UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07883

ICON Funds

(Exact name of registrant as specified in charter)

5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Address of principal executive offices) (Zip code)

Carrie Schoffman

5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-790-1600

Date of fiscal year end: September 30, 2015

Date of reporting period: September 30, 2015

Item 1. Reports to Stockholders.

2015 ANNUAL REPORT

ICON DIVERSIFIED FUNDS

INVESTMENT UPDATE

ICON Bond Fund

ICON Equity Income Fund

ICON Fund

ICON Long/Short Fund

ICON Opportunities Fund

ICON Risk-Managed Balanced Fund

1-800-764-0442 | www.iconfunds.com

You can now sign up for electronic delivery of ICON Fund shareholder reports, including prospectuses, annual reports, semiannual reports and proxy statements.

When these materials are available, you will receive an email from ICON with instructions on how to view the documents. Statements, transaction confirmations and other documents that are not available online will continue to be sent to you by U.S. mail.

Visit ICON’s website at www.iconfunds.com to learn more and sign up.

You may change or cancel your participation in eDelivery by visiting www.iconfunds.com, or you can request a hard copy of any of the materials free of charge by calling ICON Funds at 1-800-764-0442.

1-800-764-0442 • www.iconfunds.com

TABLEOF CONTENTS

ABOUT THIS REPORT (UNAUDITED)

Historical Returns

All total returns mentioned in this Report account for the change in a Fund’s per-share price and the reinvestment of any dividends, capital gain distributions and adjustments for financial statement purposes. If your account is set up to receive Fund distributions in cash rather than to reinvest them, your actual return may differ from these figures. The Funds’ performance results do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Adviser may have reimbursed certain fees or expenses of some of the Funds. If not for these reimbursements, performance would have been lower. Fund results shown, unless otherwise indicated, are at net asset value. If a sales charge (maximum 5.75%) had been deducted, results would have been lower.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance results represent past performance, and current performance may be higher or lower. Please call 1-800-764-0442 or visit www.iconfunds.com for performance results current to the most recent month-end.

Portfolio Data

This Report reflects ICON’s portfolio holdings as of September 30, 2015, the end of the reporting period. The information is not a complete analysis of every aspect of any sector, industry, security or the Funds.

There are risks associated with mutual fund investing, including the loss of principal. The likelihood of loss may be greater if you invest for a shorter period of time. There is no assurance that the investment process will consistently lead to successful results.

There are risks associated with selling short, including the risk that the ICON Long/Short Fund may have to cover its short position at a higher price than the short price, resulting in a loss. The ICON Long/Short Fund’s loss on a short sale is potentially unlimited as a loss occurs when the value of a security sold short increases. Call options involve certain risks, such as limited gains and lack of liquidity in the underlying securities, and are not suitable for all investors.

Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securities generally decreases. The ICON Bond Fund and ICON Equity Income Fund may invest up to 35% and 25% of its assets in high-yield bonds that are below investment

grade, respectively. ICON Risk-Managed Balanced Fund may invest up to 10% of its assets in high-yield bonds that are below investment grade. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher-quality bonds.

An investment concentrated in sectors and industries may involve greater risk and volatility than a more diversified investment.

Investments in foreign securities may entail unique risks, including political, market, and currency risks. Financial statements of foreign companies are governed by different accounting, auditing, and financial standards than U.S. companies and may be less transparent and uniform than in the United States. Many corporate governance standards, which help ensure the integrity of public information in the United States, do not exist in foreign countries. In general, there may be less governmental supervision of foreign stock exchanges and securities brokers and issuers. The ICON system relies on the integrity of the financial statements released to the market as part of our analysis.

Investments in other mutual fund companies may entail certain risks. For example, the Fund’s performance depends on the underlying funds in which it invests, and it is subject to the risks of the underlying funds. Additionally, an investment by the Fund or underlying fund in exchange-traded funds generally presents the same primary risks as an investment in a mutual fund.

The prospectus and statement of additional information contain this and other information about the Funds and are available by visiting www.iconfunds.com or calling 1-800-764-0442. Please read the prospectus and statement of additional information carefully.

Financial Intermediary

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may influence the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| | |

MANAGEMENT OVERVIEW (UNAUDITED) ICON BOND FUND | | |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | For the Fund’s fiscal year ended September 30, 2015, the ICON Bond Fund (the Fund) Class S shares underperformed its benchmark, the Barclays Capital U.S. Universal Index (ex-MBS). The Fund returned -0.28% while the Barclays Capital U.S. Universal Index (ex-MBS) returned 2.00%. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Investors began fiscal year 2015 anticipating a rising rate environment. As the year unfolded, a general economic malaise and declining inflation expectations produced the exact opposite, a rate rally. The U.S. Treasury market experienced volatility through the fiscal year as the yield on the 10-Year U.S. Treasury began the fiscal year at 2.49%, fell to 1.64% by the end of January 2015, due in large part to macro-economic uncertainty, rose to 2.48% at the end of May 2015, and finally finished the fiscal year at 2.04%. Corporate bond spreads experienced volatility of their own as default concerns that started primarily in the Energy sector eventually spread to other sectors of the economy. Over the course of the fiscal year, the Fund maintained a lower overall duration relative to the benchmark, causing the majority of the Fund’s underperformance as both curve return and curve carry worked against the Fund’s holdings. In the corporate bond segment of the market, the Fund maintained a relatively defensive posture as we felt spreads, specifically in the high yield segment of the market, had reached unsustainable levels. This defensive posture proved to be advantageous for the Fund as spreads began to aggressively widen, especially in the Energy sector. However, the Fund was not completely immune from the sell-off due to a small allocation to high yield bonds in the Energy sector and a specific security within the Telecommunication space. Other positions that provided positive returns for the Fund over the course of the fiscal year included preferred shares and investments in closed-end funds. Both areas provided positive returns and diversification benefits relative to the volatility in the fixed income market. In the end, the negative effects of yield curve movements proved too large to offset and the ICON Bond Fund underperformed the benchmark over the course of the fiscal year. |

| Q. | How did the Fund’s composition affect performance? |

| A. | As stated above, the Fund underperformed its benchmark during the fiscal year. Further analysis shows the underperformance stemmed from both negative curve return and negative curve carry as the Fund had a lower overall duration and virtually no exposure to long-dated U.S. Treasuries over the course of the fiscal year. The Fund had positive selection effect in the corporate bond segment of the market where holdings within the Information Technology, Financials, and Materials sectors of the market experienced larger spread movement than the broad market. Additionally, the Fund had positive selection effect from closed-end fund positions where either discount tightening was realized or activist actions resulted in bond tenders. Negative allocation effect came from the Fund’s lack of holdings in both long-dated high quality corporate bonds and long-dated U.S. Treasuries as the long end of the curve experienced strong returns. Based on our internal assumption of risk and returns, we felt as though duration extension was unwarranted and would rather look to focus on bottom up security selection. |

| Q. | What is your investment outlook for the bond market? |

| A. | The end of fiscal year 2015 saw an increase in both spread and interest rate volatility as concerns about domestic and global growth persisted. Overall, we generally believe these concerns will eventually subside and the volatility in spread product will create opportunities. Specifically, we are beginning to look for higher quality, high yield bonds in the Energy sector as risk return profiles are beginning to look attractive. While we don’t anticipate a substantial upward movement in interest rates over the course of the next 12 months, the Fund is positioned in the lower portion of its duration range as we move into fiscal year 2016. We continue to shy away from interest rate forecasts and remain steadfast in our search for issue specific opportunities. We are looking for opportunities that have the characteristics of credit upgrades, special situations, or anticipated future bond tenders. While future bond market volatility might be substantial, we believe our unique investment methodology will help the Fund navigate the changing market. |

ICON Bond Fund

Credit Diversification

September 30, 2015

| | | | |

Aaa | | | 6.8% | |

A2 | | | 1.2% | |

A3 | | | 6.5% | |

A- | | | 1.8% | * |

Baa1 | | | 9.2% | |

Baa2 | | | 9.2% | |

Baa3 | | | 5.6% | |

Ba1 | | | 10.9% | |

Ba2 | | | 8.9% | |

Ba3 | | | 0.8% | |

B1 | | | 4.1% | |

B2 | | | 5.1% | |

B3 | | | 1.5% | |

Caa1 | | | 3.5% | |

NR | | | 7.0% | |

| | | | |

| | | 82.1% | |

| | | | |

| | * | Reflects S&P Rating of A- since a Moody’s rating is unavailable for MASTR Seasoned Security Trust 2005-1, CMO as of September 30, 2015. |

Percentages are based upon U.S. Treasury obligations, collateralized mortgage obligations, corporate and foreign corporate bond investments as a percentage of net assets. Ratings based on Moody’s Investors Service, Inc.

ICON Bond Fund

Average Annual Total Return

as of September 30, 2015

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Bond Fund - Class S | | | 5/6/04 | | | | -0.28% | | | | 2.91% | | | | 4.46% | | | | 4.41% | | | | 0.86% | | | | 0.75% | |

ICON Bond Fund - Class C | | | 10/21/02 | | | | -1.10% | | | | 2.04% | | | | 3.59% | | | | 3.94% | | | | 2.27% | | | | 1.60% | |

ICON Bond Fund - Class A | | | 9/30/10 | | | | -0.44% | | | | 2.69% | | | | N/A | | | | 2.69% | | | | 1.44% | | | | 1.00% | |

ICON Bond Fund - Class A (including maximum sales charge of 4.75%) | | | 9/30/10 | | | | -5.16% | | | | N/A | | | | N/A | | | | 1.69% | | | | 1.44% | | | | 1.00% | |

Barclays Capital U.S. Universal Index | | | | | | | 2.33% | | | | 3.36% | | | | 4.80% | | | | 5.01% | | | | N/A | | | | N/A | |

Barclays Capital U.S. Universal Index (ex-MBS) | | | | | | | 2.00% | | | | 3.49% | | | | 4.78% | | | | 5.18% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

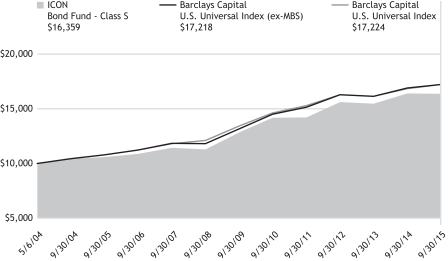

ICON Bond Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Bond Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Bond Fund’s other share classes will vary due to differences in charges and expenses. The Bond Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON BOND FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| | Corporate Bonds (63.3%) | |

| | Communications (2.1%) | |

| $ | 500,000 | | | Cincinnati Bell Telephone Co. LLC | | | 6.30 | % | | | 12/01/28 | | | $ | 467,500 | |

| | 1,290,000 | | | Cincinnati Bell, Inc. | | | 8.38 | % | | | 10/15/20 | | | | 1,298,869 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 1,766,369 | |

| | Consumer, Cyclical (5.7%) | |

| | 800,000 | | | Darden Restaurants, Inc. | | | 6.45 | % | | | 10/15/17 | | | | 870,900 | |

| | 1,300,000 | | | Darden Restaurants, Inc. | | | 7.05 | % | | | 10/15/37 | | | | 1,553,526 | |

| | 1,000,000 | | | International Game Technology(a) | | | 5.35 | % | | | 10/15/23 | | | | 915,000 | |

| | 1,000,000 | | | Pinnacle Entertainment, Inc. | | | 7.50 | % | | | 04/15/21 | | | | 1,042,500 | |

| | 500,000 | | | Pinnacle Entertainment, Inc. | | | 6.38 | % | | | 08/01/21 | | | | 529,165 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 4,911,091 | |

| | Consumer, Non-cyclical (23.0%) | |

| | 2,798,000 | | | Altria Group, Inc. | | | 9.25 | % | | | 08/06/19 | | | | 3,487,167 | |

| | 1,000,000 | | | HCA, Inc. | | | 5.25 | % | | | 04/15/25 | | | | 1,021,250 | |

| | 2,336,000 | | | Kraft Heinz Foods Co.(b) | | | 4.88 | % | | | 02/15/25 | | | | 2,492,979 | |

| | 3,000,000 | | | Hospira, Inc. | | | 5.80 | % | | | 08/12/23 | | | | 3,474,468 | |

| | 1,000,000 | | | inVentiv Health, Inc.(b) | | | 9.00 | % | | | 01/15/18 | | | | 1,032,500 | |

| | 2,565,000 | | | Lender Processing Services, Inc. / Black Knight Lending Solutions, Inc. | | | 5.75 | % | | | 04/15/23 | | | | 2,715,694 | |

| | 3,250,000 | | | Omnicare, Inc. | | | 4.75 | % | | | 12/01/22 | | | | 3,510,000 | |

| | 1,797,000 | | | Prospect Medical Holdings, Inc.(b) | | | 8.38 | % | | | 05/01/19 | | | | 1,877,865 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 19,611,923 | |

| | Energy (2.9%) | |

| | 500,000 | | | Bill Barrett Corp.(a) | | | 7.00 | % | | | 10/15/22 | | | | 325,000 | |

| | 750,000 | | | Noble Energy, Inc. | | | 5.88 | % | | | 06/01/22 | | | | 748,585 | |

| | 500,000 | | | Noble Energy, Inc. | | | 5.88 | % | | | 06/01/24 | | | | 497,500 | |

| | 1,000,000 | | | Range Resources Corp.(a) | | | 5.00 | % | | | 08/15/22 | | | | 885,000 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 2,456,085 | |

| | Financial (23.5%) | |

| | 1,366,000 | | | Ally Financial, Inc. | | | 8.00 | % | | | 03/15/20 | | | | 1,570,900 | |

| | 1,010,000 | | | E*TRADE Financial Corp. | | | 5.38 | % | | | 11/15/22 | | | | 1,070,600 | |

| | 2,500,000 | | | General Electric Capital Corp., Series A(c) | | | 7.13 | % | | | 06/15/22 | | | | 2,887,500 | |

| | 1,300,000 | | | General Electric Capital Corp., Series B(c) | | | 6.25 | % | | | 12/15/22 | | | | 1,410,500 | |

| | 600,000 | | | GFI Group, Inc. | | | 8.63 | % | | | 07/19/18 | | | | 648,000 | |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| $ | 1,015,000 | | | Highmark, Inc.(b) | | | 4.75 | % | | | 05/15/21 | | | $ | 1,053,074 | |

| | 1,000,000 | | | Highmark, Inc.(b) | | | 6.13 | % | | | 05/15/41 | | | | 1,011,381 | |

| | 1,094,000 | | | KeyCorp Capital II | | | 6.88 | % | | | 03/17/29 | | | | 1,215,504 | |

| | 2,439,000 | | | MBIA, Inc. | | | 6.63 | % | | | 10/01/28 | | | | 2,384,122 | |

| | 1,500,000 | | | NTC Capital I, Series A, FRN(c) | | | 0.81 | % | | | 01/15/27 | | | | 1,305,000 | |

| | 1,000,000 | | | Prudential Financial, Inc.(c) | | | 8.88 | % | | | 06/15/68 | | | | 1,147,750 | |

| | 2,000,000 | | | State Street Capital Trust I, FRN(c) | | | 0.88 | % | | | 05/15/28 | | | | 1,740,000 | |

| | 2,800,000 | | | USB Realty Corp., FRN(b)(c) | | | 1.44 | % | | | 01/15/17 | | | | 2,541,000 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 19,985,331 | |

| | Industrials (2.6%) | |

| | 1,260,000 | | | Ingersoll-Rand Co. | | | 6.39 | % | | | 11/15/27 | | | | 1,525,403 | |

| | 700,000 | | | Vulcan Materials Co. | | | 4.50 | % | | | 04/01/25 | | | | 686,000 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 2,211,403 | |

| | Technology (3.5%) | |

| | 1,000,000 | | | First Data Corp. | | | 11.25 | % | | | 01/15/21 | | | | 1,092,500 | |

| | 1,671,000 | | | First Data Corp. | | | 12.63 | % | | | 01/15/21 | | | | 1,898,674 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 2,991,174 | |

| | | | | | | | | | | | | | | | |

| Total Corporate Bonds

(Cost $55,099,454) | | | | | | | | | | | 53,933,376 | |

| | U.S. Treasury Obligations (6.8%) | |

| | 5,030,420 | | | Treasury Inflation Protected Security | | | 0.13 | % | | | 07/15/24 | | | | 4,799,599 | |

| | 1,000,000 | | | U.S. Treasury Note | | | 2.00 | % | | | 08/15/25 | | | | 994,714 | |

| | | | | | | | | | | | | | | | |

| Total U.S. Treasury Obligations

(Cost $5,805,361) | | | | | | | | | | | 5,794,313 | |

| | Collateralized Mortgage Obligations (7.6%) | | | | | | | | | | | | |

| | 496,411 | | | Citigroup Mortgage Loan Trust, Inc.,

Series 2013-J1, Class B3, CMO, VRN(b)(c)(d) | | | 3.56 | % | | | 10/25/43 | | | | 486,496 | |

| | 1,444,702 | | | MASTR Seasoned Securitization Trust, Inc., Series 2005-1, Class 1A1, CMO(c) | | | 6.54 | % | | | 09/25/32 | | | | 1,574,068 | |

| | 1,191,970 | | | Sequoia Mortgage Trust, Inc., Series 2013-1, Class B2, CMO, FRN(c)(d) | | | 3.64 | % | | | 02/25/43 | | | | 1,147,233 | |

| | 1,904,186 | | | Sequoia Mortgage Trust, Inc., Series 2013-10, Class B2, CMO, VRN(b)(c)(d) | | | 3.59 | % | | | 08/25/43 | | | | 1,791,775 | |

| | 1,474,117 | | | Sequoia Mortgage Trust, Inc., Series 2014-4, Class B2, CMO, VRN(b)(c)(d) | | | 3.90 | % | | | 11/25/44 | | | | 1,463,281 | |

| | | | | | | | | | | | | | | | |

| Total Collateralized Mortgage Obligations

(Cost $6,595,754) | | | | | | | | | | | 6,462,853 | |

| | Municipal Bond (1.3%) | |

| | 1,000,000 | | | Texas State Public Finance Authority, Charter School Finance Corp. | | | 7.50 | % | | | 08/15/30 | | | | 1,073,690 | |

| | | | | | | | | | | | | | | | |

| Total Municipal Bonds

(Cost $1,079,062) | | | | | | | | | | | 1,073,690 | |

| | |

| 10 | | SCHEDULEOF INVESTMENTS |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | | | |

| | Foreign Corporate Bonds (3.1%) | |

| | Consumer, Cyclical (1.7%) | |

| $ | 1,300,000 | | | Air Canada(b) | | | 8.75 | % | | | 04/01/20 | | | $ | 1,418,625 | |

| | | | | | | | | | | | | | | | |

| | Energy (1.4%) | |

| | 200,000 | | | Encana Corp. | | | 6.50 | % | | | 02/01/38 | | | | 176,460 | |

| | 1,000,000 | | | BG Energy Capital PLC(b) | | | 4.00 | % | | | 10/15/21 | | | | 1,062,042 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 1,238,502 | |

| | | | | | | | | | | | | | | | |

| Total Foreign Corporate Bonds

(Cost $2,690,541) | | | | | | | | | | | 2,657,127 | |

| | | |

| Shares or Principal Amount | | | | | | | | Value | |

| | Preferred Stocks (6.7%) | |

| | Diversified Banks (1.3%) | |

| | 10,000 | | | GMAC Capital Trust I, Series 2 | | | | | | | | | | | 255,300 | |

| | 35,686 | | | RBS Capital Funding Trust V, Series E | | | | | | | | | | | 869,668 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 1,124,968 | |

| | Diversified REIT’s (0.4%) | |

| | 20,872 | | | Winthrop Realty Trust, REIT | | | | | | | | | | | 299,722 | |

| | | | | | | | | | | | | | | | |

| | Office REIT’s (4.2%) | |

| | 70,039 | | | Equity Commonwealth, Series E | | | | | | | | | | | 1,784,593 | |

| | 69,852 | | | Gramercy Property Trust, Inc., Series B(d) | | | | | | | | | | | 1,781,226 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 3,565,819 | |

| | Specialized REIT’s (0.8%) | |

| | 28,300 | | | Digital Realty Trust, Inc., Series E(a) | | | | | | | | | | | 721,933 | |

| | | | | | | | | | | | | | | | |

| Total Preferred Stocks

(Cost $5,705,428) | | | | | | | | | | | 5,712,442 | |

| | Closed-End Mutual Funds (9.4%) | |

| | 37,949 | | | AllianceBernstein Income Fund, Inc. | | | | | | | | | | | 298,279 | |

| | 5,800 | | | BlackRock Enhanced Government Fund, Inc. | | | | | | | | | | | 79,924 | |

| | 29,661 | | | Deutsche Global High Income Fund, Inc. | | | | | | | | | | | 224,207 | |

| | 213,226 | | | Federated Enhanced Treasury Income Fund | | | | | | | | | | | 2,882,816 | |

| | 29,930 | | | First Trust Mortgage Income Fund | | | | | | | | | | | 430,693 | |

| | 13,170 | | | Firsthand Technology Value Fund, Inc.(a) | | | | | | | | | | | 112,077 | |

| | 36,360 | | | Fort Dearborn Income Securities, Inc. | | | | | | | | | | | 512,676 | |

| | 5,936 | | | LMP Real Estate Income Fund, Inc. | | | | | | | | | | | 72,894 | |

| | 29,584 | | | Montgomery Street Income Securities, Inc. | | | | | | | | | | | 514,466 | |

| | 5,201 | | | Nuveen Mortgage Opportunity Term Fund | | | | | | | | | | | 116,502 | |

| | 96,140 | | | Transamerica Income Shares, Inc. | | | | | | | | | | | 2,082,392 | |

| | 60,936 | | | Western Asset/Claymore Inflation-Linked Securities & Income Fund | | | | | | | | | | | 642,875 | |

| | | | | | | | | | | | | | | | |

| Total Closed-End Mutual Funds

(Cost $8,269,885) | | | | | | | | | | | 7,969,801 | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 11 | |

| | | | | | | | | | | | |

| | | |

| Shares or Principal Amount | | | | | | Value | |

| | | | | | | | | | | | |

| | Collateral for Securities on Loan (1.1%) | |

| $ | 974,488 | | | State Street Navigator Prime Portfolio, 0.20% | | | | | | $ | 974,488 | |

| | | | | | | | | | | | |

| Total Collateral for Securities on Loan

(Cost $974,488) | | | | | | | 974,488 | |

| | Short-Term Investments (1.1%) | |

| | 923,476 | | | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/15 | | | | | | | 923,476 | |

| | | | | | | | | | | | |

| Total Short-Term Investments

(Cost $923,476) | | | | | | | 923,476 | |

| Total Investments 100.4%

(Cost $87,143,449) | | | 85,501,566 | |

| | Liabilities Less Other Assets (0.4)% | | | (369,595 | ) |

| | | | | | | | | | | | |

| | Net Assets 100.0% | | | | | | $ | 85,131,971 | |

| | | | | | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| (a) | All or a portion of the security was on loan as of September 30, 2015. |

| (b) | 144A—Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

| (c) | Floating Rate Security. Rate disclosed is as of September 30, 2015. |

| (d) | These securities are considered to be illiquid. The aggregate value of these securities at September 30, 2015 was $6,670,011, which represent 7.8% of the Fund’s Net Assets. |

| REIT | Real Estate Investment Trust |

| | |

| 12 | | SCHEDULEOF INVESTMENTS |

| | |

MANAGEMENT OVERVIEW (UNAUDITED) ICON EQUITY INCOME FUND | | |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Equity Income Fund (the Fund) Class S shares returned -.17% for the fiscal year ending September 30, 2015, out pacing its benchmark, the S&P Composite 1500 Index, which returned -.30% during the fiscal year. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

Q. What primary factors were behind the Fund’s relative performance?

| A. | While stock returns for the fiscal year 2015 were relatively muted, the period saw notable volatility. From mid-October 2014 to mid-May 2015, the S&P Composite 1500 Index value gained over 14%. However, in just six trading days starting August 16, 2015, the same Index value fell about 10%. |

The low interest environment that has persisted over the past few years continued through fiscal year 2015. As the yield on the 10-year U.S. Treasury fell from 2.49% on September 30, 2014 to 2.04% on September 30, 2015, many investors sought higher yields in stocks, which, in turn, helped drive the demand for dividend paying stocks. This demand helped the performance of the Fund. The Utilities sector in particular, which traditionally has stocks with high dividend yields, benefited from the interest rate pressure. In September 2015, many speculated that the Federal Reserve (the FED) would raise rates for the first time since 2006. Ultimately, the FED decided not to raise rates at that time and, as previously stated, the yield on the 10-Year U.S. Treasury note fell to 2.04% by the end of September 2015.

| Q. | How did the Fund’s composition affect performance? |

| A. | At the sector level, the Consumer Staples sector had the largest positive effect on Fund’s relative performance from a total effect standpoint. Drilling down to the stock level to assess the source of this sector’s out performance, the Fund’s position in B&G Foods, Inc. was single largest positive contributor to the Fund’s performance. |

During specific periods over the course year, the overall average market value-to-price (V/P) ratio fell below 1. Because of these valuations, the Fund held increased levels of both cash and fixed income. The cash position was a positive for the Fund. However, the Fund’s fixed income

holdings created a headwind for the Fund. The Fund’s fixed income exposure primarily came from corporate bonds. While the interest rate environment was positive for government bonds, the spread between corporate bonds and government bond increased. This spread increase outpaced the improving interest rate environment leading to downward pressure on corporate bond pricing.

In addition, a sharp decline in energy commodity prices led to a steep drop in the Energy sector. While the Fund was underweight in the Energy sector relative to the benchmark, the stock selection within the Fund under performed the Energy sector holdings within the benchmark. Ultimately, the Fund’s energy exposure was the largest detractor from Fund performance. In the end, the detractors and the contributors nearly canceled each other out, leaving the Fund with only minor outperformance of the benchmark.

| Q. | What is the outlook for the ICON Equity Income Fund? |

| A. | The overall average V/P ratio for the stocks we track within our system was 1.09 as of September 30, 2015. The highest V/P at a sector level was the Financial sector with a V/P of 1.28 as of September 30, 2015. The Financial sector’s relatively high V/P ratio coupled with attractive yields on a large percentage of stocks within the sector, led to a large allocation within the Fund to the Financial sector. In addition, the Fund has an overweight position relative to the benchmark in the Utilities sector due in large part to the sector’s overall average V/P ratio of 1.11 and the large number of dividend paying stocks within the sector. We will continue to monitor the equity market to find the best combination of value and dividend for our investors. |

ICON Equity Income Fund

Sector Composition

September 30, 2015

| | | | |

Financial | | | 32.0% | |

Utilities | | | 11.1% | |

Consumer Discretionary | | | 10.6% | |

Information Technology | | | 8.6% | |

Leisure and Consumer Staples | | | 7.6% | |

Materials | | | 6.4% | |

Telecommunication & Utilities | | | 3.9% | |

Energy | | | 3.8% | |

Telecommunication Services | | | 2.0% | |

Health Care | | | 1.9% | |

Industrials | | | 1.9% | |

| | | | |

| | | 89.8% | |

| | | | |

Percentages are based upon common, convertible preferred and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Industry Composition

September 30, 2015

| | | | |

Asset Management & Custody Banks | | | 6.8% | |

Integrated Telecommunication Services | | | 5.9% | |

Multi-Utilities | | | 5.8% | |

Diversified Banks | | | 5.0% | |

Multi-line Insurance | | | 4.3% | |

Movies & Entertainment | | | 3.8% | |

Regional Banks | | | 3.8% | |

Electric Utilities | | | 3.7% | |

Tobacco | | | 3.6% | |

Automobile Manufacturers | | | 3.3% | |

Technology Hardware, Storage & Peripherals | | | 3.2% | |

Diversified Chemicals | | | 3.0% | |

Oil & Gas Refining & Marketing | | | 2.8% | |

Life & Health Insurance | | | 2.2% | |

Packaged Foods & Meats | | | 2.1% | |

Semiconductors | | | 2.1% | |

Computer & Electronics Retail | | | 2.0% | |

Biotechnology | | | 1.9% | |

Construction & Farm Machinery & Heavy Trucks | | | 1.9% | |

| | | | |

Insurance Brokers | | | 1.9% | |

Soft Drinks | | | 1.9% | |

Health Care REITs | | | 1.8% | |

Thrifts & Mortgage Finance | | | 1.8% | |

Electronic Equipment & Instruments | | | 1.7% | |

Fertilizers & Agricultural Chemicals | | | 1.7% | |

Paper Products | | | 1.7% | |

Gas Utilities | | | 1.6% | |

Semiconductor Equipment | | | 1.6% | |

Housewares & Specialties | | | 1.5% | |

Mortgage REIT’s | | | 1.4% | |

Residential REIT’s | | | 1.3% | |

Consumer Finance | | | 1.2% | |

Oil & Gas Storage & Transportation | | | 1.0% | |

Office REIT’s | | | 0.5% | |

| | | | |

| | | 89.8% | |

| | | | |

Percentages are based upon common, convertible preferred and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Average Annual Total Return

as of September 30, 2015

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Equity Income Fund - Class S | | | 5/10/04 | | | | -0.17% | | | | 9.72% | | | | 4.90% | | | | 6.13% | | | | 1.38% | | | | 1.20% | |

ICON Equity Income Fund - Class C | | | 11/8/02 | | | | -1.16% | | | | 8.62% | | | | 3.86% | | | | 6.51% | | | | 2.45% | | | | 2.20% | |

ICON Equity Income Fund - Class A | | | 5/31/06 | | | | -0.38% | | | | 9.45% | | | | N/A | | | | 4.60% | | | | 1.59% | | | | 1.45% | |

ICON Equity Income Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | -6.09% | | | | 8.17% | | | | N/A | | | | 3.94% | | | | 1.59% | | | | 1.45% | |

S&P Composite 1500 Index | | | | | | | -0.30% | | | | 13.34% | | | | 6.95% | | | | 8.62% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

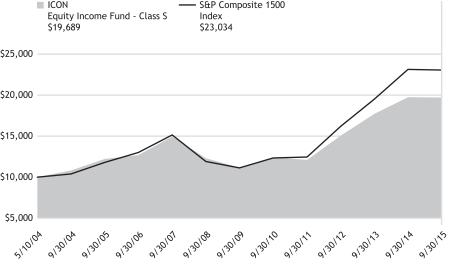

ICON Equity Income Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Equity Income Fund’s Class S shares on the Class’ inception date of 5/10/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Equity Income Fund’s other share classes will vary due to differences in charges and expenses. The Equity Income Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON EQUITY INCOME FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (85.2%) | |

| | Asset Management & Custody Banks (6.8%) | |

| | 49,100 | | | Ares Capital Corp. | | $ | 710,968 | |

| | 32,600 | | | Arlington Asset Investment Corp., Class A(a) | | | 458,030 | |

| | 18,700 | | | Invesco, Ltd. | | | 584,001 | |

| | 26,000 | | | Main Street Capital Corp.(a) | | | 693,160 | |

| | 28,700 | | | Triangle Capital Corp.(a) | | | 472,976 | |

| | | | | | | | |

| | | | | | | 2,919,135 | |

| | Automobile Manufacturers (3.3%) | |

| | 56,400 | | | Ford Motor Co. | | | 765,348 | |

| | 21,400 | | | General Motors Co. | | | 642,428 | |

| | | | | | | | |

| | | | | | | 1,407,776 | |

| | Biotechnology (1.9%) | |

| | 15,100 | | | AbbVie, Inc. | | | 821,591 | |

| | | | | | | | |

| | Computer & Electronics Retail (2.0%) | |

| | 20,900 | | | GameStop Corp., Class A(a) | | | 861,289 | |

| | | | | | | | |

| Construction & Farm Machinery & Heavy

Trucks (1.9%) |

|

| | 7,300 | | | Cummins, Inc. | | | 792,634 | |

| | | | | | | | |

| | Diversified Banks (2.1%) | |

| | 14,500 | | | JPMorgan Chase & Co. | | | 884,065 | |

| | | | | | | | |

| | Diversified Chemicals (3.0%) | |

| | 19,300 | | | Dow Chemical Co. | | | 818,320 | |

| | 49,500 | | | Huntsman Corp. | | | 479,655 | |

| | | | | | | | |

| | | | | | | 1,297,975 | |

| | Electric Utilities (3.7%) | |

| | 16,800 | | | ALLETE, Inc. | | | 848,232 | |

| | 26,800 | | | OGE Energy Corp. | | | 733,248 | |

| | | | | | | | |

| | | | | | | 1,581,480 | |

| | Electronic Equipment & Instruments (1.7%) | |

| | 84,800 | | | Daktronics, Inc. | | | 735,216 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Fertilizers & Agricultural Chemicals (1.7%) | |

| | 8,300 | | | Agrium, Inc.(a) | | $ | 742,850 | |

| | | | | | | | |

| | Gas Utilities (1.6%) | |

| | 14,000 | | | National Fuel Gas Co. | | | 699,720 | |

| | | | | | | | |

| | Health Care REITs (1.8%) | |

| | 20,800 | | | HCP, Inc., REIT | | | 774,800 | |

| | | | | | | | |

| | Housewares & Specialties (1.5%) | |

| | 13,200 | | | Tupperware Brands Corp.(a) | | | 653,268 | |

| | | | | | | | |

| | Insurance Brokers (1.9%) | |

| | 19,800 | | | Arthur J Gallagher & Co. | | | 817,344 | |

| | | | | | | | |

| Integrated Telecommunication

Services (5.9%) |

|

| | 23,300 | | | BCE, Inc. | | | 954,368 | |

| | 87,900 | | | Spark New Zealand, Ltd., ADR | | | 836,808 | |

| | 16,700 | | | Verizon Communications, Inc. | | | 726,617 | |

| | | | | | | | |

| | | | | | | 2,517,793 | |

| | Life & Health Insurance (2.2%) | |

| | 28,500 | | | Sun Life Financial, Inc. | | | 919,410 | |

| | | | | | | | |

| | Mortgage REIT’s (1.4%) | |

| | 61,000 | | | Annaly Capital Management, Inc., REIT | | | 602,070 | |

| | | | | | | | |

| | Movies & Entertainment (3.8%) | |

| | 10,100 | | | Time Warner, Inc. | | | 694,375 | |

| | 21,100 | | | Viacom, Inc., Class B | | | 910,465 | |

| | | | | | | | |

| | | | | | | 1,604,840 | |

| | Multi-line Insurance (4.3%) | |

| | 29,600 | | | Horace Mann Educators Corp. | | | 983,312 | |

| | 24,200 | | | Kemper Corp. | | | 855,954 | |

| | | | | | | | |

| | | | | | | 1,839,266 | |

| | |

| 18 | | SCHEDULEOF INVESTMENTS |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Multi-Utilities (5.8%) | |

| | 17,900 | | | Black Hills Corp. | | $ | 739,986 | |

| | 24,800 | | | CMS Energy Corp. | | | 875,936 | |

| | 10,700 | | | DTE Energy Co. | | | 859,959 | |

| | | | | | | | |

| | | | | | | 2,475,881 | |

| | Oil & Gas Refining & Marketing (2.8%) | |

| | 18,400 | | | PBF Energy, Inc., Class A | | | 519,432 | |

| | 8,500 | | | Phillips 66 | | | 653,140 | |

| | | | | | | | |

| | | | | | | 1,172,572 | |

| | Oil & Gas Storage & Transportation (1.0%) | |

| | 13,900 | | | TransCanada Corp.(a) | | | 438,962 | |

| | | | | | | | |

| | Packaged Foods & Meats (2.1%) | |

| | 24,200 | | | B&G Foods, Inc. | | | 882,090 | |

| | | | | | | | |

| | Paper Products (1.7%) | |

| | 19,200 | | | International Paper Co. | | | 725,568 | |

| | | | | | | | |

| | Regional Banks (3.8%) | |

| | 50,100 | | | Fifth Third Bancorp | | | 947,391 | |

| | 72,100 | | | First Commonwealth Financial Corp. | | | 655,389 | |

| | | | | | | | |

| | | | | | | 1,602,780 | |

| | Residential REIT’s (1.3%) | |

| | 7,300 | | | Camden Property Trust, REIT | | | 539,470 | |

| | | | | | | | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | Semiconductor Equipment (1.6%) | |

| | 45,800 | | | Applied Materials, Inc. | | $ | 672,802 | |

| | | | | | | | |

| | Semiconductors (2.1%) | |

| | 18,000 | | | Texas Instruments, Inc. | | | 891,360 | |

| | | | | | | | |

| | Soft Drinks (1.9%) | |

| | 10,200 | | | Dr. Pepper Snapple Group, Inc. | | | 806,310 | |

| | | | | | | | |

| Technology Hardware, Storage &

Peripherals (3.2%) |

|

| | 22,700 | | | Lexmark International, Inc. | | | 657,846 | |

| | 9,000 | | | Western Digital Corp. | | | 714,960 | |

| | | | | | | | |

| | | | | | | 1,372,806 | |

| | Thrifts & Mortgage Finance (1.8%) | |

| | 44,600 | | | Dime Community Bancshares, Inc. | | | 753,740 | |

| | | | | | | | |

| | Tobacco (3.6%) | |

| | 13,700 | | | Altria Group, Inc. | | | 745,280 | |

| | 17,400 | | | Reynolds American, Inc. | | | 770,298 | |

| | | | | | | | |

| | | | | | | 1,515,578 | |

| | | | | | | | |

| Total Common Stocks

(Cost $39,183,133) | | | 36,322,441 | |

| | | | | | | | | | | | | | | | |

| Shares or Principal Amount | | Interest

Rate | | | Maturity

Date | | | Value | |

| | Corporate Bonds (6.5%) | |

| | Basic Materials (0.9%) | | | | | |

| $ | 400,000 | | | Alcoa, Inc. | | | 5.13 | % | | | 10/01/24 | | | $ | 381,000 | |

| | | | | | | | | | | | | | | | |

| | Consumer, Cyclical (2.1%) | | | | | |

| | 750,000 | | | Darden Restaurants, Inc. | | | 7.05 | % | | | 10/15/37 | | | | 896,265 | |

| | | | | | | | | | | | | | | | |

| | Energy (2.1%) | | | | | |

| | 500,000 | | | California Resources Corp.(a) | | | 6.00 | % | | | 11/15/24 | | | | 297,813 | |

| | 500,000 | | | Chesapeake Energy Corp.(a) | | | 5.75 | % | | | 03/15/23 | | | | 326,093 | |

| | 500,000 | | | Denbury Resources, Inc. | | | 4.63 | % | | | 07/15/23 | | | | 270,000 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 893,906 | |

| | Financial (1.4%) | | | | | |

| | 500,000 | | | Ironshore Holdings US, Inc.(b) | | | 8.50 | % | | | 05/15/20 | | | | 587,164 | |

| | | | | | | | | | | | | | | | |

| Total Corporate Bonds

(Cost $3,263,123) |

| | | 2,758,335 | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 19 | |

| | | | | | | | | | | | |

| | | |

| Shares or Principal Amount | | | | | | Value | |

| | | | | | | | | | | | |

| | Preferred Stocks (2.7%) | | | | |

| | Consumer Finance (1.2%) | |

| | 19,600 | | | Discover Financial Services, Series B(a) | | | | | | $ | 505,876 | |

| | | | | | | | | | | | |

| | Diversified Banks (1.0%) | |

| | 17,314 | | | RBS Capital Funding Trust V, Series E | | | | | | | 421,942 | |

| | | | | | | | | | | | |

| | Office REIT’s (0.5%) | |

| | 8,329 | | | Gramercy Property Trust, Inc., Series B | | | | | | | 212,390 | |

| | | | | | | | | | | | |

| Total Preferred Stocks

(Cost $1,146,211) | | | 1,140,208 | |

| | Convertible Preferred Stock (1.9%) | |

| | Diversified Banks (1.9%) | |

| | 700 | | | Wells Fargo & Co., Series L | | | | | | | 817,600 | |

| | | | | | | | | | | | |

| Total Convertible Preferred Stocks

(Cost $828,278) | | | 817,600 | |

| | Collateral for Securities on Loan (11.2%) | |

| | 4,775,526 | | | State Street Navigator Prime Portfolio, 0.20% | | | | | | | 4,775,526 | |

| | | | | | | | | | | | |

| Total Collateral for Securities on Loan

(Cost $4,775,526) | | | 4,775,526 | |

| | Short-Term Investments (2.3%) | |

| $ | 986,907 | | | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/15 | | | | | | | 986,907 | |

| | | | | | | | | | | | |

| Total Short-Term Investments

(Cost $986,907) | | | 986,907 | |

| Total Investments 109.8%

(Cost $50,183,178) | | | 46,801,017 | |

| | Liabilities Less Other Assets (9.8)% | | | (4,158,039 | ) |

| | | | | | | | | | | | |

| | Net Assets 100.0% | | $ | 42,642,978 | |

| | | | | | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| (a) | All or a portion of the security was on loan as of September 30, 2015. |

| (b) | 144A - Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

| ADR | American Depositary Receipt |

| REIT | Real Estate Investment Trust |

| | |

| 20 | | SCHEDULEOF INVESTMENTS |

| | |

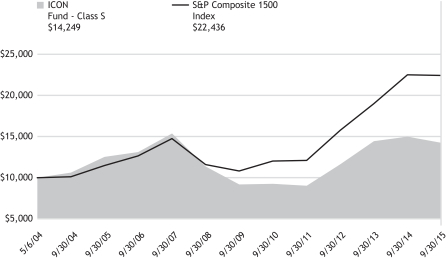

MANAGEMENT OVERVIEW (UNAUDITED) ICON FUND | | |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Fund (the Fund) Class S returned -4.75% for the fiscal year ending September 30, 2015, while its benchmark, the S&P 1500 Index, returned -.30%. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | The Fund outperformed its benchmark over the first six months of the fiscal year due in large part to overweight positions in the Consumer Discretionary and Health Care sectors. Further, an underweight position in the Energy sector, before selling it entirely in late January, as well as having no position in the Utilities sector contributed to Fund outperformance during the first six months. From late June 2015 through August 14, 2015, the day before the steep, sudden 10% drop over six trading days began, the Fund sold positions that had reached ICON’s valuation sell threshold. By August 14, the Fund had accumulated 7.4% cash. In addition, from March 31, 2015 to August 14, 2015, the Fund had gone from a 0% to a 6.2% position in the Utilities sector and from a 13.5% to a 30.7% position in the Financial sector. Despite these two sectors being known for low volatility, as measured by their below average betas, and being the most underpriced sectors according to ICON’s valuation model, Utilities and Financials dropped along with the broad market and did not provide the protection we expected. The Fund dropped more than the overall market and gave back the lead it had accumulated the first six months of the fiscal year. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The five biggest contributors to Fund performance were Skyworks Solutions, Home Depot, Mohawk Industries, Perrigo and Emergent Bio-Solutions. The leader is in the Information Technology sector, the next two are in the Consumer Discretionary sector and the last two are part of the Health Care sector. |

The five largest detractors from Fund performance were Viacom, Jazz Pharmaceuticals, Applied Materials, Lumber Liquidators and Methode Electronics. All were sold except Jazz Pharmaceuticals which remains in the portfolio. Lumber Liquidators stands out as the most notorious as the company was accused on national television of selling flooring products made from illegal chemicals.

| Q. | What is your investment outlook for the overall market? |

| A. | Over the last year, investor sentiment has been influenced by various situations including an expected rise in interest rates, a changing of the shape of the yield curve, lower oil and commodity prices, and the Energy sector’s performance dragging down earnings across all companies. Many moves in stock prices were not based on value but rather were the result of investor reaction to, and expectations for, the situations mentioned above. Some stocks we viewed as cheap didn’t rise while some we saw as over-priced moved higher. Over the long run we expect stocks to respond to value and therefore believe the market will move higher over the next year about in line with its historic average. We do not see any of the behaviors and signs we believe are typical of market peaks and expect the six-year-old bull market to resume. |

ICON Fund

Sector Composition

September 30, 2015

| | | | |

Financial | | | 37.1% | |

Consumer Discretionary | | | 23.3% | |

Health Care | | | 14.7% | |

Materials | | | 7.7% | |

Information Technology | | | 7.3% | |

Utilities | | | 6.5% | |

Industrials | | | 2.1% | |

| | | | |

| | | 98.7% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Fund

Industry Composition

September 30, 2015

| | | | |

Regional Banks | | | 13.2% | |

Biotechnology | | | 7.8% | |

Multi-line Insurance | | | 5.6% | |

Diversified Banks | | | 5.5% | |

Home Improvement Retail | | | 5.3% | |

Semiconductors | | | 4.6% | |

Specialty Chemicals | | | 4.6% | |

Multi-Utilities | | | 4.5% | |

Pharmaceuticals | | | 3.7% | |

Automobile Manufacturers | | | 3.4% | |

Consumer Finance | | | 3.4% | |

Home Furnishings | | | 3.3% | |

Health Care Distributors | | | 3.2% | |

Leisure Products | | | 3.2% | |

| | | | |

Life & Health Insurance | | | 3.2% | |

Construction Materials | | | 3.1% | |

Electronic Components | | | 2.7% | |

Real Estate Services | | | 2.7% | |

Hotels, Resorts & Cruise Lines | | | 2.5% | |

Asset Management & Custody Banks | | | 2.4% | |

Household Appliances | | | 2.3% | |

Railroads | | | 2.1% | |

Electric Utilities | | | 2.0% | |

Tires & Rubber | | | 2.0% | |

Auto Parts & Equipment | | | 1.3% | |

Investment Banking & Brokerage | | | 1.1% | |

| | | | |

| | | 98.7% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Fund

Average Annual Total Return

as of September 30, 2015

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Fund - Class S | | | 5/6/04 | | | | -4.75% | | | | 9.02% | | | | 1.30% | | | | 3.15% | | | | 1.10% | | | | 1.10% | |

ICON Fund - Class C | | | 11/28/00 | | | | -5.86% | | | | 8.17% | | | | 0.54% | | | | 2.69% | | | | 2.26% | | | | 2.25% | |

ICON Fund - Class A | | | 5/31/06 | | | | -5.13% | | | | 8.74% | | | | N/A | | | | -0.10% | | | | 1.56% | | | | 1.50% | |

ICON Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | -10.56% | | | | 7.46% | | | | N/A | | | | -0.73% | | | | 1.56% | | | | 1.50% | |

S&P Composite 1500 Index | | | | | | | -0.30% | | | | 13.34% | | | | 6.95% | | | | 4.98% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Since Inception performance results for Class C shares include returns for certain time periods that were restarted as of June 8, 2004.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

ICON Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the ICON Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the ICON Fund’s other share classes will vary due to differences in charges and expenses. The ICON Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (98.7%) | | | | |

| | Asset Management & Custody Banks (2.4%) | |

| | 94,900 | | | Janus Capital Group, Inc. | | $ | 1,290,640 | |

| | | | | | | | |

| | Auto Parts & Equipment (1.3%) | |

| | 16,900 | | | BorgWarner, Inc. | | | 702,871 | |

| | | | | | | | |

| | Automobile Manufacturers (3.4%) | |

| | 36,000 | | | Thor Industries, Inc. | | | 1,864,800 | |

| | | | | | | | |

| | Biotechnology (7.8%) | | | | |

| | 3,900 | | | Biogen, Inc.† | | | 1,138,059 | |

| | 28,900 | | | Celgene Corp.† | | | 3,126,113 | |

| | | | | | | | |

| | | | | | | 4,264,172 | |

| | Construction Materials (3.1%) | | | | |

| | 11,100 | | | Martin Marietta Materials, Inc. | | | 1,686,645 | |

| | | | | | | | |

| | Consumer Finance (3.4%) | | | | |

| | 50,800 | | | Encore Capital Group, Inc.†(a) | | | 1,879,600 | |

| | | | | | | | |

| | Diversified Banks (5.5%) | | | | |

| | 190,600 | | | Bank of America Corp. | | | 2,969,548 | |

| | | | | | | | |

| | Electric Utilities (2.0%) | | | | |

| | 39,500 | | | OGE Energy Corp. | | | 1,080,720 | |

| | | | | | | | |

| | Electronic Components (2.7%) | | | | |

| | 27,300 | | | Rogers Corp.† | | | 1,451,814 | |

| | | | | | | | |

| | Health Care Distributors (3.2%) | |

| | 9,300 | | | McKesson Corp. | | | 1,720,779 | |

| | | | | | | | |

| | Home Furnishings (3.3%) | | | | |

| | 9,800 | | | Mohawk Industries, Inc.† | | | 1,781,542 | |

| | | | | | | | |

| | Home Improvement Retail (5.3%) | |

| | 25,200 | | | Home Depot, Inc. | | | 2,910,348 | |

| | | | | | | | |

| | Hotels, Resorts & Cruise Lines (2.5%) | |

| | 18,700 | | | Wyndham Worldwide Corp. | | | 1,344,530 | |

| | | | | | | | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Household Appliances (2.3%) | | | | |

| | 8,600 | | | Whirlpool Corp. | | $ | 1,266,436 | |

| | | | | | | | |

| | Investment Banking & Brokerage (1.1%) | |

| | 22,500 | | | E*TRADE Financial Corp.† | | | 592,425 | |

| | | | | | | | |

| | Leisure Products (3.2%) | | | | |

| | 14,400 | | | Polaris Industries, Inc. | | | 1,726,128 | |

| | | | | | | | |

| | Life & Health Insurance (3.2%) | |

| | 91,700 | | | CNO Financial Group, Inc. | | | 1,724,877 | |

| | | | | | | | |

| | Multi-line Insurance (5.6%) | | | | |

| | 19,000 | | | American International Group, Inc. | | | 1,079,580 | |

| | 55,800 | | | Kemper Corp. | | | 1,973,646 | |

| | | | | | | | |

| | | | | | | 3,053,226 | |

| | Multi-Utilities (4.5%) | | | | |

| | 63,800 | | | CenterPoint Energy, Inc. | | | 1,150,952 | |

| | 36,800 | | | CMS Energy Corp. | | | 1,299,776 | |

| | | | | | | | |

| | | | | | | 2,450,728 | |

| | Pharmaceuticals (3.7%) | | | | |

| | 15,300 | | | Jazz Pharmaceuticals PLC† | | | 2,031,993 | |

| | | | | | | | |

| | Railroads (2.1%) | | | | |

| | 42,800 | | | CSX Corp. | | | 1,151,320 | |

| | | | | | | | |

| | Real Estate Services (2.7%) | | | | |

| | 46,500 | | | CBRE Group, Inc., Class A† | | | 1,488,000 | |

| | | | | | | | |

| | Regional Banks (13.2%) | | | | |

| | 92,300 | | | Fifth Third Bancorp | | | 1,745,393 | |

| | 183,700 | | | First Commonwealth Financial Corp. | | | 1,669,833 | |

| | 18,300 | | | Signature Bank† | | | 2,517,348 | |

| | 11,000 | | | SVB Financial Group† | | | 1,270,940 | |

| | | | | | | | |

| | | | | | | 7,203,514 | |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 25 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Semiconductors (4.6%) | | | | |

| | 29,500 | | | Skyworks Solutions, Inc. | | $ | 2,484,195 | |

| | | | | | | | |

| | Specialty Chemicals (4.6%) | | | | |

| | 24,800 | | | Ashland, Inc. | | | 2,495,376 | |

| | | | | | | | |

| | Tires & Rubber (2.0%) | | | | |

| | 37,800 | | | Goodyear Tire & Rubber Co. | | | 1,108,674 | |

| | | | | | | | |

| Total Common Stocks

(Cost $53,901,021) | | | 53,724,901 | |

| | Collateral for Securities on Loan (3.5%) | |

| | 1,930,400 | | | State Street Navigator Prime Portfolio, 0.20% | | | 1,930,400 | |

| | | | | | | | |

| Total Collateral for Securities

on Loan

(Cost $1,930,400) | | | 1,930,400 | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Short-Term Investments (1.4%) | |

| $ | 756,401 | | | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/15 | | $ | 756,401 | |

| | | | | | | | |

| Total Short-Term Investments

(Cost $756,401) | | | 756,401 | |

| Total Investments 103.6%

(Cost $56,587,822) | | | 56,411,702 | |

| Liabilities Less Other Assets

(3.6)% | | | (1,977,321 | ) |

| | | | | | | | |

| | Net Assets 100.0% | | $ | 54,434,381 | |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (a) | All or a portion of the security was on loan as of September 30, 2015. |

| | |

| 26 | | SCHEDULEOF INVESTMENTS |

| | |

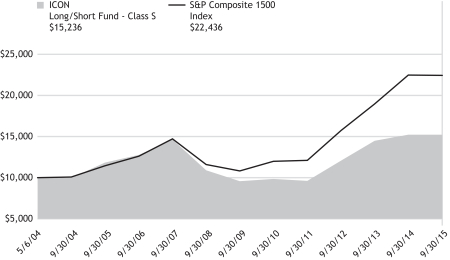

MANAGEMENT OVERVIEW (UNAUDITED) ICON LONG/SHORT FUND | | |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Long/Short Fund (the Fund) Class S returned -.11% for the fiscal year ending September 30, 2015, while its benchmark, the S&P 1500 Index, returned -.30%. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | The Fund outperformed its benchmark over the first ten months of the fiscal year due in large part to overweight positions in the Consumer Discretionary and Health Care sectors. Further, an underweight position in the Energy sector, before selling it entirely in late January, as well as having no position in the Utilities sector contributed to Fund outperformance during the first nine months. From late June 2015 through August 14, 2015, the day before the steep, sudden 10% drop over six trading days began, the Fund sold positions that had reached ICON’s valuation sell threshold. By August 14, the Fund had accumulated 6.8% cash and had a 2.37% short position. In addition, from March 31, 2015 to August 14, 2015, the Fund had gone from a 0% to a 4.0% position in the Utilities sector and from a 13.9% to a 32.7% position in the Financial sector. Despite these two sectors being known for low volatility, as measured by their below average betas, and being the most underpriced sectors according to ICON’s valuation model, Utilities and Financials dropped along with the broad market and did not provide the protection we expected. The Fund dropped more than the overall market and gave back most of the lead it had accumulated the first ten months of the fiscal year. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The five biggest contributors to Fund performance were Ligand Pharmaceuticals, Skyworks Solutions, Tractor Supply Company, Perrigo and Home Depot. Tractor Supply Company and Perrigo were sold for meeting our value-based sell threshold. The other three remain in the portfolio. |

The five largest detractors from Fund performance were Lumber Liquidators, Methode Electronics, Applied Materials, Jazz Pharmaceuticals, and McKesson. The first three were sold while Jazz

Pharmaceuticals and McKesson, both from the Health Care sector, remain in the portfolio. Lumber Liquidators stands out as the most notorious as the company was accused on national television of selling flooring products made from illegal chemicals.

| Q. | What is your investment outlook for the overall market? |

| A. | Over the last year, investor sentiment has been influenced by various situations including an expected rise in interest rates, a changing of the shape of the yield curve, lower oil and commodity prices, and the Energy sector’s performance dragging down earnings across all companies. Many moves in stock prices were not based on value but rather were the result of investor reaction to, and expectations for, the situations mentioned above. Some stocks we viewed as cheap didn’t rise while some we saw as over-priced moved higher. Over the long run we expect stocks to respond to value and therefore believe the market will move higher over the next year about in line with its historic average. We do not see any of the behaviors and signs we believe are typical of market peaks and expect the six-year-old bull market to resume. |

ICON Long/Short Fund

Sector Composition

September 30, 2015

| | | | |

Financial | | | 37.1% | |

Consumer Discretionary | | | 19.8% | |

Health Care | | | 17.0% | |

Information Technology | | | 10.7% | |

Materials | | | 6.3% | |

Utilities | | | 6.3% | |

Industrials | | | 1.7% | |

| | | | |

| | | 98.9% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Long/Short Fund

Industry Composition

September 30, 2015

| | | | |

Regional Banks | | | 12.3% | |

Biotechnology | | | 10.2% | |

Multi-line Insurance | | | 5.4% | |

Diversified Banks | | | 5.1% | |

Home Improvement Retail | | | 4.5% | |

Multi-Utilities | | | 4.3% | |

Semiconductors | | | 4.1% | |

Specialty Chemicals | | | 3.9% | |

Data Processing & Outsourced Services | | | 3.4% | |

Health Care Distributors | | | 3.4% | |

Pharmaceuticals | | | 3.4% | |

Consumer Finance | | | 3.3% | |

Electronic Components | | | 3.2% | |

Home Furnishings | | | 3.2% | |

Life & Health Insurance | | | 3.2% | |

| | | | |

Automobile Manufacturers | | | 2.7% | |

Asset Management & Custody Banks | | | 2.6% | |

Leisure Products | | | 2.6% | |

Hotels, Resorts & Cruise Lines | | | 2.5% | |

Construction Materials | | | 2.4% | |

Household Appliances | | | 2.3% | |

Real Estate Services | | | 2.1% | |

Electric Utilities | | | 2.0% | |

Insurance Brokers | | | 2.0% | |

Tires & Rubber | | | 2.0% | |

Railroads | | | 1.7% | |

Investment Banking & Brokerage | | | 1.1% | |

| | | | |

| | | 98.9% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Long/Short Fund

Average Annual Total Return

as of September 30, 2015

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Long/Short Fund - Class S | | | 5/6/04 | | | | -0.11% | | | | 9.10% | | | | 2.54% | | | | 3.76% | | | | 1.45% | | | | 1.32% | |

ICON Long/Short Fund - Class C | | | 10/17/02 | | | | -1.19% | | | | 7.94% | | | | 1.53% | | | | 4.61% | | | | 2.57% | | | | 2.38% | |

ICON Long/Short Fund - Class A | | | 5/31/06 | | | | -0.44% | | | | 8.76% | | | | N/A | | | | 1.45% | | | | 1.81% | | | | 1.63% | |

ICON Long/Short Fund - Class A (including maximum sales charge of 5.75%) | | | 5/31/06 | | | | -6.18% | | | | 7.47% | | | | N/A | | | | 0.81% | | | | 1.81% | | | | 1.63% | |

S&P Composite 1500 Index | | | | | | | -0.30% | | | | 13.34% | | | | 6.95% | | | | 8.72% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

ICON Long/Short Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Long/Short Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Long/Short Fund’s other share classes will vary due to differences in charges and expenses. The Long/Short Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON LONG/SHORT FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (98.9%) | | | | |

| | Asset Management & Custody Banks (2.6%) | |

| | 61,800 | | | Janus Capital Group, Inc. | | $ | 840,480 | |

| | | | | | | | |

| | Automobile Manufacturers (2.7%) | |

| | 17,000 | | | Thor Industries, Inc. | | | 880,600 | |

| | | | | | | | |

| | Biotechnology (10.2%) | | | | |

| | 2,300 | | | Biogen, Inc.† | | | 671,163 | |

| | 13,500 | | | Celgene Corp.† | | | 1,460,295 | |

| | 13,900 | | | Ligand Pharmaceuticals, Inc.†(a) | | | 1,190,535 | |

| | | | | | | | |

| | | | | | | 3,321,993 | |

| | Construction Materials (2.4%) | | | | |

| | 5,200 | | | Martin Marietta Materials, Inc. | | | 790,140 | |

| | | | | | | | |

| | Consumer Finance (3.3%) | | | | |

| | 29,400 | | | Encore Capital Group, Inc.†(a) | | | 1,087,800 | |

| | | | | | | | |

| Data Processing & Outsourced

Services (3.4%) |

|

| | 12,300 | | | Mastercard, Inc., Class A | | | 1,108,476 | |

| | | | | | | | |

| | Diversified Banks (5.1%) | | | | |

| | 107,100 | | | Bank of America Corp. | | | 1,668,618 | |

| | | | | | | | |

| | Electric Utilities (2.0%) | | | | |

| | 23,700 | | | OGE Energy Corp. | | | 648,432 | |

| | | | | | | | |

| | Electronic Components (3.2%) | | | | |

| | 19,700 | | | Rogers Corp.† | | | 1,047,646 | |

| | | | | | | | |

| | Health Care Distributors (3.4%) | |

| | 6,000 | | | McKesson Corp. | | | 1,110,180 | |

| | | | | | | | |

| | Home Furnishings (3.2%) | | | | |

| | 5,800 | | | Mohawk Industries, Inc.† | | | 1,054,382 | |

| | | | | | | | |

| | Home Improvement Retail (4.5%) | |

| | 12,800 | | | Home Depot, Inc. | | | 1,478,272 | |

| | | | | | | | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Hotels, Resorts & Cruise Lines (2.5%) | |

| | 11,500 | | | Wyndham Worldwide Corp. | | $ | 826,850 | |

| | | | | | | | |

| | Household Appliances (2.3%) | | | | |

| | 5,100 | | | Whirlpool Corp. | | | 751,026 | |

| | | | | | | | |

| | Insurance Brokers (2.0%) | | | | |

| | 15,500 | | | Arthur J Gallagher & Co. | | | 639,840 | |

| | | | | | | | |

| | Investment Banking & Brokerage (1.1%) | |

| | 13,500 | | | E*TRADE Financial Corp.† | | | 355,455 | |

| | | | | | | | |

| | Leisure Products (2.6%) | | | | |

| | 7,200 | | | Polaris Industries, Inc. | | | 863,064 | |

| | | | | | | | |

| | Life & Health Insurance (3.2%) | |

| | 56,300 | | | CNO Financial Group, Inc. | | | 1,059,003 | |

| | | | | | | | |

| | Multi-line Insurance (5.4%) | | | | |

| | 11,600 | | | American International Group, Inc. | | | 659,112 | |

| | 31,200 | | | Kemper Corp. | | | 1,103,544 | |

| | | | | | | | |

| | | | | | | 1,762,656 | |

| | Multi-Utilities (4.3%) | |

| | 34,600 | | | CenterPoint Energy, Inc. | | | 624,184 | |

| | 22,100 | | | CMS Energy Corp. | | | 780,572 | |

| | | | | | | | |

| | | | | | | 1,404,756 | |

| | Pharmaceuticals (3.4%) | | | | |

| | 8,400 | | | Jazz Pharmaceuticals PLC† | | | 1,115,604 | |

| | | | | | | | |

| | Railroads (1.7%) | | | | |

| | 20,400 | | | CSX Corp. | | | 548,760 | |

| | | | | | | | |

| | Real Estate Services (2.1%) | | | | |

| | 21,800 | | | CBRE Group, Inc., Class A† | | | 697,600 | |

| | | | | | | | |

| | |

| 32 | | SCHEDULEOF INVESTMENTS |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Regional Banks (12.3%) | | | | |

| | 40,300 | | | Fifth Third Bancorp | | $ | 762,073 | |

| | 112,800 | | | First Commonwealth Financial Corp. | | | 1,025,352 | |

| | 10,600 | | | Signature Bank† | | | 1,458,136 | |

| | 6,600 | | | SVB Financial Group† | | | 762,564 | |

| | | | | | | | |

| | | | | | | 4,008,125 | |

| | Semiconductors (4.1%) | | | | |

| | 15,700 | | | Skyworks Solutions, Inc. | | | 1,322,097 | |

| | | | | | | | |

| | Specialty Chemicals (3.9%) | | | | |

| | 12,600 | | | Ashland, Inc. | | | 1,267,812 | |

| | | | | | | | |

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Tires & Rubber (2.0%) | | | | |

| | 22,700 | | | Goodyear Tire & Rubber Co. | | $ | 665,791 | |

| | | | | | | | |

| Total Common Stocks

(Cost $31,819,065) | | | 32,325,458 | |

| | Collateral for Securities on Loan (7.0%) | |

| | 2,281,325 | | | State Street Navigator Prime Portfolio, 0.20% | | | 2,281,325 | |

| | | | | | | | |

| Total Collateral for

Securities on Loan

(Cost $2,281,325) | | | 2,281,325 | |

| Total Investments 105.9%

(Cost $34,100,390) | | | 34,606,783 | |

| Liabilities Less Other

Assets (5.9)% | | | (1,924,346 | ) |

| | | | | | | | |

| | Net Assets 100.0% | | $ | 32,682,437 | |

| | | | | | | | |

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (a) | All or a portion of the security was on loan as of September 30, 2015. |

| | | | |

| SCHEDULEOF INVESTMENTS | | | 33 | |

| | |

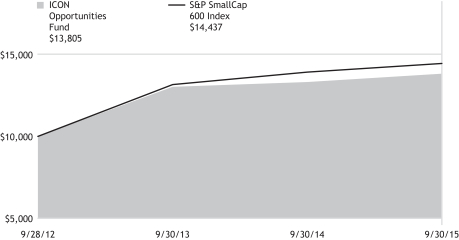

MANAGEMENT OVERVIEW (UNAUDITED) ICON OPPORTUNITIES FUND | | |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Opportunities Fund (the Fund) returned 3.75% for the fiscal year ending September 30, 2015, while its benchmark, the S&P Small-Cap 600 Index, returned 3.81%. Total returns for other periods as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | The Fund outperformed its benchmark over the first ten months of the fiscal year due in large part to overweight positions in the Consumer Discretionary and Health Care sectors. Further, an underweight position in the Energy sector, before selling it entirely in late January, as well as having no position in the Utilities sector contributed to Fund outperformance during the first nine months. From late June 2015 through August 14, 2015, the day before the steep, sudden 10% drop over six trading days began, the Fund sold positions that had reached ICON’s valuation sell threshold. By August 14, the Fund had accumulated 8.5% cash. In addition, from March 31, 2015 to August 14, 2015, the Fund had gone from a 0% to a 6.3% position in the Utilities sector and from a 14.7% to a 23.7% position in the Financial sector. Despite these two sectors being known for low volatility, as measured by their below average betas, and being the most underpriced sectors according to ICON’s valuation model, Utilities and Financials dropped along with the broad market and did not provide the protection we expected. The Fund dropped more than the overall market and gave back the lead it had accumulated the first ten months of the fiscal year. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The five biggest contributors to Fund performance were Ligand Pharmaceuticals, Cambrex, Emergent BioSolutions, Nutrisystem, and Buffalo Wild Wings. The first three are in the Health Care sector while the next two are in the Consumer Discretionary sector. |

The five largest detractors from Fund performance were Lumber Liquidators, Conn’s, Methode Electronics, Janus Capital Group, and Methanex. Lumber Liquidators stands out as the most notorious as the company was accused on national television of selling flooring products made from illegal chemicals. Conn’s stock price dropped almost 60% in

six trading days when analysts suspected the credit the company was granting customers buying appliances was resulting in growing delinquencies.

| Q. | What is your investment outlook for the overall market? |

| A. | Over the last year, investor sentiment has been influenced by various situations including an expected rise in interest rates, a changing of the shape of the yield curve, lower oil and commodity prices, and the Energy sector’s performance dragging down earnings across all companies. Many moves in stock prices were not based on value but rather were the result of investor reaction to, and expectations for, the situations mentioned above. Some stocks we viewed as cheap didn’t rise while some we saw as over-priced moved higher. Over the long run we expect stocks to respond to value and therefore believe the market will move higher over the next year about in line with its historic average. We do not see any of the behaviors and signs believe are as typical of market peaks and expect the six-year-old bull market to resume. |

ICON Opportunities Fund

Sector Composition

September 30, 2015

| | | | |

Financial | | | 29.1% | |

Consumer Discretionary | | | 15.2% | |

Health Care | | | 14.6% | |

Information Technology | | | 14.4% | |

Utilities | | | 10.3% | |

Industrials | | | 8.7% | |

Materials | | | 3.4% | |

Leisure and Consumer Staples | | | 2.1% | |

| | | | |

| | | 97.8% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Opportunities Fund

Industry Composition

September 30, 2015

| | | | |

Electric Utilities | | | 6.9% | |

Multi-line Insurance | | | 6.4% | |

Regional Banks | | | 6.4% | |

Consumer Finance | | | 6.2% | |

Electronic Equipment & Instruments | | | 6.2% | |

Pharmaceuticals | | | 5.5% | |

Asset Management & Custody Banks | | | 4.7% | |

Internet Retail | | | 4.6% | |

Automobile Manufacturers | | | 4.4% | |

Internet Software & Services | | | 3.7% | |

Biotechnology | | | 3.6% | |

Life Sciences Tools & Services | | | 3.6% | |

Construction & Farm Machinery & Heavy Trucks | | | 3.5% | |

Paper Packaging | | | 3.4% | |

| | | | |

Life & Health Insurance | | | 3.2% | |

Aerospace & Defense | | | 3.1% | |

Semiconductors | | | 2.5% | |

Gas Utilities | | | 2.3% | |

Auto Parts & Equipment | | | 2.2% | |

Insurance Brokers | | | 2.2% | |

Building Products | | | 2.1% | |

Packaged Foods & Meats | | | 2.1% | |

Electronic Components | | | 2.0% | |

Housewares & Specialties | | | 2.0% | |

Leisure Products | | | 2.0% | |

Health Care Facilities | | | 1.9% | |

Water Utilities | | | 1.1% | |

| | | | |

| | | 97.8% | |

| | | | |

Percentages are based upon common stocks as a percentage of net assets.

ICON Opportunities Fund

Average Annual Total Return

as of September 30, 2015

| | | | | | | | | | | | | | | | | | | | |

| | | Inception

Date | | | 1 Year | | | Since

Inception | | | Gross

Expense

Ratio* | | | Net

Expense

Ratio* | |

ICON Opportunities Fund | | | 9/28/12 | | | | 3.75% | | | | 11.31% | | | | 2.44% | | | | 1.50% | |

S&P Small Cap Total Return | | | | | | | 3.81% | | | | 13.03% | | | | N/A | | | | N/A | |

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

ICON Opportunities Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Opportunities Fund on the inception date of 9/28/12 to a $10,000 investment made in an unmanaged securities index on that date. The Opportunities Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

ICON OPPORTUNITIES FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| | | | | | | | |

| Shares or Principal Amount | | Value | |

| | | | | | | | |

| | Common Stocks (97.8%) | |