UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-07537

Name of Registrant: Royce Capital Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esquire |

| 745 Fifth Avenue | |

| New York, NY 10151 |

Registrant's telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31

Date of reporting period: January 1, 2019 – December 31, 2019

Item 1. Reports to Shareholders.

Royce Capital Fund 2019 Annual

Review and Report to Shareholders

December 31, 2019

Royce Capital Fund–Micro-Cap Portfolio

Royce Capital Fund–Small-Cap Portfolio

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on the Funds’ website (www.royceinvest.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary or, if you are a direct investor with the Funds, by calling 1-800-841-1180. Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1-800-841-1180 to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held with our fund complex if you invest directly with the Funds.

Table of Contents

| Annual Review | ||

| Letter to Our Shareholders | 1 | |

| Performance and Expenses | 5 | |

| Annual Report to Shareholders | ||

| Managers’ Discussions of Fund Performance and Schedules of Investments | ||

| Royce Capital Fund–Micro-Cap Portfolio | 6 | |

| Royce Capital Fund–Small-Cap Portfolio | 12 | |

| Financial Statements | 16 | |

| Notes to Financial Statements | 20 | |

| Report of Independent Registered Public Accounting Firm | 25 | |

| Understanding Your Fund’s Expenses | 26 | |

| Trustees and Officers | 27 | |

| Notes to Performance and Other Important Information | 28 |

This page is not part of theRoyce Capital Fund2019 Annual Report to Shareholders

A BIG YEAR FOR STOCKS

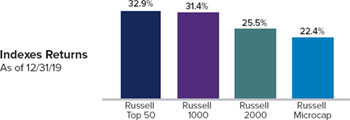

Aperiod of pauses, pivots, and rallies, 2019 ended as a highly rewarding year for equities. The major domestic and international indexes posted healthy double-digit returns, most in the range of 20-35%. The small-cap Russell 2000 Index gained 25.5% while the Russell Top 50 Mega Cap Index advanced 32.9%, the large-cap Russell 1000 Index was up 31.4%, and the Russell Microcap Index increased 22.4%—generally, bigger was better in 2019. Still, the 25.5% gain for the Russell 2000 placed it in the index’s top 27% of calendar-year showings since its 1978 inception. The advance was also impressively broad, with 70% of the stocks in the small-cap index posting positive returns, 61% advancing at least 10%, and 49% posting a calendar-year gain of 20% or more. Additionally, 10 of 11 Russell 2000 sectors were positive for the year (Energy was the sole detractor).

Although many investors think that some event, or series of events, must be present to propel share prices, there are times when the absence of negative developments is more than enough to push stocks consistently upward. This was the case in 2019, when both a

recession and a more hawkish Fed failed to materialize, which was all it took to kick-start the recovery that succeeded the dramatic downturn that saw out 2018. The Fed’s course was especially interesting. Arguably out of touch with the anxieties bred by slipping oil prices and an inverted yield curve in December 2018, the Fed raised rates and announced that 2019 would likely see at least two more hikes—all of this based on the central bank’s cautiously optimistic outlook on the U.S. economy. Once the market’s plunge showed that investors did not share this view, the Fed paused, saying it would hold the line on rates. The central bank then pivoted in July 2019, reversing course by lowering rates—which it proceeded to do again in September and October. These cuts fueled a healthy fourth quarter and helped stocks to end the year on a decidedly upbeat note.

WHAT WILL FOLLOW MEGA-CAP MANIA?

Performance in 2019 was mostly in line with previous snapbacks off precipitous declines—biotech, software, and other growth stocks were among those that did best, along with non-dividend payers and companies with high debt. The somewhat peculiar exception to the pattern was large-cap outperformance. In high-octane markets such as what we saw in 2019, small-cap stocks have typically contended with few, if any, competitors for leadership. This pattern was undone by the ongoing leadership of mega-cap stocks—including the now familiar “FAANG” group of Facebook, Apple, Amazon, Netflix, and Google—which have led the market by a substantial margin over the last 18 months. For example, from 6/30/18-12/31/19, the Russell

This page is not part of theRoyce Capital Fund2019 Annual Report to Shareholders | 1

Letter to Our Shareholders

Notable Index Performance Spreads

Russell Index Performance—6/30/18-12/31/19

Source: FactSet

Top 50 Index advanced 26.1% cumulatively compared with a paltry 3.7% gain for small-caps—and a decline of 3.9% for micro-caps.

If the dominance of mega-caps were to unwind, or even pause, we see the potential for a subsequent rotation to small-caps. We think one point effectively illustrates the size of the potential opportunity: over the last 20 years, the 50 biggest stocks in the Russell 3000 Index have averaged a combined total market cap of about four times the total market cap of the Russell 2000. At the end of 2019, however, that ratio was more than six times, which is higher than it was even at the height of the Internet bubble in 2000. We’re certainly not expecting mega-caps to collapse any time soon, which would be anomalous behavior in what we think will be an advancing market. But we do think a performance pause at their current high valuations could occur, allowing small- and micro-cap stocks to catch up.

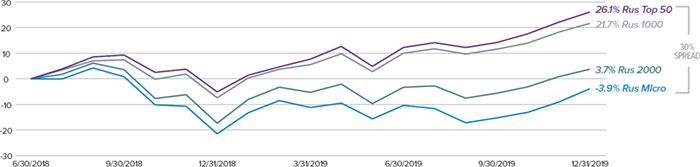

We may have seen the first seeds of such a leadership reversal in the last four months of 2019, which from our perspective provided the year’s most compelling developments. Beginning on August 27th, several reversals inverted previous market leadership patterns, each of which held through the end of 2019: small-caps outpaced large-caps, cyclicals outperformed defensives, small-cap value beat small-cap growth, and micro-caps led domestic equity performance.

August’s Reversals Held

Late August Saw Key Market Shifts That Held Through The End Of 2019

What was of particular interest to us about these reversals was their simultaneity. Leadership rotation is common, but the changes typically emerge over longer stretches of time before they take root.

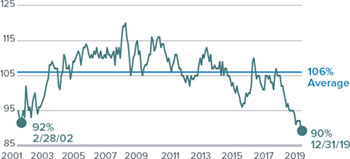

Equally important, we would also argue that valuations—both relative and absolute—must be kept in mind when looking at returns. In spite of the performance boosts that came with the late August reversals, relative valuations for small-cap versus large-cap, small-cap cyclicals versus small-cap defensives, and small-cap value versus small-cap growth still looked attractive to us. At the end of 2019, each remained near the 20-year lows they hit in late August. As the chart below shows, small-cap stocks have lagged large-caps for so long that they were relatively cheaper at the end of 2019 than at any other time since 2001 based on our preferred valuation metric, EV/EBIT, enterprise value over earnings before interest and taxes.

Small-Cap’s Relative Valuation Is Below Its Long-Term Average

Russell 2000 vs. Russell 1000 Median LTM EV/EBIT¹ (ex. Negative EBIT Companies) from 12/31/01 to 12/31/19

1Earnings before interest and taxes. Source: FactSet

BEWARE OF THE CALENDAR

When thinking about the prospects for small-cap performance, we think it’s important to avoid a common pitfall that we all stumble into occasionally—the tendency to put more emphasis on year-end

2 | This page is not part of theRoyce Capital Fund2019 Annual Report to Shareholders

LETTER TO OUR SHAREHOLDERS

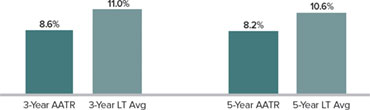

results than on other month-end periods. From the vantage point of the calendar year, small-cap performance certainly looks good. But if we look at the two-year annualized return for the Russell 2000, we see a markedly lower gain of 5.7%. Moreover, three- and five-year annualized returns for the Russell 2000 were below their respective monthly rolling averages since inception (12/31/78) at the end of 2019.

Recent 3- and 5-Year Returns Lower Than History

Russell 2000 Average Annual Total Returns vs. Long-Term Rolling Monthly Averages as of 12/31/19

Finally, the Russell 2000 finished 2019 2.2% off its most recent peak—and all-time high—reached on 8/31/18. What do these observations of historical performance suggest? Taken together, we think they suggest that, despite 2019’s strong calendar-year return, caution or pessimism about future small-cap returns and opportunities may be misplaced.

THE CASE FOR SMALL-CAP CYCLICALS

To be sure, we believe that small-cap stocks are more than capable of a strong run in 2020—and certainly resumed market leadership could be part of the equation. Even after a terrific 2019, many small-caps are still carrying what we would call a recession discount from the deep downturn at the end of 2018. Small-cap cyclicals continued to trade at a significant valuation discount to defensives at the end of 2019—based on EV/EBIT. In fact, the spread was wider than it was in October 2008, when a recession was exacerbated by the Great Financial Crisis.

These historically low relative valuations offer support for our view that late August’s performance reversals can be sustained in 2020. This confidence has led us to be active buyers in areas as diverse as energy services; healthcare devices, diagnostics, and testing; paper & packaging; semiconductors & semiconductor equipment; chemicals; and consumer finance.

Small-Cap Cyclicals Are Relatively Cheaper Than in 2008

Russell 2000 Relative Median EV/EBIT (Ex Negative EBIT)

From 12/31/99 to 12/31/19

Small-caps have also historically outpaced large-caps when the economy is growing and have lagged when it’s contracting. They have beaten large-caps, for example, in 70% of all trailing monthly rolling one-year periods—74 out of 106—when the ISM PMI rose over the last 20 years.1 This dynamic holds true for cyclicals versus defensives as well. So if the most recent slowdown is behind us, and the global economy is gradually improving (which appears to be the case), then renewed expansion supports a continuation of August’s reversals.

GOOD-BYE TO ALL THAT?

2019 closes out one of the most interesting—and challenging—decades that we have seen in more than 45 years of managing small-cap portfolios. It was a decade in which financial assets performed far better than the economy did—mostly due to frequent central bank interventions that suppressed rates and kept the capital markets flush with liquidity. We also saw developments that we would never have thought possible, such as negative interest rates. In addition, years of highly accommodative monetary policy had the unintended consequence of creating few, if any, penalties for companies that borrowed extensively.

We anticipate that each of these unusual developments should unwind to some extent over the next decade. This makes us highly confident about the prospects for select small-caps, particularly in cyclical areas, that haven’t fully participated in the decade that just passed. However, the persistence of these peculiar developments has thrown up numerous road blocks on the road back to normalization. (Indeed, one thing that has not changed over the last 10 years is the humbling nature of the prediction business.)

1The ISM PMI rose in 106 of 229 periods.

This page is not part of theRoyce Capital Fund 2019 Annual Report to Shareholders| 3

LETTER TO OUR SHAREHOLDERS

Does the Small-Cap Recovery Have Room to Run?

Russell 2000 Declines and Two Subsequent Calendar Year’s Performance from 12/31/78 through 12/31/19 (%)

Past performance is no guarantee of future results.

The question is whether or not the last decade-plus (stretching back to the 2007 market peaks and the Great Financial Crisis of 2008) of slow growth, historically low rates, and regular central bank interventions represents a “New Normal.” While our initial contention was that it did not, we now suspect that we will arrive at a blend of the old and the new. As Mark Twain is said to have quipped, “History doesn’t repeat itself, but it often rhymes.” Perhaps, then, this will result in a series of lows—low rates, low inflation, and low (by which we mean slow) economic growth—which will translate into lower U.S. equity returns than what we have seen over the last decade, along with more frequent bouts of volatility and wider variations in stock returns. While this menu may seem unpalatable, periods with more modest performance have historically been very favorable for disciplined active management approaches.

FAVORABLE CONDITIONS FOR SMALL-CAPS

The current backdrop looks quite promising to us for solid to strong small-cap performance overall thanks to the four favorable factors that we cited in July’s “Letter to Our Shareholders”—low inflation, modest valuations, moderate growth, and ample access

to capital. Together, they suggest that small-cap returns can go higher, especially the many small-cap cyclical areas that we typically like best. A few historical factors are also worth noting. Over the past 30 years, 76% of all monthly rolling one-year returns for the Russell 2000 have been positive—with an average return of 11.5%. So investors who are bearish on small-cap stocks are betting against the odds. To get a firmer sense of what 2020 may hold, we went back to the inception of the Russell 2000 and looked at the 11 calendar years when small-caps declined, as in 2018, and examined what happened in the second subsequent year. In nine of those 11 years the small-cap index advanced by an average of 14.5%. (2000 and 2002 were the exceptions.)

And two consecutive years of double-digit increases are fairly common for small-caps. Periods in which a healthy second year followed a strong one occurred in the following two-year spans: 1988-89, 1991-92, 1995-96, 2003-04, 2009-10, 2012-13, and 2016-17. With the favorable conditions we’ve outlined above in mind, we suspect that the current small-cap rally can continue, with the potential to add 2019-20 to this list.

| Sincerely, | ||

|  |  |

Charles M. Royce | Christopher D. Clark | Francis D. Gannon |

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, |

| Royce Investment Partners | Co-Chief Investment Officer, | Royce Investment Partners |

| Royce Investment Partners | ||

January 31, 2020

4 | This page is not part of theRoyce Capital Fund2019 Annual Report to Shareholders

Performance and Expenses

As of December 31, 2019

| 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | ANNUAL OPERATING EXPENSES (%) GROSS/NET |

| Royce Capital Fund–Micro-Cap Portfolio | 19.55 | 4.58 | 3.69 | 5.58 | 5.28 | 8.30 | 9.45 | 1.39/1.33 |

| Royce Capital Fund–Small-Cap Portfolio | 18.67 | 4.65 | 4.10 | 8.35 | 6.84 | 9.90 | 10.13 | 1.11/1.08 |

INDEX | ||||||||

| Russell Microcap Index | 22.43 | 6.39 | 6.57 | 11.26 | 6.16 | N/A | N/A | N/A |

| Russell 2000 Index | 25.52 | 8.59 | 8.23 | 11.83 | 7.92 | 7.59 | N/A | N/A |

| Russell 2000 Value Index | 22.39 | 4.77 | 6.99 | 10.56 | 6.92 | 9.41 | N/A | N/A |

Important Performance, Expense, and Risk Information

All performance information in thisReview and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. The Funds’ total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Funds. All performance and expense information reflects the result for each Fund’s Investment Class Shares. Gross annual operating expenses reflect each Fund’s gross total annual operating expenses and include management fees, operating expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of each fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary cost of business, to the extent necessary to maintain net operating expenses at or below 1.33% for Royce Capital Fund–Micro-Cap Portfolio, and at or below 1.08% for Royce Capital Fund–Small-Cap Portfolio through April 30, 2020.

Service Class Shares bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Royce Micro-Cap Portfolio invests primarily in micro-cap companies while Royce Small-Cap Portfolio invests primarily in small-cap companies. Investments in micro-cap and small-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Each series of Royce Capital Fund may invest up to 25% of its net assets in foreign securities. Investments in foreign securities may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see “Investing in Foreign Securities” in the prospectus.) As of 12/31/19, Royce Small-Cap Portfolio invested a significant portion of its assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any one of these stocks would cause the Portfolio’s overall value to decline to a greater degree. Royce Micro-Cap Portfolio’s broadly diversified portfolio does not ensure a profit or guarantee against loss. (Please see “Primary Risks for Fund Investors” in the prospectus.) This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell 2000 Value Index consists of the respective value stocks within the Russell 2000 as determined by Russell Investments. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

This page is not part of theRoyce Capital Fund 2019 Annual Report to Shareholders| 5

| MANAGERS’ DISCUSSION (UNAUDITED) |

| Royce Capital Fund–Micro-Cap Portfolio (RCM) |

| Jim Stoeffel Brendan Hartman |

| FUND PERFORMANCE |

Royce Capital Fund–Micro-Cap Portfolio advanced 19.6% in 2019, trailing the Russell Microcap and the Russell 2000 Indexes, which returned 22.4% and 25.5%, respectively, for the same period. |

| WHAT WORKED... AND WHAT DIDN’T |

Six of the Fund’s 10 equity sectors positively contributed to performance. Information Technology generated the most sizable impact by far, followed by Industrials and Health Care. Consumer Discretionary, Energy, and Communication Services detracted from performance, but did so modestly. On the industry level, semiconductors & semiconductor equipment (Information Technology) generated the biggest contribution, more than tripling the impact of banks (Financials) and machinery (Industrials), which followed. Conversely, energy equipment & services (Energy) was the worst-performing industry, followed by leisure products and hotels, restaurants & leisure (both in Consumer Discretionary).

The top-contributing position for the year was Ultra Clean Holdings, which develops critical subsystems for the semiconductor capital equipment and flat panel display industries. The company benefited from the recent semiconductor industry upturn and management’s decision to diversify both its customer base and service offerings. Zealand Pharma is a Copenhagen-based company that focuses on developing peptide-based therapeutics for metabolic and gastrointestinal diseases. Its two latest stage products had positive results during the year, and the company also completed its first ever acquisition, buying Encycle Therapeutics in October. Pharmaceuticals company Axsome Therapeutics also made a strong contribution, as the company had positive clinical results across its product portfolio, which includes developing therapies for central nervous system disorders. Axsome’s lead molecule, AXS-05, has been performing well in clinical trials that are expected to be finished relatively quickly because two of its ingredients were previously approved by the Food and Drug Administration.

Red Lion Hotels was the portfolio’s largest detractor in 2019, as the company suffered a setback in its efforts to transition from company-owned hotels to a franchise model. Selling its company-owned units took longer than anticipated, and Red Lion experienced greater-than-expected attrition in its newly acquired franchisees—factors that led us to sell our stake. We also saw poor performance from branded fitness and apparel product maker, Nautilus, which suffered through two consecutive failed product launches that resulted in a decision to remove the CEO. While we liked several strategic decisions that the company made over the past several years, we sold our position when our confidence in management’s ability to effectively judge the rapidly changing fitness markets was shaken. We also expected that it would take at least a year to rebuild its product pipeline. Correvio Pharma also hampered performance during the year. The pharmaceuticals company develops and discovers cardiovascular drugs for the treatment of atrial arrhythmia, congestive heart failure, and bacterial skin infections. We exited our position after the company’s atrial fibrillation drug, which is used extensively in Europe, failed to gain approval from an FDA Advisory Panel.

The Fund’s relative underperformance versus the Russell Microcap was driven entirely by sector allocation—stock selection was additive. Consumer Discretionary was the largest source of underperformance due to stock selection in multiple industries, including specialty retail and hotels, restaurants & leisure. Health Care also hurt relative performance due to our underexposure to the sector, particularly to biotechnology, which was the strongest contributor to the micro-cap index’s returns. The portfolio’s cash holdings were an additional drag on relative performance in 2019. Conversely, we saw very strong relative outperformance in Information Technology, driven mainly by savvy stock selection, though our overexposure to the sector helped modestly. Industrials and Materials were also additive thanks to successful stock selection. At the industry level, the aforementioned biotechnology group (Health Care) and energy equipment & services (Energy) hurt relative performance most, while semiconductors & semiconductor equipment and software (both in Information Technology) helped.

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| Ultra Clean Holdings | 1.27 | Red Lion Hotels | -0.61 | |||

| Zealand Pharma | 1.25 | Nautilus | -0.48 | |||

| Axsome Therapeutics | 1.07 | Correvio Pharma | -0.46 | |||

| NeoGenomics | 0.95 | Kirkland’s | -0.45 | |||

| Adesto Technologies | 0.78 | Independence Contract Drilling | -0.41 | |||

| 1Includes dividends | 2Net of dividends | |||||

| CURRENT POSITIONING AND OUTLOOK |

While issues surrounding trade have finally begun to stabilize, we find ourselves in the midst of what promises to be an eventful U.S. election cycle, with outcomes that could have major implications for investors. Despite this uncertainty, we remain generally constructive on the U.S. economy, particularly because the current Fed tightening cycle appears to have ended. Along with a possible truce in the trade wars, we believe the favorable backdrop should support underlying growth for our overweighted sectors, such as Information Technology and Industrials. Valuations look relatively attractive to us in many corners of the micro-cap world, even as recent returns show that the performance gap between micro-caps and large-caps is gradually beginning to narrow. We took advantage of these opportunities for much of the second half of 2019 as micro-cap stocks were selling at their steepest discount to large-caps since 2001. We don’t know if this recent upward move will last, but after a long period of underperformance for micro-caps, we anticipate some degree of mean reversion. |

| 6 | Royce Capital Fund 2019 Annual Report to Shareholders |

|

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RCMCX RCMSX | |

| Performance and Expenses | ||||||||||||||||

| Average Annual Total Return (%) Through 12/31/19 | ||||||||||||||||

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCM | 7.99 | 19.55 | 4.58 | 3.69 | 5.58 | 5.28 | 8.30 | 9.45 | ||||||||

| Annual Gross Operating Expenses: 1.39% Annual Net Operating Expenses: 1.33% | ||||||||||||||||

| 1 Not annualized | ||||||||||||||||

Morningstar Style Map™As of 12/31/19

TheMorningstar Style Mapis theMorningstar Style BoxTM with the center 75% of fund holdings plotted as theMorningstar Ownership ZoneTM. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 28 for additional information.

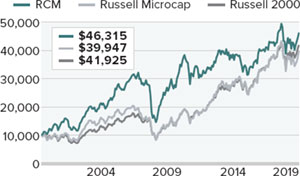

Value of $10,000

Invested on 6/30/00 (Russell Microcap Inception) as of 12/31/19 ($)

Includes reinvestment of distributions.

| Top 10 Positions | ||

| % of Net Assets | ||

| Photronics | 1.5 | |

| Ultra Clean Holdings | 1.4 | |

| Zealand Pharma | 1.3 | |

| Northwest Pipe | 1.3 | |

| Nova Measuring Instruments | 1.3 | |

| QAD Cl. A | 1.2 | |

| NeoPhotonics Corporation | 1.2 | |

| Adesto Technologies | 1.2 | |

| OrthoPediatrics Corporation | 1.2 | |

| Axsome Therapeutics | 1.1 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Information Technology | 24.8 | |

| Industrials | 22.5 | |

| Financials | 13.6 | |

| Health Care | 11.5 | |

| Consumer Discretionary | 8.0 | |

| Materials | 3.7 | |

| Real Estate | 2.8 | |

| Energy | 2.6 | |

| Communication Services | 1.9 | |

| Consumer Staples | 0.2 | |

| Cash and Cash Equivalents | 8.4 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RCM | |

| 2019 | 19.6 | |

| 2018 | -9.0 | |

| 2017 | 5.2 | |

| 2016 | 19.7 | |

| 2015 | -12.5 | |

| 2014 | -3.6 | |

| 2013 | 21.0 | |

| 2012 | 7.6 | |

| 2011 | -12.1 | |

| 2010 | 30.1 | |

| 2009 | 57.9 | |

| 2008 | -43.3 | |

| 2007 | 4.0 | |

| 2006 | 21.1 | |

| 2005 | 11.6 |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 12/31/19 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 70 | 93 | ||

| From 6/30/00 (Russell Microcap Inception) | 88 | 78 | ||

| Portfolio Diagnostics | ||||

| Fund Net Assets | $159 million | |||

| Number of Holdings | 129 | |||

| Turnover Rate | 26% | |||

| Average Market Capitalization1 | $512 million | |||

| Weighted Average P/B Ratio2 | 2.0x | |||

| Active Share3 | 89% | |||

| U.S. Investments (% of Net Assets) | 78.1% | |||

| Non-U.S. Investments (% of Net Assets) | 13.5% | |||

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information All performance information in thisReportreflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.royceinvest.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCM’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund–Micro-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.33% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell Microcap). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

Royce Capital Fund 2019 Annual Report to Shareholders | 7

|

Schedule of Investments

| Royce Capital Fund – Micro-Cap Portfolio | |||||||

| Common Stocks – 91.6% | |||||||

| SHARES | VALUE | ||||||

| COMMUNICATION SERVICES – 1.9% | |||||||

| ENTERTAINMENT - 0.6% | |||||||

| Gaia Cl. A1 | 120,800 | $ | 965,192 | ||||

| INTERACTIVE MEDIA & SERVICES - 0.9% | |||||||

| QuinStreet1 | 99,800 | 1,527,938 | |||||

| MEDIA - 0.4% | |||||||

| Marchex Cl. B1 | 153,900 | 581,742 | |||||

| Total (Cost $2,497,112) | 3,074,872 | ||||||

| CONSUMER DISCRETIONARY – 8.0% | |||||||

| AUTO COMPONENTS - 2.2% | |||||||

| Fox Factory Holding1,2 | 16,000 | 1,113,120 | |||||

| Stoneridge1 | 61,000 | 1,788,520 | |||||

| Unique Fabricating1 | 173,300 | 668,938 | |||||

| 3,570,578 | |||||||

| HOTELS, RESTAURANTS & LEISURE - 1.5% | |||||||

| Century Casinos1 | 161,100 | 1,275,912 | |||||

| Lindblad Expeditions Holdings1 | 70,900 | 1,159,215 | |||||

| 2,435,127 | |||||||

| HOUSEHOLD DURABLES - 0.6% | |||||||

| Lovesac Company (The)1,2 | 64,000 | 1,027,200 | |||||

| INTERNET & DIRECT MARKETING RETAIL - 0.3% | |||||||

| Rubicon Project (The)1 | 50,200 | 409,632 | |||||

| LEISURE PRODUCTS - 0.7% | |||||||

| MasterCraft Boat Holdings1 | 69,117 | 1,088,593 | |||||

| SPECIALTY RETAIL - 1.9% | |||||||

| Citi Trends | 54,986 | 1,271,276 | |||||

| Shoe Carnival | 47,100 | 1,755,888 | |||||

| 3,027,164 | |||||||

| TEXTILES, APPAREL & LUXURY GOODS - 0.8% | |||||||

| Vera Bradley1 | 104,200 | 1,229,560 | |||||

| Total (Cost $9,943,918) | 12,787,854 | ||||||

| CONSUMER STAPLES – 0.2% | |||||||

| BEVERAGES - 0.2% | |||||||

| †Eastside Distilling1 | 88,300 | 260,485 | |||||

| Total (Cost $371,974) | 260,485 | ||||||

| ENERGY – 2.6% | |||||||

| ENERGY EQUIPMENT & SERVICES - 1.7% | |||||||

| Natural Gas Services Group1 | 52,100 | 638,746 | |||||

| Newpark Resources1 | 203,800 | 1,277,826 | |||||

| Pason Systems | 12,600 | 127,208 | |||||

| Profire Energy1 | 486,229 | 705,032 | |||||

| 2,748,812 | |||||||

| OIL, GAS & CONSUMABLE FUELS - 0.9% | |||||||

| Ardmore Shipping1 | 154,800 | 1,400,940 | |||||

| Total (Cost $4,070,913) | 4,149,752 | ||||||

| FINANCIALS – 13.6% | |||||||

| BANKS - 6.5% | |||||||

| Allegiance Bancshares1 | 29,400 | 1,105,440 | |||||

| BayCom Corporation1 | 52,182 | 1,186,619 | |||||

| Caribbean Investment Holdings1 | 1,751,547 | 777,233 | |||||

| County Bancorp | 59,600 | 1,527,548 | |||||

| HarborOne Bancorp1 | 134,691 | 1,480,254 | |||||

| HomeTrust Bancshares | 44,700 | 1,199,301 | |||||

| Investar Holding | 57,200 | 1,372,800 | |||||

| Midway Investments1,3 | 1,751,577 | 0 | |||||

| TriState Capital Holdings1 | 66,472 | 1,736,249 | |||||

| 10,385,444 | |||||||

| CAPITAL MARKETS - 3.7% | |||||||

| B. Riley Financial | 70,700 | 1,780,226 | |||||

| Canaccord Genuity Group | 222,500 | 829,310 | |||||

| INTL FCStone1 | 24,000 | 1,171,920 | |||||

| Silvercrest Asset Management Group Cl. A | 90,300 | 1,135,974 | |||||

| †Sprott | 410,400 | 941,813 | |||||

| 5,859,243 | |||||||

| DIVERSIFIED FINANCIAL SERVICES - 0.2% | |||||||

| Waterloo Investment Holdings1,3 | 1,302,000 | 390,600 | |||||

| INSURANCE - 0.2% | |||||||

| Health Insurance Innovations Cl. A1,2 | 17,000 | 327,930 | |||||

| THRIFTS & MORTGAGE FINANCE - 3.0% | |||||||

| Meridian Bancorp | 30,600 | 614,754 | |||||

| PCSB Financial | 71,300 | 1,443,825 | |||||

| Territorial Bancorp | 41,900 | 1,296,386 | |||||

| Western New England Bancorp | 141,254 | 1,360,276 | |||||

| 4,715,241 | |||||||

| Total (Cost $22,179,842) | 21,678,458 | ||||||

| HEALTH CARE – 11.5% | |||||||

| BIOTECHNOLOGY - 2.2% | |||||||

| BioSpecifics Technologies1 | 16,900 | 962,286 | |||||

| Dynavax Technologies1 | 94,000 | 537,680 | |||||

| Zealand Pharma1 | 59,358 | 2,097,446 | |||||

| 3,597,412 | |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES - 5.5% | |||||||

| †Apyx Medical1 | 77,400 | 654,804 | |||||

| AtriCure1 | 38,600 | 1,254,886 | |||||

| Chembio Diagnostics1 | 169,300 | 772,008 | |||||

| CryoLife1 | 52,589 | 1,424,636 | |||||

| Mesa Laboratories | 4,700 | 1,172,180 | |||||

| OrthoPediatrics Corporation1 | 39,500 | 1,856,105 | |||||

| †Profound Medical1 | 35,300 | 400,966 | |||||

| Surmodics1 | 27,878 | 1,154,986 | |||||

| 8,690,571 | |||||||

| LIFE SCIENCES TOOLS & SERVICES - 2.7% | |||||||

| Harvard Bioscience1 | 376,668 | 1,148,838 | |||||

| NeoGenomics1 | 61,900 | 1,810,575 | |||||

| Quanterix Corporation1 | 54,300 | 1,283,109 | |||||

| 4,242,522 | |||||||

| PHARMACEUTICALS - 1.1% | |||||||

| †Axsome Therapeutics1,2 | 17,600 | 1,819,136 | |||||

| Total (Cost $9,895,277) | 18,349,641 | ||||||

| INDUSTRIALS – 22.5% | |||||||

| AEROSPACE & DEFENSE - 1.3% | |||||||

| Astronics Corporation1 | 31,026 | 867,177 | |||||

| CPI Aerostructures1 | 174,544 | 1,174,681 | |||||

| 2,041,858 | |||||||

| COMMERCIAL SERVICES & SUPPLIES - 1.7% | |||||||

| Acme United | 50,865 | 1,210,078 | |||||

| Heritage-Crystal Clean1 | 47,334 | 1,484,868 | |||||

| 2,694,946 | |||||||

| CONSTRUCTION & ENGINEERING - 3.5% | |||||||

| †Ameresco Cl. A1 | 94,000 | 1,645,000 | |||||

| Construction Partners Cl. A1 | 93,200 | 1,572,284 | |||||

| †IES Holdings1 | 9,000 | 230,940 | |||||

| Northwest Pipe1 | 62,900 | 2,095,199 | |||||

| 5,543,423 |

8 | Royce Capital Fund 2019 Annual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

|

December 31, 2019

Royce Capital Fund – Micro-Cap Portfolio (continued) |

| SHARES | VALUE | ||||||

| INDUSTRIALS (continued) | |||||||

| ELECTRICAL EQUIPMENT - 1.5% | |||||||

| American Superconductor1 | 130,500 | $ | 1,024,425 | ||||

| Encore Wire | 22,800 | 1,308,720 | |||||

| 2,333,145 | |||||||

| INDUSTRIAL CONGLOMERATES - 0.4% | |||||||

| Raven Industries | 17,000 | 585,820 | |||||

| MACHINERY - 7.5% | |||||||

| Alimak Group | 80,300 | 1,196,825 | |||||

| CIRCOR International1 | 20,200 | 934,048 | |||||

| Exco Technologies | 125,900 | 768,847 | |||||

| Graham Corporation | 78,620 | 1,720,206 | |||||

| Lindsay Corporation | 12,200 | 1,171,078 | |||||

| Luxfer Holdings | 65,400 | 1,210,554 | |||||

| Lydall1 | 38,500 | 790,020 | |||||

| †Porvair | 133,350 | 1,179,924 | |||||

| Spartan Motors | 72,200 | 1,305,376 | |||||

| †Wabash National | 61,100 | 897,559 | |||||

| Westport Fuel Systems1 | 345,300 | 818,361 | |||||

| 11,992,798 | |||||||

| MARINE - 1.0% | |||||||

| Clarkson | 42,000 | 1,682,904 | |||||

| PROFESSIONAL SERVICES - 3.9% | |||||||

| CRA International | 22,106 | 1,204,114 | |||||

| GP Strategies1 | 88,608 | 1,172,284 | |||||

| Heidrick & Struggles International | 38,100 | 1,238,250 | |||||

| Kforce | 30,200 | 1,198,940 | |||||

| Resources Connection | 84,754 | 1,384,033 | |||||

| 6,197,621 | |||||||

| ROAD & RAIL - 0.7% | |||||||

| Marten Transport | 50,041 | 1,075,381 | |||||

| TRADING COMPANIES & DISTRIBUTORS - 1.0% | |||||||

| Lawson Products1 | 15,800 | 823,180 | |||||

| †Transcat1 | 25,300 | 806,058 | |||||

| 1,629,238 | |||||||

| Total (Cost $26,330,218) | 35,777,134 | ||||||

| INFORMATION TECHNOLOGY – 24.8% | |||||||

| COMMUNICATIONS EQUIPMENT - 1.6% | |||||||

| Digi International1 | 97,400 | 1,725,928 | |||||

| EMCORE Corporation1 | 149,300 | 453,872 | |||||

| Harmonic1 | 37,900 | 295,620 | |||||

| 2,475,420 | |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 5.7% | |||||||

| Fabrinet1 | 21,369 | 1,385,566 | |||||

| FARO Technologies1 | 18,400 | 926,440 | |||||

| †LightPath Technologies Cl. A1 | 232,800 | 168,780 | |||||

| †Luna Innovations1 | 87,000 | 634,230 | |||||

| nLIGHT1 | 60,900 | 1,235,052 | |||||

| Novanta1 | 11,300 | 999,372 | |||||

| †PAR Technology1 | 15,300 | 470,322 | |||||

| PC Connection | 34,300 | 1,703,338 | |||||

| Vishay Precision Group1 | 44,700 | 1,519,800 | |||||

| 9,042,900 | |||||||

| IT SERVICES - 0.6% | |||||||

| Cass Information Systems | 16,148 | 932,385 | |||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 14.3% | |||||||

| Adesto Technologies1,2 | 219,100 | 1,862,350 | |||||

| Aehr Test Systems1 | 349,500 | 699,000 | |||||

| Axcelis Technologies1 | 19,800 | 477,081 | |||||

| AXT1 | 244,300 | 1,062,705 | |||||

| Brooks Automation | 23,500 | 986,060 | |||||

| †Camtek | 104,900 | 1,136,067 | |||||

| Cohu | 67,700 | 1,546,945 | |||||

| CyberOptics Corporation1 | 42,600 | 782,988 | |||||

| Everspin Technologies1 | 106,400 | 559,664 | |||||

| †Ichor Holdings1 | 45,300 | 1,507,131 | |||||

| NeoPhotonics Corporation1 | 221,200 | 1,950,984 | |||||

| Nova Measuring Instruments1 | 53,800 | 2,035,254 | |||||

| Onto Innovation1 | 11,300 | 412,902 | |||||

| PDF Solutions1 | 98,400 | 1,661,976 | |||||

| Photronics1 | 153,300 | 2,416,008 | |||||

| Silicon Motion Technology ADR | 26,900 | 1,364,099 | |||||

| Ultra Clean Holdings1 | 95,300 | 2,236,691 | |||||

| 22,697,905 | |||||||

| SOFTWARE - 2.2% | |||||||

| Agilysys1 | 61,800 | 1,570,338 | |||||

| QAD Cl. A | 38,800 | 1,976,084 | |||||

| 3,546,422 | |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS - 0.4% | |||||||

| AstroNova | 50,700 | 695,604 | |||||

| Total (Cost $26,328,731) | 39,390,636 | ||||||

| MATERIALS – 3.7% | |||||||

| CHEMICALS - 1.1% | |||||||

| FutureFuel Corporation | 62,400 | 773,136 | |||||

| Trecora Resources1 | 133,200 | 952,380 | |||||

| 1,725,516 | |||||||

| METALS & MINING - 2.6% | |||||||

| †Altius Minerals | 46,300 | 426,436 | |||||

| Haynes International | 39,870 | 1,426,548 | |||||

| Major Drilling Group International1 | 299,700 | 1,308,613 | |||||

| Universal Stainless & Alloy Products1 | 61,400 | 914,860 | |||||

| 4,076,457 | |||||||

| Total (Cost $6,589,772) | 5,801,973 | ||||||

| REAL ESTATE – 2.8% | |||||||

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITS) - 1.4% | |||||||

| Community Healthcare Trust | 32,200 | 1,380,092 | |||||

| †Postal Realty Trust Cl. A | 50,400 | 854,280 | |||||

| 2,234,372 | |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.4% | |||||||

| FRP Holdings1 | 23,440 | 1,167,546 | |||||

| Marcus & Millichap1 | 29,900 | 1,113,775 | |||||

| 2,281,321 | |||||||

| Total (Cost $2,998,434) | 4,515,693 | ||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $111,206,191) | 145,786,498 |

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2019 Annual Report to Shareholders | 9 |

|

| December 31, 2019 |

Schedule of Investments |

|

Royce Capital Fund – Micro-Cap Portfolio (continued) |

| VALUE | |||

| REPURCHASE AGREEMENT – 7.8% | |||

| Fixed Income Clearing Corporation, 0.25% dated 12/31/19, due 1/2/20, maturity value $12,409,172 (collateralized by obligations of various U.S. Government Agencies, 2.25% due 11/15/24, valued at $12,657,795) | |||

| (Cost $12,409,000) | $ | 12,409,000 | |

| COLLATERAL RECEIVED FOR SECURITIES LOANED – 0.2% | |||

| Money Market Funds | |||

| Federated Government Obligations Fund (7 day yield-1.49%) | |||

| (Cost $218,823) | 218,823 | ||

| TOTAL INVESTMENTS – 99.6% | |||

| (Cost $123,834,014) | 158,414,321 | ||

| CASH AND OTHER ASSETS LESS LIABILITIES – 0.4% | 684,157 | ||

| NET ASSETS – 100.0% | $ | 159,098,478 | |

ADR – American Depository Receipt

New additions in 2019. |

Non-income producing. |

All or a portion of these securities were on loan at December 31, 2019. |

Securities for which market quotations are not readily available represent 0.2% of net assets. These securities have been valued at their fair value under procedures approved by the Fund’s Board of Trustees. These securities are defined as Level 3 securities due to the use of significant unobservable inputs in the determination of fair value. See Notes to Financial Statements. |

Bold indicates the Fund’s 20 largest equity holdings in terms of December 31, 2019, market value.

10 | Royce Capital Fund 2019 Annual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

|

This page is intentionally left blank.

Royce Capital Fund 2019 Annual Report to Shareholders | 11

MANAGER’S DISCUSSION (UNAUDITED)

Royce Capital Fund–Small-Cap Portfolio (RCS)

Jay Kaplan, CFA

FUND PERFORMANCE

Royce Capital Fund–Small-Cap Portfolio, which uses a disciplined contrarian value approach, increased 18.7% in 2019, trailing respective gains of 25.5% and 22.4% for its small-cap benchmarks, the Russell 2000 and Russell 2000 Value Indexes, for the same period.

WHAT WORKED… AND WHAT DIDN’T

For the calendar year, seven of the portfolio’s 11 equity sectors finished in the black. Three sectors dominated the positive contributors—Information Technology, Industrials, and Financials—while Utilities was essentially flat, and Energy, Consumer Staples, and Communication Services detracted. At the industry level, electronic equipment, instruments & components (Information Technology) led, followed by banks and thrifts & mortgage finance (both in Financials), as well as machinery (Industrials). Oil, gas & consumable fuels (Energy) was the largest detractor at the industry level, followed by specialty retail, textiles, apparel & luxury goods (both in Consumer Discretionary), and food & staples retailing (Consumer Staples).

Insight Enterprises contributed most at the position level, as it did for the six-month period ended 6/30/19. The company provides information technology hardware and software for large and small enterprises and was key to the electronic equipment, instruments & components group’s strong performance in 2019. Insight continued to execute profitably in 2019, with steadily increasing revenues and better-than-expected earnings. The company also saw its sales grow as a result of its acquisition of PCM in August, which expands the firm’s reach into higher-margin end markets that are expected to drive additional improvement in the future.

Another company in the same industry was also a top contributor—PC Connection, a direct marketer of technology products and services, including computer systems as well as software and peripheral equipment. The company beat earnings estimates in the second and third quarters while also exceeding consensus revenue estimates in three out of the last four quarters—both evidence of the kind of successful execution we like from our holdings. The contribution for Genworth MI Canada, which provides private residential mortgage insurance, also stood out. The company’s stock began to rise in July when Genworth Financial, a related U.S. firm, agreed to sell its shares of Genworth MI Canada to Brookfield Business Partners in order to win regulatory approval for its own acquisition by a Chinese company. The firm also had steadily growing revenues and net income throughout 2019.

The specialty retail industry was home to the Fund’s worst performing position, footwear retailer Designer Brands (formerly known as DSW). The company has faced challenges as many leading brands are opting for more direct customer relationships. In December, the company also reported a decline in its gross margins related to unseasonably warm fall weather, which hindered performance, and tariff concerns that led to an inventory pullback and a cut in marketing investments in anticipation of lower spending by consumers that didn’t materialize. Confident that the company can right itself and navigate the secular shifts affecting retailers, we added shares in 2019. We made the opposite decision with coal producer Alliance Resource Partners by selling our stake. We opted to build our position in ArcBest, a freight and logistics solutions specialist that saw its business stall in 2019. We think that the firm’s long-term prospects are solid, especially if the economy reaccelerates in 2020.

Both stock selection and, to a lesser degree, sector allocation hurt performance versus the Russell 2000 in 2019. Consumer Discretionary and Health Care hurt most. Underperformance in the first sector was almost entirely the result of poor stock selection while in Health Care both our lower exposure and ineffective stock picks created a disadvantage. Specialty retail (Consumer Discretionary) fared worst on an industry basis relative to the benchmark, followed by biotechnology, which dominated results in Health Care. The portfolio’s cash position also detracted from relative results. Conversely, our overweight in Information Technology and underweight in Utilities helped relative results. Electronic equipment, instruments & components (Information Technology) was the top relative contributing industry, followed by machinery (Industrials).

| Top Contributors to Performance | Top Detractors from Performance | |||||

| For 2019 (%)1 | For 2019 (%)2 | |||||

| Insight Enterprises | 1.46 | Designer Brands Cl. A | -0.62 | |||

| Genworth MI Canada | 1.32 | Alliance Resource Partners L.P. | -0.53 | |||

| PC Connection | 1.27 | ArcBest | -0.50 | |||

| Meritor | 1.00 | Spirit Airlines | -0.47 | |||

| Allegiant Travel | 0.94 | G-III Apparel Group | -0.45 | |||

| 1Includes dividends | 2Net of dividends | |||||

CURRENT POSITIONING AND OUTLOOK

The market’s shift to value proved short-lived as the Russell 2000 Value trailed its growth counterpart in 2019’s fourth quarter. Whether growth’s resurgence will last or value can reassert itself is of course an open question. The fear of recession has diminished, with green shoots indicating that the global slowdown may have bottomed. Details on a China trade deal are still vague, however, and this is not the first time that an agreement has appeared close, so economic reacceleration may remain elusive. In the meantime, the Fed is holding the line on rates, and yield curve inversion is over for now. In other words, the outlook remains uncertain before we even consider geopolitical tensions or the November elections. In this environment, we have been adding select positions that look attractively valued and capable of rebounding in energy services and pharmaceuticals.

| 12 | Royce Capital Fund 2019 Annual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RCPFX RCSSX |

Performance and Expenses

Average Annual Total Return (%) Through 12/31/19

| JUL-DEC 20191 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (12/27/96) | |||||||||

| RCS | 9.36 | 18.67 | 4.65 | 4.10 | 8.35 | 6.84 | 9.90 | 10.13 | ||||||||

Annual Gross Operating Expenses: 1.11% Annual Net Operating Expenses: 1.08%

1Not annualized

TheMorningstar Style Map is theMorningstar Style Box™ with the center 75% of fund holdings plotted as theMorningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 28 for additional information.

Value of $10,000

Invested on 12/27/96 as of 12/31/19 ($)

Includes reinvestment of distributions.

Top 10 Positions

% of Net Assets

| Insight Enterprises | 2.6 | |

| Genworth MI Canada | 2.5 | |

| Miller Industries | 2.5 | |

| Sanmina Corporation | 2.2 | |

| WSFS Financial | 2.2 | |

| Spirit Airlines | 2.1 | |

| Designer Brands Cl. A | 2.1 | |

| G-III Apparel Group | 2.1 | |

| Caleres | 2.0 | |

| Shoe Carnival | 1.9 |

Portfolio Sector Breakdown

% of Net Assets

| Industrials | 27.3 | |

| Financials | 26.3 | |

| Consumer Discretionary | 15.5 | |

| Information Technology | 11.8 | |

| Energy | 6.4 | |

| Health Care | 2.3 | |

| Real Estate | 1.5 | |

| Communication Services | 0.9 | |

| Consumer Staples | 0.9 | |

| Materials | 0.7 | |

| Cash and Cash Equivalents | 6.4 |

Calendar Year Total Returns (%)

| YEAR | RCS | |

| 2019 | 18.7 | |

| 2018 | -8.3 | |

| 2017 | 5.4 | |

| 2016 | 21.0 | |

| 2015 | -11.8 | |

| 2014 | 3.2 | |

| 2013 | 34.8 | |

| 2012 | 12.5 | |

| 2011 | -3.3 | |

| 2010 | 20.5 | |

| 2009 | 35.2 | |

| 2008 | -27.2 | |

| 2007 | -2.1 | |

| 2006 | 15.6 | |

| 2005 | 8.6 |

Upside/Downside Capture Ratios

Periods Ended 12/31/19 (%)

| UPSIDE | DOWNSIDE | |

| 10-Year | 68 | 66 |

| From 12/31/96 (Start of Fund’s First Full Quarter) | 91 | 74 |

Portfolio Diagnostics

| Fund Net Assets | $399 million | |

| Number of Holdings | 84 | |

| Turnover Rate | 111% | |

| Average Market Capitalization1 | $1,152 million | |

| Weighted Average P/B Ratio2 | 1.6x | |

| Active Share3 | 96% | |

| U.S. Investments (% of Net Assets) | 86.7% | |

| Non-U.S. Investments (% of Net Assets) | 6.9% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average.This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Shareis the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in thisReportreflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Current performance may be higher or lower than performance quoted. The Fund’s total returns do not reflect any deduction for charges or expenses of the variable contracts investing in the Fund. Returns as of the most recent month-end may be obtained at www.royceinvest.com. All performance and risk information reflects the result of the Investment Class (its oldest class). Shares of RCS’s Service Class bear an annual distribution expense that is not borne by the Investment Class; if those expenses were reflected, total returns would have been lower. Certain immaterial adjustments were made to the net assets of Royce Capital Fund-Small-Cap Portfolio at 12/31/17 for financial reporting purposes, and as a result the calendar year total returns based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Gross operating expenses reflect the Fund’s total gross operating expenses for the Investment Class and include management fees and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Investment Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.08% through April 30, 2020. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2019. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters.

Royce Capital Fund 2019 Annual Report to Shareholders | 13

Schedule of Investments

Royce Capital Fund – Small-Cap Portfolio

Common Stocks – 93.6%

| SHARES | VALUE | ||||||

| COMMUNICATION SERVICES – 0.9% | |||||||

| MEDIA - 0.9% | |||||||

| Saga Communications Cl. A | 123,383 | $ | 3,750,843 | ||||

| Total (Cost $4,993,347) | 3,750,843 | ||||||

| CONSUMER DISCRETIONARY – 15.5% | |||||||

| AUTO COMPONENTS - 0.9% | |||||||

| Gentex Corporation | 66,516 | 1,927,634 | |||||

| Stoneridge1 | 58,805 | 1,724,162 | |||||

| 3,651,796 | |||||||

| HOTELS, RESTAURANTS & LEISURE - 1.5% | |||||||

| Hilton Grand Vacations1 | 171,509 | 5,898,195 | |||||

| HOUSEHOLD DURABLES - 1.0% | |||||||

| La-Z-Boy | 124,486 | 3,918,819 | |||||

| SPECIALTY RETAIL - 9.6% | |||||||

| American Eagle Outfitters | 456,965 | 6,717,385 | |||||

| Caleres | 334,917 | 7,954,279 | |||||

| Designer Brands Cl. A | 522,466 | 8,223,615 | |||||

| †Rent-A-Center | 262,133 | 7,559,916 | |||||

| Shoe Carnival | 205,836 | 7,673,566 | |||||

| 38,128,761 | |||||||

| TEXTILES, APPAREL & LUXURY GOODS - 2.5% | |||||||

| G-III Apparel Group1 | 244,665 | 8,196,278 | |||||

| Steven Madden | 45,506 | 1,957,213 | |||||

| 10,153,491 | |||||||

| Total (Cost $61,410,283) | 61,751,062 | ||||||

| CONSUMER STAPLES – 0.9% | |||||||

| FOOD & STAPLES RETAILING - 0.9% | |||||||

| Village Super Market Cl. A | 151,570 | 3,516,424 | |||||

| Total (Cost $4,131,932) | 3,516,424 | ||||||

| ENERGY – 6.4% | |||||||

| ENERGY EQUIPMENT & SERVICES - 2.3% | |||||||

| †DMC Global | 46,706 | 2,098,967 | |||||

| Helmerich & Payne | 111,500 | 5,065,445 | |||||

| †Solaris Oilfield Infrastructure Cl. A | 133,100 | 1,863,400 | |||||

| 9,027,812 | |||||||

| OIL, GAS & CONSUMABLE FUELS - 4.1% | |||||||

| †Bonanza Creek Energy1 | 221,308 | 5,165,329 | |||||

| †Dorchester Minerals L.P. | 40,700 | 794,057 | |||||

| †Laredo Petroleum1,2 | 1,976,400 | 5,672,268 | |||||

| †Penn Virginia1 | 161,226 | 4,893,209 | |||||

| 16,524,863 | |||||||

| Total (Cost $24,150,201) | 25,552,675 | ||||||

| FINANCIALS – 26.3% | |||||||

| BANKS - 12.3% | |||||||

| Ames National | 198,702 | 5,575,578 | |||||

| Bar Harbor Bankshares | 11,665 | 296,175 | |||||

| Camden National | 139,729 | 6,435,918 | |||||

| City Holding Company | 75,160 | 6,159,362 | |||||

| CNB Financial | 199,719 | 6,526,817 | |||||

| Codorus Valley Bancorp | 76,235 | 1,755,692 | |||||

| Financial Institutions | 94,182 | 3,023,242 | |||||

| Landmark Bancorp | 57,520 | 1,440,876 | |||||

| MidWestOne Financial Group | 83,692 | 3,032,161 | |||||

| National Bankshares | 145,868 | 6,553,849 | |||||

| Northrim BanCorp | 125,081 | 4,790,602 | |||||

| Unity Bancorp | 158,138 | 3,569,175 | |||||

| 49,159,447 | |||||||

| CAPITAL MARKETS - 2.9% | |||||||

| Houlihan Lokey Cl. A | 119,515 | 5,840,698 | |||||

| Moelis & Company Cl. A | 61,701 | 1,969,496 | |||||

| Pzena Investment Management Cl. A | 414,047 | 3,569,085 | |||||

| 11,379,279 | |||||||

| INSURANCE - 3.0% | |||||||

| James River Group Holdings | 96,135 | 3,961,724 | |||||

| Kingstone Companies | 227,675 | 1,764,481 | |||||

| Reinsurance Group of America | 38,836 | 6,332,598 | |||||

| 12,058,803 | |||||||

| THRIFTS & MORTGAGE FINANCE - 8.1% | |||||||

| Genworth MI Canada | 227,550 | 9,956,791 | |||||

| Southern Missouri Bancorp | 93,767 | 3,596,902 | |||||

| Timberland Bancorp | 110,777 | 3,294,508 | |||||

| TrustCo Bank Corp. NY | 758,182 | 6,573,438 | |||||

| WSFS Financial | 198,200 | 8,718,818 | |||||

| 32,140,457 | |||||||

| Total (Cost $89,963,274) | 104,737,986 | ||||||

| HEALTH CARE – 2.3% | |||||||

| BIOTECHNOLOGY - 0.5% | |||||||

| †Catalyst Pharmaceuticals1 | 542,600 | 2,034,750 | |||||

| HEALTH CARE PROVIDERS & SERVICES - 1.3% | |||||||

| AMN Healthcare Services1 | 31,541 | 1,965,320 | |||||

| Ensign Group (The) | 54,614 | 2,477,837 | |||||

| †Pennant Group1 | 22,357 | 739,346 | |||||

| 5,182,503 | |||||||

| PHARMACEUTICALS - 0.5% | |||||||

| †Supernus Pharmaceuticals1 | 91,900 | 2,179,868 | |||||

| Total (Cost $8,232,567) | 9,397,121 | ||||||

| INDUSTRIALS – 27.3% | |||||||

| AEROSPACE & DEFENSE - 1.3% | |||||||

| Magellan Aerospace | 357,100 | 3,866,487 | |||||

| †Vectrus1 | 24,171 | 1,239,005 | |||||

| 5,105,492 | |||||||

| AIRLINES - 5.6% | |||||||

| Allegiant Travel | 39,893 | 6,942,977 | |||||

| Hawaiian Holdings | 233,955 | 6,852,542 | |||||

| Spirit Airlines1 | 211,632 | 8,530,886 | |||||

| 22,326,405 | |||||||

| COMMERCIAL SERVICES & SUPPLIES - 2.5% | |||||||

| Herman Miller | 89,303 | 3,719,470 | |||||

| Kimball International Cl. B | 297,582 | 6,151,020 | |||||

| 9,870,490 | |||||||

| CONSTRUCTION & ENGINEERING - 0.5% | |||||||

| Comfort Systems USA | 38,169 | 1,902,725 | |||||

| ELECTRICAL EQUIPMENT - 0.5% | |||||||

| EnerSys | 25,987 | 1,944,607 | |||||

| MACHINERY - 6.5% | |||||||

| Alamo Group | 15,907 | 1,997,124 | |||||

| †Commercial Vehicle Group1 | 838,788 | 5,326,304 | |||||

| Federal Signal | 58,222 | 1,877,660 | |||||

| Meritor1 | 262,428 | 6,872,989 | |||||

| Miller Industries | 264,932 | 9,836,925 | |||||

| 25,911,002 | |||||||

| PROFESSIONAL SERVICES - 6.3% | |||||||

| Heidrick & Struggles International | 226,261 | 7,353,482 | |||||

| Kforce | 47,446 | 1,883,606 |

14 | Royce Capital Fund 2019 Annual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

December 31, 2019

Royce Capital Fund – Small-Cap Portfolio (continued)

| SHARES | VALUE | ||||||

| INDUSTRIALS (continued) | |||||||

| PROFESSIONAL SERVICES (continued) | |||||||

| Korn Ferry | 167,007 | $ | 7,081,097 | ||||

| Resources Connection | 210,780 | 3,442,037 | |||||

| Robert Half International | 57,964 | 3,660,427 | |||||

| TrueBlue1 | 81,748 | 1,966,857 | |||||

| 25,387,506 | |||||||

| ROAD & RAIL - 3.3% | |||||||

| ArcBest | 220,818 | 6,094,577 | |||||

| Old Dominion Freight Line | 10,104 | 1,917,537 | |||||

| Saia1 | 19,800 | 1,843,776 | |||||

| Werner Enterprises | 92,539 | 3,367,494 | |||||

| 13,223,384 | |||||||

| TRADING COMPANIES & DISTRIBUTORS - 0.8% | |||||||

| †BMC Stock Holdings1 | 107,832 | 3,093,700 | |||||

| Total (Cost $98,395,309) | 108,765,311 | ||||||

| INFORMATION TECHNOLOGY – 11.8% | |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS - 9.3% | |||||||

| Fabrinet1 | 60,802 | 3,942,402 | |||||

| Insight Enterprises1 | 145,952 | 10,258,966 | |||||

| PC Connection | 116,503 | 5,785,539 | |||||

| Sanmina Corporation1 | 260,093 | 8,905,584 | |||||

| Vishay Intertechnology | 277,299 | 5,903,696 | |||||

| Vishay Precision Group1 | 70,500 | 2,397,000 | |||||

| 37,193,187 | |||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 2.5% | |||||||

| Advanced Energy Industries1 | 28,108 | 2,001,289 | |||||

| Kulicke & Soffa Industries | 220,326 | 5,992,867 | |||||

| MKS Instruments | 17,791 | 1,957,188 | |||||

| 9,951,344 | |||||||

| Total (Cost $34,657,353) | 47,144,531 | ||||||

| MATERIALS – 0.7% | |||||||

| METALS & MINING - 0.7% | |||||||

| †Mayville Engineering1 | 297,847 | 2,793,805 | |||||

| Total (Cost $4,001,430) | 2,793,805 | ||||||

| REAL ESTATE – 1.5% | |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT - 1.5% | |||||||

| Marcus & Millichap1 | 157,119 | 5,852,683 | |||||

| Total (Cost $5,070,007) | 5,852,683 | ||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $335,005,703) | 373,262,441 | ||||||

| REPURCHASE AGREEMENT– 6.6% | |||||||

| Fixed Income Clearing Corporation, 0.25% dated 12/31/19, due 1/2/20, maturity value $26,456,367 (collateralized by obligations of various U.S. Government Agencies, 2.00%- 2.25% due 5/31/24-11/15/24, valued at $26,987,900) | |||||||

| (Cost $26,456,000) | 26,456,000 | ||||||

| TOTAL INVESTMENTS – 100.2% | |||||||

| (Cost $361,461,703) | 399,718,441 | ||||||

| LIABILITIES LESS CASH AND OTHER ASSETS – (0.2)% | (976,743 | ||||||

| NET ASSETS – 100.0% | $ | 398,741,698 |

ADR- American Depository Receipt

| † | New additions in 2019. |

| 1 | Non-income producing. |

| 2 | All or a portion of these securities were on loan at December 31, 2019. |

Bold indicates the Fund’s 20 largest equity holdings in terms of December 31, 2019, market value.

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2019 Annual Report to Shareholders | 15 |

| Statements of Assets and Liabilities | December 31, 2019 |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| ASSETS: | ||||||||

| Investments at value (including collateral on loaned securities)1 | $ | 146,005,321 | $ | 373,262,441 | ||||

| Repurchase agreements (at cost and value) | 12,409,000 | 26,456,000 | ||||||

| Cash and foreign currency | 560 | 25,299 | ||||||

| Receivable for investments sold | 382,262 | 165,272 | ||||||

| Receivable for capital shares sold | 1,105,899 | 72,002 | ||||||

| Receivable for dividends and interest | 87,756 | 438,899 | ||||||

| Receivable for securities lending income | 689 | 331 | ||||||

| Prepaid expenses and other assets | 2,056 | 4,582 | ||||||

| Total Assets | 159,993,543 | 400,424,826 | ||||||

| LIABILITIES: | ||||||||

| Payable for collateral on loaned securities | 218,823 | – | ||||||

| Payable for investments purchased | 360,679 | 1,035,272 | ||||||

| Payable for capital shares redeemed | 88,697 | 188,352 | ||||||

| Payable for investment advisory fees | 155,259 | 323,176 | ||||||

| Payable for trustees’ fees | 9,205 | 19,225 | ||||||

| Accrued expenses | 62,402 | 117,103 | ||||||

| Total Liabilities | 895,065 | 1,683,128 | ||||||

| Net Assets | $ | 159,098,478 | $ | 398,741,698 | ||||

| ANALYSIS OF NET ASSETS: | ||||||||

| Paid-in capital | $ | 122,388,694 | $ | 354,930,532 | ||||

| Total distributable earnings (loss) | 36,709,784 | 43,811,166 | ||||||

| Net Assets | $ | 159,098,478 | $ | 398,741,698 | ||||

| Investment Class | $ | 132,008,250 | $ | 173,491,361 | ||||

| Service Class | 27,090,228 | 225,250,337 | ||||||

| SHARES OUTSTANDING (unlimited number of $.001 par value): | ||||||||

| Investment Class | 13,537,817 | 21,175,851 | ||||||

| Service Class | 2,839,477 | 28,117,574 | ||||||

| NET ASSET VALUES (Net Assets ÷ Shares Outstanding): | ||||||||

| (offering and redemption price per share) | ||||||||

| Investment Class | $9.75 | $8.19 | ||||||

| Service Class | 9.54 | 8.01 | ||||||

| Investments at identified cost | $ | 111,425,014 | $ | 335,005,703 | ||||

| Market value of loaned securities2 | 4,923,692 | 2,605,674 | ||||||

| See Notes to Financial Statements for information on non-cash collateral on loaned securities. |

| 2 | Market value of loaned securities backed by non-cash collateral is as of prior business day. |

| 16 |Royce Capital Fund 2019 Annual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| Statements of Operations | Year Ended December 31, 2019 |

| Micro-Cap | Small-Cap | |||||||

| Portfolio | Portfolio | |||||||

| INVESTMENT INCOME: | ||||||||

| INCOME: | ||||||||

| Dividends | $ | 1,265,678 | $ | 6,941,933 | ||||

| Foreign withholding tax | (24,787 | ) | (153,119 | ) | ||||

| Interest | 37,195 | 99,972 | ||||||

| Securities lending | 80,682 | 1,111 | ||||||

| Total income | 1,358,768 | 6,889,897 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees | 1,849,735 | 3,208,931 | ||||||

| Distribution fees | 43,849 | 375,151 | ||||||

| Administrative and office facilities | 86,323 | 157,912 | ||||||

| Shareholder reports | 58,323 | 68,532 | ||||||

| Trustees’ fees | 44,473 | 92,315 | ||||||

| Audit | 27,950 | 33,472 | ||||||

| Custody | 23,523 | 54,093 | ||||||

| Shareholder servicing | 14,687 | 14,314 | ||||||

| Legal | 6,451 | 13,728 | ||||||

| Other expenses | 9,054 | 24,719 | ||||||

| Total expenses | 2,164,368 | 4,043,167 | ||||||

| Compensating balance credits | (353 | ) | (571 | ) | ||||

| Fees waived by investment adviser | (82,461 | ) | (125,890 | ) | ||||

| Expenses reimbursed by investment adviser | (73,339 | ) | (81,511 | ) | ||||

| Net expenses | 2,008,215 | 3,835,195 | ||||||

| Net investment income (loss) | (649,447 | ) | 3,054,702 | |||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | ||||||||

| NET REALIZED GAIN (LOSS): | ||||||||

| Investments | 2,085,590 | 3,755,867 | ||||||

| Foreign currency transactions | 6,706 | 8,487 | ||||||

| NET CHANGE IN UNREALIZED APPRECIATION (DEPRECIATION): | ||||||||

| Investments | 24,781,451 | 33,770,864 | ||||||

| Other assets and liabilities denominated in foreign currency | (1,490 | ) | (50 | ) | ||||

| Net realized and unrealized gain (loss) on investments and foreign currency | 26,872,257 | 37,535,168 | ||||||

| NET INCREASE (DECREASE) IN NET ASSETS FROM INVESTMENT OPERATIONS | $ | 26,222,810 | $ | 40,589,870 | ||||

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | Royce Capital Fund 2019 Annual Report to Shareholders | 17 |

Statements of Changes in Net Assets

| Micro-Cap Portfolio | Small-Cap Portfolio | |||||||||||||||

| Year Ended 12/31/19 | Year Ended 12/31/18 | Year Ended 12/31/19 | Year Ended 12/31/18 | |||||||||||||

| INVESTMENT OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | (649,447 | ) | $ | (640,551 | ) | $ | 3,054,702 | $ | 2,028,315 | ||||||

| Net realized gain (loss) on investments and foreign currency | 2,092,296 | 14,233,957 | 3,764,354 | 46,496,665 | ||||||||||||

| Net change in unrealized appreciation (depreciation) on investments and foreign currency | 24,779,961 | (26,943,361 | ) | 33,770,814 | (72,052,141 | ) | ||||||||||

| Net increase (decrease) in net assets from investment operations | 26,222,810 | (13,349,955 | ) | 40,589,870 | (23,527,161 | ) | ||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| Total distributable earnings | ||||||||||||||||

| Investment Class | (11,752,195 | ) | (6,692,693 | ) | (21,338,300 | ) | (3,942,054 | ) | ||||||||

| Service Class | (2,426,040 | ) | (764,616 | ) | (27,129,064 | ) | (1,828,028 | ) | ||||||||

| Total distributions | (14,178,235 | ) | (7,457,309 | ) | (48,467,364 | ) | (5,770,082 | ) | ||||||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

| Value of shares sold | ||||||||||||||||

| Investment Class | 10,068,959 | 20,188,911 | 15,075,395 | 20,508,660 | ||||||||||||

| Service Class | 16,944,428 | 8,396,343 | 315,873,262 | 3,049,574 | ||||||||||||

| Distributions reinvested | ||||||||||||||||

| Investment Class | 11,752,195 | 6,692,693 | 21,338,300 | 3,942,054 | ||||||||||||

| Service Class | 2,426,040 | 764,616 | 27,129,064 | 1,828,028 | ||||||||||||

| Value of shares redeemed | ||||||||||||||||

| Investment Class | (28,638,535 | ) | (45,283,517 | ) | (43,316,043 | ) | (62,882,019 | ) | ||||||||

| Service Class | (7,600,024 | ) | (24,574,409 | ) | (205,170,757 | ) | (153,628,193 | ) | ||||||||

| Net increase (decrease) in net assets from capital share transactions | 4,953,063 | (33,815,363 | ) | 130,929,221 | (187,181,896 | ) | ||||||||||

| Net Increase (Decrease) in Net Assets | 16,997,638 | (54,622,627 | ) | 123,051,727 | (216,479,139 | ) | ||||||||||

| NET ASSETS: | ||||||||||||||||

| Beginning of year | 142,100,840 | 196,723,467 | 275,689,971 | 492,169,110 | ||||||||||||

| End of year | $ | 159,098,478 | $ | 142,100,840 | $ | 398,741,698 | $ | 275,689,971 | ||||||||

| 18|Royce Capital Fund 2019 Annual Report to Shareholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

Financial Highlights

This table is presented to show selected data for a share outstanding throughout each year and to assist shareholders in evaluating a Fund’s performance for the periods presented. Per share amounts have been determined on the basis of the weighted average number of shares outstanding during the period.

| Ratio of Expenses to Average Net Assets | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net Asset Value, Beginning of Period | Net Investment Income (Loss) | Net Realized and Unrealized Gain (Loss) on Investments and Foreign Currency | Total from Investment Operations | Distributions from Net Investment Income | Distributions from Net Realized Gain on Investments and Foreign Currency | Total Distributions | Net Asset Value, End of Period | Total Return | Net Assets, End of Period (in thousands) | Prior to Fee Waivers, Expense Reimbursements and Balance Credits | Prior to Fee Waivers and Expense Reimbursements | Net of Fee Waivers and Expense Reimbursements | Ratio of Net Investment Income (Loss) to Average Net Assets | Portfolio Turnover Rate | |||||||||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio–Investment Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2019 | $ | 8.97 | $ | (0.04 | ) | $ | 1.77 | $ | 1.73 | $ | – | $ | (0.95 | ) | $ | (0.95 | ) | $ | 9.75 | 19.55 | % | $ | 132,008 | 1.43 | % | 1.43 | % | 1.33 | % | (0.41 | )% | 26 | % | ||||||||||||||||||||||||||||

| 2018 | 10.39 | (0.03 | ) | (0.90 | ) | (0.93 | ) | – | (0.49 | ) | (0.49 | ) | 8.97 | (9.13 | ) | 127,457 | 1.39 | 1.39 | 1.33 | (0.30 | ) | 28 | |||||||||||||||||||||||||||||||||||||||

| 2017 | 11.11 | (0.02 | ) | 0.58 | 0.56 | (0.08 | ) | (1.20 | ) | (1.28 | ) | 10.39 | 5.29 | 164,656 | 1.38 | 1.38 | 1.38 | (0.22 | ) | 30 | |||||||||||||||||||||||||||||||||||||||||

| 2016 | 9.34 | 0.03 | 1.81 | 1.84 | (0.07 | ) | – | (0.07 | ) | 11.11 | 19.71 | 177,444 | 1.36 | 1.36 | 1.36 | 0.02 | 57 | ||||||||||||||||||||||||||||||||||||||||||||

| 2015 | 11.37 | 0.03 | (1.45 | ) | (1.42 | ) | – | (0.61 | ) | (0.61 | ) | 9.34 | (12.46 | ) | 369,991 | 1.32 | 1.32 | 1.32 | 0.27 | 51 | |||||||||||||||||||||||||||||||||||||||||

| Micro-Cap Portfolio–Service Class | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||