UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-10263

GuideStone Funds

(Exact name of registrant as specified in charter)

2401 Cedar Springs Road

Dallas, TX 75201-1407

(Address of principal executive offices) (Zip code)

Rodney R. Miller, Esq.

GuideStone Financial Resources of the Southern Baptist Convention

2401 Cedar Springs Road

Dallas, TX 75201-1407

(Name and address of agent for service)

Registrant’s telephone number, including area code: 214-720-2142

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

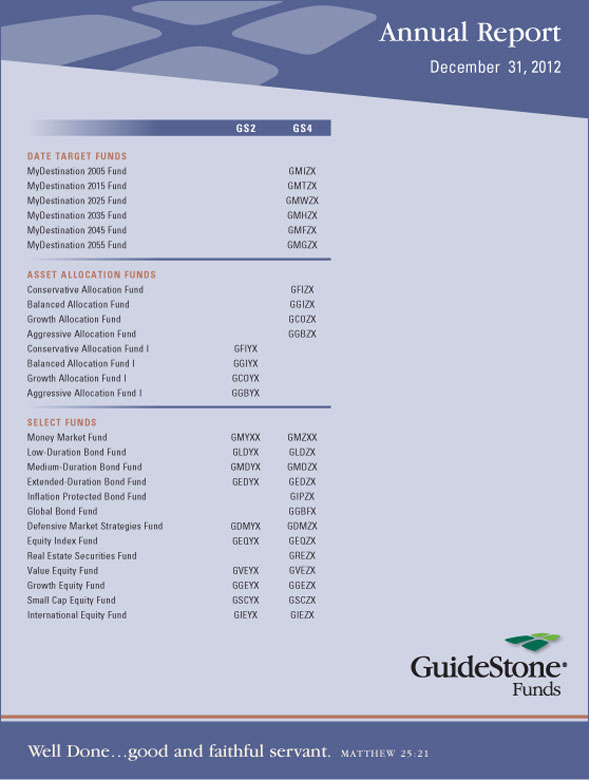

Annual Report

December 31, 2012

Gs2

Gs4

DATE TARGET FunDs

MyDestination 2005 Fund

GMIZX

MyDestination 2015 Fund

GMTZX

MyDestination 2025 Fund

GMWZX

MyDestination 2035 Fund

GMHZX

MyDestination 2045 Fund

GMFZX

MyDestination 2055 Fund

GMGZX

AssET AllocATion FunDs

Conservative Allocation Fund

GFIZX

Balanced Allocation Fund

GGIZX

Growth Allocation Fund

GCOZX

Aggressive Allocation Fund

GGBZX

Conservative Allocation Fund I

GFIYX

Balanced Allocation Fund I

GGIYX

Growth Allocation Fund I

GCOYX

Aggressive Allocation Fund I

GGBYX

sElEcT FunDs

Money Market Fund

GMYXX

GMZXX

Low-Duration Bond Fund

GLDYX

GLDZX

Medium-Duration Bond Fund

GMDYX

GMDZX

Extended-Duration Bond Fund

GEDYX

GEDZX

Inflation Protected Bond Fund

GIPZX

Global Bond Fund

GGBFX

Defensive Market Strategies Fund

GDMYX

GDMZX

Equity Index Fund

GEQYX

GEQZX

Real Estate Securities Fund

GREZX

Value Equity Fund

GVEYX

GVEZX

Growth Equity Fund

GGEYX

GGEZX

Small Cap Equity Fund

GSCYX

GSCZX

International Equity Fund

GIEYX

GIEZX

GuideStone Funds

Privacy Notice

NOTICE CONCERNING YOUR PRIVACY RIGHTS

This notice will provide you with information concerning our policies with respect to nonpublic personal information that we collect about you in connection with the following financial products and services provided and/or serviced by the entities listed below: individual retirement accounts (“IRAs”) and/or personal mutual fund accounts.

The confidentiality of your information is important to us as we recognize that you depend on us to keep your information confidential, as described in this notice.

We collect nonpublic personal information about you with regard to your IRA and/or personal mutual fund accounts from the following sources:

| | • | | Information we receive from you on applications or other forms; |

| | • | | Information about your transactions with us, our affiliates or others (including our third-party service providers); |

| | • | | Information we receive from others such as service providers, broker-dealers and your personal agents or representatives; and |

| | • | | Information you and others provide to us in correspondence sent to us, whether written, electronic or by telephone. |

We may disclose such nonpublic personal financial information about you to one or more of our affiliates as permitted by law. An affiliate of an organization means any entity that controls, is controlled by or is under common control with that organization. GuideStone Funds, GuideStone Financial Resources of the Southern Baptist Convention (“GuideStone Financial Resources”), GuideStone Capital Management (“GSCM”), GuideStone Trust Services (“GSTS”), GuideStone Financial Services (“GFS”) and GuideStone Advisors (“GA”) are affiliates of one another. GuideStone Funds, GuideStone Financial Resources, GSCM, GSTS, GFS, GA and Foreside Funds Distributors LLC do not sell your personal information to nonaffiliated third parties.

We may also disclose any of the personal information that we collect about you to nonaffiliated third parties as permitted by law. For example, we may provide your information to nonaffiliated companies that provide account services or that perform marketing services on our behalf and to other financial institutions with whom we have joint marketing agreements. We restrict access to nonpublic personal information about you to those of our employees who need to know that information in order for us to provide products and services to you. We also maintain physical, electronic and procedural safeguards to guard your personal information.

These procedures will continue to remain in effect after you cease to receive financial products and services from us.

If you have any questions concerning our customer information policy, please contact a customer relations specialist at 1-888-98-GUIDE (1-888-984-8433).

TABLE OF CONTENTS

This report has been prepared for shareholders of GuideStone Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current prospectus, which contains more complete information about the Funds. Investors are reminded to read the prospectus carefully before investing. Past performance is no guarantee of future results. Share prices will fluctuate and there may be a gain or loss when shares are redeemed. Fund shares are distributed by Foreside Funds Distributors LLC, 400 Berwyn Park, 899 Cassatt Road, Berwyn, PA 19312.

1

LETTER FROM THE PRESIDENT

Dear Shareholder:

We are pleased to present you with the 2012 GuideStone Funds Annual Report. This report reflects our unwavering commitment to integrity in financial reporting; we believe this helps you stay fully informed of your investments. We hope that you will find this information valuable when making investment decisions.

During the first quarter of 2012, GuideStone Funds became the first Christian-based, socially screened fund family to win the Lipper Award for Best Overall Small Fund Group in the U.S., ranking No. 1 out of 182 fund families with up to $40 billion in assets. This notable achievement speaks to the investment expertise of GuideStone Capital Management and its multi-manager investment process.

Since winning the Lipper award, we have continued to augment the products and services delivered to our shareholders. Several examples of our ongoing commitment are noted below:

We have made it easier to invest with GuideStone Funds. Investors may now open a GuideStone Funds personal investment account, traditional IRA or Roth IRA online. Enrollment specialists are also available by phone to assist with rollovers and transfers from other financial institutions.

We have updated your tax forms to reflect changes in cost basis reporting. Investors who sold or exchanged shares within personal investment accounts will receive an IRS Form 1099-B. This form will now report the adjusted cost basis and the holding period for covered shares purchased after January 1, 2012.

We have added additional online tools to track investment performance. Our dynamic, interactive charts allow investors to track the growth of a hypothetical $10,000 investment into any GuideStone Fund. Additionally, investors may explore the chart’s other features which include timing of dividend payments, broad market index comparisons and Morningstar® Ratings.

We invite you to learn more about the new products and services offered by GuideStone Funds. Please visit our website at www.GuideStoneFunds.org or contact us at 1-888-98-GUIDE (1-888-984-8433). Thank you for entrusting GuideStone Funds with your investment assets, and we look forward to continuing to serve you.

| | |

| Sincerely, |

|

|

|

John R. Jones, CFA President |

2

GuideStone Funds shares are distributed by Foreside Funds Distributors LLC, not an advisor affiliate.

For each fund with at least a three-year history, a Morningstar Rating is based on a Morningstar risk-adjusted return measure that accounts for variation in a fund’s monthly historical performance (reflecting sales charges and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. Within each asset class, the top 10%, the next 22.5%, 35%, 22.5%, and the bottom 10% receive 5, 4, 3, 2 or 1 star, respectively. Each fund is rated exclusively against U.S. domiciled funds. The Overall Morningstar Rating™ is based on the weighted average of the number of stars assigned to the fund’s applicable time periods. The 5-yr. rating accounts for 60% and the 3-yr. rating for 40%.

Lipper Inc., a Reuters Company, is a nationally-recognized organization that compares the performance of mutual funds having similar investment objectives. The comparison is made across registered mutual funds, ranking the funds with similar objectives according to total returns. These investment returns are calculated after operating expenses have been deducted from each fund, but the rankings do not take sales charges into account. Lipper rankings are subject to change monthly, and past rankings are no guarantee of future results. Lipper ranked 16 out of 20 GuideStone Funds (GS4 class) above median for the five-year period as of December 31, 2012.

About the Best Overall Small Company Lipper Award: GuideStone Funds ranked No. 1 out of 182 eligible companies in the small company category. To be considered for the Small Company Lipper award, companies must have at least three distinct portfolios in each of the following asset classes-equity, bond, or mixed-asset as well as at least 36 months of performance history as of the end of the calendar year of the respective evaluation year. The overall group award is given to the group with the lowest average decile ranking for Lipper’s Consistent Return measure of its respective asset class results over the three-year period. All rankings are for the three-year period as of November 30, 2011. In cases of identical results the lower average percentile rank will determine the winner. Lipper, a wholly owned subsidiary of Reuters, is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries, and media organizations. ©2011 Lipper a subsidiary of Thomson Reuters.

3

FROM THE CHIEF INVESTMENT OFFICER

| | |

Rodric E. Cummins, CFA | | Youngsters learn at an early age that the most basic fundamental in baseball is to “keep your eye on the ball,” despite the pressures and distractions of the game situation. In 2012, there was plenty of noise to distract investors from the fundamentals of investing, not the least of which was the political fury in the fourth quarter. In the face of the world’s large-scale debt and economic problems, investment markets surprised on the upside with an exceptional year. Positive economic growth, historically low interest rates, and calming assurances from global central banks provided a rich environment for investors in financial assets. Disciplined investors that maintained a well-diversified portfolio of risky assets, such as stocks and low quality bonds, were well rewarded. |

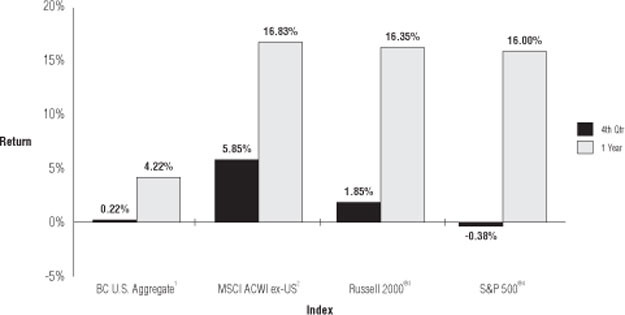

Non-U.S. markets led global stocks higher during the fourth quarter with the MSCI ACWI Ex-U.S. returning 5.85%, pushing the 2012 annual return to a very impressive 16.83%. U.S. stocks posted similar returns for the year as the Russell 3000® Index was up 16.42%. Interest rates continued to fall and credit spreads narrowed, resulting in solid gains for bonds. The Barclays Capital U.S. Aggregate Bond Index returned 4.22% for the year. More risky segments of the bond market, such as long maturity bonds and high yield bonds, produced double-digit returns.

Global economies remain mired in a long-term deleveraging phase, putting enormous strains on financial systems and policymakers in efforts to reduce debt. In an economic sense, one man’s expenses are another man’s income, so reducing spending in an effort to reduce debt naturally constrains economic growth. Fragile economic conditions promote volatility in the capital markets, which will most certainly continue into 2013. Volatility is further amplified by political systems that are called upon for thoughtful and timely decision-making. The risk of unintended policy mistakes is very real, as investors have learned in Japan over the past two decades. Yet, a well-managed deleveraging phase by policymakers can create an environment in which financial assets do very well, as we have seen in the U.S. beginning in 2009. This is a unique and challenging period for all investors, one that can produce a wide range of outcomes over short time periods for risk-based portfolios. We believe that well-diversified portfolios will continue to serve investors well, so long as investors can maintain a steady hand and a long-term perspective on risk taking. Very conservative investors may experience less volatility, but with interest rates at 100-year lows, these portfolios will struggle to offset the effects of inflation.

Each and every day across financial markets around the world, our investment process scours the globe in search for the best investment ideas for your portfolio. It is a highly disciplined process that never sleeps: it is built upon the foundation of strong intellectual capital and experience that is disbursed globally, sorting fact from noise; and it is a process that is not distracted by complex market conditions. In short, we are very intentional about keeping our eye on the ball and delivering to you industry leading investment management services.

As we turn the corner into a new year, we want to express our thankfulness for the opportunity to serve you, our customer, in the important task of managing your investment portfolio. Thank you for your trust and Happy New Year from the team at GuideStone.

*This report may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to GuideStone Funds, market or regulatory developments. The views expressed are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed are subject to change at any time based upon economic, market, or other conditions and GuideStone Funds undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed (including any forward-looking statement) may not be relied upon as investment advice or as an indication of GuideStone Funds’ trading intent.

4

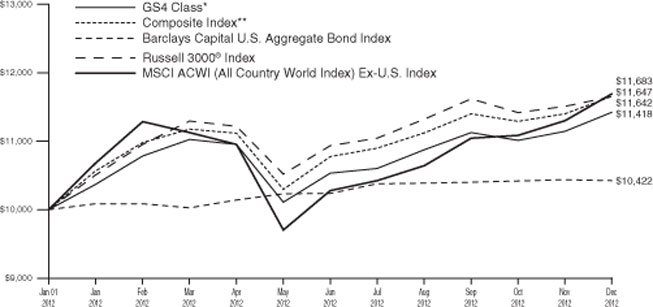

|

| Asset Class Performance Comparison |

The following graph illustrates the performance of the major assets classes during 2012.

1The Barclays Capital U.S. Aggregate Bond Index represents securities that are SEC-registered, taxable and dollar denominated. The index covers the U.S. investment grade bond market, with index components for government and corporate securities, mortgage pass-through securities and asset-backed securities.

2The MSCI ACWI (All Country World Index) Ex-U.S. Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed (excluding the United States) and emerging markets.

3The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure that larger stocks do not distort the performance and characteristics of the actual small-cap opportunity set.

4The S&P 500® Index is an unmanaged index (with no defined investment objective) of common stocks, includes reinvestment of dividends and is a registered trademark of McGraw-Hill Co., Inc. The S&P 500® Index includes 500 of the largest stocks (in terms of market value) in the United States.

5

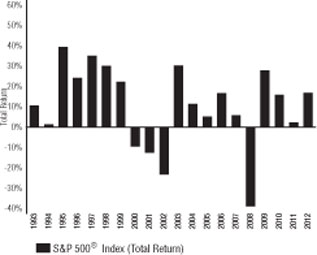

S&P 500® Index Returns

The U.S. large cap equity market, as represented by the S&P 500® Index, posted a positive annual return of 16%. This was the fourth consecutive year of positive results and ninth out of the last ten years. Similar to last year, the start of this year was generally positive, peaking in early April, up about 13% year to date at that time. However, the large cap market pulled back sharply over the next two months until reaching the low point for the year in early June, down almost 10% during this short period. From this point until year-end, this index rallied by approximately 13% to finish the year on a positive note. The best performing sectors in this index this calendar year were Financials, Consumer Discretionary and Telecommunications. The sectors in the index that lagged the most this year were Utilities, Energy and Consumer Staples. Factors such as higher beta, higher price-to-earnings, lower return on equity and smaller market capitalization made the largest positive contributions to performance this year.

The S&P 500® Index includes 500 leading companies in major industries of the U.S. economy. The index represents about 75% of U.S. equity market capitalization. It is a capitalization-weighted index calculated on a total return basis with dividends reinvested. Constituents are selected by a team of Standard & Poor’s economists and analysts.

Data Source: Bloomberg and S&P website

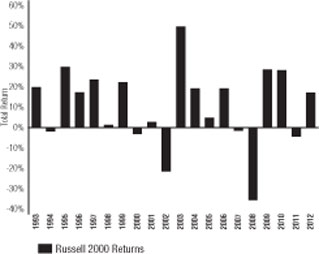

Russell 2000® Index Returns

The U.S. small cap equity market, as represented by the Russell 2000® Index, posted a positive return of 16.35% for the year. This was another volatile year with the index getting off to a good start, peaking in late March, up over 14% year to date at that time. However, the small cap market pulled back noticeably afterwards and bottomed in early June, down almost 13% over this short period. From this point until year-end, this index rallied by approximately 16% to finish the year strong. Two of last year’s worst performing sectors, Materials & Processing and Consumer Discretionary, in this index reversed course in 2012 and were the two best performers for this calendar year along with Financials. The sectors in the index that lagged the most this year were Energy, Technology and Utilities. Factors such as lower beta, lower price-to-earnings and smaller market capitalization made the largest positive contributions to performance this year.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure that larger stocks do not distort the performance and characteristics of the actual small-cap opportunity set.

Data Source: Russell Investments

6

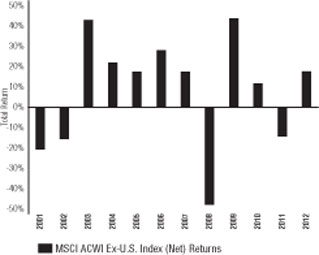

MSCI ACWI Ex-U.S. Index (Net) Returns

The non-U.S. equity market, as represented by the MSCI ACWI Ex-U.S. Index (net), posted a positive return of 16.83% for the year. However, this was a volatile year for international equity markets. The year started with a very positive tone and this index was up over 13% by mid-March. However, non-U.S. markets in aggregate pulled back sharply over the next couple of months due to increasing concerns over Greece and the Euro debt crisis. As a result of these headline issues, this index sold off almost 16% from mid-March until early June. At this juncture, strong assurances made by the European Central Bank helped to calm investors and from this point forward until year-end, this index gained some positive traction and rallied by approximately 23% from its early June low point. The best performing markets during this calendar year were Turkey, Egypt and the Philippines. The markets which did the worst were Morocco, Israel and Brazil. The sectors that led performance results this year were Financials and Consumer Discretionary. The sectors in the index that lagged the most this year were Energy, Utilities and Telecommunications.

The MSCI ACWI (All Country World Index) Ex-U.S. Index is designed to provide a broad measure of stock performance in both developed and emerging markets, excluding the U.S. This index is comprised of approximately 1,800 stocks ranging across 23 developed, non-U.S. equity markets and 21 emerging markets countries. This market capitalization-weighted index is maintained by Morgan Stanley Capital International and represents approximately 85% of the global equity opportunity set outside of the U.S.

Data Source: Factset, MSCI

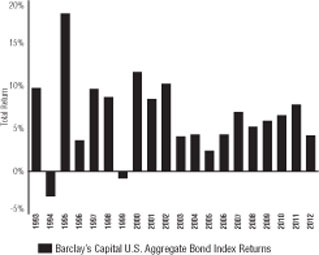

Barclays Capital U.S. Aggregate Bond Index Returns

The broad U.S. bond market, as measured by the Barclays Capital U.S. Aggregate Bond Index, posted a positive return of 4.21% for the year. Areas of the market that performed the best consisted of debt securities that possessed the following characteristics: longer maturity, corporate issued and lower credit quality. Also, commercial mortgage-backed securities did quite well during this period. Corporate bonds benefitted from improving underlying corporate fundamentals, strong balance sheets, cash positions and high demand (investors’ seeking higher yielding securities). Investors’ preference for income yield replaced their appetite for risk aversion and this change in sentiment versus a year ago increased downward pressure on U.S. Treasury securities relative to riskier corporate bonds.

The Barclays Capital U.S. Aggregate Bond Index is a broad-based benchmark representing approximately 8,200 U.S. dollar-denominated, taxable fixed income securities. To be included in this market capitalization-weighted index, bonds must be rated investment grade quality by Moody’s and Standard & Poor’s and have a maturity of at least one year. The types of fixed income instruments in this index primarily consist of U.S. Treasury securities, government-related securities, mortgage-backed securities, asset-backed securities and corporate bonds.

Data Source: Factset

7

Federal Reserve

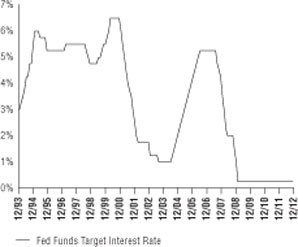

The Federal Reserve (“Fed”) maintained the same targeted Fed Funds level of 0-0.25% for the fourth consecutive year. Although the Fed formally met to review this rate level on eight separate occasions during the year, no meaningful action on changing this rate was taken. The last time an action was taken was December 2008 when the Fed cut rates to their current levels. The Fed maintained an accommodative monetary policy stance throughout the year as unemployment levels had remained elevated, and inflation had been fairly muted. The Fed accomplished this objective by extending the average maturity of its holdings of U.S. Treasury securities through the “Operation Twist” program announced last year. Additionally, the Fed injected liquidity into the financial system through its purchases of agency mortgage-backed securities at a rate of $40 billion per month through the end of the year. In mid-December, the Fed announced that it intends to keep the target range at this level of 0-0.25% as long as the unemployment rate remains above 6.5%, inflation is below 2.5% and longer term inflation expectations “continue to be well anchored”. Previous guidance from the Fed expressed its belief that the federal funds rate could likely remain at current levels until mid-2015. This change in the Fed’s attempt at expressing specific guideposts was intended to be more helpful to investors than it had been in the past. The Fed will continue to closely monitor economic and financial developments in its efforts to foster maximum employment and price stability.

The Federal Reserve (“Fed”) is the central bank of the United States. It was created by Congress to provide the nation with a safer, more flexible, and more stable monetary and financial system. The Federal Funds Rate is the interest rate at which depository institutions lend balances at the Fed to other depository institutions overnight. The rate is one tool the Fed can use in their efforts of controlling the supply of money. Changes in the Federal Funds Rate trigger a chain of events that affect other short-term interest rates, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services.

Data Source: Bloomberg, Federal Reserve

U.S. Treasury Yield Curve

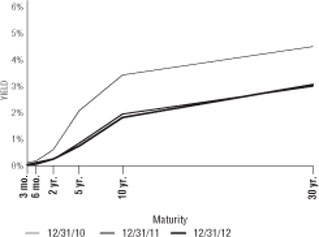

Short-term rates remained at historically low levels as the Federal Reserve (the “Fed”), through its aggressively accommodative monetary policy, maintained the target federal funds rate at 0-0.25% in an effort to stimulate economic growth all year long. The very short end of the curve where the maturity is less than two years remained basically unchanged again this year. Starting at the 5-year maturity level and longer, there was some minimal reduction in yield levels as the yield curve flattened marginally compared to the end of 2011. At year-end 2012, yields on the 2-year, 5-year, 10-year and 30-year U.S. Treasury securities were 0.25%, 0.72%, 1.76% and 2.95%, respectively.

The Treasury yield curve illustrates the relationship between yields on short-term, intermediate-term and long-term Treasury securities. Normally, the shape of the yield curve is upward sloping with rates increasing from the short end of the curve moving higher to the long end. The short end of the curve is impacted more by monetary policy (demand for money) while inflationary expectations and market forces impact the long end of the curve.

Data Source: Bloomberg

8

About Your Expenses

As a shareholder of the Funds, you incur ongoing costs, including advisory fees and to the extent applicable, shareholder services fees, as well as other Fund expenses. This example is intended to help you to understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. It is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2012 to December 31, 2012.

Actual Expenses

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses attributable to your investment during this period.

Hypothetical Example for Comparison Purposes

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. Thus, you should not use the hypothetical account values and expenses to estimate the actual ending account balance or your expenses for the period. Rather, these figures are provided to enable you to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only. Therefore, the second section of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | | | | | | | | | | | | | | | |

Actual |

Fund | | Class | | Beginning

Account Value

07/01/12 | | Ending

Account Value

12/31/12 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

MyDestination 2005 | | | | GS4 | | | | $ | 1,000.00 | | | | $ | 1,040.43 | | | | | 0.20 | % | | | $ | 1.03 | |

MyDestination 2015 | | | | GS4 | | | | | 1,000.00 | | | | | 1,053.89 | | | | | 0.15 | | | | | 0.75 | |

MyDestination 2025 | | | | GS4 | | | | | 1,000.00 | | | | | 1,067.53 | | | | | 0.15 | | | | | 0.75 | |

MyDestination 2035 | | | | GS4 | | | | | 1,000.00 | | | | | 1,085.07 | | | | | 0.20 | | | | | 1.05 | |

MyDestination 2045 | | | | GS4 | | | | | 1,000.00 | | | | | 1,085.56 | | | | | 0.20 | | | | | 1.05 | |

MyDestination 2055 | | | | GS4 | | | | | 1,000.00 | | | | | 1,084.31 | | | | | 0.20 | | | | | 1.05 | |

Conservative Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,033.08 | | | | | 0.12 | | | | | 0.61 | |

Balanced Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,059.34 | | | | | 0.12 | | | | | 0.62 | |

Growth Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,079.54 | | | | | 0.12 | | | | | 0.63 | |

Aggressive Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,095.40 | | | | | 0.12 | | | | | 0.63 | |

Conservative Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,034.20 | | | | | 0.15 | | | | | 0.79 | |

Balanced Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,061.41 | | | | | 0.13 | | | | | 0.69 | |

Growth Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,080.79 | | | | | 0.15 | | | | | 0.78 | |

Aggressive Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,096.51 | | | | | 0.15 | | | | | 0.79 | |

Money Market | | | | GS2 | | | | | 1,000.00 | | | | | 1,000.47 | | | | | 0.19 | | | | | 0.94 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,000.08 | | | | | 0.27 | | | | | 1.35 | |

Low-Duration Bond | | | | GS2 | | | | | 1,000.00 | | | | | 1,020.04 | | | | | 0.36 | | | | | 1.83 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,018.72 | | | | | 0.57 | | | | | 2.89 | |

Medium-Duration Bond | | | | GS2 | | | | | 1,000.00 | | | | | 1,033.83 | | | | | 0.48 | | | | | 2.45 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,032.88 | | | | | 0.63 | | | | | 3.22 | |

9

About Your Expenses (Continued)

| | | | | | | | | | | | | | | | | | | | | | | | | |

Actual |

Fund | | Class | | Beginning

Account Value

07/01/12 | | Ending

Account Value

12/31/12 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

Extended-Duration Bond | | | | GS2 | | | | $ | 1,000.00 | | | | $ | 1,071.77 | | | | | 0.52 | % | | | $ | 2.72 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,069.30 | | | | | 0.75 | | | | | 3.90 | |

Inflation Protected Bond | | | | GS4 | | | | | 1,000.00 | | | | | 1,025.01 | | | | | 0.64 | | | | | 3.28 | |

Global Bond | | | | GS4 | | | | | 1,000.00 | | | | | 1,068.27 | | | | | 0.81 | | | | | 4.19 | |

Defensive Market Strategies (3) | | | | GS2 | | | | | 1,000.00 | | | | | 1,035.44 | | | | | 1.04 | | | | | 5.33 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,034.15 | | | | | 1.30 | | | | | 6.66 | |

Equity Index | | | | GS2 | | | | | 1,000.00 | | | | | 1,060.65 | | | | | 0.23 | | | | | 1.19 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,059.90 | | | | | 0.38 | | | | | 1.97 | |

Real Estate Securities | | | | GS4 | | | | | 1,000.00 | | | | | 1,025.20 | | | | | 1.05 | | | | | 5.33 | |

Value Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,083.84 | | | | | 0.67 | | | | | 3.49 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,082.13 | | | | | 0.91 | | | | | 4.76 | |

Growth Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,053.84 | | | | | 0.86 | | | | | 4.44 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,052.83 | | | | | 1.05 | | | | | 5.44 | |

Small Cap Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,078.07 | | | | | 1.00 | | | | | 5.21 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,076.57 | | | | | 1.19 | | | | | 6.23 | |

International Equity (3) | | | | GS2 | | | | | 1,000.00 | | | | | 1,146.55 | | | | | 1.13 | | | | | 6.08 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,144.28 | | | | | 1.37 | | | | | 7.37 | |

|

HYPOTHETICAL (assuming a 5% return before expenses) |

Fund | | Class | | Beginning

Account Value

07/01/12 | | Ending

Account Value

12/31/12 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

MyDestination 2005 | | | | GS4 | | | | $ | 1,000.00 | | | | $ | 1,024.13 | | | | | 0.20 | % | | | $ | 1.02 | |

MyDestination 2015 | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.40 | | | | | 0.15 | | | | | 0.74 | |

MyDestination 2025 | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.41 | | | | | 0.15 | | | | | 0.74 | |

MyDestination 2035 | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.13 | | | | | 0.20 | | | | | 1.02 | |

MyDestination 2045 | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.13 | | | | | 0.20 | | | | | 1.02 | |

MyDestination 2055 | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.13 | | | | | 0.20 | | | | | 1.02 | |

Conservative Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.53 | | | | | 0.12 | | | | | 0.61 | |

Balanced Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.53 | | | | | 0.12 | | | | | 0.61 | |

Growth Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.53 | | | | | 0.12 | | | | | 0.61 | |

Aggressive Allocation | | | | GS4 | | | | | 1,000.00 | | | | | 1,024.53 | | | | | 0.12 | | | | | 0.61 | |

Conservative Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,024.36 | | | | | 0.15 | | | | | 0.79 | |

Balanced Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,024.47 | | | | | 0.13 | | | | | 0.67 | |

Growth Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,024.38 | | | | | 0.15 | | | | | 0.76 | |

Aggressive Allocation I | | | | GS2 | | | | | 1,000.00 | | | | | 1,024.38 | | | | | 0.15 | | | | | 0.76 | |

Money Market | | | | GS2 | | | | | 1,000.00 | | | | | 1,024.20 | | | | | 0.19 | | | | | 0.95 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,023.79 | | | | | 0.27 | | | | | 1.36 | |

Low-Duration Bond | | | | GS2 | | | | | 1,000.00 | | | | | 1,023.33 | | | | | 0.36 | | | | | 1.83 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,022.27 | | | | | 0.57 | | | | | 2.89 | |

Medium-Duration Bond | | | | GS2 | | | | | 1,000.00 | | | | | 1,022.72 | | | | | 0.48 | | | | | 2.44 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,021.97 | | | | | 0.63 | | | | | 3.20 | |

Extended-Duration Bond | | | | GS2 | | | | | 1,000.00 | | | | | 1,022.51 | | | | | 0.52 | | | | | 2.65 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,021.37 | | | | | 0.75 | | | | | 3.81 | |

Inflation Protected Fund | | | | GS4 | | | | | 1,000.00 | | | | | 1,021.90 | | | | | 0.64 | | | | | 3.27 | |

10

| | | | | | | | | | | | | | | | | | | | | | | | | |

HYPOTHETICAL (assuming a 5% return before expenses) |

Fund | | Class | | Beginning

Account Value

07/01/12 | | Ending

Account Value

12/31/12 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

Global Bond | | | | GS4 | | | | $ | 1,000.00 | | | | $ | 1,021.09 | | | | | 0.81 | % | | | $ | 4.09 | |

Defensive Market Strategies (3) | | | | GS2 | | | | | 1,000.00 | | | | | 1,019.90 | | | | | 1.04 | | | | | 5.29 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,018.59 | | | | | 1.30 | | | | | 6.61 | |

Equity Index | | | | GS2 | | | | | 1,000.00 | | | | | 1,023.98 | | | | | 0.23 | | | | | 1.17 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,023.23 | | | | | 0.38 | | | | | 1.93 | |

Real Estate Securities Fund | | | | GS4 | | | | | 1,000.00 | | | | | 1,019.87 | | | | | 1.05 | | | | | 5.31 | |

Value Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,021.78 | | | | | 0.67 | | | | | 3.39 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,020.57 | | | | | 0.91 | | | | | 4.62 | |

Growth Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,020.82 | | | | | 0.86 | | | | | 4.37 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,019.84 | | | | | 1.05 | | | | | 5.35 | |

Small Cap Equity | | | | GS2 | | | | | 1,000.00 | | | | | 1,020.13 | | | | | 1.00 | | | | | 5.06 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,019.14 | | | | | 1.19 | | | | | 6.06 | |

International Equity (3) | | | | GS2 | | | | | 1,000.00 | | | | | 1,019.47 | | | | | 1.13 | | | | | 5.72 | |

| | | | GS4 | | | | | 1,000.00 | | | | | 1,018.27 | | | | | 1.37 | | | | | 6.93 | |

| (1) | Expenses include the effect of contractual waivers by GuideStone Capital Management. The Date Target Funds’ and Asset Allocation Funds’ proportionate share of the operating expenses of the Select Funds is not reflected in the tables above. |

| (2) | Expenses are equal to the Fund’s annualized expense ratios for the period July 1, 2012 through December 31, 2012, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). |

| (3) | The expense ratios for the Defensive Market Strategies Fund and the International Equity Fund include the impact of dividend and interest expense on securities sold short. |

11

ABBREVIATIONS AND FOOTNOTES

INVESTMENT ABBREVIATIONS:

| | | | |

ADR | | — | | American Depository Receipt |

AGM | | — | | Assured Guaranty Municipal Corporation |

CONV | | — | | Convertible |

ETF | | — | | Exchange Traded Fund |

GDR | | — | | Global Depository Receipt |

IO | | — | | Interest Only (Principal amount shown is notional) |

LLC | | — | | Limited Liability Company |

LOC | | — | | Letter of Credit |

LP | | — | | Limited Partnership |

NVDR | | — | | Non-Voting Depository Receipt |

PIK | | — | | Payment-in-Kind Bonds |

PIPE | | — | | Private Investment in Public Equity |

PLC | | — | | Public Limited Company |

PO | | — | | Principal Only |

REIT | | — | | Real Estate Investment Trust |

SPDR | | — | | Standard & Poor’s Depositary Receipt |

STEP | | — | | Stepped Coupon Bonds: Interest rates shown reflect the rates currently in effect. |

STRIP | | — | | Stripped Security |

TBA | | — | | To be announced |

VVPR | | — | | Voter Verified Paper Record |

144A | | — | | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may not be resold subject to that rule except to qualified institutional buyers. As of December 31, 2012, the total market values and percentages of net assets for 144A securities by fund were as follows: |

| | | | | | | | | | |

Fund | | Value of

144A Securities | | Percentage of

Net Assets |

Low-Duration Bond | | | $ | 176,551,808 | | | | | 21.70 | % |

Medium-Duration Bond | | | | 114,004,879 | | | | | 13.07 | |

Extended-Duration Bond | | | | 48,693,205 | | | | | 10.34 | |

Global Bond | | | | 26,948,483 | | | | | 11.57 | |

Defensive Market Strategies | | | | 16,622,848 | | | | | 4.16 | |

Small Cap Equity | | | | 3,659,353 | | | | | 0.82 | |

International Equity | | | | 920,460 | | | | | 0.06 | |

INVESTMENT FOOTNOTES:

| | | | |

‡‡ | | — | | All or a portion of the security was held as collateral for open futures, options, securities sold short and/or swap contracts. |

@ | | — | | Illiquid. |

* | | — | | Non-income producing security. |

# | | — | | Security in default. |

§ | | — | | Security purchased with the cash proceeds from securities loaned. |

† | | — | | Variable rate security. Interest rates shown reflect the rates currently in effect. Maturity date for money market instruments is the date of the next interest rate reset. |

W | | — | | Interest rates shown reflect the effective yields as of December 31, 2012. |

¥ | | — | | Affiliated fund. |

D | | — | | Security either partially or fully on loan. |

+ | | — | | Security is valued at fair value. As of December 31, 2012, the total market values and percentages of net assets for Fair Valued securities by fund were as follows: |

| | | | | | | | | | |

Fund | | Value of

Fair

Valued

Securities | | Percentage of

Net Assets |

Low-Duration Bond | | | $ | — | | | | | — | % |

Medium-Duration Bond | | | | 14 | | | | | — | |

Global Bond | | | | 186,221 | | | | | 0.08 | |

Equity Index | | | | — | | | | | — | |

Small Cap Equity | | | | 561,127 | | | | | 0.13 | |

International Equity | | | | — | | | | | — | |

12

ABBREVIATIONS AND FOOTNOTES

FOREIGN BOND FOOTNOTES:

| | | | | | |

(A) | | | — | | | Par is denominated in Australian Dollars (AUD). |

(B) | | | — | | | Par is denominated in Brazilian Real (BRL). |

(C) | | | — | | | Par is denominated in Canadian Dollars (CAD). |

(E) | | | — | | | Par is denominated in Euro (EUR). |

(G) | | | — | | | Par is denominated in Singapore Dollars (SGD). |

(J) | | | — | | | Par is denominated in Japanese Yen (JPY). |

(K) | | | — | | | Par is denominated in Norwegian Krone (NOK). |

(M) | | | — | | | Par is denominated in Mexican Pesos (MXN). |

(N) | | | — | | | Par is denominated in Indonesian Rupiahs (IDR). |

(O) | | | — | | | Par is denominated in Switzerland Francs (CHF). |

(P) | | | — | | | Par is denominated in Peruvian Nuevos Soles (PEN). |

(R) | | | — | | | Par is denominated in Malaysian Ringgits (MYR). |

(S) | | | — | | | Par is denominated in South African Rand (ZAR). |

(U) | | | — | | | Par is denominated in British Pounds (GBP). |

(W) | | | — | | | Par is denominated in South KoreanWon (KRW). |

(Z) | | | — | | | Par is denominated in New Zealand Dollars (NZD). |

COUNTERPARTY ABBREVIATIONS:

| | | | |

BAR | | — | | Counterparty to contract is Barclays Capital. |

BNP | | — | | Counterparty to contract is BNP Paribas. |

BOA | | — | | Counterparty to contract is Bank of America. |

CITI | | — | | Counterparty to contract is Citibank NA London. |

CITIC | | — | | Counterparty to contract is Citicorp. |

CITIG | | — | | Counterparty to contract is Citigroup Global Markets, Inc. |

CME | | — | | Counterparty to contract is Chicago Mercantile Exchange. |

CS | | — | | Counterparty to contract is Credit Suisse International. |

DEUT | | — | | Counterparty to contract is Deutsche Bank AG. |

GSC | | — | | Counterparty to contract is Goldman Sachs Capital Markets, LP. |

HKSB | | — | | Counterparty to contract is Hong Kong & Shanghai Bank. |

HSBC | | — | | Counterparty to contract is HSBC Securities. |

JPM | | — | | Counterparty to contract is JPMorgan Chase Bank. |

KS | | — | | Counterparty to contract is Knight Securities. |

MLCS | | — | | Counterparty to contract is Merrill Lynch Capital Services, Inc. |

MSCS | | — | | Counterparty to contract is Morgan Stanley Capital Services. |

NT | | — | | Counterparty to contract is Northern Trust Corporation. |

RBC | | — | | Counterparty to contract is Royal Bank of Canada. |

RBS | | — | | Counterparty to contract is Royal Bank of Scotland. |

SG | | — | | Counterparty to contract is Societe Generale. |

SS | | — | | Counterparty to contract is State Street Global Markets. |

UBS | | — | | Counterparty to contract is UBS AG. |

WEST | | — | | Counterparty to contract is Westpac Pollock. |

13

MyDestination 2005 Fund

The Fund, through investments in the underlying Select Funds, combined a greater percentage of exposure to fixed income securities with a smaller percentage to equity securities. The Fund followed an allocation glide path designed to become more conservative over time, and the December 2012 targeted allocations were approximately 46.50% Fixed Income Select Funds, 28.36% U.S. Equity Select Funds, 8.14% Non-U.S. Equity Select Fund and 17.00% Real Return Select Funds.

As a fund of funds, its performance was based on the performance of the underlying Select Funds. The Fund generated a positive return of 8.92% for the one-year period ending December 31, 2012, which benefited from positive absolute performance from all of the Fixed Income Select Funds, Equity Select Funds and Real Return Select Funds. Overall exposure to the Equity Select Funds was a primary contributor to the Fund’s performance, led by positive investment results of the International Equity Fund. The Value Equity Fund and Growth Equity Fund also made significant contributions. Within the Fund’s fixed income allocation, absolute return was most positively influenced by its exposure to both the Low-Duration Bond Fund and the Medium-Duration Bond Fund, returning 4.15% and 7.68%, respectively, for 2012.

U.S. equity exposure continued to contribute positively to the performance of the Fund. The year began with a very impressive start with the S&P 500® Index’s surging over 12.00% during the first quarter. As the year progressed, equities withstood a series of political and macroeconomic concerns to finish the year with a gain of 16.00%. Serving as a driving force for the market rally was the continued support by the Federal Reserve to keep interest rates low and to encourage economic demand. Following this progression, U.S. consumer confidence and housing improved, China’s economy bounced back and accommodating monetary policies were announced in Europe. Consequently, the riskier segments within stocks and bonds benefited the most from this overall market optimism.

Consistent with the Fund’s conservative asset allocation, the Real Estate Securities Fund and Small Cap Equity Fund were the weakest absolute contributors. However, the Fund’s total equity exposure provided the majority of absolute return for the one-year period ending December 31, 2012. Further, the performance dispersion between U.S. equity and non-U.S. equity markets was not largely significant. Within U.S. equity markets, however, value-oriented equities provided a marginal benefit over growth-oriented equities for the year as measured by the Russell 1000® Value Index and Russell 1000® Growth Index. Both segments provided a material benefit to absolute performance.

In addition to the Federal Reserve’s low interest rate policy, the bond market also benefited from an environment of low inflationary pressures and sluggish economic growth. All major bond market sectors posted positive returns for the year, led by emerging markets debt which generated an annual return of 18.04%. As a further indication of risk sentiment, broad market performance, measured by the Barclays Capital U.S. Aggregate Bond Index, gained 4.22% for the year, while the riskier Barclays Capital U.S. Corporate High Yield - 2% Issuer Capped Index posted a gain of 15.77% for 2012. Both the Low-Duration Bond Fund and Medium-Duration Bond Fund equally provided beneficial contributions to the Fund.

The Fund outperformed its composite benchmark in 2012 (8.92% versus 8.47%), with its exposure to the Fixed Income Select Funds entirely accounting for the positive relative performance. The largest detractors to relative performance were the Inflation Protected Bond Fund, Defensive Market Strategies Fund and Small Cap Equity Fund. The Fund’s relative performance was most positively impacted by exposure to the Low-Duration Bond Fund, which benefited from tactically utilizing spread sectors that trade at a yield premium relative to their U.S. Treasury counterparts and maintaining diversified exposure to multiple spread sectors.

The Fund attempted to achieve its objective by investing in the Select Funds. The Fund is managed to a retirement date (“target date”) by adjusting the percentage of fixed income securities and equity securities to become more conservative each year until reaching the retirement year and then approximately 15 years thereafter. The target date in the name of the Fund is the approximate date when an investor plans to start withdrawing money. This Fund may be suitable for investors who want a simplified “one fund” retirement solution, are willing to pay slightly higher fees to get a diversified mix of investments that becomes more conservative over time and retired at an age that was near the year 2005. The Fund’s value will fluctuate due to changes in interest rates. There is a risk that the issuer of a fixed-income investment may fail to pay interest or even principal due in a timely manner or at all. The Fund’s value will fluctuate due to business developments concerning a particular issuer, industry or country, as well as general market and economic conditions. The Fund is subject to risks presented by investments in foreign issuers and changes in currency exchange rates relative to the U.S. dollar may negatively affect the values of foreign investments held by the Select Funds. By investing in this Fund, you will incur the expenses of the Fund, in addition to those of the underlying Select Funds. The principal risks of the Fund will change depending on the asset mix of the Select Funds in which it invests. You may directly invest in the Select Funds. The Fund’s value will go up and down in response to changes in the share prices of the investments that it owns. The amount invested in the Fund is not guaranteed to increase, is not guaranteed against loss nor is the amount of the original investment guaranteed at the target date. It is possible to lose money by investing in the Fund.

Please see page 16 for information regarding specific portfolio allocations. Portfolio holdings are subject to change and risk at any time.

14

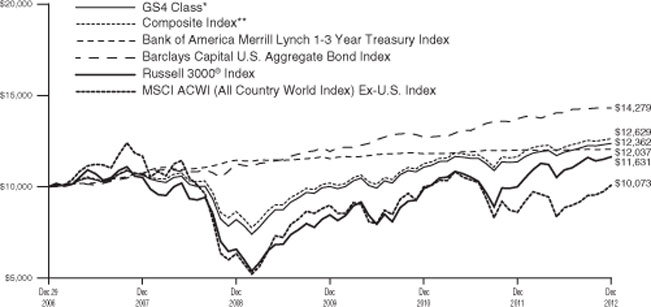

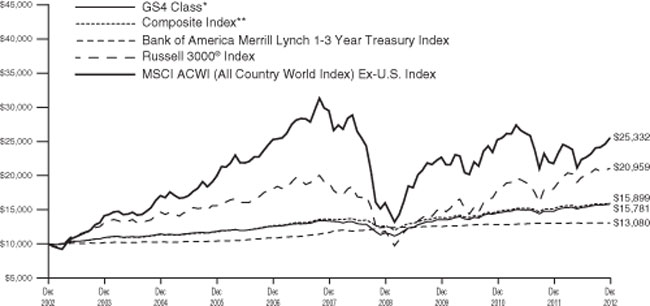

MyDestination 2005 Fund

| | | | |

| Average Annual Total Returns as of 12/31/12 |

| | GS4 Class* | | Benchmark** |

One Year | | 8.92% | | 8.47% |

Five Year | | 3.04% | | 3.34% |

Since Inception | | 3.59% | | 3.91% |

Inception Date | | 12/29/06 | | |

Total Fund Operating Expenses (April 28, 2012 Prospectus, as amended on November 30, 2012)(1) | | 1.15% | | |

(1)The Fund’s shareholders indirectly bear the expenses of the GS4 Class shares of the Select Funds in which the Fund invests. Current information regarding the Fund’s Operating Expenses can be found in the Financial Highlights.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at www.GuideStoneFunds.org. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The graph illustrates the results of a hypothetical $10,000 investment in the GS4 Class of the Fund since December 29, 2006 (commencement of operations), with all dividends and capital gains reinvested, with the Fund’s composite benchmark index.

*These returns reflect expense waivers by the Fund’s investment adviser. Without these waivers, returns would have been lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

**Represents a composite index as of December 2012, consisting of 30.00% of the Bank of America Merrill Lynch 1-3 Year Treasury Index, 16.50% of the Barclays Capital U.S. Aggregate Bond Index, 15.00% of the Barclays Capital U.S. TIPS Index,

13.25% of the S&P 500® Index, 2.00% of the Dow Jones U.S. Select Real Estate Securities IndexSM, 6.75% of the Russell 1000® Value Index, 6.75% of the Russell 1000® Growth Index, 1.61% of the Russell 2000® Index and 8.14% of the MSCI ACWI (All Country World Index) Ex-U.S. Index.

The construction of the composite index corresponds to the target percentage allocations to the underlying asset classes as represented by the Fund’s investment in the Select Funds. As the target percentage allocations to the underlying investments change according to the MyDestination Funds® glide path, the target percentage allocations to the composite index also change.

Unlike a mutual fund, the performance of an index assumes no taxes, transaction costs, management fees or other expenses.

15

| | | | |

MYDESTINATION 2005 FUND SCHEDULE OF INVESTMENTS | | | December 31, 2012 | |

| | | | | | | | | | | | |

| | | Shares | | | Value | |

MUTUAL FUNDS — 99.7% | | | | | | | | | | | | |

GuideStone Money Market

Fund (GS4 Class)¥ | | | | | 1,736,846 | | | | | $ | 1,736,846 | |

GuideStone Low-Duration

Bond Fund (GS4 Class)¥ | | | | | 1,714,401 | | | | | | 23,178,698 | |

GuideStone Medium-Duration Bond Fund (GS4 Class)¥ | | | | | 882,657 | | | | | | 12,957,406 | |

GuideStone Inflation Protected

Bond Fund (GS4 Class)¥ | | | | | 1,035,073 | | | | | | 11,644,573 | |

GuideStone Defensive Market

Strategies Fund

(GS4 Class)¥ | | | | | 977,893 | | | | | | 10,365,666 | |

GuideStone Real Estate

Securities Fund

(GS4 Class)¥ | | | | | 160,071 | | | | | | 1,696,755 | |

GuideStone Value Equity Fund (GS4 Class)¥ | | | | | 332,505 | | | | | | 5,379,933 | |

GuideStone Growth Equity

Fund (GS4 Class)¥ | | | | | 262,632 | | | | | | 5,320,915 | |

GuideStone Small Cap Equity

Fund (GS4 Class)¥ | | | | | 84,628 | | | | | | 1,348,977 | |

GuideStone International

Equity Fund

(GS4 Class)¥ | | | | | 511,531 | | | | | | 6,685,711 | |

| | | | | | | | | | | | |

| | | | |

Total Mutual Funds

(Cost $74,563,460) | | | | | | | | | | | 80,315,480 | |

| | | | | | | | | | | | |

| | |

TOTAL INVESTMENTS — 99.7%

(Cost $74,563,460) | | | | | | 80,315,480 | |

| | | | |

Other Assets in Excess of

Liabilities — 0.3% | | | | | | | | | | | 266,744 | |

| | | | | | | | | | | | |

NET ASSETS — 100.0% | | | | | | | | | | $ | 80,582,224 | |

| | | | | | | | | | | | |

PORTFOLIO SUMMARY (based on net assets)

| | | | |

| | | % | |

Bond Funds | | | 59.3 | |

Domestic Equity Funds | | | 29.9 | |

International Equity Fund | | | 8.3 | |

Money Market Fund | | | 2.2 | |

Futures Contracts | | | 2.1 | |

| | | | |

| | | 101.8 | |

| | | | |

VALUATION HIERARCHY

The following is a summary of the inputs used, as of December 31, 2012, in valuing the Fund’s investments carried at fair value:

| | | | | | | | | | | | | | | | | | | | |

| | | Total

Value | | Level 1

Quoted Prices | | Level 2

Other Significant

Observable Inputs | | Level 3

Significant

Unobservable Inputs |

Assets: | | | | | | | | | | | | | | | | | | | | |

Investments in Securities: | | | | | | | | | | | | | | | | | | | | |

Mutual Funds | | | $ | 80,315,480 | | | | $ | 80,315,480 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

Total Assets - Investments in Securities | | | $ | 80,315,480 | | | | $ | 80,315,480 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | | |

Other Financial Instruments*** | | | | | | | | | | | | | | | | | | | | |

Futures Contracts | | | $ | 6,912 | | | | $ | 6,912 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

Total Assets - Other Financial Instruments | | | $ | 6,912 | | | | $ | 6,912 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

***Other financial instruments are derivative instruments not reflected in the Schedule of Investments, such as futures, forwards and swap contracts, which are valued at the unrealized appreciation (depreciation) on the investment. Details of these investments can be found in the Notes to Financial Statements.

| | | | |

| 16 | | See Notes to Financial Statements. | | |

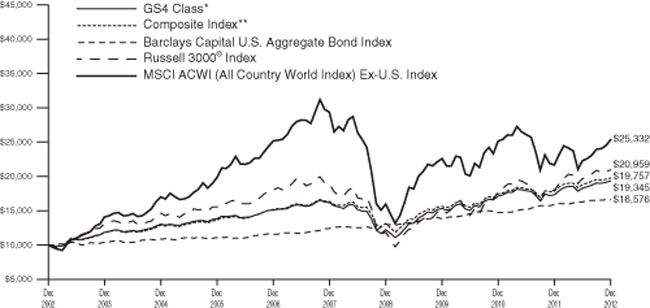

MyDestination 2015 Fund

The Fund, through investments in the underlying Select Funds, combined a greater percentage of exposure to equity securities with a smaller percentage to fixed income securities. The Fund followed an allocation glide path designed to become more conservative over time, and the December 2012 targeted allocations were approximately 29.25% Fixed income Select Funds, 41.12% U.S. Equity Select Funds, 11.38% Non-U.S. Equity Select Fund and 18.25% Real Return Select Funds.

As a fund of funds, its performance was based on the performance of the underlying Select Funds. The Fund generated a positive return of 11.46% for the one-year period ended December 31, 2012, which benefited from positive absolute performance from all of the Fixed Income Select Funds, Equity Select Funds, and Real Return Select Funds. Overall exposure to the Equity Select Funds was a primary contributor to the Fund’s performance led by positive investment results of the International Equity Fund. The Value Equity Fund and Growth Equity Fund also made significant contributions. Within the Fund’s fixed income allocation, absolute return was most positively influenced by its exposure to both the Extended-Duration Bond Fund and the Global Bond Fund, returning 15.06% and 12.52%, respectively, for 2012.

U.S. equity exposure continued to contribute positively to the performance of the Fund. The year began with a very impressive start with the S&P 500® Index’s surging over 12.00% during the first quarter. As the year progressed, equities withstood a series of political and macroeconomic concerns to finish the year with a gain of 16.00%. Serving as a driving force for the market rally was continued support by the Federal Reserve to keep interest rates low and to encourage economic demand. Following this progression, U.S. consumer confidence and housing improved, China’s economy bounced back and accommodating monetary policies were announced in Europe. Consequently, the riskier segments within stocks and bonds benefited the most from this overall market optimism.

Consistent with the Fund’s asset allocation, the Real Estate Securities Fund and Small Cap Equity Fund were the weakest absolute contributors. However, the Fund’s total equity exposure provided the majority of absolute return for the one-year period ending December 31, 2012. Further, the performance dispersion between U.S. equity and non-U.S. equity markets was not largely significant. Within U.S. equity markets, however, value-oriented equities provided a marginal benefit over growth-oriented equities for the year as measured by the Russell 1000® Value Index and Russell 1000® Growth Index. Both segments provided a material benefit to absolute performance.

In addition to the Federal Reserve’s low interest rate policy, the bond market also benefited from an environment of low inflationary pressures and sluggish economic growth. All major bond market sectors posted positive returns for the year, led by emerging markets debt which generated an annual return of 18.04%. As a further indication of risk sentiment, broad market performance, measured by the Barclays Capital U.S. Aggregate Bond Index, gained 4.22% for the year, while the riskier Barclays Capital U.S. Corporate High Yield – 2% Issuer Capped Index posted a gain of 15.77% for 2012. Both the Medium-Duration Bond Fund and Inflation Protected Bond Fund materially provided beneficial contributions to the Fund.

The Fund underperformed its composite benchmark in 2012 (11.46% versus 11.95%), with its exposure to the Equity Income Select Funds entirely attributable to underperformance. The largest detractors to relative performance were the Inflation Protected Bond Fund, Defensive Market Strategies Fund and Small Cap Equity Fund. The Fund’s relative performance was most positively impacted by exposure to the Medium-Duration Bond Fund, which benefited from exposure to and security selection in non-U.S. Treasury sectors. Generally, the Fund was underweight U.S. Treasuries in favor of spread sectors, which outperformed U.S. Treasuries for the year.

The Fund attempted to achieve its objective by investing in the Select Funds. The Fund is managed to a retirement date (“target date”) by adjusting the percentage of fixed income securities and equity securities to become more conservative each year until reaching the retirement year and then approximately 15 years thereafter. The target date in the name of the Fund is the approximate date when an investor plans to start withdrawing money. This Fund may be suitable for investors who want a simplified “one fund” retirement solution, are willing to pay slightly higher fees to get a diversified mix of investments that becomes more conservative over time and plan to retire at an age that is near the year 2015. The Fund’s value will fluctuate due to changes in interest rates. There is a risk that the issuer of a fixed-income investment may fail to pay interest or even principal due in a timely manner or at all. The Fund’s value will fluctuate due to business developments concerning a particular issuer, industry or country, as well as general market and economic conditions. The Fund is subject to risks presented by investments in foreign issuers, and changes in currency exchange rates relative to the U.S. dollar may negatively affect the values of foreign investments held by the Select Funds. By investing in this Fund, you will incur the expenses of the Fund, in addition to those of the underlying Select Funds. The principal risks of the Fund will change depending on the asset mix of the Select Funds in which it invests. You may directly invest in the Select Funds. The Fund’s value will go up and down in response to changes in the share prices of the investments that it owns. The amount invested in the Fund is not guaranteed to increase, is not guaranteed against loss nor is the amount of the original investment guaranteed at the target date. It is possible to lose money by investing in the Fund.

Please see page 19 for information regarding specific portfolio allocations. Portfolio holdings are subject to change and risk at any time.

17

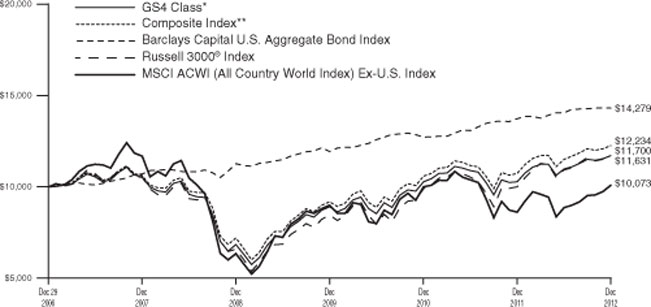

MyDestination 2015 Fund

| | | | |

| Average Annual Total Returns as of 12/31/12 |

| | GS4 Class* | | Benchmark** |

One Year | | 11.46% | | 11.95% |

Five Year | | 2.84% | | 3.56% |

Since Inception | | 3.38% | | 4.00% |

Inception Date | | 12/29/06 | | |

Total Fund Operating Expenses (April 28, 2012 Prospectus, as amended on November 30, 2012)(1) | | 1.09% | | |

(1)The Fund’s shareholders indirectly bear the expenses of the GS4 Class shares of the Select Funds in which the Fund invests. Current information regarding the Fund’s Operating Expenses can be found in the Financial Highlights.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at www.GuideStoneFunds.org. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The graph illustrates the results of a hypothetical $10,000 investment in the GS4 Class of the Fund since December 29, 2006 (commencement of operations), with all dividends and capital gains reinvested, with the Fund’s composite benchmark index.

*These returns reflect expense waivers by the Fund’s investment adviser. Without these waivers, returns would have been lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

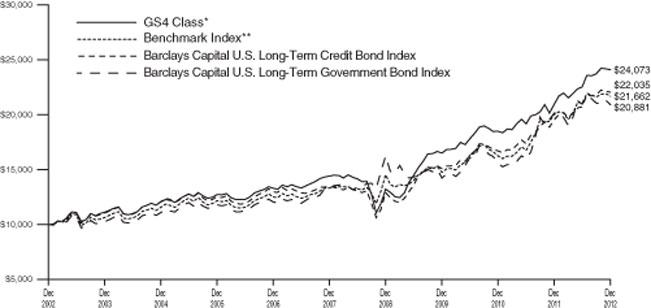

**Represents a composite index as of December 2012, consisting of 9.25% of the Bank of America Merrill Lynch 1-3 Year Treasury Index, 12.50% of the Barclays Capital U.S. Aggregate Bond Index, 1.75% of the Barclays Capital U.S. Long-Term Government Bond Index, 1.75% of the Barclays Capital U.S. Long-Term Credit Bond Index, 13.00% of the Barclays Capital U.S. TIPS Index, 2.00% of the Barclays Capital Global Aggregate Bond Index — Unhedged, 1.00% of the Barclays U.S. Corporate High Yield — 2% Issuer Capped Index, 1.00% of the J.P. Morgan Emerging Markets Bond Index Plus, 20.00% of the S&P 500® Index, 5.25% of the Dow Jones U.S. Select Real Estate Securities IndexSM, 9.35% of the Russell 1000® Value Index, 9.35% of the Russell 1000® Growth Index, 2.42% of the Russell 2000® Index and 11.38% of the MSCI ACWI (All Country World Index) Ex-U.S. Index.

The construction of the composite index corresponds to the target percentage allocations to the underlying asset classes as represented by the Fund’s investment in the Select Funds. As the target percentage allocations to the underlying investments change according to the MyDestination Funds® glide path, the target percentage allocations to the composite index also change.

Unlike a mutual fund, the performance of an index assumes no taxes, transaction costs, management fees or other expenses.

18

| | |

MYDESTINATION 2015 FUND SCHEDULE OF INVESTMENTS | | December 31, 2012 |

| | | | | | | | | | | | |

| | | Shares | | | Value | |

MUTUAL FUNDS — 100.0% | |

GuideStone Money Market

Fund (GS4 Class)¥ | | | | | 4,696,654 | | | | | $ | 4,696,654 | |

GuideStone Low-Duration

Bond Fund

(GS4 Class)¥ | | | | | 2,315,613 | | | | | | 31,307,086 | |

GuideStone Medium-Duration Bond Fund

(GS4 Class)¥ | | | | | 2,909,411 | | | | | | 42,710,156 | |

GuideStone Extended-Duration Bond Fund

(GS4 Class)¥ | | | | | 692,771 | | | | | | 12,871,681 | |

GuideStone Inflation Protected Bond Fund

(GS4 Class)¥ | | | | | 3,881,793 | | | | | | 43,670,168 | |

GuideStone Global Bond Fund (GS4 Class)¥ | | | | | 1,361,263 | | | | | | 14,129,910 | |

GuideStone Defensive Market Strategies Fund

(GS4 Class)¥ | | | | | 6,403,982 | | | | | | 67,882,208 | |

GuideStone Real Estate

Securities Fund

(GS4 Class)¥ | | | | | 1,789,219 | | | | | | 18,965,722 | |

GuideStone Value Equity Fund (GS4 Class)¥ | | | | | 2,053,269 | | | | | | 33,221,896 | |

GuideStone Growth Equity

Fund (GS4 Class)¥ | | | | | 1,581,922 | | | | | | 32,049,744 | |

GuideStone Small Cap Equity Fund

(GS4 Class)¥ | | | | | 553,892 | | | | | | 8,829,041 | |

GuideStone International

Equity Fund

(GS4 Class)¥ | | | | | 3,219,183 | | | | | | 42,074,716 | |

| | | | | | | | | | | | |

| | | | |

Total Mutual Funds

(Cost $314,050,297) | | | | | | | | | | | 352,408,982 | |

| | | | | | | | | | | | |

| | |

TOTAL INVESTMENTS — 100.0%

(Cost $314,050,297) | | | | | | 352,408,982 | |

| | | | |

Other Assets in Excess of

Liabilities — 0.0% | | | | | | | | | | | 167,396 | |

| | | | | | | | | | | | |

NET ASSETS — 100.0% | | | | | | | | | | $ | 352,576,378 | |

| | | | | | | | | | | | |

PORTFOLIO SUMMARY (based on net assets)

| | | | |

| | | % | |

Domestic Equity Funds | | | 45.6 | |

Bond Funds | | | 41.0 | |

International Equity Fund | | | 12.0 | |

Money Market Fund | | | 1.4 | |

Futures Contracts | | | 1.3 | |

| | | | |

| | | 101.3 | |

| | | | |

VALUATION HIERARCHY

The following is a summary of the inputs used, as of December 31, 2012, in valuing the Fund’s investments carried at fair value:

| | | | | | | | | | | | | | | | | | | | |

| | | Total

Value | | Level 1

Quoted Prices | | Level 2

Other Significant

Observable Inputs | | Level 3

Significant

Unobservable Inputs |

Assets: | | | | | | | | | | | | | | | | | | | | |

Investments in Securities: | | | | | | | | | | | | | | | | | | | | |

Mutual Funds | | | $ | 352,408,982 | | | | $ | 352,408,982 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

Total Assets - Investments in Securities | | | $ | 352,408,982 | | | | $ | 352,408,982 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | | |

Other Financial Instruments*** | | | | | | | | | | | | | | | | | | | | |

Futures Contracts | | | $ | 16,379 | | | | $ | 16,379 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

Total Assets - Other Financial Instruments | | | $ | 16,379 | | | | $ | 16,379 | | | | $ | — | | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | |

***Other financial instruments are derivative instruments not reflected in the Schedule of Investments, such as futures, forwards and swap contracts, which are valued at the unrealized appreciation (depreciation) on the investment. Details of these investments can be found in the Notes to Financial Statements.

| | | | |

| | See Notes to Financial Statements. | | 19 |

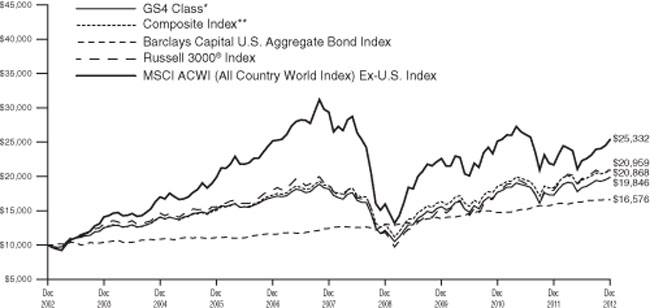

MyDestination 2025 Fund

The Fund, through investments in the underlying Select Funds, combined a greater percentage of exposure to equity securities with a much smaller percentage to fixed income securities. The Fund followed an allocation glide path designed to become more conservative over time, and the December 2012 targeted allocations were approximately 24.00% Fixed Income Select Funds, 49.35% U.S. Equity Select Funds, 17.15% Non-U.S. Equity Select Fund and 9.50% Real Return Select Funds.

As a fund of funds, its performance was based on the performance of the underlying Select Funds. The Fund generated a positive return of 13.90% for the one-year period ended December 31, 2012, which benefited from positive absolute performance from all of the Fixed Income Select Funds, Equity Select Funds and Real Return Select Funds. Overall exposure to the Equity Select Funds was a primary contributor to the Fund’s performance led by positive investment results of the International Equity Fund. The Value Equity Fund and Growth Equity Fund also made significant contributions. Within the Fund’s fixed income allocation, absolute return was most positively influenced by its exposure to both the Extended-Duration Bond Fund and the Global Bond Fund, returning 15.06% and 12.52%, respectively, for 2012.

U.S. equity exposure continued to contribute positively to the performance of the Fund. The year began with a very impressive start with the S&P 500® Index’s surging over 12.00% during the first quarter. As the year progressed, equities withstood a series of political and macroeconomic concerns to finish the year with a gain of 16.00%. Serving as a driving force for the market rally was the continued support by the Federal Reserve to keep interest rates low and to encourage economic demand. Following this progression, U.S. consumer confidence and housing improved, China’s economy bounced back and accommodating monetary policies were announced in Europe. Consequently, the riskier segments within stocks and bonds benefited the most from this overall market optimism.

Consistent with the Fund’s asset allocation, the Low-Duration Bond Fund and Inflation Protected Bond Fund were the weakest absolute contributors. However, the Fund’s total equity exposure provided the majority of absolute return for the one-year period ending December 31, 2012. Further, the performance dispersion between U.S. equity and non-U.S. equity markets was not largely significant. Within U.S. equity markets, however, value-oriented equities provided a marginal benefit over growth-oriented equities for the year as measured by the Russell 1000® Value Index and Russell 1000® Growth Index. Both segments provided a material benefit to absolute performance.

In addition to the Federal Reserve’s low interest rate policy, the bond market also benefited from an environment of low inflationary pressures and sluggish economic growth. All major bond market sectors posted positive returns for the year, led by emerging markets debt which generated an annual return of 18.04%. As a further indication of risk sentiment, broad market performance, measured by the Barclays Capital U.S. Aggregate Bond Index, gained 4.22% for the year, while the riskier Barclays Capital U.S. Corporate High Yield - 2% Issuer Capped Index posted a gain of 15.77% for 2012. The Fund’s allocation to fixed income holdings contributed meaningfully to absolute performance. Both the Extended-Duration Bond Fund and Global Bond Fund materially provided beneficial contributions to the Fund.

The Fund underperformed its composite benchmark in 2012 (13.90% versus 14.11%), with its exposure to the Equity Income Select Funds entirely attributable to underperformance. The largest detractors to relative performance were the Inflation Protected Bond Fund, Defensive Market Strategies Fund and Small Cap Equity Fund. The Fund’s relative performance was most positively impacted by exposure to the Extended-Duration Bond Fund, which benefited from significant underweight to the U.S. Treasury sector. Further, the Fund favored higher yielding corporate bonds, non-U.S. bonds and high yield bonds.

The Fund attempted to achieve its objective by investing in the Select Funds. The Fund is managed to a retirement date (“target date”) by adjusting the percentage of fixed income securities and equity securities to become more conservative each year until reaching the retirement year and then approximately 15 years thereafter. The target date in the name of the Fund is the approximate date when an investor plans to start withdrawing money. This Fund may be suitable for investors who want a simplified “one fund” retirement solution, are willing to pay slightly higher fees to get a diversified mix of investments that becomes more conservative over time and plan to retire at an age that is near the year 2025. The Fund’s value will fluctuate due to changes in interest rates. There is a risk that the issuer of a fixed-income investment may fail to pay interest or even principal due in a timely manner or at all. The Fund’s value will fluctuate due to business developments concerning a particular issuer, industry or country, as well as general market and economic conditions. The Fund is subject to risks presented by investments in foreign issuers and changes in currency exchange rates relative to the U.S. dollar may negatively affect the values of foreign investments held by the Select Funds. By investing in this Fund, you will incur the expenses of the Fund, in addition to those of the underlying Select Funds. The principal risks of the Fund will change depending on the asset mix of the Select Funds in which it invests. You may directly invest in the Select Funds. The Fund’s value will go up and down in response to changes in the share prices of the investments that it owns. The amount invested in the Fund is not guaranteed to increase, is not guaranteed against loss nor is the amount of the original investment guaranteed at the target date. It is possible to lose money by investing in the Fund.

Please see page 22 for information regarding specific portfolio allocations. Portfolio holdings are subject to change and risk at any time.

20

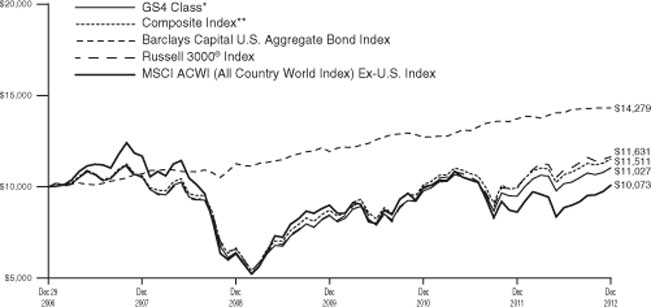

MyDestination 2025 Fund

| | | | |

| Average Annual Total Returns as of 12/31/12 |

| | GS4 Class* | | Benchmark** |

One Year | | 13.90% | | 14.11% |

Five Year | | 2.13% | | 2.90% |

Since Inception | | 2.65% | | 3.42% |

Inception Date | | 12/29/06 | | |

Total Fund Operating Expenses (April 28, 2012 Prospectus, as amended on November 30, 2012)(1) | | 1.16% | | |

(1)The Fund’s shareholders indirectly bear the expenses of the GS4 Class shares of the Select Funds in which the Fund invests. Current information regarding the Fund’s Operating Expenses can be found in the Financial Highlights.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at www.GuideStoneFunds.org. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The graph illustrates the results of a hypothetical $10,000 investment in the GS4 Class of the Fund since December 29, 2006 (commencement of operations), with all dividends and capital gains reinvested, with the Fund’s composite benchmark index.

*These returns reflect expense waivers by the Fund’s investment adviser. Without these waivers, returns would have been lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.