united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22153

Dunham Funds

(Exact name of registrant as specified in charter)

10251 Vista Sorrento Pkwy, Ste. 200, San Diego, CA 92121

(Address of principal executive offices) (Zip code)

Richard Malinowski

Gemini Fund Services, LLC., 80 Arkay Drive, Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 10/31

Date of reporting period: 4/30/17

Item 1. Reports to Stockholders.

This Semi-annual Report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act Of 1995. Forward-looking statements also include those preceded by, followed by or that include the words “believes”, “expects”, “anticipates” or similar expressions. Such statements should be viewed with caution. actual results or experience could differ materially from the forward-looking statements as a result of many factors. Each Fund makes no commitments to disclose any revisions to forward-looking statements, or any facts, events or circumstances after the date hereof that may bear upon forward-looking statements. In addition, prospective purchasers of the Funds should consider carefully the information set forth herein and the applicable fund’s prospectus. Other factors and assumptions not identified above may also have been involved in the derivation of these forward-looking statements, and the failure of these other assumptions to be realized may also cause actual results to differ materially from those projected.

Dear Fellow Shareholders,

The past six months have been exciting, to say the least. Headlines have bounced from a surprise in U.S. election results, to two increases in the Fed Funds Rate, to a significant rally in equities, to geopolitical uncertainty overseas, and to domestic political excitement, euphoria, and disappointment. While some of these headlines are not uncommon, the convergence of all of these events in such a short period would prompt most financial markets-focused academics to assume that significantly increased volatility would have coincided with this information maelstrom. Instead, volatility subsided to low levels that have not been seen in over a decade, since before the Global Financial Crisis.

While this most recent rally in the equity markets has generally resulted in all-time highs for many broad asset classes, the “per unit of earnings” prices are not at all-time highs. For example, the S&P 500 Index boasted an average Price-to-Earnings ratio of close to 21.3 at the end of the most recent fiscal quarter. This is a far-cry from the 26.5 ratio seen in 2009 or 30.6 ratio in 1999. Therefore, while equity fundamentals and prices do not appear outrageous, we do believe that there are opportunities in both the traditional equity and fixed income markets, as well as in alternative asset classes.

When looking overseas, the increased concerns over geopolitical events, such as the Dutch and French elections, have provided investment opportunities for those who remain calm amidst the panic. Foreign markets, developing markets in particular, have not seen the same rebound and rally over the past decade experienced by U.S. equities. In fact, while U.S. equities have nearly doubled in value from their 2007 highs, emerging markets stocks are still underwater and developed markets stocks are barely positive. As these regions continue to make progress implementing the complex processes needed to revitalize their economies, additional intermediate-term and long-term opportunities may surface.

As the Federal Open Market Committee has acted on their confidence that the U.S. economy is on stronger footing by increasing the Fed Funds Rate an additional 0.5 percent in the December and March meetings, the most interest-rate sensitive fixed income securities have experienced significant declines. Fed Chair, Janet Yellen, has reiterated her commitment to additional increases this year, which are expected to further stress those same securities that have broadly benefitted from close to nine years of record-low interest rates. Similar to the dispersion and uncertainty seen in the equity markets, the disconnect for many investors between what asset classes have historically been strong performers and those that should benefit most in the new environment to come is prevalent in the fixed income markets.

We remain committed to providing you with the highest level of service and an investment experience that is tailored to your specific goals. We thank you for your continued trust and the confidence you have placed in us. We take that trust very seriously and look forward to servicing your investment needs for years to come.

Sincerely,

Jeffrey A. Dunham

President

Dunham & Associates Investment Counsel, Inc.

April 30, 2017

1

Dunham Floating Rate Bond Fund

Message from the Sub-Adviser (Newfleet Asset Management, LLC)

After shocking the world and financial markets with his surprise victory, President-Elect Trump set out to deliver on his campaign promises of economic growth, healthcare and tax reform, and border security. Over the first few months of the fiscal period, U.S. stocks soared while returns on bonds suffered. Investor optimism was gleaming at the prospects for America. The latter half of the fiscal period became more of a reality check for investors. Following the inauguration, the new administration suffered a few setbacks that led investors to reassess the speed, or even the likelihood, at which the new president’s policies would come to fruition. U.S. stocks continued their upward trajectory, albeit at a reduced pace, while bond returns recovered. Over the six-month period ended April 30, 2017, U.S. stocks, as measured by the S&P 500, gained 13.3 percent. Over the same period, interest rates on the 10-year U.S. Treasury fluctuated within an 85 basis point range, hitting their low of 1.78 percent a few days prior to the election, undulating throughout the fiscal period until they reached their high of 2.63 percent in mid-March, before settling at 2.28 percent to end the fiscal period. The Federal Reserve increased the Fed Funds Rate by 25 basis points in December of 2016 and again in March of 2017. As bond prices fall when interest rates rise, returns on U.S. bonds declined. U.S. investment-grade bonds, as measured by the Bloomberg Barclays U.S. Aggregate Total Return Bond Index, lost 0.7 percent over the six-month period ended April 30, 2017. The increase in rates was mimicked by the performance of bank loans, as measured by the S&P / LSTA Leveraged Loan Index. Bank loans gained 3.0 percent over the fiscal period. The London Interbank Offered Rate (“LIBOR”) continued its upward trend during the fiscal period. Three-month LIBOR began the fiscal period at 0.88 percent, generally its lowest point of the six-month period, before beginning a steady climb to its high of 1.17 percent at end of the fiscal period.

U.S. stocks rallied over the six-month period ended April 30, 2017, and bank loan returns were meaningfully positive, as well. At the beginning of the fiscal period, the average bank loan in the Fund had a price of $99.72. By the middle of the fiscal period, the average bank loan price rose to $100.02, before dipping to $99.88 by the end of the fiscal six-month period. The Sub-Adviser remains optimistic about the asset class’ potential as interest rates rise and investor sentiment towards the loan space allows the price to continue to increase. At the beginning of the fiscal six-month period, approximately 22 bank loans in the Fund had a price lower than $95, which represented approximately 7.25 percent of the bank loans in the Fund. By the end of the fiscal six-month period, the Fund held approximately 20 bank loans with a price below $95, which represented approximately 6.25 percent of the bank loans in the Fund.

The yields on bank loans, as measured by the S&P / LSTA Leveraged Loan 100 Index, generally moved in the opposite direction from broader Treasury yield movements over the fiscal period. Bank loans, in general, began the fiscal six-month period with a yield-to-maturity of 5.1 percent, approximately 1.4 percent less than their traditional high-yield bond counterparts, as measured by the BofA Merrill Lynch High-Yield Bond Cash Pay Index. Bank loans underperformed traditional high-yield bonds over the first half of fiscal period by nearly 100 basis points, and trailed by nearly 150 basis points over the second half of the fiscal six-month period. Over the entire period, bank loans underperformed traditional high-yield bonds by nearly 250 basis points. The yield gap between the bank loans and traditional high-yield bonds saw an overall expansion over the fiscal period. At the end of the fiscal six months, the yields on bank loans stood at 4.5 percent and traditional high-yield bonds ended at 6.0 percent. The Fund held approximately 5.8 percent of its assets in traditional high-yield bonds that, from an allocation perspective, enhanced relative performance during the fiscal period.

The Sub-Adviser continued to focus on higher rated first lien loans within the bank loan space, limiting its exposure to bank loans rated CCC and lower. The exposure to lower-rated loans, second lien loans, and traditional bonds has been limited to instances where the Sub-Adviser has determined that the additional reward is expected to significantly outweigh the additional risk. However, with the significant increase in lower-rated securities over the second half of the six-month period, some of the Fund’s bonds also benefitted. For example, the Fund held the CC-rated traditional bonds issued by FTS International, Inc. (30283WAB0) (holding percentage*: 0.03 percent), a provider of oil field services and high-pressure hydraulic fracturing, operating throughout the United States. The company’s bonds increased 53.6 percent on a total return basis over the first half of the six-month period. The second half of the six-month period saw the total return of the bonds lose 2.7 percent. As oil prices rallied from their January 2016 lows and traded in the $45 to $55 range throughout the first half of the fiscal period, many energy-related issuers saw increases in their bank loans over the first half of the fiscal period, such as Fieldwood Energy, LLC (BL1112129) (holding percentage*: 0.07 percent). Another provider of oil and gas services, the company acquires and develops oil and gas opportunity assets throughout the United States. Fieldwood’s bank loan saw a price increase from $60.00 at the beginning of the fiscal period to $79.37 midway through the fiscal period. The second half of the fiscal period saw the price of the bank loans drop from $79.37 to $78.81, as oil prices generally declined from the $55 range to the $49 range. A contributor to the Fund’s performance over the entire six-month period was Drillships Financing Holding, Inc. (BL1037748) (holding percentage*: 0.08 percent), which operates as a financing holding company and a subsidiary of Ocean Rig UDW, Inc. Ocean Rig offers offshore drilling services to the oil and natural gas exploration industry, operating ultra-deepwater semi-submergible offshore drilling rigs, and specializes in drilling in harsh environments. The bank loans saw a 46.0 percent increase in its price from the beginning of the fiscal period through the end.

The Sub-Adviser remains constructive on markets but believes there are still a number of uncertainties to monitor going forward, including the unfolding of Trump’s economic policies, the strength of the U.S. dollar, and commodities prices. The Sub-Adviser expects U.S. growth in the 2 percent to 2.5 percent range for the year and believes the Fed will remain data dependent but will raise rates two more times this year. The Sub-Adviser believes global growth will be driven by emerging markets, and expects an improvement in global growth this year after hitting a bottom last year. The Sub-Adviser believes there will be continued increases in LIBOR and remains encouraged by historically low default rates, both of which should benefit bank loan investors by the floating rate feature offered by bank loans.

| * | Holdings percentage(s) as of 4/30/2017. |

| ** | Holdings percentage(s) as of the date prior to the sale of the security. |

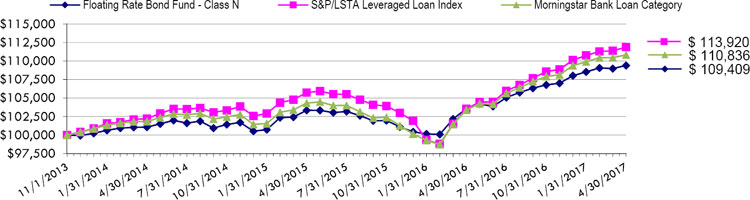

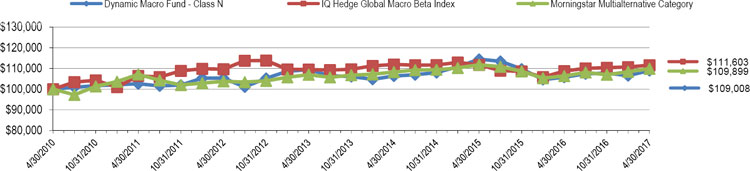

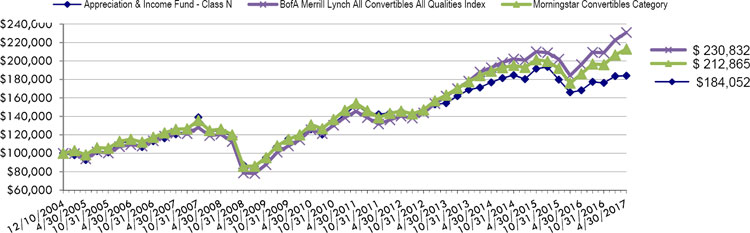

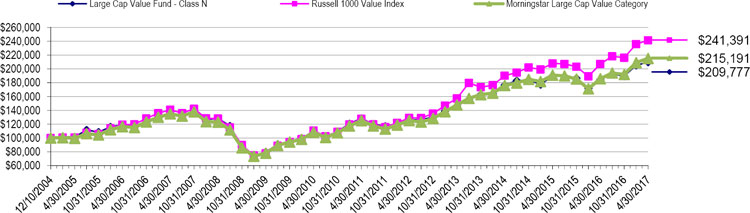

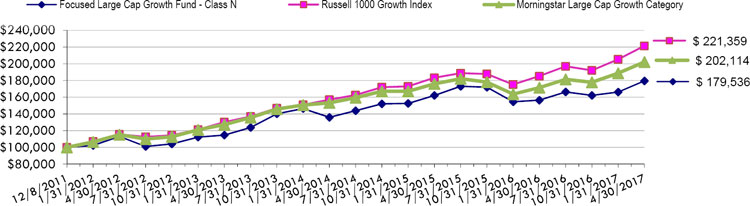

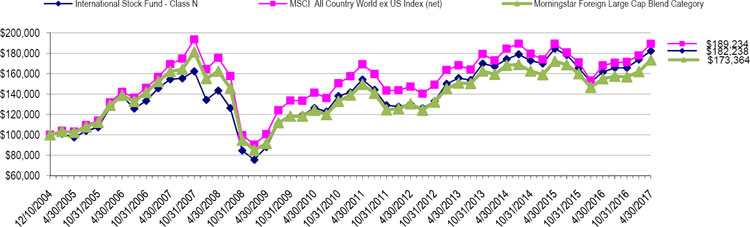

Growth of $100,000 Investment

Total Returns as of April 30, 2017

| Annualized | ||||||||

| One | Annualized | Since Inception | ||||||

| Six Months | Year | Three Years | (11/1/13) | |||||

| Class N | 2.47% | 5.65% | 2.68% | 2.61% | ||||

| Class C | 2.25% | 4.94% | 1.97% | 1.86% | ||||

| Class A with load of 4.50% | (2.30)% | 0.56% | 0.86% | 0.99% | ||||

| Class A without load | 2.33% | 5.27% | 2.42% | 2.33% | ||||

| S&P/LSTA Leverage Loan Index | 3.03% | 8.05% | 3.05% | 4.60% | ||||

| Morningstar Bank Loan Category | 2.70% | 7.21% | 2.86% | 2.99% |

The S&P/LSTA U.S. Leveraged Loan 100 Index is designed to reflect the performance of the largest facilities in the leveraged loan market. Investors cannot invest directly in an index or benchmark.

The Morningstar Bank Loan Category is generally representative of mutual funds that primarily invest in floating-rate bank loans instead of bonds. These bank loans generally offer interest payments that typically float above a common short-term benchmark such as the London interbank offered rate, or LIBOR.

As disclosed in the Trust’s latest registration statement, the Fund’s total annual operating expenses, including cost of underlying funds, are 1.20% for Class N, 1.95% for Class C and 1.45% for Class A. Class A shares are subject to a sales load of 4.50% and a deferred sales charge of up to 0.75%. The performance data quoted here represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance data quoted. The investment return and NAV will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated assuming reinvestment of all dividends and capital gains distributions, if any. The returns do not reflect the deductions of taxes a shareholder would pay on the redemption of fund shares or fund distributions. For performance information current to the most recent month-end, please call 1-800-442-4358 or visit our website www.dunham.com

2

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund |

| April 30, 2017 |

| Shares | Value | |||||||||||||||

| COMMON STOCK - 0.1% | ||||||||||||||||

| ELECTRIC - 0.1% | ||||||||||||||||

| Speedstar Holding Corp. | 23,349 | $ | — | |||||||||||||

| Vistra Energy Corp. | 10,588 | 158,291 | ||||||||||||||

| TOTAL COMMON STOCK (Cost - $148,234) | 158,291 | |||||||||||||||

| EXCHANGE TRADED FUND - 1.0% | ||||||||||||||||

| DEBT FUND - 1.0% | ||||||||||||||||

| PowerShares Senior Loan Portfolio | 56,935 | 1,325,447 | ||||||||||||||

| TOTAL EXCHANGE TRADED FUND (Cost - $1,319,832) | ||||||||||||||||

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | |||||||||||||

| BANK LOANS - 88.0% | ||||||||||||||||

| CONSUMER DISCRETIONARY - 24.3% | ||||||||||||||||

| Advantage Sales & Marketing, Inc. | $ | 182,000 | 7.6723 | % | 7/24/2022 | 174,447 | ||||||||||

| Advantage Sales & Marketing, Inc. | 285,000 | 4.4218 | 7/24/2021 | 278,944 | ||||||||||||

| Affinity Gaming LLC | 18,455 | 4.6496 | 6/30/2023 | 18,616 | ||||||||||||

| Altice US Finance I Corp | 334,811 | 3.3712 | 7/28/2025 | 335,194 | ||||||||||||

| AMC Entertainment Holdings, Inc. | 161,595 | 3.9196 | 12/16/2023 | 162,335 | ||||||||||||

| American Axle & Manufacturing Holdings, Inc. | 285,000 | 3.4054 | 4/6/2024 | 283,991 | ||||||||||||

| Aristocrat International Pty L | 600,187 | 3.4032 | 10/20/2021 | 605,940 | ||||||||||||

| Accuride | 369,175 | 8.1496 | 11/16/2023 | 373,328 | ||||||||||||

| Bass Pro Group LLC | 655,000 | 5.8996 | 6/8/2018 | 660,322 | ||||||||||||

| Bass Pro Group LLC | 655,000 | 6.1496 | 12/16/2026 | 639,490 | ||||||||||||

| Boyd Gaming Corp. | 874,475 | 3.6718 | 9/16/2023 | 879,442 | ||||||||||||

| Caesars Entertainment | 129,617 | 1.5000 | — | 159,429 | ||||||||||||

| Caesars Entertainment Operating | 305,000 | 3.6498 | 4/4/2024 | 303,589 | ||||||||||||

| Caesars Entertainment Operating | 526,848 | 10.2500 | 1/28/2018 | 602,911 | ||||||||||||

| Caesars Entertainment Resort | 815,331 | 7.1723 | 10/12/2020 | 819,412 | ||||||||||||

| Caesars Growth Properties Holding | 400,000 | 4.1665 | 5/8/2021 | 402,688 | ||||||||||||

| Caesars Growth Properties Holding | 249,714 | 3.7500 | 5/8/2021 | 251,274 | ||||||||||||

| CBAC Borrower LLC | 98,750 | 8.2500 | 7/2/2020 | 99,244 | ||||||||||||

| CBS Radio, Inc. | 295,333 | 4.6562 | 10/16/2023 | 297,918 | ||||||||||||

| CDS US Intermediate Holdings | 173,360 | 5.1496 | 7/8/2022 | 175,130 | ||||||||||||

| Charter Communications Operating LLC | 136,620 | 3.1723 | 1/16/2022 | 137,332 | ||||||||||||

| Charter Communications Operating LLC | 700,920 | 3.4223 | 1/16/2024 | 705,213 | ||||||||||||

| Charter Communications Operating LLC | 323,451 | 3.1723 | 6/30/2020 | 325,507 | ||||||||||||

| CityCenter Holdings LLC | 565,000 | 3.9062 | 4/18/2024 | 566,554 | ||||||||||||

| Cooper Standard Auto | 189,022 | 3.8996 | 11/2/2023 | 189,760 | ||||||||||||

| CSC Holdings LLC | 1,045,275 | 3.4062 | 7/16/2025 | 1,046,488 | ||||||||||||

| Delta 2 Lux Sarl | 385,000 | 4.2500 | 1/31/2024 | 386,011 | ||||||||||||

| Eldorado Resorts, Inc. | 127,725 | 6.2500 | 7/24/2022 | 127,446 | ||||||||||||

| Eldorado Resorts, Inc. | 590,000 | 5.2500 | 4/16/2024 | 589,817 | ||||||||||||

| Federal-Mogul Holdings Corp. | 983,126 | 4.9062 | 4/16/2021 | 984,001 | ||||||||||||

| Floor & Decor Outlets of America | 261,685 | 4.6723 | 9/30/2023 | 262,666 | ||||||||||||

| Gates Global LLC | 635,952 | 4.4076 | 3/31/2024 | 639,968 | ||||||||||||

| Gateway Casinos & Entertainment | 165,000 | 4.8040 | 2/22/2023 | 167,440 | ||||||||||||

| Graton Economic Development | 117,405 | 4.9601 | 8/31/2022 | 118,139 | ||||||||||||

| Greektown Holdings LLC | 170,000 | 4.1704 | 4/24/2024 | 170,496 | ||||||||||||

| Harbor Freight Tools | 394,515 | 4.4223 | 8/18/2023 | 394,073 | ||||||||||||

| Hilton Worldwide Finance LLC | 1,533,572 | 3.1704 | 10/24/2023 | 1,547,950 | ||||||||||||

| iHeart Communications, Inc. | 910,000 | 7.9223 | 1/30/2019 | 779,998 | ||||||||||||

| Intelsat Jackson Holdings S.A. | 370,000 | 3.9018 | 6/30/2019 | 365,984 | ||||||||||||

| KAR Auction Services, Inc. | 306,184 | 3.3598 | 3/12/2021 | 309,293 | ||||||||||||

| KAR Auction Services, Inc. | 74,250 | 4.6723 | 3/8/2023 | 74,970 | ||||||||||||

| Laureate Education, Inc. | 597,845 | 8.6557 | 3/16/2021 | 598,592 | ||||||||||||

| Laureate Education, Inc. | 449,681 | 5.6562 | 4/26/2024 | 450,151 | ||||||||||||

| Leslie’s Poolmart, Inc. | 318,501 | 4.8996 | 8/16/2023 | 320,624 | ||||||||||||

| Libbey Glass, Inc. | 243,843 | 4.1557 | 4/8/2021 | 236,527 | ||||||||||||

| Lions Gate Entertainment Corp. | 251,200 | 4.1496 | 12/8/2023 | 253,006 | ||||||||||||

| MCC Iowa LLC | 296,655 | 3.6723 | 1/28/2021 | 298,834 | ||||||||||||

| McGraw-Hill Global Education | 263,013 | 5.1723 | 5/4/2022 | 260,999 | ||||||||||||

| Mediacom Illinois LLC | 154,445 | 3.4223 | 2/16/2024 | 155,475 | ||||||||||||

See accompanying notes to financial statements.

3

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| CONSUMER DISCRETIONARY (Continued) - 24.3% | ||||||||||||||||

| MGM Growth Properties | $ | 373,230 | 3.672 | % | 4/24/2023 | $ | 374,564 | |||||||||

| Michaels Stores, Inc. | 527,583 | 3.9173 | 1/30/2023 | 527,253 | ||||||||||||

| Mission Broadcasting, Inc. | 19,910 | 4.1562 | 1/16/2024 | 20,114 | ||||||||||||

| Mohegan Tribal Gaming Authority | 249,375 | 5.1723 | 10/12/2023 | 251,531 | ||||||||||||

| Neiman Marcus Group LTD, Inc. | 267,245 | 4.4054 | 10/24/2020 | 213,944 | ||||||||||||

| Nexstar Broadcasting, Inc. | 205,363 | 4.1562 | 1/16/2024 | 207,472 | ||||||||||||

| Numericable US LLC | 650,000 | 3.9062 | 8/1/2025 | 648,102 | ||||||||||||

| Numericable US LLC | 159,600 | 4.4223 | 1/14/2025 | 159,999 | ||||||||||||

| Party City Holdings, Inc. | 531,410 | 4.1708 | 8/20/2022 | 531,853 | ||||||||||||

| Penn National Gaming, Inc. | 125,000 | 3.6496 | 1/20/2024 | 126,016 | ||||||||||||

| PetSmart, Inc. | 536,445 | 4.1518 | 3/12/2022 | 493,715 | ||||||||||||

| Playa Resorts Holdings | 365,000 | 4.1576 | 4/28/2024 | 366,303 | ||||||||||||

| Scientific Games International | 531,267 | 5.1562 | 9/30/2021 | 539,858 | ||||||||||||

| Serta Simmons International | 305,235 | 4.5337 | 11/8/2023 | 306,642 | ||||||||||||

| ServiceMaster Co. LLC | 874,800 | 3.6496 | 11/8/2023 | 885,874 | ||||||||||||

| Sinclair Television | 368,452 | 3.4223 | 1/4/2024 | 369,741 | ||||||||||||

| Six Flags Entertainment Corp. | 343,273 | 3.4232 | 6/30/2022 | 347,063 | ||||||||||||

| Speedstar Holding Corp. | 5,149 | 9.9051 | 4/12/2022 | 3,778 | ||||||||||||

| SRAM Corporation | 261,108 | 4.6850 | 3/16/2024 | 261,108 | ||||||||||||

| St George’s University | 222,252 | 6.3996 | 7/6/2022 | 225,309 | ||||||||||||

| Station Casinos LLC | 877,909 | 3.6562 | 6/8/2023 | 878,607 | ||||||||||||

| TI Group Automotive Systems LLC | 303,384 | 3.9223 | 6/30/2022 | 305,027 | ||||||||||||

| Transtar Holding Co. | 6,701 | 5.5000 | 4/12/2022 | 6,523 | ||||||||||||

| Transtar Holding Co. | 16,970 | 5.5000 | 4/12/2022 | 12,946 | ||||||||||||

| Tribune Co. | 23,631 | 4.1723 | 12/28/2020 | 23,838 | ||||||||||||

| Tribune Co. | 295,270 | 4.1723 | 1/26/2024 | 297,808 | ||||||||||||

| UFC Holdings LLC | 604,973 | 4.4062 | 8/18/2023 | 609,462 | ||||||||||||

| Univision Communications, Inc. | 2,476,298 | 3.9223 | 3/16/2024 | 2,463,334 | ||||||||||||

| US Farathane LLC | 270,685 | 5.1496 | 12/24/2021 | 273,900 | ||||||||||||

| Ziggo BV | 890,000 | 3.6562 | 4/16/2025 | 891,157 | ||||||||||||

| 32,609,799 | ||||||||||||||||

| CONSUMER STAPLES - 5.4% | ||||||||||||||||

| Albertsons LLC | 251,107 | 4.4218 | 12/20/2022 | 252,505 | ||||||||||||

| Albertsons LLC | 460,877 | 4.1723 | 8/24/2021 | 463,013 | ||||||||||||

| Amplify Snack Brands, Inc. | 158,525 | 6.6498 | 9/2/2023 | 156,049 | ||||||||||||

| ARAMARK Corp. | 410,000 | 3.1522 | 3/28/2024 | 414,100 | ||||||||||||

| Chobani LLC | 279,325 | 5.4223 | 10/10/2023 | 284,213 | ||||||||||||

| Coty, Inc. | 390,499 | 3.6498 | 10/28/2022 | 393,550 | ||||||||||||

| Dole Food Co, Inc. | 540,000 | 4.1554 | 4/6/2024 | 542,533 | ||||||||||||

| Galleria Co | 205,952 | 4.1498 | 9/28/2023 | 208,012 | ||||||||||||

| Hostess Brands LLC | 375,569 | 4.1723 | 8/4/2022 | 379,443 | ||||||||||||

| Jacobs Douwe Egberts | 105,001 | 3.6498 | 7/2/2022 | 105,525 | ||||||||||||

| JBS USA Lux | 655,000 | 3.6498 | 10/30/2022 | 658,861 | ||||||||||||

| Kronos, Inc. | 698,250 | 5.0346 | 10/31/2023 | 701,623 | ||||||||||||

| Kronos, Inc. | 120,000 | 9.2846 | 10/31/2024 | 125,385 | ||||||||||||

| Milk Specialties Co. | 341,285 | 5.1496 | 8/16/2023 | 344,913 | ||||||||||||

| Prestige Brands, Inc. | 193,693 | 3.9223 | 1/26/2024 | 195,727 | ||||||||||||

| Reynolds Group Holdings, Inc. | 839,354 | 4.1723 | 2/4/2023 | 844,554 | ||||||||||||

| Rite Aid Corp. | 430,000 | 5.0473 | 6/20/2021 | 431,612 | ||||||||||||

| TKC Holdings, Inc. | 275,000 | 4.8998 | 1/31/2023 | 278,208 | ||||||||||||

| US Foods, Inc. | 465,483 | 3.9223 | 6/28/2023 | 470,284 | ||||||||||||

| 7,250,110 | ||||||||||||||||

| ENERGY - 2.6% | ||||||||||||||||

| Blackhawk Mining LLC | 135,849 | 10.6723 | 2/16/2022 | 132,162 | ||||||||||||

| Chesapeake Energy Corp. | 55,000 | 8.5523 | 8/24/2021 | 59,546 | ||||||||||||

| Chief Exploration & Development | 172,000 | 7.6518 | 5/16/2021 | 166,195 | ||||||||||||

| Contura Energy, Inc. | 370,000 | 6.1518 | 3/18/2024 | 367,342 | ||||||||||||

| Drillships Financing Holding | 140,276 | 8.0000 | 4/1/2021 | 106,084 | ||||||||||||

| Drillships Ocean Ventures, Inc. | 109,200 | 7.5000 | 7/24/2021 | 101,874 | ||||||||||||

| Fieldwood Energy LLC | 134,102 | 8.3750 | 9/30/2020 | 105,689 | ||||||||||||

See accompanying notes to financial statements.

4

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| ENERGY - 2.6% (Continued) | ||||||||||||||||

| Fieldwood Energy LLC | $ | 81,748 | 8.3750 | % | 9/30/2020 | $ | 74,663 | |||||||||

| Fieldwood Energy LLC | 180,554 | 8.1723 | 9/1/2020 | 177,244 | ||||||||||||

| Gavilan Resources LLC | 290,000 | 7.1498 | 2/29/2024 | 288,550 | ||||||||||||

| Jonah Energy LLC | 243,000 | 7.6723 | 5/12/2021 | 232,673 | ||||||||||||

| MEG Energy Corp. | 594,194 | 4.5390 | 1/1/2024 | 595,866 | ||||||||||||

| Paragon Offshore Finance Co | 174,258 | 5.7500 | 7/16/2021 | 68,178 | ||||||||||||

| Peabody Energy Corp. | 290,000 | 5.6498 | 4/1/2022 | 291,873 | ||||||||||||

| Seadrill Operating LP | 811,214 | 4.1496 | 2/20/2021 | 552,031 | ||||||||||||

| Ultra Resources, Inc. | 190,000 | 4.1584 | 4/12/2024 | 189,525 | ||||||||||||

| 3,509,495 | ||||||||||||||||

| FINANCIALS - 3.5% | ||||||||||||||||

| Alixpartners LLP | 860,000 | 4.1498 | 4/4/2024 | 868,445 | ||||||||||||

| Asurion LLC | 188,460 | 4.9223 | 11/4/2023 | 190,109 | ||||||||||||

| Asurion LLC | 16,733 | 4.4223 | 7/8/2020 | 16,874 | ||||||||||||

| Asurion LLC | 301,588 | 4.4223 | 8/4/2022 | 303,944 | ||||||||||||

| Asurion LLC | 230,000 | 8.6723 | 3/4/2021 | 233,952 | ||||||||||||

| Avolon | 25,000 | 3.9032 | 3/20/2022 | 25,402 | ||||||||||||

| Delos Finance | 300,000 | 3.3996 | 10/6/2023 | 304,013 | ||||||||||||

| iStar Financial, Inc. | 20,657 | 4.9043 | 6/30/2020 | 20,915 | ||||||||||||

| Lightstone Generation | 127,796 | 5.6723 | 1/30/2024 | 128,654 | ||||||||||||

| Lightstone Generation | 7,884 | 5.6723 | 1/30/2024 | 7,937 | ||||||||||||

| Lonestar Intermediate | 215,000 | 10.1723 | 9/1/2021 | 224,137 | ||||||||||||

| TransUnion LLC | 883,246 | 3.6723 | 4/8/2023 | 891,858 | ||||||||||||

| VF Holdings Corp. | 651,825 | 4.4223 | 6/30/2023 | 655,084 | ||||||||||||

| Walter Investments | 953,918 | 4.9223 | 12/18/2020 | 864,569 | ||||||||||||

| 4,735,893 | ||||||||||||||||

| HEALTHCARE - 11.5% | ||||||||||||||||

| 21st Century Oncology, Inc. | 146,612 | 7.2746 | 4/30/2022 | 133,710 | ||||||||||||

| Acadia Healthcare Co, Inc. | 303,559 | 4.1496 | 2/16/2023 | 304,318 | ||||||||||||

| Akorn, Inc. | 258,135 | 5.4223 | 4/16/2021 | 261,202 | ||||||||||||

| Alere, Inc. | 533,080 | 4.4223 | 6/20/2022 | 536,243 | ||||||||||||

| American Renal Holdings Co, Inc. | 83,338 | 4.7500 | 8/20/2019 | 84,068 | ||||||||||||

| Amneal Pharmaceuticals LLC | 465,924 | 4.6576 | 10/31/2019 | 470,949 | ||||||||||||

| Ardent Legacy Acquisitions, Inc. | 192,075 | 6.6496 | 8/4/2021 | 193,155 | ||||||||||||

| Capsugel Holdings US, Inc. | 401,785 | 4.1723 | 8/1/2021 | 402,707 | ||||||||||||

| Change Healthcare Holdings | 995,000 | 3.9223 | 2/29/2024 | 999,234 | ||||||||||||

| CHG Healthcare Services, Inc. | 144,868 | 4.9223 | 6/8/2023 | 146,905 | ||||||||||||

| CHS/Community Health Systems | 1,099,725 | 4.0767 | 1/28/2021 | 1,094,282 | ||||||||||||

| CHS/Community Health Systems | 271,751 | 3.8268 | 1/1/2020 | 271,099 | ||||||||||||

| Concordia Healthcare Corp. | 147,563 | 5.4165 | 10/20/2021 | 99,732 | ||||||||||||

| ConvaTec, Inc. | 94,000 | 3.4223 | 10/24/2021 | 94,882 | ||||||||||||

| DaVita, Inc. | 740,970 | 3.9223 | 6/24/2021 | 749,676 | ||||||||||||

| DJO Finance LLC | 157,200 | 4.4109 | 6/8/2020 | 153,938 | ||||||||||||

| Endo Luxembourg Finance I Co | 505,000 | 5.4084 | 4/28/2024 | 509,671 | ||||||||||||

| Endo Luxembourg Finance I Co | 614,225 | 4.1496 | 9/26/2022 | 614,437 | ||||||||||||

| Envision Healthcare Corp. | 726,975 | 4.1496 | 11/30/2023 | 735,790 | ||||||||||||

| Greatbatch Ltd | 93,441 | 4.6518 | 10/28/2022 | 94,142 | ||||||||||||

| Grifols Worldwide Operations | 160,000 | 3.4204 | 2/1/2025 | 160,562 | ||||||||||||

| HCA, Inc. | 202,396 | 3.1723 | 3/16/2023 | 203,357 | ||||||||||||

| HLF Financing | 185,000 | 6.6723 | 2/16/2023 | 185,439 | ||||||||||||

| IASIS Healthcare LLC | 296,134 | 4.5000 | 5/3/2018 | 297,578 | ||||||||||||

| IASIS Healthcare LLC | 35,000 | 5.2500 | 4/28/2021 | 34,825 | ||||||||||||

| IMS Health, Inc. | 322,225 | 3.1503 | 3/8/2024 | 325,850 | ||||||||||||

| inVentiv Health, Inc. | 335,160 | 4.8140 | 11/8/2023 | 337,511 | ||||||||||||

| Kindred Healthcare, Inc. | 170,251 | 4.6551 | 4/8/2021 | 171,156 | ||||||||||||

| Mallinckrodt International | 100,000 | 3.8996 | 9/24/2024 | 100,097 | ||||||||||||

| MultiPlan, Inc. | 121,310 | 4.8996 | 6/8/2023 | 123,054 | ||||||||||||

See accompanying notes to financial statements.

5

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| HEALTHCARE (Continued) - 11.5% | ||||||||||||||||

| National Mentor Holdings, Inc. | $ | 264,075 | 4.3996 | % | 2/1/2021 | $ | 266,303 | |||||||||

| National Surgical Hospitals Inc. | 115,935 | 4.6723 | 5/31/2022 | 116,370 | ||||||||||||

| NVA Holdings, Inc. | 206,174 | 8.1496 | 8/14/2022 | 209,267 | ||||||||||||

| NVA Holdings, Inc. | 96,612 | 4.6496 | 8/14/2021 | 98,092 | ||||||||||||

| Ortho-Clinical Diag Holding | 655,930 | 4.9223 | 6/30/2021 | 653,624 | ||||||||||||

| Pharmaceutical Product Development | 550,053 | 4.4103 | 8/18/2022 | 553,686 | ||||||||||||

| Quorum Health Corp. | 220,240 | 6.7846 | 4/28/2022 | 220,240 | ||||||||||||

| Sedgwick, Inc. | 125,000 | 6.9223 | 2/28/2022 | 125,729 | ||||||||||||

| Select Medical Corp. | 300,000 | 4.6554 | 3/6/2024 | 304,125 | ||||||||||||

| Sterigenics-Nordion Holdings LLC | 243,200 | 4.1498 | 5/16/2022 | 242,973 | ||||||||||||

| Surgery Center Holding, Inc. | 208,289 | 4.9004 | 11/4/2020 | 209,851 | ||||||||||||

| Team Health, Inc. | 574,194 | 3.9223 | 2/6/2024 | 570,157 | ||||||||||||

| US Renal Care, Inc. | 719,817 | 5.3996 | 12/30/2022 | 684,276 | ||||||||||||

| Valeant Pharmaceuticals International ^ | 1,324,392 | 5.8998 | 3/31/2022 | 1,333,980 | ||||||||||||

| 15,478,242 | ||||||||||||||||

| INDUSTRIALS - 13.7% | ||||||||||||||||

| 84 Lumber Co. | 467,063 | 6.9204 | 10/24/2023 | 472,901 | ||||||||||||

| Accudyne Industries | 740,000 | 4.1496 | 12/12/2019 | 737,532 | ||||||||||||

| ADS Waste Holdings, Inc. | 988,250 | 3.9223 | 11/10/2023 | 997,688 | ||||||||||||

| Air Canada | 144,000 | 3.9054 | 10/6/2023 | 145,103 | ||||||||||||

| American Airlines, Inc. | 499,550 | 3.6562 | 12/14/2023 | 500,839 | ||||||||||||

| American Airlines, Inc. | 89,000 | 3.6723 | 4/28/2023 | 89,243 | ||||||||||||

| American Airlines, Inc. | 431,088 | 3.1723 | 6/28/2020 | 433,013 | ||||||||||||

| APEX Tool Group LLC | 357,744 | 4.5000 | 2/1/2020 | 352,603 | ||||||||||||

| Aspen Merger Sub, Inc. | 137,310 | 5.4223 | 9/28/2023 | 137,933 | ||||||||||||

| Brand Energy | 473,776 | 4.9117 | 11/26/2020 | 475,934 | ||||||||||||

| Brickman Group Holdings, Inc. | 249,000 | 7.6553 | 12/16/2021 | 251,024 | ||||||||||||

| Brickman Group Holdings, Inc. | 684,633 | 4.2959 | 12/18/2020 | 688,484 | ||||||||||||

| Casella Waste Systems, Inc. | 399,000 | 3.9062 | 10/16/2023 | 401,494 | ||||||||||||

| Columbus McKinnon Corp. | 92,331 | 4.1496 | 2/1/2024 | 93,197 | ||||||||||||

| Filtration Group, Inc. | 514,964 | 4.3140 | 11/24/2020 | 518,118 | ||||||||||||

| Fortress Merger Sub, Inc. | 145,635 | 5.1498 | 10/20/2023 | 147,455 | ||||||||||||

| Gardner Denver, Inc. | 730,274 | 4.4002 | 7/30/2020 | 731,150 | ||||||||||||

| Harland Clarke Holdings Corp. | 270,793 | 6.6496 | 2/8/2022 | 272,181 | ||||||||||||

| Harland Clarke Holdings Corp. | 154,995 | 7.1496 | 1/1/2022 | 155,964 | ||||||||||||

| HD Supply, Inc. | 347,305 | 3.8996 | 8/12/2021 | 350,234 | ||||||||||||

| HD Supply, Inc. | 513,420 | 3.8996 | 10/16/2023 | 518,446 | ||||||||||||

| Headwaters, Inc. | 500,347 | 4.1723 | 3/24/2022 | 501,848 | ||||||||||||

| Husky Injection Molding | 717,837 | 4.4223 | 6/30/2021 | 722,854 | ||||||||||||

| McJunkin Red Man Corp. | 433,975 | 5.1723 | 11/8/2019 | 438,656 | ||||||||||||

| Navistar, Inc. | 295,243 | 5.1576 | 8/8/2020 | 299,487 | ||||||||||||

| NN, Inc. | 190,000 | 4.9022 | 4/4/2021 | 190,357 | ||||||||||||

| NN, Inc. | 217,740 | 5.4223 | 10/20/2022 | 217,672 | ||||||||||||

| PAE Holding Corp. | 212,875 | 6.6723 | 10/20/2022 | 215,137 | ||||||||||||

| Piscine US Acquisitions | 324,188 | 5.6496 | 12/20/2023 | 326,958 | ||||||||||||

| Prime Security Service | 471,199 | 4.4223 | 5/2/2022 | 476,757 | ||||||||||||

| Pro Mach Group, Inc. | 621,819 | 4.9223 | 10/22/2021 | 625,706 | ||||||||||||

| Quikrete Co, Inc. | 815,955 | 4.4223 | 11/16/2023 | 819,272 | ||||||||||||

| Rexnord LLC | 368,203 | 3.9091 | 8/20/2023 | 369,946 | ||||||||||||

| Science Applications International | 231,946 | 3.5382 | 5/4/2022 | 233,468 | ||||||||||||

| Sedgwick, Inc. | 195,000 | 6.8140 | 2/28/2022 | 196,219 | ||||||||||||

| Sedgwick, Inc. | 670,193 | 3.9223 | 2/28/2021 | 671,366 | ||||||||||||

| SiteOne Landscape Supply Holding | 208,074 | 5.6665 | 4/28/2022 | 210,416 | ||||||||||||

| Spin Holdcorp | 389,832 | 4.3463 | 11/14/2019 | 390,848 | ||||||||||||

| TransDigm, Inc. | 80,718 | 4.1510 | 6/4/2021 | 80,970 | ||||||||||||

| TransDigm, Inc. | 1,033,584 | 4.1723 | 6/8/2023 | 1,033,584 | ||||||||||||

| TransDigm, Inc. | 392,385 | 4.1648 | 5/14/2022 | 392,583 | ||||||||||||

See accompanying notes to financial statements.

6

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| INDUSTRIALS - 13.7% (Continued) | ||||||||||||||||

| United Airlines, Inc. | $ | 495,000 | 3.4019 | % | 3/31/2024 | $ | 497,255 | |||||||||

| Waste Industries USA, Inc. | 539,754 | 3.9223 | 2/28/2020 | 544,701 | ||||||||||||

| WEX, Inc. | 297,750 | 4.6723 | 6/30/2023 | 301,496 | ||||||||||||

| XPO Logistics, Inc. | 205,000 | 3.4057 | 10/31/2021 | 206,552 | ||||||||||||

| 18,434,644 | ||||||||||||||||

| INFORMATION TECHNOLOGY - 9.1% | ||||||||||||||||

| Alorica, Inc. | 56,907 | 5.9223 | 6/30/2022 | 57,832 | ||||||||||||

| Applied Systems, Inc. | 157,482 | 7.6496 | 1/24/2022 | 159,188 | ||||||||||||

| Avaya, Inc. | 183,889 | 6.4218 | 5/28/2020 | 154,269 | ||||||||||||

| Avaya, Inc. | 200,000 | 8.6620 | 1/24/2018 | 205,819 | ||||||||||||

| Blackboard, Inc. | 971,866 | 6.1562 | 6/30/2021 | 975,024 | ||||||||||||

| BMC Software, Inc. | 722,533 | 5.1723 | 9/10/2020 | 727,684 | ||||||||||||

| Cologix, Inc. | 220,000 | 4.1532 | 3/20/2024 | 220,412 | ||||||||||||

| Cologix, Inc. | 110,000 | 4.1518 | 12/16/2021 | 110,550 | ||||||||||||

| Cologix, Inc. | 40,000 | 8.1532 | 3/20/2025 | 40,467 | ||||||||||||

| Cypress Semiconductor Corp. | 288,750 | 4.9054 | 7/4/2021 | 292,120 | ||||||||||||

| Dell International LLC | 1,167,375 | 3.6723 | 9/8/2023 | 1,173,107 | ||||||||||||

| Donnelley Financial Solutions | 68,937 | 5.1498 | 9/28/2023 | 69,640 | ||||||||||||

| First Data Corp. | 184,725 | 4.1665 | 7/8/2022 | 185,995 | ||||||||||||

| First Data Corp. | 1,746,400 | 3.6718 | 4/26/2024 | 1,748,583 | ||||||||||||

| Go Daddy Operating Co. LLC | 385,752 | 3.6723 | 2/16/2024 | 387,706 | ||||||||||||

| Infor US, Inc. | 1,248,760 | 3.8996 | 1/31/2022 | 1,248,079 | ||||||||||||

| Leidos Holdings, Inc. | 211,470 | 3.4223 | 8/16/2023 | 213,717 | ||||||||||||

| Masergy Communications, Inc. | 119,700 | 5.6312 | 12/16/2023 | 120,823 | ||||||||||||

| Mitchell International, Inc. | 156,000 | 8.6723 | 10/12/2021 | 157,950 | ||||||||||||

| Mitchell International, Inc. | 365,641 | 4.5346 | 10/11/2020 | 368,155 | ||||||||||||

| MKS Instruments, Inc. Term | 224,631 | 3.9223 | 4/30/2023 | 227,019 | ||||||||||||

| ON Semiconductor Corp. | 174,743 | 3.4223 | 4/1/2023 | 175,808 | ||||||||||||

| Presidio, Inc. | 179,842 | 4.4001 | 2/2/2022 | 182,231 | ||||||||||||

| Rackspace Hosting, Inc. | 367,080 | 4.5340 | 11/4/2023 | 370,149 | ||||||||||||

| Radiate HoldCo LLC | 289,524 | 4.1723 | 1/31/2024 | 290,954 | ||||||||||||

| Sophia LP | 309,749 | 4.3996 | 9/30/2022 | 309,671 | ||||||||||||

| SS&C Technologies, Inc. | 24,785 | 3.4223 | 7/8/2022 | 24,994 | ||||||||||||

| SS&C Technologies, Inc. | 289,934 | 3.4223 | 7/8/2022 | 292,381 | ||||||||||||

| Tempo Acquisition LLC | 560,000 | 4.1562 | 4/30/2024 | 560,420 | ||||||||||||

| Veritas US, Inc. | 687,397 | 6.7746 | 1/28/2023 | 685,036 | ||||||||||||

| Western Digital Corp. | 407,005 | 3.9223 | 4/28/2023 | 411,329 | ||||||||||||

| 12,147,112 | ||||||||||||||||

| MATERIALS- 7.9% | ||||||||||||||||

| ABC Supply Co, Inc. | 589,311 | 3.9223 | 11/1/2023 | 593,690 | ||||||||||||

| Alpha 3 BV | 150,000 | 4.1496 | 2/1/2024 | 151,054 | ||||||||||||

| Anchor Glass Container Corp. | 244,000 | 8.9076 | 12/8/2024 | 249,338 | ||||||||||||

| Anchor Glass Container Corp. | 185,535 | 4.4121 | 12/8/2024 | 187,321 | ||||||||||||

| Berlin Packaging LLC | 394,576 | 4.6532 | 9/30/2021 | 397,289 | ||||||||||||

| Berry Plastics Group, Inc. | 417,785 | 3.4057 | 1/6/2021 | 420,717 | ||||||||||||

| Berry Plastics Group, Inc. | 371,696 | 3.4057 | 2/8/2020 | 374,340 | ||||||||||||

| Berry Plastics Group, Inc. | 130,000 | 3.6496 | 1/20/2024 | 130,914 | ||||||||||||

| Berry Plastics Group, Inc. | 358,069 | 3.6622 | 9/30/2022 | 360,823 | ||||||||||||

| BWAY Corp. | 490,000 | 4.3998 | 4/4/2024 | 487,680 | ||||||||||||

| CPG International, Inc. | 275,725 | 4.8996 | 9/30/2020 | 277,535 | ||||||||||||

| CPI Acquisition, Inc. | 1,008,336 | 5.6584 | 8/16/2022 | 945,733 | ||||||||||||

| Dubois Chemicals, Inc. | 30,000 | 4.8812 | 3/15/2024 | 30,275 | ||||||||||||

| Dubois Chemicals, Inc. | 125,000 | 4.8812 | 3/16/2024 | 126,146 | ||||||||||||

| Duke Finance LLC | 125,000 | 6.1496 | 2/20/2024 | 126,875 | ||||||||||||

| FMG Resources | 208,172 | 3.9223 | 6/30/2019 | 209,810 | ||||||||||||

| Huntsman International LLC | 591,876 | 4.1723 | 3/31/2023 | 600,387 | ||||||||||||

| Ineos Group Holdings Ltd | 1,209,133 | 3.9223 | 4/1/2022 | 1,221,352 | ||||||||||||

See accompanying notes to financial statements.

7

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| MATERIALS- 7.9% (Continued) | ||||||||||||||||

| Ineos US Finance LLC | $ | 104,738 | 3.9223 | % | 3/31/2024 | $ | 105,701 | |||||||||

| Kraton Polymers | 207,981 | 5.1723 | 1/6/2022 | 211,183 | ||||||||||||

| MacDermid, Inc. | 154,689 | 4.6723 | 6/8/2020 | 155,766 | ||||||||||||

| New Arclin US Holdings | 275,000 | 5.3996 | 2/14/2024 | 277,837 | ||||||||||||

| Omnova Solutions, Inc. | 576,105 | 5.4223 | 8/24/2023 | 583,306 | ||||||||||||

| PKC Holding Corp. | 30,000 | 4.6584 | 4/16/2024 | 30,150 | ||||||||||||

| PQ Corp. | 92,304 | 5.4223 | 11/4/2022 | 93,655 | ||||||||||||

| Royal Holdings, Inc. | 257,240 | 4.3996 | 6/20/2022 | 259,892 | ||||||||||||

| Solenis International LP | 346,971 | 4.3142 | 8/1/2021 | 348,742 | ||||||||||||

| Summit Materials | 386,123 | 3.9223 | 7/18/2022 | 390,225 | ||||||||||||

| Tricorbraun, Inc. | 317,386 | 4.8996 | 11/30/2023 | 321,155 | ||||||||||||

| Tricorbraun, Inc. | 31,818 | 4.8040 | 11/30/2023 | 32,196 | ||||||||||||

| Univar, Inc. | 845,099 | 3.9223 | 6/30/2022 | 848,864 | ||||||||||||

| 10,549,951 | ||||||||||||||||

| REAL ESTATE - 2.1% | ||||||||||||||||

| Capital Automotive L.P. | 140,000 | 4.1665 | 3/24/2024 | 141,365 | ||||||||||||

| Capital Automotive L.P. | 390,000 | 7.1665 | 3/24/2025 | 399,506 | ||||||||||||

| Communications Sales & Leasing | 586,836 | 4.1723 | 10/24/2022 | 586,194 | ||||||||||||

| DTZ US Borrower LLC | 589,500 | 4.3500 | 11/4/2021 | 592,899 | ||||||||||||

| ESH Hospitality Inc | 346,374 | 3.6723 | 8/30/2023 | 348,586 | ||||||||||||

| Geo Group, Inc. | 230,000 | 3.4218 | 3/22/2024 | 230,575 | ||||||||||||

| Realogy Group LLC | 453,261 | 3.4196 | 7/20/2022 | 457,510 | ||||||||||||

| 2,756,635 | ||||||||||||||||

| TELECOMMUNICATION SERVICES - 4.9% | ||||||||||||||||

| Aerial Merger Sub, Inc. | 75,000 | 4.3500 | 9/2/2019 | 76,453 | ||||||||||||

| Aerial Merger Sub, Inc. | 235,000 | 4.8500 | 2/29/2024 | 238,624 | ||||||||||||

| Atlice Financinf SA | 420,000 | 3.9062 | 7/16/2025 | 420,420 | ||||||||||||

| Global Tel*Link Corp. | 295,612 | 5.0000 | 5/24/2020 | 296,044 | ||||||||||||

| Level 3 Financing, Inc. | 1,825,000 | 3.4062 | 2/22/2024 | 1,832,820 | ||||||||||||

| Sable International Finance LTD. | 463,000 | 5.9223 | 12/30/2022 | 466,241 | ||||||||||||

| SBA Senior Finance II LLC | 442,512 | 3.4223 | 3/24/2021 | 445,763 | ||||||||||||

| SBA Senior Finance II LLC | 158,183 | 3.4223 | 6/10/2022 | 158,897 | ||||||||||||

| Securus Technologies Holdings | 83,938 | 5.3996 | 4/30/2020 | 84,042 | ||||||||||||

| Securus Technologies Holdings | 139,926 | 4.7500 | 4/30/2020 | 140,101 | ||||||||||||

| Sprint Communications | 460,000 | 3.6723 | 2/2/2024 | 461,079 | ||||||||||||

| UPC Financing Partnership | 1,235,000 | 4.1477 | 4/16/2025 | 1,240,792 | ||||||||||||

| Virgin Media Investment Holdings | 660,000 | 4.1477 | 2/1/2025 | 663,336 | ||||||||||||

| 6,524,612 | ||||||||||||||||

| UTILITIES - 3.0% | ||||||||||||||||

| APLP Holdings LP | 390,883 | 5.3996 | 4/12/2023 | 393,326 | ||||||||||||

| Calpine Construction Finance | 664,321 | 3.4223 | 5/4/2020 | 665,982 | ||||||||||||

| Calpine Corp. | 263,013 | 3.8996 | 6/1/2023 | 264,329 | ||||||||||||

| Dayton Power & Light Co | 93,765 | 4.4223 | 8/24/2022 | 95,113 | ||||||||||||

| Dynergy, Inc. | 671,000 | 4.4076 | 2/8/2024 | 671,631 | ||||||||||||

| Helix Gen Funding LLC | 35,000 | 4.8696 | 3/8/2024 | 35,394 | ||||||||||||

| NRG Energy, Inc. | 960,076 | 3.4223 | 6/30/2023 | 964,978 | ||||||||||||

| Talen Energy Supply LLC | 199,500 | 5.1576 | 7/6/2023 | 198,502 | ||||||||||||

| Talen Energy Supply LLC | 335,000 | 5.0000 | 4/15/2024 | 333,325 | ||||||||||||

| Tex Operations Co. LLC | 53,571 | 3.9223 | 8/4/2023 | 53,520 | ||||||||||||

| Tex Operations Co. LLC | 232,071 | 3.9223 | 8/4/2023 | 231,853 | ||||||||||||

| Texas Comp Elec Hold LLC | 635,000 | 11.5000 | 10/1/2020 | 444 | ||||||||||||

| Vistra Operations Co. | 119,700 | 4.4062 | 12/14/2023 | 120,252 | ||||||||||||

| 4,028,649 | ||||||||||||||||

| TOTAL BANK LOANS (Cost - $117,482,125) | 118,025,142 | |||||||||||||||

| BONDS & NOTES - 6.3% | ||||||||||||||||

| AIRLINES - 0.0% | ||||||||||||||||

| American Airlines Group, Inc. ^ - 144A | 45,000 | 4.6250 | 3/1/2020 | 45,956 | ||||||||||||

| AUTO PARTS & EQUIPMENT - 0.2% | ||||||||||||||||

| Schaeffler Verwaltung Zwei Gmb - 144A | 200,000 | 4.1250 | 9/15/2021 | 203,250 | ||||||||||||

See accompanying notes to financial statements.

8

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| BUILDING MATERIALS - 0.1% | ||||||||||||||||

| Standard Industries, Inc. - 144A | $ | 95,000 | 5.5000 | % | 2/15/2023 | $ | 99,038 | |||||||||

| CHEMICALS - 0.2% | ||||||||||||||||

| Hexion US Finance Corp. | 105,000 | 6.6250 | 4/15/2020 | 99,750 | ||||||||||||

| Ineos Group Holdings SA - ^ 144A | 200,000 | 5.6250 | 8/1/2024 | 204,000 | ||||||||||||

| WR Grace & Co-Conn - 144A | 25,000 | 5.1250 | 10/1/2021 | 26,906 | ||||||||||||

| 330,656 | ||||||||||||||||

| COAL - 0.2% | ||||||||||||||||

| Alliance Resource Operating Partners LP - 144A | 257,000 | 7.5000 | 5/1/2025 | 267,601 | ||||||||||||

| Peabody Energy Corp. - 144A | 15,000 | 6.0000 | 3/31/2022 | 15,356 | ||||||||||||

| 282,957 | ||||||||||||||||

| COMPUTERS - 0.5% | ||||||||||||||||

| Diamond 1 Finance Corp. - 144A ^ | 570,000 | 5.4500 | 6/15/2023 | 615,911 | ||||||||||||

| Harland Clarke Holdings Corp. - 144A | 60,000 | 8.3750 | 8/15/2022 | 61,950 | ||||||||||||

| 677,861 | ||||||||||||||||

| DIVERSIFIED FINANANCIAL SERVICES - 0.2% | ||||||||||||||||

| Intl Lease Finance Corp. | 120,000 | 3.8750 | 4/15/2018 | 122,240 | ||||||||||||

| Springleaf Finance Corp. | 170,000 | 5.2500 | 12/15/2019 | 173,011 | ||||||||||||

| 295,251 | ||||||||||||||||

| ELECTRIC - 0.0% | ||||||||||||||||

| Talen Energy Supply LLC - 144A | 18,000 | 5.1250 | 7/15/2019 | 17,775 | ||||||||||||

| ENTERTAINMENT - 0.1% | ||||||||||||||||

| Scientific Games International, Inc. - 144A | 145,000 | 7.0000 | 1/1/2022 | 155,602 | ||||||||||||

| FOOD - 0.1% | ||||||||||||||||

| Dole Food Co., Inc. - 144A | 175,000 | 7.2500 | 6/15/2025 | 182,219 | ||||||||||||

| HEALTHCARE-SERVICES - 0.4% | ||||||||||||||||

| CHS/Community Health Systems, Inc. | 60,000 | 6.2500 | 3/31/2023 | 61,275 | ||||||||||||

| Eagle Holding Co II LLC - 144A | 25,000 | 7.6250 | 5/15/2022 | 25,531 | ||||||||||||

| Surgery Center Holdings, Inc. - 144A | 130,000 | 8.8750 | 4/15/2021 | 138,450 | ||||||||||||

| Tenet Healthcare Corp. | 275,000 | 4.6312 | 6/15/2020 | 277,750 | ||||||||||||

| Tenet Healthcare Corp. | 25,000 | 5.0000 | 3/1/2019 | 25,172 | ||||||||||||

| Tenet Healthcare Corp. | 75,000 | 6.0000 | 10/1/2020 | 79,125 | ||||||||||||

| 607,303 | ||||||||||||||||

| HOLDING COMPANIES - DIVERSIFICATION - 0.1% | ||||||||||||||||

| Argos Merger Sub, Inc. - 144A | 140,000 | 7.1250 | 3/15/2023 | 128,275 | ||||||||||||

| HOME BUILDERS - 0.2% | ||||||||||||||||

| TRI Pointe Holdings, Inc. | 70,000 | 4.3750 | 6/15/2019 | 72,450 | ||||||||||||

| TRI Pointe Group, Inc. | 130,000 | 4.8750 | 7/1/2021 | 135,525 | ||||||||||||

| 207,975 | ||||||||||||||||

| LEISURE TIME - 0.1% | ||||||||||||||||

| NCL Corp. LTD. - 144A | 125,000 | 4.7500 | 12/15/2021 | 128,438 | ||||||||||||

| LODGING - 0.0% | ||||||||||||||||

| Boyd Gaming Corp. | 40,000 | 6.8750 | 5/15/2023 | 43,200 | ||||||||||||

| MACHINERY-DIVERSIFIED - 0.1% | ||||||||||||||||

| CNH Industrial Capital LLC | 95,000 | 4.3750 | 4/5/2022 | 97,095 | ||||||||||||

| MEDIA - 0.7% | ||||||||||||||||

| Cequel Communications Escrow - 144A | 34,000 | 6.3750 | 9/15/2020 | 35,126 | ||||||||||||

| Charter Communications Operating LLC | 225,000 | 4.4640 | 7/23/2022 | 239,226 | ||||||||||||

| iHeartCommunications, Inc. | 95,000 | 9.0000 | 12/15/2019 | 78,731 | ||||||||||||

| SFR Group SA - 144A | 410,000 | 6.0000 | 5/15/2022 | 428,963 | ||||||||||||

| Univision Communications, Inc. - 144A | 200,000 | 5.1250 | 5/15/2023 | 204,000 | ||||||||||||

| 986,046 | ||||||||||||||||

| MINING - 0.1% | ||||||||||||||||

| Vedanta Resources PLC - 144A | 100,000 | 9.5000 | 7/18/2018 | 109,750 | ||||||||||||

See accompanying notes to financial statements.

9

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||||||

| Security | Amount | Rate | Date | Value | ||||||||||||

| OIL & GAS - 0.9% | ||||||||||||||||

| Alta Mesa Holdings LP - 144A | $ | 135,000 | 7.8750 | % | 12/15/2024 | $ | 142,425 | |||||||||

| Carrizo Oil & Gas, Inc. ^ | 140,000 | 6.2500 | 4/15/2023 | 141,750 | ||||||||||||

| Chesapeake Energy Corp. ^ | 170,000 | 6.6250 | 8/15/2020 | 172,550 | ||||||||||||

| Denbury Resources, Inc. | 140,000 | 5.5000 | 5/1/2022 | 105,000 | ||||||||||||

| Diamondback Energy, Inc. - 144A | 30,000 | 4.7500 | 11/1/2024 | 30,225 | ||||||||||||

| EP Energy LLC / Everest Acquisition Finance, Inc. - 144A | 160,000 | 8.0000 | 11/29/2024 | 168,200 | ||||||||||||

| FTS International, Inc. | 50,000 | 6.2500 | 5/1/2022 | 43,500 | ||||||||||||

| FTS International, Inc. - 144A | 120,000 | 8.6312 | 6/15/2020 | 121,200 | ||||||||||||

| MEG Energy Corp. - 144A ^ | 115,000 | 6.5000 | 1/15/2025 | 113,994 | ||||||||||||

| Noble Holding International Ltd. | 35,000 | 7.7500 | 1/15/2024 | 32,113 | ||||||||||||

| RSP Permian, Inc. - 144A | 90,000 | 5.2500 | 1/15/2025 | 91,800 | ||||||||||||

| 1,162,757 | ||||||||||||||||

| PACKAGING & CONTAINERS - 0.5% | ||||||||||||||||

| Ardagh Packaging Finance PLC - 144A | 235,000 | 6.0000 | 2/15/2025 | 243,519 | ||||||||||||

| Ardagh Packaging Finance PLC - 144A | 200,000 | 4.2500 | 9/15/2022 | 204,340 | ||||||||||||

| Reynolds Group - 144A | 230,000 | 4.6584 | 7/15/2021 | 235,750 | ||||||||||||

| Reynolds Group | 50,000 | 5.7500 | 10/15/2020 | 51,562 | ||||||||||||

| 735,171 | ||||||||||||||||

| PHARMACEUTICALS - 0.1% | ||||||||||||||||

| Capsugel SA - 144A | 19,000 | 7.0000 | 5/15/2019 | 18,957 | ||||||||||||

| VRX Escrow Corp. - 144A | 70,000 | 5.3750 | 3/15/2020 | 60,287 | ||||||||||||

| 79,244 | ||||||||||||||||

| PRIVATE EQUITY - 0.1% | ||||||||||||||||

| Icahn Enterprises LP - 144A | 60,000 | 6.2500 | 2/1/2022 | 62,550 | ||||||||||||

| REITS - 0.1% | ||||||||||||||||

| IStar Financial, Inc. | 30,000 | 4.8750 | 7/1/2018 | 30,450 | ||||||||||||

| IStar Financial, Inc. | 165,000 | 5.0000 | 7/1/2019 | 167,269 | ||||||||||||

| 197,719 | ||||||||||||||||

| RETAIL - 0.1% | ||||||||||||||||

| Cumberland Farms, Inc. - 144A | 125,000 | 6.7500 | 5/1/2025 | 130,019 | ||||||||||||

| SEMICONDUCTORS - 0.6% | ||||||||||||||||

| Broadcom Corp. - 144A | 355,000 | 2.3750 | 1/15/2020 | 355,455 | ||||||||||||

| Broadcom Corp. - 144A | 160,000 | 3.0000 | 1/15/2022 | 161,438 | ||||||||||||

| NXP Bv - 144A | 200,000 | 4.1250 | 6/1/2021 | 209,750 | ||||||||||||

| 726,643 | ||||||||||||||||

| SOFTWARE - 0.3% | ||||||||||||||||

| First Data Corp. - 144A | 190,000 | 5.3750 | 8/15/2023 | 198,075 | ||||||||||||

| First Data Corp. - 144A | 90,000 | 5.0000 | 1/15/2024 | 92,385 | ||||||||||||

| First Data Corp. - 144A | 25,000 | 5.7500 | 1/15/2024 | 26,031 | ||||||||||||

| 316,491 | ||||||||||||||||

| TELECOMMUNICATIONS - 0.3% | ||||||||||||||||

| Frontier Communications Corp. ^ | 105,000 | 6.2500 | 9/15/2021 | 97,650 | ||||||||||||

| Intelsat Jackson Holdings SA - ^ 144A | 7,000 | 8.0000 | 2/15/2024 | 7,543 | ||||||||||||

| T-Mobile USA, Inc. | 205,000 | 6.0000 | 4/15/2024 | 222,630 | ||||||||||||

| Verizon Communications, Inc. | 78,000 | 3.1250 | 3/16/2022 | 79,248 | ||||||||||||

| 407,071 | ||||||||||||||||

| TOTAL BONDS & NOTES (Cost - $8,317,276) | 8,416,312 | |||||||||||||||

| ASSET BACKED SECURITIES - 1.0% | ||||||||||||||||

| Home Equity Loan Trust 2007-HS | 115,736 | 6.1100 | 6/25/2037 | 116,512 | ||||||||||||

| Morgan Stanley Capital I Trust | 795,775 | 5.8090 | 12/12/2049 | 799,645 | ||||||||||||

| VOLT XXXIII LLC - 144A | 396,150 | 3.5000 | 3/25/2055 | 398,677 | ||||||||||||

| TOTAL ASSET BACKED SECURITIES (Cost - $1,317,514) | 1,314,834 | |||||||||||||||

| PRIVATE PLACEMENTS - 0.2% | ||||||||||||||||

| Wheels Up | 18,704 | 7.5546 | 6/1/2024 | 18,611 | ||||||||||||

| Wheels Up | 251,296 | 5.0000 | 6/1/2024 | 250,039 | ||||||||||||

| TOTAL PRIVATE PLACEMENTS (Cost - 270,970) | 268,650 | |||||||||||||||

See accompanying notes to financial statements.

10

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Floating Rate Bond Fund (Continued) |

| April 30, 2017 |

| Security | Shares | Value | ||||||||||

| RIGHTS - 0.0% | ||||||||||||

| TRA Rights | 10,588 | $ | 14,294 | |||||||||

| TOTAL RIGHTS (Cost - $17,470) | ||||||||||||

| Interest | ||||||||||||

| SHORT-TERM INVESTMENT - 8.3% | Rate | |||||||||||

| MONEY MARKET FUND - 8.3% | ||||||||||||

| Fidelity Institutional Money Market Funds - Government Portfolio | 11,095,571 | 0.60% | + | 11,095,571 | ||||||||

| TOTAL SHORT-TERM INVESTMENT - (Cost - $11,095,571) | ||||||||||||

| COLLATERAL FOR SECURITIES LOANED - 1.1% | ||||||||||||

| Mount Vernon Prime Portfolio (Cost - $1,493,995) | 1,493,995 | 1.12% | + | 1,493,995 | ||||||||

| TOTAL INVESTMENTS - 106.0% (Cost - $141,434,658) | 142,112,536 | |||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS - (6.0)% | (7,939,177 | ) | ||||||||||

| NET ASSETS - 100.0% | $ | 134,173,359 | ||||||||||

REITS - Real Estate Investment Trusts.

144A- Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers.

| ^ | All or a portion of these securities are on loan. Total loaned securities had a value of $957,681 at April 30, 2017. |

| + | Variable rate security. Interest rate is as of April 30, 2017. |

| Portfolio Composition * - (Unaudited) | ||||||||||

| Bank Loans | 83.1 | % | Packaging & Containers | 0.5 | % | |||||

| Short-Term Investment | 7.8 | % | Semiconductors | 0.5 | % | |||||

| Other ** | 1.8 | % | Computers | 0.5 | % | |||||

| Collateral for Securities Loaned | 1.1 | % | Healthcare Services | 0.4 | % | |||||

| Asset Backed Securities | 0.9 | % | Telecommunications | 0.3 | % | |||||

| Exchange Traded Fund | 0.9 | % | Diversified Financial Services | 0.2 | % | |||||

| Oil & Gas | 0.8 | % | Software | 0.2 | % | |||||

| Media | 0.7 | % | Chemicals | 0.2 | % | |||||

| Total | 100.0 | % | ||||||||

| * | Based on total value of investments as of April 30, 2017 |

| ** | Groupings less than 0.20% of holdings. |

Percentage may differ from Schedule of Investments which are based on Fund net assets.

See accompanying notes to financial statements.

11

Dunham Corporate/Government Bond Fund

Message from the Sub-Adviser (Newfleet Asset Management, LLC)

Investment-grade bonds, as measured by the Barclays Aggregate Bond Index, lost 0.7 percent in the six-month period ended April 30, 2017 after a 2.8 percent increase during the previous fiscal six-month period. Treasuries in the middle of the yield curve, as measured by the BofA ML Treasuries 5-7 Years Index, ended the fiscal six-month period down 1.2 percent, while long-term Treasuries, as measured by the BofA ML Treasuries 10+ Years Index, saw a sharp decrease of 4.8 percent over the same six months. Corporate bonds, as measured by the BofA ML U.S. Corporate Bond Master Index, outpaced intermediate-term Treasury bonds, rising 0.3 percent over the fiscal six-month period. High-yield bonds, as measured by the BofA ML High-Yield Bond Cash Pay Index, surged 5.5 percent, outperforming the intermediate-term Treasury bonds by a whopping 6.7 percent during the period.

The Fund continued to balance risk versus reward by choosing to emphasize, relative to the benchmark, lower duration bonds and overweighting lower credit quality securities, in anticipation of rising interest rates. The Fund began the six-month period with an average effective duration of 5.34 years and ended the period with an average effective duration of 5.46 years, while the benchmark index had an average effective duration of 5.59 years and 5.96 years, respectively. This allocation generally benefitted performance of the Fund over the six-month period, as Treasury yields fluctuated in a relatively wide range of 85 basis points. Interest rates on the 10-year U.S. Treasury fluctuated within an 85 basis point range, hitting their low of 1.78 percent a few days prior to the election, undulating throughout the fiscal period until they reached their high of 2.63 percent in mid-March, before settling at 2.28 percent to end the fiscal period. The overweights to corporate high-yield securities and corporate investment-grade securities were the largest contributors to performance over the fiscal quarter. The Sub-Adviser invested roughly 13 percent to the corporate high-yield sector, while the index held less than 1 percent in high-yield securities. The Sub-Adviser invested roughly 30 percent to corporate investment-grade securities, which was nearly 4.5 percent greater than the index’s allocation to that sector.

A contributor to the Fund during the first half of the fiscal six-month period included Scientific Games International, Inc. 6.625% due 5/15/2021 (80874YAQ3) (holding percentage*: 0.11 percent). The company develops and services lottery games and wagering systems. The bonds continued to trade well on solid third calendar quarter 2016 results with revenues up 7.2 percent year-over-year and EBITDA up 2.8 percent year-over-year. The company has deleveraged over 1x over the past year, to 7.5x. The company’s management also continues to note its commitment to reduce debt using cash flow. Most of the strong third calendar quarter 2016 cash flow was used for debt reduction, affirming management’s commitment to deleverage. The bonds gained 14.1 percent over the first half of the fiscal period. The bonds continued to perform well over the second half of the fiscal period, gaining an additional 6.3 percent. A contributor to the Fund during the second half of the fiscal six-month period included Petroleos Mexicanos SA (PEMEX) 6.875% due 8/4/2026 (71654QCB6) (holding percentage*: 0.25 percent). The company provides services for oil and gas exploration and production, offering its services to companies operating throughout Mexico. PEMEX bonds have been lifted by an overall recovery in Mexico sovereign valuations, which reflected the softer trade rhetoric that came from the Trump administration during the fiscal period. In addition, the fourth calendar quarter earnings report was supportive, as the company stated that it is on track with cost reduction efforts in a push to improve efficiency and cash flow. The bonds rose 6.7 percent over the second half of the fiscal period.

A detractor from the Fund during the first half of the fiscal six-month period included Universal Health Services, Inc. 5.000% due 6/1/2026 (913903AT7) (holding percentage**: 0.11 percent), a healthcare management company operating acute care hospitals, behavioral health centers, and surgery centers throughout the United States and Puerto Rico. Buzzfeed published a negative article regarding UHS’s behavioral health practices. The article essentially claimed that the company coded a disproportionately high percentage of patients with suicidal ideation with the implication that they were doing this to enhance admissions. The article also highlighted a handful of cases where patients felt they were wrongly admitted to UHS’s inpatient facilities. Management has strongly denied the claims and defended its positions with a number of metrics. The bonds lost 4.7 percent from the beginning of the fiscal period through December 13, 2016, at which time the Sub-Adviser exited all positions, as it felt the upside/downside was no longer attractive. A detractor from the Fund during the second half of the fiscal six-month period was PetSmart, Inc. 7.125% due 3/15/2023 (04021LAA8) (holding percentage*: 0.16 percent), a specialty retailer of pet services and solutions, operating pet superstores and pet hotels in the United States and Canada, as well as providing pet supplies and products online. The company was caught up in negativity that impacted all retailers in the first calendar quarter. Many investors fear that consumers’ shift to online retail will hurt specialty brick and mortar retailers more than expected. That sentiment resulted in the bonds losing 5.2 percent over the second half of the six-month fiscal period ended April 30, 2017.

The Sub-Adviser remains constructive on markets but believes there are still a number of uncertainties to monitor going forward, including the unfolding of Trump’s economic policies, the strength of the U.S. dollar, and commodities prices. The Sub-Adviser expects U.S. growth in the 2 percent to 2.5 percent range for the year and believes the Fed will remain data dependent but will raise rates two more times this year. The Sub-Adviser believes that housing and consumer fundamentals are still in good shape and feels good about mortgage credit and the Fund’s exposure to ABS. The Sub-Adviser believes global growth will be driven by emerging markets, and expects an improvement in global growth this year after hitting a bottom last year. The Sub-Adviser continues to believe it is important to stay diversified and granular, keeping small positions and maintaining liquidity. The Sub-Adviser has slightly reduced its double-B exposure, opting for a slight increase in single-Bs, and is considering further opportunities in emerging markets debt. The Sub-Adviser believes that the prospect of continued volatility in the bond market will present opportunities and feels they are positioned well to take advantage of those opportunities as they arise.

| * | Holdings percentage(s) as of 4/30/2017. |

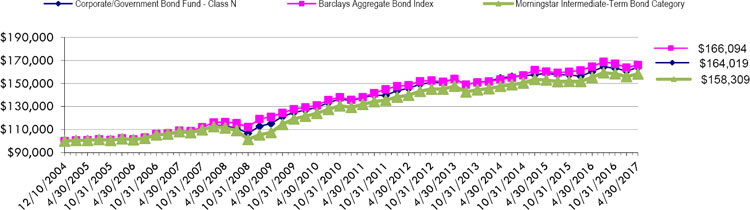

Growth of $100,000 Investment

Total Returns as of April 30, 2017

| Annualized | Annualized | Annualized | Annualized Since Inception | |||

| Six Months | One Year | Three Years | Five Years | Ten Years | (12/10/04) | |

| Class N | 0.02% | 2.28% | 1.96% | 2.37% | 4.33% | 4.07% |

| Class C | (0.34)% | 1.47% | 1.19% | 1.60% | 3.55% | 3.30% |

| Class A with load of 4.50% | (4.50)% | (2.50)% | 0.15% | 1.18% | 3.60% | 3.33%* |

| Class A without load | (0.03)% | 2.10% | 1.71% | 2.12% | 4.08% | 3.84%* |

| Barclays Aggregate Bond Index | (0.67)% | 0.83% | 2.66% | 2.27% | 4.30% | 4.18% |

| Morningstar Intermediate-Term Bond Category | (0.13)% | 1.85% | 2.37% | 2.51% | 3.88% | 3.78% |

| * | Class A commenced operations on January 3, 2007. |

The Barclays Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed-rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark.

The Morningstar Intermediate-Term Bond Category is generally representative of intermediate-term bond mutual funds that primarily invest in corporate and other investment-grade U.S. fixed-income securities and typically have durations of 3.5 to 6.0 years.

As disclosed in the Trust’s latest registration statement, the Fund’s total annual operating expenses, including underlying funds, are 1.14% for Class N, 1.89% for Class C and 1.39% for Class A. Class A shares are subject to a sales load of 4.50% and a deferred sales charge of up to 0.75%. The performance data quoted here represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance data quoted. The investment return and NAV will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated assuming reinvestment of all dividends and capital gains distributions, if any. The returns do not reflect the deductions of taxes a shareholder would pay on the redemption of fund shares or fund distributions. For performance information current to the most recent month-end, please call 1-800-442-4358 or visit our website www.dunham.com

12

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Corporate/Government Bond Fund |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||

| Security | Amount | Rate% | Date | Value | ||||||||

| CORPORATE BONDS & NOTES - 56.7% | ||||||||||||

| AEROSPACE / DEFENSE - 0.2% | ||||||||||||

| TransDigm, Inc. | $ | 75,000 | 6.000 | 7/15/2022 | $ | 77,437 | ||||||

| TransDigm, Inc. | 35,000 | 6.500 | 5/15/2025 | 35,875 | ||||||||

| 113,312 | ||||||||||||

| AIRLINES ABS - 0.6% | ||||||||||||

| America West Airlines 2001-1 Pass Through Trust | 68,224 | 7.100 | 4/2/2021 | 74,109 | ||||||||

| United Airlines 2007-1 Pass Through Trust | 229,204 | 6.636 | 7/2/2022 | 247,540 | ||||||||

| 321,649 | ||||||||||||

| AUTO MANUFACTURERS - 1.1% | ||||||||||||

| Daimler Finance LLC - 144A | 165,000 | 2.200 | 10/30/2021 | 162,500 | ||||||||

| Ford Motor Credit Co. LLC. | 270,000 | 5.750 | 2/1/2021 | 297,770 | ||||||||

| General Motors Financial Co., Inc. | 105,000 | 3.500 | 7/10/2019 | 107,640 | ||||||||

| General Motors Financial Co., Inc. | 60,000 | 4.200 | 3/1/2021 | 62,763 | ||||||||

| 630,673 | ||||||||||||

| AUTO PARTS & EQUIPMENT - 0.5% | ||||||||||||

| Cooper Standard Auto - 144A | 110,000 | 5.625 | 11/15/2026 | 111,787 | ||||||||

| Delphi Automotive PLC | 105,000 | 3.150 | 11/19/2020 | 107,264 | ||||||||

| TI Group Automotive Systems, LLC - 144A | 60,000 | 8.750 | 7/15/2023 | 64,500 | ||||||||

| 283,551 | ||||||||||||

| AUTOMOBILE ABS - 5.0% | ||||||||||||

| AmeriCredit Automobile Receivables Trust 2013-5 | 220,000 | 2.860 | 12/9/2019 | 222,401 | ||||||||

| Avis Budget Rental Car Funding AESOP LLC - 144A | 115,000 | 2.970 | 2/20/2020 | 116,720 | ||||||||

| California Republic Auto Receivables Trust 2014-3 A4 | 337,362 | 1.790 | 3/16/2020 | 337,923 | ||||||||

| Centre Point Funding LLC - 144A | 133,103 | 2.610 | 8/20/2021 | 131,258 | ||||||||

| Drive Auto Receivables Trust 2015-A - 144A | 255,000 | 2.560 | 6/15/2020 | 256,481 | ||||||||

| Drive Auto Receivables Trust 2015-D - 144A | 249,913 | 3.060 | 5/17/2021 | 251,405 | ||||||||

| Drive Auto Receivables Trust 2016-B - 144A | 160,000 | 2.980 | 1/18/2022 | 161,320 | ||||||||

| Drive Auto Receivables Trust 2017-A - 144A | 165,000 | 3.380 | 11/15/2021 | 166,768 | ||||||||

| DT Auto Owner Trust 2016-4 - 144A | 195,000 | 2.740 | 10/17/2022 | 195,820 | ||||||||

| Exeter Automobile Recievables Trust 2016-4A C - 144A | 160,000 | 2.82 | 5/16/2022 | 161,300 | ||||||||

| Flagship Credit Auto Trust 2016-1 A - 144A | 97,231 | 2.770 | 12/15/2020 | 97,960 | ||||||||

| Ford Credit Auto Owner Trust 2013-B D | 194,000 | 1.820 | 11/15/2019 | 194,235 | ||||||||

| Santander Drive Auto Receivables Trust 2014-4 | 120,000 | 3.090 | 4/15/2022 | 121,844 | ||||||||

| Santander Drive Auto Receivables Trust 2016-1 | 160,000 | 3.100 | 11/16/2020 | 162,930 | ||||||||

| Westlake Automobile Receivables Trust 2016-3 - 144A | 240,000 | 2.070 | 12/15/2021 | 239,540 | ||||||||

| 2,817,905 | ||||||||||||

| BANKS - 9.0% | ||||||||||||

| Banco de Credito del Peru - 144A | 120,000 | 6.125 | + | 4/24/2027 | 132,600 | |||||||

| Banco de Credito e Inversiones - 144A | 325,000 | 4.000 | 2/11/2023 | 334,786 | ||||||||

| Banco Internacional del Peru SAA -144A | 125,000 | 6.625 | + | 3/19/2029 | 137,187 | |||||||

| Banco Santander Chile - 144A | 150,000 | 3.875 | 9/20/2022 | 156,953 | ||||||||

| Bank of America Corp. | 55,000 | 2.000 | 1/11/2018 | 55,148 | ||||||||

| Bank of America Corp. | 175,000 | 5.625 | 7/1/2020 | 192,342 | ||||||||

| Bank of America Corp. | 286,000 | 4.200 | 8/26/2024 | 294,923 | ||||||||

| Bank of New York Mellon | 135,000 | 2.800 | 5/4/2026 | 131,919 | ||||||||

| Bank of New York Mellon | 110,000 | 4.950 | + | Perpetual | 114,538 | |||||||

| Barclays Bank PLC - 144A | 270,000 | 6.050 | 12/4/2017 | 276,664 | ||||||||

| Capital One Financial Corp. | 135,000 | 4.200 | 10/29/2025 | 136,185 | ||||||||

| Capital One Financial Corp. | 135,000 | 3.750 | 7/28/2026 | 130,527 | ||||||||

| Citigroup, Inc. ^ | 130,000 | 4.050 | 7/30/2022 | 136,277 | ||||||||

| Citigroup, Inc. | 160,000 | 6.250 | + | Perpetual | 174,400 | |||||||

| Goldman Sachs Group, Inc. | 185,000 | 5.750 | 1/24/2022 | 208,939 | ||||||||

| JPMorgan Chase & Co. | 40,000 | 6.125 | 6/27/2017 | 40,274 | ||||||||

| JPMorgan Chase & Co. | 35,000 | 5.300 | + | Perpetual | 36,577 | |||||||

| KeyCorp | 140,000 | 5.000 | + | Perpetual | 140,350 | |||||||

| M&T Bank Corp. | 55,000 | 5.125 | + | Perpetual | 55,688 | |||||||

| Morgan Stanley | 185,000 | 4.100 | 5/22/2023 | 192,291 | ||||||||

| Morgan Stanley | 150,000 | 4.350 | 9/8/2026 | 155,428 | ||||||||

| Morgan Stanley | 225,000 | 6.375 | 7/24/2042 | 292,449 | ||||||||

| PNC Financial Services Group, Inc. | 255,000 | 4.850 | + | Perpetual | 256,147 | |||||||

| PNC Financial Services Group, Inc. | 140,000 | 5.000 | + | Perpetual | 141,740 | |||||||

| Santander Holdings USA, Inc. | 135,000 | 3.700 | 5/24/2019 | 135,985 | ||||||||

| SunTrust Banks, Inc. ^ | 30,000 | 5.625 | + | Perpetual | 31,538 | |||||||

| UBS AG | 650,000 | 7.625 | 8/17/2022 | 760,500 | ||||||||

| Wells Fargo & Co. | 70,000 | 3.069 | 1/24/2023 | 70,849 | ||||||||

See accompanying notes to financial statements.

13

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Corporate/Government Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||

| Security | Amount | Rate% | Date | Value | ||||||||

| BANKS (Continued) - 9.0% | ||||||||||||

| Zions Bancorporation | $ | 115,000 | 4.500 | 6/13/2023 | $ | 121,222 | ||||||

| 5,044,426 | ||||||||||||

| BEVERAGES - 0.4% | ||||||||||||

| Anheuser-Busch InBev Finance, Inc. | 65,000 | 3.3000 | 2/1/2023 | 66,863 | ||||||||

| Anheuser-Busch InBev Finance, Inc. ^ | 135,000 | 3.6500 | 2/1/2026 | 137,820 | ||||||||

| 204,683 | ||||||||||||

| BUILDING MATERIALS - 0.9% | ||||||||||||

| Building Materials Corp. - 144A | 105,000 | 6.000 | 10/15/2025 | 112,613 | ||||||||

| Masco Corp. | 50,000 | 3.500 | 4/1/2021 | 51,500 | ||||||||

| Masco Corp. | 60,000 | 5.950 | 3/15/2022 | 68,120 | ||||||||

| Masco Corp. | 25,000 | 4.450 | 4/1/2025 | 26,709 | ||||||||

| Owens Corning | 135,000 | 3.400 | 8/15/2026 | 131,722 | ||||||||

| Vulcan Materials Co. | 135,000 | 6.000 | 4/1/2027 | 136,625 | ||||||||

| 527,289 | ||||||||||||

| CHEMICALS - 1.0% | ||||||||||||

| Equate Petrochemical BV - 144A | 200,000 | 4.250 | 11/3/2026 | 204,034 | ||||||||

| NewMarket Corp. | 305,000 | 4.100 | 12/15/2022 | 315,600 | ||||||||

| SPCM SA - 144A | 20,000 | 4.875 | 9/15/2025 | 20,275 | ||||||||

| 539,909 | ||||||||||||

| COMMERCIAL MBS - 3.7% | ||||||||||||

| Aventura Mall Trust 2013-AVM A - 144A | 155,000 | 3.743 | + | 12/5/2032 | 164,175 | |||||||

| Aventura Mall Trust 2013-AVM C - 144A | 100,000 | 3.743 | + | 12/5/2032 | 103,403 | |||||||

| BAMLL Commercial Mortgage Securities Trust 2015-200P - 144A | 105,000 | 3.218 | 4/14/2033 | 106,531 | ||||||||

| Citigroup Commercial Mortgage Trust 2008-C7 AM | 95,000 | 6.144 | + | 12/10/2049 | 96,946 | |||||||

| Cold Storage Trust 2017-ICE3 -144A | 160,000 | 1.994 | + | 4/15/2024 | 160,000 | |||||||

| GAHR Commercial Mortgage Trust 2015-NRF CFX - 144A | 105,000 | 3.495 | + | 12/15/2034 | 106,910 | |||||||

| GS Mortgage Securities Corp Trust 2012-ALOHA - 144A | 132,000 | 3.551 | 4/10/2034 | 138,875 | ||||||||

| JP Morgan Chase Commercial Mortgage Securities Trust 2011-C4 A3 - 144A | 100,000 | 4.388 | 7/15/2046 | 107,365 | ||||||||

| JP Morgan Chase Commercial Mortgage Securities Trust 2011-C4 A4 - 144A | 94,155 | 4.106 | 7/15/2046 | 96,338 | ||||||||

| LB Commercial Mortgage Trust 2007- C3 A4 | 73,117 | 6.012 | + | 7/15/2044 | 73,322 | |||||||

| LB-UBS Commercial Mortgage Trust 2007-C7 A3 | 46,563 | 5.866 | + | 9/15/2045 | 47,121 | |||||||

| Morgan Stanley Bank of America Merrill Lynch Trust 2013-C13 AS | 240,000 | 4.266 | 11/15/2046 | 256,533 | ||||||||

| Morgan Stanley Capital Barclays Bank Trust 2016-MART - 144A | 110,000 | 2.200 | 9/13/2031 | 108,741 | ||||||||

| Morgan Stanley Capital I Trust 2007-IQ14 AM | 83,396 | 5.744 | + | 4/15/2049 | 83,302 | |||||||

| Motel 6 Trust CMO 2015-MTL6 Class B - 144A | 170,000 | 3.298 | 2/5/2030 | 170,758 | ||||||||

| One Market Plaza Trust 2017-1MKT - 144A | 105,000 | 3.614 | 2/10/2032 | 109,690 | ||||||||

| Wells Fargo Commercial Mortgage Trust 2015-LC20 B | 165,000 | 3.719 | 4/15/2050 | 166,323 | ||||||||

| 2,096,333 | ||||||||||||

| COMMERCIAL SERVICES - 0.7% | ||||||||||||

| Prime Security Services Borrower LLC - 144A | 55,000 | 9.250 | 5/15/2023 | 60,225 | ||||||||

| S&P Global, Inc. | 140,000 | 4.000 | 6/15/2025 | 147,137 | ||||||||

| Team Health Holdings, Inc. - 144A | 70,000 | 6.375 | 2/1/2025 | 68,513 | ||||||||

| Verisk Analytics, Inc. | 135,000 | 4.000 | 6/15/2025 | 138,330 | ||||||||

| 414,205 | ||||||||||||

| COMPUTERS - 0.9% | ||||||||||||

| Apple, Inc. | 125,000 | 3.250 | 2/23/2026 | 127,794 | ||||||||

| Diamond 1 Finance Corp. - 144A ^ | 30,000 | 5.450 | 6/15/2023 | 32,416 | ||||||||

| Diamond 1 Finance Corp. - 144A | 25,000 | 6.020 | 6/15/2026 | 27,506 | ||||||||

| Diamond 1 Finance Corp. - 144A | 55,000 | 8.100 | 7/15/2036 | 69,205 | ||||||||

| DXC Technology Co. - 144A | 35,000 | 4.250 | 4/15/2024 | 35,914 | ||||||||

| Harland Clarke Holdings Corp. - 144A | 30,000 | 8.375 | 8/15/2022 | 30,975 | ||||||||

| Hewlett Packard Enterprise Co. | 80,000 | 3.600 | 10/15/2020 | 82,758 | ||||||||

| Hewlett Packard Enterprise Co. | 80,000 | 4.900 | 10/15/2025 | 84,202 | ||||||||

| 490,770 | ||||||||||||

| DIVERSIFIED FINANCIAL SERVICES - 1.2% | ||||||||||||

| Air Lease Corp. | 140,000 | 2.625 | 9/4/2018 | 141,090 | ||||||||

| Brookfield Finance LLC | 114,000 | 4.000 | 4/1/2024 | 117,098 | ||||||||

| Jefferies Group LLC | 60,000 | 5.125 | 1/20/2023 | 64,859 | ||||||||

| Macquarie Group Ltd.- 144A | 125,000 | 6.250 | 1/14/2021 | 139,409 | ||||||||

| Navient Corp. | 62,000 | 6.500 | 6/15/2022 | 64,170 | ||||||||

| Navient Corp. | 30,000 | 7.250 | 9/25/2023 | 31,500 | ||||||||

| OM Asset Management Plc | 135,000 | 4.800 | 7/27/2026 | 136,098 | ||||||||

| 694,224 | ||||||||||||

See accompanying notes to financial statements.

14

| SCHEDULE OF INVESTMENTS (Unaudited) |

| Dunham Corporate/Government Bond Fund (Continued) |

| April 30, 2017 |

| Principal | Interest | Maturity | ||||||||||

| Security | Amount | Rate% | Date | Value | ||||||||

| ELECTRIC - 0.6% | ||||||||||||

| Dominion Resources, Inc. | $ | 15,000 | 2.962 | 7/1/2019 | $ | 15,216 | ||||||

| Duke Energy Corp. | 140,000 | 2.650 | 9/1/2026 | 132,551 | ||||||||

| Southern Power Co. | 170,000 | 4.150 | 12/1/2025 | 177,896 | ||||||||

| 325,663 | ||||||||||||

| ELECTRONICS - 0.3% | ||||||||||||

| Flextronics International Ltd. | 135,000 | 4.750 | 6/15/2025 | 143,605 | ||||||||

| ENERGY - ALTERNATE RESOURCES - 0.2% | ||||||||||||

| TerraForm Power Operating LLC. - 144A | 110,000 | 6.375 | 2/1/2023 | 114,263 | ||||||||

| ENTERTAINMENT - 0.3% | ||||||||||||

| Eldorado Resorts, Inc. - 144A | 15,000 | 6.000 | 4/1/2025 | 15,563 | ||||||||

| Gateway Casinos & Entertainment Ltd. - 144A | 45,000 | 8.250 | 3/1/2024 | 46,125 | ||||||||

| Pinnacle Entertainment, Inc. - 144A | 40,000 | 5.625 | 5/1/2024 | 41,400 | ||||||||

| Scientific Games International, Inc. | 65,000 | 6.625 | 5/15/2021 | 62,968 | ||||||||

| Scientific Games International, Inc. - 144A | 10,000 | 7.000 | 1/1/2022 | 10,731 | ||||||||

| 176,787 | ||||||||||||

| FOOD - 0.5% | ||||||||||||

| Post Holdings, Inc. - 144A | 65,000 | 5.750 | 3/1/2027 | 67,844 | ||||||||

| Safeway, Inc. | 85,000 | 7.250 | 2/1/2031 | 82,663 | ||||||||

| Smithfield Foods, Inc. - 144A | 36,000 | 4.250 | 2/1/2027 | 36,807 | ||||||||

| Whole Foods Market, Inc. ^ | 110,000 | 5.200 | 12/3/2025 | 115,455 | ||||||||

| 302,769 | ||||||||||||

| GAS - 0.2% | ||||||||||||

| NGL Energy Partners LP | 105,000 | 5.125 | 7/15/2019 | 105,263 | ||||||||

| HEALTHCARE PRODUCTS - 0.5% | ||||||||||||

| Abbott Laboratories | 30,000 | 3.400 | 11/30/2023 | 30,481 | ||||||||

| Abbott Laboratories | 110,000 | 3.750 | 11/30/2026 | 111,569 | ||||||||

| Fresenius US Finance II, Inc. - 144A | 80,000 | 6.625 | 5/15/2022 | 74,000 | ||||||||

| Fresenius US Finance II, Inc. - 144A | 25,000 | 4.500 | 1/15/2023 | 25,875 | ||||||||

| Hill-Rom Holdings, Inc. - 144A | 63,000 | 5.000 | 2/15/2025 | 63,945 | ||||||||

| 305,870 | ||||||||||||