UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| | |

Investment Company Act file number: | | 811-08587 |

Jennison 20/20 Focus Fund

|

| Exact name of registrant as specified in charter: |

| | |

Gateway Center 3, 100 Mulberry Street, Newark, New Jersey 07102 |

| Address of principal executive offices: |

Deborah A. Docs

Gateway Center 3,

100 Mulberry Street,

Newark, New Jersey 07102

|

| Name and address of agent for service: |

Registrant’s telephone number, including area code: 800-225-1852

Date of fiscal year end: 1/31/2009

Date of reporting period: 1/31/2009

Item 1 – Reports to Stockholders

| | |

| JANUARY 31, 2009 | | ANNUAL REPORT |

Jennison 20/20 Focus Fund

FUND TYPE

Large-capitalization stock

OBJECTIVE

Long-term growth of capital

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current prospectus.

The views expressed in this report and information about the Fund’s portfolio holdings are for the period covered by this report and are subject to change thereafter.

JennisonDryden, Jennison, Prudential Financial, and the Rock Prudential logo are registered service marks of The Prudential Insurance Company of America, Newark, NJ, and its affiliates.

March 16, 2009

Dear Shareholder:

We hope you find the annual report for the Jennison 20/20 Focus Fund informative and useful. Because market volatility climbed sharply in 2008, we understand that this is a difficult time to be an investor. While it is impossible to predict what the future holds, we continue to believe a prudent response to uncertainty is to maintain a diversified portfolio, including stock and bond mutual funds consistent with your tolerance for risk, time horizon, and financial goals.

A diversified asset allocation offers two potential advantages: it limits your exposure to any particular asset class, plus it provides a better opportunity to invest some of your assets in the right place at the right time. Your financial professional can help you create a diversified investment plan that may include mutual funds covering all the basic asset classes and that reflects your personal investor profile and risk tolerance. Keep in mind that diversification and asset allocation strategies do not assure a profit or protect against loss in declining markets.

JennisonDryden Mutual Funds give you a wide range of choices that can help you make progress toward your financial goals. Our funds offer the experience, resources, and professional discipline of four leading asset managers. JennisonDryden equity funds are advised by Jennison Associates LLC, Quantitative Management Associates LLC (QMA), or PREI® (Prudential Real Estate Investors). Prudential Investment Management, Inc. (PIM) advises the JennisonDryden fixed income and money market funds through its unit Prudential Fixed Income Management. Jennison Associates, QMA, and PIM are registered investment advisers and Prudential Financial companies. PREI is a unit of PIM.

Thank you for choosing JennisonDryden Mutual Funds.

Sincerely,

Judy A. Rice, President

Jennison 20/20 Focus Fund

| | |

| Jennison 20/20 Focus Fund | | 1 |

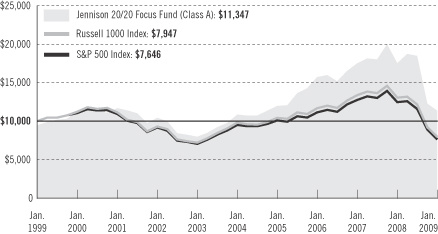

Your Fund’s Performance

Fund objective

The investment objective of the Jennison 20/20 Focus Fund is long-term growth of capital. There can be no assurance that the Fund will achieve its investment objective.

Performance data quoted represent past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the past performance data quoted. An investor may obtain performance data as of the most recent month-end by visiting our website at www.jennisondryden.com or by calling (800) 225-1852. The maximum initial sales charge is 5.50% (Class A shares). Gross operating expenses: Class A, 1.23%; Class B, 1.93%; Class C, 1.93%; Class R, 1.68%; Class Z, 0.93%. Net operating expenses apply to: Class A, 1.21%; Class B, 1.93%; Class C, 1.93%; Class R, 1.43%; Class Z, 0.93%, after contractual reduction through 5/31/2008 for Class A and through 5/31/2010 for Class R.

| | | | | | | | | | | |

| Cumulative Total Returns as of 1/31/09 | | | | | | | | | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception1 |

Class A | | –35.16 | % | | 4.88 | % | | 20.07 | % | | — |

Class B | | –35.68 | | | 0.93 | | | 11.30 | | | — |

Class C | | –35.60 | | | 1.04 | | | 11.42 | | | — |

Class R | | –35.24 | | | N/A | | | N/A | | | 2.50% (6/14/04) |

Class Z | | –34.98 | | | 6.11 | | | 22.96 | | | — |

Russell 1000® Index2 | | –39.04 | | | –18.69 | | | –20.53 | | | ** |

S&P 500 Index3 | | –38.63 | | | –19.52 | | | –23.54 | | | *** |

Lipper Multi-Cap Core Funds Avg.4 | | –39.09 | | | –19.97 | | | 1.25 | | | **** |

Lipper Large-Cap Core Funds Avg.5 | | –38.14 | | | –20.73 | | | –22.22 | | | ***** |

| | | | | | | | | | | |

| Average Annual Total Returns6 as of 12/31/08 | | | | | | |

| | | One Year | | | Five Years | | | Ten Years | | | Since Inception1 |

Class A | | –43.12 | % | | 0.23 | % | | 1.79 | % | | — |

Class B | | –43.31 | | | 0.43 | | | 1.59 | | | — |

Class C | | –40.86 | | | 0.61 | | | 1.60 | | | — |

Class R | | –39.97 | | | N/A | | | N/A | | | 0.52% (6/14/04) |

Class Z | | –39.65 | | | 1.62 | | | 2.62 | | | — |

Russell 1000® Index2 | | –37.60 | | | –2.04 | | | –1.09 | | | ** |

S&P 500 Index3 | | –36.99 | | | –2.19 | | | –1.38 | | | *** |

Lipper Multi-Cap Core Funds Avg.4 | | –38.79 | | | –2.61 | | | 0.82 | | | **** |

Lipper Large-Cap Core Funds Avg.5 | | –37.23 | | | –2.88 | | | –1.72 | | | ***** |

The 0.05% contractual reduction applicable to the Class A distribution and service (12b-1) fees expired as of May 31, 2008. After May 31, 2008, the distribution and service (12b-1) fees are 0.30% of 1% of the average daily net assets of the Class A shares.

| | |

| 2 | | Visit our website at www.jennisondryden.com |

The cumulative total returns do not reflect the deduction of applicable sales charges. If reflected, the applicable sales charges would reduce the cumulative total returns performance quoted. Class A shares are subject to a maximum front-end sales charge of 5.50%. Under certain circumstances, Class A shares may be subject to a contingent deferred sales charge (CDSC) of 1%. Class B and Class C shares are subject to a maximum CDSC of 5% and 1%, respectively. Class R and Class Z shares are not subject to a sales charge.

Source: Prudential Investments LLC and Lipper Inc. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of such fee waivers and/or expense reimbursements, total returns would be lower.

1Inception date returns are provided for any share class with less than 10 calendar years of returns.

2The Russell 1000 Index is an unmanaged index that consists of the stocks of the 1,000 largest firms in the Russell 3000® Index, an index that represents approximately 98% of the U.S. market.

3The Standard & Poor’s 500 Composite Stock Price Index (S&P 500 Index) is an unmanaged index of 500 stocks of large U.S. public companies. It gives an indication of how stock prices in the United States have performed.

4The Lipper Multi-Cap Core Funds Average (Lipper Average) represents returns based on the average return of all funds in the Lipper Multi-Cap Core Funds category. Funds in the Lipper Average invest in a variety of market-capitalization ranges without concentrating 75% of their equity assets in any one market-capitalization range over an extended period of time.

5The Lipper Large-Cap Core Funds Average (Lipper Average) invests at least 75% of their equity assets in companies with market capitalization (on a three-year weighted basis) above Lipper’s USDE large-cap floor. Large-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500 Index. Although Lipper classifies the Fund in the Lipper Multi-Cap Core Funds Category, the returns for the Lipper Large-Cap Core Funds Average are also shown; as we believe the Lipper Large-Cap Core Funds Average is more consistent with the management of the Fund.

6The average annual total returns take into account applicable sales charges. Class A, Class B, Class C, and Class R shares are subject to an annual distribution and service (12b-1) fee of up to 0.30%, 1.00%, 1.00%, and 0.75%, respectively. Approximately seven years after purchase, Class B shares will automatically convert to Class A shares on a quarterly basis. Class Z shares are not subject to an annual 12b-1 fee. The returns in the tables do not reflect the deduction of taxes that a shareholder would pay on Fund dividends and distributions or following the redemption of Fund shares.

**Russell 1000 Index Closest Month-End to Inception cumulative total return as of 1/31/09 is –18.37% for Class R. Russell 1000 Index Closest Month-End to Inception average annual total return as of 12/31/08 is –2.54% for Class R.

***S&P 500 Index Closest Month-End to Inception cumulative total return as of 1/31/09 is –19.23% for Class R. S&P 500 Index Closest Month-End to Inception average annual total return as of 12/31/08 is –2.70% for Class R.

****Lipper Multi-Cap Core Funds Average Closest Month-End to Inception cumulative total return as of 1/31/09 is –19.32% for Class R. Lipper Multi-Cap Core Funds Average Closest Month-End to Inception average annual total return as of 12/31/08 is –3.12% for Class R.

*****Lipper Large-Cap Core Funds Average Closest Month-End to Inception cumulative total return as of 1/31/09 is –20.15% for Class R. Lipper Large-Cap Core Funds Average Closest Month-End to Inception average annual total return as of 12/31/08 is –3.27% for Class R.

Investors cannot invest directly in an index. The returns for the S&P 500 Index and the Russell 1000 Index would be lower if they included the effects of sales charges, operating expenses of a mutual fund, or taxes that may be paid by an investor. Returns for the Lipper Average reflect the deduction of operating expenses, but not sales charges or taxes. The Since Inception returns for the S&P 500 Index, Russell 1000 Index, and Lipper Average are measured from the closest month-end to inception date, and not from the Fund’s actual inception date.

| | |

| Jennison 20/20 Focus Fund | | 3 |

Your Fund’s Performance (continued)

| | | |

| Five Largest Growth Holdings expressed as a percentage of net assets as of 1/31/09 | | | |

Gilead Sciences, Inc., Biotechnology | | 3.6 | % |

Research in Motion Ltd., Communications Equipment | | 3.4 | |

Google, Inc. (Class A), Internet Software & Services | | 3.4 | |

Baxter International, Inc., Healthcare Equipment & Supplies | | 3.3 | |

QUALCOMM, Inc., Communications Equipment | | 2.9 | |

Holdings reflect only long-term investments and are subject to change.

| | | |

| Five Largest Value Holdings expressed as a percentage of net assets as of 1/31/09 | | | |

Symantec Corp., Software | | 3.3 | % |

Southwestern Energy Co., Oil, Gas & Consumable Fuels | | 2.8 | |

SLM Corp., Consumer Finance | | 2.7 | |

Freeport-McMoRan Copper & Gold, Inc., Metals & Mining | | 2.7 | |

Cadbury PLC (United Kingdom) (ADR), Food Products | | 2.7 | |

Holdings reflect only long-term investments and are subject to change.

| | | |

| Five Largest Industries expressed as a percentage of net assets as of 1/31/09 | | | |

Oil, Gas & Consumable Fuels | | 13.5 | % |

Biotechnology | | 8.6 | |

Communications Equipment | | 8.2 | |

Healthcare Equipment & Supplies | | 5.5 | |

Food Products | | 5.3 | |

Industry weightings reflect only long-term investments and are subject to change.

| | |

| 4 | | Visit our website at www.jennisondryden.com |

Strategy and Performance Overview

How did the Fund perform?

The Jennison 20/20 Focus Fund’s Class A shares fell 35.16% for the 12-months ended January 31, 2009. The decline was smaller than the 38.63% drop in the S&P 500 Index, the 39.04% drop in the Russell 1000® Index, the 39.09% drop in the Lipper Multi-Cap Core Funds Average, and the 38.14% drop in the Lipper Large-Cap Core Funds Average.

How is the Fund managed?

The Fund is composed of two concentrated portfolios—one invests in growth stocks and one invests in value stocks. The growth portfolio looks for shares of companies with the potential to continue to generate above-average gains in earnings. The value portfolio looks for firms with undervalued shares that have potential to rise to their true value over time. The Fund aims to provide attractive returns while reducing volatility that would normally result from following a single investment style through changing market conditions. It may hold up to 45 stocks split roughly between its two portfolios.

In a concentrated portfolio, prudent stock selection is very important. The key component of Jennison’s growth and value investment philosophies is bottom-up stock selection, which is based on in-house analysis of corporate fundamentals such as return on assets rather than on overarching themes. Jennison’s research and highly interactive investment process are critical to selecting stocks that it strongly believes will outperform on an intermediate- and long-term basis with limited downside potential in the short run. Sector and industry allocations in a portfolio are the result of Jennison’s bottom-up stock selection process, which constructs a portfolio one stock at a time.

Spiros “Sig” Segalas manages the growth portfolio, which is compared to the style-specific Russell 1000® Growth Index (the Growth Index). David Kiefer manages the value portfolio, which is compared to the style-specific Russell 1000® Value Index (the Value Index).

What were conditions like in the U.S. stock market?

The 12-month reporting period that began February 1, 2008 was a difficult time for virtually all styles of equity investing. Problems in the U.S. subprime mortgage market spread throughout the nation’s financial system, creating a full-blown liquidity/credit crisis that roiled financial markets around the world. In this challenging environment, every sector in the Growth Index and the Value Index ended the reporting period in negative territory. Financials, materials, industrials, and energy were the sectors that declined the most in the Growth Index, while financials, materials, and industrials were the sectors that declined the most in the Value Index.

| | |

| Jennison 20/20 Focus Fund | | 5 |

Strategy and Performance Overview (continued)

The third quarter of 2008 proved exceptionally tumultuous, culminating in an alarming series of events. In September, the U.S. government took over mortgage giants Fannie Mae and Freddie Mac, and the Federal Reserve (the Fed) bailed out American International Group (AIG), one of the world’s largest insurance companies. In that same month, Lehman Brothers Holdings failed and some of its North American businesses were purchased by Barclays Capital Inc., while Bank of America agreed to acquire Merrill Lynch & Co. Commercial bank Washington Mutual Inc. failed and the bulk of its businesses were sold to J.P. Morgan Chase & Co. Wachovia Corp. also sought a buyer in September and the commercial bank was sold the following month to Wells Fargo & Co. Meanwhile, Goldman Sachs and Morgan Stanley converted to commercial banks in September, signaling the end of the era of traditional investment banking on Wall Street.

With an unprecedented level of coordination and cooperation, the Fed and the U.S. Department of the Treasury presided over efforts to resuscitate credit markets and stabilize the financial system such as the creation of the $700 billion Troubled Asset Relief Program (TARP), which was signed into law in early October. (The Treasury Department largely used the first $350 billion to take stakes in financial institutions and make loans to certain auto manufacturers.) The ongoing correction in the housing market, debt deflation, rising unemployment, and sluggish production and consumption patterns reflect the most severe economic recession in the United States in recent history. Inflation worries dissipated as commodity prices fell sharply. In an effort to stimulate growth in the United States, the Fed’s policy setting arm, the Federal Open Market Committee (FOMC), lowered its target for the federal funds rate on overnight loans between banks from 3.00% in February 2008 to a range of zero to 0.25% in December 2008, a record low.

By the end of 2008, liquidity conditions in the financial markets had improved somewhat from the panicked state of the autumn, but this did little to rekindle borrowers’ demand for funds or lenders’ willingness to loan them money. Corporations across the globe offered cautious outlooks for 2009. Significant cost-savings plans were announced, including workforce reductions and cuts in capital expenditures.

After the FOMC met in late January 2009, it announced that the Fed stands ready, if necessary, to expand the size and duration of its program that supports the mortgage and housing markets by purchasing large amounts of federal agency debt securities and mortgage-backed securities. Additionally, the Fed still plans to implement a program to facilitate lending to individuals and small businesses and is still prepared to buy longer-term U.S. Treasury securities if purchases would help conditions in the private credit markets.

| | |

| 6 | | Visit our website at www.jennisondryden.com |

What sectors and specific holdings contributed most to the growth portfolio?

Although every sector in the growth portfolio and the Growth Index ended the reporting period in the red, the growth portfolio still solidly outperformed the Growth Index. The growth portfolio’s positions in information technology had the strongest positive impact on its performance versus the Growth Index. An overweight exposure to the healthcare sector also provided considerable benefit to the growth portfolio’s relative performance. Favorable stock selection in consumer discretionary, materials, and financials also helped, as the growth portfolio posted smaller declines in these sectors than the Growth Index. A smaller exposure to the industrials sector was another source of relative gain for the growth portfolio.

The top contributor to the growth portfolio was Gilead Sciences Inc., whose products include an antifungal agent, antiviral treatments, and cardiovascular drugs. The company receives royalties from other products, including a flu treatment, Tamiflu, and the macular degeneration drug, Macugen. Jennison believes Gilead possesses excellent longer-term fundamentals, including strong sales for Atripla and Truvada, drugs that treat patients infected with the human immunodeficiency virus (HIV) that can lead to acquired immune deficiency syndrome (AIDS). Changes in the prices of these two drugs would have little effect on demand for them. Proceeds from their sales and strong royalty streams from Tamiflu fund pipeline products in the early stages of development.

Energy holding First Solar Inc. was a major contributor to the growth portfolio’s return. First Solar designs and manufactures solar-power modules via its proprietary thin-film semiconductor technology, which has enabled First Solar to cut the average cost of manufacturing its solar modules to among the lowest in the world and offer better pricing to customers. The growth portfolio sold its First Solar shares in September amid concerns that tight credit could limit investment in solar projects, falling oil prices could curtail a sense of urgency for alternative energy sources, and a free-fall in the price of polycrystalline silicon could hurt the cost-effectiveness of the company’s thin-film technology.

Another key contributor to the growth portfolio’s return was Occidental Petroleum, a global oil and gas exploration and production company. The growth segment bought shares in November because Jennison likes Occidental’s strong balance sheet, ability to generate cash, and its focus on generating production growth and high returns. This stands in contrast to most exploration and production companies that focus solely on production growth and tend to overspend. Jennison believes that cutting costs is the key to high returns in the current environment of lower oil prices.

Late in the reporting period, the growth portfolio purchased shares of the nation’s largest pharmacy benefits management company, Medco Health Solutions Inc., which performed well. Jennison likes the industry’s positive fundamental outlook and

| | |

| Jennison 20/20 Focus Fund | | 7 |

Strategy and Performance Overview (continued)

expects Medco’s growth to be fueled by generic drugs, specialty pharmacy, new business, and improvements in its capital structure, i.e., the ratio of debt to equity on its balance sheet.

What sectors and specific holdings detracted most from the growth portfolio?

The growth portfolio had underweight positions in the energy and consumer staples sectors, which detracted from its performance versus the Growth Index. Moreover, the growth segment’s consumer staples position declined more than that of the Growth Index for the reporting period.

Global oilfield services company Schlumberger Ltd. was the largest detractor from the growth portfolio’s return. Shares of Schlumberger fell as earnings estimates for oil services companies were severely cut because their clients, oil and gas exploration and production companies, slashed their budgets amid the economic slowdown. In the United States, rig count, the leading indicator of activity for oil services companies, is down and may decline further. The growth segment sold its Schlumberger shares in mid-December at a loss.

Another drag on the growth segment’s return was Alcon Inc., one of the world’s leading developers, manufacturers, and marketers of drugs, devices, surgical equipment, and care products to treat eye diseases. Alcon shares hit a rough patch in October after the firm’s earnings for the quarter ended September 30, 2008 missed expectations. The stock had climbed in June on news that Swiss pharmaceutical company Novartis planned to buy a 25% stake in Alcon in a first step toward majority ownership. After Alcon’s disappointing results, Novartis reiterated its belief that majority ownership in Alcon would enhance Novartis’ longer-term growth prospects through greater access to the fast-growing eye-care market, a high-demand specialty field with 2007 sales of about $25 billion.

The growth portfolio held shares of Thermo Fisher Scientific, which provides a wide range of consumables such as disposable laboratory glassware, instruments, and services to scientists, engineers, manufacturers, and regulators. The growth portfolio sold its Thermo Fisher position in November over concerns that the economic recession could hurt the company’s efforts to increase its earnings from industrial sales.

Exposure to Google shares also detracted from the growth portfolio’s return. In November 2008, shares of the Internet giant fell below $300 for the first time since October 2005. This occurred as several Wall Street analysts cut their fourth-quarter earnings estimates on indications that Google, like other Internet companies, was

| | |

| 8 | | Visit our website at www.jennisondryden.com |

suffering from a marked slowdown in online advertising amid the financial crisis. Google has made strides to increase its revenue earned each time an Internet user clicks on one of its search advertisements, but the flagging economy has made its efforts less effective. Ad budgets continue to decrease overall. However, advertisers and other media buyers continue to find search to be the most compelling online ad format as search budgets appear to be holding up better than other advertising categories.

Google shares recovered some ground in January 2009 after it reported what Jennison considered to be solid results for the fourth quarter of 2008. The manager believes that Google remains compelling from a risk/reward perspective and that it has defensive characteristics, such as a highly measurable return on investment, and offers significant upside potential in an economic recovery.

What sectors and specific holdings contributed most to the value portfolio?

The value portfolio outperformed the Value Index for the 12-month reporting period. Maintaining an underweight exposure to financials coupled with favorable stock selection in that sector resulted in a meaningful gain in the value portfolio versus the Value Index. Jennison does not make macro sector calls, but its stock-by-stock review of opportunities among financial firms led it to conclude there were significant risks embedded in the fundamentals of most companies, especially banks.

Favorable stock selection among industrials combined with a lower exposure to that sector made a strong positive contribution to the relative performance of the value segment versus the Value Index. Indeed, the only sector in the value portfolio that finished the reporting period in the black was industrials, posting a double-digit gain. Among other sectors, favorable security selection within consumer discretionary, information technology, and healthcare also helped the value portfolio outperform the Value Index.

Goldman Sachs was the top contributor to the value portfolio by a wide margin. The value segment bought Goldman Sachs shares in late November in the belief that the stock price had bottomed. The shares had declined amid speculation that Goldman Sachs would post its first ever quarterly loss as a public company because market turmoil pressured revenues from investment banking and proprietary trading. There was also concern about potential write-downs from emerging market equity investments. However, Jennison believed that Goldman still had solid profits from its initial emerging markets investment, such as Industrial and Commercial Bank of China.

Goldman Sachs remains one of the few capital markets platforms that has not been constrained by the credit crisis. Granted, the company took a fourth-quarter loss, its

| | |

| Jennison 20/20 Focus Fund | | 9 |

Strategy and Performance Overview (continued)

first since it went public in 1999. Yet Goldman Sachs has not had to cope with an impaired balance sheet like many of its prime competitors nor has it suffered the severe losses experienced by the rest of the industry. Goldman Sachs was also one of a select few institutions that initially refused TARP money that it was forced to accept. (Jennison expects the firm to be one of the first to pay back TARP funds to the federal government.) Goldman Sachs is taking advantage of investment opportunities created by widening spreads, which offer greater potential for profitability with the advantage of lower levels of debt on its balance sheet. Jennison believes that Goldman Sachs’ shares, which are trading at a significant discount to its tangible book value, offer considerable potential for price appreciation, given the attractive risk/reward ratio.

Southwestern Energy, which primarily focuses on the exploration and production of natural gas, was another major contributor to the value portfolio’s return. Jennison views the firm as a high-quality player in the business with a healthy asset base. The company continues to see increased efficiencies and production from its Fayetteville Shale operation and maintains a strong financial position following the sale of certain non-core assets earlier in the year. Southwestern Energy’s strong resource growth and profitability should improve as production in the Fayetteville Shale field matures.

Consumer discretionary holding H&R Block was also a key contributor to the value segment’s return. H&R Block’s new management has restructured the company to focus on its industry-leading tax preparation franchise, which is energized and taking market share from its competitors under new leadership. Earlier in 2008, H&R Block sold its Option One mortgage business and securities brokerage unit, H&R Block Financial Advisors. It held on to RSM McGladrey, the fifth largest accounting firm in the United States. Jennison believes that H&R Block holds a dominant competitive position, and as it heads into its seasonally strong third quarter, H&R Block is expected to outperform, especially given its cost saving initiatives.

The value portfolio bought HMO Aetna in December after prices of its shares and the shares of its peers collapsed amid concern about rising medical costs and the impact a Democratic-controlled Congress and White House might have on the industry. Aetna shares also fell as the market focused heavily on the firm’s 2009 pension losses. Later in December, HMO shares rallied as investors recognized that medical costs should be under control in a weakening economy. Meanwhile, Aetna’s shares rose as an increase in pension funding expense was attributed to accounting practices only. Aetna’s pension plan remains almost fully funded, and Jennison does not expect the pension plan to suffer another sizable hit. The manager believes that Aetna’s valuation is compelling with its shares trading as low as six times earnings.

| | |

| 10 | | Visit our website at www.jennisondryden.com |

What sectors and specific holdings detracted most from the value portfolio?

The value portfolio underperformed the Value Index in the consumer staples, utilities, energy, telecommunications, and materials sectors. Century Aluminum was the largest detractor from the value portfolio’s return. Rising global inventories have caused a large decline in the price of aluminum, which Jennison believes to be temporary. At current metal prices (under $1.00 per pound), much of the world capacity for aluminum is operating below cash cost. Many smelters have already shut down, and Jennison expects further closures, project delays, and production cuts to help boost the price of aluminum. Therefore, Jennison remains comfortable with the value portfolio’s position in Century Aluminum.

A position in XL Capital, an insurance and reinsurance company, hurt the performance of the value portfolio amid growing concern about the health and viability of the insurance industry. The value portfolio had bought XL shares in July at a discount to the company’s tangible book value. XL used proceeds from the sale of the shares to recapitalize its balance sheet after spinning off its financial products division, which held the company’s troubled financial assets such as collateralized debt obligations.

Jennison expected rating agencies to remove XL from credit watch after the company recapitalized, which occurred in early August. However, XL was not immune to the worsening credit crunch in October. Insurance company shares generally came under pressure because of markdowns on their portfolios of corporate bonds and alternative investments. Moreover, there was renewed concern that rating agencies might downgrade XL when the planned sale of its life reinsurance subsidiary fell through. Clients trimmed exposures to XL and its ability to write new insurance premiums suffered. The value portfolio sold its XL shares at a loss in January of 2009.

Shares of Sirius XM Radio also declined, detracting from the value portfolio’s return. Investors worried the company might have difficulty refinancing its bonds that mature in 2009 amid the tumultuous conditions in the capital markets. This could potentially force Sirius to restructure or declare bankruptcy. Weakness in auto sales and declining consumer confidence also weighed on the stock, since new car manufacturers are the satellite radio company’s largest market. The value portfolio continues to hold Sirius shares, as Jennison believes the Sirius franchise is still valuable.

Shares of Sprint fell as investor patience with the company’s turnaround wore thin. Jennison believes the firm’s management took the right steps to stabilize its business, build up cash, and loosen covenants. However, the value portfolio sold its Sprint position in October. Sprint was considered too risky for the concentrated portfolio.

| | |

| Jennison 20/20 Focus Fund | | 11 |

Strategy and Performance Overview (continued)

Were there significant changes to the Fund?

The growth portfolio bought shares of Baxter International in May as Jennison believes the firm’s fundamentals are among the best in the medical technology industry. The firm’s growth accelerated in the latest reported quarter, as gross profit margins hit another high-water mark and earnings per share increased 21% (beating consensus estimates). Baxter’s initial revenue and earnings expectations point to another strong year in 2009. Its core medical products and services business continues to benefit from sharper execution, better returns, and favorable competitive dynamics. It is one of only a few medical technology firms that currently enjoy positive pricing trends. Jennison believes that Baxter’s liquidity position and free cash flow are also sound, and that Baxter has an attractive mix of businesses and potential for further increases in its gross profit margins.

Williams Cos., an integrated oil and natural gas exploration and production company, also owns large interstate gas pipelines and smaller feeder pipelines that funnel gas from wells to interstate pipes. The value portfolio bought Williams shares in the fourth quarter of 2008 as its stock price declined due to bearish market conditions. There was nothing fundamentally wrong with the company. Jennison believes that Williams’ exploration and production properties are located in some of the most attractive basins in the United States, and its pipeline segment generates consistently attractive returns that should underpin its earnings. The company is also evaluating a variety of structural changes, such as potentially separating one or more of the firm’s principal business units to enhance shareholder value.

The growth portfolio bought shares of Genentech, which currently markets three blockbuster drugs: Rituxan, which fights non-Hodgkin’s lymphoma; Avastin, a treatment for colorectal and non-small cell lung cancers; and Herceptin for breast cancer. Lung cancer drug Tarceva rounds out the company’s oncology portfolio. Genentech’s highly touted oncology products and research pipeline are widely considered to be among the most attractive in the biotechnology industry. Jennison believes the company stands to benefit from positive news flow on Rituxan and Avastin as clinical data come back from studies in ovarian, prostate, pancreatic, and renal cancer.

The growth portfolio took profits on its position in Roche Holding, a pharmaceuticals and diagnostics firm that sells its products in more than 150 countries. Roche markets many of its bestsellers with affiliates Genentech and Chugai Pharmaceutical. During 2008, Roche bought full control of Genentech’s oncology products and research pipeline.

Jennison thought American International Group’s (AIG) leading global property/casualty and life insurance businesses would protect it on the downside. The

| | |

| 12 | | Visit our website at www.jennisondryden.com |

investment team estimated these businesses together could generate over $12 billion in earnings in 2009. AIG also had a great financial services franchise, including one of the world’s premier airplane leasing businesses. AIG’s financial products business, which historically had been highly profitable while navigating complicated financial markets, had become a troublesome business unit. In late spring of 2008, AIG appeared to be raising capital defensively, reflecting recent rating agency downgrades and the possibility that it might have to post collateral on its credit default swap exposures. Jennison believed that the amount of capital being raised would dilute future earnings unless the company made a clear case for how it might leverage it for future growth opportunities. Therefore, the value portfolio sold its AIG shares in May.

The value portfolio took profits in April on its position in Wal-Mart, as Jennison believed other investments had more attractive risk/reward profiles. Wal-Mart shares had gained as its merchandising initiatives put in place two years ago bore fruit. A combination of tough economic times, the fiscal stimulus, and Wal-Mart’s refocus on its all-important value proposition—always low prices—positioned the company well.

What is Jennison’s outlook for the stock market for the remainder of the year?

Shortly after the reporting period ended, President Obama signed into law the $787 billion American Recovery and Reinvestment Act of 2009, which aims to boost growth through aggressive infrastructure spending, tax cuts, and other measures. These extraordinary measures, TARP, and the promise to take further steps if necessary suggest that all efforts are being brought to bear on stabilizing the financial system and stimulating economic growth in the United States. The more optimistic forecasts hope for stability by mid-2009 and a nascent economic recovery by year-end.

Jennison adjusted its profit growth forecast and now expects earnings of companies in the S&P 500 Index to fall in 2009, which would make two consecutive years of declines. Under this scenario, profits will have fallen more than 50% from peak to trough, marking their worst performance since the 1930s.

Jennison’s earnings forecasts for companies held by the growth portfolio reflect expectations of the challenging economic environment in 2009. Most of these companies generate significant free cash flow and face no refinancing hurdles in the currently prohibitive environment for corporate debt funding. Most also have strong competitive positions and appear to be managing well in the face of slowing demand. These factors should allow the growth portfolio’s holdings to generate profit growth better than the market average and maintain strong capital positions, which, in turn, should lead to outperformance.

| | |

| Jennison 20/20 Focus Fund | | 13 |

Strategy and Performance Overview (continued)

While Jennison is disappointed with the value portfolio’s performance in 2008, it has always stated that it would underperform in this type of market, where emotions dictate actions and fundamental analysis is marginalized. Fear currently dominates the market. The value investment team continues to look for companies it believes are attractively valued, have strong free cash flow, strong balance sheets that should enable them to survive the downturn (without external sources of capital), steadily rising earnings, and lower risk of profit margin compression. Jennison expects performance to return to historical levels as the market inevitably refocuses on fundamentals. As in past cycles, equity markets will likely rally in anticipation of an economic recovery before statistics show that business activity has picked up.

| | |

| 14 | | Visit our website at www.jennisondryden.com |

Comments on Largest Holdings—Growth Portfolio

| 3.6% | Gilead Sciences, Inc., Biotechnology |

Please see the section that discusses shares that contributed most to the growth portfolio.

| 3.4% | Research in Motion Ltd., Communications Equipment |

BlackBerry maker Research in Motion’s share price rose on indications that new subscriber growth is exceeding expectations. News of this strength prompted several Wall Street analysts to raise their earnings projections and target prices. Research in Motion also benefitted from perceptions that its pressured profit margins may start improving. Jennison believes that the company potentially is a long-term winner, and its stock price should continue to gain as smart phone sales remain healthy, even in a tough economic environment.

| 3.4% | Google, Inc. (Class A), Internet Software & Services |

Please see section that discusses shares that detracted most from the growth portfolio.

| 3.3% | Baxter International, Inc., Healthcare Equipment & Supplies |

Please see section that discusses significant changes to the Fund.

| 2.9% | QUALCOMM, Inc., Communications Equipment |

Jennison believes that QUALCOMM is a quality company with a solid balance sheet, strong cash flow, competitive industry position, and attractive growth prospects. Last quarter, third generation technology (3G) licenses were finally issued in China. Subsequently, Jennison expects growth in China to be significant for QUALCOMM’s two main business segments. This anticipated growth should offset a significant portion of the expected revenue declines in North America and Europe, where weak demand will most likely persist through 2009. Jennison views QUALCOMM as an attractively priced company that should maintain relatively strong business fundamentals during the current economic downturn.

| | |

| Jennison 20/20 Focus Fund | | 15 |

Comments on Largest Holdings—Value Portfolio

| 3.3% | Symantec Corp., Software |

Security software maker Symantec reported another strong fiscal quarter at the end of January 2009, driven by cost cutting initiatives that enabled it to surpass expectations. Jennison believes this performance emphasizes the defensive or stable nature of Symantec’s business, which has a high percentage of recurring revenue to sustain top-line growth and a high level of variable costs to support earnings. Symantec still trades at low levels relative to its peer group, and Jennison expects the stock to outperform in the future.

| 2.8% | Southwestern Energy Co., Oil, Gas & Consumable Fuels |

Please see the section that discusses shares that contributed most to the value portfolio.

| 2.7% | SLM Corp., Consumer Finance |

SLM, commonly known as Sallie Mae, provides student loans. Jennison believed that SLM had little credit risk and therefore limited downside potential, since 80% of its business was explicitly guaranteed by the U.S. government. Furthermore, Jennison expected SLM to benefit from increases in federal funding for higher education under the American Recovery and Reinvestment Act of 2009. However, SLM’s stock price recently traded lower after the Obama administration announced a proposal to replace the Federal Family Education Loan Program with a government-run Direct Loan Program. This proposal, which will likely be passed by a largely Democratic Congress, would eliminate fees paid to private banks that provide loans to students. Jennison trimmed its SLM position out of concern that the share price could decline further if the market focuses on SLM’s potential near-term funding risks and ignores its low-cost loan servicing business. The value portfolio still has exposure to SLM as the investment team believes that its other businesses (loan servicing and private student loans) are worth more than its current stock price.

| 2.7% | Freeport-McMoRan Copper & Gold, Inc., Metals & Mining |

Shares of Freeport-McMoRan Copper & Gold have declined given the pronounced weakness in the commodities market and the subsequent fall in metal prices. Since reaching a high of about $4.00 per pound, copper prices have fallen to about $1.50 per pound. Despite the likelihood of lower demand over the near to intermediate term, Jennison retains its long-term bullish outlook because of the supply/demand imbalance for copper, especially due to growth in the developing world. Moreover, Jennison has confidence in the company’s nimble and skilled management team, which has reacted to the drop in copper price by cutting production forecasts for 2009 and 2010. The bulk of this reduction has come from mines with higher production costs in North America.

| 2.7% | Cadbury PLC (United Kingdom) (ADR), Food Products |

Cadbury recently announced the sale of its Australian beverage business, which completes the transformation of Cadbury into a producer of only confectionery goods. Jennison believes Cadbury is trading at a very attractive price, and the divestiture should boost Cadbury’s ongoing growth rates, while also favorably affecting future profit margin growth. Given the current state of the credit markets, there was concern about the potential cost to refinance a large amount of bonds that come due in June of 2009. In a press release, Cadbury’s management stated that all net cash proceeds from the sale of the beverage business will be applied toward paying down its bonds.

| | |

| 16 | | Visit our website at www.jennisondryden.com |

Fees and Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemptions, as applicable, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses, as applicable. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on August 1, 2008, at the beginning of the period, and held through the six-month period ended January 31, 2009. The example is for illustrative purposes only; you should consult the Prospectus for information on initial and subsequent minimum investment requirements.

The Fund’s transfer agent may charge additional fees to holders of certain accounts that are not included in the expenses shown in the table on the following page. These fees apply to individual retirement accounts (IRAs) and Section 403(b) accounts. As of the close of the six-month period covered by the table, IRA fees included an annual maintenance fee of $15 per account (subject to a maximum annual maintenance fee of $25 for all accounts held by the same shareholder). Section 403(b) accounts are charged an annual $25 fiduciary maintenance fee. Some of the fees may vary in amount, or may be waived, based on your total account balance or the number of JennisonDryden Funds, including the Fund, that you own. You should consider the additional fees that were charged to your Fund account over the six-month period when you estimate the total ongoing expenses paid over the period and the impact of these fees on your ending account value, as these additional expenses are not reflected in the information provided in the expense table. Additional fees have the effect of reducing investment returns.

Actual Expenses

The first line for each share class in the table on the following page provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value ÷ $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During the Six-Month Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before

| | |

| Jennison 20/20 Focus Fund | | 17 |

Fees and Expenses (continued)

expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

Jennison 20/20

Focus Fund | | Beginning Account

Value

August 1, 2008 | | Ending Account

Value January 31, 2009 | | Annualized

Expense Ratio

Based on the

Six-Month Period | | | Expenses Paid

During the

Six-Month Period* |

| | | | | | | | | | | | | | |

| Class A | | Actual | | $ | 1,000.00 | | $ | 615.00 | | 1.24 | % | | $ | 5.03 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,018.90 | | 1.24 | % | | $ | 6.29 |

| | | | | | | | | | | | | | |

| Class B | | Actual | | $ | 1,000.00 | | $ | 612.60 | | 1.94 | % | | $ | 7.86 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,015.38 | | 1.94 | % | | $ | 9.83 |

| | | | | | | | | | | | | | |

| Class C | | Actual | | $ | 1,000.00 | | $ | 612.90 | | 1.94 | % | | $ | 7.87 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,015.38 | | 1.94 | % | | $ | 9.83 |

| | | | | | | | | | | | | | |

| Class R | | Actual | | $ | 1,000.00 | | $ | 614.50 | | 1.44 | % | | $ | 5.84 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,017.90 | | 1.44 | % | | $ | 7.30 |

| | | | | | | | | | | | | | |

| Class Z | | Actual | | $ | 1,000.00 | | $ | 615.50 | | 0.94 | % | | $ | 3.82 |

| | | Hypothetical | | $ | 1,000.00 | | $ | 1,020.41 | | 0.94 | % | | $ | 4.77 |

| | | | | | | | | | | | | | |

* Fund expenses (net of fee waivers or subsidies, if any) for each share class are equal to the annualized expense ratio for each share class (provided in the table), multiplied by the average account value over the period, multiplied by the 184 days in the six-month period ended January 31, 2009, and divided by the 366 days in the Fund’s fiscal year ended January 31, 2009 ( to reflect the six-month period). Expenses presented in the table include the expenses of any underlying portfolios in which the Fund may invest.

| | |

| 18 | | Visit our website at www.jennisondryden.com |

Portfolio of Investments

as of January 31, 2009

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

LONG-TERM INVESTMENTS 96.0% | | | |

COMMON STOCKS | | | |

| |

Biotechnology 8.6% | | | |

| 479,900 | | Celgene Corp.(a) | | $ | 25,410,705 |

| 338,900 | | Genentech, Inc.(a) | | | 27,532,236 |

| 773,100 | | Gilead Sciences, Inc.(a) | | | 39,250,287 |

| | | | | |

| | | | | 92,193,228 |

| |

Capital Markets 4.2% | | | |

| 1,520,000 | | Charles Schwab Corp. (The) | | | 20,656,800 |

| 302,700 | | Goldman Sachs Group, Inc. (The) | | | 24,436,971 |

| | | | | |

| | | | | 45,093,771 |

| |

Chemicals 1.8% | | | |

| 259,900 | | Monsanto Co. | | | 19,767,994 |

| |

Commercial Services & Supplies 2.3% | | | |

| 786,100 | | Waste Management, Inc. | | | 24,518,459 |

| |

Communications Equipment 8.2% | | | |

| 1,340,100 | | Cisco Systems, Inc.(a) | | | 20,061,297 |

| 909,900 | | QUALCOMM, Inc. | | | 31,437,045 |

| 657,900 | | Research In Motion Ltd.(a)(b) | | | 36,447,660 |

| | | | | |

| | | | | 87,946,002 |

| |

Computers & Peripherals 1.4% | | | |

| 172,162 | | Apple, Inc.(a) | | | 15,516,961 |

| |

Consumer Finance 2.7% | | | |

| 2,577,500 | | SLM Corp.(a)(b) | | | 29,512,375 |

| |

Diversified Consumer Services 4.9% | | | |

| 1,091,900 | | Career Education Corp.(a)(b) | | | 23,803,420 |

| 1,388,600 | | H&R Block, Inc. | | | 28,785,678 |

| | | | | |

| | | | | 52,589,098 |

| |

Food Products 5.3% | | | |

| 892,032 | | Cadbury PLC (United Kingdom)(ADR) | | | 28,812,634 |

| 1,675,600 | | ConAgra Foods, Inc. | | | 28,652,760 |

| | | | | |

| | | | | 57,465,394 |

See Notes to Financial Statements.

| | |

| Jennison 20/20 Focus Fund | | 19 |

Portfolio of Investments

as of January 31, 2009 continued

| | | | | |

| Shares | | Description | | Value (Note 1) |

| | | | | |

COMMON STOCKS (Continued) | | | |

| |

Healthcare Equipment & Supplies 5.5% | | | |

| 268,700 | | Alcon, Inc.(b) | | $ | 23,011,468 |

| 612,400 | | Baxter International, Inc. | | | 35,917,260 |

| | | | | |

| | | | | 58,928,728 |

| |

Healthcare Providers & Services 4.4% | | | |

| 837,700 | | Aetna, Inc. | | | 25,968,700 |

| 479,600 | | Medco Health Solutions, Inc.(a) | | | 21,548,428 |

| | | | | |

| | | | | 47,517,128 |

| |

Household Products 2.4% | | | |

| 396,200 | | Colgate-Palmolive Co. | | | 25,768,848 |

| |

Internet & Catalog Retail 2.7% | | | |

| 498,600 | | Amazon.com, Inc.(a)(b) | | | 29,327,652 |

| |

Internet Software & Services 5.1% | | | |

| 106,700 | | Google, Inc. (Class A)(a) | | | 36,121,151 |

| 1,314,800 | | IAC/InterActiveCorp(a)(b) | | | 19,327,560 |

| | | | | |

| | | | | 55,448,711 |

| |

IT Services 2.1% | | | |

| 453,000 | | Visa, Inc. (Class A)(b) | | | 22,355,550 |

| |

Media 2.4% | | | |

| 1,409,700 | | Comcast Corp. (Class A)(b) | | | 20,652,105 |

| 45,164,840 | | Sirius XM Radio, Inc.(a)(b) | | | 5,419,781 |

| | | | | |

| | | | | 26,071,886 |

| |

Metals & Mining 3.8% | | | |

| 3,495,400 | | Century Aluminum Co.(a) | | | 12,408,670 |

| 1,151,500 | | Freeport-McMoRan Copper & Gold, Inc. | | | 28,948,710 |

| | | | | |

| | | | | 41,357,380 |

| |

Multi-Utilities 2.5% | | | |

| 620,400 | | Sempra Energy | | | 27,198,336 |

| |

Oil, Gas & Consumable Fuels 13.5% | | | |

| 292,600 | | Occidental Petroleum Corp. | | | 15,961,330 |

| 1,091,700 | | Petroleo Brasileiro SA (Brazil)(ADR)(b) | | | 28,602,540 |

| 940,600 | | Southwestern Energy Co.(a) | | | 29,769,989 |

See Notes to Financial Statements.

| | |

| 20 | | Visit our website at www.jennisondryden.com |

| | | | | | |

| Shares | | Description | | Value (Note 1) | |

| | | | | | |

COMMON STOCKS (Continued) | | | | |

| |

Oil, Gas & Consumable Fuels (cont’d.) | | | | |

| 1,429,000 | | Suncor Energy, Inc.(b) | | $ | 27,508,250 | |

| 1,908,900 | | Williams Cos., Inc. (The) | | | 27,010,935 | |

| 431,600 | | XTO Energy, Inc. | | | 16,008,044 | |

| | | | | | |

| | | | | 144,861,088 | |

| |

Pharmaceuticals 4.9% | | | | |

| 1,535,212 | | Schering-Plough Corp. | | | 26,958,323 | |

| 633,900 | | Teva Pharmaceutical Industries Ltd. (Israel)(ADR)(b) | | | 26,275,155 | |

| | | | | | |

| | | | | 53,233,478 | |

| |

Software 4.6% | | | | |

| 727,300 | | Adobe Systems, Inc.(a) | | | 14,044,163 | |

| 2,284,400 | | Symantec Corp.(a) | | | 35,019,852 | |

| | | | | | |

| | | | | 49,064,015 | |

| |

Wireless Telecommunication Services 2.7% | | | | |

| 1,476,100 | | NII Holdings, Inc.(a)(b) | | | 28,636,340 | |

| | | | | | |

| | Total long-term investments

(cost $1,233,258,387) | | | 1,034,372,422 | |

| | | | | | |

SHORT-TERM INVESTMENT 24.9% | | | | |

| |

Affiliated Money Market Mutual Fund | | | | |

| 268,085,668 | | Dryden Core Investment Fund - Taxable Money Market Series

(cost $268,085,668; includes $225,756,496 of cash collateral received for securities on loan; Note 3)(c)(d) | | | 268,085,668 | |

| | | | | | |

| | Total Investments 120.9%

(cost $1,501,344,055; Note 5) | | | 1,302,458,090 | |

| | Liabilities in excess of other assets (20.9%) | | | (225,173,103 | ) |

| | | | | | |

| | Net Assets 100.0% | | $ | 1,077,284,987 | |

| | | | | | |

The following abbreviation is used in the portfolio descriptions:

ADR—American Depositary Receipt.

| (a) | Non-income producing security. |

| (b) | All or a portion of a security is on loan. The aggregate market value of such securities is $174,541,677; cash collateral of $225,756,496 (included in liabilities) was received with which the Fund purchased highly liquid short-term investments. |

| (c) | Represents security, or portion thereof, purchased with the cash collateral received for securities on loan. |

| (d) | Prudential Investments LLC, the manager of the Fund, also serves as the manager of the Dryden Core Investment Fund-Taxable Money Market Series. |

See Notes to Financial Statements.

| | |

| Jennison 20/20 Focus Fund | | 21 |

Portfolio of Investments

as of January 31, 2009 continued

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

Level 1—quoted prices in active markets for identical securities

Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The following is a summary of the inputs used as of January 31, 2009 in valuing the Fund’s assets carried at fair value:

| | | | | |

Valuation inputs | | Investments

in Securities | | Other Financial

Instruments* |

Level 1—Quoted Prices | | $ | 1,302,458,090 | | — |

Level 2—Other Significant Observable Inputs | | | — | | — |

Level 3—Significant Unobservable Inputs | | | — | | — |

| | | | | |

Total | | $ | 1,302,458,090 | | — |

| | | | | |

| * | Other financial instruments are derivative instruments not reflected in the Portfolio of Investments, such as futures, forwards and swap contracts, which are valued at the unrealized appreciation/depreciation on the instrument. |

As of January 31, 2008 and January 31, 2009, the Fund did not use any significant unobservable inputs (Level 3) in determining the valuation of investments.

See Notes to Financial Statements.

| | |

| 22 | | Visit our website at www.jennisondryden.com |

The industry classification of portfolio holdings and liabilities in excess of other assets shown as a percentage of net assets as of January 31, 2009 were as follows:

| | | |

Affiliated Money Market Mutual Fund (including 21.0% of collateral received for securities on loan) | | 24.9 | % |

Oil, Gas & Consumable Fuels | | 13.5 | |

Biotechnology | | 8.6 | |

Communications Equipment | | 8.2 | |

Healthcare Equipment & Supplies | | 5.5 | |

Food Products | | 5.3 | |

Internet Software & Services | | 5.1 | |

Pharmaceuticals | | 4.9 | |

Diversified Consumer Services | | 4.9 | |

Software | | 4.6 | |

Healthcare Providers & Services | | 4.4 | |

Capital Markets | | 4.2 | |

Metals & Mining | | 3.8 | |

Consumer Finance | | 2.7 | |

Internet & Catalog Retail | | 2.7 | |

Wireless Telecommunication Services | | 2.7 | |

Multi-Utilities | | 2.5 | |

Media | | 2.4 | |

Household Products | | 2.4 | |

Commercial Services & Supplies | | 2.3 | |

IT Services | | 2.1 | |

Chemicals | | 1.8 | |

Computers & Peripherals | | 1.4 | |

| | | |

| | 120.9 | |

Liabilities in excess of other assets | | (20.9 | ) |

| | | |

| | 100.0 | % |

| | | |

See Notes to Financial Statements.

| | |

| Jennison 20/20 Focus Fund | | 23 |

Statement of Assets and Liabilities

as of January 31, 2009

| | | | |

Assets | | | | |

Investments, at value including securities on loan of $174,541,677: | | | | |

Unaffiliated investments (cost $1,233,258,387) | | $ | 1,034,372,422 | |

Affiliated investments (cost $268,085,668) | | | 268,085,668 | |

Cash | | | 159,578 | |

Receivable for investments sold | | | 7,717,669 | |

Receivable for Fund shares sold | | | 3,499,677 | |

Dividends and interest receivable | | | 621,385 | |

Foreign tax reclaims receivable | | | 44,949 | |

Prepaid expenses | | | 26,028 | |

| | | | |

Total assets | | | 1,314,527,376 | |

| | | | |

| |

Liabilities | | | | |

Payable to broker for collateral for securities on loan (Note 3) | | | 225,756,496 | |

Payable for investments purchased | | | 6,724,886 | |

Payable for Fund shares reacquired | | | 3,020,081 | |

Management fee payable | | | 686,675 | |

Accrued expenses and other liabilities | | | 496,873 | |

Distribution fee payable | | | 376,500 | |

Affiliated transfer agent fee payable | | | 178,177 | |

Deferred trustees’ fees | | | 2,701 | |

| | | | |

Total liabilities | | | 237,242,389 | |

| | | | |

| |

Net Assets | | $ | 1,077,284,987 | |

| | | | |

| | | | | |

Net assets were comprised of: | | | | |

Shares of beneficial interest, at par | | $ | 116,505 | |

Paid-in capital in excess of par | | | 1,580,066,784 | |

| | | | |

| | | 1,580,183,289 | |

Accumulated net investment loss | | | (2,701 | ) |

Accumulated net realized loss on investment transactions | | | (304,009,636 | ) |

Net unrealized depreciation on investments | | | (198,885,965 | ) |

| | | | |

Net assets, January 31, 2009 | | $ | 1,077,284,987 | |

| | | | |

See Notes to Financial Statements.

| | |

| 24 | | Visit our website at www.jennisondryden.com |

| | | |

Class A | | | |

Net asset value and redemption price per share | | | |

($559,684,535 ÷ 59,471,312 shares of beneficial interest issued and outstanding) | | $ | 9.41 |

Maximum sales charge (5.50% of offering price) | | | .55 |

| | | |

Maximum offering price to public | | $ | 9.96 |

| | | |

| |

Class B | | | |

Net asset value, offering price and redemption price per share | | | |

($96,771,824 ÷ 11,284,111 shares of beneficial interest issued and outstanding) | | $ | 8.58 |

| | | |

| |

Class C | | | |

Net asset value, offering price and redemption price per share | | | |

($163,325,082 ÷ 19,033,543 shares of beneficial interest issued and outstanding) | | $ | 8.58 |

| | | |

| |

Class R | | | |

Net asset value, offering price and redemption price per share | | | |

($27,768,414 ÷ 2,973,869 shares of beneficial interest issued and outstanding) | | $ | 9.34 |

| | | |

| |

Class Z | | | |

Net asset value, offering price and redemption price per share | | | |

($229,735,132 ÷ 23,742,156 shares of beneficial interest issued and outstanding) | | $ | 9.68 |

| | | |

See Notes to Financial Statements.

| | |

| Jennison 20/20 Focus Fund | | 25 |

Statement of Operations

Year Ended January 31, 2009

| | | | |

Net Investment Loss | | | | |

Income | | | | |

Unaffiliated dividend income (net of foreign withholding taxes of $188,815) | | $ | 14,179,284 | |

Affiliated income from securities loaned, net | | | 1,443,572 | |

Affiliated dividend income | | | 1,241,151 | |

| | | | |

Total income | | | 16,864,007 | |

| | | | |

| |

Expenses | | | | |

Management fee | | | 10,059,956 | |

Distribution fee—Class A | | | 2,038,357 | |

Distribution fee—Class B | | | 1,444,054 | |

Distribution fee—Class C | | | 2,064,232 | |

Distribution fee—Class R | | | 92,732 | |

Transfer agent’s fees and expenses (including affiliated expense of $870,400)(Note 3) | | | 1,928,000 | |

Custodian’s fees and expenses | | | 197,000 | |

Reports to shareholders | | | 172,000 | |

Registration fees | | | 129,000 | |

Trustees’ fees | | | 52,000 | |

Interest expense (Note 7) | | | 30,802 | |

Legal fees and expenses | | | 26,000 | |

Audit fee | | | 21,000 | |

Insurance | | | 15,000 | |

Miscellaneous | | | 14,376 | |

| | | | |

Total expenses | | | 18,284,509 | |

| | | | |

Net investment loss | | | (1,420,502 | ) |

| | | | |

| |

Realized And Unrealized Loss On Investments | | | | |

Net realized loss on investment transactions | | | (298,844,180 | ) |

Net change in unrealized depreciation on investments | | | (293,278,487 | ) |

| | | | |

Net loss on investments | | | (592,122,667 | ) |

| | | | |

Net Decrease In Net Assets Resulting From Operations | | $ | (593,543,169 | ) |

| | | | |

See Notes to Financial Statements.

| | |

| 26 | | Visit our website at www.jennisondryden.com |

Statement of Changes in Net Assets

| | | | | | | | |

| | | Year Ended January 31, | |

| | | 2009 | | | 2008 | |

Increase (Decrease) In Net Assets | | | | | | | | |

Operations | | | | | | | | |

Net investment loss | | $ | (1,420,502 | ) | | $ | (1,940,796 | ) |

Net realized gain (loss) on investment transactions | | | (298,844,180 | ) | | | 84,572,477 | |

Net change in unrealized appreciation (depreciation) on investments | | | (293,278,487 | ) | | | (92,809,877 | ) |

| | | | | | | | |

Net decrease in net assets resulting from operations | | | (593,543,169 | ) | | | (10,178,196 | ) |

| | | | | | | | |

| | |

Distributions from net realized gains (Note 1) | | | | | | | | |

Class A | | | (406,192 | ) | | | (90,684,266 | ) |

Class B | | | (93,619 | ) | | | (23,207,940 | ) |

Class C | | | (123,937 | ) | | | (27,731,523 | ) |

Class R | | | (8,900 | ) | | | (739,618 | ) |

Class Z | | | (140,750 | ) | | | (24,530,237 | ) |

| | | | | | | | |

| | | (773,398 | ) | | | (166,893,584 | ) |

| | | | | | | | |

| | |

Fund share transactions (Net of share conversions) (Note 6) | | | | | | | | |

Net proceeds from shares sold | | | 657,427,982 | | | | 441,861,512 | |

Net asset value of shares issued in reinvestment of dividends and distributions | | | 668,428 | | | | 146,800,608 | |

Cost of shares reacquired | | | (378,061,379 | ) | | | (281,070,116 | ) |

| | | | | | | | |

Net increase in net assets from Fund share transactions | | | 280,035,031 | | | | 307,592,004 | |

| | | | | | | | |

Total increase (decrease) | | | (314,281,536 | ) | | | 130,520,224 | |

| | |

Net Assets | | | | | | | | |

Beginning of year | | | 1,391,566,523 | | | | 1,261,046,299 | |

| | | | | | | | |

End of year | | $ | 1,077,284,987 | | | $ | 1,391,566,523 | |

| | | | | | | | |

See Notes to Financial Statements.

| | |

| Jennison 20/20 Focus Fund | | 27 |

Notes to Financial Statements

Jennison 20/20 Focus Fund (the “Fund”), is registered under the Investment Company Act of 1940 as a non-diversified, open-end management investment company. The investment objective of the Fund is long-term growth of capital. The Fund normally invests at least 80% of its total assets in up to 40 equity-related securities of U.S. companies that are selected by the Fund’s two portfolio managers (up to 20 by each) as having strong capital appreciation potential.

Note 1. Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Securities Valuation: Securities listed on a securities exchange (other than options on securities and indices) are valued at the last sale price on such exchange on the day of valuation or, if there was no sale on such day, at the mean between the last reported bid and asked prices, or at the last bid price on such day in the absence of an asked price. Securities traded via Nasdaq are valued at the Nasdaq Official Closing Price (“NOCP”) on the day of valuation, or if there was no NOCP, at the last sale price. Securities that are actively traded in the over-the-counter market, including listed securities for which the primary market is believed by Prudential Investments LLC (“PI” or “Manager”) in consultation with the subadviser, to be over-the-counter, are valued at market value using prices provided by an independent pricing agent or principal market maker. Prices may be obtained from independent pricing services which use information provided by market makers or estimates of market values obtained from yield data relating to investments or securities with similar characteristics.

Securities for which reliable market quotations are not readily available, or whose values have been affected by events occurring after the close of the security’s foreign market and before the Fund’s normal pricing time, are valued at fair value in accordance with the Board of Trustees’ approved fair valuation procedures. When determining the fair valuation of securities, some of the factors influencing the valuation include, the nature of any restrictions on disposition of the securities; assessment of the general liquidity of the securities; the issuer’s financial condition and the markets in which it does business; the cost of the investment; the size of the holding and the capitalization of issuer; the prices of any recent transactions or bids/offers for such securities or any comparable securities; any available analyst media or

| | |

| 28 | | Visit our website at www.jennisondryden.com |

other reports or information deemed reliable by the investment adviser regarding the issuer or the markets or industry in which it operates. Using fair value to price securities may result in a value that is different from a security’s most recent closing price and from the price used by other mutual funds to calculate their net asset values. As of January 31, 2009, there were no securities valued in accordance with such procedures.

Investments in mutual funds are valued at their net asset value as of the close of the New York Stock Exchange on the date of valuation.

Short-term debt securities which mature in sixty days or less are valued at amortized cost, which approximates market value. The amortized cost method involves valuing a security at its cost on the date of purchase and thereafter assuming a constant amortization to maturity of the difference between the principal amount due at maturity and cost. Short-term debt securities which mature in more than sixty days are valued at current market quotations.

Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars on the following basis:

(i) market value of investment securities, other assets and liabilities-at the current rates of exchange;

(ii) purchases and sales of investment securities, income and expenses—at the rates of exchange prevailing on the respective dates of such transactions.

The Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of portfolio securities held at the end of the fiscal year. Similarly, the Fund does not isolate the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of portfolio securities sold during the fiscal year. Accordingly, realized foreign currency gains or losses are included in the reported net realized gains or losses on investment transactions.

Net realized gains or losses on foreign currency transactions represent net foreign exchange gains or losses from the holding of foreign currencies, currency gains or losses realized between the trade date and settlement date on securities transactions, and the difference between the amount of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains or losses from valuing foreign currency denominated assets and liabilities (other than investments) at fiscal year end exchange rates are reflected as a component of net unrealized appreciation (depreciation) on investments and foreign currencies.

| | |

| Jennison 20/20 Focus Fund | | 29 |

Notes to Financial Statements

continued

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of domestic origin as a result of, among other factors, the possibility of political or economic instability, or the level of governmental supervision and regulation of foreign securities markets.

Securities Lending: The Fund may lend its portfolio securities to broker-dealers. The loans are secured by collateral at least equal, at all times, to the market value of the securities loaned. Loans are subject to termination at the option of the borrower or the Fund. Upon termination of the loan, the borrower will return to the lender securities identical to the loaned securities. Should the borrower of the securities fail financially, the Fund has the right to repurchase the securities using the collateral in the open market. The Fund recognizes income, net of any rebate and securities lending agent fees, for lending its securities in the form of fees or interest on the investment of any cash received as collateral. The Fund also continues to receive interest and dividends or amounts equivalent thereto, on the securities loaned and recognizes any unrealized gain or loss in the market price of the securities loaned that may occur during the term of the loan.

Securities Transactions and Net Investment Income: Securities transactions are recorded on the trade date. Realized and unrealized gains and losses from security and currency transactions are calculated on the identified cost basis. Dividend income is recorded on the ex-dividend date. Interest income, including amortization of premium and accretion of discount on debt securities, as required, is recorded on the accrual basis.

Net investment income or loss (other than distribution fees which are charged directly to the respective class) and unrealized and realized gains or losses are allocated daily to each class of shares based upon the relative proportion of net assets of each class at the beginning of the day.

Dividends and Distributions: The Fund expects to pay dividends from net investment income and distributions from net realized capital gains, if any, at least annually.

Dividends and distributions which are determined in accordance with federal income tax regulations and which may differ from generally accepted accounting principles, are recorded on the ex-dividend date. Permanent book/tax differences relating to income and gains are reclassified amongst undistributed net investment income, accumulated net realized gain or loss and paid-in capital in excess of par, as appropriate.

| | |

| 30 | | Visit our website at www.jennisondryden.com |

Taxes: It is the Fund’s policy to continue to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its taxable net investment income and capital gains, if any, to its shareholders. Therefore, no federal income tax provision is required.

Withholding taxes on foreign dividends are recorded net of reclaimable amounts, at the time the related income is earned.

Estimates: The preparation of the financial statements requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Note 2. Agreements

The Fund has a management agreement with PI. Pursuant to this agreement, PI has responsibility for all investment advisory services and supervises the subadviser’s performance of such services. PI has entered into a subadvisory agreement with Jennison Associates LLC (“Jennison”). The subadvisory agreement provides that Jennison furnishes investment advisory services in connection with the management of the Fund. In connection therewith, Jennison is obligated to keep certain books and records of the Fund. PI pays for the services of Jennison, the cost of compensation of officers, occupancy and certain clerical and bookkeeping costs of the Fund. The Fund bears all other costs and expenses.

The management fee paid to PI is accrued daily and payable monthly, at an annual rate of .75 of 1% of the Fund’s average daily net assets up to and including $1 billion and .70 of 1% of such average daily net assets in excess of $1 billion. The effective management fee rate was .74 of 1% of the average daily net assets for the year ended January 31, 2009.

There are two Portfolio Managers at Jennison, both of which manage approximately 50% of the Fund’s assets. In general, in order to maintain an approximately equal division of assets between the two portfolio managers, all daily cash inflows (i.e. subscriptions and reinvested distributions) and outflows (i.e. redemptions and expense items) are divided between the two portfolio managers as PI deems appropriate. In addition, periodic rebalancing of the portfolio’s assets may occur to account for market fluctuations in order to maintain an approximately equal allocation between the two portfolio managers.

The Fund has a distribution agreement with Prudential Investment Management Services LLC (“PIMS”), which acts as the distributor of the Class A, Class B, Class C,

| | |

| Jennison 20/20 Focus Fund | | 31 |

Notes to Financial Statements

continued