UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07619

Nuveen Investment Trust

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Mutual Funds

Nuveen Equity Funds

For investors seeking long-term capital appreciation.

Annual Report

June 30, 2012

| | | | | | | | | | |

| | | Share Class / Ticker Symbol |

| | | | | |

| Fund Name | | Class A | | Class B | | Class C | | Class R3 | | Class I |

Nuveen Multi-Manager Large-Cap Value Fund | | NNGAX | | NNGBX | | NNGCX | | NMMTX | | NNGRX |

Nuveen NWQ Multi-Cap Value Fund | | NQVAX | | NQVBX | | NQVCX | | NMCTX | | NQVRX |

Nuveen NWQ Large-Cap Value Fund | | NQCAX | | — | | NQCCX | | NQCQX | | NQCRX |

Nuveen NWQ Small/Mid-Cap Value Fund | | NSMAX | | — | | NSMCX | | NSQRX | | NSMRX |

Nuveen NWQ Small-Cap Value Fund | | NSCAX | | — | | NSCCX | | NSCOX | | NSCRX |

Nuveen Tradewinds Value Opportunities Fund | | NVOAX | | NVOBX | | NVOCX | | NTVTX | | NVORX |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Table of Contents

Chairman’s

Letter to Shareholders

Dear Shareholders,

Investors have many reasons to remain cautious. The challenges in the Euro area are casting a shadow over global economies and financial markets. The political support for addressing fiscal issues is eroding as the economic and social impacts become more visible. At the same time, member nations appear unwilling to provide adequate financial support or to surrender sufficient sovereignty to strengthen the banks or unify the Euro area financial system. The gains made in reducing deficits, and the hard-won progress on winning popular acceptance of the need for economic austerity, are at risk. To their credit, European political leaders press on to find compromise solutions, but there is increasing concern that time will begin to run out.

In the U.S., strong corporate earnings have enabled the equity markets to withstand much of the downward pressures coming from weakening job creation, slower economic growth and political uncertainty. The Fed remains committed to low interest rates but has refrained from predicting another program of quantitative easing unless economic growth were to weaken significantly or the threat of recession appears on the horizon. Pre-election maneuvering has added to the already highly partisan atmosphere in the Congress. The end of the Bush-era tax cuts and implementation of the spending restrictions of the Budget Control Act of 2011, both scheduled to take place at year-end, loom closer.

During the last year, U.S. based investors have experienced a sharp decline and a strong recovery in the equity markets. The experienced investment teams at Nuveen keep their eye on a longer time horizon and use their practiced investment disciplines to negotiate through market peaks and valleys to achieve long-term goals for investors. Experienced professionals pursue investments that will weather short-term volatility and at the same time, seek opportunities that are created by markets that overreact to negative developments. Monitoring this process is an important consideration for the Fund Board as it oversees your Nuveen Fund on your behalf.

As always, I encourage you to contact your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

August 23, 2012

Portfolio Managers’ Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other fac-tors. The Funds disclaim any obli-gation to update publicly or revise any forward-looking statements or views expressed herein.

The Nuveen Multi-Manager Large Cap Value Fund is co-managed by Institutional Capital LLC (ICAP), Nuveen Asset Management, LLC, and Symphony Asset Management LLC. Nuveen Asset Management and Symphony are affiliates of Nuveen Investments. Jerrold Sensor, CFA, and Thomas Wenzel, CFA, oversee the portion of the Fund’s assets managed by ICAP, while Keith Hembre, CFA and Walter French oversee the Fund’s assets managed by Nuveen Asset Management. Gunther Stein and Ross Sakamoto oversee the portion of the Fund’s assets managed by Symphony. After the reporting period ended, on August 1, 2012, Thomas Cole, CFA was named portfolio manager for the portion of the Fund’s assets managed by ICAP and Joel Drescher was named portfolio manager for the portion of the Fund’s assets managed by Symphony. The Fund’s current portfolio managers will continue to serve as portfolio managers for the Fund.

The Nuveen NWQ Multi-Cap Value Fund, Nuveen NWQ Large-Cap Value Fund, Nuveen NWQ Small/Mid-Cap Value Fund and Nuveen NWQ Small-Cap Value Fund feature equity management by NWQ Investment Management Company, LLC (NWQ), an affiliate of Nuveen Investments. Jon Bosse is the Chief Investment Officer of NWQ and manages the Multi-Cap Value and Large-Cap Value Funds. Phyllis Thomas manages the Nuveen Small/Mid-Cap Value and Small-Cap Value Funds.

The Nuveen Tradewinds Value Opportunities Fund features portfolio management by Tradewinds Global Investors, LLC (Tradewinds), an affiliate of Nuveen Investments. During the reporting period, Tradewinds announced that Dave Iben, Co-President and Chief Investment Officer of Tradewinds, decided to leave the firm during the second calendar quarter. Emily Alejos and Drew Thelen have assumed investment leadership and oversight responsibilities, now serving as Co-Chief Investment Officers for Tradewinds. As integral members of the Tradewinds investment team, Emily and Drew have worked together for more than five years. Each brings significant investment experience to the next stage of Tradewinds’ development. Effective April 1, 2012, Joann Barry, CFA and F. Rowe Michels, CFA were named portfolio managers of the Fund, and David Iben no longer serves as portfolio manager.

What factors affected the U.S. economic and equity market environments during the twelve-month reporting period ended June 30, 2012?

During the reporting period, the U.S. economy’s progress toward recovery from recession remained sluggish. The Federal Reserve (Fed) maintained its efforts to improve the overall economic environment by continuing to hold the benchmark Fed Funds rate at the record low level of zero to 0.25% that it had established in December 2008. At its June 2012 meeting, the central bank affirmed its opinion that economic conditions would likely

warrant keeping the rate at “exceptionally low levels” through at least late 2014. The Fed also announced that it would extend its so-called Operation Twist program, whereby it is lengthening the average maturity of its holdings of U.S. Treasury securities, through the end of December 2012. The goals of this program are to lower longer-term interest rates, make broader financial conditions more accommodating, support a stronger economic recovery and help ensure that inflation remains at levels consistent with the Fed’s mandates of maximum employment and price stability.

In the second quarter of 2012, the U.S. economy slowed to an annualized growth rate of 1.5%, according to initial estimates for U.S. gross domestic product (GDP). While this marked the twelfth consecutive quarter of positive growth, it was also a significant slowdown from the previous few quarters. The Consumer Price Index (CPI) rose 1.7% year-over-year as of June 2012, the same figure as May 2012, which was the lowest twelve-month rate of change since February 2011. Core CPI (which excludes food and energy) increased 2.2% during the period, remaining above the Fed’s unofficial objective of 2.0% or lower for this inflation measure. However, the number was slightly below the 2.3% figure reported in the previous three months. Labor market conditions continued to be slow to improve, with the national unemployment rate registering 8.2% in June 2012. While this figure was down from 9.1% one year ago, it was still a slight uptick from the 8.1% reading in April 2012. The housing market remained the major weak spot in the economy, beleaguered by a high level of distressed properties and difficult credit conditions. For the twelve months ended May 2012 (the most recent data available at the time this report was prepared), the average home price in the Standard & Poor’s (S&P)/Case-Shiller Index of 20 major metropolitan areas lost 0.7%. Housing prices remained at the lowest levels since spring 2003, down more than one-third from their summer 2006 peak. In addition, the U.S. economic picture continued to be clouded by concerns about the European debt crisis and global financial markets in general and efforts to reduce the U.S. federal deficit.

The U.S. equity market appreciated during the reporting period notwithstanding increased concerns regarding global economic growth and a sovereign debt crisis in Europe that have plagued stocks more recently. The best performing sectors in the Russell 1000 Value Index for the year were consumer discretionary, health care and utilities. The worst performing sectors were energy, finance, and materials & processing. Energy stocks performed poorly mostly due to extremely weak natural gas prices, concern that high gasoline prices globally were placing a strain on economic growth, and worries over whether China could maintain a sufficient economic growth rate to drive continued demand growth (an issue for commodities generally).

During the reporting period, global equity markets experienced periods of extreme volatility. The coordinated move by central banks provided a psychological boost in equity markets, but the impact proved to be short lived. Global markets rebounded in the first quarter of 2012, as there were positive returns in broad indices. The Volatility Index (VIX) declined, ending the first quarter at a five-year low and implying a generally confident view among investors. However, the second quarter saw equity declines driven by macro uncertainty. The U.S. financial sector notably retracted first quarter gains, with major banks suffering from Eurozone headwinds via capital markets operations. Energy

companies also broadly traded lower, as investors extrapolated extended soft cyclical demand indefinitely into the future. U.S. treasuries and the U.S. dollar displayed resilience, however, since investors continue to flock to these perceived safe havens.

How did the Funds perform during the twelve-month reporting period ended June 30, 2012?

The tables in the Fund Performance and Expense Ratios section of this report provide Class A Share total returns for the Funds for the one-year, five-year, ten-year and since inception periods ended June 30, 2012. Each Funds’ Class A Share total returns are compared with the performance of their corresponding market indexes and peer group averages. A more detailed account of each Fund’s performance is provided later in this report.

What strategies were used to manage the Funds during the reporting period? How did these strategies influence performance?

Nuveen Multi-Manager Large-Cap Value Fund

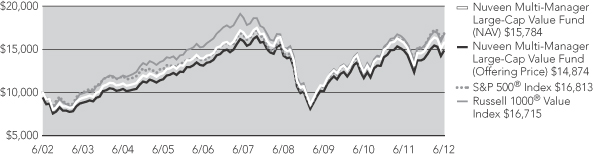

The Nuveen Multi-Manager Large-Cap Value Fund’s Class A Shares at net asset value (NAV) outperformed the comparative Lipper classification average, but underperformed both the S&P 500® and the Russell 1000® Value indexes over the twelve-month period ended June 30, 2012.

The Fund uses three separate sub-advisers to seek large capitalization value stocks with the potential for long-term capital appreciation. ICAP uses a value-oriented investment strategy that attempts to identify stocks offering the best relative value and stable to rising earnings from a universe of large and mid-sized companies. It then selects a portion of those stocks that are identified to have a catalyst for change and monitors these holdings closely to determine if circumstances change. For the Nuveen Asset Management portion of the Fund, we create proprietary models to help establish quantitative links between economic/market variables, investment factors and equity market returns. Our proprietary models analyze macroeconomic and market data and other statistics to determine what we believe will be the key drivers of performance in the current economy. We also use historical analysis of these drivers to estimate equity market return and the relative contribution to market returns for a comprehensive list of investment factors. We evaluate each stock in the investable universe to determine its sensitivity to the expected returns for each factor and estimate a potential contribution for each stock. The Fund’s portfolio will include stocks that we believe target the highest expected returns within the established risk budget. Symphony seeks to deliver consistent returns though an investment process that combines quantitative screens and fundamental research. The portfolio construction process utilizes a proprietary optimizer designed to potentially generate an optimal risk reward balance versus the stated benchmark.

The ICAP managed portion of the Fund gained modest value in absolute terms but lagged the results of the Russell 1000 Value Index. The past year was a volatile investment environment, as the stock market dropped sharply in the third quarter of 2011, rebounded strongly in the period’s subsequent two quarters and then pulled back

modestly in the second quarter of 2012. Both security selection and sector allocation detracted from the portfolio’s relative performance. The financials and energy sectors added to results compared with the Russell benchmark, while the health care and consumer staples groups detracted. The portfolio benefited the most from being overweight in consumer staples and underweight in financials. However, the Fund had no exposure to utilities, which, given that sector’s strength, was a negative factor.

Throughout the reporting period, we consistently followed our bottom-up stock-selection investment process. We selected investments individually, based on our assessment of their valuation and prospects for price improvement compared with other stocks. We bought or added to stocks that we believed offered good value as well as a potential catalyst for a rising stock price and continued to sell or reduce exposure to securities that, in our view, offered limited upside potential. We adjusted the portfolio as market conditions changed or when we found opportunities to buy and sell securities that we believed would add value for our shareholders. As one example, the portfolio’s weighting in the capital spending sector increased after we bought shares of diversified conglomerate General Electric and diesel engine manufacturer Cummins Inc. Meanwhile, in the technology sector, we added shares of network communications company Cisco Systems. In contrast, we eliminated the Fund’s stake in beverage and snack food maker PepsiCo and restaurant chain McDonald’s and we reduced the portfolio’s weighting in The Coca-Cola Company, the global beverage giant. On an individual basis, the Fund’s top contributors to relative performance were software maker Microsoft, the Coca-Cola Company and U.K. based wireless communications provider, Vodafone.

The three largest relative detractors were auto-parts manufacturer Johnson Controls, insurance company MetLife and Procter & Gamble, maker of household and personal care products. Johnson Controls was hurt by its high exposure to the underperforming automotive sector. The prospects for continued low interest rates and, accordingly, lower investment income, weighed on shares of MetLife. Procter & Gamble lagged, as increased price competition and higher commodity costs hurt the firm’s profit margins.

The portion of the portfolio managed by Nuveen Asset Management was overweight energy and information technology and underweight staples, utilities, industrials and consumer discretionary. The largest single sector overweight was information technology. This position contributed negatively to the Fund’s relative performance versus the index. Performance attributable to the individual stock holdings within each sector was a negative for the Fund during the reporting period, with the stock picks within the consumer discretionary sector having the largest negative impact. The holdings within the energy, health care and staples sectors were also a negative for the Fund. Holdings within the utilities, industrials and information technology sectors resulted in positive relative performance for the Fund.

For the portion of the portfolio managed by Symphony, we remained invested in companies with relatively strong fundamentals. We benefited from stock selection in the information technology sector, health care and consumer staples sectors. In particular, Expedia and Hewlett-Packard positively contributed to performance. Stock selection in the energy and consumer discretionary sectors detracted from performance. Also negatively impacting performance was Visteon Corporation.

Nuveen NWQ Multi-Cap Value Fund

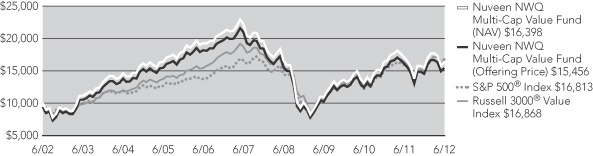

Class A Shares at net asset value (NAV) for the Nuveen NWQ Multi-Cap Value Fund underperformed S&P 500® and the Russell 3000® Value indexes and its Lipper classification average for the twelve-month period ended June 30, 2012.

The Fund seeks long-term capital appreciation by investing in equity securities of companies with large, medium and small market capitalizations that are selected on an opportunistic basis. Generally, the Fund’s managers look for undervalued companies where catalysts exist that may help unlock value or improve profitability. Such catalysts can be new management, improving fundamentals, renewed management focus, industry consolidation or company restructuring.

During the reporting period, three holdings received takeover bids, including Motorola Mobility Holdings, Northgate Minerals and Petrohawk Energy. Motorola Mobility received an all cash takeover offer from Google Inc. at $40 per share. The catalyst for the acquisition was Motorola’s extensive patent portfolio, which Google plans to use to protect its Android franchise. Northgate Minerals Corp. was acquired by AuRico Gold in an all stock deal. We trimmed our position on strength after the deal was announced, and subsequently repurchased the shares at a lower price. Petrohawk Energy Inc. accepted an all cash takeover offer from BHP Billiton Ltd. for $38.75 per share, a 65% premium to the stock’s previous day closing price.

Several positions detracted from performance, including General Motors. The company declined on concerns regarding the slowing economy and the potential impact on volumes and pricing, as well as struggles with restructuring efforts at its European and Brazilian operations.

Hartford Financial Services Group declined given fundamental challenges in its life operations and the continued low interest rate environment that is pressuring margins. Responding to shareholder pressure, the company recently announced a strategic restructuring whereby it will focus on property casualty by divesting its life and retirement businesses, and put its annuity business into runoff. Lastly, Talisman Energy Inc. underperformed given a sharp decline in natural gas prices and ongoing delays at its Yme project in the North Sea. Historical capital allocation decisions have also been a concern. We believe these issues should subside as new management appears capable at resolving the prior management’s challenges.

We strategically added several positions throughout the reporting period, including American International Group (AIG), Best Buy Co., Canadian Natural Resources, Cisco Systems and Hewlett-Packard. We also eliminated several positions due to more attractive investment opportunities. These included Amgen, Genworth Financial, Hess Corporation, Philip Morris International, Aurizon Mines, Merck & Co., Motorola Solutions and Vertex Pharmaceutical.

Nuveen NWQ Large-Cap Value Fund

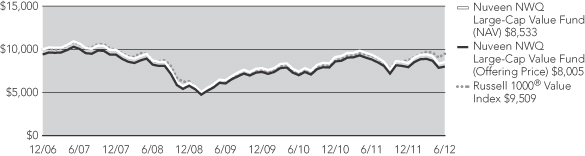

Class A Shares at net asset value (NAV) for the Nuveen NWQ Large-Cap Value Fund underperformed its comparative Lipper classification average and the Russell 1000® Value Index for the twelve-month period ended June 30, 2012.

The Fund seeks long-term capital appreciation by investing in equity securities of companies with large market capitalizations that are selected on an opportunistic basis. Generally, the Fund’s managers look for undervalued companies where catalysts exist that may help unlock value or improve profitability. Such catalysts can be new management, improving fundamentals, renewed management focus, industry consolidation or company restructuring.

Several positions positively contributed to performance including Motorola Mobility Holdings, CA Inc. and Phillip Morris International Inc. Motorola Mobility received an all cash takeover offer from Google Inc. at $40 per share. The catalyst for the acquisition was Motorola’s extensive patent portfolio, which Google plans to use to protect its Android franchise. CA Inc. appreciated as management announced that it will return $2.5 billion of capital to shareholders through 2014 by raising its dividend 400% and repurchasing shares (equating to roughly 80% of the company’s free cash flows). These are actions that we have strongly supported. CA’s strengthened management team has made strides to improve the company’s market position and enhance shareholder value through a strategic restructuring and increased focus on internal operations. Philip Morris International Inc. benefited from market share gains in Japan due to supply disruptions by their main competitor Japan Tobacco, and favorable fundamental trends in various markets in Europe.

Declines in the Fund’s energy and finance holdings contributed significantly to underperformance for the year. The Fund’s energy stocks performed poorly due to declining crude oil prices, sluggish demand, and extremely weak natural gas prices. Natural gas prices reached 10 year lows during the period as mild winter weather and falling coal prices resulted in a glut of gas in North America storage. Financial stocks were pressured by concerns of the European sovereign debt crisis, historically low interest rates, and uncertainty regarding the implementation of new regulations. We believe the fundamentals and operating metrics of the Fund’s bank and insurance holdings have improved significantly since the 2008 financial crisis, while valuations reflect extremely low expectations. Several other positions which detracted from performance included General Motors, Hartford Financial Services Group and Talisman Energy. General Motors declined on concerns regarding the slowing economy and the potential impact on volumes and pricing, as well as struggles with restructuring efforts at its European and Brazilian operations. While GM Europe remains a challenge as weak demand and structural overcapacity is pressuring margins, a new product lineup coming out in 2013 that will replace the GMT900 truck platform looks very promising. Overall the GM investment case remains attractive as the company has a healthy balance sheet and is well positioned in emerging markets, particularly China. Hartford Financial Services Group declined given fundamental challenges in its life operations and the continued low interest rate environment that is pressuring margins. Lastly, Talisman Energy Inc. underperformed given a sharp decline in natural gas prices and ongoing delays at its Yme project in the North Sea.

We strategically added several positions throughout the reporting period, including American International Group (AIG), Best Buy Co., Canadian Natural Resources, Cisco Systems and Hewlett-Packard. We also eliminated several positions due to more attractive

investment opportunities. These included Amgen, Genworth Financial, Hess Corporation, Lockhead Martin Corp. and Motorola Solutions.

Nuveen NWQ Small/Mid-Cap Value Fund

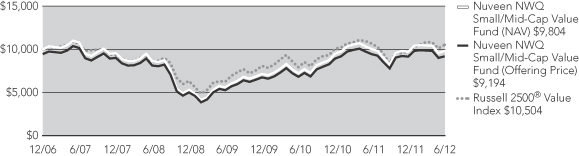

The Fund’s Class A Shares at net asset value (NAV) outperformed the Russell 2500® Value Index and its Lipper classification average for the twelve-month period ended June 30, 2012.

The Fund continued to follow its disciplined investment approach which seeks long-term capital appreciation by investing in equity securities of companies with small- to mid-market capitalizations selected using an analyst-driven, value-oriented process. The portfolio manager looks for undervalued companies where catalysts exist to unlock value or improve profitability. Such catalysts can be new management, improving fundamentals, renewed management focus, industry consolidation or company restructuring.

For the twelve-month reporting period, performance was driven by strong stock selection in the health care and consumer discretionary sectors. This was offset by weakness in materials and processing and durables. Several positions contributed to performance including Vertex Pharmaceuticals. The company’s shares rose sharply during the period after announcing interim data from Phase II studies of KALYDECO + VX-809, its combo drug for treatment of a small portion of the cystic fibrosis population. Shares of Elizabeth Arden rose during the period as the company announced several new fragrance licensing agreements and further clarified the timeline for the global relaunch of the Elizabeth Arden brand. Shares were particularly strong on the announcement that the company had acquired the global licenses for Justin Bieber fragrances. The Arden relaunch remains the company’s single biggest opportunity. Also positively contributing to performance was Northgate Minerals. The company was our best performing gold stock as the company entered into a definitive agreement to be acquired by AuRico Gold in an all-stock deal. The new entity will have five operating gold mines and a sixth scheduled to come online in 2012.

Several positions detracted from performance including Thompson Creek. The company’s shares declined on concerns over a funding gap for the company’s Mt. Milligan project in central British Columbia. The company’s copper and gold project at Mt. Milligan should add growth and diversification to the company in the longer term. Real estate operator Forestar underperformed during the period as a result of the mid-cycle economic slowdown and the perception that housing prices could decline again. Our energy stocks declined in conjunction with a weak energy market as oil prices plunged on fears of slowing growth. We continue to believe that rising global demand and limited supply will support oil prices going forward. Denbury Resources detracted from performance, after weather delays prompted the company to lower production guidance at their Bakken Development. We strategically added several positions throughout the reporting period, including Inter Parfums Inc. and TriMas Corporation. We also eliminated several positions due to more attractive investment opportunities, these included Arch Coal and Graftech.

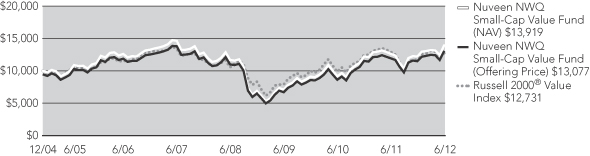

Nuveen NWQ Small-Cap Value Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed the Russell 2000® Value Index and its Lipper classification average for the twelve-month period ended June 30, 2012.

Over the reporting period, the Fund continued to follow its disciplined investment approach. The Fund seeks long-term capital appreciation by investing in equity securities of companies with small market capitalizations selected using an analyst-driven, value-oriented process. NWQ seeks to provide superior risk-adjusted returns through an analyst-driven, value-oriented process. Portfolio managers look for undervalued companies where catalysts exist to unlock value or improve profitability. Such catalysts can be new management, improving fundamentals, renewed management focus, industry consolidation or company restructuring.

Stock selection in the consumer discretionary, technology and consumer staples sectors drove the Fund’s performance. Several positions positively contributed to performance including Smart Balance. Shares of Smart Balance rose sharply in June (2012) after the company’s announcement that it had acquired Udi, the number one producer by sales of gluten-free food products. Also positively contributing to performance was Standard Microsystems. The company’s shares rose during the second quarter following the announced acquisition of the company by Microchip Technology at a significant premium. Under the terms of the agreement, Microchip Technology will acquire all outstanding common stock of Standard Microsystems.

Shares of Elizabeth Arden rose during the period as the company announced several new fragrance licensing agreements and further clarified the timeline for the global relaunch of the Elizabeth Arden brand. Shares were particularly strong on the announcement that the company had acquired the global licenses for Justin Bieber fragrances. The Arden relaunch remains the company’s single biggest opportunity.

Several positions detracted from performance during the reporting period. In particular, the performance of stocks within the energy sector reflected the sharp decline in crude oil prices late in the reporting period. Shares of Carrizo Oil & Gas fell as oil prices weakened due to well-supplied oil inventories, sluggish demand and a strengthening U.S. dollar. While the backdrop of further economic weakness and lower crude prices does have us monitoring the risk/reward of our investments, we continue to find shares of Carrizo extremely attractive. Also detracting from performance was Thompson Creek. The company’s shares declined on concerns over a funding gap for the company’s Mt. Milligan project in central British Columbia. The company’s copper and gold project at Mt. Milligan should add growth and diversification to the company in the longer term. Lastly, real estate operator Forestar underperformed during the period as a result of the mid cycle economic slowdown and the perception that housing prices could decline again.

We strategically added several positions throughout the reporting period, including Inter Parfums Inc., Neenah Paper Inc., GP Strategies Corp., Homestreet Inc. and Methode Electronics. We also eliminated several positions due to more attractive investment opportunities. These included Golfsmith and Temple-Inland.

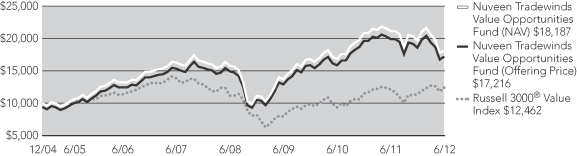

Nuveen Tradewinds Value Opportunities Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed the Russell 3000 Value Index and the Lipper classification average for the twelve-month period ended June 30, 2012. It should be noted that the Fund has held, and is expected to continue to

hold, securities that are not included in the comparative index shown in this report. Due to the difference between the securities held by the Fund and the composition of the index, we would expect there to be some differences over time between the Fund and the index in terms of performance, composition, and/or risk profile.

The Fund seeks long-term capital appreciation by investing in equity securities of companies with varying market capitalizations selected using an eclectic, value-oriented process.

Appreciation in select technology companies had a positive effect on performance. One of these top contributors was Microsoft Corporation. The company is expected to have major upgrades throughout the next few years, which we believe will drive sales upwards.

Another top contributor to performance was Georgia Gulf Corporation, a producer of chlorovinyls, aromatics and building products. Westlake Chemical offered $30/share in a hostile bid; Georgia Gulf shares were trading above the bid while rumors were swirling that it would take at least $40 to get the deal done. We eventually sold this position after the shares reached what we believed was fair value. Wal-Mart Stores, the world’s largest retailer operating discount stores, supercenters and warehouse clubs was also a top performer. The company experienced an increase in stock price after Investor Day announced a number of positive points on sales, expenses and income guidance. Investors also reacted positively to favorable trends in earnings per share and annual dividend growth. The shares reached fair value, and as a result, we trimmed and eventually sold out of our position in this name.

As has been the case for some time now, one of the areas where we have seen extensive business sustainability yet declining stock prices is in select gold mining companies. Toward the end of 2011, underperformance in gold producers was due to production shortfalls, continued rising input costs and relatively lackluster fourth quarter stock performance following capital flight out of commodities stocks. In 2012, the price-to-earnings measures for some of the gold firms we hold have dipped lower than the average for the general global market, despite historical premium valuations. We have maintained substantial exposures to these companies over the last few years as they have commonly been offered at what we view as “sale prices” in relation to the assets they control. We see recent spot price declines as temporary deviations from the long-term trend of a growing level of demand relative to fewer available quantities of the metal, placing well-resourced producers in a strong operating position. Kinross Gold Corp. is an international gold mining company based in Canada, with operations and development projects in Canada, U.S. and Russia among other countries. During the reporting period, the company drew investor apprehension due to labor and cost challenges at its Tasiast mine in Mauritania and tax negotiations at its Ecuadorian Fruta del Norte project.

Newcrest Mining is a gold mining firm that also produces copper as a byproduct of its activities. The company’s shares have suffered from weakness in gold spot prices. We continue to see the company’s abundant reserves, relatively large production volumes, and diversified mining assets as attractive at current prices.

In the energy sector, Arch Coal Inc. was a bottom performer in the last half of 2011 after the company missed revenue estimates and cut the year’s EPS forecast due to lost production in one of its mines. The company is the second largest coal producer in the U.S. and the second largest by reserves. Price dynamics in natural gas have caused declines in demand for coal, and Arch also suffered after a recent decision to cut its dividend. While sentiment remains negative in the short-term, we believe the company’s recent debt restructuring dramatically reduces liquidity concerns.

Risk Considerations

Mutual fund investing involves risk; principal loss is possible. Equity investments such as those held by the Funds are subject to market risk and common stock risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets.

Investments in small- and mid-cap companies such as those held in the Nuveen Multi- Manager Large-Cap Value Fund, the Nuveen NWQ Small/Mid-Cap Value Fund, the Nuveen Small-Cap Value Fund, and the Nuveen Tradewinds Value Opportunities Fund are subject to greater volatility.

The Nuveen Multi-Manager Large-Cap Value Fund is also subject to the risk that the sub- advisers’ investment decisions may not complement one another.

Fund Performance and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown on the following twelve pages.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

Fund Performance and Expense Ratios (continued)

Nuveen Multi-Manager Large-Cap Value Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | 10-Year* | |

Class A Shares at NAV | | | 0.19% | | | | -1.43% | | | | 4.67% | |

Class A Shares at maximum Offering Price | | | -5.60% | | | | -2.59% | | | | 4.05% | |

S&P 500® Index** | | | 5.45% | | | | -0.22% | | | | 5.33% | |

Russell 1000® Value Index** | | | 3.01% | | | | -2.19% | | | | 5.28% | |

Lipper Large-Cap Value Funds Classification Average** | | | -0.15% | | | | -2.65% | | | | 4.34% | |

| | | |

Class B Shares w/o CDSC | | | -0.56% | | | | -2.16% | | | | 4.04% | |

Class B Shares w/CDSC | | | -4.51% | | | | -2.31% | | | | 4.04% | |

Class C Shares | | | -0.51% | | | | -2.16% | | | | 3.89% | |

Class R3 Shares | | | 0.04% | | | | -1.71% | | | | 4.39% | |

Class I Shares | | | 0.45% | | | | -1.19% | | | | 4.93% | |

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios |

Class A Shares | | | 1.22% | | | 1.18% |

Class B Shares | | | 1.97% | | | 1.93% |

Class C Shares | | | 1.97% | | | 1.93% |

Class R3 Shares | | | 1.49% | | | 1.43% |

Class I Shares | | | 0.97% | | | 0.93% |

The Fund’s investment adviser has agreed to waive fees and/or reimburse expenses through October 31, 2012, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.95% (1.20% after October 31, 2012) of the average daily net assets of any class of Fund shares. The expense limitation expiring October 31, 2012, may be terminated or modified prior to that date only with the approval of the Board of Trustees of the Fund. The expense limitation in effect thereafter may be terminated or modified only with the approval of shareholders of the Fund.

| * | The returns for Class A, B, C and I Shares are actual. The returns for Class R3 Shares are actual for the periods since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expenses, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

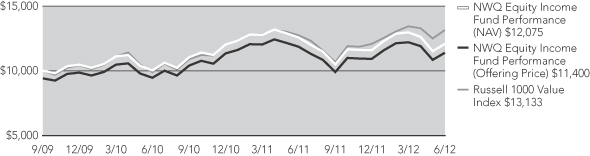

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen NWQ Multi-Cap Value Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | 10-Year* | |

Class A Shares at NAV | | | -4.29% | | | | -5.97% | | | | 5.07% | |

Class A Shares at maximum Offering Price | | | -9.81% | | | | -7.08% | | | | 4.45% | |

S&P 500® Index** | | | 5.45% | | | | 0.22% | | | | 5.33% | |

Russell 3000® Value Index** | | | 2.64% | | | | -2.10% | | | | 5.37% | |

Lipper Multi-Cap Core Funds Classification Average** | | | -1.69% | | | | -0.99% | | | | 5.29% | |

| | | | | | | | | | | | |

Class B Shares w/o CDSC | | | -4.98% | | | | -6.67% | | | | 4.44% | |

Class B Shares w/CDSC | | | -8.78% | | | | -6.85% | | | | 4.44% | |

Class C Shares | | | -4.98% | | | | -6.67% | | | | 4.29% | |

Class R3 Shares | | | -4.48% | | | | -6.22% | | | | 4.80% | |

Class I Shares | | | -4.02% | | | | -5.73% | | | | 5.34% | |

Effective December 6, 2002, based on shareholder approval, the Nuveen NWQ Multi-Cap Value Fund acquired the assets and performance history of the PBHG Special Equity Fund. The Fund had no assets prior to the acquisition. In addition, on December 14, 2001, the PBHG Special Equity Fund acquired the assets of the NWQ Special Equity Portfolio. The information presented for the Nuveen NWQ Multi-Cap Value Fund prior to the acquisition date represents the expense adjusted performance of the predecessor funds.

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 1.38% | |

Class B Shares | | | 2.13% | |

Class C Shares | | | 2.13% | |

Class R3 Shares | | | 1.63% | |

Class I Shares | | | 1.13% | |

| * | The returns for Class I Shares are actual. The returns for Class A, B and C shares are actual for the period since class inception on 12/09/02; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. The returns for Class R3 Shares are actual for the periods since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen NWQ Large-Cap Value Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | Since

Inception* | |

Class A Shares at NAV | | | -7.99% | | | | -4.17% | | | | -2.61% | |

Class A Shares at maximum Offering Price | | | -13.27% | | | | -5.30% | | | | -3.64% | |

Russell 1000® Value Index** | | | 3.01% | | | | -2.19% | | | | -0.92% | |

Lipper Large-Cap Value Funds Classification Average** | | | -0.15% | | | | -2.65% | | | | 1.20% | |

| | | |

Class C Shares | | | -8.64% | | | | -4.88% | | | | -3.32% | |

Class R3 Shares | | | -8.19% | | | | -4.41% | | | | -2.85% | |

Class I Shares | | | -7.73% | | | | -3.93% | | | | -2.36% | |

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 1.20% | |

Class C Shares | | | 1.95% | |

Class R3 Shares | | | 1.45% | |

Class I Shares | | | 0.95% | |

| * | Since inception returns for Class A, C and I Shares, and the comparative index and Lipper classification average, are from 12/15/06. The returns for Class A, C and I Shares are actual. The returns for Class R3 Shares are actual for the periods since class inception on 9/29/09; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen NWQ Small/Mid-Cap Value Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | Since

Inception* | |

Class A Shares at NAV | | | -1.41% | | | | -1.68% | | | | -0.33% | |

Class A Shares at maximum Offering Price | | | -7.05% | | | | -2.84% | | | | -1.39% | |

Russell 2500® Value Index** | | | -1.49% | | | | -0.20% | | | | 0.84% | |

S&P Lipper Small-Cap Core Funds Classification Average** | | | -3.77% | | | | 0.08% | | | | 1.53% | |

| | | |

Class C Shares | | | -2.13% | | | | -2.44% | | | | -1.10% | |

Class R3 Shares | | | -1.63% | | | | -2.16% | | | | -0.79% | |

Class I Shares | | | -1.16% | | | | -1.68% | | | | -0.30% | |

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 1.88% | | | | 1.33% | |

Class C Shares | | | 2.62% | | | | 2.08% | |

Class R3 Shares | | | 2.13% | | | | 1.58% | |

Class I Shares | | | 1.62% | | | | 1.08% | |

The investment adviser has agreed to waive fees and/or reimburse expenses through October 31, 2012 so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 1.10% (1.45% after October 31, 2012) of the average daily net assets of any class of Fund shares. The expense limitation expiring October 31, 2012, may be terminated or modified prior to that date only with the approval of the Board of Trustees of the Fund. The expense limitation in effect thereafter may be terminated or modified only with the approval of shareholders of the Fund.

| * | Since inception returns for Class A, C and I Shares, and the comparative index and Lipper classification average, are from 12/15/06. The returns for Class A, C and I Shares are actual. The returns for Class R3 Shares are actual for the periods since class inception on 9/29/09; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen NWQ Small-Cap Value Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | Since

Inception* | |

Class A Shares at NAV | | | 3.09% | | | | -2.32% | | | | 4.22% | |

Class A Shares at maximum Offering Price | | | -2.84% | | | | -3.47% | | | | 3.41% | |

Russell 2000® Value Index** | | | -1.44% | | | | -1.05% | | | | 3.71% | |

Lipper Small-Cap Core Funds Classification Average** | | | -3.77% | | | | 0.08% | | | | 4.66% | |

| | | |

Class C Shares | | | 2.36% | | | | -3.03% | | | | 3.47% | |

Class R3 Shares | | | 2.85% | | | | -2.57% | | | | 3.96% | |

Class I Shares | | | 3.38% | | | | -2.07% | | | | 4.49% | |

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | |

Expense

Ratios | |

Class A Shares | | | 1.43% | |

Class C Shares | | | 2.18% | |

Class R3 Shares | | | 1.68% | |

Class I Shares | | | 1.18% | |

| * | Since inception returns for Class A, C and I Shares, and the comparative index and Lipper classification average, are from 12/08/04. The returns for Class A, C and I Shares are actual. The returns for Class R3 Shares are actual for the periods since class inception on 9/29/09; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen Tradewinds Value Opportunities Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year* | | | Since

Inception* | |

Class A Shares at NAV | | | -12.46% | | | | 2.62% | | | | 8.92% | |

Class A Shares at maximum Offering Price | | | -17.49% | | | | 1.41% | | | | 8.07% | |

Russell 3000® Value Index** | | | 2.64% | | | | -2.10% | | | | 3.33% | |

Lipper Global Multi-Cap Core Funds Classification Average** | | | -7.23% | | | | -2.55% | | | | 3.12% | |

| | | |

Class B Shares w/o CDSC | | | -13.14% | | | | 1.85% | | | | 8.10% | |

Class B Shares w/ CDSC | | | -16.34% | | | | 1.69% | | | | 8.10% | |

Class C Shares | | | -13.11% | | | | 1.85% | | | | 8.10% | |

Class R3 Shares | | | -12.67% | | | | 2.36% | | | | 8.64% | |

Class I Shares | | | -12.27% | | | | 2.87% | | | | 9.19% | |

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 1.20% | |

Class B Shares | | | 1.95% | |

Class C Shares | | | 1.95% | |

Class R3 Shares | | | 1.45% | |

Class I Shares | | | 0.95% | |

| * | Since inception returns for Class A, B, C and I Shares, and the comparative index and Lipper classification average, are from 12/08/04. The returns for Class A, B, C and I Shares are actual. The returns for Class R3 Shares are actual for the periods since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expense, which are primarily differences in distribution and service fees. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Holding Summaries as of June 30, 2012

This data relates to the securities held in each Fund’s portfolio of investments. It should not be construed as a measure of performance for the Fund itself.

Nuveen Multi-Manager Large-Cap Value Fund

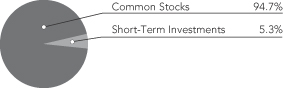

Portfolio Allocation1

Nuveen NWQ Multi-Cap Value Fund

Portfolio Allocation1

| | | | |

Portfolio Composition1 | | | |

| Oil, Gas & Consumable Fuels | | | 11.6% | |

| Pharmaceuticals | | | 10.3% | |

| Insurance | | | 7.0% | |

| Commercial Banks | | | 5.7% | |

| Diversified Financial Services | | | 4.5% | |

| Media | | | 3.8% | |

| Industrial Conglomerates | | | 3.5% | |

| Diversified Telecommunication Services | | | 3.3% | |

| Health Care Providers & Services | | | 2.9% | |

| Semiconductors & Equipment | | | 2.6% | |

| Aerospace & Defense | | | 2.5% | |

| Communication Equipment | | | 2.1% | |

| Capital Markets | | | 2.1% | |

| Consumer Finance | | | 2.1% | |

| Food Products | | | 2.1% | |

| IT Services | | | 1.9% | |

| Chemicals | | | 1.8% | |

| Software | | | 1.7% | |

| Electric Utilities | | | 1.7% | |

| Health Care Equipment & Supplies | | | 1.6% | |

| Machinery | | | 1.6% | |

| Computers & Peripherals | | | 1.5% | |

| Household Products | | | 1.5% | |

| Internet Software & Services | | | 1.5% | |

| Wireless Telecommunication Services | | | 1.4% | |

| Multiline Retail | | | 1.4% | |

| Energy Equipment & Services | | | 1.0% | |

| Short-Term Investments | | | 1.3% | |

| Other | | | 14.0% | |

| | | | |

| Portfolio Composition1 | | | |

| Insurance | | | 14.8% | |

| Oil, Gas & Consumable Fuels | | | 14.0% | |

| Pharmaceuticals | | | 12.5% | |

| Software | | | 7.7% | |

| Metals & Mining | | | 7.7% | |

| Semiconductors & Equipment | | | 6.0% | |

| Media | | | 5.9% | |

| Diversified Financial Services | | | 5.0% | |

| Machinery | | | 3.6% | |

| Specialty Retail | | | 3.6% | |

| IT Services | | | 2.8% | |

| Computers & Peripherals | | | 2.5% | |

| Short-Term Investments | | | 0.2% | |

| Other | | | 13.7% | |

| | | | |

Top Five Common Stock

Holdings1 | |

| Pfizer Inc. | | | 3.0% | |

| Exxon Mobil Corporation | | | 2.9% | |

| General Electric Company | | | 2.6% | |

| Wells Fargo & Company | | | 2.6% | |

| Merck & Company Inc. | | | 2.5% | |

| | | | |

| Top Five Common Stock Holdings1 | |

| CA Inc. | | | 7.7% | |

| Pfizer Inc. | | | 4.4% | |

| Sanofi-Aventis | | | 4.4% | |

| Apache Corporation | | | 4.0% | |

| Talisman Energy Inc. | | | 3.8% | |

| 1 | As a percentage of total investments as of June 30, 2012. Holdings are subject to change. |

Nuveen NWQ Large-Cap Value Fund

Portfolio Allocation1

Nuveen NWQ Small/Mid-Cap Value Fund

Portfolio Allocation1

| | | | |

| Portfolio Composition1 | | | |

| Insurance | | | 15.6% | |

| Oil, Gas & Consumable Fuels | | | 13.8% | |

| Pharmaceuticals | | | 12.5% | |

| Software | | | 9.6% | |

| Media | | | 6.4% | |

| Metals & Mining | | | 6.3% | |

| Diversified Financial Services | | | 4.8% | |

| Machinery | | | 3.3% | |

| Communication Equipment | | | 3.0% | |

| Computers & Peripherals | | | 2.3% | |

| Food & Staples Retailing | | | 2.2% | |

| Automobiles | | | 2.2% | |

| Short-Term Investments | | | 4.1% | |

| Other | | | 13.9% | |

| | | | |

| Portfolio Composition1 | | | |

| Insurance | | | 13.0% | |

| Electronic Equipment & Instruments | | | 9.6% | |

| Semiconductors & Equipment | | | 7.9% | |

| Machinery | | | 6.7% | |

| Paper & Forest Products | | | 5.6% | |

| Metals & Mining | | | 5.3% | |

| Commercial Banks | | | 5.1% | |

| Personal Products | | | 5.0% | |

| Hotels, Restaurants & Leisure | | | 4.9% | |

| Oil, Gas & Consumable Fuels | | | 4.5% | |

| Real Estate Management & Development | | | 4.1% | |

| Food Products | | | 4.1% | |

| Building Products | | | 3.1% | |

| Aerospace & Defense | | | 3.0% | |

| Specialty Retail | | | 2.7% | |

| Short-Term Investments | | | 1.1% | |

| Other | | | 14.3% | |

| | | | |

| Top Five Common Stock Holdings1 | |

| CA Inc. | | | 7.1% | |

| Pfizer Inc. | | | 4.7% | |

| Talisman Energy Inc. | | | 4.1% | |

| Sanofi-Aventis | | | 4.1% | |

| AngloGold Ashanti Limited, Sponsored ADR | | | 3.8% | |

| | | | |

| Top Five Common Stock Holdings1 | |

| Bob Evans Farms | | | 4.9% | |

| Elizabeth Arden, Inc. | | | 4.8% | |

| Forestar Real Estate Group Inc. | | | 4.1% | |

| Allied World Assurance Holdings | | | 3.5% | |

| Clearwater Paper Corporation | | | 3.2% | |

| 1 | As a percentage of total investments as of June 30, 2012. Holdings are subject to change. |

Holding Summaries as of June 30, 2012 (continued)

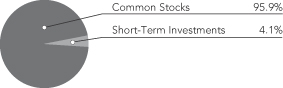

Nuveen NWQ Small-Cap Value Fund

Portfolio Allocation1

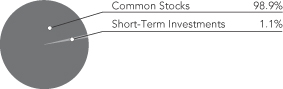

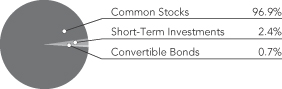

Nuveen Tradewinds Value Opportunities Fund

Portfolio Allocation1

| | | | |

| Portfolio Composition1 | | | |

| Machinery | | | 8.1% | |

| Insurance | | | 7.4% | |

| Commercial Banks | | | 7.1% | |

| Semiconductors & Equipment | | | 6.8% | |

| Personal Products | | | 6.7% | |

| Food Products | | | 5.7% | |

| Apparel, Accessories & Luxury Goods | | | 5.0% | |

| Paper & Forest Products | | | 5.0% | |

| Hotels, Restaurants & Leisure | | | 4.8% | |

| Metals & Mining | | | 4.6% | |

| Electronic Equipment & Instruments | | | 4.2% | |

| Real Estate Management & Development | | | 3.9% | |

| Oil, Gas & Consumable Fuels | | | 3.9% | |

| Building Products | | | 3.3% | |

| Thrifts & Mortgage Finance | | | 3.1% | |

| Short-Term Investments | | | 5.3% | |

| Other | | | 15.1% | |

| | | | |

| Portfolio Composition1 | | | |

| Oil, Gas & Consumable Fuels | | | 16.1% | |

| Metals & Mining | | | 15.8% | |

| Insurance | | | 11.3% | |

| Electric Utilities | | | 6.4% | |

| Pharmaceuticals | | | 4.1% | |

| Food & Staples Retailing | | | 4.0% | |

| Energy Equipment & Services | | | 3.8% | |

| Food Products | | | 3.6% | |

| Aerospace & Defense | | | 3.1% | |

| Software | | | 2.6% | |

| Wireless Telecommunication Services | | | 2.4% | |

| Capital Markets | | | 2.2% | |

| Chemicals | | | 2.0% | |

| Diversified Telecommunication Services | | | 2.0% | |

| Electronic Equipment & Instruments | | | 1.6% | |

| Communication Equipment | | | 1.6% | |

| Short-Term Investments | | | 2.4% | |

| Other | | | 15.0% | |

| | | | |

| Top Five Common Stock Holdings1 | |

| Bob Evans Farms | | | 4.8% | |

| Elizabeth Arden, Inc. | | | 4.5% | |

| Forestar Real Estate Group Inc. | | | 3.9% | |

| Carrizo Oil & Gas, Inc. | | | 3.9% | |

| Albany International Corporation, Class A | | | 3.5% | |

| | | | |

| Top Five Common Stock Holdings1 | |

| Barrick Gold Corporation | | | 4.0% | |

| Cameco Corporation | | | 3.6% | |

| Kinross Gold Corporation | | | 3.5% | |

| Newmont Mining Corporation | | | 3.1% | |

| American International Group | | | 3.1% | |

| | | | |

| Country Allocation1 | | | |

| United States | | | 64.3% | |

| Canada | | | 14.1% | |

| France | | | 3.2% | |

| Russia | | | 3.0% | |

| Australia | | | 2.6% | |

| Brazil | | | 1.6% | |

| Israel | | | 1.5% | |

| Japan | | | 1.2% | |

| Switzerland | | | 1.1% | |

| Finland | | | 1.0% | |

| Turkey | | | 1.0% | |

| South Africa | | | 1.0% | |

| South Korea | | | 0.6% | |

| Belgium | | | 0.5% | |

| Italy | | | 0.5% | |

| Indonesia | | | 0.4% | |

| Short-Term Investments | | | 2.4% | |

| 1 | As a percentage of total investments as of June 30, 2012. Holdings are subject to change. |

Expense Examples

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the respective Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Multi-Manager Large-Cap Value Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | (5% annualized return

before expenses) | |

| | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 1,071.10 | | | $ | 1,067.00 | | | $ | 1,067.70 | | | $ | 1,070.10 | | | $ | 1,072.50 | | | | | $ | 1,019.10 | | | $ | 1,015.32 | | | $ | 1,015.37 | | | $ | 1,017.75 | | | $ | 1,020.34 | |

| Expenses Incurred During Period | | $ | 5.97 | | | $ | 9.87 | | | $ | 9.82 | | | $ | 7.36 | | | $ | 4.69 | | | | | $ | 5.82 | | | $ | 9.62 | | | $ | 9.57 | | | $ | 7.17 | | | $ | 4.57 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.16%, 1.92%, 1.91%, 1.43% and ..91% for Classes A, B, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

Nuveen NWQ Multi-Cap Value Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | (5% annualized return

before expenses) | |

| | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 1,060.30 | | | $ | 1,056.50 | | | $ | 1,056.50 | | | $ | 1,059.10 | | | $ | 1,062.40 | | | | | $ | 1,018.75 | | | $ | 1,014.97 | | | $ | 1,015.07 | | | $ | 1,017.50 | | | $ | 1,020.19 | |

| Expenses Incurred During Period | | $ | 6.30 | | | $ | 10.18 | | | $ | 10.07 | | | $ | 7.58 | | | $ | 4.82 | | | | | $ | 6.17 | | | $ | 9.97 | | | $ | 9.87 | | | $ | 7.42 | | | $ | 4.72 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.23%, 1.99%, 1.97%, 1.48% and 0.94% for Classes A, B, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

Nuveen NWQ Large-Cap Value Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | (5% annualized return

before expenses) | |

| | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 1,022.50 | | | $ | 1,019.30 | | | $ | 1,021.90 | | | $ | 1,024.30 | | | | | $ | 1,019.29 | | | $ | 1,015.66 | | | $ | 1,018.20 | | | $ | 1,020.74 | |

| Expenses Incurred During Period | | $ | 5.63 | | | $ | 9.29 | | | $ | 6.74 | | | $ | 4.18 | | | | | $ | 5.62 | | | $ | 9.27 | | | $ | 6.72 | | | $ | 4.17 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.09%, 1.85%, 1.34% and .83% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

Expense Examples (continued)

Nuveen NWQ Small/Mid-Cap Value Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 1,018.20 | | | $ | 1,014.60 | | | $ | 1,017.30 | | | $ | 1,019.80 | | | | | $ | 1,018.20 | | | $ | 1,014.57 | | | $ | 1,017.16 | | | $ | 1,019.54 | |

| Expenses Incurred During Period | | $ | 6.72 | | | $ | 10.37 | | | $ | 7.77 | | | $ | 5.37 | | | | | $ | 6.72 | | | $ | 10.37 | | | $ | 7.77 | | | $ | 5.37 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.34%, 2.07%, 1.55% and 1.07% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

Nuveen NWQ Small-Cap Value Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 1,067.30 | | | $ | 1,063.10 | | | $ | 1,065.60 | | | $ | 1,068.70 | | | | | $ | 1,017.75 | | | $ | 1,014.02 | | | $ | 1,016.56 | | | $ | 1,019.00 | |

| Expenses Incurred During Period | | $ | 7.35 | | | $ | 11.18 | | | $ | 8.58 | | | $ | 6.07 | | | | | $ | 7.17 | | | $ | 10.92 | | | $ | 8.37 | | | $ | 5.92 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.43%, 2.18%, 1.67% and 1.18% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

Nuveen Tradewinds Value Opportunities Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | | | | | A Shares | | | B Shares | | | C Shares | | | R3 Shares | | | I Shares | |

| Beginning Account Value (1/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (6/30/12) | | $ | 939.40 | | | $ | 935.60 | | | $ | 936.00 | | | $ | 938.10 | | | $ | 940.20 | | | | | $ | 1,019.10 | | | $ | 1,015.42 | | | $ | 1,015.37 | | | $ | 1,018.05 | | | $ | 1,020.29 | |

| Expenses Incurred During Period | | $ | 5.59 | | | $ | 9.14 | | | $ | 9.19 | | | $ | 6.60 | | | $ | 4.44 | | | | | $ | 5.82 | | | $ | 9.52 | | | $ | 9.57 | | | $ | 6.87 | | | $ | 4.62 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.16%, 1.90%, 1.91%, 1.37% and ..92% for Classes A, B, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).