UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22563 |

|

Mairs & Power Funds Trust |

(Exact name of registrant as specified in charter) |

|

332 Minnesota Street, Suite W1520, St. Paul, MN | | 55101 |

(Address of principal executive offices) | | (Zip code) |

|

Andrea C. Stimmel, Treasurer, 332 Minnesota Street, Suite W1520, St. Paul, MN 55101 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 651-222-8478 | |

|

Date of fiscal year end: | December 31, 2018 | |

|

Date of reporting period: | December 31, 2018 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

Investing for the long-term

ANNUAL REPORT

DECEMBER 31, 2018

- GROWTH FUND (MPGFX)

est. 1958

- BALANCED FUND (MAPOX)

est. 1961

- SMALL CAP FUND (MSCFX)

est. 2011

Beginning in February 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Mairs & Power Funds' shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Mairs & Power Funds or from your Financial Intermediary. Instead, the reports will be made available on the Mairs & Power Funds' website, and you will be notified each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically for the Mairs & Power Funds, you will not be affected by this change and you need not take any action.

Mairs & Power Funds Direct Shareholders

You may elect to receive shareholder reports and other communications electronically or in paper from the Mairs & Power Funds by electing one of the following options:

1. Receive Fund Communications by Email: Contact Shareholder Servicing at (800) 304-7404 or by consenting through the direct shareholder portal online at www.mairsandpower.com. You may also elect to receive account statements, tax forms and confirmations through this means.

2. Receive Fund Communications by Mail: Contact Shareholder Servicing at (800) 304-7404.

You may elect to continue receiving paper copies of the shareholder reports and other communication, free of charge, by contacting Shareholding Servicing at (800) 304-7404 or your financial intermediary.

Mairs & Power Funds Shareholder through a Financial Intermediary (such as broker-dealer or bank)

Contact your Financial Intermediary to make your election. Your election will apply to all Mairs & Power Funds held through your Financial Intermediary.

Mairs & Power W1520 First National Bank Building, 332 Minnesota Street, St. Paul, Minnesota 55101 www.mairsandpower.com

MAIRS & POWER FUNDS MARKET COMMENTARY (unaudited)

December 31, 2018

2018 was like a tale of two years with first and second halves presenting very different markets and investment results. In the first half of the year the market continued its historic decade-long bull run, remaining focused on a narrow group of large cap growth stocks primarily in the Technology sector while value, Industrials and Health Care stocks remained out of favor. But when the market turned down as Technology reversed course, volatility returned with a vengeance and investor confidence was severely tested. There was no Santa Claus rally this year as the fourth quarter of 2018 posted the worst December in decades.

For the fourth quarter, the S&P 500 Total Return (TR) Index fell 13.52%, pulling it down 4.38% for the full year. Similarly, the Dow Jones Industrial Average TR was down 11.31% and 3.48% and the Bloomberg Barclays U.S. Government/Credit Bond Index return was up 1.46% and down 0.42% over the same periods.

Outlook

As we turn the page from 2018 to 2019, the questions looming in investors' minds are: "Is this the start of a bear market or is it merely a correction, an interruption but not an end, to the longest bull market in history?" "Is this economic expansion nearing an end or can economic growth continue into 2019 and beyond?" We don't predict market swings and we cannot predict when a recession will occur. However, we remain cautious for 2019 as we are seeing a number of yellow flags signaling an increasing risk of a recession. In addition, the continuing trade tiff, a year-end government shutdown and overall political uncertainty are unnerving the markets and shaking investor confidence.

Our first area of concern is interest rates. In December, the Federal Reserve (Fed) raised the Fed funds rate for the fourth time this year and the ninth time since beginning a normalization process that began three years ago. They have signaled the possibility of two more hikes in 2019, but are watching the data closely and have indicated a willingness to change course as appropriate. It takes time for the broader economy to feel the effect of rising interest rates and we are now starting to see the impact. Small and mid-sized businesses, the primary engines of job creation, are less confident in the outlook. Mortgage rates and consumer loan rates have risen. As a result, construction activity, new home sales and auto sales have declined slightly versus the past year.

Our second area of concern is growth. Where last year saw synchronized global growth, now we are seeing a synchronized global slowdown. GDP (gross domestic product) growth in the U.S. is projected between 1.75% and 2% for 2019, down from 3%+ in 20181. The ISM-Manufacturing Index, while still in expansion mode, has turned down. Two measures that track truck tonnage and shipments, considered reliable barometers of the U.S. economy, have fallen sharply in the past three months and are now projecting a decline in activity. Both Europe and China are experiencing slower growth and some emerging economies are struggling.

Finally, we are watching both the level and quality of corporate profits. S&P 500 earnings per share grew more than 20% in 2018, but we are now projecting it to grow 8% in 20191. Federal tax cuts benefited earnings growth in 2018 but that tailwind disappears this year. In addition, we are seeing signs of inflation in wages, transportation and other input costs. The impact of higher tariffs is becoming evident as manufacturers see materials costs rising, especially for steel. Some report being able to pass along price increases, but pricing-driven earnings growth is generally less valuable to the market than growth from selling more units. Valuation measures such as dividend yield, price-to-earnings and price-to-cash flows have declined and are now at levels in-line with long-term averages. However, equity valuations remain vulnerable in a rising rate environment and could have room for further contraction, particularly if earnings growth disappoints.

Past Performance is not a guarantee of future results.

1 Source FactSet Research Systems Inc.

Dividend yield is the ratio of a company's annual dividend compared to its share price.

Price-to-earnings is the ratio for valuing a company that measures its current share price relative to its per-share earnings.

Price-to-cash flow ratio is a stock valuation indicator that measures the value of a stock's price to its cash flow per share.

1

MAIRS & POWER FUNDS MARKET COMMENTARY (unaudited) (continued)

Earnings per share is the portion of a company's profit allocated to each share of common stock.

Institute for Supply Management (ISM)-Manufacturing Index monitors employment, production, inventories, new orders and supplier deliveries and is based on surveys of more than 300 manufacturing firms by the ISM.

S&P 500 TR (Total Return) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

Dow Jones Industrial Average TR Index is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. It is not possible to invest directly in an index.

Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

2

MAIRS & POWER GROWTH FUND (unaudited)

To Our Shareholders: December 31, 2018

In our Semi-Annual Report this year we noted that the Mairs & Power Growth Fund "has performed well over the long-term in part because it has tended to perform better when the market is performing poorly." The year just ended presents a textbook case as the Fund performed as expected, besting both its peer group index and the overall market in the second half to finish a difficult year ahead of both. In the fourth quarter, the Mairs & Power Growth Fund declined 11.76%, the S&P 500 TR benchmark fell 13.52% and the Lipper Multi Cap Core Funds Index of peers lost 14.96%. For the full year 2018, the Growth Fund was down 4.34%, while the S&P 500 TR benchmark was down 4.38% and the Lipper Multi Cap Core Funds was down 7.72%.

Our Market Commentary above describes "a tale of two years" with very different first and second halves. The market focus on a narrow group of large cap growth stocks primarily in the Technology sector presented significant headwinds to the Fund's relative performance that continued through the first half. But when the market turned, the Fund performed much better than the market during a difficult second half, a hallmark of our conservative approach. The ensuing volatility also provided us with an opportunity to increase positions in stocks we like which we believe will benefit investors over the long term.

Stock selection built on our conservative investment framework was the key to the Fund's second half outperformance. The Health Care sector returned to investor favor in the second half and outperformed the overall market. The names that worked for us included Abbott Laboratories (ABT), Medtronic PLC (MDT), and Bio-Techne Corp. (TECH), each of which outpaced both the market and the sector. In the volatile Tech sector, Apple Inc. (AAPL) and Facebook, Inc. (FB) fell particularly hard in the second half. The Fund does not hold these names and so neither rode them up nor down. Names in the Fund that held up relatively well include Alphabet Inc. Class C (GOOG) in the Communication Services sector and two Tech stocks new to the Fund, Microsoft Corporation (MSFT) and VISA Inc. (V).

MAIRS & POWER GROWTH FUND (MPGFX)

Top Relative Performers

| Fourth Quarter (9/30/18 – 12/31/18) | | Year To Date (12/31/17 – 12/31/18) | |

Hormel Foods Corp. | | | 22.33 | % | | Abbott Laboratories | | | 33.42 | % | |

Roche Holdings Ltd. | | | 16.57 | % | | Hormel Foods Corp. | | | 24.07 | % | |

Abbott Laboratories | | | 12.51 | % | | Medtronic PLC | | | 19.57 | % | |

Ecolab Inc. | | | 7.79 | % | | Ecolab Inc. | | | 15.47 | % | |

Johnson & Johnson | | | 7.51 | % | | Pfizer Inc. | | | 29.20 | % | |

Weak Relative Performers

| Fourth Quarter (9/30/18 – 12/31/18) | | Year To Date (12/31/17 – 12/31/18) | |

Donaldson Company | | | -11.71 | % | | Schlumberger NV | | | -40.25 | % | |

Bio-Techne Corp. | | | -15.45 | % | | Principal Financial Group, Inc. | | | -30.61 | % | |

Schlumberger NV | | | -26.58 | % | | General Mills, Inc. | | | -27.17 | % | |

Tennant Company | | | -17.62 | % | | 3M Company | | | -12.53 | % | |

Principal Financial Group, Inc. | | | -10.27 | % | | U.S. Bancorp | | | -7.98 | % | |

Performance shown is relative to the S&P 500 TR Index as of December 31, 2018. Relative return is the difference between the absolute return and the performance of the market, in which the position is held. Relative contribution is used for ranking, which considers average daily weightings for each holding. Past performance does not guarantee future results.

3

MAIRS & POWER GROWTH FUND (unaudited) (continued)

Microsoft has successfully navigated a difficult transition from a stagnant revenue base back to growth by shifting focus from its core Office product to a subscription and expanding its cloud platform called Azure. We see this as a great opportunity for Microsoft to compete successfully against Amazon Web Services. Visa, not just a credit card company, is categorized in the Tech sector for a reason. The company is the leader in digital payments and much better positioned than competitors to facilitate movement of money both within the U.S. and globally. Another new name to the Fund is Illinois-based Littelfuse, Inc. (LFUS), a specialty electronics supplier in the automotive industry. As cars in general and electric powered vehicles in particular become more computerized, automobiles need a greater number of specialty fuses per vehicle, which Littelfuse provides. Even if vehicle unit sales were flat, the component piece would still continue to grow. Littelfuse is a great example of a company looking forward to where the world is going and establishing a durable competitive advantage in their market. It is the kind of company we like to own. Other strong second half performers we have discussed in the past included Ecolab Inc. (ECL) in the Materials sector and Hormel Foods Corp. (HRL) in Consumer Staples.

General Electric Company (GE), Patterson Companies, Inc. (PDCO), Stratasys Ltd (SSYS), and The Western Union Company (WU) were eliminated from the Fund during 2018 as we determined that each company had lost their respective durable competitive advantage.

We remain cautious on the market outlook near-term and believe there is an increasing risk of a recession occurring sometime in the next few years. As the Fund's second half performance illustrates, however, we remain confident that we are well positioned to weather whatever challenges the market may present.

Mark L. Henneman

Lead Manager | | Andrew R. Adams

Co-Manager | |

The Fund's investment objective, risks, charges and expenses must be considered carefully before investing. The summary prospectus or full prospectus contains this and other important information about the Fund and they may be obtained by calling Shareholder Services at (800) 304-7404 or by visiting www.mairsandpower.com. Read the summary prospectus or full prospectus carefully before investing.

All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or an offer of a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

All investments have risks. The Growth Fund is designed for long-term investors. Equity investments are subject to market fluctuations and the Fund's share price can fall because of weakness in the broad market, a particular industry or specific holdings. Investments in small and midcap companies generally are more volatile. International investing risks include among others political, social or economic instability, difficulty in predicting international trade patterns, taxation and foreign trading practices and greater fluctuations in price than U.S. corporations.

Diversification does not guarantee profit or protect against loss.

S&P 500 TR (Total Return) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

Lipper Multi-Cap Core Funds Index measures the performance of the 30 largest mutual funds that invest in a variety of capitalization ranges, without concentrating 75% or more of their equity assets in any one market capitalization range over an extended period of time, as determined by Lipper, Inc. It is not possible to invest directly in an index.

4

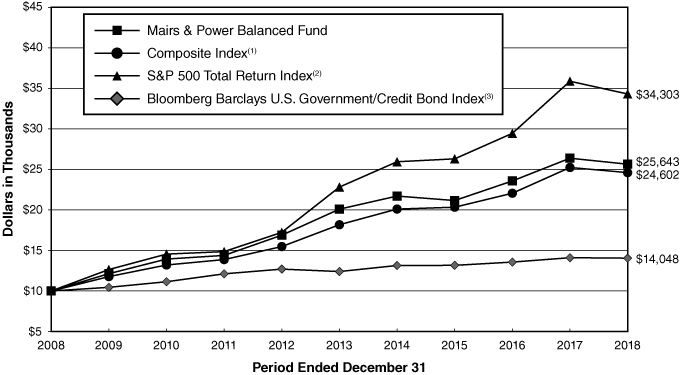

Mairs & Power Growth Fund

PERFORMANCE INFORMATION (unaudited) December 31, 2018

Ten years of investment performance (through December 31, 2018)

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund 10 years ago.

Average annual total returns for periods ended December 31, 2018

| | 1 year | | 5 years | | 10 years | | 20 years | |

Mairs & Power Growth Fund | | | -4.34 | % | | | 6.15 | % | | | 12.44 | % | | | 8.91 | % | |

S&P 500 Total Return Index(1) | | | -4.38 | % | | | 8.49 | % | | | 13.12 | % | | | 5.62 | % | |

Performance data quoted represents past performance and does not guarantee future results. All performance information shown includes the reinvestment of dividend and capital gain distributions, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. For the most recent month-end performance figures, visit the Fund's website at www.mairsandpower.com or call Shareholder Services at (800) 304-7404.

(1) The S&P 500 Total Return Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

5

Mairs & Power Growth Fund

FUND INFORMATION (unaudited) December 31, 2018

Portfolio Managers

Mark L. Henneman, CFA, lead manager since July 1, 2013, co-manager from January 1, 2006 through June 30, 2013, University of Minnesota, MBA Finance 1990

Andrew R. Adams, CFA, co-manager since January 1, 2015, University of Wisconsin-Madison, MS Finance 1997

General Information

Fund Symbol | | | MPGFX | | |

Net Asset Value (NAV) Per Share | | $ | 106.45 | | |

Expense Ratio | | | 0.64 | % | |

Portfolio Turnover Rate | | | 9.25 | % | |

Sales Charge | | | None1 | | |

Fund Inception Year | | | 1958 | | |

Portfolio Composition

Top Ten Portfolio Holdings

(Percent of Total Net Assets) 2

Ecolab Inc | | | 4.8 | % | |

US Bancorp/MN | | | 4.8 | | |

Alphabet Inc | | | 4.7 | | |

| 3M Co | | | 4.5 | | |

Medtronic PLC | | | 4.1 | | |

Johnson & Johnson | | | 3.9 | | |

Hormel Foods Corp | | | 3.9 | | |

Walt Disney Co/The | | | 3.4 | | |

Donaldson Co Inc | | | 3.2 | | |

Abbott Laboratories | | | 3.2 | | |

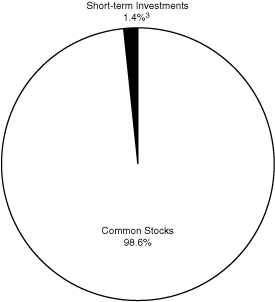

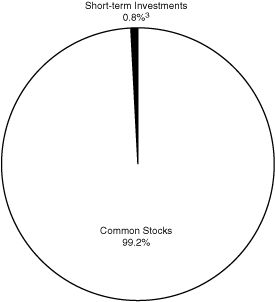

Portfolio Diversification

(Percent of Total Net Assets)

Common Stocks 98.6% | |

Industrials | | | 26.2 | % | |

Health Care | | | 23.2 | | |

Financials | | | 11.9 | | |

Information Technology | | | 11.4 | | |

Materials | | | 8.6 | | |

Communication Services | | | 8.1 | | |

Consumer Staples | | | 5.3 | | |

Energy | | | 1.4 | | |

Real Estate | | | 1.3 | | |

Consumer Discretionary | | | 1.2 | | |

Short-term Investments 1.4%3 | | | 1.4 | | |

| | | | 100.0 | % | |

1 Although the Fund is no-load, investment management fees and other expenses still apply.

2 All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or offer for a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

3 Represents short-term investments and other assets and liabilities (net).

The Schedule of Investments and portfolio diversification utilize Global Industry Classification Standard (GICS®) which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Mairs & Power, Inc. (the "Adviser").

6

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS 98.6% | |

| | | COMMUNICATION SERVICES 8.1% | |

| | 178,100 | | | Alphabet Inc (a) | | $ | 184,442,141 | | |

| | 1,215,000 | | | Walt Disney Co/The | | | 133,224,750 | | |

| | | | 317,666,891 | | |

| | | CONSUMER DISCRETIONARY 1.2% | |

| | 90,500 | | | Garrett Motion Inc (a) | | | 1,116,770 | | |

| | 250,000 | | | Gentherm Inc (a) | | | 9,995,000 | | |

| | 80,000 | | | Home Depot Inc/The | | | 13,745,600 | | |

| | 360,000 | | | Target Corp | | | 23,792,400 | | |

| | | | 48,649,770 | | |

| | | CONSUMER STAPLES 5.3% | |

| | 1,460,000 | | | General Mills Inc | | | 56,852,400 | | |

| | 3,560,000 | | | Hormel Foods Corp | | | 151,940,800 | | |

| | | | 208,793,200 | | |

| | | ENERGY 1.4% | |

| | 135,000 | | | Core Laboratories NV (c) | | | 8,054,100 | | |

| | 1,315,000 | | | Schlumberger Ltd (c) | | | 47,445,200 | | |

| | | | 55,499,300 | | |

| | | FINANCIALS 11.9% | |

| | 800,000 | | | American Express Co | | | 76,256,000 | | |

| | 1,170,000 | | | Associated Banc-Corp | | | 23,154,300 | | |

| | 570,000 | | | Charles Schwab Corp/The | | | 23,672,100 | | |

| | 1,380,000 | | | Great Western Bancorp Inc | | | 43,125,000 | | |

| | 1,540,000 | | | Principal Financial Group Inc | | | 68,021,800 | | |

| | 4,095,000 | | | US Bancorp/MN | | | 187,141,500 | | |

| | 1,010,000 | | | Wells Fargo & Co | | | 46,540,800 | | |

| | | | 467,911,500 | | |

| | | HEALTH CARE 23.2% | |

| | 1,725,000 | | | Abbott Laboratories | | | 124,769,250 | | |

| | 290,000 | | | Baxter International Inc | | | 19,087,800 | | |

| | 700,000 | | | Bio-Techne Corp | | | 101,304,000 | | |

| | 310,000 | | | Eli Lilly & Co | | | 35,873,200 | | |

| | 1,180,000 | | | Johnson & Johnson | | | 152,279,000 | | |

| | 1,765,000 | | | Medtronic PLC (e) | | | 160,544,400 | | |

| | 1,460,000 | | | Pfizer Inc | | | 63,729,000 | | |

| | 3,480,000 | | | Roche Holding AG (d) | | | 108,158,400 | | |

| | 305,000 | | | UnitedHealth Group Inc | | | 75,981,600 | | |

| | 690,000 | | | Zimmer Holdings Inc | | | 71,566,800 | | |

| | | | 913,293,450 | | |

7

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS (continued) | |

| | | INDUSTRIALS 26.2% | |

| | 925,000 | | | 3M Co | | $ | 176,249,500 | | |

| | 1,055,000 | | | CH Robinson Worldwide Inc | | | 88,714,950 | | |

| | 2,920,000 | | | Donaldson Co Inc | | | 126,698,800 | | |

| | 1,910,000 | | | Fastenal Co | | | 99,873,900 | | |

| | 345,000 | | | Generac Holdings Inc (a) | | | 17,146,500 | | |

| | 2,820,000 | | | Graco Inc | | | 118,017,000 | | |

| | 890,000 | | | Honeywell International Inc | | | 117,586,800 | | |

| | 1,220,000 | | | nVent Electric PLC (c) | | | 27,401,200 | | |

| | 1,060,000 | | | Pentair PLC (c) | | | 40,046,800 | | |

| | 143,000 | | | Proto Labs Inc (a) | | | 16,128,970 | | |

| | 74,446 | | | Resideo Technologies Inc (a) | | | 1,529,865 | | |

| | 160,000 | | | Snap-on Inc | | | 23,246,400 | | |

| | 810,000 | | | Tennant Co | | | 42,209,100 | | |

| | 1,800,000 | | | Toro Co/The | | | 100,584,000 | | |

| | 385,000 | | | United Parcel Service Inc, Class B | | | 37,549,050 | | |

| | | | 1,032,982,835 | | |

| | | INFORMATION TECHNOLOGY 11.4% | |

| | 730,000 | | | Badger Meter Inc | | | 35,923,300 | | |

| | 1,290,000 | | | Corning Inc | | | 38,970,900 | | |

| | 820,000 | | | Cray Inc (a) | | | 17,703,800 | | |

| | 1,375,000 | | | Fiserv Inc (a) | | | 101,048,750 | | |

| | 180,000 | | | Littelfuse Inc | | | 30,866,400 | | |

| | 1,000,000 | | | Microsoft Corp | | | 101,570,000 | | |

| | 90,000 | | | Motorola Solutions Inc | | | 10,353,600 | | |

| | 203,072 | | | NVE Corp | | | 17,776,923 | | |

| | 855,000 | | | QUALCOMM Inc | | | 48,658,050 | | |

| | 335,000 | | | Visa Inc | | | 44,199,900 | | |

| | | | 447,071,623 | | |

| | | MATERIALS 8.6% | |

| | 1,720,000 | | | Bemis Co Inc | | | 78,948,000 | | |

| | 1,275,000 | | | Ecolab Inc | | | 187,871,250 | | |

| | 1,670,000 | | | HB Fuller Co | | | 71,258,900 | | |

| | | | 338,078,150 | | |

| | | REAL ESTATE 1.3% | |

| | 607,200 | | | CoreSite Realty Corp | | | 52,966,056 | | |

| | | | TOTAL COMMON STOCKS

(cost $2,239,479,378) | | $ | 3,882,912,775 | | |

8

Mairs & Power Growth Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | SHORT-TERM INVESTMENTS 1.2% | |

| 46,545,998 | | | First American Government Obligations Fund, Class X, 2.36% (b)

(cost $46,545,998) | | $ | 46,545,998 | | |

| | TOTAL INVESTMENTS 99.8%

(cost $2,286,025,376) | | $ | 3,929,458,773 | | |

| | | OTHER ASSETS AND LIABILITIES (NET) 0.2% | | | 9,484,031 | | |

| | | TOTAL NET ASSETS 100.0% | | $ | 3,938,942,804 | | |

(a) Non-income producing.

(b) The rate quoted is the annualized seven-day effective yield as of December 31, 2018.

(c) Foreign security denominated in U.S. dollars. As of December 31, 2018, these securities represented $122,947,300 or 3.1% of total net assets.

(d) American Depositary Receipt.

(e) Issuer headquartered overseas but considered domestic. In determining whether a security is foreign or domestic, the Adviser will generally look at the location of the headquarters of the issuer. However, if the issuer is believed by the Adviser to be headquartered in a jurisdiction primarily for tax purposes, the Adviser will consider the following additional factors: 1) the location of the primary exchange trading its securities; 2) where it derives the majority of its revenues; and/or 3) where it earns the majority of its profits.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

See accompanying Notes to Financial Statements.

9

MAIRS & POWER BALANCED FUND (unaudited)

To Our Shareholders: December 31, 2018

As a difficult year for investors drew to a close, the Mairs & Power Balanced Fund outperformed its benchmark, finishing the quarter down 6.73% compared to the composite index (60% S&P 500 TR Index and 40% Bloomberg Barclays U.S. Government/Credit Bond Index) which lost 7.63%. For the full year 2018 the Fund was down 2.80% compared to its benchmark index which lost 2.52%.

Our Market Commentary above describes "a tale of two years" with very different first and second halves. The market focus on a narrow group of large cap growth stocks primarily in the Technology sector presented significant headwinds to the Fund's relative performance that continued through the first half. But when the market turned, the Fund performed much better than the market during a difficult second half, a hallmark of our conservative approach. The ensuing volatility also provided us with an opportunity to increase positions in stocks we like which we believe will benefit investors over the long-term.

Stock selection built on our conservative investment framework was key to the Fund's second half performance. We are overweight in the Health Care sector which returned to investor favor in the second half, outperforming the overall market and contributing significantly to the Fund's relative performance in both the fourth quarter and the year. The names that worked for us included Abbott Laboratories (ABT), Medtronic PLC (MDT), Eli Lilly and Co. (LLY) and Pfizer Inc. (PFE), outpacing both the market and the sector. Hormel Foods Corp. (HRL) in the Consumer Staples sector was also a significant positive contributor in both periods.

Our financial holdings adversely impacted relative results as our regional and money center bank holdings reacted negatively to the continued flattening of the yield curve. The Fund remains underweight in the Tech sector, which was a negative factor for the year but helped relative performance in the second half when the whole group fell out of favor. Names in the Fund that held up relatively well include Alphabet Inc. Class C (GOOG) in the Communication Services sector and two Tech stocks new to the Fund, Microsoft Corporation (MSFT) and VISA Inc. (V).

MAIRS & POWER BALANCED FUND (MAPOX)

Top Relative Performers

| Fourth Quarter (9/30/18 – 12/31/18) | | Year To Date (12/31/17 – 12/31/18) | |

Hormel Foods Corp. | | | 22.33 | % | | Abbott Laboratories | | | 33.42 | % | |

Eli Lilly and Company | | | 21.91 | % | | Eli Lilly and Company | | | 44.83 | % | |

Roche Holdings Ltd. | | | 16.57 | % | | Medtronic PLC | | | 19.57 | % | |

Abbot Laboratories | | | 12.51 | % | | Pfizer Inc. | | | 29.20 | % | |

Ecolab, Inc. | | | 7.79 | % | | Hormel Foods Corp. | | | 24.07 | % | |

Weak Relative Performers

| Fourth Quarter (9/30/18 – 12/31/18) | | Year To Date (12/31/17 – 12/31/18) | |

Schlumberger NV | | | -26.58 | % | | Principal Financial Group, Inc. | | | -30.61 | % | |

Principal Financial Group, Inc. | | | -10.27 | % | | Schlumberger NV | | | -40.25 | % | |

Donaldson Company, Inc. | | | -11.71 | % | | 3M Company | | | -12.53 | % | |

Bio-Techne Corporation | | | -15.45 | % | | U.S. Bancorp | | | -7.98 | % | |

Honeywell Intl. Inc. | | | -3.10 | % | | General Mills, Inc. | | | -27.17 | % | |

Performance shown is relative to the S&P 500 TR Index as of December 31, 2018. Relative return is the difference between the absolute return and the performance of the market, in which the position is held. Relative contribution is used for ranking, which considers average daily weightings for each holding. Past performance does not guarantee future results.

10

MAIRS & POWER BALANCED FUND (unaudited) (continued)

Microsoft has successfully navigated a difficult transition from a stagnant revenue base back to growth by shifting focus from its core Office products to a subscription-based cloud platform named Azure. We see this as a great opportunity for Microsoft to compete successfully against Amazon Web Services. We traded out of our position in Western Union Company (WU), which has a deteriorating competitive position, replacing it with VISA based on its leadership position in digital payments and the strength of its global network.

General Electric Company (GE), Patterson Companies, Inc. (PDCO), ALLETE Inc. (ALE) and Physicians Realty Trust (DOC) were also eliminated from the Fund during 2018 as we determined that each company had experienced deterioration in its durable competitive advantage to the point where they were no longer attractive as components of the Balanced Fund.

Turning to the fixed income side, the bond market produced mixed results in 2018. The Fed raised rates four times last year, hiking short-term rates 100 basis points (one percentage point) while longer-term Treasury yields only rose by about 30 basis points, causing the yield curve to flatten. In addition, the gap between the yield on Corporate bonds and U.S. Treasuries of the same maturity (known as the corporate bond spread) widened as Corporate yields rose, due to a variety of factors, by nearly 100 basis points to 4.2%. While rising yields certainly make Corporate debt more attractive today than a year ago, bond prices generally drop as yields rise. As a result, the Corporate Bond Index fell 2.5% and the Government Credit Bond Index was down 0.42% while Short-Term Treasuries performed the best posting roughly a 1% gain for the year.

In selecting corporate debt for the Fund, we identify what we believe to be high quality companies whose bonds carry a yield advantage over the index. Our low turnover philosophy has helped us hold onto that yield advantage over the years, generating excess fixed income returns. In addition, during this prolonged period of historically low interest rates, we have deliberately and incrementally positioned the portfolio toward short maturity instruments, maintaining a portfolio duration that is less than the benchmark. As a result, we hold a lower risk portfolio for a rising rate environment. At the end of the day, fixed income investors generally earn their coupons. We believe we will continue to win by investing in debt instruments issued by high quality companies possessing strong durable competitive advantages.

Kevin V. Earley

Lead Manager | | Ronald L. Kaliebe

Co-Manager | | Robert W. Thompson

Co-Manager | |

The Fund's investment objective, risks, charges and expenses must be considered carefully before investing. The summary prospectus or full prospectus contains this and other important information about the Fund and they may be obtained by calling Shareholder Services at (800) 304-7404 or by visiting www.mairsandpower.com. Read the summary prospectus or full prospectus carefully before investing.

All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or an offer of a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

All investments have risks. The Balanced Fund is designed for long-term investors. Equity investments are subject to market fluctuations and the Fund's share price can fall because of weakness in the broad market, a particular industry or specific holdings. Investments in small and midcap companies generally are more volatile. International investing risks include among others political, social or economic instability, difficulty in predicting international trade patterns, taxation and foreign trading practices, and greater fluctuations in price than U.S. corporations. The Fund is subject to yield and share price variances with changes in interest rates and market conditions. Investors should note that if interest rates rise significantly from current levels, bond total returns will decline and may even turn negative in the short-term. There is also a chance that some of the Fund's holdings may have their credit rating downgraded or may default.

Diversification does not guarantee profit or protect against loss.

11

MAIRS & POWER BALANCED FUND (unaudited) (continued)

Composite Index reflects an unmanaged portfolio of 60% of the S&P 500 TR Index and 40% of the Bloomberg Barclays U.S. Government/Credit Bond Index. It is not possible to invest directly in an index.

Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

S&P 500 TR (Total Return) Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

A coupon is the annual interest rate paid on a bond, expressed as a percentage of the face value.

Basis Point is a unit of measure for interest rates and other percentages in finance.

12

Mairs & Power Balanced Fund

PERFORMANCE INFORMATION (unaudited) December 31, 2018

Ten years of investment performance (through December 31, 2018)

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund 10 years ago.

Average annual total returns for periods ended December 31, 2018

| | 1 year | | 5 years | | 10 years | | 20 years | |

Mairs & Power Balanced Fund | | | -2.80 | % | | | 5.00 | % | | | 9.87 | % | | | 6.89 | % | |

Composite Index(1) | | | -2.52 | % | | | 6.24 | % | | | 9.42 | % | | | 5.49 | % | |

S&P 500 Total Return Index(2) | | | -4.38 | % | | | 8.49 | % | | | 13.12 | % | | | 5.62 | % | |

Bloomberg Barclays U.S.

Government/Credit Bond Index(3) | | | -0.42 | % | | | 2.53 | % | | | 3.46 | % | | | 4.54 | % | |

Performance data quoted represents past performance and does not guarantee future results. All performance information shown includes the reinvestment of dividend and capital gain distributions, but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. For the most recent month-end performance figures, visit the Fund's website at www.mairsandpower.com or call Shareholder Services at (800) 304-7404.

(1) The Composite Index reflects an unmanaged portfolio comprised of 60% of the S&P 500 Total Return Index and 40% of the Bloomberg Barclays U.S. Government/Credit Bond Index. It is not possible to invest directly in an index.

(2) The S&P 500 Total Return Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. It tracks both the capital gains of a group of stocks over time and assumes that any cash distributions, such as dividends, are reinvested back into the index. It is not possible to invest directly in an index.

(3) The Bloomberg Barclays U.S. Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the U.S. Aggregate Index. It includes investment-grade, U.S. dollar-denominated, fixed-rate treasuries, government-related and corporate securities. It is not possible to invest directly in an index.

13

Mairs & Power Balanced Fund

FUND INFORMATION (unaudited) December 31, 2018

Portfolio Managers

Kevin V. Earley, CFA, lead manager since April 1, 2018, co-manager from January 1, 2015 through March 31, 2018, University of Minnesota, MBA Finance 1990

Ronald L. Kaliebe, CFA, co-manager since April 1, 2018, lead manager from July 1, 2013 through March 31, 2018, co-manager from January 1, 2006 through June 30, 2013, University of

Wisconsin-Madison, MBA Finance 1980

Robert W. Thompson, CFA, co-manager since April 1, 2018, University of Minnesota, MBA Finance 1995

General Information

Fund Symbol | | MAPOX | |

Net Asset Value (NAV) Per Share | | $ | 86.79 | | |

Expense Ratio | | | 0.72 | % | |

Portfolio Turnover Rate | | | 9.01 | % | |

Sales Charge | | | None1 | | |

Fund Inception Year | | | 1961 | | |

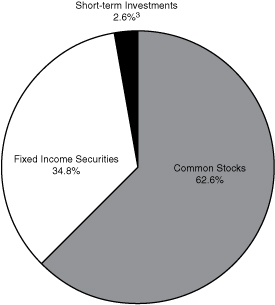

Portfolio Composition

Top Ten Common Stock Holdings

(Percent of Total Net Assets) 2

US Bancorp/MN | | | 3.0 | % | |

Medtronic PLC | | | 2.8 | | |

| 3M Co | | | 2.7 | | |

Johnson & Johnson | | | 2.7 | | |

Alphabet Inc | | | 2.6 | | |

Abbott Laboratories | | | 2.6 | | |

Honeywell International Inc | | | 2.6 | | |

Ecolab Inc | | | 2.5 | | |

Roche Holding AG | | | 2.0 | | |

Hormel Foods Corp | | | 2.0 | | |

Portfolio Diversification

(Percent of Total Net Assets)

Fixed Income Securities 34.8% | |

Corporate Bonds | | | 31.5 | % | |

Asset Backed Securities | | | 3.2 | | |

Federal Agency Obligations | | | 0.1 | | |

Common Stocks 62.6% | |

Health Care | | | 16.6 | | |

Industrials | | | 14.7 | | |

Financials | | | 10.0 | | |

Consumer Staples | | | 4.6 | | |

Communications Services | | | 4.3 | | |

Materials | | | 4.3 | | |

Information Technology | | | 3.4 | | |

Energy | | | 2.3 | | |

Consumer Discretionary | | | 2.0 | | |

Utilities | | | 0.4 | | |

Short-term Investments 2.6%3 | | | 2.6 | | |

| | | | 100.0 | % | |

1 Although the Fund is no-load, investment management fees and other expenses still apply.

2 All holdings in the portfolio are subject to change without notice and may or may not represent current or future portfolio composition. The mention of specific securities is not intended as a recommendation or offer for a particular security, nor is it intended to be a solicitation for the purchase or sale of any security.

3 Represents short-term investments and other assets and liabilities (net).

The Schedule of Investments and portfolio diversification utilize Global Industry Classification Standard (GICS®) which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

14

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES 34.8% | |

| | | FEDERAL AGENCY OBLIGATIONS 0.1% | |

$ | 1,000,000 | | | Federal Farm Credit Banks | | | 4.000 | % | | 12/18/28 | | $ | 1,001,246 | | |

| | | CORPORATE BONDS 31.5% | |

| | | COMMUNICATION SERVICES 1.4% | |

| | 500,000 | | | CenturyLink Inc | | | 6.150 | % | | 09/15/19 | | | 506,389 | | |

| | 1,000,000 | | | Time Warner Cable Inc | | | 4.125 | % | | 02/15/21 | | | 1,004,096 | | |

| | 1,000,000 | | | Viacom Inc | | | 4.250 | % | | 09/01/23 | | | 996,097 | | |

| | 1,150,000 | | | AT&T Inc | | | 3.800 | % | | 03/01/24 | | | 1,138,399 | | |

| | 2,000,000 | | | Viacom Inc | | | 3.875 | % | | 04/01/24 | | | 1,961,749 | | |

| | 1,000,000 | | | Interpublic Group of Cos Inc/The | | | 4.200 | % | | 04/15/24 | | | 999,471 | | |

| | 1,000,000 | | | CBS Corp | | | 3.500 | % | | 01/15/25 | | | 953,148 | | |

| | 2,000,000 | | | Comcast Corp | | | 4.250 | % | | 01/15/33 | | | 1,986,351 | | |

| | 1,000,000 | | | Verizon Communications Inc | | | 4.400 | % | | 11/01/34 | | | 963,792 | | |

| | 1,000,000 | | | AT&T Inc | | | 4.500 | % | | 05/15/35 | | | 897,802 | | |

| | | | 11,407,294 | | |

| | | CONSUMER DISCRETIONARY 2.6% | |

| | 1,000,000 | | | Ford Motor Credit Co LLC | | | 2.375 | % | | 03/12/19 | | | 998,340 | | |

| | 1,000,000 | | | Best Buy Co Inc | | | 5.500 | % | | 03/15/21 | | | 1,031,127 | | |

| | 555,000 | | | Kohl's Corp | | | 4.000 | % | | 11/01/21 | | | 571,928 | | |

| | 1,000,000 | | | eBay Inc | | | 3.800 | % | | 03/09/22 | | | 1,004,168 | | |

| | 500,000 | | | Whirlpool Corp | | | 4.700 | % | | 06/01/22 | | | 511,654 | | |

| | 1,000,000 | | | Block Financial LLC | | | 5.500 | % | | 11/01/22 | | | 1,028,237 | | |

| | 1,000,000 | | | General Motors Financial Co Inc | | | 3.700 | % | | 05/09/23 | | | 951,430 | | |

| | 1,000,000 | | | General Motors Financial Co Inc | | | 4.250 | % | | 05/15/23 | | | 976,619 | | |

| | 2,702,000 | | | LKQ Corp | | | 4.750 | % | | 05/15/23 | | | 2,539,880 | | |

| | 500,000 | | | Hyatt Hotels Corp | | | 3.375 | % | | 07/15/23 | | | 492,191 | | |

| | 1,000,000 | | | Advance Auto Parts Inc | | | 4.500 | % | | 12/01/23 | | | 1,023,507 | | |

| | 1,000,000 | | | General Motors Financial Co Inc | | | 3.950 | % | | 04/13/24 | | | 949,710 | | |

| | 500,000 | | | Tiffany & Co | | | 3.800 | % | | 10/01/24 | | | 501,392 | | |

| | 2,000,000 | | | Coach Inc | | | 4.250 | % | | 04/01/25 | | | 1,948,387 | | |

| | 250,000 | | | General Motors Co | | | 4.000 | % | | 04/01/25 | | | 233,673 | | |

| | 1,000,000 | | | General Motors Financial Co Inc | | | 4.300 | % | | 07/13/25 | | | 947,622 | | |

| | 1,064,000 | | | Block Financial LLC | | | 5.250 | % | | 10/01/25 | | | 1,077,537 | | |

| | 2,500,000 | | | Ford Motor Co | | | 4.346 | % | | 12/08/26 | | | 2,227,014 | | |

| | 1,000,000 | | | General Motors Co | | | 4.200 | % | | 10/01/27 | | | 901,341 | | |

| | 1,000,000 | | | Metropolitan Opera Association Inc | | | 4.349 | % | | 10/01/32 | | | 993,786 | | |

| | | | 20,909,543 | | |

15

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | CONSUMER STAPLES 0.9% | |

$ | 2,430,000 | | | Land O' Lakes Inc (g) | | | 6.000 | % | | 11/15/22 | | $ | 2,536,067 | | |

| | 1,000,000 | | | Walgreens Boots Alliance Inc | | | 3.800 | % | | 11/18/24 | | | 984,793 | | |

| | 500,000 | | | Land O' Lakes Inc (g) | | | 7.250 | % | | 07/14/27 | | | 485,000 | | |

| | 1,949,000 | | | Land O' Lakes Capital Trust I (g) | | | 7.450 | % | | 03/15/28 | | | 2,012,343 | | |

| | 1,500,000 | | | Land O' Lakes Inc (g) | | | 7.000 | % | | 12/18/28 | | | 1,462,500 | | |

| | | | 7,480,703 | | |

| | | ENERGY 1.0% | |

| | 1,170,000 | | | ONEOK Inc | | | 4.250 | % | | 02/01/22 | | | 1,181,036 | | |

| | 140,000 | | | Gulf South Pipeline Co LP | | | 4.000 | % | | 06/15/22 | | | 138,727 | | |

| | 500,000 | | | Western Gas Partners LP | | | 4.000 | % | | 07/01/22 | | | 495,718 | | |

| | 1,020,000 | | | TechnipFMC PLC (c) | | | 3.450 | % | | 10/01/22 | | | 1,006,422 | | |

| | 1,500,000 | | | Sunoco Logistics Partners Operations LP | | | 3.450 | % | | 01/15/23 | | | 1,450,519 | | |

| | 2,300,000 | | | Murphy Oil Corp | | | 6.875 | % | | 08/15/24 | | | 2,287,571 | | |

| | 500,000 | | | Kinder Morgan Energy Partners LP | | | 4.250 | % | | 09/01/24 | | | 497,005 | | |

| | 1,000,000 | | | Boardwalk Pipelines LP | | | 4.950 | % | | 12/15/24 | | | 1,014,068 | | |

| | 500,000 | | | Murphy Oil Corp (f) | | | 5.875 | % | | 12/01/42 | | | 380,441 | | |

| | | | 8,451,507 | | |

| | | FINANCIALS 13.7% | |

| | 500,000 | | | Hartford Financial Services Group Inc/The | | | 6.000 | % | | 01/15/19 | | | 500,381 | | |

| | 1,355,000 | | | BB&T Corp | | | 2.250 | % | | 02/01/19 | | | 1,354,169 | | |

| | 1,000,000 | | | Morgan Stanley | | | 2.450 | % | | 02/01/19 | | | 999,510 | | |

| | 500,000 | | | Royal Bank of Scotland Group PLC (c) | | | 5.250 | % | | 02/15/19 | | | 496,893 | | |

| | 1,000,000 | | | Wells Fargo & Co | | | 2.125 | % | | 04/22/19 | | | 997,048 | | |

| | 500,000 | | | BB&T Corp | | | 6.850 | % | | 04/30/19 | | | 506,144 | | |

| | 1,000,000 | | | Capital One Bank USA NA | | | 2.300 | % | | 06/05/19 | | | 996,614 | | |

| | 250,000 | | | WR Berkley Corp | | | 6.150 | % | | 08/15/19 | | | 254,602 | | |

| | 500,000 | | | Protective Life Corp | | | 7.375 | % | | 10/15/19 | | | 513,977 | | |

| | 500,000 | | | Credit Suisse/New York NY (c) | | | 5.400 | % | | 01/14/20 | | | 507,734 | | |

| | 500,000 | | | Prospect Capital Corp | | | 4.000 | % | | 01/15/20 | | | 496,302 | | |

| | 500,000 | | | Morgan Stanley | | | 5.500 | % | | 01/26/20 | | | 511,359 | | |

| | 500,000 | | | Hartford Financial Services Group Inc/The | | | 5.500 | % | | 03/30/20 | | | 513,066 | | |

| | 450,000 | | | Compass Bank | | | 5.500 | % | | 04/01/20 | | | 460,008 | | |

| | 1,000,000 | | | HSBC Holdings PLC (c) | | | 3.400 | % | | 03/08/21 | | | 997,405 | | |

| | 1,000,000 | | | Nationwide Financial Services Inc (g) | | | 5.375 | % | | 03/25/21 | | | 1,036,182 | | |

16

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | FINANCIALS (continued) | |

$ | 500,000 | | | Markel Corp | | | 5.350 | % | | 06/01/21 | | $ | 520,418 | | |

| | 1,000,000 | | | Capital One Financial Corp | | | 4.750 | % | | 07/15/21 | | | 1,024,773 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 5.250 | % | | 07/27/21 | | | 519,046 | | |

| | 500,000 | | | Aflac Inc | | | 4.000 | % | | 02/15/22 | | | 510,226 | | |

| | 3,000,000 | | | Primerica Inc | | | 4.750 | % | | 07/15/22 | | | 3,097,827 | | |

| | 2,833,000 | | | Infinity Property & Casualty Corp | | | 5.000 | % | | 09/19/22 | | | 2,903,521 | | |

| | 2,000,000 | | | OneBeacon US Holdings Inc | | | 4.600 | % | | 11/09/22 | | | 2,012,812 | | |

| | 1,000,000 | | | Standard Chartered PLC (c) (g) | | | 3.950 | % | | 01/11/23 | | | 975,555 | | |

| | 500,000 | | | First American Financial Corp | | | 4.300 | % | | 02/01/23 | | | 501,961 | | |

| | 2,000,000 | | | Wells Fargo & Co | | | 3.450 | % | | 02/13/23 | | | 1,958,036 | | |

| | 4,073,000 | | | Assurant Inc | | | 4.000 | % | | 03/15/23 | | | 4,105,190 | | |

| | 1,000,000 | | | Markel Corp | | | 3.625 | % | | 03/30/23 | | | 993,968 | | |

| | 1,500,000 | | | Citigroup Inc | | | 3.500 | % | | 05/15/23 | | | 1,472,617 | | |

| | 500,000 | | | Morgan Stanley | | | 4.100 | % | | 05/22/23 | | | 500,722 | | |

| | 3,000,000 | | | Liberty Mutual Group Inc (g) | | | 4.250 | % | | 06/15/23 | | | 3,024,649 | | |

| | 500,000 | | | Assurant Inc | | | 4.200 | % | | 09/27/23 | | | 501,457 | | |

| | 500,000 | | | Ameriprise Financial Inc | | | 4.000 | % | | 10/15/23 | | | 514,311 | | |

| | 500,000 | | | CNA Financial Corp | | | 7.250 | % | | 11/15/23 | | | 567,115 | | |

| | 500,000 | | | Pacific Life Insurance Co (g) | | | 7.900 | % | | 12/30/23 | | | 589,281 | | |

| | 1,000,000 | | | Moody's Corp | | | 4.875 | % | | 02/15/24 | | | 1,052,218 | | |

| | 1,000,000 | | | HSBC Holdings PLC (c) | | | 4.250 | % | | 03/14/24 | | | 992,411 | | |

| | 1,000,000 | | | NASDAQ OMX Group Inc/The | | | 4.250 | % | | 06/01/24 | | | 1,007,433 | | |

| | 540,000 | | | Wintrust Financial Corp | | | 5.000 | % | | 06/13/24 | | | 538,196 | | |

| | 2,250,000 | | | Assured Guaranty US Holdings Inc | | | 5.000 | % | | 07/01/24 | | | 2,327,093 | | |

| | 3,088,000 | | | Legg Mason Inc | | | 3.950 | % | | 07/15/24 | | | 3,043,640 | | |

| | 1,500,000 | | | Symetra Financial Corp | | | 4.250 | % | | 07/15/24 | | | 1,471,456 | | |

| | 1,500,000 | | | Stifel Financial Corp | | | 4.250 | % | | 07/18/24 | | | 1,516,917 | | |

| | 1,000,000 | | | Citigroup Inc | | | 4.000 | % | | 08/05/24 | | | 987,955 | | |

| | 3,000,000 | | | Synchrony Financial | | | 4.250 | % | | 08/15/24 | | | 2,760,220 | | |

| | 1,000,000 | | | Bank of America Corp | | | 4.200 | % | | 08/26/24 | | | 991,800 | | |

| | 2,800,000 | | | Brown & Brown Inc | | | 4.200 | % | | 09/15/24 | | | 2,784,057 | | |

| | 2,000,000 | | | Old Republic International Corp | | | 4.875 | % | | 10/01/24 | | | 2,078,894 | | |

| | 2,000,000 | | | TIAA Asset Management Finance Co LLC (g) | | | 4.125 | % | | 11/01/24 | | | 2,037,188 | | |

| | 3,000,000 | | | American Express Co | | | 3.625 | % | | 12/05/24 | | | 2,932,727 | | |

| | 3,500,000 | | | Associated Banc-Corp | | | 4.250 | % | | 01/15/25 | | | 3,519,331 | | |

17

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | FINANCIALS (continued) | |

$ | 4,000,000 | | | Kemper Corp | | | 4.350 | % | | 02/15/25 | | $ | 3,948,667 | | |

| | 1,050,000 | | | TCF National Bank | | | 4.600 | % | | 02/27/25 | | | 995,489 | | |

| | 1,000,000 | | | Compass Bank | | | 3.875 | % | | 04/10/25 | | | 958,624 | | |

| | 250,000 | | | Liberty Mutual Insurance Co (g) | | | 8.500 | % | | 05/15/25 | | | 303,664 | | |

| | 1,000,000 | | | Prudential Insurance Co of America/The (g) | | | 8.300 | % | | 07/01/25 | | | 1,234,263 | | |

| | 3,000,000 | | | American International Group Inc | | | 3.750 | % | | 07/10/25 | | | 2,872,347 | | |

| | 1,000,000 | | | Synchrony Financial | | | 4.500 | % | | 07/23/25 | | | 911,886 | | |

| | 2,000,000 | | | Janus Capital Group Inc | | | 4.875 | % | | 08/01/25 | | | 1,962,766 | | |

| | 3,000,000 | | | HSBC Holdings PLC (c) | | | 4.250 | % | | 08/18/25 | | | 2,911,768 | | |

| | 4,000,000 | | | Capital One Financial Corp | | | 4.200 | % | | 10/29/25 | | | 3,848,499 | | |

| | 1,520,000 | | | Legg Mason Inc | | | 4.750 | % | | 03/15/26 | | | 1,553,168 | | |

| | 2,000,000 | | | Hanover Insurance Group Inc/The | | | 4.500 | % | | 04/15/26 | | | 2,002,069 | | |

| | 1,000,000 | | | Wells Fargo & Co | | | 4.100 | % | | 06/03/26 | | | 976,531 | | |

| | 2,000,000 | | | MSCI Inc (g) | | | 4.750 | % | | 08/01/26 | | | 1,895,000 | | |

| | 3,290,000 | | | Old Republic International Corp | | | 3.875 | % | | 08/26/26 | | | 3,141,553 | | |

| | 500,000 | | | Morgan Stanley | | | 4.350 | % | | 09/08/26 | | | 485,902 | | |

| | 1,000,000 | | | Citigroup Inc | | | 4.300 | % | | 11/20/26 | | | 961,621 | | |

| | 1,000,000 | | | JPMorgan Chase & Co | | | 4.125 | % | | 12/15/26 | | | 975,681 | | |

| | 4,000,000 | | | Mercury General Corp | | | 4.400 | % | | 03/15/27 | | | 3,868,527 | | |

| | 250,000 | | | Provident Cos Inc | | | 7.250 | % | | 03/15/28 | | | 293,224 | | |

| | 500,000 | | | Farmers Exchange Capital (g) | | | 7.050 | % | | 07/15/28 | | | 580,242 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.250 | % | | 11/15/30 | | | 459,445 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.000 | % | | 02/15/31 | | | 452,884 | | |

| | 500,000 | | | Goldman Sachs Group Inc/The | | | 4.300 | % | | 12/15/32 | | | 456,107 | | |

| | 250,000 | | | Citigroup Inc (f) | | | 4.000 | % | | 06/27/34 | | | 224,125 | | |

| | 538,000 | | | Bank of America Corp | | | 4.000 | % | | 08/15/34 | | | 478,854 | | |

| | 1,000,000 | | | Goldman Sachs Group Inc/The | | | 4.000 | % | | 01/30/35 | | | 876,836 | | |

| | 300,000 | | | Goldman Sachs Group Inc/The (f) | | | 3.750 | % | | 05/31/36 | | | 251,314 | | |

| | 500,000 | | | Swiss Re Treasury US Corp (g) | | | 4.250 | % | | 12/06/42 | | | 487,211 | | |

| | 500,000 | | | Principal Financial Group Inc | | | 4.350 | % | | 05/15/43 | | | 463,838 | | |

| | 2,500,000 | | | M&T Bank Corp (f) | | | 5.125 | % | | 12/29/49 | | | 2,368,750 | | |

| | | | 110,677,270 | | |

| | | HEALTH CARE 1.7% | |

| | 700,000 | | | Express Scripts Holding Co | | | 2.250 | % | | 06/15/19 | | | 697,021 | | |

| | 1,000,000 | | | Quest Diagnostics Inc | | | 4.700 | % | | 04/01/21 | | | 1,027,862 | | |

| | 1,000,000 | | | Laboratory Corp of America Holdings | | | 3.750 | % | | 08/23/22 | | | 1,005,571 | | |

18

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | HEALTH CARE (continued) | |

$ | 1,000,000 | | | Laboratory Corp of America Holdings | | | 4.000 | % | | 11/01/23 | | $ | 1,007,770 | | |

| | 2,000,000 | | | Mylan Inc/PA | | | 4.200 | % | | 11/29/23 | | | 1,951,032 | | |

| | 500,000 | | | Wyeth LLC | | | 6.450 | % | | 02/01/24 | | | 572,527 | | |

| | 3,000,000 | | | Actavis Funding SCS (c) | | | 3.800 | % | | 03/15/25 | | | 2,928,671 | | |

| | 1,500,000 | | | Baxalta Inc | | | 4.000 | % | | 06/23/25 | | | 1,466,492 | | |

| | 1,000,000 | | | Celgene Corp | | | 3.875 | % | | 08/15/25 | | | 962,662 | | |

| | 1,000,000 | | | Biogen Inc | | | 4.050 | % | | 09/15/25 | | | 995,439 | | |

| | 1,000,000 | | | Express Scripts Holding Co | | | 4.500 | % | | 02/25/26 | | | 1,013,533 | | |

| | | | 13,628,580 | | |

| | | INDUSTRIALS 2.2% | |

| | 65,000 | | | Masco Corp | | | 7.125 | % | | 03/15/20 | | | 67,901 | | |

| | 500,000 | | | IDEX Corp | | | 4.200 | % | | 12/15/21 | | | 507,332 | | |

| | 500,000 | | | GATX Corp | | | 4.750 | % | | 06/15/22 | | | 518,938 | | |

| | 500,000 | | | Penske Truck Leasing Co Lp / PTL Finance Corp (g) | | | 4.875 | % | | 07/11/22 | | | 517,678 | | |

| | 2,000,000 | | | Dun & Bradstreet Corp/The (f) | | | 4.625 | % | | 12/01/22 | | | 2,025,000 | | |

| | 1,850,000 | | | MasTec Inc | | | 4.875 | % | | 03/15/23 | | | 1,794,500 | | |

| | 1,000,000 | | | GATX Corp | | | 3.900 | % | | 03/30/23 | | | 1,000,201 | | |

| | 500,000 | | | Ingersoll-Rand Global Holding Co Ltd | | | 4.250 | % | | 06/15/23 | | | 512,363 | | |

| | 1,000,000 | | | Flowserve Corp | | | 4.000 | % | | 11/15/23 | | | 987,181 | | |

| | 2,126,000 | | | Air Lease Corp | | | 4.850 | % | | 02/01/24 | | | 2,125,869 | | |

| | 2,717,000 | | | Oshkosh Corp | | | 5.375 | % | | 03/01/25 | | | 2,710,208 | | |

| | 2,000,000 | | | Tennant Co | | | 5.625 | % | | 05/01/25 | | | 1,885,000 | | |

| | 500,000 | | | Toro Co/The | | | 7.800 | % | | 06/15/27 | | | 597,717 | | |

| | 500,000 | | | Fluor Corp | | | 4.250 | % | | 09/15/28 | | | 487,083 | | |

| | 2,000,000 | | | Eaton Corp | | | 4.000 | % | | 11/02/32 | | | 1,975,228 | | |

| | | | 17,712,199 | | |

| | | INFORMATION TECHNOLOGY 4.2% | |

| | 500,000 | | | Broadridge Financial Solutions Inc | | | 3.950 | % | | 09/01/20 | | | 505,004 | | |

| | 81,000 | | | Hewlett-Packard Co | | | 3.750 | % | | 12/01/20 | | | 81,968 | | |

| | 750,000 | | | Hewlett-Packard Co | | | 4.300 | % | | 06/01/21 | | | 762,451 | | |

| | 500,000 | | | Diamond 1 Finance Corp / Diamond 2 Finance Corp (g) | | | 4.420 | % | | 06/15/21 | | | 499,175 | | |

| | 2,000,000 | | | NetApp Inc | | | 3.375 | % | | 06/15/21 | | | 1,992,431 | | |

| | 2,000,000 | | | Western Union Co/The | | | 3.600 | % | | 03/15/22 | | | 1,992,245 | | |

| | 500,000 | | | Motorola Solutions Inc | | | 3.750 | % | | 05/15/22 | | | 496,151 | | |

| | 2,000,000 | | | Symantec Corp | | | 3.950 | % | | 06/15/22 | | | 1,923,414 | | |

19

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | INFORMATION TECHNOLOGY (continued) | |

$ | 1,000,000 | | | Hewlett-Packard Co | | | 4.050 | % | | 09/15/22 | | $ | 1,013,935 | | |

| | 1,000,000 | | | DXC Technology Co | | | 4.450 | % | | 09/18/22 | | | 1,020,406 | | |

| | 1,025,000 | | | Fiserv Inc | | | 3.500 | % | | 10/01/22 | | | 1,017,935 | | |

| | 2,000,000 | | | Autodesk Inc | | | 3.600 | % | | 12/15/22 | | | 1,982,984 | | |

| | 1,352,000 | | | Total System Services Inc | | | 3.750 | % | | 06/01/23 | | | 1,341,001 | | |

| | 500,000 | | | Western Union Co/The | | | 4.250 | % | | 06/09/23 | | | 503,089 | | |

| | 2,000,000 | | | Diamond 1 Finance Corp / Diamond 2 Finance Corp (g) | | | 5.450 | % | | 06/15/23 | | | 2,035,280 | | |

| | 1,000,000 | | | Altera Corp | | | 4.100 | % | | 11/15/23 | | | 1,035,330 | | |

| | 1,000,000 | | | Juniper Networks Inc | | | 4.500 | % | | 03/15/24 | | | 1,007,433 | | |

| | 500,000 | | | Motorola Solutions Inc | | | 4.000 | % | | 09/01/24 | | | 486,571 | | |

| | 2,000,000 | | | Lam Research Corp | | | 3.800 | % | | 03/15/25 | | | 2,000,104 | | |

| | 1,031,000 | | | Arrow Electronics Inc | | | 4.000 | % | | 04/01/25 | | | 1,004,234 | | |

| | 1,000,000 | | | Juniper Networks Inc | | | 4.350 | % | | 06/15/25 | | | 997,500 | | |

| | 2,000,000 | | | Hewlett Packard Enterprise Co (f) | | | 4.900 | % | | 10/15/25 | | | 2,015,725 | | |

| | 1,500,000 | | | Dell International LLC / EMC Corp (g) | | | 6.020 | % | | 06/15/26 | | | 1,506,783 | | |

| | 1,000,000 | | | Trimble Inc | | | 4.900 | % | | 06/15/28 | | | 984,625 | | |

| | 4,000,000 | | | Intel Corp | | | 4.000 | % | | 12/15/32 | | | 4,097,145 | | |

| | 1,500,000 | | | Western Union Co/The | | | 6.200 | % | | 11/17/36 | | | 1,448,844 | | |

| | | | 33,751,763 | | |

| | | MATERIALS 2.9% | |

| | 500,000 | | | Carpenter Technology Corp | | | 5.200 | % | | 07/15/21 | | | 500,520 | | |

| | 500,000 | | | Freeport-McMoRan Inc | | | 4.000 | % | | 11/14/21 | | | 486,250 | | |

| | 175,000 | | | Mosaic Co/The | | | 3.750 | % | | 11/15/21 | | | 175,799 | | |

| | 500,000 | | | Barrick Gold Corp (c) | | | 3.850 | % | | 04/01/22 | | | 502,509 | | |

| | 1,000,000 | | | Domtar Corp | | | 4.400 | % | | 04/01/22 | | | 1,005,051 | | |

| | 1,000,000 | | | RPM International Inc | | | 3.450 | % | | 11/15/22 | | | 990,549 | | |

| | 2,000,000 | | | Crown Americas LLC / Crown Americas Capital Corp IV | | | 4.500 | % | | 01/15/23 | | | 1,952,500 | | |

| | 1,000,000 | | | Carpenter Technology Corp | | | 4.450 | % | | 03/01/23 | | | 971,639 | | |

| | 1,402,000 | | | Reliance Steel & Aluminum Co | | | 4.500 | % | | 04/15/23 | | | 1,417,833 | | |

| | 2,000,000 | | | Nucor Corp | | | 4.000 | % | | 08/01/23 | | | 2,030,695 | | |

| | 1,000,000 | | | BP Capital Markets PLC (c) | | | 3.994 | % | | 09/26/23 | | | 1,020,762 | | |

| | 2,000,000 | | | Mosaic Co/The | | | 4.250 | % | | 11/15/23 | | | 2,010,255 | | |

| | 1,000,000 | | | International Paper Co | | | 3.650 | % | | 06/15/24 | | | 1,004,016 | | |

| | 1,000,000 | | | Steel Dynamics Inc | | | 5.500 | % | | 10/01/24 | | | 990,000 | | |

| | 1,000,000 | | | Freeport-McMoRan Inc | | | 4.550 | % | | 11/14/24 | | | 922,500 | | |

20

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | CORPORATE BONDS (continued) | |

| | | MATERIALS (continued) | |

$ | 756,000 | | | Eastman Chemical Co | | | 3.800 | % | | 03/15/25 | | $ | 729,012 | | |

| | 865,000 | | | Union Carbide Corp | | | 7.500 | % | | 06/01/25 | | | 1,000,154 | | |

| | 2,000,000 | | | DowDuPont Inc | | | 4.493 | % | | 11/15/25 | | | 2,059,152 | | |

| | 200,000 | | | Worthington Industries Inc | | | 4.550 | % | | 04/15/26 | | | 199,103 | | |

| | 782,000 | | | HB Fuller Co | | | 4.000 | % | | 02/15/27 | | | 656,880 | | |

| | 1,250,000 | | | Dow Chemical Co/The | | | 4.250 | % | | 10/01/34 | | | 1,145,490 | | |

| | 1,000,000 | | | Alcoa Inc | | | 5.950 | % | | 02/01/37 | | | 923,963 | | |

| | 1,000,000 | | | Newmont Mining Corp | | | 4.875 | % | | 03/15/42 | | | 945,581 | | |

| | | | 23,640,213 | | |

| | | REAL ESTATE 0.2% | |

| | 1,000,000 | | | CBRE Services Inc | | | 5.250 | % | | 03/15/25 | | | 1,041,720 | | |

| | 350,000 | | | CBRE Services Inc | | | 4.875 | % | | 03/01/26 | | | 358,854 | | |

| | | | 1,400,574 | | |

| | | UTILITIES 0.7% | |

| | 250,000 | | | United Utilities PLC (c) | | | 5.375 | % | | 02/01/19 | | | 250,347 | | |

| | 1,000,000 | | | Exelon Generation Co LLC | | | 4.250 | % | | 06/15/22 | | | 1,013,750 | | |

| | 1,565,000 | | | National Fuel Gas Co | | | 3.750 | % | | 03/01/23 | | | 1,526,980 | | |

| | 1,060,000 | | | PSEG Power LLC | | | 4.300 | % | | 11/15/23 | | | 1,081,941 | | |

| | 1,500,000 | | | National Fuel Gas Co | | | 3.950 | % | | 09/15/27 | | | 1,400,744 | | |

| | | | 5,273,762 | | |

| | | TOTAL CORPORATE BONDS | | | 254,333,408 | | |

| | | ASSET BACKED SECURITIES 3.2% | |

| | 111,749 | | | Continental Airlines 2010-1 Class B Pass Through Trust | | | 6.000 | % | | 01/12/19 | | | 111,772 | | |

| | 184,970 | | | Delta Air Lines 2011-1 Class A Pass Through Trust | | | 5.300 | % | | 04/15/19 | | | 185,617 | | |

| | 350,876 | | | Delta Air Lines 2012-1 Class B Pass Through Trust (g) | | | 6.875 | % | | 05/07/19 | | | 353,929 | | |

| | 383,445 | | | America West Airlines 2000-1 Pass Through Trust | | | 8.057 | % | | 07/02/20 | | | 403,192 | | |

| | 432,539 | | | American Airlines 2011-1 Class A Pass Through Trust | | | 5.250 | % | | 01/31/21 | | | 439,935 | | |

| | 307,937 | | | Air Canada 2013-1 Class B Pass Through Trust (c) (g) | | | 5.375 | % | | 05/15/21 | | | 311,016 | | |

| | 633,341 | | | Northwest Airlines 2002-1 Class G-2 Pass Through Trust (h) | | | 6.264 | % | | 11/20/21 | | | 642,651 | | |

| | 339,824 | | | United Airlines 2014-1 Class B Pass Through Trust | | | 4.750 | % | | 04/11/22 | | | 337,072 | | |

| | 160,710 | | | Continental Airlines 2007-1 Class A Pass Through Trust | | | 5.983 | % | | 04/19/22 | | | 167,733 | | |

| | 255,048 | | | Southwest Airlines Co 2007-1 Pass Through Trust | | | 6.150 | % | | 08/01/22 | | | 265,990 | | |

21

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Par Value | | Security Description | | Fair Value | |

| | | FIXED INCOME SECURITIES (continued) | |

| | | ASSET BACKED SECURITIES (continued) | |

$ | 597,640 | | | Delta Air Lines 2007-1 Class B Pass Through Trust (g) (h) | | | 8.021 | % | | 08/10/22 | | $ | 650,590 | | |

| | 53,895 | | | United Airlines 2014-2 Class B Pass Through Trust | | | 4.625 | % | | 09/03/22 | | | 53,599 | | |

| | 444,247 | | | American Airlines 2014-1 Class B Pass Through Trust | | | 4.375 | % | | 10/01/22 | | | 438,250 | | |

| | 1,000,000 | | | United Airlines 2015-1 Class A Pass Through Trust | | | 3.700 | % | | 12/01/22 | | | 985,300 | | |

| | 526,123 | | | US Airways 2010-1 Class A Pass Through Trust | | | 6.250 | % | | 04/22/23 | | | 547,694 | | |

| | 2,239,522 | | | American Airlines 2015-1 Class B Pass Through Trust | | | 3.700 | % | | 05/01/23 | | | 2,169,425 | | |

| | 1,200,831 | | | Delta Air Lines 2015-1 Class B Pass Through Trust | | | 4.250 | % | | 07/30/23 | | | 1,192,905 | | |

| | 738,387 | | | American Airlines 2015-2 Class B Pass Through Trust | | | 4.400 | % | | 09/22/23 | | | 721,330 | | |

| | 278,463 | | | US Airways 2011-1 Class A Pass Through Trust | | | 7.125 | % | | 10/22/23 | | | 302,578 | | |

| | 3,123,673 | | | American Airlines 2016-1 Class B Pass Through Trust | | | 5.250 | % | | 01/15/24 | | | 3,143,664 | | |

| | 963,830 | | | Spirit Airlines Pass Through Trust 2015-1B | | | 4.450 | % | | 04/01/24 | | | 941,083 | | |

| | 1,392,110 | | | Continental Airlines 2012-2 Class A Pass Through Trust | | | 4.000 | % | | 10/29/24 | | | 1,369,975 | | |

| | 1,061,775 | | | American Airlines 2017-1 Class B Pass Through Trust | | | 4.950 | % | | 02/15/25 | | | 1,055,617 | | |

| | 842,611 | | | United Airlines 2013-1 Class A Pass Through Trust | | | 4.300 | % | | 08/15/25 | | | 846,824 | | |

| | 911,616 | | | American Airlines 2016-3 Class B Pass Through Trust | | | 3.750 | % | | 10/15/25 | | | 869,044 | | |

| | 718,348 | | | US Airways 2013-1 Class A Pass Through Trust | | | 3.950 | % | | 11/15/25 | | | 712,027 | | |

| | 1,914,352 | | | United Airlines 2016-1 Class B Pass Through Trust | | | 3.650 | % | | 01/07/26 | | | 1,814,806 | | |

| | 1,963,700 | | | Hawaiian Airlines 2013-1 Class A Pass Through Certificates | | | 3.900 | % | | 01/15/26 | | | 1,885,348 | | |

| | 391,500 | | | United Airlines 2014-1 Class A Pass Through Trust | | | 4.000 | % | | 04/11/26 | | | 385,158 | | |

| | 1,512,716 | | | American Airlines 2014-1 Class A Pass Through Trust | | | 3.700 | % | | 10/01/26 | | | 1,456,141 | | |

| | 385,059 | | | American Airlines 2015-1 Class A Pass Through Trust | | | 3.375 | % | | 05/01/27 | | | 363,765 | | |

| | 169,269 | | | American Airlines 2015-2 Class AA Pass Through Trust | | | 3.600 | % | | 09/22/27 | | | 162,430 | | |

| | 551,889 | | | American Airlines 2015-2 Class A Pass Through Trust | | | 4.000 | % | | 09/22/27 | | | 524,626 | | |

| | 112,185 | | | Spirit Airlines Pass Through Trust 2015-1A | | | 4.100 | % | | 04/01/28 | | | 110,468 | | |

| | | | 25,921,554 | | |

| | TOTAL FIXED INCOME SECURITIES

(cost $285,992,472) | | $ | 281,256,208 | | |

22

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS 62.6% | |

| | | COMMUNICATION SERVICES 4.3% | |

| | 20,200 | | | Alphabet Inc (a) | | $ | 20,919,322 | | |

| | 125,000 | | | Walt Disney Co/The | | | 13,706,250 | | |

| | | | 34,625,572 | | |

| | | CONSUMER DISCRETIONARY 2.0% | |

| | 15,900 | | | Garrett Motion Inc (a) | | | 196,206 | | |

| | 67,000 | | | Home Depot Inc/The | | | 11,511,940 | | |

| | 67,000 | | | Target Corp | | | 4,428,030 | | |

| | | | 16,136,176 | | |

| | | CONSUMER STAPLES 4.6% | |

| | 166,000 | | | General Mills Inc | | | 6,464,040 | | |

| | 77,000 | | | Hershey Co/The | | | 8,252,860 | | |

| | 380,000 | | | Hormel Foods Corp | | | 16,218,400 | | |

| | 54,000 | | | Kimberly-Clark Corp | | | 6,152,760 | | |

| | | | 37,088,060 | | |

| | | ENERGY 2.3% | |

| | 78,000 | | | Chevron Corp | | | 8,485,620 | | |

| | 70,000 | | | Exxon Mobil Corp | | | 4,773,300 | | |

| | 151,000 | | | Schlumberger Ltd (c) | | | 5,448,080 | | |

| | | | 18,707,000 | | |

| | | FINANCIALS 10.0% | |

| | 129,000 | | | American Express Co | | | 12,296,280 | | |

| | 239,000 | | | Associated Banc-Corp | | | 4,729,810 | | |

| | 105,000 | | | Great Western Bancorp Inc | | | 3,281,250 | | |

| | 140,000 | | | JPMorgan Chase & Co | | | 13,666,800 | | |

| | 271,000 | | | Principal Financial Group Inc | | | 11,970,070 | | |

| | 27,000 | | | Travelers Cos Inc/The | | | 3,233,250 | | |

| | 527,000 | | | US Bancorp/MN | | | 24,083,900 | | |

| | 167,000 | | | Wells Fargo & Co | | | 7,695,360 | | |

| | | | 80,956,720 | | |

| | | HEALTH CARE 16.6% | |

| | 285,000 | | | Abbott Laboratories | | | 20,614,050 | | |

| | 57,000 | | | Baxter International Inc | | | 3,751,740 | | |

| | 33,500 | | | Bio-Techne Corp | | | 4,848,120 | | |

| | 98,500 | | | Bristol-Myers Squibb Co | | | 5,120,030 | | |

| | 134,000 | | | Eli Lilly & Co | | | 15,506,480 | | |

| | 167,000 | | | Johnson & Johnson | | | 21,551,350 | | |

23

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | COMMON STOCKS (continued) | |

| | | HEALTH CARE (continued) | |

| | 251,000 | | | Medtronic PLC (e) | | $ | 22,830,960 | | |

| | 253,000 | | | Pfizer Inc | | | 11,043,450 | | |

| | 522,000 | | | Roche Holding AG (d) | | | 16,223,760 | | |

| | 51,500 | | | UnitedHealth Group Inc | | | 12,829,680 | | |

| | | | 134,319,620 | | |

| | | INDUSTRIALS 14.7% | |

| | 115,000 | | | 3M Co | | | 21,912,100 | | |

| | 153,000 | | | CH Robinson Worldwide Inc | | | 12,865,770 | | |

| | 195,000 | | | Donaldson Co Inc | | | 8,461,050 | | |

| | 77,000 | | | Emerson Electric Co | | | 4,600,750 | | |

| | 117,000 | | | Fastenal Co | | | 6,117,930 | | |

| | 367,000 | | | Graco Inc | | | 15,358,950 | | |

| | 156,000 | | | Honeywell International Inc | | | 20,610,720 | | |

| | 137,000 | | | nVent Electric PLC (c) | | | 3,077,020 | | |

| | 137,000 | | | Pentair PLC (c) | | | 5,175,860 | | |

| | 26,000 | | | Resideo Technologies Inc (a) | | | 534,300 | | |

| | 110,000 | | | Toro Co/The | | | 6,146,800 | | |

| | 138,000 | | | United Parcel Service Inc, Class B | | | 13,459,140 | | |

| | | | 118,320,390 | | |

| | | INFORMATION TECHNOLOGY 3.4% | |

| | 244,000 | | | Corning Inc | | | 7,371,240 | | |

| | 22,000 | | | International Business Machines Corp | | | 2,500,740 | | |

| | 75,000 | | | Microsoft Corp | | | 7,617,750 | | |

| | 12,000 | | | Motorola Solutions Inc | | | 1,380,480 | | |

| | 100,000 | | | QUALCOMM Inc | | | 5,691,000 | | |

| | 21,500 | | | Visa Inc | | | 2,836,710 | | |

| | | | 27,397,920 | | |

| | | MATERIALS 4.3% | |

| | 185,000 | | | Bemis Co Inc | | | 8,491,500 | | |

| | 139,000 | | | Ecolab Inc | | | 20,481,650 | | |

| | 136,000 | | | HB Fuller Co | | | 5,803,120 | | |

| | | | 34,776,270 | | |

| | | UTILITIES 0.4% | |

| | 65,000 | | | Xcel Energy Inc | | | 3,202,550 | | |

| | | | TOTAL COMMON STOCKS

(cost $343,021,369) | | $ | 505,530,278 | | |

24

Mairs & Power Balanced Fund

SCHEDULE OF INVESTMENTS (continued) December 31, 2018

Shares | | Security Description | | Fair Value | |

| | | SHORT-TERM INVESTMENTS 1.9% | |

| 15,210,468 | | | First American Government Obligations Fund, Class X, 2.36% (b)

(cost $15,210,468) | | $ | 15,210,468 | | |

| | TOTAL INVESTMENTS 99.3%

(cost $644,224,309) | | $ | 801,996,954 | | |

| | | OTHER ASSETS AND LIABILITIES (NET) 0.7% | | | 5,457,976 | | |

| | | TOTAL NET ASSETS 100.0% | | $ | 807,454,930 | | |

(a) Non-income producing.

(b) The rate quoted is the annualized seven-day effective yield as of December 31, 2018.

(c) Foreign security denominated in U.S. dollars. As of December 31, 2018, these securities represented $26,602,453 or 3.3% of total net assets.

(d) American Depositary Receipt.

(e) Issuer headquartered overseas but considered domestic. In determining whether a security is foreign or domestic, the Adviser will generally look at the location of the headquarters of the issuer. However, if the issuer is believed by the Adviser to be headquartered in a jurisdiction primarily for tax purposes, the Adviser will consider the following additional factors: 1) the location of the primary exchange trading its securities; 2) where it derives the majority of its revenues, and/or 3) where it earns the majority of its profits.

(f) Step Bonds – Securities for which the coupon rate of interest will adjust on specified future date(s). The rate disclosed represents the coupon rate in effect as of December 31, 2018.

(g) Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. These securities, with the exception of those securities deemed illiquid within footnote (h), have been determined to be liquid under the Funds' Liquidity Risk Management Program. As of December 31, 2018, these securities represented $24,533,596 or 3.0% of total net assets.

(h) Securities are deemed illiquid. As of December 31, 2018, these securities represented $1,293,241 or 0.2% of total net assets.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor's Financial Services LLC ("S&P"). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Adviser.

See accompanying Notes to Financial Statements.

25

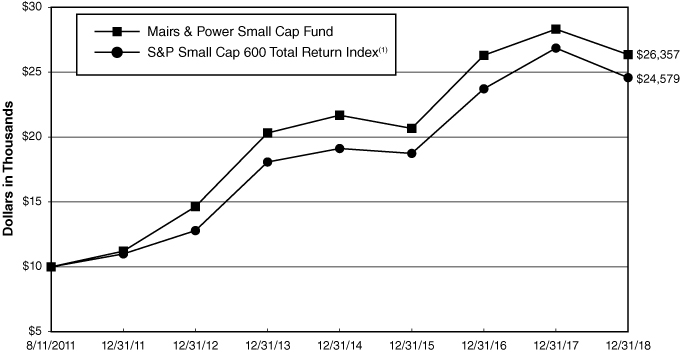

MAIRS & POWER SMALL CAP FUND (unaudited)

To Our Shareholders: December 31, 2018

The market sold off sharply in the fourth quarter of the year and small cap stocks were no exception. Nevertheless, the Mairs & Power Small Cap Fund outperformed both the index and peer group. The Fund finished the quarter down 17.03% while the S&P 600 Total Return Index and the Morningstar Small Blend Category were down 20.10% and 19.32% respectively. For the year the Fund finished down 6.91%, also ahead of the index and peer group which were down 8.48% and 12.66% respectively.

Sector allocation played a small role in relative performance for the year with Energy being the only sector of note, declining over 40% in 2018 as the worst performing sector in small cap. The Fund's significantly underweight position in the sector meaningfully contributed to relative outperformance for the year. In fact, for most of 2018, the Fund held just one energy stock.

Stock selection was the primary driver of relative outperformance in 2018. Among the several strong contributors to relative performance in 2018 were Marcus Corp (MCS) and Workiva Inc. (WK). Marcus, a Milwaukee-based company up 55.46% for the year, primarily owns and operates movie theaters in the Midwest but also owns and manages a number of hotels as well. Management has made a big push over the last several years to invest in its movie theaters with amenities like power reclining seats, in-theater beverage and food service, and restaurants and bars in some theater lobbies, all of which have been well-received by consumers. In our opinion, Marcus is in a strong competitive position as it owns the bulk of its properties and therefore has stronger cash flow than peers who have to make lease payments on the majority of their properties. This gives Marcus the ability to continue to invest aggressively in its theaters while its competitors cannot, further widening its advantage.

MAIRS & POWER SMALL CAP FUND (MSCFX)

Top Relative Performers

| Fourth Quarter (9/30/18 – 12/31/18) | | Year To Date (12/31/17 – 12/31/18) | |

Black Hills Corp. | | | 29.04 | % | | Marcus Corporation | | | 55.46 | % | |

United Fire Group, Inc | | | 29.96 | % | | Workiva, Inc. | | | 76.19 | % | |

Casey's General Stores, Inc. | | | 19.58 | % | | United Fire Group, Inc. | | | 39.53 | % | |

EMC Insurance Group, Inc. | | | 50.19 | % | | Gentherm Inc. | | | 34.40 | % | |

Glacier Bancorp, Inc. | | | 13.15 | % | | Premier Inc. | | | 36.44 | % | |