UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21210

Alpine Income Trust

(Exact name of registrant as specified in charter)

2500 Westchester Avenue, Suite 215

Purchase, New York 10577

(Address of principal executive offices)(Zip code)

(Name and Address of Agent for Service) | Copy to: |

Samuel A. Lieber

Alpine Woods Capital Investors, LLC

2500 Westchester Avenue, Suite 215

Purchase, New York 10577 | Rose DiMartino

Attorney at Law

Willkie Farr & Gallagher

787 7th Avenue, 40th Floor

New York, New York 10019 |

Registrant’s telephone number, including area code: (914) 251-0880

Date of fiscal year end: October 31

Date of reporting period: November 1, 2014 – April 30, 2015

Item 1: Shareholder Report

Equity & Income Funds

| Alpine Dynamic Dividend Fund | Alpine Equity Income Fund |

| Institutional Class (ADVDX) | Institutional Class (ADBYX) |

| Class A (ADAVX) | Class A (ADABX) |

| Alpine Accelerating Dividend Fund | Alpine Ultra Short Municipal Income Fund |

| Institutional Class (AADDX) | Institutional Class (ATOIX) |

| Class A (AAADX) | Class A (ATOAX) |

| Alpine Financial Services Fund | Alpine High Yield Managed Duration |

| Institutional Class (ADFSX) | Municipal Fund |

| Class A (ADAFX) | Institutional Class (AHYMX) |

| Alpine Small Cap Fund | Class A (AAHMX) |

| Institutional Class (ADINX) | |

| Class A (ADIAX) | |

| Alpine Transformations Fund | |

| Institutional Class (ADTRX) | |

| Class A (ADATX) | |

April 30,

2015

Semi-Annual Report

Table of Contents

Additional Alpine Funds are offered in the Alpine Equity Trust. These Funds include:

| Alpine International Real Estate Equity Fund | Alpine Emerging Markets Real Estate Fund |

| | |

| Alpine Realty Income & Growth Fund | Alpine Global Infrastructure Fund |

| | |

| Alpine Cyclical Advantage Property Fund | |

Alpine’s Real Estate Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing in funds of the Alpine Equity Trust. The statutory and summary prospectuses contain this and other important information about the investment company, and it may be obtained by calling 1-888-785-5578, or visiting www.alpinefunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible.

Alpine’s Investment Outlook

President’s Letter

Dear Shareholders:

GLOBAL INVESTMENT: CURRENT STATE OF PLAY

This report of the first half of fiscal 2015 is being written on a day when the Dow Jones Industrial Average has reached a new all-time high. In the last report, we noted “...prospects for modest economic growth supported by abundant cheap global liquidity, combined with lower energy costs, will continue to favor capital markets and global equities more broadly.” The realization of these trends was stimulated by the unprecedented intervention in global bond markets by major central banks. Thus we observed that “just as the U.S. stock market outperformed much of the world during 2014 as a result of the combination of cheap money and improving economic fundamentals, we believe that 2015 will see a global broadening of market performance to include small cap stocks in the U.S., as well increased international opportunities.” We can now add that both bond and stock markets daily volatility could increase materially above the historically subdued levels of recent years. This might create attractive opportunities to buy stocks.

For the past six years, global equity markets have performed well despite an historically lackluster economic recovery. Meanwhile, many retail and pension investors have continued to reduce equity exposure in favor of fixed income. Daily volatility has been generally muted and even short term mini-panics or financial blips over this period have been followed by long term buyers providing support by buying the dip in prices. Witness the initial Euro scare over a possible Greek default back in the summer of 2011 which is still unresolved, although hopefully a resolution is close at hand. Similarly, the Fed-induced ‘Taper Tantrum’ in May of 2013. It is now two years later and interest rates are still historically low. The collapse in gold prices during 2013, and crude oil prices since last summer have also had only modest impact on the underlying economy.

The Greek problem reflected inattention to questionable credit underwriting. It is Alpine’s view that these mini-scares did not reflect the underlying economic reality, but rather were a product of secondary financial effects. The ‘Taper Tantrum’ was a product of excessive volume of so called ‘carry trades’, dependent upon disproportionate financial spreads and easy money. Both gold and oil prices were seen as inflation benefiting alternatives to stocks and bonds, but

became financial assets as greater ease and access to investment facilitated investor speculation. Even traditional alternative investments such as agricultural commodities, including corn and soybeans, have deteriorated after years of heightened financial investment.

All of these situations were the product of broad caution over traditional equities after the bust of 2008, fueled by unprecedented liquidity created by the world’s central banks. While quantitative easing (QE) by the central banks was indeed designed to elevate asset prices, QE cannot target which assets get elevated. Liquidity surges, like flood waters move where they can flow easily. So investment in sovereign debt or inflation hedges became very crowded trades. Uniquely, these mini bubble busts benefited from several broad trends that we believe will continue to have long term economic impact. I will discuss these trends in terms of how Alpine sees their potential for creating or altering investment potential as well as their impact on the current investment cycle.

TECHNOLOGICAL TREND

Of course technological change continues to affect how we live, work, play, create and destroy. It influences all of the other trends, but it is not a trend per se, rather a factor of which we must all be aware. Much of our focus is on data, communication, research and entertainment. Advances in these areas have helped shape the trends upon which we focus.

DISINTERMEDIATION TREND

Broadening the dissemination of goods, services and information from limited, local or monopolistic sources has aided transparency, lowered prices and increased availability. Think of Amazon, Priceline, AirBnB, or Uber to name a few companies that inserted themselves between consumers and traditional brands of service providers.

GLOBALIZATION TREND

The ability to send or source goods, services, capital, data and ideas to or from almost anywhere on earth, has lowered prices and costs, but has also brought about some homogenization, albeit often with best practices. Think not just about how many countries Apple sources parts for its iPhone (11), or of Boeing jets made with Chinese wings, British engines and Japanese batteries, but of call centers for U.S. air travel or financial services operating from New Delhi or Manila.

1

URBANIZATION TREND

Due to both demographics and aforementioned trends, the pace of urbanization should grow. Jobs, information, capital and opportunity to prosper and differentiate oneself are often greater in cities than in rural settings, so long term migration trends from rural agriculture to urban industry continues in Asia, Africa and Latin America. The U.N. forecasts that this will double the population in cities, over the next 35 years, even though total global population growth will only be 50% by 2050. Newly expanding cities may benefit from modern infrastructure and ensuing cost or efficiency advances, so providers of such products and services could benefit.

DEMOCRACY TREND

The mixing of different people, different places, with varied education and cultural backgrounds can bring about a continual clash of ideas. Historically, immigrants were either co-opted and assimilated, or stayed together, yet apart from the mainstream. However, today, access to broadband for news, entertainment or communication allows for greater visibility and cross pollination of ideas, experiences and possibilities, as well as daily realities and hardships around the world. While some fear that social networks and consumer market algorithms may actually stifle transparency and new ideas, and even worse, in some places nationalism or religious fanaticism will not even tolerate such a ‘Clash of Ideas’. Hence, the ‘Arab Spring’ of democratic aspirations brought about violent reactions; leading to police states, coups and chaos. However, over time, we believe that transparency and knowledge can influence tradition and cross cultural barriers, leading to transformation and even revolution. If broadly embraced by a people, such grassroots change is inherently democratic. While many young democracies look to us as less than fair and open, we believe that they will become more representative over a few generations. As a rule, democracies provide greater opportunity for the creation and dissemination of wealth, as well as higher levels of legal protection for investors and enhanced corporate governance.

GROWTH ...

So where do these come together in Alpine Funds? It informs us where to invest, by company, industry and country. Alpine believes that business models that utilize or are part of these trends have better prospects for achieving low cost, broad distribution which can enable scale and with it, greater opportunities for revenue growth and/or margin enhancement. Naturally, this assumes the products and services offered are competitive. That said, companies with superior products will always stand out, as will low price leaders. However, the equity markets are rewarding companies which can grow both future earnings and market share with high price/earnings multiples. Companies which are less likely to have strong growth prospects, risk trading at low prices unless they take advantage of cheap financing to

buy back shares, or pay an attractive dividends. Alpine also focuses on companies which we believe are undervalued by the market, as they could become the target for take overs by others.

...AND VALUE

Mergers and acquisitions (M&A) continues to be a major investment theme for equities as divergent valuations, cheap financing and the market’s emphasis on growth is driving consolidation. Prominently, big pharma companies who cut their research and development budgets last decade, are now scrambling to buy new drugs or promising compounds to feed their large distribution capacity. This has stimulated the boom in biotech stocks over the past years. This theme should continue at least until interest rates rise materially.

LOOKING FORWARD

The durability of the current stock market rally is dependent on low interest rates and lots of financial liquidity. This has enhanced the impact of the underlying economic trends we discussed earlier. However, if the liquidity is rapidly removed from the system, there could be a destabilizing shock, both to the markets and to the economy. For that reason, we believe central banks will take a very gradual approach to raising interest rates after further job growth, wage gains and even inflation is apparent. We believe the global nature of the economic slowdown will continue to be a moderating factor on the pace of future interest rate rises. Therefore, Alpine will continue to focus on undervalued companies with attractive dividend paying potential and companies which can potentially benefit from disintermediation, globalization, urbanization, democracy and, of course, improvements in technology.

Thank you for your interest and support.

Samuel A. Lieber

President

Past performance is not a guarantee of future results. The specific market, sector or investment conditions that contribute to a Fund’s performance may not be replicated in future periods.

Mutual fund investing involves risk. Principal loss is possible. Please refer to individual fund letters for risks specific to that fund.

This letter and the letters that follow represent the opinions of the Funds’ management and are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice.

2

| Disclosures and Definitions |  |

Please refer to the Schedule of Portfolio Investments for each Fund’s holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

Favorable tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws. Alpine may not be able to anticipate the level of dividends that companies will pay in any given timeframe.

The Funds’ distributions may consist of net investment income, net realized capital gains and/or a return of capital. If a distribution includes anything other than net investment income, the Funds will provide a notice of the best estimate of its distribution sources when distributed, which will be posted on the Funds’ website: www.alpinefunds.com, or can be obtained by calling 1-800-617-7616. We estimate that the Alpine Series and Income Trusts did not pay any distributions during the fiscal semi-annual period ending April 30, 2015 through a return of capital. A return of capital distribution does not necessarily reflect the Funds’ performance and should not be confused with “yield” or “income.” Final determination of the Federal income tax characteristics of distributions paid during the calendar year will be provided on U.S. Form 1099-DIV, which will be mailed to shareholders. Please consult your tax advisor for further information.

All investments involve risk. Principal loss is possible. A small portion of the S&P 500 yield may include return of capital; the 10-year Treasury yield does not include return of capital; Corporate bonds and High Yield Bonds generally do not have return of capital; a portion of the dividend paid by REITs and REIT preferred stock may be deemed a return of capital for tax purposes in the event the company pays a dividend greater than its taxable income. A stock may trade with more or less liquidity than a bond depending on the number of shares and bonds outstanding, the size of the company, and the demand for the securities. The REIT and REIT preferred stock market are smaller than the broader equity and bond markets and often trade with less liquidity than these markets depending upon the size of the individual issue and the demand of the securities. Treasury notes are guaranteed by the U.S. Government and thus they are considered to be safer than other asset classes. Tax features of a Treasury Note, Corporate bond, Stock, High Yield bond, REITs and REIT preferred stock may vary based on an individual circumstances. Consult a tax professional for additional information. Neither the Fund nor any of its representatives may give tax advice. Investors should consult their tax advisor for information concerning their particular situation.

Standard & Poor’s Financial Services LLC (S&P) is a financial services company, a division of McGraw Hill Financial that publishes financial research and analysis on stocks and bonds. S&P is considered one of the Big Three credit-rating agencies, which also include Moody’s Investor Service and Fitch Ratings.

S&P assigns rating on a scale of ‘D’ to ‘AAA’, with ‘D’ the lowest/weakest rating, indicating a default, and ‘AAA’ the highest/strongest rating, indicating the strongest credit quality in S&P’s spectrum of credit ratings.

S&P incorporates a broad number of credit areas of each entity/municipality when assigning a bond rating to an entity’s debt instrument, including: (a) financial position, which encompasses liquidity metrics, cash reserves, non-liquid assets, liabilities, and other financial metrics; (b) debt position, which includes long and short-term bonded debt and other privately-placed notes/bonds, leases and other off-balance sheet liabilities; (c) pension and Other Post-Employment Benefits (OPEB); (d) socio economic indices; (e) the aptitude and sophistication of management.

Earnings Growth and Earnings Per Share Growth are not measures of the Funds’ future performance.

Diversification does not assure a profit or protect against loss in a declining market.

Must be preceded or accompanied by a prospectus.

Quasar Distributors, LLC, distributor.

Equity Income Funds – Definitions

Barclays High Yield Municipal Bond Index is the Muni High Yield component of the Barclays Municipal Bond Index. The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market.

Barclays 1 Year Municipal Bond Index is a total return benchmark of BAA3 ratings or better designed to measure returns for tax exempt assets.

Basis Point is a value equaling one one-hundredth of a percent (1/100 of 1%).

Beta measures the sensitivity of the investment to the movements of its benchmark. A beta higher than 1.0 indicates the investment has been more volatile than the benchmark and a beta of less than 1.0 indicates that the investment has been less volatile than the benchmark.

Bloomberg 10-Year U.S. Muni General Obligation AAA Index is populated with U.S. municipal general obligations (G.O.) with an average rating of AAA from Moody’s and S&P, with an average maturity of ten years. The option-free yield curve is built using option-adjusted

3

| Disclosures and Definitions (Continued) | |

spread (OAS) model. Furthermore, the index is derived from contributed pricing from the Municipal Securities Rulemaking Board (MSRB), new issues calendars and other proprietary contributed prices.

The Bovespa Index is a total return index weighted by traded volume and is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Dividend Yield is the yield a company pays out to its shareholders in the form of dividends. It is calculated by taking the amount of dividends paid per share over a specific period of time and dividing by the stock’s price.

Dow Jones Industrial Average is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Earnings Per Share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company’s profitability.

Free cash flow (FCF) is a measure of financial performance calculated as operating cash flow minus capital expenditures. FCF represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

Hang Seng Property Index is a capitalization-weighted index of all the stocks designed to measure the performance of the property sector of the Hang Seng Index.

KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions

Modified Duration is the approximate percentage change in a bond’s price for a 100 basis points change in yield, assuming that the bond’s expected cash flow does not change when the yield changes.

MSCI All Country World Index Gross USD is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets.

MSCI Emerging Markets Index USD is a free float-adjusted market cap weighted index that is designed to measure equity market performance in the global emerging markets.

MSCI Europe Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed markets in Europe.

Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

NASDAQ Financial-100 Index includes 100 of the largest domestic and international financial securities listed on the NASDAQ Stock Market based on market capitalization. They include companies classified according to the Industry Classification Benchmark as Financials, which are included within the NASDAQ Bank, NASDAQ Insurance, and NASDAQ Other Finance Indexes.

Price/Earnings Ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Normalized earnings – earnings metric that shows you what earnings look like smoothed out in the long run, taking into account the cyclical changes in an economy or stock.

Russell 2000® Index is a small-cap stock market index of the bottom 2,000 stocks in the Russell 3000® Index. The Russell 2000 is by far the most common benchmark for mutual funds that identify themselves as “small-cap”, while the S&P 500® index is used primarily for large capitalization stocks.

Russell 3000® Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Source: Russell Investment Group. Russell is the owner of the trademarks and copyrights related to the Russell Indexes.

S&P 500® Index is a float-adjusted, market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance.

S&P Municipal Bond Short Intermediate Index consists of bonds in the S&P Municipal Bond Index with a minimum maturity of one year and a maximum maturity of up to, but not including, eight years as measured from the Rebalancing Date.

The S&P 500® Index, and the S&P Municipal Bond Short Intermediate Index (the “Indices”) are products of S&P Dow Jones Indices LLC and have been licensed for use by Alpine Woods Capital Investors, LLC. Copyright © 2014 by

4

| | |

S&P Dow Jones Indices LLC. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written the permission of S&P Dow Jones Indices LLC. S&P Dow Jones Indices LLC, its affiliates, and third party licensors make no representation or warranty, express or implied, with respect to the Index and none of such parties shall have any liability for any errors, omissions, or interruptions in the Index or the data included therein.

Up/Down Capture Ratio – The Up Capture Ratio measures the manager’s overall performance to the benchmark’s overall performance, considering only quarters that are positive in the benchmark. An Up Capture Ratio of more than 1.0 indicates a manager who outperforms the relative benchmark in the benchmark’s positive quarters. The Down capture ratio is the ratio of the manager’s overall performance to the benchmark’s overall performance, considering only quarters that are negative in the benchmark. A Down Capture Ratio of less than 1.0 indicates a manager who outperforms the relative benchmark in the benchmark’s negative quarters and protects more of a portfolio’s value during down markets.

Weighted Average Maturity is the average time it takes for securities in a portfolio to mature, weighted in proportion to the dollar amount that is invested in the portfolio. Weighted average maturity (WAM) measures the sensitivity of fixed-income portfolios to interest rate changes. Portfolios with longer WAMs are more sensitive to changes in interest rates because the longer a bond is held, the greater the opportunity for interest rates to move up or down and affect the performance of the bonds in the portfolio.

Yield Co – A publicly-traded company structured as a C-Corporation that is formed to own operating assets (often infrastructure assets) that are intended to produce a predictable cash flow, which is distributed to investors as dividends.

An investor cannot invest directly in an index.

5

Equity Manager Reports

| | Alpine Dynamic Dividend Fund | |

| | | |

| | Alpine Accelerating Dividend Fund | |

| | | |

| | Alpine Financial Services Fund | |

| | | |

| | Alpine Small Cap Fund | |

| | | |

| | Alpine Transformations Fund | |

| | | |

| | Alpine Equity Income Fund | |

6

Alpine Dynamic Dividend Fund |  |

| | | | | | | | | | | | | | | |

| Comparative Annualized Returns as of 4/30/15 (Unaudited) | | | | |

| | | | | |

| | | 6 Months(1) | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Since Inception(2) | |

| Alpine Dynamic Dividend Fund — Institutional Class | | | 8.74 | % | | | 11.25 | % | | | 11.52 | % | | | 6.82 | % | | | 2.66 | % | | | 5.35 | % | | |

| Alpine Dynamic Dividend Fund — Class A (Without Load) | | | 8.61 | % | | | 10.98 | % | | | 11.25 | % | | | N/A | | | N/A | | | 12.50 | % | | |

| Alpine Dynamic Dividend Fund — Class A (With Load) | | | 2.71 | % | | | 5.00 | % | | | 9.14 | % | | | N/A | | | N/A | | | 10.61 | % | | |

| MSCI All Country World Daily Total Return Index (Net Div) | | | 4.97 | % | | | 7.46 | % | | | 12.24 | % | | | 9.58 | % | | | 6.98 | % | | | 7.93 | % | | |

| Lipper Global Equity Income Funds Average(3) | | | 3.19 | % | | | 3.13 | % | | | 10.47 | % | | | 8.94 | % | | | 4.81 | % | | | 6.60 | % | | |

| Lipper Global Equity Income Funds Ranking(3) | | | N/A | (4) | | | 1/139 | | | 19/90 | | | 65/66 | | | 20/20 | | | 15/15 | | |

| Gross Expense Ratio (Institutional Class): 1.44%(5) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Institutional Class): 1.38%(5) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Gross Expense Ratio (Class A): 1.69%(5) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Class A): 1.63%(5) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (1) | Not annualized. |

| | (2) | Institutional Class shares commenced on September 22, 2003 and Class A shares commenced on December 30, 2011. Returns for indices are since September 22, 2003. |

| | (3) | The since inception return represents the period beginning September 25, 2003 (Institutional Class only). |

| | (4) | FINRA does not recognize rankings for less than one year. |

| | (5) | As disclosed in the prospectus dated February 27, 2015. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. Returns for the Class A shares with sales charge reflect a maximum sales charge of 5.50%. Performance for the Class A shares without sales charges does not reflect this load.

The MSCI All Country World Daily Total Return Index (Net Div) USD is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets. Source: MSCI. MSCI data may not be reproduced or used for any other purpose. The Lipper Global Equity Income Funds Average is an average of funds that by prospectus language and portfolio practice seek relatively high current income and growth of income by investing at least 65% of their portfolio in dividend-paying securities of domestic and foreign companies. Lipper rankings for the periods shown are based on fund total returns with dividends and distributions reinvested and do not reflect sales charges. The Lipper Global Equity Income Funds Average are unmanaged and do not reflect the deduction of direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Global Equity Income Funds Average reflects fees charged by the underlying funds. The performance for the Alpine Dynamic Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Alpine Dynamic Dividend Fund has a contractual expense waiver that continues through March 1, 2016. Where a Fund’s gross and net expense ratios are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower.

To the extent that the Fund’s historical performance resulted from gains derived from participation in Initial Public Offerings (“IPOs”) and/or Secondary Offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary Offerings in the future.

7

Alpine Dynamic Dividend Fund (Continued) | |

Portfolio Distributions* (Unaudited)

Top 10 Holdings* (Unaudited)

| 1. | | Apple, Inc. | 1.96% |

| 2. | | Novartis AG-SP ADR | 1.69% |

| 3. | | McKesson Corp. | 1.53% |

| 4. | | Avago Technologies, Ltd. | 1.37% |

| 5. | | Brit PLC-Morgan Stanley BV | 1.37% |

| 6. | | Teva Pharmaceutical Industries, Ltd.-SP ADR | 1.33% |

| 7. | | Snap-on, Inc. | 1.32% |

| 8. | | Clariant AG | 1.31% |

| 9. | | Canadian Pacific Railway, Ltd. | 1.26% |

| 10. | | Thermo Fisher Scientific, Inc. | 1.23% |

| * | Portfolio Distributions percentages are based on total net investments. Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio holdings sector distributions are as of 04/30/15 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. |

| | | |

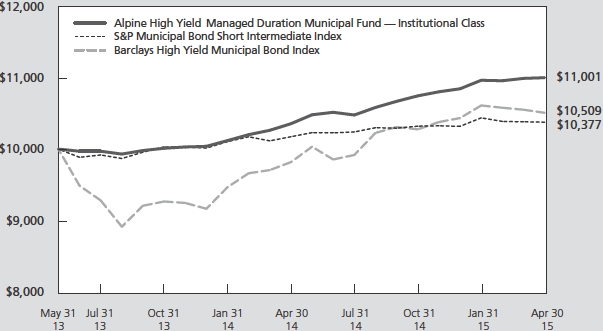

| | Value of a $10,000 Investment (Unaudited) | |

| | | |

|

| |

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmarks. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees, if applicable. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

8

Alpine Dynamic Dividend Fund (Continued) | |

Commentary

Dear Investor:

We are pleased to report the results for the Alpine Dynamic Dividend Fund for the six month period ending April 30, 2015. For this period, the Fund generated a total return of 8.74% versus the MSCI All Country World Daily Total Return Index (Net Dividend), which had a total return of 4.97%. All returns include reinvestment of all distributions. The Fund distributed $0.12 per share during the period. All references in this letter to the Fund’s performance relate to the Fund’s Institutional Class.

ECONOMIC ANALYSIS

In the six month period ending April 30, 2015, the stock market exhibited remarkable resiliency, continuing the momentous bull market that began in March 2009 despite significant volatility in commodities, currencies and interest rates. After a brief sell-off toward the end of calendar 2014 spurred in part by a rapid collapse in oil prices (by the end of the year, West Texas Intermediate (WTI) Cushing crude oil spot prices were down over 50% from their summer highs), global equities were able to stage an impressive rally, with the MSCI All Country World Daily Total Return Index (Net Dividend) delivering a 4.97% total return in the six month period.

The global rally has arguably been fueled in large part by the ultra-low interest rates seen throughout the developed world as a result of the extraordinarily accommodative monetary policy of central banks. As a recent example, in March 2015 the European Central Bank (ECB) embarked upon its own version of Quantitative Easing (QE), pledging an asset-purchase program worth about 1.1 trillion Euros through at least the end of September 2016. The MSCI Europe Index was still able to offset the 10% depreciation of the Euro against the U.S. Dollar, generating a 6.49% total return in the 6 month period ended April 30, 2015. In contrast, the U.S. Federal Reserve, having completed a third round of QE in October 2014, is contemplating the first Federal Funds rate hike in nearly a decade. The fear of rising interest rates had an impact on interest-sensitive stocks, as evidenced by the 1.1% decline in the S&P 500 Utilities Sector Index, contrasting with the 4.39% total return of the S&P 500® Index in the period.

Emerging markets were also able to offset currency headwinds, with the MSCI Emerging Markets Index up 3.92% for the six month period. The Hong Kong Hang Seng Index led the way with a total return of 18.06% in U.S. Dollars, as the Shanghai-Hong Kong Stock Connect program, launched in November 2014, allowed Chinese mainland investors to invest in the Hong Kong market, and vice versa. In addition, there was speculation of further government stimulus in China. This exuberance did not filter through to all emerging markets, however.

The Ibovespa Brasil Sao Paulo Stock Exchange Index, for example, declined by 15.56% in U.S. Dollars for the six month period as investors feared the crippling combination of rising inflation and a potential economic contraction.

PORTFOLIO ANALYSIS

For the six month period ending April 30, 2015, the industrials, consumer discretionary and health care sectors had the greatest positive effect on the Fund’s total return. While still making a positive absolute contribution, the financials and telecommunication services sectors had the smallest impact. Energy was the only sector with a negative absolute contribution. On a relative basis, the industrials sector generated the largest outperformance versus the MSCI All Country World Daily Total Return Index (Net Dividend), followed by consumer staples and utilities sectors. Financials, energy and telecommunication services were the worst relative performers.

PORTFOLIO ANALYSIS

The top five contributors to the Fund’s performance for the six month period ended April 30, 2015 based on contribution to return were China CNR Corp, China Railway Construction Corp, Avago Technologies, Walgreens Boots Alliance, and Apple.

China CNR Corp is one of two railcar original equipment manufacturers (OEMs) in China. The stock more than doubled due to a number of factors: (1) merger with CSR Corp – the other railcar OEM in China, (2) sizeable contract awards both domestically and internationally, (3) China’s new ‘One Belt, One Road’ policy, which promotes rail development in countries adjacent to China, and (4) the narrowing of the spread between the company’s A- and H-shares.

China Railway Construction Corp is a large railway construction contractor in China. Similar to China CNR Corp, the company benefited from supportive railway polices from the Chinese government, such as ‘One Belt, One Road’. The stock also benefited from a narrowing of the spread between the company’s A- and H-shares. Additionally, it benefited from the expectation that China’s fixed asset investment will remain strong in 2015.

Semiconductor manufacturer Avago Technologies received a boost from the announcement of its strategic and accretive acquisition of Emulex. From a fundamental standpoint, Avago continued to benefit from the roll out of next generation (4G LTE) wireless networks, which is stimulating demand for the company’s radiofrequency (RF) filtering products. The company also benefited from the recent merger of two of its competitors: TriQuint and RF Micro Devices, a long term positive for the industry.

9

Alpine Dynamic Dividend Fund (Continued) | |

Walgreen Boots Alliance, one of the largest drugstore chains in the world with over 13,000 stores, received accolades from investors following the first analyst meeting led by its newly revamped management team, as the company laid out a strategic plan to enhance margins by refreshing stores, improving merchandising and utilization of floor space, and reducing promotional spend. Walgreen also continued to capitalize on the wave of generic drug launch activity through its distribution agreement with AmerisourceBergen. Finally, investors cheered its progress in reaping purchasing benefits from the Alliance Boots acquisition.

Apple continued its impressive run following the successful launch and uptake of the iPhone 6 and 6 Plus mobile phones. The higher price point of these phones enhanced margins, leading to a couple rounds of earnings upgrades by the Street. The company also announced a strong start to its recently launched Apple Watch, and it expanded its capital allocation plan, as the Board increased the share repurchase authorization from $90 billion to $140 billion and approved an 11% increase to the company’s quarterly dividend.

The following companies had the largest adverse impact on the performance of the Fund based on contribution to return for the six month period ended April 30, 2015: Rumo Logistica Operadora Multimodal, Canadian Energy Services & Technology Corp, Pilgrim’s Pride, Abengoa S.A., and Freeport-McMoRan.

Rumo Logistica Operadora Multimodal is a railway concession operator in Brazil, formed through the merger of America Latina Logistica and Rumo Logistica Operadora Multimodal. Stock performance suffered as financial results continued to deteriorate, partly as a result of the slowdown in the Brazilian economy. New management has laid out short- and long-term plans to optimize costs and deploy new capital.

Canadian Energy Services & Technology Corp, the market leader in Canadian oil and gas drilling fluids, suffered from a severe decline in commodity oil and gas prices, which resulted in pricing and margin pressure on the company’s core products as customers scaled back spending. The company also was negatively impacted by a very early and protracted spring break-up in Canada. The Fund has since exited the position.

Pilgrim’s Pride, one of the country’s largest chicken producers, was negatively affected by the tough combination of avian flu-related demand shocks and rising supply, which the market feared would pressure chicken prices. While the company delivered stronger than expected earnings, investors were more focused on the potential for downside volatility for this cyclical industry following an extended period of strong volumes and margins. The Fund no longer owns the stock.

Spanish engineering and construction company, Abengoa S.A. saw its stock decline sharply amidst investor confusion over the accounting treatment of recently

issued bonds. Fortunately, the stock then recovered a good portion of its loss as the company announced a strategic agreement with infrastructure investor EIG Global Energy Partners to jointly invest in a portfolio of Abengoa’s projects under construction. Management reassured investors with positive free cash flow guidance for 2015 and a nearly EUR 2B asset disposal program, but investors remained in a “wait and see” mode.

Freeport-McMoRan, historically one of the world’s largest copper miners, buckled under pressure from the ill-timed debt-financed acquisition of McMoRan Exploration and Plains Exploration & Production. The consequently leveraged balance sheet left little room for error, and investors soured on the stock as management significantly increased its oil and gas-related capex budget in a period when oil and gas spot prices were plummeting. The Fund has since exited the position.

In order to achieve its dividend, the Fund participated in a number of dividend capture strategies including (1) purchasing shares in the stock of a regular dividend payer before an upcoming ex-date and selling after the ex-date, (2) purchasing shares before an anticipated special dividend and selling opportunistically after the ex-date of the dividend, and (3) purchasing additional shares in stocks that the Fund already owns before the ex-date and selling the original shares after the ex-date, thus receiving a dividend on a larger position while still maintaining qualified dividend income eligibility (“QDI”) on its position. These strategies have resulted in higher turnover and associated transaction costs for the Fund. While there is the potential for market loss on the shares that are held for a short period, we seek to use these strategies to generate additional income with limited impact on the construction of the core portfolio.

We have hedged a portion of our currency exposures to the Euro, the Swiss Franc, the Japanese Yen and the British Pound. The currency hedging mitigated the overall negative impact of currency on the portfolio. We have also used leverage at times both in the execution of the strategy of the Fund and to help manage net outflows during the semi-annual period.

SUMMARY

We believe that global macroeconomic conditions generally remain positive for stocks, although the market environment remains fairly uncertain. In developed markets, we are mindful that expectations have continued to rise as growth has returned and financial risks have largely faded. In the United States, fiscal policy is no longer a drag, but investors face a new uncertainty as we approach the first rate hike in many years.

In Europe, we are seeing evidence of a tentative recovery, with improving money supply trends, declining unemployment and rising business confidence. And in contrast to the Fed’s removal of the monetary punch bowl, the party is just getting started in Europe, with its own version of quantitative easing now under way. In

10

Alpine Dynamic Dividend Fund (Continued) | |

emerging markets, overall economic growth is expected to be comfortably in excess of developed markets, with China and India likely to drive the Asian region to strong growth. We are particularly encouraged by China’s reform measures aimed at sweeping away bureaucratic barriers to economic growth as the country looks to rebalance economic activity away from exports and investment-oriented industries towards consumer-oriented demand.

Beyond the macroeconomic environment, the Fund continues to emphasize its focus on what we view as high quality companies with strong balance sheets and strong potential to grow earnings and dividends amidst an uncertain macro environment. Despite the extended bull

market we have experienced in several markets across the globe, we believe there are still plenty of opportunities to invest in companies with a history of paying strong dividends at attractive prices with potential for solid earnings growth. We will continue to adapt our investment approach as economic conditions change and look forward to discussing the portfolio and the prospects for the Fund in future communications.

Sincerely,

Brian Hennessey

Joshua E. Duitz

Portfolio Managers

This letter represents the opinions of the Fund’s management and is subject to change, is not guaranteed and should not be considered a recommendation to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice. Views expressed may vary from those of the firm as a whole. Past performance is no guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The fund is subject to risks, including the following:

Credit Risk – Credit risk refers to the possibility that the issuer of a security will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation.

Currency Risk – The value of investments in securities denominated in foreign currencies increases or decreases as the rates of exchange between those currencies and the U.S. dollar change. Currency conversion costs and currency fluctuations could erase investment gains or add to investment losses. Currency exchange rates can be volatile, and are affected by factors such as general economic conditions, the actions of the U.S. and foreign governments or central banks, the imposition of currency controls and speculation.

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the market. Companies that issue dividend paying-stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future. The Fund may hold securities for short periods of time related to the dividend payment periods and may experience loss during these periods.

Emerging Market Securities Risk – The risks of foreign investments are heightened when investing in issuers in emerging market countries. Emerging market countries tend to have economic, political and legal systems that are less fully developed and are less stable than those of more developed countries. They are often particularly sensitive to market movements because their market prices tend to reflect speculative expectations. Low trading volumes may result in a lack of liquidity and in extreme price volatility.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer than expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions Risk – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. The Fund may enter into foreign currency transactions to try to manage this risk. The Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the Adviser to accurately predict the direction of changes in currency exchange rates. The Fund may enter into forward foreign currency exchange contracts in order to protect against possible losses on foreign investments resulting from adverse changes in the relationship between the U.S. dollar and foreign currencies. Although this method attempts to protect the value of the Fund’s portfolio securities against a decline in the value of a currency, it does not eliminate fluctuations in the underlying prices of the securities and while such contracts tend to minimize the risk of loss due to a decline in the value of the hedged currency, they tend to limit any potential gain which might result should the value of such currency increase.

11

Alpine Dynamic Dividend Fund (Continued) | |

Foreign Securities Risk – The Fund’s investments in securities of foreign issuers or issuers with significant exposure to foreign markets involve additional risk. Foreign countries in which the Fund may invest may have markets that are less liquid, less regulated and more volatile than U.S. markets. The value of the Fund’s investments may decline because of factors affecting the particular issuer as well as foreign markets and issuers generally, such as unfavorable government actions, and political or financial instability. Lack of information may also affect the value of these securities. The risks of foreign investment are heightened when investing in issuers of emerging market countries.

Growth Stock Risk – Growth stocks are stocks of companies believed to have above-average potential for growth in revenue and earnings. Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market while the market concentrates on undervalued stocks.

Initial Public Offerings and Secondary Offerings Risk – The Fund may invest a portion of its assets in shares of IPOs or secondary offerings of an issuer. IPOs and secondary offerings may have a magnified impact on the performance of a Fund with a small asset base. The impact of IPOs and secondary offerings on a Fund’s performance likely will decrease as the Fund’s asset size increases, which could reduce a Fund’s returns. IPOs and secondary offerings may not be consistently available to the Fund for investing. IPO and secondary offering shares frequently are volatile in price due to the absence of a prior public market, the small number of shares available for trading and limited information about the issuer. Therefore, the Fund may hold IPO and secondary offering shares for a very short period of time. This may increase the turnover of the Fund and may lead to increased expenses for the Fund, such as commissions and transaction costs. In addition, IPO and secondary offering shares can experience an immediate drop in value if the demand for the securities does not continue to support the offering price.

Leverage Risk – The Fund may use leverage to purchase securities. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting, a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

Qualified Dividend Tax Risk – Favorable U.S. federal tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws.

Small and Medium Capitalization Company Risk – Securities of small or medium capitalization companies are more likely to experience sharper swings in market values, less liquid markets, in which it may be more difficult for the Adviser to sell at times and at prices that the Adviser believes appropriate and generally are more volatile than those of larger companies.

Swaps Risk – Swap agreements are derivative instruments that can be individually negotiated and structured to address exposure to a variety of different types of investments or market factors. Depending on their structure, swap agreements may increase or decrease the Fund’s exposure to long- or short-term interest rates, foreign currency values, mortgage securities, corporate borrowing rates, or other factors such as security prices or inflation rates. The Fund also may enter into swaptions, which are options to enter into a swap agreement. Since these transactions generally do not involve the delivery of securities or other underlying assets or principal, the risk of loss with respect to swap agreements and swaptions generally is limited to the net amount of payments that the Fund is contractually obligated to make. There is also a risk of a default by the other party to a swap agreement or swaption, in which case the Fund may not receive the net amount of payments that the Fund contractually is entitled to receive.

Undervalued Stock Risk – The Fund may pursue strategies that may include investing in securities, which, in the opinion of the Adviser, are undervalued. The identification of investment opportunities in undervalued securities is a difficult task and there is no assurance that such opportunities will be successfully recognized or acquired. While investments in undervalued securities offer opportunities for above-average capital appreciation, these investments involve a high degree of financial risk and can result in substantial losses.

Please refer to pages 3-5 for other important disclosures and definitions.

12

| Alpine Accelerating Dividend Fund | |

| Comparative Annualized Returns as of 4/30/15 (Unaudited) |

| | 6 Months(1) | | 1 Year | | 3 Years | | 5 Years | | Since Inception(2) |

| Alpine Accelerating Dividend Fund — Institutional Class | | 7.36 | % | | | 11.10% | | | | 15.25% | | | | 13.15% | | | | 14.42% | |

| Alpine Accelerating Dividend Fund — Class A (Without Load) | | 7.24 | % | | | 10.90% | | | | 14.98% | | | | N/A | | | | 16.48% | |

| Alpine Accelerating Dividend Fund — Class A (With Load) | | 1.36 | % | | | 4.78% | | | | 12.82% | | | | N/A | | | | 14.52% | |

| S&P 500® Index | | 4.39 | % | | | 12.97% | | | | 16.72% | | | | 14.32% | | | | 14.37% | |

| Dow Jones Industrial Average | | 3.78 | % | | | 10.11% | | | | 13.29% | | | | 12.99% | | | | 12.98% | |

| Lipper Equity Income Funds Average(3) | | 2.96 | % | | | 7.82% | | | | 13.68% | | | | 12.08% | | | | 14.03% | |

| Lipper Equity Income Funds Ranking(3) | | N/A | (4) | | | 47/497 | | | | 68/359 | | | | 83/291 | | | | 110/273 | |

| Gross Expense Ratio (Institutional Class): 2.25%(5) | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Institutional Class): 1.35%(5) | | | | | | | | | | | | | | | | | | | |

| Gross Expense Ratio (Class A): 2.50%(5) | | | | | | | | | | | | | | | | | | | |

| Net Expense Ratio (Class A): 1.60%(5) | | | | | | | | | | | | | | | | | | | |

| | (1) | Not annualized. |

| | (2) | Institutional Class shares commenced on November 5, 2008 and Class A shares commenced on December 30, 2011. Returns for indices are since November 5, 2008. |

| | (3) | The since inception data represents the period beginning November 6, 2008 (Institutional Class only). |

| | (4) | FINRA does not recognize rankings for less than one year. |

| | (5) | As disclosed in the prospectus dated February 27, 2015. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. Returns for the Class A shares with sales charge reflect a maximum sales charge of 5.50%. Performance for the Class A shares without sales charges does not reflect this load.

The S&P 500® Index is a float-adjusted market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally the leaders in their industry. The Lipper Equity Income Funds Average is an average of funds that seek relatively high current income and income growth through investing 60% or more of their respective portfolios in equities. Lipper rankings for the periods shown are based on fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500® Index, the Dow Jones Industrial Average, and the Lipper Equity Income Funds Average are unmanaged and do not reflect direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Equity Income Funds Average reflects fees charged by the underlying funds. The performance for the Alpine Accelerating Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Alpine Accelerating Dividend Fund has a contractual expense waiver that continues through March 1, 2016. Where a Fund’s gross and net expense ratios are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower.

To the extent that the Fund’s historical performance resulted from gains derived from participation in Initial Public Offerings (“IPOs”) and/or Secondary Offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary Offerings in the future.

13

| Alpine Accelerating Dividend Fund (Continued) | |

Portfolio Distributions* (Unaudited)

| | | |

| Top 10 Holdings* (Unaudited) | |

| | 1. | Apple, Inc. | | | 3.71 | % | |

| | 2. | PepsiCo, Inc. | | | 1.81 | % | |

| | 3. | Abbott Laboratories | | | 1.76 | % | |

| | 4. | Becton, Dickinson & Co. | | | 1.75 | % | |

| | 5. | Johnson & Johnson | | | 1.65 | % | |

| | 6. | Amgen, Inc. | | | 1.59 | % | |

| | 7. | PPG Industries, Inc. | | | 1.58 | % | |

| | 8. | CBS Corp.-Class B | | | 1.55 | % | |

| | 9. | CVS Health Corp. | | | 1.53 | % | |

| | 10. | Avago Technologies, Ltd. | | | 1.52 | % | |

| | | | | | | | | |

| | * | Portfolio Distributions percentages are based on total net investments. Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio holdings sector distributions are as of 04/30/15 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. | |

| | | | |

| | | | | |

| | | | | |

| | | | | |

Value of a $10,000 Investment (Unaudited)

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees, if applicable. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

14

| Alpine Accelerating Dividend Fund (Continued) | |

Commentary

For the six months ended April 30, 2015, the Alpine Accelerating Dividend Fund generated a total return of 7.36%. This compares with a total return of 4.39% for the S&P 500® Index for the same period. During the six months ended April 30, 2015, the Fund steadily increased its monthly per share distribution from $0.0421 in October, 2014 to $0.0427 in April, 2015. All references in this letter to the Fund’s performance relate to the performance of the Fund’s Institutional Class.

PERFORMANCE DRIVERS

The Fund generally prefers to take a conservative investment stance with regard to portfolio construction and security selection during times of economic and geopolitical uncertainty. We believe the six months ended April 30, 2015 was such a time. For this reason, the Fund had an average cash holding of 3.7% during the six month period and a portfolio beta less than 1.0 during the same span.

On a sector basis, health care, information technology, and financials had the largest positive impact on the absolute performance of the Fund. The energy, telecommunication services, and utilities sectors had the smallest impact. On a relative basis, the financials sector generated the largest outperformance versus the S&P500® Index, followed by health care and consumer staples sectors. Consumer discretionary, telecommunication services, and energy were the worst relative performers, although only consumer discretionary had a negative relative return versus the Index.

PORTFOLIO ANALYSIS

The top five stocks contributing to the Fund’s performance during the six months ended April 30, 2015, based on contribution to total return, were Avago Technologies, Walgreens Boots Alliance, Amerisource Bergen, Aetna, and Apple.

| | • | Semiconductor manufacturer Avago Technologies received a boost from the announcement of its strategic and accretive acquisition of Emulex. From a fundamental standpoint, Avago continued to benefit from the roll out of next generation (4G LTE) wireless networks, which is stimulating demand for the company’s radiofrequency (RF) filtering products. The company also benefited from the recent merger of two of its competitors: TriQuint and RF Micro Devices, a long term positive for the industry. |

| | | |

| | • | Shares of Walgreens Boots Alliance have enjoyed a strong performance in the six months ended April 30, 2015 as investors shook off earlier disappointment in August 2014 when the company announced its decision not to re-domicile abroad and undergo a tax inversion to reduce corporate income taxes. The subsequent rally in the shares came as the management team transitioned from a CEO/CFO combination that came from Walgreens to a team from Alliance Boots, led by Vice Chairman Stefano Pessina, upon completion of the merger between the companies in December 2014. |

| | | |

| | • | AmerisourceBergen (ABC) continues to deliver better than expected earnings driven by its successful partnership with Walgreens Boots Alliance and the Walgreens Boots Alliance Development JV, as well as the continued tailwind from generic drug distribution. Also, investors have begun looking to drug distribution companies like ABC as a great way to play the biosimilars theme. We believe ABC is well-positioned to benefit from biosimilar distribution given its leading specialty distribution franchise, the largest amongst its peers. |

| | | |

| | • | Along with its peers in the managed care industry, Aetna stock has enjoyed strong multiple expansion during the six months ended April 30, 2015 as investors gained additional comfort with the long-term growth prospects of the industry and earnings estimates headed higher given still benign medical cost trends. For Aetna, in particular, the company reported a strong end of the 2014 calendar year and has already raised its 2015 EPS guidance twice as the fundamentals of its business have continued to improve. |

| | | |

| | • | Apple stock continues to be a strong performer given the recent successful launch and uptake of the iPhone 6 and 6 Plus mobile phones. The company’s December 2014 quarterly results, which reflected the all-important holiday period, were well ahead of expectations with close to 75MM iPhone units sold, an increase of 46% from the prior year. Importantly, the iPhone 6’s richer average selling price led to better than expected earnings for the company, leading to a round of estimate upgrades from Wall Street. |

| | | |

| Holdings in Bristow Group, Aecon Group, Qualcomm, Suncor Energy, and Applied Materials had the largest adverse impact on the performance of the Fund over the fiscal half year. |

15

| Alpine Accelerating Dividend Fund (Continued) | |

| | • | The sharp and sudden sell-off in crude oil that began near the end of September 2014 along with the consistent strengthening of the US dollar against nearly all major currencies proved a challenging combination for Bristow Group, one of the largest providers of helicopter services to the oil and gas industry. Lower crude oil prices, if sustained, could lessen future demand for Bristow’s transportation services to offshore oil rigs, while the stronger dollar has directly impacted revenues and earnings for the company. The company reduced guidance in early February 2015 to take into account negative impact of foreign currency exchange effects. |

| | | |

| | • | Similar to Bristow, Aecon Group shares were negatively impacted by the sharp and sudden sell-off in crude oil that began near the end of September 2014. As one of Canada’s largest engineering and construction companies, Aecon has quite of bit of exposure to the Canadian oil sands industry. The lower crude oil price has dented the longer-term growth outlook of the oil sands given the relatively high margin cost of production. Additionally, the weakening of the Canadian dollar versus the US dollar has itself caused the US dollar value of the Fund’s Aecon investment to decline during the sixth month period from October 2014 to April 2015. |

| | | |

| | • | Shares of Qualcomm have continued to struggle of late given its challenges in China as well as some competitive loss of market share in its chip division. In China, the company received a nearly $1B fine and agreed to reduce the royalty rate it charges to handset makers in the country. On the chip side of the business, it recently became clear that Samsung, an important customer, has chosen to use its own application processor chip in its new Galaxy S6 phones rather than continue to use Qualcomm’s chip as it has in prior phones. |

| | | |

| | • | The sharp and sudden sell-off in crude oil that began near the end of September 2014 has taken a toll on the shares of nearly all exploration and production companies in the oil and gas sector. Suncor Energy was no exception and saw its shares come under pressure during the crude sell-off. The Canadian oil sands have a relatively high margin cost of production, so the lower crude prices, if sustained, could pressure the future growth outlook for the company given its primary assets are in the oil sands. |

| | | |

| | • | Shares of Applied Materials had a significant one-day sell-off near the end of April 2015 in the wake of the surprising news that it was abandoning its planned merger with Tokyo Electron. The announcement |

caught investors off-guard as many had assumed the merger was nearing the finish line and that the company was poised to realize significant synergies from the deal. Without the financial benefits of the transaction, the shares adjusted to a standalone valuation at a lower level.

SUMMARY & OUTLOOK

As we look towards the balance of 2015, we see a market environment that remains fairly uncertain. While European Central Bank’s quantitative easing seems to be just what the doctor ordered for European equities, the investment outlook in the US is a bit more complicated. The strong dollar is dramatically and negatively impacting foreign sales and earnings for US multinationals. Additionally, investors continue to try to read the Federal Reserve tea leaves to determine when the Federal Open Market Committee (FOMC) will begin raising the Fed Funds rate. Some prominent investors are comparing this so called “lift off” of short rates to 1937 when a premature tightening by the Fed sent the US economy back into a recession. While we are not nearly so bearish, we think the path ahead could be a bit choppy with spurts of volatility likely to keep US equities from rallying alongside their European peers. What’s more, valuations appear rich to us, leaving the market susceptible to a pullback should earnings growth or the economic data prove disappointing.

As it relates to the Fund, we have continued to enhance the core strategy of focusing on quality companies with strong balance sheets that have been increasing and/or accelerating dividends. We will emphasize stocks with a longer and consistent track record of dividend increases, as we believe these companies have the potential to outperform through the cycle. We aim to invest in stocks with multiple years of continuous dividend increases and make these stocks the foundation of the Fund. Many of the Fund’s holdings already fit into this category, but we are on the lookout for more such ideas. On top of this foundation, we will continue to invest in stocks with shorter, but still meaningful track records of dividend increases. In conclusion, similar to the stocks in which we seek to invest, the Fund aims to provide a steadily rising distribution to its investors. We thank our shareholders for their support and look forward to continued success over the next year.

Sincerely,

Andrew Kohl

Portfolio Manager

16

| Alpine Accelerating Dividend Fund (Continued) | |

This letter represents the opinions of the Fund’s management and is subject to change, is not guaranteed and should not be considered a recommendation to buy or sell any security. The information provided is not intended to be, and is not, a forecast of future events, a guarantee of future results, or investment advice. Views expressed may vary from those of the firm as a whole. Past performance is no guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The Fund is subject to risks, including the following:

Currency Risk – The value of investments in securities denominated in foreign currencies increases or decreases as the rates of exchange between those currencies and the U.S. dollar change. Currency conversion costs and currency fluctuations could erase investment gains or add to investment losses. Currency exchange rates can be volatile, and are affected by factors such as general economic conditions, the actions of the U.S. and foreign governments or central banks, the imposition of currency controls and speculation.

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the market. Companies that issue dividend paying-stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future or the anticipated acceleration of dividends could not occur.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer than expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions Risk – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. The Fund may enter into foreign currency transactions to try to manage this risk. The Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the Adviser to accurately predict the direction of changes in currency exchange rates.

Foreign Securities Risk – The Fund’s investments in securities of foreign issuers or issuers with significant exposure to foreign markets involve additional risk. Foreign countries in which the Fund may invest may have markets that are less liquid, less regulated and more volatile than U.S. markets. The value of the Fund’s investments may decline because of factors affecting the particular issuer as well as foreign markets and issuers generally, such as unfavorable government actions, and political or financial instability. Lack of information may also affect the value of these securities. The risks of foreign investments are heightened when investing in issuers in emerging market countries.

Growth Stock Risk – Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market while the market concentrates on undervalued stocks. Although the Fund will not concentrate its investments in any one industry or industry group, it may, like many growth funds, weight its investments toward certain industries, thus increasing its exposure to factors adversely affecting issuers within those industries.

Initial Public Offerings and Secondary Offerings Risk – The Fund may invest a portion of its assets in shares of IPOs or secondary offerings of an issuer. IPOs and secondary offerings may have a magnified impact on the performance of a Fund with a small asset base. The impact of IPOs and secondary offerings on a Fund’s performance likely will decrease as the Fund’s asset size increases, which could reduce a Fund’s returns. IPOs and secondary offerings may not be consistently available to the Fund for investing. IPO and secondary offering shares frequently are volatile in price due to the absence of a prior public market, the small number of shares available for trading and limited information about the issuer. Therefore, the Fund may hold IPO and secondary offering shares for a very short period of time. This may increase the turnover of the Fund and may lead to increased expenses for the Fund, such as commissions and transaction costs. In addition, IPO and secondary offering shares can experience an immediate drop in value if the demand for the securities does not continue to support the offering price.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting, a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

17

| Alpine Accelerating Dividend Fund (Continued) | |

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Micro Capitalization Company Risk – Stock prices of micro capitalization companies are significantly more volatile, and more vulnerable to adverse business and economic developments than those of larger companies. Micro capitalization companies often have narrower markets for their goods and/or services and more limited managerial and financial resources than larger, more established companies, including small or medium capitalization companies.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

Small and Medium Capitalization Company Risk – Securities of small or medium capitalization companies are more likely to experience sharper swings in market values, less liquid markets, in which it may be more difficult for the Adviser to sell at times and at prices that the Adviser believes appropriate and generally are more volatile than those of larger companies.

Undervalued Stock Risk – The Fund may pursue strategies that may include investing in securities, which, in the opinion of the Adviser, are undervalued. The identification of investment opportunities in undervalued securities is a difficult task and there is no assurance that such opportunities will be successfully recognized or acquired. While investments in undervalued securities offer opportunities for above-average capital appreciation, these investments involve a high degree of financial risk and can result in substantial losses.

Please refer to pages 3-5 for other important disclosures and definitions.

18

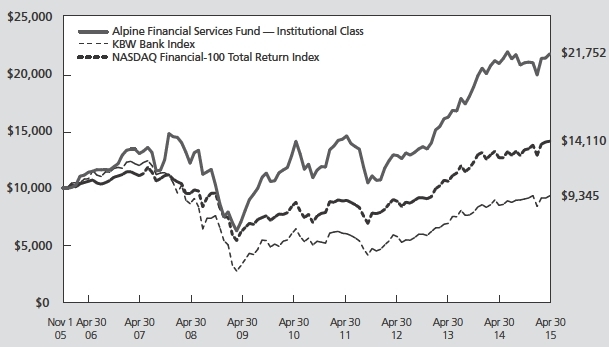

| | Alpine Financial Services Fund | |

| Comparative Annualized Returns as of 4/30/15 (Unaudited) |

| | | | 6 Months(1) | | | 1 Year | | | 3 Years | | | 5 Years | | | Since Inception(2) |

| Alpine Financial Services Fund — Institutional Class | | | 3.79 | % | | | 4.10 | % | | | 19.17 | % | | | 9.05 | % | | | 8.53% | |

| Alpine Financial Services Fund — Class A (Without Load) | | | 3.66 | % | | | 3.89 | % | | | 18.89 | % | | | N/A | | | 23.30% | |

| Alpine Financial Services Fund — Class A (With Load) | | | -2.05 | % | | | -1.84 | % | | | 16.67 | % | | | N/A | | | 21.23% | |

| KBW Bank Index | | | 3.13 | % | | | 9.83 | % | | | 17.47 | % | | | 7.69 | % | | | -0.68% | |

| NASDAQ Financial-100 Total Return Index | | | 5.66 | % | | | 11.47 | % | | | 16.82 | % | | | 9.97 | % | | | 3.69% | |

| S&P 500® Index | | | 4.39 | % | | | 12.97 | % | | | 16.72 | % | | | 14.32 | % | | | 8.19% | |

| Lipper Financial Services Funds Average(3) | | | 2.81 | % | | | 9.11 | % | | | 16.37 | % | | | 9.06 | % | | | 1.77% | |

| Lipper Financial Services Funds Ranking(3) | | | N/A(4) | | | 77/83 | | | 11/78 | | | 39/67 | | | 1/50 | |

| Gross Expense Ratio (Institutional Class): 1.49%(5) | | | | | | | | | | | | | | | | | | | | |