UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22208

Valued Advisers Trust

(Exact name of registrant as specified in charter)

Huntington Asset Services, Inc. 2960 N. Meridian Street, Suite 300 Indianapolis, IN 46208

(Address of principal executive offices) (Zip code)

Capitol Services, Inc.

615 S. Dupont Hwy.

Dover, DE 19901

(Name and address of agent for service)

With a copy to:

John H. Lively, Esq.

The Law Offices of John H. Lively & Associates, Inc.

A member firm of The 1940 Act Law GroupTM

11300 Tomahawk Creek Parkway,

Suite 310

Leawood, KS 66221

Registrant’s telephone number, including area code: 317-917-7000

Date of fiscal year end: 1/31

Date of reporting period: 1/31/15

Item 1. Reports to Stockholders.

Golub Group Equity Fund

Annual Report

January 31, 2015

Fund Adviser:

Golub Group, LLC

1850 Gateway Drive, Suite 100

San Mateo, CA 94404

Toll Free (866) 954-6682

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE FOR THE FISCAL YEAR ENDING JANUARY 31, 2015 – (Unaudited)

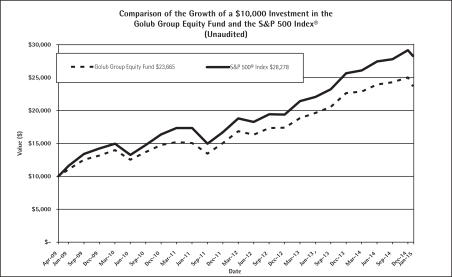

The Golub Group Equity Fund (“Fund”) returned 8.74% for the fiscal year ending January 31, 2015. In comparison, our benchmark, the S&P 500 Index®*, gained 14.22% during the same period. Since inception on April 1, 2009, the Fund has returned 136.65% as compared to the 182.78% return of the benchmark.

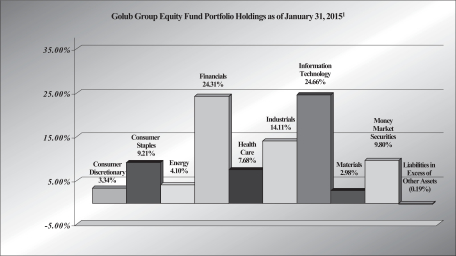

Performance for the period was led by strong returns from the Healthcare, Industrial, and Consumer Staples. Despite being underweight relative to the benchmark (9.9% of portfolio weight vs. 14.1% benchmark weight), the portfolio benefited most from its allocation to Healthcare, which was the second best performing sector in the S&P 500. Healthcare stocks returned 27% for the period paced by strong returns in Hospira and Teva Pharmaceuticals. Our overweight position in Industrials (16.0% of portfolio weight vs. 11.2% benchmark weight) was our second largest contributor to performance as the U.S. and global economy continue to show modest improvement. Consumer Staples (10.5% of portfolio) returned 14.8% outpacing the benchmark. Our Technology holdings continued their strong performance with our top performing stock, Apple, driving results. Apple, Hospira and Northrop Grumman, were the largest positive contributors and returned 67.4%, 45.0% and 41.5% respectively. Ebay ended the period as our largest holding followed by Bank of America, Microsoft and Citigroup.

Despite significantly reducing our exposure to the energy sector early in the year, the sector was the largest detractor to performance. In addition, the Fund’s underweight position in the Consumer Cyclical sector (6.8% of portfolio weight vs. 10.5% benchmark weight) acted as a drag as the Consumer Cyclical sector was a strong performer on rebounding consumer confidence and spending. Lastly, our cash position, which closed the period at 9.8% of the Fund and generated virtually no return for the year, acted as a drag on performance. National Oilwell Varco was our worst performing stock falling 16.2% during the period.

During the period, we added the following four (4) new positions to the Fund: CR Bard, Deere, Owens-Illinois, and Flowserve. During the period we sold the following eight (8) positions in their entirety: Chevron, Intel, Exxon, Cisco, Johnson and Johnson, and United Parcel Service.

In addition to the stock and security selection, Golub Group, LLC (the “Adviser”) continues to waive fees and reimburse expenses above the Fund’s expense limitation cap. Had the Adviser not waived and reimbursed these expenses, the performance of the Fund would have been lower.

1

We remain focused on our long term discipline of investing in high-quality, large-cap, dividend-paying businesses that trade at attractive valuations and are confident that our style of investing is particularly well-suited for the period ahead.

Sincerely,

Golub Group, LLC

* The S&P 500® Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. Individuals cannot invest directly in the Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

The views in the foregoing discussion were those of the Fund’s Adviser as of January 31, 2015 and may not reflect its views on the date this Annual Report is first published or anytime thereafter. These views are intended to assist shareholders in understanding their investment in the Fund and do not constitute investment advice.

The performance information quoted above represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling the Fund at 1-866-954-6682. Fee waivers and expense reimbursements have positively impacted Fund performance. An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing. The Fund’s Prospectus contains this and other important information. For information on the Fund’s expense ratio, please see the Financial Highlights Table found within the accompanying Annual Report.

2

Investment Results – (Unaudited)

Total Returns*

(For the periods ended January 31, 2015)

| Average Annual | ||||||||||||||||

| 1 Year | 3 Year | 5 Year | Since Inception (April 1, 2009) | |||||||||||||

Golub Group Equity Fund | 8.74% | 14.99% | 12.84% | 15.90% | ||||||||||||

S&P 500® Index** | 14.22% | 17.47% | 15.60% | 19.49% | ||||||||||||

| Total annual operating expenses, as disclosed in the most recent supplement to the Fund’s prospectus, dated May 30, 2014, were 1.46% of average daily net assets (1.26% after fee waivers/expense reimbursements by the Adviser.) The Adviser has contractually agreed to waive or limit its fees and assume other expenses of the Fund until May 31, 2015, so that Total Annual Fund Operating Expenses do not exceed 1.25%. This contractual arrangement may only be terminated by mutual consent of the Adviser and the Fund, and it will automatically terminate upon the termination of the investment advisory agreement between the Fund and the Adviser. This operating expense limitation does not apply to: (i) interest, (ii) taxes, (iii) brokerage commissions, (iv) other expenditures which are capitalized in accordance with generally accepted accounting principles, (v) other extraordinary expenses not incurred in the ordinary course of the Fund’s business, (vi) dividend expense on short sales, (vii) expenses incurred under a plan of distribution under Rule 12b-1, and (viii) expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, incurred by the Fund in any fiscal year. The operating expense limitation also excludes any “Fees and Expense of Acquired Funds,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including ETFs, that have their own expenses. The Adviser may recoup the sum of all fees previously waived or expenses reimbursed during any of the previous three (3) years, less any reimbursement previously paid, provided total expenses do not exceed the limitation set forth above or at the time of the original waiver, whichever is lower. | ||||||||||||||||

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance of the Fund may be lower or higher than the performance quoted. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Performance data current to the most recent month end may be obtained by calling 1-866-954-6682.

* Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower.

** The S&P 500® Index is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Fund’s portfolio. Individuals cannot invest directly in the Index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

The Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Fund is distributed by Unified Financial Securities, Inc., member FINRA.

3

Investment Results – (Unaudited) (continued)

The chart above assumes an initial investment of $10,000 made on April 1, 2009 (commencement of Fund operations) and held through January 31, 2015. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call 1-866-954-6682. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Unified Financial Securities, Inc., member FINRA.

4

Fund Holdings – (Unaudited)

| 1 | As a percentage of net assets. |

The investment objective of the Golub Group Equity Fund is to provide long-term capital appreciation. A secondary objective is to provide current income.

Availability of Portfolio Schedule – (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available at the SEC’s website at www.sec.gov. The Fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

5

Summary of Fund’s Expenses – (Unaudited)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees, distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning and held for the entire period from August 1, 2014 to January 31, 2015.

Actual Expenses

The “Actual” line of the table provide information about actual account values and actual expenses. You may use the information on this line for the class of shares you hold, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the “Actual” line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The “Hypothetical” line of the table provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios for each class of shares and an assumed rate of return of 5% per year before expenses, which are not the Fund’s actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the “Actual” and “Hypothetical” lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value | Ending Account Value | Expenses Paid During the Period Ended | ||||||||||

| August 1, 2014 | January 31, 2015 | January 31, 2015 | ||||||||||

Golub Group Equity Fund | ||||||||||||

Actual* | $ | 1,000.00 | $ | 998.30 | $ | 6.30 | ||||||

Hypothetical** | $ | 1,000.00 | $ | 1,018.90 | $ | 6.36 | ||||||

| * | Expenses are equal to the Fund’s annualized net expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 184/365. |

| ** | Assumes a 5% return before expenses. |

6

Schedule of Investments

January 31, 2015

| Shares | Fair Value | |||||||

| Common Stocks – 90.39% | ||||||||

| Consumer Discretionary 3.34% | ||||||||

| 47,335 | General Motors Co. | $ | 1,544,068 | |||||

|

| |||||||

| Consumer Staples 9.21% | ||||||||

| 8,575 | Anheuser-Busch InBev NV ADR | 1,046,750 | ||||||

| 33,950 | Coca-Cola Co./The | 1,397,722 | ||||||

| 9,265 | Diageo PLC ADR | 1,094,474 | ||||||

| 7,670 | PepsiCo, Inc. | 719,293 | ||||||

|

| |||||||

| 4,258,239 | ||||||||

|

| |||||||

| Energy 4.10% | ||||||||

| 12,330 | Devon Energy Corp. | 743,129 | ||||||

| 21,215 | National Oilwell Varco, Inc. | 1,154,733 | ||||||

|

| |||||||

| 1,897,862 | ||||||||

|

| |||||||

| Financials 24.31% | ||||||||

| 41,170 | American International Group, Inc. | 2,011,978 | ||||||

| 148,900 | Bank of America Corp. | 2,255,835 | ||||||

| 48,420 | Bank of New York Mellon Corp./The | 1,743,120 | ||||||

| 13,050 | Berkshire Hathaway, Inc. – Class B* | 1,878,026 | ||||||

| 46,715 | Citigroup, Inc. | 2,193,269 | ||||||

| 22,350 | Wells Fargo & Co. | 1,160,412 | ||||||

|

| |||||||

| 11,242,640 | ||||||||

|

| |||||||

| Health Care 7.68% | ||||||||

| 5,835 | C.R. Bard, Inc. | 997,960 | ||||||

| 16,710 | Hospira, Inc.* | 1,059,915 | ||||||

| 26,300 | Teva Pharmaceutical Industries Ltd. ADR | 1,495,418 | ||||||

|

| |||||||

| 3,553,293 | ||||||||

|

| |||||||

| Industrials 14.11% | ||||||||

| 8,260 | Deere & Co. | 703,669 | ||||||

| 5,675 | FedEx Corp. | 959,699 | ||||||

| 25,110 | Flowserve Corp. | 1,368,244 | ||||||

| 74,935 | General Electric Co. | 1,790,197 | ||||||

| 6,300 | Northrop Grumman Corp. | 988,785 | ||||||

| 6,225 | United Technologies Corp. | 714,506 | ||||||

|

| |||||||

| 6,525,100 | ||||||||

|

| |||||||

| Information Technology 24.66% | ||||||||

| 13,250 | Apple, Inc. | 1,552,370 | ||||||

| 43,035 | eBay, Inc.* | 2,280,855 | ||||||

| 20,770 | Fiserv, Inc.* | 1,506,448 | ||||||

| 3,655 | Google, Inc. – Class A* | 1,964,745 | ||||||

| 1,050 | Google, Inc. – Class C* | 561,246 | ||||||

| 55,535 | Microsoft Corp. | 2,243,614 | ||||||

| 20,735 | QUALCOMM, Inc. | 1,295,108 | ||||||

|

| |||||||

| 11,404,386 | ||||||||

|

| |||||||

See accompanying notes which are an integral part of the financial statements.

7

Schedule of Investments (continued)

January 31, 2015

| Shares | Fair Value | |||||||

| Common Stocks – (continued) | ||||||||

| Materials 2.98% | ||||||||

| 58,995 | Owens-Illinois, Inc.* | $ | 1,377,533 | |||||

|

| |||||||

Total Common Stocks (Cost $34,042,822) | 41,803,121 | |||||||

|

| |||||||

| Money Market Securities – 9.80% | ||||||||

| 4,533,375 | Fidelity Institutional Money Market Portfolio – Institutional Class, 0.11%(a) | 4,533,375 | ||||||

|

| |||||||

Total Money Market Securities (Cost $4,533,375) | 4,533,375 | |||||||

|

| |||||||

Total Investments (Cost $38,576,197) 100.19% | 46,336,496 | |||||||

|

| |||||||

Liabilities in Excess of Other Assets (0.19)% | (87,400 | ) | ||||||

|

| |||||||

TOTAL NET ASSETS 100.00% | $ | 46,249,096 | ||||||

|

| |||||||

| (a) | Rate disclosed is the seven day yield as of January 31, 2015. |

| * | Non-income producing security. |

| ADR | – American Depositary Receipt |

See accompanying notes which are an integral part of the financial statements.

8

Statement of Assets and Liabilities

January 31, 2015

Assets | ||||

Investments in securities at fair value (cost $38,576,197) | $ | 46,336,496 | ||

Dividends receivable | 15,322 | |||

Prepaid expenses | 4,084 | |||

Total Assets | 46,355,902 | |||

Liabilities | ||||

Payable for fund shares redeemed | 19,550 | |||

Payable to Adviser | 33,135 | |||

Payable to administrator, fund accountant, transfer agent, and chief compliance officer | 27,623 | |||

Payable to custodian | 1,206 | |||

Payable to trustees | 647 | |||

Other accrued expenses | 24,645 | |||

Total Liabilities | 106,806 | |||

Net Assets | $ | 46,249,096 | ||

Net Assets consist of: | ||||

Paid-in capital | $ | 36,540,771 | ||

Accumulated undistributed net investment loss | (22,009 | ) | ||

Accumulated undistributed net realized gain from investments | 1,970,035 | |||

Net unrealized appreciation on investments | 7,760,299 | |||

Net Assets | $ | 46,249,096 | ||

Shares outstanding (unlimited number of shares authorized, no par value) | 2,571,630 | |||

Net asset value, offering and redemption price per share | $ | 17.98 |

9

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

For the year ended January 31, 2015

Investment Income | ||||

Dividend income (net of foreign taxes withheld of $12,410) | $ | 728,346 | ||

Total investment income | 728,346 | |||

Expenses | ||||

Investment Adviser | 460,081 | |||

Administration | 45,095 | |||

Fund accounting | 25,000 | |||

Transfer agent | 35,244 | |||

Legal | 17,911 | |||

Registration | 6,448 | |||

Custodian | 7,520 | |||

Audit | 15,000 | |||

Trustee | 5,421 | |||

Printing | 15,445 | |||

Miscellaneous | 7,026 | |||

Total expenses | 640,191 | |||

Fees waived by Adviser | (64,918 | ) | ||

Net operating expenses | 575,273 | |||

Net investment income | 153,073 | |||

Net Realized and Unrealized Gain on Investments | ||||

Net realized gain on investment securities transactions | 4,334,747 | |||

Net change in unrealized appreciation/(depreciation) of investment securities | (868,271 | ) | ||

Net realized and unrealized gain on investments | 3,466,476 | |||

Net increase in net assets resulting from operations | $ | 3,619,549 |

10

See accompanying notes which are an integral part of the financial statements.

Statements of Changes in Net Assets

For the Year Ended January 31, 2015 | For the Year Ended January 31, 2014 | |||||||

Increase in Net Assets due to: Operations | ||||||||

Net investment income | $ | 153,073 | $ | 215,423 | ||||

Net realized gain on investment securities transactions | 4,334,747 | 2,997,985 | ||||||

Net change in unrealized appreciation (depreciation) of investments | (868,271 | ) | 3,420,746 | |||||

Net increase in net assets resulting from operations | 3,619,549 | 6,634,154 | ||||||

Distributions From: | ||||||||

Net investment income | (162,447 | ) | (220,112 | ) | ||||

Net realized gains | (3,625,526 | ) | (1,972,205 | ) | ||||

Total distributions | (3,787,973 | ) | (2,192,317 | ) | ||||

Capital Transactions | ||||||||

Proceeds from shares sold | 11,749,584 | 7,788,369 | ||||||

Reinvestment of distributions | 3,787,973 | 2,192,317 | ||||||

Amount paid for shares redeemed | (10,204,265 | ) | (5,855,754 | ) | ||||

Net increase in net assets resulting from | 5,333,292 | 4,124,932 | ||||||

Total Increase in Net Assets | 5,164,868 | 8,566,769 | ||||||

Net Assets | ||||||||

Beginning of year | 41,084,228 | 32,517,459 | ||||||

End of year | $ | 46,249,096 | $ | 41,084,228 | ||||

Accumulated undistributed net investment loss included in net assets at end of year | $ | (22,009 | ) | $ | (12,635 | ) | ||

Share Transactions | ||||||||

Shares sold | 602,198 | 438,267 | ||||||

Shares issued in reinvestment of distributions | 204,755 | 121,931 | ||||||

Shares redeemed | (525,320 | ) | (333,667 | ) | ||||

Net increase in share transactions | 281,633 | 226,531 | ||||||

11

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

(For a share outstanding during each year)

| For the Year Ended January 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

Selected Per Share Data |

| |||||||||||||||||||

Net asset value, beginning of year | $17.94 | $15.76 | $14.00 | $14.58 | $12.85 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Investment operations: | ||||||||||||||||||||

Net investment income | 0.07 | 0.10 | (a) | 0.14 | (a) | 0.15 | (a) | 0.11 | (a) | |||||||||||

Net realized and unrealized gain on investments | 1.54 | 3.09 | 2.12 | 0.20 | 2.09 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations | 1.61 | 3.19 | 2.26 | 0.35 | 2.20 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Less distributions to shareholders: | ||||||||||||||||||||

From net investment income | (0.07 | ) | (0.10 | ) | (0.14 | ) | (0.14 | ) | (0.09 | ) | ||||||||||

From net realized gains | (1.50 | ) | (0.91 | ) | (0.36 | ) | (0.79 | ) | (0.38 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (1.57 | ) | (1.01 | ) | (0.50 | ) | (0.93 | ) | (0.47 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $17.98 | $17.94 | $15.76 | $14.00 | $14.58 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return(b) | 8.74 | % | 20.20 | % | 16.34 | % | 2.65 | % | 17.20 | % | ||||||||||

Ratios and Supplemental Data: |

| |||||||||||||||||||

Net assets, end of year (000) | $46,249 | $41,084 | $32,517 | $23,946 | $19,574 | |||||||||||||||

Ratio of expenses to average net assets after expense waiver and reimbursement | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||

Ratio of expenses to average net assets before expense waiver and reimbursement | 1.39 | % | 1.45 | % | 1.57 | % | 1.75 | % | 2.21 | % | ||||||||||

Ratio of net investment income to average net assets after expense waiver and reimbursement | 0.33 | % | 0.58 | % | 0.95 | % | 1.03 | % | 0.82 | % | ||||||||||

Ratio of net investment income to average net assets before expense waiver and reimbursement | 0.19 | % | 0.38 | % | 0.63 | % | 0.53 | % | (0.14 | )% | ||||||||||

Portfolio turnover rate | 34.45 | % | 29.83 | % | 16.79 | % | 27.33 | % | 23.15 | % | ||||||||||

| (a) | Net investment income per share is calculated by dividing net investment income by the average shares outstanding throughout the year. |

| (b) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

12

See accompanying notes which are an integral part of the financial statements.

Notes to the Financial Statements

January 31, 2015

NOTE 1. ORGANIZATION

The Golub Group Equity Fund (the “Fund”) was organized as an open-end diversified series of the Valued Advisers Trust (the “Trust”) on April 1, 2009. The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees (the “Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds authorized by the Board. The Fund’s investment adviser is Golub Group, LLC (the “Adviser”). The investment objective of the Fund is to provide long-term capital appreciation. A secondary objective is to provide current income.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Securities Valuation – All investments in securities are recorded at their estimated fair value as described in Note 3.

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of and during the fiscal year ended January 31, 2015, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the year, the Fund did not incur any interest or penalties. The Fund is subject to examination by U.S. federal tax authorities for the last three tax year ends and the interim tax period since then.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income - The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. The specific identification method is used for determining gains or losses for financial statement and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Discounts and premiums on securities purchased are accreted or amortized using the effective interest method. The ability of issuers of debt securities held by the Fund to meet their obligations may be affected by economic and political developments in a specific country or region.

13

Notes to the Financial Statements (continued)

January 31, 2015

Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Dividends and Distributions – The Fund intends to distribute all or substantially all of its net investment income, if any, as dividends to its shareholders on at least an annual basis. The Fund intends to distribute its net realized long term capital gains and its net realized short term capital gains, if any, at least once a year. Dividends to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Fund. There were no such material reclassifications made as of January 31, 2015.

NOTE 3. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

Fair value is defined as the price that a Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| • | Level 1 – quoted prices in active markets for identical securities |

| • | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value

14

Notes to the Financial Statements (continued)

January 31, 2015

measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities, including common stocks, are generally valued by using market quotations, but may be valued on the basis of prices furnished by a pricing service when the Adviser believes such prices more accurately reflect the fair value of such securities. Securities that are traded on any stock exchange are generally valued by the pricing service at the last quoted sale price. Lacking a last sale price, an exchange traded security is generally valued by the pricing service at its last bid price. Securities traded in the NASDAQ over-the-counter market are generally valued by the pricing service at the NASDAQ Official Closing Price.

When using the market quotations or close prices provided by the pricing service and when the market is considered active, the security will be classified as a Level 1 security. Sometimes, an equity security owned by the Fund will be valued by the pricing service with factors other than market quotations or when the market is considered inactive. When this happens, the security will be classified as a Level 2 security. When market quotations are not readily available, when the Adviser determines that the market quotation or the price provided by the pricing service does not accurately reflect the current fair value, or when restricted or illiquid securities are being valued, such securities are valued as determined in good faith by the Adviser, in conformity with guidelines adopted by and subject to review by the Board. These securities are generally categorized as Level 3 securities.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending net asset value (“NAV”) provided by the service agent of the funds. These securities are categorized as Level 1 securities.

In accordance with the Trust’s good faith pricing guidelines, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Adviser would appear to be the amount which the owner might reasonably expect to receive for them upon their current sale. Methods which are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Good faith pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before a Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations. Good faith pricing may also be used in instances when the bonds the Fund invests in may default or otherwise cease to have market quotations readily available. Any fair valuation pricing done outside the Fund’s approved pricing methods must be approved by the Pricing Committee of the Board.

15

Notes to the Financial Statements (continued)

January 31, 2015

The following is a summary of the inputs used to value the Fund’s investments as of January 31, 2015:

| Valuation Inputs | ||||||||||||||||

| Assets | Level 1 Quoted Prices in Active Markets | Level 2 Other Significant Observable Inputs | Level 3 Significant | Total | ||||||||||||

Common Stocks* | $ | 41,803,121 | $ | – | $ | – | $ | 41,803,121 | ||||||||

Money Market Securities | 4,533,375 | – | – | 4,533,375 | ||||||||||||

Total | $ | 46,336,496 | $ | – | $ | – | $ | 46,336,496 | ||||||||

| * | Refer to the Schedule of Investments for industry classifications. |

The Fund did not hold any investments at any time during the reporting period in which significant unobservable inputs were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period. The Fund did not hold any derivative instruments during the reporting period.

The Trust recognizes transfers between fair value hierarchy levels at the end of the reporting period. There were no transfers between any levels as of January 31, 2015 and the previous reporting period end.

NOTE 4. FEES AND OTHER TRANSACTIONS WITH AFFILIATES

Under the terms of the investment advisory agreement, on behalf of the Fund (the “Agreement”), the Adviser manages the Fund’s investments subject to oversight of the Board. As compensation for its services, the Fund is obligated to pay the Adviser a fee computed and accrued daily and paid monthly at an annual rate of 1.00% of the average daily net assets of the Fund. For the fiscal year ended January 31, 2015, the Adviser earned a fee of $460,081 from the Fund before the waivers described below. At January 31, 2015, the Fund owed the Adviser $33,135.

The Adviser has contractually agreed to waive or limit its fee and reimburse certain Fund operating expenses, until May 31, 2015, so that the ratio of total annual operating expenses does not exceed 1.25%. This operating expense limitation does not apply to interest, taxes, brokerage commissions, other expenditures which are capitalized in accordance with generally accepted accounting principles, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, dividend expense on short sales, expenses incurred under a plan of distribution under Rule 12b-1, and expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, incurred by the Fund in any fiscal year. The operating expense limitation also excludes any “Acquired Fund Fees and Expenses.” Acquired Fund Fees and Expenses represent the pro rata expense indirectly incurred by the Fund as a result of investing in other investment companies, including ETFs, closed-end funds and money market funds that have their own expenses. The Adviser may be entitled to the reimbursement of any fees waived or expenses reimbursed pursuant to the agreement provided overall expenses fall below the limitations set forth above. The Adviser may recoup the sum of all fees previously waived or expenses reimbursed during any of the previous three (3) years, less any reimbursement previously paid, provided total expenses do not exceed the limitation set forth above. For the year ended January 31, 2015, the Adviser waived fees of $64,918.

16

Notes to the Financial Statements (continued)

January 31, 2015

The amounts subject to repayment by the Fund, pursuant to the aforementioned conditions, at January 31, 2015 are as follows:

| Amount | Recoverable through January 31, | |||

| $91,129 | 2016 | |||

| $74,349 | 2017 | |||

| $64,918 | 2018 | |||

The Trust retains Huntington Asset Services, Inc. (“HASI”) to manage the Fund’s business affairs and provide the Fund with administrative and compliance services, including all regulatory reporting and necessary office equipment and personnel. For the fiscal year ended January 31, 2015, HASI earned fees of $45,095 for administrative and compliance services provided to the Fund. At January 31, 2015, HASI was owed $12,553 from the Fund for administrative and compliance services. Certain officers and one Trustee of the Trust are members of management and/or employees of HASI. HASI is a wholly-owned subsidiary of Huntington Bancshares, Inc., the parent company of Unified Financial Securities, Inc. (the “Distributor”) and Huntington National Bank, the custodian of the Fund’s investments (the “Custodian”). For the fiscal year ended January 31, 2015, the Custodian earned fees of $7,520 for custody services provided to the Fund. At January 31, 2015, the Custodian was owed $1,206 from the Fund for custody services.

The Trust also retains HASI to act as the Fund’s transfer agent and to provide fund accounting services. For the fiscal year ended January 31, 2015, HASI earned fees of $35,244 for transfer agent services to the Fund. At January 31, 2015, the Fund owed HASI $8,820 for transfer agent services. For the fiscal year ended January 31, 2015, HASI earned fees of $25,000 from the Fund for fund accounting services. At January 31, 2015, HASI was owed $6,250 from the Fund for fund accounting services.

The Fund has adopted a Distribution Plan pursuant to Rule 12b-1 under the 1940 Act (the “Plan”). The Plan provides that the Fund will pay the Distributor and/or any registered securities dealer, financial institution or any other person (the “Recipient”) a shareholder servicing fee of 0.25% of the average daily net assets of the Fund in connection with the promotion and distribution of the Fund’s shares or the provision of personal services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, the printing and mailing of sales literature and servicing shareholder accounts (“12b-1 Expenses”). The Fund or Distributor may pay all or a portion of these fees to any recipient who renders assistance in distributing or promoting the sale of shares, or who provides certain shareholder services, pursuant to a written agreement. The Plan is a compensation plan, which means that the Plan will benefit shareholders because an effective sales program typically is necessary in order for the Fund to reach and maintain a sufficient size to achieve efficiently its investment objectives and to realize economies of scale. The Plan is not active and will not be activated prior to May 31, 2015.

Unified Financial Securities, Inc. acts as the principal distributor of the Fund’s shares. There were no payments made by the Fund to the Distributor during the fiscal year ended January 31, 2015. An officer of the Trust is an officer of the Distributor and such person may be deemed to be an affiliate of the Distributor.

17

Notes to the Financial Statements (continued)

January 31, 2015

NOTE 5. PURCHASES AND SALES OF SECURITIES

For the fiscal year ended January 31, 2015, purchases and sales of investment securities, other than short-term investments and short-term U.S. government obligations, were as follows:

| Amount | ||||

Purchases | ||||

U.S. Government Obligations | $ | – | ||

Other | 15,865,603 | |||

Sales | ||||

U.S. Government Obligations | $ | – | ||

Other | 14,406,937 | |||

NOTE 6. ESTIMATES

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

NOTE 7. BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a) (9) of the Investment Company Act of 1940. At January 31, 2015, Charles Schwab Corporation owned, as record shareholder, 94% of the outstanding shares of the Fund. It is not known whether Charles Schwab Corporation or any of the underlying beneficial owners owned or controlled 25% or more of the voting securities of the Fund.

NOTE 8. FEDERAL TAX INFORMATION

At January 31, 2015, the net unrealized appreciation (depreciation) of investments for tax purposes was as follows:

Gross Appreciation | $ | 8,445,438 | ||

Gross (Depreciation) | (685,658 | ) | ||

Net Appreciation (Depreciation) on Investments | $ | 7,759,780 |

At January 31, 2015, the aggregate cost of securities for federal income tax purposes was $38,576,716 for the Fund.

The tax characterization of distributions for the fiscal years ended January 31, 2015 and January 31, 2014, were as follows:

| 2015 | 2014 | |||||||

Distributions paid from: | ||||||||

Ordinary Income* | $ | 310,062 | $ | 463,691 | ||||

Long-Term Capital Gain | 3,477,911 | 1,728,626 | ||||||

| $ | 3,787,973 | $ | 2,192,317 | |||||

| * | Short-term capital gain distributions are treated as ordinary income for tax purposes. |

18

Notes to the Financial Statements (continued)

January 31, 2015

At January 31, 2015, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

Undistributed Ordinary Income | $ | 18,625 | ||

Undistributed long-term capital gains | 1,951,929 | |||

Accumulated capital and other losses | (22,009 | ) | ||

Unrealized appreciation (depreciation) | 7,759,780 | |||

| $ | 9,708,325 |

At January 31, 2015, the difference between book basis and tax basis unrealized appreciation (depreciation) is attributable to the tax deferral of losses on wash sales in the amount of $519.

Under current tax law, net investment losses after December 31 and capital losses realized after October 31 of a Fund’s fiscal year may be deferred and treated as occurring on the first business day of the following fiscal year for tax purposes. The Fund deferred losses as follows:

Qualified Late Year |

| $22,009 |

NOTE 9. COMMITMENTS AND CONTINGENCIES

The Fund indemnifies its officers and trustees for certain liabilities that may arise from their performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

NOTE 10. SUBSEQUENT EVENT

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date these financial statements were issued. Based upon this evaluation, management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

NOTE 11. PROXY VOTING RESULTS (UNAUDITED)

On December 19, 2014 a special meeting of the shareholders of the Trust was held at the offices of the Trust for the purpose of electing each nominee to the Board of Trustees.

Below are the voting results for all funds from the special meeting of the Trust:

To elect each nominee to the Board of Trustees:

| For | Against | Abstain | ||||||||||

Ira Cohen | 280,591,916 | 20,930,930 | – | |||||||||

Andrea N. Mullins | 296,332,857 | 5,189,989 | – | |||||||||

R. Jeffrey Young | 280,517,160 | 21,005,685 | – | |||||||||

19

Report of Independent Registered Public Accounting Firm

To the Shareholders of Golub Group Equity Fund and

Board of Trustees of Valued Advisers Trust

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Golub Group Equity Fund (the “Fund”), a series of Valued Advisers Trust, as of January 31, 2015, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights for the periods ended prior to January 31, 2012, were audited by other auditors whose report dated March 22, 2011 expressed an unqualified opinion on those financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of January 31, 2015, by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Golub Group Equity Fund as of January 31, 2015, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

COHEN FUND AUDIT SERVICES, LTD.

Cleveland, Ohio

March 30, 2015

20

Additional Federal Income Tax Information (Unaudited)

The Form 1099-DIV you received in January 2015 will show the tax status of all distributions paid to your account in calendar year 2014. Shareholders are advised to consult their own tax adviser with respect to the tax consequences of their investment in the Fund. As required by the Internal Revenue Code and/or regulations, shareholders must be notified regarding the status of qualified dividend income for individuals and the dividends received deduction for corporations.

Qualified Dividend Income. The Fund designates approximately 100% or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for the reduced tax rate of 15%.

Dividends Received Deduction. Corporate shareholders are generally entitled to take the dividends received deduction on the portion of the Fund’s dividend distribution that qualifies under tax law. For the Fund’s fiscal year 2015 ordinary income dividends, 100% qualifies for the corporate dividends received deduction.

For the year ended January 31, 2015, the Fund designated $3,477,911 as long-term capital gain distributions.

21

Trustees and Officers (Unaudited)

The Board of Trustees supervises the business activities of the Trust. Each Trustee serves as a trustee until termination of the Trust unless the Trustee dies, resigns, retires or is removed.

The following tables provide information regarding the Trustees and Officers.

The following table provides information regarding each of the Independent Trustees.

| Name, Address*, (Age), Position with Trust**, Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

| Ira Cohen, 55, Independent Trustee, June 2010 to present. | Independent financial services consultant, since February 2005. | Trustee and Audit Committee Chairman, Griffin Institutional Access Real Estate Fund, since May 2014; Trustee for Angel Oak Funds Trust, since October 2014. | ||

| Andrea N. Mullins, 47, Independent Trustee, December 2013 to present. | Private investor; Independent Contractor, Seabridge Wealth Management, LLC, since April 2014; Principal Financial Officer and Treasurer, Eagle Family of Funds (mutual fund family) and Vice President, Eagle Asset Management, Inc. (investment adviser) each from 2004 to 2010. | None. | ||

| * | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | As of the date of this report, the Trust consists of 13 series. |

The following table provides information regarding the Trustee who is considered an “interested person” of the Trust, as that term is defined under the 1940 Act. Based on the experience of the Trustee, the Trust concluded that the individual described below should serve as a Trustee.

| Name, Address*, (Age), Position with Trust**, Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

| R. Jeffrey Young, 50, Trustee and Chairman, June 2010 to present. | Principal Executive Officer and President, Valued Advisers Trust, since February 2010; Senior Vice President, Huntington Asset Services, Inc. since January 2010 and Director since May 2014; Director, Unified Financial Securities since May 2014; Chief Executive Officer, Huntington Funds since February 2010; Chief Executive Officer, The Huntington Strategy Shares since November 2010; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2011 to February 2013; Trustee, Valued Advisers Trust, from August 2008 to January 2010; and Managing Director and Chief Operating Officer of Professional Planning Consultants, from 2007 to 2010. | Trustee and Chairman, Capitol Series Trust, since September 2013. | ||

| * | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | As of the date of this report, the Trust consists of 13 series. |

22

The following table provides information regarding the Officers of the Trust:

| Name, Address*, (Age), Position with Trust,** Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

| R. Jeffrey Young, 50, Trustee and Chairman, June 2010 to present; Principal Executive Officer and President, Valued Advisers Trust since February 2010; | Senior Vice President, Huntington Asset Services, Inc., since January 2010 and Director since May 2014; Director, Unified Securities, since May 2014; Chief Executive Officer, Huntington Funds, since February 2010; Chief Executive Officer, The Huntington Strategy Shares, since November 2010; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2011 to February 2013; Trustee, Valued Advisers Trust, from August 2008 to January 2010; and Managing Director and Chief Operating Officer of Professional Planning Consultants, from 2007 to 2010. | Trustee and Chairman, Capitol Series Trust, since September 2013. | ||

| John C. Swhear, 53, Chief Compliance Officer, AML Officer and Vice President, August 2008 to present. | Vice President of Legal Administration and Compliance for Huntington Asset Services, Inc., the Trust’s administrator, since April 2007 and Director since May 2014; Chief Compliance Officer of Unified Financial Securities, Inc., the Trust’s distributor, since May 2007 and Director since May 2014; President, Unified Series Trust, since March 2012, and Senior Vice President from May 2007 to March 2012; Chief Compliance Officer and AML Officer, Capitol Series Trust, since September 2013; Secretary, Huntington Funds, from April 2010 to February 2012; President and Chief Executive Officer, Dreman Contrarian Funds, from March 2010 to March 2011, and Vice President and Acting Chief Executive Officer, from 2007 to March 2010. | None. | ||

| Carol J. Highsmith, 49, Vice President, August 2008 to present; Secretary, March 2014 to present | Employed in various positions with Huntington Asset Services, Inc., the Trust’s administrator, since November 1994; currently Vice President of Legal Administration; Secretary, Cross Shore Discovery Fund since May 2014. | None. | ||

| Matthew J. Miller, 38, Vice President, December 2011 to present. | Employed in various positions with Huntington Asset Services, Inc., the Trust’s administrator, since July 1998; currently Vice President of Relationship Management; Vice President, Huntington Funds, since February 2010; President and Chief Executive Officer, Capitol Series Trust, since September 2013. | None. | ||

| Bryan W. Ashmus, 42, Treasurer and Principal Financial Officer, December 2013 to present. | Vice President, Financial Administration, Huntington Asset Services, Inc., the Trust’s administrator, since September 2013; Chief Financial Officer and Treasurer, The Huntington Strategy Shares and The Huntington Funds, since November 2013; Vice President, Treasurer Services, Citi Fund Services Ohio, Inc., from May 2005 to September 2013. | None. | ||

| * | The address for each trustee and officer is 2960 N. Meridian St., Suite 300, Indianapolis, IN 46208. |

| ** | As of the date of this report, the Trust consists of 13 series. |

OTHER INFORMATION

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the trustees and is available without charge, upon request. You may call toll-free at (866) 954-6682 to request a copy of the SAI or to make shareholder inquiries.

23

VALUED ADVISERS TRUST

PRIVACY POLICY

The following is a description of the policies of the Valued Advisers Trust (the “Trust”) regarding disclosure of nonpublic personal information that shareholders provide to a series of the Trust (each, a “Fund”) or that the Fund collects from other sources. In the event that a shareholder holds shares of a Fund through a broker-dealer or other financial intermediary, the privacy policy of the financial intermediary would govern how shareholder nonpublic personal information would be shared with nonaffiliated third parties.

Categories of Information A Fund May Collect. A Fund may collect the following nonpublic personal information about its shareholders:

| • | Information the Fund receives from a shareholder on applications or other forms, correspondence, or conversations (such as the shareholder’s name, address, phone number, social security number, and date of birth); and |

| • | Information about the shareholder’s transactions with the Fund, its affiliates, or others (such as the shareholder’s account number and balance, payment history, cost basis information, and other financial information). |

Categories of Information A Fund May Disclose. A Fund may not disclose any nonpublic personal information about its current or former shareholders to unaffiliated third parties, except as required or permitted by law. A Fund is permitted by law to disclose all of the information it collects, as described above, to its service providers (such as the Fund’s custodian, administrator, transfer agent, accountant and legal counsel) to process shareholder transactions and otherwise provide services to the shareholder.

Confidentiality and Security. Each Fund shall restrict access to shareholder nonpublic personal information to those persons who require such information to provide products or services to the shareholder. Each Fund shall maintain physical, electronic, and procedural safeguards that comply with federal standards to guard shareholder nonpublic personal information.

Disposal of Information. The Funds, through their transfer agent, have taken steps to reasonably ensure that the privacy of a shareholder’s nonpublic personal information is maintained at all times, including in connection with the disposal of information that is no longer required to be maintained by the Funds. Such steps shall include, whenever possible, shredding paper documents and records prior to disposal, requiring off-site storage vendors to shred documents maintained in such locations prior to disposal, and erasing and/or obliterating any data contained on electronic media in such a manner that the information can no longer be read or reconstructed.

24

PROXY VOTING

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted those proxies is available without charge upon request by (1) calling the Fund at (866) 954-6682 and (2) from Fund documents filed with the Securities and Exchange Commission (“SEC”) on the SEC’s website at www.sec.gov.

Trustees

R. Jeffrey Young, Chairman

Ira Cohen

Andrea N. Mullins

Officers

R. Jeffrey Young, Principal Executive Officer and President

Bryan W. Ashmus, Principal Financial Officer and Treasurer

John C. Swhear, Chief Compliance Officer, AML Officer and Vice-President

Carol J. Highsmith, Vice President and Secretary

Matthew J. Miller, Vice President

Investment Adviser

Golub Group, LLC

1850 Gateway Drive, Suite 100

San Mateo, CA 94404

Distributor

Unified Financial Securities, Inc.

2960 North Meridian Street, Suite 300

Indianapolis, IN 46208

Independent Registered Public Accounting Firm

Cohen Fund Audit Services, Ltd.

1350 Euclid Avenue, Suite 800

Cleveland, OH 44115

Legal Counsel

The Law Offices of John H. Lively & Associates, Inc.,

A member firm of The 1940 Act Law GroupTM

11300 Tomahawk Creek Pkwy, Suite 310

Leawood, KS 66211

Custodian

Huntington National Bank

41 S. High St.

Columbus, OH 43215

Administrator, Transfer Agent And Fund Accountant

Huntington Asset Services, Inc.

2960 North Meridian Street, Suite 300

Indianapolis, IN 46208

This report is intended only for the information of shareholders or those who have received the Fund’s prospectus which contains information about the Fund’s management fee and expenses. Please read the prospectus carefully before investing.

Distributed by Unified Financial Securities, Inc.

Member FINRA/SIPC

ANNUAL REPORT

January 31, 2015

Angel Oak Multi-Strategy Income Fund

Angel Oak Capital Advisors, LLC

One Buckhead Plaza

3060 Peachtree Road NW

Suite 500

Atlanta, GA 30305

(404) 953-4900

2015 Outlook

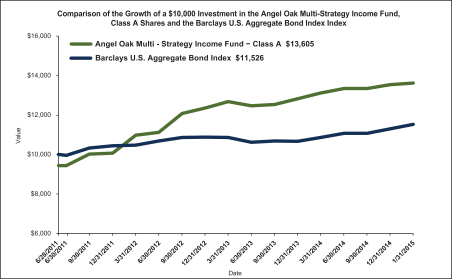

The Angel Oak Multi-Strategy Income Fund (the “Fund”) delivered solid performance for the fiscal year ended January 31, 2015, with the Institutional shares (ANGIX) returning 4.60% and the A shares (ANGLX) returning 4.41%, while its benchmark, the Barclays U.S. Aggregate Bond Index1, returned 6.61% over the same time period.

In the face of the very different rate and duration-driven return environments of 2013 and 2014, ANGIX delivered consistent 3.9% to 7.8% total returns each year. In contrast, the Fund’s benchmark was down 2% in 2013, as interest rates increased. Conversely, during 2014’s interest rate declines, the Fund’s benchmark gained approximately 6%.

Throughout both periods, ANGIX demonstrated minimal correlation2 to interest rates, as its returns were driven by the low-volatility, high-current-income profile of its structured credit instruments.

Looking back to 2014

In 2014, the markets continued their focus on the Federal Reserve’s influence over interest rates. There was much debate over rate direction, with the 10-year U.S. Treasury note giving back the gain it had reached by the end of 2013. Depending on which way investors anticipated rates moving, fixed-income portfolios were affected differently. Investors that anticipated rates staying low in 2014 were the clear winners, but in our opinion, the bet on lower interest rates, meant investors assumed more risk.

Over the course of the past year, a number of economic perceptions began to diverge between the Fed and the marketplace. Viewing domestic economic growth, increasing employment and a housing recovery in optimistic terms, the Fed saw the proverbial glass as half full. On the other hand, the markets generally saw the glass as half empty due to weaker overseas growth prospects and a variety of vexing geopolitical problems. Periodic, positive data reports on employment, such as U.S. GDP growth, the housing market and consumption, were often overlooked by a marketplace more concerned with distant global challenges.

| 1 | The Barclays U.S. Aggregate Bond Index is comprised of securities from the Barclays Government/Corporate Bond Index, Mortgage Securities Index, and the Asset Based Index. Total return includes price appreciation/depreciation and income as a percentage of the original investment. Indices are rebalanced monthly by market capitalization. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an index. Investments cannot be made in an index. |

| 2 | Correlation measures how closely in tandem the values of a security move in relation to each other over time. A correlation of +1 indicates the two returns move perfectly together, 0 (zero) indicates the movements are entirely random, or not at all correlated, and -1 indicates equal movement in opposite directions. |

1

While we expect to see a comparable level of volatility continue through 2015, one welcome theme did begin emerging at year-end: the return of non-correlative behavior among asset classes and geographies after years of moving in lockstep.

Correlations finally breaking down

We saw the first signs of a breakdown in correlation toward the end of 2014, led by the massive decline in oil prices. The initial response to this drop was the knee-jerk reaction of the herd: High-yield bonds, equities and emerging markets, whether related to energy or not, all suffered in the immediate risk-off environment. Certain asset classes, however, such as non-agency Residential Mortgage-Backed Securities (“RMBS”) and Commercial Mortgage-Backed Securities (“CMBS”), held their ground. Within a couple of days, we saw markets isolating energy-related equities, bonds and geographies. Finally, other equities and asset classes came roaring back to life as the markets paid more attention to the underlying fundamentals across various sectors and geographies.

For 2015, we anticipate a continued shift away from the recent over-correlation of risk-on assets. Since the financial crisis of a half-decade ago, the correlation among different asset classes and geographies has grown especially strong. When the Fed and other central banks intervened in the markets with an unprecedented series of Quantitative Easing (“QE”) policies, investors generally followed the herd toward a risk-on stance involving all asset classes, including equities, commodities, high yield “junk” bonds and emerging market securities. At the first sign of trouble – whether it was the U.S. ratings downgrade, the Eurozone crisis of 2011 or Fed QE tapering in 2013 – the herd assumed a risk-off attitude and sold all asset classes indiscriminately. Soon the behaviors of most asset classes and countries grew closely correlated as year-over-year equities, commodities, high-yield bonds, emerging markets, CMBS and RMBS all outperformed or underperformed as a group, depending on global risk tolerance.

We believe returns will not be driven only by broad increases or decreases in macro-risk premiums and supply technical, as they have been since the crisis. Even as central banks diverge, with the Fed getting ready to start tightening just as the European Central Bank starts kicking its own monetary easing program into high gear, other regions around the globe are diverging in their growth patterns. Europe and Russia are both facing a major slowdown, for example, just as the U.S. and some emerging markets see continued growth. We further believe that more focus on fundamentals and differentiation within equity sectors, global and domestic markets and high-yield corporate bonds, RMBS, CMBS, and Collateralized Loan Obligations (“CLOs”) can be expected as well, based on their underlying credit exposures.

As this breakdown in correlation continues through 2015, we believe that active investment selection based on bottom-up, fundamental analysis will emerge as the primary driver behind investment performance.

2

All eyes on The Fed

The Fed’s extraordinarily accommodative monetary policy, particularly QE has been a historic volatility depressant in the current post-crisis period. As illustrated below, even though interest rate volatility fell to historic lows during the year, it began rising again in the fall of 2014, after the Fed’s historic QE program came to a close.

We believe volatility has increased because of one particular elephant in the interest rate room: the uncertainty surrounding the future supply and demand of agency mortgages.

As a result of QE, the Fed has become the largest single participant in the agency mortgage market over the past three years. Currently, the Fed owns approximately $2 trillion in agency mortgages, representing about 37% of the agency mortgage market. Based on current prepayment speeds, the Fed’s portfolio is paying down debt at a rate of approximately $20 billion per month, nearly enough to absorb all of the mortgage origination supply in the U.S.

With its enormous purchasing capacity, the Fed has distorted both the market for mortgages and, subsequently, volatility. By not hedging the optionality of the mortgage-backed securities it owns, the Fed has placed downward pressure on volatility. Moreover, for six years the Fed has been on hold at 0% with the one rate it does control directly, the federal funds target rate. The Fed has been very clear that it plans to keep its target rate and its overall monetary policy in an extraordinarily accommodative posture for a considerable time. The result is the Fed will continue to be cautious, selective and patient in its approach to raising rates.

While the lack of mortgage hedging and an ultra-accommodative target rate has caused volatility to plummet in the post-crisis period, in our view, this will likely change going forward.

Confused and complacent, the markets have correctly banked on Fed dovishness. We believe, however, that this period of extremes is coming to an end.

The Fed’s softer language, which counsels “patience,” may be setting the tone for a midyear interest rate hike. However, median fed funds projections have come down significantly. Even with a much more reasonable trajectory, there is a disparity in the dots, ranging from a 0.50% to a 4.00% fed funds rate by the end of 2016. The pace and trajectory of Fed hikes can help soften the blow of an initial rate move by forecasting a slower pace and potentially lowering the terminal fed funds rate.

Regardless of the disparity in rate hike projections, the Fed’s extraordinarily accommodative monetary policy appears to be working. The growth data ended 2014 with a bang. Driven in part by acceleration in consumer spending, the U.S. economy expanded at a 5% seasonally adjusted rate by the end of the third quarter, its strongest

3

pace since 2003. Having dropped approximately 13% in the third quarter, gasoline prices fell another 36% in the fourth quarter, providing additional spending resources to consumers for continued growth in the near term.

Despite the robust growth data, however, inflation data continued to bounce along the bottom. The core personal consumption expenditures price index (“PCE”), the Fed’s preferred inflation gauge, fell to 1.4% in November, from 1.6% in October. This marked the 31st straight month that the core PCE missed the Fed’s 2.0% target. Many market analysts in search of signs of impending Fed tightening have chosen to disregard the low inflation data in favor of focusing on the growth data. We think such pundits may be better served by recollecting the Fed’s dual mandate to hold employment to a maximum level and to maintain price stability. While the Fed appears to have made progress on the unemployment front, there clearly is more work to do on the inflation side.

The fundamentals of this recovery remain positive despite the lack of wage gains, relatively non-existent inflation and a 50% drop in gasoline prices over the past six months. We believe inflation data will begin to trend downward in 2015 because of the falling price of crude oil. We anticipate that the Fed will fail to adhere to its price stability mandate for an extended period, which will give it a tremendous amount of flexibility to attain maximum employment and rid the labor markets of its post-crisis slack.

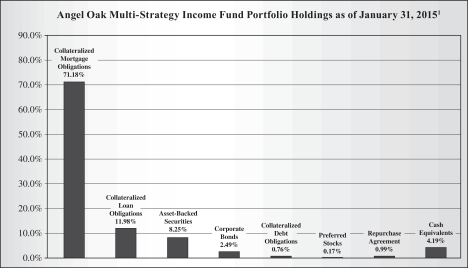

Structured Credit still in favor for 2015

An overweight to the structured credit markets such as RMBS, CMBS and CLOs improved portfolio income for ANGIX in 2014. However, the Fund’s lower sensitivity to interest rates (duration3) relative to the benchmark proved negative to performance.

Non-agency RMBS were the portfolio’s best-performing asset class. Management’s decision to continue a major allocation of 55-70% to the sector throughout the year proved positive for performance, as the asset class’s price volatility remained muted, its correlation to interest rates stayed minimal and price appreciation added to total return in 2014.

For the remainder of the portfolio, an increased exposure to non-agency CMBS improved the Fund’s total return by more than 1.00%, which proved to be a major benefit for Fund shareholders.

Throughout the first half of 2014, the Fund decreased exposure to CLOs, but not for fundamental reasons. As an explosion of new CLOs dramatically increased supply, we

| 3 | Duration is a measure, expressed as a number of years, of the sensitivity of the price of a fixed-income investment to a change in interest rates. The larger the duration number, the greater the interest-rate risk or reward for bond prices. |

4

expected additional pressures to be placed on spreads while anticipating that investor demand would remain the same. Our decrease in allocation during this high-supply period contributed to the Fund’s performance.

| YTD 12/31/2014 | ||||||||||||

Asset Class | Allocation % | Total Return | Attribution To Fund | |||||||||

ABS Other | 2.69 | % | 9.99 | % | 0.27 | % | ||||||

CLO | 14.79 | % | 2.23 | % | 0.33 | % | ||||||

CMBS | 21.79 | % | 9.64 | % | 2.10 | % | ||||||

Corporated | 2.55 | % | 4.47 | % | 0.11 | % | ||||||

NA CMO | 68.15 | % | 7.53 | % | 5.13 | % | ||||||

Rate Hedge | -1.12 | % | ||||||||||

Net Total Return | 5.84 | % | ||||||||||

Data reflects estimated performance for the Angel Oak Multi Strategy Income Fund – Class I (ANGIX)

Looking forward to 2015, we will continue to position the Fund within the floating-rate structured credit category while maintaining caution toward higher-rate, longer-term durations in anticipation of an eventual return to a higher-interest-rate environment over the next two years. The key question for investors then might be “What should be done in an environment characterized by a modestly improving economy, interest rate volatility and the beginnings of some divergence in risk appetite?”

FOR ANGEL OAK, OUR ANSWER IS AS FOLLOWS:

® Overweight current income and cash flow through the volatility. We believe that anyone can be right about an interest rate call. (If they are not, just wait 15 minutes). Our preference is to avoid the noise and conjecture around rates and just endeavor to earn outsized income through the rate storm. That said, we intend to position the portfolio for eventually higher interest rates.

® Focus on value and fundamentals when valuations become less justifiable. Fundamentals are improving, but the market and media remain skeptical of the recovery in housing. This has the effect of setting low expectations on home prices, voluntary prepayments, the Millennial generation’s lack of household formation, wage growth and access to credit. On the other hand, it also represents a ripe environment for opportunity and a solid entry point in vintage mortgages, as well as new outside-the-box originations.

From the entry point perspective, the trading tone for structured credit has been rather listless for the past 12 months. While we have not seen any over exuberance in equities, emerging markets and high-yield bonds year over year, we believe that the weaker tone in structured credit during the third and fourth quarters of 2014 will set the stage for a stronger tone in the first half of 2015.

5

Structured credit’s current lower visibility and reduced liquidity, caused by a lack of participation from the “herd,” offers the potential for outsized opportunities throughout 2015. In addition to traditional structured credit, we continue to look at off-the-beaten-path opportunities, such as Corporate credit in the regional financial sector (Regional and Community Banks).

Legacy RMBS point to opportunity

The year 2015 should bring about continued expansion in mortgage credit. The overwhelming majority of legacy borrowers have been unable to access the mortgage market since 2007, creating higher pent-up demand among Alt-A, Option ARM and sub-prime borrowers.

The best prime borrowers have had access to mortgage credit for years, leading to sustained Voluntary Prepayment Rate4 (“VPR”) speeds well into the double digits. While we expect to see some burnout in these speeds in 2015, there is also a risk of adverse selection as the loan count in these pools continues to dwindle, bringing large extension risks into play.