UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-08629

HARTFORD SERIES FUND, INC.

(Exact name of registrant as specified in charter)

5 Radnor Corporate Center, Suite 300, 100 Matsonford Road, Radnor, Pennsylvania 19087

(Address of Principal Executive Offices) (Zip Code)

Edward P. Macdonald, Esquire

Hartford Funds Management Company, LLC

5 Radnor Corporate Center, Suite 300

100 Matsonford Road

Radnor, Pennsylvania 19087

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (610) 386-4068

Date of fiscal year end: December 31

Date of reporting period: December 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F. Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

HARTFORDFUNDS

| HARTFORD SERIES FUND, INC.

2013 Annual Report

|

A MESSAGE FROM THE PRESIDENT

Dear Fellow Shareholders:

Thank you for investing in Hartford HLS Funds.

Market Review

U.S. equities (as represented by the S&P 500 Index) generated their strongest year since 1997 in 2013, rising 32.39% for the year. During the fourth quarter, equities rose without looking back, pushing the S&P 500 Index and the Dow Jones Industrial Average to new all-time highs. Despite previously cheering delays to quantitative-easing tapering, the stock market received an additional boost at the end of the year following the U.S. Federal Reserve’s (Fed) announcement of a $10-billion-a-month reduction in bond purchases beginning in January.

The Fed’s decision to begin tapering its bond purchases is generally considered a vote of confidence in the recovering U.S. economy. Consumer spending has stabilized, the housing market is showing steady improvement, the unemployment rate is slowly declining and economic growth clocked in at a healthy 4.1% in the third quarter. Equities have also recovered since the market low in March 2009: The S&P 500 Index has gained 173% from the market low through December 31, 2013.

Signs of improvement are also visible outside the U.S. Europe appears to have begun its own economic recovery, and emerging markets have reversed their recent lackluster performance. Fiscal policy continues to wield significant influence in today’s economy and central banks across the globe are maintaining their accommodative stances, including the appointment of Janet Yellen, who is widely expected to continue current monetary policies, to succeed Ben Bernanke as U.S. Federal Reserve chairman.

It’s important to stay abreast of domestic and international economic developments while balancing your individual investment goals. Meeting with your financial advisor on a regular basis to examine your current investment strategy can help you determine whether you are on the right track:

| • | Is your portfolio fully diversified with an appropriate mix of stocks and bonds? |

| • | Is your portfolio incorporating both domestic and international holdings to take advantage of the global economic recovery? |

| • | Are your investments still in line with your risk tolerance and investment time horizon? |

Your financial advisor can help you choose options within our fund family to navigate today’s markets with confidence.

Thank you again for investing with Hartford HLS Funds.

James Davey

President

Hartford HLS Funds

1The S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

2The Dow Jones Industrial Average is an unmanaged, price-weighted index of 30 of the largest, most widely held stocks traded on the New York Stock Exchange.

Table of Contents

This report is prepared for the general information of contract owners and is not an offer of contracts. It should not be used in connection with any offer, except in conjunction with the appropriate product prospectus which contains all pertinent product information including the applicable sales, administrative and other charges.

| American Funds Asset Allocation HLS Fund inception 4/30/2008 | |

| (advised by Hartford Funds Management Company, LLC) | |

| Investment Goal: Seeks high total return (including income and capital gains) consistent with preservation of capital over the long term. | |

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Asset Allocation HLS Fund IB | 23.40 | % | 14.88 | % | 6.94 | % | ||||||

| Barclays U.S. Aggregate Bond Index | -2.02 | % | 4.44 | % | 4.49 | % | ||||||

| S&P 500 Index | 32.39 | % | 17.94 | % | 7.59 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

Barclays U.S. Aggregate Bond Index represents the U.S. investment-grade fixed-rate bond market. This index is unmanaged, and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 0.86% and the gross total annual operating expense ratio for Class IB shares was 1.26%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Asset Allocation HLS Fund returned 23.40% for the twelve-month period ended December 31, 2013, versus the returns of 32.39% for the S&P 500 Index and -2.02% for the Barclays U.S. Aggregate Bond Index. The Fund outperformed the 19.17% average return of the Variable Products-Underlying Funds Lipper Mixed-Asset Target Allocation Growth Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Asset Allocation HLS Fund is directly related to the performance of the American Funds Insurance Series – Asset Allocation Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Asset Allocation Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Asset Allocation HLS Fund’s financial statements.

| 2 |

| American Funds Blue Chip Income and Growth HLS Fund inception 4/30/2008 | |

| (advised by Hartford Funds Management Company, LLC) | |

| Investment Goal: Seeks to produce income exceeding the average yield on U.S. stocks generally and to provide an opportunity for growth of principal consistent with sound common stock investing. | |

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Blue Chip Income and Growth HLS Fund IB | 32.55 | % | 16.24 | % | 6.50 | % | ||||||

| S&P 500 Index | 32.39 | % | 17.94 | % | 7.59 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.00% and the gross total annual operating expense ratio for Class IB shares was 1.50%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Blue Chip Income and Growth HLS Fund returned 32.55% for the twelve-month period ended December 31, 2013, versus the return of 32.39% for the S&P 500 Index. The Fund outperformed the 31.34% average return of the Variable Products-Underlying Funds Lipper Large-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Blue Chip Income and Growth HLS Fund is directly related to the performance of the American Funds Insurance Series – Blue Chip Income and Growth Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Blue Chip Income and Growth Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Blue Chip Income and Growth HLS Fund’s financial statements.

| 3 |

| American Funds Bond HLS Fund inception 4/30/2008 | |

| (advised by Hartford Funds Management Company, LLC) | |

| Investment Goal: Seeks to maximize current income and preservation of capital. | |

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Bond HLS Fund IB | -2.37 | % | 5.27 | % | 2.66 | % | ||||||

| Barclays U.S. Aggregate Bond Index | -2.02 | % | 4.44 | % | 4.49 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

Barclays U.S. Aggregate Bond Index represents the U.S. investment-grade fixed-rate bond market. This index is unmanaged, and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 0.93% and the gross total annual operating expense ratio for Class IB shares was 1.18%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Bond HLS Fund returned -2.37% for the twelve-month period ended December 31, 2013, versus the return of -2.02% for the Barclays U.S. Aggregate Bond Index. The Fund underperformed the -1.87% average return of the Variable Products-Underlying Funds Lipper Intermediate Investment Grade Debt Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Bond HLS Fund is directly related to the performance of the American Funds Insurance Series – Bond Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Bond Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Bond HLS Fund’s financial statements.

| 4 |

American Funds Global Bond HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

| Investment Goal: Seeks a high level of total return over the long term. |

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Global Bond HLS Fund IB | -3.03 | % | 4.19 | % | 3.41 | % | ||||||

| Barclays Global Aggregate Index | -2.60 | % | 3.91 | % | 3.47 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

Barclays Global Aggregate Index represents the global investment-grade fixed-income markets. This index is unmanaged and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.13% and the gross total annual operating expense ratio for Class IB shares was 1.63%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Global Bond HLS Fund returned -3.03% for the twelve-month period ended December 31, 2013, versus the return of -2.60% for the Barclays Global Aggregate Index. The Fund underperformed the -2.05% average return of the Variable Products-Underlying Funds Lipper Global Income Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Global Bond HLS Fund is directly related to the performance of the American Funds Insurance Series – Global Bond Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Global Bond Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Global Bond HLS Fund’s financial statements.

| 5 |

| American Funds Global Growth and Income HLS Fund inception 4/30/2008 | |

| (advised by Hartford Funds Management Company, LLC) | |

| Investment Goal: Seeks growth of capital over time and current income. | |

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Global Growth and Income HLS Fund IB | 22.16 | % | 16.10 | % | 4.41 | % | ||||||

| MSCI All Country World Index | 23.44 | % | 15.53 | % | 3.98 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

MSCI All Country World Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indices. This index is unmanaged, and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.17% and the gross total annual operating expense ratio for Class IB shares was 1.72%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

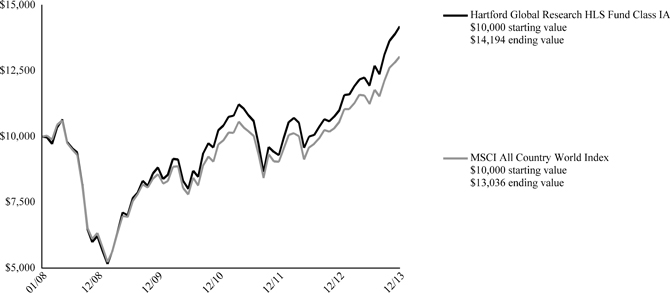

The Class IB shares of the American Funds Global Growth and Income HLS Fund returned 22.16% for the twelve-month period ended December 31, 2013, versus the return of 23.44% for the MSCI All Country World Index. The Fund underperformed the 26.58% average return of the Variable Products-Underlying Funds Lipper Global Multi-Cap Growth Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Global Growth and Income HLS Fund is directly related to the performance of the American Funds Insurance Series – Global Growth and Income Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Global Growth and Income Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Global Growth and Income HLS Fund’s financial statements.

| 6 |

American Funds Global Growth HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks long-term growth of capital.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Global Growth HLS Fund IB | 28.77 | % | 17.68 | % | 6.71 | % | ||||||

| MSCI All Country World Index | 23.44 | % | 15.53 | % | 3.98 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

MSCI All Country World Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indices. This index is unmanaged, and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.14% and the gross total annual operating expense ratio for Class IB shares was 1.89%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

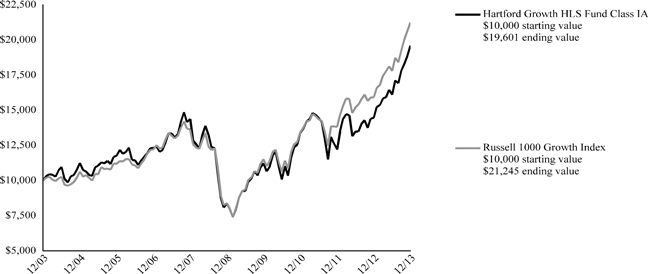

The Class IB shares of the American Funds Global Growth HLS Fund returned 28.77% for the twelve-month period ended December 31, 2013, versus the return of 23.44% for the MSCI All Country World Index. The Fund outperformed the 22.86% average return of the Variable Products-Underlying Funds Lipper Global Multi-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Global Growth HLS Fund is directly related to the performance of the American Funds Insurance Series – Global Growth Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Global Growth Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Global Growth HLS Fund’s financial statements.

| 7 |

American Funds Global Small Capitalization HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks growth of capital over time.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

| Average Annual Total Returns (as of 12/31/13) |

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Global Small Capitalization HLS Fund IB | 27.89 | % | 18.97 | % | 3.49 | % | ||||||

| MSCI All Country World Small Cap Index | 29.18 | % | 21.20 | % | 8.06 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

MSCI All Country World Small Cap Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance of smaller capitalization companies in both developed and emerging markets. This index is unmanaged and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.31% and the gross total annual operating expense ratio for Class IB shares was 1.86%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Global Small Capitalization HLS Fund returned 27.89% for the twelve-month period ended December 31, 2013, versus the return of 29.18% for the MSCI All Country World Small Cap Index. The Fund underperformed the 29.41% average return of the Variable Products-Underlying Funds Lipper Global Small/Mid-Cap Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Global Small Capitalization HLS Fund is directly related to the performance of the American Funds Insurance Series – Global Small Capitalization Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Global Small Capitalization Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Global Small Capitalization HLS Fund’s financial statements.

| 8 |

American Funds Growth HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks growth of capital.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

Average Annual Total Returns (as of 12/31/13)

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Growth HLS Fund IB | 29.78 | % | 19.09 | % | 6.23 | % | ||||||

| S&P 500 Index | 32.39 | % | 17.94 | % | 7.59 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 0.89% and the gross total annual operating expense ratio for Class IB shares was 1.39%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Growth HLS Fund returned 29.78% for the twelve-month period ended December 31, 2013, versus the return of 32.39% for the S&P 500 Index. The Fund underperformed the 34.00% average return of the Variable Products-Underlying Funds Lipper Large-Cap Growth Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Growth HLS Fund is directly related to the performance of the American Funds Insurance Series – Growth Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Growth Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Growth HLS Fund’s financial statements.

| 9 |

American Funds Growth-Income HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks long-term growth of capital and income over time.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

Average Annual Total Returns (as of 12/31/13)

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds Growth-Income HLS Fund IB | 33.14 | % | 17.29 | % | 6.69 | % | ||||||

| S&P 500 Index | 32.39 | % | 17.94 | % | 7.59 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 0.83% and the gross total annual operating expense ratio for Class IB shares was 1.28%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds Growth-Income HLS Fund returned 33.14% for the twelve-month period ended December 31, 2013, versus the return of 32.39% for the S&P 500 Index. The Fund outperformed the 31.34% average return of the Variable Products-Underlying Funds Lipper Large-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds Growth-Income HLS Fund is directly related to the performance of the American Funds Insurance Series – Growth-Income Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – Growth-Income Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds Growth-Income HLS Fund’s financial statements.

| 10 |

American Funds International HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks long-term growth of capital over time.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

Average Annual Total Returns (as of 12/31/13)

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds International HLS Fund IB | 21.23 | % | 13.29 | % | 2.28 | % | ||||||

| MSCI All Country World ex USA Index | 15.78 | % | 13.32 | % | 1.03 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

MSCI All Country World ex USA Index is a broad-based, unmanaged, market capitalization weighted, total return index that measures the performance of both developed and emerging stock markets, excluding the U.S. The index is calculated to exclude companies and share classes which cannot be freely purchased by foreigners.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.08% and the gross total annual operating expense ratio for Class IB shares was 1.68%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds International HLS Fund returned 21.23% for the twelve-month period ended December 31, 2013, versus the return of 15.78% for the MSCI All Country World ex USA Index. The Fund outperformed the 19.87% average return of the Variable Products-Underlying Funds Lipper International Multi-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds International HLS Fund is directly related to the performance of the American Funds Insurance Series – International Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – International Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds International HLS Fund’s financial statements.

| 11 |

American Funds New World HLS Fund inception 4/30/2008

(advised by Hartford Funds Management Company, LLC)

Investment Goal: Seeks long-term capital appreciation.

Performance Overview 4/30/08 - 12/31/13

The chart above represents the hypothetical growth of a $10,000 investment in Class 1B.

Average Annual Total Returns (as of 12/31/13)

| 1 Year | 5 Years | Since Inception▲ | ||||||||||

| American Funds New World HLS Fund IB | 11.06 | % | 14.43 | % | 2.93 | % | ||||||

| MSCI All Country World Index | 23.44 | % | 15.53 | % | 3.98 | % | ||||||

| MSCI Emerging Markets Index | -2.27 | % | 15.15 | % | -0.28 | % | ||||||

| ▲ | Inception: 04/30/2008 |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website at www.hartfordfunds.com.

Total returns presented above were calculated using the Fund’s net asset value available to shareholders for sale or redemption of Fund shares on December 31, 2013, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses.

MSCI All Country World Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indices. This index is unmanaged, and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

MSCI Emerging Markets Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance in the global emerging markets, consisting of 24 emerging market country indices. This index is unmanaged and its results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes.

You cannot invest directly in an index.

As of the Fund's current prospectus dated May 1, 2013, the net total annual operating expense ratio for Class IB shares was 1.35% and the gross total annual operating expense ratio for Class IB shares was 2.20%. Actual expenses may be higher. Please see the accompanying Financial Highlights for expense ratios for the year ended December 31, 2013.

Net operating expenses are the expenses paid to own the Fund. If the net operating expenses shown are lower than the gross operating expenses, then the net operating expenses reflect contractual fee waivers and expense reimbursements that may not be renewed. Contractual waivers or reimbursements remain in effect for as long as the Fund is a part of a master-feeder fund structure unless terminated or changed by the Fund or its Board of Directors if the fund structure changes. For more information about the fee arrangement and expiration dates, please see the expense table in the prospectus.

Gross operating expenses shown are before management fee waivers or expense caps. Performance information may reflect historical or current expense waivers or reimbursements, without which, performance would have been lower. For more information on fee waivers and/or expense reimbursements, please see the expense table in the prospectus.

The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable life insurance, variable annuity or qualified retirement plan product level. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance.

All investments are subject to risk including the possible loss of principal. For a discussion of the Fund’s risks, please see the Main Risks section of this report. For more detailed information on the risks associated with an investment in the Fund, please see the prospectus.

How did the Fund perform?

The Class IB shares of the American Funds New World HLS Fund returned 11.06% for the twelve-month period ended December 31, 2013, versus the returns of 23.44% for the MSCI All Country World Index and -2.27% for the MSCI Emerging Markets Index. The Fund outperformed the -0.14% average return of the Variable Products-Underlying Funds Lipper Emerging Markets Funds peer group, a group of funds with investment strategies similar to those of the Fund.

The performance of the American Funds New World HLS Fund is directly related to the performance of the American Funds Insurance Series – New World Fund Class 1, in which the Fund invests. The financial statements of the American Funds Insurance Series – New World Fund Class 1, including the Schedule of Investments, are provided in the accompanying report and should be read in conjunction with the American Funds New World HLS Fund’s financial statements.

| 12 |

| American Funds Asset Allocation HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 2,800 | American Funds Insurance Series - Asset Allocation Fund Class 1 | $ | 62,981 | |||||||||

| Total investment companies | ||||||||||||

| (cost $50,114) | $ | 62,981 | ||||||||||

| Total investments | ||||||||||||

| (cost $50,114) ▲ | 100.0 | % | $ | 62,981 | ||||||||

| Other assets and liabilities | — | % | (20 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 62,961 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $50,435 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 12,546 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 12,546 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 62,981 | ||

| Total | $ | 62,981 |

| American Funds Blue Chip Income and Growth HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 3,317 | American Funds Insurance Series - Blue Chip Income and Growth Fund Class 1 | $ | 43,521 | |||||||||

| Total investment companies | ||||||||||||

| (cost $31,861) | $ | 43,521 | ||||||||||

| Total investments | ||||||||||||

| (cost $31,861) ▲ | 100.0 | % | $ | 43,521 | ||||||||

| Other assets and liabilities | — | % | (19 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 43,502 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $32,455 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 11,066 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 11,066 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 43,521 | ||

| Total | $ | 43,521 |

The accompanying notes are an integral part of these financial statements.

| 13 |

| American Funds Bond HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 22,078 | American Funds Insurance Series - Bond Fund Class 1 | $ | 236,895 | |||||||||

| Total investment companies | ||||||||||||

| (cost $238,447) | $ | 236,895 | ||||||||||

| Total investments | ||||||||||||

| (cost $238,447) ▲ | 100.0 | % | $ | 236,895 | ||||||||

| Other assets and liabilities | — | % | (49 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 236,846 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $239,186 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | — | ||

| Unrealized Depreciation | (2,291 | ) | ||

| Net Unrealized Depreciation | $ | (2,291 | ) |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 236,895 | ||

| Total | $ | 236,895 |

| American Funds Global Bond HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.1% | ||||||||||||

| 1,433 | American Funds Insurance Series - Global Bond Fund Class 1 | $ | 17,021 | |||||||||

| Total investment companies | ||||||||||||

| (cost $17,560) | $ | 17,021 | ||||||||||

| Total investments | ||||||||||||

| (cost $17,560) ▲ | 100.1 | % | $ | 17,021 | ||||||||

| Other assets and liabilities | (0.1 | )% | (14 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 17,007 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $17,571 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | — | ||

| Unrealized Depreciation | (550 | ) | ||

| Net Unrealized Depreciation | $ | (550 | ) |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 17,021 | ||

| Total | $ | 17,021 |

The accompanying notes are an integral part of these financial statements.

| 14 |

| American Funds Global Growth and Income HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 4,208 | American Funds Insurance Series - Global Growth and Income Fund Class 1 | $ | 52,731 | |||||||||

| Total investment companies | ||||||||||||

| (cost $35,301) | $ | 52,731 | ||||||||||

| Total investments | ||||||||||||

| (cost $35,301) ▲ | 100.0 | % | $ | 52,731 | ||||||||

| Other assets and liabilities | — | % | (19 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 52,712 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $36,974 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 15,757 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 15,757 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 52,731 | ||

| Total | $ | 52,731 |

| American Funds Global Growth HLS Fund |

| Schedule of Investments |

December 31, 2013 (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.1% | ||||||||||||

| 814 | American Funds Insurance Series - Global Growth Fund Class 1 | $ | 24,524 | |||||||||

| Total investment companies | ||||||||||||

| (cost $16,229) | $ | 24,524 | ||||||||||

| Total investments | ||||||||||||

| (cost $16,229) ▲ | 100.1 | % | $ | 24,524 | ||||||||

| Other assets and liabilities | (0.1 | )% | (15 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 24,509 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $17,424 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation. | $ | 7,100 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 7,100 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 24,524 | ||

| Total | $ | 24,524 |

The accompanying notes are an integral part of these financial statements.

| 15 |

| American Funds Global Small Capitalization HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 2,384 | American Funds Insurance Series - Global Small Capitalization Fund Class 1 | $ | 61,247 | |||||||||

| Total investment companies | ||||||||||||

| (cost $43,306) | $ | 61,247 | ||||||||||

| Total investments | ||||||||||||

| (cost $43,306) ▲ | 100.0 | % | $ | 61,247 | ||||||||

| Other assets and liabilities | — | % | (23 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 61,224 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $45,340 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 15,907 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 15,907 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 61,247 | ||

| Total | $ | 61,247 |

| American Funds Growth HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 4,470 | American Funds Insurance Series - Growth Fund Class 1 | $ | 351,084 | |||||||||

| Total investment companies | ||||||||||||

| (cost $184,643) | $ | 351,084 | ||||||||||

| Total investments | ||||||||||||

| (cost $184,643) ▲ | 100.0 | % | $ | 351,084 | ||||||||

| Other assets and liabilities | — | % | (66 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 351,018 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $193,787 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 157,297 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 157,297 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 351,084 | ||

| Total | $ | 351,084 |

The accompanying notes are an integral part of these financial statements.

| 16 |

| American Funds Growth-Income HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 3,898 | American Funds Insurance Series - Growth-Income Fund Class 1 | $ | 197,730 | |||||||||

| Total investment companies | ||||||||||||

| (cost $113,342) | $ | 197,730 | ||||||||||

| Total investments | ||||||||||||

| (cost $113,342) ▲ | 100.0 | % | $ | 197,730 | ||||||||

| Other assets and liabilities | — | % | (41 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 197,689 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $117,212 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 80,518 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 80,518 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 197,730 | ||

| Total | $ | 197,730 |

| American Funds International HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 10,671 | American Funds Insurance Series - International Fund Class 1 | $ | 226,448 | |||||||||

| Total investment companies | ||||||||||||

| (cost $165,370) | $ | 226,448 | ||||||||||

| Total investments | ||||||||||||

| (cost $165,370) ▲ | 100.0 | % | $ | 226,448 | ||||||||

| Other assets and liabilities | — | % | (48 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 226,400 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $171,216 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 55,232 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 55,232 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 226,448 | ||

| Total | $ | 226,448 |

The accompanying notes are an integral part of these financial statements.

| 17 |

| American Funds New World HLS Fund |

| Schedule of Investments |

| December 31, 2013 |

| (000’s Omitted) |

| Shares | Market Value ╪ | |||||||||||

| INVESTMENT COMPANIES - 100.0% | ||||||||||||

| 1,368 | American Funds Insurance Series - New World Fund Class 1 | $ | 34,321 | |||||||||

| Total investment companies | ||||||||||||

| (cost $29,306) | $ | 34,321 | ||||||||||

| Total investments | ||||||||||||

| (cost $29,306) ▲ | 100.0 | % | $ | 34,321 | ||||||||

| Other assets and liabilities | — | % | (17 | ) | ||||||||

| Total net assets | 100.0 | % | $ | 34,304 | ||||||||

| Note: | Percentage of investments as shown is the ratio of the total market value to total net assets. |

| ▲ | At December 31, 2013, the cost of securities for federal income tax purposes was $29,851 and the aggregate gross unrealized appreciation and depreciation based on that cost were: |

| Unrealized Appreciation | $ | 4,470 | ||

| Unrealized Depreciation | — | |||

| Net Unrealized Appreciation | $ | 4,470 |

| ╪ | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

At December 31, 2013, the investment valuation hierarchy levels were:

| Assets: | ||||

| Investment in Securities - Level 1 | $ | 34,321 | ||

| Total | $ | 34,321 |

The accompanying notes are an integral part of these financial statements.

| 18 |

[This page is intentionally left blank]

| 19 |

| Hartford Series Fund, Inc. |

| Statements of Assets and Liabilities |

| December 31, 2013 |

| (000’s Omitted) |

|

| American Funds Asset Allocation HLS Fund | American Funds Blue Chip Income and Growth HLS Fund | American Funds Bond HLS Fund | ||||||||||

| Assets: | ||||||||||||

| Investments in underlying funds, at market value @ | $ | 62,981 | $ | 43,521 | $ | 236,895 | ||||||

| Receivables: | ||||||||||||

| Investment securities sold | 8 | 5 | 166 | |||||||||

| Fund shares sold | — | — | — | |||||||||

| Other assets | 6 | 5 | 13 | |||||||||

| Total assets | 62,995 | 43,531 | 237,074 | |||||||||

| Liabilities: | ||||||||||||

| Payables: | ||||||||||||

| Investment securities purchased | — | — | — | |||||||||

| Fund shares redeemed | 8 | 6 | 165 | |||||||||

| Investment management fees | 9 | 7 | 26 | |||||||||

| Distribution fees | 4 | 2 | 13 | |||||||||

| Accrued expenses | 13 | 14 | 24 | |||||||||

| Total liabilities | 34 | 29 | 228 | |||||||||

| Net assets | $ | 62,961 | $ | 43,502 | $ | 236,846 | ||||||

| Summary of Net Assets: | ||||||||||||

| Capital stock and paid-in-capital | $ | 37,382 | $ | 25,120 | $ | 230,028 | ||||||

| Undistributed net investment income | 672 | 648 | 3,495 | |||||||||

| Accumulated net realized gain | 12,040 | 6,074 | 4,875 | |||||||||

| Unrealized appreciation (depreciation) of investments | 12,867 | 11,660 | (1,552 | ) | ||||||||

| Net assets | $ | 62,961 | $ | 43,502 | $ | 236,846 | ||||||

| Shares authorized | 200,000 | 200,000 | 200,000 | |||||||||

| Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

| Class IB: Net asset value per share | $ | 12.63 | $ | 12.31 | $ | 9.75 | ||||||

| Shares outstanding | 4,986 | 3,535 | 24,304 | |||||||||

| Net assets | $ | 62,961 | $ | 43,502 | $ | 236,846 | ||||||

| @ Cost of investments in underlying funds | $ | 50,114 | $ | 31,861 | $ | 238,447 | ||||||

The accompanying notes are an integral part of these financial statements.

| 20 |

| American Funds Global Bond HLS Fund | American Funds Global Growth and Income HLS Fund | American Funds Global Growth HLS Fund | American Funds Global Small Capitalization HLS Fund | American Funds Growth HLS Fund | American Funds Growth-Income HLS Fund | American Funds International HLS Fund | American Funds New World HLS Fund | |||||||||||||||||||||||

| $ | 17,021 | $ | 52,731 | $ | 24,524 | $ | 61,247 | $ | 351,084 | $ | 197,730 | $ | 226,448 | $ | 34,321 | |||||||||||||||

| 2 | 30 | 9 | 35 | 197 | 110 | 176 | — | |||||||||||||||||||||||

| — | — | — | — | — | — | — | 3 | |||||||||||||||||||||||

| 2 | 6 | 4 | 7 | 39 | 20 | 30 | 6 | |||||||||||||||||||||||

| 17,025 | 52,767 | 24,537 | 61,289 | 351,320 | 197,860 | 226,654 | 34,330 | |||||||||||||||||||||||

| — | — | — | — | — | — | — | 3 | |||||||||||||||||||||||

| 2 | 30 | 9 | 35 | 197 | 110 | 176 | — | |||||||||||||||||||||||

| 3 | 9 | 6 | 11 | 58 | 30 | 42 | 8 | |||||||||||||||||||||||

| 1 | 3 | 1 | 3 | 19 | 11 | 12 | 2 | |||||||||||||||||||||||

| 12 | 13 | 12 | 16 | 28 | 20 | 24 | 13 | |||||||||||||||||||||||

| 18 | 55 | 28 | 65 | 302 | 171 | 254 | 26 | |||||||||||||||||||||||

| $ | 17,007 | $ | 52,712 | $ | 24,509 | $ | 61,224 | $ | 351,018 | $ | 197,689 | $ | 226,400 | $ | 34,304 | |||||||||||||||

| $ | 16,304 | $ | 19,617 | $ | 11,184 | $ | 39,058 | $ | 148,924 | $ | 92,128 | $ | 149,536 | $ | 22,922 | |||||||||||||||

| 13 | 1,526 | 196 | 171 | 2,087 | 1,910 | 2,228 | 330 | |||||||||||||||||||||||

| 1,229 | 14,139 | 4,834 | 4,054 | 33,566 | 19,263 | 13,558 | 6,037 | |||||||||||||||||||||||

| (539 | ) | 17,430 | 8,295 | 17,941 | 166,441 | 84,388 | 61,078 | 5,015 | ||||||||||||||||||||||

| $ | 17,007 | $ | 52,712 | $ | 24,509 | $ | 61,224 | $ | 351,018 | $ | 197,689 | $ | 226,400 | $ | 34,304 | |||||||||||||||

| 200,000 | 200,000 | 200,000 | 200,000 | 200,000 | 200,000 | 200,000 | 200,000 | |||||||||||||||||||||||

| $ | 0.001 | $ | 0.001 | $ | 0.001 | $ | 0.001 | $ | 0.001 | $ | 0.001 | $ | 0.001 | $ | 0.001 | |||||||||||||||

| $ | 9.66 | $ | 11.24 | $ | 12.56 | $ | 9.47 | $ | 13.09 | $ | 13.26 | $ | 10.27 | $ | 9.17 | |||||||||||||||

| 1,760 | 4,691 | 1,951 | 6,465 | 26,824 | 14,913 | 22,042 | 3,742 | |||||||||||||||||||||||

| $ | 17,007 | $ | 52,712 | $ | 24,509 | $ | 61,224 | $ | 351,018 | $ | 197,689 | $ | 226,400 | $ | 34,304 | |||||||||||||||

| $ | 17,560 | $ | 35,301 | $ | 16,229 | $ | 43,306 | $ | 184,643 | $ | 113,342 | $ | 165,370 | $ | 29,306 | |||||||||||||||

The accompanying notes are an integral part of these financial statements.

| 21 |

| Hartford Series Fund, Inc. |

| Statements of Operations |

| For the Year Ended December 31, 2013 |

| (000’s Omitted) |

|

| American Funds Asset Allocation HLS Fund | American Funds Blue Chip Income and Growth HLS Fund | American Funds Bond HLS Fund | ||||||||||

| Investment Income: | ||||||||||||

| Dividends from underlying funds | $ | 1,054 | $ | 893 | $ | 4,636 | ||||||

| Total investment income | 1,054 | 893 | 4,636 | |||||||||

| Expenses: | ||||||||||||

| Investment management fees | 451 | 323 | 1,047 | |||||||||

| Transfer agent fees | — | — | — | |||||||||

| Distribution fees - Class IB | 173 | 108 | 523 | |||||||||

| Custodian fees | — | — | — | |||||||||

| Accounting services fees | 7 | 4 | 21 | |||||||||

| Board of Directors' fees | 2 | 2 | 6 | |||||||||

| Audit fees | 11 | 10 | 12 | |||||||||

| Other expenses | 15 | 13 | 55 | |||||||||

| Total expenses (before waivers) | 659 | 460 | 1,664 | |||||||||

| Expense waivers | (277 | ) | (215 | ) | (523 | ) | ||||||