UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22563 |

|

Mairs & Power Funds Trust |

(Exact name of registrant as specified in charter) |

|

332 Minnesota Street, Suite W1520, St. Paul, MN | | 55101 |

(Address of principal executive offices) | | (Zip code) |

|

Andrea C. Stimmel, Treasurer, 332 Minnesota Street, Suite W1520, St. Paul, MN 55101 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 651-222-8478 | |

|

Date of fiscal year end: | December 31, 2016 | |

|

Date of reporting period: | December 31, 2016 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

Investing for the long-term

ANNUAL REPORT

DECEMBER 31, 2016

- GROWTH FUND (MPGFX)

est. 1958

- BALANCED FUND (MAPOX)

est. 1961

- SMALL CAP FUND (MSCFX)

est. 2011

Mairs & Power W1520 First National Bank Building, 332 Minnesota Street, St. Paul, Minnesota 55101 www.mairsandpower.com

MAIRS & POWER FUNDS MARKET COMMENTARY (unaudited)

December 31, 2016

The end of the year provides finality, if only in turning the calendar to a new year. For investors, the end of 2016 saw uncertainty replaced by absolute certainty in two important areas – the election and interest rates. With the election of Donald Trump and a Republican Congress, the market expects quick legislative action on a fiscal stimulus package, tax cuts and reduced regulations, all of which could provide a boost to economic growth and corporate profits. As a result, the stock market reacted positively and finished the year strong. In addition, after months of guessing by investors on the timing and magnitude of interest rate moves, at its year-end meeting the Federal Reserve (Fed) confirmed its confidence in the state of the economy and raised the federal funds rate by 0.25% and indicated its intention to bump rates higher in 2017, potentially more than once. Unlike stocks, bond prices reacted negatively post-election in anticipation that a stronger economy would put additional upward pressure on interest rates.

Between Election Day and year end, the S&P 500 hit eight all time highs, reaching 2,271.72 on December 13 and closed the year at 2,238.83, a total return of 11.96% for the year. For the fourth quarter, the S&P 500 Total Return (TR) was 3.82%. The Dow Jones Industrial Average TR was 8.66% for the quarter and 16.50% for the year. Our other key benchmark, the Bloomberg Barclays U.S. Government/Credit Bond Index return was a negative 3.39% for the fourth quarter and a positive 3.05% for the full year.

Leading all sectors, financials gained more than 20% in the fourth quarter as the potential beneficiaries of corporate tax cuts and a rollback of onerous federal government regulations. In addition, rising interest rates should help profits with wider lending margins.

Outlook

We enter 2017 with contradictory signals in the equity markets. As the post-election "Trump Bump" pushed stock valuations up, price-to-earnings multiples climbed above their long-term averages in a rising interest rate environment – an unusual combination. On the positive side, several economic indicators improved in the fourth quarter not only in the U.S. but, surprisingly, in Europe and Japan as well. The U.S. unemployment rate dropped to 4.6%, consumer confidence continued to rise and the Purchasing Managers' Index, which measures the outlook for manufacturing, reached a two year high. It appears that as growth is starting to accelerate globally, the expected stimulus package from the new administration may boost the economy further.

While stronger economic growth and accelerating earnings growth create a tail wind for the market, rising interest rates typically create a head wind. Investors may be disappointed if the new administration struggles to implement its economic policies as it faces the reality of trying to get things done in Washington. The market could be quite unforgiving if growth in the economy and corporate earnings aren't as strong as expected.

These competing positive and cautionary scenarios play out against a backdrop of a re-assertive Federal Reserve. If the economy heats up, the Fed may become even more aggressive in boosting interest rates. While it's important to stay abreast of macro factors, our primary focus remains on what companies are in our investment portfolios and where we see opportunities. As we start the New Year with significant changes on the horizon, we remain confident in our long-term investment approach, which involves continuing to seek out opportunities overlooked by the market and focus on good companies with durable competitive advantages.

S&P 500 TR (Total Return) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

Dow Jones Industrial Average TR Index is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. It is not possible to invest directly in an index.

1

MAIRS & POWER FUNDS MARKET COMMENTARY (unaudited) (continued)

Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

Price to earnings is a ratio of a company's share price to its per-share earnings.

Purchasing Managers' Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

2

MAIRS & POWER GROWTH FUND (unaudited)

To Our Shareholders: December 31, 2016

The Growth Fund finished the year well ahead of its benchmark index and peer group, gaining 15.38% compared to 11.96% for the S&P 500 Total Return (TR) benchmark and 12.27% for the Lipper Multi Cap Core Funds Index of peers, respectively. For the fourth quarter the Fund gained 2.54%, compared with 3.82% for the S&P 500 Total Return (TR) and 3.81% for the Lipper Index.

Stock selection drove portfolio performance in 2016, with acquisitions, exposure to industrials and our multi-cap approach being the most important factors. The announced purchases of Valspar (VAL) by Sherwin Williams (SHW), St. Jude (STJ) by Abbott Labs (ABT) and G&K Services (GK) by Cintas (CTAS) helped performance early in the year and we are working hard to find replacements for these three very fine companies. Our exposure to industrial stocks, which had lagged significantly in 2014 and 2015, paid off early in the year as the market realized that the sector had become too cheap. Portfolios also benefited from our multi-cap strategy where several small and mid-cap stocks, such as Donaldson (DCI), Toro (TTC), and Badger Meter (BMI), were strong performers.

MAIRS & POWER GROWTH FUND (MPGFX)

Top Performers

| Fourth Quarter (9/30/16 – 12/31/16) | | Year To Date (12/31/15 – 12/31/16) | |

WELLS FARGO & CO. | | | 20.64 | % | | TORO CO. | | | 41.16 | % | |

U.S. BANCORP | | | 15.95 | % | | DONALDSON CO., INC. | | | 34.86 | % | |

TORO CO. | | | 15.63 | % | | H.B. FULLER CO. | | | 20.51 | % | |

DONALDSON CO., INC. | | | 8.90 | % | | ST. JUDE MEDICAL, INC. | | | 17.86 | % | |

GRACO, INC. | | | 8.46 | % | | VALSPAR CORP. | | | 12.95 | % | |

Weak Performers

| Fourth Quarter (9/30/16 – 12/31/16) | | Year To Date (12/31/15 – 12/31/16) | |

ZIMMER BIOMET HOLDINGS | | | -24.45 | % | | CRAY INC. | | | -48.17 | % | |

MEDTRONIC PLC | | | -21.38 | % | | ROCHE HOLDINGS LTD | | | -29.19 | % | |

PENTAIR LTD. | | | -16.54 | % | | HORMEL FOODS CORP. | | | -23.92 | % | |

BEMIS CO., INC. | | | -10.07 | % | | MEDTRONIC PLC | | | -19.36 | % | |

ECOLAB, INC. | | | -7.52 | % | | ECOLAB, INC. | | | -9.48 | % | |

Past performance is no guarantee of future results.

The market rally in the second half of the year, and particularly at year-end following the election, was driven by strong performance in the financial sector based on a rising interest rate environment and expectations that the new administration and Congress will enact more favorable tax and regulatory policies. Financial holdings in the portfolio benefited but the Fund did not fully participate as more defensive health care and consumer stocks in particular were weak. We still like the companies we hold in these overlooked sectors and view the recent weakness as an opportunity to selectively add new names and increase existing positions.

Speaking of the financial sector, U.S. Bank (USB) was a top contributor to performance in both the fourth quarter and the full year (the Fund's 6th top performer year-to-date) and is our largest holding. While valuations among financial stocks, including USB, are at the high end of their trading range, we remain comfortable with our position. The bank is well run and consistently posts lower (better) efficiency ratios and its return on assets and return on equity are leading among its peers. While a large multi-state bank and one of the largest in the U.S., it escapes the most intensive regulatory microscope the very largest banks of over $750 billion in assets operate under. In addition, we believe U.S. Bank is very well positioned under several different economic scenarios. If the expectations for lower corporate taxes, a lighter regulatory touch and a rising and steepening yield curve bear out as the market expects, the bank will benefit. But given its operating strengths and solid management, even if the most optimistic scenario does not pan out we believe the bank will perform well.

3

MAIRS & POWER GROWTH FUND (unaudited) (continued)

Our long-term investment approach allows us to get to know management teams and observe closely how they build on opportunities and face challenges under a variety of conditions. Toro (TTC) is one example. The stock was a top performer in both the quarter and the year. While Toro is currently "priced for perfection," we still like the stock but are using the current rich valuation as an opportunity to lighten up and deploy the profits where we find other opportunities. C.E.O. Mike Hoffman, who retired in 2016, and his executive team have executed extraordinarily well over the years. Another exemplary C.E.O. who also retired this year is Jeff Ettinger at Hormel (HRL), another long-term portfolio holding. Both executives stepped into their respective C.E.O. roles about the same time and deserve credit for building excellent companies, strong management teams and enviable records. Their shareholders have been amply rewarded by their stewardship. Toro under Mike Hoffman's tenure has averaged 14.94% annual return and Hormel under Jeff Ettinger has averaged 17.47%, compared with the S&P 500 which averaged 7.43% over the same period. We wish them both well.

Given the relatively small number of technology companies in our region, it is one sector for which we look at a broader geographic area to find exposure in the sector. One new name we added in the technology sector in 2016 is Alphabet (GOOG), the holding company parent of Google, the leader in on-line search. While the company is headquartered outside of the Upper Midwest where many of our investments are located, it is an example of a stock that fits our investment approach in most other ways. The company enjoys above-average growth, maintains a durable competitive advantage globally and is attractively valued.

We also exited some positions in 2016. When MTS Systems (MTSC) announced the acquisition of sensor maker PCB Group for $580 million, we decided it was time to exit the stock. In addition to our concerns about execution of the current business, we did not believe the strategy behind the acquisition was sound. It added to the company's existing sensor business, where the company does not enjoy a strong competitive advantage, it diluted MTS' durable competitive advantage in its core test business, and added substantial leverage to the balance sheet.

Mark L. Henneman

Lead Manager | | Andrew R. Adams

Co-Manager | |

The Fund's investment objective, risks, charges and expenses must be considered carefully before investing. The summary prospectus or full prospectus contains this and other important information about the Fund and they may be obtained by calling Shareholder Services at (800) 304-7404 or by visiting www.mairsandpower.com. Read the summary prospectus or full prospectus carefully before investing.

All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or an offer of a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

All investments have risks. The Growth Fund is designed for long-term investors. Equity investments are subject to market fluctuations and the Fund's share price can fall because of weakness in the broad market, a particular industry or specific holdings. Investments in small and midcap companies generally are more volatile. International investing risks include among others political, social or economic instability, difficulty in predicting international trade patterns, taxation and foreign trading practices and greater fluctuations in price than U.S. corporations.

Diversification does not guarantee profit or protect against loss.

S&P 500 Total Return (TR) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

Lipper Multi-Cap Core Funds Index measures the performance of the 30 largest mutual funds that invest in a variety of capitalization ranges, without concentrating 75% or more of their equity assets in any one market capitalization range over an extended period of time, as determined by Lipper, Inc. It is not possible to invest directly in an index.

4

Mairs & Power Growth Fund

PERFORMANCE INFORMATION (unaudited) December 31, 2016

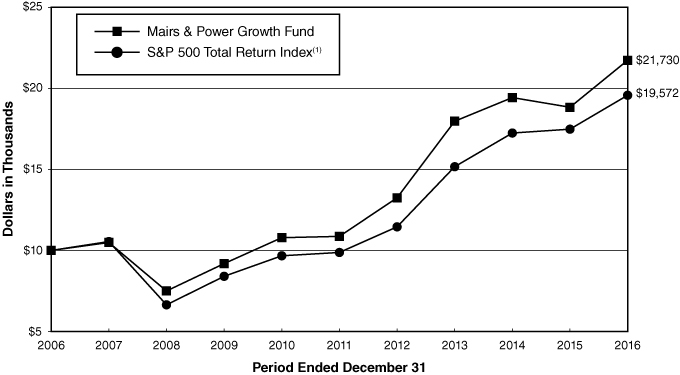

Ten years of investment performance (through December 31, 2016)

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund 10 years ago.

Average annual total returns for periods ended December 31, 2016

| | | 1 year | | 5 years | | 10 years | | 20 years | |

Mairs & Power Growth Fund | | | 15.38 | % | | | 14.86 | % | | | 8.07 | % | | | 10.18 | % | |

S&P 500 Total Return Index(1) | | | 11.96 | % | | | 14.66 | % | | | 6.95 | % | | | 7.68 | % | |

Performance data quoted represents past performance and does not guarantee future results. All performance information shown includes the reinvestment of dividend and capital gain distributions, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. For the most recent month-end performance figures, visit the Fund's website at www.mairsandpower.com or call Shareholder Services at (800) 304-7404.

(1) The S&P 500 Total Return Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

5

Mairs & Power Growth Fund

FUND INFORMATION (unaudited) December 31, 2016

Portfolio Managers

Mark L. Henneman, lead manager since July 1, 2013, co-manager from January 1, 2006 through June 30, 2013, University of Minnesota, MBA Finance 1990

Andrew R. Adams, co-manager since January 1, 2015, University of Wisconsin-Madison, MS Finance 1997

General Information

Fund Symbol | | | MPGFX | | |

Net Asset Value (NAV) Per Share | | $ | 113.83 | | |

Expense Ratio | | | 0.66 | % | |

Portfolio Turnover Rate | | | 10.99 | % | |

Sales Charge | | | None1 | | |

Fund Inception Year | | | 1958 | | |

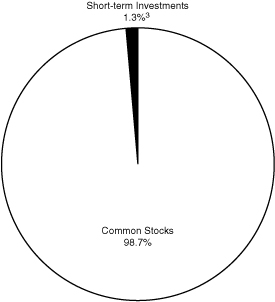

Portfolio Composition

Top Ten Portfolio Holdings

(Percent of Total Net Assets)2

US Bancorp/MN | | | 4.9 | % | |

Ecolab Inc | | | 4.3 | | |

St Jude Medical Inc | | | 4.0 | | |

| 3M Co | | | 3.9 | | |

Graco Inc | | | 3.8 | | |

Honeywell International Inc | | | 3.6 | | |

Donaldson Co Inc | | | 3.3 | | |

Johnson & Johnson | | | 3.3 | | |

Bemis Co Inc | | | 3.2 | | |

Medtronic PLC | | | 3.0 | | |

Portfolio Diversification

(Percent of Total Net Assets)

Common Stocks 98.7% | |

Industrials | | | 29.0 | % | |

Health Care | | | 21.8 | | |

Financials | | | 12.7 | | |

Materials | | | 12.3 | | |

Information Technology | | | 9.6 | | |

Consumer Discretionary | | | 5.3 | | |

Consumer Staples | | | 5.2 | | |

Energy | | | 2.8 | | |

Short-term Investments 1.3%3 | | | 1.3 | | |

| | | | 100.0 | % | |

1 Although the Fund is no-load, investment management fees and other expenses still apply.

2 All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or offer for a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

3 Represents short-term investments and other assets and liabilities (net).

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Mairs & Power, Inc. (the "Adviser").

6

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS December 31, 2016

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS 98.7% | |

| | | CONSUMER DISCRETIONARY 5.3% | |

| | 270,000 | | | Gentherm Inc (b) | | $ | 9,139,500 | | |

| | 1,420,000 | | | Target Corp | | | 102,566,600 | | |

| | 1,160,000 | | | Walt Disney Co/The | | | 120,895,200 | | |

| | | | 232,601,300 | | |

| | | CONSUMER STAPLES 5.2% | |

| | 2,020,000 | | | General Mills Inc | | | 124,775,400 | | |

| | 3,055,000 | | | Hormel Foods Corp | | | 106,344,550 | | |

| | | | 231,119,950 | | |

| | | ENERGY 2.8% | |

| | 1,450,000 | | | Schlumberger Ltd (a) | | | 121,727,500 | | |

| | | FINANCIALS 12.7% | |

| | 680,000 | | | American Express Co | | | 50,374,400 | | |

| | 1,760,000 | | | Associated Banc-Corp | | | 43,472,000 | | |

| | 790,000 | | | Great Western Bancorp Inc | | | 34,436,100 | | |

| | 1,630,000 | | | Principal Financial Group Inc | | | 94,311,800 | | |

| | 270,000 | | | Travelers Cos Inc/The | | | 33,053,400 | | |

| | 4,155,000 | | | US Bancorp/MN | | | 213,442,350 | | |

| | 1,580,000 | | | Wells Fargo & Co | | | 87,073,800 | | |

| | | | 556,163,850 | | |

| | | HEALTH CARE 21.8% | |

| | 580,000 | | | Abbott Laboratories | | | 22,277,800 | | |

| | 990,000 | | | Baxter International Inc | | | 43,896,600 | | |

| | 890,000 | | | Bio-Techne Corp | | | 91,518,700 | | |

| | 1,260,000 | | | Johnson & Johnson | | | 145,164,600 | | |

| | 1,865,000 | | | Medtronic PLC (e) | | | 132,843,950 | | |

| | 1,305,000 | | | Patterson Cos Inc | | | 53,544,150 | | |

| | 2,760,000 | | | Pfizer Inc | | | 89,644,800 | | |

| | 3,360,000 | | | Roche Holding AG (d) | | | 95,860,800 | | |

| | 2,180,000 | | | St Jude Medical Inc | | | 174,814,200 | | |

| | 245,000 | | | UnitedHealth Group Inc | | | 39,209,800 | | |

| | 685,000 | | | Zimmer Holdings Inc | | | 70,692,000 | | |

| | | | 959,467,400 | | |

| | | INDUSTRIALS 29.0% | |

| | 950,000 | | | 3M Co | | | 169,641,500 | | |

| | 1,335,000 | | | CH Robinson Worldwide Inc | | | 97,802,100 | | |

| | 3,450,000 | | | Donaldson Co Inc | | | 145,176,000 | | |

| | 750,000 | | | Emerson Electric Co | | | 41,812,500 | | |

7

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS (continued) | |

| | | INDUSTRIALS (continued) | |

| | 1,440,000 | | | Fastenal Co | | $ | 67,651,200 | | |

| | 160,000 | | | G&K Services Inc, Class A | | | 15,432,000 | | |

| | 540,000 | | | Generac Holdings Inc (b) | | | 21,999,600 | | |

| | 2,170,000 | | | General Electric Co | | | 68,572,000 | | |

| | 2,010,000 | | | Graco Inc | | | 167,010,900 | | |

| | 1,370,000 | | | Honeywell International Inc | | | 158,714,500 | | |

| | 1,660,000 | | | Pentair PLC (a) | | | 93,076,200 | | |

| | 250,000 | | | Proto Labs Inc (b) | | | 12,837,500 | | |

| | 145,000 | | | Snap-on Inc | | | 24,834,150 | | |

| | 2,190,000 | | | Toro Co/The | | | 122,530,500 | | |

| | 590,000 | | | United Parcel Service Inc, Class B | | | 67,637,600 | | |

| | | | 1,274,728,250 | | |

| | | INFORMATION TECHNOLOGY 9.6% | |

| | 57,000 | | | Alphabet Inc (b) | | | 43,993,740 | | |

| | 1,250,000 | | | Badger Meter Inc | | | 46,187,500 | | |

| | 1,350,000 | | | Corning Inc | | | 32,764,500 | | |

| | 2,070,000 | | | Cray Inc (b) (f) | | | 42,849,000 | | |

| | 780,000 | | | Fiserv Inc (b) | | | 82,898,400 | | |

| | 348,891 | | | NVE Corp (f) | | | 24,921,284 | | |

| | 1,020,000 | | | QUALCOMM Inc | | | 66,504,000 | | |

| | 930,000 | | | Stratasys Ltd (a) (b) | | | 15,382,200 | | |

| | 3,050,000 | | | Western Union Co/The | | | 66,246,000 | | |

| | | | 421,746,624 | | |

| | | MATERIALS 12.3% | |

| | 2,920,000 | | | Bemis Co Inc | | | 139,634,400 | | |

| | 1,609,999 | | | Ecolab Inc | | | 188,724,082 | | |

| | 2,481,600 | | | HB Fuller Co | | | 119,886,096 | | |

| | 890,000 | | | Valspar Corp/The | | | 92,212,900 | | |

| | | | 540,457,478 | | |

| | | | | TOTAL COMMON STOCKS

(cost $2,422,146,824) | | $ | 4,338,012,352

| | |

| | | SHORT-TERM INVESTMENTS 1.0% | |

| 42,271,848

| | | First American Government Obligations Fund, Class Z, 0.42% (c)

(cost $42,271,848) | | $ | 42,271,848

| | |

8

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Shares | | Security Description | | Fair Value | |

| | | TOTAL INVESTMENTS 99.7%

(cost $2,464,418,672) | | $ | 4,380,284,200

| | |

| | | OTHER ASSETS AND LIABILITIES (NET) 0.3% | | | 12,188,390 | | |

| | | TOTAL NET ASSETS 100.0% | | $ | 4,392,472,590 | | |

(a) Foreign security denominated in U.S. dollars. As of December 31, 2016, these securities represented $230,185,900 or 5.2% of total net assets.

(b) Non-income producing.

(c) The rate quoted is the annualized seven-day effective yield as of December 31, 2016.

(d) American Depositary Receipt.

(e) Issuer headquartered overseas but considered domestic. In determining whether a security is foreign or domestic, the Adviser will generally look at the location of the headquarters of the issuer. However, if the issuer is believed by the Adviser to be headquartered in a jurisdiction primarily for tax purposes, the Adviser will consider the following additional factors: 1) the location of the primary exchange trading its securities; 2) where it derives the majority of its revenues, and/or 3) where it earns the majority of its profits.

(f) Affiliated company at December 31, 2016.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

See accompanying Notes to Financial Statements.

9

MAIRS & POWER BALANCED FUND (unaudited)

To Our Shareholders: December 31, 2016

The Balanced Fund finished the year ahead of its benchmark composite index (60% S&P 500 Total Return Index and 40% Bloomberg Barclays U.S. Government/Credit Bond Index) gaining 11.42% compared to 8.48% for the benchmark. For the fourth quarter, the Fund gained 1.32% compared to 0.93% for the benchmark. Stock selection remains the major driver of the Fund's relative performance year-to-date.

The market rally in the second half of the year, and particularly at year-end following the election, was driven by strong performance in the financial sector based on a rising interest rate environment and expectations that the new administration and Congress will enact more favorable tax and regulatory policies. U.S. Bank (USB) was a top contributor to performance in both the fourth quarter and the full year and is our largest holding. While valuations among financial stocks, including USB, are at the high end of their trading range, we remain comfortable with our position. The bank is well run and consistently posts lower (better) efficiency ratios and its return on assets and return on equity are among the highest among its peers. While a large multi-state bank and one of the largest in the US, it escapes the most intensive regulatory microscope the very largest banks of over $750 billion in assets operate under. In addition, we believe U.S. Bank is very well positioned under several different economic scenarios. If the expectations for lower corporate taxes, a lighter regulatory touch and a rising and steepening yield curve bear out as the market expects, the bank will benefit. But given its operating strengths and solid management, even if the most optimistic scenario does not pan out, we believe the bank will perform well.

MAIRS & POWER BALANCED FUND (MAPOX)

Top Performers

| Fourth Quarter (9/30/16 – 12/31/16) | | Year To Date (12/31/15 – 12/31/16) | |

JPMORGAN CHASE & CO. | | | 25.76 | % | | CORNING INC. | | | 20.81 | % | |

ASSOCIATED BANC-CORP. | | | 22.26 | % | | JPMORGAN CHASE & CO. | | | 18.72 | % | |

WELLS FARGO & CO. | | | 20.64 | % | | PRINCIPAL FINANCIAL GROUP | | | 16.67 | % | |

U.S. BANCORP | | | 15.95 | % | | VALSPAR CORP. | | | 12.95 | % | |

CHEVRON CORP | | | 10.54 | % | | U.S. BANCORP | | | 8.43 | % | |

Weak Performers

| Fourth Quarter (9/30/16 – 12/31/16) | | Year To Date (12/31/15 – 12/31/16) | |

MEDTRONIC PLC | | | -21.38 | % | | BRISTOL-MYERS SQUIBB CO. | | | -27.01 | % | |

PENTAIR LTD. | | | -16.54 | % | | ABBOTT LABORATORIES | | | -26.43 | % | |

ABBOTT LABORATORIES | | | -12.99 | % | | HORMEL FOODS CORP. | | | -23.92 | % | |

HORMEL FOODS CORP. | | | -12.05 | % | | MEDTRONIC PLC | | | -19.36 | % | |

ECOLAB, INC. | | | -7.52 | % | | PFIZER INC. | | | -11.34 | % | |

Past performance is no guarantee of future results.

Our long-term investment approach allows us to get to know management teams and observe closely how they build on opportunities and face challenges under a variety of conditions. Toro (TTC) is one example. The stock was a strong performer in both the quarter and the year. C.E.O. Mike Hoffman, who retired in 2016, and his executive team have executed extraordinarily well over the years. Another exemplary C.E.O who also retired this year is Jeff Ettinger at Hormel (HRL), another long-term portfolio holding. Both executives stepped into their respective C.E.O. roles about the same time and deserve credit for building excellent companies, strong management teams and enviable records. Their shareholders have been amply rewarded by their stewardship. Toro under Mike Hoffman's tenure has averaged 14.94% annual return and Hormel under Jeff Ettinger has averaged 17.47%, compared with the S&P 500 which averaged 7.43% over the same period. We wish them both well.

Given the relatively small number of technology companies in our region, it is one sector for which we look at a broader geographic area to find exposure in the sector. One new name we added in the technology sector in

10

MAIRS & POWER BALANCED FUND (unaudited) (continued)

2016 is Alphabet (GOOG), the holding company parent of Google, the leader in on-line search. While the company is headquartered outside of the Upper Midwest where many of our investments are located, it is an example of a stock that fits our investment approach in most other ways. The company enjoys above-average growth, maintains a durable competitive advantage globally and is attractively valued.

We also exited some positions in 2016. We no longer felt comfortable with the long-term strategy at MTS Systems (MTSC) and MDU Resources (MDU) and sold our positions. In the energy sector, we traded out of ConocoPhillips (COP) into Chevron (CVX), viewing the latter as better managed with a stronger balance sheet.

On the fixed income side of the portfolio, we saw a 25 basis point (0.25%) rate hike from the Fed at year end, as discussed in the Market Recap above. While the rising rates put downward pressure on bond prices, particularly in the fourth quarter, high quality corporate bonds, which make up a substantial portion of the fixed income portfolio, performed reasonably well in this environment. The question on fixed income investors' minds is: "What's next?" While we do expect continued rate hikes from the Fed in 2017, we do not view modest increases from current low levels as a reason to "head for the hills." The more pertinent issue for investors is to watch how the new administration's policies unfold. If President Trump's threats of imposing tariffs spark a trade war, investors will have to become much more sensitive to who owns U.S. Treasury securities and whether those holders are buyers or sellers. With China as the largest holder of Treasuries, this issue will be at the front of fixed income investors' concerns. As we anticipate increased volatility on the fixed income side, we are not going to cash but are taking a defensive posture, remaining on the short end of maturities and looking for securities with a large and defensible payout.

Ronald L. Kaliebe

Lead Manager | | Kevin V. Earley

Co-Manager | |

The Fund's investment objective, risks, charges and expenses must be considered carefully before investing. The summary prospectus or full prospectus contains this and other important information about the Fund and they may be obtained by calling Shareholder Services at (800) 304-7404 or by visiting www.mairsandpower.com. Read the summary prospectus or full prospectus carefully before investing.

All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or an offer of a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

All investments have risks. The Balanced Fund is designed for long-term investors. Equity investments are subject to market fluctuations and the Fund's share price can fall because of weakness in the broad market, a particular industry or specific holdings. Investments in small and midcap companies generally are more volatile. International investing risks include among others political, social or economic instability, difficulty in predicting international trade patterns, taxation and foreign trading practices, and greater fluctuations in price than U.S. corporations. The Fund is subject to yield and share price variances with changes in interest rates and market conditions. Investors should note that if interest rates rise significantly from current levels, bond total returns will decline and may even turn negative in the short-term. There is also a chance that some of the Fund's holdings may have their credit rating downgraded or may default.

Diversification does not guarantee profit or protect against loss.

Composite Index reflects an unmanaged portfolio of 60% of the S&P 500 TR Index and 40% of the Bloomberg Barclays U.S. Government/Credit Bond Index. It is not possible to invest directly in an index.

Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

S&P 500 Total Return (TR) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

11

Mairs & Power Balanced Fund

PERFORMANCE INFORMATION (unaudited) December 31, 2016

Ten years of investment performance (through December 31, 2016) __________________________

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund 10 years ago.

Average annual total returns for periods ended December 31, 2016

| | | 1 year | | 5 years | | 10 years | | 20 years | |

Mairs & Power Balanced Fund | | | 11.42 | % | | | 10.38 | % | | | 6.85 | % | | | 8.48 | % | |

Composite Index(1) | | | 8.48 | % | | | 9.72 | % | | | 6.24 | % | | | 7.07 | % | |

S&P 500 Total Return Index(2) | | | 11.96 | % | | | 14.66 | % | | | 6.95 | % | | | 7.68 | % | |

Bloomberg Barclays U.S.

Government/Credit Bond Index(3) | | | 3.05 | % | | | 2.29 | % | | | 4.40 | % | | | 5.32 | % | |

Performance data quoted represents past performance and does not guarantee future results. All performance information shown includes the reinvestment of dividend and capital gain distributions, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. For the most recent month-end performance figures, visit the Fund's website at www.mairsandpower.com or call Shareholder Services at (800) 304-7404.

(1) The Composite Index reflects an unmanaged portfolio comprised of 60% of the S&P 500 Total Return Index and 40% of the Bloomberg Barclays U.S. Government/Credit Bond Index. It is not possible to invest directly in an index.

(2) The S&P 500 Total Return Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

(3) The Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

12

Mairs & Power Balanced Fund

FUND INFORMATION (unaudited) December 31, 2016

Portfolio Managers

Ronald L. Kaliebe, lead manager since July 1, 2013, co-manager from January 1, 2006 through

June 30, 2013, University of Wisconsin-Madison, MBA Finance 1980

Kevin V. Earley, co-manager since January 1, 2015, University of Minnesota, MBA Finance 1990

General Information

Fund Symbol | | MAPOX | |

Net Asset Value (NAV) Per Share | | $ | 87.29 | | |

Expense Ratio | | | 0.72 | % | |

Portfolio Turnover Rate | | | 14.10 | % | |

Sales Charge | | | None1 | | |

Fund Inception Year | | | 1961 | | |

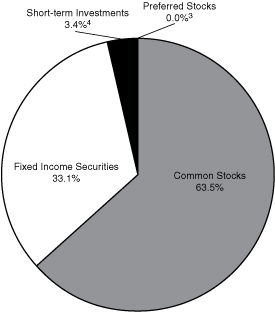

Portfolio Composition

Top Ten Common Stock Holdings

(Percent of Total Net Assets)2

US Bancorp/MN | | | 2.9 | % | |

United Parcel Service Inc, Class B | | | 2.7 | | |

Ecolab Inc | | | 2.5 | | |

Medtronic PLC | | | 2.5 | | |

Honeywell International Inc | | | 2.2 | | |

Johnson & Johnson | | | 2.1 | | |

Exxon Mobil Corp | | | 2.1 | | |

Pfizer Inc | | | 2.0 | | |

Graco Inc | | | 1.9 | | |

| 3M Co | | | 1.9 | | |

Portfolio Diversification

(Percent of Total Net Assets)

Fixed Income Securities 33.1% | |

Corporate Bonds | | | 29.9 | % | |

Asset Backed Securities | | | 2.6 | | |

Preferred Securities | | | 0.4 | | |

Federal Agency Obligations | | | 0.2 | | |

Common Stocks 63.5% | |

Industrials | | | 14.8 | % | |

Health Care | | | 14.3 | | |

Financials | | | 10.2 | | |

Materials | | | 5.8 | | |

Energy | | | 5.5 | | |

Information Technology | | | 5.5 | | |

Consumer Staples | | | 3.4 | | |

Consumer Discretionary | | | 2.8 | | |

Utilities | | | 1.2 | | |

Preferred Stocks 0.0%3 | | | 0.0 | % | |

Short-term Investments 3.4%4 | | | 3.4 | % | |

| | | | 100.0 | % | |

1 Although the Fund is no-load, investment management fees and other expenses still apply.

2 All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or offer for a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

3 Percentage is less than 0.05%.

4 Represents short-term investments and other assets and liabilities (net).

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

13

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES 33.1% | |

| | | FEDERAL AGENCY OBLIGATIONS 0.2% | |

$ | 500,000 | | | Federal Farm Credit Banks | | | 3.590 | % | | 12/27/28 | | $ | 500,169 | | |

| | 1,000,000 | | | Federal Home Loan Banks | | | 3.500 | % | | 12/22/31 | | | 995,553 | | |

| | | | 1,495,722 | | |

| | | CORPORATE BONDS 29.9% | |

| | | CONSUMER DISCRETIONARY 3.1% | |

| | 250,000 | | | ServiceMaster Co LLC/The | | | 7.100 | % | | 03/01/18 | | | 260,625 | | |

| | 500,000 | | | Best Buy Co Inc | | | 5.000 | % | | 08/01/18 | | | 522,945 | | |

| | 1,000,000 | | | Ford Motor Credit Co LLC | | | 3.000 | % | | 12/20/18 | | | 1,000,651 | | |

| | 1,000,000 | | | Time Warner Cable Inc | | | 4.125 | % | | 02/15/21 | | | 1,033,842 | | |

| | 1,000,000 | | | Best Buy Co Inc | | | 5.500 | % | | 03/15/21 | | | 1,090,000 | | |

| | 555,000 | | | Kohl's Corp | | | 4.000 | % | | 11/01/21 | | | 582,034 | | |

| | 500,000 | | | Whirlpool Corp | | | 4.700 | % | | 06/01/22 | | | 545,771 | | |

| | 750,000 | | | Newell Rubbermaid Inc | | | 4.000 | % | | 06/15/22 | | | 777,263 | | |

| | 1,000,000 | | | Block Financial LLC | | | 5.500 | % | | 11/01/22 | | | 1,053,488 | | |

| | 1,000,000 | | | Staples Inc | | | 4.375 | % | | 01/12/23 | | | 1,001,888 | | |

| | 2,000,000 | | | Kohl's Corp | | | 3.250 | % | | 02/01/23 | | | 1,977,130 | | |

| | 1,000,000 | | | Wyndham Worldwide Corp | | | 3.900 | % | | 03/01/23 | | | 998,216 | | |

| | 1,975,000 | | | LKQ Corp | | | 4.750 | % | | 05/15/23 | | | 1,965,125 | | |

| | 500,000 | | | Hyatt Hotels Corp | | | 3.375 | % | | 07/15/23 | | | 493,108 | | |

| | 1,000,000 | | | Viacom Inc | | | 4.250 | % | | 09/01/23 | | | 1,000,795 | | |

| | 2,000,000 | | | Viacom Inc | | | 3.875 | % | | 04/01/24 | | | 1,941,044 | | |

| | 1,000,000 | | | Tiffany & Co | | | 3.800 | % | | 10/01/24 | | | 991,101 | | |

| | 2,000,000 | | | Coach Inc | | | 4.250 | % | | 04/01/25 | | | 2,011,108 | | |

| | 1,000,000 | | | Ford Motor Credit Co LLC | | | 4.134 | % | | 08/04/25 | | | 1,001,202 | | |

| | 2,000,000 | | | Priceline Group Inc/The | | | 3.600 | % | | 06/01/26 | | | 1,978,008 | | |

| | 1,000,000 | | | Ford Motor Co | | | 4.346 | % | | 12/08/26 | | | 1,010,498 | | |

| | 1,000,000 | | | Metropolitan Opera Association Inc | | | 4.349 | % | | 10/01/32 | | | 978,027 | | |

| | 2,000,000 | | | Comcast Corp | | | 4.250 | % | | 01/15/33 | | | 2,081,330 | | |

| | | | 26,295,199 | | |

| | | CONSUMER STAPLES 0.9% | |

| | 525,000 | | | Cargill Inc (g) | | | 6.000 | % | | 11/27/17 | | | 546,411 | | |

| | 2,250,000 | | | Land O' Lakes Inc (g) | | | 6.000 | % | | 11/15/22 | | | 2,452,500 | | |

| | 1,000,000 | | | Walgreens Boots Alliance Inc | | | 3.800 | % | | 11/18/24 | | | 1,017,775 | | |

| | 1,949,000 | | | Land O'Lakes Capital Trust I (g) | | | 7.450 | % | | 03/15/28 | | | 2,104,920 | | |

| | 500,000 | | | Altria Group Inc | | | 4.250 | % | | 08/09/42 | | | 492,060 | | |

| | 1,000,000 | | | Cargill Inc (g) | | | 4.100 | % | | 11/01/42 | | | 958,049 | | |

| | | | 7,571,715 | | |

14

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | ENERGY 1.7% | |

$ | 250,000 | | | ConocoPhillips Co | | | 6.650 | % | | 07/15/18 | | $ | 267,696 | | |

| | 2,000,000 | | | ConocoPhillips Co | | | 4.200 | % | | 03/15/21 | | | 2,124,442 | | |

| | 140,000 | | | Gulf South Pipeline Co LP | | | 4.000 | % | | 06/15/22 | | | 141,817 | | |

| | 500,000 | | | Western Gas Partners LP | | | 4.000 | % | | 07/01/22 | | | 508,158 | | |

| | 1,020,000 | | | FMC Technologies Inc | | | 3.450 | % | | 10/01/22 | | | 1,020,440 | | |

| | 1,500,000 | | | Sunoco Logistics Partners Operations LP | | | 3.450 | % | | 01/15/23 | | | 1,465,314 | | |

| | 575,000 | | | DCP Midstream Operating LP | | | 3.875 | % | | 03/15/23 | | | 553,081 | | |

| | 2,000,000 | | | Halliburton Co | | | 3.500 | % | | 08/01/23 | | | 2,030,822 | | |

| | 1,000,000 | | | Diamond Offshore Drilling Inc | | | 3.450 | % | | 11/01/23 | | | 860,000 | | |

| | 2,300,000 | | | Murphy Oil Corp | | | 6.875 | % | | 08/15/24 | | | 2,449,500 | | |

| | 500,000 | | | Kinder Morgan Energy Partners LP | | | 4.250 | % | | 09/01/24 | | | 510,622 | | |

| | 1,000,000 | | | ConocoPhillips Co | | | 3.350 | % | | 11/15/24 | | | 994,241 | | |

| | 1,000,000 | | | Boardwalk Pipelines LP | | | 4.950 | % | | 12/15/24 | | | 1,026,769 | | |

| | 500,000 | | | Murphy Oil Corp (f) | | | 6.125 | % | | 12/01/42 | | | 468,428 | | |

| | 500,000 | | | Apache Corp | | | 4.250 | % | | 01/15/44 | | | 492,911 | | |

| | | | 14,914,241 | | |

| | | FINANCIALS 12.9% | |

| | 500,000 | | | M&I Marshall & Ilsley Bank | | | 5.000 | % | | 01/17/17 | | | 500,529 | | |

| | 500,000 | | | Citigroup Inc | | | 5.500 | % | | 02/15/17 | | | 502,337 | | |

| | 250,000 | | | Bank of America Corp | | | 5.700 | % | | 05/02/17 | | | 253,407 | | |

| | 500,000 | | | Royal Bank of Scotland Group PLC (a) | | | 4.250 | % | | 07/15/17 | | | 502,256 | | |

| | 500,000 | | | Comerica Bank | | | 5.200 | % | | 08/22/17 | | | 511,231 | | |

| | 500,000 | | | Bank of America Corp | | | 6.000 | % | | 09/01/17 | | | 514,489 | | |

| | 500,000 | | | American Express Bank FSB | | | 6.000 | % | | 09/13/17 | | | 515,457 | | |

| | 500,000 | | | Bear Stearns Cos LLC/The | | | 6.400 | % | | 10/02/17 | | | 517,973 | | |

| | 500,000 | | | Prudential Financial Inc | | | 6.000 | % | | 12/01/17 | | | 519,475 | | |

| | 500,000 | | | Barclays Bank PLC (a) (g) | | | 6.050 | % | | 12/04/17 | | | 516,543 | | |

| | 1,000,000 | | | Morgan Stanley | | | 5.950 | % | | 12/28/17 | | | 1,040,830 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 5.950 | % | | 01/18/18 | | | 520,871 | | |

| | 500,000 | | | Wachovia Corp | | | 5.750 | % | | 02/01/18 | | | 521,298 | | |

| | 250,000 | | | Lincoln National Corp | | | 7.000 | % | | 03/15/18 | | | 264,089 | | |

| | 500,000 | | | SunTrust Bank/Atlanta GA | | | 7.250 | % | | 03/15/18 | | | 530,378 | | |

| | 500,000 | | | Morgan Stanley | | | 6.625 | % | | 04/01/18 | | | 528,764 | | |

| | 1,000,000 | | | Jefferies Group LLC | | | 5.125 | % | | 04/13/18 | | | 1,033,647 | | |

| | 500,000 | | | Bank of America Corp | | | 6.875 | % | | 04/25/18 | | | 531,455 | | |

| | 500,000 | | | Provident Cos Inc | | | 7.000 | % | | 07/15/18 | | | 537,191 | | |

| | 500,000 | | | MetLife Inc | | | 6.817 | % | | 08/15/18 | | | 539,050 | | |

| | 500,000 | | | Hartford Financial Services Group Inc/The | | | 6.000 | % | | 01/15/19 | | | 538,040 | | |

15

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | FINANCIALS (continued) | |

$ | 500,000 | | | Royal Bank of Scotland Group PLC (a) | | | 5.250 | % | | 02/15/19 | | $ | 516,885 | | |

| | 500,000 | | | BB&T Corp | | | 6.850 | % | | 04/30/19 | | | 554,157 | | |

| | 250,000 | | | WR Berkley Corp | | | 6.150 | % | | 08/15/19 | | | 272,327 | | |

| | 500,000 | | | Protective Life Corp | | | 7.375 | % | | 10/15/19 | | | 566,313 | | |

| | 500,000 | | | Prospect Capital Corp | | | 5.125 | % | | 11/15/19 | | | 488,784 | | |

| | 500,000 | | | Credit Suisse/New York NY (a) | | | 5.400 | % | | 01/14/20 | | | 536,069 | | |

| | 500,000 | | | Prospect Capital Corp | | | 4.000 | % | | 01/15/20 | | | 477,937 | | |

| | 500,000 | | | Morgan Stanley | | | 5.500 | % | | 01/26/20 | | | 542,066 | | |

| | 500,000 | | | Hartford Financial Services Group Inc/The | | | 5.500 | % | | 03/30/20 | | | 545,964 | | |

| | 450,000 | | | Compass Bank | | | 5.500 | % | | 04/01/20 | | | 471,541 | | |

| | 1,000,000 | | | Barclays PLC (a) | | | 3.250 | % | | 01/12/21 | | | 1,000,974 | | |

| | 2,000,000 | | | American International Group Inc | | | 3.300 | % | | 03/01/21 | | | 2,048,566 | | |

| | 1,000,000 | | | HSBC Holdings PLC (a) | | | 3.400 | % | | 03/08/21 | | | 1,016,879 | | |

| | 1,000,000 | | | Nationwide Financial Services Inc (g) | | | 5.375 | % | | 03/25/21 | | | 1,092,241 | | |

| | 500,000 | | | Markel Corp | | | 5.350 | % | | 06/01/21 | | | 545,767 | | |

| | 1,000,000 | | | Capital One Financial Corp | | | 4.750 | % | | 07/15/21 | | | 1,081,575 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 5.250 | % | | 07/27/21 | | | 547,995 | | |

| | 500,000 | | | Genworth Holdings Inc | | | 7.625 | % | | 09/24/21 | | | 461,250 | | |

| | 500,000 | | | Aflac Inc | | | 4.000 | % | | 02/15/22 | | | 528,779 | | |

| | 2,000,000 | | | Primerica Inc | | | 4.750 | % | | 07/15/22 | | | 2,142,550 | | |

| | 2,000,000 | | | OneBeacon US Holdings Inc | | | 4.600 | % | | 11/09/22 | | | 1,993,854 | | |

| | 1,000,000 | | | Invesco Finance PLC (a) | | | 3.125 | % | | 11/30/22 | | | 1,007,375 | | |

| | 1,000,000 | | | Standard Chartered PLC (a) (g) | | | 3.950 | % | | 01/11/23 | | | 977,229 | | |

| | 2,000,000 | | | Wells Fargo & Co | | | 3.450 | % | | 02/13/23 | | | 2,007,198 | | |

| | 4,073,000 | | | Assurant Inc | | | 4.000 | % | | 03/15/23 | | | 4,101,662 | | |

| | 1,000,000 | | | Markel Corp | | | 3.625 | % | | 03/30/23 | | | 1,002,643 | | |

| | 1,000,000 | | | General Motors Financial Co Inc | | | 3.700 | % | | 05/09/23 | | | 983,987 | | |

| | 1,500,000 | | | Citigroup Inc | | | 3.500 | % | | 05/15/23 | | | 1,495,158 | | |

| | 500,000 | | | Morgan Stanley | | | 4.100 | % | | 05/22/23 | | | 513,261 | | |

| | 2,000,000 | | | Liberty Mutual Group Inc (g) | | | 4.250 | % | | 06/15/23 | | | 2,093,950 | | |

| | 2,000,000 | | | E*TRADE Financial Corp | | | 4.625 | % | | 09/15/23 | | | 2,040,000 | | |

| | 500,000 | | | Ameriprise Financial Inc | | | 4.000 | % | | 10/15/23 | | | 524,377 | | |

| | 500,000 | | | CNA Financial Corp | | | 7.250 | % | | 11/15/23 | | | 591,066 | | |

| | 500,000 | | | Pacific Life Insurance Co (g) | | | 7.900 | % | | 12/30/23 | | | 594,913 | | |

| | 1,000,000 | | | Moody's Corp | | | 4.875 | % | | 02/15/24 | | | 1,081,089 | | |

| | 1,000,000 | | | NASDAQ OMX Group Inc/The | | | 4.250 | % | | 06/01/24 | | | 1,028,995 | | |

| | 500,000 | | | Wintrust Financial Corp | | | 5.000 | % | | 06/13/24 | | | 494,370 | | |

| | 1,250,000 | | | Assured Guaranty US Holdings Inc | | | 5.000 | % | | 07/01/24 | | | 1,320,147 | | |

16

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | FINANCIALS (continued) | |

$ | 2,060,000 | | | Legg Mason Inc | | | 3.950 | % | | 07/15/24 | | $ | 2,067,404 | | |

| | 500,000 | | | Symetra Financial Corp | | | 4.250 | % | | 07/15/24 | | | 494,064 | | |

| | 1,500,000 | | | Stifel Financial Corp | | | 4.250 | % | | 07/18/24 | | | 1,489,698 | | |

| | 1,000,000 | | | Citigroup Inc | | | 4.000 | % | | 08/05/24 | | | 1,007,747 | | |

| | 1,500,000 | | | Synchrony Financial | | | 4.250 | % | | 08/15/24 | | | 1,526,922 | | |

| | 1,000,000 | | | Bank of America Corp | | | 4.200 | % | | 08/26/24 | | | 1,018,704 | | |

| | 2,800,000 | | | Brown & Brown Inc | | | 4.200 | % | | 09/15/24 | | | 2,820,675 | | |

| | 2,000,000 | | | Old Republic International Corp | | | 4.875 | % | | 10/01/24 | | | 2,083,810 | | |

| | 1,000,000 | | | TIAA Asset Management Finance Co LLC (g) | | | 4.125 | % | | 11/01/24 | | | 1,010,034 | | |

| | 2,000,000 | | | American Express Co | | | 3.625 | % | | 12/05/24 | | | 2,008,290 | | |

| | 2,000,000 | | | Associated Banc-Corp | | | 4.250 | % | | 01/15/25 | | | 1,982,030 | | |

| | 4,000,000 | | | Kemper Corp | | | 4.350 | % | | 02/15/25 | | | 3,976,696 | | |

| | 1,050,000 | | | TCF National Bank | | | 4.600 | % | | 02/27/25 | | | 1,019,810 | | |

| | 1,000,000 | | | Lincoln National Corp | | | 3.350 | % | | 03/09/25 | | | 996,023 | | |

| | 250,000 | | | Liberty Mutual Insurance Co (g) | | | 8.500 | % | | 05/15/25 | | | 306,656 | | |

| | 3,000,000 | | | American International Group Inc | | | 3.750 | % | | 07/10/25 | | | 3,019,362 | | |

| | 1,000,000 | | | Synchrony Financial | | | 4.500 | % | | 07/23/25 | | | 1,027,166 | | |

| | 1,000,000 | | | Janus Capital Group Inc | | | 4.875 | % | | 08/01/25 | | | 1,030,440 | | |

| | 3,000,000 | | | HSBC Holdings PLC (a) | | | 4.250 | % | | 08/18/25 | | | 3,027,444 | | |

| | 1,000,000 | | | Capital One Financial Corp | | | 4.200 | % | | 10/29/25 | | | 1,003,326 | | |

| | 1,520,000 | | | Legg Mason Inc | | | 4.750 | % | | 03/15/26 | | | 1,573,297 | | |

| | 2,000,000 | | | Hanover Insurance Group Inc/The | | | 4.500 | % | | 04/15/26 | | | 2,009,724 | | |

| | 1,000,000 | | | Wells Fargo & Co | | | 4.100 | % | | 06/03/26 | | | 1,013,189 | | |

| | 2,000,000 | | | Voya Financial Inc | | | 3.650 | % | | 06/15/26 | | | 1,955,550 | | |

| | 2,000,000 | | | MSCI Inc (g) | | | 4.750 | % | | 08/01/26 | | | 1,990,000 | | |

| | 2,000,000 | | | Old Republic International Corp | | | 3.875 | % | | 08/26/26 | | | 1,902,430 | | |

| | 500,000 | | | Morgan Stanley | | | 4.350 | % | | 09/08/26 | | | 512,374 | | |

| | 1,000,000 | | | National Rural Utilities Cooperative Finance Corp | | | 3.000 | % | | 11/15/26 | | | 946,536 | | |

| | 1,000,000 | | | Citigroup Inc | | | 4.300 | % | | 11/20/26 | | | 1,009,128 | | |

| | 1,000,000 | | | JPMorgan Chase & Co | | | 4.125 | % | | 12/15/26 | | | 1,020,656 | | |

| | 250,000 | | | Provident Cos Inc | | | 7.250 | % | | 03/15/28 | | | 295,771 | | |

| | 1,000,000 | | | JPMorgan Chase & Co (f) | | | 3.000 | % | | 03/21/28 | | | 932,366 | | |

| | 1,000,000 | | | Royal Bank of Canada (a) | | | 3.000 | % | | 05/10/28 | | | 859,317 | | |

| | 500,000 | | | Farmers Exchange Capital (g) | | | 7.050 | % | | 07/15/28 | | | 577,725 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.250 | % | | 11/15/30 | | | 482,761 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.000 | % | | 02/15/31 | | | 491,499 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.300 | % | | 12/15/32 | | | 488,100 | | |

| | 1,000,000 | | | JPMorgan Chase & Co (f) | | | 3.250 | % | | 01/31/33 | | | 963,535 | | |

17

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | FINANCIALS (continued) | |

$ | 649,000 | | | Lloyds Bank PLC (a) (f) | | | 3.400 | % | | 01/31/33 | | $ | 580,015 | | |

| | 250,000 | | | Citigroup Inc (f) | | | 4.000 | % | | 06/27/34 | | | 240,469 | | |

| | 538,000 | | | Bank of America Corp | | | 4.000 | % | | 08/15/34 | | | 512,361 | | |

| | 1,000,000 | | | Prudential Financial Inc | | | 4.050 | % | | 11/15/34 | | | 973,193 | | |

| | 1,000,000 | | | Goldman Sachs Group Inc/The | | | 4.000 | % | | 01/30/35 | | | 969,976 | | |

| | 1,000,000 | | | Berkshire Hathaway Finance Corp | | | 4.400 | % | | 05/15/42 | | | 1,052,754 | | |

| | 500,000 | | | MetLife Inc | | | 4.125 | % | | 08/13/42 | | | 492,083 | | |

| | 500,000 | | | Swiss Re Treasury US Corp (g) | | | 4.250 | % | | 12/06/42 | | | 488,279 | | |

| | 500,000 | | | Pacific LifeCorp (g) | | | 5.125 | % | | 01/30/43 | | | 511,066 | | |

| | 500,000 | | | Berkshire Hathaway Finance Corp | | | 4.300 | % | | 05/15/43 | | | 516,566 | | |

| | 500,000 | | | Principal Financial Group Inc | | | 4.350 | % | | 05/15/43 | | | 494,379 | | |

| | 2,000,000 | | | M&T Bank Corp (f) | | | 5.125 | % | | 12/29/49 | | | 1,935,000 | | |

| | | | 111,435,603 | | |

| | | HEALTH CARE 1.0% | |

| | 500,000 | | | UnitedHealth Group Inc | | | 6.000 | % | | 02/15/18 | | | 524,255 | | |

| | 1,000,000 | | | Quest Diagnostics Inc | | | 4.700 | % | | 04/01/21 | | | 1,073,319 | | |

| | 1,000,000 | | | Laboratory Corp of America Holdings | | | 3.750 | % | | 08/23/22 | | | 1,026,175 | | |

| | 1,000,000 | | | Laboratory Corp of America Holdings | | | 4.000 | % | | 11/01/23 | | | 1,024,543 | | |

| | 1,000,000 | | | Mylan Inc/PA | | | 4.200 | % | | 11/29/23 | | | 1,001,205 | | |

| | 500,000 | | | Wyeth LLC | | | 6.450 | % | | 02/01/24 | | | 608,818 | | |

| | 2,000,000 | | | Actavis Funding SCS (a) | | | 3.800 | % | | 03/15/25 | | | 2,002,356 | | |

| | 1,000,000 | | | Express Scripts Holding Co | | | 4.500 | % | | 02/25/26 | | | 1,029,473 | | |

| | | | 8,290,144 | | |

| | | INDUSTRIALS 2.4% | |

| | 500,000 | | | Masco Corp | | | 7.125 | % | | 03/15/20 | | | 562,500 | | |

| | 150,000 | | | Pentair Finance SA (a) | | | 3.625 | % | | 09/15/20 | | | 152,618 | | |

| | 500,000 | | | Pentair Finance SA (a) | | | 5.000 | % | | 05/15/21 | | | 532,829 | | |

| | 500,000 | | | IDEX Corp | | | 4.200 | % | | 12/15/21 | | | 512,647 | | |

| | 500,000 | | | GATX Corp | | | 4.750 | % | | 06/15/22 | | | 538,138 | | |

| | 500,000 | | | Penske Truck Leasing Co Lp / PTL Finance Corp (g) | | | 4.875 | % | | 07/11/22 | | | 536,556 | | |

| | 2,000,000 | | | Dun & Bradstreet Corp/The | | | 4.375 | % | | 12/01/22 | | | 2,026,536 | | |

| | 2,000,000 | | | Crown Americas LLC / Crown Americas Capital Corp IV | | | 4.500 | % | | 01/15/23 | | | 2,040,000 | | |

| | 1,000,000 | | | GATX Corp | | | 3.900 | % | | 03/30/23 | | | 998,560 | | |

| | 500,000 | | | Ingersoll-Rand Global Holding Co Ltd (a) | | | 4.250 | % | | 06/15/23 | | | 528,819 | | |

| | 1,000,000 | | | Flowserve Corp | | | 4.000 | % | | 11/15/23 | | | 1,012,541 | | |

| | 2,126,000 | | | Air Lease Corp | | | 4.850 | % | | 02/01/24 | | | 2,115,370 | | |

| | 500,000 | | | Pitney Bowes Inc | | | 4.625 | % | | 03/15/24 | | | 492,506 | | |

| | 1,375,000 | | | Oshkosh Corp | | | 5.375 | % | | 03/01/25 | | | 1,402,500 | | |

18

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | INDUSTRIALS (continued) | |

$ | 500,000 | | | Toro Co/The | | | 7.800 | % | | 06/15/27 | | $ | 607,394 | | |

| | 500,000 | | | General Electric Capital Corp | | | 3.500 | % | | 05/15/32 | | | 476,113 | | |

| | 2,000,000 | | | Eaton Corp | | | 4.000 | % | | 11/02/32 | | | 1,971,672 | | |

| | 2,000,000 | | | General Electric Capital Corp | | | 4.000 | % | | 02/14/33 | | | 1,951,392 | | |

| | 1,000,000 | | | Pitney Bowes Inc | | | 5.250 | % | | 01/15/37 | | | 999,830 | | |

| | 590,000 | | | Eaton Corp | | | 4.150 | % | | 11/02/42 | | | 576,710 | | |

| | 500,000 | | | Lockheed Martin Corp | | | 4.070 | % | | 12/15/42 | | | 493,526 | | |

| | | | 20,528,757 | | |

| | | INFORMATION TECHNOLOGY 3.4% | |

| | 500,000 | | | Broadridge Financial Solutions Inc | | | 6.125 | % | | 06/01/17 | | | 508,700 | | |

| | 500,000 | | | Broadridge Financial Solutions Inc | | | 3.950 | % | | 09/01/20 | | | 524,258 | | |

| | 81,000 | | | Hewlett-Packard Co | | | 3.750 | % | | 12/01/20 | | | 83,866 | | |

| | 750,000 | | | Hewlett-Packard Co | | | 4.300 | % | | 06/01/21 | | | 784,936 | | |

| | 2,000,000 | | | NetApp Inc | | | 3.375 | % | | 06/15/21 | | | 2,031,260 | | |

| | 1,000,000 | | | eBay Inc | | | 3.800 | % | | 03/09/22 | | | 1,033,131 | | |

| | 500,000 | | | Motorola Solutions Inc | | | 3.750 | % | | 05/15/22 | | | 505,384 | | |

| | 2,000,000 | | | Symantec Corp | | | 3.950 | % | | 06/15/22 | | | 1,979,486 | | |

| | 1,000,000 | | | Computer Sciences Corp | | | 4.450 | % | | 09/15/22 | | | 1,035,408 | | |

| | 1,000,000 | | | Hewlett-Packard Co | | | 4.050 | % | | 09/15/22 | | | 1,034,933 | | |

| | 1,025,000 | | | Fiserv Inc | | | 3.500 | % | | 10/01/22 | | | 1,043,863 | | |

| | 3,000,000 | | | Autodesk Inc | | | 3.600 | % | | 12/15/22 | | | 3,006,507 | | |

| | 2,000,000 | | | Fidelity National Information Services Inc | | | 3.500 | % | | 04/15/23 | | | 2,025,466 | | |

| | 1,352,000 | | | Total System Services Inc | | | 3.750 | % | | 06/01/23 | | | 1,342,800 | | |

| | 2,000,000 | | | Diamond 1 Finance Corp / Diamond 2 Finance Corp (g) | | | 5.450 | % | | 06/15/23 | | | 2,121,478 | | |

| | 1,000,000 | | | Altera Corp | | | 4.100 | % | | 11/15/23 | | | 1,075,840 | | |

| | 500,000 | | | Motorola Solutions Inc | | | 4.000 | % | | 09/01/24 | | | 500,583 | | |

| | 2,000,000 | | | Lam Research Corp | | | 3.800 | % | | 03/15/25 | | | 2,002,180 | | |

| | 500,000 | | | Arrow Electronics Inc | | | 4.000 | % | | 04/01/25 | | | 487,160 | | |

| | 1,000,000 | | | Juniper Networks Inc | | | 4.350 | % | | 06/15/25 | | | 1,008,374 | | |

| | 4,000,000 | | | Intel Corp | | | 4.000 | % | | 12/15/32 | | | 4,123,820 | | |

| | 1,500,000 | | | Western Union Co/The | | | 6.200 | % | | 11/17/36 | | | 1,564,211 | | |

| | | | 29,823,644 | | |

| | | MATERIALS 2.6% | |

| | 500,000 | | | Valspar Corp/The | | | 6.050 | % | | 05/01/17 | | | 506,845 | | |

| | 500,000 | | | Carpenter Technology Corp | | | 5.200 | % | | 07/15/21 | | | 504,984 | | |

| | 500,000 | | | Freeport-McMoRan Inc | | | 4.000 | % | | 11/14/21 | | | 487,500 | | |

| | 175,000 | | | Mosaic Co/The | | | 3.750 | % | | 11/15/21 | | | 179,721 | | |

| | 500,000 | | | Barrick Gold Corp (a) | | | 3.850 | % | | 04/01/22 | | | 507,256 | | |

19

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | MATERIALS (continued) | |

$ | 1,000,000 | | | Domtar Corp | | | 4.400 | % | | 04/01/22 | | $ | 1,028,864 | | |

| | 1,000,000 | | | RPM International Inc | | | 3.450 | % | | 11/15/22 | | | 991,591 | | |

| | 500,000 | | | Carpenter Technology Corp | | | 4.450 | % | | 03/01/23 | | | 478,470 | | |

| | 500,000 | | | Freeport-McMoRan Inc | | | 3.875 | % | | 03/15/23 | | | 458,750 | | |

| | 1,402,000 | | | Reliance Steel & Aluminum Co | | | 4.500 | % | | 04/15/23 | | | 1,410,530 | | |

| | 1,750,000 | | | Barrick Gold Corp (a) | | | 4.100 | % | | 05/01/23 | | | 1,795,222 | | |

| | 2,000,000 | | | Nucor Corp | | | 4.000 | % | | 08/01/23 | | | 2,102,426 | | |

| | 1,000,000 | | | BP Capital Markets PLC (a) | | | 3.994 | % | | 09/26/23 | | | 1,051,115 | | |

| | 2,000,000 | | | Mosaic Co/The | | | 4.250 | % | | 11/15/23 | | | 2,016,682 | | |

| | 1,000,000 | | | Steel Dynamics Inc | | | 5.500 | % | | 10/01/24 | | | 1,060,000 | | |

| | 1,000,000 | | | Freeport-McMoRan Inc | | | 4.550 | % | | 11/14/24 | | | 937,500 | | |

| | 756,000 | | | Eastman Chemical Co | | | 3.800 | % | | 03/15/25 | | | 762,418 | | |

| | 865,000 | | | Union Carbide Corp | | | 7.500 | % | | 06/01/25 | | | 1,041,364 | | |

| | 2,000,000 | | | CF Industries Inc | | | 5.150 | % | | 03/15/34 | | | 1,700,000 | | |

| | 1,250,000 | | | Dow Chemical Co/The | | | 4.250 | % | | 10/01/34 | | | 1,231,949 | | |

| | 1,000,000 | | | Alcoa Inc | | | 5.950 | % | | 02/01/37 | | | 972,750 | | |

| | 1,000,000 | | | Newmont Mining Corp | | | 4.875 | % | | 03/15/42 | | | 938,251 | | |

| | | | 22,164,188 | | |

| | | REAL ESTATE 0.3% | |

| | 1,250,000 | | | CBRE Services Inc | | | 5.000 | % | | 03/15/23 | | | 1,289,487 | | |

| | 1,000,000 | | | CBRE Services Inc | | | 5.250 | % | | 03/15/25 | | | 1,031,160 | | |

| | 350,000 | | | CBRE Services Inc | | | 4.875 | % | | 03/01/26 | | | 348,731 | | |

| | | | 2,669,378 | | |

| | | TELECOMMUNICATION SERVICES 0.6% | |

| | 500,000 | | | CenturyLink Inc | | | 6.150 | % | | 09/15/19 | | | 535,000 | | |

| | 3,000,000 | | | AT&T Inc | | | 3.000 | % | | 06/30/22 | | | 2,944,830 | | |

| | 500,000 | | | Qwest Capital Funding Inc | | | 6.875 | % | | 07/15/28 | | | 453,750 | | |

| | 1,000,000 | | | Verizon Communications Inc | | | 4.400 | % | | 11/01/34 | | | 986,986 | | |

| | | | 4,920,566 | | |

| | | UTILITIES 1.0% | |

| | 500,000 | | | Commonwealth Edison Co | | | 6.150 | % | | 09/15/17 | | | 516,432 | | |

| | 1,000,000 | | | Tampa Electric Co | | | 6.100 | % | | 05/15/18 | | | 1,059,235 | | |

| | 250,000 | | | Vectren Utility Holdings Inc | | | 5.750 | % | | 08/01/18 | | | 261,398 | | |

| | 250,000 | | | South Jersey Gas Co | | | 7.125 | % | | 10/22/18 | | | 267,942 | | |

| | 250,000 | | | United Utilities PLC (a) | | | 5.375 | % | | 02/01/19 | | | 262,006 | | |

| | 1,170,000 | | | ONEOK Inc | | | 4.250 | % | | 02/01/22 | | | 1,175,850 | | |

| | 785,000 | | | SCANA Corp | | | 4.125 | % | | 02/01/22 | | | 793,156 | | |

20

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | UTILITIES (continued) | |

$ | 1,000,000 | | | Exelon Generation Co LLC | | | 4.250 | % | | 06/15/22 | | $ | 1,035,060 | | |

| | 900,000 | | | National Fuel Gas Co | | | 3.750 | % | | 03/01/23 | | | 877,621 | | |

| | 1,060,000 | | | PSEG Power LLC | | | 4.300 | % | | 11/15/23 | | | 1,095,635 | | |

| | 1,550,000 | | | Dominion Resources Inc/VA | | | 3.625 | % | | 12/01/24 | | | 1,559,698 | | |

| | | | 8,904,033 | | |

| | | TOTAL CORPORATE BONDS | | | 257,517,468 | | |

| | | ASSET BACKED SECURITIES 2.6% | |

| | 220,865 | | | Continental Airlines 1997-4 Class B Pass Through Trust | | | 6.900 | % | | 07/02/18 | | | 220,997 | | |

| | 631,115 | | | Delta Air Lines 2012-1 Class B Pass Through Trust (g) | | | 6.875 | % | | 05/07/19 | | | 676,871 | | |

| | 299,202 | | | American Airlines 2011-1 Class B Pass Through Trust (g) | | | 7.000 | % | | 07/31/19 | | | 309,494 | | |

| | 49,319 | | | Continental Airlines 1999-1 Class B Pass Through Trust | | | 6.795 | % | | 02/02/20 | | | 50,429 | | |

| | 355,586 | | | Continental Airlines 2010-1 Class B Pass Through Trust | | | 6.000 | % | | 07/12/20 | | | 362,485 | | |

| | 260,120 | | | Delta Air Lines 2011-1 Class A Pass Through Trust | | | 5.300 | % | | 10/15/20 | | | 273,932 | | |

| | 407,337 | | | America West Airlines 2000-1 Pass Through Trust | | | 8.057 | % | | 01/02/22 | | | 460,046 | | |

| | 592,962 | | | American Airlines 2011-1 Class A Pass Through Trust | | | 5.250 | % | | 07/31/22 | | | 635,181 | | |

| | 430,429 | | | United Airlines 2014-1 Class B Pass Through Trust | | | 4.750 | % | | 10/11/23 | | | 439,037 | | |

| | 177,295 | | | Continental Airlines 2007-1 Class A Pass Through Trust | | | 5.983 | % | | 10/19/23 | | | 196,585 | | |

| | 332,192 | | | Southwest Airlines Co 2007-1 Pass Through Trust | | | 6.150 | % | | 02/01/24 | | | 366,673 | | |

| | 844,524 | | | Delta Air Lines 2007-1 Class B Pass Through Trust (g) | | | 8.021 | % | | 02/10/24 | | | 970,189 | | |

| | 67,817 | | | United Airlines 2014-2 Class B Pass Through Trust | | | 4.625 | % | | 03/03/24 | | | 69,092 | | |

| | 554,421 | | | American Airlines 2014-1 Class B Pass Through Trust | | | 4.375 | % | | 04/01/24 | | | 554,421 | | |

| | 1,000,000 | | | United Airlines 2015-1 Class A Pass Through Trust | | | 3.700 | % | | 06/01/24 | | | 1,014,400 | | |

| | 657,824 | | | US Airways 2010-1 Class A Pass Through Trust | | | 6.250 | % | | 10/22/24 | | | 730,974 | | |

| | 1,963,640 | | | American Airlines 2015-1 Class B Pass Through Trust | | | 3.700 | % | | 11/01/24 | | | 1,926,724 | | |

| | 1,402,427 | | | Delta Air Lines 2015-1 Class B Pass Through Trust | | | 4.250 | % | | 01/30/25 | | | 1,435,805 | | |

| | 940,513 | | | American Airlines 2015-2 Class B Pass Through Trust | | | 4.400 | % | | 03/22/25 | | | 929,979 | | |

| | 348,010 | | | US Airways 2011-1 Class A Pass Through Trust | | | 7.125 | % | | 04/22/25 | | | 403,483 | | |

| | 3,212,681 | | | American Airlines 2016-1 Class B Pass Through Trust | | | 5.250 | % | | 07/15/25 | | | 3,310,989 | | |

| | 1,321,632 | | | Continental Airlines 2012-2 Class A Pass Through Trust | | | 4.000 | % | | 04/29/26 | | | 1,361,281 | | |

| | 902,156 | | | United Airlines 2013-1 Class A Pass Through Trust | | | 4.300 | % | | 02/15/27 | | | 930,303 | | |

| | 839,070 | | | US Airways 2013-1 Class A Pass Through Trust | | | 3.950 | % | | 05/15/27 | | | 860,046 | | |

| | 2,057,179 | | | Hawaiian Airlines 2013-1 Class A Pass Through Certificates | | | 3.900 | % | | 07/15/27 | | | 2,066,848 | | |

| | 1,367,933 | | | American Airlines 2014-1 Class A Pass Through Trust | | | 3.700 | % | | 04/01/28 | | | 1,374,773 | | |

| | 488,176 | | | American Airlines 2015-2 Class A Pass Through Trust | | | 4.000 | % | | 03/22/29 | | | 498,525 | | |

| | | | 22,429,562 | | |

21

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Par Value/Shares | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | PREFERRED SECURITIES 0.4% | |

$ | 20,000 | | | American Financial Group Inc/OH | | | 6.250 | % | | 09/30/54 | | $ | 501,000 | | |

| | 10,000 | | | NextEra Energy Capital Holdings Inc | | | 5.700 | % | | 03/01/72 | | | 242,600 | | |

| | 20,000 | | | Protective Life Corp | | | 6.000 | % | | 09/01/42 | | | 503,800 | | |

| | 20,000 | | | Qwest Corp | | | 6.875 | % | | 10/01/54 | | | 484,000 | | |

| | 10,000 | | | Raymond James Financial Inc | | | 6.900 | % | | 03/15/42 | | | 253,900 | | |

| | 20,000 | | | Selective Insurance Group Inc | | | 5.875 | % | | 02/09/43 | | | 479,400 | | |

| | 20,000 | | | Verizon Communications Inc | | | 5.900 | % | | 02/15/54 | | | 521,800 | | |

| | 40,000 | | | WR Berkley Corp | | | 5.625 | % | | 04/30/53 | | | 904,400 | | |

| | | | 3,890,900 | | |

| | TOTAL FIXED INCOME SECURITIES

(cost $282,320,450) | | $ | 285,333,652 | | |

| | | COMMON STOCKS 63.5% | |

| | | CONSUMER DISCRETIONARY 2.8% | |

| | 72,000 | | | Home Depot Inc/The | | | | | | | | | | $ | 9,653,760 | | |

| | 195,000 | | | Target Corp | | | | | | | | | | | 14,084,850 | | |

| | | | 23,738,610 | | |

| | | CONSUMER STAPLES 3.4% | |

| | 111,000 | | | General Mills Inc | | | | | | | | | | | 6,856,470 | | |

| | 46,000 | | | Hershey Co/The | | | | | | | | | | | 4,757,780 | | |

| | 375,000 | | | Hormel Foods Corp | | | | | | | | | | | 13,053,750 | | |

| | 40,000 | | | Kimberly-Clark Corp | | | | | | | | | | | 4,564,800 | | |

| | | | 29,232,800 | | |

| | | ENERGY 5.5% | |

| | 130,000 | | | Chevron Corp | | | | | | | | | | | 15,301,000 | | |

| | 203,000 | | | Exxon Mobil Corp | | | | | | | | | | | 18,322,780 | | |

| | 166,000 | | | Schlumberger Ltd (a) | | | | | | | | | | | 13,935,700 | | |

| | | | 47,559,480 | | |

| | | FINANCIALS 10.2% | |

| | 78,000 | | | American Express Co | | | | | | | | | | | 5,778,240 | | |

| | 414,000 | | | Associated Banc-Corp | | | | | | | | | | | 10,225,800 | | |

| | 158,000 | | | JPMorgan Chase & Co | | | | | | | | | | | 13,633,820 | | |

| | 271,000 | | | Principal Financial Group Inc | | | | | | | | | | | 15,680,060 | | |

| | 35,000 | | | Travelers Cos Inc/The | | | | | | | | | | | 4,284,700 | | |

| | 485,000 | | | US Bancorp/MN | | | | | | | | | | | 24,914,450 | | |

| | 240,000 | | | Wells Fargo & Co | | | | | | | | | | | 13,226,400 | | |

| | | | 87,743,470 | | |

22

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS (continued) | |

| | | HEALTH CARE 14.3% | |

| | 355,000 | | | Abbott Laboratories | | $ | 13,635,550 | | |

| | 84,000 | | | AbbVie Inc | | | 5,260,080 | | |

| | 131,000 | | | Baxter International Inc | | | 5,808,540 | | |

| | 123,500 | | | Bristol-Myers Squibb Co | | | 7,217,340 | | |

| | 76,000 | | | Eli Lilly & Co | | | 5,589,800 | | |

| | 160,000 | | | Johnson & Johnson | | | 18,433,600 | | |

| | 302,500 | | | Medtronic PLC (e) | | | 21,547,075 | | |

| | 137,000 | | | Patterson Cos Inc | | | 5,621,110 | | |

| | 523,000 | | | Pfizer Inc | | | 16,987,040 | | |

| | 527,000 | | | Roche Holding AG (d) | | | 15,035,310 | | |

| | 51,000 | | | UnitedHealth Group Inc | | | 8,162,040 | | |

| | | | 123,297,485 | | |

| | | INDUSTRIALS 14.8% | |

| | 91,000 | | | 3M Co | | | 16,249,870 | | |

| | 147,000 | | | CH Robinson Worldwide Inc | | | 10,769,220 | | |

| | 26,000 | | | Deluxe Corp | | | 1,861,860 | | |

| | 246,000 | | | Emerson Electric Co | | | 13,714,500 | | |

| | 435,000 | | | General Electric Co | | | 13,746,000 | | |

| | 197,000 | | | Graco Inc | | | 16,368,730 | | |

| | 167,000 | | | Honeywell International Inc | | | 19,346,950 | | |

| | 138,000 | | | Pentair PLC (a) | | | 7,737,660 | | |

| | 80,000 | | | Toro Co/The | | | 4,476,000 | | |

| | 204,100 | | | United Parcel Service Inc, Class B | | | 23,398,024 | | |

| | | | 127,668,814 | | |

| | | INFORMATION TECHNOLOGY 5.5% | |

| | 7,300 | | | Alphabet Inc (b) | | | 5,634,286 | | |

| | 420,000 | | | Corning Inc | | | 10,193,400 | | |

| | 60,000 | | | International Business Machines Corp | | | 9,959,400 | | |

| | 125,000 | | | QUALCOMM Inc | | | 8,150,000 | | |

| | 637,000 | | | Western Union Co/The | | | 13,835,640 | | |

| | | | 47,772,726 | | |

| | | MATERIALS 5.8% | |

| | 194,000 | | | Bemis Co Inc | | | 9,277,080 | | |

| | 186,000 | | | Ecolab Inc | | | 21,802,920 | | |

| | 156,000 | | | HB Fuller Co | | | 7,536,360 | | |

| | 107,000 | | | Valspar Corp/The | | | 11,086,270 | | |

| | | | 49,702,630 | | |

23

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2016

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS (continued) | |

| | | UTILITIES 1.2% | |

| | 88,000 | | | ALLETE Inc | | $ | 5,648,720 | | |

| | 108,000 | | | Xcel Energy Inc | | | 4,395,600 | | |

| | | | 10,044,320 | | |

| | | | TOTAL COMMON STOCKS

(cost $386,450,756) | | $ | 546,760,335 | | |

| | | PREFERRED STOCKS 0.0% (h) | |

| | | UTILITIES 0.0% (h) | |

| | 10,000 | | | SCE Trust I | | $ | 233,200 | | |

| | | | | TOTAL PREFERRED STOCKS

(cost $250,000) | | $ | 233,200

| | |

| | | SHORT-TERM INVESTMENTS 1.9% | |

| 16,322,390 | | | First American Government Obligations Fund, Class Z, 0.42% (c)

(cost $16,322,390) | | $ | 16,322,390 | | |

| | | | TOTAL INVESTMENTS 98.5%

(cost $685,343,596) | | $ | 848,649,577 | | |

| | | | | OTHER ASSETS AND LIABILITIES (NET) 1.5% | | | 12,775,964 | | |

| | | | | TOTAL NET ASSETS 100.0% | | $ | 861,425,541 | | |

(a) Foreign security denominated in U.S. dollars. As of December 31, 2016, these securities represented $39,046,567 or 4.5% of total net assets.

(b) Non-income producing.

(c) The rate quoted is the annualized seven-day effective yield as of December 31, 2016.

(d) American Depositary Receipt.

(e) Issuer headquartered overseas but considered domestic. In determining whether a security is foreign or domestic, the Adviser will generally look at the location of the headquarters of the issuer. However, if the issuer is believed by the Adviser to be headquartered in a jurisdiction primarily for tax purposes, the Adviser will consider the following additional factors: 1) the location of the primary exchange trading its securities; 2) where it derives the majority of its revenues, and/or 3) where it earns the majority of its profits.

(f) Step Bonds – securities for which the interest rate will adjust on specified future date(s). The rate disclosed represents the interest rate in effect as of December 31, 2016.

(g) Securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. These securities have been determined to be liquid under guidelines established by the Fund's Board of Trustees. As of December 31, 2016, these securities represented $20,835,104 or 2.4% of total net assets.

(h) Percentage is less than 0.05%.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

See accompanying Notes to Financial Statements.

24

MAIRS & POWER SMALL CAP FUND (unaudited)

To Our Shareholders: December 31, 2016

Small cap stocks rallied hard in the fourth quarter with the Mairs & Power Small Cap Fund up 9.27%, the S&P 600 Total Return Index up 11.13% and the Morningstar Small Blend Category up 9.49%. For the year, the Fund finished up 27.27%, outpacing both the index and peer group which were up 26.56% and 20.78% respectively.

Sector allocation played a larger role than typical in relative performance for the year. A relative overweight position in the strongest performing sector, basic materials, helped relative performance, as did an underweight position in the poorest performing sector, healthcare. Stock selection by sector was mostly a positive contributor to relative performance with the notable exception of the technology sector.

This was due, in large part, to our position in Cray Inc. (CRAY). Cray had been highlighted as a huge driver of positive performance at the end of 2015, and we did trim the position significantly on that outperformance. However, the stock was the worst performer in 2016 and also the largest detractor from Fund performance. While the company continues to be very well positioned from a competitive standpoint in high performance computing, that industry has clearly slowed. Customers have pushed out upgrading systems as the pace of processing improvement from chip manufacturers has slowed. We expect customers will eventually make the decision to upgrade systems, and Cray should at least win its fair share of system upgrades, but the slowing pace has hurt the industry and the company's longer term growth trajectory.

MAIRS & POWER SMALL CAP FUND (MSCFX)