File No. 333-

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON FEBRUARY 27, 2014

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [ ]

Post-Effective Amendment No. [ ]

EQ Advisors Trust

(Exact Name of Registrant as Specified in Charter)

1290 Avenue of the Americas

New York, New York 10104

(Address of Principal Executive Offices)

(212) 554-1234

(Registrant’s Area Code and Telephone Number)

STEVEN M. JOENK

AXA Equitable Funds Management Group, LLC

1290 Avenue of the Americas

New York, New York 10104

(Name and Address of Agent for Service)

With copies to:

PATRICIA LOUIE, ESQ. AXA Equitable Funds Management Group, LLC 1290 Avenue of the Americas New York, New York 10104 | MARK C. AMOROSI, ESQ. K&L Gates LLP 1601 K Street, N.W. Washington, DC 20006 |

Approximate Date of Proposed Public Offering:

As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on the 30th day after filing pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: Class IA, Class IB and Class K shares of beneficial interest in the series of the registrant designated as the Multimanager Aggressive Equity Portfolio, Multimanager Technology Portfolio, Multimanager Core Bond Portfolio, Multimanager Mid Cap Growth Portfolio, Multimanager Mid Cap Value Portfolio, EQ/Large Cap Core PLUS Portfolio, EQ/Large Cap Value PLUS Portfolio, and EQ/International Core PLUS Portfolio.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 333-17217 and 811-07953).

EQ ADVISORS TRUST

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Contractholder Voting Instructions

Part A - Proxy Statement/Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibits

AXA EQUITABLE LIFE INSURANCE COMPANY

1290 Avenue of the Americas

New York, New York 10104

, 2014

Dear Contractholder:

Enclosed is a notice and Combined Proxy Statement and Prospectus relating to a Special Meeting of Shareholders of each of the following Portfolios:

| • | Multimanager Aggressive Equity Portfolio, |

| • | Multimanager Technology Portfolio, |

| • | Multimanager Core Bond Portfolio, |

| • | Multimanager Mid Cap Growth Portfolio, |

| • | Multimanager Mid Cap Value Portfolio, |

| • | Multimanager Large Cap Core Equity Portfolio, |

| • | Multimanager Large Cap Value Portfolio, and |

| • | Multimanager International Equity Portfolio (together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a series of AXA Premier VIP Trust (“VIP Trust”). The Special Meeting of Shareholders of the Acquired Portfolios is scheduled to be held at VIP Trust’s offices, 1290 Avenue of the Americas, New York, New York 10104, on May 21, 2014 at , Eastern time (the “Meeting”). At the Meeting, the shareholders of the Acquired Portfolios who are entitled to vote at the Meeting will be asked to approve the proposals described below.

VIP Trust’s Board of Trustees (the “Board”) has called the Meeting to request shareholder approval of the reorganization of each Acquired Portfolio from a series of VIP Trust into a corresponding series of EQ Advisors Trust (an “Acquiring Portfolio”) (a “Reorganization”) as set forth below:

| • | the Multimanager Aggressive Equity Portfolio into the Multimanager Aggressive Equity Portfolio, a newly created series of EQ Advisors Trust, |

| • | the Multimanager Technology Portfolio into the Multimanager Technology Portfolio, a newly created series of EQ Advisors Trust, |

| • | the Multimanager Core Bond Portfolio into the Multimanager Core Bond Portfolio, a newly created series of EQ Advisors Trust, |

| • | the Multimanager Mid Cap Growth Portfolio into the Multimanager Mid Cap Growth Portfolio, a newly created series of EQ Advisors Trust, |

| • | the Multimanager Mid Cap Value Portfolio into the Multimanager Mid Cap Value Portfolio, a newly created series of EQ Advisors Trust, |

| • | the Multimanager Large Cap Core Equity Portfolio into the EQ/Large Cap Core PLUS Portfolio, |

| • | the Multimanager Large Cap Value Portfolio into the EQ/Large Cap Value PLUS Portfolio, and |

| • | the Multimanager International Equity Portfolio into the EQ/International Core PLUS Portfolio. |

The Board of Trustees of VIP Trust has approved the proposed Reorganizations and recommends that you vote “FOR” the relevant proposals. Although the Board has determined that a vote “FOR” the proposals is in your best interest, the final decision is yours.

Each Acquiring Portfolio is managed by AXA Equitable Funds Management Group, LLC and is sub-advised by one or more investment sub-advisers. In each case, if a Reorganization is approved and implemented, each Contractholder that invests indirectly in an Acquired Portfolio will automatically become a Contractholder that invests indirectly in the corresponding Acquiring Portfolio.

As an owner of a variable life insurance policy and/or a variable annuity contract or certificate that participates in one or more of the Acquired Portfolios through the investment divisions of a separate account or accounts established by AXA Equitable Life Insurance Company (“AXA Equitable”), you are entitled to instruct AXA Equitable how to vote the Acquired Portfolio shares related to your interest in those accounts as of the close of business on February 28, 2014. The attached Notice of Special Meeting of Shareholders and Combined Proxy Statement and Prospectus concerning the Meeting describe the matters to be considered at the Meeting.

You are cordially invited to attend the Meeting. Since it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your voting instructions by completing, dating, and signing the enclosed voting instruction card and returning it in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. For further information on how to instruct an insurance company, please see the Contractholder Voting Instructions included herein. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may provide voting instructions in person, even though you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. Please respond promptly in order to save additional costs of proxy solicitation and in order to make sure you are represented.

Very truly yours,

Steven M. Joenk Managing Director AXA Equitable Life Insurance Company |

ii

AXA PREMIER VIP TRUST

Multimanager Aggressive Equity Portfolio

Multimanager Technology Portfolio

Multimanager Core Bond Portfolio

Multimanager Mid Cap Growth Portfolio

Multimanager Mid Cap Value Portfolio

Multimanager Large Cap Core Equity Portfolio

Multimanager Large Cap Value Portfolio

Multimanager International Equity Portfolio

1290 Avenue of the Americas

New York, New York 10104

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON MAY 21, 2014

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of each of the following Portfolios, each of which is a series of AXA Premier VIP Trust (“VIP Trust”), will be held on May 21, 2014, at , Eastern time, at the offices of VIP Trust, located at 1290 Avenue of the Americas, New York, New York 10104 (the “Meeting”):

| • | Multimanager Aggressive Equity Portfolio, |

| • | Multimanager Technology Portfolio, |

| • | Multimanager Core Bond Portfolio, |

| • | Multimanager Mid Cap Growth Portfolio, |

| • | Multimanager Mid Cap Value Portfolio, |

| • | Multimanager Large Cap Core Equity Portfolio, |

| • | Multimanager Large Cap Value Portfolio, and |

| • | Multimanager International Equity Portfolio (together, the “Acquired Portfolios”). |

The Meeting will be held to act on the following proposals:

1. To approve the Agreement and Plan of Reorganization and Termination adopted by the Board of Trustees of VIP Trust (the “Board”) (the “Shell Reorganization Plan”) with respect to the reorganization of the Multimanager Aggressive Equity Portfolio, a series of VIP Trust, into the Multimanager Aggressive Equity Portfolio, a newly created series of EQ Advisors Trust (“EQ Trust”).

2. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Technology Portfolio, a series of VIP Trust, into the Multimanager Technology Portfolio, a newly created series of EQ Trust.

3. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Core Bond Portfolio, a series of VIP Trust, into the Multimanager Core Bond Portfolio, a newly created series of EQ Trust.

4. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Mid Cap Growth Portfolio, a series of VIP Trust, into the Multimanager Mid Cap Growth Portfolio, a newly created series of EQ Trust.

5. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Mid Cap Value Portfolio, a series of VIP Trust, into the Multimanager Mid Cap Value Portfolio, a newly created series of EQ Trust.

6. To approve the Agreement and Plan of Reorganization and Termination adopted by the Board (the “Merger Plan”) with respect to the reorganization of the Multimanager Large Cap Core Equity Portfolio, a series of VIP Trust, into the EQ/Large Cap Core PLUS Portfolio, a series of EQ Trust.

7. To approve the Merger Plan with respect to the reorganization of the Multimanager Large Cap Value Portfolio, a series of VIP Trust, into the EQ/Large Cap Value PLUS Portfolio, a series of EQ Trust.

8. To approve the Merger Plan with respect to the reorganization of the Multimanager International Equity Portfolio, a series of VIP Trust, into the EQ/International Core PLUS Portfolio, a series of EQ Trust.

9. To transact other business that may properly come before the Meeting or any adjournments thereof.

The Board unanimously recommends that you vote in favor of the relevant proposal(s).

Please note that owners of variable life insurance policies and/or variable annuity contracts or certificates (the “Contractholders”) issued by AXA Equitable Life Insurance Company, MONY Life Insurance Company, MONY Life Insurance Company of America or another insurance company (each, an “Insurance Company”) who have invested in shares of one or more of the Acquired Portfolios through the investment divisions of a separate account or accounts of an Insurance Company will be given the opportunity, to the extent required by law, to provide the applicable Insurance Company with voting instructions on the above proposals.

You should read the Combined Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote and the Contractholders entitled to provide voting instructions at the Meeting and any adjournments or postponements thereof has been fixed as the close of business on February 28, 2014. If you attend the Meeting, you may vote or provide your voting instructions in person.

ii

YOUR VOTE IS IMPORTANT

Please return your proxy or voting instruction card promptly

Regardless of whether you plan to attend the Meeting, you should vote or provide voting instructions by promptly completing, dating, and signing the enclosed proxy or voting instruction card for the Portfolio in which you directly or indirectly own shares and returning it in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the 12-digit control number that appears on the enclosed proxy or voting instruction card and following the simple instructions. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The Board recommends that you vote or provide voting instructions to vote “FOR” the proposals.

By order of the Board,

Patricia Louie Vice President and Secretary |

Dated: , 2014

New York, New York

iii

AXA EQUITABLE LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY

MONY LIFE INSURANCE COMPANY OF AMERICA

CONTRACTHOLDER VOTING INSTRUCTIONS

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

MULTIMANAGER AGGRESSIVE EQUITY PORTFOLIO,

MULTIMANAGER TECHNOLOGY PORTFOLIO,

MULTIMANAGER CORE BOND PORTFOLIO,

MULTIMANAGER MID CAP GROWTH PORTFOLIO,

MULTIMANAGER MID CAP VALUE PORTFOLIO,

MULTIMANAGER LARGE CAP CORE EQUITY PORTFOLIO,

MULTIMANAGER LARGE CAP VALUE PORTFOLIO, AND

MULTIMANAGER INTERNATIONAL EQUITY PORTFOLIO,

EACH A SERIES OF AXA PREMIER VIP TRUST

TO BE HELD ON , 2014

Dated: , 2014

GENERAL

These Contractholder Voting Instructions are being furnished by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company (“MONY”), MONY Life Insurance Company of America (“MLOA”) or another insurance company (each, an “Insurance Company” and together, the “Insurance Companies”) to owners of their variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) who, as of February 28, 2014 (the “Record Date”), had net premiums or contributions allocated to the investment divisions of their separate account or accounts (the “Separate Accounts”) that are invested in shares of one or more of the following Portfolios:

| • | Multimanager Aggressive Equity Portfolio, |

| • | Multimanager Technology Portfolio, |

| • | Multimanager Core Bond Portfolio, |

| • | Multimanager Mid Cap Growth Portfolio, |

| • | Multimanager Mid Cap Value Portfolio, |

| • | Multimanager Large Cap Core Equity Portfolio, |

| • | Multimanager Large Cap Value Portfolio, and |

| • | Multimanager International Equity Portfolio (together, the “Acquired Portfolios”). |

Each Acquired Portfolio is a series of AXA Premier VIP Trust (“VIP Trust”), a Delaware statutory trust that is registered with the Securities and Exchange Commission as an open-end management investment company.

To the extent required by applicable law, each Insurance Company will offer Contractholders the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the Acquired Portfolios (the “Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposals (the “Proposals”) that will be considered at the Special Meeting of Shareholders of the Acquired Portfolios referred to in the preceding Notice and at any adjournments or postponements (the “Meeting”). The enclosed Combined Proxy Statement and Prospectus, which you should retain for future reference, sets forth concisely information about the proposed reorganizations involving the Acquired Portfolios and corresponding series of EQ Advisors Trust that a Contractholder should know before completing the enclosed voting instruction card.

AXA Equitable Financial Services Company, LLC, a wholly owned subsidiary of AXA Financial, Inc., is the parent company of each named Insurance Company other than MONY. AXA Financial, Inc. is a wholly owned subsidiary of AXA, a French insurance holding company. The principal executive offices of AXA Equitable Financial Services Company, LLC and AXA Financial, Inc. are located at 1290 Avenue of the Americas, New York, New York 10104. Protective Life Insurance Company is the parent company of MONY. The principal executive office of Protective Life Insurance Company is located at 2801 Highway 280 South, Birmingham, Alabama 35223.

These Contractholder Voting Instructions and the accompanying voting instruction card, together with the enclosed proxy materials, are being mailed to Contractholders on or about , 2014.

HOW TO INSTRUCT AN INSURANCE COMPANY

To instruct an Insurance Company as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contractholders are asked to promptly complete their voting instructions on the enclosed voting instruction card(s), sign and date the voting instruction card(s), and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contractholders also may provide voting instructions by telephone at 1-800-690-6903 or by Internet at our website at www.proxyvote.com.

If a voting instruction card is not marked to indicate voting instructions but is signed and timely returned, it will be treated as an instruction to vote the Shares in favor of the Proposal(s).

The number of Shares held in the investment division of a Separate Account corresponding to an Acquired Portfolio for which a Contractholder may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the corresponding Acquired Portfolio. Each whole share of an Acquired Portfolio is entitled to one vote as to each matter with respect to which it is entitled to vote and each fractional share is entitled to a

ii

proportionate fractional vote. At any time prior to an Insurance Company’s voting at the Meeting, a Contractholder may revoke his or her voting instructions with respect to that investment division by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and providing voting instructions in person at the Meeting.

HOW AN INSURANCE COMPANY WILL VOTE

An Insurance Company will vote the Shares for which it receives timely voting instructions from Contractholders in accordance with those instructions. Shares in each investment division of a Separate Account for which an Insurance Company receives a voting instruction card that is signed and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares “FOR” the applicable Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives no timely voting instructions from Contractholders, or that are attributable to amounts retained by an Insurance Company as surplus or seed money, will be voted by the applicable Insurance Company either “FOR” or “AGAINST” the applicable Proposals, or as an abstention, in the same proportion as the Shares for which Contractholders have provided voting instructions to the Insurance Company. As a result of such proportional voting by the Insurance Companies, it is possible that a small number of Contractholders could determine whether the Proposals are approved.

OTHER MATTERS

The Insurance Companies are not aware of any matters, other than the specified Proposals, to be acted on at the Meeting. If any other matters come before the Meeting, an Insurance Company will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by directors, officers and employees of AXA Equitable Funds Management Group, LLC, the investment manager of VIP Trust, or its affiliates as well as officers and agents of VIP Trust. The principal solicitation will be by mail but voting instructions may also be solicited by telephone, fax, personal interview, the Internet or other permissible means.

If the quorum necessary to transact business is not established or the vote required to approve a Proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments or postponements of the Meeting in accordance with applicable law to permit further solicitation of voting instructions. The persons named as proxies will vote in their discretion on any such adjournment or postponement.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign and date the voting instruction card and mail it in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-800-690-6903 or by Internet at our website at www.proxyvote.com.

iii

PROXY STATEMENT

for

Multimanager Aggressive Equity Portfolio,

Multimanager Technology Portfolio,

Multimanager Core Bond Portfolio,

Multimanager Mid Cap Growth Portfolio,

Multimanager Mid Cap Value Portfolio,

Multimanager Large Cap Core Equity Portfolio,

Multimanager Large Cap Value Portfolio, and

Multimanager International Equity Portfolio,

each a series of AXA Premier VIP Trust

and

PROSPECTUS

for

Multimanager Aggressive Equity Portfolio,

Multimanager Technology Portfolio,

Multimanager Core Bond Portfolio,

Multimanager Mid Cap Growth Portfolio,

Multimanager Mid Cap Value Portfolio,

EQ/Large Cap Core PLUS Portfolio,

EQ/Large Cap Value PLUS Portfolio, and

EQ/International Core PLUS Portfolio,

each a series of EQ Advisors Trust

Dated

, 2014

1290 Avenue of the Americas

New York, New York 10104

1-877-222-2144

This Combined Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being furnished to owners of variable life insurance policies and/or variable annuity contracts or certificates (the “Contracts”) (the “Contractholders”) issued by AXA Equitable Life Insurance Company (“AXA Equitable”), MONY Life Insurance Company, MONY Life Insurance Company of America or another insurance company (each, an “Insurance Company” and together, the “Insurance Companies”) who, as of

THE SECURITIES AND EXCHANGE COMMISSION AND THE COMMODITY FUTURES TRADING COMMISSION HAVE NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OF THIS PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

February 28, 2014, had net premiums or contributions allocated to the investment divisions of an Insurance Company’s separate account or accounts (the “Separate Accounts”) that are invested in shares of beneficial interest in one or more of the following Portfolios that are series of AXA Premier Trust (“VIP Trust”):

| • | Multimanager Aggressive Equity Portfolio, |

| • | Multimanager Technology Portfolio, |

| • | Multimanager Core Bond Portfolio, |

| • | Multimanager Mid Cap Growth Portfolio |

| • | Multimanager Mid Cap Value Portfolio, |

| • | Multimanager Large Cap Core Equity Portfolio, |

| • | Multimanager Large Cap Value Portfolio, and |

| • | Multimanager International Equity Portfolio. |

Each of the Multimanager Aggressive Equity, Multimanager Technology, Multimanager Core Bond, Multimanager Mid Cap Growth, Multimanager Mid Cap Value, Multimanager Large Cap Core Equity, Multimanager Large Cap Value, and Multimanager International Equity Portfolios that is a series of VIP Trust is referred to herein as an “Acquired Portfolio” and together as the “Acquired Portfolios.” Each Acquired Portfolio is a series of VIP Trust, an open-end management investment company registered with the Securities and Exchange Commission (“SEC”). This Proxy Statement/Prospectus also is being furnished to the Insurance Companies as the record owners of shares and to other shareholders that were invested in one or more of the Acquired Portfolios as of February 28, 2014. Contractholders are being provided the opportunity to instruct the applicable Insurance Company to approve or disapprove the proposals contained in this Proxy Statement/Prospectus in connection with the solicitation by the Board of Trustees of VIP Trust (“VIP Board”) of proxies to be used at the Special Meeting of Shareholders of the Acquired Portfolios to be held at 1290 Avenue of the Americas, New York, New York 10104, on May 21, 2014, at , Eastern time, or any adjournment or postponement thereof (the “Meeting”).

ii

The proposals described in this Proxy Statement/Prospectus are as follows:

| Proposal | Shareholders Entitled to Vote on the Proposal | |

| 1. To approve the Agreement and Plan of Reorganization and Termination between VIP Trust and EQ Advisors Trust (“EQ Trust”) (the “Shell Reorganization Plan”) with respect to the reorganization of the Multimanager Aggressive Equity Portfolio, a series of VIP Trust, into the Multimanager Aggressive Equity Portfolio, a newly created series of EQ Trust (the “New Multimanager Aggressive Equity Portfolio”). | Shareholders of the Multimanager Aggressive Equity Portfolio. | |

| 2. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Technology Portfolio, a series of VIP Trust, into the Multimanager Technology Portfolio, a newly created series of EQ Trust (the “New Multimanager Technology Portfolio”). | Shareholders of the Multimanager Technology Portfolio. | |

| 3. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Core Bond Portfolio, a series of VIP Trust, into the Multimanager Core Bond Portfolio, a newly created series of EQ Trust (the “New Multimanager Core Bond Portfolio”). | Shareholders of the Multimanager Core Bond Portfolio. | |

| 4. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Mid Cap Growth Portfolio, a series of VIP Trust, into the Multimanager Mid Cap Growth Portfolio, a newly created series of EQ Trust (the “New Multimanager Mid Cap Growth Portfolio”). | Shareholders of the Multimanager Mid Cap Growth Portfolio. | |

| 5. To approve the Shell Reorganization Plan with respect to the reorganization of the Multimanager Mid Cap Value Portfolio, a series of VIP Trust, into the Multimanager Mid Cap Value Portfolio, a newly created series of EQ Trust (the “New Multimanager Mid Cap Value Portfolio”). | Shareholders of the Multimanager Mid Cap Value Portfolio. | |

| 6. To approve the Agreement and Plan of Reorganization and Termination between VIP Trust and EQ Trust (the “Merger Plan”) with respect to the reorganization of the Multimanager Large Cap Core Equity Portfolio, a series of VIP Trust, into the EQ/Large Cap Core PLUS Portfolio, a series of EQ Trust. | Shareholders of the Multimanager Large Cap Core Equity Portfolio. | |

| 7. To approve the Merger Plan with respect to the reorganization of the Multimanager Large Cap Value Portfolio, a series of VIP Trust, into the EQ/Large Cap Value PLUS Portfolio, a series of EQ Trust. | Shareholders of the Multimanager Large Cap Value Portfolio. | |

| 8. To approve the Merger Plan with respect to the reorganization of the Multimanager International Equity Portfolio, a series of VIP Trust, into the EQ/International Core PLUS Portfolio, a series of EQ Trust. | Shareholders of the Multimanager International Equity Portfolio. |

iii

Each reorganization referred to in Proposals 1 – 8 above is referred to herein as a “Reorganization” and together as the “Reorganizations.” Each of the New Multimanager Aggressive Equity, New Multimanager Technology, New Multimanager Core Bond, New Multimanager Mid Cap Growth, New Multimanager Mid Cap Value, EQ/Large Cap Core PLUS, EQ/Large Cap Value PLUS, and EQ/International Core PLUS Portfolios is referred to herein as an “Acquiring Portfolio” and together as the “Acquiring Portfolios.” The Shell Reorganization Plan and Merger Plan are sometimes referred to herein as the “Reorganization Plans.”

Each Reorganization is intended to qualify for federal income tax purposes as a tax-free reorganization under section 368(a) of the Internal Revenue Code of 1986, as amended.

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the Proposals that you should know before voting or providing voting instructions. Additional information about EQ Trust has been filed with the SEC and is available upon oral or written request. This Proxy Statement/Prospectus is being provided to the Insurance Companies and mailed to Contractholders and other shareholders on or about , 2014. This Proxy Statement/Prospectus and a proxy or voting instruction card also will be available at www.proxyvote.com on or about , 2014. It is expected that one or more representatives of each Insurance Company will attend the Meeting in person or by proxy and will vote shares held by the Insurance Company in accordance with voting instructions received from its Contractholders and in accordance with voting procedures established by VIP Trust.

The Prospectus of VIP Trust, dated May 1, 2013, as supplemented, with respect to the Acquired Portfolios has been filed with the SEC (File Nos. 333-70754 and 811-10509) and is incorporated by reference into this Proxy Statement/Prospectus.

The Statement of Additional Information dated ___, 2014, relating to the Reorganizations has been filed with the SEC (File No. 333-___) and is incorporated by reference into this Proxy Statement/Prospectus.

The Annual Report to Shareholders of VIP Trust with respect to the Acquired Portfolios for the fiscal year ended December 31, 2013, has been filed with the SEC (File Nos. 333-70754 and 811-10509).

For a free copy of any of these documents, please call 1-877-522-5035 or write VIP Trust at the address above.

Because the New Multimanager Aggressive Equity, New Multimanager Technology, New Multimanager Core Bond, New Multimanager Mid Cap Growth, and New Multimanager Mid Cap Value Portfolios have not yet commenced operations as of the date of this Proxy Statement/Prospectus, no prospectus, statement of additional information, or annual report is available for these Portfolios at this time.

iv

For a free copy of any of the above documents, please call 1-877-522-5035 or write VIP Trust at the address above.

Each Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, each Trust must file certain reports and other information with the SEC. You can copy and review information about the Trusts at the SEC’s Public Reference Room in Washington, DC, and at certain of the following SEC Regional Offices: New York Regional Office, 3 World Financial Center, Suite 400, New York, New York 10281; Miami Regional Office, 801 Brickell Avenue, Suite 1800, Miami, Florida 33131; Chicago Regional Office, 175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604; Denver Regional Office, 1801 California Street, Suite 1500, Denver, Colorado 80202; Los Angeles Regional Office, 5670 Wilshire Boulevard, 11th Floor, Los Angeles, California 90036; Boston Regional Office, 33 Arch Street, 23rd Floor, Boston, MA 02110; Philadelphia Regional Office, The Mellon Independence Center, 701 Market Street, Philadelphia, PA 19106; Atlanta Regional Office, 3475 Lenox Road, N.E., Suite 1000, Atlanta, GA 30326; Fort Worth Regional Office, Burnett Plaza, Suite 1900, 801 Cherry Street, Unit 18, Fort Worth, TX 76102; Salt Lake Regional Office, 15 W. South Temple Street, Suite 1800, Salt Lake City, UT 84101; San Francisco Regional Office, 44 Montgomery Street, Suite 2600, San Francisco, CA 94104. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Reports and other information about the Trusts are available on the IDEA Database on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information from the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Washington, DC 20549, at prescribed rates.

v

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 7 | ||||

| 7 | ||||

| 8 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 8 | |||

| 11 | ||||

| 11 | ||||

| 13 | ||||

| 13 | ||||

| 17 | ||||

| 18 | ||||

| 19 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 19 | |||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 28 | ||||

| 29 | ||||

| 29 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 30 | |||

| 33 | ||||

| 33 | ||||

| 35 | ||||

| 35 |

vi

| 40 | ||||

| 41 | ||||

| 41 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 41 | |||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 46 | ||||

| 51 | ||||

| 52 | ||||

| 52 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 53 | |||

| 56 | ||||

| 56 | ||||

| 58 | ||||

| 58 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 65 | |||

| 68 | ||||

| 68 | ||||

| 70 | ||||

| 71 | ||||

| 75 | ||||

| 77 | ||||

| 77 | ||||

Comparison of Investment Objectives, Policies, and Strategies | 78 | |||

| 81 | ||||

| 81 | ||||

| 83 | ||||

| 84 |

vii

| 88 | ||||

| 90 | ||||

| 90 | ||||

Comparison of Investment Objectives, Policies and Strategies | 91 | |||

| 94 | ||||

| 94 | ||||

| 97 | ||||

| 98 | ||||

| 98 | ||||

| 100 | ||||

| 100 | ||||

Potential Benefits of the Reorganizations to FMG LLC and its Affiliates | 102 | |||

| 103 | ||||

| 109 | ||||

| 111 | ||||

| 112 | ||||

| 112 | ||||

| 112 | ||||

| 112 | ||||

| 115 | ||||

| 117 | ||||

| 117 | ||||

| 140 | ||||

| 143 | ||||

| 143 | ||||

Payments to Broker-Dealers and Other Financial Intermediaries | 143 | |||

| 144 | ||||

| 147 | ||||

| 149 | ||||

| 149 | ||||

| 150 | ||||

| 160 | ||||

| 160 | ||||

| 162 | ||||

| 162 | ||||

| 163 | ||||

| 163 | ||||

| A-1 | ||||

APPENDIX B — Merger Plan | B-1 | |||

| C-1 | ||||

| D-1 |

viii

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Reorganization Plans, copies of the forms of which are attached hereto as Appendix A and Appendix B.

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in one or more of the Acquired Portfolios as of February 28, 2014 to approve the Reorganization Plan (with respect to the Acquired Portfolio in which they are invested), whereby each Acquired Portfolio will be reorganized into the corresponding Acquiring Portfolio. (Each Acquired Portfolio and each Acquiring Portfolio is sometimes referred to herein as a “Portfolio.”)

Each Acquired Portfolio’s shares are divided into three classes, designated Class A, Class B, and Class K shares (the “Acquired Portfolio Shares”). Each Acquiring Portfolio’s shares also are divided into three classes, designated Class IA, Class IB, and Class K shares (the “Acquiring Portfolio Shares”). The rights and preferences of each class of Acquiring Portfolio Shares are substantially similar to the rights and preferences of the corresponding class of Acquired Portfolio Shares.

The Reorganization Plans provide, with respect to each Reorganization, for:

| • | the transfer of all of the assets of the Acquired Portfolio to the corresponding Acquiring Portfolio in exchange solely for Acquiring Portfolio Shares having an aggregate net asset value equal to the Acquired Portfolio’s net assets and the Acquiring Portfolio’s assumption of all the liabilities of the Acquired Portfolio; |

| • | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contractholders) of those Acquiring Portfolio Shares; and |

| • | the complete termination of the Acquired Portfolio. |

A comparison of the investment objective(s), policies, and strategies and principal risks of each Acquired Portfolio and its corresponding Acquiring Portfolio is included in “Comparison of Investment Objectives, Policies, and Strategies” and “Comparison of Principal Risk Factors” below. The Portfolios have identical distribution procedures, purchase procedures, exchange rights and redemption procedures, which are discussed in “Additional Information about the Acquiring Portfolios” below. Each Portfolio offers its shares to Separate Accounts and certain other eligible investors. Shares of each Portfolio are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of a Reorganization.

Subject to shareholder approval, each Reorganization is expected to be effective at the close of business on , 2014, or on a later date the Trusts decide upon (the

1

“Closing Date”). As a result of each Reorganization, each shareholder invested in shares of one or more of the Acquired Portfolios would become an owner of shares of the corresponding Acquiring Portfolio. Each such shareholder would hold, immediately after the Closing Date, Class IA, Class IB, or Class K shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class A, Class B, or Class K Acquired Portfolio Shares, as applicable, that were held by the shareholder as of the Closing Date. Similarly, each Contractholder whose Contract values are invested in shares of one or more of the Acquired Portfolios would become an indirect owner of shares of the corresponding Acquiring Portfolio. Each such Contractholder would indirectly hold, immediately after the Closing Date, Class IA, Class IB, or Class K shares of the applicable Acquiring Portfolio having an aggregate value equal to the aggregate value of the Class A, Class B, or Class K Acquired Portfolio Shares, as applicable, that were indirectly held by the Contractholder as of the Closing Date. The consummation of any one Reorganization is not contingent on the consummation of any other Reorganization. VIP Trust believes that there will be no adverse tax consequences to shareholders or Contractholders as a direct result of the Reorganizations. Please see “Additional Information about the Reorganizations — Federal Income Tax Consequences of the Reorganizations” below for further information.

The VIP Board has unanimously approved each Reorganization Plan with respect to the Acquired Portfolios involved therein. Accordingly, the VIP Board is submitting the Reorganization Plans for approval by the respective Acquired Portfolio’s shareholders. In considering whether to approve a proposal (a “Proposal”), you should review the Proposal for the Acquired Portfolio(s) in which you were a direct or indirect holder on the Record Date (as defined under “Voting Information”). In addition, you should review the information in this Proxy Statement/Prospectus that relates to all of the Proposals and the Reorganization Plans generally. The VIP Board recommends that you vote “FOR” the Proposals to approve the Reorganization Plans.

PROPOSAL 1: APPROVAL OF THE SHELL REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE MULTIMANAGER AGGRESSIVE EQUITY PORTFOLIO INTO THE NEW MULTIMANAGER AGGRESSIVE EQUITY PORTFOLIO, A NEWLY CREATED SERIES OF EQ TRUST.

This Proposal 1 requests your approval of the Shell Reorganization Plan, pursuant to which the Multimanager Aggressive Equity Portfolio will be reorganized into the New Multimanager Aggressive Equity Portfolio.

In considering whether you should approve this Proposal, you should note that:

| • | The New Multimanager Aggressive Equity Portfolio is newly organized and has no assets, operating history, or performance information of its own as of the date of this Proxy Statement/Prospectus. The New Multimanager Aggressive Equity Portfolio has been created as a shell series of EQ Trust solely for the purposes of acquiring the Multimanager Aggressive Equity Portfolio’s |

2

assets and continuing its business investment operations, and will not conduct any investment operations until after the closing of the Reorganization. If shareholders of the Multimanager Aggressive Equity Portfolio approve its Reorganization, the New Multimanager Aggressive Equity Portfolio will assume and publish the operating history and performance record of the Multimanager Aggressive Equity Portfolio. |

| • | The New Multimanager Aggressive Equity Portfolio and the Multimanager Aggressive Equity Portfolio have substantially identical investment objectives, policies, and strategies. Each Portfolio seeks to achieve long-term growth of capital by investing primarily in the securities of large-capitalization growth companies. In addition, each Portfolio’s assets are allocated among three or more investment sub-advisers (each, an “Adviser”), each of which manages its portion of the Portfolio using a different but complementary investment strategy. A portion or portions of each Portfolio are actively managed by an Adviser (the “Active Allocated Portion” or the “Active Allocated Portions”) and a portion of each Portfolio seeks to track the performance of the Russell 3000® Growth Index (the “Index Allocated Portion”). There are, however, differences in the Portfolios’ primary investment policies and strategies of which you should be aware. |

The primary difference between the two Portfolios is that FMG LLC currently may limit the equity exposure of the Multimanager Aggressive Equity Portfolio at times when market volatility is increasing above specific thresholds by reducing investments in securities, shorting or selling long futures and options positions on an index, increasing cash levels, and/or shorting and index. FMG LLC will not employ this volatility management strategy in managing the New Multimanager Aggressive Equity Portfolio. However, it is anticipated that the Multimanager Aggressive Equity Portfolio will discontinue using this strategy effective on or before April 30, 2014, and therefore at the time of the Reorganization it is expected that the investment objectives, policies, and strategies of each Portfolio will be identical. For a detailed comparison of the Portfolios’ investment policies and strategies, see “Comparison of Investment Objectives, Policies, and Strategies” below.

| • | The Portfolios have substantially similar risk profiles, although there are differences of which you should be aware. Each Portfolio’s principal risks include equity risk, foreign securities risk, and large-cap company risk. However, because it currently employs the volatility management strategy described above, the Multimanager Aggressive Equity Portfolio also is subject to cash management risk, custom benchmark risk, derivatives risk, futures contract risk, leverage risk, short position risk, and volatility management risk as principal risks, which are not principal risks of the New Multimanager Aggressive Equity Portfolio. For a detailed comparison of each Portfolio’s risks, see “Comparison of Principal Risk Factors” below. |

3

| • | FMG LLC (the “Manager”) serves as the investment manager and administrator for the Multimanager Aggressive Equity Portfolio and will serve as the investment manager and administrator for the New Multimanager Aggressive Equity Portfolio after the Reorganization. FMG LLC has received an exemptive order from the SEC that generally permits FMG LLC and each Trust’s Board of Trustees to appoint, dismiss and replace each Portfolio’s Adviser(s) and to amend the advisory agreements between FMG LLC and the Advisers without obtaining shareholder approval (except with respect to Affiliated Advisers (as defined herein)). FMG LLC has appointed six Advisers to manage distinct portions of the assets of the Multimanager Aggressive Equity Portfolio. In particular, AllianceBernstein L.P., which is responsible for the management of the Index Allocated Portion of the Multimanager Aggressive Equity Portfolio, and ClearBridge Investments, LLC, Scotia Institutional Asset Management US, Ltd., Marsico Capital Management, LLC, T. Rowe Price Associates, Inc., and Westfield Capital Management Company, L.P., which are responsible for the management of portions of the Active Allocated Portion of the Multimanager Aggressive Equity Portfolio, currently serve as Advisers to the Multimanager Aggressive Equity Portfolio, and it is anticipated that they will also serve as Advisers to the New Multimanager Aggressive Equity Portfolio after the Reorganization. For a detailed description of the Manager and the Advisers, please see “Additional Information about the Acquiring Portfolios — The Manager” and “ — The Advisers” below. |

| • | Class A shareholders of the Multimanager Aggressive Equity Portfolio will receive Class IA shares of the New Multimanager Aggressive Equity Portfolio, Class B shareholders of the Multimanager Aggressive Equity Portfolio will receive Class IB shares of the New Multimanager Aggressive Equity Portfolio, and Class K shareholders of the Multimanager Aggressive Equity Portfolio will receive Class K shares of the New Multimanager Aggressive Equity Portfolio pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganizations” and “Additional Information about the Acquiring Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the New Multimanager Aggressive Equity Portfolio’s Class IA, Class IB, and Class K shares, for the fiscal year following the Reorganization, will be lower than those of the Multimanager Aggressive Equity Portfolio’s Class A, Class B, and Class K shares, respectively, for the fiscal year ended December 31, 2013. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

4

| • | The maximum management fee for the Multimanager Aggressive Equity Portfolio is equal to an annual rate of 0.600% of its average daily net assets, while the maximum management fee for the New Multimanager Aggressive Equity Portfolio is equal to an annual rate of 0.580% of its average daily net assets. The management fee schedule for the Multimanager Aggressive Equity Portfolio is equal to an annual rate of 0.600% of the Portfolio’s average daily net assets up to and including $750 million, 0.550% of the Portfolio’s average daily net assets in excess of $750 million and up to and including $1.75 billion, 0.525% of the Portfolio’s average daily net assets in excess of $1.75 billion and up to and including $4.75 billion, 0.500% of the Portfolio’s average daily net assets in excess of $4.75 billion and up to and including $9.75 billion, and 0.475% of the Portfolio’s average daily net assets thereafter. The management fee schedule for the New Multimanager Aggressive Equity Portfolio is equal to an annual rate of 0.580% of the Portfolio’s average daily net assets up to and including $2 billion, 0.550% of the Portfolio’s average daily net assets in excess of $2 billion and up to and including $3 billion, 0.525% of the Portfolio’s average daily net assets in excess of $3 billion and up to and including $6 billion, 0.500% of the Portfolio’s average daily net assets in excess of $6 billion and up to and including $11 billion, and 0.475% of the Portfolio’s average daily net assets thereafter. |

| • | The administration fee schedule for the Multimanager Aggressive Equity Portfolio is equal to its proportionate share of an asset-based administration fee for the Multimanager Aggressive Equity Portfolio and certain other of VIP Trust’s multi-adviser portfolios, which is equal to an annual rate of 0.15% of these portfolios’ total average daily net assets up to and including $15 billion; 0.125% of these portfolios’ total average daily net assets in excess of $15 billion up to and including $30 billion; and 0.100% of these portfolios’ total average daily net assets in excess of $30 billion, plus an annual flat fee of $32,500 if the Multimanager Aggressive Equity Portfolio’s total average net assets are less than $5 billion. The administration fee schedule for the New Multimanager Aggressive Equity Portfolio is equal to its proportionate share of an asset-based administration fee for the New Multimanager Aggressive Equity Portfolio and certain other of EQ Trust’s portfolios, which is equal to an annual rate of 0.15% of these portfolios’ aggregate average daily net assets up to and including $20 billion; 0.110% of these portfolios’ aggregate average daily net assets in excess of $20 billion up to and including $25 billion; and 0.100% of these portfolios’ aggregate average daily net assets in excess of $25 billion, plus an annual flat fee of $32,500 if the New Multimanager Aggressive Equity Portfolio’s total average net assets are less than $5 billion. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

5

| • | Following the Reorganization, the combined Portfolio will be managed in accordance with the investment objective, policies, and strategies of the New Multimanager Aggressive Equity Portfolio. It is not expected that the New Multimanager Aggressive Equity Portfolio will revise any of its investment policies following the Reorganization to reflect those of the Multimanager Aggressive Equity Portfolio. FMG LLC has reviewed the Multimanager Aggressive Equity Portfolio’s investment objective, policies, and strategies and determined that they are substantially similar to the New Multimanager Aggressive Equity Portfolio’s investment objective, policies, and strategies. Thus, FMG LLC believes that, if the Reorganization is approved, a substantial portion of the Multimanager Aggressive Equity Portfolio’s holdings could be transferred to and held by the New Multimanager Aggressive Equity Portfolio. However, it is expected that some of those holdings may not remain at the time of the Reorganization due to normal portfolio turnover. It is also expected that, if the Reorganization is approved, the Multimanager Aggressive Equity Portfolio’s holdings that are not compatible with the New Multimanager Aggressive Equity Portfolio’s investment objective, policies, and strategies will be liquidated in an orderly manner in connection with the Reorganization, and the proceeds of these sales held in temporary investments or reinvested in assets that are consistent with those investment objective, policies, and strategies. The portion of the Multimanager Aggressive Equity Portfolio’s assets that will be liquidated in connection with the Reorganization will depend on market conditions and on the assessment by the Manager and the New Multimanager Aggressive Equity Portfolio’s Advisers of the compatibility of those holdings with the New Multimanager Aggressive Equity Portfolio’s anticipated portfolio composition and investment objective, policies, and strategies at the time of the Reorganization. The need for the Portfolio to sell investments in connection with the Reorganization may result in its selling securities at a disadvantageous time and price and could result in it realizing gains (or losses) that would not otherwise have been realized and incurring transaction costs that would not otherwise have been incurred. |

| • | The New Multimanager Aggressive Equity Portfolio will bear its proportionate share (based on the fraction that the shareholder accounts of the Multimanager Aggressive Equity Portfolio bears to the aggregate shareholder accounts of all Acquired Portfolios covered by the Shell Reorganization Plan, i.e., those mentioned below, at the Valuation Time) of 50% of the first $300,000 of the expenses of the Reorganizations of the Multimanager Aggressive Equity, Multimanager Technology, Multimanager Core Bond, Multimanager Mid Cap Growth, and Multimanager Mid Cap Value Portfolios, subject to an aggregate maximum of $150,000 for these Portfolios. FMG LLC generally will bear the expenses of the Reorganizations of these Portfolios in excess of this amount, subject to certain limitations. For additional information, please refer to “Additional Information About the Reorganizations — Terms of the Reorganization Plans” below. |

6

Comparative Fee and Expense Tables

The following tables show the fees and expenses of each class of shares of the Multimanager Aggressive Equity Portfolio and the estimated pro forma fees and expenses of each class of shares of the Acquiring Portfolio after giving effect to the proposed Reorganization. The Acquiring Portfolio is newly organized and has not had any operations of its own to date. Fees and expenses for the Multimanager Aggressive Equity Portfolio are based on those incurred by each class of its shares for the fiscal year ended December 31, 2013. The pro forma fees and expenses of the Acquiring Portfolio Shares assume that the Reorganization has been in effect for the year ended December 31, 2013. The tables below do not reflect any Contract-related fees and expenses, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

Shareholder Fees

(fees paid directly from your investment)

Multimanager Aggressive | Pro Forma New Multimanager Aggressive Equity Portfolio (assuming the Reorganization is approved) | |||

Not applicable. | Not applicable. |

Annual Operating Expenses

(expenses that you may pay each year as a percentage of the value of your investment)

| Multimanager Aggressive Equity Portfolio | Pro Forma New Multimanager Aggressive Equity Portfolio (assuming the Reorganization is approved) | |||||||||||||||||||||||

| Class A | Class B | Class K | Class IA | Class IB | Class K | |||||||||||||||||||

Management Fee | 0.58 | % | 0.58 | % | 0.58 | % | 0.58 | % | 0.58 | % | 0.58 | % | ||||||||||||

Distribution and/or Service | 0.25 | % | 0.25 | % | None | 0.25 | % | 0.25 | % | None | ||||||||||||||

Other Expenses | 0.20 | % | 0.20 | % | 0.20 | % | 0.18 | % | 0.18 | % | 0.18 | % | ||||||||||||

Total Annual Portfolio Operating Expenses | 1.03 | % | 1.03 | % | 0.78 | % | 1.01 | % | 1.01 | % | 0.76 | % | ||||||||||||

This example is intended to help you compare the costs of investing in the Portfolios with the cost of investing in other investment options. The example assumes that:

| • | You invest $10,000 in a Portfolio for the time periods indicated; |

| • | Your investment has a 5% return each year; and |

| • | The Portfolio’s operating expenses remain the same. |

7

This example does not reflect any Contract-related fees and expenses, including redemption fees (if any) at the Contract level. If such fees and expenses were reflected, the total expenses would be higher. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

Multimanager Aggressive Equity Portfolio | ||||||||||||||||

Class A | $ | 105 | $ | 328 | $ | 569 | $ | 1,259 | ||||||||

Class B | $ | 105 | $ | 328 | $ | 569 | $ | 1,259 | ||||||||

Class K | $ | 80 | $ | 249 | $ | 433 | $ | 966 | ||||||||

Pro Forma New Multimanager Aggressive Equity Portfolio (assuming the Reorganization is approved) | ||||||||||||||||

Class IA | $ | 103 | $ | 322 | $ | 558 | $ | 1,236 | ||||||||

Class IB | $ | 103 | $ | 322 | $ | 558 | $ | 1,236 | ||||||||

Class K | $ | 80 | $ | 249 | $ | 483 | $ | 966 | ||||||||

Each Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect a Portfolio’s performance. During the fiscal year ended December 31, 2013, the portfolio turnover rate for the Multimanager Aggressive Equity Portfolio was 72% of the average value of the Portfolio. The New Multimanager Aggressive Equity Portfolio has not yet commenced operations and therefore, the New Multimanager Aggressive Equity Portfolio does not have a portfolio turnover rate to report.

Comparison of Investment Objectives, Policies, and Strategies

The following table compares the investment objectives and principal investment policies and strategies of the Multimanager Aggressive Equity Portfolio with those of the New Multimanager Aggressive Equity Portfolio. Each Trust’s Board may change the investment objective of a Portfolio without a vote of the Portfolio’s shareholders. For more detailed information about each Portfolio’s investment strategies and risks, see Appendix C.

| Acquiring Portfolio | Acquired Portfolio | |||

New Multimanager Aggressive Equity Portfolio | Multimanager Aggressive Equity Portfolio | |||

Investment Objective | Seeks to achieve long-term growth of capital. | Seeks to achieve long-term growth of capital with an emphasis on risk-adjusted returns and managing volatility in the Portfolio. However, effective on or before April 30, 2014, the investment objective of this Portfolio will be changed so that it is identical to the investment objective of the Acquiring Portfolio. |

8

| Acquiring Portfolio | Acquired Portfolio | |||

New Multimanager Aggressive Equity Portfolio | Multimanager Aggressive Equity Portfolio | |||

Principal Investment Strategies | Under normal circumstances, the Portfolio intends to invest at least 80% of its net assets, plus borrowings for investment purposes, in equity securities. For purposes of this Portfolio, equity securities shall include common stocks, preferred stocks, and other equity securities, and financial instruments that derive their value from such securities. The Portfolio invests primarily in securities of large capitalization growth companies. For purposes of this Portfolio, large capitalization companies are companies with market capitalization within the range of the Russell 3000® Growth Index at the time of investment (market capitalization range of approximately $27.9 million to $500.5 billion as of December 31, 2012). The Portfolio intends to invest primarily in common stocks, but may also invest in other equity securities that an Adviser believes provide opportunities for capital growth. The size of companies in the Russell 3000® Growth Index changes with market conditions, which can result in changes to the market capitalization range of companies in the index. | Same. | ||

The Manager will generally allocate the Portfolio’s assets among three or more Advisers, each of which will manage its portion of the Portfolio using different yet complementary investment strategies. Under normal circumstances, one portion of the Portfolio is an Index Allocated Portion and the other portions of the Portfolio will be Active Allocated Portions.

Under normal circumstances, the Manager anticipates allocating approximately 50% of the Portfolio’s net assets to the Index Allocated Portion and the remaining 50% of net assets among the Active Allocated Portions. These percentages are targets established by the Manager and actual allocations between the portions may deviate from these targets by up to 20% of the Portfolio’s net assets. | Same. |

9

| Acquiring Portfolio | Acquired Portfolio | |||

New Multimanager Aggressive Equity Portfolio | Multimanager Aggressive Equity Portfolio | |||

| The Index Allocated Portion of the Portfolio seeks to track the performance (before fees and expenses) of the Russell 3000® Growth Index with minimal tracking error. This strategy is commonly referred to as an indexing strategy. Generally, the Index Allocated Portion utilizes a stratified sampling construction process in which the Index Allocated Portion invests in a subset of the companies represented in the Russell 3000® Growth Index based on the Adviser’s analysis of key risk factors and characteristics. Such factors and characteristics include industry weightings, market capitalizations, return variability and yield. | Same. | |||

| No corresponding strategy. | The Manager also may utilize futures and options, such as exchange traded futures and options contracts on securities indices, to manage equity exposure. When market volatility is increasing above specific thresholds set for the Portfolio, the Manager may limit equity exposure either by reducing investments in securities, shorting or selling long futures and options positions on an index, increasing cash levels, and/or shorting an index. However, effective on or before April 30, 2014, the Portfolio will no longer utilize this strategy. | |||

No corresponding strategy. | The Portfolio may invest up to 25% of its assets in derivatives. It is anticipated that the Portfolio’s derivative instruments will consist primarily of exchange-traded futures and options contracts on securities indices, but the Portfolio also may utilize other types of derivatives. The Portfolio may maintain a significant percentage of its assets in cash and cash equivalent instruments, some of which may serve as margin or collateral for the Portfolio’s obligations under derivative transactions. However, effective on or before April 30, 2014, the Portfolio will no longer utilize this strategy. |

10

| Acquiring Portfolio | Acquired Portfolio | |||

New Multimanager Aggressive Equity Portfolio | Multimanager Aggressive Equity Portfolio | |||

| Each Active Allocated Portion invests primarily in equity securities of companies whose above-average prospective earnings growth is not fully reflected, in the view of the Adviser, in current market valuations. The Active Allocated Portions may invest up to 25% of their total assets in securities of foreign companies, including companies based in developing countries. An Adviser may sell a security for a variety of reasons, such as to make other investments believed by an Adviser to offer superior investment opportunities. | Same. |

Comparison of Principal Risk Factors

An investment in a Portfolio is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money by investing in a Portfolio. The following table compares the principal risks of an investment in each Portfolio. For an explanation of each such risk, see “Additional Information about the Reorganizations — Description of Risk Factors” below.

Risks | New Multimanager Aggressive Equity Portfolio | Multimanager Aggressive Equity Portfolio | ||||||

Cash Management Risk | X | |||||||

Currency Risk | X | X | ||||||

Custom Benchmark Risk | X | |||||||

Derivatives Risk | X | |||||||

Emerging Markets Risk | X | X | ||||||

Equity Risk | X | X | ||||||

Foreign Securities Risk | X | X | ||||||

Futures Contract Risk | X | |||||||

Index Strategy Risk | X | X | ||||||

Large-Cap Company Risk | X | X | ||||||

Leverage Risk | X | |||||||

Mid-Cap and Small-Cap Company Risk | X | X | ||||||

Short Position Risk | X | |||||||

Volatility Management Risk | X | |||||||

Comparative Performance Information

The Acquiring Portfolio is newly organized and has no assets, operating history or performance information of its own as of the date of this Proxy Statement/Prospectus. After the Reorganization, which is subject to shareholder approval, the Acquiring Portfolio, as the successor to the Acquired Portfolio, will assume and publish the operating history and performance record of the Class A, Class B, and Class K shares of the Acquired Portfolio.

11

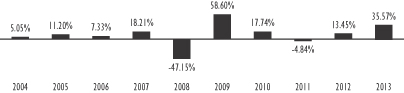

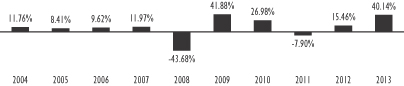

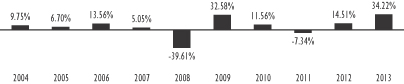

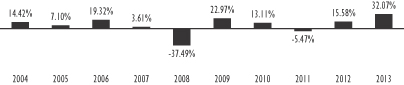

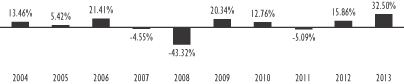

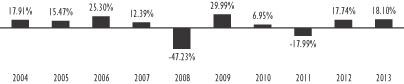

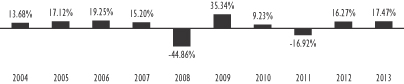

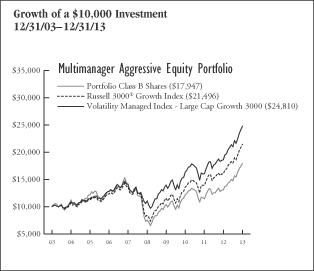

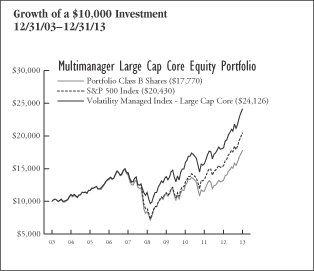

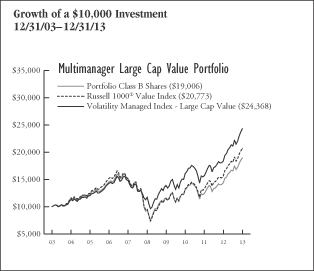

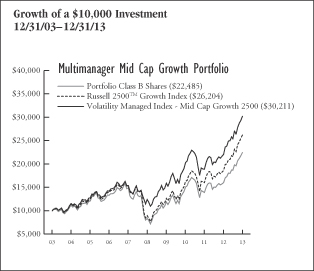

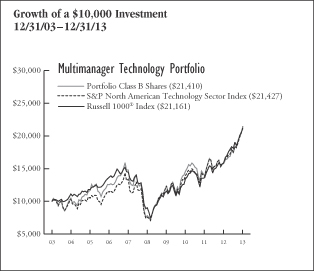

The bar charts and tables below provide some indication of the risks of investing in the Multimanager Aggressive Equity Portfolio by showing changes in the Portfolio’s performance from year to year and by showing how the Portfolio’s average annual total returns for the past one year, five years and since inception through December 31, 2013 compared to the returns of a broad-based market index. The additional broad-based market index shows how the Multimanager Aggressive Equity Portfolio’s performance compared with the returns of a volatility managed index. Past performance is not an indication of future performance.

The performance results do not reflect any Contract-related fees and expenses, which would reduce the performance results.

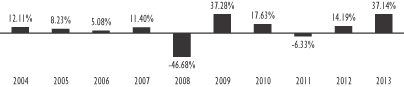

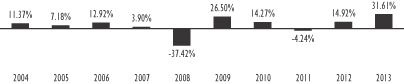

Multimanager Aggressive Equity Portfolio - Calendar Year Total Returns (Class B)

Best Quarter (% and time period) 17.70% (2009 2nd Quarter) | Worst Quarter (% and time period) -25.44% (2008 4th Quarter) | |||||||||||||||||

Multimanager Aggressive Equity Portfolio

Average Annual Total Returns | One Year | Five Years | Ten Years/ Since Inception | |||||||||

Multimanager Aggressive Equity Portfolio — Class A | 37.21% | 19.02% | 6.24% | |||||||||

Multimanager Aggressive Equity Portfolio — Class B | 37.14% | 18.83% | 6.02% | |||||||||

Multimanager Aggressive Equity Portfolio — Class K (Inception Date: August 26, 2011) | 37.55% | N/A | 22.96% | |||||||||

Russell 3000® Growth Index* | 34.23% | 20.56% | 7.95% | |||||||||

Volatility Managed Index — Large Cap Growth 3000** | 33.31% | 17.56% | 9.51% | |||||||||

| * | Russell 3000® Growth Index measures the performance of those Russell 3000® Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. |

| ** | The Volatility Managed Index — Large Cap Growth 3000 is an index that applies a formula to a blend of the S&P 500 Index and the Russell 3000® Growth Index adjusting the equity exposure of the S&P 500 Index when certain volatility levels are reached. The S&P 500 Index is a weighted index of common stocks of 500 leading companies in leading industries of the U.S. economy, capturing 75% coverage of U.S. equities. The S&P 500 Index is capitalization weighted, thereby giving greater weight to companies with the largest market capitalizations. |

12

The following table shows the capitalization of the Multimanager Aggressive Equity Portfolio as of December 31, 2013, and the Acquiring Portfolio on a pro forma combined basis as of December 31, 2013, after giving effect to the proposed Reorganization. The Acquiring Portfolio is newly organized and did not have any operations of its own as of the date of this Proxy Statement/Prospectus. Pro forma net assets may not total and net asset values per share may not recalculate due to rounding of net assets.

| Net Assets (in millions) | Net Asset Value Per Share | Shares Outstanding | ||||||||||

Multimanager Aggressive Equity Portfolio — Class A | $ | 1,029.1 | $ | 39.98 | 27,742,251 | |||||||

Adjustments | $ | — | $ | — | ||||||||

Pro forma New Multimanager Aggressive Equity Portfolio — Class IA | $ | 1,029.1 | $ | 39.98 | 27,742,251 | |||||||

Multimanager Aggressive Equity Portfolio — Class B | $ | 85.9 | $ | 39.25 | 2,188,065 | |||||||

Adjustments | $ | — | $ | — | ||||||||

Pro forma New Multimanager Aggressive Equity Portfolio — Class IB | $ | 85.9 | $ | 39.25 | 2,188,065 | |||||||

Multimanager Aggressive Equity Portfolio — Class K | $ | 8.2 | $ | 39.98 | 204,639 | |||||||

Adjustments | $ | — | $ | — | ||||||||

Pro Forma New Multimanager Aggressive Equity Portfolio — Class K | $ | 8.2 | $ | 39.98 | 204,639 | |||||||

AFTER CAREFUL CONSIDERATION, THE VIP BOARD UNANIMOUSLY APPROVED THE SHELL REORGANIZATION PLAN WITH RESPECT TO THE MULTIMANAGER AGGRESSIVE EQUITY PORTFOLIO. ACCORDINGLY, THE BOARD HAS SUBMITTED THE SHELL REORGANIZATION PLAN FOR APPROVAL BY THIS PORTFOLIO’S SHAREHOLDERS. THE BOARD RECOMMENDS THAT YOU VOTE “FOR” PROPOSAL 1.

PROPOSAL 2: APPROVAL OF THE SHELL REORGANIZATION PLAN WITH RESPECT TO THE REORGANIZATION OF THE MULTIMANAGER TECHNOLOGY PORTFOLIO INTO THE NEW MULTIMANAGER TECHNOLOGY PORTFOLIO, A NEWLY CREATED SERIES OF EQ TRUST.

This Proposal 2 requests your approval of the Shell Reorganization Plan, pursuant to which the Multimanager Technology Portfolio will be reorganized into the New Multimanager Technology Portfolio.

13

In considering whether you should approve this Proposal, you should note that:

| • | The New Multimanager Technology Portfolio is newly organized and has no assets, operating history, or performance information of its own as of the date of this Proxy Statement/Prospectus. The New Multimanager Technology Portfolio has been created as a shell series of EQ Trust solely for the purposes of acquiring the Multimanager Technology Portfolio’s assets and continuing its business investment operations, and will not conduct any investment operations until after the closing of the Reorganization. If shareholders of the Multimanager Technology Portfolio approve its Reorganization, the New Multimanager Technology Portfolio will assume and publish the operating history and performance record of the Multimanager Technology Portfolio. |

| • | The New Multimanager Technology Portfolio and the Multimanager Technology Portfolio have identical investment objectives, policies, and strategies. Each Portfolio intends to invest at least 80% of its net assets, plus borrowings for investment purposes, in equity securities of companies principally engaged in the technology sector. In addition, each Portfolio’s assets are allocated among three or more investment sub-advisers (each, an “Adviser”), each of which manages its portion of the Portfolio using a different but complementary investment strategy. A portion or portions of each Portfolio are actively managed by an Adviser (the “Active Allocated Portion” or the “Active Allocated Portions”); a portion of each Portfolio seeks to track the performance of the S&P North American Technology Sector Index (the “Index Allocated Portion”); and a portion of each Portfolio invests in exchange traded funds (“ETFs”) (the “ETF Allocated Portion”). For a detailed comparison of the Portfolios’ investment policies and strategies, see “Comparison of Investment Objectives, Policies, and Strategies” below. |

| • | The principal risks of the New Multimanager Technology Portfolio are the same as the principal risks of the Multimanager Technology Portfolio. Each Portfolio’s principal risks include equity risk, ETF risk, foreign securities risk, and technology sector risk. For a detailed comparison of each Portfolio’s principal risks, please see “Comparison of Principal Risk Factors” below. |

| • | FMG LLC (the “Manager”) serves as the investment manager and administrator for the Multimanager Technology Portfolio and will serve as the investment manager and administrator for the New Multimanager Technology Portfolio after the Reorganization. FMG LLC has received an exemptive order from the SEC that generally permits FMG LLC and each Trust’s Board of Trustees to appoint, dismiss and replace each Portfolio’s Adviser(s) and to amend the advisory agreements between FMG LLC and the Advisers without obtaining shareholder approval (except with respect to Affiliated Advisers (as defined herein)). FMG LLC has appointed three Advisers to manage distinct portions of the Multimanager Technology Portfolio. In particular, Allianz Global Investors U.S. LLC and Wellington Management Company, LLP, which are responsible for the management of portions of the Active Allocated |

14

Portion of the Multimanager Technology Portfolio, and SSgA Funds Management, Inc., which is responsible for the management of the Index Allocated Portion of the Multimanager Technology Portfolio, currently serve as Advisers to the Multimanager Technology Portfolio and it is anticipated that they will also serve as Advisers for the New Multimanager Technology Portfolio after the Reorganization. In addition, FMG LLC is responsible for the management of the ETF Allocated Portion of the Multimanager Technology Portfolio, and it is anticipated that it would also manage the ETF Allocated Portion of the New Multimanager Technology Portfolio after the Reorganization. For a detailed description of the Manager and the Advisers, please see “Additional Information about the Acquiring Portfolios — The Manager” and “ — The Advisers” below. |

| • | Class A shareholders of the Multimanager Technology Portfolio will receive Class IA shares of the New Multimanager Technology Portfolio, Class B shareholders of the Multimanager Technology Portfolio will receive Class IB shares of the New Multimanager Technology Portfolio, and Class K shareholders of the Multimanager Technology Portfolio will receive Class K Shares of the New Multimanager Technology Portfolio pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganizations” and “Additional Information about the Acquiring Portfolios” below for more information. |

| • | It is estimated that the annual operating expense ratios for the New Multimanager Technology Portfolio’s Class IA, Class IB, and Class K shares, for the fiscal year following the Reorganization, will be lower than those of the Multimanager Technology Portfolio’s Class A, Class B, and Class K shares, respectively, for the fiscal year ended December 31, 2013. For a more detailed comparison of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |

| • | The maximum management fee for each Portfolio is equal to an annual rate of 0.950% of its average daily net assets. The management fee schedule for the Multimanager Technology Portfolio is equal to an annual rate of 0.950% of the Portfolio’s average daily net assets up to and including $750 million, 0.900% of the Portfolio’s average daily net assets in excess of $750 million and up to and including $1.75 billion, 0.875% of the Portfolio’s average daily net assets in excess of $1.75 billion and up to and including $4.75 billion, 0.850% of the Portfolio’s average daily net assets in excess of $4.75 billion and up to and including $9.75 billion, and 0.825% of the Portfolio’s average daily net assets thereafter. The management fee schedule for the New Multimanager Technology Portfolio is equal to an annual rate of 0.950% of the Portfolio’s average daily net assets up to and including $2 billion, 0.900% of the Portfolio’s average daily net assets in excess of $2 billion and up to and |

15

including $3 billion, 0.875% of the Portfolio’s average daily net assets in excess of $3 billion and up to and including $6 billion, 0.850% of the Portfolio’s average daily net assets in excess of $6 billion and up to and including $11 billion, and 0.825% of the Portfolio’s average daily net assets thereafter. |

| • | The administration fee schedule for the Multimanager Technology Portfolio is equal to its proportionate share of an asset-based administration fee for the Multimanager Technology Portfolio and certain other of VIP Trust’s multi-adviser portfolios, which is equal to an annual rate of 0.15% of these portfolios’ total average daily net assets up to and including $15 billion; 0.125% of these portfolios’ total average daily net assets in excess of $15 billion up to and including $30 billion; and 0.100% of these portfolios’ total average daily net assets in excess of $30 billion, plus an annual flat fee of $32,500 if the Multimanager Technology Portfolio’s total average net assets are less than $5 billion. The administration fee schedule for the New Multimanager Technology Portfolio is equal to its proportionate share of an asset-based administration fee for the New Multimanager Technology Portfolio and certain other of EQ Trust’s portfolios, which is equal to an annual rate of 0.15% of these portfolios’ aggregate average daily net assets up to and including $20 billion; 0.110% of these portfolios’ aggregate average daily net assets in excess of $20 billion up to and including $25 billion; and 0.100% of these portfolios’ aggregate average daily net assets in excess of $25 billion, plus an annual flat fee of $32,500 if the New Multimanager Technology Portfolio’s total average net assets are less than $5 billion. For a more detailed description of the fees and expenses of the Portfolios, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Portfolios” below. |