UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07883

ICON Funds

(Exact name of registrant as specified in charter)

5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Address of principal executive offices) (Zip code)

Erik L. Jonson 5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-790-1600

Date of fiscal year end: September 30, 2012

Date of reporting period: September 30, 2012

Item 1. Reports to Stockholders.

2012 ANNUAL REPORT

ICON DIVERSIFIED FUNDS

INVESTMENT UPDATE

ICON Bond Fund

ICON Equity Income Fund

ICON Fund (formerly ICON Core Equity Fund)

ICON Long/Short Fund

ICON Risk-Managed Equity Fund

1-800-764-0442 | www.iconfunds.com

AR-DIV-12-K31247

You can now sign up for electronic delivery of ICON Fund shareholder reports, including prospectuses, annual reports, semiannual reports and proxy statements.

When these materials are available, you will receive an email from ICON with instructions on how to view the documents. Statements, transaction confirmations and other documents that are not available online will continue to be sent to you by U.S. mail.

Visit ICON’s website at www.iconfunds.com to learn more and sign up.

You may change or cancel your participation in eDelivery by visiting www.iconfunds.com, or you can request a hard copy of any of the materials free of charge by calling ICON Funds at 1-800-764-0442.

1-800-764-0442 • www.iconfunds.com

TABLEOF CONTENTS

ABOUT THIS REPORT (UNAUDITED)

Historical Returns

All total returns mentioned in this Report account for the change in a Fund’s per-share price and the reinvestment of any dividends, capital gain distributions and adjustments for financial statement purposes. If your account is set up to receive Fund distributions in cash rather than to reinvest them, your actual return may differ from these figures. The Funds’ performance results do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Adviser may have reimbursed certain fees or expenses of some of the Funds. If not for these reimbursements, performance would have been lower. Fund results shown, unless otherwise indicated, are at net asset value. If a sales charge (maximum 5.75%) had been deducted, results would have been lower.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance results represent past performance, and current performance may be higher or lower. Please call 1-800-764-0442 or visit www.iconfunds.com for performance results current to the most recent month-end.

Portfolio Data

This Report reflects ICON’s views, opinions and portfolio holdings as of September 30, 2012, the end of the reporting period. The information is not a complete analysis of every aspect of any sector, industry, security or the Funds.

Opinions and forecasts regarding industries, companies and/or themes, and portfolio composition and holdings are subject to change at any time based on market and other conditions, and should not be construed as a recommendation of any specific security, industry or sector. Each Fund’s holdings as of September 30, 2012 are included in each Fund’s Schedule of Investments.

According to ICON, value investing is an analytical approach to investing that employs various factors, including projecting earnings growth estimates, in an effort to determine whether securities are over- or underpriced relative to ICON’s estimates of their intrinsic value. Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies. ICON’s value-to-price ratio (“V/P”) is a ratio of intrinsic value, as calculated using ICON’s proprietary valuation methodology, of a broad range of domestic and international securities

within ICON’s system as compared to the current market price of those securities. The ICON system relies on the integrity of the financial statements released to the market as part of our analysis.

This Report contains statements regarding industry or sector themes, new market themes, investment outlook, relative strength, value-to-price ratios, and investment team expectations, beliefs, goals and the like that are based on current expectations, recent individual stock performance relative to current market prices, estimates of company values and other information supplied to the market by the companies we follow. Words such as “expects,” “suggests,” “anticipates,” “targets,” “goals,” “value,” “intrinsic value,” “indicates,” “believes,” “considers,” “estimates,” variations of such words and similar expressions are intended to identify forward looking statements, which are not statements of historical fact. Forward looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to assess. These risks and uncertainties are based on a number of important factors, including, among others: stock price fluctuations; the integrity and accuracy of historical and projected financial and other information supplied by companies to the public or assumptions based on such information supplied; interest rates; bond yields; future earnings growth rates; the risks noted in this Report and other factors beyond the control of our investment team but used by the investment team to influence their assumptions. Therefore, actual outcome may differ materially from what is expressed in such forward looking statements.

There are risks associated with mutual fund investing, including the loss of principal. The likelihood of loss may be greater if you invest for a shorter period of time. There is no assurance that the investment process will consistently lead to successful results.

There are risks associated with selling short, including the risk that the ICON Long/Short Fund may have to cover its short position at a higher price than the short price, resulting in a loss. The ICON Long/Short Fund’s loss on a short sale is potentially unlimited as a loss occurs when the value of a security sold short increases. Call options involve certain risks, such as limited gains and lack of liquidity in the underlying securities, and are not suitable for all investors.

Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securities generally decreases. The ICON Bond Fund may invest up to 25% of its assets in high-yield bonds that are below investment grade. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher-quality bonds.

An investment concentrated in sectors and industries may involve greater risk and volatility than a more diversified investment.

Investments in foreign securities may entail unique risks, including political, market, and currency risks. Financial statements of foreign companies are governed by different accounting, auditing, and financial standards than U.S. companies and may be less transparent and uniform than in the United States. Many corporate governance standards, which help ensure the integrity of public information in the United States, do not exist in foreign countries. In general, there may be less governmental supervision of foreign stock exchanges and securities brokers and issuers. The ICON system relies on the integrity of financial statements released to the market as part of our analysis.

The prospectus and statement of additional information contain this and other information about the Funds and are available by visiting www.iconfunds.com or calling 1-800-764-0442. Please read the prospectus and statement of additional information carefully.

Comparative Indexes

The comparative indexes discussed in this Report are meant to provide a basis for judging a Fund’s performance against specific securities indexes. Each index shown accounts for both change in the security price and reinvestment of dividends and distributions (except as noted), but does not reflect the costs of managing a mutual fund. The Funds’ portfolios may significantly differ in holdings and composition from the index. Individuals cannot invest directly in an index.

| • | | The unmanaged Standard & Poor’s (“S&P”) Composite 1500 Index (“S&P Composite 1500 Index”) is a broad-based capitalization-weighted index comprising 1,500 stocks of large-cap, mid-cap, and small-cap U.S. companies. |

| • | | The unmanaged Barclays Capital U.S. Universal Index (ex-MBS) represents the union of the U.S. Aggregate Index, the U.S. High-Yield Corporate Index, the 144A Index, the Eurodollar Index and the Emerging Markets Index. All securities in this market-value weighted index have at least one year remaining to maturity and meet certain minimum issue size criteria. |

Index returns and statistical data included in this Report are provided by FactSet Research Systems.

Financial Intermediary

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may influence the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| | | | |

MANAGEMENT OVERVIEW ICON BOND FUND | | Class C Class S Class A | | IOBCX IOBZX IOBAX |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | For the Fund’s fiscal year ended September 30, 2012, the ICON Bond Fund outperformed its benchmark, the Barclays Capital US Universal Index ex MBS. The Fund’s Class S shares returned 9.93%, while the Barclays Capital US Universal ex MBS Index returned 7.48%. Class C shares returned 8.98% (8.13% with contingent deferred sales charge applied) while the Fund’s Class A shares returned 9.66% (4.49% with maximum sales charge). Total returns for other periods as of September 30, 2012 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Mirroring a trend seen in the equity markets, the fixed income market stabilized somewhat during fiscal year 2012 as investors shifted their focus towards solid fundamentals and away from European macro-economic concerns. Virtually all segments of the fixed income market produced positive returns during the fiscal year, with the largest returns coming from the corporate segment. Historically low default rates coupled with higher than normal credit spreads appealed to investors looking for more attractive yield opportunities than those presented by the US treasury market. The ICON Bond Fund’s focus on the corporate segment of the fixed income market was one of the main reasons the Fund outperformed its benchmark over the 12-month period. |

During the first six months of the fiscal year, the U.S. Generic Government 10-year Treasury security maintained a relatively tight yield range, trading right around 2%. Throughout this six-month period, corporate bonds led the fixed income segment of the market with especially strong returns coming from junk rated securities. The ICON Bond Fund performed well during this time period, as we had a significant underweight in the treasury segment of the market relative to the benchmark and a large overweight in the corporate segment with an emphasis on high yield. The second six months of the fiscal year began with a rather aggressive treasury rally, as yields on the U.S. Generic Government 10-year Treasury security fell from around 2% to approximately 1.6%. While corporate bonds still fared well during the second half of the fiscal year, the returns declined significantly as investor focus shifted more towards the relative safety of US treasuries and instruments with higher credit ratings. The ICON Bond Fund continued to outperform its benchmark in the second half of the fiscal

year. ICON model valuations pointed us towards a general increase in our treasury exposure and improvement in overall fund credit quality.

| Q. | How did the Fund’s composition affect performance? |

| A. | The Fund’s overweight position in corporate bonds contributed positively to Fund performance. Additionally, appropriately timed treasury exposure and improvement of fund credit quality resulted in the Fund’s outperforming its benchmark when investor sentiment shifted in the middle of the fiscal year. The Fund’s corporate bond allocation also resulted in relative outperformance as ICON’s valuation metrics guided us towards an overweight position in the investment grade and high yield segment of the market. Both of these areas outperformed the broad fixed income benchmark during the fiscal year. Finally, a small allocation to floating rate securities (that is, securities with variable interest rates) within the Fund contributed positively to overall performance. |

| Q. | What is your investment outlook for the bond market? |

| A. | ICON’s valuation system, which is quantitatively based on comparing historical relationships across the credit curve to current relationships, continues to see the most value within the corporate segment of the fixed income market. More specifically, we see a unique distribution of attractive valuations with opportunity in mid- to long-term high quality corporates and also in shorter term high yield bonds. Historically low default rates and wider than normal credit spreads provide investors with attractive yield opportunities for the risk they are taking. In the Treasury segment of the fixed income market, the yield curve has flattened out over the course of the last few months, with short-term interest rates nearing long-term interest rates, as the Federal Reserve continues to remain active in the market by implementing their most recent quantitative easing program. While we continue to see value in corporates, we remain cautious on treasury bonds. Although yields remain historically low, Fed intervention seems to be providing a general ceiling above rates for the time being and we don’t foresee a substantial upward movement in yields at this time. |

ICON Bond Fund

Credit Diversification

September 30, 2012

| | | | |

Aaa | | | 18.8% | |

Aa2 | | | 4.9% | |

Aa3 | | | 1.7% | |

A1 | | | 3.6% | |

A2 | | | 2.7% | |

A3 | | | 4.2% | |

Baa1 | | | 17.3% | |

Baa2 | | | 13.7% | |

Baa3 | | | 12.2% | |

Ba1 | | | 2.6% | |

Ba2 | | | 3.4% | |

| | | | |

Ba3 | | | 4.3% | |

B1 | | | 1.2% | |

B2 | | | 1.4% | |

B3 | | | 1.1% | |

| | | | |

| | | 93.1% | |

| | | | |

Percentages are based upon U.S. Treasury obligations, corporate and foreign corporate bond investments as a percentage of net assets.

Ratings based on Moody’s Investors Service, Inc.

ICON Bond Fund

Average Annual Total Return

as of September 30, 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Bond Fund - Class C | | | 10/21/02 | | | | 8.98% | | | | 5.52% | | | | 4.93% | | | | 2.16% | | | | 1.60% | |

Barclays Capital U.S. Universal Index (ex-MBS) | | | | | | | 7.48% | | | | 6.61% | | | | 6.20% | | | | N/A | | | | N/A | |

ICON Bond Fund - Class S | | | 5/6/04 | | | | 9.93% | | | | 6.42% | | | | 5.43% | | | | 1.18% | | | | 0.75% | |

Barclays Capital U.S. Universal Index (ex-MBS) | | | | | | | 7.48% | | | | 6.61% | | | | 5.98% | | | | N/A | | | | N/A | |

ICON Bond Fund - Class A | | | 9/30/10 | | | | 9.66% | | | | N/A | | | | 4.70% | | | | 5.83% | | | | 1.01% | |

ICON Bond Fund - Class A (including maximum sales charge of 4.75%) | | | 9/30/10 | | | | 4.49% | | | | N/A | | | | 2.18% | | | | 5.83% | | | | 1.01% | |

Barclays Capital U.S. Universal Index (ex-MBS) | | | | | | | 7.48% | | | | 6.61% | | | | 5.96% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Advisor has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

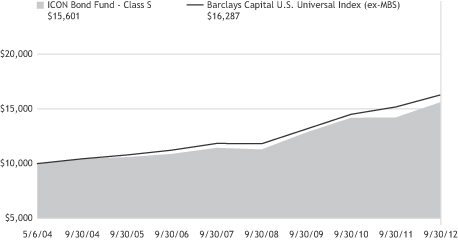

ICON Bond Fund

Value of a $10,000 Investment

through September 30, 2012

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Fund’s other share classes will vary due to differences in charges and expenses. The Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON BOND FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2012

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| | Corporate Bonds (73.6%) | | | | | | | | | | | | |

| $ | 220,000 | | | ACE INA Holdings, Inc. | | | 8.88 | % | | | 08/15/29 | | | $ | 335,095 | |

| | 500,000 | | | Ally Financial, Inc. | | | 6.75 | % | | | 12/01/14 | | | | 533,880 | |

| | 152,000 | | | Altria Group, Inc. | | | 9.25 | % | | | 08/06/19 | | | | 215,826 | |

| | 450,000 | | | Altria Group, Inc. | | | 9.95 | % | | | 11/10/38 | | | | 756,612 | |

| | 1,000,000 | | | Ameren Energy Generating Co.(a) | | | 7.00 | % | | | 04/15/18 | | | | 970,000 | |

| | 1,440,000 | | | American Express Bank FSB(b) | | | 0.53 | % | | | 06/12/17 | | | | 1,390,195 | |

| | 1,000,000 | | | American Express Co. | | | 7.00 | % | | | 03/19/18 | | | | 1,265,613 | |

| | 900,000 | | | American International Group, Inc. | | | 4.25 | % | | | 05/15/13 | | | | 918,207 | |

| | 500,000 | | | AmeriGas Finance LLC/AmeriGas Finance Corp. | | | 7.00 | % | | | 05/20/22 | | | | 538,750 | |

| | 500,000 | | | Amgen, Inc. | | | 3.88 | % | | | 11/15/21 | | | | 537,261 | |

| | 900,000 | | | AT&T, Inc. | | | 5.80 | % | | | 02/15/19 | | | | 1,119,477 | |

| | 300,000 | | | AutoNation, Inc. | | | 5.50 | % | | | 02/01/20 | | | | 320,250 | |

| | 800,000 | | | Avnet, Inc. | | | 6.00 | % | | | 09/01/15 | | | | 875,575 | |

| | 500,000 | | | B&G Foods, Inc. | | | 7.63 | % | | | 01/15/18 | | | | 540,000 | |

| | 1,000,000 | | | Ball Corp. | | | 5.00 | % | | | 03/15/22 | | | | 1,047,500 | |

| | 950,000 | | | Bank of America NA(b) | | | 0.69 | % | | | 06/15/17 | | | | 873,580 | |

| | 1,000,000 | | | BB&T Corp. | | | 5.25 | % | | | 11/01/19 | | | | 1,157,196 | |

| | 950,000 | | | Berkshire Hathaway Finance Corp. | | | 4.25 | % | | | 01/15/21 | | | | 1,082,277 | |

| | 700,000 | �� | | Berkshire Hathaway Finance Corp.(a) | | | 3.00 | % | | | 05/15/22 | | | | 725,672 | |

| | 500,000 | | | CA, Inc. | | | 5.38 | % | | | 12/01/19 | | | | 572,976 | |

| | 450,000 | | | Central Garden and Pet Co. | | | 8.25 | % | | | 03/01/18 | | | | 477,000 | |

| | 400,000 | | | Chesapeake Energy Corp.(a) | | | 9.50 | % | | | 02/15/15 | | | | 440,500 | |

| | 550,000 | | | CIT Group, Inc. | | | 5.00 | % | | | 08/15/22 | | | | 572,223 | |

| | 9,000 | | | Citigroup, Inc. | | | 6.00 | % | | | 08/15/17 | | | | 10,483 | |

| | 450,000 | | | Coca-Cola Co. | | | 4.88 | % | | | 03/15/19 | | | | 536,413 | |

| | 450,000 | | | Comcast Cable Holdings, LLC | | | 9.46 | % | | | 11/15/22 | | | | 671,866 | |

| | 1,000,000 | | | Commercial Metals Co. | | | 7.35 | % | | | 08/15/18 | | | | 1,052,500 | |

| | 400,000 | | | Constellation Brands, Inc. | | | 7.25 | % | | | 09/01/16 | | | | 458,000 | |

| | 114,000 | | | Cox Communications, Inc. | | | 7.63 | % | | | 06/15/25 | | | | 143,512 | |

| | 450,000 | | | Dean Foods Co. | | | 6.90 | % | | | 10/15/17 | | | | 479,250 | |

| | 400,000 | | | DISH DBS Corp. | | | 7.13 | % | | | 02/01/16 | | | | 442,000 | |

| | 800,000 | | | Dollar General Corp. | | | 4.13 | % | | | 07/15/17 | | | | 836,000 | |

| | 500,000 | | | Ecolab, Inc. | | | 4.35 | % | | | 12/08/21 | | | | 567,236 | |

| | 300,000 | | | Endo Health Solutions, Inc. | | | 7.00 | % | | | 07/15/19 | | | | 323,250 | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 11 | |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| $ | 450,000 | | | Entergy Corp. | | | 3.63 | % | | | 09/15/15 | | | $ | 473,382 | |

| | 500,000 | | | ERP Operating L.P. | | | 5.38 | % | | | 08/01/16 | | | | 573,528 | |

| | 750,000 | | | Exelon Generation Co., LLC | | | 6.20 | % | | | 10/01/17 | | | | 892,646 | |

| | 900,000 | | | Exelon Generation Co., LLC | | | 4.00 | % | | | 10/01/20 | | | | 954,542 | |

| | 500,000 | | | Fiserv, Inc. | | | 4.75 | % | | | 06/15/21 | | | | 547,015 | |

| | 400,000 | | | Ford Motor Credit Co., LLC | | | 8.00 | % | | | 06/01/14 | | | | 441,742 | |

| | 1,000,000 | | | Ford Motor Credit Co., LLC | | | 5.63 | % | | | 09/15/15 | | | | 1,093,068 | |

| | 900,000 | | | Gap, Inc. | | | 5.95 | % | | | 04/12/21 | | | | 1,002,527 | |

| | 500,000 | | | General Electric Capital Corp. | | | 4.75 | % | | | 09/15/14 | | | | 537,731 | |

| | 1,000,000 | | | General Electric Capital Corp.(b) | | | 0.64 | % | | | 05/11/16 | | | | 973,094 | |

| | 500,000 | | | Google, Inc. | | | 3.63 | % | | | 05/19/21 | | | | 562,523 | |

| | 1,000,000 | | | HCP, Inc. | | | 5.65 | % | | | 12/15/13 | | | | 1,055,436 | |

| | 1,500,000 | | | HCP, Inc. | | | 6.30 | % | | | 09/15/16 | | | | 1,718,452 | |

| | 500,000 | | | HCP, Inc. | | | 6.70 | % | | | 01/30/18 | | | | 599,598 | |

| | 450,000 | | | Hospira, Inc. | | | 6.05 | % | | | 03/30/17 | | | | 520,331 | |

| | 500,000 | | | Hospira, Inc. | | | 5.60 | % | | | 09/15/40 | | | | 528,066 | |

| | 500,000 | | | International Lease Finance Corp. | | | 4.88 | % | | | 04/01/15 | | | | 519,706 | |

| | 300,000 | | | Jarden Corp. | | | 7.50 | % | | | 01/15/20 | | | | 331,500 | |

| | 474,700 | | | JC Penney Corp., Inc. | | | 7.95 | % | | | 04/01/17 | | | | 490,128 | |

| | 800,000 | | | JC Penney Corp., Inc.(a) | | | 5.75 | % | | | 02/15/18 | | | | 760,000 | |

| | 450,000 | | | John Hancock Life Insurance Co.(c)(d) | | | 7.38 | % | | | 02/15/24 | | | | 564,696 | |

| | 1,200,000 | | | Johnson & Johnson | | | 2.95 | % | | | 09/01/20 | | | | 1,302,521 | |

| | 1,000,000 | | | JPMorgan Chase Bank NA(b) | | | 0.73 | % | | | 06/13/16 | | | | 963,778 | |

| | 450,000 | | | Juniper Networks, Inc. | | | 3.10 | % | | | 03/15/16 | | | | 470,835 | |

| | 900,000 | | | Kellogg Co. | | | 4.00 | % | | | 12/15/20 | | | | 1,008,932 | |

| | 500,000 | | | Life Technologies Corp. | | | 3.50 | % | | | 01/15/16 | | | | 526,285 | |

| | 400,000 | | | Limited Brands, Inc. | | | 5.63 | % | | | 02/15/22 | | | | 431,000 | |

| | 900,000 | | | Lockheed Martin Corp. | | | 4.25 | % | | | 11/15/19 | | | | 1,018,563 | |

| | 1,400,000 | | | Lorillard Tobacco Co.(a) | | | 6.88 | % | | | 05/01/20 | | | | 1,718,660 | |

| | 500,000 | | | Mead Johnson Nutrition Co. | | | 4.90 | % | | | 11/01/19 | | | | 570,531 | |

| | 450,000 | | | Medco Health Solutions, Inc. | | | 2.75 | % | | | 09/15/15 | | | | 470,716 | |

| | 350,000 | | | Merrill Lynch & Co., Inc. | | | 5.45 | % | | | 02/05/13 | | | | 355,348 | |

| | 900,000 | | | Microsoft Corp. | | | 5.30 | % | | | 02/08/41 | | | | 1,184,647 | |

| | 900,000 | | | Morgan Stanley(b) | | | 0.94 | % | | | 10/15/15 | | | | 857,542 | |

| | 950,000 | | | Morgan Stanley(e) | | | 3.50 | % | | | 10/15/20 | | | | 941,388 | |

| | 1,000,000 | | | National City Corp. | | | 6.88 | % | | | 05/15/19 | | | | 1,234,526 | |

| | 900,000 | | | Novartis Capital Corp. | | | 4.40 | % | | | 04/24/20 | | | | 1,061,424 | |

| | 900,000 | | | PepsiCo, Inc. | | | 5.00 | % | | | 06/01/18 | | | | 1,069,688 | |

| | 600,000 | | | Pitney Bowes, Inc.(a) | | | 4.75 | % | | | 05/15/18 | | | | 629,739 | |

| | 750,000 | | | PPL Energy Supply LLC(a) | | | 6.50 | % | | | 05/01/18 | | | | 887,599 | |

| | 900,000 | | | Reynolds American, Inc. | | | 7.25 | % | | | 06/01/13 | | | | 937,324 | |

| | |

| 12 | | SCHEDULEOF INVESTMENTS |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| $ | 1,000,000 | | | Rowan Cos., Inc. | | | 7.88 | % | | | 08/01/19 | | | $ | 1,239,773 | |

| | 1,350,000 | | | Southern Copper Corp. | | | 5.38 | % | | | 04/16/20 | | | | 1,517,620 | |

| | 1,000,000 | | | Suntrust Banks, Inc.(b) | | | 0.76 | % | | | 04/01/15 | | | | 973,212 | |

| | 500,000 | | | Tennessee Gas Pipeline Co. | | | 7.00 | % | | | 10/15/28 | | | | 668,026 | |

| | 400,000 | | | Toll Brothers Finance Corp. | | | 6.75 | % | | | 11/01/19 | | | | 456,276 | |

| | 1,000,000 | | | Torchmark Corp. | | | 6.38 | % | | | 06/15/16 | | | | 1,139,811 | |

| | 450,000 | | | TransDigm, Inc. | | | 7.75 | % | | | 12/15/18 | | | | 497,250 | |

| | 850,000 | | | Valmont Industries, Inc. | | | 6.63 | % | | | 04/20/20 | | | | 1,011,968 | |

| | 500,000 | | | Ventas Realty L.P./Ventas Capital Corp. | | | 4.75 | % | | | 06/01/21 | | | | 549,516 | |

| | 450,000 | | | Vornado Realty L.P. | | | 4.25 | % | | | 04/01/15 | | | | 475,554 | |

| | 500,000 | | | Wachovia Corp. | | | 5.25 | % | | | 08/01/14 | | | | 537,438 | |

| | 450,000 | | | Wal-Mart Stores, Inc. | | | 4.13 | % | | | 02/01/19 | | | | 513,253 | |

| | 500,000 | | | Wal-Mart Stores, Inc. | | | 4.25 | % | | | 04/15/21 | | | | 587,978 | |

| | 900,000 | | | Wells Fargo Bank NA(b) | | | 0.65 | % | | | 05/16/16 | | | | 875,043 | |

| | 1,000,000 | | | Willis North America, Inc. | | | 6.20 | % | | | 03/28/17 | | | | 1,139,592 | |

| | 450,000 | | | Windstream Corp. | | | 8.13 | % | | | 08/01/13 | | | | 472,500 | |

| | | | | | | | | | | | | | | | |

| Total Corporate Bonds

(Cost $64,014,746) | | | | | | | | | | | 68,221,742 | |

| | U.S. Treasury Obligations (16.1%) | | | | | | | | | | | | |

| | 2,500,000 | | | U.S. Treasury Note | | | 2.13 | % | | | 08/15/21 | | | | 2,644,530 | |

| | 2,500,000 | | | U.S. Treasury Note | | | 1.25 | % | | | 01/31/19 | | | | 2,553,320 | |

| | 1,500,000 | | | U.S. Treasury Note | | | 2.00 | % | | | 02/15/22 | | | | 1,560,117 | |

| | 1,500,000 | | | U.S. Treasury Note | | | 0.63 | % | | | 08/31/17 | | | | 1,500,937 | |

| | 2,000,000 | | | U.S. Treasury Note | | | 3.63 | % | | | 02/15/20 | | | | 2,356,876 | |

| | 2,000,000 | | | U.S. Treasury Note | | | 2.38 | % | | | 07/31/17 | | | | 2,169,376 | |

| | 2,000,000 | | | U.S. Treasury Note | | | 1.88 | % | | | 08/31/17 | | | | 2,122,968 | |

| | | | | | | | | | | | | | | | |

| Total U.S. Treasury Obligations

(Cost $14,042,078) | | | | | | | | | | | 14,908,124 | |

| | Foreign Corporate Bonds (3.4%) | | | | | | | | | | | | |

| | 900,000 | | | AngloGold Ashanti Holdings PLC | | | 5.38 | % | | | 04/15/20 | | | | 945,000 | |

| | 1,000,000 | | | Gold Fields Orogen Holding BVI, Ltd.(c)(d) | | | 4.88 | % | | | 10/07/20 | | | | 1,017,108 | |

| | 900,000 | | | Vale Overseas, Ltd. | | | 8.25 | % | | | 01/17/34 | | | | 1,165,378 | |

| | | | | | | | | | | | | | | | |

| Total Foreign Corporate Bonds

(Cost $3,014,159) | | | | | | | | | | | 3,127,486 | |

| | Collateral for Securities on Loan (5.6%) | | | | | | | | | | | | |

| | 5,182,350 | | | State Street Navigator Prime Portfolio | | | | | | | | | | | 5,182,350 | |

| | | | | | | | | | | | | | | | |

| Total Collateral for Securities on Loan

(Cost $5,182,350) | | | | | | | | | | | 5,182,350 | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 13 | |

| | | | | | | | | | | | |

| Shares or Principal Amount | | | | | | Value | |

| | | | | | | | | | | | |

| | Short-Term Investment (7.3%) | | | | | | | | |

| $ | 6,815,975 | | | State Street Euro Dollar Time Deposit (USD),

0.01%, 10/01/12 | | | | | | $ | 6,815,975 | |

| | | | | | | | | | | | |

| Total Short-Term Investments

(Cost $6,815,975) | | | | | | | 6,815,975 | |

| Total Investments 106.0%

(Cost $93,069,308) | | | | | | | 98,255,677 | |

| | Liabilities Less Other Assets (6.0)% | | | | | | | (5,587,500 | ) |

| | | | | | | | | | | | |

| | Net Assets 100.0% | | | | | | $ | 92,668,177 | |

| | | | | | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| (a) | All or a portion of the security was on loan as of September 30, 2012. |

| (b) | Floating Rate Security. Rate disclosed is as of September 30, 2012. |

| (c) | Security was acquired pursuant to Rule 144A of the Securities Act of 1933 and may be deemed to be restricted for resale. |

| (d) | These securities are considered to be illiquid. The aggregate value of the these securities at September 30, 2012 was $1,581,804, which represent 1.7% of the Fund’s Net Assets. |

| (e) | Step Bond – the coupon is at a fixed rate and resets at a specific date and rate. The rate disclosed is as of September 30, 2012. |

| | |

| 14 | | SCHEDULEOF INVESTMENTS |

| | | | |

MANAGEMENT OVERVIEW ICON EQUITY INCOME FUND | | Class S Class C Class A | | IOEZX IOECX IEQAX |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | For the fiscal year ending September 30, 2012, the ICON Equity Income Fund, Class S shares, returned 24.43%, lagging its S&P Composite 1500 Index benchmark, which rose 30.18%. The Fund’s Class A shares returned 24.10% (and 16.95% with maximum sales charge) and the Fund’s Class C shares returned 23.31% (22.31% with contingent deferred sales charge) during the same period. Total returns for other periods as of September 30, 2012 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Concerns regarding Europe’s economic woes spreading to the US were validated by sub-2% year-over-year GDP growth reported for the first two quarters of 2011. Over the course of the 12-month fiscal year, these concerns have abated somewhat. GDP year-over-year growth rates have held above 2% since the last quarter of 2011, moderating the anticipated adverse effect for the European crises. Action by the Federal Reserve, and, in particular, the Fed’s continued quantitative easing, has also proven generally positive for the equity markets. Still, as the broad market rose, dividend paying stocks, including those in the Fund, had a difficult time keeping pace. Stocks in the Fund’s benchmark with reported dividend yields 2% or higher had a weighted average return of 28% versus a 32% return for stocks with dividend yields below 2%. This underperformance created a head wind for the Equity Income Fund and the Fund’s dividend paying holdings proved detrimental to the Fund’s relative performance. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The ICON Equity Income Fund’s composition can be analyzed by both asset class and the individual securities that reflect each asset class. The Fund held fixed income securities over the course of the fiscal year, including both corporate bonds and preferred equities. Yields, on average, fell over the course of the year and there was a general tightening of corporate spreads relative to treasuries, which was beneficial to the Fund’s fixed-income holdings. Financial bonds in particular benefitted from these corporate spreads. For example, the Fund held a position in 2020 Goldman Sachs bonds priced at 99.31 on September 30, 2011 and by the end of the fiscal year the bond had |

| | appreciated to 111.60. While this 12% gain is impressive for a fixed-income security, it is not enough, even with the interest paid over the year, to compete with the 30.18% returns for the broad equity market over the same 12-month period. As a result, the 6% weighted average in fixed income securities held by the Fund during the fiscal year was a net detractor from the Fund’s relative performance. |

The fixed-income positions alone do not fully explain the Fund’s underperformance, however. The Fund’s equity holdings likewise lagged the Fund’s S&P 1500 benchmark. This underperformance is due primarily to the Fund’s exposure in the Financials and Energy sectors. In the Financials sector, for example, the Fund’s asset management industry holdings had a weighted average return of about 12% compared to a 34% return for the industry’s benchmark’s position. In contrast, the Fund’s overweight of the Consumer Discretionary sector was a positive factor and helped offset some of the underperformance from the Fund’s Energy and Financials sector holdings.

Derivative products also played a role in Fund performance. In light of the liquidity and general lack of availability of convertible bonds, the Fund occasionally held a combination of fixed-income securities paired with long equity call options to approximate a convertible bond. Over the past year, these positions were a net positive for the Fund. For example, the Fund held a blended position of Delphi Financial Group Bonds and corresponding positions of long Delphi Financial Group calls. On December 21, 2011 Delphi was bought out at $43.875 per share. This buy out price put the call options in the money and the price of the option rose substantially, contributing to Fund performance.

| Q. | What is your investment outlook for the overall market? |

| A. | In light of the most recent round of quantitative easing initiated by the Federal Reserve in September 2012 and an overall average value-to-price ratio for the domestic market of 1.39 as we head into fiscal year 2013, we are optimistic regarding the opportunities for the ICON Equity Income Fund. Additionally, we have seen a number of companies increase the size of their dividends or paying dividends for the first time. This, in turn, may create more opportunities for the Fund and our investors. |

ICON Equity Income Fund

Sector Composition

September 30, 2012

| | | | |

Industrials | | | 17.8% | |

Financial | | | 15.9% | |

Consumer Discretionary | | | 15.8% | |

Energy | | | 11.3% | |

Health Care | | | 9.5% | |

Consumer Staples | | | 8.1% | |

Information Technology | | | 7.9% | |

Utilities | | | 5.9% | |

Materials | | | 2.8% | |

| | | | |

| | | 95.0% | |

| | | | |

Percentages are based upon common and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Industry Composition

September 30, 2012

| | | | |

Integrated Oil & Gas | | | 8.2% | |

Pharmaceuticals | | | 5.0% | |

Integrated Telecommunication Services | | | 4.8% | |

Systems Software | | | 4.2% | |

Industrial Conglomerates | | | 4.1% | |

Asset Management & Custody Banks | | | 2.9% | |

Aerospace & Defense | | | 2.7% | |

Leisure Products | | | 2.7% | |

Diversified Banks | | | 2.6% | |

Industrial Machinery | | | 2.6% | |

Cable & Satellite | | | 2.4% | |

Health Care Equipment | | | 2.4% | |

Movies & Entertainment | | | 2.4% | |

Tobacco | | | 2.4% | |

Other Diversified Financial Services | | | 2.2% | |

Packaged Foods & Meats | | | 2.1% | |

Biotechnology | | | 2.1% | |

Consumer Finance | | | 2.1% | |

Mortgage REIT’s | | | 2.1% | |

Specialized REIT’s | | | 2.0% | |

Environmental & Facilities Services | | | 1.8% | |

Oil & Gas Drilling | | | 1.8% | |

Electrical Components & Equipment | | | 1.8% | |

Internet Software & Services | | | 1.6% | |

| | | | |

Advertising | | | 1.6% | |

Restaurants | | | 1.6% | |

Steel | | | 1.6% | |

General Merchandise Stores | | | 1.4% | |

Brewers | | | 1.4% | |

Computer & Electronics Retail | | | 1.4% | |

Thrifts & Mortgage Finance | | | 1.3% | |

Construction & Farm Machinery & Heavy Trucks | | | 1.3% | |

Oil & Gas Refining & Marketing | | | 1.3% | |

Soft Drinks | | | 1.3% | |

Publishing | | | 1.2% | |

Industrial Gases | | | 1.2% | |

Air Freight & Logistics | | | 1.2% | |

Office Electronics | | | 1.2% | |

Railroads | | | 1.2% | |

Diversified Support Services | | | 1.1% | |

Wireless Telecommunication Services | | | 1.0% | |

Computer Storage & Peripherals | | | 1.0% | |

Home Improvement Retail | | | 1.0% | |

Other Industries (each less than 1%) | | | 1.7% | |

| | | | |

| | | 95.0% | |

| | | | |

Percentages are based upon common and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Average Annual Total Return

as of September 30, 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Equity Income Fund - Class C | | | 11/8/02 | | | | 23.31% | | | | -0.86% | | | | 5.97% | | | | 2.53% | | | | 2.20% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 7.47% | | | | N/A | | | | N/A | |

ICON Equity Income Fund - Class S | | | 5/10/04 | | | | 24.43% | | | | 0.14% | | | | 4.98% | | | | 3.99% | | | | 1.20% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 5.90% | | | | N/A | | | | N/A | |

ICON Equity Income Fund - Class A | | | 5/31/06 | | | | 24.10% | | | | -0.13% | | | | 2.52% | | | | 1.91% | | | | 1.45% | |

ICON Equity Income Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | 16.95% | | | | -1.31% | | | | 1.56% | | | | 1.91% | | | | 1.45% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 4.34% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

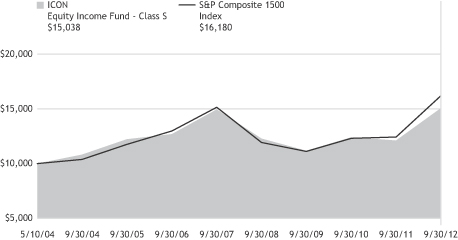

ICON Equity Income Fund

Value of a $10,000 Investment

through September 30, 2012

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Fund’s Class S shares on the Class’ inception date of 5/10/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Fund’s other share classes will vary due to differences in charges and expenses. The Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON EQUITY INCOME FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2012

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (92.9%) | |

| | 3,800 | | | 3M Co. | | $ | 351,196 | |

| | 3,400 | | | Air Products & Chemicals, Inc. | | | 281,180 | |

| | 8,000 | | | Altria Group, Inc. | | | 267,120 | |

| | 28,100 | | | Annaly Capital Management, Inc., REIT(a) | | | 473,204 | |

| | 5,200 | | | AstraZeneca PLC, ADR | | | 248,872 | |

| | 6,400 | | | AT&T, Inc. | | | 241,280 | |

| | 4,100 | | | Baxter International, Inc. | | | 247,066 | |

| | 5,400 | | | BCE, Inc. | | | 237,276 | |

| | 4,500 | | | BP PLC, ADR | | | 190,620 | |

| | 8,400 | | | CA, Inc. | | | 216,426 | |

| | 3,500 | | | Caterpillar, Inc. | | | 301,140 | |

| | 3,400 | | | Chevron Corp. | | | 396,304 | |

| | 12,800 | | | CSX Corp. | | | 265,600 | |

| | 6,500 | | | Darden Restaurants, Inc. | | | 362,375 | |

| | 6,600 | | | Dr. Pepper Snapple Group, Inc. | | | 293,898 | |

| | 5,600 | | | Eaton Corp.(a) | | | 264,656 | |

| | 8,400 | | | Emerson Electric Co. | | | 405,468 | |

| | 15,600 | | | ENI SpA, ADR | | | 683,904 | |

| | 7,700 | | | Ensco PLC, Class A | | | 420,112 | |

| | 10,400 | | | Entertainment Properties Trust, REIT | | | 462,072 | |

| | 6,700 | | | Exxon Mobil Corp. | | | 612,715 | |

| | 13,500 | | | Federated Investors, Inc., Class B(a) | | | 279,315 | |

| | 15,000 | | | GameStop Corp., Class A(a) | | | 315,000 | |

| | 26,000 | | | General Electric Co. | | | 590,460 | |

| | 7,000 | | | Hasbro, Inc. | | | 267,190 | |

| | 11,300 | | | Healthcare Services Group, Inc. | | | 258,431 | |

| | 4,500 | | | HJ Heinz Co. | | | 251,775 | |

| | 5,600 | | | Illinois Tool Works, Inc. | | | 333,032 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | 11,200 | | | j2 Global, Inc.(a) | | $ | 367,584 | |

| | 5,900 | | | Johnson & Johnson | | | 406,569 | |

| | 12,300 | | | JPMorgan Chase & Co. | | | 497,904 | |

| | 4,400 | | | Lockheed Martin Corp. | | | 410,872 | |

| | 7,300 | | | Lowe’s Cos., Inc. | | | 220,752 | |

| | 1,900 | | | M&T Bank Corp. | | | 180,804 | |

| | 10,100 | | | Mattel, Inc. | | | 358,348 | |

| | 7,200 | | | Medtronic, Inc. | | | 310,464 | |

| | 25,100 | | | Microsoft Corp. | | | 747,478 | |

| | 7,100 | | | Molson Coors Brewing Co., Class B | | | 319,855 | |

| | 8,300 | | | Nippon Telegraph & Telephone Corp., ADR | | | 196,793 | |

| | 9,400 | | | Nucor Corp. | | | 359,644 | |

| | 7,100 | | | Omnicom Group, Inc. | | | 366,076 | |

| | 61,900 | | | PDL BioPharma, Inc.(a) | | | 476,011 | |

| | 25,500 | | | People’s United Financial, Inc. | | | 309,570 | |

| | 20,200 | | | Pfizer, Inc. | | | 501,970 | |

| | 15,500 | | | Republic Services, Inc. | | | 426,405 | |

| | 6,500 | | | Reynolds American, Inc. | | | 281,710 | |

| | 6,000 | | | Rogers Communications, Inc., Class B | | | 242,400 | |

| | 5,200 | | | Target Corp. | | | 330,044 | |

| | 10,000 | | | Thomson Reuters Corp. | | | 288,600 | |

| | 5,900 | | | Time Warner Cable, Inc. | | | 560,854 | |

| | 6,100 | | | Time Warner, Inc. | | | 276,513 | |

| | 6,300 | | | Unilever PLC, ADR | | | 230,076 | |

| | 3,900 | | | United Parcel Service, Inc., Class B | | | 279,123 | |

| | 2,800 | | | United Technologies Corp. | | | 219,212 | |

| | 9,500 | | | Valero Energy Corp. | | | 300,960 | |

| | 9,300 | | | Verizon Communications, Inc. | | | 423,801 | |

| | 5,200 | | | Viacom, Inc., Class B | | | 278,668 | |

| | |

| 20 | | SCHEDULEOF INVESTMENTS |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | 11,800 | | | Waddell & Reed Financial, Inc., Class A | | $ | 386,686 | |

| | 5,900 | | | Walgreen Co. | | | 214,996 | |

| | 17,500 | | | Wells Fargo & Co. | | | 604,275 | |

| | 5,900 | | | Western Digital Corp. | | | 228,507 | |

| | 36,500 | | | Xerox Corp. | | | 267,910 | |

| | | | | | | | |

| Total Common Stocks

(Cost $19,509,798)

| | | 21,389,121 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Preferred Stock (2.1%) | |

| | 18,400 | | | Capital One Capital II(a) | | $ | 474,904 | |

| | | | | | | | |

| Total Preferred Stocks

(Cost $472,753) | | | 474,904 | |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | Corporate Bonds (4.0%) | |

| $ | 350,000 | | | Commercial Metals Co. | | | 7.35% | | | | 08/15/18 | | | $ | 368,375 | |

| | 500,000 | | | Goldman Sachs Group, Inc. | | | 5.38% | | | | 03/15/20 | | | | 557,983 | |

| | | | | | | | | | | | | | | | |

| Total Corporate Bonds

(Cost $879,430) |

| | | 926,358 | |

| | | | | | | | |

| Underlying Security/Expiration Date/Exercise Price | | Contracts* | | | Value | |

| Call Options Purchased (0.2%) | | | | | |

Archer-Daniels-Midland Co., January 2013, $35.00 | | | 69 | | | $ | 276 | |

Commercial Metals Co., December 2012, $13.00 | | | 200 | | | | 19,000 | |

Goldman Sachs Group, Inc., January 2013, $120.00 | | | 42 | | | | 16,485 | |

| | | | | | | | |

Total Call Options Purchased

(Cost $88,318) | | | | 35,761 | |

| | | | | | |

| |

| Shares or Principal Amount | | Value | |

| Collateral for Securities on Loan (7.2%) | |

| 1,657,072 | | State Street Navigator Prime Portfolio | | $ | 1,657,072 | |

| | | | | | |

| | Total Collateral for Securities on Loan

(Cost $1,657,072) | | | 1,657,072 | |

| Short-Term Investment (0.5%) | |

| $121,480 | | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/12 | | | 121,480 | |

| | | | | | |

Total Short-Term Investments

(Cost $121,480) | | | 121,480 | |

Total Investments 106.9%

(Cost $22,728,851) | | | 24,604,696 | |

| Liabilities Less Other Assets (6.9)% | | | (1,578,027 | ) |

| | | | | | |

Net Assets 100.0%

| | $ | 23,026,669 | |

| | | | | | |

The accompanying notes are an integral part of the financial statements.

| * | All options have 100 units per contract. |

| (a) | All or a portion of the security was on loan as of September 30, 2012. |

| ADR | American Depositary Receipt |

| REIT | Real Estate Investment Trust |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 21 | |

| | | | |

MANAGEMENT OVERVIEW ICON FUND | | Class C Class S Class A | | ICNCX ICNZX ICNAX |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | The ICON Fund, Class S, returned 28.57% for the fiscal year ended September 30, 2012, underperforming the 30.18% return for the S&P 1500 Composite Index. Class A shares of the Fund returned 28.25% (and 20.82% with maximum sales charge) over the same period. Class C shares of the Fund returned 27.54% for the time period. Total returns for other periods as of September 30, 2012 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| | The S&P 1500 Index gained 30.18% during the fiscal year. On September 30, 2011 we measured an overall domestic market value-to-price (V/P) ratio of 1.52 and never got close to a neutral reading of 1.00 (that is, fair value under ICON’s methodology), over the course of the next 12 months. With value as our guide, we were correctly bullish over this period. We generally minimized cash and, as noted below, tilted toward industries and sectors where we saw the greatest value. |

To take advantage of a 30% gain in the market, investors had to work through two drops of nearly 10%: one in November 2011 and the other in April through May of 2012. ICON did not attempt short term “market timing” and instead rode through these declines, focused on the longer-term value objective. The top three performing sector indexes for the year were Consumer Discretionary, Telecommunication Services and Financials; while the bottom three performing sector indexes were Utilities, Consumer Staples and Energy. Industry and sector leadership was far from steady throughout the year, with a severe theme reversal during the April-May downturn. Cyclical and economically sensitive issues, and in particular issues within the Industrials, Consumer Discretionary and Information Technology sectors, led through the April 2 high, but suffered the worst during the April-May decline. While Energy was the third worst performing sector index over the entire year, it was the best during the June 4 through September 30 advance. We attribute the inconsistent industry and sector behavior to investors frequently changing their outlook for the economy. As their views changed, their sector preferences changed quite a few times over the last year.

| Q. | How did the Fund’s composition affect performance? |

| A. | The largest contributors to Fund performance came from the Consumer Discretionary sector. Cable & satellite providers, Comcast Corp. and Time Warner Cable Inc., as well as movies & entertainment company Walt Disney Co., were among the top 5 largest holdings of the Fund. Combined, these three companies provided just over 7% in total returns to the Fund. Apparel retail companies also contributed to the Fund’s performance, as retailer TJX Cos. returned just over 63% for the year. The Consumer Discretionary sector was the Fund’s largest weighted sector at more than double its benchmark weight. Apple Inc., one of the Fund’s largest holdings, performed well in 2012, growing over 75% with the success of several new product launches and increased sales revenue. |

The Fund was underweight the Health Care sector, positioned at less than one third of the benchmark, yet this sector produced the two largest detractors to Fund performance. Questcor Pharmaceuticals Inc. dropped over 60% in a week after insurer Aetna Inc. said it would limit coverage of the company’s top-selling drug, H.P. Acthar, used to treat multiple sclerosis and infant seizures. Also, Health Care services company Bio-Reference Laboratories Inc. experienced a sharp decline after reports surfaced accusing the company of fraud and poor business practices. These two stocks caused Health Care to be the only sector that produced a negative return to the Fund’s overall performance.

| Q. | What is your investment outlook for the overall market? |

| A. | Going into the new fiscal year, ICON’s valuation system shows a market value-to-price (V/P) ratio of 1.39, suggesting there is still plenty of room for the market to appreciate towards fair value. Because of this valuation reading, we believe we are still in a bull market and we continue to position the Fund in industries that show great value according to our methodology. As fiscal year 2012 ends and fiscal year 2013 begins, the Fund is heavily tilted towards the Consumer Discretionary, Industrials, and Information Technology sectors. |

ICON Fund

Sector Composition

September 30, 2012

| | | | |

Consumer Discretionary | | | 29.6% | |

Industrials | | | 24.9% | |

Information Technology | | | 16.5% | |

Financial | | | 9.9% | |

Materials | | | 8.1% | |

Energy | | | 7.7% | |

Health Care | | | 3.3% | |

| | | | |

| | | 100.0% | |

| | | | |

Percentages are based upon common stock as a percentage of net assets.

ICON Fund

Industry Composition

September 30, 2012

| | | | |

Cable & Satellite | | | 13.6% | |

Industrial Machinery | | | 6.6% | |

IT Consulting & Other Services | | | 6.4% | |

Computer Hardware | | | 6.2% | |

Movies & Entertainment | | | 5.7% | |

Oil & Gas Equipment & Services | | | 5.7% | |

Railroads | | | 5.6% | |

Industrial Gases | | | 5.4% | |

Construction & Farm Machinery & Heavy Trucks | | | 4.4% | |

Electrical Components & Equipment | | | 4.3% | |

Apparel Retail | | | 4.1% | |

Home Improvement Retail | | | 3.5% | |

Other Diversified Financial Services | | | 2.9% | |

| | | | |

Diversified Banks | | | 2.8% | |

Consumer Finance | | | 2.8% | |

Steel | | | 2.8% | |

Footwear | | | 2.7% | |

Industrial Conglomerates | | | 2.5% | |

Communications Equipment | | | 2.3% | |

Biotechnology | | | 2.2% | |

Oil & Gas Drilling | | | 1.9% | |

Computer Storage & Peripherals | | | 1.6% | |

Air Freight & Logistics | | | 1.5% | |

Regional Banks | | | 1.4% | |

Pharmaceuticals | | | 1.1% | |

| | | | |

| | | 100.0% | |

| | | | |

Percentages are based upon common stock as a percentage of net assets.

ICON Fund

Average Annual Total Return

as of September 30, 2012

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Fund - Class C | | | 11/28/00 | | | | 27.54% | | | | -5.89% | | | | 3.30% | | | | 1.89% | | | | 2.27% | | | | 2.25% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 8.34% | | | | 3.15% | | | | N/A | | | | N/A | |

ICON Fund - Class S | | | 5/6/04 | | | | 28.57% | | | | -5.44% | | | | N/A | | | | 1.79% | | | | 2.52% | | | | 1.25% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 8.34% | | | | 5.56% | | | | N/A | | | | N/A | |

ICON Fund - Class A | | | 5/31/06 | | | | 28.25% | | | | -5.99% | | | | N/A | | | | -3.17% | | | | 2.52% | | | | 1.50% | |

ICON Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | 20.82% | | | | -7.10% | | | | N/A | | | | -4.07% | | | | 2.52% | | | | 1.50% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | N/A | | | | 4.34% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Since Inception performance results for Class C shares include returns for certain time periods that were restarted as of June 8, 2004.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

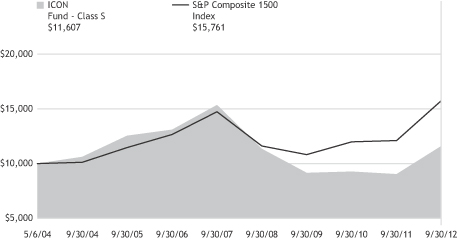

ICON Fund

Value of a $10,000 Investment

through September 30, 2012

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Fund’s other share classes will vary due to differences in charges and expenses. The Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON FUND (FORMERLY, ICON CORE EQUITY FUND)

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2012

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (100.0%) | |

| | 22,100 | | | Accenture PLC, Class A | | $ | 1,547,663 | |

| | 5,000 | | | Apple, Inc. | | | 3,336,300 | |

| | 22,100 | | | BB&T Corp. | | | 732,836 | |

| | 15,800 | | | Cash America International, Inc. | | | 609,406 | |

| | 27,800 | | | Caterpillar, Inc. | | | 2,391,912 | |

| | 15,600 | | | Celgene Corp.† | | | 1,191,840 | |

| | 105,500 | | | Comcast Corp., Class A | | | 3,773,735 | |

| | 61,800 | | | CSX Corp. | | | 1,282,350 | |

| | 18,400 | | | Dover Corp. | | | 1,094,616 | |

| | 21,600 | | | Eaton Corp.(a) | | | 1,020,816 | |

| | 32,100 | | | EMC Corp.† | | | 875,367 | |

| | 48,100 | | | Emerson Electric Co. | | | 2,321,787 | |

| | 38,700 | | | Ezcorp, Inc., Class A† | | | 887,391 | |

| | 11,600 | | | F5 Networks, Inc.† | | | 1,214,520 | |

| | 9,600 | | | FedEx Corp. | | | 812,352 | |

| | 58,200 | | | General Electric Co. | | | 1,321,722 | |

| | 16,400 | | | Halliburton Co. | | | 552,516 | |

| | 24,100 | | | Illinois Tool Works, Inc. | | | 1,433,227 | |

| | 9,100 | | | International Business Machines Corp. | | | 1,887,795 | |

| | 39,000 | | | JPMorgan Chase & Co. | | | 1,578,720 | |

| | 62,300 | | | Lowe’s Cos., Inc. | | | 1,883,952 | |

| | 17,000 | | | National Oilwell Varco, Inc. | | | 1,361,870 | |

| | 6,400 | | | Nike, Inc., Class B | | | 607,424 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | 29,300 | | | Noble Corp. | | $ | 1,048,354 | |

| | 26,400 | | | Nucor Corp. | | | 1,010,064 | |

| | 27,700 | | | Praxair, Inc. | | | 2,877,476 | |

| | 30,700 | | | Questcor Pharmaceuticals, Inc.†(a) | | | 567,950 | |

| | 15,900 | | | Schlumberger, Ltd. | | | 1,150,047 | |

| | 42,300 | | | Steel Dynamics, Inc. | | | 475,029 | |

| | 37,300 | | | Time Warner Cable, Inc. | | | 3,545,738 | |

| | 49,100 | | | TJX Cos., Inc. | | | 2,199,189 | |

| | 14,500 | | | Union Pacific Corp. | | | 1,721,150 | |

| | 30,200 | | | Viacom, Inc., Class B | | | 1,618,418 | |

| | 27,700 | | | Walt Disney Co. | | | 1,448,156 | |

| | 43,600 | | | Wells Fargo & Co. | | | 1,505,508 | |

| | 18,500 | | | Wolverine World Wide, Inc. | | | 820,845 | |

| | | | | | | | |

| Total Common Stocks

(Cost $40,210,439) | | | 53,708,041 | |

| | Collateral for Securities on Loan (2.7%) | |

| | 1,490,742 | | | State Street Navigator Prime Portfolio | | | 1,490,742 | |

| | | | | | | | |

| Total Collateral for Securities

on Loan

(Cost $1,490,742) | | | 1,490,742 | |

| Total Investments 102.7%

(Cost $41,701,181) | | | 55,198,783 | |

| Liabilities Less Other Assets

(2.7)% | | | (1,467,785 | ) |

| | | | | | | | |

| | Net Assets 100.0% | | $ | 53,730,998 | |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (a) | All or a portion of the security was on loan as of September 30, 2012. |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 27 | |

| | | | |

MANAGEMENT OVERVIEW ICON LONG/SHORT FUND | | Class C Class S Class A | | IOLCX IOLZX ISTAX |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | For the 12-months ended September 30, 2012, the ICON Long/Short Fund returned 25.41% for Class S shares, 24.15% for Class C shares (23.15% with contingent deferred sales charge) and 25.09% for Class A shares (17.87% with maximum sales charge), underperforming the 30.18% return for the Fund’s stated benchmark, the S&P 1500 Composite Index. Total returns and performance statistics for other periods as of September 30, 2012 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| | The S&P Composite 1500 Index gained 30.18% during the fiscal year. On September 30, 2011 we measured an overall market value-to-price (V/P) ratio of 1.52 and never got close to a neutral reading of 1.00, or fair value under ICON’s methodology, over the course of the last 12 months. With value as our guide, we were correctly bullish over this period. We generally reduced cash, retained only a minimal short position in the Fund and, as noted below, tilted toward the industries and sectors where we saw the greatest value. |

To take advantage of a 30% gain in the market, investors had to work through two drops of approximately 10%: one in November 2011 and the other in April through May of 2012. ICON did not attempt short term “market timing” and instead rode through these declines, focused on the longer-term value objective. The top three performing sector indexes for the year were Consumer Discretionary, Telecommunications Services and Financials; while the bottom three performing sector indexes were Utilities, Consumer Staples and Energy. Industry and sector leadership was far from steady throughout the year, with a severe theme reversal during the April-May downturn. Cyclical and economically sensitive issues, including those in the Industrials, Consumer Discretionary and Information Technology sectors, led through the April 2 high, but suffered the worst during the April-May decline. While Energy was the third worst performing sector index over the entire year, it was the best performer during the June 4 through September 30 advance. We attribute the inconsistent industry and sector behavior to investors frequently changing their outlook for the economy. As their views changed, their sector preferences changed quite a few times over the last year.

| Q. | How did the Fund’s composition affect performance? |

| A. | The largest contributors to Fund performance came from the Consumer Discretionary sector. Cable & satellite providers, Comcast Corp. and Time Warner Cable Inc., were among the top 5 largest holdings of the Fund. Combined, these two companies provided just under 4% in total return to the Fund. Apparel retail companies also contributed strongly to the Fund’s performance, as retailer TJX Cos. returned just over 63% for the year. The Consumer Discretionary sector was one of the Fund’s largest weighted sectors at almost twice its benchmark weight. Apple Inc., the Fund’s largest holding, performed well in 2012, growing over 75% with the success of several new product launches and increased sales revenue. |

The Fund was underweight the Health Care sector, positioned at less than one half of the benchmark. This sector nonetheless proved to be a significant detractor to Fund performance when Questcor Pharmaceuticals Inc. dropped over 60% in a week after insurer Aetna Inc. said it would limit coverage of the company’s top-selling drug, H.P. Acthar, which is used to treat multiple sclerosis and infant seizures. The Fund’s position in EZCorp Inc., the largest U.S. pawn-shop broker and pay day lender chain, likewise detracted from performance. EZCorp Inc. shares declined sharply after missing analysts��� earnings expectations and perceived legislative threats.

The Fund had minimal short positions over the past year. The Fund uses shorts as a strategy to increase returns, and in 2012’s rising market, we saw few opportunities to short.

| Q. | What is your investment outlook for the overall market? |

| A. | Going into the new fiscal year, ICON’s valuation system shows an overall market V/P ratio of 1.39, suggesting there is still plenty of room for the market to appreciate towards fair value. Because of this valuation reading, we believe we are still in a bull market and we continue to position the Fund long in industries that show great value according to our methodology. As fiscal year 2012 ends and fiscal year 2013 begins, the Fund is heavily tilted towards the Consumer Discretionary, Industrials, and Information Technology sectors. Still, we remain vigilant and will look for opportunities to add to the Fund’s short positions as they arise. |

ICON Long/Short Fund

Sector Composition

September 30, 2012

| | | | |

Consumer Discretionary | | | 31.6% | |

Information Technology | | | 22.4% | |

Industrials | | | 21.2% | |

Health Care | | | 8.9% | |

Financial | | | 6.6% | |

Energy | | | 4.6% | |

Materials | | | 3.3% | |

| | | | |

| | | 98.6% | |

| | | | |

Percentages are based upon long positions as a percentage of net assets.

ICON Long/Short Fund

Industry Composition

September 30, 2012

| | | | |

Cable & Satellite | | | 10.5% | |

IT Consulting & Other Services | | | 9.5% | |

Industrial Conglomerates | | | 6.6% | |

Computer Hardware | | | 6.4% | |

Home Improvement Retail | | | 4.8% | |

Railroads | | | 4.4% | |

Homefurnishing Retail | | | 4.0% | |

Oil & Gas Equipment & Services | | | 3.2% | |

Communications Equipment | | | 3.1% | |

Health Care Services | | | 3.1% | |

Construction & Farm Machinery & Heavy Trucks | | | 3.0% | |

Apparel Retail | | | 2.9% | |

Industrial Machinery | | | 2.7% | |

Biotechnology | | | 2.5% | |

Air Freight & Logistics | | | 2.5% | |

General Merchandise Stores | | | 2.5% | |

Health Care Equipment | | | 2.4% | |

Apparel, Accessories & Luxury Goods | | | 2.1% | |

| | | | |

Diversified Banks | | | 2.1% | |

Housewares & Specialties | | | 2.0% | |

Electrical Components & Equipment | | | 2.0% | |

Computer Storage & Peripherals | | | 1.9% | |

Industrial Gases | | | 1.9% | |

Other Diversified Financial Services | | | 1.9% | |

Footwear | | | 1.5% | |

Data Processing & Outsourced Services | | | 1.4% | |

Regional Banks | | | 1.4% | |

Consumer Finance | | | 1.3% | |

Movies & Entertainment | | | 1.2% | |

Other Industries (each less than 1%) | | | 3.8% | |

| | | | |

| | | 98.6% | |

| | | | |

Percentages are based upon long positions as a percentage of net assets.

ICON Long/Short Fund

Average Annual Total Return

as of September 30, 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Long/Short Fund - Class C | | | 10/17/02 | | | | 24.15% | | | | -4.81% | | | | 3.92% | | | | 3.14% | | | | 2.70% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 7.61% | | | | N/A | | | | N/A | |

ICON Long/Short Fund - Class S | | | 5/6/04 | | | | 25.41% | | | | -3.83% | | | | 2.26% | | | | 7.76% | | | | 1.65% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 5.56% | | | | N/A | | | | N/A | |

ICON Long/Short Fund - Class A | | | 5/31/06 | | | | 25.09% | | | | -4.11% | | | | -1.41% | | | | 3.23% | | | | 1.91% | |

ICON Long/Short Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | 17.87% | | | | -5.23% | | | | -2.33% | | | | 3.23% | | | | 1.91% | |

S&P Composite 1500 Index | | | | | | | 30.18% | | | | 1.36% | | | | 4.34% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

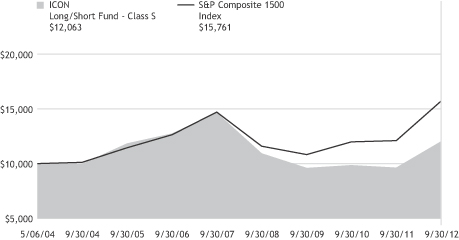

ICON Long/Short Fund

Value of a $10,000 Investment

through September 30, 2012

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Fund’s other share classes will vary due to differences in charges and expenses. The Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON LONG/SHORT FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2012

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | Common Stocks (98.6%) | | | | |

| | 9,500 | | | Accenture PLC, Class A(x) | | $ | 665,285 | |

| | 2,400 | | | Apple, Inc.(x) | | | 1,601,424 | |

| | 10,800 | | | BB&T Corp. | | | 358,128 | |

| | 16,200 | | | Bed Bath & Beyond, Inc.† | | | 1,020,600 | |

| | 26,900 | | | Bio-Reference Labs, Inc.†(a) | | | 768,802 | |

| | 8,700 | | | Caterpillar, Inc.(x) | | | 748,548 | |

| | 8,200 | | | Celgene Corp.†(x) | | | 626,480 | |

| | 11,100 | | | Cognizant Technology Solutions Corp., Class A†(x) | | | 776,112 | |

| | 38,500 | | | Comcast Corp., Class A(x) | | | 1,377,145 | |

| | 29,700 | | | CSX Corp.(x) | | | 616,275 | |

| | 15,000 | | | Danaher Corp.(x) | | | 827,250 | |

| | 8,600 | | | Dover Corp. | | | 511,614 | |

| | 2,000 | | | Ecolab, Inc. | | | 129,620 | |

| | 10,400 | | | Emerson Electric Co. | | | 502,008 | |

| | 14,300 | | | Ezcorp, Inc., Class A† | | | 327,899 | |

| | 7,500 | | | F5 Networks, Inc.† | | | 785,250 | |

| | 7,400 | | | FedEx Corp. | | | 626,188 | |

| | 36,600 | | | General Electric Co.(x) | | | 831,186 | |

| | 8,200 | | | Halliburton Co. | | | 276,258 | |

| | 16,800 | | | Home Depot, Inc. | | | 1,014,216 | |

| | 2,900 | | | Illinois Tool Works, Inc. | | | 172,463 | |

| | 4,600 | | | International Business Machines Corp.(x) | | | 954,270 | |

| | 9,600 | | | Jarden Corp. | | | 507,264 | |

| | 11,600 | | | JPMorgan Chase & Co. | | | 469,568 | |

| | 6,300 | | | Lowe’s Cos., Inc. | | | 190,512 | |

| | 800 | | | Mastercard, Inc., Class A | | | 361,184 | |

| | 3,600 | | | National Oilwell Varco, Inc. | | | 288,396 | |

| | 3,900 | | | Nike, Inc., Class B | | | 370,149 | |

| | 4,400 | | | Noble Corp.†(x) | | | 157,432 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | 7,700 | | | Norfolk Southern Corp. | | $ | 489,951 | |

| | 4,600 | | | Praxair, Inc. | | | 477,848 | |

| | 12,900 | | | Questcor Pharmaceuticals, Inc.†(a) | | | 238,650 | |

| | 4,500 | | | Reliance Steel & Aluminum Co. | | | 235,575 | |

| | 15,100 | | | ResMed, Inc. | | | 611,097 | |

| | 3,400 | | | Schlumberger, Ltd.(x) | | | 245,922 | |

| | 9,800 | | | Target Corp. | | | 622,006 | |

| | 13,300 | | | Time Warner Cable, Inc.(x) | | | 1,264,298 | |

| | 16,600 | | | TJX Cos., Inc.(x) | | | 743,514 | |

| | 3,300 | | | V.F. Corp. | | | 525,888 | |

| | 5,900 | | | Valero Energy Corp. | | | 186,912 | |

| | 6,000 | | | Walt Disney Co.(x) | | | 313,680 | |

| | 15,000 | | | Wells Fargo & Co. | | | 517,950 | |

| | 12,600 | | | Western Digital Corp. | | | 487,998 | |

| | | | | | | | |

| Total Common Stocks

(Cost $21,419,851) | | | 24,822,815 | |

| | Collateral for Securities on Loan (2.3%) | |

| | 568,361 | | | State Street Navigator Prime Portfolio | | | 568,361 | |

| | | | | | | | |

| Total Collateral for Securities

on Loan

(Cost $568,361) | | | 568,361 | |

| | Short-Term Investment (30.6%) | |

| $ | 7,709,409 | | | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/12 | | | 7,709,409 | |

| | | | | | | | |

| Total Short-Term Investments

(Cost $7,709,409) | | | 7,709,409 | |

| Total Investments 131.5%

(Cost $29,697,621) | | | 33,100,585 | |

| Liabilities Less Other Assets

(31.5)% | | | (7,938,595 | ) |

| | | | | | | | |

| | Net Assets 100.0% | | $ | 25,161,990 | |

| | | | | | | | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 33 | |

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (x) | All or a portion of the security is pledged as collateral for securities sold short. |

| (a) | All or a portion of the security was on loan as of September 30, 2012. |

| | |

| 34 | | SCHEDULEOF INVESTMENTS |

ICON LONG/SHORT FUND

SCHEDULEOF SECURITIES SOLD SHORT

SEPTEMBER 30, 2012

| | | | | | | | |

| Shares | | | Short Security | | Value | |

| | 2,000 | | | SL Green Realty Corp., REIT | | $ | 160,140 | |

| | 3,300 | | | Texas Industries, Inc. | | | 134,145 | |

| | | | | | | | |

| Total Securities Sold Short

(Proceeds $234,016) | | $ | 294,285 | |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| REIT | Real Estate Investment Trust |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 35 | |

| | | | |

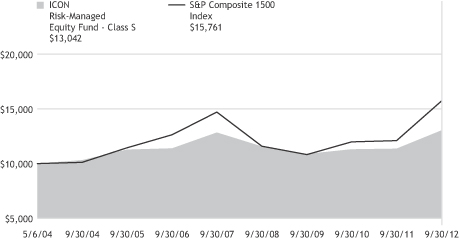

MANAGEMENT OVERVIEW ICON RISK-MANAGED EQUITY FUND | | Class C Class S Class A | | IOCCX IOCZX IOCAX |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | The ICON Risk-Managed Equity Fund, Class S, returned 14.65% for the fiscal year ended September 30, 2012, underperforming the 30.18% return for the S&P 1500 Composite Index. Class A shares of the Fund returned 14.28% (and 7.71% with maximum sales charge) and Class C shares returned 13.47% for the time period (12.47% with maximum contingent deferred sales charge). Total returns for other periods as of September 30, 2012 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

The S&P 1500 Index gained 30.18% during the fiscal year. On September 30, 2011 we measured an overall market value-to-price (V/P) ratio of 1.52 and never got close to a neutral reading of 1.00, or fair value under ICON’s methodology, over the course of the next 12 months. With value as our guide, we were correctly bullish over this period. We generally minimized cash and, as noted below, tilted toward our industries and sectors where we saw the greatest value.

To take advantage of a 30% gain in the market, investors had to work through two drops of approximately 10%: one in November 2011 and the other in April through May of 2012. ICON did not attempt short term “market timing” and instead rode through these declines, focused on the longer-term value objective. The top three performing sector indexes for the year were Consumer Discretionary, Telecommunication Services and Financials; while the bottom three performing sector indexes were Utilities, Consumer Staples and Energy. Industry and sector leadership was far from steady throughout the year, however, with a severe theme reversal during the April-May downturn. Cyclical and economically sensitive issues, including Industrials, Consumer Discretionary and Information Technology, led through the April 2 high, but suffered during the April-May decline. While Energy was the third worst performing sector index over the entire year, it was the best during the June 4 through September 30 advance. We attribute the inconsistent industry and sector behavior to investors frequently changing their outlook for the economy. As their views changed, their sector preferences changed quite a few times over the last year.

We believe we were able to reduce both the Fund’s downside capture and volatility this fiscal year through our disciplined implementation of the Fund’s core hedging strategy: writing S&P 500 Index call options and using some of the proceeds to buy S&P 500 Index out-of-the-money put options. This hedging strategy provided a downside cushion throughout the period, but most notably during two sharp declines. In a roughly two-week period, from November 8 to November 25, 2011, the S&P 1500 Index fell 9.24%. Over that same period, the Class S shares of the Fund fell 6.64%. Then, after a sharp rally, the Index dropped 8.96% between May 1 and June 4, 2012 while the Class S shares of the Fund declined 5.98% over the same period. The hedge also helped reduce the Fund’s volatility. Over the full fiscal year the Fund’s beta was 0.57 for the Class S shares. There is generally a trade-off for reducing downside capture and dampening volatility: while the hedge did what it was intended to do by helping reduce losses and creating a more stable ride, it also reduced the Fund’s upside capture.

| Q. | How did the Fund’s composition affect performance? |

| A. | Throughout the year the Fund held its largest positions in the Information Technology, Industrials, and Consumer Discretionary sectors. The largest contributor to performance came from the computer hardware industry. Apple, the Fund’s largest holding, had a strong year in 2012, growing over 75%. Also producing positive gains to the Fund were holdings in the apparel retail, IT consulting & other services, and railroads industries. |

The Fund’s Energy sector allocations produced the largest detractors to Fund performance. In particular, the Fund was negatively impacted by holdings in the oil & gas drilling and coal & consumable fuels industries. Although the Fund’s weighted average position in the Energy sector was only 0.30% less than the S&P 1500 Composite Index position in the Energy sector for the fiscal year, the Fund’s industry tilts returned approximately only half that of the benchmark’s Energy exposure.

| Q. | What is your investment outlook for the overall market? |

| A. | Going into the new fiscal year, ICON’s valuation system shows an overall market V/P of 1.39, suggesting there is still plenty of room for the market to appreciate towards fair value. Because of this valuation reading, we believe we are still in a bull market and we continue to position the Fund in industries that show great value according to our methodology. As fiscal year 2012 ends and fiscal year 2013 begins, the Fund is heavily tilted towards the Consumer Discretionary, Industrials, and Information Technology sectors. |

ICON Risk-Managed Equity Fund

Sector Composition

September 30, 2012

| | | | |

Information Technology | | | 23.8% | |

Consumer Discretionary | | | 23.3% | |