| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| |

| Investment Company Act file number 811-21503 |

| |

| The FBR Funds |

|

| (Exact name of registrant as specified in charter) |

| |

| 1001 Nineteenth Street North |

| Arlington, VA 22209 |

|

| (Address of principal executive offices) (Zip code) |

| |

| Registrant’s telephone number, including area code: 703.469.1040 |

| |

| |

| William Ginivan |

| General Counsel |

| Friedman, Billings, Ramsey Group, Inc. |

| Potomac Tower |

| 1001 Nineteenth Street North |

| Arlington, VA 22209 |

|

| (Name and address of agent for service) |

| |

| |

| Date of fiscal year end: October 31, 2006 |

| |

| Date of reporting period: October 31, 2006 |

| |

ITEM 1. REPORT TO SHAREHOLDERS

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17CRF 270.30e-1).

THE FBR FUNDS

FBR Pegasus FundTM

FBR Large Cap Financial Fund

FBR Large Cap Technology Fund

FBR Small Cap Fund

FBR Small Cap Financial Fund

FBR Small Cap Technology Fund

FBR Gas Utility Index Fund

FBR Fund for Government Investors

Annual Report

October 31, 2006

[THIS PAGE INTENTIONALLY LEFT BLANK]

The FBR Funds

Annual Letter to Shareholders

Dear Shareholder,

The stock market ended our 2006 fiscal year on a high note amid speculation that the economy is headed for a ‘soft landing’. Investors showed a preference for the old-economy large-cap stocks as the Dow Jones Industrial Average surpassed and ultimately closed above 12,000, setting a new all-time high. The broader market, as measured by the S&P 500, hovered near multi-year highs. We are pleased that each of our equity funds provided investors with double-digit returns and that seventy percent were able to outperform the market over the time period in review1,2.

The biggest event internally for us this year was the expected retirement of long time Chairman of the Board of Trustees, F. David Fowler. Mr. Fowler had been an FBR Funds Trustee since our inception and was elevated to Chairman in 2003. Under his leadership, the Board has acted on behalf of shareholders with the utmost integrity and sense of fiduciary responsibility. We have complete confidence in our new Chairman, Michael Willner, who will continue the long standing tradition of acting in the best interest of our fellow shareholders. We will miss Mr. Fowler‘s leadership, but his legacy will continue on with The FBR Funds. It is also important to note that we added two new independent trustees, William Cole - a former Ernst & Young Partner, and Reena Aggarwal - the Deputy Dean of the Georgetown University Business School. We are pleased that your Board of Trustees remains eighty percent independent and look forward to working with them as we continue to grow our business.

Almost ten years ago The FBR Funds began providing investors with highly specialized and focused mutual funds. Our three original funds will celebrate their ten-year anniversary at the start of 2007. Over the years, we have expanded our offerings organically and through acquisition to reach our current fund line-up. We are continually evaluating new opportunities that will allow us to strengthen our fund product offerings and enhance our intellectual talent pool. We are excited to share with you that our Board of Trustees unanimously voted to allow us to move forward with plans to launch two new traditional asset class funds in the first quarter of the new year. Details about the new offerings will be available shortly.

As in prior years, what follows is a discussion from each of the portfolio managers with respect to their funds’ performance and outlook. In general, The FBR Funds are about respecting your money. Our goal is to achieve attractive returns that are balanced, focused on the long-term and ever mindful of the downside risks associated with investing. If you would like more timely updates, fbrfunds.com provides daily prices, monthly performance data, portfolio holdings and other important fund information.

2

All of us at The FBR Funds want to thank you for your continued support, and we look forward to serving your investment needs in the years ahead. As always, we welcome your questions and comments. You can reach us via e-mail at funds@fbr.com or toll free at 888.200.4710.

Sincerely,

David Ellison

President and Trustee

The FBR Funds

1 The FBR Pegasus FundTM commenced operations on November 15, 2005.

2 Past Performance is No Guarantee of Future Results. The current performance may be lower or higher than performance data quoted. To obtain performance data current to the most recent month-end please call 888.200.4710 or visit www.fbrfunds.com. Investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost.

3

The FBR Funds

FBR Pegasus FundTM

Management Overview

Co-Portfolio Managers: Robert C. Barringer, CFA, Ryan Kelley, CFA and Winsor Aylesworth

Over the recent fiscal year, how did the Fund perform?

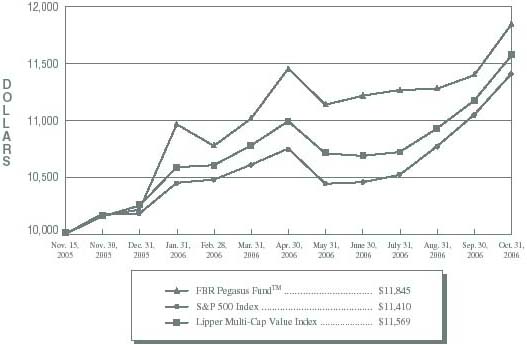

The Pegasus Fund appreciated 18.45% from its inception on November 15, 2005 through October 31, 2006. During this time period, the S&P 500 Index and the Lipper Multi-Cap Value Index returned 14.10% and 15.69%, respectively.

What factors contributed to the Fund’s performance?

The Fund benefited from overweight positions in energy, basic materials and utilities which contributed positively to performance. Underweight positions in healthcare, consumer staples and technology helped minimize exposure to the sectors that detracted the most from performance relative to the benchmarks. During the Fund’s first fiscal year, our investment process led us to overweight beneficial sectors as they contained the highest number of companies with the combination of financial strength, attractive valuation and proven records of consistent growth that we seek.

What is the outlook for the Fund?

We believe the outlook for the Fund is bright, and remain confident in the consistent and disciplined investment process we employ to manage the Fund. A beneficial aspect of our investment process is that we are able to identify the companies and sectors on an ongoing basis that have the most attractive investment characteristics. At any one point in the market, there are usually numerous investment opportunities, such as these, that are being overlooked or misunderstood by the market. Our process affords us the confidence to position the Fund to take advantage of these opportunities when they present themselves.

Currently, we continue to believe that the sectors and companies in which we are invested are attractively valued, even though they have provided solid performance. Financial services, energy, industrials, basic materials and utilities are a few of the areas in which we are most optimistic. It is within these sectors that we are finding the most opportunities to own companies with better than average balance sheets, reasonable valuations and track records of creating value for shareholders over time.

|

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change. |

4

The FBR Funds

FBR Pegasus FundTM

Comparison of Changes in Value of $10,000 Investment in

Fund Shares(1)(2) vs. Various Indices(1)(3)

| | | | | | | | | | | |

| Total Returns—For the Periods Ended October 31, 2006(4) |

| | | | | | | | | Cumulative

Since

Inception(5) | | |

| | | | | | | | |

| | |

FBR Pegasus FundTM(1)(2) | | | | | | | | 18.45% | | |

S&P 500 Index(1)(3) | | | | | | | | 14.10% | | |

Lipper Multi-Cap Value Index(1)(3) | | | | | | | | 15.69% | | |

| | | | | | | | | | | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data curernt to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are unmanaged, do not incur expenses and are not available for investment. The performance of the indices includes reinvested dividends, and does not reflect sales charges or expenses, except for the Lipper Multi-Cap Value Index which reflects fund expenses. |

| (2) | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to represent the broad domestic economy through changes in aggregate market value of 500 stocks representing all major industries. The Lipper Multi-Cap Value Index is an equally weighted index of the largest thirty funds within the multi-cap value fund classification as defined by Lipper Inc. The index is rebalanced quarterly. Lipper Analytical Services, Inc., is a nationally recognized organization that reports on mutual fund total return performance and calculates fund rankings. Each Lipper Average is based on a universe of funds with similar investment objectives. |

| (4) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | For the period November 15, 2005 (commencement of investment operations) through October 31, 2006. |

5

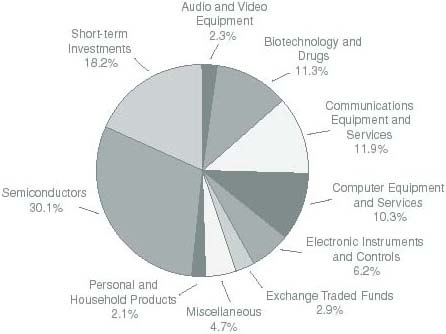

The FBR Funds

FBR Pegasus FundTM

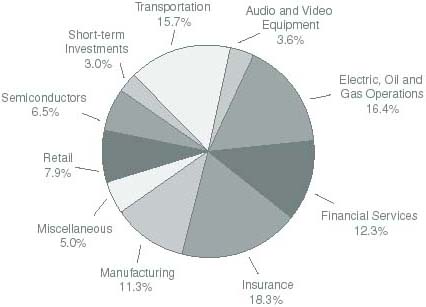

Portfolio Summary

October 31, 2006

The following chart provides a visual breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

6

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | COMMON STOCKS — 97.3% | | | | |

| | | | Airlines — 1.5% | | | | |

| | 13,417 | | Southwest Airlines Co. | | $ | 201,658 | |

| | | | | |

| |

| | | | Audio and Video Equipment — 3.6% | | | | |

| | 11,667 | | Sony Corp. ADR | | | 478,114 | |

| | | | | |

| |

| | | | Auto and Truck Parts — 2.0% | | | | |

| | 3,000 | | Genuine Parts Co. | | | 136,560 | |

| | 1,815 | | Magna International, Inc., Class A | | | 135,762 | |

| | | | | |

| |

| | | | | | | 272,322 | |

| | | | | |

| |

| | | | Banks - Regional — 6.9% | | | | |

| | 3,400 | | Allied Irish Banks PLC ADR | | | 185,776 | |

| | 2,956 | | Bank of Montreal | | | 183,272 | |

| | 1,110 | | Comerica, Inc. | | | 64,591 | |

| | 2,630 | | KeyCorp | | | 97,678 | |

| | 7,300 | | The Bank of Nova Scotia | | | 320,543 | |

| | 1,100 | | UnionBanCal Corp. | | | 63,338 | |

| | | | | |

| |

| | | | | | | 915,198 | |

| | | | | |

| |

| | | | Biotechnology and Drugs — 3.2% | | | | |

| | 4,900 | | Novartis AG ADR | | | 297,577 | |

| | 6,000 | | Schering-Plough Corp. | | | 132,840 | |

| | | | | |

| |

| | | | | | | 430,417 | |

| | | | | |

| |

| | | | Capital Goods - Miscellaneous — 0.8% | | | | |

| | 1,400 | | W.W. Grainger, Inc. | | | 101,892 | |

| | | | | |

| |

| | | | Chemicals - Plastics and Rubber — 1.5% | | | | |

| | 5,000 | | The Dow Chemical Co. | | | 203,950 | |

| | | | | |

| |

| | | | Communications Equipment — 1.1% | | | | |

| | 125 | | Research in Motion Ltd.* | | | 14,685 | |

| | 12,300 | | Tellabs, Inc.* | | | 129,642 | |

| | | | | |

| |

| | | | | | | 144,327 | |

| | | | | |

| |

| | | | Communications Services — 1.1% | | | | |

| | 1,100 | | America Movil S.A. de C.V. ADR, Series L | | | 47,157 | |

| | 1,439 | | AT&T, Inc. | | | 49,286 | |

7

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Communications Services — 1.1% (continued) | | | | |

| | 1,800 | | Nippon Telegraph and Telephone Corp. ADR | | $ | 45,234 | |

| | | | | |

| |

| | | | | | | 141,677 | |

| | | | | |

| |

| | | | Construction Services — 1.0% | | | | |

| | 2,679 | | Lennar Corp., Class A | | | 127,199 | |

| | | | | |

| |

| | | | Electric Utilities — 2.6% | | | | |

| | 3,876 | | Edison International | | | 172,249 | |

| | 4,100 | | PG&E Corp. | | | 176,874 | |

| | | | | |

| |

| | | | | | | 349,123 | |

| | | | | |

| |

| | | | Electronic Instruments and Controls — 1.8% | | | | |

| | 3,133 | | TDK Corp. ADR | | | 245,001 | |

| | | | | |

| |

| | | | Food Processing — 1.0% | | | | |

| | 2,000 | | Bunge Ltd. | | | 128,220 | |

| | | | | |

| |

| | | | Insurance - Accident and Health — 1.1% | | | | |

| | 2,500 | | Aetna, Inc. | | | 103,050 | |

| | 2,400 | | UnumProvident Corp. | | | 47,472 | |

| | | | | |

| |

| | | | | | | 150,522 | |

| | | | | | |

| |

| | | | Insurance - Life — 3.3% | | | | |

| | 3,397 | | Prudential Financial, Inc. | | | 261,331 | |

| | 4,300 | | Sun Life Financial, Inc. | | | 180,815 | |

| | | | | |

| |

| | | | | | | 442,146 | |

| | | | | |

| |

| | | | Insurance - Property and Casualty — 13.8% | | | | |

| | 2,354 | | ACE Ltd. | | | 134,767 | |

| | 143 | | Berkshire Hathaway, Inc., Class B* | | | 502,644 | |

| | 457 | | Everest Re Group Ltd. | | | 45,325 | |

| | 4,770 | | Loews Corp. | | | 185,648 | |

| | 845 | | Safeco Corp. | | | 49,171 | |

| | 4,000 | | The Allstate Corp. | | | 245,440 | |

| | 3,098 | | The Chubb Corp. | | | 164,659 | |

| | 2,269 | | The Hartford Financial Services Group, Inc. | | | 197,789 | |

| | 5,354 | | The St. Paul Travelers Companies, Inc. | | | 273,749 | |

| | 1,500 | | W.R. Berkley Corp. | | | 55,290 | |

| | | | | |

| |

| | | | | | | 1,854,482 | |

| | | | | |

| |

8

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Investment Services — 5.5% | | | | |

| | 1,750 | | Ameriprise Financial, Inc. | | $ | 90,125 | |

| | 6,276 | | Morgan Stanley | | | 479,675 | |

| | 1,098 | | The Bear Stearns Companies, Inc. | | | 166,182 | |

| | | | | |

| |

| | | | | | | 735,982 | |

| | | | | |

| |

| | | | Iron and Steel — 1.7% | | | | |

| | 4,038 | | Mittal Steel Company N.V., Class A NYS | | | 172,625 | |

| | 755 | | United States Steel Corp. | | | 51,038 | |

| | | | | |

| |

| | | | | | | 223,663 | |

| | | | | |

| |

| | | | Metal Mining — 0.8% | | | | |

| | 2,200 | | Alcan, Inc. | | | 103,642 | |

| | | | | |

| |

| | | | Oil and Gas Operations — 13.4% | | | | |

| | 1,077 | | Apache Corp. | | | 70,350 | |

| | 1,800 | | Canadian Natural Resources Ltd. | | | 93,870 | |

| | 3,400 | | Chevron Corp. | | | 228,480 | |

| | 1,200 | | CNOOC Ltd. ADR | | | 100,584 | |

| | 3,475 | | ConocoPhillips | | | 209,334 | |

| | 1,225 | | Devon Energy Corp. | | | 81,879 | |

| | 2,600 | | EnCana Corp. | | | 123,474 | |

| | 950 | | Hess Corp. | | | 40,280 | |

| | 1,200 | | Marathon Oil Corp. | | | 103,680 | |

| | 900 | | Murphy Oil Corp. | | | 42,444 | |

| | 425 | | Newfield Exploration Co.* | | | 17,336 | |

| | 2,360 | | Occidental Petroleum Corp. | | | 110,778 | |

| | 1,000 | | Questar Corp. | | | 81,480 | |

| | 2,973 | | Royal Dutch Shell PLC, Class A ADR | | | 206,980 | |

| | 3,142 | | Sempra Energy | | | 166,652 | |

| | 2,100 | | Valero Energy Corp. | | | 109,893 | |

| | | | | |

| |

| | | | | | | 1,787,494 | |

| | | | | |

| |

| | | | Oil Well Services and Equipment — 0.4% | | | | |

| | 500 | | ENSCO International, Inc. | | | 24,485 | |

| | 500 | | Noble Corp. | | | 35,050 | |

| | | | | |

| |

| | | | | | | 59,535 | |

| | | | | |

| |

9

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Photography — 2.4% | | | | |

| | 8,500 | | FUJIFILM Holdings Corp. ADR | | $ | 316,115 | |

| | | | | |

| |

| | | | Railroads — 12.2% | | | | |

| | 5,850 | | Burlington Northern Santa Fe Corp. | | | 453,551 | |

| | 2,155 | | Canadian Pacific Railway Ltd. | | | 121,736 | |

| | 7,822 | | CSX Corp. | | | 279,011 | |

| | 7,164 | | Norfolk Southern Corp. | | | 376,611 | |

| | 4,388 | | Union Pacific Corp. | | | 397,684 | |

| | | | | |

| |

| | | | | | | 1,628,593 | |

| | | | | |

| |

| | | | Retail - Drugs — 3.6% | | | | |

| | 11,000 | | Walgreen Co. | | | 480,480 | |

| | | | | |

| |

| | | | Retail - Grocery — 1.2% | | | | |

| | 2,500 | | Whole Foods Market, Inc. | | | 159,600 | |

| | | | | |

| |

| | | | Retail - Specialty — 3.2% | | | | |

| | 7,904 | | Costco Wholesale Corp. | | | 421,916 | |

| | | | | |

| |

| | | | Semiconductors — 6.6% | | | | |

| | 4,935 | | Kyocera Corp. ADR | | | 443,212 | |

| | 24,950 | | STMicroelectronics N.V. NYS | | | 433,132 | |

| | | | | |

| |

| | | | | | | 876,344 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $12,342,215) | | | 12,979,612 | |

| | | | | |

| |

10

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | PAR | | | | (NOTE 2) | |

|

| | | | REPURCHASE AGREEMENTS — 3.0% | | | | |

| | $403,000 | | With Mizuho Securities, Inc. dated 10/31/06 at 5.25% to be repurchased at $403,059 on 11/1/06, collateralized by U.S. Treasury Note, 5.125% due 5/15/16, value $413,592 (Cost $403,000) | | $ | 403,000 | |

| | | | | |

| |

| | | | Total Investments — 100.3% (Cost $12,745,215) | | | 13,382,612 | |

| | | | | | | | |

| | | | Liabilities Less Other Assets — (0.3%) | | | (33,420 | ) |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 13,349,192 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| ADR | | American Depositary Receipts |

| NYS | | New York Shares |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

11

| The FBR Funds |

|

| FBR Large Cap Financial Fund |

| Management Overview |

Portfolio Manager: David Ellison

Over the recent fiscal year, how did the Fund perform?

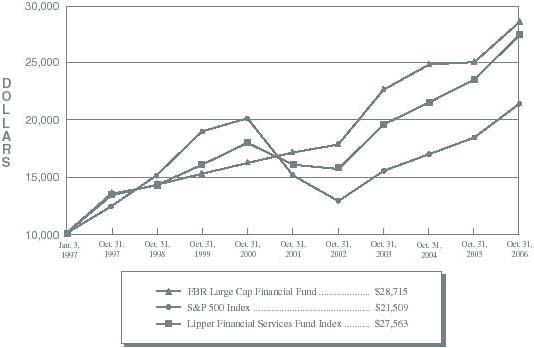

For the one-year period ended October 31, 2006, the FBR Large Cap Financial Fund appreciated 14.21%. This compares to the Lipper Financial Services Fund Index and the S&P 500 Index, which returned 16.70% and 16.34% for the same period, respectively.

What factors contributed to the Fund’s performance?

We believe that the overall positive performance of the Fund was primarily due to investor confidence in the constancy of financial institutions. Despite a difficult operating environment, industry fundamentals remained relatively stable, which led to continued strong valuations for the financial sector.

During fiscal year 2006, the Fund slightly underperformed the relevant indices. The positive performance of the financial services sector as a whole can be primarily attributed to brokerages, asset management companies and REITs. Historically, the Fund has underweighted these sub-sectors in favor of the more conventional bank and thrift business models providing less exposure to capital markets activities. In 2006, we broadened the Fund’s exposure to these sectors. The Fund lagged the financial services sector, which in turn lagged the broader market, as telecommunication services, energy, and utilities outperformed.

What is the outlook for the Fund and the financial services sector?

We believe the outlook for financial institutions is positive despite a difficult operating environment. A number of concerns surrounding the financial services industry have weighed heavily on valuations over the last couple of years. These include 1) rising short-term interest rates, 2) an inverted yield curve (the difference between long and short dated debt securities), 3) possible credit problems associated with a slow down and softening in the residential housing market, 4) pricing pressure in capital market activities, most noticeably on stock trading commission rates, 5) sluggish commercial loan demand, and finally 6) anemic merger and acquisition activity. In spite of this backdrop, we believe the financial services sector will perform well as these concerns are addressed or resolved by the management teams at each company, industry regulators and the Federal Reserve.

The Fund will continue to own financial stocks that follow low-risk business strategies and trade below average peer valuations. This strict attention to relative and absolute valuation has the intended effect of reducing the overall downside volatility associated with macro changes in the capital markets, such as the direction of interest rates and the deterioration of credit quality. It will also provide the best opportunity for solid performance over the long-term, as these companies are generally managed well and continue to deliver consistent earnings growth.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

12

| The FBR Funds |

|

| FBR Large Cap Financial Fund |

| |

| Comparison of Changes in Value of $10,000 Investment in |

| Fund Shares(1)(2) vs. Various Indices(1)(3) |

| Total Returns—For the Periods Ended October 31, 2006(4) |

| | | | | | | | | Annualized | |

| | | | | | Annualized | | Since | |

| | | One Year | | Five Year | | Inception(5) | |

| | |

| |

| |

| |

FBR Large Cap Financial Fund(1)(2) | | 14.21 | % | | 10.85 | % | | 11.33 | % | |

S&P 500 Index(1)(3) | | 16.34 | % | | 7.24 | % | | 8.10 | % | |

Lipper Financial Services Fund Index(1)(3) | | 16.70 | % | | 11.38 | % | | 10.86 | % | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher. The investment return and principal will fluctuate so that investors' shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end please call 888.200.4710 or visit www.fbrfunds.com.

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are unmanaged, do not incur expenses and are not available for investment. The performance of the indices includes reinvested dividends, and does not reflect sales charges or expenses, except for the Lipper Financial Services Fund Index which reflects fund expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to represent the broad domestic economy through changes in aggregate market value of 500 stocks representing all major industries. The Lipper Financial Services Fund Index is an equally weighted index of the largest thirty funds within the financial services fund classification as defined by Lipper Inc. The index is rebalanced quarterly. Lipper Analytical Services, Inc., is a nationally recognized organization that reports on mutual fund total return performance and calculates fund rankings. Each Lipper Average is based on a universe of funds with similar investment objectives. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | For the period January 3, 1997 (commencement of investment operations) through October 31, 2006. Certain purchases made by shareholders within this period would have been subject to an initial maximum sales charge of up to 5.50%. As a result, total returns for such shareholders would have been lower. |

13

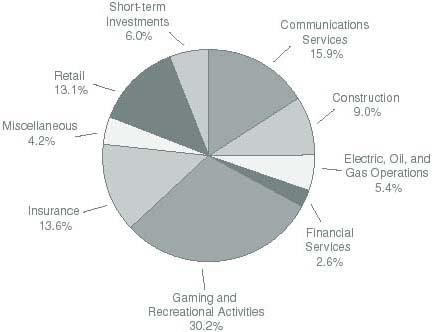

| The FBR Funds |

|

| FBR Large Cap Financial Fund |

| Portfolio Summary |

| October 31, 2006 |

The following chart provides a visual breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

14

| The FBR Funds |

|

| FBR Large Cap Financial Fund |

| Portfolio of Investments |

| October 31, 2006 |

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 98.0% | | | | |

| | | | Banks - Money Centers — 14.0% | | | | |

| | 22,000 | | Bank of America Corp. | | $ | 1,185,140 | |

| | 18,000 | | Citigroup, Inc. | | | 902,880 | |

| | 25,000 | | JP Morgan Chase & Co. | | | 1,186,000 | |

| | 7,357 | | Wachovia Corp. | | | 408,314 | |

| | | | | |

| |

| | | | | | | 3,682,334 | |

| | | | | |

| |

| | | | Banks - Regional — 21.1% | | | | |

| | 8,000 | | Capital One Financial Corp. | | | 634,640 | |

| | 17,000 | | Comerica, Inc. | | | 989,230 | |

| | 30,000 | | KeyCorp. | | | 1,114,200 | |

| | 80,000 | | Mitsubishi UFJ Financial Group, Inc. ADR | | | 1,020,000 | |

| | 27,000 | | National City Corp. | | | 1,005,750 | |

| | 10,000 | | SunTrust Banks, Inc. | | | 789,900 | |

| | | | | |

| |

| | | | | | | 5,553,720 | |

| | | | | |

| |

| | | | Consumer Financial Services — 10.9% | | | | |

| | 19,000 | | CIT Group, Inc. | | | 988,950 | |

| | 12,000 | | Fannie Mae (Federal National Mortgage) | | | 711,120 | |

| | 17,000 | | Freddie Mac (Federal Home Loan) | | | 1,172,830 | |

| | | | | |

| |

| | | | | | | 2,872,900 | |

| | | | | |

| |

| | | | Insurance - Accident and Health — 2.6% | | | | |

| | 35,000 | | UnumProvident Corp. | | | 692,300 | |

| | | | | |

| |

| | | | Insurance - Life — 13.1% | | | | |

| | 19,000 | | Genworth Financial, Inc., Class A | | | 635,360 | |

| | 8,000 | | Lincoln National Corp. | | | 506,480 | |

| | 16,000 | | MetLife, Inc. | | | 914,080 | |

| | 15,000 | | Principal Financial Group, Inc. | | | 847,350 | |

| | 7,000 | | Prudential Financial, Inc. | | | 538,510 | |

| | | | | |

| |

| | | | | | | 3,441,780 | |

| | | | | |

| |

| | | | Insurance - Property and Casualty — 8.2% | | | | |

| | 9,000 | | American International Group, Inc. | | | 604,530 | |

| | 24,000 | | CNA Financial Corp.* | | | 898,800 | |

| | 1,000 | | Everest Re Group Ltd. | | | 99,180 | |

| | 1,000 | | MBIA, Inc. | | | 62,020 | |

15

| The FBR Funds |

|

| FBR Large Cap Financial Fund |

| Portfolio of Investments (continued) |

| October 31, 2006 |

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Insurance - Property and Casualty — 8.2% (continued) | | | | |

| | 1,000 | | MGIC Investment Corp. | | $ | 58,760 | |

| | 5,000 | | The Hartford Financial Services Group, Inc. | | | 435,850 | |

| | | | | |

| |

| | | | | | | 2,159,140 | |

| | | | | |

| |

| | | | Investment Services — 23.4% | | | | |

| | 18,000 | | Ameriprise Financial, Inc. | | | 927,000 | |

| | 11,000 | | Lehman Brothers Holdings, Inc. | | | 856,240 | |

| | 11,000 | | Merrill Lynch & Company, Inc. | | | 961,620 | |

| | 16,000 | | Morgan Stanley | | | 1,222,880 | |

| | 7,000 | | The Bear Stearns Companies, Inc. | | | 1,059,450 | |

| | 6,000 | | The Goldman Sachs Group, Inc. | | | 1,138,740 | |

| | | | | |

| |

| | | | | | | 6,165,930 | |

| | | | | |

| |

| | | | Savings and Loans - Savings Banks — 4.7% | | | | |

| | 20,000 | | Astoria Financial Corp. | | | 580,200 | |

| | 20,000 | | Sovereign Bancorp, Inc. | | | 477,200 | |

| | 4,000 | | Washington Mutual, Inc. | | | 169,200 | |

| | | | | |

| |

| | | | | | | 1,226,600 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $22,090,284) | | | 25,794,704 | |

| | | | | |

| |

| | | | | | | | |

| | PAR | | | | | | |

| | | | | | |

| | | | REPURCHASE AGREEMENT — 3.6% | | | | |

| | $941,000 | | With Mizuho Securities, Inc. dated 10/31/06 at 5.25% to be repurchased at $941,137 on 11/1/06, collateralized by U.S. Treasury Note, 5.125% due 5/15/16, value $965,733 (Cost $941,000) | | | 941,000 | |

| | | | | |

| |

| | | | Total Investments — 101.6% (Cost $23,031,284) | | | 26,735,704 | |

| | | | | | | | |

| | | | Liabilities Less Other Assets — (1.6%) | | | (422,524 | ) |

| | | | | |

| |

| | | | Net Assets — 100.0% | | $ | 26,313,180 | |

| | | | | |

| |

| * | | Non-income producing security |

| ADR | | American Depositary Receipts |

| | | |

| | | |

| The accompanying notes are an integral part of the financial statements. |

| | | |

| | | 16 |

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Management Overview |

Portfolio Managers: David Ellison and Winsor Aylesworth

Over the recent fiscal year, how did the Fund perform?

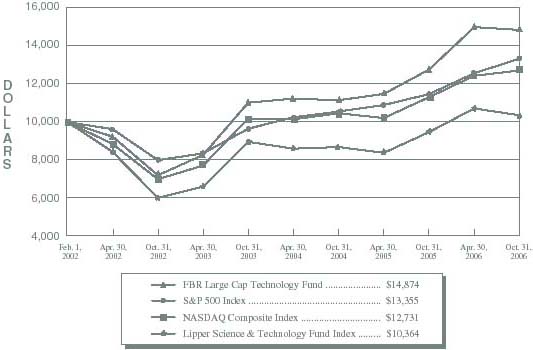

For the one-year period ended October 31, 2006, the FBR Large Cap Technology Fund appreciated 16.40%. This compares to the Lipper Science & Technology Fund Index, the S&P 500 Index, and the NASDAQ Composite Index which returned 9.43%, 16.34%, and 12.49% for the same period respectively.

What factors contributed to the Fund’s performance?

Investors enjoyed a successful year as the Fund earned double digit returns and outpaced its peer group and benchmarks over the course of our fiscal year. The Fund’s investments continue to mirror our belief that reasonably valued technology companies with minimal debt, a history of profitability and a track record of consistent growth in book value will serve us best over the long term.

The technology sector continues to act as a good surrogate for the domestic and global economy. The year is ending with generally growing economies as interest rates have stabilized and energy prices have eased throughout the world. The success of the iPod, the desirability of hi-definition televisions, the digital camera revolution and the new gaming consoles by Microsoft, Sony and Nintendo has stimulated much of the consumer demand in this sector.

What is the outlook for the Fund and the technology sector?

As we look towards 2007, the consumer will be offered newer, better, faster and cheaper technology solutions for all the things that may have caught his or her eye in 2006. As hi-definition televisions continue to proliferate, we expect to see another round of upgrades for DVD players, HD Camcorders and other peripheral products and devices.

Corporately, the new Microsoft operating system due out in early 2007 will drive new spending. As the world economies expand and interact, corporations and governments will be faced with increasingly complex challenges that can only be solved and effectively addressed by upgraded technology solutions. So, by most measures, the demand for technology should remain strong. Companies that are capable of meeting this demand and that have the capital available to invest in innovation should benefit. Of course, the markets don’t move in just one direction. Hence, we can expect the market to correct or pause over the course of the next fiscal year. By following the Fund’s proven strategy of buying large, low leveraged, growing companies at “value” prices, we are able to provide the downside protection we strive for during turbulent market conditions. Our outlook for the Fund

17

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Management Overview (continued) |

in 2007 is positive knowing we are positioned to participate in any technology rally that may occur, and that we are somewhat insulated from the downside volatility that accompanies the sector because of our strict attention to valuation.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

18

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| |

| Comparison of Changes in Value of $10,000 Investment in |

| Fund Shares(1)(2) vs. Various Indices(1)(3) |

Total Returns—For the Periods Ended October 31, 2006(4) |

| | | | | | Annualized | | |

| | | | | | Since | | |

| | | One Year | | | Inception(5) | | |

| | |

| |

| |

FBR Large Cap Technology Fund(1)(2) | | 16.40 | % | | 8.73 | % | |

S&P 500 Index(1)(3) | | 16.34 | % | | 6.28 | % | |

NASDAQ Composite Index(1)(3) | | 12.49 | % | | 5.21 | % | |

Lipper Science & Technology Fund Index(1)(3) | | 9.43 | % | | 0.76 | % | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data curernt to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are unmanaged, do not incur expenses and are not available for investment. The performance of the indices includes reinvested dividends, and does not reflect sales charges or expenses, except for the Lipper Science & Technology Fund Index which reflects fund expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to represent the broad domestic economy through changes in aggregate market value of 500 stocks representing all major industries. The NASDAQ Composite Index is a broad-based capitalization-weighted index of all NASDAQ National Market and Small Cap stocks. The Lipper Technology & Science Fund Index is an equally weighted index of the largest thirty funds within the science and technology fund classification as defined by Lipper Inc. The index is rebalanced quarterly. Lipper Analytical Services, Inc., is a nationally recognized organization that reports on mutual fund total return performance and calculates fund rankings. Each Lipper Average is based on a universe of funds with similar investment objectives. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | For the period February 1, 2002 (commencement of investment operations) through October 31, 2006. |

19

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Portfolio Summary |

| October 31, 2006 |

The following chart provides a visual breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

20

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Portfolio of Investments |

| October 31, 2006 |

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | COMMON STOCKS — 81.8% | | | | |

| | | | Audio and Video Equipment — 2.4% | | | | |

| | 23,000 | | Sony Corp. ADR | | $ | 942,540 | |

| | | | | |

| |

| | | | Biotechnology and Drugs — 11.7% | | | | |

| | 6,375 | | ALTANA AG ADR | | | 355,406 | |

| | 2,600 | | AmerisourceBergen Corp. | | | 122,720 | |

| | 7,700 | | Biogen Idec, Inc.* | | | 366,520 | |

| | 15,800 | | Merck & Company, Inc. | | | 717,636 | |

| | 18,405 | | Novartis AG ADR | | | 1,117,736 | |

| | 65,175 | | Schering-Plough Corp. | | | 1,442,974 | |

| | 13,900 | | Serono S.A. ADR | | | 302,881 | |

| | 7,000 | | Watson Pharmaceuticals, Inc.* | | | 188,370 | |

| | | | | |

| |

| | | | | | | 4,614,243 | |

| | | | | |

| |

| | | | Business Services — 0.8% | | | | |

| | 3,600 | | International Business Machines Corp. | | | 332,388 | |

| | | | | |

| |

| | | | Capital Goods - Miscellaneous — 1.3% | | | | |

| | 4,000 | | Cummins, Inc. | | | 507,920 | |

| | | | | |

| |

| | | | Communications Equipment — 8.5% | | | | |

| | 10,150 | | Comverse Technology, Inc.* | | | 220,966 | |

| | 4,500 | | Garmin Ltd. | | | 240,345 | |

| | 28,167 | | LM Ericsson Telephone Co. ADR | | | 1,065,276 | |

| | 68,500 | | Motorola, Inc. | | | 1,579,609 | |

| | 24,700 | | Tellabs, Inc.* | | | 260,338 | |

| | | | | |

| |

| | | | | | | 3,366,534 | |

| | | | | |

| |

| | | | Communications Services — 3.8% | | | | |

| | 43,325 | | AT&T, Inc. | | | 1,483,881 | |

| | | | | |

| |

| | | | Computer Hardware — 0.4% | | | | |

| | 2,000 | | Apple Computer, Inc.* | | | 162,160 | |

| | | | | |

| |

| | | | Computer Peripherals — 4.5% | | | | |

| | 29,675 | | Canon, Inc. ADR | | | 1,584,348 | |

| | 5,000 | | Hewlett-Packard Co. | | | 193,700 | |

| | | | | |

| |

| | | | | | | 1,778,048 | |

| | | | | |

| |

21

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Portfolio of Investments (continued) |

| October 31, 2006 |

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Computer Services — 2.2% | | | | |

| | 9,800 | | Computer Sciences Corp.* | | $ | 517,930 | |

| | 8,500 | | NCR Corp.* | | | 352,920 | |

| | | | | |

| |

| | | | | | | 870,850 | |

| | | | | |

| |

| | | | Computer Storage Devices — 2.7% | | | | |

| | 17,575 | | EMC Corp.* | | | 215,294 | |

| | 13,200 | | SanDisk Corp.* | | | 634,920 | |

| | 9,500 | | Seagate Technology | | | 214,510 | |

| | | | | |

| |

| | | | | | | 1,064,724 | |

| | | | | |

| |

| | | | Electronic Instruments and Controls — 6.4% | | | | |

| | 7,500 | | Agilent Technologies, Inc.* | | | 267,000 | |

| | 12,425 | | American Power Conversion Corp. | | | 375,608 | |

| | 5,400 | | Arrow Electronics, Inc.* | | | 161,190 | |

| | 35,265 | | AU Optronics Corp. ADR | | | 478,899 | |

| | 9,375 | | Jabil Circuit, Inc. | | | 269,156 | |

| | 9,600 | | Molex, Inc. | | | 335,040 | |

| | 8,025 | | TDK Corp. ADR | | | 627,555 | |

| | | | | |

| |

| | | | | | | 2,514,448 | |

| | | | | |

| |

| | | | Office Equipment — 0.9% | | | | |

| | 20,000 | | Xerox Corp.* | | | 340,000 | |

| | | | | |

| |

| | | | Personal and Household Products — 2.2% | | | | |

| | 17,375 | | McKesson Corp. | | | 870,314 | |

| | | | | |

| |

| | | | Photography — 1.2% | | | | |

| | 12,390 | | FUJIFILM Holdings Corp. ADR | | | 460,784 | |

| | | | | |

| |

| | | | Retail - Catalog and Mail Order — 0.7% | | | | |

| | 4,100 | | CDW Corp. | | | 269,247 | |

| | | | | |

| |

| | | | Semiconductors — 31.1% | | | | |

| | 8,950 | | Advanced Micro Devices, Inc.* | | | 190,367 | |

| | 8,000 | | Analog Devices, Inc. | | | 254,560 | |

| | 31,950 | | Applied Materials, Inc. | | | 555,611 | |

| | 40,400 | | Flextronics International Ltd.* | | | 468,640 | |

| | 11,442 | | Freescale Semiconductor, Inc., Class B* | | | 450,014 | |

22

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Portfolio of Investments (continued) |

| October 31, 2006 |

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Semiconductors — 31.1% (continued) | | | | |

| | 48,100 | | Infineon Technologies AG ADR* | | $ | 584,896 | |

| | 51,800 | | Intel Corp. | | | 1,105,412 | |

| | 9,500 | | Intersil Corp. | | | 222,775 | |

| | 11,775 | | KLA-Tencor Corp. | | | 578,977 | |

| | 11,800 | | Kyocera Corp. ADR | | | 1,059,758 | |

| | 8,600 | | Lam Research Corp.* | | | 425,270 | |

| | 11,700 | | Marvell Technology Group Ltd.* | | | 213,876 | |

| | 17,900 | | Maxim Integrated Products, Inc. | | | 537,179 | |

| | 11,200 | | Microchip Technology, Inc. | | | 368,816 | |

| | 40,650 | | Micron Technology, Inc.* | | | 587,393 | |

| | 16,875 | | National Semiconductor Corp. | | | 409,894 | |

| | 8,700 | | Novellus Systems, Inc.* | | | 240,555 | |

| | 53,000 | | STMicroelectronics N.V. NYS | | | 920,080 | |

| | 114,004 | | Taiwan Semiconductor Manufacturing Company Ltd. ADR | | | 1,105,838 | |

| | 52,800 | | Texas Instruments, Inc. | | | 1,593,503 | |

| | 16,900 | | Xilinx, Inc. | | | 431,119 | |

| | | | | |

| |

| | | | | | | 12,304,533 | |

| | | | | |

| |

| | | | Software and Programming — 1.0% | | | | |

| | 10,500 | | Check Point Software Technologies Ltd.* | | | 217,560 | |

| | 5,800 | | Microsoft Corp. | | | 166,518 | |

| | | | | |

| |

| | | | | | | 384,078 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $30,120,170) | | | 32,266,692 | |

| | | | | |

| |

| | | | | | | | |

| | | | EXCHANGE TRADED FUNDS — 3.0% | | | | |

| | 16,000 | | PowerShares Dynamic Biotechnology & Genome Portfolio* | | | 296,800 | |

| | 16,000 | | streetTRACKS® Morgan Stanley Technology ETF | | | 880,160 | |

| | | | | |

| |

| | | | Total Exchange Traded Funds (Cost $1,087,973) | | | 1,176,960 | |

| | | | | |

| |

23

| The FBR Funds |

|

| FBR Large Cap Technology Fund |

| Portfolio of Investments (continued) |

| October 31, 2006 |

|

| | | | | | VALUE | |

| | PAR | | | | (NOTE 2) | |

|

| | | | REPURCHASE AGREEMENT — 18.9% | | | | |

| $ | 7,440,000 | | With Mizuho Securities, Inc. dated 10/31/06 at 5.25% to be repurchased at $7,441,085 on 11/1/06, collateralized by U.S. Treasury Note, 5.125% due 5/15/16, value $7,635,552 (Cost $7,440,000) | | $ | 7,440,000 | |

| | | | | |

| |

| | | | Total Investments — 103.7% (Cost $38,648,143) | | | 40,883,652 | |

| | | | | | | | |

| | | | Liabilities Less Other Assets — (3.7%) | | | (1,476,359 | ) |

| | | | | |

| |

| | | | Net Assets — 100.0% | | $ | 39,407,293 | |

| | | | | |

| |

| * | | Non-income producing security |

| ADR | | American Depositary Receipts |

| NYS | | New York Shares |

| | | |

| | | |

| | | |

| The accompanying notes are an integral part of the financial statements. |

| | | |

| | | 24 |

The FBR Funds

FBR Small Cap Fund

Management Overview

Investment Sub Adviser: Akre Capital Management, LLC

Portfolio Manager: Charles T. Akre, Jr.

As I write this 2006 year end report, I have the occasion to think about it in terms of our nearly ten years of operation. Our achievement has been significant. We have compounded shareholders capital (per share) at an annual rate of 17.50% from inception1 through November 30, 2006. This of course is in no way predictive of future results, but is significant because of a) its very high absolute rate, and b) the Fund’s return relative to many different indices. For example, during the same time period, the S&P 500 Index (“S&P”) compounded at 8.34%, the Russell 2000 Index at 9.56%, and the Lipper Small Cap Growth Index at 9.56%.

The FBR Small Cap Fund returned 24.53%, 20.83% and 17.15% for the one-year, five-years and since inception time periods ended October 31, 2006, respectively2.

Recently, the financial media has compared fund managers based on the number of years they “beat” the S&P. The case of Bill Miller at Legg Mason is the most notable. When I examined what their compound annual returns had been, I found it significantly below our returns. By way of comparison during our first four calendar years of operation, we provided investors with returns that lagged the S&P twice, and over our entire nine year history, we bested the S&P merely six years.

The focus on beating the market on a calendar basis is, I believe, both misleading and wrong focused. My question is “Which would you rather have over the course of nearly ten years? A 17+% average annual return or a low teens annual return where the Fund has “beat” the S&P for a long string of consecutive years?”

For me the answer is obvious both on its face and because I understand well the level of risk undertaken in achieving our results.

In all of the nine prior years’ reports to shareholders, I have spent some time sharing with you our investment process and style. Briefly, we look for high returns on capital businesses, run by honest, diligent and fair managers, where an opportunity exists to reinvest excess profits to continue to earn above average returns on capital. When we find one of these, we describe it as our “little compounding machines.”

We then add that we are unwilling to pay very much for these opportunities, which is our way of saying that valuation at purchase is very important.

|

| 1 | The FBR Small Cap Fund commenced operations on January 3, 1997 |

| |

| 2 | Past Performance is No Guarantee of Future Results. The current performance may be lower or higher than performance data quoted. To obtain performance data current to the most recent month-end please call 888.200.4710 or visit www.fbrfunds.com. Investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. |

25

The FBR Funds

FBR Small Cap Fund

Management Overview (continued)

On average, the outcome of our process has produced investments with more growth, higher returns on capital, more often than not stronger balance sheets and lower valuations, than the overall “market”.

We believe it is intuitive that with these characteristics our returns are more likely to be above market (on average) with below market levels of risk.

This in essence is our risk profile. When we identify these outstanding businesses we want to own lots of them, and accordingly our portfolio doesn’t resemble the run of the mill mutual fund with 50 or 100 separate holdings. You can expect it never will.

I read in academic studies that fully 90% of the value added by diversification is achieved with only nine holdings. We are very comfortable with our process and say again, “examine the results.”

It has been traditional to comment on the market outlook in general and small-cap stocks in particular. As we have shared with you in the past, we have no-clue where the market is headed, or how small-cap stocks will perform in the coming year. You can be certain that we will remain true to the process which has caused the over nine years of results we spoke of at the outset.

Several months ago the Trustees of the Fund asked us if we would consider reopening the Fund. Our response then was that we believe we are likely to have some opportunities in the next year or two, and therefore agree that reopening the Fund makes sense. This remains our view today.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

26

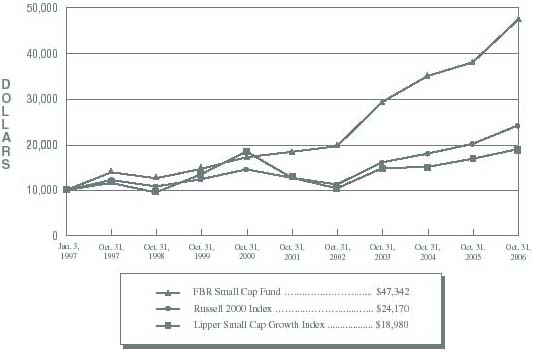

The FBR Funds

FBR Small Cap Fund

Comparison of Changes in Value of $10,000 Investment in

Fund Shares(1)(2) vs. Various Indices(1)(3)

| | Total Returns—For the Periods Ended October 31, 2006(4) | |

| | | | | | | | | | | | Annualized | |

| | | | | | | | Annualized | | Since | |

| | | | One Year | | Five Year | | Inception(5) | |

| | | |

| |

| |

| |

| | FBR Small Cap Fund(1)(2) | | | 24.53 | % | | | 20.83 | % | | | 17.15 | % | |

| | Russell 2000 Index(1)(3) | | | 19.98 | % | | | 13.75 | % | | | 9.39 | % | |

| | Lipper Small Cap Growth Index(1)(3) | | | 12.57 | % | | | 8.36 | % | | | 6.73 | % | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are umanaged, do not incur expenses and are not available for investment. The performance of the indices includes reinvested dividends, and does not reflect sales charges or expenses, except for the Lipper Small Cap Growth Fund Index which reflects fund expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | Russell 2000 Index is comprised of the smallest of the 2000 companies of the Russell 3000 Index, representing approximately 8% of the Russell 3000’s total market-capitalization. The Lipper Small Cap Growth Fund Index is an equally weighted index of the largest thirty funds within the small-cap fund classification as defined by Lipper Inc. The index is rebalanced quarterly. Lipper Analytical Services, Inc., is a nationally recognized organization that reports on mutual fund total return performance and calculates fund rankings. Each Lipper Average is based on a universe of funds with similar investment objectives. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | For the period January 3, 1997 (commencement of investment operations) through October 31, 2006. Certain purchases made by shareholders within this period would have been subject to an initial maximum sales charge of up to 5.50%. As a result, total returns for such shareholders would have been lower. |

27

The FBR Funds

FBR Small Cap Fund

Portfolio Summary

October 31, 2006

The following chart provides a visual breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

28

The FBR Funds

FBR Small Cap Fund

Portfolio of Investments

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | COMMON STOCKS — 93.6% | | | | |

| | | | Banks - Regional — 0.1% | | | | |

| | 50,000 | | Bancshares of Florida, Inc.* | | $ | 1,044,500 | |

| | | | | |

| |

| | | | | | | | |

| | | | Biotechnology and Drugs — 0.4% | | | | |

| | 228,100 | | Bradley Pharmaceuticals, Inc.* | | | 3,968,940 | |

| | | | | |

| |

| | | | | | | | |

| | | | Casinos and Gaming — 29.5% | | | | |

| | 1,600,000 | | Bally Technologies, Inc.* | | | 31,760,000 | |

| | 42,822 | | Florida Gaming Corp.* | | | 541,698 | |

| | 20,000 | | International Game Technology | | | 850,200 | |

| | 212,300 | | Isle of Capri Casinos, Inc.* | | | 5,328,730 | |

| | 992,000 | | Monarch Casino & Resort, Inc.*† | | | 22,002,560 | |

| | 4,100,000 | | Penn National Gaming, Inc.* | | | 149,937,001 | |

| | 1,471,407 | | Pinnacle Entertainment, Inc.* | | | 44,524,776 | |

| | 157,500 | | Shuffle Master, Inc.* | | | 4,406,850 | |

| | 234,861 | | Station Casinos, Inc. | | | 14,162,118 | |

| | | | | |

| |

| | | | | | | 273,513,933 | |

| | | | | |

| |

| | | | | | | | |

| | | | Communications Services — 15.9% | | | | |

| | 4,107,256 | | American Tower Corp., Class A* | | | 147,943,361 | |

| | | | | |

| |

| | | | | | | | |

| | | | Construction - Supplies and Fixtures — 5.7% | | | | |

| | 730,850 | | American Woodmark Corp. | | | 27,034,142 | |

| | 902,300 | | Simpson Manufacturing Company, Inc. | | | 25,616,297 | |

| | | | | |

| |

| | | | | | | 52,650,439 | |

| | | | | |

| |

| | | | Construction Services — 3.3% | | | | |

| | 566,666 | | D.R. Horton, Inc. | | | 13,276,984 | |

| | 600,000 | | Toll Brothers, Inc.* | | | 17,346,000 | |

| | | | | |

| |

| | | | | | | 30,622,984 | |

| | | | | |

| |

| | | | Consumer Financial Services — 2.5% | | | | |

| | 873,000 | | AmeriCredit Corp.* | | | 22,322,610 | |

| | 28,200 | | White River Capital, Inc.* | | | 517,470 | |

| | | | | |

| |

| | | | | | | 22,840,080 | |

| | | | | |

| |

| | | | Electric Utilities — 2.4% | | | | |

| | 1,000,000 | | The AES Corp.* | | | 21,990,000 | |

| | | | | |

| |

29

The FBR Funds

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | Insurance - Miscellaneous — 1.8% | | | | |

| | 50,000 | | Brown & Brown, Inc. | | $ | 1,463,000 | |

| | 393,500 | | Hilb Rogal and Hobbs Co. | | | 15,708,520 | |

| | | | | |

| |

| | | | | | | 17,171,520 | |

| | | | | |

| |

| | | | Insurance - Property and Casualty — 11.3% | | | | |

| | 80 | | Berkshire Hathaway, Inc., Class B* | | | 281,200 | |

| | 61,000 | | Investors Title Co. | | | 3,127,165 | |

| | 255,400 | | Markel Corp.* | | | 102,032,300 | |

| | | | | |

| |

| | | | | | | 105,440,665 | |

| | | | | |

| |

| | | | Office Equipment — 2.5% | | | | |

| | 1,085,400 | | Global Imaging Systems, Inc.* | | | 23,629,158 | |

| | | | | |

| |

| | | | | | | | |

| | | | Oil and Gas Operations — 3.0% | | | | |

| | 397,890 | | MarkWest Hydrocarbon, Inc. | | | 13,062,729 | |

| | 211,800 | | Penn Virginia Corp. | | | 15,154,290 | |

| | | | | |

| |

| | | | | | | 28,217,019 | |

| | | | | |

| |

| | | | Recreational Activities — 0.8% | | | | |

| | 603,800 | | Dover Motorsports, Inc. | | | 3,188,064 | |

| | 60,000 | | International Speedway Corp., Class A | | | 3,114,600 | |

| | 19,000 | | International Speedway Corp., Class B | | | 986,100 | |

| | | | | |

| |

| | | | | | | 7,288,764 | |

| | | | | |

| |

| | | | Retail - Specialty — 13.1% | | | | |

| | 3,445,336 | | 99 Cents Only Stores* | | | 41,309,579 | |

| | 107,900 | | Big 5 Sporting Goods Corp. | | | 2,593,916 | |

| | 1,500,000 | | CarMax, Inc.* | | | 66,450,000 | |

| | 356,508 | | O’Reilly Automotive, Inc.* | | | 11,511,643 | |

| | | | | |

| |

| | | | | | | 121,865,138 | |

| | | | | |

| |

| | | | Software and Programming — 0.2% | | | | |

| | 32,000 | | MICROS Systems, Inc.* | | | 1,589,760 | |

| | | | | |

| |

| | | | | | | | |

| | | | Transportation Services — 1.1% | | | | |

| | 464,997 | | Dynamex, Inc.* | | | 9,853,286 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $476,369,650) | | | 869,629,547 | |

| | | | | |

| |

30

The FBR Funds

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE | |

| | SHARES | | | | (NOTE 2) | |

|

| | | | PREFERRED STOCK — 0.5% | | | | |

| | | | Insurance - Life — 0.5% | | | | |

| | 200,000 | | ING Groep N.V., 6.125% (Cost $5,000,000) | | $ | 4,996,000 | |

| | | | | |

| |

| | | | | | | | |

| PAR | | | | | | |

| | | | | | |

| | | | REPURCHASE AGREEMENT — 6.0% | | | | |

| $ | 56,217,000 | | With Mizuho Securities, Inc. dated 10/31/06 at 5.25% to be repurchased at $56,225,198 on 11/1/06, collateralized by U.S. Treasury Note, 5.125% due 5/15/16, value $57,694,597 (Cost $56,217,000) | | | 56,217,000 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Investments — 100.1% (Cost $537,586,650) | | | 930,842,547 | |

| | | | | | | | |

| | | | Liabilities Less Other Assets — (0.1%) | | | (1,252,417 | ) |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 929,590,130 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| † | | Affiliated issuer as defined in the Investment Company Act of 1940 (ownership of at least 5% of the outstanding voting securities of an issuer) |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

31

The FBR Funds

FBR Small Cap Financial Fund

Management Overview

Portfolio Manager: David Ellison

Over the recent fiscal year, how did the Fund perform?

For the one-year period ended October 31, 2006, the FBR Small Cap Financial Fund appreciated 11.81%. This compares to the Lipper Financial Services Fund Index and the Russell 2000 Index, which returned 16.70% and 19.98% for the same period respectively.

What factors contributed to the Fund’s performance?

We believe that the overall positive performance of the Fund was primarily due to investor confidence in the constancy of financial institutions. Despite a difficult operating environment, industry fundamentals remained relatively stable, which led to continued strong valuations for the financial sector.

During fiscal year 2006, the Fund underperformed the relevant indices. The positive performance of the financial services sector as a whole can be primarily attributed to brokerages, asset management companies and REITs. Although less than in fiscal year 2005, the Fund was underweight in these sub-sectors in fiscal year 2006 in favor of the traditional small-cap banking business model. This was a major reason why the Fund lagged its financial services peer group, which in turn lagged the broader market, as telecommunication services, energy, and utilities outperformed.

The environment was characterized by a further flattening and eventual inversion of the yield curve, the unraveling of an inflated housing market, and doubts about the ability of the consumer to meet debt obligations. Certain fundamentals held up better than expected, illustrated by: stable asset quality, lower yet still positive core deposit and loan growth, and only slightly lower returns on average assets and average equity. However, the inverted yield curve placed downward pressure on the net interest incomes of small banks, resulting in decreasing sequential earnings per share (“EPS”) growth. The rise in short-term interest rates also increased liability costs, while the lack of similar increases in yielding assets strained lending profit margins. Small financial companies typically generate the bulk of their profits from their loans, while their larger counterparts have more diversified profit sources, including brokerage, trading, money management and investment banking.

What is the outlook for the Fund and the financial services sector?

Despite the current difficult operating environment, we believe the outlook for small-cap financial services companies is positive as industry fundamentals remain favorable. While there continues to be near-term pressure on profits, we expect these will abate and more normalized EPS growth rates will return. We believe that negative trends in interest rates have been the primary contributor to slower EPS growth over the last year. When this negative trend slows or reverses, EPS growth will improve and stock prices should follow. Finally, acquisition activity, which has been below historical levels, could also increase, resulting in a noticeable benefit to smaller banks and thrifts.

32

The FBR Funds

FBR Small Cap Financial Fund

Management Overview (continued)

We will continue to concentrate the Fund’s assets in small-cap financial companies that have a history of effective capital management, adhere to low-risk business strategies, and trade at below average valuations. This strategy has the intended effect of reducing the downside risk associated with investing in the financial sector over the long-term.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

33

The FBR Funds

FBR Small Cap Financial Fund

Comparison of Changes in Value of $10,000 Investment in

Fund Shares(1)(2) vs. Various Indices(1)(3)

| | Total Returns—For the Periods Ended October 31, 2006(4) | |

| | | | | | | | | | | | Annualized | |

| | | | | | | | Annualized | | Since | |

| | | | One Year | | Five Year | | Inception(5) | |

| | | |

| |

| |

| |

| | FBR Small Cap Financial Fund(1)(2) | | | 11.81 | % | | | 17.39 | % | | | 16.36 | % | |

| | Russell 2000 Index(1)(3) | | | 19.98 | % | | | 13.75 | % | | | 9.39 | % | |

| | Lipper Financial Services Fund Index(1)(3) | | | 16.70 | % | | | 11.38 | % | | | 10.86 | % | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are unmanaged, do not incur expenses and are not available for investment. The performance of the indices includes reinvested dividends, and does not reflect sales charges or expenses, except for the Lipper Financial Services Fund Index which reflects fund expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | Russell 2000 Index is comprised of the smallest of the 2000 companies of the Russell 3000 Index, representing approximately 8% of the Russell 3000’s total market-capitalization. The Lipper Financial Services Fund index is an equally weighted index of the largest thirty funds within the financial services fund classification as defined by Lipper Inc. The index is rebalanced quarterly. Lipper Analytical Services, Inc., is a nationally recognized organization that reports on mutual fund total return performance and calculates fund rankings. Each Lipper Average is based on a universe of funds with similar investment objectives. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | For the period January 3, 1997 (commencement of investment operations) through October 31, 2006. Certain purchases made by shareholders within this period would have been subject to an initial maximum sales charge of up to 5.50%. As a result, total returns for such shareholders would have been lower. |

34

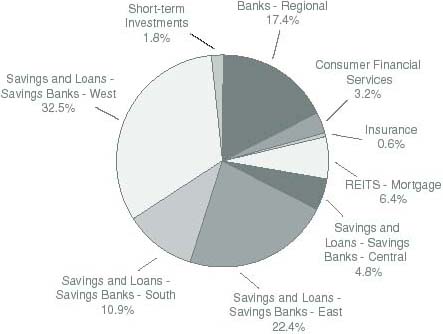

The FBR Funds

FBR Small Cap Financial Fund

Portfolio Summary

October 31, 2006

The following chart provides a visual breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

35

The FBR Funds

FBR Small Cap Financial Fund

Portfolio of Investments

October 31, 2006

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 98.2% | | | |

| | | | Banks - Regional — 17.4% | | | |

| | 183,113 | | Bancorp Rhode Island, Inc. | | $ | 7,813,432 |

| | 662,895 | | Bank Mutual Corp. | | | 8,034,287 |

| | 234,328 | | Banner Corp. | | | 10,183,895 |

| | 35,000 | | Beverly National Corp. | | | 822,500 |

| | 42,727 | | Greenville First Bancshares, Inc.* | | | 894,703 |

| | 235,770 | | ITLA Capital Corp. | | | 13,467,183 |

| | 70,000 | | Patriot National Bancorp, Inc. | | | 1,722,000 |

| | 303,123 | | Taylor Capital Group, Inc. | | | 10,563,837 |

| | 169,118 | | Yardville National Bancorp | | | 6,741,043 |

| | | | | |

|

| | | | | | | 60,242,880 |

| | | | | |

|

| | | | Consumer Financial Services — 3.2% | | | |

| | 61,569 | | Advanta Corp., Class B | | | 2,415,968 |

| | 125,000 | | AmeriCredit Corp.* | | | 3,196,250 |

| | 162,391 | | ASTA Funding, Inc. | | | 5,527,789 |

| | | | | |

|

| | | | | | | 11,140,007 |

| | | | | |

|

| | | | Insurance - Life — 0.4% | | | |

| | 27,000 | | Stancorp Financial Group, Inc. | | | 1,233,630 |

| | | | | |

|

| | | | | | | |

| | | | Insurance - Property and Casualty — 0.2% | | | |

| | 50,000 | | Affirmative Insurance Holdings, Inc. | | | 830,500 |

| | | | | |

|

| | | | | | | |

| | | | REITs - Mortgage — 6.4% | | | |

| | 10,000 | | Affordable Residential Communities, Inc.* | | | 109,800 |

| | 280,000 | | Annaly Mortgage Management, Inc. | | | 3,673,600 |

| | 295,000 | | Anworth Mortgage Asset Corp. | | | 2,678,600 |

| | 65,000 | | Impac Mortgage Holdings, Inc. | | | 615,550 |

| | 30,000 | | KKR Financial Corp. | | | 804,900 |

| | 275,600 | | Luminent Mortgage Capital, Inc. | | | 2,924,116 |

| | 440,000 | | MFA Mortgage Investments, Inc. | | | 3,484,800 |

| | 25,000 | | New Century Financial Corp. | | | 984,500 |

| | 28,650 | | New York Mortgage Trust, Inc. | | | 110,876 |

| | 133,800 | | Opteum, Inc., Class A | | | 1,109,202 |

| | 225,000 | | Thornburg Mortgage, Inc. | | | 5,778,000 |

| | | | | |

|

| | | | | | | 22,273,944 |

| | | | | |

|

36

The FBR Funds

FBR Small Cap Financial Fund

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Savings and Loans - Savings Banks - Central — 4.8% | | | |

| | 86,000 | | Capitol Federal Financial | | $ | 3,259,400 |

| | 125,000 | | Flagstar Bancorp, Inc. | | | 1,878,750 |

| | 101,698 | | HMN Financial, Inc. | | | 3,395,696 |

| | 184,679 | | MAF Bancorp, Inc. | | | 7,957,818 |

| | | | | |

|

| | | | | | | 16,491,664 |

| | | | | |

|

| | | | Savings and Loans - Savings Banks - East — 22.4% | | | |

| | 566,497 | | Dime Community Bancshares, Inc. | | | 7,902,633 |

| | 172,461 | | Flushing Financial Corp. | | | 3,033,589 |

| | 30,740 | | Harleysville Savings Financial Corp. | | | 537,950 |

| | 99,308 | | Hingham Institution for Savings | | | 3,600,412 |

| | 2,213,156 | | Hudson City Bancorp, Inc. | | | 30,386,632 |

| | 105,000 | | Investors Bancorp, Inc.* | | | 1,562,400 |

| | 106,745 | | MASSBANK Corp. | | | 3,558,878 |

| | 271,675 | | Parkvale Financial Corp. | | | 9,101,113 |

| | 130,439 | | PennFed Financial Services, Inc. | | | 2,394,860 |

| | 158,250 | | People’s Bank | | | 6,440,775 |

| | 36,000 | | Provident Financial Services, Inc. | | | 660,240 |

| | 78,688 | | TF Financial Corp. | | | 2,536,901 |

| | 91,748 | | WSFS Financial Corp. | | | 5,912,241 |

| | | | | |

|

| | | | | | | 77,628,624 |

| | | | | |

|

| | | | Savings and Loans - Savings Banks - South — 10.9% | | | |

| | 960,163 | | BankUnited Financial Corp., Class A | | | 25,895,596 |

| | 578,693 | | Franklin Bank Corp.* | | | 11,695,386 |

| | | | | |

|

| | | | | | | 37,590,982 |

| | | | | |

|

| | | | Savings and Loans - Savings Banks - West — 32.5% | | | |

| | 72,000 | | Beverly Hills Bancorp, Inc. | | | 604,080 |

| | 325,900 | | Downey Financial Corp. | | | 22,447,992 |

| | 470,000 | | FirstFed Financial Corp.* | | | 29,031,899 |

| | 80,335 | | Harrington West Financial Group, Inc. | | | 1,364,088 |

| | 270,471 | | Pacific Premier Bancorp, Inc.* † | | | 3,286,223 |

| | 311,100 | | PFF Bancorp, Inc. | | | 9,647,211 |

| | 596,000 | | Sterling Financial Corp. | | | 19,822,960 |

| | 1,124,734 | | Washington Federal, Inc. | | | 26,138,818 |

| | | | | |

|

| | | | | | | 112,343,271 |

| | | | | |

|

| | | | Total Common Stocks (Cost $252,066,057) | | | 339,775,502 |

| | | | | |

|

37

The FBR Funds

FBR Small Cap Financial Fund

Portfolio of Investments (continued)

October 31, 2006

|

| | | | | | VALUE |

| PAR | | | | (NOTE 2) |

|

| | | | REPURCHASE AGREEMENT — 1.8% | | | |

| $ | 6,367,000 | | With Mizuho Securities, Inc. dated 10/31/06 at 5.25% to be repurchased at $6,367,929 on 11/1/06, collateralized by U.S. Treasury Note, 5.125% due 5/15/16, value $6,534,349 (Cost $6,367,000) | | $ | 6,367,000 |

| | | | | |

|

| | | | | | | |

| | | | Total Investments — 100.0% (Cost $258,433,057) | | | 346,142,502 |

| | | | | | | |

| | | | Other Assets Less Liabilities — N.M. | | | 12,244 |

| | | | | |

|

| | | | | | | |

| | | | Net Assets — 100.0% | | $ | 346,154,746 |

| | | | | |

|

|

| * | | Non-income producing security |

| † | | Affiliated issuer as defined in the Investment Company Act of 1940 (ownership of at least 5% of the outstanding voting securities of an issuer) |

| N.M. | | Not meaningful |

The accompanying notes are an integral part of the financial statements.

38

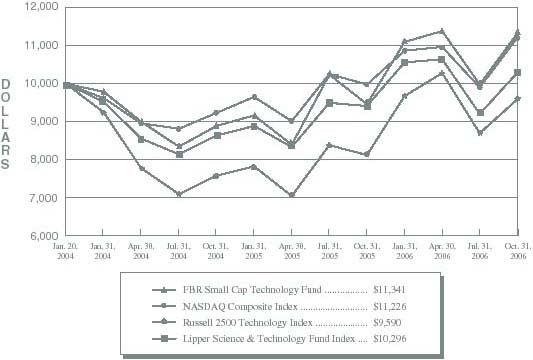

The FBR Funds

FBR Small Cap Technology Fund

Management Overview

Portfolio Manager: Robert C. Barringer, CFA

Over the recent fiscal year, how did the Fund perform?

For the one-year period ended October 31, 2006, the FBR Small Cap Technology Fund appreciated 19.87%. This compares to the Lipper Science & Technology Fund Index, the NASDAQ Composite Index, and the Russell 2500 Technology Index which returned 9.43%, 12.49%, and 18.28% for the same period, respectively.

What factors contributed to the Fund’s performance?

The Fund performed well this year, particularly relative to the Lipper Science & Technology Fund Index and the NASDAQ Composite Index. In a reversal of the trend from the previous year, small-cap technology stocks outperformed their larger peers, just as small-caps outperformed their large-cap peers in the overall market. We believe the small-cap indices performed better in the face of a rising short-term interest rate environment because most investors are anticipating a relatively soft landing for the economy and a possible rate cut by the Federal Reserve.

Over the course of the fiscal year, our investment process identified the semiconductor sector, more specifically the semi-cap equipment manufacturing group, as reaching near peak valuations. As a result, we captured some of the gains and decreased our overall exposure to the sector. The same disciplined process led us to overweight the software and programming sector, where we were able to purchase companies with terrific business models that have virtually no debt, and generate high levels of free cash flow at very attractive valuations.

What is the outlook for the Fund and the technology sector?

The outlook for the sector remains bright as consumers and corporations continue to adopt the use of technology solutions across all areas of life. We believe this trend will continue to drive demand for the foreseeable future. Technology spending is increasingly a business necessity, and failure to stay on the leading edge can create competitive disadvantages. Corporate spending on technology should remain robust as healthy balance sheets with ample cash and operational earnings are invested to support business models.