UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07239

Name of Registrant: Vanguard Horizon Funds

| |

| Address of Registrant: | P.O. Box 2600 |

| | Valley Forge, PA 19482 |

| |

| Name and address of agent for service: | Heidi Stam, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2015 – March 31, 2016

Item 1: Reports to Shareholders

Semiannual Report | March 31, 2016

Vanguard Strategic Equity Fund

Vanguard’s Principles for Investing Success

We want to give you the best chance of investment success. These principles, grounded in Vanguard’s research and experience, can put you on the right path.

Goals. Create clear, appropriate investment goals.

Balance. Develop a suitable asset allocation using broadly diversified funds. Cost. Minimize cost.

Discipline. Maintain perspective and long-term discipline.

A single theme unites these principles: Focus on the things you can control.

We believe there is no wiser course for any investor.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisor’s Report. | 8 |

| Fund Profile. | 10 |

| Performance Summary. | 11 |

| Financial Statements. | 12 |

| About Your Fund’s Expenses. | 25 |

| Trustees Approve Advisory Arrangement. | 27 |

| Glossary. | 28 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Pictured is a sailing block on the Brilliant, a 1932 schooner docked in Mystic, Connecticut. A type of pulley, the sailing block helps coordinate the setting of the sails. At Vanguard, the intricate coordination of technology and people allows us to help millions of clients around the world reach their financial goals.

Your Fund’s Total Returns

| |

| Six Months Ended March 31, 2016 | |

| | Total |

| | Returns |

| Vanguard Strategic Equity Fund | 3.38% |

| MSCI US Small + Mid Cap 2200 Index | 5.06 |

| Mid-Cap Core Funds Average | 3.97 |

| Mid-Cap Core Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | |

| | | | | |

| Your Fund’s Performance at a Glance | | | | |

| September 30, 2015, Through March 31, 2016 | | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Strategic Equity Fund | $30.82 | $28.42 | $0.507 | $2.967 |

1

Chairman’s Letter

Dear Shareholder,

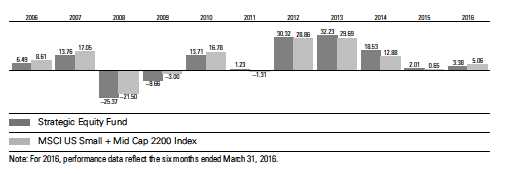

Amid considerable stock market volatility, Vanguard Strategic Equity Fund returned 3.38% for the six months ended March 31, 2016. The fund’s benchmark, the MSCI US Small + Mid Cap 2200 Index, returned 5.06%, and the average return for its peers was 3.97%.

Anyone hoping that the financial markets might become a bit more settled after the Federal Reserve’s long-anticipated rate increase—announced December 16—would have been disappointed. Stocks retreated from December through mid-February before rebounding to finish the period higher. These sharp shifts led investors to favor safer assets, a trend that generally benefited larger-capitalization stocks and more defensive sectors.

Returns for the fund ranged from double-digit gains in utilities and materials to a double-digit decline in energy. Compared with its benchmark, the fund displayed strong stock selection in the health care sector, which was offset by subpar returns from its energy, consumer staples, and consumer discretionary holdings.

Stocks charted an uneven course

en route to a solid outcome

The broad U.S. stock market returned about 7% for the six months. The period began and ended strongly, with fluctuations in the middle as China’s economic slowdown and falling oil and commodity prices worried investors.

Stocks rallied in March as investors again seemed encouraged by news about monetary policy, especially after the Fed indicated that it would raise interest rates fewer times in 2016 than previously anticipated. International stocks returned about 3% for the period after surging more than 8% in March. Stocks from emerging markets and from developed Pacific markets outperformed developed European stocks, which were nearly flat. U.S. dollar-based investors benefited as many foreign currencies strengthened against the dollar, a turnabout from the trend of recent years.

Bonds produced gains following a subpar start

The broad U.S. taxable bond market returned 2.44% for the fiscal half year. Returns were weak in the first three months, which culminated with the Fed’s quarter-percentage-point interest rate increase in December.

But with stocks volatile and the Fed indicating it would proceed cautiously with future rate hikes, bonds rallied in the final three months. The yield of the 10-year U.S. Treasury note closed at 1.77% at the end of March, down from 2.05% six months earlier. (Bond prices and yields move in opposite directions.)

| | | | |

| Market Barometer | | | |

| |

| | | | Total Returns |

| | | Periods Ended March 31, 2016 |

| | Six | One | Five Years |

| | Months | Year | (Annualized) |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 7.75% | 0.50% | 11.35% |

| Russell 2000 Index (Small-caps) | 2.02 | -9.76 | 7.20 |

| Russell 3000 Index (Broad U.S. market) | 7.30 | -0.34 | 11.01 |

| FTSE All-World ex US Index (International) | 3.09 | -8.53 | 0.70 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 2.44% | 1.96% | 3.78% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 3.20 | 3.98 | 5.59 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.06 | 0.08 | 0.04 |

| |

| CPI | | | |

| Consumer Price Index | 0.08% | 0.85% | 1.28% |

3

Returns for money market funds and savings accounts remained limited by the Fed’s still-low target rate of 0.25%–0.5%.

International bond markets (as measured by the Barclays Global Aggregate Index ex USD) returned almost 7%. Like stocks, international bond returns for U.S.-based investors benefited from dollar weakness. Even in local currencies, however, international bond returns were solidly positive, boosted in part by additional stimulus measures in Europe and Asia to combat weak growth and low inflation.

Selection among consumer-related stocks crimped the fund’s return

Vanguard Quantitative Equity Group, the fund’s advisor, uses a disciplined, data-driven process to assess the relative attractiveness of stocks—with the goal of providing a long-term return greater than that of the benchmark while tightly controlling risk. Similar to a traditional fund manager, QEG analyzes criteria that research has shown can contribute to long-term outperformance, including valuation, revenue and earnings growth, dividend policy, reinvestment decisions, and balance sheet quality.

A proprietary computer model helps QEG systematically screen and rank stocks within each of the industry groups in the fund’s investable universe—in this case, well over 2,000 small- and mid-cap stocks. This investment process has been developed and refined over more than three decades, and is supported by an experienced in-house research team.

| | | |

| Expense Ratios | | |

| Your Fund Compared With Its Peer Group | | |

| | | Peer Group |

| | Fund | Average |

| Strategic Equity Fund | 0.21% | 1.18% |

| The fund expense ratio shown is from the prospectus dated January 28, 2016, and represents estimated costs for the current fiscal year. For the six months ended March 31, 2016, the fund’s annualized expense ratio was 0.19%. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2015. |

|

|

|

| |

| Peer group: Mid-Cap Core Funds. | | |

4

QEG generally keeps your fund’s sector exposures aligned closely with those of the index; it doesn’t favor or shun a particular sector in the attempt to improve performance relative to the benchmark. Positioning within industry sub-groups can make a difference, but what often matters more is how the fund’s 400-plus holdings perform.

This strategy has produced above-benchmark returns for the fund over its last five fiscal years, but, as with any active

|

| |

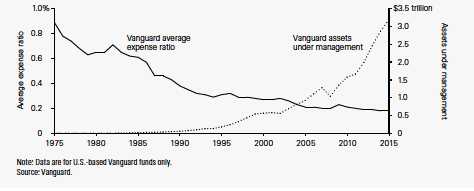

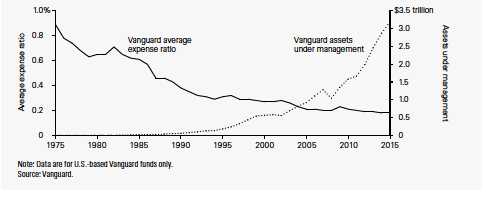

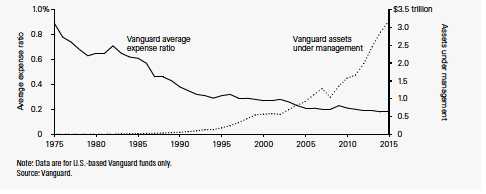

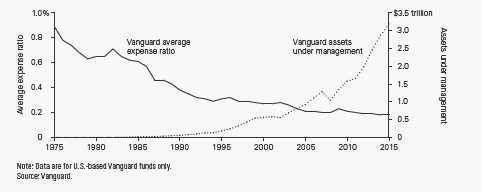

| Vanguard’s growth translates into lower costs for you |

| |

| Research indicates that lower-cost investments have tended to outperform higher-cost ones. |

| So it’s little wonder that funds with lower expense ratios—including those at Vanguard—have |

| dominated the industry’s cash inflows in recent years. |

| |

| Vanguard has long been a low-cost leader, with expenses well below those of many other |

| investment management companies. That cost difference remains a powerful advantage for |

| Vanguard clients. Why? Because a lower expense ratio allows a fund to pass along a greater |

| share of its returns to its investors. |

| |

| What’s more, as you can see in the chart below, we’ve been able to lower our costs continually |

| as our assets under management have grown. Our steady growth has not been an explicit |

| business objective. Rather, we focus on putting our clients’ interests first at all times, and |

| giving them the best chance for investment success. But economies of scale—the cost |

| efficiencies that come with our growth—have allowed us to keep lowering our fund costs, |

| even as we invest in our people and technology. |

| |

| The benefit of economies of scale |

5

investment strategy, it works better under some market conditions than others.

For the six months under review, the fund trailed its benchmark, as investors’ concerns about the global macroeconomic environment took precedence over company-specific fundamentals.

Compared with the benchmark, the fund’s health care holdings were a bright spot. The screening process here led to outperformance in the biotechnology segment and among tools and services stocks in the life sciences field.

At the other end of the spectrum, the fund lagged in the beleaguered energy sector. Some of the fund’s refining and marketing holdings struggled amid a gasoline glut and refinery production cutbacks.

The screening process met with even less success among consumer-related stocks. In consumer staples, food producers and retailers in particular disappointed. And in consumer discretionary, stocks in the auto parts, footwear, and hospitality segments weighed on the fund’s performance.

The Advisor’s Report that follows this letter provides additional details about the management of the fund during the fiscal half year.

Consider rebalancing to manage your risk

Let’s say you’ve taken the time to carefully create an appropriate asset allocation for your investment portfolio. Your efforts have produced a diversified mix of stock, bond, and money market funds tailored to your goals, time horizon, and risk tolerance.

But what should you do when your portfolio drifts from its original asset allocation as the financial markets rise or fall? Consider rebalancing to bring it back to the proper mix.

Just one year of outsized returns can throw your allocation out of whack. Take 2013 as an example. That year, the broad stock market (as measured by the Russell 3000 Index) returned 33.55% and the broad taxable bond market (as measured by the Barclays U.S. Aggregate Bond Index) returned –2.02%. A hypothetical portfolio that tracked the broad domestic market indexes and started the year with 60% stocks and 40% bonds would have ended with a more aggressive mix of 67% stocks and 33% bonds.

Rebalancing to bring your portfolio back to its original targets would require you to shift assets away from areas that have been performing well toward those that have been falling behind. That isn’t easy or intuitive. It’s a way to minimize risk rather than maximize returns and to stick with your investment plan through different types of markets. (You can read more about our approach in Best Practices for Portfolio Rebalancing at vanguard.com/research.)

It’s not necessary to check your portfolio every day or every month, much less rebalance it that frequently. It may be more appropriate to monitor it annually or semiannually and rebalance when your allocation swings 5 percentage points or more from its target.

6

It’s important, of course, to be aware of the tax implications. You’ll want to consult with your tax advisor, but generally speaking, it may be a good idea to make any asset changes within a tax-advantaged retirement account or to direct new cash flows into the underweighted asset class.

However you go about it, keeping your asset allocation from drifting too far off target can help you stay on track with the investment plan you’ve crafted to meet your financial goals.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

April 13, 2016

7

Advisor’s Report

For the fiscal half year ended March 31, 2016, Vanguard Strategic Equity Fund had a total return of 3.38%, underperforming its benchmark by 1.68 percentage points. Overall, stocks fared well during the period, with the broad U.S. equity market, as measured by the MSCI US Investable Market Index, returning 7.31%. (Index returns are based on MSCI indexes.) Large-capitalization stocks performed better than smaller-caps, and value-oriented stocks outpaced growth stocks. Developed market equities didn’t do as well as their U.S. counterparts. Emerging markets stocks staged a recovery compared with the prior six-month period, climbing more than 6%.

Performances by sector within the benchmark were mixed. The best performers were utilities, consumer staples, and materials, while energy and health care posted declines.

In late 2015, the U.S. economy continued to grow, but at a slower pace. Fourth-quarter real GDP came in at 1.4%, compared with 2.0% in the third quarter, with the deceleration attributed primarily to downturns in nonresidential fixed investment, exports, and state and local government spending. Corporate profits decreased 8.1% in the final quarter of 2015, reflecting the largest quarterly decline since the first quarter of 2011. However, the U.S. job market improved further. In March, total nonfarm payrolls rose by 215,000, and the unemployment rate stood at 5.0%.

Oil prices declined significantly in the first quarter of 2016 but have since recovered, increasing over 40% from their mid-February low. This volatility spilled over into the global stock markets, as they saw similar price movements in the same quarter. The U.S. Federal Reserve raised interest rates in December, after keeping rates near zero since 2008. Additional interest rate hikes are expected later this year, but changes are likely to be gradual and will depend on global economic data. Meanwhile, several of the world’s central banks, including the European Central Bank and the Bank of Japan, are experimenting with negative interest rates in an attempt to spur economic growth.

Although we seek to understand the impact of macroeconomic factors on portfolio performance, our investment process is centered on specific stock fundamentals. We use a disciplined, quantitative approach, not technical analysis of stock price movements. Our model aims to systematically identify stocks within each industry group in our investment universe that are more likely to exhibit long-term outperformance.

Our model focuses on five key themes that we believe attractive stocks tend to exhibit: high quality (healthy balance sheets and consistent cash flow generation); effective management decisions regarding the use of capital (sound investment policies that favor internal over external funding); consistent earnings growth (a demonstrated ability to increase earnings year

8

after year); strong momentum (a market confirmation of our view); and reasonable valuations (we try to avoid overpriced stocks). This framework helps us to identify and take advantage of inefficiencies in the market caused by persistent biases in investor behavior.

Using the results of our model, we then construct and review our portfolio daily with the goal of maximizing expected return while minimizing exposure to risks that our research indicates do not improve returns, such as deviations from sector weightings relative to the benchmark.

For this period, the management decisions, quality, and valuation components of our model made positive contributions to performance. The growth and momentum components of the model, however, did not perform as expected. As a result, our stock selection was positive in three sectors, more or less flat in two, and negative in five. The strongest selection results were in health care, utilities, and materials; the poorest results were in consumer discretionary, consumer staples, and energy.

At the individual stock level, the largest performance contributions came from overweight positions in Affymetrix, Ionis Pharmaceuticals, and Charles River Laboratories. (As of the end of the period, Affymetrix and Ionis Pharmaceuticals were no longer held by the fund.) In addition, when comparing the portfolio’s performance with that of its benchmark, we benefited from underweighting or avoiding poorly performing stocks such as Endo International and Alkermes plc.

Unfortunately, we were not able to avoid all bad performers. Overweight positions in Outerwall, Skechers U.S.A., and American Axle & Manufacturing Holdings detracted from results. Also, underweighting Mattel and Michael Kors Holdings, which were not identified for inclusion in the fund by our model, hurt our overall performance relative to our benchmark.

We continue to believe that constructing a portfolio that focuses on the key fundamentals described above will benefit investors over the long term, while recognizing that risk can reward or punish us in the near term. We look forward to the second half of the fiscal year, feeling that the fund offers a strong mix of stocks with attractive valuation and growth characteristics relative to its underlying benchmark.

We thank you for your investment.

Portfolio Managers:

Michael R. Roach, CFA

James P. Stetler, Principal

Binbin Guo, Principal, Head of Equity

Research and Portfolio Strategies

April 19, 2016

9

Strategic Equity Fund

Fund Profile

As of March 31, 2016

| | | | |

| Portfolio Characteristics | | |

| | | MSCI US | DJ |

| | | Small + | U.S. Total |

| | | Mid Cap | Market |

| | Fund 2200 Index | FA Index |

| Number of Stocks | 398 | 2,166 | 3,900 |

| Median Market Cap | $4.1B | $6.2B | $52.5B |

| Price/Earnings Ratio | 18.1x | 27.1x | 21.8x |

| Price/Book Ratio | 2.3x | 2.4x | 2.7x |

| Return on Equity | 14.0% | 13.4% | 17.5% |

| Earnings Growth | | | |

| Rate | 13.5% | 10.3% | 8.0% |

| Dividend Yield | 2.0% | 1.7% | 2.1% |

| Foreign Holdings | 0.6% | 0.0% | 0.0% |

| Turnover Rate | | | |

| (Annualized) | 68% | — | — |

| Ticker Symbol | VSEQX | — | — |

| Expense Ratio1 | 0.21% | — | — |

| 30-Day SEC Yield | 1.70% | — | — |

| Short-Term Reserves | 0.0% | — | — |

| | | | |

| Sector Diversification (% of equity exposure) |

| | | MSCI US | |

| | | Small + | DJ |

| | | Mid Cap | U.S. Total |

| | | 2200 | Market |

| | Fund | Index | FA Index |

| Consumer | | | |

| Discretionary | 16.1% | 16.3% | 13.6% |

| Consumer Staples | 5.1 | 5.1 | 9.2 |

| Energy | 4.4 | 4.5 | 6.1 |

| Financials | 22.5 | 22.4 | 17.4 |

| Health Care | 9.8 | 9.7 | 13.7 |

| Industrials | 14.1 | 14.2 | 10.7 |

| Information | | | |

| Technology | 15.4 | 15.4 | 20.1 |

| Materials | 5.8 | 5.8 | 3.2 |

| Telecommunication | | | |

| Services | 0.9 | 0.9 | 2.5 |

| Utilities | 5.9 | 5.7 | 3.5 |

| | | |

| Volatility Measures | | |

| | MSCI US | DJ |

| | Small + | U.S. Total |

| | Mid Cap | Market |

| | 2200 Index | FA Index |

| R-Squared | 0.97 | 0.90 |

| Beta | 0.98 | 1.05 |

| These measures show the degree and timing of the fund’s |

| fluctuations compared with the indexes over 36 months. |

| | | |

| Ten Largest Holdings (% of total net assets) |

| Tyson Foods Inc. | Packaged Foods & | |

| | Meats | 1.1% |

| FirstEnergy Corp. | Electric Utilities | 1.0 |

| Sealed Air Corp. | Paper Packaging | 1.0 |

| Avery Dennison Corp. | Paper Packaging | 0.9 |

| Cintas Corp. | Diversified Support | |

| | Services | 0.9 |

| Best Buy Co. Inc. | Computer & | |

| | Electronics Retail | 0.9 |

| Everest Re Group Ltd. | Reinsurance | 0.9 |

| Centene Corp. | Managed Health | |

| | Care | 0.9 |

| Leggett & Platt Inc. | Home Furnishings | 0.9 |

| Darden Restaurants Inc. | Restaurants | 0.9 |

| Top Ten | | 9.4% |

| The holdings listed exclude any temporary cash investments and equity index products. |

|

Investment Focus

1 The expense ratio shown is from the prospectus dated January 28, 2016, and represents estimated costs for the current fiscal year. For the six

months ended March 31, 2016, the annualized expense ratio was 0.19%.

10

Strategic Equity Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

Fiscal-Year Total Returns (%): September 30, 2005, Through March 31, 2016

| | | | | |

| Average Annual Total Returns: Periods Ended March 31, 2016 | | | |

| |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Strategic Equity Fund | 8/14/1995 | -5.85% | 11.60% | 6.25% |

See Financial Highlights for dividend and capital gains information.

11

Strategic Equity Fund

Financial Statements (unaudited)

Statement of Net Assets

As of March 31, 2016

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (99.6%)1 | | |

| Consumer Discretionary (16.1%) | |

| | Best Buy Co. Inc. | 1,617,700 | 52,478 |

| | Leggett & Platt Inc. | 1,065,132 | 51,552 |

| | Darden Restaurants Inc. | 768,861 | 50,976 |

| | American Eagle | | |

| | Outfitters Inc. | 3,020,800 | 50,357 |

| | Big Lots Inc. | 978,700 | 44,325 |

| | Cooper Tire | | |

| | & Rubber Co. | 1,006,961 | 37,278 |

| | Abercrombie | | |

| | & Fitch Co. | 1,103,978 | 34,819 |

| | Hasbro Inc. | 423,500 | 33,922 |

| | Foot Locker Inc. | 458,914 | 29,600 |

| ^ | Outerwall Inc. | 791,143 | 29,264 |

| * | American Axle & | | |

| | Manufacturing | | |

| | Holdings Inc. | 1,878,039 | 28,903 |

| | DR Horton Inc. | 720,000 | 21,766 |

| * | NVR Inc. | 12,200 | 21,135 |

| | Brinker International Inc. | 438,698 | 20,158 |

| * | Boyd Gaming Corp. | 956,570 | 19,763 |

| * | Helen of Troy Ltd. | 186,200 | 19,307 |

| ^ | World Wrestling | | |

| | Entertainment Inc. | | |

| | Class A | 1,055,512 | 18,640 |

| * | Express Inc. | 857,029 | 18,349 |

| * | Michael Kors | | |

| | Holdings Ltd. | 317,049 | 18,059 |

| * | Smith & Wesson | | |

| | Holding Corp. | 675,680 | 17,987 |

| * | Skechers U.S.A. Inc. | | |

| | Class A | 570,084 | 17,359 |

| | Carter’s Inc. | 157,366 | 16,583 |

| | Nordstrom Inc. | 284,755 | 16,291 |

| * | Madison Square | | |

| | Garden Co. Class A | 96,884 | 16,118 |

| | Whirlpool Corp. | 82,767 | 14,926 |

| | Jack in the Box Inc. | 226,522 | 14,468 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Wyndham Worldwide | | |

| | Corp. | 171,748 | 13,127 |

| | PVH Corp. | 131,400 | 13,017 |

| * | Penn National Gaming Inc. | 761,419 | 12,708 |

| | News Corp. Class B | 956,072 | 12,668 |

| * | Strayer Education Inc. | 257,500 | 12,553 |

| * | MSG Networks Inc. | 662,218 | 11,450 |

| | Interpublic Group | | |

| | of Cos. Inc. | 498,620 | 11,443 |

| | Gannett Co. Inc. | 688,059 | 10,417 |

| | Nutrisystem Inc. | 495,102 | 10,333 |

| * | BJ’s Restaurants Inc. | 242,200 | 10,068 |

| | Caleres Inc. | 351,900 | 9,955 |

| | Tower International Inc. | 341,290 | 9,283 |

| | News Corp. Class A | 708,200 | 9,044 |

| | GameStop Corp. Class A | 252,100 | 7,999 |

| | Cablevision Systems | | |

| | Corp. Class A | 189,800 | 6,263 |

| ^ | Cracker Barrel Old | | |

| | Country Store Inc. | 40,000 | 6,107 |

| * | Denny’s Corp. | 553,200 | 5,731 |

| | Cato Corp. Class A | 137,900 | 5,316 |

| | Bloomin’ Brands Inc. | 294,100 | 4,962 |

| | Sinclair Broadcast | | |

| | Group Inc. Class A | 149,615 | 4,601 |

| * | Burlington Stores Inc. | 75,266 | 4,233 |

| | Sturm Ruger & Co. Inc. | 60,630 | 4,146 |

| * | Michaels Cos. Inc. | 123,800 | 3,463 |

| * | Grand Canyon | | |

| | Education Inc. | 67,652 | 2,891 |

| | AMC Entertainment | | |

| | Holdings Inc. | 100,600 | 2,816 |

| | Children’s Place Inc. | 32,600 | 2,721 |

| | Cheesecake Factory Inc. | 47,873 | 2,542 |

| * | Pinnacle Entertainment Inc. | 58,041 | 2,037 |

| | DineEquity Inc. | 18,571 | 1,735 |

| | Oxford Industries Inc. | 21,200 | 1,425 |

| * | Liberty Media Corp. | | |

| | Class A | 36,464 | 1,409 |

| | Ethan Allen Interiors Inc. | 42,962 | 1,367 |

| * | Unifi Inc. | 44,600 | 1,022 |

12

Strategic Equity Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| * | ServiceMaster Global | | |

| | Holdings Inc. | 26,200 | 987 |

| | Libbey Inc. | 43,000 | 800 |

| | | | 935,022 |

| Consumer Staples (5.1%) | | |

| | Tyson Foods Inc. Class A | 946,696 | 63,107 |

| ^ | Cal-Maine Foods Inc. | 812,700 | 42,187 |

| | Bunge Ltd. | 586,161 | 33,218 |

| | Dean Foods Co. | 1,676,787 | 29,042 |

| * | SUPERVALU Inc. | 3,937,323 | 22,679 |

| | Clorox Co. | 146,505 | 18,468 |

| * | USANA Health | | |

| | Sciences Inc. | 131,000 | 15,906 |

| * | Pilgrim’s Pride Corp. | 577,077 | 14,658 |

| *,^ | Herbalife Ltd. | 206,513 | 12,713 |

| | ConAgra Foods Inc. | 284,400 | 12,690 |

| | Ingles Markets Inc. | | |

| | Class A | 228,951 | 8,586 |

| | Universal Corp. | 120,500 | 6,846 |

| ^ | Natural Health | | |

| | Trends Corp. | 205,201 | 6,802 |

| | Fresh Del Monte | | |

| | Produce Inc. | 99,841 | 4,200 |

| | Campbell Soup Co. | 44,900 | 2,864 |

| ^ | Coty Inc. Class A | 67,900 | 1,890 |

| * | Central Garden & Pet Co. | 33,600 | 549 |

| * | Seneca Foods Corp. | | |

| | Class A | 4,400 | 153 |

| | | | 296,558 |

| Energy (4.4%) | | |

| | Tesoro Corp. | 545,500 | 46,919 |

| | PBF Energy Inc. Class A | 1,413,112 | 46,915 |

| | Noble Corp. plc | 3,585,705 | 37,112 |

| | Western Refining Inc. | 836,100 | 24,322 |

| | Ensco plc Class A | 1,852,422 | 19,210 |

| | Alon USA Energy Inc. | 1,743,823 | 17,996 |

| | Rowan Cos. plc Class A | 1,091,127 | 17,567 |

| | Core Laboratories NV | 149,600 | 16,817 |

| | HollyFrontier Corp. | 208,300 | 7,357 |

| | Plains GP Holdings LP | | |

| | Class A | 727,820 | 6,325 |

| | Chesapeake Energy Corp. | 1,250,000 | 5,150 |

| * | Cameron International | | |

| | Corp. | 54,526 | 3,656 |

| | CVR Energy Inc. | 119,095 | 3,108 |

| | Atwood Oceanics Inc. | 201,131 | 1,844 |

| | | | 254,298 |

| Financials (22.4%) | | |

| | Everest Re Group Ltd. | 263,260 | 51,975 |

| | Regions Financial Corp. | 6,392,877 | 50,184 |

| * | MGIC Investment Corp. | 6,327,730 | 48,534 |

| | Assured Guaranty Ltd. | 1,855,360 | 46,941 |

| | Voya Financial Inc. | 1,307,400 | 38,921 |

| | Huntington | | |

| | Bancshares Inc. | 4,014,900 | 38,302 |

| | Navient Corp. | 3,163,358 | 37,865 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | AmTrust Financial | | |

| | Services Inc. | 1,307,156 | 33,829 |

| | Digital Realty Trust Inc. | 351,319 | 31,088 |

| | Lamar Advertising Co. | | |

| | Class A | 498,968 | 30,687 |

| | Hospitality Properties | | |

| | Trust | 1,118,171 | 29,699 |

| | MSCI Inc. Class A | 397,462 | 29,444 |

| | KeyCorp | 2,565,993 | 28,329 |

| | Aspen Insurance | | |

| | Holdings Ltd. | 527,400 | 25,157 |

| | Communications Sales | | |

| | & Leasing Inc. | 1,130,407 | 25,152 |

| | DuPont Fabros | | |

| | Technology Inc. | 597,109 | 24,201 |

| | Universal Insurance | | |

| | Holdings Inc. | 1,322,925 | 23,548 |

| | Popular Inc. | 802,061 | 22,947 |

| | GEO Group Inc. | 652,585 | 22,625 |

| | EPR Properties | 316,000 | 21,052 |

| | Kimco Realty Corp. | 697,200 | 20,065 |

| | Weingarten Realty | | |

| | Investors | 530,135 | 19,891 |

| | CoreSite Realty Corp. | 281,617 | 19,716 |

| | Sovran Self Storage Inc. | 165,100 | 19,474 |

| | Ryman Hospitality | | |

| | Properties Inc. | 338,700 | 17,436 |

| * | Walker & Dunlop Inc. | 716,400 | 17,387 |

| | Government Properties | | |

| | Income Trust | 952,295 | 16,998 |

| | Spirit Realty Capital Inc. | 1,503,356 | 16,913 |

| | CyrusOne Inc. | 367,558 | 16,779 |

| *,^ | Credit Acceptance Corp. | 92,361 | 16,768 |

| | First American | | |

| | Financial Corp. | 428,000 | 16,311 |

| | Regency Centers Corp. | 202,700 | 15,172 |

| | Corrections Corp. | | |

| | of America | 461,132 | 14,779 |

| | Great Western | | |

| | Bancorp Inc. | 537,620 | 14,661 |

| | CBL & Associates | | |

| | Properties Inc. | 1,227,050 | 14,602 |

| ^ | Lexington Realty Trust | 1,668,692 | 14,351 |

| | Equity LifeStyle | | |

| | Properties Inc. | 189,300 | 13,768 |

| | Reinsurance Group of | | |

| | America Inc. Class A | 138,820 | 13,361 |

| *,^ | World Acceptance Corp. | 343,586 | 13,029 |

| | Summit Hotel | | |

| | Properties Inc. | 1,057,800 | 12,662 |

| *,^ | LendingTree Inc. | 125,439 | 12,265 |

| | Washington Federal Inc. | 529,900 | 12,002 |

| | Omega Healthcare | | |

| | Investors Inc. | 319,300 | 11,271 |

| | Cathay General Bancorp | 393,800 | 11,156 |

13

Strategic Equity Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Hersha Hospitality Trust | | |

| | Class A | 512,813 | 10,943 |

| | Equinix Inc. | 32,294 | 10,680 |

| | PrivateBancorp Inc. | 275,800 | 10,646 |

| | Mack-Cali Realty Corp. | 399,641 | 9,392 |

| | Gaming and Leisure | | |

| | Properties Inc. | 298,959 | 9,244 |

| | Axis Capital Holdings Ltd. | 162,600 | 9,018 |

| | RLJ Lodging Trust | 392,400 | 8,978 |

| | Ashford Hospitality | | |

| | Trust Inc. | 1,343,418 | 8,571 |

| ^ | Apple Hospitality | | |

| | REIT Inc. | 386,841 | 7,663 |

| | Heritage Insurance | | |

| | Holdings Inc. | 477,261 | 7,622 |

| * | Realogy Holdings Corp. | 209,916 | 7,580 |

| | Pennsylvania REIT | 328,677 | 7,182 |

| | Unum Group | 229,054 | 7,082 |

| * | Santander Consumer | | |

| | USA Holdings Inc. | 661,637 | 6,941 |

| *,^ | Cowen Group Inc. | | |

| | Class A | 1,809,804 | 6,895 |

| | Gramercy Property Trust | 799,249 | 6,754 |

| | HCI Group Inc. | 199,900 | 6,657 |

| | Camden Property Trust | 78,000 | 6,559 |

| | Mid-America Apartment | | |

| | Communities Inc. | 62,165 | 6,354 |

| | Macerich Co. | 76,457 | 6,058 |

| | Validus Holdings Ltd. | 121,951 | 5,755 |

| | CubeSmart | 161,500 | 5,378 |

| | Synovus Financial Corp. | 185,752 | 5,370 |

| * | BofI Holding Inc. | 247,200 | 5,275 |

| | UDR Inc. | 134,001 | 5,163 |

| | First Industrial Realty | | |

| | Trust Inc. | 219,500 | 4,991 |

| | Extra Space Storage Inc. | 53,028 | 4,956 |

| | Alexandria Real Estate | | |

| | Equities Inc. | 53,900 | 4,899 |

| | Care Capital Properties Inc. | 163,891 | 4,399 |

| | NorthStar Realty | | |

| | Finance Corp. | 334,023 | 4,382 |

| * | INTL. FCStone Inc. | 147,000 | 3,929 |

| | Nelnet Inc. Class A | 89,812 | 3,536 |

| | RAIT Financial Trust | 1,114,800 | 3,500 |

| | Central Pacific | | |

| | Financial Corp. | 158,300 | 3,446 |

| | TCF Financial Corp. | 255,995 | 3,138 |

| * | Flagstar Bancorp Inc. | 144,100 | 3,092 |

| | Post Properties Inc. | 51,000 | 3,047 |

| | Senior Housing | | |

| | Properties Trust | 169,013 | 3,024 |

| | National Health | | |

| | Investors Inc. | 43,630 | 2,902 |

| | Associated Banc-Corp | 159,550 | 2,862 |

| | Primerica Inc. | 62,445 | 2,781 |

| | Ramco-Gershenson | | |

| | Properties Trust | 139,900 | 2,522 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Select Income REIT | 99,462 | 2,293 |

| | Progressive Corp. | 65,000 | 2,284 |

| * | Piper Jaffray Cos. | 43,700 | 2,166 |

| | Brixmor Property | | |

| | Group Inc. | 83,600 | 2,142 |

| | CenterState Banks Inc. | 130,000 | 1,936 |

| | Old National Bancorp | 155,879 | 1,900 |

| * | First NBC Bank Holding Co. | 85,200 | 1,754 |

| | International | | |

| | Bancshares Corp. | 63,900 | 1,576 |

| | Universal Health Realty | | |

| | Income Trust | 26,700 | 1,502 |

| | Medical Properties | | |

| | Trust Inc. | 103,200 | 1,340 |

| | Maiden Holdings Ltd. | 96,600 | 1,250 |

| | Cardinal Financial Corp. | 56,200 | 1,144 |

| | Great Southern | | |

| | Bancorp Inc. | 28,000 | 1,040 |

| | Agree Realty Corp. | 12,000 | 462 |

| | Getty Realty Corp. | 20,412 | 405 |

| | Monmouth Real Estate | | |

| | Investment Corp. | 18,800 | 224 |

| | One Liberty Properties Inc. | 8,100 | 181 |

| | United Fire Group Inc. | 3,100 | 136 |

| | Capital Bank Financial Corp. | 3,900 | 120 |

| | Federal Agricultural | | |

| | Mortgage Corp. | 1,700 | 64 |

| | EMC Insurance Group Inc. | 1,000 | 26 |

| | | | 1,304,408 |

| Health Care (9.7%) | | |

| * | Centene Corp. | 840,619 | 51,757 |

| * | Hologic Inc. | 1,464,714 | 50,533 |

| * | Quintiles Transnational | | |

| | Holdings Inc. | 701,503 | 45,668 |

| * | Charles River Laboratories | | |

| | International Inc. | 599,025 | 45,490 |

| * | Molina Healthcare Inc. | 679,209 | 43,802 |

| * | Amsurg Corp. | 507,643 | 37,870 |

| * | INC Research Holdings Inc. | | |

| | Class A | 780,013 | 32,144 |

| * | United Therapeutics Corp. | 197,949 | 22,057 |

| | CR Bard Inc. | 104,000 | 21,078 |

| * | AMN Healthcare | | |

| | Services Inc. | 578,925 | 19,458 |

| * | PAREXEL International | | |

| | Corp. | 308,787 | 19,370 |

| * | VCA Inc. | 278,700 | 16,078 |

| | Chemed Corp. | 116,300 | 15,753 |

| | ResMed Inc. | 271,283 | 15,686 |

| * | Amedisys Inc. | 283,442 | 13,702 |

| * | PRA Health Sciences Inc. | 304,500 | 13,020 |

| | Bruker Corp. | 324,866 | 9,096 |

| * | LifePoint Health Inc. | 127,728 | 8,845 |

| * | Infinity | | |

| | Pharmaceuticals Inc. | 1,596,095 | 8,411 |

| * | Natus Medical Inc. | 204,570 | 7,862 |

14

Strategic Equity Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Universal Health | | |

| | Services Inc. Class B | 60,122 | 7,498 |

| * | ICU Medical Inc. | 71,263 | 7,418 |

| * | Sucampo Pharmaceuticals | | |

| | Inc. Class A | 588,000 | 6,427 |

| *,^ | Merrimack | | |

| | Pharmaceuticals Inc. | 602,103 | 5,040 |

| * | Prestige Brands | | |

| | Holdings Inc. | 88,038 | 4,700 |

| | PDL BioPharma Inc. | 1,342,300 | 4,470 |

| * | Alere Inc. | 81,647 | 4,132 |

| | Owens & Minor Inc. | 93,837 | 3,793 |

| * | Array BioPharma Inc. | 1,143,256 | 3,373 |

| *,^ | NewLink Genetics Corp. | 182,344 | 3,319 |

| | Quality Systems Inc. | 216,851 | 3,305 |

| *,^ | Sequenom Inc. | 2,272,456 | 3,204 |

| * | Masimo Corp. | 64,971 | 2,718 |

| * | LHC Group Inc. | 66,100 | 2,350 |

| | Phibro Animal Health | | |

| | Corp. Class A | 83,084 | 2,247 |

| * | Emergent BioSolutions Inc. | 45,300 | 1,647 |

| *,^ | Insys Therapeutics Inc. | 67,641 | 1,082 |

| * | Surgical Care Affiliates Inc. | 17,753 | 822 |

| * | Triple-S Management Corp. | |

| | Class B | 32,000 | 795 |

| *,^ | Orexigen Therapeutics Inc. | 939,300 | 528 |

| | | | 566,548 |

| Industrials (14.0%) | | |

| | Cintas Corp. | 590,914 | 53,070 |

| | Huntington Ingalls | | |

| | Industries Inc. | 364,450 | 49,908 |

| * | Spirit AeroSystems | | |

| | Holdings Inc. Class A | 1,073,108 | 48,676 |

| * | Hawaiian Holdings Inc. | 973,195 | 45,925 |

| | AO Smith Corp. | 550,346 | 41,997 |

| | Pitney Bowes Inc. | 1,893,000 | 40,775 |

| | Masco Corp. | 1,219,345 | 38,348 |

| | Owens Corning | 809,300 | 38,264 |

| * | Wabash National Corp. | 2,815,314 | 37,162 |

| * | JetBlue Airways Corp. | 1,700,100 | 35,906 |

| | Trinity Industries Inc. | 1,828,946 | 33,488 |

| * | United Rentals Inc. | 454,200 | 28,247 |

| * | American Woodmark Corp. | 360,482 | 26,888 |

| | BWX Technologies Inc. | 749,436 | 25,151 |

| | Alaska Air Group Inc. | 305,546 | 25,061 |

| ^ | Greenbrier Cos. Inc. | 863,700 | 23,873 |

| * | Meritor Inc. | 2,451,546 | 19,760 |

| | Deluxe Corp. | 313,182 | 19,571 |

| | Comfort Systems | | |

| | USA Inc. | 420,300 | 13,353 |

| | Stanley Black | | |

| | & Decker Inc. | 125,233 | 13,176 |

| | GATX Corp. | 254,959 | 12,111 |

| | Aircastle Ltd. | 448,800 | 9,981 |

| | CEB Inc. | 149,007 | 9,645 |

| | General Cable Corp. | 721,900 | 8,814 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Interface Inc. Class A | 469,196 | 8,699 |

| | RR Donnelley & Sons Co. | 499,994 | 8,200 |

| * | Virgin America Inc. | 208,587 | 8,043 |

| | Briggs & Stratton Corp. | 311,836 | 7,459 |

| | Allison Transmission | | |

| | Holdings Inc. | 270,000 | 7,285 |

| | ManpowerGroup Inc. | 84,900 | 6,913 |

| | Herman Miller Inc. | 211,665 | 6,538 |

| | ADT Corp. | 154,469 | 6,373 |

| | Global Brass & Copper | | |

| | Holdings Inc. | 251,500 | 6,275 |

| | Steelcase Inc. Class A | 399,339 | 5,958 |

| | Hyster-Yale Materials | | |

| | Handling Inc. | 83,607 | 5,568 |

| | Standex International Corp. | 62,650 | 4,875 |

| | Graco Inc. | 56,720 | 4,762 |

| | Douglas Dynamics Inc. | 202,203 | 4,633 |

| | Korn/Ferry International | 160,300 | 4,535 |

| | Equifax Inc. | 31,761 | 3,630 |

| * | Dycom Industries Inc. | 54,719 | 3,539 |

| | Manitowoc Co. Inc. | 666,011 | 2,884 |

| | SkyWest Inc. | 128,300 | 2,565 |

| | Ennis Inc. | 108,100 | 2,113 |

| | Griffon Corp. | 110,800 | 1,712 |

| | Heidrick & Struggles | | |

| | International Inc. | 56,200 | 1,332 |

| | Tetra Tech Inc. | 39,519 | 1,178 |

| | John Bean | | |

| | Technologies Corp. | 17,200 | 970 |

| * | Babcock & Wilcox | | |

| | Enterprises Inc. | 38,500 | 824 |

| * | ACCO Brands Corp. | 64,300 | 577 |

| | National Presto | | |

| | Industries Inc. | 6,000 | 502 |

| | Federal Signal Corp. | 37,200 | 493 |

| | | | 817,585 |

| Information Technology (15.3%) | |

| *,^ | Advanced Micro | | |

| | Devices Inc. | 17,331,703 | 49,395 |

| | Booz Allen Hamilton | | |

| | Holding Corp. Class A | 1,611,238 | 48,788 |

| | CSRA Inc. | 1,775,176 | 47,752 |

| | CDW Corp. | 1,144,700 | 47,505 |

| * | Aspen Technology Inc. | 1,280,696 | 46,272 |

| * | Cirrus Logic Inc. | 1,258,437 | 45,820 |

| * | Manhattan Associates Inc. | 734,841 | 41,790 |

| | NVIDIA Corp. | 1,055,800 | 37,618 |

| * | Tech Data Corp. | 486,400 | 37,341 |

| * | First Data Corp. Class A | 2,785,094 | 36,039 |

| | Computer Sciences Corp. | 994,108 | 34,187 |

| | DST Systems Inc. | 276,270 | 31,155 |

| | SYNNEX Corp. | 287,438 | 26,614 |

| * | Synaptics Inc. | 322,509 | 25,717 |

| * | ARRIS International plc | 1,100,608 | 25,226 |

| | Broadridge Financial | | |

| | Solutions Inc. | 414,100 | 24,560 |

15

Strategic Equity Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Avnet Inc. | 505,236 | 22,382 |

| | Lexmark International Inc. | | |

| | Class A | 653,379 | 21,842 |

| *,^ | Fitbit Inc. Class A | 1,305,096 | 19,772 |

| * | Gartner Inc. | 191,996 | 17,155 |

| * | MicroStrategy Inc. Class A | 91,600 | 16,462 |

| * | Ciena Corp. | 854,285 | 16,249 |

| * | CACI International Inc. | | |

| | Class A | 143,277 | 15,288 |

| | EarthLink Holdings Corp. | 2,549,800 | 14,457 |

| * | GoDaddy Inc. Class A | 406,747 | 13,150 |

| | Lam Research Corp. | 127,900 | 10,565 |

| | Leidos Holdings Inc. | 207,117 | 10,422 |

| * | Blackhawk Network | | |

| | Holdings Inc. | 267,636 | 9,180 |

| | Science Applications | | |

| | International Corp. | 171,000 | 9,121 |

| | Jabil Circuit Inc. | 445,152 | 8,578 |

| * | Inphi Corp. | 221,195 | 7,375 |

| * | Gigamon Inc. | 235,900 | 7,318 |

| * | Sykes Enterprises Inc. | 233,100 | 7,035 |

| | CSG Systems | | |

| | International Inc. | 153,794 | 6,945 |

| * | ON Semiconductor Corp. | 710,537 | 6,814 |

| * | Mellanox | | |

| | Technologies Ltd. | 111,969 | 6,083 |

| | Ingram Micro Inc. | 124,363 | 4,466 |

| | MAXIMUS Inc. | 83,963 | 4,420 |

| * | Angie’s List Inc. | 507,000 | 4,091 |

| | Heartland Payment | | |

| | Systems Inc. | 36,844 | 3,558 |

| * | Cadence Design | | |

| | Systems Inc. | 140,000 | 3,301 |

| * | ePlus Inc. | 38,400 | 3,092 |

| *,^ | Ambarella Inc. | 68,437 | 3,059 |

| | Western Union Co. | 130,363 | 2,515 |

| * | Sanmina Corp. | 106,000 | 2,478 |

| * | Super Micro Computer Inc. | 65,488 | 2,232 |

| * | Flextronics | | |

| | International Ltd. | 158,252 | 1,909 |

| * | F5 Networks Inc. | 17,695 | 1,873 |

| * | Advanced Energy | | |

| | Industries Inc. | 50,300 | 1,750 |

| * | Monster Worldwide Inc. | 373,800 | 1,219 |

| * | Photronics Inc. | 95,271 | 992 |

| | | | 892,927 |

| Materials (5.8%) | | |

| | Sealed Air Corp. | 1,152,833 | 55,347 |

| | Avery Dennison Corp. | 744,990 | 53,721 |

| | Bemis Co. Inc. | 803,864 | 41,624 |

| * | Chemtura Corp. | 1,116,482 | 29,475 |

| * | Berry Plastics Group Inc. | 811,861 | 29,349 |

| *,^ | Trinseo SA | 426,150 | 15,687 |

| | Domtar Corp. | 342,884 | 13,887 |

| | Cabot Corp. | 281,214 | 13,591 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Graphic Packaging | | |

| | Holding Co. | 1,007,401 | 12,945 |

| | Reliance Steel | | |

| | & Aluminum Co. | 115,759 | 8,009 |

| | AptarGroup Inc. | 93,300 | 7,316 |

| | Newmont Mining Corp. | 244,782 | 6,506 |

| | Westlake Chemical Corp. | 129,389 | 5,991 |

| | Commercial Metals Co. | 343,860 | 5,835 |

| * | Axalta Coating | | |

| | Systems Ltd. | 184,815 | 5,397 |

| | Huntsman Corp. | 377,378 | 5,019 |

| | Neenah Paper Inc. | 76,100 | 4,845 |

| * | Ferro Corp. | 395,358 | 4,693 |

| | Kaiser Aluminum Corp. | 49,711 | 4,203 |

| | Mercer International Inc. | 394,796 | 3,731 |

| * | US Concrete Inc. | 45,049 | 2,684 |

| * | Kraton Performance | | |

| | Polymers Inc. | 110,500 | 1,912 |

| | Worthington Industries Inc. | 42,773 | 1,524 |

| * | Koppers Holdings Inc. | 55,200 | 1,240 |

| * | AK Steel Holding Corp. | 158,577 | 655 |

| | | | 335,186 |

| Telecommunication Services (0.9%) | |

| | Telephone & Data | | |

| | Systems Inc. | 454,872 | 13,687 |

| * | Level 3 | | |

| | Communications Inc. | 206,113 | 10,893 |

| | Frontier | | |

| | Communications Corp. | 1,217,000 | 6,803 |

| | Inteliquent Inc. | 337,605 | 5,419 |

| * | Cincinnati Bell Inc. | 1,327,700 | 5,138 |

| ^ | Windstream Holdings Inc. | 413,342 | 3,175 |

| * | General Communication | | |

| | Inc. Class A | 91,400 | 1,674 |

| | Cogent Communications | | |

| | Holdings Inc. | 37,085 | 1,447 |

| | Shenandoah | | |

| | Telecommunications Co. | 49,400 | 1,321 |

| * | Vonage Holdings Corp. | 140,400 | 642 |

| * | United States Cellular Corp. | 9,600 | 439 |

| * | FairPoint | | |

| | Communications Inc. | 19,500 | 290 |

| | | | 50,928 |

| Utilities (5.9%) | | |

| | FirstEnergy Corp. | 1,660,870 | 59,741 |

| | UGI Corp. | 1,253,182 | 50,491 |

| | WGL Holdings Inc. | 611,302 | 44,240 |

| | Entergy Corp. | 508,726 | 40,332 |

| | Vectren Corp. | 626,800 | 31,691 |

| | AES Corp. | 1,952,105 | 23,035 |

| | New Jersey | | |

| | Resources Corp. | 509,883 | 18,575 |

| | Ameren Corp. | 367,776 | 18,426 |

| | CMS Energy Corp. | 362,700 | 15,393 |

| | Pinnacle West | | |

| | Capital Corp. | 115,791 | 8,692 |

16

Strategic Equity Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | NiSource Inc. | 253,776 | 5,979 |

| | PNM Resources Inc. | 166,127 | 5,602 |

| | Atmos Energy Corp. | 53,434 | 3,968 |

| | ONE Gas Inc. | 59,586 | 3,641 |

| | American States Water Co. | 90,088 | 3,546 |

| | Avista Corp. | 74,239 | 3,027 |

| * | Talen Energy Corp. | 324,800 | 2,923 |

| | Unitil Corp. | 37,500 | 1,593 |

| | | | 340,895 |

| Total Common Stocks | | |

| (Cost $5,322,326) | | 5,794,355 |

| Temporary Cash Investments (2.3%)1 | |

| Money Market Fund (2.3%) | | |

| 2,3 | Vanguard Market | | |

| | Liquidity Fund, | | |

| | 0.495% | 134,680,975 | 134,681 |

| |

| | | Face | |

| | | Amount | |

| | | ($000) | |

| U.S. Government and Agency Obligations (0.0%) |

| 4 | Federal Home Loan Bank | | |

| | Discount Notes, | | |

| | 0.501%, 5/3/16 | 100 | 100 |

| 4 | Federal Home Loan Bank | | |

| | Discount Notes, | | |

| | 0.411%, 6/2/16 | 100 | 100 |

| 4,5 | Federal Home Loan Bank | | |

| | Discount Notes, 0.401%– | | |

| | 0.516%, 8/31/16 | 1,100 | 1,098 |

| 5 | United States Treasury | | |

| | Bill, 0.428%, 8/4/16 | 300 | 299 |

| | | | 1,597 |

| Total Temporary Cash Investments | |

| (Cost $136,278) | | 136,278 |

| Total Investments (101.9%) | | |

| (Cost $5,458,604) | | 5,930,633 |

| | |

| | Amount |

| | ($000) |

| Other Assets and Liabilities (-1.9%) | |

| Other Assets | |

| Investment in Vanguard | 483 |

| Receivables for Accrued Income | 8,098 |

| Receivables for Capital Shares Issued | 5,520 |

| 5Other Assets | 157 |

| Total Other Assets | 14,258 |

| Liabilities | |

| Payables for Investment Securities | |

| Purchased | (5,133) |

| Collateral for Securities on Loan | (109,708) |

| Payables for Capital Shares Redeemed | (2,648) |

| Payables to Vanguard | (7,373) |

| Other Liabilities | (8) |

| Total Liabilities | (124,870) |

| Net Assets (100%) | |

| Applicable to 204,776,822 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 5,820,021 |

| Net Asset Value Per Share | $28.42 |

| | |

| At March 31, 2016, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 5,322,609 |

| Undistributed Net Investment Income | 14,318 |

| Accumulated Net Realized Gains | 10,441 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 472,029 |

| Futures Contracts | 624 |

| Net Assets | 5,820,021 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Includes partial security positions on loan to broker-dealers. The total value of securities on loan is $107,199,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 100.0% and 1.9%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $109,708,000 of collateral received for securities on loan.

4 The issuer operates under a congressional charter; its securities are generally neither guaranteed by the U.S. Treasury nor backed by the full faith and credit of the U.S. government.

5 Securities with a value of $1,298,000 and cash of $100,000 have been segregated as initial margin for open futures contracts.

REIT—Real Estate Investment Trust.

See accompanying Notes, which are an integral part of the Financial Statements.

17

Strategic Equity Fund

Statement of Operations

| |

| | Six Months Ended |

| | March 31, 2016 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends | 54,552 |

| Interest1 | 43 |

| Securities Lending | 5,952 |

| Total Income | 60,547 |

| Expenses | |

| The Vanguard Group—Note B | |

| Investment Advisory Services | 767 |

| Management and Administrative | 3,885 |

| Marketing and Distribution | 613 |

| Custodian Fees | 35 |

| Shareholders’ Reports | 35 |

| Trustees’ Fees and Expenses | 2 |

| Total Expenses | 5,337 |

| Net Investment Income | 55,210 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 38,281 |

| Futures Contracts | 122 |

| Realized Net Gain (Loss) | 38,403 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 97,688 |

| Futures Contracts | 822 |

| Change in Unrealized Appreciation (Depreciation) | 98,510 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 192,123 |

| 1 Interest income from an affiliated company of the fund was $40,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

18

Strategic Equity Fund

Statement of Changes in Net Assets

| | |

| | Six Months Ended | Year Ended |

| | March 31, | September 30, |

| | 2016 | 2015 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 55,210 | 84,421 |

| Realized Net Gain (Loss) | 38,403 | 613,463 |

| Change in Unrealized Appreciation (Depreciation) | 98,510 | (608,999) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 192,123 | 88,885 |

| Distributions | | |

| Net Investment Income | (93,924) | (60,071) |

| Realized Capital Gain | (549,653) | (257,765) |

| Total Distributions | (643,577) | (317,836) |

| Capital Share Transactions | | |

| Issued | 388,312 | 1,082,468 |

| Issued in Lieu of Cash Distributions | 602,796 | 301,093 |

| Redeemed | (459,083) | (807,310) |

| Net Increase (Decrease) from Capital Share Transactions | 532,025 | 576,251 |

| Total Increase (Decrease) | 80,571 | 347,300 |

| Net Assets | | |

| Beginning of Period | 5,739,450 | 5,392,150 |

| End of Period1 | 5,820,021 | 5,739,450 |

| 1 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $14,318,000 and $53,032,000. |

See accompanying Notes, which are an integral part of the Financial Statements.

19

Strategic Equity Fund

Financial Highlights

| | | | | | |

| | Six Months | | | | | |

| | Ended | | | | | |

| For a Share Outstanding | March 31, | | | Year Ended September 30, |

| Throughout Each Period | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 |

| Net Asset Value, | | | | | | |

| Beginning of Period | $30.82 | $32.02 | $27.34 | $21.02 | $16.30 | $16.30 |

| Investment Operations | | | | | | |

| Net Investment Income | . 292 | . 466 | . 361 | . 4261 | .249 | .210 |

| Net Realized and Unrealized Gain (Loss) | | | | | | |

| on Investments | .782 | .207 | 4.679 | 6.244 | 4.667 | .017 |

| Total from Investment Operations | 1.074 | .673 | 5.040 | 6.670 | 4.916 | .227 |

| Distributions | | | | | | |

| Dividends from Net Investment Income | (. 507) | (. 354) | (. 360) | (. 350) | (.196) | (. 227) |

| Distributions from Realized Capital Gains | (2.967) | (1.519) | — | — | — | — |

| Total Distributions | (3.474) | (1.873) | (.360) | (.350) | (.196) | (.227) |

| Net Asset Value, End of Period | $28.42 | $30.82 | $32.02 | $27.34 | $21.02 | $16.30 |

| |

| Total Return2 | 3.38% | 2.01% | 18.53% | 32.23% | 30.32% | 1.23% |

| |

| Ratios/Supplemental Data | | | | | | |

| Net Assets, End of Period (Millions) | $5,820 | $5,739 | $5,392 | $4,239 | $3,254 | $2,756 |

| Ratio of Total Expenses to | | | | | | |

| Average Net Assets | 0.19% | 0.21% | 0.27% | 0.28% | 0.29% | 0.30% |

| Ratio of Net Investment Income to | | | | | | |

| Average Net Assets | 1.89% | 1.41% | 1.19% | 1.75%1 | 1.25% | 1.09% |

| Portfolio Turnover Rate | 68% | 70% | 60% | 64% | 67% | 73% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Net investment income per share and the ratio of net investment income to average net assets include $.043 and 0.18%, respectively, resulting from a special dividend received in connection with a merger between T-Mobile US Inc. and Metro PCS Communications Inc. in May 2013.

2 Total returns do not include account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable account service fees.

See accompanying Notes, which are an integral part of the Financial Statements.

20

Strategic Equity Fund

Notes to Financial Statements

Vanguard Strategic Equity Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

Futures contracts are valued at their quoted daily settlement prices. The aggregate settlement values of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the six months ended March 31, 2016, the fund’s average investments in long and short futures contracts represented less than 1% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period.

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (September 30, 2012–2015), and for the period ended March 31, 2016, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

21

Strategic Equity Fund

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are subject to termination by the fund at any time, and are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan.

6. Credit Facility: The fund and certain other funds managed by The Vanguard Group (“Vanguard”) participate in a $3.1 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.10% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate based upon the higher of the one-month London Interbank Offered Rate, federal funds effective rate, or overnight bank funding rate plus an agreed-upon spread.

The fund had no borrowings outstanding at March 31, 2016, or at any time during the period then ended.

7. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

B. In accordance with the terms of a Funds’ Service Agreement (the “FSA”) between Vanguard and the fund, Vanguard furnishes to the fund investment advisory, corporate management, administrative, marketing, and distribution services at Vanguard’s cost of operations (as defined by the FSA). These costs of operations are allocated to the fund based on methods and guidelines approved by the board of trustees. Vanguard does not require reimbursement in the current period for certain costs of operations (such as deferred compensation/benefits and risk/insurance costs); the fund’s liability for these costs of operations is included in Payables to Vanguard on the Statement of Net Assets.

22

Strategic Equity Fund

Upon the request of Vanguard, the fund may invest up to 0.40% of its net assets as capital in Vanguard. At March 31, 2016, the fund had contributed to Vanguard capital in the amount of $483,000, representing 0.01% of the fund’s net assets and 0.19% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and employees, respectively, of Vanguard.

C. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the market value of the fund’s investments as of March 31, 2016, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 5,794,355 | — | — |

| Temporary Cash Investments | 134,681 | 1,597 | — |

| Futures Contracts—Assets1 | 45 | — | — |

| Futures Contracts—Liabilities1 | (8) | — | — |

| Total | 5,929,073 | 1,597 | — |

| 1 Represents variation margin on the last day of the reporting period. | | | |

D. At March 31, 2016, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| E-mini S&P Mid-Cap 400 Index | June 2016 | 89 | 12,827 | 432 |

| E-mini Russell 2000 Index | June 2016 | 114 | 12,649 | 192 |

| | | | | 624 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

E. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will

23

Strategic Equity Fund

reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes. The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year.

At March 31, 2016, the cost of investment securities for tax purposes was $5,458,983,000.

Net unrealized appreciation of investment securities for tax purposes was $471,650,000, consisting of unrealized gains of $892,613,000 on securities that had risen in value since their purchase and $420,963,000 in unrealized losses on securities that had fallen in value since their purchase.

F. During the six months ended March 31, 2016, the fund purchased $1,947,011,000 of investment securities and sold $1,996,823,000 of investment securities, other than temporary cash investments.

G. Capital shares issued and redeemed were:

| | |

| | Six Months Ended | Year Ended |

| | March 31, 2016 | September 30, 2015 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 13,404 | 32,774 |

| Issued in Lieu of Cash Distributions | 21,011 | 9,610 |

| Redeemed | (15,893) | (24,537) |

| Net Increase (Decrease) in Shares Outstanding | 18,522 | 17,847 |

H. Management has determined that no material events or transactions occurred subsequent to March 31, 2016, that would require recognition or disclosure in these financial statements.

24

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

25

| | | | |

| Six Months Ended March 31, 2016 | | | |

| |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Strategic Equity Fund | 9/30/2015 | 3/31/2016 | Period |

| Based on Actual Fund Return | $1,000.00 | $1,033.79 | $0.97 |

| Based on Hypothetical 5% Yearly Return | 1,000.00 | 1,024.05 | 0.96 |

| The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that period is 0.19%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period (183/366). |

|

|

|

26

Trustees Approve Advisory Arrangement

The board of trustees of Vanguard Strategic Equity Fund has renewed the fund’s investment advisory arrangement with The Vanguard Group, Inc. (Vanguard)—through its Quantitative Equity Group.

The board determined that continuing the fund’s internalized management structure was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of the advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the arrangement. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board reviewed the quality of the fund’s investment management services over both the short and long term, and took into account the organizational depth and stability of the advisor. The board considered that Vanguard has been managing investments for more than three decades. The Quantitative Equity Group adheres to a sound, disciplined investment management process; the team has considerable experience, stability, and depth.

The board concluded that Vanguard’s experience, stability, depth, and performance, among other factors, warranted continuation of the advisory arrangement.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance relative to a benchmark index and peer group. The board concluded that the performance was such that the advisory arrangement should continue. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below its peer-group average. Information about the fund’s expenses appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section.

The board does not conduct a profitability analysis of Vanguard because of Vanguard’s unique “at-cost” structure. Unlike most other mutual fund management companies, Vanguard is owned by the funds it oversees, and produces “profits” only in the form of reduced expenses for fund shareholders.

The benefit of economies of scale

The board concluded that the fund’s at-cost arrangement with Vanguard ensures that the fund will realize economies of scale as it grows, with the cost to shareholders declining as fund assets increase.

The board will consider whether to renew the advisory arrangement again after a one-year period.

27

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.