UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: (811-22708)

Brown Advisory Funds

(Exact name of Registrant as specified in charter)

(Exact name of Registrant as specified in charter)

901 South Bond Street Suite 400

Baltimore, MD 21231

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

David M. Churchill

Principal Executive Officer

Brown Advisory Funds

901 South Bond Street Suite 400

Baltimore, MD 21231

(Name and address of agent for service)

(Name and address of agent for service)

(410) 537-5400

Registrant's telephone number, including area code

Date of fiscal year end: June 30

Date of reporting period: June 30, 2016

Item 1. Reports to Stockholders.

ANNUAL REPORT

June 30, 2016

Brown Advisory Growth Equity Fund

Brown Advisory Value Equity Fund

Brown Advisory Flexible Equity Fund

Brown Advisory Equity Income Fund

Brown Advisory Sustainable Growth Fund

Brown Advisory Small-Cap Growth Fund

Brown Advisory Small-Cap Fundamental Value Fund

Brown Advisory Multi-Strategy Fund

Brown Advisory Global Leaders Fund

Brown Advisory Intermediate Income Fund

Brown Advisory Total Return Fund

Brown Advisory Strategic Bond Fund

Brown Advisory Maryland Bond Fund

Brown Advisory Tax Exempt Bond Fund

Brown Advisory Mortgage Securities Fund

Brown Advisory – WMC Strategic European Equity Fund

Brown Advisory – WMC Japan Alpha Opportunities Fund

Brown Advisory – Somerset Emerging Markets Fund

Brown Advisory Emerging Markets Small-Cap Fund

The views in the report contained herein were those of the Funds’ investment adviser, Brown Advisory LLC, or, for the sub-advised funds, of the respective sub-adviser, as of June 30, 2016 and may not reflect their views on the date this report is first published or anytime thereafter. This report may contain discussions about certain investments both held and not held in the portfolio as of June 30, 2016. All current and future holdings are subject to risk and are subject to change. While these views are intended to assist shareholders in understanding their investment in each Fund, they do not constitute investment advice, are not a guarantee of future performance and are not intended as an offer or solicitation with respect to the purchase or sale of any security. Performance figures include the reinvestment of dividend and capital gain distributions.

The Global Industry Classification Standard (GICS®) was developed by and is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS® is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Administrator, U.S. Bancorp Fund Services, LLC.

TOPIX Index Values and TOPIX Marks are subject to the proprietary rights owned by the Tokyo Stock Exchange, Inc.

TABLE OF CONTENTS

| Brown Advisory Growth Equity Fund | ||

| A Message to our Shareholders, June 30, 2016 | 1 | |

| Performance Chart and Analysis | 3 | |

| Schedule of Investments, June 30, 2016 | 4 | |

| Brown Advisory Value Equity Fund | ||

| A Message to our Shareholders, June 30, 2016 | 5 | |

| Performance Chart and Analysis | 7 | |

| Schedule of Investments, June 30, 2016 | 8 | |

| Brown Advisory Flexible Equity Fund | ||

| A Message to our Shareholders, June 30, 2016 | 9 | |

| Performance Chart and Analysis | 11 | |

| Schedule of Investments, June 30, 2016 | 12 | |

| Brown Advisory Equity Income Fund | ||

| A Message to our Shareholders, June 30, 2016 | 13 | |

| Performance Chart and Analysis | 15 | |

| Schedule of Investments, June 30, 2016 | 16 | |

| Brown Advisory Sustainable Growth Fund | ||

| A Message to our Shareholders, June 30, 2016 | 17 | |

| Performance Chart and Analysis | 19 | |

| Schedule of Investments, June 30, 2016 | 20 | |

| Brown Advisory Small-Cap Growth Fund | ||

| A Message to our Shareholders, June 30, 2016 | 21 | |

| Performance Chart and Analysis | 23 | |

| Schedule of Investments, June 30, 2016 | 24 | |

| Brown Advisory Small-Cap Fundamental Value Fund | ||

| A Message to our Shareholders, June 30, 2016 | 26 | |

| Performance Chart and Analysis | 28 | |

| Schedule of Investments, June 30, 2016 | 29 | |

| Brown Advisory Multi-Strategy Fund | ||

| A Message to our Shareholders, June 30, 2016 | 30 | |

| Performance Chart and Analysis | 32 | |

| Schedule of Investments, June 30, 2016 | 33 | |

| Brown Advisory Global Leaders Fund | ||

| A Message to our Shareholders, June 30, 2016 | 34 | |

| Performance Chart and Analysis | 36 | |

| Schedule of Investments, June 30, 2016 | 37 | |

| Brown Advisory Intermediate Income Fund | ||

| A Message to our Shareholders, June 30, 2016 | 38 | |

| Performance Chart and Analysis | 39 | |

| Schedule of Investments, June 30, 2016 | 40 | |

| Brown Advisory Total Return Fund | ||

| A Message to our Shareholders, June 30, 2016 | 43 | |

| Performance Chart and Analysis | 44 | |

| Schedule of Investments, June 30, 2016 | 45 | |

| Brown Advisory Strategic Bond Fund | ||

| A Message to our Shareholders, June 30, 2016 | 48 | |

| Performance Chart and Analysis | 50 | |

| Schedule of Investments, June 30, 2016 | 51 | |

| Brown Advisory Maryland Bond Fund | ||

| A Message to our Shareholders, June 30, 2016 | 54 | |

| Performance Chart and Analysis | 55 | |

| Schedule of Investments, June 30, 2016 | 56 | |

| Brown Advisory Tax Exempt Bond Fund | ||

| A Message to our Shareholders, June 30, 2016 | 59 | |

| Performance Chart and Analysis | 60 | |

| Schedule of Investments, June 30, 2016 | 61 |

| Brown Advisory Mortgage Securities Fund | ||

| A Message to our Shareholders, June 30, 2016 | 64 | |

| Performance Chart and Analysis | 65 | |

| Schedule of Investments, June 30, 2016 | 66 | |

| Schedule of Securities Sold Short, June 30, 2016 | 73 | |

| Brown Advisory – WMC Strategic European Equity Fund | ||

| A Message to our Shareholders, June 30, 2016 | 74 | |

| Performance Chart and Analysis | 76 | |

| Schedule of Investments, June 30, 2016 | 77 | |

| Brown Advisory – WMC Japan Alpha Opportunities Fund | ||

| A Message to our Shareholders, June 30, 2016 | 79 | |

| Performance Chart and Analysis | 81 | |

| Schedule of Investments, June 30, 2016 | 82 | |

| Brown Advisory – Somerset Emerging Markets Fund | ||

| A Message to our Shareholders, June 30, 2016 | 85 | |

| Performance Chart and Analysis | 87 | |

| Schedule of Investments, June 30, 2016 | 88 | |

| Brown Advisory Emerging Markets Small-Cap Fund | ||

| A Message to our Shareholders, June 30, 2016 | 90 | |

| Performance Chart and Analysis | 91 | |

| Schedule of Investments, June 30, 2016 | 92 | |

| Statements of Assets and Liabilities | 94 | |

| Statements of Operations | 99 | |

| Statements of Changes in Net Assets | 104 | |

| Financial Highlights | 114 | |

| Notes to Financial Statements | 158 | |

| Report of Independent Registered Public Accounting Firm | 179 | |

| Additional Information | 180 |

GLOSSARY OF TERMS

Alpha refers to the abnormal rate of return on a security or portfolio in excess of what would be predicted by an equilibrium model like the capital asset pricing model (CAPM).

Barclays 1-10 Year Blended Municipal Bond Index is a market index of high quality, domestic fixed income securities with maturities of less than 10 years.

Barclays Intermediate US Aggregate Bond Index represents domestic taxable investment-grade bonds with index components for government and corporate securities, mortgage pass-through securities and asset-backed securities with average maturities and durations in the intermediate range. This index represents a sector of the Barclays US Aggregate Bond Index.

Barclays Mortgage Backed Securities Index is a market value-weighted index which covers the mortgage-backed securities component of the Barclays US Aggregate Bond Index. The index is composed of agency mortgage-backed passthrough securities of the Government National Mortgage Association (Ginnie Mae), the Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (Freddie Mac) with a minimum $150 million par amount outstanding and a weighted-average maturity of at least 1 year. The index includes reinvestment of income.

Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS, ABS and CMBS.

Barclays US Corporate High Yield Index measures the US Dollar denominated, high-yield, fixed-rate corporate bond market.

Basis point(s) (bps) is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. 1% is equal to 100 basis points.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

Book value is the net asset value of a company, calculated by total assets minus intangible assets (patents, goodwill) and liabilities.

CAPEX, or capital expenditures, are funds used by a company to acquire or upgrade physical assets such as property, industrial buildings or equipment. It is often used to undertake new projects or investments by the firm. This type of outlay is also made by companies to maintain or increase the scope of their operations.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Correlation is a statistical measurement of how two securities move in relation to each other.

Dividend Yield is a financial ratio that shows how much a company pays out in dividends each year relative to its share price. In the absence of any capital gains, the dividend yield is the return on investment for a stock.

Downside Capture is a statistical measure of a fund’s performance in down markets. For example, a fund with downside capture of 90% would only have declined 90% as much as the related index during the same down market period.

Duration is a measure of the sensitivity of the price of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year. The term can apply to actual data from previous periods or estimated data for future periods.

Earnings per share (EPS) is calculated by taking the total earnings divided by the number of shares outstanding.

Earnings Yield is the earnings per share for the most recent 12-month period divided by the current market price per share. The earnings yield shows the percentage of each dollar invested in the stock that was earned by the company.

EBITDA is the Earnings Before Interest, Taxes, Depreciation and Amortization. An approximate measure of a company’s operating cash flow based on data from the company’s income statement.

Enterprise Value (EV) is a measure of a company’s value, often used as an alternative to straightforward market capitalization. Enterprise Value is calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Forward price to earnings ratio uses forecasted earnings, rather than current earnings, to calculate the price to earnings ratio.

Free Cash Flow is the operating cash flows (net income plus amortization and depreciation) minus capital expenditures and dividends. Free cash flow is the amount of cash that a company has left over after it has paid all of its expenses, including investments.

Gross Domestic Product (GDP) is the monetary value of all the goods and services produced by an economy over a specified period. It includes consumption, government purchases, investments, and exports minus imports.

MSCI All Country World Index ex-U.S. is a market capitalization weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies.

MSCI Emerging Markets Asia Small-Cap Index captures small-cap representation across 8 Emerging Markets countries.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

GLOSSARY OF TERMS

MSCI Emerging Markets Small-Cap Index is a free float-adjusted market capitalization index that is designed to measure small cap equity market performance in the global emerging markets.

MSCI Europe Index is an index that captures large and mid cap representation across 15 developed market countries in Europe.

Price to Book Value Ratio (P/B) is ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share.

Price to earnings ratio (P/E) is a common tool for comparing the prices of different common stocks and is calculated by dividing the current market price of a stock by the earnings per share.

Return of Capital (ROC) is a return from an investment that is not considered income. The return of capital is when some or all of the money an investor has in an investment is paid back to him or her, thus decreasing the value of the investment.

Return on Capital Employed (ROCE) is a financial ratio that measures a company’s profitability and the efficiency with which its capital is employed. Return on Capital Employed (ROCE) is calculated as: ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed.

Return on Equity (ROE) is the amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested.

Return on Invested Capital (ROIC) is a calculation used to assess a company’s efficiency at allocating the capital under its control to profitable investments. ROIC is typically calculated by taking a company’s net income, subtracting dividends the company paid out and dividing that amount by the company’s total capital.

Russell Global Large Cap Index measures the performance of the largest securities in the Russell Global Index, based on market capitalization.

Russell 1000® Growth Index measures the performance of the large-cap growth segment of the of the U.S. equity universe. It includes those Russell 1000® companies with higher price to book value ratios and higher forecasted growth values.

Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® companies with lower price to book value ratios and lower expected growth values.

Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price to book value ratios and higher forecasted growth values.

Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index.

Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000® companies with lower price to book value ratios and lower forecasted growth values.

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies representing approximately 98% of the investable U.S. equity market.

S&P Balanced Equity and Bond – Moderate Index is the moderate profile of the S&P Balanced Equity and Bond Series which combines investable S&P indices for core equity and fixed income to provide a regulary rebalanced multi-asset measure for conservative, moderate and growth risk-reward profiles.

S&P 500 Index (“S&P 500”) is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks.

Tier 1 Capital Ratio is a comparison between a banking firm’s core equity capital and total risk-weighted assets. A firm’s core equity capital is known as its Tier 1 capital and is the measure of a bank’s financial strength based on the sum of its equity capital and disclosed reserves, and sometimes non-redeemable, non-cumulative preferred stock. A firm’s risk-weighted assets include all assets that the firm holds that are systematically weighted for credit risk. Central banks typically develop the weighting scale for different asset classes, such as cash and coins, which have zero risk, versus a letter or credit, which carries more risk.

TOPIX Total Return U.S. Dollar Hedged Index is a market capitalization-weighted index of all companies listed on the First Section of the Tokyo Stock Exchange, hedged to eliminate the impact of the change in value between the US Dollar and Japanese Yen. The unhedged version of this index, known as the TOPIX Total Return Index, does not eliminate the change in value between the US Dollar and Japanese Yen.

Turnover refers to a fund buying or selling securities. (The fund “turns over” its portfolio.) A fund pays transaction costs, such as commissions, when it buys and sells securities. Additionally, a higher turnover rate may result in higher taxes when the fund shares are held in a taxable account.

Yield Curve is a line that plots the yields of securities having equal credit quality but different maturity dates.

Yield Spread is the difference between yields on differing securities, calculated by deducting the yield of one security from another.

The broad based market indexes referenced in the following management commentaries are considered representative of their indicated market, the indexes are unmanaged and do not reflect the deduction of fees, such as, investment management and fund accounting fees, or taxes associated with a mutual fund. Investors cannot invest directly in an index.

Brown Advisory Growth Equity Fund

A Message to Our Shareholders

June 30, 2016

Dear Shareholder:

During the year ended June 30, 2016, the Brown Advisory Growth Equity Fund Investor Shares (the “Fund”) increased 0.34% in value. During the same period, the Russell 1000 Growth Index (the “Index”), the Fund’s benchmark, increased 3.02%.

Terrorist attacks and political uncertainty are just some of the issues investors wrestled with that sent equity markets on a roller coaster ride during the past 12 months. Despite the turbulence, the Fund and the Index both ended the period with a positive return.

The U.K. vote to leave the European Union roiled worldwide financial markets, partly due to concerns about Europe’s fragile growth trajectory. Amid the setback for broader markets, the Fund gave back the gains made in the prior months. Interest rate-sensitive stocks—especially those in financial services—were hit especially hard by the Brexit vote. The referendum threw yet another wrench into the Federal Reserve’s projections for an increase in the main interest rate. The yield on 10-year Treasuries dipped toward a historic low, pushing up shares with above-average dividend yields, such as those in consumer staples, utilities, and telecommunications sectors. We tend to be very underweight utilities and other high-dividend-paying stocks because they rarely meet our growth criteria.

Health care was the best performing sector compared with its counterpart in the benchmark during this time period. As a group, our health care positions held up better than the Index, due in part to the underweight to biotechnology, which fell 22%, and several individual holdings that outperformed, including long-time holding Intuitive Surgical. It was not that long ago that short-sighted investors left the stock for dead while the company worked through a sluggish cycle in hospital spending and rolled out a new version of its robotic surgical system. Procedure growth for the new system is performing better than many analysts expected, and international procedure growth is accelerating. On the negative side of health care, Alexion has been one of our biggest detractors. While the competitive environment has improved for Alexion, its results have been impaired by the strengthening U.S. dollar. Most biotech companies don’t have to deal with foreign currency issues as their revenues are predominantly domestic. Rather than avoid companies with overseas exposure, we look for those with unique products or services that are not easily replicated by competitors that benefit from the advantage of residing in a country with a weakening currency. For some of our companies, currency fluctuations will be a temporary headwind to near-term earnings. Over the long run, companies such as Alexion—which produces lifesaving drugs for the global market—have the potential to ultimately benefit from geographical diversification and the generation of revenues worldwide.

The recent volatility continues to provide opportunities to initiate new positions in what we believe to be exceptional business models and in some cases add to those that we already own. One example of this activity is our swap from Colfax to Westinghouse Air Brake Technologies (Wabtec). Wabtec is a leading manufacturer of electronic control and braking technology for the global rail industry. The recent declines in North America rail volume caused by the dislocation across the industrial landscape has created, in our belief, an excellent opportunity to invest in a best-in-breed industrial company trading at a very compelling valuation. There are several factors that make Wabtec an attractive long-term investment opportunity. Its electronic control system has become the industry standard, and new regulations will require that it be installed on new and existing trains over the next few years. The company recently announced the acquisition of a European company, gaining exposure to the commuter rail market and reducing the cyclicality of the business. We sold our position in Colfax, which is also a high quality industrial company. However, Colfax’s end markets are much more cyclical and we have much less confidence in its ability to grow through the global downturn. Although Colfax and Wabtec have both traded lower, we believe Wabtec possesses a superior business model.

We eliminated the last remaining pure energy stock in the portfolio during this period. As the price of oil declined and subsequently bottomed in February, energy stock valuations in our view signaled that investment in oilfield service stocks was predicated on the notion that the price of oil would quickly rebound. Our skill set is not predicting the short term direction of commodity prices. As such, we continued to reduce our exposure to energy and have now eliminated all of the pure energy stocks in the portfolio. We used the proceeds from the sale of FMC Technologies which is an oilfield service company, to purchase SBA Communications. SBA owns and operates cellular communication towers primarily in North America and Brazil. We have been watching SBA for several years, but it had never traded at a valuation we were willing to pay. Concerns about the deprecation of Brazil’s currency and general market weakness created an excellent opportunity in which to build our position. The business model has been stable with long term predictable lease terms. Also, the company has several new drivers for potential growth, including increasing mobile usage and reoccurring upgrades in communication hardware which has led to higher revenue per unit.

www.brownadvisoryfunds.com

1

Brown Advisory Growth Equity Fund

A Message to Our Shareholders

June 30, 2016

Despite the specter of slowing global growth we continue to find high quality growth companies. We have tried to use the recent market volatility to our advantage by capturing them at attractive valuations. At times, the market becomes preoccupied with short-term noise created by such things as foreign currency fluctuations or interest rates. Our focus has always been on business models that, in our belief, provide a truly differentiated product or customer experience. We believe this has the potential to translate into a sustainable long term growth rate.

Sincerely,

Kenneth M. Stuzin, CFA

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in medium capitalization companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

2

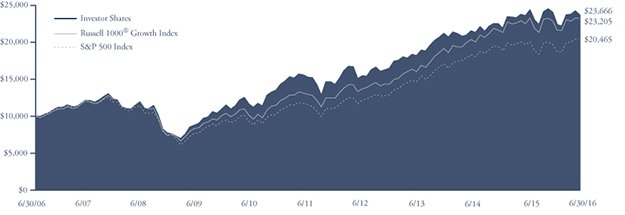

Brown Advisory Growth Equity Fund

Performance Chart and Analysis

June 30, 2016

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against broad-based securities market indices. The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price to book and higher forecasted growth values. The S&P 500 Index is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The indexes are unmanaged and do not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Average Annual Total Return | One | Five | Ten | |

as of 6/30/16 | Year | Year | Year | |

Institutional Shares1 | 0.49% | 9.32% | 9.16% | |

| Investor Shares | 0.34% | 9.16% | 9.00% | |

| Advisor Shares | 0.09% | 8.90% | 8.61% | |

Russell 1000® Growth Index | 3.02% | 12.35% | 8.78% | |

| S&P 500 Index | 3.99% | 12.10% | 7.42% |

Institutional Shares | Investor Shares | Advisor Shares | ||

Gross Expense Ratio2 | 0.72% | 0.87% | 1.12% | |

Net Expense Ratio2 | 0.72% | 0.87% | 1.12% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

2 | Per the Fund’s prospectus dated October 30, 2015. |

www.brownadvisoryfunds.com

3

Brown Advisory Growth Equity Fund

Schedule of Investments

June 30, 2016

Shares | Security Description | Value $ | ||||||

| Common Stocks — 95.1% | ||||||||

| Consumer Discretionary — 14.5% | ||||||||

| 147,410 | Amazon.com, Inc.* | 105,489,544 | ||||||

| 1,577,207 | Starbucks Corp. | 90,090,064 | ||||||

| 1,048,990 | TripAdvisor, Inc.* | 67,450,057 | ||||||

| 590,398 | Under Armour, Inc. — Class A* | 23,692,672 | ||||||

| 910,296 | Under Armour, Inc. — Class C* | 33,134,784 | ||||||

| 319,857,121 | ||||||||

| Consumer Staples — 10.6% | ||||||||

| 534,173 | Costco Wholesale Corp. | 83,886,528 | ||||||

| 864,858 | Estee Lauder Companies, Inc. | 78,719,375 | ||||||

| 779,564 | Mead Johnson Nutrition Co. | 70,745,433 | ||||||

| 233,351,336 | ||||||||

| Financials — 1.0% | ||||||||

| 858,735 | Charles Schwab Corp. | 21,734,583 | ||||||

| Health Care — 14.9% | ||||||||

| 429,598 | Alexion Pharmaceuticals, Inc.* | 50,159,862 | ||||||

| 1,110,603 | Bristol-Myers Squibb Co. | 81,684,851 | ||||||

| 661,938 | DaVita HealthCare Partners, Inc.* | 51,181,046 | ||||||

| 878,471 | Express Scripts Holding Co.* | 66,588,102 | ||||||

| 119,327 | Intuitive Surgical, Inc.* | 78,924,071 | ||||||

| 328,537,932 | ||||||||

| Industrials — 8.3% | ||||||||

| 888,752 | Danaher Corp. | 89,763,952 | ||||||

| 1,032,895 | Fastenal Co. | 45,850,209 | ||||||

| 666,950 | Wabtec Corp. | 46,839,899 | ||||||

| 182,454,060 | ||||||||

| Information Technology — 39.9% | ||||||||

| 532,631 | Adobe Systems, Inc.* | 51,020,723 | ||||||

| 882,158 | Akamai Technologies, Inc.* | 49,339,097 | ||||||

| 62,606 | Alphabet, Inc. — Class A* | 44,045,199 | ||||||

| 88,060 | Alphabet, Inc. — Class C* | 60,946,326 | ||||||

| 1,227,875 | Amphenol Corp. | 70,394,074 | ||||||

| 456,039 | ANSYS, Inc.* | 41,385,539 | ||||||

| 872,090 | Cognizant Technology Solutions Corp.* | 49,918,432 | ||||||

| 842,808 | Facebook, Inc.* | 96,316,098 | ||||||

| 347,489 | FleetCor Technologies, Inc.* | 49,736,101 | ||||||

| 2,187,741 | Genpact, Ltd.* | 58,718,968 | ||||||

| 553,138 | National Instruments Corp. | 15,155,981 | ||||||

| 602,146 | NetSuite, Inc.* | 43,836,229 | ||||||

| 724,855 | NXP Semiconductors NV* | 56,785,141 | ||||||

| 495,942 | PayPal Holdings, Inc.* | 18,106,842 | ||||||

| 952,132 | salesforce.com, Inc.* | 75,608,802 | ||||||

| 1,316,005 | Visa, Inc. | 97,608,091 | ||||||

| 878,921,643 | ||||||||

| Materials — 3.5% | ||||||||

| 645,843 | Ecolab, Inc. | 76,596,980 | ||||||

| Telecommunication Services — 2.4% | ||||||||

| 504,081 | SBA Communications Corp.* | 54,410,503 | ||||||

| Total Common Stocks (Cost $1,485,144,893) | 2,095,864,158 | |||||||

| Short-Term Investments — 4.0% | ||||||||

| Money Market Funds — 4.0% | ||||||||

| 88,142,557 | Cash Account Trust — Government | |||||||

| & Agency Securities Portfolio — | ||||||||

| Institutional Shares, 0.34%# | 88,142,557 | |||||||

| Total Short-Term Investments (Cost $88,142,557) | 88,142,557 | |||||||

| Total Investments — 99.1% (Cost $1,573,287,450) | 2,184,006,715 | |||||||

| Other Assets in Excess of Liabilities — 0.9% | 19,410,231 | |||||||

| NET ASSETS — 100.0% | $ | 2,203,416,946 | ||||||

| PORTFOLIO HOLDINGS | |

| % of Net Assets | |

| Information Technology | 39.9% |

| Health Care | 14.9% |

| Consumer Discretionary | 14.5% |

| Consumer Staples | 10.6% |

| Industrials | 8.3% |

| Money Market Funds | 4.0% |

| Materials | 3.5% |

| Telecommunication Services | 2.4% |

| Financials | 1.0% |

| Other Assets and Liabilities | 0.9% |

| 100.0% |

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2016. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

4

Brown Advisory Value Equity Fund

A Message to Our Shareholders

June 30, 2016

Dear Shareholder:

During the year ended June 30, 2016, the Brown Advisory Value Equity Fund Investor Shares (the “Fund”) declined 8.74%, while the Russell 1000 Value Index, the Fund’s benchmark, increased 2.86%.

During the year, the U.S. equity market took investors on a wild ride but was unable to break out of a trading range. Our underperformance was a tale of two halves: Stock selection was the biggest factor in the first six months while sector allocation dominated the final six months.

In the final six months of 2015, a variety of factors impaired Fund results. Fears of a global slowdown resulting from China’s currency devaluation impacted our energy, material, and industrial holdings, especially Plains GP Holdings, Potash and Joy Global. Company-specific weakness in Micron and Apple—a strong performer last year—weighed on the strategy. Poor company outlooks affected the performance of Viacom and Ameriprise.

In the first six months of 2016 (the second half of this reporting period), the sharp decline in interest rates to record lows inverted the age-old adage of “buy bonds for income and stocks for capital gains.” As of now, equities yield more than bonds and it will be difficult to eke out much of a return on bonds without a capital gain component. Of course, to generate capital gains, rates would need to go even lower.

Several events along the way exacerbated the sharp decline in rates, but the two large forces were, 1) the move by Japan and European central banks to drive interest rates into negative yields and 2) the Brexit decision in the U.K. These events caused equity investors to move away from risk assets and instead chase yield in perceived safe havens such as utilities and telecom services. Both sectors had benchmark-leading returns exceeding 20%, and we were hurt by not having exposure to these traditionally defensive areas. Worth noting, during the period between these two events, the Fund’s performance was quite strong and kept pace with the benchmark.

During the year, consumer staples was our top performing sector—a bright spot for us among the traditionally defined defensive sectors. Philip Morris and Unilever, our two consumer staples holdings, gained 32% and 15% respectively.

In health care, political headlines focused on aggressive industry pricing practices undermined investor sentiment and weighed on our pharmaceutical names. Despite the overhang, drug price inflation has very little impact on the revenues of our pharmaceutical holdings. We remain confident in the long-term fundamentals of our health care holdings and believe they represent great value at current prices.

We believe the low and negative rate environment is distorting saving, consumption and investment. We see sizable misallocations of capital: stable businesses such as utilities and staples have traded at record high valuations, Merger & Acquisitions valuations have increased every month and corporations have been hesitant to increase capital expenditures because of the uncertainty of growth and a proper rate to discount the cash flows. Importantly, our portfolio investment allocations are based on bottom up value seeking—improving fundamentals and solid cash flows not recognized by the market—rather than on a macro call on the movement of interest rates.

Our overweight sectors (consumer discretionary, technology and financials) are currently valued at 13x forward earnings, while our underweights (utilities, telecom, energy, materials, staples) are currently valued at 22x forward earnings.

During the year we eliminated 16 holdings and added 10 to the portfolio, not including several corporate actions. Our portfolio turnover was driven by selling companies heavily dependent on macro factors in favor of companies with promising valuations.

We took advantage of market dislocations to add a number of quality companies across sectors at what we believe to be attractive prices. Centene, Target, CarMax, Liberty Media and Wells Fargo are U.S.-centric companies featuring historically steady growth, high returns on capital and low earnings variability. We believe they are undervalued. In addition to Wells Fargo, we diversified our financial holdings by adding Towers Watson and Comerica, while swapping out Northern Trust. We believe that General Dynamics is a much more defensive industrial company than the ones we sold, with good visibility for potential growth in its defense business and an underappreciated outlook for its competitively positioned Gulfsteam business jets.

We eliminated some of our weakest performers, including Viacom, Plains GP Holdings, Joy Global, Copa Airlines and Oceaneering among others. We sold these companies because of pricing pressures and structural challenges in their end markets. Their exposure to external factors outside of management control overwhelmed the business attributes that originally attracted us to these companies.

www.brownadvisoryfunds.com

5

Brown Advisory Value Equity Fund

A Message to Our Shareholders

June 30, 2016

The investor bias toward safety appears unsustainable to us. Our overweight sectors combine modest valuation with supportive business fundamentals. For example, key characteristics of our consumer discretionary holdings include companies with what we believe to be durable competitive advantage, innovation, strong consumer value propositions and attractive financial metrics. Our technology holdings maintain strong cash flow and profitability metrics with what we believe are good growth prospects. Our financial holdings have continued to take market share and cut costs even as Federal Reserve policymakers signal a postponement of their next increase in the main interest rate. For the defensive sectors, we believe the high current valuation, low growth prospects, and poor business models, along with the inevitable rise in rates, will likely provide sub-par returns for investors over the intermediate to long term.

Sincerely,

Doron S. Eisenberg, CFA

Portfolio Manager

Michael L. Foss, CFA

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in medium capitalization companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. Diversification does not guarantee a profit or protect from loss in a declining market. Earnings growth is not a measure of the Fund’s future performance.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

6

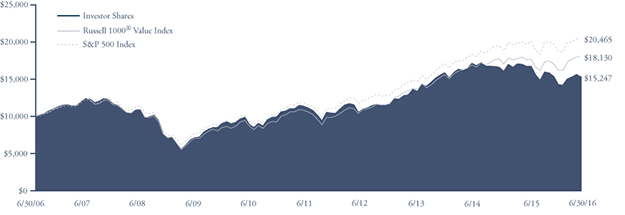

Brown Advisory Value Equity Fund

Performance Chart and Analysis

June 30, 2016

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against broad-based securities market indices. The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® companies with lower price to book ratios and lower expected growth values. The S&P 500 Index is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The indexes are unmanaged and do not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Average Annual Total Return | One | Five | Ten | |

as of 6/30/16 | Year | Year | Year | |

Institutional Shares1 | -8.57% | 6.73% | 4.46% | |

| Investor Shares | -8.74% | 6.57% | 4.31% | |

| Advisor Shares | -8.97% | 6.33% | 3.93% | |

Russell 1000® Value Index | 2.86% | 11.35% | 6.13% | |

| S&P 500 Index | 3.99% | 12.10% | 7.42% |

Institutional Shares | Investor Shares | Advisor Shares | ||

Gross Expense Ratio2 | 0.75% | 0.90% | 1.15% | |

Net Expense Ratio2 | 0.75% | 0.90% | 1.15% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

2 | Per the Fund’s prospectus dated October 30, 2015. |

www.brownadvisoryfunds.com

7

Brown Advisory Value Equity Fund

Schedule of Investments

June 30, 2016

Shares | Security Description | Value $ | ||||||

| Common Stocks — 89.2% | ||||||||

| Consumer Discretionary — 12.7% | ||||||||

| 21,167 | BorgWarner, Inc. | 624,850 | ||||||

| 25,796 | CarMax, Inc.* | 1,264,778 | ||||||

| 30,064 | Garmin, Ltd. | 1,275,315 | ||||||

| 29,361 | Liberty Media Group* | 556,978 | ||||||

| 28,529 | Liberty Media SiriusXM Group* | 880,690 | ||||||

| 20,432 | Michael Kors Holdings, Ltd.* | 1,010,975 | ||||||

| 14,756 | Target Corp. | 1,030,264 | ||||||

| 6,643,850 | ||||||||

| Consumer Staples — 6.4% | ||||||||

| 16,459 | Philip Morris International, Inc. | 1,674,210 | ||||||

| 35,780 | Unilever NV ADR | 1,679,513 | ||||||

| 3,353,723 | ||||||||

| Energy — 5.4% | ||||||||

| 16,195 | Occidental Petroleum Corp. | 1,223,694 | ||||||

| 58,913 | Suncor Energy, Inc. | 1,633,658 | ||||||

| 2,857,352 | ||||||||

| Financials — 21.4% | ||||||||

| 15,811 | Ameriprise Financial, Inc. | 1,420,618 | ||||||

| 40,056 | Charles Schwab Corp. | 1,013,817 | ||||||

| 12,694 | Comerica, Inc. | 522,104 | ||||||

| 31,815 | JPMorgan Chase & Co. | 1,976,984 | ||||||

| 169,026 | Regions Financial Corp. | 1,438,411 | ||||||

| 40,784 | SunTrust Banks, Inc. | 1,675,407 | ||||||

| 18,721 | Synovus Financial Corp. | 542,722 | ||||||

| 8,777 | T. Rowe Price Group, Inc. | 640,458 | ||||||

| 20,016 | Wells Fargo Co. | 947,357 | ||||||

| 8,154 | Willis Towers Watson PLC | 1,013,624 | ||||||

| 11,191,502 | ||||||||

| Health Care — 14.6% | ||||||||

| 33,613 | AbbVie, Inc. | 2,080,981 | ||||||

| 9,664 | Centene Corp.* | 689,720 | ||||||

| 38,881 | Hologic, Inc.* | 1,345,282 | ||||||

| 21,191 | Merck & Co., Inc. | 1,220,813 | ||||||

| 11,863 | Novartis AG ADR | 978,816 | ||||||

| 27,051 | Teva Pharmaceutical Industries, Ltd. ADR | 1,358,772 | ||||||

| 7,674,384 | ||||||||

| Industrials — 6.1% | ||||||||

| 7,594 | General Dynamics Corp. | 1,057,389 | ||||||

| 51,271 | General Electric Co. | 1,614,011 | ||||||

| 10,016 | PACCAR, Inc. | 519,530 | ||||||

| 3,190,930 | ||||||||

| Information Technology — 22.6% | ||||||||

| 16,043 | Apple, Inc. | 1,533,711 | ||||||

| 11,967 | Check Point Software Technologies, Ltd.* | 953,531 | ||||||

| 65,036 | Cisco Systems, Inc. | 1,865,883 | ||||||

| 40,464 | CommScope Holding Co, Inc.* | 1,255,598 | ||||||

| 47,346 | eBay, Inc.* | 1,108,370 | ||||||

| 19,409 | Microchip Technology, Inc. | 985,201 | ||||||

| 22,055 | Micron Technology, Inc.* | 303,477 | ||||||

| 24,053 | Microsoft Corp. | 1,230,792 | ||||||

| 18,349 | PayPal Holdings, Inc.* | 669,922 | ||||||

| 18,441 | QUALCOMM, Inc. | 987,884 | ||||||

| 25,076 | Yahoo, Inc.* | 941,854 | ||||||

| 11,836,223 | ||||||||

| Total Common Stocks (Cost $37,311,741) | 46,747,964 | |||||||

| Real Estate Investment Trusts — 5.0% | ||||||||

| 42,063 | Forest City Realty Trust, Inc. | 938,425 | ||||||

| 24,085 | W.P. Carey, Inc. | 1,671,981 | ||||||

| Total Real Estate Investment Trusts (Cost $2,224,322) | 2,610,406 | |||||||

| Short-Term Investments — 2.9% | ||||||||

| Money Market Funds — 2.9% | ||||||||

| 1,516,074 | Cash Account Trust — Government | |||||||

| & Agency Securities Portfolio — | ||||||||

| Institutional Shares, 0.34%# | 1,516,074 | |||||||

| Total Short-Term Investments (Cost $1,516,074) | 1,516,074 | |||||||

| Total Investments — 97.1% (Cost $41,052,137) | 50,874,444 | |||||||

| Other Assets in Excess of Liabilities — 2.9% | 1,522,506 | |||||||

| NET ASSETS — 100.0% | $ | 52,396,950 | ||||||

| PORTFOLIO HOLDINGS | |

| % of Net Assets | |

| Information Technology | 22.6% |

| Financials | 21.4% |

| Health Care | 14.6% |

| Consumer Discretionary | 12.7% |

| Consumer Staples | 6.4% |

| Industrials | 6.1% |

| Energy | 5.4% |

| Real Estate Investment Trusts | 5.0% |

| Money Market Funds | 2.9% |

| Other Assets and Liabilities | 2.9% |

| 100.0% |

ADR — American Depositary Receipt

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2016. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

8

Brown Advisory Flexible Equity Fund

A Message to Our Shareholders

June 30, 2016

Dear Shareholder:

During the year ended June 30, 2016, the Brown Advisory Flexible Equity Fund Investor Shares (the “Fund”) decreased 4.30%. The S&P 500 Index, the Fund’s benchmark, increased 3.99% during the same period.

Our investment results over time and relative to the S&P 500 Index benchmark have been good, despite recently lagging the market. In the past, periods of underperformance for our strategy have usually coincided with a narrowness in the focus of the markets, when just a few stocks or a particular economic sector do extremely well and the broader market lags behind. However, stocks that have recently performed well are not where we first look for new ideas—though we don’t rule them out. This approach differs from that of many investors but has served us well in the long run.

Narrowness in market focus has been a factor recently in our performance, but any manager with a portfolio that differs from the market is likely going to have periods of underperformance from time to time. There isn’t an investment Superman, Superwoman or Superteam that always out-performs the market averages. Our performance has rebounded strongly after previous lagging periods, and that is again our goal. As with the prior cases of underperformance, we are sticking with our investment disciplines rather than chasing what has been hot lately. Anything can happen in markets in short periods of time, but in the long term the market has tended to find its way back to rewarding good business performance purchased on a reasonable valuation basis. We have a strong investment team with great continuity and the same disciplines and approach as always.

The top contributor to return during the year was Edwards Lifesciences Corp., a manufacturer of devices to treat cardiovascular disease. Edwards Lifesciences rose because of strong revenue and earnings results and increased earnings guidance for the future. Additional large contributors to the Fund’s results in the period include Alphabet, Inc. Class A & C (formerly known as Google), a leader in on-line search; Lowe’s Companies, Inc., a leading home improvements retailer; Visa, Inc., a global payments processor; and Yahoo! Inc., an internet company. With the exception of Yahoo!, these have each been prominent companies and leaders in their fields. Each was purchased at times when we believe they offered exceptional value for the money from a long-term perspective, which has become better appreciated in the last year. Yahoo!, or at least its namesake business, is not exceptional but the sum of its various parts, the largest being Alibaba, the Chinese Internet retailer, showed that the shares were trading at a meaningful discount to the sum of its parts. Yahoo! shares have risen given the actions the company has taken to better realize the value of these parts for shareholders.

The biggest detractor to returns was Kinder Morgan, Inc., a pipeline transportation company, as its stock fell 49% during the year. As we discussed in our semi-annual report, we viewed Kinder Morgan’s fuel transport business as having low sensitivity to energy prices. But its reliance on capital markets to fund construction of new pipelines and expand capacity at existing lines was costly when investors’ appetite waned for funding new energy investments. Kinder was forced to either cut its investment projects or its dividend, and it chose to reduce its dividend by 75%, from $2 to 50 cents per share. The cash flows supporting the previous $2 dividend and debt service were largely intact, so we kept our stock and added to the holding as the company made good progress in improving its financial position.

Other meaningful detractors to the Fund’s performance were Charles Schwab Corp., a financial services company; Express Scripts, a pharmacy benefits manager; Copa Holdings, a Latin American airline; and Teva Pharmaceutical, a branded and proprietary pharmaceuticals manufacturer. We exited Copa during the year and continue to hold the others. We added to Teva, given the better value at the lower prices.

We added two new holdings and eliminated five since our December 31, 2015, Semi-Annual Report to shareholders. We purchased what we believe are good companies whose stocks sold off too much in our view and trimmed other holdings that held up well. We also eliminated holdings where our views of their long-term business opportunities had changed and invested in companies at good valuations with stronger near-term business trends and future prospects.

A weak earnings report and an increasingly competitive environment for credit cards prompted us to eliminate American Express. We sold Franklin Resources while maintaining our weighting in asset management companies with our investments in Ameriprise Financial and T. Rowe Price. Franklin Resources has been hit hard by recent investor withdrawals, especially involving international investments. We sold International Business Machines, an information technology company, as its various business initiatives have not sufficiently increased revenues and earnings. We exited Oceaneering International, a provider of offshore oil and services, because low oil prices have dimmed the outlook for offshore oil drilling relative to onshore drilling in shale formations in the U.S. The technology gains in onshore oil production from U.S. shale make offshore development less competitive, even with a rebound in oil prices. We eliminated California Resources shares that were distributed as part of a spinoff from Occidental Petroleum, an integrated energy company.

www.brownadvisoryfunds.com

9

Brown Advisory Flexible Equity Fund

A Message to Our Shareholders

June 30, 2016

We eliminated Owens Corning, a producer of building materials. The investment had done well since it was purchased in late 2011 as a play on a future pick up in housing activity. Housing activity has recovered and probably will continue to do so, but we believe Owens Corning shares no longer offer as much potential for future return.

We initiated new investments in Aetna, a leading health care insurance provider, and General Dynamics, an aerospace and defense company.

Aetna has had a strong competitive position and its pending acquisition of Humana has the potential to provide even greater scale in the commercial, Medicaid and Medicare Advantage markets and a more balanced mix of businesses across its portfolio. The company has invested in health care management businesses for future growth potential. Management has a proven track record of executing on strategic initiatives and good capital allocation. Valuation is attractive relative to peers, and may have the potential for above-average profit growth from the combination of Aetna and Humana.

General Dynamics is notably less expensive than other defense companies. This discounted valuation is mostly due to near-term concerns over the company’s Gulfstream commercial jets business, which we expect will be resolved over time. Defense spending worldwide has the potential to increase in the near future. General Dynamics has delivered attractive business results. It has had a strong management team, a good balance sheet, rising free cash flow and a history of increasing shareholder returns through dividends and repurchases.

We look for what we believe are bargains among long-term attractive businesses with shareholder-oriented managers. These bargains can arise due to short-term investor perceptions, temporary business difficulties that should improve, or as-yet-undiscovered opportunities and unrecognized changes for the better. We remain optimistic about the long-term outlook for equities of good companies purchased at reasonable prices and our ability to find them.

Sincerely,

R. Hutchings Vernon, CFA

Portfolio Manager

Michael L. Foss, CFA

Portfolio Manager

Past performance is not a guarantee of future results.

Mutual fund investing involves risk. Principal loss is possible. The Flexible Equity Fund may invest in securities of foreign issuers. Investments in such securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. These risks are greater for investments in emerging markets. The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in smaller and medium-sized companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

10

Brown Advisory Flexible Equity Fund

Performance Chart and Analysis

June 30, 2016

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against the broad-based securities market index. The S&P 500 Index (“Index”) is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The Index is unmanaged and does not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Since | ||||

| Average Annual Total Return | One | Five | Inception | |

as of 6/30/16 | Year | Year | (11/30/06) | |

Institutional Shares1 | -4.16% | 11.19% | 5.06% | |

| Investor Shares | -4.30% | 11.01% | 4.90% | |

Advisor Shares2 | -4.56% | 10.75% | 4.62% | |

| S&P 500 Index | 3.99% | 12.10% | 6.58% |

| Institutional Shares | Investor Shares | Advisor Shares | ||

Gross Expense Ratio3 | 0.76% | 0.91% | 1.16% | |

Net Expense Ratio3 | 0.76% | 0.91% | 1.16% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects periods during which fee waivers were in effect. In the absence of such waivers, total return would have been reduced. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

2 | Performance information for Advisor Shares, prior to commencement of operations on January 24, 2007, is based on the performance of Investor Shares, and adjusted for the higher expenses applicable to Advisor Shares. |

3 | Per the Fund’s prospectus dated October 30, 2015. |

www.brownadvisoryfunds.com

11

Brown Advisory Flexible Equity Fund

Schedule of Investments

June 30, 2016

Shares | Security Description | Value $ | ||||||

| Common Stocks — 96.6% | ||||||||

| Consumer Discretionary — 17.4% | ||||||||

| 173,055 | Best Buy Co., Inc. | 5,295,483 | ||||||

| 249,534 | CarMax, Inc.* | 12,234,652 | ||||||

| 163,235 | Lowe’s Companies, Inc. | 12,923,315 | ||||||

| 9,648 | Priceline Group, Inc.* | 12,044,660 | ||||||

| 90,273 | TJX Companies, Inc. | 6,971,784 | ||||||

| 95,822 | Walt Disney Co. | 9,373,308 | ||||||

| 58,843,202 | ||||||||

| Consumer Staples — 1.5% | ||||||||

| 47,838 | PepsiCo, Inc. | 5,067,958 | ||||||

| Energy — 5.2% | ||||||||

| 541,946 | Kinder Morgan, Inc. | 10,145,229 | ||||||

| 98,419 | Occidental Petroleum Corp. | 7,436,540 | ||||||

| 17,581,769 | ||||||||

| Financials — 19.7% | ||||||||

| 77,136 | Ameriprise Financial, Inc. | 6,930,670 | ||||||

| 227,689 | Bank of America Corp. | 3,021,433 | ||||||

| 124,003 | Berkshire Hathaway, Inc.* | 17,954,395 | ||||||

| 336,875 | Charles Schwab Corp. | 8,526,306 | ||||||

| 123,881 | JPMorgan Chase & Co. | 7,697,965 | ||||||

| 413,539 | Regions Financial Corp. | 3,519,217 | ||||||

| 73,593 | T. Rowe Price Group, Inc. | 5,370,081 | ||||||

| 284,898 | Wells Fargo & Co. | 13,484,222 | ||||||

| 66,504,289 | ||||||||

| Health Care — 13.6% | ||||||||

| 49,062 | Aetna, Inc. | 5,991,942 | ||||||

| 31,994 | Anthem, Inc. | 4,202,092 | ||||||

| 100,217 | Edwards Lifesciences Corp.* | 9,994,641 | ||||||

| 141,975 | Express Scripts Holding Co.* | 10,761,705 | ||||||

| 57,539 | Merck & Co., Inc. | 3,314,822 | ||||||

| 233,913 | Teva Pharmaceutical Industries, Ltd. ADR | 11,749,450 | ||||||

| 46,014,652 | ||||||||

| Industrials — 9.1% | ||||||||

| 190,695 | Canadian National Railway Co. | 11,262,447 | ||||||

| 18,142 | Canadian Pacific Railway, Ltd. | 2,336,508 | ||||||

| 27,122 | General Dynamics Corp. | 3,776,467 | ||||||

| 106,608 | United Rentals, Inc.* | 7,153,397 | ||||||

| 58,412 | United Technologies Corp. | 5,990,151 | ||||||

| 30,518,970 | ||||||||

| Information Technology — 28.2% | ||||||||

| 62,039 | Accenture PLC | 7,028,398 | ||||||

| 7,155 | Alphabet, Inc. — Class A* | 5,033,757 | ||||||

| 14,792 | Alphabet, Inc. — Class C* | 10,237,543 | ||||||

| 102,161 | Apple, Inc. | 9,766,592 | ||||||

| 134,545 | eBay, Inc.* | 3,149,698 | ||||||

| 136,481 | MasterCard, Inc. | 12,018,517 | ||||||

| 168,505 | Microsoft Corp. | 8,622,401 | ||||||

| 135,645 | PayPal Holdings, Inc.* | 4,952,399 | ||||||

| 132,138 | QUALCOMM, Inc. | 7,078,633 | ||||||

| 244,107 | Visa, Inc. | 18,105,416 | ||||||

| 242,432 | Yahoo, Inc.* | 9,105,746 | ||||||

| 95,099,100 | ||||||||

| Telecommunication Services — 1.9% | ||||||||

| 63,773 | Crown Castle International Corp. | 6,468,495 | ||||||

| Total Common Stocks (Cost $276,274,880) | 326,098,435 | |||||||

| Warrants — 0.1% | ||||||||

| 20,000 | Wells Fargo & Co.*, Exercise price | |||||||

| $33.90 expires 10/28/2018 | 272,400 | |||||||

| Total Warrants (Cost $221,300) | 272,400 | |||||||

| Short-Term Investments — 3.5% | ||||||||

| Money Market Funds — 3.5% | ||||||||

| 11,833,570 | Cash Account Trust — Government | |||||||

| & Agency Securities Portfolio — | ||||||||

| Institutional Shares, 0.34%# | 11,833,570 | |||||||

| Total Short-Term Investments (Cost $11,833,570) | 11,833,570 | |||||||

| Total Investments — 100.2% (Cost $288,329,750) | 338,204,405 | |||||||

| Liabilities in Excess of Other Assets — (0.2)% | (567,547 | ) | ||||||

| NET ASSETS — 100.0% | $ | 337,636,858 | ||||||

| PORTFOLIO HOLDINGS | |

| % of Net Assets | |

| Information Technology | 28.2% |

| Financials | 19.7% |

| Consumer Discretionary | 17.4% |

| Health Care | 13.6% |

| Industrials | 9.1% |

| Energy | 5.2% |

| Money Market Funds | 3.5% |

| Telecommunication Services | 1.9% |

| Consumer Staples | 1.5% |

| Warrants | 0.1% |

| Other Assets and Liabilities | (0.2)% |

| 100.0% |

ADR — American Depositary Receipt

| * | Non-Income Producing |

| # | Annualized seven-day yield as of June 30, 2016. |

The accompanying notes are an integral part of these financial statements.

www.brownadvisoryfunds.com

12

Brown Advisory Equity Income Fund

A Message to Our Shareholders

June 30, 2016

Dear Shareholder:

During the year ended June 30, 2016, the Brown Advisory Equity Income Fund Investor Shares (the “Fund”) rose 1.15%. The S&P 500 Index, the Fund’s benchmark, increased 3.99% during the same period.

U.S. large-cap equity investors realized lower returns over the past year than in the prior several years as a variety of events drove rapid shifts up and down in investor sentiment and created increased volatility in stock prices. Worries over the impact of lower oil and commodity prices in the fall accelerated into concerns about slowing economic growth in China and elsewhere during the winter, when the market hit its low point. Those fears dissipated during the spring and the market subsequently rallied, but then it fell sharply in the early summer when the U.K. vote to leave the European Union surprised many investors.

For the Fund’s benchmark, the volatile sequence of events during the year corresponded with strong performance from the traditionally defensive sectors of the market such as consumer staples, telecommunications and utilities. The Fund’s consumer staples holdings, in particular, stood out in terms of performance, led by large jumps in the stock prices of tobacco companies Altria (MO) and Philip Morris International (PM). A combination of product price increases, market share gains and new product innovation propelled both stocks higher. The Fund is currently overweight the consumer staples sector. Strong performance of the holdings in that sector more than made up for the drag produced by not having any exposure to telecommunications and utilities, which also rose sharply during the period.

The Fund’s financial sector holdings also performed well, thanks to a diversity of holdings within the sector. Commercial insurer Cincinnati Financial rose on steady earnings improvement. Timber Real Estate Investment Trust (“REIT”) Weyerhaeuser (WY) gained following the completion of its merger with timber REIT counterpart Plum Creek Timber. Currently, REITs like Weyerhaeuser are included in the financial sector of the S&P 500 Index for reporting purposes, but a new stand-alone, REIT-specific sector is expected to be created by the end of 2016.

As for the other areas within financials, the outlook of lower interest rates for a longer period of time will likely hamper the near-term earnings growth of the Fund’s bank holdings JPMorgan Chase (JPM) and Wells Fargo (WFC). Asset manager T. Rowe Price (TROW) and jumbo mortgage financing REIT Redwood Trust (RWT) were eliminated on the expectation that the rates of future earnings and dividend growth at both companies will be reduced in the current environment. We believe that two new additions in the sector, diversified financial services provider Ameriprise Financial and insurance brokerage and consulting firm Willis Towers Watson (WLTW), have the potential to buck the trend within the sector and increase their rates of cash returned to shareholders within the foreseeable future.

The Fund’s worst performing stocks during the year were both in the energy sector, where continued weakness in commodity prices took their toll on pipeline operators Kinder Morgan (KMI) and Plains GP Holdings (PAGP). Reduced activity by oil and natural gas producers led to lower utilization of the transportation and storage assets of both companies, as well as a dramatic scaling-back of their previously ambitious growth plans. As a result of the more difficult multi-year outlooks for the companies, the Fund reduced its position in Kinder Morgan and eliminated Plains GP. Other holdings within energy, namely Black Stone Minerals (BSM) and Total (TOT), were also eliminated and the Fund is currently underweight the sector.

Consumer discretionary is another sector where the Fund is underweight following the eliminations of GameStop (GME) and Garmin (GRMN) during the period. In short, the prospective earnings growth of both companies does not look as favorable as it once did. GameStop’s core business of selling console video gaming software is entering into decline, and the company diversified into less attractive areas such as sales of mobile devices. At Garmin, the results at several of its business units are either in decline (such as portable navigation devices) or have been disappointing (wearable fitness devices).

Among other sectors, the Fund’s industrials sector weighting increased with the addition of defense and commercial aerospace manufacturer General Dynamics (GD). Also, the information technology sector weighting increased with the purchase of Cisco Systems (CSCO). General Dynamics is expected to benefit as the U.S. and its international allies increase their defense spending to confront rising global threats and terrorism. Cisco Systems has been a stable cash generator in the networking equipment space where the dividend yield is expected to rise over the next several years. While operating in different business sectors, both companies have been industry leaders that have produced strong predictable cash flows and have management teams that have been committed to returning capital to shareholders through increased dividends.

Investing in stocks with high dividend yields is currently popular, but the Fund is not oriented toward simply investing in any individual stock for the sake of its yield alone. We believe a more important factor for long-term performance is the underlying

www.brownadvisoryfunds.com

13

Brown Advisory Equity Income Fund

A Message to Our Shareholders

June 30, 2016

business model. The Fund’s preference remains to allocate capital toward companies with defensible business characteristics, where we believe the business models have proven to be resilient and adaptable to changing market and economic conditions. In a period of heightened economic uncertainty and increased volatility in global markets, this business-model-centric orientation strives to provide downside protection combined with the potential for a meaningful level of income generation for you, its investors.

Sincerely,

Mike L. Foss, CFA

Portfolio Manager

Brian E. Graney, CFA

Portfolio Manager

Past performance does not guarantee future results.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. Investments in smaller and medium capitalization companies generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock. The value of the Fund’s investments in REITs and Real Estate may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs. The Fund may invest in ETFs, which may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Investments in foreign securities entail certain risks not associated with investments in domestic securities, such as volatility of currency exchange rates, and in some cases, political and economic instability and relatively illiquid markets. Investing in Master Limited Partnerships (“MLPs”) entails risk related to fluctuations in energy prices, decreases in supply of or demand for energy commodities, unique tax consequences due to the partnership structure and various other risks. Privately Placement issued securities are restricted securities that are not publicly traded. Delay or difficulty in selling such securities may result in a loss to the Fund.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of fund holdings, please refer to the Schedule of Investments provided in this report.

Definitions for terms and indices are provided in the Glossary of Terms.

www.brownadvisoryfunds.com

14

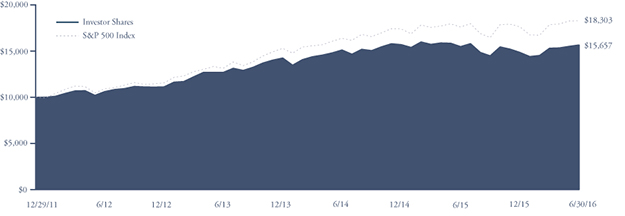

Brown Advisory Equity Income Fund

Performance Chart and Analysis

June 30, 2016

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT

The following chart reflects the change in value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Fund as measured against a broad-based securities market index. The S&P 500 Index (“Index”) is a market-value weighted index representing the performance of 500 widely held, publicly traded large capitalization stocks. The Index is unmanaged and does not reflect the deduction of fees, such as investment management fees. Investors cannot invest directly in an index.

| Since | ||||

| Average Annual Total Return | One | Inception | ||

as of 6/30/16 | Year | (12/29/11) | ||

Institutional Shares1 | 1.31% | 10.65% | ||

| Investor Shares | 1.15% | 10.47% | ||

| Advisor Shares | 0.90% | 10.20% | ||

| S&P 500 Index | 3.99% | 14.36% |

Institutional Shares | Investor Shares | Advisor Shares | ||

Gross Expense Ratio2 | 0.75% | 0.90% | 1.15% | |

Net Expense Ratio2 | 0.75% | 0.90% | 1.15% |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at brownadvisoryfunds.com/performance.html. The performance table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data does not reflect the imposition of the redemption fee of 1.00% on shares redeemed within 14 days, and if it did, performance would have been lower.

1 | Performance information for the Institutional Shares, prior to commencement of operations on October 19, 2012, is based on the performance of Investor Shares, and adjusted for the lower expenses applicable to Institutional Shares. |

2 | Per the Fund’s prospectus dated October 30, 2015. |

www.brownadvisoryfunds.com

15

Brown Advisory Equity Income Fund

Schedule of Investments

June 30, 2016

Shares | Security Description | Value $ | ||||||

| Common Stocks — 87.3% | ||||||||

| Consumer Discretionary — 9.8% | ||||||||

| 59,258 | Best Buy Co., Inc. | 1,813,295 | ||||||

| 31,063 | McDonald’s Corp. | 3,738,121 | ||||||

| 50,247 | Target Corp. | 3,508,245 | ||||||

| 57,483 | V.F. Corp. | 3,534,630 | ||||||

| 12,594,291 | ||||||||

| Consumer Staples — 14.9% | ||||||||

| 102,507 | Altria Group, Inc. | 7,068,883 | ||||||

| 83,596 | Coca-Cola Co. | 3,789,406 | ||||||

| 45,058 | Philip Morris International, Inc. | 4,583,300 | ||||||

| 81,480 | Unilever NV ADR | 3,824,671 | ||||||

| 19,266,260 | ||||||||

| Energy — 4.5% | ||||||||

| 69,329 | Kinder Morgan, Inc. | 1,297,839 | ||||||

| 37,309 | Occidental Petroleum Corp. | 2,819,068 | ||||||

| 58,911 | Suncor Energy, Inc. | 1,633,602 | ||||||

| 5,750,509 | ||||||||

| Financials — 14.3% | ||||||||

| 28,810 | Ameriprise Financial, Inc. | 2,588,579 | ||||||

| 41,235 | Cincinnati Financial Corp. | 3,088,089 | ||||||

| 24,680 | Erie Indemnity Co. | 2,451,711 | ||||||

| 50,929 | JPMorgan Chase & Co. | 3,164,728 | ||||||

| 74,141 | OneBeacon Insurance Group, Ltd. | 1,023,146 | ||||||

| 76,189 | Wells Fargo & Co. | 3,606,025 | ||||||

| 20,515 | Willis Towers Watson PLC | 2,550,220 | ||||||

| 18,472,498 | ||||||||

| Health Care — 12.5% | ||||||||

| 59,941 | AbbVie, Inc. | 3,710,947 | ||||||

| 31,165 | Johnson & Johnson | 3,780,315 | ||||||

| 46,458 | Merck & Co., Inc. | 2,676,446 | ||||||

| 43,385 | Novartis AG ADR | 3,579,696 | ||||||

| 46,970 | Teva Pharmaceutical Industries, Ltd. ADR | 2,359,303 | ||||||

| 16,106,707 | ||||||||

| Industrials — 13.1% | ||||||||

| 12,853 | General Dynamics Corp. | 1,789,652 | ||||||

| 109,095 | General Electric Co. | 3,434,311 | ||||||

| 79,261 | Healthcare Services Group, Inc. | 3,279,820 | ||||||

| 76,053 | Nielsen Holdings PLC | 3,952,474 | ||||||

| 29,299 | PACCAR, Inc. | 1,519,739 | ||||||

| 27,820 | United Technologies Corp. | 2,852,941 | ||||||

| 16,828,937 | ||||||||

| Information Technology — 17.1% | ||||||||

| 26,625 | Accenture PLC | 3,016,346 | ||||||