| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT |

| OF |

| REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act file number: 811-07537 |

| Name of Registrant: Royce Capital Fund |

| Address of Registrant: 745 Fifth Avenue |

| New York, NY 10151 |

| Name and address of agent for service: | John E. Denneen, Esq. | |||

| 745 Fifth Avenue | ||||

| New York, NY 10151 |

| Registrant’s telephone number, including area code: (212) 508-4500 |

| Date of fiscal year end: December 31, 2013 |

| Date of reporting period: January 1, 2014 – June 30, 2014 |

Item 1. Reports to Shareholders.

|

SEMIANNUAL

REVIEW AND REPORT

TO SHAREHOLDERS

Royce Capital Fund– Micro-Cap Portfolio Royce Capital Fund– Small-Cap Portfolio | |||

www.roycefunds.com |  | ||

| Performance and Expenses | Through June 30, 2014 |

| Average Annual Total Returns | Annual | ||||||||||||||||||||

| Since Inception | Operating | ||||||||||||||||||||

| Fund | Year-to-Date1 | One-Year | Five-Year | 10-Year | 15-Year | (12/27/96) | Expenses | ||||||||||||||

| Royce Capital Fund–Micro-Cap Portfolio | 1.01 | % | 18.32 | % | 14.33 | % | 7.36 | % | 11.30 | % | 11.73 | % | 1.34 | % | |||||||

| Royce Capital Fund–Small-Cap Portfolio | 1.94 | 22.19 | 17.81 | 9.44 | 12.02 | 12.15 | 1.05 | ||||||||||||||

| Russell Microcap Index2 | 1.56 | 24.98 | 20.03 | 6.67 | n.a. | n.a. | n.a. | ||||||||||||||

| Russell 2000 Index | 3.19 | 23.64 | 20.21 | 8.70 | 8.01 | 8.51 | n.a. | ||||||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. The Funds’ total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Funds. All performance and expense information reflects the result for each Fund’s Investment Class Shares. Service Class Shares bear an annual distribution expense that is not borne by the Investment Class; if the expenses were reflected, total returns would have been lower. Operating expenses reflect the Funds’ total annual operating expenses for the Investment Class as of the Funds’ most current prospectus and include management fees, other expenses and, in the case of Royce Capital Fund–Micro-Cap Portfolio, acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Series of Royce Capital Fund invest primarily in securities of micro-cap, small-cap and/or mid-cap companies, which may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Each series of Royce Capital Fund may invest up to 25% of their respective net assets in foreign securities. Investments in foreign securities may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see “Investing in Foreign Securities” in the prospectus.) Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Distributor: Royce Fund Services, Inc. |

| This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders |

| Table of Contents | |

| Semiannual Review | |

| Performance and Expenses Table | Inside Cover |

| Letter to Our Shareholders | 2 |

| 2014 In Quotes | 31 |

| Postscript: There’s No Such Thing as a Sure Thing | Inside Back Cover |

| Semiannual Report to Shareholders | 7 |

| |

| This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders | 1 |

Charles M. Royce, President The long-running, and probably unresolvable, debate about active versus passive investment strategies has taken on new life in the years since the onset of the Financial Crisis, often to the detriment of active approaches. To take one example, Morningstar compiled data showing that inflows into equity mutual funds have been dwarfed by those into equity ETFs (exchange traded funds) measuring from the momentous year of 2008. For the six calendar years from 2008-2013, traditional equity funds have taken in $5.52 billion while ETFs have attracted $389.08 billion. That’s quite a disparity. It seems to be no secret that many active managers have struggled to keep pace with their respective equity indexes in these often eventful years. These years have also seen a raft of studies purporting to show that most investment managers are unable to consistently beat the market, i.e., regularly outperform a relevant index such as the Russell 2000 or S&P 500 Indexes. Perhaps unsurprisingly, we would offer two caveats before one embraces uncritically the notion that passive Continued on page 4... | Letter to Our Shareholders No Drama Whatever other opinions we may all hold about the stock market’s behavior over the last six years, we think everyone can agree that it has certainly been dramatic. The action began in earnest in the fall of 2008, although it is important to recall that small-cap stock prices had actually been falling for more than a year prior to that—the peak for the Russell 2000 Index having been established on July 13, 2007. Yet the full effects of the bear were unleashed by the events of the Financial Crisis, which keyed the dangerously precipitous nosedive of share prices in the fall of 2008. The tumult lasted until small-caps finally hit a bottom on March 9, 2009. The fear and anxiety the descent created, however, reached into the next several years. The feeling of extraordinary fragility that characterized the early days of the recovery in the spring of 2009 did not magically evaporate when markets began to find their feet again. In fact, one could argue that these emotions dominated the behavior of investors at least until the end of 2012. The three years from 2010 through 2012 were eventful, even if the stress and excitement they generated did not equal that of the first six months of 2009. In fact, much of the market’s most extreme moves in that entire four-year span (2009-2012) took place in the first six months of those years, driven in large part by events both actual and potential. The recession in the U.S., debt issues in Europe, and slow growth in China were all very real, while a double-dip recession here at home, default in Europe, and implosion in China fortunately failed to materialize. By the end of 2012, with the stock market climbing and the economy expanding, investors seemed to recognize that, in spite of high volatility and political uncertainty, equity returns had been solidly positive since the March 2009 bottom. This improved confidence helped to spur a different kind of dramatic arc. The long, slow recovery entered a new phase in 2013—a heady, and virtually correction-free, bull run in which returns for each of the major domestic stock indexes topped 30%. | ||

| 2 | This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders |

The curtain opened on 2014, then, on the heels of one of the better calendar-year performances in the history of domestic equities, which followed four consecutive years of mostly rising stock prices in an uncertain economy. So the question now is, what is the next act for equities? Some argue that the economy is not strong enough to really take flight. They worry about the rich valuations sported by large numbers of stocks. Others see the relative absence of volatility as a sign of complacency and fret that stocks are about to enter a destructive bear phase. There are those who point to increasingly unsettled international situations, such as in Ukraine, Syria, and Iraq, and argue that the market cannot continue to pretend that events in these nations take place far offstage, not in an increasingly intertwined global economy. | Quality companies, particularly those in our chosen small-cap space, have not yet emerged as leaders, but they have inched closer over the last two years. Correlation levels throughout the market are falling. These are excellent conditions, in our view, for disciplined active management approaches, especially those with a long-term investment horizon. | |||

We, however, are in accord with the more widespread consensus that sees the U.S. economy as gradually normalizing. As evidence we would point to the following: The deficit continues to fall, the Fed continues to wind down the rate of its monthly bond purchases, and interest rates, though they remain close to zero, look likely to rise again in the near future as they did last year between May and December. Inflation is tame, commodity prices stable. Volatility, as measured by the VIX, finished the first half of 2014 at low levels not seen since 2007. Add an increasingly robust M&A market, and it seems to us that the recipe for ongoing growth—and bullishness, however mild, at least compared to last year—seems almost complete. And this process of normalization looks likely to accelerate as the Fed’s role recedes further and further into the background, setting the stage for a more dynamic pace of growth. | ||||

So while there remain voices who insist that stocks are overvalued, we think the case for additional gains, which could include a correction along the way, remains persuasive. It seems to us that the relatively lower returns of the first half of 2014 indicate not an end to a bull phase, but a chance for the market to catch its breath and assess its surroundings. It may be that investors need a break from all the drama, a respite from the unrelenting pace of the last six years. So the desire to stand back for a moment and evaluate what is happening seems eminently reasonable. How many investors have enjoyed more than a few moments of true calm since before the recession began back in 2007? Ultimately, we suspect that both the expanding economy and slower pace of returns will result in more fundamentally focused investors. | ||||

| Indeed, the indications that the strength of companies and the businesses they manage are beginning to matter more than indexes and the macro events that move them go back to the spring of 2012, when quality stocks—those with high returns on invested capital—enjoyed a brief run of outperformance. This nascent phenomenon re-started—again, briefly—in May 2013 when the 10-year Treasury rate reached a bottom. Quality companies, particularly those in our chosen small-cap space, have not yet emerged as leaders, but they have inched closer over the last two years. Correlation levels throughout the market are falling. These are excellent conditions, in our view, for disciplined active management approaches, especially those with a long-term investment horizon. | ||||

| This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders | 3 |

investing is always better: First, a number of managers have consistently outperformed the market over long- term periods and especially within the small-cap asset category. In fact, we believe strongly in the idea that it is not necessary for all managers to beat the market in order for active management to be validated as an approach. Our second note of caution relates to time periods. While it would be nice to outperform an index every year, it is just as unrealistic to expect that as it would be to expect an index to outperform active management every year. It is also unrealistic to expect a high degree of outperformance in the long term without experiencing some short-term underperformance periods. A willingness to stick to one’s approach, regardless of market movements and trends, is critical to long-term outperformance in our opinion. This is especially important during market extremes because there are active managers who exhibit style drift or other changes in their discipline when their investment style falls out of favor or is stressed, such as during the tech bubble. Successful active management also entails a willingness to think independently in terms of sector and industry weightings. It is not unusual for the most successful managers to be significantly out of sync relative to a Continued on page 6... | |||

| Letter to Our Shareholders | ||

| No Direction Home U.S. stocks turned in a respectable performance in the first half of 2014. If results were not as lofty as they were in the first half of 2013 (and they were not), they were achieved in a more tranquil domestic environment than in the first halves of 2010, 2011, or 2012. One consequence of the more relaxed atmosphere of the first half was that stocks did not seem to know quite what to do with themselves. While the overvalued/not-quite-overvalued-yet argument goes on, the market has not established a clear direction so far in 2014. The bull has so far remained in place during the current cycle; he simply slowed his run to a brisk walk in the first half. For the year-to-date period ended June 30, 2014, the major domestic indexes remained in the black. The small-cap Russell 2000 Index gained 3.2%, taking a back seat to the more tech-oriented Nasdaq Composite, which advanced 5.5% in the first half, and the large-cap S&P 500 and Russell 1000 Indexes, which scored respective gains of 7.1% and 7.3% for the year-to-date period ended June 30, 2014. The year began on a more moderate note following a red-hot second half of 2013. Nevertheless, 2014’s opening quarter was the seventh consecutive quarter of positive performance for the Russell 2000, which rose 1.1%. Large-caps led for the quarter—the S&P 500 and Russell 1000 gained 1.8% and 2.0%, respectively, while the Nasdaq Composite rose 0.5%. Small-caps reached a first-half high on March 4, and the only correction so far this year was the 9.1% drop for the Russell 2000 from that date through May 15, 2014. April was thus the cruelest month, but a series of mini-rallies from mid-May through the end of June made the second quarter mostly positive. The Russell 2000 posted its eighth consecutive positive quarter, up 2.0%. Once again, large-cap outperformed, with the S&P 500 advancing 5.2% and the Russell 1000 up 5.1% for the second quarter. The Nasdaq bounced back strong as well, climbing 5.0% in the second quarter and leaving only the small-cap index out of the five-percent club. Small-cap held onto leadership outside the U.S. In the first quarter, the Russell Global ex-U.S. Small Cap Index was up 3.2% while the Russell Global ex-U.S. Large Cap Index rose 0.8%. Results were stronger in the second quarter and, as in the first, closer to their domestic counterparts than we have seen in a while. For the second quarter, the Russell Global ex-U.S. Small Cap was up 4.2% versus 5.0% for the Russell Global ex-U.S. Large Cap. Year-to-date, non-U.S. small-caps had the edge, with the Russell Global ex-U.S. Small Cap returning 7.5% versus a gain of 5.8% for the Russell Global ex-U.S. Large Cap. After a challenging first quarter, many Asian equities bounced back in the second and finished closer to the European indexes, most of which had been on a tear prior to cooling off in the second quarter. Moving back to the U.S., mid-caps and micro-caps were equally solid in the first quarter. The Russell Midcap Index was up 3.5% versus a gain of 3.0% for the Russell Microcap Index in 2014’s first three months. This pattern broke down around the time of the March 4 small-cap high and can be seen in the second-quarter results for each index. The Russell Midcap continued its notable 2014 performance, rising 5.0% in the second quarter. This gave mid-caps an impressive 8.7% advance on a year-to-date basis. In contrast, micro-caps |

| 4 | This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders |

| U.S. stocks turned in a respectable performance in the first half of 2014. If results were not as lofty as they were in the first half of 2013 (and they were not), they were achieved in a more tranquil domestic environment than in the first halves of 2010, 2011, or 2012. We are very bullish about the prospects for active small-cap management... we have reached a point at which active management in small-cap stocks simply makes more sense, especially for long-term investors. |

| This page is not part of the Royce Capital Fund 2014 Semiannual Report to Shareholders | 5 |

benchmark index with respect to industry and sector weightings (commonly referred to as tracking error). In addition, active managers are not required to invest cash inflows at the time of receipt when market conditions or prices may not be conducive. They may screen for quality and use buy/sell triggers as a means of reducing risk. While a passive manager must own everything, an active manager has the freedom to look for attractive stocks across the targeted universe. All of this helps to explain why we remain so fond of small-caps and so confident in the effectiveness and value of active approaches in the asset class. Active small-cap managers can capture valuation opportunities beyond their respective indexes—an opportunity that would be lost if one were limited to owning only the constituents that make up the index. For example, the Russell 2000, while quite broad, only includes about 2,000 of the more than 4,100 companies1 that make up the domestic small-cap universe (those with market caps up to $2.5 billion). While self-serving, we nevertheless think that the small-cap asset class is ideally suited for active management given its enormous size, lack of institutional focus, and limited research availability. 1 Source: Reuters as of 6/30/14 | Letter to Our Shareholders Know This We feel somewhat fortunate in that we do not need to choose a side in the “overvalued versus ongoing bull market” debate. Rather than trying to make a correct market call, our attention has been focused on those potential opportunities that can materialize even in a widespread bull market. Corrections can arrive at any time, of course, and it has been a while since we have seen one of any significance. The last downturn of more than 10% for the Russell 2000 occurred in the fall of 2012. And share prices recovered so quickly from the 9.1% March-May decline this year that the down phase barely registered. This might lead one to argue that the market is being set up for at least a decent-sized pullback. Our sense, however, is that we are more likely to see smaller ones in the 5-10% range as part of the ongoing bull phase. Against the backdrop of an economy that looks poised for faster growth, a Fed tapering at a healthy clip, and an interest-rate environment in which a steady rate of increase is much more of a “when” than an “if,” less severe downturns look more likely. Small-cap valuations on the whole are above average, though not unreasonably so given near-zero interest rates and low inflation. A number of anomalies remain in the market, and in many cases we see a wide disparity between what look to us like expensive stocks and those that look inexpensive on an absolute basis. The market seems to be in the process of sorting that out—certainly those areas of the market that do not interest us, and that did well in 2012 and 2013, have been more volatile so far in 2014. In addition, we are still seeing companies that look attractively valued to us based on their fundamentals. All in all, it is looking more and more like a stock-picker’s market to us. We could see the second half of the year being pretty similar to the first in terms of the overall returns for stocks. More important, we think there are still enough opportunities out there to keep returns in positive territory through the end of 2014. This could make the market’s next act a very happy one for active small-cap managers. Sincerely, | ||||||

|  |  | |||||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | |||||

| President | Co-Chief Investment Officer, Royce & Associates | Co-Chief Investment Officer, Royce & Associates | |||||

| July 31, 2014 | |||||||

| 6 | Royce Capital Fund 2014 Semiannual Report to Shareholders |

| Table of Contents |

| Semiannual Report to Shareholders | ||||||||||

| Managers’ Discussions of Fund Performance | ||||||||||

| Royce Capital Fund–Micro-Cap Portfolio | 8 | |||||||||

| Royce Capital Fund–Small-Cap Portfolio | 10 | |||||||||

| Schedules of Investments and Financial Statements | 12 | |||||||||

| Notes to Financial Statements | 22 | |||||||||

| Understanding Your Fund’s Expenses | 26 | |||||||||

| Trustees and Officers | 27 | |||||||||

| Board Approval of Investment Advisory Agreements | 28 | |||||||||

| Notes to Performance and Other Important Information | 30 | |||||||||

| Royce Capital Fund 2014 Semiannual Report to Shareholders | 7 |

| Royce Capital Fund–Micro-Cap Portfolio |

AVERAGE ANNUAL TOTAL RETURNS Through 6/30/14 | ||||||||||

| January–June 20141 | 1.01 | % | ||||||||

| One-Year | 18.32 | |||||||||

| Three-Year | 3.99 | |||||||||

| Five-Year | 14.33 | |||||||||

| 10-Year | 7.36 | |||||||||

| 15-Year | 11.30 | |||||||||

| Since Inception (12/27/96) | 11.73 | |||||||||

| ANNUAL EXPENSE RATIO | ||||||||||

| Operating Expenses | 1.34 | % | ||||||||

| 1 Not annualized. | ||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||

| Year | RCM | Year | RCM | |||||||

| 2013 | 21.0 | % | 2005 | 11.6 | % | |||||

| 2012 | 7.6 | 2004 | 13.8 | |||||||

| 2011 | -12.1 | 2003 | 49.2 | |||||||

| 2010 | 30.1 | 2002 | -12.9 | |||||||

| 2009 | 57.9 | 2001 | 29.7 | |||||||

| 2008 | -43.3 | 2000 | 18.5 | |||||||

| 2007 | 4.0 | 1999 | 28.1 | |||||||

| 2006 | 21.1 | 1998 | 4.1 | |||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||

| Total Energy Services | 1.4 | % | ||||||||

| Kennedy-Wilson Holdings | 1.3 | |||||||||

| Patriot Transportation Holding | 1.3 | |||||||||

| Foster (L.B.) Company | 1.2 | |||||||||

| Tesco Corporation | 1.2 | |||||||||

| Universal Stainless & Alloy Products | 1.1 | |||||||||

| Resources Connection | 1.1 | |||||||||

| Stein Mart | 1.1 | |||||||||

| Marten Transport | 1.1 | |||||||||

| U.S. Physical Therapy | 1.0 | |||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||

| Industrials | 24.4 | % | ||||||||

| Consumer Discretionary | 14.1 | |||||||||

| Information Technology | 13.7 | |||||||||

| Health Care | 9.3 | |||||||||

| Materials | 8.8 | |||||||||

| Energy | 8.5 | |||||||||

| Financials | 8.2 | |||||||||

| Consumer Staples | 0.9 | |||||||||

| Utilities | 0.1 | |||||||||

| Miscellaneous | 4.1 | |||||||||

| Cash and Cash Equivalents | 7.9 | |||||||||

| |||||||||

Manager’s Discussion Royce Capital Fund–Micro-Cap Portfolio (RCM) finished the year-to-date period ended June 30, 2014 with an advance of 1.0% versus respective gains of 1.6% for its benchmark, the Russell Microcap Index, and 3.2% for the small-cap Russell 2000 Index for the same period. Following a wonderfully bullish 2013, stocks as a group cooled down in the opening months of 2014, though returns for the most part remained solidly in the black. The Fund’s participation was more limited than we would prefer. The year began with many share prices accelerating at a slower pace than they did in the torrid second half of 2013. The Fund, however, fell out of step with the market as a whole—and micro-caps more specifically—during both that highly bullish phase and the more moderate market that ushered in 2014. RCM was down 0.8% in the first quarter versus a gain of 3.0% for the Russell Microcap and 1.1% for the Russell 2000. The Fund’s results improved in the second quarter, which saw the year’s only correction so far. In fact, its performance from the interim small-cap high on March 4 through the end of June was better than both the micro-cap and small-cap indexes, which gave a boost to quarterly results. For the second quarter, RCM advanced 1.8% compared to a decline of 1.4% for the Russell Microcap and an increase of 2.0% for the Russell 2000. A look at longer-term periods showed a healthier advantage. The Fund outpaced the Russell Microcap for the 10-year period ended June 30, 2014. (Data for this index only goes back to June 30, 2000.) RCM also beat the Russell 2000 for the 15-year and since inception (12/27/96) periods ended June 30, 2014. The Fund’s average annual total return since inception was 11.7%. We are very proud of RCM’s long-term performance record. The Fund’s overweight in Energy was a factor as 2014 wore on—the sector’s strong second-quarter results made it the portfolio’s top-performing sector for the year-to-date period ended June 30, 2014. In the micro-cap space we have invested in a large number of E&P (exploration & production) companies and energy services businesses. While the former are often more volatile, we have found a number of conservatively capitalized services companies that we think are well-managed businesses. We also believe that Triangle Petroleum offers an attractive, though high-risk/high-reward opportunity. A Denver-based E&P business, its share price was volatile through much of the first half, though its overall direction was up. | |||||||||

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 6/30/141 | |||||||||||

| Furiex Pharmaceuticals | 0.42% | ||||||||||

| VASCO Data Security International | 0.41 | ||||||||||

| Super Micro Computer | 0.30 | ||||||||||

| Triangle Petroleum | 0.28 | ||||||||||

| Kennedy-Wilson Holdings | 0.27 | ||||||||||

| 1 Includes dividends. | |||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCM’s Service Class bear an annual distribution expense that is not borne by the Investment Class. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2014. | |||||||||||

| 8 | Royce Capital Fund 2014 Semiannual Report to Shareholders |

Performance and Portfolio Review Moving quickly, in just two years, from exploration to production helped attract interest in the stock. We liked its prospects going forward, modestly trimming our shares in the first half. The Fund’s top performer was Furiex Pharmaceuticals, which was acquired by Forest Laboratories at a healthy premium. The announcement came in April, when we sold our position. We were drawn first to its royalty & revenues on two approved drugs and to promising results for an IBS (irritable bowel syndrome) drug. VASCO Data Security International specializes in bank security and develops security systems to secure and manage access to user digital assets. Its stock made two significant upticks in the first half. In February, its shares rose on better-than-expected fourth quarter of 2013 earnings and a strong outlook for fiscal 2014. Increased revenues and ongoing earnings strength saw the shares getting another major boost late in April, especially with HSBC, USA, its customer, offering VASCO authentication solutions to its retail customers. A disappointing holiday season and a miserably cold winter spelled tough times for many consumer stocks in both the Discretionary and Staples sectors. Seeing better times ahead, we held onto our shares of Shoe Carnival, a family footwear retailer based in Indiana. The company has a history of strong top-line growth and what we think are reasonable and intelligent plans to both grow and improve its business. It was RCM’s fifteenth-largest holding at the end of June. After a very successful 2013, we were not shocked to see some pullback for transportation and real estate business Patriot Transportation Holding. The stock is thinly traded and tightly held, so transactions tend to have an outsized effect on its shares. Earnings cooled down a bit during the first half, but we think its core strategic business realignment remains on track. Over the past several years, we have been finding some of the most attractive micro-cap valuations in more economically sensitive sectors. The Fund’s largest sector weightings at the end of the period reflected this, with Industrials at 24.4% and Information Technology at 13.7%. The portfolio also remained overweight versus the Russell Microcap in other cyclical sectors, most notably Energy and Materials. Our view is that many portfolio holdings in these (and other) sectors can benefit from a faster-growing economy in which the Fed’s quantitative easing program comes to a close and interest rates are rising. Such an environment is likely to reward disciplined active approaches that focus on fundamentals such as strong balance sheets and high returns on invested capital. So while we remain frustrated by the Fund’s recent performance record, we are confident in its prospects going forward. |

GOOD IDEAS AT THE TIME | |

| Shoe Carnival | -0.38% |

| Patriot Transportation Holding | -0.25 |

| Destination Maternity | -0.24 |

| TGC Industries | -0.22 |

| Global Power Equipment Group | -0.22 |

| 1 Net of dividends. | |

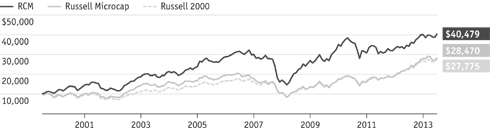

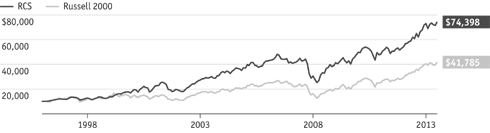

| ROYCE CAPITAL FUND–MICRO-CAP PORTFOLIO VS. RUSSELL MICROCAP AND RUSSELL 2000 Value of $10,000 Invested on 6/30/00 (Russell Microcap Inception) | |||

| |||

| Includes reinvestment of distributions. |

| FUND INFORMATION AND PORTFOLIO DIAGNOSTICS | |||

| Fund Net Assets | $579 million | ||

| Number of Holdings | 206 | ||

| Turnover Rate | 12% | ||

| Average Market Capitalization1 | $437 million | ||

| Weighted Average P/E Ratio2,3 | 21.9x | ||

| Weighted Average P/B Ratio2 | 1.7x | ||

| U.S. Investments (% of Net Assets) | 78.2% | ||

| Non-U.S. Investments (% of Net Assets) | 13.9% | ||

| Ticker Symbol | |||

| Investment Class | RCMCX | ||

| Service Class | RCMSX | ||

1Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. | |||

2Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings of its underlying stocks. | |||

| STATISTICAL MEASURES Five-Year Period Ended 6/30/14 | |||

| Sharpe Ratio | Standard Deviation | ||

| RCM | 0.84 | 17.87 | |

| Russell Microcap | 1.04 | 19.40 | |

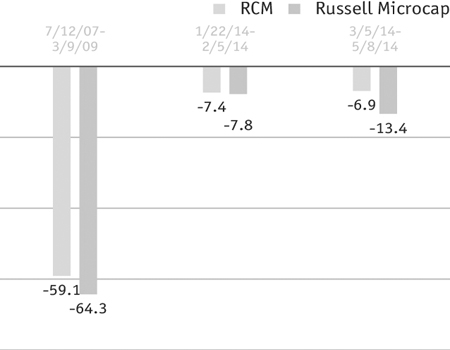

| DOWN MARKET PERFORMANCE COMPARISON All Down Periods of 7.5% or Greater Over the Last 7 Years, in Percentages (%) | |||

| |||

| Royce Capital Fund 2014 Semiannual Report to Shareholders | 9 |

| Royce Capital Fund–Small-Cap Portfolio |

AVERAGE ANNUAL TOTAL RETURNS Through 6/30/14 | ||||||||||

| January–June 20141 | 1.94 | % | ||||||||

| One-Year | 22.19 | |||||||||

| Three-Year | 12.40 | |||||||||

| Five-Year | 17.81 | |||||||||

| 10-Year | 9.44 | |||||||||

| 15-Year | 12.02 | |||||||||

| Since Inception (12/27/96) | 12.15 | |||||||||

| ANNUAL EXPENSE RATIO | ||||||||||

| Operating Expenses | 1.05 | % | ||||||||

| 1 Not annualized. | ||||||||||

| CALENDAR YEAR TOTAL RETURNS | ||||||||||

| Year | RCS | Year | RCS | |||||||

| 2013 | 34.8 | % | 2005 | 8.6 | % | |||||

| 2012 | 12.5 | 2004 | 25.0 | |||||||

| 2011 | -3.3 | 2003 | 41.1 | |||||||

| 2010 | 20.5 | 2002 | -13.8 | |||||||

| 2009 | 35.2 | 2001 | 21.0 | |||||||

| 2008 | -27.2 | 2000 | 33.3 | |||||||

| 2007 | -2.1 | 1999 | 8.2 | |||||||

| 2006 | 15.6 | 1998 | 8.9 | |||||||

| TOP 10 POSITIONS % of Net Assets | ||||||||||

| Steven Madden | 3.2 | % | ||||||||

| Plantronics | 3.1 | |||||||||

| Unit Corporation | 3.0 | |||||||||

| NETGEAR | 3.0 | |||||||||

| Vishay Intertechnology | 3.0 | |||||||||

| Genesco | 3.0 | |||||||||

| Fabrinet | 3.0 | |||||||||

| Buckle (The) | 2.7 | |||||||||

| Chemed Corporation | 2.6 | |||||||||

| Genworth MI Canada | 2.5 | |||||||||

| PORTFOLIO SECTOR BREAKDOWN % of Net Assets | ||||||||||

| Consumer Discretionary | 25.0 | % | ||||||||

| Information Technology | 24.9 | |||||||||

| Financials | 14.6 | |||||||||

| Industrials | 9.1 | |||||||||

| Energy | 6.4 | |||||||||

| Health Care | 5.5 | |||||||||

| Materials | 4.8 | |||||||||

| Consumer Staples | 1.8 | |||||||||

| Miscellaneous | 1.7 | |||||||||

| Cash and Cash Equivalents | 6.2 | |||||||||

|

Manager’s Discussion Royce Capital Fund–Small-Cap Portfolio (RCS) was up 1.9% for the year-to-date period ended June 30, 2014 versus a 3.2% gain for its small-cap benchmark, the Russell 2000 Index, for the same period. The first quarter saw a widespread slowdown in the speed of small-cap returns following the dynamic second half of 2013, which was not entirely unexpected considering last year’s blistering pace. RCS rose 0.7% for the first quarter of 2014, trailing its benchmark’s 1.1% advance. A slight downturn that lasted from early March through mid-May made for a rockier second quarter, though June was in general a positive month that did much to bring small-cap results back into the black. For the second quarter, the Fund rose 1.2% compared to 2.0% for the small-cap index. RCS did, however, beat the Russell 2000 from the index’s early March high through the end of June. Although we always like to see the Fund hold a down-market advantage, in light of the last few years of relative underperformance, this edge during a brief bearish phase offered mostly cold comfort. The Fund did outpace the benchmark for much longer-term periods. RCS beat the Russell 2000 for the 10-, 15-year, and since inception (12/27/96) periods ended June 30, 2014. The Fund’s average annual total return since inception was 12.1%. We are very proud of the Fund’s long-term performance record. When selecting stocks for RCS’s portfolio, we focus first on balance sheets, looking for businesses with low debt, which is frequently a sign of financial strength. We next look for high returns on invested capital (ROIC). Like a strong balance sheet, high ROICs are in our view a proxy for quality. We also want the company to be trading for what we believe is an attractively low share price vis-à-vis its worth as a business. In order to evaluate this, we typically use capitalization rates, which we define as operating income divided by enterprise value. We want to understand the return on our investment as if we were buying the whole company. Our challenge through the most recent cycle has been the unfashionable status of this disciplined, value-oriented approach. With a still highly accommodative Federal Reserve pouring money into the economy while keeping interest rates essentially at zero, the cost of debt is historically low and access to cash is extremely easy. This has the effect of reducing the appeal of conservatively capitalized, steadily growing businesses while increasing the demand for both fast growth |

| GOOD IDEAS THAT WORKED Top Contributors to Performance Year-to-Date through 06/30/141 | |||||||||||

| Unit Corporation | 0.91% | ||||||||||

| Matrix Service | 0.68 | ||||||||||

| Synaptics | 0.61 | ||||||||||

| World Wrestling Entertainment Cl. A | 0.59 | ||||||||||

| Vishay Intertechnology | 0.53 | ||||||||||

| 1 Includes dividends. | |||||||||||

Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCS’s Service Class bear an annual distribution expense that is not borne by the Investment Class. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees and other expenses. Regarding the two “Good Ideas” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2014. |

| 10 | Royce Capital Fund 2014 Semiannual Report to Shareholders |

Performance and Portfolio Review |

| (often regardless of profitability) and high yield (often regardless of underlying quality). While there have been some signs that this is changing, a large-scale flight to quality has not yet occurred, certainly not in the small-cap space. We remain, however, squarely focused on both long-term and absolute results and are hopeful for a shift in sentiment in which fundamentals will matter more than momentum and yield. Five of RCS’s eight equity sectors contributed to first-half returns, with Energy holding a considerable edge, followed by notable net gains for Information Technology. The Fund’s two top performers both came from the energy equipment & services industry. Unit Corporation is a long-time position—and the Fund’s third largest at the end of June—that we have owned continuously since 2002. It operates primarily as a contract drilling company, though it also explores for and produces oil and natural gas, and engages in midstream activities. These related businesses make it an outlier in an otherwise rigidly specialized industry. Unit reported double-digit production growth, introduced a new advanced drilling rig, and enjoyed continued strength from its midstream operations. Matrix Service builds natural gas storage tanks and provides construction and maintenance services to the oil, gas, power, petrochemical, industrial, and metals industries. Increased demand for its services, a complementary acquisition, and ongoing strength for natural gas helped both operating results and its stock price. We reduced our position as its price soared. Shoe Carnival is a family footwear retailer that endured the same dismal results that most other retailers did in the first half, including The Buckle and Ascena Retail Group. We held our position in Shoe Carnival and added shares of The Buckle as its stock price declined. In the case of the former, we like its plan to expand the number of stores and raise the quality of the women’s shoes it sells. After a turn as the portfolio’s top contributor in 2013, Nu Skin Enterprises earned a less esteemed status for the semiannual period. The company develops and distributes personal skin care products worldwide. Its share price suffered mightily after an article in a Chinese newspaper accused the firm in January of running a pyramid scheme, and an investigation by the Chinese government followed. The firm paid modest fines in March and began to tighten up its training procedures. We were hopeful that Nu Skin could right itself at the end of June. |

GOOD IDEAS AT THE TIME | |

| Shoe Carnival | -0.68% |

| Nu Skin Enterprises Cl. A | -0.54 |

| Buckle (The) | -0.41 |

| Ascena Retail Group | -0.34 |

| TESSCO Technologies | -0.30 |

| 1 Net of dividends. | |

| ROYCE CAPITAL FUND-SMALL-CAP PORTFOLIO VS. RUSSELL 2000 Value of $10,000 Invested on 12/27/96 | |

| |

| Includes reinvestment of distributions. | |

| FUND INFORMATION AND PORTFOLIO DIAGNOSTICS | ||||

| Fund Net Assets | $970 million | |||

| Number of Holdings | 76 | |||

| Turnover Rate | 16% | |||

| Average Market Capitalization1 | $1,404 million | |||

| Weighted Average P/E Ratio2,3 | 17.1x | |||

| Weighted Average P/B Ratio2 | 1.9x | |||

| U.S. Investments (% of Net Assets) | 83.8% | |||

| Non-U.S. Investments (% of Net Assets) | 10.0% | |||

| Symbol | ||||

| Investment Class | RCPFX | |||

| Service Class | RCSSX | |||

1Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. | ||||

2Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings of its underlying stocks. | ||||

3 The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (2% of portfolio holdings as of 6/30/14). | ||||

| STATISTICAL MEASURES Five-Year Period Ended 6/30/14 | ||||

| Sharpe Ratio | Standard Deviation | |||

| RCS | 1.12 | 15.70 | ||

| Russell 2000 | 1.10 | 18.23 | ||

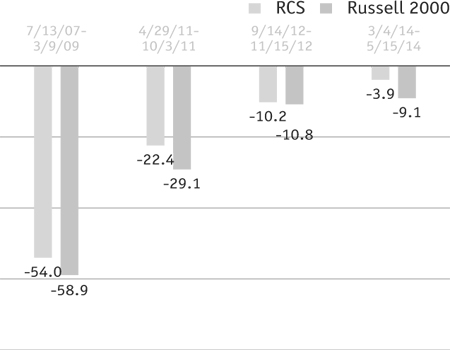

| DOWN MARKET PERFORMANCE COMPARISON All Down Periods of 7.5% or Greater Over the Last 7 Years, in Percentages (%) | ||||

| ||||

| Royce Capital Fund 2014 Semiannual Report to Shareholders | 11 |

Schedules of Investments

| Royce Capital Fund–Micro-Cap Portfolio |

| SHARES | VALUE | ||||

| COMMON STOCKS – 92.1% | |||||

| Consumer Discretionary – 14.1% | |||||

| Auto Components - 0.9% | |||||

Drew Industries | 100,979 | $ | 5,049,960 | ||

| Diversified Consumer Services - 3.2% | |||||

American Public Education 1 | 150,770 | 5,183,473 | |||

Capella Education | 96,472 | 5,247,112 | |||

JTH Holding Cl. A 1 | 128,500 | 4,280,335 | |||

Lincoln Educational Services | 823,193 | 3,696,136 | |||

| 18,407,056 | |||||

| Household Durables - 0.9% | |||||

Cavco Industries 1 | 62,004 | 5,288,941 | |||

| Internet & Catalog Retail - 0.3% | |||||

Vitacost.com 1 | 258,500 | 1,618,210 | |||

| Leisure Products - 1.2% | |||||

Black Diamond 1 | 62,409 | 700,229 | |||

LeapFrog Enterprises Cl. A 1 | 350,000 | 2,572,500 | |||

| 250,100 | 3,636,454 | ||||

| 6,909,183 | |||||

| Specialty Retail - 6.9% | |||||

Buckle (The) | 76,025 | 3,372,469 | |||

Cato Corporation (The) Cl. A | 152,300 | 4,706,070 | |||

Citi Trends 1 | 145,386 | 3,119,984 | |||

Destination Maternity | 204,500 | 4,656,465 | |||

| 146,143 | 1,486,274 | ||||

Kirkland’s 1 | 290,180 | 5,382,839 | |||

Shoe Carnival | 272,100 | 5,618,865 | |||

Stein Mart | 463,478 | 6,437,710 | |||

Zumiez 1 | 186,700 | 5,151,053 | |||

| 39,931,729 | |||||

| Textiles, Apparel & Luxury Goods - 0.7% | |||||

Culp | 150,149 | 2,614,094 | |||

Perry Ellis International 1 | 98,330 | 1,714,875 | |||

| 4,328,969 | |||||

| Total (Cost $63,097,386) | 81,534,048 | ||||

| Consumer Staples – 0.9% | |||||

| Beverages - 0.1% | |||||

Truett-Hurst Cl. A 1 | 126,100 | 641,849 | |||

| Food Products - 0.6% | |||||

Asian Citrus Holdings | 2,786,100 | 625,492 | |||

Sipef | 28,400 | 2,426,619 | |||

| 1,303,907 | 495,485 | ||||

| 3,547,596 | |||||

| Personal Products - 0.2% | |||||

Medifast 1 | 25,800 | 784,578 | |||

| Total (Cost $4,476,285) | 4,974,023 | ||||

| Energy – 8.5% | |||||

| Energy Equipment & Services - 6.2% | |||||

Canadian Energy Services & Technology | 47,400 | 1,484,568 | |||

Dawson Geophysical | 87,429 | 2,504,841 | |||

Geospace Technologies 1 | 34,912 | 1,922,953 | |||

Gulf Island Fabrication | 273,163 | 5,878,468 | |||

Natural Gas Services Group 1 | 175,400 | 5,798,724 | |||

Tesco Corporation | 313,880 | 6,698,199 | |||

TGC Industries 1 | 672,840 | 3,666,978 | |||

Total Energy Services | 369,200 | 8,037,595 | |||

| 35,992,326 | |||||

| Oil, Gas & Consumable Fuels - 2.3% | |||||

Ardmore Shipping | 53,600 | 741,288 | |||

Contango Oil & Gas 1 | 33,907 | 1,434,605 | |||

| 69,400 | 1,211,030 | ||||

Sprott Resource 1 | 1,087,300 | 3,219,969 | |||

Synergy Resources 1 | 158,100 | 2,094,825 | |||

Triangle Petroleum 1 | 392,504 | 4,611,922 | |||

| 13,313,639 | |||||

| Total (Cost $31,184,127) | 49,305,965 | ||||

| Financials – 8.2% | |||||

| Banks - 1.1% | |||||

BCB Holdings 1 | 1,303,907 | 295,675 | |||

| 44,600 | 813,950 | ||||

Pacific Continental | 238,800 | 3,278,724 | |||

TriState Capital Holdings 1 | 152,972 | 2,161,494 | |||

| 6,549,843 | |||||

| Capital Markets - 3.8% | |||||

FBR & Co. 1 | 152,816 | 4,145,898 | |||

Gluskin Sheff + Associates | 53,200 | 1,587,450 | |||

GMP Capital | 330,700 | 2,640,517 | |||

INTL FCStone 1 | 232,569 | 4,632,774 | |||

JMP Group | 242,751 | 1,837,625 | |||

Silvercrest Asset Management Group Cl. A | 113,200 | 1,948,172 | |||

U.S. Global Investors Cl. A | 198,700 | 699,424 | |||

Westwood Holdings Group | 72,527 | 4,354,521 | |||

| 21,846,381 | |||||

| Consumer Finance - 0.3% | |||||

EZCORP Cl. A 1 | 164,900 | 1,904,595 | |||

| Diversified Financial Services - 0.4% | |||||

PICO Holdings 1 | 96,835 | 2,300,800 | |||

| Insurance - 0.6% | |||||

Blue Capital Reinsurance Holdings | 80,500 | 1,585,850 | |||

Navigators Group 1 | 22,536 | 1,511,039 | |||

| 3,096,889 | |||||

| Real Estate Management & Development - 2.0% | |||||

AV Homes 1 | 107,700 | 1,760,895 | |||

Kennedy-Wilson Holdings | 282,230 | 7,569,408 | |||

Midland Holdings 1 | 4,513,000 | 2,270,941 | |||

| 11,601,244 | |||||

| Total (Cost $40,071,738) | 47,299,752 | ||||

| Health Care – 9.3% | |||||

| Biotechnology - 0.7% | |||||

BioSpecifics Technologies 1 | 39,100 | 1,054,136 | |||

| 12 | Royce Capital Fund 2014 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

June 30, 2014 (unaudited) |

| SHARES | VALUE | ||||

| Health Care (continued) | |||||

| Biotechnology (continued) | |||||

Dyax Corporation 1 | 162,116 | $ | 1,556,314 | ||

Harvard Apparatus Regenerative Technology 1 | 72,367 | 756,235 | |||

Lexicon Pharmaceuticals 1 | 570,379 | 918,310 | |||

| 4,284,995 | |||||

| Health Care Equipment & Supplies - 4.8% | |||||

Cerus Corporation 1 | 538,057 | 2,232,937 | |||

CryoLife | 199,189 | 1,782,742 | |||

Cynosure Cl. A 1 | 102,100 | 2,169,625 | |||

| 454,800 | 709,488 | ||||

Exactech 1 | 91,717 | 2,314,020 | |||

Merit Medical Systems 1 | 164,135 | 2,478,438 | |||

Novadaq Technologies 1 | 25,479 | 419,894 | |||

Orthofix International 1 | 26,400 | 957,000 | |||

RTI Surgical 1 | 318,700 | 1,386,345 | |||

STAAR Surgical 1 | 96,500 | 1,621,200 | |||

SurModics 1 | 164,378 | 3,520,977 | |||

Symmetry Medical 1 | 120,300 | 1,065,858 | |||

Synergetics USA 1 | 438,900 | 1,360,590 | |||

Syneron Medical 1 | 390,385 | 4,028,773 | |||

Trinity Biotech ADR Cl. A | 67,770 | 1,560,743 | |||

| 27,608,630 | |||||

| Health Care Providers & Services - 2.4% | |||||

| 72,500 | 2,190,950 | ||||

CorVel Corporation 1 | 92,321 | 4,171,063 | |||

PDI 1 | 318,120 | 1,393,366 | |||

U.S. Physical Therapy | 175,160 | 5,988,720 | |||

| 13,744,099 | |||||

| Life Sciences Tools & Services - 0.2% | |||||

Harvard Bioscience 1 | 289,468 | 1,317,079 | |||

| Pharmaceuticals - 1.2% | |||||

| 109,500 | 954,840 | ||||

| 41,500 | 1,323,020 | ||||

Unichem Laboratories | 374,164 | 1,404,709 | |||

Vetoquinol | 52,008 | 2,576,543 | |||

| 312,878 | 628,885 | ||||

| 6,887,997 | |||||

| Total (Cost $37,534,429) | 53,842,800 | ||||

| Industrials – 24.4% | |||||

| Aerospace & Defense - 0.9% | |||||

AeroVironment 1 | 67,000 | 2,130,600 | |||

American Science and Engineering | 27,300 | 1,899,807 | |||

CPI Aerostructures 1 | 96,100 | 1,217,587 | |||

| 5,247,994 | |||||

| Building Products - 2.2% | |||||

AAON | 107,308 | 3,596,964 | |||

Quanex Building Products | 232,400 | 4,152,988 | |||

WaterFurnace Renewable Energy | 180,800 | 5,135,699 | |||

| 12,885,651 | |||||

| Commercial Services & Supplies - 2.3% | |||||

Courier Corporation | 175,418 | 2,617,237 | |||

Ennis | 293,449 | 4,478,032 | |||

Heritage-Crystal Clean 1 | 86,734 | 1,702,588 | |||

Hudson Technologies 1 | 319,100 | 922,199 | |||

Team 1 | 39,700 | 1,628,494 | |||

US Ecology | 34,200 | 1,674,090 | |||

| 13,022,640 | |||||

| Construction & Engineering - 2.3% | |||||

Layne Christensen 1 | 213,312 | 2,837,050 | |||

MYR Group 1 | 169,338 | 4,289,331 | |||

Severfield 1 | 3,294,845 | 3,129,532 | |||

Sterling Construction 1 | 306,147 | 2,871,659 | |||

| 13,127,572 | |||||

| Electrical Equipment - 2.9% | |||||

Global Power Equipment Group | 369,588 | 5,972,542 | |||

Graphite India | 1,667,608 | 2,920,982 | |||

LSI Industries | 648,613 | 5,175,932 | |||

Powell Industries | 42,100 | 2,752,498 | |||

| 16,821,954 | |||||

| Machinery - 6.6% | |||||

AIA Engineering | 81,093 | 1,046,274 | |||

CIRCOR International | 20,000 | 1,542,600 | |||

Foster (L.B.) Company | 131,946 | 7,140,917 | |||

FreightCar America | 227,391 | 5,693,871 | |||

Gorman-Rupp Company (The) | 55,837 | 1,974,955 | |||

Graham Corporation | 145,020 | 5,048,146 | |||

Kadant | 129,031 | 4,961,242 | |||

Key Technology 1 | 292,129 | 3,599,029 | |||

RBC Bearings | 44,122 | 2,826,014 | |||

Semperit AG Holding | 75,842 | 4,647,309 | |||

| 38,480,357 | |||||

| Marine - 0.3% | |||||

Clarkson | 47,200 | 1,934,635 | |||

| Professional Services - 4.1% | |||||

CRA International 1 | 217,706 | 5,018,123 | |||

Exponent | 37,297 | 2,764,081 | |||

GP Strategies 1 | 189,108 | 4,894,115 | |||

Kforce | 217,700 | 4,713,205 | |||

Resources Connection | 492,588 | 6,457,829 | |||

| 23,847,353 | |||||

| Road & Rail - 2.4% | |||||

Marten Transport | 277,785 | 6,208,495 | |||

Patriot Transportation Holding 1 | 216,240 | 7,561,913 | |||

| 13,770,408 | |||||

| Trading Companies & Distributors - 0.4% | |||||

Houston Wire & Cable | 186,700 | 2,316,947 | |||

| Total (Cost $109,303,279) | 141,455,511 | ||||

| Information Technology – 13.7% | |||||

| Communications Equipment - 1.4% | |||||

| 255,140 | 648,056 | ||||

COM DEV International | 303,700 | 1,215,312 | |||

Digi International 1 | 297,084 | 2,798,531 | |||

KVH Industries 1 | 255,100 | 3,323,953 | |||

| 7,985,852 | |||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2014 Semiannual Report to Shareholders | 13 |

Schedules of Investments

| Royce Capital Fund–Micro-Cap Portfolio (continued) |

| SHARES | VALUE | ||||

| Information Technology (continued) | |||||

| Electronic Equipment, Instruments & Components - 2.9% | |||||

CUI Global 1 | 267,062 | $ | 2,243,321 | ||

Electro Rent | 122,800 | 2,054,444 | |||

Fabrinet 1 | 237,669 | 4,895,981 | |||

GSI Group 1 | 333,300 | 4,242,909 | |||

| 247,465 | 774,566 | ||||

Pure Technologies | 39,000 | 261,328 | |||

Vishay Precision Group 1 | 131,800 | 2,169,428 | |||

| 16,641,977 | |||||

| Internet Software & Services - 0.5% | |||||

QuinStreet 1 | 320,700 | 1,767,057 | |||

Zix Corporation 1 | 411,700 | 1,408,014 | |||

| 3,175,071 | |||||

| IT Services - 0.4% | |||||

EPAM Systems 1 | 41,248 | 1,804,600 | |||

ServiceSource International 1 | 60,275 | 349,595 | |||

| 2,154,195 | |||||

| Semiconductors & Semiconductor Equipment - 4.6% | |||||

Advanced Energy Industries 1 | 179,900 | 3,463,075 | |||

AXT 1 | 829,991 | 1,776,181 | |||

Brooks Automation | 433,400 | 4,667,718 | |||

Cascade Microtech 1 | 61,600 | 841,456 | |||

GSI Technology 1 | 513,861 | 3,062,611 | |||

Integrated Silicon Solution 1 | 360,599 | 5,326,047 | |||

Photronics 1 | 245,300 | 2,109,580 | |||

Rudolph Technologies 1 | 159,293 | 1,573,815 | |||

Ultra Clean Holdings 1 | 103,300 | 934,865 | |||

Xcerra Corporation 1 | 347,600 | 3,163,160 | |||

| 26,918,508 | |||||

| Software - 3.3% | |||||

ePlus 1 | 79,496 | 4,626,667 | |||

| 92,500 | 1,770,450 | ||||

Monotype Imaging Holdings | 151,242 | 4,260,487 | |||

SeaChange International 1 | 215,100 | 1,722,951 | |||

TeleNav 1 | 296,400 | 1,686,516 | |||

VASCO Data Security International 1 | 428,129 | 4,966,297 | |||

| 19,033,368 | |||||

| Technology Hardware, Storage & Peripherals - 0.6% | |||||

| 137,593 | 1,018,188 | ||||

Super Micro Computer 1 | 102,511 | 2,590,453 | |||

| 3,608,641 | |||||

| Total (Cost $67,431,982) | 79,517,612 | ||||

| Materials – 8.8% | |||||

| Chemicals - 2.0% | |||||

BioAmber 1 | 66,979 | 666,441 | |||

Burcon NutraScience 1 | 148,556 | 588,282 | |||

C. Uyemura & Co. | 23,900 | 1,217,354 | |||

FutureFuel Corporation | 196,100 | 3,253,299 | |||

Quaker Chemical | 55,788 | 4,283,960 | |||

Societe Internationale de Plantations d’Heveas | 28,985 | 1,390,708 | |||

| 11,400,044 | |||||

| Metals & Mining - 6.8% | |||||

Alamos Gold | 162,900 | 1,647,243 | |||

Argonaut Gold 1 | 253,100 | 1,048,406 | |||

Endeavour Mining 1 | 750,000 | 583,384 | |||

Endeavour Silver 1 | 466,100 | 2,544,906 | |||

Geodrill 1 | 1,217,200 | 935,387 | |||

Gold Standard Ventures 1 | 700,000 | 553,000 | |||

Goldgroup Mining 1 | 652,000 | 103,875 | |||

Haynes International | 81,170 | 4,593,410 | |||

Horsehead Holding Corporation 1 | 287,803 | 5,255,283 | |||

Imdex 1 | 1,677,092 | 996,291 | |||

| 1,019,096 | 2,934,997 | ||||

Olympic Steel | 203,228 | 5,029,893 | |||

Phoscan Chemical 1 | 2,968,200 | 834,506 | |||

Pilot Gold 1 | 1,669,325 | 2,284,068 | |||

Silvercorp Metals | 486,600 | 1,031,592 | |||

Synalloy Corporation | 126,641 | 2,079,445 | |||

Universal Stainless & Alloy Products 1 | 200,736 | 6,519,905 | |||

Western Copper and Gold 1 | 720,000 | 554,400 | |||

| 39,529,991 | |||||

| Total (Cost $45,534,221) | 50,930,035 | ||||

| Utilities – 0.1% | |||||

| Independent Power & Renewable Electricity Producer - 0.1% | |||||

Alterra Power 1 | 1,844,000 | 604,845 | |||

| Total (Cost $2,120,432) | 604,845 | ||||

| Miscellaneous 5 – 4.1% | |||||

| Total (Cost $22,942,293) | 24,008,391 | ||||

| TOTAL COMMON STOCKS | |||||

(Cost $423,696,172) | 533,472,982 | ||||

| REPURCHASE AGREEMENT – 8.0% | |||||

Fixed Income Clearing Corporation, | 46,310,000 | ||||

| 14 | Royce Capital Fund 2014 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

June 30, 2014 (unaudited) |

| VALUE | ||||||

| COLLATERAL RECEIVED FOR SECURITIES | ||||||

LOANED – 2.9% | ||||||

| Money Market Funds | ||||||

Federated Government Obligations Fund | $ | 16,866,398 | ||||

| TOTAL INVESTMENTS – 103.0% | ||||||

(Cost $486,872,570) | 596,649,380 | |||||

| LIABILITIES LESS CASH | ||||||

AND OTHER ASSETS – (3.0)% | (17,614,643 | ) | ||||

| NET ASSETS – 100.0% | $ | 579,034,737 | ||||

| Royce Capital Fund–Small-Cap Portfolio |

| SHARES | VALUE | ||||

| COMMON STOCKS – 93.8% | |||||

| Consumer Discretionary – 25.0% | |||||

| Automobiles - 0.8% | |||||

Thor Industries | 126,715 | $ | 7,206,282 | ||

| Media - 1.0% | |||||

Saga Communications Cl. A | 228,454 | 9,759,555 | |||

| Specialty Retail - 14.8% | |||||

American Eagle Outfitters | 800,315 | 8,979,534 | |||

Ascena Retail Group 1 | 752,980 | 12,875,958 | |||

Buckle (The) | 586,319 | 26,009,111 | |||

Cato Corporation (The) Cl. A | 493,311 | 15,243,310 | |||

GameStop Corporation Cl. A | 89,272 | 3,612,838 | |||

Genesco 1 | 352,308 | 28,935,056 | |||

Guess? | 387,254 | 10,455,858 | |||

Shoe Carnival | 775,713 | 16,018,474 | |||

Stein Mart | 1,568,778 | 21,790,326 | |||

| 143,920,465 | |||||

| Textiles, Apparel & Luxury Goods - 8.4% | |||||

Barry (R.G.) | 147,573 | 2,796,508 | |||

Crocs 1 | 720,678 | 10,831,790 | |||

Deckers Outdoor 1 | 126,797 | 10,946,385 | |||

G-III Apparel Group 1 | 227,537 | 18,580,672 | |||

Steven Madden 1 | 886,868 | 30,419,572 | |||

| 349,370 | 7,640,722 | ||||

| 81,215,649 | |||||

| Total (Cost $177,569,934) | 242,101,951 | ||||

| Consumer Staples – 1.8% | |||||

| Food & Staples Retailing - 0.6% | |||||

Village Super Market Cl. A | 256,171 | 6,053,321 | |||

| Personal Products - 1.2% | |||||

Inter Parfums | 194,975 | 5,761,511 | |||

Nu Skin Enterprises Cl. A | 75,677 | 5,597,071 | |||

| 11,358,582 | |||||

| Total (Cost $13,223,654) | 17,411,903 | ||||

| Energy – 6.4% | |||||

| Energy Equipment & Services - 5.5% | |||||

Helmerich & Payne | 34,400 | 3,994,184 | |||

Matrix Service 1 | 316,801 | 10,387,905 | |||

Oil States International 1 | 81,386 | 5,216,029 | |||

Total Energy Services | 199,800 | 4,349,706 | |||

Unit Corporation 1 | 422,354 | 29,070,626 | |||

| 53,018,450 | |||||

| Oil, Gas & Consumable Fuels - 0.9% | |||||

Cimarex Energy | 61,518 | 8,825,372 | |||

| Total (Cost $27,296,496) | 61,843,822 | ||||

| Financials – 14.6% | |||||

| Banks - 3.0% | |||||

Ames National | 219,219 | 5,072,728 | |||

Camden National | 248,298 | 9,624,030 | |||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2014 Semiannual Report to Shareholders | 15 |

Schedules of Investments

| Royce Capital Fund–Small-Cap Portfolio (continued) |

| SHARES | VALUE | ||||

| Financials (continued) | |||||

| Banks (continued) | |||||

City Holding Company | 317,540 | $ | 14,327,405 | ||

| 29,024,163 | |||||

| Capital Markets - 2.0% | |||||

Federated Investors Cl. B | 621,601 | 19,219,903 | |||

| Insurance - 5.3% | |||||

Allied World Assurance Company Holdings | 350,775 | 13,336,465 | |||

Aspen Insurance Holdings | 301,609 | 13,699,081 | |||

Montpelier Re Holdings | 266,121 | 8,502,566 | |||

Reinsurance Group of America | 201,000 | 15,858,900 | |||

| 51,397,012 | |||||

| Thrifts & Mortgage Finance - 4.3% | |||||

Genworth MI Canada | 663,700 | 23,642,038 | |||

TrustCo Bank Corp. NY | 2,776,786 | 18,548,931 | |||

| 42,190,969 | |||||

| Total (Cost $90,917,109) | 141,832,047 | ||||

| Health Care – 5.5% | |||||

| Health Care Providers & Services - 5.5% | |||||

Chemed Corporation | 262,356 | 24,588,004 | |||

Magellan Health 1 | 114,636 | 7,134,945 | |||

MEDNAX 1 | 207,220 | 12,049,843 | |||

U.S. Physical Therapy | 285,169 | 9,749,928 | |||

| Total (Cost $27,429,300) | 53,522,720 | ||||

| Industrials – 9.1% | |||||

| Aerospace & Defense - 0.9% | |||||

Cubic Corporation | 196,000 | 8,723,960 | |||

| Commercial Services & Supplies - 2.0% | |||||

Horizon North Logistics | 452,200 | 3,246,195 | |||

UniFirst Corporation | 155,850 | 16,520,100 | |||

| 19,766,295 | |||||

| Machinery - 3.4% | |||||

Alamo Group | 309,287 | 16,729,334 | |||

Kennametal | 91,195 | 4,220,504 | |||

Miller Industries 6 | 611,445 | 12,583,538 | |||

| 33,533,376 | |||||

| Road & Rail - 1.0% | |||||

Knight Transportation | 395,800 | 9,408,166 | |||

| Trading Companies & Distributors - 1.8% | |||||

Applied Industrial Technologies | 337,453 | 17,118,991 | |||

| Total (Cost $67,279,036) | 88,550,788 | ||||

| Information Technology – 24.9% | |||||

| Communications Equipment - 7.5% | |||||

NETGEAR 1 | 836,019 | 29,068,381 | |||

Plantronics | 616,130 | 29,605,046 | |||

TESSCO Technologies 6 | 438,749 | 13,921,506 | |||

| 72,594,933 | |||||

| Electronic Equipment, Instruments & Components - 9.9% | |||||

Fabrinet 1 | 1,397,388 | 28,786,193 | |||

| 615,397 | 6,449,361 | ||||

Littelfuse | 7,431 | 690,711 | |||

MTS Systems | 11,496 | 778,969 | |||

PC Connection | 914,261 | 18,906,917 | |||

Rofin-Sinar Technologies 1 | 480,502 | 11,551,268 | |||

Vishay Intertechnology | 1,872,153 | 28,999,650 | |||

| 96,163,069 | |||||

| IT Services - 3.9% | |||||

Convergys Corporation | 1,010,692 | 21,669,237 | |||

ManTech International Cl. A | 558,185 | 16,477,621 | |||

| 38,146,858 | |||||

| Semiconductors & Semiconductor Equipment - 3.6% | |||||

Cabot Microelectronics 1 | 19,233 | 858,754 | |||

IXYS Corporation | 491,829 | 6,059,333 | |||

MKS Instruments | 418,800 | 13,083,312 | |||

| 117,500 | 10,650,200 | ||||

Teradyne | 195,700 | 3,835,720 | |||

| 34,487,319 | |||||

| Total (Cost $205,444,344) | 241,392,179 | ||||

| Materials – 4.8% | |||||

| Chemicals - 2.8% | |||||

Innophos Holdings | 136,910 | 7,881,908 | |||

Innospec | 444,599 | 19,193,339 | |||

| 27,075,247 | |||||

| Containers & Packaging - 0.5% | |||||

UFP Technologies 1 | 177,566 | 4,277,565 | |||

| Metals & Mining - 0.1% | |||||

Reliance Steel & Aluminum | 18,300 | 1,348,893 | |||

| Paper & Forest Products - 1.4% | |||||

Schweitzer-Mauduit International | 320,004 | 13,971,375 | |||

| Total (Cost $42,212,568) | 46,673,080 | ||||

| Miscellaneous 5 – 1.7% | |||||

| Total (Cost $16,012,608) | 16,889,252 | ||||

| TOTAL COMMON STOCKS | |||||

(Cost $667,385,049) | 910,217,742 | ||||

| REPURCHASE AGREEMENT – 6.2% | |||||

Fixed Income Clearing Corporation, | 59,813,000 | ||||

| 16 | Royce Capital Fund 2014 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

June 30, 2014 (unaudited) |

| VALUE | ||||||

| COLLATERAL RECEIVED FOR SECURITIES | ||||||

LOANED – 0.5% | ||||||

| Money Market Funds | ||||||

Federated Government Obligations Fund | $ | 5,276,965 | ||||

| TOTAL INVESTMENTS – 100.5% | ||||||

(Cost $732,475,014) | 975,307,707 | |||||

| LIABILITIES LESS CASH | ||||||

AND OTHER ASSETS – (0.5)% | (4,846,467 | ) | ||||

| NET ASSETS – 100.0% | $ | 970,461,240 | ||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2014 Semiannual Report to Shareholders | 17 |

| Statements of Assets and Liabilities | June 30, 2014 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| ASSETS: | ||||||||

| Investments at value (including collateral on loaned securities) | ||||||||

Non-Affiliated Companies | $ | 550,339,380 | $ | 882,540,302 | ||||

Affiliated Companies | – | 32,954,405 | ||||||

| Repurchase agreements (at cost and value) | 46,310,000 | 59,813,000 | ||||||

| Cash and foreign currency | 67,709 | 276 | ||||||

| Receivable for investments sold | 1,400,087 | 1,071,736 | ||||||

| Receivable for capital shares sold | 513,723 | 9,602,851 | ||||||

| Receivable for dividends and interest | 400,892 | 600,180 | ||||||

| Prepaid expenses and other assets | 5,203 | 10,145 | ||||||

Total Assets | 599,036,994 | 986,592,895 | ||||||

| LIABILITIES: | ||||||||

| Payable for collateral on loaned securities | 16,866,398 | 5,276,965 | ||||||

| Payable for investments purchased | 1,727,588 | 8,988,019 | ||||||

| Payable for capital shares redeemed | 755,174 | 956,711 | ||||||

| Payable for investment advisory fees | 580,078 | 777,106 | ||||||

| Accrued expenses | 73,019 | 132,854 | ||||||

Total Liabilities | 20,002,257 | 16,131,655 | ||||||

Net Assets | $ | 579,034,737 | $ | 970,461,240 | ||||

| ANALYSIS OF NET ASSETS: | ||||||||

| Paid-in capital | $ | 416,765,795 | $ | 582,162,071 | ||||

| Undistributed net investment income (loss) | (2,622,729 | ) | 1,796,361 | |||||

| Accumulated net realized gain (loss) on investments and foreign currency | 55,112,550 | 143,670,276 | ||||||

| Net unrealized appreciation (depreciation) on investments and foreign currency | 109,779,121 | 242,832,532 | ||||||

Net Assets | $ | 579,034,737 | $ | 970,461,240 | ||||

Investment Class | $ | 539,262,573 | $ | 735,592,582 | ||||

Service Class | 39,772,164 | 234,868,658 | ||||||

| SHARES OUTSTANDING (unlimited number of $.001 par value): | ||||||||

Investment Class | 41,606,833 | 51,854,001 | ||||||

Service Class | 3,099,531 | 16,797,834 | ||||||

| NET ASSET VALUES (Net Assets ÷ Shares Outstanding): | ||||||||

(offering and redemption price per share) | ||||||||

Investment Class | $12.96 | $14.19 | ||||||

Service Class | 12.83 | 13.98 | ||||||

Investments at identified cost | $ | 440,562,570 | $ | 672,662,014 | ||||

Market value of loaned securities | 16,153,361 | 5,133,683 | ||||||

| 18 | Royce Capital Fund 2014 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| Statements of Changes in Net Assets |

| Micro-Cap Portfolio | Small-Cap Portfolio | |||||||||||||||

| Six months ended | Six months ended | |||||||||||||||

| 6/30/14 | Year ended | 6/30/14 | Year ended | |||||||||||||

| (unaudited) | 12/31/13 | (unaudited) | 12/31/13 | |||||||||||||

| INVESTMENT OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | (927,677 | ) | $ | (2,172,035 | ) | $ | 1,224,971 | $ | 664,506 | ||||||

Net realized gain (loss) on investments and foreign currency | 18,961,668 | 44,622,348 | 49,857,994 | 94,251,658 | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments and foreign currency | (13,369,494 | ) | 68,959,434 | (33,709,837 | ) | 169,490,816 | ||||||||||

| Net increase (decrease) in net assets from investment operations | 4,664,497 | 111,409,747 | 17,373,128 | 264,406,980 | ||||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| Net investment income | ||||||||||||||||

Investment Class | – | (2,773,314 | ) | – | (7,334,482 | ) | ||||||||||

Service Class | – | (129,808 | ) | – | (2,049,052 | ) | ||||||||||

Net realized gain on investments and foreign currency | ||||||||||||||||

Investment Class | – | (14,533,900 | ) | – | (38,123,021 | ) | ||||||||||

Service Class | – | (1,029,260 | ) | – | (11,915,684 | ) | ||||||||||

| Total distributions | – | (18,466,282 | ) | – | (59,422,239 | ) | ||||||||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

| Value of shares sold | ||||||||||||||||

Investment Class | 17,500,628 | 40,124,309 | 58,015,631 | 94,415,549 | ||||||||||||

Service Class | 6,240,190 | 9,376,424 | 6,863,630 | 36,125,376 | ||||||||||||

| Distributions reinvested | ||||||||||||||||

Investment Class | – | 17,307,214 | – | 45,457,503 | ||||||||||||

Service Class | – | 1,159,068 | – | 13,964,736 | ||||||||||||

| Value of shares redeemed | ||||||||||||||||

Investment Class | (55,468,184 | ) | (115,122,181 | ) | (72,528,389 | ) | (187,804,627 | ) | ||||||||

Service Class | (7,321,826 | ) | (12,649,040 | ) | (8,368,281 | ) | (10,480,881 | ) | ||||||||

| Net increase (decrease) in net assets from capital share transactions | (39,049,192 | ) | (59,804,206 | ) | (16,017,409 | ) | (8,322,344 | ) | ||||||||

NET INCREASE (DECREASE) IN NET ASSETS | (34,384,695 | ) | 33,139,259 | 1,355,719 | 196,662,397 | |||||||||||

| NET ASSETS: | ||||||||||||||||

Beginning of period | 613,419,432 | 580,280,173 | 969,105,521 | 772,443,124 | ||||||||||||

End of period | $ | 579,034,737 | $ | 613,419,432 | $ | 970,461,240 | $ | 969,105,521 | ||||||||

UNDISTRIBUTED NET INVESTMENT INCOME (LOSS) AT END OF PERIOD | $ | (2,622,729 | ) | $ | (1,695,052 | ) | $ | 1,796,361 | $ | 571,390 | ||||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. | Royce Capital Fund 2014 Semiannual Report to Shareholders | 19 |

| Statements of Operations | Six Months Ended June 30, 2014 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| INVESTMENT INCOME: | ||||||||

| Income: | ||||||||

Dividends | $ | 2,868,433 | $ | 6,407,548 | ||||

Foreign withholding tax | (93,230 | ) | (86,946 | ) | ||||

Securities lending | 103,900 | 55,348 | ||||||

| Total income | 2,879,103 | 6,375,950 | ||||||

| Expenses: | ||||||||

Investment advisory fees | 3,596,797 | 4,662,045 | ||||||

Distribution fees | 48,625 | 281,015 | ||||||

Custody | 51,094 | 47,926 | ||||||

Administrative and office facilities | 31,878 | 49,231 | ||||||

Trustees’ fees | 26,694 | 41,814 | ||||||

Audit | 19,627 | 17,800 | ||||||

Shareholder reports | 14,085 | 29,500 | ||||||

Shareholder servicing | 7,655 | 6,726 | ||||||

Legal | 2,444 | 3,784 | ||||||

Other expenses | 7,946 | 11,243 | ||||||

| Total expenses | 3,806,845 | 5,151,084 | ||||||

| Compensating balance credits | (65 | ) | (105 | ) | ||||

| Net expenses | 3,806,780 | 5,150,979 | ||||||

| Net investment income (loss) | (927,677 | ) | 1,224,971 | |||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | ||||||||

| Net realized gain (loss): | ||||||||

Investments | 18,969,302 | 49,859,425 | ||||||

Foreign currency transactions | (7,634 | ) | (1,431 | ) | ||||

| Net change in unrealized appreciation (depreciation): | ||||||||

Investments and foreign currency translations | (13,367,236 | ) | (33,709,609 | ) | ||||

Other assets and liabilities denominated in foreign currency | (2,258 | ) | (228 | ) | ||||

| Net realized and unrealized gain (loss) on investments and foreign currency | 5,592,174 | 16,148,157 | ||||||

| NET INCREASE (DECREASE) IN NET ASSETS FROM INVESTMENT OPERATIONS | $ | 4,664,497 | $ | 17,373,128 | ||||

| 20 | Royce Capital Fund 2014 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS. |

| This table is presented to show selected data for a share outstanding throughout each period and to assist shareholders in evaluating a Fund’s performance for the periods presented. Per share amounts have been determined on the basis of the weighted average number of shares outstanding during the period. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Realized | Distributions from Net | Ratio of Expenses to Average Net Assets | Ratio of Net | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Asset Value, Beginning of Period | Net Investment Income (Loss) | and Unrealized Gain (Loss) on Investments and Foreign Currency | Total from Investment Operations | Distributions from Net Investment Income | Realized Gain on Investments and Foreign Currency | Total Distributions | Net Asset Value, End of Period | Total Return | Net Assets, End of Period (in thousands) | Prior to Fee Waivers and Balance Credits | Prior to Fee Waivers | Net of Fee Waivers | Investment Income (Loss) to Average Net Assets | Portfolio Turnover Rate | |||||||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio – Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2014 | $ | 12.83 | $ | (0.02 | ) | $ | 0.15 | $ | 0.13 | $ | – | $ | – | $ | – | $ | 12.96 | 1.01 | %1 | $ | 539,263 | 1.30 | %2 | 1.30 | %2 | 1.30 | %2 | (0.30 | )%2 | 12 | % | ||||||||||||||||||||||||||||

| 2013 | 10.95 | (0.04 | ) | 2.32 | 2.28 | (0.06 | ) | (0.34 | ) | (0.40 | ) | 12.83 | 20.99 | 572,666 | 1.32 | 1.32 | 1.32 | (0.36 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| 2012 | 10.41 | 0.04 | 0.74 | 0.78 | – | (0.24 | ) | (0.24 | ) | 10.95 | 7.60 | 543,516 | 1.33 | 1.33 | 1.33 | 0.39 | 21 | ||||||||||||||||||||||||||||||||||||||||||

| 2011 | 12.18 | (0.03 | ) | (1.45 | ) | (1.48 | ) | (0.29 | ) | – | (0.29 | ) | 10.41 | (12.10 | ) | 569,498 | 1.32 | 1.32 | 1.32 | (0.31 | ) | 35 | |||||||||||||||||||||||||||||||||||||

| 2010 | 9.52 | (0.01 | ) | 2.87 | 2.86 | (0.20 | ) | – | (0.20 | ) | 12.18 | 30.10 | 676,654 | 1.32 | 1.32 | 1.32 | (0.09 | ) | 35 | ||||||||||||||||||||||||||||||||||||||||

| 2009 | 6.03 | (0.01 | ) | 3.50 | 3.49 | – | – | – | 9.52 | 57.88 | 522,092 | 1.33 | 1.33 | 1.33 | (0.13 | ) | 33 | ||||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio – Service Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2014 | $ | 12.72 | $ | (0.04 | ) | $ | 0.15 | $ | 0.11 | $ | – | $ | – | $ | – | $ | 12.83 | 0.86 | %1 | $ | 39,772 | 1.57 | %2 | 1.57 | %2 | 1.57 | %2 | (0.58 | )%2 | 12 | % | ||||||||||||||||||||||||||||

| 2013 | 10.87 | (0.07 | ) | 2.30 | 2.23 | (0.04 | ) | (0.34 | ) | (0.38 | ) | 12.72 | 20.65 | 40,753 | 1.60 | 1.60 | 1.58 | (0.62 | ) | 30 | |||||||||||||||||||||||||||||||||||||||

| 2012 | 10.35 | 0.03 | 0.73 | 0.76 | – | (0.24 | ) | (0.24 | ) | 10.87 | 7.45 | 36,764 | 1.59 | 1.59 | 1.55 | 0.27 | 21 | ||||||||||||||||||||||||||||||||||||||||||

| 2011 | 12.13 | (0.11 | ) | (1.39 | ) | (1.50 | ) | (0.28 | ) | – | (0.28 | ) | 10.35 | (12.26 | ) | 26,096 | 1.60 | 1.60 | 1.49 | (0.46 | ) | 35 | |||||||||||||||||||||||||||||||||||||

| 2010 | 9.49 | (0.08 | ) | 2.91 | 2.83 | (0.19 | ) | – | (0.19 | ) | 12.13 | 29.90 | 17,022 | 1.63 | 1.63 | 1.40 | (0.12 | ) | 35 | ||||||||||||||||||||||||||||||||||||||||

| 2009 | 6.02 | (0.03 | ) | 3.50 | 3.47 | – | – | – | 9.49 | 57.64 | 6,907 | 1.73 | 1.73 | 1.58 | (0.36 | ) | 33 | ||||||||||||||||||||||||||||||||||||||||||

| Small-Cap Portfolio – Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| †2014 | $ | 13.92 | $ | 0.02 | $ | 0.25 | $ | 0.27 | $ | – | $ | – | $ | – | $ | 14.19 | 1.94 | %1 | $ | 735,592 | 1.04 | %2 | 1.04 | %2 | 1.04 | %2 | 0.32 | %2 | 16 | % | |||||||||||||||||||||||||||||

| 2013 | 11.03 | 0.03 | 3.75 | 3.78 | (0.14 | ) | (0.75 | ) | (0.89 | ) | 13.92 | 34.75 | 736,917 | 1.05 | 1.05 | 1.05 | 0.13 | 43 | |||||||||||||||||||||||||||||||||||||||||

| 2012 | 10.07 | 0.15 | 1.10 | 1.25 | (0.01 | ) | (0.28 | ) | (0.29 | ) | 11.03 | 12.50 | 623,830 | 1.06 | 1.06 | 1.06 | 1.37 | 62 | |||||||||||||||||||||||||||||||||||||||||

| 2011 | 10.45 | 0.01 | (0.35 | ) | (0.34 | ) | (0.04 | ) | – | (0.04 | ) | 10.07 | (3.28 | ) | 651,243 | 1.05 | 1.05 | 1.05 | 0.11 | 36 | |||||||||||||||||||||||||||||||||||||||

| 2010 | 8.68 | 0.04 | 1.74 | 1.78 | (0.01 | ) | – | (0.01 | ) | 10.45 | 20.52 | 630,227 | 1.06 | 1.06 | 1.06 | 0.47 | 34 | ||||||||||||||||||||||||||||||||||||||||||