UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3373

Westcore Trust

(exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

David T. Buhler, Secretary

Westcore Trust

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: December 31

Date of reporting period: June 30, 2013

Item 1. Reports to Stockholders.

INTENTIONALLY LEFT BLANK

DEAR FELLOW SHAREHOLDER:

The first six months of 2013 were very rewarding to equity investors. The S&P 500® Index provided a 13.82% total return. The upward momentum has continued into the third quarter with the Index up nearly 20% for the year through the end of July.

We want to share three thoughts about the equity market. First, the year is not over. Second, the stock market and the economy seldom move in sync. Third, there have been 14 years in the last 40 years when the S&P 500® provided a total return of greater than 20%.

The first six months were not as kind to bond investors. The Barclays U.S. Aggregate Bond Index had a negative total return of -2.44%. This did not surprise investors because bond yields were at historic lows at the beginning of the year.

As you know, many views about the economy, stocks and bonds are expressed daily in the media. In our observation, it’s worth noting that the slow economic recovery from the Great Recession of 2008-09 continues and that we currently see no economic crisis building on the horizon. Additionally, stocks appear to be fairly-valued based on historical data and bonds appear to be expensive.

At the moment, bonds are presenting a dilemma to many investors because of their low yields and high valuations. While each investor’s situation is different, it may be helpful to keep in mind that stocks are typically more volatile than bonds. Therefore, if stability in your portfolio is important to you, bonds should likely remain a part of your investment selection. And, it is useful to remember that having a diversified portfolio will normally mean that all of your investments won’t be delivering high returns at the same time.

In the following pages of this report, you will find a brief commentary on each Westcore fund provided by the portfolio management team. You can also review the individual holdings of each fund.

As we let you know this spring, the Westcore Blue Chip Dividend Fund has made important changes to its investment objective and strategy. The Fund is now investing in a more focused portfolio of large companies, but has expanded its investment universe to include companies around the globe. Additionally, the Fund’s emphasis is on finding companies that the investment team believes will grow their dividends at an above-average rate. More details are available in the Fund’s commentary.

Thank you for being a part of the Westcore family of investors.

CFA is a trademark owned by the CFA Institute.

Diversification does not ensure a profit or guarantee against loss.

The Shareholder Letter and the Manager Commentaries included in this shareholder report contain certain forward-looking statements about the factors that may affect the performance of the Funds in the future. These statements are based on Fund management’s predictions and expectations concerning certain future events and their expected impact on the Funds, such as performance of the economy as a whole and of specific industry sectors, changes in the levels of interest rates, the impact of developing world events, and other factors that may influence the future performance of the Funds. Management believes these forward-looking statements to be reasonable, although they are inherently uncertain and difficult to predict. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed.

PAGE 1 |

|

Investing primarily in equity securities of large companies with growth potential.

Ross G. Moscatelli, CFA Portfolio Manager Craig W. Juran, CFA Portfolio Manager

CFA is a trademark owned by the CFA Institute.

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc. Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns | | | | | | | | | |

| | | | | | | | | | | | Since | Inception |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | Date |

| Retail Class (WTEIX) | 8.67% | | 12.72% | | 16.85% | | 4.77% | | 6.97% | | 8.51% | 6/1/1988 |

| Institutional Class | | | | | | | | | | | | |

| (WILGX) | 8.70 | | 12.93 | | 17.03 | | 4.91 | | 7.05 | | 8.54 | 9/28/2007 |

| Russell 1000® | | | | | | | | | | | | |

| Growth Index | 11.80 | | 17.07 | | 18.68 | | 7.47 | | 7.40 | | 9.44 | |

| Lipper Large-Cap | | | | | | | | | | | | |

| Growth Index | 10.18 | | 16.38 | | 16.06 | | 5.26 | | 6.24 | | 8.44 | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.11%, Net: 1.11%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.32%, Net: 0.92%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.15% for the Fund’s Retail Class for such period. In addition, the Adviser has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level Other Expenses for the Institutional Class in the same proportion as the Retail Class waivers/reimbursements as well as reimburse the Institutional class-specific Other Expenses until at least April 30, 2014. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Craig W. Juran is a registered representative of ALPS Distributors, Inc.

- During the first six months of the year, U.S. equity markets delivered strong returns fueled by low interest rates, an improving housing market, better employment trends, and the belief that the U.S. economy was finally starting to heal from the recession which started more than five years ago. Although equity markets experienced increased volatility during the second quarter, the biggest dislocations happened in the fixed income markets as the Federal Reserve signaled a potential end to Quantitative Easing (QE) causing investors to consider the possibility of higher interest rates. The prospect of QE reduction along with slower macroeconomic data from China and emerging markets ignited a new round of fear-induced selling in equity markets in the second quarter. This caused a short but powerful 6% correction in May and June, with international markets (especially emerging markets) experiencing a more significant correction. As fear subsided, however, equity markets recovered and continued to march ahead.

- Against this backdrop, the Westcore Growth Fund lagged its benchmark, the Russell 1000® Growth Index. Most of the underperformance was associated with more defensive-type equities outperforming traditional growth companies within the large-cap space.

- Holdings in financials, health care and energy produced the strongest returns relative to the benchmark during the first half of 2013. The Fund’s strongest individual performers were Gilead Sciences Inc., Google Inc. and Biogen Idec Inc. Gilead is a dominant player in the market for HIV therapies and we believe its recent acquisition of Pharmasset Inc. positions Gilead to introduce the first all-oral drug regimen for hepatitis C in 2014. Google’s prospects continued to improve as investors became more excited about its new products, such as Google Glass, a wearable computer with an optical head-mounted display, and accelerating revenue opportunities in mobile search advertising. Biogen Idec, which specializes in drugs for neurological disorders and cancer, continued to receive positive data associated with its drug for treating multiple sclerosis.

- The Fund’s weakest sectors relative to the benchmark were consumer staples, materials and information technology. From a company standpoint, the Fund’s largest detractors during the first six months were Apple Inc., Aruba Networks Inc., and Onyx Pharmaceuticals Inc. Although Apple announced a $60 billion stock buyback program, investors remained concerned about its lack of new products and slowing iPhone sales. Aruba Networks provides access management, network infrastructure and mobility application solutions for mobile enterprise networks. It delivered poor results in the first quarter and lowered future expectations, as a slowing global economy dampened demand for enterprise spending. This led investors to question the long-term growth associated with its end markets. Health care sector holding Onyx Pharmaceuticals experienced weakness in the period and we exited the position.

- With the U.S. economy improving, the housing market healing, commodity prices declining, low interest and inflation rates persisting, and central banks around the world adding liquidity as a way to promote growth, we are encouraged by the longer-term prospects for equities. As the economic impact of the U.S. federal sequester (automatic budget cuts which started in 2013) and higher taxes start to fade, we believe there is a strong possibility that the economy will pick up steam in the second half of the year, potentially driving corporate profits higher. Although the road may be bumpy at times, in our opinion, the fundamental backdrop for large-cap growth companies remains compelling.

PAGE 2 |

|

| Stock Performance | | | | |

(for the year ended 6/30/13) | | | | |

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

Gilead Sciences Inc. | 2.50% | | 0.90% | |

Google Inc. | 4.09 | | 0.89 | |

Biogen Idec Inc. | 1.92 | | 0.79 | |

Home Depot Inc. | 2.89 | | 0.70 | |

LinkedIn Corp. | 1.34 | | 0.68 | |

| | | | | |

5 Lowest | | | | |

Brookdale Senior Living Inc. | 0.46% | | -0.12% | |

VMware Inc. | 0.19 | | -0.16 | |

Onyx Pharmaceuticals Inc. | 0.50 | | -0.20 | |

Aruba Networks Inc. | 0.58 | | -0.50 | |

Apple Inc. | 6.16 | | -1.90 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| Top Ten Holdings | | |

(as of 6/30/13) | | |

Apple Inc. | 4.7% | |

Google Inc. | 4.5 | |

Microsoft Corp. | 4.3 | |

Visa Inc. | 3.3 | |

Home Depot Inc. | 3.2 | |

Amazon.com Inc. | 2.4 | |

Honeywell International Inc. | 2.3 | |

Costco Wholesale Corp. | 2.3 | |

Starbucks Corp. | 2.2 | |

Express Scripts Holding Co. | 2.2 | |

Total (% of Net Assets) | 31.4% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| Morningstar Ratings | | |

| | | Number | |

| | Morningstar | of Funds | |

| | Rating™ | in Large Growth | |

| | as of 6/30/13 | Category | |

Overall | ««« | 1,488 | |

3 Year | ««« | 1,488 | |

5 Year | ««« | 1,308 | |

10 Year | ««« | 863 | |

Morningstar Ratings shown represent the Retail Class. Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

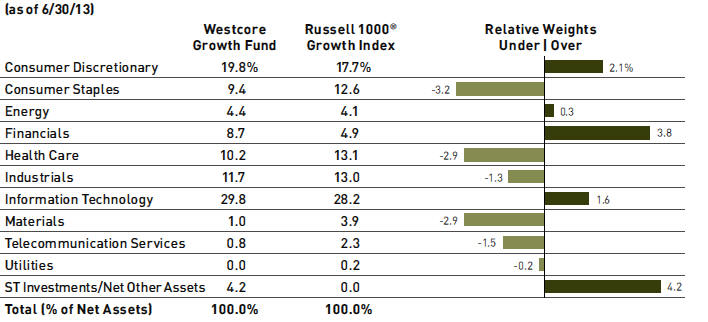

| Portfolio Characteristics | | | | | | |

(as of 6/30/13) | | | | | | |

| | Westcore | | Russell 1000® | |

| | Growth Fund | | Growth Index | |

Weighted Average Market Capitalization ($ Bil) | $84.3 | | $90.0 | |

Price/Earnings (1 year trailing) | 20.9x | | 19.0x | |

EPS Growth (3 year historical) | 23.0% | | 19.5% | |

Beta | 1.1 | | 1.0 | |

Number of Holdings | 57 | | 575 | |

Portfolio Turnover Rate | 174% | | — | |

| | | | | | |

Please see page 30 for definition of terms. | | | | | | |

| | | | | | | |

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

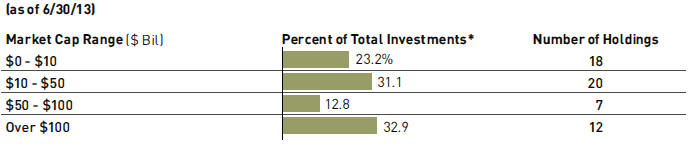

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

| | PAGE 3 |

|

Investing in a diversified portfolio of equity securities of primarily medium-sized companies with growth potential.

| | |

Mitch S. Begun, CFA Lead Portfolio Manager Portfolio Manager

F. Wiley Reed, CFA Lead Portfolio Manager

Adam C. Bliss Portfolio Manager | Brian C. Fitzsimons, CFA

Jeffrey J. Loehr, CFA Portfolio Manager |

CFA is a trademark owned by the CFA Institute.

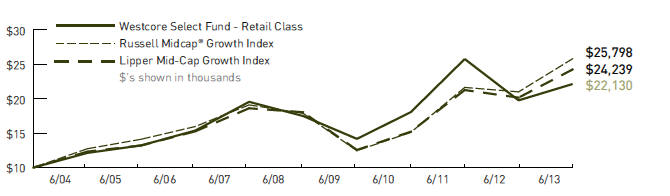

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc.

Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns | | | | | | | | | |

| | | | | | | | | | | | Since | Inception |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | Date |

Retail Class (WTMGX) | 15.55% | | 21.32% | | 14.20% | | 5.73% | | 7.14% | | 10.25% | 8/1/1986 |

Institutional Class | | | | | | | | | | | | |

(WIMGX) | 15.75 | | 21.69 | | 14.42 | | 5.89 | | 7.24 | | 10.28 | 9/28/2007 |

Russell Midcap® | | | | | | | | | | | | |

Growth Index | 14.70 | | 22.88 | | 19.53 | | 7.61 | | 9.94 | | 10.15 | |

Lipper Mid-Cap | | | | | | | | | | | | |

Growth Index | 14.26 | | 20.24 | | 16.81 | | 6.09 | | 9.26 | | 9.42 | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.06%, Net: 1.06%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 0.94%, Net: 0.88%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.15% for the Fund’s Retail Class for such period. In addition, the Adviser has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level Other Expenses for the Institutional Class in the same proportion as the Retail Class waivers/reimbursements as well as reimburse the Institutional class-specific Other Expenses until at least April 30, 2014. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

- In the first half of 2013, the Westcore MIDCO Growth Fund outperformed its benchmark, the Russell Midcap® Growth Index.

- Domestic small- and mid-cap equities surged to all-time highs in the first half of 2013. While equity markets rose, the threat of the Fed tapering its Quantitative Easing strategy sparked a sharp rise in interest rates in the second quarter. Taking a step back, we view interest rates going higher as primarily a sign that the U.S. economy is improving. Strong demand for housing and autos along with benign inflation continued to provide a solid backdrop for equities.

- The three sectors that contributed most to the Fund’s performance relative to its benchmark in the first half of 2013 were information technology, materials and consumer discretionary. The Fund’s best performing stock was consumer discretionary sector holding Netflix Inc. The company has evolved into the industry leader for streaming video content as new original content, along with exclusive content, helped retain existing customers and attract new subscribers. Within information technology, both LinkedIn Corp. and Splunk Inc. were top contributors. LinkedIn, the world’s largest online professional network, continued to monetize its unique asset through product innovation and solid execution. Splunk’s software solutions, which collect and index data at a massive scale, have become increasingly embedded in enterprise decision-making and analytic processes. The Fund’s underweighted position, along with stock selection drove outperformance in the materials sector.

- Just two sectors detracted from the Fund’s performance relative to its benchmark in the first half of 2013—consumer staples and health care. The Fund’s worst performing stock was information technology sector holding Aruba Networks Inc. Aruba, a leader in enterprise Wi-Fi solutions, saw increased competition in the second quarter and gave a disappointing growth outlook. We exited the position in the period. Also within information technology, Akamai Technologies Inc. was a notable underperformer. This Internet content delivery network provider lowered its revenue growth forecast due to reduced demand for media solutions. We sold the stock on concerns about longer-term pricing pressure for its solutions. Thoratec Corp., a leading provider of healthcare equipment for heart failure patients, was also a drag on the portfolio. Its results were disappointing in the face of intense competition and we exited the position. The Fund’s underperformance in the consumer staples sector was driven primarily by its underweighted position in the sector.

- As of the end of the first half of 2013, the Fund was overweighted primarily in the information technology and consumer discretionary sectors, and underweighted primarily in the materials, financials and consumer staples sectors.

- From our vantage point, the slowing global growth environment remains the biggest concern. Tensions are rising in many emerging markets and China has seen material weakness in its economy. It is becoming increasingly clear to us that the U.S. economy is decoupling from the emerging markets with steady growth and has the potential for acceleration in the second half of 2013. We believe the United States is in the middle innings of a multi-year business up-cycle. While decoupling is a word that most investors do not believe can exist in this global economy, in our opinion, the data suggest otherwise at this point, so stay tuned. We are optimistic about growth prospects for the United States and have positioned the Fund accordingly.

| PAGE 4 | |

|

| WESTCORE MIDCO GROWTH FUND (WTMGX (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

Netflix Inc. | 1.84% | | 1.73% | |

LinkedIn Corp. | 2.51 | | 1.17 | |

Splunk Inc. | 2.08 | | 0.97 | |

Pandora Media Inc. | 1.15 | | 0.70 | |

ServiceNow Inc. | 1.63 | | 0.64 | |

| | | | | |

5 Lowest | | | | |

TIBCO Software Inc. | 0.81% | | -0.25% | |

Thoratec Corp. | 1.37 | | -0.29 | |

Akamai Technologies Inc. | 0.92 | | -0.31 | |

Rackspace Hosting Inc. | 0.58 | | -0.45 | |

Aruba Networks Inc. | 0.46 | | -0.47 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| | | |

(as of 6/30/13) | | |

LinkedIn Corp. | 2.5% | |

Splunk Inc. | 2.4 | |

Discovery Communications Inc. | 2.3 | |

Sirius XM Radio Inc. | 2.2 | |

ServiceNow Inc. | 2.2 | |

Ralph Lauren Corp. | 2.1 | |

Workday Inc. | 2.1 | |

Netflix Inc. | 2.1 | |

Ingersoll-Rand PLC | 2.1 | |

Pandora Media Inc. | 2.1 | |

Total (% of Net Assets) | 22.1% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Mid-Cap Growth | |

| | as of 6/30/13 | Category | |

Overall | «« | 637 | |

3 Year | «« | 637 | |

5 Year | ««« | 563 | |

10 Year | «« | 417 | |

Morningstar Ratings shown represent the Retail Class. Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

Portfolio Characteristics |

(as of 6/30/13)

| | Westcore MIDCO | | Russell Midcap® | |

| | Growth Fund | | Growth Index | |

Weighted Average Market Capitalization ($ Bil) | $8.7 | | $10.5 | |

Price/Earnings (1 year trailing) | 25.3x | | 21.3x | |

EPS Growth (3 year historical) | 22.2% | | 20.4% | |

Beta | 1.2 | | 1.0 | |

Number of Holdings | 68 | | 460 | |

Portfolio Turnover Rate | 123% | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 5 |

|

Investing primarily in the common stock of a limited number of medium-sized companies selected for their growth potential.

| | |

Mitch S. Begun, CFA Lead Portfolio Manager Portfolio Manager

F. Wiley Reed, CFA Lead Portfolio Manager

Adam C. Bliss Portfolio Manager | Brian C. Fitzsimons, CFA

Jeffrey J. Loehr, CFA Portfolio Manager |

CFA is a trademark owned by the CFA Institute.

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc.

Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns |

| | | | | | | | | | | | | |

| | | | | | | | | | | | Since | Inception |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | Date |

Retail Class (WTSLX) | 16.57% | | 11.98% | | 7.02% | | 4.82% | | 8.27% | | 10.98% | 10/1/1999 |

Russell Midcap® | | | | | | | | | | | | |

Growth Index | 14.70 | | 22.88 | | 19.53 | | 7.61 | | 9.94 | | 5.85 | |

Lipper Mid-Cap | | | | | | | | | | | | |

Growth Index | 14.26 | | 20.24 | | 16.81 | | 6.09 | | 9.26 | | 5.04 | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.07%, Net: 1.07%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.15% for the Fund’s Retail Class for such period. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Westcore Select Fund is a non-diversified fund and investing in non-diversified funds generally will be more volatile and a loss of principal could be greater than investing in more diversified funds.

- In the first half of 2013, the Westcore Select Fund outperformed its benchmark, the Russell Midcap® Growth Index.

- Domestic small- and mid-cap equities surged to all-time highs in the first half of 2013. While equity markets rose, the threat of the Fed tapering its Quantitative Easing strategy sparked a sharp rise in interest rates in the second quarter. Taking a step back, we view interest rates going higher as primarily a sign that the U.S. economy is improving. Strong demand for housing and autos along with benign inflation continued to provide a solid backdrop for equities.

- The sectors that contributed most to the Fund’s performance relative to its benchmark in the first half of 2013 were information technology, materials and industrials. Within information technology, both LinkedIn Corp. and Splunk Inc. were top contributors. LinkedIn, the world’s largest online professional network, continued to monetize its unique asset through product innovation and solid execution. Splunk’s software solutions, which collect and index data at a massive scale, have become increasingly embedded in enterprise decision-making and analytic processes. Industrials sector holding, Kansas City Southern, performed well as investors came to appreciate this rail operator’s accelerating growth profile. We believe its rail network is positioned to benefit from two long-term trends: the “near-shoring” of manufacturing to Mexico and increasing U.S. oil production. Rockwood Holdings Inc. was the Fund’s best performer in the materials sector. This diversified chemical company saw strength in its lithium segment and announced the divestiture of its ceramic business for attractive terms.

- The sectors that detracted most from performance relative to the benchmark were health care, consumer staples and consumer discretionary. The Fund’s worst performing stock was information technology sector holding Aruba Networks Inc. Aruba, a leader in enterprise Wi-Fi solutions, saw increased competition in the second quarter and gave a disappointing growth outlook. We exited the position. Also within information technology, Akamai Technologies Inc. was a notable underperformer. This Internet content delivery network provider lowered its revenue growth forecast due to reduced demand media solutions. We sold the stock on concerns about longer-term pricing pressure for its solutions. Thoratec Corp., a leading provider of healthcare equipment for heart failure patients, was also a drag on performance. Disappointing results in the face of intense competition led us to exit the position. The Fund’s underperformance in the consumer staples sector was driven primarily by its underweighted position while stock selection led to underperformance in the consumer discretionary sector.

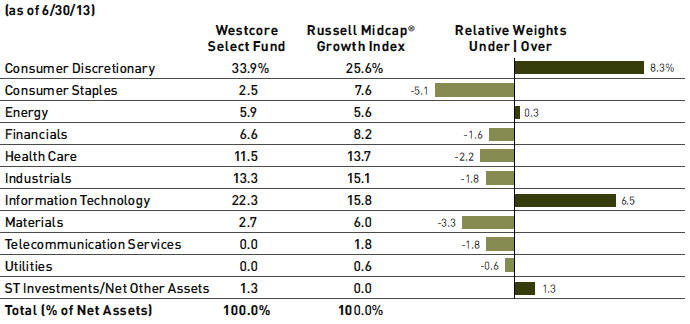

- As of the end of the first half of 2013, the Fund was overweighted primarily in the information technology and consumer discretionary sectors, and underweighted primarily in the consumer staples and materials sectors.

- From our vantage point, the slowing global growth environment remains the biggest concern. Tensions are rising in many emerging markets and China has seen material weakness in its economy. It is becoming increasingly clear to us that the U.S. economy is decoupling from the emerging markets with steady growth and has the potential for acceleration in the second half of 2013. We believe the United States is in the middle innings of a multi-year business up-cycle. While decoupling is a word that most investors do not believe can exist in this global economy, in our opinion, the data suggest otherwise at this point, so stay tuned. We are optimistic about growth prospects for the United States and have positioned the Fund accordingly.

PAGE 6 |

|

| WESTCORE SELECT FUND (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

LinkedIn Corp. | 4.48% | | 2.11% | |

Splunk Inc. | 3.68 | | 1.75 | |

Kansas City Southern | 3.90 | | 1.25 | |

Express Inc. | 3.17 | | 1.15 | |

Rockwood Holdings Inc. | 1.96 | | 1.02 | |

| | | | | |

5 Lowest | | | | |

Palo Alto Networks Inc. | 2.08% | | -0.20% | |

TIBCO Software Inc. | 1.50 | | -0.33 | |

Akamai Technologies Inc. | 1.55 | | -0.52 | |

Thoratec Corp. | 2.90 | | -0.62 | |

Aruba Networks Inc. | 0.67 | | -0.70 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| | | |

(as of 6/30/13) | | |

LinkedIn Corp. | 4.4% | |

Splunk Inc. | 4.3 | |

WABCO Holdings Inc. | 3.7 | |

BorgWarner Inc. | 3.7 | |

ServiceNow Inc. | 3.6 | |

Ralph Lauren Corp. | 3.6 | |

Michael Kors Holdings Ltd. | 3.6 | |

Pandora Media Inc. | 3.5 | |

Gartner Inc. | 3.4 | |

SVB Financial Group | 3.4 | |

Total (% of Net Assets) | 37.2% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Mid-Cap Growth | |

| | as of 6/30/13 | Category | |

Overall | «« | 637 | |

3 Year | « | 637 | |

5 Year | «« | 563 | |

10 Year | ««« | 417 | |

Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

Portfolio Characteristics |

(as of 6/30/13)

| | Westcore | | Russell Midcap® | |

| | Select Fund | | Growth Index | |

Weighted Average Market Capitalization ($ Bil) | $9.5 | | $10.5 | |

Price/Earnings (1 year trailing) | 24.4x | | 21.3x | |

EPS Growth (3 year historical) | 30.6% | | 20.4% | |

Beta | 1.2 | | 1.0 | |

Number of Holdings | 32 | | 460 | |

Portfolio Turnover Rate | 125% | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

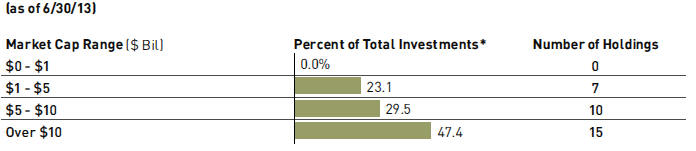

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 7 |

|

Investing in large, well-established, dividend-paying companies both in the United States and in developed foreign markets.

| | |

Troy Dayton, CFA Portfolio Manager Portfolio Manager

Derek R. Anguilm, CFA Portfolio Manager Manager | Mark M. Adelmann, CFA, CPA

Lisa Z. Ramirez, CFA Portfolio |

CFA is a trademark owned by the CFA Institute.

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc.

Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns |

| | | | | | | | | | | | Since | | Inception | |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | | Date | |

Retail Class (WTMVX) | 11.00% | | 17.96% | | 15.40% | | 4.19% | | 6.51% | | 8.56% | | 6/1/1988 | |

Institutional Class | | | | | | | | | | | | | | |

(WIMVX) | 11.21 | | 18.34 | | 15.57 | | 4.37 | | 6.61 | | 8.60 | | 9/28/2007 | |

S&P 500® Index | 13.82 | | 20.60 | | 18.45 | | 7.01 | | 7.30 | | 9.71 | | | |

Lipper Large-Cap | | | | | | | | | | | | | | |

Core Index | 13.87 | | 21.55 | | 17.09 | | 6.03 | | 6.48 | | 8.90 | | | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.17%, Net: 1.15%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.06%, Net: 0.92%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

As of April 30, 2013, the Westcore Blue Chip Dividend Fund’s objective changed to long-term capital appreciation primarily through investments in large, well-established dividend paying companies.

Denver Investments (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.15% for the Fund’s Retail Class for such period. In addition, the Adviser has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level Other Expenses for the Institutional Class in the same proportion as the Retail Class waivers/reimbursements as well as reimburse the Institutional class-specific Other Expenses until at least April 30, 2014. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Lisa Z. Ramirez is a registered representative of ALPS Distributors, Inc.

- Late in the second quarter we began to transition the Westcore Blue Chip Dividend Fund to a more focused portfolio of companies that, in our view, offer the opportunity of a growing dividend payment. We believe that coupling competitive advantage and quality considerations with a global perspective is the best starting point to find dividend-paying companies that, we believe, can weather economic cycles.

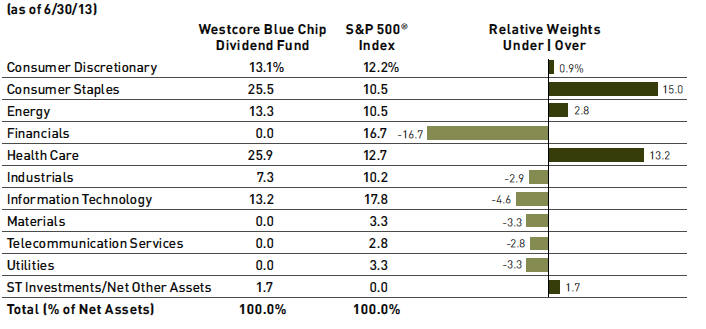

- The Westcore Blue Chip Dividend Fund underperformed its benchmark the S&P 500® Index in the first half of 2013. While we seek to outperform both the U.S. and global large-cap benchmarks over longer periods of time, the portfolio’s more concentrated focus and exposure to global companies may result in more volatility versus the benchmark in shorter timeframes. Our primary focus is on companies’ expected dividend yield and growth over a rolling 5-year timeframe.

- An illustration of this is British American Tobacco PLC (“BTI”). Had an investor purchased the stock in 2002 at a dividend yield of approximately 5%, by the end of 2012 the investor would be receiving a nearly 32% yield on initial investment (assuming dividend reinvestment). The equity value of the investment also compounded at over 21% per year. Of course, over that decade-long period the company’s stock price fluctuated, both outperforming and underperforming broad market indexes. This period was no exception, as BTI’s share price detracted from overall Fund performance. Our focus remains on the cash generating power of the company that we expect should benefit Fund shareholders in the form of cash dividends. While we cannot guarantee that companies held in the portfolio will perform as strongly as BTI, we think that it serves as an excellent reminder of the power of a dividend growth approach.

- The stocks in the portfolio currently generate a trailing one-year return on equity more than 3% above the average of those in the benchmark and on average do so without the use of higher debt. Additionally, we believe the portfolio is invested in companies at attractive valuations relative to the benchmark.

- During the first half of 2013 Microsoft Corp. was the portfolio’s top performer relative to the benchmark based on rate of return. It has grown its dividend at a five-year compound annual growth rate of 14.3% as a result of growing free cash flow and reducing shares outstanding. While the demand for technology-based goods is volatile quarter-to-quarter, long-term operating results and outlook remain steady, and we believe Microsoft should continue growing its dividend above 10% per year. Ball Corp.’s results disappointed as revenue growth slowed and earnings missed expectations. While Ball has grown its dividend, current yield remains low. Our belief that the company has a diminished ability to increase its payout in the near term led us to sell the stock.

- With the current worry over prospective returns in the bond market and uncertainty created by the possibility of Federal Reserve action, we believe that now is a great time to consider an investment in the Westcore Blue Chip Dividend Fund. We seek to build a portfolio of companies with strong and growing dividends and look forward to discussing the results of our efforts through these letters.

PAGE 8 |

|

| WESTCORE BLUE CHIP DIVIDEND FUND (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

Microsoft Corp. | 3.47% | | 0.97% | |

AmerisourceBergen Corp. | 2.76 | | 0.70 | |

H.J. Heinz Co. | 1.83 | | 0.66 | |

Activision Blizzard Inc. | 1.03 | | 0.61 | |

Campbell Soup Co. | 1.32 | | 0.59 | |

| | | | | |

5 Lowest | | | | |

Coca-Cola Co. | 1.06% | | -0.14% | |

Ball Corp. | 2.64 | | -0.19 | |

LVMH Moet Hennessy | | | | |

Louis Vuitton SA | 1.12 | | -0.23 | |

British American | | | | |

Tobacco PLC | 1.11 | | -0.24 | |

Nestle S.A. | 1.06 | | -0.25 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| | | |

(as of 6/30/13) | | |

Raytheon Co. | 3.7% | |

General Dynamics Corp. | 3.6 | |

Microsoft Corp. | 3.6 | |

AmerisourceBergen Corp. | 3.5 | |

Occidental Petroleum Corp. | 3.5 | |

Mattel Inc. | 3.4 | |

Darden Restaurants Inc. | 3.4 | |

Roche Holding AG | 3.3 | |

Chevron Corp. | 3.3 | |

Total SA | 3.3 | |

Total (% of Net Assets) | 34.6% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Large Blend | |

| | as of 6/30/13 | Category | |

Overall | ««« | 1,381 | |

3 Year | ««« | 1,381 | |

5 Year | «« | 1,254 | |

10 Year | ««« | 774 | |

Morningstar Ratings shown represent the Retail Class. Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

Portfolio Characteristics |

(as of 6/30/13)

| | Westcore Blue Chip | | S&P 500® | |

| | Dividend Fund | | Index | |

Weighted Average Market Capitalization ($ Bil) | $99.1 | | $102.7 | |

Price/Cash Flow (1 year trailing) | 10.9x | | 11.9x | |

Price/Book Value | 3.1x | | 2.7x | |

Price/Earnings (1 year trailing) | 14.9x | | 16.7x | |

Beta | 0.9 | | 1.0 | |

Number of Holdings | 30 | | 500 | |

Portfolio Turnover Rate | 78% | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 9 |

|

Investing in medium-sized, dividend-paying companies whose stocks appear to be undervalued.

| | |

Troy Dayton, CFA Portfolio Manager Portfolio Manager

Derek R. Anguilm, CFA Portfolio Manager | Mark M. Adelmann, CFA, CPA

Lisa Z. Ramirez, CFA Portfolio Manager |

CFA is a trademark owned by the CFA Institute.

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc. Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns |

| | | | | | | | | | | | Since | Inception |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | Date |

Retail Class | | | | | | | | | | | | |

(WTMCX) | 15.71% | | 25.61% | | 17.02% | | 5.68% | | 8.77% | | 8.89% | 10/1/1998 |

Russell Midcap® | | | | | | | | | | | | |

Value Index | 16.10 | | 27.65 | | 19.53 | | 8.87 | | 10.92 | | 9.83 | |

Lipper Mid-Cap | | | | | | | | | | | | |

Value Index | 16.22 | | 28.11 | | 18.17 | | 7.81 | | 9.83 | | 9.33 | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.27%, Net: 1.26%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.25% for the Fund’s Retail Class for such period. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Lisa Z. Ramirez is a registered representative of ALPS Distributors, Inc.

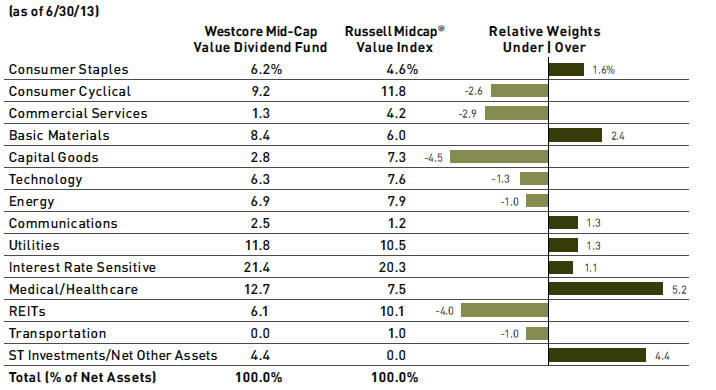

- The Westcore Mid-Cap Value Dividend Fund underperformed its benchmark the Russell Midcap® Value Index for the first half of 2013.

- The Federal Reserve attempted to provide clarity as to when it would begin to taper its quantitative easing programs. In so doing, the Fed is attempting to orchestrate a gradual movement of interest rates toward levels that more fairly reflect the current economic environment. History suggests this is a very difficult thing to accomplish. The stock market may also be recalibrating as investors feel less certain they will be protected by Federal Reserve actions.

- The strongest contributors to the Fund’s relative performance thus far in 2013 were the medical/ healthcare, energy and interest rate sensitive sectors. During the first quarter, supply disruptions at Questcor Pharmaceuticals, Inc. were tied to SKU changes required by Medicaid. This soft spot was short-lived as investors were encouraged by prescription trends that have regained strength and surpassed prior levels. Furthermore, investors seemed enthusiastic when Questcor announced the acquisition of a product that will provide it with international exposure while eliminating a potential long-term competing product. The outperformance in energy was partly due to the portfolio’s underweighted position in this sector and partly to strong performance within oil services. Disability insurer and group benefits provider, Unum Group, was the leader within the interest rate sensitive sector and the Fund’s top performer for the first six months. Investors rewarded the company’s stable-to- modestly improving operating results. Job growth was also an important factor in Unum’s strong performance as was the rising interest rate environment. We believe these two factors will continue to benefit the company’s results going forward.

- Relative returns were dampened by results in the technology, consumer cyclical and commercial services sectors. After a strong 2012 and first quarter 2013, investors were not satisfied that Dillard’s Inc. reported a quarter that was in-line with, but not as strong as previous quarters. Dillard’s, a Fund holding in the consumer cyclical sector, is a turnaround story that has historically been successful. We still see ample opportunity for sales growth and margin improvement as the company continues to close underperforming stores and introduces higher-end, unique vendor products. Silver producer, Hecla Mining Co. underperformed in the first half of the year as silver prices were under severe pressure. After Hecla announced the acquisition of Aurizon Mines, we elected to sell the position as we believe the price paid was excessive and were alarmed by the impact on the balance sheet.

- Most investors would agree Federal Reserve quantitative easing drove interest rates down to artificially low, unsustainable levels in an effort to stimulate stock prices, housing activity and associated home prices, and consumer net worth and by association, consumer confidence. While slower than expected, improvements in these areas now bring the capital markets to a critical juncture. Investors may for the first time in years be seeing negative total returns from their bond portfolios this quarter. The mantra that rewarded investors the past four to five years has been “don’t fight the Fed.” This particularly rewarded investors in lower-quality, less-liquid bonds and stocks with weaker fundamentals. It will be interesting to see what “don’t fight the Fed” will mean for the markets as they cautiously change direction. We believe the Fund’s focus on high- quality; dividend paying companies is well positioned for this environment.

PAGE 10 |

|

| WESTCORE MID-CAP VALUE DIVIDEND FUND (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

Unum Group | 2.19% | | 0.91% | |

AXIS Capital Holdings Ltd. | 2.22 | | 0.79 | |

Questcor Pharmaceuticals Inc. | 1.19 | | 0.74 | |

Tyson Foods Inc. | 2.47 | | 0.73 | |

Omnicare Inc. | 2.37 | | 0.71 | |

| | | | | |

5 Lowest | | | | |

Alexandria Real Estate | | | | |

Equities Inc. | 1.30% | | -0.03% | |

Silgan Holdings Inc. | 0.68 | | -0.03 | |

Dillard's Inc. | 2.00 | | -0.06 | |

Ball Corp. | 1.99 | | -0.12 | |

Hecla Mining Co. | 0.65 | | -0.64 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| | | |

(as of 6/30/13) | | |

Questcor Pharmaceuticals Inc. | 2.9% | |

Reinsurance Group of America Inc. | 2.8 | |

Tyson Foods Inc. | 2.6 | |

Plantronics Inc. | 2.6 | |

American Water Works Co. Inc. | 2.5 | |

Westar Energy Inc. | 2.4 | |

The NASDAQ OMX Group Inc. | 2.3 | |

Quest Diagnostics Inc. | 2.2 | |

UGI Corp. | 2.2 | |

Home Properties Inc. | 2.1 | |

Total (% of Net Assets) | 24.6% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | | |

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Mid-Cap Value | |

| | as of 6/30/13 | Category | |

Overall | ««« | 369 | |

3 Year | ««« | 369 | |

5 Year | «« | 312 | |

10 Year | ««« | 176 | |

Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

| Portfolio Characteristics | | | | | | |

(as of 6/30/13)

| | Westcore Mid-Cap | | Russell Midcap® | |

| | Value Dividend Fund | | Value Index | |

Weighted Average Market Capitalization ($ Bil) | $7.4 | | $9.8 | |

Price/Cash Flow (1 year trailing) | 9.5x | | 11.9x | |

Price/Book Value | 2.3x | | 2.0x | |

Price/Earnings (1 year trailing) | 14.5x | | 15.5x | |

Beta | 0.9 | | 1.0 | |

Number of Holdings | 55 | | 563 | |

Portfolio Turnover Rate | 42% | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 11 |

|

Investing in small-company stocks that appear to be undervalued.

| | |

Troy Dayton, CFA Portfolio Manager Portfolio Manager

Derek R. Anguilm, CFA Portfolio Manager | Mark M. Adelmann, CFA, CPA

Lisa Z. Ramirez, CFA Portfolio Manager |

CFA is a trademark owned by the CFA Institute.

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc.

Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns |

| | | | | | | | | | | | Since | | Inception | |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | | Date | |

Retail Class (WTSCX) | 14.69% | | 17.33% | | 13.12% | | 5.25% | | 7.78% | | 8.35% | | 12/28/1993 | |

Institutional Class | | | | | | | | | | | | | | |

(WISCX) | 14.75 | | 17.48 | | 13.25 | | 5.39 | | 7.87 | | 8.39 | | 9/28/2007 | |

Russell 2000® Index | 15.86 | | 24.21 | | 18.67 | | 8.77 | | 9.53 | | 8.51 | | | |

Lipper Small-Cap | | | | | | | | | | | | | | |

Core Index | 14.45 | | 24.89 | | 17.90 | | 8.38 | | 9.72 | | 9.51 | | | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.51%, Net: 1.31%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 2.08%, Net: 1.19%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.30% for the Fund’s Retail Class for such period. In addition, the Adviser has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level Other Expenses for the Institutional Class in the same proportion as the Retail Class waivers/reimbursements as well as reimburse the Institutional class-specific Other Expenses until at least April 30, 2014. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

Lisa Z. Ramirez is a registered representative of ALPS Distributors, Inc.

- Despite second quarter outperformance, the Westcore Small-Cap Opportunity Fund underperformed its benchmark the Russell 2000® Index for the first half of 2013.

- The Federal Reserve attempted to provide clarity as to when it would begin to taper its quantitative easing programs. In so doing, the Fed is attempting to orchestrate a gradual movement of interest rates toward levels that more fairly reflect the current economic environment. History suggests this is a very difficult thing to accomplish. The stock market may also be recalibrating as investors feel less certain they will be protected by Federal Reserve actions.

- In mid-2013, the best contributors to relative performance were the interest rate sensitive, energy and basic materials sectors. Independent financial services distribution company, National Financial Partners Corp., was the standout performer in the interest rate sensitive sector. During the period Madison Dearborn Partners LLC, a private equity firm, offered to buy the company validating our opinion that National Financial was undervalued. We sold the stock and re-deployed the proceeds. KapStone Paper & Packaging Corp. was the standout in basic materials. KapStone’s recently announced acquisition of Longview Fibre and Packaging, Inc. increases its containerboard exposure and adds to its Kraft Paper business. Additionally, the acquisition will bring wallpaper to the company’s mix of products.

- Weak first half relative contributors were the commercial services, medical/healthcare and consumer cyclical sectors. Commercial services holding, Central Garden & Pet Co. has experienced disappointing revisions recently with uncharacteristically cooler weather impacting demand for its garden products. Further, increased inventory and higher marketing costs have impaired near-term cash flows. The new CEO indicated the company will embark on further cost cutting measures with a balanced approach focusing on greater profitability, sales growth and strong customer service. Medical/ healthcare holding, Orthofix International N.V., had a disappointing quarter as its stimulation business, one of its higher-margin units, has continued to be weak. Furthermore, every business unit outside of biologics has seemingly become impaired. With a lack of clarity on business improvement, we sold the stock.

- Most investors would agree Federal Reserve quantitative easing drove interest rates down to artificially low, unsustainable levels in an effort to stimulate stock prices, housing activity and associated home prices, and consumer net worth and by association, consumer confidence. While slower than expected, improvements in these areas now bring the capital markets to a critical juncture. Investors may for the first time in years be seeing negative total returns from their bond portfolios this quarter. The mantra that rewarded investors the past four to five years has been “don’t fight the Fed.” This particularly rewarded investors in lower-quality, less-liquid bonds and stocks with weaker fundamentals. It will be interesting to see what “don’t fight the Fed” will mean for the markets as they cautiously change direction. We believe the Fund’s focus on high-quality, cash flow driven companies allows it to be well positioned for this environment.

PAGE 12 |

|

| WESTCORE SMALL-CAP OPPORTUNITY FUND (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

KapStone Paper & | | | | |

Packaging Corp. | 1.96% | | 1.23% | |

PAREXEL International Corp. | 1.82 | | 1.17 | |

Monotype Imaging Holdings Inc. | 2.10 | | 1.14 | |

National Financial | | | | |

Partners Corp. | 1.63 | | 0.92 | |

Schweitzer-Mauduit | | | | |

International Inc. | 3.09 | | 0.87 | |

| | | | | |

5 Lowest | | | | |

Schawk Inc. | 0.57% | | -0.22% | |

Tetra Tech Inc. | 0.92 | | -0.50 | |

Hecla Mining Co. | 0.60 | | -0.59 | |

Orthofix International N.V. | 1.71 | | -0.63 | |

Central Garden & Pet Co. | 1.75 | | -0.76 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

| | | |

(as of 6/30/13) | | |

Schweitzer-Mauduit International Inc. | 3.7% | |

U.S. Physical Therapy Inc. | 2.7 | |

Express Inc. | 2.5 | |

PharMerica Corp. | 2.5 | |

Horace Mann Educators Corp. | 2.5 | |

LifePoint Hospitals Inc. | 2.5 | |

Plantronics Inc. | 2.3 | |

AmTrust Financial Services Inc. | 2.3 | |

Marten Transport Ltd. | 2.2 | |

West Pharmaceutical Services Inc. | 2.1 | |

Total (% of Net Assets) | 25.3% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | | |

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Small Blend | |

| | as of 6/30/13 | Category | |

Overall | «« | 621 | |

3 Year | « | 621 | |

5 Year | «« | 548 | |

10 Year | «« | 339 | |

Morningstar Ratings shown represent the Retail Class. Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

| Portfolio Characteristics | | | | | | |

(as of 6/30/13)

| | Westcore Small-Cap | | Russell 2000® | |

| | Opportunity Fund | | Index | |

Weighted Average Market Capitalization ($ Mil) | | $1,394.0 | | | $1,587.0 | |

Price/Cash Flow (1 year trailing) | | 10.9x | | | 13.3x | |

Price/Book Value | | 2.1x | | | 2.3x | |

Price/Earnings (1 year trailing) | | 17.9x | | | 18.4x | |

Beta | | 0.9 | | | 1.0 | |

Number of Holdings | | 60 | | | 1,934 | |

Portfolio Turnover Rate | | 60% | | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 13 |

|

Investing primarily in small-cap, dividend paying stocks that appear to be undervalued.

| | |

Troy Dayton, CFA Portfolio Manager Portfolio Manager

Derek R. Anguilm, CFA Portfolio Manager | Mark M. Adelmann, CFA, CPA

Lisa Z. Ramirez, CFA Portfolio Manager |

CFA is a trademark owned by the CFA Institute.

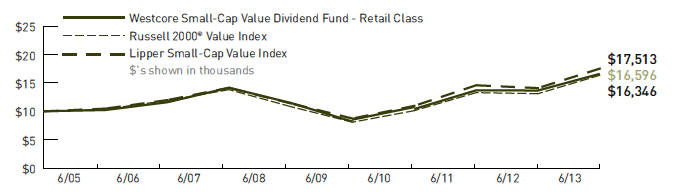

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Lipper Index data provided by Lipper, Inc.

Please see pages 28 and 29 for index definitions.

| Average Annual Total Returns |

| | | | | | | | | | | | Since | Inception |

| | 6 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Inception | Date |

Retail Class (WTSVX) | 17.23% | | 21.50% | | 16.83% | | 7.66% | | — | | 6.11% | 12/13/2004 |

Institutional Class | | | | | | | | | | | | |

(WISVX) | 17.41 | | 21.76 | | 16.96 | | 7.77 | | — | | 6.17 | 9/28/2007 |

Russell 2000® | | | | | | | | | | | | |

Value Index | 14.39 | | 24.77 | | 17.33 | | 8.59 | | — | | 5.72 | |

Lipper Small-Cap | | | | | | | | | | | | |

Value Index | 14.09 | | 24.29 | | 16.92 | | 8.98 | | — | | 6.74 | |

Retail Class Annual Expense Ratio (per the current prospectus) — Gross: 1.40%, Net: 1.31%

Institutional Class Annual Expense Ratio (per the current prospectus) — Gross: 1.25%, Net: 1.15%

The performance data quoted represents past performance and does not guarantee future results. Performance information for the institutional class shares prior to their inception date is based on the performance of the retail class. Current performance may be lower or higher than the performance quoted. To obtain current performance as of the most recent month-end, please call 800.392.CORE (2673) or visit us online at www.westcore.com. Average annual total returns and yield figures reflect the reinvestment of dividends, capital gains distributions, all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return and yield figures would have been lower. Total return and yield figures represent past performance. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Westcore fund shares are not insured by the FDIC, the Federal Reserve Board or any other agency and are subject to investment risk.

Denver Investments (the “Adviser”) contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level other expenses from April 30, 2013 until at least April 30, 2014, so that the ratio of expenses to average net assets as reported in the Fund’s Financial Highlights will be no more than 1.30% for the Fund’s Retail Class for such period. In addition, the Adviser has contractually agreed to waive the investment advisory and/or administration fees and/or to reimburse Fund level Other Expenses for the Institutional Class in the same proportion as the Retail Class waivers/reimbursements as well as reimburse the Institutional class-specific Other Expenses until at least April 30, 2014. This agreement may not be terminated or modified prior to this date except with the approval of the Board of Trustees.

Investing in small-cap funds generally will be more volatile and loss of principal could be greater than investing in larger-cap funds.

Lisa Z. Ramirez is a registered representative of ALPS Distributors, Inc.

- The Westcore Small-Cap Value Dividend Fund outperformed its benchmark, the Russell 2000 Value® Index, for the first half of 2013.

- The Federal Reserve attempted to provide clarity as to when it would begin to taper its quantitative easing programs. In so doing, the Fed is attempting to orchestrate a gradual movement of interest rates toward levels that more fairly reflect the current economic environment. History suggests this is a very difficult thing to accomplish. The stock market may also be recalibrating as investors feel less certain they will be protected by Federal Reserve actions.

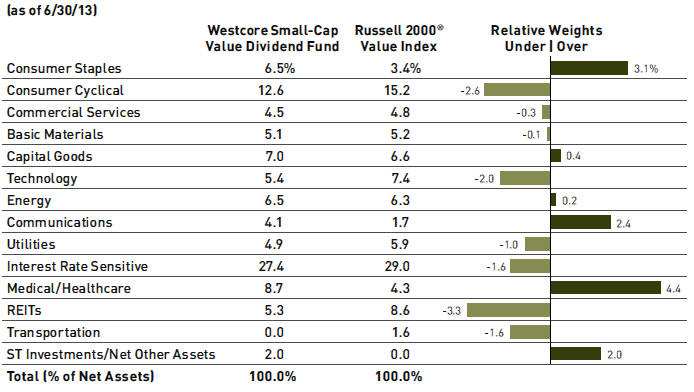

- The interest rate sensitive, medical/healthcare and energy sectors were the most significant contributors to relative performance in the first six months of the year. Endurance Specialty Holdings, Ltd., a worldwide insurance underwriter of personal and commercial property, was the strongest performer within the interest rate sensitive holdings. The stock benefitted from investors growing comfortable with the idea of a more “normal” year for crop insurance. If realized, this could result in significant earnings improvement versus 2012. We continue to like its mix of insurance and reinsurance lines, as well as its meaningful scale in the crop insurance area. Within medical/healthcare, supply disruptions at Questcor Pharmaceuticals, Inc. were tied to SKU changes required by Medicaid. This soft spot was short-lived as investors were encouraged by prescription trends that have regained strength and surpassed prior levels. Furthermore, investors seemed enthusiastic when Questcor announced the acquisition of a product that will provide it with international exposure, while eliminating a potential long-term competing product. Questcor ended the first half as the Fund’s best performer.

- The sectors that produced the most disappointing relative contributions were consumer cyclical, commercial services and technology. The Brink’s Company, within the commercial services sector, was among the Fund’s weakest holdings. While results for the second quarter were better than expected largely due to solid performance in Venezuela and the Asia Pacific region, investors continue to focus on concerns in the North America market. Management continues to shed unprofitable business units in order to improve operating margins. We see the potential for future improvements in cash flow and profits for Brink’s. In technology, semiconductor holding, Intersil Corp., had disappointing results. Investors are looking for more clarity from the new CEO and yet-to-be-named CFO as to their goals and time table for achievement. We continue to believe the semiconductor industry is experiencing a favorable upswing in demand.

- Most investors would agree Federal Reserve quantitative easing drove interest rates down to artificially low, unsustainable levels in an effort to stimulate stock prices, housing activity and associated home prices, and consumer net worth and by association, consumer confidence. While slower than expected, improvements in these areas now bring the capital markets to a critical juncture. Investors may for the first time in years be seeing negative total returns from their bond portfolios this quarter. The mantra that rewarded investors the past four to five years has been “don’t fight the Fed.” This particularly rewarded investors in lower-quality, less-liquid bonds and stocks with weaker fundamentals. It will be interesting to see what “don’t fight the Fed” will mean for the markets as they cautiously change direction. We believe the Fund’s focus on high-quality, dividend paying companies is well positioned for this environment.

PAGE 14 |

|

| WESTCORE SMALL-CAP VALUE DIVIDEND FUND (continued) |

| |

(for the year ended 6/30/13)

| | Average | | Contribution | |

5 Highest | Weight | | to Return | |

| | | | | |

Questcor Pharmaceuticals Inc. | 1.55% | | 0.99% | |

West Pharmaceutical | | | | |

Services Inc. | 3.49 | | 0.95 | |

Schweitzer-Mauduit | | | | |

International Inc. | 2.85 | | 0.76 | |

Endurance Specialty | | | | |

Holdings Ltd. | 2.56 | | 0.75 | |

Plantronics Inc. | 3.13 | | 0.62 | |

| | | | | |

5 Lowest | | | | |

Intersil Corp. | 1.27% | | -0.03% | |

Brady Corp. | 0.39 | | -0.06 | |

Cabot Corp. | 0.43 | | -0.14 | |

The Brink's Co. | 2.04 | | -0.22 | |

Hecla Mining Co. | 0.29 | | -0.28 | |

Past performance does not guarantee future results. These stocks do not represent all of the securities purchased, sold or recommended by the Funds’ Adviser. To request a complete list of the contribution of each Fund holding to overall Fund performance during the period, please call 800.392.CORE (2673) or email invest@westcore.com.

Please see page 29 for a description of the methodology used to construct this chart.

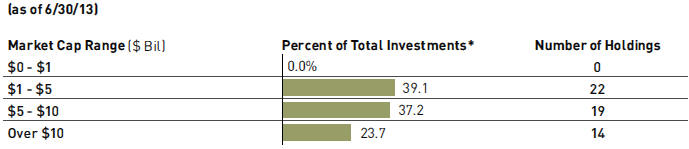

(as of 6/30/13)

West Pharmaceutical Services Inc. | 3.7% | |

Schweitzer-Mauduit International Inc. | 3.2 | |

Plantronics Inc. | 3.0 | |

Questcor Pharmaceuticals Inc. | 2.8 | |

MAXIMUS Inc. | 2.7 | |

Endurance Specialty Holdings Ltd. | 2.7 | |

Tidewater Inc. | 2.3 | |

Buckeye Technologies Inc. | 2.2 | |

Portland General Electric Co. | 2.1 | |

Compass Minerals International Inc. | 2.0 | |

Total (% of Net Assets) | 26.7% | |

Top ten holdings do not include any cash, cash equivalents or exchange traded fund investments and are subject to change. There are no guarantees that the Fund will continue to remain invested in any particular holding.

| | | | |

| | | Number | |

| | Morningstar | of Funds in | |

| | Rating™ | Small Value | |

| | as of 6/30/13 | Category | |

Overall | ««« | 295 | |

3 Year | ««« | 295 | |

5 Year | ««« | 254 | |

Morningstar Ratings shown represent the Retail Class. Morningstar proprietary ratings reflect historical risk-adjusted performance as of 6/30/13 and are subject to change every month.

Please see page 29 for more detail regarding Morningstar Ratings.

| Portfolio Characteristics | | | | | | |

(as of 6/30/13)

| | Westcore Small-Cap | | Russell 2000® | |

| | Value Dividend Fund | | Value Index | |

Weighted Average Market Capitalization ($ Mil) | | $1,892.0 | | | $1,367.0 | |

Price/Cash Flow (1 year trailing) | | 11.9x | | | 11.4x | |

Price/Book Value | | 2.1x | | | 1.7x | |

Price/Earnings (1 year trailing) | | 17.6x | | | 15.8x | |

Beta | | 0.9 | | | 1.0 | |

Number of Holdings | | 64 | | | 1,392 | |

Portfolio Turnover Rate | | 36% | | | — | |

Please see page 30 for definition of terms.

Sector classifications presented herein are based on the sector categorization methodology of the Adviser to the Funds which may result in the sector designations for one Fund being different than another Fund’s sector designations.

*Total Investments for this chart excludes short-term investments, including money market mutual funds.

Market capitalization ranges were determined by the Adviser to the Fund and are for presentation purposes only. These market capitalization ranges do not necessarily correlate to the benchmark’s market capitalization ranges.

PAGE 15 |

|

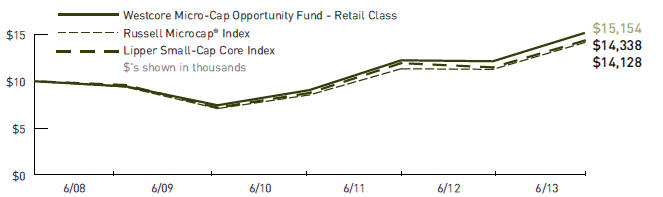

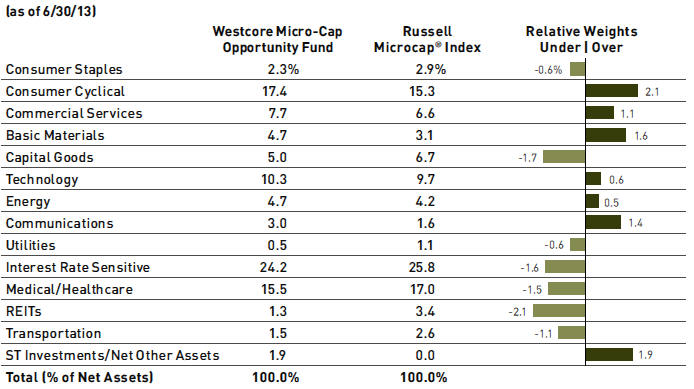

Investing primarily in micro-cap companies whose stocks appear to be undervalued.

Jon K. Tesseo Portfolio Manager

Paul A. Kuppinger, CFA Portfolio Manager

CFA is a trademark owned by the CFA Institute.