Table of Contents

OMB APPROVAL

OMB Number: 3235-0570

Expires: August 31, 2011

Estimated average burden hours per response: 18.9

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08895

ING Funds Trust

(Exact name of registrant as specified in charter)

| 7337 E. Doubletree Ranch Rd., Scottsdale, AZ | 85258 | |

| (Address of principal executive offices) | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | March 31 | |

Date of reporting period: | March 31, 2011 | |

Table of Contents

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Table of Contents

Annual Report

March 31, 2011

Classes A, B, C, I, O, R and W

Fixed-Income Funds

| n | ING GNMA Income Fund |

| n | ING High Yield Bond Fund |

| n | ING Intermediate Bond Fund |

| E-Delivery Sign-up – details inside |

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully.

MUTUAL FUNDS |

|

Table of Contents

| 1 | ||||

| 2 | ||||

| 4 | ||||

| 10 | ||||

| 12 | ||||

| 13 | ||||

| 15 | ||||

| 16 | ||||

| 18 | ||||

| 21 | ||||

| 38 | ||||

| 60 | ||||

| 61 | ||||

| 65 | ||||

| Go Paperless with E-Delivery! | | ||

Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs.

Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll.

You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail.

| ||||

PROXY VOTING INFORMATION

A description of the policies and procedures that the Funds use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Funds’ website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Funds’ website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. This report contains a summary portfolio of investments or portfolio of investments for the Funds. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Funds’ Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Funds’ Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Fund by calling Shareholder Services toll-free at (800) 992-0180.

Table of Contents

Living in Interesting Times

Dear Shareholder,

To say that the 12 months ended March 31, 2011 were eventful would be an understatement. During that time the global economic boat was rocked by market troubles, sovereign debt crises, natural and man-made disasters, doubts about the sustainability of U.S. economic growth and worries that the central banks might not be able to keep things on an even keel. The final three months of the period were perhaps the most volatile, with political upheavals in the Middle East and Libya, the earthquake and tsunami in Japan and renewed fears of a sovereign debt crisis in Europe.

Despite all these challenges, corporate earnings were robust and markets sailed on to deliver solid returns. Investors shifted between “safe-harbor” assets such as fixed income and commodities as the storms appeared, but returned to “risk assets” such as stocks and high yield bonds when the seas got smoother.

Any uncertainty about economic recovery in the United States seemed to be mitigated by encouraging data. After period-end, however, came another challenge: ratings agency Standard & Poor’s lowered its outlook for the U.S. to “negative,” a warning that the AAA rating on U.S. Treasuries might be cut in the future.

We’ve heard the arguments — possibly correct — that credit agency ratings are poor predictors of sovereign debt defaults, currency collapses and other financial crises. But that argument misses an important point: any suggestion that the U.S. might become a bad credit risk is a scary thought, not only for our pocketbook concerns but for our stature in the world.

Though few investors needed to be told that the country’s debt trajectory is unsustainable, the markets were spooked in the immediate aftermath of the announcement. Sentiment began climbing back by the end of the day, though, and continued to rally as corporations began another (so-far) impressive reporting season. Perhaps in the current milieu of extreme events, even the prospect of a fiscally weakening superpower has to be put into perspective; after all, the U.S. dollar is still the main refuge of safety-seeking investors around the globe.

Remember that the ebb and flow of current events is noise that will diminish over time; it should not distract you from your long-term goals. We can’t predict the next trouble spot, but we can hew to a well-defined investment plan. As we’ve noted many times before, it’s important to discuss any proposed changes thoroughly with your advisor before taking action. Thank you for your continued confidence in ING Funds. We look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

ING Funds

April 21, 2011

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and the ING Funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

For more complete information, or to obtain a prospectus for any ING Fund, please call your investment professional or ING Investments Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund’s investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this information and other information about the fund. Check with your investment professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

Table of Contents

MARKET PERSPECTIVE: YEAR ENDED MARCH 31, 2011

In our semi annual report we described markets, from stocks to bonds to currencies, continually buffeted by news and events relating to three main themes: the fitful US economic recovery, the sovereign debt crisis in the Eurozone and growth dynamics in China. Most equities markets were down slightly, while fixed income enjoyed 6% to 7% returns. But in the second half of our fiscal year risk appetite recovered despite the grave concerns that remained — and new crises that emerged.

In the U.S., attention seemed fixated on employment and housing. Since the latest recession ended in June 2009, the unemployment rate had been stuck between 9.4% and 10.1%. At last employment reports showed improvement to 9.0% in January and 8.9% in February. But economists were baffled by the restrained pace of job creation, averaging 136,000 in the latest three months, and by the labor force participation rate, at 64.2%, the lowest since March 1984.

In housing, sales of new and existing homes slumped after the expiry in April of a program of tax credits for home buyers and languished thereafter. House prices (based on the S&P/Case-Shiller 20-city Composite Index), having shown annual increases from February 2010 started falling again in October and our fiscal year ended with the index less than 1% above the trough recorded in May 2009.

Brighter spots domestically included gross domestic product (“GDP”) growth, which accelerated to 3.1% annualized in the fourth quarter of 2010, eight straight months of rising consumer spending and purchasing managers’ indices signaling the busiest manufacturing and service sectors in years. The Federal Reserve in November announced a second round of quantitative easing and would buy $600 billion in Treasury notes and bonds. The mixed mid-term election results forced a “compromise” stimulus package worth an estimated $858 billion for 2011.

Internationally however, the Eurozone sovereign debt crisis lingered. The bail-outs started in May with fiscally profligate Greece facing default on its bonds, followed by Ireland in November, its banks laid low by excessive lending on property. As our fiscal year ended, chronically low-growth Portugal, its government newly toppled and credit rating cut to barely investment grade, looked to be next. Meanwhile Eurozone leaders squabbled about a European Stability Mechanism, created to resolve the crisis once and for all.

Investors also watched nervously as China, having grown at 10.3% in 2010, displacing Japan as the world’s second largest economy and the U.S. as the world’s biggest manufacturer, wrestled to restrain inflation near 5% and a housing bubble, but also boost domestic consumption. The authorities increased banks’ reserve ratio requirements seven times, raised interest rates three times and resolved to raise the minimum wage on average by 13% annually through 2015.

Then in January, popular revolt erupted in North Africa. In short order dictatorships in Tunisia and Egypt fell, to be replaced by… no-one knew exactly what. By March Libya, a significant oil producer, was effectively in a civil war, with western allies joining the fray on the rebels’ side. Unrest spread to the Middle East and the price of oil, already on an upward trajectory as demand improved, firmly established itself above $100 per barrel.

As if this were not enough, a massive earthquake and tsunami hit Japan on March 11, causing perhaps $300 billion in local damage,

disruption of global supplies of electrical and digital components and possible nuclear fall-out.

In U.S. fixed income markets the Barclays Capital U.S. Aggregate Bond Index of investment grade bonds returned 5.12% in the fiscal year, with a small loss in the second half as risk appetite returned. Within this the Barclays Capital U.S. Treasury Index returned 4.53%, underperforming the 7.46% on the Barclays Capital Corporate Investment Grade Bond Index. Both outperformed the 4.37% return on the Barclays Capital U.S. Mortgage Backed Securities (“MBS”) Index, which lagged after the end of the Federal Reserve’s first round of quantitative easing targeted at mortgage backed securities. But all paled against the Barclays Capital High Yield Bond -2% Issuer Constrained Composite Index which gained an equity-like14.25%.

U.S. equities, represented by the S&P 500® Index including dividends, rose 15.65% in the 12 months through March 2011, including its best September since 1939 and best December since 1991. Prices were supported by strong earnings reports, with operating earnings per share for S&P 500® companies recording their fifth straight quarter of annual growth. Equities also benefited from improved risk appetite through the quantitative easing initiative and stimulus package referred to above.

In currencies, Eurozone angst during the fiscal year vied with pessimism about the dollar in a stalling economy and the perceived dollar-negative threat of another energy crisis. In the end the dollar fell 3.01% against the euro, 6.84% against the pound and 9.91% to the yen, which briefly made a post-war high in anticipation of yen repatriation to fund earthquake-related damage.

In international markets, based on MSCI indices in local currencies with reinvested dividends, the MSCI Japan® Index lost 10.02%, mostly after the earthquake struck. Despite generally favorable corporate earnings, declining export-dependent GDP and 24 months of falling prices also depressed sentiment. The MSCI Europe ex UK® Index returned 4.39%, with Germany up 14.14% and Ireland, Greece, Italy and Spain all falling, broadly reflecting the two-tier economy that had developed, with economic statistics favoring more soundly based countries at the expense of the peripherals. Powered by its sizeable materials and energy sectors, the MSCI UK® Index advanced 7.45%, defying the prospect of severe public spending cuts intended to eliminate an 11% budget deficit, a shock 0.5% quarterly fall in fourth quarter GDP and inflation rising to 4.4%.

Parentheses denote a negative number.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

2

Table of Contents

BENCHMARK DESCRIPTIONS

| Index | Description | |

| S&P/Case-Shiller 20-City Composite Home Price Index | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor’s. | |

| Barclays Capital U.S. Aggregate Bond Index | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |

| Barclays Capital U.S. Treasury Index | An unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded. | |

| Barclays Capital Corporate Investment Grade Bond Index | The corporate component of the Barclays Capital U.S. Credit Index. The U.S. Credit Index includes publicly-issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. The index includes both corporate and non-corporate sectors. The corporate sectors are industrial, utility and finance, which includes both U.S. and non-U.S. corporations. | |

| Barclays Capital U.S. MBS Index | An unmanaged index composed of fixed-income security mortgage pools sponsored by GNMA, FNMA and FHLMC, including GNMA Graduated Payment Mortgages. | |

| Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | An unmanaged index that includes all fixed income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |

| S&P 500® Index | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | |

| MSCI Japan® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan. | |

| MSCI Europe ex UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |

| MSCI UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |

| Barclays Capital Corporate High Yield Index | An unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment grade. |

3

Table of Contents

| ING GNMA INCOME FUND | PORTFOLIO MANAGERS’ REPORT |

Investment Type Allocation

as of March 31, 2011

(as a percent of net assets)

U.S. Government Agency Obligations | 105.1% | |||

Other Assets and Liabilities — Net | (5.1)% | |||

Net Assets | 100.0% | |||

Portfolio holdings are subject to change daily.

ING GNMA Income Fund (the “Fund”) seeks a high level of current income, consistent with liquidity and safety of principal, through investment primarily in Government National Mortgage Association (“GNMA”) mortgage-backed securities (also known as GNMA Certificates) that are guaranteed as to the timely payment of principal and interest by the U.S. government. The Fund is managed by Peter Guan, Jeff Dutra and Justin McWhorter, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

Securities issued by the U.S. Treasury are backed by the full faith and credit of the federal government. Securities issued by individual agencies and organizations may be backed by the full faith and credit of the federal government as to principal or interest but are not direct obligations of the U.S. Treasury. Securities of some agencies

and organizations are backed solely by the entity’s own resources or by the ability of the entity to borrow from the U.S. Treasury. Government securities also include certain mortgage-related securities that are sponsored by a U.S. government agency or organization and are not direct obligations of the U.S. government.

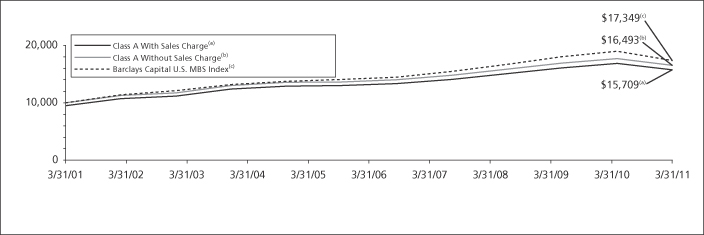

Performance: For the one year ended March 31, 2011, the Fund’s Class A shares, excluding sales charges, provided a total return of 5.26% compared to the Barclays Capital U.S. Mortgage-Backed Securities (“MBS”) Index which returned 4.37%, for the same period.

Portfolio Specifics: The portfolio was well positioned for an environment characterized by tight spreads and low rates, and took advantage the excess yield offered by premium securities. Despite historically low interest rates, higher coupon mortgages performed well due to relatively benign prepayments for most of the year. Additionally, GNMA mortgages benefitted from broad-based investor demand seeking explicit government credit guarantees. Finally, the Fund’s focus on securities with prepayment protection and high current income performed better than “generic” positions found in the index.

The fiscal year started with the conclusion of quantitative easing round one (QE 1): the dominating $1.5 billion mortgage-backed securities (“MBS”) purchase program by the U.S. Federal Reserve and U.S. Treasury department. Many investors fled mortgages toward the end of the program, expecting meaningful underperformance without government sponsorship. Mortgages spreads did not widen; instead they remained steadfast versus their U.S. Treasury equivalents as investors were flush with cash, underweight MBS exposure, and new supply of agency residential mortgage-backed securities (“RMBS”) remained light. For most of the year Ginnie Mae bonds outperformed agency MBS on broad-based support due to their explicit government guarantee and their superior prepayment experience.

Agency MBS showed some signs of stress in the middle of last year as persistently low interest rates ultimately led to an acceleration of prepayments for higher quality borrowers with home equity. Higher prepayments resulted in faster amortization of mortgage pools which, combined with high dollar prices, led to lower yields for investors. Mortgage securities repriced lower following this event. As 2010 ended the U.S. Treasury market demonstrated increased levels of volatility with 10-year Treasury rates rising 0.50% in December alone. “QE 2” was introduced to further support financial markets and keep mortgage rates relatively affordable. Mortgages weathered these events quite well and continued to provide investors with incremental yield.

As we close out this fiscal year, in our opinion, economic indicators point to modest improvements in the general economy and the elevated prepayment speeds experienced in fourth quarter 2010 have decreased substantially. We believe the market expects this decline in voluntary prepayments to continue as rates have returned to higher levels, housing prices continue to struggle and government stimulus programs fade. Throughout the year our security selection focused on MBS pools and collateralized mortgage obligations (“CMOs”) with implicit protection from prepays (newer pools whose prepayment risk is minimal for several months) and explicit protection (cash flows that are structurally locked out from near-term prepayments).

Current Strategy & Outlook: The housing market continues to struggle with prices expected to fall an additional 10% nationally over the next few quarters. To date, the government’s efforts to improve housing have been only modestly effective and further efforts to drive rates lower have had limited impact as mortgage rates are already at historically low levels. We believe foreclosure problems along with a weak job market are likely to weigh on the ability of non-prime borrowers and those without sufficient home equity to take full advantage of very low rates. These observations imply that only the best borrowers will continue to benefit from low rates and the divergence between good and marginal borrower prepayments will widen further.

With this in mind, we continue to manage the Fund seeking to benefit from high current income investments. The predominant focus remains on specified Ginnie Mae pools and CMOs that provide more attractive current income while minimizing prepayment risks. We are paying special attention to pools with lower loan balances, those with loans possessing more attractive credit characteristics and those that are sufficiently seasoned to reduce their prepayment sensitivity to interest rate movements. In addition, we will continue to seek Ginnie Mae CMOs that provide structural prepayment and extension protection.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

4

Table of Contents

| PORTFOLIO MANAGERS’ REPORT | ING GNMA INCOME FUND |

Average Annual Total Returns for the Periods Ended March 31, 2011 |

| |||||||||||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | Since | ||||||||||||||||||||||||

Including Sales Charge: | ||||||||||||||||||||||||||||

Class A(1) | 2.68 | % | 4.83 | % | 4.62 | % | — | — | ||||||||||||||||||||

Class B(2) | (0.52 | )% | 4.73 | % | 4.34 | % | — | — | ||||||||||||||||||||

Class C(3) | 3.38 | % | 5.05 | % | 4.35 | % | — | — | ||||||||||||||||||||

Class I | 5.57 | % | 6.16 | % | — | 5.35 | % | — | ||||||||||||||||||||

Class W | 5.51 | % | — | — | — | 6.31 | % | |||||||||||||||||||||

Excluding Sales Charge: | ||||||||||||||||||||||||||||

Class A | 5.26 | % | 5.85 | % | 5.13 | % | — | — | ||||||||||||||||||||

Class B | 4.48 | % | 5.06 | % | 4.34 | % | — | — | ||||||||||||||||||||

Class C | 4.38 | % | 5.05 | % | 4.35 | % | — | — | ||||||||||||||||||||

Class I | 5.57 | % | 6.16 | % | — | 5.35 | % | — | ||||||||||||||||||||

Class W | 5.51 | % | — | — | — | 6.31 | % | |||||||||||||||||||||

Barclays Capital U.S. MBS Index | 4.37 | % | 6.48 | % | 5.66 | % | 5.54 | %(4) | 6.20 | %(5) | ||||||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING GNMA Income Fund against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| (4) | Since inception performance for index is shown from January 1, 2002. |

| (5) | Since inception performance for index is shown from January 1, 2008. |

5

Table of Contents

| ING HIGH YIELD BOND FUND | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation

as of March 31, 2011

(as a percent of net assets)

Consumer Discretionary | 23.0% | |||

Energy | 13.9% | |||

Financials | 12.3% | |||

Telecommunication Services | 8.5% | |||

Health Care | 7.8% | |||

Industrials | 7.7% | |||

Materials | 6.1% | |||

Information Technology | 5.6% | |||

Consumer Staples | 5.4% | |||

Utilities | 2.6% | |||

Other Asset-Backed Securities | 0.7% | |||

Other Assets and Liabilities — Net* | 6.4% | |||

Net Assets | 100.0% | |||

| * | Includes short-term investments related to BlackRock Liquidity Funds, TempFund, Institutional Class. |

Portfolio holdings are subject to change daily.

ING High Yield Bond Fund (the “Fund”) seeks to provide investors with a high level of current income and total return. The Fund is managed by Randall Parrish, CFA, and Matthew Toms, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

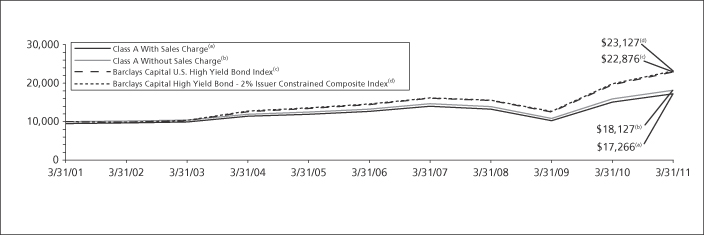

Performance: For the one year ended March 31, 2011, the Fund’s Class A shares, excluding sales charges, provided a total return of 14.22%, including a return of capital of $0.02 per share, compared to the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index and the Barclays Capital Corporate High Yield Index, which returned 14.26% and 14.31%, respectively, for the same period.

Portfolio Specifics: High yield bonds posted significant gains for the fiscal period, driven by tightening of credit spreads and by a QE-2-induced gain in Treasuries. Lower quality bonds outperformed higher quality, though the differential was less than one might expect in a strong market due to the Treasury gains. There was also limited dispersion of returns across industry sectors, with only electric utilities significantly lagging the overall market and most of the outperforming sectors driven by issuer-specific gains. We have begun in recent months to see early signs of excesses in the credit markets and a few re-leveraging transactions, but this is not yet widespread and remains at least offset by credit-positive events such as initial public offerings (IPOs) and debt retirement.

Our expectations for the past 12 months were generally fulfilled, as the U.S. economic recovery remained on track and corporate fundamentals

continued to improve. The high yield market return for the period exceeded our expectations, largely due to a more favorable interest rate environment than we anticipated. The Fund’s overweight to lower quality bonds helped performance as credit spreads narrowed. The Fund also benefited from several sector-specific positions. Of note, we were overweight television broadcasters, a group that benefited from both the general economic recovery and a record political ad season, and underweight electric utilities — specifically independent power producers — that suffered from weak power pricing fundamentals. The Fund also benefited from security selection across a range of sectors including metals and mining (overweight coal producers), energy (overweight oil, underweight natural gas), automotive (overweight suppliers that benefited from a rebound in domestic sales and production) and healthcare.

Current Strategy & Outlook: We continue to believe the U.S. economic recovery is on track, a view that is supported by signs of increased hiring activity. Issuer fundamentals continue to improve, as evidenced by 19 consecutive months of ratings upgrades exceeding downgrades. The combination of improving fundamentals and wide open capital markets has resulted in a virtual absence of defaults that is likely to persist beyond 2011. Credit spreads appear to offer more than adequate compensation for default risk in the longer term, though high dollar prices and low all-in yields limit potential upside. Potential threats to this scenario include unrest in the Middle East and resulting higher oil prices, heightened sovereign concerns and increased concerns about inflation or a tightening of U.S. monetary or fiscal policy.

In keeping with our view of economic recovery and improving credit fundamentals, we continue to maintain a slight cyclical bias and an overweight to single-B rated credits (underweight BBs), though we modestly reduced credit risk into market strength in the March quarter. We continue to maintain an overweight to the energy space — particularly oil-focused exploration and production companies, as well as an overweight to coal stocks and an underweight to utilities. We have reduced the Fund’s position in television broadcasters as this 2010 investment theme has played out.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

Top Ten Holdings*

as of March 31, 2011

(as a percent of net assets)

CCO Holdings LLC / CCO Holdings Capital Corp., | 1.3% | |||

Ally Financial, Inc., 8.000%, due 03/15/20 | 1.2% | |||

Ford Motor Credit Co., LLC, 8.125%, due 01/15/20 | 0.9% | |||

Cequel Communications Holdings I, LLC and Cequel Capital Corp., 8.625%, due 11/15/17 | 0.8% | |||

HCA, Inc., 7.875%, due 02/15/20 | 0.8% | |||

Caesars Entertainment Operating Co., Inc., | 0.8% | |||

Foresight Energy LLC / Foresight Energy Corp., | 0.7% | |||

Intelsat Luxembourg S.A., 11.500%, due 02/04/17 | 0.7% | |||

HCA, Inc., 7.250%, due 09/15/20 | 0.7% | |||

GSC Partners CDO Fund Ltd., 2.237%, due 12/16/15 | 0.7% |

| * | Excludes short-term investments related to BlackRock Liquidity Funds, TempFund, Institutional Class. |

Portfolio holdings are subject to change daily.

6

Table of Contents

| PORTFOLIO MANAGERS’ REPORT | ING HIGH YIELD BOND FUND |

Average Annual Total Returns for the Periods Ended March 31, 2011 |

| |||||||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | |||||||||||||||||||||

Including Sales Charge: | ||||||||||||||||||||||||

Class A(1) | 11.35 | % | 5.42 | % | 5.61 | % | — | |||||||||||||||||

Class B(2) | 8.35 | % | 5.34 | % | 5.34 | % | — | |||||||||||||||||

Class C(3) | 12.22 | % | 5.62 | % | 5.33 | % | — | |||||||||||||||||

Class I | 14.86 | % | — | — | 11.91 | % | ||||||||||||||||||

Excluding Sales Charge: | ||||||||||||||||||||||||

Class A | 14.22 | % | 6.44 | % | 6.13 | % | — | |||||||||||||||||

Class B | 13.35 | % | 5.63 | % | 5.34 | % | — | |||||||||||||||||

Class C | 13.22 | % | 5.62 | % | 5.33 | % | — | |||||||||||||||||

Class I | 14.86 | % | — | — | 11.91 | % | ||||||||||||||||||

Barclays Capital Corporate High Yield Index | 14.31 | % | 9.12 | % | 8.63 | % | 14.50 | %(4) | ||||||||||||||||

Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | 14.26 | % | 9.18 | % | 8.75 | % | 14.61 | %(4) | ||||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING High Yield Bond Fund against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s performance may be lower or higher than the performance data

shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| (4) | Since inception performance for the indices is shown from August 1, 2008. |

7

Table of Contents

| ING INTERMEDIATE BOND FUND | PORTFOLIO MANAGERS’ REPORT |

Investment Type Allocation

as of March 31, 2011

(as a percent of net assets)

Corporate Bonds/Notes | 41.0% | |||

U.S. Government Agency Obligations | 25.8% | |||

Collateralized Mortgage Obligations | 14.1% | |||

Asset-Backed Securities | 9.5% | |||

U.S. Treasury Obligations | 8.9% | |||

Foreign Government Bonds | 6.3% | |||

Preferred Stock | 0.3% | |||

Municipal Bonds | 0.1% | |||

Purchased Options | 0.1% | |||

Other Assets and Liabilities — Net* | (6.1)% | |||

Net Assets | 100.0% | |||

| * | Includes short-term investments related to BlackRock Liquidity Funds, TempFund, Institutional Class and securities lending collateral. |

Portfolio holdings are subject to change daily.

ING Intermediate Bond Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity. The Fund is managed by Christine Hurtsellers, Matthew Toms and Michael Mata, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

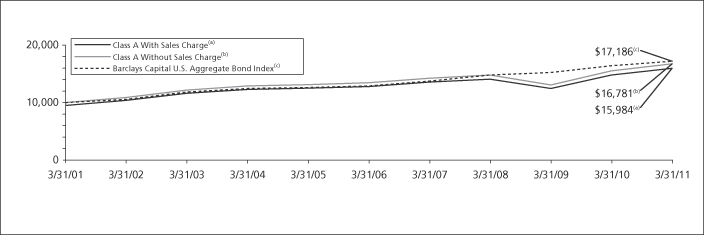

Performance: For the one year ended March 31, 2011, the Fund’s Class A shares, excluding sales charges, provided a total return of 8.00% compared to the Barclays Capital U.S. Aggregate Bond Index, which returned 5.12%, for the same period.

Portfolio Specifics: Our duration and yield curve positioning helped a bit in the first half of the year. Then our longer duration posture coming into the fourth quarter of 2010 detracted from performance materially, which led to an overall drag on performance for the Fund’s duration and yield curve positioning over the entire period. Futures, options and interest rate swaps were used in duration and yield curve management which in total had a slight negative relative return impact for the reporting period.

Sector allocation was a significant contributor to the Fund’s relative performance over the year. Outperformance of non-Treasury or spread sectors, where the Fund was overweight, helped results. Spread sectors such as high yield, commercial mortgage backed securities (“CMBS”) and investment grade credit outperformed as economic growth continued and risk assets moved higher in price. Our overweight allocations to these sectors consequently drove relative performance over the period. Underweight exposure to U.S. Treasury holdings and agency debentures, in order to fund spread allocations, helped performance. The Fund’s underweight to agency mortgages slightly hurt performance.

Security selection within investment grade corporate bonds, high yield, agency mortgages and CMBS were all significant contributors to the Fund’s outperformance throughout 2010, and as we began 2011. Our continued favoring of financials, industrials and cyclical

subsector issues among corporate bond holdings helped portfolio performance. Security selection was a contributor among asset-backed securities (“ABS”); however, it was a detractor within our allocation to U.S. Treasuries. Credit default swaps were used as part of our sector management and security selection which in total had a positive impact to the Fund’s relative outperformance of our benchmark.

Current Strategy & Outlook: As the Fund’s fiscal year comes to a close, we clearly see the global economy recovering at two speeds. Recovery in most emerging countries remains strong, while the recovery in developed markets is less pronounced. Even within developed countries, we see substantial variations in growth rates, with poor performance and bailouts occurring in peripheral Europe (Portugal, Italy, Ireland, Greece and Spain — referred to as the “PIIGS”). We see better, but still relatively weak economic growth in Japan, Great Britain and New Zealand. We believe Japan will recover from the tragic earthquake and tsunami. However, the country’s growth prospects, in our view, remain low and less than 1% over the next year. This leaves the United States, Canada, Australia and Germany as the bright spots among the developed countries.

Inflation pressure remains high in several emerging markets. The global outlook seems to be weighted to the downside, with tension in the Middle East, elevated oil prices, PIIGS still in trouble and growth in China slowing.

In the U.S., we have adjusted our growth forecast for first quarter gross domestic product (“GDP”) to 2-2.5%. This is in light of higher energy prices, instability in the Middle East and the impact following the natural disasters in Japan. However, we believe that several positive underpinnings remain that support an ongoing expansion in the U.S. The uptick in job growth (albeit slight) and decline in unemployment are positive for economic growth. The number of hours worked has also increased, which is positive for labor income. This, in turn, should help retail sales and the consumption component of GDP. Finally, interest rates remain relatively low, which reduces household debt obligations and supports balance sheet repair.

Continued expansion of the U.S. economy should support risk assets and could help them to perform well during the remainder of the year. Given this, the portfolio remains overweight to most spread sectors. In particular, we continue to like investment grade corporate credit and CMBS. Strong earnings and clean balance sheets make for attractive credit fundamentals of corporate debt. We also continue to overweight non-agency residential mortgage-backed securities, as we see their supply/demand technical factors remaining supportive and their underlying fundamentals as likely to continue to aid current valuations.

Agency mortgages continue to see good flows and demand. Interest rate volatility, news of the Treasury selling mortgages and convexity(1) selling have met with solid demand. Collectively, this has helped to keep periods of weakness contained and supportive for the asset class. Against this backdrop, the portfolio is slightly overweight the sector.

Elsewhere, credit fundamentals and technical factors remain positive for ABS. We are constructive in our view of the U.S. consumer and, reflecting this, the portfolio has an overweight to consumer-related ABS, such as credit card and auto receivables.

In off-Index sectors, we continue to see value in high yield and in emerging market debt (“EMD”). We believe the US economic expansion and strong corporate credit fundamentals are supportive for the high yield sector. In our opinion, corporate credit looks like it will continue to outperform as defaults remain low and we see no catalyst for a pick-up in defaults for 2011. Strong fundamentals remain intact in emerging markets. So far the political uncertainties in North Africa and Middle East remain mostly contained to regions and countries with modest direct economic impact to the markets. However, we continue to monitor this situation closely as we are with the situation in Japan. We are staying conservative in our sovereign and corporate selections in this space and favoring more liquid names and issues within this sector.

| (1) | Convexity is a measure of the rate at which duration changes as market interest rates change, and as a result a measure of the speed with which bond prices react to interest rate changes. |

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions. Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

Top Ten Holdings*

as of March 31, 2011

(as a percent of net assets)

Brazil Notas do Tesouro Nacional Series F, | 3.1% | |||

U.S. Treasury Note, 4.250%, due 11/15/40 | 2.6% | |||

U.S. Treasury Note, 3.625%, due 02/15/21 | 2.5% | |||

Federal Home Loan Mortgage Corporation, | 1.9% | |||

Federal National Mortgage Association, | 1.8% | |||

U.S. Treasury Note, 1.250%, due 03/15/14 | 1.8% | |||

Federal National Mortgage Association, | 1.7% | |||

MBNA Credit Card Master Note Trust, | 1.7% | |||

Federal Home Loan Mortgage Corporation, | 1.6% | |||

Mexican Udibonos, 4.000%, due 06/13/19 | 1.4% |

| * | Excludes short-term investments related to securities lending collateral. |

Portfolio holdings are subject to change daily.

8

Table of Contents

| PORTFOLIO MANAGERS’ REPORT | ING INTERMEDIATE BOND FUND |

Average Annual Total Returns for the Periods Ended March 31, 2011 |

| |||||||||||||||||||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | Since | Since | Since | ||||||||||||||||||||||||||||||

Including Sales Charge: | ||||||||||||||||||||||||||||||||||||

Class A(1) | 5.26 | % | 3.49 | % | 4.80 | % | — | — | — | — | ||||||||||||||||||||||||||

Class B(2) | 2.21 | % | 3.40 | % | 4.50 | % | — | — | — | — | ||||||||||||||||||||||||||

Class C(3) | 6.21 | % | 3.73 | % | 4.51 | % | — | — | — | — | ||||||||||||||||||||||||||

Class I | 8.35 | % | 4.83 | % | — | 5.14 | % | — | — | — | ||||||||||||||||||||||||||

Class O | 8.00 | % | 4.51 | % | — | — | 4.03 | % | — | — | ||||||||||||||||||||||||||

Class R | 7.72 | % | 4.23 | % | — | — | — | 3.51 | % | — | ||||||||||||||||||||||||||

Class W | 8.29 | % | — | — | — | — | — | 4.59 | % | |||||||||||||||||||||||||||

Excluding Sales Charge: | ||||||||||||||||||||||||||||||||||||

Class A | 8.00 | % | 4.51 | % | 5.31 | % | — | — | — | — | ||||||||||||||||||||||||||

Class B | 7.21 | % | 3.73 | % | 4.50 | % | — | — | — | — | ||||||||||||||||||||||||||

Class C | 7.21 | % | 3.73 | % | 4.51 | % | — | — | — | — | ||||||||||||||||||||||||||

Class I | 8.35 | % | 4.83 | % | — | 5.14 | % | — | — | — | ||||||||||||||||||||||||||

Class O | 8.00 | % | 4.51 | % | — | — | 4.03 | % | — | — | ||||||||||||||||||||||||||

Class R | 7.72 | % | 4.23 | % | — | — | — | 3.51 | % | — | ||||||||||||||||||||||||||

Class W | 8.29 | % | — | — | — | — | — | 4.59 | % | |||||||||||||||||||||||||||

Barclays Capital U.S. Aggregate Bond Index | 5.12 | % | 6.03 | % | 5.56 | % | 5.44 | %(4) | 5.25 | %(5) | 4.77 | %(6) | 5.57 | %(7) | ||||||||||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Intermediate Bond Fund against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| (4) | Since inception performance for index is shown from January 1, 2002. |

| (5) | Since inception performance for index is shown from August 1, 2004. |

| (6) | Since inception performance for index is shown from April 1, 2004. |

| (7) | Since inception performance for index is shown from January 1, 2008. |

9

Table of Contents

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from October 1, 2010 to March 31, 2011. The Funds’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The left section of the table shown below, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The right section of the table shown below, “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Actual Fund Return | Hypothetical (5% return before expenses) | |||||||||||||||||||||||||||||||

Beginning | Ending | Annualized | Expenses Paid | Beginning | Ending | Annualized | Expenses Paid | |||||||||||||||||||||||||

ING GNMA Income Fund |

| |||||||||||||||||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,013.50 | 0.93 | % | $ | 4.67 | $ | 1,000.00 | $ | 1,020.29 | 0.93 | % | $ | 4.68 | ||||||||||||||||

Class B | 1,000.00 | 1,009.70 | 1.68 | 8.42 | 1,000.00 | 1,016.55 | 1.68 | 8.45 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,008.70 | 1.68 | 8.41 | 1,000.00 | 1,016.55 | 1.68 | 8.45 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,015.00 | 0.63 | 3.16 | 1,000.00 | 1,021.79 | 0.63 | 3.18 | ||||||||||||||||||||||||

Class W | 1,000.00 | 1,014.70 | 0.68 | 3.42 | 1,000.00 | 1,021.54 | 0.68 | 3.43 | ||||||||||||||||||||||||

ING High Yield Bond Fund |

| |||||||||||||||||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,072.80 | 1.10 | % | $ | 5.68 | $ | 1,000.00 | $ | 1,019.45 | 1.10 | % | $ | 5.54 | ||||||||||||||||

Class B | 1,000.00 | 1,068.70 | 1.85 | 9.54 | 1,000.00 | 1,015.71 | 1.85 | 9.30 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,067.40 | 1.85 | 9.54 | 1,000.00 | 1,015.71 | 1.85 | 9.30 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,075.40 | 0.73 | 3.78 | 1,000.00 | 1,021.29 | 0.73 | 3.68 | ||||||||||||||||||||||||

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 182/365 to reflect the most recent fiscal half-year. |

10

Table of Contents

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| Actual Fund Return | Hypothetical (5% return before expenses) | |||||||||||||||||||||||||||||||

Beginning | Ending | Annualized | Expenses Paid | Beginning | Ending | Annualized | Expenses Paid | |||||||||||||||||||||||||

ING Intermediate Bond Fund |

| |||||||||||||||||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,008.60 | 0.68 | % | $ | 3.41 | $ | 1,000.00 | $ | 1,021.54 | 0.68 | % | $ | 3.43 | ||||||||||||||||

Class B | 1,000.00 | 1,005.80 | 1.43 | 7.15 | 1,000.00 | 1,017.80 | 1.43 | 7.19 | ||||||||||||||||||||||||

Class C | 1,000.00 | 1,005.80 | 1.43 | 7.15 | 1,000.00 | 1,017.80 | 1.43 | 7.19 | ||||||||||||||||||||||||

Class I | 1,000.00 | 1,010.20 | 0.38 | 1.90 | 1,000.00 | 1,023.04 | 0.38 | 1.92 | ||||||||||||||||||||||||

Class O | 1,000.00 | 1,009.70 | 0.68 | 3.41 | 1,000.00 | 1,021.54 | 0.68 | 3.43 | ||||||||||||||||||||||||

Class R | 1,000.00 | 1,007.30 | 0.93 | 4.65 | 1,000.00 | 1,020.29 | 0.93 | 4.68 | ||||||||||||||||||||||||

Class W | 1,000.00 | 1,010.00 | 0.43 | 2.15 | 1,000.00 | 1,022.79 | 0.43 | 2.17 | ||||||||||||||||||||||||

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 182/365 to reflect the most recent fiscal half-year. |

11

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Shareholders and Board of Trustees

ING Funds Trust

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments or summary portfolios of investments, as indicated, of ING GNMA Income Fund, ING High Yield Bond Fund, and ING Intermediate Bond Fund, each a series of ING Funds Trust, as of March 31, 2011, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of March 31, 2011, by correspondence with the custodian and brokers, or by other appropriate auditing procedures when replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the aforementioned funds as of March 31, 2011, and the results of their operations, the changes in their net assets, and the financial highlights for the periods specified in the first paragraph above, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

May 23, 2011

12

Table of Contents

STATEMENTS OF ASSETS AND LIABILITIES AS OF MARCH 31, 2011

ING GNMA Income Fund | ING High Yield Bond Fund | ING Intermediate Bond Fund | ||||||||||

ASSETS: | ||||||||||||

Investments in securities at value+* | $ | 824,601,202 | $ | 118,309,769 | $ | 795,221,709 | ||||||

Short-term investments at value** | — | 7,240,000 | 18,028,029 | |||||||||

Cash | 17,547,569 | 13,545 | 1,765,216 | |||||||||

Cash collateral for futures | — | — | 1,608,030 | |||||||||

Derivatives collateral (Note 2) | — | — | 1,124,000 | |||||||||

Foreign currencies at value*** | — | 13,424 | 1,605,951 | |||||||||

Receivables: | ||||||||||||

Investment securities sold | 1,983,268 | 250,850 | 17,617,103 | |||||||||

Investment securities sold on a delayed-delivery or when-issued basis | — | — | 28,206,852 | |||||||||

Fund shares sold | 849,878 | 129,005 | 762,928 | |||||||||

Dividends and interest | 3,825,497 | 2,505,050 | 6,912,152 | |||||||||

Unrealized appreciation on forward foreign currency contracts | — | — | 277,096 | |||||||||

Upfront payments made on swap agreements | — | — | 761,027 | |||||||||

Unrealized appreciation on swap agreements | — | — | 91,629 | |||||||||

Prepaid expenses | 47,895 | 43,051 | 58,373 | |||||||||

Total assets | 848,855,309 | 128,504,694 | 874,040,095 | |||||||||

LIABILITIES: | ||||||||||||

Payable for investment securities purchased | 1,167,122 | 1,257,288 | 23,319,616 | |||||||||

Payable for investment securities purchased on a delayed-delivery or when-issued basis | 61,253,682 | — | 79,118,398 | |||||||||

Payable for fund shares redeemed | 839,774 | 481,946 | 926,424 | |||||||||

Payable upon receipt of securities loaned | — | — | 17,095,000 | |||||||||

Unrealized depreciation on forward foreign currency contracts | — | — | 1,149,142 | |||||||||

Upfront payments received on swap agreements | — | — | 853,029 | |||||||||

Unrealized depreciation on swap agreements | — | — | 1,032,528 | |||||||||

Income distribution payable | — | 148,927 | 175,556 | |||||||||

Payable to affiliates | 604,025 | 102,452 | 339,123 | |||||||||

Payable for trustees fees | 4,040 | 582 | 3,930 | |||||||||

Other accrued expenses and liabilities | 232,064 | 104,437 | 324,918 | |||||||||

Written options, at fair value^ | — | — | 185,282 | |||||||||

Total liabilities | 64,100,707 | 2,095,632 | 124,522,946 | |||||||||

NET ASSETS | $ | 784,754,602 | $ | 126,409,062 | $ | 749,517,149 | ||||||

NET ASSETS WERE COMPRISED OF: | ||||||||||||

Paid-in capital | $ | 760,772,365 | $ | 165,216,298 | $ | 893,089,645 | ||||||

Undistributed (distributions in excess of) net investment income | 3,173,437 | (148,927 | ) | 20,849,573 | ||||||||

Accumulated net realized loss | (8,594,865 | ) | (47,037,827 | ) | (189,857,941 | ) | ||||||

Net unrealized appreciation | 29,403,665 | 8,379,518 | 25,435,872 | |||||||||

NET ASSETS | $ | 784,754,602 | $ | 126,409,062 | $ | 749,517,149 | ||||||

| ||||||||||||

+ Including securities loaned at value | $ | — | $ | — | $ | 16,762,640 | ||||||

* Cost of investments in securities | $ | 795,197,537 | $ | 109,930,768 | $ | 767,405,574 | ||||||

** Cost of short-term investments | $ | — | $ | 7,240,000 | $ | 18,694,000 | ||||||

*** Cost of foreign currencies | $ | — | $ | 12,907 | $ | 1,588,272 | ||||||

^ Premiums received on written options | $ | — | $ | — | $ | 138,744 | ||||||

See Accompanying Notes to Financial Statements

13

Table of Contents

STATEMENTS OF ASSETS AND LIABILITIESASOF MARCH 31, 2011 (CONTINUED)

ING GNMA Income Fund | ING High Yield Bond Fund | ING Intermediate Bond Fund | ||||||||||

Class A: | ||||||||||||

Net assets | $ | 593,080,019 | $ | 86,017,002 | $ | 315,999,882 | ||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 67,110,117 | 11,003,929 | 33,149,230 | |||||||||

Net asset value and redemption price per share | $ | 8.84 | $ | 7.82 | $ | 9.53 | ||||||

Maximum offering price per share (2.50%)(1) | $ | 9.07 | $ | 8.02 | $ | 9.77 | ||||||

Class B: | ||||||||||||

Net assets | $ | 11,262,318 | $ | 6,863,990 | $ | 9,378,956 | ||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 1,281,522 | 878,954 | 985,954 | |||||||||

Net asset value and redemption price per share(2) | $ | 8.79 | $ | 7.81 | $ | 9.51 | ||||||

Class C: | ||||||||||||

Net assets | $ | 104,196,036 | $ | 11,937,873 | $ | 33,994,317 | ||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 11,848,489 | 1,527,641 | 3,571,526 | |||||||||

Net asset value and redemption price per share(2) | $ | 8.79 | $ | 7.81 | $ | 9.52 | ||||||

Class I: | ||||||||||||

Net assets | $ | 68,995,622 | $ | 21,590,197 | $ | 332,193,292 | ||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 7,797,460 | 2,763,252 | 34,855,041 | |||||||||

Net asset value and redemption price per share | $ | 8.85 | $ | 7.81 | $ | 9.53 | ||||||

Class O: | ||||||||||||

Net assets | n/a | n/a | $ | 41,334,977 | ||||||||

Shares authorized | n/a | n/a | unlimited | |||||||||

Par value | n/a | n/a | $ | 0.001 | ||||||||

Shares outstanding | n/a | n/a | 4,334,556 | |||||||||

Net asset value and redemption price per share | n/a | n/a | $ | 9.54 | ||||||||

Class R: | ||||||||||||

Net assets | n/a | n/a | $ | 14,339,377 | ||||||||

Shares authorized | n/a | n/a | unlimited | |||||||||

Par value | n/a | n/a | $ | 0.001 | ||||||||

Shares outstanding | n/a | n/a | 1,502,297 | |||||||||

Net asset value and redemption price per share | n/a | n/a | $ | 9.54 | ||||||||

Class W: | ||||||||||||

Net assets | $ | 7,220,607 | n/a | $ | 2,276,348 | |||||||

Shares authorized | unlimited | n/a | unlimited | |||||||||

Par value | $ | 0.001 | n/a | $ | 0.001 | |||||||

Shares outstanding | 815,350 | n/a | 239,013 | |||||||||

Net asset value and redemption price per share | $ | 8.86 | n/a | $ | 9.52 | |||||||

| (1) | Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced. |

| (2) | Redemption price per share may be reduced for any applicable contingent deferred sales charges. |

See Accompanying Notes to Financial Statements

14

Table of Contents

STATEMENTS OF OPERATIONSFORTHE YEAR ENDED MARCH 31, 2011

ING GNMA Income Fund | ING High Yield Bond Fund | ING Intermediate Bond Fund | ||||||||||

INVESTMENT INCOME: | ||||||||||||

Dividends(1) | $ | — | $ | 7,655 | $ | 190,165 | ||||||

Interest, net of foreign taxes withheld* | 36,888,213 | 9,894,519 | 44,109,386 | |||||||||

Securities lending income, net | — | — | 30,314 | |||||||||

Total investment income | 36,888,213 | 9,902,174 | 44,329,865 | |||||||||

EXPENSES: | ||||||||||||

Investment management fees | 3,797,189 | 593,791 | 1,336,224 | |||||||||

Distribution and service fees: | ||||||||||||

Class A | 1,504,355 | 210,964 | 865,772 | |||||||||

Class B | 183,744 | 95,926 | 146,537 | |||||||||

Class C | 1,086,740 | 114,023 | 418,540 | |||||||||

Class O | — | — | 105,944 | |||||||||

Class R | — | — | 77,812 | |||||||||

Transfer agent fees: | ||||||||||||

Class A | 374,272 | 126,878 | 332,175 | |||||||||

Class B | 11,861 | 14,476 | 14,426 | |||||||||

Class C | 67,739 | 17,135 | 40,425 | |||||||||

Class I | 7,852 | 3,685 | 157,872 | |||||||||

Class O | — | — | 40,484 | |||||||||

Class R | — | — | 15,250 | |||||||||

Class W | 4,974 | — | 2,241 | |||||||||

Administrative service fees | 807,906 | 116,429 | 786,012 | |||||||||

Shareholder reporting expense | 67,599 | 11,587 | 62,115 | |||||||||

Registration fees | 98,510 | 84,501 | 107,991 | |||||||||

Professional fees | 79,491 | 12,584 | 63,071 | |||||||||

Custody and accounting expense | 96,986 | 22,163 | 160,855 | |||||||||

Trustee fees | 27,336 | 3,762 | 19,739 | |||||||||

Miscellaneous expense | 37,388 | 6,625 | 36,244 | |||||||||

Interest expense | — | 325 | 4,243 | |||||||||

Total expenses | 8,253,942 | 1,434,854 | 4,793,972 | |||||||||

Net recouped (waived and reimbursed) fees | — | (40,009 | ) | 37,746 | ||||||||

Net expenses | 8,253,942 | 1,394,845 | 4,831,718 | |||||||||

Net investment income | 28,634,271 | 8,507,329 | 39,498,147 | |||||||||

REALIZED AND UNREALIZED GAIN (LOSS): | ||||||||||||

Net realized gain (loss) on: | ||||||||||||

Investments | 6,946,705 | 4,791,701 | 27,376,800 | |||||||||

Foreign currency related transactions | — | — | (5,189,262 | ) | ||||||||

Futures | — | — | (3,913,986 | ) | ||||||||

Swaps | — | — | (1,807,626 | ) | ||||||||

Written options | — | — | 778,450 | |||||||||

Net realized gain | 6,946,705 | 4,791,701 | 17,244,376 | |||||||||

Net change in unrealized appreciation or depreciation on: | ||||||||||||

Investments | 3,703,788 | 2,145,736 | 4,209,708 | |||||||||

Foreign currency related transactions | — | 517 | (740,875 | ) | ||||||||

Futures | — | — | 293,525 | |||||||||

Swaps | — | — | 342,500 | |||||||||

Written options | — | — | (46,538 | ) | ||||||||

Net change in unrealized appreciation or depreciation | 3,703,788 | 2,146,253 | 4,058,320 | |||||||||

Net realized and unrealized gain | 10,650,493 | 6,937,954 | 21,302,696 | |||||||||

Increase in net assets resulting from operations | $ | 39,284,764 | $ | 15,445,283 | $ | 60,800,843 | ||||||

| ||||||||||||

* Foreign taxes withheld | $ | — | $ | — | $ | 1,530 | ||||||

(1) Dividends from affiliates | $ | — | $ | 5,813 | $ | 21,653 | ||||||

See Accompanying Notes to Financial Statements

15

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

ING GNMA Income Fund | ING High Yield Bond Fund | |||||||||||||||

Year Ended 2011 | Year Ended 2010 | Year Ended 2011 | Year Ended 2010 | |||||||||||||

FROM OPERATIONS: | ||||||||||||||||

Net investment income | $ | 28,634,271 | $ | 29,543,007 | $ | 8,507,329 | $ | 8,892,559 | ||||||||

Net realized gain (loss) | 6,946,705 | 5,839,917 | 4,791,701 | (3,193,568 | ) | |||||||||||

Net change in unrealized appreciation or depreciation | 3,703,788 | (287,645 | ) | 2,146,253 | 30,507,815 | |||||||||||

Increase in net assets resulting from operations | 39,284,764 | 35,095,279 | 15,445,283 | 36,206,806 | ||||||||||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||

Net investment income: | ||||||||||||||||

Class A | (24,627,310 | ) | (25,155,664 | ) | (6,170,719 | ) | (6,986,125 | ) | ||||||||

Class B | (637,962 | ) | (1,099,922 | ) | (641,089 | ) | (1,093,360 | ) | ||||||||

Class C | (3,671,286 | ) | (3,140,989 | ) | (746,145 | ) | (827,545 | ) | ||||||||

Class I | (3,133,728 | ) | (1,916,719 | ) | (798,345 | ) | (28,023 | ) | ||||||||

Class Q(1) | — | (2,079 | ) | — | — | |||||||||||

Class W | (346,694 | ) | (333,523 | ) | — | — | ||||||||||

Return of capital: | ||||||||||||||||

Class A | — | — | (181,532 | ) | (229,275 | ) | ||||||||||

Class B | — | — | (14,496 | ) | (38,943 | ) | ||||||||||

Class C | — | — | (25,403 | ) | (29,726 | ) | ||||||||||

Class I | — | — | (45,501 | ) | (1,015 | ) | ||||||||||

Total distributions | (32,416,980 | ) | (31,648,896 | ) | (8,623,230 | ) | (9,234,012 | ) | ||||||||

FROM CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

Net proceeds from sale of shares | 252,757,052 | 275,408,526 | 61,128,322 | 29,719,990 | ||||||||||||

Reinvestment of distributions | 27,473,342 | 26,412,537 | 6,221,442 | 5,568,334 | ||||||||||||

| 280,230,394 | 301,821,063 | 67,349,764 | 35,288,324 | |||||||||||||

Cost of shares redeemed | (282,047,139 | ) | (287,481,142 | ) | (55,515,327 | ) | (33,208,010 | ) | ||||||||

Net increase (decrease) in net assets resulting from |

| (1,816,745 | ) |

| 14,339,921 |

|

| 11,834,437 |

|

| 2,080,314 |

| ||||

Net increase in net assets | 5,051,039 | 17,786,304 | 18,656,490 | 29,053,108 | ||||||||||||

NET ASSETS: | ||||||||||||||||

Beginning of year | 779,703,563 | 761,917,259 | 107,752,572 | 78,699,464 | ||||||||||||

End of year | $ | 784,754,602 | $ | 779,703,563 | $ | 126,409,062 | $ | 107,752,572 | ||||||||

Undistributed (distributions in excess of) net investment income at end of year | $ | 3,173,437 | $ | 3,564,888 | $ | (148,927 | ) | $ | (305,010 | ) | ||||||

| ||||||||||||||||

(1) Effective November 20, 2009, Class Q shareholders of ING GNMA Income Fund converted into Class W shares of the Fund. |

| |||||||||||||||

See Accompanying Notes to Financial Statements

16

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

ING Intermediate Bond Fund | ||||||||

Year Ended March 31, 2011 | Year Ended March 31, 2010 | |||||||

FROM OPERATIONS: | ||||||||

Net investment income | $ | 39,498,147 | $ | 44,636,689 | ||||

Net realized gain (loss) | 17,244,376 | (32,149,489 | ) | |||||

Net change in unrealized appreciation or depreciation | 4,058,320 | 143,166,080 | ||||||

Increase in net assets resulting from operations | 60,800,843 | 155,653,280 | ||||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

Net investment income: | ||||||||

Class A | (15,674,008 | ) | (27,470,003 | ) | ||||

Class B | (566,077 | ) | (1,318,758 | ) | ||||

Class C | (1,594,653 | ) | (2,996,473 | ) | ||||

Class I | (15,443,401 | ) | (23,534,860 | ) | ||||

Class O | (1,909,958 | ) | (2,840,820 | ) | ||||

Class R | (664,621 | ) | (1,102,439 | ) | ||||

Class W | (113,308 | ) | (164,336 | ) | ||||

Total distributions | (35,966,026 | ) | (59,427,689 | ) | ||||

FROM CAPITAL SHARE TRANSACTIONS: | ||||||||

Net proceeds from sale of shares | 183,546,425 | 145,033,805 | ||||||

Reinvestment of distributions | 29,932,608 | 47,744,888 | ||||||

| 213,479,033 | 192,778,693 | |||||||

Cost of shares redeemed | (279,861,986 | ) | (468,048,167 | ) | ||||

Net decrease in net assets resulting from capital share transactions | (66,382,953 | ) | (275,269,474 | ) | ||||

Net decrease in net assets | (41,548,136 | ) | (179,043,883 | ) | ||||

NET ASSETS: | ||||||||

Beginning of year | 791,065,285 | 970,109,168 | ||||||

End of year | $ | 749,517,149 | $ | 791,065,285 | ||||

Undistributed net investment income at end of year | $ | 20,849,573 | $ | 21,509,983 | ||||

See Accompanying Notes to Financial Statements

17

Table of Contents

+

Selected data for a share of beneficial interest outstanding throughout each year or period.

| Income (loss) from investment operations | Less distributions | Ratios to average net assets | Supplemental data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) on investments | Total from investment operations | From net investment income | From net realized gains | From return of capital | Total distributions | Net asset value, end of year or period | Total Return(1) | Expenses before reductions/additions(2)(3) | Expenses net of fee waivers and/or recoupments, if any(2)(3) | Expenses net of all reductions/additions(2)(3) | Net investment income (loss)(2)(3) | Net assets, end of year or period | Portfolio turnover rate | |||||||||||||||||||||||||||||||||||||||||||||||||

Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | (%) | (%) | (%) | (%) | ($000’s) | (%) | ||||||||||||||||||||||||||||||||||||||||||||||||

ING GNMA Income Fund | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class A | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

03-31-11 | 8.75 | 0.32 | 0.13 | 0.45 | 0.36 | — | — | 0.36 | 8.84 | 5.26 | 0.93 | 0.93 | 0.93 | 3.63 | 593,080 | 193 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-10 | 8.71 | 0.33 | • | 0.07 | 0.40 | 0.36 | — | — | 0.36 | 8.75 | 4.68 | 0.94 | 0.94 | 0.94 | 3.83 | 589,813 | 114 | |||||||||||||||||||||||||||||||||||||||||||||||

03-31-09 | 8.54 | 0.37 | 0.18 | 0.55 | �� | 0.38 | — | — | 0.38 | 8.71 | 6.62 | 0.96 | 0.96 | 0.96 | 4.33 | 606,856 | 39 | |||||||||||||||||||||||||||||||||||||||||||||||

03-31-08 | 8.35 | 0.37 | 0.20 | 0.57 | 0.38 | — | — | 0.38 | 8.54 | 7.00 | 0.96 | 0.96 | 0.96 | 4.45 | 515,916 | 32 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-07 | 8.30 | 0.37 | 0.09 | 0.46 | 0.41 | — | — | 0.41 | 8.35 | 5.72 | 0.95 | 0.94 | 0.94 | 4.49 | 515,469 | 99 | ||||||||||||||||||||||||||||||||||||||||||||||||

Class B | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

03-31-11 | 8.70 | 0.26 | • | 0.13 | 0.39 | 0.30 | — | — | 0.30 | 8.79 | 4.48 | 1.68 | 1.68 | 1.68 | 2.90 | 11,262 | 193 | |||||||||||||||||||||||||||||||||||||||||||||||

03-31-10 | 8.66 | 0.27 | • | 0.06 | 0.33 | 0.29 | — | — | 0.29 | 8.70 | 3.89 | 1.69 | 1.69 | 1.69 | 3.08 | 25,704 | 114 | |||||||||||||||||||||||||||||||||||||||||||||||

03-31-09 | 8.49 | 0.30 | 0.18 | 0.48 | 0.31 | — | — | 0.31 | 8.66 | 5.86 | 1.71 | 1.71 | 1.71 | 3.57 | 38,718 | 39 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-08 | 8.30 | 0.31 | 0.19 | 0.50 | 0.31 | — | — | 0.31 | 8.49 | 6.24 | 1.71 | 1.71 | 1.71 | 3.70 | 45,963 | 32 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-07 | 8.26 | 0.30 | 0.09 | 0.39 | 0.35 | — | — | 0.35 | 8.30 | 4.84 | 1.70 | 1.69 | 1.69 | 3.73 | 58,568 | 99 | ||||||||||||||||||||||||||||||||||||||||||||||||

Class C | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

03-31-11 | 8.71 | 0.25 | 0.13 | 0.38 | 0.30 | — | — | 0.30 | 8.79 | 4.38 | 1.68 | 1.68 | 1.68 | 2.88 | 104,196 | 193 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-10 | 8.67 | 0.27 | • | 0.06 | 0.33 | 0.29 | — | — | 0.29 | 8.71 | 3.92 | 1.69 | 1.69 | 1.69 | 3.09 | 103,103 | 114 | |||||||||||||||||||||||||||||||||||||||||||||||

03-31-09 | 8.50 | 0.30 | 0.18 | 0.48 | 0.31 | — | — | 0.31 | 8.67 | 5.88 | 1.71 | 1.71 | 1.71 | 3.59 | 73,209 | 39 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-08 | 8.31 | 0.31 | 0.20 | 0.51 | 0.32 | — | — | 0.32 | 8.50 | 6.23 | 1.71 | 1.71 | 1.71 | 3.70 | 36,218 | 32 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-07 | 8.27 | 0.31 | 0.08 | 0.39 | 0.35 | — | — | 0.35 | 8.31 | 4.85 | 1.70 | 1.69 | 1.69 | 3.73 | 37,280 | 99 | ||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

03-31-11 | 8.76 | 0.34 | 0.14 | 0.48 | 0.39 | — | — | 0.39 | 8.85 | 5.57 | 0.63 | 0.63 | 0.63 | 3.92 | 68,996 | 193 | ||||||||||||||||||||||||||||||||||||||||||||||||

03-31-10 | 8.72 | 0.36 | • | 0.07 | 0.43 | 0.39 | — | — | 0.39 | 8.76 | 5.00 | 0.64 | 0.64 | 0.64 | 4.15 | 52,880 | 114 | |||||||||||||||||||||||||||||||||||||||||||||||