| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT |

| OF |

| REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act file number: 811-03599 |

| Name of Registrant: The Royce Fund |

| Address of Registrant: 745 Fifth Avenue |

| New York, NY 10151 |

| Name and address of agent for service | John E. Denneen, Esq. 745 Fifth Avenue New York, NY 10151 |

Registrant’s telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2018

Date of reporting period: January 1, 2018 – June 30, 2018

Item 1. Reports to Shareholders.

|

| JUNE 30, 2018 | ||

| 2018 Semiannual | ||

| Review and Report to Shareholders | ||

| Royce Dividend Value Fund | |||

| Royce Global Financial Services Fund | |||

| Royce International Discovery Fund (formerly named Royce International Micro-Cap Fund) | |||

| Royce International Premier Fund | |||

| Royce Low-Priced Stock Fund | |||

| Royce Micro-Cap Fund | |||

| Royce Micro-Cap Opportunity Fund | |||

| Royce Opportunity Fund | |||

| Royce Pennsylvania Mutual Fund | |||

| Royce Premier Fund | |||

| Royce Small-Cap Leaders Fund | |||

| Royce Small-Cap Value Fund | |||

| Royce Small/Mid-Cap Premier Fund | |||

| Royce Smaller-Companies Growth Fund | |||

| Royce Special Equity Fund | |||

| Royce Special Equity Multi-Cap Fund | |||

| Royce Total Return Fund | |||

| roycefunds.com |  | ||

| Table of Contents | |||

| Semiannual Review | |||

| Letter to Our Shareholders | 2 | ||

| Performance and Expenses | 6 | ||

| The Royce Funds and Rolling Returns | 7 | ||

| Semiannual Report to Shareholders | |||

| Managers’ Discussions of Fund Performance | |||

Royce Dividend Value Fund | 8 | ||

Royce Global Financial Services Fund | 10 | ||

Royce International Discovery Fund (formerly named Royce International Micro-Cap Fund) | 12 | ||

Royce International Premier Fund | 14 | ||

Royce Low-Priced Stock Fund | 16 | ||

Royce Micro-Cap Fund | 18 | ||

Royce Micro-Cap Opportunity Fund | 20 | ||

Royce Opportunity Fund | 22 | ||

Royce Pennsylvania Mutual Fund | 24 | ||

Royce Premier Fund | 26 | ||

Royce Small-Cap Leaders Fund | 28 | ||

Royce Small-Cap Value Fund | 30 | ||

Royce Small/Mid-Cap Premier Fund | 32 | ||

Royce Smaller-Companies Growth Fund | 34 | ||

Royce Special Equity Fund | 36 | ||

Royce Special Equity Multi-Cap Fund | 38 | ||

Royce Total Return Fund | 40 | ||

| Schedules of Investments and Financial Statements | 42 | ||

| Notes to Financial Statements | 104 | ||

| Understanding Your Fund’s Expenses | 119 | ||

| Trustees and Officers | 121 | ||

| Board Approval of Investment Advisory Agreements | 122 | ||

| Notes to Performance and Other Important Information | 125 |

| This page is not part of the 2018 Semiannual Report to Shareholders | 1 |

Letter to Our Shareholders

| During the first six months of 2018, small-cap stocks enjoyed the good times bred by a bull market that at this writing has not yet slowed down. Although the first half began with higher volatility and stalled equities prices—and ended with a series of wild days that made the bullish second quarter feel more tumultuous than it was—the overall direction of U.S. markets has remained positive, particularly for smaller stocks. For the year-to-date period ended June 30, 2018, the small-cap Russell 2000 Index gained 7.7%, well ahead of both the large-cap Russell 1000 (+2.9%) and S&P 500 (+2.6%) Indexes, while making a new historical high on June 20. Returns were even higher for micro-cap stocks—the Russell Microcap Index advanced 10.7% for the same period. This mostly welcome absolute and relative performance took place against the backdrop of an accelerating U.S. economy, a strong job |

| market, and, in many cases, sterling corporate profit growth while at the same time global economic progress slowed, most notably in China and other large emerging markets. The major non-U.S. indexes slipped deeper into negative territory during the first half, as the combination of slower international growth, rising emerging market instability, a stronger dollar, and heightened trade war worries led investors to prefer all things domestic. (In fact, 35 of the 45 non-U.S. small-cap markets that we follow had declines in the first half of 2018, though only 26 were negative when measured in local currencies.) Still, growth continued to skew positive outside the U.S., with the important economies of Japan and Germany continuing to look solid. In this context, then, you would expect a small-cap specialist to be quite content, if not happy. This might especially be the case considering that small-caps—as well as micro-caps—have been true to their historical habit of outpacing larger companies through an economic expansion. Yet as much as we were pleased with first-half |

Equity Indexes Average Annual Total Return as of 6/30/18 (%)

| YEAR-TO-DATE1 | 1-YEAR | 5-YEAR | |||||||||||||||||||||||||

| Micro-Cap | 10.7 | Small-Cap Growth | 21.9 | Small-Cap Growth | 13.6 | ||||||||||||||||||||||

| Small-Cap Growth | 9.7 | Micro-Cap | 20.2 | Large-Cap | 13.4 | ||||||||||||||||||||||

| Small-Cap | 7.7 | Small-Cap | 17.6 | Micro-Cap | 12.8 | ||||||||||||||||||||||

| Small-Cap Value | 5.4 | Large-Cap | 14.5 | Small-Cap | 12.5 | ||||||||||||||||||||||

| Large-Cap | 2.9 | Small-Cap Value | 13.1 | Small-Cap Value | 11.2 | ||||||||||||||||||||||

1 Not annualized.

Small-Cap is represented by Russell 2000; Small-Cap Value is represented by Russell 2000 Value, Small-Cap Growth is represented by Russell 2000 Growth, Large-Cap is represented by Russell 1000, Micro-Cap is represented by Russell Microcap. For details on The Royce Funds’ performance in the period, please turn to the Managers’ Discussions that begin on page 8. Past performance is no guarantee of future results.

| 2 | This page is not part of the 2018 Semiannual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| results, we find ourselves far from blissful. A closer look at small-cap performance in the first half reveals some genuine historical oddities in spite of all looking well on the surface. Our main concern is the disconnect between the confidence of the management teams we’ve been meeting with and the relatively underwhelming performance for many cyclical industries. We anticipated that stocks in these industries would do better owing to their recent earnings strength and ongoing prospects as well as to the healthy state of the U.S. economy (each, of course, being related to the other). |

| OBSTACLE ON THE TRACK The Troublesome 10-Year Treasury Yield |

| Another related concern is the way in which the ongoing weakness of the 10-year Treasury yield is at odds with the quickened pace of U.S. economic growth—when the 10-year has been sluggish in the past, it’s often been seen as a symptom of economic weakness, and not without some justification. The fact that the economy has arguably been some distance down the road to normal for at least a couple of years remains a source of concern to us. |

| Road to Normalization: Economy vs Markets |

|

| 1 Quarterly data. Source: Bloomberg |

| We invite you to consider the following five points: through the end of June, the U.S. economy had grown for 109 consecutive months, GDP growth has converged with its long-term average, unemployment reached an 18-year low in June, personal consumption expenditure inflation hit the Fed’s 2% target in May, and short rates were rising. Additionally, we’re also seeing the early signs of inflation. Most are registering in increased commodity, raw material, and other input costs, which is historically familiar economic territory. History also shows, however, that these developments are also typically coincident with rising interest rates. So far, though, the 10-year Treasury yield has stubbornly refused to acquiesce to history—making the 10-year the major obstacle on the path back to normal in our view. |

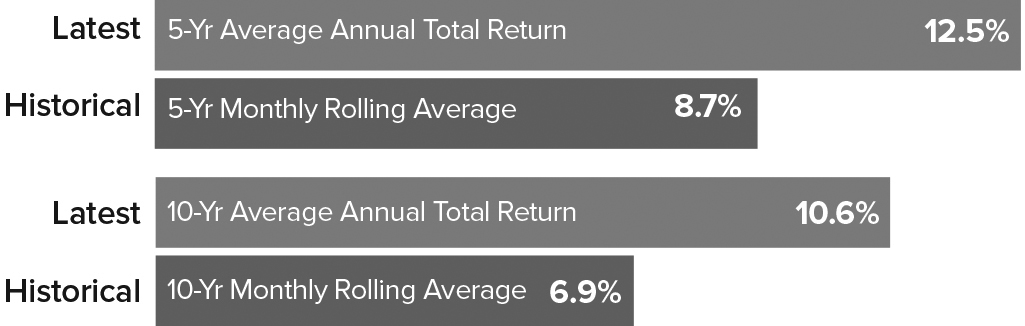

| From our perspective as highly active, valuation-sensitive small-cap specialists, the most frustrating have been those periods when the 10-year yield has fallen back. It seems to us that nearly every time it has declined over the last 18 months, the market has witnessed a subsequent flight to high yielding or growth stocks while value and economically sensitive issues struggled to keep pace. It almost seems as if investors became temporarily convinced that we had slipped back into the 2010-2015 era of quantitative easing and zero interest rates. We think it bears emphasizing that, for all its uncertainty, the current environment could not be more different. Yet the disconnect persisted into June. The critical question, then, is, what happens next? More pertinently for our investors, the question can be phrased in a more specific way as, are we likely to see a shift in small-cap style and sector leadership? We believe that we will. The second quarter saw an admittedly short-term sign when the Russell 2000 Value Index shook off five straight quarters of underperformance to outpace its small-cap growth counterpart, up 8.3% versus 7.2%. But exactly when, and under what conditions, a longer-running shift materializes remains to be seen, of course. To be sure, the kind of leadership change that we expect—from growth to value and from defensives to cyclicals—seldom occurs without a fair bit of volatility. SMALL-CAP HIGHS Returns, Valuations–and Risks Putting the issue of market turbulence aside for a moment, the timing does seem apt to us for a change. First, the two-year cumulative return at the end of June for the Russell 2000 was 46.5%—which is a wonderful, but sadly not a sustainable, pace. Second, the one-, five-, and 10-year average annual total returns for the small-cap index for the period ended June 30, 2018 were all comfortably ahead of their long-term monthly rolling averages. |

| Recent Small-Cap Returns Higher Than History Russell 2000 through 6/30/18 |

| This page is not part of the 2018 Semiannual Report to Shareholders | 3 |

| When we look at the same information for the Russell 2000 Growth Index, the contrast is even more stark, with its latest five-year return significantly in excess of its historical rolling average (+13.6% vs. +8.6%). This is one important reason why we expect a leadership shift in the form of a reversion to the mean that would favor small-cap value outperforming small-cap growth over the next five years. |

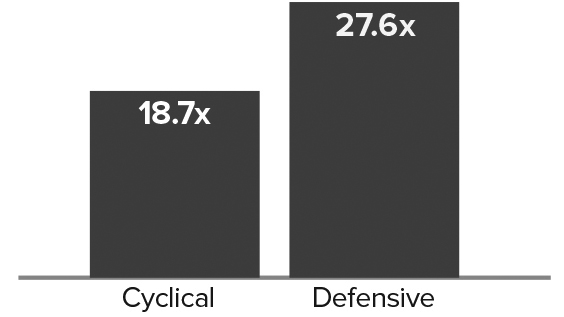

| The state of small-cap valuations also looks unsustainably high to us, particularly if we see a continued, and more consistent, rise in the 10-year yield. While the P/E ratio for the Russell 2000 did not look especially rich at the end of June, another valuation metric, the last twelve months enterprise value to earnings before interest and taxes (EV/EBIT)—which we use most frequently when examining companies—tells a different story, one that reveals higher-than-average historical valuations. The currently elevated state of returns and valuations could mean that we are entering a longish period of multiple compression, which is one reason why we prefer select small-caps with strong earnings prospects and/or modest valuations. If we see increased volatility over the balance of the year, these types of stocks look better positioned to cope with it effectively. |

| Cyclicals Cheaper than Defensives Median LTM EV/EBIT1 Ex. Negative EBIT for Russell 2000 as of 6/30/18 |

|

| Based on earnings and cash flow quality—as well as confident management teams—we are seeing superior fundamentals in selected cyclical areas that other investors are avoiding. For example, the supply/demand dynamics in a number of industries, such as semiconductors & semiconductor equipment, transportation, and chemicals, look favorable to us and do not appear to us to be fully reflected in their current valuations. Many cyclical companies appear much better positioned for intermediate-term growth than defensive and/or growth stocks. While many cyclical stocks have lagged the field over the last 18 months, they are also more reasonably priced than defensives based on EV to EBIT. We remain convinced that fundamentally strong small-cap companies, especially those with attractive-to-reasonable valuations, will become more appealing to investors as confidence in the U.S. economy continues to build. |

| 1 Last Twelve Months Enterprise Value/Earnings Before Interest and Taxes |

| Many Small-Caps Sell at a Significant Discount Bottom Three Deciles in Russell 2000 Median LTM EV/EBIT1 Ex. Negative EBIT as of 6/30/18 |

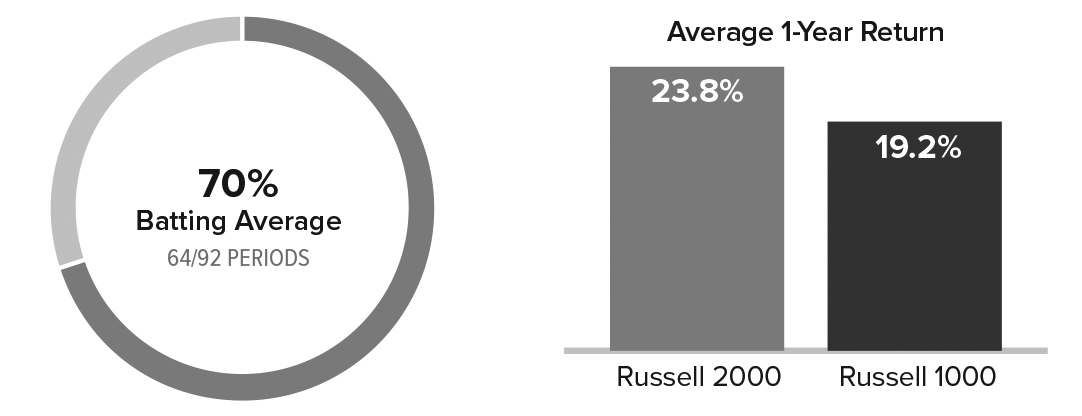

| There’s a related point that may be equally important when considering valuations: The sheer size and diversity of the small-cap asset class means that there are almost always opportunities to find what we think are promising or quality businesses trading at attractive discounts. Based on EV/EBIT, the bottom three deciles of the Russell 2000 were trading at sizable discounts compared to the median for the index as a whole at the end of June. VOLATILITY AND INTEREST RATES Both On the Rise During the first quarter, the Russell 2000 moved 1% or more in 33% of its trading days compared to 18% in all of 2017. Another volatility measure, the CBOE Russell 2000 Volatility Index (“RVX”), measures market expectations of near-term volatility conveyed by Russell 2000 stock index option prices. The RVX has averaged 24.0% per year since its inception on January 2, 2004 through June 30, 2018. Its average in 2017 was 15.9%, and its year-to-date average through the end of June 2018 was 17.5%. Eighteen months of lower volatility suggests—strongly to us—that increased volatility is likely. We also believe that the upward trend in rates is under way—and suspect that the 10-year yield will begin to move up more consistently over the next year. We see both rising rates and increased volatility as healthy. In fact, looking once more at history, we find that periods of rising rates have been favorable for small-cap stocks on both an absolute and relative basis. When the 10-Year Treasury yield was rising, the Russell 2000 outperformed the large-cap Russell 1000 in 70% of monthly rolling one-year periods for the 20-year period ended June 30, 2018 with an average one-year return of 23.8% versus 19.2% for large-cap. Our expectations for small-cap returns are more modest, though we do expect this historical relative return spread pattern to hold up. |

| 4 | This page is not part of the 2018 Semiannual Report to Shareholders |

LETTER TO OUR SHAREHOLDERS

| How Have Small-Caps Performed When Rates Were Rising? Russell 2000 vs Russell 1000 Trailing Monthly Rolling 1-Year Returns When 10-Year Treasury Yield was Rising From 6/30/98 through 6/30/18 | |

| |

| 10-Year Treasury Yield rose in 92 of 229 periods | |

| More specifically, we see rising rates as a phenomenon that should also be helpful to risk-conscious active managers in the small-cap space—primarily because it fosters an environment where better balance sheet companies are likely to be rewarded for their fiscal prudence. In other words, risk management matters. This is relevant today because of the increased leverage—specifically financial leverage—within the Russell 2000. And as rates continue to move up, the overall small-cap index looks increasingly risky. As active managers, we have the ability to screen and scrutinize small-cap businesses with better balance sheets and shy away from those that we see as having excess financial leverage. (It is worth mentioning that the market has largely ignored better balance sheet companies for much of the last 10 years.) Most of our strategies gravitate toward companies with low debt. We would rather focus on companies that have great operating leverage—but not financial leverage. With rising rates, inflation, and economic growth becoming established, the market seems to be transitioning into an environment that will favor similar qualities. | |

REASONS TO BE CHEERFUL | |

| We are therefore of two minds about the current cycle. On the one hand, we think that we could see some consolidation or a correction—the latter certainly seems more probable now than it did | |

| a year ago. Yet we remain optimistic about small-cap earnings growth and like the fundamentals of our holdings across our strategies in terms of balance sheets, cash flows, and earnings strength. It is in cyclical areas, including Industrials, the more cyclical precincts of technology, and Materials, and that we have most often uncovered what we judge to be the best combination of value, quality, and/ or growth prospects. And this has always been a function of our bottom-up process rather than a top down view of the economy. This is why many of our portfolios have had perennially higher weightings in those sectors (and while others we manage have had high weightings in Financials and Consumer Discretionary). We also long ago developed the practice of leaning into those areas of the asset class where we see excess pessimism. Investments in industries that the rest of the market is abandoning have often borne fruit, though we have learned through decades of small-cap asset management that it usually requires a great deal of patience—measured in years in many cases—before the arrival of a bountiful harvest. We think it’s worth noting that the three changes in the market environment that we expect—lower returns, higher volatility, and value/cyclical leadership—have all historically been coincident with leadership for active management. We see signs of progress that in our view place us squarely on the road to normalization, which was evident in the modest increases in bond yields and the reemergence of value’s leadership in 2018’s second quarter. We saw other equally positive signs in July, including stabilizing macro indicators from outside the U.S., a welcome rebound in the performance of many industrial companies, and ongoing earnings strength for several cyclical areas. We expect to see more signs of normalizing markets to emerge as the year goes on. |

| Sincerely, |

|  |  | ||

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon | ||

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, | ||

| Royce & Associates, LP | Co-Chief Investment Officer, | Royce & Associates, LP | ||

| Royce & Associates, LP | ||||

| July 30, 2018 |

| This page is not part of the 2018 Semiannual Report to Shareholders | 5 |

Performance and Expenses

| Performance and Expenses | |||||||||||||||||||||

| ANNUAL OPERATING EXPENSES (%) | |||||||||||||||||||||

| YTD1 | 1-YR | 5-YR | 10-YR | 15-YR | 20-YR | 45-YR/SINCE INCEPTION | INCEPTION DATE | GROSS | NET | ||||||||||||

| Royce Dividend Value Fund | -2.02 | 10.66 | 8.57 | 9.16 | N/A | N/A | 8.87 | 5/3/04 | 1.39 | 1.34 | |||||||||||

| Royce Global Financial Services Fund | 2.65 | 14.45 | 10.82 | 9.51 | N/A | N/A | 8.59 | 12/31/03 | 1.77 | 1.58 | |||||||||||

| Royce International Discovery Fund | -6.21 | 3.96 | 8.03 | N/A | N/A | N/A | 3.62 | 12/31/10 | 2.79 | 1.44 | |||||||||||

| Royce International Premier Fund | -3.08 | 10.77 | 10.10 | N/A | N/A | N/A | 7.65 | 12/31/10 | 1.65 | 1.44 | |||||||||||

| Royce Low-Priced Stock Fund | 9.34 | 18.75 | 6.61 | 4.82 | 7.51 | 8.52 | 10.25 | 12/15/93 | 1.61 | 1.58 | |||||||||||

| Royce Micro-Cap Fund | 10.22 | 13.91 | 6.36 | 5.52 | 8.64 | 8.67 | 11.02 | 12/31/91 | 1.60 | 1.58 | |||||||||||

| Royce Micro-Cap Opportunity Fund | 7.79 | 22.73 | 10.32 | N/A | N/A | N/A | 14.07 | 8/31/10 | 1.28 | 1.24 | |||||||||||

| Royce Opportunity Fund | 4.05 | 17.23 | 11.40 | 11.15 | 11.48 | 11.93 | 12.61 | 11/19/96 | 1.18 | 1.18 | |||||||||||

| Royce Pennsylvania Mutual Fund | 5.70 | 17.23 | 10.63 | 8.92 | 10.40 | 9.77 | 13.50 | N/A | 0.92 | 0.92 | |||||||||||

| Royce Premier Fund | 2.59 | 16.81 | 10.56 | 8.62 | 11.51 | 10.64 | 11.81 | 12/31/91 | 1.16 | 1.16 | |||||||||||

| Royce Small-Cap Leaders Fund | 3.64 | 12.87 | 7.50 | 7.99 | 9.66 | N/A | 9.66 | 6/30/03 | 1.59 | 1.49 | |||||||||||

| Royce Small-Cap Value Fund | 7.11 | 17.71 | 7.30 | 5.61 | 10.20 | N/A | 9.74 | 6/14/01 | 1.51 | 1.49 | |||||||||||

| Royce Small/Mid-Cap Premier Fund | -3.14 | 11.09 | 8.04 | 8.84 | 9.83 | 10.64 | 12.28 | 12/27/95 | 1.32 | 1.32 | |||||||||||

| Royce Smaller-Companies Growth Fund | 10.38 | 16.87 | 11.34 | 8.00 | 11.05 | N/A | 11.73 | 6/14/01 | 1.49 | 1.49 | |||||||||||

| Royce Special Equity Fund | -0.32 | 7.92 | 7.71 | 9.67 | 9.13 | 9.33 | 9.20 | 5/1/98 | 1.17 | 1.17 | |||||||||||

| Royce Special Equity Multi-Cap Fund | -5.67 | 2.76 | 6.20 | N/A | N/A | N/A | 8.97 | 12/31/10 | 1.39 | 1.24 | |||||||||||

| Royce Total Return Fund | 0.59 | 11.23 | 9.75 | 8.70 | 9.28 | 9.01 | 10.83 | 12/15/93 | 1.21 | 1.21 | |||||||||||

| INDEX | |||||||||||||||||||||

| Russell 2000 | 7.66 | 17.57 | 12.46 | 10.60 | 10.50 | 8.03 | N/A | N/A | N/A | N/A | |||||||||||

| Russell Microcap | 10.71 | 20.21 | 12.78 | 10.63 | 9.44 | N/A | N/A | N/A | N/A | N/A | |||||||||||

| Russell 2000 Value | 5.44 | 13.10 | 11.18 | 9.88 | 9.93 | 8.67 | N/A | N/A | N/A | N/A | |||||||||||

| Russell 2500 | 5.46 | 16.24 | 12.29 | 10.74 | 10.99 | 9.11 | N/A | N/A | N/A | N/A | |||||||||||

| Russell 1000 | 2.85 | 14.54 | 13.37 | 10.20 | 9.54 | 6.74 | N/A | N/A | N/A | N/A | |||||||||||

| Russell Global ex-U.S. Small Cap | -3.78 | 9.17 | 8.03 | 4.97 | 10.21 | 7.72 | N/A | N/A | N/A | N/A | |||||||||||

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Investment and Service Class shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund (2% for Royce International Discovery and International Premier Funds). Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.roycefunds.com. All performance and expense information reflects results of the Funds’ oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Gross annual operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and service fees, other expenses, and any applicable acquired fund fees and expenses. Net annual operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business, to the extent necessary to maintain net operating expenses at or below: 1.24% for Royce Micro-Cap Opportunity and Special Equity Multi-Cap Funds; 1.34% for Royce Dividend Value Fund; 1.44% for Royce International Discovery and International Premier Funds; 1.49% for Royce Global Financial Services, Low-Priced Stock, Micro-Cap, Small-Cap Leaders, and Small-Cap Value Funds through April 30, 2019; at or below 1.99% for Royce International Discovery Fund through April 30, 2028. Acquired fund fees and expenses reflect the estimated amount of fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies.

Service Class shares bear an annual distribution expense that is not borne by the Funds’ Investment Class. If such distribution expenses had been reflected for Funds showing Investment Class performance, returns would have been lower. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see “Primary Risks for Fund Investors” in the prospectus.) Certain Funds invest a significant portion of their respective assets in foreign companies that may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see “Investing in Foreign Securities” in the prospectus.) Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. (Please see “Primary Risk of Fund Investors” in the prospectus.) Certain Funds generally invest a significant portion of their assets in a limited number of stocks, which may involve considerably more risk than a more broadly diversified portfolio because a decline in the value of any of these stocks would cause their overall value to decline to a greater degree. A broadly diversified portfolio, however, does not ensure a profit or guarantee against loss. This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Value Index consists of the respective value stocks within the Russell 2000 as determined by Russell Investments. The Russell 2500 is an unmanaged, capitalization-weighted index of the 2,500 smallest publicly traded U.S. companies in the Russell 3000 index. The Russell 1000 is an unmanaged, capitalization-weighted index of domestic large-cap stocks. It measures the performance of the 1,000 largest publicly traded U.S. companies in the Russell 3,000 Index. The Russell Global ex-U.S. Small Cap Index is an index of global small-cap stocks, excluding the United States. The performance of an index does not represent exactly any particular investment as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

| 6 | This page is not part of the 2018 Semiannual Report to Shareholders |

The Royce Funds and Rolling Returns

We believe strongly in the idea that a long-term perspective is crucial for determining the success of an investment approach. Flourishing in an up market is wonderful, but surviving a bear market by losing less (or not at all) is equally desirable. In any case, the true tests of a portfolio’s mettle are results over bull and bear periods. This is why we prefer to examine results that include up and down market phases—primarily by looking at rolling return periods.

| When evaluating fund performance, it is common practice to review results for the most recent year (often the calendar year) along with its related longer-term trailing periods. However, a calendar-year return is not necessarily any more or less important to consider than any other 12-month period (or related trailing period). It is also true that few investors buy mutual funds on New Year’s Eve and then sell exactly five or 10 years later. Of course, the reality is that trailing returns ending last month or last quarter are the most commonly available and easily comparable results, so these otherwise arbitrary periods often drive investor decisions and flows. |

| Keeping in mind that investors will buy and sell at any time throughout any given year, we think it makes sense to examine performance over a larger series of dates. We believe rolling returns offer a more effective measure because they provide a more accurate and in-depth picture of a portfolio’s performance. Rather than “point-in-time” results anchored by the end of the month or quarter, |

| rolling returns account for the fact that investors typically do not invest at the beginning of the current five- or 10-year period but instead are in fact investing over many periods. |

| So instead of assuming that an investment was made on January 1, rolling returns calculate all of the periods starting not only in January, but also in February, March, April, etc. For example, a monthly five-year rolling return accounts for all of the five-year returns beginning at a given inception date and advancing one month sequentially. This method allows an investor to evaluate the consistency of a fund’s performance over time—including the ups and downs of market cycles. |

| We believe that rolling returns provide a particularly robust analytical tool for evaluating manager performance, especially during volatile periods when simply shifting the performance date range one or two months in either direction can paint a very different picture. |

| Royce Funds1 vs. The Benchmark2 |

| Monthly Rolling Average Annual Return Periods and Relative Results Since Fund Inception or Most Recent 20 Years through June 30, 2018 |

| Average Annual 10-Year Rolling Return | Average Annual 5-Year Rolling Return | |||||||||||||||||||||||||||||||||||||||||||

| FUND | PERIODS BEATING THE INDEX | FUND AVG (%)3 | INDEX AVG (%)3 | PERIODS BEATING THE INDEX | FUND AVG (%)3 | INDEX AVG (%)3 | ||||||||||||||||||||||||||||||||||||||

| U.S. EQUITY | ||||||||||||||||||||||||||||||||||||||||||||

| Low-Priced Stock | 54/121 | 45% | 7.2 | 6.9 | 107/181 | 59% | 8.3 | 8.7 | ||||||||||||||||||||||||||||||||||||

| Micro-Cap | 60/97 | 62% | 7.5 | 6.4 | 92/157 | 59% | 8.3 | 8.3 | ||||||||||||||||||||||||||||||||||||

| Opportunity | 96/121 | 79% | 9.0 | 6.9 | 127/181 | 70% | 11.6 | 8.7 | ||||||||||||||||||||||||||||||||||||

| Pennsylvania Mutual | 79/121 | 65% | 8.4 | 6.9 | 115/181 | 64% | 10.3 | 8.7 | ||||||||||||||||||||||||||||||||||||

| Premier | 114/121 | 94% | 10.0 | 6.9 | 119/181 | 66% | 11.2 | 8.7 | ||||||||||||||||||||||||||||||||||||

| Small/Mid-Cap Premier | 68/121 | 56% | 8.7 | 7.9 | 119/181 | 66% | 10.0 | 9.7 | ||||||||||||||||||||||||||||||||||||

| Special Equity | 100/121 | 83% | 9.2 | 6.9 | 105/181 | 58% | 10.6 | 8.7 | ||||||||||||||||||||||||||||||||||||

| Total Return | 60/121 | 50% | 7.8 | 6.9 | 103/181 | 57% | 9.6 | 8.7 | ||||||||||||||||||||||||||||||||||||

| 1 Included are all Royce Funds with at least 20 years of history. |

| 2 The Russell 2000 Index is the benchmark for most funds. Royce Micro-Cap Fund is compared to the Russell Microcap Index from the inception of that index. Royce Small/Mid-Cap Premier Fund is compared to the Russell 2500 Index. |

| 3 Average return shown is the average of all month-end trailing five- and 10-year total returns. |

| Past performance is no guarantee of future results. For more information on performance please see page 6. |

| This page is not part of the 2018 Semiannual Report to Shareholders | 7 |

| MANAGERS’ DISCUSSION |

| Royce Dividend Value Fund (RDV) |

|

| Chuck Royce Jay Kaplan, CFA |

| FUND PERFORMANCE |

| The first half of 2018 was another period of lower-than-average volatility in which small-cap growth stocks beat small-cap value, and small-cap companies that pay no dividends outpaced those that do. Additionally, the Fund’s preference for more economically cyclical dividend-paying stocks, as opposed to those more sensitive to interest rates, worked doubly against it in the more bullish second quarter, when the former group lagged while the latter rallied. Finally, investors responded to tariff and trade war talk by selling off many non-U.S. stocks, which hurt Fund performance because more than a quarter of the portfolio was invested in companies headquartered outside the U.S. at the end of the first half. Needless to say, this made for a less than ideal environment for our risk-conscious dividend value approach. Royce Dividend Value Fund was down 2.0% for the year-to-date period ended June 30, 2018, significantly trailing its small-cap benchmark, the Russell 2000 Index, which gained 7.7% for the same period. |

| WHAT WORKED... AND WHAT DIDN’T |

| Seven of the Fund’s 11 equity sectors finished the first half in the red, with the most significant detractions coming from Financials and Industrials, the portfolio’s two largest sectors and its most substantial overweights versus the Russell 2000. The capital markets group (Financials)—also a significant overweight in the Fund—detracted most at the industry level. A perennial area of concentration for the portfolio owing to the number of dividend-paying asset management companies within it, the group saw disappointing performances from several holdings, most prominently Federated Investors, where outflows from a large equity mutual fund as well increased competition in money market funds—resulting in downward pressure on fees—helped to keep investors selling. We chose to hold our shares in the expectation that the firm will be able to rebound. DENTSPLY SIRONA, a dental equipment and consumables manufacturer from the Health Care sector, was the biggest detractor at the position level as the company remained in the midst of turnaround efforts aimed at improving topline growth and operating margins. We were content to be patient at the end of June. |

| Global staffing and services company Manpower Group detracted most in the Industrials sector, and second most in the portfolio overall. Earnings remained positive in 2018’s first half, prospects in a still-tightening global labor market appear strong, and recent acquisitions expanded its global footprint. Its shares fell mostly on a change in a tax subsidy rate in France for companies that provide temporary labor and loftier expectations for growth than even strong earnings earlier in the year could meet. We remained confident in its core global business at the end of June. Thor Industries is a leading manufacturer of RVs (recreational vehicles) and has emerged as an innovative industry leader over the last several years. The firm announced record fiscal second-quarter sales in March, but also reported higher raw material and commodity costs. Along with concerns that its industry may have hit a sales peak, this was enough to drive investors away. We held our stake at the end of June. |

| As for positions that made positive contributions to first-half results, the leader was Norway’s TGS-NOPEC Geophysical, which provides geoscience data to oil and gas companies worldwide. Its revenue and earnings were boosted by improving exploration and production spending, higher oil prices, and the longer-term need for energy companies to replenish reserves, which is driving increased spending on seismic data. A top contributor from 2017, alternative asset manager KKR & Co. was a happy exception in the capital markets industry. The firm announced in May that it would make the switch from being a limited partnership to a corporation—one that pays dividends—news that encouraged additional investment in its stock. Relative to the Russell 2000, three sectors hurt results most. Poor stock picks were the culprits in the Financial sector, while in Health Care, a combination of lower exposure and stock selection miscues detracted. In Industrials, a mix of higher exposure and ineffective stock picks also hurt relative results. Conversely, a more modest positive contribution on a relative basis came from superior stock selection in Energy. |

| Top Contributors to Performance | |||

| Year-to-Date Through 6/30/18 (%)1 | |||

| TGS-NOPEC Geophysical | 0.70 | ||

| KKR & Co. L.P. | 0.47 | ||

| HEICO Corporation Cl. A | 0.34 | ||

| FLIR Systems | 0.29 | ||

| Expeditors International of Washington | 0.26 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance | |||

| Year-to-Date Through 6/30/18 (%)2 | |||

| DENTSPLY SIRONA | -0.69 | ||

| ManpowerGroup | -0.61 | ||

| Federated Investors Cl. B | -0.39 | ||

| Thor Industries | -0.36 | ||

| Jupiter Fund Management | -0.35 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| The market’s behavior is curious to us. On the one hand, we hear optimism and solid progress from the management teams we meet with, see solid earnings reports, and observe consistently strong macroeconomic data. On the other hand, small-cap market leadership has stubbornly remained with defensive and yield-oriented stocks, while cyclicals have lagged. Despite new highs for the Russell 2000, we are therefore far from ebullient. We are continuing to reduce the portfolio’s exposure to companies with higher valuations and expectations while modestly raising cash levels. We do anticipate a change in market leadership to more cyclical stocks, but admit that changes in leadership seldom occur without turbulence. If higher volatility reemerges, we aim to be able to take advantage of what may be temporarily lower prices. |

| 8 | The Royce Funds 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RYDVX RDVIX RDIIX RDVCX |

| Performance and Expenses Average Annual Total Return (%) Through 6/30/18 | ||||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | 10-YR | SINCE INCEPTION (5/3/04) | |||||||

| RDV | -2.02 | 10.66 | 8.44 | 8.57 | 9.16 | 8.87 | ||||||

| Annual Gross Operating Expenses: 1.39% Annual Net Operating Expenses: 1.34% | ||||||||||||

| 1 Not annualized | ||||||||||||

| Relative Risk Adjusted Returns: Monthly Rolling Sharpe Ratios Since Inception Through 6/30/18 On a monthly rolling risk-adjusted basis, the Fund outperformed the Russell 2000 in 96% of all 10-year periods and 59% of all 5-year periods. | ||||||||||||

| PERIODS BEATING THE INDEX | FUND AVG (%)1 | INDEX AVG (%)1 | ||||||||||||

| 10-year | 48/50 | 96% | 0.48 | 0.43 | ||||||||||

| 5-year | 65/110 | 59% | 0.58 | 0.54 | ||||||||||

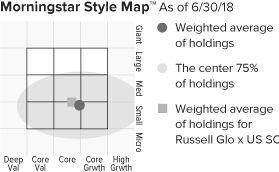

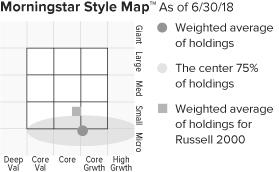

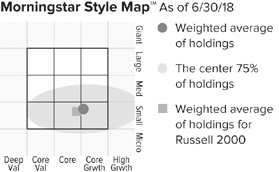

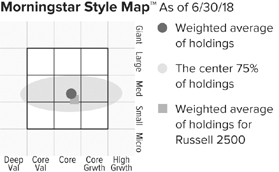

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 125 for additional information. |

Value of $10,000

| Top 10 Positions | ||

| % of Net Assets | ||

| FLIR Systems | 2.9 | |

| KKR & Co. L.P. | 2.5 | |

| Reliance Steel & Aluminum | 2.3 | |

| HEICO Corporation Cl. A | 2.1 | |

| AptarGroup | 2.1 | |

| TGS-NOPEC Geophysical | 2.0 | |

| IDEX Corporation | 2.0 | |

| Applied Industrial Technologies | 1.9 | |

| Expeditors International of Washington | 1.9 | |

| Quaker Chemical | 1.9 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 29.3 | |

| Financials | 28.6 | |

| Materials | 13.9 | |

| Consumer Discretionary | 9.2 | |

| Information Technology | 7.1 | |

| Energy | 4.9 | |

| Health Care | 3.7 | |

| Utilities | 1.0 | |

| Consumer Staples | 0.6 | |

| Real Estate | 0.4 | |

| Cash and Cash Equivalents | 1.3 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RDV | |

| 2017 | 21.7 | |

| 2016 | 16.4 | |

| 2015 | -5.7 | |

| 2014 | -2.1 | |

| 2013 | 30.7 | |

| 2012 | 16.9 | |

| 2011 | -4.5 | |

| 2010 | 30.1 | |

| 2009 | 37.7 | |

| 2008 | -31.5 | |

| 2007 | -0.0 | |

| 2006 | 19.9 | |

| 2005 | 7.3 | |

| Upside/Downside Capture Ratios | |||

| Periods Ended 6/30/18 (%) | |||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 86 | 86 | ||

| From 6/30/04 (Start of Fund’s First Full Quarter) | 86 | 77 | ||

| Portfolio Diagnostics | |||

| Fund Net Assets | $166 million | ||

| Number of Holdings | 97 | ||

| Turnover Rate | 7% | ||

| Average Market Capitalization1 | $4,121 million | ||

| Weighted Average P/E Ratio2,3 | 16.8x | ||

| Weighted Average P/B Ratio2 | 2.7x | ||

| Active Share4 | 97% | ||

| U.S. Investments (% of Net Assets) | 72.0% | ||

| Non-U.S. Investments (% of Net Assets) | 26.7% | ||

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (5% of portfolio holdings as of 6/30/18). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information |

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. All performance and risk information reflects results of the Service Class (its oldest class). Certain immaterial adjustments were made to the net assets of Royce Dividend Value Fund at 6/30/15 for financial reporting purposes, and as a result the net asset values for shareholder transactions on that date and the calendar year Total Returns (%) based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Gross operating expenses reflect the Fund’s total gross annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Service Class’s net annual operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.34% through April 30, 2019. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2018. The Sharpe Ratio is calculated for a specified period by dividing a fund’s annualized excess returns by its annualized standard deviation. The higher the Sharpe ratio, the better the fund’s historical risk-adjusted performance. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| The Royce Funds 2018 Semiannual Report to Shareholders | 9 |

| MANAGERS’ DISCUSSION |

| Royce Global Financial Services (RFS) |

|

| Chuck Royce Chris Flynn |

| FUND PERFORMANCE |

| After returning more than 22% in 2017, it was not surprising that the Fund saw a moderation in its pace of gains in the first half. Moreover, two elements that supported performance last year— international holdings and high weighting in asset management companies—both detracted from first-half returns. Additionally, there were significant reversals among individual holdings, as two of 2017’s winners gave back some returns and landed among the bottom five detractors, while another holding made the opposite journey, bouncing back from being one of 2017’s laggards to one of the first half’s top contributors. Royce Global Financial Services posted a modest gain of 2.6% for the first half of 2018, which trailed both the Russell 2000, which advanced 7.7%, and the Russell 25000 Financial Services Indexes, which was up 4.6%. |

| WHAT WORKED... AND WHAT DIDN’T |

| The company making the biggest positive contribution to first-half performance was Virtu Financial, which uses its technology to act as a market maker and liquidity provider to the global financial markets. Based in New York City, the firm announced impressive first-quarter results in profits and earnings, thanks to increased volatility, high trading volumes, and better-than-expected progress integrating a large acquisition. In our view, the company’s business model is well positioned to benefit from the increased volatility in financial markets that we expect to see in the coming years. We discussed Popular, one of the largest Puerto Rico-based banks, in our 2017 commentary, providing our rationale for sticking with this holding, even though it lagged in that year. Strong earnings so far in 2018, along with an opportunistic, accretive acquisition, have led the stock to outperform as there are more signs of Puerto Rico recovering from last year’s devastating hurricanes. |

| As for positions that detracted, U.S. Global Investors is a specialty asset manager focused mostly on emerging markets, precious metals, and, more recently, digital currencies. Its shares surged in 2017 after its investment in a blockchain technology company. We were wary of this enthusiasm and sold nearly half our position, which proved prescient as its stock declined significantly in the first half of 2018 when the price of the highly volatile cryptocurrency Ethereum collapsed in March. Jupiter Fund Management, a U.K. based asset manager, fell after strong appreciation in 2017 as investors became concerned about ongoing investments in the business which will lead to cost increases in excess of revenue growth, along with continued fee declines and outflows for their funds. We held our position this year as we see a strong, well-managed franchise positioning its business for long-term growth. The Fund’s relative results are often driven by the fortunes of international versus U.S. stocks and asset managers versus the overall financial sector. Both factors hampered relative returns in the first half. As a result of stock price declines in local markets for most countries, which were exacerbated by a stronger dollar, holdings in only one of the 20 non-U.S. geographies where the Fund has investments contributed to returns. This marked a stark reversal from 2017, when holdings in 14 of 20 countries contributed. The Fund’s perennially large concentration in asset management & custody banks also detracted, though most came from international based asset managers due to the factors referenced above. However, most of our alternative asset management holdings, an area we have been emphasizing over the past few years, saw solid gains during the first half. |

| Top Contributors to Performance | |||

| Year-to-Date Through 6/30/18 (%)1 | |||

| Virtu Financial Cl. A | 1.44 | ||

| FRP Holdings | 0.64 | ||

| Sprott | 0.60 | ||

| Popular | 0.57 | ||

| BofI Holding | 0.49 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance | |||

| Year-to-Date Through 6/30/18 (%)2 | |||

| U.S. Global Investors Cl. A | -0.67 | ||

| Jupiter Fund Management | -0.43 | ||

| Altus Group | -0.38 | ||

| Clarkson | -0.34 | ||

| SEI Investments | -0.30 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| We began the year anticipating increased volatility, lower overall returns for small-cap stocks, rising interest rates, and strength for those global financial businesses that appeared best positioned to operate effectively in this type of environment. We saw little in the first half—either at the company or macro levels—that led us to significantly alter this view. Despite some short-term reversals, we remain firmly committed to global investing for this Fund, particularly as we believe our investors can participate in the long-term growth of some of the leading niche financial companies outside the U.S., many of which are relatively unknown to domestic investors. Moreover, we anticipate that in the coming years, the current wide valuation disparity between U.S. and international stocks will narrow, favoring international stock performance. The largest portion of the portfolio remains invested in asset management companies where we see sustained positive trends for the specialty traditional asset managers, alternative asset managers, and wealth managers we hold. The second largest area is regional banks, generally those where we see a differentiated franchise. Our exposure to banks has grown larger because we see an unusually supportive environment, including accelerating loan growth, widening interest margins, decreasing regulatory burdens, and continued low credit losses. While we remain guardedly optimistic about small-cap returns, we think the portfolio is well positioned to take advantage of the undervalued opportunities within the financial services sector. |

| 10 | The Royce Funds 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RYFSX RGFIX |

| Performance and Expenses | ||||||||||||||

| Average Annual Total Return (%) Through 6/30/18 | ||||||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | 10-YR | SINCE INCEPTION (12/31/03) | |||||||||

| RFS | 2.65 | 14.45 | 8.05 | 10.82 | 9.51 | 8.59 | ||||||||

| Annual Gross Operating Expenses: 1.77% Annual Net Operating Expenses: 1.58% | ||||||||||||||

| 1 Not annualized | ||||||||||||||

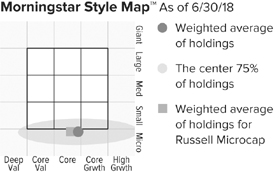

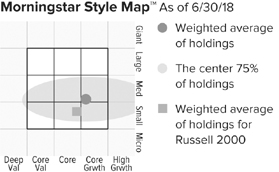

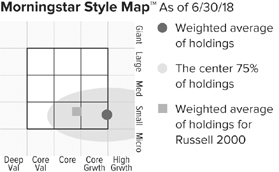

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 125 for additional information. |

Value of $10,000

| Top 10 Positions | ||

| % of Net Assets | ||

| E-L Financial | 2.9 | |

| Popular | 2.6 | |

| First Citizens BancShares Cl. A | 2.3 | |

| Virtu Financial Cl. A | 2.2 | |

| Franco-Nevada Corporation | 2.1 | |

| FRP Holdings | 2.1 | |

| Sprott | 2.0 | |

| BOK Financial | 1.9 | |

| FirstService Corporation | 1.9 | |

| Ashmore Group | 1.9 | |

| Portfolio Industry Breakdown | ||

| % of Net Assets (Subject to Change) | ||

| Capital Markets | 45.4 | |

| Banks | 19.4 | |

| Real Estate Management & Development | 7.0 | |

| Insurance | 6.6 | |

| Metals & Mining | 2.1 | |

| Thrifts & Mortgage Finance | 1.9 | |

| IT Services | 1.7 | |

| Professional Services | 1.7 | |

| Trading Companies & Distributors | 1.4 | |

| Marine | 1.4 | |

| Internet Software & Services | 1.2 | |

| Software | 1.2 | |

| Investment Companies | 0.9 | |

| Hotels, Restaurants & Leisure | 0.6 | |

| Diversified Financial Services | 0.6 | |

| Consumer Finance | 0.5 | |

| Equity Real Estate Investment Trusts (REITs) | 0.3 | |

| Health Care Providers & Services | 0.0 | |

| Cash and Cash Equivalents | 6.1 | |

| Upside/Downside Capture Ratios | ||||

| Periods Ended 6/30/18 (%) | ||||

| UPSIDE | DOWNSIDE | |||

| 10-Year | 87 | 86 | ||

| Fund’s First Full Quarter (12/31/03) | 85 | 79 | ||

| Calendar Year Total Returns (%) | ||

| YEAR | RFS | |

| 2017 | 22.5 | |

| 2016 | 12.9 | |

| 2015 | -4.7 | |

| 2014 | 3.5 | |

| 2013 | 42.0 | |

| 2012 | 20.7 | |

| 2011 | -11.3 | |

| 2010 | 18.5 | |

| 2009 | 32.1 | |

| 2008 | -35.4 | |

| 2007 | -4.7 | |

| 2006 | 24.8 | |

| 2005 | 12.2 | |

| 2004 | 15.1 | |

| Portfolio Country Breakdown1,2 | ||

| % of Net Assets | ||

| United States | 54.0 | |

| Canada | 15.3 | |

| United Kingdom | 7.9 | |

| Switzerland | 3.6 | |

| India | 2.5 | |

| France | 1.6 | |

| South Africa | 1.5 | |

| Hong Kong | 1.5 | |

| 1 | Represents countries that are 1.5% or more of net assets. |

| 2 | Securities are categorized by the country of their headquarters. |

| Portfolio Diagnostics | ||

| Fund Net Assets | $57 million | |

| Number of Holdings | 96 | |

| Turnover Rate | 5% | |

| Average Market Capitalization1 | $2,121 million | |

| Weighted Average P/E Ratio2,3 | 16.1x | |

| Weighted Average P/B Ratio2 | 1.9x | |

| Active Share4 | 99% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (7% of portfolio holdings as of 6/30/18). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. Gross operating expenses reflect the Fund’s gross total annual operating expenses for the Service Class and include management fees, 12b-1 distribution and service fees, other expenses and acquired fund fees and expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse expenses to the extent necessary to maintain the Fund’s net annual operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.49% through April 30, 2019. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds, hedge funds, private equity funds, and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2018. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the benchmark went up and dividing it by the benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s benchmark (Russell 2000). It is calculated by measuring the Fund’s performance in quarters when the benchmark goes down and dividing it by the benchmark’s return in those quarters. |

| The Royce Funds 2018 Semiannual Report to Shareholders | 11 |

| MANAGERS’ DISCUSSION | ||

| Royce International Discovery Fund (RMI) (formerly named Royce International Micro-Cap Fund) | ||

|

| Jim Harvey, CFA |

| FUND PERFORMANCE Tariff and trade war talk, a strengthening dollar, and market and economic softness in China and Europe all had a dampening effect on non-U.S. stocks of all sizes in the first half of 2018. Royce International Discovery Fund was down 6.2% for the year-to-date period ended June 30, 2018, underperforming its benchmark, the Russell Global ex-U.S. Small Cap Index, which declined 3.8% for the same period. |

| WHAT WORKED... AND WHAT DIDN’T |

| Of the Fund’s 10 equity sectors, six detracted from first-half results, with the largest negative impacts coming overwhelmingly from Industrials and Consumer Discretionary, its two largest sectors at the end of June. Industrials was also a substantial overweight relative to the benchmark. At the position level, three of the portfolio’s five biggest detractors came from this same sector. Atento is Latin America’s largest provider of customer relationship management and business process outsourcing (“CRM BPO”) services. Its stock price suffered in late 2017 after a secondary offering of shares was poorly received. In March of 2018, its shares again slipped when it reported a quarterly loss. While its Latin American end markets remain volatile, Atento is the dominant player in these markets and was also trading at a hefty discount to its global peers. This led us to add shares in the first half. Asian Granito India is one of India’s top tile manufacturers. Profit and revenue growth were not enough to offset a falling rupee, rising oil prices, and the slowing pace of global growth—all of which turned market sentiment negative, with Indian small-caps hit especially hard. Uncertain about its prospects in this climate, we sold our shares in June. We also exited our position in Magellan Aerospace, a Canadian company that manufactures engine and other components for customers in Canada, the U.S., and Europe. In early May, the company reported weaker-than-expected results rooted mostly in the expense of building a new manufacturing facility and a volatile British pound. Outside of Industrials, we built our position in Eugene Technology when uneven quarterly revenue growth and concerns that the semiconductor cycle had peaked combined to bring down its share price. Based in South Korea, Eugene is a semiconductor equipment maker that specializes in single-wafer type thermal insulation equipment. We like its niche and expect a revival in demand for its products. |

| The Fund’s top contributor at the position level in 2017, Conviviality fell to being by far its most significant detractor in the first half of 2018. The firm is a liquor distributor in the U.K. that also operates franchised off-license and convenience chain stores. Conviviality unraveled in short order in 2018, after it issued a pair of profit warnings, admitted to having a large, previously undiscovered tax bill, and unsuccessfully attempted to raise capital from investors to stave off liquidation. Needless to say, its management proved to be far less capable than investors had thought during its period of early success. |

| The top contributor at the position level was Hua Hong Semiconductor, a manufacturer of 200 millimeter wafers for specialized applications. Its shares benefited from impressive sales and earnings growth as well as the Chinese government’s push to source native semiconductor production. We reduced our position as its stock rose. TCI is a Taiwanese contract manufacturer of dietary supplements, health drinks, and skin care. Its shares were nourished by strong sales and earnings growth driven mostly by Chinese consumer demand and the company’s near-term positive outlook. Norway’s Leroy Seafood Group produces and distributes seafood around the globe, with a core business producing salmon, trout, and whitefish. Concerns that salmon prices were peaking allowed us to purchase shares at historically low multiples early in 2018. When subsequent earnings were better than expected accompanied by a more positive outlook on salmon prices, its shares jumped more than 60% from previous lows, which prompted us to sell our shares. |

| Relative to the benchmark year-to-date, the portfolio’s largest disadvantage came from ineffective stock selection in the Consumer Staples and Consumer Discretionary sectors, while it benefited from better stock picking in Financials, Telecommunication Services, and Materials. |

| Top Contributors to Performance Year-to-Date Through 6/30/18 (%)1 | |||

| Hua Hong Semiconductor | 0.77 | ||

| TCI | 0.45 | ||

| Leroy Seafood Group | 0.41 | ||

| China Resources Cement Holdings | 0.36 | ||

| HT&E | 0.35 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance Year-to-Date Through 6/30/18 (%)2 | |||

| Conviviality | -1.24 | ||

| Atento | -0.58 | ||

| Asian Granito India | -0.45 | ||

| Eugene Technology | -0.36 | ||

| Magellan Aerospace | -0.35 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| The combination of a modest slowdown in international growth, rising emerging market instability, a stronger dollar, and heightened trade war concerns led investors to prefer a more limited menu of domestic offerings in the first half. In fact, 35 of the 45 non-U.S. small-cap markets that we follow had declines in the first half of 2018 (though only 26 were negative when measured in local currencies). Non-U.S. companies therefore faced major challenges, particularly in emerging market economies where fears of potential currency declines drove many investors to pull money out of these geographies. From a valuation standpoint, the U.S. market remained one of the most expensive in the world at the end of June, a distinction it has held for the better part of the past 10 years. In this environment, we continue to find attractive investment opportunities in both developed as well as emerging markets, where companies in India, Brazil, and Indonesia looked particularly interesting to us at June 30. |

| 12 | The Royce Funds 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS ROIMX |

| Performance and Expenses | ||||||||||||

| Average Annual Total Return (%) Through 6/30/18 | ||||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | SINCE INCEPTION (12/31/10) | ||||||||

| RMI | -6.21 | 3.96 | 5.48 | 8.03 | 3.62 | |||||||

| Annual Gross Operating Expenses: 2.79% Annual Net Operating Expenses: 1.44% | ||||||||||||

| 1 Not annualized | ||||||||||||

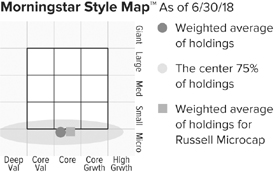

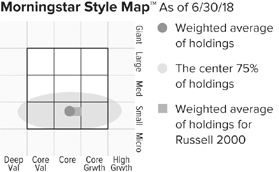

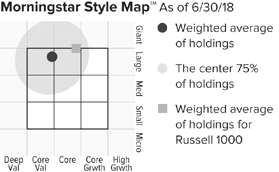

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 125 for additional information. |

Value of $10,000

| Top 10 Positions | ||

| % of Net Assets | ||

| Sonae SGPS | 2.6 | |

| DFDS | 2.5 | |

| Nilfisk Holding | 2.3 | |

| Outsourcing | 2.3 | |

| Biffa | 2.3 | |

| Kyowa Exeo | 2.1 | |

| Restore | 2.1 | |

| Zenkoku Hosho | 2.1 | |

| Hilton Food Group | 2.0 | |

| Atento | 1.9 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 24.5 | |

| Consumer Discretionary | 13.8 | |

| Information Technology | 13.1 | |

| Financials | 13.1 | |

| Materials | 8.1 | |

| Consumer Staples | 7.3 | |

| Real Estate | 6.5 | |

| Health Care | 4.0 | |

| Energy | 3.7 | |

| Telecommunication Services | 2.0 | |

| Cash and Cash Equivalents | 3.9 | |

| Calendar Year Total Returns (%) | ||

| YEAR | RMI | |

| 2017 | 27.7 | |

| 2016 | 6.3 | |

| 2015 | -1.0 | |

| 2014 | -2.4 | |

| 2013 | 18.9 | |

| 2012 | 13.6 | |

| 2011 | -21.5 | |

| Portfolio Country Breakdown1,2 | ||

| % of Net Assets | ||

| Japan | 20.0 | |

| United Kingdom | 10.4 | |

| Canada | 5.9 | |

| South Korea | 5.5 | |

| Denmark | 4.8 | |

| China | 4.8 | |

| Hong Kong | 4.4 | |

| Taiwan | 4.1 | |

| Brazil | 3.9 | |

| Australia | 3.4 | |

| 1 | Represents countries that are 3% or more of net assets. |

| 2 | Securities are categorized by the country of their headquarters. |

| Portfolio Diagnostics | ||

| Fund Net Assets | $8 million | |

| Number of Holdings | 81 | |

| Turnover Rate | 112% | |

| Average Market Capitalization1 | $1,221 million | |

| Weighted Average P/E Ratio2,3 | 16.4x | |

| Weighted Average P/B Ratio2 | 2.1x | |

| Active Share4 | 98% | |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (5% of portfolio holdings as of 6/30/18). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

| Important Performance and Expense Information |

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 2% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.roycefunds.com. Gross operating expenses reflect total gross annual operating expenses and include management fees, 12b-1 distribution and service fees, and other expenses. Net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive its fees and/or reimburse operating expenses, to the extent necessary to maintain the Fund’s net annual operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.44% through April 30, 2019 and at or below 1.99% through April 30, 2028. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2018. |

| The Royce Funds 2018 Semiannual Report to Shareholders | 13 |

| MANAGERS’ DISCUSSION | ||

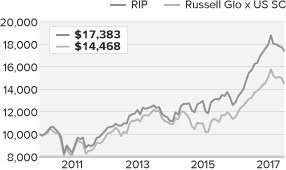

| Royce International Premier Fund (RIP) |

|

| David Nadel Mark Rayner, CA |

| FUND PERFORMANCE Tariff and trade war talk, a strengthening dollar, market and economic softness in China, and slower growth in Europe all had a dampening effect on non-U.S. stocks in the first half of 2018. In spite of these challenges, the Fund maintained its advantage over its benchmark, the Russell Global ex-U.S. Small Cap Index, outpacing the index for the one, three-, five-year, and since inception (12/31/10) periods ended June 30, 2018. Royce International Premier Fund fell 3.1% for the year-to-date period ended June 30, 2018, losing slightly less than the Russell Global ex-U.S. Small Cap Index, which declined 3.8% for the same period. Most international indexes slipped into negative territory during 2018’s first six months due to the combination of the modest slowdown in international growth, rising emerging market instability, a stronger dollar, and heightened trade war concerns. However, we were encouraged that several holdings continued to execute well in the first half, and several saw otherwise positive stock market performances in their respective currencies undone by U.S. dollar strength. |

| WHAT WORKED... AND WHAT DIDN’T |

| During the first half, the sectors making the largest negative impact on performance were Information Technology (the portfolio’s second-largest weighting at the end of June) and Consumer Discretionary. Only three of the portfolio’s nine equity sectors made positive contributions to year-to-date results, and only Health Care had a meaningful effect. |

| At the industry level, IT services (Information Technology) detracted most, followed by the construction & engineering group (Industrials). The portfolio’s top two detractors at the position level came from these two respective industries. They were also chiefly responsible for India and Switzerland having the first- and second-biggest negative effects on performance at the country level. Vakrangee is an Indian company that operates a network of outlets providing everyday transactional services to mostly rural consumers, primarily in under-served areas. During the first quarter, the company faced questions about corporate governance and its internal investment policy, among other issues. Although Vakrangee refuted these allegations, the cloud overhanging the firm’s credibility gave us pause, and we exited our position in April. Burkhalter Holding is the leading provider of electrical engineering services in Switzerland. Its stock price was hurt by increasing talk that competition would pressure pricing. Seeing these issues as more temporal than structural, we added shares in the first half. Two companies in the software industry contributed most in the first half. Bravura Solutions is an Australian funds-management software business. Following several high-profile contract signings and the successful monetization off its innovative Sonata platform, Bravura benefited from several broker upgrades, which helped solidify its status as the industry leader in one of the world’s most attractive pension markets. We trimmed our position slightly in the first half. SimCorp is a Danish company that provides software to the asset management industry. Its shares advanced in mid-May on the release of fiscal first-quarter results that showed a 23% advance in revenue with 26% operating margins. With the shares re-rated far more quickly than we anticipated, we began to exit our position as its stock climbed. |

| Relative to the benchmark year-to-date, the portfolio’s overall advantage came from sector allocation. However, the Fund also gained an edge from stock selection in Health Care, in addition to our overweight in the sector. Superior stock picks gave the portfolio another advantage in Industrials, most meaningfully in machinery and commercial services & supplies. Finally, the strength of the U.S. dollar also gave the Fund’s cash position a relative advantage. Conversely, stock selection was a detractor versus the international small-cap index in Information Technology, especially in the software, IT services, and electronic equipment, instruments & components groups. The Fund’s significantly lower exposure, as well as ineffective stock picks, hurt relative results in Real Estate, while stock selection was an issue in Consumer Discretionary. |

| Top Contributors to Performance Year-to-Date Through 6/30/18 (%)1 | |||

| Bravura Solutions | 1.09 | ||

| SimCorp | 0.53 | ||

| TGS-NOPEC Geophysical | 0.53 | ||

| Sartorius Stedim Biotech | 0.41 | ||

| DiaSorin | 0.39 | ||

| 1 Includes dividends | |||

| Top Detractors from Performance Year-to-Date Through 6/30/18 (%)2 | |||

| Vakrangee | -0.90 | ||

| Burkhalter Holding | -0.80 | ||

| SH Kelkar & Company | -0.61 | ||

| OdontoPrev | -0.54 | ||

| ITE Group | -0.49 | ||

| 2 Net of dividends | |||

| CURRENT POSITIONING AND OUTLOOK |

| At the end of June, the bulk of the portfolio’s assets remained invested in four sectors—Industrials, Information Technology, Health Care, and Materials—with the first two groups accounting for more than half of its assets. With the pace of non-U.S. growth having slowed in the first half, we used our Quality at a Reasonable Price (‘QARP’) approach to find high-quality companies trading at what we thought were low or reasonable valuations. Our goal, as always, is to find businesses that look well-positioned to deliver high returns over full market cycles. Our focus is on companies that are market leaders, typically with global reach and/or expertise, attributes that we suspect will prove timely in a period of growing U.S. dollar strength. In the first half, we added three new holdings: EPS Holdings, a Japanese clinical testing services business, ITE Group, a U.K.-based company that organizes trade exhibitions and conferences worldwide, and Kardex, a Swiss firm with a global business that offers intra-logistic services as well as automated storage solutions and material handling systems. |

| 14 | The Royce Funds 2018 Semiannual Report to Shareholders |

| PERFORMANCE AND PORTFOLIO REVIEW | TICKER SYMBOLS RYIPX RIPNX RINPX RIPIX |

| Performance and Expenses | ||||||||||

| Average Annual Total Return (%) Through 6/30/18 | ||||||||||

| JAN-JUN 20181 | 1-YR | 3-YR | 5-YR | SINCE INCEPTION (12/31/10) | ||||||

| RIP | -3.08 | 10.77 | 11.07 | 10.10 | 7.65 | |||||

| Annual Gross Operating Expenses: 1.65% Annual Net Operating Expenses: 1.44% | ||||||||||

| 1 Not annualized | ||||||||||

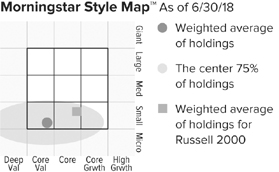

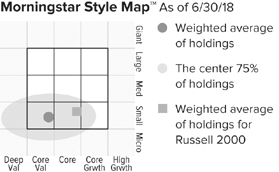

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 125 for additional information. |

Value of $10,000

| Top 10 Positions | ||

| % of Net Assets | ||

| USS | 3.0 | |

| VZ Holding | 2.9 | |

| Partners Group Holding | 2.8 | |

| Meitec Corporation | 2.7 | |

| IPH | 2.3 | |

| Equiniti Group | 2.3 | |

| TOTVS | 2.3 | |

| OdontoPrev | 2.3 | |

| TravelSky Technology | 2.3 | |

| As One | 2.2 | |

| Portfolio Sector Breakdown | ||

| % of Net Assets | ||

| Industrials | 26.2 | |

| Information Technology | 22.8 | |

| Health Care | 17.2 | |

| Materials | 9.3 | |

| Financials | 7.6 | |

| Consumer Discretionary | 6.5 | |

| Real Estate | 4.0 | |