united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-21720

Northern Lights Fund Trust

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450 Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

1209 Orange Street Wilmington, DE 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-490-4300

Date of fiscal year end: 9/30

Date of reporting period: 9/30/23

Item 1. Reports to Stockholders.

Deer Park Total Return Credit Fund

Class A Shares: DPFAX

Class C Shares: DPFCX

Class I Shares: DPFNX

Annual Report

September 30, 2023

www.deerparkfund.com

1-888-868-9501

Distributed by Northern Lights Distributors, LLC

Member FINRA/SIPC

November 30, 2023

Dear Investor,

The Deer Park Total Return Credit Fund (the “Fund”) is an open-end mutual fund that invests primarily in legacy non-agency mortgage backed securities (“RMBS”) and legacy asset backed securities (“ABS”) which we believe have an attractive fundamental backdrop. The Fund seeks to target a distribution yield of 3-6% and a mid-to-high single-digit total return with little correlation to both investment grade and high yield bonds, though actual distributions and performance will vary, and the Fund may have periods of negative performance (please see important disclosures below regarding the Fund’s distribution yield and performance).

Market Performance for the Fiscal Year Ended September 30, 2023

The Fund’s Class I Shares returned -2.37% over the fiscal year ended September 30, 2023 (the “Investment Period”), and 3.45% annualized since the Fund’s inception on October 16, 2015. In aggregate, the Fund’s Class I Shares distributed approximately $0.59/share over the fiscal year based on a specified distribution policy of $0.045/ share during the first two months of the Investment Period and $0.05/share per month in the remaining ten. This may have included a portion of return of capital.

The Fund’s distribution policy is to make monthly distributions to shareholders. The level of monthly distributions (including return of capital) is not fixed. However, this distribution policy is subject to change. Shareholders should not assume that the source of a distribution from the Fund is net profit. A portion of the distributions consist of a return of capital based on the character of the distributions received from the underlying holdings. The final determination of the source and tax characteristics of all distributions will be made after the end of the year. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares. There is no assurance that the Fund will continue to declare distributions or that they will continue at these rates.

| As of September 30, 2023 | Q4 2022 | Q1 2023 | Q2 2023 | Q3 2023 | One Year | Three Year | Since Inception* |

| DPFNX Class I (NAV) | -2.35% | -0.68% | 0.57% | 0.10% | -2.37% | -0.78% | 3.45% |

| DPFAX Class A (NAV) | -2.42% | -0.74% | 0.51% | -0.08% | -2.73% | -1.06% | 3.17% |

| DPFAX Class A (Max Load) | -8.03% | -6.46% | -5.32% | -5.83% | -8.32% | -2.99% | 2.41% |

| DPFCX Class C (NAV) | -2.61% | -0.93% | 0.31% | -0.27% | -3.47% | -1.82% | 0.86% |

| Bloomberg US Aggregate Bond Index | 1.87% | 2.96% | -0.84% | -3.23% | 0.64% | -5.21% | 0.50% |

| HFRX Fixed Income – Credit | 2.51% | 1.68% | 1.30% | -0.11% | 5.48% | -0.94% | 1.49% |

| * | Inception date for the I and A share classes is October 16, 2015. Inception date the C share class is April 6, 2017. Total returns are calculated with the traded NAV on September 29, 2023.Performance for periods longer than one year is annualized. |

The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. For performance information current to the most recent month-end, please call toll-free (888) 868-9501.

The Fund’s total annual operating expenses are 2.44%, 3.19%, and 2.19% for the Class A, C, and I shares, respectively. The Fund’s investment advisor has contractually agreed to waive management fees and to make payments to limit Fund expenses until at least January 31, 2024. After this fee waiver, the expense ratios are 2.04%, 2.79%, and 1.79% for the Class A, C, and I shares, respectively. These fee waivers and expense reimbursements are subject to possible recoupment from the Fund in future years. The maximum sales load for the Class A shares is 5.75%. A fund’s performance, especially for very short periods of time, should not be the sole factor in making your investment decisions.

1

Performance Statistics

The chart below shows performance statistics of the Fund relative to the Bloomberg Barclays U.S. Aggregate Bond Index and the HFRX Fixed Income – Credit Index from November 2015 (the first full month of Fund performance) through September 2023.

| Nov. 2015 - Sep. 2023 | Deer Park Total Return Credit I | Bloomberg Barclays US Aggregate Bond Index | HFRX Fixed Income - Credit Index |

| Annualized Return | 3.38% | 0.56% | 1.43% |

| Cumulative Return | 30.06% | 4.51% | 11.87% |

| Standard Deviation | 6.84% | 4.72% | 5.10% |

| Gain Deviation | 3.51% | 3.26% | 3.43% |

| Loss Deviation | 5.92% | 3.39% | 3.77% |

| Sharpe Ratio | 0.29 | -0.18 | 0.00 |

| Max Drawdown | -15.80% | -17.18% | -14.26% |

| Deer Park Fund Correlation to: | 1.00 | 0.24 | 0.66 |

Past performance is not indicative of future results. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

Please see additional information in the Important Risk Disclosures section at the end of this letter regarding the terms used in this table.

Since inception of the Fund on October 16, 2015 through September 30, 2023, the Fund’s performance was positive or flat 81% of the trading days and negative only 19% of the trading days. This compares favorably to the Bloomberg Barclays US Aggregate Bond Index shown below.

| Daily Statistics | Deer Park Total Return Credit I | Bloomberg Barclays US Aggregate Bond Index |

| Positive/Flat Days | 1614 | 1056 |

| Negative Days | 387 | 945 |

| % Positive/Flat Days | 81% | 53% |

| % Negative Days | 19% | 47% |

Past performance is not indicative of future results. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

Market & Portfolio Update:

The financial markets were exceptionally volatile in the 12 months ended September 30, 2023 with investor sentiment whipsawed by push-pull expectations for the Fed’s tightening efforts, a rising AI narrative, slowing economic growth, and some market participants hoping for a Fed pivot to pause rate hikes and return to QE. The extent of uncertainty remains high as the narrative around outcomes continues to evolve.

2

The Fed has raised the Fed Funds rate 525 basis points since March 2022 (through September 30, 2023), the largest increase since 1980. We believe that the general market consensus is that, after that 525 bps of interest rate increases since March 2022, we are nearing ‘peak rates.’ As often stated by the Federal Reserve (the “Fed”), interest rate increases operate on a long and variable lag with timing and effects that are difficult to predict. This is especially the case with the recent increase in longer-dated Treasury rates (e.g., 10-year Treasury yield above 4.50% at the end of September 2023) and the anticipated further economic slowing this increase may have on the economy.

While the markets are taking solace from the hopes that interest rate increases may be done, the Fed’s message of keeping interest rates ‘higher for longer’ appears to have changed mid-term expectations. Fed Chairman Powell has clearly messaged that they do not want to make the mistake the Fed made in the 1970’s and ease interest rates before fully extinguishing inflationary pressures. Historically, there has been a lag between when the Fed hikes interest rates and when the resulting effects are observed in credit markets. Often, this delay has several quarters or even over a year from the time that interest rates increase to the point that they result in higher corporate interest costs and the potential onset of an economic recession. Notably, given the effect of the pandemic relief stimulus and the significant refinancing wave that occurred as a result of years of near-zero interest rates, we may see an even more prolonged lag effect from the Fed’s current rate increases.

Credit spreads have widened across the majority of credit products beginning in 2022 and continuing into 2023, including in the Non-Agency RMBS space. In our view, given the price decline and spread widening, RMBS offers historically attractive default-adjusted return opportunities, especially relative to investment grade and high-yield corporate bonds. The current spread levels in RMBS would historically indicate credit stress and an impending default cycle. However, in our view, the fundamentals in RMBS remain sound, and technical market factors (forced selling, low liquidity, slower prepayment assumptions) are not representative of underlying collateral performance characteristics. We believe that the price/yield levels across most investment grade and high yield corporate bonds do not reflect the potential risk associated with a potential recessionary environment. We feel the current price levels offer an attractive relative value entry point for mortgage credit and especially for RMBS which possess additional upside optionality associated with positive convexity, forbearance recoveries, increased prepayments, and excess spread recoveries.

3

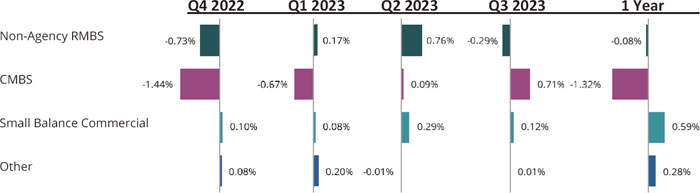

Performance Attribution

Please see the below Performance Attribution for the Investment Period. The performance of these sectors reflected the impact of the broader credit market spread widening effect.

The attribution data will not match the performance results of the Fund as it is an estimate and does not include Fund expenses, the results of residual cash balances and other timing considerations. Past performance is not indicative of future results. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

Legacy RMBS

Legacy Non-Agency RMBS remains the largest holding in the Fund’s portfolio, and these positions were roughly flat (-0.08% contribution to return) over the Investment Period. As mentioned earlier, recent market volatility has resulted in increased spread levels across the Legacy Non-Agency RMBS bonds. Deer Park is hoping to utilize their position as one of the largest and most knowledgeable investors in the Legacy RMBS sector and selectively purchase bonds at what they believe are attractive prices.

CMBS

The Fund’s CMBS positions contributed negatively to performance in the first half of the Investment Period, but contributed positively during the second half of the Investment Period. Uncertainty in the CMBS market has contributed to many investors’ broad-brush dismissal of the entire commercial real estate sector. However, about 70% of conduit CMBS loans have been refinancing before or within three months of their scheduled maturity date. We believe that the market’s expectation that the majority of commercial real estate assets will be unable to refinance and default seems too draconian. This creates the opportunity to analyze bonds to select those with high-quality assets and the highest probability of repayment.

Other Investment Notes

The Fund did not have exposure to derivatives during the Investment Period. We believe the Fund invested in a manner consistent with the objectives or investment strategy detailed in the fund’s prospectus throughout the Investment Period.

4

Market Outlook

We continue to have a very positive outlook on the portfolio and believe that positive performance trends continue to support the long-term return potential for these positions. In our view, traditional fixed-income investors have largely overlooked the RMBS space. Trading activity in this sector has been impacted by liquidity-driven technical factors that have created what we believe is a compelling investment opportunity; (1) technical price impact of forced selling; (2) stable-to-improved collateral performance characteristics due to years of home price appreciation and deleveraging of risk; (3) further long-term return potential from unique facets within the RMBS sector. The RMBS space is trading at levels we have not seen in years and offering what we believe are attractive Default-Adjusted Yields with what we believe is diminishing credit risk. Current market conditions are seeing a dearth of bid activity, offering liquidity providers an opportune time to actively select RMBS bonds with attractive return potential.

5

Important Risk Disclosures:

Investors should carefully consider the investment objectives, risks, charges and expenses of the Deer Park Total Return Credit Fund. This and other important information about the Fund is contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling (888) 868-9501. The Prospectus should be read carefully before investing. The Deer Park Total Return Credit Fund is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. Princeton Fund Advisors, LLC, and Northern Lights Distributors are not affiliated. Mutual Funds involve risk including the possible loss of principal.

ABS, RMBS and CMBS are subject to credit risk because underlying loan borrowers may default. Additionally, these securities are subject to prepayment risk because the underlying loans held by the issuers may be paid off prior to maturity. The value of these securities may go down as a result of changes in prepayment rates on the underlying mortgages or loans. During periods of declining interest rates, prepayment rates usually increase and the Fund may have to reinvest prepayment proceeds at a lower interest rate. CMBS are less susceptible to this risk because underlying loans may have prepayment penalties or prepayment lock out periods. There is a risk that issuers and counterparties will not make payments on securities and other investments held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes.

Standard Deviation measures the average deviations of a return series from its mean. Gain Deviation is the Standard Deviation of all positive returns. Loss Deviation is the Standard Deviation of all negative returns. Sharpe Ratio is a statistical measure that uses standard deviation and excess return over a risk-free rate of return to determine reward per unit of risk. A higher Sharpe ratio implies a better historical risk-adjusted performance. The Sharpe ratio has been calculated using the Citi 3-month Treasury Bill Index for the risk-free rate of return. Correlation is a statistic that measures the degree to which two return series move in relation to each other. Loan-to-Value is calculated by dividing the amount borrowed (mortgage amount) by the appraised value of the property, expressed as a percentage. The House Price Index (HPI) is a broad measure of the movement of single-family property prices in the United States.

The Bloomberg Barclays U.S. Aggregate Bond Index provides a measure of the performance of the U.S. investment grades bond market. The value of the Fund’s investments in fixed income securities will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities. HFRX Fixed Income - Credit Index includes strategies with exposure to credit across a broad continuum of credit sub-strategies, including Corporate, Sovereign, and Asset Backed. Investment thesis across all strategies is predicated on realization of a valuation discrepancy between the related credit instruments.

Foreign investing involves risks not typically associated with U.S. investments, including adverse fluctuations in foreign currency values, adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards. Investing in emerging markets imposes risks different from, or greater than, risks of investing in foreign developed countries.

Lower-quality fixed income securities, known as “high yield” or “junk” bonds, present greater risk than bonds of higher quality, including an increased risk of default. An economic downturn or period of rising interest rates could adversely affect the market for these bonds and reduce the Fund’s ability to sell its bonds. The lack of a liquid market for these bonds could decrease the Fund’s share price.

Repayment of defaulted securities and obligations of distressed issuers (including insolvent issuers or issuers in payment or covenant default, in workout or restructuring or in bankruptcy or in solvency proceedings) is subject to significant uncertainties. Investments in defaulted securities and obligations of distressed issuers are considered speculative as are junk bonds in general.

The value of a specific security can be more volatile than the market as a whole and can perform differently from the value of the market as a whole. The value of securities of smaller issuers can be more volatile than those of larger issuers. The value of certain types of securities can be more volatile due to increased sensitivity to adverse issuer, political, regulatory, market, or economic developments. Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations.

The advisor’s and sub-advisor’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests (long or short) may prove to be incorrect and may not produce the desired results. Additionally, the advisor’s judgments about the potential performance of the sub-advisor may also prove incorrect and may not produce the desired results. Overall equity and fixed income securities and derivatives market risks may affect the value of individual instruments in which the Fund invests. Factors such as domestic and foreign economic growth and market conditions, interest rate levels, and political events affect the securities and derivatives markets. When the value of the Fund’s investments goes down, your investment in the Fund decreases in value and you could lose money.

Smaller companies may have limited product lines, markets or financial resources, and they may be dependent on a limited management group. Securities of smaller companies may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. Underlying funds are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in an underlying fund and may be higher than other mutual funds that invest directly in stocks and bonds. Underlying funds are subject to specific risks, depending on the nature of the fund.

7975-NLD 11/20/2023

6

| Deer Park Total Return Credit Fund |

| PORTFOLIO REVIEW (Unaudited) |

| September 30, 2023 |

The Fund’s performance figures* for the period ended September 30, 2023, compared to its benchmarks:

| Annualized | Annualized | ||||

| Annualized | Annualized | Inception** - | Inception*** - | ||

| One Year | Three Year | Five Year | September 30, 2023 | September 30, 2023 | |

| Class A Shares | (2.73)% | (1.06)% | (0.12)% | 3.17% | — |

| Class A Shares with load | (8.32)% | (2.99)% | (1.30)% | 2.41% | — |

| Class C Shares | (3.47)% | (1.82)% | (0.87)% | — | 0.86% |

| Class I Shares | (2.37)% | (0.78)% | 0.15% | 3.45% | — |

| Bloomberg Capital U.S. Aggregate Bond Index | 0.64% | (5.21)% | 0.10% | 0.50% | 0.19% |

| HFRX Fixed Income - Credit Index | 5.47% | (0.94)% | 1.12% | 1.49% | 1.37% |

| * | The performance data quoted here represents past performance. The performance comparison includes reinvestment of all dividends and distributions and has been adjusted for the Class A maximum applicable sales charge of 5.75%. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than the original cost. Total returns are calculated with the traded NAV on September 29, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or on the redemption of Fund shares. The Fund’s total annual operating expenses, including underlying funds, before fee waivers and/or expense reimbursements are 2.44%, 3.19% and 2.19%, respectively, for Class A, Class C and Class I shares per the January 30, 2023 prospectus. The Fund’s total annual operating expenses, including underlying funds, after fee waivers and/or expense reimbursements are 2.04%, 2.79% and 1.79%, respectively, for Class A, Class C and Class I shares per the January 30, 2023 prospectus. Class A shares are subject to a maximum sales charge of 5.75% imposed on purchases. For certain of the periods shown, the Fund’s adviser waived and/or reimbursed certain expenses of the Fund. Absent this arrangement, the Fund’s performance would have been lower. For performance information current to the most recent month-end, please call toll free (888) 868-9501. |

| ** | Commencement of operations is October 16, 2015. |

| *** | Commencement of operations is April 6, 2017. |

The Bloomberg Capital U.S. Aggregate Bond Index is commonly used as a benchmark by both passive and active investors to measure portfolio performance relative to the U.S. dollar-denominated investment grade fixed-rate taxable bond market. It is also an informational measure of broad market returns commonly applied to fixed income instruments. The index contains approximately 8,200 fixed income issues and is valued at around $15 trillion, representing 43% of the total U.S. bond market. Investors cannot invest directly in the index.

HFRX Fixed Income - Credit Index includes strategies with exposure to credit across a broad continuum of credit sub-strategies, including Corporate, Sovereign, Distressed, Convertible, Asset Backed, Capital Structure Arbitrage, Multi-Strategy and other Relative Value and Event Driven sub-strategies. Investment thesis across all strategies is predicated on realization of a valuation discrepancy between the related credit instruments. Strategies may also include and utilize equity securities, credit derivatives, government fixed income, commodities, currencies or other hybrid securities. Investors cannot invest directly in the index.

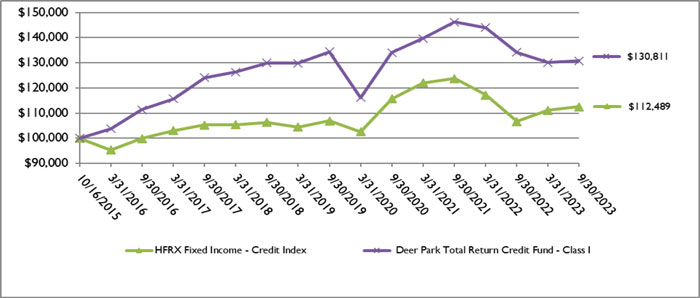

Comparison of the Change in Value of a $100,000 Investment

7

| Deer Park Total Return Credit Fund |

| PORTFOLIO REVIEW (Unaudited)(Continued) |

| September 30, 2023 |

The Fund’s top asset classes and industry sectors as of September 30, 2023, are as follows:

| Percent of Net | ||||

| Portfolio Composition: | Assets | |||

| Agency Asset Backed Securities | ||||

| Collateralized Mortgage Obligations | 0.6 | % | ||

| Agency CMBS | 0.6 | % | ||

| Non Agency Asset Backed Securities | ||||

| Collateralized Mortgage Obligations | 31.8 | % | ||

| Residential Mortgage | 27.5 | % | ||

| Non Agency CMBS | 25.3 | % | ||

| Home Equity | 16.0 | % | ||

| Manufactured Housing | 2.4 | % | ||

| Other ABS | 0.7 | % | ||

| Whole Business | 0.1 | % | ||

| Short-Term Investment | 0.7 | % | ||

| Liabilities In Excess Of Other Assets + | (5.7 | )% | ||

| 100.0 | % | |||

| + | Includes Reverse Repurchase Agreements |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

8

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| AGENCY ASSET BACKED SECURITIES — 1.2% | ||||||||||||||

| AGENCY CMBS — 0.6% | ||||||||||||||

| 2,553,595 | Freddie Mac Military Housing Bonds Series 2015-R1 C3(b),(d) | 5.9280 | 11/25/52 | $ | 2,118,884 | |||||||||

| 2,925,944 | Government National Mortgage Association Series 2007-15 IO(a),(b) | 1.5960 | 03/16/47 | 30,895 | ||||||||||

| 4,325,182 | Government National Mortgage Association Series 2015-6 IO(a),(b) | 0.4750 | 02/16/51 | 45,751 | ||||||||||

| 2,619,044 | Government National Mortgage Association Series 2013-15 IO(a),(b) | 0.5620 | 08/16/51 | 54,642 | ||||||||||

| 828,765 | Government National Mortgage Association Series 2012-72 IO(a),(b) | 0.5610 | 11/16/52 | 6,322 | ||||||||||

| 253,231 | Government National Mortgage Association Series 2015-122 IO(a),(b) | 0.5840 | 05/16/57 | 320 | ||||||||||

| 2,256,814 | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 0.6% | ||||||||||||||

| 1,050,666 | Fannie Mae REMICS Series 2012-90 SA(a),(c) | SOFR30A + 5.936% | 0.6210 | 08/25/42 | 70,222 | |||||||||

| 4,501,794 | Fannie Mae REMICS Series 2012-144 SH(a),(c) | SOFR30A + 5.986% | 0.6710 | 01/25/43 | 388,463 | |||||||||

| 3,871,149 | Fannie Mae REMICS Series 2017-16 CS(a),(c) | SOFR30A + 5.936% | 0.6210 | 03/25/47 | 318,683 | |||||||||

| 2,484,576 | Fannie Mae REMICS Series 2017-14 DS(a),(c) | SOFR30A + 5.936% | 0.6210 | 03/25/47 | 207,343 | |||||||||

| 2,450,151 | Fannie Mae REMICS Series 2017-68 SN(a),(c) | SOFR30A + 6.036% | 0.7210 | 09/25/47 | 237,209 | |||||||||

| 1,882,089 | Fannie Mae REMICS Series 2018-64 SE(a),(c) | SOFR30A + 6.086% | 0.7710 | 09/25/48 | 156,565 | |||||||||

| 635,082 | Freddie Mac REMICS Series 4238 NS(a),(c) | SOFR30A + 6.586% | 1.2720 | 02/15/42 | 52,412 | |||||||||

| 3,454,100 | Freddie Mac REMICS Series 4416 DS(a),(c) | SOFR30A + 5.986% | 0.6720 | 12/15/44 | 269,476 | |||||||||

| 201,443 | Freddie Mac REMICS Series 4583 ST(a),(c) | SOFR30A + 5.886% | 0.5720 | 05/15/46 | 15,203 | |||||||||

| 1,793,058 | Freddie Mac REMICS Series 4685 SA(a),(c) | SOFR30A + 5.986% | 0.6720 | 05/15/47 | 165,696 | |||||||||

| 3,844,444 | Freddie Mac REMICS Series 4718 SC(a),(c) | SOFR30A + 6.036% | 0.7220 | 09/15/47 | 359,143 | |||||||||

| 1,254,530 | Freddie Mac REMICS Series 4796 AS(a),(c) | SOFR30A + 6.086% | 0.7720 | 05/15/48 | 110,631 | |||||||||

| 10,518,089 | Government National Mortgage Association Series 2019-111 SK(a),(c) | TSFR1M + 3.316% | 0.0001 | 09/20/49 | 74,524 | |||||||||

| 2,425,570 | ||||||||||||||

| TOTAL AGENCY ASSET BACKED SECURITIES (Cost $18,513,107) | 4,682,384 | |||||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% | ||||||||||||||

| 36,767 | Adjustable Rate Mortgage Trust 2005-4 Series 2005-4 3A1(b) | 4.8040 | 08/25/35 | 35,657 | ||||||||||

| 1,680,494 | Adjustable Rate Mortgage Trust 2007-1 Series 2007-1 5A1(c) | TSFR1M + 0.414% | 5.7340 | 03/25/37 | 1,893,124 | |||||||||

| 139,155 | Alternative Loan Trust 2003-4CB Series 2003-4CB B1(b) | 6.1280 | 04/25/33 | 71,693 | ||||||||||

| 93,111 | Alternative Loan Trust 2003-J2 Series 2003-J2 B1 | 6.0000 | 10/25/33 | 67,971 | ||||||||||

| 720,053 | Alternative Loan Trust 2004-8CB Series 2004-8CB M3(c) | TSFR1M + 2.964% | 8.2840 | 06/25/34 | 823,505 | |||||||||

| 339,569 | Alternative Loan Trust 2005-22T1 Series 2005-22T1 A2(a),(c) | TSFR1M + 4.956% | 0.0001 | 06/25/35 | 11,661 | |||||||||

See accompanying notes to financial statements.

9

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 568,918 | Alternative Loan Trust 2005-45 Series 2005-45 2A1(c) | 12MTA + 2.050% | 6.6760 | 10/20/35 | $ | 400,826 | ||||||||

| 1,129,553 | Alternative Loan Trust 2005-50CB Series 2005-50CB 3A1 | 6.0000 | 11/25/35 | 433,329 | ||||||||||

| 335,034 | Alternative Loan Trust 2005-56 Series 2005-56 5A1(c) | TSFR1M + 0.754% | 6.0740 | 11/25/35 | 264,473 | |||||||||

| 599,783 | Alternative Loan Trust 2005-65CB Series 2005-65CB 2A4 | 5.5000 | 12/25/35 | 416,883 | ||||||||||

| 413,992 | Alternative Loan Trust 2005-65CB Series 2005-65CB 1A5(c) | TSFR1M + 0.864% | 5.5000 | 01/25/36 | 258,887 | |||||||||

| 1,630,196 | Alternative Loan Trust 2006-32CB Series 2006-32CB A8(a),(c) | TSFR1M + 5.156% | 0.0001 | 11/25/36 | 71,393 | |||||||||

| 465,743 | Alternative Loan Trust 2006-36T2 Series 2006-36T2 1A9(c) | TSFR1M + 1.014% | 6.3340 | 12/25/36 | 153,265 | |||||||||

| 163,966 | Alternative Loan Trust 2006-HY10 Series 2006-HY10 2A1(b) | 4.3380 | 05/25/36 | 142,435 | ||||||||||

| 294,588 | Alternative Loan Trust 2006-J3 Series 2006-J3 2A1 | 4.7500 | 12/29/23 | 201,571 | ||||||||||

| 159,122 | Alternative Loan Trust 2006-J5 Series 2006-J5 1A4 | 6.5000 | 09/25/36 | 84,343 | ||||||||||

| 21,915,571 | Alternative Loan Trust 2006-OA10 Series 2006-OA10 XBI(a),(e) (i) | 0.0001 | 08/25/46 | 5,746 | ||||||||||

| 5,276,636 | Alternative Loan Trust 2006-OA10 Series 2006-OA10 XAD(a),(e) (i) | 0.0001 | 08/25/46 | 491 | ||||||||||

| 1,065,567 | Alternative Loan Trust 2006-OA11 Series 2006-OA11 A1B(c) | TSFR1M + 0.494% | 5.8140 | 09/25/46 | 983,367 | |||||||||

| 13,499,933 | Alternative Loan Trust 2006-OA14 Series 2006-OA14 X2(a),(b) (i) | 0.0001 | 11/25/46 | 68 | ||||||||||

| 5,579,674 | Alternative Loan Trust 2006-OA17 Series 2006-OA17 2X(a),(b) | 0.9710 | 12/20/46 | 375,163 | ||||||||||

| 225,289 | Alternative Loan Trust 2006-OA19 Series 2006-OA19 A1(c) | TSFR1M + 0.294% | 5.6190 | 02/20/47 | 171,771 | |||||||||

| 36,910,986 | Alternative Loan Trust 2006-OA2 Series 2006-OA2 X1P(a),(b) (i) | 0.0490 | 05/20/46 | 273,444 | ||||||||||

| 1,985,720 | Alternative Loan Trust 2006-OA7 Series 2006-OA7 2A1(c) | 12MTA + 0.940% | 5.3700 | 06/25/46 | 1,647,182 | |||||||||

| 78 | Alternative Loan Trust 2006-OC6 Series 2006-OC6 2A2A(c) (i) | TSFR1M + 0.434% | 5.7540 | 07/25/36 | 4,718 | |||||||||

| 149,687 | Alternative Loan Trust Resecuritization 2006-22R Series 2006-22R 2A2 | 6.2500 | 05/25/36 | 83,119 | ||||||||||

| 1,190,767 | American Home Mortgage Assets Trust 2005-1 Series 2005-1 3A22(c) | TSFR1M + 0.774% | 6.0940 | 11/25/35 | 938,286 | |||||||||

| 456,728 | American Home Mortgage Assets Trust 2006-1 Series 2006-1 1A2(c) | TSFR1M + 0.304% | 5.6240 | 05/25/46 | 379,297 | |||||||||

| 187,869 | American Home Mortgage Assets Trust 2006-2 Series 2006-2 1A1(c) | 12MTA + 0.960% | 5.5860 | 09/25/46 | 161,384 | |||||||||

| 144,327 | American Home Mortgage Assets Trust 2007-5 Series 2007-5 A1(c) | TSFR1M + 0.494% | 5.8140 | 06/25/47 | 124,805 | |||||||||

| 2,862,497 | American Home Mortgage Investment Trust 2005-4 Series 2005-4 1A2(c) | TSFR1M + 0.874% | 6.1940 | 11/25/45 | 2,819,820 | |||||||||

| 498,954 | American Home Mortgage Investment Trust 2006-3 Series 2006-3 11A2(c) | TSFR1M + 0.574% | 5.8940 | 12/25/46 | 479,512 | |||||||||

| 4,197,727 | American Home Mortgage Investment Trust 2007-2 Series 2007-2 12A1(c) | TSFR1M + 0.654% | 5.9740 | 03/25/37 | 1,537,161 | |||||||||

| 859,814 | Banc of America Alternative Loan Trust 2006-5 Series 2006-5 CBIO(a) | 6.0000 | 06/25/46 | 153,090 | ||||||||||

| 1,425,048 | Banc of America Alternative Loan Trust 2006-6 Series 2006-6 CBIO(a) | 6.0000 | 07/25/46 | 179,223 | ||||||||||

| 172,767 | Banc of America Alternative Loan Trust 2006-8 Series 2006-8 1A5(a),(c) | TSFR1M + 772.262% | 6.0000 | 11/25/36 | 31,539 | |||||||||

| 343,009 | Banc of America Alternative Loan Trust 2006-8 Series 2006-8 XIO(a) | 6.0000 | 11/25/46 | 69,862 | ||||||||||

| 2,917,708 | Banc of America Funding 2005-C Trust Series 2005-C M2(c) | TSFR1M + 0.764% | 6.0890 | 05/20/35 | 2,087,690 | |||||||||

| 61,589 | Banc of America Funding 2005-F Trust Series 2005-F 1A1(c) | TSFR1M + 0.734% | 6.0590 | 09/20/35 | 43,434 | |||||||||

| 1,383,564 | Banc of America Funding 2006-D Trust Series 2006-D 1A2(c) | TSFR1M + 0.674% | 5.9990 | 05/20/36 | 411,909 | |||||||||

See accompanying notes to financial statements.

10

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 471,426 | Banc of America Mortgage 2007-1 Trust Series 2007-1 2IO(a) | 6.0000 | 01/25/37 | $ | 69,147 | |||||||||

| 567,712 | BCAP, LLC 2008-RR3 Trust Series 2008-RR3 A1B(b),(d) | 6.6940 | 10/25/36 | 172,860 | ||||||||||

| 1,703,688 | BCAP, LLC 2009-RR4 Trust Series 2009-RR4 1A2(b),(d) | 52.0660 | 06/26/37 | 449,790 | ||||||||||

| 81,450 | Bear Stearns ALT-A Trust Series 2004-7 1A1(b) (i) | 2.6250 | 10/25/34 | 55,783 | ||||||||||

| 732,774 | Bear Stearns ALT-A Trust 2003-5 Series 2003-5 M(b) | 4.7380 | 12/25/33 | 668,652 | ||||||||||

| 262,905 | Bear Stearns ALT-A Trust 2003-6 Series 2003-6 B1(b) | 4.6160 | 01/25/34 | 153,472 | ||||||||||

| 1,524,666 | Bear Stearns ALT-A Trust 2005-10 Series 2005-10 11A1(c) | TSFR1M + 0.614% | 5.9340 | 01/25/36 | 1,465,957 | |||||||||

| 1,001,322 | Bear Stearns ALT-A Trust 2005-3 Series 2005-3 1A1(b) | 3.8720 | 04/25/35 | 862,919 | ||||||||||

| 227,937 | Bear Stearns ALT-A Trust 2005-7 Series 2005-7 25A1(b) | 4.6810 | 09/25/35 | 93,132 | ||||||||||

| 1,280,070 | Bear Stearns ALT-A Trust 2006-4 Series 2006-4 23A4(b) | 4.0170 | 08/25/36 | 856,719 | ||||||||||

| 386,341 | Bear Stearns ALT-A Trust 2007-2 Series 2007-2 1A1(c) | TSFR1M + 0.454% | 5.7740 | 04/25/37 | 333,712 | |||||||||

| 180,157 | Bear Stearns ARM Trust 2004-6 Series 2004-6 2A2(b) | 3.8350 | 09/25/34 | 132,583 | ||||||||||

| 310,020 | Bear Stearns ARM Trust 2005-12 Series 2005-12 23A1(b) | 4.6410 | 02/25/36 | 277,410 | ||||||||||

| 70,764 | Bear Stearns ARM Trust 2007-4 Series 2007-4 22A1(b) | 4.0680 | 06/25/47 | 63,059 | ||||||||||

| 30,678 | Bear Stearns Asset Backed Securities I Trust Series 2004-AC5 A2(c) | TSFR1M + 0.514% | 5.8340 | 10/25/34 | 26,168 | |||||||||

| 216,991 | Bear Stearns Asset Backed Securities Trust Series 2003-AC4 M1(e) | 5.6580 | 09/25/33 | 152,207 | ||||||||||

| 44,451 | Bear Stearns Asset Backed Securities Trust Series 2003-AC5 B(c) | TSFR1M + 4.989% | 10.3090 | 10/25/33 | 55,397 | |||||||||

| 36,106 | Bear Stearns Asset Backed Securities Trust Series 2003-AC6 M2(c) | TSFR1M + 2.764% | 8.0840 | 11/25/33 | 25,213 | |||||||||

| 1,580,001 | Bear Stearns Mortgage Funding Trust 2006-AR1 Series 2006-AR1 2A2(c) | TSFR1M + 0.634% | 5.9540 | 08/25/36 | 1,946,997 | |||||||||

| 318,883 | Bear Stearns Mortgage Funding Trust 2006-AR5 Series 2006-AR5 1A1(c) | TSFR1M + 0.274% | 5.5940 | 12/25/46 | 260,807 | |||||||||

| 2,670,405 | Bear Stearns Mortgage Funding Trust 2006-AR5 Series 2006-AR5 1A2(c) | TSFR1M + 0.324% | 5.6440 | 12/25/46 | 2,688,729 | |||||||||

| 2,504,110 | Bear Stearns Mortgage Funding Trust 2007-AR1 Series 2007-AR1 1A2(c) | TSFR1M + 0.324% | 5.6440 | 01/25/37 | 2,409,905 | |||||||||

| 148,656 | Bear Stearns Mortgage Funding Trust 2007-AR3 Series 2007-AR3 1A1(c) | TSFR1M + 0.254% | 5.5740 | 03/25/37 | 125,115 | |||||||||

| 1,950,440 | Bear Stearns Mortgage Funding Trust 2007-AR3 Series 2007-AR3 1A2(c) | TSFR1M + 0.294% | 5.6140 | 03/25/37 | 2,012,050 | |||||||||

| 1,659,605 | Bear Stearns Mortgage Funding Trust 2007-AR3 Series 2007-AR3 21A2(c) | TSFR1M + 0.494% | 5.8140 | 04/25/37 | 1,635,829 | |||||||||

| 22,127 | Bear Stearns Mortgage Funding Trust 2007-SL1 Series 2007-SL1 1A(c) | TSFR1M + 0.434% | 5.7540 | 03/25/37 | 22,602 | |||||||||

| 392,367 | Chase Mortgage Finance Trust Series 2005-S3 Series 2005-S3 A10 | 5.5000 | 11/25/35 | 283,665 | ||||||||||

| 23,060 | Chase Mortgage Finance Trust Series 2007-A1 Series 2007-A1 5A2(b) | 5.3060 | 02/25/37 | 20,978 | ||||||||||

| 43,077 | Chase Mortgage Finance Trust Series 2007-A1 Series 2007-A1 7A1(b) | 5.4630 | 02/25/37 | 42,385 | ||||||||||

| 570,406 | ChaseFlex Trust Multi-Class Mortgage Pass-Through Series 2007-M1 2AV2(c) | TSFR1M + 0.344% | 4.0530 | 08/25/37 | 444,337 | |||||||||

| 669,489 | Chevy Chase Funding, LLC Mortgage-Backed Series 2003-4A B1(b),(d) | 5.7400 | 10/25/34 | 605,894 | ||||||||||

| 37,077 | Chevy Chase Funding, LLC Mortgage-Backed Series 2004-2A A2(c),(d) | TSFR1M + 0.434% | 5.7540 | 05/25/35 | 35,019 | |||||||||

| 525,469 | Chevy Chase Funding, LLC Mortgage-Backed Series 2004-4A B1(b),(d) | 4.6640 | 10/25/35 | 385,504 | ||||||||||

| 437,602 | Chevy Chase Funding, LLC Mortgage-Backed Series 2007-2A A2(c),(d) | TSFR1M + 0.294% | 5.6140 | 05/25/48 | 272,076 | |||||||||

See accompanying notes to financial statements.

11

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 484,506 | CHL Mortgage Pass-Through Trust 2003-48 Series 2003-48 B1(b) | 5.3380 | 10/25/33 | $ | 27,635 | |||||||||

| 240,070 | CHL Mortgage Pass-Through Trust 2003-58 Series 2003-58 M(b) | 4.6990 | 02/19/34 | 213,242 | ||||||||||

| 27,043 | CHL Mortgage Pass-Through Trust 2004-25 Series 2004-25 1A2(c) | TSFR1M + 0.894% | 6.2140 | 02/25/35 | 21,278 | |||||||||

| 5,289,552 | CHL Mortgage Pass-Through Trust 2004-29 Series 2004-29 2X(a),(b) (i) | 0.001 | 02/25/35 | 53 | ||||||||||

| 40,103 | CHL Mortgage Pass-Through Trust 2005-11 Series 2005-11 3A3(b) | 3.5620 | 04/25/35 | 28,873 | ||||||||||

| 20,491 | CHL Mortgage Pass-Through Trust 2005-11 Series 2005-11 4A1(c) | TSFR1M + 0.384% | 5.7040 | 04/25/35 | 18,537 | |||||||||

| 253,116 | CHL Mortgage Pass-Through Trust 2005-11 Series 2005-11 4A2(c) | TSFR1M + 0.434% | 5.7540 | 04/25/35 | 141,330 | |||||||||

| 211,897 | CHL Mortgage Pass-Through Trust 2005-14 Series 2005-14 A3 | 5.5000 | 07/25/35 | 77,458 | ||||||||||

| 286,538 | CHL Mortgage Pass-Through Trust 2005-2 Series 2005-2 2A3(c) | TSFR1M + 0.794% | 6.1140 | 03/25/35 | 259,090 | |||||||||

| 76,989 | CHL Mortgage Pass-Through Trust 2006-HYB3 Series 2006-HYB3 2A1A(b) | 3.9380 | 05/20/36 | 70,939 | ||||||||||

| 101,074 | CHL Mortgage Pass-Through Trust 2007-HYB2 Series 2007-HYB2 3A1(b) | 3.7280 | 02/25/47 | 86,931 | ||||||||||

| 258,967 | CHL Mortgage Pass-Through Trust 2007-J3 Series 2007-J3 A9 | 6.0000 | 07/25/37 | 108,880 | ||||||||||

| 64,598 | Citicorp Mortgage Securities Trust Series 2006-4 Series 2006-4 1A12 | 6.0000 | 08/25/36 | 39,683 | ||||||||||

| 34,027 | Citicorp Mortgage Securities Trust Series 2007-7 Series 2007-7 APO(f) | 0.0001 | 08/25/37 | 23,385 | ||||||||||

| 39,089 | Citigroup Mortgage Loan Trust 2004-HYB2 Series 2004-HYB2 1A(b) | 5.3240 | 03/25/34 | 36,437 | ||||||||||

| 134,173 | Citigroup Mortgage Loan Trust 2005-3 Series 2005-3 2A2B(b) | 5.2130 | 08/25/35 | 109,936 | ||||||||||

| 67,027 | Citigroup Mortgage Loan Trust 2006-AR1 Series 2006-AR1 2A1(c) | H15T1Y + 2.400% | 6.3800 | 03/25/36 | 61,242 | |||||||||

| 66,691 | Citigroup Mortgage Loan Trust 2007-10 Series 2007-10 22AA(b) | 4.3800 | 09/25/37 | 58,734 | ||||||||||

| 40,334 | Citigroup Mortgage Loan Trust 2007-AR8 Series 2007-AR8 2A1A(b) | 4.3890 | 07/25/37 | 34,941 | ||||||||||

| 25,553 | Citigroup Mortgage Loan Trust, Inc. Series 2004-HYB1 A31(b) | 4.1830 | 02/25/34 | 25,539 | ||||||||||

| 433,860 | Citigroup Mortgage Loan Trust, Inc. Series 2005-9 1A1(c) | TSFR1M + 0.374% | 5.6940 | 11/25/35 | 363,204 | |||||||||

| 61,757 | CitiMortgage Alternative Loan Trust Series 2007-A1 Series 2007-A1 1A1 | 6.0000 | 01/25/37 | 53,793 | ||||||||||

| 1,103,610 | CitiMortgage Alternative Loan Trust Series 2007-A4 Series 2007-A4 1A7 | 5.7500 | 04/25/37 | 968,085 | ||||||||||

| 2,924,354 | CitiMortgage Alternative Loan Trust Series 2007-A6 Series 2007-A6 1A2(a),(c) | TSFR1M + 5.286% | 0.0001 | 06/25/37 | 70,876 | |||||||||

| 95,714 | Countrywide Asset-Backed Certificates Series 2005-IM3 A3(c) | TSFR1M + 0.614% | 5.9340 | 03/25/36 | 93,856 | |||||||||

| 264,542 | Credit Suisse First Boston Mortgage Securities Series 2002-AR21 CB1(b) | 3.9010 | 06/25/32 | 251,861 | ||||||||||

| 1,056,762 | Credit Suisse First Boston Mortgage Securities Series 2003-1 DB2(b) | 6.6550 | 02/25/33 | 787,523 | ||||||||||

| 87,188 | Credit Suisse First Boston Mortgage Securities Series 2003-AR9 CB1(b) | 4.2570 | 03/25/33 | 82,690 | ||||||||||

| 690,681 | Credit Suisse First Boston Mortgage Securities Series 2004-AR1 6M2(c) | TSFR1M + 2.214% | 7.5340 | 02/25/34 | 709,305 | |||||||||

| 941,414 | Credit Suisse First Boston Mortgage Securities Series 2004-AR7 CB1(c) | TSFR1M + 1.264% | 6.5840 | 11/25/34 | 879,599 | |||||||||

| 568,329 | Credit Suisse First Boston Mortgage Securities Series 2005-1 1A4 | 5.5000 | 02/25/35 | 494,062 | ||||||||||

| 544,792 | CSFB Mortgage-Backed Trust Series 2004-7 Series 2004-7 DB1(b) | 5.9880 | 11/25/34 | 278,595 | ||||||||||

| 66,540 | Deutsche Alt-A Securities Inc Mortgage Loan Trust Series 2005-5 1A3(b) | 5.5000 | 11/25/35 | 96,315 | ||||||||||

| 660,393 | Deutsche Alt-A Securities Mortgage Loan Trust Series 2006-AR5 23A | 6.0000 | 10/25/23 | 344,642 | ||||||||||

See accompanying notes to financial statements.

12

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 1,096,989 | Deutsche Alt-A Securities Mortgage Loan Trust Series 2007-OA5 A3(c) | TSFR1M + 0.514% | 5.8340 | 08/25/47 | $ | 804,541 | ||||||||

| 1,003,227 | Deutsche Mortgage Securities Inc REMIC Trust Series 2008-RS1 4A2(c),(d) | US0001M + 0.250% | 5.6830 | 05/28/37 | 479,625 | |||||||||

| 12,088 | DSLA Mortgage Loan Trust 2004-AR3 Series 2004-AR3 B2(c) | TSFR1M + 1.764% | 7.0920 | 08/25/35 | 10,547 | |||||||||

| 244,551 | DSLA Mortgage Loan Trust 2004-AR3 Series 2004-AR3 B3(c) | TSFR1M + 1.989% | 7.3170 | 07/19/44 | 132,189 | |||||||||

| 3,201,247 | DSLA Mortgage Loan Trust 2007-AR1 Series 2007-AR1 2A1B(c) (h) | TSFR1M + 0.294% | 5.6220 | 04/19/47 | 3,234,947 | |||||||||

| 122,963 | Fannie Mae REMIC Trust 2003-W1 Series 2003-W1 M(b) | 2.4880 | 12/25/42 | 96,879 | ||||||||||

| 1,150,197 | Global Mortgage Securitization Ltd. Series 2005-A B1(d) | 5.2500 | 04/25/32 | 1,118,340 | ||||||||||

| 1,502 | GreenPoint Mortgage Funding Trust 2006-AR3 Series 2006-AR3 3A1(c) | TSFR1M + 0.574% | 5.8940 | 04/25/36 | 3,533 | |||||||||

| 1,560,768 | GreenPoint Mortgage Funding Trust Series 2006-AR6 Series 2006-AR6 A4(c) | TSFR1M + 0.794% | 6.1140 | 10/25/46 | 1,065,584 | |||||||||

| 330,639 | GreenPoint Mortgage Loan Trust 2004-1 Series 2004-1 A(c) | TSFR1M + 1.264% | 6.5840 | 10/25/34 | 258,982 | |||||||||

| 1,310,297 | GSMPS Mortgage Loan Trust 2003-3 Series 2003-3 B1(b),(d) | 7.0320 | 06/25/43 | 88,555 | ||||||||||

| 199,915 | GSR Mortgage Loan Trust 2003-1 Series 2003-1 A11(c) | H15T1Y + 1.750% | 6.7800 | 03/25/33 | 191,087 | |||||||||

| 155,788 | GSR Mortgage Loan Trust 2003-2F Series 2003-2F 2A5 | 4.7500 | 03/25/32 | 142,175 | ||||||||||

| 13,271 | GSR Mortgage Loan Trust 2004-7 Series 2004-7 1A2(b) | 4.2310 | 06/25/34 | 12,847 | ||||||||||

| 1,978,257 | GSR Mortgage Loan Trust 2006-4F Series 2006-4F 4A1(c) | TSFR1M + 0.464% | 5.7840 | 05/25/36 | 345,726 | |||||||||

| 1,043,814 | GSR Mortgage Loan Trust 2006-9F Series 2006-9F 6A1(c) | TSFR1M + 0.464% | 5.7840 | 10/25/36 | 92,975 | |||||||||

| 16,745 | GSR Mortgage Loan Trust 2006-AR2 Series 2006-AR2 1B2(c) | TSFR1M + 0.894% | 6.2140 | 12/25/35 | 5,374 | |||||||||

| 98,845 | GSR Mortgage Loan Trust 2006-AR2 Series 2006-AR2 2A1(b) | 3.5740 | 04/25/36 | 66,281 | ||||||||||

| 1,210,322 | GSR Mortgage Loan Trust 2006-OA1 Series 2006-OA1 2A2(c) | TSFR1M + 0.634% | 5.9540 | 08/25/46 | 301,502 | |||||||||

| 458,875 | HarborView Mortgage Loan Trust 2005-12 Series 2005-12 1A1A(c) | 12MTA + 2.000% | 6.6260 | 10/19/35 | 248,327 | |||||||||

| 3,407,862 | HarborView Mortgage Loan Trust 2005-13 Series 2005-13 2A11(c) | TSFR1M + 0.674% | 6.0020 | 02/19/36 | 1,618,209 | |||||||||

| 116,072 | HarborView Mortgage Loan Trust 2005-6 Series 2005-6 A1B(c) | US0006M + 0.760% | 6.3880 | 07/19/45 | 92,556 | |||||||||

| 1,293,804 | HarborView Mortgage Loan Trust 2005-6 Series 2005-6 B1(c) | US0006M + 0.825% | 6.4530 | 07/19/45 | 946,134 | |||||||||

| 15,009,905 | HarborView Mortgage Loan Trust 2005-8 Series 2005-8 1X(a),(b) | 0.0001 | 09/19/35 | 150 | ||||||||||

| 11,400,008 | HarborView Mortgage Loan Trust 2006-1 Series 2006-1 X1(a),(b) | 0.0001 | 03/19/36 | 114 | ||||||||||

| 3,849,028 | HarborView Mortgage Loan Trust 2006-10 Series 2006-10 2A1B(c) (h) | TSFR1M + 0.354% | 5.6820 | 11/19/36 | 3,397,565 | |||||||||

| 1,344,682 | HarborView Mortgage Loan Trust 2006-12 Series 2006-12 2A13(c) | TSFR1M + 0.594% | 5.9220 | 12/19/36 | 1,224,619 | |||||||||

| 1,013,165 | HarborView Mortgage Loan Trust 2006-14 Series 2006-14 2A1B(c) | TSFR1M + 0.514% | 5.8420 | 02/19/37 | 1,442,784 | |||||||||

| 105,748 | HarborView Mortgage Loan Trust 2006-7 Series 2006-7 2A1A(c) | TSFR1M + 0.514% | 5.8420 | 09/19/46 | 93,655 | |||||||||

| 2,061,657 | HarborView Mortgage Loan Trust 2007-1 Series 2007-1 2A1B(c) | TSFR1M + 0.474% | 5.8020 | 03/19/37 | 2,930,440 | |||||||||

| 1,620,520 | HarborView Mortgage Loan Trust 2007-3 Series 2007-3 2A1B(c) | TSFR1M + 0.574% | 5.9020 | 05/19/47 | 1,337,215 | |||||||||

| 4,230,605 | HarborView Mortgage Loan Trust 2007-7 Series 2007-7 2A1B(c) | TSFR1M + 2.114% | 6.4340 | 10/25/37 | 3,413,423 | |||||||||

| 85,010 | HomeBanc Mortgage Trust 2004-2 Series 2004-2 M1(c) | TSFR1M + 1.089% | 6.4090 | 12/25/34 | 78,716 | |||||||||

| 336,455 | HomeBanc Mortgage Trust 2005-1 Series 2005-1 B1(c) | TSFR1M + 1.989% | 2.1580 | 03/25/35 | 218,065 | |||||||||

See accompanying notes to financial statements.

13

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 43,910 | HomeBanc Mortgage Trust 2005-1 Series 2005-1 B2(c) | TSFR1M + 2.064% | 2.1580 | 03/25/35 | $ | 28,434 | ||||||||

| 305,615 | Impac CMB Trust Series 2004-11 Series 2004-11 2A2(c) | TSFR1M + 0.854% | 6.1740 | 03/25/35 | 271,326 | |||||||||

| 28,142 | Impac CMB Trust Series 2004-4 Series 2004-4 1M6(c) | TSFR1M + 2.364% | 7.6840 | 09/25/34 | 27,627 | |||||||||

| 220,881 | Impac CMB Trust Series 2005-2 Series 2005-2 1M1(c) | TSFR1M + 0.759% | 6.0790 | 04/25/35 | 201,511 | |||||||||

| 377,654 | Impac CMB Trust Series 2005-2 Series 2005-2 1M3(c) | TSFR1M + 0.879% | 6.1990 | 04/25/35 | 340,656 | |||||||||

| 54,112 | Impac CMB Trust Series 2005-2 Series 2005-2 2M2(c) | TSFR1M + 1.239% | 6.5590 | 04/25/35 | 48,903 | |||||||||

| 36,075 | Impac CMB Trust Series 2005-2 Series 2005-2 2B(c) | TSFR1M + 2.589% | 7.9090 | 04/25/35 | 34,260 | |||||||||

| 3,238 | Impac CMB Trust Series 2005-6 Series 2005-6 2B2(c) | TSFR1M + 3.489% | 8.8090 | 10/25/35 | 3,149 | |||||||||

| 210,943 | Impac Secured Assets CMN Owner Trust Series 2002-2 M1 | 6.5000 | 04/25/33 | 117,803 | ||||||||||

| 900,165 | Impac Secured Assets CMN Owner Trust Series 2004-1 M2(e) | 5.5260 | 03/25/34 | 729,360 | ||||||||||

| 1,555,800 | IndyMac IMJA Mortgage Loan Trust 2007-A1 Series 2007-A1 A4 | 6.0000 | 08/25/37 | 608,882 | ||||||||||

| 1,475,253 | IndyMac IMJA Mortgage Loan Trust 2007-A3 Series 2007-A3 A1 | 6.2500 | 11/25/37 | 652,790 | ||||||||||

| 4,431,683 | IndyMac IMSC Mortgage Loan Trust 2007-HOA1 Series 2007-HOA1 A22(c) | TSFR1M + 0.474% | 5.7940 | 07/25/47 | 3,179,263 | |||||||||

| 75,103 | IndyMac INDA Mortgage Loan Trust 2006-AR3 Series 2006-AR3 1A1(b) | 3.7330 | 12/25/36 | 64,079 | ||||||||||

| 961,289 | IndyMac INDX Mortgage Loan Trust 2004-AR13 Series 2004-AR13 B1(b) | 3.4340 | 01/25/35 | 721,617 | ||||||||||

| 1,391,918 | IndyMac INDX Mortgage Loan Trust 2004-AR14 Series 2004-AR14 2A1A(c) | TSFR1M + 0.834% | 6.1540 | 01/25/35 | 981,414 | |||||||||

| 95,538 | IndyMac INDX Mortgage Loan Trust 2004-AR5 Series 2004-AR5 2A1B(c) | TSFR1M + 0.914% | 6.2340 | 08/25/34 | 82,217 | |||||||||

| 738,076 | IndyMac INDX Mortgage Loan Trust 2004-AR6 Series 2004-AR6 2A(b) | 4.4720 | 10/25/34 | 695,091 | ||||||||||

| 901,829 | IndyMac INDX Mortgage Loan Trust 2004-AR9 Series 2004-AR9 5M2(c) | TSFR1M + 1.914% | 7.2340 | 11/25/34 | 653,765 | |||||||||

| 195,708 | IndyMac INDX Mortgage Loan Trust 2005-AR2 Series 2005-AR2 2A1B(c) | TSFR1M + 0.894% | 6.2140 | 02/25/35 | 138,615 | |||||||||

| 279,128 | IndyMac INDX Mortgage Loan Trust 2005-AR23 Series 2005-AR23 2A1(b) | 3.9380 | 11/25/35 | 224,210 | ||||||||||

| 299,688 | IndyMac INDX Mortgage Loan Trust 2005-AR4 Series 2005-AR4 2A1A(c) | TSFR1M + 0.674% | 5.9940 | 03/25/35 | 293,803 | |||||||||

| 226,023 | IndyMac INDX Mortgage Loan Trust 2006-AR21 Series 2006-AR21 A1(c) | TSFR1M + 0.354% | 5.6740 | 08/25/36 | 206,780 | |||||||||

| 486,076 | IndyMac INDX Mortgage Loan Trust 2006-AR29 Series 2006-AR29 A2(c) | TSFR1M + 0.274% | 5.5940 | 11/25/36 | 470,782 | |||||||||

| 595,578 | IndyMac INDX Mortgage Loan Trust 2006-AR29 Series 2006-AR29 A3(c) | TSFR1M + 0.454% | 5.7740 | 11/25/36 | 579,401 | |||||||||

| 38,293 | IndyMac INDX Mortgage Loan Trust 2006-AR5 Series 2006-AR5 2A1(b) | 3.4250 | 05/25/36 | 34,959 | ||||||||||

| 71,791 | IndyMac INDX Mortgage Loan Trust 2006-AR6 Series 2006-AR6 2A1A(c) | TSFR1M + 0.514% | 5.8340 | 06/25/46 | 55,494 | |||||||||

| 137,056 | IndyMac INDX Mortgage Loan Trust 2006-AR8 Series 2006-AR8 A3A(c) | TSFR1M + 0.574% | 5.8940 | 07/25/46 | 169,492 | |||||||||

| 1,362,658 | IndyMac INDX Mortgage Loan Trust 2007-FLX3 Series 2007-FLX3 A2(c) | TSFR1M + 0.654% | 5.9740 | 06/25/37 | 1,462,142 | |||||||||

| 356,466 | JP Morgan Alternative Loan Trust Series 2006-A2 5A1(b) | 3.9770 | 05/25/36 | 201,596 | ||||||||||

| 957,411 | JP Morgan Mortgage Trust 2005-A1 Series 2005-A1 IB2(b) | 4.6660 | 02/25/35 | 847,949 | ||||||||||

| 57,172 | JP Morgan Mortgage Trust 2006-A6 Series 2006-A6 3A2(b) | 4.3800 | 10/25/36 | 41,401 | ||||||||||

| 136,870 | JP Morgan Mortgage Trust 2006-A7 Series 2006-A7 2A2(b) | 3.9010 | 01/25/37 | 111,165 | ||||||||||

| 129,528 | JP Morgan Mortgage Trust 2006-S3 Series 2006-S3 1A12 | 6.5000 | 08/25/36 | 43,264 | ||||||||||

See accompanying notes to financial statements.

14

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 1,683,356 | Lehman Mortgage Trust 2005-3 Series 2005-3 1A5 | 5.5000 | 01/25/36 | $ | 831,072 | |||||||||

| 38,765 | Lehman Mortgage Trust 2005-3 Series 2005-3 2A7 | 6.0000 | 01/25/36 | 31,221 | ||||||||||

| 1,304,347 | Lehman XS Trust Series 2005-5N Series 2005-5N 3A3C(c) | TSFR1M + 0.614% | 5.9340 | 11/25/35 | 780,160 | |||||||||

| 1,631,292 | Lehman XS Trust Series 2006-18N Series 2006-18N A4(c) | TSFR1M + 0.494% | 5.8140 | 12/25/36 | 1,316,249 | |||||||||

| 643,209 | Lehman XS Trust Series 2007-12N Series 2007-12N 1A3A(c) | TSFR1M + 0.514% | 5.8340 | 07/25/47 | 611,955 | |||||||||

| 124,121 | Lehman XS Trust Series 2007-16N Series 2007-16N 2A2(c) | TSFR1M + 1.814% | 7.1340 | 09/25/47 | 106,359 | |||||||||

| 793,536 | Lehman XS Trust Series 2007-7N Series 2007-7N 1A2(c) | TSFR1M + 0.594% | 5.9140 | 06/25/47 | 696,105 | |||||||||

| 436,304 | MASTR Alternative Loan Trust 2006-2 Series 2006-2 2A3(c) | TSFR1M + 0.464% | 5.7840 | 03/25/36 | 46,837 | |||||||||

| 283,598 | MASTR Alternative Loan Trust 2006-2 Series 2006-2 2A1(c) | TSFR1M + 0.514% | 5.8340 | 03/25/36 | 30,790 | |||||||||

| 361,026 | MASTR Asset Securitization Trust 2004-1 Series 2004-1 B1(b) | 5.4920 | 02/25/34 | 289,048 | ||||||||||

| 42,361 | MASTR Asset Securitization Trust 2004-3 Series 2004-3 4A11 | 5.5000 | 03/25/34 | 1,825 | ||||||||||

| 561,319 | Mellon Residential Funding Cor Mor Pas Thr Tr Series 1999-TBC3 A2(b) | 5.8930 | 10/20/29 | 565,082 | ||||||||||

| 581,509 | Merrill Lynch Alternative Note Asset Trust Series 2007-OAR4 A1(c) | TSFR1M + 0.614% | 5.9340 | 08/25/37 | 495,430 | |||||||||

| 50,863 | Merrill Lynch Mortgage Investors Trust MLMI Series 2003-A1 M2(b) | 4.5120 | 12/25/32 | 48,001 | ||||||||||

| 3,520,737 | Merrill Lynch Mortgage Investors Trust Series 2005-A6 M2(c) | TSFR1M + 1.089% | 6.4090 | 08/25/35 | 3,118,088 | |||||||||

| 3,558,158 | Merrill Lynch Mortgage Investors Trust Series MLCC Series 2003-G XA2(a),(b) | 0.1730 | 01/25/29 | 11,522 | ||||||||||

| 287,904 | Merrill Lynch Mortgage Investors Trust Series MLCC Series 2007-3 M1(b) | 3.4270 | 09/25/37 | 66,827 | ||||||||||

| 29,727 | Merrill Lynch Mortgage Investors Trust Series MLMI Series 2004-A1 M1(b) | 4.1690 | 02/25/34 | 21,305 | ||||||||||

| 414,839 | Morgan Stanley Mortgage Loan Trust 2004-11AR Series 2004-11AR 1B1(c) | TSFR1M + 0.714% | 6.0340 | 01/25/35 | 331,781 | |||||||||

| 67,027 | MortgageIT Trust 2005-2 Series 2005-2 1M2(c) | TSFR1M + 0.924% | 6.2440 | 05/25/35 | 64,426 | |||||||||

| 21,824 | MortgageIT Trust 2005-2 Series 2005-2 2M2(c) | TSFR1M + 1.764% | 7.0940 | 05/25/35 | 19,802 | |||||||||

| 123,485 | Nomura Asset Acceptance Corp Alternative Loan Series 2004-AR1 5M1(c) | TSFR1M + 1.214% | 6.5340 | 08/25/34 | 133,512 | |||||||||

| 221,815 | Nomura Asset Acceptance Corp Alternative Loan Series 2006-AF1 2A(b) | 5.0230 | 06/25/36 | 161,869 | ||||||||||

| 249,829 | NovaStar Mortgage Funding Trust Series 2006-MTA1 Series 2006-MTA1 2A1A(c) | TSFR1M + 0.494% | 0.4760 | 09/25/46 | 225,884 | |||||||||

| 4,230,027 | OPTONE 68402SAC3 DEL TR 2016-1 Series 2016-1A SAC3(a),(b),(d) | 4.9340 | 02/26/38 | 2,388,019 | ||||||||||

| 695,000 | Prime Mortgage Trust 2006-CL1 Series 2006-CL1 M3(c) | TSFR1M + 0.834% | 6.1540 | 02/25/35 | 560,732 | |||||||||

| 325,067 | RAAC Series 2004-SP3 Trust Series 2004-SP3 MII4(c) | TSFR1M + 2.889% | 8.2090 | 09/25/34 | 218,756 | |||||||||

| 3,888 | RALI Series 2003-QS9 Trust Series 2003-QS9 A2(c) | TSFR1M + 0.564% | 5.8840 | 05/25/30 | 3,314 | |||||||||

| 3,357,902 | RALI Series 2005-QO1 Trust Series 2005-QO1 A3(c) | TSFR1M + 0.494% | 5.8140 | 08/25/35 | 1,177,139 | |||||||||

| 190,749 | RALI Series 2005-QS7 Trust Series 2005-QS7 CB | 5.5000 | 06/25/35 | 165,717 | ||||||||||

| 1,596,537 | RALI Series 2006-QA8 Trust Series 2006-QA8 A1(c) | TSFR1M + 0.494% | 5.8140 | 09/25/36 | 1,421,681 | |||||||||

| 1,558,766 | RALI Series 2006-QO7 Trust Series 2006-QO7 1A1(c) | 12MTA + 0.800% | 5.2300 | 09/25/46 | 1,331,015 | |||||||||

| 316,096 | RALI Series 2006-QO8 Trust Series 2006-QO8 1A3A(c) | TSFR1M + 0.514% | 5.8340 | 10/25/46 | 292,111 | |||||||||

| 33,159,251 | RALI Series 2006-QS12 Trust Series 2006-QS12 AV(a),(b) (i) | 0.4650 | 09/25/36 | 404,732 | ||||||||||

See accompanying notes to financial statements.

15

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 266,755 | RALI Series 2006-QS16 Trust Series 2006-QS16 A10 | 6.0000 | 11/25/36 | $ | 194,715 | |||||||||

| 140,905 | RALI Series 2006-QS7 Trust Series 2006-QS7 A4(c) | TSFR1M + 0.514% | 5.8340 | 06/25/36 | 100,056 | |||||||||

| 1,724,683 | RALI Series 2007-QH3 Trust Series 2007-QH3 A2(c) | TSFR1M + 0.534% | 5.8540 | 04/25/37 | 3,548,509 | |||||||||

| 467,053 | RALI Series 2007-QH5 Trust Series 2007-QH5 AI2(c) | TSFR1M + 0.614% | 5.9340 | 06/25/37 | 267,057 | |||||||||

| 599,609 | RALI Series 2007-QH7 Trust Series 2007-QH7 1A2(c) | TSFR1M + 0.654% | 5.9740 | 08/25/37 | 351,246 | |||||||||

| 6,258 | RAMP Series 2004-SL1 Trust Series 2004-SL1 MI6(c) | TSFR1M + 2.014% | 8.2840 | 10/25/31 | 5,719 | |||||||||

| 8,685,502 | Reperforming Loan REMIC Trust 2005-R1 Series 2005-R1 1AS(a),(b),(d) | 0.8200 | 03/25/35 | 287,176 | ||||||||||

| 8,435,495 | Reperforming Loan REMIC Trust 2005-R2 Series 2005-R2 1AS(a),(b),(d) | 0.4190 | 06/25/35 | 209,824 | ||||||||||

| 9,380,122 | Reperforming Loan REMIC Trust 2006-R1 Series 2006-R1 AS(a),(b) | 0.3350 | 01/25/36 | 257,218 | ||||||||||

| 863,804 | Residential Asset Securitization Trust 2003-A4 Series 2003-A4 B1 | 5.7500 | 05/25/33 | 591,252 | ||||||||||

| 14,940,778 | Residential Asset Securitization Trust 2005-A11CB Series 2005-A11 1AX(a),(b) | 0.3660 | 10/25/35 | 171,224 | ||||||||||

| 265,324 | Residential Asset Securitization Trust 2005-A16 Series 2005-A16 A3 | 6.0000 | 02/25/36 | 118,260 | ||||||||||

| 2,125,529 | Residential Asset Securitization Trust 2007-A9 Series 2007-A9 AX(a),(b) | 7.0000 | 09/25/37 | 630,937 | ||||||||||

| 1,120,940 | RFMSI Series 2007-S6 Trust Series 2007-S6 2A5(c) | TSFR1M + 0.614% | 5.9340 | 06/25/37 | 703,762 | |||||||||

| 159,614 | SACO I, Inc. Series 1999-3 1B1(b),(d) (i) | 4.9850 | 04/25/39 | 147,240 | ||||||||||

| 79,056 | Sequoia Mortgage Trust 9 Series 9 B1(c) | TSFR1M + 1.239% | 6.5640 | 09/20/32 | 67,493 | |||||||||

| 2,896,444 | Structured Adjustable Rate Mortgage Loan Trust Series 2005-10 M1(c) | TSFR1M + 0.789% | 6.1090 | 06/25/35 | 2,846,733 | |||||||||

| 1,072,675 | Structured Adjustable Rate Mortgage Loan Trust Series 2005-18 4A1(b) | 3.8310 | 09/25/35 | 698,796 | ||||||||||

| 2,019,410 | Structured Asset Mortgage Investments II Trust Series 2005-AR5 X2(a),(b) | 0.4660 | 07/19/35 | 27,352 | ||||||||||

| 180,897 | Structured Asset Mortgage Investments II Trust Series 2006-AR3 11A1(c) | TSFR1M + 0.534% | 5.8540 | 04/25/36 | 157,482 | |||||||||

| 2,997,026 | Structured Asset Mortgage Investments II Trust Series 2006-AR3 12A3(c) | TSFR1M + 0.654% | 5.9740 | 05/25/36 | 2,253,704 | |||||||||

| 35,511,364 | Structured Asset Mortgage Investments II Trust Series 2006-AR7 X(a) | 0.9000 | 08/25/36 | 832,244 | ||||||||||

| 10,380 | Structured Asset Mortgage Investments II Trust Series AR7 A10(c) (i) | TSFR1M + 0.514% | 5.8340 | 08/25/36 | 11,739 | |||||||||

| 1,790,375 | Structured Asset Mortgage Investments II Trust Series 2005-AR2 1A1(c) | TSFR1M + 0.574% | 5.8940 | 05/25/45 | 1,609,660 | |||||||||

| 926,207 | Structured Asset Mortgage Investments II Trust Series 2007-AR7 2A1(b) | 3.6050 | 05/25/47 | 746,670 | ||||||||||

| 32,657,454 | Structured Asset Mortgage Investments II Trust Series 2007-AR6 X2(a) | 0.5000 | 08/25/47 | 583,919 | ||||||||||

| 2,462,798 | Structured Asset Mortgage Investments II Trust Series AR6 A2(c) | 12MTA + 1.730% | 6.1600 | 08/25/47 | 2,620,611 | |||||||||

| 389,268 | Structured Asset Securities Corp Assistance Loan Series 2003-AL1 B1(d) | 3.3560 | 04/25/31 | 385,168 | ||||||||||

| 189,524 | Structured Asset Securities Corp Mortgage Series 2003-9A B1II(b) | 6.0100 | 03/25/33 | 172,957 | ||||||||||

| 451,613 | Structured Asset Securities Corporation Series 2005-RF4 B1(b),(d) | 4.3910 | 07/25/35 | 320,406 | ||||||||||

| 447,860 | SunTrust Alternative Loan Trust 2006-1F Series 2006-1F 1A4 | 6.0000 | 04/25/36 | 190,147 | ||||||||||

| 24,169,714 | WaMu Mortgage Pass-Through Certificates Series 2005-AR15 X(a),(b) | 0.0001 | 11/25/45 | 15,457 | ||||||||||

| 439,404 | WaMu Mortgage Pass-Through Certificates Series 2006-AR4 2A1A(c) | COF 11 + 1.500% | 4.5820 | 05/25/46 | 363,989 | |||||||||

| 380,105 | Washington Mutual Mortgage Pass-Through Series 2006-5 1A2 | 6.0000 | 07/25/36 | 284,444 | ||||||||||

See accompanying notes to financial statements.

16

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS — 31.8% (Continued) | ||||||||||||||

| 1,100,114 | Washington Mutual Mortgage Pass-Through Series 2007-1 1A3(c) | TSFR1M + 0.484% | 5.8040 | 02/25/37 | $ | 725,796 | ||||||||

| 324,700 | Washington Mutual Mortgage Pass-Through Series 2007-OA1 1A(c) | 12MTA + 0.710% | 5.1400 | 12/25/46 | 265,586 | |||||||||

| 124,867,493 | ||||||||||||||

| HOME EQUITY — 16.0% | ||||||||||||||

| 176,034 | ABFC 2004-OPT1 Trust Series 2004-OPT1 M6(c) | TSFR1M + 5.364% | 10.6840 | 12/25/32 | 166,399 | |||||||||

| 340,586 | ABFC 2004-OPT3 Trust Series 2004-OPT3 M1(c) | TSFR1M + 0.864% | 6.1840 | 09/25/33 | 341,363 | |||||||||

| 481,733 | ABFC 2004-OPT4 Trust Series 2004-OPT4 M3(c) | TSFR1M + 2.289% | 7.6090 | 08/25/33 | 436,840 | |||||||||

| 562,272 | Accredited Mortgage Loan Trust 2005-3 Series 2005-3 M6(c) | TSFR1M + 1.164% | 6.4840 | 09/25/35 | 364,156 | |||||||||

| 114,000 | Accredited Mortgage Loan Trust 2005-4 Series 2005-4 M3(c) | TSFR1M + 0.574% | 5.8940 | 12/25/35 | 81,550 | |||||||||

| 338,700 | ACE Securities Corp Home Equity Loan Trust Series Series 2003-FM1 M6(c) | TSFR1M + 5.364% | 10.6840 | 11/25/32 | 272,885 | |||||||||

| 141,259 | ACE Securities Corp Home Equity Loan Trust Series Series 2003-NC1 M4(c) | TSFR1M + 5.364% | 10.6840 | 07/25/33 | 113,773 | |||||||||

| 464,823 | ACE Securities Corp Home Equity Loan Trust Series Series 2003-HE1 M5(c) | TSFR1M + 5.364% | 10.6840 | 11/25/33 | 435,777 | |||||||||

| 33,875 | ACE Securities Corp Home Equity Loan Trust Series Series 2004-OP1 M2(c) | TSFR1M + 1.689% | 7.0090 | 04/25/34 | 32,023 | |||||||||

| 80,583 | ACE Securities Corp Home Equity Loan Trust Series Series 2004-OP1 M4(c) | TSFR1M + 3.114% | 8.4340 | 04/25/34 | 73,067 | |||||||||

| 245,351 | ACE Securities Corp Home Equity Loan Trust Series Series 2004-OP1 M5(c) | TSFR1M + 3.489% | 8.8090 | 04/25/34 | 193,627 | |||||||||

| 1,418,184 | ACE Securities Corp Home Equity Loan Trust Series Series 2004-RM2 M5(c) | TSFR1M + 1.509% | 6.8290 | 01/25/35 | 1,006,213 | |||||||||

| 372,476 | Aegis Asset Backed Securities Trust Mortgage Series 2004-1 M3(c) | TSFR1M + 2.444% | 7.7640 | 04/25/34 | 175,900 | |||||||||

| 192,973 | Aegis Asset Backed Securities Trust Mortgage Series 2004-1 B1(c) | TSFR1M + 2.894% | 8.2140 | 04/25/34 | 14,784 | |||||||||

| 623,163 | AFC Home Equity Loan Trust Series 1999-2 1A(c) | TSFR1M + 0.924% | 6.2440 | 06/25/29 | 367,773 | |||||||||

| 3,157,162 | Ameriquest Mortgage Securities Asset-Backed Series 2002-3 M4(c) | TSFR1M + 3.339% | 8.6590 | 08/25/32 | 2,714,869 | |||||||||

| 297,741 | Argent Securities Inc Asset-Backed Pass-Through Series 2003-W10 M3(c) | TSFR1M + 2.889% | 3.4330 | 01/25/34 | 233,745 | |||||||||

| 285,921 | Argent Securities Inc Asset-Backed Pass-Through Series 2006-M2 A2C(c) | TSFR1M + 0.264% | 5.5840 | 09/25/36 | 92,741 | |||||||||

| 102,868 | Asset Backed Securities Corp Home Equity Loan Series 2004-HE3 M6(c) | TSFR1M + 4.239% | 9.5590 | 06/25/34 | 93,177 | |||||||||

| 328,556 | Asset Backed Securities Corp Home Equity Loan Series 2004-HE9 M2(c) | TSFR1M + 1.914% | 7.2340 | 12/25/34 | 235,770 | |||||||||

| 199,370 | Asset Backed Securities Corp Home Equity Loan Series 2005-HE2 M4(c) | TSFR1M + 1.344% | 6.2540 | 02/25/35 | 192,455 | |||||||||

| 790,274 | Asset Backed Securities Corp Home Equity Loan Series 2005-HE2 M5(c) | TSFR1M + 1.989% | 6.6840 | 02/25/35 | 759,682 | |||||||||

| 57,666 | Bayview Financial Acquisition Trust Series 2006-D 1A4(e) | 6.5960 | 12/28/36 | 57,664 | ||||||||||

| 2,430,000 | Bayview Financial Mortgage Pass-Through Trust Series 2005-C B2(c) | TSFR1M + 2.139% | 6.7830 | 06/28/44 | 2,140,356 | |||||||||

| 4,756,909 | Bayview Financial Mortgage Pass-Through Trust Series 2004-D B2(c) | TSFR1M + 5.364% | 10.6850 | 08/28/44 | 5,289,762 | |||||||||

| 293,321 | Bear Stearns Asset Backed Securities I Trust Series 2004-FR2 M6(c) | TSFR1M + 2.964% | 5.0570 | 06/25/34 | 261,286 | |||||||||

| 112,763 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE6 M5(c) | TSFR1M + 4.239% | 5.2440 | 08/25/34 | 100,116 | |||||||||

| 182,516 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE7 M6(c) | TSFR1M + 5.739% | 11.0590 | 08/25/34 | 168,103 | |||||||||

| 912,695 | Bear Stearns Asset Backed Securities I Trust Series 2004-FR3 M5(c) | TSFR1M + 2.964% | 5.2630 | 09/25/34 | 797,600 | |||||||||

| 542,598 | Bear Stearns Asset Backed Securities I Trust Series 2004-FR3 M4(c) | TSFR1M + 2.814% | 5.2630 | 09/25/34 | 485,401 | |||||||||

See accompanying notes to financial statements.

17

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| HOME EQUITY — 16.0% (Continued) | ||||||||||||||

| 454,479 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE8 M3(c) | TSFR1M + 2.214% | 7.5340 | 09/25/34 | $ | 434,131 | ||||||||

| 618,958 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE8 M4(c) | TSFR1M + 2.739% | 8.0590 | 09/25/34 | 623,566 | |||||||||

| 708,000 | Bear Stearns Asset Backed Securities I Trust Series 2004-BO1 M9B(c) | TSFR1M + 6.114% | 11.4340 | 10/25/34 | 708,621 | |||||||||

| 376,533 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE9 M4(c) | TSFR1M + 2.739% | 5.3710 | 11/25/34 | 363,593 | |||||||||

| 188,378 | Bear Stearns Asset Backed Securities I Trust Series 2004-HE10 M5(c) | TSFR1M + 2.814% | 5.6280 | 12/25/34 | 196,729 | |||||||||

| 731,384 | Bear Stearns Asset Backed Securities I Trust Series 2006-HE10 23A(c) | TSFR1M + 0.254% | 4.7170 | 12/25/36 | 897,345 | |||||||||

| 158,089 | Bear Stearns Asset Backed Securities Trust Series 1999-2 MF1(e) | 8.2200 | 10/25/29 | 207,092 | ||||||||||

| 38,451 | Bear Stearns Asset Backed Securities Trust Series 1999-2 AF2(e) | 8.4100 | 10/25/29 | 38,273 | ||||||||||

| 73,148 | Bear Stearns Asset Backed Securities Trust Series 2003-HE1 M5(c) | TSFR1M + 3.489% | 5.5550 | 01/25/34 | 78,958 | |||||||||

| 86,246 | Bear Stearns Asset Backed Securities Trust Series 2003-HE1 M4(c) | TSFR1M + 2.964% | 5.5550 | 01/25/34 | 80,144 | |||||||||

| 112,358 | Bear Stearns Asset Backed Securities Trust Series 2004-HE1 M6(c) | TSFR1M + 6.114% | 5.7270 | 02/25/34 | 119,647 | |||||||||

| 514,705 | Bear Stearns Asset Backed Securities Trust Series 2004-HE2 M6(c) | TSFR1M + 4.989% | 5.2980 | 03/25/34 | 497,671 | |||||||||

| 9,927 | Bear Stearns Asset Backed Securities Trust Series 2004-HE2 M4(c) | TSFR1M + 2.739% | 5.2980 | 03/25/34 | 9,628 | |||||||||

| 73,228 | Bear Stearns Asset Backed Securities Trust Series 2004-HE5 M2(c) | TSFR1M + 1.989% | 7.3090 | 07/25/34 | 62,410 | |||||||||

| 51,739 | Bear Stearns Asset Backed Securities Trust Series 2004-HE5 M6(c) | TSFR1M + 5.739% | 11.0590 | 07/25/34 | 41,084 | |||||||||

| 923,475 | CDC Mortgage Capital Trust 2003-HE2 Series 2003-HE2 M2(c) | TSFR1M + 2.964% | 8.2840 | 10/25/33 | 906,403 | |||||||||

| 602,930 | CDC Mortgage Capital Trust 2004-HE1 Series 2004-HE1 M1(c) | TSFR1M + 0.969% | 6.2890 | 06/25/34 | 695,125 | |||||||||

| 581,470 | CDC Mortgage Capital Trust 2004-HE1 Series 2004-HE1 M2(c) | TSFR1M + 1.914% | 7.2340 | 06/25/34 | 576,150 | |||||||||

| 358,357 | CDC Mortgage Capital Trust 2004-HE3 Series 2004-HE3 M2(c) | TSFR1M + 1.914% | 6.2200 | 11/25/34 | 338,459 | |||||||||

| 277,929 | Centex Home Equity Loan Trust 2001-b Series 2001-B A5(e) | 7.3300 | 07/25/32 | 209,192 | ||||||||||

| 48,684 | Centex Home Equity Loan Trust 2003-A Series 2003-A M2(c) | TSFR1M + 1.844% | 7.1640 | 03/25/33 | 45,097 | |||||||||

| 658,373 | Centex Home Equity Loan Trust 2004-B Series 2004-B M5(c) | TSFR1M + 1.689% | 7.0090 | 03/25/34 | 607,682 | |||||||||

| 83,580 | Centex Home Equity Loan Trust 2004-D Series 2004-D MV2(c) | TSFR1M + 1.149% | 6.4690 | 09/25/34 | 80,573 | |||||||||

| 182,009 | Citigroup Global Markets Mortgage Securities VII, Series 2002-WMC1 M1(c) | TSFR1M + 1.464% | 6.7840 | 01/25/32 | 190,937 | |||||||||

| 77,450 | Citigroup Mortgage Loan Trust 2007-AMC2 Series 2007-AMC2 A3A(c) | TSFR1M + 0.194% | 5.5140 | 01/25/37 | 53,581 | |||||||||

| 323,859 | Citigroup Mortgage Loan Trust 2007-OPX1 Series 2007-OPX1 A4B(e) | 6.3330 | 01/25/37 | 115,483 | ||||||||||

| 4,418,377 | Citigroup Mortgage Loan Trust, Inc. Series 2005-HE4 M5(c) | TSFR1M + 1.089% | 6.4090 | 10/25/35 | 2,311,054 | |||||||||

| 116,328 | Conseco Finance Corporation/Old Series 2002-A B1(c) | TSFR1M + 5.364% | 10.6970 | 04/15/32 | 116,720 | |||||||||

| 180,382 | Conseco Finance Home Equity Loan Trust 2002-B Series 2002-B B1(c) | TSFR1M + 5.364% | 10.6970 | 05/15/33 | 181,014 | |||||||||

| 78,867 | Credit Suisse First Boston Mortgage Securities Series 2002-HE16 M2(c) | TSFR1M + 2.114% | 7.4340 | 10/25/32 | 76,979 | |||||||||

| 114,483 | Credit Suisse First Boston Mortgage Securities Series 2004-FRE1 B3(c) | TSFR1M + 3.364% | 3.9100 | 04/25/34 | 101,950 | |||||||||

| 488,289 | CWHEQ Revolving Home Equity Loan Trust Series Series 2005-B 2A(c),(d) | TSFR1M + 0.294% | 5.6270 | 05/15/35 | 482,424 | |||||||||

| 122,024 | Delta Funding Home Equity Loan Trust 1999-3 Series 1999-3 M1(e) | 8.1000 | 01/15/30 | 80,355 | ||||||||||

| 778,987 | EMC Mortgage Loan Trust 2002-A Series 2002-AA M2(c),(d) | TSFR1M + 2.664% | 7.9840 | 05/25/39 | 776,510 | |||||||||

See accompanying notes to financial statements.

18

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| HOME EQUITY — 16.0% (Continued) | ||||||||||||||

| 441,101 | EquiFirst Mortgage Loan Trust 2004-3 Series 2004-3 M9(c) | TSFR1M + 4.014% | 9.3340 | 12/25/34 | $ | 374,692 | ||||||||

| 3,910,253 | First NLC Trust 2005-1 Series 2005-1 M2(c) | TSFR1M + 0.759% | 2.6290 | 05/25/35 | 2,880,687 | |||||||||

| 305,240 | GE Capital Mortgage Funding Corp 1999-HE3 Trust Series 1999-HE3 M(b) | 7.7750 | 10/25/29 | 298,949 | ||||||||||

| 54,313 | GE Capital Mortgage Services Inc 1999-HE2 Trust Series 1999-HE2 B1(b) | 7.9050 | 07/25/29 | 28,461 | ||||||||||

| 51,718 | GSAA Home Equity Trust 2006-3 Series 2006-3 A1(c) | TSFR1M + 0.274% | 5.5940 | 03/25/36 | 18,460 | |||||||||

| 229,987 | Home Equity Asset Trust Series 2002-4 M2(c) | TSFR1M + 2.664% | 7.9840 | 03/25/33 | 214,424 | |||||||||

| 135,035 | Home Equity Asset Trust Series 2003-8 M3(c) | TSFR1M + 2.464% | 7.7840 | 04/25/34 | 129,268 | |||||||||

| 296,287 | Home Equity Asset Trust Series 2003-8 B1(c) | TSFR1M + 2.614% | 7.9340 | 04/25/34 | 279,876 | |||||||||

| 202,168 | Home Equity Asset Trust Series 2004-3 B1(c) | TSFR1M + 2.714% | 8.0340 | 08/25/34 | 605,324 | |||||||||

| 770,660 | Home Equity Asset Trust Series 2004-8 M4(c) | TSFR1M + 1.614% | 6.9340 | 03/25/35 | 703,314 | |||||||||

| 177,370 | Home Equity Asset Trust 2002-2 Series 2002-2 M2(c) | TSFR1M + 1.964% | 7.2790 | 06/25/32 | 159,381 | |||||||||

| 215,407 | Home Equity Asset Trust 2004-6 Series 2004-6 M5(c) | TSFR1M + 1.764% | 7.0840 | 12/25/34 | 205,750 | |||||||||

| 1,143,915 | Home Equity Asset Trust 2005-4 Series 2005-4 M7(c) | TSFR1M + 1.794% | 4.4540 | 10/25/35 | 1,150,605 | |||||||||

| 464,290 | Home Equity Mortgage Loan Asset-Backed Trust Series 2001-C M2(c) | TSFR1M + 2.289% | 7.6090 | 12/25/32 | 464,411 | |||||||||

| 105,693 | Home Equity Mortgage Loan Asset-Backed Trust Series 2003-A MF1(e) | 4.9790 | 04/25/33 | 152,785 | ||||||||||

| 156,564 | Home Equity Mortgage Loan Asset-Backed Trust Series 2004-C M4(c) | TSFR1M + 1.539% | 4.2480 | 03/25/35 | 134,947 | |||||||||

| 344,441 | Home Equity Mortgage Loan Asset-Backed Trust Series 2004-C M5(c) | TSFR1M + 1.689% | 4.2480 | 03/25/35 | 292,537 | |||||||||

| 293,558 | Home Equity Mortgage Loan Asset-Backed Trust Series 2004-C M6(c) | TSFR1M + 1.989% | 4.2480 | 03/25/35 | 245,930 | |||||||||

| 453,975 | IMC Home Equity Loan Trust 1998-1 Series 1998-1 M1(e) | 7.5300 | 06/20/29 | 423,208 | ||||||||||

| 612 | IMC Home Equity Loan Trust 1998-5 Series 1998-5 A6(e) | 6.5600 | 03/15/37 | 605 | ||||||||||

| 133,609 | Mastr Asset Backed Securities Trust 2004-FRE1 Series 2004-FRE1 M6(c) | TSFR1M + 2.214% | 6.8340 | 07/25/34 | 109,348 | |||||||||

| 97,560 | Mastr Asset Backed Securities Trust 2004-HE1 Series 2004-HE1 M8(c) | TSFR1M + 3.864% | 9.1840 | 09/25/34 | 78,540 | |||||||||

| 24,381 | Mastr Asset Backed Securities Trust 2004-OPT2 Series 2004-OPT2 M4(c) | TSFR1M + 1.614% | 6.9340 | 09/25/34 | 24,324 | |||||||||

| 662,362 | Mastr Asset Backed Securities Trust 2004-OPT2 Series 2004-OPT2 M8(c) | TSFR1M + 2.964% | 8.2840 | 09/25/34 | 481,717 | |||||||||

| 52,367 | Mastr Asset Backed Securities Trust 2005-NC1 Series 2005-NC1 M5(c) | TSFR1M + 1.314% | 6.6340 | 12/25/34 | 51,205 | |||||||||

| 1,088,197 | Merrill Lynch Mortgage Investors Trust Series Series 2003-HE1 M2(c) | TSFR1M + 2.589% | 7.9090 | 07/25/34 | 1,041,844 | |||||||||

| 701,486 | Merrill Lynch Mortgage Investors Trust Series Series 2004-HE2 B3(c) | TSFR1M + 5.364% | 10.6840 | 08/25/35 | 648,743 | |||||||||

| 122,683 | Merrill Lynch Mortgage Investors Trust Series Series 2005-NC1 B2(c) | TSFR1M + 2.064% | 7.3840 | 10/25/35 | 114,619 | |||||||||

| 732,187 | Morgan Stanley A.B.S Capital I Inc Trust 2003-NC10 Series 2003-NC10 B2(c) | TSFR1M + 5.739% | 11.0590 | 10/25/33 | 778,486 | |||||||||

| 420,215 | Morgan Stanley A.B.S Capital I Inc Trust 2003-NC8 Series 2003-NC8 B1(c) | TSFR1M + 5.514% | 10.8340 | 09/25/33 | 401,663 | |||||||||

| 568,546 | Morgan Stanley A.B.S Capital I Inc Trust 2003-NC8 Series 2003-NC8 B2(c) | TSFR1M + 5.739% | 11.0590 | 09/25/33 | 510,168 | |||||||||

| 492,840 | Morgan Stanley A.B.S Capital I Inc Trust 2005-HE2 Series 2005-HE2 M5(c) | TSFR1M + 1.134% | 6.4540 | 01/25/35 | 406,705 | |||||||||

| 1,100,106 | Morgan Stanley A.B.S Capital I Inc Trust 2005-NC1 Series 2005-NC1 M5(c) | TSFR1M + 1.209% | 6.5290 | 01/25/35 | 984,510 | |||||||||

| 263,916 | Morgan Stanley A.B.S Capital I Inc Trust 2007-HE3 Series 2007-HE3 A2A(c) | TSFR1M + 0.174% | 5.4940 | 12/25/36 | 128,964 | |||||||||

See accompanying notes to financial statements.

19

| DEER PARK TOTAL RETURN CREDIT FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| September 30, 2023 |

| Principal | Coupon | |||||||||||||

| Amount ($) | Spread | Rate (%) | Maturity | Fair Value | ||||||||||

| NON-AGENCY ASSET BACKED SECURITIES — 103.8% (Continued) | ||||||||||||||

| HOME EQUITY — 16.0% (Continued) | ||||||||||||||

| 20,949,213 | Morgan Stanley Mortgage Loan Trust 2007-7AX Series 2007-7AX 2A4(c) | TSFR1M + 0.754% | 6.0740 | 04/25/37 | $ | 774,656 | ||||||||

| 5,261,451 | Morgan Stanley Mortgage Loan Trust 2007-7AX Series 2007-7AX 2A6(c) | TSFR1M + 0.754% | 6.0740 | 04/25/37 | 194,557 | |||||||||

| 781,492 | New Century Home Equity Loan Trust 2003-6 Series 2003-6 M4(c) | TSFR1M + 4.877% | 10.1970 | 01/25/34 | 787,050 | |||||||||