UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22298

Starboard Investment Trust

(Exact name of registrant as specified in charter)

116 South Franklin Street, Post Office Box 69, Rocky Mount, North Carolina 27802

(Address of principal executive offices) (Zip code)

Terrence O. Davis

116 South Franklin Street, Post Office Box 69, Rocky Mount, North Carolina 27802

(Name and address of agent for service)

Registrant's telephone number, including area code: 252-972-9922

Date of fiscal year end: August 31

Date of reporting period: August 31, 2014

Item 1. REPORTS TO STOCKHOLDERS.

Statements in this Annual Report that reflect projections or expectations of future financial or economic performance of the Roumell Opportunistic Value Fund ("Fund") and of the market in general and statements of the Fund's plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include, without limitation, general economic conditions such as inflation, recession and interest rates. Past performance is not a guarantee of future results. An investment in the Fund is subject to investment risks, including the possible loss of some or the entire principal amount invested. There can be no assurance that the Fund will be successful in meeting its investment objective. Investment in the Fund is also subject to the following risks: market risk, opportunistic investment strategy risk, sector risk, non-diversified fund risk, investment advisor risk, new fund risk, operating risk, common stocks risk, preferred stock risk, warrants risk, convertible securities risk, large-cap securities risk, small-cap and mid-cap securities risk, micro-cap securities risk, risks related to investing in other investment companies, interest rate and credit risk, maturity risk, inflation risk, investment-grade securities risk, lower-rated securities or "junk bonds" risk, risks of investing in municipal securities, risks of investing in REITs, risk of investing in corporate debt securities, government debt markets may be illiquid or disrupted, foreign securities risk, and currency risk. More information about these risks and other risks can be found in the Fund's prospectus. The performance information quoted in this annual report represents past performance, which is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. An investor may obtain performance data current to the most recent month-end by visiting ncfunds.com. An investor should consider the investment objectives, risks, and charges and expenses of the Fund carefully before investing. The prospectus contains this and other information about the Fund. A copy of the prospectus is available at ncfunds.com or by calling Shareholder Services at 800-773-3863. The prospectus should be read carefully before investing. |

This Annual Report was first distributed to shareholders on or about October 30, 2014.

For More Information on Your Roumell Opportunistic Value Fund:

See Our Web site @ ncfunds.com.

or

Call Our Shareholder Services Group at 800-773-3863.

August 31, 2014

For the year ended August 31, 2014, the return on the Institutional class shares was (0.12)%. The return on the Class A shares was (0.38)%, the return on the Class C shares was (1.09)%. This compares to 18.10% for the Russell 2000 Value Index, 13.66% for the 60% Russell 2000 Value Index/40% Barclays Government Credit Index, and 25.25% for the S&P 500 over the same period. These returns were attained with an allocation of about 36% in cash, 43% in equities, and 21% in fixed income during the fiscal year.

Please see the table below for the Fund's historical performance information through the calendar quarter ended September 30, 2014.

| Average Annual Total Returns (Unaudited) | | | Net | Gross |

Period Ended September 30, 2014 | Past 1 Year | Since Inception* | Expense Ratio** | Expense Ratio*** |

Roumell Opportunistic Value Fund – Institutional Class Shares | (5.52)% | 1.88% | 1.32% | 1.62% |

Roumell Opportunistic Value Fund –Class A Shares | (5.80)% | 1.63% | 1.57% | 1.87% |

| After tax with sales charge**** | (2.08)% | 1.24% | N/A | N/A |

Roumell Opportunistic Value Fund –Class C Shares | (6.54)% | (5.86)% | 2.32% | 2.62% |

After tax with deferred sales charge**** | (2.35)% | (4.84)% | N/A | N/A |

60% Russell 2000 Value Index, and 40% Barclays Capital U.S. Government Credit Index | 4.11% | 7.71% | N/A | N/A |

| S&P 500 Total Return Index | 19.73% | 15.18% | N/A | N/A |

The quoted performance data represents past performance, which is not a guarantee of future results. Investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain more current performance data regarding the Fund, including performance data current to the Fund's most recent month-end, please visit ncfunds.com or call the Fund at (800)773-3863. Fee waivers and expenses reimbursements have positively impacted Fund performance.

*The Fund's inception date is December 31, 2010.

**The Advisor has entered into an Operating Plan with the Fund's administrator through January 1, 2015, under which it has agreed to (i) to pay the administrator a fee based on the daily average net assets of the Fund when net assets are below $77 million; (ii) if these payments are less than a designated minimum, then the Advisor pays a fee that makes up the difference; and (iii) to assume expenses of the Fund outlined in the Operating Plan that are not covered by the fee paid under Fund Accounting and Administration Agreement. These measures are intended to limit the Fund's operating expenses to 1.23% of the average daily net assets, exclusive of brokerage fees and commissions, portfolio transaction fees, registration fees, taxes, borrowing costs (such as interest or dividend expenses on securities sold short), acquired fund fees and expenses, extraordinary expenses, and distribution and/or service (12b-1) fees. The Fund's net expense ratio will be higher than 1.23% to the extent the Fund incurs expenses excluded from this arrangement. The Fund also charges a 1.00% redemption fee on the Institutional Class shares, Class A shares, and Class C shares within 60 days of their issuance. The Operating Plan can only be terminated prior to the conclusion of the current term with the approval of the Fund's Board of Trustees. More recent expense ratios are found in the Financial Highlights.

***Gross expense ratio includes acquired fund fees and expenses and other expenses.

****A maximum sales charge imposed on purchases of 4.50% is charged to the Class A shares. A maximum deferred sales charge of 1.00% is applied to the Class C shares. For the fiscal year ended August 31, 2014, the after tax with sales charge return on the Class A shares was 1.22%. The after tax with the deferred sales charge return on the Class C shares was 0.93%.

The Pervasiveness of Short-Termism

Imagine the following scenario. An investment manager watches a stock fall sharply to $10. Through thorough analysis, the manager determines that the company's risk of insolvency is virtually zero and that, in better times, the stock will be worth $30 or more. The manager, of course, should buy the stock. But if he has to worry about short-term performance, he will be reluctant to buy at $10 on the fear that the stock will fall to $5, despite his high conviction that it will ultimately rise to $30. We believe this scenario frequently plays out in various forms in the stock and bond markets. The lesson, of course, is that pressures of short-term performance lead to poor investment decisions.

The average holding period for New York Stock Exchange (NYSE) listed stocks has declined to less than one year from eight years in the 1950s and 1960s.1 The increasing pervasiveness of short-termism creates a favorable environment for opportunistic investors. It is therefore incumbent upon investment managers to cultivate a client base who themselves appreciate the steep cost of impatience and the myriad opportunities available to those who are not constrained by it.

According to Jeremy Grantham, Cofounder and Chief Investment Strategist of GMO LLC, "The central truth of the investment business is that investment behavior is driven by career risk…. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority 'go with the flow,' either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest."

In addition to career risk, recency bias—or the inclination to give too much weight to recent experiences—can drive short-term behavior. Many investors want to be in the market after it surges, and they want out after it declines. The Wall Street Journal profiled a married couple, two doctors living in Texas, who sold all of their stock investments after losing half of their savings in the 2008 bear market. Not until the stock market reached new highs did the couple decide to get back in the market. Therein lies the irony of the investment business. Clients generally want more equity exposure when investment opportunities are few, and redemptions are highest when investment opportunities are great, as they were at the depths of the 2008–2009 bear market.

Career risk and recency bias affect not only the behavior of investors but also that of analysts who sell research for the Wall Street firms. Mirroring similar behavior by investors, Wall Street research analysts compound mispricing in the stock market. We sampled analyst coverage on 60 randomly selected companies from the S&P 500. Of the 1,510 analyst ratings, only 85, or 5.6%, were negative. Yet in the prior five years, on average 37% of stocks in the S&P 500 generated a negative return (including dividends) in each year.

The analyst community tends to be bullish during periods of high prices and more bearish when prices are low, in direct contrast to a profitable investment strategy. Seventy-one

percent of analysts covering Amazon.com, Inc. had bullish ratings when that stock peaked at the end of 1999. Most analysts ignored the fact that it traded for 22x revenue and was unprofitable. When the stock bottomed in the fall of 2001, only 45% of analysts were bullish. Similarly, 69% of analysts covering Wells Fargo & Co. were bullish when that stock peaked in the fall of 2007. As it bottomed in the spring of 2009, only 40% of analysts had bullish ratings.

The analyst community in aggregate simply does not accurately portray risk or opportunity in its rating systems. Wall Street firms are in the business of selling securities as well as servicing corporate clients. An analyst's positive bent, therefore, serves two purposes. It can help sell securities, and it can also help ingratiate analysts with management teams who may be or may become clients. Although regulatory changes preclude analysts from receiving direct compensation from investment banking activity, make no mistake, conflicts remain. Moreover, analysts rarely stray too far from the herd, because if you are wrong with the herd you keep your job. If you are wrong and against the herd, you're fired.

Conventional daily performance reporting adds to the difficulty of maintaining a long-term view. Most people innately feel the need to be proactive because it's hard to distinguish inactivity from laziness. A 2007 study2 concluded that, as a result of action bias, soccer goalkeepers remain in the center of the goal only 6% of the time during penalty kicks, despite the ball being kicked to the center 29% of the time. Investors' collective proclivity toward action and impatience is exactly the reason why value investing has historically been so effective. We believe opportunities for those investors who truly take a multiyear view offer the best reward relative to risk, primarily because of the pervasiveness of impatience elsewhere. Most investors shun these opportunities, which in turn get priced far below intrinsic value.

Value stocks often take a while to return to intrinsic value; these companies are typically under-earning their potential at the time the stocks are purchased. These issues can make for a bumpy ride for the investor. Revered value investor Seth Klarman has said:

Value investors have a perspective that allows them not to suffer these interim losses, but to relish or at least appreciate them—because interim price declines allow an investor to average down, to buy more at an even better price, which results in much greater profits over time than if prices had not declined at all. It is critical that you remind your clients, your investment team, and, as often as necessary, yourself that you can only control your process and approach—that you cannot forecast the vagaries of the market, which in any case are an opportunity and not a problem for value investors.

2 M. Bar-Eli, O. H. Azar, I. Ritov, Y. Keidar-Levin, and G. Schein, "Action Bias among Elite Soccer Goalkeepers: The Case of Penalty Kicks," Journal of Economic Psychology 28 (2007): 606–21.

We agree that volatility provides opportunity. For example, we often take advantage of lower prices in our securities because of our belief in the underlying value of our investment rationale. We believe the best strategy for retail and institutional investors is to select good portfolio managers and stick with them through the volatility. We do not manage for a given quarter or a given year. We manage with a three-year time horizon because the impact of company fundamentals on stocks is diminished over shorter investment periods. To quote Benjamin Graham, the father of value investing, "In the short run the market is a voting machine. In the long run it's a weighing machine."

Top Three Holdings

To our delight, the CEOs of our top three holdings presented at our annual investor conference in September. Bill Gates has written about the importance of backing the right people. In a recent Wall Street Journal article, Gates remarked, "There's an essential human factor in every business endeavor. It doesn't matter if you have a perfect product, production plan and marketing pitch; you'll still need the right people to lead and implement those plans." We have found that our investments have a higher likelihood of making money when we have met management. Some investors take the approach that meeting management can lead to excessive emotional attachment to an investment. Our experience has been that, while one must be vigilant about overemphasizing a relationship in spite of fundamentals, building relationships with management teams is beneficial. We believe making a firsthand assessment of the people behind the business is important to the investment thesis.

SeaChange International, Inc., SEAC. SeaChange, which comprised 6.90% of the portfolio as of August 31, 2014, is a cash-rich, debt-free company with highly desirable software assets that are well positioned to take advantage of cable content distribution. This is our second foray in SeaChange. We exited SEAC in the fourth quarter of 2013 after a dramatic increase in its stock price. Earlier this year, another buying opportunity presented itself as the company announced disappointing top-line revenue that we viewed as noise, which in no way undermined the long-term strength of this unique story. We believe the larger-than-expected decline in its legacy platforms (Axiom, Middleware, Streamers), and the longer sales cycle of next-generation software, concerned investors who do not fully appreciate the below-the-surface dynamism regarding the adoption of its next-gen software tools.

The "noise" from the first quarter not surprisingly persisted in the second quarter. Upon a further weakening in SEAC's stock price, we bought additional shares, thereby reducing our cost basis. In our view, the fundamental thesis of this story has not changed. Although total revenues will decline this year, the driver of the decline is legacy product revenue, which will decrease to about 10% of total revenue. While management believes the company will keep most of what remains from legacy business, any further declines won't have a material impact on overall revenues simply due to how small legacy business has become. Regarding the longer-than-anticipated sales cycle for next-generation products, we believe any concern is more than offset by the stickiness of the revenue, which is due to high switching costs. SEAC has been selected by nearly 50 cable operators, compared to just five in 2011, a clear signal of successful R&D investment. We believe penetration of its 80 million current customer subscribers will rise toward 100% over time from less than 20% today; this is important as it represents built-in organic growth since cable companies pay license fees on a per subscriber basis.

Finally, we believe deeply in SEAC's CEO, Raghu Rau, and the board, in our view, is competent and shareholder friendly. In fact, we believe SEAC's software remains a highly desirable strategic asset for a larger company, and the board would sell the company at the right price. For reference, Cisco Systems acquired NDS, a SEAC competitor, in 2012 for 5x revenue. In 2013, SEAC displaced NDS at Liberty Global, Europe's largest cable operator. We believe valuing SEAC at 2–2.5x revenue is reasonable and would provide us an attractive return.

Sizmek, Inc., SZMK. Sizmek, which comprised 6.90% of the portfolio as of August 31, 2014, manages, distributes, and analyzes online advertising campaigns. The online advertising market has strong secular tailwinds; Raymond James estimates U.S. online ad spending to grow 15% per year for the next three years. Sizmek is a major player in this market, having served 1.5 trillion advertisements in 2013. Sizmek's predecessor company, Digital Generation, sold its TV advertising distribution business in 2013, an event that resulted in a $3/share special dividend to our Fund. The company now focuses exclusively on the online advertising market, and is building a true global platform business that provides advertisers a full suite of end-to-end capabilities (ad serving, analytics, and verification).

Online advertising consists of three basic categories: banner/display, video, and mobile, growing annually at roughly 5%, 25%, and 30%, respectively. While banner makes up more than 50% of SZMK's distribution business, the company is heavily focused on the faster growing video market, with a much smaller presence in mobile. Worldwide, display advertising accounts for roughly $30 billion of the more than $40 billion spent on online advertising. SZMK is positioning itself as a globally integrated platform with a differentiated open-stack architecture able to manage cross-platform advertising campaigns. Roumell Asset Management's independent software consultant has spent considerable time analyzing SZMK's open-stack MDX platform and has reported back highly favorable results. Recently, the company has established new relationships with Tommy Hilfiger, Audi, Toyota, and Volkswagen, and expanded its existing relationships with Time and Unilever. SZMK was also chosen by the German media agency of McDonald's to manage its online World Cup campaign.

A plethora of point solution companies exist, but very few of these have end-to-end capabilities. The dominant player in the space, Google's DoubleClick, is a closed system and requires its ad-serve clients to use its analytic tools. SZMK's customers can choose the company's ad-serving and verification services but are not required to choose Sizmek's analytic products. SZMK is estimated to have the second largest market share, albeit a distant second. Recently, SZMK hired Patrick Meehan from Google, where as head of platform sales he was responsible for large holding-company relationships. He was previously director of agency sales and account management at DoubleClick. The company's three-year goal is to collapse the technologies and tools now in separate silos and move toward a SaaS business model.

In our view, the company is cheap. SZMK is debt-free, and has roughly $100 million in cash with a market capitalization of approximately $300 million. The company has made several acquisitions over the past few years totaling about $400 million (after impairments). SZMK has about $185 million in revenue resulting in an enterprise value to revenue of roughly 1x, while peers trade at an average of roughly 2.5x. Moreover, operational metrics are steadily improving. To wit, management has boosted Earnings before Interest, Taxes, and Depreciation (EBITDA) margins from 5% in 2011 to 14% in 2013 and has a goal of reaching 30% in the medium term. Many of its peers have growth but no margin. SZMK's revenues are growing (profitably) at about 15% annually. We believe after the sale of its legacy TV ad distribution business and resulting emergence as a stand-alone online company, few investors understand the potential value of SZMK. To our knowledge, the company has two firms providing research coverage. Finally, we believe SZMK is a highly desired strategic asset.

Recently, we met with CEO Neil Nguyen and once again walked away with a high level of confidence that Neil possesses a clear vision and the requisite execution skills to grow SZMK into a leading online ad management company. Scott Ginsburg, SZMK's founder, and Neil own roughly 14% of the company. In summary, a debt-free, cash-rich balance sheet, cheap valuation, secular tailwinds, and strong leadership result in what we believe is a compelling investment opportunity.

Rosetta Stone, Inc., RST. Rosetta Stone is the global leader in technology-enabled language learning. The company offers language-learning and reading instruction to consumers, businesses, government entities, and schools via packaged software and online subscriptions. The language offerings emphasize a unique "dynamic immersion" methodology that relies on the associative pairing of images, texts, and sounds to mimic the way people naturally learn native languages. In the past two years, the company has made four acquisitions aimed at strengthening its own language reach and to better leverage its brand by cross-selling related products. Rosetta generates roughly 20% of revenue from overseas and is headquartered in Arlington, Virginia.

RST is a company in transition led by Stephen Swad, CEO, who was brought in three years ago to build a profitable and sustainable business model. Readers may recall seeing Rosetta Stone kiosks in airports a few years back. Today, those (low ROI) kiosks are gone and more of the company's consumer business is delivered online or through selling agreements with retailers such as Amazon, Costco, and Apple's iTunes. However, the consumer business is not the company's primary attraction to us. The company is emphasizing its Enterprise & Education (E&E) business, where its high level of service and support is a differentiated and valued attribute. For instance, a number of agencies within the U.S. Department of Defense contract with RST to provide language learning to its employees and receive a dedicated website and access to key support personnel. Coaching support is highly correlated with language-learning success. E&E revenue is now $115 million annually, with renewal rates of 75%. The company's total SaaS subscription revenue is now about $140 million and represents roughly 50% of total revenue.

One of RST's primary cross-selling opportunities results from its 2013 acquisition of K–12 instructional reading software company Lexia for $22.5 million. RST's products are already used in 20,000 (out of 125,000) K–12 schools in North America. The company's purchase of Fit Brains, a top-five player in brain exercise software (a space in which industry leader Lumosity is spending heavily to increase its popularity), provides another opportunity to leverage the brand. Overall, the company enjoys 80%-plus gross margins and is looking to leverage R&D investments, and reduce sales and marketing expenses, while taking advantage of the already significant sunk brand costs to create a profitable business model with high recurring revenues. The company has guided for approximately $20 million in EBITDA in 2014 and will generate about $10 million in free cash flow this year, which will be held back by integration costs that will likely decline in 2015.

RST is unleveraged and possesses a healthy cash balance. By year-end, we anticipate RST will have $70 million in cash, or roughly 35% of its current $200 million market capitalization. If you back-out an additional $70 million spent on recent acquisitions, the implied value for RST's core business is a mere $60 million. What is the brand worth? It's a difficult question to answer, but we believe nonetheless that it is a significant off-balance-sheet asset. In the last five years, the company has spent more than $500 million on sales and marketing and enjoys a 74% brand recognition rate. Looked at another way, the company's year-end enterprise value of $130 million is less than 1x its highly recurring SaaS revenue, 80% of which comes from its growing E&E business. SaaS companies typically trade for generous multiples of revenue.

In January, The Economist summed up the digital language learning space as follows: "Technology is starting to change language learning. [Berlitz] is a bit of a digital dawdler. Most of its smartphone apps are repurposed versions of its old books.... Rosetta Stone, an American technology company, provides a contrast, supplementing technology with human teaching rather than vice versa. Its software has a clever interface that eschews traditional drills in favour of pictures and examples that gradually and intuitively build vocabulary and grammar skills.… From 2006 to 2009 the company more than tripled R&D spending, customising each language offering and adding cultural and social features. Well-built tablet and smartphone apps let students learn anywhere."

Why is it cheap? The primary reason involves recent negative sales trends in RST's consumer segment. The emergence of free apps for people looking to "get by" for their upcoming trip to Europe has undoubtedly taken market share in this segment. Second, investors are understandably skeptical of the company's ability to integrate recent acquisitions. Our variant view is that while total revenues have been roughly flat over the last three years, the 20% decline in product revenue is masking 48% growth in the more profitable subscription business. Moreover, according to independent sources, the industry is growing. For instance, the global e-learning market research firm Ambient Insight estimates that global digital English-language-learning products are growing by double digits. Universities, K–12 schools, companies, and government entities are all increasingly using technology. RST's institutional business lies in front of this trend.

We sat down with CEO Steve Swad and his team and believe they have a credible vision and well-articulated growth strategy. Steve has taken more than 60% of his total compensation in stock for the last two years. Key industry contacts indicate real excitement within the company's sales force stemming from the new direction and underscore our belief in Steve and his team.

At day's end, we believe RST "weighs" far more today than its price implies. To wit, a mere two times the current SaaS-based revenue plus its estimated year-end cash balance equates to roughly $300 million, compared to the current $200 million market capitalization. This exercise ascribes no value to the company's consumer business, which generates $200 million in revenue. At the price we paid, the odds of a good return appear to us to be strongly in our favor.

Best Regards,

Jim Roumell

Lead Portfolio Manager

Roumell Opportunistic Value Fund

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | | | | | |

| Institutional Class Shares | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| Performance Update (Unaudited) | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

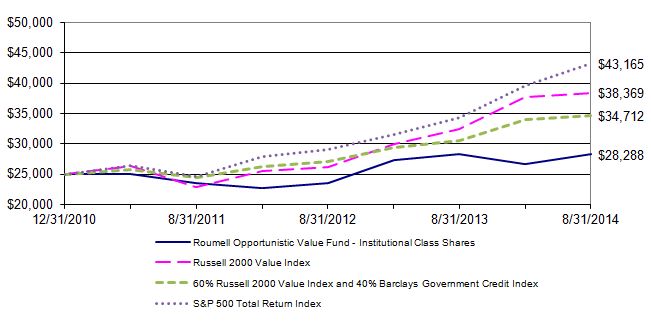

| For the period from December 31, 2010 (Date of Initial Public Investment) to August 31, 2014 | |

| | | | | | | | | | | | | | | | | | |

| Comparison of the Change in Value of a $25,000 Investment | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | |

| | | | | | | | | | | | | | | | | | |

| This graph assumes the minimum initial investment of $25,000 at December 31, 2010 (Date of Initial Public Investment). All dividends and distributions are reinvested. This graph depicts the performance of the Roumell Opportunistic Value Fund Institutional Class Shares (the "Fund") versus the Russell 2000 Value Index, a blend of 60% of the Russell 2000 Value Index and 40% of the Barclays Government Credit Index, and the S&P 500 Total Return Index. It is important to note that the Fund is a professionally managed mutual fund while the indices are not available for investment and are unmanaged. The comparison is shown for illustrative purposes only. |

| | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns | |

| | | | | | | | | | | | | | | | | Gross | |

| | As of | | | | | | One | | Since | | Inception | | Expense | |

| | August 31, 2014 | | | | | Year | | Inception | Date | | Ratio* | |

| | Institutional Class Shares | | | | -0.12% | | 3.43% | | 12/31/10 | | 1.23% | |

| | Russell 2000 Value Index | | | | 18.10% | | 12.35% | | N/A | | N/A | |

| | 60% Russell 2000 Value Index and | | | | | | | | | | |

| | | 40% Barclays Government Credit Index | | 13.66% | | 9.34% | | N/A | | N/A | |

| | S&P 500 Total Return Index | | | | 25.25% | | 15.99% | | N/A | | N/A | |

| | | | | | | | | | | | | | | | | | |

| * The gross expense ratio shown is from the Fund's prospectus dated December 30, 2013. | |

| | | | | | | | | | | | | | | | | | |

| Performance quoted above represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com. |

| | | | | | | | | | | | | | | | | | |

| The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestments of distributions. |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | | | | | |

| Class A Shares | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| Performance Update (Unaudited) | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

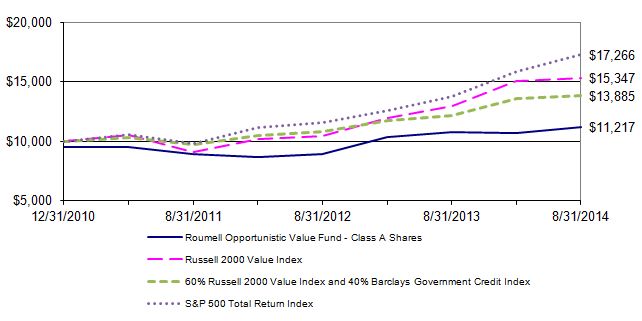

| For the period from December 31, 2010 (Date of Initial Public Investment) to August 31, 2014 |

| | | | | | | | | | | | | | | | | | |

| Comparison of the Change in Value of a $10,000 Investment | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | |

| | | | | | | | | | | | | | | | | | |

| This graph assumes an initial investment of $10,000 ($9,550 after maximum sales load of 4.50%) at December 31, 2010 (Date of Initial Public Investment). All dividends and distributions are reinvested. This graph depicts the performance of the Roumell Opportunistic Value Fund Class A Shares (the "Fund") versus the Russell 2000 Value Index, a blend of 60% of the Russell 2000 Value Index and 40% of the Barclays Government Credit Index, and the S&P 500 Total Return Index. It is important to note that the Fund is a professionally managed mutual fund while the indices are not available for investment and are unmanaged. The comparison is shown for illustrative purposes only. |

| | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns | |

| | | | | | | | | | | | | | | | | Gross | |

| | As of | | | | | | One | | Since | | Inception | | Expense | |

| | August 31, 2014 | | | | | Year | | Inception | Date | | Ratio* | |

| | Class A Shares - No Sales Load | | | -0.38% | | 3.18% | | 12/31/10 | | 1.48% | |

| | Class A Shares - 4.50% Maximum Sales Load | -4.84% | | 1.89% | | 12/31/10 | | 1.48% | |

| | Russell 2000 Value Index | | | | 18.10% | | 12.35% | | N/A | | N/A | |

| | 60% Russell 2000 Value Index and | | | | | | | | | | |

| | | 40% Barclays Government Credit Index | | 13.66% | | 9.34% | | N/A | | N/A | |

| | S&P 500 Total Return Index | | | | 25.25% | | 15.99% | | N/A | | N/A | |

| * The gross expense ratio shown is from the Fund's prospectus dated December 30, 2013. | |

| | | | | | | | | | | | | | | | | | |

| Performance quoted above represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com. |

| | | | | | | | | | | | | | | | | | |

| The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestments of distributions. |

| | | | | | | | | | | | | | | | | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | | | | | |

| Class C Shares | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| Performance Update (Unaudited) | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

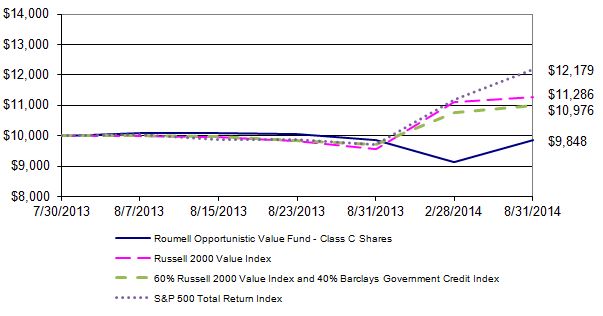

| For the period from July 30, 2013 (Date of Initial Public Investment) to August 31, 2014 | |

| | | | | | | | | | | | | | | | | | |

| Comparison of the Change in Value of a $10,000 Investment | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | |

| | | | | | | | | | | | | | | | | | |

| This graph assumes an initial investment of $10,000 at July 30, 2013 (Date of Initial Public Investment) and includes the 1% maximum deferred sales charge. All dividends and distributions are reinvested. This graph depicts the performance of the Roumell Opportunistic Value Fund Class C Shares (the "Fund") versus the Russell 2000 Value Index, a blend of 60% of the Russell 2000 Value Index and 40% of the Barclays Government Credit Index, and the S&P 500 Total Return Index. It is important to note that the Fund is a professionally managed mutual fund while the indices are not available for investment and are unmanaged. The comparison is shown for illustrative purposes only. |

| | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns | |

| | | | | | | | | | | | | | | | | Gross | |

| | As of | | | | | | One | | Since | | Inception | | Expense |

| | August 31, 2014 | | | | | Year | | Inception | | Date | | Ratio* | |

| | Class C Shares | | | | | | -1.09% | | -1.40% | | 07/30/13 | | 2.23% | |

| | Russell 2000 Value Index | | | | 18.10% | | 11.71% | | N/A | | N/A | |

| | 60% Russell 2000 Value Index and | | | | | | | | | | |

| | | 40% Barclays Government Credit Index | | 13.66% | | 8.91% | | N/A | | N/A | |

| | S&P 500 Total Return Index | | | | 25.25% | | 19.72% | | N/A | | N/A | |

| | | | | | | | | | | | | | | | | | |

| * The gross expense ratio shown is from the Fund's prospectus dated December 30, 2013. | |

| | | | | | | | | | | | | | | | | | |

| Performance quoted above represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com. |

| | | | | | | | | | | | | | | | | | |

| The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestments of distributions. |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | |

| | | | | | | | | | |

| Schedule of Investments | | | | | | | |

| | | | | | | | | | |

| As of August 31, 2014 | | | | | | | |

| | | | | | Shares | | Cost | | Value (Note 1) |

| | | | | | | | | | |

| COMMON STOCKS - 53.90% | | | | | | | |

| | | | | | | | | | |

| Business Services - 12.43% | | | | | | | |

| * | Rosetta Stone, Inc. | | | 278,530 | $ | 2,807,880 | $ | 2,437,138 |

| * | Sizmek, Inc. | | | 348,570 | | 3,285,245 | | 3,067,416 |

| | | | | | | | | | 5,504,554 |

| Consumer Discretionary - 6.03% | | | | | | |

| * | Aeropostale, Inc. | | | 96,420 | | 845,348 | | 404,000 |

| | Apple, Inc. | | | 8,770 | | 549,867 | | 898,925 |

| | Samsung Electronics Co. Ltd. | | 1,360 | | 1,425,398 | | 1,368,209 |

| | | | | | | | | | 2,671,134 |

| Energy - 7.64% | | | | | | | |

| * | Athabasca Oil Corp. | | | 69,000 | | 467,906 | | 502,649 |

| * | BPZ Resources, Inc. | | | 856,970 | | 2,262,324 | | 2,099,577 |

| * | Gordon Creek Energy, Inc. | | | 27,566 | | 52,224 | | 1,648 |

| * | InterOil Corp. | | | 6,900 | | 347,393 | | 418,485 |

| * | Village Main Reef Ltd. | | | 8,925,000 | | 335,666 | | 360,034 |

| | | | | | | | | | 3,382,393 |

| Health Care - 2.76% | | | | | | | |

| * | Itamar Medical Ltd. | | | 215,000 | | 92,837 | | 124,928 |

| | Transcept Pharmaceuticals, Inc. | | 498,550 | | 1,345,992 | | 1,096,810 |

| | | | | | | | | | 1,221,738 |

| Information Technology - 17.23% | | | | | | |

| | Compuware Corp. | | | 64,390 | | 650,782 | | 602,046 |

| * | Covisint Corp. | | | 111,890 | | 771,086 | | 538,191 |

| * | DSP Group, Inc. | | | 188,270 | | 1,311,443 | | 1,690,665 |

| * | EnerNOC, Inc. | | | 62,200 | | 1,178,944 | | 1,221,608 |

| * | Quantum Corp. | | | 410,130 | | 479,321 | | 512,663 |

| * | SeaChange International, Inc. | | | 404,510 | | 3,769,729 | | 3,070,231 |

| | | | | | | | | | 7,635,404 |

| Materials - 1.08% | | | | | | | |

| * | Colossus Minerals, Inc. | | | 1,159,672 | | 1,670,855 | | 150,758 |

| * | The Phaunos Timber Fund | | | 821,000 | | 316,342 | | 328,727 |

| | | | | | | | | | 479,485 |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | (Continued) |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | |

| | | | | | | | | | |

| Schedule of Investments - Continued | | | | | | | |

| | | | | | | | | | |

| As of August 31, 2014 | | | | | | | |

| | | | | | Shares | | Cost | | Value (Note 1) |

| | | | | | | | | | |

| Real Estate - 6.73% | | | | | | | |

| * | Keck Seng Investments | | | 660,000 | | $ 559,221 | $ | 579,089 |

| * | Lai Sun Development Company Ltd. | | 52,363,000 | | 1,470,879 | | 1,364,798 |

| * | WCI Communities, Inc. | | | 52,000 | | 947,175 | | 1,037,400 |

| | | | | | | | | | 2,981,287 |

| | | | | | | | | | |

| | Total Common Stocks (Cost $26,943,857) | | | | | | 23,875,995 |

| | | | | | | | | | |

| CLOSED-END FUND - 2.90% | | | | | | | |

| | American Select Portfolio | | | 120,160 | | 1,152,342 | | 1,284,510 |

| | | | | | | | | | |

| | Total Closed-End Fund (Cost $1,152,342) | | | | | | 1,284,510 |

| | | | Shares | | Dividend Rate | | Maturity Date | | |

| PREFERRED STOCKS - 7.64% | | | | | | |

| | MVC Capital, Inc. | 33,950 | | 7.250% | | 1/15/2023 | | 870,478 |

| | Oxford Lane Capital Corp. | 65,000 | | 8.500% | | 12/31/2017 | | 1,677,000 |

| | SandRidge Energy, Inc. | 8,200 | | 8.500% | | 12/31/2049 | | 836,400 |

| | | | | | | | | | 3,383,878 |

| | | | | | | | | | |

| | Total Preferred Stocks (Cost $3,315,132) | | | | | | 3,383,878 |

| | | | Par | | Interest Rate | | Maturity Date | | |

| CONVERTIBLE BOND - 2.07% | | | | | | | |

| | Tower Group International Ltd. | $ | 966,000 | | 5.000% | | 9/15/2014 | | 915,889 |

| | | | | | | | | | 915,889 |

| | | | | | | | | | |

| | Total Convertible Bond (Cost $964,650) | | | | | | 915,889 |

| | | | | | | | | | |

| CORPORATE BONDS - 9.63% | Par | | Interest Rate | | Maturity Date | | |

| ᶐ | Athabasca Oil Corp. | 1,319,000 | | 7.500% | | 11/19/2017 | | 1,201,076 |

| | Clayton Williams Energy, Inc. | $ | 841,000 | | 7.750% | | 4/1/2019 | | 887,255 |

| | Goodrich Petroleum Corp. | 1,304,000 | | 8.875% | | 3/15/2019 | | 1,369,200 |

| | Resolute Energy Corp. | 786,000 | | 8.500% | | 5/1/2020 | | 809,580 |

| | | | | | | | | | 4,267,111 |

| | | | | | | | | | |

| | Total Corporate Bonds (Cost $4,115,997) | | | | | | 4,267,111 |

| | | | | | | | | | |

| | | | | | | | | | (Continued) |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | |

| | | | | | | | | | |

| Schedule of Investments - Continued | | | | | | | |

| | | | | | | | | | |

| As of August 31, 2014 | | | | | | | |

| | | | | | | | | | Value (Note 1) |

| WARRANT - 0.01% | Shares | | Strike Price | | Exercise Date | | |

| | Colossus Minerals, Inc. (a) | 580,998 | | $ 1.00 | | 3/17/2019 | $ | 5,810 |

| | | | | | | | | | |

| | Total Warrant (Cost $0) | | | | | | | 5,810 |

| | | | | | | | | | |

| SHORT-TERM INVESTMENT - 24.96% | | | | Shares | | |

| § | Federated Treasury Obligations Fund, 0.01% | | 11,056,609 | $ | 11,056,609 |

| | | | | | | | | | |

| | Total Short-Term Investment (Cost $11,056,609) | | | | 11,056,609 |

| | | | | | | | | | |

| Total Value of Investments (Cost $47,548,587) - 101.11% | | | $ | 44,789,802 |

| | | | | | | | | | |

| Liabilities in Excess of Other Assets - (1.11)% | | | | | | (492,026) |

| | | | | | | | | | |

| Net Assets - 100.00% | | | | | | $ | 44,297,776 |

| | | | | | | | | | |

| | * | Non-income producing investment | | | | | | |

| | § | Represents 7 day effective yield | | | | | | |

| | ᶐ | Rule 144-A Security | | | | | | | |

| | | | | | | | | | |

| | (a) | Security is fair valued and represents 0.01% of net assets. | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | (Continued) |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | |

| | | | | | | | | | |

| Schedule of Investments - Continued | | | | | | | |

| | | | | | | | | | |

| As of August 31, 2014 | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | Summary of Investments | | | | | | | |

| | | | | | % of Net | | | | |

| | | Sector | | | Assets | | Value | | |

| | | Business Services | | | 12.43% | $ | 5,504,554 | | |

| | | Consumer Discretionary | | | 6.03% | | 2,671,134 | | |

| | | Energy | | | 7.64% | | 3,382,393 | | |

| | | Health Care | | | 2.76% | | 1,221,738 | | |

| | | Information Technology | | | 17.23% | | 7,635,404 | | |

| | | Materials | | | 1.08% | | 479,485 | | |

| | | Real Estate | | | 6.73% | | 2,981,287 | | |

| | | Closed-End Fund | | | 2.90% | | 1,284,510 | | |

| | | Preferred Stocks | | | 7.64% | | 3,383,878 | | |

| | | Convertible Bond | | | 2.07% | | 915,889 | | |

| | | Corporate Bonds | | | 9.63% | | 4,267,111 | | |

| | | Warrant | | | 0.01% | | 5,810 | | |

| | | Short-Term Investment | | | 24.96% | | 11,056,609 | | |

| | | Liabilities in Excess of Other Assets | | -1.11% | | (492,026) | | |

| | | Total | | | 100.00% | $ | 44,297,776 | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| See Notes to Financial Statements | | | | | | | |

| | | | | | | | | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | |

| | | | | | | |

| Statement of Assets and Liabilities | | |

| | | | | | | |

| As of August 31, 2014 | | | |

| | | | | | | |

| Assets: | | | | | |

| Investments, at value (cost $47,548,587) | $ | 44,789,802 |

| Cash | | | | | 25,442 |

| Receivables: | | | |

| | Fund shares sold | | | 1,409 |

| | Dividends and interest | | 151,360 |

| Total assets | | | 44,968,013 |

| | | | | | | |

| Liabilities: | | | | |

| Payables: | | | | |

| | Investments purchased | | 571,345 |

| | Fund shares repurchased | | 49,845 |

| Accrued expenses | | | |

| | Advisory fees | | | 34,933 |

| | Administration fees | | 11,771 |

| | Distribution and service fees - Class A Shares and Class C Shares | | 2,343 |

| Total liabilities | | | 670,237 |

| | | | | | | |

| Net Assets | | | $ | 44,297,776 |

| | | | | | | |

| Net Assets Consist of: | | | |

| Paid in Beneficial Interest | $ | 43,569,746 |

| Undistributed net investment income | | 360,883 |

| Accumulated net realized gain on investments | | 3,125,932 |

| Net unrealized depreciation on investments | | (2,758,785) |

| Total Net Assets | | $ | 44,297,776 |

| Institutional Class Shares of beneficial interest outstanding, no par value (a) | | 3,793,543 |

| Net Assets | | $ | 39,841,966 |

| Net Asset Value, Offering Price and Redemption Price Per Share (b) | $ | 10.50 |

| Class A Shares of beneficial interest outstanding, no par value (a) | | 193,682 |

| Net Assets | | $ | 2,022,224 |

| Net Asset Value and Redemption Price Per Share (b) | $ | 10.44 |

| Offering Price Per Share ($10.44 ÷ 95.50%) | $ | 10.93 |

| Class C Shares of beneficial interest outstanding, no par value (a) | | 263,891 |

| Net Assets | | $ | 2,433,586 |

| Net Asset Value, Offering Price and Redemption Price Per Share (b)(c) | $ | 9.22 |

| | | | | | | |

| (a) | Unlimited Authorized Shares | | |

| (b) | The fund charges a 1% redemption fee on redemptions made within 60 days of initial purchase. |

| (c) | Contingent deferred sales charge for Class C Shares is imposed on proceeds redeemed within |

| one year of purchase date (note 1). | | |

| | | | | | | |

| See Notes to Financial Statements | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | |

| | | | | | | |

| Statement of Operations | | |

| | | | | | | |

| | | | | | | |

| For the Year ended August 31, 2014 | | |

| | | | | | | |

| Investment Income: | | |

| Interest | | | $ | 691,231 |

| Dividends (net of foreign taxes withheld of $3,780) | | 404,589 |

| | | | | | | |

| Total Investment Income | | 1,095,820 |

| | | | | | | |

| Expenses: | | | | |

| Advisory fees (note 2) | | 403,478 |

| Administration fees (note 2) | | 135,955 |

| Distribution and service fees - Class A Shares (note 3) | | 6,286 |

| Distribution and service fees - Class C Shares (note 3) | | 20,394 |

| | | | | | | |

| Total Expenses | | 566,113 |

| | | | | | | |

| Net Investment Income | | 529,707 |

| | | | | | | |

| Realized and Unrealized Gain (Loss) on Investments: | | |

| | | | | | | |

| | Net realized gain from investments and foreign currency transactions | | 3,036,028 |

| | Distributions of net realized gains from underlying investment companies | 51,058 |

| Total realized gain | | 3,087,086 |

| | | | | | | |

| Net change in unrealized appreciation on investments and translation of | | |

| | assets and liabilities in foreign currency | | (3,774,240) |

| | | | | | | |

| Net Realized and Unrealized Gain (Loss) on Investments | | (687,154) |

| | | | | | | |

| Net Decrease in Net Assets Resulting from Operations | $ | (157,447) |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| See Notes to Financial Statements | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | |

| | | | | | | | | | | |

| Statements of Changes in Net Assets | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| For the Year ended August 31, | | | | | 2014 | | 2013 |

| | | | | | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | | | $ | 529,707 | $ | 77,321 |

| Net realized gain from investments and foreign | | | | |

| | currency transactions | | | | | 3,036,028 | | 2,676,127 |

| Distributions of net realized gains from underlying investment | | |

| | companies | | | | | 51,058 | | - |

| | Net change in unrealized appreciation (depreciation) on | | | | |

| | on investments and translation of assets and liabilities | | | | |

| | in foreign currency | | | | | (3,774,240) | | 1,924,396 |

| | | | | | | | | | | |

| Net (Decrease) Increase in Net Assets Resulting from Operations | (157,447) | | 4,677,844 |

| | | | | | | | | | | |

Distributions to Shareholders: (note 5) | | | | | | |

| Net investment income | | | | | | | |

| | Institutional Class Shares | | | | (131,223) | | (169,985) |

| | Class A Shares | | | | | (4,611) | | (11,086) |

| | Class C Shares | | | | | (5,882) | | - |

| | | | | | | | | | | |

| Net realized gains | | | | | | | |

| | Institutional Class Shares | | | | (2,142,814) | | - |

| | Class A Shares | | | | | (147,821) | | - |

| | Class C Shares | | | | | (114,528) | | - |

| | | | | | | | | | | |

| Decrease in Net Assets Resulting from Distributions | | (2,546,879) | | (181,071) |

| | | | | | | | | | | |

| Beneficial Interest Transactions: | | | | | | |

| Shares sold | | | | | 26,903,496 | | 17,785,572 |

| Redemption fees | | | | | 1,675 | | 344 |

| Reinvested dividends and distributions | | | | 2,045,628 | | 161,618 |

| Shares repurchased | | | | | (18,733,750) | | (5,334,117) |

| | | | | | | | | | | |

| Increase from Beneficial Interest Transactions | | 10,217,049 | | 12,613,417 |

| | | | | | | | | | | |

| Net Increase in Net Assets | | | | | 7,512,723 | | 17,110,190 |

| | | | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of Year | | | | | 36,785,053 | | 19,674,863 |

| End of Year | | | | $ | 44,297,776 | $ | 36,785,053 |

| | | | | | | | | | | |

| Undistributed Net Investment Income | | | $ | 360,883 | $ | 1,842 |

| See Notes to Financial Statements | | | | | | (Continued) |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | |

| | | | | | | | | | | |

| Statements of Changes in Net Assets (continued) | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| For the Year ended August 31, | 2014 | | | | 2013 | | |

| | | | | | | | | | | |

| Share Information: | | | | | | | |

| Institutional Class Shares | Shares | | Amount | | Shares | | Amount |

| | Shares sold | 2,231,388 | $ | 24,030,091 | | 1,513,598 | $ | 16,237,651 |

| | Redemption fees | - | | 1,548 | | - | | 344 |

| | Reinvested dividends | | | | | | | |

| | | and distributions | 171,100 | | 1,774,205 | | 15,546 | | 150,992 |

| | Shares repurchased | (1,622,933) | | (17,179,993) | | (476,166) | | (5,206,363) |

| Net Increase in Beneficial | | | | | | | |

| Interest and Shares | 779,555 | $ | 8,625,851 | | 1,052,978 | $ | 11,182,624 |

| | | | | | | | | | | |

| Class A Shares | Shares | | Amount | | Shares | | Amount |

| | Shares sold | 78,347 | $ | 827,249 | | 87,457 | $ | 927,154 |

| | Redemption fees | - | | 127 | | - | | - |

| | Reinvested dividends | | | | | | | |

| | | and distributions | 14,647 | | 151,013 | | 1,097 | | 10,626 |

| | Shares repurchased | (129,323) | | (1,347,764) | | (12,217) | | (127,754) |

| Net Increase (Decrease) in | | | | | | | |

| Beneficial Interest and Shares | (36,329) | $ | (369,375) | | 76,337 | $ | 810,026 |

| | | | | | | | | | | |

| Class C Shares | Shares | | Amount | | Shares | | Amount |

| | Shares sold | 211,343 | $ | 2,046,156 | | 61,762 | $ | 620,767 |

| | Reinvested dividends | | | | | | | |

| | | and distributions | 13,132 | | 120,410 | | - | | - |

| | Shares repurchased | (22,346) | | (205,993) | | - | | - |

| Net Increase in Beneficial | | | | | | | |

| Interest and Shares | 202,129 | $ | 1,960,573 | | 61,762 | $ | 620,767 |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| See Notes to Financial Statements | | | | | | |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | | | |

| | | | | | | | | | | | | |

| Financial Highlights | | | | | | | | | |

| | | | | | | | | | | | | |

| For a share outstanding during the | | Institutional Class Shares |

| fiscal year or period ended August 31, | | 2014 | | 2013 | | 2012 | | 2011 (d) | |

| | | | | | | | | | | | | |

| Net Asset Value, Beginning of Period | $ | 11.15 | $ | 9.31 | $ | 9.42 | $ | 10.00 | |

| | | | | | | | | | | | | |

| Income (Loss) from Investment Operations | | | | | | | | | |

| Net investment income | | 0.13 | | 0.03 | | 0.09 | | 0.03 | |

| Net realized and unrealized gain (loss) | | | | | | | | | |

| | on investments | | (0.16) | | 1.89 | | (0.13) | | (0.61) | |

| Total from Investment Operations | | (0.03) | | 1.92 | | (0.04) | | (0.58) | |

| | | | | | | | | | | | | |

| Less Distributions: | | | | | | | | | |

| From net investment income | | (0.03) | | (0.08) | | (0.07) | | - | |

| From realized gains | | (0.59) | | - | | - | | - | |

| Total Distributions | | (0.62) | | (0.08) | | (0.07) | | - | |

| | | | | | | | | | | | | |

| Paid in Beneficial Interest: | | | | | | | | | |

From redemption fees (note 1) | | 0.00 | (e) | 0.00 | (e) | 0.00 | (e) | - | |

| Total Paid in Beneficial Interest | | 0.00 | (e) | 0.00 | (e) | 0.00 | (e) | - | |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | $ | 10.50 | $ | 11.15 | $ | 9.31 | $ | 9.42 | |

| | | | | | | | | | | | | |

| Total Return | | (0.12)% | (c) | 20.71% | (c) | (0.36)% | | (5.80)% | (b) |

| | | | | | | | | | | | | |

| Net Assets, End of Period (in thousands) | $ | 39,842 | $ | 33,617 | $ | 18,249 | $ | 12,368 | |

| | | | | | | | | | | | | |

| Ratios of: | | | | | | | | | | |

| Total Expenses to Average Net Assets | | 1.23% | | 1.23% | | 1.23% | | 1.23% | (a) |

| Net Investment Income to Average Net Assets | 1.27% | | 0.31% | | 1.10% | | 1.08% | (a) |

| | | | | | | | | | | | | |

| Portfolio turnover rate | | 92.74% | | 77.73% | | 49.34% | | 33.08% | (b) |

| | | | | | | | | | | | | |

| (a) | Annualized. | | | | | | | | | |

| (b) | Not annualized. | | | | | | | | | |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United |

| States of America and, consequently, the net asset value for financial reporting purposes and |

| the returns based upon those net asset values may differ from the net asset values and returns |

| for shareholder transactions. | | | | | | | | | |

| (d) | For a share outstanding for the initial period from December 31, 2010 (Date of Initial Public |

| Investment) to August 31, 2011. | | | | | | | | | |

| (e) | Actual amount is less than $0.01 per share. | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| See Notes to Financial Statements | | | | | | | | (Continued) |

ROUMELL OPPORTUNISTIC VALUE FUND

| Financial Highlights | | | | | | | | | |

| | | | | | | | | | | | | |

| For a share outstanding during the | | Class A Shares |

| fiscal year or period ended August 31, | | 2014 | | 2013 | | 2012 | | 2011 (e) | |

| | | | | | | | | | | | | |

| Net Asset Value, Beginning of Period | $ | 11.10 | $ | 9.28 | $ | 9.41 | $ | 10.00 | |

| | | | | | | | | | | | | |

| Income (Loss) from Investment Operations | | | | | | | | | |

| Net investment income | | 0.12 | | 0.01 | | 0.08 | | 0.03 | |

| Net realized and unrealized gain (loss) | | | | | | | | | |

| | on investments | | (0.17) | | 1.88 | | (0.15) | | (0.62) | |

| Total from Investment Operations | | (0.05) | | 1.89 | | (0.07) | | (0.59) | |

| | | | | | | | | | | | | |

| Less Distributions: | | | | | | | | | |

| From net investment income | | (0.02) | | (0.07) | | (0.06) | | - | |

| From realized gains | | (0.59) | | - | | - | | - | |

| Total Distributions | | (0.61) | | (0.07) | | (0.06) | | - | |

| | | | | | | | | | | | | |

| Paid in Beneficial Interest: | | | | | | | | | |

From redemption fees (note 1) | | 0.00 | (f) | - | | 0.00 | (f) | - | |

| Total Paid in Beneficial Interest | | 0.00 | (f) | - | | 0.00 | (f) | - | |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | $ | 10.44 | $ | 11.10 | $ | 9.28 | $ | 9.41 | |

| | | | | | | | | | | | | |

| Total Return (c) | | (0.38)% | (d) | 20.46% | (d) | (0.56)% | | (6.00)% | (b) |

| | | | | | | | | | | | | |

| Net Assets, End of Period (in thousands) | $ | 2,022 | $ | 2,553 | $ | 1,426 | $ | 1,674 | |

| | | | | | | | | | | | | |

| Ratios of: | | | | | | | | | | |

| Total Expenses to Average Net Assets | | 1.48% | | 1.48% | | 1.48% | | 1.48% | (a) |

| Net Investment Income to Average Net Assets | 1.02% | | 3.00% | | 0.89% | | 0.73% | (a) |

| | | | | | | | | | | | | |

| Portfolio turnover rate | | 92.74% | | 77.73% | | 49.34% | | 33.08% | (b) |

| | | | | | | | | | | | | |

| (a) | Annualized. | | | | | | | | | |

| (b) | Not annualized. | | | | | | | | | |

| (c) | Total return does not reflect sales charge, if any. | | | | | | | |

| (d) | Includes adjustments in accordance with accounting principles generally accepted in the United |

| States of America and, consequently, the net asset value for financial reporting purposes and | |

| the returns based upon those net asset values may differ from the net asset values and returns | |

| for shareholder transactions. | | | | | | | | | |

| (e) | For a share outstanding for the initial period from December 31, 2010 (Date of Initial Public | |

| Investment) to August 31, 2011. | | | | | | | | | |

| (f) | Actual amount is less than $0.01 per share. | | | | | | | | |

| | | | | | | | | | | | | |

| See Notes to Financial Statements | | | | | | | | (Continued) |

| ROUMELL OPPORTUNISTIC VALUE FUND | | | | | |

| | | | | | | | | |

| Financial Highlights | | | | | |

| | | | | | | | | |

| For a share outstanding during the | | Class C Shares |

| fiscal year or period ended August 31, | | 2014 | | 2013 | (e) |

| | | | | | | | | |

| Net Asset Value, Beginning of Period | $ | 9.95 | $ | 10.00 | |

| | | | | | | | | |

| Income (Loss) from Investment Operations | | | | | |

| Net investment income (loss) | | 0.03 | | (0.01) | |

| Net realized and unrealized loss on investments | | (0.15) | | (0.04) | |

| Total from Investment Operations | | (0.12) | | (0.05) | |

| | | | | | | | | |

| Less Distributions: | | | | | |

| From net investment income | | (0.02) | | - | |

| From realized gains | | (0.59) | | - | |

| Total Distributions | | (0.61) | | - | |

| | | | | | | | | |

| Net Asset Value, End of Period | $ | 9.22 | $ | 9.95 | |

| | | | | | | | | |

| Total Return (c) | | (1.09)% | (d) | (0.50)% | (b)(d) |

| | | | | | | | | |

| Net Assets, End of Period (in thousands) | $ | 2,434 | $ | 615 | |

| | | | | | | | | |

| Ratios of: | | | | | | | |

| Total Expenses to Average Net Assets | | 2.23% | | 2.23% | (a) |

| Net Investment Income (Loss) to Average Net Assets | | 0.27% | | (1.20)% | (a) |

| | | | | | | | | |

| Portfolio turnover rate | | 92.74% | | 77.73% | (b) |

| | | | | | | | | |

| (a) | Annualized. | | | | | |

| (b) | Not annualized. | | | | | |

| (c) | Total return does not reflect sales charge, if any. | | | | | |

| (d) | Includes adjustments in accordance with accounting principles generally accepted in the United | |

| States of America and, consequently, the net asset value for financial reporting purposes and | | |

| the returns based upon those net asset values may differ from the net asset values and returns | | |

| for shareholder transactions. | | | | | |

| (e) | For a share outstanding for the initial period from July 30, 2013 (Date of Initial Public | | | |

| Investment) to August 31, 2013. | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| See Notes to Financial Statements | | | | | |

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

| 1. | Organization and Significant Accounting Policies |

The Roumell Opportunistic Value Fund ("Fund") is a series of the Starboard Investment Trust ("Trust"). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the "1940 Act"), as an open-end management investment company. The Fund is a separate non-diversified series of the Trust.

The Fund commenced operations on December 31, 2010. The investment objective of the Fund is to seek capital appreciation and income. Roumell Asset Management, LLC ("Roumell Asset Management" or the "Advisor") seeks to achieve the Fund's investment objective by using an opportunistic investment strategy. The Advisor is an opportunistic capital allocator (OCA) with a deep value bias in selecting individual securities. The Advisor will wait until an investment situation is presented where, in its opinion, the odds of success are favorable relative to the risks. In the absence of such situations, the Fund will stay liquid and on the sidelines invested in Cash and Cash Equivalents. The Advisor's approach to opportunistic investing emphasizes purchasing securities at a meaningful, quantifiable discount to its calculation of intrinsic value taking into consideration the understandability of the business model, the safety of the capital structure, and the competency of the company's management. Using this opportunistic strategy, however, may result in the Advisor finding many suitable investment opportunities for the Fund during certain periods, but finding very few during other periods.

The Fund currently has an unlimited number of authorized shares, which are divided into three classes - Institutional Class Shares, Class A Shares, and Class C Shares. Each class of shares has equal rights as to assets of the Fund, and the classes are identical except for differences in sales charges and ongoing distribution and service fees. Class A Shares are subject to an initial sales charge of 4.50%. Class C Shares are subject to a contingent deferred sales charge of 1% of the proceeds redeemed within one year of the purchase date. Class A Shares and Class C Shares are subject to distribution plan fees, which are further discussed in Note 3. All share classes are subject to redemption fees within 60 days of the issuance of such shares of 1.00%. Income, expenses (other than distribution and service fees), and realized and unrealized gains or losses on investments are allocated to each class of shares based upon its relative net assets. All classes have equal voting privileges, except where otherwise required by law or when the Trustees determine that the matter to be voted on affects only the interests of the shareholders of a particular class.

(Continued)

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

The following accounting policies have been consistently followed by the Fund and are in conformity with accounting principles generally accepted in the United States of America ("GAAP").

Investment Valuation

The Fund's investments in securities are carried at value. Securities listed on an exchange or quoted on a national market system are valued at the last sales price as of 4:00 p.m. Eastern Time. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. Other securities traded in the over-the-counter market and listed securities for which no sale was reported on that date are valued at the most recent bid price. Securities and assets for which representative market quotations are not readily available (e.g., if the exchange on which the security is principally traded closes early or if trading of the particular security is halted during the day and does not resume prior to the Fund's net asset value calculation) or which cannot be accurately valued using the Fund's normal pricing procedures are valued at fair value as determined in good faith under policies approved by the Trustees. A security's "fair value" price may differ from the price next available for that security using the Fund's normal pricing procedures. Instruments with maturities of 60 days or less are valued at amortized cost, which approximates market value.

Fair Value Measurement

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1: quoted prices in active markets for identical securities

Level 2: other significant observable inputs (including quoted prices for similar securities, interest rates, credit risk, etc.)

Level 3: significant unobservable inputs (including the Fund's own assumptions in determining fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

(Continued)

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the inputs as of August 31, 2014 for the Fund's assets measured at fair value:

| Investments in Securities (a) | | Total | | Level 1 | | Level 2 | | Level 3(b) |

| Common Stocks* | $ | | 23,875,995 | $ | | 23,725,237 | $ | | 150,758 - | $ | | - - |

| Closed-End Fund | | 1,284,510 | | 1,284,510 | | - - | | - - |

| Preferred Stocks | | 3,383,878 | | 1,706,878 | | 1,677,000- | | - - |

| Convertible Bond | | 915,889 | | - | | 915,889 | | - - |

| Corporate Bonds | | 4,267,111 | | - | | 4,267,111 | | - |

| Warrant | | 5,810 | | - | | - | | 5,810 |

| Short-Term Investment | | 11,056,609 | | 11,056,609 | | - | | - - |

| Total | $ | 44,789,802 | $ | 37,773,234 | $ | 7,010,758 | $ | 5,810 |

*Refer to Schedule of Investments for breakdown by Sector

(a) As of August 31, 2014, $1,677,000 transferred from Level 1 to Level 2 based on the valuation input levels assigned to securities on August 31, 2013. This was a result of the security transferring from an active market at the time of pricing to an inactive market. It is the Fund's policy to record transfers at the end of the year.

(b) At the beginning and the end of the reporting period, Level 3 investments were not considered a material portion of the Fund.

Foreign Currency Translation

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. Purchases and sales of securities and income items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date.

(Continued)

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes, and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income is recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded as soon as the Fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums. Gains and losses are determined on the identified cost basis, which is the same basis used for federal income tax purposes.

Expenses

The Fund bears expenses incurred specifically on its behalf as well as a portion of general expenses, which are allocated according to methods reviewed annually by the Trustees.

Distributions

The Fund may declare and distribute dividends from net investment income (if any) quarterly. Distributions from capital gains (if any) are generally declared and distributed annually. Dividends and distributions to shareholders are recorded on ex-date.

Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in the net assets from operations during the reported period. Actual results could differ from those estimates.

(Continued)

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

Fees on Redemptions

The Fund charges a redemption fee of 1.00% on redemptions of Fund shares occurring within 60 days following the issuance of such shares. The redemption fee is not a fee to finance sales or sales promotion expenses, but is paid to the Fund to defray the costs of liquidating an investor and discouraging short-term trading of the Fund's shares. No redemption fee will be imposed on the redemption of shares representing dividends or capital gains distributions, or on amounts representing capital appreciation of shares.

Federal Income Taxes

No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

| 2. | Transactions with Affiliates and Service Providers |

Advisor

As full compensation for the investment advisory services provided to the Fund, the Advisor receives a monthly fee equal to an annualized rate of 0.92% of the Fund's average daily net assets. The fee paid to the Advisor is calculated by multiplying the average daily net assets of the Fund, computed at the end of each month and payable within five days thereafter.

Administrator

Fund Accounting and Administration Agreement: The Administrator provides the Fund with administrative, fund accounting, and compliance services. The Administrator receives compensation from the Fund at a maximum annual rate of 0.31% and is responsible for the coordination and payment of vendor services and other Fund expenses from such compensation. Pursuant to this arrangement, the Administrator pays the following expenses: (i) compensation and expenses of any employees of the Trust and of any other persons rendering any services to the Fund; (ii) clerical and shareholder service staff salaries; (iii) office space and other office expenses; (iv) fees and expenses incurred by the Fund in connection with membership in investment company organizations; (v) fees and expenses of counsel to the Trustees who are not interested persons of the Fund and Trust;

(Continued)

ROUMELL OPPORTUNISTIC VALUE FUND

Notes to Financial Statements

(vi) fees and expenses of counsel to the Fund and Trust engaged to assist with preparation of Fund and Trust documents and filings and provide other ordinary legal services; (vii) fees and expenses of independent public accountants to the Fund, including fees and expense for tax preparation; (viii) expenses of registering shares under federal and state securities laws; (ix) insurance expenses; (x) fees and expenses of the custodian, shareholder servicing, dividend disbursing and transfer agent, administrator, distributor, and accounting and pricing services agents of the Fund; (xi) compensation for a chief compliance officer for the Trust; (xii) expenses, including clerical expenses, of issue, sale, redemption, or repurchase of shares of the Fund; (xiii) the cost of preparing and distributing reports and notices to shareholders; (xiv) the cost of printing or preparing prospectuses and statements of additional information for delivery to the Fund's current shareholders; (xv) the cost of printing or preparing documents, statements or reports to shareholders; and (xvi) other expenses not specifically assumed by the Fund or Advisor. The Administrator cannot recoup from the Fund any Fund expenses in excess of the administration fees payable under the Fund Accounting and Administration Agreement.