UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811-21494 |

Nuveen Floating Rate Income Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

| | |

| Registrant’s telephone number, including area code: | | (312) 917-7700 |

| | |

| Date of fiscal year end: | | July 31 |

| | |

| Date of reporting period: | | July 31, 2021 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Closed-End Funds

31 July 2021

Nuveen

Closed-End Funds

| | |

| NSL | | Nuveen Senior Income Fund |

| JFR | | Nuveen Floating Rate Income Fund |

| JRO | | Nuveen Floating Rate Income Opportunity Fund |

| JSD | | Nuveen Short Duration Credit Opportunities Fund |

| JQC | | Nuveen Credit Strategies Income Fund |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #2 or (ii) by logging into your Investor Center account at www.computershare.com/investor and clicking on “Communication Preferences”. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Table of Contents

3

Chair’s Letter to Shareholders

Dear Shareholders,

More than a year has passed since the World Health Organization declared COVID-19 a global pandemic in March 2020, resulting in a year marked by a global economic downturn, financial market turbulence and some immeasurable losses of life. Although the health crisis persists, with the widespread distribution of vaccines in the U.S. and extraordinary economic interventions by governments and central banks around the world, we collectively look forward to what our “new normal” might be.

Rebounding global economic activity has driven both gross domestic product growth and inflation higher, especially in the U.S. Vaccinations have enabled a further reopening of economies while governments and central banks have taken extraordinary measures to support the recoveries. Since the crisis began, the U.S. government has enacted six relief measures totaling $5.3 trillion to support individuals and families, small and large businesses, state and local governments, education, public health and vaccinations. Currently, Congress is working on an infrastructure spending plan, although its final shape and whether it passes remains to be seen. The U.S. Federal Reserve (Fed) and other central banks around the world have acknowledged the economic progress to date but remain committed to sustaining the recovery by maintaining accommodative monetary conditions. However, as economies have reopened, the surge in consumer demand has outpaced supply chain capacity, resulting in a jump in inflation indicators in recent months. Whether inflation persists is a subject of debate by economists and some market observers, while the Fed and other central banks believe it to be more transitory. Additionally, the recent impact of the COVID-19 delta variant is likely to be factored into central bank forecasts, which could complicate the timing of monetary policy changes.

While the markets’ longer-term outlook has brightened, we expect intermittent bouts of volatility to continue. There are some signs that the first economies to recover – including China, the U.S. and Europe not far behind – have reached their growth peaks and are moving toward stabilization, while the delta variant is adding caution to the growth outlook. Markets are closely monitoring central bank signals, particularly if inflation remains elevated, as a sooner-than-expected shift to monetary tightening could slow the economic recovery. Additionally, as more virulent strains of COVID-19 such as the delta variant have spread, both case counts and hospitalizations are rising again, and vaccination rollouts have been uneven around the country and around the world. The recovery hinges on controlling the virus, and estimates vary considerably on when economic activity might be fully restored and what level of public inoculation would be sufficient to contain the spread of the virus, particularly in light of new variants. On the political front, the Biden administration’s full policy agenda and the potential for Congressional gridlock remain to be seen, either of which could cause investment outlooks to shift. Short-term market fluctuations can provide your Fund opportunities to invest in new ideas as well as upgrade existing positioning while providing long-term value for shareholders. For more than 120 years, the careful consideration of risk and reward has guided Nuveen’s focus on delivering long-term results to our shareholders.

If you have concerns about what’s coming next, it may be an opportune time to assess your portfolio. We encourage you to review your time horizon, risk tolerance and investment goals with your financial professional.

On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Terence J. Toth

Chair of the Board

September 22, 2021

4

Portfolio Managers’ Comments

Nuveen Senior Income Fund (NSL)

Nuveen Floating Rate Income Fund (JFR)

Nuveen Floating Rate Income Opportunity Fund (JRO)

Nuveen Short Duration Credit Opportunities Fund (JSD)

Nuveen Credit Strategies Income Fund (JQC)

The Funds’ are sub-advised by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser (the “Adviser”). On December 31, 2020, the Funds’ previous sub-adviser, Symphony Asset Management, LLC (“Symphony”), also an affiliate of the Adviser, was merged with and into NAM (the “Reorganization”). Effective as of the date of the Reorganization, NAM assumed the portfolio management responsibilities for the Funds’ investment portfolio and, as previously approved by the Fund’s Board of Trustees, the Funds’ entered into an amended and restated sub-advisory agreement with NAM, the terms of which were substantially identical to the prior sub-advisory agreement with Symphony. Scott Caraher and Kevin Lorenz, CFA, continue as portfolio managers for the Funds.

Here the portfolio management team discusses economic and market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period ended July 31, 2021. For more information on the Funds’ investment objectives and policies, please refer to the Shareholder Update section of the report.

What factors affected the economy and the markets during the twelve-month annual reporting period ended July 31, 2021?

Supported by massive fiscal and monetary stimulus and economic reopening, the U.S. economy rebounded more quickly than expected from the deep downturn caused by the COVID-19 crisis and containment measures. The federal government’s relief measures have totaled approximately $5.3 trillion across six aid packages that have allocated direct payments to individuals and families, expanded unemployment insurance, provided loans to large and small businesses, funded hospitals and health agencies, and supported state and local governments, education and public health/vaccination. (Additionally, in August 2021, after the close of this reporting period, the Senate approved a $1 trillion infrastructure and jobs plan, which moves to the House for consideration.) The U.S. Federal Reserve (Fed) has maintained short-term interest rates near zero and enacted credit facilities to help keep the financial system stable, lowering borrowing costs for businesses and individuals. Gross domestic product (GDP) expanded at an annualized rate of 6.3% in the first quarter and 6.5% in the second quarter, according to the “advance” estimate released by the Bureau of Economic Analysis, after shrinking 3.5% (annualized) in 2020 compared to 2019’s annual level.

By the start of this reporting period, markets had largely stabilized from the initial health crisis shock. In March 2020, equity and commodity markets sold off and safe-haven assets rallied as countries initiated quarantines, restricted travel and shuttered factories and businesses, while an ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia amplified price volatility. In late 2020, the announcement of high efficacy rates in several COVID-19 vaccine trials, followed by regulatory authorizations and public vaccination drives across Western countries, improved the outlook for 2021, which contributed to risk-on sentiment in the markets. Increasing vaccination rates and certain surprisingly strong economic readings in the first few months of 2021 led to rising inflation concerns. However, recent Fed commentary pointed to Fed Fund rate hikes by 2023, calming market fears of inaction.

The loan market enjoyed solid performance during the twelve-month reporting period, supported by healthy economic data, better-than-expected corporate earnings and further improvement in credit fundamentals. Loans also benefited

5

Portfolio Managers’ Comments (continued)

from an improving supply and demand backdrop in the second half of the reporting period. On the supply side, issues brought to market were generally absorbed given the level of demand for loans amid the global search for yield. In terms of demand, following heavy outflows during the first five months of the reporting period (August 1, 2020 – December 31, 2020), loan mutual funds and exchange-traded funds (ETFs) garnered a combined $32 billion of inflows over the next seven months ending July 31, 2021. Meanwhile, collateralized loan obligations (CLO) demand also remained robust. It’s notable that investor demand for loans stayed strong despite a fairly benign rate backdrop, an indication that longer-term investors continued to maintain a positive outlook for growth while preparing themselves for potentially higher rates.

For the reporting period, lower quality, discounted and higher spread assets outperformed. These assets tend to have more price appreciation potential and higher coupons to drive returns.

What key strategies were used to manage the Funds during this twelve-month reporting period ended July 31, 2021?

The Funds invested predominantly in first-lien, senior secured corporate loans. NAM generally focuses on loans of issuers with businesses in defensive sectors that have strong asset coverage, as well as loans of larger issuance and facility sizes. These loans are generally referred to as broadly syndicated loans. Consistent with their investment policies, the Funds also invest opportunistically in below investment grade corporate bonds to seek relative value opportunities across the capital structure.

How did the Funds perform during this twelve-month reporting period ended July 31, 2021?

For the twelve-month reporting period ended July 31, 2021, all five Funds outperformed the Credit Suisse Leveraged Loan Index. For purposes of this Performance Commentary references to relative performance are in comparison to the Credit Suisse Leveraged Loan Index.

For the reporting period, relative outperformance for the NSL, JFR, JRO and JSD portfolios was driven by increased allocations to B-rated senior loans. Select exposure to energy-related companies given higher energy prices also contributed to relative performance. In particular, the post-reorganization equity of exploration and production (E&P) company California Resources notched gains due to the energy rally and the firm’s earnings. Similarly, loans issued by Fieldwood Energy found favor in the “risk-on” market environment and on approval of its debt restructuring plan. Lastly, the term loans of deep-water marine transportation specialist Harvey Gulf International Marine, Inc. also contributed. The Funds’ portfolios continue to maintain exposure to these companies.

Offsetting some of the portfolios’ relative outperformance were individual positions that included Diamond Sports Group LLC, a media and entertainment company. Its loans were volatile due to potential restructuring talks and disappointing earnings results during the reporting period. The portfolios’ exposure to the specialty pharmaceutical company, Endo Health Solutions, Inc., also hurt relative performance as the company faced continued costs from opioid lawsuits. The Funds’ portfolios continue to maintain exposure to these companies.

The Funds noted above (NSL, JFR, JRO and JSD) are managed in a similar manner. However, JQC has a different mandate, and therefore, has a relatively higher credit quality profile in its loan portfolio compared to the other Funds. During the reporting period, the JQC portfolio’s relative outperformance was driven by select exposure to some of the same energy-related companies previously mentioned. Among the most notable contributors was the post-reorganization equity of E&P company California Resources and loans issued by Fieldwood Energy. Additionally, the portfolio’s overweight to and security selection within Transportation, including exposure to the loans of American Airlines, aided relative performance during the reporting period. The Fund’s portfolio continues to maintain exposure to these companies.

6

Fund Leverage

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of the Funds’ common shares relative to their comparative benchmarks was the Funds’ use of leverage through bank borrowings, Term Preferred Shares (Term Preferred) for NSL, JFR and JRO, Taxable Fund Preferred Shares (TFP) for NSL, JFR, JRO and JSD and reverse repurchase agreements for JQC. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that a Fund pays on its leveraging instruments are lower than the interest the Fund earns on its portfolio securities that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value. All this will make the shares’ total return performance more variable over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when shortterm interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term interest rates. While fund leverage expenses are somewhat higher than their recent lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

The Funds’ use of leverage had a positive impact on total return performance during this reporting period.

During the current fiscal period, JFR and JRO used cancellable interest rate swaps to partially hedge the interest cost of leverage. Each Fund received payments based upon pre-determined fixed rates and paid one-month LIBOR plus a fixed spread. After a non-callable period, the swap counterparty owns the right on future monthly dates to terminate the swap at par. The purpose of the cancellable interest rate swap is to convert a fixed rate Term Preferred Share issuance to floating rate, and the cancellation dates of the swap correspond to dates on which the Funds can call the Term Preferred Share issue. Collectively, these interest rate swap contracts had a negligible impact on the Funds’ total return performance during the period.

As of July 31, 2021, the Funds’ percentages of leverage are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | |

| | | NSL | | | JFR | | | JRO | | | JSD | | | JQC | |

Effective Leverage* | | | 36.35 | % | | | 36.47 | % | | | 36.52 | % | | | 36.38 | % | | | 36.72 | % |

Regulatory Leverage* | | | 36.35 | % | | | 36.47 | % | | | 36.52 | % | | | 36.38 | % | | | 30.01 | % |

| * | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of reverse repurchase agreements, certain derivatives and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

7

Fund Leverage (continued)

THE FUNDS’ LEVERAGE

Bank Borrowings

As noted previously, the Funds employ leverage through the use of bank borrowings. The Funds’ bank borrowing activities are as shown in the accompanying table. Paydowns reflect on-going leverage management activity that seeks to maintain each Fund’s leverage ratio within a specified internal operating range.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | Outstanding

Balance as of

August 1, 2020 | | | Draws | | | Paydowns | | | Outstanding

Balance as of

July 31, 2021 | | | Average

Balance

Outstanding | | | | | | Draws | | | Paydowns | | | Outstanding

Balance as of

September 28, 2021 | |

NSL | | $ | 86,200,000 | | | $ | 33,100,000 | | | $ | (25,000,000 | ) | | $ | 94,300,000 | | | $ | 91,798,082 | | | | | | | $ | — | | | $ | — | | | $ | 94,300,000 | |

JFR | | $ | 208,100,000 | | | $ | 80,300,000 | | | $ | (50,000,000 | ) | | $ | 238,400,000 | | | $ | 227,504,384 | | | | | | | $ | — | | | $ | — | | | $ | 238,400,000 | |

JRO | | $ | 164,900,000 | | | $ | 44,600,000 | | | $ | (45,000,000 | ) | | $ | 164,500,000 | | | $ | 160,261,096 | | | | | | | $ | — | | | $ | — | | | $ | 164,500,000 | |

JSD | | $ | 8,500,000 | | | $ | 11,000,000 | | | $ | — | | | $ | 19,500,000 | | | $ | 14,519,178 | | | | | | | $ | — | | | $ | — | | | $ | 19,500,000 | |

JQC | | $ | 402,000,000 | | | $ | 25,000,000 | | | $ | (25,000,000 | ) | | $ | 402,000,000 | | | $ | 399,021,918 | | | | | | | $ | — | | | $ | — | | | $ | 402,000,000 | |

Refer to Notes to Financial Statements, Note 9 – Fund Leverage for further details.

Reverse Repurchase Agreements

As noted previously, in addition to bank borrowings, JQC also used reverse repurchase agreements, in which the Fund sells to a counterparty a security that it holds with a contemporaneous agreement to repurchase the same security at an agreed-upon price and date. The Fund’s transactions in reverse repurchase agreements are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

Outstanding

Balance as of

August 1, 2020 | | | Sales | | | Purchases | | | Outstanding

Balance as of

July 31, 2021 | | | Average Balance

Outstanding | | | | | | Sales | | | Purchases | | | Outstanding

Balance as of

September 28, 2021 | |

| | $117,000,000 | | | | $ — | | | | $25,000,000 | | | | $142,000,000 | | | | $135,082,192 | | | | | | | | $ — | | | | $ — | | | | $142,000,000 | |

Refer to Notes to Financial Statements, Note 9 – Fund Leverage for further details.

Term Preferred Shares

As noted previously, in addition to bank borrowings, the following Funds also issued Term Preferred. The Funds' transactions in Term Preferred are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | Outstanding

Balance as of

August 1, 2020 | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

July 31, 2021 | | | Average Balance

Outstanding | | | | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

September 28, 2021 | |

NSL* | | $ | 33,000,000 | | | $ | — | | | $ | (33,000,000 | ) | | $ | — | | | $ | 17,219,178 | | | | | | | $ | — | | | $ | — | | | $ | — | |

JFR** | | $ | 90,000,000 | | | $ | — | | | $ | (90,000,000 | ) | | $ | — | | | $ | 81,076,923 | | | | | | | $ | — | | | $ | — | | | $ | — | |

JRO*** | | $ | 45,000,000 | | | $ | — | | | $ | (45,000,000 | ) | | $ | — | | | $ | 41,732,673 | | | | | | | $ | — | | | $ | — | | | $ | — | |

| * | For the period August 1, 2020 through October 12, 2020. |

| ** | For the period August 1, 2020 through December 8, 2020. |

| *** | For the period August 1, 2020 through November 9, 2020. |

8

Refer to Notes to Financial Statements, Note 5 – Fund Shares for further details on Term Preferred.

Taxable Fund Preferred Shares

As noted previously, in addition to bank borrowings, NSL, JFR, JRO and JSD also issued TFP. The Funds’ transactions in TFP are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | Outstanding

Balance as of

August 1, 2020 | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

July 31, 2021 | | | Average

Balance

Outstanding | | | | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

September 27, 2021 | |

NSL* | | $ | — | | | $ | 40,000,000 | | | $ | — | | | $ | 40,000,000 | | | $ | 40,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 40,000,000 | |

JFR** | | $ | — | | | $ | 100,000,000 | | | $ | — | | | $ | 100,000,000 | | | $ | 100,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 100,000,000 | |

JRO*** | | $ | — | | | $ | 75,000,000 | | | $ | — | | | $ | 75,000,000 | | | $ | 75,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 75,000,000 | |

JSD | | $ | 70,000,000 | | | $ | — | | | $ | — | | | $ | 70,000,000 | | | $ | 70,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 70,000,000 | |

| * | For the period October 5, 2020 (first issuance date of shares) through July 31, 2021. |

| ** | For the period December 4, 2020 (first issuance date of shares) through July 31, 2021. |

| *** | For the period November 5, 2020 (first issuance date of shares) through July 31, 2021. |

Refer to Notes to Financial Statements, Note 5 – Fund Shares for further details on TFP.

9

Common Share Information

DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of July 31, 2021, the Funds’ fiscal and tax year end, and may differ from previously issued distribution notifications.

NSL, JFR, JRO and JSD

Effective with each Fund’s distribution payable April 1, 2021, NSL, JFR, JRO and JSD have implemented a level distribution policy. The level distribution policy is intended to provide shareholders with stable, but not guaranteed, cash flow, independent of the amount or timing of income earned or capital gains realized by the Funds. The Funds intend to distribute all or substantially all of their net investment income through their regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, in order to maintain its level distribution amount, each Fund may pay out more or less than its net investment income during the period. As a result, distributions sources may include net investment income, realized gains and return of capital. You should not draw any conclusions about the Fund’s investment performance from the amount of the distribution or from the terms of the level distribution program. A return of capital is a non-taxable distribution of a portion of a Fund’s capital. A return of capital distribution does not necessarily reflect a Fund’s investment performance and should not be confused with “yield” or “income.”

JQC

JQC has a capital return plan where a supplemental amount is expected to be included in the Fund’s regular monthly distribution. Under this program, the Fund’s regular monthly distribution is expected to include net investment income, return of capital and potentially capital gains for tax purposes. On September 20, 2021 (subsequent to the close of this reporting period), JQC announced that its Board of Trustees approved the adoption of a level distribution policy. The level distribution policy will become effective with the Fund’s distribution payable November 1, 2021.

The amounts and sources of distributions reported in this notice are for financial reporting purposes and are not being provided for tax reporting purposes. The actual amounts and character of the distributions for tax reporting purposes will be reported to shareholders on Form 1099-DIV, which will be sent to shareholders shortly after calendar year-end. Because distribution source estimates are updated throughout the current fiscal year based on a Fund’s performance, those estimates may differ from both the tax information reported to you in your Fund’s 1099 statement, as well as the ultimate economic sources of distributions over the life of your investment. The figures in the table below provide the sources of distributions and may include amounts attributed to realized gains and/or returns of capital. More details about each Fund’s distributions are available on www.nuveen.com/en-us/closed-end-funds.

Data as of July 31, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Month

Percentage of Distributions | | | Calendar YTD

Per Share Amounts | |

| Fund | | Net

Investment

Income | | | Realized

Gains | | | Return of

Capital | | | Total

Distributions | | | Net

Investment

Income | | | Realized

Gains | | | Return of

Capital | |

NSL | | | 100.00 | % | | | 0.00 | % | | | 0.00 | % | | $ | 0.3835 | | | $ | 0.3835 | | | $ | 0.0000 | | | $ | 0.0000 | |

JFR | | | 100.00 | % | | | 0.00 | % | | | 0.00 | % | | $ | 0.6245 | | | $ | 0.6245 | | | $ | 0.0000 | | | $ | 0.0000 | |

JRO | | | 100.00 | % | | | 0.00 | % | | | 0.00 | % | | $ | 0.6150 | | | $ | 0.6150 | | | $ | 0.0000 | | | $ | 0.0000 | |

JSD | | | 100.00 | % | | | 0.00 | % | | | 0.00 | % | | $ | 0.9410 | | | $ | 0.9410 | | | $ | 0.0000 | | | $ | 0.0000 | |

JQC | | | 35.18 | % | | | 0.00 | % | | | 64.82 | % | | $ | 0.8516 | | | $ | 0.2996 | | | $ | 0.0000 | | | $ | 0.5520 | |

10

The following table provides information regarding Fund distributions and total return performance over various time periods. This information is intended to help you better understand whether Fund returns for the specified time periods were sufficient to meet Fund distributions.

Data as of July 31, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Annualized | | | Cumulative | |

| Fund | | Inception

Date | | | Latest

Monthly

Per Share

Distribution | | | Current

Distribution on

NAV | | | 1-Year

Return on

NAV | | | 5-Year

Return on

NAV | | | Fiscal YTD

Distributions

on NAV | | | Fiscal

YTD Return

on NAV | |

NSL | | | 10/26/1999 | | | $ | 0.0340 | | | | 6.70 | % | | | 17.48 | % | | | 4.70 | % | | | 6.30 | % | | | 17.48 | % |

JFR | | | 3/25/2004 | | | $ | 0.0580 | | | | 6.72 | % | | | 17.36 | % | | | 4.89 | % | | | 6.03 | % | | | 17.36 | % |

JRO | | | 7/27/2004 | | | $ | 0.0575 | | | | 6.72 | % | | | 17.42 | % | | | 4.93 | % | | | 5.99 | % | | | 17.42 | % |

JSD | | | 5/25/2011 | | | $ | 0.0865 | | | | 6.69 | % | | | 18.24 | % | | | 4.66 | % | | | 6.06 | % | | | 18.24 | % |

JQC | | | 6/25/2003 | | | $ | 0.0509 | | | | 8.84 | % | | | 13.42 | % | | | 4.26 | % | | | 12.32 | % | | | 13.42 | % |

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closed-end-funds, along with other Nuveen closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE REPURCHASES

During August 2021 (subsequent to the close of the reporting period), the Funds’ Board of Trustees reauthorized an open-market share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding common shares.

As of July 31, 2021, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired their outstanding common shares as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | |

| | | NSL | | | JFR | | | JRO | | | JSD | | | JQC | |

Common shares cumulatively repurchased and retired | | | 15,400 | | | | 147,593 | | | | 39,400 | | | | 10,000 | | | | 5,473,400 | |

Common shares authorized for repurchase | | | 3,860,000 | | | | 5,690,000 | | | | 4,050,000 | | | | 1,005,000 | | | | 13,560,000 | |

During the current reporting period, the Funds did not repurchase any of their outstanding common shares.

OTHER COMMON SHARE INFORMATION

As of July 31, 2021, the Funds’ common share prices were trading at a premium/ (discount) to their common share NAVs and trading at an average premium/(discount) to NAV during the current reporting period, as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | NSL | | | JFR | | | JRO | | | JSD | | | JQC | |

Common share NAV | | | $6.09 | | | | $10.36 | | | | $10.27 | | | | $15.52 | | | | $6.91 | |

Common share pirce | | | $5.74 | | | | $9.76 | | | | $9.69 | | | | $14.40 | | | | $6.53 | |

Premium/(Discount) to NAV | | | (5.75 | )% | | | (5.79 | )% | | | (5.65 | )% | | | (7.22 | )% | | | (5.50 | )% |

Average premium/(discount) to NAV | | | (9.77 | )% | | | (9.86 | )% | | | (10.12 | )% | | | (10.49 | )% | | | (9.15 | )% |

11

| | |

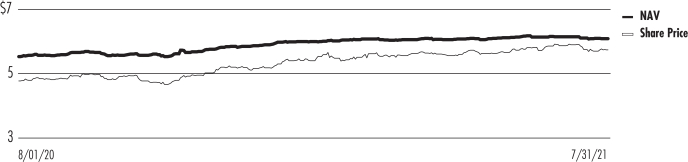

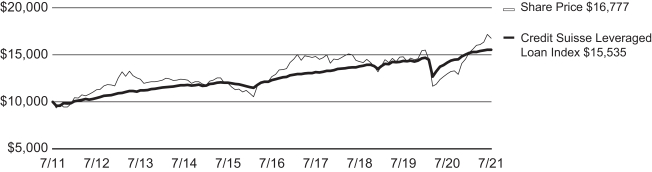

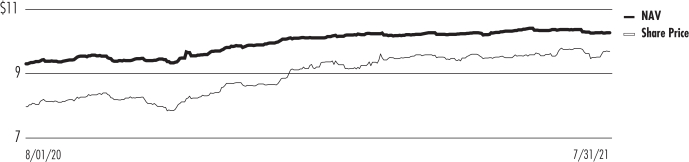

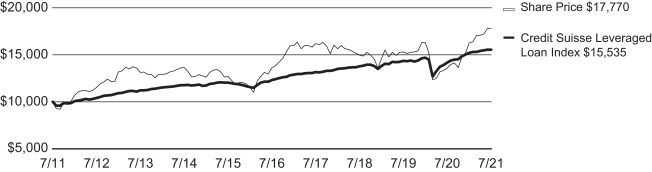

| NSL | | Nuveen Senior Income Fund Performance Overview and Holding Summaries as of July 31, 2021 |

Refer to Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| NSL at Common Share NAV | | | 17.48% | | | | 4.70% | | | | 5.25% | |

| NSL at Common Share Price | | | 28.97% | | | | 5.72% | | | | 5.31% | |

| Credit Suisse Leveraged Loan Index | | | 9.60% | | | | 4.75% | | | | 4.50% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

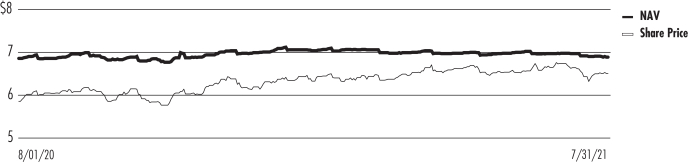

Daily Common Share NAV and Share Price

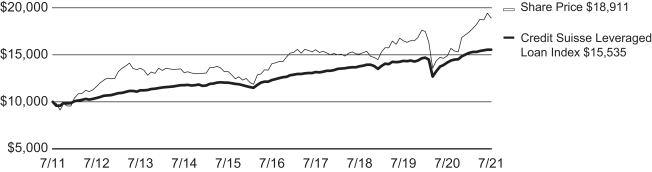

Growth of an Assumed $10,000 Investment as of July 31, 2021 — Common Share Price

12

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

Variable Rate Senior Loan

Interests | | | 139.1% | |

| Corporate Bonds | | | 11.0% | |

| Common Stocks | | | 3.6% | |

| Warrants | | | 0.1% | |

| Convertible Preferred Securities | | | 0.1% | |

| Common Stock Rights | | | 0.0% | |

| Short-Term Investment Companies | | | 4.4% | |

| Other Assets Less Liabilities | | | (1.4)% | |

| Net Assets Plus Borrowings and Taxable Fund Preferred Shares, net of deferred offering costs | | | 156.9% | |

| Borrowings | | | (40.1)% | |

| Taxable Fund Preferred Shares, net of deferred offering costs | | | (16.8)% | |

Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| B.C. Unlimited Liability Company | | | 2.0% | |

| Seattle Spinco, Inc. | | | 1.4% | |

| Parexel International Corporation | | | 1.2% | |

| Delta 2 (LUX) S.a.r.l. | | | 1.2% | |

| PetSmart, Inc. | | | 1.1% | |

Portfolio Composition

(% of total investments)

| | | | |

| Media | | | 10.8% | |

| Hotels, Restaurants & Leisure | | | 10.5% | |

| Software | | | 7.7% | |

| Health Care Providers & Services | | | 6.0% | |

| Oil, Gas & Consumable Fuels | | | 4.4% | |

| Pharmaceuticals | | | 4.0% | |

| Commercial Services & Supplies | | | 3.7% | |

| IT Services | | | 3.3% | |

| Diversified Telecommunication Services | | | 2.8% | |

| Life Sciences Tools & Services | | | 2.6% | |

| Insurance | | | 2.3% | |

| Entertainment | | | 2.1% | |

| Specialty Retail | | | 2.0% | |

| Communications Equipment | | | 1.8% | |

| Auto Components | | | 1.7% | |

| Technology Hardware, Storage & Peripherals | | | 1.6% | |

| Professional Services | | | 1.5% | |

| Airlines | | | 1.5% | |

| Road & Rail | | | 1.4% | |

| Health Care Technology | | | 1.3% | |

| Building Products | | | 1.3% | |

| Internet Software & Services | | | 1.2% | |

| Personal Products | | | 1.2% | |

| Electric Utilities | | | 1.2% | |

| Other1 | | | 19.3% | |

| Short-Term Investment Companies | | | 2.8% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed income investments)

| | | | |

| BBB | | | 10.0% | |

| BB or Lower | | | 86.1% | |

| N/R (not rated) | | | 3.9% | |

Total | | | 100% | |

| 1 | See Portfolio of Investments for details on “other” Portfolio Composition. |

13

| | |

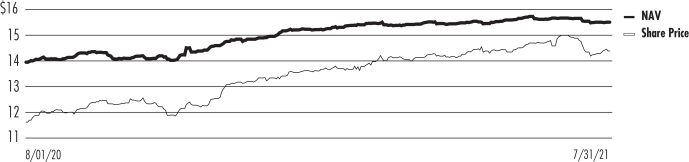

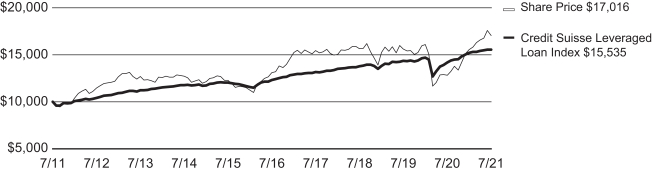

| JFR | | Nuveen Floating Rate Income Fund Performance Overview and Holding Summaries as of July 31, 2021 |

Refer to Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JFR at Common Share NAV | | | 17.36% | | | | 4.89% | | | | 5.38% | |

| JFR at Common Share Price | | | 30.14% | | | | 5.52% | | | | 5.82% | |

| Credit Suisse Leveraged Loan Index | | | 9.60% | | | | 4.75% | | | | 4.50% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2021 — Common Share Price

14

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Variable Rate Senior Loan Interests | | | 138.1% | |

| Corporate Bonds | | | 11.0% | |

| Common Stocks | | | 3.6% | |

| Long-Term Investment Companies | | | 2.0% | |

| Asset-Backed Securities | | | 0.6% | |

| Warrants | | | 0.1% | |

| Convertible Preferred Securities | | | 0.0% | |

| Common Stock Rights | | | 0.0% | |

| Short-Term Investment Companies | | | 6.8% | |

| Other Assets Less Liabilities | | | (5.0)% | |

| Net Assets Plus Borrowings and Taxable Fund Preferred Shares, net of deferred offering costs | | | 157.2% | |

| Borrowings | | | (40.4)% | |

| Taxable Fund Preferred Shares, net of deferred offering costs | | | (16.8)% | |

Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| B.C. Unlimited Liability Company | | | 2.4% | |

| Parexel International Corporation | | | 1.3% | |

| Clear Channel Outdoor Holdings, Inc. | | | 1.2% | |

| Caesars Resort Collection, LLC | | | 1.1% | |

| Seattle Spinco, Inc. | | | 1.1% | |

Portfolio Composition

(% of total investments)

| | | | |

| Media | | | 11.3% | |

| Hotels, Restaurants & Leisure | | | 11.1% | |

| Software | | | 6.9% | |

| Health Care Providers & Services | | | 6.1% | |

| Oil, Gas & Consumable Fuels | | | 4.2% | |

| Pharmaceuticals | | | 4.0% | |

| Commercial Services & Supplies | | | 3.4% | |

| Life Sciences Tools & Services | | | 2.8% | |

| IT Services | | | 2.7% | |

| Diversified Telecommunication Services | | | 2.5% | |

| Insurance | | | 2.4% | |

| Entertainment | | | 2.1% | |

| Communications Equipment | | | 2.0% | |

| Specialty Retail | | | 1.9% | |

| Technology Hardware, Storage & Peripherals | | | 1.6% | |

| Auto Components | | | 1.4% | |

| Building Products | | | 1.3% | |

| Road & Rail | | | 1.3% | |

| Professional Services | | | 1.3% | |

| Airlines | | | 1.2% | |

| Health Care Technology | | | 1.2% | |

| Interactive Media & Services | | | 1.2% | |

| Personal Products | | | 1.1% | |

| Other1 | | | 19.2% | |

| Long-Term Investment Companies | | | 1.2% | |

| Asset-Backed Securities | | | 0.4% | |

| Short-Term Investment Companies | | | 4.2% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed income investments)

| | | | |

| BBB | | | 10.5% | |

| BB or Lower | | | 85.9% | |

| N/R (not rated) | | | 3.6% | |

Total | | | 100% | |

| 1 | See Portfolio of Investments for details on “other” Portfolio Composition. |

15

| | |

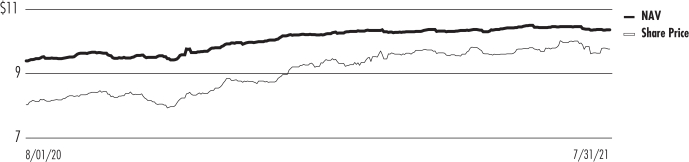

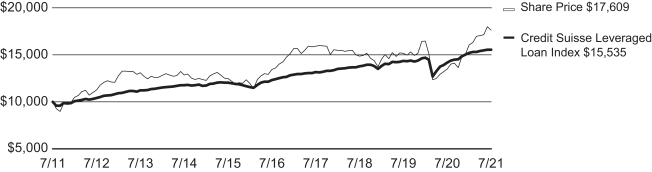

| JRO | | Nuveen Floating Rate Income Opportunity Fund Performance Overview and Holding Summaries as of July 31, 2021 |

Refer to Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JRO at Common Share NAV | | | 17.42% | | | | 4.93% | | | | 5.64% | |

| JRO at Common Share Price | | | 30.14% | | | | 5.42% | | | | 5.92% | |

| Credit Suisse Leveraged Loan Index | | | 9.60% | | | | 4.75% | | | | 4.50% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2021 — Common Share Price

16

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Variable Rate Senior Loan Interests | | | 138.6% | |

| Corporate Bonds | | | 11.4% | |

| Common Stocks | | | 3.7% | |

| Asset-Backed Securities | | | 0.6% | |

| Warrants | | | 0.1% | |

| Convertible Preferred Securities | | | 0.0% | |

| Common Stock Rights | | | 0.0% | |

| Short-Term Investment Companies | | | 6.3% | |

| Other Assets Less Liabilities | | | (3.3)% | |

| Net Assets Plus Borrowings and Taxable Fund Preferred Shares, net of deferred offering costs | | | 157.4% | |

| Borrowings | | | (39.5)% | |

| Taxable Fund Preferred Shares, net of deferred offering costs | | | (17.9)% | |

Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| B.C. Unlimited Liability Company | | | 2.4% | |

| Parexel International Corporation | | | 1.2% | |

Clear Channel Outdoor

Holdings, Inc. | | | 1.2% | |

| Caesars Resort Collection, LLC, Term Loan | | | 1.2% | |

| Seattle Spinco, Inc. | | | 1.2% | |

Portfolio Composition

(% of total investments)

| | | | |

| Media | | | 11.8% | |

| Hotels, Restaurants & Leisure | | | 11.1% | |

| Software | | | 7.0% | |

| Health Care Providers & Services | | | 6.4% | |

| Oil, Gas & Consumable Fuels | | | 4.0% | |

| Commercial Services & Supplies | | | 3.7% | |

| Pharmaceuticals | | | 3.4% | |

| IT Services | | | 3.2% | |

| Life Sciences Tools & Services | | | 2.8% | |

| Diversified Telecommunication Services | | | 2.5% | |

| Entertainment | | | 2.3% | |

| Insurance | | | 2.2% | |

| Communications Equipment | | | 1.9% | |

| Specialty Retail | | | 1.9% | |

| Technology Hardware, Storage & Peripherals | | | 1.5% | |

| Road & Rail | | | 1.5% | |

| Building Products | | | 1.5% | |

| Auto Components | | | 1.4% | |

| Health Care Technology | | | 1.3% | |

| Capital Markets | | | 1.3% | |

| Airlines | | | 1.3% | |

| Professional Services | | | 1.3% | |

| Interactive Media & Services | | | 1.2% | |

| Other1 | | | 19.2% | |

| Asset-Backed Securities | | | 0.4% | |

| Short-Term Investment Companies | | | 3.9% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed income investments)

| | | | |

| BBB | | | 9.9% | |

| BB or Lower | | | 86.3% | |

| N/R (not rated) | | | 3.8% | |

Total | | | 100% | |

| 1 | See Portfolio of Investments for details on “other” Portfolio Composition. |

17

| | |

| JSD | | Nuveen Short Duration Credit Opportunities Fund Performance Overview and Holding Summaries as of July 31, 2021 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JSD at Common Share NAV | | | 18.24% | | | | 4.66% | | | | 5.31% | |

| JSD at Common Share Price | | | 32.61% | | | | 5.34% | | | | 5.46% | |

| Credit Suisse Leveraged Loan Index | | | 9.60% | | | | 4.75% | | | | 4.50% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2021 — Common Share Price

18

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Variable Rate Senior Loan Interests | | | 138.5% | |

| Corporate Bonds | | | 12.2% | |

| Common Stocks | | | 3.4% | |

| Warrants | | | 0.1% | |

| Convertible Preferred Securities | | | 0.1% | |

| Common Stock Rights | | | 0.0% | |

| Short-Term Investment Companies | | | 6.8% | |

| Other Assets Less Liabilities | | | (4.1)% | |

| Net Assets Plus Borrowings and Taxable Fund Preferred Shares, net of deferred offering costs | | | 157.0% | |

| Borrowings | | | (12.5)% | |

| Taxable Fund Preferred, net of deferred offering costs | | | (44.5)% | |

Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| PPD, Inc. | | | 1.8% | |

| Caesars Resort Collection, LLC | | | 1.6% | |

| Delta 2 (LUX) S.a.r.l. | | | 1.3% | |

| PetSmart, Inc. | | | 1.1% | |

| Seattle Spinco, Inc. | | | 1.1% | |

Portfolio Composition

(% of total investments)

| | | | |

| Hotels, Restaurants & Leisure | | | 10.0% | |

| Media | | | 9.5% | |

| Software | | | 7.7% | |

| Health Care Providers & Services | | | 6.4% | |

| Pharmaceuticals | | | 4.4% | |

| Oil, Gas & Consumable Fuels | | | 4.3% | |

| Commercial Services & Supplies | | | 4.0% | |

| IT Services | | | 3.8% | |

| Life Sciences Tools & Services | | | 3.3% | |

| Diversified Telecommunication Services | | | 2.9% | |

| Specialty Retail | | | 2.2% | |

| Entertainment | | | 1.6% | |

| Insurance | | | 1.6% | |

| Auto Components | | | 1.6% | |

| Electric Utilities | | | 1.6% | |

| Airlines | | | 1.5% | |

| Road & Rail | | | 1.4% | |

| Professional Services | | | 1.4% | |

| Communications Equipment | | | 1.3% | |

| Technology Hardware, Storage & Peripherals | | | 1.2% | |

| Health Care Equipment & Supplies | | | 1.2% | |

| Construction & Engineering | | | 1.2% | |

| Capital Markets | | | 1.2% | |

| Health Care Technology | | | 1.2% | |

| Other1 | | | 19.3% | |

| Short-term Investment Companies | | | 4.2% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed income investments)

| | | | |

| BBB | | | 9.3% | |

| BB or Lower | | | 86.9% | |

| N/R (not rated) | | | 3.8% | |

Total | | | 100% | |

| 1 | See Portfolio of Investments for details on “other” Portfolio Composition. |

19

| | |

| JQC | | Nuveen Credit Strategies Income Fund Performance Overview and Holding Summaries as of July 31, 2021 |

Refer to Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JQC at Common Share NAV | | | 13.42% | | | | 4.26% | | | | 4.77% | |

| JQC at Common Share Price | | | 26.98% | | | | 6.15% | | | | 6.58% | |

| Credit Suisse Leveraged Loan Index | | | 9.60% | | | | 4.75% | | | | 4.50% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2021 — Common Share Price

20

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Variable Rate Senior Loan Interests | | | 140.0% | |

| Corporate Bonds | | | 19.3% | |

| Common Stocks | | | 1.1% | |

| Convertible Bonds | | | 0.2% | |

| Warrants | | | 0.1% | |

| Common Stock Rights | | | 0.0% | |

| Short-Term Investment Companies | | | 1.4% | |

| Other Assets Less Liabilities | | | (4.0)% | |

| Net Assets Plus Borrowings and Reverse Repurchase Agreements | | | 158.1% | |

| Borrowings | | | (42.9)% | |

| Reverse Repurchase Agreements | | | (15.2)% | |

Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| Parexel International Corporation, Term Loan B | | | 1.5% | |

| Sabre GLBL, Inc., Term Loan B | | | 1.2% | |

| Life Time Fitness Inc , Term Loan B | | | 1.2% | |

| Quikrete Holdings, Inc., Term Loan, First Lien | | | 1.1% | |

| Ziggo Financing Partnership, Term Loan I | | | 1.1% | |

Portfolio Composition

(% of total investments)

| | | | |

| Hotels, Restaurants & Leisure | | | 11.1% | |

| Media | | | 10.0% | |

| Health Care Providers & Services | | | 9.5% | |

| Software | | | 8.2% | |

| Pharmaceuticals | | | 4.1% | |

| Insurance | | | 3.5% | |

| Commercial Services & Supplies | | | 3.5% | |

| Diversified Telecommunication Services | | | 3.4% | |

| Airlines | | | 3.1% | |

| IT Services | | | 2.8% | |

| Oil, Gas & Consumable Fuels | | | 2.8% | |

| Food & Staples Retailing | | | 2.6% | |

| Communications Equipment | | | 2.6% | |

| Life Sciences Tools & Services | | | 2.0% | |

| Machinery | | | 1.9% | |

| Personal Products | | | 1.9% | |

| Specialty Retail | | | 1.8% | |

| Building Products | | | 1.7% | |

| Leisure Products | | | 1.4% | |

| Chemicals | | | 1.4% | |

| Other1 | | | 19.8% | |

| Short-Term Investment Companies | | | 0.9% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed income investments)

| | | | |

| BBB | | | 14.6% | |

| BB or Lower | | | 83.9% | |

| N/R (not rated) | | | 1.5% | |

Total | | | 100% | |

| 1 | See Portfolio of Investments for details on “other” Portfolio Composition. |

21

Shareholder Meeting Report

The annual meeting of shareholders was held on April 6, 2021 for NSL, JFR, JRO, JSD and JQC. The meeting was held virtually due to public health concerns regarding the ongoing COVID-19 pandemic; at this meeting the shareholders were asked to elect Board members.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | NSL | | | JFR | | | JRO | | | JSD | | | JQC | |

| | | Common and

Preferred

shares voting

together as a

class | | | Preferred

Shares | | | Common and

Preferred

shares voting

together as a

class | | | Preferred

Shares | | | Common and

Preferred

shares voting

together as a

class | | | Preferred

Shares | | | Common and

Preferred

shares voting

together as a

class | | | Preferred

Shares | | | Common

Shares | |

Approval of the Board Members was reached as follows: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Jack B. Evans | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For | | | 15,269,981 | | | | — | | | | 19,925,265 | | | | — | | | | 12,844,141 | | | | — | | | | 4,221,956 | | | | — | | | | 79,954,539 | |

Withhold | | | 14,250,010 | | | | — | | | | 26,258,372 | | | | — | | | | 18,826,046 | | | | — | | | | 4,260,206 | | | | — | | | | 25,140,111 | |

Total | | | 29,519,991 | | | | — | | | | 46,183,637 | | | | — | | | | 31,670,187 | | | | — | | | | 8,482,162 | | | | — | | | | 105,094,650 | |

Matthew Thornton III | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For | | | 21,919,584 | | | | — | | | | 35,265,261 | | | | — | | | | 23,644,579 | | | | — | | | | 5,846,342 | | | | — | | | | 98,430,207 | |

Withhold | | | 7,600,407 | | | | — | | | | 10,918,376 | | | | — | | | | 8,025,608 | | | | — | | | | 2,635,820 | | | | — | | | | 6,664,443 | |

Total | | | 29,519,991 | | | | — | | | | 46,183,637 | | | | — | | | | 31,670,187 | | | | — | | | | 8,482,162 | | | | — | | | | 105,094,650 | |

William C. Hunter | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For | | | — | | | | 40,000 | | | | — | | | | 66,000 | | | | — | | | | 75,000 | | | | — | | | | 47,000 | | | | — | |

Withhold | | | — | | | | — | | | | — | | | | 34,000 | | | | — | | | | — | | | | — | | | | 23,000 | | | | — | |

Total | | | — | | | | 40,000 | | | | — | | | | 100,000 | | | | — | | | | 75,000 | | | | — | | | | 70,000 | | | | — | |

Albin F. Moschner | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For | | | — | | | | 40,000 | | | | — | | | | 66,000 | | | | — | | | | 75,000 | | | | — | | | | 47,000 | | | | 80,005,675 | |

Withhold | | | — | | | | — | | | | — | | | | 34,000 | | | | — | | | | — | | | | — | | | | 23,000 | | | | 25,088,975 | |

Total | | | — | | | | 40,000 | | | | — | | | | 100,000 | | | | — | | | | 75,000 | | | | — | | | | 70,000 | | | | 105,094,650 | |

22

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees

Nuveen Senior Income Fund

Nuveen Floating Rate Income Fund

Nuveen Floating Rate Income Opportunity Fund

Nuveen Short Duration Credit Opportunities Fund

Nuveen Credit Strategies Income Fund:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Senior Income Fund, Nuveen Floating Rate Income Fund, Nuveen Floating Rate Income Opportunity Fund, Nuveen Short Duration Credit Opportunities Fund and Nuveen Credit Strategies Income Fund (the Funds), including the portfolios of investments, as of July 31, 2021, the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the five-year period then ended. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of July 31, 2021, the results of their operations and their cash flows for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of July 31, 2021, by correspondence with custodians and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

September 28, 2021

23

| | |

| NSL | | Nuveen Senior Income Fund Portfolio of Investments July 31, 2021 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon (2) | | | Reference

Rate (2) | | | Spread (2) | | | Maturity (3) | | | Ratings (4) | | | Value | |

| |

| | | | LONG-TERM INVESTMENTS – 153.9% (97.2% of Total Investments) | |

| |

| | | | VARIABLE RATE SENIOR LOAN INTERESTS – 139.1% (87.9% of Total Investments) (2) | |

| |

| | | | Aerospace & Defense – 1.5% (1.0% of Total Investments) | |

| | | | | | | |

| $ | 313 | | | Dynasty Acquisition Co., Inc., Term Loan B1 | | | 3.647% | | | | 3-Month LIBOR | | | | 3.500% | | | | 4/08/26 | | | | B– | | | $ | 302,924 | |

| | 168 | | | Dynasty Acquisition Co., Inc., Term Loan B2 | | | 3.647% | | | | 3-Month LIBOR | | | | 3.500% | | | | 4/08/26 | | | | B– | | | | 162,862 | |

| | 731 | | | Maxar Technologies Ltd., Term Loan B | | | 2.850% | | | | 1-Month LIBOR | | | | 2.750% | | | | 10/05/24 | | | | B | | | | 725,116 | |

| | 964 | | | TransDigm, Inc., Term Loan E | | | 2.342% | | | | 1-Month LIBOR | | | | 2.250% | | | | 5/30/25 | | | | Ba3 | | | | 948,089 | |

| | 795 | | | TransDigm, Inc., Term Loan F | | | 2.342% | | | | 1-Month LIBOR | | | | 2.250% | | | | 12/09/25 | | | | Ba3 | | | | 782,569 | |

| | 687 | | | TransDigm, Inc., Term Loan G | | | 2.342% | | | | 1-Month LIBOR | | | | 2.250% | | | | 8/22/24 | | | | Ba3 | | | | 676,992 | |

| | 3,658 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | | | | | | | | | 3,598,552 | |

| |

| | | | Airlines – 2.3% (1.5% of Total Investments) | |

| | | | | | | |

| | 920 | | | AAdvantage Loyalty IP Ltd., Term Loan | | | 5.500% | | | | 3-Month LIBOR | | | | 4.750% | | | | 4/20/28 | | | | Ba2 | | | | 947,493 | |

| | 189 | | | American Airlines, Inc., Incremental Term Loan | | | 2.093% | | | | 1-Month LIBOR | | | | 2.000% | | | | 12/14/23 | | | | Ba3 | | | | 184,697 | |

| | 760 | | | American Airlines, Inc., Term Loan, First Lien | | | 1.840% | | | | 1-Month LIBOR | | | | 1.750% | | | | 1/29/27 | | | | Ba3 | | | | 706,446 | |

| | 963 | | | Kestrel Bidco, Inc., Term Loan B | | | 4.000% | | | | 6-Month LIBOR | | | | 3.000% | | | | 12/11/26 | | | | BB– | | | | 932,275 | |

| | 1,075 | | | SkyMiles IP Ltd., Term Loan B | | | 4.750% | | | | 3-Month LIBOR | | | | 3.750% | | | | 10/20/27 | | | | Baa1 | | | | 1,137,113 | |

| | 1,496 | | | United Airlines, Inc., Term Loan B | | | 4.500% | | | | 1-Month LIBOR | | | | 3.750% | | | | 4/21/28 | | | | Ba1 | | | | 1,500,836 | |

| | 5,403 | | | Total Airlines | | | | | | | | | | | | | | | | | | | | | | | 5,408,860 | |

| |

| | | | Auto Components – 1.7% (1.1% of Total Investments) | |

| | | | | | | |

| | 124 | | | Adient US LLC, Term Loan B | | | 3.592% | | | | 1-Month LIBOR | | | | 3.500% | | | | 4/08/28 | | | | BB– | | | | 123,882 | |

| | 1,363 | | | Clarios Global LP, Term Loan B | | | 3.342% | | | | 1-Month LIBOR | | | | 3.250% | | | | 4/30/26 | | | | B1 | | | | 1,354,463 | |

| | 825 | | | DexKo Global Inc., Term Loan | | | 4.500% | | | | 1-Month LIBOR | | | | 3.500% | | | | 7/24/24 | | | | B1 | | | | 825,614 | |

| | 746 | | | Les Schwab Tire Centers, Term Loan B | | | 4.000% | | | | 6-Month LIBOR | | | | 3.250% | | | | 11/02/27 | | | | B | | | | 746,873 | |

| | 898 | | | Superior Industries International, Inc., Term Loan B, First Lien | | | 4.092% | | | | 1-Month LIBOR | | | | 4.000% | | | | 5/23/24 | | | | Ba3 | | | | 898,521 | |

| | 3,956 | | | Total Auto Components | | | | | | | | | | | | | | | | | | | | | | | 3,949,353 | |

| |

| | | | Automobiles – 0.2% (0.1% of Total Investments) | |

| | | | | | | |

| | 518 | | | Wand NewCo 3, Inc., Term Loan | | | 3.092% | | | | 1-Month LIBOR | | | | 3.000% | | | | 2/05/26 | | | | B1 | | | | 511,757 | |

| |

| | | | Banks – 0.1% (0.0% of Total Investments) | |

| | | | | | | |

| | 157 | | | iQor US, Inc., Exit Term Loan | | | 7.589% | | | | 1-Month LIBOR | | | | 7.500% | | | | 9/15/27 | | | | N/R | | | | 161,171 | |

| |

| | | | Beverages – 1.0% (0.6% of Total Investments) | |

| | | | | | | |

| | 617 | | | Arterra Wines Canada, Inc., Term Loan | | | 4.250% | | | | 3-Month LIBOR | | | | 3.500% | | | | 11/25/27 | | | | B1 | | | | 616,900 | |

| | 469 | | | City Brewing Company, LLC, Term Loan | | | 4.250% | | | | 3-Month LIBOR | | | | 3.500% | | | | 4/05/28 | | | | B+ | | | | 466,948 | |

| | 1,185 | | | Triton Water Holdings, Inc, Term Loan | | | 4.000% | | | | 3-Month LIBOR | | | | 3.500% | | | | 3/31/28 | | | | B1 | | | | 1,177,740 | |

| | 2,271 | | | Total Beverages | | | | | | | | | | | | | | | | | | | | | | | 2,261,588 | |

| |

| | | | Biotechnology – 0.8% (0.5% of Total Investments) | |

| | | | | | | |

| | 2,004 | | | Grifols Worldwide Operations USA, Inc., Term Loan B | | | 2.084% | | | | 1-Week LIBOR | | | | 2.000% | | | | 11/15/27 | | | | BB+ | | | | 1,980,111 | |

| |

| | | | Building Products – 2.0% (1.3% of Total Investments) | |

| | | | | | | |

| | 300 | | | All-Star Bidco AB, Term Loan, (WI/DD) | | | TBD | | | | TBD | | | | TBD | | | | TBD | | | | N/R | | | | 299,625 | |

| | 1,133 | | | Cornerstone Building Brands, Inc., Term Loan B | | | 3.750% | | | | 1-Month LIBOR | | | | 3.250% | | | | 4/12/28 | | | | B+ | | | | 1,132,132 | |

| | 104 | | | LBM Acquisition LLC, Term Loan, (WI/DD) | | | TBD | | | | TBD | | | | TBD | | | | TBD | | | | B+ | | | | 102,827 | |

| | 465 | | | LBM Acquisition LLC, Term Loan B | | | 4.500% | | | | 3-Month LIBOR | | | | 3.750% | | | | 12/17/27 | | | | B+ | | | | 461,564 | |

| | 160 | | | Potters Industries, LLC, Term Loan B | | | 4.750% | | | | 3-Month LIBOR | | | | 4.000% | | | | 12/14/27 | | | | B | | | | 160,100 | |

| | 2,091 | | | Quikrete Holdings, Inc., Term Loan, First Lien | | | 2.592% | | | | 1-Month LIBOR | | | | 2.500% | | | | 1/31/27 | | | | BB– | | | | 2,069,238 | |

| | 427 | | | Resideo Funding, Inc., Term Loan | | | 2.750% | | | | 3-Month LIBOR | | | | 2.250% | | | | 2/12/28 | | | | BBB– | | | | 425,719 | |

| | 162 | | | Resideo Funding, Inc., Term Loan | | | 2.750% | | | | 1-Month LIBOR | | | | 2.250% | | | | 2/12/28 | | | | BBB– | | | | 160,970 | |

| | 4,842 | | | Total Building Products | | | | | | | | | | | | | | | | | | | | | | | 4,812,175 | |

| |

| | | | Capital Markets – 1.3% (0.8% of Total Investments) | |

| | | | | | | |

| | 185 | | | RPI Intermediate Finance Trust, Term Loan B1 | | | 1.842% | | | | 1-Month LIBOR | | | | 1.750% | | | | 2/11/27 | | | | BBB– | | | | 184,202 | |

| | 1,999 | | | Sequa Mezzanine Holdings L.L.C., Extended Term Loan, (cash 6.750%, PIK 1.000%) | | | 7.750% | | | | 3-Month LIBOR | | | | 6.750% | | | | 7/31/23 | | | | B– | | | | 2,028,059 | |

24

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon (2) | | | Reference

Rate (2) | | | Spread (2) | | | Maturity (3) | | | Ratings (4) | | | Value | |

| |

| | | | Capital Markets (continued) | |

| | | | | | | |

| $ | 823 | | | Sequa Mezzanine Holdings L.L.C., Term Loan, Second Lien, (cash 5.000%, PIK 6.750%) | | | 11.750% | | | | 3-Month LIBOR | | | | 10.750% | | | | 7/31/24 | | | | CCC– | | | $ | 812,850 | |

| | 3,007 | | | Total Capital Markets | | | | | | | | | | | | | | | | | | | | | | | 3,025,111 | |

| |

| | | | Chemicals – 1.0% (0.7% of Total Investments) | |

| | | | | | | |

| | 323 | | | ASP Unifrax Holdings, Inc., Term Loan B | | | 3.897% | | | | 3-Month LIBOR | | | | 3.750% | | | | 12/14/25 | | | | B– | | | | 317,278 | |

| | 373 | | | Atotech B.V., Term Loan B | | | 3.000% | | | | 3-Month LIBOR | | | | 2.500% | | | | 3/18/28 | | | | B+ | | | | 371,911 | |

| | 500 | | | INEOS Styrolution US Holding LLC, Term Loan B | | | 3.250% | | | | 1-Month LIBOR | | | | 2.750% | | | | 1/29/26 | | | | BB+ | | | | 499,250 | |

| | 659 | | | Ineos US Finance LLC, Term Loan B | | | 2.107% | | | | 2-Month LIBOR | | | | 2.000% | | | | 3/31/24 | | | | BBB– | | | | 651,136 | |

| | 398 | | | Lonza Group AG, Term Loan B | | | 4.750% | | | | 3-Month LIBOR | | | | 4.000% | | | | 5/14/28 | | | | B2 | | | | 398,498 | |

| | 177 | | | Sparta US HoldCo LLC, Term Loan, (WI/DD) | | | TBD | | | | TBD | | | | TBD | | | | TBD | | | | B+ | | | | 177,184 | |

| | 2,430 | | | Total Chemicals | | | | | | | | | | | | | | | | | | | | | | | 2,415,257 | |

| |

| | | | Commercial Services & Supplies – 5.6% (3.5% of Total Investments) | |

| | | | | | | |

| | 499 | | | Amentum Government Services Holdings LLC, Term Loan B | | | 5.500% | | | | 3-Month LIBOR | | | | 4.750% | | | | 1/31/27 | | | | B1 | | | | 500,620 | |

| | 523 | | | Brand Energy & Infrastructure Services, Inc., Term Loan | | | 5.250% | | | | 3-Month LIBOR | | | | 4.250% | | | | 6/21/24 | | | | B– | | | | 514,566 | |

| | 4,293 | | | Delta 2 (LUX) S.a.r.l., Term Loan | | | 3.500% | | | | 1-Month LIBOR | | | | 2.500% | | | | 2/01/24 | | | | B+ | | | | 4,267,795 | |

| | 433 | | | Garda World Security Corporation, Term Loan B | | | 4.340% | | | | 1-Month LIBOR | | | | 4.250% | | | | 10/30/26 | | | | BB+ | | | | 432,851 | |

| | 1,037 | | | GFL Environmental, Inc., Term Loan | | | 3.500% | | | | 3-Month LIBOR | | | | 3.000% | | | | 5/30/25 | | | | BB– | | | | 1,037,557 | |

| | 275 | | | KAR Auction Services, Inc., Term Loan B6 | | | 2.375% | | | | 1-Month LIBOR | | | | 2.250% | | | | 9/19/26 | | | | Ba3 | | | | 271,649 | |

| | 500 | | | Madison IAQ LLC, Term Loan | | | 3.750% | | | | 3-Month LIBOR | | | | 3.250% | | | | 6/21/28 | | | | B1 | | | | 496,383 | |

| | 506 | | | PAE Holding Corporation, Term Loan B | | | 5.250% | | | | 1-Month LIBOR | | | | 4.500% | | | | 10/19/27 | | | | B | | | | 508,444 | |

| | 144 | | | Prime Security Services Borrower, LLC, Term Loan | | | 3.500% | | | | 1-Month LIBOR | | | | 2.750% | | | | 9/23/26 | | | | BB– | | | | 143,979 | |

| | 94 | | | Prime Security Services Borrower, LLC, Term Loan | | | 3.500% | | | | 3-Month LIBOR | | | | 2.750% | | | | 9/23/26 | | | | BB– | | | | 93,257 | |

| | 187 | | | Prime Security Services Borrower, LLC, Term Loan | | | 3.500% | | | | 6-Month LIBOR | | | | 2.750% | | | | 9/23/26 | | | | BB– | | | | 186,513 | |

| | 94 | | | Prime Security Services Borrower, LLC, Term Loan | | | 3.500% | | | | 12-Month LIBOR | | | | 2.750% | | | | 9/23/26 | | | | BB– | | | | 93,257 | |

| | 680 | | | Robertshaw US Holding Corp, Term Loan, First Lien | | | 4.500% | | | | 1-Month LIBOR | | | | 3.500% | | | | 2/28/25 | | | | CCC+ | | | | 655,464 | |

| | 89 | | | Sabert Corporation, Term Loan B | | | 5.500% | | | | 1-Month LIBOR | | | | 4.500% | | | | 12/10/26 | | | | B | | | | 89,499 | |

| | 748 | | | Spin Holdco, Inc., Term Loan | | | 4.750% | | | | 3-Month LIBOR | | | | 4.000% | | | | 3/04/28 | | | | B– | | | | 748,499 | |

| | 1,926 | | | Travelport Finance (Luxembourg) S.a.r.l., Term Loan, (cash 2.500%, PIK 6.500%), (DD1) | | | 2.500% | | | | 3-Month LIBOR | | | | 1.500% | | | | 2/28/25 | | | | B– | | | | 1,964,690 | |

| | 368 | | | West Corporation, Term Loan B1 | | | 4.500% | | | | 3-Month LIBOR | | | | 3.500% | | | | 10/10/24 | | | | BB+ | | | | 356,040 | |

| | 730 | | | WEX, Inc., Term Loan | | | 2.342% | | | | 1-Month LIBOR | | | | 2.250% | | | | 4/01/28 | | | | Ba2 | | | | 722,728 | |

| | 13,126 | | | Total Commercial Services & Supplies | | | | | | | | | | | | | | | | | | | | | | | 13,083,791 | |

| |

| | | | Communications Equipment – 2.4% (1.5% of Total Investments) | |

| | | | | | | |

| | 1,647 | | | CommScope, Inc., Term Loan B | | | 3.342% | | | | 1-Month LIBOR | | | | 3.250% | | | | 4/04/26 | | | | Ba3 | | | | 1,633,882 | |

| | 50 | | | MetroNet Systems Holdings, LLC, Delayed Draw Term Loan, (5) | | | 4.500% | | | | 1-Month LIBOR | | | | 3.750% | | | | 6/02/28 | | | | B2 | | | | 50,106 | |

| | 450 | | | MetroNet Systems Holdings, LLC, Term Loan, First Lien | | | 4.500% | | | | 1-Month LIBOR | | | | 3.750% | | | | 6/02/28 | | | | B2 | | | | 450,956 | |

| | 638 | | | MLN US HoldCo LLC, Term Loan, First Lien | | | 4.603% | | | | 1-Month LIBOR | | | | 4.500% | | | | 11/30/25 | | | | B3 | | | | 583,411 | |

| | 968 | | | Plantronics Inc, Term Loan B | | | 2.592% | | | | 1-Month LIBOR | | | | 2.500% | | | | 7/02/25 | | | | Ba2 | | | | 948,376 | |

| | 3 | | | Riverbed Technology, Inc., Term Loan B | | | 7.000% | | | | 2-Month LIBOR | | | | 6.000% | | | | 12/31/25 | | | | B2 | | | | 2,959 | |

| | 1,240 | | | Riverbed Technology, Inc., Term Loan B | | | 7.000% | | | | 3-Month LIBOR | | | | 6.000% | | | | 12/31/25 | | | | B2 | | | | 1,174,929 | |

| | 878 | | | Univision Communications, Inc., Term Loan C5 | | | 3.750% | | | | 1-Month LIBOR | | | | 2.750% | | | | 3/15/24 | | | | B | | | | 875,933 | |

| | 5,874 | | | Total Communications Equipment | | | | | | | | | | | | | | | | | | | | | | | 5,720,552 | |

| |

| | | | Construction & Engineering – 1.6% (1.0% of Total Investments) | |

| | | | | | | |

| | 300 | | | AECOM Technology Corporation , Term Loan B | | | 1.842% | | | | 1-Month LIBOR | | | | 1.750% | | | | 4/13/28 | | | | BBB– | | | | 299,813 | |

| | 465 | | | Aegion Corporation, Term Loan | | | 5.500% | | | | 3-Month LIBOR | | | | 4.750% | | | | 5/17/28 | | | | B | | | | 469,650 | |

| | 1,124 | | | Brown Group Holding, LLC, Term Loan B | | | 3.250% | | | | 3-Month LIBOR | | | | 2.750% | | | | 6/07/28 | | | | B+ | | | | 1,117,698 | |

| | 125 | | | FrontDoor Inc, Term Loan B | | | 2.342% | | | | 1-Month LIBOR | | | | 2.250% | | | | 6/17/28 | | | | Ba2 | | | | 124,974 | |

| | 250 | | | Osmose Utilities Services, Inc., Term Loan | | | 3.750% | | | | 3-Month LIBOR | | | | 3.250% | | | | 6/17/28 | | | | B | | | | 248,126 | |

| | 216 | | | Pike Corporation, Incremental Term Loan B | | | 3.100% | | | | 1-Month LIBOR | | | | 3.000% | | | | 1/21/28 | | | | Ba3 | | | | 215,272 | |

| | 1,218 | | | Traverse Midstream Partners LLC, Term Loan | | | 6.500% | | | | 1-Month LIBOR | | | | 5.500% | | | | 9/27/24 | | | | B | | | | 1,220,351 | |

| | 3,698 | | | Total Construction & Engineering | | | | | | | | | | | | | | | | | | | | | | | 3,695,884 | |

| |

| | | | Containers & Packaging – 1.3% (0.8% of Total Investments) | |

| | | | | | | |

| | 880 | | | Berry Global, Inc., Term Loan Z | | | 1.850% | | | | 1-Month LIBOR | | | | 1.750% | | | | 7/01/26 | | | | BBB– | | | | 870,927 | |

| | 326 | | | Reynolds Consumer Products LLC, Term Loan | | | 1.842% | | | | 1-Month LIBOR | | | | 1.750% | | | | 2/04/27 | | | | BBB– | | | | 322,954 | |