As filed with the Securities and Exchange Commission on March 5, 2019

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-01800

U.S. GLOBAL INVESTORS FUNDS

Three Canal Plaza, Suite 600

Portland, Maine 04101

Jessica Chase, Principal Executive Officer

Three Canal Plaza, Suite 600

Portland, Maine 04101

207-347-2000

Date of fiscal year end: December 31

Date of reporting period: January 1, 2018 – December 31, 2018

ITEM 1. REPORT TO STOCKHOLDERS.

U.S. Global Investors Funds

Annual Report

December 31, 2018

Beginning on January 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund or your financial intermediary electronically by contacting the Fund at (800) 873-8637, or by contacting your financial intermediary directly.

You may elect to receive all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at (800) 873-8637, or by contacting your financial intermediary directly. Your election to receive reports in paper will apply to all Funds held with U.S. Global Investors Funds.

U.S. Global Investors Funds

Annual Report

December 31, 2018

Table of Contents

| Letter to Shareholders (unaudited) | 1 |

| Definitions for Management Teams’ Perspectives (unaudited) | 7 |

| Management Team’s Perspective (unaudited) | 9 |

| Portfolios of Investments | 43 |

| Notes to Portfolios of Investments | 82 |

| Statements of Assets and Liabilities | 98 |

| Statements of Operations | 102 |

| Statements of Changes in Net Assets | 106 |

| Notes to Financial Statements | 112 |

| Financial Highlights | 127 |

| Report of Independent Registered Public Accounting Firm | 138 |

| Trustees and Officers (unaudited) | 140 |

| Approval of Investment Advisory Agreement (unaudited) | 142 |

| Additional Information (unaudited) | 147 |

| Expense Example (unaudited) | 149 |

Nasdaq Symbols

U.S. Global Investors Funds

| Investor Class | |

| U.S. Government Securities Ultra-Short Bond Fund | UGSDX |

| Near-Term Tax Free Fund | NEARX |

| All American Equity Fund | GBTFX |

| Holmes Macro Trends Fund | MEGAX |

| Global Resources Fund | PSPFX |

| World Precious Minerals Fund | UNWPX |

| Gold and Precious Metals Fund | USERX |

| Emerging Europe Fund | EUROX |

| China Region Fund | USCOX |

| Institutional Class | |

| Global Resources Fund | PIPFX |

| World Precious Minerals Fund | UNWIX |

| Atlantic Fund Services 3 Canal Plaza, Suite 600 Portland, ME 04101 |

| U.S. Global Investors Funds | (unaudited) |

Dear Fellow Shareholder,

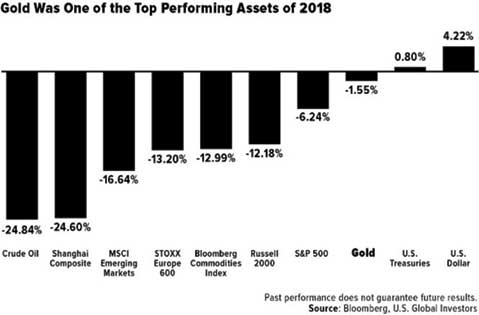

King Dollar was on top in 2018, one of the few major assets to end the year in the black on steady interest rate hikes and robust economic growth in the U.S. But greenback strength is a double-edged sword, as you know. Although good for U.S. consumers, it can hamper exporters, commodities, oil, gold and more.

So will rates continue to rise in 2019? If so, the dollar will follow suit, putting additional pressure on other assets. I think there are a number of signs that the rate hike we saw in December could be the last one this cycle. Significantly, Federal Reserve Chairman Jerome Powell said that “we will be patient” with further tightening.

Under the circumstances, I’m very pleased with how well gold performed last year. It did what most investors expect it to do. Stocks began to sell off late in the year, boosting investor demand for safe haven assets. The yellow metal remarkably beat the S&P 500 Index for the month of December, the fourth quarter and the year. It’s also outperforming the market so far in the 21st century, even with dividends reinvested.

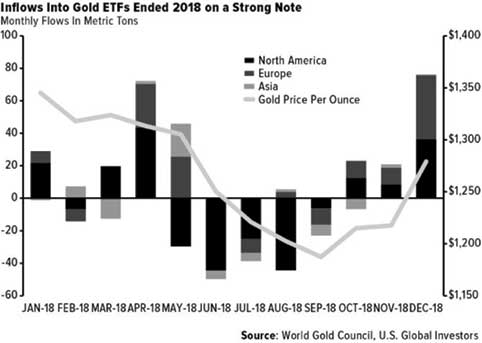

It wasn’t just physical gold that investors were drawn to. Inflows into global gold ETFs surged late in 2018, attracting as much as $3.1 billion, or 76 metric tons, in December alone, the best month of the year.

| U.S. Global Investors Funds | (unaudited) |

Is Gold Ready to Break Out?

Throughout the year, I saw multiple signs that lead me to believe that the gold market has found a bottom. One of those signs was Vanguard’s decision to change the name and investment strategy of its Precious Metals and Mining Fund. In September, the company lowered the fund’s exposure to metals and mining, from 80 percent to 25 percent, effectively orphaning gold investors and giving them no way to participate in a potential rally.

This isn’t the first time Vanguard has done this to investors. Back in 2001, it removed the word “gold” from what was then the Gold and Precious Metals Fund. The change coincided with a decade-long precious metals bull run that saw gold rally from an average price of $271 an ounce in 2001 to an all-time high of more than $1,900 in September 2011. That’s more than a sevenfold increase.

Another sign that this could be a bottom is the prevalence of merger and acquisition (M&A) activity among big-name gold producers. In September 2018, Barrick Gold and Randgold Resources announced a merger worth $6.5 billion, creating the world’s largest gold miner. That title didn’t stand for long, however, after Newmont Mining said it would be buying Goldcorp for a cool $10 billion. Whereas Barrick-Randgold produced a combined 6.6 million ounces of gold in 2017, Newmont-Goldcorp was responsible for as much as nearly 8 million ounces.

I see this news as positive overall for the metals and mining industry, which has long signaled the need for consolidation. As I explained in a Frank Talk Live segment back in October, it’s when an industry has found a bottom that you start to see big M&A deals. A couple of years

| U.S. Global Investors Funds | (unaudited) |

ago, the very talented people at Visual Capitalist showed in an infographic that mining M&As peaked in the aftermath of the financial crisis.

Gold Royalty Companies Are the “Best Bet,” Says Paradigm Capital

It’s no secret that I’m a fan of royalty and streaming companies such as Franco-Nevada and Wheaton Precious Metals. I’ve long admired these companies for generating profits and creating value, even when the metals market is flat or weak. We own significant positions in royalty and streaming companies in our Gold and Precious Metals Fund (USERX) and World Precious Minerals Fund (UNWPX).

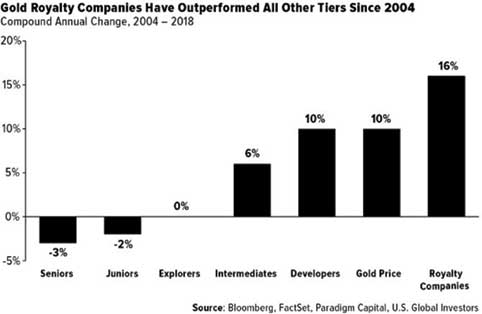

Paradigm Capital reaffirmed my conviction in the royalty model. The Canadian investment dealer recently shared its research into the long-term performance of the various “tiers” in gold mining, from juniors to seniors, from explorers to developers. The royalty companies—which include not just Franco and Wheaton but also Royal Gold, Sandstorm and Osisko Royalties— are the “best bet” when seeking to “make money in gold equities,” according to Paradigm’s senior analyst, Don MacLean. He adds: “Royalty companies have the best business model in the sector, by far.”

Below, you can see that royalty companies have outperformed all other tiers, including gold itself. Royalty companies collectively delivered 16 percent in compound annual growth from 2004 to 2018. Put another way, they returned a massive 884 percent in cumulative change, compared to gold at 300 percent.

Many junior and senior producers have struggled over the same time period, but Paradigm writes that gold equities are like “coiled springs” and should outperform the precious metal if a “meaningful” gold rally of 10 percent or more occurs. At the end of 2018, large-cap seniors led the rally, followed by intermediates and royalty companies. This is in line with past gold

| U.S. Global Investors Funds | (unaudited) |

equity rallies, Paradigm says, as the largest producers have historically performed best at the start.

Diana Widmaier-Picasso, co-founder of Menē Photo courtesy of Menē

Active Management Can Help You Invest in Attractive Companies Before the Street Does

One of our favorite companies this past year was newcomer Mene, a gold and platinum jewelry designer and manufacturer. You might not have heard the name yet, but you could soon enough.

Founded in 2017 by Roy Sebag, co-founder of gold financial services firm Goldmoney, and Diana Widmaier-Picasso, granddaughter of—you guessed it—Pablo Picasso, Mene's mission is to disrupt the gold jewelry market by selling directly to the consumer and pricing its merchandise fairly and transparently. Unlike traditional sellers like Tiffany & Co. and Cartier, which sometimes have high premiums, Mene prices its jewelry based on the changing value of gold. It then charges a 15 percent to 20 percent design and production fee on top of that.

What also sets the company apart is that its jewelry—from earrings to necklaces, bracelets to charms—is made of 24-karat gold or platinum. No alloys, no insets of diamonds or other stones. That’s done to help the pieces retain their value over time.

Here at U.S. Global Investors, we believe gold is money and a timeless investment. Mene, which takes its name from the Aramaic word for “money,” has clearly run with that idea, going so far as to trademark the phrase “investment jewelry.”

It’s a business model that seems to have resonated with consumers and investors alike. In its first 10 months of operation, Mene did as much as $7 million in sales in more than 53 countries, as of October 2018.

The reason I tell you this is to highlight our potential ability to find and invest in little-known yet promising companies before they become overvalued. In the case of Mene, we managed to get in even earlier, before shares in the company were made available to the public. The jeweler went public on the Toronto Stock Exchange (TSX) in November, but thanks to active management and our industry relationships, we were able to buy shares privately seven months prior to that. So even before its stock was available to retail investors, Mene accounted for 2.46 percent of the Gold and Precious Metals Fund (USERX) as of September 30.

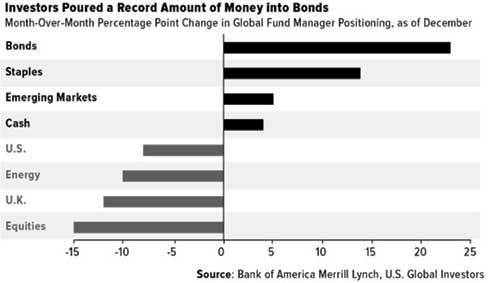

Fund Managers De-Risked in Favor of Bonds and Cash

Late last year, as volatility heightened, fund managers turned incredibly bearish on risk assets and bullish on defensive positions such as bonds, staples and cash. According to Zero Hedge’s analysis of a Bank of America Merrill Lynch report, December represented “the biggest ever one-month rotation into bonds class as investors dumped equities around the globe while bond allocations rose 23 percentage points to net 35 percent underweight.” What’s more, fund

| U.S. Global Investors Funds | (unaudited) |

managers’ average cash levels stood at 4.7 percent in November, above the 10-year average, according to Morningstar data.

Equity outflows were particularly pronounced. According to Lipper data, as much as $46 billion fled U.S. stock mutual funds and ETFs in the week ended December 13. That’s the most ever for a one-week period. It’s very possible that the selling was related to end-of-year tax-loss harvesting, but again, we’ve never seen outflows of that magnitude.

Within the bond category, ultrashort vehicles were most favored. In November, ultrashort bond funds, such as our U.S. Government Securities Ultra-Short Bond Fund (UGSDX), saw the greatest inflows compared to other categories, attracting a remarkable $5.7 billion. That’s the most in at least a decade, according to Morningstar.

Investors might also want to consider short-term municipal bonds, the kind our Near-Term Tax Free Fund (NEARX) invests in, as they’ve historically done well during times of geopolitical and economic uncertainty.

To get the latest insights and commentary on gold, commodities, emerging markets, bitcoin and much, much more, subscribe to our award-winning Investor Alert and to my personal CEO blog, Frank Talk. Both can be reached by visiting usfunds.com.

Thank you for your continued trust and confidence in U.S. Global Investors. We wish you and your family good health and prosperity in 2019.

Sincerely,

Frank E. Holmes

CEO and Chief Investment Officer

U.S. Global Investors, Inc.

| U.S. Global Investors Funds | (unaudited) |

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors. Though the Near-Term Tax Free Fund seeks minimal fluctuations in share price, it is subject to the risk that the credit quality of a portfolio holding could decline, as well as risk related to changes in the economic conditions of a state, region or issuer. These risks could cause the fund’s share price to decline. Tax-exempt income is federal income tax free. A portion of this income may be subject to state and local taxes and at times the alternative minimum tax. The Near-Term Tax Free Fund may invest up to 20% of its assets in securities that pay taxable interest. Income or fund distributions attributable to capital gains are usually subject to both state and federal income taxes.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity. The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000. The Russell 3000 Index consists of the 3,000 largest U.S. companies as determined by total market capitalization. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Gold and Precious Metals Fund, World Precious Minerals Fund, Near-Term Tax Free Fund and U.S. Government Securities Ultra- Short Bond Fund as a percentage of net assets as of 12/31/2018: Barrick Gold Corp. 0.00%; Randgold Resources Ltd 0.00%; Newmont Mining Corp. 1.01% in Gold and Precious Metals Fund; Goldcorp Inc. 0.00%; Franco-Nevada Corp. 0.00%; Wheaton Precious Metals Corp. 2.50% in Gold and Precious Metals Fund, 0.20% in World Precious Minerals Fund; Royal Gold Inc. 0.00%; Sandstorm Gold Ltd. 3.22% in Gold and Precious Metals Fund; Osisko Gold Royalties Ltd. 1.07% in Gold and Precious Metals Fund, 1.31% in World Precious Minerals Fund; Mene Inc. 2.95% in Gold and Precious Metals Fund, 0.92% in World Precious Minerals Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

| Definitions for Management Teams’ Perspectives | (unaudited) |

Benchmark Index Definitions

Returns for indices reflect no deduction for fees, expenses or taxes, unless noted.

The Bloomberg Barclays U.S. Treasury Bills 6-9 Months Total Return Index tracks the performance of U.S. Treasury Bills with a maturity of six to nine months.

The Bloomberg Barclays 3-Year Municipal Bond Index is a total return benchmark designed for municipal assets. The index includes bonds with a minimum credit rating of BAA3, that are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million and have a maturity of two to four years.

The FTSE Gold Mines Index encompasses all gold mining companies that have a sustainable and attributable gold production of at least 300,000 ounces a year and that derive 75% or more of their revenue from mined gold.

The Hang Seng Composite Index is a market-capitalization weighted index that covers about 95% of the total market capitalization of companies listed on the Main Board of the Hong Kong Stock Exchange.

The MSCI Emerging Markets Europe 10/40 Index (Net Total Return) is a free float-adjusted market capitalization index that is designed to measure equity performance in the emerging market countries of Europe (Czech Republic, Greece, Hungary, Poland, Russia and Turkey). The index is calculated on a net return basis (i.e., reflects the minimum possible dividend reinvestment after deduction of the maximum rate withholding tax). The index is periodically rebalanced relative to the constituents’ weights in the parent index.

The NYSE Arca Gold Miners Index is a modified market capitalization-weighted index comprised of publicly-traded companies involved primarily in the mining for gold and silver.

The S&P Global Natural Resources Index (Net Total Return) includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified, liquid and investable equity exposure across 3 primary commodity-related sectors: Agribusiness, Energy, and Metals & Mining. The index is calculated on a net return basis (i.e., reflects the minimum possible dividend reinvestment after deduction of the maximum rate withholding tax).

The S&P 500 Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The S&P Composite 1500 Index is a broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, the S&P 500 and the S&P 600.

Other Index Definitions

The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity.

| Definitions for Management Teams’ Perspectives | (unaudited) |

The Caixin China Manufacturing Purchasing Manager’s Index is a composite indicator designed to provide an overall view of activity in the manufacturing sector and acts as a leading indicator for the whole economy. When the PMI is below 50.0 this indicates that the manufacturing economy is declining and a value above 50.0 indicates an expansion of the manufacturing economy.

The Citigroup Economic Surprise Indices are objective and quantitative measures of economic news. They are defined as weighted historical standard deviations of data surprises (actual releases vs Bloomberg survey median).

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Hang Seng Index is a capitalization-weighted index of 33 companies that represent approximately 70 percent of the total market capitalization of The Stock Exchange of Hong Kong.

The MSCI Emerging Markets Europe Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the emerging markets countries of Europe (Czech Republic, Hungary, Poland, Russia, and Turkey).

The NAHB Housing Market Index is derived from a monthly survey, and gauges builder perceptions of current single-family home sales and sales expectations for the next six months, as well as rating traffic of prospective buyers. Scores from each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

The Philadelphia Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The Purchasing Manager’s Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

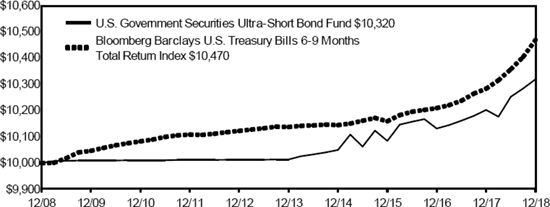

| U.S. Government Securities Ultra-Short Bond Fund | (unaudited) |

Management Team’s Perspective

Introduction

The U.S. Government Securities Ultra-Short Bond Fund (UGSDX) is designed to be used as an investment that takes advantage of the security of U.S. Government bonds and obligations, while simultaneously pursuing a higher level of current income than money market funds offer. The fund’s dollar-weighted average effective maturity is two years or less.

Performance Graph

U.S. Government Securities Ultra-Short Bond Fund

| Average Annual Performance | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year |

| U.S. Government Securities Ultra-Short Bond Fund | 1.15% | 0.60% | 0.32% |

| Bloomberg Barclays U.S. Treasury Bills 6-9 Months Total Return Index | 1.81% | 0.65% | 0.46% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations and reimbursements to maintain a minimum yield, without which returns would have been lower. The above returns for the U.S. Government Securities Ultra-Short Bond Fund include the fund’s results as a money market fund through the date of its conversion (December 20, 2013) to an ultra-short bond fund, and therefore are not representative of the fund’s results had it operated as an ultra-short bond fund for the full term of the periods shown. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.03%. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 0.45%. The Adviser can modify or terminate this arrangement at any time. In addition, returns may include the effects of additional voluntary waivers of fees and reimbursements of expenses by the Adviser, including waivers and reimbursements to maintain a minimum net yield for the fund.

See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

| U.S. Government Securities Ultra-Short Bond Fund | (unaudited) |

The Year in Review – Economic and Political Issues that Affected the Fund

2018 started off with synchronized global growth across key economies. However, within a few months, it became clear that growth trajectories between the U.S. and the rest of the world were diverging. U.S. bonds were affected in 2018 as a result of the surge in GDP growth following the December 2017 tax cut and the steady pace of Federal Reserve rate hikes. Personal income tax cuts, together with low unemployment, boosted household disposable income and powered strong consumer spending growth. A lower corporate tax rate, combined with a continued U.S. boom in oil and gas fracking, supported business investment. A congressional budget deal in February led to strong U.S. military spending, while spending by state and local governments also picked up. Faster GDP growth led to tight labor markets and rising inflation. In response, the Fed continued down the path of rate normalization and the unwinding of quantitative easing, increasing interest rates four times during the year and boosting rates by a cumulative 100 basis points. While higher interest rates began impacting the economy, U.S. trade tariffs instituted throughout the year also hurt growth, both domestically and abroad. One sector hit by the Fed’s moves was the interest-sensitive housing market, where sales and construction slowed in 2018.

Interest rates were very volatile throughout the year, and a general flattening trend saw a part of the yield curve (three-year/five-year yields) invert for the first time since 2007. Long yields made fresh multi-year highs in 2018, with the 10-year Treasury yield’s move above the prior highs of 2013 and 2014 at the 3 percent to 3.05 percent range, to its 2018 high of 3.25 percent in October. Following a retest of the 3.05 percent breakout in late October, the long yield attempted a move to new highs but failed to move past 3.25 percent. The ensuing move lower was swift, with the 10-year yield ending 2018 at 2.68 percent. The short end of the curve spent most of 2018 rising faster than the long end, and thus the two-year/10-year spread flattened to its narrowest spread in a decade.

Investment Highlights

The U.S. Government Securities Ultra-Short Bond Fund returned 1.15 percent for the year ended December 31, 2018, underperforming its benchmark, the Bloomberg Barclays U.S. Treasury Bills 6-9 Months Total Return Index, which returned 1.81 percent.

Current Outlook

2019 is shaping up as a year where volatility will persist as investors await clarity around policy decisions from central banks and monitor trade negotiations between the U.S. and China. The Fed’s renewed focus on contained inflation, risk management and a lack of certainty about equilibrium or neutral rates suggests a more dovish direction moving forward. Furthermore, monetary policy has been tightening for two years and fiscal stimulus is waning. As a result, the economy is facing a more serious moderation in growth and inflation, and as such the Fed is likely to act cautiously regarding its policy path.

| U.S. Government Securities Ultra-Short Bond Fund | (unaudited) |

The section labeled Portfolio of Investments contains a complete list of the fund’s holdings.

Portfolio Allocation by Issuer Based on Total Investments | | December 31, 2018 | |

| Federal Farm Credit Bank | | | 75.6 | % |

| Federal Home Loan Bank | | | 24.4 | % |

| Total | | | 100.0 | % |

| Portfolio Allocation by Maturity | | | | | December 31, 2018 | |

| 1-3 Months | | $ | 11,990,725 | | | | 27.9 | % |

| 3-12 Months | | | 17,482,071 | | | | 40.7 | % |

| 1-3 Years | | | 13,498,054 | | | | 31.4 | % |

| | | $ | 42,970,850 | | | | 100.0 | % |

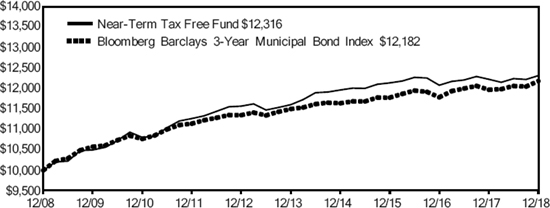

| Near-Term Tax Free Fund | (unaudited) |

Management Team’s Perspective

Introduction

The Near-Term Tax Free Fund (NEARX) seeks to provide a high level of current income exempt from federal income taxation and to preserve capital. However, a portion of any distribution may be subject to federal and/or state income taxes. The Near-Term Tax Free Fund will maintain a weighted average maturity of less than five years.

Performance Graph

Near-Term Tax Free Fund

| Average Annual Performance | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year |

| Near-Term Tax Free Fund | 0.73% | 1.19% | 2.10% |

| Bloomberg Barclays 3-Year Municipal Bond Index | 1.76% | 1.16% | 1.99% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 0.99%. The Adviser has contractually agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, extraordinary expenses, taxes, brokerage commissions and interest) to not exceed 0.45% on an annualized basis through April 30, 2019.

See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

The Year in Review – Economic and Political Issues that Affected the Fund

Looking back on 2018, the municipal market was pressured in the first quarter as a result of the interest-rate environment, stronger inflation data and rising bond yields. The Federal Reserve raised interest rates again at its mid-March policy meeting, bringing the federal funds rate to a 1.50 percent to 1.75 percent range. The Fed also alerted investors they should expect another two rate hikes later in the year, followed by three more in 2019. After running below the Fed’s 2 percent target rate for most of the previous six

| Near-Term Tax Free Fund | (unaudited) |

years, inflation data started to firm up throughout the quarter. As a result, a majority of Fed members believed inflation would rise above the 2 percent threshold throughout 2018. During the first quarter, the front end of the curve outperformed the long end, while lower quality credit outperformed higher quality. Technical conditions were impacted by the record $62.5 billion in supply that was pulled forward and priced ahead of the passage of the Tax Cuts and Jobs Act in December 2017. The pull forward led to a new-issue total of $63 billion in the first quarter, down roughly 32 percent from the previous year. As expected, the elimination of advanced refundings had a significant negative impact on supply as well.

Municipal bonds had positive returns in the second quarter as demand improved following the U.S. Treasury-led selloff in the first quarter. New municipal bond issuance totaled $96 billion in the second quarter, down 12 percent from the previous year. Both municipal and U.S. Treasury yields were volatile during the quarter. The 10-year Treasury bond yield surpassed 3.1 percent in May, reaching its highest level since 2011. By the end of the month, bond yields had declined. Municipals outperformed Treasuries on a total return basis on both the short and long end of the curve. For the first time since the financial crisis, banks reduced their municipal bond holdings as a result of the corporate tax cuts enacted in December 2017, which made municipal bonds less appealing. Demand picked up from households in many high-tax states such as California and New York. The Tax Cuts and Jobs Act of 2017 capped the state and local tax deduction (SALT) at $10,000. The change in the SALT deduction made the attractiveness of municipal bonds increase in certain high-tax locations. The Fed raised rates in June to a 1.75 percent to 2.00 percent target range and anticipated to carry out two more rate hikes in the remainder of the year. Inflation moved higher during the quarter, while U.S. economic data on job creation, consumer spending, housing and manufacturing and services generally remained robust, keeping the economy on its upward trajectory.

During the third quarter, municipal bonds fell short of Treasuries’ performance due to more than expected supply coming to the secondary market. The Federal Reserve raised the federal funds rate to a target range of between 2.00 percent and 2.25 percent in September and announced it expected one more rate increase in 2018 and three more in 2019. Noting the strength of the U.S. economy and inflation near the 2 percent target, the Fed removed language that interest rate policy would remain “accommodative.” Standard & Poor’s (S&P) released a September 2018 report in which it subjected state financial operations to the stresses of moderate and severe recessions and then compared 2018 reserves to expected drawdowns. Only 20 states had reserves sufficient to cover loss of revenue and increased social service spending during a moderate recession, and overall the states showed an average revenue shortfall of 9.9 percent. S&P went further and made adjustments for dependence on more cyclical revenue streams, level of social-service spending and fixed costs, including pensions. After the adjustments, 14 states were considered low risk, 21 moderate and 14 elevated. S&P contended, however, that states have the capacity to make fiscal adjustments in response to a downturn. S&P also noted, however, that there were 19 state downgrades from the beginning of 2016 through August 2018, compared with just four upgrades, and observed that this ratio was abnormal this far into a recovery.

In the last quarter of the year, the Fed raised the federal funds rate in December to a target range of 2.25 percent to 2.50 percent, for a grand total of four quarter-point hikes in 2018. The Fed lowered its inflation and growth expectations for 2019 and subsequently reduced its rate hike projections for the following year from three hikes to two. Although Fed Chair Powell was arguably “dovish” at the December press conference, markets were hoping for more flexibility as they navigate the balance sheet tapering. Municipal bonds ended the quarter on positive performance that was on par with their taxable peers, assisted by a sell-off in equity markets that led to fixed-income and other safe haven demand.

Investment Highlights

For the year ended December 31, 2018, the Near-Term Tax Free Fund returned 0.73 percent, underperforming its benchmark, the Bloomberg Barclays 3-Year Municipal Bond Index, which gained 1.76 percent.

Strengths

| ● | The fund’s allocation to bonds from New Jersey, Utah and South Carolina outperformed. |

| | |

| ● | The fund benefited from its allocation to airports, higher education and school district bonds, which all outperformed. |

| Near-Term Tax Free Fund | (unaudited) |

| ● | The fund’s allocation toward the short-end of the yield curve outperformed. |

Weaknesses

| ● | The fund’s allocation to bonds from New York and Missouri underperformed. |

| ● | The fund’s exposure to housing and utilities bonds underperformed. |

| ● | The fund’s allocation towards the long end of the yield curve underperformed. |

Current Outlook

Opportunities

After hiking interest rates four times in 2018, the Federal Reserve seems open to keep increases on hold at least through early 2019. Although hard economic data has generally remained solid in the U.S., signs of a slowdown in the rest of the world and a muted inflation environment provide leeway for the Fed to wait and see how the economy evolves. Chairman Powell affirmed that there is no preset path for rates and that the Fed will be agile in shifting its policy if necessary to keep the economy strong. This stance is positive for financial markets broadly, and creates the backdrop for a calmer interest rate environment that is especially supportive for fixed income assets.

Threats

State and local government sectors could come under pressure if the U.S. economy slows enough to constrain revenues from sales and income tax receipts. State governments may be forced to rein in their spending, while pension underfunding remains a significant concern.

The section labeled Portfolio of Investments contains a complete list of the fund’s holdings.

| Top 10 Area Concentrations | |

| (Based on Net Assets) | December 31, 2018 |

| Texas | 26.11% |

| New York | 11.87% |

| Florida | 9.33% |

| Washington | 6.24% |

| Illinois | 4.87% |

| South Carolina | 2.98% |

| Missouri | 2.89% |

| Pennsylvania | 2.81% |

| Michigan | 2.54% |

| North Carolina | 2.54% |

| Total Top 10 Areas | 72.18% |

| Near-Term Tax Free Fund | (unaudited) |

| Municipal Bond Ratings* | |

| Based on Total Municipal Bonds | December 31, 2018 |

| Bond | Percentage |

| AAA | 12.5% |

| AA | 62.6% |

| A | 18.2% |

| BBB | 6.0% |

| Not Rated | 0.7% |

| Total | 100.0% |

| * | Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). “Not Rated” is used to classify securities for which a rating is not available. Credit quality ratings for each issue are obtained from Moody’s and S&P Global Ratings, and the higher rating for each issue is used. |

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

Management Team’s Perspective

Introduction

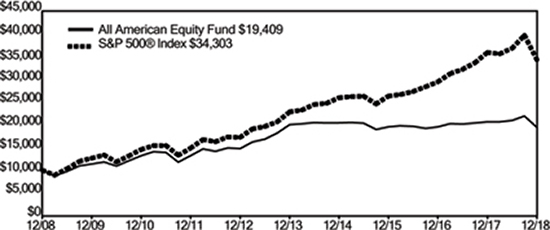

The principal objective of the All American Equity Fund (GBTFX) is to seek capital appreciation by investing primarily in a broadly diversified portfolio of domestic common stocks. The fund invests in large-capitalization stocks while retaining the flexibility to seek out promising individual stock opportunities, including stocks with meaningful dividend yields.

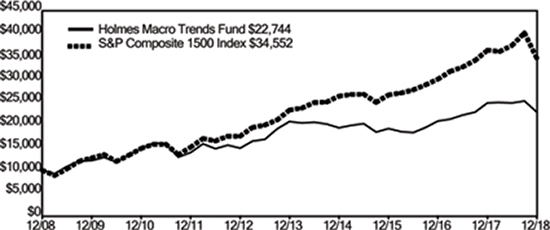

The Holmes Macro Trends Fund (MEGAX) invests in companies with good growth prospects and strong positive earnings momentum. The fund’s primary objective is to seek long-term capital appreciation.

Performance Graphs

All American Equity Fund

| Average Annual Performance | | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year |

| All American Equity Fund | (6.07)% | (0.61)% | 6.86% |

| S&P 500® Index | (4.38)% | 8.49% | 13.12% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.79%. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 2.20%. The Adviser can modify or terminate this arrangement at any time.

See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

Holmes Macro Trends Fund

| Average Annual Performance | | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year |

| Holmes Macro Trends Fund | (8.28)% | 1.87% | 8.56% |

| S&P Composite 1500 Index | (4.96)% | 8.25% | 13.20% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.83%. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 2.20%. The Adviser can modify or terminate this arrangement at any time.

See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

The Year in Review – Economic and Political Issues that Affected the Funds

In 2017, the S&P 500 Index set a record of 12 consecutive months of price appreciation. This was an accomplishment that has not occurred for over 90 years. But as investors, we understand prices don’t continue to drift higher without checking investor sentiment, and it was definitely checked in 2018.

Early in the year, the tax cuts continued to help the markets find traction and propelled the market higher until around October. The dollar remained strong all year, creating a small headwind for U.S. exports. And as almost every global market slowed or stopped quantitative easing—the exception being Japan—the Federal Reserve raised rates four times. The market didn’t appear to care, however, until late in the year.

In October the markets started to fall apart as tariff talks caused investors to question economic growth patterns. Investors’ emotions created so much disquiet that we were left with the worst December performance since 1931. The capitalization-weighted S&P 500 fell 4.39 percent, with dividends reinvested.

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

With regard to investing style, growth stocks were the strongest for the year. Although they fell 0.01 percent (including dividends), they still outperformed value, which lost 8.97 (including dividends). Health care was the strongest sector of the year, up 4.6 percent. The S&P 500 Energy Index declined 20.5 percent. West Texas Intermediate (WTI) crude fell 24.8 percent, with the majority of the losses happening between October and the end of the year. The commodity closed the year at $45 per barrel.

Investment Highlights

The Holmes Macro Trends Fund (MEGAX) fell 8.28 percent in 2018, underperforming its benchmark, the S&P Composite 1500 Index, which gave back 4.96 percent. The All American Equity Fund (GBTFX) declined 6.07 percent for the year, underperforming its benchmark, the S&P 500 Index.

Overall growth-oriented stocks outperformed value and dividend-oriented companies, while the lagging sectors, energy and materials, just didn’t grab investor attention. The primary driver of underperformance in 2018 was the fact that the funds had more exposure to smaller and growth-oriented companies than their benchmarks. Our investment model was effectively out of favor with money flows, evidenced by the fact that the market did not reward securities we selected based on growth metrics. We believe this is transitory and that our growth at a reasonable price (GARP) investment style will ultimately be rewarded.

Our funds are actively managed, and because the holding period is generally not a consideration in investment decisions, the portfolios’ turnover rate might fluctuate from year to year as the funds adjust their portfolio composition. The funds’ annual portfolio turnovers were, and are expected to continue to be, more than 100 percent.

All American Equity Fund

Strengths

| ● | The fund’s allocation in consumer staples and utilities helped fund performance. |

| ● | Stock selection was better than the index in the industrials and consumer staples sectors. |

| ● | Ball Corporation, Valero Energy and Keurig Dr Pepper were the best contributors to fund performance. |

Weaknesses

| ● | The fund’s allocation in financials and energy didn’t seem to add to the bottom line. |

| ● | Investments in Constellation Brands, Affiliated Managers Group and Southwest Airlines were the worst contributors to performance. |

Holmes Macro Trends Fund

Strengths

| ● | Stock selection was strong in information technology and consumer staples companies. |

| ● | The fund’s underweight position in technology was beneficial, as was the fund’s overweighing of the consumer discretionary sector. |

| ● | Medifast and Electro Scientific Industries were among the best performers in the fund. |

Weaknesses

| ● | Sector allocations in the energy and materials sectors did not perform as well as anticipated. |

| ● | Stock selection in the consumer discretionary and health care sectors seemed to be a drag on the fund. |

| ● | Cutera and Chemours failed to live up to expectations and were among the worst contributors to the fund’s performance. |

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

Current Outlook

Opportunities

| ● | Strong hiring in 2018 pushed the unemployment rate to its lowest level in almost 50 years, with jobless rates near 3.7 percent for the end of the year. As such, workers saw the fastest wage growth in nine years. |

| ● | The University of Michigan said its consumer sentiment index reading at the end of the year was unchanged at 97.5, keeping most of the gains consumers have registered over the last two years. The last time the sentiment index was consistently above 90 was between 1997 and 2000, when it recorded a four-year average of 105.3. |

| ● | U.S. consumer spending gathered momentum the last quarter of the year, with retail sales rising 0.9 percent in December, helping to calm investor fears of an imminent economic slowdown. |

Threats

| ● | Goldman Sachs predicts that 2019 will be another poor year for risk-adjusted investment returns due to slowing economic growth, shrinking central bank balance sheets and continued bouts of volatility. UBS Group wealth managers wrote that gold may rise to $1,300 an ounce in 2019 as volatility grows. |

| ● | The Commerce Department showed a steep drop in new orders for U.S. manufactured goods. Factory orders tumbled 2.1 percent in the third quarter. Durable goods orders led the way lower, dropping 4.3 percent amid a 12 percent plunge in orders for transportation equipment. |

| ● | OPEC producers and allies surprised the market with a larger-than-expected deal to reduce output. The group will collectively curb production by 1.2 million barrels a day, higher than the 1 million barrel-a-day scenario that was earlier floated. |

The section labeled Portfolio of Investments contains a complete list of the funds’ holdings.

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

All American Equity Fund

| Top 10 Equity Holdings (Based on Net Assets) | December 31, 2018 |

| CMS Energy Corp. | 5.19% |

| Electric - Integrated | |

| Yum! Brands, Inc. | 4.40% |

| Retail - Restaurants | |

| Mondelez International, Inc. | 4.00% |

| Food - Miscellaneous/Diversified | |

| Amgen, Inc. | 3.72% |

| Medical - Biomedical/Genetics | |

| Zoetis, Inc. | 3.71% |

| Medical - Drugs | |

| Visa, Inc. | 3.70% |

| Finance - Credit Card | |

| Baxter International, Inc. | 3.59% |

| Medical Products | |

| Cognizant Technology Solutions Corp. | 3.47% |

| Computer Services | |

| Tyson Foods, Inc. | 3.38% |

| Food - Meat Products | |

| American Tower Corp. REIT | 3.23% |

| REITS - Diversified | |

| Total Top 10 Equity Holdings | 38.39% |

| Portfolio Allocation by Industry Sector* | |

| Based on Total Investments | December 31, 2018 |

| Consumer, Non-cyclical | 27.9% |

| Financial | 18.3% |

| Consumer, Cyclical | 18.2% |

| Technology | 12.9% |

| Energy | 7.4% |

| Utilities | 5.6% |

| Exchange Traded Funds | 5.0% |

| Industrial | 3.2% |

| Other | 1.5% |

| Total | 100.0% |

| * | Summary information above may differ from the portfolio schedule included in the financial statements due to the use of different classifications of securities for presentation purposes. |

| All American Equity Fund & Holmes Macro Trends Fund | (unaudited) |

Holmes Macro Trends Fund

| Top 10 Equity Holdings (Based on Net Assets) | December 31, 2018 |

| Kimberly-Clark Corp. | 4.61% |

| Consumer Products - Miscellaneous | |

| AbbVie, Inc. | 4.43% |

| Medical - Drugs | |

| Ciena Corp. | 4.21% |

| Telecom Equipment Fiber Optics | |

| TEGNA, Inc. | 4.00% |

| Television | |

| The Home Depot, Inc. | 3.76% |

| Retail - Building Products | |

| Pool Corp. | 3.71% |

| Distribution/Wholesale | |

| S&P Global, Inc. | 3.67% |

| Commercial Services - Finance | |

| Trex Co., Inc. | 3.42% |

| Building & Construction Products - Miscellaneous | |

| Ingevity Corp. | 3.18% |

| Chemicals - Specialty | |

| Electro Scientific Industries, Inc. | 2.94% |

| Lasers - System/Components | |

| Total Top 10 Equity Holdings | 37.93% |

| Portfolio Allocation by Industry Sector* | |

| Based on Total Investments | December 31, 2018 |

| Consumer, Non-cyclical | 31.9% |

| Communications | 16.1% |

| Industrial | 14.7% |

| Consumer, Cyclical | 13.4% |

| Basic Materials | 9.6% |

| Exchange Traded Funds | 5.4% |

| Financial | 3.6% |

| Technology | 3.5% |

| Other | 1.8% |

| Total | 100.0% |

| * | Summary information above may differ from the portfolio schedule included in the financial statements due to the use of different classifications of securities for presentation purposes. |

| Global Resources Fund | (unaudited) |

Management Team’s Perspective

Introduction

The Global Resources Fund (PSPFX and PIPFX) is a non-diversified natural resources fund with the principal objective of seeking long-term growth of capital while providing protection against inflation and monetary instability. The fund invests in companies involved in the exploration, production and processing of petroleum, natural gas, coal, alternative energies, chemicals, mining, iron and steel, and paper and forest products around the globe.

Performance Graph

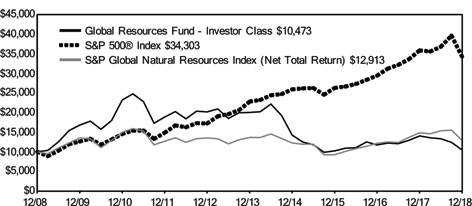

Global Resources Fund

| Average Annual Performance | | | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year | Since Inception (Institutional Class) |

| Global Resources Fund - Investor Class | (25.48)% | (12.17)% | 0.46% | n/a |

| Global Resources Fund - Institutional Class (Inception 3/1/10) | (24.66)% | (11.42)% | n/a | (4.56)% |

| S&P 500® Index | (4.38)% | 8.49% | 13.12% | 11.91% |

| S&P Global Natural Resources Index (Net Total Return) | (13.08)% | (1.12)% | 2.59% | 0.20% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.59% for the Investor Class and 3.55% for the Institutional Class. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 1.90% for the Investor Class. Also pursuant to a voluntary agreement, the Adviser has agreed to waive all class specific expenses of the Institutional Class. The Adviser can modify or terminate these arrangements at any time. See Definitions for Management Teams’ Perspectives for index definitions. Please visit our website at www.usfunds.com for updated performance information for different time periods.

| Global Resources Fund | (unaudited) |

The Year in Review – Economic and Political Issues that Affected the Fund

The Bloomberg Commodity Index dropped 13 percent in 2018, posting its first decline in three years. All major commodities dropped, with crude oil, copper and gold prices falling 25, 20 and 1.6 percent respectively. Prospects for a trade war between China and the U.S., following President Donald Trump’s imposing tariffs on certain imports of Chinese goods, set off negative investor sentiment toward growth, specifically in China, the world’s largest consumer of raw materials.

These trade war fears were exacerbated by the global manufacturing sector slowdown, following a two-year global synchronized upward trajectory in manufacturing activity. This was evidenced by JP Morgan’s Global Manufacturing Purchasing Manager’s Index (PMI) barometer, which peaked in December 2017 at 54.5, and fell steadily to fresh lows of 51.5 in December 2018. China’s manufacturing sector actually contracted in December, after weakening throughout the year. U.S. and eurozone manufacturers also ended the year with a lower reading.

Crude oil’s drop was driven by the rapid and unexpected volume growth out of U.S. producers, which led the nation to become the world’s largest producer of crude, ahead of Russia and Saudi Arabia. This supply shock was made worse by waivers to U.S. sanctions on Iran, which allowed certain nations to continue importing Iranian crude. The price drop was only marginally offset by a fresh agreement among members of the Organization of Petroleum Exporting Countries (OPEC) to limit production.

The base metals complex, highly susceptible to manufacturing activity globally, dropped as fears of a trade war between the U.S. and China raised concerns over China’s ability to maintain its gross domestic product (GDP) growth forecasts. Copper, nickel and zinc posted double-digit drops in 2018, a reflection of lower GDP and PMI readings, suggesting weaker demand for the metals.

Gold was the best performing major commodity in 2018, declining marginally by 1.6 percent, after posting two consecutive annual advances. The weaker global PMIs, coupled with an earnings’ slowdown in the U.S., have resulted in Federal Reserve officials communicating a slower pace to the ongoing tightening cycle.

Investment Highlights

Overview

For the year ended December 31, 2018, the Investor Class of the Global Resources Fund dropped 25.48 percent and the Institutional Class dropped 24.66 percent, trailing the fund’s benchmark, the S&P Global Natural Resources Index (Net Total Return), which dropped 13.08 percent.

The fund employed a defensive investment position targeting value-driven opportunities with lower-than-average beta. However, to maintain varying degrees of investment exposure to the commodities market, the fund utilized a number of rolling call option positions to hedge the fund’s benchmark risks and provide optionality to upswings in commodities stocks. The options hedging model was highly successful in early 2018, but later offset by paying premiums that expired out of the money. The fund has greater exposure to income-yielding securities, and as such pays a yield in excess of 4 percent, the highest dividend yield of any of its peers.

Because the fund is actively managed and holding period is generally not a consideration in investment decisions, the portfolio turnover rate may fluctuate from year to year as the fund adjusts its portfolio composition. The fund’s annual portfolio turnover was, and is expected to continue to be, more than 100 percent.

Strengths

| ● | The U.S. dollar slipped from its 2018 high as Federal Reserve Chairman Jerome Powell hinted he's ready to pause rate hikes while he assesses risks to the U.S. economy. Major economists now |

| Global Resources Fund | (unaudited) |

coincide that a weaker U.S. dollar may be in the cards, which conversely should benefit commodity prices and overall import demand from emerging markets.

| ● | The fund’s overweight in precious metals, renewable energy, oil services, oil refiners and oil explorers and producers (E&Ps) as well as its underweight in industrials stocks had a positive contribution to the fund in excess of its benchmark. The fund’s cash holdings also provided a positive contribution. |

| ● | The fund had superior stock selection in the precious metals, industrials, oil services and integrated oil sectors. The best performing stocks were OceanaGold, EVRAZ and Grupa Lotos. |

Weaknesses

| ● | The Bloomberg Commodity Index, a measure of a basket of commodities, ended the year down for the first time in three years. All major commodities dropped, with crude oil, copper and gold prices falling. Prospects for a trade war between China and the U.S. set off negative investor sentiment toward growth, specifically in China, the world’s largest consumer of raw materials. |

| ● | The fund’s overweight in junior resource stocks and industrial chemicals, as well as its underweight in integrated oil, base and industrial metals stocks, had a negative contribution to the fund relative to its benchmark. |

| ● | The fund had inferior stock selection in the oil refiners, oil E&Ps, agricultural and industrial chemical sectors. The worst performing stocks were CruzSur Energy (formerly Pentanova Energy), Pacific Infrastructure and Daqo New Energy. |

Current Outlook

Opportunities

| ● | Goldman Sachs, Morgan Stanley and Citi all agree that commodities as a complex are compelling. Interestingly, there have been seven Fed rate hike cycles over the past 50 years, and all but one of those cycles have coincided with commodities outperforming the market. |

| ● | Japanese bank Nomura is bearish on the U.S. dollar. The bank notes that U.S. growth is already losing momentum, and even with a few more hikes, Fed policy rates would settle at their lowest level in history for the end of a hiking cycle. The punchline is that “U.S. yields are simply not high enough to make up for the U.S. growing twin deficits, and lack of foreign capital inflows,” concludes the report. |

| ● | China is taking steps to address U.S. complaints that Beijing engages in unfair trade practices. The Wall Street Journal reported: “Chinese officials are also considering making changes to the Made in China 2025 Plan, a state-led industrial policy aimed at enabling Chinese companies to dominate a number of industries such as artificial intelligence and robotics.” This policy is a focal point of the U.S. complaints against China. |

Threats

| ● | The main issue for base metals in 2019 is whether Chinese infrastructure stimulus can offset slowing property demand, according to BMO analysts. “It is fair to say the jury is still out on whether efforts thus far are sufficient,” referring to the amount of stimulus promised by Chinese Premier Li Keqiang, and the central bank. |

| ● | The strength of U.S. economic indicators appears to be fading. The Citigroup U.S. Economic Surprise Index, which measures whether economic data have exceeded or fallen short of analysts’ estimates, fell to the lowest in more than a year. The Fed’s Beige Book report showed fading optimism over growth prospects at U.S. firms even as most districts continued to report a modest expansion. |

| Global Resources Fund | (unaudited) |

| ● | The U.S. NAHB Housing Market Index declined to 56 points in December versus 60 points the previous month, and dropped to the lowest level since May 2015. In addition, the drop now constitutes the largest two-month drop since October 2001, highlighting the negative momentum in a key end market for natural resources. |

The section labeled Portfolio of Investments contains a complete list of the fund’s holdings.

| Top 10 Equity Holdings (Based on Net Assets) | December 31, 2018 |

| Pacific Infrastructure Ventures, Inc. | 6.76% |

| Real Estate Operating/Development | |

| OceanaGold Corp. | 2.37% |

| Gold Mining | |

| Grupa Lotos SA | 2.23% |

| Oil Refining & Marketing | |

| Vestas Wind Systems A/S | 2.21% |

| Energy - Alternate Sources | |

| Centamin PLC | 2.20% |

| Gold Mining | |

| Polskie Gornictwo Naftowe i Gazownictwo SA | 2.19% |

| Oil Companies - Integrated | |

| Anglo American PLC | 2.11% |

| Diversified Minerals | |

| Hudbay Minerals, Inc. | 2.10% |

| Metal - Copper | |

| AGL Energy, Ltd. | 2.00% |

| Electric - Integrated | |

| China Shenhua Energy Co., Ltd. | 2.00% |

| Coal | |

| Total Top 10 Equity Holdings | 26.17% |

| Global Resources Fund | (unaudited) |

| Portfolio Allocation by Industry Sector* | |

| Based on Total Investments | December 31, 2018 |

| Metals & Mining | 29.8% |

| Oil, Gas & Consumable Fuels | 16.2% |

| Chemicals | 15.5% |

| Precious Metals & Minerals | 7.6% |

| Real Estate | 7.3% |

| Electric - Generation | 5.0% |

| Building Products | 4.9% |

| Energy Equipment & Services | 3.7% |

| Paper & Forest Products | 3.1% |

| Other | 6.9% |

| Total | 100.0% |

| * | Summary information above may differ from the portfolio schedule included in the financial statements due to the use of different classifications of securities for presentation purposes. |

| Precious Metals and Minerals Funds | (unaudited) |

Management Team’s Perspective

Introduction

The World Precious Minerals Fund (UNWPX and UNWIX) and the Gold and Precious Metals Fund (USERX) pursue an objective of long-term capital growth through investments in gold, precious metals and mining companies. The World Precious Minerals Fund focuses on equity securities of companies principally engaged in the exploration, mining and processing of precious minerals such as gold, silver, platinum and diamonds. Although this fund has the latitude to invest in a broad range of precious minerals, it currently remains focused on the gold sector. The Gold and Precious Metals Fund focuses on the equity securities of established gold and precious metals companies and pursues current income as a secondary objective.

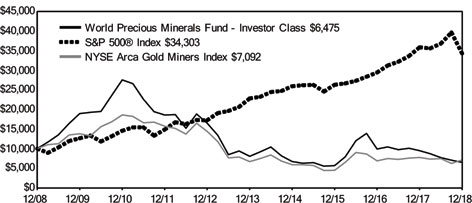

World Precious Minerals Fund

| Average Annual Performance | | | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year | Since Inception (Institutional Class) |

| World Precious Minerals Fund - Investor Class | (31.67)% | (4.19)% | (4.25)% | n/a |

| World Precious Minerals Fund - Institutional Class (Inception 3/1/10) | (31.20)% | (3.72)% | n/a | (10.95)% |

| S&P 500® Index | (4.38)% | 8.49% | 13.12% | 11.91% |

| NYSE Arca Gold Miners Index | (8.21)% | 1.22% | (3.38)% | (6.92)% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.85% for the Investor Class and 2.23% for the Institutional Class. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 1.90%. Also pursuant to a voluntary agreement, the Adviser has agreed to waive all class specific expenses of the Institutional Class. The Adviser can modify or terminate these arrangements at any time. See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

| Precious Metals and Minerals Funds | (unaudited) |

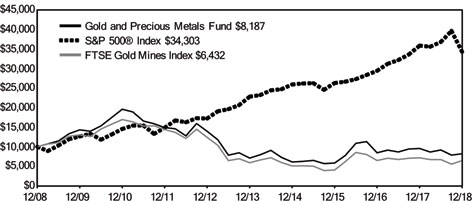

Gold and Precious Metals Fund

| Average Annual Performance | | For the Periods Ended December 31, 2018 |

| | One Year | Five Year | Ten Year |

| Gold and Precious Metals Fund | (14.29)% | 2.90% | (1.98)% |

| S&P 500® Index | (4.38)% | 8.49% | 13.12% |

| FTSE Gold Mines Index | (10.04)% | 1.69% | (4.32)% |

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. For all or a portion of the periods, the fund had expense limitations, without which returns would have been lower. Returns greater than one year are annualized.

Gross expense ratio as stated in the most recent prospectus is 1.66%. Pursuant to a voluntary arrangement, the Adviser has agreed to limit total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, taxes, brokerage commissions and interest) to not exceed 1.90%. The Adviser can modify or terminate this arrangement at any time.

See Definitions for Management Teams’ Perspectives for index definitions.

Please visit our website at www.usfunds.com for updated performance information for different time periods.

The Year in Review - Economic and Political Issues that Affected the Funds

Gold started the year above $1,300 an ounce, but by the end of the first quarter, momentum was waning and the dollar started to pick up strength, particularly against the Turkish lira, as economic conditions worsened. It was reported in April that the Turkish central bank transferred approximately 220 tons of its gold reserves stored in the U.S. Federal Reserve system back to Turkey and that two other banks were in the process of transferring 95 tons of gold reserves from the U.S. back to Turkey. The race was then on to see who could front-run their sell before Turkey hit the market. Hedge funds and other large speculators pared bullish bets on bullion to the lowest in more than two years. Gold racked up six consecutive months of declines, its longest losing streak in five years, and pushed the gold futures market for speculators to the first net short position since late 2001.

Turkey’s gold selling found many central banks were willing buyers. The World Gold Council (WGC) reported that central banks added a net total of 193.3 tonnes of gold to their reserves in the first six months of 2018, representing an 8 percent increase from the same period in 2017, and the strongest first half of

| Precious Metals and Minerals Funds | (unaudited) |

the year since 2015. Russia has been a steady buyer of gold, and India, Poland and Hungary also added to their gold reserves in 2018.

The U.S. Treasury reported that Russia sold $81 billion worth of U.S. government debt and bought more gold in July than in any other month in 2018. The yuan’s share in the Russian central bank’s foreign-exchange and gold assets almost tripled in a matter of three months, jumping from only 1 percent in the third quarter to 2.8 percent. “The rise in the share of yuan assets reflects Russia’s intentions to diversify away from major currencies. The International Monetary Fund (IMF) approved adding the yuan, China’s currency, into the IMF’s foreign exchange basket. This is the first time the IMF has ever added a new currency to its foreign exchange basket. The IMF’s acceptance opens the door for potentially putting the yuan on par with the U.S. dollar,” according to Reuters.

By September, the urgency of the currency crisis in Turkey had abated and by the middle of the month we began seeing weekly updates of its central bank adding to its gold holdings after selling off about 15 percent of its reserves. With these weekly updates of growing gold reserves in Turkey, gold prices closed out the year with three consecutive monthly gains. Although gold finished the year with a negative return, it did outperform the S&P 500 Index for the year.

For the exploration & development gold companies, access to capital in 2018 was a major impediment. Many investment banks have left aside the business of funding smaller mining projects, leaving an opening for less traditional sources of capital for raising money. RBC Capital Markets reported that of the approximately $925 million raised by junior precious metals companies for the first part of 2018, only 14 percent has come from traditional equity sources, with the rest from alternative lenders such as royalty and streaming companies. The shift in funding has largely been driven by investors blindly buying gold mining stock ETFs for the exposure to gold’s beta, and not conducting any due diligence on the investment merits of the underlying securities held by the ETF.

At the end of July, Vanguard announced that it was restructuring and changing the name of its $2.3 billion Precious Metals and Mining Fund. The fund, renamed the Global Capital Cycles Fund, reduced its exposure to mining stocks to just 25 percent from 80 percent. This move showed that negative sentiment and bearishness on gold and precious metals had hit a bottom, as Vanguard is one of the largest fund companies. Its rotation out of gold mining stocks could lead to some near-term weakness in share prices but could certainly be a buying opportunity as well. In terms of timing, Avi Gilbert, creator of Elliotwavetrader.net, noted: “You don’t see these types of moves at market tops.”

The net result is that there are many cheap non-index gold companies that may see the first benefits of industry consolidation as the seniors scramble to replace their depleting resource base and falling production profile. Gold company CEOs, however, are paralyzed with fear that they will lose their jobs (finally) if they do one more bad deal. The world’s major gold producers had cut back on mergers and acquisitions (M&As) with industry transactions totaling just $8.95 billion in 2017, tumbling by a third from the previous year, according to Bloomberg. In a rush to boost output in 2011, when gold was at an all-time high of $1,921.17 an ounce, companies spent a record $38.7 billion on acquisitions.

Barrick Gold, the world’s largest producer of gold, reported a decline in first-quarter production as planned maintenance weighed on output, as expected. The gold miner produced only 1.05 million ounces in the first quarter of the year, which is the lowest quarterly production amount for Barrick in 16 years. This emphasized the notion that the world may have hit “peak gold” supply, where most of the world’s gold has already been discovered, and it’s become much more difficult to find new deposits. 2018 may well have been the year when shareholder activism in the gold space wrecked management’s perverse malaise. Paulson & Co launched a successful bid to oust the management and board of Detour Gold by year end. Gold giant Barrick, likely seeing the writing on the wall, announced a friendly merger with Randgold Resources to bring its highly successful management team into Barrick to create the world’s largest gold mining company. Mark Bristow, CEO of Randgold, will be become the CEO of the newly combined company. The installment of Bristow may mark a shift from gold mines being run by financial “artists” back to true scientists.

Investment Highlights

For the year ended December 31, 2018, the World Precious Minerals Fund Investor Class lost 31.67 percent, and the Institutional Class fell 31.20 percent. The fund’s benchmark, the NYSE Arca Gold Miners Index, declined 8.21 percent on a total return basis.

| Precious Metals and Minerals Funds | (unaudited) |

The strategy of the World Precious Minerals Fund favors junior exploration and development stocks and mid-tiered producing stocks. These lower-capitalization stocks have historically outperformed senior gold mining companies over longer periods, as senior gold miners have typically acquired proven assets of junior gold companies rather than explored for new mining projects with capital-constrained budgets.

The Gold and Precious Metals Fund declined 14.29 percent for the year, slightly underperforming its benchmark, the FTSE Gold Mines Index, which fell 10.04 percent on a total return basis. While focusing on established, gold-producing companies, the Gold and Precious Metals Fund holds a higher weighting of mid-tier stocks compared to its benchmark.

Both funds employed a defensive investment position from time to time in the past year with higher-than-average cash balances on hand to protect the liquidity of the funds. However, to maintain varying degrees of investment exposure to the gold market, the funds utilized some call options positions and directional ETFs, which are more liquid than options, to hedge the funds’ benchmark risks and provide optionality to upswings in gold stocks.

Gold finished the year down just 1.58 percent, while silver fell 8.53 percent. Palladium ended the year strongest with a gain of 18.59 percent, primarily driven by a shift in Europe to gasoline engines from diesel and a greater need for pollution reduction, particularly in China. This increases the demand for palladium, which is used in pollution-scrubbing catalytic converters. Platinum sank 14.49 percent on weakening demand relative to palladium.

Strengths

| ● | Wesdome Gold Mines became our largest position over the course of the year and was the best contributor to returns for both Gold and Precious Metals Fund (USERX) and World Precious Minerals Fund (UNWPX) with a 103.53 percent return. |

| ● | St Barbara was the second best dollar gainer for USERX, with a 17.89 percent gain. The second best contributor to UNWPX was avoiding the third largest gold mining company, Goldcorp, which fell 22.95 percent in the past year. |

| ● | Kirkland Lake Gold was the third best performer for USERX, with a 22.02 percent gain, before the fund took final profits following returns that approached 200 percent in the prior year. The third best contributor to UNWPX was Canyon Resources, which surged almost threefold on the awarding of the Martap Bauxite license in Cameroon. |

Weaknesses

| ● | Rye Patch Gold was the biggest detractor for USERX, losing 44.33 percent before being taken over by Alio Gold on poor restart results for the Florida Canyon Mine in Nevada. For UNWPX, tax-loss selling played a role in pushing down returns across the junior mining and exploration space as we closed out the year. Barsele Minerals, despite finishing the first nine months of the year with positive returns, was our most significant dollar decliner with a price drop of 46.82 percent by year end on no negative headline news. |

| ● | Leagold Mining was the second biggest dollar detractor for USERX with the share price down 39.39 percent for the year. TriStar Gold, down 38.18 percent, was the second largest dollar detractor for UNWPX, with the bulk of the losses coming in the fourth quarter. |

| ● | In the third quarter, Anglogold Ashanti hired Kevin Dushnisky, co-president of Barrick Gold, as its new CEO. USERX did not own any Anglogold, but the market seemed to reward the change in leadership with the shares finishing the year up 22.41 percent. There was little material news to support the rerating. Roxgold finished the year down 46.92 percent and was the third worst performer for UNWPX. One of the largest holders of Roxgold was the Vanguard Precious Metals and Minerals Fund, which announced it was changing the investment objective and significantly down-weighting its gold exposure. The holding remained an overhang on the market until the position was sold from Vanguard’s portfolio at year end. |

| Precious Metals and Minerals Funds | (unaudited) |

Current Outlook

Opportunities

| ● | Goldman Sachs economists released three reasons to buy gold after this year’s selloff. Firstly, it forecasts emerging market growth stabilization and maintains a constructive outlook on emerging market currencies. Secondly, it views the recent gold ETF and Commodity Futures Trading Commission (CFTC) net specs liquidation as a one-off cleaning up on speculative positions. And thirdly, it views the rising interest rate environment as not necessarily bearish for gold, as many believe. |