UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File number: 811-10405

Alpine Series Trust

(Exact name of registrant as specified in charter)

2500 Westchester Avenue, Suite 215

Purchase, New York 10577

(Address of principal executive offices)(Zip code)

(Name and Address of Agent for

Service) | Copy to: |

| | |

Samuel A. Lieber

Alpine Woods Capital Investors, LLC

2500 Westchester Avenue, Suite 215

Purchase, New York 10577 | Rose DiMartino

Attorney at Law

Willkie Farr & Gallagher

787 7th Avenue, 40th Floor

New York, New York 10019 |

Registrant’s telephone number, including area code: (914) 251-0880

Date of fiscal year end: October 31, 2013

Date of reporting period: November 1, 2012 – October 31, 2013

Item 1: Shareholder Report.

Table of Contents

Additional Alpine Funds are offered in the Alpine Equity Trust. These Funds include:

| Alpine International Real Estate Equity Fund | Alpine Global Infrastructure Fund |

| Alpine Realty Income & Growth Fund | Alpine Global Consumer Growth Fund |

| Alpine Cyclical Advantage Property Fund | |

| Alpine Emerging Markets Real Estate Fund | |

Alpine’s Real Estate Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing in funds of the Alpine Equity Trust. The statutory and summary prospectuses contain this and other important information about the investment company, and it may be obtained by calling 1-888-785-5578, or visiting www.alpinefunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible.

Alpine’s Investment Outlook

President’s Letter

Dear Investors:

The fiscal year ended October 31, 2013 presented a difficult and complex year for investors across capital markets. However, like 2012, it has produced positive returns as economic and business momentum remain favorable. We are nearly five years past the trough of the global financial crisis which occurred from November, 2008 through early March, 2009. The positive performance of stocks since that time may appear to have moved ahead of the economic recovery in the real economy, however, this must be considered in the context of the extreme trough of valuations after the 2008 financial crisis. Generally, the price of many equities today, as measured against typical parameters such as price to earnings multiples, earnings yield relative to treasury yields, share price to cash flow, discounted cash flows, or EV/EBITDA (enterprise value divided by earnings before interest taxes depreciation and amortization), are typically less expensive than during the 2007 peak. Thus, in the context of a normalized business cycle we believe that the most relevant question becomes where are corporate earnings and overall business activity trending? Given the slow pace of recovery, Alpine believes that we are only in the middle of a protracted economic cycle.

The slow pace of recovery as measured by job creation, business capital expenditures, per capita income growth, new business formation, the pace of car and home sales, as well as retail consumption patterns amongst other components of gross domestic product (GDP), suggests that the tepid economy is far from testing the limits of capacity or productivity. This has contributed to the continued lack of material goods inflation, despite the sustained efforts of the global central bankers to provide inexpensive financial liquidity. The lack of growth is evident from the recent earnings reports of the S&P 500® Index companies, which in many cases reflected positive earnings growth with minimal or even declining top line revenue trends. Companies have wrung productivity gains through technological streamlining, enhanced production processes, cost containment and reducing

costs of capital through refinancing or restructuring debt. Increasingly, market participants are concerned that companies may be approaching the limits of such profit margin enhancements. Going forward, we believe the market’s focus may turn to macro factors underpinning the prospects for economic growth which, if positive, should stimulate incremental demand for goods and services, boost aggregate revenues, and ultimately drive returns.

The year began with the traditional economic concerns as it became increasingly evident that the more than thirty-year trend of declining interest rates was nearing an end. The tug-of-war between inflation and deflation seemed to be tilting in the direction of the former as 2012 rolled into 2013, but swung abruptly in the second calendar quarter back to worries over U.S. economic slowing due to reduced government spending as sequestration cuts were implemented. Then the Federal Reserve (Fed) upset the capital markets shortly after interest rates hit record lows at the end of April when Fed Chairman Bernanke announced a process through which the economy would be weaned off the current Quantitative Easing (QE) program, the mechanism by which the Federal Reserve is making $85 billion of monthly purchases of treasury and mortgage backed securities in order to keep interest rates low. The Fed proposed that they would ‘taper’ down QE from $85 billion to $0 in the coming year contingent on the domestic economy showing signs of recovery. Thus, two new words entered the economists’ lexicon this year: ‘sequestration’ and ‘taper’.

Due to the inability of the President and Congress to find common ground between ideology and political opportunism, there has been limited fiscal stimulus deployed towards economic recovery over the past three years. This is in stark contrast to historical precedent where economic stimulus typically extended for two to three years after a recession. Since some lawmakers, investors and economists believed that more stimulus would only inflate the existing debt position, they argued for austerity measures, which precluded more fiscal deficit spending. Sequestration came into play earlier this year as a force majeure created by Congress in

1

anticipation of their inability to come to terms with both current and future fiscal responsibilities. Most economists forecasted that the sequestration process, which indiscriminately reduced spending across the U.S. government, would impact the economy by over a half percent of GDP. In effect, Congress chose to impose the burden of deficit reduction now, rather than waiting until a future date, even if the economy might be on a more stable footing then. It is clear that uncertainty surrounding government policy has significantly dampened business investment sentiment.

In the wake of the financial crisis the Fed was left as the only entity which could provide economic stimulus in the form of cheap money. However, low interest rates alone would not been enough to stimulate economic activity because the lending operations of many domestic financial institutions were significantly impaired by the near collapse of 2008. Since the onset of the crisis the Fed has utilized numerous tools in order to repair the credit mechanism in the economy. In 2012, the Fed acknowledged the potential of a deflationary effect from diminished fiscal spending combined with restricted bank lending practices, and launched the current wave of its QE program which targeted the open-ended purchase of mortgage and treasury bonds from the banks at a profit. We believe the program almost certainly has helped to stabilize the U.S. banking system, to raise the value of financial assets, and even to stimulate modest job growth. Unfortunately, the liquidity introduced into global markets through the latest QE measures also introduced distortions into the economy including excess leverage and speculation in some segments of the capital markets. Thus in our opinion, the limitless duration of open-ended easing could not go on indefinitely without causing more problems. The market became both concerned that the taper would undermine the renewed strength of our banking system and feared the unknown potential level where unsupported interest rates might settle (presumably higher). This forced many investors holding positions in interest sensitive investments to sell, hedge or otherwise reduce much of their interest rate exposure. As a result of the sudden unwinding of these positions, prices fell sharply in May and June of this year. Bond yields, foreign sovereign yields and mortgage yields rose precipitously as the market began discounting the potential impact of Fed tapering.

The market’s knee-jerk reaction to the May taper announcement proved to be premature as the Fed, in fact, did not begin tapering in September as most expected. In fact, since the sell-off in May, the Fed has gone to great lengths to communicate its decision making parameters and to strengthen the credibility of

its forward guidance on interest rates. Indeed, in recent comments by prospective Fed Governor Janet Yellen, after the close of our Funds’ fiscal year, she emphasized that when tapering does occur it will be done in accordance with improvement in economic data and will be at a very gradual pace. Thus, bonds have rallied somewhat as we enter a new phase in the seemingly never ending dance of the capital markets.

Despite tapering concerns, which have at times had traders responding to changes in sentiment on what often seems to be a daily basis, the overall direction and tone of the markets has been positive. Indeed, the S&P 500® Index, as well as other indices, surpassed the price levels of 2007 in April of this year, establishing new highs through the end of the fiscal year. As we reported in the past, the equity markets continue to climb a ‘wall of worry’, two steps forward, one step back, looking over a shoulder both to see how far we have advanced as well as whether danger lurks in our shadow. This could be a very positive stance for investment markets, provided that the fundamentals are supportive. In this light, let us return to the story of limited top-line revenue growth as opposed to bottom-line earnings growth.

Without broad economic growth, revenue growth is dependent upon market share gains or an expanding demand for specific goods and services. For most economies to grow there has to be job creation first and foremost, followed by income growth which should be sustained by enhanced productive capacity. As we closely monitor business trends and capital flows it is becoming increasingly apparent that the world’s more robust economies, notably the developed economies of North America and Asia, are at the nascent stages of a durable recovery, even if broad growth has yet to be sustained. Specifically, the United States and Japan are showing positive, if not consistent, trends in new orders and capital investment. While such investment is not as broad based as we would like to see across different segments of the economy, automobile sales, new building starts (both commercial and residential), as well as selective capital goods hold the potential for a sustained capital goods cycle.

Outside the United States, the traditional engines of global economic growth appear to be aligning in part due to significant monetary easing utilizing QE type policies in both Japan and Great Britain as well as, to a limited degree, the Eurozone. This is providing scope for these countries domestic banking sectors to heal and for capital markets to begin re-pricing risk more favorably in terms of higher stock prices and increasing money flows moving along the capital stack toward a higher risk/ reward profile. Japan is riding the wave of ‘Abenomics’,

2

pushing both aggressive monetary loosening and increasing fiscal reforms into the economy. If both the business and consumer segments of the economy can be kick started, then markets could continue pricing in a reflation of growth expectations across the economy, which in turn could create a virtuous cycle across other countries given Japan’s oversized role in the global economy. While the overall economic picture in Europe remains difficult due to continued high unemployment and a weak banking system, particularly in Southern Europe, the economies in Germany and Great Britain continue to motor along. Emblematic of this stage of recovery in Europe is Ireland, which was arguably one of the major beneficiaries of the prior period of excess capital in the early part of last decade. Following a period of fiscal austerity and recapitalization of its banking system, there is strong evidence for recovery as property prices rise and investment capital begins to flow into new business formation ultimately leading to job growth.

With respect to the larger emerging markets we can look to continued solid growth out of China, in spite of the fact that China faces challenges of its own in terms of its banking structure and lending channels. Nonetheless, China’s current account surpluses and foreign capital reserves provide significant support for them to maintain stability as the economy continues its transformation from a pure low priced exporter towards a higher value added producer with a growing consumer base. We note that a number of trends of internet retail demand are globally led by the Chinese consumer, both in terms of the double-digit growth rate of retail sales to the single day record for sales volume ($5.75 billion of sales were recorded by Alibaba.com on November 11 of this year). We believe that the business cycle in many other emerging markets will remain a bit choppy over the first half of next year, however, to a certain extent, the developing economies have been able to take advantage of the delay in Fed tapering, to implement agendas to address the uncertain growth outlook and the expected rise in bond yields. We expect such adjustments could drive business capital expenditure to offset fading governmental economic support (be it fiscal or monetary) to set the stage for the next phase of global economic activity.

While we believe that as economies begin to pick up steam over the next two to three years there will be greater consumer demand for goods and services which may again lead to an excess rate of expansion in prices as well as activity, none of this appears to be present in traditional measures of inflation. The price of gold fell by 23.11% over the fiscal year, while silver declined by 32.03%. As uncertainties over China’s growth trajectory worked through the global economy, resource-based

countries saw their currencies decline, notably the Australian Dollar was down 8.87%, Brazilian Real down 9.33%, South African Rand down 10.73% and Indonesian Rupiah down 12.49%. It’s worth noting that Japan was able to depreciate what many believed was an overvalued Yen, leading to an 18.9% fall, which corresponded with significant monetary stimulus and Quantitative Easing in an effort to raise equity prices and jumpstart inflation in its economy. Just to emphasize that currency markets are especially sensitive to global flows of capital, it is worth noting that the largest currency declines during the fiscal year occurred in the Syrian Pound and the Iranian Rial, both of which dropped by over 50% as those countries endured the hardships of civil war and economic blockade respectively.

In summary, we believe the current data suggest that establishing a new trend in global inflation, economic activity and capital availability could be a few years away. Interest rates could remain low relative to history, with the prospect for the yield curve tilting higher over time. This implies relatively appealing prospects for equities, assuming valuations remain sensible. At this time current equity valuations appear reasonable, notwithstanding the selective exuberance of the crowd searching for “the next new thing”, be it web retailers, new energy technology or social media related stocks.

In our view other issues that the capital markets would look at favorably include Congress providing a modicum of current fiscal stimulus over the next twelve to twenty-four months via appropriate tax incentives combined with enacting a program to tackle the long term entitlement pressures before they become more corrosive in 2020. In the meantime, the prospect of reasonable earnings growth, moderate top line expansion, rising corporate capex and gradual strengthening of the employment market could lead to a more traditional balance between the corporate sector, government and public expenditures and thereby provide a sustained basis for equity total returns over the next few years.

We appreciate your interest and support.

Sincerely,

Samuel A. Lieber

President

Past performance is not a guarantee of future results. The specific market, sector or investment conditions that contribute to a Fund’s performance may not be replicated in future periods.

3

Mutual fund investing involves risk. Principal loss is possible. Please refer to individual fund letters for risks specific to that fund.

This letter and the letters that follow represent the opinions of the Funds’ management and are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice.

4

| Disclosures and Definitions |  |

Equity Income Disclosures –

Please refer to the Schedule of Portfolio Investments for each Fund’s holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

Current and future portfolio holdings are subject to risk.

Favorable tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws. Alpine may not be able to anticipate the level of dividends that companies will pay in any given timeframe.

The Funds’ monthly distributions may consist of net investment income, net realized capital gains and / or a return of capital. If a distribution includes anything other than net investment income, the Funds will provide a notice of the best estimate of its distribution sources when distributed, which will be posted on the Funds’ website, www.alpinefunds.com A return of capital distribution does not necessarily reflect the Fund’s performance and should not be confused with “yield” or “income.” Final determination of the federal income tax characteristics of distributions paid during calendar year 2013 will be provided on U.S. Form 1099-DIV, which will be mailed to shareholders. Please consult your tax advisor for further information.

All investments involve risk. Principal loss is possible. A small portion of the S&P 500 yield may include return of capital; the 10-year Treasury yield does not include return of capital; Corporate Bonds and High Yield Bonds generally do not have return of capital; a portion of the dividend paid by REITs and REIT preferred stock may be deemed a return of capital for tax purposes in the event the company pays a dividend greater than its taxable income. A stock may trade with more or less liquidity than a bond depending on the number of shares and bonds outstanding, the size of the company, and the demand for the securities. The REIT and REIT preferred stock market are smaller than the broader equity and bond markets and often trade with less liquidity than these markets depending upon the size of the individual issue and the demand of the securities. Treasury notes are guaranteed by the U.S. government and thus they are considered to be safer than other asset classes. Tax features of a Treasury Note, Corporate Bond, Stock, High Yield Bond, REITs and REIT preferred stock may vary based on an individual circumstances. Consult a tax professional for additional information.

Neither the Fund nor any of its representatives may give tax advice. Investors should consult their tax advisor for information concerning their particular situation.

Earnings Growth and EPS Growth are not measures of the Funds’ future performance.

Diversification does not assure a profit or protect against loss in a declining market.

Must be preceded or accompanied by a prospectus.

Quasar Distributors, LLC, distributor.

Equity Income Definitions

Average Weight refers to the average weight of the holding in the portfolio during the reporting period

A Basis Point is a value equaling one one-hundredth of a percent (1/100 of 1%).

Barclays Capital High Yield Municipal Bond Index is the Muni High Yield component of the Municipal Bond Index. The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market.

Beta measures the sensitivity of the investment to the movements of its benchmark. A beta higher than 1.0 indicates the investment has been more volatile than the benchmark and a beta of less than 1.0 indicates that the investment has been less volatile than the benchmark.

Big data is the term for a collection of data sets so large and complex that it becomes difficult to process using on-hand database management tools or traditional data processing applications. The challenges include capture, curation, storage, search, sharing, transfer, analysis, and visualization. The trend to larger data sets is due to the additional information derivable from analysis of a single large set of related data, as compared to separate smaller sets with the same total amount of data, allowing correlations to be found to “spot business trends, determine quality of research, prevent diseases, combat crime, and determine real-time roadway traffic conditions.”

Capex (aka Capitalization Expenditure) are funds used by a company to acquire or upgrade physical assets such as property, industrial buildings or equipment. This type of outlay is made by companies to maintain or increase the scope of their operations.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Custom Balanced Benchmark reflects an unmanaged portfolio (rebalanced monthly) of 60% of the S&P 500 Index, which is a market capitalization-weighted index of 500 large capitalization stocks commonly used to represent the U.S. equity market, and 40% of the Barclays Capital U.S. Aggregate Bond Index (BCAG), which is a widely recognized, unmanaged index of U.S. dollar-denominated investment-grade fixed income securities. The Fund may, however, invest up to 75% of its total assets in equity securities.

Earnings Growth is a measure of a company’s net income over a specific period, generally one year, is a key indicator for measuring a company’s success, and the driving force behind stock price appreciation.

Earnings Per Share Growth is a measure of a company’s net income over a specific period, generally one year, is a key indicator for measuring a company’s success, and the driving force behind stock price appreciation.

5

| Disclosures and Definitions (continued) | |

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is essentially Net Income with Interest, Taxes, Depreciation, and Amortization added back to it. EBITDA can be used to analyze and compare profitability between companies and industries because it eliminates the effects of financing and accounting decisions. However, this is a non-GAAP measure that allows a greater amount of discretion as to what is (and is not) included in the calculation. This also means that companies often change the items included in their EBITDA calculation from one reporting period to the next.

EV (Enterprise Value) is a measure of a company’s value.

First Tier Security is any eligible security that: (i) is a rated security that has received a short-term rating from the requisite NRSROs in the highest short-term rating category for debt obligations (within which there may be sub-categories or gradations indicating relative standing); or (ii) is an unrated security that is of comparable quality to a security meeting the requirements for a rated security as determined by the Fund’s Board of Trustees; or (iii) is a security issued by a registered investment company that is a money market fund; or (iv) is a Government security.

Hedge involves making an investment to reduce the risk of adverse price movements in an asset. Normally, a hedge consists of taking an offsetting position in a related security, such as a futures contract.

KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions.

Lipper Mixed-Asset Target Allocation Growth Funds Average is an average of funds that, by portfolio practice, maintain a mix of between 60%-80% equity securities, with the remainder invested in bonds, cash, and cash equivalents.

MSCI Emerging Markets Index USD is a free float-adjusted market cap weighted index that is designed to measure equity market performance in the global emerging markets. Source: MSCI. MSCI data may not be reproduced or used for any other purpose.

MSCI Europe Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed markets in Europe. Source: MSCI. MSCI data may not be reproduced or used for any other purpose.

MSCI All Country World Index Gross USD is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

NASDAQ Financial-100 Index includes 100 of the largest domestic and international financial securities listed on the NASDAQ Stock Market based on market capitalization. They include companies classified according to the Industry Classification Benchmark as Financials, which are included within the NASDAQ Bank, NASDAQ Insurance, and NASDAQ Other Finance Indexes.

Price/Earnings Ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Normalized earnings – earnings metric that shows you want earnings look like smoothed out in the long run, taking into account the cyclical changes in an economy or stock.

Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 Index companies with higher price-to-value ratios and higher forecasted growth values.

Russell 2000® Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 Index companies with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

S&P MidCap 400® Index is a float-adjusted market capitalization-weighted index of 400 medium-capitalization domestic stocks chosen for market size, liquidity, and industry group representation.

S&P 500® Index is a float-adjusted, market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance.

S&P 500® Financials Index comprises those companies included in the S&P 500 that are classified as members of the GICS® financials sector.

S&P Municipal Bond Short Intermediate Index consists of bonds in the S&P Municipal Bond Index with a minimum maturity of one year and a maximum maturity of up to, but not including, eight years as measured from the Rebalancing Date.

S&P 500® Utilities Index comprises those companies included in the S&P 500 that are classified as members of the GICS® utilities sector.

Variable Rate Demand Note (VRDN): A debt instrument that represents borrowed funds that are payable on demand and accrue interest based on a prevailing money market rate, such as the prime rate. The interest rate applicable to the borrowed funds is specified from the outset of the debt, and is typically equal to the specified money market rate plus an extra margin.

Yield Curves: A line that plots interest rates of bonds with equal credit quality but various maturity dates on a specific date.

An investor cannot invest directly in an index.

6

EQUITY MANAGER REPORTS

| | Alpine Dynamic Dividend Fund |

| | |

| | Alpine Accelerating Dividend Fund |

| | |

| | Alpine Financial Services Fund |

| | |

| | Alpine Innovators Fund |

| | |

| | Alpine Transformations Fund |

| | |

| | Alpine Foundation Fund |

7

| Alpine Dynamic Dividend Fund |  |

| Comparative Annualized Returns as of 10/31/13 (unaudited) | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Since Inception(1) | |

| Alpine Dynamic Dividend Fund — Institutional Class | | | 17.02 | % | | | 5.67 | % | | | 7.24 | % | | | 3.84 | % | | | 4.48 | % | | |

| Alpine Dynamic Dividend Fund — Class A (Without Load) | | | 16.73 | % | | | N/A | | | N/A | | | N/A | | | 13.64 | % | | |

| Alpine Dynamic Dividend Fund — Class A (With Load) | | | 10.40 | % | | | N/A | | | N/A | | | N/A | | | 10.19 | % | | |

| MSCI All Country World Index Gross USD | | | 23.89 | % | | | 10.85 | % | | | 14.00 | % | | | 8.14 | % | | | 8.32 | % | | |

| S&P 500® Index | | | 27.18 | % | | | 16.56 | % | | | 15.17 | % | | | 7.46 | % | | | 7.54 | % | | |

| Lipper Global Equity Income Funds Average(2) | | | 19.91 | % | | | 10.36 | % | | | 11.76 | % | | | 6.36 | % | | | 6.81 | % | | |

| Lipper Global Equity Income Funds Ranking(2) | | | 89/113 | | | 61/62 | | | 48/49 | | | 18/18 | | | 15/15 | | |

| Gross Expense Ratio (Institutional Class): 1.28%(3) | | | | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Institutional Class): 1.28%(3) | | | | | | | | | | | | | | | | | | | | | | |

| Gross Expense Ratio (Class A): 1.53%(3) | | | | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Class A): 1.53%(3) | | | | | | | | | | | | | | | | | | | | | | |

| | (1) | Institutional Class shares commenced on September 22, 2003 and Class A shares commenced on December 30, 2011. Returns for indices are since September 22, 2003. |

| | (2) | The since inception return represents the period beginning September 25, 2003 (Institutional Class only). |

| | (3) | As disclosed in the prospectus dated February 28, 2013. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. Returns for the Class A shares with sales charge reflect a maximum sales charge of 5.50%. Performance for the Class A shares without sales charges does not reflect this load.

The MSCI All Country World Index Gross USD is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets. Source: MSCI. MSCI data may not be reproduced or used for any other purpose. The S&P 500® Index is a float-adjusted market capitalization index of 500 common stocks chosen for market size, liquidity and industry group representation to represent U.S. equity performance. The Lipper Global Equity Income Funds Average is an average of funds that by prospectus language and portfolio practice seek relatively high current income and growth of income by investing at least 65% of their portfolio in dividend-paying securities of domestic and foreign companies. Lipper rankings for the periods shown are based on fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500® Index and the Lipper Global Equity Income Funds Average are unmanaged and do not reflect the deduction of direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Global Equity Income Funds Average reflects fees charged by the underlying funds. The performance for the Alpine Dynamic Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Alpine Dynamic Dividend Fund has a contractual expense waiver that continues through February 28, 2014. Where a Fund’s gross and net expense ratios are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower.

To the extent that the Fund’s historical performance resulted from gains derived from participation in Initial Public Offerings (“IPOs”) and/or Secondary Offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary Offerings in the future.

8

| Alpine Dynamic Dividend Fund (continued) | |

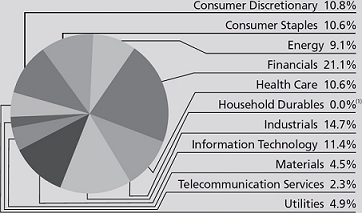

Portfolio Distributions* (unaudited)

| Top 10 Holdings* (unaudited) | |

| 1. | | Vodafone Group PLC-ADR | 2.29 | % |

| 2. | | QUALCOMM, Inc. | 1.94 | % |

| 3. | | Apple, Inc. | 1.88 | % |

| 4. | | RR Donnelley & Sons Co. | 1.80 | % |

| 5. | | Nestle SA | 1.74 | % |

| 6. | | Roche Holding AG | 1.61 | % |

| 7. | | Canadian Pacific Railway, Ltd. | 1.52 | % |

| 8. | | Corrections Corp. of America | 1.48 | % |

| 9. | | Novartis AG-ADR | 1.47 | % |

| 10. | | Avago Technologies, Ltd. | 1.47 | % |

| * | Portfolio Distributions percentages are based on total investments. Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio holdings and sector distributions are as of 10/31/13 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. |

(1) Amount is less than 0.05%.

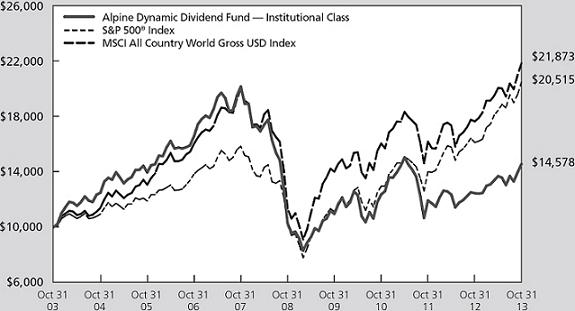

Value of a $10,000 Investment (unaudited)

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmarks. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees, if applicable. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

9

| Alpine Dynamic Dividend Fund (continued) | |

Commentary

For the fiscal year ended October 31, 2013, the Alpine Dynamic Dividend Fund generated a total return of 17.02% versus our benchmark, the MSCI All Country World Index Gross USD, which had a total return of 23.89%. On December 13, 2012, we were named co-portfolio managers of this Fund. From that date until October 31, 2013, the total return was 17.29% versus the benchmark return of 19.56%. All returns include reinvestment of all distributions. The Fund distributed $0.284 per share during the fiscal year. All references in this letter to the Fund’s performance relate to the Fund’s Institutional Class.

As previously announced in January 2013, we reduced the distribution rate during the period to align the Fund’s distribution rate with our assessment of the Fund’s long-term return potential as well as our projected levels of dividend income available to the Fund and to provide the Fund more flexibility to seek capital appreciation.

PERFORMANCE DRIVERS

While most major markets across the world exhibited positive returns in the 12 month period ended October 31, 2013, the dichotomy in returns between developed and emerging markets was striking, with the S&P 500® Index and the MSCI Europe Index, up 27.18% and 28.51% respectively, far outperforming the MSCI Emerging Market Index’s 6.90% return. We believe the performance of the indices themselves masked differing sensitivities to rising interest rates among different sectors: the S&P 500 Financials Index, a perceived beneficiary of rising interest rates, returned 31.91%, while the S&P 500 Utilities Index was up only 9.51% for the 12 month period.

To get a sense of the drivers of these diverging returns, it helps to examine some of the important macroeconomic events during the period. The downward pressure on global interest rates that had fueled the broad rally for high yielding securities reversed abruptly in May 2013, as there was speculation that the Federal Reserve (the “Fed”) might reduce its bond purchases. The 10 year Treasury yield rose from a low of 1.6% in early May to 3.0% by September 2013 as Fed Chairman Bernanke confirmed that the Fed would likely begin tapering its quantitative easing program by the end of the year.

Stocks have since resumed their upward climb as the Fed backed away from its earlier inclination to taper its bond-buying program. Leading indicators such as industrial production and consumer confidence surveys have continued to improve across many regions, particularly in Europe, with Chancellor Angela Merkel’s resounding

victory in German national elections providing strong support for the European unification process.

For the twelve month period, the industrials and consumer staples sectors had the greatest positive effect on the Fund’s total return on a relative basis. In the industrials sector, the Fund benefited from its exposure to companies that had a specific catalyst such as a new CEO at Canadian Pacific, and a successful debt refinancing and operational restructuring at R.R. Donnelley. In the consumer staples sector, the Fund benefited from its exposure to companies that had unique growth levers such as Walgreen’s highly accretive alliance with drug distributor AmerisourceBergen and Energizer’s successful migration from slow growth batteries to faster growing, higher gross margin personal care categories. On a relative basis, the consumer discretionary and energy sectors that had the greatest negative effect on total return. The Fund was adversely impacted by its exposure to companies in the consumer discretionary sector that were directly impacted by the hike in payroll taxes, colder-than-normal weather in the spring, and persistently high gasoline prices in the United States. In the energy sector, the Fund under-performed due primarily to its overweight to international services companies that were affected by delays in capital spending by major oil companies.

PORTFOLIO ANALYSIS

The top five contributors to the Fund’s performance for the fiscal year ending October 31, 2013 based on contribution to total return were R.R. Donnelley & Sons (100.18%), Vodafone Group Plc (51.95%), McKesson Corp (68.39%), Walgreen Company (72.44%), and Canadian Pacific Railway Ltd (55.87%).

R.R. Donnelly (average weight 1.16%) was the Fund’s top-performing stock for the year as the company delivered earnings that exceeded expectations, showing great progress in shifting its revenue mix from secularly declining segments such as Books and Directories towards growth segments including Logistics Services and Global Turnkey Solutions. R.R. Donnelly may have reached an inflection point as it has begun to show organic growth in its traditional print business. The company has also refinanced a portion of their debt at lower interest rates.

Vodafone (average weight 1.97%) is a multinational telecommunications company. The stock outperformed initially due to speculation that the company would sell its stake in Verizon Wireless to Verizon Communications. After the deal was announced, Vodafone continued to outperform due to the higher than expected price that Verizon Communications agreed to pay for the stake, and

10

| Alpine Dynamic Dividend Fund (continued) | |

due to the announcement of the large dividend that Vodafone will pay once the sale is completed. There is currently speculation that AT&T may bid for Vodafone once the Verizon Wireless sale closes in 2014.

McKesson Corp (average weight 1.46%) is a San Francisco-based pharmaceutical distributor and medical supplies wholesaler. The company is a key beneficiary of the increased volumes of pharmaceutical drugs resulting from the Affordable Care Act, and has generated consistently higher operating margins and returns on capital than its peers. We believe the stock will continue to outperform due to its accretive acquisition of European drug distributor Celesio AG, as well as the tailwind from elevated generic drug launches in 2014 and 2015.

Walgreen Company (average weight 1.34%) is the nation’s largest drugstore chain with over 8,000 mostly freestanding stores. The stock has outperformed peers partly due to its highly accretive 10 year drug distribution agreement with AmerisourceBergen announced in March 2013. Between this deal and the acquisition of Alliance Boots (Europe’s largest drug wholesaler), Walgreens effectively tripled its generic drug buying power, leading to significant cost savings.

Canadian Pacific Railway (average weight 1.54%) was a top-performing stock for the fiscal year as the new CEO Hunter Harrison’s efforts to restructure the railway began to bear fruit. The restructuring has included headcount reduction, running more efficient (longer) trains, and a fuel conservation strategy. These changes have been implemented faster than the original timetable set out by the new management team resulting in a lower operating ratio. We believe the company will be able to increase their customer base by offering better services.

The bottom five contributors to the Fund’s performance for the fiscal year ending October 31, 2013 based on contribution to total return were Subsea 7 (-18.35%), Tronox Ltd (-25.33%), Apple Inc (-9.75%), American Eagle Outfitters (-24.06%), and Petrofac Ltd (-30.73%).

Subsea 7 (average weight 0.74%) is one of three main competitors in subsea construction, one of the fastest growing segments of the oil services industry. Having earned a reputation for its strong risk management and conservative bidding practices, the market was justifiably surprised when Subsea 7 announced that the full-life project loss on its $1 billion contract with Petrobras would be up to three times higher than estimated just three months previously, wiping out as much as a third of annual operating income at the company. We no longer have a position in Subsea 7.

Tronox Ltd (average weight 0.05%) is the only vertically integrated producer of titanium dioxide (TiO2), a whitening/brightening pigment used in paints, plastics,

paper, sunscreen and food coloring with no effective substitutes. Due to an extended destocking period in China and weak end markets in Europe, the Board of Tronox decided to cancel the special dividend for which we were invested in the stock and we sold the position.

Apple (average weight 2.42%) was an underperformer as the company’s product cycle failed to impress consumers and growth came to a halt in the high end of the mobile smart phone market. In addition, Apple lacked a product in the faster growing mass market channel. Some investor activism helped the shares rebound nicely from their lows but it wasn’t enough to completely offset the earlier underperformance.

American Eagle Outfitters (average weight 1.17%) is a mall-based retailer of denim and other casual apparel and accessories aimed at young men and women ages 15-25. Following six quarters of impressive performance, the increasingly promotional environment in the teen retail space caught up with American Eagle, driving negative returns and declining margins.

Petrofac Ltd (average weight 0.52%) is an oil and gas-focused engineering, procurement and construction company with a strong reputation as a primary contractor able to execute large capital projects in a range of competencies from upstream to downstream facilities. The stock underperformed as a dearth of project awards in the increasingly competitive onshore markets led to pressure on revenues and margins. We no longer have a position in Petrofac.

In order to achieve its dividend, the Fund participated in a number of dividend capture strategies including (1) purchasing shares in the stock of a regular dividend payer before an upcoming ex-date and selling after the ex-date, (2) purchasing shares before an anticipated special dividend and selling opportunistically after the ex-date of the dividend, and (3) purchasing additional shares in stocks that the Fund already owns before the ex-date and selling the original shares after the ex-date, thus receiving a dividend on a larger position while still maintaining qualified dividend income eligibility (“QDI”) on its position. Although these strategies have resulted in higher turnover and associated transaction costs for the Fund overall the Fund’s turnover rate has decreased as we have relied less upon these strategies this year. While there is the potential for market loss on the shares that are held for a short period, we seek to use these strategies to generate additional income with limited impact on the construction of the core portfolio.

We have hedged a portion of our currency exposures to the Swiss Franc, Japanese Yen and British Pound. We have also used leverage at times both in the execution of the strategy of the Fund and to help manage significant amounts of net outflows during the fiscal year.

11

| Alpine Dynamic Dividend Fund (continued) | |

SUMMARY & OUTLOOK

We believe the Alpine Dynamic Dividend Fund has been reinvigorated in order to best pursue its investment objective: to seek high current dividend income that qualifies for the reduced U.S. Federal income tax rates created by the “Jobs and Growth Tax Relief Reconciliation Act of 2003” while also focusing on total return for long-term growth of capital. We have shifted to a team-based structure that incorporates both top-down and bottom-up stock picking. The investment team includes experienced Alpine portfolio managers and research analysts who provide analysis and recommendations on stocks within the sectors they cover. We, along with our CEO, CIO and Senior Investment Risk Strategist, comprise a committee that provides strategic oversight to the Fund and monitors sector and regional exposures, as well as quantitative and qualitative risk factors.

While we are concerned that there may be lingering effects of the U.S. government shutdown and the political squabbling over the debt ceiling, there are many bright spots in the U.S. economy. Auto sales have improved, and there has been a broad-based gain in

manufacturing activity. The energy renaissance spurred by hydraulic fracturing technologies has created a durable cost advantage for many domestic industries reliant on fossil fuels, a trend that is starting to manifest itself in rising margins. The Affordable Care Act, despite all the negative politically-charged rhetoric, has created a potential tailwind for multiple subsectors of the healthcare industry. Europe continues to stabilize with many leading economists now forecasting growth for the first time in several years. And with the valuation of stocks in many emerging markets countries at historical lows relative to their developed market counterparts, we believe there are attractive risk/reward opportunities. The Fund maintains its focus on, what we believe are high quality companies with strong balance sheets and strong potential to grow earnings and dividends amidst an uncertain macro environment.

Sincerely,

Brian Hennessey

Joshua Duitz

Co-Portfolio Managers

12

| Alpine Dynamic Dividend Fund (continued) | |

This letter represents the opinions of the Fund’s management and is subject to change, is not guaranteed and should not be considered a recommendation to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice. Views expressed may vary from those of the firm as a whole. Past performance is no guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The Fund is subject to risks, including the following:

Credit Risk – Credit risk refers to the possibility that the issuer of a security will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation.

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the market. Companies that issue dividend paying-stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future. The Fund may hold securities for short periods of time related to the dividend payment periods and may experience loss during these periods.

Emerging Market Securities Risk – The risks of foreign investments are heightened when investing in issuers in emerging market countries. Emerging market countries tend to have economic, political and legal systems that are less fully developed and are less stable than those of more developed countries. They are often particularly sensitive to market movements because their market prices tend to reflect speculative expectations. Low trading volumes may result in a lack of liquidity and in extreme price volatility.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer than expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions Risk – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. The Fund may enter into foreign currency transactions to try to manage this risk. The Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the Adviser to accurately predict the direction of changes in currency exchange rates. The Fund may enter into forward foreign currency exchange contracts in order to protect against possible losses on foreign investments resulting from adverse changes in the relationship between the U.S. dollar and foreign currencies. Although this method attempts to protect the value of the Fund’s portfolio securities against a decline in the value of a currency, it does not eliminate fluctuations in the underlying prices of the securities and while such contracts tend to minimize the risk of loss due to a decline in the value of the hedged currency, they tend to limit any potential gain which might result should the value of such currency increase.

Foreign Securities Risk – The Fund’s investments in securities of foreign issuers or issuers with significant exposure to foreign markets involve additional risk. Foreign countries in which the Fund may invest may have markets that are less liquid, less regulated and more volatile than U.S. markets. The value of the Fund’s investments may decline because of factors affecting the particular issuer as well as foreign markets and issuers generally, such as unfavorable government actions, and political or financial instability. Lack of information may also affect the value of these securities. The risks of foreign investment are heightened when investing in issuers of emerging market countries.

Growth Stock Risk – Growth stocks are stocks of companies believed to have above-average potential for growth in revenue and earnings. Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market while the market concentrates on undervalued stocks.

13

| Alpine Dynamic Dividend Fund (continued) | |

Initial Public Offerings (IPO) and Secondary Offerings Risk – The Fund may invest a portion of its assets in shares of IPOs or secondary offerings of an issuer. IPOs and secondary offerings may have a magnified impact on the performance of a Fund with a small asset base. The impact of IPOs and secondary offerings on a Fund’s performance likely will decrease as the Fund’s asset size increases, which could reduce a Fund’s returns. IPOs and secondary offerings may not be consistently available to the Fund for investing. IPO and secondary offering shares frequently are volatile in price due to the absence of a prior public market, the small number of shares available for trading and limited information about the issuer. Therefore, the Fund may hold IPO and secondary offering shares for a very short period of time. This may increase the turnover of the Fund and may lead to increased expenses for the Fund, such as commissions and transaction costs. In addition, IPO and secondary offering shares can experience an immediate drop in value if the demand for the securities does not continue to support the offering price.

Leverage Risk – The Fund may use leverage to purchase securities. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting, a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Micro Capitalization Company Risk – Stock prices of micro capitalization companies are significantly more volatile, and more vulnerable to adverse business and economic developments than those of larger companies. Micro capitalization companies often have narrower markets for their goods and/or services and more limited managerial and financial resources than larger, more established companies, including small or medium capitalization companies.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

Qualified Dividend Tax Risk – Favorable U.S. federal tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws.

Small- and Medium-Capitalization Company Risk – Securities of small- or medium-capitalization companies are more likely to experience sharper swings in market values, and may be less liquid, in which case it may be more difficult for the Adviser to sell at times and at prices that the Adviser believes appropriate and generally are more volatile than those of larger companies.

Swaps Risk – Swap agreements are derivative instruments that can be individually negotiated and structured to address exposure to a variety of different types of investments or market factors. Depending on their structure, swap agreements may increase or decrease the Fund’s exposure to long- or short-term interest rates, foreign currency values, mortgage securities, corporate borrowing rates, or other factors such as security prices or inflation rates. The Fund also may enter into swaptions, which are options to enter into a swap agreement. Since these transactions generally do not involve the delivery of securities or other underlying assets or principal, the risk of loss with respect to swap agreements and swaptions generally is limited to the net amount of payments that the Fund is contractually obligated to make. There is also a risk of a default by the other party to a swap agreement or swaption, in which case the Fund may not receive the net amount of payments that the Fund contractually is entitled to receive.

Undervalued Stock Risk – The Fund may pursue strategies that may include investing in securities, which, in the opinion of the Adviser, are undervalued. The identification of investment opportunities in undervalued securities is a difficult task and there is no assurance that such opportunities will be successfully recognized or acquired. While investments in undervalued securities offer opportunities for above-average capital appreciation, these investments involve a high degree of financial risk and can result in substantial losses.

Please refer to pages 5-6 for other important disclosures and definitions.

14

| Alpine Accelerating Dividend Fund | |

| Comparative Annualized Returns as of 10/31/13 (unaudited) |

| | | 1 Year | | 3 Years | | Since Inception(1) |

| Alpine Accelerating Dividend Fund — Institutional Class | | | 25.94% | | | | 14.26% | | | | 14.76% | |

| Alpine Accelerating Dividend Fund — Class A (Without Load) | | | 25.55% | | | | N/A | | | | 19.37% | |

| Alpine Accelerating Dividend Fund — Class A (With Load) | | | 18.65% | | | | N/A | | | | 15.75% | |

| S&P 500® Index | | | 27.18% | | | | 16.56% | | | | 14.34% | |

| Dow Jones Industrial Average | | | 21.82% | | | | 14.82% | | | | 13.22% | |

| Lipper Equity Income Funds Average(2) | | | 23.47% | | | | 14.53% | | | | 15.18% | |

| Lipper Equity Income Funds Ranking(2) | | | 102/388 | | | | 165/293 | | | | 158/262 | |

| Gross Expense Ratio (Institutional Class): 3.26%(3) | | | | | | | | | | | | |

| Net Expense Ratio (Institutional Class): 1.35%(3) | | | | | | | | | | | | |

| Gross Expense Ratio (Class A): 3.51%(3) | | | | | | | | | | | | |

| Net Expense Ratio (Class A): 1.60%(3) | | | | | | | | | | | | |

| | (1) | Institutional Class shares commenced on November 5, 2008 and Class A shares commenced on December 30, 2011. Returns for indices are since November 5, 2008. |

| | (2) | The since inception data represents the period beginning November 6, 2008 (Institutional Class only). |

| | (3) | As disclosed in the prospectus dated February 28, 2013. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. Returns for the Class A shares with sales charge reflect a maximum sales charge of 5.50%. Performance for the Class A shares without sales charges does not reflect this load.

The S&P 500® Index is a float-adjusted market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally the leaders in their industry. The Lipper Equity Income Funds Average is an average of funds that seek relatively high current income and income growth through investing 60% or more of their respective portfolios in equities. Lipper rankings for the periods shown are based on fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500® Index, the Dow Jones Industrial Average, and the Lipper Equity Income Funds Average are unmanaged and do not reflect direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Equity Income Funds Average reflects fees charged by the underlying funds. The performance for the Alpine Accelerating Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Alpine Accelerating Dividend Fund has a contractual expense waiver that continues through February 28, 2014. Where a Fund’s gross and net expense ratios are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower.

To the extent that the Fund’s historical performance resulted from gains derived from participation in Initial Public Offerings (“IPOs”) and/or Secondary Offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary Offerings in the future.

15

| Alpine Accelerating Dividend Fund (continued) | |

Portfolio Distributions* (unaudited)

Top 10 Holdings* (unaudited)

| 1. | | Apple, Inc. | 1.81 | % |

| 2. | | QUALCOMM, Inc. | 1.60 | % |

| 3. | | Dick’s Sporting Goods, Inc. | 1.60 | % |

| 4. | | GNC Holdings, Inc.-Class A | 1.56 | % |

| 5. | | PepsiCo, Inc. | 1.55 | % |

| 6. | | International Business Machines Corp. | 1.55 | % |

| 7. | | The J.M. Smucker Co. | 1.54 | % |

| 8. | | Comcast Corp.-Class A | 1.54 | % |

| 9. | | Energizer Holdings, Inc. | 1.53 | % |

| 10. | | General Mills, Inc. | 1.51 | % |

| * | Portfolio Distributions percentages are based on total investments. Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio holdings and sector distributions are as of 10/31/13 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. |

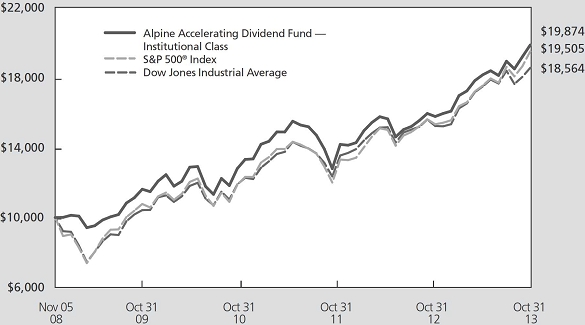

Value of a $10,000 Investment (unaudited)

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees, if applicable. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

16

| Alpine Accelerating Dividend Fund (continued) | | |

Commentary

For the fiscal year ended October 31, 2013, the Alpine Accelerating Dividend Fund generated a total return of 25.94%. This compares with a total return of 27.18% for the S&P 500® Index for the same period. During the last twelve months, the Fund steadily increased its monthly per share distribution from $0.0398 in November, 2012 to $0.0409 in October, 2013. All references in this letter to the Fund’s performance relate to the performance of the Fund’s Institutional Class.

PERFORMANCE DRIVERS

The Fund generally prefers to take a conservative investment stance with regard to portfolio construction and security selection during times of economic and geopolitical uncertainty. We believe the twelve months ended October 31, 2013 was such a time. For this reason, the Fund had an average cash holding of 7.7% during the fiscal year and a portfolio beta less than 1.0 during the same span.

On a sector basis, the financials had the largest impact on the absolute performance of the Fund, followed by health care and consumer discretionary. Telecommunication was the only sector to generate a negative return over the past 12 months. On a relative basis, consumer staples generated the largest outperformance versus the S&P 500®, followed by energy and industrials. Materials, consumer discretionary, and telecommunication services were the worst relative performers.

PORTFOLIO ANALYSIS

The top five contributors to the Fund’s performance during the twelve months ended October 31, 2013, based on contribution to total return were CBS (+85.03%), Walgreen (+72.71%), AmerisourceBergen (+69.72%), Nike (+69.13%), and Bristow Group (+64.36%).

| • | Demand for quality content in the digital world continues to drive CBS’ (average weight 1.57%) profit and its stock price higher. The media giant is capitalizing on its strong catalog of new and old shows by signing deals with online digital content providers. In addition, strong ratings on its broadcast network have enabled the company to generate solid increases in its advertising rates and to sign profitable re-transmission agreements with many of its affiliate stations. |

| • | Walgreens’ (average weight 1.55%) shares rebounded nicely during the fiscal year as the fundamentals in its core US pharmacy operations |

| | improved. The company also began to recognize some of the synergies from the 2012 Alliance Boots merger. Finally, midway through the year, Walgreens entered into a well-received new distribution agreement with AmerisourceBergen for branded and generic drugs. |

| • | In March 2013, AmerisourceBergen (average weight 1.40%) unveiled what it described as a “game-changing” partnership with Walgreens, including a 10 year distribution agreement for branded and generic drugs along with access to generic drugs sourced through Walgreens joint venture with Alliance Boots. In addition to the earnings accretive nature of the distribution deal, the shares enjoyed meaningful P/E multiple expansion during the fiscal year as investors began to factor in the longer term benefits of the partnership. |

| • | Nike (average weight 1.27%) remains a force in the thriving global footwear segment. The company continues to grow in the United States fueled by a strong demand for athletic wear. Sales and future orders exceeded expectations for most of the past year. Meanwhile, management has been aggressively working to right size its Chinese operations. The better-than-expected performance led to rising earnings and a higher P/E multiple for the shares. |

| • | As a leading provider of offshore helicopter services to the oil and gas industry, Bristow (average weight 1.33%) continued to pursue its goal of 10-15% annual earnings per share (EPS) growth as energy companies continue to increase spending for offshore exploration and production of oil and natural gas. In addition, in March, Bristow won a $2.5 billion search and rescue contract with the British government that could potentially add as much as $1.00 per share of earnings later this decade. |

Tower Group International (-75.03%), Oi S.A. (-26.16%), Two Harbors (-19.05%), Apple (-9.85%), and Potash Corporation of Saskatchewan (-18.05%) had the largest adverse impact on the performance of the Fund over the fiscal year.

| • | After a solid start to the year, including the consummation of a merger with a Bermuda-based reinsurer, Tower Group (average weight 0.68%) surprised the market with the announcement of a massive reserve charge that led to a ratings downgrade from The A.M. Best ratings agency, further pressuring the shares. Despite a seemingly |

17

| Alpine Accelerating Dividend Fund (continued) | | |

| | | inexpensive valuation in the aftermath of an extreme sell-off, we opted to exit the position given a lack of current financial statements and the high probability that Tower Group will eliminate its dividend. |

| • | The Brazilian telecommunications industry has struggled this year and Oi S.A.(average weight 0.09%) has been caught in the downdraft. Investors continued to sell shares of Oi as they became frustrated with the slow pace of operational improvements despite multiple years of restructuring. Even the proposed merger with Portugal Telecom hasn’t succeeded in reversing the sell-off. |

| • | Two Harbors (average weight 0.67%) shares declined during the fiscal year as its business of investing in mortgage-backed securities came under pressure as the market wrestled with the prospect of the end of the Fed’s QE3 program. As a result, mortgage REITs like Two Harbors were forced to lower their dividends. |

| • | After peaking in late November 2012, the shares of Apple (average weight 1.67%) fell as the company’s product cycle failed to impress consumers and growth came to a halt in the high end of the mobile smart phone market. In addition, Apple lacked a product in the faster growing mass market channel. Some investor activism helped the shares rebound nicely from their lows but it wasn’t enough to completely offset the earlier underperformance. |

| • | Shares of Potash Corp. (average weight 1.02%) suffered a two-day decline of nearly 25% when competitor Uralkali unexpectedly withdrew from its marketing alliance with partner Belaruskali and embarked on a new strategy favoring volume over price. Uralkali’s decision threw the potash market into turmoil and led to a sharp decline in sales of the nutrient as the market struggled to find a new equilibrium. |

SUMMARY & OUTLOOK

As we look toward 2014, we see a market environment that appears fairly similar to that of the preceding year. The United States continues to grow below trend while contending with a partisan environment in Washington D.C. and the prospect of the Federal Reserve’s tapering of QE3 at some point during the year. In Europe, growth continues to be sluggish and the specter of deflation cannot be overlooked. Indeed, the European Central Bank just cut the main refinance rate by another 25 basis points to stave off the deflationary risk and to stimulate the Euro area economies. Emerging markets (EM) appear to be undergoing a difficult transition from a world awash in liquidity to one where liquidity isn’t quite so abundant. Many EM countries could be forced to slow their economies down to balance external current account deficits and tame inflation if QE3 induced liquidity dries up should the Fed begin to taper in 2014. This macro backdrop and our view that equity market valuations are fairly robust, lead us to continue to take a conservative investment stance.

As such, the Fund seeks to continue to emphasize its focus on what we believe are quality companies with strong balance sheets that have a demonstrated track record of increasing and/or accelerating dividends. In addition, we remain on the lookout for stocks with the potential to initiate, grow, or accelerate their dividends over time. Although this strategy may lag behind the market in periods of robust returns, we believe it provides a more attractive risk/return profile over the long run. In conclusion, similar to the stocks in which we seek to invest, the Fund aims to provide a steadily rising distribution to its investors.

We thank our shareholders for their support and look forward to continued success over the next year.

Sincerely,

Bryan Keane

Andrew Kohl

Co-Portfolio Managers

18

| Alpine Accelerating Dividend Fund (continued) | | |

This letter represents the opinions of the Fund’s management and is subject to change, is not guaranteed and should not be considered a recommendation to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice. Views expressed may vary from those of the firm as a whole. Past performance is no guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The Fund is subject to risks, including the following:

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the market. Companies that issue dividend-paying stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future or the anticipated acceleration of dividends could not occur.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer-than-expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions Risk – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. The Fund may enter into foreign currency transactions to try to manage this risk. The Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the Adviser to accurately predict the direction of changes in currency exchange rates.

Foreign Securities Risk – The Fund’s investments in securities of foreign issuers or issuers with significant exposure to foreign markets involve additional risk. Foreign countries in which the Fund may invest may have markets that are less liquid, less regulated and more volatile than U.S. markets. The value of the Fund’s investments may decline because of factors affecting the particular issuer as well as foreign markets and issuers generally, such as unfavorable government actions, and political or financial instability. Lack of information may also affect the value of these securities. The risks of foreign investments are heightened when investing in issuers in emerging market countries.

Growth Stock Risk – Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out-of-favor and underperform the overall equity market while the market concentrates on undervalued stocks. Although the Fund will not concentrate its investments in any one industry or industry group, it may, like many growth funds, weight its investments toward certain industries, thus increasing its exposure to factors adversely affecting issuers within those industries.

Initial Public Offerings (IPO) and Secondary Offerings Risk – The Fund may invest a portion of its assets in shares of IPOs or Secondary Offerings of an issuer. IPOs and Secondary Offerings may have a magnified impact on the performance of a Fund with a small asset base. The impact of IPOs and Secondary Offerings on a Fund’s performance likely will decrease as the Fund’s asset size increases, which could reduce a Fund’s returns. IPOs and Secondary Offerings may not be consistently available to the Fund for investing. IPO and Secondary Offering shares frequently are volatile in price due to the absence of a prior public market, the small number of shares available for trading and limited information about the issuer. Therefore, the Fund may hold IPO and Secondary Offering shares for a very short period of time. This may increase the turnover of the Fund and may lead to increased expenses for the Fund, such as commissions and transaction costs. In addition, IPO and Secondary Offering shares can experience an immediate drop in value if the demand for the securities does not continue to support the offering price.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Micro-Capitalization Company Risk – Stock prices of micro-capitalization companies are significantly more volatile, and more vulnerable to adverse business and economic developments than those of larger companies. Micro-capitalization companies often have more narrow markets for their goods and/or services and more limited managerial and financial resources than larger, more established companies, including small- or medium-capitalization companies.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

19

| Alpine Accelerating Dividend Fund (continued) | | |