UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22208

Valued Advisers Trust

(Exact name of registrant as specified in charter)

| | |

Huntington Asset Services, Inc. 2960 N. Meridian Street, Suite 300 | | Indianapolis, IN 46208 |

| (Address of principal executive offices) | | (Zip code) |

Capitol Services, Inc.

615 S. Dupont Hwy.

Dover, DE 19901

(Name and address of agent for service)

With a copy to:

John H. Lively, Esq.

The Law Offices of John H. Lively & Associates, Inc.

A member firm of The 1940 Act Law Group

11300 Tomahawk Creek Parkway,

Suite 310

Leawood, KS 66221

Registrant’s telephone number, including area code: 317-917-7000

Date of fiscal year end: 5/31

Date of reporting period: 5/31/14

Item 1. Reports to Stockholders.

ANNUAL REPORT

May 31, 2014

BFS Equity Fund

185 Asylum Street — City Place II — Hartford, CT 06103 — (855) 575-2430

Letter to Shareholders

Dear Fellow Shareholders,

Welcome to the first annual report of the BFS Equity Fund (the “Fund”). The report covers the period from the launch of the Fund on November 8, 2013 through May 31, 2014 – the end of the Fund’s fiscal year. Thus the report covers a period of slightly less than seven months.

On the day of the launch on November 8, 2013, approximately $1.1 million was invested in the Fund, and over the subsequent period covered by this report, investors added more than $11 million to the Fund. With the positive investment performance of the Fund during the period under review, the BFS Equity Fund completed its fiscal year on May 31, 2014 with assets of $12.7 million.

This report includes a commentary from the Lead Portfolio Manager – Keith LaRose – and Co-Portfolio Managers, Tom Sargent and Tim Foster. You will also find a listing of the portfolio holdings as of May 31, 2014, financial statements and detailed information about the performance and positioning of the BFS Equity Fund.

The Fund’s launch took place during the 5th year of this bull market, which commenced on March 6, 2009 with the S&P 500® Index (“S&P 500”)1 bottoming at 666.79. At the inception of the Fund, the price of the S&P 500 had climbed 165.6% to close at 1770.61 on November 8, 2013. While not negative on the prospects of the U.S. economy or on the stock market at the time of the Fund’s launch, the Fund’s Portfolio Managers were naturally somewhat cautious in initiating stock positions in many stocks near their all-time highs. Accordingly, the Fund during its initial phase was positioned somewhat defensively in order to weather a potential pullback in the market.

In fact, there was a mild correction in the early part of 2014. As some shareholders may remember, the price of the S&P 500, having gained 4.39% from the date of the Fund’s launch through the end of 2013, sold off from January 15, 2014 through the first several days of February. The price of the S&P 500 dropped 5.76% during this period so that as of the close of the market on February 3, 2014, the price of the S&P 500 was lower than on the date of the Fund’s inception.

It was largely during this period when the market was whipsawing +/- 5% that the Fund’s managers were constructing the portfolio. The process was also complicated by the harsh winter which caused U.S. GDP to decline 2.9% during the first quarter, thereby negatively impacting the shares of many stocks. The

1

end result of our investment strategy is the Fund’s portfolio of 50 quality growth stocks purchased with a risk-mitigating approach and positioned to provide a margin of safety in the case of economic or market weakness. More than 85% of the Fund’s companies pay dividends, and a considerable number are so-called “dividend aristocrats” – companies which have increased their dividend payouts annually for the past 25 years. While the total return of the Fund has lagged the S&P 500 and the Dow Jones Industrial Average2 from its launch through May 31, 2014, we, at Bradley, Foster & Sargent, believe the Fund’s ownership of shares in these quality companies with strong brands and robust cash flow should be able to withstand market corrections, even bear markets and perform well over the long-term.

The Portfolio Managers of the BFS Equity Fund and I are shareholders together with you, and we appreciate the trust that you have placed in us to manage your assets. Kindly contact us via email through our website – www.bfsinvest.com or www.bfsfunds.com – or by telephone at 860-527-8050 with any questions or concerns about the Fund that are not addressed in this report.

Sincerely,

Robert H. Bradley

President and CEO

Bradley, Foster & Sargent, Inc.

| 1 | | The S&P 500® Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| 2 | | The Dow Jones Industrial Average® is a widely recognized unmanaged index of equity prices and is representative of a narrower market and range of securities than is found in the Fund’s portfolio. The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

2

Portfolio Managers’ Letter

TO OUR SHAREHOLDERS

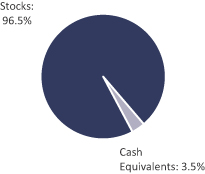

The BFS Equity Fund (the “Fund”) had a total return of 7.4% for the period November 8, 2013 through May 31, 2014, the close of our first fiscal year. This compared to a total return of 11.4% for the S&P 500® Index (“S&P 500”) and 8.7% for the Dow Jones Industrial Average for the same period. At our fiscal year-end, the Fund had net assets of $12.7 million with a cash position of 3.5%.

MARKET COMMENTARY

The U.S. equity markets were strong during the fourth quarter of 2013 with the S&P 500 up 10.5%. For the full calendar year of 2013, the S&P 500 was up 32.4%, the best year since 1997. During the fourth quarter of 2013, when the Fund was launched, economic activity appeared to be accelerating, and this caused the yield on the U.S. 10-Year Treasury Note to climb from approximately 2.5% at the beginning of the quarter to 3.0% by year-end. However, the economy failed to shift into a higher gear, as the cold weather hampered growth and international geopolitical concerns during the first quarter of 2014 worried investors. In fact, GDP in the U.S. during the first quarter declined 2.9%. This caused U.S. interest rates to fall once again, confounding many investors. The poor weather and geopolitical difficulties in the first quarter of 2014 caused a brief, sharp sell-off in the U.S. equity markets in the second half of January and early February, with the S&P 500 falling 5.8% during this period. Despite the weak economy, we remained optimistic about the long-term prospects for corporate earnings growth, and we continued to maintain the view that moderate economic growth combined with low interest rates is a positive investment backdrop. During this period of uncertainty, we remained focused on the longer-term horizon which enabled us to establish numerous high quality positions at reasonable valuations. Since the inception of the Fund in November 2013, we have been of the opinion that the long awaited normalization process for U.S. interest rates is underway and that the Federal Reserve will bring its quantitative easing program to an end during the fourth quarter of 2014. Accordingly, we have held a strong preference for companies that benefit from economic expansion and rising interest rates.

INVESTMENT STRATEGY

Our investment strategy is to seek to buy shares in high-quality businesses identified through our bottom-up research process. We do not acquire shares for short-term speculative trading. When evaluating the attractiveness of a

3

particular holding, we have a three to five year time horizon. Although our top-down macro-economic views play a role with respect to both sector and security selection, our decisions are driven to a greater extent by our analysis of the absolute and relative attractiveness of each company. Our equity investment process has two main principles: identifying quality companies and investing in the stocks of these companies at favorable valuations, which often happens after an event or a change of circumstances. We are keenly focused on making solid intermediate and long-term judgments, as opposed to rotating toward the flavor of the moment in an attempt to achieve short-term results. Investment risks and opportunities are analyzed company-by-company, and for each holding, we seek to judge whether all the key factors are incorporated into the company’s stock price. As such, we will endeavor to deliver attractive risk-adjusted results over a full market cycle as opposed to a boom and bust pattern of performance.

INVESTMENT COMMENTARY

During the 6+ month period under review, the U.S. stock market remained in a relatively narrow trading range between the close of the S&P 500 on February 3, 2014 of 1742 and the high of 1924 on the closing day of our fiscal year, May 31, 2014. With the S&P 500 trading at approximately 16 times 2014 estimated earnings (roughly in line with its 40-year historical average), we had ample opportunity to deploy capital at reasonable prices into the shares of quality businesses that were already familiar to us. At the end of the fiscal year, the Fund had positions in 50 holdings and was well diversified. Based on our bottom-up security selection, the Fund is moderately overweight in several areas of the market including Industrials (15.0% of the Fund compared to 10.5% for the S&P 500) and Health Care (15.6% of the Fund compared to 13.3% for the S&P 500).

Energy

In the Energy sector, the Fund has significant investments (9.1% of Fund assets). The Fund’s holdings in the Energy sector were up 17.0% for the period November 8, 2013 through May 31, 2014, compared to an increase of 12.4% of the S&P 500 Energy sector for the same period. The Energy sector is benefiting from the energy revolution taking place in the United States. The remarkable technology of horizontal drilling has ushered in an energy boom in the U.S. by opening up new opportunities for expanded production from domestic oil and gas shale plays. EOG Resources and Continental Resources, both of which focus primarily on oil exploration and production, were our big winners – up 25.3% and 24.7% respectively. Both EOG and Continental are benefiting from strong oil

4

production and reserve growth from key shale plays in the Bakken and the South Central Oklahoma Oil Preserve. Both companies have valuable acreage positions in these two highly prolific shale formations in the United States with a drilling inventory that should last for years.

Financials

The Fund has substantial holdings in the Financials sector (15.1% of Fund assets). While the Fund’s holdings were up 2.7% for the period under review, they underperformed the S&P 500 Financials sector by 7.7%. Our holdings were purposefully weighted toward larger financial institutions that we view as inexpensive. In our opinion, they are healthy and well-capitalized, and we believe that they are poised to deliver attractive total returns over a longer-term time horizon through earnings growth, return of capital through share buybacks, and increased dividends. However, reduced regulatory pressure and loan growth are necessary to unleash this potential. This clearly did not materialize during our partial fiscal year. Wells Fargo was our best performer in the Financials sector, up 20.3%, followed by American Express, up 11.7%, and M&T Bank Corp., up 9.6%. This was not enough to offset the negative performance from Bank of America, down 9.9%, State Street down 8.6% and Goldman Sachs, down 8.2%. Although our Financials sector positions, in aggregate, underperformed its S&P 500 Financials sector benchmark, we believe that with strong U.S. economic growth, higher interest rates, and less regulation, our portfolio choices will produce solid long-term results.

CLOSING COMMENTS

2013 was a terrific year for the U.S. stock market. The stock market, which was undervalued at the start of 2013, is now, we believe, closer to fair value. Accordingly, our outlook for the market in 2014 is more modest. Yet we believe that the BFS Equity Fund is well positioned in its holdings to take advantage of the promising long-term performance from these fine businesses with outstanding management teams. We believe these top-in-class companies will deliver solid long-term risk adjusted results for our investors. We will continue to keep our eye on the long-term horizon, avoid short-term noise, and remain opportunistic with respect to capital deployment. We, at Bradley, Foster & Sargent, Inc., look forward to serving you through our management of the BFS Equity Fund. We welcome you and thank you for placing your capital under our care.

| | | | |

| Keith LaRose | | Timothy Foster | | Thomas Sargent |

| Lead Portfolio Manager | | Co-Portfolio Manager | | Co-Portfolio Manager |

5

ANNUAL PERFORMANCE REVIEW

(Unaudited)

The Fund underperformed the S&P 500 by 4.0% and the Dow Jones Industrial Average by 1.4% for the period November 8, 2013 through May 31, 2014.

Key Detractors from Relative Results

| | • | | Relative returns from holdings in the Financials sector (up 2.7% compared to up 10.4% for the S&P 500 Financials sector) detracted from results. Bank of America (down 9.9%), State Street (down 8.6%) and Goldman Sachs (down 8.2% until time of sale) as well as JP Morgan (up 6.2% but less than the S&P 500 Financials sector benchmark) produced underperformance in this sector. |

| | • | | The Fund’s overweight position and holdings in the Industrial Sector (up 7.0% compared with up 11.7% for the S&P 500 Industrial sector) detracted from results. Kansas City Southern (down 15.7% until time of sale) was the biggest negative in the Fund in this sector. |

Key Contributors to Relative Results

| | • | | The Fund’s holdings in the Energy sector (up 17.0% compared with up 12.4% for the S&P 500 Energy sector) helped results. EOG (up 25.3%) and CLR (up 24.7%) were the strongest contributors for the Fund in this sector. |

| | • | | Strong returns for the Fund’s holdings in the Materials sector (up 24.1% compared with the S&P 500 Materials sector up 14.4%) aided results. Westlake Chemical (up 40.2%) was a notable contributor. |

FUND INFORMATION (Unaudited)

ASSET ALLOCATION

(As a percentage of total investments)

| | | | |

TEN LARGEST HOLDINGS (%) | | FUND | |

Danaher | | | 4.6 | |

Walt Disney | | | 4.0 | |

JPMorgan Chase | | | 3.7 | |

United Technologies | | | 3.7 | |

Microsoft | | | 3.2 | |

Wells Fargo | | | 3.2 | |

Johnson & Johnson | | | 3.2 | |

Google – Class A | | | 3.0 | |

Home Depot | | | 2.8 | |

EOG Resources | | | 2.7 | |

| | | | | | | | |

SECTOR DIVERSIFICATION (%) | | FUND | | | S&P 500 | |

Health Care | | | 15.6 | | | | 13.3 | |

Financials | | | 15.1 | | | | 16.1 | |

Industrial | | | 15.0 | | | | 10.5 | |

Consumer Discretionary | | | 13.6 | | | | 11.9 | |

Consumer Staples | | | 11.7 | | | | 9.5 | |

Technology | | | 11.4 | | | | 18.9 | |

Energy | | | 9.1 | | | | 10.8 | |

Materials | | | 3.8 | | | | 3.5 | |

Telecommunication Services | | | 1.2 | | | | 2.4 | |

Utilities | | | 0.0 | | | | 3.1 | |

Cash Equivalents | | | 3.5 | | | | 0.0 | |

6

Investment Results (Unaudited)

Total Returns* (For the period ended May 31, 2014)

| | | | |

| | | Since Inception (November 8, 2013) | |

BFS Equity Fund | | | 7.36% | |

S&P 500® Index** | | | 11.39% | |

Dow Jones Industrial Average®*** | | | 8.73% | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Current performance of a Fund may be lower or higher than the performance quoted.

* Return figures reflect any change in price per share and assume the reinvestment of all distributions.

** The S&P 500® Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

*** The Dow Jones Industrial Average® is a widely recognized unmanaged index of equity prices and is representative of a narrower market and range of securities than is found in the Fund’s portfolio. The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

AVAILABILITY OF PORTFOLIO SCHEDULE (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q will be available at the SEC’s website at www.sec.gov. The Fund’s Form N-Q may be reviewed and copied at the Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

SUMMARY OF FUND’S EXPENSES (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period, and held for the six month period, December 1, 2013 to May 31, 2014.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number in the first line under the heading entitled

7

“Expenses Paid During the Period Ended May 31, 2014” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | |

| | | Beginning

Account

Value | | | Ending

Account

Value | | | Expenses

Paid During

the Period Ended | |

| | | | | | May 31, 2014 | | | May 31, 2014* | |

| BFS Equity Fund | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,050.50 | | | $ | 6.39 | |

Hypothetical ** (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.70 | | | $ | 6.29 | |

| * | | Expenses are equal to the Fund’s annualized expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 182/365. |

| ** | | Assumes a 5% return before expenses. |

8

Schedule of Investments

May 31, 2014

| | | | | | | | |

| Shares | | | | | Fair Value | |

| | COMMON STOCKS – 96.35% | |

| | |

| | | | Aerospace & Defense 3.65% | | | | |

| | 4,000 | | | United Technologies Corp. | | $ | 464,880 | |

| | | | | | | | |

| | |

| | | | Beverages 3.60% | | | | |

| | 2,300 | | | Constellation Brands, Inc. – Class A* | | | 193,499 | |

| | 3,000 | | | PepsiCo, Inc. | | | 264,990 | |

| | | | | | | | |

| | | | | | | 458,489 | |

| | | | | | | | |

| | | | Biotechnology 1.72% | | | | |

| | 475 | | | Celgene Corp.* | | | 72,689 | |

| | 1,800 | | | Gilead Sciences, Inc.* | | | 146,178 | |

| | | | | | | | |

| | | | | | | 218,867 | |

| | | | | | | | |

| | | | Capital Markets 1.18% | | | | |

| | 2,300 | | | State Street Corp. | | | 150,121 | |

| | | | | | | | |

| | |

| | | | Chemicals 3.76% | | | | |

| | 1,500 | | | Monsanto Co. | | | 182,775 | |

| | 900 | | | Praxair, Inc. | | | 119,016 | |

| | 2,200 | | | Westlake Chemical Corp. | | | 177,870 | |

| | | | | | | | |

| | | | | | | 479,661 | |

| | | | | | | | |

| | | | Commercial Banks 5.57% | | | | |

| | 2,500 | | | M&T Bank Corp. | | | 303,425 | |

| | 8,000 | | | Wells Fargo & Co. | | | 406,240 | |

| | | | | | | | |

| | | | | | | 709,665 | |

| | | | | | | | |

| | | | Computers & Peripherals 2.23% | | | | |

| | 450 | | | Apple, Inc. | | | 284,850 | |

| | | | | | | | |

| | |

| | | | Consumer Finance 2.51% | | | | |

| | 3,500 | | | American Express Co. | | | 320,250 | |

| | | | | | | | |

| | |

| | | | Diversified Financial Services 4.85% | | | | |

| | 10,000 | | | Bank of America Corp. | | | 151,400 | |

| | 8,400 | | | JPMorgan Chase & Co. | | | 466,788 | |

| | | | | | | | |

| | | | | | | 618,188 | |

| | | | | | | | |

| | | | Diversified Telecommunication 1.18% | | | | |

| | 3,000 | | | Verizon Communications, Inc. | | | 149,880 | |

| | | | | | | | |

| | |

| | | | Electronic Equipment, Instruments & Components 1.73% | | | | |

| | 2,300 | | | Amphenol Corp. – Class A | | | 220,340 | |

| | | | | | | | |

| | |

| | | | Food & Staples Retailing 3.05% | | | | |

| | 1,800 | | | Costco Wholesale Corp. | | | 208,836 | |

| | 2,500 | | | Walgreen Co. | | | 179,775 | |

| | | | | | | | |

| | | | | | | 388,611 | |

| | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

9

Schedule of Investments (continued)

May 31, 2014

| | | | | | | | |

| Shares | | | | | Fair Value | |

| | COMMON STOCKS – (continued) | |

| | |

| | | | Food Products 2.47% | | | | |

| | 4,000 | | | Nestle SA ADR | | $ | 314,300 | |

| | | | | | | | |

| | |

| | | | Health Care Equipment & Supplies 1.66% | | | | |

| | 2,900 | | | Covidien PLC | | | 212,019 | |

| | | | | | | | |

| | |

| | | | Hotels, Restaurants & Leisure 3.89% | | | | |

| | 2,000 | | | McDonalds Corp. | | | 202,860 | |

| | 4,000 | | | Starbucks Corp. | | | 292,960 | |

| | | | | | | | |

| | | | | | | 495,820 | |

| | | | | | | | |

| | | | Household Products 2.55% | | | | |

| | 2,500 | | | Colgate-Palmolive Co. | | | 171,000 | |

| | 1,900 | | | Procter & Gamble Co. | | | 153,501 | |

| | | | | | | | |

| | | | | | | 324,501 | |

| | | | | | | | |

| | | | Industrial Conglomerates 5.46% | | | | |

| | 7,500 | | | Danaher Corp. | | | 588,225 | |

| | 4,000 | | | General Electric Co. | | | 107,160 | |

| | | | | | | | |

| | | | | | | 695,385 | |

| | | | | | | | |

| | | | Internet Software & Services 2.96% | | | | |

| | 660 | | | Google, Inc. – Class A* | | | 377,289 | |

| | | | | | | | |

| | |

| | | | Life Sciences Tools & Services 2.29% | | | | |

| | 2,500 | | | Thermo Fisher Scientific, Inc. | | | 292,275 | |

| | | | | | | | |

| | |

| | | | Machinery 1.43% | | | | |

| | 2,000 | | | Deere & Co. | | | 182,340 | |

| | | | | | | | |

| | |

| | | | Media 3.95% | | | | |

| | 6,000 | | | Walt Disney Co./The | | | 504,060 | |

| | | | | | | | |

| | |

| | | | Oil, Gas & Consumable Fuels 9.06% | | | | |

| | 1,700 | | | Continental Resources, Inc.* | | | 238,612 | |

| | 3,200 | | | EOG Resources, Inc. | | | 338,560 | |

| | 1,400 | | | Exxon Mobil Corp. | | | 140,742 | |

| | 3,000 | | | Occidental Petroleum Corp. | | | 299,070 | |

| | 5,000 | | | Plains GP Holdings LP(a) | | | 138,000 | |

| | | | | | | | |

| | | | | | | 1,154,984 | |

| | | | | | | | |

| | | | Pharmaceuticals 9.90% | | | | |

| | 4,000 | | | Johnson & Johnson | | | 405,840 | |

| | 4,000 | | | Merck & Co., Inc. | | | 231,440 | |

| | 2,600 | | | Novartis AG ADR | | | 234,156 | |

| | 8,000 | | | Pfizer, Inc. | | | 237,040 | |

| | 5,000 | | | Zoetis, Inc. | | | 153,500 | |

| | | | | | | | |

| | | | | | | 1,261,976 | |

| | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

10

Schedule of Investments (continued)

May 31, 2014

| | | | | | | | |

| Shares | | | | | Fair Value | |

| | COMMON STOCKS – (continued) | |

| | |

| | | | Professional Services 1.89% | | | | |

| | 5,000 | | | Nielsen NV | | $ | 241,300 | |

| | | | | | | | |

| | |

| | | | Real Estate Investment Trust 1.00% | | | | |

| | 2,000 | | | WP Carey, Inc. | | | 127,280 | |

| | | | | | | | |

| | |

| | | | Road & Rail 1.04% | | | | |

| | 2,200 | | | Canadian National Railway Co. | | | 133,276 | |

| | | | | | | | |

| | |

| | | | Software 4.48% | | | | |

| | 2,500 | | | Adobe Systems, Inc.* | | | 161,350 | |

| | 10,000 | | | Microsoft Corp. | | | 409,400 | |

| | | | | | | | |

| | | | | | | 570,750 | |

| | | | | | | | |

| | | | Specialty Retail 2.83% | | | | |

| | 4,500 | | | Home Depot, Inc./The | | | 361,035 | |

| | | | | | | | |

| | |

| | | | Textiles, Apparel & Luxury Goods 2.93% | | | | |

| | 2,500 | | | Luxottica Group SpA ADR | | | 142,475 | |

| | 3,000 | | | NIKE, Inc. | | | 230,730 | |

| | | | | | | | |

| | | | | | | 373,205 | |

| | | | | | | | |

| | | | Tobacco 1.53% | | | | |

| | 2,000 | | | Genesee & Wyoming, Inc. – Class A* | | | 194,700 | |

| | | | | | | | |

| | | | Total Common Stocks (Cost $11,502,377) | | | 12,280,297 | |

| | | | | | | | |

| | |

| | | | Money Market Securities 3.52% | | | | |

| | 448,023 | | | Fidelity Institutional Money Market Funds – Prime Money Market Portfolio, 0.06%(b) | | | 448,023 | |

| | | | | | | | |

| | | | Total Money Market Securities (Cost $448,023) | | | 448,023 | |

| | | | | | | | |

| | | | Total Investments 99.87% (Cost $11,950,400) | | | 12,728,320 | |

| | | | | | | | |

| | | | Other Assets in Excess of Liabilities 0.13% | | | 16,743 | |

| | | | | | | | |

| | | | TOTAL NET ASSETS 100.00% | | $ | 12,745,063 | |

| | | | | | | | |

| (a) | | Master Limited Partnership. |

| (b) | | Rate disclosed is the seven day yield as of May 31, 2014. |

| * | | Non-income producing security. |

| ADR | | – American Depositary Receipt |

See accompanying notes which are an integral part of these financial statements.

11

Statement of Assets and Liabilities

May 31, 2014

| | | | |

Assets | | | | |

Investments in securities at fair value (cost $11,950,400) | | $ | 12,728,320 | |

Cash | | | 1,776 | |

Receivable for fund shares sold | | | 4,303 | |

Dividends receivable | | | 17,152 | |

Tax reclaims receivable | | | 4,454 | |

Receivable from Adviser | | | 16,165 | |

Deferred offering costs | | | 19,185 | |

Prepaid expenses | | | 1,873 | |

Total Assets | | | 12,793,228 | |

Liabilities | | | | |

Payable to administrator, fund accountant, and transfer agent | | | 17,096 | |

Payable to custodian | | | 1,198 | |

Distribution fees accrued | | | 2,629 | |

Other accrued expenses | | | 27,242 | |

Total Liabilities | | | 48,165 | |

Net Assets | | $ | 12,745,063 | |

Net Assets consist of: | | | | |

Paid-in capital | | $ | 12,113,432 | |

Accumulated undistributed net investment income | | | 32,183 | |

Accumulated net realized loss from investments | | | (178,472 | ) |

Net unrealized appreciation on investments | | | 777,920 | |

Net Assets | | $ | 12,745,063 | |

Shares outstanding (unlimited number of shares authorized, no par value) | | | 1,188,037 | |

Net asset value, offering and redemption price per share | | $ | 10.73 | |

12

See accompanying notes which are an integral part of these financial statements.

Statement of Operations

For the period ended May 31, 2014(a)

| | | | |

Investment Income | | | | |

Dividend income (net of foreign taxes withheld of $908) | | $ | 105,282 | |

Total investment income | | | 105,282 | |

Expenses | | | | |

Investment Adviser | | | 40,611 | |

Distribution (12b-1) | | | 13,537 | |

Administration | | | 21,486 | |

Fund accounting | | | 14,097 | |

Transfer agent | | | 28,825 | |

Legal | | | 13,711 | |

Custodian | | | 8,354 | |

Audit | | | 16,500 | |

Trustee | | | 1,649 | |

Offering costs | | | 24,580 | |

Organizational costs | | | 8,750 | |

Miscellaneous | | | 11,708 | |

Report Printing | | | 7,160 | |

24f-2 | | | 1,529 | |

Pricing | | | 1,272 | |

Registration | | | 328 | |

Total expenses | | | 214,097 | |

Fees waived and reimbursed by Adviser | | | (146,030 | ) |

Net operating expenses | | | 68,067 | |

Net investment income | | | 37,215 | |

Net Realized and Unrealized Gains/(Losses) on Investments | | | | |

Net realized loss on investment securities transactions | | | (178,580 | ) |

Net change in unrealized appreciation on investment securities | | | 777,920 | |

Net realized and unrealized gain on investments | | | 599,340 | |

Net increase in net assets resulting from operations | | $ | 636,555 | |

| (a) | | For the period November 8, 2013 (commencement of operations) to May 31, 2014. |

13

See accompanying notes which are an integral part of these financial statements.

Statement of Changes in Net Assets

| | | | |

| Increase in Net Assets due to: | | For the Period Ended May 31, 2014(a) | |

Operations | | | | |

Net investment income | | $ | 37,215 | |

Net realized loss on investment securities transactions | | | (178,580 | ) |

Net change in unrealized appreciation on investment securities | | | 777,920 | |

Net increase in net assets resulting from operations | | | 636,555 | |

Distributions From | | | | |

Net investment income | | | (4,924 | ) |

Total distributions | | | (4,924 | ) |

Capital Transactions | | | | |

Proceeds from shares sold | | | 12,239,160 | |

Reinvestment of distributions | | | 2,913 | |

Amount paid for shares redeemed | | | (128,641 | ) |

Net increase in net assets resulting from capital transactions | | | 12,113,432 | |

Total Increase in Net Assets | | | 12,745,063 | |

Net Assets | | | | |

Beginning of period | | | – | |

End of period | | $ | 12,745,063 | |

Accumulated undistributed net investment income | | $ | 32,183 | |

Share Transactions | | | | |

Sold | | | 1,200,263 | |

Issued in reinvestment of distributions | | | 280 | |

Redeemed | | | (12,506 | ) |

Net increase in share transactions | | | 1,188,037 | |

| (a) | | For the period November 8, 2013 (commencement of operations) to May 31, 2014. |

14

See accompanying notes which are an integral part of these financial statements.

Financial Highlights

(For a share outstanding during the period)

| | | | |

| | | For the Period Ended

May 31, 2014(a) | |

Selected Per Share Data: | |

Net asset value, beginning of period | | | $10.00 | |

| | | | |

| |

Income from investment operations: | | | | |

| |

Net investment income | | | 0.04 | |

| |

Net realized and unrealized gain on investments | | | 0.70 | |

| | | | |

| |

Total from investment operations | | | 0.74 | |

| | | | |

| |

Less distributions to shareholders from: | | | | |

| |

From investment income | | | (0.01 | ) |

| | | | |

| |

Total distributions | | | (0.01 | ) |

| | | | |

Net asset value, end of period | | | $10.73 | |

| | | | |

| |

Total Return(b) | | | 7.36 | %(c) |

| | | | |

Ratios and Supplemental Data: | |

Net assets, end of period (000) | | | $12,745 | |

| |

Ratio of expenses to average net assets | | | 1.25 | %(d) |

| |

Ratio of expenses to average net assets before waiver | | | 3.93 | %(d) |

| |

Ratio of net investment income to average net assets | | | 0.68 | %(d) |

| |

Ratio of net investment loss to average net assets before waiver | | | (2.00 | )%(d) |

| |

Portfolio turnover rate | | | 46.50 | %(c) |

| (a) | | For the period November 8, 2013 (commencement of operations) to May 31, 2014. |

| (b) | | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends, if any. |

15

See accompanying notes which are an integral part of these financial statements.

Notes to the Financial Statements

May 31, 2014

NOTE 1 – ORGANIZATION

The BFS Equity Fund (the “Fund”) was organized as an open-end diversified series of the Valued Advisers Trust (the “Trust”) on July 23, 2013 and commenced operations on November 8, 2013. The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Trustees to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds authorized by the Board of Trustees (the “Board”). The Fund’s investment adviser is Bradley, Foster & Sargent, Inc. (the “Adviser”). The investment objective of the Fund is long-term appreciation through growth of principal and income.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with the generally accepted accounting principles in the United States of America (“GAAP”).

Securities Valuation – All investments in securities are recorded at their estimated fair value as described in Note 3.

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of, and during the period ended May 31, 2014, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the year, the Fund did not incur any interest or penalties. The Fund is subject to examination by U.S. federal tax authorities for all tax years since inception.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income - The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. The Fund has chosen high cost as its standing (default) tax lot identification method for all shareholders. Interest income is recorded on an accrual basis and dividend income is recorded on the ex-dividend date except in the case of foreign securities, in which case dividends are generally recorded as soon as such information becomes available. Discounts and premiums on securities purchased are accreted or amortized using the effective interest method. The ability of issuers of debt securities held by the Fund to meet their obligations may be affected by economic and political developments in a specific country or region. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

16

Notes to the Financial Statements (continued)

May 31, 2014

Dividends and Distributions – The Fund intends to distribute its net realized long term and short term capital gains, if any, at least once a year. Dividends to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Fund. For the period ended May 31, 2014, the Fund made the following reclassifications of net assets.

| | | | |

| Paid-in Capital | | Accumulated Undistributed Net Investment Income | | Accumulated Net Realized Gain/(Loss) on Investments |

$– | | $(108) | | $108 |

NOTE 3 – SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

Fair value is defined as the price that a Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. Accounting principles generally accepted in the United States of America (“GAAP”) have established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| | • | | Level 1 – quoted prices in active markets for identical securities |

| | • | | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| | • | | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

17

Notes to the Financial Statements (continued)

May 31, 2014

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities, including common stocks, are generally valued by using market quotations, but may be valued on the basis of prices furnished by a pricing service when the Adviser believes such prices more accurately reflect the fair value of such securities. Securities that are traded on any stock exchange are generally valued by the pricing service at the last quoted sale price. Lacking a last sale price, an exchange traded security is generally valued by the pricing service at its last bid price. Securities traded in the NASDAQ over-the-counter market are generally valued by the pricing service at the NASDAQ Official Closing Price.

When using the market quotations or close prices provided by the pricing service and when the market is considered active, the security will be classified as a Level 1 security. Sometimes, an equity security owned by the Fund will be valued by the pricing service with factors other than market quotations or when the market is considered inactive. When this happens, the security will be classified as a Level 2 security. When market quotations are not readily available, when the Adviser determines that the market quotation or the price provided by the pricing service does not accurately reflect the current fair value, or when restricted or illiquid securities are being valued, such securities are valued as determined in good faith by the Adviser, in conformity with guidelines adopted by and subject to review by the Board. These securities will generally be categorized as Level 3 securities.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending net asset value (“NAV”) provided by the service agent of the funds. These securities will be categorized as Level 1 securities.

In accordance with the Trust’s good faith pricing guidelines, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Adviser would appear to be the amount which the owner might reasonably expect to receive for them upon their current sale. Methods which are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Good faith pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before a Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations. Good faith pricing may also be used in instances when the bonds the Fund invests in may default or otherwise cease to have market quotations readily available.

18

Notes to Financial Statements (continued)

May 31, 2014

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2014:

| | | | | | | | | | | | | | | | |

| | | Valuation Inputs | | | | |

| Assets | | Level 1 Quoted Prices in

Active Markets | | | Level 2 Other Significant Observable Inputs | | | Level 3 Significant Unobservable Inputs | | | Total | |

Common Stocks* | | $ | 12,280,297 | | | $ | – | | | $ | – | | | $ | 12,280,297 | |

Money Market Securities | | | 448,023 | | | | – | | | | – | | | | 448,023 | |

Total | | $ | 12,728,320 | | | $ | – | | | $ | – | | | $ | 12,728,320 | |

| * | | Refer to Schedule of Investments for industry classifications. |

The Fund did not hold any investments at any time during the reporting period in which other significant observable inputs (Level 2) were used in determining fair value. The Fund did not hold any assets at any time during the reporting period in which significant unobservable inputs were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

The Trust recognizes transfers between fair value hierarchy levels at the end of the reporting period. There were no transfers between any levels during the period ended May 31, 2014.

NOTE 4 – FEES AND OTHER TRANSACTIONS WITH AFFILIATES

Under the terms of the investment advisory agreement, on behalf of the Fund (the “Agreement”), the Adviser manages the Fund’s investments subject to oversight of the Board. As compensation for its services, the Fund is obligated to pay the Adviser a fee computed and accrued daily and paid monthly at an annual rate of 0.75% of the average daily net assets of the Fund. For the period ended May 31, 2014, the Adviser earned a fee of $40,611 from the Fund before the waivers described below. At May 31, 2014, the Adviser owed $16,165 to the Fund, including fee waivers and expense reimbursements.

The Adviser has contractually agreed to waive or limit its fee and reimburse certain Fund operating expenses, until September 30, 2015, so that the ratio of total annual operating expenses does not exceed 1.00%. This operating expense limitation does not apply to interest, taxes, brokerage commissions, other expenditures which are capitalized in accordance with generally accepted accounting principles, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, dividend expense on short sales, expenses incurred under a plan of distribution under Rule 12b-1, and expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, incurred by the Fund in any fiscal year. The operating expense limitation also excludes any “Fees and Expenses of Acquired Funds” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including ETFs, that have their own expenses. The Adviser may be entitled to recoup the sum of all fees previously waived or expenses reimbursed during any of the previous three (3) years, less any reimbursement previously paid, provided total expenses do not exceed the limitation set forth above. For the period November 8, 2013 (commencement of operations) through May 31, 2014, expenses totaling $146,030 were waived or reimbursed by the Adviser and may be subject to potential recoupment by the Adviser until May 31, 2017.

19

Notes to Financial Statements (continued)

May 31, 2014

The Trust retains Huntington Asset Services, Inc. (“HASI”) to manage the Fund’s business affairs and provide the Fund with administrative services, including all regulatory reporting and necessary office equipment and personnel. For the period ended May 31, 2014, HASI earned fees of $21,486 for administrative and compliance services provided to the Fund. At May 31, 2014, HASI was owed $6,333 from the Fund for administrative and compliance services. Certain officers of the Trust are members of management and/or employees of HASI. HASI is a wholly-owned subsidiary of Huntington Bancshares, Inc., the parent company of Unified Financial Securities, Inc. (the “Distributor”) and Huntington National Bank, the custodian of the Fund’s investments (the “Custodian”). For the period ended May 31, 2014, the Custodian earned fees of $8,354 for custody services provided to the Fund. At May 31, 2014, the Custodian was owed $1,198 from the Fund for custody services.

The Trust also retains HASI to act as the Fund’s transfer agent and to provide fund accounting services. For the period ended May 31, 2014, HASI earned fees of $28,825 for transfer agent services and reimbursement for out-of-pocket expenses incurred in providing transfer agent services to the Fund. At May 31, 2014, the Fund owed HASI $6,596 for transfer agent services and out-of-pocket expenses. For the period ended May 31, 2014, HASI earned fees of $14,097 from the Fund for fund accounting services. At May 31, 2014, HASI was owed $4,167 from the Fund for fund accounting services.

The Fund has adopted a Distribution Plan pursuant to Rule 12b-1 under the 1940 Act (the “Plan”). The Plan provides that the Fund will pay the Distributor and/or any registered securities dealer, financial institution or any other person (the “Recipient”) a shareholder servicing fee of 0.25% of the average daily net assets of the Fund in connection with the promotion and distribution of the Fund’s shares or the provision of personal services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, the printing and mailing of sales literature and servicing shareholder accounts (“12b-1 Expenses”). The Fund or Distributor may pay all or a portion of these fees to any recipient who renders assistance in distributing or promoting the sale of shares, or who provides certain shareholder services, pursuant to a written agreement. The Plan is a compensation plan, which means that the Plan will benefit shareholders because an effective sales program typically is necessary in order for the Fund to reach and maintain a sufficient size to achieve efficiently its investment objectives and to realize economies of scale. For the period ended May 31, 2014, 12b-1 expense incurred by the Fund was $13,537. The Fund owed $2,629 for 12b-1 fees as of May 31, 2014.

Unified Financial Securities, Inc. acts as the principal distributor of the Fund’s shares. An officer of the Trust is an officer of the Distributor and such person may be deemed to be an affiliate of the Distributor.

NOTE 5 – INVESTMENTS

For the period ended May 31, 2014, purchases and sales of investment securities, other than short-term investments and short-term U.S. government obligations, were as follows:

| | | | | | | | |

| | | Purchases | | | Sales | |

| | $ | 16,375,740 | | | $ | 4,694,780 | |

There were no purchases or sales of long-term U.S. government obligations during the period ended May 31, 2014.

20

Notes to Financial Statements (continued)

May 31, 2014

NOTE 6 – ESTIMATES

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

NOTE 7 – BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a) (9) of the Investment Company Act of 1940. At May 31, 2014, Charles Schwab & Co. (“Schwab”) owned, as record shareholder, 51% of the outstanding shares of the Fund. It is not known whether Schwab or any of the underlying beneficial owners owned or controlled 25% or more of the voting securities of the Fund. As a result, Schwab may be deemed to control the Fund.

NOTE 8 – FEDERAL TAX INFORMATION

At May 31, 2014, the net unrealized appreciation (depreciation) of investments for tax purposes was as follows:

| | | | |

Gross Unrealized Appreciation | | $ | 840,103 | |

Gross Unrealized (Depreciation) | | | (85,158 | ) |

Net Unrealized Appreciation | | $ | 754,945 | |

At May 31, 2014, the aggregate cost of securities for federal income tax purposes was $11,973,375 for the Fund.

At May 31, 2014, the Fund’s most recent fiscal year end, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

| | | | |

Undistributed ordinary income | | $ | 30,704 | |

Undistributed long-term capital gains | | | – | |

Accumulated capital and other losses | | | (154,018 | ) |

Unrealized Appreciation | | | 754,945 | |

| | | $ | 631,631 | |

The difference between book and tax basis appreciation was attributable primarily to the tax deferral of losses on wash sales in the amount of $22,975.

The tax character of distributions paid for the fiscal period ended May 31, 2014 was as follows:

| | | | |

| | | 2014 | |

Distributions paid from: | | | | |

Ordinary Income | | $ | 4,924 | |

| | | $ | 4,924 | |

Certain capital losses incurred after October 31, and within the current taxable year, are deemed to arise on the first business day of the Fund’s following taxable year. For the tax year ended May 31, 2014, the Fund deferred post October capital losses in the amount of $154,018.

21

Notes to Financial Statements (continued)

May 31, 2014

NOTE 9 – COMMITMENTS AND CONTINGENCIES

The Fund indemnifies its officers and trustees for certain liabilities that may arise from performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

NOTE 10 – SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date these financial statements were issued. There were no items requiring adjustment of financial statements or additional disclosure.

22

Report of Independent Registered Public Accounting Firm

To the Shareholders of BFS Equity Fund and

Board of Trustees of Valued Advisers Trust

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of BFS Equity Fund (the “Fund”), a series of Valued Advisers Trust, as of May 31, 2014, and the related statements of operations and changes in net assets, and the financial highlights for the period November 8, 2013 (commencement of operations) through May 31, 2014. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2014 by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the BFS Equity Fund as of May 31, 2014, the results of its operations, the changes in its net assets, and its financial highlights for the period November 8, 2013 (commencement of operations) through May 31, 2014, in conformity with accounting principles generally accepted in the United States of America.

COHEN FUND AUDIT SERVICES, LTD.

Cleveland, Ohio

July 29, 2014

23

Additional Federal Income Tax Information (Unaudited):

Qualified Dividend Income: For the period ended May 31, 2014, the Fund designates 100% of the dividends distributed during the fiscal year as amounts which can be taken into account as a dividend for the purpose of the maximum tax rate under section 1(h)(11) of the Internal Revenue Code.

Dividends Received Deduction: For the period ended May 31, 2014, the Fund designates 100% of the dividends distributed during the fiscal year as qualifying for the dividends-received deduction for corporate shareholders.

The Funds will notify shareholders in January 2015 of amounts for use in preparing 2014 income tax returns.

24

The following table provides information regarding each of the Independent Trustees.

| | | | |

Name, Address*, (Age),

Position with Trust**, Term

of Position with Trust | | Principal Occupation During Past 5 Years | | Other Directorships |

| | |

| Ira Cohen, 55, Independent Trustee, June 2010 to present. | | Independent financial services consultant, since February 2005. | | Trustee, Griffin Institutional Access Real Estate Fund, since June 2014. |

| | |

| Andrea N. Mullins, 47, Independent Trustee, December 2013 to present. | | Private investor; Independent Contractor, Seabridge Wealth Management, LLC, since April 2014; Principal Financial Officer and Treasurer, Eagle Family of Funds (mutual fund family) and Vice President, Eagle Asset Management, Inc. (investment adviser), each from 2004 to 2010. | | None. |

| * | | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | | As of the date of this SAI, the Trust consists of 14 series. |

The following table provides information regarding the Trustee who is considered an “interested person” of the Trust, as that term is defined under the 1940 Act. Based on the experience of the Trustee, the Trust concluded that the individual described below should serve as a Trustee.

| | | | |

Name, Address*, (Age),

Position with Trust**, Term

of Position with Trust | | Principal Occupation During Past 5 Years | | Other Directorships |

| | |

| R. Jeffrey Young, 49, Trustee and Chairman, June 2010 to present. | | Senior Vice President, Huntington Asset Services, Inc., the Trust’s administrator, since January 2010, Director since May 2014; Chief Executive Officer, Huntington Funds, since February 2010; Chief Executive Officer, Huntington Strategy Shares, since November 2010; Director, Unified Financial Securities, Inc., the Trust’s distributor, since May 2014; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2011 to February 2013; Trustee, Valued Advisers Trust, from August 2008 to January 2010; and Managing Director and Chief Operating Officer of Professional Planning Consultants, from 2007 to 2010. | | Trustee, Capitol Series Trust, since September 2013. |

| * | | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | | As of the date of this SAI, the Trust consists of 14 series. |

25

The following table provides information regarding the Officers of the Trust:

| | | | |

Name, Address*, (Age),

Position with Trust,** Term

of Position with Trust | | Principal Occupation During Past 5 Years | | Other Directorships |

| | |

| R. Jeffrey Young, 49, Trustee and Chairman, June 2010 to present; Principal Executive Officer and President, Valued Advisers Trust since February 2010; | | Senior Vice President, Huntington Asset Services, Inc., the Trust’s administrator, since January 2010, Director since May 2014; Chief Executive Officer, Huntington Funds, since February 2010; Chief Executive Officer, Huntington Strategy Shares, since November 2010; Director, Unified Financial Securities, Inc., the Trust’s distributor, since May 2014; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2011 to February 2013; Trustee, Valued Advisers Trust, from August 2008 to January 2010; and Managing Director and Chief Operating Officer, Professional Planning Consultants, from 2007 to 2010. | | Trustee, Capitol Series Trust, since September 2013. |

| | |

| John C. Swhear, 53, Chief Compliance Officer, AML Officer and Vice President, August 2008 to present. | | Vice President of Legal Administration and Compliance, Huntington Asset Services, Inc., the Trust’s administrator, since April 2007, Director since May 2014; Chief Compliance Officer, Unified Financial Securities, Inc., the Trust’s distributor, since May 2007, Director since May 2014; President, Unified Series Trust, since March 2012, and Senior Vice President from May 2007 to March 2012; Chief Compliance Officer and AML Officer, Capitol Series Trust, since September 2013; Secretary, Huntington Funds, from April 2010 to February 2012; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2010 to March 2011, and Vice President and Acting Chief Executive Officer, from 2007 to March 2010. | | None. |

| | |

| Carol J. Highsmith, 49, Vice President, August 2008 to present; Secretary, March 2014 to present | | Employed in various positions with Huntington Asset Services, Inc., the Trust’s administrator, since November of 1994; currently Vice President of Legal Administration. | | None. |

| | |

| Matthew J. Miller, 38, Vice President, December 2011 to present. | | Employed in various positions with Huntington Asset Services, Inc., the Trust’s administrator, since July of 1998; currently Vice President of Relationship Management; Vice President, Huntington Funds, since February 2010; President and Chief Executive Officer, Capitol Series Trust, since September 2013. | | None. |

| | |

| Bryan W. Ashmus, 41, Principal Financial Officer and Treasurer, December 2013 to present. | | Vice President, Financial Administration, Huntington Asset Services, Inc., the Trust’s administrator, since September 2013; Chief Financial Officer and Treasurer, Huntington Strategy Shares and Huntington Funds, since November 2013; Vice President, Treasurer Services, Citi Fund Services Ohio, Inc., from 2005 to 2013. | | None. |

| * | | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | | As of the date of this SAI, the Trust consists of 14 series. |

26

VALUED ADVISERS TRUST

PRIVACY POLICY

The following is a description of the policies of the Valued Advisers Trust (the “Trust”) regarding disclosure of nonpublic personal information that shareholders provide to a series of the Trust (each, a “Fund”) or that the Fund collects from other sources. In the event that a shareholder holds shares of a Fund through a broker-dealer or other financial intermediary, the privacy policy of the financial intermediary would govern how shareholder nonpublic personal information would be shared with nonaffiliated third parties.

Categories of Information a Fund May Collect. A Fund may collect the following nonpublic personal information about its shareholders:

| | • | | Information the Fund receives from a shareholder on applications or other forms, correspondence, or conversations (such as the shareholder’s name, address, phone number, social security number, and date of birth); and |

| | • | | Information about the shareholder’s transactions with the Fund, its affiliates, or others (such as the shareholder’s account number and balance, payment history, cost basis information, and other financial information). |

Categories of Information a Fund May Disclose. A Fund may not disclose any nonpublic personal information about its current or former shareholders to unaffiliated third parties, except as required or permitted by law. A Fund is permitted by law to disclose all of the information it collects, as described above, to its service providers (such as the Fund’s custodian, administrator, transfer agent, accountant and legal counsel) to process shareholder transactions and otherwise provide services to the shareholder.

Confidentiality and Security. Each Fund shall restrict access to shareholder nonpublic personal information to those persons who require such information to provide products or services to the shareholder. Each Fund shall maintain physical, electronic, and procedural safeguards that comply with federal standards to guard shareholder nonpublic personal information.

Disposal of Information. The Funds, through their transfer agent, have taken steps to reasonably ensure that the privacy of a shareholder’s nonpublic personal information is maintained at all times, including in connection with the disposal of information that is no longer required to be maintained by the Funds. Such steps shall include, whenever possible, shredding paper documents and records prior to disposal, requiring off-site storage vendors to shred documents maintained in such locations prior to disposal, and erasing and/or obliterating any data contained on electronic media in such a manner that the information can no longer be read or reconstructed.

27

OTHER INFORMATION

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the trustees and is available without charge, upon request. You may call toll-free at (855) 575-2430 to request a copy of the SAI or to make shareholder inquiries.

28

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted those proxies during the most recent twelve month period ended June 30, will be available without charge upon request by (1) calling the Fund at (855) 575-2430 and (2) from Fund documents filed with the Securities and Exchange Commission (“SEC”) on the SEC’s website at www.sec.gov.

TRUSTEES

R. Jeffrey Young, Chairman

Ira Cohen

Andrea N. Mullins

OFFICERS

R. Jeffrey Young, Principal Executive Officer and President

Bryan W. Ashmus, Principal Financial Officer and Treasurer

John C. Swhear, Chief Compliance Officer, AML Officer and Vice-President

Carol J. Highsmith, Vice President and Secretary

Matthew J. Miller, Vice President

INVESTMENT ADVISER

Bradley, Foster & Sargent, Inc.

185 Asylum Street, City Place II

Hartford, Connecticut 06103

DISTRIBUTOR

Unified Financial Securities, Inc.

2960 North Meridian Street, Suite 300

Indianapolis, IN 46208

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Cohen Fund Audit Services, Ltd.

1350 Euclid Avenue, Suite 800

Cleveland, OH 44115

LEGAL COUNSEL

The Law Offices of John H. Lively & Associates, Inc.

A member firm of The 1940 Act Law Group TM

11300 Tomahawk Creek Parkway, Suite 310

Leawood, KS 66211

CUSTODIAN

Huntington National Bank

41 South High Street

Columbus, OH 43215

ADMINISTRATOR, TRANSFER AGENT AND FUND ACCOUNTANT

Huntington Asset Services, Inc.

2960 North Meridian Street, Suite 300

Indianapolis, IN 46208

This report is intended only for the information of shareholders or those who have received the Fund’s prospectus which contains information about the Fund’s management fee and expenses. Please read the prospectus carefully before investing.

Distributed by Unified Financial Securities, Inc.

Member FINRA/SIPC

ANNUAL REPORT

May 31, 2014

CLOUD CAPITAL FUNDS

Cloud Capital Strategic Large Cap Fund

Cloud Capital Strategic Mid Cap Fund

Fund Adviser:

Cloud Capital LLC

5314 South Yale, Suite 606

Tulsa, OK 74135

Toll Free (877) 670-2227

Management’s Discussion of Fund Performance

We welcome and thank all new and existing shareholders of the Cloud Capital mutual funds.

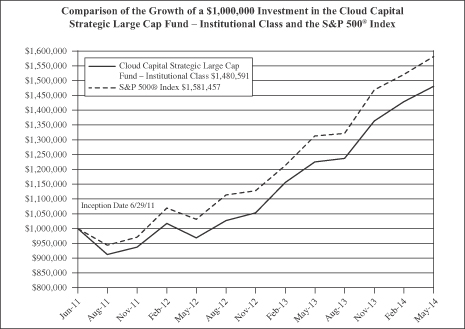

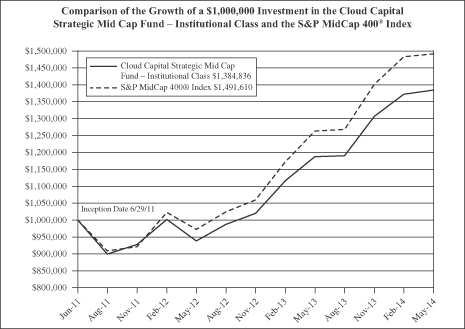

In the fiscal year ended May 31, 2014, both the Cloud Capital Strategic Large Cap Fund (the “Large Cap Fund”) and the Cloud Capital Strategic Mid Cap Fund (the “Mid Cap Fund”) (each a “Fund” and, collectively the “Funds”) experienced strong growth. The Large Cap Fund gained 20.8%, ahead of S&P 500® Index total return by 0.4% and ahead of its peer group by 1.7%. The Mid Cap Fund gained 16.7% for the year, short of the S&P MidCap 400® Index total return by 1.4%. The expenses of operating the Mid Cap Fund were responsible for much of the lag against the benchmark’s performance.

The Funds endured a terrible start, opening into a 20% market correction, but have largely managed to overcome that. The Large Cap Fund is within 20 bps of its benchmark over the last two years, and ranks in the top quartile of the Large Blend peer group for the trailing twelve months. The Mid Cap Fund has been slower to recover, but is beginning to catch up to its benchmark and peer group.

The U.S. market has extended its bull run for over five years now, setting new historical highs regularly over the past year, despite slow growth in the overall economy. While portfolios grow, we at Cloud Capital LLC (“Cloud Capital”) can’t help but remember the beginning of 2007, when disparities between the stock market and the economy were growing and were largely ignored. While we want to continue to enjoy the fruits of the market rally as long as possible, it is also important to us to have our shareholders’ assets in a position of safety when the rally concludes.

The Funds are now operating at a lower gross expense ratio with the waiver of a management fee, which should bolster performance even more going forward.

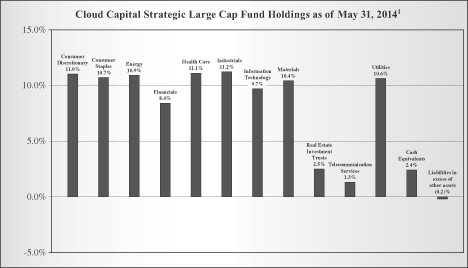

In the Large Cap Fund, the stock selections within the portfolio were very successful over the past year, with the Large Cap Fund outperforming the benchmark in all ten GICS Sectors. The sector-neutral approach employed in the Fund also enhanced performance, winning seven of ten sectors versus the benchmark.

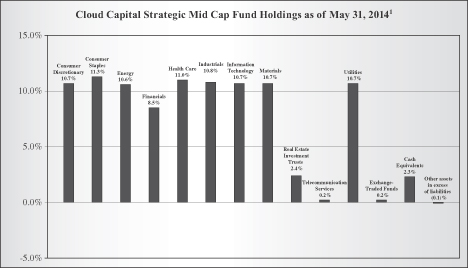

During that same period, the Mid Cap Fund found greater success in the sector-neutral strategy, with eight of ten GICS sectors besting the benchmark allocation. All ten sectors gained at least 13.8% over the fiscal year, led by the Health Care sector with 25.3%. Cash drag had a greater effect on the Mid Cap Fund than the Large Cap Fund during this period, and hindered performance against the index, which doesn’t have to concern itself with liquidity or operating expenses.

Although the market appears to be resuming historical cyclical growth, the truth is the after-effects of continued stimulus that have flowed into the market over the past

1

several years are still unclear. The core strategy of the Funds, which has historically outperformed the benchmark 76% of the time over rolling one-year periods, would benefit greatly from a return to the good old days. However, we are vigilant for unforeseen consequences of artificially driving the markets through stimulus, and especially the effects of withdrawing that support, as will have to eventually happen.

Again, we thank our shareholders for their continued confidence in Cloud Capital LLC, and with another fiscal year behind us, we look forward to many more years of serving them.

Sincerely,

Randy Cloud

Cloud Capital LLC, President

2

Cloud Capital Strategic Large Cap Fund

Investment Results – (Unaudited)

Total Returns *

(For the periods ended May 31, 2014)

| | | | | | | | |

| | | | | | Average Annual

Returns | |

| | | One Year | | | Since Inception

(June 29, 2011) | |

Cloud Capital Strategic Large Cap Fund –Institutional Class | | | 20.81 | % | | | 14.35 | % |

S&P 500® Index** | | | 20.45 | % | | | 16.96 | % |

Total annual operating expenses, as disclosed in the Fund’s prospectus dated February 26, 2014, were 1.41% of average daily net assets (0.91% after fee waivers/expense reimbursements by Cloud Capital LLC (the Adviser)). The Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Large Cap Fund effective February 1, 2014 through September 30, 2015, so that Total Annual Fund Operating Expenses does not exceed 1.40%. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, and indirect expenses (such as “Acquired Fund Fees and Expenses”). The Adviser shall not be entitled to reimbursement for any advisory fees waived for the period February 1, 2014 through September 30, 2015. However, for the periods prior to this, the Adviser may be entitled to the reimbursement of any fees waived or expenses reimbursed pursuant to prior expense limitation agreements provided overall expenses fall below the limitations set forth above. The Adviser may recoup the sum of all fees previously waived or expenses reimbursed during any of the previous three (3) years, less any reimbursement previously paid, provided total expenses do not exceed the limitation set forth above. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Current performance of a Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-877-670-2227.

* Return figures reflect any change in price per share and assume the reinvestment of all distributions.

** The S&P 500® Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The Index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company and may be obtained by calling 1-877-670-2227. Please read it carefully before investing.

The Fund is distributed by Unified Financial Securities, Inc., Member FINRA.

3

The chart above assumes an initial investment of $1,000,000 made on June 29, 2011 (commencement of Fund operations) and held through May 31, 2014. THE FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund’s shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.