UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08764 |

|

PACE® Select Advisors Trust |

(Exact name of registrant as specified in charter) |

|

1285 Avenue of the Americas, New York, New York | | 10019-6028 |

(Address of principal executive offices) | | (Zip code) |

|

Mark F. Kemper, Esq. UBS Global Asset Management 1285 Avenue of the Americas New York, NY 10019-6028 |

(Name and address of agent for service) |

Copy to: Jack W. Murphy, Esq. Dechert LLP 1900 K Street, N.W. Washington, DC 20006 |

Registrant’s telephone number, including area code: | 212-821 3000 | |

|

Date of fiscal year end: | July 31 | |

|

Date of reporting period: | July 31, 2015 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

PACE® Select Advisors Trust

Annual Report

PACE® Select Advisors Trust

Table of contents | |

Introduction | | | 2 | | |

Portfolio Advisor's and Sub-Advisors' commentaries and Portfolios of investments | |

| PACE® Money Market Investments | | | 4 | | |

| PACE® Mortgage-Backed Securities Fixed Income Investments | | | 11 | | |

| PACE® Intermediate Fixed Income Investments | | | 28 | | |

| PACE® Strategic Fixed Income Investments | | | 55 | | |

| PACE® Municipal Fixed Income Investments | | | 87 | | |

| PACE® International Fixed Income Investments | | | 99 | | |

| PACE® High Yield Investments | | | 112 | | |

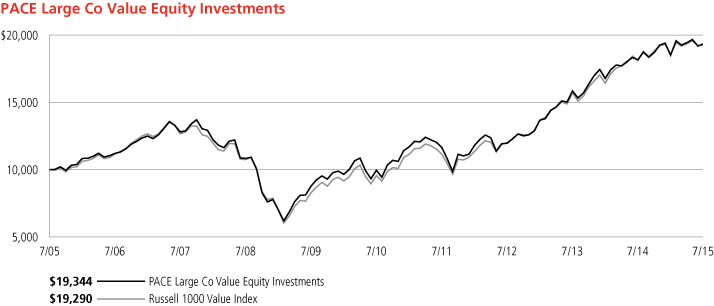

| PACE® Large Co Value Equity Investments | | | 129 | | |

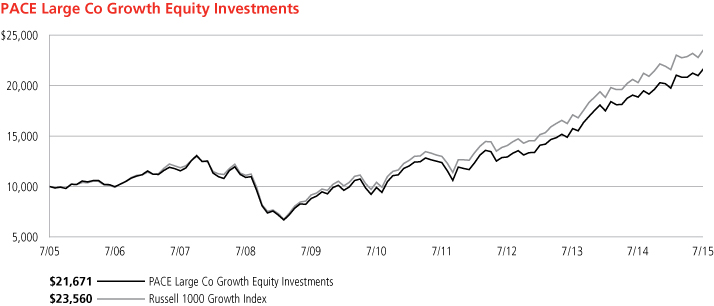

| PACE® Large Co Growth Equity Investments | | | 146 | | |

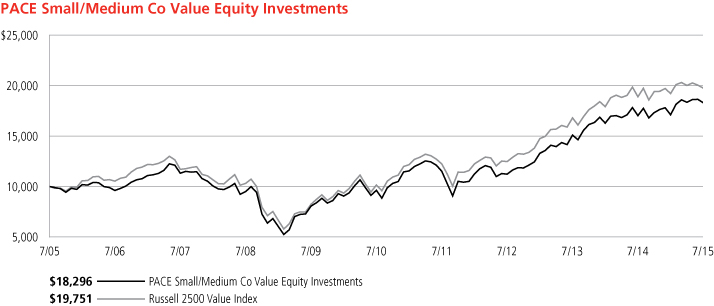

| PACE® Small/Medium Co Value Equity Investments | | | 155 | | |

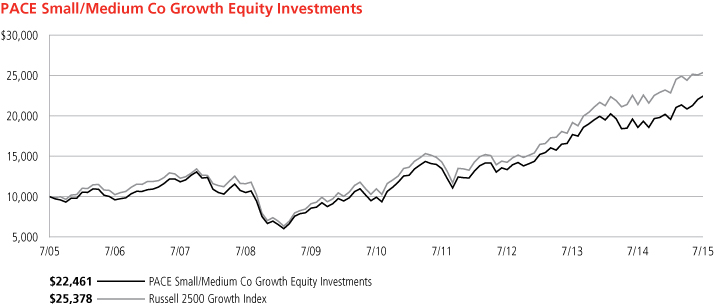

| PACE® Small/Medium Co Growth Equity Investments | | | 166 | | |

| PACE® International Equity Investments | | | 178 | | |

| PACE® International Emerging Markets Equity Investments | | | 194 | | |

| PACE® Global Real Estate Securities Investments | | | 206 | | |

| PACE® Alternative Strategies Investments | | | 214 | | |

Understanding your Portfolio's expenses | | | 256 | | |

Statement of assets and liabilities | | | 262 | | |

Statement of operations | | | 270 | | |

Statement of changes in net assets | | | 274 | | |

Statement of cash flows | | | 280 | | |

Financial highlights | | | 283 | | |

Notes to financial statements | | | 312 | | |

Report of independent registered public accounting firm | | | 361 | | |

Tax information | | | 362 | | |

General information | | | 363 | | |

Board approvals of sub-advisory agreements | | | 364 | | |

Supplemental information, trustees and officers | | | 382 | | |

PACE Select Advisors Trust offers multiple share classes representing interests in 15 separate Portfolios. (PACE Money Market Investments offers only one share class.) Different classes of shares and/or Portfolios are offered by separate prospectuses.

For more information on a portfolio or class of shares, contact your financial advisor. He or she can send you a current prospectus relating to a portfolio or class of shares. Investors should carefully read and consider a mutual fund's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other information about a mutual fund. For a current prospectus, contact UBS Global Asset Management (Americas) Inc. at 888-793 8637, or visit us on the Web at www.ubs.com/globalam-us.

Derivatives vary in complexity, involve risks which are different from, and may be greater than, the risks associated with investing in securities or other instruments. Please see the funds' prospectuses for more complete discussion of the risks associated with investing in derivatives.

1

PACE Select Advisors Trust

Introduction

September 18, 2015

Dear PACE Shareholder,

We are pleased to provide you with the annual report for the PACE portfolios (the "Portfolios"), comprising the PACE Select Advisors Trust. This report includes summaries of the performance of each Portfolio, as well as commentaries from the investment advisor and sub-advisors regarding the events that affected Portfolio performance during the 12 months ended July 31, 2015. Please note that the opinions of the sub-advisors do not necessarily represent those of UBS Global Asset Management (Americas) Inc., the Portfolios' investment advisor.

Global growth generally improves

Growth in the US fluctuated during the reporting period. The US Commerce Department reported that gross domestic product ("GDP") expanded at a 4.3% seasonally adjusted annualized rate during the third quarter of 2014. GDP growth then moderated to 2.1% during the fourth quarter and 0.6% for the first quarter of 2015. However, the US economy then improved, as the Commerce Department's second estimate for second quarter GDP was 3.7%.1

The US Federal Reserve Board (the "Fed") largely maintained its accommodative monetary policy during the reporting period, and continued to hold the fed funds rate at a historically low range between 0% and 0.25%. (The federal funds rate or the "fed funds rate," is the rate US banks charge one another for funds they borrow on an overnight basis.) However, at its March 2015 meeting, the Fed said that it "... anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2% objective over the medium term." Finally, at the central bank's meeting that concluded in June 2015, the Fed said that it "...currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run."

In terms of the global economy, the International Monetary Fund's ("IMF") July 2015 World Economic Outlook Update said "A setback to activity in the first quarter of 2015, mostly in North America, has resulted in a small downward revision to global growth for 2015 relative to the April 2015 World Economic Outlook. Nevertheless, the underlying drivers for a gradual acceleration in economic activity in advanced economies—easy financial conditions, more neutral fiscal policy in the euro area, lower fuel prices, and improving confidence and labor market conditions—remain intact." The IMF projects that 2015 growth in the eurozone will be 1.5%, versus 0.8% in 2014. Japan's economy is expected to expand 0.8% in 2015, an improvement from the 0.1% contraction in 2014. In contrast, the IMF sees growth in emerging market countries decelerating in 2015, with GDP of 4.2% compared to 4.6% in 2014.

US equities post superior results

While it experienced several setbacks, the US equity market generated strong results during the reporting period. Investor sentiment was challenged at times given some mixed global economic data and corporate profit figures, as well as numerous geopolitical issues. All told, the US stock market, as measured by the S&P 500 Index,2 gained 11.21% for the 12 months ended July 31, 2015. In contrast, international equities produced weak results, as they were dragged down by growth concerns, fluctuating oil prices and the crisis in Greece. International developed

1 Based on the Commerce Department's second estimate announced on August 27, 2015, after the reporting period had ended.

2 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

2

PACE Select Advisors Trust

market equities, as measured by the MSCI EAFE Index (net),3 fell 0.27% during the period. Emerging market equities, as measured by the MSCI Emerging Markets Index (net),4 declined 13.38% over the same period.

Mixed returns in the fixed income market

The global fixed income market was also volatile at times during the reporting period. This was triggered by incoming economic data, uncertainties surrounding future monetary policy and—as was the case for the equity market—unfolding geopolitical events. Against this backdrop, the yield on the 10-year US Treasury fell from 2.58% to 2.20% during the reporting period, and the overall US bond market, as measured by the Barclays US Aggregate Index,5 gained 2.82%. Riskier fixed income securities generated weaker results for the 12 months ended July 31, 2015. High yield bonds, as measured by the BofA Merrill Lynch US High Yield Cash Pay Constrained Index6 returned 0.22%, whereas emerging markets debt, as measured by the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global),7 declined 1.28%.

Sincerely,

Mark E. Carver

President, PACE Select Advisors Trust

Managing Director, UBS Global Asset Management (Americas) Inc.

This report is intended to assist investors in understanding how the Portfolios performed during the 12-month period ended July 31, 2015. The views expressed in the Advisor's and Sub-Advisors' comments sections are as of the end of the reporting period, reflect performance results gross of fees and expenses, and are those of the investment advisor (with respect to PACE Money Market Investments only) and sub-advisors. Sub-advisors' comments on Portfolios that have more than one sub-advisor are reflective of their portion of the Portfolio only. The views and opinions in this report were current as of September 18, 2015. They are not guarantees of future performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the investment advisor and sub-advisors reserve the right to change their views about individual securities, sectors and markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Portfolio's future investment intent.

3 The MSCI EAFE Index (net) is an index of stocks designed to measure the investment returns of developed economies outside of North America. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

4 The MSCI Emerging Markets Index (net) is a market capitalization-weighted index composed of different emerging market countries in Europe, Latin America and the Pacific Basin. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

5 The Barclays US Aggregate Index is an unmanaged broad based index designed to measure the US dollar-denominated, investment grade, taxable bond market. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed, asset-backed and commercial mortgage-backed sectors. Investors should note that indices do not reflect the deduction of fees and expenses.

6 The BofA Merrill Lynch US High Yield Cash Pay Constrained Index is an unmanaged index of publicly placed, non-convertible, coupon-bearing US dollar-denominated, below investment grade corporate debt with a term to maturity of at least one year. The index is market-capitalization-weighted, so that larger bond issuers have a greater effect on the index's return. However, the representation of any single bond issuer is restricted to a maximum of 2% of the total index. Investors should note that indices do not reflect the deduction of fees and expenses.

7 The J.P. Morgan Emerging Markets Bond Index Global (EMBI Global) is an unmanaged index which is designed to track total returns for US dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans and Eurobonds. Investors should note that indices do not reflect the deduction of fees and expenses.

3

PACE Select Advisors Trust

PACE Money Market Investments

On September 22, 2015, the Portfolio's Board of Trustees ("the Board") approved a new policy on behalf of the Portfolio to invest at least 99.5% of its total assets in cash, government securities and/or repurchase agreements that are collateralized fully by cash or government securities to allow the Portfolio to qualify as a government money market fund, as defined under the amended Rule 2a-7 of the Investment Company Act of 1940. In addition, the Board approved changing the Portfolio's name to PACE Government Money Market Investments to ensure that the Portfolio is understood to be a government money market fund. In connection with the change to the Portfolio's name, the Portfolio also will adopt a non-fundamental investment policy that the Portfolio invests, under normal circumstances, at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in government securities, including government securities subject to repurchase agreements. The changes are expected to become effective on or about November 28, 2015.

Performance (unaudited)

For the 12 months ended July 31, 2015, the Portfolio returned 0.01% before the deduction of the maximum PACE program fee.1 Please remember that the PACE program fee is assessed outside the Portfolio at the PACE program account level. The program fee does not impact the determination of the Portfolio's net asset value per share. For comparison purposes, the median return of the Lipper Money Market Funds category was 0.01%. (Returns over various time periods are shown in the "Performance at a glance" table on page 6. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.) For a detailed commentary on the market environment in general during the period, please refer to page 2.

Advisor's Comments

Throughout the reporting period, the US Federal Reserve Board (the "Fed") continued to hold the federal funds rate at a historically low range between 0% and 0.25%. The federal funds rate, or the "fed funds rate," is the rate US banks charge one another for funds they borrow on an overnight basis. (For more details on the Fed's actions, see page 2.) This continued to depress yields on a wide range of short-term investments. As a result, the Portfolio's yield remained low during the reporting period.

We tactically adjusted the Portfolio's weighted average maturity ("WAM") throughout the 12-month review period. When the reporting period began, the Portfolio had a WAM of 40 days. This was decreased to 38 days at the end of the reporting period.

PACE Select Advisors Trust – PACE Money Market Investments

Investment Advisor:

UBS Global Asset Management (Americas) Inc.

Portfolio Manager:

Robert Sabatino

Objective:

Current income consistent with preservation of capital and liquidity

Investment process:

The Portfolio is a money market mutual fund and seeks to maintain a stable price of $1.00 per share, although it may be possible to lose money by investing in this Portfolio. The Portfolio invests in a diversified portfolio of high-quality money market instruments of governmental and private issuers. Security selection is based on the assessment of relative values and changes in market and economic conditions.

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

4

PACE Select Advisors Trust

PACE Money Market Investments

Sub-advisor's comments – concluded

At the issuer level, we maintained a high level of diversification, investing in smaller positions with the goal of reducing risk and keeping the Portfolio highly liquid. To that end, we typically purchased up to 3% in single nongovernment issuers throughout the reporting period. (The Portfolio is generally able to hold up to 5% in any one issuer, subject to certain exceptions.)

Several adjustments were made to the Portfolio's sector positioning during the 12-month period. We increased the Portfolio's exposures to repurchase agreements, US government and agency obligations and certificates of deposit. Conversely, we reduced our allocation to commercial paper and modestly pared our exposure to short-term corporate obligations. (Repurchase agreements are transactions in which the seller of a security agrees to buy it back at a predetermined time and price or upon demand.)

5

PACE Select Advisors Trust

PACE Money Market Investments

Performance at a glance (unaudited)

Average annual total returns for periods ended 07/31/15 | | 1 year | | 5 years | | 10 years | |

PACE Money Market Investments1 | | | 0.01 | % | | | 0.01 | % | | | 1.29 | % | |

Lipper Money Market Funds median | | | 0.01 | | | | 0.01 | | | | 1.27 | | |

Most recent calendar quarter-end returns (unaudited)

Average annual total returns for periods ended 06/30/15 | | 1 year | | 5 years | | 10 years | |

PACE Money Market Investments1 | | | 0.01 | % | | | 0.01 | % | | | 1.31 | % | |

For PACE Money Market Investments1 , the 7-day current yield for the period ended July 31, 2015 was 0.01% after fee waivers and/or expense reimbursements; the yield was (0.70)% before fee waivers and/or expense reimbursements. The Portfolio's yield quotation more closely reflects the current earnings of the Portfolio than the total return quotation. Yields will fluctuate and reflect fee waivers and/or expense reimbursements.

1 Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions. The return of an investment will fluctuate. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the payable dates. Current performance may be higher or lower than the performance data quoted.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

An investment in PACE Money Market Investments is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Portfolio seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Portfolio.

Not FDIC Insured. May lose value. No bank guarantee.

6

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio statistics (unaudited)

Characteristics | | 07/31/15 | |

Net assets (mm) | | $ | 168.5 | | |

Number of holdings | | | 52 | | |

Weighted average maturity | | | 38 days | | |

Portfolio composition1 | | 07/31/15 | |

Commercial paper | | | 45.4 | % | |

Repurchase agreements | | | 22.2 | | |

Certificates of deposit | | | 17.2 | | |

US government and agency obligations | | | 14.0 | | |

Short-term corporate obligation | | | 1.2 | | |

Other assets less liabilities | | | 0.02 | | |

Total | | | 100.0 | % | |

Top ten holdings1 | | 07/31/15 | |

Repurchase agreement with Goldman Sachs, Inc., 0.120% due 08/03/15 | | | 16.0 | % | |

Repurchase agreement with Barclays Capital, Inc., 0.130% due 08/03/15 | | | 5.9 | | |

Natixis, 0.080% due 08/03/15 | | | 3.0 | | |

Federal Home Loan Bank, 0.065% due 08/05/15 | | | 3.0 | | |

Working Capital Management Co., 0.150% due 08/03/15 | | | 3.0 | | |

Federal Home Loan Bank, 0.070% due 08/12/15 | | | 3.0 | | |

Atlantic Asset Securitization LLC, 0.140% due 08/07/15 | | | 3.0 | | |

Pfizer, Inc., 0.090% due 08/13/15 | | | 3.0 | | |

Starbird Funding Corp., 0.280% due 09/21/15 | | | 2.9 | | |

Federal Home Loan Bank, 0.170% due 12/09/15 | | | 2.9 | | |

Total | | | 45.7 | % | |

1 Weightings represent percentages of the Portfolio's net assets as of July 31, 2015. The Portfolio is actively managed and its composition will vary over time.

2 Represent less than 0.05% of net assets as of July 31, 2015.

7

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

US government and agency obligations—13.95% | |

Federal Home Loan Bank

0.065%, due 08/05/151 | | $ | 5,000,000 | | | $ | 4,999,964 | | |

0.070%, due 08/12/151 | | | 5,000,000 | | | | 4,999,893 | | |

0.170%, due 12/09/151 | | | 5,000,000 | | | | 4,996,931 | | |

Federal Home Loan Mortgage Corp.*

0.170%, due 11/04/151 | | | 1,000,000 | | | | 999,551 | | |

Federal National Mortgage

Association*

0.231%, due 03/21/161 | | | 2,000,000 | | | | 1,997,010 | | |

US Treasury Bills

0.180%, due 02/04/161 | | | 1,500,000 | | | | 1,498,597 | | |

0.100%, due 02/04/161 | | | 3,000,000 | | | | 2,996,572 | | |

US Treasury Notes

2.000%, due 04/30/16 | | | 1,000,000 | | | | 1,013,160 | | |

Total US government and agency obligations

(cost—$23,501,678) | | | | | 23,501,678 | | |

Certificates of deposit—17.21% | |

Banking-non-US—10.09% | |

Credit Industriel et Commercial

0.140%, due 08/05/15 | | | 3,000,000 | | | | 3,000,000 | | |

Mizuho Bank Ltd.

0.250%, due 09/01/15 | | | 2,000,000 | | | | 2,000,000 | | |

0.280%, due 10/20/15 | | | 2,000,000 | | | | 2,000,000 | | |

Natixis

0.255%, due 08/03/152 | | | 2,000,000 | | | | 2,000,000 | | |

Norinchukin Bank

0.160%, due 08/17/15 | | | 2,000,000 | | | | 2,000,000 | | |

0.160%, due 08/20/15 | | | 3,000,000 | | | | 3,000,000 | | |

Rabobank Nederland NV

0.295%, due 10/13/15 | | | 2,000,000 | | | | 2,000,000 | | |

Toronto-Dominion Bank

0.520%, due 02/23/16 | | | 1,000,000 | | | | 1,000,000 | | |

| | | | 17,000,000 | | |

Banking-US—7.12% | |

BMO Harris Bank N.A.

0.310%, due 10/08/15 | | | 2,000,000 | | | | 2,000,000 | | |

Citibank N.A.

0.200%, due 10/01/15 | | | 2,000,000 | | | | 2,000,000 | | |

HSBC Bank USA N.A.

0.280%, due 08/03/15 | | | 2,000,000 | | | | 2,000,000 | | |

0.400%, due 12/07/15 | | | 2,000,000 | | | | 2,000,000 | | |

JPMorgan Chase Bank N.A.

0.320%, due 10/28/15 | | | 2,000,000 | | | | 2,000,000 | | |

State Street Bank & Trust Co.

0.220%, due 11/09/15 | | | 2,000,000 | | | | 2,000,000 | | |

| | | | 12,000,000 | | |

Total certificates of deposit

(cost—$29,000,000) | | | | | 29,000,000 | | |

Commercial paper1—45.39% | |

Asset backed-miscellaneous—24.62% | |

Albion Capital Corp.

0.190%, due 08/20/15 | | | 1,000,000 | | | | 999,900 | | |

| | | Face

amount | | Value | |

Commercial paper1—(continued) | |

Asset backed-miscellaneous—(concluded) | |

Antalis US Funding Corp.

0.210%, due 08/21/15 | | $ | 2,000,000 | | | $ | 1,999,767 | | |

Atlantic Asset Securitization LLC

0.140%, due 08/07/15 | | | 5,000,000 | | | | 4,999,883 | | |

Barton Capital Corp.

0.257%, due 08/17/152 | | | 2,000,000 | | | | 2,000,000 | | |

Cancara Asset Securitisation LLC

0.170%, due 08/03/15 | | | 2,000,000 | | | | 1,999,981 | | |

Fairway Finance Co. LLC

0.260%, due 08/17/15 | | | 2,000,000 | | | | 1,999,769 | | |

Gotham Funding Corp.

0.160%, due 08/10/15 | | | 3,000,000 | | | | 2,999,880 | | |

Liberty Street Funding LLC

0.250%, due 10/26/15 | | | 2,000,000 | | | | 1,998,806 | | |

LMA Americas LLC

0.140%, due 08/03/15 | | | 4,000,000 | | | | 3,999,969 | | |

Manhattan Asset Funding Co. LLC

0.180%, due 08/25/15 | | | 4,000,000 | | | | 3,999,520 | | |

Starbird Funding Corp.

0.280%, due 09/21/15 | | | 5,000,000 | | | | 4,998,017 | | |

Victory Receivables Corp.

0.190%, due 08/10/15 | | | 4,500,000 | | | | 4,499,786 | | |

Working Capital Management Co.

0.150%, due 08/03/15 | | | 5,000,000 | | | | 4,999,958 | | |

| | | | 41,495,236 | | |

Banking-non-US—7.71% | |

Australia & New Zealand Banking

Group Ltd.

0.276%, due 08/13/152 | | | 2,000,000 | | | | 2,000,000 | | |

Caisse Centrale Desjardins

0.170%, due 08/11/15 | | | 1,000,000 | | | | 999,953 | | |

Mitsubishi UFJ Trust & Banking Corp.

0.160%, due 08/17/15 | | | 3,000,000 | | | | 2,999,786 | | |

National Australia Bank Ltd.

0.415%, due 01/08/16 | | | 2,000,000 | | | | 1,996,311 | | |

Natixis

0.080%, due 08/03/15 | | | 5,000,000 | | | | 4,999,978 | | |

| | | | 12,996,028 | | |

Banking-US—2.96% | |

Bedford Row Funding Corp.

0.110%, due 08/17/15 | | | 3,000,000 | | | | 2,999,853 | | |

0.470%, due 01/04/16 | | | 2,000,000 | | | | 1,995,927 | | |

| | | | 4,995,780 | | |

Electric-integrated—1.19% | |

CNPC Finance HK Ltd.

0.400%, due 08/04/15 | | | 2,000,000 | | | | 1,999,933 | | |

Finance-non-captive diversified—1.19% | |

General Electric Capital Corp.

0.350%, due 10/02/15 | | | 2,000,000 | | | | 1,998,794 | | |

8

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Commercial paper1—(concluded) | |

Insurance-life—1.78% | |

MetLife Short Term Funding LLC

0.150%, due 08/24/15 | | $ | 3,000,000 | | | $ | 2,999,713 | | |

Machinery-agriculture & construction—2.97% | |

Caterpillar Financial Services Corp.

0.100%, due 08/04/15 | | | 2,000,000 | | | | 1,999,983 | | |

0.110%, due 09/14/15 | | | 3,000,000 | | | | 2,999,597 | | |

| | | | 4,999,580 | | |

Pharmaceuticals—2.97% | |

Pfizer, Inc.

0.090%, due 08/13/15 | | | 5,000,000 | | | | 4,999,850 | | |

Total commercial paper

(cost—$76,784,914) | | | | | 76,484,914 | | |

Short-term corporate obligation—1.19% | |

Finance-non-captive diversified—1.19% | |

General Electric Capital Corp

2.250%, due 11/09/15

(cost—$2,010,309) | | | 2,000,000 | | | | 2,010,309 | | |

Repurchase agreements—22.22% | |

Repurchase agreement dated

07/31/15 with Barclays Capital, Inc.,

0.130% due 08/03/15, collateralized

by $10,200,000 US Treasury Note,

1.625% due 07/31/20;

(value—$10,200,000);

proceeds: $10,000,108 | | | 10,000,000 | | | | 10,000,000 | | |

Repurchase agreement dated

07/31/15 with Goldman Sachs & Co.,

0.120% due 08/03/15, collateralized

by $27,451,000 Federal Home Loan

Mortgage Corp. obligation,

1.840% due 04/08/20;

(value—$27,540,094);

proceeds: $27,000,270 | | | 27,000,000 | | | | 27,000,000 | | |

| | | Face

amount | | Value | |

Repurchase agreements—(concluded) | |

Repurchase agreement dated

07/31/15 with State Street Bank

and Trust Co., 0.000% due

08/03/15, collateralized by

$417,935 Federal Home Loan

Mortgage Corp. obligation,

1.960% due 11/07/22 and $49,820

Federal National Mortgage

Association obligation,

2.170% due 11/07/22;

(value—$450,464);

proceeds: $441,000 | | $ | 441,000 | | | $ | 441,000 | | |

Total repurchase agreements

(cost—$37,441,000) | | | | | 37,441,000 | | |

Total investments

(cost—$168,437,901 which

approximates cost for federal

income tax purposes)—99.96% | | | | | 168,437,901 | | |

Other assets in excess of

liabilities—0.04% | | | | | 65,216 | | |

Net assets (applicable to 168,501,248

shares of beneficial interest

outstanding equivalent to $1.00

per share)—100.00% | | | | $ | 168,503,117 | | |

For a listing of defined portfolio acronyms that are used throughout the Portfolio of investments as well as the tables that follow, please refer to page 254.

9

PACE Select Advisors Trust

PACE Money Market Investments

Portfolio of investments—July 31, 2015

Fair valuation summary

The following is a summary of the fair valuations according to the inputs used as of July 31, 2015 in valuing the Portfolio's investments:

Assets

Description | | Unadjusted

quoted prices in

active markets for

identical investments

(Level 1) | | Other significant

observable inputs

(Level 2) | | Unobservable

inputs

(Level 3) | | Total | |

US government and agency obligations | | $ | — | | | $ | 23,501,678 | | | $ | — | | | $ | 23,501,678 | | |

Certificates of deposit | | | — | | | | 29,000,000 | | | | — | | | | 29,000,000 | | |

Commercial paper | | | — | | | | 76,484,914 | | | | — | | | | 76,484,914 | | |

Short-term corporate obligation | | | — | | | | 2,010,309 | | | | — | | | | 2,010,309 | | |

Repurchase agreements | | | — | | | | 37,441,000 | | | | — | | | | 37,441,000 | | |

Total | | $ | — | | | $ | 168,437,901 | | | $ | — | | | $ | 168,437,901 | | |

At July 31, 2015, there were no transfers between Level 1 and Level 2.

Issuer breakdown by country or territory of origin (unaudited)

| | | Percentage of

total investments | |

United States | | | 81.0 | % | |

Japan | | | 7.1 | | |

France | | | 5.9 | | |

Australia | | | 2.4 | | |

Netherlands | | | 1.2 | | |

Canada | | | 1.2 | | |

China | | | 1.2 | | |

Total | | | 100.0 | % | |

Portfolio footnotes

* On September 7, 2008, the Federal Housing Finance Agency placed the Federal National Mortgage Association and the Federal Home Loan Mortgage Corporation into conservatorship, and the US Treasury guaranteed the debt issued by those organizations.

1 Rates shown are the discount rates at date of purchase unless otherwise noted.

2 Variable or floating rate security. The interest rate shown is the current rate as of July 31, 2015 and changes periodically. The maturity date reflects earlier of reset date or stated maturity date.

See accompanying notes to financial statements.

10

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Performance (unaudited)

For the 12 months ended July 31, 2015, the Portfolio's Class P shares gained 3.04% before the deduction of the maximum PACE Select program fee.1 In comparison, the Barclays US Mortgage-Backed Securities Index (the "benchmark") rose 3.54%, and the Lipper US Mortgage Funds category posted a median return of 3.24%.3 (Returns for all share classes over various time periods are shown in the "Performance at a glance" table on page 14. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.) For a detailed commentary on the market environment in general during the reporting period, please refer to page 2.

Sub-advisor's comments2

(Please note that while the sub-advisor outperformed the benchmark on a gross-of-fees basis, the Portfolio underperformed net of fees, as reported in the "Performance at a glance" table. As stated in footnote two, the comments that follow address performance on a gross-of-fees basis.)

The Portfolio outperformed its benchmark during the reporting period. Positioning within the agency mortgage-backed security ("MBS") sector was neutral to modestly positive for performance. An overall underweight to agency MBS contributed to results as they lagged like-duration Treasuries. However, less exposure to lower coupon Freddie Mac ("FHLMC") and Fannie Mae ("FNMA") mortgages during the first half of the period detracted from returns, as these securities outperformed higher coupons given elevated prepayment concerns. An underweight to 15-year conventional FNMA and FHLMC securities detracted from returns, as they outperformed the broader market and like-duration Treasuries. Additionally, an underweight to Ginnie Mae ("GNMA") bonds for most of the period contributed to results as they underperformed FHLMC and FNMA mortgages.

An allocation to non-agency MBS contributed to results as prices on selected securities rose amid strong demand and continued limited supply.

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

2 All sub-advisors discuss performance on a gross-of-fees basis—meaning that no fees or expenses are reflected in their sleeves'/sleeve's performance. Alternately, Portfolio performance is shown net of fees, which does factor in fees and expenses associated with the Portfolio.

3 Barclays US Mortgage-Backed Securities Index, as calculated by the investment advisor, which as of July 31, 2015 had a duration of approximately 4.34 years.

PACE Select Advisors Trust – PACE Mortgage-Backed Securities Fixed

Income Investments

Investment Sub-Advisor:

Pacific Investment Management Company LLC ("PIMCO")

Portfolio Managers:

Daniel Hyman and Michael Cudzil

Objective:

Current income

Investment process:

The Portfolio invests primarily in government fixed income securities which include US bonds, including those backed by mortgages, and related repurchase agreements. Mortgage-backed securities include "to be announced" or "TBA" securities, which usually are traded on a forward commitment basis with an approximate principal amount and no defined maturity date; issued or guaranteed by US government agencies and instrumentalities. The Portfolio also invests, to a lesser extent, in investment grade bonds of private issuers, including those backed by mortgages or other assets. The Portfolio may invest in bonds of varying maturities, but normally limits its duration to within +/- 50% of the effective duration of the Portfolio's benchmark index.3 (Duration is a measure of a portfolio's sensitivity to interest rate changes.) The Portfolio may engage in short selling with respect to securities issued by the US Treasury and certain TBA securities coupon trades. PIMCO establishes duration targets based on its expectations for changes in interest rates, and then positions the Portfolio to take advantage of yield curve shifts. PIMCO decides to buy and sell specific bonds based on an analysis of their values relative to other similar securities.

11

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Sub-advisor's comments – concluded

An underweight to US duration detracted from performance as the yield on the 10-year US Treasury fell 38 basis points (0.38%). (Duration measures a portfolio's sensitivity to interest rate changes.)

Overall, derivative usage was positive during the reporting period, primarily due to income generated from selling mortgage pool options as a way to manage interest rate and volatility risk within the sector. This was partially offset by negative price action of synthetic interest-only agency MBS that were traded as total return swaps. The Portfolio also used interest rate swaps to adjust interest rate and yield curve exposures, as well as to substitute for physical securities. Additionally, options on swaps were used to manage interest rate and volatility exposures, as well as to generate income in expected interest rate scenarios. Government futures were utilized to adjust interest rate exposures and replicate government bond positions.

Special considerations

The Portfolio may be appropriate for long-term investors seeking current income who are able to withstand short-term fluctuations in the fixed income markets in return for potentially higher returns over the long term. The yield and value of the Portfolio change every day and can be affected by changes in interest rates, general market conditions, and other political, social and economic developments, as well as specific matters relating to the issuers in which the Portfolio invests. It is important to note that an investment in the Portfolio is only one component of a balanced investment plan.

12

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Illustration of an assumed investment of $10,000 in Class P shares of the Portfolio (unaudited)

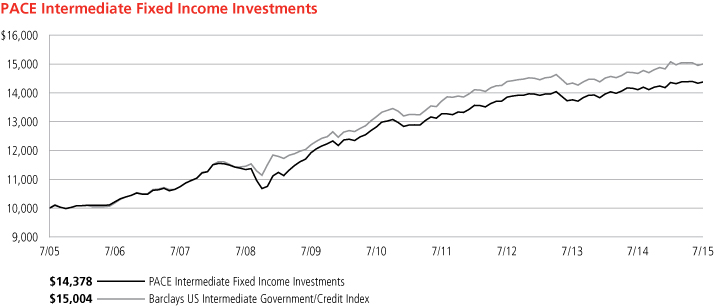

The following graph depicts the performance of PACE Mortgage-Backed Securities Fixed Income Investments Class P shares versus the Barclays US Mortgage-Backed Securities Index over the 10 years ended July 31, 2015. Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that PACE Mortgage-Backed Securities Fixed Income Investments is a professionally managed portfolio while the Index is not available for investment and is unmanaged. The comparison is shown for illustration purposes only.

13

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Performance at a glance (unaudited)

Average annual total returns for periods ended 07/31/15 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | 2.86 | % | | | 2.45 | % | | | 4.25 | % | |

Class C2 | | | 2.27 | | | | 1.93 | | | | 3.73 | | |

Class Y3 | | | 3.12 | | | | 2.71 | | | | 4.53 | | |

Class P4 | | | 3.04 | | | | 2.70 | | | | 4.51 | | |

After deducting maximum sales charge | |

Class A1 | | | (1.74 | ) | | | 1.50 | | | | 3.78 | | |

Class C2 | | | 1.52 | | | | 1.93 | | | | 3.73 | | |

Barclays US Mortgage-Backed Securities Index5 | | | 3.54 | | | | 2.85 | | | | 4.68 | | |

Lipper US Mortgage Funds median | | | 3.24 | | | | 2.97 | | | | 4.18 | | |

Most recent calendar quarter-end returns (unaudited)

Average annual total returns for periods ended 06/30/15 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | 1.97 | % | | | 2.58 | % | | | 4.16 | % | |

Class C2 | | | 1.38 | | | | 2.06 | | | | 3.63 | | |

Class Y3 | | | 2.23 | | | | 2.83 | | | | 4.44 | | |

Class P4 | | | 2.14 | | | | 2.82 | | | | 4.41 | | |

After deducting maximum sales charge | |

Class A1 | | | (2.64 | ) | | | 1.64 | | | | 3.68 | | |

Class C2 | | | 0.63 | | | | 2.06 | | | | 3.63 | | |

The annualized gross and net expense ratios, respectively, for each class of shares as in the November 28, 2014 prospectuses, were as follows: Class A—1.07% and 0.97%; Class C—1.59% and 1.47%; Class Y—0.87% and 0.72%; and Class P—0.90% and 0.72%. Net expenses reflect fee waivers and/or expense reimbursements, if any, pursuant to an agreement that is in effect to cap the expenses. The Portfolio and UBS Global Asset Management (Americas) Inc. ("UBS Global AM") have entered into a written fee waiver/expense reimbursement agreement pursuant to which UBS Global AM is contractually obligated to (1) waive its management fees through November 30, 2015 to the extent necessary to reflect the lower sub-advisory fee paid by UBS Global AM to Pacific Investment Management Company LLC, the Portfolio's investment sub-advisor; and (2) waive its management fees and/or reimburse expenses so that the Portfolio's ordinary total operating expenses of each class through November 30, 2015 (excluding dividend expense, borrowing costs, and interest expense relating to short sales, and expenses attributable to investment in other investment companies, interest, taxes, brokerage commissions and extraordinary expenses) would not exceed Class A—0.97%; Class C—1.47%; Class Y—0.72%; and Class P—0.72%. The Portfolio has agreed to repay UBS Global AM for any waived fees/reimbursed expenses (pursuant to item (2)) to the extent that it can do so over the following three fiscal years without causing the Portfolio's expenses in any of those three years to exceed these expense caps. The fee waiver/expense reimbursement agreement may be terminated by the Portfolio's board at any time and also will terminate automatically upon the expiration or termination of the Portfolio's advisory contract with UBS Global AM. Upon termination of the agreement, however, UBS Global AM's three year recoupment rights will survive.

1 Maximum sales charge for Class A shares is 4.5%. Class A shares bear ongoing 12b-1 service fees.

2 Maximum contingent deferred sales charge for Class C shares is 0.75% imposed on redemptions and is reduced to 0% after one year. Class C shares bear ongoing 12b-1 service and distribution fees.

3 The Portfolio offers Class Y shares to a limited group of eligible investors, including certain qualifying retirement plans. Class Y shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees.

4 Class P shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees, but Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance.

5 The Barclays US Mortgage-Backed Securities Index is an unmanaged index which primarily covers the mortgage-backed pass-through securities issued by Ginnie Mae (formally known as the Government National Mortgage Association or GNMA), Freddie Mac (formally known as Federal Home Loan Mortgage Corporation or FHLMC), and Fannie Mae (formally known as Federal National Mortgage Association or FNMA). Investors should note that indices do not reflect the deduction of fees and expenses.

Prior to February 17, 2015, if an investor sold or exchanged shares less than 90 days after purchase, a redemption fee of 1.00% of the amount sold or exchanged was deducted at the time of the transaction, except as noted otherwise in the prospectus. For sales or exchanges taking place on or after February 17, 2015 but prior to August 3, 2015, there is a reduction in the redemption holding period from 90 days to 30 days. Effective August 3, 2015, the 1.00% redemption fee imposed on sales or exchanges of any class of shares of the portfolios made during the holding periods specified in the prospectus was eliminated. Please refer to the prospectus for further information.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. The return and principal value of an investment will fluctuate, so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the ex-dividend dates. Current performance may be higher or lower than the performance data quoted. For month-end performance figures, please visit http://globalam-us.ubs.com/corpweb/performance.do.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

14

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio statistics (unaudited)

Characteristics | | 07/31/15 | |

Weighted average duration | | | 3.28 yrs. | | |

Weighted average maturity | | | 4.27 yrs. | | |

Average coupon | | | 2.50 | % | |

Net assets (mm) | | $ | 529.4 | | |

Number of holdings | | | 521 | | |

Portfolio composition1 | | 07/31/15 | |

Bonds | | | 149.2 | % | |

Investments sold short | | | (32.7 | ) | |

Options and swaps | | | (0.3 | ) | |

Cash equivalents and other assets less liabilities | | | (16.2 | ) | |

Total | | | 100.0 | % | |

Asset allocation1 | | 07/31/15 | |

US government agency mortgage pass-through certificates | | | 122.9 | % | |

Collateralized mortgage obligations | | | 13.9 | | |

Asset-backed securities | | | 6.2 | | |

US government obligations | | | 4.9 | | |

Stripped mortgage-backed securities | | | 1.3 | | |

Options and swaps | | | (0.3 | ) | |

Investments sold short | | | (32.7 | ) | |

Cash equivalents and other assets less liabilities | | | (16.2 | ) | |

Total | | | 100.0 | % | |

1 Weightings represent percentages of the Portfolio's net assets as of July 31, 2015. The Portfolio is actively managed and its composition will vary over time.

15

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

US government obligations—4.85% | |

US Treasury Notes

1.875%, due 05/31/221 | | $ | 8,700,000 | | | $ | 8,675,536 | | |

2.000%, due 07/31/22 | | | 6,200,000 | | | | 6,224,461 | | |

2.000%, due 02/15/25 | | | 10,950,000 | | | | 10,760,937 | | |

Total US government obligations

(cost—$25,690,599) | | | 25,660,934 | | |

Government national mortgage association

certificates—34.06% | |

GNMA

3.000%, due 01/15/45 | | | 22,999,999 | | | | 23,429,501 | | |

3.000%, due 02/15/45 | | | 999,999 | | | | 1,018,673 | | |

3.000%, due 07/15/45 | | | 1,000,000 | | | | 1,018,674 | | |

4.000%, due 12/15/41 | | | 2,089,726 | | | | 2,246,230 | | |

4.500%, due 09/15/39 | | | 1,389,420 | | | | 1,522,331 | | |

4.500%, due 11/15/39 | | | 320,600 | | | | 349,016 | | |

4.500%, due 05/15/40 | | | 153,445 | | | | 166,796 | | |

4.500%, due 06/15/40 | | | 675,403 | | | | 734,668 | | |

5.000%, due 12/15/34 | | | 295,978 | | | | 330,630 | | |

5.000%, due 04/15/38 | | | 235,251 | | | | 261,034 | | |

5.000%, due 05/15/38 | | | 8,361 | | | | 9,269 | | |

5.000%, due 08/15/39 | | | 621,012 | | | | 689,326 | | |

5.000%, due 09/15/39 | | | 824,951 | | | | 915,170 | | |

5.000%, due 10/15/39 | | | 8,569 | | | | 9,498 | | |

5.000%, due 12/15/39 | | | 22,826 | | | | 25,350 | | |

5.000%, due 02/15/40 | | | 391,102 | | | | 434,273 | | |

5.000%, due 05/15/40 | | | 601,571 | | | | 667,932 | | |

5.000%, due 09/15/40 | | | 13,235 | | | | 14,695 | | |

5.000%, due 05/15/41 | | | 169,529 | | | | 189,840 | | |

5.500%, due 08/15/35 | | | 53,919 | | | | 61,277 | | |

5.500%, due 02/15/38 | | | 6,492 | | | | 7,307 | | |

5.500%, due 04/15/38 | | | 549,089 | | | | 617,083 | | |

5.500%, due 05/15/38 | | | 558,681 | | | | 629,353 | | |

5.500%, due 06/15/38 | | | 296,377 | | | | 333,607 | | |

5.500%, due 10/15/38 | | | 1,447,478 | | | | 1,629,287 | | |

5.500%, due 11/15/38 | | | 80,299 | | | | 90,422 | | |

5.500%, due 12/15/38 | | | 16,380 | | | | 18,437 | | |

5.500%, due 03/15/39 | | | 278,021 | | | | 313,977 | | |

5.500%, due 05/15/39 | | | 139,385 | | | | 156,893 | | |

5.500%, due 09/15/39 | | | 693,476 | | | | 780,516 | | |

5.500%, due 01/15/40 | | | 11,386 | | | | 12,823 | | |

5.500%, due 03/15/40 | | | 978,686 | | | | 1,101,523 | | |

5.500%, due 05/15/40 | | | 60,500 | | | | 68,060 | | |

6.500%, due 02/15/29 | | | 1,228 | | | | 1,402 | | |

6.500%, due 01/15/36 | | | 12,261 | | | | 13,991 | | |

6.500%, due 09/15/36 | | | 327,957 | | | | 383,580 | | |

6.500%, due 02/15/37 | | | 17,923 | | | | 20,799 | | |

6.500%, due 04/15/37 | | | 12,418 | | | | 14,171 | | |

6.500%, due 01/15/38 | | | 12,063 | | | | 13,819 | | |

6.500%, due 06/15/38 | | | 41,440 | | | | 47,822 | | |

6.500%, due 07/15/38 | | | 43,760 | | | | 53,691 | | |

6.500%, due 11/15/38 | | | 11,365 | | | | 13,711 | | |

7.500%, due 08/15/21 | | | 3,014 | | | | 3,121 | | |

8.000%, due 02/15/23 | | | 584 | | | | 645 | | |

8.250%, due 04/15/19 | | | 94,347 | | | | 100,939 | | |

10.500%, due 02/15/19 | | | 15,543 | | | | 15,633 | | |

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(continued) | |

10.500%, due 06/15/19 | | $ | 19,686 | | | $ | 19,799 | | |

10.500%, due 07/15/19 | | | 25,191 | | | | 25,336 | | |

10.500%, due 07/15/20 | | | 2,150 | | | | 2,163 | | |

10.500%, due 08/15/20 | | | 19,826 | | | | 20,265 | | |

GNMA II

2.500%, due 03/20/45 | | | 994,527 | | | | 969,863 | | |

3.000%, due 07/20/451 | | | 9,999,000 | | | | 10,184,309 | | |

5.000%, due 12/20/33 | | | 444,616 | | | | 494,793 | | |

5.000%, due 01/20/34 | | | 252,253 | | | | 281,700 | | |

5.000%, due 02/20/38 | | | 344,503 | | | | 374,566 | | |

5.000%, due 04/20/38 | | | 392,944 | | | | 427,992 | | |

5.000%, due 08/20/41 | | | 51,109 | | | | 56,688 | | |

5.000%, due 12/20/42 | | | 69,549 | | | | 77,441 | | |

5.000%, due 08/20/43 | | | 6,804,647 | | | | 7,388,720 | | |

9.000%, due 04/20/25 | | | 10,281 | | | | 11,794 | | |

9.000%, due 12/20/26 | | | 3,529 | | | | 3,748 | | |

9.000%, due 01/20/27 | | | 10,835 | | | | 11,180 | | |

9.000%, due 09/20/30 | | | 1,175 | | | | 1,180 | | |

9.000%, due 10/20/30 | | | 3,846 | | | | 4,024 | | |

9.000%, due 11/20/30 | | | 5,210 | | | | 5,310 | | |

GNMA II ARM

1.625%, due 07/20/17 | | | 1,470 | | | | 1,492 | | |

1.625%, due 09/20/21 | | | 77,969 | | | | 80,530 | | |

1.625%, due 06/20/22 | | | 69,075 | | | | 71,730 | | |

1.625%, due 04/20/24 | | | 108,600 | | | | 112,194 | | |

1.625%, due 08/20/25 | | | 20,555 | | | | 21,386 | | |

1.625%, due 09/20/25 | | | 26,801 | | | | 27,907 | | |

1.625%, due 04/20/26 | | | 135,288 | | | | 140,074 | | |

1.625%, due 06/20/26 | | | 58,150 | | | | 60,387 | | |

1.625%, due 08/20/26 | | | 29,806 | | | | 31,016 | | |

1.625%, due 04/20/27 | | | 33,611 | | | | 34,959 | | |

1.625%, due 07/20/27 | | | 11,050 | | | | 11,499 | | |

1.625%, due 04/20/30 | | | 11,444 | | | | 11,904 | | |

1.625%, due 05/20/30 | | | 124,215 | | | | 129,206 | | |

1.625%, due 07/20/30 | | | 63,949 | | | | 66,530 | | |

1.750%, due 01/20/23 | | | 50,002 | | | | 51,594 | | |

1.750%, due 03/20/23 | | | 25,217 | | | | 26,042 | | |

1.750%, due 01/20/24 | | | 58,980 | | | | 60,892 | | |

1.750%, due 02/20/25 | | | 15,356 | | | | 15,900 | | |

1.750%, due 03/20/26 | | | 14,798 | | | | 15,366 | | |

1.750%, due 01/20/27 | | | 83,088 | | | | 84,030 | | |

1.750%, due 01/20/28 | | | 13,876 | | | | 14,404 | | |

1.750%, due 02/20/28 | | | 9,614 | | | | 9,948 | | |

2.000%, due 01/20/25 | | | 7,034 | | | | 7,248 | | |

2.000%, due 05/20/25 | | | 7,813 | | | | 8,072 | | |

2.000%, due 09/20/26 | | | 4,715 | | | | 4,880 | | |

2.000%, due 01/20/27 | | | 5,578 | | | | 5,801 | | |

2.000%, due 02/20/27 | | | 11,457 | | | | 11,849 | | |

2.000%, due 04/20/27 | | | 3,676 | | | | 3,887 | | |

2.000%, due 08/20/27 | | | 31,373 | | | | 33,355 | | |

2.000%, due 04/20/30 | | | 12,612 | | | | 13,077 | | |

2.000%, due 05/20/30 | | | 395,195 | | | | 409,786 | | |

2.000%, due 07/20/30 | | | 21,094 | | | | 21,951 | | |

2.000%, due 08/20/30 | | | 109,042 | | | | 113,487 | | |

2.500%, due 04/20/18 | | | 1,996 | | | | 2,005 | | |

16

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(concluded) | |

2.500%, due 11/20/21 | | $ | 16,787 | | | $ | 17,205 | | |

2.500%, due 03/20/25 | | | 25,300 | | | | 26,116 | | |

2.500%, due 07/20/30 | | | 42,620 | | | | 45,114 | | |

2.500%, due 08/20/30 | | | 4,175 | | | | 4,313 | | |

2.500%, due 10/20/30 | | | 14,481 | | | | 14,846 | | |

3.000%, due 04/20/18 | | | 2,586 | | | | 2,645 | | |

3.000%, due 05/20/25 | | | 52,468 | | | | 55,529 | | |

3.000%, due 06/20/25 | | | 19,733 | | | | 20,533 | | |

3.500%, due 03/20/25 | | | 10,168 | | | | 10,263 | | |

4.000%, due 01/20/18 | | | 34,249 | | | | 35,441 | | |

4.000%, due 05/20/18 | | | 2,717 | | | | 2,743 | | |

4.000%, due 06/20/19 | | | 14,502 | | | | 14,731 | | |

GNMA TBA

3.000% | | | 2,000,000 | | | | 2,034,062 | | |

| 3.500% | | | 6,000,000 | | | | 6,261,872 | | |

| 4.000% | | | 3,000,000 | | | | 3,187,033 | | |

| 4.500% | | | 4,000,000 | | | | 4,334,688 | | |

| 6.000% | | | 1,000,000 | | | | 1,128,403 | | |

GNMA II TBA

3.000% | | | 20,000,000 | | | | 20,340,624 | | |

| 3.500% | | | 35,000,000 | | | | 36,460,153 | | |

| 4.000% | | | 27,000,000 | | | | 28,631,073 | | |

| 4.500% | | | 14,000,000 | | | | 15,086,095 | | |

Total government national mortgage

association certificates

(cost—$178,874,228) | | | 180,325,536 | | |

Federal home loan mortgage corporation

certificates*—27.91% | |

FHLMC

3.000%, due 04/01/43 | | | 467,423 | | | | 470,015 | | |

3.000%, due 05/01/43 | | | 486,827 | | | | 489,458 | | |

3.000%, due 12/01/44 | | | 336,044 | | | | 337,547 | | |

3.000%, due 04/01/45 | | | 239,999 | | | | 240,948 | | |

3.000%, due 05/01/45 | | | 249,999 | | | | 250,988 | | |

3.000%, due 06/01/45 | | | 6,510,006 | | | | 6,535,752 | | |

3.500%, due 09/01/32 | | | 864,354 | | | | 911,331 | | |

4.000%, due 01/01/37 | | | 688,934 | | | | 733,489 | | |

4.000%, due 07/01/43 | | | 350,044 | | | | 375,463 | | |

4.000%, due 06/01/44 | | | 1,823,535 | | | | 1,936,937 | | |

5.000%, due 10/01/25 | | | 111,602 | | | | 122,702 | | |

5.000%, due 11/01/27 | | | 10,066 | | | | 11,093 | | |

5.000%, due 10/01/29 | | | 387,837 | | | | 426,623 | | |

5.000%, due 09/01/33 | | | 328,729 | | | | 362,419 | | |

5.000%, due 01/01/34 | | | 60,961 | | | | 67,725 | | |

5.000%, due 06/01/34 | | | 21,127 | | | | 23,401 | | |

5.000%, due 04/01/35 | | | 59,446 | | | | 65,394 | | |

5.000%, due 05/01/35 | | | 239,248 | | | | 264,829 | | |

5.000%, due 07/01/35 | | | 1,923,507 | | | | 2,130,471 | | |

5.000%, due 08/01/35 | | | 69,868 | | | | 77,354 | | |

5.000%, due 10/01/35 | | | 56,643 | | | | 62,585 | | |

5.000%, due 12/01/35 | | | 6,264 | | | | 6,897 | | |

5.000%, due 02/01/37 | | | 171,474 | | | | 188,589 | | |

5.000%, due 06/01/37 | | | 99,715 | | | | 109,771 | | |

5.000%, due 07/01/38 | | | 489,024 | | | | 537,473 | | |

| | | Face

amount | | Value | |

Federal home loan mortgage corporation

certificates*—(continued) | |

5.000%, due 11/01/38 | | $ | 531,905 | | | $ | 584,927 | | |

5.000%, due 06/01/39 | | | 125,682 | | | | 138,441 | | |

5.000%, due 08/01/39 | | | 52,016 | | | | 57,470 | | |

5.000%, due 03/01/40 | | | 14,121 | | | | 15,636 | | |

5.000%, due 07/01/40 | | | 801,107 | | | | 886,387 | | |

5.000%, due 08/01/40 | | | 112,443 | | | | 124,563 | | |

5.000%, due 09/01/40 | | | 322,915 | | | | 355,025 | | |

5.000%, due 11/01/40 | | | 519,610 | | | | 575,762 | | |

5.000%, due 02/01/41 | | | 886,196 | | | | 981,658 | | |

5.000%, due 03/01/41 | | | 60,033 | | | | 66,471 | | |

5.000%, due 04/01/41 | | | 2,053,267 | | | | 2,263,370 | | |

5.000%, due 05/01/41 | | | 420,399 | | | | 464,891 | | |

5.000%, due 06/01/41 | | | 129,073 | | | | 142,973 | | |

5.000%, due 07/01/41 | | | 78,401 | | | | 86,534 | | |

5.000%, due 08/01/44 | | | 180,376 | | | | 200,164 | | |

5.500%, due 06/01/28 | | | 2,828 | | | | 3,157 | | |

5.500%, due 02/01/32 | | | 3,585 | | | | 4,021 | | |

5.500%, due 12/01/32 | | | 4,970 | | | | 5,574 | | |

5.500%, due 02/01/33 | | | 96,446 | | | | 107,705 | | |

5.500%, due 05/01/33 | | | 1,891 | | | | 2,116 | | |

5.500%, due 06/01/33 | | | 299,746 | | | | 339,300 | | |

5.500%, due 12/01/33 | | | 110,910 | | | | 124,813 | | |

5.500%, due 12/01/34 | | | 90,228 | | | | 101,363 | | |

5.500%, due 06/01/351 | | | 1,590,338 | | | | 1,785,934 | | |

5.500%, due 07/01/35 | | | 10,807 | | | | 12,122 | | |

5.500%, due 10/01/35 | | | 371,017 | | | | 416,865 | | |

5.500%, due 12/01/35 | | | 241,660 | | | | 270,829 | | |

5.500%, due 06/01/36 | | | 884,253 | | | | 991,652 | | |

5.500%, due 12/01/361 | | | 1,469,871 | | | | 1,641,677 | | |

5.500%, due 03/01/37 | | | 181,859 | | | | 203,250 | | |

5.500%, due 07/01/37 | | | 95,600 | | | | 104,782 | | |

5.500%, due 10/01/37 | | | 9,267 | | | | 10,345 | | |

5.500%, due 04/01/38 | | | 282,001 | | | | 314,793 | | |

5.500%, due 05/01/38 | | | 33,824 | | | | 37,757 | | |

5.500%, due 12/01/38 | | | 6,179 | | | | 6,973 | | |

5.500%, due 01/01/39 | | | 126,091 | | | | 140,753 | | |

5.500%, due 09/01/39 | | | 387,269 | | | | 436,361 | | |

5.500%, due 02/01/40 | | | 18,682 | | | | 20,855 | | |

5.500%, due 03/01/40 | | | 14,665 | | | | 16,389 | | |

5.500%, due 05/01/40 | | | 253,222 | | | | 282,667 | | |

5.500%, due 02/01/41 | | | 74,216 | | | | 82,963 | | |

5.500%, due 03/01/41 | | | 267,977 | | | | 299,215 | | |

6.000%, due 11/01/37 | | | 2,448,639 | | | | 2,766,065 | | |

7.000%, due 08/01/25 | | | 373 | | | | 422 | | |

9.000%, due 04/01/25 | | | 30,329 | | | | 30,575 | | |

11.000%, due 12/01/15 | | | 52 | | | | 52 | | |

11.000%, due 06/01/19 | | | 229 | | | | 230 | | |

11.000%, due 09/01/20 | | | 194 | | | | 197 | | |

11.500%, due 01/01/16 | | | 272 | | | | 274 | | |

11.500%, due 01/01/18 | | | 444 | | | | 444 | | |

11.500%, due 06/01/19 | | | 11,309 | | | | 11,450 | | |

FHLMC ARM

2.262%, due 01/01/28 | | | 16,406 | | | | 17,024 | | |

2.332%, due 11/01/27 | | | 80,297 | | | | 83,450 | | |

2.356%, due 04/01/29 | | | 116,987 | | | | 122,950 | | |

17

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Federal home loan mortgage corporation

certificates*—(concluded) | |

2.388%, due 07/01/24 | | $ | 148,129 | | | $ | 149,926 | | |

2.398%, due 10/01/23 | | | 52,542 | | | | 54,270 | | |

2.456%, due 11/01/29 | | | 320,451 | | | | 336,924 | | |

2.486%, due 06/01/28 | | | 262,024 | | | | 276,762 | | |

2.511%, due 07/01/28 | | | 110,099 | | | | 114,989 | | |

2.511%, due 12/01/29 | | | 59,978 | | | | 62,539 | | |

2.589%, due 01/01/29 | | | 171,597 | | | | 183,019 | | |

2.590%, due 10/01/27 | | | 206,754 | | | | 220,424 | | |

2.594%, due 11/01/25 | | | 187,668 | | | | 200,231 | | |

2.630%, due 10/01/27 | | | 199,028 | | | | 211,742 | | |

2.750%, due 01/01/30 | | | 30,308 | | | | 30,530 | | |

FHLMC TBA

3.000%1 | | | 46,000,000 | | | | 46,136,250 | | |

| 3.500% | | | 28,000,000 | | | | 28,932,977 | | |

| 4.000% | | | 19,000,000 | | | | 20,125,157 | | |

| 4.500% | | | 15,000,000 | | | | 16,237,404 | | |

Total federal home loan mortgage

corporation certificates

(cost—$146,346,500) | | | 147,754,034 | | |

Federal housing administration certificates—0.06% | |

FHA GMAC

7.400%, due 02/01/212 | | | 67,806 | | | | 67,696 | | |

FHA Reilly

6.896%, due 07/01/20 | | | 238,642 | | | | 238,642 | | |

Total federal housing administration

certificates

(cost—$306,803) | | | 306,338 | | |

Federal national mortgage association

certificates*—60.83% | |

FNMA

2.000%, due 05/01/28 | | | 292,357 | | | | 291,505 | | |

2.000%, due 08/01/28 | | | 401,245 | | | | 400,076 | | |

2.000%, due 10/01/28 | | | 1,948,079 | | | | 1,942,409 | | |

2.354%, due 03/01/23 | | | 1,821,377 | | | | 1,826,474 | | |

2.500%, due 06/01/28 | | | 400,763 | | | | 410,521 | | |

2.500%, due 07/01/28 | | | 3,198,361 | | | | 3,276,455 | | |

2.500%, due 08/01/28 | | | 122,763 | | | | 125,760 | | |

2.500%, due 07/01/29 | | | 518,456 | | | | 526,761 | | |

2.500%, due 12/01/29 | | | 28,982 | | | | 29,446 | | |

2.500%, due 01/01/30 | | | 1,884,042 | | | | 1,914,224 | | |

2.500%, due 04/01/30 | | | 25,179 | | | | 25,582 | | |

2.500%, due 05/01/301 | | | 48,089,462 | | | | 48,859,841 | | |

2.500%, due 06/01/30 | | | 7,033,207 | | | | 7,145,876 | | |

2.500%, due 07/01/301 | | | 51,192,642 | | | | 52,012,736 | | |

2.500%, due 08/01/30 | | | 1,171,099 | | | | 1,189,828 | | |

3.000%, due 10/01/42 | | | 873,832 | | | | 883,289 | | |

3.000%, due 01/01/43 | | | 3,426,553 | | | | 3,462,537 | | |

3.000%, due 04/01/43 | | | 1,301,564 | | | | 1,314,634 | | |

3.000%, due 05/01/43 | | | 1,362,932 | | | | 1,376,368 | | |

3.000%, due 06/01/43 | | | 191,690 | | | | 193,555 | | |

3.000%, due 09/01/43 | | | 1,526,034 | | | | 1,539,810 | | |

3.330%, due 07/01/22 | | | 3,886,000 | | | | 4,121,486 | | |

3.500%, due 11/01/25 | | | 963,561 | | | | 1,021,673 | | |

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(continued) | |

3.500%, due 03/01/42 | | $ | 770,090 | | | $ | 802,208 | | |

3.500%, due 12/01/42 | | | 3,002,968 | | | | 3,129,002 | | |

3.500%, due 03/01/43 | | | 1,659,083 | | | | 1,728,670 | | |

3.500%, due 05/01/43 | | | 6,121,343 | | | | 6,395,361 | | |

3.500%, due 05/01/44 | | | 75,000 | | | | 77,905 | | |

3.500%, due 06/01/45 | | | 604,393 | | | | 627,807 | | |

3.500%, due 07/01/45 | | | 12,355,379 | | | | 12,834,487 | | |

3.600%, due 08/01/23 | | | 817,000 | | | | 880,589 | | |

3.765%, due 12/01/25 | | | 3,000,000 | | | | 3,218,824 | | |

4.000%, due 03/01/19 | | | 35,664 | | | | 37,414 | | |

4.000%, due 06/01/19 | | | 44,434 | | | | 46,618 | | |

4.000%, due 07/01/25 | | | 37,208 | | | | 39,047 | | |

4.000%, due 08/01/25 | | | 93,542 | | | | 98,971 | | |

4.000%, due 09/01/25 | | | 93,666 | | | | 99,228 | | |

4.000%, due 10/01/25 | | | 33,891 | | | | 36,052 | | |

4.000%, due 11/01/25 | | | 286,307 | | | | 305,478 | | |

4.000%, due 01/01/26 | | | 498,187 | | | | 529,735 | | |

4.000%, due 02/01/26 | | | 2,064,443 | | | | 2,202,344 | | |

4.000%, due 03/01/26 | | | 1,650,660 | | | | 1,758,426 | | |

4.000%, due 04/01/26 | | | 3,774,600 | | | | 4,026,990 | | |

4.000%, due 05/01/39 | | | 233,640 | | | | 250,356 | | |

4.000%, due 09/01/39 | | | 536,974 | | | | 577,314 | | |

4.000%, due 12/01/41 | | | 1,634,027 | | | | 1,757,573 | | |

4.000%, due 07/01/42 | | | 2,622,279 | | | | 2,828,845 | | |

4.000%, due 09/01/42 | | | 9,934,581 | | | | 10,686,520 | | |

4.000%, due 10/01/42 | | | 7,244,189 | | | | 7,792,512 | | |

4.500%, due 11/01/17 | | | 17,529 | | | | 18,279 | | |

4.500%, due 02/01/18 | | | 433,500 | | | | 452,054 | | |

4.500%, due 04/01/18 | | | 2,523,640 | | | | 2,631,652 | | |

4.500%, due 05/01/18 | | | 68,032 | | | | 70,944 | | |

4.500%, due 06/01/18 | | | 92,070 | | | | 96,010 | | |

4.500%, due 05/01/19 | | | 6,826 | | | | 7,119 | | |

4.500%, due 09/01/19 | | | 136,877 | | | | 143,235 | | |

4.500%, due 08/01/20 | | | 64,965 | | | | 67,808 | | |

4.500%, due 05/01/21 | | | 350,451 | | | | 365,451 | | |

4.500%, due 03/01/23 | | | 13,415 | | | | 14,432 | | |

4.500%, due 08/01/41 | | | 1,499,501 | | | | 1,654,545 | | |

5.000%, due 05/01/17 | | | 155,001 | | | | 162,260 | | |

5.000%, due 12/01/17 | | | 355,981 | | | | 372,653 | | |

5.000%, due 03/01/23 | | | 7,360 | | | | 7,976 | | |

5.000%, due 05/01/23 | | | 179,311 | | | | 194,547 | | |

5.000%, due 09/01/23 | | | 652,016 | | | | 720,709 | | |

5.000%, due 07/01/24 | | | 926,401 | | | | 1,024,002 | | |

5.000%, due 03/01/25 | | | 40,463 | | | | 44,725 | | |

5.000%, due 07/01/27 | | | 954,870 | | | | 1,055,470 | | |

5.000%, due 10/01/34 | | | 47,753 | | | | 52,784 | | |

5.000%, due 08/01/41 | | | 51,754 | | | | 57,351 | | |

5.500%, due 07/01/27 | | | 238,733 | | | | 267,681 | | |

5.500%, due 02/01/32 | | | 12,139 | | | | 13,616 | | |

5.500%, due 11/01/32 | | | 141,847 | | | | 159,062 | | |

5.500%, due 03/01/33 | | | 148,189 | | | | 166,048 | | |

5.500%, due 12/01/33 | | | 1,793 | | | | 2,032 | | |

5.500%, due 04/01/34 | | | 105,840 | | | | 119,635 | | |

5.500%, due 01/01/35 | | | 136,311 | | | | 152,840 | | |

5.500%, due 04/01/36 | | | 92,958 | | | | 104,261 | | |

18

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(continued) | |

5.500%, due 05/01/37 | | $ | 448,726 | | | $ | 507,014 | | |

5.500%, due 07/01/37 | | | 232,343 | | | | 262,661 | | |

5.500%, due 06/01/39 | | | 2,189,911 | | | | 2,475,028 | | |

5.500%, due 11/01/39 | | | 838,297 | | | | 949,924 | | |

6.000%, due 11/01/21 | | | 83,044 | | | | 88,548 | | |

6.000%, due 01/01/23 | | | 242,835 | | | | 260,640 | | |

6.000%, due 03/01/23 | | | 399,166 | | | | 439,956 | | |

6.000%, due 11/01/26 | | | 48,692 | | | | 55,171 | | |

6.000%, due 02/01/32 | | | 84,925 | | | | 96,291 | | |

6.000%, due 09/01/32 | | | 8,768 | | | | 9,934 | | |

6.000%, due 10/01/32 | | | 9,336 | | | | 10,586 | | |

6.000%, due 12/01/32 | | | 27,190 | | | | 31,120 | | |

6.000%, due 01/01/33 | | | 150,973 | | | | 171,337 | | |

6.000%, due 02/01/33 | | | 32,453 | | | | 36,770 | | |

6.000%, due 09/01/34 | | | 249,678 | | | | 284,196 | | |

6.000%, due 04/01/35 | | | 1,093 | | | | 1,239 | | |

6.000%, due 05/01/35 | | | 149,126 | | | | 169,208 | | |

6.000%, due 06/01/35 | | | 34,947 | | | | 39,927 | | |

6.000%, due 07/01/35 | | | 92,610 | | | | 105,408 | | |

6.000%, due 08/01/35 | | | 111,209 | | | | 126,110 | | |

6.000%, due 09/01/35 | | | 2,623 | | | | 2,989 | | |

6.000%, due 01/01/36 | | | 71,820 | | | | 81,396 | | |

6.000%, due 06/01/36 | | | 3,286 | | | | 3,727 | | |

6.000%, due 09/01/36 | | | 81,550 | | | | 92,943 | | |

6.000%, due 10/01/36 | | | 27,514 | | | | 31,236 | | |

6.000%, due 12/01/36 | | | 341,924 | | | | 391,792 | | |

6.000%, due 01/01/37 | | | 22,343 | | | | 25,312 | | |

6.000%, due 03/01/37 | | | 33,820 | | | | 38,769 | | |

6.000%, due 12/01/37 | | | 136,098 | | | | 154,203 | | |

6.000%, due 01/01/38 | | | 799,858 | | | | 906,498 | | |

6.000%, due 08/01/38 | | | 2,273 | | | | 2,576 | | |

6.000%, due 11/01/38 | | | 859,225 | | | | 981,855 | | |

6.000%, due 05/01/39 | | | 103,350 | | | | 118,153 | | |

6.000%, due 11/01/40 | | | 1,184,038 | | | | 1,356,805 | | |

6.500%, due 07/01/19 | | | 10,487 | | | | 12,037 | | |

6.500%, due 10/01/36 | | | 572,701 | | | | 657,316 | | |

6.500%, due 02/01/37 | | | 8,673 | | | | 10,332 | | |

6.500%, due 07/01/37 | | | 71,463 | | | | 82,021 | | |

6.500%, due 08/01/37 | | | 157,691 | | | | 180,989 | | |

6.500%, due 09/01/37 | | | 158,316 | | | | 181,706 | | |

6.500%, due 12/01/37 | | | 255,694 | | | | 293,472 | | |

6.500%, due 08/01/38 | | | 3,374 | | | | 3,872 | | |

6.500%, due 05/01/40 | | | 2,585,482 | | | | 2,967,479 | | |

7.500%, due 11/01/26 | | | 20,377 | | | | 20,867 | | |

8.000%, due 11/01/26 | | | 14,802 | | | | 15,506 | | |

9.000%, due 02/01/26 | | | 16,712 | | | | 19,057 | | |

10.500%, due 08/01/20 | | | 88 | | | | 89 | | |

10.500%, due 04/01/22 | | | 9 | | | | 9 | | |

FNMA ARM

1.356%, due 03/01/44 | | | 354,476 | | | | 363,688 | | |

1.645%, due 07/01/30 | | | 21,430 | | | | 21,751 | | |

1.680%, due 10/01/26 | | | 210,876 | | | | 213,793 | | |

2.205%, due 02/01/26 | | | 37,262 | | | | 37,401 | | |

2.220%, due 09/01/26 | | | 22,021 | | | | 22,117 | | |

2.366%, due 05/01/30 | | | 43,282 | | | | 45,156 | | |

| | | Face

amount | | Value | |

Federal national mortgage association

certificates*—(concluded) | | | |

2.377%, due 02/01/30 | | $ | 5,587 | | | $ | 5,615 | | |

2.546%, due 03/01/25 | | | 99,763 | | | | 104,640 | | |

2.621%, due 12/01/27 | | | 22,457 | | | | 23,351 | | |

FNMA TBA

3.000% | | | 30,500,000 | | | | 30,944,089 | | |

| 3.500% | | | 37,500,000 | | | | 38,848,270 | | |

| 4.000% | | | 10,000,000 | | | | 10,613,671 | | |

| 4.500% | | | 9,500,000 | | | | 10,289,316 | | |

| 5.000% | | | 4,000,000 | | | | 4,417,033 | | |

| 5.500% | | | 3,000,000 | | | | 3,365,156 | | |

| 6.000% | | | 1,000,000 | | | | 1,134,966 | | |

Total federal national mortgage

association certificates

(cost—$318,621,279) | | | 322,062,390 | | |

Collateralized mortgage obligations—13.91% | | | |

Alternative Loan Trust,

Series 2003-16T1, Class A2

0.661%, due 09/25/333 | | | 91,595 | | | | 90,283 | | |

Series 2004-J7, Class 2A1

0.967%, due 09/25/343 | | | 125,999 | | | | 123,494 | | |

ARM Trust,

Series 2005-8, Class 3A21

2.774%, due 11/25/353 | | | 1,411,435 | | | | 1,198,861 | | |

BAMLL Commercial Mortgage

Securities Trust, Series 2015-ASHF,

Class A

1.407%, due 01/15/283,4 | | | 500,000 | | | | 497,174 | | |

BCAP LLC 2010-RR1 Trust,

Series 2010-RR1, Class 1A4

2.792%, due 03/26/373,4 | | | 315,719 | | | | 250,547 | | |

BCAP LLC 2011-RR6-I Trust,

Series 2011-RR6, Class 11A1

0.437%, due 07/26/353,4 | | | 121,827 | | | | 120,560 | | |

BCAP LLC 2011-RR10 Trust,

Series 2011-RR10, Class 3A5

2.648%, due 06/26/353,4 | | | 407,400 | | | | 408,033 | | |

BCAP LLC 2011-RR11 Trust,

Series 2011-R11, Class 8A5

0.387%, due 07/26/363,4 | | | 412,564 | | | | 390,652 | | |

Series 2011-R11, Class 22A1

1.673%, due 10/26/353,4 | | | 243,537 | | | | 243,842 | | |

BCAP LLC 2013-RR1 Trust,

Series 2013-RR1, Class 3A4 | |

7.425%, due 10/26/373,4 | | | 482,468 | | | | 448,187 | | |

BCAP LLC 2013-RR5 Trust,

Series 2013-RR5, Class 5A1 | |

0.986%, due 11/26/463,4 | | | 372,547 | | | | 357,555 | | |

BCAP LLC 2014-RR1 Trust,

Series 2014-RR1, Class 3A1 | |

0.347%, due 03/26/373,4 | | | 123,860 | | | | 121,126 | | |

Bear Stearns ARM Trust, | |

Series 2002-011, Class 1A2

2.595%, due 02/25/333 | | | 14,895 | | | | 13,877 | | |

19

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 2004-002, Class 12A2

2.699%, due 05/25/343 | | $ | 84,406 | | | $ | 82,447 | | |

Bear Stearns Asset-Backed

Securities Trust,

Series 2003-AC5, Class A1

5.750%, due 10/25/335 | | | 1,205,741 | | | | 1,255,677 | | |

Series 2004-AC3, Class A2

6.000%, due 06/25/345 | | | 1,509,048 | | | | 1,542,426 | | |

Chevy Chase Mortgage Funding

Corp., Series 2004-1, Class A1

0.471%, due 01/25/353,4 | | | 151,964 | | | | 136,602 | | |

CHL Mortgage Pass-Through Trust,

Series 2003-HYB1, Class 1A1

2.704%, due 05/19/333 | | | 7,106 | | | | 6,988 | | |

CSMC Trust,

Series 2013-5R, Class 1A1

0.449%, due 02/27/363,4 | | | 663,735 | | | | 629,462 | | |

Series 2013-MH1, Class A

4.792%, due 05/27/533,6 | | | 1,078,426 | | | | 1,115,340 | | |

FHLMC REMIC,

Series 0023, Class KZ

6.500%, due 11/25/23 | | | 30,273 | | | | 34,029 | | |

Series 0159, Class H

4.500%, due 09/15/21 | | | 7,274 | | | | 7,616 | | |

Series 1003, Class H

0.937%, due 10/15/203 | | | 12,917 | | | | 13,076 | | |

Series 1349, Class PS

7.500%, due 08/15/22 | | | 1,592 | | | | 1,800 | | |

Series 1502, Class PX

7.000%, due 04/15/23 | | | 214,007 | | | | 235,986 | | |

Series 1534, Class Z

5.000%, due 06/15/23 | | | 94,906 | | | | 101,970 | | |

Series 1573, Class PZ

7.000%, due 09/15/23 | | | 31,881 | | | | 35,575 | | |

Series 1658, Class GZ

7.000%, due 01/15/24 | | | 15,400 | | | | 17,374 | | |

Series 1694, Class Z

6.500%, due 03/15/24 | | | 132,395 | | | | 147,736 | | |

Series 1775, Class Z

8.500%, due 03/15/25 | | | 3,948 | | | | 4,584 | | |

Series 2400, Class FQ

0.687%, due 01/15/323 | | | 266,881 | | | | 270,473 | | |

Series 2411, Class FJ

0.537%, due 12/15/293 | | | 29,940 | | | | 30,093 | | |

Series 2614, Class WO

0.000%, due 05/15/334,7 | | | 2,036,347 | | | | 1,846,148 | | |

Series 3096, Class FL

0.587%, due 01/15/363 | | | 262,054 | | | | 263,340 | | |

Series 3114, Class PF

0.587%, due 02/15/363 | | | 1,320,284 | | | | 1,330,069 | | |

Series 3153, Class UF

0.617%, due 05/15/363 | | | 287,547 | | | | 289,363 | | |

Series 3339, Class LI

6.293%, due 07/15/373,4,8 | | | 1,735,342 | | | | 253,556 | | |

Series 3442, Class MT

0.187%, due 07/15/343,4 | | | 168,815 | | | | 166,297 | | |

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 3667, Class FW

0.737%, due 02/15/383 | | $ | 259,130 | | | $ | 262,372 | | |

Series 3671, Class FQ

1.037%, due 12/15/363 | | | 2,594,046 | | | | 2,651,177 | | |

Series 3864, Class NT

5.500%, due 03/15/393 | | | 1,372,290 | | | | 1,502,168 | | |

Series 4037, Class PI

3.000%, due 04/15/274,8 | | | 5,934,801 | | | | 593,777 | | |

Series 4136, Class EZ

3.000%, due 11/15/42 | | | 1,844,172 | | | | 1,697,967 | | |

Series 4182, Class YI

2.500%, due 03/15/284,8 | | | 8,401,132 | | | | 862,548 | | |

Series 4255, Class SN

11.769%, due 05/15/353 | | | 675,965 | | | | 727,286 | | |

Series 4263, Class SD

11.767%, due 11/15/433,4 | | | 913,657 | | | | 1,058,538 | | |

Series 4265, Class ES

13.163%, due 11/15/433,4 | | | 2,129,166 | | | | 2,203,534 | | |

Series 4326, Class SB

11.636%, due 04/15/443,4 | | | 537,783 | | | | 560,130 | | |

FNMA REMIC,

Trust 1987-002, Class Z

11.000%, due 11/25/17 | | | 4,838 | | | | 4,887 | | |

Trust 1988-007, Class Z

9.250%, due 04/25/18 | | | 49,178 | | | | 52,559 | | |

Trust 1992-129, Class L

6.000%, due 07/25/22 | | | 4,062 | | | | 4,395 | | |

Trust 1992-158, Class ZZ

7.750%, due 08/25/22 | | | 12,000 | | | | 13,422 | | |

Trust 1993-037, Class PX

7.000%, due 03/25/23 | | | 165,106 | | | | 183,864 | | |

Trust 1993-250, Class Z

7.000%, due 12/25/23 | | | 138 | | | | 138 | | |

Trust 1997-022, Class F

0.644%, due 03/25/273 | | | 167,548 | | | | 164,746 | | |

Trust 2002-060, Class F1

0.591%, due 06/25/323 | | | 118,247 | | | | 118,016 | | |

Trust 2006-112, Class LF

0.741%, due 11/25/363 | | | 3,586,650 | | | | 3,629,339 | | |

Trust 2007-067, Class FB

0.511%, due 07/25/373 | | | 1,051,908 | | | | 1,057,526 | | |

Trust 2009-033, Class FB

1.011%, due 03/25/373 | | | 1,681,772 | | | | 1,716,810 | | |

Trust 2010-035, Class EF

0.741%, due 04/25/403 | | | 441,676 | | | | 446,935 | | |

Trust 2010-141, Class FA

0.691%, due 12/25/403 | | | 939,447 | | | | 947,563 | | |

Trust 2012-090, Class FB

0.631%, due 08/25/423 | | | 466,049 | | | | 468,317 | | |

Trust 2012-111, Class HS

3.508%, due 10/25/423 | | | 230,226 | | | | 189,619 | | |

Trust 2012-128, Class FK

0.541%, due 11/25/423 | | | 755,180 | | | | 765,895 | | |

Trust 2013-010, Class US

7.542%, due 02/25/433 | | | 349,487 | | | | 349,002 | | |

20

PACE Select Advisors Trust

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2015

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Trust 2013-028, Class YS

5.960%, due 07/25/423,4,8 | | $ | 1,730,858 | | | $ | 346,689 | | |

Trust 2013-030, Class GI

3.000%, due 01/25/434,8 | | | 5,254,636 | | | | 790,663 | | |

Trust 2013-030, Class JI

3.000%, due 04/25/434,8 | | | 1,807,975 | | | | 252,020 | | |

Trust 2013-034, Class PS

5.960%, due 08/25/423,4,8 | | | 1,372,011 | | | | 270,651 | | |

Trust 2013-044, Class ZG

3.500%, due 03/25/42 | | | 1,088,828 | | | | 1,044,014 | | |

Trust 2013-045, Class IK

3.000%, due 02/25/434,8 | | | 3,352,699 | | | | 499,322 | | |

Trust 2013-116, Class IY

3.000%, due 09/25/434,8 | | | 1,028,838 | | | | 143,778 | | |

Trust G92-040, Class ZC