UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07443

Name of Registrant:

Vanguard Whitehall Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: October 31

Date of reporting period: November 1, 2008 – October 31, 2009

Item 1: Reports to Shareholders

|

| Vanguard Selected Value Fund |

| Annual Report |

|

|

| October 31, 2009 |

|

|

|

|

> Vanguard Selected Value Fund returned more than 22% for the 12 months ended October 31, 2009, significantly outperforming its comparative standards.

> Financial and consumer discretionary stocks—two of the fund’s largest sectors—contributed the most to its success.

> Over the past ten years, the fund’s average annual return of about 8% was ahead of the comparable return of the Russell Midcap Value Index and the average result for peer funds.

| |

| Contents | |

| Your Fund’s Total Returns | 1 |

| President’s Letter | 2 |

| Advisors’ Report | 8 |

| Results of Proxy Voting | 11 |

| Fund Profile | 12 |

| Performance Summary | 13 |

| Financial Statements | 15 |

| Your Fund’s After-Tax Returns | 25 |

| About Your Fund’s Expenses | 26 |

| Glossary | 28 |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.)

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

Cover photograph: Veronica Coia.

| | | | |

| Your Fund’s Total Returns | | | |

| |

| |

| |

| |

| Fiscal Year Ended October 31, 2009 | | | | |

| | | | Ticker | Total |

| | | | Symbol | Returns |

| Vanguard Selected Value Fund | | | VASVX | 22.77% |

| Russell Midcap Value Index | | | | 14.52 |

| Mid-Cap Value Funds Average1 | | | | 18.37 |

| |

| |

| Your Fund’s Performance at a Glance | | | | |

| October 31, 2008–October 31, 2009 | | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Selected Value Fund | $12.48 | $14.78 | $0.417 | $0.000 |

1 Derived from data provided by Lipper Inc.

1

President’s Letter

Dear Shareholder,

Vanguard Selected Value Fund returned 22.77% for the 12 months ended October 31, 2009—its third-best fiscal year ever. This is especially welcome coming on the heels of last year’s performance, the fund’s (and the markets’) worst showing since its inception in 1996. The fund handily outperformed the 14.52% return of its benchmark—the Russell Midcap Value Index—and the 18.37% average return of peer funds for the period.

Much of the fund’s success can be attributed to the stock-selection skills of its advisors—Barrow, Hanley, Mewhinney & Strauss, Inc., and Donald Smith & Co., Inc.—especially in financial and consumer discretionary stocks. These two sizable sectors benefited as investors became more confident about credit markets and the economy.

If you hold shares in a taxable account, you may wish to review the table and discussion on after-tax returns for the fiscal year that appear later in this report.

A vicious bear market quickly turned bullish

A year ago, the global financial system stood on the brink of collapse as the expanding U.S. credit crisis precipitated the deepest worldwide recession since World War II. Since then, markets have pulled back from the depths and, in fact, have rallied impressively. Although U.S. unemployment has risen to double digits

2

and signs of a robust recovery are hard to find, the global economy has begun to revive. For the first time in more than a year, U.S. gross domestic product registered growth, as reported by the Commerce Department for the third quarter of calendar 2009.

U.S. stocks recorded positive returns for the fiscal year ended October 31 as the market’s losses during the first four months of the period—marking the final plunge of a historic bear market—were erased by a remarkable rally beginning in March. Global stocks did even better, thanks to some renewed strength in developed markets and a powerful upswing in emerging markets that actually had some prognosticators worrying about a new asset bubble. Reminders of the markets’ travails are nevertheless apparent in the index returns for the past three years, where negative figures are the rule. Even the five-year returns for U.S. stocks as of October 31 were barely positive, further evidence of the long-term damage done by the collapse of the real estate bubble.

The bond market experienced an equally dramatic turnaround

The stock market’s rapid fall and recovery were matched by an equally dramatic turnaround in the bond market. At the end of 2008, as the credit markets virtually shut down, risk-averse investors flocked to U.S. Treasury bonds. The effect was to widen the difference between the lower yields of Treasuries and the higher yields of corporate bonds to a margin not seen since the Great Depression.

| | | |

| Market Barometer | | | |

| | | Average Annual Total Returns |

| | | Periods Ended October 31, 2009 |

| | One Year | Three Years | Five Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 11.20% | –6.84% | 0.71% |

| Russell 2000 Index (Small-caps) | 6.46 | –8.51 | 0.59 |

| Dow Jones U.S. Total Stock Market Index | 11.34 | –6.55 | 1.06 |

| MSCI All Country World Index ex USA (International) | 34.79 | –2.49 | 7.58 |

| |

| Bonds | | | |

| Barclays Capital U.S. Aggregate Bond Index | | | |

| (Broad taxable market) | 13.79% | 6.35% | 5.05% |

| Barclays Capital Municipal Bond Index | 13.60 | 4.17 | 4.15 |

| Citigroup 3-Month Treasury Bill Index | 0.28 | 2.50 | 2.94 |

| |

| CPI | | | |

| Consumer Price Index | –0.18% | 2.32% | 2.52% |

3

Central banks around the world responded to the economic slowdown by lowering interest rates and implementing other aggressive stimulus programs. Meanwhile, governments boosted spending in hopes of reversing the recessionary tide. As fears of a worldwide depression eased, investors’ appetite for risk returned to more normal levels. The receding pessimism increased demand for corporate bonds, raising their prices and bringing down their yields.

Over the past 12 months, both taxable and municipal bonds returned more than 13%.

However, the Fed’s easy-money campaign had a predictable effect on short-term savings vehicles such as money market funds, whose yields track prevailing short-term rates. In December 2008, the Fed reduced its target for the federal funds rate, a benchmark for the interest rates paid by money market instruments and other very short-term securities, to between 0% and 0.25%. The Fed has said it expects to maintain its target at this level “for an extended period.”

Favorable stock selection boosted performance

Every stock sector in the fund advanced for the year, in many cases overcoming first-half losses on the way to significant double-digit gains. The advisors’ stock selection was rewarding in most sectors, especially two of the largest—financials and consumer discretionary. These two sectors were responsible for more than half of the fund’s 12-month return.

| | |

| Expense Ratios1 | | |

| Your Fund Compared With Its Peer Group | | |

| | | Mid-Cap |

| | | Value Funds |

| | Fund | Average |

| Selected Value Fund | 0.45% | 1.41% |

1 The fund expense ratio shown is from the prospectus dated February 27, 2009, and represents estimated costs for the current fiscal year based on the fund's net assets as of the prospectus date. For the fiscal year ended October 31, 2009, the fund's expense ratio was 0.52%.

The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2008.

4

For some time, the advisors have maintained relatively light exposure to the financial sector. This positioning helped the fund sidestep some of the damage to this sector over much of the last two years. And when financial stocks began to recover, the fund managed to be in the right place at the right time: Its relatively limited selection of financial services stocks returned about 20%, while the index’s financial sector declined. For example, the share price of consumer-finance company Capital One Financial—the fund’s largest holding on October 31—approximately doubled after the stock was added to the portfolio during the first half of the fiscal year.

The advisors’ above-benchmark exposure to consumer discretionary stocks proved rewarding throughout the year. During the first half, while stock prices were still falling, the fund profited from investments in some retailers that were well-positioned among cost-conscious consumers. With the spring rally under way, and consumers regaining some confidence, recreation-oriented companies posted strong gains. Top-ten holding Royal Caribbean Cruises, for example, benefited from signs that price-discounting pressure is starting to ease.

In Selected Value’s relatively concentrated portfolio of about 60 stocks, the performance of any single holding can have an outsized impact on the fund’s total return. This can be a plus: Propelled by rising gold prices, shares of Canadian mining company Yamana Gold

| |

| Total Returns | |

| Ten Years Ended October 31, 2009 | |

| | Average |

| | Annual Return |

| Selected Value Fund | 8.06% |

| Russell Midcap Value Index | 6.59 |

| Mid-Cap Value Funds Average1 | 6.35�� |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1 Derived from data provided by Lipper Inc.

5

more than doubled in value, making it one of the fund’s best-performing stocks (the company is not included in the all-U.S. benchmark index). On the other hand, the shortfalls are equally apparent in a small portfolio. Among the detractors were Hill-Rom Holdings (medical technologies), Omnicare (pharmaceutical services for long-term care facilities), and New York Community Bancorp.

For more information on the fund’s positioning and performance during the year, please see the Advisors’ Report that follows this letter.

In ten-year performance, the fund is ahead of the pack

Bolstered by especially strong results in fiscal year 2009, the Selected Value Fund has put some distance between its long-term performance and that of its comparative standards. For the ten years ended October 31, the fund’s 8.06% average annual return was more than a percentage point higher than the comparable returns of its benchmark index and peer-group average.

In a decade that included two major bear markets, the fund significantly outpaced the broad U.S. stock market, which was essentially flat. (The Dow Jones U.S. Total Stock Market Index returned 0.06% per year, on average.) It’s worth remembering, however, that the advisors’ focus on a small number of out-of-favor, medium-sized companies often produces results that differ meaningfully from those of the market as a whole.

A word on expenses

The fund’s expense ratio has risen over the past fiscal year. The explanation is threefold.

First, the fund’s average net assets, the asset base used in calculating the expense ratio, declined from the average level in the prior fiscal year. With a smaller denominator, the fund’s fixed expenses have accounted for a modestly higher percentage of fund assets.

Second, the Vanguard funds’ contracts with external advisors typically include breakpoint pricing. As assets rise above a breakpoint threshold, advisory fees are paid at a lower rate. When assets fall, as they have during fiscal 2009, a smaller portion of assets is subject to the lower rate, causing the overall rate to increase. Over time, breakpoint pricing has helped shareholders benefit from the economies of scale produced by growth in the fund’s assets.

Finally, Vanguard’s contracts with external advisors generally include an incentive-fee provision that is contingent on the advisors’ performance relative to their benchmarks. This fee structure helps to ensure that the interests of the fund shareholders and advisors remain aligned. Over the past year, the advisory fee increased as the fund’s relative performance improved. The fund’s financial statements include more information about Vanguard Selected Value Fund’s incentive fee.

Timeless principles work well in today’s changeable markets

Over the last two years, stocks have taken investors on a roller-coaster ride. After soaring to record highs in October 2007, the U.S. stock market in 2008 suffered its worst calendar year since the 1930s, then turned around this past spring. Investors were given a strong dose of reality—not only by the volatile stock market but also by the demise of some major financial institutions and the persistence of the longest recession in seven decades.

What lessons did we learn? We were reminded of the value of some timeless investment principles—including diversification, balance, and taking a long-term view. Although diversification didn’t immunize investors from the market declines, it certainly insulated them from the worst of it. And patience is often rewarded: Many investors who did not panic and sell out as stocks sank have recovered a substantial share of their paper losses.

Now that the economy and the markets have pulled back from the brink, it’s a good time to reevaluate your long-term investment objectives, time frame, and risk tolerance, and to make sure your investments are appropriately diversified. Within such a portfolio, Vanguard Selected Value Fund—with its advisors’ disciplined, low-turnover strategy—can provide low-cost exposure to the potential opportunities associated with under-appreciated midsized companies.

Thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

November 12, 2009

7

Advisors’ Report

For the fiscal year ended October 31, 2009, Vanguard Selected Value Fund returned 22.77%. Your fund is managed by two independent advisors. This provides exposure to distinct, yet complementary, investment approaches, enhancing the fund’s diversification. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage and amount of fund assets each manages, and a brief description of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal period and of

how portfolio positioning reflects this assessment. These comments were prepared on November 16, 2009.

Barrow, Hanley, Mewhinney & Strauss, Inc.

Portfolio Managers:

James P. Barrow, Founding Partner

Mark Giambrone, Partner

This past year has been an extremely volatile period for the equity markets. We began last November amid substantial fear about the depths of the economic downturn and a critical need for meaningful government intervention, which led to a substantial sell-off in the markets. The fiscal year ended with a growing belief that things have stabilized,

| | | |

| Vanguard Selected Value Fund Investment Advisors | |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| Barrow, Hanley, Mewhinney | 71 | 2,032 | Conducts fundamental research on individual stocks |

| & Strauss, Inc. | | | exhibiting traditional value characteristics: price/ |

| | | | earnings and price/book ratios below the market |

| | | | average and dividend yields above the market average. |

| Donald Smith & Co., Inc. | 25 | 710 | Conducts fundamental research on the lowest price- |

| | | | to-tangible-book value companies. Research focuses |

| | | | on underlying quality of book value and assets, and |

| | | | on long-term earnings potential. |

| Cash Investments | 4 | 109 | These short-term reserves are invested by Vanguard |

| | | | in equity index products to simulate investment in |

| | | | stocks. Each advisor may also maintain a modest |

| | | | cash position. |

8

liquidity is returning to the debt markets, and improvement may be on the horizon—all leading to a substantial recovery in the markets. We are pleased with our portfolio’s performance over this time frame, as it has substantially outperformed its benchmark.

As we noted earlier in the year, the dramatic sell-off created opportunities for us to invest in high-quality companies that we believed would not only weather the storm but would also recover significantly when they emerged on the other side. This approach led us to companies such as Capital One Financial, Newell Rubbermaid, Computer Sciences, and International Game Technology, whose performance benefited the portfolio. More recently we’ve found different opportunities in more stable, high-quality businesses that were left behind in the recent rally but that we believe represent tremendous value, such as insurer Chubb, food distributor Sysco, Fidelity National Financial, and PNC Financial Services Group.

We continue to be overweighted in sectors that have tremendous valuation potential and should achieve earnings stability or a meaningful rebound in earnings as the economy continues to stabilize, such as industrials, consumer discretionary, and health care. Our overweighted position in health care detracted from performance for the fiscal year because of concerns about potential health care reform in Washington. We think current valuations reflect a worst-case scenario and believe these valuations will lift once the outcome of the debate is clear in late 2009 or in 2010. While we have been underweighted in financials, we continue to find selective opportunities in the sector and our position is steadily increasing.

We continue to be underweighted in sectors where valuations don’t seem to be much favored by the current and future economic environment or where company fundamentals do not match our investment parameters. These include materials, telecommunication services, consumer staples, and information technology.

Donald Smith & Co., Inc.

Portfolio Managers: Donald G. Smith, Chief Investment Officer

Richard L. Greenberg, CFA, Senior Vice President

At the end of October 2009, we continued to hold a concentrated portfolio of low price-to-tangible-book value stocks with attractive long-term earnings potential. As a group, the portfolio stocks were selling at 83% of tangible book value and 7.5 times our estimate of “normalized earnings,” which have been smoothed for the ups and downs of the economy and the business cycle. In contrast, the S&P 500 Index sells at about 345% of tangible book value and 14.8 times normalized earnings.

Our universe of low price-to-book value stocks has performed much better since the market hit bottom in March, and we are pleased that our portfolio returned more than its benchmark. Depressed cyclical industries, such as technology,

9

paper and paper products, retailers, and travel (airlines and cruise operators) have rebounded as economic prospects brightened.

Our top-performing stocks over the past year included apparel and home furnishings retailer Dillard’s, Yamana Gold, paper manufacturer Domtar, and three technology companies: Flextronics International, Micron Technology, and Semiconductor Manufacturing International. The two insurance companies whose book values had been hurt by temporary portfolio markdowns, CNA Financial and Unum Group, experienced substantial price appreciation as rebounding financial markets helped book values to recover. We added to our holdings of both companies earlier in the fiscal year.

We eliminated our positions in five stocks: Ashland, American Financial Group, Puget Energy, Qimonda, and Spansion. (Puget Energy was acquired by an investor group in February.) We scaled back our holdings in Flextronics International, Micron Technology, Pinnacle West Capital (which owns an Arizona utility and develops real estate), Royal Caribbean Cruises, and Yamana Gold. On the purchases side, we participated in a secondary offering of Transatlantic Holdings and then sold the stock after 23.5%

appreciation. We also added Aspen Insurance Holdings, Southwest Airlines, and Tesoro (an oil refiner and marketer) to the portfolio over the past year, all at discounts to tangible book value. In general, we sold stocks that had performed well and added to our positions in underperformers that met our investment criteria.

Our largest industry weightings at the fiscal year-end included insurance, technology, airlines, and utilities. As mentioned, the book values of insurance companies have rebounded substantially. CNA Financial, the largest holding in our portfolio, has seen tangible book value grow from about $20 per share last December to $35 per share as of September 30, a 75% appreciation. The stock was selling at $21.77 on October 31—only 62% of book value.

Overall, our portfolio remains attractively valued, though large moves in many of the stocks and in the overall market have made it more difficult to find new, attractively valued companies that meet our strict investment criteria. As opportunities emerge, however, our portfolio’s sizable allocation to cash will put us in a position to take advantage of them.

10

Results of Proxy Voting

At a special meeting of shareholders on July 2, 2009, fund shareholders approved the following two proposals:

Proposal 1—Elect trustees for each fund.*

The individuals listed in the table below were elected as trustees for each fund. All trustees with the exception of Messrs. McNabb and Volanakis (both of whom already served as directors of The Vanguard Group, Inc.) served as trustees to the funds prior to the shareholder meeting.

| | | |

| | | | Percentage |

| Trustee | For | Withheld | For |

| John J. Brennan | 267,380,786 | 8,631,474 | 96.9% |

| Charles D. Ellis | 256,520,935 | 19,491,324 | 92.9% |

| Emerson U. Fullwood | 257,085,311 | 18,926,948 | 93.1% |

| Rajiv L. Gupta | 266,612,131 | 9,400,128 | 96.6% |

| Amy Gutmann | 267,915,925 | 8,096,335 | 97.1% |

| JoAnn Heffernan Heisen | 266,998,335 | 9,013,925 | 96.7% |

| F. William McNabb III | 267,044,346 | 8,967,914 | 96.8% |

| André F. Perold | 256,971,735 | 19,040,525 | 93.1% |

| Alfred M. Rankin, Jr. | 266,847,723 | 9,164,536 | 96.7% |

| Peter F. Volanakis | 266,899,599 | 9,112,660 | 96.7% |

| * Results are for all funds within the same trust. | | | |

Proposal 2—Update and standardize the funds’ fundamental policies regarding:

(a) Purchasing and selling real estate.

(b) Issuing senior securities.

(c) Borrowing money.

(d) Making loans.

(e) Purchasing and selling commodities.

(f) Concentrating investments in a particular industry or group of industries.

(g) Eliminating outdated fundamental investment policies not required by law.

The revised fundamental policies are clearly stated and simple, yet comprehensive, making oversight and compliance more efficient than under the former policies. The revised fundamental policies will allow the funds to respond more quickly to regulatory and market changes, while avoiding the costs and delays associated with successive shareholder meetings.

| | | | | |

| | | | | Broker | Percentage |

| Selected Value Fund | For | Abstain | Against | Non-Votes | For |

| 2a | 118,113,958 | 2,668,089 | 3,934,973 | 6,724,883 | 89.9% |

| 2b | 117,628,170 | 2,972,266 | 4,116,582 | 6,724,884 | 89.5% |

| 2c | 114,478,655 | 2,877,848 | 7,360,517 | 6,724,882 | 87.1% |

| 2d | 115,008,695 | 2,852,851 | 6,855,472 | 6,724,884 | 87.5% |

| 2e | 114,940,879 | 2,883,130 | 6,893,009 | 6,724,884 | 87.4% |

| 2f | 117,599,707 | 2,849,677 | 4,267,636 | 6,724,882 | 89.5% |

| 2g | 118,910,580 | 2,843,751 | 2,962,689 | 6,724,882 | 90.5% |

11

Selected Value Fund

Fund Profile

As of October 31, 2009

| | | |

| Portfolio Characteristics | | |

| | | Comparative | Broad |

| | Fund | Index1 | Index2 |

| Number of Stocks | 64 | 549 | 4,310 |

| Median Market Cap | $5.3B | $4.9B | $28.3B |

| Price/Earnings Ratio | 40.2x | 149.8x | 30.3x |

| Price/Book Ratio | 1.2x | 1.4x | 2.1x |

| Yield3 | 1.8% | 2.3% | 1.9% |

| Return on Equity | 13.7% | 12.0% | 19.4% |

| Earnings Growth Rate | 3.8% | 1.0% | 9.3% |

| Foreign Holdings | 4.3% | 0.0% | 0.0% |

| Turnover Rate | 30% | — | — |

| Expense Ratio4 | 0.45% | — | — |

| Short-Term Reserves | 8.7% | — | —- |

| | | |

| Sector Diversification (% of equity exposure) |

| | | Comparative | Broad |

| | Fund | Index1 | Index2 |

| Consumer Discretionary | 16.3% | 12.4% | 10.0% |

| Consumer Staples | 5.1 | 6.5 | 10.3 |

| Energy | 6.0 | 9.6 | 11.6 |

| Financials | 27.2 | 28.0 | 16.3 |

| Health Care | 9.0 | 4.2 | 11.9 |

| Industrials | 17.4 | 10.9 | 10.4 |

| Information Technology | 6.1 | 6.9 | 19.1 |

| Materials | 3.0 | 7.4 | 3.8 |

| Telecommunication | | | |

| Services | 0.1 | 2.4 | 2.8 |

| Utilities | 9.8 | 11.7 | 3.8 |

| | |

| Volatility Measures5 | |

| | Fund Versus | Fund Versus |

| | Comparative Index1 | Broad Index2 |

| R-Squared | 0.95 | 0.92 |

| Beta | 0.82 | 1.01 |

| | |

| Ten Largest Holdings6 (% of total net assets) |

| Capital One | | |

| Financial Corp. | consumer finance | 2.5% |

| Pinnacle West | | |

| Capital Corp. | electric utilities | 2.3 |

| Newell Rubbermaid Inc. | housewares and | |

| | specialties | 2.3 |

| Eaton Corp. | industrial machinery | 2.2 |

| PNC Financial Services | | |

| Group Inc. | regional banks | 2.2 |

| Royal Caribbean | hotels, resorts, and | |

| Cruises Ltd. | cruise lines | 2.2 |

| Stanley Works | industrial machinery | 2.2 |

| Computer Sciences Corp. | data processing and | |

| | outsourced services | 2.2 |

| International Game | | |

| Technology | casinos and gaming | 2.1 |

| MDU Resources | | |

| Group Inc. | multi-utilities | 2.0 |

| Top Ten | | 22.2% |

Investment Focus

1 Russell Midcap Value Index.

2 Dow Jones U.S. Total Stock Market Index.

3 30-day SEC yield for the fund; annualized dividend yield for the indexes. See the Glossary.

4 The expense ratio shown is from the prospectus dated February 27, 2009, and represents estimated costs for the current fiscal year based on the fund’s net assets as of the prospectus date. For the fiscal year ended October 31, 2009, the fund’s expense ratio was 0.52%.

5 For an explanation of R-squared, beta, and other terms used here, see the Glossary.

6 The holdings listed exclude any temporary cash investments and equity index products.

12

Selected Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

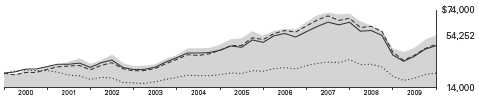

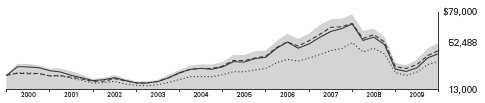

Cumulative Performance: October 31, 1999–October 31, 2009

Initial Investment of $25,000

| | | | |

| | | Average Annual Total Returns | Final Value |

| | | Periods Ended October 31, 2009 | of a $25,000 |

| | One Year | Five Years | Ten Years | Investment |

| Selected Value Fund1 | 22.77% | 2.92% | 8.06% | $54,252 |

| Dow Jones U.S. Total Stock Market Index | 11.34 | 1.06 | 0.06 | 25,140 |

| Russell Midcap Value Index | 14.52 | 2.05 | 6.59 | 47,343 |

| Mid-Cap Value Funds Average2 | 18.37 | 1.60 | 6.35 | 46,276 |

1 Total returns do not reflect the 1% fee assessed on redemptions after March 23, 2005, of shares held for less than one year; the 1% fee assessed until March 23, 2005, on shares purchased on or after August 7, 2001, and held for less than five years; or the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Derived from data provided by Lipper Inc.

13

Selected Value Fund

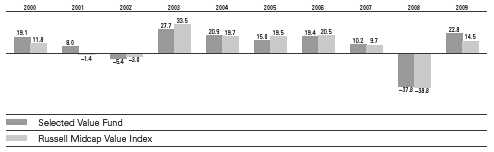

Fiscal-Year Total Returns (%): October 31, 1999–October 31, 2009

Average Annual Total Returns: Periods Ended September 30, 2009

This table presents average annual total returns through the latest calendar quarter—rather than through the end

of the fiscal period. Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception Date | One Year | Five Years | Ten Years |

| Selected Value Fund1 | 2/15/1996 | 3.05% | 3.97% | 8.02% |

1 Total returns do not reflect the 1% fee assessed on redemptions after March 23, 2005, of shares held for less than one year; the 1% fee assessed until March 23, 2005, on shares purchased on or after August 7, 2001, and held for less than five years; or the account service fee that may be applicable to certain accounts with balances below $10,000.

Note: See Financial Highlights table for dividend and capital gains information.

14

Selected Value Fund

Financial Statements

Statement of Net Assets

As of October 31, 2009

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (87.4%)1 | | |

| Consumer Discretionary (14.5%) | |

| | Newell Rubbermaid Inc. | 4,500,000 | 65,295 |

| * | Royal Caribbean | | |

| | Cruises Ltd. | 3,130,020 | 63,320 |

| | International Game | | |

| | Technology | 3,319,100 | 59,213 |

| * | Hanesbrands Inc. | 2,316,400 | 50,081 |

| * | GameStop Corp. Class A | 2,011,000 | 48,847 |

| | Family Dollar Stores Inc. | 1,476,700 | 41,791 |

| | Advance Auto Parts Inc. | 911,300 | 33,955 |

| | Dillard’s Inc. Class A | 2,451,900 | 33,395 |

| | Service Corp. | | |

| | International | 2,486,200 | 17,080 |

| | | | 412,977 |

| Consumer Staples (4.2%) | | |

| | Sysco Corp. | 1,648,400 | 43,600 |

| | Reynolds American Inc. | 794,000 | 38,493 |

| | Lorillard Inc. | 487,800 | 37,912 |

| | | | 120,005 |

| Energy (5.1%) | | |

| | Murphy Oil Corp. | 876,400 | 53,583 |

| | Spectra Energy Corp. | 1,575,700 | 30,127 |

| | El Paso Corp. | 2,628,600 | 25,787 |

| | Overseas Shipholding | | |

| | Group Inc. | 472,900 | 18,561 |

| | Tesoro Corp. | 1,090,600 | 15,421 |

| | | | 143,479 |

| Financials (24.2%) | | |

| | Capital One Financial | | |

| | Corp. | 1,955,900 | 71,585 |

| | PNC Financial Services | | |

| | Group Inc. | 1,297,212 | 63,485 |

| | Annaly Capital | | |

| | Management Inc. | 3,411,900 | 57,695 |

| | Willis Group Holdings Ltd. | 2,076,800 | 56,074 |

| | Axis Capital Holdings Ltd. | 1,746,900 | 50,468 |

| * | CNA Financial Corp. | 2,312,035 | 50,333 |

| | Fidelity National | | |

| | Financial Inc. Class A | 3,385,400 | 45,940 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Chubb Corp. | 827,300 | 40,141 |

| * | SLM Corp. | 4,012,400 | 38,920 |

| | Fifth Third Bancorp | 3,756,400 | 33,582 |

| | Unum Group | 1,517,200 | 30,268 |

| | New York Community | | |

| | Bancorp Inc. | 2,764,500 | 29,829 |

| | Validus Holdings Ltd. | 1,114,173 | 28,188 |

| | Ameriprise Financial Inc. | 635,300 | 22,026 |

| | People’s United | | |

| | Financial Inc. | 1,335,897 | 21,414 |

| | SunTrust Banks Inc. | 1,039,500 | 19,865 |

| | XL Capital Ltd. Class A | 900,100 | 14,771 |

| | American National | | |

| | Insurance Co. | 140,326 | 11,716 |

| | Aspen Insurance | | |

| | Holdings Ltd. | 141,000 | 3,638 |

| | | | 689,938 |

| Health Care (7.7%) | | |

| | Omnicare Inc. | 2,378,900 | 51,551 |

| | Quest Diagnostics Inc. | 870,700 | 48,698 |

| | Cardinal Health Inc. | 1,315,500 | 37,281 |

| | CIGNA Corp. | 1,303,400 | 36,287 |

| * | Coventry Health Care Inc. | 1,807,600 | 35,845 |

| * | CareFusion Corp. | 457,750 | 10,240 |

| | | | 219,902 |

| Industrials (15.5%) | | |

| | Eaton Corp. | 1,058,600 | 63,992 |

| | Stanley Works | 1,395,700 | 63,128 |

| | Goodrich Corp. | 1,039,400 | 56,491 |

| | L-3 Communications | | |

| | Holdings Inc. | 654,700 | 47,328 |

| | ITT Corp. | 919,900 | 46,639 |

| * | Air France-KLM ADR | 2,952,913 | 45,180 |

| | Ryder System Inc. | 1,050,700 | 42,606 |

| | SPX Corp. | 540,400 | 28,522 |

| | Avery Dennison Corp. | 756,100 | 26,955 |

| | Southwest Airlines Co. | 2,603,371 | 21,868 |

| | | | 442,709 |

15

| | | | |

| Selected Value Fund | | | |

| |

| |

| |

| | | | | Market |

| | | | | Value• |

| | | | Shares | ($000) |

| Information Technology (4.8%) | |

| * | Computer Sciences Corp. | 1,237,800 | 62,769 |

| * | Micron Technology Inc. | 6,468,416 | 43,921 |

| * | Flextronics International | | |

| | Ltd. | | 2,978,613 | 19,301 |

| * | Semiconductor | | | |

| | Manufacturing | | | |

| | International Corp. ADR | 4,626,200 | 11,195 |

| | | | | 137,186 |

| Materials (2.6%) | | | |

| | Yamana Gold Inc. | | 3,588,100 | 38,213 |

| * | Domtar Corp. | | 861,316 | 36,081 |

| | | | | 74,294 |

| Utilities (8.8%) | | | |

| | Pinnacle West | | | |

| | Capital Corp. | | 2,133,059 | 66,807 |

| | MDU Resources | | | |

| | Group Inc. | | 2,803,600 | 58,175 |

| | Xcel Energy Inc. | | 2,853,900 | 53,825 |

| | Centerpoint Energy Inc. | 3,633,600 | 45,783 |

| * | RRI Energy Inc. | | 2,846,200 | 15,000 |

| | NV Energy Inc. | | 1,035,700 | 11,869 |

| | | | | 251,459 |

| Total Common Stocks | | | |

| (Cost $2,552,324) | | | 2,491,949 |

| Temporary Cash Investments (12.5%)1 | |

| Money Market Fund (12.1%) | | |

| 2 | Vanguard Market Liquidity | | |

| | Fund, 0.225% | 345,201,555 | 345,202 |

| | | |

| | | Face | Market |

| | | Amount | Value• |

| | | ($000) | ($000) |

| U.S. Government and Agency Obligations (0.4%) |

| 3,4 | Fannie Mae | | |

| | Discount Notes, | | |

| | 0.351%, 11/12/09 | 1,500 | 1,500 |

| 3,4 | Fannie Mae | | |

| | Discount Notes, | | |

| | 0.180%, 3/10/10 | 1,000 | 1,000 |

| 3,4 | Freddie Mac | | |

| | Discount Notes, | | |

| | 0.260%, 12/22/09 | 8,000 | 7,999 |

| | | | 10,499 |

| Total Temporary Cash Investments | |

| (Cost $355,698) | | 355,701 |

| Total Investments (99.9%) | | |

| (Cost $2,908,022) | | 2,847,650 |

| Other Assets and Liabilities (0.1%) | |

| Other Assets | | 18,202 |

| Liabilities | | (14,435) |

| | | | 3,767 |

| Net Assets (100%) | | |

| Applicable to 192,964,917 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 2,851,417 |

| Net Asset Value Per Share | | $14.78 |

| |

| |

| At October 31, 2009, net assets consisted of: |

| | | | Amount |

| | | | ($000) |

| Paid-in Capital | | 3,326,643 |

| Undistributed Net | | |

| Investment Income | | 29,601 |

| Accumulated Net | | |

| Realized Losses | | (444,432) |

| Unrealized Appreciation | | |

| (Depreciation) | | |

| Investment Securities | | (60,372) |

| Futures Contracts | | (23) |

| Net Assets | | 2,851,417 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 91.2% and 8.7%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 The issuer operates under a congressional charter; its securities are not backed by the full faith and credit of the U.S. government.

4 Securities with a value of $10,499,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

16

| |

| Selected Value Fund | |

| |

| |

| Statement of Operations | |

| |

| | Year Ended |

| | October 31, 2009 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1 | 56,328 |

| Interest2 | 1,979 |

| Security Lending | 275 |

| Total Income | 58,582 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 5,906 |

| Performance Adjustment | 1,085 |

| The Vanguard Group—Note C | |

| Management and Administrative | 4,674 |

| Marketing and Distribution | 661 |

| Custodian Fees | 36 |

| Auditing Fees | 24 |

| Shareholders’ Reports and Proxies | 128 |

| Trustees’ Fees and Expenses | 5 |

| Total Expenses | 12,519 |

| Expenses Paid Indirectly | (288) |

| Net Expenses | 12,231 |

| Net Investment Income | 46,351 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | (257,146) |

| Futures Contracts | 9,896 |

| Foreign Currencies | 144 |

| Realized Net Gain (Loss) | (247,106) |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 701,531 |

| Futures Contracts | 2,355 |

| Change in Unrealized Appreciation (Depreciation) | 703,886 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 503,131 |

1 Dividends are net of foreign withholding taxes of $33,000.

2 Interest income from an affiliated company of the fund was $1,869,000.

See accompanying Notes, which are an integral part of the Financial Statements.

17

| | |

| Selected Value Fund | | |

| |

| |

| Statement of Changes in Net Assets | | |

| |

| | Year Ended October 31, |

| | 2009 | 2008 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 46,351 | 82,975 |

| Realized Net Gain (Loss) | (247,106) | (192,386) |

| Change in Unrealized Appreciation (Depreciation) | 703,886 | (1,518,492) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 503,131 | (1,627,903) |

| Distributions | | |

| Net Investment Income | (78,192) | (80,704) |

| Realized Capital Gain1 | — | (338,084) |

| Total Distributions | (78,192) | (418,788) |

| Capital Share Transactions | | |

| Issued | 465,114 | 428,618 |

| Issued in Lieu of Cash Distributions | 69,913 | 371,336 |

| Redeemed2 | (531,001) | (1,321,353) |

| Net Increase (Decrease) from Capital Share Transactions | 4,026 | (521,399) |

| Total Increase (Decrease) | 428,965 | (2,568,090) |

| Net Assets | | |

| Beginning of Period | 2,422,452 | 4,990,542 |

| End of Period3 | 2,851,417 | 2,422,452 |

1 Includes fiscal 2008 short-term gain distributions totaling $35,553,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net of redemption fees for fiscal 2009 and 2008 of $297,000 and $1,028,000, respectively.

3 Net Assets—End of Period includes undistributed net investment income of $29,601,000 and $61,298,000.

See accompanying Notes, which are an integral part of the Financial Statements.

18

| | | | | |

| Selected Value Fund | | | | | |

| |

| |

| Financial Highlights | | | | | |

| |

| |

| For a Share Outstanding | | | Year Ended October 31, |

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $12.48 | $22.11 | $21.38 | $18.99 | $16.76 |

| Investment Operations | | | | | |

| Net Investment Income | .254 | .3901 | .400 | .350 | .300 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | 2.463 | (8.100) | 1.700 | 3.180 | 2.190 |

| Total from Investment Operations | 2.717 | (7.710) | 2.100 | 3.530 | 2.490 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (.417) | (.370) | (.320) | (.290) | (.260) |

| Distributions from Realized Capital Gains | — | (1.550) | (1.050) | (.850) | — |

| Total Distributions | (.417) | (1.920) | (1.370) | (1.140) | (.260) |

| Net Asset Value, End of Period | $14.78 | $12.48 | $22.11 | $21.38 | $18.99 |

| |

| Total Return2 | 22.77% | –37.79% | 10.15% | 19.38% | 14.96% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $2,851 | $2,422 | $4,991 | $4,326 | $3,707 |

| Ratio of Total Expenses to | | | | | |

| Average Net Assets3 | 0.52% | 0.38% | 0.42% | 0.45% | 0.51% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 1.93% | 2.21% | 1.74% | 1.75% | 1.81% |

| Portfolio Turnover Rate | 30% | 23% | 33% | 37% | 28% |

1 Calculated based on average shares outstanding.

2 Total returns do not reflect the 1% fee assessed on redemptions after March 23, 2005, of shares held for less than one year; the 1% fee assessed until March 23, 2005, on shares purchased on or after August 7, 2001, and held for less than five years; or the account service fee that may be applicable to certain accounts with balances below $10,000.

3 Includes performance-based investment advisory fee increases (decreases) of 0.05%, (0.03%), (0.02%), (0.05%), and (0.02%).

See accompanying Notes, which are an integral part of the Financial Statements.

19

Selected Value Fund

Notes to Financial Statements

Vanguard Selected Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the va lues of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

20

Selected Value Fund

4. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2006–2009), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

5. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

6. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

7. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold. Fees assessed on redemptions of capital shares are credited to paid-in capital.

B. Barrow, Hanley, Mewhinney & Strauss, Inc., and Donald Smith & Co., Inc., each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Barrow, Hanley, Mewhinney & Strauss, Inc., is subject to quarterly adjustments based on performance for the preceding three years relative to the Russell Midcap Value Index. The basic fee of Donald Smith & Co., Inc., is subject to quarterly adjustments based on performance since July 31, 2005, relative to the MSCI Investable Market 2500 Index.

The Vanguard Group manages the cash reserves of the fund on an at-cost basis.

For the year ended October 31, 2009, the aggregate investment advisory fee represented an effective annual basic rate of 0.25% of the fund’s average net assets, before an increase of $1,085,000 (0.05%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At October 31, 2009, the fund had contributed capital of $609,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.24% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended October 31, 2009, these arrangements reduced the fund’s expenses by $288,000 (an annual rate of 0.01% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

21

Selected Value Fund

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the fund’s investments as of October 31, 2009, based on the inputs

used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 2,491,949 | — | — |

| Temporary Cash Investments | 345,202 | 10,499 | — |

| Futures Contracts—Liabilities1 | (3,005) | — | — |

| Total | 2,834,146 | 10,499 | — |

| 1 Represents variation margin on the last day of the reporting period. | | | |

F. At October 31, 2009, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | Number of | Aggregate | Unrealized |

| | | Long (Short) | Settlement | Appreciation |

| Futures Contracts | Expiration | Contracts | Value | (Depreciation) |

| S&P 500 Index | December 2009 | 352 | 90,904 | 451 |

| E-mini S&P 500 Index | December 2009 | 352 | 18,181 | (474) |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended October 31, 2009, the fund realized net foreign currency gains of $144,000, which increased distributable net income for tax purposes; accordingly, such gains have been reclassified from accumulated net realized losses to undistributed net investment income.

For tax purposes, at October 31, 2009, the fund had $35,499,000 of ordinary income available for distribution. The fund had available capital loss carryforwards totaling $443,851,000 to offset future net capital gains of $194,512,000 through October 31, 2016, and $249,339,000 through October 31, 2017.

22

Selected Value Fund

At October 31, 2009, the cost of investment securities for tax purposes was $2,908,022,000. Net unrealized depreciation of investment securities for tax purposes was $60,372,000, consisting of unrealized gains of $388,438,000 on securities that had risen in value since their purchase and $448,810,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended October 31, 2009, the fund purchased $623,727,000 of investment securities and sold $745,625,000 of investment securities, other than temporary cash investments.

| | |

| I. Capital shares issued and redeemed were: | | |

| | Year Ended October 31, |

| | 2009 | 2008 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 36,852 | 24,952 |

| Issued in Lieu of Cash Distributions | 6,144 | 19,762 |

| Redeemed | (44,143) | (76,343) |

| Net Increase (Decrease) in Shares Outstanding | (1,147) | (31,629) |

J. In preparing the financial statements as of October 31, 2009, management considered the impact of subsequent events occurring through December 8, 2009, for potential recognition or disclosure in these financial statements.

23

Report of Independent Registered Public Accounting Firm

To the Trustees of Vanguard Whitehall Funds and the Shareholders of Vanguard Selected Value Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Selected Value Fund (the "Fund") at October 31, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements") are the responsibility of the Fund's management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of th e Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2009 by correspondence with the custodian and broker and by agreement to the underlying ownership records of Vanguard Market Liquidity Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

December 8, 2009

|

| Special 2009 tax information (unaudited) for Vanguard Selected Value Fund |

This information for the fiscal year ended October 31, 2009, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $66,651,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 96.0% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

24

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2009. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| | | |

| Average Annual Total Returns: Selected Value Fund1 | | | |

| Periods Ended October 31, 2009 | | | |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | 22.77% | 2.92% | 8.06% |

| Returns After Taxes on Distributions | 21.99 | 1.97 | 7.23 |

| Returns After Taxes on Distributions and Sale of Fund Shares | 15.25 | 2.43 | 6.85 |

1 Total returns do not reflect the 1% fee assessed on redemptions after March 23, 2005, of shares held for less than one year; the 1% fee assessed until March 23, 2005, on shares purchased on or after August 7, 2001, and held for less than five years; or the account service fee that may be applicable to certain accounts with balances below $10,000.

25

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading “Expenses Paid During Period.”

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund’s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| | | |

| Six Months Ended October 31, 2009 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Selected Value Fund | 4/30/2009 | 10/31/2009 | Period1 |

| Based on Actual Fund Return | $1,000.00 | $1,220.48 | $2.80 |

| Hypothetical 5% Yearly Return | 1,000.00 | 1,022.68 | 2.55 |

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include the 1% fee on redemptions of shares held for less than one year, nor do they include the account service fee described in the prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

1 The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that period is 0.50%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

26

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

27

Glossary

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by stocks or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

28

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

29

This page intentionally left blank.

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 156 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at www.vanguard.com.

| |

| Interested Trustees | Emerson U. Fullwood |

| | Born 1948. Trustee Since January 2008. Principal |

| John J. Brennan1 | Occupation(s) During the Past Five Years: Executive |

| Born 1954. Trustee Since May 1987. Chairman of | Chief Staff and Marketing Officer for North America |

| the Board. Principal Occupation(s) During the Past | and Corporate Vice President (retired 2008) of Xerox |

| Five Years: Chairman of the Board and Director/Trustee | Corporation (photocopiers and printers); Director of |

| of The Vanguard Group, Inc., and of each of the | SPX Corporation (multi-industry manufacturing), the |

| investment companies served by The Vanguard Group; | United Way of Rochester, the Boy Scouts of America, |

| Chief Executive Officer (1996–2008) and President | Amerigroup Corporation (direct health and medical |

| (1989–2008) of The Vanguard Group and of each of the | insurance carriers), and Monroe Community College |

| investment companies served by The Vanguard Group; | Foundation. |

| Chairman of the Financial Accounting Foundation; | |

| Governor of the Financial Industry Regulatory Authority | Rajiv L. Gupta |

| (FINRA); Director of United Way of Southeastern | Born 1945. Trustee Since December 2001.2 Principal |

| Pennsylvania. | Occupation(s) During the Past Five Years: Chairman |

| | and Chief Executive Officer (retired 2009) and President |

| F. William McNabb III1 | (2006–2008) of Rohm and Haas Co. (chemicals); Board |

| Born 1957. Trustee Since July 2009. Principal | Member of American Chemistry Council; Director of |

| Occupation(s) During the Past Five Years: Director of | Tyco International, Ltd. (diversified manufacturing and |

| The Vanguard Group, Inc., since 2008; Chief Executive | services) and Hewlett-Packard Co. (electronic computer |

| Officer and President of The Vanguard Group and of | manufacturing); Trustee of The Conference Board. |

| each of the investment companies served by The | |

| Vanguard Group since 2008; Director of Vanguard | Amy Gutmann |

| Marketing Corporation; Managing Director of The | Born 1949. Trustee Since June 2006. Principal |

| Vanguard Group (1995–2008). | Occupation(s) During the Past Five Years: President of |

| | the University of Pennsylvania; Christopher H. Browne |

| | Distinguished Professor of Political Science in the School |

| Independent Trustees | of Arts and Sciences with secondary appointments |

| | at the Annenberg School for Communication and the |

| Charles D. Ellis | Graduate School of Education of the University of |

| Born 1937. Trustee Since January 2001. Principal | Pennsylvania; Director of Carnegie Corporation of |

| Occupation(s) During the Past Five Years: Applecore | New York, Schuylkill River Development Corporation, |

| Partners (pro bono ventures in education); Senior | and Greater Philadelphia Chamber of Commerce; |

| Advisor to Greenwich Associates (international business | Trustee of the National Constitution Center. |

| strategy consulting); Successor Trustee of Yale University; | |

| Overseer of the Stern School of Business at New York | |

| University; Trustee of the Whitehead Institute for | |

| Biomedical Research. | |

| | |

| JoAnn Heffernan Heisen | Executive Officers | |

| Born 1950. Trustee Since July 1998. Principal | | |

| Occupation(s) During the Past Five Years: Corporate | Thomas J. Higgins1 | |

| Vice President and Chief Global Diversity Officer since | Born 1957. Chief Financial Officer Since September |

| 2006 (retired 2008) and Member of the Executive | 2008. Principal Occupation(s) During the Past Five |

| Committee (retired 2008) of Johnson & Johnson | Years: Principal of The Vanguard Group, Inc.; Chief |

| (pharmaceuticals/consumer products); Vice President | Financial Officer of each of the investment companies |

| and Chief Information Officer of Johnson & Johnson | served by The Vanguard Group since 2008; Treasurer |

| (1997–2005); Director of the University Medical Center | of each of the investment companies served by The |

| at Princeton and Women’s Research and Education | Vanguard Group (1998–2008). |

| Institute; Member of the Advisory Board of the Maxwell | | |

| School of Citizenship and Public Affairs at Syracuse | | |

| University. | Kathryn J. Hyatt1 | |

| | Born 1955. Treasurer Since November 2008. Principal |

| | Occupation(s) During the Past Five Years: Principal of |

| F. Joseph Loughrey | The Vanguard Group, Inc.; Treasurer of each of the |

| Born 1949. Trustee Since October 2009. Principal | investment companies served by The Vanguard |

| Occupation(s) During the Past Five Years: President and | Group since 2008; Assistant Treasurer of each of the |

| Chief Operating Officer since 2005 (retired 2009) and | investment companies served by The Vanguard Group |

| Vice Chairman of the Board (2008–2009) of Cummins | (1988–2008). | |

| Inc. (industrial machinery); Director of SKF AB (industrial | | |

| machinery), Hillenbrand, Inc. (specialized consumer | | |

| services), Sauer-Danfoss Inc. (machinery), the Lumina | Heidi Stam1 | |

| Foundation for Education, and the Columbus Community | Born 1956. Secretary Since July 2005. Principal |

| Education Coalition; Chairman of the Advisory Council | Occupation(s) During the Past Five Years: Managing |

| for the College of Arts and Letters at the University of | Director of The Vanguard Group, Inc., since 2006; |

| Notre Dame. | General Counsel of The Vanguard Group since 2005; |

| | Secretary of The Vanguard Group and of each of the |

| | investment companies served by The Vanguard Group |

| André F. Perold | since 2005; Director and Senior Vice President of |

| Born 1952. Trustee Since December 2004. Principal | Vanguard Marketing Corporation since 2005; Principal |

| Occupation(s) During the Past Five Years: George Gund | of The Vanguard Group (1997–2006). |

| Professor of Finance and Banking, Harvard Business | | |

| School; Chair of the Investment Committee of HighVista | | |

| Strategies LLC (private investment firm). | Vanguard Senior Management Team |

| |

| Alfred M. Rankin, Jr. | R. Gregory Barton | Michael S. Miller |

| Born 1941. Trustee Since January 1993. Principal | Mortimer J. Buckley | James M. Norris |

| Occupation(s) During the Past Five Years: Chairman, | Kathleen C. Gubanich | Glenn W. Reed |

| President, and Chief Executive Officer of NACCO | Paul A. Heller | George U. Sauter |

| Industries, Inc. (forklift trucks/housewares/lignite); | | |

| Director of Goodrich Corporation (industrial products/ | | |

| aircraft systems and services); Deputy Chairman of | Founder | |

| the Federal Reserve Bank of Cleveland; Trustee of | | |

| University Hospitals of Cleveland, The Cleveland | | |

| Museum of Art, and Case Western Reserve University. | John C. Bogle | |

| | Chairman and Chief Executive Officer, 1974–1996 |

| |

| Peter F. Volanakis | | |

| Born 1955. Trustee Since July 2009. Principal | | |

| Occupation(s) During the Past Five Years: President | | |

| since 2007 and Chief Operating Officer since 2005 | | |

| of Corning Incorporated (communications equipment); | | |

| President of Corning Technologies (2001–2005); Director | | |

| of Corning Incorporated and Dow Corning; Trustee of | | |

| the Corning Incorporated Foundation and the Corning | | |

| Museum of Glass; Overseer of the Amos Tuck School | | |

| of Business Administration at Dartmouth College. | | |

1 These individuals are “interested persons” as defined in the Investment Company Act of 1940.

2 December 2002 for Vanguard Equity Income Fund, Vanguard Growth Equity Fund, the Vanguard Municipal Bond Funds, and the Vanguard

State Tax-Exempt Funds.

|  |

| P.O. Box 2600 |

| Valley Forge, PA 19482-2600 |

Connect with Vanguard® > www.vanguard.com

| |

| Fund Information > 800-662-7447 | All comparative mutual fund data are from Lipper Inc. |