UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: | 811-21673 |

THE ALLIANCEBERNSTEIN POOLING PORTFOLIOS

| (Exact name of registrant as specified in charter) |

| 1345 Avenue of the Americas, New York, New York | 10105 | |

| (Address of principal executive offices) | (Zip code) |

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: August 31, 2009

Date of reporting period: February 28, 2009

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

SEMI-ANNUAL REPORT

AllianceBernstein Pooling Portfolios

U.S. Value

U.S. Large Cap Growth

Global Real Estate Investment

International Value

International Growth

Small-Mid Cap Value

Small-Mid Cap Growth

Short Duration Bond

Intermediate Duration Bond

Inflation-Protected Securities

High-Yield

February 28, 2009

Semi-Annual Report

Investment Products Offered

| • | Are Not FDIC Insured |

| • | May Lose Value |

| • | Are Not Bank Guaranteed |

The investment return and principal value of an investment in the Fund will fluctuate as the prices of the individual securities in which it invests fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. You should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For a free copy of the Fund’s prospectus, which contains this and other information, visit our web site at www.alliancebernstein.com or call your financial advisor or AllianceBernstein® at (800) 227-4618. Please read the prospectus carefully before you invest.

You may obtain performance information current to the most recent month-end by visiting www.alliancebernstein.com.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AllianceBernstein’s web site at www.alliancebernstein.com, or go to the Securities and Exchange Commission’s (the “Commission”) web site at www.sec.gov, or call AllianceBernstein at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s web site at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

AllianceBernstein Investments, Inc. is an affiliate of AllianceBernstein L.P., the manager of the AllianceBernstein funds, and is a member of FINRA.

AllianceBernstein® and the AB Logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.

April 24, 2009

This report provides management’s discussion of fund performance for the AllianceBernstein Pooling Portfolios (collectively, the “Portfolios”; individually, the “Portfolio”) for the semi-annual reporting period ended February 28, 2009. Please note that effective November 24, 2008, AllianceBernstein Pooling Portfolios—Global Value Portfolio and Global Research Growth Portfolio have been liquidated.

The tables on pages 25-26 show each Portfolio’s performance for the six- and 12-month periods ended February 28, 2009, compared to their respective benchmarks. Additional performance can be found on pages 27-28. Each Portfolio’s benchmark is as follows: US Value Portfolio—Russell 1000 Value Index; US Large Cap Growth Portfolio—Russell 1000 Growth Index; Global Real Estate Investment Portfolio—Financial Times Stock Exchange (FTSE) European Public Real Estate Association (EPRA) National Association of Real Estate Investment Trusts (NAREIT) Global Real Estate (RE) Index; International Value Portfolio—Morgan Stanley Capital International (MSCI) Europe, Australasia and Far East (EAFE) Index; International Growth Portfolio—MSCI EAFE Index and MSCI EAFE Growth Index; Small-Mid Cap Value Portfolio—Russell 2500 Value Index; Small-Mid Cap Growth Portfolio—Russell 2500 Growth Index; Short Duration Bond Portfolio—Merrill Lynch 1-3 Year Treasury Index; Intermediate Duration Bond Portfolio—Barclays Capital US Aggregate

Index; Inflation-Protected Securities Portfolio—Barclays Capital 1-10 Year Inflation Protected Securities (TIPS) Index; High-Yield Portfolio—Barclays Capital US High Yield 2% Issuer Cap.

US Value Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in a diversified portfolio of equity securities of US companies with relatively larger market capitalizations as compared to the overall US equity market. The Portfolio’s investment policies emphasize investment in companies that AllianceBernstein L.P.’s (the “Adviser’s”) Bernstein unit (“Bernstein”) determines to be undervalued. In selecting securities for the Portfolio, Bernstein uses its fundamental research to identify companies whose long-term earnings power and dividend-paying capability are not reflected in the current market price of their securities. Under normal circumstances, the Portfolio invests at least 80% of its net assets in equity securities issued by US companies.

Investment Results

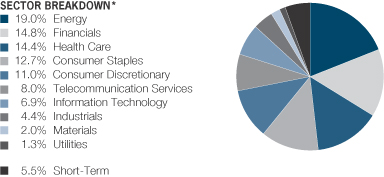

The Portfolio underperformed the benchmark, the Russell 1000 Value Index, for the six- and 12-month periods ended February 28, 2009, although both posted declines. Stock selection in financials and an underweight in utilities accounted for the largest drag on relative returns. Sector selection was a contributor to relative performance.

For the 12-month period, stock selection in financials and utilities

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 1 |

accounted for most of the Portfolio’s underperformance. Global recession fears also undermined many of the Portfolio’s consumer-related holdings. In utilities the Portfolio’s underweight in outperforming electric utility stocks hurt. The US Value Investment Policy Group’s (the “Group’s”) extensive analysis of financial companies focused primarily on the Portfolio’s holdings’ ability to absorb significant economic losses resulting from deteriorating credit-market conditions. However, the Group clearly underestimated the severity and abruptness of mark-to-market losses and rating-agency downgrades that ultimately prevented these firms from accessing credit markets or raising equity without heavy dilution.

Market Review and Investment Strategy

US equities collapsed over the reporting period ended February 28, 2009, amid continuing disarray in the global credit markets and a deepening recession. Growth stocks outperformed value stocks during both six- and 12-month periods.

The Group follows a central tenet of seeking to keep Portfolio risk in-line with the value opportunities it identifies. The Portfolio seeks to capture value while controlling tracking error. The Group selects about 150 large-cap US stocks, emphasizing the most attractively valued companies and industries by identifying companies priced below their long-term earnings power. The Group applies quantitative tools to control risk. Amid growing financial and economic

uncertainty, US markets remain highly volatile. Investor anxieties are evident in the Group’s measure of the value opportunity—the discount to fair value—which has widened dramatically over the past fiscal year to near-historical highs. As the Group knows from successfully managing the Portfolio through past crises, if the analysis of long-term earnings power remains focused, continues to balance opportunity against the risks entailed and applies the Portfolio’s time-tested value philosophy and portfolio-management techniques, the strategy may over time recapture its losses. Accordingly, the Portfolio reflects a balanced exposure to stocks across sectors that offer compelling value opportunities identified by the Group’s research.

US Large Cap Growth Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in equity securities of US companies with relatively larger market capitalizations as compared to the overall US equity market. The Portfolio focuses on a relatively small number of large, intensively researched US companies that the Adviser believes have strong management, superior industry positions, excellent balance sheets and superior earnings growth prospects.

Under normal circumstances, the Portfolio invests at least 80% of its net assets in equity securities issued by large-cap US companies. For these purposes, “large-cap US companies” are those that, at the time of investment, have market capitalizations

| 2 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

within the range of market capitalizations of companies appearing in the Russell 1000 Growth Index. While the market capitalizations of companies in the Russell 1000 Growth Index ranged from $30 million to almost $392 billion as of October 31, 2008, the Portfolio normally will invest in common stocks of companies with market capitalizations of at least $5 billion at the time of purchase.

The Adviser relies heavily on the fundamental analysis and research of its internal research staff to select the Portfolio’s investments. The Adviser looks for companies whose substantially above average prospective earnings growth is not fully reflected in current market valuations.

Investment Results

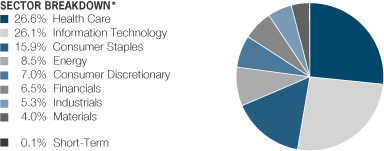

The Portfolio outperformed the benchmark, the Russell 1000 Growth Index, for the six-month period ended February 28, 2009, although both posted declines. The Portfolio benefitted from favorable relative performance from a number of health care stocks and a significant overweight position in the sector. Within consumer discretionary, sector allocation was neutral for the six-month period, but favorable stock selection boosted relative performance. Relative stock selection in the materials sector contributed to relative returns as well. Technology and energy holdings along with an overweight position in the financials sector detracted from relative returns.

For the 12-month period ended February 28, 2009, the Portfolio

outperformed the benchmark, although again, both posted negative returns. During the period, capital markets became more risk averse in the face of rapidly deteriorating global economic growth. Benefitting relative returns was a significant overweight in the health care sector, coupled with favorable stock selection, with six of the top ten contributing stocks coming from the health care sector. Positive positioning and relative stock selection in the consumer discretionary sector as well as favorable stock selection in the materials sector also contributed to relative returns. In the financials sector, an overweight position and unfavorable stock selection in the sector detracted the most from performance, along with unfavorable stock selection in the information technology sector.

Market Review and Investment Strategy

The period ended February 28, 2009, was marked by a wholesale flight to safety in the capital markets as evidence mounted that a global economy was entering a recession. The Standard & Poor’s (S&P) 500 Stock Index’s return for 2008 was the worst single year in the reported history of the index. No equity sector was spared from 2008’s broad downturn as every sector of the market declined in the quarter. During the period, consumer staples stocks plunged the least, while energy and financials fared worst. Volatility and risk aversion intensified as panicky investors overwhelmingly based decisions on an urgent desire to flee any hint of risk.

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 3 |

In short, economies and financial markets are stuck in a vicious cycle. Fears of an economic depression are accelerating the deleveraging in financial markets. As a result, credit is tightening, and consumers, corporations and municipal governments are spending less, which slows the economy further. But the cycle can be broken. While the current crisis is as severe as any in modern history, the magnitude and global scope of the policy response in both developed and developing economies is unparalleled. Some market adjustments in progress include major fiscal stimulus plans, aggressive monetary easing, government guarantees of bank deposits and liabilities, a plunge in oil prices and lower interbank lending rates.

Certainly, the current economic conditions are grim. Unemployment has been rising quickly and credit markets are still not functioning properly. Given the difficult environment and reduced earnings visibility for many of the companies in the S&P 500 Stock Index, the Portfolio’s US Large Cap Growth Investment Team (the “Team”) has positioned the Portfolio conservatively. The Team has focused on companies with relative earnings stability such as those in the health care and consumer staples sectors. During the period, the Portfolio remained underweight in those sectors with the greatest amount of economic sensitivity. This positioning proved prudent, as the Portfolio’s overweight in health care was a leading contributor to performance for both six- and 12-month periods.

Global Real Estate Investment Portfolio

Investment Objective and Policies

The Portfolio seeks total return from a combination of income and long-term growth of capital. The Portfolio invests primarily in equity securities of real estate investment trusts, or REITs, and other real estate industry companies, such as real estate operating companies, or REOCs. Under normal circumstances, the Portfolio invests at least 80% of its net assets in these types of securities. The Portfolio’s investment policies emphasize investment in real estate companies Bernstein believes have strong property fundamentals and management teams. The Portfolio seeks to invest in real estate companies whose underlying portfolios are diversified geographically and by property type. The Portfolio may invest up to 20% of its total assets in mortgage-backed securities, which are securities that directly or indirectly represent participations in, or are collateralized by and payable from, mortgage loans secured by real property. The Portfolio has many of the same risks as direct ownership of real estate, including the risk that the value of real estate could decline due to a variety of factors affecting the real estate market. In addition, REITs are dependent on the capability of their managers, may have limited diversification and could be significantly affected by changes in tax laws.

Investment Results

The Portfolio outperformed the benchmark, the FTSE EPRA/NAREIT Global RE Index for the

| 4 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

six- and 12-month periods ended February 28, 2009. The Portfolio and the benchmark posted negative returns for both periods. Performance versus the benchmark was driven by favorable security selection, sector and country exposure.

During the six-month period, global economic growth experienced a marked decline as the financial crisis continued to evolve. The failure or near failure of a number of prominent US and UK financial institutions underscored the severity of this economic cycle. The growing contagion of the crisis to credit and equity markets around the world also intensified for the period, and a massive reduction in the financial leverage of the private sector and a retrenchment of global consumers is now being experienced. As a consequence, world economies appear to have entered a synchronized downturn. It is not possible to determine the ultimate impact of the crisis on real estate fundamentals; however, the Portfolio’s REIT Investment Policy Group (the “Group”) believes it will be negative to commercial real estate demand, and has continued to position the Portfolio to withstand a prolonged period of subpar economic growth and reduced liquidity availability.

Absolute returns of real estate securities were poor for the reporting period due to investor anxiety related to dysfunctional capital markets, liquidity shortages and recession fears. However, defensive positioning focused on diversification and exposure to companies with a reliable

cash flow stream helped drive the Portfolio’s outperformance compared to the benchmark.

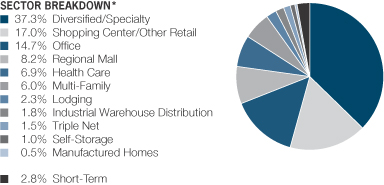

During the six-month period, security selection in the retail and diversified sectors drove performance. In the US, Europe and Brazil, the Group has been able to identify attractively valued companies in segments of the retail markets where fundamentals are stronger and cash flows can be expected to be relatively more resilient. For example, the Portfolio holds and overweights a position in an owner of retail factory outlets which offers an attractive value proposition to well-known brands that can retail their products, incurring occupancy costs that are much lower than in regional malls or strip malls. Consumers like this retail format because they can find their favorite brands at a lower price point than in the malls, so consumer traffic has been positive. In addition, the company has been very conservative in managing its balance sheet and enjoys no maturities of significance over the next two years. Some of the Portfolio’s investments in European retail REITs also performed well, supported by solid supply fundamentals, stable demand, rent indexation (CPI or other indicative index of general price increase which rents are indexed to) and a conservative capital structure complemented with a robust interest coverage ratio.

Some of the Portfolio’s US and HK investments with exposure to development businesses were key detractors from performance for the

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 5 |

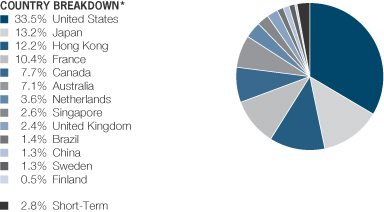

six-month period. These companies were penalized by the market on the expectation that they will suffer volume declines during the current economic downturn. While the Group is of a view that the earnings may be weaker in the near future, the strength of their development platforms and balance sheet should support these companies’ ability to navigate successful through the downturn. HK residential developers, in particular, have suffered from investor fears related to layoffs and retrenchment of the financial services sector, which figures prominently as a driver of HK’s economy. The Group believes that, with a solid supply-demand backdrop, demand for apartments will revive once the economy stabilizes and household confidence improves.

In addition to retail exposures described above, the Portfolio’s US health care positions also contributed to relative performance for the 12-month period ended February 28, 2009. Health care REITs own real estate that is leased to nursing homes, assisted living, independent living and hospital operators, in addition to specialized office space leased as medical offices. Most of the contracts with health care operators are structured on a “triple net basis” where the tenant pays for insurance, taxes and maintenance. This reduces the risk to the owner and increases the reliability of the income stream. Cash-flow consistency has become very attractive to investors as risk aversion has increased. Facility occupancies have stabilized for the assisted living and

independent living subsectors of health care real estate, and business fundamentals are stable. Generally, as investor fears of the impact of US housing declines on seniors’ enrollment in assisted living and nursing home facilities diminished, sentiment toward health care real estate stocks improved and health care real estate stocks outperformed.

US niche investments also positively contributed for the period. For example, the Portfolio’s overweight position in a company that invests in, repositions and develops data-center specialized real estate was a contributor. This space demands custom structural design, power supply and climate control. Favorable fundamentals in this market niche suggest that it may be less affected by the cyclical downturn. Canadian REITs also contributed to performance as relative to other countries: liquidity and financing availability has been greater in Canada, underpinned by a banking system that appears to have fared better during this credit crisis. For the 12-month period, security selection in HK lagged the benchmark. In this region, companies that combine development activities with more stable rental property business detracted from relative performance as low risk appetite prevailed in the global equity markets and investors, fearing the impact of a global liquidity squeeze, were particularly anxious about development strategies where cash flows are less reliable than in the own-to-lease businesses.

| 6 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Market Review and Investment Strategy

The decline in global real estate markets was pronounced for both the six- and 12-month periods ended February 28, 2009, with the FTSE EPRA/NAREIT Global RE Index declining -55.35% and -59.53%, respectively. Most of the decline experienced by the index materialized in the six-month period, as the impact and severity of the credit turmoil escalated and risk aversion among investors intensified. During the latter part of the 12-month period, concerns about the impact of the credit cycle on consumers, economic growth and real estate valuations dominated capital markets sentiment and contributed to high equity volatility. The global credit squeeze has been felt across markets as the cost of borrowing has increased and availability of credit has diminished in most major markets.

While fundamentals vary by region of the world and by property type, in general, new commercial real estate construction during the period has been subdued, partly due to high construction costs. As a result, commercial real estate has entered the downturn with robust occupancy rates, a manageable supply of new space in the pipeline and in-place rents which, in many cases, are below prevailing market rents (thus giving some owners an opportunity to increase cash flows as leases expire and new rents are set).

The Group believes the Portfolio is well positioned to withstand a period of turmoil. Stock selection emphasizes

companies with ample dividend coverage, reasonable leverage and high-quality tenants. The Portfolio’s global scope should allow the Group to uncover new opportunities while focusing on stocks unduly penalized by the market turmoil, attractively valued stocks in markets less affected by the credit crisis, and niche segments where demand dynamics are relatively insulated from the ongoing demand slowdown.

International Value Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in a diversified portfolio of equity securities of established companies selected from more than 40 industries and from more than 40 developed and emerging market countries. The Portfolio’s investment policies emphasize investment in companies that Bernstein determines to be undervalued. In selecting securities for the Portfolio, Bernstein uses its fundamental research to identify companies whose long-term earnings power is not reflected in the current market price of their securities.

Investment Results

The Portfolio underperformed the benchmark, the MSCI EAFE Index, for the six- and 12-month periods ended February 28, 2009, although both posted declines. For both periods, underperformance was due primarily to negative security selection, and hurt most by the Portfolio’s financial holdings. Security selection in the capital equipment sector also hurt relative performance during both

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 7 |

periods, though to a lesser degree. Sector selection was negative for both periods, hurt by the Portfolio’s overweight of the industrial commodities sector.

The stocks the Portfolio owns, often characterized by uncertainty over their near-term prospects, tend to outperform in the long run. In periods of heightened risk aversion, however, investors shun these stocks. Thus, stock selection was negative across most sectors, as low-priced stocks underperformed almost everywhere. While the International Value Investment Policy Group’s (the “Group’s”) analysis of financial companies was extremely detailed, it focused on their ability to absorb severe credit losses. The Group underestimated the impact that an extended period of risk aversion would have on the liquidity of credit markets, where some of the Portfolio’s holdings faced severe refinancing risks. Nor did the Group foresee how regulators and ratings agencies would react to these conditions.

Market Review and Investment Strategy

Global equity markets have declined during the period ended February 28, 2009, following turmoil in the financial system that threatened to plunge the global economy into a deep and prolonged recession. Global industrial production is plummeting, unemployment is rising quickly, and credit markets remain nearly frozen. The US led much of the developed world into recession, while emerging-market economies that have powered global

growth in recent years, such as China, have also slowed sharply.

The Group follows a central tenet of seeking to keep portfolio risk in-line with the value opportunities it identifies. The Portfolio selects attractively valued stocks by using rigorous research to identify companies priced below the long-term earnings power. After a lengthy period of compression, valuation spreads have widened. The Group continues to take advantage of investor overreaction to economic and industrial stresses, using its deep research capabilities to look for investment opportunities arising from current market volatility.

International Growth Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in an international portfolio of equity securities of companies located in both developed and emerging market countries. The Portfolio’s investment process relies upon comprehensive fundamental company research produced by the Adviser’s large research team of analysts covering both developed and emerging markets around the globe. Research-driven stock selection is expected to be the primary driver of returns relative to the Portfolio’s benchmark and other decisions, such as country selection, are generally the result of the stock selection process. The Portfolio invests, under normal circumstances, in the equity securities of companies located in at least three countries (and normally substantially more) other than the United States.

| 8 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Investment Results

The Portfolio’s broad-based benchmark has changed from the MSCI AC World Index (Ex-US) to the MSCI EAFE Index. The former benchmark includes both developed (other than the US) and emerging markets in its performance calculations. The Portfolio does not make substantial investments in emerging markets. The MSCI EAFE Index is a more appropriate broad-based benchmark for the Portfolio since it has minimal emerging markets exposure and also excludes the performance of US issuers. Performance of the MSCI EAFE Growth Index as a secondary benchmark for the Portfolio is also included.

The Portfolio underperformed the MSCI EAFE Growth Index and the MSCI EAFE Index for the six- and 12-month periods ended February 28, 2009; both benchmarks and the Portfolio posted declines. For the six-month period, an overweight in health care and an underweight in technology relative to the benchmark most benefited performance, as did solid stock selection in energy, consumer staples and health care. These benefits however, were offset by poor stock selection in financials, materials and utilities.

For the 12-month period, performance was negatively impacted by poor stock performance in the financials, materials and industrials sectors. This underperformance overwhelmed the performance of stocks in the consumer staples and energy sectors. Returns were helped by an overweight in

health care relative to benchmark that performed well versus an underweight in technology that did poorly.

Market Review and Investment Strategy

Equity markets have continued to decline during the period ended February 28, 2009. 2008 was a challenging year for equity investors, as fears about the health of the global economy and the impact it would have on corporate earnings, translated into collapsing stock prices. The six-month period ended February 28, 2009, was dominated by concerns about financial market contagion. As the credit crisis evolved, the economic environment deteriorated and investors began to shun risky assets in favor of safety, certainty and security. This wholesale flight to safety reached a climax toward the end of 2008, as further evidence of the severity of the global slowdown emerged. The International Growth Portfolio Oversight Group (the “Group”) expected a slowdown, but was surprised by its severity, the speed with which it occurred and the financial turmoil it created. Sentiment has been badly affected, and this is likely to have a continued detrimental impact on activity and therefore corporate prospects.

Governments everywhere have been quick to realize this, and elicited a massive policy response, designed to restore calm to troubled markets and sow the seeds of an eventual recovery. The Group believes this will work. The Portfolio has consequently been adjusted so as to increase exposure to stable growth companies that have

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 9 |

strong balance sheets and reliable revenue streams that may better help them weather the current storm. This has been balanced with exposure to companies that the Group believes are likely to be early beneficiaries of a recovery. Although the market upheaval has been painful to equity investors generally, and to the Portfolio in particular, the Group believes that the Portfolio is well positioned to do well in the rebound it expects. The Group is convinced that during turbulent times, like now, it is important to maintain investment discipline and keep true to one’s process, as this should increase the chances of achieving investment success. The Portfolio’s overall investment strategy, with a focus on research driven stock selection, remains intact. During the reporting period, the Group continued to place emphasis on companies it believes will exhibit future growth rates that exceed the market’s expectations. The Portfolio continues to hold diversified stocks which exhibit positive relative earnings potential and price momentum characteristics, with strong representation in both developed and emerging markets, and in a wide array of economic sectors.

Small-Mid Cap Value Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in a diversified portfolio of equity securities of small- to mid-capitalization US companies, generally representing 60-110 companies. For these purposes, “small- and mid-cap companies” are

those that, at the time of investment, fall within the capitalization range between the smallest company in the Russell 2500 Value Index and the greater of $5 billion or the market capitalization of the largest company in the Russell 2500 Value Index. Under normal circumstances, the Portfolio invests at least 80% of its net assets in these types of securities. The Portfolio’s investment policies emphasize investment in companies that Bernstein determines to be undervalued. In selecting securities for the Portfolio, Bernstein uses its fundamental research to identify companies whose long-term earnings power is not reflected in the current market price of their securities. The Portfolio may also invest up to 20% of its total assets in equity securities issued by non-US companies.

Investment Results

The Portfolio underperformed the benchmark, the Russell 2500 Value Index, for the six- and 12-month periods ended February 28, 2009, although both posted declines. Underperformance was driven primarily by adverse stock selection for both periods.

For the six-month period, the Portfolio’s underperformance occurred between September and November 2008, as investor anxiety over the economy and the state of the capital markets worsened. Underperformance was driven primarily by adverse stock selection which was spread across a number of sectors but concentrated in stocks with more cyclical exposure, such as industrial commodities and

| 10 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

capital equipment. Stock selection was also a detractor in utilities, as a result of concerns over capital markets access for some of the Portfolio’s holdings in the sector. Stock selection in financials was a relative contributor for the period, as several of the Portfolio’s insurance and bank holdings benefited from having more stable investment and loan portfolios and investors sought companies where there was less risk of losses and eroding book value. Sector selection was modestly negative as beneficial overweights in technology and consumer staples were offset by an underweight in utilities. Holdings in the utilities sector showed strong relative performance as investors sought more defensive names as anxiety over the economy increased.

For the 12-month period ended February 28, 2009, many of the same themes emerged which is not surprising given the powerful volatility and performance trends that emerged over the second half of 2008. Sector selection was essentially neutral as the Portfolio’s overweight position in consumer staples and underweight position in financials were offset by an underweight in utilities. Adverse stock selection was again broadly based as returns to value and quality factors were muted or negative over the 12-month period. Again, it was more pronounced in sectors with more economic exposure—such as capital equipment and industrial resources. Stock selection in financials continued to be the Portfolio’s strongest relative contributor.

Market Review and Investment Strategy

Investor anxiety over depressed global economic growth and continued financial contagion for the period ended February 28, 2009, has deepened the value opportunity in smaller cap markets. The Small/Mid Cap Value Investment Policy Group (the “Group”) seeks to capture a diverse array of compelling opportunities—including many in cyclical industries—while guarding against the risk of a prolonged economic downturn. The effects of investors’ indiscriminate sell-off of any stock with perceived exposure to the global economy and the distorting influence of hedge-fund delevering—which disproportionately benefited smaller stocks, especially in the third quarter of 2008—have created a higher quality and larger cap bias to this opportunity in the smaller cap universe. As a result, the Group has increased both the quality and relative market cap within the Portfolio, while keeping valuations attractive.

The opportunity is also remarkably diverse, spanning many industries and sectors. However, since companies and sectors sensitive to the economic cycle performed worse in 2008, many have become very attractively valued. Over the fourth quarter and into 2009, the Group has increased the Portfolio’s exposure to sectors such as energy and technology while reducing exposure to financials. In the Group’s analysis, investors have overreacted to the threats posed by the financial crisis and recession; many cyclicals today are valued as if their earnings will never recover. But recessions end, credit

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 11 |

markets ease and companies address their problems. Thus historically, cyclical stocks purchased when investor anxiety was acute have rebounded hugely after past downturns have eased.

Even with the pullback in oil prices, the Group remains sensitive to the fact that the causes of investor anxiety, fears over ongoing financial contagion and slowing economic growth, may continue for some time. Further, the risk from this prolonged anxiety—that companies with perceived exposure to the consumer and the economy will underperform—is higher than average in the short term. Offsetting this risk somewhat, in the Group’s view, is the quality and business model strength of the companies it’s adding to the Portfolio. The Group believes this will allow the Portfolio to navigate the current environment and in many cases emerge stronger as weaker competitors fall by the wayside. Further, the Group feels that the longer-term return potential for these companies is compelling given their current valuations and have begun adding them to the Portfolio where the Group believes that the risk is justified by the potential returns.

Small-Mid Cap Growth Portfolio

Investment Objective and Policies

The Portfolio seeks long-term growth of capital. The Portfolio invests primarily in a diversified portfolio of equity securities with relatively smaller market capitalizations as compared to the overall US equity market. Under normal circumstances, the Portfolio invests at least 80% of its net assets in

small- and mid-cap companies. For these purposes, “small- and mid-cap companies” are those that, at the time of investment, have market capitalizations in the greater of the range of companies constituting the Russell 2500 Growth Index or between $1 and $6 billion. The market caps of companies in the Russell 2500 Growth Index ranged from $10 million to $6.1 billion as of October 31, 2008. Because the Portfolio’s definition of small- to mid-cap companies is dynamic, the upper limit on market capitalization will change with the markets.

Normally, the Portfolio invests in US companies that the Adviser believes have strong management, superior industry positions, excellent balance sheets and superior earnings growth prospects. The Adviser relies heavily on the fundamental analysis and research of its internal research staff to select the Portfolio’s investments. The Portfolio may also invest up to 20% of its total assets in equity securities issued by non-US companies.

Investment Results

The Portfolio outperformed the benchmark, the Russell 2500 Growth Index, for both the six- and 12-month periods ended February 28, 2009, although the Portfolio and the benchmark suffered sharp declines during both periods. A wholesale flight to safety intensified throughout the six-month period, as evidence mounted that the global economy was entering a recession. Weakness was widespread, with all sectors posting declines in excess of 30% during both the six- and 12-month periods.

| 12 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Stock selection in the consumer/commercial services sector was the largest positive contributor in both six- and 12-month periods, which more than offset disappointing relative returns in the industrial and health care sectors. Favorable sector allocations also provided a modest boost throughout both periods, as the Portfolio benefited from an underweight in the very poor-performing industrials sector and an overweight in health care throughout much of the reporting period.

Market Review and Investment Strategy

For the reporting period ended February 28, 2009, US equities, as represented by the S&P 500 declined sharply, as global growth slowed and the financial crises came to a head. The biggest declines came during the three-month period following the demise of Lehman Brothers, as investors appetite for risk virtually disappeared. Small- and mid-cap growth investors suffered even greater declines given the generally riskier profile of smaller-capitalization stocks.

Sector allocations within the Portfolio changed modestly for the six-month period under review, as the Portfolio’s Small Cap Growth Investment Team (the “Team”) moved its consumer/commercial services exposure from slightly below benchmark to a sizeable overweight in the latter part of the reporting period. These purchases were funded by shifting from a marketweight in health care to an underweight, and an elimination of an overweight in technology. The Portfo-

lio’s largest overweights as of February 28, 2009, were consumer/commercial services and energy; the largest underweights were industrials and health care. Worth noting, active sector exposures have been reined in to below average levels, as the Team seeks to manage Portfolio risk in the currently volatile environment. Consistent with the Team’s discipline, investments throughout the reporting period emphasized companies whose earnings growth potential had been underestimated by the marketplace.

Short Duration Bond Portfolio

Investment Objective and Policies

The Portfolio seeks a moderate rate of income that is subject to taxes. The Portfolio invests primarily in investment-grade, US Dollar-denominated fixed-income securities. Under normal circumstances, the Portfolio invests at least 80% of its net assets in fixed-income securities. The Portfolio seeks to maintain a relatively short duration of one to three years under normal market conditions. The Portfolio may invest in many types of fixed-income securities, including corporate bonds, notes, US Government and agency securities, asset-backed securities, mortgage-related securities and inflation-protected securities, as well as other securities of US and non-US issuers.

Investment Results

The Portfolio underperformed the benchmark, the Merrill Lynch 1-3 Year Treasury Index, for the six- and 12-month periods ended February 28, 2009. A broad liquidity

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 13 |

crisis stemming from the credit crunch contributed to underperformance. Treasury yields fell and spreads widened across all fixed-income markets. Detracting from the Portfolio’s relative performance for both periods was an underweight in US government debt as well as exposure to agency MBS, agency debt, commercial mortgage-backed securities (CMBS), subprime-related ABS and Alt-A mortgage (home loans made with less than full documentation) securities, which all underperformed treasuries. (Leverage did not have any meaningful impact on performance.)

Market Review and Investment Strategy

For the reporting period ended February 28, 2009, the spreading financial crisis and its impact on the global economy drove fixed-income yield spreads sharply wider. Investor risk aversion significantly increased as economic data pointed to a continued deteriorating economy. During the reporting period the US Federal Reserve (the “Fed”) responded to the crisis with multiple interest rate cuts, which aimed to restore confidence in the financial markets and put the economy on firmer footing. The Fed funds rate was reduced by a total of 200 basis points (bps) for the reporting period, leaving the interest rate at between 0.0% and 0.25% at the end of the reporting period.

There was heightened demand for US Treasuries during the semi-annual period as investors sought less-risky assets in light of the subprime market volatility. US Treasury holdings

outperformed spread sectors on both an absolute and duration-adjusted basis for the period. Shorter-term yields fell most, with two-year yields losing 140 bps to yield 0.98% while the ten-year yield lost 80 bps to end the period at 3.02%. Longer-maturity (15+ year) US Treasuries at 9.40% outperformed both shorter-term (1-3 Year) US Treasuries at 3.05% and Intermediate-term (5-10 Year) US Treasuries at 6.88% during the six-month period, according to Merrill Lynch. The US Investment Grade/Liquid Markets/Structured Products Investment Team (the “Team”) significantly increased the Portfolio’s weighting in MBS while also adding exposure to investment-grade corporates and agency debentures. The Team reduced the positions in subprime asset-backed securities (ABS) and non-agency mortgages for the period under review.

Intermediate Duration Bond Portfolio

Investment Objective and Policies

The Portfolio seeks a moderate to high rate of income that is subject to taxes. The Portfolio may invest in many types of debt securities including corporate bonds, notes, US Government and agency securities, asset-backed securities, mortgage-related securities, and inflation-protected securities as well as other securities of US and non-US issuers. Under normal circumstances, the Portfolio invests at least 80% of its net assets in fixed-income securities. The Portfolio seeks to maintain a relatively longer duration of three to six years under normal market conditions. The Portfolio may

| 14 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

invest up to 20% of its total assets in debt securities denominated in currencies other than the US Dollar. The Portfolio may also invest up to 20% of its assets in hybrid instruments, which have characteristics of futures, options, currencies and securities.

Investment Results

The Portfolio underperformed the benchmark, the Barclays Capital US Aggregate Index, for the six- and 12-month periods ended February 28, 2009. For both periods the following positions detracted from performance: underweights in Treasuries and agencies; exposure to subprime-related ABS and Alt-A mortgage securities; overweights in investment-grade corporates and CMBS; and positions in high-yield and emerging markets. The Fund’s exposure to subprime-related ABS and Alt-A mortgage securities detracted from performance despite their AAA and AA ratings. Leverage did not impact performance for either six- or 12-month period.

Market Review and Investment Strategy

The spreading financial crisis and its impact on the global economy drove fixed-income yield spreads sharply wider during the reporting period ended February 28, 2009. Investor risk aversion significantly increased as economic data pointed to a continued deteriorating economy. During the reporting period the US Federal Reserve responded to the crisis with multiple interest rate cuts, which aimed to restore confidence in the financial markets and put the economy on firmer footing. The Fed funds rate

was reduced, leaving the interest rate between 0.0% and 0.25% at the end of the reporting period.

There was heightened demand for US Treasuries during the reporting period as investors sought less-risky assets in light of the credit crisis market volatility. For the six-month period, US Treasury holdings outperformed spread sectors on both an absolute and duration adjusted basis. During the period, shorter-term yields fell most, with two-year yields losing 140 bps to yield 0.98%, while the ten-year yields lost 80 bps to end the period at 3.02%. According to Merrill Lynch, longer maturity (15+ year) US Treasuries, which returned 9.40% outperformed both shorter-term (1-3 Year) Treasuries at 3.05% and Intermediate-term (5-10 Year) US Treasuries at 6.88% during the six-month period

During the six-month period the Portfolio’s US Investment Grade: Core Fixed Income Team (the “Team”) continued to underweight Treasuries and agencies in favor of overweight allocations to the corporate sector and in AAA-rated super-senior commercial mortgage-backed securities. In the Team’s view, these sectors represent an outstanding opportunity for investors to benefit from attractive excess returns over government bonds. Current valuations in investment-grade corporates are at the widest levels since the Depression, and imply a default rate nearly four times investment-grade defaults’ experience during that period. While the breadth and depth of the global slowdown is

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 15 |

unknown, and the recovery—for both the credit markets and the economy—will take time, worst-case scenarios, coupled with significant liquidity premiums, are priced into today’s valuations. As risk aversion begins to abate and valuations align with fundamentals, the Team believes investment-grade corporates and CMBS should again outperform.

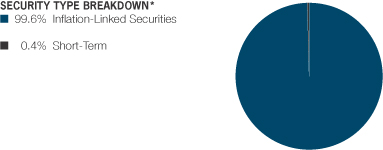

Inflation-Protected Securities Portfolio

Investment Objective and Policies

The Portfolio seeks a total return that exceeds the rate of inflation over the long term with income that is subject to taxes. The Portfolio invests primarily in US Dollar-denominated inflation-protected securities. Under normal circumstances, the Portfolio invests at least 80% of its net assets in inflation-protected securities. The Portfolio’s investments in inflation-protected securities include inflation-protected debt securities of varying maturities issued by US or non-US governments, their agencies or instrumentalities and by corporations, and inflation derivatives. The Portfolio seeks to maintain a duration within three years (plus or minus) of the duration of the Barclays Capital US 1-10 Year TIPS Index, which as of October 31, 2008, was 3.04 years.

Assets not invested in inflation-protected securities may be invested in other types of debt securities, including corporate bonds, notes, US Government and agency securities, asset-backed securities, and mortgage-related securities as well as other securities of US and non-US issuers.

Investment Results

The Portfolio modestly underperformed the benchmark, the Barclays Capital 1-10 Year TIPS Index, for the six- and 12-month periods ended February 28, 2009, although both posted declines. For both periods, the Portfolio’s longer duration relative to the index contributed to the underperformance. For the six-month reporting period, TIPS real yields rose, especially in the short-term as the TIPS real yield curve flattened and negatively impacted performance. The inflation accrual for the six-month period was -7.8% on an annualized basis, resulting in a negative absolute return for the Portfolio.

Market Review and Investment Strategy

For the period ended February 28, 2009, the credit crisis entered a new and more menacing phase late in the year with fear of counterparty risk paralyzing interbank lending. The inability to access capital led to a crisis for financial institutions, causing the failure of Lehman Brothers, prompting rapid-fire acquisitions, driving long-standing independent firms to merge and forcing the government to intervene. Extreme risk aversion that seized the markets following the September 2008 bankruptcy of Lehman Brothers accelerated into the fourth quarter of 2008 as massive global deleveraging continued. Tumult in the financial markets bled into the real economy, in the US and across the globe. Economic data for virtually every country showed sharp if not historic declines. Investors flocked to the safety of governments and credit

| 16 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

markets sold off violently. The yield on US Treasury bills even reached near zero, showing that investors were willing to forgo a return on their investment in exchange for a safe place to park their cash. While global government bond yields hit or neared record lows, yield spreads on investment-grade corporate bonds shot to peaks unseen since the 1930s, and the MSCI World Index declined -40.71% for the full year 2008 in US dollars—the worst annual loss since the equity benchmark’s inception in 1970.

The drumbeat of negative economic news continued into 2009 as global equity markets declined further. The US unemployment rate surged to its highest level in 25 years as payrolls fell and the unemployment rate jumped to 8.1%. The housing market continued to struggle and the Commerce Department reported that US gross domestic product (GDP) fell by -6.3% in the fourth quarter of 2008. In response to the financial and economic crisis central banks lowered rates, governments pledged record fiscal stimulus and the Obama administration announced several government sponsored programs to aid homeowners and restore the flow of credit to consumers and small businesses.

US Treasuries posted a solid return of 5.67% for the six month reporting period benefiting from a flight to quality. US Treasury yields fell sharply across the maturity spectrum with shorter term yields falling most. The two-year yield declined 140 bps to end the period at 0.97%, while the ten

year yield declined 80 bps to end the period at 3.01%. The yield curve steepened 60 bps between the two and ten year yield. TIPS as represented by the benchmark posted an absolute return -6.73% for the six-month period. Ten-year TIPS underperformed comparable maturity Treasuries by approximately 1,183 bps.

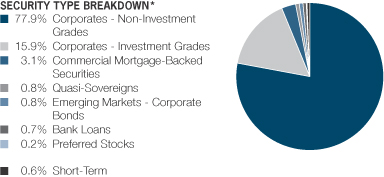

High-Yield Portfolio

Investment Objective and Policies

The Portfolio seeks a high total return by maximizing current income and, to the extent consistent with that objective, capital appreciation. The Portfolio invests primarily in high-yield debt securities. Under normal circumstances, the Portfolio invests at least 80% of its net assets in these types of securities. The Portfolio invests in high-yield, below investment-grade debt securities, commonly known as “junk bonds.” The Portfolio seeks to maximize current income by taking advantage of market developments, yield disparities, and variations in the creditworthiness of issuers.

Investment Results

The Portfolio underperformed the benchmark, the Barclays Capital US High Yield 2% Issuer Cap Index, for the six- and 12-month periods ended February 28, 2009, although both posted declines. For both periods the Portfolio’s industry allocation detracted from relative performance, while security selection was positive. An overweight in financial-related holdings and an underweight in consumer noncyclicals were primary detractors from performance. The Portfolio’s overweight in telecommunications, which

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 17 |

outperformed, contributed positively. Security selection within electric and energy holdings was positive, while media and automotive security selection detracted for both periods. The Portfolio’s use of leverage also detracted for the six- and 12-month periods.

Market Review and Investment Strategy

The credit crisis intensified for the periods ended February 28, 2009, with fear of counterparty risk paralyzing interbank lending. The inability to access capital led to a crisis for financial institutions, causing the failure of Lehman Brothers in September 2008, prompting rapid-fire acquisitions, driving long-standing independent firms to merge and forcing government intervention. The extreme risk aversion that seized the markets in September accelerated into the fourth quarter of 2008, as massive global deleveraging continued. Tumult in the financial markets bled into the real economy, both in the US and across the globe. Economic data for virtually every country showed sharp if not historic declines. Investors flocked to the safety of governments and credit markets sold off violently. The yield on US Treasury bills even reached near zero, showing that investors were willing to forgo a return on their investment in exchange for a safe place to park their cash. While global government bond yields hit or neared record lows, yield spreads on investment-grade corporate bonds shot to peaks unseen since the 1930s, and the MSCI World Index, which measures global developed market

equity performance, declined 40.71% for the full year 2008 in US dollars—the worst annual loss since the equity benchmark’s inception in 1970.

The drumbeat of negative economic news continued for the reporting period ended February 28, 2009, as global equity markets declined further. The US unemployment rate surged to its highest level in 25 years as payrolls fell; the unemployment rate jumped to 8.1%. The housing market also continued to struggle. In response to the financial and economic crisis central banks lowered rates, governments pledged record fiscal stimulus and the Obama administration announced several government-sponsored programs to aid homeowners and restore the flow of credit to consumers and small businesses.

US high-yield debt followed the equity markets lower during the reporting period and turned in its worst annual performance on record for the calendar year 2008. For the six-month period, high-yield returned -21.50%, according to the Barclays Capital US High Yield 2% Issuer Cap Index. Spreads almost doubled, moving from 778 bps to 1,524 bps by period end. By quality tier, lower-rated high-yield debt significantly underperformed higher-rated debt. By industry, banking, brokerage, automotive, gaming and building materials were among the worst performing industries adversely affected by the significant economic downturn.

Wider high-yield spreads from market turmoil have created opportunities;

| 18 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

however, uncertainty regarding investors’ appetite for risk remains a concern. With the continuing credit crisis and recession, the Portfolio’s Global Credit Investment Team (the “Team”) does expect defaults to increase from the historic lows of the past few years. However, a lot of “bad news” is already reflected in security prices. Recovery in the second half of 2009 will depend on a variety of factors, but most critical will be whether consumers and businesses respond to economic incentives and start to take on risk. While there are some unusual

and unique features in this downturn that have resulted in a particularly hard landing, the Team believes that forces for an eventual recovery are being marshaled. Central banks have slashed interest rates, governments have pledged record fiscal stimulus, programs are being enacted to loosen credit and corporations are liquidating their inventories. In the Team’s view, therefore, even if the tough environment creates a worse-than-expected outcome in the first half of 2009, a second half recovery may still be the best bet.

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 19 |

HISTORICAL PERFORMANCE

An Important Note About the Value of Historical Performance

The performance shown on the following pages represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting our website at www.alliancebernstein.com.

The investment return and principal value of an investment in the Portfolios will fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. You should consider the investment objectives, risks, charges and expenses of the Portfolios carefully before investing. For a free copy of the Portfolios’ prospectus, which contains this and other information, contact your AllianceBernstein representative or call 800.227.4618. You should read the prospectus carefully before you invest.

Please note: Shares of the Portfolios are offered exclusively to mutual funds advised by, and certain institutional clients of, AllianceBernstein that seek a blend of asset classes for investment. These share classes are not currently offered for direct investment from the general public. The AllianceBernstein Pooling Portfolios can be purchased at the relevant net asset value (NAV) without a sales charge or other fee. However, there are sales charges in connection to purchases of other AllianceBernstein share classes invested in these Pooling Portfolios. For additional information regarding other retail share classes and their sales charges and fees, please visit www.alliancebernstein.com. All fees and expenses related to the operation of the Portfolios have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

Benchmark Disclosures

None of the indices listed below reflect fees and expenses associated with the active management of a mutual fund portfolio.

The unmanaged Russell 1000 Value Index contains those securities in the Russell 1000 Index with a less-than-average growth orientation. The unmanaged Russell 1000 Index is composed of 1000 of the largest capitalized companies that are traded in the United States.

The unmanaged Russell 1000 Growth Index contains those securities in the Russell 1000 Index with a greater-than-average growth orientation.

The unmanaged Russell 1000 Index is composed of 1000 of the largest capitalized companies that are traded in the US.

The unmanaged Financial Times Stock Exchange (FTSE) European Public Real Estate Association (EPRA)/National Association of Real Estate Investment Trust (NAREIT) Global RE Index is a free-floating, market capitalization-weighted index structured in such a way that it can be considered to represent general trends in all eligible real estate stocks worldwide. The Index is designed to reflect the stock performance of companies engaged in specific aspects of the North American, European and Asian real estate markets.

The unmanaged MSCI Europe, Australasia and Far East (EAFE) Index is a market capitalization index that measures stock performance in 21 countries in Europe, Australasia and the Far East. Returns for this Index are net. In calculating net returns, the dividend is reinvested after deduction of withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties.

(Historical Performance continued on next page)

| 20 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

The unmanaged MSCI EAFE Growth Index is a subset of the MSCI EAFE Index and generally represents approximately 50% of the free float-adjusted market capitalization of each appropriate Single Country Index and consists of those securities classified by MSCI as most representing the growth style.

The unmanaged Russell 2500 Value Index contains those securities in the Russell 2500 Index with a less-than-average growth orientation. The unmanaged Russell 2500 Index includes 2500 small- and mid-cap US stocks.

The unmanaged Russell 2500 Growth Index contains those securities in the Russell 2500 Index with a greater-than-average growth orientation. The unmanaged Russell 2500 Index includes 2500 small- and mid-cap US stocks.

The unmanaged Merrill Lynch 1-3 Year Treasury Index is composed of US government securities, including agency securities, with remaining maturities of one to three years.

The unmanaged Barclays Capital US Aggregate Index covers the US investment-grade fixed-rate bond market, including government and credit securities, agency mortgage pass through securities, asset-backed securities and commercial mortgage-backed securities.

The unmanaged Barclays Capital 1-10 Year TIPS Index is the 1-10 year maturity component of the unmanaged Barclays Capital US Treasury Inflation Notes Index and consists of inflation-protection securities issued by the US Treasury.

The unmanaged Barclays Capital US High Yield 2% Issuer Cap covers the universe of fixed-rate, non-investment grade debt. Pay-in-kind (PIK) bonds, Eurobonds, and debt issues from countries designated as emerging markets (e.g., Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-emerging market countries are included. Original issue zeroes, step-up coupon structures and 144-As are also included in the Index.

An investor cannot invest directly in an index, and its results are not indicative of the performance of any specific investment, including the Portfolio.

A Word About Risk

US Value Portfolio

Value investing does not guarantee a profit or eliminate risk. Not all companies whose stocks are considered to be value stocks are able to turn their business around or successfully employ corrective strategies which would result in stock prices that rise as initially expected.

US Large Cap Growth Portfolio

The Portfolio concentrates its investments in a limited number of issues and an investment in the Portfolio is therefore subject to greater risk and volatility than investments in a more diversified portfolio. Growth investing does not guarantee a profit or eliminate risk. The stocks of these companies can have relatively high valuations. Because of these high valuations, an investment in a growth stock can be more risky than an investment in a company with more modest growth expectations.

Global Real Estate Investment Portfolio

An investment in the Portfolio is subject to certain risks associated with the direct ownership of real estate and with the real estate industry in general, including declines in the value of real estate, general and local economic conditions and interest rates. The Portfolio concentrates its investments in real estate-related investments and may therefore be subject to greater risks and volatility than a fund with a more diversified Portfolio. The Portfolio’s assets may be invested in foreign securities, which may

(Historical Performance continued on next page)

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 21 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

magnify these fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. Investment in the Portfolio includes risks not associated with funds that invest exclusively in US issues. Because the Portfolio will invest in foreign currency-denominated securities, these fluctuations may be magnified by changes in foreign exchange rates.

International Value Portfolio

Value investing does not guarantee a profit or eliminate risk. Not all companies whose stocks are considered to be value stocks are able to turn their business around or successfully employ corrective strategies which would result in stock prices that rise as initially expected. Substantially all of the Portfolio’s assets will be invested in foreign securities which may magnify fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. Because the Portfolio may invest in emerging markets and in developing countries, an investment also has the risk that market changes or other factors affecting emerging markets and developing countries, including political instability and unpredictable economic conditions, may have a significant effect on the Portfolio’s net asset value.

International Growth Portfolio

Substantially all of the Portfolio’s assets will be invested in foreign securities which may magnify fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. The Portfolio may invest in securities of emerging market nations. These investments have additional risks, such as illiquid or thinly traded markets, company management risk, heightened political instability and currency volatility. Accounting standards and market regulations in emerging market nations are not the same as those in the US.

Small-Mid Cap Value Portfolio

Value investing does not guarantee a profit or eliminate risk. Not all companies whose stocks are considered to be value stocks are able to turn their business around or successfully employ corrective strategies which would result in stock prices that rise as initially expected. The Portfolio concentrates its investments in the stocks of small- to mid-capitalization companies, which tend to be more volatile than large-cap companies. Small- and mid-cap stocks may have additional risks because these companies tend to have limited product lines, markets or financial resources. The Portfolio can invest in foreign securities which may magnify these fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. Because the Portfolio may invest in emerging markets and in developing countries, an investment also has the risk that market changes or other factors affecting emerging markets and developing countries, including political instability and unpredictable economic conditions, may have a significant effect on the Portfolio’s net asset value.

Small-Mid Cap Growth Portfolio

The Portfolio concentrates its investments in the stocks of small- to mid-capitalization companies, which tend to be more volatile than large-cap companies. Small-cap stocks may have additional risks because these companies tend to have limited product lines, markets, financial resources or less liquidity (i.e., more difficulty when buying and selling more than the average daily trading volume of certain investment shares). The Portfolio can invest in foreign securities. Foreign markets can be more volatile than the US market due to increased risks of adverse issuer, political, regulatory, market or economic developments. In addition, because the Portfolio will

(Historical Performance continued on next page)

| 22 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

invest in foreign currency-denominated securities, fluctuations in the value of the Portfolio’s investments may be magnified by changes in foreign exchange rates.

Short Duration Bond Portfolio

The Portfolio’s assets can be invested in foreign securities which may magnify asset value fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. Because the Portfolio may invest in emerging markets and in developing countries, an investment also has the risk that market changes or other factors affecting emerging markets and developing countries, including political instability and unpredictable economic conditions, may have an impact on the Portfolio’s asset value. Price fluctuation in the Portfolio’s securities may be caused by changes in the general level of interest rates or changes in bond credit quality ratings. Please note, as interest rates rise, existing bond prices fall and can cause the value of an investment in the Portfolio to decline. Changes in interest rates have a greater effect on bonds with longer maturities than on those with shorter maturities. Investments in the Portfolio are not guaranteed because of fluctuation in the net asset value of the underlying fixed-income related investments. Similar to direct bond ownership, bond funds have the same interest rate, inflation and credit risks that are associated with the underlying bonds owned by the Portfolio. Portfolio purchasers should understand that, in contrast to owning individual bonds, there are ongoing fees and expenses associated with owning shares of bond funds. The Portfolio may also invest a portion of its assets in below investment-grade securities which are subject to greater risk than higher-rated securities.

Intermediate Duration Bond Portfolio

The Portfolio may invest in convertible debt securities, preferred stock and dividend paying stocks, US government obligations and foreign fixed-income securities. The Portfolio may invest in mortgage-related and other asset-backed securities which are subject to prepayment risk; the risk that early payments on principal on some mortgage-related securities may occur during periods of falling mortgage rates and expose the Portfolio to a lower rate of return upon reinvestment of principal. The Portfolio may invest a portion of its assets in foreign securities, which may magnify fluctuations. Price fluctuations may also be caused by changes in interest rates or bond quality ratings. These changes have a greater effect on bonds with longer maturities than on those with shorter maturities. Please note, as interest rates rise, existing bond prices fall and can cause the value of an investment in the Portfolio to decline. Investments in the Portfolio are not guaranteed because of fluctuation in the net asset value of the underlying fixed-income related investments. Similar to direct bond ownership, bond funds have the same interest rate, inflation and credit risks that are associated with the underlying bonds owned by the Portfolio. Portfolio purchasers should understand that, in contrast to owning individual bonds, there are ongoing fees and expenses associated with owning shares of bond funds. The Portfolio may invest in high-yield bonds, otherwise known as “junk bonds,” which involves a greater risk of default and price volatility than other bonds. Investing in below investment grade presents special risks, including credit risk. The Portfolio is also subject to leverage risk. When a fund borrows money or otherwise leverages its portfolio, it may be volatile because leverage tends to exaggerate the effect of any increase or decrease in the value of a fund’s investments. A fund may create leverage through the use of reverse repurchase agreements, forward contracts or dollar rolls or by borrowing money.

Inflation-Protected Securities Portfolio

Among the principal risks of investing in the Portfolio are interest-rate risk, credit risk and market risk. Interest rate risk is the risk that changes in interest rates will affect

(Historical Performance continued on next page)

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 23 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

the value of income-producing securities. Credit risk is the risk that a security issuer or the counterparty to certain derivatives will be unable or unwilling to make timely payments of income or principal. Market risk is the risk of losses from adverse changes in the market. To the extent the Portfolio invests in securities of non-US issuers, it may have non-US issuer risk and currency risk.

High-Yield Portfolio

The Portfolio can invest in foreign securities, including emerging markets, which may magnify fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. Price fluctuation in the Portfolio’s securities may be caused by changes in the general level of interest rates or changes in bond credit quality ratings. Please note, as interest rates rise, existing bond prices fall and can cause the value of an investment in the Portfolio to decline. Changes in interest rates have a greater effect on bonds with longer maturities than on those with shorter maturities. High-yield bonds, otherwise known as “junk bonds,” involve a greater risk of default and price volatility than other bonds. Investing in non-investment-grade securities presents special risks, including credit risk. Investments in the Portfolio are not guaranteed because of fluctuation in the net asset value of the underlying fixed-income related investments. Similar to direct bond ownership, bond funds have the same interest rate, inflation and credit risks that are associated with the underlying bonds owned by the Portfolio. Portfolio purchasers should understand that, in contrast to owning individual bonds, there are ongoing fees and expenses associated with owning shares of bond funds.

All Portfolios

While the equity Portfolios invest principally in common stocks and other equity securities and the fixed-income Portfolios invest principally in bonds and fixed-income securities, in order to achieve their investment objectives, the Portfolios may at times use certain types of investment derivatives, such as options, futures, forwards and swaps. These instruments involve risks different from, and in certain cases, greater than, the risks presented by more traditional investments. These risks are fully discussed in the Portfolios’ prospectus.

(Historical Performance continued on next page)

| 24 | • ALLIANCEBERNSTEIN POOLING PORTFOLIOS |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

US VALUE PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein US Value Portfolio | -44.97% | -49.48% | ||||

Russell 1000 Value Index | -44.71% | -47.35% | ||||

US LARGE CAP GROWTH PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein US Large Cap Growth Portfolio | -38.50% | -39.02% | ||||

Russell 1000 Growth Index | -39.90% | -40.03% | ||||

GLOBAL REAL ESTATE INVESTMENT PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein Global Real Estate Investment Portfolio | -51.84% | -55.85% | ||||

FTSE EPRA/NAREIT Global RE Index | -55.35% | -59.53% | ||||

INTERNATIONAL VALUE PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein International Value Portfolio | -51.14% | -57.06% | ||||

MSCI EAFE Index | -44.58% | -50.22% | ||||

INTERNATIONAL GROWTH PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein International Growth Portfolio | -45.60% | -52.29% | ||||

MSCI EAFE Index | -44.58% | -50.22% | ||||

MSCI EAFE Growth Index | -43.75% | -49.07% | ||||

See Historical Performance and Benchmark disclosures on pages 20-24.

(Historical Performance continued on next page)

| ALLIANCEBERNSTEIN POOLING PORTFOLIOS • | 25 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

SMALL-MID CAP VALUE PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein Small-Mid Cap Value Portfolio | -47.50% | -46.25% | ||||

Russell 2500 Value Index | -46.05% | -43.69% | ||||

SMALL-MID CAP GROWTH PORTFOLIO

| THE PORTFOLIO VS. ITS BENCHMARK PERIODS ENDED FEBRUARY 28, 2009 | Returns | |||||