UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-07537

Name of Registrant: Royce Capital Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

Name and address of agent for service:

John E. Denneen, Esq.

745 Fifth Avenue

New York, NY 10151

Registrant's telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2019

Date of reporting period: January 1, 2019 – June 30, 2019

Item 1. Reports to Shareholders.

|

| JUNE 30, 2019 | ||

| 2019 Semiannual | ||

| Review and Report to Shareholders | ||

| Royce Capital Fund– | ||||

| Micro-Cap Portfolio | ||||

| Royce Capital Fund– | ||||

| Small-Cap Portfolio | ||||

| Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on the Funds’ website (www.roycefunds.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary or, if you are a direct investor with the Funds, by calling 1-800-841-1180. Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1-800-841-1180 to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held with our fund complex if you invest directly with the Funds. | ||||

| roycefunds.com |  | |||

| Table of Contents | |||

| Semiannual Review | |||

| Letter to Our Shareholders | 1 | ||

| Performance and Expenses | 5 | ||

| Semiannual Report to Shareholders | |||

| Managers’ Discussions of Fund Performance and Schedules of Investments | |||

Royce Capital Fund–Micro-Cap Portfolio | 6 | ||

Royce Capital Fund–Small-Cap Portfolio | 12 | ||

| Financial Statements | 16 | ||

| Notes to Financial Statements | 20 | ||

| Understanding Your Fund’s Expenses | 25 | ||

| Trustees and Officers | 26 | ||

| Board Approval of Investment Advisory Agreement | 27 | ||

| Notes to Performance and Other Important Information | 29 |

| This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders |

Letter to Our Shareholders

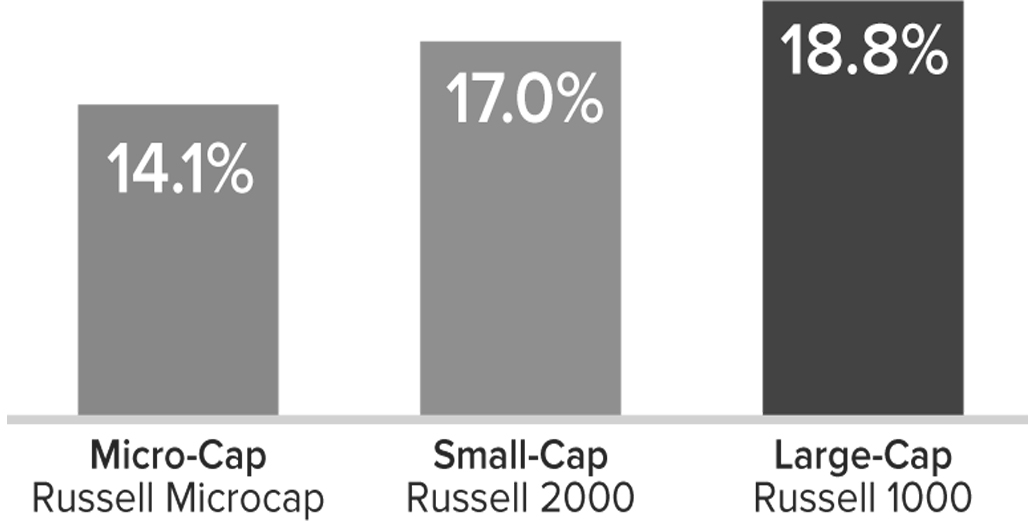

| The first six months of 2019 offered equity investors almost everything they could have hoped for following the high anxiety of a recession scare and the bearish fourth quarter of 2018, when the small-cap Russell 2000 Index fell 20.2%. Stocks immediately showed great resilience, and then some, by roaring back in the first half of the year. A highly welcome double-digit rebound in the first quarter was followed by a seesawing second quarter that saw more motion than progress. This was an understandable pause that gave the market time to digest the prior advance. The upshot was a solid advance rise in the year’s first six months, a period that saw low trading volumes and little volatility, which was mostly confined to a small decline in May. During the first half, the Russell 2000 advanced 17.0% while its large-cap sibling, the Russell 1000 Index, was even better, up 18.8%. In fact, performance in the first half generally trended higher the further up the market capitalization scale you traveled. |

| Equity Indexes Total Returns Year-to-Date through 6/30/19 |  |

| Some questioned the substance of this rally, observing that the same risks that fueled last year’s decline were still with us. The list is long and, by now, familiar. Most of the anxiety continues to circulate around the issue of global growth—or the widely rumored imminent lack of it—and its probable negative impact on corporate profits. There wasn’t much in the way of fresh answers to these concerns at the end of June beyond the admittedly consequential Fed pivot to a more dovish stance (as well as subsequent and similar actions promised from the European Central Bank). Yet, while the Fed’s words and actions went some way to reassuring investors that it was prepared to give the markets a dose of stimulus, the effect on economic growth was pretty much nil. Moreover, the increasing tensions around trade and tariffs remain an issue at this writing. With no resolution forthcoming, many companies were lowering expectations and/or offering a more muted outlook, with predictably negative effects on the stocks of many economically sensitive businesses. It’s not surprising, then, that equity investors showed a marked preference for safety in the form of large-cap stocks, or chose to bet on better times further down the road by vacuuming up shares of growth issues regardless of capitalization size. Some additional context is also important: large-caps, growth stocks, and defensive areas (that is, bond proxies) have historically done better in low or declining interest rate environments, an atmosphere that has characterized much of the decade following the Financial Crisis, with its record-low interest rates (and the |

| For details on The Royce Funds’ performance in the period, please turn to the Managers’ Discussions that begin on page 8. Past performance is no guarantee of future results. |

| This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders | 1 |

LETTER TO OUR SHAREHOLDERS

| ‘easy money’ that came with them). With rates still near historic lows, these same stocks have led the market over the last two-plus years. All of this notwithstanding, we believe that the long-term case for small-cap stocks is strong, as we will explain through the course of this letter. PESSIMISTS, OPTIMISTS—AND US By periodically inverting the otherwise mostly flat yield curve, the bond market maintained its saturnine insistence that the economy was slowing and potentially, perhaps inevitably, moving toward recession. To be sure, many observers point to the inverted yield curve as iron-clad proof that the current slackening momentum in the pace of growth in the U.S., along with the advanced age of the expansion, is a prelude to a recession. More optimistic voices argue that large-cap stocks spent much of the first half making new all-time highs, that the labor market continues to strengthen, and that the economy continues to expand in spite of a raft of dismal headlines. |

| THE CASE FOR SMALL-CAP LEADERSHIP |

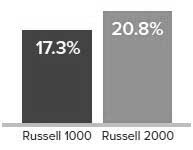

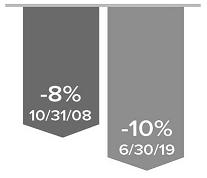

| Our first argument is in favor of small-cap returning to market leadership. We make it on the grounds of reversion to the mean, one of our longest-held investment principles. Looking at first-half performance, the resilience of small-cap stocks seemed both apropos and encouraging to us given that we continue to see solid fundamentals for many companies, attractively joined with historically average, or below average, valuation levels. However, small-caps lagged large-caps not only in the first half but also for the one-year period ended June 30, 2019, when the Russell 2000 fell 3.3% versus a gain of 10.0% for the large-cap index. This performance divergence has created a historical oddity that can be seen in the spread between |

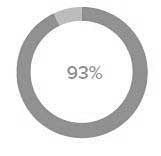

| small- and large-cap returns. It rarely happens over the course of a 12-month period that small-caps are in the red while large-caps are in the black. In fact, it’s happened less than 7% of the time over the past 20 years—in 16 out of 229 monthly rolling 12-month periods. What are the implications of this peculiar divergence in performance? In 93% of the following 12-month periods—only 13 of the 14 currently have subsequent periods to measure—small-caps bounced back to outpace large-caps. It’s true that small-caps have historically tended to lag their large-cap siblings when yields are falling—and have often done the same when economic growth is slowing. The resumption of small-cap leadership, then, is contingent on these conditions changing. When rates rise (or simply normalize) and/or the economy reaccelerates, and history strongly suggests that both should, we would expect small-cap to recapture leadership. |

| What Happened After 12-Month Periods When Large-Caps Rose and Small-Caps Fell? 16 out of 229 Trailing 1-Year Periods from 6/30/99 to 6/30/19 |

| Median Return for Subsequent 12 Months (14/229 Periods)  | % of Periods Russell 2000 Outperformed in Subsequent 12 Months (13/14 Periods)  |

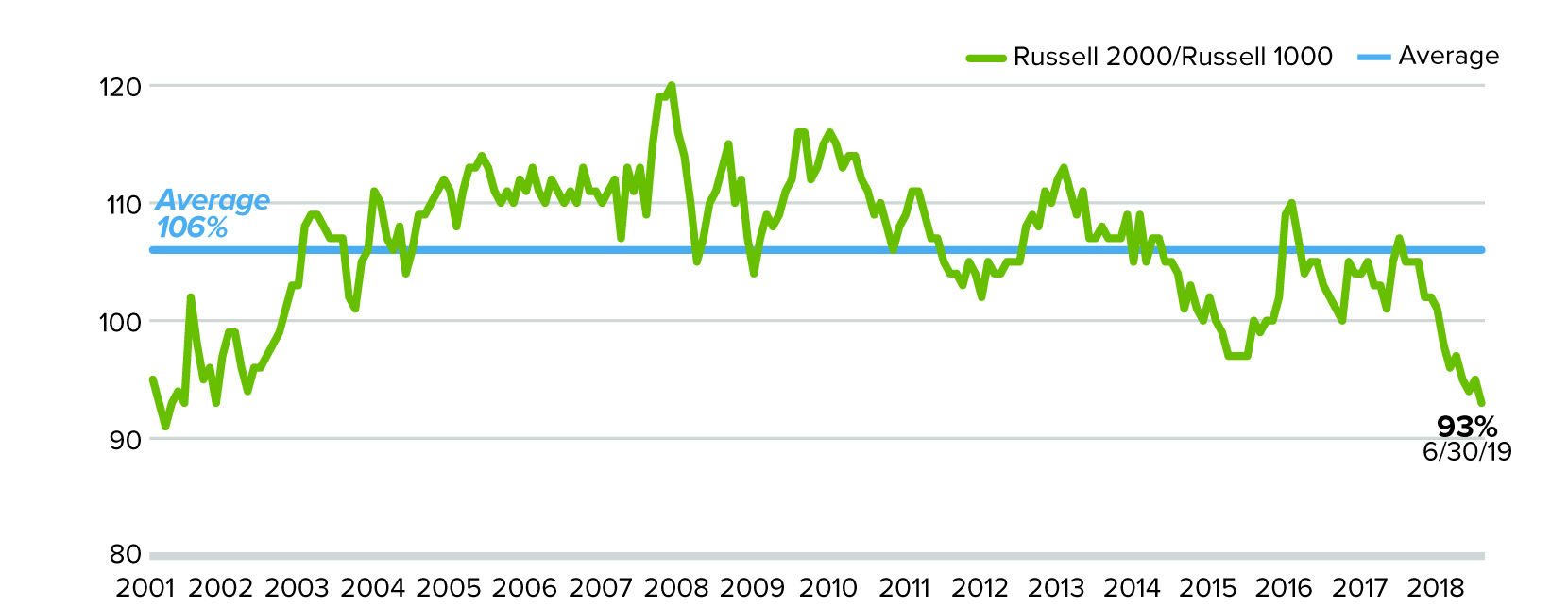

| One additional observation on relative performance: From December 31, 1978 through June 30, 2019, the five-year monthly rolling average return was 10.6% for the Russell 2000 and 11.7% for the Russell 1000, while the five-year average annual total returns for the small- and large-cap indexes for the period ended June 30, 2019 were 7.1% and 10.5%, respectively. With small-caps well below their long-term average, we expect performance to improve to a greater degree than for large-caps, which finished June much closer to their long-term average. Our confidence in mean reversion is further grounded in the relative valuation spread between the Russell 2000 and the Russell 1000 at the end of June, which was significantly below its long-term average based on each index’s median last 12-months’ EV/EBIT (enterprise value over earnings before interest and taxes). In fact, small-caps have lagged large-caps for such an extended period of time that they finished June at their cheapest relative to large-caps since 2001. |

| 2 | This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| So while no one thinks that stocks are currently bargain priced, it’s also true that the vast and diverse universe of small-cap stocks contains a considerable number of attractive risk/reward opportunities based on the combination of reasonable to attractive valuations (again measured by median EV/EBIT) and profitability. |

| THE VALUATION SITUATION When looking for investment candidates, we typically survey the small-cap market for what looks to us like excess pessimism—which is precisely what we’ve been seeing in certain cyclical areas over the last couple of years. Our practice is to then investigate how much of that negative sentiment is already reflected in the current stock price of a given company. So it was significant that at the end of June, cyclical stocks were selling at a greater discount to the Russell 2000 than they had during the fall of 2008—in the teeth of the Financial Crisis. To us, that is the very definition of excess pessimism. |

| Small-Cap Cyclical Discount Russell 2000 Relative Median EV/EBIT1 (Ex Negative EBIT) Cyclical/Russell 2000 |

Source: FactSet

| We suspect that these relatively inexpensive valuations are in large part the result of investors placing undue emphasis on daily macro headlines when trying to understand or anticipate small-cap market movements. (The frequently missed distinction between slower economic growth and a recession is an example of the trouble this can lead to.) We think that investors often fail to fully appreciate the “reaction function,” the response of businesses, central banks, and governments to slowdowns. While we are by no means macro forecasters, it would not surprise us if the global economy grew a little faster over the next year. If history is any guide, this reacceleration could boost small-cap stocks, which have done well on both an absolute and relative basis, especially versus large-caps, when the ISM Manufacturing Index (a common proxy for economic conditions) is on the rise. As unlikely as it currently seems, additional growth could come from a U.S.-China |

| Small-Cap’s Relative Valuation Is Significantly Below Its Long-Term Average Russell 2000 vs. Russell 1000 Median LTM EV/EBIT1 (ex. Negative EBIT Companies) from 12/31/01 to 6/30/19 |

Source: FactSet

| trade deal that addresses tariffs and stokes even modest growth in China, which would likely spur increased activity in Europe as well. Moreover, we expect profitable companies in select cyclical areas to do better regardless of which route the global economy takes in the short term. For example, and in spite of reports of revisions, earnings prospects for the second half of 2019 look solid for many of our small-cap cyclical holdings, especially given the relatively weaker third and fourth quarters of 2018 with which 2019’s two second-half quarters will be compared. We often seek to identify opportunities at the intersection of quality and value—that is, companies with average or better profitability and lower-than-average valuations. There were three cyclical sectors that had higher-than-average profitability and lower-than-average valuations at the end of June—Industrials, Consumer Discretionary, and Materials.2 The relative attractiveness of these and other cyclical areas dovetails nicely with our bottom-up approaches, where the search for fundamentally sound, well-managed companies with solid growth potential has more recently led us overwhelmingly to cyclical businesses. SMALL-CAP STOCKS AND THE URGE TO MERGE The appeal of small-cap stocks can also be seen in recent merger & acquisition (M&A) activity. The number of small-cap M&A deals in the U.S. hit a 10-year high in June, with 503 transactions announced for the trailing four quarters through the end of that month, according to Bloomberg data. This is the largest number of deals in the asset class since before the Financial Crisis. |

| 1 Enterprise Value/Earnings before interest and taxes. |

| 2 Based on the relation between each sector’s average return on equity (ROE) for the five years ended 6/30/19 (excluding companies with negative ROE) and median EV/EBIT (excluding companies with negative earnings). Cyclical are defined as follows: Communication Services, Consumer Discretionary, Energy, Financials, Industrials, Information Technology, and Materials. |

| This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders | 3 |

LETTER TO OUR SHAREHOLDERS

| We anticipate that this trend will continue for a variety of reasons. CEO’s are under relentless pressure to grow profits. If they believe organic growth opportunities are limited, then inorganic paths such as acquisitions begin to make sense. Along similar lines, the CEO of a small-cap company might look more favorably on a buyout offer at a significant stock price premium if he or she sees limited opportunities for their own organic growth. However paradoxical, we can see how a further deceleration in economic growth could lead to an acceleration in M&A deals. With their attractive relative valuations, many small-cap companies should continue to be attractive takeover targets. We also think that many better-managed small-cap businesses will continue to be active as acquirers. We meet with many management teams that run companies with strong balance sheets and are eager to find ways to grow. With interest rates so low, many acquisitions are likely to be accretive, which increases their attraction to a potential buyer. THE NEXT LEG OF THE JOURNEY Disagreements about the condition of the market and state of the economy have created opportunities for active managers and other discerning stock pickers because there’s so little consensus about what constitutes value or quality. Somewhat counterintuitively, this has made us generally quite comfortable with what we’re holding in each of our strategies. Of course, our overall cyclical tilt would not immunize any of our portfolios from a recession. However, the market has provided opportunities to build portfolios that we think are not only inexpensive, but that we think should also provide healthy returns going forward in our most valuation-sensitive strategies. We also expect that many of our high-quality holdings (specifically those in Industrials and Information Technology) could outperform cyclicals in general in the event of a recession thanks to their status as market leaders in global niches as opposed to being one of many players in a highly fragmented commodity business. Across all of our strategies, we’ve been adding or holding positions in areas such as technology, industrials, and many other areas that we |

| think should do well under present or improved conditions. Equally important, many of these holdings already have valuations that seem to reflect a high probability of an imminent recession. Any economic news that shows improvement—or simply the absence of worsening conditions—may lift these stocks. In framing this promising picture of the long-term possibilities for small-cap cyclicals, we also recognize that the lengthy list of current risks is creating an even higher level of uncertainty than usual. However, having done this for as long as we have—four decades and counting—we are also highly aware that the markets seldom do what’s most expected. Given today’s widespread concerns about slowing growth, increasing trade tensions, and the extended economic cycle, the most surprising outcome—as we’ve suggested—might be a rally catalyzed by improved growth. When looking forward, we believe it’s appropriate to be humble about our own forecasts and respectful of those that differ from ours. With what seems like ever increasing tariff and trade tensions, there is a plausible negative scenario of slowing Chinese growth that tips languishing European economies into recession and pushes global yields even lower. This would in all likelihood lead to greater instability in global financial markets as well as breeding heightened risk aversion. While we think this outcome is less likely than others, we also believe that investors should remain mindful of the reaction function we mentioned earlier. Additionally, environments that feature increased uncertainty, turbulence, and market volatility often provide opportunities for companies with leading market positions and strong balance sheets to solidify or expand market share. Volatile environments have also been historically favorable for active small-cap managers. We also see four favorable factors in the current market environment—low inflation, modest valuations, moderate growth, and increased access to capital—that we think support solid-to-strong small-cap performance in the intermediate term regardless current anxieties. These four factors paint an attractive picture in our view, one that small-cap investors might be at risk of missing if they pay more attention to the macro picture than to company fundamentals, where we think the real action is. |

| Sincerely, |

|  |  | ||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | ||

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, | ||

| Royce & Associates, LP | Co-Chief Investment Officer, | Royce & Associates, LP | ||

| Royce & Associates, LP | ||||

| July 31, 2019 |

| 4 | This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders |

Performance and Expenses

| Performance and Expenses |

| As of June 30, 2019 |

| YTD1 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | ANNUAL OPERATING EXPENSES (%) GROSS/NET | ||||||||||||||

| Royce Capital Fund–Micro-Cap Portfolio | 10.70 | -8.72 | 8.19 | 1.16 | 7.54 | 5.25 | 8.68 | 9.29 | 1.39/1.33 | |||||||||||||

| Royce Capital Fund–Small-Cap Portfolio | 8.51 | -7.10 | 7.18 | 2.52 | 9.90 | 7.08 | 9.56 | 9.93 | 1.11/1.08 | |||||||||||||

INDEX | ||||||||||||||||||||||

| Russell Microcap Index | 14.15 | -10.39 | 11.19 | 5.52 | 12.54 | 6.28 | N/A | N/A | N/A | |||||||||||||

| Russell 2000 Index | 16.98 | -3.31 | 12.30 | 7.06 | 13.45 | 8.15 | 7.77 | N/A | N/A | |||||||||||||

| Russell 2000 Value Index | 13.47 | -6.24 | 9.81 | 5.39 | 12.40 | 7.28 | 8.64 | N/A | N/A | |||||||||||||

| 1 Not annualized. | ||||||||||||||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. The Funds’ total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Funds. All performance and expense information reflects the result for each Fund’s Investment Class Shares. Gross annual operating expenses reflect each Fund’s gross total annual operating expenses and include management fees, operating expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of each fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary cost of business, to the extent necessary to maintain net operating expenses at or below 1.33% for Royce Capital Fund–Micro-Cap Portfolio, and at or below 1.08% for Royce Capital Fund–Small-Cap Portfolio through April 30, 2020.

Service Class Shares bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Royce Micro-Cap Portfolio invests primarily in micro-cap companies while Royce Small-Cap Portfolio invests primarily in small-cap companies. Investments in micro-cap and small-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Each series of Royce Capital Fund may invest up to 25% of its net assets in foreign securities. Investments in foreign securities may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see “Investing in Foreign Securities” in the prospectus.) As of 6/30/19, Royce Small-Cap Portfolio invested a significant portion of its assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any one of these stocks would cause the Portfolio’s overall value to decline to a greater degree. Royce Micro-Cap Portfolio’s broadly diversified portfolio does not ensure a profit or guarantee against loss. (Please see “Primary Risks for Fund Investors” in the prospectus.) This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell 2000 Value Index consists of the respective value stocks within the Russell 2000 as determined by Russell Investments. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

| This page is not part of the Royce Capital Fund 2019 Semiannual Report to Shareholders | 5 |

| MANAGERS’ DISCUSSION |

| Royce Capital Fund–Micro-Cap Portfolio (RCM) |

|

| Jim Stoeffel Brendan Hartman |

| FUND PERFORMANCE |

| For the year-to-date period ended June 30, 2019, Royce Capital Fund–Micro-Cap Portfolio underperformed both of its benchmarks. The Fund gained 10.7%, while the Russell Microcap and Russell 2000 Indexes returned 14.1% and 17.0%, respectively, for the same period. We were pleased, however, that the Fund outpaced the micro-cap index for the one-year period ended June 30, 2019. |

| WHAT WORKED...AND WHAT DIDN’T |

| Eight of the Fund’s 10 equity sectors generated positive returns in 2019’s first half. Our persistent large weighting in Information Technology worked in our favor as it was the top contributor at the sector level. Industrials and Health Care followed Information Technology while Communication Services and Consumer Staples detracted, but with only minor impacts. At the industry level, the greatest source of positive performance came from semiconductors & semiconductor equipment (Information Technology), which saw strong results from Adesto Technologies, the second-largest contributing position in the overall portfolio. Through a series of acquisitions, the company has transformed itself from a niche memory provider to a more comprehensive systems provider targeting industrial “Internet-of-Things” applications. Recent results have exceeded expectations as management has successfully integrated its acquisitions and is beginning to garner new product wins. We maintained our position in the shares as we believe the transformation is in the very early stages. |

| Machinery (Industrials) and software (Information Technology) followed as the next top-contributing industries. The best-performing position for the year-to-date period was Quanterix Corporation, a medical technology provider that offers ultra-high sensitivity immunoassay platforms used in testing protein biomarkers. Its shares benefited as the company’s leading edge technology drove significant growth in critical life sciences research applications in areas such as neurology, oncology, and cardiology, among others. We also saw a strong contribution from Kornit Digital, a digital printing specialist for the apparel and textile industries thanks to this machinery company’s recent record revenue growth. |

| The top detractors at the industry level were specialty retail and leisure products—both in Consumer Discretionary. After a series of successful new product offerings, health and fitness products company Nautilus suffered through two consecutive failed product launches, with a resulting decision to remove the CEO. While we like a number of the strategic decisions the company has made over the past several years, we sold our position as we expect it will take at least a year to rebuild a new product pipeline, and our confidence in management’s ability to effectively navigate the rapidly changing fitness market was shaken. Independence Contract Drilling operates a fleet of state-of the-art drilling rigs throughout North America. Its shares have been hurt by the ongoing slowdown in drilling activity in the U.S. While the outlook for the industry remains cloudy given volatile oil prices, we held our position as we believe its shares trade well below the underlying asset value of its high-end rigs. |

| Relative to the Russell Microcap, both stock selection and sector allocation hindered performance for the year-to-date period. Health Care hampered relative results most due to both poor stock selection—most notably in biotechnology—and our underexposure, particularly in pharmaceuticals. Consumer Discretionary came next, mostly due to poor stock selection. The specialty retail group hampered results most, as home décor, furniture, and accessories company Kirkland’s suffered a setback in its efforts to redefine itself as an omnichannel retailer capable of competing with the likes of Amazon and Wayfair. While we believe there is an opportunity for well-run retailers to effectively reimagine their business models in the e-commerce age, we moved on from the stock given management’s recent struggles to execute toward their vision. Conversely, Information Technology was the top contributor due to our overweight in the sector, most impactfully in semiconductors & semiconductor equipment. Industrials followed, with construction & engineering the sector’s strongest industry thanks to savvy stock selection. |

| Top Contributors to Performance | ||||

| Year-to-Date Through 6/30/19 (%)1 | ||||

| Quanterix Corporation | 0.62 | |||

| Adesto Technologies | 0.57 | |||

| Kornit Digital | 0.57 | |||

| NeoGenomics | 0.56 | |||

| Zealand Pharma | 0.55 | |||

| 1 Includes dividends | ||||

| Top Detractors from Performance | ||||

| Year-to-Date Through 6/30/19 (%)2 | ||||

| Nautilus | -0.44 | |||

| Kirkland’s | -0.41 | |||

| Independence Contract Drilling | -0.31 | |||

| Harvard Bioscience | -0.26 | |||

| NeoPhotonics Corporation | -0.22 | |||

| 2 Net of dividends | ||||

| CURRENT POSITIONING AND OUTLOOK |

| We remain generally constructive on the U.S. economy despite the increasing uncertainty around trade and late cycle economic concerns. Our constructive stance was further enhanced by the end of the current Fed tightening cycle, which we think should support what we view as attractive fundamentals and valuations for holdings in various technological and industrial areas, as well as in certain pockets of medical technology, where we have been increasingly active. We also continued to incrementally build our exposure to Information Technology. Indeed, we remain optimistic about the overall prospects for micro-cap stocks in the current environment. Anticipating better growth in the U.S. relative to the rest of the globe, we stayed primarily focused on companies that derive most of their revenues from domestic activities. |

| 6 | Royce Capital Fund 2019 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RCMCX RCMSX |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 6/30/19 | ||||||||||||||||

| JAN-JUN 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCM | 10.70 | -8.72 | 8.19 | 1.16 | 7.54 | 5.25 | 8.68 | 9.29 | ||||||||

| Annual Gross Operating Expenses: 1.39% Annual Net Operating Expenses: 1.33% | ||||||||||||||||

| 1 Not annualized | ||||||||||||||||

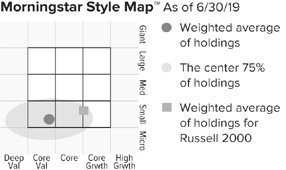

The Morningstar Style Map is the Morningstar Style BoxTM with the center 75% of fund holdings plotted as the Morningstar Ownership ZoneTM. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 29 for additional information. |

Value of $10,000

as of 6/30/19 ($)

Includes reinvestment of distributions.

| Top 10 Positions | ||

| % of Net Assets | ||

| Stoneridge | 1.4 | |

| NeoGenomics | 1.3 | |

| Adesto Technologies | 1.2 | |

| Northwest Pipe | 1.2 | |

| Quanterix Corporation | 1.1 | |

| Ultra Clean Holdings | 1.1 | |

| Rudolph Technologies | 1.1 | |

| Construction Partners Cl. A | 1.0 | |

| Vishay Precision Group | 1.0 | |

| B. Riley Financial | 1.0 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 22.1 | |

| Information Technology | 21.1 | |

| Financials | 13.1 | |

| Health Care | 12.0 | |

| Consumer Discretionary | 9.9 | |

| Energy | 4.1 | |

| Materials | 4.1 | |

| Real Estate | 3.0 | |

| Communication Services | 2.5 | |

| Consumer Staples | 2.0 | |

| Cash and Cash Equivalents | 6.1 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCM | |

| 2018 | -9.0 | |

| 2017 | 5.2 | |

| 2016 | 19.7 | |

| 2015 | -12.5 | |

| 2014 | -3.6 | |

| 2013 | 21.0 | |

| 2012 | 7.6 | |

| 2011 | -12.1 | |

| 2010 | 30.1 | |

| 2009 | 57.9 | |

| 2008 | -43.3 | |

| 2007 | 4.0 | |

| 2006 | 21.1 | |

| 2005 | 11.6 | |

| 2004 | 13.8 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 6/30/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 73 | 88 | ||

| From 6/30/00 (Russell Microcap Inception) | 88 | 79 | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $148 million | |

| Number of Holdings | 140 | |

| Turnover Rate | 8% | |

| Average Market Capitalization1 | $458 million | |

| Weighted Average P/B Ratio2 | 1.8x | |

| Active Share3 | 90% | |

| U.S. Investments (% of Net Assets) | 81.7% | |

| Non-U.S. Investments (% of Net Assets) | 12.2% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCM’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund-Micro-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net assets values differ from the adjusted net values and calendar year total returns reported in the Financial Highlights. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.33% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell Microcap). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| Royce Capital Fund 2019 Semiannual Report to Shareholders | 7 |

Schedule of Investments

| Royce Capital Fund - Micro-Cap Portfolio |

| Common Stocks – 93.9% |

| SHARES | VALUE | ||||||

| COMMUNICATION SERVICES – 2.5% | |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES - 0.6% | |||||||

ORBCOMM 1 | 117,500 | $ | 851,875 | ||||

| ENTERTAINMENT - 0.6% | |||||||

Gaia Cl. A 1 | 113,200 | 858,056 | |||||

| INTERACTIVE MEDIA & SERVICES - 1.0% | |||||||

QuinStreet 1 | 89,900 | 1,424,915 | |||||

| MEDIA - 0.3% | |||||||

Marchex Cl. B 1 | 113,300 | 532,510 | |||||

| Total (Cost $2,920,307) | 3,667,356 | ||||||

| CONSUMER DISCRETIONARY – 9.9% | |||||||

| AUTO COMPONENTS - 2.6% | |||||||

| 16,500 | 1,361,415 | ||||||

Stoneridge 1 | 64,500 | 2,034,975 | |||||

Unique Fabricating 1 | 173,300 | 469,643 | |||||

| 3,866,033 | |||||||

| HOTELS, RESTAURANTS & LEISURE - 2.4% | |||||||

Century Casinos 1 | 131,500 | 1,275,550 | |||||

Lindblad Expeditions Holdings 1 | 62,400 | 1,120,080 | |||||

Red Lion Hotels 1 | 155,000 | 1,102,050 | |||||

| 3,497,680 | |||||||

| HOUSEHOLD DURABLES - 1.4% | |||||||

Cavco Industries 1 | 5,504 | 867,100 | |||||

Lovesac Company (The) 1 | 39,400 | 1,224,158 | |||||

| 2,091,258 | |||||||

| LEISURE PRODUCTS - 0.7% | |||||||

MasterCraft Boat Holdings 1 | 52,917 | 1,036,644 | |||||

| SPECIALTY RETAIL - 1.7% | |||||||

Citi Trends | 47,886 | 700,094 | |||||

Haverty Furniture | 49,100 | 836,173 | |||||

Shoe Carnival | 35,000 | 966,000 | |||||

| 2,502,267 | |||||||

| TEXTILES, APPAREL & LUXURY GOODS - 1.1% | |||||||

Culp | 30,649 | 582,331 | |||||

Vera Bradley 1 | 90,100 | 1,081,200 | |||||

| 1,663,531 | |||||||

| Total (Cost $10,735,015) | 14,657,413 | ||||||

| CONSUMER STAPLES – 2.0% | |||||||

| BEVERAGES - 0.7% | |||||||

| 76,900 | 945,870 | ||||||

| FOOD PRODUCTS - 1.3% | |||||||

Farmer Bros. 1 | 47,800 | 782,486 | |||||

John B. Sanfilippo & Son | 15,000 | 1,195,350 | |||||

| 1,977,836 | |||||||

| Total (Cost $3,105,013) | 2,923,706 | ||||||

| ENERGY – 4.1% | |||||||

| ENERGY EQUIPMENT & SERVICES - 3.3% | |||||||

Gulf Island Fabrication 1 | 92,634 | 657,701 | |||||

Independence Contract Drilling 1 | 301,600 | 476,528 | |||||

Natural Gas Services Group 1 | 61,100 | 1,008,150 | |||||

Newpark Resources 1 | 160,000 | 1,187,200 | |||||

Profire Energy 1 | 486,229 | 734,206 | |||||

Total Energy Services | 139,300 | 878,636 | |||||

| 4,942,421 | |||||||

| OIL, GAS & CONSUMABLE FUELS - 0.8% | |||||||

Ardmore Shipping 1 | 136,000 | 1,108,400 | |||||

| Total (Cost $7,346,954) | 6,050,821 | ||||||

| FINANCIALS – 13.1% | |||||||

| BANKS - 6.0% | |||||||

Allegiance Bancshares 1 | 29,000 | 966,860 | |||||

BayCom Corporation 1 | 45,682 | 1,000,436 | |||||

Caribbean Investment Holdings 1 | 1,751,547 | 355,900 | |||||

County Bancorp | 59,600 | 1,018,564 | |||||

HarborOne Bancorp 1 | 63,100 | 1,181,863 | |||||

HomeTrust Bancshares | 44,700 | 1,123,758 | |||||

Investar Holding | 46,200 | 1,101,870 | |||||

| 1,751,577 | 0 | ||||||

TriState Capital Holdings 1 | 51,072 | 1,089,876 | |||||

Two River Bancorp | 72,400 | 1,039,664 | |||||

| 8,878,791 | |||||||

| CAPITAL MARKETS - 3.6% | |||||||

B. Riley Financial | 73,200 | 1,526,952 | |||||

Canaccord Genuity Group | 257,900 | 1,181,627 | |||||

INTL FCStone 1 | 12,300 | 486,957 | |||||

Silvercrest Asset Management Group Cl. A | 90,300 | 1,266,909 | |||||

Westwood Holdings Group | 23,427 | 824,631 | |||||

| 5,287,076 | |||||||

| DIVERSIFIED FINANCIAL SERVICES - 0.3% | |||||||

| 1,302,000 | 390,600 | ||||||

| INSURANCE - 0.5% | |||||||

| 30,400 | 787,968 | ||||||

| THRIFTS & MORTGAGE FINANCE - 2.7% | |||||||

Meridian Bancorp | 16,300 | 291,607 | |||||

PCSB Financial | 62,600 | 1,267,650 | |||||

Territorial Bancorp | 41,900 | 1,294,710 | |||||

Western New England Bancorp | 130,954 | 1,223,110 | |||||

| 4,077,077 | |||||||

| Total (Cost $22,040,773) | 19,421,512 | ||||||

| HEALTH CARE – 12.0% | |||||||

| BIOTECHNOLOGY - 2.9% | |||||||

BioSpecifics Technologies 1 | 20,300 | 1,212,113 | |||||

Dynavax Technologies 1 | 64,800 | 258,552 | |||||

Progenics Pharmaceuticals 1 | 215,200 | 1,327,784 | |||||

Zealand Pharma 1 | 68,758 | 1,494,751 | |||||

| 4,293,200 | |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES - 5.4% | |||||||

| 19,600 | 131,712 | ||||||

AtriCure 1 | 38,600 | 1,151,824 | |||||

Chembio Diagnostics 1 | 142,400 | 867,216 | |||||

CryoLife 1 | 42,089 | 1,259,724 | |||||

Mesa Laboratories | 4,700 | 1,148,398 | |||||

OrthoPediatrics Corporation 1 | 35,000 | 1,365,000 | |||||

Surmodics 1 | 25,178 | 1,086,934 | |||||

Tactile Systems Technology 1 | 16,200 | 922,104 | |||||

| 7,932,912 | |||||||

| HEALTH CARE TECHNOLOGY - 0.1% | |||||||

| 137,661 | 228,517 | ||||||

| LIFE SCIENCES TOOLS & SERVICES - 2.9% | |||||||

Harvard Bioscience 1 | 357,168 | 714,336 | |||||

NeoGenomics 1 | 87,600 | 1,921,944 | |||||

Quanterix Corporation 1 | 49,400 | 1,669,226 | |||||

| 4,305,506 | |||||||

| PHARMACEUTICALS - 0.7% | |||||||

| 257,200 | 555,552 | ||||||

Paratek Pharmaceuticals 1 | 94,600 | 377,454 | |||||

| 8 | Royce Capital Fund 2019 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| June 30, 2019 (unaudited) |

| Royce Capital Fund - Micro-Cap Portfolio (continued) |

| SHARES | VALUE | ||||||

| HEALTH CARE (continued) | |||||||

| PHARMACEUTICALS (continued) | |||||||

Tetraphase Pharmaceuticals 1 | 253,900 | $ | 121,948 | ||||

| 1,054,954 | |||||||

| Total (Cost $13,285,394) | 17,815,089 | ||||||

| INDUSTRIALS – 22.1% | |||||||

| AEROSPACE & DEFENSE - 1.8% | |||||||

Astronics Corporation 1 | 31,026 | 1,247,866 | |||||

CPI Aerostructures 1 | 174,344 | 1,466,233 | |||||

| 2,714,099 | |||||||

| COMMERCIAL SERVICES & SUPPLIES - 1.5% | |||||||

Acme United | 50,865 | 1,148,532 | |||||

Heritage-Crystal Clean 1 | 41,634 | 1,095,391 | |||||

| 2,243,923 | |||||||

| CONSTRUCTION & ENGINEERING - 2.2% | |||||||

Construction Partners Cl. A 1 | 103,000 | 1,547,060 | |||||

Northwest Pipe 1 | 67,500 | 1,740,150 | |||||

| 3,287,210 | |||||||

| ELECTRICAL EQUIPMENT - 1.7% | |||||||

American Superconductor 1 | 117,400 | 1,089,472 | |||||

Encore Wire | 22,800 | 1,335,624 | |||||

| 2,425,096 | |||||||

| INDUSTRIAL CONGLOMERATES - 0.6% | |||||||

Raven Industries | 25,700 | 922,116 | |||||

| MACHINERY - 8.8% | |||||||

Alimak Group | 80,300 | 1,233,103 | |||||

Exco Technologies | 156,700 | 927,361 | |||||

FreightCar America 1 | 86,091 | 505,354 | |||||

Graham Corporation | 67,020 | 1,354,474 | |||||

Greenbrier Companies (The) | 16,600 | 504,640 | |||||

Helios Technologies | 20,100 | 932,841 | |||||

Kadant | 11,931 | 1,083,454 | |||||

Kornit Digital 1 | 48,200 | 1,526,012 | |||||

Lindsay Corporation | 13,100 | 1,076,951 | |||||

Luxfer Holdings | 46,400 | 1,137,728 | |||||

Lydall 1 | 38,800 | 783,760 | |||||

Spartan Motors | 96,100 | 1,053,256 | |||||

Westport Fuel Systems 1 | 345,300 | 935,763 | |||||

| 13,054,697 | |||||||

| MARINE - 0.8% | |||||||

Clarkson | 38,100 | 1,214,465 | |||||

| PROFESSIONAL SERVICES - 3.8% | |||||||

CRA International | 22,106 | 847,323 | |||||

GP Strategies 1 | 90,608 | 1,366,369 | |||||

Heidrick & Struggles International | 25,600 | 767,232 | |||||

Kforce | 32,600 | 1,143,934 | |||||

Resources Connection | 89,254 | 1,428,956 | |||||

| 5,553,814 | |||||||

| ROAD & RAIL - 0.7% | |||||||

Marten Transport | 55,841 | 1,013,514 | |||||

| TRADING COMPANIES & DISTRIBUTORS - 0.2% | |||||||

| 11,300 | 289,167 | ||||||

| Total (Cost $24,128,601) | 32,718,101 | ||||||

| INFORMATION TECHNOLOGY – 21.1% | |||||||

| COMMUNICATIONS EQUIPMENT - 1.3% | |||||||

Digi International 1 | 97,400 | 1,235,032 | |||||

EMCORE Corporation 1 | 149,300 | 491,197 | |||||

Harmonic 1 | 25,700 | 142,635 | |||||

| 1,868,864 | |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 5.0% | |||||||

ePlus 1 | 13,792 | 950,821 | |||||

Fabrinet 1 | 22,669 | 1,125,969 | |||||

| 232,800 | 211,848 | ||||||

| 30,700 | 138,150 | ||||||

nLIGHT 1 | 47,500 | 912,000 | |||||

Novanta 1 | 13,000 | 1,225,900 | |||||

PC Connection | 36,500 | 1,276,770 | |||||

Vishay Precision Group 1 | 38,000 | 1,543,940 | |||||

| 7,385,398 | |||||||

| IT SERVICES - 0.8% | |||||||

Cass Information Systems | 24,048 | 1,165,847 | |||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 11.4% | |||||||

Adesto Technologies 1 | 220,400 | 1,796,260 | |||||

Aehr Test Systems 1 | 349,500 | 576,675 | |||||

AXT 1 | 148,600 | 588,456 | |||||

Brooks Automation | 29,500 | 1,143,125 | |||||

†Camtek | 51,800 | 437,710 | |||||

Cohu | 46,800 | 722,124 | |||||

CyberOptics Corporation 1 | 36,300 | 589,149 | |||||

| 92,500 | 603,100 | ||||||

| 33,400 | 789,576 | ||||||

Nanometrics 1 | 8,900 | 308,919 | |||||

NeoPhotonics Corporation 1 | 227,300 | 950,114 | |||||

Nova Measuring Instruments 1 | 57,500 | 1,471,425 | |||||

PDF Solutions 1 | 85,700 | 1,124,384 | |||||

Photronics 1 | 164,600 | 1,349,720 | |||||

Rudolph Technologies 1 | 58,293 | 1,610,635 | |||||

Silicon Motion Technology ADR | 26,900 | 1,193,822 | |||||

Ultra Clean Holdings 1 | 117,100 | 1,630,032 | |||||

| 16,885,226 | |||||||

| SOFTWARE - 1.8% | |||||||

Agilysys 1 | 66,800 | 1,434,196 | |||||

QAD Cl. A | 31,800 | 1,278,678 | |||||

| 2,712,874 | |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS - 0.8% | |||||||

AstroNova | 43,700 | 1,129,208 | |||||

| Total (Cost $23,530,501) | 31,147,417 | ||||||

| MATERIALS – 4.1% | |||||||

| CHEMICALS - 2.0% | |||||||

FutureFuel Corporation | 62,400 | 729,456 | |||||

Quaker Chemical | 5,288 | 1,072,829 | |||||

Trecora Resources 1 | 115,400 | 1,104,378 | |||||

| 2,906,663 | |||||||

| METALS & MINING - 2.1% | |||||||

Haynes International | 39,870 | 1,268,265 | |||||

Major Drilling Group International 1 | 254,700 | 822,711 | |||||

Universal Stainless & Alloy Products 1 | 63,700 | 1,019,200 | |||||

| 3,110,176 | |||||||

| Total (Cost $6,023,402) | 6,016,839 | ||||||

| REAL ESTATE – 3.0% | |||||||

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITS) - 1.4% | |||||||

Community Healthcare Trust | 32,200 | 1,269,002 | |||||

†Postal Realty Trust Cl. A | 50,400 | 793,800 | |||||

| 2,062,802 | |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.6% | |||||||

FRP Holdings 1 | 23,440 | 1,307,249 | |||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2019 Semiannual Report to Shareholders | 9 |

| Schedule of Investments | June 30, 2019 (unaudited) |

| Royce Capital Fund - Micro-Cap Portfolio (continued) |

| SHARES | VALUE | ||||||

| REAL ESTATE (continued) | |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT (continued) | |||||||

Marcus & Millichap 1 | 33,900 | $ | 1,045,815 | ||||

| 2,353,064 | |||||||

| Total (Cost $3,100,777) | 4,415,866 | ||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $116,216,737) | 138,834,120 | ||||||

| REPURCHASE AGREEMENT – 6.6% | |||||||

| Fixed Income Clearing Corporation, 0.50% dated 6/28/19, due 7/1/19, maturity value $9,737,406 (collateralized by obligations of various U.S. Government Agencies, 1.75% due 05/31/22, valued at $9,935,991) | |||||||

| (Cost $9,737,000) | 9,737,000 | ||||||

| COLLATERAL RECEIVED FOR SECURITIES LOANED – 0.6% | |||||||

| Money Market Funds | |||||||

Federated Government Obligations Fund (7 day yield-2.2655%) | |||||||

| (Cost $868,441) | 868,441 | ||||||

| TOTAL INVESTMENTS – 101.1% | |||||||

| (Cost $126,822,178) | 149,439,561 | ||||||

| LIABILITIES LESS CASH AND OTHER ASSETS – (1.1)% | (1,640,919 | ) | |||||

| NET ASSETS – 100.0% | $ | 147,798,642 | |||||

ADR – American Depository Receipt

| † | New additions in 2019. |

| 1 | Non-income producing. |

| 2 | All or a portion of these securities were on loan at June 30, 2019. |

| 3 | Securities for which market quotations are not readily available represent 0.3% of net assets. These securities have been valued at their fair value under procedures approved by the Fund’s Board of Trustees. These securities are defined as Level 3 securities due to the use of significant unobservable inputs in the determination of fair value. See Notes to Financial Statements. |

Bold indicates the Fund’s 20 largest equity holdings in terms of June 30, 2019, market value.

| 10 | Royce Capital Fund 2019 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| This page is intentionally left blank. |

| Royce Capital Fund 2019 Semiannual Report to Shareholders | 11 |

| MANAGER’S DISCUSSION |

| Royce Capital Fund–Small-Cap Portfolio (RCS) |

|

| Jay Kaplan, CFA |

| FUND PERFORMANCE |

| Royce Capital Fund–Small-Cap Portfolio increased 8.5% for the year-to-date period ended June 30, 2019, trailing respective gains of 17.0% and 13.5% for its small-cap benchmarks, the Russell 2000 and Russell 2000 Value Indexes, for the same period. |

| WHAT WORKED... AND WHAT DIDN’T |

| Five of the portfolio’s 11 equity sectors finished the year-to-date period in the black. Industrials, Information Technology, and Financials were the strongest contributors, while Materials and Health Care were more muted. Three sectors finished in the red, with Consumer Discretionary making the biggest detraction, followed by much smaller negative impacts from Energy and Communication Services. (Real Estate, Utilities, and Consumer Staples were essentially flat.) |

| At the industry level, electronic equipment, instruments & components (Information Technology) was the strongest positive contributor in 2019’s first half. The rising shares of Insight Enterprises, which provides information technology hardware and software for large and small enterprises, helped both this industry and the portfolio as a whole. Investors seemed drawn to its improved margins and earnings, along with its solid outlook for the rest of the year. We took some gains as its stock rose. Machinery (Industrials) was the second-biggest industry contributor, boosted by Meritor, which supplies drivetrain, braking, and other aftermarket solutions for commercial and industrial vehicles. Improved revenues and better-than-expected earnings were driven largely by higher North American truck production. It was the portfolio’s second-largest holding at the end of June. |

| Specialty retail (Consumer Discretionary) detracted most at the industry level, due in part to poor performance from Caleres and top-10 holding, Shoe Carnival. Several factors hurt Caleres, such as reduced traffic and same-store sales growth at the firm’s Famous Footwear retailer (which accounts for about half of its profits); near-term margin pressure from having to clear excess inventory at hefty discounts in advance of new, much improved back-to-school styles from Famous Footwear’s largest vendor; and the negative impact that the threatened next round of U.S. tariffs on China-made goods would have on consumer prices and demand. Few retailers were immune from these anxieties, but it seemed to us that the shares of apparel and footwear companies, which also included Shoe Carnival, were among the hardest hit. Ever contrarian and always thinking about the long run, we began to build our stake in Caleres in late June. |

| G-III Apparel Group lost most in the textiles, apparel & luxury goods group, the second-biggest industry detractor. Its stock suffered from the same tariff worries that helped hurt Caleres and Shoe Carnival as well as from poor results from its retail arm. We like that G-III is preparing to move some production out of China. It also maintains a strong wholesale business, powered by popular brands such as DKNY, Donna Karan, and Tommy Hilfiger. ArcBest is a freight and logistics solutions specialist that saw its business stall in the first quarter. Believing in its long-term prospects and thinking that its shares were punished disproportionately by recession fears, we held our position at the end of June. |

| Relative to the Russell 2000, both poor stock picking and sector allocation were sources of first-half underperformance. Stock selection in Consumer Discretionary hurt most, particularly in specialty retail. Stock selection also hurt in Information Technology, primarily in electronic equipment, instruments & components, and in Industrials, where professional services and road & rail detracted most. Materials was the sole source of first-half outperformance, thanks mostly to savvy stock selection in metals & mining—the only industry in this sector where we had exposure. |

| Top Contributors to Performance | ||||

| Year-to-Date Through 6/30/19 (%)1 | ||||

| Insight Enterprises | 0.91 | |||

| Meritor | 0.86 | |||

| Advanced Energy Industries | 0.56 | |||

| Camden National | 0.51 | |||

| Apogee Enterprises | 0.50 | |||

| 1 Includes dividends | ||||

| Top Detractors from Performance | ||||

| Year-to-Date Through 6/30/19 (%)2 | ||||

| G-III Apparel Group | -0.66 | |||

| ArcBest | -0.52 | |||

| Caleres | -0.42 | |||

| Shoe Carnival | -0.35 | |||

| Celestica | -0.33 | |||

| 2 Net of dividends | ||||

| CURRENT POSITIONING AND OUTLOOK |

| There’s been an ongoing slugfest among investors: in one corner, large-cap indexes have been routinely reaching new highs, the labor market is strong, and the economy is growing; on the opposite side of the ring, small-caps have been lagging large-caps—which seldom happens in a vibrant economy—the yield curve was flat or inverted through much of the first half, and economies outside the U.S. are slowing more quickly and appreciably than our own. So optimism, including the more cautious variety, is facing off against a pessimism that sees recession as imminent. Needless to say, only one of these combatants will be able to claim victory. For our part, we are squarely in the guarded optimism camp. We see growth slowing at a marginal pace—and certainly not contracting, which is the key distinction. Many of our holdings finished June at prices that looked to us like a recession had already been priced in. We have therefore been adding to positions in select cyclical areas such as trucking, trucks and automobile components, and footwear manufactures and retailers. We have not found many new opportunities, however, due to the otherwise mostly elevated state of many small-cap valuations. Recent relative performance challenges notwithstanding, we are comfortable with how we’ve positioned the portfolio in the face of ongoing uncertainty. |

| 12 | Royce Capital Fund 2019 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RCPFX RCSSX |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 6/30/19 | ||||||||||||||||

| JAN-JUN 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCS | 8.51 | -7.10 | 7.18 | 2.52 | 9.90 | 7.08 | 9.56 | 9.93 | ||||||||

| Annual Gross Operating Expenses: 1.11% Annual Net Operating Expenses: 1.08% | ||||||||||||||||

| 1 Not annualized | ||||||||||||||||

Relative Returns: Monthly Rolling Average Annual Return Periods

| On a monthly rolling basis, the Fund outperformed the Russell 2000 in 59% of all 10-year periods; 57% of all 5-year periods; and 51% of all 1-year periods. |

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||

| 10-year | 71/121 | 59% | 8.8 | 7.8 | ||||||||

| 5-year | 104/181 | 57% | 9.7 | 8.8 | ||||||||

| 1-year | 116/229 | 51% | 11.6 | 9.6 | ||||||||

The Morningstar Style Map is the Morningstar Style BoxTM with the center 75% of fund holdings plotted as the Morningstar Ownership ZoneTM. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 29 for additional information. |

Value of $10,000

Includes reinvestment of distributions.

| Top 10 Positions | ||

| % of Net Assets | ||

| Hilton Grand Vacations | 2.5 | |

| Meritor | 2.5 | |

| Insight Enterprises | 2.4 | |

| Miller Industries | 2.4 | |

| Allegiant Travel | 2.3 | |

| Designer Brands Cl. A | 2.1 | |

| Kulicke & Soffa Industries | 2.1 | |

| Shoe Carnival | 2.0 | |

| Sanmina Corporation | 2.0 | |

| Camden National | 2.0 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 29.8 | |

| Financials | 24.7 | |

| Information Technology | 16.1 | |

| Consumer Discretionary | 15.1 | |

| Energy | 2.7 | |

| Consumer Staples | 1.7 | |

| Communication Services | 1.6 | |

| Health Care | 1.0 | |

| Real Estate | 1.0 | |

| Materials | 0.5 | |

| Cash and Cash Equivalents | 5.8 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCS | |

| 2018 | -8.3 | |

| 2017 | 5.4 | |

| 2016 | 21.0 | |

| 2015 | -11.8 | |

| 2014 | 3.2 | |

| 2013 | 34.8 | |

| 2012 | 12.5 | |

| 2011 | -3.3 | |

| 2010 | 20.5 | |

| 2009 | 35.2 | |

| 2008 | -27.2 | |

| 2007 | -2.1 | |

| 2006 | 15.6 | |

| 2005 | 8.6 | |

| 2004 | 25.0 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 6/30/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 72 | 70 | ||

| From 12/31/96 (Start of Fund’s First Full Quarter) | 92 | 75 | ||

| Portfolio Diagnostics | ||

| Fund Net Assets | $276 million | |

| Number of Holdings | 84 | |

| Turnover Rate | 84% | |

| Average Market Capitalization1 | $1,110 million | |

| Weighted Average P/B Ratio2 | 1.7x | |

| Active Share3 | 96% | |

| U.S. Investments (% of Net Assets) | 87.4% | |

| Non-U.S. Investments (% of Net Assets) | 6.8% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.roycefunds.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCS’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund-Small-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net assets values differ from the adjusted net values and calendar year total returns reported in the Financial Highlights. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.08% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| Royce Capital Fund 2019 Semiannual Report to Shareholders | 13 |

Schedule of Investments

| Royce Capital Fund - Small-Cap Portfolio | ||||||||

| Common Stocks – 94.2% | ||||||||

| SHARES | VALUE | |||||||

| COMMUNICATION SERVICES – 1.6% | ||||||||

| MEDIA - 1.6% | ||||||||

Saga Communications Cl. A | 141,036 | $ | 4,405,965 | |||||

| Total (Cost $6,074,969) | 4,405,965 | |||||||

| CONSUMER DISCRETIONARY – 15.1% | ||||||||

| AUTO COMPONENTS - 2.7% | ||||||||

Cooper-Standard Holdings 1 | 9,200 | 421,544 | ||||||

Gentex Corporation | 84,116 | 2,070,095 | ||||||

Stoneridge 1 | 41,205 | 1,300,018 | ||||||

†Tower International | 193,551 | 3,774,244 | ||||||

| 7,565,901 | ||||||||

| HOTELS, RESTAURANTS & LEISURE - 2.9% | ||||||||

Cheesecake Factory | 28,315 | 1,237,932 | ||||||

Hilton Grand Vacations 1 | 214,809 | 6,835,222 | ||||||

| 8,073,154 | ||||||||

| HOUSEHOLD DURABLES - 0.9% | ||||||||

La-Z-Boy | 80,986 | 2,483,031 | ||||||

| INTERNET & DIRECT MARKETING RETAIL - 0.1% | ||||||||

| 33,322 | 411,527 | |||||||

| SPECIALTY RETAIL - 6.2% | ||||||||

American Eagle Outfitters | 167,865 | 2,836,918 | ||||||

Caleres | 138,617 | 2,761,251 | ||||||

Designer Brands Cl. A | 300,866 | 5,767,601 | ||||||

Shoe Carnival | 204,736 | 5,650,714 | ||||||

| 17,016,484 | ||||||||

| TEXTILES, APPAREL & LUXURY GOODS - 2.3% | ||||||||

G-III Apparel Group 1 | 167,365 | 4,923,878 | ||||||

Steven Madden | 39,606 | 1,344,624 | ||||||

| 6,268,502 | ||||||||

| Total (Cost $47,474,348) | 41,818,599 | |||||||

| CONSUMER STAPLES – 1.7% | ||||||||

| FOOD & STAPLES RETAILING - 1.7% | ||||||||

Village Super Market Cl. A | 174,078 | 4,614,808 | ||||||

| Total (Cost $4,659,952) | 4,614,808 | |||||||

| ENERGY – 2.7% | ||||||||

| ENERGY EQUIPMENT & SERVICES - 1.3% | ||||||||

Helmerich & Payne | 71,800 | 3,634,516 | ||||||

| OIL, GAS & CONSUMABLE FUELS - 1.4% | ||||||||

†Alliance Resource Partners L.P. | 199,200 | 3,382,416 | ||||||

Unit Corporation 1 | 40,713 | 361,938 | ||||||

| 3,744,354 | ||||||||

| Total (Cost $7,182,133) | 7,378,870 | |||||||

| FINANCIALS – 24.7% | ||||||||

| BANKS - 11.9% | ||||||||

Ames National | 149,942 | 4,063,428 | ||||||

Bar Harbor Bankshares | 64,381 | 1,711,891 | ||||||

Camden National | 120,348 | 5,520,363 | ||||||

City Holding Company | 35,010 | 2,669,863 | ||||||

CNB Financial | 149,719 | 4,228,064 | ||||||

Codorus Valley Bancorp | 53,660 | 1,234,180 | ||||||

Financial Institutions | 70,182 | 2,045,805 | ||||||

Landmark Bancorp | 36,981 | 885,695 | ||||||

MidWestOne Financial Group | 53,069 | 1,483,809 | ||||||

National Bankshares | 99,057 | 3,856,289 | ||||||

Northrim BanCorp | 81,481 | 2,905,612 | ||||||

Unity Bancorp | 109,438 | 2,484,243 | ||||||

| 33,089,242 | ||||||||

| CAPITAL MARKETS - 2.9% | ||||||||

Houlihan Lokey Cl. A | 28,015 | 1,247,508 | ||||||

Moelis & Company Cl. A | 117,271 | 4,098,621 | ||||||

Pzena Investment Management Cl. A | 312,511 | 2,684,470 | ||||||

| 8,030,599 | ||||||||

| INSURANCE - 2.6% | ||||||||

James River Group Holdings | 27,335 | 1,282,011 | ||||||

Kingstone Companies | 204,395 | 1,768,017 | ||||||

Reinsurance Group of America | 26,036 | 4,062,397 | ||||||

| 7,112,425 | ||||||||

| THRIFTS & MORTGAGE FINANCE - 7.3% | ||||||||

Genworth MI Canada | 163,350 | 5,169,122 | ||||||

Southern Missouri Bancorp | 70,381 | 2,451,370 | ||||||

Timberland Bancorp | 77,177 | 2,306,049 | ||||||

TrustCo Bank Corp. NY | 618,682 | 4,899,962 | ||||||

WSFS Financial | 128,900 | 5,323,570 | ||||||

| 20,150,073 | ||||||||

| Total (Cost $60,778,056) | 68,382,339 | |||||||

| HEALTH CARE – 1.0% | ||||||||

| HEALTH CARE PROVIDERS & SERVICES - 1.0% | ||||||||

AMN Healthcare Services 1 | 21,941 | 1,190,299 | ||||||

Ensign Group (The) | 28,314 | 1,611,633 | ||||||

| Total (Cost $1,689,236) | 2,801,932 | |||||||

| INDUSTRIALS – 29.8% | ||||||||

| AEROSPACE & DEFENSE - 0.9% | ||||||||

Magellan Aerospace | 194,200 | 2,417,212 | ||||||

| AIRLINES - 5.3% | ||||||||

Allegiant Travel | 44,393 | 6,370,396 | ||||||

Hawaiian Holdings | 153,055 | 4,198,299 | ||||||

Spirit Airlines 1 | 86,432 | 4,125,399 | ||||||

| 14,694,094 | ||||||||

| BUILDING PRODUCTS - 1.0% | ||||||||

Apogee Enterprises | 67,417 | 2,928,595 | ||||||

| COMMERCIAL SERVICES & SUPPLIES - 2.5% | ||||||||

Herman Miller | 68,403 | 3,057,614 | ||||||

Kimball International Cl. B | 219,982 | 3,834,286 | ||||||

| 6,891,900 | ||||||||

| CONSTRUCTION & ENGINEERING - 0.5% | ||||||||

Comfort Systems USA | 26,269 | 1,339,456 | ||||||

| ELECTRICAL EQUIPMENT - 1.0% | ||||||||

EnerSys | 40,936 | 2,804,116 | ||||||

| MACHINERY - 7.5% | ||||||||

Alamo Group | 13,207 | 1,319,776 | ||||||

| 479,296 | 3,843,954 | |||||||

Federal Signal | 50,022 | 1,338,088 | ||||||

Meritor 1 | 280,329 | 6,797,978 | ||||||

Miller Industries | 218,355 | 6,714,416 | ||||||

Wabash National | 39,854 | 648,425 | ||||||

| 20,662,637 | ||||||||

| PROFESSIONAL SERVICES - 5.6% | ||||||||

Heidrick & Struggles International | 127,108 | 3,809,427 | ||||||

Kforce | 62,446 | 2,191,230 | ||||||

Korn Ferry | 101,271 | 4,057,929 | ||||||

Resources Connection | 162,180 | 2,596,502 | ||||||

Robert Half International | 27,164 | 1,548,619 | ||||||

TrueBlue 1 | 60,648 | 1,337,895 | ||||||

| 15,541,602 | ||||||||

| 14 | Royce Capital Fund 2019 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| June 30, 2019 (unaudited) |

| Royce Capital Fund - Small-Cap Portfolio (continued) | ||||||||

| SHARES | VALUE | |||||||

| INDUSTRIALS (continued) | ||||||||

| ROAD & RAIL - 4.5% | ||||||||

ArcBest | 154,800 | $ | 4,351,428 | |||||

Old Dominion Freight Line | 9,104 | 1,358,863 | ||||||

Saia 1 | 38,918 | 2,516,827 | ||||||

Werner Enterprises | 134,439 | 4,178,364 | ||||||

| 12,405,482 | ||||||||

| TRADING COMPANIES & DISTRIBUTORS - 1.0% | ||||||||

| 127,332 | 2,699,438 | |||||||

| Total (Cost $78,819,293) | 82,384,532 | |||||||

| INFORMATION TECHNOLOGY – 16.1% | ||||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 10.6% | ||||||||

Benchmark Electronics | 53,751 | 1,350,225 | ||||||

Fabrinet 1 | 47,186 | 2,343,729 | ||||||

Insight Enterprises 1 | 116,152 | 6,760,046 | ||||||

Methode Electronics | 46,115 | 1,317,506 | ||||||

PC Connection | 127,535 | 4,461,174 | ||||||

Sanmina Corporation 1 | 184,393 | 5,583,420 | ||||||

Vishay Intertechnology | 294,399 | 4,863,472 | ||||||

Vishay Precision Group 1 | 68,300 | 2,775,029 | ||||||

| 29,454,601 | ||||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 5.5% | ||||||||

Advanced Energy Industries 1 | 51,152 | 2,878,323 | ||||||

Kulicke & Soffa Industries | 255,126 | 5,753,091 | ||||||

MKS Instruments | 64,691 | 5,038,782 | ||||||

Silicon Motion Technology ADR | 33,900 | 1,504,482 | ||||||

| 15,174,678 | ||||||||

| Total (Cost $39,890,771) | 44,629,279 | |||||||

| MATERIALS – 0.5% | ||||||||

| METALS & MINING - 0.5% | ||||||||

| 95,182 | 1,313,512 | |||||||

| Total (Cost $1,372,799) | 1,313,512 | |||||||

| REAL ESTATE – 1.0% | ||||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.0% | ||||||||

Marcus & Millichap 1 | 87,719 | 2,706,131 | ||||||

| Total (Cost $2,627,614) | 2,706,131 | |||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $250,569,171) | 260,435,967 | |||||||

| REPURCHASE AGREEMENT – 5.7% | ||||||||

| Fixed Income Clearing Corporation, 0.50% dated 6/28/19, due 7/1/19, maturity value $15,638,652 (collateralized by obligations of various U.S. Government Agencies, 1.75% due 05/31/22, valued at $15,955,679) | ||||||||

| (Cost $15,638,000) | 15,638,000 | |||||||

| TOTAL INVESTMENTS – 99.9% | ||||||||

| (Cost $266,207,171) | 276,073,967 | |||||||

| CASH AND OTHER ASSETS LESS LIABILITIES – 0.1% | 343,862 | |||||||

| NET ASSETS – 100.0% | $ | 276,417,829 | ||||||

| ADR- American Depository Receipt | |

| † | New additions in 2019. |

| 1 | Non-income producing. |

Bold indicates the Fund’s 20 largest equity holdings in terms of June 30, 2019, market value. |

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2019 Semiannual Report to Shareholders | 15 |

| Statements of Assets and Liabilities | June 30, 2019 (unaudited) |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| ASSETS: | ||||||||

| Investments at value (including collateral on loaned securities) 1 | $ | 139,702,561 | $ | 260,435,967 | ||||

| Repurchase agreements (at cost and value) | 9,737,000 | 15,638,000 | ||||||

| Cash and foreign currency | 9,282 | 55,401 | ||||||

| Receivable for investments sold | 18,265 | 634,629 | ||||||

| Receivable for capital shares sold | 17,303 | 210,049 | ||||||

| Receivable for dividends and interest | 115,366 | 273,353 | ||||||

| Receivable for securities lending income | 16,157 | 19 | ||||||

| Prepaid expenses and other assets | 414 | 6,301 | ||||||

| Total Assets | 149,616,348 | 277,253,719 | ||||||

| LIABILITIES: | ||||||||

| Payable for collateral on loaned securities | 868,441 | – | ||||||

| Payable for investments purchased | 276,653 | 371,313 | ||||||

| Payable for capital shares redeemed | 465,559 | 143,000 | ||||||

| Payable for investment advisory fees | 141,109 | 205,818 | ||||||

| Payable for trustees’ fees | 12,551 | 27,171 | ||||||

| Accrued expenses | 53,393 | 88,588 | ||||||

| Total Liabilities | 1,817,706 | 835,890 | ||||||

| Net Assets | $ | 147,798,642 | $ | 276,417,829 | ||||

| ANALYSIS OF NET ASSETS: | ||||||||

| Paid-in capital | $ | 108,907,395 | $ | 212,918,918 | ||||

| Total distributable earnings (loss) | 38,891,247 | 63,498,911 | ||||||

| Net Assets | $ | 147,798,642 | $ | 276,417,829 | ||||

Investment Class | $ | 132,560,108 | $ | 167,294,236 | ||||

Service Class | 15,238,534 | 109,123,593 | ||||||

| SHARES OUTSTANDING (unlimited number of $.001 par value): | ||||||||

Investment Class | 13,352,353 | 19,585,969 | ||||||

Service Class | 1,566,761 | 13,085,753 | ||||||

| NET ASSET VALUES (Net Assets ÷ Shares Outstanding): | ||||||||

(offering and redemption price per share) | ||||||||

Investment Class | $9.93 | $8.54 | ||||||

Service Class | 9.73 | 8.34 | ||||||

| Investments at identified cost | $ | 117,085,178 | $ | 250,569,171 | ||||

| Market value of loaned securities2 | 2,797,383 | – | ||||||

| 1 | See Notes to Financial Statements for information on non-cash collateral on loaned securities. |

| 2 | Market value of loaned securities backed by non-cash collateral is as of prior business day. |

| 16 | Royce Capital Fund 2019 Semiannual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

Statements of Changes in Net Assets

| Micro-Cap Portfolio | Small-Cap Portfolio | |||||||||||||||

| Six Months Ended | Six Months Ended | |||||||||||||||

| 6/30/19 (unaudited) | Year Ended 12/31/18 | 6/30/19 (unaudited) | Year Ended 12/31/18 | |||||||||||||

| INVESTMENT OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | (387,357 | ) | $ | (640,551 | ) | $ | 1,616,026 | $ | 2,028,315 | ||||||

| Net realized gain (loss) on investments and foreign currency | 2,459,076 | 14,233,957 | 4,813,490 | 46,496,665 | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments and foreign currency | 12,817,940 | (26,943,361 | ) | 5,380,735 | (72,052,141 | ) | ||||||||||

| Net increase (decrease) in net assets from investment operations | 14,889,659 | (13,349,955 | ) | 11,810,251 | (23,527,161 | ) | ||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| Total distributable earnings | ||||||||||||||||

Investment Class | – | (6,692,693 | ) | – | (3,942,054 | ) | ||||||||||

Service Class | – | (764,616 | ) | – | (1,828,028 | ) | ||||||||||

| Total distributions | – | (7,457,309 | ) | – | (5,770,082 | ) | ||||||||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

| Value of shares sold | ||||||||||||||||

Investment Class | 5,738,470 | 20,188,911 | 8,801,761 | 20,508,660 | ||||||||||||

Service Class | 2,706,178 | 8,396,343 | 180,413,384 | 3,049,574 | ||||||||||||

| Distributions reinvested | ||||||||||||||||

Investment Class | – | 6,692,693 | – | 3,942,054 | ||||||||||||

Service Class | – | 764,616 | – | 1,828,028 | ||||||||||||

| Value of shares redeemed | ||||||||||||||||

Investment Class | (14,134,458 | ) | (45,283,517 | ) | (28,077,509 | ) | (62,882,019 | ) | ||||||||

Service Class | (3,502,047 | ) | (24,574,409 | ) | (172,220,029 | ) | (153,628,193 | ) | ||||||||

| Net increase (decrease) in net assets from capital share transactions | (9,191,857 | ) | (33,815,363 | ) | (11,082,393 | ) | (187,181,896 | ) | ||||||||

| Net Increase (Decrease) in Net Assets | 5,697,802 | (54,622,627 | ) | 727,858 | (216,479,139 | ) | ||||||||||

| NET ASSETS: | ||||||||||||||||