a part of "Other expenses" in the Statement of Operations. The Trust expects to renew this line of credit for one year durations each April at then current market rates and terms.

No amounts were borrowed for the benefit of the Fund under the line of credit during the six months ended June 30, 2016.

6. Fund Share Transactions

Proceeds and payments on Fund shares as shown in the Statement of Changes in Net Assets are in respect of the following numbers of shares:

| (Unaudited) Six months ended June 30, 2016 | Year ended December 31, 2015 | ||||||||||

Shares sold | 170,738 | 431,818 | |||||||||

| Shares issued in reinvestment of dividend distributions | 1,831,046 | 2,291,751 | |||||||||

Less shares redeemed | (1,910,180 | ) | (3,377,227 | ) | |||||||

Net increase (decrease) in shares outstanding | 91,604 | (653,658 | ) | ||||||||

7. Investment Transactions

The aggregate cost of purchases and proceeds from sales other than short-term obligations for the six months ended June 30, 2016, were $196,645,747 and $230,814,351, respectively. The amount of purchase and sales activity impacts the portfolio turnover rate reported in the Financial Highlights.

8. Shareholder Concentration

At June 30, 2016, two unaffiliated shareholder accounts owned an aggregate of 29.3% of the outstanding shares of the Fund. The Fund has no knowledge about whether any portion of those shares was owned beneficially by such accounts. Affiliated shareholder accounts owned 60.2% of the outstanding shares of the Fund. Subscription and redemption activity by concentrated accounts may have a significant effect on the operations of the Fund.

9. Subsequent Events

Management has evaluated the events and transactions that have occurred through the date the financial statements were issued and noted no items requiring adjustment of the financial statements or additional disclosure.

10. Information Regarding Pending and Settled Legal Proceedings