UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08764 |

|

PACE® Select Advisors Trust |

(Exact name of registrant as specified in charter) |

|

1285 Avenue of the Americas, New York, New York | | 10019-6028 |

(Address of principal executive offices) | | (Zip code) |

|

Keith A. Weller, Esq. UBS Asset Management One North Wacker Drive Chicago, IL 60606 |

(Name and address of agent for service) |

|

Copy to: |

Stephen H. Bier, Esq. Dechert LLP 1095 Avenue of the Americas New York, NY 10036-6797 |

|

Registrant’s telephone number, including area code: | 212-821 3000 | |

|

Date of fiscal year end: | July 31 | |

|

Date of reporting period: | July 31, 2019 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

(a) Copy of the report transmitted to shareholders:

PACE® Select Advisors Trust

Annual Report | July 31, 2019

Table of contents | | Page | |

Introduction | | | 3 | | |

Portfolio Advisor's and Subadvisors' commentaries and Portfolios of investments | | | |

PACE® Government Money Market Investments | | | 6 | | |

PACE® Mortgage-Backed Securities Fixed Income Investments | | | 10 | | |

PACE® Intermediate Fixed Income Investments | | | 32 | | |

PACE® Strategic Fixed Income Investments | | | 70 | | |

PACE® Municipal Fixed Income Investments | | | 102 | | |

PACE® Global Fixed Income Investments | | | 113 | | |

PACE® High Yield Investments | | | 130 | | |

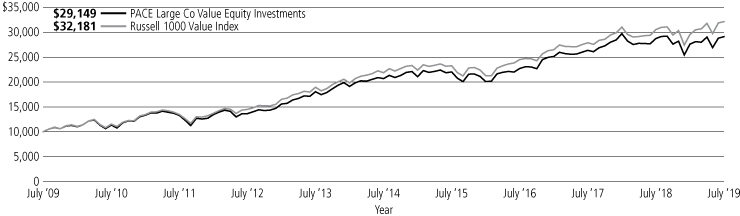

PACE® Large Co Value Equity Investments | | | 160 | | |

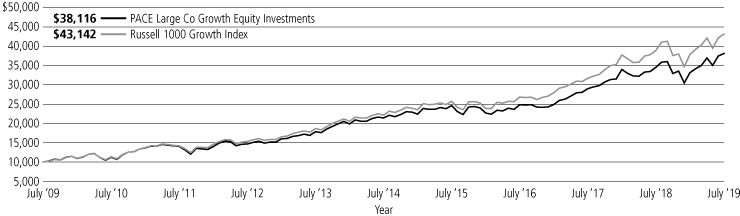

PACE® Large Co Growth Equity Investments | | | 173 | | |

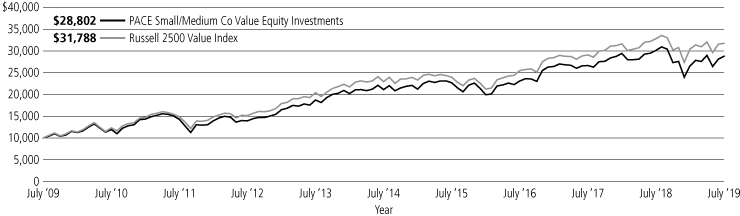

PACE® Small/Medium Co Value Equity Investments | | | 181 | | |

PACE® Small/Medium Co Growth Equity Investments | | | 189 | | |

PACE® International Equity Investments | | | 200 | | |

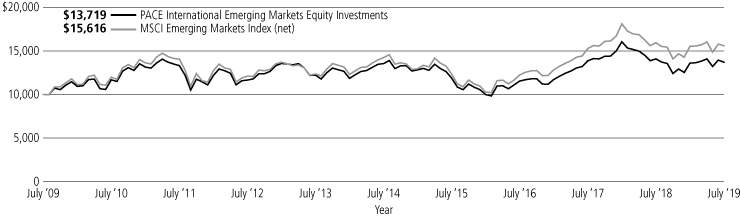

PACE® International Emerging Markets Equity Investments | | | 214 | | |

PACE® Global Real Estate Securities Investments | | | 224 | | |

PACE® Alternative Strategies Investments | | | 232 | | |

Understanding your Portfolio's expenses | | | 263 | | |

Statement of assets and liabilities | | | 268 | | |

Statement of operations | | | 276 | | |

Statement of changes in net assets | | | 280 | | |

Statement of cash flows | | | 286 | | |

Financial highlights | | | 289 | | |

Notes to financial statements | | | 318 | | |

Report of independent registered public accounting firm | | | 368 | | |

Tax information | | | 369 | | |

General information | | | 370 | | |

Board approvals of investment management and administration agreement and

subadvisory agreements | | | 371 | | |

Supplemental information, trustees and officers | | | 381 | | |

1

This page intentionally left blank.

2

September 18, 2019

Dear PACE Shareholder,

We are pleased to provide you with the annual report for the PACE portfolios (the "Portfolios"), comprising the PACE Select Advisors Trust. This report includes summaries of the performance of each Portfolio, as well as commentaries from the investment advisor and subadvisors regarding the events that affected Portfolio performance during the 12 months ended July 31, 2019 (the "reporting period"). Please note that the opinions of the subadvisors do not necessarily represent those of UBS Asset Management (Americas) Inc.

Headwinds for global growth

As the reporting period began, the US economy reached a new record for the longest expansion on record, exceeding the previous mark of 120 months.1 However, trade conflicts, less robust manufacturing activity and several other factors have led to moderating global growth. Looking back, the US Commerce Department reported that gross domestic product ("GDP") grew at 3.4% and 2.2% seasonally adjusted annualized rates during the third and fourth quarters of 2018, respectively. GDP growth then bounced back to 3.1% during the first quarter of 2019. Finally, the US Commerce Department's initial estimate for second quarter GDP growth in the US was 2.1%.

Headwinds facing the economy were acknowledged by the US Federal Reserve Board (the "Fed"). After raising interest rates four times in 2018, in July 2019 the Fed started to reverse course, saying it would pause from additional rate hikes as it monitored incoming economic data. At its meeting that concluded on March 20, 2019, most Federal Open Market Committee ("FOMC")2 members indicated that they did not feel additional rate hikes would be needed in 2019. After its June 2019 meeting, Fed Chair Jerome Powell said, "The case for somewhat more accommodative policy has strengthened" and the market anticipated one or two rate cuts by the end of the year. Finally, at its meeting in July 2019, the Fed lowered its target rate from a range between 2.25% and 2.50% to a range between 2.00% and 2.25%. This marked the first rate cut since 2008.

From a global perspective, in its July 2019 World Economic Outlook Update, the International Monetary Fund ("IMF") said, "Global growth remains subdued. Since the April World Economic Outlook (WEO) report, the United States further increased tariffs on certain Chinese imports and China retaliated by raising tariffs on a subset of US imports. Additional escalation was averted following the June G20 summit. Global technology supply chains were threatened by the prospect of US sanctions, Brexit-related uncertainty continued, and rising geopolitical tensions roiled energy prices...Risks to the forecast are mainly to the downside. They include further trade and technology tensions that dent sentiment and slow investment; a protracted increase in risk aversion that exposes the financial vulnerabilities continuing to accumulate after years of low interest rates; and mounting disinflationary pressures that increase debt service difficulties, constrain the monetary policy space to counter downturns, and make adverse shocks more persistent than normal." From a regional perspective, the IMF projects 2019 growth in the eurozone will be 1.3%, versus 1.9% in 2018. Japan's economy is expected to expand 0.9% in 2019, compared to 0.8% in 2018. Elsewhere, the IMF projects that overall growth in emerging market countries will decelerate to 4.1% in 2019, versus 4.5% in 2018.

Global equities generate mixed results

The global equity market generated mixed results during the reporting period. US equities experienced several setbacks, but they proved to be only temporary in nature, as the market reached several new all-time record highs. Supporting the market were corporate profits that often exceeded expectations, hopes for a resolution between the US and China trade war, and the Fed lowering interest rates to support the economy. All told, the S&P 500 Index3 gained 7.99% during the 12 months ended July 31, 2019. Returns were weaker outside the US, as slower growth,

1 Source: The National Bureau of Economic Research, 7/19

2 The Federal Open Market Committee ("FOMC") is a policy-making body of the Federal Reserve System responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments.

3 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

3

political issues and concerns over trade disputes negatively impacted investor sentiment. International developed equities, as measured by the MSCI EAFE Index (net),4 returned -2.60% during the reporting period, while emerging markets equities, as measured by the MSCI Emerging Markets Index (net),5 fell 2.18%.

The fixed income market produces solid results

The global fixed income market posted solid results during the reporting period. In the US, both short- and long-term Treasury yields declined (bond yields and prices move in the opposite direction). Periods of investor risk aversion, the Fed's monetary policy reversal and modest inflation helped to push yields lower. For the 12 month reporting period as a whole, the yield on the US 10-year Treasury fell from 2.96% to 2.02%. Government bond yields outside the US also generally moved lower, as the European Central Bank, the Bank of Japan and the Bank of

4 The MSCI EAFE Index (net) is an index of stocks designed to measure the investment returns of developed economies outside of North America. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

5 The MSCI Emerging Markets Index (net) is a market capitalization-weighted index composed of different emerging market countries in Europe, Latin America, and the Pacific Basin. Net total return indices reinvest dividends after the deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The index is constructed and managed with a view to being fully investable from the perspective of international institutional investors. Investors should note that indices do not reflect the deduction of fees and expenses.

4

England largely maintained their highly accommodative monetary policies. The overall US bond market, as measured by the Bloomberg Barclays US Aggregate Index,6 returned 8.08% for the 12 months ended July 31, 2019. Returns of riskier fixed income securities were also positive. High yield bonds, as measured by the ICE BofAML US High Yield Cash Pay Constrained Index,7 returned 6.95% during the reporting period. Elsewhere, emerging markets debt, as measured by the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global),8 gained 10.33%.

Sincerely,

Igor Lasun

President, PACE Select Advisors Trust

Executive Director, UBS Asset Management (Americas) Inc.

This report is intended to assist investors in understanding how the Portfolios performed during the 12-month period ended July 31, 2019. The views expressed in the Advisor's and Subadvisors' comments sections are as of the end of the reporting period, reflect performance results gross of fees and expenses, and are those of the investment advisor and subadvisors. Subadvisors' comments on Portfolios that have more than one subadvisor are reflective of their portion of the Portfolio only. The views and opinions in this report were current as of September 18, 2019. They are not guarantees of future performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the investment advisor and subadvisors reserve the right to change their views about individual securities, sectors and markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Portfolio's future investment intent.

Mutual funds are sold by prospectus only. You should read it carefully and consider a fund's investment objectives, risks, charges, expenses and other important information contained in the prospectus before investing. Prospectuses for most of our funds can be obtained from your financial advisor, by calling UBS Funds at 800-647 1568 or by visiting our Website at www.ubs.com/am-us.

6 The Bloomberg Barclays US Aggregate Index is an unmanaged broad based index designed to measure the US dollar-denominated, investment-grade, taxable bond market. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed, asset-backed and commercial mortgage-backed sectors. Investors should note that indices do not reflect the deduction of fees and expenses.

7 The ICE BofAML US High Yield Cash Pay Constrained Index is an unmanaged index of publicly placed, non-convertible, coupon-bearing US dollar denominated, below investment grade corporate debt with a term to maturity of at least one year. The index is market capitalization weighted, so that larger bond issuers have a greater effect on the index's return. However, the representation of any single bond issuer is restricted to a maximum of 2% of the total index. Investors should note that indices do not reflect the deduction of fees and expenses.

8 The J.P. Morgan Emerging Markets Bond Index Global (EMBI Global) is an unmanaged index which is designed to track total returns for US dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans and Eurobonds. Investors should note that indices do not reflect the deduction of fees and expenses.

5

PACE Government Money Market Investments

Performance

The seven-day current yield for the Fund as of July 31, 2019 was 1.74% (after fee waivers/expense reimbursements).1 For more information on the Fund's performance, refer to "Yields and characteristics at a glance" on page 7. Please remember that the PACE program fee is assessed outside the Portfolio at the PACE program account level. The program fee does not impact the determination of the Portfolio's net asset value per share. For a detailed commentary on the market environment in general during the period, please refer to page 3.

Advisor's comments

The Federal Reserve Board (Fed) initially continued to normalize monetary policy during the reporting period. For example, the Fed raised rates at its meetings in September and December 2018, for a total of four rate hikes in 2018. With its December 2018 increase, the federal funds rate moved to a range between 2.25% and 2.50%. In addition, the Fed continued reducing its balance sheet. However, at its meeting in January 2019, the Fed announced that it would take a less aggressive stance on future rate hikes. Then, as expected, the Fed lowered rates at its meeting in July 2019—the first cut since 2008. While the yields on a wide range of short-term investments moved higher over the period, yields still remain low by historical comparison. As a result, the Portfolio's yield remained low during the reporting period.

We tactically adjusted the Portfolio's weighted average maturity ("WAM") throughout the 12-month review period. When the reporting period began, the Portfolio had a WAM of 22 days. This was increased to 34 days at the end of the reporting period.

A number of adjustments were made to the Portfolio's sector and issuer positioning during the 12-month period. We modestly reduced the Portfolio's exposure to US government and agency obligations and slightly pared its allocation to repurchase agreements. (Repurchase agreements are transactions in which the seller of a security agrees to buy it back at a predetermined time and price or upon demand.)

Mutual funds are sold by prospectus only. You should read it carefully and consider a fund's investment objectives, risks, charges, expenses and other important information contained in the prospectus before investing. Prospectuses for most of our funds can be obtained from your financial advisor, by calling UBS Funds at 800-647 1568 or by visiting our Website at www.ubs.com/am-us.

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

PACE Select Advisors Trust – PACE Government Money Market Investments

Investment Advisor:

UBS Asset Management (Americas) Inc.

Portfolio Manager:

Robert Sabatino

Objective:

Current income consistent with preservation of capital and liquidity

Investment process:

The Portfolio is a money market mutual fund and seeks to maintain a stable price of $1.00 per share, although it may be possible to lose money by investing in this Portfolio. The Portfolio invests in a diversified portfolio of high-quality money market instruments of governmental issuers. Security selection is based on the assessment of relative values and changes in market and economic conditions.

6

PACE Government Money Market Investments

Yields and characteristics at a glance—July 31, 2019 (unaudited)

Yields and characteristics | |

Seven-day current yield after fee waivers and/or expense reimbursements1 | | | 1.74 | % | |

Seven-day effective yield after fee waivers and/or expense reimbursements1 | | | 1.75 | | |

Seven-day current yield before fee waivers and/or expense reimbursements1 | | | 1.19 | | |

Seven-day effective yield before fee waivers and/or expense reimbursements1 | | | 1.19 | | |

Weighted average maturity2 | | | 34 days | | |

Portfolio composition3 | |

US government and agency obligations | | | 79.2 | % | |

Repurchase agreements | | | 21.5 | | |

Other assets less liabilities | | | (0.7 | ) | |

Total | | | 100.0 | % | |

You could lose money by investing in PACE Government Money Market Investments. Although the portfolio seeks to preserve the value of your investment at $1.00 per share, the portfolio cannot guarantee it will do so. An investment in PACE Government Money Market Investments is not insured or guaranteed by the Federal Deposit Insurance Corporation ("FDIC") or any other government agency. PACE Government Money Market Investments' sponsor has no legal obligation to provide financial support to PACE Government Money Market Investments, and you should not expect that the portfolio's sponsor will provide financial support to PACE Government Money Market Investments at any time.

Not FDIC insured. May lose value. No bank guarantee.

1 Yields will fluctuate and reflect fee waivers and/or expense reimbursements, if any, unless otherwise noted. Performance data quoated represents past performance. Past performance does not guarantee future results. Current performance may be higher or lower than the performance data quoted.

2 The Portfolio is actively managed and its weighted average maturity will differ over time.

3 Weightings represent percentages of the Portfolio's net assets as of the date indicated. The Portfolio is actively managed and its composition will vary over time.

7

PACE Government Money Market Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

US government and agency obligations—79.2% | |

Federal Farm Credit Bank

2.070%, due 12/12/191 | | $ | 1,250,000 | | | $ | 1,240,441 | | |

2.400%, due 11/25/191 | | | 1,300,000 | | | | 1,289,947 | | |

Federal Home Loan Bank

2.025%, due 01/06/201 | | | 2,000,000 | | | | 1,982,225 | | |

2.080%, due 11/13/191 | | | 1,000,000 | | | | 993,991 | | |

2.085%, due 11/04/191 | | | 1,500,000 | | | | 1,491,747 | | |

2.090%, due 10/01/191 | | | 2,000,000 | | | | 1,992,917 | | |

2.090%, due 10/25/191 | | | 4,000,000 | | | | 3,980,261 | | |

2.140%, due 08/20/191 | | | 5,000,000 | | | | 4,994,353 | | |

2.145%, due 08/23/191 | | | 5,000,000 | | | | 4,993,446 | | |

2.150%, due 08/14/191 | | | 7,000,000 | | | | 6,994,565 | | |

2.150%, due 09/06/191 | | | 2,000,000 | | | | 1,995,700 | | |

2.150%, due 09/16/191 | | | 5,000,000 | | | | 4,986,264 | | |

2.180%, due 08/08/191 | | | 3,000,000 | | | | 2,998,728 | | |

2.200%, due 08/09/191 | | | 5,000,000 | | | | 4,997,556 | | |

2.215%, due 08/21/191 | | | 2,500,000 | | | | 2,496,924 | | |

2.215%, due 09/04/191 | | | 5,000,000 | | | | 4,989,540 | | |

2.215%, due 09/13/191 | | | 6,000,000 | | | | 5,984,126 | | |

2.240%, due 08/20/191 | | | 5,000,000 | | | | 4,994,089 | | |

2.245%, due 08/21/191 | | | 2,000,000 | | | | 1,997,506 | | |

2.330%, due 09/04/191 | | | 3,000,000 | | | | 2,993,398 | | |

2.330%, due 09/06/191 | | | 3,500,000 | | | | 3,491,845 | | |

2.335%, due 09/03/191 | | | 1,000,000 | | | | 997,860 | | |

2.340%, due 09/16/191 | | | 5,000,000 | | | | 4,985,050 | | |

2.345%, due 08/28/191 | | | 3,000,000 | | | | 2,994,724 | | |

2.348%, due 08/23/191 | | | 2,000,000 | | | | 1,997,130 | | |

2.349%, due 08/30/191 | | | 2,000,000 | | | | 1,996,215 | | |

2.367%, due 08/21/191 | | | 4,000,000 | | | | 3,994,740 | | |

2.372%, due 08/16/191 | | | 2,000,000 | | | | 1,998,023 | | |

2.378%, due 08/14/191 | | | 2,000,000 | | | | 1,998,283 | | |

2.400%, due 08/01/191 | | | 1,000,000 | | | | 1,000,000 | | |

2.400%, due 09/11/191 | | | 1,000,000 | | | | 997,267 | | |

2.400%, due 10/21/191 | | | 1,500,000 | | | | 1,491,900 | | |

2.400%, due 06/17/20 | | | 2,000,000 | | | | 2,000,000 | | |

2.410%, due 10/25/191 | | | 1,000,000 | | | | 994,310 | | |

2.415%, due 08/15/191 | | | 1,000,000 | | | | 999,061 | | |

2.430%, due 09/25/191 | | | 3,000,000 | | | | 2,988,862 | | |

2.435%, due 10/01/191 | | | 2,000,000 | | | | 1,991,748 | | |

2.437%, due 09/20/191 | | | 1,000,000 | | | | 996,615 | | |

2.440%, due 10/02/191 | | | 2,000,000 | | | | 1,991,596 | | |

2.440%, due 10/17/191 | | | 400,000 | | | | 397,912 | | |

2.440%, due 10/21/191 | | | 1,500,000 | | | | 1,491,765 | | |

2.510%, due 05/28/20 | | | 1,000,000 | | | | 1,000,000 | | |

1 mo. USD LIBOR - 0.025%,

2.342%, due 10/09/192 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.015%,

2.257%, due 05/20/202 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.020%,

2.340%, due 05/08/202 | | | 2,500,000 | | | | 2,500,000 | | |

1 mo. USD LIBOR - 0.030%,

2.330%, due 11/07/192 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.055%,

2.270%, due 01/14/202 | | | 1,000,000 | | | | 1,000,000 | | |

1 mo. USD LIBOR - 0.065%,

2.235%, due 10/18/192 | | | 2,000,000 | | | | 2,000,000 | | |

| | | Face

amount | | Value | |

US government and agency obligations—(concluded) | |

1 mo. USD LIBOR - 0.070%,

2.297%, due 10/09/192 | | $ | 2,000,000 | | | $ | 2,000,000 | | |

1 mo. USD LIBOR - 0.080%,

2.161%, due 09/27/192 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.090%,

2.289%, due 09/10/192 | | | 1,000,000 | | | | 1,000,000 | | |

1 mo. USD LIBOR - 0.100%,

2.172%, due 08/21/192 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.105%,

2.167%, due 08/20/192 | | | 2,000,000 | | | | 2,000,000 | | |

1 mo. USD LIBOR - 0.110%,

2.215%, due 08/13/192 | | | 2,000,000 | | | | 2,000,000 | | |

3 mo. USD LIBOR - 0.265%,

2.311%, due 08/02/192 | | | 2,000,000 | | | | 1,999,997 | | |

SOFR + 0.010%,

2.400%, due 01/24/202 | | | 2,000,000 | | | | 2,000,000 | | |

SOFR + 0.025%,

2.415%, due 04/22/202 | | | 2,000,000 | | | | 2,000,000 | | |

SOFR + 0.065%,

2.455%, due 11/15/192 | | | 1,000,000 | | | | 1,000,000 | | |

Federal Home Loan Mortgage Corp.

2.340%, due 10/17/191 | | | 2,500,000 | | | | 2,487,487 | | |

US Treasury Bill

1.673%, due 12/26/191 | | | 3,000,000 | | | | 2,975,181 | | |

Total US government and agency

obligations

(cost—$146,145,295) | | | 146,145,295 | | |

Repurchase agreement—21.5% | |

Repurchase agreement dated

07/31/19 with Goldman Sachs & Co.,

2.510% due 08/01/19, collateralized by

$14,566,000 Federal Farm Credit Bank

obligation, 2.080% to 3.000% due

10/01/25 to 05/16/36, $3,000

Federal Home Loan Mortgage Corp.

obligation, 2.750% due 06/19/23,

$24,670,000 Federal Home Loan Banks

obligations, 1.875 to 3.300% due

11/29/21 to 09/08/28 and $101

US Treasury Inflation Index Notes,

Zero Coupon due 08/15/22 to 11/15/29;

(value—$40,494,000); proceeds: $39,702,768

(cost—$39,700,000) | | | 39,700,000 | | | | 39,700,000 | | |

Total investments

(cost—$185,845,295 which

approximates cost for federal

income tax purposes)—100.7% | | | 185,845,295 | | |

Liabilities in excess of other assets—(0.7)% | | | | | (1,243,367 | ) | |

Net assets—100.0% | | $ | 184,601,928 | | |

8

PACE Government Money Market Investments

Portfolio of investments—July 31, 2019

For a listing of defined portfolio acronyms that are used throughout the Portfolio of investments as well as the tables that follow, please refer to page 261.

Fair valuation summary

The following is a summary of the fair valuations according to the inputs used as of July 31, 2019 in valuing the Portfolio's investments. In the event a Portfolio holds investments for which fair value is measured using the NAV per share practical expedient (or its equivalent), a separate column will be added to the fair value hierarchy table; this is intended to permit reconciliation to the amounts presented in the Portfolio of investments:

Description | | Unadjusted

quoted prices in

active markets for

identical investments

(Level 1) | | Other significant

observable inputs

(Level 2) | | Unobservable

inputs

(Level 3) | | Total | |

US government and agency obligations | | $ | — | | | $ | 146,145,295 | | | $ | — | | | $ | 146,145,295 | | |

Repurchase agreement | | | — | | | | 39,700,000 | | | | — | | | | 39,700,000 | | |

Total | | $ | — | | | $ | 185,845,295 | | | $ | — | | | $ | 185,845,295 | | |

At July 31, 2019, there were no transfers between Level 1 and Level 2.

Portfolio footnotes

1 Rate shown is the discount rate at the date of purchase unless otherwise noted.

2 Variable or floating rate security. The interest rate shown is the rate in effect as of period end and changes periodically.

See accompanying notes to financial statements.

9

PACE Mortgage-Backed Securities Fixed Income Investments

Performance

For the 12 months ended July 31, 2019, the Portfolio's Class P shares returned 6.53% before the deduction of the maximum PACE Select program fee.1 In comparison, the Bloomberg Barclays US Mortgage-Backed Securities Index (the "benchmark") returned 6.76%, and the Lipper US Mortgage Funds category posted a median return of 6.40%. (Returns for all share classes over various time periods are shown in the "Performance at a glance" table on page 12. Please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.) For a detailed commentary on the market environment in general during the reporting period, please refer to page 3.

Subadvisor's comments2

(Please note that while the subadvisor outperformed the benchmark on a gross-of-fees basis, the Portfolio underperformed net of fees, as reported in the "Performance at a glance" table. As stated in footnote two, the comments that follow address performance on a gross-of-fees basis.)

The Portfolio generated a positive return and outperformed its benchmark during the reporting period. Overall, US interest rate strategies were modestly positive for performance. Near-benchmark US duration exposure was neutral for performance. (Duration measures a portfolio's sensitivity to interest rate changes.) Yield curve positioning, including a focus on the intermediate portion of the yield curve, modestly contributed to results, as intermediate yields outperformed short- and long-end yields during the period.

Agency mortgage-backed security (MBS) strategies contributed to performance. An average overweight to agency MBS detracted from performance as the sector lagged like-duration Treasuries. However, this was more than offset by relative value positioning within the sector, which added to performance. Exposure to select non-agency mortgages contributed to results, as these securities remained well-supported by the improving US housing market. Non-mortgage securitized debt exposure, including holdings of collateralized loan obligations, was positive for returns.

Overall, derivative usage was neutral to modestly positive for performance during the period. The use of interest rate swaps to short- and long-end US swap rates detracted from returns, as swap rates outperformed Treasury rates. The Fund used interest rate swaps and constant maturity swaps to adjust interest rate and yield curve exposures, as well as to substitute for physical securities. The Portfolio benefited from the income generated from selling mortgage pool options as a way to manage interest rate and volatility risk within the sector. Additionally, options on swaps were primarily used to manage interest rate exposure and volatility. The purchase of options on swaps detracted from performance due to premium payments made. Total return swaps, used to replicate broad exposure to interest only agency mortgages, while limiting idiosyncratic risk of owning individual bonds, was neutral for performance.

1 Class P shares held through the PACE Select Advisors Program are subject to a maximum Program fee of 2.50%, which, if included, would have reduced performance. Class P shares held through other advisory programs also may be subject to a program fee, which, if included, would have reduced performance.

2 Performance is discussed on a gross-of-fees basis—meaning that no fees or expenses are reflected in their sleeves'/sleeve's performance. Alternately, Portfolio performance is shown net of fees, which does factor in fees and expenses associated with the Portfolio.

PACE Select Advisors Trust – PACE Mortgage-Backed Securities Fixed

Income Investments

Investment Manager:

UBS Asset Management (Americas) Inc. ("UBS AM")

Investment Subadvisor:

Pacific Investment Management Company LLC ("PIMCO")

Portfolio Management Team:

UBS AM: Mabel Lung, CFA, Gina Toth, CFA, Fred Lee, CFA, Joseph Sciortino and Steve Bienashski

PIMCO: Daniel Hyman and Michael Cudzil

Objective:

Current income

Investment process:

The subadvisor utilizes a strategy that involves buying or

selling specific bonds based on an analysis of their values

relative to other similar bonds.

10

PACE Mortgage-Backed Securities Fixed Income Investments

Mutual funds are sold by prospectus only. You should read it carefully and consider a fund's investment objectives, risks, charges, expenses and other important information contained in the prospectus before investing. Prospectuses for most of our funds can be obtained from your financial advisor, by calling UBS Funds at 800-647 1568 or by visiting our Website at www.ubs.com/am-us.

Special considerations

The Portfolio may be appropriate for long-term investors seeking current income who are able to withstand short-term fluctuations in the fixed income markets in return for potentially higher returns over the long term. The yield and value of the Portfolio change every day and can be affected by changes in interest rates, general market conditions, and other political, social and economic developments, as well as specific matters relating to the issuers in which the Portfolio invests. It is important to note that an investment in the Portfolio is only one component of a balanced investment plan.

11

PACE Mortgage-Backed Securities Fixed Income Investments

Performance at a glance (unaudited)

Average annual total returns for periods ended 07/31/19 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | 6.27 | % | | | 2.38 | % | | | 3.10 | % | |

Class Y2 | | | 6.44 | | | | 2.64 | | | | 3.35 | | |

Class P3 | | | 6.53 | | | | 2.64 | | | | 3.36 | | |

After deducting maximum sales charge | |

Class A1 | | | 2.29 | | | | 1.60 | | | | 2.70 | | |

Bloomberg Barclays US Mortgage-Backed Securities Index4 | | | 6.76 | | | | 2.76 | | | | 3.19 | | |

Lipper US Mortgage Funds median | | | 6.40 | | | | 2.55 | | | | 3.23 | | |

Most recent calendar quarter-end returns (unaudited)

Average annual total returns for periods ended 06/30/19 | | 1 year | | 5 years | | 10 years | |

Before deducting maximum sales charge | |

Class A1 | | | 5.82 | % | | | 2.22 | % | | | 3.19 | % | |

Class Y3 | | | 6.08 | | | | 2.48 | | | | 3.45 | | |

Class P4 | | | 6.16 | | | | 2.48 | | | | 3.46 | | |

After deducting maximum sales charge | |

Class A1 | | | 1.87 | | | | 1.45 | | | | 2.79 | | |

The annualized gross and net expense ratios, respectively, for each class of shares as in the November 28, 2018 prospectuses, were as follows: Class A—1.09% and 0.97%; Class Y—1.01% and 0.72%; and Class P—0.93% and 0.72%. Net expenses reflect fee waivers and/or expense reimbursements, if any, pursuant to an agreement that is in effect to cap the expenses. The Portfolio and UBS Asset Management (Americas) Inc. ("UBS AM") have entered into a written fee waiver/expense reimbursement agreement pursuant to which UBS AM is contractually obligated to waive its management fees and/or reimburse expenses so that the Portfolio's ordinary total operating expenses of each class through November 30, 2019 (excluding dividend expense, borrowing costs, and interest expense relating to short sales, and expenses attributable to investment in other investment companies, interest, taxes, brokerage commissions and extraordinary expenses) would not exceed Class A—0.97%; Class Y—0.72%; and Class P—0.72%. The Portfolio has agreed to repay UBS AM for any waived fees/reimbursed expenses to the extent that it can do so over the following three fiscal years without causing the Portfolio's expenses in any of those three years to exceed these expense caps and that UBS AM has not waived the right to do so. The fee waiver/expense reimbursement agreement may be terminated by the Portfolio's board at any time and also will terminate automatically upon the expiration or termination of the Portfolio's advisory contract with UBS AM. Upon termination of the agreement, however, UBS AM's three year recoupment rights will survive.

1 Maximum sales charge for Class A shares is 3.75%. Class A shares bear ongoing 12b-1 service fees of 0.25% annually.

2 The Portfolio offers Class Y shares to a limited group of eligible investors, including certain qualifying retirement plans. Class Y shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees.

3 Class P shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees, but Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance.

4 The Bloomberg Barclays US Mortgage-Backed Securities Index is an unmanaged index which primarily covers the mortgage-backed passthrough securities issued by Ginnie Mae (formally known as the Government National Mortgage Association or GNMA), Freddie Mac (formally known as Federal Home Loan Mortgage Corporation or FHLMC), and Fannie Mae (formally known as Federal National Mortgage Association or FNMA). Investors should note that indices do not reflect the deduction of fees and expenses.

Prior to August 3, 2015, a 1% redemption fee was imposed on sales or exchanges of any class of shares of the Portfolio made during the specified holding period.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. The return and principal value of an investment will fluctuate, so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the ex-dividend dates. Current performance may be higher or lower than the performance data quoted. For month-end performance figures, please visit www.ubs.com/us-mutualfundperformance.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

12

PACE Mortgage-Backed Securities Fixed Income Investments

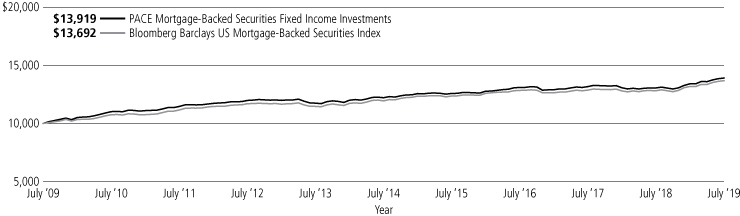

Illustration of an assumed investment of $10,000 in Class P shares of the Portfolio (unaudited)

The following graph depicts the performance of PACE Mortgage-Backed Securities Fixed Income Investments Class P shares versus the Bloomberg Barclays US Mortgage-Backed Securities Index over the 10 years ended July 31, 2019. Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that PACE Mortgage-Backed Securities Fixed Income Investments is a professionally managed portfolio while the Index is not available for investment and is unmanaged. The comparison is shown for illustration purposes only.

PACE Mortgage-Backed Securities Fixed Income Investments

13

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio statistics—July 31, 2019 (unaudited)

Characteristics | |

Weighted average duration | | | 2.40 yrs. | | |

Weighted average maturity | | | 2.70 yrs. | | |

Average coupon | | | 3.28 | % | |

Top ten holdings (long holdings)1 | | Percentage of

net assets | |

FNMA TBA, 3.000% | | | 19.4 | % | |

GNMA TBA, 4.000% | | | 10.4 | | |

GNMA TBA, 3.500% | | | 9.8 | | |

FNMA TBA, 3.500% | | | 5.2 | | |

FNMA TBA, 4.500% | | | 5.0 | | |

GNMA TBA, 3.000% | | | 5.0 | | |

FNMA TBA, 4.000% | | | 3.5 | | |

FNMA TBA, 2.500% | | | 2.9 | | |

US Treasury Note, 3.000%, due 09/30/25 | | | 2.7 | | |

GNMA TBA, 5.000% | | | 2.2 | | |

Total | | | 66.1 | % | |

Asset allocation1 | | Percentage of

net assets | |

US government agency mortgage pass-through certificates | | | 131.8 | % | |

Collateralized mortgage obligations | | | 26.6 | | |

Asset-backed securities | | | 17.2 | | |

US government obligations | | | 4.7 | | |

Commercial mortgage-backed securities | | | 0.9 | | |

Short-term investment | | | 0.8 | | |

Repurchase agreement | | | 0.2 | | |

Stripped mortgage-backed securities | | | 0.2 | | |

Options, swaptions, futures, swaps | | | 0.0 | † | |

Investments sold short | | | (9.0 | ) | |

Cash equivalents and other assets less liabilities | | | (73.4 | ) | |

Total | | | 100.0 | % | |

† Amount is less than 0.05%

1 The Portfolio is actively managed and its composition will vary over time.

14

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

US government obligations—4.7% | |

US Treasury Notes

2.250%, due 03/31/26 | | $ | 1,100,000 | | | $ | 1,123,504 | | |

2.500%, due 02/28/26 | | | 2,200,000 | | | | 2,280,610 | | |

2.625%, due 12/31/25 | | | 2,100,000 | | | | 2,191,301 | | |

2.750%, due 08/31/25 | | | 1,500,000 | | | | 1,573,945 | | |

3.000%, due 09/30/251 | | | 9,200,000 | | | | 9,791,531 | | |

Total US government obligations

(cost—$16,059,587) | | | 16,960,891 | | |

Government national mortgage association

certificates—49.6% | |

GNMA

3.000%, due 11/15/421 | | | 90,040 | | | | 92,172 | | |

3.000%, due 02/15/431 | | | 573,129 | | | | 587,639 | | |

3.000%, due 05/15/431 | | | 1,245,939 | | | | 1,275,876 | | |

3.000%, due 06/15/431 | | | 410,945 | | | | 420,313 | | |

3.000%, due 07/15/431 | | | 114,640 | | | | 117,394 | | |

3.000%, due 01/15/451 | | | 421,520 | | | | 432,088 | | |

3.000%, due 02/15/451 | | | 44,066 | | | | 45,106 | | |

3.000%, due 07/15/451 | | | 613,176 | | | | 627,680 | | |

3.000%, due 10/15/451 | | | 948,418 | | | | 970,795 | | |

3.500%, due 11/15/42 | | | 694,496 | | | | 721,554 | | |

3.500%, due 03/15/45 | | | 288,005 | | | | 299,614 | | |

3.500%, due 04/15/45 | | | 636,811 | | | | 663,894 | | |

4.000%, due 12/15/41 | | | 1,345,108 | | | | 1,426,596 | | |

4.000%, due 01/15/47 | | | 142,600 | | | | 149,902 | | |

4.000%, due 02/15/47 | | | 858,577 | | | | 910,855 | | |

4.000%, due 04/15/47 | | | 1,166,133 | | | | 1,236,893 | | |

4.000%, due 05/15/47 | | | 138,220 | | | | 146,638 | | |

4.000%, due 06/15/47 | | | 126,732 | | | | 134,448 | | |

4.000%, due 07/15/47 | | | 152,663 | | | | 161,976 | | |

4.000%, due 08/15/47 | | | 218,687 | | | | 231,051 | | |

4.000%, due 12/15/47 | | | 58,149 | | | | 60,836 | | |

4.500%, due 09/15/391 | | | 575,586 | | | | 621,505 | | |

4.500%, due 06/15/401 | | | 287,343 | | | | 310,275 | | |

4.500%, due 12/15/451 | | | 31,164 | | | | 33,544 | | |

4.500%, due 07/15/461 | | | 8,226 | | | | 8,874 | | |

4.500%, due 08/15/461 | | | 12,659 | | | | 13,653 | | |

4.500%, due 09/15/461 | | | 232,935 | | | | 246,922 | | |

4.500%, due 10/15/461 | | | 560,647 | | | | 605,048 | | |

4.500%, due 01/15/471 | | | 792,273 | | | | 854,908 | | |

5.000%, due 12/15/34 | | | 148,654 | | | | 157,788 | | |

5.000%, due 04/15/38 | | | 89,380 | | | | 94,988 | | |

5.000%, due 08/15/39 | | | 78,825 | | | | 82,991 | | |

5.000%, due 12/15/39 | | | 6,229 | | | | 6,607 | | |

5.000%, due 05/15/40 | | | 262,292 | | | | 289,736 | | |

5.000%, due 09/15/40 | | | 3,428 | | | | 3,609 | | |

5.000%, due 05/15/41 | | | 36,091 | | | | 37,998 | | |

5.500%, due 08/15/35 | | | 22,222 | | | | 25,127 | | |

5.500%, due 02/15/38 | | | 2,254 | | | | 2,546 | | |

5.500%, due 04/15/38 | | | 209,436 | | | | 232,334 | | |

5.500%, due 05/15/38 | | | 226,012 | | | | 250,807 | | |

5.500%, due 06/15/38 | | | 106,545 | | | | 116,194 | | |

5.500%, due 10/15/38 | | | 564,601 | | | | 625,967 | | |

5.500%, due 11/15/38 | | | 34,584 | | | | 38,346 | | |

5.500%, due 12/15/38 | | | 6,496 | | | | 7,204 | | |

5.500%, due 03/15/39 | | | 31,852 | | | | 34,083 | | |

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(continued) | |

5.500%, due 05/15/39 | | $ | 50,928 | | | $ | 56,468 | | |

5.500%, due 09/15/39 | | | 265,597 | | | | 294,544 | | |

5.500%, due 01/15/40 | | | 4,753 | | | | 5,201 | | |

5.500%, due 03/15/40 | | | 308,784 | | | | 341,167 | | |

6.500%, due 02/15/29 | | | 532 | | | | 585 | | |

6.500%, due 01/15/36 | | | 10,520 | | | | 11,580 | | |

6.500%, due 09/15/36 | | | 186,716 | | | | 213,456 | | |

6.500%, due 02/15/37 | | | 10,632 | | | | 11,997 | | |

6.500%, due 04/15/37 | | | 6,987 | | | | 7,880 | | |

6.500%, due 01/15/38 | | | 6,235 | | | | 6,863 | | |

6.500%, due 06/15/38 | | | 26,968 | | | | 30,576 | | |

6.500%, due 07/15/38 | | | 20,681 | | | | 23,959 | | |

6.500%, due 11/15/38 | | | 6,034 | | | | 7,159 | | |

7.500%, due 08/15/21 | | | 253 | | | | 253 | | |

8.000%, due 02/15/23 | | | 159 | | | | 167 | | |

10.500%, due 07/15/20 | | | 28 | | | | 28 | | |

10.500%, due 08/15/20 | | | 2,976 | | | | 2,984 | | |

GNMA II

2.500%, due 04/20/47 | | | 871,764 | | | | 872,542 | | |

3.000%, due 09/20/47 | | | 2,012,197 | | | | 2,057,067 | | |

3.500%, due 04/20/45 | | | 10,947 | | | | 11,405 | | |

3.500%, due 11/20/45 | | | 669,650 | | | | 698,357 | | |

3.500%, due 04/20/46 | | | 811,886 | | | | 844,465 | | |

3.500%, due 05/20/46 | | | 1,661,288 | | | | 1,723,909 | | |

3.500%, due 04/20/47 | | | 577,231 | | | | 600,863 | | |

3.500%, due 07/20/47 | | | 4,996,937 | | | | 5,196,264 | | |

3.500%, due 08/20/47 | | | 485,789 | | | | 508,712 | | |

3.500%, due 09/20/47 | | | 198,345 | | | | 207,247 | | |

3.500%, due 11/20/47 | | | 678,830 | | | | 708,612 | | |

3.500%, due 12/20/47 | | | 131,960 | | | | 138,151 | | |

3.500%, due 01/20/48 | | | 3,020,867 | | | | 3,154,844 | | |

3.500%, due 02/20/48 | | | 2,489,839 | | | | 2,590,220 | | |

3.500%, due 03/20/48 | | | 4,188,063 | | | | 4,329,330 | | |

3.500%, due 09/20/48 | | | 3,144,016 | | | | 3,251,759 | | |

3.750%, due 05/20/30 | | | 545,479 | | | | 566,850 | | |

4.000%, due 12/20/40 | | | 608,363 | | | | 631,359 | | |

4.000%, due 07/20/41 | | | 49,417 | | | | 51,339 | | |

4.000%, due 03/20/47 | | | 1,469,470 | | | | 1,539,318 | | |

4.000%, due 12/20/47 | | | 68,333 | | | | 73,155 | | |

4.000%, due 01/20/48 | | | 188,024 | | | | 199,893 | | |

4.000%, due 03/20/48 | | | 486,728 | | | | 513,703 | | |

4.000%, due 04/20/48 | | | 1,109,595 | | | | 1,164,794 | | |

4.000%, due 05/20/48 | | | 274,466 | | | | 290,583 | | |

4.000%, due 06/20/48 | | | 358,347 | | | | 378,556 | | |

4.000%, due 07/20/48 | | | 116,977 | | | | 123,900 | | |

4.000%, due 06/20/49 | | | 1,989,290 | | | | 2,067,773 | | |

4.000%, due 07/20/49 | | | 2,810,906 | | | | 2,924,422 | | |

4.500%, due 10/20/44 | | | 497,032 | | | | 517,274 | | |

4.500%, due 02/20/45 | | | 396,922 | | | | 408,485 | | |

4.500%, due 08/20/45 | | | 255,797 | | | | 270,398 | | |

4.500%, due 02/20/46 | | | 196,150 | | | | 204,255 | | |

4.500%, due 04/20/48 | | | 158,530 | | | | 165,374 | | |

4.500%, due 05/20/48 | | | 473,730 | | | | 493,681 | | |

4.500%, due 06/20/48 | | | 1,235,990 | | | | 1,288,426 | | |

4.500%, due 10/20/48 | | | 495,891 | | | | 519,563 | | |

4.500%, due 03/20/49 | | | 179,803 | | | | 187,375 | | |

15

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(continued) | |

4.500%, due 04/20/49 | | $ | 5,958,936 | | | $ | 6,209,893 | | |

4.500%, due 05/20/49 | | | 814,346 | | | | 852,375 | | |

4.500%, due 07/20/49 | | | 500,000 | | | | 524,645 | | |

5.000%, due 12/20/33 | | | 210,355 | | | | 226,493 | | |

5.000%, due 01/20/34 | | | 104,917 | | | | 113,030 | | |

5.000%, due 02/20/38 | | | 129,974 | | | | 141,710 | | |

5.000%, due 04/20/38 | | | 157,716 | | | | 173,620 | | |

5.000%, due 08/20/41 | | | 19,098 | | | | 20,971 | | |

5.000%, due 12/20/42 | | | 29,082 | | | | 32,015 | | |

5.000%, due 08/20/43 | | | 2,457,941 | | | | 2,699,331 | | |

5.000%, due 09/20/48 | | | 483,178 | | | | 523,496 | | |

5.000%, due 10/20/48 | | | 507,414 | | | | 534,210 | | |

5.000%, due 11/20/48 | | | 804,516 | | | | 835,145 | | |

5.000%, due 02/20/49 | | | 1,096,748 | | | | 1,151,367 | | |

5.000%, due 03/20/49 | | | 1,413,857 | | | | 1,485,589 | | |

5.000%, due 04/20/49 | | | 165,475 | | | | 173,906 | | |

5.500%, due 09/20/48 | | | 587,646 | | | | 620,822 | | |

6.000%, due 10/20/38 | | | 4,689 | | | | 5,219 | | |

6.500%, due 09/20/32 | | | 2,730 | | | | 2,982 | | |

6.500%, due 11/20/38 | | | 10,829 | | | | 11,234 | | |

6.500%, due 12/20/38 | | | 5,216 | | | | 5,455 | | |

7.000%, due 03/20/28 | | | 39,704 | | | | 40,021 | | |

9.000%, due 04/20/25 | | | 4,871 | | | | 5,311 | | |

9.000%, due 12/20/26 | | | 2,570 | | | | 2,661 | | |

9.000%, due 01/20/27 | | | 8,272 | | | | 8,369 | | |

9.000%, due 09/20/30 | | | 1,005 | | | | 1,007 | | |

9.000%, due 10/20/30 | | | 3,260 | | | | 3,357 | | |

9.000%, due 11/20/30 | | | 4,184 | | | | 4,210 | | |

GNMA II ARM

1 year CMT + 1.500%,

3.625%, due 06/20/222 | | | 17,445 | | | | 17,534 | | |

1 year CMT + 1.500%,

3.625%, due 04/20/242 | | | 41,434 | | | | 41,473 | | |

1 year CMT + 1.500%,

3.625%, due 05/20/252 | | | 3,697 | | | | 3,788 | | |

1 year CMT + 1.500%,

3.625%, due 04/20/262 | | | 67,496 | | | | 67,699 | | |

1 year CMT + 1.500%,

3.625%, due 06/20/262 | | | 28,866 | | | | 29,466 | | |

1 year CMT + 1.500%,

3.625%, due 04/20/272 | | | 17,007 | | | | 17,150 | | |

1 year CMT + 1.500%,

3.625%, due 04/20/302 | | | 11,083 | | | | 11,471 | | |

1 year CMT + 1.500%,

3.625%, due 05/20/302 | | | 282,420 | | | | 292,392 | | |

1 year CMT + 1.500%,

3.750%, due 09/20/212 | | | 21,046 | | | | 21,093 | | |

1 year CMT + 1.500%,

3.750%, due 05/20/252 | | | 20,798 | | | | 21,112 | | |

1 year CMT + 1.500%,

3.750%, due 06/20/252 | | | 10,703 | | | | 10,828 | | |

1 year CMT + 1.500%,

3.750%, due 08/20/252 | | | 9,951 | | | | 10,145 | | |

1 year CMT + 1.500%,

3.750%, due 09/20/252 | | | 13,331 | | | | 13,720 | | |

| | | Face

amount | | Value | |

Government national mortgage association

certificates—(concluded) | | | |

1 year CMT + 1.500%,

3.750%, due 08/20/262 | | $ | 14,289 | | | $ | 14,745 | | |

1 year CMT + 1.500%,

3.750%, due 09/20/262 | | | 2,449 | | | | 2,510 | | |

1 year CMT + 1.500%,

3.750%, due 07/20/272 | | | 5,753 | | | | 5,949 | | |

1 year CMT + 1.500%,

3.750%, due 08/20/272 | | | 17,060 | | | | 17,254 | | |

1 year CMT + 1.500%,

3.750%, due 07/20/302 | | | 65,874 | | | | 68,095 | | |

1 year CMT + 1.500%,

3.750%, due 08/20/302 | | | 64,356 | | | | 66,852 | | |

1 year CMT + 1.500%,

4.000%, due 01/20/232 | | | 15,717 | | | | 15,996 | | |

1 year CMT + 1.500%,

4.000%, due 03/20/232 | | | 6,657 | | | | 6,698 | | |

1 year CMT + 1.500%,

4.000%, due 01/20/242 | | | 21,821 | | | | 21,927 | | |

1 year CMT + 1.500%,

4.000%, due 01/20/252 | | | 2,939 | | | | 3,012 | | |

1 year CMT + 1.500%,

4.000%, due 02/20/252 | | | 4,730 | | | | 4,731 | | |

1 year CMT + 1.500%,

4.000%, due 03/20/252 | | | 15,755 | | | | 15,759 | | |

1 year CMT + 1.500%,

4.000%, due 03/20/262 | | | 7,317 | | | | 7,365 | | |

1 year CMT + 1.500%,

4.000%, due 01/20/272 | | | 60,824 | | | | 60,972 | | |

1 year CMT + 1.500%,

4.000%, due 02/20/272 | | | 5,122 | | | | 5,177 | | |

1 year CMT + 1.500%,

4.000%, due 01/20/282 | | | 7,455 | | | | 7,697 | | |

1 year CMT + 1.500%,

4.000%, due 02/20/282 | | | 4,948 | | | | 4,973 | | |

1 year CMT + 1.500%,

4.125%, due 11/20/212 | | | 3,194 | | | | 3,199 | | |

1 year CMT + 1.500%,

4.125%, due 10/20/302 | | | 11,457 | | | | 11,514 | | |

GNMA II TBA

3.000% | | | 17,750,000 | | | | 18,108,120 | | |

| 3.500%1 | | | 34,300,000 | | | | 35,443,213 | | |

| 4.000% | | | 36,250,000 | | | | 37,607,808 | | |

| 4.500%1 | | | 750,000 | | | | 780,459 | | |

| 5.000% | | | 7,500,000 | | | | 7,854,492 | | |

GNMA TBA

4.000% | | | 2,500,000 | | | | 2,605,078 | | |

| 4.500%1 | | | 2,000,000 | | | | 2,111,223 | | |

Total government national mortgage

association certificates

(cost—$178,525,638) | | | 179,724,597 | | |

Federal home loan mortgage corporation certificates—10.7% | | | |

FHLMC

2.500%, due 01/01/31 | | | 278,773 | | | | 280,819 | | |

2.500%, due 11/01/31 | | | 60,606 | | | | 61,025 | | |

2.500%, due 07/01/32 | | | 171,279 | | | | 172,428 | | |

16

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Federal home loan mortgage corporation certificates—(continued) | |

2.500%, due 08/01/32 | | $ | 821,190 | | | $ | 826,700 | | |

2.500%, due 09/01/32 | | | 1,032,657 | | | | 1,039,591 | | |

2.500%, due 11/01/32 | | | 906,121 | | | | 912,212 | | |

2.500%, due 12/01/32 | | | 922,820 | | | | 929,027 | | |

2.500%, due 01/01/33 | | | 229,065 | | | | 230,604 | | |

3.000%, due 01/01/33 | | | 2,920,069 | | | | 2,982,258 | | |

3.000%, due 04/01/43 | | | 281,536 | | | | 287,846 | | |

3.000%, due 05/01/43 | | | 207,831 | | | | 211,958 | | |

3.000%, due 12/01/44 | | | 217,719 | | | | 220,629 | | |

3.000%, due 04/01/45 | | | 1,368,081 | | | | 1,392,046 | | |

3.000%, due 08/01/46 | | | 480,688 | | | | 481,947 | | |

3.000%, due 12/01/46 | | | 1,727,644 | | | | 1,754,682 | | |

3.000%, due 10/01/47 | | | 292,742 | | | | 296,936 | | |

3.500%, due 09/01/32 | | | 478,143 | | | | 497,784 | | |

4.000%, due 01/01/37 | | | 261,213 | | | | 274,394 | | |

4.000%, due 07/01/43 | | | 225,715 | | | | 238,521 | | |

4.000%, due 04/01/44 | | | 209,775 | | | | 225,316 | | |

4.000%, due 08/01/44 | | | 2,978,543 | | | | 3,191,986 | | |

4.000%, due 08/01/47 | | | 802,199 | | | | 859,601 | | |

4.000%, due 11/01/47 | | | 734,021 | | | | 766,833 | | |

4.000%, due 01/01/48 | | | 1,835,011 | | | | 1,912,482 | | |

4.000%, due 02/01/48 | | | 66,935 | | | | 69,720 | | |

4.000%, due 03/01/48 | | | 48,716 | | | | 50,731 | | |

4.000%, due 04/01/48 | | | 170,599 | | | | 177,646 | | |

4.000%, due 06/01/48 | | | 857,825 | | | | 896,469 | | |

4.000%, due 12/01/48 | | | 927,720 | | | | 975,638 | | |

4.500%, due 10/01/33 | | | 47,519 | | | | 49,125 | | |

4.500%, due 09/01/34 | | | 896,077 | | | | 934,273 | | |

4.500%, due 01/01/36 | | | 21,624 | | | | 22,669 | | |

4.500%, due 05/01/37 | | | 5,935 | | | | 6,286 | | |

4.500%, due 05/01/38 | | | 34,168 | | | | 34,746 | | |

4.500%, due 11/01/48 | | | 942,664 | | | | 991,097 | | |

5.000%, due 10/01/25 | | | 39,959 | | | | 42,429 | | |

5.000%, due 11/01/27 | | | 6,954 | | | | 7,384 | | |

5.000%, due 07/01/33 | | | 9,650 | | | | 10,126 | | |

5.000%, due 09/01/33 | | | 185,638 | | | | 203,319 | | |

5.000%, due 06/01/34 | | | 8,767 | | | | 9,615 | | |

5.000%, due 04/01/35 | | | 33,071 | | | | 35,120 | | |

5.000%, due 05/01/35 | | | 86,215 | | | | 94,706 | | |

5.000%, due 07/01/35 | | | 215,296 | | | | 234,617 | | |

5.000%, due 08/01/35 | | | 25,607 | | | | 28,119 | | |

5.000%, due 10/01/35 | | | 21,339 | | | | 23,432 | | |

5.000%, due 12/01/35 | | | 724 | | | | 794 | | |

5.000%, due 07/01/38 | | | 248,841 | | | | 271,062 | | |

5.000%, due 11/01/38 | | | 196,162 | | | | 213,852 | | |

5.000%, due 06/01/39 | | | 49,916 | | | | 54,483 | | |

5.000%, due 03/01/40 | | | 6,110 | | | | 6,672 | | |

5.000%, due 07/01/40 | | | 295,725 | | | | 322,056 | | |

5.000%, due 09/01/40 | | | 148,664 | | | | 160,691 | | |

5.000%, due 11/01/40 | | | 243,818 | | | | 262,919 | | |

5.000%, due 02/01/41 | | | 394,267 | | | | 430,552 | | |

5.000%, due 03/01/41 | | | 22,253 | | | | 24,209 | | |

5.000%, due 04/01/41 | | | 84,138 | | | | 91,240 | | |

5.000%, due 05/01/41 | | | 151,265 | | | | 165,105 | | |

5.000%, due 07/01/41 | | | 40,717 | | | | 44,465 | | |

5.000%, due 08/01/44 | | | 67,602 | | | | 73,747 | | |

5.000%, due 03/01/49 | | | 2,453,711 | | | | 2,686,301 | | |

| | | Face

amount | | Value | |

Federal home loan mortgage corporation certificates—(continued) | |

5.500%, due 06/01/283 | | $ | 1,327 | | | $ | 1,422 | | |

5.500%, due 02/01/32 | | | 1,651 | | | | 1,797 | | |

5.500%, due 12/01/32 | | | 3,074 | | | | 3,388 | | |

5.500%, due 02/01/33 | | | 42,009 | | | | 45,078 | | |

5.500%, due 05/01/33 | | | 688 | | | | 762 | | |

5.500%, due 06/01/33 | | | 164,004 | | | | 183,042 | | |

5.500%, due 12/01/33 | | | 41,513 | | | | 45,391 | | |

5.500%, due 12/01/34 | | | 39,310 | | | | 44,032 | | |

5.500%, due 06/01/35 | | | 636,036 | | | | 712,151 | | |

5.500%, due 07/01/35 | | | 4,701 | | | | 5,060 | | |

5.500%, due 10/01/35 | | | 133,724 | | | | 144,678 | | |

5.500%, due 12/01/35 | | | 100,459 | | | | 112,480 | | |

5.500%, due 06/01/36 | | | 366,564 | | | | 410,260 | | |

5.500%, due 07/01/36 | | | 21,700 | | | | 22,127 | | |

5.500%, due 12/01/36 | | | 558,248 | | | | 623,894 | | |

5.500%, due 03/01/37 | | | 73,311 | | | | 81,724 | | |

5.500%, due 07/01/37 | | | 61,446 | | | | 64,342 | | |

5.500%, due 10/01/37 | | | 3,163 | | | | 3,540 | | |

5.500%, due 04/01/38 | | | 111,821 | | | | 124,992 | | |

5.500%, due 05/01/38 | | | 11,899 | | | | 13,130 | | |

5.500%, due 12/01/38 | | | 2,110 | | | | 2,339 | | |

5.500%, due 01/01/39 | | | 50,655 | | | | 56,536 | | |

5.500%, due 09/01/39 | | | 149,836 | | | | 167,496 | | |

5.500%, due 02/01/40 | | | 7,177 | | | | 7,930 | | |

5.500%, due 03/01/40 | | | 6,724 | | | | 7,421 | | |

5.500%, due 05/01/40 | | | 94,637 | | | | 104,912 | | |

5.500%, due 03/01/41 | | | 100,946 | | | | 111,920 | | |

6.000%, due 11/01/37 | | | 898,608 | | | | 1,023,451 | | |

7.000%, due 08/01/25 | | | 140 | | | | 150 | | |

11.000%, due 09/01/20 | | | 1 | | | | 1 | | |

FHLMC ARM

1 year CMT + 2.250%,

4.543%, due 09/01/342 | | | 758,040 | | | | 798,166 | | |

12 mo. USD LIBOR + 1.765%,

4.549%, due 11/01/362 | | | 317,084 | | | | 333,123 | | |

1 year CMT + 2.182%,

4.593%, due 04/01/292 | | | 38,681 | | | | 39,450 | | |

1 year CMT + 2.131%,

4.631%, due 11/01/272 | | | 51,953 | | | | 52,921 | | |

12 mo. USD LIBOR + 1.863%,

4.664%, due 11/01/412 | | | 1,466,329 | | | | 1,529,452 | | |

1 year CMT + 2.299%,

4.669%, due 10/01/232 | | | 9,070 | | | | 9,244 | | |

1 year CMT + 2.137%,

4.677%, due 01/01/282 | | | 11,135 | | | | 11,410 | | |

12 mo. USD LIBOR + 1.781%,

4.713%, due 10/01/392 | | | 1,379,670 | | | | 1,450,776 | | |

1 year CMT + 2.282%,

4.716%, due 06/01/282 | | | 125,803 | | | | 131,402 | | |

1 year CMT + 2.259%,

4.760%, due 11/01/292 | | | 128,891 | | | | 133,901 | | |

1 year CMT + 2.224%,

4.786%, due 07/01/242 | | | 48,287 | | | | 49,310 | | |

1 year CMT + 2.439%,

4.830%, due 10/01/272 | | | 104,181 | | | | 109,048 | | |

1 year CMT + 2.282%,

4.872%, due 07/01/282 | | | 58,040 | | | | 60,399 | | |

17

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Federal home loan mortgage corporation certificates—(concluded) | |

1 year CMT + 2.463%,

4.893%, due 10/01/272 | | $ | 89,867 | | | $ | 94,015 | | |

1 year CMT + 2.359%,

4.895%, due 12/01/292 | | | 17,453 | | | | 18,142 | | |

1 year CMT + 2.415%,

4.968%, due 01/01/292 | | | 94,042 | | | | 98,677 | | |

1 year CMT + 2.415%,

5.071%, due 11/01/252 | | | 64,781 | | | | 67,763 | | |

1 year CMT + 2.625%,

5.125%, due 01/01/302 | | | 22,716 | | | | 22,876 | | |

Total federal home loan mortgage

corporation certificates

(cost—$38,486,113) | | | 38,888,561 | | |

Federal housing administration certificates—0.0%† | |

FHA GMAC

7.400%, due 02/01/21 | | | 1,838 | | | | 1,836 | | |

FHA Reilly

6.896%, due 07/01/20 | | | 26,451 | | | | 26,418 | | |

Total federal housing administration

certificates

(cost—$28,299) | | | 28,254 | | |

Federal national mortgage association certificates—71.5% | |

FNMA

2.000%, due 05/01/28 | | | 175,775 | | | | 174,966 | | |

2.000%, due 09/01/31 | | | 209,198 | | | | 206,427 | | |

2.000%, due 11/01/31 | | | 535,243 | | | | 528,190 | | |

2.000%, due 01/01/32 | | | 123,046 | | | | 121,417 | | |

2.500%, due 06/01/28 | | | 209,171 | | | | 210,831 | | |

2.500%, due 07/01/28 | | | 1,567,588 | | | | 1,580,088 | | |

2.500%, due 08/01/28 | | | 534,034 | | | | 538,216 | | |

2.500%, due 09/01/30 | | | 33,826 | | | | 34,065 | | |

2.500%, due 11/01/30 | | | 54,184 | | | | 54,567 | | |

2.500%, due 01/01/33 | | | 495,841 | | | | 493,382 | | |

2.500%, due 04/01/47 | | | 232,259 | | | | 229,378 | | |

3.000%, due 05/01/28 | | | 202,237 | | | | 206,487 | | |

3.000%, due 02/01/30 | | | 352,111 | | | | 359,485 | | |

3.000%, due 04/01/30 | | | 106,083 | | | | 108,308 | | |

3.000%, due 05/01/30 | | | 113,891 | | | | 116,284 | | |

3.000%, due 10/01/30 | | | 34,477 | | | | 35,199 | | |

3.000%, due 04/01/31 | | | 2,226,439 | | | | 2,279,206 | | |

3.000%, due 01/01/38 | | | 938,798 | | | | 956,277 | | |

3.000%, due 04/01/38 | | | 1,075,390 | | | | 1,095,408 | | |

3.000%, due 10/01/42 | | | 551,312 | | | | 561,951 | | |

3.000%, due 01/01/43 | | | 2,062,856 | | | | 2,102,585 | | |

3.000%, due 04/01/43 | | | 841,279 | | | | 857,505 | | |

3.000%, due 05/01/43 | | | 871,538 | | | | 888,348 | | |

3.000%, due 06/01/43 | | | 119,893 | | | | 122,207 | | |

3.000%, due 09/01/43 | | | 1,100,618 | | | | 1,121,619 | | |

3.000%, due 11/01/46 | | | 90,477 | | | | 91,838 | | |

3.000%, due 12/01/46 | | | 6,840,866 | | | | 6,947,220 | | |

3.500%, due 11/01/25 | | | 336,365 | | | | 347,410 | | |

3.500%, due 08/01/29 | | | 62,281 | | | | 64,379 | | |

3.500%, due 12/01/41 | | | 1,060,310 | | | | 1,111,874 | | |

3.500%, due 03/01/42 | | | 454,024 | | | | 473,003 | | |

3.500%, due 04/01/42 | | | 51,927 | | | | 53,616 | | |

3.500%, due 12/01/42 | | | 1,642,085 | | | | 1,715,873 | | |

| | | Face

amount | | Value | |

Federal national mortgage association certificates—(continued) | |

3.500%, due 03/01/43 | | $ | 932,814 | | | $ | 974,735 | | |

3.500%, due 05/01/43 | | | 3,961,259 | | | | 4,153,725 | | |

3.500%, due 07/01/43 | | | 336,644 | | | | 350,714 | | |

3.500%, due 06/01/45 | | | 4,377,055 | | | | 4,524,712 | | |

3.500%, due 08/01/45 | | | 92,006 | | | | 95,057 | | |

3.500%, due 09/01/46 | | | 1,525,935 | | | | 1,586,783 | | |

3.500%, due 08/01/47 | | | 536,037 | | | | 554,958 | | |

3.500%, due 09/01/47 | | | 675,812 | | | | 700,973 | | |

3.500%, due 11/01/47 | | | 1,008,598 | | | | 1,043,133 | | |

3.500%, due 12/01/47 | | | 904,683 | | | | 936,618 | | |

3.500%, due 02/01/48 | | | 2,298,899 | | | | 2,386,106 | | |

3.500%, due 03/01/48 | | | 1,992,262 | | | | 2,067,810 | | |

3.575%, due 02/01/26 | | | 500,000 | | | | 533,179 | | |

3.600%, due 08/01/23 | | | 780,084 | | | | 820,667 | | |

3.820%, due 01/01/29 | | | 500,000 | | | | 550,728 | | |

4.000%, due 07/01/25 | | | 11,815 | | | | 12,285 | | |

4.000%, due 09/01/25 | | | 4,535 | | | | 4,715 | | |

4.000%, due 10/01/25 | | | 7,032 | | | | 7,303 | | |

4.000%, due 11/01/25 | | | 95,314 | | | | 99,189 | | |

4.000%, due 01/01/26 | | | 264,387 | | | | 274,750 | | |

4.000%, due 02/01/26 | | | 653,114 | | | | 680,249 | | |

4.000%, due 03/01/26 | | | 52,245 | | | | 54,335 | | |

4.000%, due 04/01/26 | | | 1,293,002 | | | | 1,348,751 | | |

4.000%, due 08/01/32 | | | 7,932 | | | | 8,335 | | |

4.000%, due 06/01/33 | | | 161,448 | | | | 169,694 | | |

4.000%, due 07/01/33 | | | 342,654 | | | | 360,201 | | |

4.000%, due 08/01/33 | | | 2,807,454 | | | | 2,972,105 | | |

4.000%, due 07/01/34 | | | 931,052 | | | | 978,367 | | |

4.000%, due 07/01/35 | | | 1,841,481 | | | | 1,947,559 | | |

4.000%, due 04/01/37 | | | 1,362,368 | | | | 1,435,549 | | |

4.000%, due 03/01/38 | | | 935,954 | | | | 992,673 | | |

4.000%, due 07/01/38 | | | 3,104,333 | | | | 3,241,058 | | |

4.000%, due 08/01/38 | | | 934,055 | | | | 982,381 | | |

4.000%, due 09/01/38 | | | 1,795,171 | | | | 1,871,386 | | |

4.000%, due 05/01/39 | | | 142,198 | | | | 150,662 | | |

4.000%, due 09/01/39 | | | 313,618 | | | | 333,461 | | |

4.000%, due 09/01/40 | | | 3,013,413 | | | | 3,193,967 | | |

4.000%, due 12/01/40 | | | 3,964,103 | | | | 4,214,087 | | |

4.000%, due 04/01/41 | | | 949,596 | | | | 1,008,436 | | |

4.000%, due 11/01/41 | | | 614,295 | | | | 657,973 | | |

4.000%, due 12/01/41 | | | 886,784 | | | | 949,828 | | |

4.000%, due 07/01/42 | | | 3,740,947 | | | | 3,995,660 | | |

4.000%, due 09/01/42 | | | 5,449,123 | | | | 5,836,556 | | |

4.000%, due 10/01/42 | | | 4,134,166 | | | | 4,428,119 | | |

4.000%, due 07/01/43 | | | 426,484 | | | | 449,310 | | |

4.000%, due 08/01/44 | | | 222,981 | | | | 239,109 | | |

4.000%, due 12/01/44 | | | 49,643 | | | | 52,284 | | |

4.000%, due 06/01/45 | | | 33,034 | | | | 34,782 | | |

4.000%, due 08/01/45 | | | 2,561,873 | | | | 2,695,869 | | |

4.000%, due 02/01/47 | | | 278,866 | | | | 292,182 | | |

4.000%, due 03/01/47 | | | 146,960 | | | | 153,371 | | |

4.000%, due 04/01/47 | | | 627,741 | | | | 661,399 | | |

4.000%, due 05/01/47 | | | 741,675 | | | | 775,250 | | |

4.000%, due 06/01/47 | | | 31,755 | | | | 33,339 | | |

4.000%, due 09/01/47 | | | 329,907 | | | | 343,228 | | |

4.000%, due 10/01/47 | | | 832,720 | | | | 873,141 | | |

4.000%, due 11/01/47 | | | 70,071 | | | | 73,076 | | |

18

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Federal national mortgage association certificates—(continued) | |

4.000%, due 12/01/47 | | $ | 187,592 | | | $ | 194,954 | | |

4.000%, due 01/01/48 | | | 2,114,617 | | | | 2,204,895 | | |

4.000%, due 02/01/48 | | | 740,035 | | | | 775,698 | | |

4.000%, due 03/01/48 | | | 728,697 | | | | 762,278 | | |

4.000%, due 04/01/48 | | | 434,350 | | | | 451,716 | | |

4.000%, due 12/01/48 | | | 1,511,207 | | | | 1,587,656 | | |

4.500%, due 05/01/21 | | | 4,177 | | | | 4,280 | | |

4.500%, due 03/01/23 | | | 3,864 | | | | 3,989 | | |

4.500%, due 06/01/29 | | | 28,172 | | | | 29,551 | | |

4.500%, due 06/01/35 | | | 16,016 | | | | 16,661 | | |

4.500%, due 12/01/38 | | | 469,258 | | | | 506,349 | | |

4.500%, due 01/01/39 | | | 1,171 | | | | 1,227 | | |

4.500%, due 03/01/39 | | | 10,025 | | | | 10,800 | | |

4.500%, due 06/01/39 | | | 63,936 | | | | 68,908 | | |

4.500%, due 07/01/39 | | | 2,819 | | | | 2,970 | | |

4.500%, due 08/01/39 | | | 113,149 | | | | 121,833 | | |

4.500%, due 10/01/39 | | | 4,960 | | | | 5,345 | | |

4.500%, due 12/01/393 | | | 372,938 | | | | 403,098 | | |

4.500%, due 01/01/40 | | | 3,748 | | | | 4,077 | | |

4.500%, due 02/01/40 | | | 4,114 | | | | 4,457 | | |

4.500%, due 03/01/40 | | | 73,041 | | | | 78,772 | | |

4.500%, due 08/01/40 | | | 65,975 | | | | 71,167 | | |

4.500%, due 11/01/40 | | | 397,649 | | | | 431,424 | | |

4.500%, due 07/01/41 | | | 448,163 | | | | 483,431 | | |

4.500%, due 08/01/41 | | | 773,339 | | | | 840,266 | | |

4.500%, due 09/01/41 | | | 11,452 | | | | 12,000 | | |

4.500%, due 01/01/42 | | | 2,082,945 | | | | 2,245,950 | | |

4.500%, due 08/01/42 | | | 3,032 | | | | 3,229 | | |

4.500%, due 09/01/43 | | | 305,891 | | | | 332,380 | | |

4.500%, due 11/01/43 | | | 62,469 | | | | 67,186 | | |

4.500%, due 07/01/44 | | | 299,620 | | | | 323,970 | | |

4.500%, due 12/01/44 | | | 1,843 | | | | 1,965 | | |

4.500%, due 07/01/48 | | | 1,872,196 | | | | 1,969,958 | | |

4.500%, due 09/01/48 | | | 947,283 | | | | 1,011,566 | | |

4.500%, due 11/01/48 | | | 936,187 | | | | 982,862 | | |

4.500%, due 01/01/49 | | | 972,477 | | | | 1,033,432 | | |

12 mo. USD LIBOR + 1.731%,

4.613%, due 05/01/382 | | | 1,282,066 | | | | 1,343,699 | | |

1 year CMT + 2.221%,

4.632%, due 10/01/372 | | | 2,037,075 | | | | 2,141,881 | | |

1 year CMT + 2.034%,

4.644%, due 09/01/412 | | | 532,637 | | | | 559,027 | | |

1 year CMT + 2.237%,

4.713%, due 01/01/362 | | | 425,525 | | | | 448,304 | | |

12 mo. USD LIBOR + 1.790%,

4.915%, due 02/01/422 | | | 255,800 | | | | 265,865 | | |

1 year CMT + 2.282%,

4.936%, due 05/01/352 | | | 177,715 | | | | 187,382 | | |

5.000%, due 03/01/23 | | | 1,376 | | | | 1,416 | | |

5.000%, due 05/01/23 | | | 48,920 | | | | 50,670 | | |

5.000%, due 03/01/25 | | | 14,137 | | | | 15,003 | | |

5.000%, due 03/01/33 | | | 16,405 | | | | 17,161 | | |

5.000%, due 05/01/37 | | | 7,273 | | | | 7,638 | | |

5.000%, due 09/01/37 | | | 27,556 | | | | 28,990 | | |

5.000%, due 06/01/38 | | | 47,405 | | | | 49,906 | | |

5.000%, due 06/01/48 | | | 470,808 | | | | 509,107 | | |

5.000%, due 07/01/48 | | | 1,141,728 | | | | 1,224,187 | | |

| | | Face

amount | | Value | |

Federal national mortgage association certificates—(continued) | |

5.000%, due 10/01/48 | | $ | 865,342 | | | $ | 926,895 | | |

5.000%, due 12/01/48 | | | 14,547 | | | | 15,438 | | |

5.000%, due 01/01/49 | | | 150,155 | | | | 159,920 | | |

5.000%, due 03/01/49 | | | 196,691 | | | | 209,482 | | |

5.500%, due 11/01/321 | | | 47,884 | | | | 51,260 | | |

5.500%, due 12/01/331 | | | 1,200 | | | | 1,319 | | |

5.500%, due 04/01/341 | | | 25,133 | | | | 27,453 | | |

5.500%, due 01/01/351 | | | 118,220 | | | | 126,555 | | |

5.500%, due 04/01/361 | | | 82,745 | | | | 88,580 | | |

5.500%, due 05/01/371 | | | 175,884 | | | | 196,773 | | |

5.500%, due 07/01/371 | | | 99,864 | | | | 111,594 | | |

5.500%, due 06/01/381 | | | 129,419 | | | | 143,260 | | |

5.500%, due 11/01/391 | | | 327,576 | | | | 362,587 | | |

5.500%, due 07/01/401 | | | 438,579 | | | | 484,102 | | |

5.500%, due 02/01/421 | | | 242,603 | | | | 271,234 | | |

6.000%, due 11/01/21 | | | 21,438 | | | | 21,802 | | |

6.000%, due 01/01/23 | | | 49,869 | | | | 50,393 | | |

6.000%, due 03/01/23 | | | 76,184 | | | | 78,695 | | |

6.000%, due 11/01/26 | | | 18,287 | | | | 20,099 | | |

6.000%, due 12/01/32 | | | 10,904 | | | | 12,403 | | |

6.000%, due 02/01/33 | | | 27,476 | | | | 30,673 | | |

6.000%, due 09/01/34 | | | 115,991 | | | | 131,340 | | |

6.000%, due 05/01/35 | | | 37,286 | | | | 41,067 | | |

6.000%, due 06/01/35 | | | 13,797 | | | | 15,662 | | |

6.000%, due 07/01/35 | | | 35,363 | | | | 39,033 | | |

6.000%, due 09/01/35 | | | 1,398 | | | | 1,589 | | |

6.000%, due 01/01/36 | | | 25,858 | | | | 29,387 | | |

6.000%, due 06/01/36 | | | 226 | | | | 248 | | |

6.000%, due 09/01/36 | | | 30,548 | | | | 34,712 | | |

6.000%, due 10/01/36 | | | 16,093 | | | | 18,207 | | |

6.000%, due 12/01/36 | | | 112,178 | | | | 127,429 | | |

6.000%, due 03/01/37 | | | 14,244 | | | | 16,183 | | |

6.000%, due 10/01/37 | | | 40,121 | | | | 43,332 | | |

6.000%, due 11/01/38 | | | 337,799 | | | | 384,353 | | |

6.000%, due 05/01/39 | | | 44,000 | | | | 50,081 | | |

6.000%, due 11/01/40 | | | 467,221 | | | | 531,722 | | |

6.500%, due 10/01/36 | | | 332,933 | | | | 369,245 | | |

6.500%, due 02/01/37 | | | 3,353 | | | | 3,790 | | |

6.500%, due 07/01/37 | | | 31,483 | | | | 34,917 | | |

6.500%, due 08/01/37 | | | 27,900 | | | | 30,943 | | |

6.500%, due 09/01/37 | | | 43,447 | | | | 49,476 | | |

6.500%, due 12/01/37 | | | 79,634 | | | | 90,778 | | |

6.500%, due 08/01/38 | | | 1,129 | | | | 1,252 | | |

6.500%, due 05/01/40 | | | 1,016,221 | | | | 1,201,902 | | |

7.500%, due 11/01/26 | | | 12,244 | | | | 12,305 | | |

8.000%, due 11/01/26 | | | 4,190 | | | | 4,208 | | |

9.000%, due 02/01/26 | | | 8,000 | | | | 8,101 | | |

FNMA ARM | | | | | |

12 mo. MTA + 1.200%,

3.704%, due 03/01/442 | | | 162,212 | | | | 163,245 | | |

1 year CMT + 2.095%,

4.345%, due 09/01/262 | | | 743 | | | | 746 | | |

1 year CMT + 2.082%,

4.657%, due 02/01/262 | | | 23,404 | | | | 23,541 | | |

1 year CMT + 2.102%,

4.659%, due 05/01/302 | | | 27,495 | | | | 28,425 | | |

19

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Federal national mortgage association certificates—(concluded) | | | | | |

1 year CMT + 2.250%,

4.750%, due 02/01/302 | | $ | 3,331 | | | $ | 3,356 | | |

1 year CMT + 2.325%,

4.825%, due 03/01/252 | | | 22,556 | | | | 22,876 | | |

1 year CMT + 2.507%,

5.108%, due 12/01/272 | | | 15,790 | | | | 16,302 | | |

FNMA TBA

2.500% | | | 10,500,000 | | | | 10,503,623 | | |

| 3.000% | | | 69,700,000 | | | | 70,391,404 | | |

| 3.500% | | | 18,500,000 | | | | 18,937,207 | | |

| 4.000% | | | 12,200,000 | | | | 12,628,156 | | |

| 4.500%1 | | | 6,300,000 | | | | 6,600,641 | | |

| 4.500% | | | 11,000,000 | | | | 11,528,367 | | |

| 5.000% | | | 200,000 | | | | 212,344 | | |

| 6.000% | | | 1,000,000 | | | | 1,098,867 | | |

Total federal national mortgage

association certificates

(cost—$257,053,285) | | | 258,674,896 | | |

Collateralized mortgage obligations—26.6% | | | | | |

AREIT Trust,

Series 2018-CRE2, Class A,

1 mo. USD LIBOR + 0.980%,

3.312%, due 11/14/352,4 | | | 1,985,244 | | | | 1,985,275 | | |

ARM Trust,

Series 2005-8, Class 3A21,

4.145%, due 11/25/356 | | | 560,901 | | | | 506,452 | | |

BCAP LLC,

Series 2013-RR1, Class 3A4,

6.000%, due 10/26/374,6 | | | 338,214 | | | | 291,867 | | |

BCAP LLC Trust,

Series 2010-RR1, Class 1A4,

4.170%, due 03/26/374,6 | | | 121,567 | | | | 107,471 | | |

Series 2011-R11, Class 8A5,

2.583%, due 07/26/364,6 | | | 96,645 | | | | 93,851 | | |

Series 2011-RR10, Class 3A5,

5.003%, due 06/26/354,6 | | | 48,156 | | | | 48,021 | | |

Series 2013-RR5, Class 5A1,

12 mo. MTA + 0.840%,

0.505%, due 11/26/462,4 | | | 166,819 | | | | 167,754 | | |

Bear Stearns ARM Trust,

Series 2002-011, Class 1A2,

4.434%, due 02/25/336 | | | 4,069 | | | | 3,840 | | |

Series 2004-002, Class 12A2,

3.958%, due 05/25/346 | | | 39,771 | | | | 39,248 | | |

Bear Stearns Asset-Backed Securities Trust,

Series 2003-AC5, Class A1,

5.750%, due 10/25/337 | | | 524,256 | | | | 553,249 | | |

Series 2004-AC3, Class A2,

6.000%, due 06/25/347 | | | 734,828 | | | | 763,512 | | |

BX Commercial Mortgage Trust,

Series 2018-IND, Class A, | | | | | |

1 mo. USD LIBOR + 0.750%,

3.075%, due 11/15/352,4 | | | 5,522,441 | | | | 5,522,432 | | |

Series 2018-IND, Class D,

1 mo. USD LIBOR + 1.300%,

3.625%, due 11/15/352,4 | | | 6,496,989 | | | | 6,501,064 | | |

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Chevy Chase Mortgage Funding Corp.,

Series 2004-1, Class A1,

1 mo. USD LIBOR + 0.280%,

2.546%, due 01/25/352,4 | | $ | 62,526 | | | $ | 61,837 | | |

CHL Mortgage Pass-Through Trust,

Series 2003-HYB1, Class 1A1,

4.597%, due 05/19/336 | | | 3,569 | | | | 3,706 | | |

Series 2007-15, Class 2A2,

6.500%, due 09/25/37 | | | 32,821 | | | | 23,862 | | |

Citigroup Commercial Mortgage Trust,

Series 2019-SMRT, Class A,

4.149%, due 01/10/244 | | | 3,200,000 | | | | 3,421,908 | | |

Civic Mortgage LLC,

Series 2018-1, Class A1,

3.892%, due 06/25/224,7 | | | 195,408 | | | | 194,955 | | |

CSMC Trust,

Series 2013-MH1, Class A,

4.789%, due 05/27/534,6 | | | 1,024,168 | | | | 1,066,861 | | |

FHLMC REMIC,

Series 0023, Class KZ,

6.500%, due 11/25/23 | | | 9,329 | | | | 9,856 | | |

Series 0159, Class H,

4.500%, due 09/15/21 | | | 514 | | | | 515 | | |

Series 1003, Class H,

1 mo. USD LIBOR + 0.750%,

3.075%, due 10/15/202 | | | 1,673 | | | | 1,679 | | |

Series 1349, Class PS,

7.500%, due 08/15/22 | | | 337 | | | | 353 | | |

Series 1502, Class PX,

7.000%, due 04/15/23 | | | 64,873 | | | | 68,424 | | |

Series 1534, Class Z,

5.000%, due 06/15/23 | | | 29,343 | | | | 30,079 | | |

Series 1573, Class PZ,

7.000%, due 09/15/23 | | | 8,143 | | | | 8,658 | | |

Series 1658, Class GZ,

7.000%, due 01/15/24 | | | 4,444 | | | | 4,748 | | |

Series 1694, Class Z,

6.500%, due 03/15/24 | | | 52,549 | | | | 56,279 | | |

Series 1775, Class Z,

8.500%, due 03/15/25 | | | 1,716 | | | | 1,929 | | |

Series 2018-28, Class CA,

3.000%, due 05/25/48 | | | 1,880,208 | | | | 1,891,688 | | |

Series 2400, Class FQ,

1 mo. USD LIBOR + 0.500%,

2.825%, due 01/15/322 | | | 111,511 | | | | 112,035 | | |

Series 2411, Class FJ,

1 mo. USD LIBOR + 0.350%,

2.675%, due 12/15/292 | | | 14,249 | | | | 14,265 | | |

Series 2614, Class WO, PO,

0.000%, due 05/15/33 | | | 851,706 | | | | 785,273 | | |

Series 3096, Class FL,

1 mo. USD LIBOR + 0.400%,

2.725%, due 01/15/362 | | | 133,427 | | | | 133,576 | | |

Series 3114, Class PF, | | | | | |

1 mo. USD LIBOR + 0.400%,

2.725%, due 02/15/362 | | | 665,830 | | | | 666,550 | | |

20

PACE Mortgage-Backed Securities Fixed Income Investments

Portfolio of investments—July 31, 2019

| | | Face

amount | | Value | |

Collateralized mortgage obligations—(continued) | |

Series 3153, Class UF,

1 mo. USD LIBOR + 0.430%,

2.914%, due 05/15/362 | | $ | 155,855 | | | $ | 156,243 | | |

Series 3339, Class LI, IO, | | | | | |

1 mo. USD LIBOR + 6.480%,

4.155%, due 07/15/372 | | | 738,829 | | | | 100,273 | | |

Series 3442, Class MT, | | | | | |

1 mo. USD LIBOR,