united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22718

Two Roads Shared Trust

(Exact name of registrant as specified in charter)

17645 Wright Street, Suite 200, Omaha, NE 68137

(Address of principal executive offices) (Zip code)

Richard Malinowski, Gemini Fund Services, LLC.

80 Arkay Drive Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 12/31

Date of reporting period:12/31/18

ITEM 1. REPORTS TO SHAREHOLDERS.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Portfolio’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Portfolios’ website www.redwoodmutualfunds.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Portfolios electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by following the instructions included with paper Portfolio documents that have been mailed to you.

Dear Shareholder,

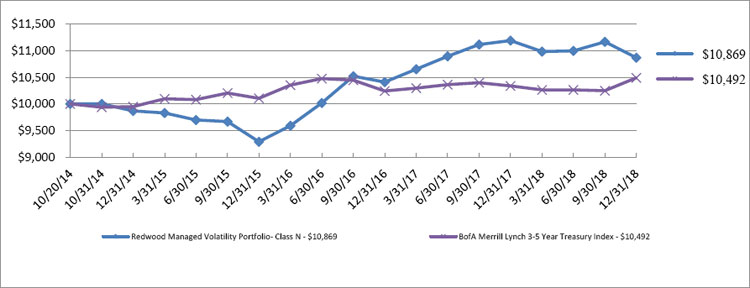

The first three quarters of 2018 witnessed stocks continuing to set new record highs before the sell-off in the fourth quarter erased all of those gains leaving the S&P 500 down for the year. Bond investors continued to face the conundrum of how to generate satisfying returns in this environment. Once again, during this year, the Bloomberg Barclays Aggregate Bond Index (“the Aggregate”) failed to produce any meaningful returns, ending the year up 1 basis point, while other fixed income benchmarks ended the year negative, such as the Bloomberg Barclays U.S. Corporate Bond Index (“the Corporate Bond Index”) ending down -2.51%. In that context, Redwood Managed Volatility Portfolio (“the Portfolio”) ending the year down -2.41%, while disappointing, is not unusual. While the Portfolio’s benchmark, the Bank of America Merrill Lynch 3-5 Year US Treasury Index (“the Benchmark”), outperformed the Portfolio in 2018, ending the year up 1.48%, the Portfolio has outperformed the Benchmark on a 2 Year and 3 Year annualized basis. (2 Year: Portfolio: +2.66%, Benchmark: +1.21%; 3 Year: Portfolio: +5.86%, Benchmark: +1.25%)

Risk Realization

As we warned of rising risk complacency in last year’s annual shareholder letter, this year began to see some of that risk come to bear and ultimately realize negative performance across a wide swath of risk assets. Just as complacency can and often does extend longer than many expect, so too can the pendulum swing to the opposite side of risk aversion when losses start to mount. Significant, unexpected losses can drive investor behavior to exacerbate those losses through additional selling. Fortunately, at Redwood, we utilize a quantitative approach, aiming to minimize the subjectivity of investing. We remained vigilant in our risk active risk management approach and the portfolio experienced peak to trough drawdown lower than the both the Aggregate and the Corporate Bond Index during the year. Our experience over time has shown that challenging environments characterized by losses are followed by more attractive environments to seek positive returns.

For the Managed Volatility Portfolio, our approach employs multiple factors that seek to be invested while markets are appreciating, but also seek to be defensive in a “risk-off” position if markets are depreciating. Whether markets are going up or down, our bias is to be ready when things change. Over time, we are confident in the value to be added from this vigilance in both risk management and return seeking.

We encourage you to talk with your financial advisor.

Thank you for your continued trust.

Sincerely,

Michael Messinger

Principal & Co-Portfolio Manager

Redwood Investment Management, LLC

The views in this report are those of the Portfolio’s management. This report contains certain forward-looking statements about factors that may affect the performance of the Portfolio in the future. These statements are based on the Portfolio’s management’s predictions and expectations concerning certain future events such as the performance of the economy as a whole and of specific industry sectors. Management believes these forward-looking statements are reasonable, although they are inherently uncertain and difficult to predict.

3165-NLD-2/15/2019

1

Redwood Managed Volatility Portfolio

PORTFOLIO REVIEW (Unaudited)

December 31, 2018

The Portfolio’s performance figures* for the periods ended December 31, 2018, compared to its benchmark:

| Since Inception | Since Inception | ||

| One Year | Class N | Class I | |

| Class N(a) | (2.87)% | 2.00% | N/A |

| Class I(b) | (2.41)% | N/A | 2.90% |

| BofA Merrill Lynch US 3-5 Year Treasury Index(c) | 1.48% | 1.15% | 0.95% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated using the traded net asset value on December 31, 2018 for Class N and Class I. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or on the redemption of Portfolio shares. The Portfolio’s total annual operating expenses, before expense waivers, are 2.68% and 2.19% for Class N shares and Class I shares, respectively, per the April 30, 2018 prospectus. The Advisor has contractually agreed to reduce the Portfolio’s fees and/or to make payments to limit Portfolio expenses until at least May 1, 2019, so that the total annual operating expenses (exclusive of any front-end or contingent deferred loads, taxes, interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, underlying fund fees and expenses or extraordinary expenses such as litigation) of the Portfolio do not exceed 1.99% and 1.49% for Class N and Class I shares, respectively. Waivers and expense payments may be recouped by the Advisor from the Portfolio, to the extent that overall expenses fall below specified limits, within three years of when the amounts were waived or recouped. For performance information current to the most recent month-end, please call toll-free 1-855-733-3863. |

| (a) | Redwood Managed Volatility Portfolio Class N commenced operations on October 20, 2014. |

| (b) | Redwood Managed Volatility Portfolio Class I commenced operations on January 15, 2015. |

| (c) | BofA Merrill Lynch US 3-5 Year Treasury Index is an unmanaged index which includes U.S. Treasury securities with maturities of 3 to 4.99 years. The index is produced by Bank of America Merrill Lynch, Pierce, Fenner & Smith, Inc. Investors can not invest directly in an index or benchmark. |

Comparison of the Change in Value of a $10,000 Investment

| PORTFOLIO ANALYSIS (Unaudited)* | ||||

| December 31, 2018 | ||||

| Percent of | ||||

| Net Assets | ||||

| Short-Term Investments | 95.2 | % | ||

| Mutual Funds | 0.6 | % | ||

| Cash, Other Assets Less Liabilities | 4.2 | % | ||

| Total | 100.0 | % | ||

| * Portfolio Analysis does not include derivative exposure | ||||

| Please refer to the Portfolio of Investments for a detailed listing of the Portfolio’s holdings. | ||||

2

Redwood Managed Volatility Portfolio

PORTFOLIO OF INVESTMENTS

December 31, 2018

| Shares | Fair Value | |||||||

| MUTUAL FUNDS - 0.6% | ||||||||

| DEBT FUNDS - 0.6% | ||||||||

| 5,160 | Salient Select Income Fund - Institutional Class | $ | 98,400 | |||||

| TOTAL MUTUAL FUNDS (Cost - $118,509) | ||||||||

| SHORT-TERM INVESTMENTS - 95.2% | ||||||||

| 2,000,000 | BlackRock Liquidity Funds FedFund Portfolio - Institutional Class - 2.31%+ | 2,000,000 | ||||||

| 2,001,265 | Dreyfus Cash Management - Institutional Class - 2.53%+ | 2,001,265 | ||||||

| 2,500,285 | Goldman Sachs Financial Square Money Market Fund - Institutional Class - 2.32%+ | 2,500,285 | ||||||

| 8,504,535 | JPMorgan U.S. Government Money Market Fund - Institutional Class - 2.28%+ | 8,504,535 | ||||||

| 2,404,577 | JPMorgan U.S. Treasury Plus Money Market Fund - Institutional Class - 2.33%+ | 2,404,577 | ||||||

| TOTAL SHORT-TERM INVESTMENTS (Cost - $17,410,662) | 17,410,662 | |||||||

| TOTAL INVESTMENTS - 95.8% (Cost - $17,529,171) | $ | 17,509,062 | ||||||

| CASH AND OTHER ASSETS LESS LIABILITIES - 4.2% | 770,896 | |||||||

| NET ASSETS - 100.0% | $ | 18,279,958 | ||||||

| + | Money market fund; interest rate reflects seven day effective yield on December 31, 2018. |

The accompanying notes are an integral part of these financial statements.

3

Redwood Managed Volatility Portfolio

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2018

| ASSETS | ||||

| Investment securities: | ||||

| At cost | $ | 17,529,171 | ||

| At value | 17,509,062 | |||

| Cash | 756,224 | |||

| Collateral Cash | 2,023 | |||

| Receivable for Portfolio shares sold | 1,371 | |||

| Dividends and interest receivable | 31,128 | |||

| Receivable from Related Parties | 10,741 | |||

| Prepaid expenses | 1,417 | |||

| TOTAL ASSETS | 18,311,966 | |||

| LIABILITIES | ||||

| Payable for Portfolio shares redeemed | 98 | |||

| Investment advisory fees payable | 23,228 | |||

| Distribution (12b-1) fees payable - Class N | 6,870 | |||

| Accrued expenses and other liabilities | 1,812 | |||

| TOTAL LIABILITIES | 32,008 | |||

| NET ASSETS | $ | 18,279,958 | ||

| Class N Shares: | ||||

| Net Assets | $ | 11,977,301 | ||

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | 1,334,104 | |||

| Net Asset Value, Offering and Redemption Price Per Share | $ | 8.98 | ||

| Class I Shares: | ||||

| Net Assets | $ | 6,302,657 | ||

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | 697,919 | |||

| Net Asset Value, Offering and Redemption Price Per Share | $ | 9.03 | ||

| Net Assets Consist of: | ||||

| Paid-in-Capital | $ | 19,459,933 | ||

| Accumulated Deficit | (1,179,975 | ) | ||

| Net Assets | $ | 18,279,958 |

The accompanying notes are an integral part of these financial statements.

4

Redwood Managed Volatility Portfolio

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2018

| INVESTMENT INCOME | ||||

| Dividends | $ | 856,047 | ||

| Interest | 62,568 | |||

| TOTAL INVESTMENT INCOME | 918,615 | |||

| EXPENSES | ||||

| Investment advisory fees | 285,922 | |||

| Distribution (12b-1) fees - Class N | 67,499 | |||

| Legal fees | 28,000 | |||

| Audit fees | 17,101 | |||

| Accounting services fees | 16,779 | |||

| Administrative services fees | 16,103 | |||

| Transfer agent fees | 14,012 | |||

| Trustees’ fees and expenses | 13,001 | |||

| Printing and postage expenses | 9,499 | |||

| Compliance officer fees | 8,200 | |||

| Custodian fees | 7,543 | |||

| Other expenses | 2,522 | |||

| TOTAL EXPENSES | 486,181 | |||

| Less: Fees waived by the Advisor | (78,365 | ) | ||

| NET EXPENSES | 407,816 | |||

| NET INVESTMENT INCOME | 510,799 | |||

| REALIZED AND UNREALIZED LOSS ON INVESTMENTS | ||||

| Net Realized Loss on Investments and Swaps | ||||

| Investments | (904,654 | ) | ||

| Total Return Swap Contracts | (212,872 | ) | ||

| Net Change in Unrealized Depreciation on | ||||

| Investments | (59,412 | ) | ||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (1,176,938 | ) | ||

| NET DECREASE IN NET ASSETS FROM OPERATIONS | $ | (666,139 | ) |

The accompanying notes are an integral part of these financial statements.

5

Redwood Managed Volatility Portfolio

STATEMENTS OF CHANGES IN NET ASSETS

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| December 31, 2018 | December 31, 2017 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 510,799 | $ | 826,385 | ||||

| Net realized gain (loss) on investments and swaps | (1,117,526 | ) | 1,521,467 | |||||

| Realized gain distributions from investment companies | — | 4,093 | ||||||

| Net change in unrealized depreciation of investments and swaps | (59,412 | ) | (43,804 | ) | ||||

| Net increase (decrease) in net assets resulting from operations | (666,139 | ) | 2,308,141 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| From net investment income: | ||||||||

| Class I | — | (761,535 | ) | |||||

| Class N | — | (1,222,014 | ) | |||||

| Total distributions paid* | ||||||||

| Class I | (728,069 | ) | — | |||||

| Class N | (1,419,371 | ) | — | |||||

| Net decrease in net assets from distributions to shareholders | (2,147,440 | ) | (1,983,549 | ) | ||||

| FROM SHARES OF BENEFICIAL INTEREST | ||||||||

| Class N: | ||||||||

| Proceeds from shares sold | 3,540,181 | 7,402,380 | ||||||

| Net asset value of shares issued in reinvestment of distributions | 1,419,371 | 1,222,014 | ||||||

| Cost of shares redeemed | (8,544,397 | ) | (10,053,136 | ) | ||||

| Net decrease in net assets from shares of beneficial interest | (3,584,845 | ) | (1,428,742 | ) | ||||

| Class I: | ||||||||

| Proceeds from shares sold | 2,621,511 | 582,322 | ||||||

| Net asset value of shares issued in reinvestment of distributions | 728,069 | 761,535 | ||||||

| Cost of shares redeemed | (7,438,534 | ) | (2,579,468 | ) | ||||

| Net decrease in net assets from shares of beneficial interest | (4,088,954 | ) | (1,235,611 | ) | ||||

| TOTAL DECREASE IN NET ASSETS | (10,487,378 | ) | (2,339,761 | ) | ||||

| NET ASSETS | ||||||||

| Beginning of Year | 28,767,336 | 31,107,097 | ||||||

| End of Year ** | $ | 18,279,958 | $ | 28,767,336 | ||||

| SHARE ACTIVITY | ||||||||

| Class N: | ||||||||

| Shares Sold | 344,788 | 688,400 | ||||||

| Shares Reinvested | 158,059 | 118,642 | ||||||

| Shares Redeemed | (847,420 | ) | (938,498 | ) | ||||

| (344,573 | ) | (131,456 | ) | |||||

| Class I: | ||||||||

| Shares Sold | 250,706 | 54,093 | ||||||

| Shares Reinvested | 80,629 | 73,366 | ||||||

| Shares Redeemed | (719,543 | ) | (239,866 | ) | ||||

| (388,209 | ) | (112,408 | ) | |||||

| Net decrease in shares of beneficial interest outstanding | (732,781 | ) | (243,864 | ) | ||||

| * | Distributions from net investment income and net realized capital gains are combined for the year ended December 31, 2018. See “New Accounting Pronouncements” in the Notes to Financial Statements for more information. The dividends and distributions to shareholders for the year ended December 31, 2017 have not been reclassified to conform to the current year presentation. |

| ** | Net Assets- End of Year includes net investment income in excess of distributions of $2,204,187 as of December 31, 2017. |

The accompanying notes are an integral part of these financial statements.

6

Redwood Managed Volatility Portfolio - Class N

FINANCIAL HIGHLIGHTS

Per share data and ratios for a share of beneficial interest outstanding throughout each period presented.

| For the | For the | For the | For the | For the | ||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Period Ended | ||||||||||||||||

| December 31, 2018 | December 31, 2017 | December 31, 2016 | December 31, 2015 | December 31, 2014 * | ||||||||||||||||

| Net Asset Value, Beginning of Period | $ | 10.37 | $ | 10.31 | $ | 9.29 | $ | 9.87 | $ | 10.00 | ||||||||||

| Decrease From Operations: | ||||||||||||||||||||

| Net investment income (a) | 0.20 | 0.26 | 0.27 | 0.09 | 0.03 | |||||||||||||||

| Net gain (loss) from investments (both realized and unrealized) | (0.49 | ) | 0.50 | 0.85 | (0.67 | ) | (0.16 | ) | ||||||||||||

| Total from operations | (0.29 | ) | 0.76 | 1.12 | (0.58 | ) | (0.13 | ) | ||||||||||||

| Less Distributions: | ||||||||||||||||||||

| From net investment income | (1.10 | ) | (0.70 | ) | (0.10 | ) | — | — | ||||||||||||

| Total Distributions | (1.10 | ) | (0.70 | ) | (0.10 | ) | — | — | ||||||||||||

| Net Asset Value, End of Period | $ | 8.98 | $ | 10.37 | $ | 10.31 | $ | 9.29 | $ | 9.87 | ||||||||||

| Total Return (b) | (2.87 | )% | 7.48 | % | 12.07 | % | (5.88 | )% | (1.30 | )% (d) | ||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||

| Net assets, end of period (in 000’s) | $ | 11,977 | $ | 17,412 | $ | 18,665 | $ | 5,072 | $ | 7,593 | ||||||||||

| Ratio of gross expenses to average net assets (e,f) | 2.42 | % | 2.06 | % | 2.15 | % | 2.40 | % | 4.67 | % (c) | ||||||||||

| Ratio of net expenses to average net assets (e) | 1.99 | % | 1.99 | % | 1.99 | % | 1.99 | % | 1.99 | % (c) | ||||||||||

| Ratio of net investment income to average net assets (g) | 1.99 | % | 2.45 | % | 2.70 | % | 0.87 | % | 1.74 | % (c) | ||||||||||

| Portfolio turnover rate | 15 | % | 20 | % | 156 | % | 629 | % | 213 | % (d) | ||||||||||

| * | Class N commenced operations on October 20, 2014. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Advisor not absorbed a portion of Portfolio expenses, total returns would have been lower. Total returns for periods less than one year are not annualized. |

| (c) | Annualized. |

| (d) | Not annualized. |

| (e) | Does not include expenses of other investment companies in which the Portfolio invests. |

| (f) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Advisor. |

| (g) | Recognition of net investment income by the Portfolio is affected by the timing of declaration of dividends by underlying investment companies in which the Portfolio invests. |

The accompanying notes are an integral part of these financial statements.

7

Redwood Managed Volatility Portfolio - Class I

FINANCIAL HIGHLIGHTS

Per share data and ratios for a share of beneficial interest outstanding throughout the period presented.

| For the | For the | For the | For the | |||||||||||||

| Year Ended | Year Ended | Year Ended | Period Ended | |||||||||||||

| December 31, 2018 | December 31, 2017 | December 31, 2016 | December 31, 2015 * | |||||||||||||

| Net Asset Value, Beginning of Period | $ | 10.45 | $ | 10.38 | $ | 9.33 | $ | 9.89 | ||||||||

| Decrease From Operations: | ||||||||||||||||

| Net investment income (a) | 0.27 | 0.32 | 0.25 | 0.16 | ||||||||||||

| Net gain (loss) from investments (both realized and unrealized) | (0.51 | ) | 0.49 | 0.92 | (0.71 | ) | ||||||||||

| Total from operations | (0.24 | ) | 0.81 | 1.17 | (0.55 | ) | ||||||||||

| Less Distributions: | ||||||||||||||||

| From net investment income | (1.18 | ) | (0.74 | ) | (0.12 | ) | (0.01 | ) | ||||||||

| Total Distributions | (1.18 | ) | (0.74 | ) | (0.12 | ) | (0.01 | ) | ||||||||

| Net Asset Value, End of Period | $ | 9.03 | $ | 10.45 | $ | 10.38 | $ | 9.33 | ||||||||

| Total Return (b) | (2.41 | )% | 7.99 | % | 12.57 | % | (5.60 | )% (d) | ||||||||

| Ratios/Supplemental Data | ||||||||||||||||

| Net assets, end of period (in 000’s) | $ | 6,303 | $ | 11,355 | $ | 12,442 | $ | 19,151 | ||||||||

| Ratio of gross expenses to average net assets (e,f) | 1.92 | % | 1.57 | % | 1.66 | % | 1.84 | % (c) | ||||||||

| Ratio of net expenses to average net assets (e) | 1.49 | % | 1.49 | % | 1.49 | % | 1.49 | % (c) | ||||||||

| Ratio of net investment income to average net assets (g) | 2.60 | % | 2.95 | % | 2.56 | % | 1.74 | % (c) | ||||||||

| Portfolio turnover rate | 15 | % | 20 | % | 156 | % | 629 | % (d) | ||||||||

| * | Class I commenced operations on January 15, 2015. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Advisor not absorbed a portion of Portfolio expenses, total returns would have been lower. Total returns for periods less than one year are not annualized. |

| (c) | Annualized. |

| (d) | Not annualized. |

| (e) | Does not include expenses of other investment companies in which the Portfolio invests. |

| (f) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Advisor. |

| (g) | Recognition of net investment income by the Portfolio is affected by the timing of declaration of dividends by underlying investment companies in which the Portfolio invests. |

The accompanying notes are an integral part of these financial statements.

8

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS

December 31, 2018

| 1. | ORGANIZATION |

Redwood Managed Volatility Portfolio (the “Portfolio”), is a series of shares of beneficial interest of the Two Roads Shared Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on June 8, 2012, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified, open-end management investment company. The Portfolio commenced investment operations on October 20, 2014. The investment objective is to seek a combination of total return and prudent management of portfolio downside volatility and downside loss.

The Portfolio offers Class N and Class I shares. Class N shares commenced operations October 20, 2014 and Class I Shares commenced operations January 15, 2015. All classes are sold at net asset value (“NAV”). Each share class represents an interest in the same assets of the Portfolio and classes are identical except for differences in their ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. The Portfolio’s income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Portfolio in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Portfolio is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update ASU 2013-08.

Security Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price. In the absence of a sale such securities shall be valued at the mean between the last bid and ask prices on the day of valuation. Total return swaps on exchange-listed securities shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the current bid and ask prices on the day of valuation on each underlying exchange-listed security. Exchange listed swaps shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the current bid and ask prices on the day of valuation. Short-term debt obligations, excluding U.S. Treasury Bills, having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost.

Valuation of Underlying Funds – The Portfolio may invest in funds of open-end or closed-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value to the methods established by the boards of directors of the Underlying Funds.

Open-end funds are valued at their respective net asset values as reported by such investment companies. The shares of many closed-end investment companies, after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or premium on shares of any closed-end investment company purchased by the Portfolio will not change. As of December 31, 2018 the Portfolio did not hold any closed-end investment companies.

9

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

The Portfolio may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Portfolio’s Board of Trustees (the “Board”). The Board has delegated execution of these procedures to a fair value team composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) Advisor. The team may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board has also engaged a third party valuation firm to, as needed, attend valuation meetings held by the Trust, review minutes of such meetings and report to the Board on a quarterly basis. The Board reviews and ratifies the execution of this process and the resultant fair value prices at least quarterly to assure the process produces reliable results.

Fair Valuation Process – The applicable investments are valued collectively via inputs from each group within the fair value team. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the Advisor, the prices or values available do not represent the fair value of the instrument; Factors which may cause the Advisor to make such a judgment include, but are not limited to, the following: only a bid price or an ask price is available; the spread between bid and ask prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that will affect the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to the Portfolio’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued via inputs from the Advisor based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If the Advisor is unable to obtain a current bid from such independent dealers or other independent parties, the fair value team shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Portfolio’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Portfolio utilizes various methods to measure the fair value of all of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Portfolio has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 –Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Portfolio’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that

10

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of December 31, 2018 for the Portfolio’s assets and liabilities measured at fair value:

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Mutual Funds | $ | 98,400 | $ | — | $ | — | $ | 98,400 | ||||||||

| Short-Term Investment | 17,410,662 | — | — | 17,410,662 | ||||||||||||

| Total Assets | $ | 17,509,062 | $ | — | $ | — | $ | 17,509,062 | ||||||||

The Portfolio did not hold any Level 3 securities during the period.

The Portfolio’s investments in financial instruments and derivatives expose it to various risks certain of which are discussed below. Please refer to the Portfolio’s prospectus and statement of additional information for a full listing of risks associated with the Portfolio’s investments which include but are not limited to active trading risk, asset allocation risk, bank loan risk, borrowing risk, cash positions risk, counterparty credit risk, credit risk, credit default swap risk, cybersecurity risk, derivatives risk, fixed income risk, gap risk, high-yield fixed income securities risk, investment companies and ETFs risk, leveraging risk, liquidity risk, managed volatility strategy risk, management risk, market risk, market events risk, model risk, money market instrument risk, rules-based strategy risk, swap risk, swaptions risk, underlying fund risk, U.S. Government securities risk and valuation risk.

Mutual Fund Risk:Mutual funds are subject to investment advisory or management and other expenses, which will be indirectly paid by the Portfolio. The Portfolio is subject to specific risks, depending on investment strategy.

Swap Agreements – The Portfolio is subject to equity price risk, interest rate risk, credit risk, currency risk, counterparty risk and/or commodity risk in the normal course of pursuing its investment objective. The Portfolio may enter into various swap transactions for investment purposes or to manage interest rate, equity, foreign exchange (currency), or credit risk. These would be two-party contracts entered into primarily to exchange the returns (or differentials in rates of returns) earned or realized on particular pre-determined investments or instruments. The basket swaps are valued at the difference between the fair value of the referenced securities in the basket less the notional value of the contract.

The gross returns to be exchanged or “swapped” between parties are calculated with respect to a notional amount, i.e., the return on or increase in value of a particular dollar amount invested at a particular interest rate, in a particular foreign currency, or in a “basket” of securities representing a particular index or market segment. Realized gains and losses from the decrease in notional value of the swap are recognized on trade date. The basket swaps are valued at the difference between the fair value of the referenced securities in the basket less the notional value of the contract.

The Portfolio maintains a control account with the value of the collateral to not be less than 25% of an Equity Notional Amount (notional being value of swap +/- amount owed to the counterparty for that month). As of December 31, 2018 the notional value of the swap was $0. The maximum risk of loss is the cash flows to be received from the counterparty until next valuation date (not the contract’s remaining life), which is monthly. The swap resets at the end of each month and as of December 31, 2018, $0 was due to the counterparty relating to the swap. The average notional value of the basket swaps that the Portfolio invested in during the year ended December 31, 2018 was $5,713,501.

11

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

Impact of Derivatives on the Statement of Operations:The following is a summary of the location of derivative investments on the Portfolio’s Statement of Operations for the year ended December 31, 2018:

| Derivative Investment Type | Location of Gain/Loss on Derivative |

| Total Return Swap Contracts | Net realized gain (loss) on total return swap contracts |

The following is a summary of the Portfolio’s realized gain (loss) on derivative investments recognized in the Statement of Operations categorized by primary risk exposure for the fiscal year ended December 31, 2018:

| Realized gain/(loss) on derivatives recognized in the Statement of Operations | ||||||||

| Total for the Fiscal | ||||||||

| Year Ended | ||||||||

| Derivative Investment Type | Equity Risk | December 31, 2018 | ||||||

| Total Return Swap Contracts | $ | (212,872 | ) | $ | (212,872 | ) | ||

The average notional value of the derivative instruments traded for the year ended December 31, 2018 as disclosed under Swap Agreements and the amounts realized and changes in unrealized gains and losses on derivative instruments during the period as disclosed above and within the Statement of Operations serve as indicators of the volume of derivative activity for the Portfolio.

Market Risk– Overall market risk may affect the value of individual instruments in which the Portfolio invests. Factors such as domestic and foreign economic growth and market conditions, real or perceived adverse economic or political conditions, inflation, changes in interest rate levels, lack of liquidity in the bond markets, volatility in the equities market or adverse investor sentiment affect the securities markets. When the value of the Portfolio’s investments goes down, your investment in the Portfolio decreases in value and you could lose money.

Security Transactions and Related Income – Security transactions are accounted for on trade date basis. Interest income is recognized on an accrual basis. Discounts are accreted and premiums are amortized on securities purchased over the lives of the respective securities. Dividend income is recorded on the ex-dividend date. Realized gains or losses from sales of securities are determined by comparing the identified cost of the security lot sold with the net sales proceeds.

Investment Companies and Exchange Traded Funds (“ETFs”) Risk– The Portfolio invests in other investment companies, including ETFs. ETFs are a type of fund bought and sold on a securities exchange. An ETF trades like common stock and represents a fixed portfolio of securities. The risks of owning an ETF generally reflect the risks of owning the underlying securities they are designed to track, although the lack of liquidity on an ETF could result in it being more volatile. When the Porfolio invests in other investment companies, including ETFs, it will bear additional expenses based on its pro rata share of the other investment company’s or ETF’s operating expenses, including the potential duplication of management fees. The Portfolio also will incur brokerage costs when it purchases and sells ETFs.

Dividends and Distributions to Shareholders –Dividends from net investment income are declared and distributed annually. Distributable net realized capital gains are declared and distributed annually. Dividends from net investment income and distributions from net realized gains are recorded on ex-dividend date and determined in accordance with federal income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (i.e., deferred losses, capital loss carry forwards) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification.

Federal Income Taxes– It is the Portfolio’s policy to qualify as a regulated investment company by complying with the provisions of the Internal Revenue Code that are applicable to regulated investment companies and to distribute

12

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

substantially all of its taxable income and net realized gains to shareholders. Therefore, no federal income tax provision has been recorded.

The Portfolio recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Portfolio’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for the open tax years (2015-2017) or expected to be taken in the Portfolio’s 2018 tax return. The Portfolio identifies its major tax jurisdictions as U.S. Federal, Nebraska, and foreign jurisdictions where the Portfolio makes significant investments; however the Portfolio is not aware of any tax positions for which it is reasonably expected that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

The Portfolio recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the period, the Portfolio did not incur any interest or penalties.

Expenses– Expenses of the Trust that are directly identifiable to a specific portfolio are charged to that portfolio. Expenses, which are not readily identifiable to a specific portfolio, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative sizes of the portfolios in the Trust.

Indemnification–The Trust indemnifies its officers and trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Portfolio enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Portfolio’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Portfolio that have not yet occurred. However, the risk of loss due to these warranties and indemnities appears to be remote.

| 3. | INVESTMENT TRANSACTIONS |

The cost of purchases and proceeds from the sale of securities, other than short-term investments, for year ended December 31, 2018, amounted to $2,470,350 and $20,972,766 respectively.

| 4. | INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES |

Advisory Fees – Redwood Investment Management, LLC serves as the Portfolio’s Investment Advisor (the “Advisor”). Pursuant to an Investment Advisory Agreement with the Portfolio, the Advisor, under the oversight of the Board, directs the daily operations of the Portfolio and supervises the performance of administrative and professional services provided by others. As compensation for its services and the related expenses borne by the Advisor, the Portfolio pays the Advisor an investment advisory fee, computed and accrued daily and paid monthly, at an annual rate of 1.25% of the Portfolio’s average daily net assets. For the year ended December 31, 2018, the Advisor earned management fees of $285,922.

The Advisor has contractually agreed to reduce its fees and/or absorb expenses of the Portfolio (The “Waiver Agreement”), until at least May 1, 2019, to ensure that total annual portfolio operating expenses after fee waiver and/or reimbursement (exclusive of any taxes, short selling expenses, interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, indirect expenses, expenses of other investment companies in which the Portfolio may invest, or extraordinary expenses such as litigation) will not exceed 1.99% and 1.49% of the Portfolio’s average daily net assets for Class N and Class I shares, respectively, subject to possible recoupment from the Portfolio in future years on a rolling three year basis (within the three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits.

If the Advisor waives any fee or reimburses any expense pursuant to the Waiver Agreement, and the Portfolio’s operating expenses are subsequently less than 1.99% or 1.49% of average underlying daily net assets attributable to Class N shares or Class I shares, respectively, the Advisor shall be entitled to be reimbursed by the Portfolio for such waived fees or reimbursed expenses, provided that such reimbursement does not cause the Portfolio’s expenses to exceed 1.99% and 1.49% of average daily net assets for Class N and Class I shares, respectively. If Portfolio operating expenses attributable

13

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

to Class N or Class I shares subsequently exceed 1.99% or 1.49%, respectively, per annum of the average daily net assets, the reimbursements shall be suspended. During the year ended December 31, 2018, the Advisor has reimbursed $78,365 in expenses to the Portfolio. Pursuant to the Waiver Agreement, cumulative expenses subject to recapture are $227,260 and the amounts will expire as follows: on December 31, 2019 - $113,344, December 31, 2020 - $35,551, and December 31, 2021 – $78,365.

The Board has adopted the Trust’s Master Distribution and Shareholder Servicing Plan (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act. The Plan provides that a monthly service and/or distribution fee is calculated by the Portfolio at an annual rate of 0.50% of its average daily net assets for Class N shares and is paid to Northern Lights Distributors, LLC (the “Distributor”) to provide compensation for ongoing shareholder servicing and distribution-related activities or services and/or maintenance of the Portfolio’s shareholder accounts not otherwise required to be provided by the Advisor. During the year ended December 31, 2018, Class N paid $67,499 in distribution fees.

The Distributor acts as the Portfolio’s principal underwriter in a continuous public offering of the Portfolio’s Class N and Class I shares.

In addition, certain affiliates of the Distributor provide services to the Portfolio as follows:

Gemini Fund Services, LLC (“GFS”)– GFS, an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to separate servicing agreements with GFS, the Portfolio pays GFS customary fees for providing administration, fund accounting, and transfer agency services to the Portfolio. Certain officers of the Trust are also officers of GFS, and are not paid any fees directly by the Portfolio for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”) – NLCS, an affiliate of GFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from the Portfolio.

Blu Giant, LLC (“Blu Giant”) –Blu Giant, an affiliate of GFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Portfolio on an ad-hoc basis. For the provision of these services, Blu Giant receives customary fees from the Portfolio.

| 5 | .AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS |

The identified cost of investments in securities owned by the Fund for federal tax purposes and its respective gross unrealized appreciation and depreciation at December 31, 2018, was as follows:

| Cost for Federal Tax purposes | $ | 17,529,243 | ||

| Unrealized Appreciation | 4 | |||

| Unrealized Depreciation | (20,185 | ) | ||

| Tax Net Unrealized Depreciation | $ | (20,181 | ) |

14

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

| 6. | DISTRIBUTION TO SHAREHOLDERS & TAX COMPONENTS OF CAPITAL |

The tax character of fund distributions paid for the fiscal years ended December 31, 2018 and December 31, 2017 was as follows:

| Fiscal Year Ended | Fiscal Year Ended | |||||||

| December 31, 2018 | December 31, 2017 | |||||||

| Ordinary Income | $ | 2,147,440 | $ | 1,983,549 | ||||

| Long-Term Capital Gain | — | — | ||||||

| Return of Capital | — | — | ||||||

| $ | 2,147,440 | $ | 1,983,549 | |||||

As of December 31, 2018, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| Undistributed | Undistributed | Post October Loss | Capital Loss | Other | Unrealized | Total | ||||||||||||||||||||

| Ordinary | Long-Term | and | Carry | Book/Tax | Appreciation/ | Accumulated | ||||||||||||||||||||

| Income | Gains | Late Year Loss | Forwards | Differences | (Depreciation) | Earnings/(Deficits) | ||||||||||||||||||||

| $ | 354,674 | $ | — | $ | — | $ | (1,514,468 | ) | $ | — | $ | (20,181 | ) | $ | (1,179,975 | ) | ||||||||||

The difference between book basis and tax basis unrealized depreciation and accumulated net realized loss from investments is primarily attributable to the tax deferral of losses on wash sales.

At December 31, 2018, the Portfolio had capital loss carry forwards for federal income tax purposes available to offset future capital gains as follows:

| Non-Expiring | Non-Expiring | |||||||||

| Short-Term | Long-Term | Total | ||||||||

| $ | 619,965 | $ | 894,503 | $ | 1,514,468 | |||||

| 7. | CONTROL OWNERSHIP |

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a Portfolio creates presumption of control of the Portfolio, under Section 2(a)9 of the 1940 Act. As of December 31, 2018, Jefferson National Life Insurance Co. held approximately 84% of the voting securities of the Portfolio.

| 8. | UNDERLYING INVESTMENTS IN OTHER INVESTMENT COMPANIES |

The Portfolio invests in other investment companies. Each underlying fund, including eachETF, is subject to specific risks, depending on the nature of the underlying fund. These risks could include liquidity risk, sector risk, foreign and related currency risk and high yield risk. Investors in the Portfolio will indirectly bear fees and expenses charged by the underlying investment companies in which the Portfolio invests in addition to the Portfolio’s direct fees and expenses.

The performance of the Fund will be directly affected by the performance of the JPMorgan U.S. Government Money Market Fund – Institutional Class. The financial statements of the Portfolio, including the portfolio of investments, can be found at the Securities and Exchange Commission’s (“SEC”) websitewww.sec.gov and should be read in conjunction with the Portfolio’s financial statements. As of December 31, 2018, the percentage of the net assets invested in the JPMorgan U.S. Government Money Market Fund – Institutional Class was 46.5%.

15

Redwood Managed Volatility Portfolio

NOTES TO FINANCIAL STATEMENTS (Continued)

December 31, 2018

| 9. | NEW ACCOUNTING PRONOUNCEMENTS |

In August 2018, the FASB issued Accounting Standards Update (“ASU”) No. 2018-13, which changes certain fair value measurement disclosure requirements. The new ASU, in addition to other modifications and additions, removes the requirement to disclose the amount and reasons for transfers between Level 1 and Level 2 of the fair value hierarchy, and the policy for the timing of transfers between levels. For investment companies, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. Early adoption is allowed. These amendments have been adapted with these financial statements.

In August 2018, the Securities and Exchange Commission adopted amendments to certain disclosure requirements under Regulation S-X to conform to US GAAP, including: (i) an amendment to require presentation of the total, rather than the components, of distributable earnings on the Statement of Assets and Liabilities; and (ii) an amendment to require presentation of the total, rather than the components, of distributions to shareholders, except for tax return of capital distributions, if any, on the Statement of Changes in Net Assets. The amendments also removed the requirement for parenthetical disclosure of undistributed net investment income on the Statement of Changes in Net Assets. These amendments have been adapted with these financial statements.

| 10. | SUBSEQUENT EVENTS |

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that no events or transactions occurred requiring adjustment or disclosure in the financial statements, other than the following:

Effective February 1, 2019, NorthStar Financial Services Group, LLC, the parent company of Gemini Fund Services, LLC (“GFS”) and its affiliated companies including Northern Lights Distributors, LLC (“NLD”), Northern Lights Compliance Services, LLC (“NLCS”) and Blu Giant, LLC (“Blu Giant”) (collectively, the “Gemini Companies”), sold its interest in the Gemini Companies to a third party private equity firm that contemporaneously acquired Ultimus Fund Solutions, LLC (an independent mutual fund administration firm) and its affiliates (collectively, the “Ultimus Companies”). As a result of these separate transactions, the Gemini Companies and the Ultimus Companies are now indirectly owned through a common parent entity, The Ultimus Group, LLC.

16

| GRANT THORNTON LLP | |

| 757 Third Ave., 9th Floor | |

| New York, NY 10017 | |

| D | +1 212.599.0100 |

| F | +1 212.370.4520 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Trustees of the Two Roads Shared Trust

and Shareholders of Redwood Managed Volatility Portfolio

Opinion on the financial statements

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of Redwood Managed Volatility Portfolio (a fund in the Two Roads Shared Trust) (the “Fund”) as of December 31, 2018, the related statement of operations for the year then ended, and the statements of changes in net assets for each of the two years in the period ended December 31, 2018, and the financial highlights for each of the three years in the period ended December 31, 2018, and the related notes (collectively referred to as the “financial statements”). The accompanying financial highlights for the year ended December 31, 2015 and for the period from October 20, 2014 (commencement of operations) through December 31, 2014 were audited by other auditors whose report thereon dated February 19, 2016 expressed an unqualified opinion on those financial highlights. In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2018, and the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended December 31, 2018, and its financial highlights for each of the three years in the period ended December 31, 2018 in conformity with accounting principles generally accepted in the United States of America.

Basis for opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of

| GT.COM | Grant Thornton LLP is the U.S. member firm of Grant Thornton International Ltd (GTIL). GTIL and each of its member firms are separate legal entities and are not a worldwide partnership. |

17

internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of December 31, 2018, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2016.

New York, New York

February 22, 2019

18

Redwood Managed Volatility Portfolio

EXPENSE EXAMPLES (Unaudited)

December 31, 2018

As a shareholder of Redwood Managed Volatility Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Redwood Managed Volatility Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2018 through December 31, 2018.

Actual Expenses

The “Actual” line in the table below provides information about actual account values and actual expenses. You may use the information below together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The “Hypothetical” line in the table below provides information about hypothetical account values and hypothetical expenses based on the Redwood Managed Volatility Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the period. You may use this information to compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | Expense Ratio | |

| Account Value | Account Value | During Period | During Period | |

| Actual * | 7/1/18 | 12/31/18 | 7/1/18-12/31/18 | 7/1/18-12/31/18 |

| Class I | 1,000.00 | $ 991.10 | $ 7.48 | 1.49% |

| Class N | 1,000.00 | 988.40 | 9.97 | 1.99% |

| Beginning | Ending | Expenses Paid | Expense Ratio | |

| Hypothetical | Account Value | Account Value | During Period* | During Period |

| (5% return before expenses) | 7/1/18 | 12/31/18 | 7/1/18-12/31/18 | 7/1/18-12/31/18 |

| Class I | 1,000.00 | $ 1,017.69 | $ 7.58 | 1.49% |

| Class N | 1,000.00 | 1,015.17 | 10.11 | 1.99% |

| * | Expenses are equal to the average account value over the period, multiplied by the Portfolio’s annualized expense ratio, multiplied by the number of days in the period (184) divided by the number of days in the fiscal year (365). |

19

Redwood Managed Volatility Portfolio

SUPPLEMENTAL INFORMATION (Unaudited)

December 31, 2018

Approval of Advisory Agreement –Redwood Managed Volatility Portfolio

At a meeting held on June 12 and 13, 2018 (the “Meeting”), the Board of Trustees (the “Board”) of Two Roads Shared Trust (the “Trust”), including all of those trustees who are not “interested persons” of the Trust (as such term is defined in the 1940 Act), which independent Trustees constitute all of the Trustees, considered the approval of an investment advisory agreement (the “Advisory Agreement”) between Redwood Investment Management, LLC (“Redwood” or the “Adviser”) and the Trust, on behalf of the Redwood Managed Volatility Portfolio (the “Fund”), a series of the Trust.

In connection with the Board’s consideration of the Advisory Agreement, the Board received written materials in advance of the Meeting, which included information regarding: (i) the nature, extent, and quality of services provided to the Fund by the Adviser; (ii) a description of the Adviser’s investment management personnel; (iii) an overview of the Adviser’s respective operations and financial condition; (iv) a description of the Adviser’s brokerage practices (including any soft dollar arrangements); (v) a comparison of the Fund’s advisory fee and overall expenses with those of comparable mutual funds; (vi) the level of profitability from the Adviser’s fund-related operations; (vii) the Adviser’s respective compliance policies and procedures, including policies and procedures for personal securities transactions, business continuity and information security; and (viii) information regarding the performance record of the Fund as compared to other funds with similar investment strategies.

Throughout the process, including at the meeting, the Board had numerous opportunities to ask questions of and request additional materials from the Adviser. During the Meeting, the Board was advised by, and met in executive session with, the Board’s independent legal counsel, and received a memorandum from such independent counsel regarding its responsibilities under applicable law.

Matters considered by the Board in connection with its approval of the Advisory Agreementincl uded, among others, the following:

Nature, Extent and Quality of Services. The Board reviewed materials provided by Redwood related to the Advisory Agreements with the Trust on behalf of the Fund, including the Advisory Agreement; a description of the manner in which investment decisions are made and executed; a review of the financial condition of Redwood; an overview of the personnel that perform advisory, compliance and operational services for the Fund, including any changes in key personnel; Redwood’s compliance policies and procedures, including its business continuity policy and information systems security policy and a Code of Ethics containing provisions reasonably necessary to prevent Access Persons, as that term is defined in Rule 17j-1 under the Investment Company Act of 1940, as amended, from engaging in conduct prohibited by Rule 17j-1(b); information regarding risk management processes; an annual review of the operation of Redwood’s compliance program; and an independent report prepared by Broadridge analyzing the performance record, fees and expenses of the Fund as compared to other mutual funds with similar investment strategies.

20

Redwood Managed Volatility Portfolio

SUPPLEMENTAL INFORMATION (Unaudited)(Continued)

December 31, 2018

In reaching its conclusions with respect to the nature and quality of services to be provided by Redwood under the Advisory Agreement, the Board considered that Redwood’s employees have extensive asset management, risk management, operations and compliance experience. The Board considered that Redwood continued to employ quantitative and tactical investment strategies in the Fund that require a level of sophistication to execute and that there have been no significant changes in Redwood’s investment strategies other than the expansion to manage additional strategies and accounts. The Board noted that Redwood had allocated appropriate resources and staff to operate its compliance program, including the implementation of trading procedures reasonably designed to mitigate conflicts among accounts, that Redwood had adopted cybersecurity and business continuity policies and procedures, that Redwood’s risk management and associated policies appeared to be operating effectively and that Redwood identified and monitored risks. The Board also considered Redwood’s brokerage practices. The Board also considered the experience and tenure of key personnel, noting the qualifications of the professional staff and that Redwood had added additional staffing as the firm continued to grow, including the recent addition of a new CCO. The Board concluded that Redwood had sufficient quality and depth of personnel, resources, investment methods and compliance policies and procedures to perform its duties under the Advisory Agreement and that the nature, overall quality and extent of the advisory services provided by Redwood to the Fund were satisfactory and reliable.

Performance. The Board considered the performance of the Fund. The Board reviewed the Fund’s performance for the one-year, three-year, and since inception periods ended April 30, 2018 as compared to the Fund’s benchmark index (BofA Merrill Lynch US Treasuries 3-5 Year Index) and against the performance of a group of peer funds (the “Peer Group”) provided by Broadridge, an independent third-party data provider. The Board considered that the Fund had outperformed the mean of each of the Peer Group, the Fund’s Morningstar category (Nontraditional Bond) and the Fund’s primary benchmark for the one-year and three-year periods, and had slightly underperformed the median of its Peer Group, but had outperformed its benchmark for the since inception period.

The Board also took into account management’s discussion of the Fund’s performance and considered the Morningstar category in which the Fund had been placed, noting the differences between the Fund’s investment strategies and the investment strategies of other funds in the Peer Group. The Board also considered that the Fund’s performance over the 3-year period suggests a consistent focus and process with respect to downside risk volatility. The Board concluded that the Fund’s performance was satisfactory and that it was meeting investment objectives.

Fees and Expenses. As to the costs of the services provided by Redwood, with respect to the Fund, the Board considered that the Fund’s advisory fee of 1.25% was above the Peer Group median. The Board also considered that the Fund’s total net operating expenses were below the median and average of the Peer Group. The Board also considered the Fund’s expense ratio, noting that Redwood had agreed to limit the Fund’s net annual operating expenses to 1.49% and 1.99% (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) borrowing costs (such as interest and dividend expense

21

Redwood Managed Volatility Portfolio

SUPPLEMENTAL INFORMATION (Unaudited)(Continued)

December 31, 2018

on securities sold short); (v) taxes; and (vi) extraordinary expenses, such as litigation expenses) of the average net assets of Class I and Class N shares of the Fund, respectively.

In considering the level of the advisory fee with respect to the Fund, the Board also took into account the cost of other accounts managed by Redwood, if any, that used a similar investment strategy, noting that differences were attributable to the differences in the management of these different kinds of accounts.

Based on the factors above, the Board concluded that the advisory fee of the Fund was not unreasonable.

Profitability. The Board considered Redwood’s profitability and whether these profits were reasonable in light of the services provided to the Fund. The Board reviewed a profitability analysis prepared by Redwood based on current asset levels of the Fund, and considered the total profits of Redwood from its relationship with the Fund. The Board noted the direct and indirect costs of operating the Fund and that Redwood continued to reimburse operating expenses of the Fund. The Board concluded that Redwood’s profitability from its relationship with the Fund was not excessive.

Economies of Scale. The Board considered whether Redwood would realize economies of scale with respect to its management of the Fund as the Fund grows and whether fee levels reflected these economies of scale for the benefit of shareholders. The Board noted that the advisory fees did not currently have breakpoints. The Board considered Redwood’s discussion of the Fund’s advisory fee structure. The Board considered the profitability analysis included in the Board Materials, and noted that while expenses of managing the Fund as a percentage of assets under management are expected to decrease as the Fund’s assets continue to grow, at current asset levels, economies of scale had not yet been reached. The Board noted that it would revisit whether economies of scale should be taken into account in the future once the Fund has achieved sufficient scale.

Other Benefits. The Board also considered the character and amount of any other direct and incidental benefits to be received by Redwood from its association with the Fund. The Board considered that no affiliate of Redwood maintains a relationship with the Fund and Redwood did not anticipate receiving any direct, indirect or ancillary material “fall-out” benefits from its relationship with the Fund.

Conclusion. The Board, having requested and received such information from Redwood as it believed reasonably necessary to evaluate the terms of the Advisory Agreement, and having been advised by independent counsel that the Board had appropriately considered and weighed all relevant factors, determined that approval of the Advisory Agreement for an additional one-year term was in the best interests of the Fund and its shareholders. In considering the Advisory Agreement renewal, the Board did not identify any one factor as all important and each Independent Trustee may have considered different factors as more important.

22

Redwood Managed Volatility Portfolio

SUPPLEMENTAL INFORMATION (Unaudited)(Continued)

December 31, 2018

Trustees and Officers. The Trustees and officers of the Trust, together with information as to their principal business occupations during the past five years and other information, are shown below. Unless otherwise noted, the address of each Trustee and Officer is 17605 Wright Street, Suite 2, Omaha, Nebraska 68130.

Independent Trustees *

| Name, Address, Year of Birth | Position(s) Held with Registrant | Term and Length Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios Overseen In The Fund Complex** | Other Directorships Held During Past 5 Years |

| Mark Garbin Year of Birth: 1951 | Trustee | Indefinite, Since 2012 | Managing Principal, Coherent Capital Management LLC (since 2008) | 8 | Northern Lights Fund Trust (since 2013); Northern Lights Variable Trust (for series not affiliated with the Funds since 2013); Forethought Variable Insurance Trust (since 2013); Northern Lights Variable Trust (since 2013); OHA Mortgage Strategies Fund (offshore), Ltd. (2014 - 2017); and Altegris KKR Commitments Master Fund (since 2014); and OFI Carlyle Private Credit Fund (since March 2018) |

| Mark D. Gersten Year of Birth: 1950 | Chairman, Trustee | Indefinite, Since 2012 | Independent Consultant (since 2012); Senior Vice President – Global Fund Administration Mutual Funds & Alternative Funds, AllianceBernstein LP (1985 – 2011). | 8 | Northern Lights Fund Trust (since 2013); Northern Lights Variable Trust (for series not affiliated with the Funds since 2013); Altegris KKR Commitments Master Fund (since 2014); previously, Ramius Archview Credit and Distressed Fund (2015-2017); and Schroder Global Series Trust (2012 to 2017) |

| Neil M. Kaufman Year of Birth: 1960 | Trustee, Audit Committee Chairman | Indefinite, Since 2012 | Managing Member, Kaufman & Associates, LLC (legal services)(Since 2016); Partner, Abrams Fensterman, Fensterman, Eisman, Formato, Ferrara & Wolf, LLP (legal services)(2010-2016) | 8 | Altegris KKR Commitments Master Fund (since 2014) |

| Anita K. Krug Year of Birth: 1969 | Trustee | Indefinite, Since 2012 | Interim Vice Chancellor for Academic Affairs (since 2018) University of Washington Bothell; Interim Dean (2017- 2018), Professor (since 2016), Associate Professor (2014-2016); and Assistant Professor (2010-2014), University of Washington School of Law | 8 | Altegris KKR Commitments Master Fund (since 2014); Centerstone Investors Trust (since 2016) |

| * | Information is as of December 31, 2018. |

| ** | As of December 31, 2018, the Trust was comprised of 20 active portfolios managed by seven unaffiliated investment advisers and two affiliated investment advisers. The term “Fund Complex” applies only to those funds that (i) are advised by a common investment adviser or by an investment adviser that is an affiliated person of the investment adviser of any of the other funds in the Trust or (ii) hold themselves out to investors as related companies for purposes of investment and investor services. The Portfolio does not hold itself out as related to any other series within the Trust for investment purpose. |

The Portfolio’s investment adviser also serves as investment adviser to the following funds: the Redwood Managed Volatility Fund, Redwood AlphaFactor® Tactical Core Fund, Redwood Managed Municipal Income Fund, Redwood Activist Leaders Fund, Redwood AlphaFactor® Tactical International Fund, Redwood Systematic Macro Trend (“SMarT”) Fund, and LeadersharesTM AlphaFactor® US Core Equity ETF, each another series of the Trust.

23

Redwood Managed Volatility Portfolio

SUPPLEMENTAL INFORMATION (Unaudited)(Continued)

December 31, 2018

Officers of the Trust*

| Name, Address, Year of Birth | Position(s) Held with Registrant | Principal Occupation(s) During Past 5 Years | Number of Portfolios Overseen In The Fund Complex** | Other Directorships Held During Past 5 Years |

| James Colantino 80 Arkay Drive Hauppauge, NY 11788 Year of Birth: 1969 | President Since Feb. 2017 Treasurer (2012 to 2017) | Senior Vice President (2012- present); Vice President (2004 to 2012); Gemini Fund Services, LLC. | N/A | N/A |

| Laura Szalyga 80 Arkay Drive Hauppauge, NY 11788 Year of Birth: 1978 | Treasurer Since Feb. 2017 | Vice President, Gemini Fund Services, LLC (since 2015); Assistant Vice President, Gemini Fund Services, LLC (2011-2014). | N/A | N/A |

| Richard A. Malinowski 80 Arkay Drive Hauppauge, NY 11788 Year of Birth: 1983 | Vice President Since Sep. 2018 Secretary Since 2013 | Senior Vice President (since 2017); Vice President and Counsel (2016-2017) and Assistant Vice President (2012 – 2016), Gemini Fund Services, LLC | N/A | N/A |

| William B. Kimme Year of Birth: 1962 | Chief Compliance Officer Since Inception | Senior Compliance Officer, Northern Lights Compliance Services, LLC (September 2011 - present) | N/A | N/A |

| * | Information is as of December 31, 2018. |

| ** | As of December 31, 2018, the Trust was comprised of 20 active portfolios managed by seven unaffiliated investment advisers and two affiliated investment advisers. The term “Fund Complex” applies only to those funds that (i) are advised by a common investment adviser or by an investment adviser that is an affiliated person of the investment adviser of any of the other funds in the Trust or (ii) hold themselves out to investors as related companies for purposes of investment and investor services. The Portfolio does not hold itself out as related to any other series within the Trust for investment purpose. |

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the Trustees and is available free of charge, upon request, by calling toll-free at 1-855-RED-FUND (733-3863).

The Portfolio’s investment adviser also serves as investment adviser to the following funds: the Redwood Managed Volatility Fund, Redwood AlphaFactor® Tactical Core Fund, Redwood Managed Municipal Income Fund, Redwood Activist Leaders Fund, Redwood AlphaFactor® Tactical International Fund, Redwood Systematic Macro Trend (“SMarT”) Fund, and LeadersharesTM AlphaFactor® US Core Equity ETF, each another series of the Trust.

24

PRIVACY NOTICE