UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Khimmara Greer

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246_ |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | May 31 | |

| Date of reporting period: | November 30, 2022 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

(a).

Institutional Class (ADLVX)

SEMI-ANNUAL REPORT

November 30, 2022

(Unaudited)

Managed by

Adler Asset Management, LLC

For information or assistance in opening an account,

please call toll-free 1-800-408-4682.

| ADLER VALUE FUND | |

| LETTER TO SHAREHOLDERS (Unaudited) | December 16, 2022 |

Dear Shareholder,

On August 16, 2018, the Adler Value Fund (the “Fund”) commenced operations. Adler Asset Management, LLC (the “Adviser”) is the Fund’s investment adviser.

Returns

The table below shows the total returns for the Fund and its benchmark, the S&P 500 Value Index, for the six-month, one-year, three-year annualized, and cumulative since inception periods ended November 30, 2022.

| Total Returns to 11/30/2022 | ||||

| Six Months | Cumulative | |||

| Ended | Three-Year | Since | ||

| 11/30/2022 | One-Year | Annualized | Inception | |

| Adler Value Fund | -3.18% | -1.84% | 10.57% | 48.35% |

| S&P 500 Value | 2.17% | 5.59% | 8.79% | 47.15% |

Performance for the Six-Month Period

During the six-month period ended November 30, 2022, the Fund underperformed its benchmark. The Fund’s more defensive holdings performed well. As recession fears have gripped the equity markets, the Fund’s deeper value, more cyclical names have not performed as well. Value stocks can and do operate in industries impacted by a potential economic slowdown with the equity market re-pricing certain stocks. The Adviser remains confident in the catalysts for the Fund’s holdings as we move through this period of economic uncertainty.

Commentary

As the six-month period progressed, equity, fixed-income, foreign exchange, and commodities markets continued to react to economic data that either validated or refuted market expectations around three key themes:

| ● | Pace of Federal Reserve interest rate increases; |

| ● | Rate of inflation; and |

| ● | Probability, timing, and severity of a potential recession. |

Investment Approach

In selecting investments for the Fund, the Adviser uses a focused-value strategy to invest in companies that, in its opinion, appear to be undervalued by the equity market but where catalysts exist, in the opinion of the Adviser, to close these valuation gaps. The Adviser seeks to exploit perceived market misjudgments in pricing by buying equity securities that appear to be undervalued because of a temporary aversion to these out-of-favor issuers.

The Adviser maintains a watch list of companies and reviews each company’s financial condition and prospects, including factors such as (but not limited to): expected future earnings, cash flow, the ability and willingness to return capital to shareholders, competitive

1

position, quality of the business franchise, and the reputation, experience, and competence of a company’s management and board of directors. The Adviser considers these factors both while the company is on the watch list and also at the time of purchase. Not all companies, at the time of purchase, are on the Adviser’s watch list, and a company may be added to the Fund’s portfolio following a precipitating event.

When added to the Fund’s portfolio, a company will generally be trading at a significant discount to its 52-week or all-time high. The Adviser’s contrarian approach, buying what it believes are fundamentally sound companies that are out-of-favor with the market, is industry, sector and market capitalization agnostic, and typically will result in a portfolio containing the securities of fewer than thirty issuers.

Portfolio Developments

The following is a discussion of recent developments concerning two of the Fund’s portfolio holdings.

Tenneco (TEN) is a leading designer, manufacturer, and marketer of automotive products for original equipment and aftermarket customers. Through its four business groups, Motorparts, Performance Solutions, Clean Air and Powertrain, Tenneco delivers solutions for the light vehicle, commercial truck, off-highway, industrial, motorsport and aftermarket. The cash sale of TEN closed at $20.00 per share during the six-month period.

Twitter (TWTR) is a leading social media company. The cash sale of TWTR closed at $54.20 per share during the six-month period.

In closing, I want to thank shareholders for their confidence in the Fund’s Adviser. The Adviser continues to assess companies that fit the Fund’s investment approach.

David Adler

Adler Asset Management, LLC

December 16, 2022

2

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-800-408-4682.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website at www.adlervaluefund.com or call 1-800-408-4682 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Fund as of November 30, 2022, please see the Schedule of Investments section of the semi-annual report. The opinions of the Fund’s adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements, include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

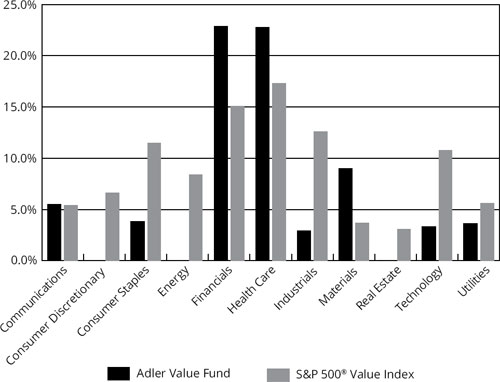

| ADLER VALUE FUND |

| PORTFOLIO INFORMATION |

| November 30, 2022 (Unaudited) |

Sector Diversification

(% of Net Assets)

| Top 10 Equity Holdings | ||

| % of Net | ||

| Security Description | Assets | |

| Bristol-Myers Squibb Company | 6.8% | |

| Pfizer, Inc | 5.3% | |

| Charles Schwab Corporation (The) | 5.0% | |

| Cigna Corporation | 4.7% | |

| Aflac, Inc. | 4.7% | |

| Valvoline, Inc. | 4.6% | |

| O-I Glass, Inc. | 4.1% | |

| Jackson Financial, Inc. - Class A | 3.8% | |

| PG&E Corporation | 3.6% | |

| Equitable Holdings, Inc. | 3.6% | |

4

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS |

| November 30, 2022 (Unaudited) |

| COMMON STOCKS — 71.8% | Shares | Value | ||||||

| Communications — 5.5% | ||||||||

| Cable & Satellite — 0.9% | ||||||||

| Altice USA, Inc. - Class A (a) | 3,400 | $ | 15,504 | |||||

| Comcast Corporation - Class A | 600 | 21,984 | ||||||

| 37,488 | ||||||||

| Entertainment Content — 1.9% | ||||||||

| Paramount Global - Class B | 4,000 | 80,320 | ||||||

| Publishing & Broadcasting — 2.7% | ||||||||

| iHeartMedia, Inc. - Class A (a) | 13,700 | 110,148 | ||||||

| Consumer Staples — 3.8% | ||||||||

| Beverages — 1.1% | ||||||||

| Diageo plc - ADR | 250 | 46,638 | ||||||

| Household Products — 2.7% | ||||||||

| Spectrum Brands Holdings, Inc. | 2,100 | 111,867 | ||||||

| Financials — 20.9% | ||||||||

| Banking — 2.3% | ||||||||

| Citigroup, Inc. | 2,000 | 96,820 | ||||||

| Broker-Dealers — 6.5% | ||||||||

| Charles Schwab Corporation (The) | 2,500 | 206,350 | ||||||

| XP, Inc. - Class A (a) | 3,595 | 62,948 | ||||||

| 269,298 | ||||||||

| Insurance — 12.1% | ||||||||

| Aflac, Inc. | 2,700 | 194,211 | ||||||

| Equitable Holdings, Inc. | 4,700 | 149,178 | ||||||

| Jackson Financial, Inc. - Class A | 4,300 | 160,605 | ||||||

| 503,994 | ||||||||

| Health Care — 22.8% | ||||||||

| Biotech & Pharma — 18.1% | ||||||||

| Bayer AG - ADR | 8,800 | 128,128 | ||||||

| Bristol-Myers Squibb Company | 3,500 | 280,980 | ||||||

| Pfizer, Inc. | 4,400 | 220,572 | ||||||

| Viatris, Inc. | 10,935 | 120,613 | ||||||

| 750,293 | ||||||||

| Health Care Facilities & Services — 4.7% | ||||||||

| Cigna Corporation | 600 | 197,334 | ||||||

5

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 71.8% (Continued) | Shares | Value | ||||||

| Industrials — 2.9% | ||||||||

| Industrial Support Services — 2.9% | ||||||||

| Grainger (W.W.), Inc. | 200 | $ | 120,612 | |||||

| Materials — 9.0% | ||||||||

| Chemicals — 4.6% | ||||||||

| Valvoline, Inc. | 5,800 | 191,284 | ||||||

| Containers & Packaging — 4.4% | ||||||||

| Berry Global Group, Inc. | 200 | 11,720 | ||||||

| O-I Glass, Inc. (a) | 10,400 | 170,664 | ||||||

| 182,384 | ||||||||

| Technology — 3.3% | ||||||||

| Technology & Electronics — 2.5% | ||||||||

| Corning, Inc. | 3,000 | 102,390 | ||||||

| Technology Hardware — 0.8% | ||||||||

| Diebold Nixdorf, Inc. (a) | 15,300 | 32,895 | ||||||

| Utilities — 3.6% | ||||||||

| Electric Utilities — 3.6% | ||||||||

| PG&E Corporation (a) | 9,600 | 150,720 | ||||||

| Total Common Stocks (Cost $2,543,042) | $ | 2,984,485 | ||||||

6

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| PREFERRED STOCKS — 2.0% | Shares | Value | ||||||

| Financials — 2.0% | ||||||||

| Banking — 2.0% | ||||||||

| Itau Unibanco Holding S.A. - ADR (Cost $80,145) | 16,800 | $ | 83,664 | |||||

| PURCHASED OPTION | Notional | |||||||||||||||

| CONTRACTS — 3.4% | Strike Price | Contracts | Value | Value | ||||||||||||

| Call Option Contracts — 3.4% | ||||||||||||||||

| Altice USA, Inc. - Class A, 01/20/23 | $ | 10.00 | 30 | $ | 13,680 | $ | 300 | |||||||||

| Altice USA, Inc. - Class A, 01/20/23 | 11.00 | 10 | 4,560 | 50 | ||||||||||||

| Altice USA, Inc. - Class A, 01/20/23 | 12.00 | 20 | 9,120 | 50 | ||||||||||||

| Bristol-Myers Squibb Company, 03/17/23 | 67.50 | 10 | 80,280 | 13,625 | ||||||||||||

| Bristol-Myers Squibb Company, 03/17/23 | 72.50 | 10 | 80,280 | 9,175 | ||||||||||||

| Citigroup, Inc., 01/20/23 | 47.50 | 10 | 48,410 | 2,870 | ||||||||||||

| Corning, Inc., 01/20/23 | 32.00 | 20 | 68,260 | 5,700 | ||||||||||||

| Corning, Inc., 01/20/23 | 35.00 | 10 | 34,130 | 1,040 | ||||||||||||

| Corning, Inc., 01/20/23 | 37.00 | 30 | 102,390 | 990 | ||||||||||||

| Diebold Nixdorf, Inc., 02/17/23 | 3.00 | 25 | 5,375 | 375 | ||||||||||||

| Diebold Nixdorf, Inc., 05/19/23 | 2.00 | 15 | 3,225 | 975 | ||||||||||||

| Diebold Nixdorf, Inc., 05/19/23 | 2.50 | 25 | 5,375 | 1,250 | ||||||||||||

| Equitable Holdings, Inc., 01/20/23 | 25.00 | 5 | 15,870 | 3,475 | ||||||||||||

| Equitable Holdings, Inc., 01/20/23 | 30.00 | 55 | 174,570 | 13,887 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 12.50 | 15 | 12,060 | 113 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 15.00 | 30 | 24,120 | 225 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 17.50 | 10 | 8,040 | 75 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 20.00 | 30 | 24,120 | 225 | ||||||||||||

| iHeartMedia, Inc., - Class A, 04/21/23 | 7.50 | 25 | 20,100 | 4,562 | ||||||||||||

| Itau Unibanco Holding S.A. - ADR, 01/20/23 | 4.50 | 10 | 4,980 | 1,132 | ||||||||||||

| Itau Unibanco Holding S.A. - ADR, 01/20/23 | 5.00 | 20 | 9,960 | 1,402 | ||||||||||||

7

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| PURCHASED OPTION | ||||||||||||||||

| CONTRACTS — 3.4% | Notional | |||||||||||||||

| (Continued) | Strike Price | Contracts | Value | Value | ||||||||||||

| Call Option Contracts — 3.4% (Continued) | ||||||||||||||||

| Jackson Financial, Inc., - Class A, 01/20/23 | $ | 25.00 | 5 | $ | 18,675 | $ | 6,750 | |||||||||

| Jackson Financial, Inc., - Class A, 01/20/23 | 30.00 | 35 | 130,725 | 30,100 | ||||||||||||

| MultiPlan Corporation, 01/20/23 | 5.00 | 110 | 16,390 | 550 | ||||||||||||

| MultiPlan Corporation, 01/20/23 | 7.50 | 10 | 1,490 | 250 | ||||||||||||

| O-I Glass, Inc., 12/16/22 | 12.00 | 5 | 8,205 | 2,250 | ||||||||||||

| Paramount Global - Class B, 01/20/23 | 30.00 | 10 | 20,080 | 50 | ||||||||||||

| Pfizer, Inc., 01/20/23 | 47.00 | 30 | 150,390 | 11,700 | ||||||||||||

| Pfizer, Inc., 01/20/23 | 50.00 | 40 | 200,520 | 7,520 | ||||||||||||

| PG&E Corporation, 01/23/23 | 10.00 | 10 | 15,700 | 5,650 | ||||||||||||

| Spectrum Brands Holdings, Inc., 01/20/23 | 75.00 | 15 | 79,905 | 3,638 | ||||||||||||

| Valvoline, Inc., 12/19/22 | 30.00 | 20 | 65,960 | 6,100 | ||||||||||||

| Viatris, Inc., 01/20/23 | 10.00 | 40 | 44,120 | 5,000 | ||||||||||||

| Viatris, Inc., 01/20/23 | 12.50 | 50 | 55,150 | 500 | ||||||||||||

| Viatris, Inc., 01/20/23 | 15.00 | 160 | 176,480 | 400 | ||||||||||||

| Total Purchased Option Contracts (Cost $213,662) | $ | 1,732,695 | $ | 141,954 | ||||||||||||

| MONEY MARKET FUNDS — 22.4% | Shares | Value | ||||||

| Federated Hermes Treasury Obligations Fund - Service Shares, 3.41% (b) (Cost $929,422) | 929,422 | $ | 929,422 | |||||

| Investments at Value — 99.6% (Cost $3,766,271) | $ | 4,139,525 | ||||||

| Other Assets in Excess of Liabilities — 0.4% | 15,370 | |||||||

| Net Assets — 100.0% | $ | 4,154,895 | ||||||

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of November 30, 2022. |

ADR - American Depositary Receipt

AG - Aktiengesellschaft

plc - Public Limited Company

S.A. - Société anonyme

See accompanying notes to financial statements.

8

| ADLER VALUE FUND |

| STATEMENT OF ASSETS AND LIABILITIES |

| November 30, 2022 (Unaudited) |

| ASSETS | ||||

| Investments in securities: | ||||

| At cost | $ | 3,766,271 | ||

| At value (Note 2) | $ | 4,139,525 | ||

| Receivable from Adviser (Note 4) | 11,152 | |||

| Dividends receivable | 11,882 | |||

| Other assets | 12,135 | |||

| Total assets | 4,174,694 | |||

| LIABILITIES | ||||

| Payable for investment securities purchased | 5,716 | |||

| Payable to administrator (Note 4) | 7,030 | |||

| Other accrued expenses | 7,053 | |||

| Total liabilities | 19,799 | |||

| NET ASSETS | $ | 4,154,895 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid-in capital | $ | 3,535,295 | ||

| Accumulated earnings | 619,600 | |||

| NET ASSETS | $ | 4,154,895 | ||

| PRICING OF INSTITUTIONAL SHARES (Note 2) | ||||

| Net assets applicable to Institutional Shares | $ | 4,154,895 | ||

| Shares of Institutional Shares outstanding (no par value, unlimited number of shares authorized) | 154,895 | |||

| Net asset value, offering and redemption price per share (Note 2) | $ | 26.82 |

See accompanying notes to financial statements.

9

| ADLER VALUE FUND |

| STATEMENT OF OPERATIONS |

| For the Six Months Ended November 30, 2022 (Unaudited) |

| INVESTMENT INCOME | ||||

| Dividends | $ | 41,221 | ||

| Foreign withholding tax on dividends | (724 | ) | ||

| Total investment income | 40,497 | |||

| EXPENSES | ||||

| Investment advisory fees (Note 4) | 19,452 | |||

| Fund accounting fees (Note 4) | 15,196 | |||

| Administration fees (Note 4) | 15,000 | |||

| Legal fees | 11,635 | |||

| Trustees’ fees and expenses (Note 4) | 9,731 | |||

| Audit and tax services fees | 8,361 | |||

| Registration and filing fees | 6,983 | |||

| Transfer agent fees (Note 4) | 6,000 | |||

| Compliance fees (Note 4) | 6,000 | |||

| Custodian and bank service fees | 4,804 | |||

| Shareholder reporting expenses | 4,208 | |||

| Insurance expense | 1,490 | |||

| Postage and supplies | 582 | |||

| Other expenses | 4,046 | |||

| Total expenses | 113,488 | |||

| Less fee reductions and expense reimbursements by the Adviser (Note 4) | (89,173 | ) | ||

| Net expenses | 24,315 | |||

| NET INVESTMENT INCOME | 16,182 | |||

| REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | ||||

| Net realized losses on investments transactions | (7,667 | ) | ||

| Net change in unrealized appreciation (depreciation) on investments | (135,934 | ) | ||

| NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | (143,601 | ) | ||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (127,419 | ) |

See accompanying notes to financial statements.

10

| ADLER VALUE FUND |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Six Months | ||||||||

| Ended | ||||||||

| November 30, | Year Ended | |||||||

| 2022 | May 31, | |||||||

| (Unaudited) | 2022 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 16,182 | $ | 132,311 | ||||

| Net realized gains (losses) from investment transactions | (7,667 | ) | 433,006 | |||||

| Net change in unrealized appreciation (depreciation) on investments | (135,934 | ) | (639,008 | ) | ||||

| Net decrease in net assets resulting from operations | (127,419 | ) | (73,691 | ) | ||||

| DISTRIBUTIONS TO SHAREHOLDERS (NOTE 2) | ||||||||

| Institutional Shares | — | (326,422 | ) | |||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

| Institutional Shares | ||||||||

| Proceeds from shares sold | 79,950 | 556,469 | ||||||

| Net asset value of shares issued in reinvestment of distributions to shareholders | — | 326,422 | ||||||

| Payments for shares redeemed | — | (75,104 | ) | |||||

| Net increase in Institutional Shares net assets from capital share transactions | 79,950 | 807,787 | ||||||

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (47,469 | ) | 407,674 | |||||

| NET ASSETS | ||||||||

| Beginning of period | 4,202,364 | 3,794,690 | ||||||

| End of period | $ | 4,154,895 | $ | 4,202,364 | ||||

| CAPITAL SHARES ACTIVITY | ||||||||

| Institutional Shares | ||||||||

| Shares sold | 3,166 | 18,654 | ||||||

| Shares reinvested | — | 11,295 | ||||||

| Shares redeemed | — | (2,634 | ) | |||||

| Net increase in shares outstanding | 3,166 | 27,315 | ||||||

| Shares outstanding, beginning of period | 151,729 | 124,414 | ||||||

| Shares outstanding, end of period | 154,895 | 151,729 | ||||||

See accompanying notes to financial statements.

11

| ADLER VALUE FUND |

| INSTITUTIONAL SHARES |

| FINANCIAL HIGHLIGHTS |

Per Share Data for a Share Outstanding Throughout Each Period

| Six Months | ||||||||||||||||||||

| Ended | ||||||||||||||||||||

| November 30, | Year Ended | Year Ended | Period Ended | Period Ended | ||||||||||||||||

| 2022 | May 31, | May 31, | May 31, | July 31, | ||||||||||||||||

| (Unaudited) | 2022 | 2021 | 2020(a) | 2019(b) | ||||||||||||||||

| Net asset value at beginning of period | $ | 27.70 | $ | 30.50 | $ | 19.82 | $ | 20.41 | $ | 20.00 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income | 0.11 | (c) | 0.95 | (c) | 0.07 | (c) | 0.49 | (d) | 0.15 | |||||||||||

| Net realized and unrealized gains (losses) on investments | (0.99 | ) | (1.35 | ) | 10.92 | (0.88 | ) | 0.26 | ||||||||||||

| Total from investment operations | (0.88 | ) | (0.40 | ) | 10.99 | (0.39 | ) | 0.41 | ||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | — | (2.30 | ) | (0.31 | ) | (0.20 | ) | — | ||||||||||||

| Net realized gains | — | (0.10 | ) | — | — | — | ||||||||||||||

| Total distributions | — | (2.40 | ) | (0.31 | ) | (0.20 | ) | — | ||||||||||||

| Net asset value at end of period | $ | 26.82 | $ | 27.70 | $ | 30.50 | $ | 19.82 | $ | 20.41 | ||||||||||

| Total return (e) | (3.18 | %) (f) | (1.64 | %) | 55.78 | % | (2.01 | %) (f) | 2.05 | % (f) | ||||||||||

| Net assets at end of period (000’s) | $ | 4,155 | $ | 4,202 | $ | 3,795 | $ | 1,458 | $ | 1,447 | ||||||||||

| Ratios/supplementary data: | ||||||||||||||||||||

| Ratio of total expenses to average net assets | 5.83 | % (g) | 5.65 | % | 8.42 | % | 13.01 | % (g) | 11.82 | % (g) | ||||||||||

| Ratio of net expenses to average net assets (h) | 1.25 | % (g) | 1.25 | % | 1.25 | % | 1.25 | % (g) | 1.26 | % (g)(i) | ||||||||||

| Ratio of net investment income to average net assets (h) | 0.83 | % (g) | 3.23 | % (j) | 0.27 | % | 2.93 | % (d)(g) | 0.81 | % (g) | ||||||||||

| Portfolio turnover rate | 12 | % (f) | 45 | % | 0 | % (k) | 4 | % (f) | 0 | % | ||||||||||

| (a) | Fund changed fiscal year to May 31. |

| (b) | Represents the period from the commencement of operations (August 16, 2018) through July 31, 2019. |

| (c) | Per share net investment income has been determined on the basis of average number of shares outstanding during the period. |

| (d) | During the period ended May 31, 2020, the Fund received a large special dividend distribution from NortonLifeLock, Inc. Had the Fund not received this special dividend distribution, the net investment income per share and ratio of net investment income to average net assets would have been $0.33 and 1.97%(g) lower, respectively. |

| (e) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced fees and reimbursed expenses (Note 4). |

| (f) | Not annualized. |

| (g) | Annualized. |

| (h) | Ratio was determined after advisory fee reductions and expense reimbursements (Note 4). |

| (i) | Includes federal excise taxes of 0.01% of average net assets with respect to the period ended July 31, 2019. |

| (j) | During the year ended May 31, 2022, the Fund received a large special dividend distribution from Meredith Corporation. Had the Fund not received this special dividend distribution, the net investment income per share and ratio of net investment income to average net assets would have been $0.82 and 2.79% lower, respectively. |

| (k) | Percentage rounds to less than 1%. |

See accompanying notes to financial statements.

12

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS |

| November 30, 2022 (Unaudited) |

1. Organization

Adler Value Fund (the “Fund”) is a non-diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report.

The investment objective of the Fund is to seek to achieve long-term growth of capital.

The Fund currently offers one class of shares: Institutional Class shares (sold without any sales loads or distribution fees and subject to a $2,500 initial investment for all accounts, except for an IRA for which the minimum initial investment is $1,000).

2. Significant Accounting Policies

The Fund follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.” The following is a summary of the Fund’s significant accounting policies used in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

New accounting pronouncements – In October 2020, the Securities and Exchange Commission (the “SEC”) adopted new regulations governing the use of derivatives by registered investment companies (“Rule 18f-4”). The Fund was required to comply with Rule 18f-4 by August 19, 2022. Rule 18f-4 imposes limits on the amount of derivatives a fund can enter into, eliminates the asset segregation framework previously used by funds to comply with Section 18 of the 1940 Act, tracks derivatives as senior securities and requires funds whose use of derivatives is more than a limited specified exposure amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. The Fund is currently complying with Rule 18f-4.

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern Time) on each day the NYSE is open for business. The Fund generally values its listed securities on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. Option contracts are valued at the closing price on the exchanges on which they are primarily traded; if no closing price is available at the time of valuation, the option will be valued at the mean of the closing bid and ask prices for that day. Investments representing shares of money market funds and other open-end investment companies not traded on an exchange are valued at their net asset value (“NAV”) as reported by such companies. When using a quoted price and when the market is considered active, the security will be classified as Level 1 within the fair value hierarchy (see next page). In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with

13

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

procedures established by and under the general supervision of the Board of Trustees of the Trust (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s NAV may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| ● | Level 1 – quoted prices in active markets for identical securities |

| ● | Level 2 – other significant observable inputs |

| ● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the Fund’s investments based on the inputs used to value the investments as of November 30, 2022:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Common Stocks | $ | 2,984,485 | $ | — | $ | — | $ | 2,984,485 | ||||||||

| Preferred Stocks | 83,664 | — | — | 83,664 | ||||||||||||

| Purchased Option Contracts | 30,695 | 111,259 | — | 141,954 | ||||||||||||

| Money Market Funds | 929,422 | — | — | 929,422 | ||||||||||||

| Total | $ | 4,028,266 | $ | 111,259 | $ | — | $ | 4,139,525 | ||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common and preferred stocks by sector and industry type. The Fund did not have any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of or during the six months ended November 30, 2022.

Share valuation – The NAV per share of each class of the Fund is calculated daily by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class. The offering price and redemption price per share of each class of the Fund is equal to the NAV per share of such class.

14

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

Investment income – Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair value of the security received. Interest income is accrued as earned. Withholding taxes on foreign dividends, if any, have been recorded in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Investment transactions – Investment transactions are accounted for on the trade date.

Realized gains and losses on investments sold are determined on a specific identification basis.

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series, the number of series in the Trust, or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – Distributions to shareholders arising from net investment income and realized capital gains, if any, are declared and paid annually to shareholders. The amount of distributions from net investment income and net realized capital gains are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. For the year ended May 31, 2021, the tax character of distributions paid to shareholders was ordinary income of $313,110 and long-term capital gain of $13,312. There were no distributions paid to shareholders during the six months ended November 30, 2022.

Purchased option contracts – The Fund may use option contracts in any manner consistent with its investment objectives and as long as its use is consistent with relevant provisions of the 1940 Act. The Fund may use options for speculative purposes as well as for the purpose of seeking to reduce the overall investment risk that would otherwise be associated with the securities in which the Fund invests. When the Fund purchases a call or put option, an amount equal to the total premium (the premium plus the commission) paid by the Fund is recorded as an asset on the Fund’s Statement of Assets and Liabilities and is subsequently marked-to-market daily. Premiums paid in the purchase of options which expire are treated as realized losses. Premiums paid in the purchase of call options which are exercised increase the cost of the security purchased. Premiums paid in the purchase of put options which are exercised decrease the proceeds used to calculate the realized capital gain or loss on the sale of the security.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of increase (decrease) in net assets from operations during the reporting period. Actual results could differ from those estimates.

15

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986, as amended (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year amounts equal to at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the 12 months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of May 31, 2022:

| Tax cost of investments | $ | 3,684,442 | ||

| Gross unrealized appreciation | $ | 762,930 | ||

| Gross unrealized depreciation | (253,745 | ) | ||

| Net unrealized appreciation | 509,185 | |||

| Undistributed long-term gains | 257,372 | |||

| Accumulated capital and other losses | (19,538 | ) | ||

| Distributable earnings | $ | 747,019 | ||

Net qualified late year ordinary losses represent losses incurred after December 31, 2021. These losses are deemed to arise on the first day of the Fund’s next taxable year. For the year ended May 31, 2022, the Fund qualified late year ordinary losses of $19,538.

The federal tax cost, unrealized appreciation (depreciation) as of November 30, 2022 is as follows:

| Tax cost of investments | $ | 3,766,274 | ||

| Gross unrealized appreciation | 857,353 | |||

| Gross unrealized depreciation | (484,102 | ) | ||

| Net unrealized appreciation | 373,251 | |||

The difference between the federal income tax cost of investments and the financial statement cost of investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are due to the tax deferral of losses on wash sales.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for the current and all open tax periods (generally, three years) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. federal.

16

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

3. Investment Transactions

During the six months ended November 30, 2022, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $358,924 and $397,844, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Adler Asset Management, LLC (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an investment advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has agreed, until December 1, 2023, to reduce its investment advisory fees and reimburse other expenses to limit total annual operating expenses (exclusive of brokerage costs; taxes; interest; borrowing costs such as interest and dividends expenses on securities sold short; costs to organize the Fund; acquired fund fees and expenses; and extraordinary expenses such as litigation and merger or reorganization costs and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding 1.25% of the Fund’s average daily net assets of the Institutional Class shares. Accordingly, during the six months ended November 30, 2022, the Adviser did not collect any of its investment advisory fees and reimbursed other operating expenses totaling $69,721.

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause the Fund’s total annual operating expenses to exceed the lesser of (i) the expense limitation then in effect, if any, and (ii) the expense limitation in effect at the time the expenses to be repaid were incurred. As of November 30, 2022, the Adviser may seek recoupment of investment advisory fee reductions and expense reimbursements no later than the dates as stated below:

| May 31, 2023 | $ | 86,012 | ||

| May 31, 2024 | 179,743 | |||

| May 31, 2025 | 180,253 | |||

| November 30, 2025 | 89,173 | |||

| Total | $ | 535,181 | ||

17

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies, and certain costs related to the pricing of the Fund’s portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers and a Trustee of the Trust are also officers of Ultimus and are not paid by the Fund for serving in such capacities.

TRUSTEE COMPENSATION

Effective October 17, 2022, each member of the Board (a “Trustee”) who is not an “interested person” (as defined by the 1940 Act, as amended) of the Trust (“Independent Trustee”) receives a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who receives a $1,700 annual retainer from the Fund, paid quarterly and the Audit Committee Chairperson who receives a $1,500 annual retainer from the Fund, paid quarterly. Each Independent Trustee also receives from the Fund a fee of $550 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to October 17, 2022, no annual retainer was designated specifically for the Audit Committee Chairperson.

PRINCIPAL HOLDER OF FUND SHARES

As of November 30, 2022, the following shareholder owned of record 25% or more of the outstanding shares of the Fund:

| NAME OF RECORD OWNER | % Ownership | |

| David R. Adler | 60% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

18

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

5. Derivative Transactions

The location on the Statement of Assets and Liabilities of the derivative positions of the Fund are as follows:

| Average | ||||||||||||||||

| Fair Value | Monthly | |||||||||||||||

| Notional Value | ||||||||||||||||

| Six Months | ||||||||||||||||

| Ended | ||||||||||||||||

| Type of | Asset | Liability | November 30, | |||||||||||||

| Derivative | Risk | Location | Derivatives | Derivatives | 2022* | |||||||||||

| Equity call options purchased | Equity | Investments in securities at value | $ | 141,954 | $ | — | $ | 1,568,677 | ||||||||

| * | The average monthly notional value generally represents the Fund’s derivative activity throughout the period. |

Realized and unrealized gains and losses associated with transactions in derivative instruments for the Fund during the six months ended November 30, 2022 are recorded in the following locations on the Statement of Operations:

| Change in | ||||||||||||||

| Unrealized | ||||||||||||||

| Type of | Realized | Appreciation | ||||||||||||

| Derivative | Risk | Location | Losses | Location | (Depreciation) | |||||||||

| Equity call options purchased | Equity | Net realized losses on investment transactions | $ | (18,758 | ) | Net change in unrealized appreciation (depreciation) on investments | $ | (88,164 | ) | |||||

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations, warranties, and general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

19

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events except for the following:

On December 27, 2022, the Fund paid a long-term capital gain distribution of $1.6617 per share to shareholders of record on December 23, 2022.

20

| ADLER VALUE FUND |

| LIQUIDITY RISK MANAGEMENT PROGRAM (Unaudited) |

The Fund has adopted and implemented a written liquidity risk management program (the “Program”) as required by Rule 22e-4 (the “Liquidity Rule”) under the Investment Company Act of 1940, as amended. The Program is reasonably designed to assess and manage the Fund’s liquidity risk, taking into consideration, among other factors, the Fund’s investment strategy and the liquidity of its portfolio investments during normal and reasonably foreseeable stressed conditions; its short- and long-term cash flow projections; and its cash holdings and access to other funding sources. The Fund’s Board of Trustees (the “Board”) approved the appointment of the Liquidity Administrator Committee, comprising of the Fund’s Adviser and certain Trust officers, to be responsible for the Program’s administration and oversight and for reporting to the Board on at least an annual basis regarding the Program’s operation and effectiveness. The annual written report assessing the Program (the “Report”) was presented to the Board at the October 17 – 18, 2022 Board meeting and covered the period from June 1, 2021 to May 31, 2022 (the “Review Period”).

During the Review Period, the Fund did not experience unusual stress or disruption to its operations related to purchase and redemption activity. Also, during the Review Period, the Fund held adequate levels of cash and highly liquid investments to meet shareholder redemption activities in accordance with applicable requirements. The Report concluded that the Program is reasonably designed to prevent violation of the Liquidity Rule and the Program has been effectively implemented.

21

| ADLER VALUE FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period June 1, 2022) and held until the end of the period (November 30, 2022).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge sales loads.

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

22

| ADLER VALUE FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued) |

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning | Ending | |||||||

| Account Value | Account Value | Expenses | ||||||

| June 1, | November 30, | Net Expense | Paid During | |||||

| Institutional Class | 2022 | 2022 | Ratio(a) | Period(b) | ||||

| Based on Actual Fund Return | $1,000.00 | $968.20 | 1.25% | $6.17 | ||||

| Based on Hypothetical 5%Return (before expenses) | $1,000.00 | $1,018.80 | 1.25% | $6.33 |

| (a) | Annualized, based on the Fund’s most recent one-half year expenses. |

| (b) | Expenses are equal to the Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

23

| ADLER VALUE FUND |

| OTHER INFORMATION (Unaudited) |

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling 1-800-408-4682, or on the SEC’s website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, 2022 is also available without charge upon request by calling 1-800-408-4682, or on the SEC’s website at www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. These filings are available upon request by calling 1-800-408-4682. Furthermore, you may obtain a copy of the filings on the SEC’s website at www.sec.gov and the Fund’s website at www.adlervaluefund.com.

24

| ADLER VALUE FUND |

| CUSTOMER PRIVACY NOTICE |

| FACTS | WHAT DOES THE ADLER VALUE FUND (the “Fund”) DO WITH YOUR PERSONAL INFORMATION? |

| Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

| What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include: |

| ■ Social Security number | |

| ■ Assets | |

| ■ Retirement Assets | |

| ■ Transaction History | |

| ■ Checking Account Information | |

| ■ Purchase History | |

| ■ Account Balances | |

| ■ Account Transactions | |

| ■ Wire Transfer Instructions | |

| When you are no longer our customer, we continue to share your information as described in this notice. |

| How? | All financial companies need to share your personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons the Fund chooses to share; and whether you can limit this sharing. |

| Does the | Can you limit | |

| Reasons we can share your personal information | Fund share? | this sharing? |

| For our everyday business purposes – | ||

| Such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus | Yes | No |

| For our marketing purposes – | ||

| to offer our products and services to you | No | We don’t share |

| For joint marketing with other financial companies | No | We don’t share |

| For our affiliates’ everyday business purposes – | ||

| information about your transactions and experiences | No | We don’t share |

| For our affiliates’ everyday business purposes – | ||

| information about your creditworthiness | No | We don’t share |

| For nonaffiliates to market to you | No | We don’t share |

| Questions? | Call 1-800-408-4682 |

25

| ADLER VALUE FUND |

| CUSTOMER PRIVACY NOTICE (Continued) |

| Who we are | |

| Who is providing this notice? | Adler Value Fund

Ultimus Fund Distributors, LLC (Distributor)

Ultimus Fund Solutions, LLC (Administrator) |

| What we do | |

| How does the Fund protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings.

Our service providers are held accountable for adhering to strict policies and procedures to prevent any misuse of your nonpublic personal information. |

| How does the Fund collect my personal information? | We collect your personal information, for example, when you

■ Open an account

■ Provide account information

■ Give us your contact information

■ Make deposits or withdrawals from your account

■ Make a wire transfer

■ Tell us where to send the money

■ Tell us who receives the money

■ Show your government-issued ID

■ Show your driver’s license

We also collect your personal information from other companies. |

| Why can’t I limit all sharing? | Federal law gives you the right to limit only

■ Sharing for affiliates’ everyday business purposes – information about your creditworthiness

■ Affiliates from using your information to market to you

■ Sharing for nonaffiliates to market to you

State laws and individual companies may give you additional rights to limit sharing. |

| Definitions | |

| Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies. |

| ■ Adler Asset Management, LLC, the investment adviser to the Fund, could be deemed to be an affiliate. | |

| Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies |

| ■ The Fund does not share with nonaffiliates so they can market to you. | |

| Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you. |

| ■ The Fund does not jointly market. | |

26

This page intentionally left blank.

This page intentionally left blank.

ADLER-SAR-22

EVOLUTIONARY TREE INNOVATORS FUND

I Class Shares (INVNX)

A Class Shares (INVTX)

Semi-Annual Report

November 30, 2022

(Unaudited)

| EVOLUTIONARY TREE INNOVATORS FUND | |

| LETTER TO SHAREHOLDERS (Unaudited) | December 20, 2022 |

Dear Fellow Shareholders,

As we exit 2022, the markets are still grappling with a collection of macro and geopolitical headwinds—namely, heightened inflation, the Federal Reserve raising rates, Putin’s war in Ukraine, and a potential recession forthcoming. However, there are glimmers of stabilization, which may set the stage for better news over time. We believe we are starting to see early signs that certain holdings in the Fund are nearing “terra firma,” supported by a combination of strong underlying business growth, evolutionary shifts/trends, and innovation-based catalysts.

To be clear, we are not “calling the bottom” in the markets (no one can time the market or the economy), but we are starting to see some stabilization for a subset of growth and innovation companies, particularly the quality innovators. To use a colloquialism, these would be the “babies thrown out with the bathwater.” The common theme for these companies is that they generally have resilient businesses and can grow despite a recessionary environment, with growth often driven by specific new products or services that are still early in adoption (what we call innovation catalysts).

For newer investors to the Evolutionary Tree Innovators Fund, we provide below a brief overview of our investment approach and why we focus on long-term drivers such as innovation versus trying to predict or side-step movements in the market or economy. For investors that are more familiar with our innovation-focused strategy, please jump to the sections on our perspective on the current environment and why we believe the underlying companies owned in the Fund are well positioned, as a group, to drive sustainable growth.

How Our Approach Enables Investors to Access Leading and Quality Innovative Businesses

The Evolutionary Tree Innovators Fund was launched to provide an attractive pathway for investing in important innovations and secular trends, or evolutionary shifts as we call them. The Fund and its adviser apply an innovation and evolution-focused framework to investing. We believe the development of innovation and its resultant pattern of evolutionary change is the primary engine of growth for companies, industries, and the economy—and, in turn, is the underlying driver of long-term wealth creation. While investors are currently focused on near-term macro drivers, such as the Fed, inflation, and the war in Ukraine, we believe innovation can still drive growth for leading innovators and remains critically important for long-term investors.

The Fund seeks to identify important innovations that are driving secular growth and evolutionary shifts for companies, industries, and the economy, and own the leading innovators at the forefront. The Fund defines an evolutionary shift as when an industry shifts from an old generation (of a product, service, or business model) over to a “next generation” or new offering that provides advantages versus the “old way” of doing things. The Fund invests in a focused portfolio of 25-35 quality innovative businesses.

1

Examples of innovations that we believe contribute to sustainable growth include technological innovation, product innovation, service or experience innovation, process or cost innovation, and/or business model innovation. In addition to contributing to sustaining growth for leading innovative businesses, new innovations may also enable innovators to take market share, create competitive advantage, and/or enhance profitability over time. Innovation is the root cause of value creation.

Perspective on the Volatile Markets and Near-term Economic Environment

While day-to-day volatility continues in the markets, the Fund experienced some stabilization in the first half of the fiscal year (May 31 through November 30) relative to prior periods, but slightly lagged its benchmark. During the first half of the fiscal year, the I Class of the Fund declined 3.00% versus the broader S&P 500 Index return of 2.61%.

The bear market has also shifted, from primarily penalizing growth equities earlier in the year to broadening out to value and cyclical stocks, and with higher rates, even bonds are now in a severe bear market. In short, the pain has expanded to most investment styles and asset classes. Given that growth stocks entered the bear market first (starting last year) and are thus potentially much further along in the retrenchment process, it is conceivable that they will have an opportunity to be one of the first to emerge out of the bear market.

Why is growth showing early signs of stabilization? We believe investors are beginning to show renewed interest in embracing secular growth companies for two reasons. First, with a slowing economy, investors are looking for companies that can grow through a potential recession, and this “search for growth” naturally brings them to innovative companies benefiting from secular trends and driving sustainable growth with new products and services. The holdings in the Fund continue delivering well-above-average growth (approximately 30% revenue growth, on a weighted-average basis) with stable-to-improving profitability, while preserving solid balance sheets. Second, increasingly investors are beginning to appreciate that, after a significant pullback, stock prices and valuations for quality companies may now be reaching attractive levels.

Our Views on Putting the Macro and Market Environment into Perspective

| 1. | While inflation is high currently, it is likely at or near peak levels and will ease gradually over time, particularly as the global economy slows. Signs of easing inflation will start to stabilize the markets and, in particular, growth stocks. We may already be seeing signs of this dynamic. It is early, but some progress is being made. |

| 2. | A slowing economy, driven by the ending of one-time pandemic subsidies and monetary policy tightening by the Fed, will begin to ease prices across a growing number of cost inputs. The recent pullback in commodity prices is already revealing this potential. |

| 3. | Technology companies, particularly software companies, are a part of the solution to the labor shortage issue, as companies look to drive cost efficiencies. Quality technology leaders may be attractively valued, in our opinion. Our 8 investment criteria lead us to quality innovators, including those in the enterprise software space. |

2

| 4. | Healthcare companies, almost a quarter of the Fund, are showing relative resilience in this economy as demand for advanced treatments continues despite the slow economy. In addition to strong demand, healthcare holdings are benefiting from a number of innovation catalysts (new products being launched). |

| 5. | A slower economy will hurt cyclical industries, which we avoid, while highlighting the value of secular growth industries and innovators, which can generally grow through difficult economic environments. Innovative businesses have multiple growth drivers such as new products, services, and market share gains— independent of the economy. |

| 6. | We believe “growth is the new value,” and lower valuations may entice investors to re-embrace growth and innovation over time. The timing of this process is unknown, particularly given the collection of macro headwinds, but we believe patience will be rewarded. |

While Inflation Remains Too High, We Are Starting to See Signs of Progress by the Fed’s Tightening Campaign

The primary driver of so much of the volatility in the markets is related to high inflation, which has led to one of the fastest tightening cycles. Until inflation is brought in check, the markets are likely to remain highly volatile. However, it is important to note that we are actually seeing early signs of progress by the Fed in reducing the sources of inflation. In fact, a number of key components of inflation have seen pretty dramatic declines from peak levels, most notably the price of oil/gasoline, shipping costs, and various commodities. There are other inputs that remain stubbornly high, such as the price of food and rent. So, the Fed has more work to do, but, again, progress is being made.

Equally important to bringing down inflation across key inputs is the Fed’s focus on preventing inflation expectations from becoming entrenched longer-term, which could lead to runaway inflation and the dreaded “stagflation” environment of high inflation plus low growth. This is one of the reasons the Fed is raising rates so aggressively—to cut off the conversion of short-term inflation into long-term “stickier” inflation. As long-term investors, this is a goal we support, even if it creates some short-term pain.

One method to track progress on this front is to study consumer inflation expectations, and the New York Fed conducts such a survey (source: www.newyorkfed.org). The good, but early, news is that we are starting to see a step in the right direction, as both 1-year and 3-year inflation expectations by consumers have peaked and are clearly coming down. The 1-year expectation of 5-6% remains too high, but is down from near 7%, while consumer inflation expectations for 3-years out are quite low.

Innovative Businesses Have Fuel—Innovation and Trends—to Power Through Recessionary Environments

We believe quality innovators that have developed and are launching new products and services may be less impacted from a recession than cyclical companies that are highly dependent on growth in the broader economy.

In general, we have found that the companies that are most protected, at least on a relative basis, are the ones that offer mission critical and highly essential products and services. One example is Service Now, an enterprise software company, that enables companies

3

to deliver phenomenal customer service experiences using its cloud-based platform. Companies are literally running big parts of their businesses on this platform. Second, companies that sell to larger organizations with stable IT budgets can also be more insulated. For example, Axon, a dominant leader in body cameras, tasers, and software technology for police departments, is benefiting from expanded funding for police tech (at both the federal and local levels) to promote transparency, accountability, and improved officer effectiveness.

In addition, companies with longer-duration contracts may also see less impact from short-term economic slumps. A great example here is nCino, which developed the Bank Operating System, a cloud-based platform for banks to manage workflows for multiple lines of business. New rollouts of nCino’s suite of offerings across loan origination or retail bank departments often take years to implement and then are used for many, many years. Companies with technology platforms and suites, such as nCino, are also fairly protected because they represent solutions for driving worker productivity, reducing complexity, and lowering costs—goals that are embraced by clients during recessionary periods.

Lastly, companies with strong and/or growing profitability with robust balance sheets are better insulated from recessions, especially in a rising rate environment. Well-funded businesses typically have balance sheets and/or strong cash flow generation that funds their growth and allows them to out-invest their competitors. As a result, these quality innovators often emerge from a recession stronger, as weaker competitors under-invest.

To be clear, no company is completely immune from the negative impact of recessions. We believe, however, that it will be the highly innovative companies that will have the fuel to drive above-average growth, on average, through recessionary environments, especially relative to less-innovative companies or those that are highly cyclical.

In addition to new innovations fueling growth for quality innovators, there is a second force that is often ignored, but equally as powerful in sustaining growth for certain businesses. This force is secular trends, or what we call evolutionary shifts: when an industry shifts from an older generation of an offering (e.g., product, service, or business model) to a next-generation offering that provides advantages to customers versus the “old way.” These shifts or secular trends can take years, even decades, to play out as consumers shift gradually over time. All of our investment holdings benefit from different secular trends, often driven by the underlying innovations they develop. Key point: In a recessionary environment, these shifts and trends are still moving forward, providing another wind at the back of these innovative businesses and helping to sustain growth.

A few standout examples illustrate this dynamic. Airbnb, for one, is driving a shift away from traditional hotels to alternative accommodations, not to mention the consumer shift toward spending more on experiences. The shift to alternative accommodations also benefits from the “trade down” effect that happens in recessions, when consumers are looking for great value. Another example is Stryker, a leader in medtech, that benefits from the shift toward less invasive and even robotic surgery for knee and hip replacements. Lastly, both Microsoft and Amazon’s AWS benefit from the shift from on-premise datacenters toward the use of public cloud-based infrastructure-as-a-service (IaaS), a shift that most companies are embracing on their Digital Transformation journeys.

4

Recent Innovation Catalysts May Further Sustain Growth & Resilience, Especially in Healthcare

Innovators continue to innovate, even in a recessionary-like environment. When innovative businesses announce a major update on a new innovation in their pipeline or when they launch a new product or service, this is considered a “catalyst”, and investors often take notice because it drives another wave of growth. In recent months, we have seen a number of new catalysts that have benefited our healthcare holdings, which comprise up to a quarter of the Fund. This was a primary driver of a rebound in a number of biotech and medtech companies held in the Fund during the quarter.

We own companies, such as Sarepta and Argenx, both biotech companies that offer treatments for severe diseases, where new treatments are often desperately needed. We have seen important new catalysts for both companies. Argenx gained FDA approval for its new treatment, Vyvgart, for an autoimmune disease called myasthenia gravis, and this launch is exceeding expectations. It also reported positive phase 3 clinical results for Vyvgart in a second large autoimmune indication, immune thrombocytopenia (ITP). Sarepta, meanwhile, has reported updates on its clinical trials for Duchenne’s muscular dystrophy (DMD), which showed strong safety and potential functional benefits for patients that normally lose their ability to move. The FDA has encouraged Sarepta to file early using an accelerated approval process, with potential launch in 2023.

Another innovation catalyst that benefited the Fund was the recent FDA approval of Revance’s Botox competitor, Daxxify, which has shown twice the durability of Botox (injected every 6 months vs every 3 months for Botox). Revance also just recently filed for FDA approval for Daxxify in cervical dystonia, a new therapeutic indication, which is supported by positive Phase 3 clinical trial results, also with the extended 6-month duration.

We have tended to overweight the Fund to healthcare-related companies because they are often some of the most innovative companies in our economy, especially those with breakthrough treatments. But healthcare companies are also some of the most resilient during recessionary times. Healthcare spending tends to be quite resilient because demand is fairly inelastic. It generally does not change much based on the economy, so demand tends to be pretty consistent. Second, the FDA and its approval process is unaffected by the economy, and we are actually seeing the FDA become more accommodative to new drug approvals, especially for treatments that offer important breakthrough benefits for patients with an unmet medical need. We are also seeing a growing number of acquisitions of biotech companies by larger pharmaceutical companies, which can, at times, provide a valuation floor for quality biotech companies.

The bottom line: The healthcare holdings are great examples—despite all the macro headwinds—of how innovation catalysts are driving strong growth (such as with Argenx’s launch of Vyvgart) or enabling companies to report important updates on their R&D pipeline (such as Sarepta), which may set these companies up for future approvals and growth. We like that these dynamics offer catalysts or idiosyncratic growth drivers that are not reliant on the broader economy.

5

Concluding Thoughts

While the markets continue to deal with a number of macro and geopolitical issues, there is underlying fundamental strength across the Fund holdings. This strength is tied directly to continued solid business growth, multi-year secular trends, and specific innovation catalysts. And, while inflation remains high currently, we are starting to see early signs of progress of bringing this down over time by the Fed. We are going to be patient and ride through these temporary storms, stay focused on our core investment strategy, and continue ownership of quality innovative businesses.

Thank you for your continued interest in, and support of, the Evolutionary Tree Innovators Fund.

6

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-833-517-1010.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website at mutualfund.evolutionarytree.com or call 1-833-517-1010 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Fund as of November 30, 2022, please see the Schedule of Investments section of the semi-annual report. The opinions of the Fund’s adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements, include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

7

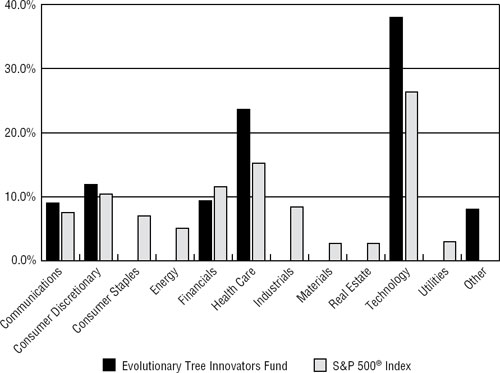

| EVOLUTIONARY TREE INNOVATORS FUND |

| PORTFOLIO INFORMATION |

| November 30, 2022 (Unaudited) |

Sector Diversification (% of Net Assets)

| Top 10 Equity Holdings | ||

| % of | ||

| Security Description | Net Assets | |

| HubSpot, Inc. | 6.9% | |

| Microsoft Corporation | 6.7% | |

| Amazon.com, Inc. | 6.7% | |

| ServiceNow, Inc. | 6.6% | |

| Sarepta Therapeuctics, Inc. | 5.8% | |

| Alphabet, Inc. - Class A | 5.7% | |

| nCino, Inc. | 5.5% | |

| Inspire Medical Systems, Inc. | 5.1% | |

| Airbnb, Inc. - Class A | 3.5% | |

| Axon Enterprise, Inc. | 3.3% | |

8

| EVOLUTIONARY TREE INNOVATORS FUND |

| SCHEDULE OF INVESTMENTS |

| November 30, 2022 (Unaudited) |

| COMMON STOCKS — 92.0% | Shares | Value | ||||||

| Communications — 9.0% | ||||||||

| Digital Media — 9.0% | ||||||||

| Alphabet, Inc. - Class A (a) | 12,755 | $ | 1,288,127 | |||||

| Bumble, Inc. - Class A (a) | 14,016 | 341,430 | ||||||

| Trade Desk, Inc. (The) - Class A (a) | 7,634 | 398,037 | ||||||

| 2,027,594 | ||||||||

| Consumer Discretionary — 12.0% | ||||||||

| Consumer Leisure — 3.5% | ||||||||

| Airbnb, Inc. - Class A (a) | 7,630 | 779,328 | ||||||

| E-Commerce — 8.5% | ||||||||

| Amazon.com, Inc. (a) | 15,660 | 1,511,817 | ||||||

| Sea Ltd. - ADR (a) | 7,098 | 414,310 | ||||||

| 1,926,127 | ||||||||

| Financials — 9.4% | ||||||||

| Financial Services — 9.4% | ||||||||

| Block, Inc. - Class A (a) | 4,561 | 309,099 | ||||||

| Charles Schwab Corporation (The) | 6,435 | 531,145 | ||||||

| Tradeweb Markets, Inc. - Class A | 9,770 | 600,464 | ||||||

| Visa, Inc. - Class A | 3,135 | 680,295 | ||||||

| 2,121,003 | ||||||||

| Health Care — 23.6% | ||||||||

| Biotechnology — 9.5% | ||||||||

| argenx SE - ADR (a) | 1,069 | 425,430 | ||||||

| Arrowhead Pharmaceuticals, Inc. (a) | 13,133 | 422,882 | ||||||

| Sarepta Therapeutics, Inc. (a) | 10,617 | 1,303,874 | ||||||

| 2,152,186 | ||||||||

| Life Sciences Tools & Services — 1.8% | ||||||||