UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-173

DODGE & COX FUNDS

(Exact name of registrant as specified in charter)

555 California Street, 40th Floor

San Francisco, CA 94104

(Address of principal executive offices) (Zip code)

Thomas M. Mistele, Esq.

555 California Street, 40th Floor

San Francisco, CA 94104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-981-1710

Date of fiscal year end: DECEMBER 31, 2016

Date of reporting period: DECEMBER 31, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following are the December 31, 2016 annual reports for the Dodge & Cox Funds, a Delaware statutory trust, consisting of six series: Dodge & Cox Stock Fund, Dodge & Cox Global Stock Fund, Dodge & Cox International Stock Fund, Dodge & Cox Balanced Fund, Dodge & Cox Income Fund, and Dodge & Cox Global Bond Fund. The reports of each series were transmitted to their respective shareholders on February 15, 2017.

DODGE & COX FUNDS®

Annual Report

December 31, 2016

Stock Fund

ESTABLISHED 1965

TICKER: DODGX

12/16 SF AR  Printed on recycled paper

Printed on recycled paper

TO OUR SHAREHOLDERS

The Dodge & Cox Stock Fund had a total return of 21.3% for the year ended December 31, 2016, compared to a return of 12.0% for the S&P 500 Index.

AN EXTRAORDINARY YEAR

The Fund’s strong absolute and relative performance in 2016 was achieved with largely the same portfolio that produced weak results in 2015. Many of the biggest contributors in 2016 were the largest detractors in 2015. The past year’s performance also improved the Fund’s longer-term relative results. The Fund’s annualized total return for the past five years was 17.0% versus 14.7% for the S&P 500.

We would like to express sincere appreciation to our fellow shareholders for your patience and confidence in Dodge & Cox. These results serve as a reminder that a single quarter or year is too short an interval over which to judge the success of our strategy. Our bottom-up, value-oriented, active investment approach requires independent thinking to build the level of conviction essential to invest in companies that are out of favor. Stock prices can move dramatically in response to the headlines of the day, but it often takes time for a company’s results to improve and for positive change to be recognized by other investors. Accordingly, maintaining a long-term investment horizon and staying the course when markets move against us are essential for our investment team, as well as for our fellow shareholders. We would be the first to acknowledge this is not easy to do, but our persistence to stick with our convictions in the face of market volatility was rewarded during this past year.

For the past 20 years, the Fund’s average annualized total return was 10.0% versus 7.7% for the S&P 500. This period encompassed large swings in Fund performance, market prices, and equity valuations, including the technology stock bubble and crash as well as the 2008-09 global financial crisis and subsequent recovery. More recently, investor concerns have been around global economic growth, lower commodity prices, and the U.S. presidential election. Uncertainty is a constant, but it can create compelling opportunities for patient, long-term, value-oriented, active investors. Our recent insight paper, “Understanding the Case for Active Management,” is summarized at the end of this letter and is available in its entirety on our website.

MARKET COMMENTARY

In 2016, global equity markets were volatile amid macroeconomic and geopolitical concerns. The U.S. equity market was one of the stronger developed markets and appreciated significantly: the S&P 500 reached an all-time high in mid-December and was up 12% for the year.

During 2015, value stocks underperformed growth stocks in the United States by one of the widest margins since the global financial crisis. This trend reversed in 2016, as U.S. value stocks outperformed growth stocks by ten percentage points,(a) benefiting many of the Fund’s value-oriented holdings. Recently, the more economically sensitive sectors of the market that are likely to benefit from an improving economy and higher interest rates (e.g.,

Energy, Financials) have accounted for a larger portion of the value category than stocks in the more defensive, stable sectors (e.g., Consumer Staples, Real Estate, Telecommunication Services, Utilities).

Equity returns for these two broad groups—more economically sensitive and more defensive sectors—have been highly correlated with interest rate movements in recent years. As interest rates declined to historically low levels and investors searched for yield in the equity market, defensive stocks with “bond-like” characteristics outperformed more cyclical stocks. In the first half of 2016, the best-performing sectors of the S&P 500 were Telecommunication Services and Utilities, while Financials and Information Technology were the worst performers. Conversely, as U.S. Treasury yields rose during the second half of 2016, especially after the U.S. presidential election, economically sensitive holdings outperformed considerably: Financials and Information Technology were the strongest sectors of the market, while Real Estate and Utilities were the weakest.

INVESTMENT STRATEGY

The Fund’s performance in 2016 mirrored this shift described above between the cyclical and defensive sectors: first half 2016 performance for the Fund was up 1% (versus up 4% for the S&P 500) and second half performance was up 20% (versus up 8%). As a result of individual security selection, the portfolio is tilted toward more economically sensitive companies: Financials comprised 29% of the portfolio, Information Technology accounted for 18%, and Energy was 9%.(b) We believe the Fund is well positioned based on our opinion that longer-term global economic growth will be better than many expect and interest rates will continue to rise. There is also a significant valuation gap between the Fund’s holdings and sectors where the Fund has little or no exposure.

Our strong price discipline is an essential characteristic of our investment strategy. We constantly weigh valuation against fundamentals and seek to invest in companies where the initial valuation reflects concerns about future earnings and cash flow prospects, while our analysis reveals the possibility of more positive developments. As long-term investors, our challenge is to assess short-term concerns while investing with an eye toward future prospects. When we see long-term value, we often add to positions as valuations decline and other investors become more pessimistic. Two examples include recent activity in the Financials and Health Care sectors, which are discussed below.

Financials

Amid heightened market volatility, we revisited and retested our thinking on many of the Fund’s holdings during 2015 and the first half of 2016. As valuations became more attractive, we concluded market conditions had created long-term investment opportunities in selected economically sensitive companies, especially in Financials. Despite low interest rates and global economic challenges, we saw opportunities because many of the portfolio’s Financials holdings traded at relatively inexpensive valuations (at

PAGE 2 § DODGE & COX STOCK FUND

levels not seen since the 2008 global financial crisis) although they had benefited from loan growth and improved credit quality since the crisis. We added to various companies, including American Express, Bank of America, Goldman Sachs, and MetLife.(c)

During the second half of 2016, Financials was the best-performing sector of the S&P 500 (up 22%), in large part due to rising interest rates. We trimmed several of the Fund’s holdings in response to higher share prices, but maintain a significant overweight position in the sector (29% versus 15% for the S&P 500). Profits are improving and strong capital positions allow the banks to return significant capital to shareholders via share buybacks and dividends, making them a compelling alternative to other dividend-paying stocks, in our view. As rates increase, profitability within the sector should improve further. The sector also stands to benefit from potential easing of financial regulation by the Trump administration (e.g., The Dodd-Frank Wall Street Reform and Consumer Protection Act could be repealed or modified).

While we trimmed Financials on a net basis during the fourth quarter, we opportunistically added to Wells Fargo (up only 5% for 2016), which detracted from relative performance and was weak among bank stocks due to regulatory infractions and fines. We were disappointed to learn about the bank’s sales practices that resulted in improper account openings, but are convinced Wells Fargo is actively addressing the issues. After a comprehensive review, we believe Wells Fargo’s superior franchise, deep management team, track record of generating higher returns than other banks, and attractive valuation at 1.6 times book value make it an attractive long-term investment opportunity. On December 31, Wells Fargo was a 3.9% position in the Fund.

Health Care

Health Care was the worst performing sector (down 2%) of the S&P 500 in 2016 amid legal, regulatory, and pricing concerns, especially in the Pharmaceuticals industry. Pharmacy benefit managers have exerted increased pricing pressure on drug manufacturers, aided by industry consolidation and higher market shares. This trend could impact long-term profitability for pharmaceutical companies. Additional risks include biosimilar and generic competition, as well as reduced drug reimbursement from government buyers and private payors.

Conversely, research and development (R&D) productivity has increased for many of the Fund’s pharmaceutical holdings. Overall industry R&D pipelines have become larger, and new drug approvals are on the upswing. These companies stand to benefit from long-term growth in emerging markets; consumers and governments have demonstrated a tendency to spend more on health care as consumer purchasing power increases. Furthermore, the Fund’s pharmaceutical holdings have reasonable valuations, strong balance sheets, high free cash flow, and cost-cutting opportunities that help mitigate risk.

After evaluating the risks versus the opportunities, the Fund remains overweight Pharmaceuticals (11% compared to 5% for the S&P 500). We added tactically to several holdings (e.g., AstraZeneca, Sanofi) as valuations became more attractive during the second half of 2016. In addition, we recently initiated new positions in Alnylam Pharmaceuticals and Bristol-Myers Squibb.

Bristol-Myers Squibb

Once a diversified pharmaceutical company facing significant patent expirations (a “cliff”), Bristol-Myers has transitioned into a focused biopharmaceutical company that is positioned to grow. Many of its competitors responded to their patent cliffs by expanding into other non-drug areas; Bristol-Myers shed its interests in those assets unrelated to the drug business (e.g., medical supply, nutritionals), focused on specialty drugs, and concentrated on only those therapeutic areas that it believed could be profitable over the long term. Its medicines help millions of people fight against such diseases as cancer, cardiovascular disease, hepatitis, HIV/AIDS, and rheumatoid arthritis.

In 2016, one of Bristol-Myers’ lead immuno-oncology trials (CheckMate-026) failed and its stock price declined significantly. We think this is a short-term setback, and believe the company’s immuno-oncology business is particularly attractive with its strong pipeline of other drugs, significant growth potential, and reasonable valuation at 20 times forward earnings. After weighing the risks versus the long-term opportunities, we initiated a position in Bristol-Myers, which accounted for 1.3% of the Fund on December 31.

IN CLOSING

While U.S. equity valuations have increased, we remain optimistic about the long-term outlook for the portfolio, which trades at a discount: 14.7 times forward earnings compared to 18.8 times for the S&P 500. The valuation disparities that characterize the current environment offer significant opportunities for active management. We believe that being patient, persistent, and having a long-term investment horizon are essential for investment success. While we do not know what the future holds, we will continue to apply the bottom-up, value-oriented investment approach that has served the Fund well for decades.

We want to express gratitude to the Fund’s shareholders for taking the long view and having confidence in Dodge & Cox. Our strategy requires patience and persistence, and we appreciate yours.

As always, we welcome your comments and questions.

For the Board of Trustees,

| | |

| |  |

Charles F. Pohl, Chairman | | Dana M. Emery, President |

January 31, 2017

| (a) | | The Russell 1000 Value Index outperformed the Russell 1000 Growth Index by 10.3 percentage points during 2016. Generally, stocks that have lower valuations are “value” stocks, while those with higher valuations are “growth” stocks. |

| (b) | | Unless otherwise specified, all weightings and characteristics are as of December 31, 2016. |

| (c) | | The use of specific examples does not imply that they are more attractive investments than the Fund’s other holdings. |

DODGE & COX STOCK FUND §PAGE 3

UNDERSTANDING THE CASE FOR ACTIVE MANAGEMENT

One of the fiercest investment debates concerns active versus passive approaches to investing: Should investors actively choose individual investments in the hopes of beating the market, or choose a fund that tracks an index and matches the return of the market, never doing better, but never doing worse?

The most frequently cited evidence against active management is that the majority of active managers fail to beat their benchmark each year. But measuring on a 12-month basis doesn’t necessarily capture the results of an active management strategy because it often takes more than a year for a strategy to come to fruition. When measurement intervals are lengthened, the results of the active versus passive comparison are significantly different—a higher percentage of active managers outperform their benchmarks. To be sure, outperformance over the long run is nowhere near a sure thing, but the data suggests active management is an eminently viable choice.

One of the attributes of successful active managers is having a high “active share,” meaning their portfolio is significantly different from an index. Another attribute is having low fees and low portfolio turnover, which reduce the drag on performance exerted by expenses. Successful active managers also tend to provide higher risk-adjusted returns, because unlike index funds, they aren’t obliged to invest in higher risk companies. Studies also show that active managers do better when they are tightly focused on specific strategies and markets and when they have a significant financial stake in their funds.

Research indicates that the average U.S. mutual fund investor earns two percentage points less per year than the average fund because many investors move in and out of funds too quickly. But if investors have the discipline to stick with good active managers through inevitable periods of underperformance, they can have meaningful prospects of outperforming the market over time.

A summary from Dodge & Cox’s insight paper titled, “Understanding the Case for Active Management.”

ANNUAL PERFORMANCE REVIEW

The Fund outperformed the S&P 500 by 9.3 percentage points in 2016.

Key Contributors to Relative Results

| | § | | Returns from holdings in the Consumer Discretionary sector (up 26% compared to up 6% for the S&P 500 sector) helped results. Time Warner Inc. (up 52%), which agreed to be acquired by AT&T, was particularly strong. Time Warner Cable (up 13% to date of merger) and Charter Communications (up 24% from date of merger) merged during the year and performed well. | |

| | § | | The Fund’s holdings in the Information Technology sector (up 25% compared to up 14% for the S&P 500 sector) aided performance. Hewlett Packard Enterprise (up 54%) and HP Inc. (up 30%) were key contributors. | |

| | § | | The Fund’s significant overweight position (27% versus 13%) in the Financials sector (up 22%, in line with the S&P 500 sector) added to relative results. Notable contributors included Goldman Sachs (up 35%) and Bank of America (up 33%). | |

| | § | | Following a weak 2015, Sprint (up 133%) was a standout performer. | |

Key Detractors from Relative Results

| | § | | The Health Care sector (down 2% for the S&P 500) faced headwinds during the year and lagged the overall market. Selected Fund holdings were weak, including Express Scripts (down 21%), Roche (down 15%), and Novartis (down 13%). | |

| | § | | Wells Fargo (up only 5%), a large position in the Fund, detracted from performance and was weak among bank stocks due to regulatory infractions and fines. | |

KEY CHARACTERISTICS OF DODGE & COX

Independent Organization

Dodge & Cox is one of the largest privately owned investment managers in the world. We remain committed to independence, with a goal of providing the highest quality investment management service to our existing clients.

Over 85 Years of Investment Experience

Dodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Experienced Investment Team

The Investment Policy Committee, which is the decision-making body for the Stock Fund, is an eight-member committee with an average tenure at Dodge & Cox of 23 years.

One Business with a Single Research Office

Dodge & Cox manages equity (domestic, international, and global), fixed income (domestic and global), and balanced investments, operating from one office in San Francisco.

Consistent Investment Approach

Our team decision-making process involves thorough, bottom-up fundamental analysis of each investment.

Long-Term Focus and Low Expenses

We invest with a three- to five-year investment horizon, which has historically resulted in low turnover relative to our peers. We manage Funds that maintain low expense ratios.

Risks: The Fund is subject to market risk, meaning holdings in the Fund may decline in value for extended periods due to the financial prospects of individual companies, or due to general market and economic conditions. Please read the prospectus and summary prospectus for specific details regarding the Fund’s risk profile.

PAGE 4 § DODGE & COX STOCK FUND

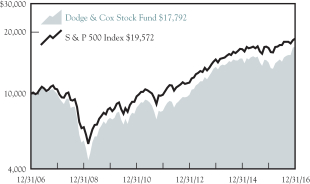

GROWTH OF $10,000 OVER 10 YEARS

FOR AN INVESTMENT MADE ON DECEMBER 31, 2006

AVERAGE ANNUAL TOTAL RETURN

FOR PERIODS ENDED DECEMBER 31, 2016

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | 20 Years | |

Dodge & Cox Stock Fund | | | 21.27 | % | | | 17.00 | % | | | 5.93 | % | | | 10.00 | % |

S&P 500 Index | | | 11.96 | | | | 14.66 | | | | 6.95 | | | | 7.68 | |

Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated. Performance is updated and published monthly. Visit the Fund’s website at dodgeandcox.com or call 800-621-3979 for current performance figures.

The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted for any income taxes payable by shareholders on these distributions or on Fund share redemptions. Index returns include dividends but, unlike Fund returns, do not reflect fees or expenses. The S&P 500 Index is a market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market.

S&P 500® is a trademark of S&P Global Inc.

FUND EXPENSE EXAMPLE

As a Fund shareholder, you incur ongoing Fund costs, including management fees and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The following example shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The example assumes a $1,000 investment held for the six months indicated.

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and expenses based on the Fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON WITH OTHER MUTUAL FUNDS

Information on the second line of the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio of the Fund and an assumed 5% annual rate of return before expenses (not the Fund’s actual return). The amount under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other mutual funds.

| | | | | | | | | | | | |

Six Months Ended

December 31, 2016 | | Beginning Account Value

7/1/2016 | | | Ending Account Value

12/31/2016 | | | Expenses Paid

During Period* | |

Based on Actual Fund Return | | $ | 1,000.00 | | | $ | 1,204.20 | | | $ | 2.85 | |

Based on Hypothetical 5% Yearly Return | | | 1,000.00 | | | | 1,022.55 | | | | 2.61 | |

| * | | Expenses are equal to the Fund’s annualized expense ratio of 0.51%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). |

The expenses shown in the table highlight ongoing costs only and do not reflect any transactional fees or account maintenance fees. Though other mutual funds may charge such fees, please note that the Fund does not charge transaction fees (e.g., redemption fees, sales loads) or universal account maintenance fees (e.g., small account fees).

DODGE & COX STOCK FUND §PAGE 5

| | | | |

| FUND INFORMATION (unaudited) | | | December 31, 2016 | |

| | | | |

| GENERAL INFORMATION | | | |

Net Asset Value Per Share | | | $184.30 | |

Total Net Assets (billions) | | | $61.6 | |

Expense Ratio | | | 0.52% | |

Portfolio Turnover Rate | | | 16% | |

30-Day SEC Yield(a) | | | 1.18% | |

Number of Companies | | | 64 | |

Fund Inception | | | 1965 | |

No sales charges or distribution fees | | | | |

Investment Manager: Dodge & Cox, San Francisco. Managed by the Investment Policy Committee, whose eight members’ average tenure at Dodge & Cox is 23 years.

| | | | | | | | |

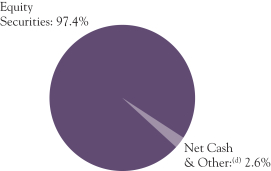

| PORTFOLIO CHARACTERISTICS | | Fund | | | S&P 500 | |

Median Market Capitalization (billions) | | | $40 | | | | $19 | |

Weighted Average Market Capitalization (billions) | | | $113 | | | | $151 | |

Price-to-Earnings Ratio(b) | | | 14.7x | | | | 18.8x | |

Foreign Securities not in the S&P 500(c) | | | 9.1% | | | | 0.0% | |

| | | | |

| TEN LARGEST HOLDINGS (%)(d) | | Fund | |

Bank of America Corp. | | | 4.0 | |

Wells Fargo & Co. | | | 3.9 | |

Capital One Financial Corp. | | | 3.8 | |

Charles Schwab Corp. | | | 3.8 | |

Hewlett Packard Enterprise Co. | | | 3.5 | |

Goldman Sachs Group, Inc. | | | 3.3 | |

Time Warner, Inc. | | | 3.1 | |

Sanofi (France) | | | 2.9 | |

Charter Communications, Inc. | | | 2.9 | |

Microsoft Corp. | | | 2.5 | |

| | | | | | | | |

| SECTOR DIVERSIFICATION(%) | | Fund | | | S&P 500 | |

Financials | | | 29.4 | | | | 14.8 | |

Information Technology | | | 17.9 | | | | 20.8 | |

Health Care | | | 16.9 | | | | 13.6 | |

Consumer Discretionary | | | 15.1 | | | | 12.0 | |

Energy | | | 9.2 | | | | 7.6 | |

Industrials | | | 4.2 | | | | 10.3 | |

Telecommunication Services | | | 1.9 | | | | 2.7 | |

Consumer Staples | | | 1.5 | | | | 9.4 | |

Materials | | | 1.0 | | | | 2.8 | |

Utilities | | | 0.0 | | | | 3.1 | |

Real Estate | | | 0.0 | | | | 2.9 | |

| (a) | SEC Yield is an annualization of the Fund’s net investment income for the trailing 30-day period. Dividends paid by the Fund may be higher or lower than implied by the SEC Yield. |

| (b) | Price-to-earnings (P/E) ratios are calculated using 12-month forward earnings estimates from third-party sources. |

| (c) | Foreign securities are U.S. dollar denominated. |

| (d) | The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation to buy, sell, or hold any particular security and is not indicative of Dodge & Cox’s current or future trading activity. |

| (e) | Net Cash & Other includes cash, short-term investments, receivables, and payables. |

PAGE 6 § DODGE & COX STOCK FUND

| | | | |

| PORTFOLIO OF INVESTMENTS | | | December 31, 2016 | |

| | | | | | | | |

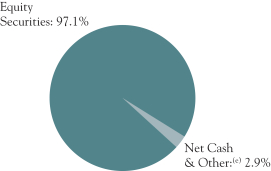

| COMMON STOCKS: 97.1% | |

| | |

| | | SHARES | | | VALUE | |

| CONSUMER DISCRETIONARY: 15.1% | |

AUTOMOBILES & COMPONENTS: 0.6% | |

Adient PLC(a) (Ireland) | | | 1,142,935 | | | $ | 66,975,991 | |

Harley-Davidson, Inc. | | | 5,610,647 | | | | 327,325,146 | |

| | | | | | | | |

| | | | 394,301,137 | |

CONSUMER DURABLES & APPAREL: 0.5% | |

Coach, Inc. | | | 8,813,900 | | | | 308,662,778 | |

| | |

MEDIA: 11.8% | | | | | | | | |

Charter Communications, Inc., Class A(a) | | | 6,094,486 | | | | 1,754,724,409 | |

Comcast Corp., Class A | | | 22,498,797 | | | | 1,553,541,933 | |

DISH Network Corp., Class A(a) | | | 9,727,476 | | | | 563,512,684 | |

News Corp., Class A | | | 4,462,806 | | | | 51,143,757 | |

Time Warner, Inc. | | | 19,778,332 | | | | 1,909,202,388 | |

Twenty-First Century Fox, Inc., Class A | | | 41,334,626 | | | | 1,159,022,913 | |

Twenty-First Century Fox, Inc., Class B | | | 9,350,000 | | | | 254,787,500 | |

| | | | | | | | |

| | | | 7,245,935,584 | |

RETAILING: 2.2% | |

Liberty Interactive Corp. QVC Group, Series A(a) | | | 12,017,275 | | | | 240,105,155 | |

Target Corp. | | | 6,161,054 | | | | 445,012,930 | |

The Priceline Group, Inc.(a) | | | 458,400 | | | | 672,041,904 | |

| | | | | | | | |

| | | | 1,357,159,989 | |

| | | | | | | | |

| | | | | | | 9,306,059,488 | |

| CONSUMER STAPLES: 1.5% | |

FOOD & STAPLES RETAILING: 1.5% | |

Wal-Mart Stores, Inc. | | | 12,988,050 | | | | 897,734,016 | |

| | |

| ENERGY: 9.2% | | | | | | | | |

Anadarko Petroleum Corp. | | | 13,395,521 | | | | 934,069,679 | |

Apache Corp. | | | 17,095,994 | | | | 1,085,082,739 | |

Baker Hughes, Inc. | | | 15,637,578 | | | | 1,015,973,443 | |

Concho Resources, Inc.(a) | | | 3,615,000 | | | | 479,349,000 | |

National Oilwell Varco, Inc. | | | 18,698,000 | | | | 700,053,120 | |

Schlumberger, Ltd. (Curacao/United States) | | | 15,499,245 | | | | 1,301,161,618 | |

Weatherford International PLC(a) (Ireland) | | | 28,007,400 | | | | 139,756,926 | |

| | | | | | | | |

| | | | 5,655,446,525 | |

| FINANCIALS: 29.4% | |

BANKS: 11.2% | |

Bank of America Corp. | | | 111,294,300 | | | | 2,459,604,030 | |

BB&T Corp. | | | 13,015,144 | | | | 611,972,071 | |

JPMorgan Chase & Co. | | | 16,797,800 | | | | 1,449,482,162 | |

Wells Fargo & Co. | | | 43,253,341 | | | | 2,383,691,622 | |

| | | | | | | | |

| | | | 6,904,749,885 | |

DIVERSIFIED FINANCIALS: 15.3% | |

American Express Co. | | | 17,197,300 | | | | 1,273,975,984 | |

Bank of New York Mellon Corp. | | | 29,763,060 | | | | 1,410,173,783 | |

Capital One Financial Corp.(b) | | | 27,167,711 | | | | 2,370,111,108 | |

Charles Schwab Corp. | | | 58,867,600 | | | | 2,323,504,172 | |

Goldman Sachs Group, Inc. | | | 8,518,700 | | | | 2,039,802,715 | |

| | | | | | | | |

| | | | 9,417,567,762 | |

INSURANCE: 2.9% | |

AEGON NV (Netherlands) | | | 71,579,823 | | | | 395,836,421 | |

MetLife, Inc. | | | 26,432,700 | | | | 1,424,458,203 | |

| | | | | | | | |

| | | | | | | 1,820,294,624 | |

| | | | | | | | |

| | | | 18,142,612,271 | |

| HEALTH CARE: 16.9% | |

HEALTH CARE EQUIPMENT & SERVICES: 6.3% | |

Anthem, Inc. | | | 1,527,685 | | | | 219,635,272 | |

Cigna Corp. | | | 8,608,217 | | | | 1,148,250,066 | |

| | | | | | | | |

| | |

| | | SHARES | | | VALUE | |

Danaher Corp. | | | 3,237,600 | | | $ | 252,014,784 | |

Express Scripts Holding Co.(a) | | | 12,534,871 | | | | 862,273,776 | |

Medtronic PLC (Ireland) | | | 6,719,600 | | | | 478,637,108 | |

UnitedHealth Group, Inc. | | | 5,830,760 | | | | 933,154,830 | |

| | | | | | | | |

| | | | 3,893,965,836 | |

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES: 10.6% | |

Alnylam Pharmaceuticals, Inc.(a)(b) | | | 5,430,735 | | | | 203,326,718 | |

AstraZeneca PLC ADR (United Kingdom) | | | 32,659,383 | | | | 892,254,344 | |

Bristol-Myers Squibb Co. | | | 14,113,900 | | | | 824,816,316 | |

Merck & Co., Inc. | | | 7,767,900 | | | | 457,296,273 | |

Novartis AG ADR (Switzerland) | | | 20,392,957 | | | | 1,485,422,988 | |

Roche Holding AG ADR (Switzerland) | | | 31,020,799 | | | | 885,023,396 | |

Sanofi ADR (France) | | | 44,130,728 | | | | 1,784,646,640 | |

| | | | | | | | |

| | | | | | | 6,532,786,675 | |

| | | | | | | | |

| | | | 10,426,752,511 | |

| INDUSTRIALS: 4.2% | |

CAPITAL GOODS: 0.8% | |

Johnson Controls International PLC (Ireland) | | | 11,329,351 | | | | 466,655,968 | |

| | |

TRANSPORTATION: 3.4% | | | | | | | | |

FedEx Corp. | | | 6,847,099 | | | | 1,274,929,834 | |

Union Pacific Corp. | | | 8,070,000 | | | | 836,697,600 | |

| | | | | | | | |

| | | | 2,111,627,434 | |

| | | | | | | | |

| | | | 2,578,283,402 | |

| INFORMATION TECHNOLOGY: 17.9% | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT: 0.8% | |

Maxim Integrated Products, Inc. | | | 12,095,740 | | | | 466,532,692 | |

| | |

SOFTWARE & SERVICES: 7.2% | | | | | | | | |

Alphabet, Inc., Class A(a) | | | 203,100 | | | | 160,946,595 | |

Alphabet, Inc., Class C(a) | | | 1,765,253 | | | | 1,362,457,570 | |

Dell Technologies, Inc., Class V(a) | | | 6,851,210 | | | | 376,611,014 | |

Microsoft Corp. | | | 25,147,300 | | | | 1,562,653,222 | |

Symantec Corp.(b) | | | 3,340,476 | | | | 79,803,972 | |

Synopsys, Inc.(a)(b) | | | 7,265,469 | | | | 427,645,505 | |

VMware, Inc.(a) | | | 5,955,511 | | | | 468,877,381 | |

| | | | | | | | |

| | | | 4,438,995,259 | |

TECHNOLOGY, HARDWARE & EQUIPMENT: 9.9% | |

Cisco Systems, Inc. | | | 38,202,711 | | | | 1,154,485,927 | |

Corning, Inc. | | | 18,842,000 | | | | 457,295,340 | |

Hewlett Packard Enterprise Co.(b) | | | 93,402,495 | | | | 2,161,333,734 | |

HP Inc. | | | 71,435,195 | | | | 1,060,098,294 | |

Juniper Networks, Inc. | | | 3,169,247 | | | | 89,562,920 | |

NetApp, Inc.(b) | | | 14,368,331 | | | | 506,771,034 | |

TE Connectivity, Ltd. (Switzerland) | | | 9,976,475 | | | | 691,170,188 | |

| | | | | | | | |

| | | | 6,120,717,437 | |

| | | | | | | | |

| | | | 11,026,245,388 | |

| MATERIALS: 1.0% | | | | | | | | |

Celanese Corp., Series A(b) | | | 7,779,698 | | | | 612,573,421 | |

|

| TELECOMMUNICATION SERVICES: 1.9% | |

Sprint Corp.(a) | | | 106,416,127 | | | | 896,023,789 | |

Zayo Group Holdings, Inc.(a) | | | 8,550,000 | | | | 280,953,000 | |

| | | | | | | | |

| | | | 1,176,976,789 | |

| | | | | | | | |

TOTAL COMMON STOCKS

(Cost $39,936,648,414) | | | $ | 59,822,683,811 | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 7 |

| | | | |

| PORTFOLIO OF INVESTMENTS | | | December 31, 2016 | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS: 3.0% | |

| | |

| | | PAR VALUE | | | VALUE | |

MONEY MARKET FUND: 0.1% | | | | | |

State Street Institutional Treasury Plus Money Market Fund | | $ | 62,055,950 | | | $ | 62,055,950 | |

| |

REPURCHASE AGREEMENT: 2.9% | | | | | |

Fixed Income Clearing Corporation(c) 0.10%, dated 12/30/16, due 1/3/17, maturity value $1,754,866,498 | | | 1,754,843,000 | | | | 1,754,843,000 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $1,816,898,950) | | | $ | 1,816,898,950 | |

| | | | | | | | |

TOTAL INVESTMENTS

(Cost $41,753,547,364) | | | 100.1 | % | | $ | 61,639,582,761 | |

OTHER ASSETS LESS LIABILITIES | | | (0.1 | %) | | | (39,106,902 | ) |

| | | | | | | | |

| NET ASSETS | | | 100.0 | % | | $ | 61,600,475,859 | |

| | | | | | | | |

| (b) | See Note 9 regarding holdings of 5% voting securities |

| (c) | Repurchase agreement is collateralized by Fannie Mae 5.375%, 6/12/17, Federal Farm Credit Bank 1.125%, 9/22/17, Freddie Mac 0.75%-1.00%, 7/14/17-11/28/17, U.S. Treasury Inflation Indexed Note 0.125%-2.625%, 4/15/17-7/15/17, and U.S. Treasury Notes 0.625%-1.875%, 5/15/17-12/31/17. Total collateral value is $1,789,951,128. |

In determining a company’s country designation, the Fund generally references the country of incorporation. In cases where the Fund considers the country of incorporation to be a “jurisdiction of convenience” chosen primarily for tax purposes or in other limited circumstances, the Fund uses the country designation of an appropriate broad-based market index. In those cases, two countries are listed—the country of incorporation and the country designated by an appropriate index, respectively.

ADR: American Depositary Receipt

FUTURES CONTRACTS

| | | | | | | | | | | | | | | | |

| Description | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Unrealized

Appreciation/

(Depreciation) | |

E-mini S&P 500 Index—Long Position | | | 15,431 | | | | Mar 2017 | | | $ | 1,725,340,110 | | | $ | (14,740,454 | ) |

| | |

| PAGE 8 § DODGE & COX STOCK FUND | | See accompanying Notes to Financial Statements |

| | | | |

STATEMENT OF ASSETS AND LIABILITIES | |

| |

| | | December 31, 2016 | |

ASSETS: | | | | |

Investments, at value | | | | |

Unaffiliated issuers (cost $38,193,911,466) | | $ | 55,785,466,746 | |

Affiliated issuers (cost $3,559,635,898) | | | 5,854,116,015 | |

| | | | |

| | | 61,639,582,761 | |

Cash held at broker | | | 73,297,257 | |

Receivable for investments sold | | | 93,302,447 | |

Receivable for Fund shares sold | | | 38,128,416 | |

Dividends and interest receivable | | | 61,732,289 | |

Prepaid expenses and other assets | | | 314,115 | |

| | | | |

| | | 61,906,357,285 | |

| | | | |

LIABILITIES: | | | | |

Payable for investments purchased | | | 9,628,958 | |

Payable to broker for variation margin | | | 5,595,262 | |

Payable for Fund shares redeemed | | | 262,792,748 | |

Management fees payable | | | 26,417,770 | |

Accrued expenses | | | 1,446,688 | |

| | | | |

| | | 305,881,426 | |

| | | | |

NET ASSETS | | $ | 61,600,475,859 | |

| | | | |

NET ASSETS CONSIST OF: | | | | |

Paid in capital | | $ | 40,826,136,110 | |

Undistributed net investment income | | | 7,382,075 | |

Undistributed net realized gain | | | 895,662,731 | |

Net unrealized appreciation | | | 19,871,294,943 | |

| | | | |

| | $ | 61,600,475,859 | |

| | | | |

Fund shares outstanding (par value $0.01 each,

unlimited shares authorized) | | | 334,247,521 | |

Net asset value per share | | $ | 184.30 | |

|

STATEMENT OF OPERATIONS | |

| |

| | | Year Ended

December 31, 2016 | |

INVESTMENT INCOME: | | | | |

Dividends (net of foreign taxes of $10,923,953) | | | | |

Unaffiliated issuers | | $ | 1,003,676,462 | |

Affiliated issuers | | | 293,655,555 | |

Interest | | | 778,193 | |

| | | | |

| | | 1,298,110,210 | |

| | | | |

EXPENSES: | | | | |

Management fees | | | 275,674,035 | |

Custody and fund accounting fees | | | 689,957 | |

Transfer agent fees | | | 3,594,887 | |

Professional services | | | 140,704 | |

Shareholder reports | | | 1,100,507 | |

Registration fees | | | 264,299 | |

Trustees’ fees | | | 247,500 | |

ADR depositary services fees | | | 3,658,073 | |

Miscellaneous | | | 765,153 | |

| | | | |

| | | 286,135,115 | |

| | | | |

NET INVESTMENT INCOME | | | 1,011,975,095 | |

| | | | |

REALIZED AND UNREALIZED GAIN (LOSS): | | | | |

Net realized gain (loss) | | | | |

Investments in unaffiliated issuers | | | 2,639,028,649 | |

Investments in affiliated issuers | | | 313,249,118 | |

Futures contracts | | | 14,986,913 | |

Foreign currency transactions | | | (127,784 | ) |

Net change in unrealized appreciation/depreciation | | | | |

Investments | | | 7,043,077,537 | |

Futures contracts | | | (16,453,661 | ) |

| | | | |

Net realized and unrealized gain | | | 9,993,760,772 | |

| | | | |

NET CHANGE IN NET ASSETS

FROM OPERATIONS | | $ | 11,005,735,867 | |

| | | | |

| | | | | | | | |

STATEMENT OF CHANGES IN NET ASSETS | | | | | |

| | |

| | | Year Ended

December 31, 2016 | | | Year Ended

December 31, 2015 | |

OPERATIONS: | | | | | | | | |

Net investment income | | $ | 1,011,975,095 | | | $ | 801,418,840 | |

Net realized gain | | | 2,967,136,896 | | | | 2,982,618,142 | |

Net change in unrealized appreciation/depreciation | | | 7,026,623,876 | | | | (6,397,067,953 | ) |

| | | | | | | | |

| | | 11,005,735,867 | | | | (2,613,030,971 | ) |

| | | | | | | | |

| | |

DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | | | | |

Net investment income | | | (1,006,582,969 | ) | | | (813,298,971 | ) |

Net realized gain | | | (2,967,981,956 | ) | | | (2,475,923,268 | ) |

| | | | | | | | |

Total distributions | | | (3,974,564,925 | ) | | | (3,289,222,239 | ) |

| | | | | | | | |

| | |

FUND SHARE TRANSACTIONS: | | | | | | | | |

Proceeds from sale of shares | | | 7,078,053,220 | | | | 7,399,154,348 | |

Reinvestment of distributions | | | 3,757,250,793 | | | | 3,094,798,205 | |

Cost of shares redeemed | | | (11,111,123,603 | ) | | | (10,006,695,861 | ) |

| | | | | | | | |

Net change from Fund share transactions | | | (275,819,590 | ) | | | 487,256,692 | |

| | | | | | | | |

Total change in net assets | | | 6,755,351,352 | | | | (5,414,996,518 | ) |

| | |

NET ASSETS: | | | | | | | | |

Beginning of year | | | 54,845,124,507 | | | | 60,260,121,025 | |

| | | | | | | | |

End of year (including undistributed net investment income of $7,382,075 and $7,503,253, respectively) | | $ | 61,600,475,859 | | | $ | 54,845,124,507 | |

| | | | | | | | |

| | |

SHARE INFORMATION: | | | | | | | | |

Shares sold | | | 42,458,419 | | | | 41,883,366 | |

Distributions reinvested | | | 21,705,948 | | | | 18,759,974 | |

Shares redeemed | | | (66,866,904 | ) | | | (56,738,159 | ) |

| | | | | | | | |

Net change in shares outstanding | | | (2,702,537 | ) | | | 3,905,181 | |

| | | | | | | | |

| | |

| See accompanying Notes to Financial Statements | | DODGE & COX STOCK FUND §PAGE 9 |

NOTES TO FINANCIAL STATEMENTS

NOTE 1—ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Dodge & Cox Stock Fund (the “Fund”) is one of the series constituting the Dodge & Cox Funds (the “Trust” or the “Funds”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund commenced operations on January 4, 1965, and seeks long-term growth of principal and income. Risk considerations and investment strategies of the Fund are discussed in the Fund’s Prospectus.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which require the use of estimates and assumptions by management. Actual results may differ from those estimates. Significant accounting policies are as follows:

Security valuation The Fund’s net assets are typically valued as of the normally scheduled close of trading on the New York Stock Exchange (NYSE), generally 4:00 p.m. Eastern Time, each day that the NYSE is open for business.

Portfolio securities and other financial instruments for which market quotes are readily available are valued at market value. Listed securities are generally valued using the official quoted close price or the last sale on the exchange that is determined to be the primary market for the security. Exchange-traded derivatives are valued at the settlement price determined by the relevant exchange. Security values are not discounted based on the size of the Fund’s position. Short-term securities less than 60 days to maturity may be valued at amortized cost if amortized cost approximates current value. Mutual funds are valued at their respective net asset values. All securities held by the Fund are denominated in U.S. dollars.

If market quotations are not readily available or if a security’s value is believed to have materially changed after the close of the security’s primary market but before the close of trading on the NYSE, the security is valued at fair value as determined in good faith by or under the direction of the Fund’s Board of Trustees. The Board of Trustees has appointed Dodge & Cox, the Fund’s investment manager, to make fair value determinations in accordance with the Dodge & Cox Funds Valuation Policies (“Valuation Policies”), subject to Board oversight. Dodge & Cox has established a Pricing Committee that is comprised of representatives from Treasury, Legal, Compliance, and Operations. The Pricing Committee is responsible for implementing the Valuation Policies, including determining the fair value of securities when market quotations or market-based valuations are not readily available or are deemed unreliable. The Pricing Committee considers relevant indications of value that are reasonably available to it in determining the fair value assigned to a particular security, such as the value of similar financial instruments, trading volumes, contractual restrictions on disposition, related corporate actions, and changes in economic conditions. In doing so, the Pricing Committee employs various

methods for calibrating fair valuation approaches, including a regular review of key inputs and assumptions, back-testing, and review of any related market activity.

Valuing securities through a fair value determination involves greater reliance on judgment than valuation of securities based on readily available market quotations. In some instances, lack of information and uncertainty as to the significance of information may lead to a conclusion that a prior valuation is the best indication of a security’s value. When fair value pricing is employed, the prices of securities used by the Fund to calculate its NAV may differ from quoted or published prices for the same securities.

Security transactions, investment income, expenses, and distributions Security transactions are recorded on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost.

Dividend income and corporate action transactions are recorded on the ex-dividend date, or when the Fund first learns of the dividend/corporate action if the ex-dividend date has passed. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Dividends characterized as return of capital for U.S. tax purposes are recorded as a reduction of cost of investments and/or realized gain. Interest income is recorded on the accrual basis.

Expenses are recorded on the accrual basis. Some expenses of the Trust can be directly attributed to a specific series. Expenses which cannot be directly attributed are allocated among the Funds in the Trust using methodologies determined by the nature of the expense.

Distributions to shareholders are recorded on the ex-dividend date.

Repurchase agreements The Fund enters into repurchase agreements, secured by U.S. government or agency securities, which involve the purchase of securities from a counterparty with a simultaneous commitment to resell the securities at an agreed-upon date and price. It is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default by the counterparty, the Fund has the contractual right to liquidate the collateral securities and to apply the proceeds in satisfaction of the obligation.

Foreign taxes The Fund may be subject to foreign taxes which may be imposed by certain countries in which the Fund invests. The Fund endeavors to record foreign taxes based on applicable foreign tax law. Withholding taxes are incurred on certain foreign dividends and are accrued at the time the associated dividend is recorded. The Fund files withholding tax reclaims in certain jurisdictions to recover a portion of amounts previously withheld. The Fund records a reclaim receivable based

PAGE 10 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS

on, among other things, a jurisdiction’s legal obligation to pay reclaims as well as payment history and market convention. In consideration of recent decisions rendered by European courts, the Fund has filed for additional reclaims related to prior years. A corresponding receivable is established when both the amount is known and significant contingencies or uncertainties regarding collectability are removed. These amounts, if any, are reported in “dividends and interest receivable” on the Statement of Assets and Liabilities.

Futures Contracts Futures contracts involve an obligation to purchase or sell (depending on whether the Fund has entered a long or short futures contract, respectively) an asset at a future date, at a price set at the time of the contract. Upon entering into a futures contract, the Fund is required to deposit an amount of cash or liquid assets (referred to as initial margin) in a segregated account with the clearing broker. Subsequent payments (referred to as variation margin) to and from the clearing broker are made on a daily basis based on changes in the market value of futures contracts. Futures contracts are traded publicly and their market value changes daily. Changes in the market value of open futures contracts are recorded as unrealized appreciation or depreciation in the Statement of Operations. Realized gains and losses on futures contracts are recorded in the Statement of Operations at the closing or expiration of the contracts. Cash deposited with a broker as initial margin is recorded on the Statement of Assets and Liabilities. A receivable and/or payable to brokers for daily variation margin is also recorded on the Statement of Assets and Liabilities.

Investments in futures contracts may include certain risks, which may be different from, and potentially greater than, those of the underlying securities. To the extent the Fund uses futures, it is exposed to additional volatility and potential losses resulting from leverage.

The Fund has maintained long S&P 500 futures contracts to provide equity exposure that approximates the Fund’s “net cash and other” position, which includes cash, short-term investments, receivables, and payables. During the year ended December 31, 2016, these S&P 500 futures contracts had notional values ranging from 1% to 3% of net assets.

Indemnification Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business the Trust enters into contracts that provide general indemnities to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 2—VALUATION MEASUREMENTS

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| § | | Level 1: Quoted prices in active markets for identical securities |

| § | | Level 2: Other significant observable inputs (including quoted prices for similar securities, market indices, interest rates, credit risk, forward exchange rates, etc.) |

| § | | Level 3: Significant unobservable inputs (including Fund management’s assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s holdings at December 31, 2016:

| | | | | | | | |

| Classification(a) | | LEVEL 1

(Quoted Prices) | | | LEVEL 2

(Other Significant

Observable Inputs) | |

Securities | | | | | | | | |

Common Stocks(b) | | $ | 59,822,683,811 | | | $ | — | |

Short-term Investments | | | | | | | | |

Money Market Fund | | | 62,055,950 | | | | — | |

Repurchase Agreement | | | — | | | | 1,754,843,000 | |

| | | | | | | | |

Total Securities | | $ | 59,884,739,761 | | | $ | 1,754,843,000 | |

| | | | | | | | |

Other Financial Instruments | | | | | | | | |

Futures Contracts | | | | | | | | |

Depreciation | | $ | (14,740,454 | ) | | $ | — | |

| | | | | | | | | |

| (a) | There were no transfers between Level 1 and Level 2 during the year ended December 31, 2016. There were no Level 3 securities at December 31, 2016 and 2015, and there were no transfers to Level 3 during the year. |

| (b) | All common stocks held in the Fund are Level 1 securities. For a detailed break-out of common stocks by major industry classification, please refer to the Portfolio of Investments. |

NOTE 3—RELATED PARTY TRANSACTIONS

Management fees Under a written agreement approved by a unanimous vote of the Board of Trustees, the Fund pays an annual management fee of 0.50% of the Fund’s average daily net assets to Dodge & Cox, investment manager of the Fund. The agreement further provides that Dodge & Cox shall waive its fee to the extent that such fee plus all other ordinary operating expenses of the Fund exceed 0.75% of the average daily net assets for the year.

Fund officers and trustees All officers and two of the trustees of the Trust are officers or employees of Dodge & Cox. The Trust pays a fee only to those trustees who are not affiliated with Dodge & Cox.

NOTE 4—INCOME TAX INFORMATION AND DISTRIBUTIONS TO SHAREHOLDERS

A provision for federal income taxes is not required since the Fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute all of its taxable income to shareholders. Distributions are determined in accordance with income tax regulations, and such amounts may differ from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book to tax differences at year end to reflect tax character.

DODGE & COX STOCK FUND §PAGE 11

NOTES TO FINANCIAL STATEMENTS

Book to tax differences are primarily due to differing treatments of wash sales, net short-term realized gain (loss), certain dividends, and futures contracts. At December 31, 2016, the cost of investments for federal income tax purposes was $41,799,114,906.

Distributions during the years noted below were characterized as follows for federal income tax purposes:

| | | | | | | | |

| | | Year Ended December 31, 2016 | | | Year Ended

December 31, 2015 | |

Ordinary income | | | $1,056,249,886 | | | | $813,298,971 | |

| | | ($3.183 per share) | | | | ($2.460 per share) | |

| | |

Long-term capital gain | | | $2,918,315,039 | | | | $2,475,923,268 | |

| | | ($8.899 per share) | | | | ($7.577 per share) | |

At December 31, 2016, the tax basis components of distributable earnings were as follows:

| | | | |

Unrealized appreciation | | $ | 21,008,106,160 | |

Unrealized depreciation | | | (1,167,638,305 | ) |

| | | | |

Net unrealized appreciation | | | 19,840,467,855 | |

Undistributed ordinary income | | | 54,938,850 | |

Undistributed long-term capital gain | | | 878,933,044 | |

Fund management has reviewed the tax positions for open periods (three years and four years, respectively, from filing the Fund’s Federal and State tax returns) as applicable to the Fund, and has determined that no provision for income tax is required in the Fund’s financial statements.

NOTE 5—LOAN FACILITIES

Pursuant to an exemptive order issued by the Securities and Exchange Commission (SEC), the Fund may participate in an interfund lending facility (Facility). The Facility allows the Fund to borrow money from or loan money to the Funds. Loans under the Facility are made for temporary or emergency purposes, such as to fund shareholder redemption requests. Interest on borrowings is the average of the current repurchase agreement rate and the bank loan rate. There was no activity in the Facility during the year.

All Funds in the Trust participate in a $500 million committed credit facility (Line of Credit) with State Street Bank and Trust Company, to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The maximum amount available to the Fund is $250 million. Each Fund pays an annual commitment fee on its pro-rata portion of the Line of Credit. For the year ended December 31, 2016, the Fund’s commitment fee amounted to $281,548 and is reflected as a Miscellaneous Expense in the Statement of Operations. Interest on borrowings is charged at the prevailing rate. There were no borrowings on the Line of Credit during the year.

NOTE 6—PURCHASES AND SALES OF INVESTMENTS

For the year ended December 31, 2016, purchases and sales of securities, other than short-term securities, aggregated $8,789,787,134 and $12,613,765,083, respectively.

NOTE 7—NEW ACCOUNTING GUIDANCE

In October 2016, the SEC issued a new rule, Investment Company Reporting Modernization, which, among other provisions, amends Regulation S-X to require standardized, enhanced disclosures, particularly related to derivatives, in investment company financial statements. Compliance with the guidance is required for financial statements filed with the SEC on or after August 1, 2017. Management is currently assessing the impact of this rule to the Fund’s financial statements and other filings and does not expect any impact to the Fund’s net assets or results of operations.

NOTE 8—SUBSEQUENT EVENTS

Fund management has determined that no material events or transactions occurred subsequent to December 31, 2016, and through the date of the Fund’s financial statements issuance, which require additional disclosure in the Fund’s financial statements.

PAGE 12 § DODGE & COX STOCK FUND

NOTES TO FINANCIAL STATEMENTS

NOTE 9—HOLDINGS OF 5% VOTING SECURITIES

Each of the companies listed below was considered to be an affiliate of the Fund because the Fund owned 5% or more of the company’s voting securities during all or part of the year ended December 31, 2016. Purchase and sale transactions and dividend income earned during the year on these securities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Shares at

Beginning of Year | | | Additions | | | Reductions | | | Shares at

End of Year | | | Dividend

Income (a) | | | Value at

End of Year | |

ADT Corp. | | | 11,138,437 | | | | — | | | | (11,138,437 | ) | | | — | | | $ | 2,450,456 | | | $ | — | |

Alnylam Pharmaceuticals, Inc. | | | — | | | | 5,430,735 | | | | — | | | | 5,430,735 | | | | — | (b) | | | 203,326,718 | |

Capital One Financial Corp. | | | 29,786,611 | | | | — | | | | (2,618,900 | ) | | | 27,167,711 | | | | 47,658,578 | | | | 2,370,111,108 | |

Celanese Corp., Series A | | | 7,219,998 | | | | 1,029,700 | | | | (470,000 | ) | | | 7,779,698 | | | | 10,190,289 | | | | 612,573,421 | |

Hewlett Packard Enterprise Co. | | | 90,984,995 | | | | 5,017,500 | | | | (2,600,000 | ) | | | 93,402,495 | | | | 21,776,824 | | | | 2,161,333,734 | |

NetApp, Inc. | | | 21,532,731 | | | | 900,000 | | | | (8,064,400 | ) | | | 14,368,331 | | | | 16,053,775 | | | | 506,771,034 | |

Symantec Corp. | | | 54,111,000 | | | | — | | | | (50,770,524 | ) | | | 3,340,476 | | | | 195,525,633 | | | | — | (c) |

Synopsys, Inc. | | | 9,193,469 | | | | — | | | | (1,928,000 | ) | | | 7,265,469 | | | | — | (b) | | | — | (c) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | 293,655,555 | | | $ | 5,854,116,015 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| (a) | Net of foreign taxes, if any |

| (c) | Company was not an affiliate at year end |

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | |

SELECTED DATA AND RATIOS (for a share outstanding throughout each year) | | Year Ended December 31, | |

| | | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

| | | | |

Net asset value, beginning of year | | | $162.77 | | | | $180.94 | | | | $168.87 | | | | $121.90 | | | | $101.64 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 3.05 | | | | 2.42 | | | | 2.83 | | | | 2.11 | | | | 1.98 | |

Net realized and unrealized gain (loss) | | | 30.56 | | | | (10.55 | ) | | | 14.60 | | | | 46.97 | | | | 20.26 | |

| | | | |

Total from investment operations | | | 33.61 | | | | (8.13 | ) | | | 17.43 | | | | 49.08 | | | | 22.24 | |

| | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (3.03 | ) | | | (2.46 | ) | | | (2.80 | ) | | | (2.11 | ) | | | (1.98 | ) |

Net realized gain | | | (9.05 | ) | | | (7.58 | ) | | | (2.56 | ) | | | — | | | | — | |

| | | | |

Total distributions | | | (12.08 | ) | | | (10.04 | ) | | | (5.36 | ) | | | (2.11 | ) | | | (1.98 | ) |

| | | | |

Net asset value, end of year | | | $184.30 | | | | $162.77 | | | | $180.94 | | | | $168.87 | | | | $121.90 | |

| | | | |

Total return | | | 21.27 | % | | | (4.47 | )% | | | 10.43 | % | | | 40.55 | % | | | 22.01 | % |

Ratios/supplemental data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (millions) | | | $61,600 | | | | $54,845 | | | | $60,260 | | | | $54,848 | | | | $39,841 | |

Ratio of expenses to average net assets | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % | | | 0.52 | % |

Ratio of net investment income to average net assets | | | 1.83 | % | | | 1.36 | % | | | 1.62 | % | | | 1.45 | % | | | 1.72 | % |

Portfolio turnover rate | | | 16 | % | | | 15 | % | | | 17 | % | | | 15 | % | | | 11 | % |

See accompanying Notes to Financial Statements

DODGE & COX STOCK FUND §PAGE 13

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Trustees of Dodge & Cox Funds and Shareholders of Dodge & Cox Stock Fund

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Dodge & Cox Stock Fund (one of the series constituting Dodge & Cox Funds, hereafter referred to as the “Fund”) as of December 31, 2016, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities as of December 31, 2016 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

February 15, 2017

PAGE 14 § DODGE & COX STOCK FUND

SPECIAL 2016 TAX INFORMATION

(unaudited)

The following information is provided pursuant to provisions of the Internal Revenue Code:

The Fund designates up to a maximum amount of $1,307,555,855 of its distributions paid to shareholders in 2016 as qualified dividends (treated for federal income tax purposes in the hands of shareholders as taxable at a maximum rate of 20%).

For shareholders that are corporations, the Fund designates 91% of its ordinary dividends paid to shareholders in 2016 as dividends from domestic corporations eligible for the corporate dividends received deduction, provided that the shareholder otherwise satisfies applicable requirements to claim that deduction.

BOARD APPROVAL OF FUNDS’ INVESTMENT MANAGEMENT AGREEMENTS AND MANAGEMENT FEES

(unaudited)

The Board of Trustees is responsible for overseeing the performance of the Dodge & Cox Funds’ investment manager and determining whether to continue the Investment Management Agreements between the Funds and Dodge & Cox each year (the “Agreements”). At a meeting of the Board of Trustees of the Trust held on December 14, 2016, the Trustees, by a unanimous vote (including a separate vote of those Trustees who are not “interested persons” (as defined in the Investment Company Act of 1940) (the “Independent Trustees”)), approved the renewal of the Agreements for an additional one-year term through December 31, 2017 with respect to each Fund. During the course of the year, the Board received extensive information and materials relating to the investment management and administrative services provided by Dodge & Cox and the performance of each of the Funds.

INFORMATION RECEIVED

In 2016, the Board requested and received a series of special presentations relating to the proposed renewal of the Funds’ Agreements. These presentations, which took place over the course of the year, covered, among other things, (i) a report about asset management industry trends and the competitive landscape for Dodge & Cox and the Funds; (ii) an extensive presentation regarding economies of scale, which included materials describing key enhancements over the past 15 years in the scope of services that Dodge & Cox furnishes to the Funds; (iii) a detailed presentation by Morningstar® representatives regarding the format, methodology, and content of Morningstar’s 15(c) report; (iv) materials describing peer fund management fees (including funds with breakpoints) and expense ratios and Dodge & Cox’s separate account advisory fee schedules as compared to those of peer firms; and (v) reports by outside counsel regarding mutual fund litigation trends and developments.

In addition to the foregoing and in advance of the meeting, the Board, including each of the Independent Trustees, requested, received, and reviewed materials relating to the Agreements and the services provided by Dodge & Cox. The Independent Trustees retained Morningstar to prepare an independent expense and

performance summary for each Fund and comparable funds managed by other advisers identified by Morningstar. The Morningstar materials included information regarding advisory fee rates, expense ratios, and transfer agency, custodial, and distribution expenses, as well as appropriate performance comparisons to each Fund’s peer group and an index or combination of indices. The Morningstar materials also included a comparison of expenses of various share classes offered by comparable funds. The materials reviewed by the Board contained information concerning, among other things, Dodge & Cox’s profitability, financial results and condition, advisory fee revenue and separate account fee schedules. The Board additionally considered the Funds’ brokerage commissions, turnover rates, sales and redemption data, and the significant investment that Dodge & Cox makes in research used in managing the Funds. The Board received and reviewed memoranda and related materials addressing, among other things, Dodge & Cox’s services to the Funds; how Dodge & Cox Funds’ fees compare to fees of peer group funds; the different fees, services, costs, and risks associated with other accounts managed by Dodge & Cox as compared to the Dodge & Cox Funds; and the ways in which the Funds realize economies of scale. Throughout the process of reviewing the services provided by Dodge & Cox and preparing for the meeting, the Independent Trustees found Dodge & Cox to be open, forthright, detailed, and very helpful in answering questions about all issues. The Board received copies of the Agreements and a memorandum from the independent legal counsel to the Independent Trustees discussing the factors generally regarded as appropriate to consider in evaluating advisory arrangements. The Trust’s Contract Review Committee, consisting solely of Independent Trustees, met with the independent legal counsel on November 3, 2016 and again on December 14, 2016 to discuss whether to renew the Agreements. The Board, including the Independent Trustees, subsequently concluded that the existing Agreements are fair and reasonable and voted to approve the Agreements. In considering the Agreements, the Board, including the Independent Trustees, did not identify any single factor or particular information as all-important or controlling. In reaching the decision to approve the Agreements, the Board considered several factors, discussed below, to be key factors and reached the conclusions described below.

NATURE, QUALITY, AND EXTENT OF THE SERVICES

The Board considered that Dodge & Cox provides a wide range of services to the Funds in addition to portfolio management and that the quality of these services has been excellent in all respects. The extensive nature of services provided by Dodge & Cox has been documented in materials provided to the Board and in presentations made to the Board throughout the year. In particular, the Board considered the nature, quality, and extent of portfolio management, administrative, and shareholder services performed by Dodge & Cox. With regard to portfolio management services, the Board considered Dodge & Cox’s established long-term history of care and conscientiousness in the management of the Funds; its demonstrated consistency in investment approach and depth; the

DODGE & COX STOCK FUND §PAGE 15

background and experience of the Dodge & Cox Investment Policy Committee, International Investment Policy Committee, Global Stock Investment Policy Committee, Fixed Income Investment Policy Committee, and Global Bond Investment Policy Committee, and research analysts responsible for managing the Funds; Dodge & Cox’s methods for assessing the regulatory and investment climate in various jurisdictions; its overall high level of attention to its core investment management function; and its commitment to the Funds and their shareholders. The Board also considered analysis provided by Morningstar regarding the degree of active management in the Dodge & Cox equity funds and concluded that Dodge & Cox is an active, high conviction manager of equity portfolios, not a “closet index” manager.

In the area of administrative and shareholder services, the Board considered the excellent quality of Dodge & Cox’s work in areas such as compliance, legal services, trading, proxy voting, technology, oversight of the Funds’ transfer agent and custodian, tax compliance, and shareholder communication through its website and other means. The Board also noted Dodge & Cox’s diligent disclosure policy, its favorable compliance record, and its reputation as a trusted, shareholder-friendly mutual fund family.

In addition, the Board considered that Dodge & Cox manages approximately $180 billion in Fund assets with fewer professionals than most comparable funds, and that on average these professionals have more experience and longer tenure than investment professionals at comparable funds. The Board also noted that Dodge & Cox is an investment research-oriented firm with no other business endeavors to distract management’s attention from its research efforts or to present material conflicts of interest with the operations of the Funds, that its investment professionals adhere to a consistent investment approach across the Funds, and that due to its careful and deliberate strategy with respect to new products, Dodge & Cox has had remarkable stability in its mutual fund product offerings over the course of the past 86 years and has the fewest funds of any of the 25 largest mutual fund families by assets. The Board further considered the favorable stewardship grades given by Morningstar to each of the Funds and the “Gold” analyst rating awarded by Morningstar to all of the Funds except the Global Bond Fund. The Board concluded that it was satisfied with the nature, extent, and quality of investment management and other services provided to the Funds by Dodge & Cox.

INVESTMENT PERFORMANCE

The Board considered short-term and long-term investment performance for each Fund (including periods of outperformance or underperformance) as compared to both relevant indices and the performance of such Fund’s peer group. The Board noted that, as of November 30, 2016, the Funds had strong absolute and relative year-to-date performance, and were also generally solid performers over longer periods. The Board determined after extensive review and inquiry that Dodge & Cox’s historic, long-term, team-oriented, bottom-up investment approach remains consistent and that Dodge & Cox continues to be distinguished by its integrity, transparency, and independence. The Board

considered that the performance of the Funds is the result of value-oriented investment management process that emphasizes a long-term investment horizon, comprehensive independent research, team approach, price discipline, low cost, and low portfolio turnover. The Board also considered that the investment performance delivered by Dodge & Cox to the Funds appeared to be consistent with the relevant performance delivered for other clients of Dodge & Cox. The Board concluded that Dodge & Cox has delivered favorable long-term performance for Fund investors consistent with the long-term investment strategies being pursued by the Funds.

COSTS AND ANCILLARY BENEFITS

Costs of Services to Funds: Fees and Expenses. The Board considered each Fund’s management fee rate and expense ratio relative to each Fund’s peer group and relative to management fees charged by Dodge & Cox to other clients. In particular, the Board considered that the Funds continue to be substantially below their peer group median in expense ratios and that many media and industry reports specifically comment on the low expense ratios of the Funds, which have been a defining characteristic of the Funds for many years. The Board also evaluated the operating structures of the Funds and Dodge & Cox, noting that the Funds do not charge front-end sales commissions or distribution fees, and Dodge & Cox bears, among other things, the significant cost of third party research, reimbursement for shareholder recordkeeping and administrative costs to third-party retirement plan administrators, and administrative and office overhead. The Board noted that expenses are well below industry averages.

When compared to peer group funds, the Funds are in the quartile with the lowest expense ratios. The Board also considered that the Funds receive numerous administrative, regulatory compliance, legal, technology, and shareholder support services from Dodge & Cox without any additional administrative fee and the fact that the Funds have relatively low transaction costs and portfolio turnover rates. The Board noted the Funds’ unusual single-share-class structure and reviewed Morningstar data (including asset-weighted average expense ratios) showing that the few peer group funds with lower expense ratios often have other share classes with significantly higher expense ratios. In this regard, the Board considered that many of the Funds’ shareholders would not be eligible to purchase comparably priced shares of many peer group funds, which typically make their lower-priced share classes available only to institutional investors. The Board determined that the Funds provide access for small investors to high quality investment management at a relatively low cost. The Board also considered that the Funds’ are priced to scale, i.e., management fee rates begin at relatively low levels with the result that, even without breakpoints, the Funds’ management fee rates are lower than those of many peer funds whose fee schedules include breakpoints. With respect to non-U.S. funds sponsored and managed by Dodge & Cox that are comparable to the Funds in many respects, the Board noted that the fee rates charged by Dodge & Cox are the same as or higher than the fee rates charged to the Funds.

PAGE 16 § DODGE & COX STOCK FUND

The Board reviewed information regarding the fee rates Dodge & Cox charges to separate accounts that have investment programs similar to those of the Funds, including instances where separate account fees are lower than Fund fees. The Board considered the significant differences in the nature and scope of services Dodge & Cox provides to the Funds as compared to other client accounts, as well as material differences in regulatory, litigation, and other risks as between Dodge & Cox Funds and other types of clients. The Board noted that different markets exist for mutual fund and institutional separate account management services and that a comparison of Fund fee rates and separate account fee rates must consider the fact that separate account clients bear additional costs and responsibilities that are included in the cost of a Fund. The Board further noted that many sophisticated institutional investors in the Funds that are eligible to open separate accounts at Dodge & Cox have decided for various reasons to invest in the Funds. After consideration of these matters, the Board concluded that the overall costs incurred by the Funds for the services they receive (including the management fee paid to Dodge & Cox) are reasonable and that the fees are acceptable based upon the qualifications, experience, reputation, and performance of Dodge & Cox and the low overall expense ratios of the Funds.