UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21934

RIVERNORTH FUNDS

(exact name of registrant as specified in charter)

325 North LaSalle Street, Suite 645, Chicago, IL 60654

(Address of principal executive offices) (Zip code)

Patrick W. Galley

RiverNorth Funds

325 North LaSalle Street

Chicago, IL 60654

(Name and address of agent for service)

| | | | |

| Registrant’s telephone number, including area code: 312-832-1440 |

| |

| Date of fiscal year end: September 30th | | |

|

| Date of reporting period: October 1, 2010 to September 30, 2011 |

| Item 1. | Reports to Stockholders. |

| | |

| RiverNorth Funds | | Table of Contents |

| | |

Annual Report | September 30, 2011 | | 1 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

Dear Fellow Shareholders,

We are pleased to provide you with the 2011 Annual Report for the RiverNorth Funds. This report covers the RiverNorth Core Opportunity Fund (ticker: RNCOX) and the RiverNorth/DoubleLine Strategic Income Fund (tickers: RNSIX and RNDLX). Both Funds have a fiscal year end of September 30, 2011.

The RiverNorth Core Opportunity Fund was launched in December 2006 with an investment objective of capital appreciation and income. We tactically manage the Fund’s asset allocation and generally implement the Fund’s objectives by purchasing closed-end funds and exchange-traded funds. We believe that opportunistic, discount-based investments in closed-end fund shares can earn excess returns over the closed-end fund’s benchmark index. In our opinion, the investment strategy has worked well over the past few years. Since inception (December 27, 2006), the RiverNorth Core Opportunity Fund has generated an annualized return of 5.25% (for full performance see page 3). This compares favorably to the Fund’s benchmark, the unmanaged Blend Index1, which has generated an annualized return of 1.45% over the same time period.

The Adviser, RiverNorth Capital Management, LLC, closed the RiverNorth Core Opportunity Fund to new investors on July 1, 2011. Current investors may still purchase shares. The Adviser is committed to monitoring the Fund’s size relative to our ability to effectively execute the Fund’s strategy and achieve its objectives. As of September 30, 2011, the net assets of the Fund were $488 million.

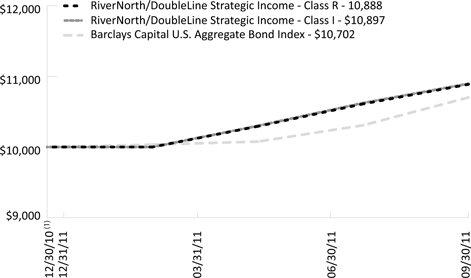

The RiverNorth/DoubleLine Strategic Income Fund was launched in December 2010 with an investment objective of current income and overall total return. We are very excited about the partnership with DoubleLine Capital, LP, a leader in fixed income asset management. RiverNorth Capital Management is the Fund’s Adviser and DoubleLine Capital is the Fund’s Sub-Adviser. Together we are tactically allocating capital across three distinct income-oriented strategies – 1) tactical closed-end fund income, 2) core fixed income and 3) opportunistic income. Although the Fund is young, we are pleased with the outcome of our investment strategy thus far. Since inception (December 30, 2010), the RiverNorth/DoubleLine Strategic Income Fund has generated a total return of 8.97% (RNSIX) and 8.88% (RNDLX). This compares favorably to the Fund’s benchmark, the Barclays Capital U.S. Aggregate Bond Index, which generated a total return of 7.02% over the same time period.

The RiverNorth/DoubleLine Strategic Income Fund has been well received by investors. As of September 30, 2011, the net assets of the Fund were $470 million.

Both Funds are designed to be flexible and opportunistic. We believe these characteristics are necessary for an investment strategy in today’s volatile market environment. Investors are concerned about the slow growth in the U.S., our country’s fiscal deficit and the escalating debt crisis in Europe. This fear and uncertainty may lead to attractive buying opportunities for ably prepared investors. We believe both Funds are well diversified2, balanced and positioned to capitalize on future market volatility.

We thank you for your investment and trust in managing your assets.

Respectfully,

| | |

| Patrick Galley, CFA | | Steve O’Neill, CFA |

1 The Blend Index consists of 60% S&P 500 Index and 40% Barclays Capital U.S. Aggregate Bond Index.

2 Diversification does not eliminate the risk of experiencing investment losses.

| | |

| 2 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

RiverNorth Core Opportunity Fund

How did the RiverNorth Core Opportunity Fund perform relative to its benchmark during the reporting period?

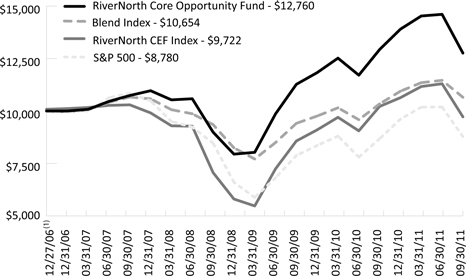

For the twelve months ended September 30, 2011, the RiverNorth Core Opportunity Fund (RNCOX; the “Fund”) returned negative 1.33%. The unmanaged Blend Index returned positive 3.06%, during the same period. The Blend Index consists of 60% S&P 500 Index and 40% Barclays Capital U.S. Aggregate Bond Index.

In order to compare the Fund’s performance to the overall taxable closed-end fund market, the Fund’s Adviser maintains the RiverNorth Closed-end Fund Index (“RiverNorth CEF Index”). We believe the RiverNorth CEF Index provides the best representation of the taxable closed-end fund market because it is constructed without discount biases and is designed to capture the broader group’s asset class diversity. Given that RNCOX invests in closed-end funds opportunistically, as opposed to exclusively, its objective is not to outperform the RiverNorth CEF Index. Therefore we encourage investors to use the RiverNorth CEF Index as a point of reference.

The RiverNorth CEF Index returned negative 4.85% over the past twelve months.

Average Annual Total Returns for Periods Ending September 30, 2011

| | | | | | |

| | | 1-Year | | 3-Year | | Since Inception(1) |

RiverNorth Core Opportunity Fund (RNCOX) | | -1.33% | | 12.37% | | 5.25% |

Blend Index(2) | | 3.06% | | 4.44% | | 1.45% |

S&P 500 Index(2) | | 1.16% | | 1.23% | | -2.55% |

RiverNorth CEF Index(3) | | -4.85% | | 11.23% | | -0.59% |

| (1) | Inception date is December 27, 2006. |

| (2) | Blend Index consists of 60% S&P 500 Index and 40% Barclays Capital U.S. Aggregate Bond Index. S&P 500 Index is a capitalization-weighted index of 500 stocks. The S&P 500 index is designed to measure performance of the broad domestic economy based on the changing aggregate market value of these 500 stocks. The Barclays Capital US Aggregate Bond Index (formerly Lehman Brothers US Aggregate Bond Index) is a benchmark index composed of US securities in Treasury, Government-Related, Corporate, and Securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $250 million. This unmanaged index does not reflect fees and expenses. The index cannot be invested in directly. The S&P 500 and Blend Indices are indices only and cannot be invested in directly. |

| (3) | The RiverNorth CEF Index measures the performance of the taxable closed-end fund market through a representative 75 Funds. The index rebalances every 12 months and is calculated using the total return of the underlying investments. Please see www.rivernorth.com for more information. The RiverNorth CEF Index is an index only and cannot be invested in directly. |

Performance data quoted represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth

| | |

Annual Report | September 30, 2011 | | 3 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

more or less than their original cost. You can obtain performance data current to the most recent month end by calling (888) 848-7569 or www.rivernorthfunds.com. Total return measures net investment income and capital gain or loss from portfolio investments. All performance shown assumes reinvestment of dividends and capital gains distributions and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

The RiverNorth Core Opportunity Fund’s Total Annual Fund Operating Expenses as disclosed in the prospectus is 2.39%. The Adviser has contractually agreed to defer the collection of fees and/or reimburse expenses, but only to the extent necessary to limit Total Annual Fund Operating Expenses (excluding brokerage fees and commissions; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; indirect expenses incurred by the underlying funds in which the Fund invests; and extraordinary expenses) to 1.60% of the average daily net assets of the Fund through January 31, 2012.

For a longer-term perspective on Fund performance, we refer you to the following chart:

Comparison of a $10,000 Investment in the RiverNorth Core Opportunity Fund, the S&P 500® Index, and the Blend Index

What contributing factors were responsible for the RiverNorth Core Opportunity Fund’s relative performance during the period?

Closed-end fund discounts generally widened during the reporting period. As a reminder, the market price of a closed-end fund can trade at a discount or premium to the fund’s net asset value. Some of the Fund’s long-term mean reversion positions were negative impacted by discount widening.

On the other hand, corporate actions completed by a number of large closed-end fund holdings were beneficial to performance. The most noteworthy corporate action was taken by the Fund’s

| | |

| 4 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

second largest holding on September 30, 2010. RNCOX started the fiscal year with 5.33% of assets allocated to NFJ Dividend, Interest & Premium Strategy Fund (“NFJ”). The discount on September 30, 2010 was 14.16%. We were anticipating a distribution increase that would bring the fund’s distribution rate closer to that of its closed-end fund peers. Three months into the fiscal year, NFJ increased its distribution rate by 200%. By June 30, 2011, the discount had narrowed to 1.05% and we had gradually sold our entire position into market strength.

The Fund also participated in a number of profitable tender offers. A closed-end fund tender offer gives shareholders the opportunity to sell shares directly to the fund. The purchase price is often equal to some percentage of the fund’s net asset value (e.g. 98% of net asset value). During the fiscal year, LMP Capital and Income Fund tendered 35%, H&Q Life Sciences Investors tendered 35%, SunAmerica Focused Alpha Growth Fund tendered 30% and DWS High Income Opportunities Fund tendered 25%. In each case, the tender offer was undersubscribed and therefore we received more than our pro-rata share.

In terms of asset allocation, the Fund’s asset class diversification beyond the traditional 60/40 portfolio partially detracted from performance in fiscal year 2011. The Fund’s benchmark, the Blend Index, consists of 60% S&P 500 Index and 40% Barclays Capital US Aggregate Bond Index.

The Fund’s allocation to international equity contributed to the underperformance of the Fund’s equity portfolio relative to the S&P 500 Index (60% of the Fund’s benchmark). The MSCI EAFE and MSCI Emerging Markets indices were down 9.36% and 16.15%, respectively, over the past twelve months. Whereas the total return of the S&P 500 was positive 1.16%. The Fund started the fiscal year with 10% of assets allocated to international equity. We used the sell-off in international equity to increase our allocation to 15% by fiscal year-end. The additional exposure was implemented by purchasing global equity closed-end funds trading at historically wide discounts and exchange-traded funds. Over the long-term, we believe the diversification of the equity portfolio will help improve risk-adjusted returns.

The Fund’s low duration and minimal exposure to U.S. government bonds and mortgage-backed securities contributed to the underperformance of the Fund’s bond portfolio relative to the Barclays Capital U.S. Aggregate Bond Index (40% of the Fund’s benchmark). The Fund held a significant cash position to help to minimize interest rate risk and to provide liquidity for the frequent trading opportunities in the closed-end fund space. Cash also helps counterbalance any incremental asset class exposure the Fund acquires through the underlying leverage found in many closed-end funds.

A tactical allocation to leveraged loan funds worked well during the fiscal year. These funds rallied in the first half of the year and we sold nearly all of our positions by June 30, 2011. Subsequently we repurchased many of the same positions when they sold off in August and September.

What was the closed-end fund environment like for the past twelve months and current outlook?

The one-year trailing average discount on the RiverNorth CEF Index was 2.80% on September 30, 2011. We started the fiscal year with an average discount of 1.57% and ended the year with an average discount of 3.81%. The range of the average discount over the past twelve months was 1.23% to 7.85%. Most of the discount volatility occurred in November/December 2010 and August 2011. Interestingly, discount volatility during these two periods occurred for very different reasons.

| | |

Annual Report | September 30, 2011 | | 5 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

The U.S. economy had picked up momentum in the second half of 2010 and with it came a rise in inflation and interest-rate expectations. In the last few months of the year, the yield on the 10-year U.S. Treasury bond jumped 100 basis points (1 basis point equals 1/100th of 1%). Almost overnight, closed-end fund investors began to panic about rising rates and their knee-jerk reaction was to sell closed-end bond funds. Year-end tax loss selling pressure exacerbated the weakness. The average discount widened from 1.57% on September 30, 2010 to 4.88% on December 14, 2010. We welcomed the discount volatility and took advantage of the sell-off by increasing our closed-end fund exposure. When discounts narrowed in early 2011, we booked gains on our short-term mean reversion trades.

The second period of discount volatility occurred under the opposite set of expectations. The U.S. economy showed signs of weakness in the second quarter of 2011. Investors began to fear a double-dip recession. Those concerns were further agitated by the rising awareness of our country’s fiscal deficit, Standard & Poor’s downgrading of U.S. government debt and the escalating debt crisis in Europe. Within a few short months, the yield on the 10-year U.S. Treasury bond dropped nearly 200 basis points. The most acute discount volatility occurred in the first week of August. The average discount widened from 3.18% on August 1, 2011 to 7.85% on August 8, 2011. Once again, we were buying closed-end funds while others were selling. RNCOX added material positions in a number of global equity and covered call funds trading at discounts in the high-teens. As of September 30, 2011, the market prices and discounts on these funds are still well-below their pre-August levels.

Looking forward, we anticipate more discount volatility. Closed-end fund investors have become fair weather fans; indiscriminately selling at the first sign of trouble. Their short-term mentality drives fairly wild swings in the closed-end fund market. That being said, if/when capital markets volatility declines, we believe discounts will narrow to levels that are considered low by historical standards. Taxable closed-end funds are currently offering yields in excess of 8% in a world where the 10-year U.S. Treasury yields less than 2%. Investors hungry for yield should continue to find value in closed-end funds.

How was the RiverNorth Core Opportunity Fund positioned at the end of September 2011?

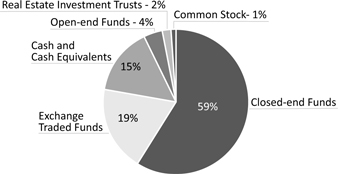

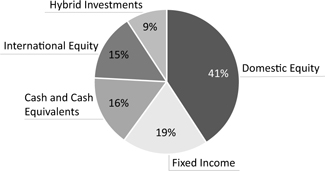

We believe the Fund is well diversified across asset classes with tactical allocations to large-cap equities and lower duration fixed income. We have increased the Fund’s overall equity exposure to 56% of assets and further diversified this exposure into international equities. The Fund’s fixed income exposure was decreased to 19% of assets following the elimination of various closed-end bond funds and exchange-traded funds.

Over the past twelve months, we have increased our cash position to 16% of assets. Given the current level of market volatility (e.g. CBOE Volatility Index above 40) and the low opportunity cost of holding cash relative to short-term bonds, we like holding cash to give us dry powder for closed-end fund trading opportunities.

The Fund’s current allocation to closed-end funds is 59% of assets. We are finding value in general equity and covered call closed-end funds. It is our view that discounts on both groups will narrow if/when Main Street sentiment improves towards stocks and we have been adding to these positions on weakness. We continue to wait for attractive buying opportunities for closed-end bond funds. We are looking for weakness in line with the levels of November/December 2010 and August 2011 before making significant investments.

| | |

| 6 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

The charts below further highlight our positioning:

RiverNorth Core Opportunity Fund

Portfolio asset allocations are approximations made by the Adviser.

Investment Vehicle Allocation(1) (percentages are based on net assets)

Asset Class Allocation(1) (percentages are based on net assets)

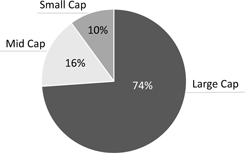

Equity Capitalization Allocation(1) (percentages are based on net assets)

| | |

Annual Report | September 30, 2011 | | 7 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

Fixed Income Allocation(1) (percentages are based on net assets)

| (1) | Investments in international markets present special risks including currency fluctuation, the potential for diplomatic and political instability, regulatory and liquidity risks, foreign taxation and differences in auditing and other financial standards. Risks of foreign investing are generally intensified for investments in emerging markets. The Fund invests in securities (Investment Companies) that have underlying exposure to high yield securities and unrated securities of similar credit quality (commonly known as junk bonds ), as well as derivatives of such securities, and therefore is likely to be subject to greater levels of interest rate, credit and liquidity risk than funds that do not invest in such securities. The underlying securities of these investments are considered predominately speculative with respect to the issuers continuing ability to make principal and interest payments. An economic downturn or period of rising interest rates could adversely affect the market for these underlying securities and therefore the Fund’s investment in securities that have high yield exposure. Small-Cap and Mid-Cap investing involves greater risk not associated with investing in more established companies, such as greater price volatility, business risk, less liquidity and increased competitive threat. Holdings are subject to change. |

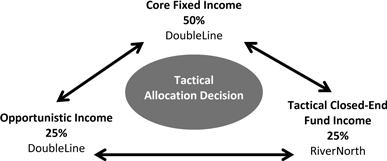

RiverNorth/DoubleLine Strategic Income Fund

The RiverNorth/DoubleLine Strategic Income Fund (RNSIX and RNDLX; the “Fund”) consists of three distinct fixed income strategies (or sleeves) and the Fund’s exposure to each sleeve is tactically managed.

RiverNorth Capital Management oversees the Tactical Closed-end Fund Income Strategy. The strategy is designed to provide diversified exposure to the fixed income market through opportunistic investments in closed-end funds. RiverNorth utilizes a combination of short-and long-term trading strategies to seek to derive value from the discount and premium spreads associated with closed-end bond funds. RiverNorth uses proprietary screening and algorithmic trading models to enhance the closed-end fund strategy. We believe that opportunistic, discount-based investments in closed-end fund shares can earn excess returns over the closed-end fund’s benchmark index.

The second sleeve is the Opportunistic Income Strategy managed by DoubleLine Capital. The strategy incorporates DoubleLine’s “best ideas” and has a flexible mandate with a current focus on non-agency and agency mortgage-backed securities (“MBS”).

| | |

| 8 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

The two niche strategies are combined with a third sleeve, the Core Fixed Income Strategy, also managed by DoubleLine. The Core Fixed Income Strategy incorporates an active asset allocation approach in an effort to mitigate risk and achieve superior risk-adjusted returns within the diverse fixed income universe. DoubleLine’s Asset Allocation Committee, led by Jeffrey Gundlach, determines which fixed income sectors to over- or underweight based upon their qualitative and quantitative analyses.

We believe the combination and the tactical management of these three unique but complementary strategies creates a novel approach to investing in today’s fixed income environment.

How did the RiverNorth/DoubleLine Strategic Income Fund perform relative to its benchmark during the reporting period?

Since inception through September 30, 2011, the Fund returned 8.97% (RNSIX) and 8.88% (RNDLX). The Barclays Capital U.S. Aggregate Bond Index returned 7.02%, during the same period.

| | |

| | | Since Inception(1) |

RiverNorth/DoubleLine Strategic Income Fund – Class I (RNSIX) | | 8.97% |

RiverNorth/DoubleLine Strategic Income Fund – Class R (RNDLX) | | 8.88% |

Barclays Capital U.S. Aggregate Bond Index(2) | | 7.02% |

| (1) | Inception date is December 30, 2010. Since Inception return is cumulative, not annualized. |

| (2) | The Barclays Capital US Aggregate Bond Index (formerly Lehman Brothers US Aggregate Bond Index) is a benchmark index composed of US securities in Treasury, Government-Related, Corporate, and Securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $250 million. This unmanaged index does not reflect fees and expenses. The index cannot be invested in directly. |

Performance data quoted represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling (888) 848-7569 or www.rivernorthfunds.com. Total return measures net investment income and capital gain or loss from portfolio investments. All performance shown assumes reinvestment of dividends and capital gains distributions and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

The RiverNorth/DoubleLine Strategic Income Fund’s Total Annual Operating Expense as disclosed in the prospectus is 1.20% for Class I Shares and 1.45% for Class R Shares. The Adviser has contractually agreed to defer the collection of fees and/or reimburse expenses, but only to the extent necessary to limit Total Annual Fund Operating Expenses (excluding brokerage fees and commissions; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; indirect expenses incurred by the Underlying Funds in which the fund invest; and extraordinary expenses) 0.95% for Class I Shares 1.20% for Class R Shares of the average daily net assets of the Fund through January 31, 2012.

| | |

Annual Report | September 30, 2011 | | 9 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

Comparison of a $10,000 Investment in the RiverNorth/DoubleLine Strategic Income Fund and the Barclays Capital U.S. Aggregate Bond Index

What contributing factors were responsible for the RiverNorth/DoubleLine Strategic Income Fund’s relative performance during the period?

RiverNorth Tactical Closed-end Income Sleeve:

Active trading of closed-end funds generated positive returns for the Fund. Additionally, tactical management of the total exposure to closed-end funds helped improve the sleeve’s performance. During the reporting period, the market price return of the closed-end fund portfolio exceeded the net asset value return due to discount narrowing.

DoubleLine Opportunistic Income Sleeve:

Long duration agency collateralized mortgage obligations such as inverse floaters had large price gains in addition to high interest returns. Non-agency MBS were flat to slightly negative in price since inception, however, they experienced high income returns given their fixed coupons and low dollar prices. Of the non-agency MBS subsectors, Prime (conforming mortgages with prime borrowers) was the best performing collateral with lower quality collateral returns lagging.

DoubleLine Core Fixed Income Sleeve:

Due to the significant drop in interest rates over the year, along with a general flight to quality, the U.S. government portion of the portfolio contributed significantly to the portfolio’s outperformance. The MBS portion also outperformed despite having a shorter duration than the Barclays Capital U.S. Aggregate Bond Index. The corporate bonds performed in line with both the

| | |

| 10 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011(Unaudited) |

credit sector of the benchmark while the allocation to emerging markets detracted from performance, particularly over the 3rd quarter.

What was the closed-end fund environment like since inception of the RiverNorth/DoubleLine Strategic Income Fund and current outlook?

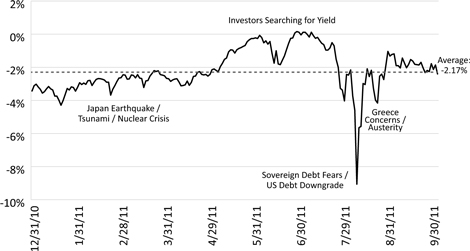

Since inception, the average discount on taxable bond funds was 2.17% (Morningstar US All Taxable Fixed Income Unweighted Index). As of September 30, 2011, roughly 17% and 49% of taxable bond funds were trading at discounts wider than 10% and 5%, respectively.

Panicky investors caused discount volatility to surge in August 2011. Reasons for the fear included, but were not limited to, the escalating debt crisis in Europe, the slowing U.S. economy and the rising awareness of our country’s fiscal deficit. The intense selling pressure pushed the average taxable bond discount from 2.42% on August 1, 2011 to 9.06% on August 8, 2011. RiverNorth welcomed the discount volatility and opportunistically increased the Fund’s closed-end fund exposure. We believe the best time to buy a closed-end fund is when others are rushing towards the exit.

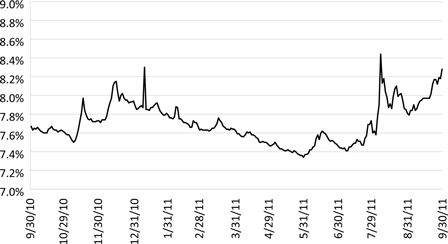

All Taxable Fixed-Income CEF Discounts

Looking forward, we anticipate more discount volatility. Investors’ risk-on/risk-off mentality to owning closed-end funds drives fairly wild swings in the market. That being said, we believe the volatility will be tempered by investors’ hunger for yield. In today’s low interest rate environment, the relatively high distribution rates on taxable closed-end funds look attractive to many buyers. Closed-end funds utilize leverage to enhance their distribution yields. As of September 30, 2011, the average distribution on taxable closed-end funds was 8.3%. This compares favorably to the 2.4% yield on the Barclays Capital U.S. Aggregate Bond Index.

| | |

Annual Report | September 30, 2011 | | 11 |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

All Taxable Closed-End Fund Yield

Source: RiverNorth Capital Management LLC and Morningstar

What was the fixed-income environment like since inception of the RiverNorth/DoubleLine Strategic Income Fund and current outlook?

The prevailing sentiment at DoubleLine entering 2011 was one of deflationary forces. Given the continued deterioration in the housing market, DoubleLine’s thoughts were for a low rate environment with potential to add duration to the portfolios at 10-year U.S. Treasury yields of 3.5%-4.0%. 2011 started the year with 10-year U.S. Treasury yields at 3.30% and investors with a risk on mentality – this pushed 10-year yields to roughly 3.75%. DoubleLine took that opportunity to add duration to the Opportunistic Income sleeve in the Fund. Concerns over the Greece’s fiscal house once again resurfaced in late spring which turned investor’s attitude towards risk as a negative and they began to exit the markets in masses returning to the safety of the now downgraded US Treasury market pushing yields to historic lows. Along the way the Federal Reserve announced shorts rates will be anchored until 2013. The third quarter ended with 10-year U.S. Treasury yields at 1.92%. Currently, we still believe rates will remain low for an extended period of time. The housing market has years of bumping along before a recovery. Short-term global monetization programs will continue to create volatility in the markets as risk trades are put on and then taken off.

| | |

| 12 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Funds | | Shareholder Letter |

| | September 30, 2011 (Unaudited) |

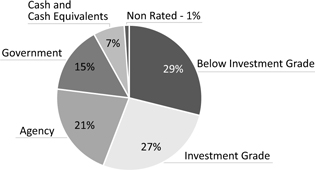

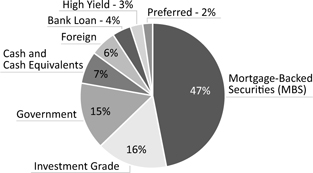

How was the Fund positioned at the end of September 2011?

Portfolio detail statistics are estimates made by the Adviser and are subject to change.

Strategy (“Sleeve”) Allocation

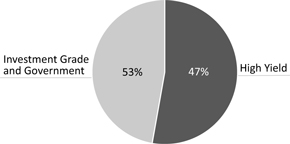

Credit Quality Distribution(1)

Sector Breakdown(1)

| (1) | Holdings subject to change. |

| | |

Annual Report | September 30, 2011 | | 13 |

| | |

RiverNorth Funds | | Disclosure of Fund Expenses |

| | September 30, 2011 (Unaudited) |

Expense Example

As a shareholder of the RiverNorth Core Opportunity Fund or RiverNorth/DoubleLine Strategic Income Fund, you incur ongoing costs which typically consist of management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period, April 1, 2011 and held for the six months ended September 30, 2011.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of other funds.

| | | | | | | | |

| | | Beginning Account Value 04/01/2011 | | Ending Account Value 09/30/2011 | | Expense Ratio(a) | | Expenses Paid During Period(b) |

RiverNorth Core Opportunity Fund | | | | | | | | |

Actual | | $1,000.00 | | $878.20 | | 1.45% | | $6.83 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,017.80 | | 1.45% | | $7.33 |

RiverNorth/DoubleLine Strategic Income Fund | | | | | | | | |

Class I Shares | | | | | | | | |

Actual | | $1,000.00 | | $1,058.00 | | 0.95% | | $4.90 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.31 | | 0.95% | | $4.81 |

Class R Shares | | | | | | | | |

Actual | | $1,000.00 | | $1,057.80 | | 1.20% | | $6.19 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,019.05 | | 1.20% | | $6.07 |

| (a) | Annualized, based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), then divided by 365. Note this expense example is typically based on a six-month period. |

| | |

| 14 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Core Opportunity Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | |

| Shares/Description | | Value | |

| CLOSED-END FUNDS - 57.94% | | | | |

| | 908,104 | | | Adams Express Co. | | $ | 8,363,638 | |

| | 532,382 | | | AllianceBernstein Income Fund, Inc. | | | 4,243,085 | |

| | 57,674 | | | Apollo Senior Floating Rate Fund, Inc. | | | 908,942 | |

| | 681,996 | | | BlackRock Credit Allocation Income Trust II, Inc. | | | 6,369,843 | |

| | 243,789 | | | BlackRock Credit Allocation Income Trust III, Inc. | | | 2,408,635 | |

| | 964,545 | | | BlackRock Credit Allocation Income Trust IV, Inc. | | | 11,072,977 | |

| | 653,052 | | | Boulder Growth & Income Fund, Inc. | | | 3,565,664 | |

| | 273,671 | | | Boulder Total Return Fund, Inc.(a) | | | 3,694,558 | |

| | 268,313 | | | Calamos Convertible and High Income Fund | | | 2,978,274 | |

| | 446,479 | | | Calamos Strategic Total Return Fund | | | 3,553,973 | |

| | 90,000 | | | Central Europe and Russia Fund, Inc. | | | 2,739,600 | |

| | 22,543 | | | ClearBridge Energy MLP Opportunity Fund, Inc. | | | 374,214 | |

| | 535,437 | | | Clough Global Equity Fund | | | 6,248,550 | |

| | 1,213,386 | | | Clough Global Opportunities Fund | | | 12,801,222 | |

| | 367,900 | | | Eaton Vance Enhanced Equity Income Fund | | | 3,598,062 | |

| | 47,537 | | | Eaton Vance Floating-Rate Income Trust | | | 669,796 | |

| | 516,789 | | | Eaton Vance Risk-Managed Diversified Equity Income Fund | | | 5,658,840 | |

| | 52,847 | | | Eaton Vance Senior Floating-Rate Trust | | | 750,956 | |

| | 444,617 | | | Eaton Vance Tax-Managed Buy-Write Opportunities Fund | | | 4,855,218 | |

| | 706,625 | | | Eaton Vance Tax-Managed Diversified Equity Income Fund | | | 6,027,511 | |

| | 1,350,049 | | | Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund | | | 13,176,478 | |

| | 1,579,368 | | | Eaton Vance Tax-Managed Global Diversified Equity Income Fund | | | 12,634,944 | |

| | 357,972 | | | Fifth Street Finance Corp. | | | 3,336,299 | |

| | 11,074 | | | First Trust Senior Floating Rate Income Fund II | | | 148,613 | |

| | 498,033 | | | Gabelli Dividend & Income Trust | | | 6,818,072 | |

| | 388,645 | | | General American Investors Co., Inc. | | | 8,923,289 | |

| | 70,892 | | | Guggenheim Build America Bonds Managed Duration Trust | | | 1,419,967 | |

| | 214,797 | | | H&Q Life Sciences Investors Fund | | | 2,246,777 | |

| | 59,150 | | | Highland Credit Strategies Fund | | | 366,730 | |

| | 344,690 | | | ING Prime Rate Trust | | | 1,764,813 | |

| | 210,602 | | | Invesco Van Kampen Dynamic Credit Opportunities Fund | | | 2,242,911 | |

| | 153,067 | | | Invesco Van Kampen Senior Income Trust | | | 645,943 | |

| | 4,316,281 | | | Liberty All Star Equity Fund | | | 17,696,752 | |

| | 247,506 | | | LMP Capital and Income Fund, Inc. | | | 2,833,944 | |

| | 473,714 | | | Macquarie Global Infrastructure Total Return Fund, Inc. | | | 7,257,298 | |

| | 365,719 | | | Morgan Stanley Emerging Markets Domestic Debt Fund, Inc. | | | 5,291,954 | |

| | 25,682 | | | Nuveen Floating Rate Income Fund | | | 260,159 | |

| | 1,272,560 | | | Nuveen Multi -Strategy Income and Growth Fund | | | 9,544,200 | |

| | 1,817,154 | | | Nuveen Multi-Strategy Income and Growth Fund 2 | | | 14,282,830 | |

| | 229,646 | | | PIMCO Income Opportunity Fund | | | 5,651,588 | |

| | 669,249 | | | PIMCO Income Strategy Fund II | | | 5,869,314 | |

| | 490,419 | | | Royce Focus Trust, Inc. | | | 2,962,131 | |

| | 1,806,506 | | | Royce Value Trust, Inc. | | | 20,016,086 | |

| | 376,477 | | | SunAmerica Focused Alpha Growth Fund,Inc. | | | 6,641,054 | |

| | 1,214,541 | | | TCW Strategic Income Fund, Inc. | | | 6,048,414 | |

| | 100,000 | | | Templeton Emerging Markets Fund | | | 1,681,000 | |

| | |

Annual Report | September 30, 2011 | | 15 |

| | |

RiverNorth Core Opportunity Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | |

| Shares/Description | | Value | |

| | 996,396 | | | Tri-Continental Corp. | | $ | 12,674,157 | |

| | 156,599 | | | Wells Fargo Advantage Multi-Sector Income Fund | | | 2,225,272 | |

| | 172,041 | | | Western Asset Global Corporate Defined Opportunity Fund, Inc. | | | 2,974,589 | |

| | 263,992 | | | Western Asset/Claymore Inflation-Linked Opportunities & Income Fund | | | 3,334,219 | |

| | 3,632,391 | | | Zweig Total Return Fund, Inc. | | | 11,005,781 | |

| | | | | | | | |

| |

| | TOTAL CLOSED-END FUNDS (Cost $279,891,203) | | | 282,859,136 | |

| | | | | | | | |

| |

| | MUTUAL FUNDS - 4.32% | | | | |

| | 533,820 | | | Calamos Convertible Fund - Class A | | | 9,603,429 | |

| | 1,111,161 | | | Eaton Vance Floating-Rate Advantaged Fund | | | 11,489,401 | |

| | | | | | | | |

| |

| | TOTAL MUTUAL FUNDS (Cost $15,487,073) | | | 21,092,830 | |

| | | | | | | | |

| |

| | EXCHANGE-TRADED FUNDS - 18.76% | | | | |

| | 100,000 | | | iShares MSCI EAFE Index Fund | | | 4,778,000 | |

| | 176,839 | | | iShares MSCI Emerging Markets Index Fund | | | 6,206,165 | |

| | 60,537 | | | iShares Russell 1000 Growth Index Fund | | | 3,183,035 | |

| | 487,153 | | | iShares S&P 100 Index Fund | | | 25,054,279 | |

| | 30,000 | | | iShares S&P Global 100 Index Fund | | | 1,608,600 | |

| | 327,568 | | | Powershares FTSE RAFI US 1000 Portfolio | | | 16,021,351 | |

| | 118,563 | | | Rydex Russell Top 50 ETF | | | 9,769,591 | |

| | 111,000 | | | SPDR Barclays Capital Convertible Securities ETF | | | 3,954,930 | |

| | 63,914 | | | SPDR S&P 500 ETF | | | 7,231,869 | |

| | 247,860 | | | Vanguard MSCI EAFE ETF | | | 7,468,022 | |

| | 175,300 | | | Vanguard MSCI Emerging Markets ETF | | | 6,280,999 | |

| | | | | | | | |

| |

| | TOTAL EXCHANGE-TRADED FUNDS (Cost $93,317,194) | | | 91,556,841 | |

| | | | | | | | |

| |

| | HOLDING & INVESTMENT MANAGEMENT COMPANIES - 0.19% | | | | |

| | 12,100 | | | Affiliated Managers Group, Inc.(a) | | | 944,405 | |

| | | | | | | | |

| |

| | TOTAL HOLDING & INVESTMENT MANAGEMENT COMPANIES (Cost $634,253) | | | 944,405 | |

| | | | | | | | |

| |

| | PREFERRED STOCKS - 0.82% | | | | |

| | 64,103 | | | General American Investors Co., Inc., Series B, 5.950% | | | 1,639,114 | |

| | |

| 16 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth Core Opportunity Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | |

| Shares/Description | | Value | |

| | 92,500 | | | Kayne Anderson MLP Investment Co., Series D, 4.950% | | $ | 2,359,675 | |

| | | | | | | | |

| |

| | TOTAL PREFERRED STOCKS (Cost $3,825,799) | | | 3,998,789 | |

| | | | | | | | |

| |

| REAL ESTATE INVESTMENT TRUSTS - 1.51% | | | | |

| | 355,035 | | | Apollo Commercial Real Estate Finance, Inc. | | | 4,675,811 | |

| | 208,533 | | | Colony Financial, Inc. | | | 2,694,246 | |

| | | | | | | | |

| |

| | TOTAL REAL ESTATE INVESTMENT TRUSTS (Cost $9,382,783) | | | 7,370,057 | |

| | | | | | | | |

| |

| | TOTAL INVESTMENTS - 83.54% (Cost $402,538,305) | | | 407,822,058 | |

| CASH - 15.48% | | | 75,567,253 | |

| OTHER ASSETS IN EXCESS OF LIABILITIES - 0.98% | | | 4,805,842 | |

| | | | | | | | |

| NET ASSETS - 100.00% | | $ | 488,195,153 | |

| | | | | | | | |

| (a) | Non-income producing security. |

Common Abbreviations:

ETF - Exchange Traded Fund.

MLP – Master Limited Partnership.

MSCI – Morgan Stanley Capital International.

S&P – Standard & Poor’s.

SPDR – Standard & Poor’s Depository Receipts.

See Notes to Financial Statements.

| | |

Annual Report | September 30, 2011 | | 17 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | |

| Shares/Description | | Value | |

CLOSED-END FUNDS - 18.48% | | | | |

919,822 | | AllianceBernstein Income Fund, Inc. | | $ | 7,330,981 | |

246,496 | | Apollo Senior Floating Rate Fund, Inc. | | | 3,884,777 | |

309,764 | | BlackRock Build America Bond Trust | | | 6,257,233 | |

257,601 | | BlackRock Credit Allocation Income Trust I, Inc. | | | 2,264,313 | |

197,900 | | BlackRock Credit Allocation Income Trust II, Inc. | | | 1,848,386 | |

283,748 | | BlackRock Credit Allocation Income Trust III, Inc. | | | 2,803,430 | |

451,650 | | BlackRock Credit Allocation Income Trust IV, Inc. | | | 5,184,942 | |

21,048 | | BlackRock Diversified Income Strategies Fund, Inc. | | | 193,431 | |

7,100 | | BlackRock Floating Rate Income Strategies Fund, Inc. | | | 90,383 | |

111,054 | | BlackRock Income Opportunity Trust, Inc. | | | 1,089,440 | |

291,594 | | BlackRock Income Trust, Inc. | | | 2,102,393 | |

95,510 | | BlackRock Limited Duration Income Trust | | | 1,517,654 | |

254,901 | | Calamos Convertible and High Income Fund | | | 2,829,401 | |

66,889 | | Calamos Convertible Opportunities and Income Fund | | | 759,190 | |

187,604 | | DWS Global High Income Fund, Inc. | | | 1,348,873 | |

37,000 | | Eaton Vance Floating-Rate Income Trust | | | 521,330 | |

148,120 | | Eaton Vance Limited Duration Income Fund | | | 2,171,439 | |

90,450 | | Eaton Vance Senior Floating-Rate Trust | | | 1,285,294 | |

10,200 | | Eaton Vance Senior Income Trust | | | 64,362 | |

167,277 | | Eaton Vance Short Duration Diversified Income Fund | | | 2,691,487 | |

49,021 | | Eaton Vance Tax-Advantaged Bond and Options Strategies Fund | | | 811,788 | |

262,641 | | Federated Enhanced Treasury Income Fund | | | 3,939,615 | |

17,815 | | First Trust Senior Floating Rate Income Fund II | | | 239,077 | |

141,450 | | First Trust Strategic High Income Fund | | | 488,003 | |

132,167 | | First Trust Strategic High Income Fund III | | | 524,703 | |

129,838 | | Guggenheim Build America Bonds Managed Duration Trust | | | 2,600,655 | |

11,600 | | Helios Advantage Income Fund, Inc. | | | 87,696 | |

29,876 | | Helios Multi-Sector High Income Fund, Inc. | | | 153,264 | |

76,503 | | Helios Strategic Income Fund, Inc. | | | 406,996 | |

142,301 | | Highland Credit Strategies Fund | | | 882,266 | |

499,867 | | ING Prime Rate Trust | | | 2,559,319 | |

248,532 | | Invesco Van Kampen Dynamic Credit Opportunities Fund | | | 2,646,866 | |

439,051 | | Invesco Van Kampen Senior Income Trust | | | 1,852,795 | |

127,328 | | Montgomery Street Income Securities, Inc. | | | 1,986,317 | |

10,780 | | Morgan Stanley Emerging Markets Debt Fund, Inc. | | | 104,243 | |

285,728 | | Morgan Stanley Emerging Markets Domestic Debt Fund, Inc. | | | 4,134,484 | |

29,058 | | Nuveen Build America Bond Opportunity Fund | | | 614,286 | |

58,900 | | Nuveen Build American Bond Term Fund | | | 1,175,055 | |

47,689 | | Nuveen Floating Rate Income Fund | | | 483,090 | |

76,724 | | Nuveen Multi-Currency Short-Term Government Income Fund | | | 998,179 | |

118,500 | | Nuveen Multi-Strategy Income and Growth Fund | | | 888,750 | |

249,844 | | Nuveen Multi-Strategy Income and Growth Fund 2 | | | 1,963,774 | |

2,891 | | Nuveen Short Duration Credit Opportunities Fund | | | 49,638 | |

56,366 | | PIMCO Income Opportunity Fund | | | 1,387,167 | |

| | |

| 18 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | |

| Shares/Description | | Value | |

14,862 | | PIMCO Income Strategy Fund | | $ | 149,066 | |

220,636 | | PIMCO Income Strategy Fund II | | | 1,934,978 | |

31,123 | | Putnam Master Intermediate Income Trust | | | 157,171 | |

347,247 | | Wells Fargo Advantage Multi-Sector Income Fund | | | 4,934,380 | |

121,248 | | Western Asset Global Corporate Defined Opportunity Fund, Inc. | | | 2,096,378 | |

66,631 | | Western Asset Inflation Management Fund, Inc. | | | 1,161,378 | |

| | | | | | |

| |

TOTAL CLOSED-END FUNDS (Cost $91,073,408) | | | 87,650,116 | |

| | | | | | |

| |

PREFERRED STOCKS - 0.88% | | | | |

3,909 | | General American Investors Co., Inc., Series B, 5.950% | | | 99,953 | |

48,014 | | The GDL Fund, Series B, 7.000% | | | 2,496,728 | |

154,100 | | Tortoise Energy Capital Corp., 5.000% | | | 1,568,738 | |

| | | | | | |

| |

TOTAL PREFERRED STOCKS (Cost $4,166,746) | | | 4,165,419 | |

| | | | | | |

| |

REAL ESTATE INVESTMENT TRUSTS - 0.63% | | | | |

150,124 | | Apollo Commercial Real Estate Finance, Inc. | | | 1,977,133 | |

79,048 | | Colony Financial, Inc. | | | 1,021,300 | |

| | | | | | |

| |

TOTAL REAL ESTATE INVESTMENT TRUSTS (Cost 3,630,934) | | | 2,998,433 | |

| | | | | | |

| | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

CORPORATE BONDS - 14.04% | |

Argentina - 0.20% | |

$400,000 | | Pan American Energy LLC(a) | | 7.88% | | 05/07/2021 | | | 404,480 | |

150,000 | | Provincia de Neuquen Argentina(b) | | 7.88% | | 04/26/2021 | | | 142,500 | |

350,000 | | YPF SA | | 10.00% | | 11/02/2028 | | | 390,250 | |

| | | | | | | | | | |

| | | | | | | | | 937,230 | |

| | | | | | | | | | |

Australia - 0.15% | | | | | | |

700,000 | | Australia & New Zealand Banking Group Ltd.(b) | | 4.88% | | 01/12/2021 | | | 728,612 | |

| | | | | | | | | | |

| | | | | | | | | 728,612 | |

| | | | | | | | | | |

Bermuda - 0.21% | | | | | | |

200,000 | | Digicel Ltd.(b) | | 8.25% | | 09/01/2017 | | | 190,000 | |

400,000 | | Inkia Energy Ltd.(a) | | 8.38% | | 04/04/2021 | | | 396,000 | |

| | |

Annual Report | September 30, 2011 | | 19 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $400,000 | | | Qtel International Finance Ltd.(a) | | 3.38% | | 10/14/2016 | | $ | 402,250 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 988,250 | |

| | | | | | | | | | | | |

| Brazil - 0.35% | | | | |

| | 400,000 | | | Banco do Nordeste do Brasil SA(a) | | 3.63% | | 11/09/2015 | | | 398,000 | |

| | 600,000 | | | Cosan Overseas Ltd. | | 8.25% | | 12/31/2049 | | | 570,000 | |

| | 200,000 | | | Globo Comunicacao e Participacoes SA(a) | | 7.25% | | 04/26/2022 | | | 208,000 | |

| | 300,000 | | | Globo Comunicacao e Participacoes SA(a)(c) | | 6.25% | | 07/20/2049 | | | 308,250 | |

| | 200,000 | | | JBS SA(a) | | 10.50% | | 08/04/2016 | | | 192,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,676,250 | |

| | | | | | | | | | | | |

| British Virgin Islands - 0.17% | | | | |

| | 100,000 | | | C10 Capital SPV Ltd.(a)(d) | | 6.72% | | 12/31/2049 | | | 47,500 | |

| | 200,000 | | | Gold Fields Orogen Holding BVI Ltd.(b) | | 4.88% | | 10/07/2020 | | | 184,711 | |

| | 200,000 | | | Gold Fields Orogen Holding BVI Ltd.(a) | | 4.88% | | 10/07/2020 | | | 184,461 | |

| | 400,000 | | | Hongkong Electric Finance Ltd. | | 4.25% | | 12/14/2020 | | | 398,774 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 815,446 | |

| | | | | | | | | | | | |

| Canada - 0.59% | | | | |

| | 250,000 | | | Hydro Quebec | | 2.00% | | 06/30/2016 | | | 255,599 | |

| | 100,000 | | | Hydro Quebec | | 7.50% | | 04/01/2016 | | | 124,389 | |

| | 600,000 | | | Pacific Rubiales Energy Corp.(a) | | 8.75% | | 11/10/2016 | | | 659,250 | |

| | 700,000 | | | Province of Ontario Canada | | 2.30% | | 05/10/2016 | | | 726,429 | |

| | 200,000 | | | PTTEP Canada International Finance Ltd.(a) | | 5.69% | | 04/05/2021 | | | 203,600 | |

| | 800,000 | | | Royal Bank of Canada | | 2.30% | | 07/20/2016 | | | 810,243 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,779,510 | |

| | | | | | | | | | | | |

| Cayman Islands - 0.70% | |

| | 200,000 | | | AES Andres Dominicana Ltd.(a) | | 9.50% | | 11/12/2020 | | | 200,000 | |

| | 400,000 | | | EGE Haina Finance Co.(a) | | 9.50% | | 04/26/2017 | | | 406,000 | |

| | 200,000 | | | Hutchison Whampoa International 10 Ltd.(a)(d) | | 6.00% | | 10/28/2049 | | | 192,500 | |

| | 100,000 | | | Industrial Subordinated Trust(b) | | 8.25% | | 07/27/2021 | | | 103,000 | |

| | 100,000 | | | Minerva Overseas II Ltd.(a) | | 10.88% | | 11/15/2019 | | | 80,000 | |

| | 350,000 | | | Odebrecht Finance Ltd.(a) | | 7.50% | | 09/29/2049 | | | 343,438 | |

| | 500,000 | | | Petrobras International Finance Co. - Pifco | | 3.88% | | 01/27/2016 | | | 501,000 | |

| | 950,000 | | | Transocean, Inc. | | 6.00% | | 03/15/2018 | | | 1,013,928 | |

| | 500,000 | | | Vale Overseas Ltd. | | 4.63% | | 09/15/2020 | | | 490,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,329,866 | |

| | | | | | | | | | | | |

| Chile - 0.28% | | | | |

| | 180,000 | | | AES Gener SA(b) | | 5.25% | | 08/15/2021 | | | 175,387 | |

| | 250,000 | | | Automotores Gildemeister SA(b) | | 8.25% | | 05/24/2021 | | | 239,375 | |

| | |

| 20 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $200,000 | | | Automotores Gildemeister SA(a) | | 8.25% | | 05/24/2021 | | $ | 191,500 | |

| | 200,000 | | | Cencosud SA(a) | | 5.50% | | 01/20/2021 | | | 201,314 | |

| | 500,000 | | | Codelco, Inc.(a) | | 3.75% | | 11/04/2020 | | | 499,558 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,307,134 | |

| | | | | | | | | | | | |

| Colombia - 0.04% | | | | | | | | |

| | 200,000 | | | BanColombia SA(b) | | 5.95% | | 06/03/2021 | | | 195,500 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 195,500 | |

| | | | | | | | | | | | |

| Cyprus - 0.02% | | | | | | | | |

| | 100,000 | | | Alfa MTN Markets Ltd. for ABH Financial Ltd(a) | | 8.20% | | 06/25/2012 | | | 100,850 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 100,850 | |

| | | | | | | | | | | | |

| El Salvador - 0.02% | | | | | | | | |

| | 100,000 | | | Telemovil Finance Co. Ltd.(a) | | 8.00% | | 10/01/2017 | | | 98,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 98,000 | |

| | | | | | | | | | | | |

| European Union - 0.30% | | | | | | | | |

| | 1,100,000 | | | Corp. Andina de Fomento | | 3.75% | | 01/15/2016 | | | 1,119,220 | |

| | 300,000 | | | Eurasian Development Bank(a) | | 7.38% | | 09/24/2014 | | | 306,744 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,425,964 | |

| | | | | | | | | | | | |

| France - 0.36% | | | | | | | | |

| | 1,150,000 | | | France Telecom SA | | 2.75% | | 09/14/2016 | | | 1,143,253 | |

| | 550,000 | | | Sanofi | | 2.63% | | 03/29/2016 | | | 569,988 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,713,241 | |

| | | | | | | | | | | | |

| Germany - 0.08% | | | | | | | | |

| | 400,000 | | | Deutsche Bank AG | | 3.25% | | 01/11/2016 | | | 392,817 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 392,817 | |

| | | | | | | | | | | | |

| Great Britain - 0.40% | | | | | | | | |

| | 500,000 | | | BP Capital Markets PLC | | 4.75% | | 03/10/2019 | | | 551,050 | |

| | 650,000 | | | British Telecommunications PLC | | 5.95% | | 01/15/2018 | | | 724,516 | |

| | 600,000 | | | HSBC Holdings PLC | | 5.10% | | 04/05/2021 | | | 619,893 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,895,459 | |

| | | | | | | | | | | | |

| Ireland - 0.04% | | | | | | | | |

| | 200,000 | | | AK Transneft OJSC Via TransCapitalInvest Ltd.(a) | | 5.67% | | 03/05/2014 | | | 201,400 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 201,400 | |

| | | | | | | | | | | | |

| Kazakhstan - 0.01% | | | | | | | | |

| | 60,000 | | | BTA Bank JSC(a)(c) | | 10.75% | | 07/01/2018 | | | 27,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 27,000 | |

| | | | | | | | | | | | |

| Luxembourg - 0.42% | | | | | | | | |

| | 200,000 | | | ArcelorMittal | | 5.38% | | 06/01/2013 | | | 204,181 | |

| | 250,000 | | | ArcelorMittal | | 3.75% | | 08/05/2015 | | | 233,753 | |

| | |

Annual Report | September 30, 2011 | | 21 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $100,000 | | | Bank of Moscow OJSC Via Kuznetski Capital(d) | | 5.97% | | 11/25/2015 | | $ | 88,500 | |

| | 660,000 | | | Covidien International Finance SA | | 2.80% | | 06/15/2015 | | | 685,207 | |

| | 500,000 | | | Gazprom OAO Via Gaz Capital SA(a) | | 5.09% | | 11/29/2015 | | | 495,000 | |

| | 200,000 | | | Russian Agricultural Bank OJSC Via RSHB Capital SA(b)(d) | | 6.00% | | 06/03/2021 | | | 172,000 | |

| | 100,000 | | | VTB Bank OJSC Via VTB Capital SA(a) | | 6.55% | | 10/13/2020 | | | 93,065 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,971,706 | |

| | | | | | | | | | | | |

| Mexico - 0.52% | | | | | | | | |

| | 100,000 | | | America Movil SAB de CV | | 6.13% | | 03/30/2040 | | | 105,000 | |

| | 200,000 | | | Banco Mercantil del Norte SA(a) | | 4.38% | | 07/19/2015 | | | 201,000 | |

| | 400,000 | | | Banco Mercantil del Norte SA(a)(d) | | 6.86% | | 10/13/2021 | | | 396,000 | |

| | 600,000 | | | Controladora Comercial Mexicana SAB de CV(a) | | 7.00% | | 06/30/2018 | | | 573,000 | |

| | 300,000 | | | Empresas ICA SAB de CV(a) | | 8.90% | | 02/04/2021 | | | 267,000 | |

| | 500,000 | | | Gruma SAB de CV(a) | | 7.75% | | 03/03/2099 | | | 500,000 | |

| | 100,000 | | | Ixe Banco SA(a) | | 9.25% | | 10/14/2020 | | | 111,500 | |

| | 300,000 | | | Sigma Alimentos SA de CV(a) | | 6.88% | | 12/16/2019 | | | 310,500 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,464,000 | |

| | | | | | | | | | | | |

| Netherlands - 0.27% | | | | | | | | |

| | 200,000 | | | Banco Continental SA via Continental Trustees Cayman Ltd.(a)(d) | | 7.38% | | 10/07/2020 | | | 194,000 | |

| | 400,000 | | | Koninklijke KPN NV | | 8.38% | | 10/01/2030 | | | 517,232 | |

| | 200,000 | | | Marfrig Holding Europe BV(b) | | 8.38% | | 05/09/2018 | | | 128,000 | |

| | 200,000 | | | VimpelCom Holdings BV(b) | | 7.50% | | 03/01/2022 | | | 161,500 | |

| | 300,000 | | | WPE International Cooperatief UA(a) | | 10.38% | | 09/30/2020 | | | 273,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,273,732 | |

| | | | | | | | | | | | |

| Norway - 0.08% | | | | | | | | |

| | 400,000 | | | Corp. Pesquera Inca SAC(a) | | 9.00% | | 02/10/2017 | | | 404,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 404,000 | |

| | | | | | | | | | | | |

| Panama - 0.02% | | | | | | | | |

| | 100,000 | | | AES El Salvador Trust(a) | | 6.75% | | 02/01/2016 | | | 98,500 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 98,500 | |

| | | | | | | | | | | | |

| Peru - 0.15% | | | | | | | | |

| | 100,000 | | | Banco de Credito del Peru(b)(d) | | 6.88% | | 09/16/2026 | | | 99,000 | |

| | 300,000 | | | Banco de Credito del Peru(a) | | 4.75% | | 03/16/2016 | | | 292,500 | |

| | 100,000 | | | Banco de Credito del Peru(a)(d) | | 9.75% | | 11/06/2069 | | | 113,000 | |

| | 200,000 | | | Banco Internacional del Peru SAA(a)(d) | | 8.50% | | 04/23/2070 | | | 204,000 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 708,500 | |

| | | | | | | | | | | | |

| | |

| 22 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| Qatar - 0.06% | | | | | | | | |

| | $250,000 | | | Ras Laffan Liquefied Natural Gas Co. Ltd. III(a) | | 5.84% | | 09/30/2027 | | $ | 276,250 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 276,250 | |

| | | | | | | | | | | | |

| Singapore - 0.13% | | | | | | | | |

| | 600,000 | | | Oversea-Chinese Banking Corp. Ltd.(d) | | 4.25% | | 11/18/2019 | | | 616,303 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 616,303 | |

| | | | | | | | | | | | |

| South Korea - 0.55% | | | | | | | | |

| | 600,000 | | | Export-Import Bank of Korea | | 3.75% | | 10/20/2016 | | | 588,627 | |

| | 600,000 | | | Industrial Bank of Korea(a) | | 3.75% | | 09/29/2016 | | | 588,030 | |

| | 850,000 | | | Korea Development Bank | | 8.00% | | 01/23/2014 | | | 944,838 | |

| | 300,000 | | | POSCO(b) | | 4.25% | | 10/28/2020 | | | 280,168 | |

| | 200,000 | | | POSCO(b) | | 5.25% | | 04/14/2021 | | | 198,723 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,600,386 | |

| | | | | | | | | | | | |

| United States - 7.92% | | | | | | | | |

| | 400,000 | | | 3M Co. | | 5.70% | | 03/15/2037 | | | 526,619 | |

| | 550,000 | | | Alcoa, Inc. | | 6.15% | | 08/15/2020 | | | 558,804 | |

| | 875,000 | | | Altria Group, Inc. | | 9.25% | | 08/06/2019 | | | 1,149,940 | |

| | 500,000 | | | American Airlines 2011-2 Class A Pass Through Trust | | 8.63% | | 10/15/2021 | | | 495,000 | |

| | 800,000 | | | American Express Credit Corp. | | 2.75% | | 09/15/2015 | | | 805,122 | |

| | 500,000 | | | Anheuser-Busch InBev Worldwide, Inc. | | 5.38% | | 11/15/2014 | | | 559,366 | |

| | 550,000 | | | Arrow Electronics, Inc. | | 3.38% | | 11/01/2015 | | | 545,176 | |

| | 75,000 | | | AT&T, Inc.(b) | | 5.35% | | 09/01/2040 | | | 78,904 | |

| | 450,000 | | | AT&T, Inc. | | 5.35% | | 09/01/2040 | | | 473,423 | |

| | 717,000 | | | Berkshire Hathaway, Inc. | | 3.20% | | 02/11/2015 | | | 754,793 | |

| | 400,000 | | | Biogen Idec, Inc. | | 6.88% | | 03/01/2018 | | | 491,170 | |

| | 700,000 | | | Boston Properties LP | | 4.13% | | 05/15/2021 | | | 674,957 | |

| | 711,000 | | | Celgene Corp. | | 3.95% | | 10/15/2020 | | | 722,671 | |

| | 450,000 | | | Citigroup, Inc. | | 6.00% | | 12/13/2013 | | | 472,967 | |

| | 650,000 | | | Comcast Corp. | | 5.85% | | 11/15/2015 | | | 738,419 | |

| | 400,000 | | | ConocoPhillips | | 6.50% | | 02/01/2039 | | | 533,762 | |

| | 100,000 | | | Credit Suisse USA, Inc. | | 4.88% | | 01/15/2015 | | | 105,430 | |

| | 200,000 | | | Credit Suisse USA, Inc. | | 5.38% | | 03/02/2016 | | | 214,362 | |

| | 100,000 | | | Daimler Finance North America LLC | | 6.50% | | 11/15/2013 | | | 109,859 | |

| | 600,000 | | | Daimler Finance North America LLC(b) | | 1.88% | | 09/15/2014 | | | 592,828 | |

| | 965,000 | | | Devon Energy Corp. | | 6.30% | | 01/15/2019 | | | 1,172,891 | |

| | 600,000 | | | DIRECTV Holdings LLC / DIRECTV Financing Co., Inc. | | 5.00% | | 03/01/2021 | | | 636,765 | |

| | 500,000 | | | Drummond Co., Inc | | 7.38% | | 02/15/2016 | | | 508,750 | |

| | 400,000 | | | Duke Energy Corp. | | 3.55% | | 09/15/2021 | | | 400,514 | |

| | 900,000 | | | General Electric Capital Corp. | | 3.75% | | 11/14/2014 | | | 940,653 | |

| | 475,000 | | | Halliburton Co. | | 6.15% | | 09/15/2019 | | | 576,913 | |

| | |

Annual Report | September 30, 2011 | | 23 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| $ | 600,000 | | | Illinois Tool Works, Inc.(b) | | 3.38% | | 09/15/2021 | | $ | 617,069 | |

| | 650,000 | | | Intel Corp. | | 3.30% | | 10/01/2021 | | | 666,485 | |

| | 400,000 | | | International Business Machines Corp. | | 1.95% | | 07/22/2016 | | | 404,252 | |

| | 650,000 | | | JP Morgan Chase & Co. | | 4.95% | | 03/25/2020 | | | 689,450 | |

| | 350,000 | | | Kellogg Co. | | 7.45% | | 04/01/2031 | | | 508,899 | |

| | 500,000 | | | Kinder Morgan Energy Partners LP | | 6.95% | | 01/15/2038 | | | 560,424 | |

| | 500,000 | | | Kraft Foods, Inc. | | 5.38% | | 02/10/2020 | | | 567,562 | |

| | 518,000 | | | Marathon Petroleum Corp.(b) | | 5.13% | | 03/01/2021 | | | 541,208 | |

| | 250,000 | | | MetLife, Inc. | | 6.38% | | 06/15/2034 | | | 294,911 | |

| | 250,000 | | | MetLife, Inc. | | 5.70% | | 06/15/2035 | | | 268,782 | |

| | 150,000 | | | Midamerican Energy Holdings Co. | | 5.95% | | 05/15/2037 | | | 177,570 | |

| | 400,000 | | | Midamerican Energy Holdings Co. | | 6.50% | | 09/15/2037 | | | 503,267 | |

| | 750,000 | | | Motorola Solutions, Inc. | | 6.00% | | 11/15/2017 | | | 831,947 | |

| | 395,000 | | | National Rural Utilities Cooperative Finance Corp. | | 10.38% | | 11/01/2018 | | | 568,920 | |

| | 625,000 | | | News America, Inc. | | 6.65% | | 11/15/2037 | | | 690,826 | |

| | 550,000 | | | Novartis Capital Corp. | | 4.40% | | 04/24/2020 | | | 623,489 | |

| | 450,000 | | | Omnicom Group, Inc. | | 4.45% | | 08/15/2020 | | | 455,439 | |

| | 350,000 | | | ONEOK Partners LP | | 6.13% | | 02/01/2041 | | | 389,496 | |

| | 850,000 | | | Pemex Project Funding Master Trust | | 6.63% | | 06/15/2035 | | | 920,125 | |

| | 650,000 | | | PNC Funding Corp. | | 4.38% | | 08/11/2020 | | | 676,153 | |

| | 400,000 | | | Safeway, Inc. | | 6.25% | | 03/15/2014 | | | 445,604 | |

| | 310,000 | | | Simon Property Group LP | | 5.65% | | 02/01/2020 | | | 340,956 | |

| | 220,000 | | | Southern Copper Corp. | | 6.75% | | 04/16/2040 | | | 218,350 | |

| | 1,100,000 | | | Southern Power Co. | | 4.88% | | 07/15/2015 | | | 1,201,557 | |

| | 200,000 | | | Southwest Airlines Co. | | 5.25% | | 10/01/2014 | | | 214,686 | |

| | 100,000 | | | Southwest Airlines Co. | | 5.75% | | 12/15/2016 | | | 111,058 | |

| | 442,000 | | | Southwest Airlines Co. | | 5.13% | | 03/01/2017 | | | 474,648 | |

| | 300,000 | | | Target Corp. | | 3.88% | | 07/15/2020 | | | 326,299 | |

| | 400,000 | | | The Boeing Co. | | 6.88% | | 03/15/2039 | | | 556,276 | |

| | 925,000 | | | The Coca-Cola Co.(b) | | 1.80% | | 09/01/2016 | | | 929,411 | |

| | 300,000 | | | The Kroger Co. | | 5.50% | | 02/01/2013 | | | 316,032 | |

| | 200,000 | | | The Kroger Co. | | 7.50% | | 01/15/2014 | | | 226,443 | |

| | 426,000 | | | The Procter & Gamble Co. | | 5.55% | | 03/05/2037 | | | 552,011 | |

| | 900,000 | | | Time Warner Cable, Inc. | | 5.00% | | 02/01/2020 | | | 958,927 | |

| | 800,000 | | | United Parcel Service, Inc. | | 3.13% | | 01/15/2021 | | | 838,178 | |

| | 950,000 | | | Valero Energy Corp. | | 6.13% | | 02/01/2020 | | | 1,057,220 | |

| | 900,000 | | | Wal-Mart Stores, Inc. | | 3.25% | | 10/25/2020 | | | 935,553 | |

| | 590,000 | | | Waste Management, Inc. | | 6.13% | | 11/30/2039 | | | 719,727 | |

| | 605,000 | | | WellPoint, Inc. | | 5.25% | | 01/15/2016 | | | 674,471 | |

| | 200,000 | | | WellPoint, Inc. | | 5.88% | | 06/15/2017 | | | 229,230 | |

| | |

| 24 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

$450,000 | | Xerox Corp. | | 4.25% | | 02/15/2015 | | $ | 476,598 | |

| | | | | | | | | | |

| | | | | | | | | 37,599,567 | |

| | | | | | | | | | |

| | | |

TOTAL CORPORATE BONDS (Cost $66,977,053) | | | | | | | 66,625,473 | |

| | | | | | | | | | |

| | | |

COLLATERALIZED MORTGAGE OBLIGATIONS - 23.28% | | | | | | | | |

| | American Home Mortgage Investment Trust | | | | | | | | |

324,823 | | Series 2007-A(b)(c) | | 6.10% | | 01/25/2037 | | | 195,186 | |

| | Banc of America Alternative Loan Trust | | | | | | | | |

195,108 | | Series 2005-6 | | 6.00% | | 07/25/2035 | | | 166,600 | |

1,025,456 | | Series 2005-6 | | 5.50% | | 07/25/2035 | | | 909,547 | |

| | Banc of America Funding Corp. | | | | | | | | |

1,412,502 | | Series 2006-2 | | 5.50% | | 03/25/2036 | | | 1,288,908 | |

| | Banc of America Merrill Lynch Commercial Mortgage, Inc. | | | | | | | | |

51,421,803 | | Series 2005-5(d) | | 0.18% | | 10/10/2045 | | | 48,645 | |

100,000 | | Series 2007-1 | | 5.45% | | 01/15/2017 | | | 107,142 | |

305,000 | | Series 2007-4(d) | | 5.92% | | 02/10/2051 | | | 322,552 | |

| | Banc of America Mortgage Securities, Inc. | | | | | | | | |

675,977 | | Series 2004-8 | | 5.50% | | 09/25/2024 | | | 688,047 | |

| | Bank of America-First Union NB Commercial Mortgage | | | | | | | | |

45,000 | | Series 2001-3(b) | | 6.56% | | 04/11/2037 | | | 44,932 | |

| | BCAP LLC Trust | | | | | | | | |

437,035 | | Series 2007-AA2(d) | | 7.50% | | 04/25/2037 | | | 379,123 | |

283,557 | | Series 2007-AA2 | | 6.00% | | 04/25/2037 | | | 196,482 | |

500,000 | | Series 2010-RR6(b)(d) | | 9.62% | | 08/26/2022 | | | 500,625 | |

| | Bear Stearns Alt-A Trust | | | | | | | | |

3,839,302 | | Series 2006-6(d) | | 5.06% | | 11/25/2036 | | | 2,166,503 | |

| | Bear Stearns Asset Backed Securities Trust | | | | | | | | |

1,379,824 | | Series 2005-HE3(d) | | 0.91% | | 03/25/2035 | | | 989,288 | |

| | Bear Stearns Commercial Mortgage Securities | | | | | | | | |

800,000 | | Series 2001-TOP2(d) | | 6.83% | | 02/15/2035 | | | 797,173 | |

150,000 | | Series 2005-PW10(d) | | 5.45% | | 12/11/2040 | | | 143,588 | |

100,000 | | Series 2006-PW13(d) | | 5.58% | | 08/11/2016 | | | 98,878 | |

| | Chase Mortgage Finance Corp. | | | | | | | | |

1,957,841 | | Series 2007-S3 | | 5.50% | | 05/25/2037 | | | 1,902,333 | |

| | Citigroup Commercial Mortgage Trust | | | | | | | | |

63,000 | | Series 2004-C1(d) | | 5.54% | | 04/15/2040 | | | 61,688 | |

250,000 | | Series 2005-C3(d) | | 4.83% | | 05/15/2043 | | | 253,819 | |

11,895 | | Series 2006-C4(d) | | 5.92% | | 03/15/2049 | | | 11,883 | |

| | Citigroup Mortgage Loan Trust, Inc. | | | | | | | | |

1,800,000 | | Series 2006-WF1(c) | | 6.08% | | 03/25/2036 | | | 1,045,584 | |

2,551,047 | | Series 2007-OPX1(c) | | 6.33% | | 01/25/2037 | | | 1,395,976 | |

| | |

Annual Report | September 30, 2011 | | 25 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $2,000,000 | | | Series 2008-AR4(b)(d) | | 5.24% | | 11/25/2038 | | $ | 1,240,000 | |

| | 1,400,000 | | | Series 2008-AR4(b)(d) | | 5.55% | | 11/25/2038 | | | 806,626 | |

| | 1,485,358 | | | Series 2010-8(b)(d) | | 12.29% | | 11/25/2036 | | | 1,142,983 | |

| | | | Citigroup/Deutsche Bank Commercial Mortgage Trust | | | | | | | | |

| | 532,900 | | | Series 2005-CD1(d) | | 0.35% | | 07/15/2044 | | | 526,462 | |

| | 35,000 | | | Series 2006-CD3 | | 5.65% | | 10/15/2048 | | | 30,817 | |

| | 250,000 | | | Series 2007-CD4 | | 5.32% | | 03/11/2012 | | | 258,912 | |

| | | | Citimortgage Alternative Loan Trust | | | | | | | | |

| | 2,171,578 | | | Series 2007-A1 | | 6.00% | | 01/25/2037 | | | 1,492,105 | |

| | 427,744 | | | Series 2007-A1(d) | | 5.17% | | 01/25/2037 | | | 64,000 | |

| | 330,750 | | | Series 2007-A3(d) | | 6.00% | | 03/25/2037 | | | 228,081 | |

| | 752,662 | | | Series 2007-A3(d) | | 5.17% | | 03/25/2037 | | | 113,803 | |

| | 2,276,469 | | | Series 2007-A6 | | 5.50% | | 06/25/2037 | | | 1,641,300 | |

| | | | Commercial Mortgage Asset Trust | | | | | | | | |

| | 250,000 | | | Series 1999-C1(d) | | 7.23% | | 01/17/2032 | | | 262,831 | |

| | | | Commercial Mortgage Pass Through Certificates | | | | | | | | |

| | 25,000 | | | Series 2006-C7(d) | | 5.97% | | 06/10/2046 | | | 23,947 | |

| | 1,231,411 | | | Series 2010-C1(b)(d) | | 2.62% | | 07/10/2046 | | | 96,714 | |

| | 100,000 | | | Series 2011-THL(b) | | 5.95% | | 08/09/2016 | | | 94,104 | |

| | | | Countrywide Alternative Loan Trust | | | | | | | | |

| | 1,256,468 | | | Series 2005-20CB | | 5.50% | | 07/25/2035 | | | 1,009,040 | |

| | 436,771 | | | Series 2005-54CB | | 5.50% | | 11/25/2035 | | | 338,770 | |

| | 1,000,000 | | | Series 2005-6CB | | 5.50% | | 04/25/2035 | | | 820,077 | |

| | 1,148,231 | | | Series 2005-86CB | | 5.50% | | 02/25/2036 | | | 815,648 | |

| | 2,375,123 | | | Series 2005-9CB(d) | | 4.82% | | 05/25/2035 | | | 269,064 | |

| | 1,337,344 | | | Series 2005-9CB(d) | | 0.73% | | 05/25/2035 | | | 977,020 | |

| | 904,870 | | | Series 2006-12CB(d) | | 5.75% | | 05/25/2036 | | | 524,055 | |

| | 4,066,563 | | | Series 2006-15CB | | 6.50% | | 06/25/2036 | | | 2,233,779 | |

| | 621,227 | | | Series 2006-30T1 | | 6.25% | | 11/25/2036 | | | 464,479 | |

| | 426,486 | | | Series 2006-32CB | | 5.50% | | 11/25/2036 | | | 313,712 | |

| | 881,991 | | | Series 2006-36T2(d) | | 26.98% | | 12/25/2036 | | | 1,280,279 | |

| | 3,775,815 | | | Series 2007-23CB(d) | | 0.73% | | 09/25/2037 | | | 1,869,312 | |

| | 3,701,128 | | | Series 2007-23CB(d) | | 6.27% | | 09/25/2037 | | | 841,144 | |

| | | | Countrywide Home Loan Mortgage Pass Through Trust | | | | | | | | |

| | 300,000 | | | Series 2005-J4 | | 5.50% | | 11/25/2035 | | | 272,360 | |

| | 1,587,841 | | | Series 2007-17 | | 6.00% | | 10/25/2037 | | | 1,473,110 | |

| | 1,466,740 | | | Series 2007-3 | | 6.00% | | 04/25/2037 | | | 1,183,770 | |

| | 2,000,000 | | | Series 2007-7 | | 5.75% | | 06/25/2037 | | | 1,660,328 | |

| | | | Credit Suisse First Boston Mortgage Securities Corp. | | | | | | | | |

| | 231,090 | | | Series 2005-10 | | 5.50% | | 11/25/2035 | | | 174,419 | |

| | 215,482 | | | Series 2005-8 | | 5.50% | | 08/25/2025 | | | 192,567 | |

| | | | Credit Suisse Mortgage Capital Certificates | | | | | | | | |

| | 498,461 | | | Series 2006-1 | | 6.00% | | 02/25/2036 | | | 345,576 | |

| | 619,059 | | | Series 2006-4 | | 5.50% | | 05/25/2021 | | | 583,538 | |

| | |

| 26 | | (888) 848-7569 | www.rivernorthfunds.com |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $1,898,655 | | | Series 2006-5 | | 6.25% | | 06/25/2036 | | $ | 1,034,934 | |

| | 3,519,237 | | | Series 2006-7 | | 5.00% | | 08/25/2036 | | | 2,763,182 | |

| | 210,752 | | | Series 2006-9 | | 6.00% | | 11/25/2036 | | | 189,407 | |

| | 80,000 | | | Series 2006-C3(d) | | 6.01% | | 06/15/2038 | | | 73,042 | |

| | 119,342,587 | | | Series 2006-C4(b)(d) | | 0.75% | | 09/15/2039 | | | 1,392,012 | |

| | 1,129,935 | | | Series 2007-2 | | 5.00% | | 03/25/2037 | | | 1,088,352 | |

| | 860,548 | | | Series 2007-3(d) | | 5.84% | | 04/25/2037 | | | 460,343 | |

| | 199,186 | | | Series 2007-4 | | 6.00% | | 06/25/2037 | | | 173,158 | |

| | | | Crest Dartmouth Street | | | | | | | | |

| | 1,000,000 | | | Series 2003-1A(b)(d) | | 1.86% | | 06/28/2038 | | | 913,750 | |

| | | | CSAB Mortgage Backed Trust | | | | | | | | |

| | 262,877 | | | Series 2007-1(d) | | 5.90% | | 05/25/2037 | | | 143,707 | |

| | | | Deutsche ALT-A Securities, Inc. Alternate Loan Trust | | | | | | | | |

| | 924,958 | | | Series 2005-6(d) | | 4.85% | | 12/25/2035 | | | 107,828 | |

| | 458,194 | | | Series 2005-6(d) | | 1.63% | | 12/25/2035 | | | 275,075 | |

| | | | Deutsche Mortgage Securities, Inc. | | | | | | | | |

| | 331,714 | | | Series 2006-PR1(b)(d) | | 11.80% | | 04/15/2036 | | | 350,062 | |

| | | | First Horizon Alternative Mortgage Securities | | | | | | | | |

| | 248,486 | | | Series 2005-FA6 | | 5.50% | | 09/25/2035 | | | 201,190 | |

| | 297,085 | | | Series 2006-FA7 | | 6.25% | | 12/25/2036 | | | 214,900 | |

| | 501,056 | | | Series 2007-FA2 | | 6.00% | | 04/25/2037 | | | 345,132 | |

| | | | GE Capital Commercial Mortgage Corp. | | | | | | | | |

| | 1,065,000 | | | Series 2002-2A(b)(d) | | 6.31% | | 08/11/2036 | | | 1,069,913 | |

| | | | GMAC Commercial Mortgage Securities, Inc. | | | | | | | | |

| | 200,000 | | | Series 2006-C1(d) | | 5.29% | | 11/10/2045 | | | 191,702 | |

| | | | Greenwich Capital Commercial Funding Corp. | | | | | | | | |

| | 10,000 | | | Series 2004-FL2A(b)(d) | | 0.63% | | 11/05/2019 | | | 9,606 | |

| | 250,000 | | | Series 2007-GG9 | | 5.44% | | 03/10/2039 | | | 260,434 | |

| | | | GS Mortgage Securities Corp. II | | | | | | | | |

| | 250,000 | | | Series 2006-GG6(d) | | 5.62% | | 04/10/2038 | | | 229,500 | |

| | 20,557,154 | | | Series 2006-GG6(b)(d) | | 0.17% | | 04/10/2038 | | | 35,996 | |

| | 20,000 | | | Series 2007-GG10(d) | | 6.00% | | 08/10/2045 | | | 20,880 | |

| | 596,854 | | | Series 2011-GC3(b)(d) | | 1.34% | | 03/10/2044 | | | 35,438 | |

| | | | GSAA Trust | | | | | | | | |

| | 1,055,518 | | | Series 2005-7(d) | | 4.48% | | 05/25/2035 | | | 1,011,543 | |

| | 890,502 | | | Series 2006-18(c) | | 5.68% | | 11/25/2036 | | | 493,752 | |

| | 301,964 | | | Series 2006-6(d) | | 5.32% | | 03/25/2036 | | | 146,183 | |

| | 1,607,043 | | | Series 2007-2(c) | | 6.10% | | 03/25/2037 | | | 952,003 | |

| | | | HSBC Asset Loan Obligation | | | | | | | | |

| | 1,383,937 | | | Series 2007-2 | | 5.50% | | 09/25/2037 | | | 1,341,604 | |

| | | | Indymac IMSC Mortgage Loan Trust | | | | | | | | |

| | 2,869,030 | | | Series 2007-F2 | | 6.50% | | 07/25/2037 | | | 1,409,856 | |

| | | | JP Morgan Alternative Loan Trust | | | | | | | | |

| | 990,368 | | | Series 2005-S1 | | 6.00% | | 12/25/2035 | | | 811,286 | |

| | |

Annual Report | September 30, 2011 | | 27 |

| | |

RiverNorth/DoubleLine Strategic Income Fund | | Schedule of Investments |

| | September 30, 2011 |

| | | | | | | | | | | | |

| Principal Amount/Description | | Rate | | Maturity | | Value | |

| | $352,709 | | | Series 2006-S1 | | 5.00% | | 02/25/2021 | | $ | 300,969 | |

| | 2,657,759 | | | Series 2006-S3(c) | | 6.12% | | 08/25/2036 | | | 2,331,131 | |

| | | | JP Morgan Chase Commercial Mortgage Securities Corp. | | | | | | | | |

| | 948,118 | | | Series 2006-LDP8(d) | | 0.75% | | 05/15/2045 | | | 19,846 | |

| | 200,000 | | | Series 2007-C1 | | 5.72% | | 11/15/2017 | | | 212,666 | |

| | 100,000 | | | Series 2007-CB18(d) | | 5.47% | | 02/12/2017 | | | 89,805 | |

| | 100,000 | | | Series 2007-CB19(d) | | 5.93% | | 05/12/2017 | | | 87,840 | |

| | 50,000 | | | Series 2007-CB19(d) | | 5.93% | | 02/12/2049 | | | 53,249 | |

| | | | JP Morgan Mortgage Acquisition Corp. | | | | | | | | |

| | 500,000 | | | Series 2006-CH2(c) | | 5.46% | | 10/25/2036 | | | 265,859 | |

| | 2,000,000 | | | Series 2007-CH1(c) | | 5.86% | | 05/25/2015 | | | 1,363,010 | |

| | | | JP Morgan Mortgage Trust | | | | | | | | |

| | 1,163,580 | | | Series 2007-S3 | | 6.00% | | 07/25/2037 | | | 1,004,126 | |

| | 710,977 | | | Series 2007-S3 | | 6.00% | | 08/25/2037 | | | 593,826 | |

| | | | LB-UBS Commercial Mortgage Trust | | | | | | | | |

| | 650,000 | | | Series 2001-C2(b) | | 7.29% | | 09/15/2034 | | | 647,245 | |

| | | | Lehman Mortgage Trust | | | | | | | | |

| | 2,046,079 | | | Series 2006-6 | | 5.50% | | 10/25/2036 | | | 1,300,453 | |

| | 5,521,426 | | | Series 2006-7(d) | | 0.48% | | 11/25/2036 | | | 742,577 | |

| | 5,521,426 | | | Series 2006-7(d) | | 7.52% | | 11/25/2036 | | | 1,517,371 | |

| | 3,438,910 | | | Series 2006-8(d) | | 0.65% | | 12/25/2036 | | | 1,505,345 | |

| | 3,438,910 | | | Series 2006-8(d) | | 6.35% | | 12/25/2036 | | | 833,935 | |