UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: (811-22708)

Brown Advisory Funds

(Exact name of Registrant as specified in charter)

901 South Bond Street Suite 400

Baltimore, MD 21231

(Address of principal executive offices) (Zip code)

David M. Churchill

President

Brown Advisory Funds

901 South Bond Street Suite 400

Baltimore, MD 21231

(Name and address of agent for service)

(410) 537-5400

Registrant's telephone number, including area code

Date of fiscal year end: June 30

Date of reporting period: June 30, 2014

Item 1. Reports to Stockholders.

ANNUAL REPORT

June 30, 2014

Brown Advisory Growth Equity Fund

Brown Advisory Value Equity Fund

Brown Advisory Flexible Equity Fund

Brown Advisory Small-Cap Growth Fund

Brown Advisory Small-Cap Fundamental Value Fund

Brown Advisory Opportunity Fund

Brown Advisory Maryland Bond Fund

Brown Advisory Intermediate Income Fund

Brown Advisory Tactical Bond Fund

Brown Advisory Equity Income Fund

Brown Advisory Sustainable Growth Fund

Brown Advisory Tax Exempt Bond Fund

Brown Advisory – Somerset Emerging Markets Fund

Brown Advisory – WMC Strategic European Equity Fund

Brown Advisory Mortgage Securities Fund

Brown Advisory – WMC Japan Alpha Opportunities Fund

The views in the report contained herein were those of the Funds’ investment adviser, Brown Advisory, LLC, or, for the sub-advised funds, of the respective sub-adviser, as of June 30, 2014 and may not reflect their views on the date this report is first published or anytime thereafter. This report may contain discussions about certain investments both held and not held in the portfolio as of June 30, 2014. All current and future holdings are subject to risk and are subject to change. While these views are intended to assist shareholders in understanding their investment in each Fund, they do not constitute investment advice, are not a guarantee of future performance and are not intended as an offer or solicitation with respect to the purchase or sale of any security. Performance figures include the reinvestment of dividend and capital gain distributions.

The Global Industry Classification Standard (GICS®) was developed by and is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS® is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Administrator, U.S. Bancorp Fund Services, LLC.

TOPIX Index Values and TOPIX Marks are subject to the proprietary rights owned by the Tokyo Stock Exchange, Inc.

TABLE OF CONTENTS

| Brown Advisory Growth Equity Fund | |||

| A Message to our Shareholders, June 30, 2014 | 1 | ||

| Performance Chart and Analysis | 3 | ||

| Schedule of Investments, June 30, 2014 | 4 | ||

| Brown Advisory Value Equity Fund | |||

| A Message to our Shareholders, June 30, 2014 | 5 | ||

| Performance Chart and Analysis | 7 | ||

| Schedule of Investments, June 30, 2014 | 8 | ||

| Brown Advisory Flexible Equity Fund | |||

| A Message to our Shareholders, June 30, 2014 | 9 | ||

| Performance Chart and Analysis | 11 | ||

| Schedule of Investments, June 30, 2014 | 12 | ||

| Brown Advisory Small-Cap Growth Fund | |||

| A Message to our Shareholders, June 30, 2014 | 13 | ||

| Performance Chart and Analysis | 15 | ||

| Schedule of Investments, June 30, 2014 | 16 | ||

| Brown Advisory Small-Cap Fundamental Value Fund | |||

| A Message to our Shareholders, June 30, 2014 | 18 | ||

| Performance Chart and Analysis | 20 | ||

| Schedule of Investments, June 30, 2014 | 21 | ||

| Brown Advisory Opportunity Fund | |||

| A Message to our Shareholders, June 30, 2014 | 22 | ||

| Performance Chart and Analysis | 24 | ||

| Schedule of Investments, June 30, 2014 | 25 | ||

| Brown Advisory Maryland Bond Fund | |||

| A Message to our Shareholders, June 30, 2014 | 27 | ||

| Performance Chart and Analysis | 28 | ||

| Schedule of Investments, June 30, 2014 | 29 | ||

| Brown Advisory Intermediate Income Fund | |||

| A Message to our Shareholders, June 30, 2014 | 34 | ||

| Performance Chart and Analysis | 35 | ||

| Schedule of Investments, June 30, 2014 | 36 | ||

| Brown Advisory Tactical Bond Fund | |||

| A Message to our Shareholders, June 30, 2014 | 38 | ||

| Performance Chart and Analysis | 39 | ||

| Schedule of Investments, June 30, 2014 | 40 | ||

| Brown Advisory Equity Income Fund | |||

| A Message to our Shareholders, June 30, 2014 | 41 | ||

| Performance Chart and Analysis | 43 | ||

| Schedule of Investments, June 30, 2014 | 44 | ||

| Brown Advisory Sustainable Growth Fund | |||

| A Message to our Shareholders, June 30, 2014 | 45 | ||

| Performance Chart and Analysis | 47 | ||

| Schedule of Investments, June 30, 2014 | 48 | ||

| Brown Advisory Tax Exempt Bond Fund | |||

| A Message to our Shareholders, June 30, 2014 | 49 | ||

| Performance Chart and Analysis | 50 | ||

| Schedule of Investments, June 30, 2014 | 51 | ||

| Brown Advisory – Somerset Emerging Markets Fund | |||

| A Message to our Shareholders, June 30, 2014 | 54 | ||

| Performance Chart and Analysis | 56 | ||

| Schedule of Investments, June 30, 2014 | 57 | ||

| Brown Advisory – WMC Strategic European Equity Fund | |||

| A Message to our Shareholders, June 30, 2014 | 59 | ||

| Performance Chart and Analysis | 61 | ||

| Schedule of Investments, June 30, 2014 | 62 | ||

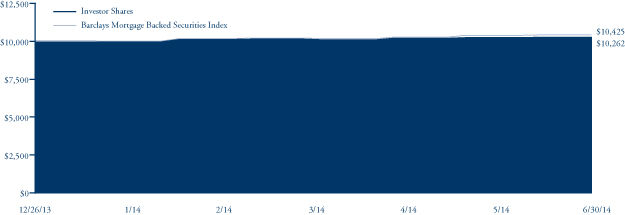

| Brown Advisory Mortgage Securities Fund | |||

| A Message to our Shareholders, June 30, 2014 | 64 | ||

| Performance Chart and Analysis | 65 | ||

| Schedule of Investments, June 30, 2014 | 66 | ||

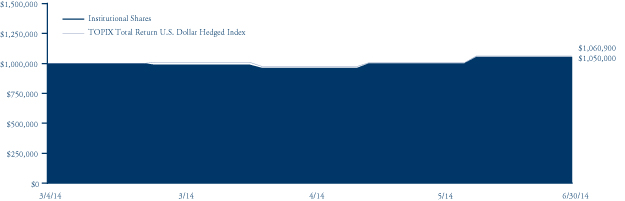

| Brown Advisory – WMC Japan Alpha Opportunities Fund | |||

| A Message to our Shareholders, June 30, 2014 | 70 | ||

| Performance Chart and Analysis | 72 | ||

| Schedule of Investments, June 30, 2014 | 73 | ||

| Statements of Assets and Liabilities | 77 | ||

| Statements of Operations | 81 | ||

| Statements of Changes in Net Assets | 85 | ||

| Financial Highlights | 93 | ||

| Notes to Financial Statements | 131 | ||

| Report of Independent Registered Public Accounting Firm | 150 | ||

| Additional Information | 151 | ||

GLOSSARY OF TERMS

Alpha refers to the abnormal rate of return on a security or portfolio in excess of what would be predicted by an equilibrium model like the capital asset pricing model (CAPM).

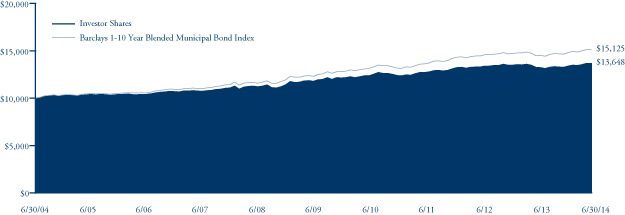

Barclays 1-10 Year Blended Municipal Bond Index is a market index of high quality, domestic fixed income securities with maturities of less than 10 years.

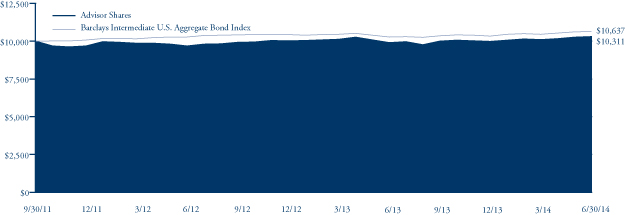

Barclays Intermediate U.S. Aggregate Bond Index represents domestic taxable investment-grade bonds with index components for government and corporate securities, mortgage pass-through securities and asset-backed securities with average maturities and durations in the intermediate range. This index represents a sector of the Barclays Capital U.S. Aggregate Index.

Barclays Mortgage Backed Securities Index is a market value-weighted index which covers the mortgage-backed securities component of the Barclays U.S. Aggregate Bond Index. The index is composed of agency mortgage-backed passthrough securities of the Government National Mortgage Association (Ginnie Mae), the Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (Freddie Mac) with a minimum $150 million par amount outstanding and a weighted-average maturity of at least 1 year. The index includes reinvestment of income.

Basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. 1% is equal to 100 basis points.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

Book value is the net asset value of a company, calculated by total assets minus intangible assets (patents, goodwill) and liabilities.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Correlation is a statistical measurement of how two securities move in relation to each other.

Dividend Yield is a financial ratio that shows how much a company pays out in dividends each year relative to its share price. In the absence of any capital gains, the dividend yield is the return on investment for a stock.

Downside Capture is a statistical measure of a fund’s performance in down markets. For example, a fund with downside capture of 90% would only have declined 90% as much as the related index during the same down market period.

Duration is a measure of the sensitivity of the price of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year. The term can apply to actual data from previous periods or estimated data for future periods.

Earnings per share (EPS) is calculated by taking the total earnings divided by the number of shares outstanding.

Earnings Yield is the earnings per share for the most recent 12-month period divided by the current market price per share. The earnings yield shows the percentage of each dollar invested in the stock that was earned by the company.

EBITDA is the Earnings Before Interest, Taxes, Depreciation and Amortization. An approximate measure of a company’s operating cash flow based on data from the company’s income statement.

Enterprise Value (EV) is a measure of a company’s value, often used as an alternative to straightforward market capitalization. Enterprise Value is calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Forward price to earnings ratio uses forecasted earnings, rather than current earnings, to calculate the price to earnings ratio.

Free Cash Flow is the operating cash flows (net income plus amortization and depreciation) minus capital expenditures and dividends. Free cash flow is the amount of cash that a company has left over after it has paid all of its expenses, including investments.

Gross Domestic Product (GDP) is the monetary value of all the goods and services produced by an economy over a specified period. It includes consumption, government purchases, investments, and exports minus imports.

GLOSSARY OF TERMS

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

MSCI Europe Index is an index that captures large and mid cap representation across 15 developed market countries in Europe.

Price to Book Value Ratio is ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share.

Price to earnings ratio (P/E) is a common tool for comparing the prices of different common stocks and is calculated by dividing the current market price of a stock by the earnings per share.

Return of Capital (ROC) is a return from an investment that is not considered income. The return of capital is when some or all of the money an investor has in an investment is paid back to him or her, thus decreasing the value of the investment.

Return on Capital Employed (ROCE) is a financial ratio that measures a company’s profitability and the efficiency with which its capital is employed. Return on Capital Employed (ROCE) is calculated as: ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed

Return on Equity (ROE) is the amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested.

Return on Invested Capital (ROIC) is a calculation used to assess a company’s efficiency at allocating the capital under its control to profitable investments. ROIC is typically calculated by taking a company’s net income, subtracting dividends the company paid out and dividing that amount by the company’s total capital.

Russell 1000® Growth Index measures the performance of the large-cap growth segment of the of the U.S. equity universe. It includes those Russell 1000® companies with higher price to book value ratios and higher forecasted growth values.

Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® companies with lower price to book value ratios and lower expected growth values.

Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price to book value ratios and higher forecasted growth values.

Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index.

Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000® companies with lower price to book value ratios and lower forecasted growth values.

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies representing approximately 98% of the investable U.S. equity market.

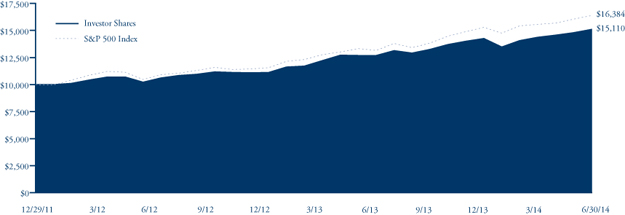

S&P 500 Index (“S&P 500”) is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks.

Tier 1 Capital Ratio is a comparison between a banking firm’s core equity capital and total risk-weighted assets. A firm’s core equity capital is known as its Tier 1 capital and is the measure of a bank’s financial strength based on the sum of its equity capital and disclosed reserves, and sometimes non-redeemable, non-cumulative preferred stock. A firm’s risk-weighted assets include all assets that the firm holds that are systematically weighted for credit risk. Central banks typically develop the weighting scale for different asset classes, such as cash and coins, which have zero risk, versus a letter or credit, which carries more risk.

TOPIX Total Return U.S. Dollar Hedged Index is a market capitalization-weighted index of all companies listed on the First Section of the Tokyo Stock Exchange.

Turnover refers to a fund buying or selling securities. (The fund “turns over” its portfolio.) A fund pays transaction costs, such as commissions, when it buys and sells securities. Additionally, a higher turnover rate may result in higher taxes when the fund shares are held in a taxable account.

Yield Curve is a line that plots the yields of securities having equal credit quality but different maturity dates.

The broad based market indexes referenced in the following management commentaries are considered representative of their indicated market, the indexes are unmanaged and do not reflect the deduction of fees, such as, investment management and fund accounting fees, or taxes associated with a mutual fund. Investors cannot invest directly in an index.

A Message to Our Shareholders

June 30, 2014

Dear Shareholder:

Dear Shareholder:

During the year ended June 30, 2014, the Brown Advisory Growth Equity Fund Investor Shares (the “Fund”) returned 18.35%. During the same period, the Fund’s benchmark, the Russell 1000® Growth Index (the “Index”) returned 26.92%.

U.S. stocks marched steadily upward during the year ended June 30, 2014, and many domestic stock indexes were trading at or near all-time highs at the end of the second quarter. We posted strong absolute returns during this period but trailed our benchmark during what was clearly a challenging period for the Fund. A confluence of unrelated factors impacted performance over the course of the fiscal year. Momentum buyers drove sharp returns in several segments of the market such as biotechnology and social media, while many investors were attracted to the slower-growing defensive names at the other end of the risk spectrum. The companies that have exhibited a history of high-quality fast-growing business models that we favor in our strategy were unloved by the market during this period. Additionally, several of our portfolio companies struggled with specific short-term issues during the year, which gave us opportunities to add to our position at what we believe to be attractive prices but nonetheless hampered our 12-month performance.

We try to remind our shareholders of how our long-term investment approach is likely to perform in various market conditions over time. Given our valuation-sensitive, quality-focused approach, these sorts of runaway markets have been a headwind to our strategy in the past, and historically we have generated the bulk of our alpha during more rational periods over the course of full market cycles.

Specifically, our underperformance for the period was the result of two main factors: underexposure to the booming biotech sector, and several short-term issues with Intuitive Surgical and Whole Foods.

We have held Intuitive Surgical for over seven years. Our thesis for the stock is the same today as when we bought it: The company manufactures a minimally invasive robotic surgery system for which there is virtually no competition. In our opinion, the business model offers an extremely attractive long-term growth trajectory in terms of the number of surgical procedures performed using the system. The stock endured several controversies during the year, ranging from false claims about safety to interim sales comparables that did not satisfy analysts’ expectations. In our opinion, much of this controversy was a distraction and narrowly focused on short-term metrics. After a considerable amount of additional due diligence, we concluded that our investment thesis for the company’s business model remains solidly intact. Whole Foods also fell far out of favor with growth investors after reporting several consecutive quarters of disappointing same-store-sales growth. We spent a great deal of time with the company’s management team in an effort to sort through these interim difficulties, and the exercise confirmed our belief that the team is still very much on track in seeking to successfully execute its long-term growth strategy.

Biotechnology stocks turned in blistering performance during the past 12 months, but our investment approach steers us toward sustainable growth business models, and we are inherently wary of stocks whose fates are so closely tied to the binary outcome of clinical trials. Thus, our exposure to this market segment has been through stocks that, in our view, offer a return profile with more limited downside relative to their upside potential. One such name that we added to the portfolio during the year is Gilead Sciences (a biotechnology company that recently received approval for Sovaldi, a new highly effective hepatitis C treatment).

One strong positive contributor was energy-service company Schlumberger, one of our longest-held positions. Over the last several years, the company has endeavored to create a step change in technology within the oil and gas industry, and its progress with this effort along with more recent efficiency initiatives caught the attention of investors. Despite Schlumberger’s size, we believe that it can grow its earnings at a healthy double-digit clip for the foreseeable future.

Although we seek to own companies for the long term, we added several new names to the portfolio and exited several others over the course of the past year. Fastenal is an industrial distribution company we have followed for a number of years while waiting for an attractive entry point. Our patience paid off, as the stock recently traded down from its typical premium valuation on non-fundamental concerns. We funded the purchase of Fastenal by exiting Roper, another industrial company. We also purchased Discovery Communications, a leading provider of cable TV content that reaches its global subscriber base through nearly 200 networks spearheaded by the Discovery Channel, TLC and Animal Planet. The business has historically offered attractive profit margins and has steadily gained market share. In order to fund the purchase of Discovery, we sold our position in NetApp, a data-storage company, as we grew concerned about its long-term growth outlook in the face of the market’s shift toward cloud-based data solutions.

www.brownadvisoryfunds.com

1

Brown Advisory Growth Equity Fund

A Message to Our Shareholders

June 30, 2014

While interim underperformance is unwelcome, it is an inevitable result for a long-term investment program that applies a rigorous investment process consistently. We have strict criteria for the types of business models we include in the portfolio. We haven’t chased returns by buying slower-growing defensive companies that pay high dividends, and we haven’t exposed the portfolio to momentum-driven stocks to chase after short-term market excitement. We are committed to owning a portfolio of high-quality business models that we believe are capable of sustaining above-average growth rates for an extended period. These companies may or may not be in favor in a given year, but we believe that their results over time will speak for themselves.

While interim underperformance is unwelcome, it is an inevitable result for a long-term investment program that applies a rigorous investment process consistently. We have strict criteria for the types of business models we include in the portfolio. We haven’t chased returns by buying slower-growing defensive companies that pay high dividends, and we haven’t exposed the portfolio to momentum-driven stocks to chase after short-term market excitement. We are committed to owning a portfolio of high-quality business models that we believe are capable of sustaining above-average growth rates for an extended period. These companies may or may not be in favor in a given year, but we believe that their results over time will speak for themselves.

Sincerely,

Kenneth M. Stuzin, CFA

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in smaller and medium capitalization companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Earnings growth is not a measure of the Fund’s future performance.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

2

Brown Advisory Growth Equity Fund

Performance Chart and Analysis

June 30, 2014

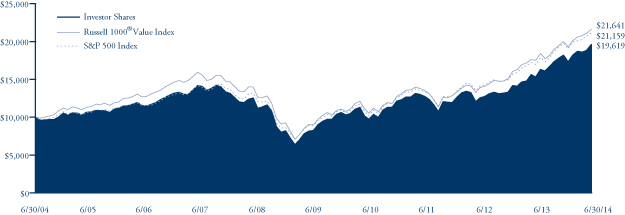

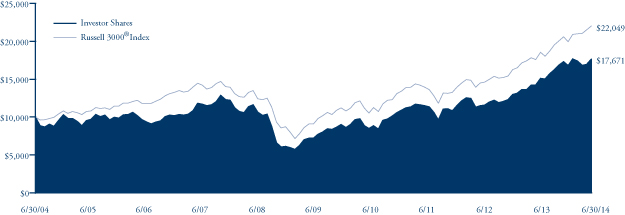

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against broad-based securities market indices. The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price to book and higher forecasted growth values. The S&P 500 Index is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The indexes are unmanaged and do not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Average Annual Total Return | One | Five | Ten |

| as of 6/30/14 | Year | Year | Year |

Institutional Shares1 | 18.46% | 19.12% | 8.90% |

| Investor Shares | 18.35% | 18.95% | 8.74% |

Advisor Shares2 | 18.02% | 18.58% | 8.36% |

Russell 1000® Growth Index | 26.92% | 19.24% | 8.20% |

| S&P 500 Index | 24.61% | 18.83% | 7.78% |

| Institutional Shares | Investor Shares | Advisor Shares | |

Gross Expense Ratio3 | 0.78% | 0.93% | 1.18% |

Net Expense Ratio3 | 0.78% | 0.93% | 1.18% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

| 1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

| 2 | Performance information for Advisor Shares, prior to commencement of operations on May 18, 2006, is based on the performance of Investor Shares, and adjusted for the higher expenses applicable to Advisor Shares. |

| 3 | Per the Fund’s prospectus dated October 31, 2013. |

www.brownadvisoryfunds.com

3

Brown Advisory Growth Equity Fund

Schedule of Investments

June 30, 2014

| Shares | Security Description | Value $ | |||||

| Common Stocks — 97.5% | |||||||

| Consumer Discretionary — 7.4% | |||||||

| 791,577 | Discovery Communications, Inc.* | 58,798,339 | |||||

| 431,903 | Fossil Group, Inc.* | 45,142,502 | |||||

| 1,327,989 | Starbucks Corp. | 102,759,789 | |||||

| 206,700,630 | |||||||

| Consumer Staples — 12.1% | |||||||

| 520,845 | Costco Wholesale Corp. | 59,980,510 | |||||

| 1,218,278 | Estee Lauder Companies, Inc. | 90,469,324 | |||||

| 1,106,613 | Mead Johnson Nutrition Co. | 103,103,133 | |||||

| 2,146,838 | Whole Foods Market, Inc. | 82,932,352 | |||||

| 336,485,319 | |||||||

| Energy — 11.3% | |||||||

| 534,512 | Core Laboratories NV | 89,295,575 | |||||

| 1,623,559 | FMC Technologies, Inc.* | 99,150,748 | |||||

| 1,066,703 | Schlumberger NV | 125,817,619 | |||||

| 314,263,942 | |||||||

| Financials — 4.3% | |||||||

| 4,382,691 | Charles Schwab Corp. | 118,025,869 | |||||

| Health Care — 16.1% | |||||||

| 704,931 | Covance, Inc.* | 60,327,995 | |||||

| 1,129,801 | DaVita HealthCare Partners, Inc.* | 81,707,208 | |||||

| 1,648,806 | Express Scripts Holding Co.* | 114,311,720 | |||||

| 1,208,427 | Gilead Sciences, Inc.* | 100,190,683 | |||||

| 223,120 | Intuitive Surgical, Inc.* | 91,880,816 | |||||

| 448,418,422 | |||||||

| Industrials — 11.4% | |||||||

| 1,238,543 | Danaher Corp. | 97,510,491 | |||||

| 1,190,574 | Fastenal Co. | 58,921,507 | |||||

| 1,009,779 | Fluor Corp. | 77,652,005 | |||||

| 687,077 | Stericycle, Inc.* | 81,363,658 | |||||

| 315,447,661 | |||||||

| Information Technology — 31.6% | |||||||

| 821,427 | Accenture PLC | 66,404,159 | |||||

| 913,038 | Amphenol Corp. | 87,962,081 | |||||

| 542,990 | ANSYS, Inc.* | 41,169,502 | |||||

| 1,080,653 | Apple, Inc. | 100,425,083 | |||||

| 1,037,289 | Cognizant Technology Solutions Corp.* | 50,733,805 | |||||

| 3,296,529 | Genpact, Ltd.* | 57,788,153 | |||||

| 106,217 | Google, Inc. — Class A* | 62,101,893 | |||||

| 106,217 | Google, Inc. — Class C* | 61,104,516 | |||||

| 1,469,552 | National Instruments Corp. | 47,598,789 | |||||

| 1,452,962 | QUALCOMM, Inc. | 115,074,590 | |||||

| 1,402,134 | Salesforce.com, Inc.* | 81,435,943 | |||||

| 505,133 | Visa, Inc. | 106,436,575 | |||||

| 878,235,089 | |||||||

| Materials — 3.3% | |||||||

| 825,936 | Ecolab, Inc. | 91,959,714 | % | ||||

| Total Common Stocks (Cost $2,082,555,223) | 2,709,536,646 | ||||||

| Short-Term Investments — 2.8% | |||||||

| Money Market Funds — 2.8% | |||||||

| 78,492,937 | DWS Cash Account Trust — Government | ||||||

| & Agency Securities Portfolio, 0.03%# | 78,492,937 | ||||||

| Total Short-Term Investments (Cost $78,492,937) | 78,492,937 | ||||||

| Total Investments — 100.3% (Cost $2,161,048,160) | 2,788,029,583 | ||||||

| Liabilities in Excess of Other Assets — (0.3)% | (8,734,029 | ) | |||||

| NET ASSETS — 100.0% | $ | 2,779,295,554 | |||||

| PORTFOLIO HOLDINGS | |||||||

| % of Net Assets | |||||||

| Information Technology | 31.6 | % | |||||

| Health Care | 16.1 | % | |||||

| Consumer Staples | 12.1 | % | |||||

| Industrials | 11.4 | % | |||||

| Energy | 11.3 | % | |||||

| Consumer Discretionary | 7.4 | % | |||||

| Financials | 4.3 | % | |||||

| Materials | 3.3 | % | |||||

| Money Market Funds | 2.8 | % | |||||

| Other Assets and Liabilities | (0.3 | )% | |||||

| 100.0 | % | ||||||

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2014. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

4

Brown Advisory Value Equity Fund

A Message to Our Shareholders

June 30, 2014

Dear Shareholder:

During the year ended June 30, 2014, the Brown Advisory Value Equity Fund Investor Shares (the “Fund”) increased 28.26 % in value. During the same period, the Russell 1000® Value Index (the “Index”), the Fund’s benchmark, increased 23.81%.

For the year ended June 30, 2014, the portfolio gained ground, in varying degrees, in all sectors vs. its benchmark. Several factors supported our performance over the past year. First, investors paid a huge premium for perceived safety in utilities and other purely defensive names in the past few years, but more recently we believe that they began to see that economic conditions were relatively healthy, especially in the U.S. Our pro-cyclical orientation has benefited from this, as we have little to no exposure in defensive areas such as consumer staples, telecom and utilities. Second, we have benefited from favorable stock selection within most sectors, and in particular within the energy space; and while our technology selections lagged those of the benchmark, we still earned strong absolute returns from technology that helped our overall performance.

Leading contributors to performance during the period included Schlumberger, Apple, Canadian Natural Resources, Best Buy and Garmin. The new CEO at Schlumberger is committed to innovation, productivity, returns on capital and better capital deployment, and his initiatives have produced very encouraging early results. Apple’s stock has recovered considerably from recent lows thanks to solid financial returns, a focus on shareholder value, and investor optimism regarding its product pipeline.

Performance detractors included Abercrombie and Fitch, Guess?, Coach, Ensco and JP Morgan. Retailing conditions remain difficult, and teen retail has been particularly challenging; we elected to sell Abercrombie upon concluding that its recovery plan would fall short of what we initially expected. In contrast, we still hold Guess?, and we added Coach to the portfolio after a string of disappointing quarters have greatly lowered investors’ expectations for this leading luxury goods maker.

Our new idea pipeline has been consistently strong throughout the trailing 12 months, with new portfolio names coming from a variety of market segments. New investments included Baxter International, a leading healthcare company; City National, a high-quality regional bank; Coach, a global luxury goods franchise; Ensco plc, a high-quality offshore rig company; Gamestop, the world’s leading video game retailer; Garmin Ltd, a GPS-focused technology products firm; Joy Global, a leading mining equipment provider; JP Morgan, a well-known global bank; Potash Corp, a key producer of nitrogen, phosphate and potash for agricultural markets; and Teva Pharmaceutical, a global leader in generic drugs.

Most of our sales over the past year were from investments that reached our price targets or offered us less appealing prospects than the new ideas listed above. Positions sold during the period included Carbo Ceramics, Cimarex Energy, Deckers Outdoors, DuPont, Eaton, Fluor, Metlife, PNC Financial and Terex. In the cases of Abercrombie & Fitch and FirstMerit, we sold our positions due to a breakdown in our investment thesis.

We believe that the Fund is well positioned for the year ahead. Notably, a large portion of our portfolio companies, in our view, are “under-earning” right now compared to their historic potential; in other words, we believe that they have plenty of room to expand their margins, during a period when many companies appear to be at peak margin levels. Another meaningful portion of the portfolio includes companies whose business franchise strength supports reliable high free cash flows. Collectively, we believe that our companies compare favorably to those of the benchmark. Our portfolio, in our view, is more global, has higher financial quality, is more Research and Development (R&D) focused, generates higher free cash flows and consists of companies that offer a competitive dividend yield, yet overall our portfolio trades at a meaningful discount to the benchmark. We have relied on this approach for many years and believe that it has the potential to produce attractive returns going forward.

Sincerely,

Richard Bernstein, CFA

Portfolio Manager

www.brownadvisoryfunds.com

5

Brown Advisory Value Equity Fund

A Message to Our Shareholders

June 30, 2014

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in medium capitalization companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. Diversification does not guarantee a profit or protect from loss in a declining market.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary on Terms.

www.brownadvisoryfunds.com

6

Brown Advisory Value Equity Fund

Performance Chart and Analysis

June 30, 2014

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against broad-based securities market indices. The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® companies with lower price to book ratios and lower expected growth values. The S&P 500 Index is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The indexes are unmanaged and do not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Average Annual Total Return | One | Five | Ten |

| as of 6/30/14 | Year | Year | Year |

Institutional Shares1 | 28.41% | 19.14% | 7.13% |

| Investor Shares | 28.26% | 18.98% | 6.97% |

Advisor Shares2 | 27.90% | 18.62% | 6.57% |

Russell 1000® Value Index | 23.81% | 19.23% | 8.03% |

| S&P 500 Index | 24.61% | 18.83% | 7.78% |

| Institutional Shares | Investor Shares | Advisor Shares | |

Gross Expense Ratio3 | 0.82% | 0.97% | 1.22% |

Net Expense Ratio3 | 0.82% | 0.97% | 1.22% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

| 1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

| 2 | Performance information for Advisor Shares, prior to commencement of operations on April 25, 2006, is based on the performance of Investor Shares, and adjusted for the higher expenses applicable to Advisor Shares. |

| 3 | Per the Fund’s prospectus dated October 31, 2013. |

www.brownadvisoryfunds.com

7

Brown Advisory Value Equity Fund

Schedule of Investments

June 30, 2014

| Shares | Security Description | Value $ | |||||

| Common Stocks — 96.0% | |||||||

| Consumer Discretionary — 11.5% | |||||||

| 239,895 | Best Buy, Inc. | 7,439,144 | |||||

| 102,175 | Coach, Inc. | 3,493,363 | |||||

| 129,079 | GameStop Corp. | 5,223,827 | |||||

| 106,785 | Garmin, Ltd. | 6,503,207 | |||||

| 193,088 | Guess?, Inc. | 5,213,376 | |||||

| 27,872,917 | |||||||

| Energy — 16.1% | |||||||

| 168,546 | Canadian Natural Resources, Ltd. | 7,737,947 | |||||

| 129,020 | ENSCO PLC | 7,169,641 | |||||

| 80,806 | National Oilwell Varco, Inc. | 6,654,374 | |||||

| 68,341 | Occidental Petroleum Corp. | 7,013,837 | |||||

| 90,760 | Schlumberger NV | 10,705,142 | |||||

| 39,280,941 | |||||||

| Financials — 22.6% | |||||||

| 283,078 | Charles Schwab Corp. | 7,623,290 | |||||

| 89,010 | City National Corp. | 6,743,398 | |||||

| 143,745 | Hartford Financial Services Group, Inc. | 5,147,508 | |||||

| 116,105 | JPMorgan Chase & Co. | 6,689,970 | |||||

| 45,273 | M&T Bank Corp. | 5,616,116 | |||||

| 113,825 | Northern Trust Corp. | 7,308,703 | |||||

| 695,701 | Regions Financial Corp. | 7,388,345 | |||||

| 208,301 | SunTrust Banks, Inc. | 8,344,538 | |||||

| 54,861,868 | |||||||

| Health Care — 11.9% | |||||||

| 80,910 | Baxter International, Inc. | 5,849,793 | |||||

| 234,340 | Hologic, Inc.* | 5,940,519 | |||||

| 84,550 | Merck & Co., Inc. | 4,891,218 | |||||

| 59,680 | Novartis AG ADR | 5,402,830 | |||||

| 130,420 | Teva Pharmaceutical Industries, Ltd. ADR | 6,836,616 | |||||

| 28,920,976 | |||||||

| Industrials — 7.2% | |||||||

| 102,460 | Joy Global, Inc. | 6,309,487 | |||||

| 135,983 | Kennametal, Inc. | 6,293,293 | |||||

| 78,757 | PACCAR, Inc. | 4,948,302 | |||||

| 17,551,082 | |||||||

| Information Technology — 20.5% | |||||||

| 112,210 | Apple, Inc. | 10,427,675 | |||||

| 56,465 | Check Point Software Technologies, Ltd.* | 3,784,849 | |||||

| 340,535 | Cisco Systems, Inc. | 8,462,295 | |||||

| 71,970 | Microchip Technology, Inc. | 3,512,856 | |||||

| 108,245 | Microsoft Corp. | 4,513,817 | |||||

| 173,275 | NetApp, Inc. | 6,328,003 | |||||

| 117,197 | Oracle Corp. | 4,749,994 | |||||

| 102,395 | QUALCOMM, Inc. | 8,109,684 | |||||

| 49,889,173 | |||||||

| Materials — 6.2% | |||||||

| 202,155 | Freeport-McMoRan Copper & Gold, Inc. | 7,378,658 | |||||

| 205,670 | Potash Corp. of Saskatchewan, Inc. | 7,807,233 | |||||

| 15,185,891 | |||||||

| Total Common Stocks (Cost $177,395,841) | 233,562,848 | ||||||

| Short-Term Investments — 3.9% | |||||||

| Money Market Funds — 3.9% | |||||||

| 9,433,414 | DWS Cash Account Trust — Government | ||||||

| & Agency Securities Portfolio, 0.03%# | 9,433,414 | ||||||

| Total Short-Term Investments (Cost $9,433,414) | 9,433,414 | ||||||

| Total Investments — 99.9% (Cost $186,829,255) | 242,996,262 | ||||||

| Other Assets in Excess of Liabilities — 0.1% | 319,421 | ||||||

| NET ASSETS — 100.0% | $ | 243,315,683 | |||||

| PORTFOLIO HOLDINGS | |||||||

| % of Net Assets | |||||||

| Financials | 22.6 | % | |||||

| Information Technology | 20.5 | % | |||||

| Energy | 16.1 | % | |||||

| Health Care | 11.9 | % | |||||

| Consumer Discretionary | 11.5 | % | |||||

| Industrials | 7.2 | % | |||||

| Materials | 6.2 | % | |||||

| Money Market Funds | 3.9 | % | |||||

| Other Assets and Liabilities | 0.1 | % | |||||

| 100.0 | % | ||||||

ADR — American Depositary Receipt

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2014. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

8

Brown Advisory Flexible Equity Fund

A Message to Our Shareholders

June 30, 2014

Dear Shareholder:

During the year ended June 30, 2014, the Brown Advisory Flexible Equity Fund Investor Shares (the “Fund”) returned 20.78%. The S&P 500 Index (the “Index”), the Fund’s benchmark, returned 24.61% during the same period. The Fund outperformed the Index for the trailing three- and five-year periods ending June 30, 2014 with annualized returns of 17.74% and 19.37% compared to the benchmark returns of 16.58% and 18.83% for the same periods, respectively. Since inception on November 30, 2006, the Fund returned 5.78% vs. the Index’s return of 6.81%. The Fund’s gross expense ratio, per the prospectus dated October 31, 2013, is 1.04%.

Performance data quoted represents past performance and is no guarantee of future results. Performance for periods greater than one year is annualized. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than original cost. Shares redeemed or exchanged within 14 days of purchase will be charged a 1.00% fee. Performance data quoted does not reflect the redemption or exchange fee. If reflected, total returns would be reduced. For the most recent month- end performance, please call 1-800-540-6807.

Five-year annualized returns of 18% to 19% are well out of the ordinary; the trailing five-year period began during a post-financial-crisis historical low point for equity markets. The long-term average earnings growth for S&P 500 Index companies is about 7%; when factoring in current dividend yields of approximately 2% for those companies, we might more reasonably expect lower annualized returns going forward. Of course, the concept of annualizing returns suggests a steadiness in returns from year to year, when in fact the opposite is closer to the truth. Economic and business progress is uneven, and investor sentiment is even more uneven, so stock index prices tend to vary widely from one period to the next.

Additionally, active investment strategies have inherent biases based on the types of stocks they favor. For example, we favor businesses with differentiated offerings or with a history of more dependable recurring revenues vs. revenues that fluctuate with commodity prices or economic cycles. We try to avoid areas of the market that are overheating thanks to a boom mentality and instead focus on what we consider to be outstanding businesses that we can own over a long period of time. Obviously, this approach might excel in certain short-term periods but lag the market during periods when performance is dominated by a hot market trend. If you really get to know your manager’s approach and tendencies, you can better prepare yourself for the inevitable periods of short-term underperformance that can occur on the way to potentially good long-term results.

The biggest contributors to the Fund’s results during the year were Google, Apple, MasterCard, United Rentals and Canadian National Railway. With the exception of United Rentals, all of the top performers are multiyear holdings in the fund. The most significant detractors to the Fund’s performance were Kinder Morgan, Kraft Foods and eBay. We added to Kinder Morgan, another long-term holding in the Fund, on short-term price weakness, while we eliminated Kraft after it separated from Mondelez and subsequently advanced to what we viewed as an expensive valuation relative to its likely future growth. eBay’s share price dipped a bit with the disclosure of a security breach in its systems, but we do not anticipate that the event will have a long-term impact on its healthy, growing e-commerce and PayPal businesses.

Recent new holdings include Copa Holdings, National Oilwell Varco, Now Inc. and Teva Pharmaceutical. The airline industry is notorious for intense price competition, high capital intensity, and unpredictable costs and passenger demand, but Copa has distinguished itself despite these obstacles to produce good results for shareholders. Similarly to eBay, oil-and-gas equipment firm National Oilwell Varco’s stock price has lagged the company’s earnings progress. We believe that the stock has the potential to be better appreciated by the market in time. Management appears focused on building value for shareholders with good capital allocation decisions, such as the spinoff of its distribution business, Now Inc. Teva is facing generic competition for Copaxone, a key multiple sclerosis drug whose patent is set to expire. The stock is trading at what we view as a low multiple, and we believe that the company and its new CEO are focused on the right things to potentially minimize the profit impact of the loss of Copaxone sales.

We sold Aaron’s, Bed, Bath & Beyond, Rogers Communications and Southwestern Energy during the period covered in this report, all based on revised assessments of their long-term business prospects.

In early May, we attended the Berkshire Hathaway Annual Meeting, as we have for many years, to hear the comments of Warren Buffett and Charlie Munger. Berkshire Hathaway is a sizable long-term holding in the fund. Our notes from this year’s meeting will be available for a time at brownadvisory.com, and afterward upon request. We encourage you to read them for the business and investment wisdom shared by Mr. Buffett and Mr. Munger.

www.brownadvisoryfunds.com

9

Brown Advisory Flexible Equity Fund

A Message to Our Shareholders

June 30, 2014

As a reminder of our approach, we look for bargains among long-term attractive businesses with shareholder-oriented managers. These bargains can arise due to short-term investor perceptions, temporary business difficulties that should improve, or as-yet undiscovered opportunities and unrecognized changes for the better. We remain optimistic about the long-term outlook for equities of good companies purchased at reasonable prices and our ability to find them.

Sincerely,

R. Hutchings Vernon

Portfolio Manager

Michael L. Foss

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The Flexible Equity Fund may invest in securities of foreign issuers. Investments in such securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in smaller companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities.

Stocks are generally perceived to have more financial risk than bonds in that bond holders have a claim on firm operations or assets that is senior to that of equity holders. In addition, stock prices are generally more volatile than bond prices. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. A stock may trade with more or less liquidity than a bond depending on the number of shares and bonds outstanding, the size of the company, and the demand for the securities. Similarly, the transaction costs involved in trading a stock may be more or less than a particular bond depending on the factors mentioned above and whether the stock or bond trades upon an exchange. Depending on the entity issuing the bond, it may or may or may not afford additional protections to the investor, such as a guarantee of return of principal by a government or bond insurance company. There is typically no guarantee of any kind associated with the purchase of an individual stock. Bonds are often owned by individuals interested in current income while stocks are generally owned by individuals seeking price appreciation with income a secondary concern. The tax treatment of returns of bonds and stocks also differs given differential tax treatment of income versus capital gain.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

10

Brown Advisory Flexible Equity Fund

Performance Chart and Analysis

June 30, 2014

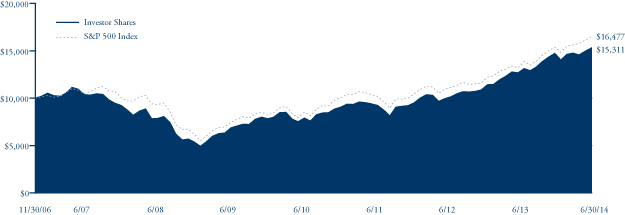

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against the broad-based securities market index. The S&P 500 (“Index”) is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The Index is unmanaged and does not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Since | |||

| Average Annual Total Return | One | Five | Inception |

| as of 6/30/14 | Year | Year | (11/30/06) |

Institutional Shares1 | 21.06% | 19.56% | 5.94% |

| Investor Shares | 20.78% | 19.37% | 5.78% |

Advisor Shares2 | 20.52% | 19.10% | 5.49% |

| S&P 500 Index | 24.61% | 18.83% | 6.81% |

| Institutional Shares | Investor Shares | Advisor Shares | |

Gross Expense Ratio3 | 0.89% | 1.04% | 1.29% |

Net Expense Ratio3 | 0.89% | 1.04% | 1.29% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

| 1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

| 2 | Performance information for Advisor Shares, prior to commencement of operations on January 24, 2007, is based on the performance of Investor Shares, and adjusted for the higher expenses applicable to Advisor Shares. |

| 3 | Per the Fund’s prospectus dated October 31, 2013. |

www.brownadvisoryfunds.com

11

Brown Advisory Flexible Equity Fund

Schedule of Investments

June 30, 2014

| Shares | Security Description | Value $ | |||||

| Common Stocks — 93.0% | |||||||

| Consumer Discretionary — 14.4% | |||||||

| 194,936 | Best Buy, Inc. | 6,044,965 | |||||

| 73,715 | CarMax, Inc.* | 3,833,917 | |||||

| 54,641 | General Motors Co. | 1,983,468 | |||||

| 77,961 | Lowe’s Companies, Inc. | 3,741,349 | |||||

| 16,445 | Time Warner Cable, Inc. | 2,422,349 | |||||

| 55,101 | TJX Companies, Inc. | 2,928,618 | |||||

| 59,557 | Walt Disney Co. | 5,106,417 | |||||

| 26,061,083 | |||||||

| Consumer Staples — 2.2% | |||||||

| 45,842 | Mondelez International, Inc. | 1,724,118 | |||||

| 25,197 | PepsiCo, Inc. | 2,251,100 | |||||

| 3,975,218 | |||||||

| Energy — 8.6% | |||||||

| 154,643 | Kinder Morgan, Inc. | 5,607,355 | |||||

| 52,112 | National Oilwell Varco, Inc. | 4,291,423 | |||||

| 54,263 | Occidental Petroleum Corp. | 5,569,012 | |||||

| 15,467,790 | |||||||

| Financials — 20.0% | |||||||

| 31,215 | American Express Co. | 2,961,367 | |||||

| 103,815 | Bank of America Corp. | 1,595,636 | |||||

| 58,884 | Berkshire Hathaway, Inc.* | 7,452,359 | |||||

| 156,602 | Charles Schwab Corp. | 4,217,292 | |||||

| 18,377 | CME Group, Inc. | 1,303,848 | |||||

| 54,606 | Franklin Resources, Inc. | 3,158,411 | |||||

| 72,977 | JPMorgan Chase & Co. | 4,204,935 | |||||

| 230,019 | Regions Financial Corp. | 2,442,802 | |||||

| 14,521 | T. Rowe Price Group, Inc. | 1,225,717 | |||||

| 143,069 | Wells Fargo Co. | 7,519,707 | |||||

| 36,082,074 | |||||||

| Health Care — 11.2% | |||||||

| 45,242 | Edwards Lifesciences Corp.* | 3,883,573 | |||||

| 88,354 | Express Scripts Holding Co.* | 6,125,583 | |||||

| 31,545 | Merck & Co., Inc. | 1,824,878 | |||||

| 76,735 | Teva Pharmaceutical Industries, Ltd. ADR | 4,022,449 | |||||

| 40,443 | Wellpoint, Inc. | 4,352,071 | |||||

| 20,208,554 | |||||||

| Industrials — 11.7% | |||||||

| 96,384 | Canadian National Railway Co. | 6,266,888 | |||||

| 10,636 | Canadian Pacific Railway, Ltd. | 1,926,605 | |||||

| 21,328 | Copa Holdings S.A. | 3,040,733 | |||||

| 12,940 | NOW, Inc.* | 468,557 | |||||

| 73,556 | Owens Corning | 2,845,146 | |||||

| 30,038 | United Rentals, Inc.* | 3,145,880 | |||||

| 30,669 | United Technologies Corp. | 3,540,736 | |||||

| 21,234,545 | |||||||

| Information Technology — 23.6% | |||||||

| 45,969 | Accenture PLC | 3,716,134 | |||||

| 51,170 | Apple, Inc. | 4,755,228 | |||||

| 54,083 | eBay, Inc.* | 2,707,395 | |||||

| 6,554 | Google, Inc. Class A* | 3,831,927 | % | ||||

| 7,199 | Google, Inc. Class C* | 4,141,441 | |||||

| 12,504 | International Business Machines Corp. | 2,266,600 | |||||

| 78,110 | Mastercard, Inc. | 5,738,742 | |||||

| 100,319 | Microsoft Corp. | 4,183,302 | |||||

| 49,324 | QUALCOMM, Inc. | 3,906,461 | |||||

| 34,818 | Visa, Inc. | 7,336,501 | |||||

| 42,583,731 | |||||||

| Telecommunication Services — 1.3% | |||||||

| 31,030 | Crown Castle International Corp. | 2,304,288 | |||||

| Total Common Stocks (Cost $127,290,186) | 167,917,283 | ||||||

| Warrants — 0.3% | |||||||

| 40,000 | Kinder Morgan, Inc.* | 111,200 | |||||

| 20,000 | Wells Fargo Co.* | 428,800 | |||||

| Total Warrants (Cost $330,001) | 540,000 | ||||||

| Short-Term Investments — 5.6% | |||||||

| Money Market Funds — 5.6% | |||||||

| 10,090,890 | DWS Cash Account Trust — Government | ||||||

| & Agency Securities Portfolio, 0.03%# | 10,090,890 | ||||||

| Total Short-Term Investments (Cost $10,090,890) | 10,090,890 | ||||||

| Total Investments — 98.9% (Cost $137,711,077) | 178,548,173 | ||||||

| Other Assets in Excess of Liabilities — 1.1% | 2,024,085 | ||||||

| NET ASSETS — 100.0% | $ | 180,572,258 | |||||

| PORTFOLIO HOLDINGS | |||||||

| % of Net Assets | |||||||

| Information Technology | 23.6 | % | |||||

| Financials | 20.0 | % | |||||

| Consumer Discretionary | 14.4 | % | |||||

| Industrials | 11.7 | % | |||||

| Health Care | 11.2 | % | |||||

| Energy | 8.6 | % | |||||

| Money Market Funds | 5.6 | % | |||||

| Consumer Staples | 2.2 | % | |||||

| Telecommunication Services | 1.3 | % | |||||

| Warrants | 0.3 | % | |||||

| Other Assets and Liabilities | 1.1 | % | |||||

| 100.0 | % | ||||||

ADR — American Depositary Receipt

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2014. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

12

Brown Advisory Small-Cap Growth Fund

A Message to Our Shareholders

June 30, 2014

Dear Shareholder:

During the year ended June 30, 2014, the Brown Advisory Small-Cap Growth Fund Investor Shares (the “Fund”) increased 18.42% in value. During the same period, the Russell 2000® Growth Index (the “Index”), the Fund’s benchmark, increased 24.73%.

The year can be divided into two distinct periods. For most of the past year, the Fund performed largely in line with its benchmark. Sound stock selection helped to mitigate the fact that we were underweight in some of the best-performing areas of the market (i.e., biotechnology & pharmaceuticals, etc.). However, the period from mid-May 2014 through the end of the second quarter proved quite challenging for our portfolio, during which we generated the bulk of the underperformance for the full year. A stock-specific event impacted results negatively, along with a vigorous benchmark rally in lower-quality stocks that, due to our focus on higher-quality names, worked to our detriment.

Heading into 2014, we were prepared for increased volatility following a near linear ascent in small-cap issues in 2013. As part of this preparation, we positioned the portfolio generally in what we viewed as higher-quality stocks, at reasonable relative valuations, and within the upper end of the small-market-capitalization spectrum. Unfortunately, our results were disappointing; to use a baseball analogy, we had a decent batting average, but our slugging percentage was weak—in other words, we saw a handful of our largest positions pull back meaningfully from recent highs.

While we are disappointed with recent performance, we are certainly not discouraged about our investment approach. We have maintained a consistent philosophy and executed a consistent process and strategy over the last eight years.

Overall sector allocation did not change dramatically over the past year. We were overweight in industrials and information technology, and underweight in consumer discretionary, energy, financials, health care and materials. At times, the Global Industry Classification Standard (GICS) methodology does not necessarily align with our internal view of the appropriate sector designations for our holdings. When making our internal adjustments, our weighting in consumer discretionary, health care and financials increases, while our weighting in information technology and industrials decreases.

Our top and bottom contributors for the year were spread across many sectors, with no particular sector driving performance on either side of the ledger. Incyte Corporation was the largest contributor. This relatively mature biotechnology company more than doubled on the strength of the launch of its drug for myelofibrosis, Jakafi, and a preliminary data release on that drug’s potential effectiveness in treating pancreatic cancer. United Rentals was the second largest contributor, benefiting from the recovery in the commercial real estate sector. Broadridge Financial Solutions, Harman International and Idex Corporation rounded out the Fund’s top-five contributors for the trailing 12 months.

The largest detractors during the period came from the consumer discretionary, health care and industrial sectors. Quiksilver reported extremely disappointing sales results, a result of a large number of small, wholesale-account closures. The new management team’s efforts to drive greater cost efficiency simply could not offset the shortfall in anticipated revenue. Ariad Pharmaceuticals was a small position, but it declined materially due to troubling safety data emanating from its FDA-approved drug, Iclusig. UTI Worldwide, a global freight forwarding company, experienced difficulties in rolling out key systems in the U.S. and also produced lackluster international results. As a result of these difficulties, the company unexpectedly moved to raise capital. In each of these cases, we viewed our original investment thesis as being violated and moved to exit the positions.

During the period, we added a number of new holdings while eliminating those that reached our price targets or that weren’t progressing as we had hoped. The period turnover was relatively low, consistent with our history and in line with our desire to be business owners and not stock traders.

We were heavily engaged in due diligence over the past year, conducting face-to-face meetings with the management teams of the majority of our portfolio companies along with dozens of other companies that we are considering as potential new ideas for the portfolio. We seek companies that offer us the potential for growth (through large and/or growing end markets and a differentiated product, service or business model), the potential for sustainable results (through favorable competitive positioning and/or strong

www.brownadvisoryfunds.com

13

Brown Advisory Small-Cap Growth Fund

A Message to Our Shareholders

June 30, 2014

management), and the potential for value creation (through high or improving margins and capital efficiency). We look to purchase these businesses at attractive prices when we have a non-consensus view. We will maintain this discipline going forward as we strive for stronger relative results going forward.

management), and the potential for value creation (through high or improving margins and capital efficiency). We look to purchase these businesses at attractive prices when we have a non-consensus view. We will maintain this discipline going forward as we strive for stronger relative results going forward.

Sincerely,

Christopher A. Berrier

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in smaller companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. Privately Placement issued securities are restricted securities that are not publicly traded. Delay or difficulty in selling such securities may result in a loss to the Fund.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

14

Brown Advisory Small-Cap Growth Fund

Performance Chart and Analysis

June 30, 2014

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund compared with the broad-based securities market index. The Russell 2000® Growth Index (“Index”) measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price to book value ratios and higher forecasted growth values. The Index is unmanaged and does not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Average Annual Total Return | One | Five | Ten |

| as of 6/30/14 | Year | Year | Year |

| Institutional Shares | 18.59% | 19.36% | 8.33% |

| Investor Shares | 18.42% | 19.29% | 8.52% |

Advisor Shares1 | 18.07% | 18.90% | 8.09% |

Russell 2000® Growth Index | 24.73% | 20.50% | 9.04% |

| Institutional Shares | Investor Shares | Advisor Shares | |

Gross Expense Ratio2 | 1.04% | 1.19% | 1.44% |

Net Expense Ratio2 | 1.04% | 1.19% | 1.44% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

| 1 | Performance information for Advisor Shares, prior to commencement of operations on April 25, 2006, is based on the performance of Investor Shares, and adjusted for the higher expenses applicable to Advisor Shares. |

| 2 | Per the Fund’s prospectus dated October 31, 2013. |

www.brownadvisoryfunds.com

15

Brown Advisory Small-Cap Growth Fund

Schedule of Investments

June 30, 2014

| Shares | Security Description | Value $ | |||||

| Common Stocks — 96.2% | |||||||

| Consumer Discretionary — 11.9% | |||||||

| 88,442 | ANN, Inc.* | 3,638,504 | |||||

| 81,315 | Ascent Capital Group, Inc.* | 5,367,603 | |||||

| 122,199 | Bright Horizons Family Solutions, Inc.* | 5,247,225 | |||||

| 26,723 | CoStar Group, Inc.* | 4,226,777 | |||||

| 28,496 | Harman International Industries, Inc. | 3,061,325 | |||||

| 276,210 | HomeAway, Inc.* | 9,617,632 | |||||

| 109,866 | Krispy Kreme Doughnuts, Inc.* | 1,755,659 | |||||

| 358,519 | Quiksilver, Inc.* | 1,283,498 | |||||

| 93,609 | Stage Stores, Inc. | 1,749,552 | |||||

| 35,947,775 | |||||||

| Consumer Staples — 3.1% | |||||||

| 41,100 | PriceSmart, Inc. | 3,577,344 | |||||

| 70,811 | Susser Holdings Corp.* | 5,715,864 | |||||

| 9,293,208 | |||||||

| Energy — 2.3% | |||||||

| 259,025 | Helix Energy Solutions Group, Inc.* | 6,814,948 | |||||

| Financials — 4.3% | |||||||

| 62,090 | City National Corp. | 4,703,938 | |||||

| 130,461 | Prosperity Bancshares, Inc. | 8,166,859 | |||||

| 12,870,797 | |||||||

| Health Care — 12.0% | |||||||

| 95,606 | Charles River Laboratories International, Inc.* | 5,116,833 | |||||

| 80,733 | Covance, Inc.* | 6,909,130 | |||||

| 85,652 | Dyax Corp.* | 822,259 | |||||

| 198,223 | Endologix, Inc.* | 3,014,972 | |||||

| 50,461 | Henry Schein, Inc.* | 5,988,207 | |||||

| 40,041 | IDEXX Laboratories, Inc.* | 5,348,276 | |||||

| 43,205 | Incyte Corp.* | 2,438,490 | |||||

| 12,733 | Receptos, Inc.* | 542,426 | |||||

| 69,756 | Seattle Genetics, Inc.* | 2,668,167 | |||||

| 4,101 | Ultragenyx Pharmaceutical, Inc.* | 184,094 | |||||

| 127,623 | Volcano Corporation* | 2,247,441 | |||||

| 23,132 | WuXi PharmaTech (Cayman), Inc. ADR* | 760,118 | |||||

| 36,040,413 | |||||||

| Industrials — 24.9% | |||||||

| 14,332 | Acuity Brands, Inc. | 1,981,399 | |||||

| 91,473 | Advisory Board Company* | 4,738,301 | |||||

| 46,999 | Colfax Corp.* | 3,503,305 | |||||

| 89,266 | Corporate Executive Board Co. | 6,089,726 | |||||

| 199,392 | DigitalGlobe, Inc.* | 5,543,098 | |||||

| 122,908 | HEICO Corp. | 6,383,842 | |||||

| 104,544 | Hexcel Corp.* | 4,275,850 | |||||

| 95,960 | IDEX Corp. | 7,747,810 | |||||

| 317,169 | Knight Transportation, Inc. | 7,539,107 | |||||

| 86,999 | Landstar System, Inc. | 5,567,936 | |||||

| 142,951 | Roadrunner Transportation | ||||||

| Services Holdings, Inc.* | 4,016,923 | ||||||

| 67,791 | Team, Inc.* | 2,780,787 | |||||

| 28,549 | United Rentals, Inc.* | 2,989,937 | |||||

| 213,291 | Waste Connections, Inc. | 10,355,278 | |||||

| 30,316 | Woodward, Inc. | 1,521,257 | |||||

| 75,034,556 | |||||||

| Information Technology — 35.8% | |||||||

| 245,610 | Applied Micro Circuits Corp.* | 2,655,044 | |||||

| 183,588 | Aruba Networks, Inc.* | 3,216,462 | |||||

| 240,940 | Broadridge Financial Solutions, Inc. | 10,032,742 | |||||

| 165,559 | BroadSoft, Inc.* | 4,369,102 | |||||

| 71,862 | Cavium, Inc.* | 3,568,667 | |||||

| 25,809 | CommVault Systems, Inc.* | 1,269,028 | |||||

| 28,374 | Concur Technologies, Inc.* | 2,648,429 | |||||

| 275,303 | CoreLogic, Inc.* | 8,358,199 | |||||

| 20,587 | Cvent, Inc.* | 598,876 | |||||

| 110,171 | E2open, Inc.* | 2,277,235 | |||||

| 305,247 | EXFO, Inc.*† | 1,465,186 | |||||

| 95,965 | Fair Isaac Corp. | 6,118,728 | |||||

| 323,970 | Genpact, Ltd.* | 5,679,194 | |||||

| 79,283 | Global Payments, Inc. | 5,775,766 | |||||

| 211,743 | Informatica Corp.* | 7,548,638 | |||||

| 167,724 | Interactive Intelligence Group, Inc.* | 9,414,348 | |||||

| 170,505 | MAXIMUS, Inc. | 7,335,125 | |||||

| 384,530 | Pegasystems, Inc. | 8,121,274 | |||||

| 29,848 | PROS Holdings, Inc.* | 789,181 | |||||

| 164,284 | Riverbed Technology, Inc.* | 3,389,179 | |||||

| 196,463 | Sapient Corp.* | 3,192,524 | |||||

| 69,865 | Synchronoss Technologies, Inc.* | 2,442,480 | |||||

| 39,045 | Ultimate Software Group, Inc.* | 5,394,848 | |||||

| 85,768 | Xoom Corp.* | 2,260,844 | |||||

| 107,921,099 | |||||||

| Materials — 1.9% | |||||||

| 76,651 | Rockwood Holdings, Inc. | 5,824,710 | |||||

| Total Common Stocks (Cost $190,947,113) | 289,747,506 | ||||||

| Private Placements — 0.8% | |||||||

| 16,600 | Greenspring Global Partners IV-B, L.P.*^† | 2,235,793 | |||||

| 54,769 | Greenspring Global Partners V-B, L.P.*~† | 69,705 | |||||

| Total Private Placements (Cost $947,657) | 2,305,498 | ||||||

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

16

Brown Advisory Small-Cap Growth Fund

Schedule of Investments

June 30, 2014

| Shares | Security Description | Value $ | |||||

| Short-Term Investments — 3.5% | |||||||

| Money Market Funds — 3.5% | |||||||

| 10,572,132 | DWS Cash Account Trust — Government | ||||||

| & Agency Securities Portfolio, 0.03%# | 10,572,132 | ||||||

| Total Short-Term Investments (Cost $10,572,132) | 10,572,132 | ||||||

| Total Investments — 100.5% (Cost $202,466,902) | 302,625,136 | ||||||

| Liabilities in Excess of Other Assets — (0.5)% | (1,540,780 | ) | |||||

| NET ASSETS — 100.0% | $ | 301,084,356 | |||||

| PORTFOLIO HOLDINGS | |||||||

| % of Net Assets | |||||||

| Information Technology | 35.8 | % | |||||

| Industrials | 24.9 | % | |||||

| Health Care | 12.0 | % | |||||

| Consumer Discretionary | 11.9 | % | |||||

| Financials | 4.3 | % | |||||

| Money Market Funds | 3.5 | % | |||||

| Consumer Staples | 3.1 | % | |||||

| Energy | 2.3 | % | |||||

| Materials | 1.9 | % | |||||

| Private Placements | 0.8 | % | |||||

| Other Assets and Liabilities | (0.5 | )% | |||||

| 100.0 | % | ||||||

ADR — American Depositary Receipt

| * | Non-Income Producing |

| ^ | Security is exempt from registration under Rule 144A of the Securities Act of 1933. Security is fair valued under the supervision of the Board of Trustees and was acquired from February 2008 to April 2014 as part of a $2,000,000 capital commitment. At June 30, 2014, $1,660,000 of the capital commitment has been fulfilled by the Fund. |

| ~ | Security is exempt from registration under Rule 144A of the Securities Act of 1933. Security is fair valued under the supervision of the Board of Trustees and was acquired from October 2012 to May 2014 as part of a $100,000 capital commitment. At June 30, 2014, $54,769 of the capital commitment has been fulfilled by the Fund. |

| † | All or a portion of this security is considered illiquid. At June 30, 2014, the total market value of securities considered illiquid was $2,455,773 or 0.8% of net assets. |

| # | Annualized seven-day yield as of June 30, 2014. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

17

Brown Advisory Small-Cap Fundamental Value Fund

A Message to Our Shareholders

June 30, 2014

Dear Shareholder: