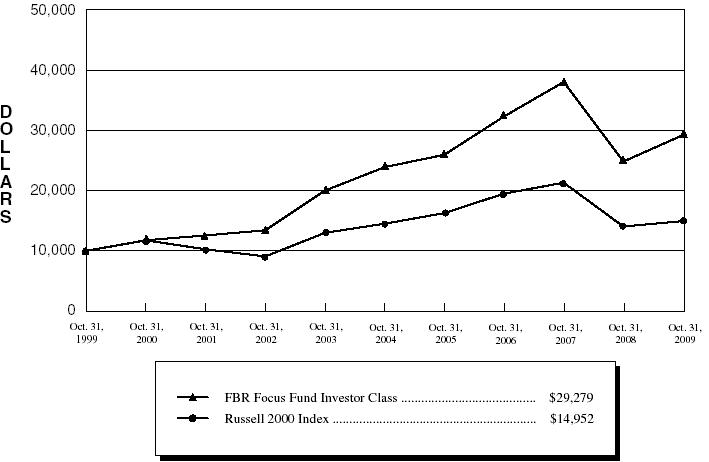

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| |

| Investment Company Act file number 811-21503 |

| |

| The FBR Funds |

|

| (Exact name of registrant as specified in charter) |

| |

| 1001 Nineteenth Street North |

| Arlington, VA 22209 |

|

| (Address of principal executive offices) (Zip code) |

| |

| Registrant’s telephone number, including area code: 703.469.1040 |

| |

| |

| William Ginivan |

| General Counsel |

| FBR Capital Markets, Inc. |

| Potomac Tower |

| 1001 Nineteenth Street North |

| Arlington, VA 22209 |

|

| (Name and address of agent for service) |

| |

| |

| Date of fiscal year end: October 31, 2009 |

| |

| Date of reporting period: October 31, 2009 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORT TO SHAREHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17CRF 270.30e-1).

THE FBR FUNDS

FBR Pegasus FundTM

FBR Pegasus Mid Cap FundTM

FBR Pegasus Small Cap FundTM

FBR Pegasus Small Cap Growth FundTM

FBR Focus Fund

FBR Large Cap Financial Fund

FBR Small Cap Financial Fund

FBR Technology Fund

FBR Gas Utility Index Fund

Annual Report

October 31, 2009

[THIS PAGE INTENTIONALLY LEFT BLANK]

The FBR Funds

Annual Letter to Shareholders

Dear Shareholder,

We are pleased to present The FBR Funds’ Annual Report for the twelve-month period ended October 31, 2009.

As we have outlined in previous communications, for each of our actively managed mutual funds our objective is to strive for downside protection in volatile markets while participating in rising ones. We firmly believe that on a relative and absolute basis, outperformance in difficult markets is one of the key drivers to creating long-term wealth for our clients.

The 2009 fiscal year can certainly be characterized as the tale of two markets coupled with emotional volatility. Over the course of the period, investors were subject to a volatile and intense nosedive from September 2008 through February 2009 and subsequent explosive and manic rally off the March lows which lasted through August before cooling in late September 2009. This type of extreme downside and upside volatility, even though it is a small sample of observations relative to our long-term prospective, provides an appropriate backdrop for investors to examine whether we have in fact delivered upon our objectives.

Did we manage to achieve our stated objectives in the face of such short-term market extremes? The answer is a resounding “yes”. I am proud to report that all of our actively managed funds, regardless of capitalization and style, outperformed their benchmarks and peers during the drawdown period, which subjected investors to less volatility. As you would expect, when the market began its rally, our funds generally performed in-line on the way back up. Examining the entire reporting period, which encompasses both extremes, we are fortunate to be able to report that all of our actively managed funds outperformed their benchmark and peers on a relative basis. Detailed performance information on each of our funds can be found within the enclosed Annual Report.

Given our long-term orientation as investors, a single twelve month period should not be the sole basis for the complete evaluation of our investment philosophy and the processes that drive our performance. At the close of our fiscal year, we offered three (3) funds with performance records exceeding ten-years and five (5) funds with a performance record exceeding five-years. During those two time frames, which incorporated asset bubbles and disappointments, bear markets, and optimism, all of these funds across the longer-term horizons outperformed their respective category average on an absolute and relative basis. We are proud of this fact and have every bit of confidence that our newer funds will deliver similar results as they continue to build long-term track records.

The difficult capital markets environment not only presented challenges for investors, it also had a major impact on the entire asset management industry. Post crisis, investors turned to the defensive fixed-income asset class, in search of yield, or to money markets funds for preservation. The flows to these conservative asset classes left many equity funds with significantly smaller assets than in prior years forcing many asset managers to evaluate and rationalize their business strategies and practice.

At The FBR Funds, we were not immune to this trend but managed to successfully navigate the turmoil primarily because of enhanced distribution and client retention efforts. We re-examined our business in light of the changing industry landscape and executed several steps to ensure we remain in the best position to capitalize on current dislocation and stress permeating our industry today. All of the actions being taken, such as exiting the money market business and internalizing the management of our largest product, though difficult, are necessary to ensure we have a solid foundation in place to continue to

2

grow our business organically as well as strategically while remaining focused and committed to delivering the highest quality solutions to our clients.

As in prior years, what follows in this report is a discussion with each portfolio manager with respect to the performance of their fund(s) over the 2009 fiscal year. It also includes their thoughts on related industry conditions and their investment outlook. We believe the comments and thoughts from our seven (7) fund managers are an important part of our annual and semi-annual communications to our shareholder. We encourage you to read them and hopefully better understand our investment process and current thinking.

All of us at The FBR Funds want to thank you for your continued support, and we look forward to serving your investment needs in the years ahead. As always, we welcome your questions and comments. You can reach us via e-mail at fbrfundsinfo@fbr.com or toll free at 888.200.4710.

Sincerely,

David Ellison

President, Chief Investment Officer and Trustee

The FBR Funds

Past performance is not guarantee of future results. The performance data quoted represents past performance and the current performance may be lower or higher than the data quoted. Investment return and principal will fluctuate so that investors’ shares, when redeemed may be worth more or less than their original value. The performance data does not reflect the deduction of redemption fees and if reflected, the redemption fee would reduce the performance quoted. To obtain performance data current to the most recent month-end call 888.888.0025.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. This and other information can be found in the Fund’s prospectus. To obtain a free prospectus please call 888.888.0025 of visit fbrfunds.com. Please read the prospectus carefully before investing. The FBR Funds are distributed by FBR Investment Services, Inc., member FINRA/SIPC.

3

The FBR Funds

FBR Pegasus FundTM

Management Overview

Portfolio Managers: Robert Barringer, CFA and Ryan Kelley, CFA

Over the last 12 months, how did the Fund perform and what factors contributed to this performance?

For the one-year period ended October 31, 2009, the Investor Class of the FBR Pegasus FundTM returned 20.12%. This compares favorably to the S&P 500 Index and the Morningstar Large Blend category average which over the same time period returned 9.80% and 11.86%, respectively.

The Fund’s strong total return of over 20% masks the extreme volatility that we experienced in the stock market over the course of the fiscal year. The credit market crisis and financial meltdown that began in the fall of 2008 caused the stock market to drop precipitously, as evidenced by the S&P 500 Index’s negative 29% return from October 31, 2008 to its low closing price on March 9, 2009. During this dramatic market drawdown, the FBR Pegasus FundTM held up better than the index, only dropping approximately 23%. Subsequently, from March 9, 2009 through the end of our reporting period, the Fund matched the extremely strong recovery of the market, as both the S&P 500 Index and the Fund soared 55%. One of our primary investment objectives is to outperform the index with less volatility, and we believe this past year’s performance is a testament to our disciplined investment process.

We are encouraged by the Fund’s relative outperformance and attribute that to two primary factors: stock selection and selective exposure to high-quality stocks in the financial sector.

First, the Fund’s performance was driven primarily by the stocks we owned, rather than by our exposure to any particular industry. According to portfolio analysis provided by Morningstar, over 93% of our outperformance versus the S&P 500 Index was attributable to our ability to chose and weight individual securities within each sector, regardless of a sector’s overall performance. To further highlight this, the Fund’s average material, telecommunication services, and energy stock returns were 59% (versus the index’s 16%), 44% (versus the index’s 5%), and 30% (versus the index’s 8%), respectively. Our stock selection process and long-term orientation worked well during the reporting period.

Second, our exposure to the financial sector helped provide better returns for our shareholders. Throughout the first half of the fiscal year, the Fund was underexposed on average to the financial sector, which performed abysmally during that time period. As financial stocks began roaring back in March 2009, we opportunistically invested in certain companies that fit our investment criteria for financials and that we felt were dramatically under-valued on a long-term basis. In fact, we became heavily over-exposed to financials in the second part of the year. For the entire fiscal year, financials performed the worst within the S&P 500, returning on average -6%, while the Fund’s financial stocks returned on average 9%. Our stock selection and timing worked well, as almost one-fourth of our overall outperformance versus the index came from owning the right financial stocks at the right time.

During this volatile fiscal year, every sector posted overall positive returns for our Fund. Materials and energy were two sectors other than financials that contributed substantially to the Fund’s outperformance versus the index. Only the information technology sector

4

The FBR Funds

FBR Pegasus FundTM

Management Overview (continued)

underperformed relative to the benchmark, as the average S&P 500 information technology stock was up 31% during the reporting period versus the Fund’s average of 28%.

Portfolio managers comments on the Fund and the related investment outlook.

The past year’s events shook many of the world’s markets and economies to the core, including, in particular, the US. The economic consequences of the bursting of the property market bubble, with all of its attendant aftershocks, are still being felt today. The leverage that was lurking in the financial system was revealed, along with the “virtuous circle” that the leverage had created, namely inflated property values in every category. Then came the other end of the spectrum, the “vicious cycle” of vastly constrained credit and lower property values, causing financing and refinancing problems, leading to further declines in values. One of the few bright spots on the economic front was continued growth in emerging markets, such as in China, which prevented the economic crisis from becoming even worse than it could have been.

The good news is that liquidity has returned to a large degree in the public credit markets as well as in the equity market, allowing companies access to needed capital in order to shore up weakened balance sheets. The stock market has recovered quite nicely from the March 2009 lows and seems to be anticipating a slow, steady recovery in the year ahead. Many of the top performing sectors were those that the market had been concerned about: those with high operating leverage and high balance sheet leverage.

There are now fundamental signs that the economy may be stabilizing, with recent trends in consumer sentiment, employment, and housing showing signs of bottoming. In addition, companies have acted quickly to maintain lean cost structures, helping to mitigate lower revenues and helping the bottom line. These moves have allowed earnings to come in ahead of expectations and should provide greater upside when revenue growth returns.

We continue to position the portfolio to benefit from a slow, steady recovery in the US and globally, and as such, we have overweight positions in the financials, materials, and technology spaces. The wild card is consumers, who have had to deal with declining values of their major asset, their home, and who are concerned about their job, and their retirement nest egg. Thus, while things may get better on the employment front, consumer spending, two thirds of GDP, may continue to be muted.

As always, we focus on picking the best run companies that are selling at reasonable valuations with solid balance sheets, a strategy which has helped us to do well in this uncertain environment.While the market has come back strongly, we believe that there are many opportunities that should perform well in the coming year as the recovery proves to be on more solid ground.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

5

The FBR Funds

FBR Pegasus FundTM

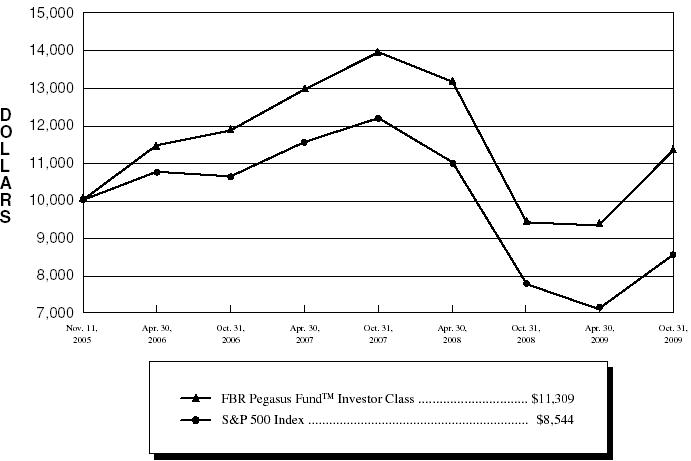

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. S&P 500 Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2009(4) | |

| | | | | | Annualized | |

| | | | | | Since | |

| | | One Year | | Inception(5) | |

| | |

| |

| |

FBR Pegasus FundTM Investor Class(1)(2) | | 20.12 | % | | 3.16 | % | |

FBR Pegasus FundTM I Class(2) | | 20.21 | % | | (10.81 | )% | |

S&P 500 Index(1)(3) | | 9.80 | % | | (3.89 | )% | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. If reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | The S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to represent the broad domestic economy through changes in aggregate market value of 500 stocks representing all major industries. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | The inception date for the Investor Class is November 15, 2005 and the inception date for the I Class is May 30, 2008. The index return is for the period beginning November 15, 2005. |

6

The FBR Funds

FBR Pegasus FundTM

Portfolio Summary

October 31, 2009

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | | % of Total Investments |

| |

|

| Finance | | 23.3 | % |

| Technology Services | 15.2 | % |

| Retail Trade | | 11.1 | % |

| Health Technology | 9.7 | % |

| Electronic Technology | 9.4 | % |

| Energy Minerals | 9.3 | % |

| Producer Manufacturing | 6.5 | % |

| Consumer Non-Durables | 5.3 | % |

| Non-Energy Minerals | 3.2 | % |

| Transportation | | 3.0 | % |

| Consumer Services | 1.0 | % |

| Communications | | 0.4 | % |

| | | | |

| Cash | | 2.6 | % |

7

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 94.5% | | | | |

| | | | Communications — 0.4% | | | | |

| | 1,850 | | America Movil S.A.B. de C.V., Series L ADR | | $ | 81,641 | |

| | | | | |

| |

| | | | Consumer Non-Durables — 5.1% | | | | |

| | 1,475 | | Colgate-Palmolive Co. | | | 115,979 | |

| | 5,000 | | Ralcorp Holdings, Inc.* | | | 268,500 | |

| | 3,502 | | The J.M. Smucker Co. | | | 184,660 | |

| | 13,800 | | Unilever PLC ADR | | | 411,655 | |

| | | | | |

| |

| | | | | | | 980,794 | |

| | | | | |

| |

| | | | Consumer Services — 1.0% | | | | |

| | 6,550 | | Carnival Corp. | | | 190,736 | |

| | | | | |

| |

| | | | Electronic Technology — 9.3% | | | | |

| | 2,200 | | Apple, Inc.* | | | 414,700 | |

| | 4,000 | | Canon, Inc. ADR | | | 150,640 | |

| | 19,100 | | Cisco Systems, Inc.* | | | 436,435 | |

| | 27,500 | | Intel Corp. | | | 525,525 | |

| | 3,900 | | Research In Motion Ltd.* | | | 229,047 | |

| | | | | |

| |

| | | | | | | 1,756,347 | |

| | | | | |

| |

| | | | Energy Minerals — 9.0% | | | | |

| | 7,252 | | Apache Corp. | | | 682,559 | |

| | 7,200 | | ConocoPhillips | | | 361,296 | |

| | 2,885 | | Occidental Petroleum Corp. | | | 218,914 | |

| | 1,830 | | PetroChina Company Ltd. ADR | | | 219,673 | |

| | 1,498 | | Royal Dutch Shell PLC, Class A ADR | | | 88,996 | |

| | 4,608 | | Suncor Energy, Inc. | | | 152,156 | |

| | | | | |

| |

| | | | | | | 1,723,594 | |

| | | | | |

| |

| | | | Finance — 22.5% | | | | |

| | 4,900 | | Ameriprise Financial, Inc. | | | 169,883 | |

| | 21,300 | | Bank of America Corp. | | | 310,554 | |

8

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Finance — 22.5% (continued) | | | | |

| | 37,000 | | Citigroup, Inc. | | $ | 151,330 | |

| | 3,525 | | Franklin Resources, Inc. | | | 368,821 | |

| | 15,300 | | Hudson City Bancorp, Inc. | | | 201,042 | |

| | 1,900 | | IntercontinentalExchange, Inc.* | | | 190,361 | |

| | 9,825 | | JPMorgan Chase & Co. | | | 410,390 | |

| | 76,400 | | KeyCorp. | | | 411,796 | |

| | 6,900 | | Manulife Financial Corp. | | | 128,271 | |

| | 7,000 | | MetLife, Inc. | | | 238,210 | |

| | 5,600 | | Morgan Stanley | | | 179,872 | |

| | 17,600 | | People’s United Financial, Inc. | | | 282,128 | |

| | 3,100 | | Prudential Financial, Inc. | | | 140,213 | |

| | 8,600 | | SunTrust Banks, Inc. | | | 164,346 | |

| | 11,975 | | T. Rowe Price Group, Inc. | | | 583,541 | |

| | 2,125 | | The Goldman Sachs Group, Inc. | | | 361,611 | |

| | | | | |

| |

| | | | | | | 4,292,369 | |

| | | | | |

| |

| | | | Health Technology — 9.5% | | | | |

| | 2,240 | | Abbott Laboratories | | | 113,277 | |

| | 4,775 | | Baxter International, Inc. | | | 258,137 | |

| | 3,325 | | Becton, Dickinson and Co. | | | 227,297 | |

| | 2,020 | | C.R. Bard, Inc. | | | 151,641 | |

| | 6,500 | | Johnson & Johnson | | | 383,825 | |

| | 11,600 | | Merck & Company, Inc. | | | 358,788 | |

| | 3,220 | | Novo Nordisk A/S ADR | | | 200,123 | |

| | 6,304 | | Pfizer, Inc. | | | 107,357 | |

| | | | | |

| |

| | | | | | | 1,800,445 | |

| | | | | |

| |

| | | | Non-Energy Minerals — 3.1% | | | | |

| | 6,000 | | BHP Billiton Ltd. ADR | | | 393,480 | |

| | 2,750 | | Freeport-McMoRan Copper & Gold, Inc.* | | | 201,740 | |

| | | | | |

| |

| | | | | | | 595,220 | |

| | | | | |

| |

9

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Producer Manufacturing — 6.4% | | | | |

| | 11,115 | | 3M Co. | | $ | 817,730 | |

| | 27,700 | | General Electric Co. | | | 395,002 | |

| | | | | |

| |

| | | | | | | 1,212,732 | |

| | | | | |

| |

| | | | Retail Trade — 10.7% | | | | |

| | 11,600 | | American Eagle Outfitters, Inc. | | | 202,884 | |

| | 3,000 | | Fastenal Co. | | | 103,500 | |

| | 4,500 | | Kohl’s Corp.* | | | 257,490 | |

| | 19,600 | | Lowe’s Companies, Inc. | | | 383,572 | |

| | 9,600 | | Target Corp. | | | 464,928 | |

| | 15,325 | | The Gap, Inc. | | | 327,036 | |

| | 4,900 | | Walgreen Co. | | | 185,367 | |

| | 2,350 | | Wal-Mart Stores, Inc. | | | 116,748 | |

| | | | | |

| |

| | | | | | | 2,041,525 | |

| | | | | |

| |

| | | | Technology Services — 14.6% | | | | |

| | 4,450 | | Accenture PLC, Class A | | | 165,006 | |

| | 3,600 | | Adobe Systems, Inc.* | | | 118,584 | |

| | 3,700 | | Automatic Data Processing, Inc. | | | 147,260 | |

| | 675 | | Google, Inc., Class A* | | | 361,881 | |

| | 3,800 | | International Business Machines Corp. | | | 458,318 | |

| | 17,650 | | Microsoft Corp. | | | 489,434 | |

| | 21,800 | | Oracle Corp. | | | 459,980 | |

| | 9,200 | | SAP AG ADR | | | 416,484 | |

| | 10,400 | | Total System Services, Inc. | | | 166,088 | |

| | | | | |

| |

| | | | | | | 2,783,035 | |

| | | | | |

| |

| | | | Transportation — 2.9% | | | | |

| | 4,350 | | Burlington Northern Santa Fe Corp. | | | 327,642 | |

| | 4,050 | | Union Pacific Corp. | | | 223,317 | |

| | | | | |

| |

| | | | | | | 550,959 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $16,249,571) | | | 18,009,397 | |

| | | | | |

| |

10

The FBR Funds

FBR Pegasus FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | MONEY MARKET FUND — 2.6% | | | | |

| | 486,364 | | JPMorgan 100% U.S. Treasury Securities Money Market Fund | | $ | 486,364 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Investments — 97.1% (Cost $16,735,935) | | | 18,495,761 | |

| | | | | | | | |

| | | | Other Assets Less Liabilities — 2.9% | | | 550,371 | |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 19,046,132 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| ADR | | American Depositary Receipts |

| PLC | | Public Liability Company |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

11

The FBR Funds

FBR Pegasus Mid Cap FundTM

Management Overview

Portfolio Manager: Ryan Kelley, CFA

Over the last 12 months, how did the Fund perform and what factors contributed to this performance?

For the one-year period ended October 31, 2009, the Investor Class of the FBR Pegasus Mid Cap FundTM returned 18.51%. This compares to the Russell Midcap Index and the Morningstar Mid Cap Blend category average, which over the same time period returned 18.75% and 18.21%, respectively.

During this fiscal year, mid-cap stocks performed the best when compared to large-cap and small-cap stocks. Indeed, while the Russell Midcap Index returned almost 19%, the Russell 1000 Index (large-cap) and the Russell 2000 Index (small-cap) rose only 11% and 6%, respectively.

We are encouraged by the Fund’s strong total return of almost 19% coupled with its low volatility. The credit market and financial crisis that began in the fall of 2008 caused the stock market to drop precipitously, and the Russell Midcap Index posted a negative 29% return from October 31, 2008 to its low closing price on March 9, 2009. During this dramatic drop, the Fund showed substantially less volatility, only dropping approximately 21%. Subsequently, from March 9, 2009 through the end of our reporting period, the Fund lagged the extremely strong recovery of the market but ended the fiscal year essentially in-line with its benchmark and its peers.

Despite an extremely volatile market, every sector in the Russell Midcap Index posted positive average returns over our fiscal year. According to Morningstar, leading sectors included information technology and consumer discretionary, posting average returns of 33% and 32%, respectively. While the Fund slightly lagged by less than 2% in each of these sectors, they were the two largest contributors to the Fund’s performance. The two sectors in which the Fund outperformed the benchmark by the greatest margin were consumer staples and materials, with the latter posting average returns of 74% versus the index’s 25%. The healthcare sector, however, was the largest detractor from the Fund’s performance as certain medical equipment producers performed poorly during the fiscal year.

Although performance is primarily driven by a fund’s investments, cash levels can both add and subtract from a fund’s relative performance. The Fund experienced some of both this year. High cash levels as the market was falling helped the Fund outperform the benchmark. However, this larger cash position caused the Fund to lag as the market soared in March and April. Additionally, in late April of 2009, a large cash inflow of approximately 33% (well above our normal level of less than 10%) of the Fund’s overall assets under management caused continued underperformance as the markets continued their strong upward trend.

Portfolio manager comments on the Fund and the related investment outlook.

We strive to provide strong long-term returns for our shareholders while protecting against the downside. We are encouraged by this year’s performance, as the Fund posted a total return of almost 19% and did so with significantly less volatility than our benchmark.

12

The FBR Funds

FBR Pegasus Mid Cap FundTM

Management Overview (continued)

The volatility in both the economy and the financial markets was dramatic, if not unprecedented, to say the least. Two issues became apparent in this turbulent market. First, fear and panic are extremely strong drivers in our modern market of instantaneous access to information, low-cost trading, and rapidly shifting money flows. Second, we believe economic resilience coupled with worldwide governmental intervention is a powerful force for stock market recovery. These two factors, when working in succession, helped to cause the extreme decline and inspiring recovery that we saw this past year.

We believe that the economic recovery has begun in earnest, although there is still much uncertainty in the market and continued mixed fundamental data flow makes it difficult for investors to become comfortable with the overall direction of the market. We continue to seek good entry points for new portfolio holdings and re-evaluate both those stocks that have done well and those that have not. Our investment philosophy, process, and discipline remain intact while we adapt to new opportunities and rapidly moving markets. We believe the Fund’s diversification and mix of low valuation stocks and higher growth stocks will continue to provide solid returns for our shareholders with less volatility over a complete business cycle.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

13

The FBR Funds

FBR Pegasus Mid Cap FundTM

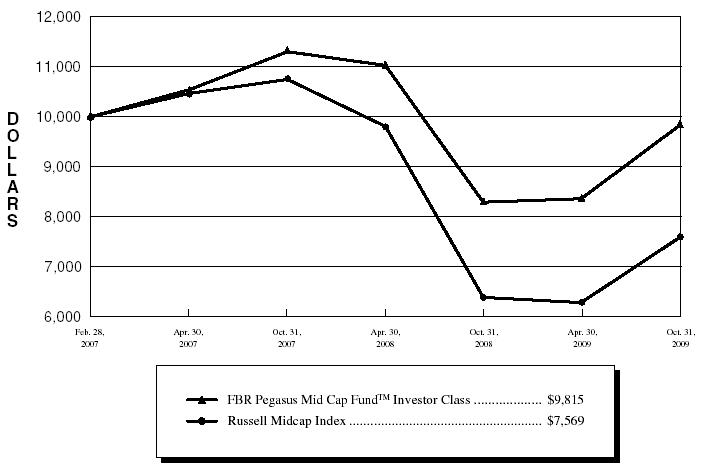

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell Midcap Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2009(4) | |

| | | | | | Annualized | |

| | | | | | Since | |

| | | One Year | | Inception(5) | |

| | |

| |

| |

FBR Pegasus Mid Cap FundTM Investor Class(1)(2) | | 18.51 | % | | (0.70 | )% | |

FBR Pegasus Mid Cap FundTM I Class(2) | | 18.78 | % | | (11.20 | )% | |

Russell Midcap Index(1)(3) | | 18.75 | % | | (9.88 | )% | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. If reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index, which represents approximately 31% of the total market capitalization of the Russell 1000 Index. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | The inception date for the Investor Class is February 28, 2007 and the inception date for the I Class is May 30, 2008. The index return is for the period beginning February 28, 2007. |

14

The FBR Funds

FBR Pegasus Mid Cap FundTM

Portfolio Summary

October 31, 2009

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | | % of Total Investments |

| |

|

| Finance | | 19.8 | % |

| Health Technology | 9.8 | % |

| Technology Services | 9.4 | % |

| Retail Trade | | 8.2 | % |

| Producer Manufacturing | 7.5 | % |

| Commercial Services | 7.0 | % |

| Consumer Non-Durables | 6.0 | % |

| Utilities | | 5.0 | % |

| Process Industries | 4.7 | % |

| Industrial Services | 4.6 | % |

| Electronic Technology | 3.7 | % |

| Consumer Durables | 3.3 | % |

| Non-Energy Minerals | 3.1 | % |

| Distribution Services | 1.8 | % |

| Energy Minerals | 1.7 | % |

| Communications | | 1.4 | % |

| Consumer Services | 1.4 | % |

| Health Services | 0.5 | % |

| | | | |

| Cash | | 1.1 | % |

15

The FBR Funds

FBR Pegasus Mid Cap FundTM

Portfolio of Investments

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 95.2% | | | | |

| | | | Commercial Services — 6.7% | | | | |

| | 3,660 | | Copart, Inc.* | | $ | 117,742 | |

| | 1,550 | | Equifax, Inc. | | | 42,439 | |

| | 2,172 | | FactSet Research Systems, Inc. | | | 139,117 | |

| | 3,525 | | Ritchie Bros. Auctioneers, Inc. | | | 77,268 | |

| | 4,850 | | SEI Investments Co. | | | 84,730 | |

| | | | | |

| |

| | | | | | | 461,296 | |

| | | | | |

| |

| | | | Communications — 1.3% | | | | |

| | 3,050 | | Telephone and Data Systems, Inc. | | | 90,341 | |

| | | | | |

| |

| | | | Consumer Durables — 3.2% | | | | |

| | 12,293 | | Activision Blizzard, Inc.* | | | 133,133 | |

| | 4,699 | | Mattel, Inc. | | | 88,952 | |

| | | | | |

| |

| | | | | | | 222,085 | |

| | | | | |

| |

| | | | Consumer Non-Durables — 5.8% | | | | |

| | 2,812 | | Alberto-Culver Co. | | | 75,418 | |

| | 3,500 | | Hansen Natural Corp.* | | | 126,525 | |

| | 5,825 | | Tyson Foods, Inc., Class A | | | 72,929 | |

| | 1,729 | | VF Corp. | | | 122,828 | |

| | | | | |

| |

| | | | | | | 397,700 | |

| | | | | |

| |

| | | | Consumer Services — 1.3% | | | | |

| | 775 | | Apollo Group, Inc., Class A* | | | 44,253 | |

| | 500 | | ITT Educational Services, Inc.* | | | 45,175 | |

| | | | | |

| |

| | | | | | | 89,428 | |

| | | | | |

| |

| | | | Distribution Services — 1.7% | | | | |

| | 6,575 | | Ingram Micro, Inc., Class A* | | | 116,049 | |

| | | | | |

| |

| | | | Electronic Technology — 3.6% | | | | |

| | 3,325 | | Dolby Laboratories, Inc., Class A* | | | 139,450 | |

| | 3,875 | | FLIR Systems, Inc.* | | | 107,764 | |

| | | | | |

| |

| | | | | | | 247,214 | |

| | | | | |

| |

| | | | Energy Minerals — 1.7% | | | | |

| | 1,077 | | Energen Corp. | | | 47,259 | |

| | 1,675 | | Pioneer Natural Resources Co. | | | 68,859 | |

| | | | | |

| |

| | | | | | | 116,118 | |

| | | | | |

| |

16

The FBR Funds

FBR Pegasus Mid Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Finance — 19.1% | | | | |

| | 4,470 | | Annaly Capital Management, Inc. | | $ | 75,588 | |

| | 3,040 | | Capitol Federal Financial | | | 92,203 | |

| | 3,325 | | Comerica, Inc. | | | 92,268 | |

| | 1,975 | | Commerce Bancshares, Inc. | | | 75,761 | |

| | 10,725 | | Hudson City Bancorp, Inc. | | | 140,926 | |

| | 16,900 | | Huntington Bancshares, Inc. | | | 64,389 | |

| | 15,350 | | KeyCorp. | | | 82,737 | |

| | 1,446 | | M&T Bank Corp. | | | 90,880 | |

| | 7,285 | | New York Community Bancorp, Inc. | | | 78,678 | |

| | 7,950 | | People’s United Financial, Inc. | | | 127,439 | |

| | 16,000 | | Regions Financial Corp. | | | 77,440 | |

| | 4,886 | | T. Rowe Price Group, Inc. | | | 238,094 | |

| | 1,725 | | The Hanover Insurance Group, Inc. | | | 72,554 | |

| | | | | |

| |

| | | | | | | 1,308,957 | |

| | | | | |

| |

| | | | Health Services — 0.5% | | | | |

| | 1,030 | | Lincare Holdings, Inc.* | | | 32,352 | |

| | | | | |

| |

| | | | Health Technology — 9.3% | | | | |

| | 380 | | Bio-Rad Laboratories, Inc., Class A* | | | 33,968 | |

| | 1,546 | | C.R. Bard, Inc. | | | 116,058 | |

| | 4,100 | | Endo Pharmaceuticals Holdings, Inc.* | | | 91,840 | |

| | 3,738 | | Forest Laboratories, Inc.* | | | 103,430 | |

| | 2,445 | | Pall Corp. | | | 77,604 | |

| | 1,685 | | Techne Corp. | | | 105,330 | |

| | 2,839 | | Varian Medical Systems, Inc.* | | | 116,343 | |

| | | | | |

| |

| | | | | | | 644,573 | |

| | | | | |

| |

| | | | Industrial Services — 4.4% | | | | |

| | 2,285 | | ENSCO International, Inc. | | | 104,630 | |

| | 3,340 | | Helmerich & Payne, Inc. | | | 126,986 | |

| | 1,087 | | Pride International, Inc.* | | | 32,132 | |

| | 1,550 | | Rowan Companies, Inc. | | | 36,038 | |

| | | | | |

| |

| | | | | | | 299,786 | |

| | | | | |

| |

| | | | Non-Energy Minerals — 3.0% | | | | |

| | 3,375 | | Compania de Minas Buenaventura S.A.A. ADR | | | 113,299 | |

| | 2,627 | | United States Steel Corp. | | | 90,605 | |

| | | | | |

| |

| | | | | | | 203,904 | |

| | | | | |

| |

17

The FBR Funds

FBR Pegasus Mid Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Process Industries — 4.4% | | | | |

| | 1,472 | | Bunge Ltd. | | $ | 83,992 | |

| | 2,475 | | Ecolab, Inc. | | | 108,801 | |

| | 2,134 | | Sigma-Aldrich Corp. | | | 110,819 | |

| | | | | |

| |

| | | | | | | 303,612 | |

| | | | | |

| |

| | | | Producer Manufacturing — 7.3% | | | | |

| | 2,953 | | Cummins, Inc. | | | 127,157 | |

| | 2,235 | | Kubota Corp. ADR | | | 85,846 | |

| | 3,580 | | Magna International, Inc., Class A | | | 141,875 | |

| | 2,712 | | Roper Industries, Inc. | | | 137,092 | |

| | | | | |

| |

| | | | | | | 491,970 | |

| | | | | |

| |

| | | | Retail Trade — 8.1% | | | | |

| | 3,690 | | Abercrombie & Fitch Co., Class A | | | 121,106 | |

| | 7,249 | | American Eagle Outfitters, Inc. | | | 126,785 | |

| | 2,525 | | BJ’s Wholesale Club, Inc.* | | | 88,451 | |

| | 2,350 | | Fastenal Co. | | | 81,075 | |

| | 3,485 | | Tiffany & Co. | | | 136,926 | |

| | | | | |

| |

| | | | | | | 554,343 | |

| | | | | |

| |

| | | | Technology Services — 9.0% | | | | |

| | 5,133 | | Check Point Software Technologies Ltd.* | | | 159,482 | |

| | 3,350 | | Cognizant Technology Solutions Corp., Class A* | | | 129,478 | |

| | 2,700 | | Global Payments, Inc. | | | 132,920 | |

| | 950 | | NetEase.com, Inc. ADR* | | | 36,689 | |

| | 4,375 | | Paychex, Inc. | | | 124,294 | |

| | 600 | | Sohu.com, Inc.* | | | 33,360 | |

| | | | | |

| |

| | | | | | | 616,223 | |

| | | | | |

| |

| | | | Utilities — 4.8% | | | | |

| | 1,816 | | Pinnacle West Capital Corp. | | | 56,877 | |

| | 1,473 | | Questar Corp. | | | 58,684 | |

| | 1,675 | | SCANA Corp. | | | 56,682 | |

| | 1,100 | | Sempra Energy | | | 56,595 | |

18

The FBR Funds

FBR Pegasus Mid Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Utilities — 4.8% (continued) | | | | |

| | 2,950 | | Westar Energy, Inc. | | $ | 56,493 | |

| | 2,173 | | Xcel Energy, Inc. | | | 40,939 | |

| | | | | |

| |

| | | | | | | 326,270 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $5,998,739) | | | 6,522,221 | |

| | | | | |

| |

| | | | | | | | |

| | | | MONEY MARKET FUND — 1.1% | | | | |

| | 75,655 | | JPMorgan 100% U.S. Treasury Securities Money Market Fund | | | 75,655 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Investments — 96.3% (Cost $6,074,394) | | | 6,597,876 | |

| | | | | | | | |

| | | | Other Assets Less Liabilities — 3.7% | | | 253,157 | |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 6,851,033 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| ADR | | American Depositary Receipts |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

19

The FBR Funds

FBR Pegasus Small Cap FundTM

Management Overview

Portfolio Manager: Robert Barringer, CFA

Over the last 12 months, how did the Fund perform and what factors contributed to this performance?

For the one-year period ended October 31, 2009, the Investor Class of the FBR Pegasus Small Cap FundTM returned 12.68%. This compares to the Russell 2000 Index and the Morningstar Small Cap Blend category average, which returned 6.46% and 11.74%, respectively.

Specific stock selection accounted for the vast majority (94%) of the overall return of the Fund versus overweighting specific sectors, which attributed approximately 6%. In particular, the Fund’s selections of individual high-quality financial stocks were the largest drivers of outperformance. Relative to the Russell 2000 Index, the Fund maintained overweight positions in savings banks and asset managers while remaining materially underweight in very hard hit regional banks during the reporting period. Individual selection in the consumer discretionary sector was the second best contributor to the Fund’s outperformance, where specific stock picks well outperformed the buoyant category.

Over the course of the reporting period, almost every single economic sector represented in the Fund’s portfolio experienced a positive return relative to its index, with one minor exception, consumer staples. Our goal is to provide investors with diversified exposure to the small-cap asset class while delivering above average risk-adjusted returns over a full market cycle. Our investment process allows us to identify companies offering what we believe are the most attractive risk/return profiles within each sector and acquire them at reasonable prices. The previous twelve months highlighted the merits of our process as we continued to achieve our stated objective.

Portfolio manager comments on the Fund and the related investment outlook.

The stock market and the economy of the US in the past year have been hit hard by the popping of the real estate bubble and all of its associated implications. Intuitively, investors would have assumed that large-cap companies would outperform in this scenario, but the large-cap asset class was severely impacted by the negative performance of large financial institutions. These financial institutions relied more heavily on complex investments and unregulated funding sources embedded in their “more sophisticated” balance sheet structure to continue to drive growth. This stance ultimately proved to be extremely risky, especially as locating adequate short-term funding became nearly impossible as a result of the credit crisis and higher capital requirements were mandated by the government. Indeed, the smaller cap companies in the financial area, by virtue of their “plain vanilla” profiles, with relatively straightforward businesses of making loans and taking in deposits from their branch network, were, with some exceptions, less impacted and performed far better than their larger brethren. Other major large-cap companies that were impacted by the credit crisis were auto companies and their manufacturers, and some other major companies with complex financial subsidiaries, such as General Electric.

20

The FBR Funds

FBR Pegasus Small Cap FundTM

Management Overview (continued)

We are now in the process of healing across the global financial system, as companies are now able to access the public debt and equity markets. Increasingly, companies across the market cap spectrum have been able to raise capital either through an initial public offering or a secondary issue, and I believe that through this healing process the stronger players will be able to acquire assets or entire companies at attractive prices. Examples of this include recent very attractive deals that a number of banks have completed with the assistance of the FDIC, in effect making them the consolidators of the banking space. Investors also seem to be looking at public real estate investment trusts to act in a similar capacity, being able to access the public markets while the private players are having more difficulty raising capital.

In the year ahead, I have positioned the portfolio to take advantage of the viewpoint that the US economy will gradually improve, and that we will move from a phase of survival to a focus on growth. One of the wildcards is how quickly we will see employment growth return or whether, as many people have voiced, we will have a “jobless recovery”. Two key issues are how and when will the government manage to back away from its aggressive stimulus program. Also important is the timing of a decision by the fed to raise interest rates and the impact of dang so on a fragile recovery.

As always, I will be looking for the best companies in each sector, with solid business models, good management, prudent balance sheets, selling at the most reasonable prices. I will tilt the portfolio towards those areas that can take advantage of a cyclical upturn in the economy, such as certain parts of industrials, material, financials, and technology. Further, I will attempt to position the portfolio to participate and capitalize on what I believe are some of the most significant and powerful, secular growth trends developing today.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

21

The FBR Funds

FBR Pegasus Small Cap FundTM

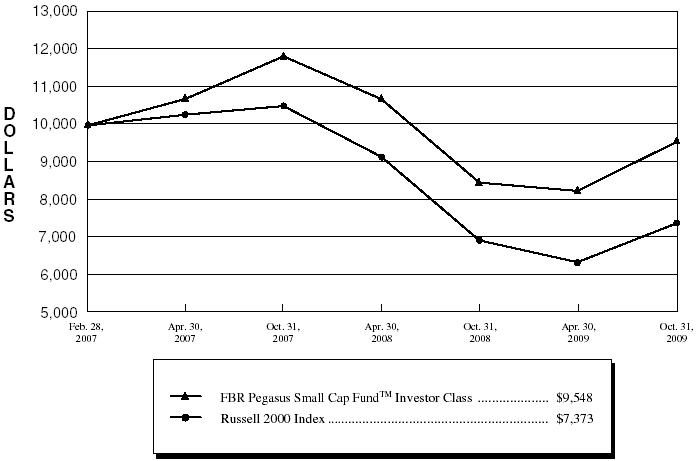

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell 2000 Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2009(4) | |

| | | | | | Annualized | |

| | | | | | Since | |

| | | One Year | | Inception(5) | |

| | |

| |

| |

FBR Pegasus Small Cap FundTM Investor Class(1)(2) | | 12.68 | % | | (1.72 | )% | |

FBR Pegasus Small Cap FundTM I Class(2) | | 12.73 | % | | (10.14 | )% | |

Russell 2000 Index(1)(3) | | 6.46 | % | | (10.76 | )% | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. If reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | The Russell 2000 Index is comprised of the smallest of the 2000 companies of the Russell 3000 Index, representing approximately 8% of the Russell 3000’s total market capitalization. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | The inception date for the Investor Class is February 28, 2007 and the inception date for the I Class is May 30, 2008. The index return is for the period beginning February 28, 2007. |

22

The FBR Funds

FBR Pegasus Small Cap FundTM

Portfolio Summary

October 31, 2009

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | | % of Total Investments |

| |

|

| Finance | | 31.8 | % |

| Electronic Technology | 11.2 | % |

| Retail Trade | | 8.0 | % |

| Technology Services | 7.3 | % |

| Producer Manufacturing | 7.3 | % |

| Energy Minerals | | 5.5 | % |

| Health Technology | 5.3 | % |

| Distribution Services | 4.7 | % |

| Process Industries | 3.1 | % |

| Transportation | | 2.8 | % |

| Commercial Services | 2.6 | % |

| Consumer Durables | 2.5 | % |

| Utilities | | 2.0 | % |

| Consumer Services | 1.9 | % |

| Industrial Services | 1.7 | % |

| Non-Energy Minerals | 1.4 | % |

| Health Services | | 0.9 | % |

23

The FBR Funds

FBR Pegasus Small Cap FundTM

Portfolio of Investments

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 94.4% | | | | |

| | | | Commercial Services — 2.5% | | | | |

| | 4,075 | | Lender Processing Services, Inc. | | $ | 162,185 | |

| | 5,910 | | SEI Investments Co. | | | 103,248 | |

| | | | | |

| |

| | | | | | | 265,433 | |

| | | | | |

| |

| | | | Consumer Durables — 2.3% | | | | |

| | 5,400 | | Lennar Corp., Class A | | | 68,040 | |

| | 2,450 | | Snap-On, Inc. | | | 89,499 | |

| | 1,900 | | The Black & Decker Corp. | | | 89,718 | |

| | | | | |

| |

| | | | | | | 247,257 | |

| | | | | |

| |

| | | | Consumer Services — 1.7% | | | | |

| | 2,500 | | DreamWorks Animation SKG, Inc., Class A* | | | 80,000 | |

| | 6,070 | | Rollins, Inc. | | | 109,746 | |

| | | | | |

| |

| | | | | | | 189,746 | |

| | | | | |

| |

| | | | Distribution Services — 4.4% | | | | |

| | 2,100 | | MSC Industrial Direct Company, Inc., Class A | | | 90,405 | |

| | 6,380 | | Patterson Companies, Inc.* | | | 162,881 | |

| | 11,500 | | Pool Corp. | | | 225,170 | |

| | | | | |

| |

| | | | | | | 478,456 | |

| | | | | |

| |

| | | | Electronic Technology — 10.6% | | | | |

| | 8,450 | | ADTRAN, Inc. | | | 194,688 | |

| | 1,850 | | Comtech Telecommunications Corp.* | | | 59,422 | |

| | 2,300 | | Cymer, Inc.* | | | 78,752 | |

| | 16,800 | | Emulex Corp.* | | | 169,680 | |

| | 8,900 | | International Rectifier Corp.* | | | 162,692 | |

| | 4,500 | | Microchip Technology, Inc. | | | 107,820 | |

| | 5,700 | | Polycom, Inc.* | | | 122,379 | |

| | 9,950 | | QLogic Corp.* | | | 174,523 | |

| | 6,300 | | Skyworks Solutions, Inc.* | | | 65,709 | |

| | | | | |

| |

| | | | | | | 1,135,665 | |

| | | | | |

| |

| | | | Energy Minerals — 5.2% | | | | |

| | 3,900 | | Arena Resources, Inc.* | | | 145,314 | |

| | 3,200 | | Concho Resources, Inc.* | | | 121,952 | |

| | 1,980 | | Energen Corp. | | | 86,882 | |

24

The FBR Funds

FBR Pegasus Small Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Energy Minerals — 5.2% (continued) | | | | |

| | 3,150 | | Goodrich Petroleum Corp.* | | $ | 80,861 | |

| | 2,000 | | Whiting Petroleum Corp.* | | | 112,800 | |

| | | | | |

| |

| | | | | | | 547,809 | |

| | | | | |

| |

| | | | Finance — 29.8% | | | | |

| | 3,475 | | Affiliated Managers Group, Inc.* | | | 220,628 | |

| | 6,835 | | American Financial Group, Inc. | | | 168,140 | |

| | 10,000 | | AmeriCredit Corp.* | | | 176,500 | |

| | 7,500 | | Arthur J. Gallagher & Co. | | | 167,325 | |

| | 21,800 | | Astoria Financial Corp. | | | 217,564 | |

| | 12,500 | | Cathay General Bancorp | | | 110,375 | |

| | 14,000 | | DiamondRock Hospitality Co.* | | | 106,540 | |

| | 13,400 | | First Horizon National Corp.* | | | 158,522 | |

| | 25,300 | | First Niagara Financial Group, Inc. | | | 324,852 | |

| | 23,300 | | Fulton Financial Corp. | | | 192,458 | |

| | 4,600 | | Knight Capital Group, Inc., Class A* | | | 77,510 | |

| | 5,275 | | optionsXpress Holdings, Inc. | | | 82,448 | |

| | 4,700 | | Platinum Underwriters Holdings Ltd. | | | 168,119 | |

| | 3,700 | | Raymond James Financial, Inc. | | | 87,357 | |

| | 4,550 | | StanCorp Financial Group, Inc. | | | 167,031 | |

| | 15,400 | | Susquehanna Bancshares, Inc. | | | 84,854 | |

| | 1,950 | | The Hanover Insurance Group, Inc. | | | 82,017 | |

| | 1,965 | | Torchmark Corp. | | | 79,779 | |

| | 5,900 | | UDR, Inc. | | | 84,842 | |

| | 7,500 | | Waddell & Reed Financial, Inc., Class A | | | 210,450 | |

| | 13,900 | | Webster Financial Corp. | | | 157,209 | |

| | 4,750 | | Zions Bancorp | | | 67,260 | |

| | | | | |

| |

| | | | | | | 3,191,780 | |

| | | | | |

| |

| | | | Health Services — 0.8% | | | | |

| | 2,100 | | Computer Programs and Systems, Inc. | | | 88,704 | |

| | | | | |

| |

| | | | Health Technology — 5.1% | | | | |

| | 12,200 | | STERIS Corp. | | | 356,973 | |

| | 1,897 | | Techne Corp. | | | 118,581 | |

| | 7,700 | | VIVUS, Inc.* | | | 60,830 | |

| | | | | |

| |

| | | | | | | 536,384 | |

| | | | | |

| |

25

The FBR Funds

FBR Pegasus Small Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Industrial Services — 1.6% | | | | |

| | 7,500 | | Rowan Companies, Inc. | | $ | 174,375 | |

| | | | | |

| |

| | | | Non-Energy Minerals — 1.3% | | | | |

| | 8,400 | | Century Aluminum Co.* | | | 72,828 | |

| | 5,000 | | Steel Dynamics, Inc. | | | 66,950 | |

| | | | | |

| |

| | | | | | | 139,778 | |

| | | | | |

| |

| | | | Process Industries — 2.9% | | | | |

| | 9,650 | | GrafTech International Ltd.* | | | 130,275 | |

| | 3,030 | | Sensient Technologies Corp. | | | 76,629 | |

| | 4,200 | | The Valspar Corp. | | | 106,554 | |

| | | | | |

| |

| | | | | | | 313,458 | |

| | | | | |

| |

| | | | Producer Manufacturing — 7.0% | | | | |

| | 1,525 | | A.O. Smith Corp. | | | 60,436 | |

| | 1,700 | | Armstrong World Industries, Inc.* | | | 63,325 | |

| | 2,210 | | Carlisle Companies, Inc. | | | 68,598 | |

| | 4,580 | | Graco, Inc. | | | 126,132 | |

| | 2,750 | | Lennox International, Inc. | | | 92,593 | |

| | 2,300 | | Lincoln Electric Holdings, Inc. | | | 109,112 | |

| | 3,400 | | Simpson Manufacturing Company, Inc. | | | 79,526 | |

| | 2,075 | | The Toro Co. | | | 76,817 | |

| | 875 | | Valmont Industries, Inc. | | | 63,236 | |

| | | | | |

| |

| | | | | | | 739,775 | |

| | | | | |

| |

| | | | Retail Trade — 7.7% | | | | |

| | 5,225 | | Abercrombie & Fitch Co., Class A | | | 171,484 | |

| | 9,000 | | American Eagle Outfitters, Inc. | | | 157,410 | |

| | 3,050 | | Jos. A. Bank Clothiers, Inc.* | | | 124,989 | |

| | 2,900 | | The Buckle, Inc. | | | 87,029 | |

| | 2,625 | | The Gymboree Corp.* | | | 111,746 | |

| | 8,500 | | Williams-Sonoma, Inc. | | | 159,630 | |

| | | | | |

| |

| | | | | | | 812,288 | |

| | | | | |

| |

| | | | Technology Services — 6.9% | | | | |

| | 4,000 | | Broadridge Financial Solutions, Inc. | | | 83,240 | |

| | 8,700 | | Jack Henry & Associates, Inc. | | | 200,709 | |

| | 3,020 | | MICROS Systems, Inc.* | | | 81,298 | |

26

The FBR Funds

FBR Pegasus Small Cap FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Technology Services — 6.9% (continued) | | | | |

| | 5,900 | | Sybase, Inc.* | | $ | 233,404 | |

| | 14,900 | | TIBCO Software, Inc.* | | | 130,375 | |

| | | | | |

| |

| | | | | | | 729,026 | |

| | | | | |

| |

| | | | Transportation — 2.7% | | | | |

| | 6,400 | | Genessee & Wyoming, Inc., Class A* | | | 185,664 | |

| | 5,250 | | Werner Enterprises, Inc. | | | 98,438 | |

| | | | | |

| |

| | | | | | | 284,102 | |

| | | | | |

| |

| | | | Utilities — 1.9% | | | | |

| | 6,300 | | Great Plains Energy, Inc. | | | 108,990 | |

| | 5,000 | | Portland General Electric Co. | | | 92,950 | |

| | | | | |

| |

| | | | | | | 201,940 | |

| | | | | |

| |

| | | | Total Common Stocks (Cost $9,427,736) | | | 10,075,976 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Investments — 94.4% (Cost $9,427,736) | | | 10,075,976 | |

| | | | | | | | |

| | | | Other Assets Less Liabilities — 5.6% | | | 595,240 | |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 10,671,216 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

27

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Management Overview

Portfolio Manager: Robert Barringer, CFA

Over the last 12 months, how did the Fund perform and what factors contributed to this performance?

For the one-year period ended October 31, 2009, the Investor Class of the FBR Pegasus Small Cap Growth FundTM returned 18.39%. This compares to the Russell 2000 Growth Index and the Morningstar Small Cap Growth category average, which returned 11.34% and 13.17%, respectively.

Nearly all of the Fund’s outperformance against its benchmark was attributable to specific stock selection in the various economic sectors represented in the portfolio rather than its relative over- or underweight positions. The main areas of outperformance were individual selections in select high-quality healthcare, industrials, consumer discretionary and technology companies. The single largest detractor to the Fund’s performance during the reporting period was a combination of individual selection and an underweight position to the energy minerals sector relative to the Russell 2000 Growth Index.

During this time frame, our investment process continued to allow us to identify high-quality small-cap companies with solid fundamentals, outsized prospects for growth and durable business models that we were able to acquire at reasonable valuations. This allowed the Fund to expose investors to less volatility than its benchmark. Over the course of the last twelve months, the Fund delivered almost 90% of the upside performance while subjecting investors to only 72% of the downside. This lower volatility is attributable to the Fund’s tighter standard deviation band of 24.40% relative to the Russell 2000 Growth Index���s 29.68%. During this tumultuous period, it was heartening to see the market recognize the lower-risk higher-return potential inherent in the types of companies we seek to own regardless of market environment and reward them accordingly.

Portfolio manager comments on the Fund and the related investment outlook.

Over the past year, the small-cap growth style more than doubled the performance of the small-cap value style largely because of its lower exposure to the harder hit segments of the market including financials, industrials and materials. Technology, in particular, was a strong performer over the Fund’s fiscal year, as hardware, semiconductor and software earnings held up a lot better than anticipated, certainly relative to expectations set by previous cycles. Technology and innovation is increasingly relied upon as a strategic asset to save money and time, and, without access to implementing the best tools available, a company can be at a competitive disadvantage. Over the past few years, individuals have been coming to view technology as essential to their personal lives and spending has remained strong and should continue for the foreseeable future.

In addition, the consumer discretionary segment performed well, in spite of what was happening to employment and the economy. While perhaps taking fewer vacations and trips to hotels, consumers continued to buy apparel and visit restaurants as eating out has

28

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Management Overview (continued)

become a regular feature of the American lifestyle. The death of the consumer was predicted, but it did not happen, even with all of the troubles with personal balance sheets, and high unemployment.

Looking ahead, I expect that the economy will slowly improve as signs of stability have shown themselves in a number of key economic statistics. The Fund’s investment style heavily emphasizes quality growth and will continue to invest in those market segments which afford the highest growth characteristics. I will continue to attempt to take advantage of those areas that have been hardest hit over the past year, such as the industrials, financials, and materials sectors. Those cyclical areas also should perform well as economic growth resumes.

As always, I will look for the best run companies with solid balance sheets, good management, and above average growth potential. In addition, I will attempt to identify and capitalize on those key secular growth stories that should provide high growth and returns over a multi-year period.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

29

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

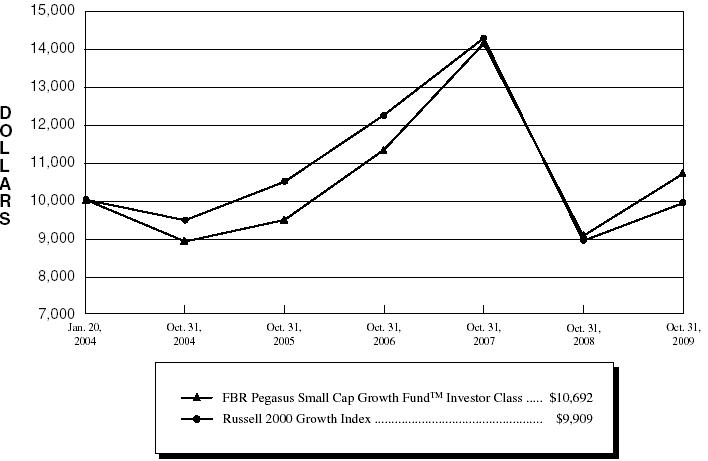

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell 2000 Growth Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2009(4) | |

| | | | | | | | | | Annualized | |

| | | | | | | Annualized | | Since | |

| | | | One Year | | Five Year | | Inception(5) | |

| | | |

| |

| |

| |

FBR Pegasus Small Cap Growth FundTM Investor Class(1)(2) | | | 18.39 | % | | 3.78 | % | | 1.16 | % | |

FBR Pegasus Small Cap Growth FundTM I Class(2) | | | 18.50 | % | | N/A | | | (10.65 | )% | |

FBR Pegasus Small Cap Growth FundTM R Class(2) | | | 17.99 | % | | N/A | | | (11.10 | )% | |

Russell 2000 Growth Index(1)(3) | | | 11.34 | % | | 0.95 | % | | (0.16 | )% | |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. If reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710 or visit www.fbrfunds.com.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the indices are unmanaged, do not incur expenses and are not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | The Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-value ratios and higher forecasted growth values. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | The inception date for the Investor Class is January 20, 2004 and the inception date for the I Class and R Class is May 30, 2008. The index return is for the period beginning January 20, 2004. |

30

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Portfolio Summary

October 31, 2009

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | | % of Total Investments |

| |

|

| Technology Services | | 19.2 | % |

| Finance | | 12.5 | % |

| Commercial Services | | 10.3 | % |

| Health Technology | | 8.9 | % |

| Health Services | | 7.7 | % |

| Electronic Technology | | 6.8 | % |

| Consumer Non-Durables | | 5.9 | % |

| Consumer Services | | 5.9 | % |

| Producer Manufacturing | | 4.8 | % |

| Transportation | | 4.0 | % |

| Energy Minerals | | 3.1 | % |

| Industrial Services | | 2.4 | % |

| Retail Trade | | 2.3 | % |

| Consumer Durables | | 2.3 | % |

| Non-Energy Minerals | | 1.5 | % |

| Distribution Services | | 1.4 | % |

| Communications | | 0.7 | % |

| | | | |

| Cash | | 0.3 | % |

31

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Portfolio of Investments

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 99.0% | | | | |

| | | | Commercial Services — 10.1% | | | | |

| | 1,825 | | Copart, Inc.* | | $ | 58,710 | |

| | 1,738 | | CoStar Group, Inc.* | | | 67,469 | |

| | 1,825 | | FactSet Research Systems, Inc. | | | 116,891 | |

| | 1,490 | | Morningstar, Inc.* | | | 76,020 | |

| | 3,900 | | SEI Investments Co. | | | 68,133 | |

| | 2,300 | | Watson Wyatt Worldwide, Inc., Class A | | | 100,234 | |

| | 3,000 | | Wright Express Corp.* | | | 83,730 | |

| | | | | |

| |

| | | | | | | 571,187 | |

| | | | | |

| |

| | | | Communications — 0.7% | | | | |

| | 6,000 | | Terremark Worldwide, Inc.* | | | 38,340 | |

| | | | | |

| |

| | | | Consumer Durables — 2.3% | | | | |

| | 3,200 | | Fossil, Inc.* | | | 85,535 | |

| | 1,100 | | Polaris Industries, Inc. | | | 46,277 | |

| | | | | |

| |

| | | | | | | 131,812 | |

| | | | | |

| |

| | | | Consumer Non-Durables — 5.8% | | | | |

| | 1,700 | | Guess?, Inc. | | | 62,135 | |

| | 2,500 | | Hansen Natural Corp.* | | | 90,375 | |

| | 3,650 | | True Religion Apparel, Inc.* | | | 94,060 | |

| | 3,175 | | Under Armour, Inc., Class A* | | | 85,249 | |

| | | | | |

| |

| | | | | | | 331,819 | |

| | | | | |

| |

| | | | Consumer Services — 6.0% | | | | |

| | 940 | | Capella Education Co.* | | | 64,766 | |

| | 450 | | Chipotle Mexican Grill, Inc., Class A* | | | 36,671 | |

| | 445 | | ITT Educational Services, Inc.* | | | 40,206 | |

| | 3,800 | | Penn National Gaming, Inc.* | | | 95,494 | |

| | 5,000 | | Rollins, Inc. | | | 90,400 | |

| | | | | |

| |

| | | | | | | 327,537 | |

| | | | | |

| |

| | | | Distribution Services — 1.3% | | | | |

| | 3,050 | | Patterson Companies, Inc.* | | | 77,867 | |

| | | | | |

| |

| | | | Electronic Technology — 6.8% | | | | |

| | 1,000 | | Hittite Microwave Corp.* | | | 36,800 | |

| | 3,100 | | Palm, Inc.* | | | 35,991 | |

32

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Electronic Technology — 6.8% (continued) | | | | |

| | 3,725 | | Polycom, Inc.* | | $ | 79,976 | |

| | 7,725 | | QLogic Corp.* | | | 135,497 | |

| | 4,100 | | Skyworks Solutions, Inc.* | | | 42,763 | |

| | 2,000 | | Supertex, Inc.* | | | 48,500 | |

| | | | | |

| |

| | | | | | | 379,527 | |

| | | | | |

| |

| | | | Energy Minerals — 3.1% | | | | |

| | 1,840 | | Comstock Resources, Inc.* | | | 75,606 | |

| | 3,675 | | Goodrich Petroleum Corp.* | | | 94,337 | |

| | | | | |

| |

| | | | | | | 169,943 | |

| | | | | |

| |

| | | | Finance — 12.4% | | | | |

| | 7,600 | | AmeriCredit Corp.* | | | 134,140 | |

| | 1,200 | | Comerica, Inc. | | | 33,300 | |

| | 11,000 | | Conseco, Inc.* | | | 57,310 | |

| | 850 | | Ebix, Inc.* | | | 52,360 | |

| | 16,400 | | Huntington Bancshares, Inc. | | | 62,484 | |

| | 4,000 | | Janus Capital Group, Inc. | | | 52,480 | |

| | 4,600 | | Legg Mason, Inc. | | | 133,906 | |

| | 4,825 | | Marshall & Ilsley Corp. | | | 25,669 | |

| | 1,275 | | Stifel Financial Corp.* | | | 66,249 | |

| | 4,700 | | TradeStation Group, Inc.* | | | 36,284 | |

| | 1,625 | | Waddell & Reed Financial, Inc., Class A | | | 45,598 | |

| | | | | |

| |

| | | | | | | 699,780 | |

| | | | | |

| |

| | | | Health Services — 7.6% | | | | |

| | 600 | | athenahealth, Inc.* | | | 22,566 | |

| | 1,380 | | Cerner Corp.* | | | 104,935 | |

| | 11,400 | | Health Grades, Inc.* | | | 49,476 | |

| | 1,640 | | Lincare Holdings, Inc.* | | | 51,512 | |

| | 650 | | MEDNAX, Inc.* | | | 33,748 | |

| | 3,900 | | VCA Antech, Inc.* | | | 92,897 | |

| | 2,825 | | WellCare Health Plans, Inc.* | | | 73,817 | |

| | | | | |

| |

| | | | | | | 428,951 | |

| | | | | |

| |

| | | | Health Technology — 8.9% | | | | |

| | 2,300 | | Crucell N.V. ADR* | | | 45,425 | |

| | 2,050 | | Dendreon Corp.* | | | 51,804 | |

| | 800 | | Human Genome Sciences, Inc.* | | | 14,952 | |

33

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Health Technology — 8.9% (continued) | | | | |

| | 1,165 | | IDEXX Laboratories, Inc.* | | $ | 59,555 | |

| | 2,700 | | Kinetic Concepts, Inc.* | | | 89,613 | |

| | 2,175 | | Techne Corp. | | | 135,959 | |

| | 1,000 | | United Therapeutics Corp.* | | | 42,540 | |

| | 7,000 | | VIVUS, Inc.* | | | 55,300 | |

| | | | | |

| |

| | | | | | | 495,148 | |

| | | | | |

| |

| | | | Industrial Services — 2.4% | | | | |

| | 750 | | Core Laboratories N.V. | | | 78,225 | |

| | 2,700 | | Superior Energy Services, Inc.* | | | 58,347 | |

| | | | | |

| |

| | | | | | | 136,572 | |

| | | | | |

| |

| | | | Non-Energy Minerals — 1.5% | | | | |

| | 3,000 | | Century Aluminum Co.* | | | 26,010 | |

| | 1,350 | | Schnitzer Steel Industries, Inc., Class A | | | 58,374 | |

| | | | | |

| |

| | | | | | | 84,384 | |

| | | | | |

| |

| | | | Producer Manufacturing — 4.8% | | | | |

| | 1,850 | | A123 Systems, Inc.* | | | 36,371 | |

| | 1,425 | | Mettler-Toledo International, Inc.* | | | 138,938 | |

| | 1,500 | | Westinghouse Air Brake Technologies Corp. | | | 55,140 | |

| | 1,525 | | Woodward Governor Co. | | | 35,853 | |

| | | | | |

| |

| | | | | | | 266,302 | |

| | | | | |

| |

| | | | Retail Trade — 2.3% | | | | |

| | 1,800 | | Aeropostale, Inc.* | | | 67,554 | |

| | 1,460 | | J. Crew Group, Inc.* | | | 59,539 | |

| | | | | |

| |

| | | | | | | 127,093 | |

| | | | | |

| |

| | | | Technology Services — 19.1% | | | | |

| | 3,400 | | Blackbaud, Inc. | | | 75,446 | |

| | 4,600 | | CommVault Systems, Inc.* | | | 90,620 | |

| | 5,045 | | Fidelity National Information Services, Inc. | | | 109,779 | |

| | 2,800 | | Global Payments, Inc. | | | 137,844 | |

| | 3,877 | | Jack Henry & Associates, Inc. | | | 89,442 | |

| | 1,500 | | JDA Software Group, Inc.* | | | 29,760 | |

| | 2,095 | | MICROS Systems, Inc.* | | | 56,397 | |

| | 700 | | MicroStrategy, Inc., Class A* | | | 61,089 | |

| | 2,575 | | Open Text Corp.* | | | 95,378 | |

34

The FBR Funds

FBR Pegasus Small Cap Growth FundTM

Portfolio of Investments (continued)

October 31, 2009

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Technology Services — 19.1% (continued) | | | | |

| | 950 | | Quality Systems, Inc. | | $ | 57,969 | |

| | 5,025 | | Quest Software, Inc.* | | | 84,269 | |

| | 3,100 | | Solera Holdings, Inc. | | | 99,882 | |

| | 1,400 | | Sybase, Inc.* | | | 55,384 | |

| | 885 | | Syntel, Inc. | | | 31,710 | |

| | | | | |

| |

| | | | | | | 1,074,969 | |

| | | | | |

| |

| | | | Transportation — 3.9% | | | | |

| | 1,875 | | Genessee & Wyoming, Inc., Class A* | | | 54,394 | |

| | 8,400 | | Heartland Express, Inc. | | | 114,240 | |