ANNUAL REPORT

September 30, 2018

FMI Large Cap Fund

Investor Class (FMIHX)

Institutional Class (FMIQX)

FMI Common Stock Fund

Investor Class (FMIMX)

Institutional Class (FMIUX)

FMI International Fund

Investor Class (FMIJX)

Institutional Class (FMIYX)

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| FMI Funds, Inc. | |

| | |

| Advised by Fiduciary Management, Inc. | |

| www.fmifunds.com | |

| | |

| | |

| | |

| | | |

FMI Funds, Inc.

TABLE OF CONTENTS

| FMI Large Cap Fund | |

| Shareholder Letter | 1 |

| Management’s Discussion of Fund Performance | 8 |

| Schedule of Investments | 10 |

| Industry Sectors | 12 |

| | |

| FMI Common Stock Fund | |

| Shareholder Letter | 13 |

| Management’s Discussion of Fund Performance | 20 |

| Schedule of Investments | 22 |

| Industry Sectors | 24 |

| | |

| FMI International Fund | |

| Shareholder Letter | 25 |

| Management’s Discussion of Fund Performance | 33 |

| Schedule of Investments | 36 |

| Schedule of Forward Currency Contracts | 40 |

| Industry Sectors | 41 |

| | |

| Financial Statements | |

| Statements of Assets and Liabilities | 42 |

| Statements of Operations | 43 |

| Statements of Changes in Net Assets | 44 |

| Financial Highlights | 47 |

| Notes to Financial Statements | 53 |

| | |

| Report of Independent Registered Public Accounting Firm | 63 |

| Expense Example | 64 |

| Directors and Officers | 66 |

| Disclosure Information | 69 |

| Additional Information | 72 |

| Tax Notice | 72 |

| Notice of Privacy Policy | 73 |

| Householding Notice | 73 |

FMI

Large Cap

Fund

September 30, 2018

Dear Fellow Shareholders:

The FMI Large Cap Fund returned 4.05%1 in the September quarter compared to 7.71% for the Standard & Poor’s 500 Index. Growth stocks continued to outperform value stocks, leaving us in the proverbial penalty box. Sectors that contributed positively to results included Finance, Consumer Durables and Producer Manufacturing. On the negative side of the sector ledger were Consumer Services, Health Technology and Electronic Technology. Cash was an additional drag. Positive performers included Berkshire Hathaway, Honeywell and TJX Companies. On the flip side, eBay, Schlumberger and Twenty-First Century Fox underperformed. We eliminated Progressive from the portfolio and added Dollar Tree and Chubb.

The seeds of any bust are inherent in the boom that outstrips the pace of whatever solid factors gave it its impetus in the first place. There are no safeguards that can protect the emotional investor from himself. – J. Paul Getty

The bull market stretched into uncharted territory in the third calendar quarter, reaching its longest duration and one of its strongest up-cycle performances on record. Investors continued to focus on the good news -- the U.S. economy, Wall Street’s version of earnings and rising stock prices…while ignoring danger signals -- overconfidence (as reflected in valuations), rising rates and inflation, unbridled debt accumulation, a burgeoning trade war and perhaps some signs of fatigue in the economy. Faith in index funds and exchange-traded funds (ETFs) continued unabated, despite the “crowded trade” nature of many of these products. High confidence in technology shares harkens back to the 1990s, with exceptionally optimistic valuations for both established and startup companies. Private equity transactions, in all but a small minority of cases, are taking place at record-high valuations and debt leverage. So-called “covenant-lite” conditions have returned to the high yield arena. Across the board there appears to be little regard for safety and downside protection.

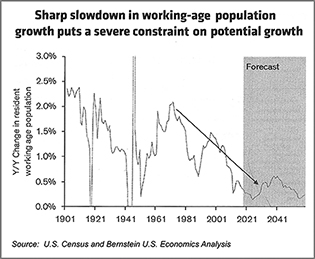

According to Bloomberg’s weekly survey, U.S. real GDP grew at an estimated rate of 3.0% in Q3 and is predicted to grow 2.8% in the December quarter. While the unemployment rate is low, the work force participation rate of 62.7% remained well below its 67% peak, and today, hovers near a 40-year low. Working age population growth continued to be soft (see chart on the right) and unless birth rates or immigration pick up, will be a source of future weakness.

____________

1 | The FMI Large Cap Fund Investor Class (FMIHX) and FMI Large Cap Fund Institutional Class (FMIQX) had a return of 4.05% and 4.10%, respectively, for the third quarter of 2018. |

The large number of working-age people who lost jobs in the last recession and were supposed to be returning to the labor force this cycle appear to be mostly idle. The evidence of this is rising wage rates (recently exceeding 3% according to the Atlanta Fed). With wages being the largest cost for most companies, margins may be at risk. Productivity gains, which have been meaningfully below long-term averages (see chart below) may not provide the offset to wage pressures unless there is a sustained increase in business improvement spending.

The benefit from lower tax rates and fewer regulations is a positive, although the lack of fiscal discipline threatens long-term prosperity. The market seems unconcerned with the potential of an economic downturn. While we are not economists, we do recognize that recessions often come out of the blue. A yield curve that is near inversion doesn’t bolster confidence that fair weather is a foregone conclusion. The CRB Metals Index is off over 15% from its recent peak. Pending home sales declined for the eighth straight month in August, down 2.3% from last year. Auto sales, at a recently annualized rate of 16.6 million, are down nearly 1.9 million units from the peak. Many technology companies are seeing inventories grow much faster than sales. Overseas economies, buyers of U.S. products, have softened, particularly in the emerging markets. Currency weakness in many of these countries is of particular concern, given high levels of dollar-denominated debt.

Across the globe, debt levels are rising significantly. The sovereign debt load has approximately doubled, and debt of all kinds is up 75% over the past decade, even though excessive debt was at the root of the last crisis. Worldwide debt-to-GDP is at a record 318%. The U.S. annual budget deficit as a percent of GDP is running at a 4.2% rate...the kind of figure one would normally see in the throes of a recession. Interestingly, it

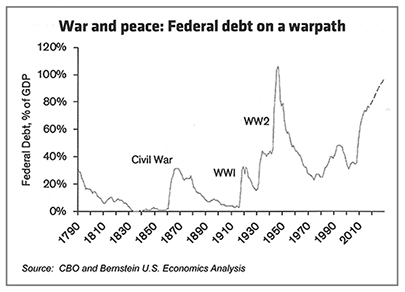

wasn’t that long ago that U.S. leaders chastised Eurozone countries for exceeding the 3% deficit-to-GDP mandate. It is highly unusual for debt ratios to be rising at this point in the economic cycle. The U.S. national debt is $21.5 trillion, an astonishing figure relative to our $20.5 trillion economy and unprecedented in non-war times (see chart from Bernstein on previous page). Unfunded welfare benefits are a multiple of our debt obligations.

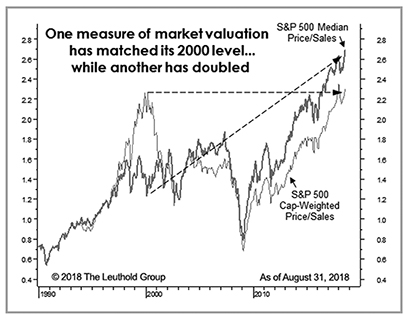

Much has been made of the strong earnings performance in recent quarters. Everyone’s skepticism meter ought to be blinking yellow when Wall Street says earnings growth is 20% while the economy is growing 5% nominally and sales growth is in the single digits. We are, of course, experiencing a one-time positive year-over-year benefit from lower corporate tax rates but once those lap, long-term earnings growth rates will likely fall significantly. Wall Street, with an assist from corporate managements, has embraced the concept of “adjusted earnings,” as discussed in previous letters. The abuse of this measurement has reached alarming levels. Based partly on our inquiry, the Leuthold Group studied actual GAAP (generally accepted accounting principles) reported, operating and “adjusted” S&P 500 earnings over a long-term (30-year) time frame. The spread between these figures has become wide. Even excluding the credit crisis quarters, the spread between reported GAAP earnings and Wall Street earnings is 23.6% (Wall Street’s version is always higher). Proponents of adjusted earnings presentation say that amortization of intangibles, stock compensation and other one-time items justify this measure. Leuthold, among other findings, determined that more than 40% of the amount companies spent on mergers & acquisitions activity ended up in the scrap heap (written off). Additionally, many companies that claim “one-time” charges often have these write-offs with great frequency. Excluding the real cost of stock options seems dubious. There may be some justification for adding back a portion of amortization to GAAP earnings, but it seems managements and Wall Street have overplayed this hand.

Using the long-term, oft-cited valuation data provided by Leuthold, stocks today are in the 9th decile on a median basis (10th being the most expensive). We regularly review 46 different valuation series, including several price-to-earnings (P/E) data sets. It would be odd, to say the least, to have most of these measures registering in the 9th or 10th deciles, while at the same time having Wall Street’s version of P/E ratios be “reasonable” or even “attractive,” as proponents like to tout. Somebody is wrong. Using a much harder-to-manipulate series, price-to-sales, tells a different story. Leuthold recently called the above chart “the scariest chart in the world.” Of course, investor sentiment usually reflects the current trajectory of stock prices. “Markets make opinions,” as the old bromide goes.

Ten years after the last financial and stock market crisis, the media has engaged in a lengthy rehash and post mortem of what transpired. It’s ironic and quite surprising to us at least, given how fresh the crisis still is in our minds, that many of the same mistakes are being repeated by investors today. A decade ago most investors scoffed at the notion that home prices could fall. A house was a surefire investment, and the proof of that was the willingness of banks to loan 95% or more against

it. Investors believed in Wall Street’s products (credit default options, mortgage-backed securities, collateralized loan obligations, etc.) and high-yield bonds. The economy was seemingly healthy, and the market saw little reason to worry about high valuations. They believed in central bankers. Today, investors have the same lofty confidence in high-flying social media, technology and med-tech shares. Many of the same aforementioned derivative investment vehicles are back in vogue, along with a cornucopia of ETFs and index products. Many mistakenly believe that these products carry not only low fees, but low risk. Do investors in the iShares U.S. Energy ETF, iShares Technology ETF or iShares Telecom ETF, for example, know that far from investing in diversified portfolios, they are putting over half their money behind just five stocks? A little over a year ago we discussed the potential liquidity issues facing many of the most popular ETFs. With turnover in many of these ETFs vastly greater than even the most liquid underlying constituent stocks, trading activity could be very interesting when markets get shaky. Junk bond spreads recently hit 315 basis points over treasuries -- half the level of two years ago and a figure not seen since 2007, according to economist David Rosenberg. The faith in central bankers seems unshaken. Finally, just like a decade ago, perception that the economy is strong appears to be overriding any concern about high valuations or other potential troublesome developments.

What we have seen as excessive and unsustainable has persisted far longer than we thought possible. On one level that makes us “wrong,” but of course that doesn’t change the reality of the aforementioned conditions. We would rather give up some of the upside than to be remorseful in hindsight. Greed usually ends in regret. That means being more cautious with our investments and expectations today. Is there a way around another crisis and lousy stock market? Anything is possible when it comes to markets and human behavior. Earnings...the good and sustainable kind...could advance at a healthy rate and inflation could stay within earshot of 2%. The big one, interest rates, though significantly higher than two years ago, could stay well below normal for an extended period. Wages and other escalating costs could recede. The political crisis between the left and right could ameliorate. The nascent trade war with China could resolve. Externalities such as terrorism, wars, natural disasters, etc., could be benign. In other words, a lot must go right and not much can go wrong given today’s valuations. We continue to hunt for attractive investments but acknowledge the environment is far from ideal. We are working diligently, with a focus on the long term. Additionally, we have our own money invested right alongside yours. Our confidence in achieving good full cycle returns remains high.

Below we highlight a couple of investments:

Dollar Tree Inc. (DLTR)

(Analyst: Matt Sullivan)

Description

Dollar Tree is a leading discount retailer in the United States and Canada, operating over 15,000 total stores. 6,812 stores, or 45%, are operated under the Dollar Tree and Dollar Tree Canada (225 stores) banners. The other 8,261 stores are operated under the Family Dollar banner, which was acquired in July of 2015. The Dollar Tree brand accounts for 51% of the combined company’s revenue, 58% of gross profit, and 67% of EBITDA (earnings before interest, taxes, depreciation, and amortization). The Family Dollar franchise accounts for the remaining 49% of revenue, 42% of gross profit, and 33% of EBITDA.

Good Business

| | • | The Dollar Tree banner has one of the best margin and return profiles in the physical retail industry. Family Dollar’s return on invested capital (ROIC) is lower but has ample opportunity to improve. Its closest competitor, Dollar General, earns very high returns on capital. We believe Family Dollar can at least partially close the ROIC gap with Dollar General. |

| | • | Dollar Tree has grown its same store sales for 41 consecutive quarters. Family Dollar’s comparable same-store sales have been less impressive, particularly recently, yet Dollar General’s comps have been positive for 28 straight years. Both the dollar and discount store business models, respectively, have proven to be defensive and should hold up well in a more difficult economic environment. |

| | | |

| | • | The customer profile, low average ticket, and types of products sold protect the business from online competition. |

| | | |

| | • | The Dollar Tree business model is unique within the retail landscape. The $1 price point and constantly changing inventory provides the customer with a differentiated, treasure hunt shopping experience. The ever-changing merchandise in the store also provides management with the ability to control the company’s gross margin. |

| | | |

| | • | Both Dollar Tree and Family Dollar are difficult to replicate. |

| | | |

| | • | The balance sheet is in good shape with net debt-to-EBITDA of approximately 1.7 times. |

| | | |

| | • | The business is easy to understand. |

Valuation

| | • | Dollar Tree shares are down by more than 20% this year. This compares to the S&P 500, which is up approximately 10% year-to-date. |

| | | |

| | • | Dollar Tree is trading at 1.1 times enterprise value-to-sales, which is about one standard deviation below its 3- and 5-year averages. |

| | | |

| | • | Dollar Tree is trading at 9.5 times enterprise value-to-EBITDA (EV/EBITDA), which is a discount to other high-quality retailers as well as the S&P 500. |

| | | |

| | • | On a sum of the parts basis using 2018 estimates, if we ascribe a 12 times EV/EBITDA multiple to the Dollar Tree banner, we believe we’re paying less than 5 times EV/EBITDA for Family Dollar. For reference, Dollar General trades at 12 times EV/EBITDA. |

| | | |

| | • | The stock is trading at approximately 14 times next year’s consensus earnings per share estimate. |

Management

| | • | Bob Sasser became Executive Chairman of the Board on September 18, 2017. He was previously Chief Executive Officer from 2004 to September 2017. From 1993 to 2003, he was Dollar Tree’s Chief Operating Officer. |

| | | |

| | • | Gary Philbin became President and Chief Executive Officer of Dollar Tree and was appointed to the board of directors on September 18, 2017. He was previously Enterprise President of Dollar Tree from December 2016 to September 2017. From July 2015 to December 2016, he served as President and Chief Operating Officer of Family Dollar. From March 2007 to July 2015, he was Chief Operating Officer of Dollar Tree. |

Investment Thesis

We believe Dollar Tree is an excellent business with a good operational management team. The Family Dollar business that was acquired in July 2015 is still a work in progress. The turnaround is taking much longer than management or Wall Street originally expected. Some analysts are beginning to lose faith that the business will ever be successfully turned around. This has created a drag on the stock price.

The stock is now much cheaper than other discount retailers as well as the market. While we’re not convinced that the Family Dollar turnaround will work, we believe the market is ascribing an excessively low multiple to the asset. This leads us to believe that there are multiple ways to win

in the stock, including a potential separation or sale of Family Dollar. A number of sell-side analysts have already started calling for a spin or sale of Family Dollar. This could be an excellent outcome if it happens relatively quickly, as opposed to later, after further struggles. If management does successfully turn Family Dollar around, the stock should do well, considering its relatively modest valuation.

Chubb Ltd. (CB)

(Analyst: Matthew Goetzinger)

Description

Chubb is one of the largest publicly traded property and casualty insurance companies globally. In aggregate, the company has operations in 54 countries and territories. Chubb provides commercial, personal property, casualty, personal accident, and supplemental health insurance to a diverse group of clients. A.M. Best rates the company as an A++ (stable) insurer, and Standard & Poor’s carries it at a AA (stable) rating. Approximately 63% of premiums are from the U.S., 13% from Europe/Eurasia & Africa, 11% from Asia, 8% from Latin America, and 5% from Bermuda and Canada.

Good Business

| | • | Chubb is a durable, differentiated multi-line insurer with an attractive small and middle market commercial book of business, as well as a highly attractive high net worth personal lines customer base. |

| | | |

| | • | For medium-to-larger-sized commercial enterprises, casualty insurance is a necessary coverage. This non-discretionary attribute, along with Chubb’s emphasis on high service levels, results in strong customer retention and predictable revenues. The company’s renewal retention ratio generally ranges between 85 to 90%. |

| | | |

| | • | The company’s disciplined risk selection and cycle management have led to consistently conservative initial loss picks, underwriting stability, and a low volatility return on equity (ROE). The company presently generates a 16% return on total capital. Incremental returns on capital are attractive. |

| | | |

| | • | Chubb currently maintains industry-low balance sheet leverage metrics across the three most important indicators of net premiums-to-shareholders’ equity (0.67 times), invested assets-to-shareholders’ equity (2.4 times), and debt-to-total capital (20%). Approximately 55% of net premiums are from shorter tail lines. |

Valuation

| | • | Over the past 25 years, Chubb’s price-to-book multiple has averaged approximately 1.5 times, ranging from a low of around 1 times to a high of over 2 times. The stock presently trades at multi-year lows. |

| | | |

| | • | Over the past 13 years, Chubb has grown book value per share at a 10% cumulative annual growth rate. |

| | | |

| | • | Downside margin of safety is supported by the company’s current low valuation multiple, excess capital, loss reserve cushion, and significant franchise value. |

Management

| | • | Chubb has a diverse and highly-respected management team, led by Evan Greenberg as Chairman and CEO. The top five executives own approximately $400 million of stock. |

| | | |

| | • | Management is compensated based upon key financial metrics (75% overall weight) of tangible book value per share growth, core operating ROE, core operating income, and the property & casualty (P&C) combined ratio. The residual quarter of incentive compensation is determined by operational and strategic goals. |

| | • | Mr. Greenberg’s management team has been a cohesive group, with backgrounds tying back to legacy ACE and supplemented by key individuals staying on from the Chubb organization. |

| | | |

| | • | Philip Bancroft has been the Chief Financial Officer of Chubb Ltd. since January of 2002. |

Investment Thesis

Chubb is a defensive and diversified P&C company serving attractive commercial and personal lines. The franchise is run by one of the industry’s most respected management teams, who are expected to continue operating the company with a disciplined focus on underwriting cycle management and maintaining a conservative balance sheet. Gradual deployment of the company’s excess capital into organic premium growth, small complimentary tuck-in acquisitions outside the U.S., and repurchases at an attractive discount to intrinsic value should continue the company’s 15-year track record of 10% compound annual growth in book value per share. Chubb’s current multi-year low valuation provides a unique opportunity to invest in one of the best businesses in property and casualty insurance.

Thank you for your confidence in the FMI Large Cap Fund.

This shareholder letter is unaudited.

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2018, the FMI Large Cap Fund the “Fund” had a total return of 12.67%1. The benchmark S&P 500 returned 17.91% in the same period. Sectors that aided relative performance included Finance, Health Services and Process Industries. Progressive Corp. drove the performance within the Finance sector, likely due to continued good earnings and underwriting performance. UnitedHealth Group appreciated strongly during the year on very solid earnings. The Nutrien/Potash combination recovered somewhat in 2018, helping the Process Industries sector. On the negative side of sector performance, Technology Services, Electronic Technology, and Industrial Services all detracted. The Fund’s cash level was also a drag on performance. The benchmark’s exposure to technology related stocks and sectors has been a major driver of performance and the Fund’s underweighting has been the opposite. The stocks that make up these sectors are generally considered growth stocks rather than value stocks. These equities are valued at extraordinary levels today. Additionally, one of our holdings in Technology Services, Cerner Corp., underperformed. Revenue growth has perhaps been slightly less than the market expected. Schlumberger declined during the period and hurt the Industrial Services sector performance. Despite higher oil prices, Schlumberger’s fundamentals have lagged. Deep water and more complex work has not come on as rapidly as anticipated, pushing back the earnings recovery.

Other stocks that helped performance included the Level 3/CenturyLink merged company, TJX Companies, JPMorgan Chase and Twenty-First Century Fox. eBay, Stanley Black & Decker, Omnicom, PACCAR and Bank of New York Mellon all detracted from relative results.

Some new additions to the Fund over the past twelve months included Quest Diagnostics, Smith & Nephew, Masco Corp., PepsiCo, Chubb Ltd. and Dollar Tree. Some stocks sold during the year included AmerisourceBergen, Devon Energy, Microsoft, Comcast and Progressive Corp. As of September 30, 2018, the Fund was significantly overweighted in Producer Manufacturing, Health Services and Commercial Services and meaningfully underweighted in Health Technology, Utilities and Electronic Technology.

Strong performance across most technology and biotechnology related sectors and retail trade (Amazon) characterized the S&P 500 over the past year. Passive investment strategies continued to see heavy inflows of money, at the expense of active strategies. Stocks generally appear overvalued and the S&P 500 index, on many valuation measures, is even more expensive than it was in the late 1990s. The growing use of “adjusted earnings” rather than GAAP earnings by Wall Street and corporate management gives a misleading P/E ratio. The current bull market is nine and a half years old and the longest on record.

The Federal Reserve has moved slowly to normalize interest rates but the price of money remains unusually cheap by historical standards. Economic growth has improved over the past twelve months but at great cost to both government and corporate balance sheets. Total debt relative to U.S. GDP is near 100% and the deficit to GDP is now 4.2%. Corporate leverage by some measures is at a fifty-year high. The unemployment rate is low but the labor force participation rate continues to be depressed. Wage rates and inflation are rising. Domestic and international political risks remain elevated.

While the conventional wisdom is that stock market risk is low because the economy is stronger, we believe valuations are so high that it leaves little room for error. We remain cautious on the stock market’s prospects over the near term. The Fund continues to sell at a discount to the S&P 500 on most valuation measures.

____________

1 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of 12.67% and 12.82%, respectively, for the fiscal year ended September 30, 2018. |

FMI Large Cap Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

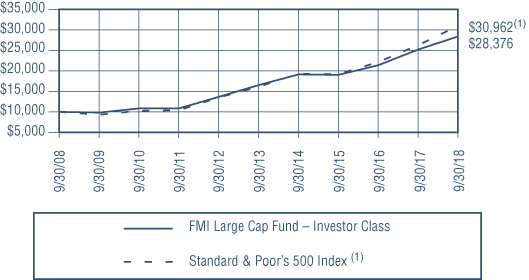

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI LARGE CAP FUND – INVESTOR CLASS AND STANDARD & POOR’S 500 INDEX(1)

AVERAGE ANNUALIZED TOTAL RETURN

| | | | | | Inception |

| | | | | | through |

| | Inception Date | 1-Year | 5-Year | 10-Year | 9/30/2018 |

| FMI Large Cap Fund – Investor Class | 12/31/01 | 12.67% | 11.43% | 10.99% | 9.28% |

| FMI Large Cap Fund – Institutional Class | 10/31/16 | 12.82% | N/A | N/A | 17.53% |

Standard & Poor’s 500 Index(1)* | | 17.91% | 13.95% | 11.97% | 7.88% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Standard & Poor’s 500 Index consists of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The Standard & Poor’s Ratings Group designates the stocks to be included in the Index on a statistical basis. A particular stock’s weighting in the Index is based on its relative total market value (i.e., its market price per share times the number of shares outstanding). Stocks may be added or deleted from the Index from time to time. |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 31, 2001 to September 30, 2018. |

An investment cannot be made directly into an index.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

September 30, 2018

| Shares | | | | Cost | | | Value | |

| COMMON STOCKS — 92.6% (a) | | | | | | |

| | | | | | | |

COMMERCIAL SERVICES SECTOR — 2.4% | | | | | | |

| | | Advertising/Marketing Services — 2.4% | | | | | | |

| | 2,135,000 | | Omnicom Group Inc. | | $ | 144,720,073 | | | $ | 145,222,700 | |

| | | | | | | | | |

COMMUNICATIONS SECTOR — 2.7% | | | | | | | | |

| | | | Specialty Telecommunications — 2.7% | | | | | | | | |

| | 7,687,000 | | CenturyLink Inc. | | | 156,339,767 | | | | 162,964,400 | |

| | | | | | | | | |

CONSUMER DURABLES SECTOR — 3.0% | | | | | | | | |

| | | | Tools & Hardware — 3.0% | | | | | | | | |

| | 1,245,000 | | Stanley Black & Decker Inc. | | | 121,553,431 | | | | 182,317,800 | |

| | | | | | | | | |

CONSUMER NON-DURABLES SECTOR — 8.5% | | | | | | | | |

| | | | Beverages: Non-Alcoholic — 2.7% | | | | | | | | |

| | 1,455,000 | | PepsiCo Inc. | | | 146,874,516 | | | | 162,669,000 | |

| | | | | | | | | | | | |

| | | | Food: Major Diversified — 3.0% | | | | | | | | |

| | 2,190,000 | | Nestlé S.A. — SP-ADR | | | 112,268,922 | | | | 182,208,000 | |

| | | | | | | | | | | | |

| | | | Household/Personal Care — 2.8% | | | | | | | | |

| | 3,090,000 | | Unilever PLC — SP-ADR | | | 136,645,902 | | | | 169,857,300 | |

| | | | | | | | | |

CONSUMER SERVICES SECTOR — 7.4% | | | | | | | | |

| | | | Movies/Entertainment — 4.1% | | | | | | | | |

| | 5,440,000 | | Twenty-First Century Fox Inc. – Cl B | | | 158,230,155 | | | | 249,260,800 | |

| | | | | | | | | | | | |

| | | | Other Consumer Services — 3.3% | | | | | | | | |

| | 5,965,000 | | eBay Inc.* | | | 124,808,363 | | | | 196,964,300 | |

| | | | | | | | | |

ELECTRONIC TECHNOLOGY SECTOR — 1.8% | | | | | | | | |

| | | | Electronic Components — 1.8% | | | | | | | | |

| | 1,210,000 | | TE Connectivity Ltd. | | | 18,936,165 | | | | 106,395,300 | |

| | | | | | | | | |

FINANCE SECTOR — 15.5% | | | | | | | | |

| | | | Investment Managers — 1.0% | | | | | | | | |

| | 1,930,000 | | Franklin Resources Inc. | | | 62,018,367 | | | | 58,691,300 | |

| | | | | | | | | | | | |

| | | | Major Banks — 6.8% | | | | | | | | |

| | 3,325,000 | | Bank of New York Mellon Corp. | | | 68,080,743 | | | | 169,541,750 | |

| | 2,148,000 | | JPMorgan Chase & Co. | | | 137,905,665 | | | | 242,380,320 | |

| | | | | | | 205,986,408 | | | | 411,922,070 | |

| | | | Multi-Line Insurance — 5.2% | | | | | | | | |

| | 1,460,000 | | Berkshire Hathaway Inc. – Cl B* | | | 88,501,453 | | | | 312,600,600 | |

| | | | | | | | | | | | |

| | | | Property/Casualty Insurance — 2.5% | | | | | | | | |

| | 1,125,000 | | Chubb Ltd. | | | 151,747,628 | | | | 150,345,000 | |

| | | | | | | | | |

HEALTH SERVICES SECTOR — 10.4% | | | | | | | | |

| | | | Health Industry Services — 3.4% | | | | | | | | |

| | 1,890,000 | | Quest Diagnostics Inc. | | | 190,864,071 | | | | 203,949,900 | |

The accompanying notes to financial statements are an integral part of this schedule.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2018

| Shares | | | | Cost | | | Value | |

| COMMON STOCKS — 92.6% (a) (Continued) | | | | | | |

| | | | | | | |

HEALTH SERVICES SECTOR — 10.4% (Continued) | | | | | | |

| | | Managed Health Care — 7.0% | | | | | | |

| | 675,000 | | Aetna Inc. | | $ | 114,835,883 | | | $ | 136,923,750 | |

| | 1,070,000 | | UnitedHealth Group Inc. | | | 76,504,985 | | | | 284,662,800 | |

| | | | | | | 191,340,868 | | | | 421,586,550 | |

HEALTH TECHNOLOGY SECTOR — 2.5% | | | | | | | | |

| | | | Medical Specialties — 2.5% | | | | | | | | |

| | 3,995,000 | | Smith & Nephew PLC — SP-ADR | | | 148,560,577 | | | | 148,174,550 | |

| | | | | | | | | |

INDUSTRIAL SERVICES SECTOR — 2.7% | | | | | | | | |

| | | | Oilfield Services/Equipment — 2.7% | | | | | | | | |

| | 2,630,000 | | Schlumberger Ltd. | | | 162,455,964 | | | | 160,219,600 | |

| | | | | | | | | |

PROCESS INDUSTRIES SECTOR — 3.4% | | | | | | | | |

| | | | Chemicals: Agricultural — 3.4% | | | | | | | | |

| | 3,521,000 | | Nutrien Ltd. | | | 159,602,854 | | | | 203,161,700 | |

| | | | | | | | | |

PRODUCER MANUFACTURING SECTOR — 8.8% | | | | | | | | |

| | | | Building Products — 1.9% | | | | | | | | |

| | 3,160,000 | | Masco Corp. | | | 119,891,733 | | | | 115,656,000 | |

| | | | | | | | | | | | |

| | | | Industrial Conglomerates — 4.7% | | | | | | | | |

| | 1,700,000 | | Honeywell International Inc. | | | 162,566,838 | | | | 282,880,000 | |

| | | | | | | | | | | | |

| | | | Trucks/Construction/Farm Machinery — 2.2% | | | | | | | | |

| | 1,965,000 | | PACCAR Inc. | | | 79,213,329 | | | | 133,993,350 | |

| | | | | | | | | |

RETAIL TRADE SECTOR — 11.3% | | | | | | | | |

| | | | Apparel/Footwear Retail — 4.3% | | | | | | | | |

| | 2,325,000 | | The TJX Companies Inc. | | | 163,877,055 | | | | 260,446,500 | |

| | | | | | | | | | | | |

| | | | Discount Stores — 7.0% | | | | | | | | |

| | 2,713,000 | | Dollar General Corp. | | | 198,620,238 | | | | 296,530,900 | |

| | 1,510,000 | | Dollar Tree Inc.* | | | 133,944,252 | | | | 123,140,500 | |

| | | | | | | 332,564,490 | | | | 419,671,400 | |

TECHNOLOGY SERVICES SECTOR — 9.4% | | | | | | | | |

| | | | Information Technology Services — 6.6% | | | | | | | | |

| | 1,270,000 | | Accenture PLC | | | 37,265,546 | | | | 216,154,000 | |

| | 2,814,000 | | Cerner Corp.* | | | 146,339,969 | | | | 181,249,740 | |

| | | | | | | 183,605,515 | | | | 397,403,740 | |

| | | | Packaged Software — 2.8% | | | | | | | | |

| | 3,214,000 | | Oracle Corp. | | | 128,504,605 | | | | 165,713,840 | |

| | | | | | | | | |

TRANSPORTATION SECTOR — 2.8% | | | | | | | | |

| | | | Air Freight/Couriers — 2.8% | | | | | | | | |

| | 2,250,000 | | Expeditors International of Washington Inc. | | | 83,243,577 | | | | 165,442,500 | |

| | | | Total common stocks | | | 3,734,922,626 | | | | 5,569,718,200 | |

The accompanying notes to financial statements are an integral part of this schedule.

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2018

| Principal Amount | | | Cost | | | Value | |

| SHORT-TERM INVESTMENTS — 7.4% (a) | | | | | | |

| | | Bank Deposit Account — 3.3% | | | | | | |

| $ | 196,701,727 | | U.S. Bank N.A., 2.05%^ | | $ | 196,701,727 | | | $ | 196,701,727 | |

| | | | | | | | | | | | |

| | | | U.S. Treasury Securities — 4.1% | | | | | | | | |

| | 50,000,000 | | U.S. Treasury Bills, 1.953%, due 10/18/18^ | | | 49,953,840 | | | | 49,951,184 | |

| | 50,000,000 | | U.S. Treasury Bills, 2.070%, due 11/23/18^ | | | 49,850,938 | | | | 49,844,773 | |

| | 150,000,000 | | U.S. Treasury Bills, 2.098%, due 12/13/18^ | | | 149,362,770 | | | | 149,353,266 | |

| | | | Total U.S. treasury securities | | | 249,167,548 | | | | 249,149,223 | |

| | | | Total short-term investments | | | 445,869,275 | | | | 445,850,950 | |

| | | | Total investments — 100.0% | | $ | 4,180,791,901 | | | | 6,015,569,150 | |

| | | | Other assets, less liabilities — 0.0% (a) | | | | | | | 2,003,535 | |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 6,017,572,685 | |

| * | Non-income producing security. |

| ^ | The rate shown is as of September 30, 2018. |

| (a) | Percentages for the various classifications relate to total net assets. |

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

The accompanying notes to financial statements are an integral part of this schedule.

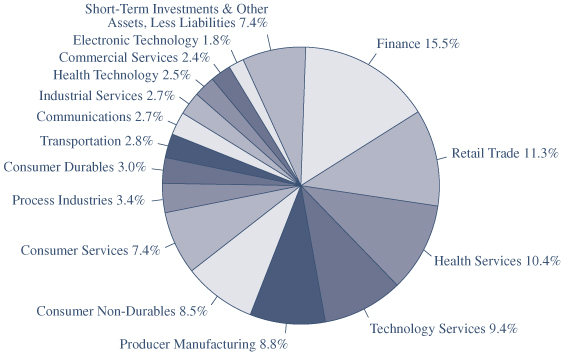

INDUSTRY SECTORSas of September 30, 2018 (Unaudited)

FMI

Common Stock

Fund

September 30, 2018

Dear Fellow Shareholders:

The FMI Common Stock Fund returned 2.88%1 in the September quarter compared to 3.58% for the Russell 2000 Index. Growth stocks continued to outperform value stocks, although not to the same degree as recent quarters or years. Equities of money-losing companies continued to outpace the moneymakers. As of September 25, 2018, of the top 50 performers (year-to-date) in the Russell 2000 benchmark, not a single one would pass our quality or valuation criteria. 35 of the top 50 Russell 2000 performers lost money over the past twelve months. These 50 companies, on a median basis, trade at 9.6 times revenue. The benchmark trades at or near record-high multiples of just about any valuation characteristic one can conjure. Given the heavy flows toward passive index investing, including the Russell 2000, it’s not an exaggeration to say that investors simply don’t seem to care what they are buying. They believe the Russell 2000 is a proxy for small cap or growth stock investing, and that’s about the extent of it. The median Russell 2000 stock has significantly lagged the Index, suggesting performance has been driven by the higher-valued and heavier-weighted stocks. Interestingly, $1 invested in the FMI Common Stock Fund at the beginning of 2009 (roughly coinciding with the start of this bull market) would be worth $3.50 today, compared to $2.38 for the median Russell 2000 stock, and $3.88 for the Russell 2000 Index. In a down market, it is likely that the movie will play in reverse, with the benchmark underperforming the median. Sectors that contributed positively to the Fund’s results in the quarter included Producer Manufacturing, Finance, and Commercial Services. On the negative side of the ledger were Health Technology, Technology Services and Consumer Non-Durable sectors. Cash continued to be a drag. Carlisle Companies, Armstrong World Industries and W.R. Berkeley were positive performers, while FirstCash, Hain Celestial Group and ViaSat detracted.

The seeds of any bust are inherent in the boom that outstrips the pace of whatever solid factors gave it its impetus in the first place. There are no safeguards that can protect the emotional investor from himself. – J. Paul Getty

The bull market stretched into uncharted territory in the third calendar quarter, reaching its longest duration and one of its strongest up-cycle performances on record. Investors continued to focus on the good news -- the U.S. economy, Wall Street’s version of earnings and rising stock prices...while ignoring danger signals -- overconfidence (as reflected in valuations), rising rates and inflation, unbridled debt accumulation, a burgeoning trade war and perhaps some signs of fatigue in the economy. Faith in index funds and exchange-traded funds (ETFs) continued unabated, despite the “crowded trade” nature of many of these products. High confidence in technology shares harkens back to the 1990s, with exceptionally optimistic valuations for both established and startup companies. Private equity transactions, in all but a small minority of cases, are taking place at record-high valuations and debt leverage. So-called “covenant-lite” conditions have returned to the high yield arena. Across the board there appears to be little regard for safety and downside protection.

____________

1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of 2.88% and 2.91%, respectively, for the third quarter of 2018. |

According to Bloomberg’s weekly survey, U.S. real GDP grew at an estimated rate of 3.0% in Q3 and is predicted to grow 2.8% in the December quarter. While the unemployment rate is low, the work force participation rate of 62.7% remained well below its 67% peak, and today, hovers near a 40-year low. Working age population growth continued to be soft (see chart on the right) and unless birth rates or immigration pick up, will be a source of future weakness.

The large number of working-age people who lost jobs in the last recession and were supposed to be returning to the labor force this cycle appear to be mostly idle. The evidence of this is rising wage rates (recently exceeding 3% according to the Atlanta Fed). With wages being the largest cost for most companies, margins may be at risk. Productivity gains, which have been meaningfully below long-term averages (see chart below) may not provide the offset to wage pressures unless there is a sustained increase in business improvement spending.

The benefit from lower tax rates and fewer regulations is a positive, although the lack of fiscal discipline threatens long-term prosperity. The market seems unconcerned with the potential of an economic downturn. While we are not economists, we do recognize that recessions often come out of the blue. A yield curve that is near inversion doesn’t bolster confidence that fair weather is a foregone conclusion. The CRB Metals Index is off over 15% from its recent peak. Pending home sales declined for the eighth straight month in August, down 2.3% from last year. Auto sales, at a recently annualized rate of 16.6 million, are down nearly 1.9 million units from the peak. Many technology companies are seeing inventories grow much faster than sales. Overseas economies, buyers of U.S. products, have softened, particularly in the emerging markets. Currency weakness in many of these countries is of particular concern, given high levels of dollar-denominated debt.

Across the globe, debt levels are rising significantly. The sovereign debt load has approximately doubled, and debt of all kinds is up 75% over the past decade, even though excessive debt was at the root of the last crisis. Worldwide debt-to-GDP is at a record 318%. The U.S. annual budget deficit as a percent of GDP is running at a 4.2% rate...the kind of figure one would normally see in the throes of a recession. Interestingly, it wasn’t that long ago that U.S. leaders chastised Eurozone countries for exceeding the 3% deficit-to-GDP mandate. It is highly unusual for debt ratios to be rising at this point in the economic cycle. The U.S. national debt is $21.5 trillion, an astonishing figure relative to our $20.5 trillion economy and unprecedented in non-war times (see above chart from Bernstein). Unfunded welfare benefits are a multiple of our debt obligations.

Much has been made of the strong earnings performance in recent quarters. Everyone’s skepticism meter ought to be blinking yellow when Wall Street says earnings growth is 20% while the economy is growing 5% nominally and sales growth is in the single digits. We are, of course, experiencing a one-time positive year-over-year benefit from lower corporate tax rates but once those lap, long-term earnings growth rates will likely fall significantly. Wall Street, with an assist from corporate managements, has embraced the concept of “adjusted earnings,” as discussed in previous letters. The abuse of this measurement has reached alarming levels. Based partly on our inquiry, the Leuthold Group studied actual GAAP (generally accepted accounting principles) reported, operating and “adjusted” S&P 500 earnings over a long-term (30-year) time frame. The spread between these figures has become wide. Even excluding the credit crisis quarters, the spread between reported GAAP earnings and Wall Street earnings is 23.6% (Wall Street’s version is always higher). Proponents of adjusted earnings presentation say that amortization of intangibles, stock compensation and other one-time items justify this measure. Leuthold, among other findings, determined that more than 40% of the amount companies spent on mergers & acquisitions activity ended up in the scrap heap (written off). Additionally, many companies that claim “one-time” charges often have these write-offs with great frequency. Excluding the real cost of stock options seems dubious. There may be some justification for adding back a portion of amortization to GAAP earnings, but it seems managements and Wall Street have overplayed this hand.

Using the long-term, oft-cited valuation data provided by Leuthold, stocks today are in the 9th decile on a median basis (10th being the most expensive). We regularly review 46 different valuation series, including several price-to-earnings (P/E) data sets. It would be odd, to say the least, to have most of these measures registering in the 9th or 10th deciles, while at the same time having Wall Street’s version of P/E ratios be “reasonable” or even “attractive,” as proponents like to tout. Somebody is wrong. Using a much harder-to-manipulate series, price-to-sales, tells a different story. Leuthold recently called the above chart “the scariest chart in the world.” Of course, investor sentiment usually reflects the current trajectory of stock prices. “Markets make opinions,” as the old bromide goes.

Ten years after the last financial and stock market crisis, the media has engaged in a lengthy rehash and post mortem of what transpired. It’s ironic and quite surprising to us at least, given how fresh the crisis still is in our minds, that many of the same mistakes are being repeated by investors today. A decade ago most investors scoffed at the notion that home prices could fall. A house was a surefire investment, and the proof of that was the willingness of banks to loan 95% or more against it. Investors believed in Wall Street’s products (credit default options, mortgage-backed securities, collateralized loan obligations, etc.) and high-yield bonds. The economy was seemingly healthy, and the market saw little reason to worry about high valuations. They believed in central bankers. Today, investors have the same lofty confidence in high-flying social media, technology and med-tech shares. Many of the same aforementioned derivative investment vehicles are back in vogue, along with a cornucopia of ETFs and index products. Many mistakenly believe that these products carry not only low fees, but low risk. Do investors in the iShares U.S. Energy ETF, iShares Technology ETF or iShares Telecom ETF, for example, know that far from investing in diversified portfolios, they are putting over half their money behind just five stocks? A little over a year ago we discussed the potential liquidity issues facing many of the most popular ETFs. With turnover in many of these ETFs vastly greater than even the most liquid underlying constituent stocks, trading activity could be very interesting when markets get shaky. Junk bond spreads recently hit 315 basis points over treasuries -- half the level of two years ago and a figure not seen since 2007, according to economist David Rosenberg. The faith in central bankers seems unshaken. Finally, just like a decade ago, perception that the economy is strong appears to be overriding any concern about high valuations or other potential troublesome developments.

What we have seen as excessive and unsustainable has persisted far longer than we thought possible. On one level that makes us “wrong,” but of course that doesn’t change the reality of the aforementioned conditions. We would rather give up some of the upside than to be remorseful in hindsight. Greed usually ends in regret. That means being more cautious with our investments and expectations today. Is there a way around another crisis and lousy stock market? Anything is possible when it comes to markets and human behavior. Earnings...the good and sustainable kind...could advance at a healthy rate and inflation could stay within earshot of 2%. The big one, interest rates, though significantly higher than two years ago, could stay well below normal for an extended period. Wages and other escalating costs could recede. The political crisis between the

left and right could ameliorate. The nascent trade war with China could resolve. Externalities such as terrorism, wars, natural disasters, etc., could be benign. In other words, a lot must go right and not much can go wrong given today’s valuations. We continue to hunt for attractive investments but acknowledge the environment is far from ideal. We are working diligently, with a focus on the long term. Additionally, we have our own money invested right alongside yours. Our confidence in achieving good full cycle returns remains high.

Below we highlight a couple of investments:

Argo Group International Holdings Ltd. (ARGO)

(Analyst: Matthew Goetzinger)

Description

Argo Group International is a diversified specialty insurance company focusing on small-to-mid-sized commercial risks. Specialty Excess and Surplus lines (35% of gross written premiums), niche Commercial Specialty (30%), and International Specialty (15%) together constitute Argo’s property and casualty business. Argo’s Lloyd’s franchise, Syndicate 1200, comprises the remaining mix of premiums written. Reinsurance accounts for 12% of the premium mix. Argo is A rated by A.M. Best.

Good Business

| | • | Argo is a durable, differentiated, and diversified specialty insurer with an attractive small-to-middle market account focus. |

| | | |

| | • | The company has significant scarcity value as one of the few remaining independent scale players in the specialty market with a top five market share. |

| | | |

| | • | Property and casualty insurance is a necessary coverage. This non-discretionary attribute, along with the company’s emphasis on high service levels, results in strong customer retention and predictable revenues. |

| | | |

| | • | Argo’s focus on safety and good risk-adjusted returns leads the company to maintain conservative customer exposures and excess reserves. Management targets 10% annual growth in book value of equity per share. |

| | | |

| | • | The company is managed with conservative leverage parameters. |

| | | |

| | • | Argo is A rated by A.M. Best and Standard & Poor’s, with a risk-based capital ratio of 200%. |

Valuation

| | • | Argo trades at just over 1 times estimated year-end book value per share. |

| | | |

| | • | The 20-year industry average property & casualty insurance book value multiple is 1.2 times, with speciality insurers typically trading at a strong valuation premium to the group. |

| | | |

| | • | Recent private market values for strong specialty insurers have been north of 1.7 times book value. |

Management

| | • | Mark Watson was named Argo’s Chief Executive Officer in January of 2000. He previously had a leadership role at a smaller niche insurer who ultimately sold to the USF&G Corp. |

| | | |

| | • | As a group, Argo’s executive management team and corporate board own 4.9% of the company’s shares outstanding. CEO Mark Watson individually holds approximately 3.3% of the shares. |

| | | |

| | • | The company’s incentive compensation plans appropriately target growth in book value per share as a key metric. |

| | | |

| | • | During the past several years Argo has capitalized on industry changes and hired key talent from larger firms like AIG and Travelers. |

Investment Thesis

Argo is a durable, differentiated specialty insurer with an attractive small-to-middle market account focus. Capitalizing on a continuation of the company’s strong underwriting track record, incremental improvements to overhead costs, and steady investment performance should result in Argo achieving a 10% return on equity, and a higher level once interest rates normalize. The stock trades at an attractive valuation.

Graham Holdings Co. (GHC)

(Analyst: Dan Sievers)

Description

Graham Holdings, formerly the Washington Post Company, is a decentralized family-controlled holding company, and the owner of Kaplan International, Test Prep, and Professional education businesses (55% of second quarter 2018 revenue); seven broadcast television stations (17% of revenues); a manufacturing division (19% of revenues); a home healthcare division (6% of revenues); a digital marketing firm called Social Code (2% of revenues); and other assets (1% of revenues).

Good Business

| | • | Following an almost decade-long restructuring, Kaplan no longer owns or operates a for-profit college. We believe that Kaplan’s education services business (International, Test Prep, and Professional/Schweser) will be able to grow over time, and we should see potential for margin improvement. |

| | | |

| | • | Graham Holdings’ seven broadcast television stations continue to exhibit durability and good profitability, adding value through local news programming while benefiting from growth in retransmission fees and political advertising in even-numbered years. |

| | | |

| | • | For Graham’s Kaplan, broadcast, home healthcare, and Social Code divisions, we believe incremental growth can be achieved with very limited incremental capital investment, leading to attractive returns on invested capital and free cash flow that can be utilized opportunistically by the corporate office to repurchase undervalued shares, or for reasonably-priced acquisitions. |

| | | |

| | • | Graham Holdings is conservatively capitalized with over $400 million in net balance sheet cash. In addition, its pension plans are overfunded by $1 billion. The value of this pension surplus to shareholders is certainly limited but may still be quite significant. |

Valuation

| | • | The company is not covered by any sell-side analysts, but based on our estimates for 2018, the company trades at a modest 6.0 times enterprise value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple. |

| | | |

| | • | Based on these same near-term 2018 estimates, we estimate a sum-of-the-parts value that offers over 35% upside. We note that Graham has an exemplary long-term record of repurchasing its shares aggressively only when the shares trade at a wide discount to their estimate of net asset value. |

Management

| | • | CEO Tim O’Shaughnessy (age 36) has, in his 4 years at Graham, exhibited financial conservatism and a long-term focus. In August of 2018, he made a $2 million open-market purchase of Graham shares at $550. Mr. O’Shaughnessy is the son-in-law to controlling shareholder and Chairman Donald Graham (age 73), who has more than 18% economic ownership in the company. |

| | | |

| | • | We note the presence (and influence) of reputable value-focused investors such as Chris Davis and Tom Gayner on the board of directors. |

Investment Thesis

Graham Holdings is covered by zero sell-side analysts and has been largely ignored by investors during a nearly decade-long restructuring at Kaplan and a period of difficult -- but necessary -- divestiture decisions, including the 2013 sale of The Washington Post, the spin-off of the very valuable Cable One (CABO) division, and the recent March 2018 divestiture of Kaplan University (now part of Purdue University Global). Today, we believe the restructuring at Kaplan is largely complete, and that the remaining set of Kaplan businesses are attractive. We believe results from this new, stronger and simpler Kaplan are likely to lead some investors to rediscover the stock in due course. In the meantime, the company is run with a long-term focus and has a fortress-like balance sheet, which provides optionality to either repurchase shares at an attractive valuation, or wait for moderately-priced acquisition opportunities to present themselves.

Thank you for your confidence in the FMI Common Stock Fund.

This shareholder letter is unaudited.

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

During the fiscal year ended September 30, 2018, the FMI Common Stock Fund the “Fund” had a total return of 6.92%1. The benchmark Russell 2000 returned 15.24% in the same period. Sectors that aided relative performance included Finance, Producer Manufacturing, and Utilities. FirstCash and Kennedy-Wilson were notable positive contributors within the Finance sector, both likely due to fundamental results being somewhat better than the market anticipated. Armstrong World Industries and Carlisle Cos. reported solid progress and the stocks responded, aiding performance in the Producer Manufacturing sector. The zero exposure to Utilities drove the outperformance of that sector. On the detractor side of the ledger, Technology Services, Distribution Services and Consumer Services, along with elevated cash, pulled down performance. TiVo Corp. and Allscripts Healthcare Solutions, all within Technology Services, underperformed over the past year. TiVo’s stock remained under a cloud due to the ongoing lawsuit with Comcast and a management change. Allscripts seemed to perform reasonably well fundamentally but the company’s complexity and uneven order rate has been off-putting to investors. Recent announcements should make the story much simpler in the future. In the Distribution Service sector, Anixter International declined in the period because of inconsistent quarterly performance. A new CEO was recently installed. Graham Holdings was off slightly during the year so it was a detractor on a relative basis to the Consumer Services sector. Technology related sectors and higher than normal cash were by far the two biggest factors in the underperformance of the Fund during the trailing 12 months.

Some stocks sold in the period include Greenlight Capital, Applied Industrial Technologies, MEDNAX, Kirby Corp., Esterline Technologies and Casey’s General Stores. Stocks added include Cars.com, Howard Hughes, Trinity Industries, Argo Group, TiVo, EnPro Industries, Hain Celestial and WABCO. As of September 30, 2018, the Fund was significantly overweighted in Distribution Services, Commercial Services and Producer Manufacturing and meaningfully underweighted in Finance, Electronic Technology and Health Technology.

The fiscal year was very similar to the prior with respect to the benchmark. Strong performance across most sectors characterized the Russell 2000 over the past year. Highly speculative companies, such as biotechnology and technology stocks, were particularly strong. Despite the Russell 2000’s strong returns, approximately one third of the companies in the index lost money over the past year. Passive investment strategies continued to see heavy inflows of money, at the expense of active strategies. Stocks generally appear overvalued and the Russell 2000 index, on many valuation measures, is even more expensive than it was in the late 1990s. The bull market in small cap stocks, with one interruption, has extended to nine and a half years, one of the longest on record and is up over 450% from the last major trough in March of 2009.

The Federal Reserve has moved slowly to normalize interest rates but the price of money remains unusually cheap by historical standards. Economic growth has improved over the past twelve months but at great cost to both government and corporate balance sheets. Total debt relative to U.S. GDP is near 100% and the deficit to GDP is now 4.2%. Corporate leverage by some measures is at a fifty-year high. The unemployment rate is low but the labor force participation rate continues to be depressed. Wage rates and inflation are rising. Domestic and international political risks remain elevated.

While the conventional wisdom is that stock market risk is low because the economy is stronger, we believe valuations are so high that it leaves little room for error. We remain cautious on the stock market’s prospects over the near term. The Fund continues to sell at a discount to the Russell 2000 on most valuation measures.

____________

1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of 6.92% and 7.02%, respectively, for the fiscal year ended September 30, 2018. |

FMI Common Stock Fund

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (Unaudited)

(Continued)

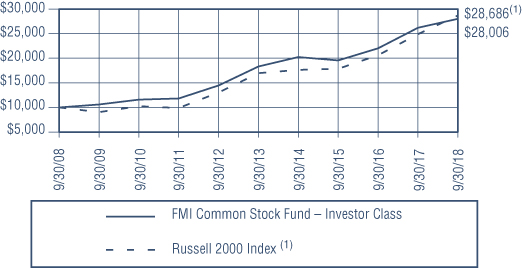

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN

FMI COMMON STOCK FUND – INVESTOR CLASS AND THE RUSSELL 2000 INDEX(1)

AVERAGE ANNUALIZED TOTAL RETURN

| | | | | | Inception |

| | Inception | | | | through |

| | Date | 1-Year | 5-Year | 10-Year | 9/30/2018 |

| FMI Common Stock Fund – | | | | | |

| Investor Class | 12/18/81 | 6.92% | 8.85% | 10.85% | 11.91% |

| FMI Common Stock Fund – | | | | | |

| Institutional Class | 10/31/16 | 7.02% | N/A | N/A | 15.15% |

Russell 2000 Index(1)* | | 15.24% | 11.07% | 11.11% | 10.67% |

The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund may be lower or higher than the performance quoted. The total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return includes change in share prices and in each case includes reinvestments of any dividends, interest and capital gain distributions. Performance data current to the most recent month-end may be obtained by visiting www.fmifunds.com or by calling 1-800-811-5311.

| (1) | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which comprises the 3,000 largest U.S. companies based on total market capitalization. |

| * | The benchmark since inception returns are calculated since inception of the Investor Class, December 18, 1981 to September 30, 2018. |

An investment cannot be made directly into an index.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

September 30, 2018

| Shares | | | | Cost | | | Value | |

| COMMON STOCKS — 81.7% (a) | | | | | | |

| | | | | | | |

COMMERCIAL SERVICES SECTOR — 14.4% | | | | | | |

| | | Advertising/Marketing Services — 3.3% | | | | | | |

| | 1,550,000 | | Interpublic Group of Cos. Inc. | | $ | 27,837,296 | | | $ | 35,448,500 | |

| | | | | | | | | | | | |

| | | | Financial Publishing/Services — 1.6% | | | | | | | | |

| | 78,000 | | FactSet Research Systems Inc. | | | 12,516,471 | | | | 17,449,380 | |

| | | | | | | | | | | | |

| | | | Miscellaneous Commercial Services — 5.3% | | | | | | | | |

| | 80,000 | | Broadridge Financial Solutions Inc. | | | 1,629,984 | | | | 10,556,000 | |

| | 1,500,000 | | Genpact Ltd. | | | 27,268,509 | | | | 45,915,000 | |

| | | | | | | 28,898,493 | | | | 56,471,000 | |

| | | | Personnel Services — 4.2% | | | | | | | | |

| | 280,000 | | ManpowerGroup Inc. | | | 19,009,958 | | | | 24,068,800 | |

| | 290,000 | | Robert Half International Inc. | | | 7,557,791 | | | | 20,410,200 | |

| | | | | | | 26,567,749 | | | | 44,479,000 | |

CONSUMER NON-DURABLES SECTOR — 1.3% | | | | | | | | |

| | | | Food: Specialty/Candy — 1.3% | | | | | | | | |

| | 520,000 | | Hain Celestial Group Inc.* | | | 15,815,962 | | | | 14,102,400 | |

| | | | | | | | | |

CONSUMER SERVICES SECTOR — 5.8% | | | | | | | | |

| | | | Cable/Satellite TV — 1.9% | | | | | | | | |

| | 23,000 | | Cable One Inc. | | | 6,979,818 | | | | 20,323,030 | |

| | | | | | | | | | | | |

| | | | Other Consumer Services — 3.9% | | | | | | | | |

| | 73,000 | | Graham Holdings Co. | | | 35,482,299 | | | | 42,288,900 | |

| | | | | | | | | |

DISTRIBUTION SERVICES SECTOR — 7.6% | | | | | | | | |

| | | | Electronics Distributors — 4.4% | | | | | | | | |

| | 280,000 | | Arrow Electronics Inc.* | | | 4,740,467 | | | | 20,641,600 | |

| | 280,000 | | ePlus Inc.* | | | 15,102,514 | | | | 25,956,000 | |

| | | | | | | 19,842,981 | | | | 46,597,600 | |

| | | | Wholesale Distributors — 3.2% | | | | | | | | |

| | 348,000 | | Anixter International Inc.* | | | 22,551,135 | | | | 24,464,400 | |

| | 117,000 | | MSC Industrial Direct Co. Inc. | | | 7,003,921 | | | | 10,308,870 | |

| | | | | | | 29,555,056 | | | | 34,773,270 | |

ELECTRONIC TECHNOLOGY SECTOR — 2.1% | | | | | | | | |

| | | | Telecommunications Equipment — 2.1% | | | | | | | | |

| | 355,000 | | ViaSat Inc.* | | | 24,867,862 | | | | 22,702,250 | |

| | | | | | | | | |

FINANCE SECTOR — 19.6% | | | | | | | | |

| | | | Finance/Rental/Leasing — 6.1% | | | | | | | | |

| | 438,000 | | FirstCash Inc. | | | 13,596,578 | | | | 35,916,000 | |

| | 400,000 | | Ryder System Inc. | | | 18,363,248 | | | | 29,228,000 | |

| | | | | | | 31,959,826 | | | | 65,144,000 | |

| | | | Property/Casualty Insurance — 7.6% | | | | | | | | |

| | 304,750 | | Argo Group International Holdings Ltd. | | | 16,023,541 | | | | 19,214,488 | |

| | 365,000 | | W.R. Berkley Corp. | | | 11,515,238 | | | | 29,174,450 | |

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2018

| Shares | | | | Cost | | | Value | |

| COMMON STOCKS — 81.7% (a) (Continued) | | | | | | |

| | | | | | | |

FINANCE SECTOR — 19.6% (Continued) | | | | | | |

| | | Property/Casualty Insurance — 7.6% (Continued) | | | | | | |

| | 35,000 | | White Mountains Insurance Group Ltd. | | $ | 31,410,325 | | | $ | 32,755,450 | |

| | | | | | | 58,949,104 | | | | 81,144,388 | |

| | | | Real Estate Development — 4.5% | | | | | | | | |

| | 177,000 | | The Howard Hughes Corp.* | | | 22,364,166 | | | | 21,986,940 | |

| | 1,220,000 | | Kennedy-Wilson Holdings Inc. | | | 25,274,389 | | | | 26,230,000 | |

| | | | | | | 47,638,555 | | | | 48,216,940 | |

| | | | Regional Banks — 1.4% | | | | | | | | |

| | 293,000 | | Zions Bancorporation | | | 7,891,512 | | | | 14,693,950 | |

| | | | | | | | | |

PROCESS INDUSTRIES SECTOR — 3.9% | | | | | | | | |

| | | | Containers/Packaging — 3.9% | | | | | | | | |

| | 387,000 | | Avery Dennison Corp. | | | 25,381,510 | | | | 41,931,450 | |

| | | | | | | | | |

PRODUCER MANUFACTURING SECTOR — 19.2% | | | | | | | | |

| | | | Auto Parts: OEM — 1.0% | | | | | | | | |

| | 89,000 | | WABCO Holdings Inc.* | | | 10,947,026 | | | | 10,496,660 | |

| | | | | | | | | | | | |

| | | | Building Products — 3.9% | | | | | | | | |

| | 600,000 | | Armstrong World Industries Inc.* | | | 26,113,541 | | | | 41,760,000 | |

| | | | | | | | | | | | |

| | | | Industrial Machinery — 4.4% | | | | | | | | |

| | 180,000 | | EnPro Industries Inc. | | | 13,414,936 | | | | 13,127,400 | |

| | 414,000 | | Woodward Inc. | | | 17,005,585 | | | | 33,476,040 | |

| | | | | | | 30,420,521 | | | | 46,603,440 | |

| | | | Metal Fabrication — 1.3% | | | | | | | | |

| | 102,000 | | Valmont Industries Inc. | | | 14,934,787 | | | | 14,127,000 | |

| | | | | | | | | | | | |

| | | | Miscellaneous Manufacturing — 6.9% | | | | | | | | |

| | 365,000 | | Carlisle Cos. Inc. | | | 29,135,573 | | | | 44,457,000 | |

| | 965,000 | | TriMas Corp.* | | | 21,230,669 | | | | 29,336,000 | |

| | | | | | | 50,366,242 | | | | 73,793,000 | |

| | | | Trucks/Construction/Farm Machinery — 1.7% | | | | | | | | |

| | 485,000 | | Trinity Industries Inc. | | | 15,852,178 | | | | 17,770,400 | |

| | | | | | | | | |

RETAIL TRADE SECTOR — 2.1% | | | | | | | | |

| | | | Specialty Stores — 2.1% | | | | | | | | |

| | 475,000 | | Penske Automotive Group Inc. | | | 16,842,025 | | | | 22,510,250 | |

| | | | | | | | | |

TECHNOLOGY SERVICES SECTOR — 5.7% | | | | | | | | |

| | | | Information Technology Services — 3.0% | | | | | | | | |

| | 2,260,000 | | Allscripts Healthcare Solutions Inc.* | | | 27,585,536 | | | | 32,205,000 | |

| | | | | | | | | | | | |

| | | | Internet Software/Services — 1.6% | | | | | | | | |

| | 615,000 | | Cars.com Inc.* | | | 16,797,883 | | | | 16,980,150 | |

| | | | | | | | | | | | |

| | | | Packaged Software — 1.1% | | | | | | | | |

| | 920,000 | | TiVo Corp. | | | 12,608,763 | | | | 11,454,000 | |

| | | | Total common stocks | | | 622,652,996 | | | | 873,465,958 | |

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2018

| Principal Amount | | | Cost | | | Value | |

| SHORT-TERM INVESTMENTS — 18.3% (a) | | | | | | |

| | | Bank Deposit Account — 4.3% | | | | | | |

| $ | 45,686,522 | | U.S. Bank N.A., 2.05%^ | | $ | 45,686,522 | | | $ | 45,686,522 | |

| | | | | | | | | | | | |

| | | | U.S. Treasury Securities — 14.0% | | | | | | | | |

| | 25,000,000 | | U.S. Treasury Bills, 1.953%, due 10/18/18^ | | | 24,976,920 | | | | 24,975,592 | |

| | 50,000,000 | | U.S. Treasury Bills, 2.070%, due 11/23/18^ | | | 49,850,937 | | | | 49,844,772 | |

| | 50,000,000 | | U.S. Treasury Bills, 2.098%, due 12/13/18^ | | | 49,787,590 | | | | 49,784,422 | |

| | 25,000,000 | | U.S. Treasury Bills, 2.166%, due 01/17/19^ | | | 24,835,750 | | | | 24,836,031 | |

| | | | Total U.S. treasury securities | | | 149,451,197 | | | | 149,440,817 | |

| | | | Total short-term investments | | | 195,137,719 | | | | 195,127,339 | |

| | | | Total investments — 100.0% | | $ | 817,790,715 | | | | 1,068,593,297 | |

| | | | Other assets, less liabilities — 0.0% (a) | | | | | | | 71,870 | |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 1,068,665,167 | |

| * | Non-income producing security. |

| ^ | The rate shown is as of September 30, 2018. |

| (a) | Percentages for the various classifications relate to total net assets. |

The accompanying notes to financial statements are an integral part of this schedule.

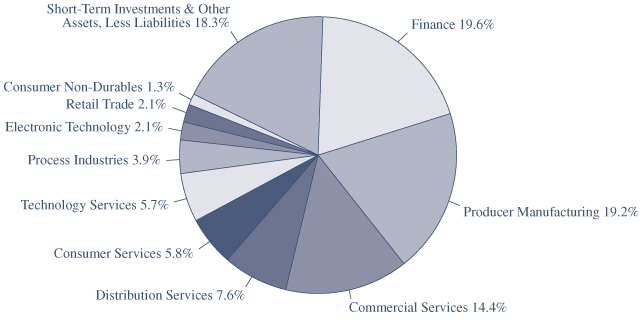

INDUSTRY SECTORS

as of September 30, 2018 (Unaudited)

FMI

International

Fund

September 30, 2018

Dear Fellow Shareholders:

From a macroeconomic standpoint, several negative data points have surfaced: there are signs that global economic growth may have peaked; capital investment disappointed; debt levels continued to rise; trade growth slowed thanks to rising trade tensions and heightened policy uncertainty; housing markets waned; and emerging market currencies and financial markets came under intense pressure. However, after a slow start to the year, developed international stock markets continue their path toward recovery. The FMI International Fund (“Fund”) added 0.51%1 in the quarter, compared with an MSCI EAFE Index return of 2.36% in local currency and 1.35% in U.S. Dollars (USD). The Consumer Services, Electronic Technology and Consumer Durables sectors performed well on a relative basis, partially offset by Producer Manufacturing, Commercial Services, and Distribution Services. Top individual gains were logged by Whitbread, Isuzu Motors and Safran, while Smiths Group, Travis Perkins and Schlumberger each declined in value. Cash detracted from overall returns.

To justify today’s expensive stock valuations, investors need to believe companies will be able to quickly grow into their current multiples. In our view, expectations are lofty and don’t leave much room for error. A number of signposts continue to give us reason for pause.

Structural Growth Challenges

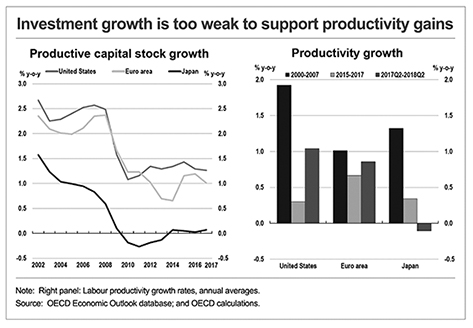

At its core, long-term economic growth is driven by a combination of three key factors: productivity growth, more people working, and people working more hours. Productivity, or the improvement in output per hour worked, can be enhanced by capital investments, as advancements in innovation and technology can help drive efficiency improvements. As capital stock ages, organic investment in property, plant and equipment and research and development (R&D), is paramount in driving future growth. In recent years, however, capital investment and productivity have fallen well short of historical norms, despite an accommodative monetary environment where money was virtually free. Instead, companies have often opted to lever up their balance sheets to acquire businesses or do share buybacks at high valuations, neither of which does much to grow the economic pie. While a momentum and growth-driven stock market might cheer on this form of capital allocation, long-term shareholder value is unlikely to be enhanced by debt-fueled financial engineering. As shown in the chart on the next page from the Organisation for Economic Co-operation and Development (OECD), current “investment growth is too weak to support productivity gains.”2 This is a major problem, and one which requires a significant change in mindset to fix. For the economy to sustainably grow at higher levels, companies must invest organically and improve their productivity.

____________

1 | The FMI International Fund Investor Class (FMIJX) and FMI International Fund Institutional Class (FMIYX) had a return of 0.51% and 0.50%, respectively, for the third quarter of 2018. |

2 | Laurence Boone – OECD Chief Economist, presentation. “OECD Interim Economic Outlook: High uncertainty weighing on global growth.” September 20, 2018. |

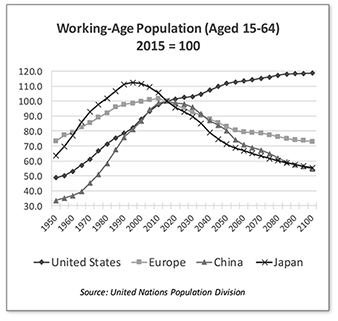

Given that faster growth has not come from productivity, economic output will be more reliant on the number of people working, and number of hours worked. Unfortunately, the outlook on this front is equally challenged. The United Nations Population Division forecasts a steady decline in working-age population in Europe, Japan and China, as illustrated in the chart on the right.3 Despite massive long-term financial implications, this structural challenge gets very little airtime from the financial press.

The Economist aptly describes the problem at hand: “A place with fewer workers must raise productivity even more to keep growing economically. It will struggle to sustain spending on public goods such as defense. The national debt will be borne on fewer shoulders. Fewer people will be around to come up with the sort of brilliant ideas that can enrich a nation. Businesses might be loath to invest. In fast-shrinking Japan, even domestic firms focus on foreign markets. The old will weigh more heavily on society, too. […] In Japan, where young people are few and lives are long, demographers expect there to be 48 people over the age of 65 for every 100 people of working age in 2020. In 1990 there were just 17.” With debt levels rising steadily and more people exiting the workforce, the math starts to break down. The current trajectory is simply not sustainable. Fortunately, there are a number of potential solutions to this predicament: countries can look to increase the number of women in the workforce, push back the retirement age (and related benefits), increase immigration, and improve birth rates. Significant policy changes would be necessary, some of which (such as higher retirement age and immigration) would likely face stiff political opposition.4 Change is never easy, but at some point, tough decisions will have to be made. Ultimately, we see this headwind getting worse before it gets better.

____________

3 | http://www.un.org/en/development/desa/population/ |

4 | “Many countries suffer from shrinking working-age populations,” The Economist, May 5, 2018. |

Corporate Debt: “Tidal Wave”

Coming out of the great financial crisis of 2008-09, the expectation was for significant deleveraging. Quite the opposite has occurred; while households and banks have repaired their balance sheets to some degree, governments, central banks, nonfinancial corporations and shadow banks have more than picked up the slack. In July, the Institute of International Finance (IIF) estimated that total global debt has reached $247 trillion (318% of GDP),5 which compares with $167 trillion in 2007 (287%).6

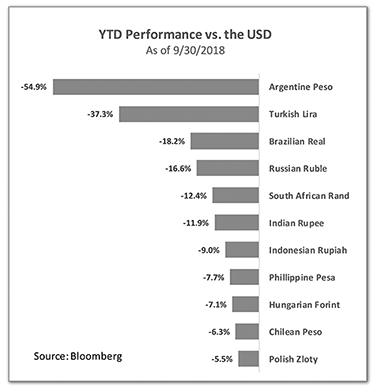

Recent reports by the McKinsey Global Institute (MGI) have studied the corporate debt sector, which often slips under the radar. Thanks to ultra-low interest rates, nonfinancial corporate debt has more than doubled over the last decade, growing by $37 trillion to reach $66 trillion in mid-2017, according to MGI. Approximately two thirds of the growth in corporate debt has come from developing countries, which comes with heightened risk, especially when loans are issued in USD.7 Turkey and Argentina are feeling this pain (see above chart), as their currencies have outright collapsed, with a significant share of debt in foreign currencies, large external financing needs and high domestic inflation, among other factors. Contagion has been limited to emerging markets thus far, and the hope is that it will remain contained.

Not surprisingly, China has accounted for more than half of the growth in global corporate debt, and now has one of the highest corporate debt ratios in the world. Approximately 30% to 35% of corporate debt in China is associated with construction and real estate,8 which we view as a major risk point. Even though a housing and/or credit crisis in China has yet to come to bear, that doesn’t mean it eventually won’t.

Globally, corporate borrowers have shifted toward bond financing instead of bank loans, as demand has been strong, with bond investors starved for yield. Unfortunately, over the past decade there has been a deterioration in credit quality. According to PIMCO, the net leverage ratio for investment grade BBB issuers has risen from 1.7 times in 2000 to 2.9 times in 2017, a significant increase. The debt rating agencies’ willingness to move the goal posts is a troubling development. Meanwhile, loan covenant quality has recently hit record lows, according to Moody’s,9 while corporate defaults are already above their 30-year average, despite an extraordinarily low interest-rate environment.10

____________

5 | “Global Debt Monitor – July 2018.” Institute of International Finance, July 19, 2018. |

6 | “IIF Quarterly Global Debt Monitor – May 2018.” Institute of International Finance, May, 2018. GDP data taken from IMF database (https://www.imf.org/external/datamapper/datasets/WEO/1). |