UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | 811-07443 |

Name of Registrant: | Vanguard Whitehall Funds |

Address of Registrant: | P.O. Box 2600 |

| | Valley Forge, PA 19482 |

Name and address of agent for service: | Anne E. Robinson, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

Registrant’s telephone number, including area code: (610) 669-1000 |

Date of fiscal year end: October 31 |

Date of reporting period: November 1, 2015 – October 31, 2016 |

Item 1: Reports to Shareholders |

|

| Annual Report | October 31, 2016 |

| Vanguard Selected Value Fund |

A new format, unwavering commitment

As you begin reading this report, you’ll notice that we’ve made some improvements to the opening sections—based on feedback from you, our clients.

Page 1 starts with a new ”Your Fund’s Performance at a Glance,” a concise, handy summary of how your fund performed during the period.

In the renamed ”Chairman’s Perspective,” Bill McNabb will focus on enduring principles and investment insights.

We’ve modified some tables, and eliminated some redundancy, but we haven’t removed any information.

At Vanguard, we’re always looking for better ways to communicate and to help you make sound investment decisions. Thank you for entrusting your assets to us.

| |

| Contents | |

| Your Fund’s Performance at a Glance. | 1 |

| Chairman’s Perspective. | 3 |

| Advisors’ Report. | 7 |

| Fund Profile. | 12 |

| Performance Summary. | 13 |

| Financial Statements. | 15 |

| Your Fund’s After-Tax Returns. | 28 |

| About Your Fund’s Expenses. | 29 |

| Glossary. | 31 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: No matter what language you speak, Vanguard has one consistent message and set of principles. Our primary focus is on you, our clients. We conduct our business with integrity as a faithful steward of your assets. This message is shown translated into seven languages, reflecting our expanding global presence.

Your Fund’s Performance at a Glance

• Vanguard Selected Value Fund returned 2.20% for the 12 months ended October 31, 2016, trailing the 7.84% return of its benchmark, the Russell Midcap Value Index, and the 4.65% average return of its mid-capitalization value fund peers.

• Value stocks performed better than their growth counterparts, while large- and small-cap stocks exceeded mid-caps.

• As always, Selected Value’s three advisors depended on extensive research as they hunted for undervalued mid-cap companies.

• The fund’s consumer discretionary, industrial, and energy holdings all lagged their benchmark counterparts. Consumer discretionary lagged the most, finishing well behind the benchmark. Within that sector, cruise lines were the main culprit. Shortfalls in industrials and energy also hurt returns.

• For the ten years ended October 31, 2016, the fund’s average annual return of 6.95% slightly trailed that of its benchmark, which bears no expenses, and surpassed that of its peers.

| |

| Total Returns: Fiscal Year Ended October 31, 2016 | |

| | Total |

| | Returns |

| Vanguard Selected Value Fund | 2.20% |

| Russell Midcap Value Index | 7.84 |

| Mid-Cap Value Funds Average | 4.65 |

| Mid-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | |

| |

| |

| Total Returns: Ten Years Ended October 31, 2016 | |

| | Average |

| | Annual Return |

| Selected Value Fund | 6.95% |

| Russell Midcap Value Index | 7.19 |

| Mid-Cap Value Funds Average | 6.34 |

| Mid-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1

| | |

| Expense Ratios | | |

| Your Fund Compared With Its Peer Group | | |

| | | Peer Group |

| | Fund | Average |

| Selected Value Fund | 0.39% | 1.25% |

The fund expense ratio shown is from the prospectus dated February 25, 2016, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2016, the fund’s expense ratio was 0.35%. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2015.

Peer group: Mid-Cap Value Funds.

2

Chairman’s Perspective

Bill McNabb

Chairman and Chief Executive Officer

Dear Shareholder,

Over the three years ended August 31, 2016, investors poured more than $1 trillion into index funds. Indexing now accounts for nearly a third of all mutual fund assets—more than double what it did a decade ago and eight times its share two decades ago.1

By contrast, active management’s commercial struggles have reflected its disappointing investment performance. Over the decade ended December 31, 2015, 82% of actively managed stock funds and 81% of active bond funds have either underperformed their benchmarks or shut down.

This subpar performance has fueled the explosion of asset growth in indexing among individual, retirement, and nonprofit investors. So what might the trend mean for the future of actively managed funds?

Our research and experience indicate that active management can survive—and even succeed—but only if it’s offered at much lower expense.

High costs, which limit a manager’s ability to deliver benchmark-beating returns to clients, are the biggest reason why active has lagged. Industrywide as of December 31, 2015, the average expense ratio for all active stock funds is 1.14%, compared with 0.76% for stock index

1 Sources: Wall Street Journal; Morningstar, Inc.; and Investment Company Institute, 2016.

3

funds. And the expense advantage is even wider for bonds; the average expense ratio for an active bond fund is 0.93%, compared with 0.43% for bond index funds.

But even these big differences understate the real gap. These days, it’s not hard to find an index fund that charges maybe 0.05% or 0.10%. So even if you have identified active managers who are skilled at selecting stocks and bonds, to match the return of a comparable (much cheaper) index fund would require significant outperformance. Think about it. Any fund that charges 1.00% in expenses—not even the high end of the range—will find it extraordinarily difficult to overcome the index fund’s head start.

Active management also has taken a hit from a regulatory environment that has been favorable to low-cost strategies. The U.S. Department of Labor several years ago mandated greater disclosure of retirement plan fees. And its new fiduciary rule, which is set to take effect in April, requires financial advisors to demonstrate that their recommendations are aligned with their clients’ best interest. Both changes encourage the use of lower-cost investments, including index funds.

The future of active management

In light of all this, people have been asking me whether active management is “dead.” My response is both yes and no. High-cost active management is dead, and rightly so. It has never been a winning proposition

| | | |

| Market Barometer | | | |

| | | Average Annual Total Returns |

| | | Periods Ended October 31, 2016 |

| | One | Three | Five |

| | Year | Years | Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 4.26% | 8.48% | 13.51% |

| Russell 2000 Index (Small-caps) | 4.11 | 4.12 | 11.51 |

| Russell 3000 Index (Broad U.S. market) | 4.24 | 8.13 | 13.35 |

| FTSE All-World ex US Index (International) | 0.64 | -0.94 | 4.09 |

| |

| Bonds | | | |

| Bloomberg Barclays U.S. Aggregate Bond Index | | | |

| (Broad taxable market) | 4.37% | 3.48% | 2.90% |

| Bloomberg Barclays Municipal Bond Index | | | |

| (Broad tax-exempt market) | 4.06 | 4.89 | 4.34 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.22 | 0.07 | 0.07 |

| |

| CPI | | | |

| Consumer Price Index | 1.64% | 1.15% | 1.32% |

4

for investors. Low-cost active funds, though, can potentially play an important role for investors who seek to outperform the market.

Paying less for your funds is the only sure-fire way to improve your odds of achieving success in active management. But even if you have found an active manager with low costs, the odds of outperforming the market are still long. You have to be able to identify talented stock and bond portfolio managers with long time horizons and clear investment strategies. Look for managers with consistent track records and the discipline to stick closely to their investment strategy.

Know what you own and why

Despite the well-deserved reputation of indexing and the challenges for active managers, there’s still a place for traditional active strategies that are low-cost, diversified, and highly disciplined, and are run by talented managers who focus on the long term.

Vanguard has always applied these principles to our active strategies, and investors have benefited as a majority of our active funds outperformed their benchmarks and bested their peers’ average annual return over the ten years ended September 30, 2016.

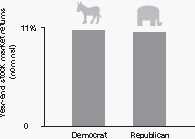

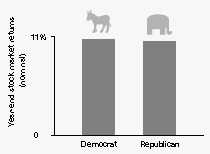

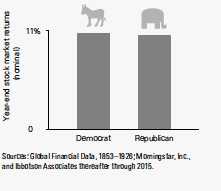

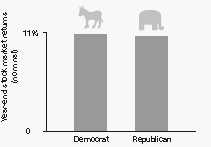

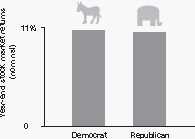

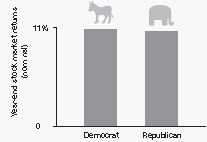

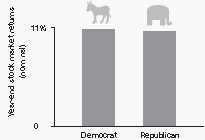

Worried about the election’s impact on your portfolio?

The 2016 presidential election season was one of the most intense and unpredictable in U.S. history. In its aftermath, investors may be left with lingering questions about what the outcome will mean for their portfolios. The answer, based on Vanguard research into decades of historical data, is that presidential elections typically have no long-term effect on market performance.

These findings hold true regardless of the market’s initial reaction. Whether there’s a swoon or bounce immediately after an election, investors shouldn’t extrapolate that performance to the long term.

As you can see in the accompanying chart, data going back to 1853 show that stock market returns are virtually identical no matter which party controls the White House. Although headlines out of Washington at any given time may still cause concern, investors

shouldn’t overreact to short-term events. Instead, it’s best to maintain a balanced and diversified portfolio and stay focused on your long-term goals.

Average annual stock market returns based on party control of the White House (1853–2015)

Sources: Global Financial Data, 1853–1926; Morningstar, Inc., and Ibbotson Associates thereafter through 2015.

5

But it’s crucial for investors to be patient. Even active managers with the best track records frequently underperform their benchmarks when their investment styles are out of favor. Such periods, though temporary, can persist. So it’s important when entrusting your assets to an active strategy to be in it for the long haul.

Make sure you know what you’re buying and what the risks are. Active strategies are becoming more complex, so it’s important to clearly understand what the investments in your portfolio are designed to accomplish and why you want to hold them. Otherwise, you run the risk of selecting strategies that don’t fit your needs or objectives.

Keeping these considerations in mind can potentially boost your chances of success in identifying active strategies that may be able to help you reach your goals.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

November 9, 2016

6

Advisors’ Report

For the fiscal year ended October 31, 2016, Vanguard Selected Value Fund returned 2.20%. Your fund is managed by three independent advisors. This provides exposure to distinct yet complementary investment approaches, enhancing the fund’s diversification. It is not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the percentage and amount of fund assets each manages, and a brief description of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal period and of how portfolio positioning reflects this assessment. (Please note that the Pzena Investment

Management discussion refers to industry sectors as defined by Russell classifications rather than the Global Industry Classification Standard used elsewhere in this report.) These comments were prepared on November 17, 2016.

Barrow, Hanley, Mewhinney &

Strauss, LLC

Portfolio Managers:

James P. Barrow,

Executive Director

Mark Giambrone,

Managing Director

The uncertainty and volatility of the last 12 months have created significant headwinds for our strategy. We began

| | | |

| Vanguard Selected Value Fund Investment Advisors | |

| |

| | Fund Assets Managed | |

| Investment Advisor | % | $ Million | Investment Strategy |

| Barrow, Hanley, Mewhinney & | 59 | 5,217 | Conducts fundamental research on individual stocks |

| Strauss, LLC | | | exhibiting traditional value characteristics: |

| | | | price/earnings and price/book ratios below the market |

| | | | average and dividend yields above the market average. |

| Pzena Investment Management, | 21 | 1,849 | Uses a fundamental, bottom-up, deep-value-oriented |

| LLC | | | investment strategy. Seeks to buy good businesses at |

| | | | low prices, focusing exclusively on companies that are |

| | | | underperforming their historically demonstrated |

| | | | earnings power. |

| Donald Smith & Co., Inc. | 18 | 1,567 | Conducts fundamental research on the lowest |

| | | | price-to-tangible book value companies. Research |

| | | | focuses on underlying quality of book value and assets, |

| | | | and on long-term earnings potential. |

| Cash Investments | 2 | 169 | These short-term reserves are invested by Vanguard in |

| | | | equity index products to simulate investment in stocks. |

| | | | Each advisor may also maintain a cash position. |

7

2016 anticipating several Federal Reserve rate increases, but global concerns sent the market plummeting early on, and investors began considering the possibility of negative interest rates in the United States. This first-quarter unease was followed by the unexpected Brexit vote toward the end of the second quarter—and all these events occurred during our own election cycle.

This scenario could not have been worse for our expectations and positioning, as we believe rates will rise slowly, economic growth will continue, and there will be some global stability. The already expensive areas of the market that benefit both from their defensive characteristics and lower-rate environments––including utilities and REITs, where we are underweight––did well over the period. Conversely, groups that need interest rates and the economy to improve steadily––including consumer discretionary, consumer finance, and industrials, where we are overweight––did poorly.

We believe we are positioned to take advantage of value in the market and that we are past the point of maximum uncertainty; we expect our performance to slowly recover throughout the year. An election year creates its own uncertainty and usually exerts some pressure on health care names (in which we are overweight); the largest overhang may not disappear until after the election. At that point, however, we expect valuations and cash flows to matter most. The portfolio is well situated to benefit from such an environment.

We continue to benefit from a pickup in merger and acquisition activity, as both St. Jude Medical and Tyco International were taken out during the period. If we are finding good companies with attractive valuations and cash flow, and the market doesn’t recognize this, a financial or strategic buyer certainly validates our process.

We are underweight utilities, technology, energy, and REITs. We believe traditional yield plays like utilities and REITs have had substantial runs thanks to a continued low interest rate environment and have very little room for valuation upside or meaningful yield relative to their own histories. We also see considerable risk to these valuation levels when interest rates rise.

Pzena Investment Management, LLC

Portfolio Managers:

Richard Pzena, Founder,

Chief Executive Officer, and

Co-Chief Investment Officer

John Flynn, Principal

Eli Rabinowich, Principal

Equity market returns were volatile over the 12 months, marked by plummeting energy prices in early 2016 and a surprise Brexit vote in June. Despite these head-winds, markets were solidly positive for the year. Our portfolio performed in line with the Russell Midcap Value Index, the fund’s benchmark, benefiting from positioning in technology and stock selection within energy and hindered

8

by the underperformance of some consumer discretionary and producer durables holdings.

Hard drive manufacturer Seagate Technology was the portfolio’s top individual contributor. We added to our position in the second quarter of 2016 as the stock declined on personal computer unit weakness that led to a severe decline in gross margins. The stock rebounded sharply during the most recent quarter as the company increased guidance on its cost-cutting efforts and end-market recovery. Also performing well in technology was Hewlett Packard Enterprise (enterprise information technology) as management continues to disassemble the business in order to unlock value. Within producer durables, Terex Corporation (machinery manufacturing) was a top contributor, helped by its continued initiatives to simplify the business and improve returns.

Staples (office supplies) and News Corp. (media and information services) were the leading detractors in the portfolio. Staples struggled as it announced that it would shut its stores in the United Kingdom, and may do the same in Continental Europe, because of declining sales. The company was hurt most from failing to get regulatory approval for its merger deal with Office Depot. We had long believed such an outcome to be possible and had limited our position size accordingly, and we believe the stock remains attractive. News Corp. shares were weak as the company showed continued deterioration in its newspapers business. The stock remains attractive based on its low valuation of 0.6 times book value and more than $3 per share in cash.

The exploitable pockets of cheapness continue to be in financial services, information technology (“old tech” companies that are more exposed to enterprise spending), and, to a growing extent, industrial cyclicals—areas where we have our largest exposures. We have significantly less exposure to sectors deemed “safe” by investors, such as health care, consumer staples, and utilities, where we believe valuations are at unattractive levels.

Donald Smith & Co., Inc.

Portfolio Managers:

Donald G. Smith, President

and Chief Investment Officer

Richard L. Greenberg, CFA,

Senior Vice President

The portfolio continues to meet our criteria of owning a concentrated selection of low price-to-tangible book value stocks with attractive long-term earnings potential. It currently sells at 106% of tangible book value and 8.2 times our estimate of “normalized earnings.” In contrast, the Standard & Poor’s 500 Index sells at over 7 times tangible book value and 17 times normalized earnings.

The rebound in precious metals and energy mirrored the rise in the underlying commodities and contributed most to returns. Top contributors included Yamana Gold (+62.6%) and Kinross Gold Corporation (+92.0%). WPX Energy (+58.3%) and Nabors (+18.5%) also contributed.

9

Continued surplus capacity and declining day rates meant that offshore drillers, such as Noble Corp. (–63.3%), did not do well.

While rebounding oil prices helped the energy sector, they also hindered the performance of previously strong airline/ aircraft leasing stocks, including JetBlue (–29.6%), Air France (–16.8%), and AerCap (–0.94%). Lower interest rates tend to push down financial stocks. Our financial exposure is primarily limited to insurance stocks, which on average lagged the market with single-digit returns. Everest Re was an exception, rising 14.4%. In technology, Ingram Micro (+24.9%) received a takeover offer from a Chinese conglomerate.

We eliminated our positions in a number of holdings, most of which had done well and met our targets. These included American National Insurance Company, Coeur Mining, New Gold, Royal Caribbean Cruises, Valero Energy Corporation, and Validus Holdings. We also trimmed positions in Aspen Insurance, Everest RE, Ingram Micro, JetBlue, Kinross Gold, WPX Energy, and XL Group, and added to our positions in AerCap, Air France-KLM, Celestica, MFA Financial, and Micron. We reduced our holdings in Yamana earlier in the period, and then bought some back later at a lower price. Three new names were added to the portfolio: Axis Capital, IAMGOLD Corporation, and Toll Brothers. Axis Capital is a Bermuda-based insurer/ reinsurer; IAMGOLD is an 800,000-ounce gold producer with mines in Africa and Canada; and Toll Brothers is a national builder of luxury homes.

Our largest position is in AerCap. The stock sells at 89% book value, below fair market value, and about 6 times our 2- to 4-year earnings estimate. AerCap has been aggressively selling planes at premiums to book value and redeploying proceeds to a stock buyback program. Our largest industry weightings are to insurance, technology, airlines/aircraft leasing, and metals.

The portfolio’s six insurance companies sell at an average of 95% of tangible book value. Hurt by low interest rates and the attendant low returns on investment portfolios, returns on equity have generally been in the high single digits. Higher interest rates, coupled with stock buyback programs at all six companies and the potential for takeover, should buoy the stocks. In technology, it appears that a better supply/demand situation has developed in memory, providing underlying support to Micron.

Finally, the precious metals stocks have been an obvious beneficiary of the recent rebound in gold and silver prices. While it may be difficult to predict the future direction of precious metal prices, several factors give us comfort in our position.

On a macro level, these factors include worldwide loose monetary policy, which has led to negative real (and in many cases nominal) interest rates in much of the developed world; strong and persistent central bank purchases of gold; rising wealth in countries with a historical affinity for gold (China and India); and a benign

10

outlook for gold supply, with few sizable projects on the horizon to replace depletion from older mines.

Our investment in the miners themselves is not necessarily predicated on rising gold prices. Each of them has company-specific projects or catalysts that have the potential to lead to sharply higher earnings, even assuming flat gold prices. The stocks are cheap on both historical price/book

value and price/revenues metrics, while cost-cutting efforts over the past few years should allow the companies to be at least cash flow breakeven, even if gold prices turn lower. Our preference has been to purchase companies that have the most sales and reserves relative to enterprise value; they also must have the balance-sheet strength to survive an extended period of lower prices.

11

Selected Value Fund

Fund Profile

As of October 31, 2016

| | | |

| Portfolio Characteristics | | |

| | | | DJ |

| | | | U.S. |

| | | Russell | Total |

| | | Midcap | Market |

| | | Value | FA |

| | Fund | Index | Index |

| Number of Stocks | 123 | 565 | 3,833 |

| Median Market Cap | $9.2B | $11.2B | $53.5B |

| Price/Earnings Ratio | 20.3x | 23.7x | 23.1x |

| Price/Book Ratio | 1.7x | 1.8x | 2.7x |

| Return on Equity | 11.7% | 10.0% | 16.6% |

| Earnings Growth | | | |

| Rate | 10.9% | 7.9% | 8.4% |

| Dividend Yield | 2.1% | 2.3% | 2.1% |

| Foreign Holdings | 10.9% | 0.0% | 0.0% |

| Turnover Rate | 27% | — | — |

| Ticker Symbol | VASVX | — | — |

| Expense Ratio1 | 0.39% | — | — |

| 30-Day SEC Yield | 1.78% | — | — |

| Short-Term | | | |

| Reserves | 1.7% | — | — |

| | | |

| Sector Diversification (% of equity exposure) |

| | | Russell | DJ |

| | | Midcap | U.S. Total |

| | | Value | Market |

| | Fund | Index | FA Index |

| Consumer | | | |

| Discretionary | 15.5% | 8.7% | 12.6% |

| Consumer Staples | 3.4 | 3.6 | 8.9 |

| Energy | 7.5 | 9.9 | 6.6 |

| Financials | 26.4 | 18.3 | 13.9 |

| Health Care | 4.0 | 4.5 | 13.4 |

| Industrials | 16.3 | 12.4 | 10.5 |

| Information | | | |

| Technology | 11.2 | 9.0 | 21.0 |

| Materials | 7.9 | 5.7 | 3.2 |

| Real Estate | 3.4 | 14.7 | 4.2 |

| Telecommunication | | | |

| Services | 0.1 | 1.5 | 2.3 |

| Utilities | 4.3 | 11.7 | 3.4 |

| | |

| Volatility Measures | | |

| | Russell | DJ |

| | Midcap | U.S. Total |

| | Value | Market |

| | Index | FA Index |

| R-Squared | 0.86 | 0.86 |

| Beta | 1.02 | 1.03 |

These measures show the degree and timing of the fund’s

fluctuations compared with the indexes over 36 months.

| | |

| Ten Largest Holdings (% of total net assets) |

| AerCap Holdings NV | Trading Companies & | |

| | Distributors | 2.1% |

| Royal Caribbean Cruises | Hotels, Resorts & | |

| Ltd. | Cruise Lines | 2.0 |

| Willis Towers Watson | | |

| plc | Insurance Brokers | 2.0 |

| Ingram Micro Inc. | Technology | |

| | Distributors | 1.9 |

| Micron Technology Inc. | Semiconductors | 1.9 |

| Capital One Financial | | |

| Corp. | Consumer Finance | 1.9 |

| Hanesbrands Inc. | Apparel, Accessories | |

| | & Luxury Goods | 1.9 |

| Reynolds American Inc. | Tobacco | 1.9 |

| Norwegian Cruise Line | Hotels, Resorts & | |

| Holdings Ltd. | Cruise Lines | 1.9 |

| Stanley Black & Decker | | |

| Inc. | Industrial Machinery | 1.9 |

| Top Ten | | 19.4% |

The holdings listed exclude any temporary cash investments and equity index products.

Investment Focus

1 The expense ratio shown is from the prospectus dated February 25, 2016, and represents estimated costs for the current fiscal year. For the fiscal year ended October 31, 2016, the expense ratio was 0.35%.

12

Selected Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

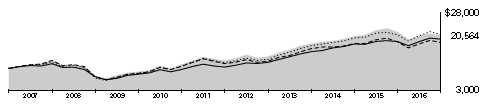

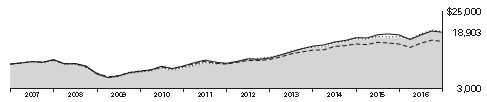

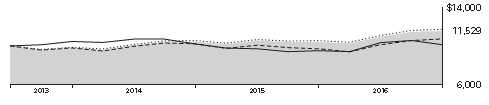

Cumulative Performance: October 31, 2006, Through October 31, 2016

Initial Investment of $10,000

| | | | |

| | Average Annual Total Returns | |

| | Periods Ended October 31, 2016 | |

| | | | | Final Value |

| | One | Five | Ten | of a $10,000 |

| | Year | Years | Years | Investment |

| Selected Value Fund | 2.20% | 12.16% | 6.95% | $19,585 |

| Russell Midcap Value Index | 7.84 | 14.07 | 7.19 | 20,033 |

| Mid-Cap Value Funds Average | 4.65 | 12.27 | 6.34 | 18,486 |

| Dow Jones U.S. Total Stock Market | | | | |

| Float Adjusted Index | 4.21 | 13.29 | 6.87 | 19,436 |

See Financial Highlights for dividend and capital gains information.

13

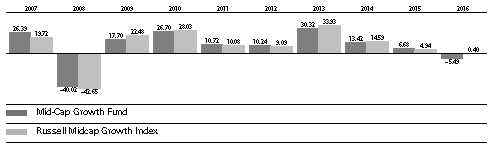

Selected Value Fund

Fiscal-Year Total Returns (%): October 31, 2006, Through October 31, 2016

Average Annual Total Returns: Periods Ended September 30, 2016

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| | | | |

| | Inception | One | Five | Ten |

| | Date | Year | Years | Years |

| Selected Value Fund | 2/15/1996 | 10.53% | 15.23% | 7.39% |

14

Selected Value Fund

Financial Statements

Statement of Net Assets

As of October 31, 2016

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (96.4%)1 | | |

| Consumer Discretionary (13.5%) | |

| | Royal Caribbean Cruises | | |

| | Ltd. | 2,344,500 | 180,222 |

| | Hanesbrands Inc. | 6,499,800 | 167,045 |

| * | Norwegian Cruise Line | | |

| | Holdings Ltd. | 4,283,100 | 166,484 |

| | Whirlpool Corp. | 989,800 | 148,292 |

| | L Brands Inc. | 1,671,200 | 120,644 |

| | Meredith Corp. | 1,495,544 | 67,823 |

| ^,2 | SeaWorld Entertainment | | |

| | Inc. | 4,546,700 | 63,699 |

| | Interpublic Group of Cos. | | |

| | Inc. | 2,152,894 | 48,203 |

| | News Corp. Class A | 3,579,375 | 43,382 |

| | Omnicom Group Inc. | 531,150 | 42,396 |

| | Dana Inc. | 2,360,300 | 36,538 |

| | Hilton Worldwide | | |

| | Holdings Inc. | 1,586,544 | 35,856 |

| * | Toll Brothers Inc. | 1,022,000 | 28,044 |

| | Staples Inc. | 3,090,600 | 22,870 |

| * | Adient plc | 343,886 | 15,650 |

| | | | 1,187,148 |

| Consumer Staples (3.0%) | | |

| | Reynolds American Inc. | 3,028,476 | 166,808 |

| | Coca-Cola European | | |

| | Partners plc | 1,820,000 | 69,961 |

| | Kellogg Co. | 337,425 | 25,351 |

| | | | 262,120 |

| Energy (7.3%) | | |

| | Devon Energy Corp. | 3,382,600 | 128,167 |

| ^ | Vermilion Energy Inc. | 2,812,100 | 110,459 |

| | PBF Energy Inc. Class A | 4,662,257 | 101,637 |

| ^ | Golar LNG Ltd. | 4,424,608 | 96,855 |

| | Murphy Oil Corp. | 1,521,653 | 39,365 |

| * | WPX Energy Inc. | 3,037,079 | 32,983 |

| | Cenovus Energy Inc. | 2,004,475 | 28,945 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Baker Hughes Inc. | 437,251 | 24,224 |

| | FMC Technologies Inc. | 637,475 | 20,571 |

| | Superior Energy Services | | |

| | Inc. | 1,120,132 | 15,861 |

| | Noble Corp. plc | 3,160,316 | 15,612 |

| | Rowan Cos. plc Class A | 996,725 | 13,226 |

| | Nabors Industries Ltd. | 885,000 | 10,531 |

| ^ | Tidewater Inc. | 556,400 | 963 |

| *,^ | Paragon Offshore plc | 870,105 | 243 |

| | | | 639,642 |

| Financials (25.9%) | | |

| | Willis Towers Watson plc | 1,392,045 | 175,258 |

| | Capital One Financial | | |

| | Corp. | 2,265,500 | 167,738 |

| | Discover Financial | | |

| | Services | 2,845,200 | 160,270 |

| | New York Community | | |

| | Bancorp Inc. | 10,701,500 | 153,673 |

| | Unum Group | 4,292,805 | 151,965 |

| | FNF Group | 3,258,500 | 117,013 |

| | KeyCorp | 7,651,825 | 108,044 |

| | Fifth Third Bancorp | 4,809,000 | 104,644 |

| | Navient Corp. | 7,757,647 | 99,143 |

| | Ameriprise Financial Inc. | 1,018,600 | 90,034 |

| | Voya Financial Inc. | 2,829,840 | 86,452 |

| | Axis Capital Holdings Ltd. | 1,509,138 | 85,976 |

| | CNA Financial Corp. | 2,259,996 | 82,648 |

| | Everest Re Group Ltd. | 401,462 | 81,705 |

| | XL Group Ltd. | 1,631,430 | 56,611 |

| | Comerica Inc. | 1,040,025 | 54,175 |

| ^ | Element Fleet | | |

| | Management Corp. | 5,546,200 | 54,044 |

| | Valley National Bancorp | 5,402,200 | 53,266 |

| | Regions Financial Corp. | 4,105,725 | 43,972 |

| | Invesco Ltd. | 1,501,950 | 42,190 |

| | Franklin Resources Inc. | 1,059,950 | 35,678 |

| | Webster Financial Corp. | 765,100 | 30,910 |

| * | SLM Corp. | 4,030,500 | 28,415 |

15

| | | |

| Selected Value Fund | | |

| |

| |

| |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Validus Holdings Ltd. | 541,925 | 27,692 |

| | Torchmark Corp. | 426,183 | 27,024 |

| | Endurance Specialty | | |

| | Holdings Ltd. | 260,000 | 23,907 |

| | MFA Financial Inc. | 3,014,000 | 22,032 |

| | Legg Mason Inc. | 639,775 | 18,374 |

| | Allstate Corp. | 269,225 | 18,280 |

| | Progressive Corp. | 495,225 | 15,604 |

| | Synovus Financial Corp. | 420,221 | 13,897 |

| | Hartford Financial Services | | |

| | Group Inc. | 313,800 | 13,842 |

| *,^ | ECN Capital Corp. | 5,545,900 | 12,115 |

| | Aspen Insurance Holdings | | |

| | Ltd. | 200,475 | 9,673 |

| | Genworth Financial Inc. | | |

| | Class A | 2,224,850 | 9,211 |

| | Assurant Inc. | 80,045 | 6,445 |

| | | | 2,281,920 |

| Health Care (3.5%) | | |

| | Cigna Corp. | 1,327,025 | 157,690 |

| | Cardinal Health Inc. | 1,903,900 | 130,779 |

| | Aetna Inc. | 154,800 | 16,618 |

| | | | 305,087 |

| Industrials (17.5%) | | |

| * | AerCap Holdings NV | 4,443,188 | 182,659 |

| | Stanley Black & Decker | | |

| | Inc. | 1,440,975 | 164,041 |

| | Owens Corning | 3,081,732 | 150,327 |

| * | Johnson Controls | | |

| | International plc | 3,438,864 | 138,655 |

| * | Spirit AeroSystems | | |

| | Holdings Inc. Class A | 2,715,407 | 136,748 |

| | Eaton Corp. plc | 2,018,900 | 128,745 |

| | KBR Inc. | 6,222,500 | 92,155 |

| * | JetBlue Airways Corp. | 5,138,340 | 89,818 |

| | Orbital ATK Inc. | 1,048,400 | 77,959 |

| | Ryder System Inc. | 1,008,600 | 69,987 |

| | CNH Industrial NV | 7,519,700 | 58,503 |

| *,^ | Air France-KLM ADR | 8,488,085 | 51,608 |

| | Terex Corp. | 2,115,440 | 50,517 |

| | Parker-Hannifin Corp. | 375,225 | 46,059 |

| | Dover Corp. | 664,325 | 44,437 |

| | AECOM | 1,380,510 | 38,447 |

| | Actuant Corp. Class A | 1,038,025 | 23,148 |

| | | | 1,543,813 |

| Information Technology (10.4%) | |

| | Ingram Micro Inc. | 4,595,009 | 170,934 |

| * | Micron Technology Inc. | 9,780,588 | 167,835 |

| | Microchip Technology Inc. | 2,250,200 | 136,250 |

| | Total System Services | | |

| | Inc. | 1,686,036 | 84,099 |

| | Hewlett Packard | | |

| | Enterprise Co. | 2,214,625 | 49,763 |

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | ON Semiconductor Corp. | 4,216,096 | 49,202 |

| | Avnet Inc. | 1,102,016 | 46,230 |

| | Seagate Technology plc | 1,257,575 | 43,147 |

| | Flex Ltd. | 2,982,200 | 42,317 |

| * | Celestica Inc. | 2,887,239 | 34,214 |

| | HP Inc. | 2,175,125 | 31,517 |

| | Genpact Ltd. | 1,016,327 | 23,365 |

| | Arrow Electronics Inc. | 304,204 | 18,593 |

| | Jabil Circuit Inc. | 711,890 | 15,192 |

| | CDW Corp. | 145,485 | 6,534 |

| | | | 919,192 |

| Materials (7.8%) | | |

| * | Kinross Gold Corp. | 42,300,000 | 163,278 |

| ^ | CRH plc ADR | 4,798,799 | 155,001 |

| | FMC Corp. | 2,840,000 | 133,168 |

| | Yamana Gold Inc. | | |

| | (New York Shares) | 20,405,340 | 72,643 |

| * | Axalta Coating Systems | | |

| | Ltd. | 2,846,500 | 71,504 |

| | Celanese Corp. Class A | 811,000 | 59,138 |

| * | IAMGOLD Corp. | 9,238,132 | 37,045 |

| | | | 691,777 |

| Real Estate (3.3%) | | |

| 2 | GEO Group Inc. | 3,840,700 | 92,023 |

| | Host Hotels & Resorts | | |

| | Inc. | 5,038,900 | 78,002 |

| | Lamar Advertising Co. | | |

| | Class A | 840,850 | 53,352 |

| | Corporate Office | | |

| | Properties Trust | 1,861,110 | 49,673 |

| | Hospitality Properties | | |

| | Trust | 583,800 | 15,973 |

| | | | 289,023 |

| Utilities (4.2%) | | |

| | Xcel Energy Inc. | 2,961,137 | 123,035 |

| | Pinnacle West Capital | | |

| | Corp. | 1,443,700 | 109,909 |

| | CenterPoint Energy Inc. | 2,167,817 | 49,426 |

| | Edison International | 558,150 | 41,013 |

| | PG&E Corp. | 312,425 | 19,408 |

| | Exelon Corp. | 483,693 | 16,480 |

| | NRG Energy Inc. | 796,234 | 8,464 |

| | | | 367,735 |

| Total Common Stocks | | |

| (Cost $6,952,508) | | 8,487,457 |

16

| | | | |

| Selected Value Fund | | | |

| |

| |

| |

| | | | | Market |

| | | | | Value• |

| | | | Shares | ($000) |

| Temporary Cash Investments (4.8%)1 | |

| Money Market Fund (4.7%) | | |

| 3,4 | Vanguard Market Liquidity | | |

| | Fund, 0.718% | 4,108,011 | 410,842 |

| |

| | | | Face | |

| | | | Amount | |

| | | | ($000) | |

| U.S. Government and Agency Obligations (0.1%) |

| 5,6 | Freddie Mac Discount Notes, | | |

| | 0.300%, 11/8/16 | | 600 | 600 |

| 6 | United States Treasury Bill, | | |

| | 0.296%–0.320%, 11/25/16 | 5,700 | 5,699 |

| 6 | United States Treasury Bill, | | |

| | 0.257–0.292%, 12/29/16 | 1,800 | 1,799 |

| 6 | United States Treasury Bill, | | |

| | 0.454%, 4/20/17 | | 200 | 200 |

| | | | | 8,298 |

| Total Temporary Cash Investments | |

| (Cost $419,115) | | | 419,140 |

| Total Investments (101.2%) | | |

| (Cost $7,371,623) | | | 8,906,597 |

| Other Assets and Liabilities (-1.2%) | |

| Other Assets | | | 20,626 |

| Liabilities 4 | | | (125,557) |

| | | | | (104,931) |

| Net Assets (100%) | | | |

| Applicable to 323,065,536 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 8,801,666 |

| Net Asset Value Per Share | | $27.24 |

| |

| | Amount |

| | ($000) |

| Statement of Assets and Liabilities | |

| Assets | |

| Investments in Securities, at Value | |

| Unaffiliated Issuers | 8,340,033 |

| Affiliated Vanguard Funds | 410,842 |

| Other Affiliated Issuers | 155,722 |

| Total Investments in Securities | 8,906,597 |

| Investment in Vanguard | 687 |

| Receivables for Investment Securities | |

| Sold | 9,597 |

| Receivables for Accrued Income | 7,197 |

| Receivables for Capital Shares Issued | 2,730 |

| Other Assets | 415 |

| Total Assets | 8,927,223 |

| Liabilities | |

| Payables for Investment Securities | |

| Purchased | (6,614) |

| Collateral for Securities on Loan | (93,713) |

| Payables to Investment Advisor | (3,716) |

| Payables for Capital Shares Redeemed | (10,483) |

| Payables to Vanguard | (10,716) |

| Other Liabilities | (315) |

| Total Liabilities | (125,557) |

| Net Assets | 8,801,666 |

17

Selected Value Fund

| |

| At October 31, 2016, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 6,888,746 |

| Undistributed Net Investment Income | 118,432 |

| Accumulated Net Realized Gains | 261,298 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 1,534,974 |

| Futures Contracts | (1,784) |

| Net Assets | 8,801,666 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Includes partial security positions on loan to broker-dealers. The total value of securities on loan is $87,621,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures

investments, the fund’s effective common stock and temporary cash investment positions represent 98.4% and 2.8%, respectively, of

net assets.

2 Considered an affiliated company of the fund as the fund owns more than 5% of the outstanding voting securities of such company.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the

7-day yield.

4 Includes $93,713,000 of collateral received for securities on loan.

5 The issuer was placed under federal conservatorship in September 2008; since that time, its daily operations have been managed by the

Federal Housing Finance Agency and it receives capital from the U.S. Treasury, as needed to maintain a positive net worth, in exchange

for senior preferred stock.

6 Securities with a value of $7,798,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

18

| |

| Selected Value Fund | |

| |

| |

| Statement of Operations | |

| |

| | Year Ended |

| | October 31, 2016 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends1 | 208,155 |

| Interest | 2,122 |

| Securities Lending—Net | 902 |

| Total Income | 211,179 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 19,809 |

| Performance Adjustment | (3,390) |

| The Vanguard Group—Note C | |

| Management and Administrative | 13,235 |

| Marketing and Distribution | 1,820 |

| Custodian Fees | 97 |

| Auditing Fees | 36 |

| Shareholders’ Reports | 163 |

| Trustees’ Fees and Expenses | 11 |

| Total Expenses | 31,781 |

| Expenses Paid Indirectly | (439) |

| Net Expenses | 31,342 |

| Net Investment Income | 179,837 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | 279,830 |

| Futures Contracts | 14,324 |

| Foreign Currencies | (32) |

| Realized Net Gain (Loss) | 294,122 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | (271,390) |

| Futures Contracts | (7,939) |

| Change in Unrealized Appreciation (Depreciation) | (279,329) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 194,630 |

| 1 Dividends are net of foreign withholding taxes of $526,000. | |

See accompanying Notes, which are an integral part of the Financial Statements.

19

| | |

| Selected Value Fund | | |

| |

| |

| Statement of Changes in Net Assets | | |

| |

| | Year Ended October 31, |

| | 2016 | 2015 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 179,837 | 163,790 |

| Realized Net Gain (Loss) | 294,122 | 379,722 |

| Change in Unrealized Appreciation (Depreciation) | (279,329) | (444,590) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 194,630 | 98,922 |

| Distributions | | |

| Net Investment Income | (150,373) | (138,609) |

| Realized Capital Gain1 | (347,588) | (401,073) |

| Total Distributions | (497,961) | (539,682) |

| Capital Share Transactions | | |

| Issued | 1,575,113 | 1,787,330 |

| Issued in Lieu of Cash Distributions | 457,613 | 496,488 |

| Redeemed | (2,591,075) | (2,333,003) |

| Net Increase (Decrease) from Capital Share Transactions | (558,349) | (49,185) |

| Total Increase (Decrease) | (861,680) | (489,945) |

| Net Assets | | |

| Beginning of Period | 9,663,346 | 10,153,291 |

| End of Period2 | 8,801,666 | 9,663,346 |

1 Includes fiscal 2016 and 2015 short-term gain distributions totaling $29,192,000 and $33,623,000, respectively. Short-term gain distributions

are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $118,432,000 and $106,036,000.

See accompanying Notes, which are an integral part of the Financial Statements.

20

| | | | | |

| Selected Value Fund | | | | | |

| |

| |

| Financial Highlights | | | | | |

| |

| |

| For a Share Outstanding | | | Year Ended October 31, |

| Throughout Each Period | 2016 | 2015 | 2014 | 2013 | 2012 |

| Net Asset Value, Beginning of Period | $28.15 | $29.49 | $28.07 | $21.01 | $18.81 |

| Investment Operations | | | | | |

| Net Investment Income | . 5271 | .478 | .415 | . 395 | .405 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | .030 | (.245) | 2.555 | 7.105 | 2.122 |

| Total from Investment Operations | .557 | .233 | 2.970 | 7.500 | 2.527 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (. 443) | (. 404) | (. 330) | (. 440) | (. 327) |

| Distributions from Realized Capital Gains | (1.024) | (1.169) | (1.220) | — | — |

| Total Distributions | (1.467) | (1.573) | (1.550) | (.440) | (.327) |

| Net Asset Value, End of Period | $27.24 | $28.15 | $29.49 | $28.07 | $21.01 |

| |

| Total Return2 | 2.20% | 0.88% | 11.02% | 36.43% | 13.64% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $8,802 | $9,663 | $10,153 | $7,019 | $4,337 |

| Ratio of Total Expenses to Average Net Assets3 | 0.35% | 0.39% | 0.41% | 0.43% | 0.38% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 2.00% | 1.62% | 1.53% | 1.70% | 2.00% |

| Portfolio Turnover Rate | 27% | 24% | 18% | 27% | 18% |

1 Calculated based on average shares outstanding.

2 Total returns do not include account service fees that may have applied in the periods shown. Fund prospectuses provide information about

any applicable account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of (0.04%), (0.02%), 0.01%, 0.02%, and (0.03%).

See accompanying Notes, which are an integral part of the Financial Statements.

21

Selected Value Fund

Notes to Financial Statements

Vanguard Selected Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

Futures contracts are valued at their quoted daily settlement prices. The aggregate settlement values of the contracts are not recorded in the Statement of Assets and Liabilities. Fluctuations in the value of the contracts are recorded in the Statement of Assets and Liabilities as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the year ended October 31, 2016, the fund’s average investments in long and short futures contracts represented 2% and 0% of net assets, respectively, based on the average of aggregate settlement values at each quarter-end during the period.

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (October 31, 2013–2016), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

22

Selected Value Fund

5. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are subject to termination by the fund at any time, and are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the absence of a default the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Assets and Liabilities for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan. During the term of the loan, the fund is entitled to all distributions made on or in respect of the loaned securities.

6. Credit Facility: The fund and certain other funds managed by The Vanguard Group (“Vanguard”) participate in a $3.1 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.10% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate based upon the higher of the one-month London Interbank Offered Rate, federal funds effective rate, or overnight bank funding rate plus an agreed-upon spread.

The fund had no borrowings outstanding at October 31, 2016, or at any time during the period then ended.

7. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

B. The investment advisory firms Barrow, Hanley, Mewhinney & Strauss, LLC, Donald Smith & Co., Inc., and Pzena Investment Management, LLC, each provide investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor. The basic fee of Barrow, Hanley, Mewhinney & Strauss, LLC, is subject to quarterly adjustments based on performance relative to the Russell Midcap Value Index for the preceding three years. The basic fee of Donald Smith & Co., Inc., is subject to quarterly adjustments based on performance relative to the MSCI Investable Market 2500 Index for the preceding five years. The basic fee of Pzena Investment Management, LLC, is subject to quarterly adjustments based on performance relative to the Russell Midcap Value Index since April 30, 2014.

23

Selected Value Fund

Vanguard manages the cash reserves of the fund as described below.

For the year ended October 31, 2016, the aggregate investment advisory fee represented an effective annual basic rate of 0.22% of the fund’s average net assets, before a decrease of $3,390,000 (0.04%) based on performance.

C. In accordance with the terms of a Funds’ Service Agreement (the “FSA”) between Vanguard and the fund, Vanguard furnishes to the fund corporate management, administrative, marketing, distribution, and cash management services at Vanguard’s cost of operations (as defined by the FSA). These costs of operations are allocated to the fund based on methods and guidelines approved by the board of trustees. Vanguard does not require reimbursement in the current period for certain costs of operations (such as deferred compensation/benefits and risk/insurance costs); the fund’s liability for these costs of operations is included in Payables to Vanguard on the Statement of Assets and Liabilities.

Upon the request of Vanguard, the fund may invest up to 0.40% of its net assets as capital in Vanguard. At October 31, 2016, the fund had contributed to Vanguard capital in the amount of $687,000, representing 0.01% of the fund’s net assets and 0.27% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and employees, respectively, of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended October 31, 2016, these arrangements reduced the fund’s expenses by $439,000 (an annual rate of 0.00% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the market value of the fund’s investments as of October 31, 2016, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 8,487,457 | — | — |

| Temporary Cash Investments | 410,842 | 8,298 | — |

| Futures Contracts—Assets1 | 6 | — | — |

| Futures Contracts—Liabilities1 | (314) | — | — |

| Total | 8,897,991 | 8,298 | — |

| 1 Represents variation margin on the last day of the reporting period. | | | |

24

Selected Value Fund

F. At October 31, 2016, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| | | | |

| | | | | ($000) |

| | | | Aggregate | |

| | | Number of | Settlement | Unrealized |

| | | Long (Short) | Value | Appreciation |

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| E-mini S&P 500 Index | December 2016 | 1,642 | 174,060 | (1,784) |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

During the year ended October 31, 2016, the fund realized net foreign currency losses of $32,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income.

The fund used a tax accounting practice to treat a portion of the price of capital shares redeemed during the year as distributions from net investment income and realized capital gains. Accordingly, the fund has reclassified $17,036,000 from undistributed net investment income, and $27,138,000 from accumulated net realized gains, to paid-in capital.

For tax purposes, at October 31, 2016, the fund had $129,021,000 of ordinary income and $259,750,000 of long-term capital gains available for distribution.

At October 31, 2016, the cost of investment securities for tax purposes was $7,372,296,000. Net unrealized appreciation of investment securities for tax purposes was $1,534,301,000, consisting of unrealized gains of $2,243,602,000 on securities that had risen in value since their purchase and $709,301,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended October 31, 2016, the fund purchased $2,352,037,000 of investment securities and sold $2,886,715,000 of investment securities, other than temporary cash investments.

25

| | |

| Selected Value Fund | | |

| |

| |

| |

| |

| I. Capital shares issued and redeemed were: | | |

| | Year Ended October 31, |

| | 2016 | 2015 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 63,300 | 62,441 |

| Issued in Lieu of Cash Distributions | 17,506 | 17,943 |

| Redeemed | (100,972) | (81,402) |

| Net Increase (Decrease) in Shares Outstanding | (20,166) | (1,018) |

J. Certain of the fund’s investments are in companies that are considered to be affiliated companies of the fund because the fund owns more than 5% of the outstanding voting securities of the company or the issuer is another member of The Vanguard Group. Transactions during the period in securities of these companies were as follows:

| | | | | | |

| | | | Current Period Transactions | |

| | Oct. 31, | | Proceeds | | | Oct. 31, |

| | 2015 | | from | | Capital Gain | 2016 |

| | Market | Purchases | Securities | | Distributions | Market |

| | Value | at Cost | Sold1 | Income | Received | Value |

| | ($000) | ($000) | ($000) | ($000) | ($000) | ($000) |

| GEO Group Inc. | — | 88,638 | — | 2,497 | — | 92,023 |

| SeaWorld Entertainment Inc. | 102,468 | — | 10,832 | 3,612 | — | 63,699 |

| SPX FLOW Inc. | 84,631 | — | 52,087 | — | — | — |

| Vanguard Market Liquidity Fund | 708,715 | NA2 | NA 2 | 2,076 | — | 410,842 |

| Vanguard Mid-Cap Value ETF | 29,626 | — | 29,453 | 283 | — | — |

| Total | 925,440 | | | 8,468 | — | 566,564 |

| 1 Includes net realized gain (loss) on affiliated investment securities sold of ($58,795,000). |

| 2 Not applicable—purchases and sales are for temporary cash investment purposes. |

K. Management has determined that no material events or transactions occurred subsequent to October 31, 2016, that would require recognition or disclosure in these financial statements.

26

Report of Independent Registered Public Accounting Firm

To the Board of Trustees of Vanguard Whitehall Funds and the Shareholders of Vanguard Selected Value Fund:

In our opinion, the accompanying statement of net assets, statement of assets and liabilities and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Selected Value Fund (constituting a separate portfolio of Vanguard Whitehall Funds, hereafter referred to as the “Fund”) at October 31, 2016, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2016 by correspondence with the custodian and brokers and by agreement to the underlying ownership records of the transfer agent, provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

December 15, 2016

Special 2016 tax information (unaudited) for Vanguard Selected Value Fund

This information for the fiscal year ended October 31, 2016, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $345,803,000 as capital gain dividends (20% rate gain distributions) to shareholders during the fiscal year.

For nonresident alien shareholders, 100% of short-term capital gain dividends distributed by the fund are qualified short-term capital gains.

The fund distributed $167,214,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 77.1% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

27

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2016. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| | | |

| Average Annual Total Returns: Selected Value Fund | | | |

| Periods Ended October 31, 2016 | | | |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | 2.20% | 12.16% | 6.95% |

| Returns After Taxes on Distributions | 0.88 | 11.16 | 6.08 |

| Returns After Taxes on Distributions and Sale of Fund Shares | 2.21 | 9.67 | 5.53 |

28

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

29

| | | |

| Six Months Ended October 31, 2016 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| Selected Value Fund | 4/30/2016 | 10/31/2016 | Period |

| Based on Actual Fund Return | $1,000.00 | $1,010.01 | $1.57 |

| Based on Hypothetical 5% Yearly Return | 1,000.00 | 1,023.58 | 1.58 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that period is 0.31%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period (184/366).

30

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but does not include the transaction costs of buying and selling portfolio securities.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

31

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

32

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 198 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. The mailing address of the trustees and officers is P.O. Box 876, Valley Forge, PA 19482. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at vanguard.com.

Interested Trustee1

F. William McNabb III