UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07443

Name of Registrant: Vanguard Whitehall Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: October 31

Date of reporting period: November 1, 2011 – October 31, 2012

Item 1: Reports to Shareholders

|

|

| Annual Report | October 31, 2012 |

| Vanguard Selected Value Fund |

|

|

|

> Vanguard Selected Value Fund returned more than 13% for the 12 months ended October 31, 2012, trailing its benchmark index but outpacing the average return of its peers.

> Holdings among banks and credit card companies helped results, but setbacks to the fund’s technology stocks detracted.

> For the ten years ended October 31, the fund’s average annual return was 10.27%, a few steps behind that of the benchmark but more than a percentage point better than the average annual return of peer funds.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 7 |

| Fund Profile. | 11 |

| Performance Summary. | 12 |

| Financial Statements. | 14 |

| Your Fund’s After-Tax Returns. | 24 |

| About Your Fund’s Expenses. | 25 |

| Glossary. | 27 |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.)

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Our cover photograph shows rigging on the HMSSurprise, a replica of an 18th-century Royal Navy frigate. It was featured in the 2003 movie Master and Commander: The Far Side of the World, which was based on Patrick O’Brian’s sea novels, set amid the Napoleonic Wars. Vanguard was named for another ship of that era, the HMSVanguard, which was the flagship of British Admiral Horatio Nelson at the Battle of the Nile.

| |

| Your Fund’s Total Returns | |

| |

| |

| |

| |

| Fiscal Year Ended October 31, 2012 | |

| |

| | Total |

| | Returns |

| Vanguard Selected Value Fund | 13.64% |

| Russell Midcap Value Index | 14.99 |

| Mid-Cap Value Funds Average | 12.00 |

| Mid-Cap Value Funds Average: Derived from data provided by Lipper Inc. | |

Your Fund’s Performance at a Glance

October 31, 2011, Through October 31, 2012

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Selected Value Fund | $18.81 | $21.01 | $0.327 | $0.000 |

1

Chairman’s Letter

Dear Shareholder,

In a strong period for U.S. stocks, especially value stocks, Vanguard Selected Value Fund returned more than 13% for the 12 months ended October 31, 2012. The fund’s performance lagged that of its benchmark, the Russell Midcap Value Index, but outpaced the average return of peer funds by more than one percentage point.

Holdings in the financial sector, which represented the fund’s largest allocation, boosted performance, but those in technology weakened it. If you hold fund shares in a taxable account, you may wish to review the information about after-tax returns for the fiscal year that appears later in this report.

U.S. stocks led the advance for global equity markets

U.S. stocks returned about 14% for the 12 months ended October 31, putting domestic equities ahead of their international counterparts. Stocks in Europe and Asia, meanwhile, posted modestly positive results. The advances came amid moves by U.S. and European central bankers to manage risks to the U.S. economy and the finances of European governments and banks. The president of the European Central Bank declared in July that policymakers would do whatever was needed to preserve the euro common currency.

2

Although investors’ worries have eased, Europe’s financial troubles are by no means resolved. Vanguard economists believe the most likely scenario is that the Eurozone will “muddle through” for several years, with occasional spikes in market volatility, as fiscal tightening persists in the face of weak economic growth.

Bonds continued their march, but leaner times may lie ahead

The broad U.S. taxable bond market returned about 5% for the 12 months. Municipal bonds delivered a robust performance, returning 9%.

As bond prices rose, the yield of the 10-year U.S. Treasury note fell to a record low in July, closing below 1.5%. (Bond yields and prices move in opposite directions.) By the end of the period, the yield had climbed, but it still remained exceptionally low by historical standards.

Bondholders have enjoyed years of healthy returns. But as Tim Buckley, our incoming chief investment officer, has noted, investors shouldn’t be surprised if future results are much more modest. As yields remain low, the opportunity for similarly strong returns diminishes.

The Federal Reserve announced on September 13 that it would continue to hold its target for short-term interest rates between 0% and 0.25% at least through mid-2015. The exceptionally low rates, in

| | | |

| Market Barometer | | | |

| |

| | | Average Annual Total Returns |

| | | Periods Ended October 31, 2012 |

| | One | Three | Five |

| | Year | Years | Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 14.97% | 13.48% | 0.53% |

| Russell 2000 Index (Small-caps) | 12.08 | 14.82 | 1.19 |

| Dow Jones U.S. Total Stock Market Index | 14.45 | 13.62 | 0.75 |

| MSCI All Country World Index ex USA (International) | 3.98 | 3.74 | -5.08 |

| |

| Bonds | | | |

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 5.25% | 6.08% | 6.38% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 9.03 | 6.84 | 6.02 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.06 | 0.08 | 0.56 |

| |

| CPI | | | |

| Consumer Price Index | 2.16% | 2.28% | 2.06% |

3

place since late 2008, kept a tight lid on returns from money market funds and savings accounts.

Financial holdings propelled the fund’s strong performance

Financial stocks made up more than one-quarter of Selected Value’s assets, on average, during the 12 months, a bit less than their 31% share of the benchmark index. Financials have been a traditional focus for value-style investing because they tend to trade at a discount to certain overall market metrics, such as price/ earnings ratios, while also offering relatively high dividend yields.

But as with other investments, there are trade-offs. Generally, established financial firms are expected to have lower rates of earnings growth than companies in other industries, such as technology. And in recent years, banks and other financial firms have had to contend with the lingering problems from mortgage defaults associated with the deep downturn in U.S. housing.

In the 2012 fiscal year, however, financial stocks were the biggest contributor to Selected Value’s advance. Regional banks benefited from a modest improvement in loan growth amid hopes for a housing recovery. Credit-card lenders also fared well as improving consumer balance sheets led to an uptick in spending and borrowing.

Expense Ratios

Your Fund Compared With Its Peer Group

| | |

| | | Peer Group |

| | Fund | Average |

| Selected Value Fund | 0.45% | 1.31% |

The fund expense ratio shown is from the prospectus dated February 27, 2012, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2012, the fund’s expense ratio was 0.38%. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2011.

Peer group: Mid-Cap Value Funds.

4

As for disappointments, setbacks for the fund’s technology stocks headed the list. Some tech firms in the portfolio saw their business suffer because of Europe’s economic troubles. The Advisors’ Report that follows this letter provides additional details about the management of the fund during the year.

The fund produced solid returns during a challenging decade

For the ten years ended October 31, the Selected Value Fund recorded an average annual return of 10.27%, slightly behind the return of the benchmark index but better than the average return of peers. Of course, the fund’s goal is to outperform both its benchmark and its peers over time. Still, given the challenges of the past decade, including the 2008–2009 financial crisis, the fund has delivered a solid performance.

The two advisors that manage the fund take a highly concentrated approach to investing. On October 31 the fund held just 64 stocks, compared with more than 500 in the benchmark index. It’s important to keep in mind that such concentration can lead to volatility. But we’re confident that the advisors’ approach to identifying significantly undervalued stocks can deliver superior results over the long term.

Total Returns

Ten Years Ended October 31, 2012

| |

| | Average |

| | Annual Return |

| Selected Value Fund | 10.27% |

| Russell Midcap Value Index | 10.63 |

| Mid-Cap Value Funds Average | 9.09 |

| Mid-Cap Value Funds Average: Derived from data provided by Lipper Inc. | |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

5

How our core purpose informs our approach to active management

At Vanguard, we sum up our core purpose this way: to take a stand for all investors, to treat them fairly, and to give them the best chance for investment success. When it comes to our actively managed funds, such as the Selected Value Fund, this commitment is reflected both in our rigorous process for selecting advisors and in our ongoing efforts to keep costs low. We believe our approach gives investors the opportunity to outperform market indexes over the long term.

But make no mistake: Outperformance is hard to come by. For one thing, competition among investors is fierce. Charles Ellis, the author of one of my favorite books on investing, Winning the Loser’s Game, points out that the competition is not between the skilled and the inept. It’s between the skilled and the skilled. “It’s like the Williams sisters playing tennis against each other,” as he put it in a recent Vanguard webcast.

Because we recognize the challenges inherent in active management, Vanguard has offered and advocated for index funds for more than 35 years. By seeking to track—rather than beat—market returns, index funds provide several benefits: low costs, diversification across a market, and limited deviation from the performance of market benchmarks.

Still, the case for indexing doesn’t preclude the potential for skilled, seasoned managers to deliver outperformance. And the chances for success can increase if those managers deliver their services at low cost, allowing investors to keep more of their returns.

As always, thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

November 14, 2012

6

Advisors’ Report

For the fiscal year ended October 31, 2012, Vanguard Selected Value Fund returned 13.64%. Your fund is managed by two independent advisors. This provides exposure to distinct yet complementary investment approaches, enhancing the fund’s diversification. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage and amount of fund assets each manages, and a brief description of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal period and of how portfolio positioning reflects this assessment. These comments were prepared on November 20, 2012.

Barrow, Hanley, Mewhinney & Strauss, LLC

Portfolio Managers:

James P. Barrow, Executive Director

Mark Giambrone, Managing Director

In the last year, the markets have weathered many concerns, beginning with a potential collapse of the European monetary union and the euro, economic

| | | | |

| Vanguard Selected Value Fund Investment Advisors | | |

| |

| | Fund Assets Managed | | |

| Investment Advisor | % | $ Million | | Investment Strategy |

| Barrow, Hanley, Mewhinney & | 74 | 3,222 | | Conducts fundamental research on individual stocks |

| Strauss, LLC | | | | exhibiting traditional value characteristics: |

| | | | | price/earnings and price/book ratios below the market |

| | | | | average and dividend yields above the market average. |

| Donald Smith & Co., Inc. | 24 | 1,025 | | Conducts fundamental research on the lowest |

| | | | | price-to-tangible-book-value companies. Research |

| | | | | focuses on underlying quality of book value and assets, |

| | | | | and on long-term earnings potential. |

| Cash Investments | 2 | 90 | | These short-term reserves are invested by Vanguard in |

| | | | | equity index products to simulate investment in stocks. |

| | | | | Each advisor may also maintain a modest cash |

| | | | | position. |

7

slowdowns in emerging markets (especially China) and the United States, and an uncertain national political landscape. Today, we see Europe still struggling but no worse off, slow and steady improvement in the United States, emerging markets stabilizing, and a U.S. election that left us exactly where we started.

All this has led to a U.S. stock market that performed nicely in the fiscal year, delivering a meaningful gain. As is usual in a strong market, our portfolio will lag initially, while the most distressed or least profitable companies are leading the rally, but will catch up as investors once again focus on solid fundamentals, good valuations, and attractive dividend yields. We continue to like the positioning of the portfolio and believe it is well situated for consistent moderate improvements in the economy.

Accordingly, we hold overweight stakes in the industrial, health care, and consumer discretionary sectors relative to the benchmark, along with a large weighting in financials. All of these sectors are positioned to benefit from an improving economic backdrop while providing us with solid fundamentals, low valuations, and healthy dividend yields. Consistently with that perspective, we have underweighted the telecommunication services, materials, and information technology sectors. We believe that traditional yield plays like utilities and REITs have had significant runs and do not offer much valuation potential or dividend support, so we remain underweighted in these sectors as well.

We are confident that we have a portfolio of significantly undervalued companies that should perform well over time or be acquired by a buyer recognizing their value. An example of the latter occurred during the fiscal year when Coventry Health Care was acquired at a nice premium by Aetna. We expect this type of activity to continue, given the health of corporate balance sheets, the considerable free cash flow being generated by most companies, the low returns received from holding cash, and the belief that merger-and-acquisition activity can be a controlled way to expand a business and add to the bottom line.

Historically, the best-performing stocks have included those that not only pay a dividend but can also grow that dividend over time. We have built a portfolio with very reasonable valuations and a current dividend yield of 3.1%, which we believe will grow nicely. The accompanying table shows the percentage increases in dividends for some of our holdings in the past year.

8

| |

| Dividend increases for fund holdings, | |

| 12 months through October 31, 2012 | |

| |

| CA | 300% |

| Cardinal Health | 10 |

| Discover Financial Services | 67 |

| Eaton | 12 |

| Golar LNG | 45 |

| Hasbro | 20 |

| L3 Communications Holdings | 11 |

| Lorillard | 19 |

| Molex | 10 |

| Omnicare | 75 |

| PNC Financial Services Group | 14 |

| SLM | 25 |

| St. Jude Medical | 10 |

| Western Union | 25 |

| Source: Barrow, Hanley, Mewhinney & Strauss. | |

An additional benefit of strong balance sheets and cash flows is that companies are able to repurchase their shares. For example, these are some of our portfolio companies that conducted buybacks over the past five years together with the percentage reductions in the number of their shares: CA, -15%; Cardinal Health, -15%; Chubb, -33%; Hasbro, -20%; L3 Communications Holdings, -22%; Rent-A-Center, -16%.

Overall, we are optimistic about the prospects for our portfolio of quality companies that have good earnings and cash flow prospects, pay above-market yields, and have below-market valuations.

Donald Smith & Co., Inc.

Portfolio Managers:

Donald G. Smith, Chief Investment Officer

Richard L. Greenberg, CFA, Senior Vice President

The portfolio at the end of October 2012 continued to meet our criteria, representing a concentrated set of stocks with low ratios of price to tangible book value and attractive long-term earnings potential. The portfolio currently sells at 81% of tangible book value and 7.9 times our estimate of “normalized earnings.” In contrast, the S&P 500 Index sells at about 400% of tangible book value and about 16 times normalized earnings.

Two technology stocks, Ingram Micro and Micron Technology, detracted from our results for the fiscal year. Weak demand for personal computers hurt Ingram’s sales and also cut into demand for the memory Micron produces for PCs. Two independent power producers, GenOn and Exelon, suffered because of low natural gas prices (a key determinant of pricing for electricity) and a continued imbalance in supply and demand. Overseas Shipholding Group declined most. Despite its 70% uncollater-alized assets, the company has had difficulty coming to terms with banks on refinancing debt due in the first quarter of 2013. We believe that its net asset value remains well above the current stock price.

9

Solid performers over the past year included Dillard’s, which continues to show a dramatic earnings-per-share turnaround, Tesoro, NRG Energy, Yamana Gold, and Montpelier Re.

We eliminated the following stocks from the portfolio after they achieved sizable gains: Domtar, Montpelier Re, Noble, Pinnacle West, and Tesoro (which had risen more than 140%). We scaled back positions in Yamana Gold, CNA Financial, Dillard’s, NV Energy, and Everest Re Group, and increased our holdings in Southwest Airlines, Royal Caribbean Cruises, and XL Group.

We added four new names, all energy-related. As we have discussed previously, while we are not particularly optimistic about oil prices (and our airline stocks would benefit from a decline), we believe that the more than 30-to-1 ratio of the price of crude oil to the price of natural gas is unsustainable on a long-term basis; the energy equivalent ratio is roughly 8 to 1. Nabors Industries, a land driller; WPX Energy, a gas-heavy exploration and production company; and NRG Energy, an independent power producer, would all benefit from rising natural gas prices. We purchased all three at below tangible book value. The fourth addition was Valero Energy, a refiner. Recent actions indicate that the company is becoming more shareholder-friendly. It should generate more free cash to return to shareholders as a large capital spending program peaks this year.

The insurance industry remains our largest weighting. The five stocks we own in this group sell at an average 70% of tangible book value. The majority of these companies are wisely buying back stock at discounts to book value.

The two technology holdings discussed earlier, Micron Technology and Ingram Micro, make up a sizeable fraction of the portfolio. Although overseas demand has been anemic because of weaker European and Asian economies, we believe the stocks reflect this declining demand and have tremendous rebound potential. Our airline stocks, another significant weighting, should benefit from industry consolidation as well as from higher load factors, better pricing, and lower fuel costs.

10

Selected Value Fund

Fund Profile

As of October 31, 2012

| | | |

| Portfolio Characteristics | | |

| | | Russell | DJ |

| | | Midcap | U.S. Total |

| | | Value | Market |

| | Fund | Index | Index |

| Number of Stocks | 64 | 562 | 3,636 |

| Median Market Cap | $7.7B | $7.2B | $34.8B |

| Price/Earnings Ratio | 16.3x | 17.0x | 16.3x |

| Price/Book Ratio | 1.4x | 1.5x | 2.1x |

| Return on Equity | 10.1% | 9.1% | 17.6% |

| Earnings Growth Rate | 5.5% | 3.1% | 10.0% |

| Dividend Yield | 2.7% | 2.3% | 2.1% |

| Foreign Holdings | 7.1% | 0.0% | 0.0% |

| Turnover Rate | 18% | — | — |

| Ticker Symbol | VASVX | — | — |

| Expense Ratio1 | 0.45% | — | — |

| 30-Day SEC Yield | 2.14% | — | — |

| Short-Term Reserves | 7.3% | — | — |

| | | |

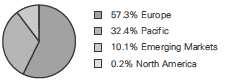

| Sector Diversification (% of equity exposure) |

| | | Russell | DJ |

| | | Midcap | U.S. Total |

| | | Value | Market |

| | Fund | Index | Index |

| Consumer Discretionary 14.3% | 9.6% | 12.1% |

| Consumer Staples | 4.3 | 4.8 | 9.5 |

| Energy | 6.7 | 9.1 | 10.4 |

| Financials | 28.7 | 30.6 | 16.6 |

| Health Care | 8.9 | 7.0 | 11.9 |

| Industrials | 15.9 | 11.0 | 10.8 |

| Information Technology | 8.7 | 9.6 | 18.3 |

| Materials | 4.1 | 6.1 | 3.9 |

| Telecommunication | | | |

| Services | 0.1 | 1.5 | 2.8 |

| Utilities | 8.3 | 10.7 | 3.7 |

| | |

| Volatility Measures | | |

| | Russell | DJ |

| | Midcap | U.S. Total |

| | Value | Market |

| | Index | Index |

| R-Squared | 0.97 | 0.97 |

| Beta | 0.93 | 0.98 |

These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months.

| | |

| Ten Largest Holdings (% of total net assets) |

| Royal Caribbean Cruises | Hotels, Resorts & | |

| Ltd. | Cruise Lines | 3.9% |

| XL Group plc Class A | Property & Casualty | |

| | Insurance | 3.0 |

| Cigna Corp. | Managed Health | |

| | Care | 2.4 |

| Capital One Financial | | |

| Corp. | Consumer Finance | 2.3 |

| SLM Corp. | Consumer Finance | 2.3 |

| Discover Financial | | |

| Services | Consumer Finance | 2.3 |

| Seadrill Ltd. | Oil & Gas Drilling | 2.3 |

| Omnicare Inc. | Health Care Services | 2.3 |

| Fifth Third Bancorp | Regional Banks | 2.3 |

| Yamana Gold Inc. | Gold | 2.2 |

| Top Ten | | 25.3% |

The holdings listed exclude any temporary cash investments and equity index products.

Investment Focus

1 The expense ratio shown is from the prospectus dated February 27, 2012, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2012, the expense ratio was 0.38%.

11

Selected Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

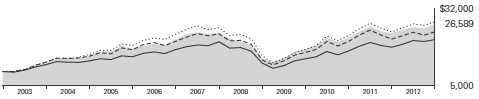

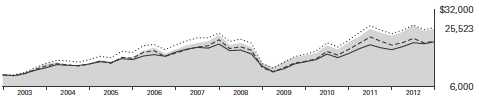

Cumulative Performance: October 31, 2002, Through October 31, 2012

Initial Investment of $10,000

| | | | |

| | | Average Annual Total Returns | |

| | Periods Ended October 31, 2012 | |

| | | | | Final Value |

| | One | Five | Ten | of a $10,000 |

| | Year | Years | Years | Investment |

| Selected Value Fund | 13.64% | 2.63% | 10.27% | $26,589 |

| Russell Midcap Value Index | 14.99 | 1.68 | 10.63 | 27,451 |

| Mid-Cap Value Funds Average | 12.00 | 0.59 | 9.09 | 23,872 |

| Dow Jones U.S. Total Stock Market | | | | |

| Index | 14.45 | 0.75 | 7.78 | 21,163 |

Mid-Cap Value Funds Average: Derived from data provided by Lipper Inc.

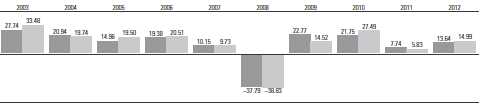

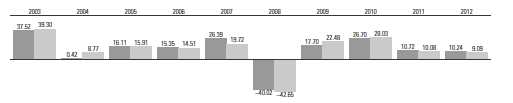

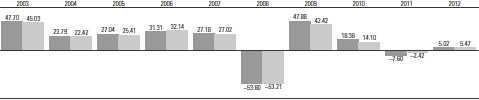

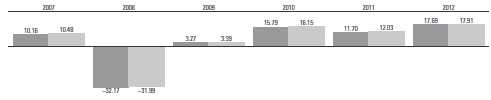

Fiscal-Year Total Returns (%): October 31, 2002, Through October 31, 2012

|

| Selected Value Fund |

| Russell Midcap Value Index |

| See Financial Highlights for dividend and capital gains information. |

12

Selected Value Fund

Average Annual Total Returns: Periods Ended September 30, 2012

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Selected Value Fund | 2/15/1996 | 27.44% | 2.71% | 10.34% |

13

Selected Value Fund

Financial Statements

Statement of Net Assets

As of October 31, 2012

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| Common Stocks (90.9%)1 | | |

| Consumer Discretionary (13.1%) | |

| | Royal Caribbean | | |

| | Cruises Ltd. | 5,046,294 | 169,909 |

| * | Hanesbrands Inc. | 2,694,900 | 90,198 |

| | International Game | | |

| | Technology | 5,370,100 | 68,952 |

| | Hasbro Inc. | 1,774,200 | 63,853 |

| | Newell Rubbermaid Inc. | 2,616,600 | 54,007 |

| | Rent-A-Center Inc. | 1,340,017 | 44,663 |

| | Dillard’s Inc. Class A | 507,834 | 39,103 |

| | Service Corp. | | |

| | International | 2,544,397 | 35,723 |

| | | | 566,408 |

| Consumer Staples (3.7%) | | |

| | Lorillard Inc. | 733,800 | 85,128 |

| | Reynolds American Inc. | 1,846,800 | 76,901 |

| | | | 162,029 |

| Energy (6.0%) | | |

| | Seadrill Ltd. | 2,467,900 | 99,555 |

| | Golar LNG Ltd. | 1,717,947 | 67,051 |

| | Spectra Energy Corp. | 1,664,900 | 48,066 |

| * | WPX Energy Inc. | 1,892,935 | 32,066 |

| * | Nabors Industries Ltd. | 435,000 | 5,868 |

| | Valero Energy Corp. | 200,500 | 5,835 |

| ^ | Overseas Shipholding | | |

| | Group Inc. | 472,900 | 530 |

| | | | 258,971 |

| Financials (26.4%) | | |

| | XL Group plc Class A | 5,245,700 | 129,779 |

| | Capital One Financial | | |

| | Corp. | 1,679,500 | 101,055 |

| | SLM Corp. | 5,721,200 | 100,579 |

| | Discover Financial | | |

| | Services | 2,442,000 | 100,122 |

| | Fifth Third Bancorp | 6,722,100 | 97,672 |

| | New York Community | | |

| | Bancorp Inc. | 6,570,300 | 91,064 |

| | CNA Financial Corp. | 2,780,982 | 81,705 |

| | Willis Group Holdings plc | 2,242,900 | 75,518 |

| | | |

| | | | Market |

| | | | Value |

| | | Shares | ($000) |

| | Essex Property Trust Inc. | 437,900 | 65,685 |

| | Ameriprise Financial Inc. | 1,106,400 | 64,581 |

| | People’s United | | |

| | Financial Inc. | 5,329,400 | 64,113 |

| | Chubb Corp. | 737,100 | 56,742 |

| | Everest Re Group Ltd. | 357,437 | 39,693 |

| | Annaly Capital | | |

| | Management Inc. | 2,320,500 | 37,453 |

| | Unum Group | 1,401,490 | 28,422 |

| | American National | | |

| | Insurance Co. | 164,858 | 12,045 |

| | | | 1,146,228 |

| Health Care (8.0%) | | |

| | Cigna Corp. | 2,051,000 | 104,601 |

| | Omnicare Inc. | 2,832,900 | 97,820 |

| | Cardinal Health Inc. | 2,018,400 | 83,017 |

| | St. Jude Medical Inc. | 1,636,000 | 62,593 |

| | | | 348,031 |

| Industrials (14.6%) | | |

| | Pentair Ltd. | 2,225,800 | 94,018 |

| | Masco Corp. | 5,836,700 | 88,076 |

| | Stanley Black & | | |

| | Decker Inc. | 1,270,200 | 88,025 |

| | Eaton Corp. | 1,552,200 | 73,295 |

| | SPX Corp. | 871,500 | 59,776 |

| | Southwest Airlines Co. | 5,205,028 | 45,908 |

| * | Air France-KLM ADR | 5,177,864 | 43,494 |

| | L-3 Communications | | |

| | Holdings Inc. | 553,300 | 40,833 |

| * | JetBlue Airways Corp. | 7,389,729 | 39,092 |

| | Exelis Inc. | 2,316,600 | 25,621 |

| | Xylem Inc. | 972,000 | 23,581 |

| | ITT Corp. | 486,000 | 10,109 |

| | | | 631,828 |

| Information Technology (7.7%) | |

| | Molex Inc. | 3,364,700 | 87,381 |

| | CA Inc. | 3,639,000 | 81,950 |

| * | Micron Technology Inc. | 12,321,916 | 66,847 |

| * | Ingram Micro Inc. | 4,190,311 | 63,693 |

| | Western Union Co. | 2,777,500 | 35,274 |

| | | | 335,145 |

14

| | |

| Selected Value Fund | | |

| |

| |

| |

| | | Market |

| | | Value |

| | Shares | ($000) |

| Materials (3.8%) | | |

| Yamana Gold Inc. | 4,783,334 | 96,671 |

| Sonoco Products Co. | 2,102,300 | 65,445 |

| | | 162,116 |

| Utilities (7.6%) | | |

| CenterPoint Energy Inc. | 3,839,300 | 83,198 |

| Xcel Energy Inc. | 2,535,300 | 71,622 |

| Pinnacle West | | |

| Capital Corp. | 1,164,800 | 61,699 |

| ONEOK Inc. | 1,010,200 | 47,783 |

| Exelon Corp. | 1,113,003 | 39,823 |

| NRG Energy Inc. | 773,000 | 16,666 |

| * GenOn Energy Inc. | 3,553,218 | 9,132 |

| NV Energy Inc. | 26,884 | 511 |

| | | 330,434 |

| Total Common Stocks | | |

| (Cost $3,148,141) | | 3,941,190 |

| Temporary Cash Investments (9.4%)1 | |

| Money Market Fund (9.3%) | | |

| 2,3 Vanguard Market | | |

| Liquidity | | |

| Fund, 0.167% | 403,069,115 | 403,069 |

| | |

| | Face | Market |

| | Amount | Value |

| | ($000) | ($000) |

| U.S. Government and Agency Obligations (0.1%) |

| 4,5 Fannie Mae Discount Notes, | | |

| 0.135%, 12/12/12 | 3,000 | 3,000 |

| 5 United States Treasury | | |

| Note/Bond, | | |

| 0.625%, 2/28/13 | 3,500 | 3,505 |

| | | 6,505 |

| Total Temporary Cash Investments | |

| (Cost $409,574) | | 409,574 |

| Total Investments (100.3%) | | |

| (Cost $3,557,715) | | 4,350,764 |

| Other Assets and Liabilities (-0.3%) | |

| Other Assets | | 7,928 |

| Liabilities3 | | (21,567) |

| | | (13,639) |

| Net Assets (100%) | | |

| Applicable to 206,470,338 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 4,337,125 |

| Net Asset Value Per Share | | $21.01 |

| |

| At October 31, 2012, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 3,558,452 |

| Undistributed Net | |

| Investment Income | 58,409 |

| Accumulated Net Realized Losses | (69,621) |

| Unrealized Appreciation | |

| (Depreciation) | |

| Investment Securities | 793,049 |

| Futures Contracts | (3,164) |

| Net Assets | 4,337,125 |

See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $151,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 93.0% and 7.3%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $269,000 of collateral received for securities on loan.

4 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the Federal Housing Finance Agency and it receives capital from the U.S. Treasury, as needed to maintain a positive net worth, in exchange for senior preferred stock.

5 Securities with a value of $5,605,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

15

| |

| Selected Value Fund | |

| |

| |

| Statement of Operations | |

| |

| | Year Ended |

| | October 31, 2012 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1 | 97,553 |

| Interest2 | 477 |

| Security Lending | 487 |

| Total Income | 98,517 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 9,301 |

| Performance Adjustment | (1,349) |

| The Vanguard Group—Note C | |

| Management and Administrative | 6,831 |

| Marketing and Distribution | 885 |

| Custodian Fees | 48 |

| Auditing Fees | 29 |

| Shareholders’ Reports | 47 |

| Trustees’ Fees and Expenses | 8 |

| Total Expenses | 15,800 |

| Expenses Paid Indirectly | (87) |

| Net Expenses | 15,713 |

| Net Investment Income | 82,804 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 204,150 |

| Futures Contracts | 29,111 |

| Realized Net Gain (Loss) | 233,261 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 215,318 |

| Futures Contracts | (6,834) |

| Change in Unrealized Appreciation (Depreciation) | 208,484 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 524,549 |

1 Dividends are net of foreign withholding taxes of $251,000.

2 Interest income from an affiliated company of the fund was $468,000.

See accompanying Notes, which are an integral part of the Financial Statements.

16

| | |

| Selected Value Fund | | |

| |

| |

| Statement of Changes in Net Assets | | |

| |

| | Year Ended October 31, |

| | 2012 | 2011 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 82,804 | 70,108 |

| Realized Net Gain (Loss) | 233,261 | 168,062 |

| Change in Unrealized Appreciation (Depreciation) | 208,484 | 37,302 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 524,549 | 275,472 |

| Distributions | | |

| Net Investment Income | (67,422) | (60,410) |

| Realized Capital Gain | — | — |

| Total Distributions | (67,422) | (60,410) |

| Capital Share Transactions | | |

| Issued | 541,729 | 636,966 |

| Issued in Lieu of Cash Distributions | 60,262 | 54,298 |

| Redeemed1 | (678,320) | (589,231) |

| Net Increase (Decrease) from Capital Share Transactions | (76,329) | 102,033 |

| Total Increase (Decrease) | 380,798 | 317,095 |

| Net Assets | | |

| Beginning of Period | 3,956,327 | 3,639,232 |

| End of Period2 | 4,337,125 | 3,956,327 |

1 Net of redemption fees for fiscal 2012 and 2011 of $177,000 and $482,000, respectively. Effective May 23, 2012, the redemption fee was eliminated.

2 Net Assets—End of Period includes undistributed net investment income of $58,409,000 and $43,027,000.

See accompanying Notes, which are an integral part of the Financial Statements.

17

| | | | | |

| Selected Value Fund | | | | | |

| |

| |

| Financial Highlights | | | | | |

| |

| |

| |

| For a Share Outstanding | | | Year Ended October 31, |

| Throughout Each Period | 2012 | 2011 | 2010 | 2009 | 2008 |

| Net Asset Value, Beginning of Period | $18.81 | $17.73 | $14.78 | $12.48 | $22.11 |

| Investment Operations | | | | | |

| Net Investment Income | .405 | .334 | .250 | .254 | .3901 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | 2.122 | 1.037 | 2.941 | 2.463 | (8.100) |

| Total from Investment Operations | 2.527 | 1.371 | 3.191 | 2.717 | (7.710) |

| Distributions | | | | | |

| Dividends from Net Investment Income | (.327) | (.291) | (.241) | (.417) | (.370) |

| Distributions from Realized Capital Gains | — | — | — | — | (1.550) |

| Total Distributions | (.327) | (.291) | (.241) | (.417) | (1.920) |

| Net Asset Value, End of Period | $21.01 | $18.81 | $17.73 | $14.78 | $12.48 |

| |

| Total Return2 | 13.64% | 7.74% | 21.75% | 22.77% | –37.79% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $4,337 | $3,956 | $3,639 | $2,851 | $2,422 |

| Ratio of Total Expenses to Average Net Assets3 | 0.38% | 0.45% | 0.47% | 0.52% | 0.38% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 2.00% | 1.74% | 1.52% | 1.93% | 2.21% |

| Portfolio Turnover Rate | 18% | 25% | 22% | 30% | 23% |

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of (0.03%), 0.04%, 0.05%, 0.05%, and (0.03%).

See accompanying Notes, which are an integral part of the Financial Statements.

18

Selected Value Fund

Notes to Financial Statements

Vanguard Selected Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the year ended October 31, 2012, the fund’s average investment in futures contracts represented 3% of net assets, based on quarterly average aggregate settlement values.

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2009–2012), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

19

Selected Value Fund

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents fees charged to borrowers plus income earned on investing cash collateral, less expenses associated with the loan.

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold. Fees assessed on redemptions of capital shares prior to May 23, 2012, were credited to paid-in capital.

B. Barrow, Hanley, Mewhinney & Strauss, LLC, and Donald Smith & Co., Inc., each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Barrow, Hanley, Mewhinney & Strauss, LLC, is subject to quarterly adjustments based on performance for the preceding three years relative to the Russell Midcap Value Index. The basic fee of Donald Smith & Co., Inc., is subject to quarterly adjustments based on performance for the preceding five years relative to the MSCI Investable Market 2500 Index.

The Vanguard Group manages the cash reserves of the fund on an at-cost basis.

For the year ended October 31, 2012, the aggregate investment advisory fee represented an effective annual basic rate of 0.23% of the fund’s average net assets, before a decrease of $1,349,000 (0.03%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At October 31, 2012, the fund had contributed capital of $600,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.24% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended October 31, 2012, these arrangements reduced the fund’s expenses by $87,000 (an annual rate of 0.00% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

20

Selected Value Fund

The following table summarizes the market value of the fund’s investments as of October 31, 2012, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 3,941,190 | — | — |

| Temporary Cash Investments | 403,069 | 6,505 | — |

| Futures Contracts—Liabilities1 | (53) | — | — |

| Total | 4,344,206 | 6,505 | — |

| 1 Represents variation margin on the last day of the reporting period. |

F. At October 31, 2012, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| S&P 500 Index | December 2012 | 251 | 88,277 | (3,080) |

| E-mini S&P 500 Index | December 2012 | 60 | 4,220 | (84) |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

For tax purposes, at October 31, 2012, the fund had $65,526,000 of ordinary income available for distribution. The fund used capital loss carryforwards of $226,427,000 to offset taxable capital gains realized during the year ended October 31, 2012. At October 31, 2012, the fund had available capital losses totaling $72,182,000 to offset future net capital gains of $49,688,000 through October 31, 2017, and $22,494,000 through October 31, 2018.

At October 31, 2012, the cost of investment securities for tax purposes was $3,557,715,000. Net unrealized appreciation of investment securities for tax purposes was $793,049,000, consisting of unrealized gains of $966,028,000 on securities that had risen in value since their purchase and $172,979,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended October 31, 2012, the fund purchased $680,273,000 of investment securities and sold $889,772,000 of investment securities, other than temporary cash investments.

21

Selected Value Fund

I. Capital shares issued and redeemed were:

| | |

| | Year Ended October 31, |

| | 2012 | 2011 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 27,462 | 33,349 |

| Issued in Lieu of Cash Distributions | 3,211 | 2,899 |

| Redeemed | (34,501) | (31,206) |

| Net Increase (Decrease) in Shares Outstanding | (3,828) | 5,042 |

J. In preparing the financial statements as of October 31, 2012, management considered the impact of subsequent events for potential recognition or disclosure in these financial statements.

22

Report of Independent Registered

Public Accounting Firm

To the Trustees of Vanguard Whitehall Funds and the Shareholders of Vanguard Selected Value Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Selected Value Fund (constituting a separate portfolio of Vanguard Whitehall Funds, hereafter referred to as the “Fund”) at October 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2012 by correspondence with the custodian and broker and by agreement to the underlying ownership records of the transfer agent, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

December 11, 2012

| |

| Special 2012 tax information (unaudited) for Vanguard Selected Value Fund |

This information for the fiscal year ended October 31, 2012, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $67,422,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 85.0% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

23

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2012. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

Average Annual Total Returns: Selected Value Fund

Periods Ended October 31, 2012

| | | |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | 13.64% | 2.63% | 10.27% |

| Returns After Taxes on Distributions | 13.35 | 2.02 | 9.57 |

| Returns After Taxes on Distributions and Sale of Fund Shares | 9.19 | 2.08 | 8.92 |

24

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

25

| | | |

| Six Months Ended October 31, 2012 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Selected Value Fund | 4/30/2012 | 10/31/2012 | Period |

| Based on Actual Fund Return | $1,000.00 | $1,041.65 | $1.96 |

| Based on Hypothetical 5% Yearly Return | 1,000.00 | 1,023.29 | 1.94 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that period is 0.38%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

26

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but does not include the transaction costs of buying and selling portfolio securities.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

27

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

28

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 180 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at vanguard.com.

| |

| InterestedTrustee1 | and Delphi Automotive LLP (automotive components); |

| | Senior Advisor at New Mountain Capital; Trustee of |

| F. William McNabb III | The Conference Board. |

| Born 1957. Trustee Since July 2009. Chairman of the | |

| Board. Principal Occupation(s) During the Past Five | Amy Gutmann |

| Years: Chairman of the Board of The Vanguard Group, | Born 1949. Trustee Since June 2006. Principal |

| Inc., and of each of the investment companies served | Occupation(s) During the Past Five Years: President |

| by The Vanguard Group, since January 2010; Director | of the University of Pennsylvania; Christopher H. |

| of The Vanguard Group since 2008; Chief Executive | Browne Distinguished Professor of Political Science |

| Officer and President of The Vanguard Group and of | in the School of Arts and Sciences with secondary |

| each of the investment companies served by The | appointments at the Annenberg School for |

| Vanguard Group since 2008; Director of Vanguard | Communication and the Graduate School of Education |

| Marketing Corporation; Managing Director of The | of the University of Pennsylvania; Member of the |

| Vanguard Group (1995–2008). | National Commission on the Humanities and Social |

| | Sciences; Trustee of Carnegie Corporation of New |

| | York and of the National Constitution Center; Chair |

| IndependentTrustees | of the U. S. Presidential Commission for the Study |

| | of Bioethical Issues. |

| Emerson U. Fullwood | |

| Born 1948. Trustee Since January 2008. Principal | JoAnn Heffernan Heisen |

| Occupation(s) During the Past Five Years: Executive | Born 1950. Trustee Since July 1998. Principal |

| Chief Staff and Marketing Officer for North America | Occupation(s) During the Past Five Years: Corporate |

| and Corporate Vice President (retired 2008) of Xerox | Vice President and Chief Global Diversity Officer |

| Corporation (document management products and | (retired 2008) and Member of the Executive |

| services); Executive in Residence and 2010 | Committee (1997–2008) of Johnson & Johnson |

| Distinguished Minett Professor at the Rochester | (pharmaceuticals/medical devices/consumer |

| Institute of Technology; Director of SPX Corporation | products); Director of Skytop Lodge Corporation |

| (multi-industry manufacturing), the United Way of | (hotels), the University Medical Center at Princeton, |

| Rochester, Amerigroup Corporation (managed health | the Robert Wood Johnson Foundation, and the Center |

| care), the University of Rochester Medical Center, | for Talent Innovation; Member of the Advisory Board |

| Monroe Community College Foundation, and North | of the Maxwell School of Citizenship and Public Affairs |

| Carolina A&T University. | at Syracuse University. |

| |

| Rajiv L. Gupta | F. Joseph Loughrey |

| Born 1945. Trustee Since December 2001.2 | Born 1949. Trustee Since October 2009. Principal |

| Principal Occupation(s) During the Past Five Years: | Occupation(s) During the Past Five Years: President |

| Chairman and Chief Executive Officer (retired 2009) | and Chief Operating Officer (retired 2009) of Cummins |

| and President (2006–2008) of Rohm and Haas Co. | Inc. (industrial machinery); Director of SKF AB |

| (chemicals); Director of Tyco International, Ltd. | (industrial machinery), Hillenbrand, Inc. (specialized |

| (diversified manufacturing and services), Hewlett- | consumer services), the Lumina Foundation for |

| Packard Co. (electronic computer manufacturing), | |

| |

| | |

| Education, and Oxfam America; Chairman of the | Executive Officers | |

| Advisory Council for the College of Arts and Letters | | |

| and Member of the Advisory Board to the Kellogg | Glenn Booraem | |

| Institute for International Studies at the University | Born 1967. Controller Since July 2010. Principal |

| of Notre Dame. | Occupation(s) During the Past Five Years: Principal |

| | of The Vanguard Group, Inc.; Controller of each of |

| Mark Loughridge | the investment companies served by The Vanguard |

| Born 1953. Trustee Since March 2012. Principal | Group; Assistant Controller of each of the investment |

| Occupation(s) During the Past Five Years: Senior Vice | companies served by The Vanguard Group (2001–2010). |

| President and Chief Financial Officer at IBM (information | | |

| technology services); Fiduciary Member of IBM’s | Thomas J. Higgins | |

| Retirement Plan Committee. | Born 1957. Chief Financial Officer Since September |

| | 2008. Principal Occupation(s) During the Past Five |

| Scott C. Malpass | Years: Principal of The Vanguard Group, Inc.; Chief |

| Born 1962. Trustee Since March 2012. Principal | Financial Officer of each of the investment companies |

| Occupation(s) During the Past Five Years: Chief | served by The Vanguard Group; Treasurer of each of |

| Investment Officer and Vice President at the University | the investment companies served by The Vanguard |

| of Notre Dame; Assistant Professor of Finance at the | Group (1998–2008). | |

| Mendoza College of Business at Notre Dame; Member | | |

| of the Notre Dame 403(b) Investment Committee; | Kathryn J. Hyatt | |

| Director of TIFF Advisory Services, Inc. (investment | Born 1955. Treasurer Since November 2008. Principal |

| advisor); Member of the Investment Advisory | Occupation(s) During the Past Five Years: Principal of |

| Committees of the Financial Industry Regulatory | The Vanguard Group, Inc.; Treasurer of each of the |

| Authority (FINRA) and of Major League Baseball. | investment companies served by The Vanguard |

| | Group; Assistant Treasurer of each of the investment |

| André F. Perold | companies served by The Vanguard Group (1988–2008). |

| Born 1952. Trustee Since December 2004. Principal | | |

| Occupation(s) During the Past Five Years: George | Heidi Stam | |

| Gund Professor of Finance and Banking at the Harvard | Born 1956. Secretary Since July 2005. Principal |

| Business School (retired 2011); Chief Investment | Occupation(s) During the Past Five Years: Managing |

| Officer and Managing Partner of HighVista Strategies | Director of The Vanguard Group, Inc.; General Counsel |

| LLC (private investment firm); Director of Rand | of The Vanguard Group; Secretary of The Vanguard |

| Merchant Bank; Overseer of the Museum of Fine | Group and of each of the investment companies |

| Arts Boston. | served by The Vanguard Group; Director and Senior |

| | Vice President of Vanguard Marketing Corporation. |

| Alfred M. Rankin, Jr. | | |

| Born 1941. Trustee Since January 1993. Principal | | |

| Occupation(s) During the Past Five Years: Chairman, | Vanguard Senior ManagementTeam |

| President, and Chief Executive Officer of NACCO | | |

| Industries, Inc. (forklift trucks/housewares/lignite); | Mortimer J. Buckley | Michael S. Miller |

| Director of Goodrich Corporation (industrial products/ | Kathleen C. Gubanich | James M. Norris |

| aircraft systems and services) and the National | Paul A. Heller | Glenn W. Reed |

| Association of Manufacturers; Chairman of the Board | Martha G. King | George U. Sauter |

| of the Federal Reserve Bank of Cleveland and of | Chris D. McIsaac | |

| University Hospitals of Cleveland; Advisory Chairman | | |

| of the Board of The Cleveland Museum of Art. | | |

| Chairman Emeritus and Senior Advisor |

| Peter F. Volanakis | | |

| Born 1955. Trustee Since July 2009. Principal | John J. Brennan | |

| Occupation(s) During the Past Five Years: President | Chairman, 1996–2009 | |

| and Chief Operating Officer (retired 2010) of Corning | Chief Executive Officer and President, 1996–2008 | |

| Incorporated (communications equipment); Director | | |

| of SPX Corporation (multi-industry manufacturing); | |

| Overseer of the Amos Tuck School of Business | Founder | |

| Administration at Dartmouth College; Advisor to the | | |

| Norris Cotton Cancer Center. | John C. Bogle | |

| Chairman and Chief Executive Officer, 1974–1996 | |

1 Mr. McNabb is considered an “interested person,” as defined in the Investment Company Act of 1940, because he is an officer of the Vanguard funds.

2 December 2002 for Vanguard Equity Income Fund, Vanguard Growth Equity Fund, the Vanguard Municipal Bond Funds, and the Vanguard State Tax-Exempt Funds.

|  |

| P.O. Box 2600 | |

| Valley Forge, PA 19482-2600 | |

Connect with Vanguard® > vanguard.com

| |

| Fund Information > 800-662-7447 | CFA® is a trademark owned by CFA Institute. |

| Direct Investor Account Services > 800-662-2739 | |

| Institutional Investor Services > 800-523-1036 | |

| Text Telephone for People | |

| With Hearing Impairment > 800-749-7273 | |

| |

| This material may be used in conjunction | |

| with the offering of shares of any Vanguard | |

| fund only if preceded or accompanied by | |

| the fund’s current prospectus. | |

| |

| All comparative mutual fund data are from Lipper Inc. or | |

| Morningstar, Inc., unless otherwise noted. | |

| |

| You can obtain a free copy of Vanguard’s proxy voting | |

| guidelines by visiting vanguard.com/proxyreporting or by | |

| calling Vanguard at 800-662-2739. The guidelines are | |

| also available from the SEC’s website, sec.gov. In | |

| addition, you may obtain a free report on how your fund | |

| voted the proxies for securities it owned during the 12 | |

| months ended June 30. To get the report, visit either | |

| vanguard.com/proxyreporting or sec.gov. | |

| |

| You can review and copy information about your fund at | |

| the SEC’s Public Reference Room in Washington, D.C. To | |

| find out more about this public service, call the SEC at | |

| 202-551-8090. Information about your fund is also | |

| available on the SEC’s website, and you can receive | |

| copies of this information, for a fee, by sending a | |

| request in either of two ways: via e-mail addressed to | |

| publicinfo@sec.gov or via regular mail addressed to the | |

| Public Reference Section, Securities and Exchange | |

| Commission, Washington, DC 20549-1520. | |

| |

| |

| | © 2012 The Vanguard Group, Inc. |

| | All rights reserved. |

| | Vanguard Marketing Corporation, Distributor. |

| |

| | Q9340 122012 |

|

|

| Annual Report | October 31, 2012 |

| Vanguard Mid-Cap Growth Fund |

|

|

|

> Vanguard Mid-Cap Growth Fund returned 10.24% for the fiscal year ended October 31, 2012.

> The fund outperformed its benchmark, the Russell Midcap Growth Index, and the average return of its mid-cap growth peers.

> The advisors’ strong stock selection within the industrial and information technology sectors helped boost the fund’s performance relative to the benchmark.

| |

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 7 |

| Fund Profile. | 11 |

| Performance Summary. | 12 |

| Financial Statements. | 14 |

| Your Fund’s After-Tax Returns. | 24 |

| About Your Fund’s Expenses. | 25 |

| Glossary. | 27 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Our cover photograph shows rigging on the HMSSurprise, a replica of an 18th-century Royal Navy frigate. It was featured in the 2003 movie Master and Commander: The Far Side of the World, which was based on Patrick O’Brian’s sea novels, set amid the Napoleonic Wars. Vanguard was named for another ship of that era, the HMSVanguard, which was the flagship of British Admiral Horatio Nelson at the Battle of the Nile.

Your Fund’s Total Returns

| |

| Fiscal Year Ended October 31, 2012 | |

| |

| | Total |

| | Returns |

| Vanguard Mid-Cap Growth Fund | 10.24% |

| Russell Midcap Growth Index | 9.09 |

| Mid-Cap Growth Funds Average | 7.02 |

| Mid-Cap Growth Funds Average: Derived from data provided by Lipper Inc. | |

Your Fund’s Performance at a Glance

October 31, 2011, Through October 31, 2012

| | | | |

| | | | Distributions Per Share |

| | Starting | Ending | Income | Capital |

| | Share Price | Share Price | Dividends | Gains |

| Vanguard Mid-Cap Growth Fund | $19.40 | $20.95 | $0.030 | $0.353 |

1

Chairman’s Letter

Dear Shareholder,

For the 12 months ended October 31, 2012, Vanguard Mid-Cap Growth Fund returned 10.24%. The fund easily outperformed its benchmark, the Russell Midcap Growth Index, which returned 9.09%, and it far exceeded the 7.02% average return of peer funds.

The fund posted positive returns in most sectors. It outperformed its market benchmark thanks in part to the advisors’ strong selections among information technology and industrial stocks.