UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22525

Managed Portfolio Series

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Brian R. Wiedmeyer, President

Managed Portfolio Series

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Ave, 5th Fl

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 765-6844

Registrant's telephone number, including area code

Date of fiscal year end: November 30, 2023

Date of reporting period: November 30, 2023

Updated August 1, 2011

Item 1. Reports to Stockholders.

TortoiseEcofin

2023 Annual Report

This combined financial report provides you with a comprehensive review of our funds that span the entire energy value chain.

Table of Contents

2023 Annual Report | November 30, 2023

Open-end fund comparison

| | Name/Ticker | | Primary focus | | Total investments

($ Millions)(1) | | Portfolio mix by asset type(1) | | Portfolio mix by ownership(1) |

| Tortoise Energy Infrastructure Total

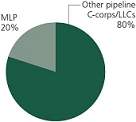

Return Fund Institutional Class (TORIX) A Class (TORTX) Inception: 5/2011 C Class (TORCX) Inception: 9/2012 | | North American pipeline companies | | $2,119.2 | |  | |  |

Tortoise Energy

Infrastructure and

Income Fund Institutional Class (INFIX)

A Class (INFRX)

Inception: 5/2011

C Class (INFFX)

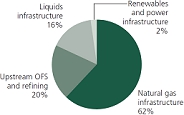

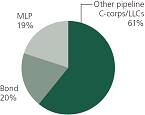

Inception: 4/2012 | | Energy infrastructure equity and debt | | $492.6 | |  | |  |

| | | | | | | Portfolio mix by sector type(1) | | Portfolio mix by geography(1) |

Ecofin Global Renewables Infrastructure Fund Institutional Class (ECOIX)

A Class (ECOAX)

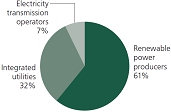

Inception: 8/2020 | | Global Securities benefiting from long-term growth associated with energy transition | | $216.8 | |  | |  |

(1)As of 11/30/2023

(unaudited)

Tortoise

2023 Annual Report

Dear shareholder,

The 2023 fiscal year offered energy investors significant opportunity with record levels of production, growing export demand, along with some regulatory clarity. Overall, performance ended the year mixed with midstream higher and both broader energy and utilities lower. Higher interest rates clearly impacted relative performance. And cash flow proved to be king. Notable events influencing performance included geopolitical tensions in Ukraine and Israel and OPEC+ decisions around crude oil supply and demand. Effects of the Inflation Reduction Act also started to surface. Finally, the U.S. energy complex remained ever important to supporting the global economy. Sustainable infrastructure continued to face significant headwinds over the fiscal year due to a variety of factors including inflation, elevated interest rates, and natural gas prices.

Energy and power infrastructure

The broad energy sector returned -4.3% for the annual fiscal period (as measured by the S&P 500 Energy Index). Energy was generally rangebound during the year, bottoming down 15% in March following the regional banking crisis, and peaking higher by 5% in September following the Organization of Petroleum Exporting Countries plus Russia’s (OPEC+) announcement to curtail crude oil supplies to the global market. The war between Russian and Ukraine remained in focus and geopolitically was magnified when the Israel and Hamas conflict intensified in October. That raised concerns about a broader Middle East conflict. The allocation for free cash flow remained an energy investor focus with lower debt, dividend growth, and share buybacks being a cornerstone of management’s playbook. These policies, along with disciplined mergers & acquisitions (M&A), were favored in the higher interest environment and in front of concerns about a slowing economy in 2024.

Global crude oil supply and demand led energy market sentiment. In the first quarter the Organization for Economic Cooperation and Development (OECD) commercial inventories built up marginally partly due to slower Chinese demand than expected coming out of COVID lockdowns. This resulted in a decision by Saudi Arabia in the summer to voluntarily reduce its oil output by 1 million barrels per day (bpd) for the month of July, with the potential for this cut to be extended. Consequently, oil stocks declined, and crude oil prices rallied in the third quarter. Though Saudi Arabia consistently extended their cuts in the second half, concerns about a global economic slowdown along with growing production in the United States and Guyana weighed on prices late in the year. To better balance the market, in November OPEC+ agreed to 2 million bpd of cuts to start 2024, leaving the oil market in a constructive position on supply and demand.

U.S. crude oil production growth exceeded expectations, growing nearly 1 million bpd in 2023 to 13.2 million bpd. That level eclipsed the previous record high of 13.0 million bpd achieved in November of 2019. The growth resulted despite rig counts and well completions falling as the year progressed. Simply, producers did more with less. Drilling laterals lengthened, completion times shortened and even the application of artificial intelligence positively impacted efficiencies. The Permian basin, the largest U.S. oilfield, remained the primary driver of growth reaching six million bpd. Aiding producer returns, oilfield service and material costs declined, resulting in lower break-even costs. The Energy Information Agency (EIA) forecasts production in 2024 to remain steady, partly due to the lower rig count and completion activity trend transpiring in 2023.

U.S. natural gas production grew as well in 2023 as the U.S. exported more liquefied natural gas (LNG) than any other country in the first half. U.S. LNG production reached nearly 12 billion cubic feet per day (bcf/d). The war in Ukraine continued to present a long-term opportunity for U.S. liquefied natural gas. LNG exports to Europe accelerated in 2022 and remained elevated in 2023. These exports, lower industrial demand, and a relatively warm winter in 2022/23 kept European natural gas storage inventories full throughout 2023 and well positioned to keep Europe adequately supplied for the 2024 winter. U.S. natural gas storage inventories also entered year-end 2023 well supplied at just above the five-year average partly due to a warm winter a year ago. Also helping inventories is growing U.S. production, that improved from 102 bcf/d to 105 bcf/d over the year. That production will help supply LNG export facilities set to come on-line starting in the second half of 2024 through year-end 2027. In that short timeframe U.S. LNG export capacity will nearly double to 25 bcf/d. The EIA forecasts natural gas production to be mostly flat in 2024 due partly to limited visibility to near-term demand improvement and, like the drilling cadence for oil, declining service activity.

Natural gas liquids (NGLs) do not receive as much attention as crude oil or natural gas because they are less visible to consumers. Nonetheless, that does not diminish their importance as NGLs are the key components in making plastics along with being a source of heat. And, at 6.8 million bpd, the U.S. is the world’s largest producer of NGLs. Growth in 2023 surpassed 600 thousand bpd with most marginal production exported to meet growing Asian petrochemical demand. The EIA forecasts NGL production to be stable in 2024.

The midstream energy sector returned 7.6% for the fiscal year (as measured by the Alerian Midstream Energy Index or AMNA), topping broader energy. Growing production volumes and inflation passed through via higher tariff rates benefitted revenues. Further, the sector’s elevated and higher free cash flow, declining leverage, attractive valuation, and share buybacks supported performance. Finally, disciplined M&A activity with synergies largely accruing to buyers offered a favorable environment for those seeking acquisition led growth.

Cash flow improved for midstream companies in 2023 following volumes and tariff increases and cost and capital expenditure discipline. Management teams targeted cash flow increasingly toward shareholders in the form of debt paydown, dividend and distribution growth, and share repurchases. Leverage targets are now generally between 3.0x – 4.0x earnings before interest, taxes, depreciation and amortization (EBITDA) with leverage being a full “turn” lower versus levels prior to 2020. And in addition to dividend and distribution growth, companies opportunistically repurchased shares, as buybacks topped $4 billion from the fourth quarter of 2022 through the third quarter of 2023. With leverage targets now largely achieved, 2024 sets up for incrementally more cash flow earmarked for dividends and buybacks.

(unaudited)

2023 Annual Report | November 30, 2023

Following hawkish interest rate actions from the Federal Reserve, the prospects of an economic recession weighed on investor psyche during much of the fiscal year. While multiple recessions occurred in the last 40 years, energy demand still increased in 38 out of the last 41 years (2008 and 2020 decreased). Due to actions taken during the recent 2020 recession that reduced capital expenditures and focused on debt paydown, we believe the energy sector, and specifically midstream, is well prepared to deal with another potential recession. With the world remaining undersupplied energy over the long-term and sector balance sheets now less levered than in past recent recessions (2001, 2008 and 2020), we believe energy is well positioned should lower economic growth materialize.

Broader market concerns about higher interest rates boosted midstream’s relative attractiveness. As higher rates due to inflation were passed through, companies generated significant free cash flow that led to little to no debt or equity capital market access requirements even for maturing debt. Additionally, the good economic growth resulted in higher energy demand. Looking at history, good performance in a higher rate environment is not surprising. In the 18 time periods when the 10-year Treasury yield increased by 50 basis points or more since 2001, midstream energy, represented by the Tortoise North American Pipeline Index, returned an average of 7.4%, compared to a S&P 500 Index average return of 5.9%, and bond returns of -2.6% represented by the Bloomberg U.S. Aggregate Bond Index.

With inflation continuing to increase in 2023, midstream provided investors inflation protection. Pipelines typically benefit from long-term contracts with inflation protection from regulated tariff escalators. Additionally, tariffs on regulated liquid pipelines include an inflation escalator aligned with the Producer Price Index (PPI). Federal Energy Regulatory Commission (FERC) indexing allowed for a tariff increase of over 13% beginning on July 1, 2023. In fact, we estimate that the cumulative total allowable tariff increase since 2020 through year-end 2024 will eclipse 26%. This contract feature serves as protection against higher operating costs.

Midstream companies remained active in M&A with many discrete assets changing hands along with a handful of corporate transactions. The commonality among all the transactions was buyer discipline. The buyers only purchased complementary assets to existing footprints where synergies were obvious and paid a price that made the transaction immediately accretive. Even in the corporate transactions, premiums paid were constructive. In the largest corporate transaction, ONEOK acquired Magellan Midstream Partners at a 22% premium. Synergies and diversification drove the rationale as both Tulsa companies transport petroleum products, with ONEOK mostly natural gas liquids and Magellan refined products and crude oil. ONEOK also estimated a tax benefit of $1.5 billion.

One major new pipeline received regulatory help with the signing of the Fiscal Responsibility Act (FRA) that resolved the mid-summer debt ceiling scuffle. That Act approved all construction and operational permits and authorizations required for the Mountain Valley Pipeline (MVP). MVP would transport 2 bcf/d of natural gas from the Marcellus through West Virginia and into Virginia. Equitrans Midstream (ETRN), MVP’s operator, now estimates pipeline completion in the first quarter of 2024. In addition, the FRA reformed the way the National Environmental Policy Act (NEPA) interacts with agencies to approve energy projects so that project developers have more confidence in permitting processes. Now, when two or more agencies are involved in review, one will be designated lead agency to reduce delays. Further, the timeframe for an Environmental Impact Statement is limited to two years and an Environmental Assessment to one year, and there are limits on the number of pages for each. Despite the improved regulatory efficiency, attaining project approvals remained challenging. For example, Navigator CO2 Ventures cancelled its proposed $3.5 billion, 1,300-mile carbon capture pipeline due to an unpredictable regulatory and government process. The pipeline concept involved transporting carbon dioxide emissions from ethanol plants to sites where the greenhouse gas would be sequestered deep underground.

Sustainable infrastructure

From a macro perspective the first half of the period was generally characterised by influences stemming from stubborn inflation, elevated interest rates, and declining energy prices, in particular natural gas. In China, the magnitude of economic recovery following the post-COVID reopening ultimately did not come to fruition.

Elevated borrowing costs were concerning for businesses which ‘borrow to grow,’ as were higher equipment costs, trade issues, permitting and transmission constraints. The period also saw banking turmoil triggered primarily by Silicon Valley Bank in early March. As such, some companies in our investment universe could not escape these varying impulses even if their secular growth remained intact.

The second half of the period opened with continued upward pressure on interest rates across the OECD and declining power prices in Europe. In response, our capital-intensive sector saw challenges amidst these elevated interest rates, notably on existing asset cash flows due to higher costs of capital, and on balance sheets due to the increased total capital needed to finance growth. Amidst such a context, the sector derated while broader market multiples expanded.

The third calendar quarter saw a further steady increase in longer-term interest rates, which created a larger headwind to valuations and spreads of capital formation for new projects, and overshadowed other drivers as the market reduced the present value of actual cash flows and questioned the value of growth for companies in the sector. Within that context, purer renewables companies that do not have other businesses have been most impacted. We therefore saw both U.S. and European valuations continue to compress. Amidst such a context the sector struggled during the quarter.

The close of the period saw a welcome improvement in performance, as interest rates began to stabilise and hopeful sentiment on potential future rate cuts for 2024 arose.

(unaudited)

Looking Ahead:

In 2024, if interest rates stabilize and then decline, we believe that would be very supportive for the sector in the future. Stability in interest rates should help reduce volatility by offering more consistent net present values of operating cash flows and growth. This is unfortunately an exogenous factor, but equally is not fundamental to operating earnings before interest and taxes (EBIT).

We maintain conviction looking ahead; electrification trends remain robust as fundamentally demand is strong, and we predict strong policy support (from the U.S.’ IRA, across to Europe). Further, valuations for the stocks in the investment universe have come down relative to history and relative to the broader market. We believe doubts surrounding growth are likely overly pessimistic, and that the mean-reverting aspects of utilities and infrastructure have been historically compelling. Over-time, in our sector, share prices will tend to correlate with earnings, and we anticipate these dynamics in 2024.

Notably, through 2023 many companies have reset priorities among growth, credit rating, and dividend. The sector will therefore enter 2024 offering a clearer picture with potentially less volatility and a focus on execution.

Moving into 2024 and considering valuations, strength in demand, attractive renewables development returns and where we are in the inflation and interest rate cycles, we believe that we are approaching an inflection point and are in an attractive spot. This sector captures structural growth in a slowing global economic environment. Companies typically deliver more stable, and more predictable non-cyclical earnings, and are positioned to protect better in falling markets while also participating in rebounds.

Concluding thoughts

Energy infrastructure remains essential for the U.S. to continue as the leading global energy producer and to meet the energy demands of consumers, both domestically and abroad. Geopolitical events further highlighted this reality. We believe that indispensable nature offers compelling opportunities for 2024 and beyond. We hope for improved performance of sustainable infrastructure and climate action investments. With strong demand for renewable energy sources, we believe the sector is well positioned heading into 2024.

The S&P 500® Index is an unmanaged market-value weighted index of stocks, which is widely regarded as the standard for measuring large-cap U.S. stock market performance. The S&P Energy Select Sector® Index is a capitalization-weighted index of S&P 500® Index companies in the energy sector involved in the development or production of energy products. The Tortoise North American Pipeline IndexSM is a float adjusted, capitalization-weighted index of energy pipeline companies domiciled in the United States and Canada. The Tortoise MLP Index® is a float-adjusted, capitalization-weighted index of energy master limited partnerships.

The Tortoise indices are the exclusive property of TIS Advisors which has contracted with S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC) to calculate and maintain the Tortoise MLP Index® and Tortoise North American Pipeline IndexSM (the “Indices”). The Indices are not sponsored by S&P Dow Jones Indices or its affiliates or its third party licensors (collectively, “S&P Dow Jones Indices LLC”). S&P Dow Jones Indices will not be liable for any errors or omission in calculating the Indices. “Calculated by S&P Dow Jones Indices” and its related stylized mark(s) are service marks of S&P Dow Jones Indices and have been licensed for use by TIS Advisors and its affiliates. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”).

Free cash flow is the cash a company produces through its operations, less the cost of total capital expenditures (growth and maintenance).

The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. The prices included in the PPI are from the first commercial transaction for many products and some services

It is not possible to invest directly in an index.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost.

(unaudited)

2023 Annual Report | November 30, 2023

Tortoise

Energy Infrastructure Total Return Fund

Basic fund facts

Investment objective: Total return

Structure: Regulated investment company

| | | Institutional | | A Class | | C Class |

| Ticker | | | TORIX | | | | TORTX | | | | TORCX | |

| Gross expense ratio(5) | | | 0.93 | % | | | 1.18 | % | | | 1.93 | % |

| Redemption fee | | | None | | | | None | | | | None | |

| Maximum front-end sales load | | | None | (1) | | | 5.50 | %(2) | | | None | (1) |

| Maximum deferred sales load | | | None | | | | None | (3) | | | 1.00 | %(4) |

| (1) | While the Institutional and C Classes have no front-end load, advisory and other expenses still apply. |

| (2) | You may qualify for sales charge discounts if you invest at least $50,000. |

| (3) | No front-end sales charge is payable on A Class investments of $1 million or more, although the fund may impose a Contingent Deferred Sales Charge (“CDSC”) of 1% on certain redemptions made within 12 months of purchase. |

| (4) | The C Class CDSC applies to redemptions made within 12 months of purchase. |

| (5) | The expense ratios reflect those in the most recent prospectus and may not agree to the financial highlights. |

Targeted investment characteristics

The fund’s targeted investments generally will have the following characteristics:

| • | Strategic assets that fuel the economy |

| • | Diversified asset base |

| • | Limited direct commodity price exposure |

| • | History of predictable, recurring cash flows |

| • | Total-return potential through growth and current income |

| • | Experienced management teams |

Top ten holdings (as of November 30, 2023)

| 1. | Cheniere Energy, Inc. | 10.1% |

| 2. | Targa Resources Corp. | 10.0% |

| 3. | The Williams Companies, Inc. | 7.7% |

| 4. | Kinder Morgan, Inc. | 7.4% |

| 5. | ONEOK, Inc. | 7.3% |

| 6. | Enbridge Inc. | 7.0% |

| 7. | MPLX LP | 4.9% |

| 8. | Plains GP Holdings, L.P. | 4.9% |

| 9. | Energy Transfer LP | 4.9% |

| 10. | Pembina Pipeline Corporation | 4.8% |

Key asset performance drivers

| • | All segments except for diversified infrastructure had positive performance. |

| • | The fund’s largest allocation to natural gas pipeline companies added the most to performance. |

| • | The fund’s allocation to diversified infrastructure detracted the most from performance. |

| Top five contributors |

| Targa Resources Corp. |

| Plains GP Holdings, L.P. |

| Magellan Midstream Partners, LP |

| The Williams Companies, Inc. |

| Energy Transfer LP |

| Bottom five contributors |

| NextEra Energy Partners LP |

| Enbridge, Inc. |

| TC Energy Corporation |

| Pembina Pipeline Corporation |

| Clearway Energy, Inc. |

(unaudited)

Tortoise

Energy Infrastructure Total Return Fund (continued)

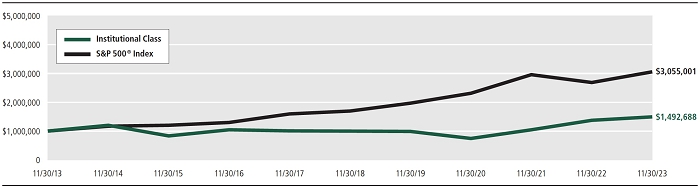

Value of $1,000,000 vs. S&P 500® Index

November 30, 2013 through November 30, 2023

This chart illustrates the performance of a hypothetical $1,000,000 investment made on November 30, 2013 and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers in effect. In the absence of such waivers, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for the index.

The performance data quoted above represents past performance on November 30, 2013 through November 30, 2023. Past performance is no guarantee of future results. The investment return and value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be obtained through the most recent month-end by calling 855-TCA-FUND (855-822-3863). Future performance may be lower or higher than the performance stated above.

The S&P 500® Index is an unmanaged market-value weighted index of stocks, which is widely regarded as the standard for measuring large-cap U.S. stock market performance. Returns include reinvested dividends. You cannot invest directly in an index.

(unaudited)

2023 Annual Report | November 30, 2023

Total returns (as of November 30, 2023)

| Ticker | | Class | | | 1 year | | | 3 years | | | 5 years | | | 10 years(1) | | | Since Inception(2) | | | Gross expense ratio(6) |

| TORIX | | Institutional | | | 8.73 | % | | | 26.19 | % | | | 8.39 | % | | | 4.09 | % | | | 6.96 | % | | | 0.93 | % |

| TORTX | | A Class (excluding load)(3) | | | 8.48 | % | | | 25.89 | % | | | 8.11 | % | | | 3.80 | % | | | 6.67 | % | | | 1.18 | % |

| TORTX | | A Class (maximum load)(3) | | | 2.53 | % | | | 23.54 | % | | | 6.89 | % | | | 3.22 | % | | | 6.19 | % | | | 1.18 | % |

| TORCX | | C Class (excluding CDSC) | | | 7.68 | % | | | 24.91 | % | | | 7.31 | % | | | 3.05 | % | | | 5.89 | % | | | 1.93 | % |

| TORCX | | C Class (including CDSC) | | | 6.68 | % | | | 24.91 | % | | | 7.31 | % | | | 3.05 | % | | | 5.89 | % | | | 1.93 | % |

| S&P 500® Index(4) | | | | | 13.84 | % | | | 9.76 | % | | | 12.51 | % | | | 11.82 | % | | | 12.45 | % | | | — | |

| TNAPT(5) | | | | | 4.92 | % | | | 21.01 | % | | | 9.57 | % | | | 6.20 | % | | | 8.11 | % | | | — | |

| (1) | The C Class Shares commenced operations on September 19, 2012. Performance shown for the C Class prior to the inception of the C Class is based on the performance of the Institutional Class Shares, adjusted for the higher expenses applicable to the C Class Shares. |

| (2) | Reflects period from May 31, 2011 through November 30, 2023. The Institutional and A Class Shares commenced operations on May 31, 2011 and C Class Shares commenced operations on September 19, 2012. Performance shown for the C Class prior to inception of the C Class Shares is based on the performance of the Institutional Class Shares, adjusted for the higher expenses applicable to C Class Shares. |

| (3) | Prior to March 30, 2019, A Class Shares were known as Investor Class Shares. |

| (4) | The S&P 500® Index is an unmanaged market-value weighted index of stocks, which is widely regarded as the standard for measuring large-cap U.S. stock market performance. Returns include reinvested dividends. You cannot invest directly in an index. |

| (5) | The Tortoise North American Pipeline IndexSM is a float-adjusted, capitalization weighted index of pipeline companies headquartered in the United States and Canada. You cannot invest directly in an index. |

| (6) | The gross expense ratio is in line with the Energy Infrastructure Total Return Fund’s most recent effective prospectus and may not reflect current year activity. |

Note: For periods over 1 year, performance reflected is for the average annual returns. Performance data shown for the A Class (maximum load) reflects a sales charge of 5.50%. Performance data shown “excluding load” does not reflect the deduction of the maximum sales load. Performance data shown for the C Class (including CDSC) reflects a contingent deferred sales charge (“CDSC”) of 1% for the first 12 months of investment. Performance data shown “excluding CDSC” does not reflect the deduction of the CDSC. If reflected, the load and CDSC would reduce the performance quoted. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855-TCA-FUND (855-822-3863).

(unaudited)

Tortoise

Energy Infrastructure and Income Fund

Basic fund facts

Investment objective: Current income and long-term capital appreciation

Structure: Regulated investment company

| | | Institutional | | A Class | | C Class |

| Ticker | | INFIX | | | INFRX | | | INFFX | |

| Gross expense ratio(5) | | | 1.13 | % | | | 1.38 | % | | | 2.13 | % |

| Redemption fee | | | None | | | | None | | | | None | |

| Maximum front-end sales load | | | None | (1) | | | 5.50 | %(2) | | | None | (1) |

| Maximum deferred sales load | | | None | | | | None | (3) | | | 1.00 | %(4) |

| (1) | While the Institutional and C Classes have no front-end load, advisory and other expenses still apply. |

| (2) | You may qualify for sales charge discounts if you invest at least $50,000. |

| (3) | No front-end sales charge is payable on A Class investments of $1 million or more, although the fund may impose a Contingent Deferred Sales Charge (“CDSC”) of 1% on certain redemptions made within 12 months of purchase. |

| (4) | The C Class CDSC applies to redemptions made within 12 months of purchase. |

| (5) | The expense ratios reflect those in the most recent prospectus and may not agree to the financial highlights. |

Targeted investment characteristics

The fund’s targeted investments generally will have the following characteristics:

| • | Securities from across the capital structure and energy value chain |

| • | Strategic assets that fuel the economy |

| • | Diversified asset base |

| • | Limited direct commodity price exposure |

| • | History of predictable, recurring cash flows |

| • | Current income through distributions |

| • | A flexible asset allocation dependent on current market opportunities |

| • | Experienced management team |

Top ten holdings (as of November 30, 2023)

| 1. | Cheniere Energy, Inc. | 8.8 | % |

| 2. | Energy Transfer LP | 5.7 | % |

| 3. | ONEOK, Inc. | 5.6 | % |

| 4. | Plains GP Holdings, L.P. | 4.8 | % |

| 5. | Enterprise Products Partners L.P. | 4.7 | % |

| 6. | The Williams Companies, Inc. | 4.5 | % |

| 7. | Targa Resources Corp. | 4.4 | % |

| 8. | ConocoPhillips | 3.8 | % |

| 9. | EQT Corporation | 3.8 | % |

| 10. | MPLX LP | 3.7 | % |

Key asset performance drivers

| • | All segments except for oil & gas production and diversified infrastructure had positive performance. |

| • | The fund’s largest allocation to natural gas pipeline companies added the most to performance. |

| • | The fund’s allocation to diversified infrastructure detracted the most from performance. |

| Top five contributors |

| Plains GP Holdings, L.P. |

| Magellan Midstream Partners, LP |

| Energy Transfer LP |

| Targa Resources Corp. |

| MPLX LP |

| |

| Bottom five contributors |

| NextEra Energy Partners LP |

| Devon Energy Corporation |

| New Fortress Energy Inc. |

| Ovintiv Inc. |

| Clearway Energy, Inc. |

(unaudited)

2023 Annual Report | November 30, 2023

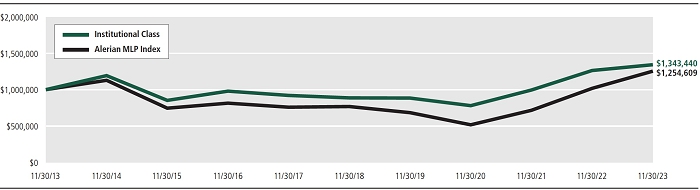

Value of $1,000,000 vs. the Alerian MLP Index

November 30, 2013 through November 30, 2023

This chart illustrates the performance of a hypothetical $1,000,000 investment made on November 30, 2013 and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers in effect. In the absence of such waivers, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for the index.

The performance data quoted above represents past performance from November 30, 2013 through November 30, 2023. Past performance is no guarantee of future results. The investment return and value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be obtained through the most recent month-end by calling 855-TCA-FUND (855-822-3863). Future performance may be lower or higher than the performance stated above.

The Alerian MLP Index is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a pricereturn basis (AMZ) and on a total-return basis (AMZX).

(unaudited)

Tortoise

Energy Infrastructure and Income Fund (continued)

Total returns (as of November 30, 2023)

| Ticker | | Class | | | 1 year | | | 3 years | | | 5 years | | | 10 years | | | Since Inception(1) | | | Gross expense ratio(3) |

| INFIX | | Institutional | | | 6.32 | % | | | 19.90 | % | | | 8.67 | % | | | 3.00 | % | | | 5.25 | % | | | 1.13 | % |

| INFRX | | A Class (excluding load) | | | 6.10 | % | | | 19.57 | % | | | 8.43 | % | | | 2.75 | % | | | 5.01 | % | | | 1.38 | % |

| INFRX | | A Class (maximum load) | | | 0.25 | % | | | 17.36 | % | | | 7.21 | % | | | 2.18 | % | | | 4.55 | % | | | 1.38 | % |

| INFFX | | C Class (excluding CDSC) | | | 5.27 | % | | | 18.71 | % | | | 7.58 | % | | | 1.96 | % | | | 4.27 | % | | | 2.13 | % |

| INFFX | | C Class (including CDSC) | | | 4.28 | % | | | 18.71 | % | | | 7.58 | % | | | 1.96 | % | | | 4.27 | % | | | 2.13 | % |

| Alerian MLP Index(2) | | | | | 23.29 | % | | | 34.51 | % | | | 10.33 | % | | | 2.29 | % | | | 5.15 | % | | | — | |

| (1) | Reflects period from fund inception on December 27, 2010 through November 30, 2023. The Institutional Class commenced operations on December 27, 2010, the A Class Shares commenced operation on May 18, 2011 and the C Class Shares commenced operations on April 2, 2012. Performance shown for the A Class and C Class prior to the inception of the A Class Shares and C Class Shares is based on the performance of the Institutional Class Shares, adjusted for the higher expenses applicable to the A Class Shares and the C Class Shares, respectively. |

| (2) | The Alerian MLP Index is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a pricereturn basis (AMZ) and on a total-return basis (AMZX). |

| (3) | The gross expense ratio is in line with the Energy Infrastructure and Income Fund’s most recent effective prospectus and may not reflect current year activity. |

Note: For periods over 1 year, performance reflected is for the average annual returns. Performance data shown for the A Class (maximum load) reflects a sales charge of 5.50%. Performance data shown “excluding load” does not reflect the deduction of the maximum sales load. Performance data shown for the C Class (including CDSC) reflects a contingent deferred sales charge (“CDSC”) of 1% for the first 18 months of investment. Performance data shown “excluding CDSC” does not reflect the deduction of the CDSC. If reflected, the load and CDSC would reduce the performance quoted. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855-TCA-FUND (855-822-3863).

(unaudited)

2023 Annual Report | November 30, 2023

Ecofin

Global Renewables Infrastructure Fund

Basic fund facts

Investment objective: Total Return

Structure: Regulated Investment Company

| | | Institutional | | A Class |

| Ticker | | ECOIX | | | ECOAX | |

| Net Expense Ratio(1) | | | 0.90 | % | | | 1.15 | % |

| Redemption fee | | | None | | | | None | |

| Maximum front-end sales load | | | None | (2) | | | 5.50 | %(3) |

| Maximum deferred sales load | | | None | | | | None | (4) |

| (1) | The expense ratios reflect those in the most recent prospectus and may not agree to the financial highlights. |

| (2) | While the Institutional Class has no front-end load, advisory and other expenses still apply. |

| (3) | You may qualify for sales charge discounts if you invest at least $50,000. |

| (4) | No front-end sales charge is payable on A Class investments of $1 million or more, although the fund may impose a Contingent Deferred Sales Charge (“CDSC”) of 1% on certain redemptions made within 12 months of purchase. |

Targeted investment characteristics

The fund’s targeted investments generally will have the following characteristics:

| • | Securities from across the capital structure and energy value chain |

| • | Strategic assets that fuel the economy |

| • | Diversified asset base |

| • | Limited direct commodity price exposure |

| • | History of predictable, recurring cash flows |

| • | Current income through distributions |

| • | A flexible asset allocation dependent on current market opportunities |

| • | Experienced management team |

Top ten holdings (as of November 30, 2023)

| 1. | | ERG SpA | | | 7.0 | % |

| 2. | | Clearway Energy, Inc. | | | 6.8 | % |

| 3. | | NextEra Energy, Inc. | | | 6.7 | % |

| 4. | | ReNew Energy Global Plc | | | 6.0 | % |

| 5. | | Atlantica Sustainable Infrastructure plc | | | 5.5 | % |

| 6. | | Dominion Resources, Inc. | | | 4.6 | % |

| 7. | | Edison International | | | 4.5 | % |

| 8. | | Exelon Corp | | | 4.4 | % |

| 9. | | Terna — Rete Elettrica Nazionale SpA | | | 4.2 | % |

| 10. | | Public Service Enterprise Group Incorporated | | | 4.2 | % |

Key asset performance drivers

| • | Two main holdings, NextEra Energy Partners (NEP) and NextEra Energy (NEE) together detracted the most from performance for the full fiscal period. NEP announced a downward revision to its growth outlook to avoid having to raise equity at a very high cost. That triggered negative market sentiment, and somewhat by association, NEE fell as well. |

| • | Renewable electricity names detracted the most from performance over the fiscal year. However, towards the end of the period we saw positive contribution from various industries, most notably, independent power producers & energy traders, electric utilities, and renewable electricity. |

| • | North American names detracted most from performance. However, towards the end of the period we saw North American names, and especially European names, positively contribute to performance. |

| Top five contributors |

| BKW Energie AG |

| Constellation Energy Corp. |

| ReNew Energy Global PLC |

| Terna — Rete Elettrica Nazionale SpA |

| Public SVC Enterprise Group |

| Bottom five contributors |

| NextEra Energy Partners LP |

| RENOVA, Inc. |

| NextEra Energy, Inc. |

| Innergex Renewable Energy, Inc. |

| Atlantica Sustainable Infrastructure plc |

(unaudited)

Ecofin

Global Renewables Infrastructure Fund (continued)

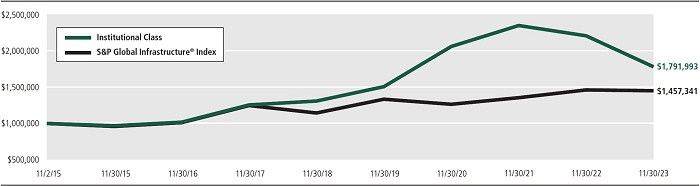

Value of $1,000,000 vs. S&P Global Infrastructure® Index (Net)

November 2, 2015 through November 30, 2023

The Fund commenced operations on August 7, 2020. This chart illustrates the performance of a hypothetical $1,000,000 investment made on November 2, 2015 and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers in effect. In the absence of such waivers, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for the index.

The performance data quoted above represents past performance on November 2, 2015 through November 30, 2023. Past performance is no guarantee of future results. The investment return and value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be obtained through the most recent month-end by calling 855-TCA-FUND (855-822-3863). Future performance may be lower or higher than the performance stated above.

The S&P Global Infrastructure® Index is designed to track 75 companies from around the world chosen to represent the listed infrastructure industry while maintaining liquidity and tradability. You cannot invest directly in an index.

(unaudited)

2023 Annual Report | November 30, 2023

Total returns (as of November 30, 2023)

| Ticker | | Class | | | 1 Year | | | 3 Years | | | 5 Years | | | Since inception | | | Gross expense ratio(5) |

| ECOIX(1)(2) | | Institutional | | | -19.47 | % | | | -4.78 | % | | | 6.41 | % | | | 7.49 | % | | | 0.90 | % |

| ECOAX(1)(3) | | A Class (excluding load) | | | -19.66 | % | | | -5.03 | % | | | 6.18 | % | | | 7.25 | % | | | 1.15 | % |

| ECOAX(1)(3) | | A Class (including load) | | | -24.08 | % | | | -6.82 | % | | | 4.98 | % | | | 6.51 | % | | | 1.15 | % |

| S&P Global Infrastructure Index (Net)(4) | | | -0.76 | % | | | 4.75 | % | | | 4.91 | % | | | 4.77 | % | | | — | |

| (1) | Fund commenced operations on August 7, 2020. |

| (2) | The performance data quoted for the period prior to August 7, 2020 is that of the Tortoise Global Renewables Infrastructure Fund Limited (the “Predecessor Fund”) and has been adjusted to reflect the Fund’s share class’ fees and expenses. The Predecessor Fund commenced operations on November 2, 2015, and was not a registered mutual fund subject to the same investment and tax restrictions as the Fund. If it had, the Predecessor Fund’s performance might have been lower. The Predecessor Fund’s shares were exchanged for the Fund’s Institutional Class shares on August 7, 2020. |

| (3) | Performance of the A Class prior to the inception of the class is based on the performance of the Predecessor Fund, adjusted for the higher expenses applicable to the class compared to the Institutional Class. |

| (4) | The S&P Global Infrastructure® Index is designed to track 75 companies from around the world chosen to represent the listed infrastructure industry while maintaining liquidity and tradability. You cannot invest directly in an index. |

| (5) | The gross expense ratio is in line with the Global Renewables Infrastructure Fund’s most recent effective prospectus and may not reflect current year activity. |

Note: For periods over 1 year, performance reflected is for the average annual returns. Performance data shown for the A Class (maximum load) reflects a sales charge of 5.50%. Performance data shown “excluding load” does not reflect the deduction of the maximum sales load.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855-TCA-FUND (855-822-3863).

(unaudited)

Mutual fund investing involves risk. Principal loss is possible. The funds are non-diversified, meaning they may concentrate their assets in fewer individual holdings than a diversified fund. Therefore, the funds are more exposed to individual stock volatility than diversified funds. Investing in specific sectors such as North American energy may involve greater risk and volatility than less concentrated investments. Risks include, but are not limited to, risks associated with energy investments, including upstream energy companies, midstream companies, downstream companies, energy company beneficiaries, master limited partnerships (MLPs), MLP affiliates, commodity price volatility, supply and demand, regulatory, environmental, operating, capital markets, terrorism, natural disaster and climate change risks. The tax benefits received by an investor investing in the funds differ from that of a direct investment in an MLP by an investor. The value of the funds’ investments in an MLP will depend largely on the MLP’s treatment as a partnership for U.S. federal income tax purposes. If the MLP is deemed to be a corporation then its income would be subject to federal taxation, reducing the amount of cash available for distribution to the funds which could result in a reduction of the funds’ values. Investments in foreign companies involve risk not ordinarily associated with investments in securities and instruments of U.S. issuers, including risks related to political, social and economic developments abroad, differences between U.S. and foreign regulatory and accounting requirements, tax risk and market practices, as well as fluctuations in foreign currencies. The funds invest in large, small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility than larger companies. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. The funds may also write call options which may limit the funds’ abilities to profit from increases in the market value of a security, but cause it to retain the risk of loss should the price of the security decline. Some funds may invest in other derivatives including options, futures and swap agreements, which can be highly volatile, illiquid and difficult to value, and changes in the value of a derivative held by the funds may not correlate with the underlying instrument or the fund’s other investments and can include additional risks such as liquidity risk, leverage risk and counterparty risk that are possibly greater than risks associated with investing directly in the underlying investments. Some funds may engage in short sales and in doing so are subject to the risk that they may not always be able to borrow a security, or close out a short position at a particular time or at an acceptable price.

Nothing contained on this communication constitutes tax, legal, or investment advice. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation.

This report reflects our views and opinions as of the date herein, which are subject to change at any time based on market and other conditions. We disclaim any responsibility to update these views. The views should not be relied on as investment advice or an indication of trading intent on behalf of the funds.

Fund holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the fund’s Schedule of Investments in this report.

(unaudited)

2023 Annual Report | November 30, 2023

Expense example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (June 1, 2023 – November 30, 2023)

Actual expenses

For each class, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Tortoise Energy Infrastructure Total Return Fund

| | | Beginning

Account Value

(06/01/2023) | | Ending

Account Value

(11/30/2023) | | Expenses Paid

During Period(1)

(06/01/2023 – 11/30/2023) |

| Institutional Class Actual(2) | | $ | 1,000.00 | | | $ | 1,184.30 | | | $ | 5.09 | |

| Institutional Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,020.41 | | | $ | 4.71 | |

| A Class Actual(2) | | $ | 1,000.00 | | | $ | 1,183.60 | | | $ | 6.46 | |

| A Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,019.15 | | | $ | 5.97 | |

| C Class Actual(2) | | $ | 1,000.00 | | | $ | 1,178.80 | | | $ | 10.54 | |

| C Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,015.39 | | | $ | 9.75 | |

| (1) | Expenses are equal to the Fund’s annualized expense ratio for the most recent six-month period of 0.93%, 1.18%, and 1.93% for the Institutional Class, A Class and C Class, respectively, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. |

| (2) | Based on the actual returns for the six-month period ended November 30, 2023 of 18.43%, 18.36% and 17.88% for the Institutional Class, A Class and C Class, respectively. |

(unaudited)

Tortoise Energy Infrastructure and Income Fund

| | | Beginning

Account Value

(06/01/2023) | | Ending

Account Value

(11/30/2023) | | Expenses Paid

During Period(1)

(06/01/2023 – 11/30/2023) |

| Institutional Class Actual(2) | | $ | 1,000.00 | | | $ | 1,153.10 | | | $ | 6.10 | |

| Institutional Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,019.40 | | | $ | 5.72 | |

| A Class Actual(2) | | $ | 1,000.00 | | | $ | 1,150.80 | | | $ | 7.44 | |

| A Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,018.05 | | | $ | 6.98 | |

| C Class Actual(2) | | $ | 1,000.00 | | | $ | 1,145.70 | | | $ | 11.46 | |

| C Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,014.39 | | | $ | 10.76 | |

| (1) | Expenses are equal to the Fund’s annualized expense ratio for the most recent six-month period of 1.13%, 1.38%, and 2.13% for the Institutional Class, A Class and C Class, respectively, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. |

| (2) | Based on the actual returns for the six-month period ended November 30, 2023 of 15.31%, 15.08% and 14.57% for the Institutional Class, A Class and C Class, respectively. |

Ecofin Global Renewables Infrastructure Fund

| | | Beginning

Account Value

(06/01/2023) | | Ending

Account Value

(11/30/2023) | | Expenses Paid

During Period(1)

(06/01/2023 – 11/30/2023) |

| Institutional Class Actual(2) | | $ | 1,000.00 | | | $ | 883.30 | | | $ | 4.58 | |

| Institutional Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,020.21 | | | $ | 4.91 | |

| A Class Actual(2) | | $ | 1,000.00 | | | $ | 881.40 | | | $ | 5.75 | |

| A Class Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,018.95 | | | $ | 6.17 | |

| (1) | Expenses are equal to the Fund’s annualized expense ratio for the most recent six-month period of 0.97% and 1.22% for the Institutional Class and A Class, respectively, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. |

| (2) | Based on the actual returns for the six-month period ended November 30, 2023 of -11.67% for the Institutional Class and -11.86% for the A Class, respectively. |

| (3) | Excluding interest expense, the actual expenses would be $4.44 and $5.61 for the Institutional Class, and C Class, respectively. |

| (4) | Excluding interest expense, the hypothetical expenses would be $4.76 and $6.02 for the Institutional Class, and C Class, respectively. |

(unaudited)

2023 Annual Report | November 30, 2023

Tortoise Energy Infrastructure Total Return

Schedule of Investments

November 30, 2023

| | | Shares | | | Value | |

| Common Stocks — 77.1% | | | | | | | | |

| Canada Crude Oil Pipelines — 11.8% | | | | | | | | |

| Enbridge, Inc. | | | 4,447,920 | | | $ | 155,098,971 | |

| Pembina Pipeline Corporation | | | 3,159,931 | | | | 105,699,744 | |

| | | | | | | | 260,798,715 | |

| | | | | | | | | |

| Canada Natural Gas/Natural Gas Liquids Pipelines — 6.3% | | | | | | | | |

| Keyera Corp. | | | 2,873,032 | | | | 72,347,178 | |

| TC Energy Corporation | | | 1,739,291 | | | | 65,258,198 | |

| | | | | | | | 137,605,376 | |

| United States Crude Oil Pipelines — 4.9% | | | | | | | | |

| Plains GP Holdings L.P. | | | 6,682,095 | | | | 107,982,655 | |

| | | | | | | | | |

| United States Natural Gas Gathering/Processing — 8.4% | | | | | | | | |

| Antero Midstream Corporation | | | 2,351,910 | | | | 31,327,441 | |

| EnLink Midstream, LLC | | | 4,134,576 | | | | 56,519,654 | |

| Equitrans Midstream Corp. | | | 5,485,143 | | | | 51,450,642 | |

| Hess Midstream LP — Class A | | | 1,195,932 | | | | 38,915,627 | |

| Kinetik Holdings, Inc. | | | 210,428 | | | | 7,651,162 | |

| | | | | | | | 185,864,526 | |

| United States Natural Gas/Natural Gas Liquids Pipelines — 44.4% | | | | | | | | |

| Cheniere Energy, Inc. | | | 1,229,610 | | | | 223,973,461 | |

| DT Midstream, Inc. | | | 449,197 | | | | 25,734,496 | |

| Excelerate Energy, Inc. | | | 296,135 | | | | 4,951,377 | |

| Kinder Morgan, Inc. | | | 9,357,102 | | | | 164,404,282 | |

| NextDecade Corp.(a) | | | 1,909,915 | | | | 9,530,476 | |

| ONEOK, Inc. | | | 2,325,146 | | | | 160,086,302 | |

| Targa Resources Corp. | | | 2,444,776 | | | | 221,129,989 | |

| The Williams Companies, Inc. | | | 4,625,026 | | | | 170,154,707 | |

| | | | | | | | 979,965,090 | |

| United States Renewables and Power Infrastructure — 1.3% | | | | | | | | |

| Clearway Energy, Inc. | | | 343,302 | | | | 8,572,251 | |

| NextEra Energy Partners LP | | | 379,501 | | | | 8,933,454 | |

| Sempra Energy | | | 143,558 | | | | 10,461,071 | |

| | | | | | | | 27,966,776 | |

| | | | | | | | | |

Total Common Stocks

(Cost $1,162,761,281) | | | | | | | 1,700,183,138 | |

| | | | | | | |

| | | Units/Shares | | | | |

| Master Limited Partnerships — 19.0% | | | | | | | | |

| United States Crude Oil Pipelines — 2.0% | | | | | | | | |

| NuStar Energy LP | | | 1,580,762 | | | | 30,097,709 | |

| Plains All American Pipeline LP | | | 826,247 | | | | 13,120,802 | |

| | | | | | | | 43,218,511 | |

| | | | | | | | | |

| United States Natural Gas Gathering/Processing — 3.0% | | | | | | | | |

| Western Midstream Partners LP | | | 2,208,889 | | | | 65,869,070 | |

| | | | | | | | | |

| United States Natural Gas/Natural Gas Liquids Pipelines — 9.0% | | | | | | | | |

| Energy Transfer LP | | | 7,771,343 | | | | 107,943,954 | |

| Enterprise Products Partners LP | | | 3,398,344 | | | | 91,007,653 | |

| | | | | | | | 198,951,607 | |

| | | | | | | | | |

| United States Other — 0.1% | | | | | | | | |

| Westlake Chemical Partners LP | | | 127,871 | | | | 2,896,278 | |

| | | | | | | | | |

| United States Refined Product Pipelines — 4.9% | | | | | | | | |

| MPLX LP | | | 2,965,031 | | | | 108,105,030 | |

| | | | | | | | | |

Total Master Limited Partnerships

(Cost $226,689,153) | | | | | | | 419,040,496 | |

| | | | | | | | | |

| Short-Term Investments — 1.9% | | | | | | | | |

| Money Market Funds — 1.9% | | | | | | | | |

| First American Government Obligations | | | | | | | | |

| Fund — Class X, 5.29%(b) | | | 42,737,622 | | | | 42,737,622 | |

| | | | | | | | | |

Total Short-Term Investments

(Cost $42,737,622) | | | | | | | 42,737,622 | |

| | | | | | | | | |

Total Investments — 98.0%

(Cost $1,432,188,056) | | | | | | | 2,161,961,256 | |

| Other Assets in Excess of Liabilities — 2.0% | | | | | | | 45,202,624 | |

| Total Net Assets — 100.0% | | | | | | $ | 2,207,163,880 | |

Percentages are stated as a percent of net assets.

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of November 30, 2023. |

See accompanying Notes to Financial Statements.

Tortoise Energy Infrastructure and Income Fund

Schedule of Investments

November 30, 2023

| | | Shares | | | Value | |

| Common Stocks — 59.9% | | | | | | | | |

| Canada Crude Oil Pipelines — 2.1% | | | | | | | | |

| Enbridge, Inc. | | | 304,484 | | | $ | 10,617,357 | |

| | | | | | | | | |

| Canada Oil & Gas Production — 1.7% | | | | | | | | |

| Ovintiv, Inc. | | | 187,315 | | | | 8,305,547 | |

| | | | | | | | | |

| United Kingdom Renewables and Power Infrastructure — 0.3% | | | | | | | | |

| Atlantica Sustainable Infrastructure PLC | | | 80,553 | | | | 1,532,118 | |

| | | | | | | | | |

| United States Crude Oil Pipelines — 4.8% | | | | | | | | |

| Plains GP Holdings L.P. | | | 1,492,912 | | | | 24,125,458 | |

| | | | | | | | | |

| United States Natural Gas Gathering/Processing — 3.3% | | | | | | | | |

| Equitrans Midstream Corp. | | | 706,020 | | | | 6,622,468 | |

| Hess Midstream LP — Class A | | | 174,587 | | | | 5,681,061 | |

| Kinetik Holdings, Inc. | | | 40,684 | | | | 1,479,270 | |

| Kodiak Gas Services, Inc. | | | 145,707 | | | | 2,568,814 | |

| | | | | | | | 16,351,613 | |

| | | | | | | | | |

| United States Natural Gas/Natural Gas Liquids Pipelines — 27.9% | | | | | | | | |

| Cheniere Energy, Inc. | | | 239,948 | | | | 43,706,529 | |

| Kinder Morgan, Inc. | | | 713,741 | | | | 12,540,429 | |

| New Fortress Energy, Inc. | | | 271,245 | | | | 10,437,508 | |

| ONEOK, Inc. | | | 404,804 | | | | 27,870,755 | |

| Targa Resources Corp. | | | 242,320 | | | | 21,917,844 | |

| The Williams Companies, Inc. | | | 610,594 | | | | 22,463,753 | |

| | | | | | | | 138,936,818 | |

| | | | | | | | | |

| United States Oil & Gas Production — 16.6% | | | | | | | | |

| ConocoPhillips | | | 164,718 | | | | 19,036,460 | |

| Coterra Energy, Inc. | | | 432,396 | | | | 11,350,395 | |

| Devon Energy Corporation | | | 170,926 | | | | 7,686,542 | |

| Diamondback Energy, Inc. | | | 67,187 | | | | 10,374,345 | |

| EQT Corporation | | | 472,972 | | | | 18,899,961 | |

| Pioneer Natural Resources Company | | | 65,074 | | | | 15,073,741 | |

| | | | | | | | 82,421,444 | |

| | | | | | | | | |

| United States Refined Product Pipelines — 1.8% | | | | | | | | |

| Phillips 66 | | | 71,185 | | | | 9,175,035 | |

| | | | | | | | | |

| United States Renewables and Power Infrastructure — 1.4% | | | | | | | | |

| Clearway Energy, Inc. — Class C | | | 154,878 | | | | 3,867,304 | |

| NextEra Energy Partners LP | | | 137,123 | | | | 3,227,875 | |

| | | | | | | | 7,095,179 | |

| | | | | | | | | |

Total Common Stocks

(Cost $212,314,201) | | | | | | | 298,560,569 | |

| | | | | | | | | |

| Corporate Bonds — 19.6% | | | | | | | | |

| Canada Crude Oil Pipelines — 0.7% | | | | | | | | |

| Enbridge, Inc., | | | | | | | | |

| 5.50% to 07/15/2027 then 3 mo. | | | | | | | | |

| Term SOFR + 3.68%, 07/15/2077 | | | 4,000,000 | | | | 3,523,407 | |

| | | | | | | | | |

| United States Natural Gas Gathering/Processing — 8.6% | | | | | | | | |

| Antero Midstream Partners LP / Antero | | | | | | | | |

| Midstream Finance Corp., | | | | | | | | |

| 5.75%, 03/01/2027(a) | | | 6,370,000 | | | | 6,232,310 | |

| Blue Racer Midstream LLC / | | | | | | | | |

| Blue Racer Finance Corp. | | | | | | | | |

| 6.63%, 07/15/2026(a) | | | 3,800,000 | | | | 3,751,951 | |

| 7.63%, 12/15/2025(a) | | | 3,575,000 | | | | 3,622,076 | |

| EnLink Midstream Partners LP, | | | | | | | | |

| 4.85%, 07/15/2026 | | | 7,550,000 | | | | 7,352,858 | |

| EnLink Midstream, LLC, | | | | | | | | |

| 5.38%, 06/01/2029 | | | 4,455,000 | | | | 4,302,568 | |

| Hess Midstream Operations LP | | | | | | | | |

| 5.13%, 06/15/2028(a) | | | 4,050,000 | | | | 3,879,090 | |

| 5.63%, 02/15/2026(a) | | | 8,125,000 | | | | 8,030,465 | |

| Targa Resources Partners LP / Targa | | | | | | | | |

| Resources Partners Finance Corp., | | | | | | | | |

| 6.50%, 07/15/2027 | | | 5,537,000 | | | | 5,594,122 | |

| | | | | | | | 42,765,440 | |

| | | | | | | | | |

| United States Natural Gas/Natural Gas Liquids Pipelines — 6.3% | | | | | | | | |

| DT Midstream, Inc., | | | | | | | | |

| 4.38%, 06/15/2031(a) | | | 6,100,000 | | | | 5,360,420 | |

| EQM Midstream Partners LP, | | | | | | | | |

| 5.50%, 07/15/2028 | | | 8,500,000 | | | | 8,269,548 | |

| NGPL PipeCo LLC, | | | | | | | | |

| 7.77%, 12/15/2037(a) | | | 9,125,000 | | | | 9,734,669 | |

| Tallgrass Energy Partners LP / | | | | | | | | |

| Tallgrass Energy Finance Corp. | | | | | | | | |

| 5.50%, 01/15/2028(a) | | | 7,925,000 | | | | 7,318,508 | |

| 6.00%, 03/01/2027(a) | | | 850,000 | | | | 818,129 | |

| | | | | | | | 31,501,274 | |

| | | | | | | | | |

| United States Oil Field Services — 1.3% | | | | | | | | |

| Archrock Partners LP / Archrock | | | | | | | | |

| Partners Finance Corp., | | | | | | | | |

| 6.88%, 04/01/2027(a) | | | 6,575,000 | | | | 6,522,097 | |

| | | | | | | | | |

| United States Other — 2.7% | | | | | | | | |

| New Fortress Energy, Inc. | | | | | | | | |

| 6.50%, 09/30/2026(a) | | | 5,000,000 | | | | 4,756,028 | |

| 6.75%, 09/15/2025(a) | | | 8,800,000 | | | | 8,539,457 | |

| | | | | | | | 13,295,485 | |

| | | | | | | | | |

Total Corporate Bonds

(Cost $99,896,131) | | | | | | | 97,607,703 | |

See accompanying Notes to Financial Statements.

2023 Annual Report | November 30, 2023

Tortoise Energy Infrastructure and Income Fund

Schedule of Investments (continued)

November 30, 2023

| | | Units/Shares | | | Value | |

| Master Limited Partnerships — 19.3% | | | | | | | | |

| United States Crude Oil Pipelines — 2.6% | | | | | | | | |

| Plains All American Pipeline LP | | | 811,156 | | | $ | 12,881,157 | |

| | | | | | | | | |

| United States Natural Gas Gathering/Processing — 2.7% | | | | | | | | |

| Western Midstream Partners LP | | | 446,900 | | | | 13,326,558 | |

| | | | | | | | | |

| United States Natural Gas Pipelines — 10.3% | | | | | | | | |

| Energy Transfer LP | | | 2,064,295 | | | | 28,673,058 | |

| Enterprise Products Partners LP | | | 870,418 | | | | 23,309,794 | |

| | | | | | | | 51,982,852 | |

| | | | | | | | | |

| United States Refined Product Pipelines — 3.7% | | | | | | | | |

| MPLX LP | | | 501,472 | | | | 18,283,669 | |

| | | | | | | | | |

Total Master Limited Partnerships

(Cost $53,629,538) | | | | | | | 96,474,236 | |

| | | | | | | |

| | | Shares | | | | |

| Short-Term Investments — 0.8% | | | | | | | | |

| Money Market Funds — 0.8% | | | | | | | | |

| First American Government Obligations Fund — Class X, 5.29%(b) | | | 4,207,989 | | | | 4,207,989 | |

| | | | | | | | | |

Total Short-Term Investments

(Cost $4,207,989) | | | | | | | 4,207,989 | |

| | | | | | | | | |

Total Investments — 99.6%

(Cost $370,047,859) | | | | | | | 496,850,497 | |

| Other Assets in Excess of Liabilities — 0.4% | | | | | | | 2,215,727 | |

| Total Net Assets — 100.0% | | | | | | $ | 499,066,224 | |

Percentages are stated as a percent of net assets.

PLC — Public Limited Company

SOFR — Secured Overnight Financing Rate

| (a) | Security is exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities may only be resold in transactions exempt from registration to qualified institutional investors. As of November 30, 2023, the value of these securities total $68,565,200 or 13.7% of the Fund’s net assets. |

| (b) | The rate shown represents the 7-day effective yield as of November 30, 2023. |

See accompanying Notes to Financial Statements.

Ecofin Global Renewables Infrastructure Fund

Schedule of Investments

November 30, 2023

| | | Shares | | | Value | |

| Common Stocks — 93.5% | | | | | | | | |

| Belgium Electricity Transmission Operators — 1.8% | | | | | | | | |

| Elia Group SA/NV | | | 38,019 | | | $ | 4,120,485 | |

| | | | | | | | | |

| Canada Renewable Power Producers — 3.6% | | | | | | | | |

| Innergex Renewable Energy, Inc. | | | 1,169,549 | | | | 8,282,815 | |

| | | | | | | | | |

| France Power — 3.4% | | | | | | | | |

| Neoen SA | | | 254,556 | | | | 7,784,499 | |

| | | | | | | | | |

| Germany Renewable Power Producers — 3.4% | | | | | | | | |

| Encavis AG(a) | | | 526,313 | | | | 7,836,559 | |

| | | | | | | | | |

| Hong Kong Renewable Power Producers — 5.0% | | | | | | | | |

| China Longyuan Power Group Corp. Ltd. | | | 7,744,829 | | | | 5,792,441 | |

| China Suntien Green Energy Corp. Ltd. | | | 11,377,782 | | | | 3,784,109 | |

| Xinyi Energy Holdings Ltd. | | | 12,103,729 | | | | 2,026,214 | |

| | | | | | | | 11,602,764 | |

| | | | | | | | | |

| India Power — 6.0% | | | | | | | | |

| ReNew Energy Global PLC(a) | | | 2,168,475 | | | | 13,964,979 | |

| | | | | | | | | |

| Italy Electricity Transmission Operators — 4.2% | | | | | | | | |

| Terna — Rete Elettrica Nazionale SpA | | | 1,215,206 | | | | 9,791,013 | |

| | | | | | | | | |

| Italy Renewable Power Producers — 6.9% | | | | | | | | |

| ERG SpA | | | 567,489 | | | | 16,276,451 | |

| | | | | | | | | |

| Japan Renewable Power Producers — 2.1% | | | | | | | | |

| RENOVA, Inc.(a) | | | 691,486 | | | | 4,930,797 | |

| | | | | | | | | |

| Portugal Electric Utilities — 4.1% | | | | | | | | |

| EDP — Energias de Portugal, S.A. | | | 2,010,160 | | | | 9,613,602 | |

| | | | | | | | | |

| Portugal Renewables Power Producer — 2.8% | | | | | | | | |

| Greenvolt-Energias Renovaveis, S.A.(a) | | | 832,587 | | | | 6,453,941 | |

| | | | | | | | | |

| Spain Integrated Utilities — 2.2% | | | | | | | | |

| EDP Renovaveis SA | | | 273,516 | | | | 4,995,537 | |

| | | | | | | | | |

| Switzerland Integrated Utilities — 1.3% | | | | | | | | |

| BKW Energie AG | | | 16,997 | | | | 2,996,799 | |

| | | | | | | | | |

| Thailand Renewable Power Producers — 1.5% | | | | | | | | |

| Super Energy Corporation PLC(a) | | | 269,437,990 | | | | 3,368,743 | |

| | | | | | | | | |

| United Kingdom Renewable Power Producers — 7.9% | | | | | | | | |

| Atlantica Sustainable Infrastructure PLC | | | 672,732 | | | | 12,795,363 | |

| Greencoat UK Wind PLC/Funds | | | 3,038,938 | | | | 5,520,738 | |

| | | | | | | | 18,316,101 | |

| | | | | | | |

| United States Electric Utilities — 22.6% | | | | | | | | |

| Avista Corp. | | | 120,355 | | | | 4,086,052 | |

| Constellation Energy Corp. | | | 20,618 | | | | 2,495,603 | |

| Edison International | | | 157,267 | | | | 10,535,315 | |

| Exelon Corp. | | | 261,956 | | | | 10,087,926 | |

| NextEra Energy, Inc. | | | 266,556 | | | | 15,596,192 | |

| Public Service Enterprise Group Incorporated | | | 155,570 | | | | 9,712,235 | |

| | | | | | | | 52,513,323 | |

| | | | | | | | | |

| United States Renewable Power Producers — 14.7% | | | | | | | | |

| Clearway Energy, Inc. | | | 627,051 | | | | 15,657,464 | |

| Dominion Energy, Inc. | | | 233,546 | | | | 10,588,976 | |

| NextEra Energy Partners LP | | | 329,284 | | | | 7,751,345 | |

| | | | | | | | 33,997,785 | |

| | | | | | | | | |

Total Common Stocks

(Cost $261,039,714) | | | | | | | 216,846,193 | |

| | | | | | | | | |

| Short-Term Investments — 1.3% | | | | | | | | |

| Money Market Funds — 1.3% | | | | | | | | |

| First American Government Obligations Fund — Class X, 5.29%(b) | | | 2,972,924 | | | | 2,972,923 | |

Total Short-Term Investments

(Cost $2,972,924) | | | | | | | 2,972,923 | |

Total Investments — 94.8%

(Cost $264,012,638) | | | | | | | 219,819,116 | |

| Other Assets in Excess of Liabilities — 5.2% | | | | | | | 12,052,837 | |

| Total Net Assets — 100.0% | | | | | | $ | 231,871,953 | |

Percentages are stated as a percent of net assets.

PLC — Public Limited Company

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of November 30, 2023. |

See accompanying Notes to Financial Statements.

2023 Annual Report | November 30, 2023

Ecofin Global Renewables Infrastructure Fund

Open Swap Contracts

November 30, 2023

| Counterparty | | Security | | Termination

Date | | Pay/Receive

on

Financing

Rate | | Financing Rate | | Payment

Frequency | | Shares | | | Notional

Amount | | | Unrealized

Appreciation

(Depreciation)* | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Morgan Stanley | | Drax Group PLC | | 8/15/24 | | Pay | | 0.200% + Federal Funds Effective Rate | | Monthly | | | 2,058,575 | | | $ | 11,351,776 | | | $ | 60,287 | |

| | | | | | | | | | | | | | | | | | | | | $ | 60,287 | |

* Based on the net swap value held at each counterparty. Unrealized appreciation (depreciation) is a receivable (payable).

See accompanying Notes to Financial Statements.

Statements of Assets & Liabilities

November 30, 2023

| | | Tortoise Energy

Infrastructure Total

Return Fund | |

| Assets: | | | |

| Investments, at fair value (cost $1,432,188,056, $370,047,859,and $264,012,638, respectively) | | $ | 2,161,961,256 | |

| Cash held as collateral | | | — | |

| Dividends & interest receivable | | | 2,883,079 | |

| Receivable for investment securities sold | | | 44,229,810 | |

| Receivable for swap contracts | | | — | |

| Receivable for capital shares sold | | | 4,039,596 | |

| Prepaid expenses and other assets | | | 36,674 | |

| Total assets | | | 2,213,150,415 | |

| | | | | |

| Liabilities: | | | | |

| Payable for investment securities purchased | | | — | |

| Payable for capital shares redeemed | | | 3,545,123 | |

| Payable to Adviser | | | 1,546,213 | |

| Payable for fund administration & accounting fees | | | 286,701 | |

| Payable for compliance fees | | | 3,470 | |

| Payable for custody fees | | | 19,413 | |

| Payable for audit & tax | | | 55,747 | |

| Payable for transfer agent fees & expenses | | | 146,144 | |

| Payable to trustees | | | 489 | |

| Payable for interest expense | | | 13,512 | |

| Accrued expenses | | | 102,115 | |

| Accrued distribution fees | | | 267,608 | |

| Total liabilities | | | 5,986,535 | |

| Net Assets | | $ | 2,207,163,880 | |

| | | | | |

| Net Assets Consist of: | | | | |

| Capital Stock | | $ | 2,579,505,205 | |

| Total accumulated loss | | | (372,341,325 | ) |

| Net Assets | | $ | 2,207,163,880 | |

| | | | | |

| Institutional Class | | | | |

| Net Assets | | $ | 1,989,434,255 | |

| Shares issued and outstanding(1) | | | 136,832,480 | |

| Net asset value, redemption price and minimum offering price per share | | $ | 14.54 | |

| | | | | |

| A Class | | | | |

| Net Assets | | $ | 198,181,413 | |

| Shares issued and outstanding(1) | | | 13,834,333 | |

| Net asset value, redemption price and minimum offering price per share | | $ | 14.33 | |

| Maximum offering price per share(2) | | $ | 15.16 | |

| | | | | |

| C Class | | | | |

| Net Assets | | $ | 19,548,212 | |

| Shares issued and outstanding(1) | | | 1,396,535 | |

| Net asset value, redemption price and minimum offering price per share | | $ | 14.00 | |

| (1) | Unlimited shares authorized. |

| (2) | The offering price is calculated by dividing the net asset value by 1 minus the maximum sales charge of 5.50%. |

See accompanying Notes to Financial Statements.

2023 Annual Report | November 30, 2023

| | | | | | | |

| | Tortoise Energy

Infrastructure and

Income Fund | | | | Ecofin Global

Renewables

Infrastructure Fund | |

| | | | | | | |

| $ | 496,850,497 | | | $ | 219,819,116 | |

| | — | | | | 11,299,146 | |

| | 2,870,080 | | | | 1,426,986 | |

| | — | | | | — | |

| | — | | | | 60,287 | |

| | 295,541 | | | | 237,227 | |

| | 27,825 | | | | 19,923 | |

| | 500,043,943 | | | | 232,862,685 | |

| | | | | | | |

| | — | | | | 194,527 | |

| | 317,868 | | | | 494,689 | |

| | 402,716 | | | | 142,285 | |

| | 100,273 | | | | 60,734 | |

| | 3,470 | | | | 3,470 | |

| | 3,355 | | | | 8,372 | |

| | 32,503 | | | | 31,996 | |

| | 38,214 | | | | 30,425 | |

| | 879 | | | | 276 | |

| | — | | | | 10,904 | |

| | 37,845 | | | | 10,735 | |

| | 40,596 | | | | 2,319 | |

| | 977,719 | | | | 990,732 | |

| $ | 499,066,224 | | | $ | 231,871,953 | |

| | | | | | | |

| $ | 792,648,434 | | | $ | 300,992,879 | |

| | (293,582,210 | ) | | | (69,120,926 | ) |

| $ | 499,066,224 | | | $ | 231,871,953 | |

| | | | | | | |

| | | | | | | |

| $ | 431,331,958 | | | $ | 230,043,269 | |

| | 56,191,807 | | | | 26,076,593 | |

| $ | 7.68 | | | $ | 8.82 | |

| | | | | | | |

| | | | | | | |

| $ | 48,598,912 | | | $ | 1,828,684 | |

| | 6,186,673 | | | | 207,457 | |

| $ | 7.86 | | | $ | 8.81 | |

| $ | 8.32 | | | $ | 9.32 | |

| | | | | | | |

| | | | | | | |

| $ | 19,135,354 | | | $ | — | |

| | 2,456,048 | | | | — | |

| $ | 7.79 | | | $ | — | |

Statements of Operations

For the Year Ended November 30, 2023

| | | | |

| | | Tortoise Energy

Infrastructure Total

Return Fund | |

| Investment Income: | | | |

| Dividends and distributions from unaffiliated common stock | | $ | 83,233,785 | |

| Distributions from master limited partnerships | | | 46,059,969 | |

| Less: return of capital on distributions from unaffilated investments | | | (66,176,790 | ) |

| Less: foreign taxes withheld | | | (3,811,343 | ) |

| Net dividends and distributions from investments | | | 59,305,621 | |

| Dividends from money market mutual funds | | | 1,938,497 | |

| Interest income | | | — | |

| Total investment income | | | 61,244,118 | |

| | | | | |

| Expenses: | | | | |

| Advisory fees (See Note 6) | | | 19,211,003 | |

| Fund administration & accounting fees (See Note 6) | | | 869,445 | |

| Transfer agent fees & expenses (See Note 6) | | | 354,882 | |

| Shareholder communication fees | | | 239,777 | |

| Custody fees (See Note 6) | | | 124,757 | |

| Registration fees | | | 84,301 | |

| Audit & tax fees | | | 55,667 | |

| Trustee fees | | | 22,958 | |

| Other | | | 24,679 | |

| Insurance fees | | | 14,800 | |

| Compliance fees (See Note 6) | | | 10,242 | |

| Legal fees | | | 24,294 | |

| Distribution fees (See Note 7): | | | | |

| A Class | | | 449,357 | |

| C Class | | | 202,966 | |

| Total expenses before income tax expense | | | 21,689,128 | |

| Interest expense on line of credit (See Note 11) | | | 13,200 | |

| Income Tax Expense | | | — | |

| Total expenses before reimbursement/recoupment | | | 21,702,328 | |

| Fee recoupment (See Note 6) | | | — | |

| Net expenses | | | 21,702,328 | |

| Net Investment Income | | | 39,541,790 | |