Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07883

ICON Funds

(Exact name of registrant as specified in charter)

5299 DTC Blvd.

Suite 1200 Greenwood Village, CO 80111

(Address of principal executive offices) (Zip code)

Carrie M. Schoffman

5299 DTC Blvd.

Suite 1200 Greenwood Village, CO 80111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-790-1600

Date of fiscal year end: September 30, 2014

Date of reporting period: September 30, 2014

Table of Contents

| Item 1. | Reports to Stockholders. |

Table of Contents

2014 ANNUAL REPORT

ICON DIVERSIFIED FUNDS

INVESTMENT UPDATE

ICON Bond Fund

ICON Equity Income Fund

ICON Fund

ICON Long/Short Fund

ICON Opportunities Fund

ICON Risk-Managed Balanced Fund

1-800-764-0442 | www.iconfunds.com

Table of Contents

You can now sign up for electronic delivery of ICON Fund shareholder reports, including prospectuses, annual reports, semiannual reports and proxy statements.

When these materials are available, you will receive an email from ICON with instructions on how to view the documents. Statements, transaction confirmations and other documents that are not available online will continue to be sent to you by U.S. mail.

Visit ICON’s website at www.iconfunds.com to learn more and sign up.

You may change or cancel your participation in eDelivery by visiting www.iconfunds.com, or you can request a hard copy of any of the materials free of charge by calling ICON Funds at 1-800-764-0442.

1-800-764-0442 • www.iconfunds.com

Table of Contents

| 2 | ||||

| 6 | ||||

Management Overview (Unaudited) and Schedules of Investments | ||||

| 9 | ||||

| 17 | ||||

| 24 | ||||

| 29 | ||||

| 35 | ||||

| 40 | ||||

| 50 | ||||

| 62 | ||||

| 68 | ||||

| 88 | ||||

| 89 | ||||

| 92 | ||||

| 95 | ||||

| 103 | ||||

Table of Contents

Historical Returns

All total returns mentioned in this Report account for the change in a Fund’s per-share price and the reinvestment of any dividends, capital gain distributions and adjustments for financial statement purposes. If your account is set up to receive Fund distributions in cash rather than to reinvest them, your actual return may differ from these figures. The Funds’ performance results do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Adviser may have reimbursed certain fees or expenses of some of the Funds. If not for these reimbursements, performance would have been lower. Fund results shown, unless otherwise indicated, are at net asset value. If a sales charge (maximum 5.75%) had been deducted, results would have been lower.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance results represent past performance, and current performance may be higher or lower. Please call 1-800-764-0442 or visit www.iconfunds.com for performance results current to the most recent month-end.

Portfolio Data

This Report reflects ICON’s views, opinions and portfolio holdings as of September 30, 2014, the end of the reporting period. The information is not a complete analysis of every aspect of any sector, industry, security or the Funds.

Opinions and forecasts regarding industries, companies and/or themes, and portfolio composition and holdings are subject to change at any time based on market and other conditions, and should not be construed as a recommendation of any specific security, industry or sector. Each Fund’s holdings as of September 30, 2014 are included in each Fund’s Schedule of Investments.

According to ICON, value investing is an analytical approach to investing that employs various factors, including projecting earnings growth estimates, in an effort to determine whether securities are over- or underpriced relative to ICON’s estimates of their intrinsic value. Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies. ICON’s value-to-price ratio (“V/P”) is a ratio of intrinsic value, as calculated using ICON’s proprietary valuation methodology, of a broad range of domestic and international securities within ICON’s system as compared to the current market price of those securities. The ICON system relies on the integrity of the financial statements released to the market as part of our analysis.

| 2 | ABOUT THIS REPORT |

Table of Contents

This Report contains statements regarding industry or sector themes, new market themes, investment outlook, relative strength, value-to-price ratios, and investment team expectations, beliefs, goals and the like that are based on current expectations, recent individual stock performance relative to current market prices, estimates of company values and other information supplied to the market by the companies we follow. Words such as “expects,” “suggests,” “anticipates,” “targets,” “goals,” “value,” “intrinsic value,” “indicates,” “believes,” “considers,” “estimates,” variations of such words and similar expressions are intended to identify forward looking statements, which are not statements of historical fact. Forward looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to assess. These risks and uncertainties are based on a number of important factors, including, among others: stock price fluctuations; the integrity and accuracy of historical and projected financial and other information supplied by companies to the public or assumptions based on such information supplied; interest rates; bond yields; future earnings growth rates; the risks noted in this Report and other factors beyond the control of our investment team but used by the investment team to influence their assumptions. Therefore, actual outcome may differ materially from what is expressed in such forward looking statements.

There are risks associated with mutual fund investing, including the loss of principal. The likelihood of loss may be greater if you invest for a shorter period of time. There is no assurance that the investment process will consistently lead to successful results.

There are risks associated with selling short, including the risk that the ICON Long/Short Fund may have to cover its short position at a higher price than the short price, resulting in a loss. The ICON Long/Short Fund’s loss on a short sale is potentially unlimited as a loss occurs when the value of a security sold short increases. Call options involve certain risks, such as limited gains and lack of liquidity in the underlying securities, and are not suitable for all investors.

Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securities generally decreases. Effective May 5, 2014 the ICON Bond Fund may invest up to 35% of its assets in high-yield bonds that are below investment grade. Prior to May 5, 2014 the Bond Fund was limited to 25% in below investment grade bonds. The ICON Equity Income Fund may invest up to 25% of its assets in high-yield bonds that are below investment grade. ICON Risk-Managed Balanced Fund may invest up to 10% of its assets in high-yield bonds that are below investment grade. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher-quality bonds.

An investment concentrated in sectors and industries may involve greater risk and volatility than a more diversified investment.

| ABOUT THIS REPORT | 3 |

Table of Contents

Investments in foreign securities may entail unique risks, including political, market, and currency risks. Financial statements of foreign companies are governed by different accounting, auditing, and financial standards than U.S. companies and may be less transparent and uniform than in the United States. Many corporate governance standards, which help ensure the integrity of public information in the United States, do not exist in foreign countries. In general, there may be less governmental supervision of foreign stock exchanges and securities brokers and issuers. The ICON system relies on the integrity of financial statements released to the market as part of our analysis.

Investments in other mutual fund companies may entail certain risks. For example, the Fund’s performance depends on the underlying funds in which it invests, and it is subject to the risks of the underlying funds. Additionally, an investment by the Fund or underlying fund in exchange-traded funds generally presents the same primary risks as an investment in a mutual fund.

The prospectus and statement of additional information contain this and other information about the Funds and are available by visiting www.iconfunds.com or calling 1-800-764-0442. Please read the prospectus and statement of additional information carefully.

Comparative Indexes

The comparative indexes discussed in this Report are meant to provide a basis for judging a Fund’s performance against specific securities indexes. Each index shown accounts for both change in the security price and reinvestment of dividends and distributions (except as noted), but does not reflect the costs of managing a mutual fund. The Funds’ portfolios may significantly differ in holdings and composition from the index. Individuals cannot invest directly in an index.

| • | The unmanaged Standard & Poor’s (“S&P”) Composite 1500 Index (“S&P Composite 1500 Index”) is a broad-based capitalization-weighted index comprising 1,500 stocks of large-cap, mid-cap, and small-cap U.S. companies. |

| • | The unmanaged Barclays Capital U.S. Universal Index (ex-MBS) represents the union of the U.S. Aggregate Index, the U.S. High-Yield Corporate Index, the 144A Index, the Eurodollar Index and the Emerging Markets Index. All securities in this market-value weighted index have at least one year remaining to maturity and meet certain minimum issue size criteria. |

| • | The unmanaged Standard & Poor’s (“S&P”) SmallCap 600 Index (“S&P SmallCap 600 Index”) is a broad-based capitalization-weighted index comprising 600 stocks of small-cap U.S. companies. |

| 4 | ABOUT THIS REPORT |

Table of Contents

Index returns and statistical data included in this Report are provided by FactSet Research Systems.

Financial Intermediary

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may influence the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| ABOUT THIS REPORT | 5 |

Table of Contents

MESSAGE FROM ICON FUNDS (UNAUDITED)

Dear Shareholder,

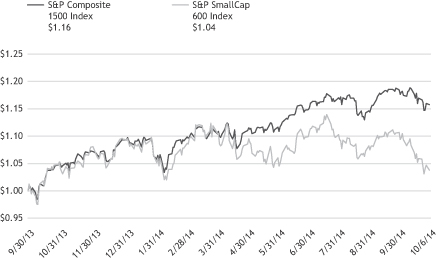

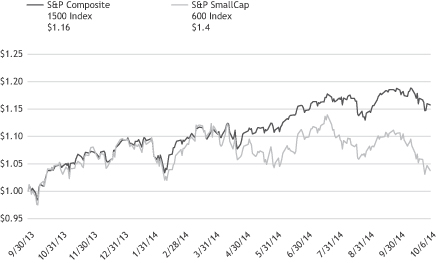

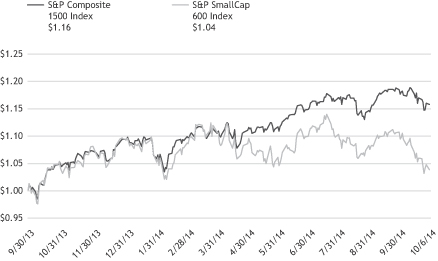

The graph below shows the S&P Composite 1500 Index and a subset of it, the S&P SmallCap 600 Index (“S&P SmallCap 600 Index”) from 9/30/13 through 10/6/14 (our fiscal year plus a few days into October). It reveals a fragmented, divergent market in 2014. The two indexes moved similarly in late 2013, then diverged in 2014. The 1500, lifted by a few large-cap stocks, moved 7.5% higher year to date through September 30, 2014, while the small-cap component of it is negative for 2014, as highlighted in the table. In addition to that divergence, there have been a few rapid, short term industry and sector theme reversals during each up and down phase, more easily seen on the Small Cap chart. We believe the divergence and the theme reversals can be explained by investors’ reaction to three situations.

Index | 9/30/13-12/31/13 | 12/31/13-9/30/14 | ||||||

S&P Composite 1500 | 10.3% | 7.5% | ||||||

S&P SmallCap 600 | 9.8% | -3.7% | ||||||

The first situation relates to investors’ reactions to a surprise negative Gross Domestic Product (GDP). Entering the first quarter of 2014, most forecasters were calling for positive real GDP. However, as the quarter unfolded it became apparent that something was wrong. Now, looking back, we know real GDP was at a negative 2.1% pace for the year. Investors flipped from favoring cyclical industries and sectors in late 2013 to favoring defensive, recession proof ones in early 2014. This theme change lasted only three and

| 6 | MESSAGE FROM ICON FUNDS |

Table of Contents

a half months for the 1500 Index and one month longer for the 600 Index, too quick for a value-based system to capture.

The second situation involves investors’ reactions to a rise in the U.S. Dollar. From June 30, 2013 through September 30, 2014, the U.S. Dollar Index (DXY) gained 7.7%, which is still 28.5% below its peak in 2002. It appears many investors and speculators adjusted their equity portfolios, attempting to guess which industries and stocks would either benefit from or be hurt by a stronger US Dollar. We have found economic reactions to currency swings to be less dramatic and slower than theory would suggest so we suspect these investors may be over reacting lately.

The last situation relates to investors’ speculation on rising interest rates. In anticipation of the Federal Reserve ending its quantitative easing program, there appeared to be a popular belief that both short-term and long-term interest rates would increase. Investors who believed this might have adjusted their equity portfolios in anticipation of higher interest rates and their behavior affected stock prices. First, it should be mentioned that ICON believes, and has stated, that interest rates can go low and stay low for many years. We see no support for higher long term interest rates. We sense, however, that we are in the minority with that outlook. We believe the many investors who expect higher interest rates bought stocks they think will benefit from higher rates and sold stocks they think will be hurt by rate increases. For example, it might be that these investors, believing that rising rates will hurt small cap stocks more than large cap stocks, bought large cap issues while avoiding small cap stocks altogether. Similarly, believing that higher rates would have a negative impact on certain industries, they avoided industries in the Consumer Discretionary sector that have an element of consumer borrowing such as the homebuilders, automobile manufacturers and home furnishing industries.

We believe investors’ reactions to a surprise negative GDP quarter, a rise in the US Dollar and an anticipated rise interest rates have contributed to moves in stocks that were not related to value of the stocks themselves. We have seen overpriced stocks (in our opinion) get bid up higher and underpriced stocks taken lower as investors try to get repositioned. This recent trend of positioning equity portfolios for anticipated higher interest rates and a rising US Dollar is stretching the valuation in some industries according to our system. However, according to our methodology, industries favored by these speculators are becoming overpriced while disfavored industries are becoming underpriced. Given this scenario, we expect this behavior to end sometime in the next year.

The first week of October 2014 our ICON market value-to-price (V/P) ratio has been in the 1.06 – 1.10 range, indicating stocks, on average, are priced

| MESSAGE FROM ICON FUNDS | 7 |

Table of Contents

below our estimate of fair value and giving us the expectation that stock prices can move higher over the next year. Over the course of the last year value has grown and prices of some stocks have kept pace, but, as seen in the graph, some have lagged behind. As mentioned above, we believe this disconnect is due to concerns about the strength of the U.S. Dollar and the expectation of rising interest rates. We are finding better value in the cyclical, economically sensitive industries rather than the so-called recession proof industries. With an overall V/P ratio of 1.10 and many industry valuation readings stretched, we will buy the best bargains we can find and have the patience to wait for investors to ultimately recognize value. Our valuation readings, coupled with various supportive conditions such as low inflation, low interest rates, no shortages of capital or commodities and modest economic growth, lead us to believe we are in a favorable setting for owning equities.

Craig Callahan D.B.A.

Chief Executive Officer

ICON Advisers, Inc.

| 8 | MESSAGE FROM ICON FUNDS |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) | Class S Class C Class A | IOBZX IOBCX IOBAX |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | For the Fund’s fiscal year ended September 30, 2014, the ICON Bond Fund (the Fund) Class S shares outperformed its benchmark, the Barclays Capital US Universal Index. The Fund returned 6.01% while the Barclays Capital U.S. Universal Index Excluding Mortgage Backed Securities returned 4.60%. Total returns for other periods and additional Class shares as of September 30, 2014, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Fiscal year 2014 caught many investors off guard as a largely anticipated bond sell-off turned into a strong rally as yields fell across the board. The yield on the U.S. Generic Government 10-year Treasury began the fiscal year at a value of 2.62%, rose above 3.00% by the end of the calendar year 2013, fell below 2.45% at the end of May 2014 in response to some macro-economic uncertainty, and finally finished the fiscal year at a value of 2.49%. In addition to the rally in the U.S. treasury market, corporate bond spreads tightened throughout the majority of the fiscal year in both investment grade and high yield corporate bonds before experiencing some volatility during the third quarter of 2014. While the ICON Bond Fund maintained a lower overall duration over the course of the time period resulting less relative curve effect, the Fund was able to outperform the broad based fixed income benchmark during the fiscal year through a combination of bond selections within the corporate bond segment of the market and active allocation to both preferred shares and closed-end fund positions. In the corporate bond space, we maintained a lower overall duration relative to the benchmark but selections in the Energy, Financials, and Telecommunications sectors of the market outperformed the market as a whole. As spreads continued to tighten we focused on other segments of the market to produce alpha for our investors, including certain preferred issues. All of our positions in this space produced positive returns, but three specific holdings within the real estate segment of the market did particularly well with one position producing a large gain due to a company issued call. Lastly, holdings within the closed-end segment of the market also produced positive returns as either net asset value (NAV) based movement or discount arbitrage opportunities were realized. The end result of these portfolio adjustments was outperformance during the period for the ICON Bond Fund in the face of a large duration based drag. |

| MANAGEMENT OVERVIEW | 9 |

Table of Contents

| Q. | How did the Fund’s composition affect performance? |

| A. | As stated above, the Fund was able to outperform its benchmark during the fiscal year. Further analysis shows the outperformance stemmed from both selection effect and allocation effect while relative curve effect (gains from interest rate movements) was negative over the fiscal year. Positive selection effect came from both the corporate bond segment of the market where selections within the Energy, Financials, and Telecommunications sectors of the market saw larger spread movement than the broad market, as well as closed-end fund positions where either discount tightening was realized or activist actions resulted in fund tender plays. Positive allocation effect came from strong performance in corporate bonds, closed-end funds, and preferred shares. Finally, negative curve effect resulted from the Fund being positioned in shorter duration securities while there was a large rate rally over the course of the fiscal year. Based on our internal assumption of risk and returns we felt as though duration extension was unwarranted and would rather look to focus on bottom up security selection. |

| Q. | What is your investment outlook for the bond market? |

| A. | The end of fiscal year 2014 saw an increase in both spread and interest rate volatility as concerns about domestic and global growth began to emerge. Overall, we generally believe these concerns are unwarranted and the volatility in spread product will create opportunities in the end. While we don’t anticipate a substantial upward movement in interest rates over the course of the next 12 months, the Fund is positioned in the lower portion of its duration range as we move into fiscal year 2015. As in fiscal year 2014, we continue to shy away from interest rate forecasts and remain steadfast in our search for issue specific opportunities. We are looking for opportunities that have the characteristics of credit upgrades, special situations, or anticipated future bond tenders. While future bond market volatility might be substantial, we believe our unique investment methodology will help the Fund navigate the changing market. |

| 10 | MANAGEMENT OVERVIEW |

Table of Contents

ICON Bond Fund

Credit Diversification

September 30, 2014

Aaa | 12.1% | |||

A1 | 4.2% | |||

A2 | 0.4% | |||

A3 | 8.4% | |||

Baa1 | 10.5% | |||

Baa2 | 5.9% | |||

Baa3 | 12.3% | |||

Ba1 | 3.7% | |||

Ba2 | 3.0% | |||

Ba3 | 4.5% | |||

B2 | 3.2% | |||

B3 | 4.2% | |||

Caa1 | 3.4% | |||

|

| |||

| 75.8% | ||||

|

|

Percentages are based upon U.S. Treasury obligations, corporate and foreign corporate bond investments as a percentage of net assets. Ratings based on Moody’s Investors Service, Inc.

| MANAGEMENT OVERVIEW | 11 |

Table of Contents

ICON Bond Fund

Average Annual Total Return

as of September 30, 2014

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON Bond Fund - | 5/6/04 | 6.01% | 5.03% | 4.63% | 4.87% | 0.89% | 0.75% | |||||||||||||||||||||

ICON Bond Fund - | 10/21/02 | 5.10% | 4.14% | 3.76% | 4.37% | 2.06% | 1.60% | |||||||||||||||||||||

ICON Bond Fund - | 9/30/10 | 5.77% | N/A | N/A | 3.48% | 1.34% | 1.00% | |||||||||||||||||||||

ICON Bond Fund - | 9/30/10 | 0.77% | N/A | N/A | 2.23% | 1.34% | 1.00% | |||||||||||||||||||||

Barclays Capital U.S. Universal Index | 4.39% | 4.66% | 4.90% | 5.24% | N/A | N/A | ||||||||||||||||||||||

Barclays Capital U.S. Universal Index (ex-MBS) | 4.60% | 5.12% | 4.92% | 5.45% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| 12 | MANAGEMENT OVERVIEW |

Table of Contents

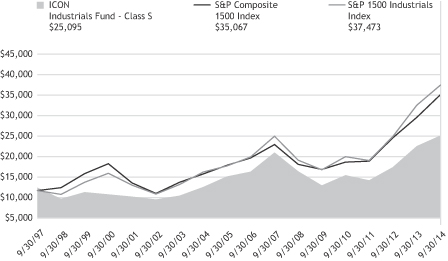

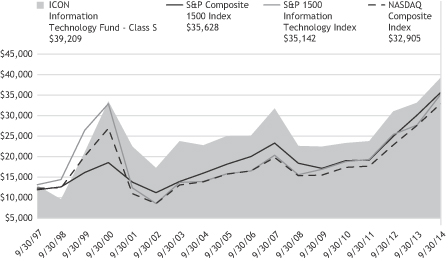

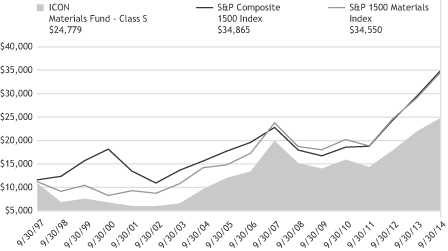

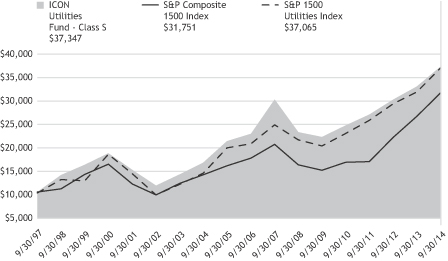

ICON Bond Fund

Value of a $10,000 Investment

through September 30, 2014

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Bond Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Bond Fund’s other share classes will vary due to differences in charges and expenses. The Bond Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| MANAGEMENT OVERVIEW | 13 |

Table of Contents

ICON BOND FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2014

| Shares or Principal Amount | Interest Rate | Maturity Date | Value | |||||||||||||

| Corporate Bonds (57.2%) | ||||||||||||||||

| $ | 2,000,000 | AIG Life Holdings, Inc. | 6.63 | % | 02/15/29 | $ | 2,456,090 | |||||||||

| 2,798,000 | Altria Group, Inc. | 9.25 | % | 08/06/19 | 3,642,459 | |||||||||||

| 1,000,000 | Brightstar Corp.(a) | 7.25 | % | 08/01/18 | 1,076,250 | |||||||||||

| 3,450,000 | Clearwire Communications LLC / Clearwire Finance, Inc.(a) | 14.75 | % | 12/01/16 | 4,286,625 | |||||||||||

| 1,000,000 | Comcast Cable Holdings LLC | 10.13 | % | 04/15/22 | 1,387,262 | |||||||||||

| 2,500,000 | Cullen/Frost Capital Trust II(b) | 1.78 | % | 03/01/34 | 2,194,746 | |||||||||||

| 1,300,000 | Everest Reinsurance Holdings, Inc.(b) | 6.60 | % | 05/01/67 | 1,358,500 | |||||||||||

| 2,000,000 | Freescale Semiconductor, Inc. | 10.75 | % | 08/01/20 | 2,220,000 | |||||||||||

| 1,000,000 | Fulton Capital Trust I Ltd. | 6.29 | % | 02/01/36 | 965,000 | |||||||||||

| 780,000 | GE Capital Franchise Finance Corp., MTN | 7.10 | % | 11/30/26 | 997,229 | |||||||||||

| 2,500,000 | General Electric Capital Corp., Series A, FRN(b) | 7.13 | % | 06/15/22 | 2,893,750 | |||||||||||

| 1,000,000 | General Electric Capital Corp., Series B(b) | 6.25 | % | 12/15/22 | 1,077,500 | |||||||||||

| 2,750,000 | General Electric Capital Corp. / LJ VP Holdings LLC(a) | 3.80 | % | 06/18/19 | 2,929,074 | |||||||||||

| 1,000,000 | Gibson Brands, Inc.(a) | 8.88 | % | 08/01/18 | 977,500 | |||||||||||

| 1,500,000 | Goodman Networks, Inc.(c) | 12.13 | % | 07/01/18 | 1,575,000 | |||||||||||

| 1,300,000 | GRD Holdings III Corp.(a) | 10.75 | % | 06/01/19 | 1,433,250 | |||||||||||

| 1,000,000 | Ingersoll-Rand Co. | 6.39 | % | 11/15/27 | 1,192,033 | |||||||||||

| 1,549,805 | Kiowa Power Partners LLC(a) | 5.74 | % | 03/30/21 | 1,613,352 | |||||||||||

| 3,500,000 | Lender Processing Services, Inc. / Black Knight Lending Solutions, Inc. | 5.75 | % | 04/15/23 | 3,657,500 | |||||||||||

| 1,000,000 | Liberty Mutual Group, Inc.(a)(b) | 7.00 | % | 03/07/67 | 1,060,000 | |||||||||||

| 1,000,000 | Masco Corp. | 5.95 | % | 03/15/22 | 1,092,500 | |||||||||||

| 2,439,000 | MBIA, Inc. | 6.63 | % | 10/01/28 | 2,487,780 | |||||||||||

| 2,500,000 | Prudential Financial, Inc.(b) | 8.88 | % | 06/15/68 | 3,015,625 | |||||||||||

| 300,000 | Prudential Holdings LLC, Series FSA(a) | 7.25 | % | 12/18/23 | 368,599 | |||||||||||

| 2,000,000 | Prudential Insurance Co. of America(a) | 8.30 | % | 07/01/25 | 2,715,978 | |||||||||||

| 1,000,000 | Regions Financial Corp. | 7.75 | % | 09/15/24 | 1,195,186 | |||||||||||

| 1,500,000 | SESI LLC | 7.13 | % | 12/15/21 | 1,657,500 | |||||||||||

| 1,000,000 | United Refining Co. | 10.50 | % | 02/28/18 | 1,065,000 | |||||||||||

| 1,500,000 | UnitedHealth Group, Inc. | 3.88 | % | 10/15/20 | 1,606,032 | |||||||||||

|

| |||||||||||||||

|

| Total Corporate Bonds (Cost $54,486,273) |

| 54,197,320 | |||||||||||||

| U.S. Treasury Obligations (12.1%) | ||||||||||||||||

| 4,000,000 | U.S. Treasury Note | 1.88 | % | 08/31/17 | 4,092,812 | |||||||||||

| 14 | SCHEDULEOF INVESTMENTS |

Table of Contents

| Shares or Principal Amount | Interest Rate | Maturity Date | Value | |||||||||||||

| $ | 3,500,000 | U.S. Treasury Note | 1.13 | % | 12/31/19 | $ | 3,369,842 | |||||||||

| 2,000,000 | U.S. Treasury Note | 0.25 | % | 02/28/15 | 2,001,718 | |||||||||||

| 2,000,000 | U.S. Treasury Note | 0.13 | % | 12/31/14 | 2,000,312 | |||||||||||

|

| |||||||||||||||

|

| Total U.S. Treasury Obligations (Cost $11,444,296) |

| 11,464,684 | |||||||||||||

| Foreign Corporate Bonds (6.5%) | ||||||||||||||||

| 1,000,000 | CHC Helicopter S.A. | 9.38 | % | 06/01/21 | 1,055,000 | |||||||||||

| 2,000,000 | Drill Rigs Holdings, Inc.(a) | 6.50 | % | 10/01/17 | 1,990,000 | |||||||||||

| 3,000,000 | Shelf Drilling Holdings Ltd.(a)(d) | 8.63 | % | 11/01/18 | 3,150,000 | |||||||||||

|

| |||||||||||||||

|

| Total Foreign Corporate Bonds (Cost $6,448,028) |

| 6,195,000 | |||||||||||||

| Shares or Principal Amount | Value | |||||||||||||||

| Closed-End Mutual Funds (8.9%) | ||||||||||||||||

| 38,036 | Brookfield High Income Fund, Inc.(d) | $ | 356,397 | |||||||||||||

| 256,678 | Diversified Real Asset Income Fund(d) | 4,550,901 | ||||||||||||||

| 30,586 | Firsthand Technology Value Fund, Inc.†(d) | 734,370 | ||||||||||||||

| 81,884 | Nuveen Diversified Currency Opportunities Fund | 872,884 | ||||||||||||||

| 62,575 | Nuveen Dividend Advantage Municipal Fund 3(d) | 855,400 | ||||||||||||||

| 12,864 | Nuveen Dividend Advantage Municipal Income Fund | 181,511 | ||||||||||||||

| 21,513 | Nuveen Municipal Advantage Fund, Inc. | 290,210 | ||||||||||||||

| 44,414 | Nuveen Quality Income Municipal Fund, Inc. | 608,028 | ||||||||||||||

|

| |||||||||||||||

|

| Total Closed-End Mutual Funds (Cost $8,205,003) | 8,449,701 | ||||||||||||||

| Preferred Stocks (7.6%) | ||||||||||||||||

| 95,482 | American Homes 4 Rent REIT, Series B(e) | 2,278,201 | ||||||||||||||

| 18,829 | Digital Realty Trust, Inc., Series E(d) | 484,658 | ||||||||||||||

| 104,543 | Equity Commonwealth, Series E(d) | 2,666,892 | ||||||||||||||

| 56,750 | Gramercy Property Trust, Inc., Series B(d) | 1,427,262 | ||||||||||||||

| 12,532 | Protective Life Corp.(d) | 322,323 | ||||||||||||||

|

| |||||||||||||||

|

| Total Preferred Stocks (Cost $7,221,331) | 7,179,336 | ||||||||||||||

| Collateral for Securities on Loan (5.4%) | ||||||||||||||||

| 5,128,327 | State Street Navigator Prime Portfolio, 0.15% | 5,128,327 | ||||||||||||||

|

| |||||||||||||||

|

| Total Collateral for Securities on Loan (Cost $5,128,327) | 5,128,327 | ||||||||||||||

| Short-Term Investments (4.6%) | ||||||||||||||||

| $ | 4,407,264 | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/14 | 4,407,264 | |||||||||||||

|

| |||||||||||||||

|

| Total Short-Term Investments (Cost $4,407,264) | 4,407,264 | ||||||||||||||

| SCHEDULEOF INVESTMENTS | 15 |

Table of Contents

| Shares or Principal Amount | Value | |||||||||

| Total Investments 102.3% (Cost $97,340,522) | $ | 97,021,632 | ||||||||

| Liabilities Less Other Assets (2.3)% | (2,189,725 | ) | ||||||||

|

| |||||||||

| Net Assets 100.0% | $ | 94,831,907 | ||||||||

|

| |||||||||

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (a) | 144A - Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

| (b) | Floating Rate Security. Rate disclosed is as of September 30, 2014. |

| (c) | Step Bond - the coupon is at a fixed rate and resets at a specific date and rate. The rate disclosed is as of September 30, 2014. |

| (d) | All or a portion of the security was on loan as of September 30, 2014. |

| (e) | Preferred Stock - the coupon is at a fixed rate and resets at a specific date and rate. The rate disclosed is as of September 30, 2014. |

| MTN | Medium Term Note |

| REIT | Real Estate Investment Trust |

| 16 | SCHEDULEOF INVESTMENTS |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) | Class S Class C Class A | IOEZX IOECX IEQAX |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Equity Income Fund (the Fund) Class S shares returned 11.36% for the fiscal year ending September 30, 2014, lagging its benchmark, the S&P Composite 1500 Index, which returned 18.57% during the fiscal year. Total returns for other periods and additional Class shares as of September 30, 2014, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Similar to the other diversified funds at ICON, the poor performance of small cap stocks that our system indicated were trading below our estimate of fair value hindered the Fund’s performance. Over the course of the fiscal year, about 20% of the Fund’s holdings had a market capitalization of less than 3 billion. These holdings only returned, on average, around 7% during the fiscal year, well below the 18.57% return of the S&P Composite 1500 Index. |

Further, at the commencement of the fiscal year the overall average value-to-price (V/P) ratio according to our methodology for the Health Care sector was below 1.00, indicating that, on average, stocks in the Health Care sector were overpriced. As a result, the Fund had little exposure to the Health Care sector, which turned out to be one of the best preforming sectors over the course of the fiscal year.

| Q. | How did the Fund’s composition affect performance? |

| A. | While the availability of dividend paying stocks in the Information Technology sector has improved over the last 5 years, stocks in the sector that were the most attractive according to our methodology did not offer attractive yields. As a result, the Fund only averaged about 6% exposure to this sector during the period. The Fund’s relatively small position in the Information Technology sector had a negative impact on performance as the sector returned around 26% over the fiscal year. |

The Fund also had an average exposure of about 13% to preferred stocks and corporate bonds during the fiscal year. While these securities proved beneficial from an income standpoint, and helped the Fund maintain a strong dividend yield, they proved to be a drag on the Fund’s overall performance compared to the benchmark. Furthermore, during the fiscal year the overall market V/P ratio fell below 1.00 according to our valuation metrics. Based on this reading, the Fund held cash during the

| MANAGEMENT OVERVIEW | 17 |

Table of Contents

fiscal year. On average the cash position was around 6%, which detracted from the Fund’s performance relative to the benchmark given the strong return in the equity market.

A substantial position in the commodity chemical industry, which had an average return of over 55%, proved to be a contributor to the Fund’s performance. However, the performance of the commodity chemical industry was not enough to overcome the negatives stated above.

| Q. | What is the outlook for the ICON Equity Income Fund? |

| A. | The overall average V/P ratio for the stocks we track within our system was 1.10 as of October 1, 2014. The dividend rich Utility sector had an average V/P ratio of 1.12 according to our methodology. Given the relatively high reading in the Utilities sector, the Fund has a large allocation in the sector. We also believe the current downward pressure on the 10-year U.S. Treasury should provide a positive environment for dividend paying stocks. Additionally, certain industries within the Consumer Discretionary sector look attractive according to our system, and as of the end of the fiscal year, the Fund held close to 20% weighting in this sector. We will continue to monitor the equity market to find the best combination of value and dividend for our investors. |

| 18 | MANAGEMENT OVERVIEW |

Table of Contents

ICON Equity Income Fund

Sector Composition

September 30, 2014

Financial | 20.9% | |||

Consumer Discretionary | 17.8% | |||

Consumer Staples | 11.9% | |||

Utilities | 10.4% | |||

Industrials | 9.5% | |||

Materials | 9.4% | |||

Information Technology | 4.6% | |||

Telecommunication | 4.4% | |||

Energy | 3.7% | |||

Health Care | 1.8% | |||

|

| |||

| 94.4% | ||||

|

|

Percentages are based upon common, convertible preferred and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Industry Composition

September 30, 2014

Electric Utilities | 5.2% | |||

Asset Management & Custody Banks | 4.6% | |||

Integrated Telecommunication Services | 4.4% | |||

Soft Drinks | 4.1% | |||

Agricultural Products | 4.0% | |||

Department Stores | 3.8% | |||

Health Care REITs | 3.8% | |||

Multi-Utilities | 3.6% | |||

Specialized REIT’s | 3.5% | |||

Paper Packaging | 3.3% | |||

Internet Software & Services | 2.3% | |||

Technology Hardware, Storage & Peripherals | 2.3% | |||

Diversified Banks | 2.2% | |||

Diversified Chemicals | 2.2% |

Packaged Foods & Meats | 2.2% | |||

Fertilizers & Agricultural Chemicals | 2.1% | |||

Home Improvement Retail | 2.1% | |||

Oil & Gas Drilling | 2.1% | |||

Diversified Support Services | 2.0% | |||

Computer & Electronics Retail | 1.9% | |||

Industrial Machinery | 1.9% | |||

Auto Parts & Equipment | 1.8% | |||

Commodity Chemicals | 1.8% | |||

Consumer Finance | 1.8% | |||

Household Appliances | 1.8% | |||

Pharmaceuticals | 1.8% | |||

Residential REIT’s | 1.8% | |||

Automobile Manufacturers | 1.7% | |||

Gas Utilities | 1.7% | |||

Restaurants | 1.7% |

| MANAGEMENT OVERVIEW | 19 |

Table of Contents

ICON Equity Income Fund

Industry Composition (continued)

September 30, 2014

Construction & Farm Machinery & Heavy Trucks | 1.6% | |||

Oil & Gas Equipment & Services | 1.6% | |||

Personal Products | 1.6% | |||

Regional Banks | 1.6% | |||

Casinos & Gaming | 1.5% | |||

Housewares & Specialties | 1.5% | |||

Insurance Brokers | 1.5% |

Office Services & Supplies | 1.5% | |||

Aerospace & Defense | 1.4% | |||

Railroads | 1.1% | |||

|

| |||

| 94.4% | ||||

|

|

Percentages are based upon common, convertible preferred and preferred stocks as a percentage of net assets.

ICON Equity Income Fund

Average Annual Total Return

as of September 30, 2014

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON Equity Income Fund - Class S | 5/10/04 | 11.36% | 12.08% | 6.20% | 6.75% | 1.53% | 1.21% | |||||||||||||||||||||

ICON Equity Income Fund - Class C | 11/8/02 | 10.26% | 10.97% | 5.14% | 7.18% | 2.42% | 2.21% | |||||||||||||||||||||

ICON Equity Income Fund - Class A | 5/31/06 | 11.07% | 11.81% | N/A | 5.21% | 1.68% | 1.46% | |||||||||||||||||||||

ICON Equity Income Fund - Class A (including maximum sales charge of 5.75%) | 5/31/06 | 4.66% | 10.50% | N/A | 4.47% | 1.68% | 1.46% | |||||||||||||||||||||

S&P Composite 1500 Index | 18.57% | 15.79% | 8.34% | 9.41% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| 20 | MANAGEMENT OVERVIEW |

Table of Contents

ICON Equity Income Fund

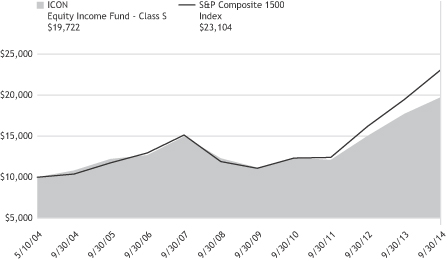

Value of a $10,000 Investment

through September 30, 2014

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Equity Income Fund’s Class S shares on the Class’ inception date of 5/10/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Equity Income Fund’s other share classes will vary due to differences in charges and expenses. The Equity Income Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| MANAGEMENT OVERVIEW | 21 |

Table of Contents

ICON EQUITY INCOME FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2014

| Shares or Principal Amount | Value | |||||||

| Common Stocks (86.6%) | ||||||||

| 8,500 | AbbVie, Inc. | $ | 490,960 | |||||

| 6,400 | Agrium, Inc.(a) | 569,600 | ||||||

| 6,300 | Apple, Inc. | 634,725 | ||||||

| 9,200 | Arthur J Gallagher & Co. | 417,312 | ||||||

| 9,700 | Avery Dennison Corp. | 433,105 | ||||||

| 22,000 | B&G Foods, Inc. | 606,100 | ||||||

| 12,900 | BCE, Inc. | 551,604 | ||||||

| 6,700 | Bristow Group, Inc. | 450,240 | ||||||

| 7,300 | Camden Property Trust, REIT | 500,269 | ||||||

| 18,300 | CMS Energy Corp. | 542,778 | ||||||

| 10,700 | Coca-Cola Enterprises, Inc. | 474,652 | ||||||

| 15,200 | Corrections Corp. of America, REIT | 522,272 | ||||||

| 4,500 | Cracker Barrel Old Country Store, Inc. | 464,355 | ||||||

| 3,300 | Cummins, Inc. | 435,534 | ||||||

| 11,500 | Dow Chemical Co. | 603,060 | ||||||

| 10,200 | Dr. Pepper Snapple Group, Inc. | 655,962 | ||||||

| 6,800 | Duke Energy Corp. | 508,436 | ||||||

| 52,000 | First Commonwealth Financial Corp. | 436,280 | ||||||

| 12,500 | GameStop Corp., Class A(a) | 515,000 | ||||||

| 17,900 | Hawaiian Electric Industries, Inc.(a) | 475,245 | ||||||

| 13,300 | HCP, Inc., REIT | 528,143 | ||||||

| 19,100 | Healthcare Services Group, Inc. | 546,451 | ||||||

| 5,900 | Helmerich & Payne, Inc. | 577,433 | ||||||

| 6,200 | Home Depot, Inc. | 568,788 | ||||||

| 7,500 | Ingredion, Inc. | 568,425 | ||||||

| 14,600 | Invesco, Ltd. | 576,408 | ||||||

| 12,500 | j2 Global, Inc. | 617,000 | ||||||

| 11,000 | Johnson Controls, Inc. | 484,000 | ||||||

| 24,500 | Knoll, Inc. | 424,095 | ||||||

| Shares or Principal Amount | Value | |||||||

| 9,800 | Laclede Group, Inc. | $ | 454,720 | |||||

| 6,500 | Las Vegas Sands Corp. | 404,365 | ||||||

| 4,600 | LyondellBasell Industries, Class A | 499,836 | ||||||

| 9,600 | Macy’s, Inc. | 558,528 | ||||||

| 22,100 | Main Street Capital Corp. | 677,144 | ||||||

| 7,100 | Nordstrom, Inc. | 485,427 | ||||||

| 2,800 | Norfolk Southern Corp. | 312,480 | ||||||

| 9,700 | Nu Skin Enterprises, Inc., Class A(a) | 436,791 | ||||||

| 7,100 | Packaging Corp. of America | 453,122 | ||||||

| 2,700 | Public Storage, REIT | 447,768 | ||||||

| 3,800 | Raytheon Co. | 386,156 | ||||||

| 8,700 | SCANA Corp. | 431,607 | ||||||

| 8,900 | Thor Industries, Inc. | 458,350 | ||||||

| 6,000 | Tupperware Brands Corp. | 414,240 | ||||||

| 8,200 | Ventas, Inc., REIT | 507,990 | ||||||

| 13,300 | Verizon Communications, Inc., Series L | 664,867 | ||||||

| 12,600 | Westar Energy, Inc. | 429,912 | ||||||

| 3,300 | Whirlpool Corp. | 480,645 | ||||||

|

| |||||||

| | Total Common Stocks (Cost $23,199,660) | 23,682,180 | ||||||

| Preferred Stocks (3.7%) | ||||||||

| 19,600 | Discover Financial Services, Series B(a) | 494,116 | ||||||

| 21,000 | Stanley Black & Decker, Inc.(a) | 518,280 | ||||||

|

| |||||||

| | Total Preferred Stocks (Cost $998,730) | 1,012,396 | ||||||

| Convertible Preferred Stocks (4.1%) | ||||||||

| 4,800 | Bunge, Ltd. | 522,000 | ||||||

| 500 | Wells Fargo & Co., Series L | 601,255 | ||||||

|

| |||||||

| | Total Convertible Preferred Stocks (Cost $1,090,147) | 1,123,255 | ||||||

| 22 | SCHEDULEOF INVESTMENTS |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| Collateral for Securities on Loan (10.4%) | ||||||||

| 2,849,625 | State Street Navigator Prime Portfolio, 0.15% | $ | 2,849,625 | |||||

|

| |||||||

| | Total Collateral for Securities on Loan (Cost $2,849,625) | 2,849,625 | ||||||

| Shares or Principal Amount | Value | |||||||

| Short-Term Investments (1.6%) | ||||||||

| $ | 425,747 | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/14 | $ | 425,747 | ||||

|

| |||||||

| | Total Short-Term Investments (Cost $425,747) | 425,747 | ||||||

| | Total Investments 106.4% (Cost $28,563,909) | 29,093,203 | ||||||

| | Liabilities Less Other Assets (6.4)% | (1,743,338 | ) | |||||

|

| |||||||

| Net Assets 100.0% | $ | 27,349,865 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| (a) | All or a portion of the security was on loan as of September 30, 2014. |

| REIT | Real Estate Investment Trust |

| SCHEDULEOF INVESTMENTS | 23 |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) | Class S Class C Class A | ICNZX ICNCX ICNAX |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Fund (the Fund) Class S returned 3.71% over the fiscal year ending September 30, 2014, but lagged its benchmark, the S & P Composite 1500 Index, which returned 18.57%. Total returns for other periods and additional Class shares as of September 30, 2014, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | A year ago, September 30, 2013, the Fund had a favorable sector weighting with Consumer Discretionary at 31.1%, Energy at 18.5%, Industrials at 16.4%, Information Technology at 11.4% and Materials at 2.6%, but the Fund lagged the rising index during the fourth quarter of 2013, due to the Fund’s 6.2% cash holdings. Over the first quarter of 2014, the cyclical sectors hurt the Fund as investors reacted to a surprise negative GDP unfolding. The Fund’s cash holdings were retained until mid-April, when the Fund’s exposure to the Health Care and Financial sectors were increased. Exposure to the Energy sector was reduced by over half in July, but the remaining positions hurt the portfolio with the drop in the price of oil in September 2014. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The five largest contributions to performance during the fiscal year came from Union Pacific, Walt Disney, Celgene, Questcor Pharmaceuticals and Apple. |

Large declines of a few stocks in the Consumer Discretionary, Energy and Materials sectors were too much for the top performing stocks to overcome relative to the benchmark. The five largest detractors from performance were Lulu Lemon Athletica, Lumber Liquidators, Dril-Quip, Oceaneering International and FMC Corporation. In general, the stocks that had the large, and usually quite sudden, declines had one thing in common, analysts revising earnings estimates downward, often accompanied by a surprise event. The downward revisions in earnings estimates were generally short term oriented, for just one or two quarters. As short term revision do not have much effect on our valuation, we continue to hold four of those stocks. Lulu Lemon was sold, the others remain in the portfolio.

| 24 | MANAGEMENT OVERVIEW |

Table of Contents

In our opinion, three situations influenced investor behavior with regard to equities. Over the first nine months of calendar year 2014, investors repositioned their portfolios for higher long-term interest rates, a rising dollar and a slowing global economy. Stock prices did not respond to value, but instead were driven by these three situations. We expect all three will prove to be passing fads.

| Q. | What is your investment outlook for the overall market? |

| A. | With our overall average market value-to-price (V/P) ratio hitting a sixteen month high of 1.15 in early October 2014, we would expect the broad market to move higher over the next twelve months, posting slightly better than average returns. With investors reacting to the three situations mentioned above, our industry and sector valuation rankings have been altered over the last six months. The current V/P ratios suggest to us that cyclical industries and sectors will lead the market higher, featuring a comeback for the Consumer Discretionary sector. |

ICON Fund

Sector Composition

September 30, 2014

Consumer Discretionary | 34.5% | |||

Health Care | 19.0% | |||

Materials | 13.4% | |||

Industrials | 9.0% | |||

Energy | 8.5% | |||

Financial | 7.7% | |||

Information Technology | 7.3% | |||

|

| |||

| 99.4% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

| MANAGEMENT OVERVIEW | 25 |

Table of Contents

ICON Fund

Industry Composition

September 30, 2014

Biotechnology | 11.7% | |||

Oil & Gas Equipment & Services | 8.5% | |||

Home Improvement Retail | 7.4% | |||

Pharmaceuticals | 7.3% | |||

Broadcasting | 6.7% | |||

Airlines | 4.7% | |||

Railroads | 4.3% | |||

Specialty Chemicals | 3.9% | |||

Paper Products | 3.7% | |||

Electronic Manufacturing Services | 3.6% | |||

Consumer Finance | 3.4% | |||

Home Furnishings | 3.4% | |||

Diversified Chemicals | 3.3% | |||

Movies & Entertainment | 3.0% | |||

Automobile Manufacturers | 2.8% |

Department Stores | 2.8% | |||

Paper Packaging | 2.5% | |||

Internet Software & Services | 2.4% | |||

Hotels, Resorts & Cruise Lines | 2.3% | |||

Regional Banks | 2.3% | |||

Asset Management & Custody Banks | 2.0% | |||

Cable & Satellite | 1.8% | |||

Leisure Products | 1.5% | |||

Specialty Stores | 1.5% | |||

Auto Parts & Equipment | 1.3% | |||

Electronic Components | 1.3% | |||

|

| |||

| 99.4% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

ICON Fund

Average Annual Total Return

as of September 30, 2014

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON Fund - Class S | 5/6/04 | 3.71% | 10.33% | 3.51% | 3.95% | 1.23% | 1.23% | |||||||||||||||||||||

ICON Fund - Class C | 11/28/00 | 2.57% | 9.67% | 2.79% | 3.33% | 2.32% | 2.26% | |||||||||||||||||||||

ICON Fund - Class A | 5/31/06 | 3.36% | 9.94% | N/A | 0.52% | 1.58% | 1.51% | |||||||||||||||||||||

ICON Fund - Class A (including maximum sales charge of 5.75%) | 5/31/06 | -2.60% | 8.65% | N/A | -0.19% | 1.58% | 1.51% | |||||||||||||||||||||

S&P Composite 1500 Index | 18.57% | 15.79% | 8.34% | 5.37% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Since Inception performance results for Class C shares include returns for certain time periods that were restarted as of June 8, 2004.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| 26 | MANAGEMENT OVERVIEW |

Table of Contents

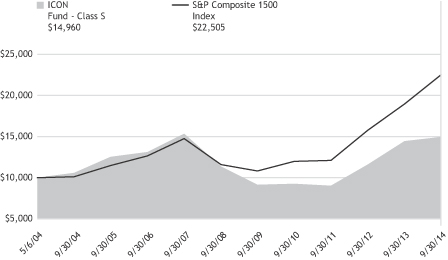

ICON Fund

Value of a $10,000 Investment

through September 30, 2014

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the ICON Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the ICON Fund’s other share classes will vary due to differences in charges and expenses. The ICON Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| MANAGEMENT OVERVIEW | 27 |

Table of Contents

ICON FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2014

| Shares or Principal Amount | Value | |||||||

| Common Stocks (99.4%) | ||||||||

| 42,700 | Alaska Air Group, Inc. | $ | 1,859,158 | |||||

| 24,800 | Ashland, Inc. | 2,581,680 | ||||||

| 7,200 | Biogen Idec, Inc.† | 2,381,832 | ||||||

| 16,900 | BorgWarner, Inc. | 889,109 | ||||||

| 33,300 | CBS Corp., Class B | 1,781,550 | ||||||

| 35,900 | Celgene Corp.† | 3,402,602 | ||||||

| 40,600 | Clearwater Paper Corp.† | 2,440,466 | ||||||

| 42,800 | CSX Corp. | 1,372,168 | ||||||

| 35,700 | Delta Air Lines, Inc. | 1,290,555 | ||||||

| 36,200 | Discovery Communications, Inc., Class A† | 1,368,360 | ||||||

| 36,200 | Discovery Communications, Inc., Class C† | 1,349,536 | ||||||

| 16,600 | Dril-Quip, Inc.† | 1,484,040 | ||||||

| 94,200 | Emergent Biosolutions, Inc.† | 2,007,402 | ||||||

| 50,800 | Encore Capital Group, Inc.†(a) | 2,250,948 | ||||||

| 38,600 | FMC Corp. | 2,207,534 | ||||||

| 28,600 | FMC Technologies, Inc.† | 1,553,266 | ||||||

| 38,200 | Home Depot, Inc. | 3,504,468 | ||||||

| 13,000 | Jazz Pharmaceuticals PLC† | 2,087,280 | ||||||

| 25,600 | Lumber Liquidators Holdings, Inc.†(a) | 1,468,928 | ||||||

| 32,000 | Macy’s, Inc. | 1,861,760 | ||||||

| 64,800 | Methode Electronics, Inc. | 2,389,176 | ||||||

| 16,800 | Mohawk Industries, Inc.† | 2,264,976 | ||||||

| 22,400 | Oceaneering International, Inc. | 1,459,808 | ||||||

| Shares or Principal Amount | Value | |||||||

| 26,400 | Packaging Corp. of America | $ | 1,684,848 | |||||

| 18,700 | Perrigo Co. PLC | 2,808,553 | ||||||

| 6,500 | Polaris Industries, Inc. | 973,635 | ||||||

| 29,300 | RigNet, Inc.† | 1,185,185 | ||||||

| 15,600 | Rogers Corp.† | 854,256 | ||||||

| 13,800 | Signature Bank† | 1,546,428 | ||||||

| 36,000 | Thor Industries, Inc. | 1,854,000 | ||||||

| 8,300 | Time Warner Cable, Inc. | 1,190,967 | ||||||

| 15,900 | Tractor Supply Co. | 978,009 | ||||||

| 13,600 | Union Pacific Corp. | 1,474,512 | ||||||

| 26,100 | Viacom, Inc., Class B | 2,008,134 | ||||||

| 29,200 | VistaPrint NV†(a) | 1,599,868 | ||||||

| 25,900 | Waddell & Reed Financial, Inc., Class A | 1,338,771 | ||||||

| 18,700 | Wyndham Worldwide Corp. | 1,519,562 | ||||||

|

| |||||||

| | Total Common Stocks (Cost $62,958,534) | 66,273,330 | ||||||

| | Collateral for Securities on Loan (3.8%) | |||||||

| 2,566,103 | State Street Navigator Prime Portfolio, 0.15% | 2,566,103 | ||||||

|

| |||||||

| | Total Collateral for Securities on Loan (Cost $2,566,103) | 2,566,103 | ||||||

| | Total Investments 103.2% (Cost $65,524,637) | 68,839,433 | ||||||

| | Liabilities Less Other Assets (3.2)% | (2,136,775 | ) | |||||

|

| |||||||

| Net Assets 100.0% | $ | 66,702,658 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (a) | All or a portion of the security was on loan as of September 30, 2014. |

| 28 | SCHEDULEOF INVESTMENTS |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) | Class S Class C Class A | IOLZX IOLCX ISTAX |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Long/Short Fund (the Fund) Class S returned 5.32% over the fiscal year but lagged its benchmark, the S & P Composite 1500 Index, which returned 18.57%. Total returns for other periods and additional Class shares as of September 30, 2014 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | A year ago, September 30, 2013, the Fund had a favorable sector weighting with Consumer Discretionary at 31.4%, Information Technology at 17.6%, Industrials at 12.3%, Energy at 11.6%, Healthcare at 6.4%, Financial at 5.8% and Materials at 3.1% but the Fund lagged the rising index that next quarter, ending December 31, 2013, due to the Fund’s 8.8% cash holdings and five short positions accounting for 7.4% of assets. By December 31, 2013, the Fund had 19.9% cash and 9.9% short positions. During the first quarter of 2014, the cyclical sectors hurt the Fund as investors reacted to a surprise negative GDP unfolding. By early April cash had increased to 34% of assets while eight short positioned totaled 16.8% of assets. In mid-April cash was reduced to minimal levels and all but two short positions were covered. The Fund’s holdings in the Healthcare and Materials sectors were increased. |

| Q. | How did the Fund’s composition affect performance? |

| A. | The five largest contributions to performance during the fiscal year came from Celgene Corporation, Jazz Pharmaceuticals, Norfolk Southern, Methode Electronics and Time Warner Cable. |

Large declines of a few stocks in the Consumer Discretionary, Energy, Materials and Healthcare sectors were too much for the top performing stocks to overcome relative to the benchmark. The five largest detractors from performance were Lumber Liquidators, Ligand Pharmaceuticals, FMC, RigNet and Dril-Quip. In general, the stocks that had the large, and usually quite sudden, declines had one thing in common, analysts revising earnings estimates downward, often accompanied by a surprise event. The downward revisions in earnings estimates were generally short term oriented, for just one or two quarters. As short term negative revisions do not have much effect on our valuation, we continue to hold those five stocks.

| MANAGEMENT OVERVIEW | 29 |

Table of Contents

In our opinion, three situations influenced investor behavior with regard to equities. Over the first nine months of calendar year 2014, investors repositioned their portfolios for higher long term interest rates, a rising dollar and a slowing global economy. Stock prices did not respond to value, but instead were driven by these three situations. We expect all three will prove to be passing fads.

| Q. | What is your investment outlook for the overall market? |

| A. | With our overall average market value-to-price (V/P) ratio hitting a sixteen month high of 1.15 in early October 2014, we would expect the broad market to move higher over the next twelve months, posting slightly better than average returns. With investors reacting to the three situations mentioned above, our industry and sector valuation rankings have been altered over the last six months. The current V/P ratios suggest to us that cyclical industries and sectors will lead the market higher, featuring a comeback for the Consumer Discretionary sector. |

ICON Long/Short Fund

Sector Composition

September 30, 2014

Consumer Discretionary | 31.5 % | |||

Health Care | 19.9% | |||

Information Technology | 17.0% | |||

Materials | 10.9% | |||

Energy | 7.9% | |||

Financial | 7.7% | |||

Industrials | 6.9% | |||

|

| |||

| 101.8% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

| 30 | MANAGEMENT OVERVIEW |

Table of Contents

ICON Long/Short Fund

Industry Composition

September 30, 2014

Biotechnology | 12.4% | |||

Home Improvement Retail | 7.9% | |||

Oil & Gas Equipment & Services | 7.9% | |||

Pharmaceuticals | 7.5% | |||

Internet Software & Services | 4.6% | |||

Railroads | 4.5% | |||

Electronic Manufacturing Services | 4.4% | |||

Broadcasting | 3.4% | |||

Electronic Components | 3.4% | |||

Paper Packaging | 3.0% | |||

Hotels, Resorts & Cruise Lines | 2.9% | |||

IT Consulting & Other Services | 2.9% | |||

Home Furnishings | 2.8% | |||

Leisure Products | 2.8% | |||

Asset Management & Custody Banks | 2.7% |

Leisure Facilities | 2.7% | |||

Specialty Stores | 2.7% | |||

Consumer Finance | 2.6% | |||

Cable & Satellite | 2.5% | |||

Housewares & Specialties | 2.5% | |||

Airlines | 2.4% | |||

Regional Banks | 2.4% | |||

Diversified Chemicals | 2.3% | |||

Paper Products | 2.1% | |||

Specialty Chemicals | 2.1% | |||

Data Processing & Outsourced Services | 1.7% | |||

Commodity Chemicals | 1.4% | |||

Automobile Manufacturers | 1.3% | |||

|

| |||

| 101.8% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

ICON Long/Short Fund

Average Annual Total Return

as of September 30, 2014

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON Long/Short Fund - Class S | 5/6/04 | 5.32% | 9.69% | 4.35% | 4.14% | 1.53% | 1.32% | |||||||||||||||||||||

ICON Long/Short Fund - Class C | 10/17/02 | 4.30% | 8.55% | 3.32% | 5.11% | 2.62% | 2.37% | |||||||||||||||||||||

ICON Long/Short Fund - Class A | 5/31/06 | 5.02% | 9.36% | N/A | 1.68% | 1.91% | 1.61% | |||||||||||||||||||||

ICON Long/Short Fund - Class A (including maximum sales charge of 5.75%) | 5/31/06 | -1.05% | 8.08% | N/A | 0.96% | 1.91% | 1.61% | |||||||||||||||||||||

S&P Composite 1500 Index | 18.57% | 15.79% | 8.34% | 9.52% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| MANAGEMENT OVERVIEW | 31 |

Table of Contents

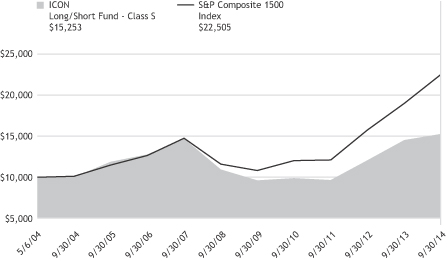

ICON Long/Short Fund

Value of a $10,000 Investment

through September 30, 2014

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Long/Short Fund’s Class S shares on the Class’ inception date of 5/6/04 to a $10,000 investment made in an unmanaged securities index on that date. Performance for the Long/Short Fund’s other share classes will vary due to differences in charges and expenses. The Long/Short Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| 32 | MANAGEMENT OVERVIEW |

Table of Contents

ICON LONG/SHORT FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2014

| Shares or Principal Amount | Value | |||||||

| Common Stocks (101.8%) | ||||||||

| 18,800 | Alaska Air Group, Inc. | $ | 818,552 | |||||

| 7,100 | Ashland, Inc. | 739,110 | ||||||

| 3,000 | Biogen Idec, Inc.† | 992,430 | ||||||

| 9,500 | Cabot Corp. | 482,315 | ||||||

| 19,800 | Cedar Fair L.P. | 935,946 | ||||||

| 14,600 | Celgene Corp.† | 1,383,788 | ||||||

| 12,000 | Clearwater Paper Corp.† | 721,320 | ||||||

| 22,200 | Cognizant Technology Solutions Corp., Class A†(x) | 993,894 | ||||||

| 22,000 | CSX Corp. | 705,320 | ||||||

| 15,600 | Discovery Communications, Inc., Class A† | 589,680 | ||||||

| 15,600 | Discovery Communications, Inc., Class C† | 581,568 | ||||||

| 5,600 | Dril-Quip, Inc.† | 500,640 | ||||||

| 44,400 | Emergent Biosolutions, Inc.† | 946,164 | ||||||

| 19,900 | Encore Capital Group, Inc.†(a) | 881,769 | ||||||

| 14,000 | FMC Corp. | 800,660 | ||||||

| 12,100 | FMC Technologies, Inc.† | 657,151 | ||||||

| 17,300 | Home Depot, Inc. | 1,587,102 | ||||||

| 14,400 | Jarden Corp.† | 865,584 | ||||||

| 6,800 | Jazz Pharmaceuticals PLC† | 1,091,808 | ||||||

| 20,700 | Ligand Pharmaceuticals, Inc., Class B† | 972,693 | ||||||

| 20,000 | Lumber Liquidators Holdings, Inc.†(a) | 1,147,600 | ||||||

| 8,000 | Mastercard, Inc., Class A | 591,360 | ||||||

| 41,700 | Methode Electronics, Inc. | 1,537,479 | ||||||

| 7,300 | Mohawk Industries, Inc.† | 984,186 | ||||||

| Shares or Principal Amount | Value | |||||||

| 7,700 | Norfolk Southern Corp. | $ | 859,320 | |||||

| 9,400 | Oceaneering International, Inc.(x) | 612,598 | ||||||

| 16,000 | Packaging Corp. of America | 1,021,120 | ||||||

| 9,800 | Perrigo Co. PLC | 1,471,862 | ||||||

| 6,500 | Polaris Industries, Inc. | 973,635 | ||||||

| 24,200 | RigNet, Inc.† | 978,890 | ||||||

| 21,200 | Rogers Corp.† | 1,160,912 | ||||||

| 7,300 | Signature Bank† | 818,038 | ||||||

| 8,700 | Thor Industries, Inc.(x) | 448,050 | ||||||

| 6,100 | Time Warner Cable, Inc.(x) | 875,289 | ||||||

| 15,400 | Tractor Supply Co. | 947,254 | ||||||

| 28,800 | VistaPrint NV†(a) | 1,577,952 | ||||||

| 18,300 | Waddell & Reed Financial, Inc., Class A | 945,927 | ||||||

| 12,400 | Wyndham Worldwide Corp. | 1,007,624 | ||||||

|

| |||||||

|

| Total Common Stocks (Cost $33,372,974) | 35,206,590 | ||||||

| | Collateral for Securities on Loan (9.9%) | |||||||

| 3,405,494 | State Street Navigator Prime Portfolio, 0.15% | 3,405,494 | ||||||

|

| |||||||

|

| Total Collateral for Securities on Loan (Cost $3,405,494) | 3,405,494 | ||||||

|

| Total Investments 111.7% (Cost $36,778,468) | 38,612,084 | ||||||

| | Liabilities Less Other Assets (11.7)% | (4,055,305 | ) | |||||

|

| |||||||

| Net Assets 100.0% | $ | 34,556,779 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| (x) | All or a portion of the security is pledged as collateral for securities sold short. |

| (a) | All or a portion of the security was on loan as of September 30, 2014. |

| SCHEDULEOF INVESTMENTS | 33 |

Table of Contents

ICON LONG/SHORT FUND

SCHEDULEOF SECURITIES SOLD SHORT

SEPTEMBER 30, 2014

| Shares | Short Security | Value | ||||||

| 11,600 | Amedisys, Inc.† | $ | 233,972 | |||||

| 225,000 | Cincinnati Bell, Inc.† | 758,250 | ||||||

|

| |||||||

|

| Total Securities Sold Short (Proceeds $999,482) | $ | 992,222 | |||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| † | Non-income producing security. |

| 34 | SCHEDULEOF INVESTMENTS |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) | ICONX |

| Q. | How did the Fund perform relative to its benchmarks? |

| A. | The ICON Opportunities Fund (the Fund) returned 2.19% over the fiscal year but lagged its benchmark, the S&P SmallCap 600 Index, which returned 5.74%. Total returns and other performance statistics as of September 30, 2014 appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | A year ago, September 30, 2013, the Fund had a favorable sector weighting with Consumer Discretionary at 18.6%, Materials at 12.4%, Information Technology at 12.1%, Financials at 10.5%, Industrials at 11.1%, Energy at 9.9%, and Healthcare at 7.3%, but the Fund lagged the rising index that next quarter due to the Fund’s 17.9% cash holdings. The cash holdings generally resulted from the Fund selling overpriced positions without buying into other positions. Although exposure to the Consumer Discretionary sector had been reduced to 11.6% by December 31, 2013, remaining positions in the sector hurt the Fund during the first quarter of 2014 as investors reacted to a surprise negative GDP unfolding. The Fund accumulated more cash until mid-April, when the Fund’s exposure to the Information Technology, Financial and Healthcare sector was increased. Unlike the S&P LargeCap 500 Index, the S&P SmallCap 600 index dropped from mid-April to mid-May. Around that dip, a minor rotation was made to increase the Fund’s exposure to the Information Technology, Consumer Discretionary and Healthcare sectors. |

While some large-cap stocks did well, pushing the S&P 500 Index to record highs in 2014, small cap stocks were generally stuck in a sideways range, not moving up as much as their large cap counterparts during advances while dropping more during declines. Amidst these oscillations, there were rapid industry and sector theme reversals.

In our opinion, three situations influenced investor behavior with regard to equities. Over the first nine months of calendar year 2014, investors repositioned their portfolios for higher long term interest rates, a rising dollar and a slowing global economy. Stock prices did not respond to value, but instead were driven by these three situations. We expect all three will prove to be passing fads.

| MANAGEMENT OVERVIEW | 35 |

Table of Contents

| Q. | What were the Fund’s greatest contributors/detractors? |

| A. | The five largest contributions to performance during the fiscal year came from Kapstone Paper & Packaging, Questcor Pharmaceuticals, Akorn, Dresser-Rand Group and Janus Capital, which was purchased based on value but enjoyed a sharp surge when a high profile bond manager joined the firm. It was sold the day of that announcement. |

The five largest detractors from performance were Lumber Liquidators, Ligand Pharmaceuticals, Conn’s, RigNet and World Acceptance. In general, the stocks that had large, and usually quite sudden, declines had one thing in common, analysts revising earnings estimates downward, often accompanied by a surprise event or announcement. The downward revisions in earnings estimates were generally short term oriented, for just one or two quarters. As short term revision do not have much effect on our valuation, we continue to hold all five of those stocks.

| Q. | What is your investment outlook for the overall market? |

| A. | With our overall average market value-to-price (V/P) ratio hitting a sixteen month high of 1.15 in early October 2014, we would expect the broad market to move higher over the next twelve months, posting slightly better than average returns. With investors reacting to the three situations mentioned above, our industry and sector valuation rankings have been altered over the last six months. The current V/P ratios suggest to us that cyclical industries and sectors will lead the market higher and that small-cap stocks will fully participate. |

ICON Opportunities Fund

Country Composition

September 30, 2014

United States | 92.6% | |||

Netherlands | 3.7% | |||

Canada | 2.4% | |||

|

| |||

| 98.7% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

ICON Opportunities Fund

Sector Composition

September 30, 2014

Information Technology | 21.5% | |||

Health Care | 20.6% | |||

Consumer Discretionary | 19.5% | |||

Materials | 18.4% | |||

Financial | 9.6% | |||

Energy | 6.1% | |||

Industrials | 3.0% | |||

|

| |||

| 98.7% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

| 36 | MANAGMENT OVERVIEW |

Table of Contents

ICON Opportunities Fund

Industry Composition

September 30, 2014

Biotechnology | 7.6% | |||

Specialty Chemicals | 7.5% | |||

Electronic Equipment & Instruments | 7.1% | |||

Life Sciences Tools & Services | 7.0% | |||

Consumer Finance | 6.8% | |||

Internet Software & Services | 6.6% | |||

Oil & Gas Equipment & Services | 6.1% | |||

Pharmaceuticals | 6.0% | |||

Automobile Manufacturers | 4.0% | |||

Paper Products | 3.7% | |||

Electronic Manufacturing Services | 3.6% | |||

Restaurants | 3.4% | |||

Home Improvement Retail | 3.1% | |||

Aerospace & Defense | 3.0% | |||

Apparel Retail | 2.7% | |||

Computer & Electronics Retail | 2.7% |

Commodity Chemicals | 2.4% | |||

Diversified Chemicals | 2.4% | |||

Paper Packaging | 2.4% | |||

Home Furnishings | 2.0% | |||

Insurance Brokers | 2.0% | |||

Footwear | 1.6% | |||

Technology Distributors | 1.6% | |||

Electronic Components | 1.5% | |||

Data Processing & Outsourced Services | 1.1% | |||

Asset Management & Custody Banks | 0.8% | |||

|

| |||

| 98.7% | ||||

|

|

Percentages are based upon common stocks as a percentage of net assets.

ICON Opportunities Fund

Average Annual Total Return

as of September 30, 2014

| Inception Date | 1 Year | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||

ICON Opportunities Fund | 9/28/12 | 2.19% | 15.28% | 12.47% | 1.52% | |||||||||||||||

S&P SmallCap 600 Index | 5.74% | 17.94% | N/A | N/A | ||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

| MANAGEMENT OVERVIEW | 37 |

Table of Contents

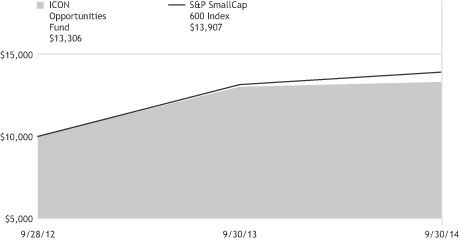

ICON Opportunities Fund

Value of a $10,000 Investment

through September 30, 2014

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Opportunities Fund on the inception date of 10/1/12 to a $10,000 investment made in an unmanaged securities index on that date. The Opportunities Fund’s performance in this chart and the performance table assumes the reinvestment of dividends and capital gain distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| 38 | MANAGEMENT OVERVIEW |

Table of Contents

ICON OPPORTUNITIES FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2014

| Shares or Principal Amount | Value | |||||||

| Common Stocks (98.7%) | ||||||||

| 8,637 | Akorn, Inc.† | $ | 313,264 | |||||

| 16,600 | Albany Molecular Research, Inc.† | 366,362 | ||||||

| 12,292 | Ascena Retail Group, Inc.† | 163,484 | ||||||

| 6,600 | Avery Dennison Corp. | 294,690 | ||||||

| 3,400 | Bristow Group, Inc. | 228,480 | ||||||

| 7,700 | Brown & Brown, Inc. | 247,555 | ||||||

| 3,079 | Buffalo Wild Wings, Inc.† | 413,417 | ||||||

| 14,800 | Cambrex Corp.† | 276,464 | ||||||

| 7,566 | Clearwater Paper Corp.† | 454,792 | ||||||

| 4,894 | Coherent, Inc.† | 300,345 | ||||||

| 10,592 | Conn’s, Inc.† | 320,620 | ||||||

| 5,449 | Curtiss-Wright Corp. | 359,198 | ||||||

| 16,500 | Daktronics, Inc. | 202,785 | ||||||

| 1,885 | Dril-Quip, Inc.† | 168,519 | ||||||

| 21,388 | Emergent Biosolutions, Inc.† | 455,778 | ||||||

| 8,873 | Encore Capital Group, Inc.† | 393,163 | ||||||

| 4,665 | FEI Co. | 351,834 | ||||||

| 6,850 | Finish Line, Inc., Class A | 171,456 | ||||||

| 152 | GameStop Corp., Class A | 6,262 | ||||||

| 5,369 | HB Fuller Co. | 213,149 | ||||||

| 3,612 | j2 Global, Inc. | 178,288 | ||||||

| 20,100 | Landec Corp.† | 246,225 | ||||||

| 9,000 | Lannett Co., Inc.† | 411,120 | ||||||

| 7,026 | Leggett & Platt, Inc. | 245,348 | ||||||

| 9,931 | Ligand Pharmaceuticals, Inc., Class B† | 466,658 | ||||||

| Shares or Principal Amount | Value | |||||||

| 8,100 | LSB Industries, Inc.† | $ | 289,251 | |||||

| 6,565 | Lumber Liquidators Holdings, Inc.† | 376,700 | ||||||

| 4,345 | Methanex Corp. | 290,246 | ||||||

| 11,771 | Methode Electronics, Inc. | 433,997 | ||||||

| 7,333 | Minerals Technologies, Inc. | 452,519 | ||||||

| 3,320 | PAREXEL International Corp.† | 209,459 | ||||||

| 11,502 | Perficient, Inc.† | 172,415 | ||||||

| 5,453 | Portfolio Recovery Associates, Inc.† | 284,810 | ||||||

| 8,440 | RigNet, Inc.† | 341,398 | ||||||

| 3,360 | Rogers Corp.† | 183,994 | ||||||

| 5,857 | Steven Madden, Ltd.† | 188,771 | ||||||

| 2,925 | SYNNEX Corp.† | 189,043 | ||||||

| 9,401 | Thor Industries, Inc. | 484,151 | ||||||

| 4,400 | Total System Services, Inc. | 136,224 | ||||||

| 8,205 | VistaPrint NV† | 449,552 | ||||||

| 1,782 | Waddell & Reed Financial, Inc., Class A | 92,112 | ||||||

| 2,304 | World Acceptance Corp.† | 155,520 | ||||||

|

| |||||||

| | Total Common Stocks (Cost $12,641,715) | 11,979,418 | ||||||

| | Total Investments 98.7% (Cost $12,641,715) | 11,979,418 | ||||||

| | Other Assets Less Liabilities 1.3% | 153,277 | ||||||

|

| |||||||

| Net Assets 100.0% | $ | 12,132,695 | ||||||

|