UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3445

The Merger Fund

(Exact name of registrant as specified in charter)

100 Summit Lake Drive

Valhalla, New York 10595

(Address of principal executive offices) (Zip code)

Roy Behren and Michael T. Shannon

100 Summit Lake Drive

Valhalla, New York 10595

(Name and address of agent for service)

1-800-343-8959

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Item 1. Reports to Stockholders.

ANNUAL REPORT

DECEMBER 31, 2012

Dear Fellow Shareholders:

The fourth quarter ending December 31, 2012 extended our track record of stable, “boring” returns. The Merger Fund® (the “Fund”) gained 1.34% during the period, our 77th gain in the 96 quarters since the Fund’s inception in 1989, bringing our full-year performance to 3.61%.

Amid continued worldwide economic, political and fiscal uncertainty, equity markets stalled but in general did not reverse their gains accrued during the first three quarters of the year. The S&P 500 lost 0.38% for the quarter, bringing its year-to-date performance down to a still-extraordinary 16.00% (of which Apple alone contributed almost 1.5%), and the MSCI World Index tacked on 2.63%, bringing its yearly tally to 16.54%. The same cannot be said for our hedge-fund or fixed-income comrades, as the HFRX Merger Arbitrage Index gained 0.27% for the quarter for a 0.95% yearly gain, with a standard deviation of 3.11% (greater than The Merger Fund‘s 2.78%) and the Barclays Aggregate Bond Index returned 0.22% for the quarter. As in the past, the Fund exhibited roughly one-fifth the “risk” (volatility) of the S&P and one-sixth the volatility of the MSCI World Index.1 The Fund’s beta correlation vs. both indices remained at approximately 0.10.

| | Average Annualized Total Return as of 12/31/2012 |

| | | | | | | | Since |

| | 3-month | YTD | 1-year | 3-year | 5-year | 10-year | Inception* |

The Merger Fund® | 1.34 | 3.61 | 3.61 | 2.89 | 2.93 | 4.26 | 6.95 |

| HFRX Merger Arbitrage Index | 0.27 | 0.95 | 0.95 | 1.47 | 3.21 | 4.22 | ** |

| Barclays Aggregate Bond Index | 0.22 | 4.23 | 4.23 | 6.21 | 5.96 | 5.19 | 7.17 |

| S&P 500 Index | -0.38 | 16.00 | 16.00 | 10.87 | 1.66 | 7.10 | 9.14 |

| MSCI The World Index | 2.63 | 16.54 | 16.54 | 7.53 | -0.60 | 8.08 | 6.44 |

| Citi 6-Month T-Bills | 0.04 | 0.11 | 0.11 | 0.15 | 0.66 | 1.84 | 3.81 |

| ** | The information is not available because the benchmark’s life is less than the period shown. |

YTD and 3-month performance is not annualized. Performance data quoted represents past performance; past performance does not guarantee future results. The performance results portrayed herein reflect the reinvestment of all interest, dividends and distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data included herein for periods prior to 2011 reflect that of Westchester Capital Management, Inc., the Fund’s prior investment advisor. Messrs. Behren and Shannon, the Fund’s current portfolio managers, assumed portfolio management duties of the Fund in 2006. Performance data current to the most recent month-end may be obtained by calling (800) 343-8959 or by visiting www.mergerfund.com. As of the latest Prospectus, the Fund’s Total Annual Operating Expenses were 1.68%. Expenses before investment related expenses were 1.33%. Investment related expenses will include acquired fund fees and expenses, interest expense, borrowing expense on securities sold short and dividends on securities sold short.

Hedge funds in general had trouble keeping up with the broader markets, with the HFRI Composite Index and the HFRI Fund of Hedge Funds Index lagging the S&P by approximately 10% each in 2012.2 Additionally, college endowments, which on average are thought to hold in excess of 50% of their assets in hedge funds, private equity and other “alternative investments” returned -0.3% as a group during their 2012 fiscal year.3

We bring up the performance of other actively managed investments because a notion has gained some traction throughout investment circles that fees paid to portfolio managers and investment advisors are a waste of money. Conjecturing that funds in general cannot outperform the market or their relevant index over the long haul, the “efficient market hypothesis” was originally proposed by Professor Eugene Fama of the University of Chicago in the 1960s4 and is currently championed by John Bogle, the retired founder of The Vanguard Group of mutual funds. Bogle is well-known for his insistence on the superiority of index funds over actively managed mutual funds. He has claimed that it is foolish to attempt to pick actively managed mutual funds in order to outperform a low-cost index fund over a long time period. This concept has been repeated in the press and apparently embraced by

1 | Three-year trailing standard deviation for The Merger Fund® was 2.78% versus 15.38% for the S&P and 16.95% for the MSCI World Index. |

2 | Bank of America Merrill Lynch Capital Strategy Group, Global Hedge Fund update, December 2012 (16% vs. 6.16% for the HF Composite and 5.25% for the Fund of Hedge Fund Index). |

| 3 | Wall Street Journal, Friday, February 1, 2013 “College Endowments Show Weak Returns” |

| 4 | A Wikipedia entry concisely explains that the Efficient Market Hypothesis asserts that financial markets are “informationally efficient.“ As a result, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given that all information available at the time the investment was made would already be reflected in the price of the security. |

many investors, as almost $150 billion was redeemed from “actively managed” stock funds in 2012. During the same period, U.S. equity and bond Exchange Traded Funds (“ETFs”) saw record inflows of approximately $187 billion combined.5 This phenomenon may also reflect the fact that many managers, of both hedge and mutual funds, have underperformed their benchmark indexes.

In our investment space, however, an investor would rather have a driver at the wheel than ride through “arbitrage-land” in the equivalent of Google’s computer-controlled, auto-piloted automobiles. The first metric we proffer would be the success rate of our investments in merger arbitrage transactions versus the complete universe of deals that would make up an index, ETF or ETN (Exchange Traded Note). As we have discussed in past letters, we believe the greater than 98% completion rate of deals in which the Fund has invested over the past several decades reflects the value that we as managers have added by being selective. An investment in either a random sampling of deals (a “dartboard portfolio”) or in every single announced deal would have yielded a success rate closer to the 90-92% range, and such a portfolio would thus provide a lower rate of return. Secondly, a manager may also add value, or “alpha” in comparison to an index of his actively managed peers, as evidenced by The Merger Fund’s outperformance versus the HFRX Merger Arbitrage index over the 1-, 3-, 10-year periods shown in the chart on the previous page. And finally, to get to the point, several passively managed merger-arbitrage investment vehicles have sprung up, presumably in response to the above-mentioned dynamics. We cannot see how it would be possible to replicate such a research-intensive strategy in an index.

We therefore submit that the results of our investment process, which encompasses financial, legal, regulatory and strategic judgment-based factors, merit permitting Westchester Capital Management to guide your tour of “arbitrage-land” as we attempt to continue providing attractive risk-adjusted returns in all market environments.

The current environment for deal activity appears promising. We would reiterate that the elements that began to emerge in 2009 are still in place, as Goldman Sachs stated in their aptly titled research piece “M&A: The Stage is Set, Confidence is Key.” And, like a broken record that is played quarterly, we agree with its authors. “Debt is cheap. Cash is up. Margins are peaking and sales growth is slowing. The S&P is up and Gross Domestic Product growth improves. Unlevered private equity dry powder [exceeds] $360bln… Merger and acquisitions in relation to equity market cap remains well below normalized levels.”6 We fully agree that confidence, which stems from economic and corporate visibility, will be the key to an uptick in activity. “Wait and see has been the dominant attitude of corporations’ approach to acquisitions because of the macroeconomic uncertainty….Once these crises find a solution there will likely be a rebound in activity driven by continuing consolidation in natural resources, industrials, technology and financial services,” explained Gene Sykes, Goldman Sachs’ global head of Mergers and Acquisitions.7

The bullish view appears to be confirmed by the sharp increase in worldwide deal activity during the fourth quarter. According to the Wall Street Journal, global mergers and acquisitions rose to the highest level in four years this quarter, as a late-year surge provided grounds for optimism in a very slow year. Companies worldwide announced $692 billion in purchases during the final three months of the year, while full-year activity reached only $2.23 trillion versus $2.42 trillion in 2011, an 8% decrease. Activity outside of the U.S. increased in the fourth quarter, with European deals growing 73% from the prior quarter to $176 billion. The Goldman Sachs report similarly observes that global deal and fee backlog at the end of December 2012 sat at the highest quarter-end level seen since the end of 2007.8

Although the tide may have recently turned, lack of confidence during the year dampened hostile transaction activity. Hostile transactions amounted to approximately $100 billion, down 33% from 2011, and hit the lowest level since 2003. Frank Aquila, co-head of Sullivan & Cromwell’s global corporate practice, noted “One of the prerequisite conditions for a hostile bid is a high degree of confidence that a company can get financing, confidence in the value of the target and confidence in getting regulatory approval. What we have had over the past 12 months has been a lack of confidence at all levels in deal making.”9

Geographically, U.S. targets accounted for 35% of the year’s merger volume. Asian companies continue to be active acquirers, as activity rose to its highest level in over a year, led by Softbank’s $38 billion dollar purchase of U.S.-based Sprint Nextel Corp. This activity reflected a trend towards cross-border takeovers, which accounted for approximately half of all announced deals in 2012. Finally, private equity activity slowed but continued in 2012, with $211 billion worth of deals, which was the least amount of activity in that space since 2009. The good news, however, is that buyers and sellers are confident enough about economic prospects that they are comfortable utilizing leverage again. During the past two quarters, strong credit markets and low interest rates have led buyout sponsors to utilize a greater percentage of borrowed funds to finance their deals. Since the financial crisis in 2008, private equity firms have contributed an average of 42% of the cost of leverage buy-outs (LBOs) with their own money, and over the past six months, that percentage has fallen to 33%, according to Thompson Reuters. Another measure of leverage, the average ratio of

| 5 | Wall Street Journal, Thursday, January 3, 2013 “Investors Sour on Pro Stock Pickers” |

| 6 | Goldman Sachs Equity Research, January 10, 2013, “M&A: The Stage is Set, Confidence is Key” |

| 7 | Bloomberg News, Thursday December 27, 2012 “Fourth-Quarter M&A Surge Spurs Optimism After 2012 Deals Decline” |

| 8 | Backlog was defined as deals that were announced within a two-year period with a completion date or withdrawal date that came after that two year period or which were considered as pending at the end of that two year period. |

| 9 | Financial Times, Friday January 11, 2013 “Hostile Deals Hit 10-year Low on Lack of Confidence” |

debt to cash flow (also known as EBITDA, or Earnings Before Interest, Taxes, Depreciation and Amortization) in these types of deals has risen to 5.5x, the highest level since early 2008 and close to the pre-crisis levels of 6-6.5x seen in 2006 and 2007.10

Another indicator we consider is the positive performance of acquirers’ stock. Well-received deals often encourage additional activity, and we have seen significant strength in the buyers’ stock prices this year. To name a few, Conagra Foods Inc.’s stock climbed 5% in the wake of its $6.7 billion agreement to purchase Ralcorp Holdings; M&T Bank Corp. announced its purchase of Hudson City Bancorp and promptly saw its own stock rise almost 5%; Intercontinental Exchange opened over 5% higher after revealing its purchase of NYSE Euronext in a $9 billion acquisition; and McKesson Corp. surged 4% on its deal to purchase PSS World Medical, Inc. The year 2012 saw acquirers’ stock prices rise on merger news in more than 50% of announced transactions. “When you announce good strategic deals these days both stock prices go up, not just the target’s price,” and that may persuade more companies to pursue transactions, Bank of America Corp’s head of M&A Steven Baronoff said at this year’s Bloomberg Dealmakers Summit.

Our Portfolio

We held 107 investments during the quarter and experienced one terminated deal, generally consistent with our historic deal-selection success rate. Reflecting a 3:1 ratio of winners to losers, 27 of those positions produced negative marks-to-market and 80 were flat to positive. We invested in 28 new situations during the quarter, and as of the end of December we held 78 positions and were 90% invested. New situations are concentrated in the U.S., as 23 of the new positions are local, one is European, two are Japanese, one is Australian and one is Singapore-based.

Winners and losers were dispersed throughout the portfolio, with no single deal accounting for a swing greater than one quarter of one percent. For the second consecutive quarter, the biggest gainer for the quarter was a European transaction. As Glencore International plc’s purchase of Xstrata plc continued to dig towards the finish line, the spread tightened enough to contribute 0.21% to the Fund’s performance.

In second place was CNOOC’s bid for Nexen, Inc. of Canada, a $15 billion oil and gas exploration and development company. Nexen finally received Canadian and Chinese regulatory approval and is currently waiting to receive its final required clearance from the U.S. Committee on Foreign Investment in the United States (CFIUS). It has been a long road for the China National Oil Company, but they navigated their way very well and when completed, the deal should provide a roadmap for future purchases by Chinese state-affiliated entities. Notably, and FINALLY, we are pleased to announce that Hertz’s Global Holdings, Inc.’s purchase of Dollar Thrifty Automotive Group has been completed. After writing about this transaction for 5 quarterly letters, and a drawn-out negotiation with the FTC, the deal squeaked through the antitrust process by Hertz agreeing to sell its Advantage (lower-end) car rental business and conceding to allow competitors to operate onsite at airports at 26 of its locations that overlapped with Dollar Thrifty.

The biggest loser was our position in the only broken deal of the quarter, Astral Media Inc. of Canada. The $2.5 billion acquisition by Canadian broadcaster BCE Inc. was originally announced in March of 2012, and was expected to close sometime in the second half. The company and shareholders (and in particular, our Canadian telecom counsel) were surprised when the CRTC, the Canadian radio and television regulatory authority, rejected the transaction on October 18th due to market concentration issues and a lack of tangible benefits to the viewing public. Although we held a small position, at less than one percent of our assets, we began the process of exiting our holdings. While this was underway, BCE, which retained the right to appeal or resubmit an application to the CRTC, decided not to terminate the merger agreement with Astral and in fact resubmitted an amended proposal to the authorities which it claimed remedied the prior shortcomings. It is not clear if the concerns have been adequately addressed, as the application will not be made public until later in the first quarter, but a public hearing will be convened and we will have further opportunity to reassess the situation and perhaps re-involve the Fund in this transaction. So for now, it will remain on the broken-deal side of the ledger, but as happened last quarter with the rejected and then-later-approved acquisition of Progress Energy Resources of Canada by Malaysia’s Petronas, we might claw this one back.

The portfolio remains diversified, and our new positions span a variety of industries, transaction structures and geography. Telecommunications was our most active industry: Deutsche Telecom rang up MetroPCS Communications for a friendly deal, Sumitomo Corp. broadcast its interest in Japanese cable and satellite corporation Jupiter Communications, and Softbank burned up the wires with three interconnected transactions, completing its purchase of eAccess Ltd, a fellow Japanese provider of diversified communication services and then following that up with a deal to buy Sprint Nextel Corporation which itself then made a bid for fellow U.S. wireless provider Clearwire Corporation. The next most active sector for the Fund was Oil and Gas. We are hoping that Freeport-McMoRan Copper & Gold hits a gusher with its simultaneous U.S. purchases of McMoRan Exploration Co., and Plains Exploration and Production Company. We also topped off the tank with a small position in Murphy Oil, which is restructuring via a planned spin-off of its refining and marketing operations.

| 10 | Wall Street Journal, Monday December 17, 2012 “Debt Loads Climb in Buyout Deals” |

Additionally, we saw transactions between related parties, who either currently do business with each other or are already partly owned by the prospective acquirer. Such situations include the buy-in of Netherlands’ CNH Global NV by Fiat Industrial, Crexus by its controlling shareholder Annaly Capital Management, Singapore-based Frasier and Neave, Ltd by Thai Beverage PCL (of Thailand of course!), McMoRan Exploration’s acquisition by related Freeport-McMoRan Copper & Gold, and even Clearwire Corp.’s proposed marriage with Sprint Nextel is somewhat incestuous given Sprint’s large ownership of and business relationship with Clearwire.

As mentioned in previous letters, transformational reorganizations and spin-offs have continued to occur, in some cases prompted by activist investors. The value of such spin-offs has risen markedly as companies continue to seek ways to unlock shareholder value in this low-growth environment. We have witnessed many instances of increased value from these transactions and are staying alert for opportunities for the Fund to realize low-volatility, low-risk rates of return. Corporate restructurings we are following closely include Pfizer, Valero Energy, Dun & Bradstreet, The McGraw-Hill Companies, Lamar Advertising, Corrections Corp. of America, Penn Gaming, Murphy Oil, CBS Corporation, Vodaphone plc and the recently completed $57 billion spin-off of AbbVie Inc. by Abbott Laboratories.

On another unrelated note, Hewlett-Packard Co. announced that it had been the victim of numerous “accounting improprieties” by members of Autonomy Corp plc, which it had acquired in a multi-billion dollar transaction at the end of 2011. The Fund had invested in this deal and held Autonomy stock through the completion of the merger. Although it is unfortunate that Hewlett-Packard has now taken a $9 billion impairment charge, we were unaffected because our positions are self-liquidating when a merger closes. In a cash deal, we receive cash for our shares, and in a stock-for-stock deal we are short the acquiring company’s shares and that short position will offset the long target shares upon completion.

Finally a brief macro note: the investment flows discussed in the first page of this letter may credibly be interpreted as the beginning of the long awaited “great rotation” out of bonds and into stocks. Although there has been much discussion about the existence of a “bond bubble,” those who have bet on a fixed income “correction” for the past several years have incurred losses. While we do not position our portfolio to have directional exposure to either stocks or bonds, there tends to be a correlation between the risk-free rate of investment (such as treasury bills), also known as the cost of capital, and the performance of absolute-return strategies such as merger arbitrage. High-quality arbitrage spreads on announced merger transactions offer rates of return which are comprised of a spread, known as a risk premium, over and above the cost of capital, to account for the potential risk of investing in merger transactions. Therefore, the strategy is naturally positioned in the event that were interest rates to rise, investments such as ours, with any element of risk, would need to provide a greater return than a risk-free investment, and market forces would consequently be expected to drive prices to accommodate this dynamic. We do not predict future stock market or interest rate levels, but we are comfortable with our exposure and tendency of low volatility in the event that rates turn up from these historic low levels.

Miscellaneous

The Fund’s total expense ratio, which we watch like a hawk, including management fee waivers currently in place, is 23% below our peer averages, again placing it in the lowest quartile of funds in the Morningstar Market Neutral Fund category.11 We are also in the lowest quartile for Investment Advisory Fees, at 32% below our peer averages in the Market Neutral Fund category.12

As noted previously, Westchester Capital Management, LLC is the portfolio manager for a ’40-Act registered mutual fund called the Dunham Monthly Distribution Fund, which provides an alternative market-neutral profile to The Merger Fund®. There is significant strategy overlap and Merger Fund shareholders will receive the benefit of any relevant ideas uncovered through our parallel investment processes.

Quarterly statistical summaries will be provided within two weeks after the end of the quarter, prior to the release of the quarterly letter. They are available electronically on the web, or we would be happy to arrange for an automatic email when it becomes available.

For convenience, investors can arrange for e-alerts of important Fund communications. Through our website at www.mergerfund.com, you can check account balances, make purchases and sales, and sign up for notification of trade confirmations, statements and shareholder communications via e-mail.

Thanks again for your support and please feel free to contact us with any questions or comments.

Sincerely,

|  |

| Roy Behren | Mike Shannon |

| 11 | Morningstar Market Neutral Fund average total expense ratio of 1.77% vs. The Merger Fund® at 1.37%. |

| 12 | Morningstar Market Neutral Fund average investment advisory fees of 1.27% vs. The Merger Fund® at 0.87%. |

Before investing in The Merger Fund®, carefully consider its investment objectives, risks, charges and expenses. For a prospectus or summary prospectus containing this and other information, please call (800) 343-8959 or view it online at www.mergerfund.com. Please read it carefully before investing.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Mutual fund investing involves risk. Principal loss is possible. The principal risk associated with the Fund’s merger arbitrage investment strategy is that certain of the proposed reorganizations in which the Fund invests may be renegotiated or terminated, in which case losses may be realized. Investments in foreign companies involved in pending mergers, takeovers and other corporate reorganizations may entail political, cultural, regulatory, legal, and tax risks different from those associated with comparable transactions in the United States. Merger arbitrage portfolios may have higher turnover rates than portfolios of typical long-only funds. This may increase the transaction costs to the Fund, which could impact the Fund’s performance. The purpose of the short sale is to protect against a decline in the market value of the acquiring company’s shares prior to the acquisition completion. However, should the acquisition be called off or otherwise not completed, the Fund may realize losses on both its long position in the target company’s shares and it short position in the acquirer’s shares.

References to other mutual funds do not construe an offer of those securities.

The views expressed are as of February 5, 2013 and are a general guide to the views of Westchester Capital Management. The views expressed are those of the fund manager, are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security. This document does not replace portfolio and fund-specific materials.

Definitions: The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. The MSCI World Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed economies. The indices are unmanaged and not available for direct investment. HFRX Indices are investable indices designed to be representative of the overall composition of the hedge fund industry. The Barclays Aggregate Bond Index is an intermediate term index comprised of investment grade bonds. The HFRX Merger Arbitrage Index is comprised of strategies which employ an investment process primarily focused on opportunities in equity and equity related instruments of companies which are currently engaged in a corporate transaction. Citi 6-Month T-Bills measures monthly return equivalents of yield averages that are not marked to market. The Six-Month Treasury Bill Indexes consist of the last three six-month Treasury bill issues. Standard Deviation is the degree by which returns vary relative to the average return. The higher the standard deviation, the greater the variability of the investment; Beta is a measure of the fund’s sensitivity to market movements. A portfolio with a beta greater than 1 is more volatile than the market and a portfolio with a beta less than 1 is less volatile than the market; A basis point (often denoted as bp) is a unit equal to 1/100 of a percentage point. The relationship between percentage changes and basis points can be summarized as follows: 1% change = 100 basis points and 0.01% = 1 basis point. Correlation is calculated using R-Squared; a measure that represents the percentage of a fund’s movements that can be explained by movements in a benchmark index. A fund with low R-squared doesn’t act much like the index. The HFRI Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to HFR Database. The HFRI Fund of Hedge Funds Index invests with multiple managers through funds or managed accounts. Alpha is a measure of performance on a risk-adjusted basis. Alpha takes the volatility (price risk) of a mutual fund and compares its risk-adjusted performance to a benchmark index. The excess return of the fund relative to the return of the benchmark index is a fund’s alpha. EBITDA is a non-GAAP metric that is measured exactly as stated. All interest payments, tax, depreciation and amortization entries in the income statement are reversed out from the bottom-line net income. It is intended to measure and enable profitability comparison between different companies by canceling the effects of different asset bases (by cancelling depreciation), different takeover histories (by cancelling amortization often stemming from goodwill), effects due to different tax structures, as well as the effects of different capital structures (by cancelling interest payments).

This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

The SEC does not endorse, indemnify, approve nor disapprove of any security.

The Merger Fund® is distributed by Quasar Distributors, LLC.

| Chart 1 | Chart 2 |

| | |

| PORTFOLIO COMPOSITION | PORTFOLIO COMPOSITION |

| By Type of Deal* | By Type of Buyer* |

| | |

|  |

| | |

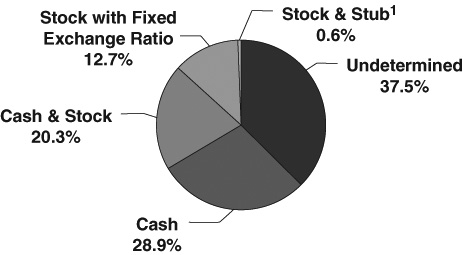

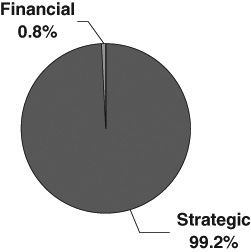

Chart 3

PORTFOLIO COMPOSITION

By Deal Terms*

| * | Data expressed as a percentage of long common stock, corporate bonds and swap contract positions as of December 31, 2012. |

| 1 | “Stub” includes assets other than cash and stock (e.g., escrow notes). |

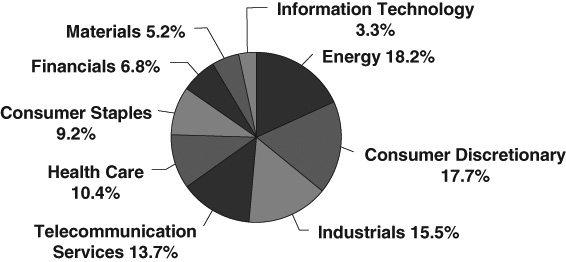

Chart 4

PORTFOLIO COMPOSITION

By Sector*

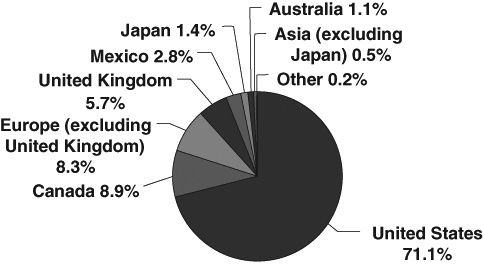

Chart 5

PORTFOLIO COMPOSITION

By Region*

| * | Data expressed as a percentage of long common stock, corporate bonds and swap contract positions as of December 31, 2012. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

Chart 6

GLOBAL MERGER ACTIVITY

Quarterly volume of announced global mergers

and acquisitions January 2003 – December 2012

Source: Bloomberg, Global Financial Advisory Mergers & Acquisitions Rankings 2012

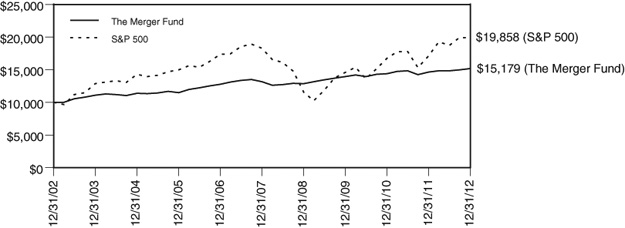

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT

IN THE MERGER FUND AND S&P 500

| | | Average |

| | | Annual Total Return |

| | 1 Yr. | 3 Yr. | 5 Yr. | 10 Yr. |

| The Merger Fund | 3.61% | 2.89% | 2.93% | 4.26% |

| The Standard & Poor’s 500 Index | 16.00% | 10.87% | 1.66% | 7.10% |

The Standard & Poor’s 500 Index (S&P 500) is a capitalization-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. This chart assumes an initial gross investment of $10,000 made on December 31, 2002. Returns shown include the reinvestment of all dividends. Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investment return and principal value will fluctuate, so that your shares, when redeemed, may be worth more or less than the original cost.

The Merger Fund

EXPENSE EXAMPLE

December 31, 2012

(Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs as described below and (2) ongoing costs, including management fees, distribution and/or service fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 for the period 7/1/12 – 12/31/12.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. Although the Fund charges no sales load or transaction fees, you will be assessed transaction-related fees for outgoing wire transfers, returned checks and stop-payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Fund’s transfer agent. If you request that a redemption be made by wire transfer, a $15.00 fee will be charged by the Fund’s transfer agent. IRAs will be charged a $15.00 annual maintenance fee. To the extent the Fund invests in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Fund invests in addition to the expenses of the Fund. Actual expenses of the underlying funds are expected to vary among the various underlying funds. These expenses are not included in the example below, but if they were, such expenses would lower the “Ending Account Value” below. The example below includes, among other fees, management fees, shareholder servicing fees, fund accounting, custody and transfer agent fees. However, the example below does not include portfolio trading commissions and related expenses, and extraordinary expenses as determined under generally accepted accounting principles.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning Account | Ending Account | Expenses Paid During |

| | Value 7/1/12 | Value 12/31/12 | Period 7/1/12 – 12/31/12* |

Actual+(1) | $1,000.00 | $1,024.30 | $7.33 |

Hypothetical++(2) | $1,000.00 | $1,017.90 | $7.30 |

| + | Excluding dividends on securities sold short, borrowing expense on securities sold short and interest expense, your actual cost of investment in the Fund would be $6.36. |

| ++ | Excluding dividends on securities sold short, borrowing expense on securities sold short and interest expense, your hypothetical cost of investment in the Fund would be $6.34. |

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.44%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). |

| (1) | Ending account values and expenses paid during the period based on a 2.43% return. This actual return is net of expenses. |

| (2) | Ending account values and expenses paid during period based on a 5.00% annual return before expenses. |

SCHEDULE OF INVESTMENTS

December 31, 2012

| Shares | | | | Value | |

| | | | |

| COMMON STOCKS — 71.47% | | | |

| | | | | | |

| | | ADVERTISING — 2.74% | | | |

| | 691,532 | | Arbitron, Inc. (h) | | $ | 32,280,714 | |

| | 2,293,200 | | Lamar Advertising Company Class A (a)(f) | | | 88,861,500 | |

| | | | | | | 121,142,214 | |

| | | | APPAREL RETAIL — 0.68% | | | | |

| | 1,534,000 | | J.C. Penney Company, Inc. (h) | | | | |

| | | | | | | 30,235,140 | |

| | | | APPAREL, ACCESSORIES & LUXURY GOODS — 2.60% | | | | |

| | 1,605,036 | | The Warnaco Group, Inc. (a)(g) | | | 114,872,426 | |

| | | | | | | | |

| | | | AUTO PARTS & EQUIPMENT — 0.57% | | | | |

| | 468,554 | | Visteon Corporation (a)(f) | | | 25,217,576 | |

| | | | | | | | |

| | | | AUTOMOBILE MANUFACTURERS — 0.43% | | | | |

| | 650,000 | | General Motors Co. (a) | | | 18,739,500 | |

| | | | | | | | |

| | | | BREWERS — 0.15% | | | | |

| | 774,215 | | Grupo Modelo, S.A. de C.V. (b) | | | 6,984,213 | |

| | | | | | | | |

| | | | BROADCASTING & CABLE TV — 0.62% | | | | |

| | 302,613 | | Astral Media, Inc. Class A (b)(h) | | | 14,064,340 | |

| | 225,300 | | Discovery Communications, Inc. Class C (a) | | | 13,180,050 | |

| | | | | | | 27,244,390 | |

| | | | CABLE & SATELLITE TV — 2.31% | | | | |

| | 2,843,758 | | Comcast Corporation Special Class A (h) | | | 102,233,100 | |

| | | | | | | | |

| | | | COMPUTER STORAGE & PERIPHERALS — 0.25% | | | | |

| | 1,137,486 | | Intermec, Inc. (a) | | | 11,215,612 | |

| | | | | | | | |

| | | | CONSTRUCTION & ENGINEERING — 2.84% | | | | |

| | 324,400 | | Chicago Bridge & Iron Company N.V. — ADR | | | 15,035,940 | |

| | 2,365,267 | | The Shaw Group Inc. (a)(g) | | | 110,245,095 | |

| | | | | | | 125,281,035 | |

| | | | CONSTRUCTION & FARM | | | | |

| | | | MACHINERY & HEAVY TRUCKS — 0.37% | | | | |

| | 742,200 | | Navistar International Corporation (a) | | | 16,157,694 | |

| | | | | | | | |

| | | | DISTILLERS & VINTNERS — 0.45% | | | | |

| | 559,700 | | Constellation Brands, Inc. Class A (a)(f) | | | 19,807,783 | |

| | | | | | | | |

| | | | DIVERSIFIED CHEMICALS — 0.95% | | | | |

| | 2,630,004 | | Huntsman Corporation (f) | | | 41,817,064 | |

| | | | | | | | |

| | | | DIVERSIFIED METALS & MINING — 0.70% | | | | |

| | 877,263 | | Freeport-McMoRan Copper & Gold, Inc. (f) | | | 30,002,395 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Shares | | | | Value | |

| | | | | | |

| | | DIVERSIFIED METALS & MINING — 0.70% (continued) | | | |

| | 310,134 | | Pilot Gold, Inc. (a)(b) | | $ | 664,105 | |

| | | | | | | 30,666,500 | |

| | | | HEALTH CARE DISTRIBUTORS — 1.64% | | | | |

| | 2,500,934 | | PSS World Medical, Inc. (a)(f) | | | 72,226,974 | |

| | | | | | | | |

| | | | HOUSEHOLD PRODUCTS — 0.43% | | | | |

| | 280,200 | | The Procter & Gamble Company (f) | | | 19,022,778 | |

| | | | | | | | |

| | | | INDUSTRIAL CONGLOMERATES — 0.96% | | | | |

| | 2,521,668 | | Fraser & Neave Ltd. (b)(h) | | | 20,023,887 | |

| | 769,500 | | Tyco International Ltd. (b)(f) | | | 22,507,875 | |

| | | | | | | 42,531,762 | |

| | | | INDUSTRIAL MACHINERY — 2.77% | | | | |

| | 230,257 | | Gardner Denver, Inc. (h) | | | 15,772,604 | |

| | 1,389,700 | | Robbins & Myers, Inc. (f) | | | 82,617,665 | |

| | 503,300 | | The Timken Company | | | 24,072,839 | |

| | | | | | | 122,463,108 | |

| | | | INTEGRATED OIL & GAS — 5.03% | | | | |

| | 1,870,100 | | BP PLC — ADR (f) | | | 77,870,964 | |

| | 1,325,200 | | Hess Corporation (f) | | | 70,182,592 | |

| | 1,241,900 | | Murphy Oil Corporation (f) | | | 73,955,145 | |

| | | | | | | 222,008,701 | |

| | | | INTEGRATED TELECOMMUNICATION SERVICES — 3.73% | | | | |

| | 464,200 | | AT&T, Inc. (h) | | | 15,648,182 | |

| | 1,884,840 | | CenturyLink, Inc. (f) | | | 73,734,941 | |

| | 196,750 | | TELUS Corporation (non-voting) (b) | | | 12,793,596 | |

| | 1,443,300 | | Verizon Communications, Inc. (f) | | | 62,451,591 | |

| | | | | | | 164,628,310 | |

| | | | INTERNET RETAIL — 0.14% | | | | |

| | 92,768 | | Liberty Ventures (a) | | | 6,285,960 | |

| | | | | | | | |

| | | | INVESTMENT BANKING & BROKERAGE — 0.50% | | | | |

| | 1,191,753 | | Jefferies Group, Inc. (h) | | | 22,130,853 | |

| | | | | | | | |

| | | | MANAGED HEALTH CARE — 4.14% | | | | |

| | 4,079,102 | | Coventry Health Care, Inc. (h) | | | 182,866,143 | |

| | | | | | | | |

| | | | MORTGAGE REITS — 0.13% | | | | |

| | 488,596 | | CreXus Investment Corporation | | | 5,985,301 | |

| | | | | | | | |

| | | | MOVIES & ENTERTAINMENT — 0.82% | | | | |

| | 1,416,100 | | News Corporation Class A (f) | | | 36,167,194 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Shares | | | | Value | |

| | | | | | |

| | | MULTI-LINE INSURANCE — 1.80% | | | |

| | 2,255,400 | | American International Group, Inc. (a)(f) | | $ | 79,615,620 | |

| | | | | | | | |

| | | | OIL & GAS EXPLORATION & PRODUCTION — 9.52% | | | | |

| | 803,700 | | Anadarko Petroleum Corporation (f) | | | 59,722,947 | |

| | 1,457,000 | | Chesapeake Energy Corporation (f) | | | 24,215,340 | |

| | 2,352,000 | | McMoRan Exploration Co. (a)(f) | | | 37,749,600 | |

| | 6,682,531 | | Nexen, Inc. (b)(f) | | | 180,027,385 | |

| | 2,523,914 | | Plains Exploration & Production Company (a)(g) | | | 118,472,523 | |

| | | | | | | 420,187,795 | |

| | | | OIL & GAS REFINING & MARKETING — 0.71% | | | | |

| | 921,700 | | Valero Energy Corporation (f) | | | 31,448,404 | |

| | | | | | | | |

| | | | OIL & GAS STORAGE & TRANSPORTATION — 0.84% | | | | |

| | 1,138,100 | | Williams Companies, Inc. (f) | | | 37,261,394 | |

| | | | | | | | |

| | | | PACKAGED FOODS & MEATS — 3.97% | | | | |

| | 2,909,300 | | Dean Foods Company (a)(f) | | | 48,032,543 | |

| | 2,816,349 | | Dole Food Company, Inc. (a)(f) | | | 32,303,523 | |

| | 1,060,951 | | Ralcorp Holdings, Inc. (a)(h) | | | 95,114,257 | |

| | | | | | | 175,450,323 | |

| | | | PERSONAL PRODUCTS — 0.15% | | | | |

| | 98,800 | | Mead Johnson Nutrition Co. | | | 6,509,932 | |

| | | | | | | | |

| | | | PHARMACEUTICALS — 3.64% | | | | |

| | 1,603,545 | | Abbott Laboratories (f) | | | 105,032,197 | |

| | 577,500 | | Eli Lilly & Company (h) | | | 28,482,300 | |

| | 1,091,822 | | Pfizer, Inc. (f) | | | 27,382,896 | |

| | | | | | | 160,897,393 | |

| | | | PUBLISHING — 1.34% | | | | |

| | 1,079,400 | | McGraw-Hill Companies, Inc. (f) | | | 59,010,798 | |

| | | | | | | | |

| | | | REGIONAL BANKS — 0.75% | | | | |

| | 280,525 | | Citizens Republic Bancorp, Inc. (a) | | | 5,321,559 | |

| | 3,305,900 | | KeyCorp (f) | | | 27,835,678 | |

| | | | | | | 33,157,237 | |

| | | | REINSURANCE — 0.16% | | | | |

| | 248,195 | | Alterra Capital Holdings Ltd. (b) | | | 6,996,617 | |

| | | | | | | | |

| | | | SECURITY & ALARM SERVICES — 1.57% | | | | |

| | 1,948,700 | | Corrections Corporation of America (f) | | | 69,120,389 | |

| | | | | | | | |

| | | | SEMICONDUCTOR EQUIPMENT — 2.72% | | | | |

| | 1,328,500 | | Cymer, Inc. (a)(h) | | | 120,136,255 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Shares | | | | Value | |

| | | | | | |

| | | SPECIALIZED FINANCE — 1.75% | | | |

| | 2,447,842 | | NYSE Euronext (f) | | $ | 77,204,937 | |

| | | | | | | | |

| | | | THRIFTS & MORTGAGE FINANCE — 1.05% | | | | |

| | 5,708,776 | | Hudson City Bancorp, Inc. (e) | | | 46,412,349 | |

| | | | | | | | |

| | | | TRUCKING — 1.13% | | | | |

| | 3,065,100 | | Hertz Global Holdings, Inc. (a)(f) | | | 49,869,177 | |

| | | | | | | | |

| | | | WIRELESS TELECOMMUNICATION SERVICES — 4.42% | | | | |

| | 1,162,103 | | Clearwire Corporation Class A (a) | | | 3,358,478 | |

| | 11,778,900 | | MetroPCS Communications, Inc. (a)(f) | | | 117,082,266 | |

| | 13,185,000 | | Sprint Nextel Corporation (a)(f) | | | 74,758,950 | |

| | | | | | | 195,199,694 | |

| | | | TOTAL COMMON STOCKS (Cost $3,057,461,267) | | | 3,156,409,645 | |

| | | | | |

| WARRANTS — 0.00% | | | | |

| | 142,642 | | Kinross Gold Corporation (a)(b) | | | 42,304 | |

| | | | TOTAL WARRANTS (Cost $540,029) | | | 42,304 | |

| | | | | | | | |

| Principal Amount | | | | |

| | | | | |

| CORPORATE BONDS — 1.14% | | | | |

| | | | McMoRan Exploration Co. | | | | |

| $ | 10,969,000 | | 11.875%, 11/15/2014 | | | 11,723,119 | |

| | | | MetroPCS Wireless, Inc. | | | | |

| | 10,338,000 | | 6.625%, 11/15/2020 | | | 11,022,893 | |

| | | | Rite Aid Corporation | | | | |

| | 24,486,000 | | 10.375%, 7/15/2016 | | | 26,016,375 | |

| | | | Sealy Mattress Co. | | | | |

| | 1,461,000 | | 10.875%, 4/15/2016 (Acquired 10/5/2012, Cost $1,598,769) (i) | | | 1,552,312 | |

| | | | TOTAL CORPORATE BONDS (Cost $50,444,364) | | | 50,314,699 | |

| | | | | | | | |

| Contracts (100 shares per contract) | | | | |

| | | | | |

| PURCHASED PUT OPTIONS — 0.46% | | | | |

| | | | Abbott Laboratories | | | | |

| | 16,036 | | Expiration: February 2013, Exercise Price: $57.50 | | | 288,648 | |

| | | | American International Group, Inc. | | | | |

| | 5,880 | | Expiration: February 2013, Exercise Price: $26.00 | | | 47,040 | |

| | 5,090 | | Expiration: February 2013, Exercise Price: $28.00 | | | 66,170 | |

| | 10,182 | | Expiration: February 2013, Exercise Price: $29.00 | | | 193,458 | |

| | | | Anadarko Petroleum Corporation | | | | |

| | 8,037 | | Expiration: February 2013, Exercise Price: $55.00 | | | 140,648 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | BP PLC — ADR | | | |

| | 18,701 | | Expiration: January 2013, Exercise Price: $35.00 | | $ | 130,907 | |

| | | | CenturyLink, Inc. | | | | |

| | 8,202 | | Expiration: January 2013, Exercise Price: $34.00 | | | 41,010 | |

| | 2,469 | | Expiration: April 2013, Exercise Price: $30.00 | | | 37,035 | |

| | | | Chesapeake Energy Corporation | | | | |

| | 14,570 | | Expiration: January 2013, Exercise Price: $14.00 | | | 72,850 | |

| | | | Constellation Brands, Inc. Class A | | | | |

| | 5,597 | | Expiration: January 2013, Exercise Price: $27.50 | | | 111,940 | |

| | | | Corrections Corporation of America | | | | |

| | 19,487 | | Expiration: March 2013, Exercise Price: $28.00 | | | 487,175 | |

| | | | Dean Foods Company | | | | |

| | 10,994 | | Expiration: March 2013, Exercise Price: $11.00 | | | 109,940 | |

| | 12,426 | | Expiration: June 2013, Exercise Price: $12.00 | | | 497,040 | |

| | | | Dole Food Company, Inc. | | | | |

| | 8,627 | | Expiration: January 2013, Exercise Price: $9.00 | | | 43,135 | |

| | 6,821 | | Expiration: January 2013, Exercise Price: $10.00 | | | 68,210 | |

| | 3,737 | | Expiration: April 2013, Exercise Price: $9.00 | | | 112,110 | |

| | | | Eli Lilly & Company | | | | |

| | 5,775 | | Expiration: January 2013, Exercise Price: $40.00 | | | 34,650 | |

| | | | General Motors Co. | | | | |

| | 3,321 | | Expiration: June 2013, Exercise Price: $19.00 | | | 99,630 | |

| | 3,179 | | Expiration: June 2013, Exercise Price: $20.00 | | | 120,802 | |

| | | | H&R Block, Inc. | | | | |

| | 4,708 | | Expiration: January 2013, Exercise Price: $10.00 | | | 11,770 | |

| | | | Hertz Global Holdings, Inc. | | | | |

| | 11,006 | | Expiration: March 2013, Exercise Price: $10.00 | | | 27,515 | |

| | 9,822 | | Expiration: March 2013, Exercise Price: $11.00 | | | 98,220 | |

| | | | Hess Corporation | | | | |

| | 3,732 | | Expiration: February 2013, Exercise Price: $37.50 | | | 57,846 | |

| | 5,604 | | Expiration: February 2013, Exercise Price: $40.00 | | | 140,100 | |

| | 3,289 | | Expiration: February 2013, Exercise Price: $42.50 | | | 120,049 | |

| | | | Huntsman Corporation | | | | |

| | 22,890 | | Expiration: January 2013, Exercise Price: $11.00 | | | 57,225 | |

| | 5,882 | | Expiration: February 2013, Exercise Price: $10.00 | | | 29,410 | |

| | | | iShares Russell 2000 Index Fund | | | | |

| | 4,650 | | Expiration: February 2013, Exercise Price: $82.00 | | | 716,100 | |

| | | | J.C. Penney Company, Inc. | | | | |

| | 4,276 | | Expiration: January 2013, Exercise Price: $16.00 | | | 94,072 | |

| | 1,951 | | Expiration: January 2013, Exercise Price: $17.50 | | | 87,795 | |

| | 9,113 | | Expiration: February 2013, Exercise Price: $15.00 | | | 423,754 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | KeyCorp | | | |

| | 33,059 | | Expiration: March 2013, Exercise Price: $7.00 | | $ | 314,060 | |

| | | | Lamar Advertising Company Class A | | | | |

| | 11,466 | | Expiration: January 2013, Exercise Price: $28.00 | | | 85,995 | |

| | | | Materials Select Sector SPDR Trust | | | | |

| | 317 | | Expiration: March 2013, Exercise Price: $38.00 | | | 51,354 | |

| | | | McGraw-Hill Companies, Inc. | | | | |

| | 10,795 | | Expiration: February 2013, Exercise Price: $40.50 | | | 53,975 | |

| | | | Mead Johnson Nutrition Co. | | | | |

| | 988 | | Expiration: February 2013, Exercise Price: $60.00 | | | 65,208 | |

| | | | Murphy Oil Corporation | | | | |

| | 1,561 | | Expiration: January 2013, Exercise Price: $47.50 | | | 7,805 | |

| | 6,076 | | Expiration: January 2013, Exercise Price: $50.00 | | | 60,760 | |

| | 2,223 | | Expiration: January 2013, Exercise Price: $52.50 | | | 33,345 | |

| | 1,766 | | Expiration: April 2013, Exercise Price: $45.00 | | | 83,885 | |

| | | | Navistar International Corporation | | | | |

| | 7,422 | | Expiration: April 2013, Exercise Price: $12.00 | | | 185,550 | |

| | | | News Corporation Class A | | | | |

| | 14,161 | | Expiration: April 2013, Exercise Price: $20.00 | | | 247,817 | |

| | | | Pfizer, Inc. | | | | |

| | 10,918 | | Expiration: March 2013, Exercise Price: $22.00 | | | 163,770 | |

| | | | The Procter & Gamble Company | | | | |

| | 2,827 | | Expiration: January 2013, Exercise Price: $55.00 | | | 16,962 | |

| | | | SPDR S&P 500 ETF Trust | | | | |

| | 933 | | Expiration: January 2013, Exercise Price: $140.00 | | | 111,027 | |

| | 9,773 | | Expiration: January 2013, Exercise Price: $141.00 | | | 1,417,085 | |

| | | | Sprint Nextel Corporation | | | | |

| | 18,788 | | Expiration: January 2014, Exercise Price: $10.00 | | | 11,554,620 | |

| | | | The Timken Company | | | | |

| | 2,517 | | Expiration: March 2013, Exercise Price: $35.00 | | | 50,340 | |

| | | | Tyco International Ltd. | | | | |

| | 7,696 | | Expiration: January 2013, Exercise Price: $24.00 | | | 46,176 | |

| | | | Valero Energy Corporation | | | | |

| | 6,144 | | Expiration: June 2013, Exercise Price: $28.00 | | | 700,416 | |

| | | | Verizon Communications, Inc. | | | | |

| | 2,157 | | Expiration: January 2013, Exercise Price: $37.00 | | | 12,942 | |

| | 4,457 | | Expiration: February 2013, Exercise Price: $36.00 | | | 42,341 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | Visteon Corporation | | | |

| | 1,412 | | Expiration: March 2013, Exercise Price: $40.00 | | $ | 31,770 | |

| | 1,867 | | Expiration: March 2013, Exercise Price: $45.00 | | | 116,688 | |

| | | | Williams Companies, Inc. | | | | |

| | 11,381 | | Expiration: February 2013, Exercise Price: $27.00 | | | 91,048 | |

| | | | Yahoo! Inc. | | | | |

| | 6,233 | | Expiration: January 2013, Exercise Price: $12.50 | | | 6,233 | |

| | | | TOTAL PURCHASED PUT OPTIONS (Cost $29,940,939) | | | 20,117,426 | |

| | | | | | | | |

| Principal Amount | | | | |

| | | | | |

| ESCROW NOTES — 0.01% | | | | |

| $ | 601,200 | | Delphi Financial Class Action Trust Escrow (a)(d) | | | 420,840 | |

| | | | TOTAL ESCROW NOTES (Cost $0) | | | 420,840 | |

| | | | | | | | |

| Shares | | | | | | |

| | | | | |

| SHORT-TERM INVESTMENTS — 21.22% | | | | |

| | 195,821,594 | | BlackRock Liquidity Funds TempFund Portfolio, 0.14% (c)(g) | | | 195,821,594 | |

| | 247,000,000 | | Fidelity Institutional Government Portfolio, 0.01% (c)(e) | | | 247,000,000 | |

| | 247,000,000 | | Goldman Sachs Financial Square Money Market Fund, 0.14% (c)(g) | | | 247,000,000 | |

| | 247,000,000 | | The Liquid Asset Portfolio, 0.15% (c)(g) | | | 247,000,000 | |

| | | | TOTAL SHORT-TERM INVESTMENTS | | | | |

| | | | (Cost $936,821,594) | | | 936,821,594 | |

| | | | TOTAL INVESTMENTS | | | | |

| | | | (Cost $4,075,208,193) — 94.30% | | $ | 4,164,126,508 | |

Percentages are stated as a percent of net assets.

ADR — American Depository Receipt

ETF — Exchange-Traded Fund

PLC — Public Limited Company

| (a) | Non-income producing security. |

| (c) | The rate quoted is the annualized seven-day yield as of December 31, 2012. |

| (d) | Security fair valued by the Adviser in good faith in accordance with the policies adopted by the Board of Trustees. |

| (e) | All or a portion of the shares have been committed as collateral for open securities sold short. |

| (f) | All or a portion of the shares have been committed as collateral for written option contracts. |

| (g) | All or a portion of the shares have been committed as collateral for swap contracts. |

| (h) | All or a portion of the shares have been committed as collateral for forward currency exchange contracts. |

| (i) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration normally to qualified institutional buyers. As of December 31, 2012, these securities represented 0.04% of total net assets. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Funds Services, LLC.

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF SECURITIES SOLD SHORT

December 31, 2012

| Shares | | | | Value | |

| | | | |

| COMMON STOCKS | | | |

| | 63,589 | | Aetna, Inc. | | $ | 2,944,171 | |

| | 1,528,270 | | ASML Holding N.V. — ADR | | | 98,435,871 | |

| | 2,843,758 | | Comcast Corporation Class A | | | 106,299,674 | |

| | 225,300 | | Discovery Communications, Inc. Class A | | | 14,302,044 | |

| | 58,170 | | Expedia, Inc. | | | 3,574,546 | |

| | 42,808 | | FirstMerit Corporation | | | 607,446 | |

| | 122,750 | | IntercontinentalExchange, Inc. | | | 15,197,677 | |

| | 92,500 | | Leucadia National Corporation | | | 2,200,575 | |

| | 212,991 | | M & T Bank Corporation | | | 20,973,224 | |

| | 10,710 | | Markel Corporation | | | 4,641,928 | |

| | 36,167 | | PVH Corporation | | | 4,014,899 | |

| | 196,750 | | TELUS Corporation (a) | | | 12,876,671 | |

| | 79,647 | | TripAdvisor, Inc. | | | 3,341,988 | |

| | | | | | | 289,410,714 | |

| | | | | | | | |

| Principal Amount | | | | |

| | | | | |

| CORPORATE BONDS | | | | |

| | | | SPX Corporation | | | | |

| $ | 2,000,000 | | 6.875%, 9/1/2017 | | | 2,240,000 | |

| | | | TOTAL SECURITIES SOLD SHORT | | | | |

| | | | (Proceeds $257,724,348) | | $ | 291,650,714 | |

ADR — American Depository Receipt

(a)Foreign security.

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF OPTIONS WRITTEN

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | | |

| CALL OPTIONS WRITTEN | | | |

| | | Abbott Laboratories | | | |

| | 16,035 | | Expiration: February 2013, Exercise Price: $65.00 | | $ | 2,605,688 | |

| | | | Aetna, Inc. | | | | |

| | 13,543 | | Expiration: January 2013, Exercise Price: $36.00 | | | 13,949,290 | |

| | 835 | | Expiration: January 2013, Exercise Price: $39.00 | | | 609,550 | |

| | 834 | | Expiration: January 2013, Exercise Price: $40.00 | | | 529,590 | |

| | | | American International Group, Inc. | | | | |

| | 5,880 | | Expiration: February 2013, Exercise Price: $30.00 | | | 3,263,400 | |

| | 6,492 | | Expiration: February 2013, Exercise Price: $32.00 | | | 2,499,420 | |

| | 10,182 | | Expiration: February 2013, Exercise Price: $33.00 | | | 3,105,510 | |

| | | | Anadarko Petroleum Corporation | | | | |

| | 8,037 | | Expiration: February 2013, Exercise Price: $65.00 | | | 8,117,370 | |

| | | | BP PLC — ADR | | | | |

| | 14,021 | | Expiration: January 2013, Exercise Price: $40.00 | | | 2,692,032 | |

| | 4,680 | | Expiration: January 2013, Exercise Price: $41.00 | | | 549,900 | |

| | | | CenturyLink, Inc. | | | | |

| | 1,221 | | Expiration: January 2013, Exercise Price: $39.00 | | | 73,260 | |

| | 11,519 | | Expiration: January 2013, Exercise Price: $40.00 | | | 201,582 | |

| | 6,106 | | Expiration: April 2013, Exercise Price: $38.00 | | | 1,175,405 | |

| | | | Chesapeake Energy Corporation | | | | |

| | 14,570 | | Expiration: January 2013, Exercise Price: $17.50 | | | 393,390 | |

| | | | Chicago Bridge & Iron Company N.V. | | | | |

| | 6,270 | | Expiration: April 2013, Exercise Price: $38.00 | | | 5,548,950 | |

| | | | Clearwire Corporation Class A | | | | |

| | 11,621 | | Expiration: January 2013, Exercise Price: $3.00 | | | 58,105 | |

| | | | Constellation Brands, Inc. Class A | | | | |

| | 3,754 | | Expiration: January 2013, Exercise Price: $32.50 | | | 1,313,900 | |

| | 1,843 | | Expiration: January 2013, Exercise Price: $35.00 | | | 322,525 | |

| | | | Corrections Corporation of America | | | | |

| | 11,873 | | Expiration: June 2013, Exercise Price: $33.00 | | | 4,867,930 | |

| | 7,614 | | Expiration: June 2013, Exercise Price: $34.00 | | | 2,741,040 | |

| | | | Dean Foods Company | | | | |

| | 16,667 | | Expiration: March 2013, Exercise Price: $15.00 | | | 3,500,070 | |

| | 12,426 | | Expiration: June 2013, Exercise Price: $16.00 | | | 2,609,460 | |

| | | | Dole Food Company, Inc. | | | | |

| | 10,783 | | Expiration: January 2013, Exercise Price: $11.00 | | | 754,810 | |

| | 10,005 | | Expiration: January 2013, Exercise Price: $12.50 | | | 100,050 | |

| | 3,737 | | Expiration: April 2013, Exercise Price: $11.00 | | | 495,152 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF OPTIONS WRITTEN (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | Eli Lilly & Company | | | |

| | 5,775 | | Expiration: January 2013, Exercise Price: $47.00 | | $ | 1,495,725 | |

| | | | Freeport-McMoRan Copper & Gold, Inc. | | | | |

| | 3,371 | | Expiration: February 2013, Exercise Price: $27.00 | | | 2,435,547 | |

| | 11,763 | | Expiration: February 2013, Exercise Price: $28.00 | | | 7,351,875 | |

| | 10,122 | | Expiration: May 2013, Exercise Price: $27.00 | | | 7,616,805 | |

| | | | General Motors Co. | | | | |

| | 3,321 | | Expiration: June 2013, Exercise Price: $25.00 | | | 1,643,895 | |

| | 3,179 | | Expiration: June 2013, Exercise Price: $26.00 | | | 1,347,896 | |

| | | | Hertz Global Holdings, Inc. | | | | |

| | 11,006 | | Expiration: March 2013, Exercise Price: $13.00 | | | 3,852,100 | |

| | 19,645 | | Expiration: March 2013, Exercise Price: $14.00 | | | 5,205,925 | |

| | | | Hess Corporation | | | | |

| | 5,614 | | Expiration: February 2013, Exercise Price: $45.00 | | | 4,785,935 | |

| | 4,349 | | Expiration: February 2013, Exercise Price: $47.50 | | | 2,772,488 | |

| | 3,289 | | Expiration: February 2013, Exercise Price: $50.00 | | | 1,447,160 | |

| | | | Huntsman Corporation | | | | |

| | 6,451 | | Expiration: January 2013, Exercise Price: $15.00 | | | 645,100 | |

| | 5,882 | | Expiration: February 2013, Exercise Price: $13.00 | | | 1,794,010 | |

| | 10,519 | | Expiration: May 2013, Exercise Price: $14.00 | | | 2,787,535 | |

| | | | IntercontinentalExchange, Inc. | | | | |

| | 2,662 | | Expiration: June 2013, Exercise Price: $110.00 | | | 4,565,330 | |

| | | | J.C. Penney Company, Inc. | | | | |

| | 4,276 | | Expiration: January 2013, Exercise Price: $20.00 | | | 461,808 | |

| | 1,951 | | Expiration: January 2013, Exercise Price: $21.00 | | | 138,521 | |

| | 9,113 | | Expiration: February 2013, Exercise Price: $18.00 | | | 2,615,431 | |

| | | | KeyCorp | | | | |

| | 33,059 | | Expiration: March 2013, Exercise Price: $8.00 | | | 2,347,189 | |

| | | | Lamar Advertising Company Class A | | | | |

| | 22,932 | | Expiration: January 2013, Exercise Price: $35.00 | | | 8,828,820 | |

| | | | Leucadia National Corporation | | | | |

| | 8,728 | | Expiration: March 2013, Exercise Price: $20.00 | | | 3,491,200 | |

| | | | M & T Bank Corporation | | | | |

| | 17 | | Expiration: January 2013, Exercise Price: $85.00 | | | 23,035 | |

| | 729 | | Expiration: April 2013, Exercise Price: $85.00 | | | 1,020,600 | |

| | 1,922 | | Expiration: April 2013, Exercise Price: $95.00 | | | 1,153,200 | |

| | | | McGraw-Hill Companies, Inc. | | | | |

| | 3,689 | | Expiration: February 2013, Exercise Price: $46.50 | | | 3,061,870 | |

| | 7,105 | | Expiration: February 2013, Exercise Price: $47.50 | | | 5,186,650 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF OPTIONS WRITTEN (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | McMoRan Exploration Co. | | | |

| | 23,520 | | Expiration: February 2013, Exercise Price: $15.00 | | $ | 2,540,160 | |

| | | | Mead Johnson Nutrition Co. | | | | |

| | 988 | | Expiration: February 2013, Exercise Price: $65.00 | | | 283,556 | |

| | | | MetroPCS Communications, Inc. | | | | |

| | 61,945 | | Expiration: January 2013, Exercise Price: $10.00 | | | 2,168,075 | |

| | 11,280 | | Expiration: January 2013, Exercise Price: $11.00 | | | 169,200 | |

| | 14,699 | | Expiration: February 2013, Exercise Price: $9.00 | | | 1,653,638 | |

| | 4,203 | | Expiration: February 2013, Exercise Price: $10.00 | | | 210,150 | |

| | 21,459 | | Expiration: May 2013, Exercise Price: $9.00 | | | 3,111,555 | |

| | 4,203 | | Expiration: May 2013, Exercise Price: $10.00 | | | 361,458 | |

| | | | Murphy Oil Corporation | | | | |

| | 1,561 | | Expiration: January 2013, Exercise Price: $55.00 | | | 749,280 | |

| | 6,869 | | Expiration: January 2013, Exercise Price: $57.50 | | | 1,923,320 | |

| | 2,223 | | Expiration: January 2013, Exercise Price: $60.00 | | | 288,990 | |

| | 1,766 | | Expiration: April 2013, Exercise Price: $55.00 | | | 1,130,240 | |

| | | | Navistar International Corporation | | | | |

| | 7,422 | | Expiration: April 2013, Exercise Price: $16.00 | | | 4,861,410 | |

| | | | News Corporation Class A | | | | |

| | 14,161 | | Expiration: April 2013, Exercise Price: $24.00 | | | 3,257,030 | |

| | | | NYSE Euronext | | | | |

| | 1,639 | | Expiration: March 2013, Exercise Price: $21.00 | | | 1,733,242 | |

| | | | Pfizer, Inc. | | | | |

| | 10,918 | | Expiration: March 2013, Exercise Price: $25.00 | | | 786,096 | |

| | | | The Procter & Gamble Company | | | | |

| | 2,802 | | Expiration: January 2013, Exercise Price: $65.00 | | | 875,625 | |

| | | | PSS World Medical, Inc. | | | | |

| | 1,208 | | Expiration: February 2013, Exercise Price: $30.00 | | | 3,020 | |

| | | | PVH Corporation | | | | |

| | 2,578 | | Expiration: March 2013, Exercise Price: $95.00 | | | 4,524,390 | |

| | | | Robbins & Myers, Inc. | | | | |

| | 6,234 | | Expiration: January 2013, Exercise Price: $60.00 | | | 31,170 | |

| | | | Sprint Nextel Corporation | | | | |

| | 18,189 | | Expiration: January 2013, Exercise Price: $5.50 | | | 400,158 | |

| | 13,507 | | Expiration: February 2013, Exercise Price: $5.50 | | | 364,689 | |

| | 41,449 | | Expiration: February 2013, Exercise Price: $6.00 | | | 207,245 | |

| | | | The Timken Company | | | | |

| | 5,034 | | Expiration: March 2013, Exercise Price: $40.00 | | | 4,278,900 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF OPTIONS WRITTEN (continued)

December 31, 2012

| Contracts (100 shares per contract) | | Value | |

| | | Tyco International Ltd. | | | |

| | 7,696 | | Expiration: January 2013, Exercise Price: $27.00 | | $ | 1,816,256 | |

| | | | Valero Energy Corporation | | | | |

| | 9,217 | | Expiration: June 2013, Exercise Price: $32.00 | | | 3,917,225 | |

| | | | Verizon Communications, Inc. | | | | |

| | 2,157 | | Expiration: January 2013, Exercise Price: $42.00 | | | 295,509 | |

| | 4,457 | | Expiration: February 2013, Exercise Price: $41.00 | | | 1,067,452 | |

| | | | Visteon Corporation | | | | |

| | 2,805 | | Expiration: March 2013, Exercise Price: $45.00 | | | 2,664,750 | |

| | 1,867 | | Expiration: March 2013, Exercise Price: $50.00 | | | 1,017,515 | |

| | | | Williams Companies, Inc. | | | | |

| | 11,381 | | Expiration: February 2013, Exercise Price: $31.00 | | | 2,572,106 | |

| | | | Xstrata PLC | | | | |

| | 10,240 | | Expiration: February 2013, Exercise Price: GBP 10.00 (a) | | | 1,272,535 | |

| | 40,960 | | Expiration: February 2013, Exercise Price: GBP 9.80 (a) | | | 6,121,472 | |

| | | | | | | 196,810,446 | |

| PUT OPTIONS WRITTEN | | | | |

| | | | iShares Russell 2000 Index Fund | | | | |

| | 2,325 | | Expiration: February 2013, Exercise Price: $78.00 | | | 174,375 | |

| | | | SPDR S&P 500 ETF Trust | | | | |

| | 933 | | Expiration: January 2013, Exercise Price: $134.00 | | | 36,387 | |

| | 9,774 | | Expiration: January 2013, Exercise Price: $135.00 | | | 430,056 | |

| | | | Sprint Nextel Corporation | | | | |

| | 9,394 | | Expiration: January 2014, Exercise Price: $4.00 | | | 685,762 | |

| | | | | | | 1,326,580 | |

| | | | TOTAL OPTIONS WRITTEN | | | | |

| | | | (Premiums received $202,586,126) | | $ | 198,137,026 | |

ADR — American Depository Receipt

ETF — Exchange-Traded Fund

GBP — British Pound

PLC — Public Limited Company

(a) Level 2 security. Please see Note 2 for more information.

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF FORWARD CURRENCY EXCHANGE CONTRACTS*

December 31, 2012

| | | | | | | | | U.S. $ | | | | | | | | U.S. $ | | | Unrealized | |

| Settlement | | Currency to | | | Value at | | | Currency to | | | Value at | | | Appreciation | |

| Date | | be Delivered | | | Dec. 31, 2012 | | | be Received | | | Dec. 31, 2012 | | | (Depreciation) | |

| 1/16/13 | | | | 1,903,391 | | Australian Dollars | | | $ | 1,974,111 | | | | 1,937,081 | | U.S. Dollars | | | $ | 1,937,081 | | | $ | (37,030 | ) |

| 1/16/13 | | | | 1,965,724 | | U.S. Dollars | | | | 1,965,724 | | | | 1,903,391 | | Australian Dollars | | | | 1,974,111 | | | | 8,387 | |

| 3/20/13 | | | | 2,627,932 | | Australian Dollars | | | | 2,713,161 | | | | 2,756,964 | | U.S. Dollars | | | | 2,756,964 | | | | 43,803 | |

| 5/8/13 | | | | 34,154,492 | | Australian Dollars | | | | 35,141,793 | | | | 34,998,192 | | U.S. Dollars | | | | 34,998,192 | | | | (143,601 | ) |

| 7/10/13 | | | | 6,705,949 | | Australian Dollars | | | | 6,869,927 | | | | 6,882,807 | | U.S. Dollars | | | | 6,882,807 | | | | 12,880 | |

| 1/9/13 | | | | 27,782,952 | | British Pounds | | | | 45,131,214 | | | | 44,645,398 | | U.S. Dollars | | | | 44,645,398 | | | | (485,816 | ) |

| 1/9/13 | | | | 6,731,217 | | U.S. Dollars | | | | 6,731,217 | | | | 4,166,200 | | British Pounds | | | | 6,767,663 | | | | 36,446 | |

| 2/26/13 | | | | 50,222,088 | | British Pounds | | | | 81,569,221 | | | | 81,191,589 | | U.S. Dollars | | | | 81,191,589 | | | | (377,632 | ) |

| 3/15/13 | | | | 56,764,667 | | British Pounds | | | | 92,190,043 | | | | 91,198,664 | | U.S. Dollars | | | | 91,198,664 | | | | (991,379 | ) |

| 1/4/13 | | | | 193,865,750 | | Canadian Dollars | | | | 194,882,480 | | | | 195,173,412 | | U.S. Dollars | | | | 195,173,412 | | | | 290,932 | |

| 3/20/13 | | | | 931,002 | | Canadian Dollars | | | | 934,387 | | | | 941,907 | | U.S. Dollars | | | | 941,907 | | | | 7,520 | |

| 6/12/13 | | | | 14,777,140 | | Canadian Dollars | | | | 14,800,922 | | | | 14,919,592 | | U.S. Dollars | | | | 14,919,592 | | | | 118,670 | |

| 1/9/13 | | | | 33,250,000 | | Euros | | | | 43,891,719 | | | | 43,271,051 | | U.S. Dollars | | | | 43,271,051 | | | | (620,668 | ) |

| 1/9/13 | | | | 43,089,739 | | U.S. Dollars | | | | 43,089,739 | | | | 33,250,000 | | Euros | | | | 43,891,719 | | | | 801,980 | |

| 1/24/13 | | | | 119,107,262 | | Euros | | | | 157,249,404 | | | | 152,509,852 | | U.S. Dollars | | | | 152,509,852 | | | | (4,739,552 | ) |

| 1/24/13 | | | | 157,227,672 | | U.S. Dollars | | | | 157,227,672 | | | | 119,107,262 | | Euros | | | | 157,249,404 | | | | 21,732 | |

| 3/7/13 | | | | 107,553,707 | | Euros | | | | 142,047,912 | | | | 142,237,627 | | U.S. Dollars | | | | 142,237,627 | | | | 189,715 | |

| 3/13/13 | | | | 15,989,193 | | Euros | | | | 21,118,440 | | | | 20,776,038 | | U.S. Dollars | | | | 20,776,038 | | | | (342,402 | ) |

| 3/13/13 | | | | 20,820,711 | | U.S. Dollars | | | | 20,820,711 | | | | 15,989,193 | | Euros | | | | 21,118,440 | | | | 297,729 | |

| 4/15/13 | | | | 2,723,288,750 | | Japanese Yen | | | | 31,461,233 | | | | 32,937,564 | | U.S. Dollars | | | | 32,937,564 | | | | 1,476,331 | |

| 2/15/13 | | | | 23,955,846 | | Singapore Dollar | | | | 19,609,622 | | | | 19,593,380 | | U.S. Dollars | | | | 19,593,380 | | | | (16,242 | ) |

| | | | | | | | | | $ | 1,121,420,652 | | | | | | | | | $ | 1,116,972,455 | | | $ | (4,448,197 | ) |

| * | JPMorgan Chase & Co. Inc. is the counterparty for all open forward currency exchange contracts held by the Fund as of December 31, 2012. |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

SCHEDULE OF SWAP CONTRACTS

December 31, 2012

| | | | | | | | | | | | Unrealized | | | |

| Termination | | | | | | | | | | Appreciation | | | |

| Date | | Security | | Shares | | | Notional | | | (Depreciation)* | | | Counterparty |

| LONG SWAP CONTRACTS | | | | | | | | | | | |

| 7/12/13 | | | Aegis Group PLC | | | 23,651,944 | | | $ | 89,748,247 | | | $ | 1,673,216 | | | JPMorgan Chase & Co. Inc. |

| 9/19/13 | | | Australian Infrastructure Fund | | | 10,428,853 | | | | 33,740,155 | | | | 409,167 | | | JPMorgan Chase & Co. Inc. |

| 7/5/13 | | | British Sky Broadcasting | | | | | | | | | | | | | | |

| | | | Group PLC | | | 3,313,600 | | | | 41,129,724 | | | | 5,813,808 | | | Merrill Lynch & Co. Inc. |

| 5/1/13 | | | Charter Hall Office REIT | | | | | | | | | | | | | | |

| | | | Contingent Consideration (a) | | | 2,032,447 | | | | — | ** | | | — | ** | | JPMorgan Chase & Co. Inc. |

| 11/20/13 | | | CNH Global N.V. (a) | | | 843,439 | | | | 33,745,994 | | | | (6,353,891 | ) | | Merrill Lynch & Co. Inc. |

| 10/10/13 | | | eAccess Ltd. (a) | | | 35,220 | | | | 25,737,771 | | | | 5,367,742 | | | JPMorgan Chase & Co. Inc. |

| 11/30/13 | | | GrainCorp. Ltd. | | | 570,719 | | | | 7,308,793 | | | | 221,203 | | | JPMorgan Chase & Co. Inc. |

| 6/25/13 | | | Grupo Modelo, S.A. de C.V. | | | 11,474,863 | | | | 102,974,044 | | | | 1,069,468 | | | JPMorgan Chase & Co. Inc. |

| 10/18/13 | | | Hillgrove Resources Ltd. | | | 13,139,699 | | | | 1,566,909 | | | | 190,952 | | | JPMorgan Chase & Co. Inc. |

| 12/6/13 | | | Jupiter Telecommunications | | | | | | | | | | | | | | |

| | | | Co., Ltd. | | | 24,479 | | | | 30,682,213 | | | | (1,485,862 | ) | | JPMorgan Chase & Co. Inc. |

| 11/2/13 | | | TELUS Corporation (non-voting) | | | 117,600 | | | | 7,653,529 | | | | 88,313 | | | The Goldman Sachs Group, Inc. |

| 2/22/13 | | | TELUS Corporation (non-voting) | | | 2,167,790 | | | | 141,082,006 | | | | 17,431,009 | | | Merrill Lynch & Co. Inc. |

| 3/8/13 | | | TNT Express NV | | | 1,229,700 | | | | 13,635,701 | | | | (1,454,198 | ) | | Merrill Lynch & Co. Inc. |

| 3/20/13 | | | TNT Express NV | | | 10,091,743 | | | | 111,903,705 | | | | (7,542,368 | ) | | JPMorgan Chase & Co. Inc. |

| 12/19/13 | | | Xstrata PLC | | | 43,473 | | | | 748,189 | | | | 9,833 | | | The Goldman Sachs Group, Inc. |

| 5/18/13 | | | Xstrata PLC | | | 7,602,860 | | | | 130,848,566 | | | | 11,590,374 | | | JPMorgan Chase & Co. Inc. |

| SHORT SWAP CONTRACTS | | | | | | | | | | | | | | |

| 10/3/13 | | | Fiat Industrial S.p.A. | | | (13,427 | ) | | | (146,492 | ) | | | (9,086 | ) | | JPMorgan Chase & Co. Inc. |

| 11/20/13 | | | Fiat Industrial S.p.A. | | | (3,215,676 | ) | | | (35,083,733 | ) | | | (671,079 | ) | | Merrill Lynch & Co. Inc. |

| 12/19/13 | | | Glencore International PLC | | | (123,598 | ) | | | (706,694 | ) | | | (1,923 | ) | | The Goldman Sachs Group, Inc. |

| 4/10/13 | | | Glencore International PLC | | | (7,575,524 | ) | | | (43,314,422 | ) | | | (2,072,826 | ) | | JPMorgan Chase & Co. Inc. |

| 10/10/13 | | | SoftBank Corporation | | | (707,370 | ) | | | (25,801,674 | ) | | | (1,653,394 | ) | | JPMorgan Chase & Co. Inc. |

| 11/2/13 | | | TELUS Corporation | | | (117,600 | ) | | | (7,723,161 | ) | | | (46,924 | ) | | The Goldman Sachs Group, Inc. |

| 2/22/13 | | | TELUS Corporation | | | (2,167,790 | ) | | | (142,365,576 | ) | | | (17,513,519 | ) | | Merrill Lynch & Co. Inc. |

| | | | | | | | | | | | | | $ | 5,060,015 | | | |

PLC — Public Limited Company

REIT – Real Estate Investment Trust

| * | Based on the net value of each broker, unrealized appreciation is a receivable and unrealized depreciation is a payable. |

| ** | Value is less than $0.50. |

| (a) | Security fair valued by the Adviser in good faith in accordance with the policies adopted by the Board of Trustees. |

The accompanying notes are an integral part of these financial statements.

The Merger Fund

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2012

| ASSETS: | | | | | | |

| Investments, at value (Cost $4,075,208,193) | | | | | $ | 4,164,126,508 | |

| Cash | | | | | | 65,828 | |

| Cash held in foreign currency (Cost $195,134,122) | | | | | | 194,898,713 | |

| Deposits at brokers | | | | | | 321,501,025 | |

| Receivable from brokers | | | | | | 257,724,348 | |

| Receivable for investments sold | | | | | | 7,138,333 | |

| Receivable for forward currency exchange contracts | | | | | | 3,306,125 | |

| Receivable for swap contracts | | | | | | 7,807,885 | |

| Receivable for fund shares issued | | | | | | 13,187,870 | |

| Dividends and interest receivable | | | | | | 16,580,765 | |

| Prepaid expenses and other receivables | | | | | | 113,178 | |

| Total Assets | | | | | | 4,986,450,578 | |

| LIABILITIES: | | | | | | | |

| Securities sold short, at value (proceeds of $257,724,348) | | $ | 291,650,714 | | | | | |

| Written option contracts, at value (premiums received $202,586,126) | | | 198,137,026 | | | | | |

| Payable for forward currency exchange contracts | | | 7,754,322 | | | | | |

| Payable for swap contracts | | | 2,747,870 | | | | | |

| Payable for closed swap contracts | | | 8,343,175 | | | | | |

| Payable for investments purchased | | | 40,408,721 | | | | | |

| Payable for fund shares redeemed | | | 13,200,013 | | | | | |

| Distribution fees payable | | | 4,437,159 | | | | | |

| Dividends and interest payable | | | 2,388,763 | | | | | |

| Accrued expenses and other liabilities | | | 1,692,956 | | | | | |

| Total Liabilities | | | | | | | 570,760,719 | |

| NET ASSETS | | | | | | $ | 4,415,689,859 | |

| NET ASSETS CONSIST OF: | | | | | | | | |

| Accumulated undistributed net investment loss | | | | | | $ | (628,060 | ) |

| Accumulated net realized loss on investments, securities | | | | | | | | |

| sold short, written option contracts expired or closed, swap contracts, | | | | | | | | |

| foreign currency translation and forward currency exchange contracts | | | | | | | (87,965,411 | ) |

| Net unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments | | $ | 88,918,315 | | | | | |

| Securities sold short | | | (33,926,366 | ) | | | | |

| Written option contracts | | | 4,449,100 | | | | | |

| Swap contracts | | | 5,060,015 | | | | | |

| Foreign currency translation | | | (235,905 | ) | | | | |

| Forward currency exchange contracts | | | (4,448,197 | ) | | | | |

| Net unrealized appreciation | | | | | | | 59,816,962 | |