UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08764 |

|

PACE® Select Advisors Trust |

(Exact name of registrant as specified in charter) |

|

1285 Avenue of the Americas, New York, New York | | 10019-6028 |

(Address of principal executive offices) | | (Zip code) |

|

Mark F. Kemper, Esq. UBS Asset Management 1285 Avenue of the Americas New York, NY 10019-6028 |

(Name and address of agent for service) |

|

Copy to: Jack W. Murphy, Esq. Dechert LLP 1900 K Street, N.W. Washington, DC 20006 |

|

Registrant’s telephone number, including area code: | 212-821 3000 | |

|

Date of fiscal year end: | July 31 | |

|

Date of reporting period: | July 31, 2017 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

PACE® Select Advisors Trust

Annual Report | July 31, 2017

Table of contents | | Page | |

Introduction | | | 3 | | |

Portfolio Advisor's and Subadvisors' commentaries and Portfolios of investments | | | |

PACE® Government Money Market Investments | | | 5 | | |

PACE® Mortgage-Backed Securities Fixed Income Investments | | | 9 | | |

PACE® Intermediate Fixed Income Investments | | | 29 | | |

PACE® Strategic Fixed Income Investments | | | 56 | | |

PACE® Municipal Fixed Income Investments | | | 89 | | |

PACE® Global Fixed Income Investments (formerly, PACE® International Fixed Income Investments) | | | 100 | | |

PACE® High Yield Investments | | | 117 | | |

PACE® Large Co Value Equity Investments | | | 141 | | |

PACE® Large Co Growth Equity Investments | | | 156 | | |

PACE® Small/Medium Co Value Equity Investments | | | 165 | | |

PACE® Small/Medium Co Growth Equity Investments | | | 176 | | |

PACE® International Equity Investments | | | 187 | | |

PACE® International Emerging Markets Equity Investments | | | 203 | | |

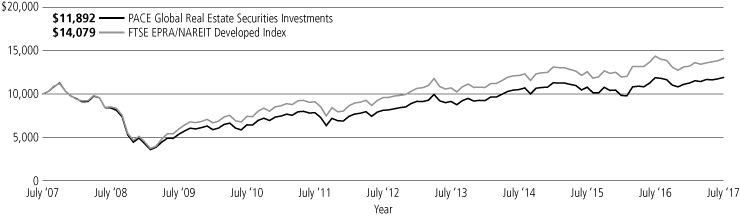

PACE® Global Real Estate Securities Investments | | | 214 | | |

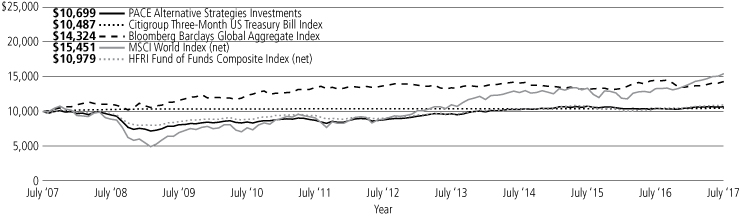

PACE® Alternative Strategies Investments | | | 222 | | |

Understanding your Portfolio's expenses | | | 262 | | |

Statement of assets and liabilities | | | 268 | | |

Statement of operations | | | 276 | | |

Statement of changes in net assets | | | 280 | | |

Statement of cash flows | | | 286 | | |

Financial highlights | | | 289 | | |

Notes to financial statements | | | 318 | | |

Report of independent registered public accounting firm | | | 369 | | |

Tax information | | | 370 | | |

General information | | | 371 | | |

Board approvals of investment management and administration agreement and

subadvisory agreements | | | 372 | | |

Supplemental information, trustees and officers | | | 387 | | |

1

This page intentionally left blank.

2

September 18, 2017

Dear PACE Shareholder,

We are pleased to provide you with the annual report for the PACE portfolios (the "Portfolios"), comprising the PACE Select Advisors Trust. This report includes summaries of the performance of each Portfolio, as well as commentaries from the investment advisor and subadvisors regarding the events that affected Portfolio performance during the 12 months ended July 31, 2017 (the "reporting period"). Please note that the opinions of the subadvisors do not necessarily represent those of UBS Asset Management (Americas) Inc.

The global economic expansion continues

The US economy continued to expand, albeit at a relatively modest pace, during the reporting period. Looking back, the US Commerce Department reported that gross domestic product ("GDP") grew at a revised 2.2% seasonally adjusted annualized rate during the second quarter of 2016, prior to the beginning of the reporting period. GDP growth then improved to a revised 2.8% rate during the third quarter of 2016—the strongest reading since the first quarter of 2015. GDP growth then moderated to a revised 1.8% rate during the fourth quarter of 2016 and 1.2% during the first quarter of 2017, respectively. Finally, second quarter 2017 GDP grew at a 2.6% rate based on the US Commerce Department's initial estimate.

Prior to the beginning of the reporting period, after taking its first step toward normalizing monetary policy in late 2015, the US Federal Reserve Board (the "Fed") kept the federal funds rate unchanged until December 2016, when it increased rates by 0.25% to a range between 0.50% and 0.75%. After keeping rates unchanged at its first meeting in 2017, the Fed again raised rates 0.25% to a range between 0.75% and 1.00% at its meeting in March 2017, and then to a range between 1.00% and 1.25% at its meeting in June 2017. In its statement following its June meeting, the Fed indicated that it may begin reducing its balance sheet later in the year, saying, "The Committee currently expects to begin implementing a balance sheet normalization program this year, provided that the economy evolves broadly as anticipated."

From a global perspective, the International Monetary Fund's ("IMF") July 2017 World Economic Outlook Update stated, "The pickup in global growth anticipated in the April World Economic Outlook remains on track, with global output projected to grow by 3.5 percent in 2017 and 3.6 percent in 2018. The unchanged global growth projections mask somewhat different contributions at the country level. U.S. growth projections are lower than in April, primarily reflecting the assumption that fiscal policy will be less expansionary going forward than previously anticipated. Growth has been revised up for Japan and especially the euro area, where positive surprises to activity in late 2016 and early 2017 point to solid momentum." From a regional perspective, the IMF estimates 2017 growth in the eurozone will be 1.9%, versus 1.6% in 2016. Japan's economy is expected to expand 1.3% in 2017, compared to 1.0% in 2016. Elsewhere, the IMF projects that overall growth in emerging markets countries will accelerate to 4.6% in 2017, versus 4.3% in 2016.

Global equities generate very strong results

While there were periods of volatility, the global equity market generated very strong results during the reporting period as a whole. After a strong start, equites experienced a setback in October 2016 given uncertainties surrounding the US elections. However, US equities rallied sharply following the elections given expectations for improving growth under the Trump administration. International equities largely followed the same pattern, as they rallied amid signs of improving growth and continued monetary policy accommodation. All told, the US stock market, as measured by the S&P 500 Index,1 gained 16.04% for the 12 months ended July 31, 2017. International developed

1 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

3

equities, as measured by the MSCI EAFE Index (net),2 rose 17.77% during the reporting period, while emerging markets equities, as measured by the MSCI Emerging Markets Index (net),3 gained 24.84%.

The fixed income market generates mixed results

The global fixed income market posted mixed results during the reporting period. In the US, Treasury yields moved sharply higher after the November elections as investors anticipated an uptick in growth and inflation. Additionally, Fed rate hikes pressured the shorter end of the yield curve. However, after peaking in mid-March 2017, yields moved lower amid skepticism about the Trump administration's growth initiatives. For the fiscal year as a whole, the yield on the US 10-year Treasury rose from 1.46% to 2.30% (bond yields and prices move in the opposite direction). The overall US bond market, as measured by the Bloomberg Barclays US Aggregate Bond Index,4 declined 0.51% for the 12 months ended July 31, 2017. Returns of riskier fixed income securities were much higher. High yield bonds, as measured by the BofA Merrill Lynch US High Yield Cash Pay Constrained Index5 gained 11.23% during the reporting period. Elsewhere, emerging markets debt, as measured by the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global),6 rose 4.59%.

Sincerely,

Mark E. Carver

President, PACE Select Advisors Trust

Managing Director, UBS Asset Management (Americas) Inc.

This report is intended to assist investors in understanding how the Portfolios performed during the 12-month period ended July 31, 2017. The views expressed in the Advisor's and Subadvisors' comments sections are as of the end of the reporting period, reflect performance results gross of fees and expenses, and are those of the investment advisor (with respect to PACE Government Money Market Investments only) and subadvisors. Subadvisors' comments on Portfolios that have more than one subadvisor are reflective of their portion of the Portfolio only. The views and opinions in this report were current as of September 18, 2017. They are not guarantees of future performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the investment advisor and subadvisors reserve the right to change their views about individual securities, sectors and markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Portfolio's future investment intent.

2 The MSCI EAFE Index (net) is an index of stocks designed to measure the investment returns of developed economies outside of North America. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

3 The MSCI Emerging Markets Index (net) is a market capitalization-weighted index composed of different emerging market countries in Europe, Latin America, and the Pacific Basin. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

4 The Bloomberg Barclays US Aggregate Bond Index is an unmanaged broad based index designed to measure the US dollar-denominated, investment-grade, taxable bond market. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed, asset-backed and commercial mortgage-backed sectors. Investors should note that indices do not reflect the deduction of fees and expenses.

5 The BofA Merrill Lynch US High Yield Cash Pay Constrained Index is an unmanaged index of publicly placed, non-convertible, coupon-bearing US dollar denominated, below investment grade corporate debt with a term to maturity of at least one year. The index is market capitalization weighted, so that larger bond issuers have a greater effect on the index's return. However, the representation of any single bond issuer is restricted to a maximum of 2% of the total index. Investors should note that indices do not reflect the deduction of fees and expenses.

6 The J.P. Morgan Emerging Markets Bond Index Global (EMBI Global) is an unmanaged index which is designed to track total returns for US dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans and Eurobonds. Investors should note that indices do not reflect the deduction of fees and expenses.

4

PACE Government Money Market Investments

Performance (Unaudited)

The seven-day current yield for the Fund as of July 31, 2017 was 0.46% (after fee waivers/expense reimbursements).1 For more information on the Fund's performance, refer to "Yields and characteristics at a glance" on page 6. Please remember that the PACE program fee is assessed outside the Portfolio at the PACE program account level. The program fee does not impact the determination of the Portfolio's net asset value per share. For a detailed commentary on the market environment in general during the period, please refer to page 3.

Advisor's comments (Unaudited)

In December 2016, the US Federal Reserve Board (the "Fed") modestly raised the federal funds rate from a low range between 0.25% and 0.50% to a range between 0.50% and 0.75%. The federal funds rate or the "fed funds rate," is the rate US banks charge one another for funds they borrow on an overnight basis. The Fed again raised rates in March and June 2017. At the end of the reporting period the fed fund rates was in a range between 1.00% and 1.25%. (For more details on the Fed's actions, see page 3.) While the yields on a wide range of short-term investments moved higher over the period, yields still remain low by historical comparison. As a result, the Portfolio's yield remained low during the reporting period.

We tactically adjusted the Portfolio's weighted average maturity ("WAM") throughout the 12-month review period. When the reporting period began, the Portfolio had a WAM of 32 days. This was increased to 40 days at the end of the reporting period.

A number of adjustments were made to the Portfolio's sector and issuer positioning during the 12-month period. We increased the Portfolio's exposure to US government and agency obligations and reduced its allocation to repurchase agreements. (Repurchase agreements are transactions in which the seller of a security agrees to buy it back at a predetermined time and price or upon demand.)

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

PACE Select Advisors Trust – PACE Government Money Market Investments

Investment Advisor:

UBS Asset Management (Americas) Inc.

Portfolio Manager:

Robert Sabatino

Objective:

Current income consistent with preservation of capital and liquidity

Investment process:

The Portfolio is a money market mutual fund and seeks to maintain a stable price of $1.00 per share, although it may be possible to lose money by investing in this Portfolio. The Portfolio invests in a diversified portfolio of high-quality money market instruments of governmental issuers. Security selection is based on the assessment of relative values and changes in market and economic conditions.

5

PACE Government Money Market Investments

Yields and characteristics at a glance—July 31, 2017 (unaudited)

Yields and characteristics | |

Seven-day current yield after fee waivers and/or expense reimbursements1 | | | 0.46 | % | |

Seven-day effective yield after fee waivers and/or expense reimbursements1 | | | 0.46 | | |

Seven-day current yield before fee waivers and/or expense reimbursements1 | | | 0.15 | | |

Seven-day effective yield before fee waivers and/or expense reimbursements1 | | | 0.15 | | |

Weighted average maturity2 | | | 40 days | | |

Portfolio composition3 | |

US government and agency obligations | | | 76.3 | % | |

Repurchase agreements | | | 24.1 | | |

Other assets less liabilities | | | (0.4 | ) | |

Total | | | 100.0 | % | |

You could lose money by investing in PACE Government Money Market Investments. Although the portfolio seeks to preserve the value of your investment at $1.00 per share, the portfolio cannot guarantee it will do so. An investment in PACE Government Money Market Investments is not insured or guaranteed by the Federal Deposit Insurance Corporation ("FDIC") or any other government agency. PACE Government Money Market Investments' sponsor has no legal obligation to provide financial support to PACE Government Money Market Investments, and you should not expect that the portfolio's sponsor will provide financial support to PACE Government Money Market Investments at any time.

Not FDIC insured. May lose value. No bank guarantee.

1 Yields will fluctuate and reflect fee waivers and/or expense reimbursements, if any, unless otherwise noted. Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be higher or lower than the performance data quoted.

2 The Portfolio is actively managed and its weighted average maturity will differ over time.

3 Weightings represent percentages of the Portfolio's net assets as of the date indicated. The Portfolio is actively managed and its composition will vary over time.

6

PACE Government Money Market Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

US government and agency obligations—76.29% | |

Federal Farm Credit Bank

0.770%, due 10/27/171 | | $ | 1,000,000 | | | $ | 998,139 | | |

1.180%, due 09/02/172 | | | 1,000,000 | | | | 1,000,940 | | |

1.203%, due 08/26/172 | | | 2,000,000 | | | | 2,000,000 | | |

1.214%, due 08/21/172 | | | 1,000,000 | | | | 1,000,037 | | |

1.279%, due 08/08/172 | | | 2,000,000 | | | | 1,999,835 | | |

1.324%, due 08/29/172 | | | 3,000,000 | | | | 3,000,000 | | |

Federal Home Loan Bank

0.630%, due 08/03/171 | | | 1,000,000 | | | | 999,965 | | |

0.750%, due 10/18/171 | | | 5,000,000 | | | | 4,991,875 | | |

0.800%, due 08/09/172 | | | 2,000,000 | | | | 2,000,101 | | |

0.910%, due 08/15/171 | | | 2,000,000 | | | | 1,999,292 | | |

0.935%, due 08/11/171 | | | 2,000,000 | | | | 1,999,481 | | |

0.950%, due 08/23/171 | | | 7,000,000 | | | | 6,995,936 | | |

0.960%, due 09/05/171 | | | 2,000,000 | | | | 1,998,133 | | |

0.970%, due 09/11/171 | | | 5,000,000 | | | | 4,994,476 | | |

0.970%, due 11/13/171 | | | 1,000,000 | | | | 997,198 | | |

0.975%, due 10/25/171 | | | 3,000,000 | | | | 2,993,094 | | |

0.995%, due 11/01/171 | | | 5,000,000 | | | | 4,987,286 | | |

1.010%, due 08/04/171 | | | 4,000,000 | | | | 3,999,663 | | |

1.019%, due 11/03/171 | | | 1,000,000 | | | | 997,389 | | |

1.020%, due 08/23/171 | | | 5,000,000 | | | | 4,996,883 | | |

1.021%, due 12/07/171 | | | 2,000,000 | | | | 1,992,889 | | |

1.025%, due 09/07/171 | | | 2,000,000 | | | | 1,997,893 | | |

1.025%, due 09/20/171 | | | 2,000,000 | | | | 1,997,153 | | |

1.025%, due 09/21/171 | | | 5,000,000 | | | | 4,992,740 | | |

1.030%, due 09/18/171 | | | 2,000,000 | | | | 1,997,253 | | |

1.040%, due 09/25/171 | | | 5,000,000 | | | | 4,992,056 | | |

1.040%, due 09/26/171 | | | 5,000,000 | | | | 4,991,911 | | |

1.046%, due 08/18/172 | | | 5,000,000 | | | | 5,000,000 | | |

1.048%, due 09/15/171 | | | 5,000,000 | | | | 4,993,450 | | |

1.050%, due 10/06/171 | | | 5,500,000 | | | | 5,489,413 | | |

1.055%, due 10/04/171 | | | 2,000,000 | | | | 1,996,249 | | |

1.076%, due 09/26/172 | | | 800,000 | | | | 799,940 | | |

1.080%, due 10/16/171 | | | 7,000,000 | | | | 6,984,040 | | |

1.080%, due 10/27/171 | | | 1,000,000 | | | | 997,390 | | |

1.080%, due 11/27/171 | | | 3,000,000 | | | | 2,989,380 | | |

1.083%, due 10/25/171 | | | 2,000,000 | | | | 1,994,886 | | |

1.102%, due 08/25/172 | | | 1,000,000 | | | | 1,000,000 | | |

1.109%, due 08/14/172 | | | 2,000,000 | | | | 2,000,000 | | |

1.125%, due 01/19/181 | | | 5,000,000 | | | | 4,973,281 | | |

1.129%, due 08/21/172 | | | 2,000,000 | | | | 2,000,000 | | |

1.129%, due 12/22/171 | | | 2,000,000 | | | | 1,991,031 | | |

1.229%, due 10/10/172 | | | 3,500,000 | | | | 3,499,965 | | |

1.243%, due 08/28/172 | | | 600,000 | | | | 599,974 | | |

1.277%, due 08/06/172 | | | 750,000 | | | | 750,114 | | |

| | | Face

amount | | Value | |

US government and agency obligations—(concluded) | |

Federal National Mortgage Association

1.275%, due 10/11/172 | | $ | 2,000,000 | | | $ | 2,000,000 | | |

US Treasury Bill

0.892%, due 09/28/171 | | | 5,000,000 | | | | 4,992,814 | | |

US Treasury Notes

0.750%, due 10/31/17 | | | 3,000,000 | | | | 2,999,535 | | |

0.875%, due 08/15/17 | | | 5,000,000 | | | | 5,000,037 | | |

1.354%, due 08/01/172 | | | 1,000,000 | | | | 1,000,100 | | |

1.358%, due 08/01/172 | | | 2,300,000 | | | | 2,300,223 | | |

1.374%, due 08/01/172 | | | 6,000,000 | | | | 6,000,751 | | |

1.875%, due 08/31/17 | | | 2,000,000 | | | | 2,001,929 | | |

Total US government and agency

obligations

(cost—$152,266,120) | | | 152,266,120 | | |

Repurchase agreements—24.07% | |

Repurchase agreement dated 07/31/17 with

Goldman Sachs & Co., 1.020% due 08/01/17,

collateralized by $20,265,000 Federal Farm

Credit Banks, 1.404% to 3.000% due

04/04/18 to 05/19/36, $1,475,000 Federal

Home Loan Bank obligations, zero coupon due

09/22/17, $787,000 US Treasury Bond, 8.125%

due 08/15/19 and $52,994,893 US Treasury

Bonds STRIPs, zero coupon due 11/15/19 to

08/15/46; (value—$48,960,000); proceeds:

$48,001,360 | | | 48,000,000 | | | | 48,000,000 | | |

Repurchase agreement dated 07/31/17 with

State Street Bank and Trust Co., 0.050% due

08/01/17, collateralized by $34,126 US Treasury

Note, 2.000% due 08/31/21; (value—$34,784);

proceeds: $34,000 | | | 34,000 | | | | 34,000 | | |

Total repurchase agreements

(cost—$48,034,000) | | | 48,034,000 | | |

Total investments

(cost—$200,300,120 which approximates cost

for federal income tax purposes)—100.36% | | | 200,300,120 | | |

Liabilities in excess of other assets—(0.36)% | | | | | (714,761 | ) | |

| Net assets—100.00% | | $ | 199,585,359 | | |

For a listing of defined portfolio acronyms that are used throughout the Portfolio of investments as well as the tables that follow, please refer to page 260.

7

PACE Government Money Market Investments

Portfolio of investments—July 31, 2017

Fair valuation summary

The following is a summary of the fair valuations according to the inputs used as of July 31, 2017 in valuing the Portfolio's investments. In the event a Portfolio holds investments for which fair value is measured using the NAV per share practical expedient (or its equivalent), a separate column will be added to the fair value hierarchy table; this is intended to permit reconciliation to the amounts presented in the Portfolio of investments:

Assets

Description | | Unadjusted

quoted prices in

active markets for

identical investments

(Level 1) | | Other significant

observable inputs

(Level 2) | | Unobservable

inputs

(Level 3) | | Total | |

US government and agency obligations | | $ | — | | | $ | 152,266,120 | | | $ | — | | | $ | 152,266,120 | | |

Repurchase agreements | | | — | | | | 48,034,000 | | | | — | | | | 48,034,000 | | |

Total | | $ | — | | | $ | 200,300,120 | | | $ | — | | | $ | 200,300,120 | | |

At July 31, 2017, there were no transfers between Level 1 and Level 2

Portfolio footnotes

1 Rate shown is the discount rate at the date of purchase unless otherwise noted.

2 Variable or floating rate security. The interest rate shown is the current rate at the period end and changes periodically.

See accompanying notes to financial statements.

8

PACE Mortgage-Backed Securities Fixed Income Investments

Performance (Unaudited)

For the 12 months ended July 31, 2017, the Portfolio's Class P shares gained 0.55% before the deduction of the maximum PACE Select program fee.1 In comparison, the Bloomberg Barclays US Mortgage-Backed Securities Index (the "benchmark") returned 0.19%, and the Lipper US Mortgage Funds category posted a median return of 0.40%. (Returns for all share classes over various time periods are shown in the "Performance at a glance" table on page 11. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.) For a detailed commentary on the market environment in general during the reporting period, please refer to page 3.

Advisor's comments (Unaudited)2

We performed in line with the benchmark during the reporting period. Overall, US interest rate strategies were negative for performance. A modest overweight to US Treasuries detracted from results as yields generally rose. Additionally, yield curve positioning, with a focus on the short end of the curve, was negative for performance as short rates underperformed the intermediate and long portions of the curve.

Relative value positioning within agency mortgage-backed securities ("MBS") contributed to returns. A modest overweight to Ginnie Mae ("GNMA") mortgages detracted from returns as the segment underperformed the broader mortgage market. However, a focus on 4 - 4.5% coupons within GNMA was positive for returns, as these coupons outperformed the broader mortgage market. An overweight to Freddie Mac securities contributed to results, as this segment outperformed the broader mortgage market. Holdings of interest-only and floating rate agency collateralized-mortgages, which benefit from increasing short-term interest rates, were additive for performance. Finally, exposure to mortgage credit, especially non-agency and commercial mortgages, added to returns.

Overall, derivative usage was positive for results during the reporting period, as the Portfolio was short long-end US swap rates, which underperformed Treasury rates. The Portfolio used interest rate swaps to adjust interest rate and yield curve exposures, as well as to substitute for physical securities. The Portfolio benefited from the income generated from selling mortgage pool options as a way to manage interest rate and volatility risk within the sector. Additionally, options on swaps were primarily used to manage interest rate exposure and volatility. They contributed to performance through income generation. Total return swaps were used to replicate broad exposure to interest-only agency mortgages while limiting the idiosyncratic risk of owning individual bonds.

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

2 All Sub-Advisors discuss performance on a gross-of-fees basis—meaning that no fees or expenses are reflected in their sleeves'/sleeve's performance. Alternately, Portfolio performance is shown net of fees, which does factor in fees and expenses associated with the Portfolio.

PACE Select Advisors Trust – PACE Mortgage-Backed Securities Fixed

Income Investments

Investment Manager:

UBS Asset Management (Americas) Inc. ("UBS AM")

Investment Subadvisor:

Pacific Investment Management Company LLC ("PIMCO")

Portfolio Management Team:

UBS AM: Mabel Lung, CFA, Gina Toth, CFA, Fred Lee, CFA, Diana To and Anthony Karaminas, CFA

PIMCO: Daniel Hyman and Michael Cudzil

Objective:

Current income

Investment process:

The Portfolio invests primarily in government fixed income securities which include US bonds, including those backed by mortgages, and related repurchase agreements. Mortgage-backed securities include "to be announced" or "TBA" securities, which usually are traded on a forward commitment basis with an approximate principal amount and no defined maturity date; issued or guaranteed by US government agencies and instrumentalities. The Portfolio also invests, to a lesser extent, in investment grade bonds of private issuers, including those backed by mortgages or other assets. The Portfolio may invest in bonds of varying maturities, but normally limits its duration

9

PACE Mortgage-Backed Securities Fixed Income Investments

Investment process

(concluded)

to within +/- 50% of the effective duration of the Portfolio's benchmark index. (Duration is a measure of a portfolio's sensitivity to interest rate changes.) The Portfolio may engage in short selling with respect to securities issued by the US Treasury and certain TBA securities coupon trades. PIMCO establishes duration targets based on its expectations for changes in interest rates, and then positions the Portfolio to take advantage of yield curve shifts. PIMCO decides to buy and sell specific bonds based on an analysis of their values relative to other similar securities.

Special considerations

The Portfolio may be appropriate for long-term investors seeking current income who are able to withstand short-term fluctuations in the fixed income markets in return for potentially higher returns over the long term. The yield and value of the Portfolio change every day and can be affected by changes in interest rates, general market conditions, and other political, social and economic developments, as well as specific matters relating to the issuers in which the Portfolio invests. It is important to note that an investment in the Portfolio is only one component of a balanced investment plan.

10

PACE Mortgage-Backed Securities Fixed Income Investments

Performance at a glance (unaudited)

Average annual total returns for periods ended 07/31/17 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | 0.30 | % | | | 1.64 | % | | | 4.04 | % | |

Class C2 | | | (0.21 | ) | | | 1.15 | | | | 3.52 | | |

Class Y3 | | | 0.63 | | | | 1.92 | | | | 4.31 | | |

Class P4 | | | 0.55 | | | | 1.92 | | | | 4.31 | | |

After deducting maximum sales charge | |

Class A1 | | | (3.45 | ) | | | 0.88 | | | | 3.64 | | |

Class C2 | | | (0.94 | ) | | | 1.15 | | | | 3.52 | | |

Bloomberg Barclays US Mortgage-Backed Securities Index5 | | | 0.19 | | | | 1.93 | | | | 4.28 | | |

Lipper US Mortgage Funds median | | | 0.40 | | | | 1.92 | | | | 3.89 | | |

Most recent calendar quarter-end returns (unaudited)

Average annual total returns for periods ended 06/30/17 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | (0.11 | )% | | | 1.71 | % | | | 4.06 | % | |

Class C2 | | | (0.53 | ) | | | 1.22 | | | | 3.54 | | |

Class Y3 | | | 0.22 | | | | 1.98 | | | | 4.33 | | |

Class P4 | | | 0.22 | | | | 1.97 | | | | 4.32 | | |

After deducting maximum sales charge | |

Class A1 | | | (3.83 | ) | | | 0.94 | | | | 3.66 | | |

Class C2 | | | (1.26 | ) | | | 1.22 | | | | 3.54 | | |

The annualized gross and net expense ratios, respectively, for each class of shares as in the November 28, 2016 prospectuses, were as follows: Class A—1.07% and 0.97%; Class C—1.60% and 1.47%; Class Y—0.89% and 0.72%; and Class P—0.91% and 0.72% Net expenses reflect fee waivers and/or expense reimbursements, if any, pursuant to an agreement that is in effect to cap the expenses. The Portfolio and UBS Asset Management (Americas) Inc. ("UBS AM") have entered into a written fee waiver/expense reimbursement agreement pursuant to which UBS AM is contractually obligated to: (1) waive its management fees through November 30, 2017 to the extent necessary to reflect the lower subadvisory fee paid by UBS AM to Pacific Investment Management Company LLC, the Portfolio's investment advisor; and (2) waive its management fees and/or reimburse expenses so that the Portfolio's ordinary total operating expenses of each class through November 30, 2017 (excluding dividend expense, borrowing costs, and interest expense relating to short sales, and expenses attributable to investment in other investment companies, interest, taxes, brokerage commissions and extraordinary expenses) would not exceed Class A—0.97%; Class C—1.47%; Class Y—0.72%; and Class P—0.72%. The Portfolio has agreed to repay UBS AM for any waived fees/reimbursed expenses (pursuant to item (2)) to the extent that it can do so over the following three fiscal years without causing the Portfolio's expenses in any of those three years to exceed these expense caps and that UBS AM has not waived the right to do so. The fee waiver/expense reimbursement agreement may be terminated by the Portfolio's board at any time and also will terminate automatically upon the expiration or termination of the Portfolio's advisory contract with UBS AM. Upon termination of the agreement, however, UBS AM's three year recoupment rights will survive.

1 Maximum sales charge for Class A shares is 3.75%. Class A shares bear ongoing 12b-1 service fees of 0.25% annually.

2 Maximum contingent deferred sales charge for Class C shares is 0.75% imposed on redemptions and is reduced to 0% after one year. Class C shares bear ongoing 12b-1 service and distribution fees of 0.25% and 0.50% annually, respectively.

3 The Portfolio offers Class Y shares to a limited group of eligible investors, including certain qualifying retirement plans. Class Y shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees.

4 Class P shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees, but Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance.

5 The Bloomberg Barclays US Mortgage-Backed Securities Index is an unmanaged index which primarily covers the mortgage-backed passthrough securities issued by Ginnie Mae (formally known as the Government National Mortgage Association or GNMA), Freddie Mac (formally known as Federal Home Loan Mortgage Corporation or FHLMC), and Fannie Mae (formally known as Federal National Mortgage Association or FNMA). Investors should note that indices do not reflect the deduction of fees and expenses.

Prior to August 3, 2015, a 1% redemption fee was imposed on sales or exchanges of any class of shares of the Portfolio made during the specified holding period.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. The return and principal value of an investment will fluctuate, so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the ex-dividend dates. Current performance may be higher or lower than the performance data quoted. For month-end performance figures, please visit www.ubs.com/us-mutualfundperformance.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

11

PACE Mortgage-Backed Securities Fixed Income Investments

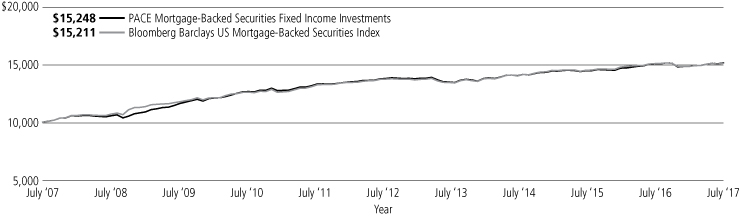

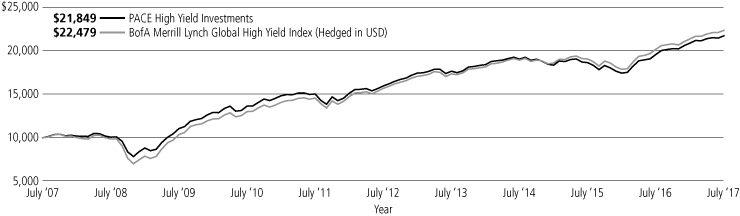

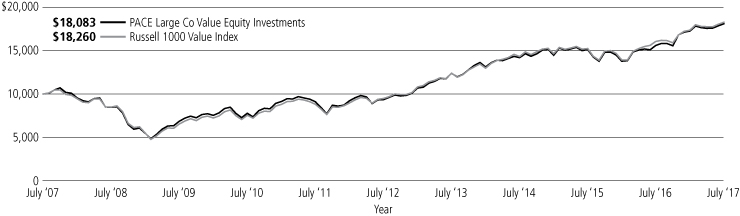

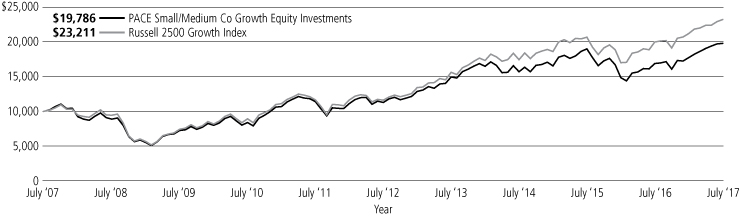

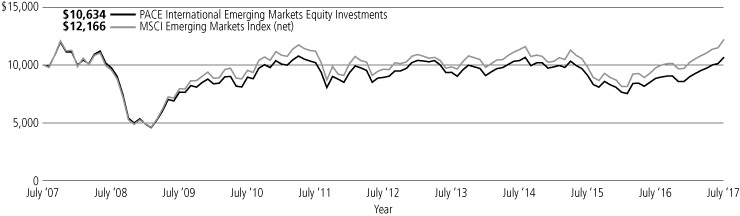

Illustration of an assumed investment of $10,000 in Class P shares of the Portfolio (unaudited)

The following graph depicts the performance of PACE Mortgage-Backed Securities Fixed Income Investments Class P shares versus the Bloomberg Barclays US Mortgage-Backed Securities Index over the 10 years ended July 31, 2017. Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that PACE Mortgage-Backed Securities Fixed Income Investments is a professionally managed portfolio while the Index is not available for investment and is unmanaged. The comparison is shown for illustration purposes only.

PACE Mortgage-Backed Securities Fixed Income Investments

12

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio statistics—July 31, 2017 (unaudited)

Characteristics | |

Weighted average duration | | | 3.47 yrs. | | |

Weighted average maturity | | | 4.82 yrs. | | |

Average coupon | | | 2.79 | % | |

Top ten holdings (long holdings)1 | | Percentage of

net assets | |

FNMA TBA, 3.500% | | | 17.8 | % | |

FNMA TBA, 3.000% | | | 9.5 | | |

FHLMC TBA, 3.500% | | | 7.9 | | |

GNMA II TBA, 3.500% | | | 7.8 | | |

FHLMC TBA, 3.000% | | | 7.8 | | |

GNMA II TBA, 4.000% | | | 5.6 | | |

FHLMC TBA, 4.500% | | | 3.6 | | |

FHLMC, 4.000% due 06/01/47 | | | 3.2 | | |

FNMA TBA, 4.500% | | | 3.0 | | |

GNMA II, 3.000% due 07/20/46 | | | 2.7 | | |

Total | | | 68.9 | % | |

Asset allocation1 | | Percentage of

net assets | |

US government agency mortgage pass-through certificates | | | 127.6 | % | |

Collateralized mortgage obligations | | | 17.9 | | |

Asset-backed securities | | | 14.7 | | |

US government obligations | | | 4.1 | | |

Stripped mortgage-backed securities | | | 1.3 | | |

Options, swaptions, and swaps | | | 0.1 | | |

Commercial mortgage-backed security | | | 0.0 | * | |

Investments sold short | | | (7.9 | ) | |

Cash equivalents and other assets less liabilities | | | (57.8 | ) | |

Total | | | 100.0 | % | |

* Amount represents less than 0.05%.

1 The Portfolio is actively managed and its composition will vary over time.

13

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

US government obligations—4.09% | |

US Treasury Notes

1.750%, due 06/30/22 | | $ | 3,375,000 | | | $ | 3,362,080 | | |

2.250%, due 11/15/25 | | | 2,700,000 | | | | 2,706,855 | | |

2.250%, due 02/15/27 | | | 9,675,000 | | | | 9,647,794 | | |

2.375%, due 05/15/27 | | | 2,500,000 | | | | 2,518,653 | | |

Total US government obligations

(cost—$18,295,417) | | | 18,235,382 | | |

Government national mortgage association

certificates—33.20% | |

GNMA

3.000%, due 11/15/42 | | | 124,328 | | | | 126,530 | | |

3.000%, due 02/15/431 | | | 644,571 | | | | 656,026 | | |

3.000%, due 05/15/431 | | | 1,784,997 | | | | 1,812,938 | | |

3.000%, due 06/15/431 | | | 560,060 | | | | 569,229 | | |

3.000%, due 07/15/43 | | | 161,376 | | | | 164,086 | | |

3.000%, due 01/15/45 | | | 444,770 | | | | 452,603 | | |

3.000%, due 02/15/45 | | | 51,858 | | | | 52,709 | | |

3.000%, due 07/15/451 | | | 704,604 | | | | 716,166 | | |

3.000%, due 08/15/45 | | | 51,622 | | | | 52,384 | | |

3.000%, due 10/15/451 | | | 1,134,957 | | | | 1,153,351 | | |

3.000%, due 12/15/451 | | | 869,115 | | | | 881,938 | | |

3.500%, due 11/15/42 | | | 891,177 | | | | 928,213 | | |

3.500%, due 03/15/451 | | | 1,217,672 | | | | 1,266,567 | | |

3.500%, due 04/15/451 | | | 890,591 | | | | 926,814 | | |

3.500%, due 09/15/451 | | | 1,011,055 | | | | 1,050,587 | | |

4.000%, due 12/15/41 | | | 1,652,884 | | | | 1,746,546 | | |

4.000%, due 01/15/47 | | | 234,258 | | | | 249,036 | | |

4.000%, due 02/15/47 | | | 1,142,291 | | | | 1,214,313 | | |

4.000%, due 04/15/47 | | | 1,136,428 | | | | 1,208,218 | | |

4.500%, due 09/15/39 | | | 906,169 | | | | 989,106 | | |

4.500%, due 06/15/40 | | | 418,758 | | | | 450,403 | | |

5.000%, due 12/15/34 | | | 200,120 | | | | 218,850 | | |

5.000%, due 04/15/38 | | | 169,957 | | | | 187,197 | | |

5.000%, due 05/15/38 | | | 5,247 | | | | 5,779 | | |

5.000%, due 08/15/39 | | | 236,434 | | | | 258,147 | | |

5.000%, due 09/15/39 | | | 506,568 | | | | 557,374 | | |

5.000%, due 10/15/39 | | | 4,996 | | | | 5,501 | | |

5.000%, due 12/15/39 | | | 14,034 | | | | 15,419 | | |

5.000%, due 05/15/40 | | | 380,055 | | | | 417,361 | | |

5.000%, due 09/15/40 | | | 8,878 | | | | 9,701 | | |

5.000%, due 05/15/41 | | | 100,457 | | | | 109,617 | | |

5.500%, due 08/15/35 | | | 32,633 | | | | 36,710 | | |

5.500%, due 02/15/38 | | | 3,417 | | | | 3,828 | | |

5.500%, due 04/15/38 | | | 295,282 | | | | 329,675 | | |

5.500%, due 05/15/38 | | | 306,322 | | | | 341,588 | | |

5.500%, due 06/15/38 | | | 163,791 | | | | 182,503 | | |

5.500%, due 10/15/38 | | | 811,051 | | | | 908,966 | | |

5.500%, due 11/15/38 | | | 45,894 | | | | 51,137 | | |

5.500%, due 12/15/38 | | | 9,507 | | | | 10,666 | | |

5.500%, due 03/15/39 | | | 71,037 | | | | 79,061 | | |

5.500%, due 05/15/39 | | | 76,924 | | | | 85,711 | | |

5.500%, due 09/15/39 | | | 390,537 | | | | 435,120 | | |

5.500%, due 01/15/40 | | | 6,533 | | | | 7,280 | | |

5.500%, due 03/15/40 | | | 462,602 | | | | 518,500 | | |

5.500%, due 05/15/40 | | | 391 | | | | 391 | | |

6.500%, due 02/15/29 | | | 838 | | | | 924 | | |

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(continued) | |

6.500%, due 01/15/36 | | $ | 11,460 | | | $ | 12,550 | | |

6.500%, due 09/15/36 | | | 198,215 | | | | 225,466 | | |

6.500%, due 02/15/37 | | | 13,763 | | | | 15,560 | | |

6.500%, due 04/15/37 | | | 10,208 | | | | 11,375 | | |

6.500%, due 01/15/38 | | | 11,475 | | | | 12,921 | | |

6.500%, due 06/15/38 | | | 32,894 | | | | 36,362 | | |

6.500%, due 07/15/38 | | | 21,971 | | | | 24,628 | | |

6.500%, due 11/15/38 | | | 7,440 | | | | 8,943 | | |

7.500%, due 08/15/21 | | | 1,272 | | | | 1,284 | | |

8.000%, due 02/15/23 | | | 383 | | | | 410 | | |

8.250%, due 04/15/19 | | | 11,113 | | | | 11,188 | | |

10.500%, due 02/15/19 | | | 7,364 | | | | 7,397 | | |

10.500%, due 06/15/19 | | | 9,534 | | | | 9,576 | | |

10.500%, due 07/15/19 | | | 5,404 | | | | 5,429 | | |

10.500%, due 07/15/20 | | | 1,353 | | | | 1,359 | | |

10.500%, due 08/15/20 | | | 8,351 | | | | 8,390 | | |

GNMA I

3.000%, due 12/15/45 | | | 78,939 | | | | 80,238 | | |

GNMA II

3.000%, due 07/20/46 | | | 11,999,991 | | | | 12,184,501 | | |

3.000%, due 10/20/46 | | | 7,516,215 | | | | 7,631,783 | | |

3.000%, due 11/20/46 | | | 4,386,084 | | | | 4,453,524 | | |

3.000%, due 07/20/47 | | | 200,000 | | | | 203,075 | | |

3.500%, due 04/20/45 | | | 15,707 | | | | 16,363 | | |

3.500%, due 11/20/45 | | | 893,995 | | | | 932,426 | | |

3.500%, due 05/20/46 | | | 2,260,851 | | | | 2,378,408 | | |

3.750%, due 05/20/30 | | | 791,675 | | | | 831,392 | | |

4.000%, due 12/20/40 | | | 917,534 | | | | 949,692 | | |

4.000%, due 07/20/41 | | | 51,892 | | | | 54,703 | | |

4.500%, due 09/20/41 | | | 394,882 | | | | 408,378 | | |

4.500%, due 07/20/44 | | | 145,945 | | | | 150,935 | | |

4.500%, due 10/20/44 | | | 760,966 | | | | 787,077 | | |

4.500%, due 02/20/45 | | | 605,333 | | | | 625,672 | | |

4.500%, due 08/20/45 | | | 411,138 | | | | 437,202 | | |

4.500%, due 02/20/46 | | | 353,806 | | | | 365,906 | | |

4.500%, due 04/20/46 | | | 56,371 | | | | 58,301 | | |

5.000%, due 12/20/33 | | | 295,570 | | | | 328,991 | | |

5.000%, due 01/20/34 | | | 158,432 | | | | 174,500 | | |

5.000%, due 02/20/38 | | | 188,786 | | | | 207,876 | | |

5.000%, due 04/20/38 | | | 234,969 | | | | 259,052 | | |

5.000%, due 08/20/41 | | | 29,204 | | | | 32,116 | | |

5.000%, due 12/20/42 | | | 42,528 | | | | 46,360 | | |

5.000%, due 08/20/43 | | | 3,502,911 | | | | 3,803,146 | | |

6.000%, due 10/20/38 | | | 7,214 | | | | 7,758 | | |

6.500%, due 09/20/32 | | | 6,286 | | | | 6,785 | | |

6.500%, due 11/20/38 | | | 11,406 | | | | 11,950 | | |

6.500%, due 12/20/38 | | | 33,454 | | | | 35,928 | | |

7.000%, due 03/20/28 | | | 47,854 | | | | 48,703 | | |

9.000%, due 04/20/25 | | | 6,929 | | | | 7,758 | | |

9.000%, due 12/20/26 | | | 3,099 | | | | 3,246 | | |

9.000%, due 01/20/27 | | | 9,675 | | | | 9,872 | | |

9.000%, due 09/20/30 | | | 1,098 | | | | 1,102 | | |

9.000%, due 10/20/30 | | | 3,582 | | | | 3,718 | | |

9.000%, due 11/20/30 | | | 4,746 | | | | 4,811 | | |

14

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(concluded) | | | |

GNMA II ARM

2.125%, due 09/20/212 | | $ | 47,912 | | | $ | 49,105 | | |

2.125%, due 06/20/222 | | | 38,639 | | | | 39,366 | | |

2.125%, due 04/20/242 | | | 56,858 | | | | 57,208 | | |

2.125%, due 05/20/252 | | | 5,635 | | | | 5,783 | | |

2.125%, due 08/20/252 | | | 14,422 | | | | 14,869 | | |

2.125%, due 09/20/252 | | | 20,145 | | | | 20,764 | | |

2.125%, due 04/20/262 | | | 98,048 | | | | 100,387 | | |

2.125%, due 06/20/262 | | | 42,245 | | | | 43,376 | | |

2.125%, due 08/20/262 | | | 22,368 | | | | 23,100 | | |

2.125%, due 09/20/262 | | | 3,600 | | | | 3,719 | | |

2.125%, due 04/20/272 | | | 25,816 | | | | 26,597 | | |

2.125%, due 07/20/272 | | | 8,292 | | | | 8,577 | | |

2.125%, due 08/20/272 | | | 25,530 | | | | 26,142 | | |

2.125%, due 04/20/302 | | | 16,935 | | | | 17,506 | | |

2.125%, due 05/20/302 | | | 393,638 | | | | 406,831 | | |

2.125%, due 07/20/302 | | | 62,796 | | | | 65,143 | | |

2.125%, due 08/20/302 | | | 86,270 | | | | 89,541 | | |

2.375%, due 01/20/232 | | | 30,425 | | | | 31,113 | | |

2.375%, due 03/20/232 | | | 14,339 | | | | 14,676 | | |

2.375%, due 01/20/242 | | | 45,187 | | | | 46,093 | | |

2.375%, due 01/20/252 | | | 4,904 | | | | 5,044 | | |

2.375%, due 02/20/252 | | | 9,138 | | | | 9,388 | | |

2.375%, due 03/20/262 | | | 11,815 | | | | 12,186 | | |

2.375%, due 01/20/272 | | | 74,518 | | | | 74,760 | | |

2.375%, due 02/20/272 | | | 7,819 | | | | 8,024 | | |

2.375%, due 01/20/282 | | | 11,185 | | | | 11,576 | | |

2.375%, due 02/20/282 | | | 7,367 | | | | 7,496 | | |

2.500%, due 04/20/182 | | | 516 | | | | 515 | | |

2.500%, due 11/20/212 | | | 9,176 | | | | 9,288 | | |

2.500%, due 03/20/252 | | | 15,904 | | | | 16,390 | | |

2.500%, due 07/20/302 | | | 27,687 | | | | 28,588 | | |

2.500%, due 08/20/302 | | | 1,912 | | | | 1,956 | | |

2.500%, due 10/20/302 | | | 12,964 | | | | 13,390 | | |

3.000%, due 04/20/182 | | | 425 | | | | 426 | | |

3.000%, due 05/20/252 | | | 34,838 | | | | 36,129 | | |

3.000%, due 06/20/252 | | | 14,849 | | | | 15,219 | | |

3.500%, due 03/20/252 | | | 7,492 | | | | 7,450 | | |

4.000%, due 01/20/182 | | | 3,712 | | | | 3,720 | | |

4.000%, due 05/20/182 | | | 311 | | | | 312 | | |

4.000%, due 06/20/192 | | | 5,758 | | | | 5,761 | | |

GNMA TBA

4.000% | | | 3,000,000 | | | | 3,153,691 | | |

| 4.500% | | | 4,500,000 | | | | 4,820,274 | | |

GNMA II TBA

2.500% | | | 1,000,000 | | | | 979,941 | | |

| 3.000% | | | 6,800,000 | | | | 6,898,547 | | |

| 3.500% | | | 33,500,000 | | | | 34,753,808 | | |

| 4.000% | | | 23,700,000 | | | | 24,926,660 | | |

| 4.500% | | | 11,000,000 | | | | 11,668,164 | | |

Total government national mortgage

association certificates

(cost—$147,753,341) | | | 147,939,454 | | |

| | | Face

amount | | Value | |

Federal home loan mortgage corporation

certificates—31.27% | |

FHLMC

2.500%, due 01/01/31 | | $ | 424,886 | | | $ | 429,156 | | |

3.000%, due 04/01/43 | | | 356,674 | | | | 359,026 | | |

3.000%, due 05/01/43 | | | 293,516 | | | | 295,450 | | |

3.000%, due 12/01/44 | | | 289,769 | | | | 290,843 | | |

3.000%, due 04/01/45 | | | 1,841,849 | | | | 1,849,793 | | |

3.000%, due 08/01/46 | | | 501,689 | | | | 500,413 | | |

3.500%, due 09/01/32 | | | 639,657 | | | | 671,451 | | |

4.000%, due 01/01/371 | | | 398,430 | | | | 421,717 | | |

4.000%, due 07/01/431 | | | 290,746 | | | | 308,686 | | |

4.000%, due 08/01/44 | | | 3,994,856 | | | | 4,265,991 | | |

4.000%, due 06/01/47 | | | 13,379,619 | | | | 14,099,953 | | |

4.500%, due 10/01/33 | | | 52,045 | | | | 54,477 | | |

4.500%, due 09/01/34 | | | 1,230,675 | | | | 1,277,198 | | |

4.500%, due 01/01/36 | | | 30,340 | | | | 32,172 | | |

4.500%, due 05/01/37 | | | 9,419 | | | | 9,980 | | |

4.500%, due 05/01/38 | | | 78,274 | | | | 81,528 | | |

5.000%, due 10/01/25 | | | 64,787 | | | | 70,508 | | |

5.000%, due 11/01/27 | | | 8,696 | | | | 9,464 | | |

5.000%, due 07/01/33 | | | 10,836 | | | | 11,184 | | |

5.000%, due 09/01/33 | | | 259,578 | | | | 288,189 | | |

5.000%, due 01/01/34 | | | 37,494 | | | | 41,089 | | |

5.000%, due 06/01/34 | | | 12,486 | | | | 13,691 | | |

5.000%, due 04/01/35 | | | 48,470 | | | | 52,750 | | |

5.000%, due 05/01/35 | | | 130,587 | | | | 143,242 | | |

5.000%, due 07/01/35 | | | 1,125,392 | | | | 1,237,747 | | |

5.000%, due 08/01/35 | | | 38,346 | | | | 42,043 | | |

5.000%, due 10/01/35 | | | 31,806 | | | | 34,851 | | |

5.000%, due 12/01/35 | | | 3,347 | | | | 3,660 | | |

5.000%, due 02/01/37 | | | 74,671 | | | | 81,936 | | |

5.000%, due 05/01/37 | | | 12,270 | | | | 12,537 | | |

5.000%, due 06/01/37 | | | 62,778 | | | | 68,854 | | |

5.000%, due 07/01/38 | | | 323,184 | | | | 354,989 | | |

5.000%, due 11/01/38 | | | 293,987 | | | | 322,914 | | |

5.000%, due 06/01/39 | | | 73,166 | | | | 80,464 | | |

5.000%, due 08/01/39 | | | 28,004 | | | | 30,762 | | |

5.000%, due 03/01/40 | | | 9,143 | | | | 10,059 | | |

5.000%, due 07/01/40 | | | 407,696 | | | | 447,798 | | |

5.000%, due 08/01/40 | | | 70,762 | | | | 77,526 | | |

5.000%, due 09/01/40 | | | 191,723 | | | | 210,200 | | |

5.000%, due 11/01/40 | | | 289,514 | | | | 317,347 | | |

5.000%, due 02/01/41 | | | 600,374 | | | | 657,344 | | |

5.000%, due 03/01/41 | | | 44,698 | | | | 49,178 | | |

5.000%, due 04/01/41 | | | 1,263,375 | | | | 1,379,971 | | |

5.000%, due 05/01/41 | | | 249,954 | | | | 273,753 | | |

5.000%, due 06/01/41 | | | 79,373 | | | | 86,837 | | |

5.000%, due 07/01/41 | | | 55,285 | | | | 60,571 | | |

5.000%, due 08/01/44 | | | 105,530 | | | | 116,224 | | |

5.500%, due 06/01/28 | | | 1,663 | | | | 1,832 | | |

5.500%, due 02/01/32 | | | 2,345 | | | | 2,621 | | |

5.500%, due 12/01/32 | | | 3,995 | | | | 4,464 | | |

5.500%, due 02/01/33 | | | 48,831 | | | | 53,841 | | |

5.500%, due 05/01/33 | | | 1,081 | | | | 1,207 | | |

5.500%, due 06/01/33 | | | 247,653 | | | | 276,857 | | |

5.500%, due 12/01/33 | | | 70,584 | | | | 79,061 | | |

5.500%, due 12/01/34 | | | 55,529 | | | | 62,208 | | |

15

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Federal home loan mortgage corporation

certificates—(concluded) | | | |

5.500%, due 06/01/351 | | $ | 930,530 | | | $ | 1,043,151 | | |

5.500%, due 07/01/35 | | | 6,628 | | | | 7,338 | | |

5.500%, due 10/01/351 | | | 216,235 | | | | 239,982 | | |

5.500%, due 12/01/35 | | | 143,101 | | | | 159,470 | | |

5.500%, due 06/01/361 | | | 531,428 | | | | 596,122 | | |

5.500%, due 07/01/36 | | | 23,225 | | | | 24,366 | | |

5.500%, due 12/01/361 | | | 794,990 | | | | 885,367 | | |

5.500%, due 03/01/37 | | | 97,983 | | | | 109,101 | | |

5.500%, due 07/01/37 | | | 65,033 | | | | 69,047 | | |

5.500%, due 10/01/37 | | | 4,842 | | | | 5,388 | | |

5.500%, due 04/01/38 | | | 175,084 | | | | 195,892 | | |

5.500%, due 05/01/38 | | | 16,349 | | | | 18,063 | | |

5.500%, due 12/01/38 | | | 3,621 | | | | 4,039 | | |

5.500%, due 01/01/39 | | | 74,013 | | | | 82,463 | | |

5.500%, due 09/01/39 | | | 223,031 | | | | 250,215 | | |

5.500%, due 02/01/40 | | | 10,948 | | | | 12,170 | | |

5.500%, due 03/01/40 | | | 9,378 | | | | 10,395 | | |

5.500%, due 05/01/40 | | | 141,702 | | | | 157,977 | | |

5.500%, due 02/01/41 | | | 71,528 | | | | 78,864 | | |

5.500%, due 03/01/41 | | | 150,728 | | | | 168,049 | | |

6.000%, due 11/01/37 | | | 1,341,167 | | | | 1,517,689 | | |

7.000%, due 08/01/25 | | | 232 | | | | 259 | | |

9.000%, due 04/01/25 | | | 25,884 | | | | 25,979 | | |

11.000%, due 06/01/19 | | | 115 | | | | 115 | | |

11.000%, due 09/01/20 | | | 90 | | | | 91 | | |

11.500%, due 06/01/19 | | | 6,035 | | | | 6,055 | | |

FHLMC ARM

2.762%, due 01/01/282 | | | 13,646 | | | | 14,030 | | |

2.804%, due 04/01/292 | | | 69,957 | | | | 71,355 | | |

2.863%, due 11/01/272 | | | 64,884 | | | | 65,939 | | |

2.874%, due 09/01/342 | | | 1,400,696 | | | | 1,476,789 | | |

2.939%, due 10/01/232 | | | 25,847 | | | | 26,457 | | |

2.962%, due 07/01/242 | | | 82,235 | | | | 83,430 | | |

2.966%, due 09/01/372 | | | 929,615 | | | | 978,683 | | |

3.036%, due 11/01/292 | | | 222,308 | | | | 230,713 | | |

3.041%, due 12/01/292 | | | 32,829 | | | | 34,076 | | |

3.044%, due 06/01/282 | | | 177,143 | | | | 185,031 | | |

3.064%, due 10/01/272 | | | 144,121 | | | | 152,100 | | |

3.093%, due 11/01/362 | | | 399,070 | | | | 417,545 | | |

3.125%, due 01/01/302 | | | 26,872 | | | | 27,009 | | |

3.139%, due 01/01/292 | | | 136,710 | | | | 144,156 | | |

3.164%, due 07/01/282 | | | 84,922 | | | | 88,361 | | |

3.175%, due 10/01/272 | | | 153,961 | | | | 161,542 | | |

3.191%, due 11/01/252 | | | 117,750 | | | | 124,253 | | |

3.401%, due 11/01/412 | | | 3,222,294 | | | | 3,375,774 | | |

3.430%, due 10/01/392 | | | 2,644,875 | | | | 2,792,490 | | |

FHLMC TBA

2.500% | | | 5,500,000 | | | | 5,545,473 | | |

| 3.000% | | | 34,500,000 | | | | 34,611,750 | | |

| 3.500% | | | 34,000,000 | | | | 34,966,876 | | |

| 4.500% | | | 15,000,000 | | | | 16,070,053 | | |

Total federal home loan mortgage

corporation certificates

(cost—$138,731,803) | | | 139,329,139 | | |

| | | Face

amount | | Value | |

Federal housing administration

certificates—0.03% | |

FHA GMAC

7.400%, due 02/01/213,4 | | $ | 9,624 | | | $ | 9,618 | | |

FHA Reilly

6.896%, due 07/01/203,4 | | | 102,417 | | | | 102,355 | | |

Total federal housing administration

certificates

(cost—$112,179) | | | 111,973 | | |

Federal national mortgage association

certificates—63.09% | |

FNMA

2.000%, due 05/01/28 | | | 244,613 | | | | 241,799 | | |

2.348%, due 09/01/19 | | | 702,986 | | | | 705,290 | | |

2.500%, due 06/01/28 | | | 300,074 | | | | 304,395 | | |

2.500%, due 07/01/28 | | | 2,308,284 | | | | 2,341,642 | | |

2.500%, due 08/01/28 | | | 719,766 | | | | 730,176 | | |

2.500%, due 09/01/30 | | | 48,542 | | | | 49,110 | | |

2.500%, due 11/01/30 | | | 75,467 | | | | 76,183 | | |

2.500%, due 10/01/46 | | | 180,550 | | | | 174,670 | | |

2.500%, due 11/01/46 | | | 493,208 | | | | 477,144 | | |

2.500%, due 01/01/47 | | | 1,294,424 | | | | 1,252,263 | | |

2.677%, due 02/01/422 | | | 807,083 | | | | 837,004 | | |

2.830%, due 09/01/412 | | | 866,595 | | | | 908,955 | | |

2.944%, due 10/01/372 | | | 3,710,453 | | | | 3,906,661 | | |

2.994%, due 05/01/352 | | | 253,902 | | | | 267,580 | | |

3.000%, due 02/01/21 | | | 2,835,424 | | | | 2,918,302 | | |

3.000%, due 10/01/22 | | | 152,983 | | | | 157,455 | | |

3.000%, due 08/01/23 | | | 134,482 | | | | 138,527 | | |

3.000%, due 04/01/24 | | | 112,439 | | | | 115,843 | | |

3.000%, due 07/01/24 | | | 1,126,026 | | | | 1,160,273 | | |

3.000%, due 05/01/28 | | | 296,756 | | | | 306,062 | | |

3.000%, due 02/01/30 | | | 551,171 | | | | 567,282 | | |

3.000%, due 04/01/30 | | | 146,458 | | | | 150,739 | | |

3.000%, due 05/01/30 | | | 139,993 | | | | 144,085 | | |

3.000%, due 08/01/30 | | | 256,816 | | | | 264,323 | | |

3.000%, due 10/01/30 | | | 44,670 | | | | 45,976 | | |

3.000%, due 11/01/30 | | | 340,189 | | | | 350,191 | | |

3.000%, due 12/01/301 | | | 384,671 | | | | 395,965 | | |

3.000%, due 04/01/311 | | | 3,201,787 | | | | 3,302,067 | | |

3.000%, due 10/01/42 | | | 686,241 | | | | 691,171 | | |

3.000%, due 01/01/43 | | | 2,641,694 | | | | 2,660,651 | | |

3.000%, due 04/01/43 | | | 1,008,686 | | | | 1,015,869 | | |

3.000%, due 05/01/43 | | | 1,074,330 | | | | 1,081,970 | | |

3.000%, due 06/01/43 | | | 149,787 | | | | 150,851 | | |

3.000%, due 09/01/43 | | | 1,307,188 | | | | 1,317,779 | | |

3.000%, due 12/01/46 | | | 2,922,465 | | | | 2,939,821 | | |

3.045%, due 01/01/362 | | | 733,160 | | | | 771,108 | | |

3.315%, due 05/01/382 | | | 2,325,242 | | | | 2,454,057 | | |

3.440%, due 02/01/32 | | | 2,500,000 | | | | 2,583,897 | | |

3.500%, due 11/01/25 | | | 592,891 | | | | 618,959 | | |

3.500%, due 08/01/29 | | | 102,916 | | | | 107,615 | | |

3.500%, due 12/01/41 | | | 1,373,434 | | | | 1,427,687 | | |

3.500%, due 03/01/42 | | | 584,486 | | | | 605,087 | | |

3.500%, due 04/01/42 | | | 75,635 | | | | 77,997 | | |

3.500%, due 12/01/42 | | | 2,267,639 | | | | 2,348,199 | | |

3.500%, due 03/01/43 | | | 1,220,737 | | | | 1,263,782 | | |

3.500%, due 05/01/43 | | | 4,938,498 | | | | 5,130,965 | | |

16

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Federal national mortgage association

certificates—(continued) | |

3.500%, due 07/01/43 | | $ | 425,929 | | | $ | 441,161 | | |

3.500%, due 06/01/45 | | | 5,730,273 | | | | 5,904,396 | | |

3.500%, due 08/01/45 | | | 121,006 | | | | 124,675 | | |

3.600%, due 08/01/23 | | | 805,907 | | | | 858,166 | | |

4.000%, due 07/01/25 | | | 18,930 | | | | 19,949 | | |

4.000%, due 08/01/25 | | | 52,425 | | | | 55,247 | | |

4.000%, due 09/01/25 | | | 46,663 | | | | 49,178 | | |

4.000%, due 10/01/25 | | | 24,011 | | | | 25,076 | | |

4.000%, due 11/01/25 | | | 166,063 | | | | 175,002 | | |

4.000%, due 01/01/26 | | | 395,852 | | | | 414,945 | | |

4.000%, due 02/01/26 | | | 1,045,809 | | | | 1,097,918 | | |

4.000%, due 03/01/26 | | | 995,025 | | | | 1,048,346 | | |

4.000%, due 04/01/26 | | | 2,247,628 | | | | 2,368,103 | | |

4.000%, due 08/01/32 | | | 10,975 | | | | 11,664 | | |

4.000%, due 06/01/33 | | | 190,303 | | | | 201,876 | | |

4.000%, due 07/01/33 | | | 676,256 | | | | 718,816 | | |

4.000%, due 07/01/34 | | | 1,219,655 | | | | 1,296,756 | | |

4.000%, due 05/01/39 | | | 173,961 | | | | 184,941 | | |

4.000%, due 09/01/39 | | | 405,239 | | | | 432,800 | | |

4.000%, due 09/01/401 | | | 4,053,972 | | | | 4,288,453 | | |

4.000%, due 12/01/401 | | | 5,291,635 | | | | 5,643,773 | | |

4.000%, due 04/01/411 | | | 1,173,153 | | | | 1,248,786 | | |

4.000%, due 11/01/411 | | | 940,779 | | | | 1,005,228 | | |

4.000%, due 12/01/411 | | | 1,198,191 | | | | 1,279,892 | | |

4.000%, due 07/01/421 | | | 5,511,486 | | | | 5,885,643 | | |

4.000%, due 09/01/421 | | | 7,237,167 | | | | 7,720,792 | | |

4.000%, due 10/01/421 | | | 5,411,904 | | | | 5,774,223 | | |

4.000%, due 12/01/44 | | | 68,006 | | | | 71,669 | | |

4.000%, due 06/01/45 | | | 46,471 | | | | 48,961 | | |

4.000%, due 08/01/45 | | | 3,151,507 | | | | 3,319,802 | | |

4.000%, due 10/01/45 | | | 2,084,598 | | | | 2,195,304 | | |

4.000%, due 12/01/45 | | | 459,312 | | | | 483,729 | | |

4.000%, due 02/01/46 | | | 368,097 | | | | 387,746 | | |

4.000%, due 05/01/46 | | | 887,654 | | | | 935,124 | | |

4.000%, due 07/01/46 | | | 2,739,389 | | | | 2,885,824 | | |

4.500%, due 05/01/19 | | | 1,590 | | | | 1,627 | | |

4.500%, due 09/01/19 | | | 41,425 | | | | 42,378 | | |

4.500%, due 08/01/20 | | | 16,392 | | | | 16,769 | | |

4.500%, due 01/01/21 | | | 104,471 | | | | 106,876 | | |

4.500%, due 05/01/21 | | | 81,231 | | | | 83,101 | | |

4.500%, due 03/01/23 | | | 7,835 | | | | 8,304 | | |

4.500%, due 06/01/35 | | | 17,239 | | | | 17,941 | | |

4.500%, due 04/01/38 | | | 160,982 | | | | 167,068 | | |

4.500%, due 01/01/39 | | | 2,029 | | | | 2,181 | | |

4.500%, due 03/01/39 | | | 14,166 | | | | 15,386 | | |

4.500%, due 06/01/39 | | | 90,672 | | | | 98,548 | | |

4.500%, due 07/01/39 | | | 3,011 | | | | 3,232 | | |

4.500%, due 08/01/39 | | | 148,406 | | | | 161,208 | | |

4.500%, due 10/01/39 | | | 6,583 | | | | 7,154 | | |

4.500%, due 12/01/39 | | | 529,201 | | | | 576,823 | | |

4.500%, due 01/01/40 | | | 4,819 | | | | 5,268 | | |

4.500%, due 02/01/40 | | | 5,370 | | | | 5,855 | | |

4.500%, due 03/01/40 | | | 98,365 | | | | 106,920 | | |

4.500%, due 08/01/40 | | | 89,973 | | | | 97,774 | | |

4.500%, due 11/01/40 | | | 509,183 | | | | 555,354 | | |

4.500%, due 07/01/41 | | | 604,341 | | | | 656,540 | | |

4.500%, due 08/01/41 | | | 1,064,934 | | | | 1,161,175 | | |

| | | Face

amount | | Value | |

Federal national mortgage association

certificates—(continued) | |

4.500%, due 09/01/41 | | $ | 36,332 | | | $ | 39,236 | | |

4.500%, due 01/01/42 | | | 2,887,137 | | | | 3,138,750 | | |

4.500%, due 08/01/42 | | | 4,790 | | | | 5,207 | | |

4.500%, due 09/01/43 | | | 414,021 | | | | 452,667 | | |

4.500%, due 11/01/43 | | | 96,011 | | | | 104,609 | | |

4.500%, due 07/01/44 | | | 425,972 | | | | 463,866 | | |

4.500%, due 12/01/44 | | | 2,768 | | | | 3,000 | | |

5.000%, due 12/01/17 | | | 34,398 | | | | 35,181 | | |

5.000%, due 03/01/23 | | | 3,420 | | | | 3,567 | | |

5.000%, due 05/01/23 | | | 86,435 | | | | 90,746 | | |

5.000%, due 09/01/23 | | | 370,492 | | | | 404,908 | | |

5.000%, due 07/01/24 | | | 536,144 | | | | 585,948 | | |

5.000%, due 03/01/25 | | | 24,020 | | | | 26,251 | | |

5.000%, due 07/01/27 | | | 543,739 | | | | 594,248 | | |

5.000%, due 03/01/33 | | | 45,417 | | | | 47,451 | | |

5.000%, due 05/01/37 | | | 14,115 | | | | 14,730 | | |

5.000%, due 09/01/37 | | | 48,524 | | | | 52,435 | | |

5.000%, due 06/01/38 | | | 104,693 | | | | 113,188 | | |

5.500%, due 06/01/23 | | | 594,244 | | | | 656,875 | | |

5.500%, due 10/01/24 | | | 8,877 | | | | 9,812 | | |

5.500%, due 11/01/25 | | | 11,807 | | | | 13,055 | | |

5.500%, due 07/01/27 | | | 135,527 | | | | 149,838 | | |

5.500%, due 11/01/32 | | | 102,855 | | | | 114,847 | | |

5.500%, due 12/01/33 | | | 1,407 | | | | 1,572 | | |

5.500%, due 04/01/34 | | | 37,326 | | | | 41,407 | | |

5.500%, due 01/01/35 | | | 128,407 | | | | 141,941 | | |

5.500%, due 04/01/36 | | | 88,157 | | | | 97,518 | | |

5.500%, due 05/01/37 | | | 262,485 | | | | 293,714 | | |

5.500%, due 07/01/37 | | | 137,485 | | | | 153,679 | | |

5.500%, due 06/01/38 | | | 230,213 | | | | 256,047 | | |

5.500%, due 06/01/39 | | | 1,259,095 | | | | 1,407,211 | | |

5.500%, due 11/01/39 | | | 475,991 | | | | 531,839 | | |

5.500%, due 07/01/40 | �� | | 645,138 | | | | 717,368 | | |

5.500%, due 02/01/42 | | | 377,064 | | | | 421,003 | | |

6.000%, due 12/01/18 | | | 1,217 | | | | 1,368 | | |

6.000%, due 07/01/19 | | | 1,036 | | | | 1,165 | | |

6.000%, due 11/01/21 | | | 48,407 | | | | 50,600 | | |

6.000%, due 01/01/23 | | | 150,042 | | | | 157,113 | | |

6.000%, due 03/01/23 | | | 196,750 | | | | 209,967 | | |

6.000%, due 09/01/25 | | | 997,748 | | | | 1,121,986 | | |

6.000%, due 11/01/26 | | | 29,361 | | | | 33,017 | | |

6.000%, due 02/01/32 | | | 77,778 | | | | 87,499 | | |

6.000%, due 12/01/32 | | | 17,137 | | | | 19,577 | | |

6.000%, due 02/01/33 | | | 30,109 | | | | 34,123 | | |

6.000%, due 09/01/34 | | | 154,946 | | | | 176,912 | | |

6.000%, due 04/01/35 | | | 342 | | | | 385 | | |

6.000%, due 05/01/35 | | | 72,223 | | | | 81,459 | | |

6.000%, due 06/01/35 | | | 22,863 | | | | 26,112 | | |

6.000%, due 07/01/35 | | | 52,274 | | | | 59,115 | | |

6.000%, due 09/01/35 | | | 2,028 | | | | 2,316 | | |

6.000%, due 01/01/36 | | | 43,504 | | | | 49,404 | | |

6.000%, due 06/01/36 | | | 350 | | | | 394 | | |

6.000%, due 09/01/36 | | | 50,536 | | | | 57,211 | | |

6.000%, due 10/01/36 | | | 17,324 | | | | 19,546 | | |

6.000%, due 12/01/36 | | | 201,018 | | | | 228,318 | | |

6.000%, due 03/01/37 | | | 22,709 | | | | 25,822 | | |

17

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Federal national mortgage association

certificates—(concluded) | | | |

6.000%, due 10/01/37 | | $ | 91,168 | | | $ | 99,980 | | |

6.000%, due 12/01/37 | | | 47,632 | | | | 53,563 | | |

6.000%, due 11/01/38 | | | 478,474 | | | | 543,853 | | |

6.000%, due 05/01/39 | | | 60,396 | | | | 68,793 | | |

6.000%, due 11/01/40 | | | 700,537 | | | | 799,245 | | |

6.500%, due 07/01/19 | | | 5,222 | | | | 5,781 | | |

6.500%, due 10/01/36 | | | 443,488 | | | | 492,192 | | |

6.500%, due 02/01/37 | | | 3,822 | | | | 4,244 | | |

6.500%, due 07/01/37 | | | 33,189 | | | | 36,737 | | |

6.500%, due 08/01/37 | | | 80,112 | | | | 88,676 | | |

6.500%, due 09/01/37 | | | 85,134 | | | | 96,431 | | |

6.500%, due 12/01/37 | | | 174,775 | | | | 196,257 | | |

6.500%, due 08/01/38 | | | 1,205 | | | | 1,333 | | |

6.500%, due 05/01/40 | | | 1,498,189 | | | | 1,736,849 | | |

7.500%, due 11/01/26 | | | 16,634 | | | | 16,764 | | |

8.000%, due 11/01/26 | | | 9,634 | | | | 9,749 | | |

9.000%, due 02/01/26 | | | 10,688 | | | | 11,141 | | |

FNMA ARM

1.932%, due 03/01/442 | | | 240,574 | | | | 244,833 | | |

2.145%, due 07/01/302 | | | 19,003 | | | | 19,245 | | |

2.480%, due 10/01/262 | | | 82,794 | | | | 83,617 | | |

2.603%, due 09/01/262 | | | 18,085 | | | | 18,130 | | |

2.742%, due 02/01/262 | | | 30,446 | | | | 30,482 | | |

2.750%, due 02/01/302 | | | 3,828 | | | | 3,839 | | |

2.881%, due 05/01/302 | | | 34,854 | | | | 36,175 | | |

3.123%, due 12/01/272 | | | 19,407 | | | | 20,162 | | |

3.125%, due 03/01/252 | | | 50,052 | | | | 51,943 | | |

FNMA TBA | |

| 2.000% | | | 1,000,000 | | | | 983,125 | | |

| 2.500% | | | 9,500,000 | | | | 9,505,191 | | |

| 3.000% | | | 42,000,000 | | | | 42,329,470 | | |

| 3.500% | | | 77,000,000 | | | | 79,399,178 | | |

| 4.500% | | | 12,500,000 | | | | 13,406,739 | | |

| 5.000% | | | 4,700,000 | | | | 5,083,578 | | |

Total federal national mortgage

association certificates

(cost—$280,587,037) | | | 281,143,291 | | |

Collateralized mortgage obligations—17.86% | | | |

Alternative Loan Trust,

Series 2004-J7, Class 2A1

2.012%, due 09/25/342 | | | 26,930 | | | | 26,887 | | |

ARM Trust, Series 2005-8, Class 3A21

3.492%, due 11/25/352 | | | 908,591 | | | | 765,235 | | |

BAMLL Commercial Mortgage Securities Trust,

Series 2015-ASHF, Class A

2.379%, due 01/15/282,5 | | | 500,000 | | | | 500,621 | | |

BCAP LLC 2010-RR1 Trust,

Series 2010-RR1, Class 1A4

3.508%, due 03/26/372,5 | | | 193,733 | | | | 160,302 | | |

BCAP LLC 2011-RR10 Trust,

Series 2011-RR10, Class 3A5

3.187%, due 06/26/352,5 | | | 189,472 | | | | 186,938 | | |

BCAP LLC 2011-RR11 Trust,

Series 2011-R11, Class 22A1

2.543%, due 10/26/352,5 | | | 64,188 | | | | 64,274 | | |

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 2011-R11, Class 8A5

1.412%, due 07/26/362,5 | | $ | 228,436 | | | $ | 216,799 | | |

BCAP LLC 2013-RR1 Trust,

Series 2013-RR1, Class 3A4

6.000%, due 10/26/372,5 | | | 448,418 | | | | 417,967 | | |

BCAP LLC 2013-RR5 Trust,

Series 2013-RR5, Class 5A1

1.572%, due 11/26/462,5 | | | 264,132 | | | | 256,394 | | |

Bear Stearns ARM Trust,

Series 2002-011, Class 1A2

3.551%, due 02/25/332 | | | 9,530 | | | | 9,105 | | |

Series 2004-002, Class 12A2

3.204%, due 05/25/342 | | | 55,890 | | | | 55,760 | | |

Bear Stearns Asset-Backed Securities Trust,

Series 2003-AC5, Class A1

5.750%, due 10/25/336 | | | 746,892 | | | | 768,275 | | |

Series 2004-AC3, Class A2

5.500%, due 06/25/346 | | | 997,631 | | | | 1,008,774 | | |

Chevy Chase Mortgage Funding Corp.,

Series 2004-1, Class A1

1.512%, due 01/25/352,5 | | | 115,594 | | | | 106,578 | | |

CHL Mortgage Pass-Through Trust,

Series 2003-HYB1, Class 1A1

3.750%, due 05/19/332 | | | 4,346 | | | | 4,296 | | |

Countrywide Commercial Mortgage Trust,

Series 2007-MF1, Class A

6.271%, due 11/12/432,5 | | | 334,169 | | | | 334,285 | | |

CSMC Trust,

Series 2013-5R, Class 1A1

1.517%, due 02/27/362,5 | | | 217,354 | | | | 213,824 | | |

Series 2013-MH1, Class A

4.791%, due 05/27/532,3,5 | | | 1,052,609 | | | | 1,087,707 | | |

FHLMC REMIC,

Series 0023, Class KZ

6.500%, due 11/25/23 | | | 18,565 | | | | 20,247 | | |

Series 0159, Class H

4.500%, due 09/15/21 | | | 3,500 | | | | 3,584 | | |

Series 1003, Class H

1.976%, due 10/15/202 | | | 6,381 | | | | 6,440 | | |

Series 1349, Class PS

7.500%, due 08/15/22 | | | 737 | | | | 804 | | |

Series 1502, Class PX

7.000%, due 04/15/23 | | | 131,680 | | | | 144,086 | | |

Series 1534, Class Z

5.000%, due 06/15/23 | | | 54,761 | | | | 57,336 | | |

Series 1573, Class PZ

7.000%, due 09/15/23 | | | 17,453 | | | | 19,053 | | |

Series 1658, Class GZ

7.000%, due 01/15/24 | | | 8,429 | | | | 9,226 | | |

Series 1694, Class Z

6.500%, due 03/15/24 | | | 86,216 | | | | 94,821 | | |

Series 1775, Class Z

8.500%, due 03/15/25 | | | 2,861 | | | | 3,305 | | |

Series 2400, Class FQ

1.726%, due 01/15/322 | | | 180,153 | | | | 180,833 | | |

Series 2411, Class FJ

1.576%, due 12/15/292 | | | 20,525 | | | | 20,525 | | |

18

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 2614, Class WO, PO

0.000%, due 05/15/33 | | $ | 1,251,494 | | | $ | 1,142,131 | | |

Series 3096, Class FL

1.626%, due 01/15/362 | | | 178,458 | | | | 178,997 | | |

Series 3114, Class PF

1.626%, due 02/15/362 | | | 927,752 | | | | 931,925 | | |

Series 3153, Class UF

1.656%, due 05/15/362 | | | 232,704 | | | | 233,733 | | |

Series 3339, Class LI, IO

5.254%, due 07/15/372 | | | 994,975 | | | | 157,210 | | |

Series 3442, Class MT

1.226%, due 07/15/342 | | | 105,218 | | | | 101,790 | | |

Series 3598, Class JI, IO

1.616%, due 10/15/372 | | | 72,617 | | | | 3,315 | | |

Series 3621, Class WI, IO

1.829%, due 05/15/372 | | | 136,311 | | | | 8,000 | | |

Series 3635, Class IB, IO

1.466%, due 10/15/372 | | | 241,093 | | | | 12,956 | | |

Series 3667, Class FW

1.776%, due 02/15/382 | | | 145,544 | | | | 146,343 | | |

Series 3671, Class FQ

2.076%, due 12/15/362 | | | 1,614,864 | | | | 1,633,022 | | |

Series 3684, Class JI, IO

1.598%, due 11/15/362 | | | 659,344 | | | | 47,019 | | |

Series 3864, Class NT

5.500%, due 03/15/392 | | | 804,873 | | | | 868,584 | | |

Series 4037, Class PI, IO

3.000%, due 04/15/27 | | | 3,934,111 | | | | 322,005 | | |

Series 4131, Class AI, IO

2.500%, due 10/15/22 | | | 2,080,050 | | | | 93,991 | | |

Series 4136, Class EZ

3.000%, due 11/15/42 | | | 1,336,414 | | | | 1,339,453 | | |

Series 4156, Class SA, IO

4.974%, due 01/15/332 | | | 2,537,611 | | | | 404,507 | | |

Series 4165, Class TI, IO

3.000%, due 12/15/42 | | | 2,455,500 | | | | 244,826 | | |

Series 4182, Class YI, IO

2.500%, due 03/15/28 | | | 6,030,704 | | | | 504,472 | | |

Series 4255, Class SN

8.994%, due 05/15/352 | | | 348,181 | | | | 403,257 | | |

Series 4263, Class SD

8.999%, due 11/15/432 | | | 406,514 | | | | 458,358 | | |

Series 4265, Class ES

9.833%, due 11/15/432 | | | 828,981 | | | | 1,044,501 | | |

Series 4324, Class IO, IO

2.109%, due 08/15/362 | | | 371,519 | | | | 23,142 | | |

Series 4338, Class SB, IO

1.880%, due 10/15/412 | | | 429,044 | | | | 25,964 | | |

Series 4367, Class GS, IO

1.651%, due 03/15/372 | | | 227,240 | | | | 13,970 | | |

Series 4394, Class WI, IO

1.778%, due 08/15/412 | | | 207,709 | | | | 12,421 | | |

Series 4438, Class WI, IO

1.663%, due 11/15/382 | | | 691,010 | | | | 39,075 | | |

Series 4457, Class DI, IO

4.000%, due 08/15/24 | | | 1,600,688 | | | | 139,112 | | |

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 4463, Class IO, IO

2.009%, due 02/15/382 | | $ | 473,039 | | | $ | 28,203 | | |

Series 4544, Class IP, IO

4.000%, due 01/15/46 | | | 4,595,576 | | | | 914,632 | | |

Trust 2513, Class AS, IO

6.774%, due 02/15/322 | | | 425,298 | | | | 87,142 | | |

Trust 3609, Class LI, IO

4.500%, due 12/15/24 | | | 770,070 | | | | 25,081 | | |

Trust 3838, Class LI, IO

4.500%, due 04/15/22 | | | 338,688 | | | | 18,989 | | |

Trust 3962, Class KS, IO

1.684%, due 06/15/382 | | | 409,855 | | | | 27,451 | | |

Trust 4076, Class SW, IO

4.824%, due 07/15/422 | | | 2,940,764 | | | | 632,087 | | |

Trust 4100, Class HI, IO

3.000%, due 08/15/27 | | | 708,782 | | | | 65,565 | | |

Trust 4182, Class QI, IO

3.000%, due 02/15/33 | | | 260,305 | | | | 24,205 | | |

Trust 4479, Class NI, IO

4.500%, due 11/15/19 | | | 458,053 | | | | 13,333 | | |

FHLMC STRIPs,

Series 303, Class C19, IO

3.500%, due 01/15/43 | | | 1,450,602 | | | | 295,687 | | |

Series 320, Class S4, IO

1.490%, due 10/15/372 | | | 3,137,075 | | | | 184,266 | | |

Series 328, Class S4, IO

2.018%, due 02/15/382 | | | 358,770 | | | | 20,797 | | |

FNMA REMIC,

Series 386, Class 14, IO

6.500%, due 04/25/38 | | | 110,523 | | | | 29,405 | | |

Series 413, Class 111, IO

4.000%, due 07/25/422 | | | 1,676,883 | | | | 318,267 | | |

Series 419, Class C3, IO

3.000%, due 11/25/43 | | | 284,246 | | | | 55,249 | | |

Trust 1988-007, Class Z

9.250%, due 04/25/18 | | | 4,298 | | | | 4,351 | | |

Trust 1992-129, Class L

6.000%, due 07/25/22 | | | 2,157 | | | | 2,282 | | |

Trust 1992-158, Class ZZ

7.750%, due 08/25/22 | | | 2,400 | | | | 2,668 | | |

Trust 1993-037, Class PX

7.000%, due 03/25/23 | | | 93,069 | | | | 100,766 | | |

Trust 1997-022, Class F

1.223%, due 03/25/272 | | | 84,520 | | | | 83,477 | | |

Trust 2002-060, Class F1

1.632%, due 06/25/322 | | | 74,973 | | | | 74,864 | | |

Trust 2003-070, Class SH

11.536%, due 07/25/232 | | | 68,428 | | | | 81,680 | | |

Trust 2007-067, Class FB

1.552%, due 07/25/372 | | | 559,987 | | | | 560,029 | | |

Trust 2009-033, Class FB

2.052%, due 03/25/372 | | | 1,033,132 | | | | 1,048,485 | | |

Trust 2010-141, Class FA

1.732%, due 12/25/402 | | | 562,549 | | | | 561,659 | | |

Trust 2010-76, Class SA, IO

5.268%, due 07/25/402 | | | 2,274,930 | | | | 385,224 | | |

19

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2017

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Trust 2011-86, Class DI, IO

3.500%, due 09/25/21 | | $ | 198,667 | | | $ | 10,507 | | |

Trust 2012-090, Class FB

1.672%, due 08/25/422 | | | 257,916 | | | | 257,127 | | |

Trust 2012-111, Class HS

2.640%, due 10/25/422 | | | 264,970 | | | | 217,754 | | |

Trust 2012-122, Class LI, IO

4.500%, due 07/25/41 | | | 1,343,946 | | | | 223,743 | | |

Trust 2012-128, Class FK

1.582%, due 11/25/422 | | | 489,010 | | | | 485,812 | | |

Trust 2012-32, Class AI, IO

3.000%, due 04/25/22 | | | 331,332 | | | | 16,495 | | |

Trust 2012-77, Class IO, IO

1.672%, due 07/25/522 | | | 589,764 | | | | 32,272 | | |

Trust 2013-028, Class YS, IO

4.918%, due 07/25/422 | | | 1,780,793 | | | | 305,703 | | |

Trust 2013-030, Class GI, IO

3.000%, due 01/25/43 | | | 3,351,808 | | | | 511,018 | | |

Trust 2013-030, Class JI, IO

3.000%, due 04/25/43 | | | 1,187,680 | | | | 181,264 | | |

Trust 2013-034, Class PS, IO

4.918%, due 08/25/422 | | | 1,013,966 | | | | 172,692 | | |

Trust 2013-044, Class ZG

3.500%, due 03/25/42 | | | 659,435 | | | | 675,716 | | |

Trust 2013-045, Class IK, IO

3.000%, due 02/25/43 | | | 2,218,884 | | | | 330,851 | | |