Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR/A

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07883

ICON Funds

(Exact name of registrant as specified in charter)

5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Address of principal executive offices) (Zip code)

Carrie M. Schoffman 5299 DTC Blvd. Suite 1200 Greenwood Village, CO 80111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-790-1600

Date of fiscal year end: September 30, 2015

Date of reporting period: March 31, 2015

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

2015 ANNUAL REPORT

ICON INTERNATIONAL FUNDS

INVESTMENT UPDATE

ICON Emerging Markets Fund

ICON International Equity Fund

1-800-764-0442 | www.iconfunds.com

Table of Contents

You can now sign up for electronic delivery of ICON Fund shareholder reports, including prospectuses, annual reports, semiannual reports and proxy statements.

When these materials are available, you will receive an email from ICON with instructions on how to view the documents. Statements, transaction confirmations and other documents that are not available online will continue to be sent to you by U.S. mail.

Visit ICON’s website at www.iconfunds.com to learn more and sign up.

You may change or cancel your participation in eDelivery by visiting www.iconfunds.com, or you can request a hard copy of any of the materials free of charge by calling ICON Funds at 1-800-764-0442.

1-800-764-0442 • www.iconfunds.com

Table of Contents

| 2 | ||||

Management Overview (Unaudited) and Schedules of Investments | ||||

| 4 | ||||

| 13 | ||||

| 24 | ||||

| 32 | ||||

| 36 | ||||

| 51 | ||||

| 52 | ||||

| 54 | ||||

| 57 | ||||

| 65 | ||||

Table of Contents

Historical Returns

All total returns mentioned in this Report account for the change in a Fund’s per-share price and the reinvestment of any dividends, capital gain distributions and adjustments for financial statement purposes. If your account is set up to receive Fund distributions in cash rather than to reinvest them, your actual return may differ from these figures. The Funds’ performance results do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Adviser may have reimbursed certain fees or expenses of some of the Funds. If not for these reimbursements, performance would have been lower. Fund results shown, unless otherwise indicated, are at net asset value. If a sales charge (maximum 5.75%) had been deducted, results would have been lower.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance results represent past performance, and current performance may be higher or lower. Please call 1-800-764-0442 or visit www.iconfunds.com for performance results current to the most recent month-end.

Portfolio Data

This Report reflects ICON’s portfolio holdings as of September 30, 2015, the end of the reporting period. The information is not a complete analysis of every aspect of any sector, industry, security or the Funds.

There are risks associated with mutual fund investing, including the loss of principal. The likelihood of loss may be greater if you invest for a shorter period of time. There is no assurance that the investment process will consistently lead to successful results.

An investment in a region fund may involve greater risk and volatility than a diversified fund. An investment concentrated in sectors and industries may involve greater risk and volatility than a more diversified investment.

Investments in foreign securities may entail unique risks, including political, market, and currency risks. Financial statements of foreign companies are governed by different accounting, auditing, and financial standards than U.S. companies and may be less transparent and uniform than in the United States. Many corporate governance standards, which help ensure the integrity of public information in the United States, do not exist in foreign countries. In general, there may be less governmental supervision of foreign

| 2 | ABOUT THIS REPORT |

Table of Contents

stock exchanges and securities brokers and issuers. The ICON system relies on the integrity of the financial statements released to the market as part of our analysis.

The prospectus and statement of additional information contain this and other information about the Funds and are available by visiting www.iconfunds.com or calling 1-800-764-0442. Please read the prospectus and statement of additional information carefully.

Financial Intermediary

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may influence the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| ABOUT THIS REPORT | 3 |

Table of Contents

| Q. | How did the Fund perform relative to its benchmark? |

| A. | The ICON Emerging Markets Fund (the Fund) Class S returned -5.61% for the fiscal year ended September 30, 2015, while its benchmark, the MSCI Emerging Markets Index, returned -18.98%. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | Unlike the previous fiscal year’s gain, the emerging markets benchmark experienced a marked decline over the course of fiscal year 2015. While the U.S. economy continued to show signs of improvement relative to the rest of the world, headwinds investors faced internationally during the period included economic growth concerns, especially with respect to that of China and many of its emerging markets peers, currency volatility, and the prospect of the Federal Reserve raising rates for the first time since 2006. However, despite these headwinds, interest rates generally remained low and monetary policy continued to be accommodative globally. |

From a country perspective, Hungary was the sole country within the emerging markets benchmark to experience positive returns during the period. China was the second best performing country, despite its negative return for the fiscal year and its significant drop in performance that began in mid-2015. Greece, dealing with debt problems and a possibility of its exit from the Eurozone, was the worst performing country in the emerging markets space. While the Fund did not participate in Hungary’s upside move, China, an average underweight for the Fund during the period, was one of the larger contributors to relative performance. Having no position in Greece during the period also contributed to performance relative to the benchmark. Lastly, the Fund’s overweight position in India was the largest contributor to relative performance while the Fund’s underweight position in South Africa detracted the most from relative performance.

From a sector perspective, although each sector in the benchmark experienced a decline during the period, the Health Care sector was the best performing sector followed by Information Technology. The Fund had an overweight position relative to the benchmark in both sectors during the period, contributing to the Fund’s performance relative to the

| 4 | MANAGEMENT OVERVIEW |

Table of Contents

benchmark. The Energy and Materials sectors were the two worst performing sectors during the period and the Fund’s underweight position in both sectors contributed to the Fund’s performance relative to the benchmark. Finally, the Financials sector, an average underweight in the Fund, was the largest contributor to relative performance while the Consumer Discretionary sector, an average overweight, was the largest and only detractor on a relative basis.

| Q. | How did the Fund’s composition affect performance? |

| A. | The top country contributors to Fund performance during the period were China, India, and Taiwan. South Korea, Brazil and South Africa detracted the most from Fund performance. Top sector contributors to Fund performance during the period included Health Care, led by the pharmaceuticals industry, and Industrials, an average sector overweight that was led by the airport services industry. The Consumer Discretionary sector, where the catalog retail industry was the largest detractor, and the Financials sector, where diversified banks was the largest detractor, detracted the most from Fund performance. |

From a total effect standpoint, countries that added the most to relative performance in addition to India included China and Brazil. Countries detracting the most from relative performance in addition to South Africa included Malaysia, an average underweight, and Taiwan. Sectors adding the most to relative performance from a total effect standpoint, in addition to Financials, included Industrials and Energy. As mentioned previously, the Consumer Discretionary sector was the only sector that detracted from relative performance from a total effect standpoint.

With equity valuations appearing to be stretched during the period, a higher than average allocation to cash was used for defensive purposes, which added significantly to benchmark relative performance. The Fund did not employ currency hedging during the period.

| Q. | What is your investment outlook for emerging markets? |

| A. | At the end of fiscal year 2015, the emerging markets value-to-price (V/P) ratio stood at 0.89, indicating that, on average, emerging markets stocks are overpriced according to our system. Having surpassed our estimates of fair value, we have built up a cash position that we intend to put toward better bargains as they present themselves. Economic growth outside of the United States remains a key concern for investors, particularly as it relates to China and many of its fellow emerging market countries. Despite the prospect of the Federal Reserve tightening monetary policy in the near term, monetary policy in general remains accommodative globally. |

| MANAGEMENT OVERVIEW | 5 |

Table of Contents

Although our system continues to indicate emerging markets in general are overvalued, there are still areas demonstrating good bargains according to our methodology. Examples of countries where we see opportunities include India and Thailand, and the Fund is overweight in both countries. Industries in which we are finding opportunities include internet software & services, health care facilities and property & casualty insurance. Guided by our disciplined, systematic and non-emotional approach to investing, we remain ready to reallocate and adapt as our investment system dictates.

ICON Emerging Markets Fund

Country Composition

September 30, 2015

India | 21.5% | |||

South Korea | 20.8% | |||

South Africa | 9.4% | |||

China | 8.5% | |||

Hong Kong | 6.5% | |||

Thailand | 4.4% | |||

Turkey | 3.2% | |||

Philippines | 2.8% | |||

Mexico | 2.6% | |||

Brazil | 2.2% | |||

Taiwan | 2.2% | |||

Malaysia | 0.9% | |||

|

| |||

| 85.0% | ||||

|

|

Percentages are based upon common and preferred stocks as a percentage of net assets.

ICON Emerging Markets Fund

Sector Composition

September 30, 2015

Financials | 26.6% | |||

Information Technology | 13.7% | |||

Consumer Discretionary | 13.1% | |||

Consumer Staples | 8.8% | |||

Industrials | 7.5% | |||

Health Care | 5.2% | |||

Telecommunication Services | 3.3% | |||

Utilities | 4.5% | |||

Materials | 1.9% | |||

Energy | 0.4% | |||

|

| |||

| 85.0% | ||||

|

|

Percentages are based upon common and preferred stocks as a percentage of net assets.

| 6 | MANAGEMENT OVERVIEW |

Table of Contents

ICON Emerging Markets Fund

Industry Composition

September 30, 2015

Diversified Banks | 11.1% | |||

Multi-Sector Holdings | 5.0% | |||

Internet Software & Services | 4.0% | |||

Health Care Facilities | 3.4% | |||

Technology Hardware, Storage & Peripherals | 3.3% | |||

Wireless Telecommunication Services | 3.3% | |||

Household Products | 3.2% | |||

Gas Utilities | 2.6% | |||

Automobile Manufacturers | 2.5% | |||

Airport Services | 2.4% | |||

Life & Health Insurance | 2.4% | |||

Property & Casualty Insurance | 2.3% | |||

Environmental & Facilities Services | 2.2% | |||

Motorcycle Manufacturers | 2.2% | |||

Semiconductors | 2.2% | |||

Thrifts & Mortgage Finance | 2.2% | |||

Tobacco | 2.2% | |||

Cable & Satellite | 2.1% | |||

Water Utilities | 1.9% | |||

IT Consulting & Other Services | 1.8% | |||

Pharmaceuticals | 1.8% | |||

Electronic Manufacturing Services | 1.4% | |||

Real Estate Development | 1.4% | |||

Reinsurance | 1.4% | |||

Casinos & Gaming | 1.3% | |||

Diversified Chemicals | 1.3% | |||

Marine Ports & Services | 1.2% | |||

Broadcasting | 1.0% | |||

Electronic Equipment & Instruments | 1.0% | |||

Specialty Stores | 1.0% | |||

Other Industries (each less than 1%) | 9.9% | |||

|

| |||

| 85.0% | ||||

|

|

Percentages are based upon common and preferred stocks as a percentage of net assets.

| MANAGEMENT OVERVIEW | 7 |

Table of Contents

ICON Emerging Markets Fund

Average Annual Total Return

as of September 30, 2015

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON Emerging Markets Fund - Class S | 2/25/97 | -5.61% | 1.23% | 3.52% | 2.58% | 2.11% | 1.88% | |||||||||||||||||||||

ICON Emerging Markets Fund - Class C | 1/25/08 | -6.68% | 0.24% | N/A | -1.11% | 4.65% | 2.78% | |||||||||||||||||||||

ICON Emerging Markets Fund - Class A | 5/31/06 | -5.84% | 1.02% | N/A | 1.48% | 4.32% | 1.95% | |||||||||||||||||||||

ICON Emerging Markets Fund - Class A (including maximum sales charge of 5.75%) | 5/31/06 | -11.27% | -0.16% | N/A | 0.84% | 4.32% | 1.95% | |||||||||||||||||||||

MSCI Emerging Markets Index | -18.98% | -3.25% | 4.60% | 5.13% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Fund’s name and investment strategy changed effective May 5, 2014. The Fund’s past performance would have been different if the current strategy had been in effect. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| 8 | MANAGEMENT OVERVIEW |

Table of Contents

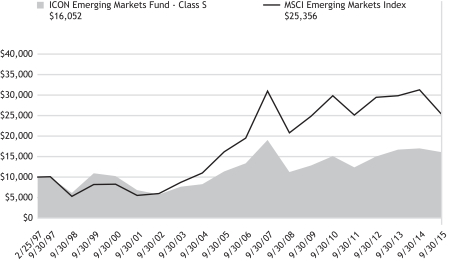

ICON Emerging Markets Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the Emerging Markets Fund’s Class S shares on the Class’ inception date of 2/25/97 to a $10,000 investment made in an unmanaged securities index on that date. The Fund’s name and investment strategy changed effective May 5, 2014. The Fund’s past performance would have been different if the current strategy had been in effect. Performance for the Emerging Markets Fund’s other share classes will vary due to differences in charges and expenses. The Emerging Markets Fund’s performance in this chart and the performance table assumes the reinvestment of dividends, capital gain distributions and tax return of capital, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| MANAGEMENT OVERVIEW | 9 |

Table of Contents

ICON EMERGING MARKETS FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| Shares or Principal Amount | Value | |||||||

| Common Stocks (84.5%) | ||||||||

| Agricultural Products (0.3%) | ||||||||

| 22,000 | Genting Plantations Bhd* | $ | 49,501 | |||||

|

| |||||||

| Airport Services (2.4%) | ||||||||

| 54,000 | Airports of Thailand PCL* | 419,138 | ||||||

|

| |||||||

| Apparel Retail (0.7%) | ||||||||

| 9,100 | Mr Price Group, Ltd.* | 127,032 | ||||||

|

| |||||||

| Automobile Manufacturers (2.5%) | ||||||||

| 17,000 | Ford Otomotiv Sanayi* | 181,668 | ||||||

| 3,600 | Maruti Suzuki India, Ltd.* | 257,060 | ||||||

|

| |||||||

| 438,728 | ||||||||

| Brewers (0.7%) | ||||||||

| 24,500 | AMBEV S.A.** | 120,013 | ||||||

|

| |||||||

| Broadcasting (1.0%) | ||||||||

| 30,000 | Zee Entertainment Enterprises, Ltd.* | 179,780 | ||||||

|

| |||||||

| Cable & Satellite (2.1%) | ||||||||

| 2,870 | Naspers, Ltd., Class N* | 359,689 | ||||||

|

| |||||||

| Casinos & Gaming (1.3%) | ||||||||

| 6,500 | Kangwon Land, Inc.* | 232,319 | ||||||

|

| |||||||

| Catalog Retail (0.7%) | ||||||||

| 750 | CJ O Shopping Co., Ltd.* | 117,430 | ||||||

|

| |||||||

| Diversified Banks (10.6%) | ||||||||

| 96,000 | Akbank T.A.S.* | 215,355 | ||||||

| 90,000 | BDO Unibank, Inc.* | 199,600 | ||||||

| 65,000 | Grupo Financiero Banorte S.A.B. de C.V., Class O** | 318,831 | ||||||

| 15,200 | HDFC Bank, Ltd.* | 248,541 | ||||||

| Shares or Principal Amount | Value | |||||||

| 88,700 | ICICI Bank, Ltd.* | $ | 365,570 | |||||

| 55,000 | Malayan Banking Bhd* | 107,297 | ||||||

| 10,800 | Standard Bank Group, Ltd.* | 105,453 | ||||||

| 25,400 | Yes Bank, Ltd.* | 283,809 | ||||||

|

| |||||||

| 1,844,456 | ||||||||

| Diversified Chemicals (1.3%) | ||||||||

| 39,400 | Tata Chemicals, Ltd.* | 230,553 | ||||||

|

| |||||||

| Diversified Support Services (0.7%) | ||||||||

| 1,200 | KEPCO Plant Service & Engineering Co., Ltd.* | 122,824 | ||||||

|

| |||||||

| Electronic Equipment & Instruments (1.0%) | ||||||||

| 4,500 | SFA Engineering Corp.* | 171,202 | ||||||

|

| |||||||

| Electronic Manufacturing Services (1.4%) | ||||||||

| 40,000 | AAC Technologies Holdings, Inc.* | 250,466 | ||||||

|

| |||||||

| Environmental & Facilities Services (2.2%) | ||||||||

| 268,000 | China Everbright International, Ltd.* | 378,579 | ||||||

|

| |||||||

| Food Distributors (0.7%) | ||||||||

| 5,700 | Hyundai Greenfood Co., Ltd.* | 123,467 | ||||||

|

| |||||||

| Gas Utilities (2.6%) | ||||||||

| 42,000 | China Resources Gas Group, Ltd.* | 107,965 | ||||||

| 10,400 | Korea Gas Corp.* | 349,278 | ||||||

|

| |||||||

| 457,243 | ||||||||

| Health Care Facilities (3.4%) | ||||||||

| 8,200 | Apollo Hospitals Enterprise, Ltd.* | 180,002 | ||||||

| 159,000 | Life Healthcare Group Holdings, Ltd.* | 409,022 | ||||||

|

| |||||||

| 589,024 | ||||||||

| 10 | SCHEDULEOF INVESTMENTS |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| Highways & Railtracks (0.6%) | ||||||||

| 32,000 | CCR S.A.** | $ | 98,232 | |||||

|

| |||||||

| Hotels, Resorts & Cruise Lines (0.7%) | ||||||||

| 1,000 | Hana Tour Service, Inc.* | 122,861 | ||||||

|

| |||||||

| Household Appliances (0.9%) | ||||||||

| 2,200 | Coway Co., Ltd.* | 155,674 | ||||||

|

| |||||||

| Household Products (3.2%) | ||||||||

| 780 | LG Household & Health Care, Ltd.* | 564,477 | ||||||

|

| |||||||

| Industrial Conglomerates (0.4%) | ||||||||

| 12,000 | Beijing Enterprises Holdings, Ltd.* | 72,369 | ||||||

|

| |||||||

| Internet Software & Services (4.0%) | ||||||||

| 240 | NAVER Corp.* | 104,025 | ||||||

| 35,045 | Tencent Holdings, Ltd.* | 591,653 | ||||||

|

| |||||||

| 695,678 | ||||||||

| IT Consulting & Other Services (1.8%) | ||||||||

| 11,200 | Infosys, Ltd.* | 197,844 | ||||||

| 12,000 | Wipro, Ltd.* | 109,640 | ||||||

|

| |||||||

| 307,484 | ||||||||

| Life & Health Insurance (2.4%) | ||||||||

| 50,000 | China Life Insurance Co. Ltd., Class H* | 174,219 | ||||||

| 49,000 | Ping An Insurance Group Co., Class H* | 245,171 | ||||||

|

| |||||||

| 419,390 | ||||||||

| Marine Ports & Services (1.2%) | ||||||||

| 47,600 | Adani Ports and Special Economic Zone* | 217,449 | ||||||

|

| |||||||

| Motorcycle Manufacturers (2.2%) | ||||||||

| 10,300 | Hero MotorCorp, Ltd.* | 376,881 | ||||||

|

| |||||||

| Multi-Sector Holdings (5.0%) | ||||||||

| 17,000 | Ayala Corp.* | 279,150 | ||||||

| 53,000 | Haci Omer Sabanci Holding* | 155,511 | ||||||

| 23,900 | Remgro, Ltd.* | 435,906 | ||||||

|

| |||||||

| 870,567 | ||||||||

| Shares or Principal Amount | Value | |||||||

| Oil & Gas Storage & Transportation (0.4%) | ||||||||

| 4,500 | Ultrapar Participacoes S.A.** | $ | 75,823 | |||||

|

| |||||||

| Personal Products (0.9%) | ||||||||

| 16,000 | Hengan International Group Co., Ltd.* | 156,451 | ||||||

|

| |||||||

| Pharmaceuticals (1.8%) | ||||||||

| 60,000 | China Medical System Holdings, Ltd.* | 68,518 | ||||||

| 3,800 | Dr. Reddy’s Laboratories, Ltd.* | 241,521 | ||||||

|

| |||||||

| 310,039 | ||||||||

| Property & Casualty Insurance (2.3%) | ||||||||

| 8,000 | Hyundai Marine & Fire Insurance Co., Ltd.* | 204,117 | ||||||

| 820 | Samsung Fire & Marine Insurance Co., Ltd.* | 193,637 | ||||||

|

| |||||||

| 397,754 | ||||||||

| Real Estate Development (1.4%) | ||||||||

| 106,000 | China Resources Land, Ltd.* | 250,299 | ||||||

|

| |||||||

| Real Estate Operating Companies (0.8%) | ||||||||

| 116,000 | Central Pattana PCL* | 143,206 | ||||||

|

| |||||||

| Reinsurance (1.4%) | ||||||||

| 20,784 | Korean Reinsurance Co.* | 250,233 | ||||||

|

| |||||||

| Semiconductors (2.2%) | ||||||||

| 94,000 | Taiwan Semiconductor Manufacturing Co., Ltd.* | 376,721 | ||||||

|

| |||||||

| Soft Drinks (0.8%) | ||||||||

| 25,000 | Arca Continental S.A.B. de C.V.** | 140,788 | ||||||

|

| |||||||

| Specialty Chemicals (0.6%) | ||||||||

| 7,900 | Asian Paints, Ltd.* | 101,419 | ||||||

|

| |||||||

| Specialty Stores (1.0%) | ||||||||

| 1,890 | Hotel Shilla Co., Ltd.* | 184,216 | ||||||

|

| |||||||

| SCHEDULEOF INVESTMENTS | 11 |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| | Technology Hardware, Storage & Peripherals (3.3%) | | ||||||

| 596 | Samsung Electronics Co., Ltd.* | $ | 571,834 | |||||

|

| |||||||

| Thrifts & Mortgage Finance (2.2%) | ||||||||

| 54,800 | LIC Housing Finance Ltd.* | 392,655 | ||||||

|

| |||||||

| Tobacco (2.2%) | ||||||||

| 75,200 | ITC, Ltd.* | 377,302 | ||||||

|

| |||||||

| Water Utilities (1.9%) | ||||||||

| 472,000 | Beijing Enterprises Water Group, Ltd.*† | 331,999 | ||||||

|

| |||||||

| | Wireless Telecommunication Services (3.3%) | | ||||||

| 15,000 | Advanced Info Service PCL* | 93,555 | ||||||

| 50,000 | Intouch Holdings PCL, Class F* | 100,597 | ||||||

| 15,200 | MTN Group, Ltd.* | 195,461 | ||||||

| 810 | SK Telecom Co., Ltd.* | 179,687 | ||||||

|

| |||||||

| 569,300 | ||||||||

|

| |||||||

| Shares or Principal Amount | Value | |||||||

|

| Total Common Stocks (Cost $15,633,119) | $ | 14,742,545 | |||||

| Preferred Stock (0.5%) | ||||||||

| Diversified Banks (0.5%) | ||||||||

| 13,750 | Itau Unibanco Holding S.A.** | 91,944 | ||||||

|

| |||||||

|

| Total Preferred Stocks (Cost $196,055) | 91,944 | ||||||

| Short-Term Investments (14.8%) | ||||||||

| $ | 2,579,245 | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/15 | 2,579,245 | |||||

|

| |||||||

|

| Total Short-Term Investments (Cost $2,579,245) | 2,579,245 | ||||||

|

| Total Investments 99.8% (Cost $18,408,419) | 17,413,734 | ||||||

| | Other Assets Less Liabilities 0.2% | 35,645 | ||||||

|

| |||||||

| Net Assets 100.0% | $ | 17,449,379 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| * | The value of foreign securities fair valued (Note 2) as of September 30, 2015 was 80.2% of net assets. |

| † | Non-income producing security. |

| ** | This security is considered a Level 1 security. See Note 2 for further details. |

| 12 | SCHEDULEOF INVESTMENTS |

Table of Contents

MANAGEMENT OVERVIEW (UNAUDITED) |

| Q. | How did the Fund perform relative to its benchmark? |

| A. | The ICON International Equity Fund (the Fund) Class S returned -3.15% for the fiscal year ended September 30, 2015, while the MSCI All Country World Index ex-United States (ACWI ex-U.S.) returned -11.78%. Total returns for other periods and additional Class shares as of September 30, 2015, appear in the subsequent pages of this Fund’s Management Overview. |

| Q. | What primary factors were behind the Fund’s relative performance? |

| A. | We finished fiscal year 2015 with global stock market losses as the global economy digested increased financial volatility and economic uncertainty. China found itself under the spotlight as continued slower growth brought forth worries about the ripple effects on the broader global economy. While other sectors and countries adjusted to this slowdown, China experienced large gyrations in its equity markets, which prompted government intervention in its markets. Japan experienced a slow recovery from recession, with the assistance of a stimulative monetary policy. However, the slow pace of the recovery begs the question of whether there is a need for further future policy action in Asia’s second largest economy. Europe generally experienced continued growth amidst the undercurrents of the domestic and global economy. Greece dominated headlines as fiscal problems and backlashes against austerity brought a real possibility of its exit from the Eurozone. As the period closed, we still saw modest upside in the global markets overall with some regions showing great bargains and others appearing slightly overpriced according to our system. |

At the beginning of the fiscal year, our valuation model signaled a modest 8% upside to fair value for global markets and pointed the Fund towards an overweight position in the cyclical sectors of the market such as Information Technology, Industrials, and Consumer Discretionary. From a regional perspective, the Fund maintained an overweight position in European equities as well as an underweight position in the Asia-Pacific region and Western Hemisphere. Emerging market equities remained overvalued according to our model and the Fund maintained an underweight position in those regions as well. Despite the ongoing issues looming over the world economy as well as rotations within the Fund that may seem contrarian, our discipline and focus on value guided our decisions, which we believe will benefit the Fund going forward.

| MANAGEMENT OVERVIEW | 13 |

Table of Contents

As a multi-cap manager, we are not restricted by market capitalization. However, following our valuation readings led to a concentration in small and mid-cap companies during the period and an underweight position in large-cap stocks relative to the benchmark. Overall, large-cap stocks outperformed their small and mid-cap peers, which detracted from the fund’s relative performance.

Currency movements worldwide throughout the fiscal year also had a negative impact on the Fund’s returns. The U.S. dollar broadly strengthened throughout the year versus most of the underlying currencies of the holdings in the Fund. Currency hedging was not used during the fiscal year.

| Q. | How did the Fund’s composition affect performance? |

| A. | The Fund’s primary contributors to benchmark relative performance came from the Industrials and Information Technology sectors. Specifically, overweight positions in the diversified support services and industrial machinery industries within the Industrials sector and semiconductors and IT consulting & other services industries within the Information Technology Sector contributed to performance relative to the benchmark. Further, an underweight position in the poor performing Financials sector, specifically in the diversified banks industry, proved beneficial. |

Conversely, the Consumer Staples sector was a detractor, as the agricultural products and food retail industries hindered the Fund’s returns. The Energy sector was another notable source of relative underperformance as the sector was the worst performing sector for the period. The oil & gas equipment & services and oil & gas drilling industries suffered losses as commodity weakness had an adverse effect on companies’ stock prices. With the slight increase in interest rates and declines in stock prices, our valuation methodology is showing us slightly fewer bargains than we saw at the beginning of the year. As such, we see modest upside to the market, with the best bargains coming from the Financials and Industrials sectors.

While all geographic regions saw losses over the period, there were areas of clear differentiation among certain countries throughout the year. Most notably, emerging market countries saw larger losses, specifically in countries such as Brazil, Indonesia, Malaysia, and Russia. Conversely, countries in the developed world, specifically those in Europe, held up better throughout the year. As the period ended, the emerging markets and the Asia-Pacific region appeared overvalued according to our system while Europe and other developed markets in general showed the most upside globally.

| 14 | MANAGEMENT OVERVIEW |

Table of Contents

| Q. | What is your investment outlook for the international equity market? |

| A. | Our system estimates that international equities, on average, still remain below our estimate of their intrinsic value. At the end of the period, international markets as a whole had an overall average value-to-price (V/P) ratio of 1.05, implying that, on average, our estimate of fair value for stocks is about 5% higher than where they are currently trading. Risk aversion amongst investors remains and corporate earnings have generally grown despite ongoing economic struggles and geopolitical concerns. While global economic growth has languished outside of the United States, interest rates remain low, thanks in great part to loose monetary policy and extraordinary central bank intervention. |

According to our valuation system, Europe represents the best opportunity from a regional perspective, with Asia-Pacific showing the least upside. Despite some improvements in sentiment and equity prices in the emerging market countries, overall they still remain overvalued according to our metrics and do not warrant an overweight exposure within the Fund. Based on our methodology, developed markets in Europe show attractive upside in countries such as Belgium, France, Germany, and Sweden. As of the end of the fiscal year 2015 we estimate that, on average, fair value for European equities is 25% higher than where prices are currently trading. Within the Western Hemisphere, Canada and Mexico look attractive to our system with Indonesia, the Philippines, and Thailand currently showing the most value in the Asia-Pacific region.

From a sector perspective, we are still tilted towards the Financials and Industrials sectors. Within our system, Energy is now the most over-valued sector, and represents an underweight position relative to the benchmark as we see little upside within this sector.

At ICON we continue to seek out industries that our system identifies as trading at a discount to fair value. Guided by our disciplined, systematic and non-emotional approach to investing, we see numerous opportunities amidst the recent turbulence and volatility. We believe it is nearly impossible to accurately time market bottoms and we believe rallies do not offer invitations. Therefore, given our current valuations, we remain almost fully invested. As market conditions dictate, we will adjust accordingly.

| MANAGEMENT OVERVIEW | 15 |

Table of Contents

ICON International Equity Fund

Country Composition

September 30, 2015

Germany | 22.6% | |||

United Kingdom | 12.8% | |||

France | 11.6% | |||

Canada | 6.7% | |||

Japan | 5.8% | |||

Switzerland | 5.4% | |||

India | 4.7% | |||

Denmark | 3.9% | |||

Norway | 2.0% | |||

Sweden | 2.0% | |||

Belgium | 1.4% | |||

Finland | 1.4% | |||

Ireland | 1.4% | |||

United States | 1.4% | |||

Netherlands | 1.3% | |||

South Korea | 1.3% | |||

Isle Of Man | 1.1% | |||

South Africa | 0.9% | |||

China | 0.8% | |||

Spain | 0.8% | |||

Australia | 0.7% | |||

Portugal | 0.7% | |||

Hong Kong | 0.4% | |||

Philippines | 0.4% | |||

|

| |||

| 91.5% | ||||

|

| |||

Percentages are based upon common, preferred and real estate investment trusts stocks as a percentage of net assets. |

| |||

ICON International Equity Fund

Sector Composition

September 30, 2015

Financials | 19.2% | |||

Industrials | 18.4% | |||

Information Technology | 12.4% | |||

Consumer Discretionary | 11.8% | |||

Consumer Staples | 9.9% | |||

Health Care | 6.0% | |||

Utilities | 5.8% | |||

Materials | 5.2% | |||

Energy | 1.9% | |||

Telecommunication Services | 0.9% | |||

|

| |||

| 91.5% | ||||

|

|

Percentages are based upon common, preferred and real estate investment trusts stocks as a percentage of net assets.

| 16 | MANAGEMENT OVERVIEW |

Table of Contents

ICON International Equity Fund

Industry Composition

September 30, 2015

Pharmaceuticals | 4.6% | |||

Diversified Banks | 4.3% | |||

Data Processing & Outsourced Services | 3.3% | |||

Life & Health Insurance | 3.3% | |||

Multi-Utilities | 3.2% | |||

Cable & Satellite | 3.1% | |||

Electronic Equipment & Instruments | 2.9% | |||

Packaged Foods & Meats | 2.9% | |||

Specialty Chemicals | 2.6% | |||

Industrial Conglomerates | 2.5% | |||

Advertising | 2.4% | |||

Airlines | 2.4% | |||

Auto Parts & Equipment | 2.4% | |||

Aerospace & Defense | 2.2% | |||

Multi-line Insurance | 2.2% | |||

Railroads | 2.1% | |||

IT Consulting & Other Services | 2.0% | |||

Research & Consulting Services | 1.8% | |||

Building Products | 1.7% | |||

Food Retail | 1.7% | |||

Household Products | 1.7% | |||

Semiconductors | 1.6% | |||

Integrated Oil & Gas | 1.5% | |||

Multi-Sector Holdings | 1.4% | |||

Personal Products | 1.3% | |||

Broadcasting | 1.2% | |||

Diversified Support Services | 1.2% | |||

Industrial Machinery | 1.2% | |||

Integrated Telecommunication Services | 1.2% | |||

Security & Alarm Services | 1.2% | |||

Automobile Manufacturers | 1.1% | |||

Diversified Capital Markets | 1.1% | |||

Airport Services | 1.0% | |||

Thrifts & Mortgage Finance | 1.0% | |||

Water Utilities | 1.0% | |||

Other Industries (each less than 1%) | 19.2% | |||

|

| |||

| 91.5% | ||||

|

|

Percentages are based upon common, preferred and real estate investment trusts stocks as a percentage of net assets.

| MANAGEMENT OVERVIEW | 17 |

Table of Contents

ICON International Equity Fund

Average Annual Total Return

as of September 30, 2015

| Inception Date | 1 Year | 5 Years | 10 Years | Since Inception | Gross Expense Ratio* | Net Expense Ratio* | ||||||||||||||||||||||

ICON International Equity Fund - Class S | 2/18/97 | -3.15% | -0.81% | 1.44% | 4.77% | 1.41% | 1.41% | |||||||||||||||||||||

ICON International Equity Fund - Class C | 2/19/04 | -4.20% | -1.89% | 0.27% | 1.90% | 2.82% | 2.56% | |||||||||||||||||||||

ICON International Equity Fund - Class A | 5/31/06 | -3.52% | -1.17% | N/A | -1.02% | 2.12% | 1.81% | |||||||||||||||||||||

ICON International Equity Fund - Class A (including maximum sales charge of 5.75%) | 5/31/06 | -9.06% | -2.33% | N/A | -1.65% | 2.12% | 1.81% | |||||||||||||||||||||

MSCI ACWI ex-U.S. | -11.78% | 2.27% | 3.49% | 4.53% | N/A | N/A | ||||||||||||||||||||||

Past performance is not a guarantee of future results. Information about these performance results and the comparative indexes can be found in the About This Report section. The Fund’s name and investment strategy changed effective January 29, 2004. The Fund’s past performance would have been different if the current strategy had been in effect. The Adviser has agreed to limit certain Fund expenses; without these limitations, returns would have been lower. The limitation provisions may be terminated in the future.

| * | Please see the most recent prospectus for details. |

Class C total returns exclude applicable sales charges. If sales charges were included returns would be lower.

| 18 | MANAGEMENT OVERVIEW |

Table of Contents

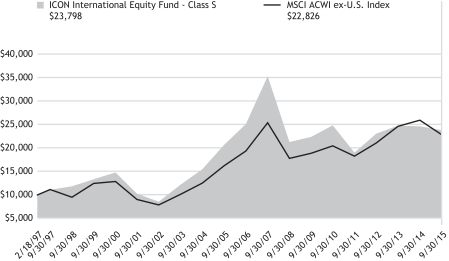

ICON International Equity Fund

Value of a $10,000 Investment

through September 30, 2015

Past performance is not a guarantee of future results. The above graph compares a $10,000 investment made in the International Equity Fund’s Class S shares on the Class’ inception date of 2/18/97 to a $10,000 investment made in an unmanaged securities index on that date. The Fund’s name and investment strategy changed effective January 29, 2004. The Fund’s past performance would have been different if the current strategy had been in effect. Performance for the International Equity Fund’s other share classes will vary due to differences in charges and expenses. The International Equity Fund’s performance in this chart and the performance table assumes the reinvestment of dividends, capital gain distributions and tax return of capital, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.

| MANAGEMENT OVERVIEW | 19 |

Table of Contents

ICON INTERNATIONAL EQUITY FUND

SCHEDULEOF INVESTMENTS

SEPTEMBER 30, 2015

| Shares or Principal Amount | Value | |||||||

| Common Stocks (89.0%) | ||||||||

| Advertising (2.4%) | ||||||||

| 19,500 | CyberAgent, Inc.*(a) | $ | 762,814 | |||||

| 50,000 | WPP PLC* | 1,040,950 | ||||||

|

| |||||||

| 1,803,764 | ||||||||

| Aerospace & Defense (2.2%) | ||||||||

| 5,400 | Airbus Group SE* | 319,788 | ||||||

| 87,000 | BAE Systems PLC* | 589,738 | ||||||

| 40,000 | Meggitt PLC* | 288,565 | ||||||

| 19,000 | Zodiac Aerospace* | 436,244 | ||||||

|

| |||||||

| 1,634,335 | ||||||||

| Airlines (2.4%) | ||||||||

| 69,300 | Air Canada†** | 557,204 | ||||||

| 6,900 | American Airlines Group, Inc.** | 267,927 | ||||||

| 37,150 | Deutsche Lufthansa AG*† | 517,157 | ||||||

| 11,500 | Southwest Airlines Co.** | 437,460 | ||||||

|

| |||||||

| 1,779,748 | ||||||||

| Airport Services (1.0%) | ||||||||

| 11,500 | Fraport AG Frankfurt Airport Services Worldwide* | 711,078 | ||||||

|

| |||||||

| Alternative Carriers (0.4%) | ||||||||

| 63,000 | TalkTalk Telecom Group PLC*(a) | 299,997 | ||||||

|

| |||||||

| Application Software (0.8%) | ||||||||

| 9,200 | SAP SE* | 596,010 | ||||||

|

| |||||||

| Asset Management & Custody Banks (0.7%) | ||||||||

| 18,000 | Deutsche Beteiligungs AG* | 501,303 | ||||||

|

| |||||||

| Auto Parts & Equipment (2.4%) | ||||||||

| 4,900 | Linamar Corp.** | 256,842 | ||||||

| 12,000 | Magna International, Inc.** | 575,586 | ||||||

| 33,000 | Martinrea International, Inc.** | 261,132 | ||||||

| 11,300 | Montupet* | 666,163 | ||||||

|

| |||||||

| 1,759,723 | ||||||||

| Shares or Principal Amount | Value | |||||||

| Automobile Manufacturers (1.1%) | ||||||||

| 7,800 | Daimler AG* | $ | 567,864 | |||||

| 50,258 | Tata Motors, Ltd.*† | 228,161 | ||||||

|

| |||||||

| 796,025 | ||||||||

| Brewers (0.9%) | ||||||||

| 18,200 | Royal Unibrew AS* | 681,433 | ||||||

|

| |||||||

| Broadcasting (1.2%) | ||||||||

| 26,000 | Mediaset Espana Comunicacion S.A.* | 284,230 | ||||||

| 12,300 | ProSiebenSat.1 Media SE* | 603,753 | ||||||

|

| |||||||

| 887,983 | ||||||||

| Building Products (1.7%) | ||||||||

| 16,000 | Assa Abloy AB* | 286,972 | ||||||

| 6,800 | Rockwool International AS, Class B* | 969,273 | ||||||

|

| |||||||

| 1,256,245 | ||||||||

| Cable & Satellite (3.1%) | ||||||||

| 11,400 | Eutelsat Communications S.A.* | 349,650 | ||||||

| 5,138 | Naspers, Ltd., Class N* | 643,930 | ||||||

| 7,300 | Numericable-SFR SAS*† | 337,948 | ||||||

| 44,000 | Quebecor, Inc., Class B** | 963,087 | ||||||

|

| |||||||

| 2,294,615 | ||||||||

| Commodity Chemicals (0.9%) | ||||||||

| 49,000 | Asahi Kasei Corp.* | 345,521 | ||||||

| 72,000 | Tosoh Corp.*(a) | 346,506 | ||||||

|

| |||||||

| 692,027 | ||||||||

| Communications Equipment (0.6%) | ||||||||

| 43,000 | ADVA Optical Networking SE†** | 460,157 | ||||||

|

| |||||||

| Construction Materials (0.7%) | ||||||||

| 4,200 | HeidelbergCement AG* | 288,422 | ||||||

| 4,630 | LafargeHolcim, Ltd.** | 241,191 | ||||||

|

| |||||||

| 529,613 | ||||||||

| | Data Processing & Outsourced Services (3.3%) | | ||||||

| 169,000 | Optimal Payments PLC*† | 828,701 | ||||||

| 20 | SCHEDULEOF INVESTMENTS |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| 33,500 | Wirecard AG* | $ | 1,604,051 | |||||

|

| |||||||

| 2,432,752 | ||||||||

| Distillers & Vintners (0.5%) | ||||||||

| 15,000 | Diageo PLC* | 403,003 | ||||||

|

| |||||||

| Diversified Banks (4.3%) | ||||||||

| 86,000 | Axis Bank, Ltd.* | 655,029 | ||||||

| 42,900 | Commerzbank AG*† | 453,100 | ||||||

| 21,000 | DnB ASA* | 273,302 | ||||||

| 57,000 | HDFC Bank, Ltd.* | 932,027 | ||||||

| 250,000 | Lloyds Banking Group PLC* | 284,615 | ||||||

| 26,000 | Nordea Bank AB* | 290,069 | ||||||

| 27,000 | Skandinaviska Enskilda Banken AB* | 288,771 | ||||||

|

| |||||||

| 3,176,913 | ||||||||

| Diversified Capital Markets (1.1%) | ||||||||

| 23,200 | Close Brothers Group PLC* | 524,757 | ||||||

| 12,000 | Deutsche Bank AG* | 323,846 | ||||||

|

| |||||||

| 848,603 | ||||||||

| Diversified Real Estate Activities (0.8%) | ||||||||

| 5,800 | Daito Trust Construction Co., Ltd.* | 589,308 | ||||||

|

| |||||||

| Diversified Support Services (1.2%) | ||||||||

| 38,000 | Babcock International Group PLC* | 525,700 | ||||||

| 6,600 | Cewe Stiftung & Co. KGAA* | 367,163 | ||||||

|

| |||||||

| 892,863 | ||||||||

| Electric Utilities (0.4%) | ||||||||

| 146,000 | Power Grid Corp. of India, Ltd.* | 295,931 | ||||||

|

| |||||||

| Electronic Components (0.4%) | ||||||||

| 20,600 | Japan Aviation Electronics Industry, Ltd.* | 309,417 | ||||||

|

| |||||||

| Electronic Equipment & Instruments (2.9%) | ||||||||

| 5,157 | Ingenico Group* | 623,153 | ||||||

| 14,240 | Isra Vision AG* | 796,637 | ||||||

| 28,595 | Jenoptik AG* | 406,531 | ||||||

| 11,400 | Spectris PLC* | 291,678 | ||||||

|

| |||||||

| 2,117,999 | ||||||||

| Fertilizers & Agricultural Chemicals (0.3%) | ||||||||

| 220,000 | Gujarat State Fertilizers & Chemicals, Ltd.* | 236,932 | ||||||

|

| |||||||

| Shares or Principal Amount | Value | |||||||

| Food Retail (1.7%) | ||||||||

| 7,000 | Casino Guichard Perrachon S.A.* | $ | 372,784 | |||||

| 10,700 | Kesko Oyj, Class B* | 379,003 | ||||||

| 385,000 | Sonae SGPS S.A.* | 474,806 | ||||||

|

| |||||||

| 1,226,593 | ||||||||

| Gas Utilities (0.5%) | ||||||||

| 12,000 | Korea Gas Corp.* | 403,014 | ||||||

|

| |||||||

| Health Care Equipment (0.8%) | ||||||||

| 32,000 | GN Store Nord AS* | 574,872 | ||||||

|

| |||||||

| Household Products (1.1%) | ||||||||

| 640 | LG Household & Health Care, Ltd.* | 463,161 | ||||||

| 16,000 | Pigeon Corp.** | 371,175 | ||||||

|

| |||||||

| 834,336 | ||||||||

| Hypermarkets & Super Centers (0.9%) | ||||||||

| 11,500 | Carrefour S.A.** | 339,756 | ||||||

| 200,000 | Robinsons Retail Holdings, Inc.* | 312,837 | ||||||

|

| |||||||

| 652,593 | ||||||||

| Industrial Conglomerates (2.5%) | ||||||||

| 3,198 | Daetwyler Holding AG*(a) | 434,128 | ||||||

| 25,000 | Indus Holding AG* | 1,118,574 | ||||||

| 3,650 | Siemens AG* | 326,080 | ||||||

|

| |||||||

| 1,878,782 | ||||||||

| Industrial Machinery (1.2%) | ||||||||

| 1,400,000 | EVA Precision Industrial Holdings, Ltd.* | 276,484 | ||||||

| 8,000 | GEA Group AG* | 305,043 | ||||||

| 5,500 | NKT Holding AS* | 290,380 | ||||||

|

| |||||||

| 871,907 | ||||||||

| Integrated Oil & Gas (1.5%) | ||||||||

| 73,300 | BP PLC** | 370,354 | ||||||

| 15,500 | Royal Dutch Shell PLC, Class B** | 366,486 | ||||||

| 8,200 | Total S.A.** | 368,340 | ||||||

|

| |||||||

| 1,105,180 | ||||||||

| | Integrated Telecommunication Services (1.2%) | | ||||||

| 20,300 | Deutsche Telekom AG* | 361,370 | ||||||

| 28,000 | Telenor ASA*(a) | 523,224 | ||||||

|

| |||||||

| 884,594 | ||||||||

| SCHEDULEOF INVESTMENTS | 21 |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| Internet Software & Services (0.8%) | ||||||||

| 10,100 | Alibaba Group Holding, Ltd., ADR†** | $ | 595,597 | |||||

|

| |||||||

| IT Consulting & Other Services (2.0%) | ||||||||

| 5,629 | Atos SE* | 432,680 | ||||||

| 8,000 | CANCOM SE* | 278,536 | ||||||

| 5,000 | Cap Gemini S.A.* | 446,514 | ||||||

| 14,000 | GFT Technologies SE* | 342,230 | ||||||

|

| |||||||

| 1,499,960 | ||||||||

| Leisure Products (0.9%) | ||||||||

| 26,000 | Amer Sports OYJ* | 661,328 | ||||||

|

| |||||||

| Life & Health Insurance (3.3%) | ||||||||

| 51,000 | Aegon N.V.* | 292,441 | ||||||

| 156,000 | Legal & General Group PLC* | 562,500 | ||||||

| 10,200 | �� | NN Group** | 292,003 | |||||

| 60,000 | Prudential PLC* | 1,265,791 | ||||||

|

| |||||||

| 2,412,735 | ||||||||

| Life Sciences Tools & Services (0.6%) | ||||||||

| 3,100 | Tecan Group AG* | 436,490 | ||||||

|

| |||||||

| Multi-line Insurance (2.2%) | ||||||||

| 4,000 | Allianz SE* | 628,371 | ||||||

| 24,400 | AXA S.A.* | 592,406 | ||||||

| 14,000 | Talanx AG* | 419,416 | ||||||

|

| |||||||

| 1,640,193 | ||||||||

| Multi-Sector Holdings (1.4%) | ||||||||

| 13,500 | Groupe Bruxelles Lambert S.A.* | 1,018,764 | ||||||

|

| |||||||

| Multi-Utilities (3.2%) | ||||||||

| 22,100 | Atco, Ltd., Class I** | 649,172 | ||||||

| 31,000 | E.ON SE* | 266,025 | ||||||

| 34,900 | Engie* | 564,699 | ||||||

| 48,500 | National Grid PLC* | 675,466 | ||||||

| 20,000 | RWE AG* | 227,274 | ||||||

|

| |||||||

| 2,382,636 | ||||||||

| Oil & Gas Storage & Transportation (0.4%) | ||||||||

| 7,800 | Enbridge, Inc.** | 289,614 | ||||||

|

| |||||||

| Packaged Foods & Meats (2.9%) | ||||||||

| 7,800 | Danone* | 492,360 | ||||||

| 14,400 | Nestle S.A.* | 1,082,961 | ||||||

| 230 | Orion Corp * | 183,158 | ||||||

| 17,000 | Saputo, Inc.** | 373,249 | ||||||

|

| |||||||

| 2,131,728 | ||||||||

| Shares or Principal Amount | Value | |||||||

| Paper Packaging (0.7%) | ||||||||

| 19,300 | Smurfit Kappa Group PLC* | $ | 519,981 | |||||

|

| |||||||

| Personal Products (1.3%) | ||||||||

| 8,400 | Kao Corp.** | 378,320 | ||||||

| 3,400 | L’Oreal S.A.* | 590,968 | ||||||

|

| |||||||

| 969,288 | ||||||||

| Pharmaceuticals (4.6%) | ||||||||

| 2,800 | Bayer AG* | 359,235 | ||||||

| 33,000 | Cipla, Ltd.* | 320,741 | ||||||

| 5,600 | Novartis AG* | 514,706 | ||||||

| 7,000 | Novo Nordisk AS, Class B* | 377,752 | ||||||

| 4,000 | Roche Holding AG* | 1,061,886 | ||||||

| 7,900 | Shire PLC* | 540,060 | ||||||

| 1,500 | Valeant Pharmaceuticals International, Inc.†** | 267,741 | ||||||

|

| |||||||

| 3,442,121 | ||||||||

| Railroads (2.1%) | ||||||||

| 3,600 | Canadian Pacific Railway, Ltd.** | 516,706 | ||||||

| 34,000 | VTG AG*(a) | 1,005,707 | ||||||

|

| |||||||

| 1,522,413 | ||||||||

| Real Estate Development (0.8%) | ||||||||

| 145,321 | Oberoi Realty, Ltd.* | 605,807 | ||||||

|

| |||||||

| Real Estate Operating Companies (0.8%) | ||||||||

| 6,000 | Deutsche EuroShop AG* | 269,799 | ||||||

| 10,200 | Vonovia SE* | 328,297 | ||||||

|

| |||||||

| 598,096 | ||||||||

| Reinsurance (0.8%) | ||||||||

| 2,200 | Muenchener Rueckversicherungs Gesellschaft AG* | 410,882 | ||||||

| 2,300 | Swiss Re AG* | 197,333 | ||||||

|

| |||||||

| 608,215 | ||||||||

| Research & Consulting Services (1.8%) | ||||||||

| 6,510 | Bertrandt AG* | 679,828 | ||||||

| 8,900 | Teleperformance* | 675,308 | ||||||

|

| |||||||

| 1,355,136 | ||||||||

| Security & Alarm Services (1.2%) | ||||||||

| 21,500 | Loomis AB, Class B* | 563,516 | ||||||

| 67,500 | Prosegur Cia de Seguridad S.A.* | 325,031 | ||||||

|

| |||||||

| 888,547 | ||||||||

| 22 | SCHEDULEOF INVESTMENTS |

Table of Contents

| Shares or Principal Amount | Value | |||||||

| Semiconductors (1.6%) | ||||||||

| 40,100 | ARM Holdings PLC* | $ | 576,125 | |||||

| 54,905 | Infineon Technologies AG* | 616,881 | ||||||

|

| |||||||

| 1,193,006 | ||||||||

| Specialized Finance (0.4%) | ||||||||

| 95,000 | Power Finance Corp., Ltd.* | 333,380 | ||||||

|

| |||||||

| Specialty Chemicals (2.6%) | ||||||||

| 111,640 | Borregaard ASA* | 672,465 | ||||||

| - | (b) | Duk San Neolux Co., Ltd.*† | - | (b) | ||||

| 35,000 | Hitachi Chemical Co., Ltd.*(a) | 482,904 | ||||||

| 29,000 | Tokyo Ohka Kogyo Co., Ltd.* | 768,767 | ||||||

|

| |||||||

| 1,924,136 | ||||||||

| Thrifts & Mortgage Finance (1.0%) | ||||||||

| 127,000 | Paragon Group of Cos. PLC* | 759,803 | ||||||

|

| |||||||

| Tires & Rubber (0.4%) | ||||||||

| 3,200 | Cie Generale des Etablissements Michelin, Class B** | 291,132 | ||||||

|

| |||||||

| Trading Companies & Distributors (0.4%) | ||||||||

| 114,000 | SIG PLC* | 299,713 | ||||||

|

| |||||||

| Trucking (0.7%) | ||||||||

| 29,000 | TransForce, Inc.**(a) | 519,153 | ||||||

|

| |||||||

| Water Utilities (1.0%) | ||||||||

| 32,700 | Pennon Group PLC* | 384,633 | ||||||

| 23,000 | United Utilities Group PLC* | 322,368 | ||||||

|

| |||||||

| 707,001 | ||||||||

|

| |||||||

|

| Total Common Stocks (Cost $72,099,089) | 66,025,621 | ||||||

| Shares or Principal Amount | Value | |||||||

| Preferred Stocks (0.9%) | ||||||||

| Home Improvement Retail (0.3%) | ||||||||

| 2,740 | Hornbach Holding AG* | $ | 220,620 | |||||

|

| |||||||

| Household Products (0.6%) | ||||||||

| 4,700 | Henkel AG & Co. KGaA* | 484,078 | ||||||

|

| |||||||

|

| Total Preferred Stocks (Cost $747,656) | 704,698 | ||||||

| Real Estate Investment Trusts (1.6%) | ||||||||

| 14,300 | Klepierre, REIT* | 648,109 | ||||||

| 173,000 | Charter Hall Group, REIT* | 531,191 | ||||||

|

| |||||||

|

| Total Real Estate Investment Trusts (Cost $1,278,562) | 1,179,300 | ||||||

| Collateral for Securities on Loan (5.1%) | ||||||||

| 3,785,339 | State Street Navigator Prime Portfolio, 0.20% | 3,785,339 | ||||||

|

| |||||||

|

| Total Collateral for Securities on Loan (Cost $3,785,339) | 3,785,339 | ||||||

| Short-Term Investments (15.1%) | ||||||||

| $ | 11,214,677 | State Street Euro Dollar Time Deposit (USD), 0.01%, 10/01/15 | 11,214,677 | |||||

|

| |||||||

|

| Total Short-Term Investments (Cost $11,214,677) | 11,214,677 | ||||||

|

| Total Investments 111.7% (Cost $89,125,323) | 82,909,635 | ||||||

| | Liabilities Less Other Assets (11.7)% | (8,684,407 | ) | |||||

|

| |||||||

| Net Assets 100.0% | $ | 74,225,228 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

| * | The value of foreign securities fair valued (Note 2) as of September 30, 2015 was 78.0% of net assets. |

| † | Non-income producing security. |

| ** | This security is considered a Level 1 security. See Note 2 for further details. |

| (a) | All or a portion of the security was on loan as of September 30, 2015. |

| (b) | Value is less than 1. |

| ADR | American Depositary Receipt |

| REIT | Real Estate Investment Trust |

| SCHEDULEOF INVESTMENTS | 23 |

Table of Contents

STATEMENTSOF ASSETSAND LIABILITIES

SEPTEMBER 30, 2015

| ICON Emerging Markets Fund | ICON International Equity Fund | |||||||

Assets | ||||||||

Investments, at cost | $ | 18,408,419 | $ | 89,125,323 | ||||

|

|

|

| |||||

Investments, at value† | 17,413,734 | 82,909,635 | ||||||

Foreign currency, at value(a) | 15,757 | 43,958 | ||||||

Receivables: | ||||||||

Fund shares sold | 49,295 | 93,574 | ||||||

Expense reimbursements due from Adviser | 36,492 | 12,169 | ||||||

Dividends | 6,551 | 52,637 | ||||||

Foreign tax reclaims | 2,661 | 65,734 | ||||||

Other assets | 9,455 | 21,774 | ||||||

|

|

|

| |||||

Total Assets | 17,533,945 | 83,199,481 | ||||||

|

|

|

| |||||

Liabilities | ||||||||

Payables: | ||||||||

Fund shares redeemed | 21,007 | 36,208 | ||||||

Advisory fees | 14,540 | 61,556 | ||||||

Transfer agent fees | 5,361 | 11,669 | ||||||

Fund accounting fees | 784 | 3,478 | ||||||

Administration fees | 726 | 3,077 | ||||||

Accrued distribution fees | 623 | 3,527 | ||||||

Trustee fees | 455 | 3,313 | ||||||

Capital gains tax | 454 | - | ||||||

Investments purchased | - | 5,006,685 | ||||||

Payable for collateral received on securities loaned | - | 3,785,339 | ||||||

Accrued expenses | 40,616 | 59,401 | ||||||

|

|

|

| |||||

Total Liabilities | 84,566 | 8,974,253 | ||||||

|

|

|

| |||||

Net Assets - all share classes | $ | 17,449,379 | $ | 74,225,228 | ||||

|

|

|

| |||||

Net Assets - Class S | $ | 16,122,801 | $ | 67,200,360 | ||||

|

|

|

| |||||

Net Assets - Class C | $ | 601,620 | $ | 3,299,387 | ||||

|

|

|

| |||||

Net Assets - Class A | $ | 724,958 | $ | 3,725,481 | ||||

|

|

|

| |||||

| 24 | FINANCIAL STATEMENTS |

Table of Contents

| ICON Emerging Markets Fund | ICON International Equity Fund | |||||||

Net Assets Consist of | ||||||||

Paid-in capital | $ | 26,190,223 | $ | 169,330,116 | ||||

Accumulated undistributed net investment income/(loss) | (19,769 | ) | (511,973 | ) | ||||

Accumulated undistributed net realized gain/(loss) | (7,724,835 | ) | (88,364,836 | ) | ||||

Unrealized appreciation/(depreciation) | (996,240 | ) | (6,228,079 | ) | ||||

|

|

|

| |||||

Net Assets | $ | 17,449,379 | $ | 74,225,228 | ||||

|

|

|

| |||||

Shares outstanding (unlimited shares authorized, no par value) | ||||||||

Class S | 1,244,546 | 5,909,082 | ||||||

Class C | 48,893 | 321,343 | ||||||

Class A | 56,144 | 331,482 | ||||||

Net asset value (offering and redemption price per share) | ||||||||

Class S | $ | 12.95 | $ | 11.37 | ||||

Class C | $ | 12.30 | $ | 10.27 | ||||

Class A | $ | 12.91 | $ | 11.24 | ||||

Class A maximum offering price (100%/(100%-maximum sales charge)) of net asset value adjusted to the nearest cent per share | $ | 13.69 | $ | 11.92 | ||||

† Includes securities on loan of | $ | - | $ | 3,656,301 | ||||

(a) Foreign currency, at cost | $ | 16,305 | $ | 44,611 | ||||

The accompanying notes are an integral part of the financial statements.

| FINANCIAL STATEMENTS | 25 |

Table of Contents

STATEMENTSOF OPERATIONS

FORTHEYEARENDED SEPTEMBER 30, 2015

| ICON Emerging Markets Fund | ICON International Equity Fund | |||||||

Investment Income | ||||||||

Interest | $ | 494 | $ | 1,143 | ||||

Dividends | 182,308 | 1,278,051 | ||||||

Income from securities lending, net | - | 47,040 | ||||||

Foreign taxes withheld | (17,285 | ) | (129,985 | ) | ||||

|

|

|

| |||||

Total Investment Income | 165,517 | 1,196,249 | ||||||

|

|

|

| |||||

Expenses | ||||||||

Advisory fees | 121,707 | 845,192 | ||||||

Audit and tax service expense | 49,042 | 51,125 | ||||||

Registration fees: | ||||||||

Class S | 16,184 | 14,011 | ||||||

Class C | 10,824 | 11,055 | ||||||

Class A | 10,251 | 10,810 | ||||||

Transfer agent fees | 29,110 | 81,953 | ||||||

Custody fees | 18,983 | 45,758 | ||||||

Distribution fees: | ||||||||

Class C | 5,911 | 40,707 | ||||||

Class A | 1,196 | 10,002 | ||||||

Administration fees | 6,085 | 42,259 | ||||||

Fund accounting fees | 2,866 | 19,707 | ||||||

Insurance expense | 2,253 | 7,403 | ||||||

Trustee fees and expenses | 1,382 | 11,444 | ||||||

Interest expense | 512 | 409 | ||||||

Other expenses | 47,970 | 97,873 | ||||||

|

|

|

| |||||

Total expenses before expense reimbursement | 324,276 | 1,289,708 | ||||||

Expense reimbursement by Adviser due to expense limitation agreement | (128,011 | ) | (34,663 | ) | ||||

|

|

|

| |||||

Net Expenses | 196,265 | 1,255,045 | ||||||

|

|

|

| |||||

Net Investment Income/(Loss) | (30,748 | ) | (58,796 | ) | ||||

|

|

|

| |||||

Net Realized and Unrealized Gain/(Loss) | ||||||||

Net realized gain/(loss) on: | ||||||||

Investments | (248,300 | ) | (4,553,855 | ) | ||||

Foreign currency | (19,620 | ) | (503,558 | ) | ||||

Net realized capital gains tax | - | (106,007 | ) | |||||

Change in unrealized net appreciation/(depreciation) on: | ||||||||

Investments and foreign currency | (787,160 | ) | 3,115,720 | |||||

Net unrealized capital gains tax | (26 | ) | 4,052 | |||||

|

|

|

| |||||

Net realized and unrealized gain/(loss) | (1,055,106 | ) | (2,043,648 | ) | ||||

|

|

|

| |||||

Net Increase/(Decrease) in Net Assets Resulting From Operations | $ | (1,085,854 | ) | $ | (2,102,444 | ) | ||

|

|

|

| |||||

The accompanying notes are an integral part of the financial statements.

| 26 | FINANCIAL STATEMENTS |

Table of Contents

(This page is intentionally left blank)

Table of Contents

STATEMENTSOF CHANGESIN NET ASSETS

| ICON Emerging Markets Fund | ||||||||

| Year Ended September 30, 2015 | Year Ended September 30, 2014 | |||||||

Operations | ||||||||

Net investment income/(loss) | $ | (30,748 | ) | $ | (44,580 | ) | ||

Net realized gain/(loss) on investments | (248,300 | ) | 2,609,559 | |||||

Net realized gain/(loss) from foreign currency | (19,620 | ) | (37,546 | ) | ||||

Net realized capital gains tax | - | (52,013 | ) | |||||

Change in net unrealized appreciation/(depreciation) | (787,186 | ) | (2,391,992 | ) | ||||

|

|

|

| |||||

Net increase/(decrease) in net assets resulting from operations | (1,085,854 | ) | 83,428 | |||||

|

|

|

| |||||

Dividends and Distributions to Shareholders | ||||||||

Net investment income | ||||||||

Class S | - | (59,304 | ) | |||||

Class A | - | (1,490 | ) | |||||

|

|

|

| |||||

Net decrease from dividends and distributions | - | (60,794 | ) | |||||

|

|

|

| |||||

Fund Share Transactions | ||||||||

Shares sold | ||||||||

Class S | 20,067,880 | 6,840,980 | ||||||

Class C | 349,016 | 123,445 | ||||||

Class A | 862,982 | 75,466 | ||||||

Reinvested dividends and distributions | ||||||||

Class S | - | 56,463 | ||||||

Class A | - | 1,270 | ||||||

Shares repurchased | ||||||||

Class S | (11,885,964 | ) | (27,023,177 | ) | ||||

Class C | (468,737 | ) | (198,478 | ) | ||||

Class A | (398,743 | ) | (562,635 | ) | ||||

|

|

|

| |||||

Net increase/(decrease) from fund share transactions | 8,526,434 | (20,686,666 | ) | |||||

|

|

|

| |||||

Total net increase/(decrease) in net assets | 7,440,580 | (20,664,032 | ) | |||||

Net Assets | ||||||||

Beginning of year | 10,008,799 | 30,672,831 | ||||||

|

|

|

| |||||

End of year | $ | 17,449,379 | $ | 10,008,799 | ||||

|

|

|

| |||||

| 28 | FINANCIAL STATEMENTS |

Table of Contents

| ICON International Equity Fund | ||||||

Year Ended 2015 | Year Ended September 30, 2014 | |||||

| $ | (58,796 | ) | $ | 210,917 | ||

| (4,553,855 | ) | 7,551,567 | ||||

| (503,558 | ) | (271,659 | ) | |||

| (106,007 | ) | (35,013 | ) | |||

| 3,119,772 | (11,815,994 | ) | ||||

|

|

|

| |||

| (2,102,444 | ) | (4,360,182 | ) | |||

|

|

|

| |||

| (71,695 | ) | - | ||||

| - | - | |||||

|

|

|

| |||

| (71,695 | ) | - | ||||

|

|

|

| |||

| 4,506,506 | 54,955,281 | |||||

| 82,616 | 194,693 | |||||

| 1,145,130 | 353,579 | |||||

| 70,812 | - | |||||

| - | - | |||||

| (15,856,511 | ) | (12,360,031 | ) | |||

| (1,251,157 | ) | (1,233,291 | ) | |||

| (1,339,594 | ) | (1,312,960 | ) | |||

|

|

|

| |||

| (12,642,198 | ) | 40,597,271 | ||||

|

|

|

| |||

| (14,816,337 | ) | 36,237,089 | ||||

| 89,041,565 | 52,804,476 | |||||

|

|

|

| |||

| $ | 74,225,228 | $ | 89,041,565 | |||

|

|

|

| |||

| FINANCIAL STATEMENTS | 29 |

Table of Contents

STATEMENTSOF CHANGESIN NET ASSETS (CONTINUED)

| ICON Emerging Markets Fund | ||||||||

| Year Ended September 30, 2015 | Year Ended September 30, 2014 | |||||||

Transactions in Fund Shares | ||||||||

Shares sold | ||||||||

Class S | 1,456,599 | 496,107 | ||||||

Class C | 26,591 | 9,218 | ||||||

Class A | 62,831 | 5,468 | ||||||

Reinvested dividends and distributions | ||||||||

Class S | - | 4,198 | ||||||

Class A | - | 94 | ||||||

Shares repurchased | ||||||||

Class S | (863,679 | ) | (1,998,939 | ) | ||||

Class C | (35,508 | ) | (15,076 | ) | ||||

Class A | (28,954 | ) | (41,663 | ) | ||||

|

|

|

| |||||

Net increase/(decrease) | 617,880 | (1,540,593 | ) | |||||

|

|

|

| |||||

Shares outstanding, beginning of year | 731,703 | 2,272,296 | ||||||

|

|

|

| |||||

Shares outstanding, end of year | 1,349,583 | 731,703 | ||||||

|

|

|

| |||||

Accumulated undistributed net investment income/(loss) | $ | (19,769 | ) | $ | (18,814 | ) | ||

|

|

|

| |||||

The accompanying notes are an integral part of the financial statements.

| 30 | FINANCIAL STATEMENTS |

Table of Contents

| ICON International Equity Fund | ||||||

Year Ended 2015 | Year Ended September 30, 2014 | |||||

| 382,453 | 4,258,487 | |||||

| 7,381 | 16,869 | |||||

| 94,725 | 28,338 | |||||

| 6,089 | - | |||||

| - | - | |||||

| (1,317,093 | ) | (986,622 | ) | |||

| (114,930 | ) | (107,336 | ) | |||

| (114,235 | ) | (106,543 | ) | |||

|

|

|

| |||

| (1,055,610 | ) | 3,103,193 | ||||

|

|

|

| |||

| 7,617,517 | 4,514,324 | |||||

|

|

|

| |||

| 6,561,907 | 7,617,517 | |||||

|

|

|

| |||

| $ | (511,973 | ) | $ | 71,689 | ||

|

|

|

| |||

| FINANCIAL STATEMENTS | 31 |

Table of Contents

| Income/(loss) from investment operations | Less dividends and | |||||||||||||||||||||||

| Net asset value, beginning of period | Net investment income/ (loss)(x) | Net realized and unrealized gains/(losses) on investments | Total from investment operations | Dividends from net investment income | Distributions from net realized gains | |||||||||||||||||||

ICON Emerging Markets Fund | ||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||

Year ended September 30, 2015 | $ | 13.72 | $ | (0.03 | ) | $ | (0.74 | ) | $ | (0.77 | ) | $ | - | $ | - | |||||||||

Year ended September 30, 2014 | 13.51 | (0.03 | ) | 0.27 | 0.24 | (0.03 | ) | - | ||||||||||||||||

Year ended September 30, 2013 | 12.21 | 0.06 | 1.33 | 1.39 | (0.09 | ) | - | |||||||||||||||||

Year ended September 30, 2012 | 10.12 | 0.11 | 2.02 | 2.13 | (0.04 | ) | - | |||||||||||||||||

Year ended September 30, 2011 | 12.35 | 0.07 | (2.30 | ) | (2.23 | ) | - | - | ||||||||||||||||

Class C | ||||||||||||||||||||||||

Year ended September 30, 2015 | 13.18 | (0.17 | ) | (0.71 | ) | (0.88 | ) | - | - | |||||||||||||||

Year ended September 30, 2014 | 13.06 | (0.11 | ) | 0.23 | 0.12 | - | - | |||||||||||||||||

Year ended September 30, 2013 | 11.84 | (0.05 | ) | 1.28 | 1.23 | (0.01 | ) | - | ||||||||||||||||

Year ended September 30, 2012 | 9.88 | 0.01 | 1.95 | 1.96 | - | - | ||||||||||||||||||

Year ended September 30, 2011 | 12.17 | (0.02 | ) | (2.27 | ) | (2.29 | ) | - | - | |||||||||||||||

Class A | ||||||||||||||||||||||||

Year ended September 30, 2015 | 13.71 | (0.07 | ) | (0.73 | ) | (0.80 | ) | - | - | |||||||||||||||

Year ended September 30, 2014 | 13.51 | (0.04 | ) | 0.27 | 0.23 | (0.03 | ) | - | ||||||||||||||||

Year ended September 30, 2013 | 12.17 | 0.04 | 1.33 | 1.37 | (0.03 | ) | - | |||||||||||||||||

Year ended September 30, 2012 | 10.10 | 0.09 | 2.00 | 2.09 | (0.02 | ) | - | |||||||||||||||||

Year ended September 30, 2011 | 12.35 | 0.04 | (2.29 | ) | (2.25 | ) | - | - | ||||||||||||||||

| 32 | FINANCIAL HIGHLIGHTS |

Table of Contents

| distributions | Ratio of expenses to average net assets | Ratio of net investment income/(loss) to average net assets | ||||||||||||||||||||||||||||||||

| Total dividends and distributions | Net asset value, end of period | Total return* | Net assets, end of period (in thousands) | Before expense limitation/ recoupment and transfer agent earnings credits | After expense limitation/ recoupment and transfer agent earnings credits | Before expense limitation/ recoupment and transfer agent earnings credits | After expense limitation/ recoupment and transfer agent earnings credits | Portfolio turnover rate(a) | ||||||||||||||||||||||||||

| $ | - | $ | 12.95 | (5.61 | )% | $ | 16,123 | 2.44 | % | 1.55 | % | (1.08 | )% | (0.19 | )% | 76.12 | % | |||||||||||||||||

| (0.03 | ) | 13.72 | 1.78 | % | 8,942 | 2.11 | % | 1.88 | %(d) | (0.42 | )% | (0.19 | )% | 92.17 | % | |||||||||||||||||||

| (0.09 | ) | 13.51 | 11.44 | % | 29,053 | 1.64 | % | 1.64 | % | 0.46 | % | 0.46 | % | 59.98 | % | |||||||||||||||||||

| (0.04 | ) | 12.21 | 21.16 | % | 37,969 | 1.50 | % | 1.50 | % | 0.96 | % | 0.96 | % | 71.84 | % | |||||||||||||||||||

| - | 10.12 | (18.06 | )% | 55,637 | 1.59 | % | 1.59 | % | 0.55 | % | 0.55 | % | 71.03 | % | ||||||||||||||||||||

| - | 12.30 | (6.68 | )% | 601 | 5.11 | % | 2.55 | %(b) | (3.88 | )% | (1.32 | )% | 76.12 | % | ||||||||||||||||||||

| - | 13.18 | 0.92 | % | 762 | 4.65 | % | 2.78 | %(b) | (2.70 | )% | (0.83 | )% | 92.17 | % | ||||||||||||||||||||

| (0.01 | ) | 13.06 | 10.44 | % | 832 | 3.76 | % | 2.56 | %(b) | (1.63 | )% | (0.43 | )% | 59.98 | % | |||||||||||||||||||

| - | 11.84 | 19.84 | % | 869 | 3.91 | % | 2.55 | %(b) | (1.28 | )% | 0.08 | % | 71.84 | % | ||||||||||||||||||||

| - | 9.88 | (18.82 | )% | 792 | 4.40 | % | 2.55 | %(b) | (2.02 | )% | (0.17 | )% | 71.03 | % | ||||||||||||||||||||

| - | 12.91 | (5.84 | )% | 725 | 4.75 | % | 1.80 | %(b) | (3.44 | )% | (0.49 | )% | 76.12 | % | ||||||||||||||||||||

| (0.03 | ) | 13.71 | 1.68 | % | 305 | 4.32 | % | 1.95 | %(b) | (2.65 | )% | (0.28 | )% | 92.17 | % | |||||||||||||||||||

| (0.03 | ) | 13.51 | 11.29 | % | 789 | 2.97 | % | 1.81 | %(b) | (0.82 | )% | 0.34 | % | 59.98 | % | |||||||||||||||||||

| (0.02 | ) | 12.17 | 20.73 | % | 690 | 2.88 | % | 1.80 | %(b) | (0.31 | )% | 0.77 | % | 71.84 | % | |||||||||||||||||||

| - | 10.10 | (18.22 | )% | 768 | 3.05 | % | 1.81 | %(b) | (0.97 | )% | 0.27 | % | 71.03 | % | ||||||||||||||||||||

| FINANCIAL HIGHLIGHTS | 33 |

Table of Contents

FINANCIAL HIGHLIGHTS (CONTINUED)

| Income/(loss) from investment operations | Less dividends and | |||||||||||||||||||||||

| Net asset value, beginning of period | Net investment income/ (loss)(x) | Net realized and unrealized gains/(losses) on investments | Total from investment operations | Dividends from net investment income | Distributions from net realized gains | |||||||||||||||||||

ICON International Equity Fund | ||||||||||||||||||||||||

Class S** | ||||||||||||||||||||||||

Year ended September 30, 2015 | $ | 11.75 | $ | - | (c) | $ | (0.37 | ) | $ | (0.37 | ) | $ | (0.01 | ) | $ | - | ||||||||

Year ended September 30, 2014 | 11.81 | 0.06 | (0.12 | ) | (0.06 | ) | - | - | ||||||||||||||||

Year ended September 30, 2013 | 11.05 | 0.07 | 0.74 | 0.81 | - | (c) | (0.05 | ) | ||||||||||||||||

Year ended September 30, 2012 | 9.22 | 0.16 | 1.78 | 1.94 | (0.11 | ) | - | |||||||||||||||||

Year ended September 30, 2011 | 12.11 | 0.14 | (2.95 | ) | (2.81 | ) | (0.08 | ) | - | |||||||||||||||

Class C | ||||||||||||||||||||||||

Year ended September 30, 2015 | 10.72 | (0.12 | ) | (0.33 | ) | (0.45 | ) | - | - | |||||||||||||||

Year ended September 30, 2014 | 10.89 | (0.08 | ) | (0.09 | ) | (0.17 | ) | - | - | |||||||||||||||

Year ended September 30, 2013 | 10.26 | (0.04 | ) | 0.67 | 0.63 | - | - | |||||||||||||||||

Year ended September 30, 2012 | 8.56 | (0.02 | ) | 1.72 | 1.70 | - | - | |||||||||||||||||

Year ended September 30, 2011 | 11.30 | - | (c) | (2.74 | ) | (2.74 | ) | - | - | |||||||||||||||

Class A*** | ||||||||||||||||||||||||

Year ended September 30, 2015 | 11.65 | (0.04 | ) | (0.37 | ) | (0.41 | ) | - | - | |||||||||||||||

Year ended September 30, 2014 | 11.75 | - | (c) | (0.10 | ) | (0.10 | ) | - | - | |||||||||||||||

Year ended September 30, 2013 | 10.99 | 0.04 | 0.73 | 0.77 | - | (c) | (0.01 | ) | ||||||||||||||||

Year ended September 30, 2012 | 9.16 | 0.11 | 1.77 | 1.88 | (0.05 | ) | - | |||||||||||||||||

Year ended September 30, 2011 | 12.04 | 0.10 | (2.94 | ) | (2.84 | ) | (0.04 | ) | - | |||||||||||||||

| (x) | Calculated using the average shares method. |

| * | The total return calculation is for the period indicated and excludes any sales charges. |

| ** | Class S shares were formerly named Class Z shares prior to January 23, 2012. |

| *** | Class I shares merged into Class A on January 23, 2012. The results of each class prior to the merger may have been different than what is presented. |

| (a) | Portfolio turnover is calculated at the Fund level and is not annualized for periods less than a year. |

| (b) | The Fund’s operating expenses, not including interest expense, are contractually limited to the amounts discussed in Note 3. The ratios in these financial highlights reflect the limitation, including the interest expense. |

| (c) | Amount less than $0.005. |

| (d) | Effective May, 5, 2014, Class S’s operating expenses, not including interest expense, were contractually limited to the amounts discussed in Note 3. The ratios in these financial highlights reflect the limitation, including the interest expense. |

| (e) | Percentage less than 0.005%. |

The accompanying notes are an integral part of the financial statements.

| 34 | FINANCIAL HIGHLIGHTS |

Table of Contents

| distributions | Ratio of expenses to average net assets | Ratio of net investment income/(loss) to average net assets | ||||||||||||||||||||||||||||||||

| Total dividends and distributions | Net asset value, end of period | Total return* | Net assets, end of period (in thousands) | Before expense limitation/ recoupment and transfer agent earnings credits | After expense limitation/ recoupment and transfer agent earnings credits(b) | Before expense limitation/ recoupment and transfer agent earnings credits | After expense limitation/ recoupment and transfer agent earnings credits | Portfolio turnover rate(a) | ||||||||||||||||||||||||||

| $ | (0.01 | ) | $ | 11.37 | (3.15 | )% | $ | 67,201 | 1.41 | % | 1.41 | % | - | %(e) | - | %(e) | 204.10 | % | ||||||||||||||||

| - | 11.75 | (0.51 | )% | 80,356 | 1.41 | % | 1.41 | % | 0.44 | % | 0.44 | % | 192.93 | % | ||||||||||||||||||||

| (0.05 | ) | 11.81 | 7.33 | % | 42,105 | 1.45 | % | 1.45 | % | 0.65 | % | 0.65 | % | 137.83 | % | |||||||||||||||||||

| (0.11 | ) | 11.05 | 21.19 | % | 56,152 | 1.39 | % | 1.39 | % | 1.47 | % | 1.47 | % | 121.82 | % | |||||||||||||||||||

| (0.08 | ) | 9.22 | (23.38 | )% | 6,826 | 1.45 | % | 1.45 | % | 1.12 | % | 1.12 | % | 91.46 | % | |||||||||||||||||||

| - | 10.27 | (4.20 | )% | 3,299 | 2.96 | % | 2.55 | % | (1.56 | )% | (1.15 | )% | 204.10 | % | ||||||||||||||||||||

| - | 10.72 | (1.56 | )% | 4,597 | 2.82 | % | 2.56 | % | (0.99 | )% | (0.73 | )% | 192.93 | % | ||||||||||||||||||||

| - | 10.89 | 6.14 | % | 5,657 | 2.77 | % | 2.56 | % | (0.63 | )% | (0.42 | )% | 137.83 | % | ||||||||||||||||||||

| - | 10.26 | 19.86 | % | 6,773 | 2.72 | % | 2.55 | % | (0.41 | )% | (0.24 | )% | 121.82 | % | ||||||||||||||||||||

| - | 8.56 | (24.25 | )% | 8,050 | 2.64 | % | 2.55 | % | (0.11 | )% | (0.02 | )% | 91.46 | % | ||||||||||||||||||||

| - | 11.24 | (3.52 | )% | 3,725 | 2.25 | % | 1.80 | % | (0.77 | )% | (0.32 | )% | 204.10 | % | ||||||||||||||||||||

| �� | - | 11.65 | (0.85 | )% | 4,089 | 2.12 | % | 1.81 | % | (0.27 | )% | 0.04 | % | 192.93 | % | |||||||||||||||||||

| (0.01 | ) | 11.75 | 7.03 | % | 5,043 | 2.19 | % | 1.81 | % | (0.06 | )% | 0.32 | % | 137.83 | % | |||||||||||||||||||

| (0.05 | ) | 10.99 | 20.61 | % | 6,309 | 2.01 | % | 1.80 | % | 0.85 | % | 1.06 | % | 121.82 | % | |||||||||||||||||||

| (0.04 | ) | 9.16 | (23.65 | )% | 2,640 | 2.03 | % | 1.80 | % | 0.56 | % | 0.79 | % | 91.46 | % | |||||||||||||||||||

| FINANCIAL HIGHLIGHTS | 35 |

Table of Contents

SEPTEMBER 30, 2015

1. Organization