Exhibit (c)(9)

|

STRICTLY CONFIDENTIAL

Project Napa

Presentation to the Special Committee of the Board of Directors

Overview of Cloud ERP Opportunity – Strategic Rationale for Napa Transaction

May 20, 2016

|

Disclaimer

This presentation has been prepared by Moelis & Company LLC (“Moelis”) for exclusive use of the Special Committee of the Board of

Directors of Orlando Corporation (“Orlando” or the “Company”) in considering the transaction described herein based on publicly available information. Moelis has not assumed any responsibility for independently verifying the information herein, Moelis makes no representation or warranty as to the accuracy, completeness or reasonableness of the information herein and Moelis disclaims any liability with respect to the information herein. In this presentation, Moelis has used certain projections, forecasts or other forward-looking statements with respect to the Company and/or other parties involved in the transaction which were prepared based on publicly available information. This presentation speaks only as of its date and Moelis assumes no obligation to update it or to advise any person that its conclusions or advice has changed.

This presentation is solely for informational purposes. This presentation is not intended to provide any basis for any decision on any transaction and is not a recommendation with respect to any transaction. The recipient should make its own independent business decision based on all other information, advice and the recipient’s own judgment. This presentation is not an offer to sell or a solicitation of an indication of interest to purchase any security, option, commodity, future, loan or currency. It is not a commitment to underwrite any security, to loan any funds or to make any investment. Moelis does not offer tax, accounting or legal advice.

Moelis provides mergers and acquisitions, restructuring and other advisory services to clients and its affiliates manage private investment partnerships. Its personnel may make statements or provide advice that is contrary to information contained in this material. Our proprietary interests may conflict with your interests. Moelis may from time to time have positions in or effect transactions in securities described in this presentation. Moelis may have advised, may seek to advise and may in the future advise or invest in companies mentioned in this presentation.

This presentation is confidential and may not be disclosed to any other person or relied upon without the prior written consent of Moelis.

[ 1 ]

|

Executive Summary

Moelis is pleased to meet with the Special Committee of the Board of Directors of Orlando to discuss Project Napa

Database, middleware and application software are key products / markets for Orlando

The market for these services is rapidly evolving, with cloud disrupting traditional on-premise delivery models

Orlando has successfully transitioned its middleware, database, and applications (CRM, HCM) capabilities, but lacks a broad Cloud ERP offering

Maintaining a leading position in ERP application software is a strategic imperative for Orlando

Napa could directly address the Orlando shortcomings in Cloud ERP

Competitors are likely to look to strengthen their Cloud ERP positions, making timing a key consideration

Addressing Orlando’s shortcomings in Cloud ERP should be viewed as a strategic imperative

[ 2 ]

|

Why is Cloud ERP a Strategic Opportunity for Orlando?

Building a leading presence in Cloud ERP can help Orlando in holistically serving the broader ERP market and in further strengthening its IaaS and PaaS business capabilities

ERP is the largest and one of the stickiest application software types, with favorable secular tailwinds

Cloud ERP strength would position Orlando to more broadly serve the larger ERP market

Strong SaaS presence in ERP creates strategic cross-selling opportunities for complementary products such as PaaS and IaaS

Gives Orlando a better ‘seat at the table’ as customers make decisions on long-term ERP strategy

Longer-term product pipeline dependent on penetrating broader market once meaningfully scaled

A comprehensive suite of ERP offerings – both on-premise and SaaS – gives Orlando the potential to become an end-to-end winner for all customer ERP needs

[ 3 ]

|

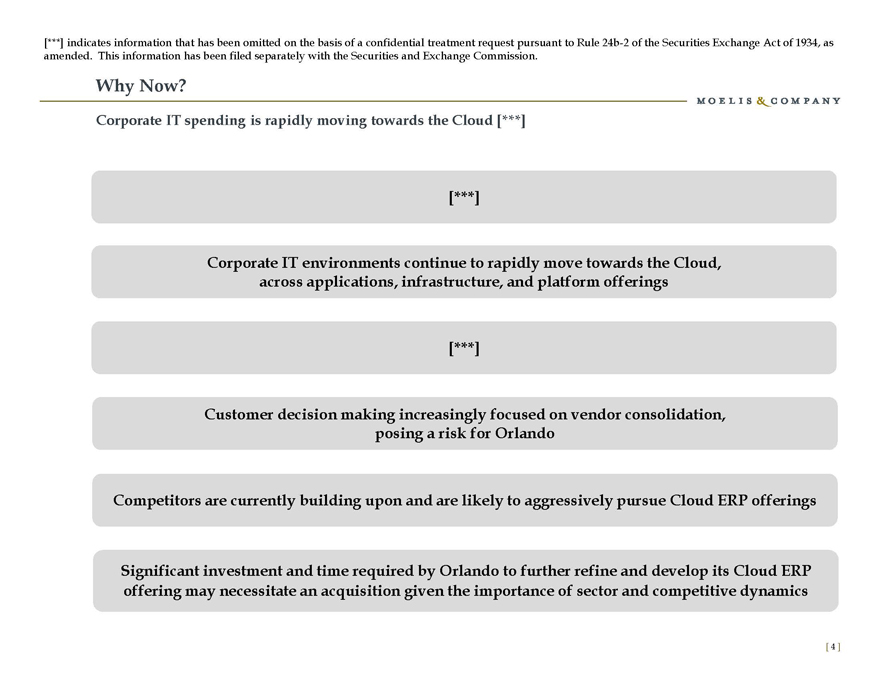

Why Now?

Corporate IT spending is rapidly moving towards the Cloud [***] [***]

Corporate IT environments continue to rapidly move towards the Cloud, across applications, infrastructure, and platform offerings

[***]

Customer decision making increasingly focused on vendor consolidation, posing a risk for Orlando

Competitors are currently building upon and are likely to aggressively pursue Cloud ERP offerings

Significant investment and time required by Orlando to further refine and develop its Cloud ERP offering may necessitate an acquisition given the importance of sector and competitive dynamics

[***] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. This information has been filed separately with the Securities and Exchange Commission. [ 4 ]

|

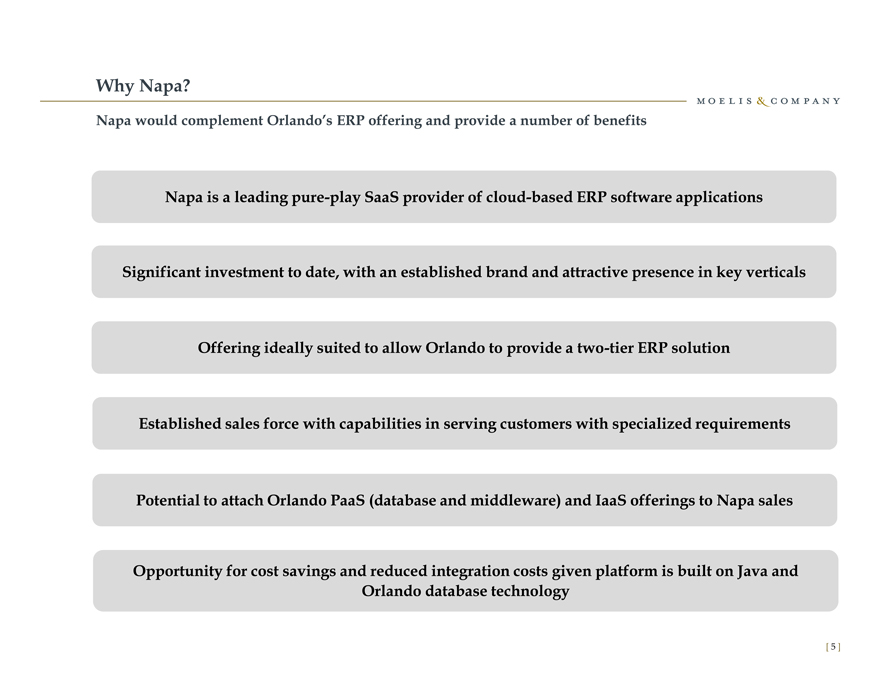

Why Napa?

Napa would complement Orlando’s ERP offering and provide a number of benefits

Napa is a leading pure-play SaaS provider of cloud-based ERP software applications

Significant investment to date, with an established brand and attractive presence in key verticals

Offering ideally suited to allow Orlando to provide a two-tier ERP solution

Established sales force with capabilities in serving customers with specialized requirements

Potential to attach Orlando PaaS (database and middleware) and IaaS offerings to Napa sales

Opportunity for cost savings and reduced integration costs given platform is built on Java and

Orlando database technology

[ 5 ]

|

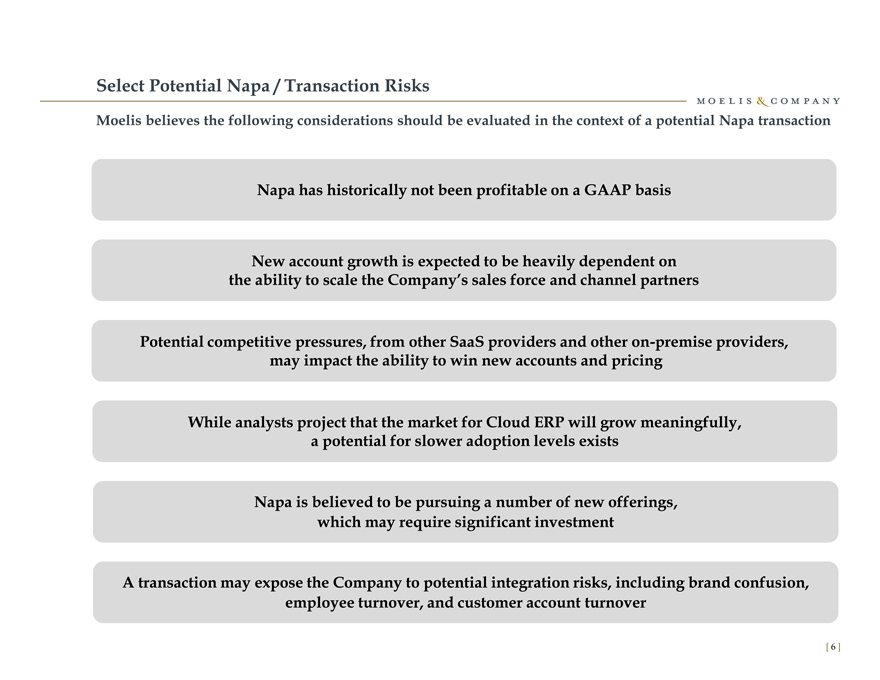

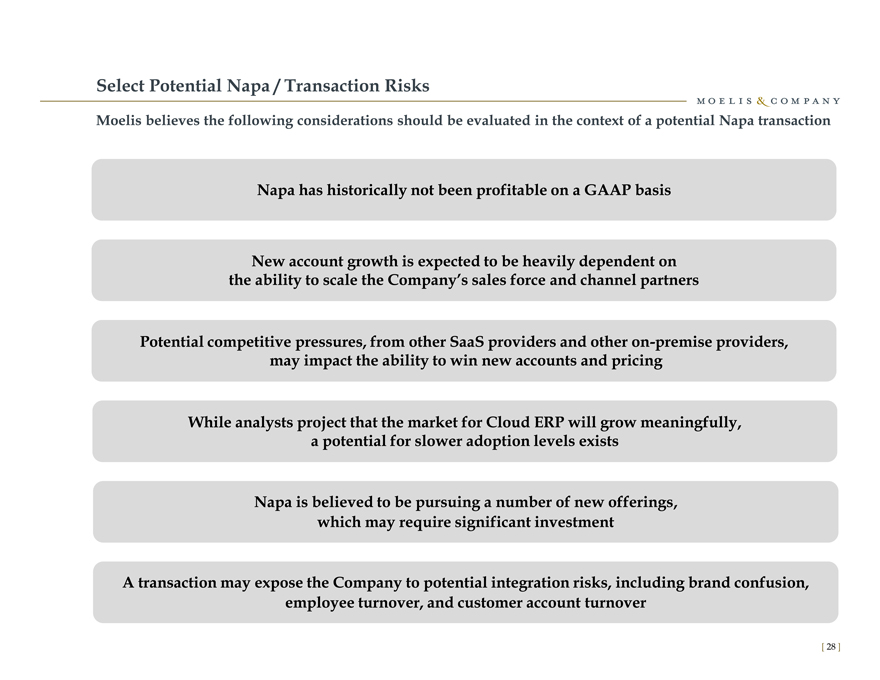

Select Potential Napa / Transaction Risks

Moelis believes the following considerations should be evaluated in the context of a potential Napa transaction

Napa has historically not been profitable on a GAAP basis

New account growth is expected to be heavily dependent on the ability to scale the Company’s sales force and channel partners

Potential competitive pressures, from other SaaS providers and other on-premise providers, may impact the ability to win new accounts and pricing

While analysts project that the market for Cloud ERP will grow meaningfully, a potential for slower adoption levels exists

Napa is believed to be pursuing a number of new offerings, which may require significant investment

A transaction may expose the Company to potential integration risks, including brand confusion, employee turnover, and customer account turnover

[ 6 ]

|

I. Why Now?

|

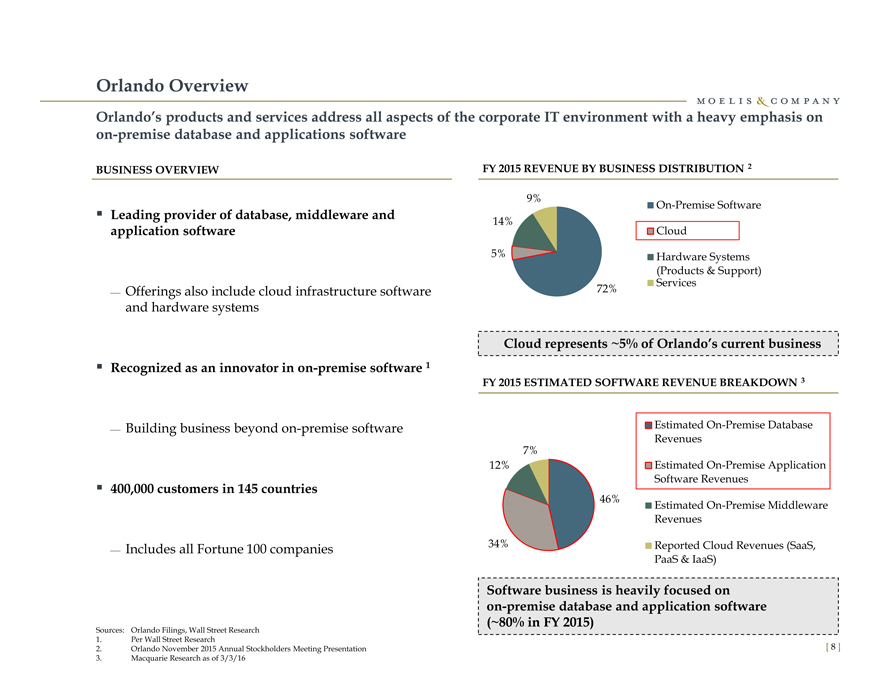

Orlando Overview

Orlando’s products and services address all aspects of the corporate IT environment with a heavy emphasis on on-premise database and applications software

BUSINESS OVERVIEW

Leading provider of database, middleware and application software

Offerings also include cloud infrastructure software and hardware systems

Recognized as an innovator in on-premise software 1

Building business beyond on-premise software

400,000 customers in 145 countries

Includes all Fortune 100 companies

Sources: Orlando Filings, Wall Street Research

Per Wall Street Research

Orlando November 2015 Annual Stockholders Meeting Presentation

Macquarie Research as of 3/3/16

FY 2015 REVENUE BY BUSINESS DISTRIBUTION 2

9% On-Premise Software

14%

Cloud

5% Hardware Systems

(Products & Support)

72% Services

Cloud represents ~5% of Orlando’s current business

FY 2015 ESTIMATED SOFTWARE REVENUE BREAKDOWN 3

Estimated On-Premise Database

Revenues

7%

12% Estimated On-Premise Application

Software Revenues

46%Estimated On-Premise Middleware

Revenues

34% Reported Cloud Revenues (SaaS,

PaaS & IaaS)

Software business is heavily focused on on-premise database and application software (~80% in FY 2015)

[ 8 ]

|

[***] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. This information has been filed separately with the Securities and Exchange Commission. Orlando’s ERP Profile [***] ORLANDO ERP OVERVIEW 3-YEAR ON-PREMISE ERP LICENSE SOFTWARE PERFORMANCE ($ in millions) ERP heavily focused around on-premise offerings FY 2013: [***] of ERP revenue FY 2014: [***] of ERP revenue [***] FY 2015: [***] of ERP revenue [***] ¹ Maintenance continues to be an attractive business FY2013A FY2014A FY2015A Cloud-based ERP accounted for [***] on 3-YEAR CLOUD ERP ARR ² an annualized revenue basis as of FY 2015 ($ in millions) Offering viewed as well-suited for complex environments [***] FY2013A FY2014A FY2015A Source: Orlando Management [ 9 ] 1. [***] based on FY 2013 – FY 2015 data 2. ARR is “Annual Renewable Revenue,” which is the booking value of the first year of a subscription contract

|

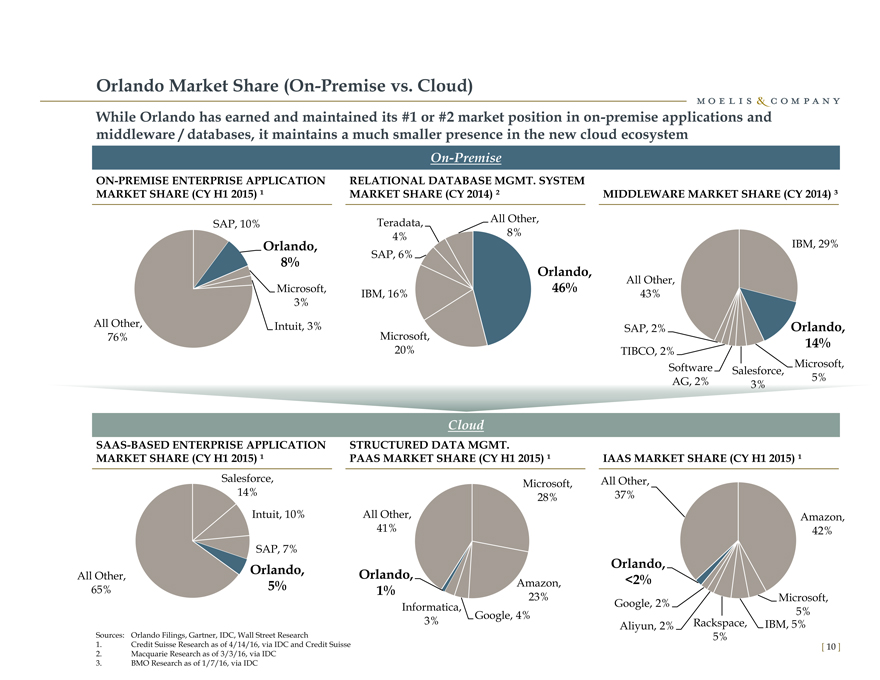

Orlando Market Share (On-Premise vs. Cloud)

While Orlando has earned and maintained its #1 or #2 market position in on-premise applications and middleware / databases, it maintains a much smaller presence in the new cloud ecosystem

On-Premise

ON-PREMISE ENTERPRISE APPLICATION RELATIONAL DATABASE MGMT. SYSTEM

MARKET SHARE (CY H1 2015) ¹ MARKET SHARE (CY 2014) ²

SAP, 10% Teradata,All Other,

4%8%

Orlando,

8% SAP, 6%

Orlando,

Microsoft, 46%

IBM, 16%

3%

All Other, Intuit, 3%

76% Microsoft,

20%

Cloud

SAAS-BASED ENTERPRISE APPLICATION STRUCTURED DATA MGMT.

MARKET SHARE (CY H1 2015) ¹ PAAS MARKET SHARE (CY H1 2015) ¹

Salesforce, Microsoft,

14% 28%

Intuit, 10% All Other,

41%

SAP, 7%

All Other, Orlando, Orlando,

65% 5% 1%Amazon,

23%

Informatica,

3%Google, 4%

Sources: Orlando Filings, Gartner, IDC, Wall Street Research

Credit Suisse Research as of 4/14/16, via IDC and Credit Suisse

Macquarie Research as of 3/3/16, via IDC

BMO Research as of 1/7/16, via IDC

MIDDLEWARE MARKET SHARE (CY 2014) ³

IBM, 29%

All Other,

43%

SAP, 2% Orlando,

TIBCO, 2% 14%

Software Salesforce, Microsoft,

AG, 2% 3%5%

IAAS MARKET SHARE (CY H1 2015) ¹

All Other,

37%

Amazon,

42%

Orlando,

<2%

Google, 2% Microsoft,

5%

Aliyun, 2% Rackspace, IBM, 5%

5%

[ 10 ]

|

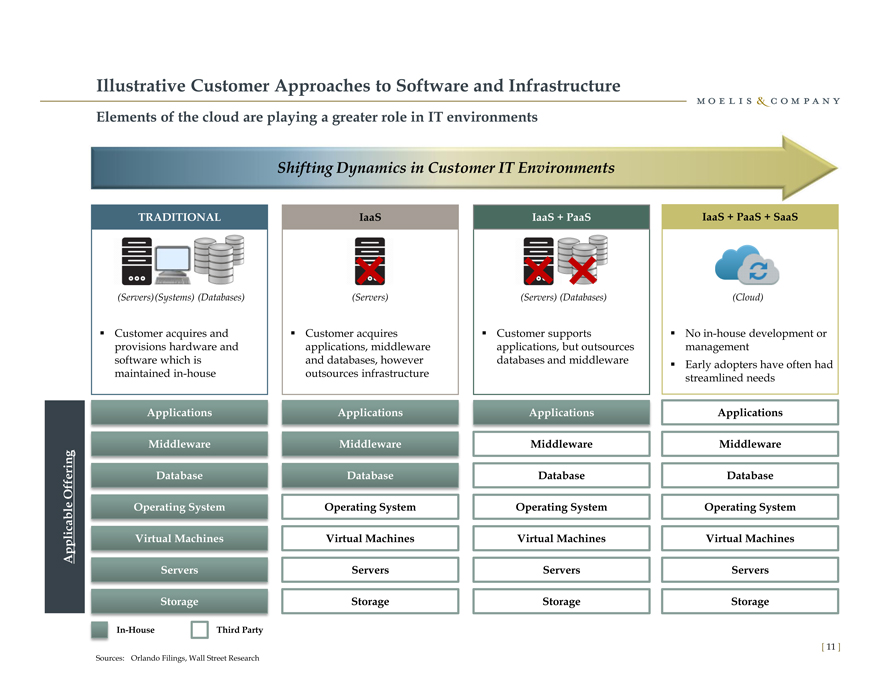

Illustrative Customer Approaches to Software and Infrastructure

Elements of the cloud are playing a greater role in IT environments

Shifting Dynamics in Customer IT Environments

TRADITIONAL

(Servers)(Systems) (Databases)

Customer acquires and provisions hardware and software which is maintained in-house

IaaS

(Servers)

Customer acquires applications, middleware and databases, however outsources infrastructure

IaaS + PaaS

(Servers) (Databases)

Customer supports applications, but outsources databases and middleware

IaaS + PaaS + SaaS

No in-house development or management

Early adopters have often had streamlined needs

ApplicationsApplicationsApplicationsApplications

MiddlewareMiddlewareMiddlewareMiddleware

Offering DatabaseDatabaseDatabaseDatabase

Operating SystemOperating SystemOperating SystemOperating System

Applicable Virtual MachinesVirtual MachinesVirtual MachinesVirtual Machines

ServersServersServersServers

StorageStorageStorageStorage

In-House Third Party

[ 11 ]

Sources: Orlando Filings, Wall Street Research

|

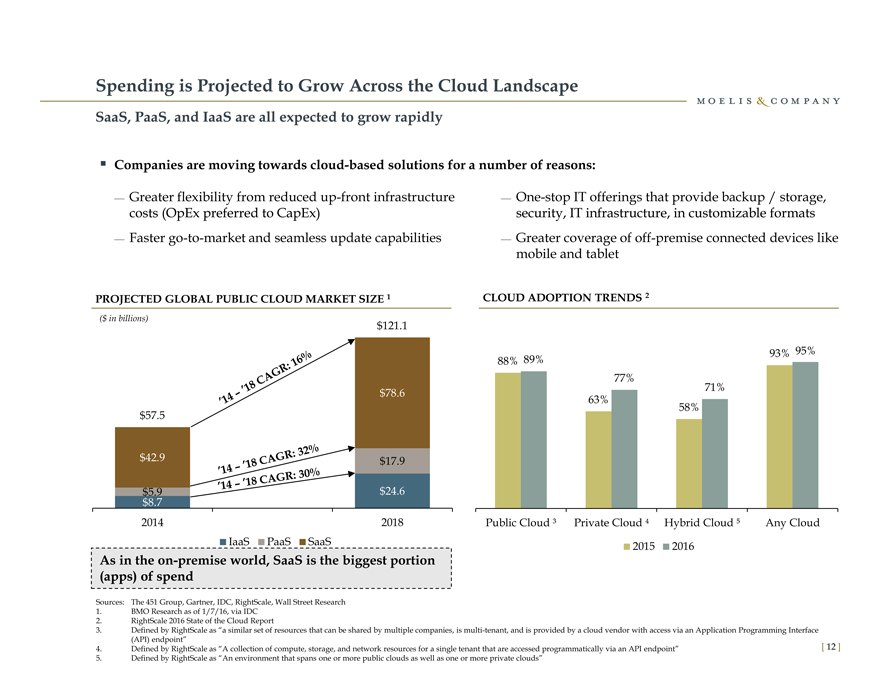

Spending is Projected to Grow Across the Cloud Landscape

SaaS, PaaS, and IaaS are all expected to grow rapidly

Companies are moving towards cloud-based solutions for a number of reasons:

Greater flexibility from reduced up-front infrastructure One-stop IT offerings that provide backup / storage,

costs (OpEx preferred to CapEx) security, IT infrastructure, in customizable formats

Faster go-to-market and seamless update capabilities Greater coverage of off-premise connected devices like

mobile and tablet

PROJECTED GLOBAL PUBLIC CLOUD MARKET SIZE 1 CLOUD ADOPTION TRENDS 2

($ in billions)

$121.1

88% 89%93% 95%

77%

$78.671%

63%

58%

$57.5

$42.9 $17.9

$5.9 $24.6

$8.7

2014 2018Public Cloud ³Private CloudHybrid CloudAny Cloud

IaaS PaaS SaaS20152016

As in the on-premise world, SaaS is the biggest portion

(apps) of spend

Sources: The 451 Group, Gartner, IDC, RightScale, Wall Street Research

1. BMO Research as of 1/7/16, via IDC

2. RightScale 2016 State of the Cloud Report

3. Defined by RightScale as “a similar set of resources that can be shared by multiple companies, is multi-tenant, and is provided by a cloud vendor with access via an Application Programming Interface

(API) endpoin

4. Defined by RightScale as “A collection of compute, storage, and network resources for a single tenant that are accessed programmatically via an API endpoint” [ 12 ]

5. Defined by RightScale as “An environment that spans one or more public clouds as well as one or more private clouds”

|

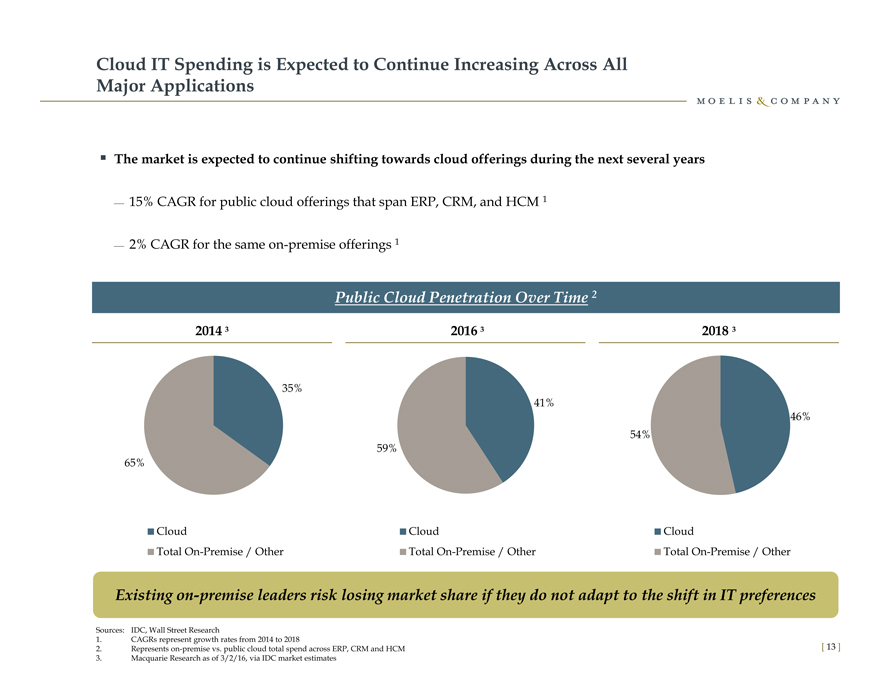

Cloud IT Spending is Expected to Continue Increasing Across All Major Applications

The market is expected to continue shifting towards cloud offerings during the next several years

15% CAGR for public cloud offerings that span ERP, CRM, and HCM 1

2% CAGR for the same on-premise offerings 1

Public Cloud Penetration Over Time 2

2014 3 2016 3 2018 3

35%

41%

46%

54%

59%

65%

Cloud Cloud Cloud

Total On-Premise / Other Total On-Premise / Other Total On-Premise / Other

Existing on-premise leaders risk losing market share if they do not adapt to the shift in IT preferences

Sources: IDC, Wall Street Research

1. CAGRs represent growth rates from 2014 to 2018

2. Represents on-premise vs. public cloud total spend across ERP, CRM and HCM [ 13 ]

3. Macquarie Research as of 3/2/16, via IDC market estimates

|

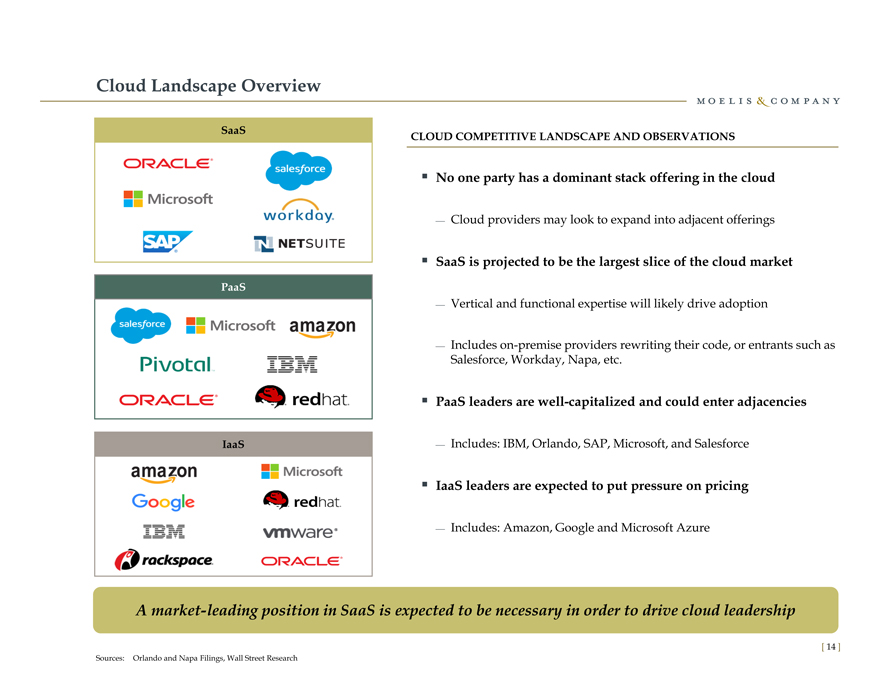

Cloud Landscape Overview

SaaS CLOUD COMPETITIVE LANDSCAPE AND OBSERVATIONS

No one party has a dominant stack offering in the cloud

Cloud providers may look to expand into adjacent offerings

SaaS is projected to be the largest slice of the cloud market

PaaS

Vertical and functional expertise will likely drive adoption

Includes on-premise providers rewriting their code, or entrants such as

Salesforce, Workday, Napa, etc.

PaaS leaders are well-capitalized and could enter adjacencies

IaaS Includes: IBM, Orlando, SAP, Microsoft, and Salesforce

IaaS leaders are expected to put pressure on pricing

Includes: Amazon, Google and Microsoft Azure

A market-leading position in SaaS is expected to be necessary in order to drive cloud leadership

[ 14 ]

|

Sources: Orlando and Napa Filings, Wall Street Research

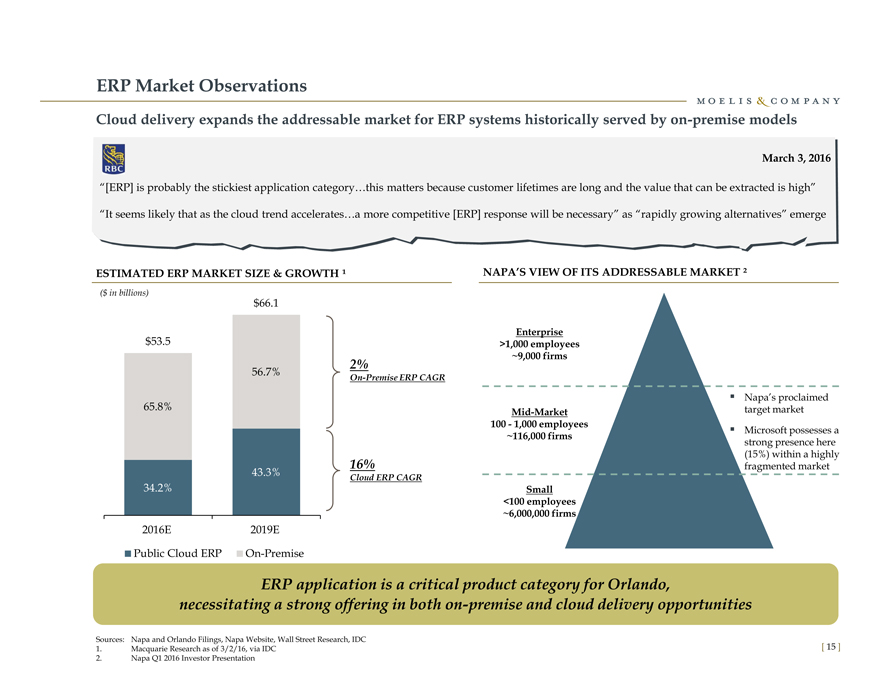

ERP Market Observations

Cloud delivery expands the addressable market for ERP systems historically served by on-premise models

March 3, 2016

“[ERP] is probably the stickiest application category…this matters because customer lifetimes are long and the value that can be extracted is high”

“It seems likely that as the cloud trend accelerates…a more competitive [ERP] response will be necessary” as “rapidly growing alternatives” emerge

ESTIMATED ERP MARKET SIZE & GROWTH ¹

NAPA’S VIEW OF ITS ADDRESSABLE MARKET ²

($ in billions)

$66.1

Enterprise

$53.5 >1,000 employees

~9,000 firms

56.7% 2%

On-Premise ERP CAGR

Napa’s proclaimed

65.8% Mid-Markettarget market

100—1,000 employees Microsoft possesses a

~116,000 firmsstrong presence here

(15%) within a highly

16%fragmented market

43.3% Cloud ERP CAGR

34.2% Small

<100 employees

~6,000,000 firms

2016E 2019E

Public Cloud ERP On-Premise

ERP application is a critical product category for Orlando, necessitating a strong offering in both on-premise and cloud delivery opportunities

Sources: Napa and Orlando Filings, Napa Website, Wall Street Research, IDC

1. Macquarie Research as of 3/2/16, via IDC [ 15 ]

2. Napa Q1 2016 Investor Presentation

|

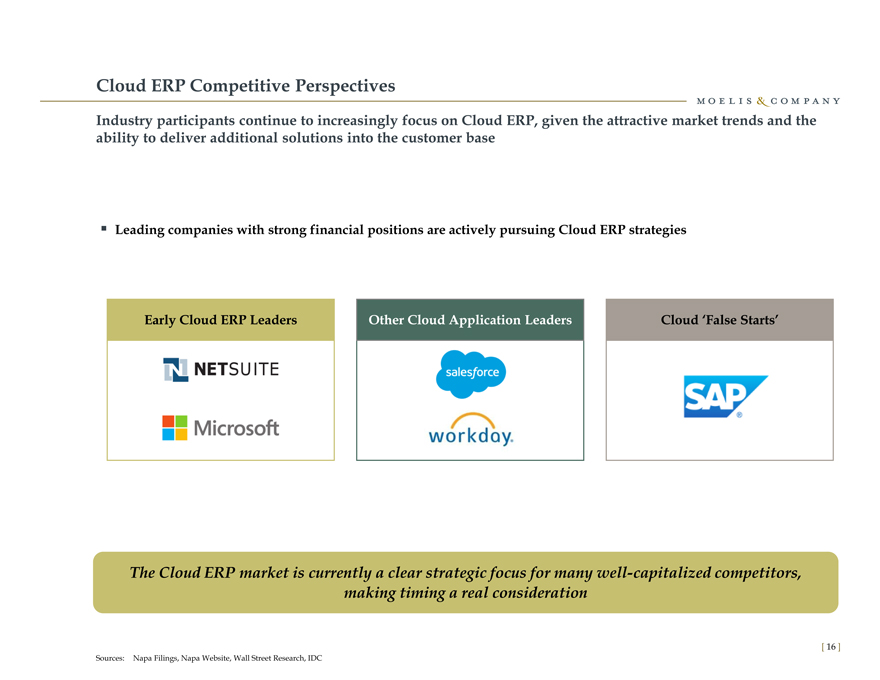

Cloud ERP Competitive Perspectives

[Graphic Appears Here]

Industry participants continue to increasingly focus on Cloud ERP, given the attractive market trends and the ability to deliver additional solutions into the customer base

Leading companies with strong financial positions are actively pursuing Cloud ERP strategies

Early Cloud ERP Leaders

Other Cloud Application Leaders

Cloud ‘False Starts’

The Cloud ERP market is currently a clear strategic focus for many well-capitalized competitors, making timing a real consideration

[ 16 ]

Sources: Napa Filings, Napa Website, Wall Street Research, IDC

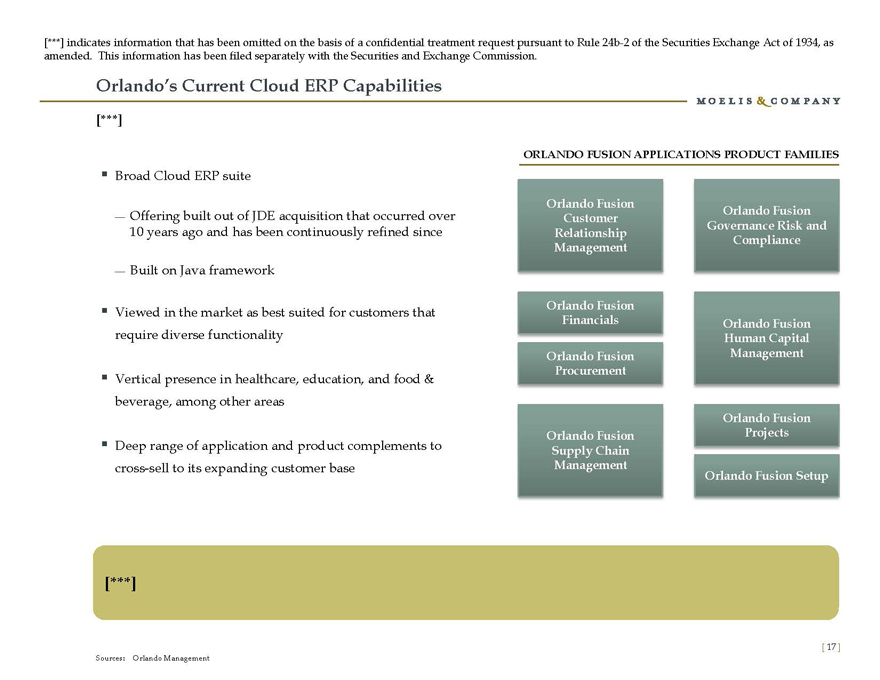

Orlando’s Current Cloud ERP Capabilities

|

Orlando’s Current Cloud ERP Capabilities

[***]

Broad Cloud ERP suite Offering built out of JDE acquisition that occurred over 10 years ago and has been continuously refined since

Built on Java framework

Viewed in the market as best suited for customers that require diverse functionality

Vertical presence in healthcare, education, and food & beverage, among other areas

Deep range of application and product complements to cross-sell to its expanding customer base

ORLANDO FUSION APPLICATIONS PRODUCT FAMILIES

[***]

Sources: Orlando Management

[***] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. This information has been filed separately with the Securities and Exchange Commission. [ 17 ]

|

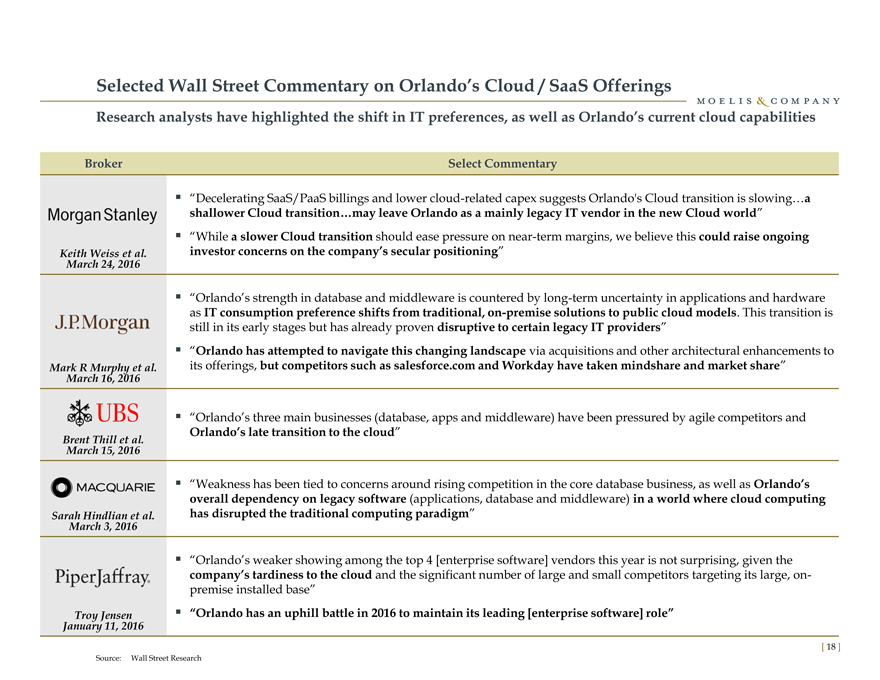

Selected Wall Street Commentary on Orlando’s Cloud / SaaS Offerings

Research analysts have highlighted the shift in IT preferences, as well as Orlando’s current cloud capabilities

Broker Select Commentary

“Decelerating SaaS/PaaS billings and lower cloud-related capex suggests Orlando’s Cloud transition is slowing…a

shallower Cloud transition…may leave Orlando as a mainly legacy IT vendor in the new Cloud world”

“While a slower Cloud transition should ease pressure on near-term margins, we believe this could raise ongoing

Keith Weiss et al. investor concerns on the company’s secular positioning”

March 24, 2016

“Orlando’s strength in database and middleware is countered by long-term uncertainty in applications and hardware

as IT consumption preference shifts from traditional, on-premise solutions to public cloud models. This transition is

still in its early stages but has already proven disruptive to certain legacy IT providers”

“Orlando has attempted to navigate this changing landscape via acquisitions and other architectural enhancements to

Mark R Murphy et al. its offerings, but competitors such as salesforce.com and Workday have taken mindshare and market share”

March 16, 2016

“Orlando’s three main businesses (database, apps and middleware) have been pressured by agile competitors and

Brent Thill et al. Orlando’s late transition to the cloud”

March 15, 2016

“Weakness has been tied to concerns around rising competition in the core database business, as well as Orlando’s

overall dependency on legacy software (applications, database and middleware) in a world where cloud computing

Sarah Hindlian et al. has disrupted the traditional computing paradigm”

March 3, 2016

“Orlando’s weaker showing among the top 4 [enterprise software] vendors this year is not surprising, given the

company’s tardiness to the cloud and the significant number of large and small competitors targeting its large, on-

premise installed base”

Troy Jensen “Orlando has an uphill battle in 2016 to maintain its leading [enterprise software] role”

January 11, 2016

[ 18 ]

Source: Wall Street Research

|

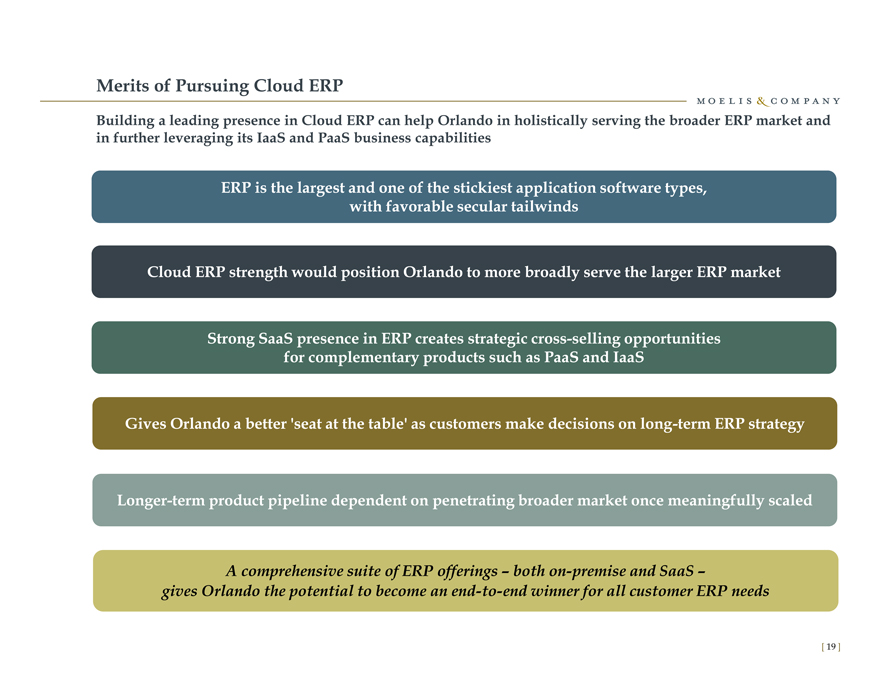

Merits of Pursuing Cloud ERP

Building a leading presence in Cloud ERP can help Orlando in holistically serving the broader ERP market and in further leveraging its IaaS and PaaS business capabilities

ERP is the largest and one of the stickiest application software types, with favorable secular tailwinds

Cloud ERP strength would position Orlando to more broadly serve the larger ERP market

Strong SaaS presence in ERP creates strategic cross-selling opportunities for complementary products such as PaaS and IaaS

Gives Orlando a better ‘seat at the table’ as customers make decisions on long-term ERP strategy

Longer-term product pipeline dependent on penetrating broader market once meaningfully scaled

A comprehensive suite of ERP offerings – both on-premise and SaaS – gives Orlando the potential to become an end-to-end winner for all customer ERP needs

[ 19 ]

|

II. Why Napa?

|

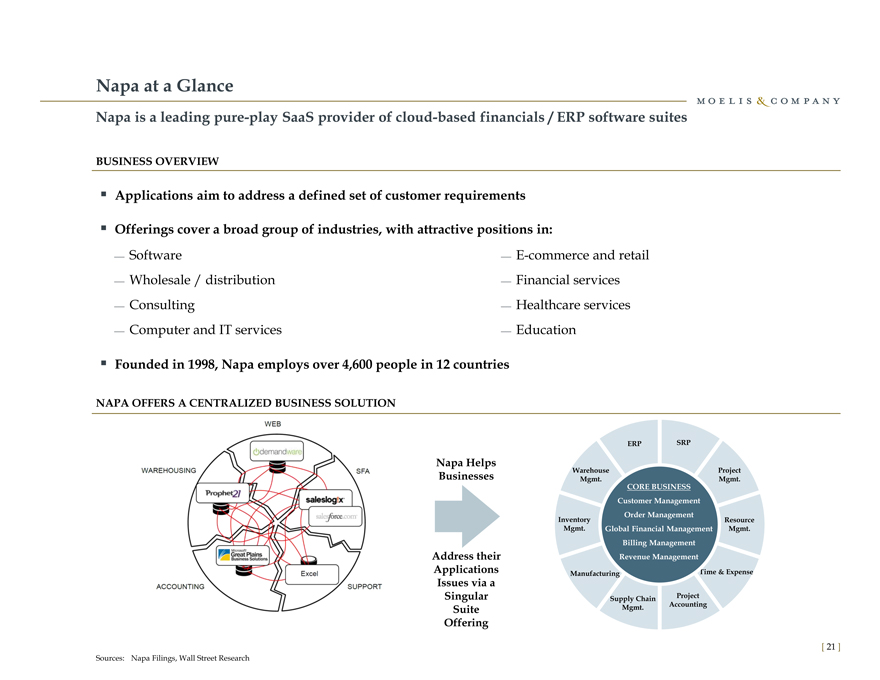

Napa at a Glance

Napa is a leading pure-play SaaS provider of cloud-based financials / ERP software suites

BUSINESS OVERVIEW

Applications aim to address a defined set of customer requirements

Offerings cover a broad group of industries, with attractive positions in:

Software E-commerce and retail

Wholesale / distribution Financial services

Consulting Healthcare services

Computer and IT services Education

Founded in 1998, Napa employs over 4,600 people in 12 countries

NAPA OFFERS A CENTRALIZED BUSINESS SOLUTION

ERP SRP

Napa Helps Warehouse Project

Businesses Mgmt. Mgmt.

CORE BUSINESS

Customer Management

Order Management

Inventory Resource

Mgmt. Global Financial Management Mgmt.

Billing Management

Address their Revenue Management

Applications Manufacturing Time & Expense

Issues via a

Singular Supply Chain Project

Suite Mgmt. Accounting

Offering

[ 21 ]

|

Sources: Napa Filings, Wall Street Research

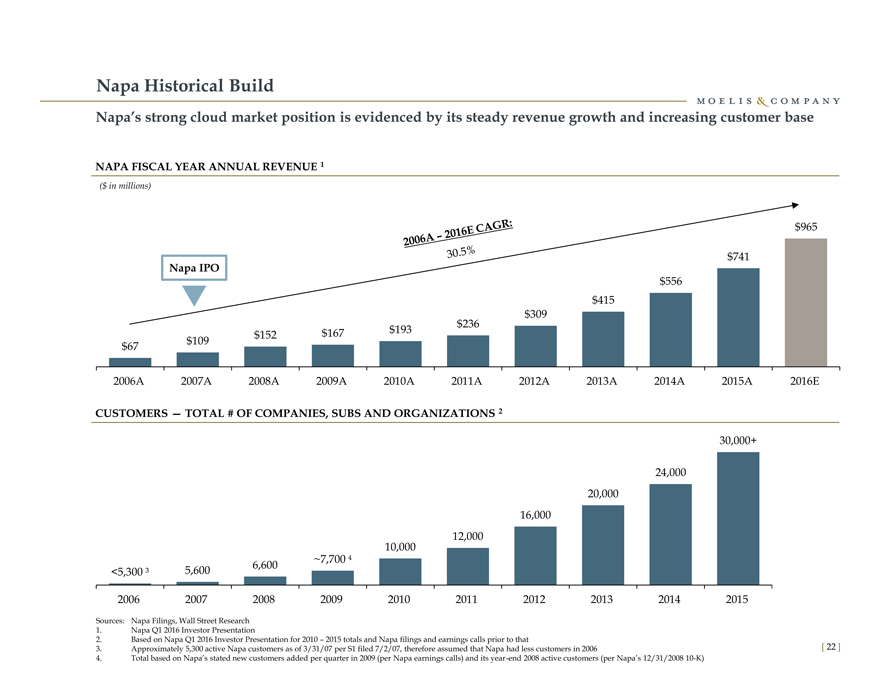

Napa Historical Build

Napa’s strong cloud market position is evidenced by its steady revenue growth and increasing customer base

NAPA FISCAL YEAR ANNUAL REVENUE 1

($ in millions)

$965

$741

Napa IPO

$556

$415

$309

$152$167$193$236

$67 $109

2006A 2007A 2008A2009A2010A2011A2012A2013A2014A2015A2016E

CUSTOMERS — TOTAL # OF COMPANIES, SUBS AND ORGANIZATIONS 2

30,000+

24,000

20,000

16,000

12,000

10,000

~7,700

<5,300 ³ 5,600 6,600

2006 2007 20082009201020112012201320142015

Sources: Napa Filings, Wall Street Research

1. Napa Q1 2016 Investor Presentation

2. Based on Napa Q1 2016 Investor Presentation for 2010 – 2015 totals and Napa filings and earnings calls prior to that

3. Approximately 5,300 active Napa customers as of 3/31/07 per S1 filed 7/2/07, therefore assumed that Napa had less customers in 2006 [ 22 ]

4. Total based on Napa’s stated new customers added per quarter in 2009 (per Napa earnings calls) and its year-end 2008 active customers (per Napa’s 12/31/2008 10-K)

|

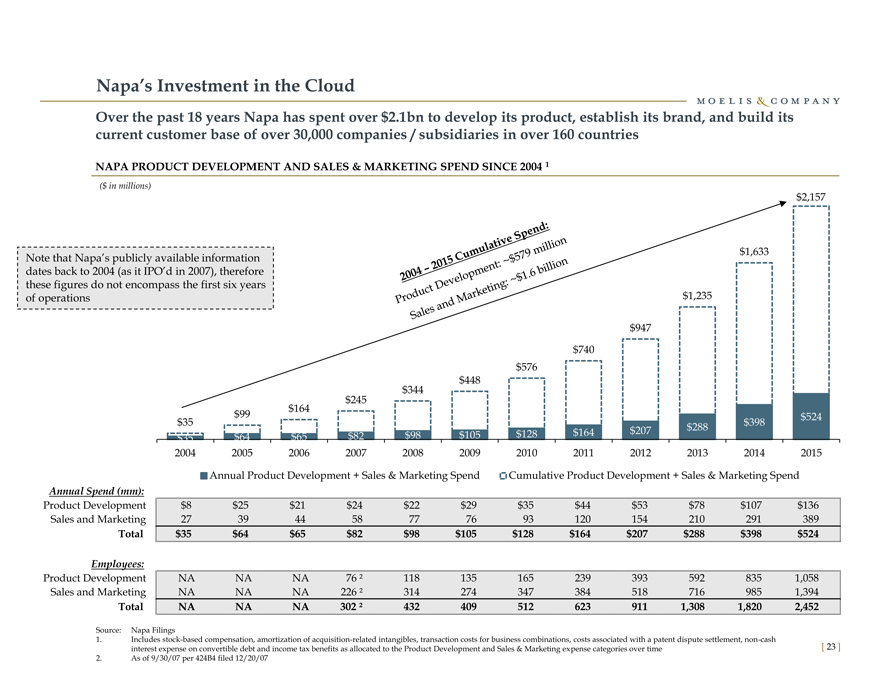

Napa’s Investment in the Cloud

[Graphic Appears Here]

Over the past 18 years Napa has spent over $2.1bn to develop its product, establish its brand, and build its current customer base of over 30,000 companies / subsidiaries in over 160 countries

NAPA PRODUCT DEVELOPMENT AND SALES & MARKETING SPEND SINCE 2004 1

($ in millions)

$2,157

Note that Napa’s publicly available information $1,633

dates back to 2004 (as it IPO’d in 2007), therefore

these figures do not encompass the first six years

of operations $1,235

$947

$740

$576

$448

$344

$245

$164

$99$524

$35 $288$398

$35 $64$65$82$98$105$128$164$207

2004 20052006200720082009201020112012201320142015

Annual Product Development + Sales & Marketing SpendCumulative Product Development + Sales & Marketing Spend

Annual Spend (mm):

Product Development $8 $25$21$24$22$29$35$44$53$78$107$136

Sales and Marketing 27 394458777693120154210291389

Total $35 $64$65$82$98$105$128$164$207$288$398$524

Employees:

Product Development NA NANA76 ²1181351652393935928351,058

Sales and Marketing NA NANA226 ²3142743473845187169851,394

Total NA NANA302 ²4324095126239111,3081,8202,452

Source: Napa Filings

1. Includes stock-based compensation, amortization of acquisition-related intangibles, transaction costs for business combinations, costs associated with a patent dispute settlement, non-cash

interest expense on convertible debt and income tax benefits as allocated to the Product Development and Sales & Marketing expense categories over time [ 23 ]

2. As of 9/30/07 per 424B4 filed 12/20/07

|

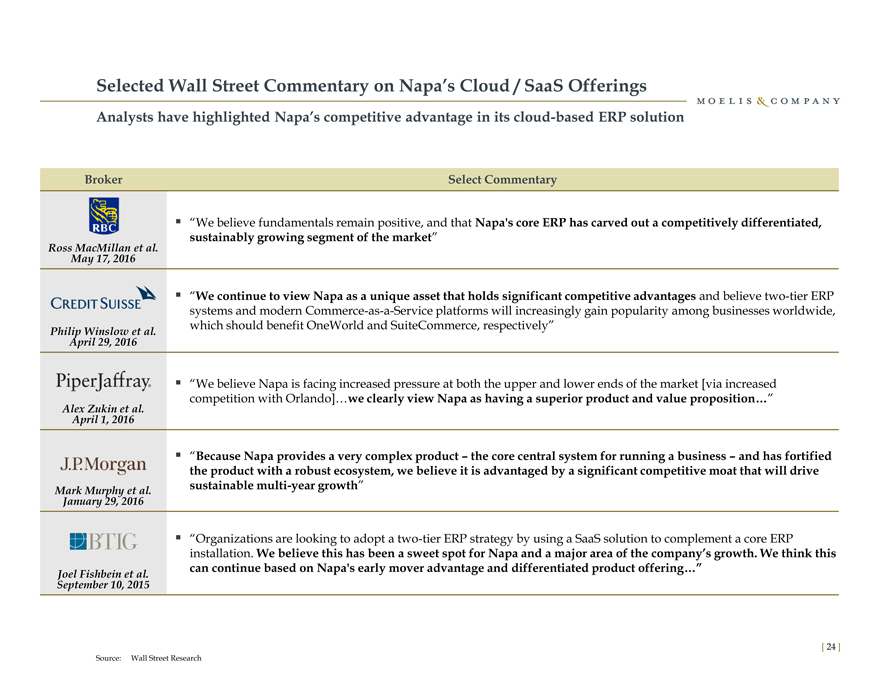

Selected Wall Street Commentary on Napa’s Cloud / SaaS Offerings

Analysts have highlighted Napa’s competitive advantage in its cloud-based ERP solution

Broker Select Commentary

“We believe fundamentals remain positive, and that Napa’s core ERP has carved out a competitively differentiated,

sustainably growing segment of the market”

Ross MacMillan et al.

May 17, 2016

“We continue to view Napa as a unique asset that holds significant competitive advantages and believe two-tier ERP

systems and modern Commerce-as-a-Service platforms will increasingly gain popularity among businesses worldwide,

Philip Winslow et al. which should benefit OneWorld and SuiteCommerce, respectively”

April 29, 2016

“We believe Napa is facing increased pressure at both the upper and lower ends of the market [via increased

competition with Orlando]…we clearly view Napa as having a superior product and value proposition…”

Alex Zukin et al.

April 1, 2016

“Because Napa provides a very complex product – the core central system for running a business – and has fortified

the product with a robust ecosystem, we believe it is advantaged by a significant competitive moat that will drive

Mark Murphy et al. sustainable multi-year growth”

January 29, 2016

“Organizations are looking to adopt a two-tier ERP strategy by using a SaaS solution to complement a core ERP

installation. We believe this has been a sweet spot for Napa and a major area of the company’s growth. We think this

Joel Fishbein et al. can continue based on Napa’s early mover advantage and differentiated product offering…”

September 10, 2015

[ 24 ]

Source: Wall Street Research

|

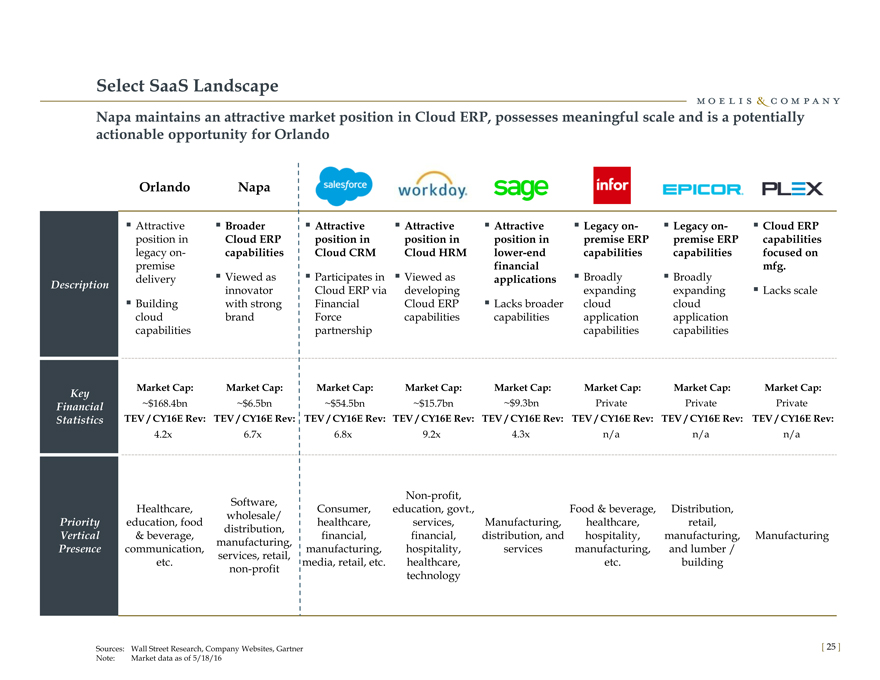

Select SaaS Landscape

Napa maintains an attractive market position in Cloud ERP, possesses meaningful scale and is a potentially actionable opportunity for Orlando

Orlando Napa

Attractive Broader Attractive Attractive Attractive Legacy on- Legacy on- Cloud ERP

position in Cloud ERPposition inposition inposition inpremise ERPpremise ERPcapabilities

legacy on- capabilitiesCloud CRMCloud HRMlower-endcapabilitiescapabilitiesfocused on

premise financialmfg.

delivery Viewed as Participates in Viewed asapplications Broadly Broadly

Description innovatorCloud ERP viadevelopingexpandingexpanding Lacks scale

Building with strongFinancialCloud ERP Lacks broadercloudcloud

cloud brandForcecapabilitiescapabilitiesapplicationapplication

capabilities partnershipcapabilitiescapabilities

Key Market Cap: Market Cap:Market Cap:Market Cap:Market Cap:Market Cap:Market Cap:Market Cap:

Financial ~$168.4bn ~$6.5bn~$54.5bn~$15.7bn~$9.3bnPrivatePrivatePrivate

Statistics TEV / CY16E Rev: TEV / CY16E Rev:TEV / CY16E Rev:TEV / CY16E Rev:TEV / CY16E Rev:TEV / CY16E Rev:TEV / CY16E Rev:TEV / CY16E Rev:

4.2x 6.7x6.8x9.2x4.3xn/an/an/a

Software,Non-profit,

Healthcare, Consumer,education, govt.,Food & beverage,Distribution,

wholesale/

Priority education, food healthcare,services,Manufacturing,healthcare,retail,

distribution,

Vertical & beverage, financial,financial,distribution, andhospitality,manufacturing,Manufacturing

manufacturing,

Presence communication, manufacturing,hospitality,servicesmanufacturing,and lumber /

services, retail,

etc. media, retail, etc.healthcare,etc.building

non-profittechnology

Sources: Wall Street Research, Company Websites, Gartner [ 25 ]

Note: Market data as of 5/18/16

|

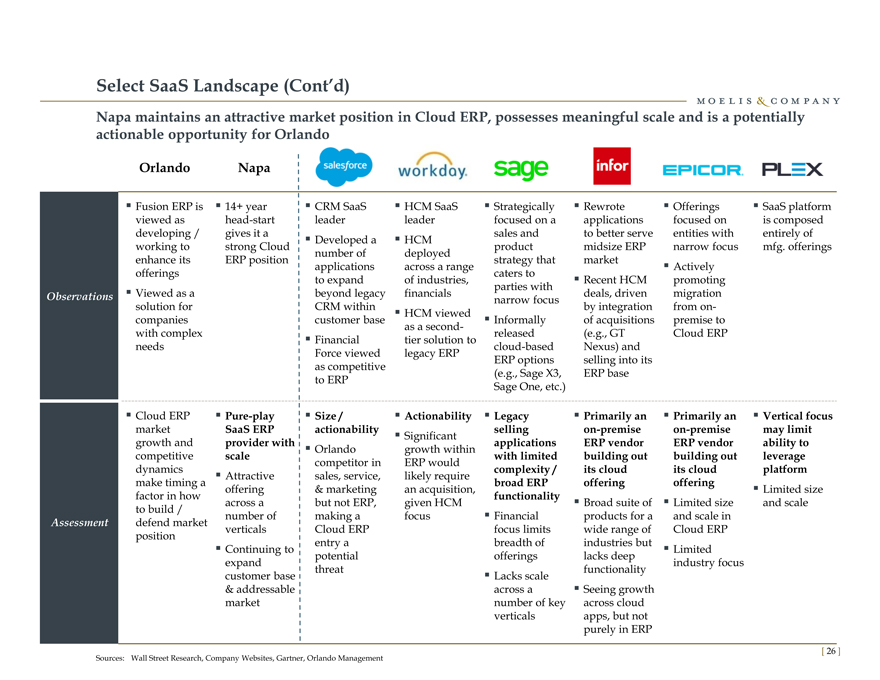

Select SaaS Landscape (Cont’d)

Napa maintains an attractive market position in Cloud ERP, possesses meaningful scale and is a potentially actionable opportunity for Orlando

Orlando Napa

Fusion ERP is 14+ year CRM SaaS HCM SaaS Strategically Rewrote Offerings SaaS platform

viewed as head-startleaderleaderfocused on aapplicationsfocused onis composed

developing / gives it a Developed a HCMsales andto better serveentities withentirely of

working to strong Cloudproductmidsize ERPnarrow focusmfg. offerings

number ofdeployed

enhance its ERP positionapplicationsacross a rangestrategy thatmarket Actively

offerings to expandof industries,caters to Recent HCMpromoting

parties with

Observations Viewed as a beyond legacyfinancialsnarrow focusdeals, drivenmigration

solution for CRM within HCM viewedby integrationfrom on-

companies customer base Informallyof acquisitionspremise to

as a second-

with complex Financialtier solution toreleased(e.g., GTCloud ERP

needs cloud-basedNexus) and

Force viewedlegacy ERPERP optionsselling into its

as competitive(e.g., Sage X3,ERP base

to ERPSage One, etc.)

Cloud ERP Pure-play Size / Actionability Legacy Primarily an Primarily an Vertical focus

market SaaS ERPactionability Significantsellingon-premiseon-premisemay limit

growth and provider with Orlandogrowth withinapplicationsERP vendorERP vendorability to

competitive scalewith limitedbuilding outbuilding outleverage

competitor inERP would

dynamics Attractivesales, service,likely requirecomplexity /its cloudits cloudplatform

make timing a offering& marketingan acquisition,broad ERPofferingoffering Limited size

factor in how across abut not ERP,given HCMfunctionality Broad suite of Limited sizeand scale

to build / number ofmaking afocus Financialproducts for aand scale in

Assessment defend market verticalsCloud ERPfocus limitswide range ofCloud ERP

position entry abreadth ofindustries but

Continuing to Limited

potentialofferingslacks deep

expandindustry focus

customer basethreat Lacks scalefunctionality

& addressableacross a Seeing growth

marketnumber of keyacross cloud

verticalsapps, but not

purely in ERP

[ 26 ]

Sources: Wall Street Research, Company Websites, Gartner, Orlando Management

|

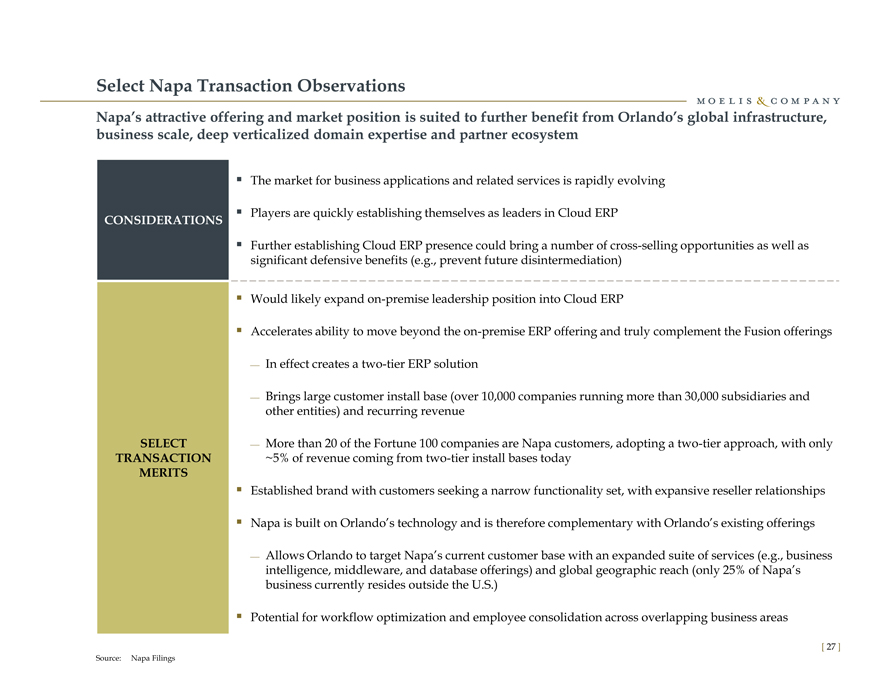

Select Napa Transaction Observations

Napa’s attractive offering and market position is suited to further benefit from Orlando’s global infrastructure, business scale, deep verticalized domain expertise and partner ecosystem

The market for business applications and related services is rapidly evolving

CONSIDERATIONS Players are quickly establishing themselves as leaders in Cloud ERP

Further establishing Cloud ERP presence could bring a number of cross-selling opportunities as well as

significant defensive benefits (e.g., prevent future disintermediation)

Would likely expand on-premise leadership position into Cloud ERP

Accelerates ability to move beyond the on-premise ERP offering and truly complement the Fusion offerings

In effect creates a two-tier ERP solution

Brings large customer install base (over 10,000 companies running more than 30,000 subsidiaries and

other entities) and recurring revenue

SELECT More than 20 of the Fortune 100 companies are Napa customers, adopting a two-tier approach, with only

TRANSACTION ~5% of revenue coming from two-tier install bases today

MERITS

Established brand with customers seeking a narrow functionality set, with expansive reseller relationships

Napa is built on Orlando’s technology and is therefore complementary with Orlando’s existing offerings

Allows Orlando to target Napa’s current customer base with an expanded suite of services (e.g., business intelligence, middleware, and database offerings) and global geographic reach (only 25% of Napa’s business currently resides outside the U.S.)

Potential for workflow optimization and employee consolidation across overlapping business areas

[ 27 ]

Source: Napa Filings

|

Select Potential Napa / Transaction Risks

Moelis believes the following considerations should be evaluated in the context of a potential Napa transaction

Napa has historically not been profitable on a GAAP basis

New account growth is expected to be heavily dependent on the ability to scale the Company’s sales force and channel partners

Potential competitive pressures, from other SaaS providers and other on-premise providers, may impact the ability to win new accounts and pricing

While analysts project that the market for Cloud ERP will grow meaningfully, a potential for slower adoption levels exists

Napa is believed to be pursuing a number of new offerings, which may require significant investment

A transaction may expose the Company to potential integration risks, including brand confusion, employee turnover, and customer account turnover

[ 28 ]

|

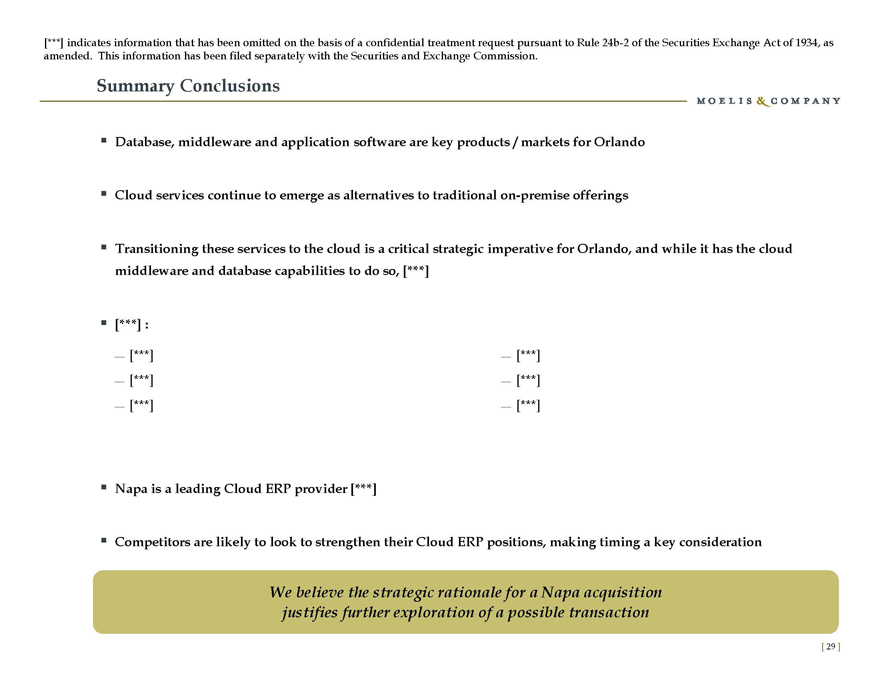

Summary Conclusions

Database, middleware and application software are key products / markets for Orlando

Cloud services continue to emerge as alternatives to traditional on-premise offerings

Transitioning these services to the cloud is a critical strategic imperative for Orlando, and while it has the cloud middleware and database capabilities to do so, [***]

[***] :

Napa is a leading Cloud ERP provider [***]

Competitors are likely to look to strengthen their Cloud ERP positions, making timing a key consideration

[***]

[***]

[***]

[***]

[***]

[***]

We believe the strategic rationale for a Napa acquisition justifies further exploration of a possible transaction

[***] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. This information has been filed separately with the Securities and Exchange Commission. [ 29 ]

|

Contact Information

Moelis & Company LLC is a U.S.-registered broker dealer and a member of FINRA & SIPC.

Moelis & Company LLC

1999 Avenue of the Stars, Suite 1900

Los Angeles, CA 90067

Tel: (310) 443-2300

399 Park Avenue, 5th Floor

New York, NY 10022

Tel: (212) 883-3800

[ 30 ]